Embed Size (px)

Citation preview

® 1994 International Monetary Fund

December 1994

IMF Staff Country Report No. 94/15

Ethiopia—Recent Economic Developments

This report on recent economic developments in Ethiopia was prepared bya staff team of the International Monetary Fund as backgrounddocumentation for the periodic consultation with this member country. Inreleasing this document for public use, confidential material may havebeen removed at the request of the member.

Copies of this report are available to the public from

International Monetary Fund • Publication Services700 19th Street, N.W. • Washington, D.C. 20431

Telephone: (202) 623-7430 • Telefax: (202) 623-7201Telex (RCA): 248331 IMF UR

Price: $15.00 a copy

International Monetary FundWashington, D.C.

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

INTERNATIONAL MONETARY FUND

ETHIOPIA

Recent Economic Developments

Prepared by a staff mission consisting of Mr. P. Heller (head-AFR),Mr. M. Kitahara (AFR), Mr. G. Taube (AFR), Mr. E. M. Ucer (AFR),

Mr. C. McDonald (AFR), and Mr. C. Shiells (PDR)

Approved by the African Department

August 29, 1994

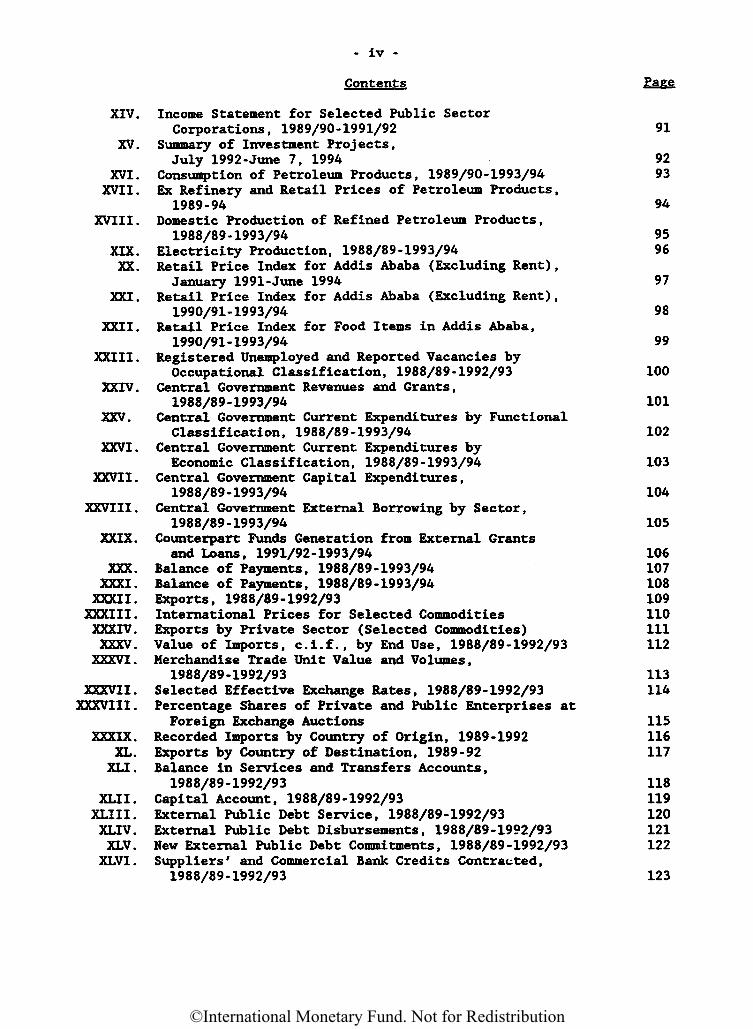

Contents Page

Basic Data vi-vii

I. Real Sector 1

1. Aggregate output and expenditure 22. Sectoral developments 2

a. Agriculture 2b. Manufacturing 10c. Energy 12d. Mining 13e. Building and construction 14f. Transportation 14

3. Employment 154. Wages 165. Prices 186. Private sector investment 197. Privatization 218. Revised GDP figures 21

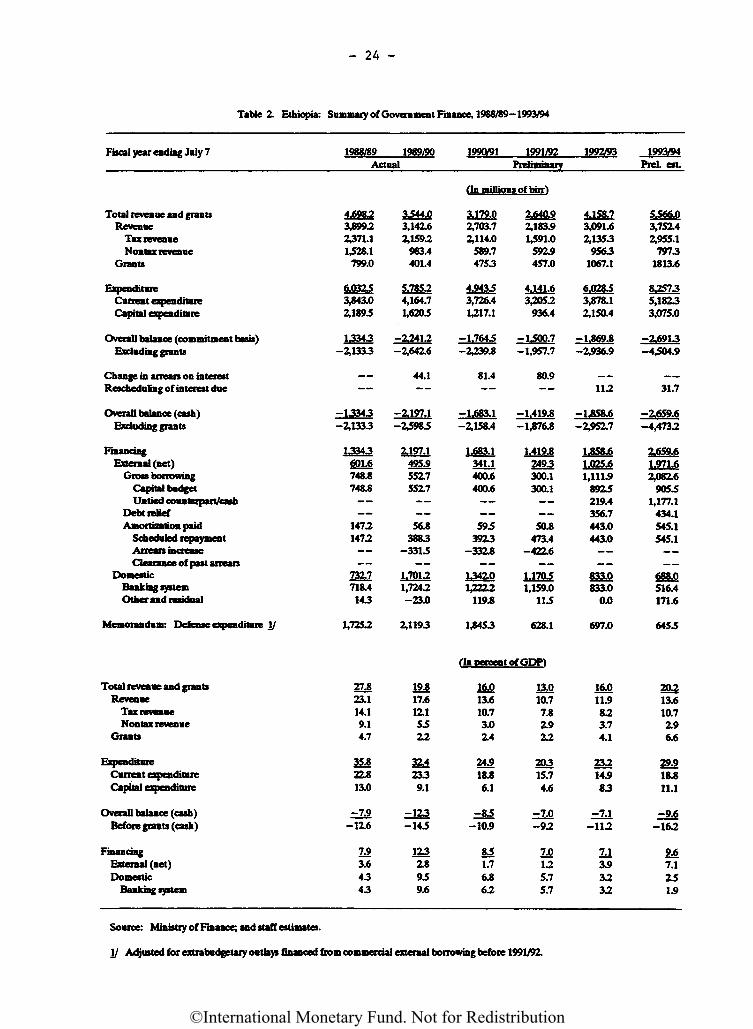

II. Public Finance 22

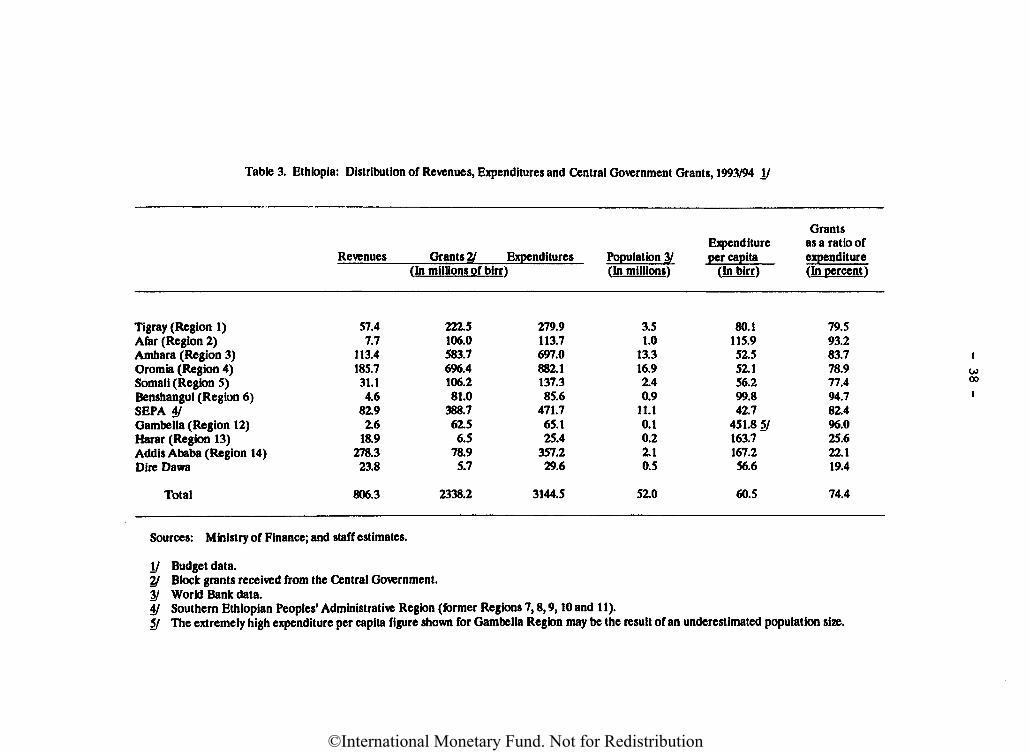

1. Overall fiscal performance 222. Revenue and grants 23

a. Overview 23b. Tax revenue 25c. Nontax revenue 28d. External grants 29

3. Public expenditures 30a. Current expenditures 30b. Capital expenditures 34

4. The regionalization policy and fiscal implications 35a. Overview 35b. Tax policy and revenues 36c. Budget preparation and implementation in 1993/94 36d. Domestic and foreign financing 39

©International Monetary Fund. Not for Redistribution

- ii -

Contents Page

III. Balance of Payments 39

1. Overall developments, 1989/90-1993/94 392. Merchandise trade 41

a. Exports 42b. Imports 44c. Terms of trade 45d. Direction of trade 45

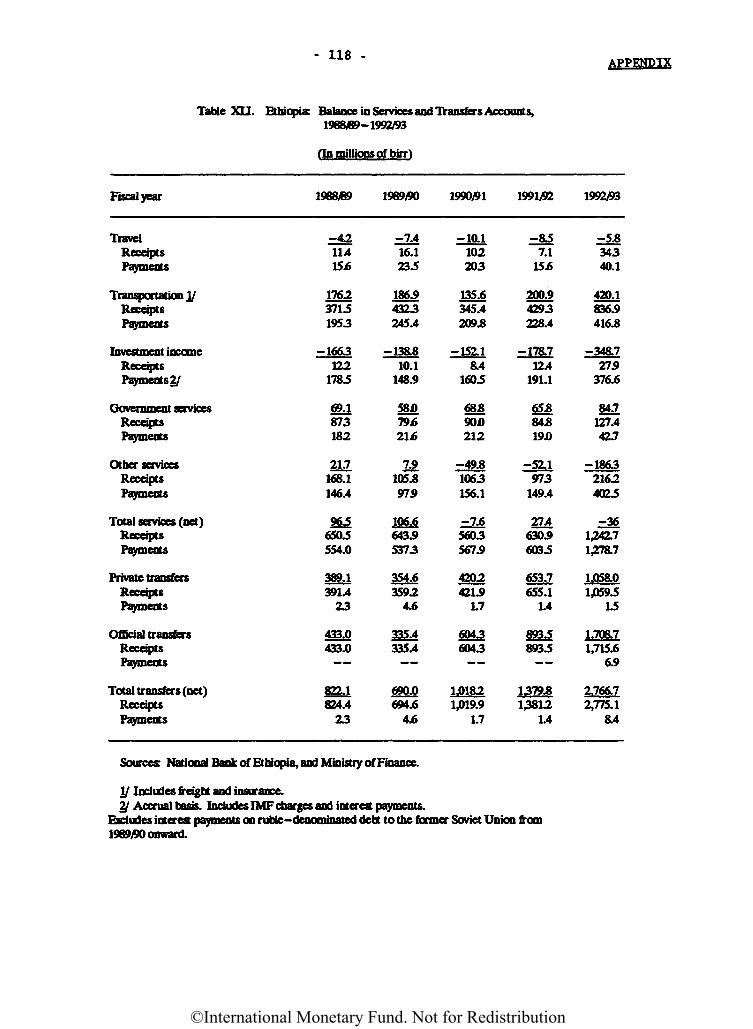

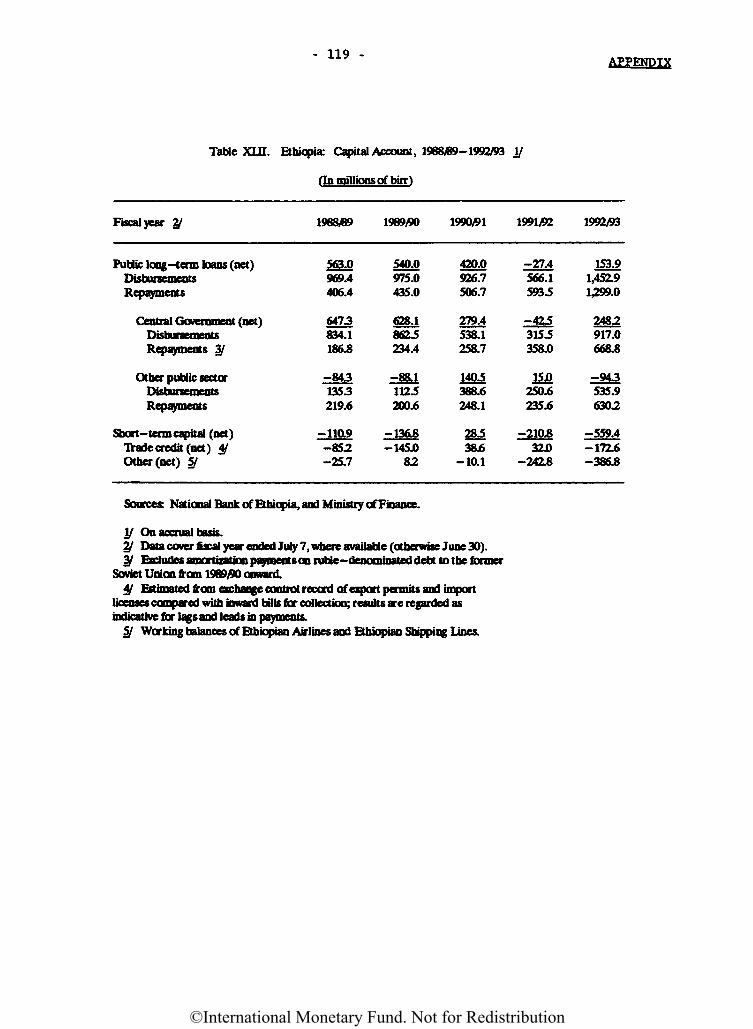

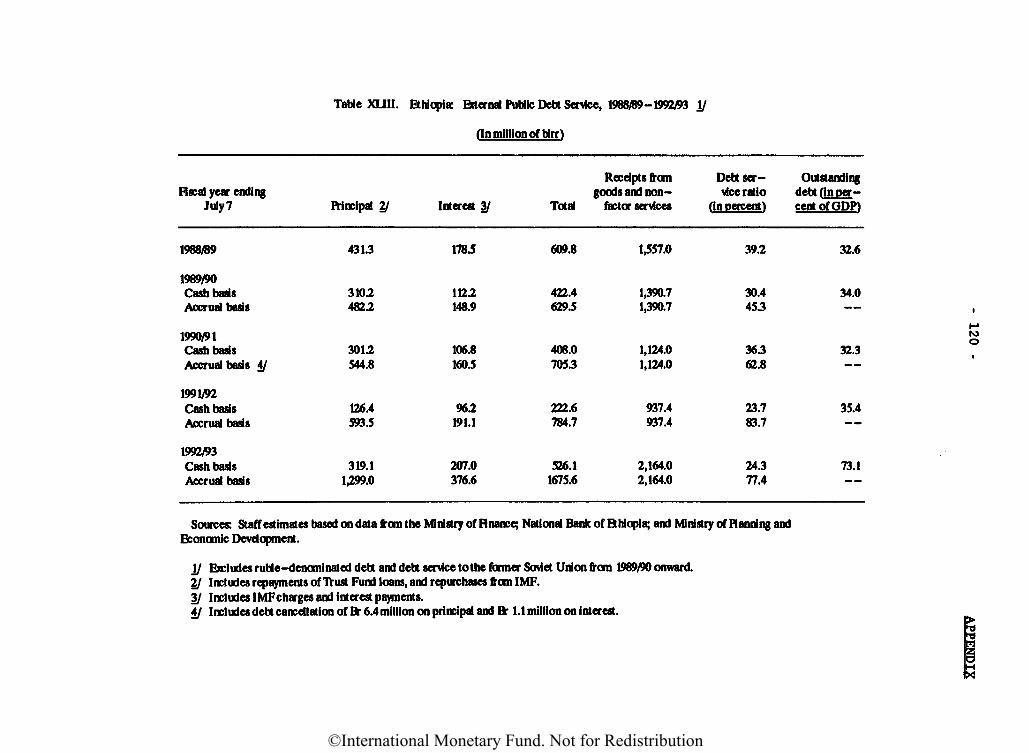

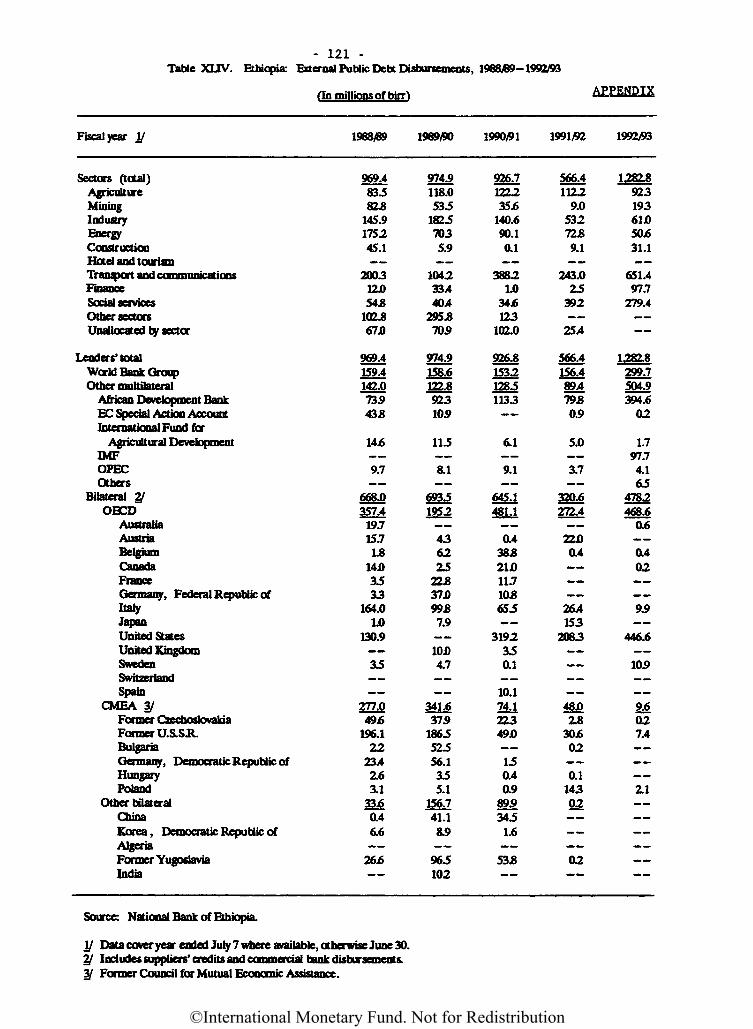

3. Services and transfers 464. Capital account 465. External debt 48

IV. Exchange and Trade System 49

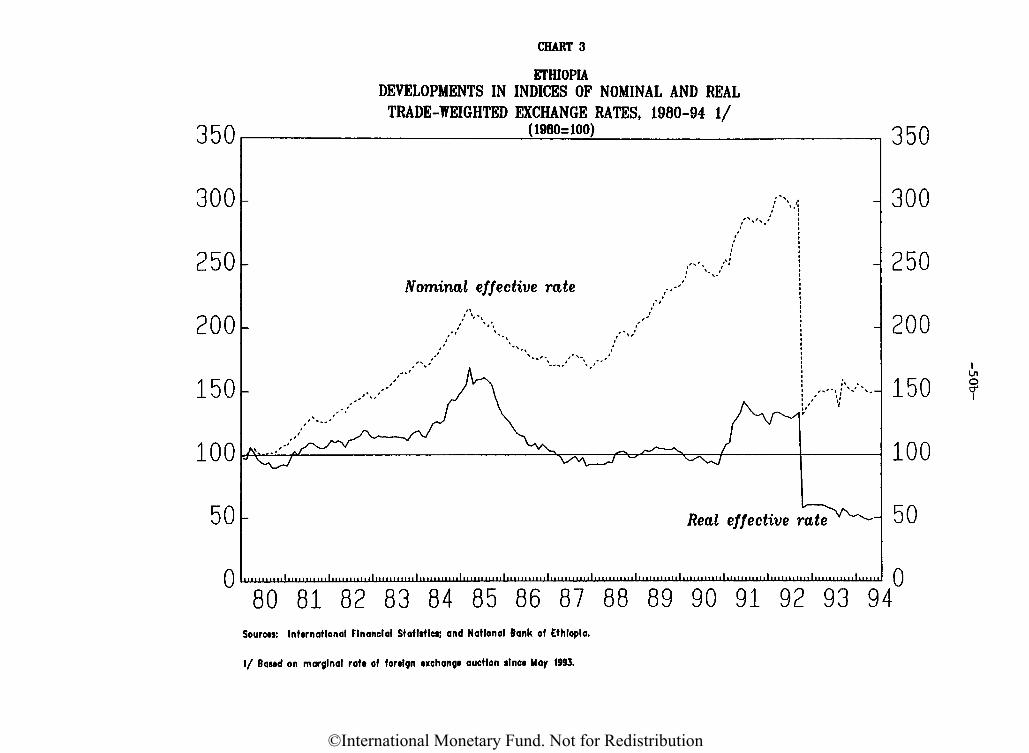

1. Exchange arrangement 492. Administration of control 523. Prescription of currency 524. Nonresident accounts 525. Imports and import payments 526. Payments for invisible transactions 537. Exports and export proceeds 548. Proceeds from invisible transactions 549. Capital 5410. Gold 55

V. Money and Credit 56

1. Monetary and credit developments 56a. Overview 56b. Credit operations of the monetary system 58c. Domestic liabilities of the monetary system 60d. Specialized banks 61

2. Financial system 623. Monetary policy instruments 63

a. Credit allocation 63b. Reserve and liquidity requirements 65c. Refinancing facilities 65d. Interest rates 65e. Payment system 66

4. Financial sector reform 67a. Restructuring and recapitalization of theAIDB 67b. New legislation 68

©International Monetary Fund. Not for Redistribution

- iii -

Contents Page

VI. Assessing Eritrea's Impact on Ethiopia's Program 69

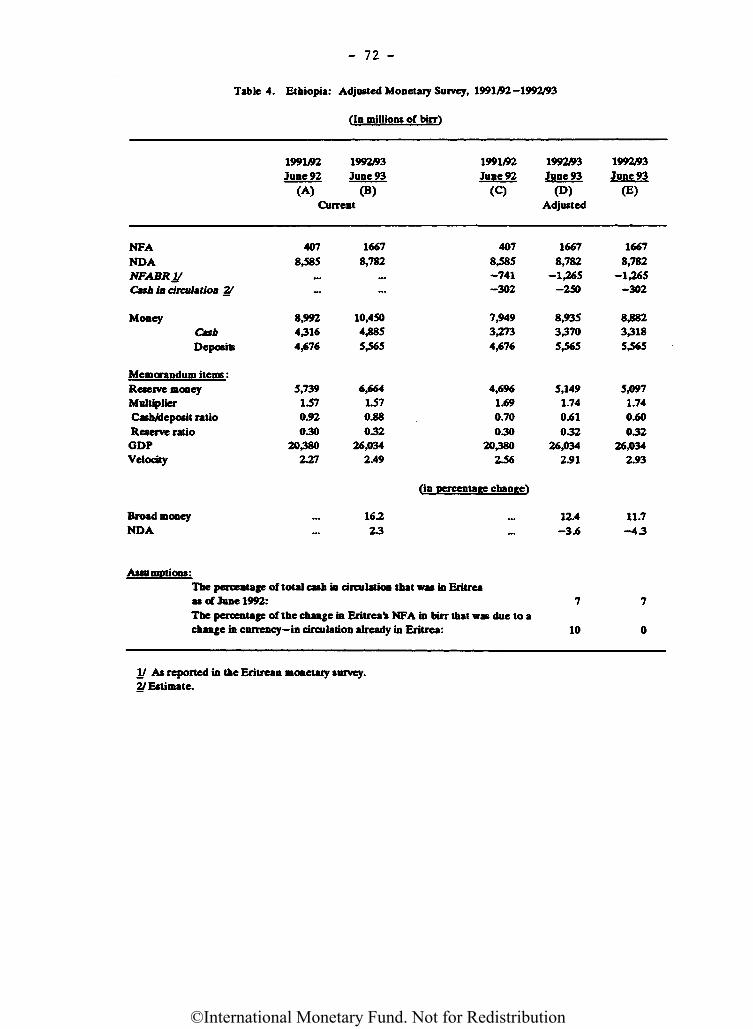

1. Overview 692. Possible adjustments 693. Numerical illustrations 71

VII. Estimation of Demand Curve for Foreign Exchange Auctions 73

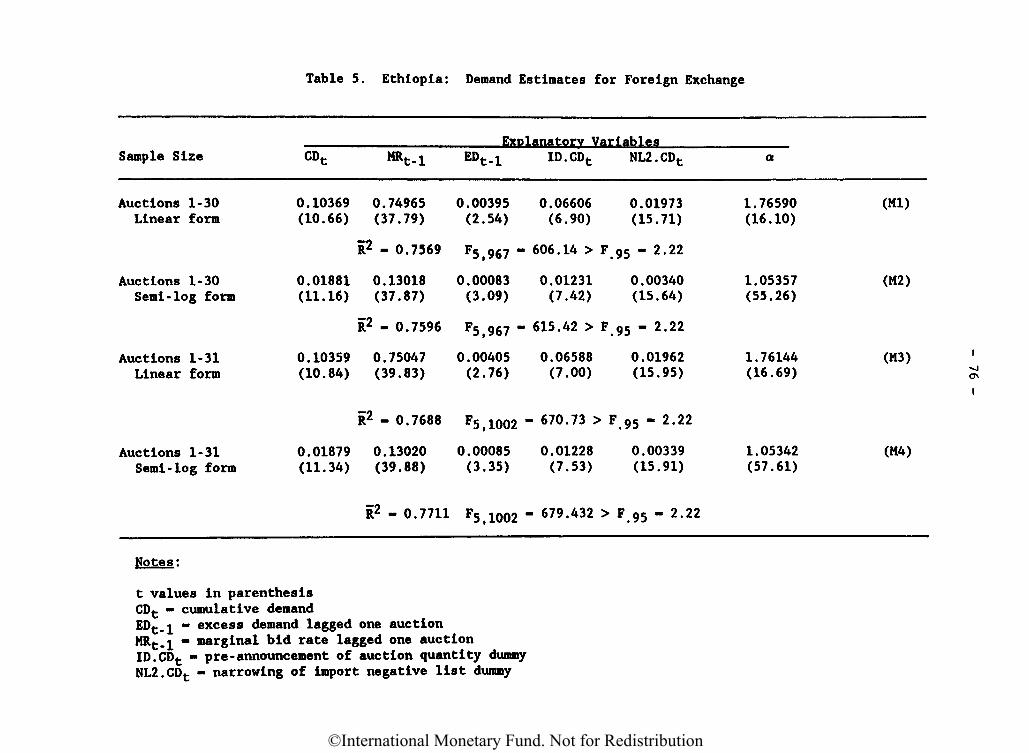

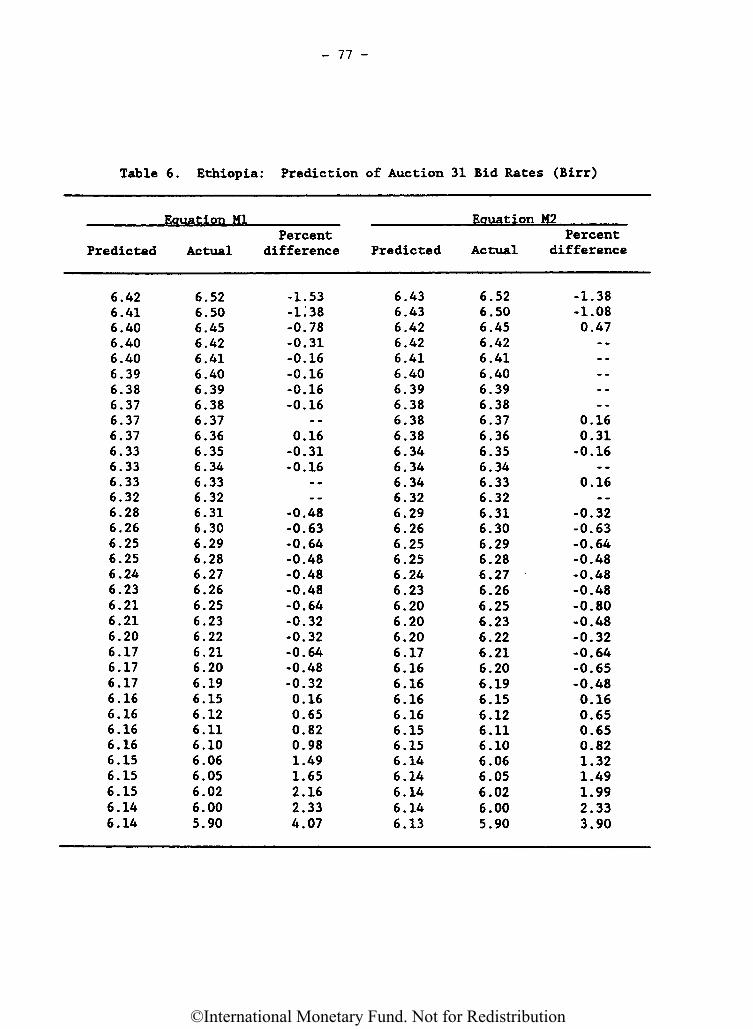

1. Specification of equations 742. Structural issues 753. Estimation results and simulations 75

Text Tables

1. Wage Structure 172. Summary of Government Finance, 1988/89-1993/94 243. Distribution of Revenues, Expenditures and

Central Government Grants, 1993/94 384. Adjusted Monetary Survey, 1991/92-1992/93 725. Demand Estimates for Foreign Exchange 766. Prediction of Auction 31 Bid Rates 77

Appendix Tables

I. Growth Rate of Sectoral GDP at Constant 1980/81Factor Cost, 1988/89-1993/94 78

II. Gross Domestic Product by Sector at CurrentFactor Cost, 1988/89-1993/94 79

III. Expenditure on Gross Domestic Product at CurrentMarket Prices, 1988/89-1993/94 80

IV. Gross Domestic Product by Sector at Constant1980/81 Factor Cost, 1988/89-1993/94 81

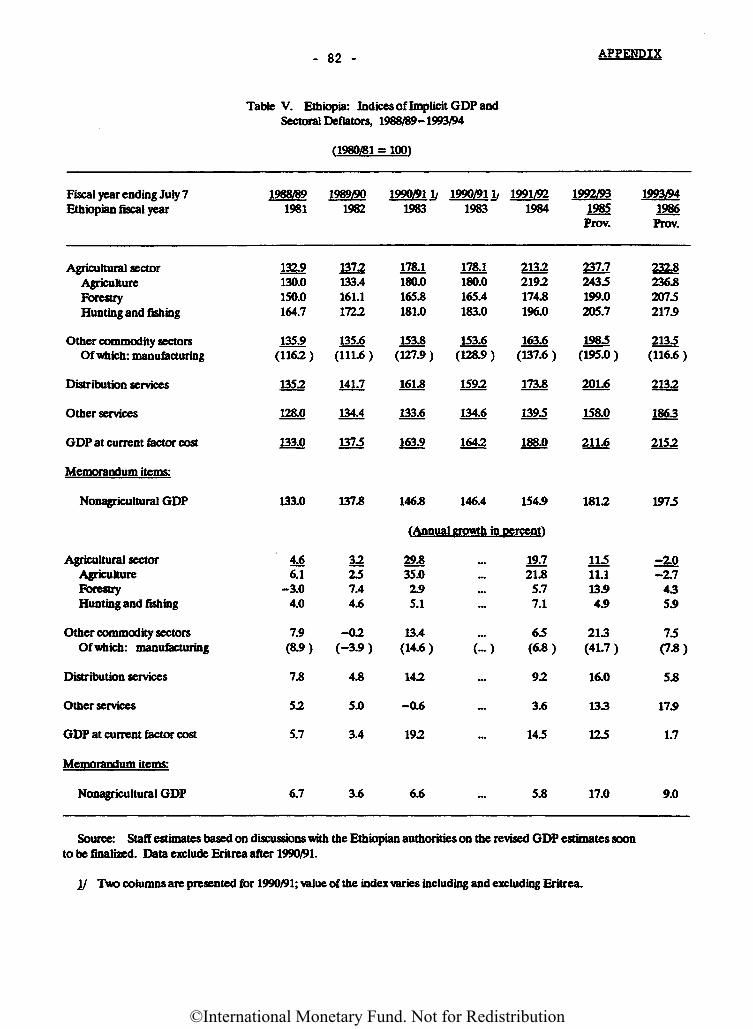

V. Indices of Implicit GDP and Sectoral Deflators,1988/89-1993/94 82

VI. Estimates of Agricultural Production of MajorCrops, 1988/89-1991/92 83

VII. Estimates of Cultivated Areas Under Major Crops,1988/89-1991/92 84

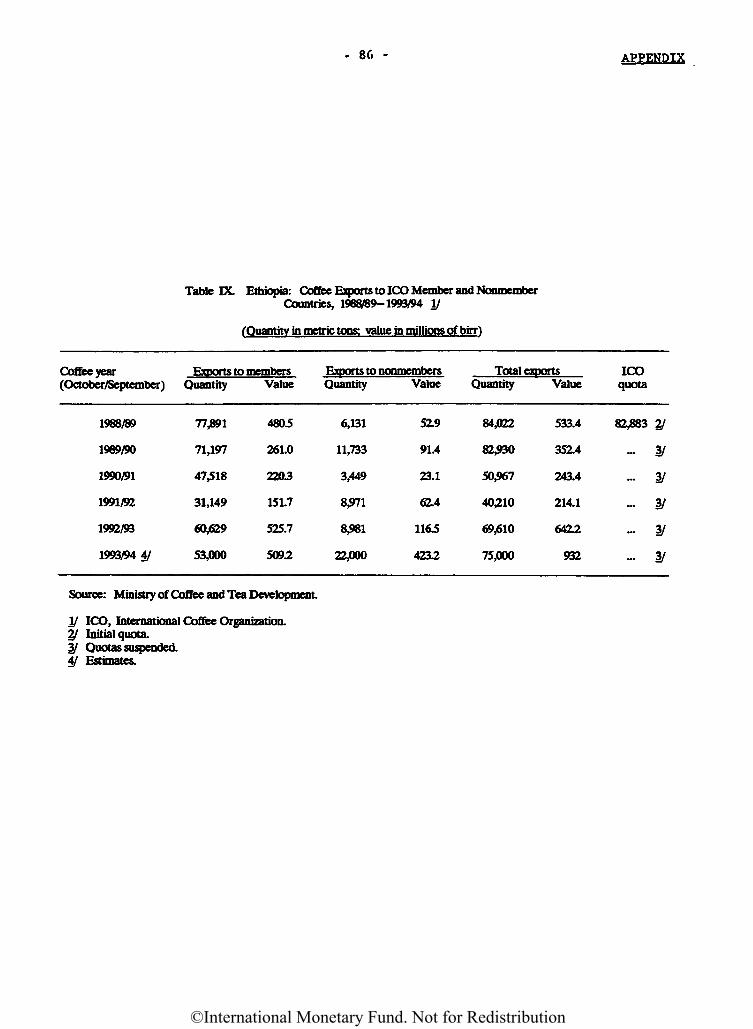

VIII. Estimates of Coffee Production, Marketing, andStocks, 1988/89-1993/94 85

IX. Coffee Exports to ICO Member and NonmemberCountries, 1988/89-1993/94 86

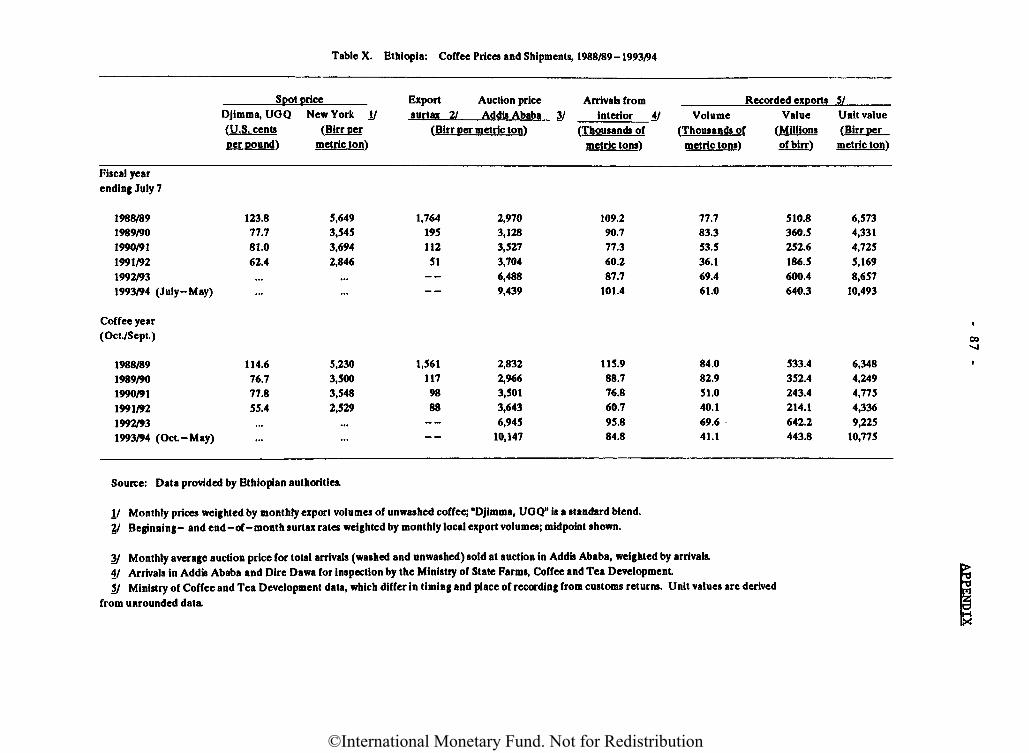

X. Coffee Prices and Shipments, 1988/89-1993/94 87XI. Monthly Export and Arrival Volumes, Coffee Prices,

and Surtax, January 1991-May 1994 88XII. Value of Manufacturing and Processing at Constant

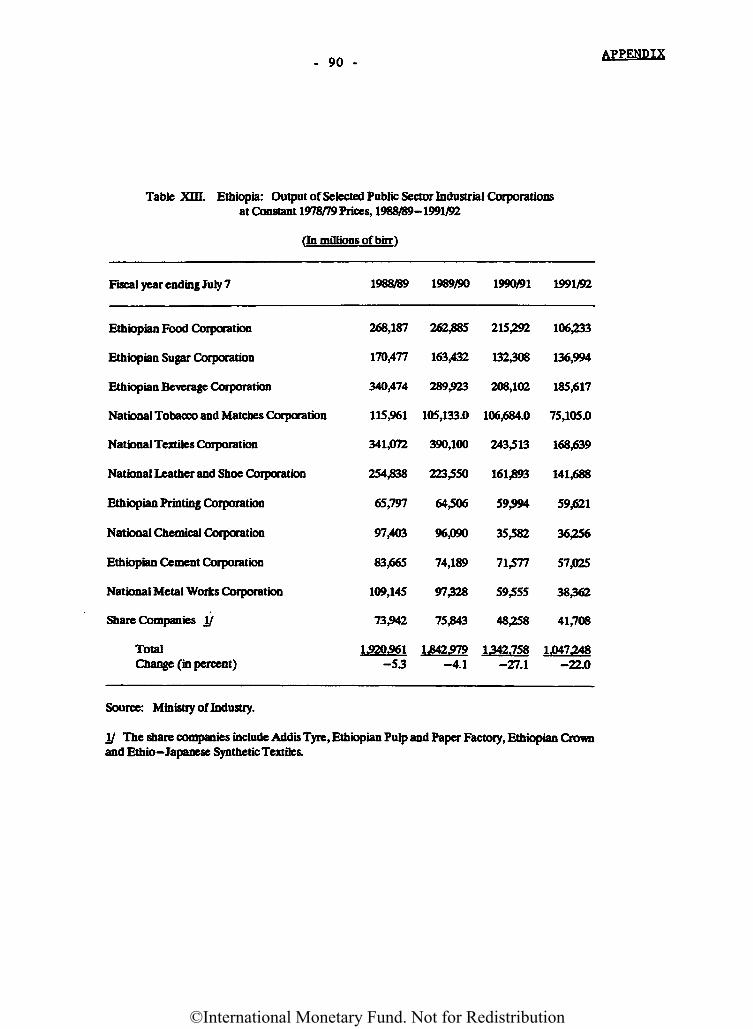

Prices, 1988/89-1991/92 89XIII. Output of Selected Public Sector Industrial

Corporations at Constant 1978/79 Prices,1988/89-1991/92 90

©International Monetary Fund. Not for Redistribution

- iv -

Contents

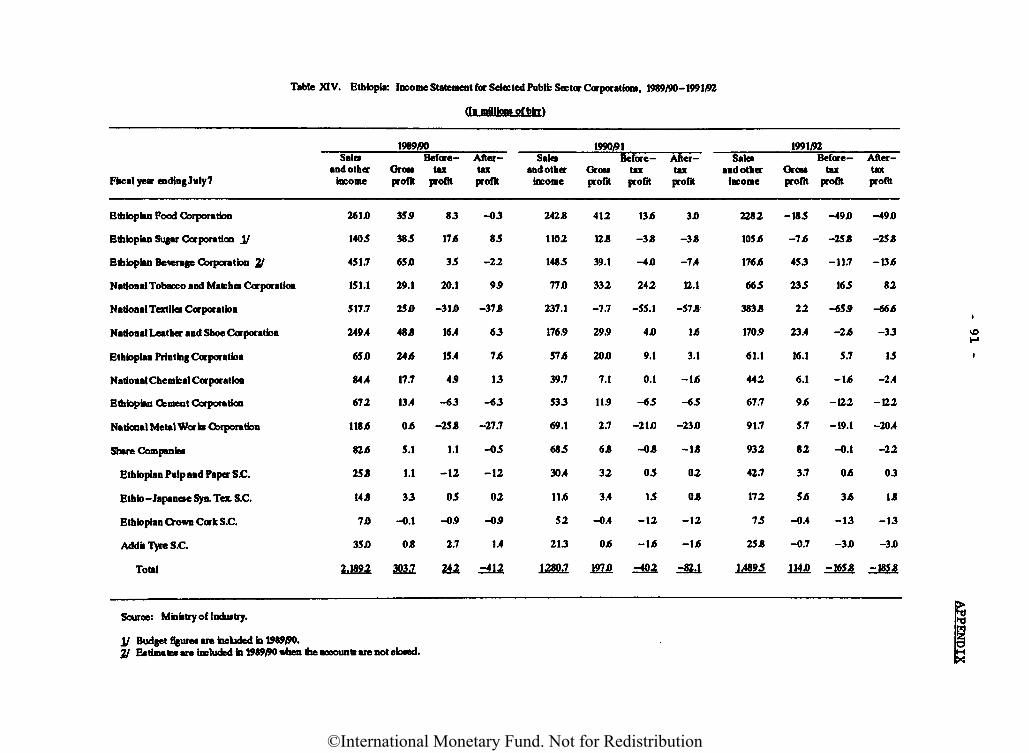

XIV. Income Statement for Selected Public SectorCorporations, 1989/90-1991/92

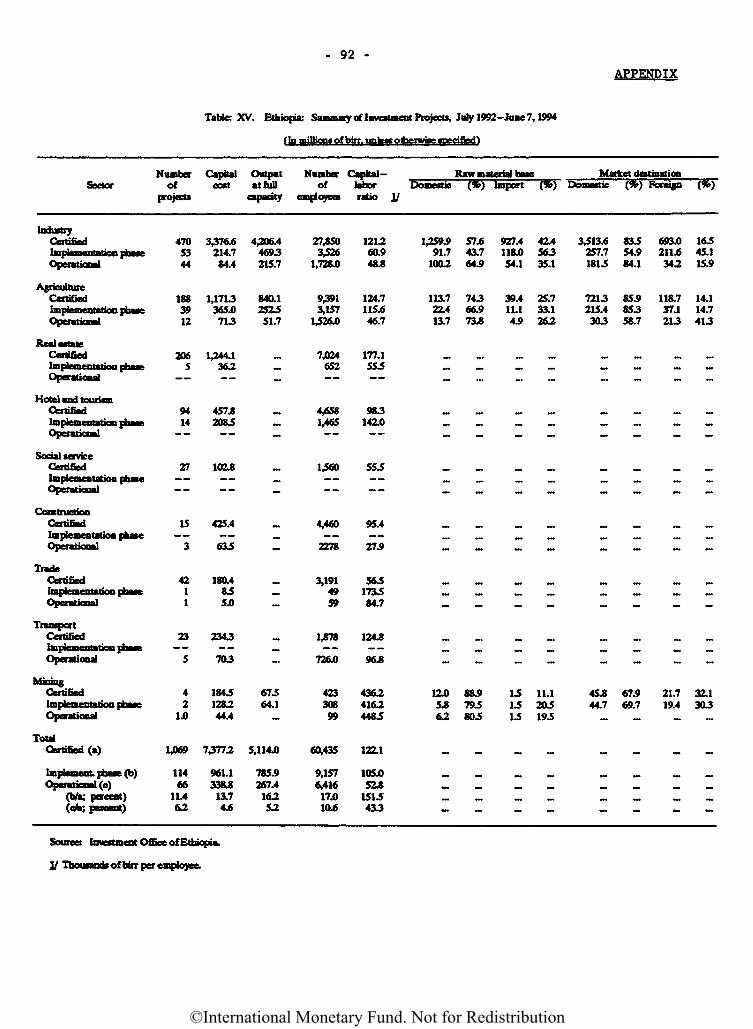

XV. Summary of Investment Projects,July 1992-June 7, 1994

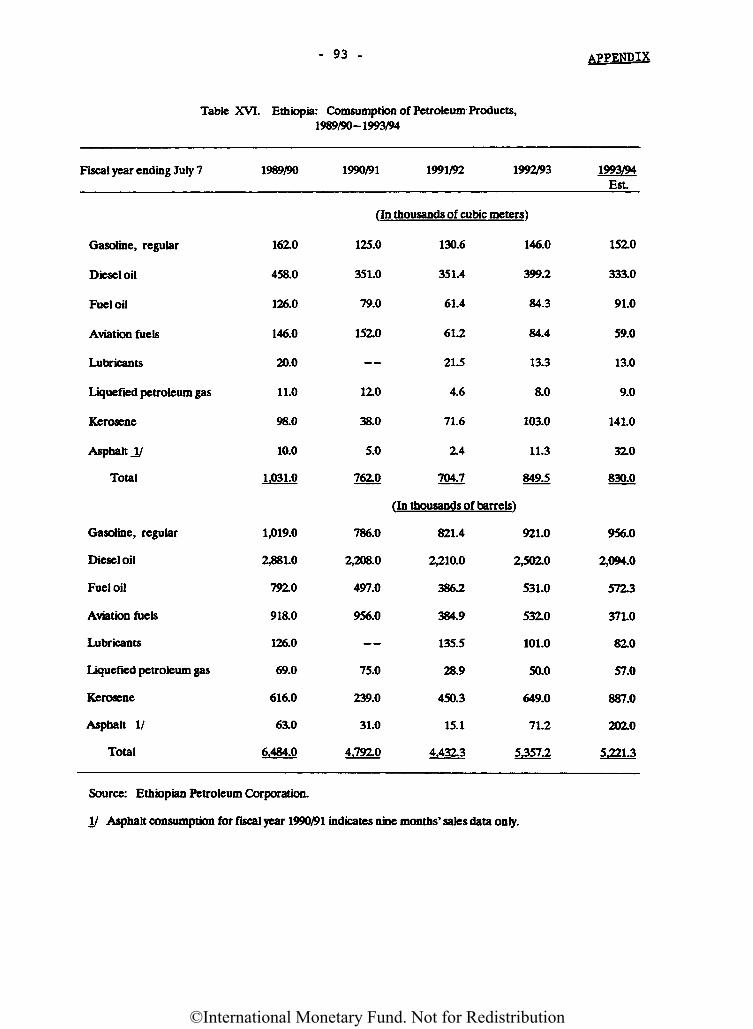

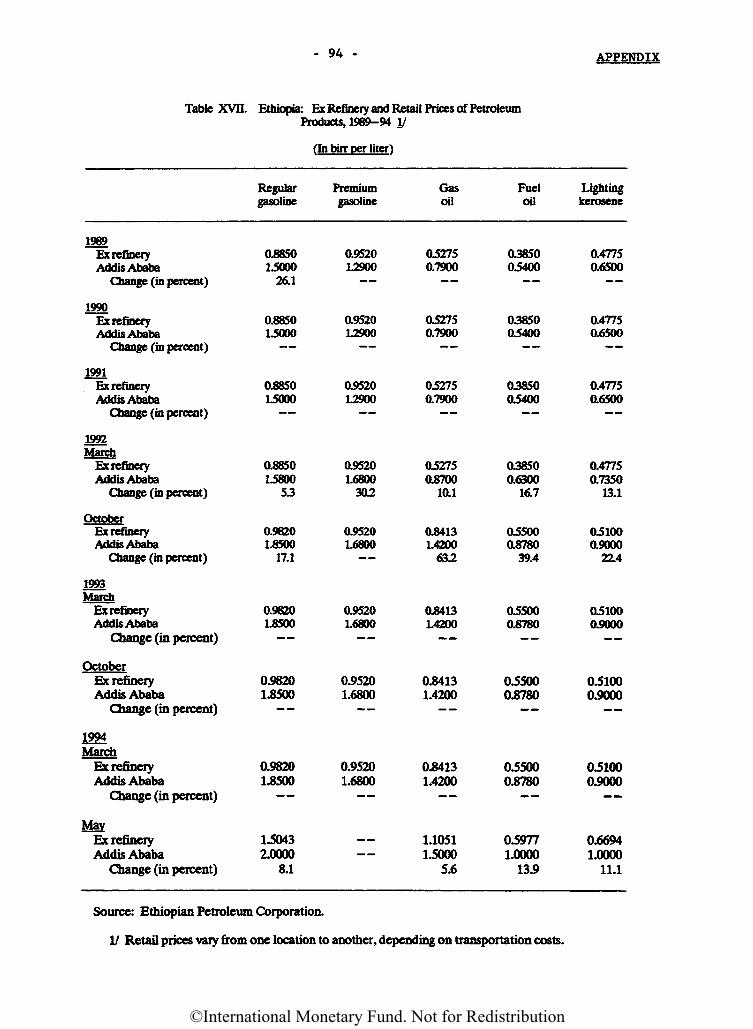

XVI. Consumption of Petroleum Products, 1989/90-1993/94XVII. Ex Refinery and Retail Prices of Petroleum Products,

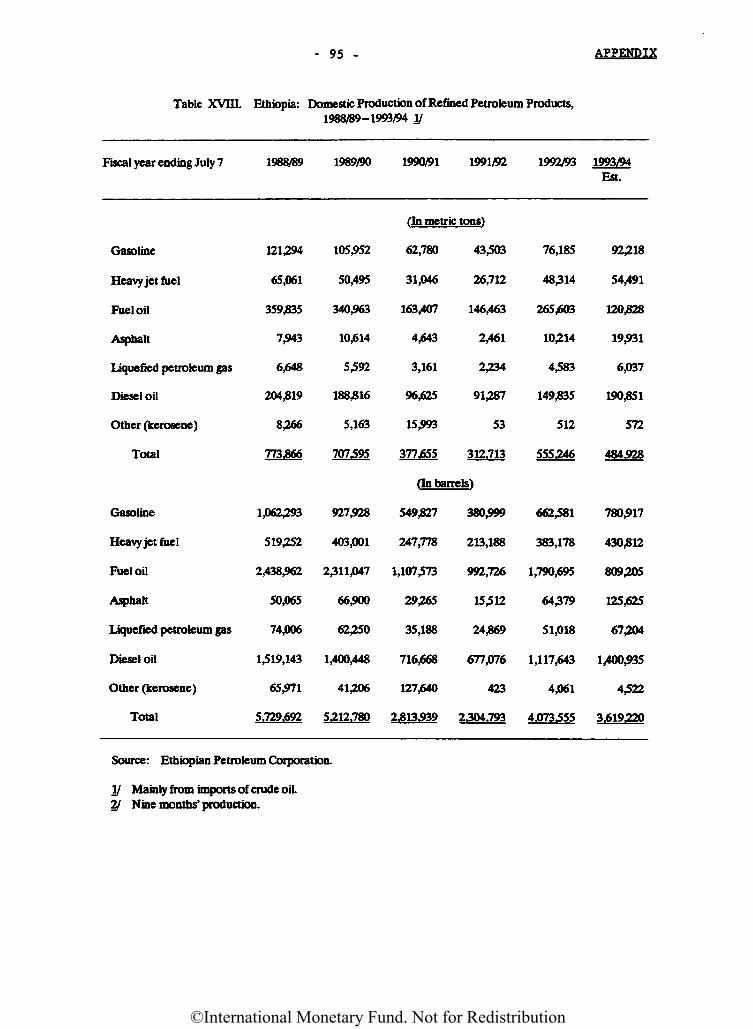

1989-94XVIII. Domestic Production of Refined Petroleum Products,

1988/89-1993/94XIX. Electricity Production, 1988/89-1993/94XX. Retail Price Index for Addis Ababa (Excluding Rent),

January 1991-June 1994XXI. Retail Price Index for Addis Ababa (Excluding Rent),

1990/91-1993/94XXII. Retail Price Index for Food Items in Addis Ababa,

1990/91-1993/94XXIII. Registered Unemployed and Reported Vacancies by

Occupational Classification, 1988/89-1992/93XXIV. Central Government Revenues and Grants,

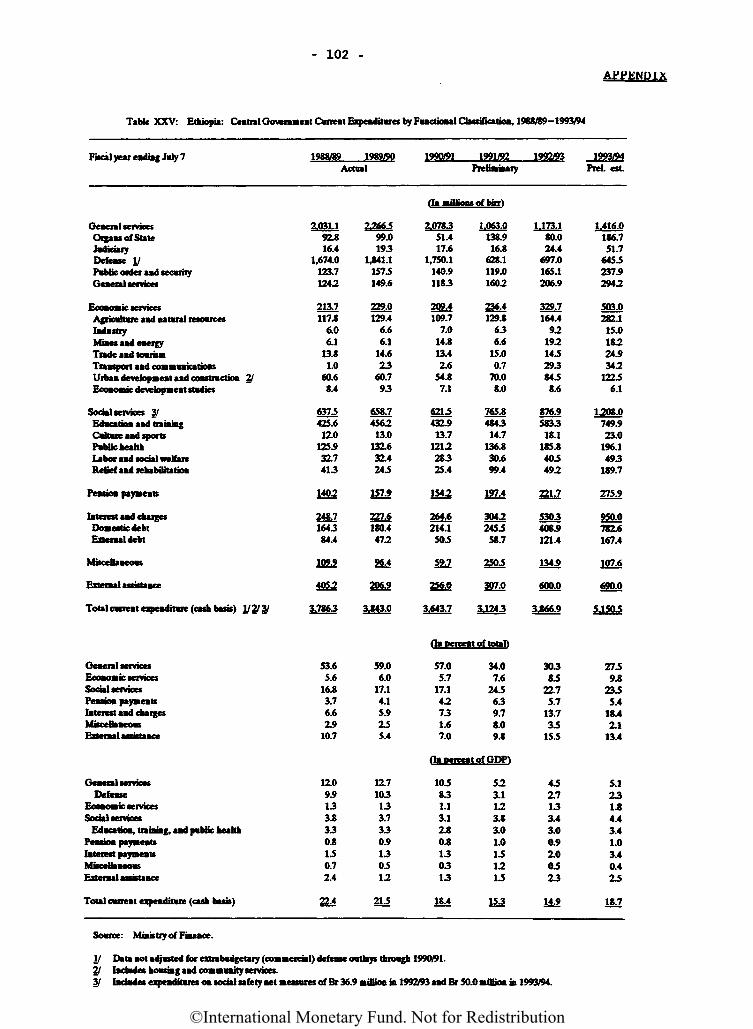

1988/89-1993/94XXV. Central Government Current Expenditures by Functional

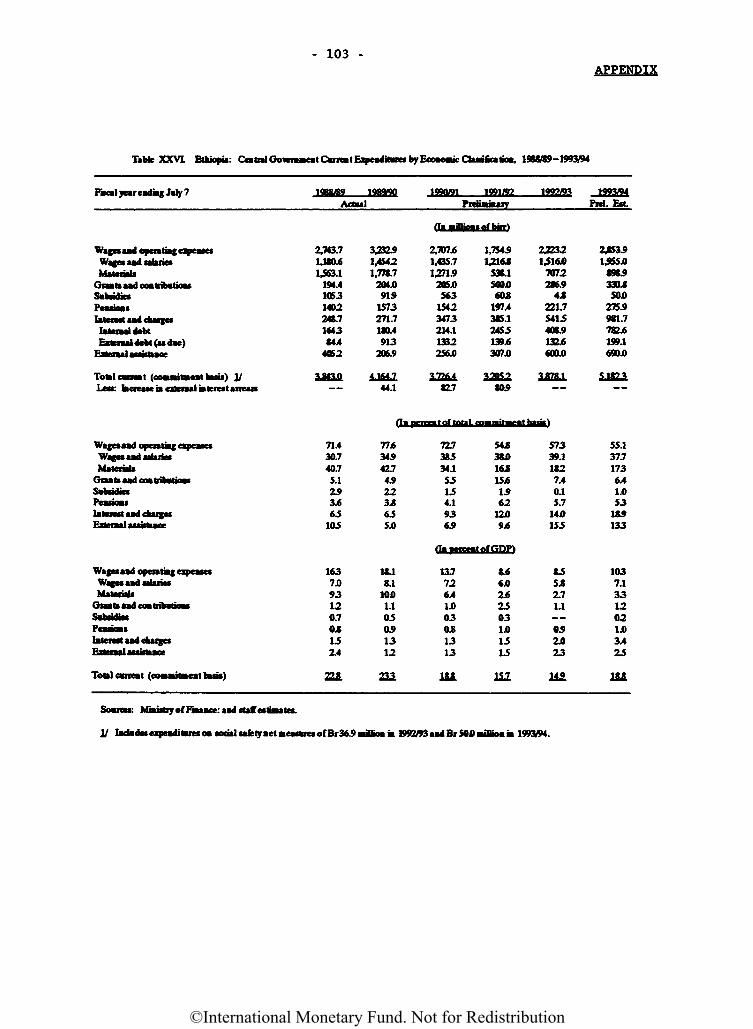

Classification, 1988/89-1993/94XXVI. Central Government Current Expenditures by

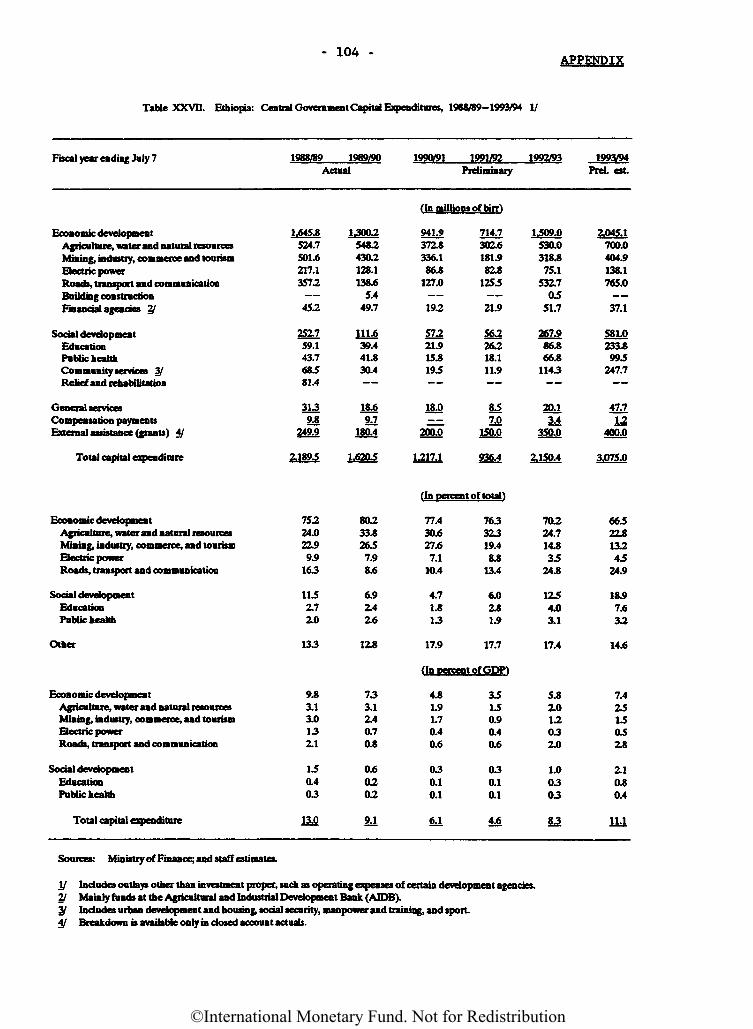

Economic Classification, 1988/89-1993/94XXVII. Central Government Capital Expenditures,

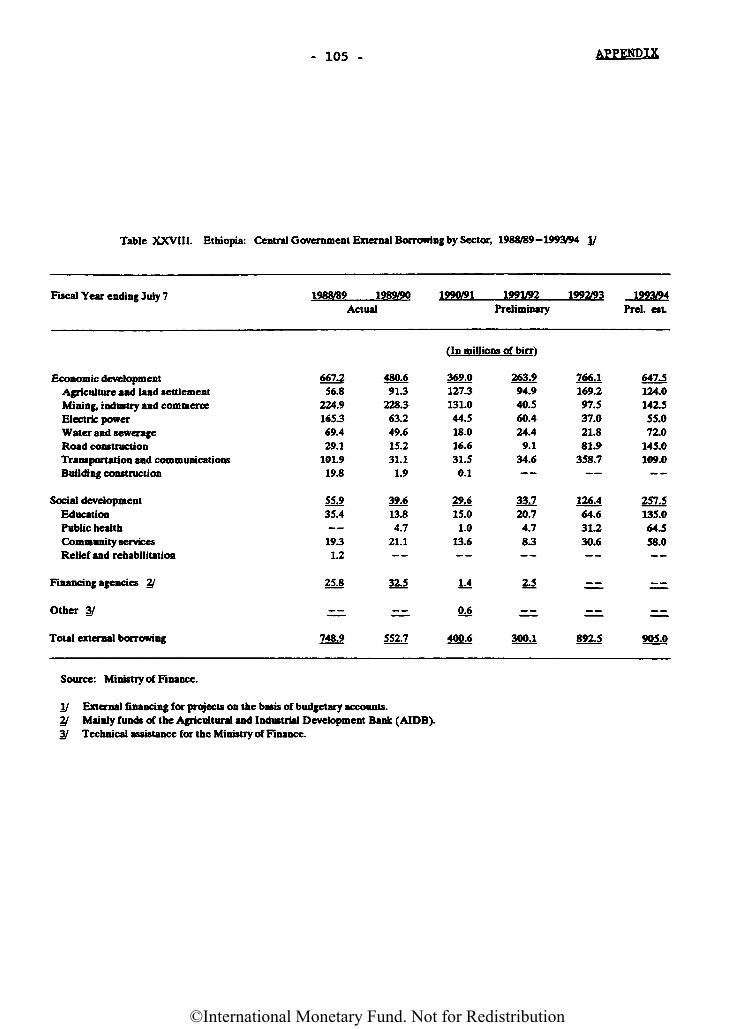

1988/89-1993/94XXVIII. Central Government External Borrowing by Sector,

1988/89-1993/94XXIX. Counterpart Funds Generation from External Grants

and Loans, 1991/92-1993/94XXX. Balance of Payments, 1988/89-1993/94XXXI. Balance of Payments, 1988/89-1993/94XXXII. Exports, 1988/89-1992/93XXXIII. International Prices for Selected CommoditiesXXXIV. Exports by Private Sector (Selected Commodities)XXXV. Value of Imports, c.i.f., by End Use, 1988/89-1992/93XXXVI. Merchandise Trade Unit Value and Volumes,

1988/89-1992/93XXXVII. Selected Effective Exchange Rates, 1988/89-1992/93XXXVIII. Percentage Shares of Private and Public Enterprises at

Foreign Exchange AuctionsXXXIX. Recorded Imports by Country of Origin, 1989-1992

XL. Exports by Country of Destination, 1989-92XLI. Balance in Services and Transfers Accounts,

1988/89-1992/93XLII. Capital Account, 1988/89-1992/93XLIII. External Public Debt Service, 1988/89-1992/93XLIV. External Public Debt Disbursements, 1988/89-1992/93XLV. New External Public Debt Commitments, 1988/89-1992/93XLVI. Suppliers' and Commercial Bank Credits Contracted,

1988/89-1992/93

Page

91

9293

94

9596

97

98

99

100

101

102

103

104

105

106107108109110111112

113114

115116117

118119120121122

123

©International Monetary Fund. Not for Redistribution

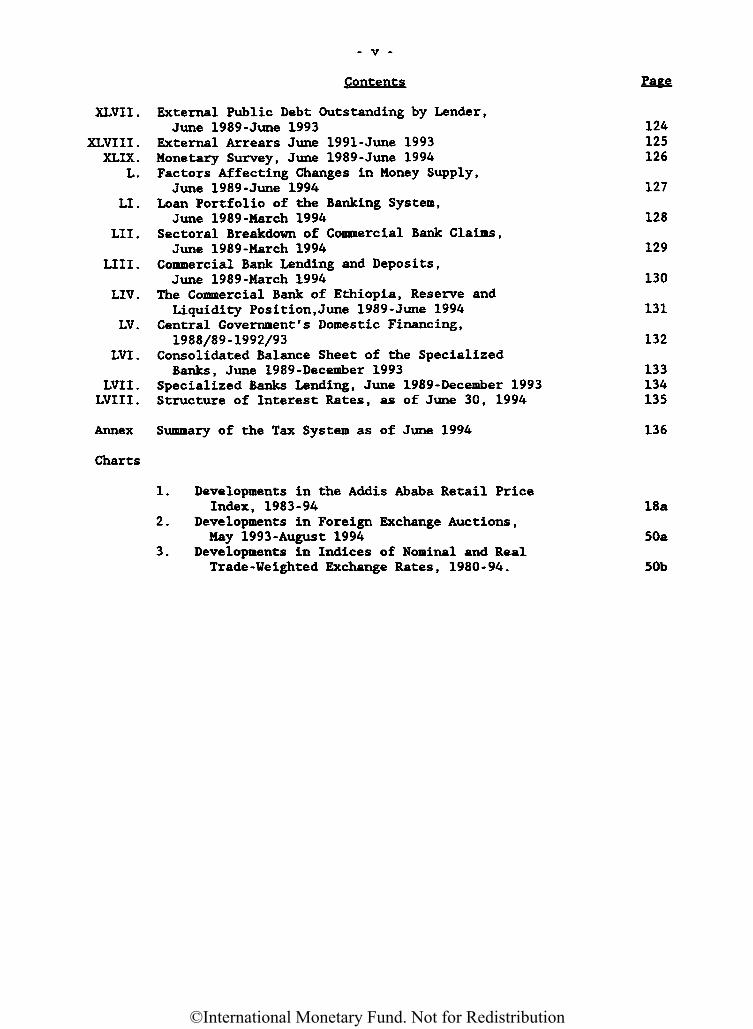

- V -

Contents

XLVII. External Public Debt Outstanding by Lender,June 1989-June 1993

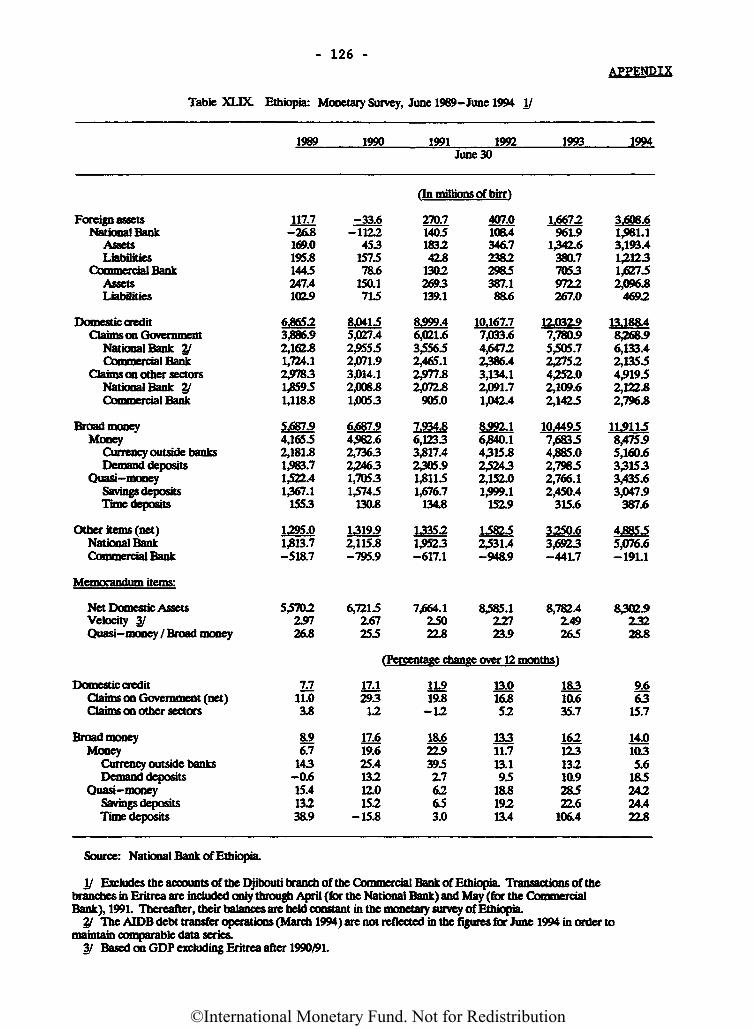

XLVIII. External Arrears June 1991-June 1993XLIX. Monetary Survey, June 1989-June 1994

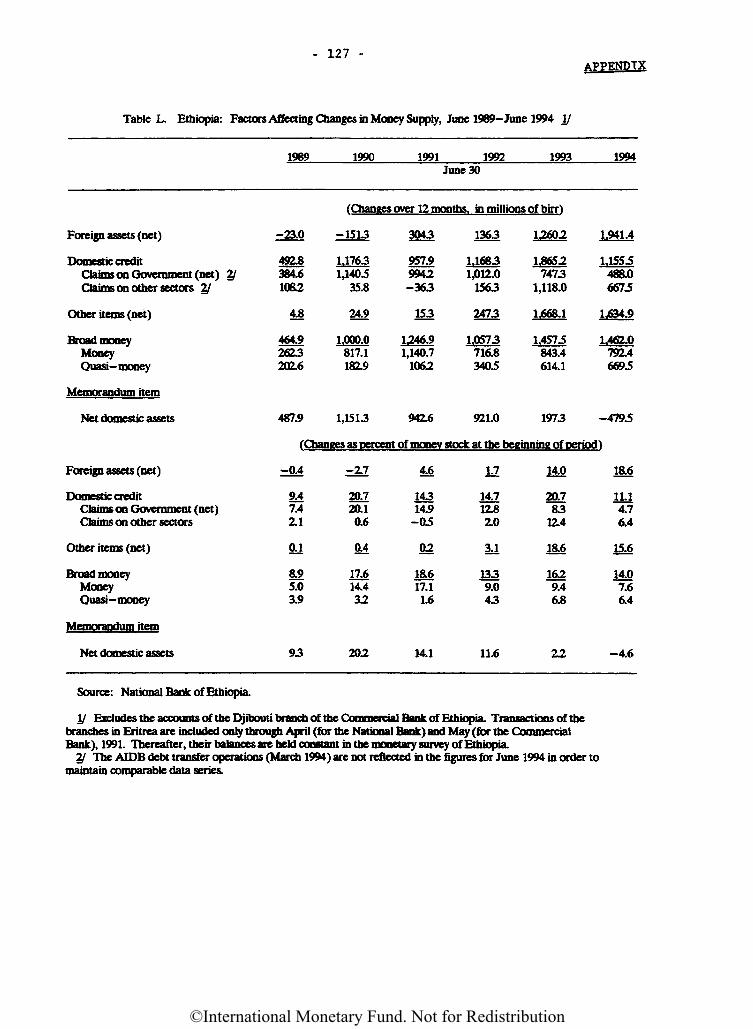

L. Factors Affecting Changes in Money Supply,June 1989-June 1994

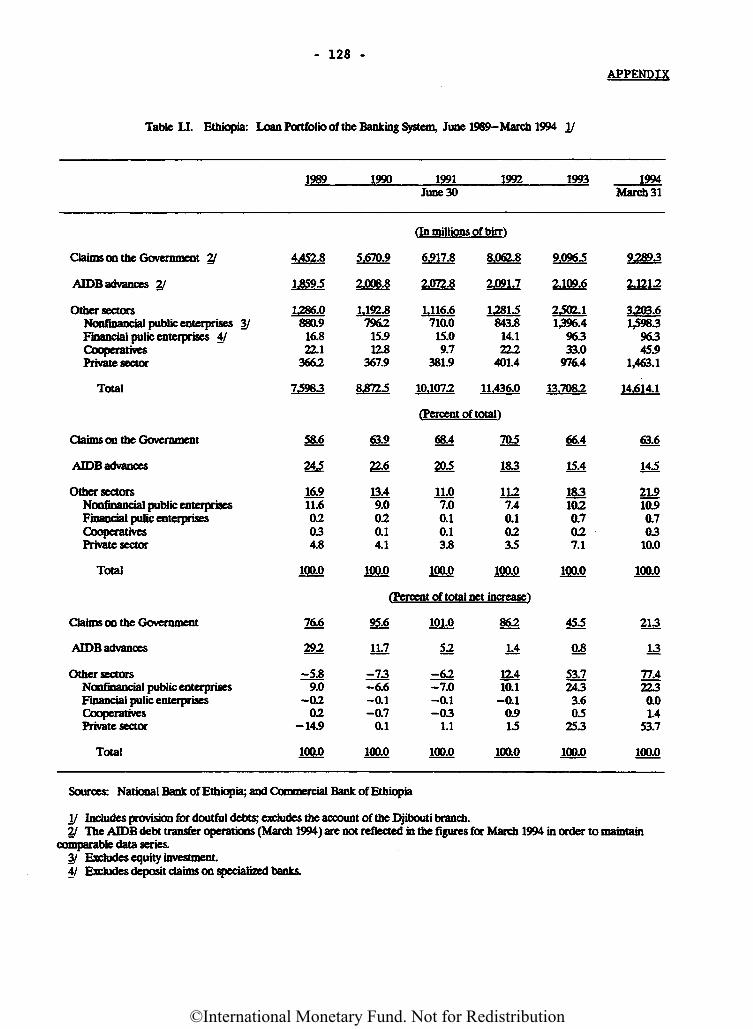

LI. Loan Portfolio of the Banking System,June 1989-March 1994

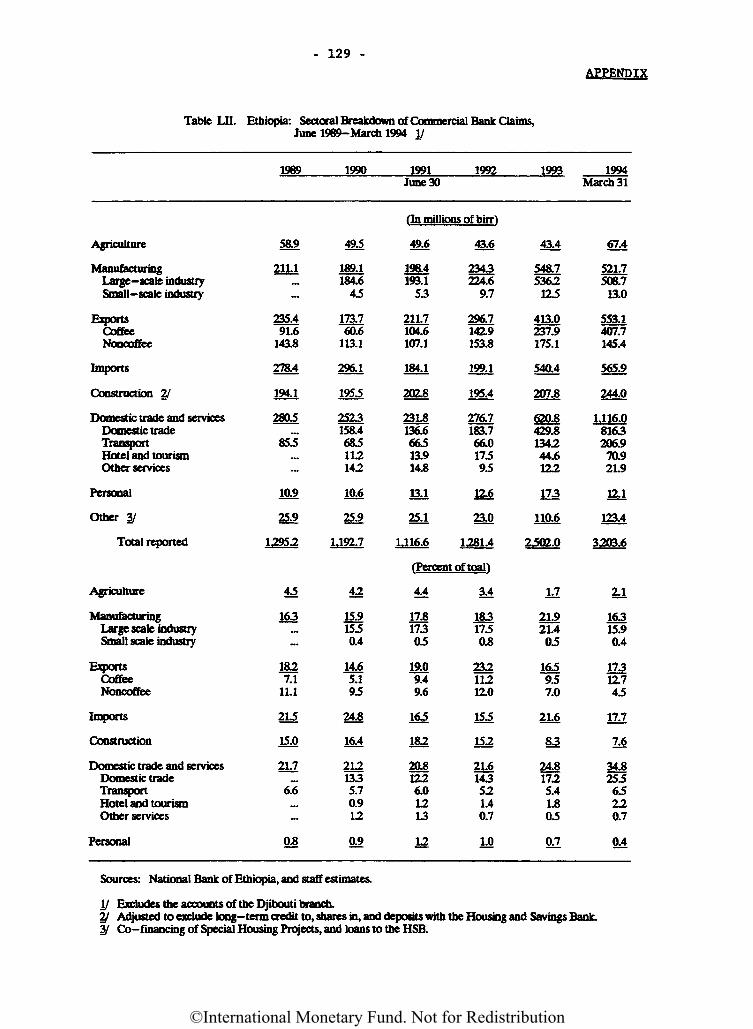

LIT. Sectoral Breakdown of Commercial Bank Claims,June 1989-March 1994

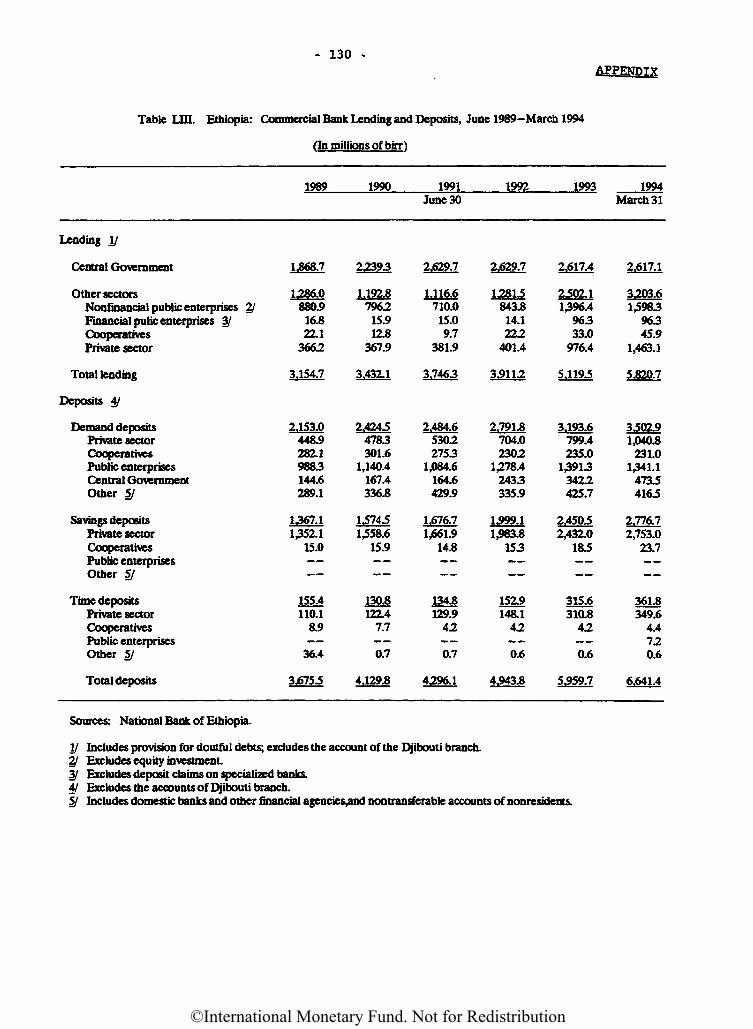

LIII. Commercial Bank Lending and Deposits,June 1989-March 1994

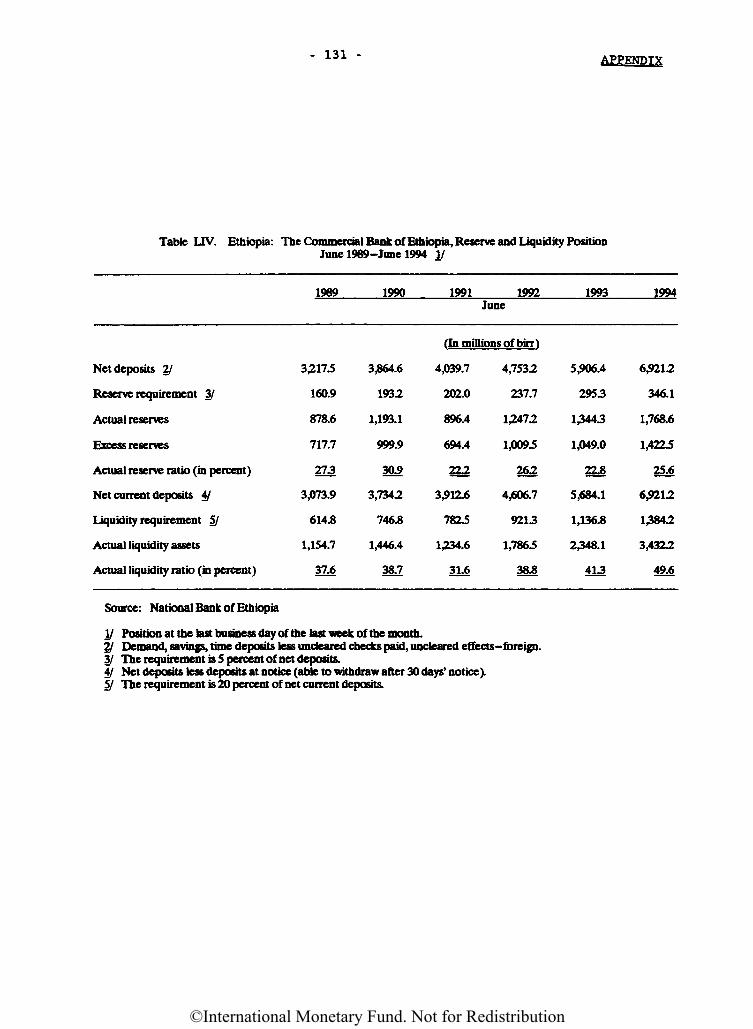

LIV. The Commercial Bank of Ethiopia, Reserve andLiquidity Position, June 1989-June 1994

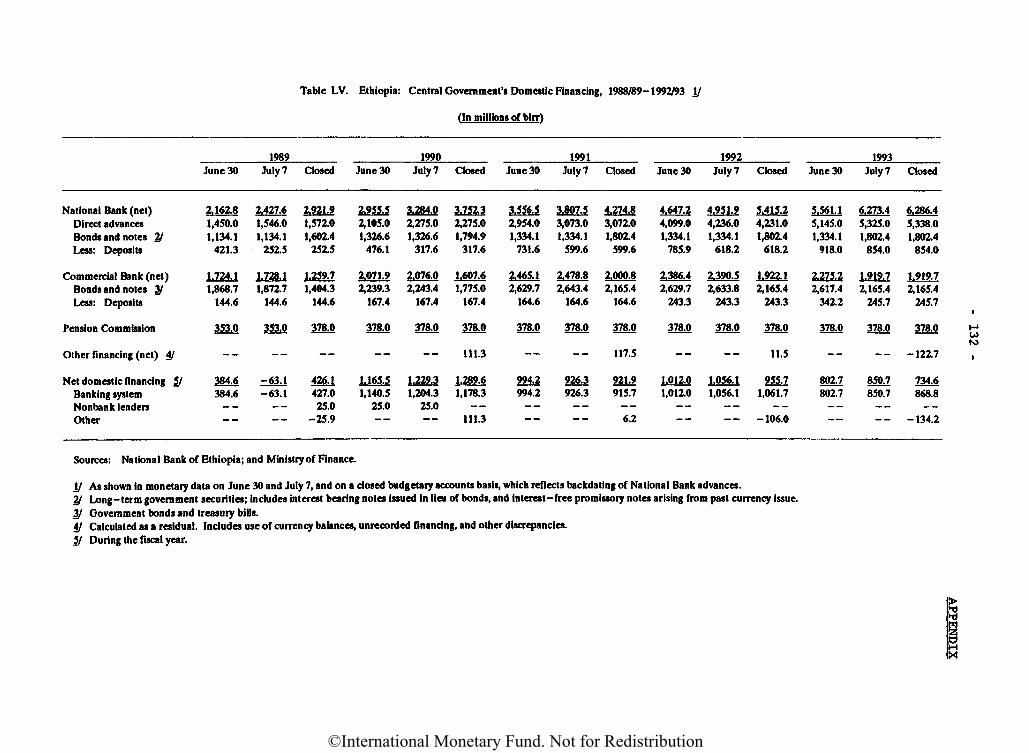

LV. Central Government's Domestic Financing,1988/89-1992/93

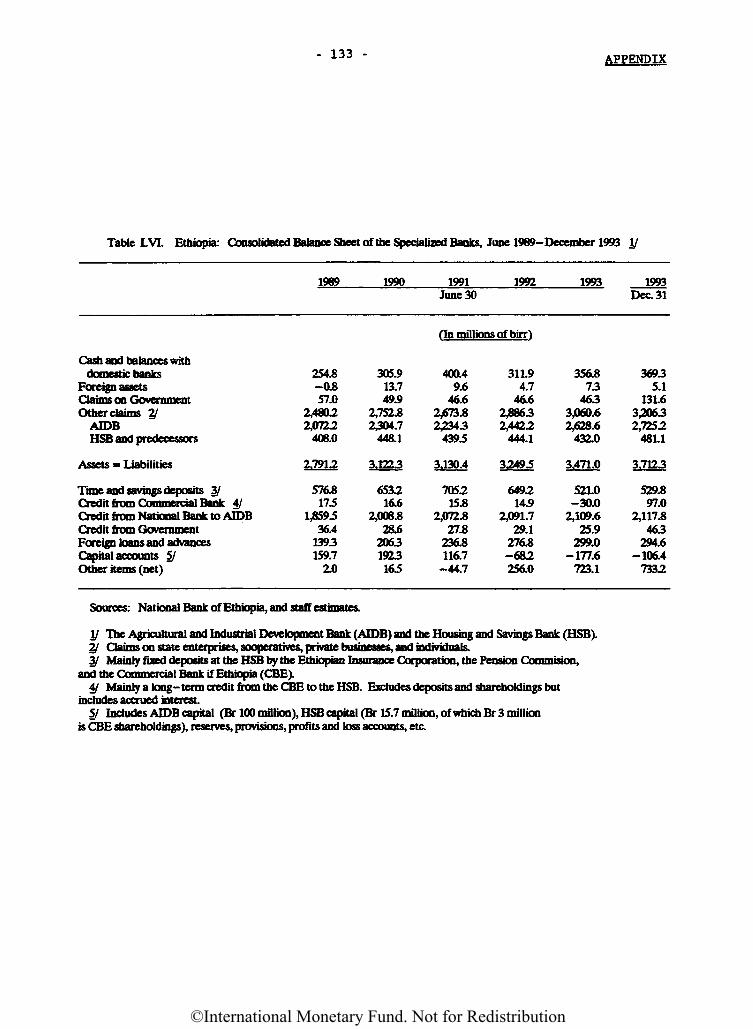

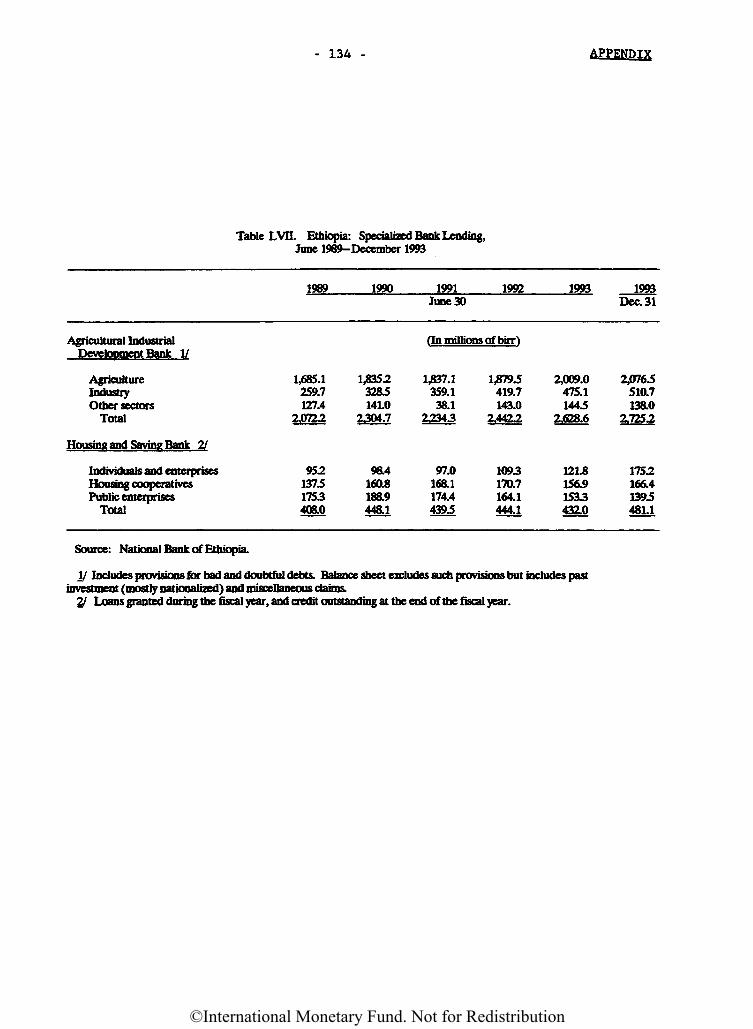

LVI. Consolidated Balance Sheet of the SpecializedBanks, June 1989-December 1993

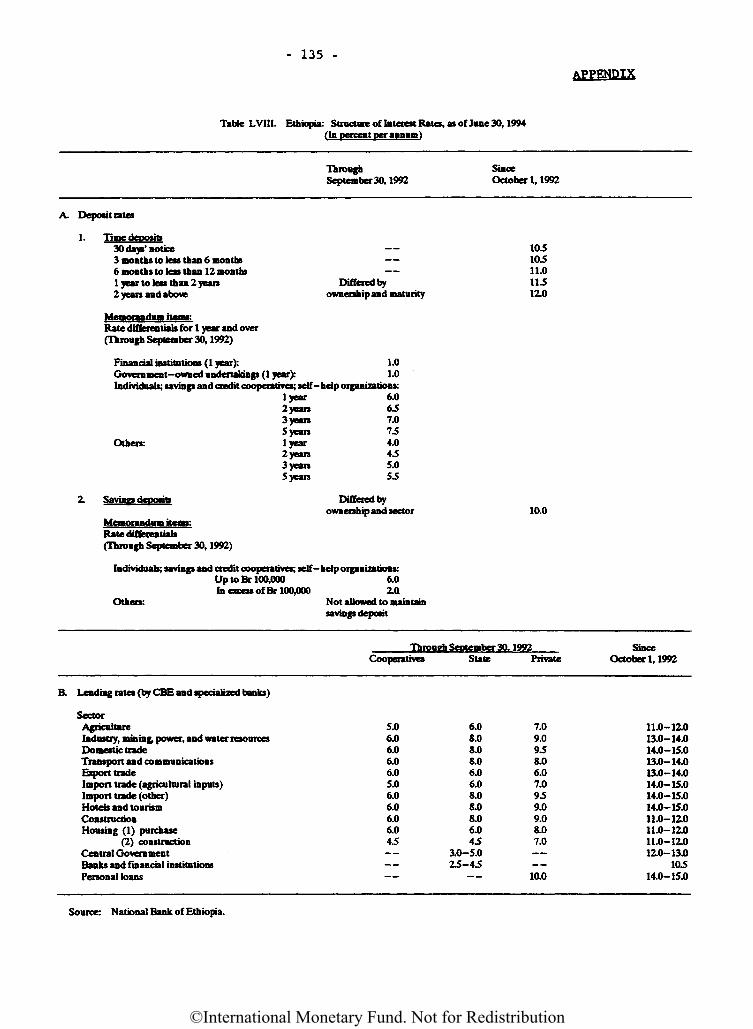

LVII. Specialized Banks Lending, June 1989-December 1993LVIII. Structure of Interest Rates, as of June 30, 1994

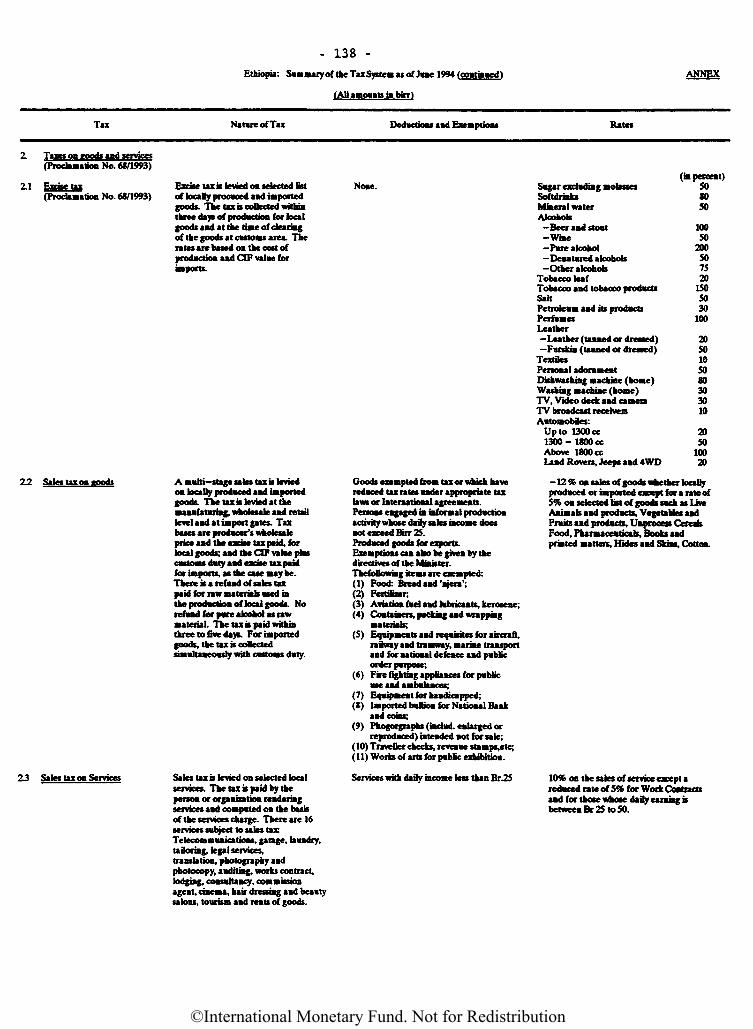

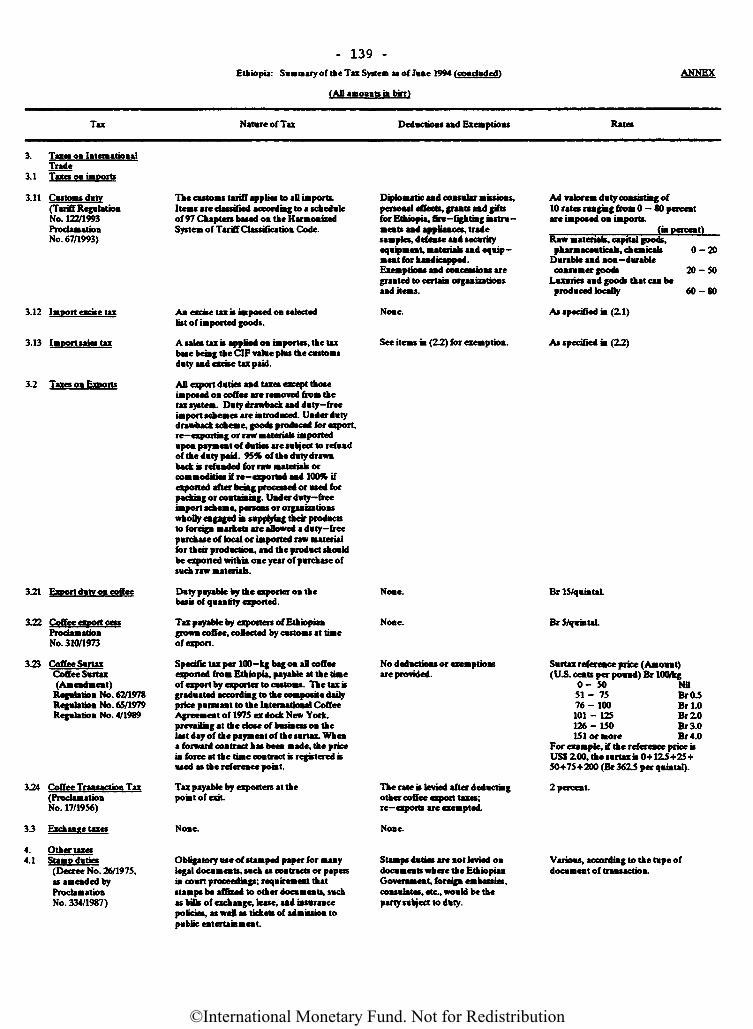

Annex Summary of the Tax System as of June 1994

Charts

1. Developments in the Addis Ababa Retail PriceIndex, 1983-94

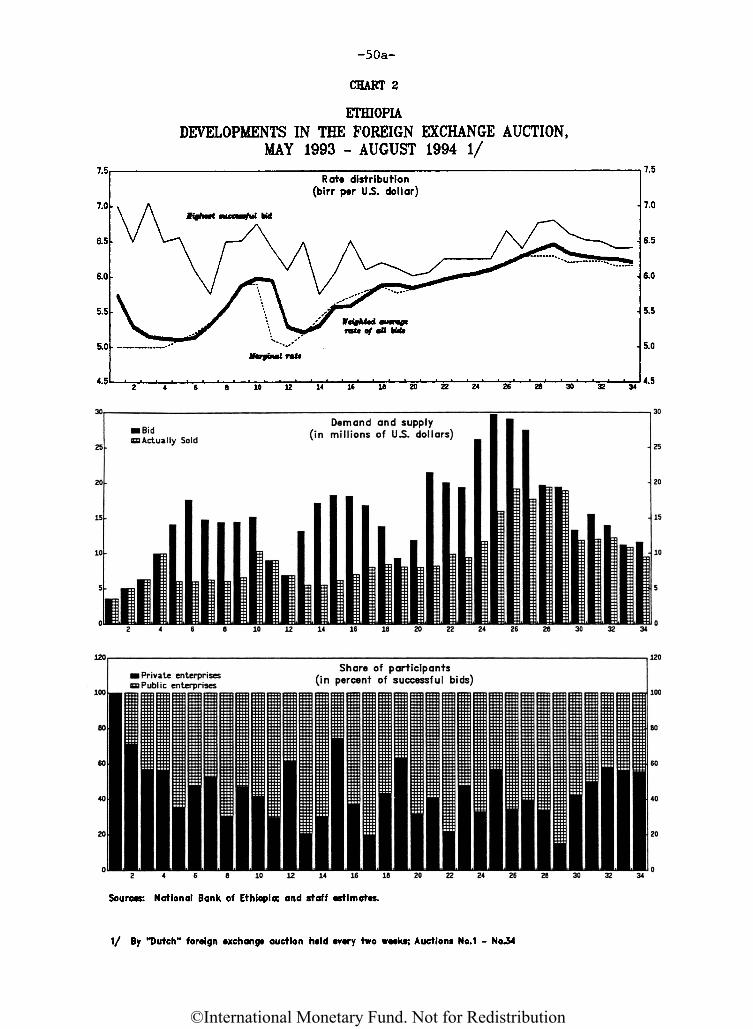

2. Developments in Foreign Exchange Auctions,May 1993-August 1994

3. Developments in Indices of Nominal and RealTrade-Weighted Exchange Rates, 1980-94.

124125126

127

128

129

130

131

132

133134135

136

18a

50a

50b

Page

©International Monetary Fund. Not for Redistribution

- vi -

Ethiopia—Basic Data

1.1 million square kilometers

GDP at currantmarkat pricaa

GDP at constantfactor cost (at1980/81 prices)

AgricultureManufacturingDistribution servicesPublic administrationAnnual real growthrate of GDP (in percent)

Investment (percentof nominal GDP)

Prices

GDP deflatorConsumer price index 5/

Government finance

RevenueForeign grantsExpenditure and netlendingCurrentCapital

Overall balance(accrual)

External interestarrears

Overall balance,cash basis

External financing (net)Domestic financing (net)Banking system

16,873.4

11,719.4

40.75.716.89.5

0.2

9.7

5.79.6

3,899.2799.0

6,043.33,853.82,189.5

-1,345.1

-1.345.1601.6743.5729.2

17,871.7

12,119.5

41.34.916.710.4

3.4

8.9

3.45.2

3142.6401.4

5785.24164.71620.5

-2241.2

44.1

-2197.1495.91701.21724.2

19,815.5

11,307.9

(In percent ofnominal GDP )

51.63.013.07.1

-6.7

7.1

(Annual percent>ajse chm&es

19.220.9

(In millions

2,703.7475.3

4,943.53,726.41,217.1

-1.764.5

81.4

-1,683.1341.1

1,342.01,222.2

20,379.8

10,325.4

57.22.211.64.9

-3.2

9.3

14.521.0

of birr)

2,183.9457.0

4,141.63,205.2936.4

-1,500.7

80.9

-1,419.8249.3

1,170.51,159.0

26,034.8

11,595.0

53.83.813.26.1

12.3

12.5

12.510.0

3,091.61,067.1

6,028.53,878.12,150.4

-1,869.8

-1,858.61,025.6833.0833.0

27,596.1

11,751.5

47.84.514.77.1

1.3

14.1

1.71.2

3,752.41,813.6

8,257.35,182.33,075.0

-2,691.3

-2,659.61,971.6688.0516.4

I/ Excluding Eritrea.y Provisional. 1990/91-1991/92 provisional for fiscal figures only.3/ Estimate.4/ GDP data exclude Eritrea after 1990/91.5/ Addis Ababa Retail Price Index average.

Area, population, and GDP per capita \/

AreaPopulation:Total (1992/93 midyear estimate)Annual growth xata

GDP par capita (1992/93)

1988/89 1989/90

52.4 Billion3 parcantSDR 82.5

1990/91 2/ 1991/92 2/ 1992/93 £/ 1993/94 3/

(Fiscal rear andad July 7)

(In millions of birr, unless otherwise specified)GPORK d^BBQgt.4 e wT'oAtet'. fGDP^ A/

©International Monetary Fund. Not for Redistribution

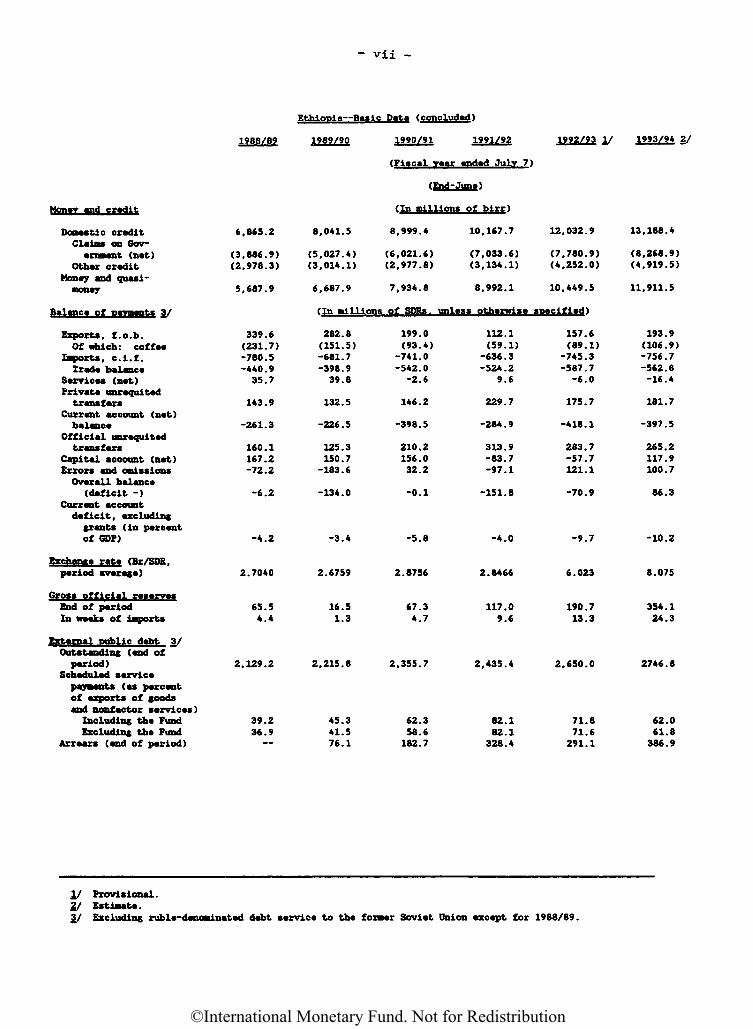

- vii -

Ethiopia—Basic Data (concluded)

1988/89 1989/90 1990/91

(Fiscal irear ended July 7

1991/92 1992/93 I/ 1993/94 2/

(End- June)

Money and credit

Domestic creditClaim* on Gov-ernment (net)

Other creditMoney and quasi -money

Balance of payments 3/

Exports, f.o.b.Of which: co£f««

Imports, c.i.f.Trad* balance

Services (net)Private unrequitedtransfers

Current account (netbalance

Official unrequitedtransfers

Capital account (net)Errors and omissionsOverall balance(deficit -)

Current accountdeficit, excludinggrants (in percentof GDP)

Exchange rate (Br/SDR.period average)

End of periodIn weeks of imports

External wiblic debt 3/Outstanding (end ofperiod)

Scheduled servicepayments (as percentof exports of goodsand nonf actor services)Including the FundExcluding the Fund

Arrears (end of period)

(In millions of birr)

6,865.2

(3,886.9)(2,978.3)

5,687.9

339.6(231.7)-780.5-440.935.7

143.9

-261.3

160.1167.2-72.2

-6.2

-4.2

2.7040

65.54.4

2,129.2

39.236.9~

8.041.5

(5.027.4)(3.014.1)

6,687.9

(In millio

282.8(151.5)-681.7-398.939.8

132.5

-226.5

125.3150.7-183.6

-134.0

-3.4

2.6759

16.51.3

2,215.8

45.341.576.1

8,999.4

(6,021.6)(2.977.8)

7,934.8

ins of SORs .

199.0(93.4)-741.0-542.0-2.6

146.2

-398.5

210.2156.032.2

-0.1

-5.8

2.8756

67.34.7

2.355.7

62.358.6182.7

10.167.7

(7,033.6)(3,134.1)

8,992.1

unless otherwise si

112.1(59.1)-636.3-524.2

9.6

229.7

-284.9

313.9-83.7-97.1

-151.8

-4.0

2.8466

117.09.6

2,435.4

82.182.1328.4

12,032.9

(7,780.9)(4,252.0)

10,449.5

sec if led)

157.6(89.1)-745.3-587.7-6.0

175.7

-418.1

283.7-57.7121.1

-70.9

-9.7

6.023

190.713.3

2,650.0

71.871.6291.1

13,188.4

(8,268.9)(4,919.5)

11,911.5

193.9(106.9)-756.7-562.6-16.4

181.7

-397.5

265.2117.9100.7

86.3

-10.2

8.075

354.124.3

2746.8

62.061.8386.9

i/ Provisional.2/ Estimate.3/ Excluding ruble-denominated debt service to the former Soviet Union except for 1988/89.

Groes officia reserves

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

I. Real Sector

1. Aggregate output and expenditure

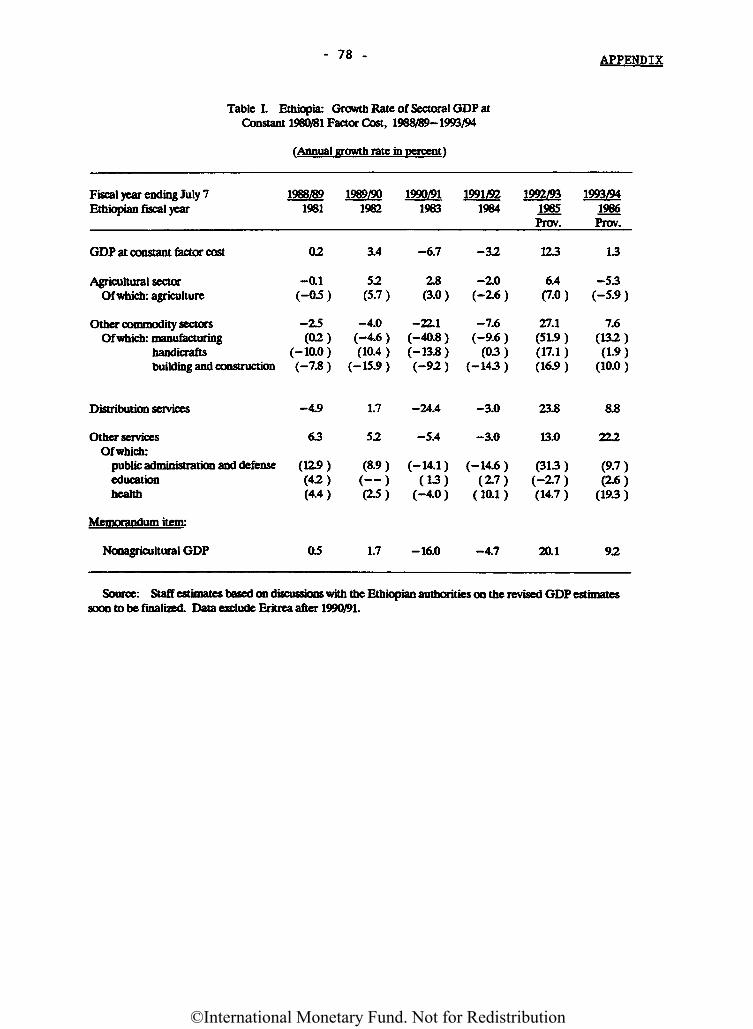

Following a period of modest and fluctuating growth in the 1980s(averaging 2.5 percent), events surrounding the collapse of the Derg regimein 1991 led to a substantial worsening of economic conditions in theEthiopian economy, as reflected in a cumulative decline in economic activityof about 10 percent during 1990/91-1991/92 (Appendix Table I). The adverseimpact of overall instability and security-related problems during thisperiod was further magnified by variable weather conditions, depressedcoffee prices, and foreign exchange scarcity, leading to a continuousdeterioration in capacity utilization in the manufacturing sector.

Agricultural production, reflecting its significant sensitivity tofavorable weather conditions, exhibited a relatively strong, albeit erratic,performance during 1989/90-1991/92--an average growth of 4 percent during1989/90-1990/91, followed by a sharp drop in 1991/92 (2.6 percent). Thelatter also reflected a significant decline in the total area undercultivation as a result of the escalation of the civil war. In contrast,economic activity in the manufacturing and construction sectors declined byan annual average of 17.1 percent and 13.1 percent, respectively, during1989/90-1991/92, mainly owing to a severe shortage of raw materials andforeign exchange. Output from distribution and other services alsocontracted by an average of 7 percent and 1 percent per annum, respectively,reflecting the overall decline in economic activity.

In 1992/93, there was a significant recovery in the economy, which wasreflected in virtually all sectors, with real GDP rebounding by anexceptional 12.3 percent. While the improved security situation in thecountry and, subsequently, the emergence of a favorable economic andpolitical climate set the stage for the recovery, a number of additionalfactors contributed to this outcome. In the agricultural sector, goodweather conditions, coupled with increases in land under cultivation andgreater fertilizer usage, led to a bumper crop, with the sector registeringa strong 7 percent growth rate. In the manufacturing sector, a smooth flowof inputs through increased availability of foreign exchange led to adramatic recovery in the capacity utilization rate, mainly in the publicenterprise sector. Growth in manufacturing rebounded by an extraordinary51.9 percent, albeit from an extremely low base. Small-scale private sectoractivity also began to develop, reflecting a modest revival from itshistorically repressed condition.

Developments during 1993/94 have been less favorable, even though theeconomy is estimated to have grown modestly (1.3 percent). An erraticdistribution and pattern of rainfall throughout the country and inadequateusage of fertilizers and pesticides during the main rainy season areestimated to have contributed to a significant drop in agricultural output.This shortfall has been further aggravated by an unusually dry short rainy

©International Monetary Fund. Not for Redistribution

- 2 -

season, leading to severe drought in some northern regions, as well as inthe southern lowlands. In addition, the pest problems that emerged duringthe 1994 short harvest in these regions, as well as in the western parts ofthe country, are estimated to have contributed to the sharp drop inharvested output. As a consequence, agricultural output is estimated tohave declined by almost 6 percent. However, growth in the non-agriculturalsector (9.2 percent), most notably in the manufacturing sector(13.2 percent), continued to be robust, thereby helping the economy maintaina positive growth for the year as a whole. This was mainly attributable tothe continued recovery in the public enterprise sector, as well as inprivate sector activity, and to an improved investment rate.

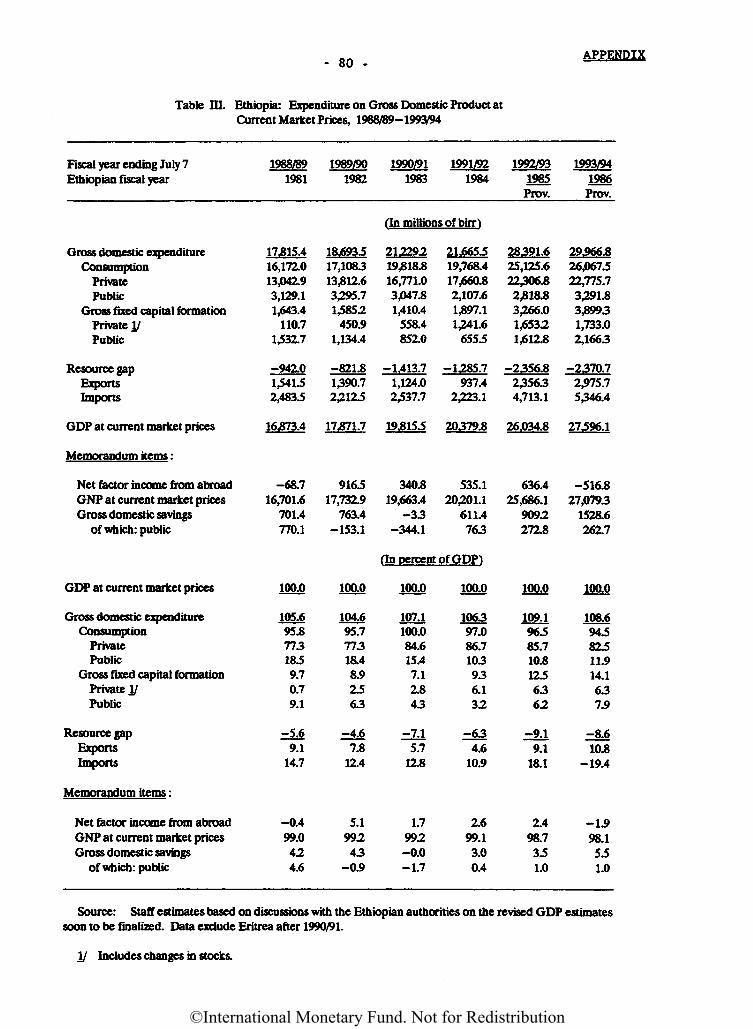

The overall investment rate in the economy, after having stagnated atabout 9 percent for four consecutive years during 1988/89-1991/92, improvedconsiderably during 1992/93-1993/94, averaging 13.3 percent of GDP (AppendixTable III) . Although still low even in comparison with the average for sub-Saharan Africa (17.3 percent in 1993), this represented almost a doubling ofinvestment as a percent of GDP, compared with the 1990/91 level. In1992/93, about half of the 12.5 percent gross capital formation rate derivedfrom the private sector. In 1993/94, the investment rate further increased,to 14.1 percent, mainly reflecting a higher rate of capital budgetimplementation by the public sector. Domestic savings, while still weak,given Ethiopia's extremely low per capita income level, also improvedmodestly during 1992/93-1993/94, after having dropped sharply to zero in1990/91. This was attributable to a slight improvement in public sectorsavings, which increased from minus 1.7 percent of GDP in 1990/91 to1 percent in 1993/94, as well as a revival in private sector savings (from1.7 percent of GDP in 1990/91 to 4.6 percent in 1993/94). Although totalconsumption declined slightly during this period, the expansion ininvestment continued to be reflected in a large resource gap, whichincreased from an average of 6 percent of GDP percent during 1989/90-1991/92to 8.8 percent during 1992/93-1993/94.

2. Sectoral developments

a. Agriculture

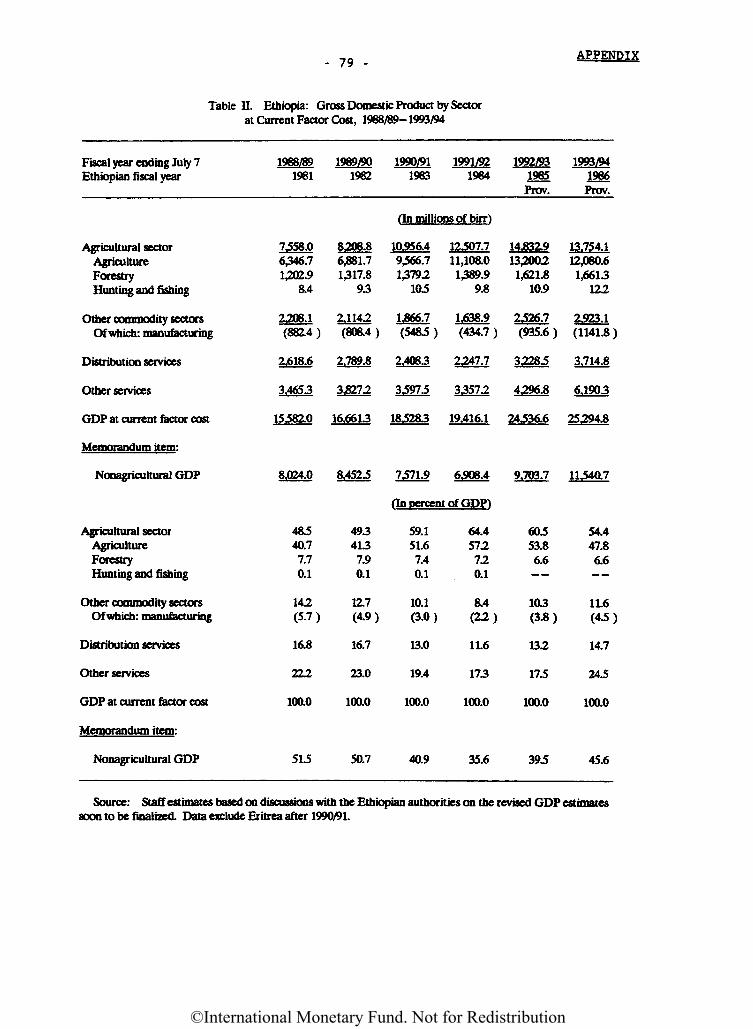

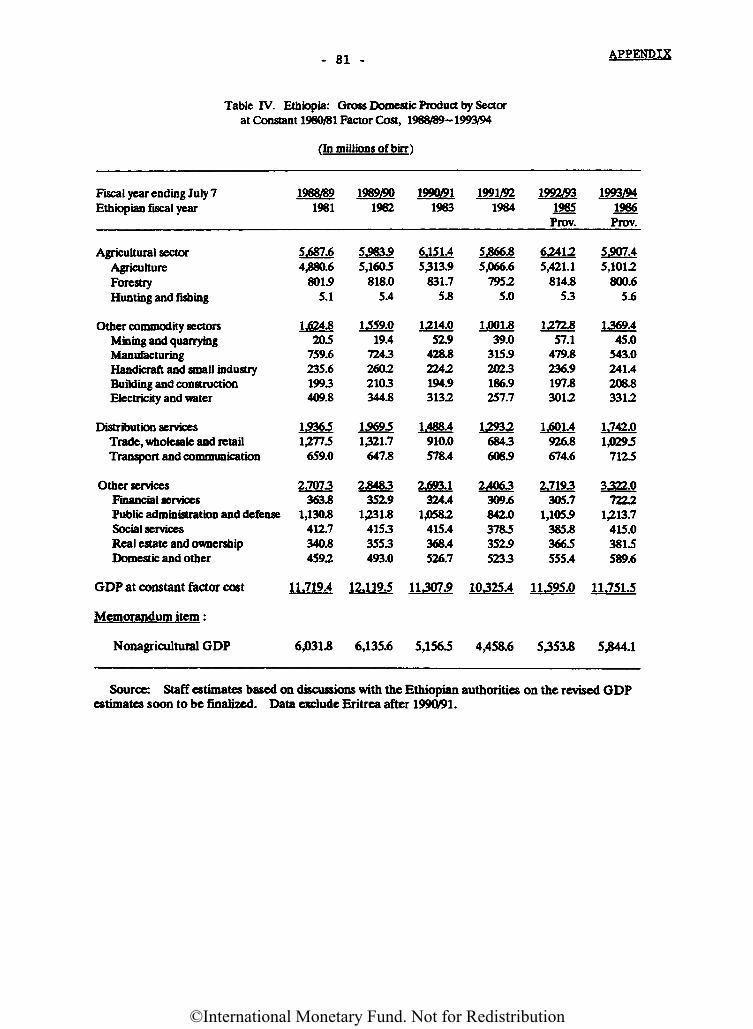

The agricultural sec tor--including principally agriculture andlivestock, but, to a marginal degree, the forestry, fishing, and huntingsub-sectors--is by far the most important sector in the Ethiopian economy,constituting more than 50 percent of GDP (1993/94) , and employing more than80 percent of the labor force (Appendix Table II).

(1) Crops

Crop production is predominantly concentrated in staple crops,which are produced by smallholder, subsistence farmers. Irrigation islimited, such that production crucially depends on the amount anddistribution of rainfall. Although the average level of rainfall variesconsiderably across the different regions, broadly, two harvests occur

©International Monetary Fund. Not for Redistribution

- 3 -

during any given year. The main harvest season (the meher crop) follows thelong rains of July-September and the second harvest (the belg crop) followsthe short rains of February-April. In some regions, mostly in the centralhighlands, the above-mentioned two rainy seasons tend to merge and theharvest generally occurs in October and January. More than 90 percent oftotal crop production takes place during the meher season, while the shortseason accounts for the remainder. However, some areas (e.g., Bale and Omoin the South, and Wello and Tigray in the North) depend crucially on thebelg rains.

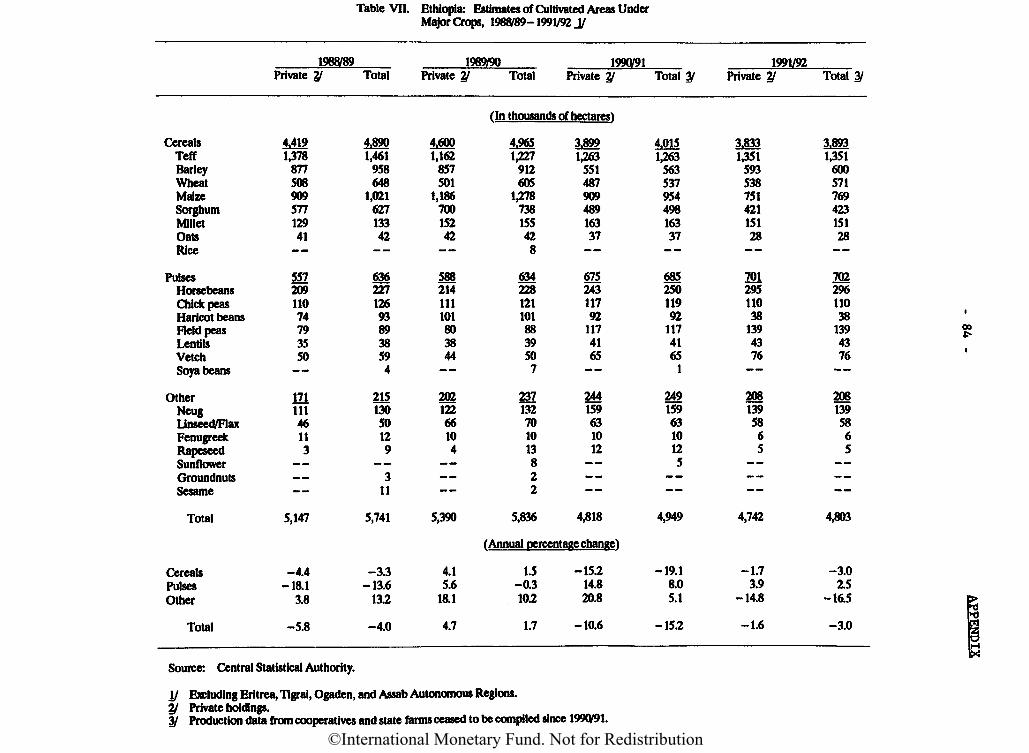

In a good year, cereal production, which mainly includes maize(28 percent of the total), teff (24 percent), barley (16 percent), wheat(13 percent), and sorghum (13 percent), is estimated at around 6 milliontons. I/ Of the total cultivated area, teff and maize cover more than50 percent, followed by barley (17 percent) and wheat and sorghum(13 percent each). Maize, sorghum, and wheat have relatively high yields,and are normally planted during the long season; nevertheless, their yields,on average, at about 12 quintals per hectare, are considered extremely loweven by African standards, mainly owing to rudimentary farming techniques aswell as limited usage of fertilizers and improved seeds. It is estimatedthat about 15 percent of total crop production is marketable while theremainder is used for self-consumption or animal feed. In general,switching across crops (particularly toward cash crops) is uncommon inEthiopia, because of the high priority that the farmers give to ensuringsubsistence through the planting of staple crops and the lack of knowledgeof the appropriate technology. 2/

Ethiopia's principal surplus areas in the production of cereals areconcentrated in the Oromiya (e.g., Arsi, and East and West Showa) and Amhara(e.g., East and West Go jam) regions, while many densely populated areas inthe north (e.g., Tigray, Wello, and Gondar) as well as the pastoral southare known as structural deficit areas. The incomes of the smallholderfarmers are particularly susceptible to drought, due to their limitedability to compensate for the impact of crop failure (e.g. lack ofalternative employment opportunities, limited asset base, isolation frommajor markets, and low level of farm technology). The majority of the4 million people in Ethiopia who are estimated to depend on food aid (evenunder normal circumstances) live in these regions. 3/

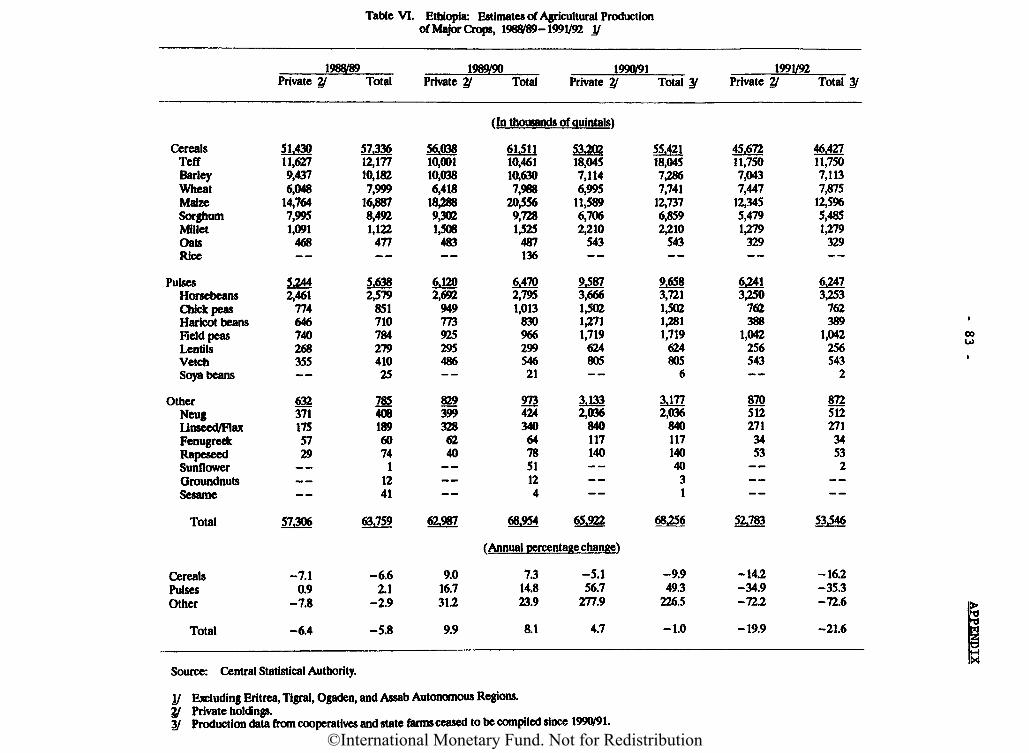

I/ Figures are averages for 1988/89-1991/92, and are stated aspercentages of total staple crop production (Tables VI, VII). Data are notavailable for 1992/93-1993/94, owing to the suspension of the annual cropsurvey conducted by the Central Statistical Authority (CSA) ; presently, theCSA is mainly involved in the preparation of the forthcoming census.

2J There has been some switching to root crops, but principally in thesouthern areas in order to cope with drought.3/ This implies, on average, an annual minimum food aid requirement of

roughly 500,000 tons, assuming an annual cereal requirement of about 120-130kilograms per person.

©International Monetary Fund. Not for Redistribution

. 4-

During 1992/93, cereal production is estimated to have grown by about9 percent, with the highest growth achieved from the relatively high-yielding maize (20 percent) and sorghum (10 percent), followed by barley(4 percent), wheat (4 percent), and teff (3 percent). In 1993/94,reflecting vagaries of the meher season as well as drought during the shortrainy season, crop production is estimated to have declined by10 percent. \J

Ethiopia's main cash crops include coffee, oil seeds, and pulses. £/Coffee. the most important cash crop and Ethiopia's principal export (seeSection III.2a for further discussion), is mostly grown in Oromiya and theSouthern Ethiopia Region, mainly by smallholder farmers (96 percent).Coffee is prepared and processed for the market in two different forms--sun-dried and washed. 3/ Exports are largely concentrated in sun-dried coffee(djimma, wollega, hararge, and sidamo) , while exports of the higher-qualitywashed coffee are constrained by a lack of infrastructure (viz. , washingstations, access roads, vehicles, training, etc.). Washed coffee isprocessed predominantly by service cooperatives (and a limited number ofstate farms), since the private sector has only recently been permitted toengage in coffee processing. There are about 130 washing stations inEthiopia, 2 of which are owned by the private sector.

As part of ongoing reforms in the coffee sector, the Ethiopian CoffeeMarketing Corporation (ECMC) was restructured into two separateenterprises--the Coffee Sales and Purchase Enterprise (CSPE) and theEthiopian Coffee Export Enterprise (ECEE)--in late 1993. While the CSPE isengaged in coffee purchases and transfers from the interior (to the twoexport auction centers at Addis Ababa and Dire Dawa) , the ECEE is in chargeof buying coffee at these auction centers from both the CSPE and individualtraders, and then exporting it. As a result of the liberalized licensingrequirements for coffee exports that were introduced in August 1993(reflecting significantly reduced issuance and renewal fees), the number of

I/ These figures are very preliminary.2/ In addition, small amounts of sugar cane and cotton are grown, mainly

in state farm plantations along the Awash river in the Afar region. Thelatter has been adversely affected during the transition to a marketeconomy, as most cotton growing state farms were dissolved, and smallholdersswitched to staple crop and livestock production, leading to a decline innational lint cotton production, to about 5,000 tons at present fromapproximately 30,000 tons during the Derg regime. There are efforts tostudy the problems of the sector with a view to reviving it. In addition,fruits and vegetables appear to have gained in importance in recent years,although no statistics have been compiled on production.I/ In dry processing, fully ripe red cherries are directly picked from

the tree and dried in the sun on raised beds, providing air circulation andavoiding soil contamination. The more capital-intensive wet processingmethod involves pulping, fermenting, as well as drying on elevated wiretrays.

©International Monetary Fund. Not for Redistribution

- 5 -

coffee exporters as well as private traders (both collectors (sebsabv) andtransporters (akrabv)̂ . have increased, thereby providing for greatercompetition in the various stages of the coffee marketing process. JL/ Themonopoly position of the ECMC in the exporting of washed coffee also endedduring 1991/92, as private exporters were allowed to participate in theauctions alongside the ECMC. 2/

Nevertheless, a number of regulations still pertain to the marketing ofcoffee; these appear to be aimed at controlling the quality and movement ofcoffee for export. These include: (i) the regulation that the amount ofcoffee that can be moved by an (unlicensed) individual must not exceed3 kilograms; (ii) the requirement that all exportable coffee must bechanneled through the auction and that all coffee sold in the domesticmarket must be coffee not acceptable for export (after inspection andgrading at the auction centers); and (iii) the restriction that privateexporters cannot make coffee purchases outside of the auctions.

In response to the sudden drop in coffee prices in mid-1989 (followingthe failure of ICO members to agree on quotas), and in order to restoreincentives to coffee growers, producer prices were increased substantially,with the increase being financed through both a reduction in the coffeeexport surtax and a direct subsidy from the budget. More recently,beginning in the 1992 coffee season ,3/> an^ in response to the volatilityof international prices, floor prices were set by the CSPE for sun-driedcoffee; these floor prices have remained unchanged since then. 4/ Owingto the recent surge in international prices (in mid-1994), these prices areno longer binding. Sun-dried coffee is regularly traded between thesabsabies and farmers on the basis of recent auction prices announced on thepublic radio and posted at local market places. As regards washed coffee,farmers receive a first payment from the service cooperatives before theirwashed coffee is sent to the auction market. They then get a second paymentif the resulting auction price is above the first payment. Currently, about60 percent of this difference is distributed to farmers 5J as a secondpayment and the remaining 40 percent is reserved (by the cooperatives) for

\J There are six types of coffee licenses: coffee export, coffeetransport, coffee cleaning, coffee collecting, coffee trade auxiliary, andcoffee washing.

2J Private exporters have been allowed in the exporting of sun-driedcoffee since late 1989.

3/ The coffee season extends from October through September.4/ These prices were set at 4.2 Br/kg for djinima, 6.15 Br/kg for sidamo,

7.0 Br/kg for nekempte, and 9.1 Br/kg for hararge. The setting of floorprices was complicated for some time because of low international prices aswell as the continuing demand in the domestic market, with domestic pricesremaining, on average, higher than the export prices.

5J The exact share varies across service cooperatives.

©International Monetary Fund. Not for Redistribution

- 6 -

management and reinvestment for farmers. There are no data on the actualproducer prices received by farmers. \J

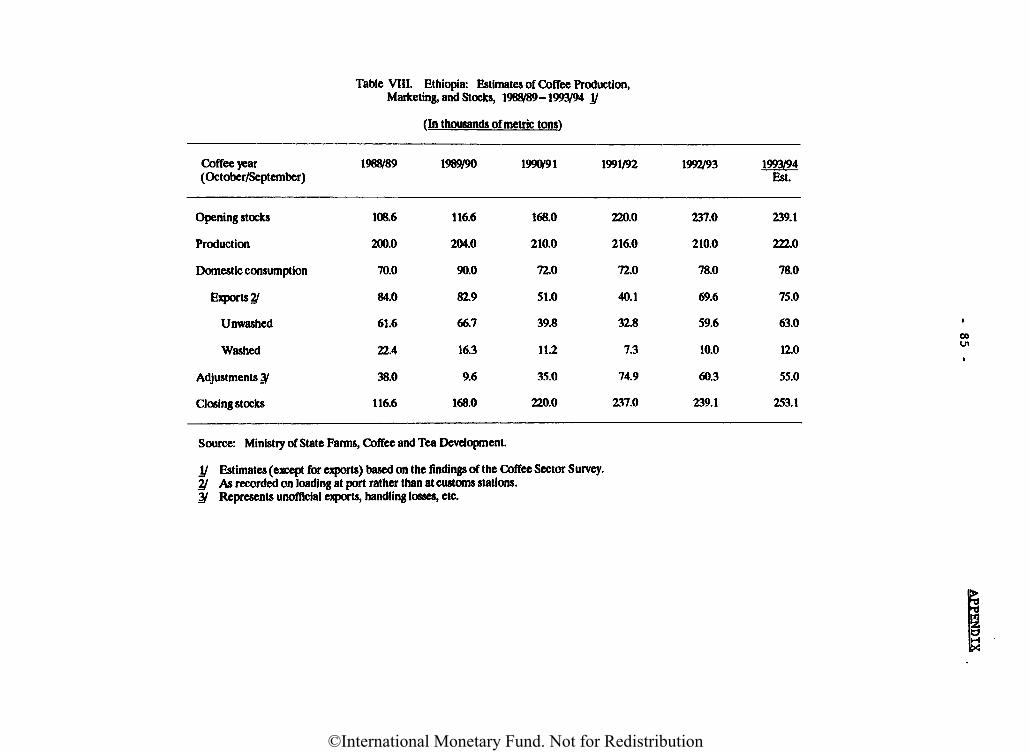

During 1989/90-1991/92, coffee production is estimated to have grownevenly, albeit modestly, by about 2.5 percent per annum, averaging slightlyabove 200,000 tons (Appendix Table VIII). After a slight decline in1992/93, production is estimated to have increased by 5.7 percent in1993/94, reaching 222,000 tons. While this may be attributed partly to thefavorable impact of recent liberalization measures as well as to increasesin international prices, the full impact of such measures on the growth incoffee production is presumably restricted in the short term to efficiencygains (during the picking of coffee beans), which is estimated to remainnear 5 percent, given the usual cycle between the planting of new coffee andits harvesting. 2/ There is very little information on changes in thetotal area planted (presently estimated at some 400,000 hectares), althoughsome additional planting is estimated to have taken place in traditionalcoffee growing areas, such as Eastern Hararge.

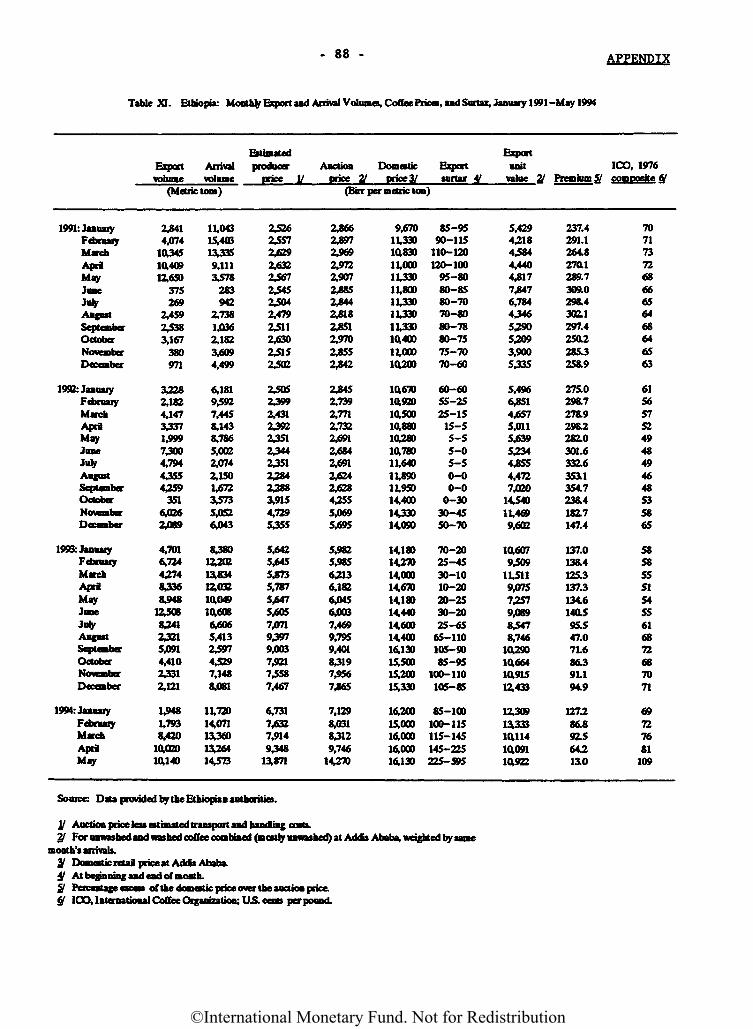

Arrivals at the auction centers, 3/ although lower than the record1989 level, increased considerably to about 67,000 tons during January-May1994, as compared with an average of 51,000 tons for the same five-monthperiod extending from 1990 through 1993 (Appendix Table XI). While this ispartly attributable to the diminished role of the parallel market in thechanneling of coffee to the international market, 4/ the continuedincreases in international prices, which have substantially reduced thedifferential between the auction price and the domestic price, appear tohave contributed to this outcome. However, existing regulations (asdiscussed above)--coupled with a traditionally high domestic demand forcoffee, estimated to absorb about 35-40 percent of total coffee production--continue to induce a diversion of exportable coffee beans to the domesticmarket through irregular channels.

Pulses (horsebeans, chickpeas, haricots, and lentils) and oilseeds(neug, flax, rapeseed, sesame, and castor beans) constitute about 12-13 percent of crop production, and 17 percent of the total land undercultivation (excluding coffee and other cash crops). 5/ They are grownmostly as rotational crops by smallholder farmers in between the meher andbelg seasons. In 1992/93, preliminary estimates suggest that productiongrew by about 3.4 percent.

JL/ However, prices can be deduced from the auction price data byadjusting for taxes and transportation and handling costs.

7J Normally, coffee trees come into production 3-4 years after plantingand are in full production at 6-8 years.3/ Arrivals at the auctions increase during October through April,

following the coffee harvest in October.4/ However, leakages to Djibouti, Somalia, and Sudan are still estimated

to be high.5/ Averages for 1989/90-1991/92.

©International Monetary Fund. Not for Redistribution

- 7 -

(2) Livestock

Ethiopia's livestock herd of 75 million is estimated to be thelargest in Africa. It is difficult to calculate the sector's value added,since a significant part of meat and dairy production is produced forsubsistence purposes and in certain regions, particularly in the highlands,livestock is utilized only to support farming. Ethiopia's livestocksubsector continues to suffer from the vagaries of unpredictable weatherconditions, disease, and the lack of a coherent plan for the development ofthe sector. Although hides and skins and leather are Ethiopia's second mostimportant export, the sector's huge potential remains largely untapped. Theimpact of the recent drought is estimated to have been substantial forlivestock herds.

(3) Fertilizer usage

Since the launching of the economic reform program, progress hasbeen made in various areas, including in the usage of fertilizer, provisionof credit and agricultural extension services to farmers, and the marketingand pricing of agricultural products. Despite the introduction of theGovernment's "New (Fertilizer) Marketing System" in 1991/92, there have beendifficulties in ensuring adequate levels of fertilizer usage by thesmallholder sector. \J The monopoly of the Agricultural Input SupplyCorporation (AISCO) in fertilizer procurement and distribution was removed,resulting in a multiple channel procurement and distribution system withsignificant private sector involvement in retailing, and to some extent, inwholesaling. At the end of 1993, more than 1,000 private retailers wereregistered by AISCO (about 900 of whom are operational) and an additional600 are expected to be registered in 1994; these retailers operate alongsideapproximately 400 service cooperatives and 400 marketing centers, the lattermanaged by AISCO. It is estimated that the share of the private retailersin fertilizer distribution will increase to over 60 percent by the end of1994. The total number of wholesalers in 1994 is likely to remain the sameas in 1993 (at around 30), because of the large scale of the operationsinvolved. Almost all fertilizer imports continue to be funded by donorsthrough AISCO; in 1992/93 a private company started to import fertilizer aswell.

Fertilizer usage in Ethiopia is considered extremely low; only about15 percent of the farmers are estimated to use fertilizers. In 1993,fertilizer sales to the peasant sector (121,000 metric tons) were about

I/ Prior to 1991/92, AISCO used about 2,900 Service Cooperatives (SC) asthe only retail outlets for fertilizer retailing. During 1990/91, aconsiderable number of SCs were destroyed and damaged as a result of thecivil unrest and ceased to function. Following the substantial reduction inthe number of retail outlets (down to about 550), AISCO, with the assistanceof the United Nations Food and Agricultural Organization (FAO), introduced aNew Marketing System.

©International Monetary Fund. Not for Redistribution

- 8 -

20 percent lower than in 1992 (156,000 metric tons). I/ The reasons forthe decline included a delay in the announcement of fertilizer prices, 2/confusion over the associated subsidy scheme, lack of retail market outletsand credit facilities, and administrative constraints placed on the newprivate sector dealers in the context of the pan-territorial pricing policypursued by the Government. The Government's efforts to promote the benefitsof fertilizer, which should have been launched at the time of priceincreases, were also limited. The 1994 sales target is about 160,000 metrictons, slightly above 1992, and is likely to be achieved, given favorablestock positions (partly owing to lower-than-expected sales during thepreceding year) and the timely announcement of prices in mid-January.However, during January-April 1994, actual sales by AISCO to the peasantsector (27,510 metric tons) were lower than the level during thecorresponding period in 1992 (33,476 metric tons), an outcome partlyattributable to the delay in the commencement of the belg rains and the lateplanting season.

After four years without a direct financial fertilizer subsidy, theGovernment reintroduced a fixed subsidy of 15 percent on both types offertilizers in February 1993, amounting to Br 26.43 per quintal for DAP andBr 23.41 per quintal for urea. In 1994, the subsidy was raised to 20-21 percent (to Br 36.96 and Br 31.98 per quintal, respectively). I/ ANational Committee, chaired by the Ministry of Agriculture, with the GeneralManagers of the Agricultural and Industrial Development Bank (AIDB),Commercial Bank of Ethiopia (CBE), and AISCO as members, was recentlyestablished (along with regional committees) , to facilitate the provision offertilizer credit to needy farmers as well as to ensure the repayment ofcredit.

(4) Rural credit

As regards rural credit schemes, the Government recently enactedthe Agricultural Cooperative Societies Proclamation (issued on February 1,1994) , which sought to promote the role of service cooperatives (named"cooperative societies" under the proclamation) in the allocation of credit

i/ There is no domestic production of fertilizers in Ethiopia. Two typesof fertilizers are imported--Diammonium Phosphate, or DAP (about 85 percent)and urea (15 percent).2/ Given the regular crop cycle in Ethiopia, in order to increase

fertilizer usage during a particular crop season, price announcements needto be made around December of the preceding year or in January. The 1993crop season price was only announced in May 1993, which was already past thebelg season and behind the planting phase of the meher season.I/ The subsidy equals the difference between the cost of fertilizer to

the Government and the price charged to the farmer. When farmers purchasedirectly from the marketing centers, they are expected to pay an additionalBr 7 per quintal, which is the margin for private traders (included as partof the subsidy).

©International Monetary Fund. Not for Redistribution

- 9 -

in the rural areas. According to the Proclamation, the functions of thecooperatives will also include acceptance of deposits and the granting ofloans to other institutions. It is expected that the AIDE and the CBE willboth be involved in the scheme (contrary to the previous credit programs,which included only the AIDE).

(5) Agricultural Marketing and Pricing

In the areas of marketing and pricing of agricultural output,significant progress has been made in reorganizing the AgriculturalMarketing Corporation (AMC) , which has now been renamed the Ethiopian GrainTrade Enterprise (EGTE) . The focus of the EGTE within the new market-oriented economy is significantly different from its past role. ]L/ Themain objective of the EGTE is to stabilize the grain market throughintervention. In a normal year, based on the probability of grain supplyfluctuations in the market-dep endent population (i.e., urban, nomadic, andproducers/consumers in deficit areas), about 300,000 tons of grain areassumed to be needed as a buffer stock and for the purpose of seasonalstabilization. Of this amount, 150,000 tons are planned to be purchasedlocally, while the rest would be supplied from abroad, principally fromdonors.

The planned operations of the EGTE were disrupted in 1993/94 because ofthe adverse impact of the drought. In order to prevent a further increasein producer prices, the EGTE purchased 18,000 tons in 1993/94 (compared with150,000 tons the preceding year). Currently, the EGTE principally focuseson stabilizing the food situation in the country through the distribution offood aid. About 30,000 tons were provided to the drought-affected regionsdirectly from EGTE's stocks. As of mid-1994, the EGTE held stocks of110,000 tons of grains, down from 160,000 tons in January 1994.

Although there is some competition at the wholesale level, which is dueto its enormous infrastructure (trucks, warehouses, credit, etc.), the EGTEis by far the biggest participant in the grain market, with a substantialinfluence on producer prices. At present, producer prices are negotiatedbetween the local committees (acting as agents for the EGTE in the

I/ Previously, farmers were forced to surrender a minimum of 50 percentof agricultural output to the AMC at fixed prices, allowing a small marginover cost. Checkpoints were established along major grain routes, andillegally transported farm produce was confiscated. One consequence was thereduction of the smooth flow of grains from surplus to deficit areas. Thisled to very low prices in surplus areas and extremely high prices in deficitareas. On the other hand, AMC purchases were mostly allocated to urbanareas, institutions (such as flour mills) and, more importantly, themilitary. Given the heavy involvement of AMC in the grain trade, grainswere transacted at artificially low prices, which bore little relation tomarket prices. In March 1990, the quota system governing the surrender ofgrains was abolished, and merchants were allowed to operate freely.

©International Monetary Fund. Not for Redistribution

- 10 -

corresponding regions) and the fanners, on the basis of indicative pricesset by the EGTE. The EGTE, in turn, sets prices in line with regional pricedevelopments in the urban and rural markets.

The reorganization at the EGTE continued during 1993/94. As a resultof its new focus on selected markets, its collection points have beenreduced from 2,000 to 500. The number of trade centers (buying and selling)have been reduced from 104 to 66 and its coordinating branches now number17, instead of 27. At the start of the reorganization process, the totalstaff numbered 4,300. Currently, its staff is 3,089 and it is intended toreduce the staff further to about 2,500. At present, the EGTE makesavailable its excess storage capacity to the private sector, nongovernmentorganizations, and AISCO. Though it is not involved in the provision ofcredit to farmers, the EGTE supplies some inputs to farmers (particularlyfertilizer) in association with private traders.

(6) Agricultural land tenure

Since 1991, when the Government announced its policy of providing thefarmers with security of land user ship and eliminated restrictions on therental of land and the hiring of labor, there have been no changes in policyon the issue of land ownership. It is expected that the issue will beconsidered following the establishment of a nationally elected govern-ment. I/

b. Manufacturing

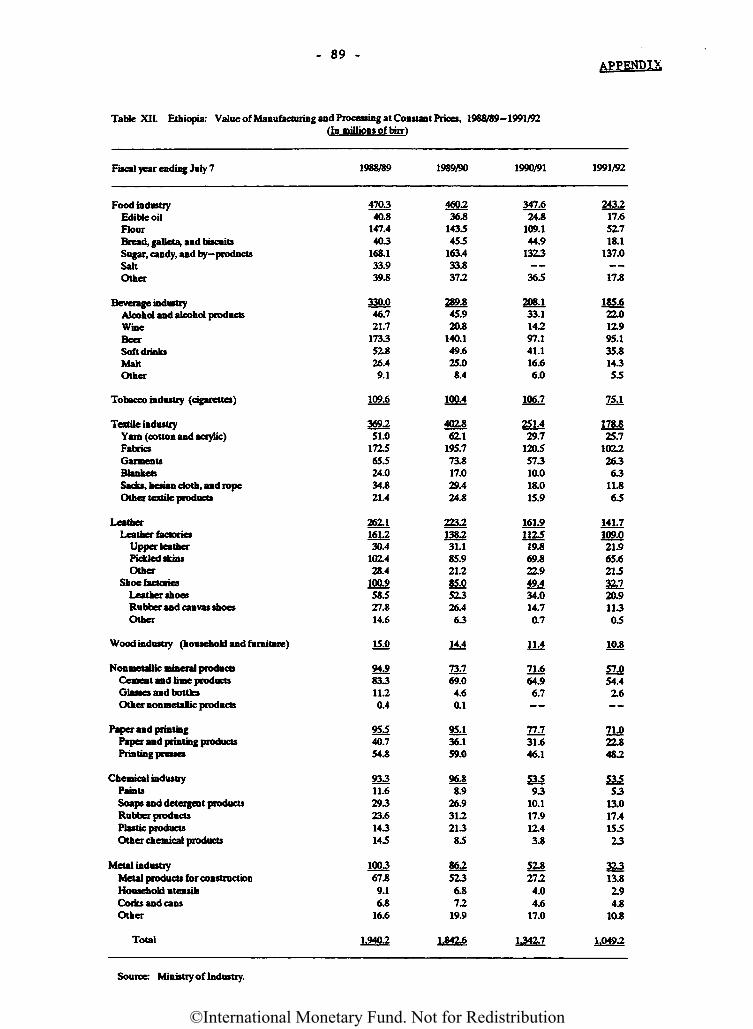

The manufacturing sector in Ethiopia is comprised of lightmanufacturing products such as construction materials, metal and chemicalproducts, and basic consumer goods such as food, beverages, and textiles.The sector is mainly dominated by about 150 public enterprises (PE) , whichcontribute more than 95 percent of the sector's value added. The productionof PEs is mostly concentrated in the food and beverages (50 percent) andtextiles industries (15.3 percent); in addition, tobacco (12.4 percent),leather and leather products (6 percent), rubber, plastic, and cement(5.5 percent) are also important subsectors. 2/ Private sectormanufacturing activity, although on a much smaller scale, follows a similarpattern. Of about 150 private sector firms, most are involved in bakeryproducts, textiles, footwear, and furniture production.

I/ For historical background of land issues, see Ethiopia: RecentEconomic Developments, SM/93/102, May 13, 1993.2/ Recent data on manufacturing pertaining to 1992/93-1993/94 are not

available because of disruptions related to the restructuring at theMinistry of Industry. Percentages reported are based on the gross value ofproduction in 1989/90, presumably a normal year, and before the onset ofacute shortages. Also see Tables XII-XIV.

©International Monetary Fund. Not for Redistribution

- 11 -

During 1989/90-1991/92, manufacturing was adversely affected by theescalation of the civil war; shortages of raw materials, foreign exchange,and fuel; and the frequent breakdowns arising from obsolete machinery andpower failures. As a result, the share of the manufacturing sector in GDPdeclined steadily, from around 5.7 percent in 1989/90 to 2.2 percent in1991/92. In 1992/93, the sector's share increased to 3.8 percent, owing toa sharp rebound following the elimination of some of these constraints(mainly the greater availability of foreign exchange). The average capacityutilization rate of the Pes climbed to almost 70 percent, from rates as lowas 20 percent in many industries at the end of 1991/92. In 1993/94, thesector's share increased further to 4.5 percent, though this was in part dueto the contraction in agricultural production.

In the short term at least, the sustainability of the recovery in themanufacturing sector is likely to be influenced by the rapidity with whichthe private sector responds to market incentives as well as by the capacityof the PEs to adapt to the more competitive market environment that has beenrecently introduced in the economy. With respect to the latter, as a resultof the Public Enterprise Proclamation enacted in August 1992, PEs electtheir own management boards, assume autonomy in their pricing and productiondecisions, and are no longer supervised by the Ministry of Industry. \JThe economic policy reforms that took place during 1992/93, most notably theliberalization of prices, the devaluation of the exchange rate, and thedismantling of the state distribution network, 2/ have created an unusualeconomic environment for PEs. Although most PEs succeeded in increasingoutput from unusually repressed levels and in improving their financialviability, the change in the cost structures following these reform measuresmade direct adherence by the PEs to the former cost-plus pricing principledifficult, partly because of low demand at the new, much higher prices.

In certain sectors, the need for restructuring is particularlypronounced. For instance, the textile sector currently suffers from seriousoverstocking, owing to a combination of supply and demand problems that havebeen developing over years, and which became acute during the transition toa market economy. On the demand side, changing tastes as well as

\J The Supervisory Authority is in charge of evaluating the performanceof PEs as well as in organizing their external auditing. The Authority isalso represented in a PE's Board of Directors for the purpose of assessingthe PE's investment budget.2/ At the level of retail trade, the private sector has already started

to play a more active role. Regarding wholesale trade, the previousinstitutions inherited from the earlier regime still occupy the dominantshare, although participation by the private sector is now allowed. Theformer institutions are now autonomous entities with their own Board ofDirectors and do not receive subsidies from the Government. The EthiopianDomestic Distribution Corporation and the Ethiopian Import-ExportCorporation were merged. The new organization will continue to be involvedin wholesale trade as well as in the importation of consumer goods.

©International Monetary Fund. Not for Redistribution

- 12 -

competitive prices offered by private sector firms--most importantly bycontraband trade from neighboring countries and increased sales of second-hand clothing--have resulted in a serious disruption in sales. Production,on the other hand, has been continuing, owing to the temporary availabilityof cotton supplies, and the concern to keep firms operating, given theirsizable work forces. The tobacco industry is faced with similar problemsarising from weak demand. Obsolete machinery is a major problem in manysectors, most notably in the food industry.

c. Energy

Ethiopia is excessively dependent on traditional fuels consistingmainly of wood, agricultural residues, and animal waste. Only about6 percent of Ethiopia's energy needs is met from modern energy sources suchas petroleum and electricity. As a result, deforestation, with its adverseimpact on soil productivity, has been an extremely serious problem.

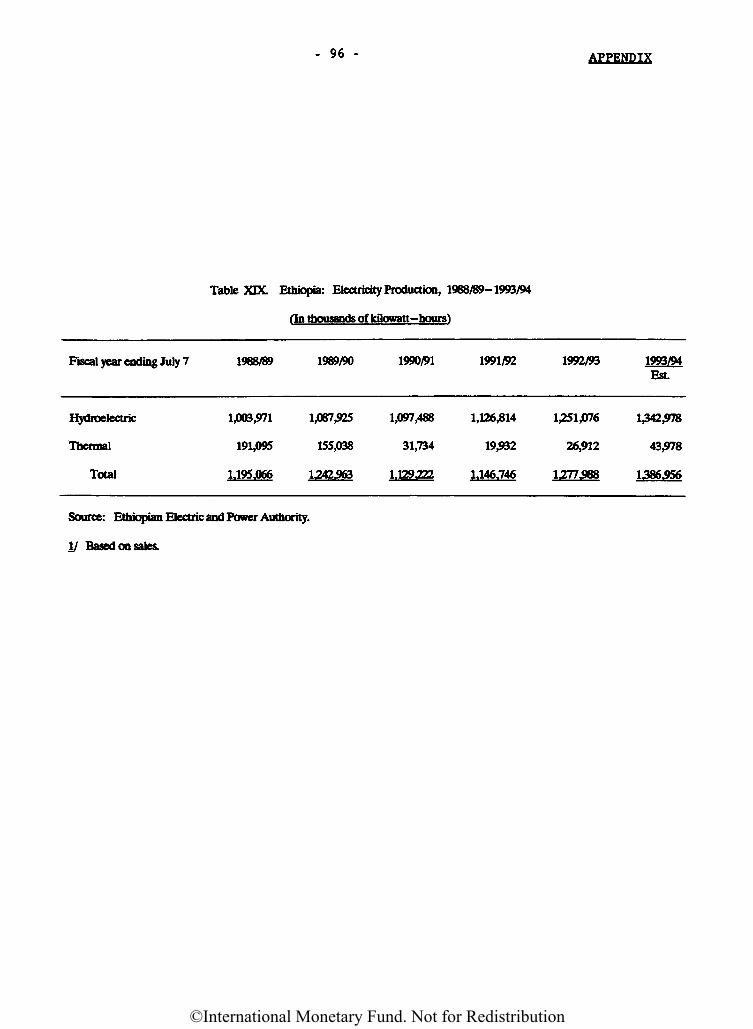

Power generated by hydroelectric plants supplies most of Ethiopia'selectricity needs (over 95 percent), with total installed electricitycapacity at about 370 megawatts. Ethiopia's rich hydroelectric potential,with 40 river basins, remains almost completely untapped. Greater effort isbeing made to develop such energy sources. The construction of a new hydro-electric plant (rated at 180 megawatts) was supposed to start in 1992 as aresult of an agreement with North Korea. The agreement, however, iscurrently being renegotiated; four other hydroelectric projects are understudy. After almost complete stagnation between 1988/89 and 1991/92,electricity production increased by 11 percent in 1992/93 and 8.5 percent in1993/94, reaching 1.3 billion kilowatt-hours (Appendix Table XIX). Althoughonly 2 percent of the hydroelectric potential has been exploited, thecountry has excess capacity at the present rate of consumption. Thus theEthiopian authorities have been looking into the possibility of marketingelectricity to neighboring countries and progress has been made in theconstruction of transmission lines for the export of electricity.

Ethiopia imports crude oil (mainly from Saudi Arabia) for processing atthe Assab petroleum refinery, which is now owned by Eritrea. Ethiopia has acontract with the Eritrean Government for processing the crude oil importedby Ethiopia; the contract is renewed every year. Petroleum products refinedat Assab are considered "Ethiopian output" and are either shipped toEthiopia or sold to Eritrea as an export; about 20 percent of the productsrefined at Assab are sold in the Eritrean market, the remainder is used inEthiopia. Transactions are settled in birr, and the prices are revisedevery quarter based on international market prices. Additional petroleumproducts are imported from outside (and paid for in convertible currencies),and principally include kerosene, gasoline, and gas oil.

Recently, important steps have been taken to develop new energy sourcesfor Ethiopia, while reducing dependence on forests and the import ofpetroleum products. Financed under a World Bank loan, a project has beeninitiated to develop the natural gas deposits situated in the Ogaden region.

©International Monetary Fund. Not for Redistribution

- 13 -

The Calub gas reserves, estimated at about 2.7 trillion cubic feet (in tworeservoirs of 0.7 and 2.0 trillion cubic feet), are significant, with theupper layer (0.7 trillion cubic feet) also estimated to contain substantialassociated liquids (LPG, gasoline, kerosene, and diesel/gas oil). Theproject's contribution is expected to reach approximately 70,000 tons of oilequivalent per year (or about 8 percent of the current consumption ofpetroleum and electricity), providing energy sources for urban consumptionamounting to about 400,000 tons/year of fuelwood (about 18 percent ofcurrent urban consumption).

d. Mining

Mining and quarrying are relatively unimportant in Ethiopia,contributing less than 1 percent of GDP. However, based on the findings ofgeological surveys, it is estimated that there is substantial potential forexpansion. The Ethiopian Mineral Resource Corporation (EMRC) is responsiblefor the overall management of Ethiopia's mineral resources (except formarble) from the early stages of exploration through production andexporting; private sector involvement is encouraged to tap the sector'spotential.

Gold. Ethiopia's most important natural resource, is concentrated inthe Legedenbi area (500 kilometers south of Addis Ababa in the Sidamoregion) . Average annual production is about 3 tons, which is fully sold tothe National Bank of Ethiopia (NBE) for export. A project financed jointlyby the AfDB is expected to increase annual production capacity to about 4.8-5 tons by the year 1996, assuming that private sector involvement increases.In addition to primary gold (produced by modern techniques), small-scaleproduction takes place in the same region. Production from such sources isestimated to be around 500 kilograms. Tantalite production is about 30 tonsper annum, and is principally produced at a pilot plant, also located aroundLegedenbi. The production potential at this particular reserve is up to 200tons, but output has been limited by the competitiveness of theinternational markets.

Potash deposits exist around the very northern tip of Ethiopia by theEritrean border (close to the Red Sea). Soda ash is produced for localconsumption only, for use in the production of glass, bottles, detergents,etc.; current production is about 20,000 tons. If access to world marketscould be ensured, production could be raised to 1 million tons. Salt isproduced in very small quantities in a localized manner; large quantitiesare mostly imported from Eritrea. A reserve is being built in the Afarregion in the north-east, which is expected to produce about 300-400 milliontons of salt. There is an iron ore deposit in the western part of Ethiopia.Although it is not expected to be very rich, the Government is undertaking afeasibility study. Marble is handled by Natural Mining Company, a privateenterprise. West Wolega, East Hararge, and Tigray have particularly richmarble deposits.

©International Monetary Fund. Not for Redistribution

- 14 -

e. Building and construction

The construction sector was particularly repressed in the last years ofthe previous government, declining by a cumulative 56 percent during1988/89-1991/92; this largely reflected shortages in construction materialsas well as the overall decline in economic activity. As a result, thesector's share in GDP declined from 3.9 percent in 1988/89 to 2.1 percent in1991/92. In 1992/93, along with the overall recovery in economic activity,the sector rebounded by about 17 percent. This strong performance continuedin 1993/94, with the sector's share reaching 2.9 percent of GDP afteranother year of strong growth (10 percent). However, the share of GDP hasremained lower than in the pre-1989/90 period.

f. Transportation

The most common form of transportation in Ethiopia is road transport,accounting for more than 90 percent of all inter-urban freight and passengermovement. The jointly owned single track Ethiopia-Djibouti railway line,although in poor condition, handles most of the remaining load. Civilaviation is/not yet very important, although Ethiopian Airlines isconsidered to have established a highly profitable network of internationaland domestic routes. Given the rural nature of the economy, nonmotorizedtransport is also significant in areas where roads have not beenconstructed.

Ethiopia's road density is among the lowest in Africa, with anestimated 15.2 kilometers of road per 1,000 square kilometers. The mainroad network extends radially from Addis Ababa with few interconnectinglinks; large areas of the country have no linkage to regional and economiccenters. The public road network in Ethiopia consists of less than20,000 kilometers of main and rural roads. Of the main roads, approximately3,500 kilometers are paved and roughly 8,000 kilometers are graveled. It isestimated that about 65 percent of these roads are in poor condition, withthe deterioration in road conditions having intensified over the last decadebecause of a lack of maintenance.

In December 1992, central control of road transport operations wasabolished and the trucking industry was deregulated. Specifically, zonaltransport offices (Ketenas), established according to the Proclamation of1976 to control and regulate commercial road transport operations, wereclosed. State control of freight rates was removed, and the centralizedsystem of route and cargo assignment to private operators was liberalized.Although the state-owned Ethiopian Freight Transport Corporation (EFTC) isstill the largest single trucking operation in Ethiopia in terms of itsmassive infrastructure (cargo reservation and maintenance facilities as wellas load capacity), private sector participation has been increasing. By theend of 1993, in addition to 4,000 trucks that operated in association withEFTC, six private companies, with a capacity of about 1,450 trucks, havebeen established.

©International Monetary Fund. Not for Redistribution

- 15 -

After having risen by about 30-40 percent following deregulation,freight rates subsequently declined to levels lower than those prevailing inthe pre-deregulation period, which is partly due to the increase in thesupply of trucks, depressed demand, and to some extent, competition fromunlicensed operators. Rates appear to vary depending on routes; this isattributable to a number of factors, some of which are associated withproblems encountered by the trucking industry, including poor roadconditions, the aging fleet and high vehicle operating costs, and animbalance in the freight cargo load between inbound and outbound routes.

With the independence of Eritrea (with its ports of Assab and Massawa,Ethiopia is now a land-locked country. Assab is the principal port forimports to and exports from Ethiopia. Imports of dry, bulk, and oil cargoesenter through Assab, while other goods, particularly food aid, enter throughDjibouti. In addition, smaller quantities enter through Massawa for thenorthern regions. The government-owned Ethiopian Shipping Lines Corporationis the major shipping company servicing Assab; it owns 11 vessels, with acombined denarius weight (DWT) of 80,000 tons.

3. Emp 1 oymen t

Because of the rural nature of the economy, the modern wage sectoremployment in Ethiopia is small. Currently, the Government provides jobsfor about 240,000 employees in the civil service, and another 245,000 areemployed in the public enterprise sector, engaged in production andservices. Current data on employment by private formal (wage or self-employed) and informal sectors are virtually nonexistent. A surveyundertaken by the Ministry of Labor and Social Affairs (MLSA) in 1983, whichincluded establishments employing 10 people and more, put private sectorwage employment at slightly less than 200,000 (out of a total of about700,000), or 37 percent of the public sector wage employment in the sameyear. Assuming that a similar relation presently prevails, the current sizeof modern sector wage employment (at those establishments employing10 people or more) may be estimated at less than 1 million.

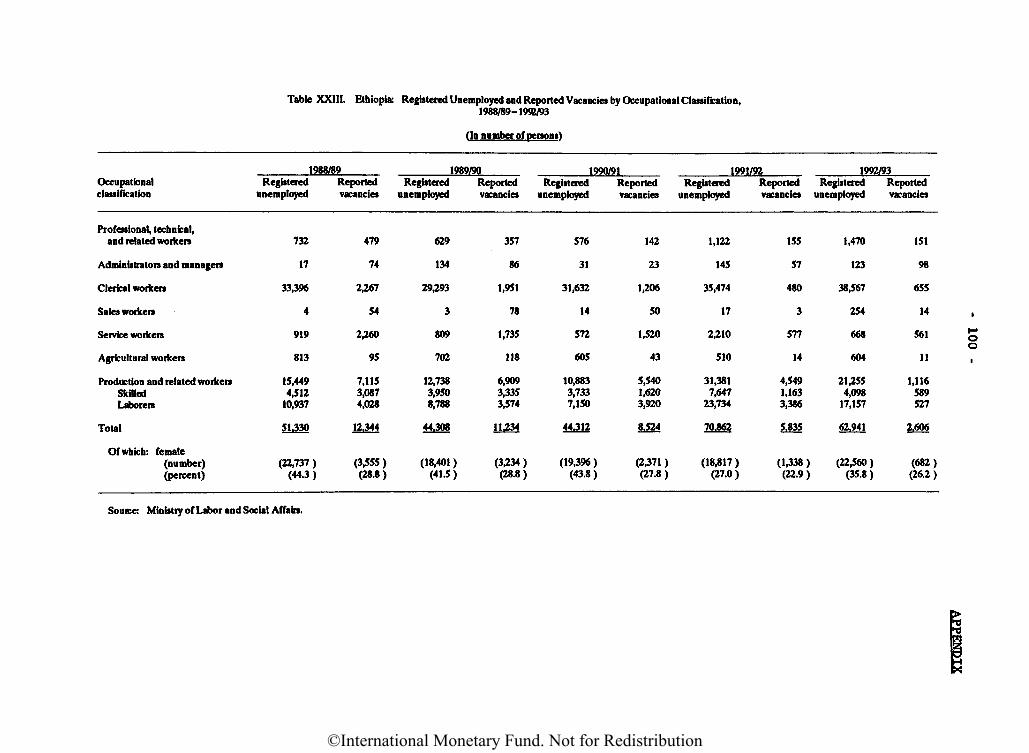

Over the last decade, high population growth coupled with less thansatisfactory improvements in the productive capacity of the economysharpened the existing imbalance in Ethiopia's labor market. On the basisof the last census conducted in 1984, Ethiopia's population is estimated tohave reached 52 million (excluding Eritrea) in 1992, from 40.7 million in1984, implying an average growth rate of 3 percent per annum. The growthrate of the urban population (6.4 percent) is estimated to have exceededthat of the rural population (2.7 percent) during this period, partly owingto migration. Given that employment opportunities have not expanded at thesame rate, it is likely that the unemployment problem has become more acutein the urban centers.

Data on the registered unemployed, vacancies, and placements, asreported by the MLSA and compiled from the Labor Exchange Offices (LEOs),suffer from a number of statistical problems, including the voluntary nature

©International Monetary Fund. Not for Redistribution

- 16 -

of registrations as well as reporting issues (e.g., cases where vacancieswere filled or applicants secured jobs by themselves are not regularlyreported to the LEO). However, an increase in the registered unemployedduring 1991/92-1992/93, coupled with a decline in reported vacancies,appears to indicate a worsening of the imbalance in the labor market(Appendix Table XXIII). While demobilization of the army, returnees fromEritrea, and an increasing number of graduates from the university areconsidered to have contributed to this outcome, some retrenchment also tookplace in the context of the recent restructuring of the ministries and thereform of the PEs. The Prime Minister's Office (PMO) is in charge of theNational Retrenchment Policy, with two committees--the RedeploymentCommittee and the Vocational Training Committee--dealing with the issue.Currently, policies are directed more toward the training of workers who arelikely to be retrenched, as privatization of PEs commences, while keepingthem on the payroll. Most retrenchment in the short term is expected totake the form of a redeployment of workers from the center to the regions;reportedly, regions are now operating with 70 percent vacancy rates, andthus there is room for most workers who are likely to be retrenched from thecentral government ministries to be redeployed at the regional level. Thereare also plans in the Government to subsidize some private sector firms toemploy retrenched workers. The revival in private sector activity isenvisaged to have dampened the unemployment problem to some extent.

Labor relations in Ethiopia are currently organized under the new LaborCode, which became effective in January 20, 1993, replacing the LaborProclamation Order of 1975. The objectives of this proclamation are (i) toestablish rules governing worker-employer relations according to basicprinciples of rights and obligations; (ii) to guarantee the right of workersand employers to form their respective associations and to engage incollective bargaining; and (iii) to strengthen and define the powers andduties of the government agency charged with ensuring that the law isadhered to with respect to collective bargaining, occupational safety,health, and the work environment. I/ In line with the new Labor Code,LEOs are now operating as service agencies, rather than regulatory placementagencies. There are about 30 offices around the country, operating more orless autonomously, partly owing to regionalization. The unemployed stillreport to the LEOs, but on a completely voluntary basis. However, noprivate employment agencies are allowed in the system, consistent with thecurrent policy stance of the International Labor Organization.

4. Wages

In October 1992, at the time of the exchange rate devaluation, theGovernment introduced significant wage increases, mainly for low-paid stateemployees. Increases were made on a progressively sliding scale, with theobjective of raising the incomes of those groups whose wages had fallensignificantly below the minimum consumption basket (calculated by the Wage

I/ See Ethiopia: Recent Economic Developments, SM/93/102, 5/13/93.

©International Monetary Fund. Not for Redistribution

- 17 -

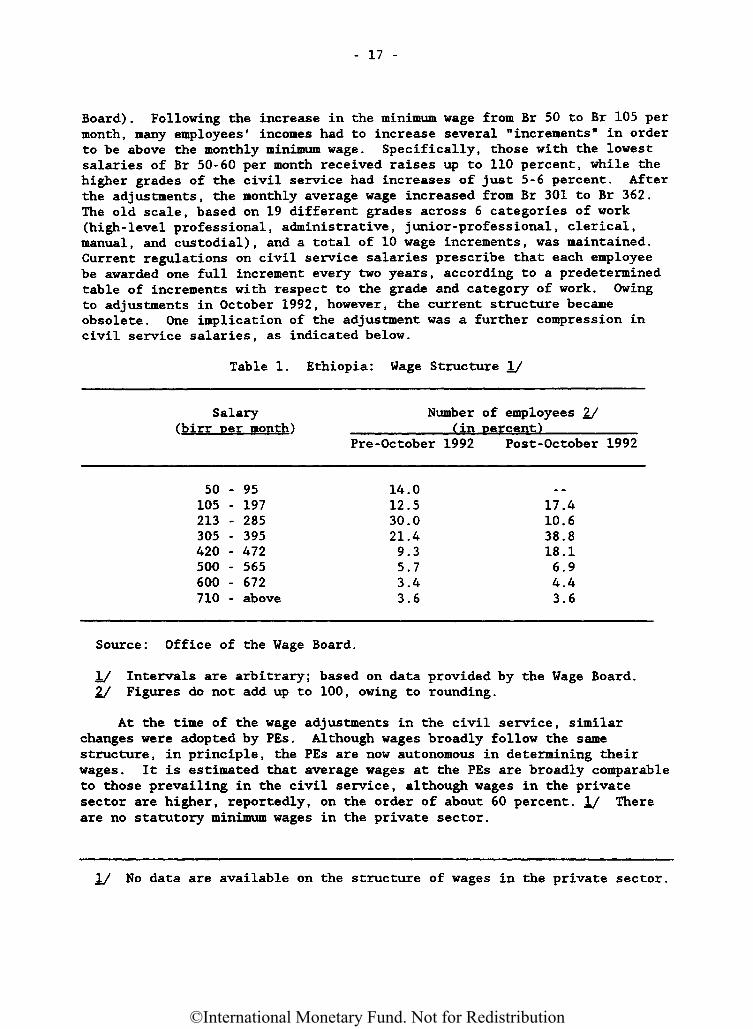

Board) . Following the increase in the minimum wage from Br 50 to Br 105 permonth, many employees' incomes had to increase several "increments11 in orderto be above the monthly minimum wage. Specifically, those with the lowestsalaries of Br 50-60 per month received raises up to 110 percent, while thehigher grades of the civil service had increases of just 5-6 percent. Afterthe adjustments, the monthly average wage increased from Br 301 to Br 362.The old scale, based on 19 different grades across 6 categories of work(high-level professional, administrative, junior-professional, clerical,manual, and custodial), and a total of 10 wage increments, was maintained.Current regulations on civil service salaries prescribe that each employeebe awarded one full increment every two years, according to a predeterminedtable of increments with respect to the grade and category of work. Owingto adjustments in October 1992, however, the current structure becameobsolete. One implication of the adjustment was a further compression incivil service salaries, as indicated below.

Table 1. Ethiopia: Wage Structure I/

Salary Number of employees 2/(birr per month) (in percent)

Pre-October 1992 Post-October 1992

50105213305420500600710

- 95- 197- 285- 395- 472- 565- 672- above

14.012.530.021.49.35.73.43.6

17.410.638.818.16.94.43.6

Source: Office of the Wage Board.

I/ Intervals are arbitrary; based on data provided by the Wage Board.7J Figures do not add up to 100, owing to rounding.

At the time of the wage adjustments in the civil service, similarchanges were adopted by PEs. Although wages broadly follow the samestructure, in principle, the PEs are now autonomous in determining theirwages. It is estimated that average wages at the PEs are broadly comparableto those prevailing in the civil service, although wages in the privatesector are higher, reportedly, on the order of about 60 percent. I/ Thereare no statutory minimum wages in the private sector.

I/ No data are available on the structure of wages in the private sector.

©International Monetary Fund. Not for Redistribution

- 18 -

A preliminary study on the reform of the civil service pay structurehas now been completed within the broader context of the civil servicereform. The study, which was prepared and carried out by the WageBoard, \J recommends modifications to the pay structure with a view todecompressing wages. Further analysis of the study is anticipated beforethe Government finalizes its decision on the magnitude and structure of payadjustments.

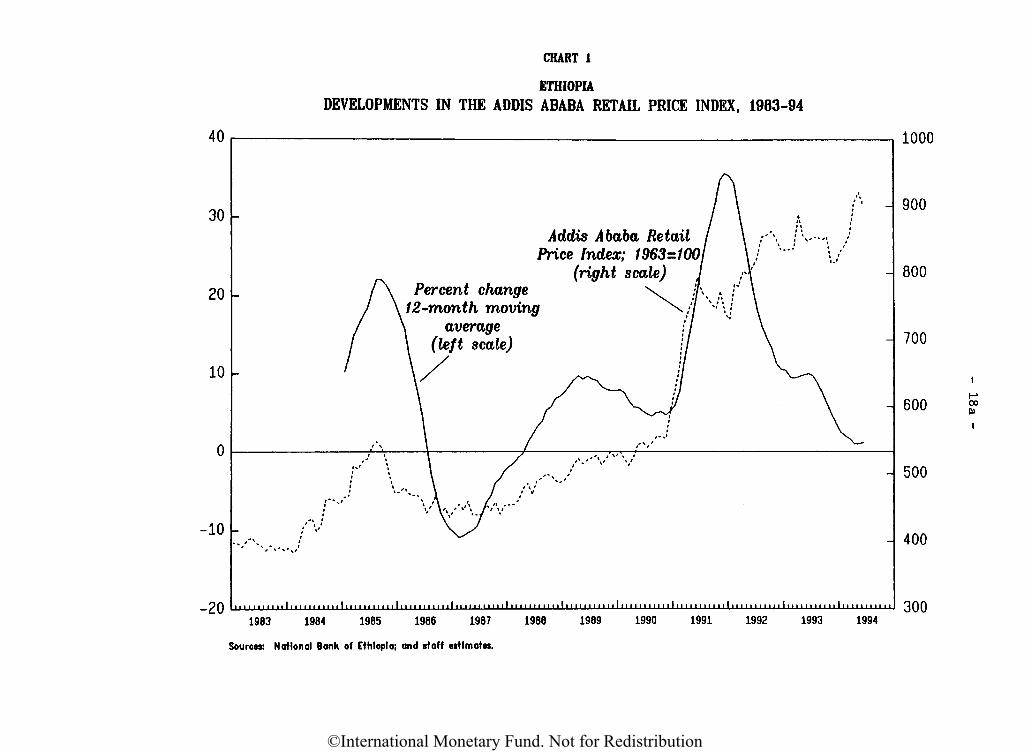

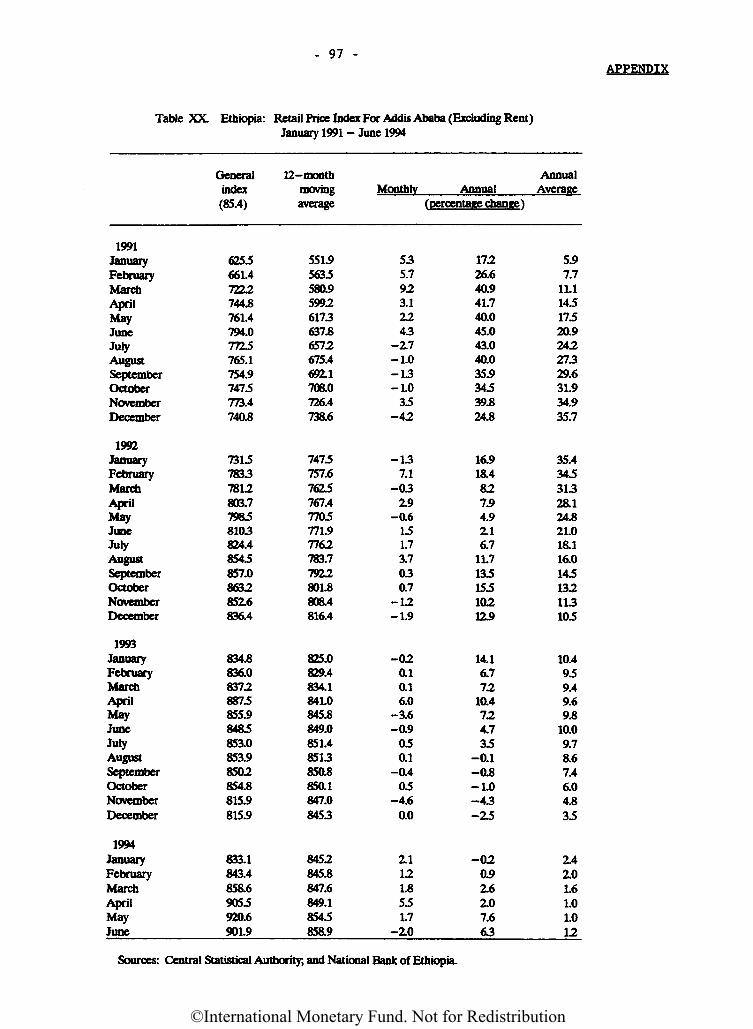

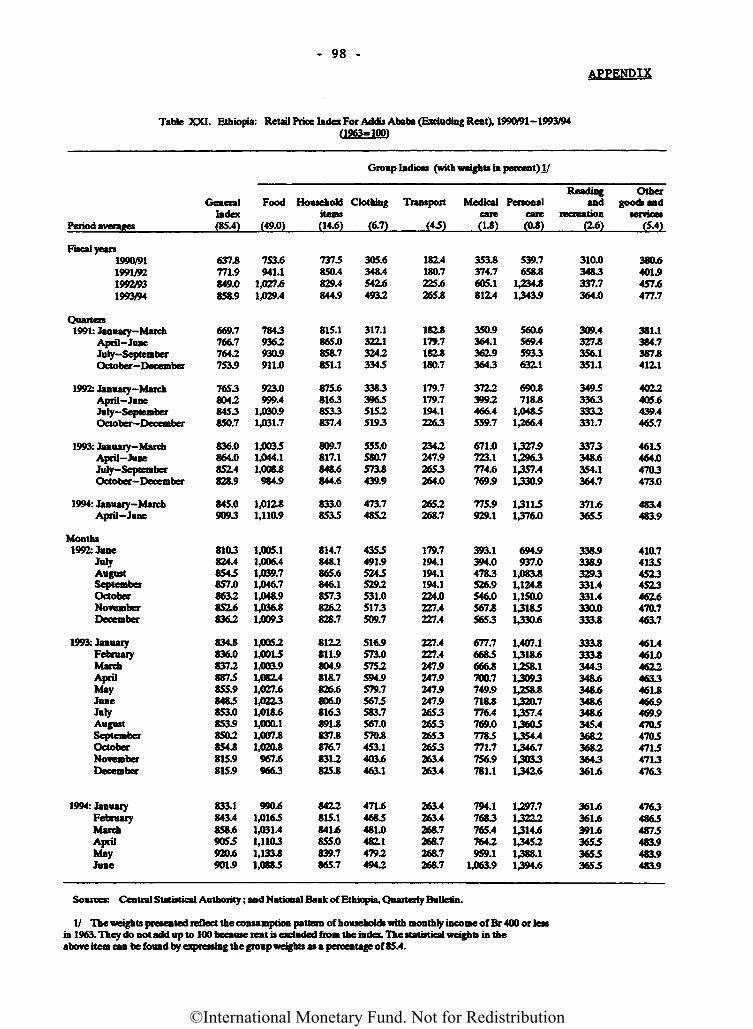

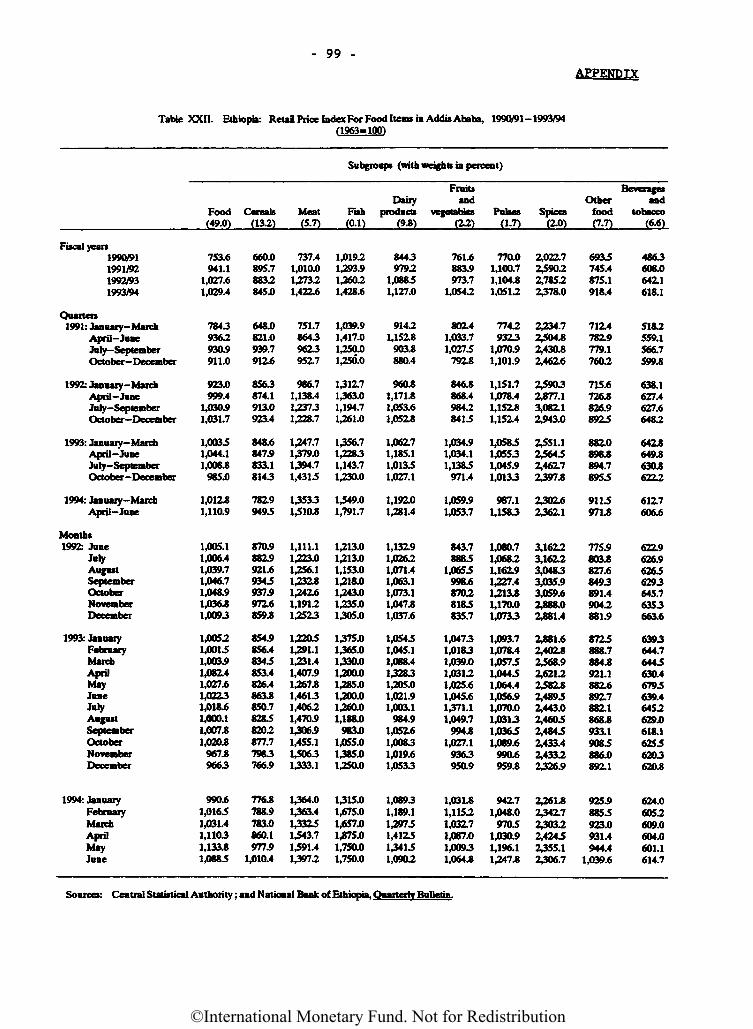

Over the years, price developments in Ethiopia have largely beeninfluenced by supply-side factors such as external shocks, volatility ofagricultural production, and shortages of foreign exchange. 2/ During1990/91-1991/92, the annual inflation rate averaged about 20 percent, assupply-side disruptions related to the end of the previous government werefurther aggravated by loose financial policies (Appendix Tables XX-XXII).During 1992/93, despite the substantial adjustment of the exchange rate ofthe birr in October 1992, inflation declined to 10 percent, owing to atightening of financial policies (including an improved fiscal position andpositive real interest rates), as well as the favorable impact of a goodmeher harvest on food prices, coupled with an overall normalization inagricultural production. Annual inflation continued to decelerate during1993/94, to 1.2 percent, mainly reflecting the continued positive effect ofthe good 1992/93 harvest as well as the tailing-off of the adverse effectsof devaluation. Inflation as measured by the GDP deflator, which reflectsdevelopments in wholesale prices to some extent, also followed a similarpattern.

During January-May 1994, there was an increase in monthly inflation,reflecting pressures developing in the cereal market. The price indexdropped in June by 2.0 percent, as a result of a decline in some other fooditems (e.g., meat and dairy products), while monthly inflation continued to

I/ The old structure within which the Wage Board used to operate has beendismantled; now the Board directly reports to the Prime Minister's Office.2/ Inflation is measured by the Addis Ababa Retail Price Index (AARPI),

which suffers from a number of statistical problems in terms of its coverageand expenditure weights. See Ethiopia: Recent Economic Developments,SM/91/122, 6/14/91.

5. Prices

©International Monetary Fund. Not for Redistribution

CHART 1

ETHIOPIADEVELOPMENTS IN THE ADDIS ABABA RETAIL PRICE INDEX, 1983-94

Sources: N at tonal Bank of Ethiopia; and staff estimates.

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

- 19 -

be positive for cereals and nonfood items as a whole. I/ On an annualbasis, reflecting the impact of the good harvests in 1992/93, the increasein food prices fell below that of nonfood prices during 1992/93-1993/94.

Ethiopia has abolished all price controls except for three productcategories, which remain subject to price controls at both the retail andthe wholesale levels. These include petroleum and petroleum products, somePharmaceuticals, and sugar for household consumption. Controls over pricesof a few essential items (cement, corrugated roofing, nails, reinforcingbars, khaki textiles, nylon textiles, traditional abujadid cloth, and cottonyarn) were eliminated in mid-1993. Price controls on spare parts, whichalso had been removed on a de facto basis in mid-1993, were removedstatutorily in July 1994. In mid-May, the retail prices of petroleumproducts were increased with a view to taking account of the impact ofadjustments in the official exchange rate on the import parity price.Utility prices remain under government control. Telephone tariffs wereadjusted in July 1994. The present electricity tariffs, which have remainedunchanged since March 1986, are currently being reviewed by the EthiopianElectric Light and Power Authority. A study on water and sewerage tariffshas been completed. Passenger transport tariffs also remain underGovernment control.

6- Private sector investment

Since the launching of the economic reform program in late 1992, theprivate sector environment in Ethiopia has improved considerably. In linewith the directives laid out in the new Investment Code (ProclamationNo. 15/1992), Regional Investment Offices (RIO) 2J nave been establishedas one-stop offices to issue licenses for domestic investments exceedingBr 250,000. The Investment Office of Ethiopia (IOE) , located in Region 14(the Addis Ababa Region) issues licenses for foreign investments (exceedingUS$500,000) and acts as the Regional Investment Office for Region 14. Inaddition, the IOE issues licenses and grants incentives on behalf of thoseAdministrative Regions that have not yet set up an investment office.

i/ About 57 percent of the AARPI is composed of food items; consequently,the seasonal pattern of inflation, as measured by the AARPI, is largelydetermined by the seasonal pattern of the food index. A simple regressionon food price inflation (covering the last ten years), including monthlyseasonal dummies and controlling for the escalation of war in 1990/91 andthe drought in 1984/85, indicates that the pattern of monthly inflation infood prices follows broadly the developments in the crop pattern.Specifically, monthly inflation is significantly lower in December andstarts increasing gradually thereafter during January through April; nosignificant trend is observed during May through July. In August, inflationappears significantly higher, and then remains stable till November.2/ There were 4 RIOs as of June 7, 1994.

©International Monetary Fund. Not for Redistribution

- 20 -

Between July 1992 and June 7, 1994, the IOE and other functioningregional investment offices have issued investment certificates to1,069 projects, of which eight were foreign investment projects (AppendixTable XV). The total capital implied by these project applications amountedto Br 7.3 billion (Br 6.9 billion issued by the IOE), of which foreigninvestment projects amounted to Br 677 million (9 percent). The totalemployment potential of the projects is estimated at some 60,000 permanentand 83,000 temporary jobs. The regional distribution of investment projectsis overwhelmingly in favor of Region 14 (75.7 percent), followed by Oromiya(12.5 percent), Region 3 (4 percent), Tigray (3.3. percent), and theSouthern Ethiopian Peoples Region (2.7 percent), while the remainder(1.8 percent) is shared by six other regions. Such a concentration ispartly attributable to delays encountered at the regional level during theinitial period following enactment of the Investment Code.

In terms of the sectoral distribution of investment licenses,manufacturing has the highest share (about 45 percent in value terms),followed by real estate (16.8 percent), agriculture (15.8 percent), hotelsand tourism (6.1 percent), and construction (5.7 percent). Manufacturinginvestment is mostly concentrated in the food and beverages sector, followedby textiles and leather products, building materials, and plastic products.The value of four cotton projects accounts for about 55 percent of theinvestment licenses issued by the IOE in the area of agriculture. As ofJune 7, 1994, 114 projects (valued at Br 961,367) were under implementationand 66 projects (valued at Br 338,940) were operational. The implementationratio (adjusted for those projects which are already operational) stillremains low, at about 13.7 percent, owing to uncertainties over theGovernment's urban land lease policy and to bottlenecks in the financingarea. As regards the latter, given that the credit needs for the proposedinvestments (as of June 7, 1994) are estimated to exceed Br 3 billion, thereis some uncertainty as to the capacity of Ethiopia's banking system toprovide the required credit for these investments.

In assessing the momentum of private investment, it would appear thatthere has been a slowdown in recent months. During 1992/93, the IOE issuedlicenses for 503 projects valued at Br 3.6 billion. A similar amount islikely to have been realized for 1993/94, as the value of total investmentlicenses issued by the IOE reached Br 3.2 billion as of June 7, 1994.However, in terms of the number of licenses issued, a considerable slowdownappears to have occurred; after a significant jump during the first quarterof 1993/94 (211 licenses), only 147 licenses were issued during January-May1994. Nevertheless, there has been no increase in the number of returnedlicenses.

As regards licensing policies, the IOE continues to guide investorinterests through its tax holidays (which extend 3 to 8 years) and tariffexemptions (mainly on machinery imports). In those areas where the IOEconcludes an excessive buildup has been taking place, investors areexplicitly advised to divert their interests to other areas. In addition to

©International Monetary Fund. Not for Redistribution

- 21 -

areas that are exclusively reserved for the Government, \J certain keyareas are exclusively reserved for the domestic private sector, such asradio and television broadcasting; printing and publishing; retail andwholesale trade; import trade; banking and insurance business; small andmedium-size air, rail and marine services (wet and dry cargo, and passengerservices); traditional commodity exports; and food processing (for the localmarket).

7. pr jva t i z a t i

Ethiopia is in the very early stages of the privatization process. APrivatization Agency has been set up (Proclamation No. 87/1994, February 17,1994) to study and execute the privatization/divestment process, and is inthe process of organizing its work activities, including the hiring ofadditional personnel. Over the next few months, the agency will review thework that has been done by other institutions (e.g., Ministry of Industry),and then formulate the exact time frame and specific modalities forprivatization. Some 29 hotels and restaurants and about 120 retail outlets,which were expected to be divested by the Government in the short term, arenow expected to be fully disposed of in the coming months. About 100 PEsare planned to be privatized; of these, about 50 will be privatized in theshort term (2-3 years). Privatization of state farms will be undertakenalong with the remaining PEs over the longer term. However, a small amountof land under the state farms (about 6,500 hectares) has been disposed of ortaken over by smallholders. In addition, a few enterprises were returned totheir original owners and some are in the process of being returned.

8. Revised GDP figures

A project was initiated in 1992 in the Ministry of Planning andEconomic Development, with technical assistance from the United NationsDevelopment Program (UNDP), to revise Ethiopia's national income accountsfor the period 1980/81-1990/91. The project is expected to be finalized,and figures published before the end of 1994. The figures include estimatesfor 1991/92-1993/94. The main objectives of the project were: (i) toidentify and correct methodological deficiencies in the old series after anin-depth study of the national accounts system; and (ii) to expand thesystem, to the extent possible, to cover hitherto uncompiled accounts. Asthe project continued, the objectives were enlarged to include estimation ofseries without Eritrea for the period 1980/81-1990/91 (for consistencypurposes) as well as to devise methodologies for the estimation of regionaldomestic products. 2/

The coverage has been increased mainly in livestock, forestry,transportation, education, government administration, and defense. Revised

I/ See Ethiopia: Recent Economic Developments, SM/93/102, 5/13/93.2/ Under the revised figures, Eritrea constitutes broadly about 7 percent

of Ethiopia.

©International Monetary Fund. Not for Redistribution

- 22 -

estimation procedures have been applied in agriculture (crops, livestock,and forestry), mining and quarrying, small-scale industries and handicrafts,water, trade, hotels, and restaurants, domestic services, and otherservices. In addition, new data sources have been used, including: (i) thenumber of economically active population (based on the 1984 Population andHousing Census); (ii) surveys on small-scale industries; (iii) the energysurvey for forestry; (iv) producer prices of various commodities; and(v) surveys on inputs to the agricultural sector. New aggregates werecompiled on "Private Final Consumption Expenditure" and the "Change inStocks."

The revised GDP figures are broadly about 25 percent higher than theold figures in constant prices; in current prices, while a similarcomparison applies for figures related to early 1980s, the differentialgrows during the latter half of the 1980s, yielding a revised series about50 percent higher than the old series. The principal reason for thedifferential appears to be that in the revised series, the value of theagricultural sector is much higher in current prices, mainly owing to theadoption of market-determined producer prices in its valuation as opposed tocontrolled prices.

II. Public Finance

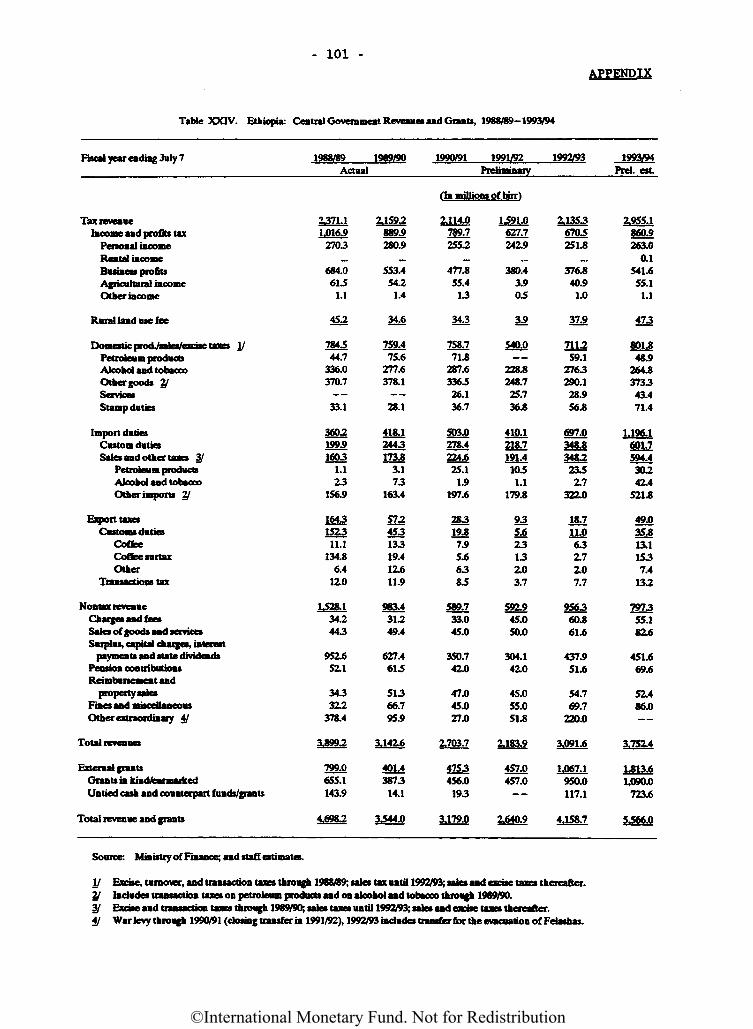

1- Overall fiscal performance

During the period 1988/89-1990/91, fiscal performance was stronglyinfluenced by the civil war, the inadequate economic policies of theprevious government with its orientation toward central planning, and thedeepening economic and political crisis in the country. A relativelyfavorable budgetary outcome was achieved in 1988/89, but in the followingyears, fiscal performance worsened sharply. In 1989/90, the overall fiscaldeficit (on a cash basis, including grants) reached a record level of12.3 percent of GDP (14.5 percent excluding grants), reflecting both verylow levels of revenues and external grants, and high governmentexpenditures. During the last years of the previous regime, militaryexpenditures were particularly large--averaging 9.7 percent of GDP duringthe period 1988/89-1990/91.