Embed Size (px)

Citation preview

ERA-Net Smart Grids Plus | From local trials towards a European Knowledge Community This project has received funding in the framework of the joint programming initiative ERA-Net Smart Grids Plus, with support from the European Union’s Horizon 2020 research and innovation programme.

Smart Grids Business Models and Market Integration

Version 1.0

Deliverable Work Package 2

Partners:

Bergische Universität Wuppertal, Germany

INESC TEC, Portugal

SINTEF Energi AS, Norway

Skagerak Nett AS, Norway

Smarter Grid Solutions, United Kingdom

27 June 2017

Deliverable No. 2 | Smart Grids Business Models and Market Integration 2

INTERNAL REFERENCE

• Deliverable No.: D2

• Deliverable Name: Smart Grids Business Models and Market Integration

• Lead Partner: SINTEF Energy Research

• Work Package No.: 2

• Task No. & Name: Task 2.1 – 2.5

• Document (File): SmartGuide WP2 - SG Business Models and Market Integration

• Issue (Save) Date: 2017-06-27

DOCUMENT SENSITIVITY

☒ Not Sensitive Contains only factual or background information; contains no new or additional analysis, recommendations or policy-relevant statements

☐ Moderately Sensitive Contains some analysis or interpretation of results; contains no recommendations or policy-relevant statements

☐ Sensitive Contains analysis or interpretation of results with policy-relevance and/or recommendations or policy-relevant statements

☐ Highly Sensitive Confidential

Contains significant analysis or interpretation of results with major policy-relevance or implications, contains extensive recommendations or policy-relevant statements, and/or contain policy-prescriptive statements. This sensitivity requires SB decision.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 3

DOCUMENT STATUS

Date Person(s) Organisation

Author(s) 2017-05-24 Kevin Cibis Bergische Universität Wuppertal

Julian Wruk Bergische Universität Wuppertal

Nuno Fonseca INESC TEC

Fabian Heyman INESC TEC

André Madureira INESC TEC

Filipe Soares INESC TEC

Bruna Tavares INESC TEC

Lovinda Ødegården SINTEF Energi

Hanne Sæle SINTEF Energi

Henrik Landsverk Skagerak Nett

Laura Kane Smarter Grid Solutions

Robert MacDonald Smarter Grid Solutions

Verification by 2017-06-02 Graham Ault Smarter Grid Solutions

Approval by 2017-06-16 Markus Zdrallek Bergische Universität Wuppertal

Deliverable No. 2 | Smart Grids Business Models and Market Integration 4

CONTENTS

ABBREVIATIONS ................................................................................................ 8

1. INTRODUCTION ........................................................................................ 13

1.1 Introduction and main challenges of SmartGuide ..................................... 13

1.1.1 Historic conditions and process of change ........................................................13

1.1.2 Overview of SmartGuide project .....................................................................13

1.2 Objectives and goals of Work Package 2 .................................................. 14

2. COUNTRY SPECIFIC LEGAL AND REGULATORY CIRCUMSTANCES OF DER PROMOTION ......................................................................................... 15

2.1 Portugal .................................................................................................... 15

2.1.1 National directives ........................................................................................15

2.1.2 Integration into existing grids ........................................................................17

2.1.3 Support schemes ..........................................................................................18

2.1.4 Future foresight/future plans ..........................................................................20

2.2 Norway ..................................................................................................... 21

2.2.1 National directives ........................................................................................21

2.2.2 Integration into existing grids ........................................................................22

2.2.3 Support schemes ..........................................................................................23

2.2.4 Future foresight/future plans ..........................................................................24

2.3 United Kingdom ........................................................................................ 24

2.3.1 National directives ........................................................................................24

2.3.2 Integration into existing grids ........................................................................27

2.3.3 DER support schemes ...................................................................................29

2.3.4 Future foresight/future plans ..........................................................................30

2.4 Germany ................................................................................................... 30

2.4.1 National directives ........................................................................................30

2.4.2 Integration into existing grids ........................................................................32

2.4.3 Support schemes ..........................................................................................33

2.4.4 Future foresight/future plans ..........................................................................34

2.5 Comparison of country specific circumstances of DER promotion ............. 36

3. DRIVERS FOR SMART GRID AND APPROACHES FOR DEPLOYMENT OF SMART GRID – FROM A DSO POINT OF VIEW .............................................. 39

3.1 Portugal .................................................................................................... 39

3.1.1 Regulatory Framework (for the DSO) ..............................................................39

3.1.2 Regulatory Framework relevant for different Smart Grid Technology ...................42

3.2 Norway ..................................................................................................... 44

Deliverable No. 2 | Smart Grids Business Models and Market Integration 5

3.2.1 Regulatory Framework (for the DSO) ..............................................................44

3.2.2 Regulatory Framework relevant for different Smart Grid Technology ...................45

3.3 United Kingdom ........................................................................................ 47

3.3.1 Regulatory Framework (for the DSO) ..............................................................47

3.3.2 Regulatory Framework relevant for different Smart Grid Technology ...................48

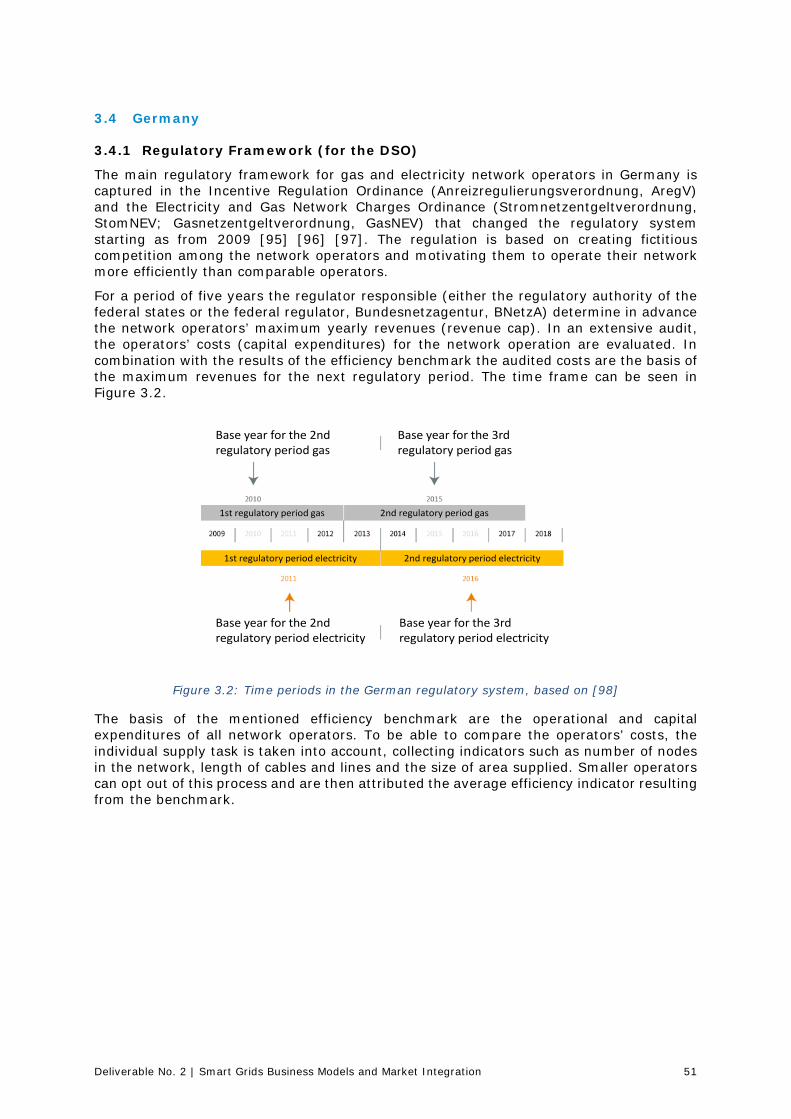

3.4 Germany ................................................................................................... 51

3.4.1 Regulatory Framework (for the DSO) ..............................................................51

3.4.2 Regulatory Framework relevant for different Smart Grid Technology ...................52

3.5 Comparison of drivers for smart grid ........................................................ 57

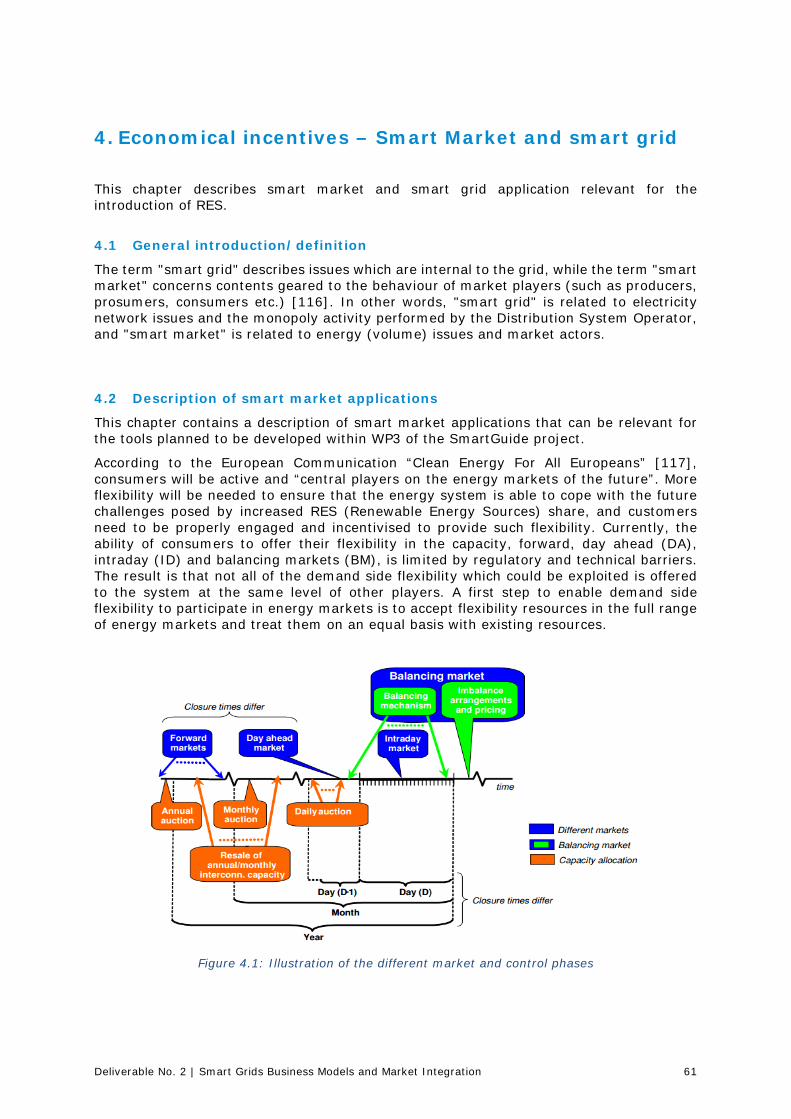

4. ECONOMICAL INCENTIVES – SMART MARKET AND SMART GRID .............. 61

4.1 General introduction/definition ................................................................ 61

4.2 Description of smart market applications ................................................. 61

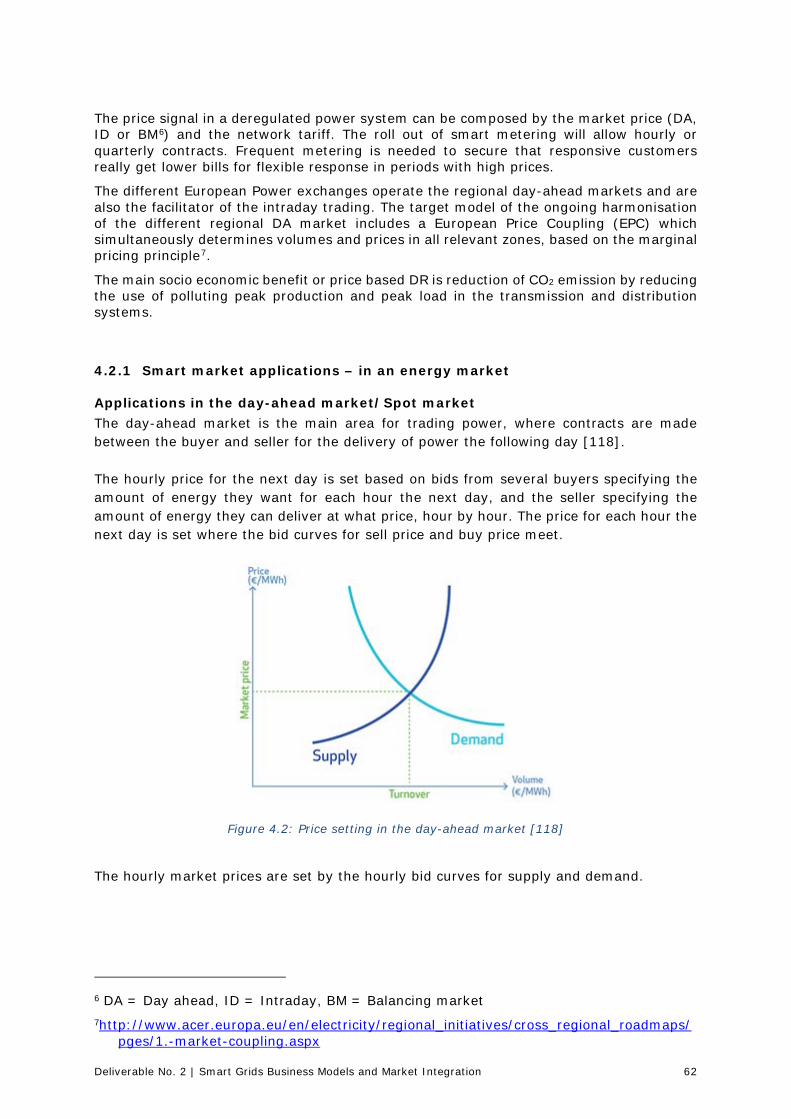

4.2.1 Smart market applications – in an energy market .............................................62

4.2.2 Smart market applications – in a balancing market ...........................................65

4.3 Country specific circumstances ................................................................. 69

4.3.1 Portugal ......................................................................................................69

4.3.2 Norway .......................................................................................................74

4.3.3 United Kingdom ............................................................................................78

4.3.4 Germany .....................................................................................................87

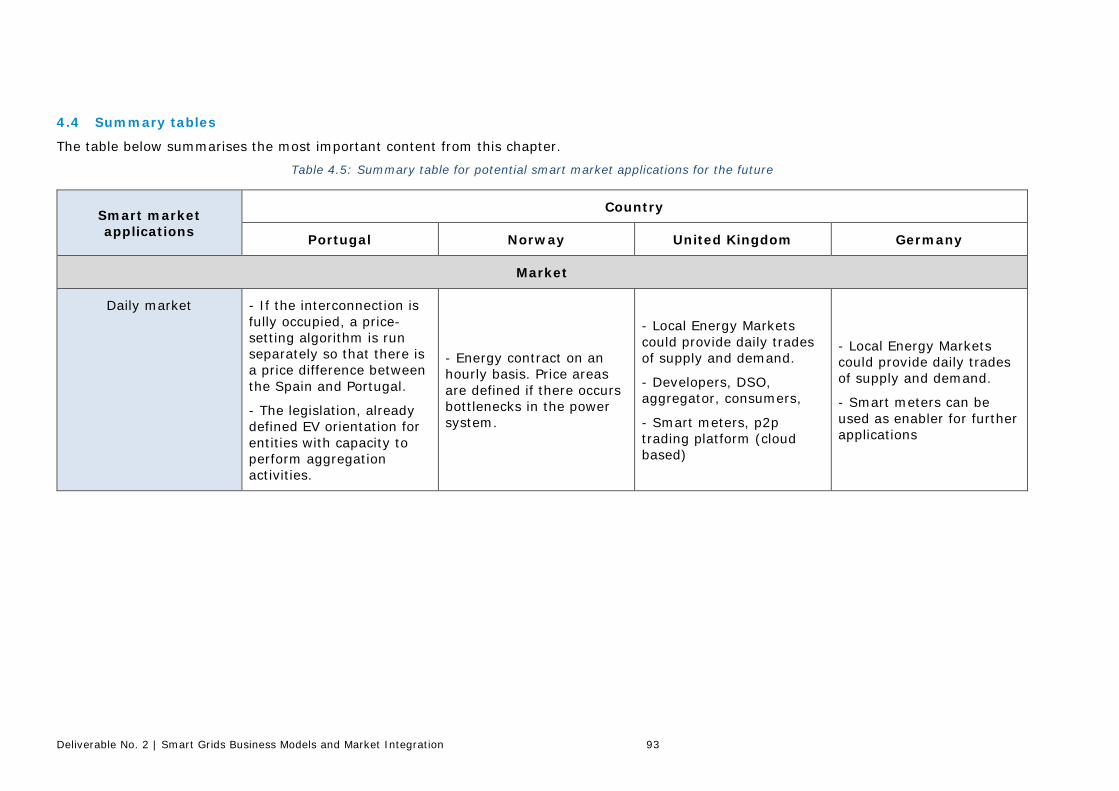

4.4 Summary tables ........................................................................................ 93

5. REVIEW OF DEVELOPMENTS OF GRID CODES FOR SMART GRID TECHNOLOGIES ................................................................................................ 98

5.1 Short overview of Network Codes ............................................................. 98

5.2 Portugal .................................................................................................. 100

5.3 Norway ................................................................................................... 104

5.4 United Kingdom ...................................................................................... 105

5.5 Germany ................................................................................................. 107

6. CONCLUSIONS ........................................................................................ 112

7. REFERENCES ........................................................................................... 114

Deliverable No. 2 | Smart Grids Business Models and Market Integration 6

FIGURES

Figure 2.1: Installed power in renewables of all technologies in Portugal 2010-2030 [10] ..........................................................................................................................18

Figure 2.2: Accumulated capacity of solar PV power in Norway (Source: Multiconsult) [20] ....................................................................................................................23

Figure 2.3: Projection of future UK CO2 emissions under the four scenarios studied in the National Grid Future Energy Scenarios ....................................................................25

Figure 2.4: Diagram of how CfD will operate ............................................................26

Figure 2.5: Increase in number of installed smart meters in the UK [40] .....................27

Figure 2.6: Cumulative contracted capacity connected to Transmission level under the Connect and Manage scheme in the UK [41] ............................................................28

Figure 2.7: Projected installed capacity of distribution generation, based on Slow Progress Scenario [30] ..........................................................................................28

Figure 2.8: Example of a distribution heatmap from SP Energy Networks ....................29

Figure 2.9: Components of both fixed feed-in tariffs and the market-premium system. Based on [52] ......................................................................................................31

Figure 2.10: Expansion of installed capacity of RES power plants in Germany [57] .......33

Figure 2.11: Share of RES in the gross electricity consumption 1999-2016 [57] ...........33

Figure 2.12: Architecture of the German energy transition [55] ..................................35

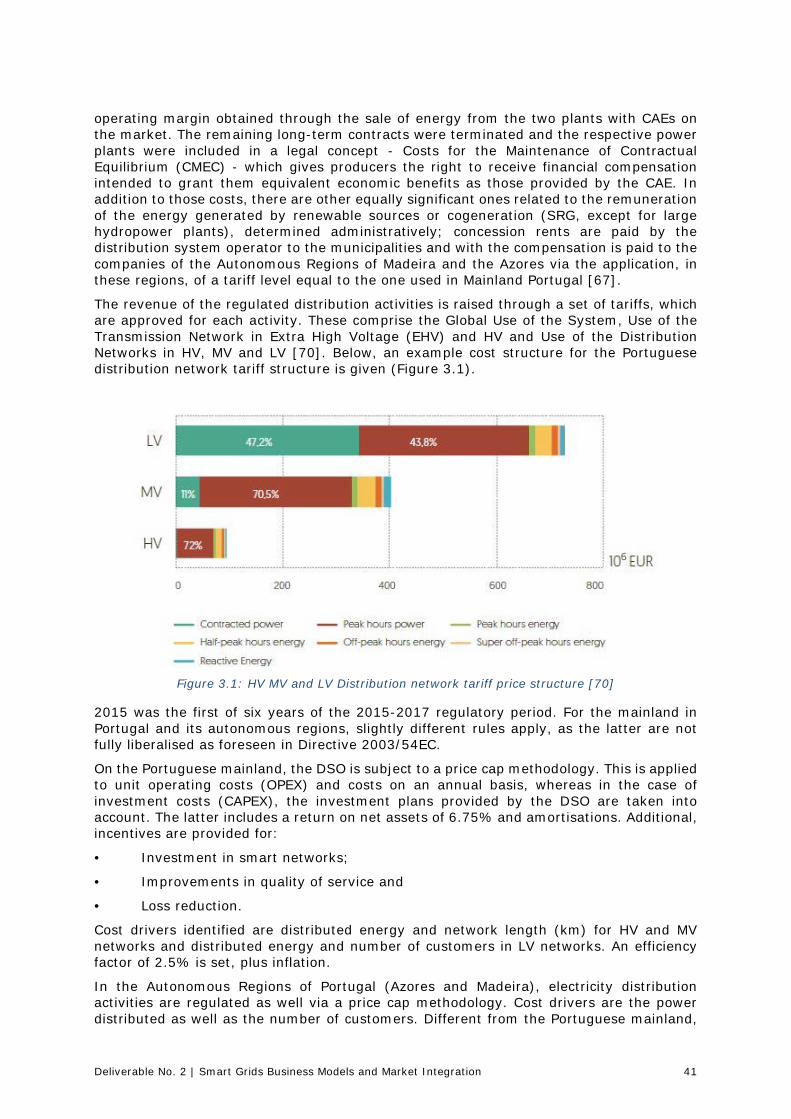

Figure 3.1: HV MV and LV Distribution network tariff price structure [70] ....................41

Figure 3.2: Time periods in the German regulatory system, based on [98] ..................51

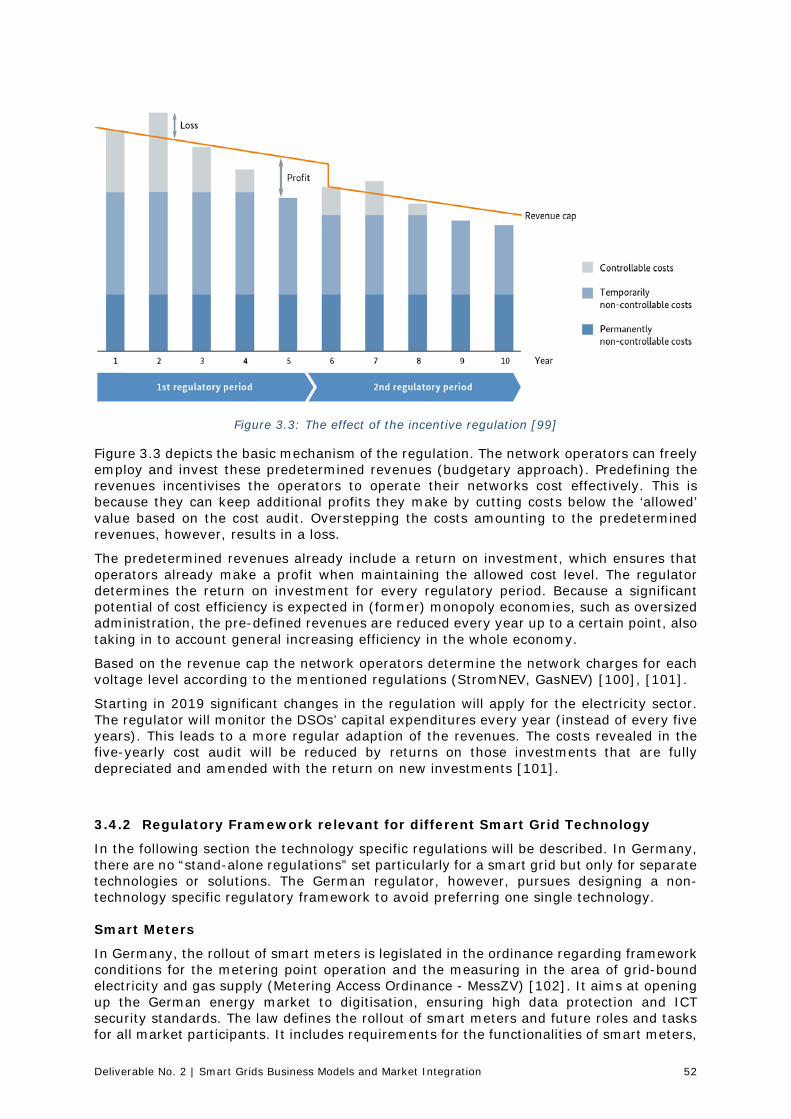

Figure 3.3: The effect of the incentive regulation [99] ...............................................52

Figure 4.1: Illustration of the different market and control phases ..............................61

Figure 4.2: Price setting in the day-ahead market [118] ............................................62

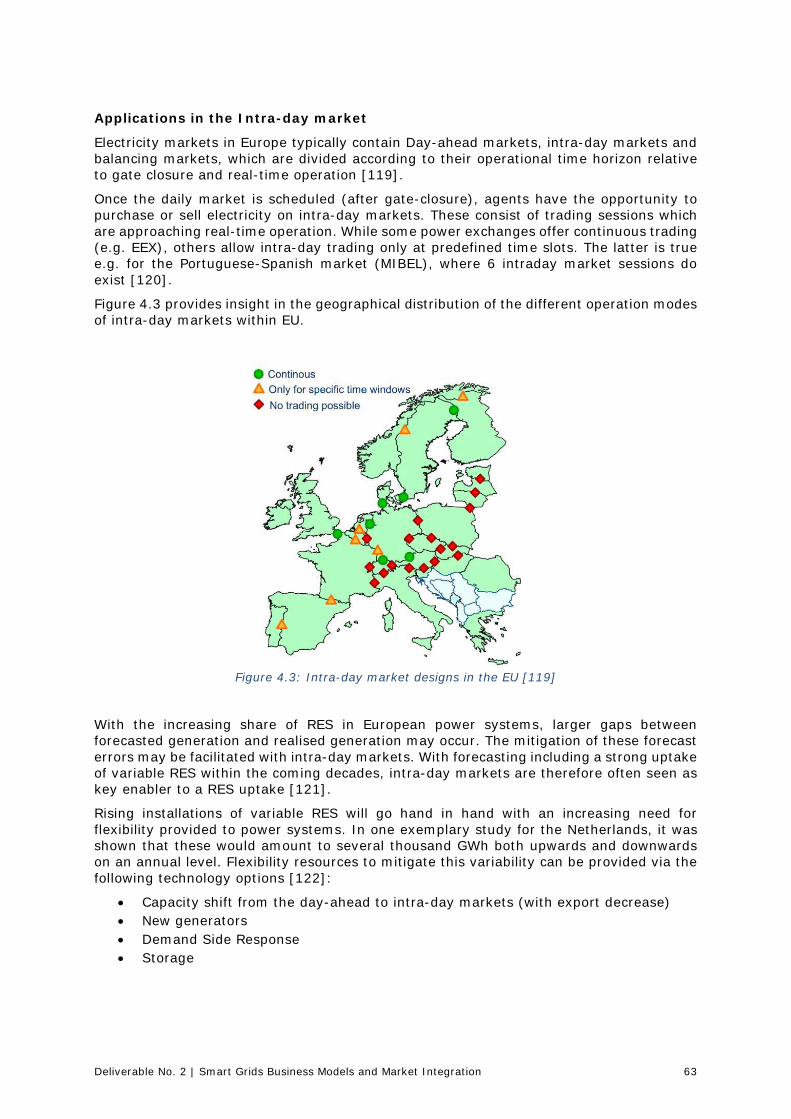

Figure 4.3: Intra-day market designs in the EU [119] ...............................................63

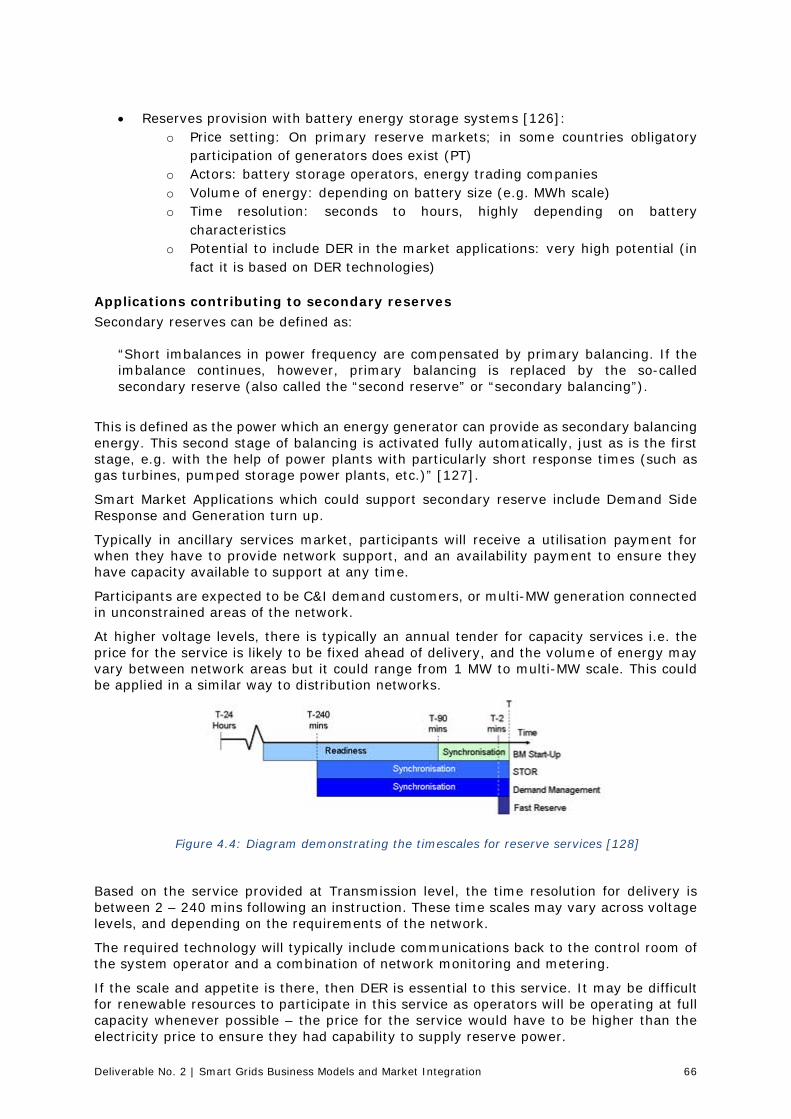

Figure 4.4: Diagram demonstrating the timescales for reserve services [128] ..............66

Figure 4.5: Share of clients and consumption by the retail energy sales companies in Portugal [137] .....................................................................................................70

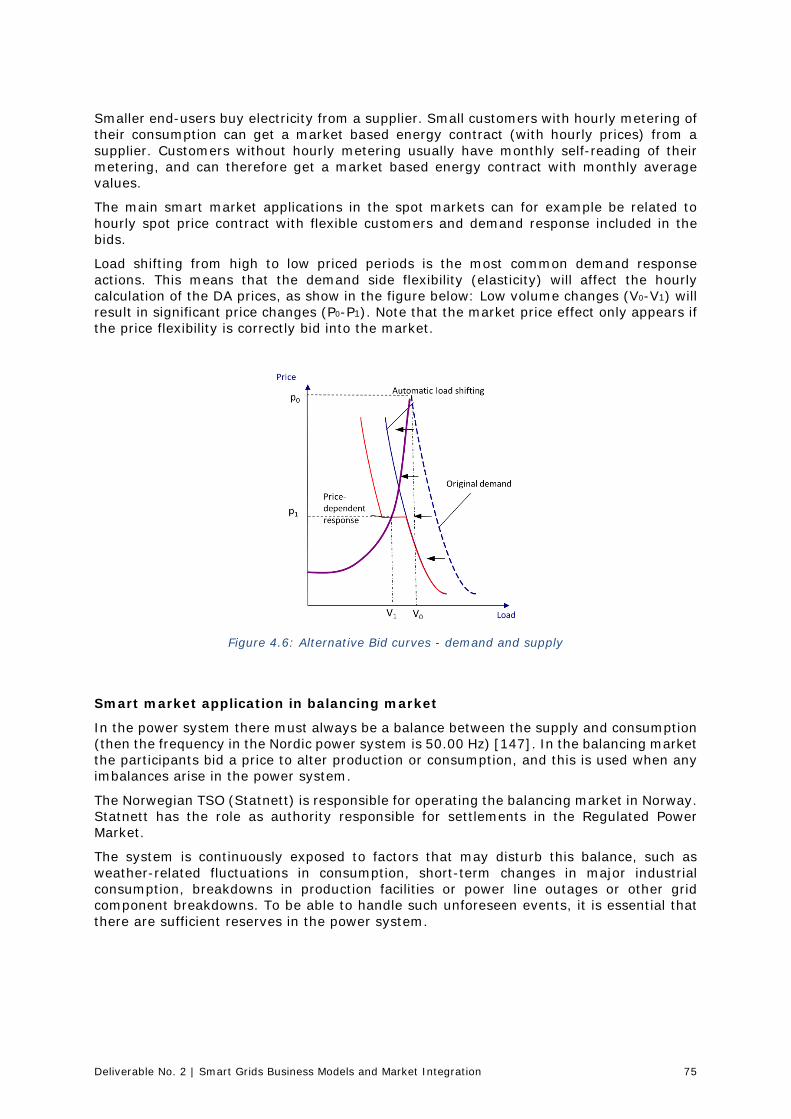

Figure 4.6: Alternative Bid curves - demand and supply ............................................75

Figure 4.7: Monopoly actors and market participants involved in smart market applications [91] ..................................................................................................78

Figure 4.8: Overview of the settlement and balancing process in the UK .....................79

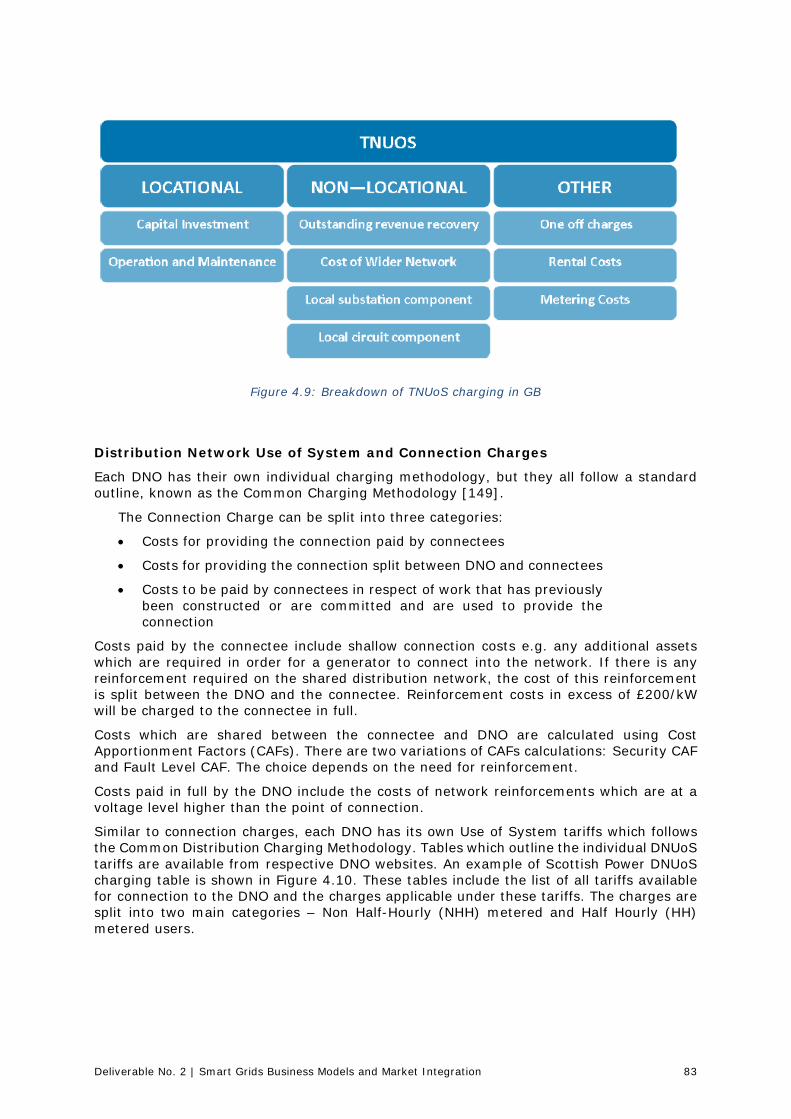

Figure 4.9: Breakdown of TNUoS charging in GB ......................................................83

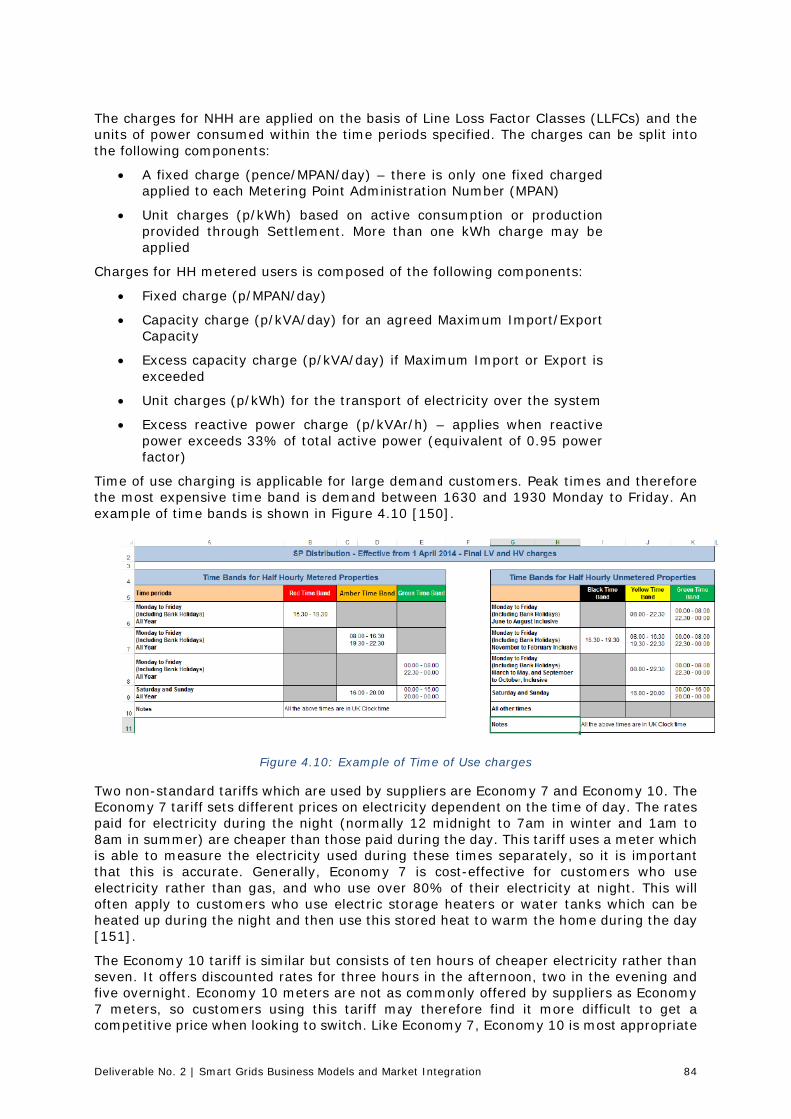

Figure 4.10: Example of Time of Use charges ...........................................................84

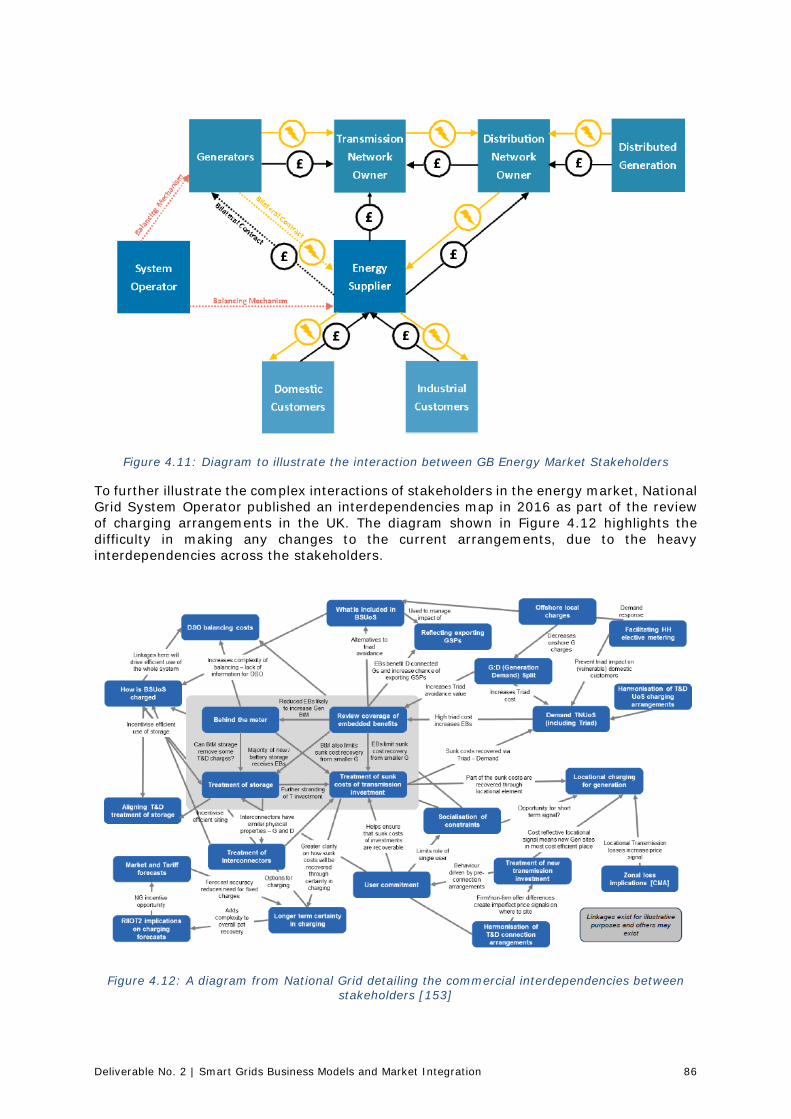

Figure 4.11: Diagram to illustrate the interaction between GB Energy Market Stakeholders ........................................................................................................86

Figure 4.12: A diagram from National Grid detailing the commercial interdependencies between stakeholders [153] ..................................................................................86

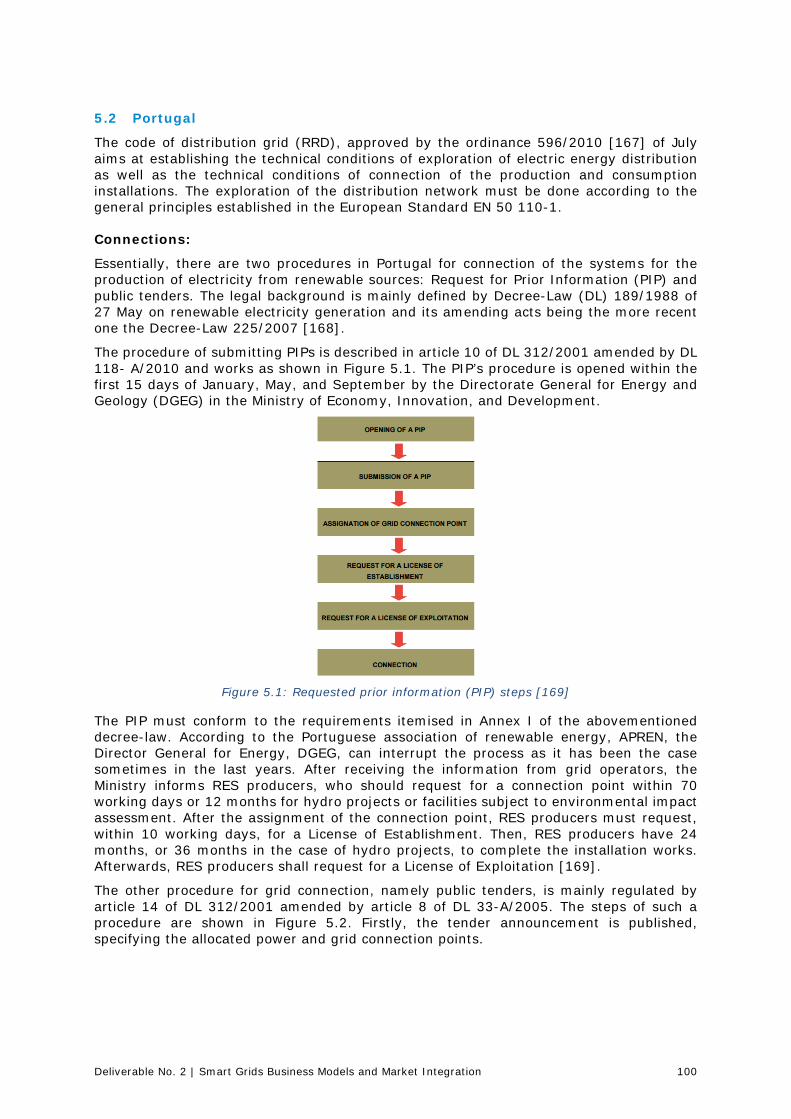

Figure 5.1: Requested prior information (PIP) steps [169] ....................................... 100

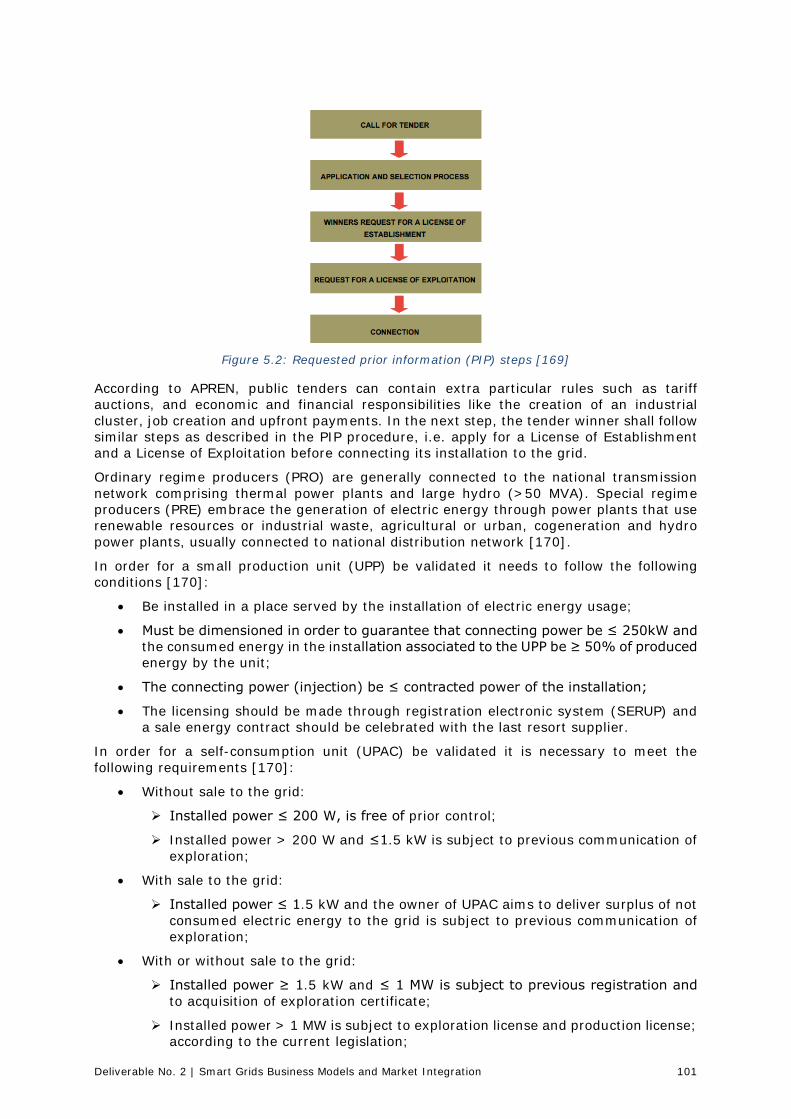

Figure 5.2: Requested prior information (PIP) steps [169] ....................................... 101

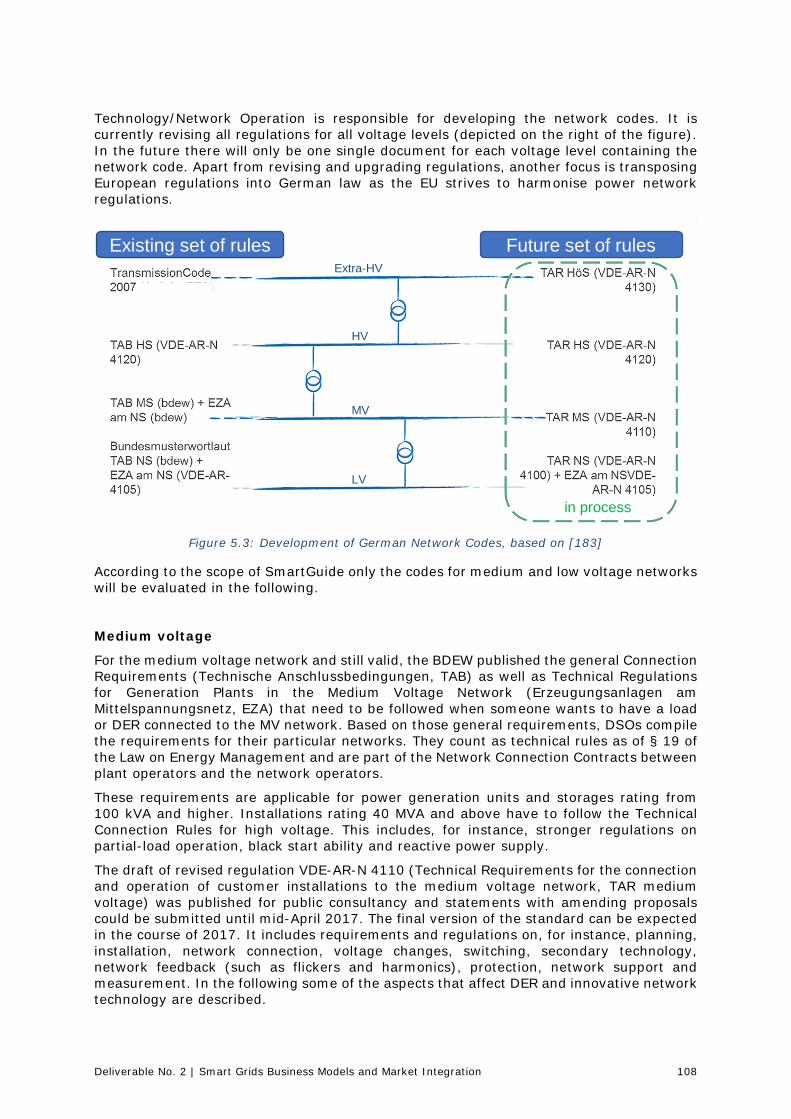

Figure 5.3: Development of German Network Codes, based on [183] ........................ 108

Deliverable No. 2 | Smart Grids Business Models and Market Integration 7

TABLES

Table 2.1: Differences between each law of small scale generation in Portugal .............19

Table 2.2: Costs of Smart Meters [39] ....................................................................27

Table 2.3: Comparing the circumstances of DER promotion in the different countries ....36

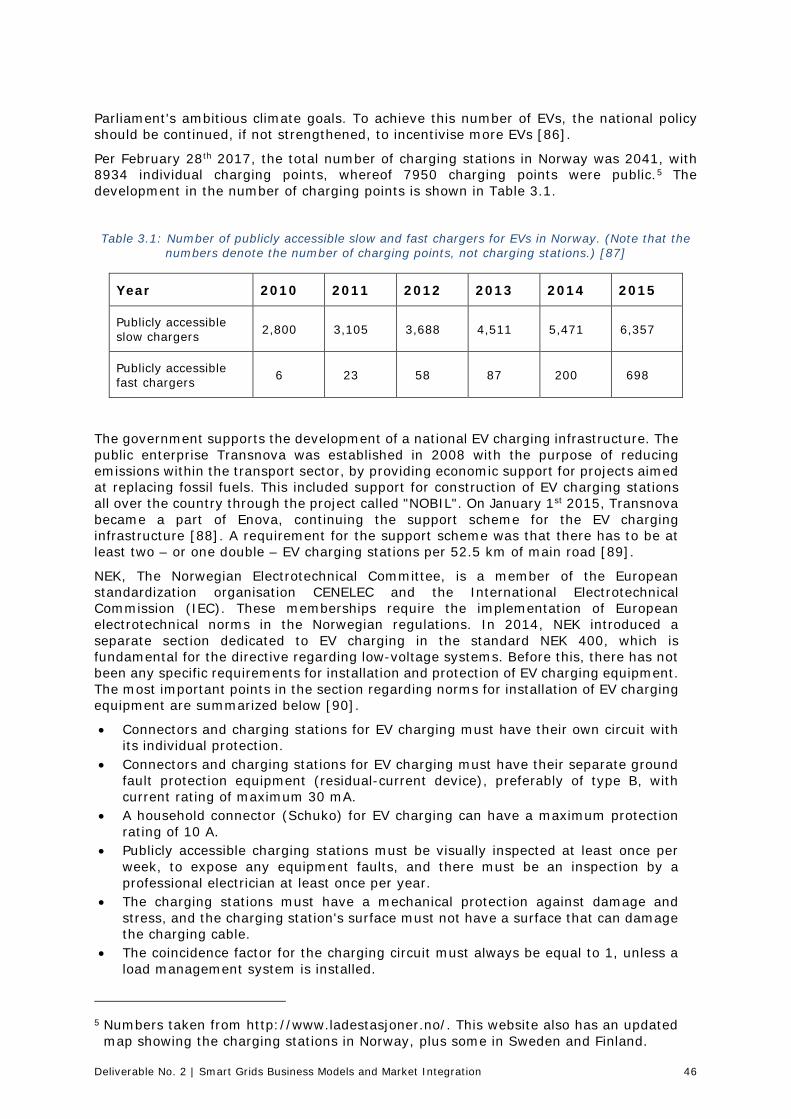

Table 3.1: Number of publicly accessible slow and fast chargers for EVs in Norway. (Note that the numbers denote the number of charging points, not charging stations.) [87] ...46

Table 3.2: Summary of RIIO-ED1 assessment categories [92] ...................................48

Table 3.3: Summary of incentives which can be linked to Smart Grid Technologies .......50

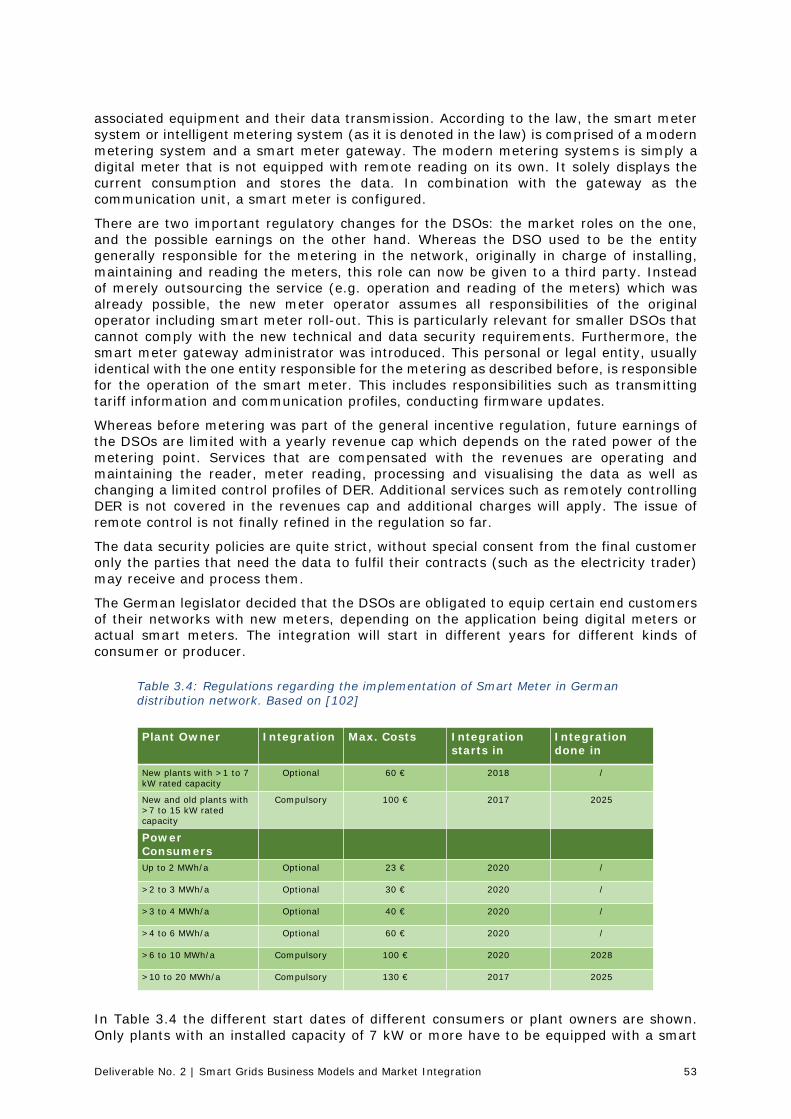

Table 3.4: Regulations regarding the implementation of Smart Meter in German distribution network. Based on [102] ......................................................................53

Table 3.5: Comparing drivers for smart grid technologies in the different countries .......57

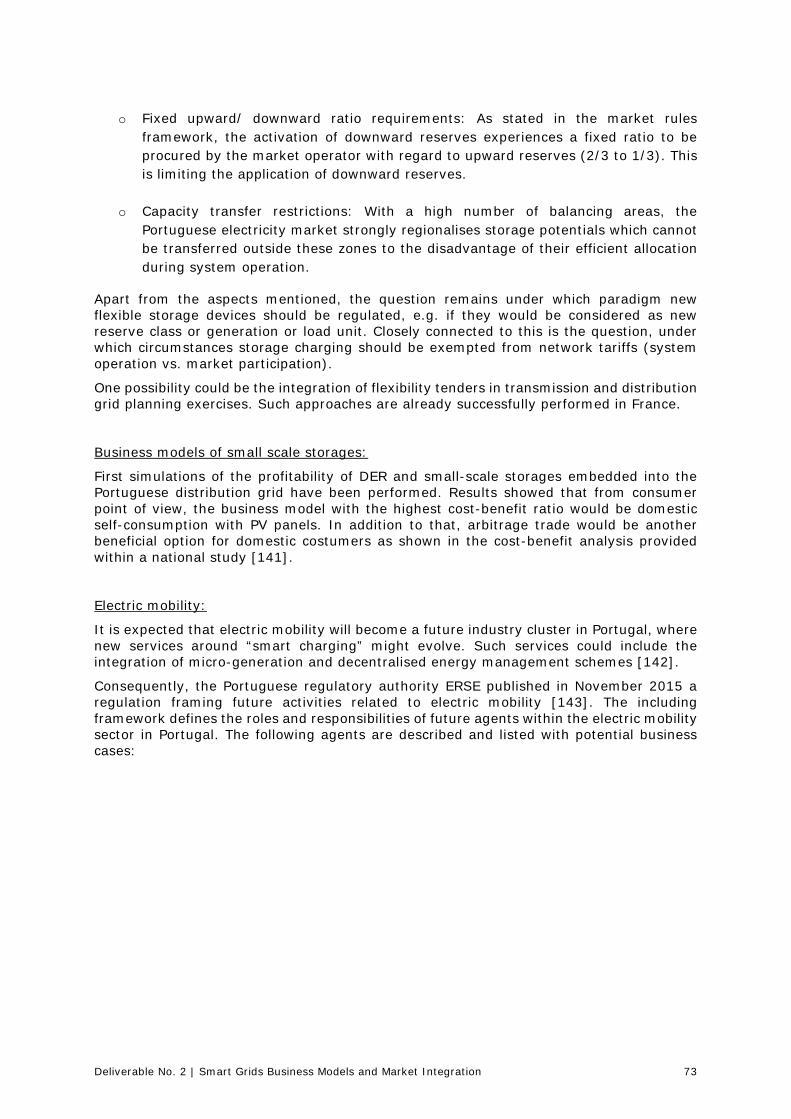

Table 4.1: Business opportunities of each agent of the electric mobility .......................74

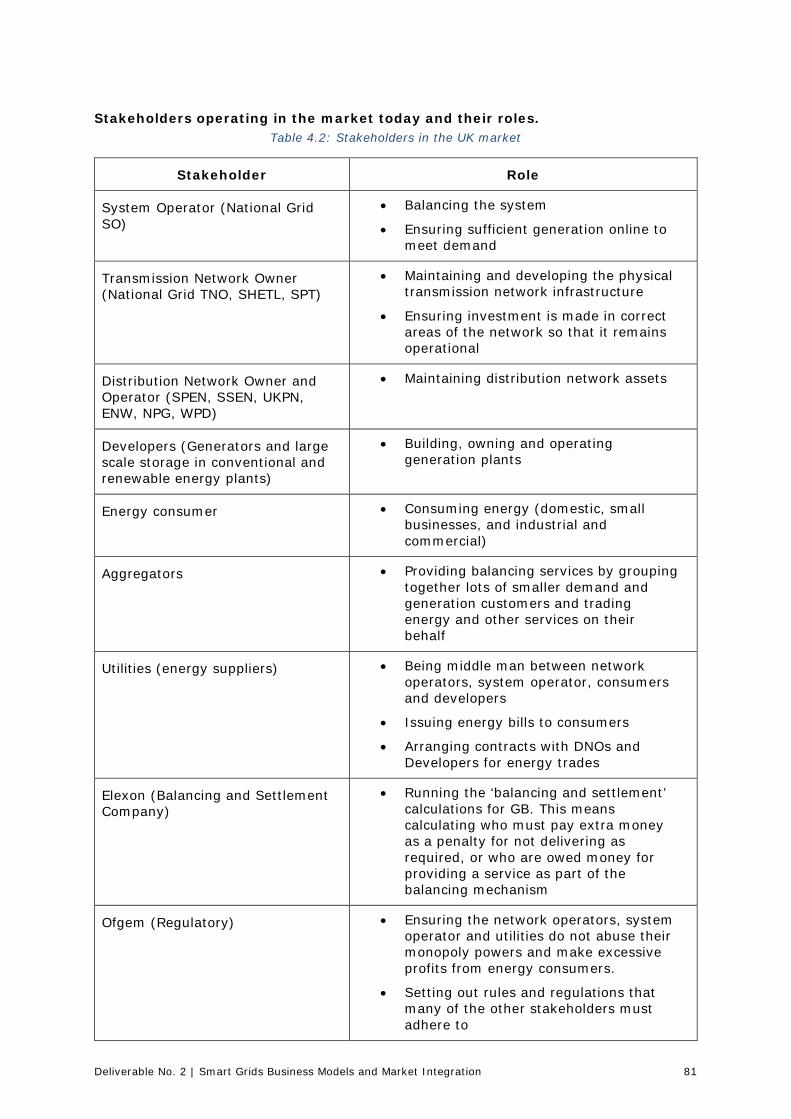

Table 4.2: Stakeholders in the UK market................................................................81

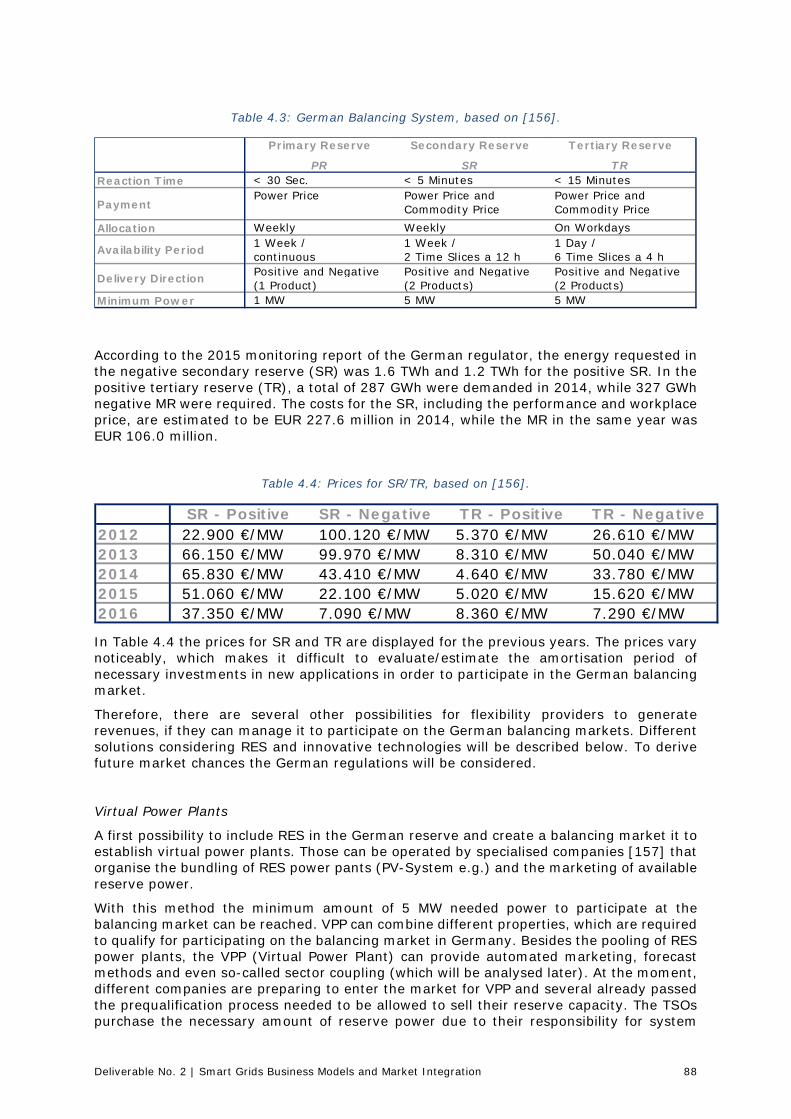

Table 4.3: German Balancing System, based on [156]. .............................................88

Table 4.4: Prices for SR/TR, based on [156]. ...........................................................88

Table 4.5: Summary table for potential smart market applications for the future ..........93

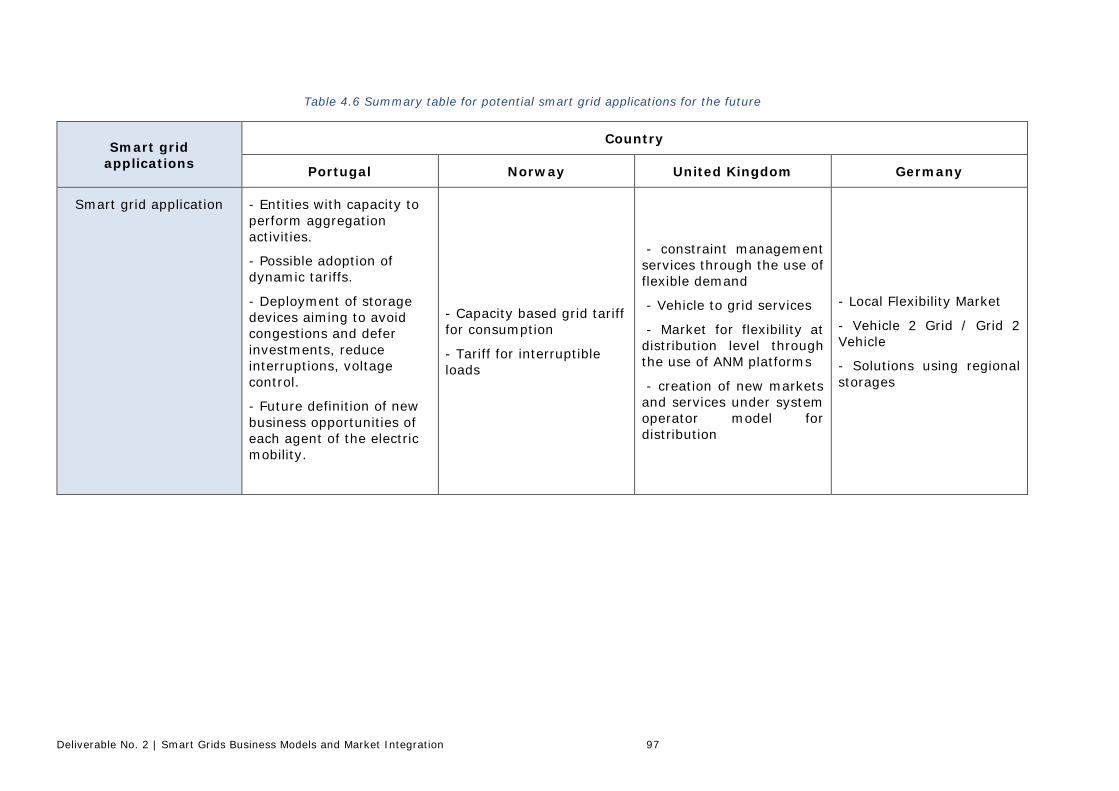

Table 4.6 Summary table for potential smart grid applications for the future ................97

Table 5.1: Values for the inductive and capacitive reactive energy of the PRE ............ 103

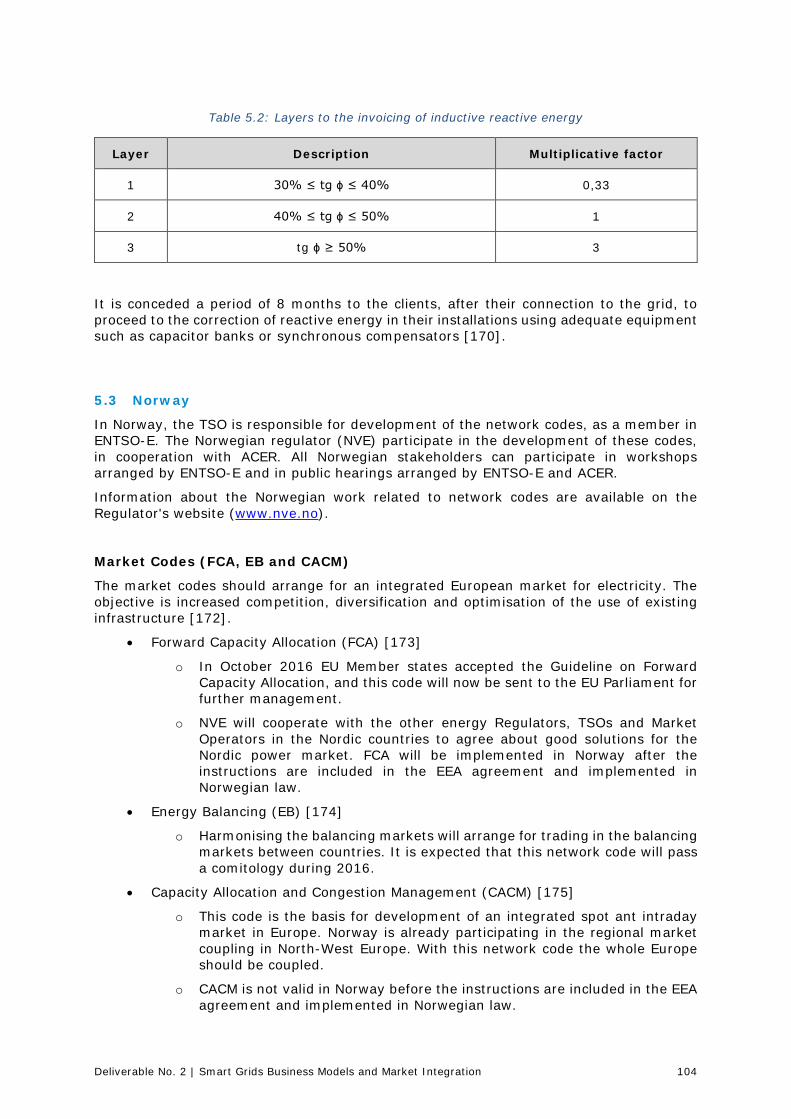

Table 5.2: Layers to the invoicing of inductive reactive energy ................................. 104

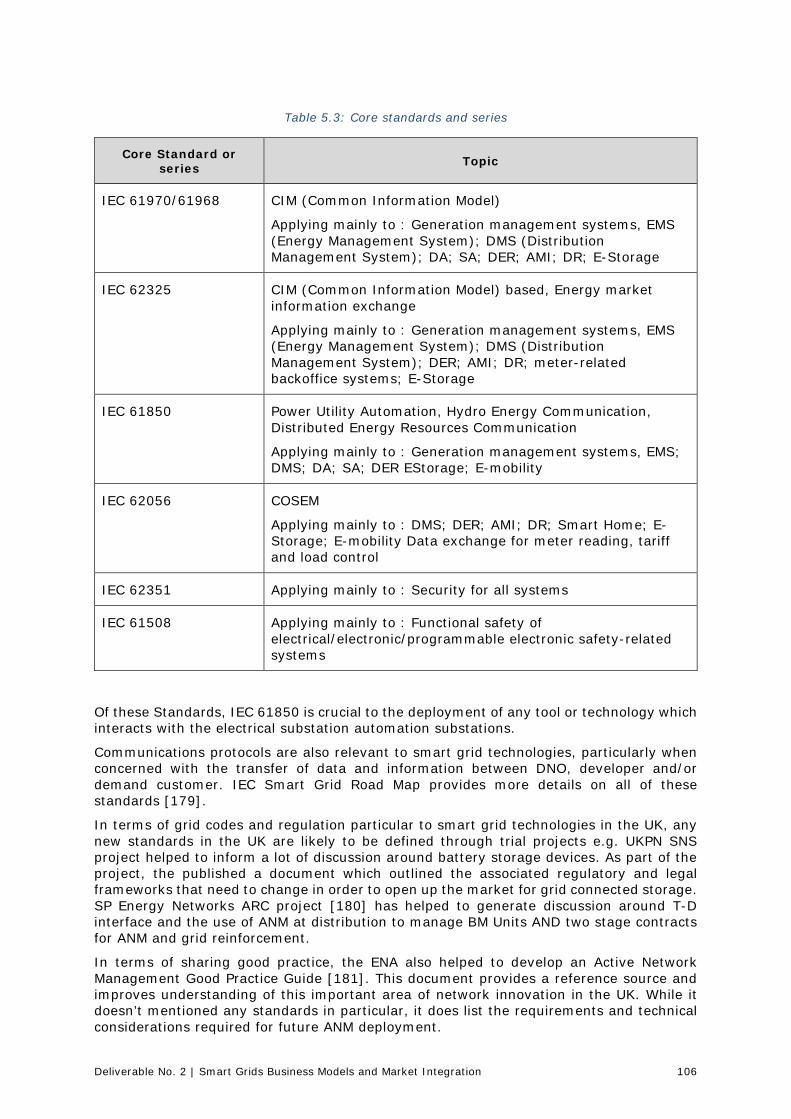

Table 5.3: Core standards and series .................................................................... 106

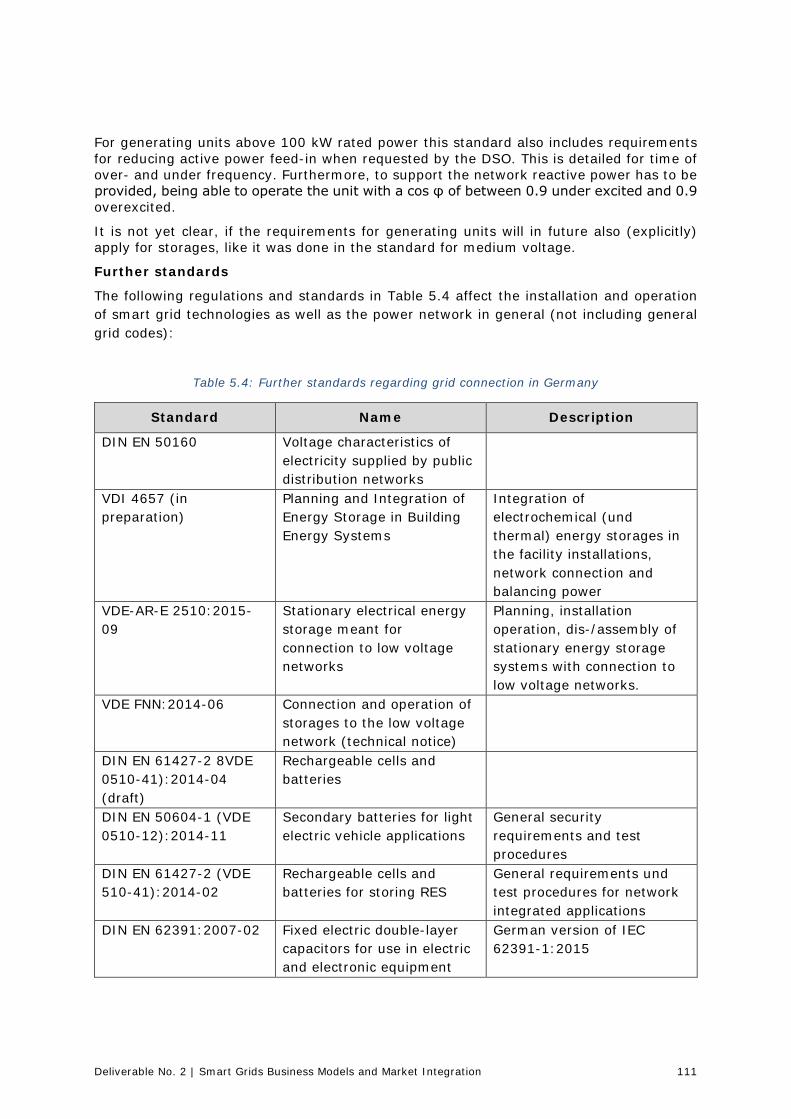

Table 5.4: Further standards regarding grid connection in Germany .......................... 111

Deliverable No. 2 | Smart Grids Business Models and Market Integration 8

ABBREVIATIONS

AbLaV Verordnung über Vereinbarungen zu abschaltbaren Lasten

AC Alternating current

ACER Agency for the Cooperation of Energy Regulators

ANM Active Network Management

APREN Portuguese association of renewable energy

AregV Anreizregulierungsverordnung

BDEW the German Association of Energy and Water Industries

BETTA British Electricity Trading Transmission Arrangements

BM Balancing market

BM Balancing Mechanism

BNetzA Bundesnetzagentur

BSC Balancing and Settlement Code

BSCCo Balancing and Settlement Code Company

BSUoS Balancing Service Use of System Charges

CACM Capacity Allocation and Congestion Management

CAE Electricity Acquisition Contracts

CAF Cost Apportionment Factors

CAPEX Case of investment costs. Capital expenditures.

CCL Climate Change Levy

CCS Combined charging system

CENS Costs of Energy Not Supplied

CfD Contracts for Difference

CHP Combined Heat and Power plants

CI Customer Interruptions

CIEG Costs arising essentially from legal decisions

CIM Common Information Model

CMEC Maintenance of Contractual Equilibrium

CML Customer Minutes Lost

COP21 Kyoto Protocol

DA Day ahead market

DCC Data and Communications Company

DCC Demand Connection Code

DCLF ICRP DC Load Flow Investment Cost Related Pricing

DER Distributed Energy Resources

DFIG Doubly fed induction generator technology

DG Distributed Generation

DGEG Direcção Geral de Geologia e Energia (Director General for Energy)

Deliverable No. 2 | Smart Grids Business Models and Market Integration 9

DIN Deutsches Institut für Normung

DL Decree-Law

DNA Decentralised network automation

DNO Distribution Network Operator

DR Demand Response

DSO Distribution System Operator

DSR Demand Side Response

EDA Electricidade dos Açores

EDP Energias de Portugal

EEA European Economic Area

EEF Energy Efficiency Fund

EEG Renewable Energies Act

EEM Empresa de Electricidade da Madeira

EEX European Energy Exchange

EHV Extra High Voltage

ENE 2020 The National Energy Strategy 2020

EnEG Energieeinsparungsgesetz

ENTSO-E European Network of Transmission System Operators for Electricity

EnWG Energiewirtschaftsgesetz

EPC European Price Coupling

ERO Early Rollout Obligation

ERSE National regulatory authority for energy services

EU European Union

EV Electric Vehicle

EZA Erzeugungsanlagen am Mittelspannungsnetz

FAI Innovation Support Fund

FES Future Energy Scenarios

FiT Feed-in Tariff

FPN Final Physical Notification

G2V Grid-to-vehicle

GasNEV Gasnetzentgeltverordnung

GAV Gross Asset Value

GDP Gross Domestic Product

GHG Greenhouse Gases

HV High voltage

HVDC high-voltage direct current

ICE The Incentive on Connections Engagement

ICT Information and Communication Technology

ID Intraday market

Deliverable No. 2 | Smart Grids Business Models and Market Integration 10

IEC International Electrotechnical Commission

IHD In-Home Displays

IIS Interruptions Incentive Scheme

KfW Kreditanstalt für Wiederaufbau, engl. Reconstruction Credit Institute

LEC Levy Exemption Certificates

LLFC Line Loss Factor Classes

LSV Ladesäulenverordnung

LV Low voltage

MessZV Messzugangsverordnung

mFRR manual Frequency Restoration Reserves

MIBEL Iberian Electricity Market

MITS Main Interconnected Transmission System

MV Medium voltage

NEEAP National Energy Efficiency Action Plan

NEK Norsk Elektroteknisk Komite

NETA New Electricity Trading Arrangements

NETS National Electricity Transmission System

NHH Non Half-Hourly

NIA National Innovation Allowance

NIC National Innovation Competition

NREAP National Renewable Energy Action Plan

NVE The Norwegian Water Resources and Energy Directorate

OFGEM Office of Gas and Electricity Markets

OLTC On Load Tap Changer

OPEX Unit operating costs/Operating expenses

PCR Primary Control Reserve

PIP Prior Information

PLC Power Line Communication

PNAEE National Action Plan for Energy Efficiency

PNAER 2020 Plano Nacional de Ação para as Energias Renováveis

PPEC Consumption Efficiency Promotion Plan

PRE Special regime producers

PRO Ordinary regime producers

PV Photovoltaic

RAV Regulatory Asset Value

REGO Renewable Energy Guarantees of Origin

RES Renewable Energy Sources

RESP Rede Eléctrica de Serviço Público

RfG Requirements for Generators

Deliverable No. 2 | Smart Grids Business Models and Market Integration 11

RIIO Revenue = Incentives + Innovation + Outputs

ROC Renewable Obligation Certificates

RPC Reactive Power Controller

RPI Retail Price Index

RQS Quality of Service Code

RRC Commercial Relations Code

RRD Code of distribution grid

RT Tariff Code

SEC Smart Energy Code

SEN National Electricity System

SGT Smart Grid Technology

SME Small and Medium Enterprises

SPT Scottish Power Transmission

SRG Special regime generation

SSF Site Specific Charges

StromNEV Stromnetzentgeltverordnung

StromNZV Stromnetzzugangsverordnung

StromStG Stromsteuergesetz

SVAC Static Var Compensator

TAB Technische Anschlussbedingungen

TC Transmission Running Costs

TNUoS Transmission Network Use of System

TOTEX Total Expenditure

ToU Time of use tariffs

TSO Transmission System Operator

UPAC Self-Consumption Units

UPP Small Production Units

V2G Vehicle-to-grid

VDE Association of Electrical, Electronic and Information Technologies

VPP Virtual Power Plant

WTG Wind Turbine Generators

Deliverable No. 2 | Smart Grids Business Models and Market Integration 12

Disclaimer

The content and views expressed in this material are those of the authors and do not necessarily reflect the views or opinion of the ERA-Net SG+ initiative. Any reference given does not necessarily imply the endorsement by ERA-Net SG+.

About ERA-Net Smart Grids Plus

ERA-Net Smart Grids Plus is an initiative of 21 European countries and regions. The vision for Smart Grids in Europe is to create an electric power system that integrates renewable energies and enables flexible consumer and production technologies. This can help to shape an electricity grid with a high security of supply, coupled with low greenhouse gas emissions, at an affordable price. Our aim is to support the development of the technologies, market designs and customer adoptions that are necessary to reach this goal. The initiative is providing a hub for the collaboration of European member-states. It supports the coordination of funding partners, enabling joint funding of RDD projects. Beyond that ERA-Net SG+ builds up a knowledge community, involving key demo projects and experts from all over Europe, to organise the learning between projects and programs from the local level up to the European level.

www.eranet-smartgridsplus.eu

The work of INESCT TEC is financed by FCT – Fundação para a Ciência e a Tecnologia (Portuguese Foundation for Science and Technology) within project SmartGP/0002/2015, under the framework of the ERA-Net Smart Grids Plus initiative.

The work of SINTEF Energi and Skagerak is mainly funded by the Norwegian Research Council, under the framework of the ERA-NET Smart Grids Plus initiative.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 13

1. Introduction

In WP2, SG Business Models and Market Integration, the analysis of country specific regulatory and legal circumstances of the use of smart grid technologies and smart market applications are performed. Additionally, country specific legal and regulatory circumstances of promotion of renewable energy sources are analysed in the European-wide context. Furthermore developments of Grid Codes focusing specifically on the integration and full value realization of smart grid technologies are reviewed.

This report presents the work that has been produced within the scope of the second work package of the SmartGuide project.

WP1 (SG Solutions and Technologies) and WP2 ran with a partial overlap so that they could influence each other in the development of a solid structure for the project that would then be input to the following work packages.

1.1 Introduction and main challenges of SmartGuide

1.1.1 Historic conditions and process of change

Future electrical distribution systems will come across many modifications mostly due to new paradigms both at conceptual and technical levels. During the last decades, the planning and operation procedures of power distribution grids have been changing, one of the main reasons being the high penetration of Distributed Energy Resources (DER), in particular Distributed Generation (DG) units based on Renewable Energy Sources (RES). The intention of developed countries, mainly in Europe, to decrease fossil fuels dependency and the policies imposing the reduction of Greenhouse Gases (GHG) emissions have contributed to the development of this paradigm. In fact, environmental concerns are behind the increase of renewable-based DG, as well as the promotion of electric mobility and integration of storage units in the distribution network. However, distribution grids, which have been designed to supply customers through unidirectional power flows coming from the transmission network, may not be able to handle technical issues brought by the inclusion of these DER.

The integration of RES in existing energy distribution systems all over Europe is being promoted following the climate and energy 20/20/20 targets of the European Union (EU). Due to the variability of these RES, in particular wind turbines and photovoltaic (PV) systems, the uncertainty associated to the balancing of generation and demand escalates. Smart Grid (SG) technologies are important to ensure cost-effective expansion of distribution systems. Naturally, the SG use cases may vary from country to country depending on specific regulatory and legal parameters as well as historical and geographical conditions, which have led to different grid topologies and operation principles. It must be accepted that there is no ‘one size fits all’ approach when it comes to smart grid implementation – each country or organisation has to first identify what they really want from their smart grid solution and develop an appropriate strategy and execution plan accordingly.

1.1.2 Overview of SmartGuide project

SmartGuide is a research project with five project partners from four associated partner countries: Norway, Portugal, the United Kingdom and Germany. The main objective of the project SmartGuide is the development of improved and generalised planning and operating guidelines for European smart distribution systems, considering RES and the demand-side that arise from smart market applications (e.g. demand response, ancillary services such as frequency control). The associated Distribution System Operators (DSOs) will provide network data in order to analyse SG technologies used in current distribution

Deliverable No. 2 | Smart Grids Business Models and Market Integration 14

networks and provide expertise of operational network planning. On this basis, country specific planning and operation principles will be derived. In a further step, these principles will be abstracted to form a European planning guideline for using smart grid technologies in distribution networks. The guideline is supposed to assist DSOs noncommittally when assessing the deployment of smart grid technologies in their network. During the project, all partners will develop different software frameworks to identify increased requirements for network reinforcement and possible SG solutions in order to upgrade existing distribution networks in a cost-efficient manner.

Within WP1 of the project, a state-of-art of the current Smart Grid (SG) solutions and technologies in each country of the participating partners was developed. It also summarized the main SG solutions and technologies explored by the literature in the last years.

1.2 Objectives and goals of Work Package 2

The overall purpose of WP2 is to describe the state-of-the-art related to smart grids business models and market integration.

The report describes country specific regulatory and legal circumstances of the use of smart grid technologies and smart market applications, country specific legal and regulatory circumstances of promotion of renewable energy sources (in an European-wide context) and the developments of Grid Codes focusing specifically on the integration and full value realization of smart grid technologies will be reviewed.

This document is divided into five main sections. The first chapter is this introduction. The second chapter describes country specific legal and regulatory circumstances of DER promotion, focusing on national directives, integration into existing grids (the success of the directives), support schemes for private customers or companies to invest in DER and foresights/future plans, including RES promotion mechanism. The third chapter describes the drivers for smart grid and approaches for deployment of smart grid from a DSO point of view. The smart grid technologies to be reviewed in this chapter are smart meters, demand side response (DSR)/management, electric vehicle charging, network automation, active voltage management, energy storage and distributed generation. For each country the existing legal and regulatory elements of relevance and their implications for rollout of smart grid technology and legal/regulatory improvements to incentivise smart grid technology should be described. The fourth chapter describes economical incentives in smart market and smart grid, where "smart market" concerns contents geared to the behaviour of market players and "smart grid" is related to electricity network issues and the monopoly activity performed by the DSO. The fifth chapter describes the Grid Codes and the status of implementation in the different countries (Portugal, Norway, UK and Germany).

Deliverable No. 2 | Smart Grids Business Models and Market Integration 15

2. Country specific legal and regulatory circumstances of DER promotion

In this chapter national regulation related to DER1 promotion are described, focusing on renewable energy resources. For the countries Portugal, Norway, UK and Germany, the following topics are included:

• National directives: Existing regulation to support DER integration. • Integration into existing grids: Review of success of regulation to date

including total installed capacity in the country due to the regulation. • Support schemes/incentive schemes: Incentive mechanisms that

supports private customers or companies to invest in DER • Foresight/future plans, incl. future RES promotion mechanisms.

2.1 Portugal

2.1.1 National directives

Energy policies in Portugal are very reliant on strategy set at European level and more specifically to the commitments made under such plan within the Kyoto Protocol (COP21). Several measures have been adopted in recent years in order to stimulate energy efficiency and reduce carbon emissions by promoting “green” investments and growth of renewable energy production. Among them are The National Energy Strategy 2020 (“ENE 2020”) [1], the Energy Efficiency Fund (EEF) [2] which encourage measures of the National Action Plan for Energy Efficiency (“PNAEE”), the Portuguese Carbon Fund and the restructuring of Green Taxation which altered a set of environmental tax rules in the energy sector [3].

According to PNAER 2020 (Plano Nacional de Ação para as Energias Renováveis) established through Council of Ministers Resolution 20/2013 of 10th April 2013 [4] the incentives to renewable energy investments until 2020 are:

• Encouraging the installation of solar thermal systems in the residential sector;

• Promoting the installation in buildings of more efficient energy systems;

• Streamlining the licensing procedures of renewable electricity plants;

• Conceding incentives to be applied to power plants dedicated to forest biomass;

• Endorsing the use of endogenous resources and excess for the production of biofuels.

Regarding the small scale generation (micro-generation and mini-generation) there are two main decree-laws that regulate this type of production of renewable electricity. All producers have grid access under both regimes. Decree-Law 363/2007, of 2nd November (revised by the Decree-Law 118-A/2010 of 8th October and by the Decree-Law 25/2013 of 8th March) regulates the production by RES up to 5.75 kW.

1 DER = Distribution Energy Resources. DER includes Distributed Generation (DG) and energy storage.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 16

The micro-generation law is characterized in two regimes [5]:

• The general regime is applicable to any type of micro-generation up to a limit of 5.75 kW (25 A single-phase);

• The special regime is applicable to renewable electricity production up to a limit of 3.68 kW (16 A single-phase).

In 2014 there were 25,000 installations in the special regime and 900 in the general regime with a total capacity of 93 MW and 4.0 MW, respectively [5].

Decree-Law 34/2011 of 8th March (revised by the Decree-Law 25/2013 of 19th February) regulates the production from 5.75 kW to 250 kW. The mini-generation law is also characterized in two regimes [5]:

• The general regime is applicable to any type of renewable energy generation technology up to 250 kW;

• The special regime is applicable to any type of renewable energy generation technology up to 3.68 kW (16 A single-phase).

In 2014 there were 1,200 installations in the special regime with a total capacity of 52 MW [5]. In September of the same year, the government ratified a decree law that aims at merging the micro-generation and mini-generation framework (Decree-Law 153/2014 of 20th October). This new regime for Small Production Units (UPP in Portuguese) and Self-Consumption Units (UPAC in Portuguese) replaces the remuneration regime previously applicable to micro and mini generation units, which continues to be applicable only to installations registered until January 2015, date on which Decree-Law 153/2014 has come into force through Ordinance 14/2015.

In Portugal, the generation of electricity from RES is mainly promoted through a Feed-in Tariff (FiT). Currently, the FiT regime continues to apply only to existing installations. A new regime for Small Production Units (UPP) and Self-Consumption Units (UPAC) has been introduced by Decree-Law 153/2014 as mentioned above, replacing the remuneration regime previously applicable to micro and mini generation units, which continues to be applicable only to installations registered until January 2015, date on which DL 153/2014 has come into force through Ordinance 14/2015 (same as above).

This new decree-law waives licensing for the activity of electricity production when its goal is self-consumption or when production is carried out by small plants. Micro production rules are meant to encourage domestic production for in-house consumption but the exceeding power may still be fed in to the Public Service Electricity Network (Rede Eléctrica de Serviço Público – RESP, in Portuguese). It is also possible to sell all the production to the RESP through a bidding system. In these cases, micro producers will take advantage of a specific tariff that varies depending on the type of energy source and the amount of power already fed in by micro producers [6].

In recent years, due to the economic crisis that the country went through, the adoption of cross-cutting measures of public expenses had been set which also affected the energy sector, including the costs associated with the remuneration of producers for instance. Lately, the period of intense subsidies to investment in renewable energy sector is over. Moreover, the current system of incentives to power guarantee (for thermal and hydroelectric power projects) is considerably distant from the preceding subsidy regime. On the other hand, important steps were taken in order the creation of a dynamic renewable market. It was introduced the possibility of produce energy from RES under the ordinary regime which means the chance to participate in a regime with a remuneration by RES (through organized markets or bilateral contracts).

Also, the tax incentives and a recent ministerial order of February 2015 established the access circumstances and financing policy for projects in the area of sustainability and efficiency. These comprise promoting the generation and distribution of energy from RES,

Deliverable No. 2 | Smart Grids Business Models and Market Integration 17

supporting energy efficiency and use of renewables in companies, homes and public infrastructures and promoting the use of sustainable mobility [3].

2.1.2 Integration into existing grids

Owners of UPACs may enter into a power purchase agreement with the last resort supplier in order to sell their surplus of electricity if they use RES and have an installed capacity of up to 1 MW, and if their electrical usage installation is connected to the public energy grid. If the UPACs have an installed capacity of more than 1.5 kW and are connected to the public energy grid, the owners are subject to pay fixed monthly compensation intended to recover part of the costs arising from measures related to energy policy, sustainability and general economic interests. The connection capacity that may be attributed each year to UPPs cannot exceed 20 MW, in accordance with the programme established annually by the Director General for Energy and Geology (DGEG). Furthermore, UPP owners may enter into power purchase agreements with the last recourse supplier to sell the electricity that they generate [7].

Portugal’s greenhouse gas emission levels developed in line with the goals defined under Kyoto Protocol. Although an increase of greenhouse gas emissions of 27% was allowed, actual emission levels lie on smaller values (around 19% in 2012). Decree-Law 141/2010 of 31st December 2010 settled as a mandatory target that, by 2020, the minimum of 31% of Portugal’s primary energy consumption should come from RES, which is higher than EU-27 average. According to Eurostat data [8], between 2008 and 2012, the renewables share in gross final energy consumption increased from 22.8% to 24.6% and the country is showing good progress towards its 2020 RES obligation. In 2012 61% of electricity in Portugal was already coming from RES. Besides, Portugal decreased its external energy dependency from 89% in 2005 to 71% in 2014. Between 2011 and 2014, a total of 2,757 MW from RES were licensed, thus achieving 11.6 GW of installed capacity [6].

Wind energy takes the leading role among national RES installed capacities. As of December 2013 there were approximately 224 wind farms and 2,540 wind turbine generators (WTG) installed in Portugal, a 42% increase from the 192 wind farms installed in 2008. As of March 2015 the number of wind farms has risen to 245 and the number of WTG almost reached the 2,500 mark (being at 2,496).

Recent studies have rated wave energy in Portugal as an energy resource with a medium-high potential. With an average annual flow of 30 MW per kilometre of water front with a depth of 50 meters, the Portuguese coast has the potential to generate approximately 10 TWh/year of electricity (about 20% of Portuguese consumption).

In 2013, biomass with combined heat and power (CHP) represented 367 MW of the installed power, while biomass without CHP represented 105 MW. As regards Municipal solid waste, it generates about 88 MW of power.

Today, biomass is one of the main export products in Portugal: in 2013 the country exported 824,000 tons of biomass worth € 111,000,000.00. Italy, the United Kingdom and Belgium are the main importers.

Reaching an annual average of 2,200 to 3,000 hours of sun in the mainland, and between 1,700 and 2,200, respectively, in the Azores and Madeira islands, Portugal has a strong potential for solar energy. According APREN (Associação de Energias Renováveis) [9], in 2015, the installed power in Portugal was 429 MW. This represented a 733.3% increase considering the mere 58.5 MW installed in 2008.

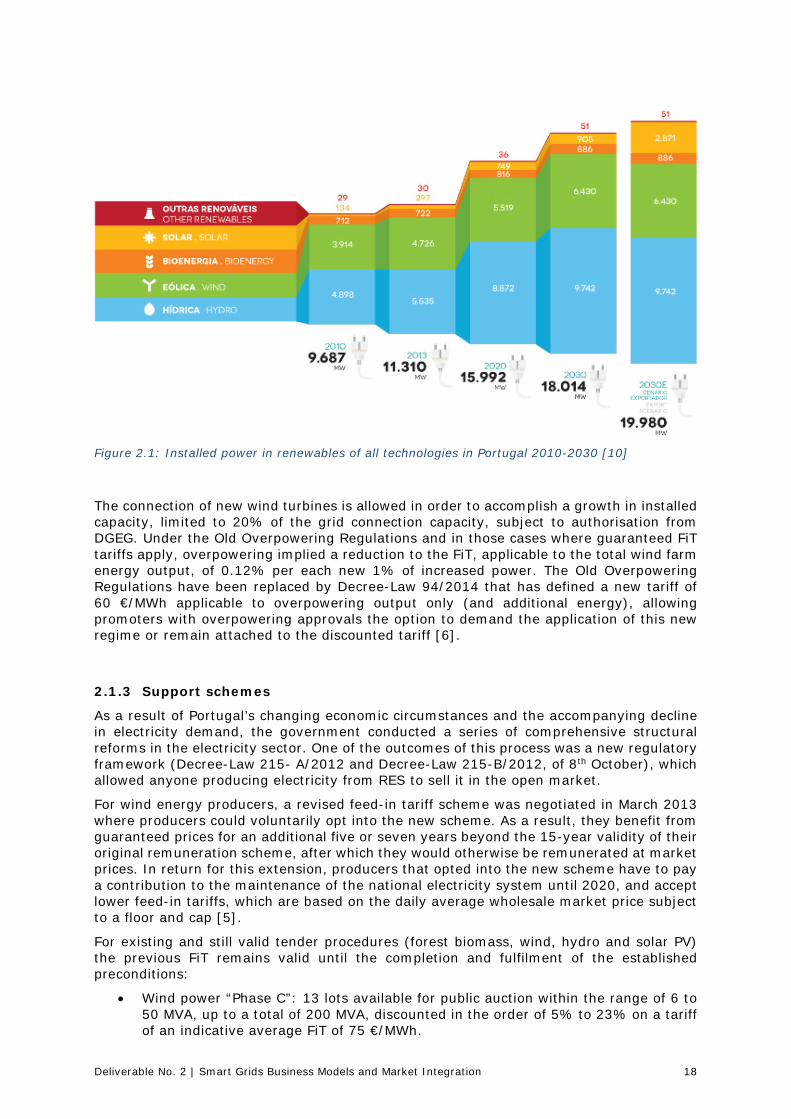

The installed power in renewables increased on all of the technologies and it is predictable that it duplicates between 2010 and 2030, replacing the generation from coal and natural gas and responding to the foreseen consumption grow for Portugal according to APREN (Associação de Energias Renováveis).

Deliverable No. 2 | Smart Grids Business Models and Market Integration 18

Figure 2.1: Installed power in renewables of all technologies in Portugal 2010-2030 [10]

The connection of new wind turbines is allowed in order to accomplish a growth in installed capacity, limited to 20% of the grid connection capacity, subject to authorisation from DGEG. Under the Old Overpowering Regulations and in those cases where guaranteed FiT tariffs apply, overpowering implied a reduction to the FiT, applicable to the total wind farm energy output, of 0.12% per each new 1% of increased power. The Old Overpowering Regulations have been replaced by Decree-Law 94/2014 that has defined a new tariff of 60 €/MWh applicable to overpowering output only (and additional energy), allowing promoters with overpowering approvals the option to demand the application of this new regime or remain attached to the discounted tariff [6].

2.1.3 Support schemes

As a result of Portugal’s changing economic circumstances and the accompanying decline in electricity demand, the government conducted a series of comprehensive structural reforms in the electricity sector. One of the outcomes of this process was a new regulatory framework (Decree-Law 215- A/2012 and Decree-Law 215-B/2012, of 8th October), which allowed anyone producing electricity from RES to sell it in the open market.

For wind energy producers, a revised feed-in tariff scheme was negotiated in March 2013 where producers could voluntarily opt into the new scheme. As a result, they benefit from guaranteed prices for an additional five or seven years beyond the 15-year validity of their original remuneration scheme, after which they would otherwise be remunerated at market prices. In return for this extension, producers that opted into the new scheme have to pay a contribution to the maintenance of the national electricity system until 2020, and accept lower feed-in tariffs, which are based on the daily average wholesale market price subject to a floor and cap [5].

For existing and still valid tender procedures (forest biomass, wind, hydro and solar PV) the previous FiT remains valid until the completion and fulfilment of the established preconditions:

• Wind power “Phase C”: 13 lots available for public auction within the range of 6 to 50 MVA, up to a total of 200 MVA, discounted in the order of 5% to 23% on a tariff of an indicative average FiT of 75 €/MWh.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 19

• Hydroelectric plants of up to 10 MW each to a total of 150 MVA: indicative average FiT of 91-95 € per MWh for a period of 25 years (Decree-Law 126/2010 of 23rd November).

• Solar photovoltaics (PV or CPV) of 2.0 MVA each, to a total of 150 MVA: an indicative average of 257 €/MWh for a period of 20 years and for the first 34 GWh per installed MW (Decree-Law 132-A/2010, of 21st December).

• Forest biomass: an indicative average of 119 €/MWh for a period of 25 years (Decree-Law 5/2011, of 10th January revised by the Decree-Law 179/2012 of 3rd August, and by Decree-Law 166/2015 of 21st August) [5].

Table 2.1 shows the difference between the reference I and other support schemes applied for each law of small scale generation.

Table 2.1: Differences between each law of small scale generation in Portugal

Micro-generation

-Reference FiT applied to each technology with different percentage: 100% for solar, 80% for wind, 40% for hydro, 70% for biomass CHP and 40% for non-renewable CHP.

-Valid for 15 years divided in two periods (e.g. reference FiT for PV: 66/145 €/MWh in 2014).

Mini-generation

- Reference FiT applied to each technology with different percentage: 100% for solar, 80% for wind, 50% for hydro, 60% for biomass and 60% for biogas.

- Reduced each year and, once defined, is valid for 15 years (e.g. 105.7 €/MWh for PV in 2014).

Small generation

- Reference FiT applied to each technology with different percentage: 100% for solar, 90% for biomass and biogas, 70% for wind and 60% for hydro.

- Is valid for 15 years for new producers and has a value of 95 €/MWh.

- If there is 2 m2 of solar thermal panels in the consumer’s installation 5 €/MWh are added or 10 €/MWh if there is an Electric Vehicle (EV) charging power outlet connected to the mobility grid in the consumer facility.

Self-consumption

- Does not benefit from a FiT.

- Has the possibility of injecting the surplus into the grid, which if paid by the last-resort supplier at 90% of the average monthly market price or trade the electricity surplus by green certificates.

- Has a mechanism to compensate the electric system through the general and economic interest costs.

The construction and operation of forest biomass power plants was promoted by the Decree-Law 5/2011, of 10th January 2011, which stipulated a favourable feed-in tariff calculus for power plants that start operating until 31st December 2016 [6].

There are other support schemes towards to integrate more DER in the grid and to improve energy efficiency. The Government has assumed a commitment to Green Growth allowing access to a fund (about 1,000 M€) in connection for energy efficiency and the efficient management of water and waste projects.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 20

Through a resolution of the municipal council, municipalities may agree a discount up to 15% of the property tax applied to buildings with high energy efficiency [6]:

• Buildings with energy class equal or higher than A, in accordance with Decree-Law 118/2013, of 20th August 2013;

• Building where the execution of construction works, reconstruction, modification, extension and maintenance, improve their energy class in at least two classes;

• A reduction of up to 50% of property tax may be applied to properties that are solely affected to the production of energy from RES.

2.1.4 Future foresight/future plans

It is foreseen that Portuguese legal rules that approach investments in the sector will be revised and readjusted. In the future, the viability of these investments should arise from commercial plans and regulated tariffs. Yet, the scientific and technological developments such as energy from the waves or PV should continue to be incentivized. A recovery of investments is expected befitting from European Union’s commitment to reinforce the interconnections in southwest Europe, from the increasing number of incentives directed towards the growth of the share of RES in production mix, from the promotion of energy efficiency measures and from the development of smart grids and smart meters in accordance with the priorities agreed in both the Europe 2020 Strategy and Partnership Agreement for Portugal 2014-2020 [3].

Due of the stable relationships with commercial partners in transmission and distribution of energy and because historically there have been no retroactive changes to legislation, it is not expected that investments in wind farms be affected by any future regulatory modifications. Extended regulated tariffs after 2020 and the market facilitator offtake obligation prolongs these favourable conditions [6].

However, Portugal possesses a significant electricity tariff debt, which could adversely affect the availability of financial incentives for smart grid and innovation programs.

Electricity tariff deficits occur in case the regulated components in the retail price for electricity are set below the cost by the energy companies (in this case EDP Distribuição).

The deficit accounted for 4.4 billion € in 2013 which corresponded to roughly 2.6% of the national GDP. The creation of the tariff deficit was partly explained by the rocketing amount of renewable subsidies made available due to the increase in installed RES capacity subject to FiT. The capacity addition lead to an increase of RES support from 528 million € to 752 million € between 2009 and 2011 [11].

This led to the inclusion of restrictive measures to reduce tariff into the economic programme for Portugal by the European Commission, curbing RES support and revising remuneration schemes (e.g. for co-generation) [11]. In return, this partly caused a 1.2% rise of network charges for low normal voltage tariffs, to be borne by all residential customers [12].

Driven by objectives of the broader “Commitment to Green Growth”, Portugal is seeking to achieve ambitious goals such as:

• Reaching 31% renewable energy in gross end-consumer power consumption by 2020 and 40% in 2030;

• Increasing self-consumption to 300 MW by 2020, lowering prices and allowing for the sale of excess production to the national grid;

• Decreasing the price of renewable energy by 30-40%;

• Reducing the Public Administration’s energy consumption by 30% in 2020 and 35% in 2030;

Deliverable No. 2 | Smart Grids Business Models and Market Integration 21

• Establishing energy interconnection, with the goals of 12% by 2020 and 25% by 2030;

• Reducing the energy consumption of buildings by 25% in 2020 and 30% in 2030;

• Encouraging export of renewable energy to other EU countries.

The IEA [5] indicates several recommendations for energy policies that Portugal’s government should take in the next years. The main recommendations are:

• Prepare an annual energy policy statement, a monitoring tool which examines implementation of energy policy;

• Develop energy plans and scenarios to 2030 and beyond consulting stakeholders to improve to understand new energy realities;

• Pursue the development of interconnections with neighbouring countries, facilitating RES integration and security of supply;

• Start the phased and cost-effective introduction of smart meters across SME and commercial sectors;

• Incorporate the additional cost of RES energy in end-user electricity prices in a transparent manner and monitor the electricity tariff deficit closely.

2.2 Norway

2.2.1 National directives

Much of the legal framework in Norway is based on decisions in EU due to the agreement of the European Economic Area (EEA). The relevant regulations for supporting integration of DER in Norway are typically motivated by environmental/climate mitigation causes, mainly aimed towards renewable energy sources.

The Green Certificate market

After Directive 2009/28/EC, Norway's goal of reaching a renewable share of 67.5% of total energy production in 2020, motivated the establishment of a joint green certificate market with Sweden. Renewable power producers receive one certificate per MWh, and the electricity suppliers have a statutory obligation to buy an amount of green certificates corresponding to a given share of the supplier's total sales volume. The joint market allows Norwegian suppliers to purchase certificates from Swedish producers, and vice versa. The common goal is to increase the renewable energy production by 28.4 TWh from 2012 to 2020 [13]. Norway will finance 13.2 TWh and Sweden will finance 15.3 TWh of the certificates each, independent of the division of production between the countries. The green certificate market started up in 1st January 2012 [14]. There is no requirement regarding size of the generation unit, as long as it uses renewable energy sources [13].

The plusskunde scheme (small prosumers)

The Norwegian regulator, NVE2, defines the term "plusskunde" (translated to "plus-customer") as a grid-connected prosumer whose net export of power is below 100 kW at all times. Such a prosumer can sign a plusskunde agreement with their DSO, and the customer is then getting a reduced network tariff for the net energy fed into the grid (compared to the network tariff other generation units have to pay) [15]. Net exported kWh the plusskunde will only be billed per kWh according to a marginal loss rate which depends on the impact that the plusskunde's exported power has on local grid losses. This marginal loss rate is mostly negative, meaning that the plusskunde earns money per net

2 NVE = The Norwegian Water Resources and Energy Directorate

Deliverable No. 2 | Smart Grids Business Models and Market Integration 22

kWh exported, in addition to revenues from selling the electricity. The prosumers with a plusskunde agreement do not pay taxes for their self-consumed electricity, even though this is not established by law at present. This exemption is practiced for all prosumers with solar panels [16].

A plusskunde may be approved for certificates for their surplus electricity production or the total production, without losing the plusskunde benefits. For green certificates to be granted for the total production, installation of an extra metering device, metering the total production, is required. In Norway, the green certificate scheme is rarely economically attractive for small prosumers. To be approved for green certificates, there is a fee of minimum 15,000 NOK for the smallest generation units [17].

Building regulations

Building regulations are encouraging buildings with low (net) energy consumption, which can be achieved by e.g. heat pumps, district heating, non-fossil boilers or solar collectors. Since July 2010, energy performance certification of buildings has been mandatory, as to increase the interest in energy effective solutions. The directive regarding technical requirements for constructions (Byggteknisk forskrift, TEK10) was revised in January 2016, including reduced requirements for buildings with their own renewable electricity generation (e.g. solar panels). The precondition is that the electricity production is at 20 kWh/m2 of total heated useable floor area [13].

2.2.2 Integration into existing grids

The number of granted green certificates has been low in Norway compared to Sweden. This is partially because most of the renewable power plants in Norway are small (≤ 10 MWp) hydropower plants with a small cumulative installed capacity. At January 2017, 565 small power plants have been approved by NVE to receive green certificates for their electricity. All of these are small hydropower plants, with a total capacity of 1.3 GWp. 92% of the power plants were granted certificates for the total production, while the rest only for parts of the production. In addition, many of the applications for constructing power plants have been rejected due to causes such as negative influence on biodiversity, fish populations, protected watercourses and outdoor activities. Only three PV installations have been granted green certificates in Norway, all of which are larger units (the smallest one is rated 70 kWp) [18].

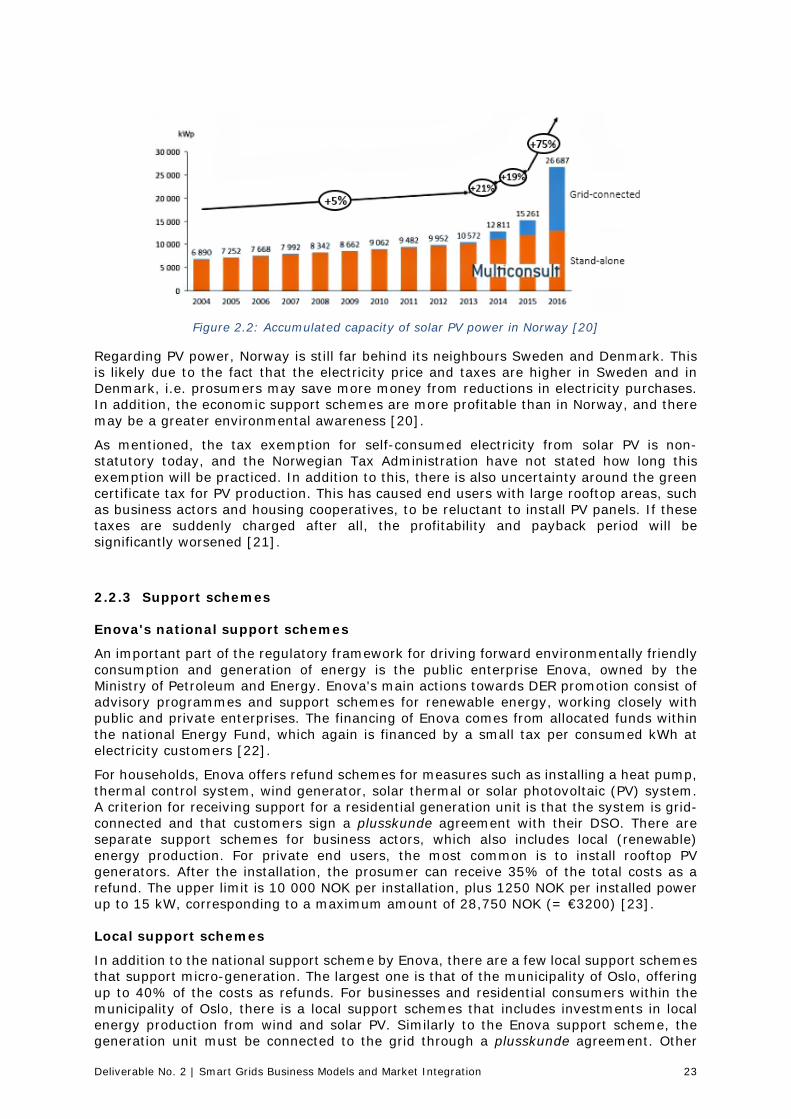

Although installation of small solar PV units on consumer level still has a long payback period due to the high investment costs, there is an increasing number of prosumers being connected to the grid. The exact number of prosumers in Norway is unknown, but it is estimated that the number of registered plusskunde prosumers is approximately 700 at April 2017 and continuously increasing [19]. Especially in 2016, the number of larger PV installations has increased among public/commercial buildings, such as storage buildings, supermarkets and educational facilities. Of the approximately 11.4 MWp installed capacity in 2016, 10 MWp was grid-connected and 7.4 out of 11.4 MWp was connected to commercial buildings. The accumulative capacity of installed PV is shown in Figure 2.2 [20].

Deliverable No. 2 | Smart Grids Business Models and Market Integration 23

Figure 2.2: Accumulated capacity of solar PV power in Norway [20]

Regarding PV power, Norway is still far behind its neighbours Sweden and Denmark. This is likely due to the fact that the electricity price and taxes are higher in Sweden and in Denmark, i.e. prosumers may save more money from reductions in electricity purchases. In addition, the economic support schemes are more profitable than in Norway, and there may be a greater environmental awareness [20].

As mentioned, the tax exemption for self-consumed electricity from solar PV is non-statutory today, and the Norwegian Tax Administration have not stated how long this exemption will be practiced. In addition to this, there is also uncertainty around the green certificate tax for PV production. This has caused end users with large rooftop areas, such as business actors and housing cooperatives, to be reluctant to install PV panels. If these taxes are suddenly charged after all, the profitability and payback period will be significantly worsened [21].

2.2.3 Support schemes

Enova's national support schemes

An important part of the regulatory framework for driving forward environmentally friendly consumption and generation of energy is the public enterprise Enova, owned by the Ministry of Petroleum and Energy. Enova's main actions towards DER promotion consist of advisory programmes and support schemes for renewable energy, working closely with public and private enterprises. The financing of Enova comes from allocated funds within the national Energy Fund, which again is financed by a small tax per consumed kWh at electricity customers [22].

For households, Enova offers refund schemes for measures such as installing a heat pump, thermal control system, wind generator, solar thermal or solar photovoltaic (PV) system. A criterion for receiving support for a residential generation unit is that the system is grid-connected and that customers sign a plusskunde agreement with their DSO. There are separate support schemes for business actors, which also includes local (renewable) energy production. For private end users, the most common is to install rooftop PV generators. After the installation, the prosumer can receive 35% of the total costs as a refund. The upper limit is 10 000 NOK per installation, plus 1250 NOK per installed power up to 15 kW, corresponding to a maximum amount of 28,750 NOK (= €3200) [23].

Local support schemes

In addition to the national support scheme by Enova, there are a few local support schemes that support micro-generation. The largest one is that of the municipality of Oslo, offering up to 40% of the costs as refunds. For businesses and residential consumers within the municipality of Oslo, there is a local support schemes that includes investments in local energy production from wind and solar PV. Similarly to the Enova support scheme, the generation unit must be connected to the grid through a plusskunde agreement. Other

Deliverable No. 2 | Smart Grids Business Models and Market Integration 24

examples of local support schemes are those of the municipality of Hvaler and the county of Vestfold, with smaller investment support [24].

In April 2016 the Norwegian Environment Agency was given the responsibility of administrating a new support scheme for municipalities, named Klimasats. The municipalities may apply for economic support for all actions that either reduce emissions of greenhouse gases or that contribute to the transition towards a low-emission society. The projects may be in cooperation with local businesses, organizations or private persons, but the municipality must have an active role [25].

2.2.4 Future foresight/future plans

The Norwegian regulator has expressed that a transition from energy-based to capacity-based tariffs is wanted. This may cause self-consumption for prosumers to be less profitable, as today they are mainly saving money per kWh not extracted from the grid. As the new tariffs will be reflecting only the marginal losses, the energy-based part of the electricity bill will be smaller. As most prosumers with PV panels are producing power outside their peak consumption, the power-based part of the bill may be as large as for an end user without local generation. The Norwegian Regulator, NVE, has indicated different tariff models through a hearing, but have not yet presented any final suggestions [26], [27].

2.3 United Kingdom

2.3.1 National directives

The UK Government has a number of road maps and incentives in place to encourage the development of a low carbon energy system across the UK.

UK Government targets, outlined in the UK Government Low Carbon Transition Plan [28], state that 30% of electricity will be generated from renewable energy sources by 2020. The devolved Scottish Government has also set its own ambitious targets, aiming for 100% of electrical demand to be met from renewable energy by 2020 [29].

The UK undertakes a process of agreeing ‘Carbon Budgets’. This implements a restriction on the total amount of greenhouse gases that the UK will emit over a 5-year period. The most recent budget was set in July 2016 for the period 2028 – 2032. If emissions rise in one sector, they must be reduced in another to ensure the budget of 1,725 million tonnes of CO2 equivalent is not exceeded. This will result in a reduction in carbon emissions of 57% by 2030 compared to 1990 levels; this is a tougher restriction than that imposed by the EU which requires a 40% cut by 2030 on 1990 levels.

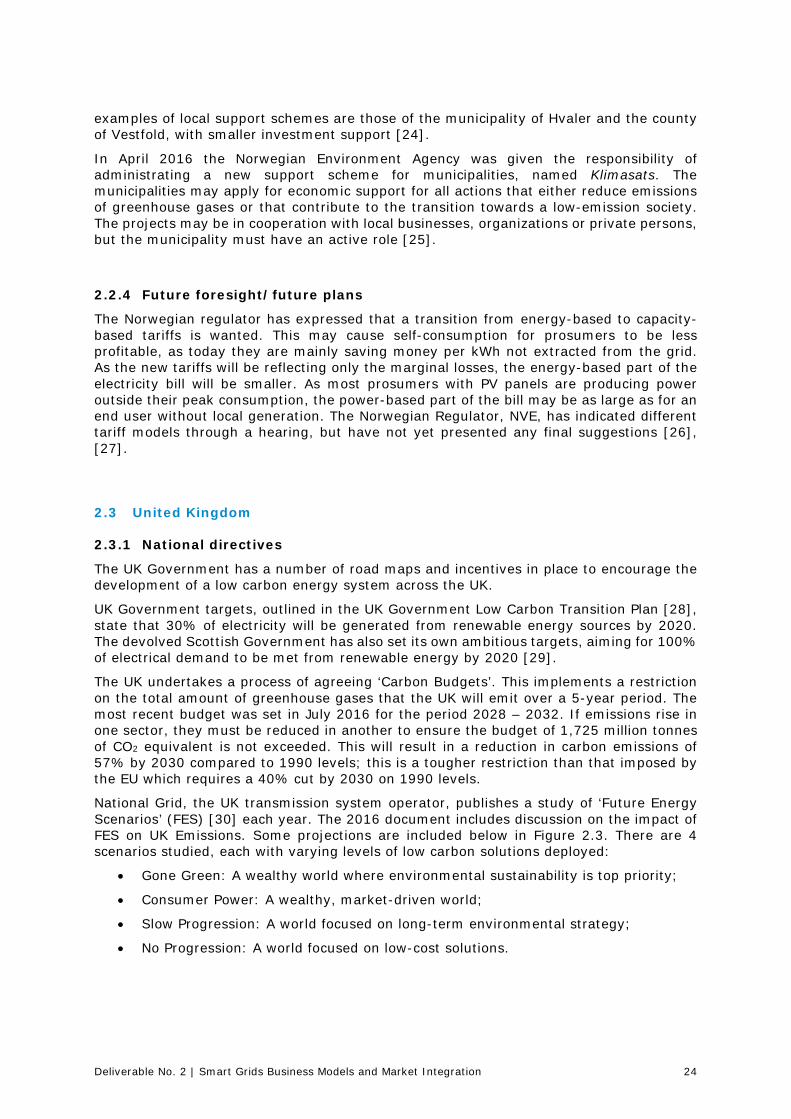

National Grid, the UK transmission system operator, publishes a study of ‘Future Energy Scenarios’ (FES) [30] each year. The 2016 document includes discussion on the impact of FES on UK Emissions. Some projections are included below in Figure 2.3. There are 4 scenarios studied, each with varying levels of low carbon solutions deployed:

• Gone Green: A wealthy world where environmental sustainability is top priority;

• Consumer Power: A wealthy, market-driven world;

• Slow Progression: A world focused on long-term environmental strategy;

• No Progression: A world focused on low-cost solutions.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 25

Figure 2.3: Projection of future UK CO2 emissions under the four scenarios studied in the National

Grid Future Energy Scenarios

The Climate Change Levy (CCL) is a tax on UK business energy use. The final supply recipient of electricity generated from renewable sources and combined heat and power were eligible for tax exception for generation before 1st August 2015. Levy Exemption Certificates (LEC) provided suppliers with evidence to the UK tax authority that electricity supplied to a UK business customer was CCL exempt. The final customer realised the exemption from the tax.

The Renewable Energy Guarantees of Origin (REGO) scheme provides transparency to consumers about the proportion of electricity that suppliers source from renewable generation. One REGO certificate is issued per MWh of eligible renewable output to generators of renewable electricity. This is evidence to the final customer that a given share of energy was produced from renewable sources.

Renewable Support Tariffs

There are two schemes in place to support the development of renewables in the UK:

• Feed-in Tariffs (FITs) for sub-5 MW generation

• Renewable Obligation Certificates (ROCs) for generation with rated export of 5 MW and greater, in March 2017 the ROC mechanism was replaced by Contracts for Difference (CfD).

Feed-in Tariffs are awarded to generators smaller than 5 MW in capacity, offering £/kWh rates that vary depending on the capacity and the generating technology used. FIT prices are set by the regulator Ofgem (Office of Gas and Electricity Markets) each year. This support mechanism is aimed at smaller generators to encourage the deployment of generation at a domestic scale. An example of FIT payments awarded to Solar PV generation is available in [31].

ROCs were introduced to the UK market in 2002, replacing an earlier incentive mechanism. ROCs introduced a significant incentive for renewable generation development in the UK. Under the scheme, generators are rewarded a ROC for each MWh of energy produced by renewable energy sources. The value of ROCs is set at a fixed rate for each year and varies in line with the Retail Price Index (RPI). The numbers of ROCs awarded per MWh varies depending on the technology to encourage investment in less-demonstrated technologies, such as marine energy. Generators can trade ROCs with other parties, with the certificates ultimately used by suppliers to demonstrate that they have met their obligations to supply a certain percentage of energy supply via low carbon sources [32]. The average ROC price in 2016 was £42.65 [33]. ROCs are only available to new generators until March 2017 [34] when they will be replaced by CfDs.

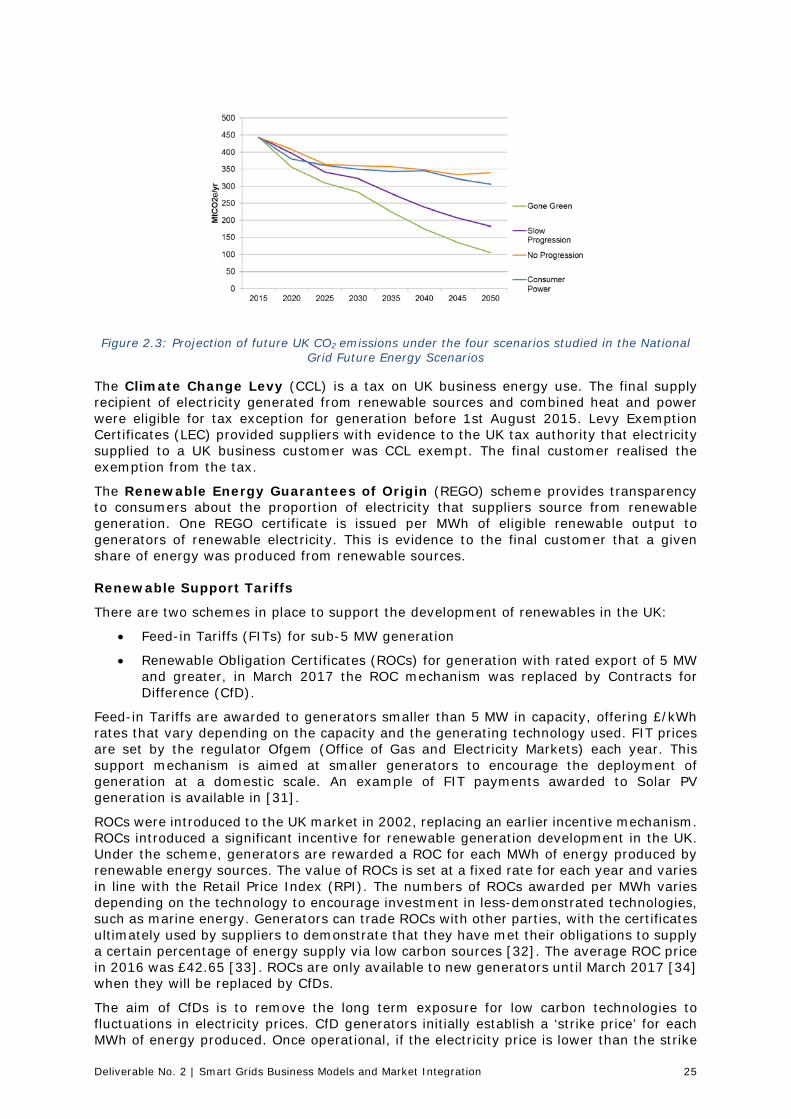

The aim of CfDs is to remove the long term exposure for low carbon technologies to fluctuations in electricity prices. CfD generators initially establish a ‘strike price’ for each MWh of energy produced. Once operational, if the electricity price is lower than the strike

Deliverable No. 2 | Smart Grids Business Models and Market Integration 26

price, a top up is paid to low carbon generators. If the electricity price is higher than the strike price, then low carbon generators must pay back the difference. The generators remain participants in the wholesale energy market. The diagram in Figure 2.4 provides a demonstration of the CfD concept.

Figure 2.4: Diagram of how CfD will operate

The results from the first CfD auction in February 2015 allocated a total of 2.1 GW of contracts with strike prices ranging from £50/MWh - £119/MWh across a range of renewable technologies [35].

Using onshore wind as an example, the previous ROC price of £42 plus the wholesale price of electricity would on average equate to approximately £80 per MWh. The CfD contract will not vary with wholesale electricity price, and therefore the cost per MWh is guaranteed over period of contract, e.g. 20-25 years.

Smart meter rollout The UK Government and energy regulator have driven, through the energy suppliers, roll-out of smart meters to homes across the UK.

The Early Rollout Obligation (ERO) [36] was announced as part of the Rollout Strategy in 2015. It required large energy suppliers to have installed, and enrolled with the Data Communications Company, a minimum number of smart meters by February 2017. The long term aim is to roll out 53 million gas and electricity meters to all homes and small businesses in the UK by the end of 2020.

The Data and Communications Company (DCC) was established in 2013 [37] and is responsible for linking all smart meters to the systems of energy suppliers, network operators, and energy service companies. DCC will develop and deliver the data and communications through external providers. The Smart Energy Code (SEC) is a new industry code which sets out the terms for the provision of the DCC’s services and specifies governance and management of smart metering.

The technical requirements of UK smart meters were defined through a consultation process, run by the UK Government [38]. The resultant document details all of the technical requirements for both gas and electricity smart meters. One important requirement is that any smart meter installed will allow switching of suppliers i.e. if supplier A installs your

Deliverable No. 2 | Smart Grids Business Models and Market Integration 27

smart meter, you will be able to move to Supplier B without having to install a new smart meter or seek any permissions for using the smart meter with another supplier.

The cost of the Smart Meter rollout is itemised in Table 2.2. The costs to suppliers will be refunded though consumer energy bills. The recent cost–benefit analysis performed by the UK Government [39] proposed there is £5 billion of net benefits to consumers, and £8.25 billion of net benefits to suppliers, achieved by rolling out smart meters.

Table 2.2: Costs of Smart Meters [39]

Item Cost (£ bn) Meters, their installation and operation, and the In-Home Displays (IHDs)

5.44

DCC related costs, including communications hubs provision

3.13

Energy suppliers’ and other industries’ IT system costs

1

Industry governance, organisational and administration costs, energy, pavement reading inefficiency and other costs

1.42

Total 10.99

The most recent progress report from the government on smart meter installations [40] states that a total of 540,100 smart meters were installed by large energy suppliers in the first quarter of 2016. The growth in the number of smart meters installed is presented in Figure 2.5 below.

Figure 2.5: Increase in number of installed smart meters in the UK [40]

2.3.2 Integration into existing grids

The introduction of renewable incentives in 20023 led to a sharp growth in the installed capacity of renewable generation at transmission and distribution level. More details on these incentive schemes are provided in Section 2.3.1.

On the transmission system, the ‘Connect and Manage’ scheme was introduced in 2011 to ensure renewable generation was provided accelerated connection dates ahead of

3 Renewable Obligation was introduced in 2002, with Feed-in Tariffs following in 2010

Deliverable No. 2 | Smart Grids Business Models and Market Integration 28

necessary reinforcement; the export from this generation was managed within the capacity limits of the existing system with compensation for export curtailment paid to generators by the System Operator.

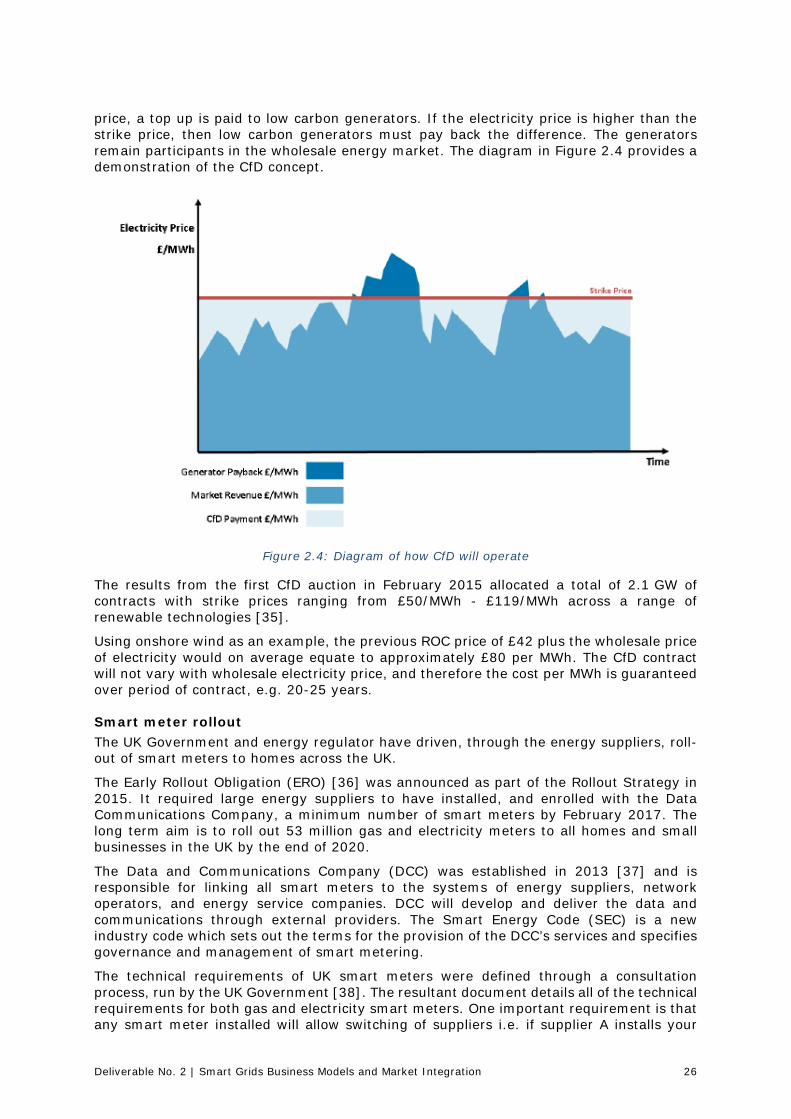

The graph below in Figure 2.6 demonstrates the increase in Connect and Manage generator capacity. It is likely that without the Connect and Manage scheme, many of these developments would have been significantly delayed, awaiting transmission reinforcement.

Figure 2.6: Cumulative contracted capacity connected to Transmission level under the Connect and

Manage scheme in the UK [41]

The projection of distribution network installed generation capacity, under National Grid’s ‘Slow Progress’ scenario, is presented in Figure 2.7.

Figure 2.7: Projected installed capacity of distribution generation, based on Slow Progress Scenario

[30]

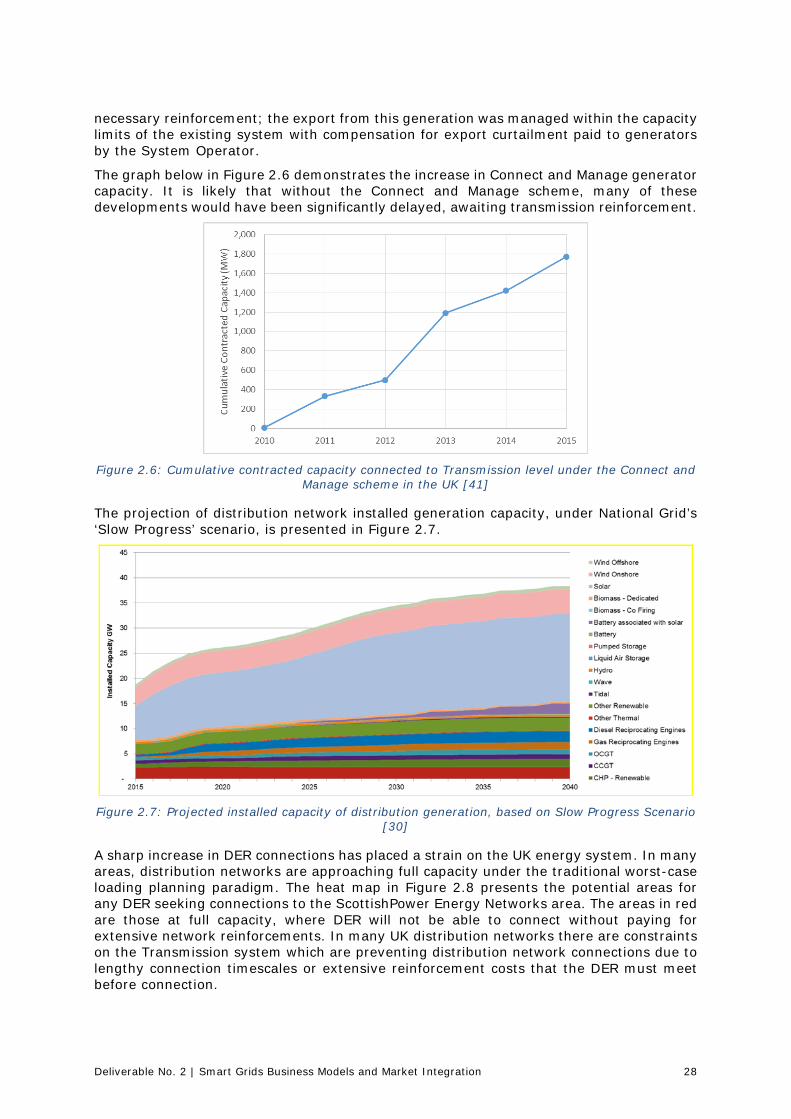

A sharp increase in DER connections has placed a strain on the UK energy system. In many areas, distribution networks are approaching full capacity under the traditional worst-case loading planning paradigm. The heat map in Figure 2.8 presents the potential areas for any DER seeking connections to the ScottishPower Energy Networks area. The areas in red are those at full capacity, where DER will not be able to connect without paying for extensive network reinforcements. In many UK distribution networks there are constraints on the Transmission system which are preventing distribution network connections due to lengthy connection timescales or extensive reinforcement costs that the DER must meet before connection.

Deliverable No. 2 | Smart Grids Business Models and Market Integration 29

Figure 2.8: Example of a distribution heatmap from SP Energy Networks

To address these constraint issues, DSOs are having to develop alternative connection options for DG developers.

In addition to capacity constraints, the increase in DER has created a number of wider system issues that have been documented in National Grid’s System Operability Framework [42] document:

• Lack of visibility and coordination at transmission level; • Low frequency demand disconnection and fault ride through capabilities; • System frequency issues due to the increase of inverter connected technologies and

reduction in spinning machines.

Electric Vehicles (EV) are a significant part of the progress towards reducing the carbon emissions from transport. EV technology has developed significantly in recent years and is discussed in greater detail in the WP1 Report [43].

Recent figures suggest that the Government is falling behind EV rollout targets. While there has been an increase in the number of EVs owned in the UK, the increase has not been as great as initially predicted.

A statistical release in September 2016 [44] notes that in the first quarter of 2016, there was a 31% increase in the number of EVs registered for the first time in the UK, 1% of the total number of new vehicle registrations. This same document captures public attitudes towards electric vehicles in the UK. Attitudes are changing slowly but there has not been a massive swing towards electric vehicles despite the incentives in place.

The majority of motorway service stations now have some fast charging points, and many cities and towns across the UK have dedicated parking bays for electric vehicles [45].

2.3.3 DER support schemes

There are a number of funding support schemes available to renewable energy developers in the UK [46]. Such schemes cover different sizes of investment, from large multi-MW wind farms to community groups looking to install small-scale DER schemes.

The Green Investment Bank [47] is an investment bank created by the UK Government, the sole shareholder, to provide initial capital to invest in the UK Green Economy. The Green Investment Bank has invested in every part of the UK and across all target sectors, including energy efficiency, waste and bioenergy, offshore wind and onshore renewables. Project expenditure ranges from £1 billion down to £2 million, with additional funds set up specifically to target smaller-scale green investments.

As an example of a smaller funding body, ‘Local Energy Scotland’ [48] provides support and funding opportunities to local communities and rural businesses. Funding support includes a start-up grant, pre-planning loan, infrastructure and innovation fund, and post-

Deliverable No. 2 | Smart Grids Business Models and Market Integration 30

consent loans. There a number of similar bodies to this across the UK. These bodies are separated by country as this type of power has been devolved to individual nation governments.

In addition to funding for developers, there is support available for individuals to purchase electric vehicles, and for installation of EV charging infrastructure. As long as the vehicle meets certain conditions [49] the government grant will contribute 35% of the cost of the car, up to a maximum of either £2,500 or £4,500 depending on the model or 20% of the cost of a van, up to a maximum of £8,000. Since the launch of the grants, there have been 80,239 eligible cars registered [50].

2.3.4 Future foresight/future plans

The change in subsidies and support schemes in the UK, coupled with changes in government personnel and policy decisions, has resulted in a reduction in confidence in the UK renewable energy industry. Connection applications for new developments at distribution level have reduced significantly according to DSOs.

Regardless of this, there are still significant planned infrastructure reinforcements that are required to accommodate the large volume of contracted, but not built, generation that is due to connect in the coming years.

The government has made some attempts to understand what is required of them to ensure a low carbon energy future is realised. A 2015 consultation launched by the Parliamentary Committee on Energy and Climate Change [51] asked for industry stakeholders to provide feedback on the current electricity system and how changes could be made to improve upon flexibility of the system, whole system coordination, improve the connection process for developers and maintain value for money for customers. Stakeholders were invited to give oral evidence at several meetings during the first half of 2016. Three reports were published in the second half of 2016 summarising all that was learned and highlighting changes required to obtain future goals.

In 2016 the regulator, Ofgem, and the department for Business, Energy and Industrial Strategy (BEIS) 4 published a number consultation documents on system flexibility and quicker and more efficient connections to the network.

The shift towards whole system coordination, and the interaction of distribution with transmission is the focus of the UK energy industry at the moment, and in particular, the creation of a Distribution System Operator and development of the overall System Operator role which has the potential to introduce more control and ancillary services to distribution-connected generation. Democratisation of the energy market can increase competition and lead to lower costs for users of the system.

2.4 Germany

2.4.1 National directives

In the early 2000, the German Federal Government started to develop a legislative proposal to increase the share of RES in the German energy mix in the following years. The main driver for the initiative was climate and environmental protection and the reduction of energy supply costs, considering long term external effects caused by conventional energy resources [52]. There are different kinds of national directives used in Germany to promote RES and improve their economic efficiency.

4 Formerly Department of Energy and Climate Change (DECC)

Deliverable No. 2 | Smart Grids Business Models and Market Integration 31

Fixed feed-in tariffs

The first national directive specified in the German Renewable Energies Act (Erneuerbare-Energien-Gesetz, EEG) are fixed feed-in tariffs. They were introduced in the first amendment Act in 2010 for the EEG 2009 to promote the installation of RES and are designed in line with the currently installed RES capacity. The tariffs are fixed for 20 years starting with the commissioning of the RES system. The costs are redirected to the German electricity consumers (apportionment), who have to pay a levy which increases their electricity tariff. The costs are therefore covered by the electricity consumers and are not paid by federal organisations [53].

Feed-In Premium