Embed Size (px)

Citation preview

1

PROJECT ON CUSTOMER

SATISFACTION IN

WESTERN UNION MONEY

TRANSFER

Name: Ronak Surana

Enrollment no.: A30606411033

Class: BBA 2011-2014

2

AKNOWLEDGEMENTS

I would like to thank my college, AGBS

Hyderabad for giving me an opportunity

to do this project. It helped me learn a lot

about the current market and about how

work takes place.

I would also like to thank my faculty for

their guidance and their ideas that helped

me bring out the project better.

I would also like to thank my friends

who helped me during the course of

study.

Last but not the least, I am thankful to

my parents for their immense support

and their blessings.

3

ABOUT THE PROJECT

I have done my project on the customer

satisfaction of Western Union Money

Transfer service, Secunderabad.

I did this project as it shows how a

money transfer service can help people

living in different countries.

During the course of this project, I went

to the Western Union office at

Secunderabad. I collected information

regarding their services from a number of

customers.

I have also gone through the company

history and profile thoroughly.

4

CONTENTS 1. INTRODUCTION TO MARKETING

2. CUSTOMER SATISFACTION

3. MONEY TRANSFER SERVICE

4. HISTORY OF WESTERN UNION

MONEY TRANSFER

5. COMPANY PROFILE

6. RESEARCH

7. RESEARCH METHODOLOGY

8. ANALYSIS AND INTERPRETATION

OF RESEARCH DATA

9. FINDING & SUGGESTIONS

10. QUESTIONNAIRE AND

BIBLIOGRAPHY

5

CHAPTER 1

INTRODUCTION

TO

MARKETING

6

INTRODUCTION:

Marketing is a process or an activity by

which individuals and groups of people get what

they need and want by creative and exchanging

services and goods with other.

Traditional people think that marketing is

telling and selling. But modern sense the

marketing is satisfied customer needs and

making good relationship with other.

Marketing deals meeting the customer needs

and satisfied those offering higher values to

customers.

Marketing needs with maintaining present

customers and growing potential customers

premising higher values.

7

MARKETING CONCEPTS:

The following concepts or very use full to business organization

Production concept

Product concept

Market concept

Societal marketing concept

Marketing is a restless, changing and dynamic field

thousands of new products, including those of entire new industries

has appeared in the market the role of marketing and market places

are recurrently changing day by day on ever increasing are

becoming more market-driven in the premium has been placed on

making sound marketing decisions and companies strategic decision

making.

Concentration on key markets or opportunities provides firms with

a chance to build a fuller picture of market conditions understand

the details of customers specific requirements, design and develop

offering adapted to meet buyer needs, establish and sustain along

term marketing presence and minimize costs while maximizing the

returns from individual market.

8

OBJECTIVE OF THE STUDY:

Study the customer satisfaction about money transfer service.

To draw out the customer satisfaction levels.

To build a good customer relationship.

To take care necessary measures to improve services offered to

customer.

To compare satisfaction of the company Vis-a-Vis major

competitors.

9

METHODOLOGY:

SOURCES OF DATA:

The data furnished in the report has been collected from two sources.

PRIMARY DATA:

The primary data for research study has been collected from the

customers by the method of questionnaire.

SECONDARY DATA:

The secondary data for research study has been collected from the

brochures, pamphlets and from internet websites.

10

SCOPE OF THE STUDY:

This study is related to Western union Money Transfer Service

only.

The study covers the opinion of customers about the Western

Union Money Transfer Service.

The study is concerned with perception of the customers of the

Western Union Money Transfer Service.

It manages to bring out how much a money transfer service can

help people.

It helped create awareness about the usefulness and positive effects

of money transfer services.

It brought out the discrepancies involved in a money transfer

process.

11

LIMITATIONS:

The following are the limitations of the project.

A survey on customers of WESTERN UNION MONEY TRANSFER

OF SERVICES restricted to Secunderabad.

1) There is a limited time to study the project it is difficult to

collect more information. Therefore a deep study is not

possible.

2) The given information by the customers may not be correct as

their opinions, attitudes etc., may differ from others.

3) It is collected only from 30 customers; therefore it cannot give

the accurate information.

4) It may not provide all the information required to find out the

customer satisfaction of Western Union Money Transfer.

12

CHAPTER 2

CUSTOMER

SATISFACTION

13

CUSTOMER

SATISFACTION:

Customer satisfaction is known as the heart of marketing. Every

business’s success in today’s world depends upon the level of

satisfaction of the customers. No business can survive without

satisfaction of customers, be it product or service.

Customer satisfaction is outlined a frame work of a five steps end-to-end

process.

The presentation tries to address a problem that many corporations get

consistently, year after year low customers satisfaction scores even

though year after year they aim towards improvements. Although we do

not claim to comprehend all the reasons behind declared in customer

satisfaction corporations experience in recent year, we be live a

substantial increase in customer satisfaction could be achieved by better

management of promises to customers and better co ordination of

actions to improve customer satisfaction.

Quality and service alone cannot produce recurrent satisfaction.

Satisfaction is distinct and separate issue. It is the customer’s entire

experience with us that determines his or her declaration of satisfaction.

This experience is not objective at all but totally subjective. It is the

customer’s call. A customer is satisfied only if and when they say they

are satisfied. Satisfaction is a based upon the customer’s perception is

his/her interpretation of the value received played back against

expectations. This declaration does not require any objective evidence. It

can be a declaration made with no reason.

14

Our interactions with the customer, the promises made to the

customer in these conversations, the customers’ expectations generated

in these conversations and the actions we take that are consistent with

those expectations combine to produce a declarations of satisfaction.

Therefore it is essential we manage these aspects of our business in pro-

active manner to excel at customer satisfaction.

CUSTOMER SATISFACTION

PROCESS:

Customer satisfaction process is not a set of surveys, a set of

“Bridge the Gaps” actions in response to Customer satisfaction surveys.

Customer satisfaction process is end-to-end, planned,

comprehensive, coordinated, and managed. Set of activities and

interactions designed to achieve the highest possible Customer

satisfaction. Actions initiated both ahead of “Customer satisfaction

surveys”, and as a response to “Customer satisfaction surveys”.

UNDER STANDING CUSTOMER

EXPECTATIONS:

How do buyers form their expectations? From past buying

experience, friends’ and associates’ advice, marketers’ and competitors’

information and promises. If marketers raise expectations too high, the

buyer is likely to be disappointed. However, if the company sets

expectations too low, it won’t attract enough buyers. Some of today’s

most successful companies are raising expectations and delivering

15

performances to match. When General Motors launched the Saturn car

division, it changed the whole buyer-seller relationship with a New Deal

for car buyers: There would be a fixed price a 30-day guarantee or

money back; and sales people on salary, not on commission. Look at

what high satisfaction can do.

A customer’s decision to be loyal or to defect is the sum of many

small encounters with the company. Consulting firm Forum Corporation

say that in order for all these small encounters to add up to customer

loyalty, companies need to create a “branded customer experience”.

Here is how San Francisco’s Joie de Vivre chain does this.

MEASURING SATISFACTION:

Many companies are systematically measuring customer

satisfaction and the factors shaping it. For example, IBM tracks how

satisfied customers are with r\each IBM salesperson they encounter, and

makes this a factor in each salesperson’s compensation.

A company would be wise to measure customer satisfaction

regularly because one key to customer retention is customer satisfaction.

A highly satisfied customer generally stays loyal longer, buys more as

the company introduces new products and upgrades existing products,

talks favorably about the company and its products, pays less attention

to competing brands and is less sensitive to price, offers product or

service ideas to company, and costs less to serve than new customers

because transactions are routine.

The link between customer satisfaction and customer loyalty,

however, it is not proportional. Suppose customer satisfaction is rated on

a scale from one to five. At a very low level of customer satisfaction,

customers are likely to abandon the company and even bad-mouth it. At

levels two to four, customers are fairly satisfied but still find it easy to

switch when a better offer comes along. AT level five, t6he customer is

very likely to repurchase and even spread good word of mouth about the

company. High satisfaction or delight creates an emotional bond with

the brand or company, not just a rational preference. Xerox’s senior

16

management found out that its “completely satisfied” customers were six

times more likely to repurchase Xerox products over the following 18

months than its “very satisfied” customers.

When customers rate their satisfaction with an element of the

company’s performance-say, delivery-the company needs to recognize

that customers vary in how they define good delivery. It could mean

early delivery, on-time delivery, order completeness, and so on. The

company must also realize that two customers can report being “highly

satisfied” for different reasons. One may be easily satisfied most of the

time and the other might be hard to please but was pleased on this

occasion.

A number of methods exist to measure customer satisfaction.

Periodic surveys can track customer satisfaction directly. Respondents

can also be asked additional questions to measure repurchase intention

and the likelihood or willingness to recommend the company and brand

to others. Paramount attributes the success of its five theme parks to the

thousands of Web-based guest surveys it sends to customers who have

agreed to be contacted. During the past year, the company conducted

more than 55 Web-based surveys and netted 100,000 individual

responses that described guest satisfaction on topics including rides,

dining, shopping, games, and shows.

Companies can monitor the customer loss rate and contact

customers who have stopped buying or who have switched to another

supplier to learn by this happened. Finally, companies can hire mystery

shoppers to pose as potential buyers and report on strong and weak

points experienced in buying the company’s and competitors’ products.

Managers themselves can enter company and competitor sales situation

where they are unknown and experienced firsthand the treatment they

receive, or phone their own company with questions and complaints to

see hoe the calls are handle.

For customer satisfaction surveys, it’s important that companies

ask the right questions. Frederick Reichheld suggests that perhaps only

one question really matters: “Would you recommend this product or

service to a friend?” He maintains that marketing departments typically

17

focus surveys on the areas they can control, such as brand image,

pricing, and product features. According to Reichheld, a customer’s

willingness to recommend to a friend results from how well the

customer is treated by front-line employees, which in turn is determined

by all the functional areas that contribute to a customer’s experience.

In addition to tracking customer value expectation and satisfaction,

companies need to monitor their competitors’ performance in these

areas. One company was pleased to find that 80 percent of his customers

said they were satisfied. Then the CEO found out that its leading

competitor had a 90 percent customer satisfaction score. He was further

dismayed when he learned that this competitor was aiming for a 95

percent satisfaction score.

For customer-centered companies, customer satisfaction is both a

goal and a marketing tool. Companies need to be especially concerned

today with their customer satisfaction level because the Internet provides

a tool for consumers to spread bad word of mouthas well as good

word of mouthto the rest of the world. On Web sites like

troublebenz.com and lemonmb.com, angry Mercedes-Benz owners have

been airing their complaints on everything from faulty key fobs and

leaky sunroofs to balky electronic that leave drivers and their passengers

stranded.

Companies that do achieve high customer satisfaction ratings make

sure their target market knows it. When J .D. Power began to rate

national home mortgage leaders, Countrywide was quick to advertise its

number-one ranking in customer satisfaction. Dell Computer’ meteoric

growth in the computer systems industry can be partly attributed to

achieving and advertising its number-one rank in customer satisfaction.

The University of Michigan’s Claes Fornell has developed the

American Customer Satisfaction Index (ACSI) to measure the perceived

satisfaction consumers feel with different firms. Industries, economic

sectors, and national economies. Examples of firms that led their

respective industries with high ACSI scores in 2003 are Dell (78),

Cadillac (87), FedEx (82), Google (82), Heinz (88), Kenmore (84),

Southwest Airlines (75), and Yahoo! (78).

18

CHAPTER 3

MONEY

TRANSFER

SERVICE

&

REMITTANCE

19

HISTORY OF MONEY

TRANSFER SERVICE:

Money transfer service is not a new thing to mankind. People have been

travelling to distant places for earning since centuries. Migration has

been an integral part of human life

A person earning in far-off country has to send money home to his

family. The process of sending of money home is the most important

part of earning in a foreign country. Sending this money home is called

remittance.

REMITTANCE:

A remittance is a transfer of money by a foreign worker to his or her

home country.

Remittances are not a new phenomenon in the world, being a normal

concomitant to migration which has always been a part of human

history. Several European countries, for example Spain, Italy and Ireland

were heavily dependent on remittances received from their emigrants

during the 19th and 20th centuries. In the case of Spain, remittances

amounted to the 21% of all of its current account income in 1946. All of

those countries created policies on remittances developed after

significant research efforts in the field. For instance, Italy was the first

country in the world to enact a law to protect remittances in 1901 while

Spain was the first country to sign an international treaty (with

Argentina in 1960) to lower the cost of the remittances received.

20

EFFECTS, IMPORTANCE

AND BENEFITS:

The remittances in a way are a major force in driving the economy of

home country. The remittances sent by the citizens who are working

abroad offers an import source of funds for many developing nations. In

some cases these funds from remittances even exceed the aid received

from the developed world.

The remittances received in home countries are used for meeting the

expenses of the worker’s family; however it is difficult to track the

expenditure as it is form of private transfers. As per the economists,

recipients may use funds for buying necessities like food, clothing and

housing. It does not lead to development because these are not strictly

investments. Some other economists opined that funds received from

abroad are used for developing the domestic financial system. The

remittances can be sent via wire transfer, to banks and other financial

institutions. These funds are used for the consumption of goods and

services. It can also be used for other purposes like constructing house,

building or any other investments.

As per the research, migrants returning from abroad invest their funds in

developing their own business and they recognize the business trends in

their home country and utilise their work experience abroad for creating

a company in their home country. The inflow of money from

remittances is compared to commodity like oil that have high demand

source. Government can spend money on poorly-planned projects and

get into trouble if the demand for that commodity slows down. As the

remittances are not held by the government unlike oil revenues, they are

sent to individuals for spending.

21

Money sent home by migrants constitutes the second largest financial

inflow to many developing countries, exceeding international aid.

Estimates of remittances to developing countries vary from International

Fund for Agricultural Development's US$301 billion (including

informal flows) to the World Bank's US$250 billion for 2006 (excluding

informal flows). Remittances contribute to economic growth and to the

livelihoods of people worldwide. Moreover, remittance transfers can

also promote access to financial services for the sender and recipient,

thereby increasing financial and social inclusion.

Remittances also foster, in the receiving countries, a further economic

dependence on the global economy instead of building sustainable, local

economies.

As remittance receivers often have a higher propensity to own a bank

account, remittances promote access to financial services for the sender

and recipient, an essential aspect of leveraging remittances to promote

economic development.

The stability of remittance flows despite financial crises and economic

downturns make them a reliable financial resource for developing

countries. As migrant remittances are sent cumulatively over the years

and not only by new migrants, remittances are able to be persistent over

time. At the state level, countries with diversified migration destinations

are likely to have more sustainable remittance flows.

22

TYPES OF REMITTANCES:

The remittances can be classified into four types including Family

Remittances, Community Remittances, Migrant Worker Remittances

and Social Worker Remittances.

Family Remittances: It refers to remittances that are sent by individual

immigrants working in the foreign locations to their family, relatives or

friends in their home country. These remittances are sent every month

and they assist the families of the migrants to survive. These remittances

also help the poor families to fight against the poverty. The family

remittances are regarded as the major form of remittances across the

world where millions of workers are working hard in distant land away

from their home for earning their livelihood.

Community Remittances: It refers to the remittance that is sent by

individual immigrants generally and also includes the remittance sent by

various hometown associations to organisations and communities in

their home country. This money has been used for the developmental

activities of communities such as in building infrastructure, church,

parks, and roads. It also offers health care to the poor. The community

remittances are also used for offering health benefits, education; and

employment to big communities who need these facilities in the home

countries.

Migrant worker Remittances – These remittances refers to the cash

transfers done by migrant workers for sending the money to the families,

friends and relatives back home. The migrant worker remittances make

up a large chunk of money inflows into home country by the people who

have migrated to foreign locations in the search of money, job or

education.

23

Social Remittances – These remittances basically comprise of various

ideas, practices, and social capital that make up the backbone of many

remittances that flows from workers of one country to another. Thus

social remittances assist the traditions and culture of one race or

community, to socialize with the cultures and traditions of another

community. Social Remittances help in the bonding of people and do not

have money associated with them.

24

WAYS OF MAKING

PAYMENT:

One can make payment for the remittance in your bank in many ways as

mentioned below.

(a) Certified Personal Check or Personal Check – This check needs to be

drawn on the account and should be payable to the branch of bank from

where you are sending money.

(b) Cashier’s Check – This payment method involves the check to be

purchased from your account and it should be payable to branch of bank

from where you are sending money. You should ensure that your name

is printed on the check.

(c) Wire Transfer – This method involves the wire transfer from your

account. The account number and routing number are used for sending

money in this case.

(d) ACH Debit Authorization – This method involves the debit of money

from account upon the authorization through the Automated Clearing

House (ACH). ACH refers to an electronic processing facility that

allows the bank to debit (or credit) an account with another bank. It acts

as an electronic substitute for checks in the banks. The form used

requires you to fill the information related to the bank account including

the bank’s routing number and account number that is available on the

check.

(e) Account Debit – In case user has maintained an account with the

branch of the bank, he can authorize the bank to debit that account.

25

(f) Cash – Customer can also make the payment in person up to $2500.

(g) Debit or Credit Card – Banks can also charge the valid debit or credit

card up to amount of $5000 if customer comes in person for sending

money and up to $1000 when customer applies by mail or fax.

REMITTANCE IN INDIA:

India continues to be the top recipient of global remittance flow at $52

billion in 2011, the World Bank has said in a report.

Remittance is defined as the sum of money paid to someone at a

distance. A 'remittance transfer' refers to the transfer of money from an

individual, usually a person who has emigrated from her city or country

of origin, to another individual, usually a relative who remains at home.

Migrant remittance flow to developing countries, including India, will be

around $317 billion this year, a lower-than-expected fall from the year-

ago level, but will return to the recovery path in years to come, the

World Bank has said.

Remittance flow to developing countries will touch $317 billion in 2011,

and going forward, the inflows to these nations are expected to remain

almost flat in 2012, (with a modest rise of 1.4 per cent) and grow by 3.9

per cent in 2012, the World Bank said in its Migration and Development

Brief.

26

FACTS RELATED TO

REMITTANCE:

The facts related to the remittances are mentioned below:

(1) As per the report submitted by the World Bank, almost US$250

billion was sent through remittance throughout the world in the year

2006. The amount of money sent via remittance has been increasing

steadily with thirty percent growth every year

(2) The share of the global remittances sent to the developing nations

rises from fifty seven percent in 1995 to seventy two percent in 2005. It

was equivalent to an amount of $167 billion in the time period of ten

years.

(3) India is the leading remittance receiver globally and accounts for the

maximum remittance received every year. In the year 2006, $26.9 billion

was remitted to India and it increased up to $55.06 billion in 2009. India

is followed by China at second position with $22.52 billion in 2006 to

$40.5 billion in 2008. These two are followed by Philippines ($17.3

billion); Mexico ($21.2 billion) and Poland.

(4) A large chunk of remittances from the US is directed to Asian

countries including India ( 26 billion USD), Philippines (16 billion

USD) and China (23 billion USD). In the year 2003.2004, five out of

seven top remittance recipient countries belonged to Asia. The Asian

countries were India, Philippines, China, Pakistan and Bangladesh. Non

Asian countries in the top seven include Mexico and France.

(5) The Asian countries like India, China and non Asian such as Mexico

and France accounts for a third of global remittances.

27

(6) The remittances make up a high share of GDP gross domestic

product in only two countries including the Philippines and Serbia and

Montenegro.

(7) In fact, approx ten percent of the population globally is involved

directly with remittances.

(8) USA tops the list of countries that offers the largest amount of

remittances, with $31 billion of remittance is sent every year from USA

to other countries.

28

CHAPTER 4

HISTORY OF

WESTERN UNION

MONEY

TRANSFER

29

HISTORY:

Western union began as a telegraph company, sending

messages to millions of people worldwide. Today, Western union is a

global leader in money transfer services. Because money transfers

service is available in over 200 countries at more than 2, 70,000 agent

locations. India is the largest remittance market in the world.

Western Union Money Transfer commenced its operations in India in

1993 with few agents. Today, the Western Union family extends to more

than 36,000 locations across 3500 cities.

Today, Western Union serves millions of customers in India and their

service has created a lifeline for NRIs.

1851

A group of businessmen in Rochester, New York and Mississippi

Valley printing Telegraph company Western Union’s Predecessor

Company.

1856

The New York and Mississippi Valley printing telegraph company

changes its name to Western Union Telegraph Company, signifying the

union of “western” telegraph lines with eastern lines into one system.

30

1861

Western Union completes the first transcontinental telegraph line,

providing fast, coast-to-coast communications during the U.S. Civil

War.

1869

Western Union introduces the first stock ticker, providing brokerage

firms with New York stock Exchange quotations.

1871

Western Union Money Transfer service was introduced and became the

company’s primary business.

1884

Western Union is selected as one of the original 11 stocks tracked in

the first Dow Jones Average.

1914

Western Union introduces the first consumer charge card.

1920

Western Union introduces teletypewriter, joining branches and

individual companies.

31

1933

Singing telegrams are introduced.

1935

The first inter-city facsimile service is introduced.

1943

Western Union pioneers the first commercial inter-city microwave

system.

1958

Western Union introduces Telex, a direct-dial consumer to consumer

teleprinter service.

1964

Western Union launches the use of a transcontinental microwave radio

beam system, replacing poles and wires spanning the continent.

1970

Western Union Mailgram messages offer next-day delivery through the

postal service.

32

1974

Western Union launches Westar I, the first commercial

communications satellite in the United States.

1980

Revenue from the Money Transfer service (originally known as money

order service) exceeds that from the telegram service for the first time in

Western Union history.

1982

Western Union is the first company with five satellites in orbit.

1989

Quick collect provides creditors a service for securing fast collection of

payments via fiat-rate money transfers.

Rapid Money Transfer Service becomes available outside North

America.

1992

Western Union Money Order service provides customers with a fast,

easy way to get money orders.

33

1993

Dinero en Minutos (Money in Minutes) service is introduced, making

fund sent to Mexico from the U.S. available in minutes.

1993

The Western Union phone card service is the first branded, pre-paid,

and disposable telephone card offered in the United States.

1994

First financial Management Corporation acquires Western Union

financial Services, Inc.

1995

First financial management corporation completes a $7 billion merger

with first data corporation (NYSE:FDC) Western Union financial

services, Inc. becomes a first data corporation subsidiary.

1996

Western Union opens its North America head quarters in Englewood,

Colorada.

International presence continues to expand with new regional offices in

Paris, Vienna, and Hong Kong.

34

1998

The Western Union Money Transfer service expands to reach 50,000

Agent locations worldwide, the world’s largest money-transfer network.

International Regional Operating Centers open in Brussels and Costa

Rica.

1999

By the end of the year, there are more than 80,000 Western Union

agent locations in more than 140 countries and territories and the globe.

2000

Western Union launches westernunion.com, bringing the convenience

of money transfers to the Internet.

2001

Western Union celebrates its 150-year anniversary by reaching more

than 100,000 Agent locations worldwide.

2002

Christina Gold named president, Western Union Financial Services,

Inc.

2005

The Western Union Agent network, combined with subsidiary Orlandi

Valuta, exceeds 250,000 locations.

35

2006

Western Union discontinues its historic telegram services, completing

its transformation to a financial services company.

For more than 150 years, Western Union has been connecting people.

2009

In May 2009, Western Union announced their intention to acquire

Custom House from Peter Gustavson. The deal closed in September

2009, with Western Union purchasing Custom House for $370 million

USD. Its acquisition led the company to be re-branded as Western Union

Business Solutions.

2010

Hikmet Ersec takes over as the president of Western Union Business

Solutions on September 1, 2010.

2011

In January 2011, Western Union acquired the 100% of Angelo Costa,

CEO Francesco Costa, a group active in money transfer and services to

immigrants. Angelo Costa has a network of 7,500 points of sale in

various European countries. The agreement was signed for $ 200

million.

In July 2011, Western Union acquired Travelex's Global Business

Payments division for £606 Million.

36

PRESIDENTS OF THE

COMPANY:

Hiram Sibley (1856–1866)

Jeptha Wade (1866–1867)

William Orton (1867–1878)

Norvin Green (1878–1893)

Thomas Eckert (1893–1902)

Robert Clowry (1902–1910)

Theodore Vail (1910–1914)

Newcomb Carlton (1914–1933)

Roy White (1933–1941)

Albert Williams (1941–1948)

Walter P. Marshall (1948–1964)

Russell McFall (1965–1979)

Robert Flanagan (1979–1984)

Roland Berner (1984)

Robert Leventhal (1984–1988)

Robert Amman (1988–1994)

Alan Silberstein (1994–2001)

Christina Gold (2006–2010)

Hikmet Ersek (2010–Present)

37

CHAPTER 5

COMPANY

PROFILE

38

A GLOBAL LEADER:

Western Union employees nearly 7,000 people around the world.

Employees live and work in more than 200 different countries and

speak 75 languages and dialects.

Western Union has more than 5,00,000 agent locations in more

than 200 countries.

Western Union is a global leader Money Transfer Services.

Western Union is an industry leader with more than $5 billion

revenue, and total assets worth nearly $8 billion.

Western Union helps consumer and business send money, bill

payments quickly, reliably.

Western Union provides consumers with financial, convenience

and control.

Western Union offers services through agent locations around the

world.

Western Union Money Transfer is a part of, First Data Corp., which

is a fortune 500 company who also is world leader in Money Transfer

Business with over 2,70,000 locations spread over more than 200

countries. Western Union with its state-of-the-art technology offers

safe, reliable, legal and fraud free instant money transfer services duly

approved by Reserve Bank of India.

39

SAFE:

The safest easiest and fastest way to transfer money from

anywhere in the world to India is through Western Union Money

Transfer. For disbursement at Paul Merchants Ltd., offices authorized by

Reserve Bank of India, Western Union Financial Services USA is the

largest and most trusted service in the world and has been in existence

since 1871, and currently has and electronically transfer network of over

2,70,000 locations to make money transfer for immediate payout in 200

countries including India. Paul Merchants Ltd. Is the market leader in

the Money transfer with conveniently located offices throughout India

so, if you intend to send money to someone in India then make sure, you

do it through Western Union Money Transfer to Paul Merchants for

disbursement. The person you are sending money to, will receive it just

minutes after you have sent it to any of the Paul merchants locations.

EASY:

Money Transfer made easy to transfer the Money you don’t need

to have a Bank Account. Simply bring your Money to any Western

Union agent and fill out a short

Form to pay a service fee. Get a receipt with Money Transfer Control

Number. In form your receiver of the Transfer and advice him to collect

Money at any of Paul Merchants locations listed in our website. The

receiver will be required to present proper photo identification and will

be paid immediately. Paul Merchants and Western Union are much more

convenient than any Bank.

40

LEGAL:

Money Transfer through Western Union is totally legal and authorized

By Reserve Bank of India. Paul Merchants Limited (PML) is the

flagship company of renowned “PAUL MERCHANTS” group based at

Chadigarh, a Conglomerate having prominent interests in fields like

Forex, International Money Transfer, Finance, Immigration, Tours &

Travels and Holidays, Packages and Air Ticketing. Paul Merchants

Limited was incorporated on 13th

July 1984 and its Scrips are listed on

Delhi Stock Exchange. Riding high upon its vision and philosophy

Of remaining ahead of Times, PML has made paradigmic developments

in all the fields of its operations PML has established itself has a leading

member of the regions star studded financial services sector lobby.

PML had made a humble beginning in the field of international Money

Transfer after signing an agency agreement with Western Union

Financial Services Inc., New Jersey, U.S.A. PML had obtained a

specific approval from the Reserve Bank of India, Central Office, and

Mumbai for this purpose. Western Union Financial Services Inc. is

world’s number one Money Transfer company with over 2,70,000 agent

locations covering more than 200 countries. Staff and thoughtfully

entered strategic alliance is that today PML is ranked as the highest

revenue generating principal agent of Western Union in whole of south

Asia and is making momentous contribution to the foreign exchange

reserves of India in the form of Western Union inward remittances.

PML is being managed professionally by a group of experienced

professionals having wide experience in their respective fields under the

innovative leadership of its chairman cum managing director, Mr. S.

Paul who himself has an experienced of over 30 years in various lines of

business over the year the Board of directors of PML has conducted the

Business with a profuse dignity, which inspires everyone associated with

the company. PML has a dedicated and fully trained team of over 300

employees who are having expertise in their respective fields. The

company offices are equipped with all modern infrastructures required

for extending quality service to valuable customer, with the company’s

41

concept of providing “Total Services” in the Forex, Money Transfer &

travel sectors and its belief in providing “Service up to the utmost

satisfaction of the customer” the company is poised to achieve greater

heights in the near future.

PAUL MERCHANTS is one of the primary agents of the Western

Union.

PAUL MERCHANTS HAVING THE FOLLOWING PARTNERS:

State bank of Patiala (SBOP)

Kerala state Financial Enterprises Ltd.

Trinethra

Capital Local Area Bank

HP Gas

Punjab & Sind Bank (P & SB)

Hindustan Petroleum Corporation Ltd.

Bharat Petroleum Corporation Ltd.(BPCL)

Professional Courier

E-SEVA

COX & KING

PHEROZ Framroze

42

EMITRA

State Bank of Indore (SBOI)

Sify-I-Way

Tick Business Solutions

CMS Computer Solutions

Easy Bill (HERO Honda)

43

AREAS OF OPERATIONS:

SERVICES PROVIDED:

ONLINE

Western Union's website, westernunion.com, allows users to send and

receive funds to others, pay bills, or purchase gift cards.

The domain westernunion.com attracted at least 8.7 million visitors

annually by 2008 according to an online study.

BIDPAY

As the Internet became an arena for commerce at the turn of the

millennium, Western Union started its online services. BidPay was

renamed "Western Union Auction Payments" in 2004 before being

renamed back to BidPay. BidPay ceased operations on December 31,

2005, and was purchased for US$1.8 million in March 2006 by

CyberSource Corp. who announced their intention to re-launch BidPay.

BidPay was later discontinued by CyberSource effective December 31,

2007.

WESTERN UNION MOBILE

In October 2007, Western Union announced plans to introduce a mobile

money transfer service with the GSM Association, a global trade

association representing more than 700 mobile operators in 218

countries and covering 2.5 billion mobile subscribers.

44

The proliferation of mobile phones in developed and developing

economies provides a widely accessible consumer device capable of

delivering mobile financial services ranging from text notifications

associated with Western Union cash delivery services to phone-based

remittance options. Western Union's mobile money transfer service

offering will connect its core money transfer platform to m-bank or m-

wallet platforms provided by mobile operators and / or locally regulated

financial institutions.

SENDING AND RECEIVING FUNDS

The most important service that Western Union provides is the transfer

of money from one place/country to other. Money can be transferred in

cash or as cheques. Alternatively, a sender may forward funds online to

a recipient by using Western Union's online site, westernunion.com.

TRANSFER FEES

Fees differ based on originating and receiver countries and type of

transfer. Generally, fees are less if using the website rather than using a

partner agent location.

PAST SERVICES

Along with satellite telecommunications, Western Union was also active

in other forms of telecommunication services:

WU phone parlors near Times Square, 2008

Common carrier terrestrial microwave networks

45

Business communications networks such as Telex and TWX,

which was acquired from AT&T and renamed Telex II by Western

Union

Landline-based leased voice and data communication circuits

Long distance telephone service

Airfone air-ground radiotelephone service from 1981 to 1986

Cellular phone service for a very short time in the early 1980s (the

phones were made by 2-way radio manufacturer E.F. Johnson

Company)

46

WESTERN UNION EXECUTIVE

BOARD: CEO – Hikmet Ersek

Chairman of the Board – Jack Greenberg

Director – Roberto Mendoza

Director – Michael Miles

Director – Linda Levinson

Director – Dennis Stevenson

Director – Betsy Holden

Director – Richard Goodman

Director – Dinyar Devitre

Director – Wulf Von Schimmelmann

CFO – Scott Scheirman

Human Resources – Paula Larson

Marketing – Diane Scott

Integration – Robin Heller

Global Consumer Financial Services – Stewart Stockdale

CIO – John Thompson

CMO – Gail Galuppo

Corporate Affairs – Anne McCarthy

Legal & Secretary – John Dye

The Western Union Foundation – Luella Chavez D’Angelo

Western Union Business Solutions – Raj Agarwal

Latin America & Caribbean – Odilon Almeida

North America – Victoria Lopez Negrete

Asia Pacific – Drina Yue

Electronic Channels – Khalid Fellahi

Europe & CIS – Jan Hillered

Middle East & Africa – Jean Claude Farah

47

MONEY TRANSFER

PROCESS:

PROCEDURE FOR MONEY

TRANSFER TO INDIA FROM

ABROAD:

Person sending money from abroad, approaches the nearest

WESTERN UNION agent location submits the money along

with the name and address of receiver.

A long with the receipt, the location officer gives a secret

10digit code called the MTCN (Money Transfer Control

Number). This code can be verified at every Western Union

location and helps to identify the genuine receiver.

The sender informs the receiver about the code as well as the

amount sent.

Upon receipt of the code, the receiver approaches the nearest

Western Union agent location along with the code and his

identity proof.

The location officer issues the money immediately to the

receiver after verifying the code and any of the Western Union

48

accepted photo identity card. The entire process takes a few

minutes.

SAMPLE FORM FOR SENDING MONEY

49

PROCEDURE FOR RECEIVING MONEY IN INDIA:

The receiver must be physically present for transaction and possess

all the five basic information:

Sender’s Name

Country sent from

Amount expected

MTCN (Money Transfer Control Number)

Receiver’s Name

If any of these are not available, the payment should not be made.

The receiver should produce one of the 10 valid photo IDs for

personal identification:

Passport

Voter card

Driving License

Pan card

Employee Id (Armed Forces & Para military Services)

50

Employee Id of RBI,SEBI,TRAI & IRDI (Serving, not

retired)

Ration Card

Central Govt. Employee ID

State Govt. Employee ID

Loyalty Card

Employee Id of police (again, in service)

Bank pass book with photo

Payment is not to be made in cash for an amount of over

Rs.50,000/-Only an account’s payee cheque should be issued.

51

CHAPTER 6

RESEARCH

52

PROBLEM DEFINITION

In the case, the topic is to know the

“customer satisfaction towards

“WESTERN UNION MONEY

TRANSFER” because of good marketing,

the basic problem is to know the

satisfaction of the consumer is at present

towards WESTERN UNION MONEY

TRANSFER. What people think about it?

The main problem is to know how many

people are interested in using the services

of WESTERN UNION MONEY

TRANSFER.

53

OBJECTIVES OF THE STUDY:-

The main objective of the study can be explained as below:-

To know how many persons are willing to use

WESTERN UNION MONEY TRANSFER service.

To know the different criteria that the customer

undertakes while using money exchange services.

Through customer satisfaction, we can know the current

position of WESTERN UNION MONEY TRANSFER

in the market.

Also the study will provide detail about the money

exchange and remittance service and the financial

position of the company will be known.

SCOPE OF THE STUDY:-

Scope of the study is to know the customer satisfaction

about WESTERN UNION MONEY TRANSFER in Hyderabad

city.

54

RESEARCH COMPONENT

Research design: Research design is the plan for collecting the information

related to the study. Research design explains the methods

that are used for collecting the information. The research

design will focus attention on the different methods that are

used for collection of the data. Also it will help to solve the

problem. Different forms of collecting the data will be tasted

in the research design.

In this case, survey method is used to collect the necessary

data in the survey method, the personal interview is used to

collect the information from the respondents, and

questionnaires are used. The respondents are visited

personally, and the detail information is collected related to the

study. The question mainly focuses attention on the consumer

behavior to fulfill the objective of the study.

55

CHAPTER 7

RESEARCH

METHODOLOGY

56

RESEARCH METHODOLOGY

“Research is an organized inquiry designed and carried out to

provide information for solving problems.”

-Fred Kerlinger.

“Research is careful inquiry or examination to discover new

information or relationships and to existing knowledge.”

- Francis Rammel.

The nature of the project work has been exploratory as no

hypothesis is taken to be tested. Though the conclusions

drawn could be taken as the hypothesis and further tested by

the research work undertaken in the relevant field. The

reason for choosing the exploratory research design is the

fact the project report has been primarily based upon the

secondary sources of data and whose authenticity could be

assured of.

The reluctance of the company's personnel in parting with

much of information led the project report to be based

substantially on the secondary source of data. The sources of

data used in data collection are the following:

57

Primary sources:

In order to gather information about the various products, I

personally visited a number of retail markets and collected

data pertaining to the prices of the products offered. The

market visits were useful in knowing the comparative prices

and quality of the offered brands vis-à-vis the competitive

brands. Detail regarding the packaging of the products were

collected were collected and I also inquired about the various

sales promotion schemes followed by the three companies.

By interviewing these retailers valuable information was

collected. I inquired from them about their marketing

advertising and distribution strategies.

Secondary sources:

Information was collected from secondary sources such as

public libraries, newspapers, business magazines.

Beside these the use of Internet was also made in collecting

relevant information. The data collected from the above

mentioned sources has been adequately structured and used

at appropriate places in the report. This particular way of

data collection was used because of its low cost (except data

58

collected through surfing the internet) and less time

consumption. The information gathered included:

Their annual reports

Pamphlets.

Posters.

Press clippings.

News releases

Newsletters.

Pictures.

Websites

59

CHAPTER 8

ANALYSIS &

INTERPRETATION

OF RESEARCH

DATA

60

SERVICES WESTERN UNION MONEY

TRANSFER, SECUNDERABAD:

Response No. of Respondents Percentage

Satisfied 12 40

Dissatisfied 5 16.66

Very much satisfied 13 43.34

Very much

dissatisfied

Total 30 100

The customers were asked about the services of Western Union Money

Transfer, Secunderabad. 43.3% of the Respondents are very much

satisfied with the services of organization where are only 16.66% of

customers are dissatisfied service.

0

20

40

60

80

100

120

No.of

Respondents

percentages

Satisfied

Dissatisfied

Verymuchsatisfied

Verymuchdissatisfi

ed

Total

61

SOURCE OF INFORMATION:

The customer responded that they came to know about money transfer

service through television were 60% where as others came to know

about the western union services through friends and magazine.

0

20

40

60

80

100

120

No.of Respondents percentages

Television

Magazine

Friends

Agents

Total

Response No. of Respondents percentage

Television 18 60

Magazine 3 10

Friends 7 23.3

Agents 2 6.7

Total 30 100

62

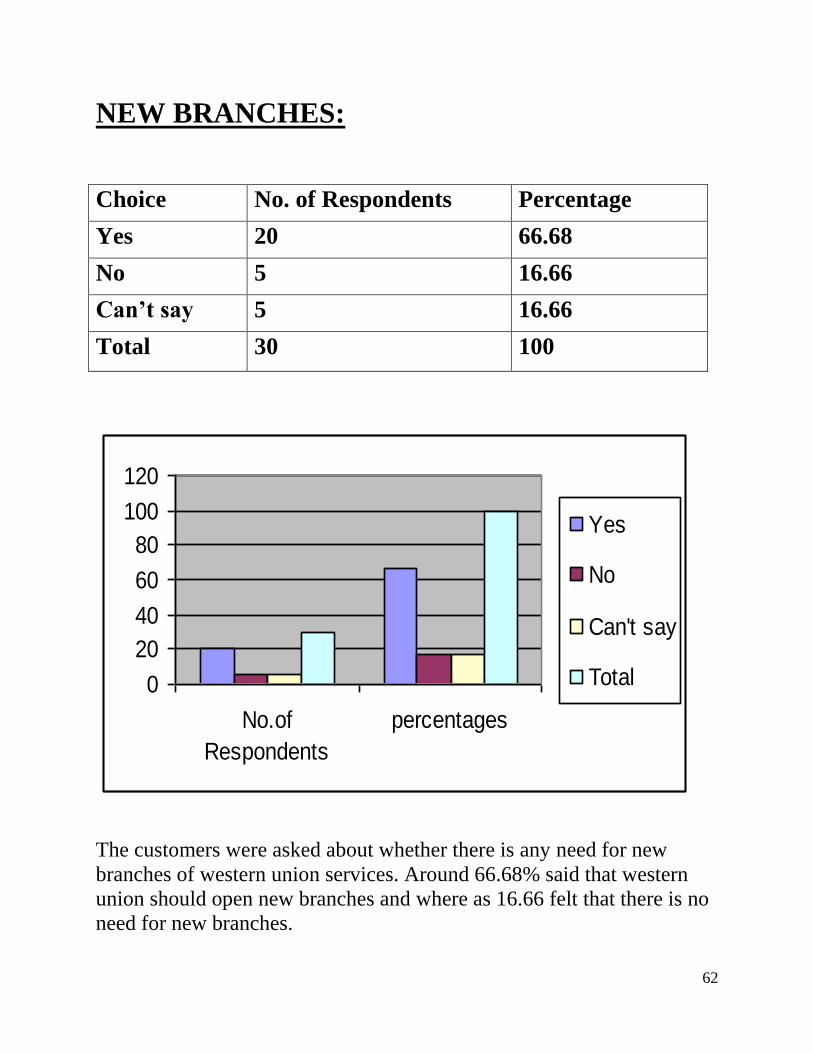

NEW BRANCHES:

Choice No. of Respondents Percentage

Yes 20 66.68

No 5 16.66

Can’t say 5 16.66

Total 30 100

The customers were asked about whether there is any need for new

branches of western union services. Around 66.68% said that western

union should open new branches and where as 16.66 felt that there is no

need for new branches.

0

20

40

60

80

100

120

No.of

Respondents

percentages

Yes

No

Can't say

Total

63

SERVICES EXPECTED:

Services No. of Respondents Percentage

Online services 12 40

International

Exchange

10 33.33

Depositary

participate

08 26.67

Total 30 100

The customers were asked about the new services they are expecting

from western union. 33.33% of the respondents said that they were

expecting International Exchange where as 40% of the customers said

that they want Online Services only. 26.67% of the customers said that

they were Expecting Depositary Participate services.

0

20

40

60

80

100

120

No.of Respondents percentages

Onlineser

vices

Internatio

nalExcha

nge

Depositar

y

Participat

eTotal

64

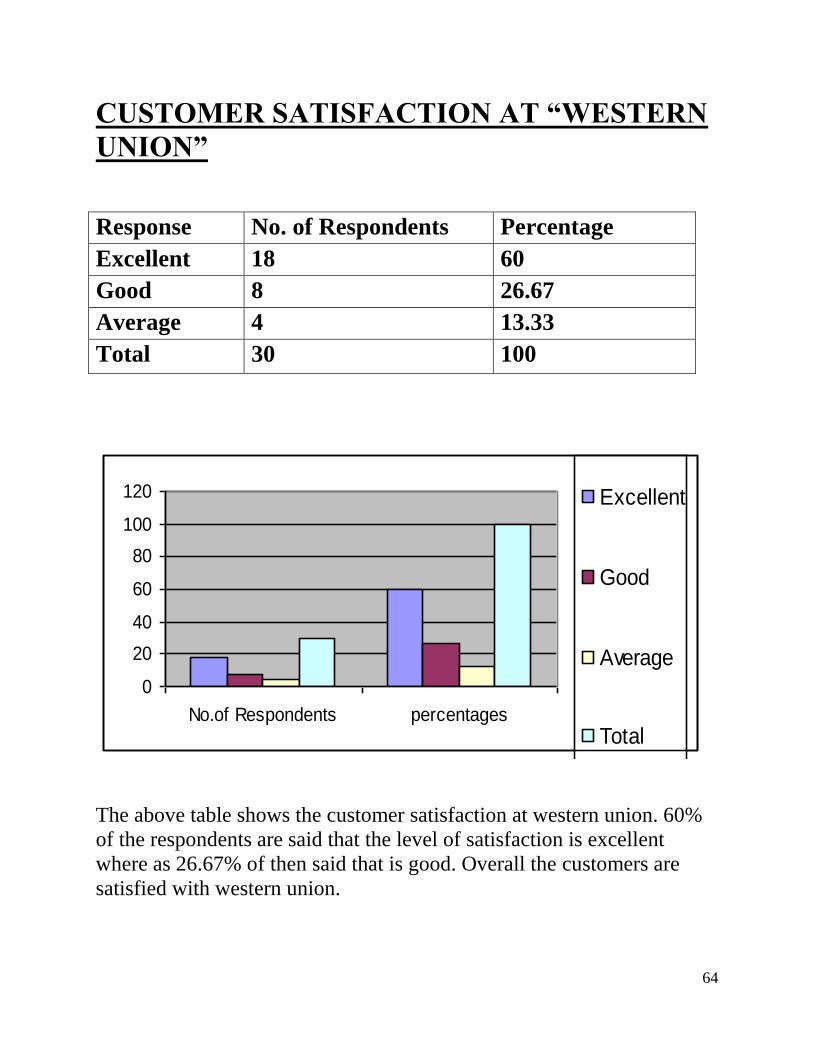

CUSTOMER SATISFACTION AT “WESTERN

UNION”

Response No. of Respondents Percentage

Excellent 18 60

Good 8 26.67

Average 4 13.33

Total 30 100

The above table shows the customer satisfaction at western union. 60%

of the respondents are said that the level of satisfaction is excellent

where as 26.67% of then said that is good. Overall the customers are

satisfied with western union.

0

20

40

60

80

100

120

No.of Respondents percentages

Excellent

Good

Average

Total

65

FINANCIAL DETAILS SECRECY:

Options No. of Respondents Percentage

Yes 13 43.33

No 17 56.67

Total 30 100

The customers were asked whether they would like the financial details

to be passed to other. 56.67% of customers said that they would like to

maintain secrecy of their financial details, where as 43.33% of them said

that they would like to pass on the details to others.

0

20

40

60

80

100

120

No.of Respondents percentages

Yes

No

Total

66

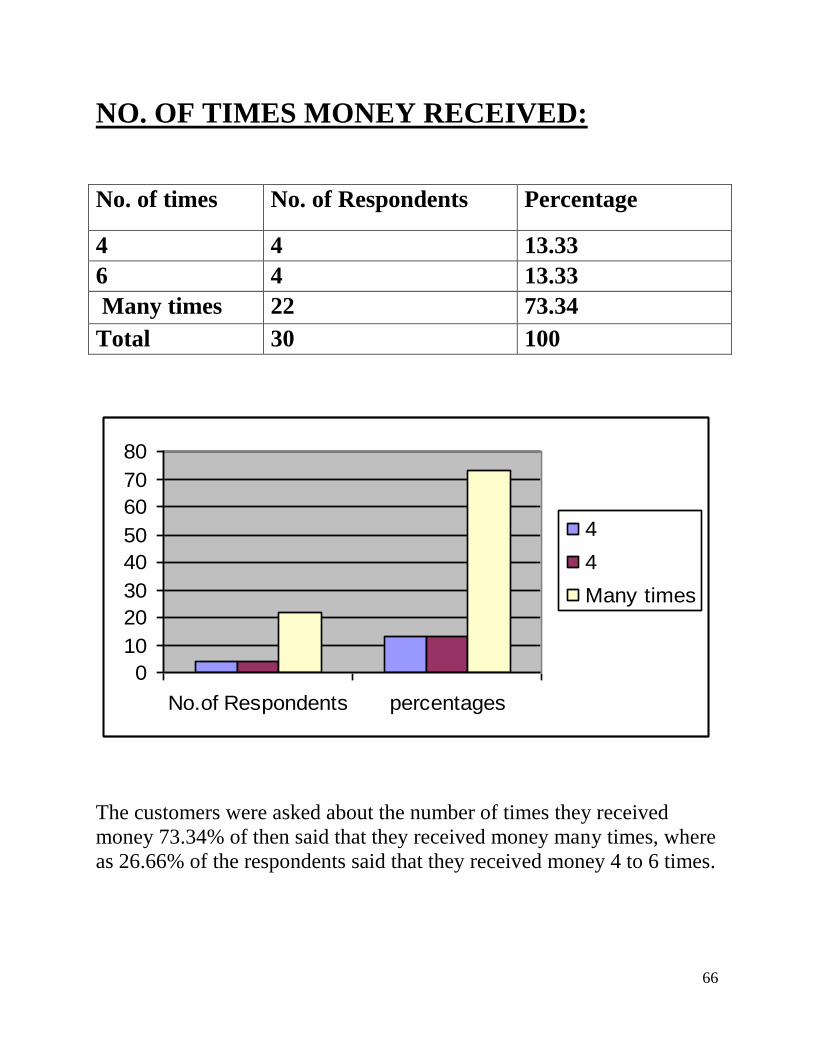

NO. OF TIMES MONEY RECEIVED:

No. of times No. of Respondents Percentage

4 4 13.33

6 4 13.33

Many times 22 73.34

Total 30 100

The customers were asked about the number of times they received

money 73.34% of then said that they received money many times, where

as 26.66% of the respondents said that they received money 4 to 6 times.

0

10

20

30

40

50

60

70

80

No.of Respondents percentages

4

4

Many times

67

PROBLEM FACED:

Problem faced No. of Respondent Percentage

Yes 5 16.7

No 25 83.3

Total 30 100

The customers were asked whether they faced any problem while

receiving money. 83.3% of them said that they didn’t face any problem

where as 16.7% of customers were faced problem while receiving the

money.

0

20

40

60

80

100

120

No.of Respondents percentages

Yes

No

total

68

ANY DEFECTS:

Response No. of Respondents Percentage

Yes 3 10

No 27 90

Total 30 100

The customers were asked whether they find any defects in western

union. 90% of customers did not find any defects in western union

where as 10% of the respondents find defects.

0

20

40

60

80

100

120

No.of Respondents percentages

Yes

No

total

69

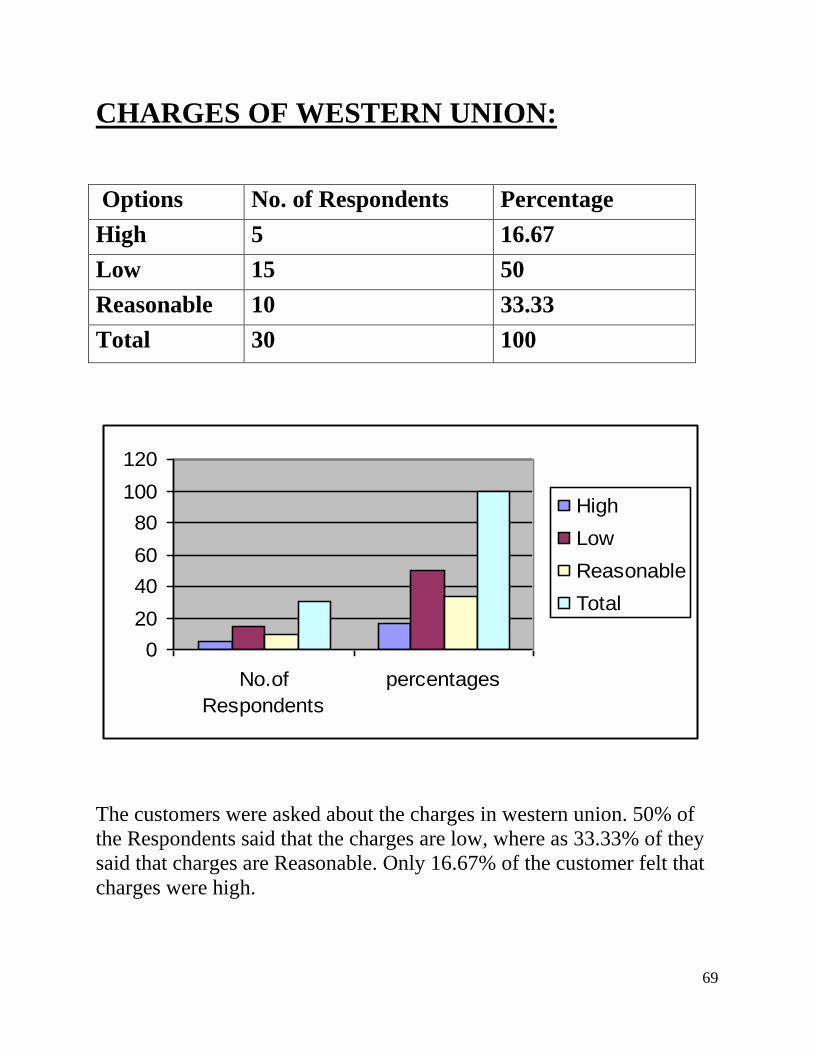

CHARGES OF WESTERN UNION:

Options No. of Respondents Percentage

High 5 16.67

Low 15 50

Reasonable 10 33.33

Total 30 100

The customers were asked about the charges in western union. 50% of

the Respondents said that the charges are low, where as 33.33% of they

said that charges are Reasonable. Only 16.67% of the customer felt that

charges were high.

0

20

40

60

80

100

120

No.of

Respondents

percentages

High

Low

Reasonable

Total

70

MANAGEMENT TREATMENT:

Treatment No. of Respondents Percentage

Partial 5 16.67

Impartial 20 66.66

Reasonable 5 16..66

Total 30 100

The customers were asked how the Management treats them in

organization. 66.67% of the customers said that they were treated

equally.

0

20

40

60

80

100

120

No.of

Respondents

percentages

Partial

Impartial

Reasonable

Total

71

WESTERN UNION MONEY TRANSFER

SERVICE:

Options No. of Respondents Percentage

Good 22 73.33

Bad 8 26.67

Total 30 100

The customers were asked whether the services of western union are

good or bad. 73.33% of them said that it is good, where as 26.67% of

them said that western union services are bad.

0

20

40

60

80

100

120

No.of Respondents percentages

Good

Bad

Total

72

CUSTOMER RELUCTANCE TO WORK:

Reluctance to

work

No. of Respondents Percentages

Yes 20 66.67

No 10 33.33

Total 30 100

The customers were asked if western union is making the customer

reluctant to work hard. 66.67% of them said yes, it is making the people

reluctant to work hard, where as 33.33% of them said no.

0

20

40

60

80

100

120

No.of Respondents percentages

Yes

No

Total

73

CHOICE FOR PREFERANCE WESTERN

UNION:

Preference No. of Respondents Percentage

Easy Finance only 6 20

Moderate price 10 33.33

Durability 14 46.66

Total 30 100

The customers were asked were asked why they prefer western union.

46.66% of them preferred it for Durability where as 33.33% of them

opted it for Moderate price and 20% of them opted it for Easy Finance.

0

20

40

60

80

100

120

No.of

Respondents

percentages

Easy

Finance

OnlyModerate

price

Durability

Total

74

CHAPTER 9

FINDINGS

AND

SUGGESTIONS

75

FINDINGS:

After observing the customers opinions, I found the following details:

It is found that the service is in a very good position in the area.

In the month of December 2011, it has the highest turnover.

In the month of December 2011, it also made the highest number

of transactions.

Customers came from different and far-off places.

Most of the customers were satisfied with the service provided by

Western Union Money Transfer services.

Compared to all other money transfer services, the Western Union

Money Transfer service is reliable, legal, and cheaper and this

service convenient to the all types of customers.

In Western union money transfer service, Paul Merchants is in the

number one position in south Asia.

Western union money transfer service is available in more than

200 countries. Therefore all types of customers all over the world

will get benefit from this service.

This service is provided all over the world by 5, 00,000 agent

locations.

Western union money transfer service and Paul merchants are

providing best service to Indians as well NRI’S, in money transfer

service.

76

SUGGESTIONS:

Many customers responded that western union money transfer

service is not offering domestic money transfer service. So my

suggestion is that they start domestic money transfer service

also.

Western union money transfer service is not giving any

discounts to the customers. So my suggestion is that if some

discounts are offered to customers, it will help to increase the

transactions.

Many people do not know about service provided by Western

union international, therefore it should increase its

advertisements, marketing and network to make it known to

people.

People are unaware about transfer services. So my suggestion is

to increase the awareness in people about service offered by

western union.

Increasing the agent locations so that each and every person will

know about the service provided by the western union money

transfer.

Service offered by western union is best but it needs to improve

the service to rural people also. Because many people from rural

areas go to foreign countries for employment.

The service offered by western union international money

transfer is better compared to other competitors like UAE

Exchange, instant cash etc.

77

CONCLUSION

Today, businesses around the world, both large and small, cannot ignore the impact that the global economy is having on their performance. Globalisation, the internet, and information transparency have led to an increasingly mobile workforce, ever more fickle customers, and rapidly changing technologies and business models. One result of this seemingly inexorable trend is that companies are less able to predict - let alone control - the short-term shape of their own markets.

As a result, more and more organisations are choosing to adopt a marketing-led philosophy to enable them to win market share and capture and retain the hearts and minds of current and prospective customers. Marketing is becoming more important as organisations around the world strive to develop products and services that appeal to their customers and aim to differentiate their offering in the increasingly-crowded global marketplace.

These complex issues heighten the need for effective marketing whilst expanding its scope beyond the ‘marketing function’. Put simply, marketing is no longer the sole prerogative of a single ‘function’, even if the leadership on marketing comes from that function, together with the framework within which marketing strategies are conceived, developed, planned, executed, reviewed and improved.

78

CHAPTER 10

QUESTIONNAIRE

AND

BIBLIOGRAPHY

79

QUESTIONNAIRE

NAME:

OCCUPTION:

GENDER:

AGE:

1. How do you feel about the services of “WESTERN

UNION MONEY TRANSFER”?

A) Satisfied

B) Dissatisfied

C) Very much satisfied

D) Very much dissatisfied

2. How did you come to know about money transfer service?

A) From television

B) From Magazine

C) From Friends

D) From Agent

80

3. What major purpose would you use this money transfer

service?

4. Do you think WESTERN UNION requires many more

branches for effective services?

A) Yes

B) No

C) Can’t say

5. Do you demand any of the services below?

A) Online service

B) International Exchange

C) Depositary participate services

81

6. How much would you rate customer satisfaction “At

Western Union”?

A) Excellent

B) Good

C) Average

7. Would you like to share your money transfer’s financial

details with others?

A) Yes

B) No

8. How many times you received money from abroad?

A) 4

B) 6

C) Many times

82

8. Have you faced any problem while receiving your money

in Western Union?

A) Yes

If yes, please mention

B) No

9. Would you like to point out any defects you found in

money transfer services?

A) Yes

If yes, please mention

C) No

83

10.What do you feel about the charges at Western Union

services?

A) High

B) Low

9. Reasonable

11. How does the management treat customers?

A) Partial

B) Impartial

C) Indifferent

12. Do you think Western Union makes customer reluctant to

work hard?

A) Yes

B) No

84

13. Why “most of the customers prefer Western Union

service”? Mention if any other reason.

A) Easy process

B) Moderate price

C) Durability

D) Other reason

14. Any other suggestions you would like to give to improve

the services of Western Union Money transfer.

85

BIBLIOGRAPHY

http://www.westernunion.com

http://en.wikipedia.org/

http://www.remittance.in/

http://www.google.com/

NEW RULES OF MARKETING

-David Meerman Scott

WORD OF MARKETING

-Andy Sernovitz