Embed Size (px)

Citation preview

European Financial Management, 2011doi: 10.1111/j.1468-036X.2011.00604.x

International Capital Flows into theEuropean Private Equity Market

Gael Imad’EddineUniversite Lille Nord de France – SKEMA Business School, 2 rue de Mulhouse, 59020 Lille (France)E-mail: [email protected]

Armin SchwienbacherUniversite Lille Nord de France – SKEMA Business School, 2 rue de Mulhouse, 59020 Lille, FranceE-mail: [email protected]

Abstract

In this paper, we explore the relationship between institutional investors and fundsmanagers, a relatively little studied field in private equity. We study this relationshipwithin the context of international investment flows. We address the followingquestion: When building risk-return exposure to European private companies,which US limited partners (LPs) are more likely to invest in US funds investing inEuropean targets as opposed to in European funds investing locally? We build ourresearch using a two-level analysis. We first look at which US LPs are more likelyto invest in funds focusing on Europe (regardless of whether a US or Europeanfund) to identify the active global players. And second, using only the subsample ofLPs investing in Europe-focused funds, we study which types of LPs are more likelyto provide capital to European funds investing locally as opposed to US funds witha European focus. We find that financial institutions with facilities in Europe, suchas banks and insurance companies, are more prone to invest directly in Europeanfunds. This is consistent with the transaction cost hypothesis whereby LPs maybenefit from lower costs to access valuable information to screen European funds.The presence of local facilities may further capture size effects. We also find thatpension funds often invest directly in European funds although those funds do not

We would like to thank Yasuhiro Arikawa, Jean-Gabriel Cousin, Douglas Cumming,Eric De Bodt, Michel Levasseur, Hideaki Miyajima, Mark Kamstra, Piet Sercu, LaurentVilanova, Peter Wirtz and the anonymous referee for their comments, as well as participantsof the European Financial Management Symposium 2010 Entrepreneurial Finance &Venture Capital Markets and the seminar and conference participants of the Lille Schoolof Management Research Center, the KUL-LSM Finance Workshop, the Waseda UniversityFinance and the University of Lyon. All remaining errors are our responsibility.

C© 2011 Blackwell Publishing Ltd

2 Gael Imad’Eddine and Armin Schwienbacher

possess local facilities in Europe. This may be due to their larger size that drivesthem to invest abroad or their increased experience in investing in private equity.

Keywords: private equity, international capital flows, fund management

JEL classification: F21, F3, G23, G24

1. Introduction

In September 2007, CalPers, the giant Californian pension fund, and Standard LifeInvestment Private Equity (SLIPE), a UK based investment firm, announced that CalPerswas committing €400 million into European private equity. ‘We are delighted to havebeen selected for this mandate by CalPers, the largest public pension fund in the US.This is testimony to the expertise and professionalism of our private equity team andour strong track record in the European private equity market. This is our fourth majorsegregated mandate from a North American client. Over 50% of our assets undermanagement are now from North America’,1 declared David Currie, Chief ExecutiveOfficer of SLIPE. This is just one of many other examples of partnerships between USinstitutional investors and European fund managers. The private equity2 (PE) markethas evolved into a truly global market in the last two decades, creating important capitalflows around the world.

On the one hand, such flows have been witnessed through the internationalisation ofinvestment activities of funds themselves (Megginson, 2004), investing more and moreglobally in companies outside their own national borders and continent. On the otherhand, this globalisation trend is also observed at the fundraising level of PE funds thatnow raise capital internationally. Institutional investors have become increasingly activein investing directly into PE funds outside their home country, making countries withlarge institutional investors exporters of PE capital and thus important fund providers forventure capital (VC) and buyout funds worldwide. The European market has benefitedfrom the flow of capital from US limited partners (LPs), who are major contributors tothe international PE market. PEREP Analytics, a new data provider for the EuropeanPE industry, indicates that over 25% of the capital supplied to European PE funds stemsfrom North America. Therefore, developing capabilities and reputation to attract capitalcommitments from US LPs are a key element of successful fundraising for Europeanfund managers active in private equity. This in turn can be beneficial to Europeancompanies (namely, for startups receiving venture capital as well as mature companiesfor buyout capital) as it facilitates their access to more competitive PE capital throughincreased supply of capital.

This paper aims at contributing to this gap in the literature by providing a betterunderstanding about which European-focused funds (either US or European funds) aremost capable of attracting US commitments, and which US LPs are more willing toinvest directly in European funds rather than US funds with a European focus. Morespecifically, our analysis examines how US investors provide financing to European

1 This information is available on both the CalPers and SLIPE websites: http://uk.standardlifeinvestments.com/content/press/press_releases/calpers_commits_400_million_euro_to_european_private_equity.html2 ‘Private equity’ includes both venture capital and buyout.

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 3

companies that aim at attracting VC or buyout capital, either by receiving capital fromUS funds with a European investment focus or European funds with a local investmentfocus.

This research question provides insights into the access of US investors to marketsoutside their home country. Since the US market has become more mature andcompetitive, investors have been seeking new opportunities worldwide (Megginson,2004). Understanding what affects global PE capital commitments is important fromthe LP perspective, given the potential difficulties in investing in less mature markets.Investing outside the US leads to additional costs related to differences in the legalenvironment, culture and geographical distance. While US capital also flows to Asiaand (other) emerging markets, the European market is characterised by smaller legal andcultural differences with the US.

This research question also has important policy implications. While US and Europeanfunds with a European focus ultimately fuel European firms, the two strategies arepotentially very different in nature and may have different consequences. The importanceof geographical proximity between the funds and the investee on the value-addingcapacity has been well documented, especially for the venture capital segment (Makelaand Maula, 2008; Bengtsson and Ravid, 2009; Tykvova and Schertler, 2010). A betterunderstanding of what enables European funds to attract large international (especiallyUS) LPs contributes to promoting the development of a more active buyout and venturecapital market in Europe. Several studies have addressed this policy issue from theinvestment perspective (for instance, Diller and Kaserer, 2009) but rarely from thefundraising perspective. Our paper aims at identifying drivers of the development of anactive European market from the fundraising perspective.

Given our specific research question, we focus only on direct investments made byLPs into limited partnership funds in the USA and Europe.3 The distinction betweenfund origin (i.e., whether the fund is from the USA or Europe) and geographical focus(i.e., where the fund invests its capital) is important here, and is, therefore, at the heart ofour analysis. In the context of an LP perspective, the geographical risk-return exposureis indeed better measured by examining the geographical focus rather than fund origin.

Our analysis provides several key results. Since our study is centered on US LPsinvesting in funds with a European focus, we first identify the LPs that are considered asactive ‘global players’ and thus fuel the European PE market, regardless of the countryof origin of the funds. We find that insurance companies, banks and pension funds arethe main providers of US money to European PE target companies, with pension fundsclearly being the largest providers. As predicted by the transaction costs hypothesis, wealso find that financial LPs (i.e., banks and insurance companies) are more likely toinvest in European funds as opposed to US funds. Moreover, LPs with local facilitiesin Europe have a greater propensity to invest directly in European funds, rather thanthrough US based vehicles with a European focus. This means that European fundmanagers (so-called general partners [GPs]) are more likely to get funding from US LPsif LPs have direct facilities in Europe in the form of branch offices. This gives thembetter access to information. This is particularly the case for insurance companies and

3 As robustness, we tried to extend the analysis to Asia, but faced severe lack of observations.LP investments in Asian funds are highly underrepresented in the database we used(VentureXpert). Therefore, we provide here an analysis for US and Europe only, wheredata is more available and, thus, more reliable.

C© 2011 Blackwell Publishing Ltd

4 Gael Imad’Eddine and Armin Schwienbacher

banks. An alternative reason may be that the presence of local facilities proxies for sizeof the LP. Our results are consistent with both stories, although we find no support forcorporate LPs (which favours the former story). Further, we find no significant impacton performance, suggesting that owning local facilities may lead to lower screening costsbut not to selecting better performing European funds.

Pension funds are also more prone to invest in European funds with a local focus ratherthan US funds with a European focus, although they typically do not have facilities inEurope. However, our analysis suggests that the size of capital under pension fundmanagement may allow pension funds to lower average costs of collecting information(i.e., relative of their capital under management). Moreover, they may benefit fromextensive experience. Further investigations provided in the paper point out a possiblereason for this conjecture: when investing in Europe, pension funds predominantlyinvest in less established funds where asymmetric information is relatively more severebut where deal conditions are potentially better.

Our work spans several strands of literature. The first relates to studies on theEuropean VC and buyout market, given our particular focus on this market (see, e.g.,Cumming, 2002; Da Rin et al., 2006; Hege et al., 2009). These studies, however, focuson investments by funds into companies and not capital commitments of LPs into PEfunds. General trends in the globalisation of venture capital are discussed by Megginson(2004), evidencing that cross-border investments by VC funds have become increasinglyimportant. Our study particularly focuses on drivers of cross-border investments fromthe US to Europe.

We further rely on studies focusing on the functioning of the fundraising process forPE funds and LP contracts (e.g., Gompers and Lerner, 1996, 1998; Jeng and Wells,2000; Mayer et al., 2005; Litvak, 2004). Within this strand of research, the paper that isclosest to ours is that by Lerner et al. (2007) that analyses the capital supply by differentinstitutional investors in the USA to PE funds and the associated returns. However, theiranalysis abstracts from geographical focus of investments made. Jeng and Wells (2000)and Mayer et al. (2005) offer an analysis of VC supply for (primarily) Europe, evidencingwhich macroeconomic variables foster the most the supply of capital into the market. Incontrast, Gompers and Lerner (1998) examine what has driven the overall fundraisingactivities in the US market and to what extent its past surges were driven by regulatoryand taxation changes that made private equity more attractive as an alternative asset class.LP agreements are examined in Gompers and Lerner (1996), Lerner and Schoar (2004)and Litvak (2004). We contribute to this strand by examining the source of these funds,in particular the means by which US capital is being allocated to European companies.

Finally, our study relates to the very large literature on international capital flows andits diversification impact on alternative asset classes such as private equity (see, e.g.,Froot et al., 2001; Froot and Teo, 2004). These studies treat private equity as a singleasset class; our study instead focuses on investment funds. Other studies have focused onthis topic in relation to the investment behaviour of style investments (see, e.g., Wermer,2002; Barberis and Shleifer, 2003). The importance of styles within the PE segmenthas been examined by Cumming et al. (2009). Our contribution here is to study thespecific investment strategy adopted by LPs to achieve exposure to the European PEmarket.

The remainder of our paper is structured as follows. The next section provides atheoretical discussion of why different types of LP may affect the choice of investmentstrategy. Section 3 details the source of our data, the sample considered and theconstruction of our variables. Section 4 provides a general overview of capital flows

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 5

Fig. 1. US LPs global players choice of investment.

This figure presents the structure of investment strategy of US LPs for investing in European privatecompanies: the US limited partners can either choose a European private equity fund (with a Europeanfocus) or a US private equity fund with a European focus.

into Europe by relying on summary statistics of our sample. Section 5 presents our mainfindings. Section 6 concludes.

2. Theory

In this section, we develop hypotheses that provide possible explanations as to whydifferent types of fund providers (LPs) may differ in their propensity to invest directlyin European funds with a local focus as opposed to investing in US funds targetingEuropean companies. This is depicted in Figure 1.

2.1. The ‘local facilities’ hypothesis

Investments in private equity are illiquid for many years. Once the money is invested, theLP has to wait up to a decade before getting the investment back. The only way an LPcan penalise a bad GP is to refuse to add money into a new fund. Therefore, acquiringinformation to screen competent GPs is a critical step for an LP prior to making acommitment. The process of reducing information asymmetries, however, bears somecosts that lead to transaction costs for the LP. It seems logical that on average thesecosts would be higher for European funds than for US funds from the perspective of USLPs. We cite as an example the screening costs and the anticipated ex-post verificationcosts, which are aggravated by geographical distance. Another issue is the unfamiliarityof the legal environment; contracting with a partner outside the US legal system incursadditional costs to properly secure the deal because the LP must invest resources to learnabout rights and obligations.

Therefore, we conjecture that transaction costs can be a barrier for US LPs to investdirectly in European funds. We identify two ways to acquire information and therebyovercome these transaction costs. First, LPs with suitable branch offices in Europe are

C© 2011 Blackwell Publishing Ltd

6 Gael Imad’Eddine and Armin Schwienbacher

more likely to invest directly in European PE funds with a local focus, while LPs withoutown facilities in Europe prefer diversifying their portfolio towards European companiesthrough US funds with a European focus. In contrast, US GPs are more likely to beknown by US LPs. Financial institutions such as banks and insurance companies arelikely to have appropriate facilities in Europe to support the direct investment of capitalinto local funds. It is important to note that the branch network is an exogenous factorfrom the perspective of PE investments: it is the legacy from the history of the consideredinstitutions. PE investments are generally a smaller part of the overall activities of LPs.Instead, the extent of the branch network of banks and insurance companies is largelydriven by retail services offered in different countries. However, the existence of thoselocal branches can provide access to local information at lower cost, which may alsopromote capital commitments to local PE funds. This leads us to conjecture that USLPs with local facilities in Europe will be more associated with direct investments intoEuropean funds as opposed to US funds with a European focus.

Another way to acquire information is derived from the financial capacity of the LP.Since screening costs are typically fixed, large players should find it less costly (perdollar invested) to spend money on screening experienced GPs. The financial means ofa university endowment are likely to be smaller than a pension fund. When they decide toinvest abroad, LPs can pay for advice. The quality of this advice depends on the amountspent. Thus, if the LPs do not have local facilities there is always the possibility ofpurchasing the expertise. These fixed costs do not represent the same burden relative tothe size of the overall investment activity. Larger LPs may benefits from scale economies.It is recognised that the largest LPs in the US are pension funds (Lerner et al., 2007).

Note however that local facilities could be also simply capture a size effect.4 Largerinstitutions acting as LPs are more likely to invest directly in European funds for at leasttwo reasons: first, they can reach economies of scale by lowering the research costsper dollar invested; second, they might have exhausted their most valuable investmentopportunities in their home market (here the US market) in terms of talented GPs, giventhe significant amount of capital under management. In both cases, it creates incentivesto invest abroad such as into European funds. In the empirical analysis, we will addressthis alternative explanation in order to disentangle the possible size effect from thepostulated informational effect from local facilities.

2.2. Established participants hypothesis

This second hypothesis builds on the findings of Lerner et al. (2007), namely, that fundproviders that have supplied capital to the VC and buyout markets for a long time havebuilt up significant knowledge that enables them to select and at times participate inthe fundraising of the most promising funds. This avoids that these same fund providersbear the same level of asymmetric information as institutional investors who have onlyrecently started to invest in private equity through direct commitments into individualfunds. Therefore, we expect LPs with significant prior experience in selecting GPs tobe more likely to maintain their European exposure through direct investments intoEuropean local funds as opposed to with US funds with a European focus.

Lerner et al. (2007) document the fact that established LPs have a ‘seat at the table’ attheir US funds; i.e., US GPs may reward their LPs for their earlier contributions so that

4 We thank the anonymous reviewer for pointing this out.

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 7

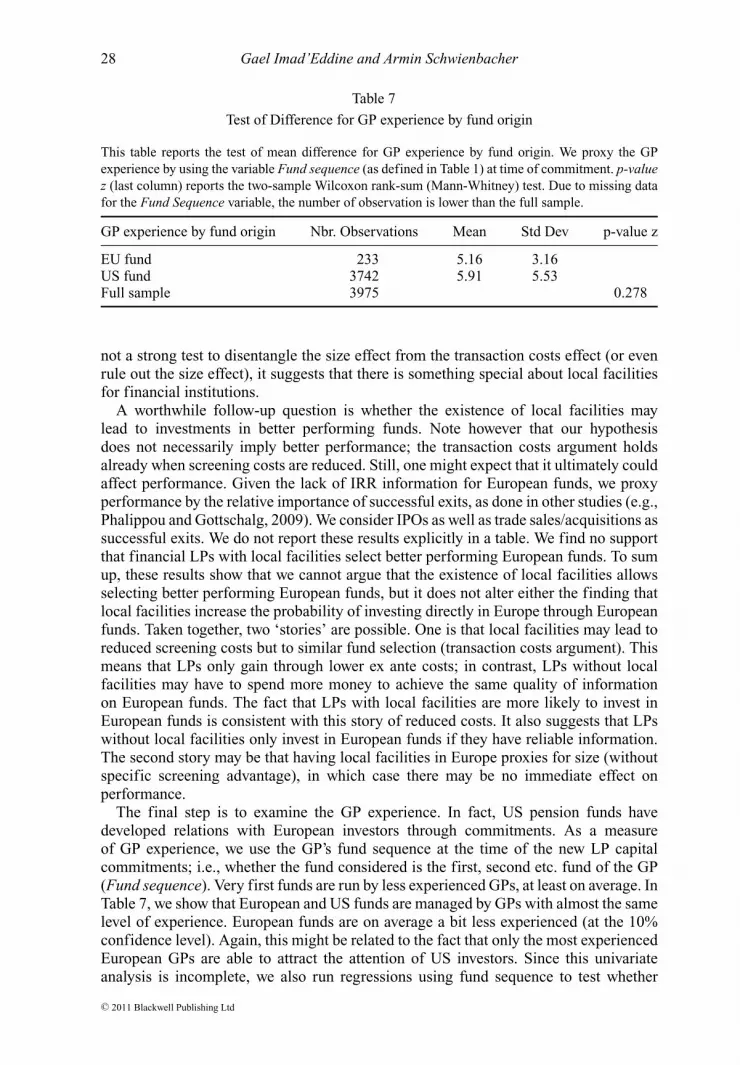

the most successful GPs can restrict the fundraising to former LPs even if they can raisemore money. In case these US GPs are precisely those expanding to Europe, we might aswell expect the opposite result since US LPs prefer to use these privileged opportunitiesto earn higher returns. Whether the ‘experience effect’ or the ‘seat effect’ dominates isan empirical question that we shall examine in Section 4.

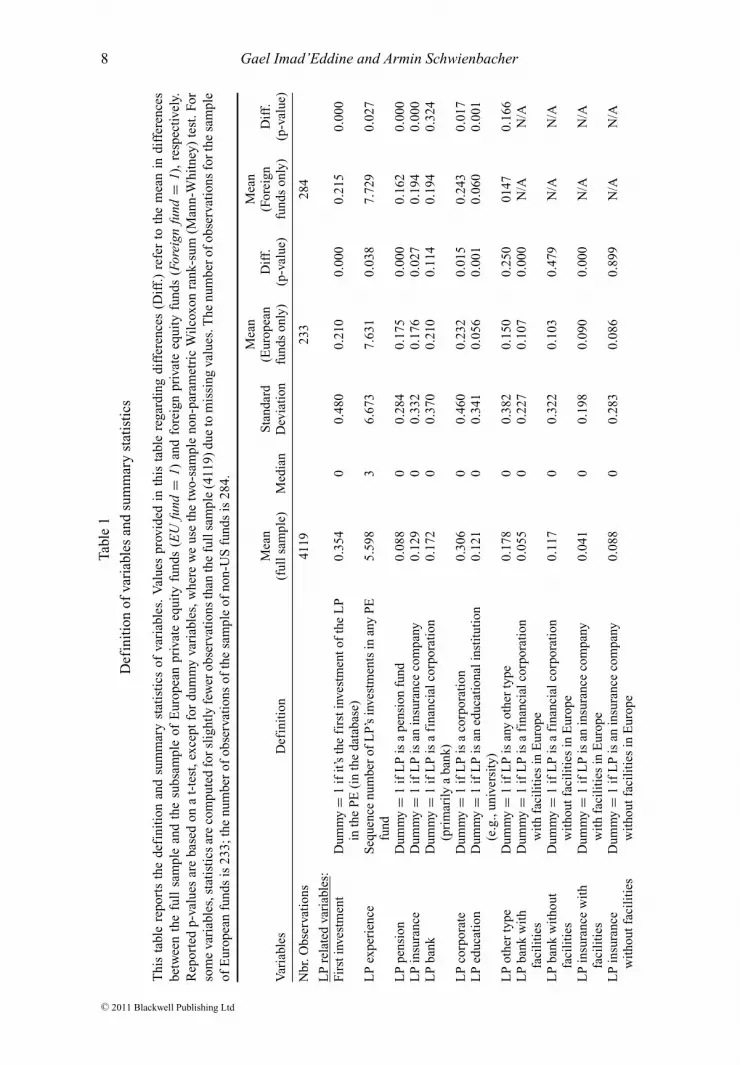

3. Data Source and Sample Selection

We gather information on LP investments into VC and buyout funds from theVentureXpert database (Thomson Financial). This database provides the most com-prehensive information on PE transactions available and is also widely used in research.While most other studies use information on specific deals (direct investments by fundsinto portfolio companies), we primarily rely on a separate database of VentureXpert thatprovides information on LPs that have invested in funds covered by the database. Thisincludes most of the major institutional investors in the USA.

Our sample is limited to US LPs that provide capital commitments into VC and buyoutfunds (and thus we exclude commitments into funds-of-funds) either in the USA or inEurope. We extract all observations on LPs included in the database that have completeinformation on the variables needed for our study. In total, our sample comprises4119 commitments (GP-LP pairs) spanning the period 1981–2002 (the ‘vintage years’).Importantly, we only consider US LPs, given the focus of our research question. Thenationality of the GP is based on the nation of the ultimate owner. European branches ofUS GPs are therefore considered as US GPs.

Variables used in this study are defined in Table 1. However, a note is warranted forthe constructed measures of investment focus of funds, namely, whether a VC or buyoutfund invests in Europe or elsewhere. Since this information is not directly available inthe database (obviously, the nationality of funds is available), we proxy it by lookingat the first three investments a fund has made. A fund with US (Europe, outside theUSA) focus is one that has made at least two of these three investments in the US(Europe, outside the US). By definition, any fund considered as having a Europeanfocus (Focus EU = 1) is also considered a fund with foreign focus (Foreign focus =1).The rationale behind this methodology is that fund managers are most likely to stickto the objectives stated in their prospectus in their first investments, since they are drawnup quickly after the funds have been raised (and thus before market conditions may havechanged). For later investments, fund managers are more likely to drift away from theirstated objectives – either due to strategic considerations or major changes in marketconditions – so that using all investments of a fund may lead to a less precise measureof the fund’s initial geographical focus. Cumming et al. (2009) document this styledrift phenomenon in the PE industry.5 According to a Coller Capital survey of 2008,

5 Coller Capital, a leading institutional investor in private equity, conducted the ‘2008 GlobalPrivate Equity Barometer survey’, which identifies style drift as one of the most importantissues facing institutional investors. Coller Capital reports that style drift by private equityinvestors is perceived negatively by 84% of fund limited partners. The report also confirmsthat 75% of respondents, who are predominately institutional investors, view style driftas important, because style-inconsistent investments could lead to underperformance, andcould indicate that the private equity managers lack the necessary knowledge and skills tosuccessfully manage these portfolios. (Cumming et al., 2009).

C© 2011 Blackwell Publishing Ltd

8 Gael Imad’Eddine and Armin Schwienbacher

Tabl

e1

Def

init

ion

ofva

riab

les

and

sum

mar

yst

atis

tics

Thi

sta

ble

repo

rts

the

defi

niti

onan

dsu

mm

ary

stat

isti

csof

vari

able

s.V

alue

spr

ovid

edin

this

tabl

ere

gard

ing

diff

eren

ces

(Dif

f.)

refe

rto

the

mea

nin

diff

eren

ces

betw

een

the

full

sam

ple

and

the

subs

ampl

eof

Eur

opea

npr

ivat

eeq

uity

fund

s(E

Ufu

nd=

1)an

dfo

reig

npr

ivat

eeq

uity

fund

s(F

orei

gnfu

nd=

1),

resp

ectiv

ely.

Rep

orte

dp-

valu

esar

eba

sed

ona

t-te

st,e

xcep

tfo

rdu

mm

yva

riab

les,

whe

rew

eus

eth

etw

o-sa

mpl

eno

n-pa

ram

etri

cW

ilco

xon

rank

-sum

(Man

n-W

hitn

ey)

test

.For

som

eva

riab

les,

stat

isti

csar

eco

mpu

ted

for

slig

htly

few

erob

serv

atio

nsth

anth

efu

llsa

mpl

e(4

119)

due

tom

issi

ngva

lues

.The

num

ber

ofob

serv

atio

nsfo

rth

esa

mpl

eof

Eur

opea

nfu

nds

is23

3;th

enu

mbe

rof

obse

rvat

ions

ofth

esa

mpl

eof

non-

US

fund

sis

284.

Mea

nM

ean

Mea

nS

tand

ard

(Eur

opea

nD

iff.

(For

eign

Dif

f.V

aria

bles

Def

init

ion

(ful

lsam

ple)

Med

ian

Dev

iati

onfu

nds

only

)(p

-val

ue)

fund

son

ly)

(p-v

alue

)

Nbr

.Obs

erva

tion

s41

1923

328

4

LP

rela

ted

vari

able

s:Fi

rsti

nves

tmen

tD

umm

y=

1if

it’s

the

firs

tinv

estm

ento

fth

eL

Pin

the

PE

(in

the

data

base

)0.

354

00.

480

0.21

00.

000

0.21

50.

000

LP

expe

rien

ceS

eque

nce

num

ber

ofL

P’s

inve

stm

ents

inan

yP

Efu

nd5.

598

36.

673

7.63

10.

038

7.72

90.

027

LP

pens

ion

Dum

my

=1

ifL

Pis

ape

nsio

nfu

nd0.

088

00.

284

0.17

50.

000

0.16

20.

000

LP

insu

ranc

eD

umm

y=

1if

LP

isan

insu

ranc

eco

mpa

ny0.

129

00.

332

0.17

60.

027

0.19

40.

000

LP

bank

Dum

my

=1

ifL

Pis

afi

nanc

ialc

orpo

rati

on(p

rim

arily

aba

nk)

0.17

20

0.37

00.

210

0.11

40.

194

0.32

4

LP

corp

orat

eD

umm

y=

1if

LP

isa

corp

orat

ion

0.30

60

0.46

00.

232

0.01

50.

243

0.01

7L

Ped

ucat

ion

Dum

my

=1

ifL

Pis

aned

ucat

iona

lins

titu

tion

(e.g

.,un

iver

sity

)0.

121

00.

341

0.05

60.

001

0.06

00.

001

LP

othe

rty

peD

umm

y=

1if

LP

isan

yot

her

type

0.17

80

0.38

20.

150

0.25

001

470.

166

LP

bank

wit

hfa

cili

ties

Dum

my

=1

ifL

Pis

afi

nanc

ialc

orpo

rati

onw

ith

faci

liti

esin

Eur

ope

0.05

50

0.22

70.

107

0.00

0N

/AN

/A

LP

bank

wit

hout

faci

liti

esD

umm

y=

1if

LP

isa

fina

ncia

lcor

pora

tion

wit

hout

faci

liti

esin

Eur

ope

0.11

70

0.32

20.

103

0.47

9N

/AN

/A

LP

insu

ranc

ew

ith

faci

liti

esD

umm

y=

1if

LP

isan

insu

ranc

eco

mpa

nyw

ith

faci

liti

esin

Eur

ope

0.04

10

0.19

80.

090

0.00

0N

/AN

/A

LP

insu

ranc

ew

itho

utfa

cili

ties

Dum

my

=1

ifL

Pis

anin

sura

nce

com

pany

wit

hout

faci

liti

esin

Eur

ope

0.08

80

0.28

30.

086

0.89

9N

/AN

/A

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 9

LP

corp

orat

ew

ith

faci

liti

esD

umm

y=

1if

LP

isa

corp

orat

ion

wit

hfa

cili

ties

inE

urop

e0.

145

00.

123

0.15

00.

814

N/A

N/A

LP

corp

orat

ew

itho

utfa

cili

ties

Dum

my

=1

ifL

Pis

aco

rpor

atio

nw

itho

utfa

cili

ties

inE

urop

e0.

160

00.

367

0.08

10.

000

N/A

N/A

LP

fina

ncia

lwit

hfa

cili

ties

Dum

my

=1

ifL

Pis

afi

nanc

ialL

P(i

nsur

ance

orba

nk)

wit

ha

Eur

opea

nfa

cili

ty0.

096

00.

294

0.19

70.

000

N/A

N/A

LP

fina

ncia

lw

itho

utfa

cili

ties

Dum

my

=1

ifL

Pis

afi

nanc

ialL

P(i

nsur

ance

orba

nk)

wit

hout

aE

urop

ean

faci

lity

0.20

60

0.40

40.

189

0.50

8N

/AN

/A

GP

&fu

ndre

late

dva

riab

les:

Fun

dse

quen

ceS

eque

nce

num

ber

ofth

efu

ndat

the

tim

eof

the

deal

5.83

34

5.37

75.

163

0.20

54.

777

0.28

5

Fun

dsi

zeF

und

size

inm

illi

ons

ofU

SD

799.

138

8.5

1092

.711

34.6

0.00

198

2.4

0.09

9V

Cfu

ndD

umm

y=

1if

fund

’sin

vest

men

tfoc

usis

vent

ure

capi

tal

0.43

30

0.49

10.

253

0.00

00.

292

0.00

0

Buy

outf

und

Dum

my

=1

iffu

nd’s

inve

stm

entf

ocus

isbu

yout

0.42

40

0.49

40.

712

0.00

00.

676

0.00

0O

ther

fund

Dum

my

=1

iffu

nd’s

inve

stm

entf

ocus

isne

ithe

rV

Cor

buyo

ut0.

143

00.

350.

035

0.00

00.

032

0.00

0

US

fund

Dum

my

=1

iffu

ndis

from

the

US

0.93

11

0.24

80.

000

0.00

00.

000

0.00

0E

Ufu

ndD

umm

y=

1if

fund

isfr

omE

urop

e0.

057

00.

227

1.00

00.

000

0.82

00.

000

Fore

ign

fund

Dum

my

=1

iffu

ndis

notf

rom

the

US

0.06

90

0.24

81.

000

0.00

01.

000

0.00

0Fo

cus

US

Dum

my

=1

iffu

ndfo

cuse

son

US

inve

stm

ents

0.84

00

0.36

70.

077

0.00

00.

116

0.00

0Fo

cus

EU

Dum

my

=1

iffu

ndfo

cuse

son

Eur

opea

nin

vest

men

ts0.

096

00.

294

0.82

80.

000

0.68

00.

000

Focu

sfo

reig

nD

umm

y=

1if

fund

focu

ses

onno

n-U

Sin

vest

men

ts(i

ncl.

Eur

ope)

0.16

00

0.36

60.

914

0.00

00.

877

0.00

0

EU

Fun

dE

UD

umm

y=

1if

EU

fund

=1

and

Focu

sE

U=

10.

044

00.

205

0.83

70.

000

0.69

00.

000

Mar

ketc

ondi

tion

vari

able

:F

undr

aisi

ngN

atur

allo

gari

thm

ofth

ede

flat

edto

tala

mou

ntra

ised

byth

eP

Ein

dust

ryin

the

cons

ider

edye

ar

10.1

4510

.249

0.92

910

.336

0.06

210

.311

0.01

7

C© 2011 Blackwell Publishing Ltd

10 Gael Imad’Eddine and Armin Schwienbacher

the style drift practice is generally perceived negatively. Therefore, it is unlikely thatthe first investments would deviate from the objectives stated in the prospectus. Theseobjectives were assessed by the LPs to determine their exposure to certain asset classesand geographical diversification. Nevertheless, style drifts exists in private equity andcan occur later in the life cycle of funds based on economic reasons such as majorchanges in market potentials and opportunities.

It is important to note that we only include direct investments by LPs into funds butdo not consider investments made by LPs in private equity through the intermediation offunds-of-funds, who may also offer LPs an exposure to PE investments. This limitationstems from the data available in VentureXpert. To our knowledge, there is no separatedatabase available that would allow us to consider this alternative investment option.This leads to an important limitation of our study that inevitably affects the scope ofour analysis and conclusions. But it should be noted that investments in funds-of-fundsis an even more ‘distant’ way to make investments. As we are concerned with whichLPs are better able to make more direct investments, those opting for funds-of-fundsare even less able to overcome the information asymmetry issue of distant geographicalexposure.

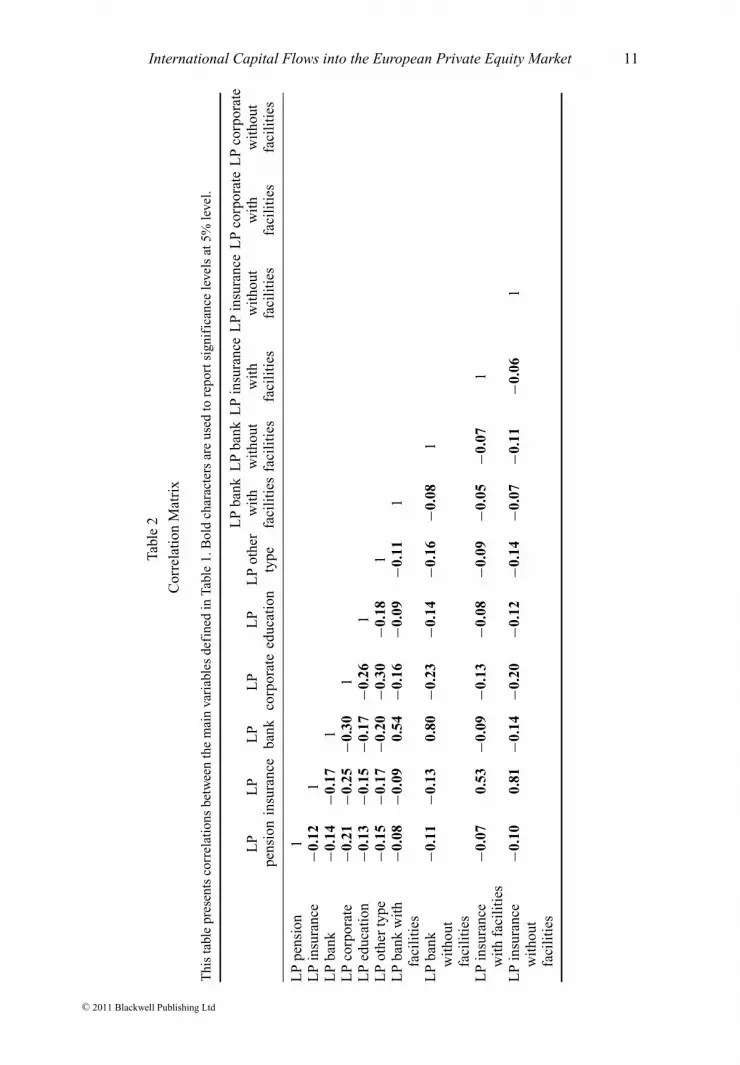

We use several dummies to identify the LP types: insurance companies (LP insurance),banks (LP bank), corporations (LP corporate), educational institutions and endowments(LP education), pension funds (LP pension) and one dummy for all other types (LPother). We also include a VC/buyout dummy in some regressions to allow us to identifythe type of funds. Our database is composed of VC funds, pure buyout funds andsome others funds. We use two definitions of the LP experience: the age of the LP atthe time of the investment (LP experience); and the ‘first investment’ dummy (Firstinvestment). We also include market condition variables. Throughout the analysis, weuse a measure of aggregate PE fundraising (the variable Fundraising).6 Year dummiesare always included unless stated otherwise. Other regression results are available uponrequest from the authors. Apart these three market condition variables, our variablesdo not show any correlation issue in the multivariate analysis. A complete correlationmatrix is provided in Table 2.

Lastly, in order to establish whether an LP owns local facilities in Europe we use theORBIS database provided by Bureau Van Dyck and complement the information bysearching the Internet when necessary. The database offers information on the existenceof subsidiaries and whether it is a sister company (in which case we can also obtaininformation on the parent company). Our variable that captures the existence of localfacilities in Europe takes the value of one if the LP has a subsidiary or a sister firm inEurope at the time of the commitment, and zero otherwise. This variable gives usefulinformation about the presence of the LP in Europe through a subsidiary (or a sistercompany). Our asymmetric information hypothesis would lead us to predict a positiveeffect for financial institutions with local facilities, but not necessarily for pension funds.Local facilities is unlikely to impact corporate LPs either, since these are essentiallyoperational facilities that provide little gains in terms of access to financial investments.

6 As robustness, we considered other market variables that are based on the MSCI IndexEurope and that control for the post-1997 period. These measures are essentially exchangeablein our estimation with our variable Fundraising. Thus, we only include Fundraising to controlfor market conditions. The other coefficients are not affected by the choice of any one ofthese alternative measures.

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 11

Tabl

e2

Cor

rela

tion

Mat

rix

Thi

sta

ble

pres

ents

corr

elat

ions

betw

een

the

mai

nva

riab

les

defi

ned

inTa

ble

1.B

old

char

acte

rsar

eus

edto

repo

rtsi

gnif

ican

cele

vels

at5%

leve

l.

LP

bank

LP

bank

LP

insu

ranc

eL

Pin

sura

nce

LP

corp

orat

eL

Pco

rpor

ate

LP

LP

LP

LP

LP

LP

othe

rw

ith

wit

hout

wit

hw

itho

utw

ith

wit

hout

pens

ion

insu

ranc

eba

nkco

rpor

ate

educ

atio

nty

pefa

cili

ties

faci

liti

esfa

cili

ties

faci

liti

esfa

cili

ties

faci

liti

es

LP

pens

ion

1L

Pin

sura

nce

−0.1

21

LP

bank

−0.1

4−0

.17

1L

Pco

rpor

ate

−0.2

1−0

.25

−0.3

01

LP

educ

atio

n−0

.13

−0.1

5−0

.17

−0.2

61

LP

othe

rty

pe−0

.15

−0.1

7−0

.20

−0.3

0−0

.18

1L

Pba

nkw

ith

faci

liti

es−0

.08

−0.0

90.

54−0

.16

−0.0

9−0

.11

1

LP

bank

wit

hout

faci

liti

es

−0.1

1−0

.13

0.80

−0.2

3−0

.14

−0.1

6−0

.08

1

LP

insu

ranc

ew

ith

faci

liti

es−0

.07

0.53

−0.0

9−0

.13

−0.0

8−0

.09

−0.0

5−0

.07

1

LP

insu

ranc

ew

itho

utfa

cili

ties

−0.1

00.

81−0

.14

−0.2

0−0

.12

−0.1

4− 0

.07

−0.1

1−0

.06

1

C© 2011 Blackwell Publishing Ltd

12 Gael Imad’Eddine and Armin Schwienbacher

Tab

le2

Con

tinu

ed.

LP

bank

LP

bank

LP

insu

ranc

eL

Pin

sura

nce

LP

corp

orat

eL

Pco

rpor

ate

LP

LP

LP

LP

LP

LP

othe

rw

ith

wit

hout

wit

hw

itho

utw

ith

wit

hout

pens

ion

insu

ranc

eba

nkco

rpor

ate

educ

atio

nty

pefa

cili

ties

faci

liti

esfa

cili

ties

faci

liti

esfa

cili

ties

faci

liti

es

LP

corp

orat

ew

ith

faci

liti

es−0

.14

−0.1

6−0

.18

0.63

−0.1

6−0

.19

−0.1

0−0

.15

−0.0

8−0

.13

1

LP

corp

orat

ew

itho

utfa

cili

ties

−0.1

4−0

.16

−0.1

90.

65−0

.17

−0.2

0−0

.10

−0.1

5−0

.09

−0.1

3−0

.18

1

Firs

tinv

estm

ent

−0.1

5−0

.13

0.16

0.19

−0.0

6−0

.09

−0.0

40.

21−0

.09

−0.0

9−0

.06

0.30

LP

expe

rien

ce0.

150.

16−0

.14

−0.1

50.

060.

000.

05−0

.20

0.09

0.12

0.04

−0.2

2V

Cfu

nd−0

.06

−0.0

00.

060.

10−0

.08

−0.0

5−0

.02

0.08

−0.0

20.

01−0

.02

0.14

Buy

outf

und

0.01

0.01

0.02

−0.0

5−0

.01

0.04

0.05

−0.0

10.

03− 0

.01

−0.0

1−0

.06

Oth

erfu

nd0.

06−0

.00

−0.0

9−0

.05

0.10

0.02

−0.0

3−0

.09

−0.0

0−0

.00

0.03

−0.1

0F

undr

aisi

ng0.

17−0

.05

−0.0

4−0

.20

0.08

0.13

0.05

−0.0

90.

01−0

.06

−0.0

4−0

.22

Firs

tinv

estm

ent

LP

expe

rien

ceV

Cfu

ndB

uyou

tfun

dO

ther

fund

Firs

tinv

estm

ent

1L

Pex

peri

ence

−0.6

41

VC

fund

0.19

−0.0

91

Buy

outf

und

−0.1

50.

10−0

.66

1O

ther

fund

−0.0

5−0

.01

−0.4

1−0

.41

1F

undr

aisi

ng−0

.46

0.43

−0.2

00.

22−0

.01

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 13

4. International Capital Flows to European Companies through Private Equity

In this section, we document some observations with regards to capital flows based onLP capital commitments into the European PE market.

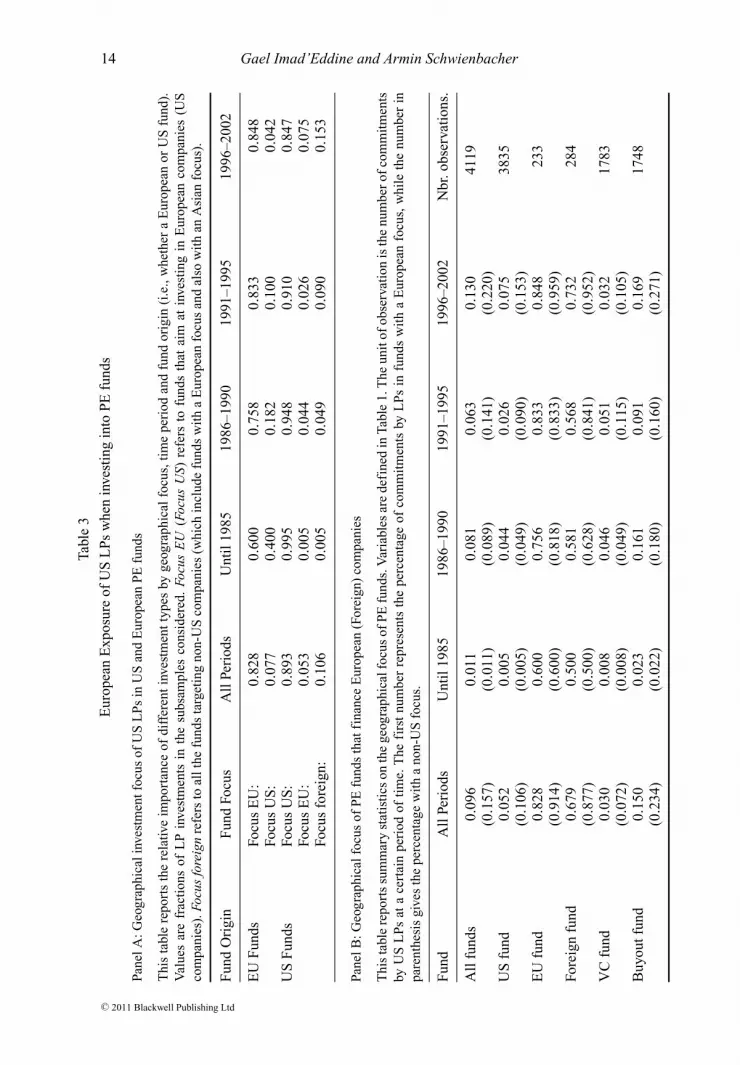

4.1. Analysis of how geographical focus has evolved over time

The interest by US LPs for Europe-focused funds has increased over time. Panel A inTable 3 shows that European funds have increased their deals with US LPs over time,especially in the latest period of our sample (1996–2002). The geographical focuson European targets by US funds has increased, reaching 7.5% of the LP capitalcommitments in the most recent period of 1996–2002. This is impressive growthcompared to before 1985, where Europe accounts for only 0.5% of LP commitments inUS funds. When looking at all the funds (Table 3, Panel C), we see that the Europeanprivate corporate market has increased in importance significantly over time. Before1985, it represented only 0.9% of US LP commitments, while 7.2% in the last period. Thisgrowth is due to increased interest of US funds focusing on European private companies,and also to the development of European PE funds investing on the European continent.When looking at funds focusing on Europe (either US funds or European funds), thepercentage value grows from 1% before 1985, to 12.9% in the last period of 1996–2002.This shows that the overall growth of the European PE market is due to both Europeanfunds attracting US LPs, as well as increase of European interest by US funds.

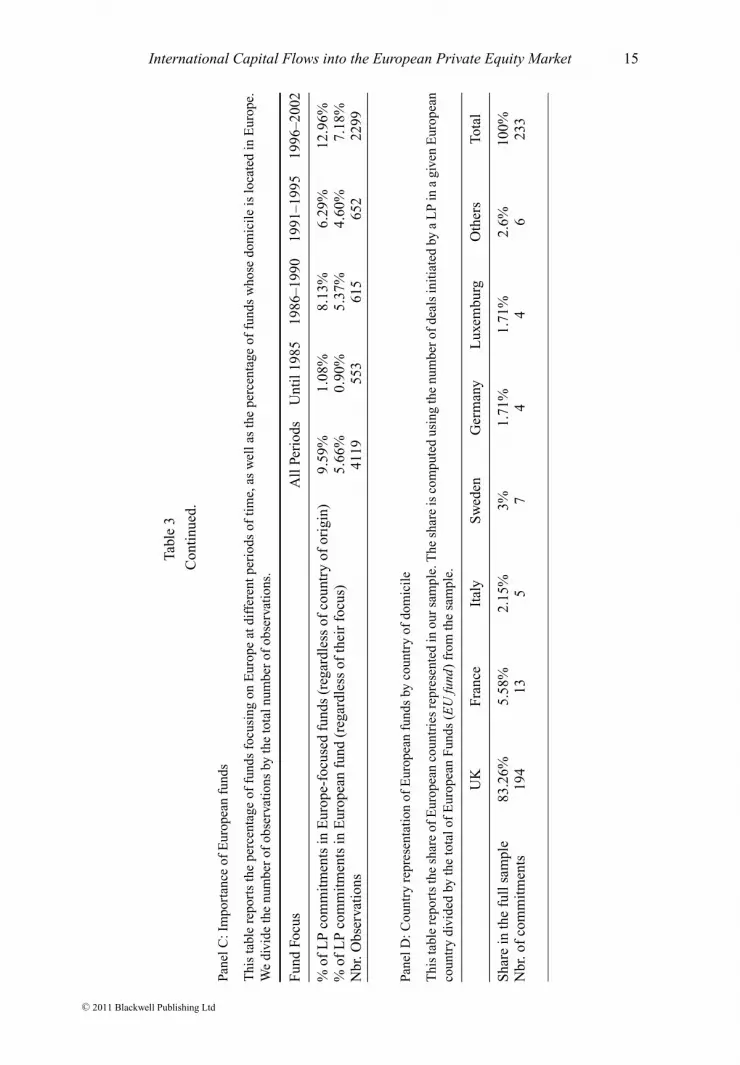

A closer look at the composition of the European funds (Table 3, Panel D) showsthat the vast majority of capital commitments by US LPs goes to UK funds (83.26%).The UK has a well developed PE market – primarily buyout – and large institutionalinvestors capable of channeling capital to the market. Other countries, including Franceand Germany, attract US LPs to a much lower magnitude.7

4.2. Analysis of how LP types differ from each other

Table 1 provides summary statistics on the relative importance of the different LP types.Overall, the bulk of the commitments to PE funds is by financial institutions (banks).In our sample, 30.6% of the deals are by corporate-affiliated LPs. This fraction has,however, been decreasing over time. Since 1985, the share has been decreasing steadilyfrom 50.8% down to 21.5% (values not reported in Table 1). The second largest providersof funds are financial institutions with 17.2%, followed by insurance companies with12.9%. Put together they represent 30% of the capital commitments into funds. Again,these shares have evolved over our sample period. Financial LPs started at around 26.8%,then dropped to 15.2%. Insurance companies contributed 12.3% of commitments until1985, about 17% from 1986 to 1995, but then only 10.7% in the most recent period

7 Assessing the representativeness of our sample is extremely difficult, since there areno alternative data available from other studies or general statistics from professionalassociations. The only data we could find are from PEREP’s 2007 survey available onthe European Private Equity and Venture Capital Association (EVCA) website. Our data arefor a longer time period than just 2007, which makes comparison difficult. At first sight, itis unclear whether the survey excludes investments in funds-of-funds, but we see that thetrends remain similar. According to the survey, the UK share is decreasing while increasingin the rest of Europe.

C© 2011 Blackwell Publishing Ltd

14 Gael Imad’Eddine and Armin Schwienbacher

Tabl

e3

Eur

opea

nE

xpos

ure

ofU

SL

Ps

whe

nin

vest

ing

into

PE

fund

s

Pane

lA:G

eogr

aphi

cali

nves

tmen

tfoc

usof

US

LP

sin

US

and

Eur

opea

nP

Efu

nds

Thi

sta

ble

repo

rts

the

rela

tive

impo

rtan

ceof

diff

eren

tin

vest

men

tty

pes

byge

ogra

phic

alfo

cus,

tim

epe

riod

and

fund

orig

in(i

.e.,

whe

ther

aE

urop

ean

orU

Sfu

nd).

Val

ues

are

frac

tion

sof

LP

inve

stm

ents

inth

esu

bsam

ples

cons

ider

ed.

Focu

sE

U(F

ocus

US)

refe

rsto

fund

sth

atai

mat

inve

stin

gin

Eur

opea

nco

mpa

nies

(US

com

pani

es).

Focu

sfo

reig

nre

fers

toal

lthe

fund

sta

rget

ing

non-

US

com

pani

es(w

hich

incl

ude

fund

sw

ith

aE

urop

ean

focu

san

dal

sow

ith

anA

sian

focu

s).

Fun

dO

rigi

nF

und

Focu

sA

llPe

riod

sU

ntil

1985

1986

–199

019

91–1

995

1996

–200

2

EU

Fun

dsFo

cus

EU

:0.

828

0.60

00.

758

0.83

30.

848

Focu

sU

S:

0.07

70.

400

0.18

20.

100

0.04

2U

SF

unds

Focu

sU

S:

0.89

30.

995

0.94

80.

910

0.84

7Fo

cus

EU

:0.

053

0.00

50.

044

0.02

60.

075

Focu

sfo

reig

n:0.

106

0.00

50.

049

0.09

00.

153

Pane

lB:G

eogr

aphi

calf

ocus

ofP

Efu

nds

that

fina

nce

Eur

opea

n(F

orei

gn)

com

pani

es

Thi

sta

ble

repo

rts

sum

mar

yst

atis

tics

onth

ege

ogra

phic

alfo

cus

ofP

Efu

nds.

Var

iabl

esar

ede

fine

din

Tabl

e1.

The

unit

ofob

serv

atio

nis

the

num

ber

ofco

mm

itm

ents

byU

SL

Ps

ata

cert

ain

peri

odof

tim

e.T

hefi

rst

num

ber

repr

esen

tsth

epe

rcen

tage

ofco

mm

itm

ents

byL

Ps

infu

nds

wit

ha

Eur

opea

nfo

cus,

whi

leth

enu

mbe

rin

pare

nthe

sis

give

sth

epe

rcen

tage

wit

ha

non-

US

focu

s.

Fun

dA

llPe

riod

sU

ntil

1985

1986

–199

019

91–1

995

1996

–200

2N

br.o

bser

vati

ons.

All

fund

s0.

096

0.01

10.

081

0.06

30.

130

4119

(0.1

57)

(0.0

11)

(0.0

89)

(0.1

41)

(0.2

20)

US

fund

0.05

20.

005

0.04

40.

026

0.07

538

35(0

.106

)(0

.005

)(0

.049

)(0

.090

)(0

.153

)E

Ufu

nd0.

828

0.60

00.

756

0.83

30.

848

233

(0.9

14)

(0.6

00)

(0.8

18)

(0.8

33)

(0.9

59)

Fore

ign

fund

0.67

90.

500

0.58

10.

568

0.73

228

4(0

.877

)(0

.500

)(0

.628

)(0

.841

)(0

.952

)V

Cfu

nd0.

030

0.00

80.

046

0.05

10.

032

1783

(0. 0

72)

(0.0

08)

(0.0

49)

(0.1

15)

(0.1

05)

Buy

outf

und

0.15

00.

023

0.16

10.

091

0.16

917

48(0

.234

)(0

.022

)(0

.180

)(0

.160

)(0

.271

)

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 15

Tabl

e3

Con

tinu

ed.

Pane

lC:I

mpo

rtan

ceof

Eur

opea

nfu

nds

Thi

sta

ble

repo

rts

the

perc

enta

geof

fund

sfo

cusi

ngon

Eur

ope

atdi

ffer

entp

erio

dsof

tim

e,as

wel

las

the

perc

enta

geof

fund

sw

hose

dom

icil

eis

loca

ted

inE

urop

e.W

edi

vide

the

num

ber

ofob

serv

atio

nsby

the

tota

lnum

ber

ofob

serv

atio

ns.

Fun

dFo

cus

All

Peri

ods

Unt

il19

8519

86–1

990

1991

–199

519

96–2

002

%of

LP

com

mit

men

tsin

Eur

ope-

focu

sed

fund

s(r

egar

dles

sof

coun

try

ofor

igin

)9.

59%

1.08

%8.

13%

6.29

%12

.96%

%of

LP

com

mit

men

tsin

Eur

opea

nfu

nd(r

egar

dles

sof

thei

rfo

cus)

5.66

%0.

90%

5.37

%4.

60%

7.18

%N

br.O

bser

vati

ons

4119

553

615

652

2299

Pane

lD:C

ount

ryre

pres

enta

tion

ofE

urop

ean

fund

sby

coun

try

ofdo

mic

ile

Thi

sta

ble

repo

rts

the

shar

eof

Eur

opea

nco

untr

ies

repr

esen

ted

inou

rsa

mpl

e.T

hesh

are

isco

mpu

ted

usin

gth

enu

mbe

rof

deal

sin

itia

ted

bya

LP

ina

give

nE

urop

ean

coun

try

divi

ded

byth

eto

talo

fE

urop

ean

Fun

ds(E

Ufu

nd)

from

the

sam

ple.

UK

Fran

ceIt

aly

Sw

eden

Ger

man

yL

uxem

burg

Oth

ers

Tota

l

Sha

rein

the

full

sam

ple

83.2

6%5.

58%

2.15

%3%

1.71

%1.

71%

2.6%

100%

Nbr

.of

com

mit

men

ts19

413

57

44

623

3

C© 2011 Blackwell Publishing Ltd

16 Gael Imad’Eddine and Armin Schwienbacher

(1996–2002). Educational institutions and endowments have instead increased theirshare during the sample period from 4.9% to 13.8% in the last time period considered.

5. Empirical Analysis

In this section, we present empirical results on the investment behaviour of US LPsinvesting in VC and buyout funds. We focus on LP capital commitments targetingfunds with Europe as a geographical focus — i.e., those who aim at ultimately providingfinance to European mature corporations (through buyouts) and startups (through venturecapital). In Section 5.1, we investigate which US LPs invest in funds with Europe as ageographical focus. Since such a focus can be achieved either by investing in US fundstargeting European investments or in European funds investing locally, we rely for ourdependent variable on a dummy variable that captures whether a fund (US or European)takes such a geographical focus. This allows us to investigate which US LP types areglobal players (i.e., seeking international exposure into PE assets) as opposed to thoseinvesting only in US focused funds. For each LP type not all LPs are global investors.However, we aim to identify LP type has a higher propensity to be global players. InSection 5.2, we then focus on this ‘global player’ subsample, to investigate which of thetwo strategies presented in Figure 1 is preferred. This will allow us to test the empiricalpredictions developed in Section 2.

5.1. Which US fund providers have a European focus?

To investigate which US institutional investors are more likely to invest in fundswith a European focus, we regress the geographical focus of funds (Focus EU) onLP characteristics and several control variables. In all our regressions we use logisticregression models with standard errors robust to clustering at the fund level.8 Our mainvariables of interest are the ones related to the specific LP type. This regression allows usto identify the types most prone to be global players targeting the European PE market.

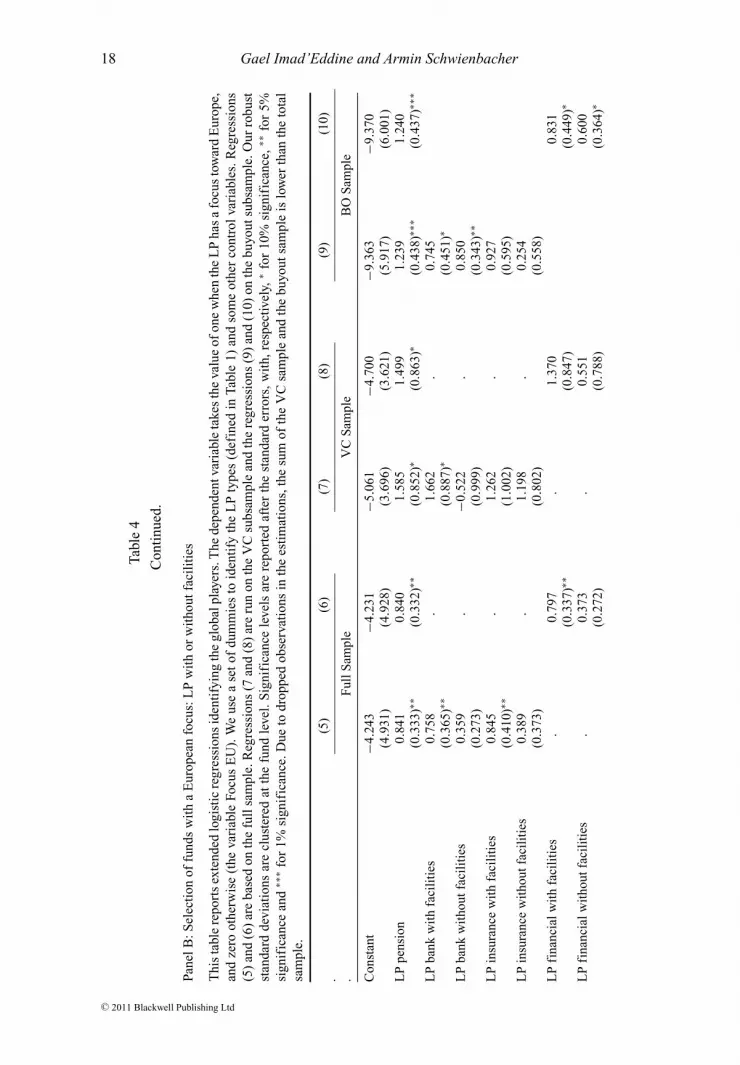

Results are provided in Table 4, Panels A and B. Panel A shows results for the LP typewithout taking into account the existence of European facilities. Panel B shows resultsincluding these European facilities.

Regressions (1)–(2) are based on the full sample, while regressions (3) & (4) areon investments in VC and buyout funds subsamples respectively. We use the group ofLP corporate as reference group to analyse the effect of the different LP types. Theyshow some interesting findings. For the full sample (i.e., regardless of fund type), onlypension funds are most likely to invest in funds with a geographical focus on Europe,regardless of whether through US funds or European funds. Pension funds seem to putthe most effort into achieving European exposure through direct investments into USand/or European funds.9 However, from an absolute magnitude perspective, pension

8 This may be due to the fact that a GP can attract more than one LP.9 Since some funds may be present more than once in our database (whenever they attractedmore than one LP reported in the database), we checked for clustered effects in the regressionanalysis. Our results are robust to any clustering effect at the fund level. Without usingthe clustered robust methodology, these regressions show that pension funds, insurancecompanies and bank-related LPs are all significant. The significance of banks and pensionfunds is largely reduced due to controlling for the clustering effect in residuals.

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 17Ta

ble

4

Reg

ress

ion

anal

ysis

ofth

eE

urop

ean

focu

sby

US

LP

s

Pane

lA:S

elec

tion

offu

nds

wit

ha

Eur

opea

nfo

cus:

byL

Pty

pe.

Thi

sta

ble

repo

rts

the

logi

stic

regr

essi

ons

iden

tify

ing

the

glob

alpl

ayer

s.T

hede

pend

entv

aria

ble

take

sth

eva

lue

ofon

ew

hen

the

LP

has

afo

cus

tow

ard

Eur

ope,

and

zero

othe

rwis

e(t

heva

riab

leFo

cus

EU

).W

eus

ea

set

ofdu

mm

ies

toid

enti

fyth

eL

Pty

pes

(def

ined

inTa

ble

1)an

dso

me

othe

rco

ntro

lva

riab

les.

Reg

ress

ions

(1)

and

(2)

are

base

don

the

full

sam

ple.

Reg

ress

ions

(3)

and

(4)

are

run

onth

esu

bsam

ple

ofre

spec

tivel

yth

eV

Csu

bsam

ple

and

the

buyo

utsu

bsam

ple.

Our

robu

stst

anda

rdde

viat

ions

are

clus

tere

dat

the

fund

leve

l.S

igni

fica

nce

leve

lsar

ere

port

edaf

ter

the

stan

dard

erro

rs,w

ith,

resp

ectiv

ely,

*fo

r10

%si

gnif

ican

ce,*

*fo

r5%

sign

ific

ance

and

***

for

1%si

gnif

ican

ce.D

ueto

drop

ped

obse

rvat

ions

inth

ees

tim

atio

ns,t

hesu

mof

the

VC

sam

ple

and

the

buyo

utsa

mpl

eis

low

erth

anth

eto

tal

sam

ple.

(1)

(2)

(3)

(4)

. .F

ullS

ampl

eV

CS

ampl

eB

uyou

tSam

ple

Con

stan

t−8

.269

−4.2

36−4

.036

−9.0

55(4

.943

)∗(5

.008

)(3

.896

)(6

.085

)L

Ppe

nsio

n0.

596

0.55

11.

015

0.80

8(0

.228

)∗∗∗

(0.2

52)∗∗

(0.5

75)∗

(0.2

99)∗∗

∗L

Pin

sura

nce

0.27

60.

247

0.64

30.

0621

(0.2

26)

(0.2

35)

(0.5

67)

(0.3

02)

LP

bank

0.31

10.

230

−0.0

738

0.40

7(0

.213

)(0

.215

)(0

.625

)(0

.243

)∗L

Ped

ucat

ion

0.07

16−0

.014

8−0

.179

0.10

2(0

.290

)(0

.288

)(0

.643

)(0

.430

)L

Pot

her

type

0.00

906

−0.0

142

−0.3

430.

122

(0.2

20)

(0.2

19)

(0.5

24)

(0.3

00)

Firs

tinv

estm

ent

−0.6

03−0

.485

−0.9

65−0

.310

(0.2

75)∗∗

(0.2

47)∗∗

(0.4

64)∗∗

(0.3

04)

VC

fund

.−1

.390

(0.4

53)∗∗

∗O

ther

fund

.0.

0289

(0.6

78)

Fun

drai

sing

0.56

40.

220

0.16

60.

832

(0.4

90)

(0.4

99)

(0.3

75)

(0.5

68)

Obs

erva

tion

s37

1737

1716

5115

32P

seud

oR

–squ

ared

0.12

80.

164

0.11

90.

124

Wal

dch

i280

.13

81.5

250

.71

51.3

8P

rob

>ch

i20

00

0Y

ear

dum

mie

sY

esY

esY

esY

es

C© 2011 Blackwell Publishing Ltd

18 Gael Imad’Eddine and Armin Schwienbacher

Tabl

e4

Con

tinu

ed.

Pane

lB:S

elec

tion

offu

nds

wit

ha

Eur

opea

nfo

cus:

LP

wit

hor

wit

hout

faci

liti

es

Thi

sta

ble

repo

rts

exte

nded

logi

stic

regr

essi

ons

iden

tify

ing

the

glob

alpl

ayer

s.T

hede

pend

entv

aria

ble

take

sth

eva

lue

ofon

ew

hen

the

LP

has

afo

cus

tow

ard

Eur

ope,

and

zero

othe

rwis

e(t

heva

riab

leFo

cus

EU

).W

eus

ea

set

ofdu

mm

ies

toid

enti

fyth

eL

Pty

pes

(def

ined

inTa

ble

1)an

dso

me

othe

rco

ntro

lva

riab

les.

Reg

ress

ions

(5)

and

(6)

are

base

don

the

full

sam

ple.

Reg

ress

ions

(7an

d(8

)ar

eru

non

the

VC

subs

ampl

ean

dth

ere

gres

sion

s(9

)an

d(1

0)on

the

buyo

utsu

bsam

ple.

Our

robu

stst

anda

rdde

viat

ions

are

clus

tere

dat

the

fund

leve

l.S

igni

fica

nce

leve

lsar

ere

port

edaf

ter

the

stan

dard

erro

rs,w

ith,

resp

ectiv

ely,

∗fo

r10

%si

gnif

ican

ce,∗∗

for

5%si

gnif

ican

cean

d∗∗

∗fo

r1%

sign

ific

ance

.Due

todr

oppe

dob

serv

atio

nsin

the

esti

mat

ions

,the

sum

ofth

eV

Csa

mpl

ean

dth

ebu

yout

sam

ple

islo

wer

than

the

tota

lsa

mpl

e.

(5)

(6)

(7)

(8)

(9)

(10)

. .F

ullS

ampl

eV

CS

ampl

eB

OS

ampl

e

Con

stan

t−4

.243

−4.2

31−5

.061

−4.7

00−9

.363

−9.3

70(4

.931

)(4

.928

)(3

.696

)(3

.621

)(5

.917

)(6

.001

)L

Ppe

nsio

n0.

841

0.84

01.

585

1.49

91.

239

1.24

0(0

.333

)∗∗(0

.332

)∗∗(0

.852

)∗(0

.863

)∗(0

.438

)∗∗∗

(0.4

37)∗∗

∗L

Pba

nkw

ith

faci

liti

es0.

758

.1.

662

.0.

745

(0.3

65)∗∗

(0.8

87)∗

(0.4

51)∗

LP

bank

wit

hout

faci

liti

es0.

359

.−0

.522

.0.

850

(0.2

73)

(0.9

99)

(0.3

43)∗∗

LP

insu

ranc

ew

ith

faci

liti

es0.

845

.1.

262

.0.

927

(0.4

10)∗∗

(1.0

02)

(0.5

95)

LP

insu

ranc

ew

itho

utfa

cili

ties

0.38

9.

1.19

8.

0.25

4(0

.373

)(0

.802

)(0

.558

)L

Pfi

nanc

ialw

ith

faci

liti

es.

0.79

7.

1.37

00.

831

(0.3

37)∗∗

(0.8

47)

(0.4

49)∗

LP

fina

ncia

lwit

hout

faci

liti

es.

0.37

3.

0.55

10.

600

(0.2

72)

(0.7

88)

(0.3

64)∗

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 19

LP

corp

orat

ew

ith

faci

liti

es0.

457

0.45

60.

944

0.87

60.

682

0.69

5(0

.337

)(0

.333

)(0

.649

)(0

.649

)(0

.494

)(0

.485

)L

Ped

ucat

ion

0.27

30.

272

0.41

50.

316

0.53

10.

535

(0.4

00)

(0.3

97)

(0.8

61)

(0.8

64)

(0.6

50)

(0.6

47)

LP

othe

rty

pe0.

268

0.26

70.

225

0.13

80.

542

0.54

4(0

.349

)(0

.347

)(0

.707

)(0

.706

)(0

.540

)(0

.537

)Fi

rsti

nves

tmen

t−0

.410

−0.4

15−0

.726

−0.9

67−0

.224

−0.1

87(0

.235

)∗(0

.247

)∗(0

.426

)∗(0

.453

)∗∗(0

.285

)(0

.292

)V

Cfu

nd−1

.381

−1.3

80.

.

(0.4

54)∗∗

∗(0

.455

)∗∗∗

Oth

erfu

nd0.

0221

0.02

28.

.

(0.6

82)

(0.6

84)

Fun

drai

sing

0.19

60.

195

0.20

70.

183

0.82

20.

821

(0.4

95)

(0.4

95)

(0.3

61)

(0.3

55)

(0.5

60)

(0.5

68)

Obs

erva

tion

s37

1737

1716

5116

5115

3215

32P

seud

oR

-squ

ared

0.16

70.

167

0.14

00.

126

0.12

90.

127

Wal

dch

i258

.65

85.1

67.6

460

.36

64.2

358

.65

Pro

b>

chi2

00

00

00

Yea

rdu

mm

ies

Yes

Yes

Yes

Yes

Yes

Yes

C© 2011 Blackwell Publishing Ltd

20 Gael Imad’Eddine and Armin Schwienbacher

funds, insurance companies and banks all appear to be global players, although onlypension funds have a statistically significant coefficient.

In unreported analysis, we grouped the three LP types (pension fund, insurancecompany and bank) into one dummy variable and ran again the regressions robustto clustering at the fund level. The coefficient of this aggregate variable is significantboth at the 5% and 10% levels depending on the specification (primarily inclusionor exclusion of the VC and buyout fund dummy). This therefore provides reinforcingevidence for these LP types to be a distinct group.

In these regressions, we do not separate US funds from European funds. The coefficienttells us about the probability to invest in a fund that eventually focuses on Europeantargets. On average in our sample, Europe-focused funds are statistically larger than thosefocusing on the US. This is explained by the fact that US LPs, especially pension funds,primarily invest in buyout funds when investing in European funds.10 Lerner et al. (2007)present pension funds as smart investors able to screen for successful GPs. Their sizeand skills allow them to invest in funds focusing on Europe to achieve diversification.

Moreover, further results suggest that less experienced institutional investors are lesslikely to diversify towards Europe, especially if it is their very first direct investmentinto a PE fund (First investment). This result is intuitive. If it is the first investment,LPs have little knowledge of competent GPs. So it is even harder for them to assess thequality of GPs when it comes to investing in funds with foreign focus. These LPs have ahigher probability of choosing a fund focusing on the US market, for which novice LPsmay more easily assess the risk and return profile.

Given that the level of activities in the PE market is highly cyclical and stronglycorrelated with conditions in public markets, we include a fundraising variable whichexpresses the annual level of deflated fundraising worldwide. The amount raised canimpact investment strategy since if this amount rises dramatically, LPs might want todiversify internationally, keeping domestic opportunities constant.

In Regression (2), we include a VC dummy and find a significant negative impact(since we also include the Other fund dummy, the reference group here is the buyoutsub-sample). This is intuitive, as Europe-focused funds raising capital from US investorsare predominantly buyout funds (see Section 4). The recent development of EuropeanPE is mainly due to buyout opportunities. EVCA and several studies reveal weak returnsfrom VC investments in Europe. Hege et al. (2009) report that even US VC funds sufferfrom weak returns when investing in European companies. Caselli et al. (2009) showthat VC investments in Italy have little impact on innovation in the ventures they investin.

When we split the sample between VC investments and buyout investments, we areable to go a step further in the analysis than just adding a dummy variable. Interestingly,there are some differences between VC and buyout funds as shown by regressions (3)& (4). LP past experience seems to matter in the VC subsample. Indeed, if it is thefirst investment the LP tends to shy away from European-focused funds. Pension fundsremain main providers of capital for both European focused VC and buyout funds; bankshave a marginal interest in European buyout funds.

10 As such, our European sample is not representative of the average European fund but rathera distinct sample of GPs capable of attracting US capital. This is also due to the fact that thebulk of capital commitments made in European focused funds is made in the buyout sector,where funds are typically larger.

C© 2011 Blackwell Publishing Ltd

International Capital Flows into the European Private Equity Market 21

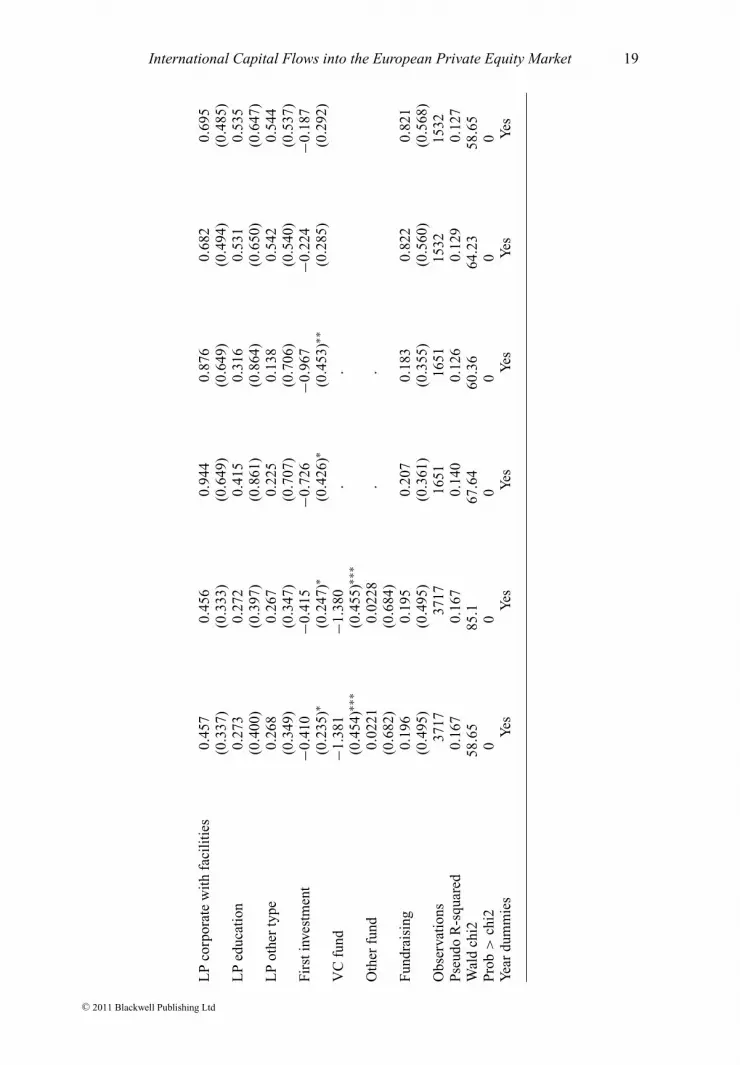

Regressions (5) to (10) use a finer definition of LPs by dividing each type intotwo subgroups: those with facilities in Europe and those without. The existence oflocal facilities in Europe may proxy for better familiarity with and access to localinvestment opportunities. Odd regressions (5, 7 & 9) split all LP types into two subgroups(with/without facilities). Pension funds, educational institutions and the category ofother LPs (LP other type) are not divided because we found either no or only veryfew observations with facilities in Europe. For the even regressions (6, 8 & 10), LPbank and LP insurance are put together as financial LPs and then again divided into LPfinancial with facilities and LP financial without facilities. The reference group for allthese regressions is LP corporate without facilities. Our result for LP pension remainsunaffected. For the full sample banks and insurance companies are more prone to beinternational players only when they hold local facilities. Corporate LPs with facilitiesdo not significantly differ from the corporate LPs without facilities. This confirms thespecificity for financial LPs, next to pension funds.

When we look at the two subsamples separately, results are then less clear for thefinancial LPs (and there is still no effect for LP corporate). LP bank with facilitieshas a positive and significant effect for both subsamples (10% level); for the buyoutsubsample, we find that the coefficient of LP bank without facilities is also significantand positive (5% level). This indicates that the effect found on the financial LPs is mainlydriven by banks. The existence of facilities does not seem to matter however for buyoutinvestments.

In this section we identified one group of investors that is more likely to be globalplayers, namely, pension funds (LP pension). Insurance companies and banks have asimilar impact economically speaking, albeit not significant statistically. These resultsare, however, drawn from the full sample. When we look at the effect of fund type (VCor buyout), the results give a less clear picture. It appears that the results are largelydriven by commitments to VC funds where LP characteristics matter rather than buyoutfunds. The existence of facilities in Europe has an impact especially for financial LPs.In particular, the effect is strongest for banks.11

5.2. Which investment strategies do US LPs use to target the European PE market?