Embed Size (px)

Citation preview

What must be the Relation between Liquidity Ratios and

Profitability of the Banks in a Transition Economy?

The Case of Kyrgyzstan

Gulnaz Atabaeva1 , Farida Tashbaeva2, Nurlan Atabaev2 , Ibrahim Keles3

1Alatoo International University, Kyrgyzstan

2American University of Central Asia, Kyrgyzstan

3International Black Sea University, Georgia

Abstract

Liquidity and profitability are two main concerns of banks.

Stakeholders have different priorities for those aspects:

shareholders demand profit maximization, and the depositors

expect liquidity maximization, that is to be able to withdraw their

deposits whenever they need. Thus, banks are often challenged

with the need to satisfy these two stakeholder groups. This article

aims to determine the trade-off among liquidity and profitability in

Kyrgyzstan's banking sector for 2001-2019.

This article investigates the trade-off between liquidity and

profitability in the Kyrgyz banking system by focusing on ratios

such as liquidity, return on assets, return on equity, loan volume,

net interest margin, deposit volume, and exchange rate using the

Vector Auto Regression approach and Augmented Dickey-Fuller

test methods. Data were obtained from the National Bank of the

Kyrgyz Republic's publications.

The findings of this work showed a negative correlation between

liquidity and the economic development of Kyrgyzstan. The high

rate of the Kyrgyz banking system's liquidity ratio does not

positively impact economic growth. Besides this, no significant

relation among liquidity ratio and deposit volume was observed

for Kyrgyzstan.

Keywords: Credit Volume, Deposit Volume, Liquidity Ratio,

Profitability, Return on Assets, Return on Equity, Vector Auto

Regression.

JEL Classification Codes: E51, E52, E58.

Received 03 January 2022

Revised 25 February 2022

Accepted 04 March 2022

Citation: Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

Copyright: © 2022 by the authors. This article is an Open Access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

corresponding authors:

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

2

1. Introduction

Banks are powerful actors in the finance sector and contributes to a big share of the

economy (Met et al., 2008). Amongs the various functions of banks, their primary role is to collect

funds from the public and distribute those funds as credits to businesses. In addition, banks provide

services such as collection and payment of credit instruments, discounting bills of exchange,

foreign currency exchange, check/cheque payment, remittance of funds, etc. To provide these

services, banks perform several activities on both asset and liability sides of the balance sheet. For

example, on the assets side of the balance sheet, loans receivables occur as a result of loaning

money. The responsibilities of the bank appear on the liability side of the balance sheet as deposits.

To increase profitability, bank managers will try to convert deposits into loans as much as possible.

But at the same time, to maintain liquidity, they will try to keep those deposits on hand. So there

is an inherent tradeoff and persistent decision dilemma between profitability and liquidity ratio

(Malik et al. 2016).

The banking sector helps develop and expand new businesses to drive economic

development and employment, and banks are required to balance the demand and supply of

liquidity appropriately. Concerns about liquidity issue arise because of potential failures in

resource management and unfavorable economic conditions may lead to excessive cash drawings

by the banks' depositors (Waleed et al. 2016).

The banking sector's liquidity ratio is one of the economic standards and requirements

tracked by the commercial banks of the Kyrgyz Republic (NBKR, 2017). During the last 19 years,

the Kyrgyz Republic's banking sector is maintain a high liquidity ratio. A high liquidity ratio is an

indicator of stability in the banking sector and provides a high degree of safety for depositors

(Westerfield, 1921). Nevertheless, there are opposing sides to the high liquidity ratio. As stated by

Brealey et al. (2011) and Westerfield (1921), a high liquidity ratio is not favorable for a bank's

profitability. By holding on to a high amount of liquid assets, banks do not invest these assets into

their loan portfolio; hence, interest revenue falls, and profitability falls. Consequently, lesser

investments and loan can be obtained by small and medium businesses, and these businesses fail

to grow prosper, leading to further GDP decreases. In other words, the banking sector's high

liquidity ratio likely affects the economy of the Kyrgyz Republic.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

3

A considerable relationship among bank profitability and bank liquidity was suggested by

many researchers (Tran et al. 2016). Several theories have been introduced to explain the

relationship between liquidity and profitability of banks. These include liquidity management

theories such as The Real Bills Doctrine (Humphrey, 1982), The Shift-Ability Theory (Mitchell,

1923), The Anticipated Income Theory (Prochnow, 1949). More recently, Osborne et al. (2012)

judged that greater liquidity results in higher cost and lower profitability for banks, and is not

entirely a bad outcome since, the trade-off theory proposes that higher liquidity rates decrease the

bank's risks for the coming periods and effectively compensate investors for the possibility of

bankruptcy risk (Osborne et al. (2012).

The aim of this study to analyse the association concerning a bank's liquidity and

profitability and show results for the Kyrgyz banks. The findings of the study suggested a

significant relationship net interest margin, Return on Equity, and Return on Assets which are the

main parameters of the liquidity and profitability of the Kyrgyz banks.

2. Literature Review

Banks are the leading, complex, and difficult to govern institutions, having an implicit 'too

big to fail' guarantee in most countries (Becht et al. 2011). Like other businesses, banks are profit-

oriented, and they have investors expecting dividends. To survive and develop, they must have

profitable operations. On top of that, they must also provide and ensure sufficient liquidity. They

must satisfy the withdrawal needs of their clients (Tursoy, 2018). As a result of these, bank actively

manages their liquidity, that is balancing the cost of attaining higher liquidity and the cost of

inefficient allocation of such liquidity (Jahan et al. 2014).

Djalilov & Piesse (2016) analyzed profitability factors in Central and Eastern Europe and

former USSR countries' banking systems for the 2000–2013 period using the

Generalized Method of Moments (GMM). Their findings showed that profitability endures, and

there are different factors affecting bank profitability of their banking system. Their results showed

that Central and Eastern Europe banking systems are more competitive, and credit risk and

profitability are positively correlated. On the former USSR countries' banking systems side, credit

risk and profitability are negatively correlated. Additionally, government spending and monetary

freedom negatively influence bank profitability, as well.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

4

Faizulayev & Wada (2019) studied the Eurasian Economic Union banks' financial

performance by using Generalized Least Square (GLS) approach for 2011–2017. Liquidity and

credit risk are the leading indicators of the profitability of the banks. In another transition country's

banking system, the Albanian banking system, was analyzed by Shijaku (2017) for 2008–2015

with 16 banks. His findings showed that greater concentration hurt bank stability and indicated

that bank stability is associated with macroeconomic circumstances and capital ratio and opposite

with operational efficiency. In the same line of investigation, Haji-Zada (2017) proposed that real

GDP growth rate, exchange rate, corruption, and the political risk are the parameters affecting

credit risk in Kyrgyzstan. The higher credit risk hurts liquidity and profitability. Thus, the real

GDP growth rate positively impacts liquidity and profitability, and the exchange rate, corruption,

and political risk hurt liquidity and profitability.

The impact of state ownership and business models on bank stability at the Eurasian

Economic Union (EAEU) 's three founding states (Russia, Kazakhstan, and Belarus) were

examined by Pak (2019) for 2008–2016 period and found that state ownership and the probability

of survival have positive relation but have a negative association with the Basel III Net Stable

Funding Ratio (NSFR). The diversification in funding structures develops their financial stability.

Generally, improved capitalization and less dependence on short-term borrowing enhance the

weak structural liquidity. Moreover, the same author (Pak, 2020) examined the bank profitability

for the same group of countries. She found a substantial degree of stability in net interest margin

(NIM) and a lack of persistence in return on assets (ROA).

Erdogan & Aksoy (2016) investigated the determining factors of banks' profits and the

regulations' outcomes by using the Prais-Winsten regression method. Their results showed a

positive correlation between capital, size, off-balance-sheet transactions, liquidity and loans and

performance, and a negative correlation among quality of loans, concentration, and performance.

The Ukrainian banking system was analyzed according to deposit activity (Kichurchak,

2019) and devaluation of the national currency (Sobolieva-Tereshchenko, O., & Zhukova, 2020).

The importance of two parameters on banks' stability in transition economies was analyzed, and it

was thought that a similar importance level is valid for Kyrgyzstan.

Morris & Shin (2016) determine the liquidity ratio as the possible amount of cash on the

asset side to short term liability amounts. So, possible money is defined as liquid assets (such as

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

5

marketable securities and account receivable) plus other assets (such as advances paid to

employees or suppliers). Ratio analysis is one of the most popular tools that use financial

statements to estimate the company performance and compare the company with other companies

in the same industry by manipulating financial information such as balance sheets and income

statements. A sudden stop in an organization is usually defined as a sudden slowdown in

investments or positive cash flows, with an associated shift from sizeable current account deficits

into smaller deficits or small surpluses (Morris & Shin, 2016).

Tovar-García & Ruslana Kozubekova (2016) found that Kyrgyz banks with higher capital

ratios and liquidity charge higher interest rates on loans. But charging higher interest rates does

not give a guaranty for higher profitability.

3. Data and Methodology

The data on banking activities was collected from the website of NBKR, specifically from

the Bulletin of the National Bank of the Kyrgyz Republic, from the statistics on Deposits in

commercial banks by the end of the period, and from the statistics on Issued Credits of commercial

banks by the end of the period. The timeframe of all variables is from January 2007 to December

2019 monthly. The dataset included the following variables:

LC- Liquidity Ratio

ROA-Return on Assets

ROE-Return on Equity

DNIM- Net Interest Margin

DEPD/DEPS-Deposit Volume

VAR - Vector Autoregression model

ADF- Augmented Dickey-Fuller test

LOD/LOS-Issued Loans

DER-Exchange rate

TRAS/TRADES- Issued loans for trade

INDD-Issued loans for industry

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

6

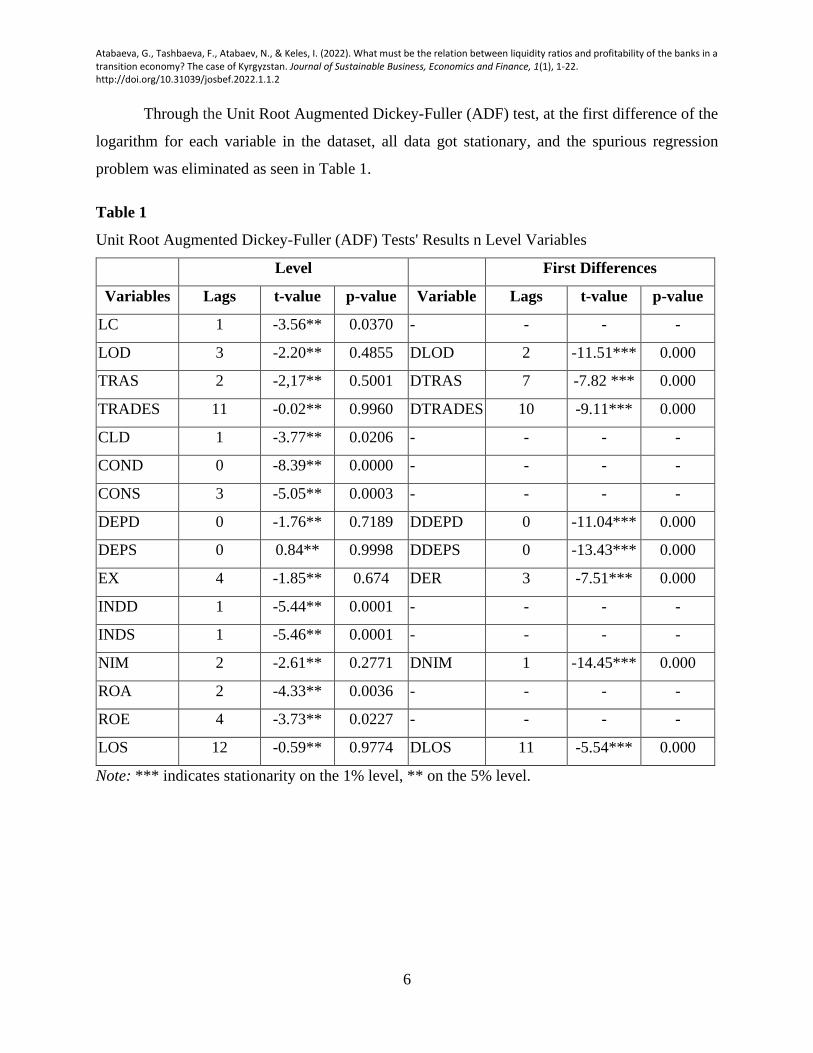

Through the Unit Root Augmented Dickey-Fuller (ADF) test, at the first difference of the

logarithm for each variable in the dataset, all data got stationary, and the spurious regression

problem was eliminated as seen in Table 1.

Table 1

Unit Root Augmented Dickey-Fuller (ADF) Tests' Results n Level Variables

Level First Differences

Variables Lags t-value p-value Variable Lags t-value p-value

LC 1 -3.56** 0.0370 - - - -

LOD 3 -2.20** 0.4855 DLOD 2 -11.51*** 0.000

TRAS 2 -2,17** 0.5001 DTRAS 7 -7.82 *** 0.000

TRADES 11 -0.02** 0.9960 DTRADES 10 -9.11*** 0.000

CLD 1 -3.77** 0.0206 - - - -

COND 0 -8.39** 0.0000 - - - -

CONS 3 -5.05** 0.0003 - - - -

DEPD 0 -1.76** 0.7189 DDEPD 0 -11.04*** 0.000

DEPS 0 0.84** 0.9998 DDEPS 0 -13.43*** 0.000

EX 4 -1.85** 0.674 DER 3 -7.51*** 0.000

INDD 1 -5.44** 0.0001 - - - -

INDS 1 -5.46** 0.0001 - - - -

NIM 2 -2.61** 0.2771 DNIM 1 -14.45*** 0.000

ROA 2 -4.33** 0.0036 - - - -

ROE 4 -3.73** 0.0227 - - - -

LOS 12 -0.59** 0.9774 DLOS 11 -5.54*** 0.000

Note: *** indicates stationarity on the 1% level, ** on the 5% level.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

7

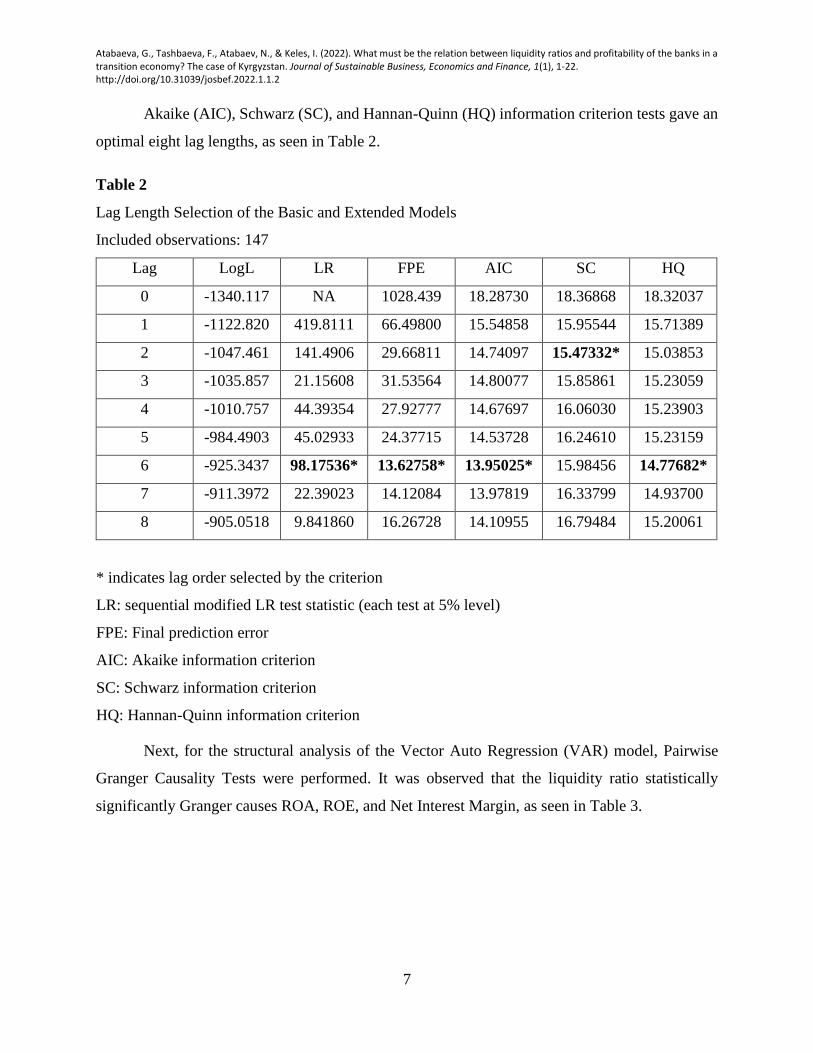

Akaike (AIC), Schwarz (SC), and Hannan-Quinn (HQ) information criterion tests gave an

optimal eight lag lengths, as seen in Table 2.

Table 2

Lag Length Selection of the Basic and Extended Models

Included observations: 147

Lag LogL LR FPE AIC SC HQ

0 -1340.117 NA 1028.439 18.28730 18.36868 18.32037

1 -1122.820 419.8111 66.49800 15.54858 15.95544 15.71389

2 -1047.461 141.4906 29.66811 14.74097 15.47332* 15.03853

3 -1035.857 21.15608 31.53564 14.80077 15.85861 15.23059

4 -1010.757 44.39354 27.92777 14.67697 16.06030 15.23903

5 -984.4903 45.02933 24.37715 14.53728 16.24610 15.23159

6 -925.3437 98.17536* 13.62758* 13.95025* 15.98456 14.77682*

7 -911.3972 22.39023 14.12084 13.97819 16.33799 14.93700

8 -905.0518 9.841860 16.26728 14.10955 16.79484 15.20061

* indicates lag order selected by the criterion

LR: sequential modified LR test statistic (each test at 5% level)

FPE: Final prediction error

AIC: Akaike information criterion

SC: Schwarz information criterion

HQ: Hannan-Quinn information criterion

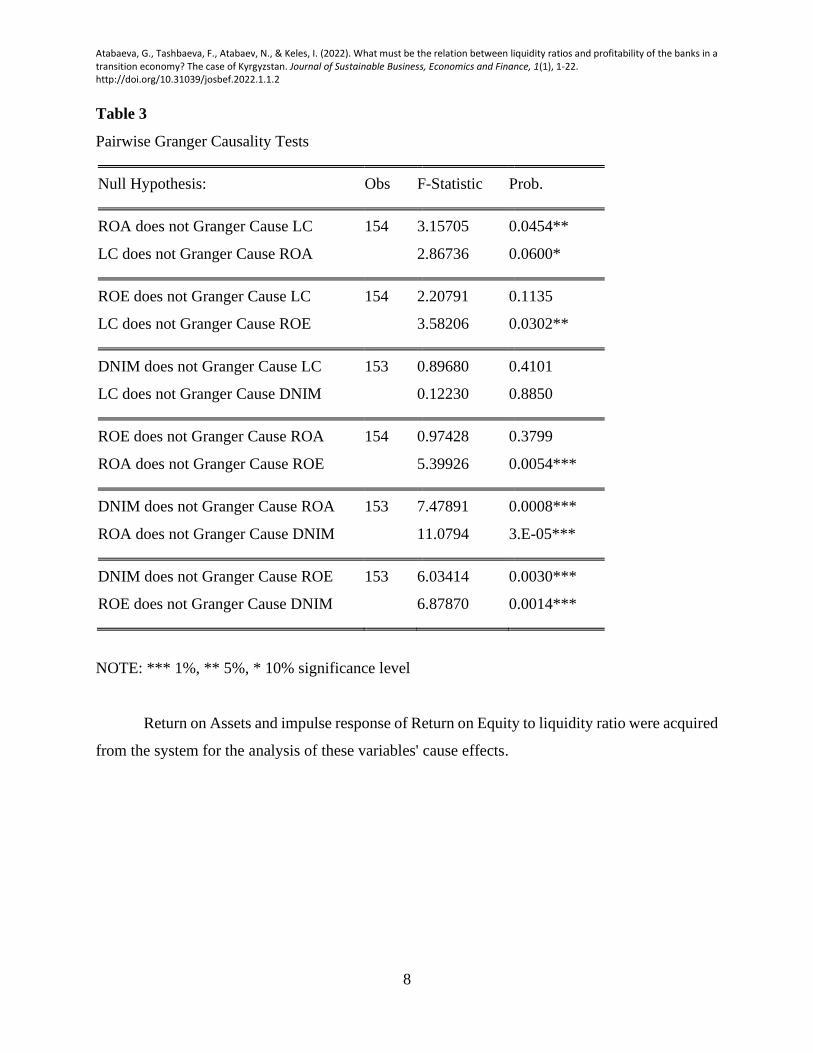

Next, for the structural analysis of the Vector Auto Regression (VAR) model, Pairwise

Granger Causality Tests were performed. It was observed that the liquidity ratio statistically

significantly Granger causes ROA, ROE, and Net Interest Margin, as seen in Table 3.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

8

Table 3

Pairwise Granger Causality Tests

Null Hypothesis: Obs F-Statistic Prob.

ROA does not Granger Cause LC 154 3.15705 0.0454**

LC does not Granger Cause ROA 2.86736 0.0600*

ROE does not Granger Cause LC 154 2.20791 0.1135

LC does not Granger Cause ROE 3.58206 0.0302**

DNIM does not Granger Cause LC 153 0.89680 0.4101

LC does not Granger Cause DNIM 0.12230 0.8850

ROE does not Granger Cause ROA 154 0.97428 0.3799

ROA does not Granger Cause ROE 5.39926 0.0054***

DNIM does not Granger Cause ROA 153 7.47891 0.0008***

ROA does not Granger Cause DNIM 11.0794 3.E-05***

DNIM does not Granger Cause ROE 153 6.03414 0.0030***

ROE does not Granger Cause DNIM 6.87870 0.0014***

NOTE: *** 1%, ** 5%, * 10% significance level

Return on Assets and impulse response of Return on Equity to liquidity ratio were acquired

from the system for the analysis of these variables' cause effects.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

9

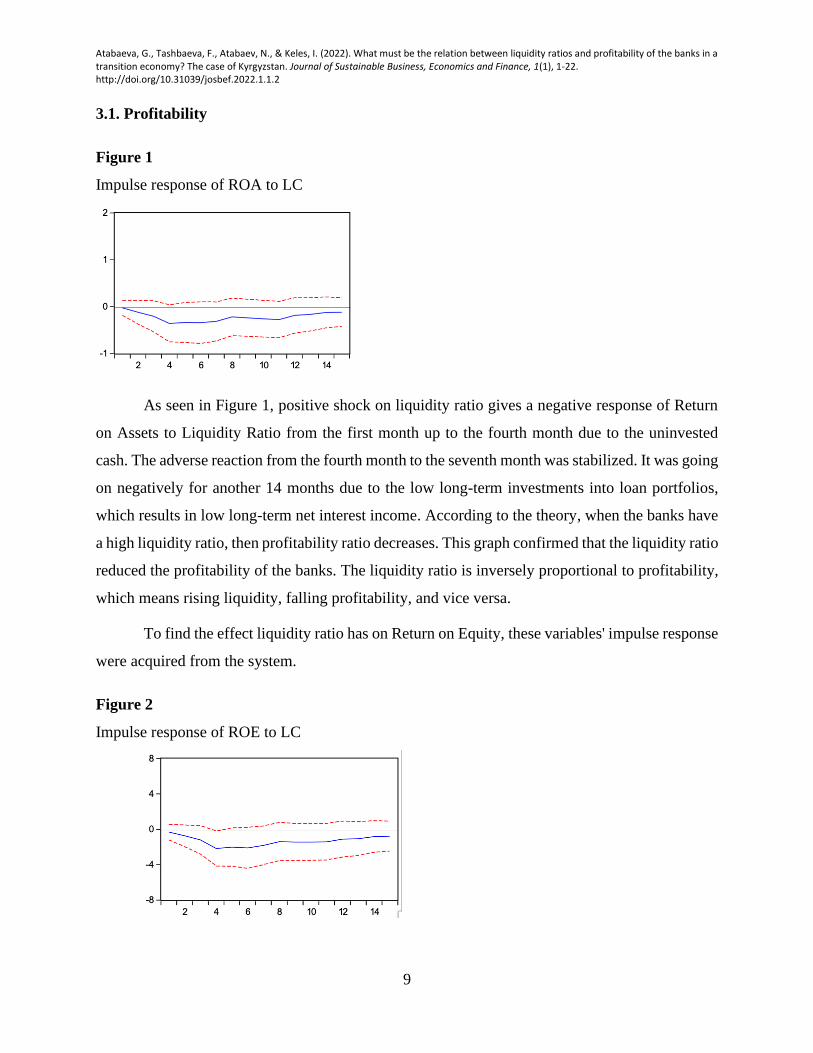

3.1. Profitability

Figure 1

Impulse response of ROA to LC

As seen in Figure 1, positive shock on liquidity ratio gives a negative response of Return

on Assets to Liquidity Ratio from the first month up to the fourth month due to the uninvested

cash. The adverse reaction from the fourth month to the seventh month was stabilized. It was going

on negatively for another 14 months due to the low long-term investments into loan portfolios,

which results in low long-term net interest income. According to the theory, when the banks have

a high liquidity ratio, then profitability ratio decreases. This graph confirmed that the liquidity ratio

reduced the profitability of the banks. The liquidity ratio is inversely proportional to profitability,

which means rising liquidity, falling profitability, and vice versa.

To find the effect liquidity ratio has on Return on Equity, these variables' impulse response

were acquired from the system.

Figure 2

Impulse response of ROE to LC

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

10

An impulse response of return on equity (ROE) to liquidity ratio is seen in Figure 2. There,

the positive shock in liquidity ratio gives an adverse reaction from ROE and short-term and long-

term. If a liquidity ratio increases, then return on equity decreases and vice versa. As Figure 2

shows, starting from the first month to the fourth month, return on equity decreased, it was

stabilized from the fourth month up to the seventh month, and it was going on correlate negatively

for another 14 months. This illustrates that a liquidity ratio negatively impacts profitability and on

the return mentioned above on assets when the banks increase the liquidity ratio, which means that

profitability decreases.

To find the effect liquidity ratio has on Net Interest Margin, these variables' impulse

response was also acquired from the system.

Figure 3

Impulse response of DNIM to LC

Figure 3 shows the impulse response of Net Interest Margin to liquidity ratio. A negative

shock in liquidity ratio gives a positive reaction of Net Interest Margin and short-term and long-

term due to the investments into government securities, which offers a high-interest revenue. So,

the fact that liquidity ratio increases when Net Interest Margin increases because the government

securities in a mostly short-term circulation, with high-interest rates, gives a high-interest revenue

and adds more profitability into the banking sector. This illustrates that banks invest in government

securities. As a result, liquidity ratio and profitability increases. The investment into a short -term

securities during the one-year liquidity ratio has a positive impact on profitability.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

11

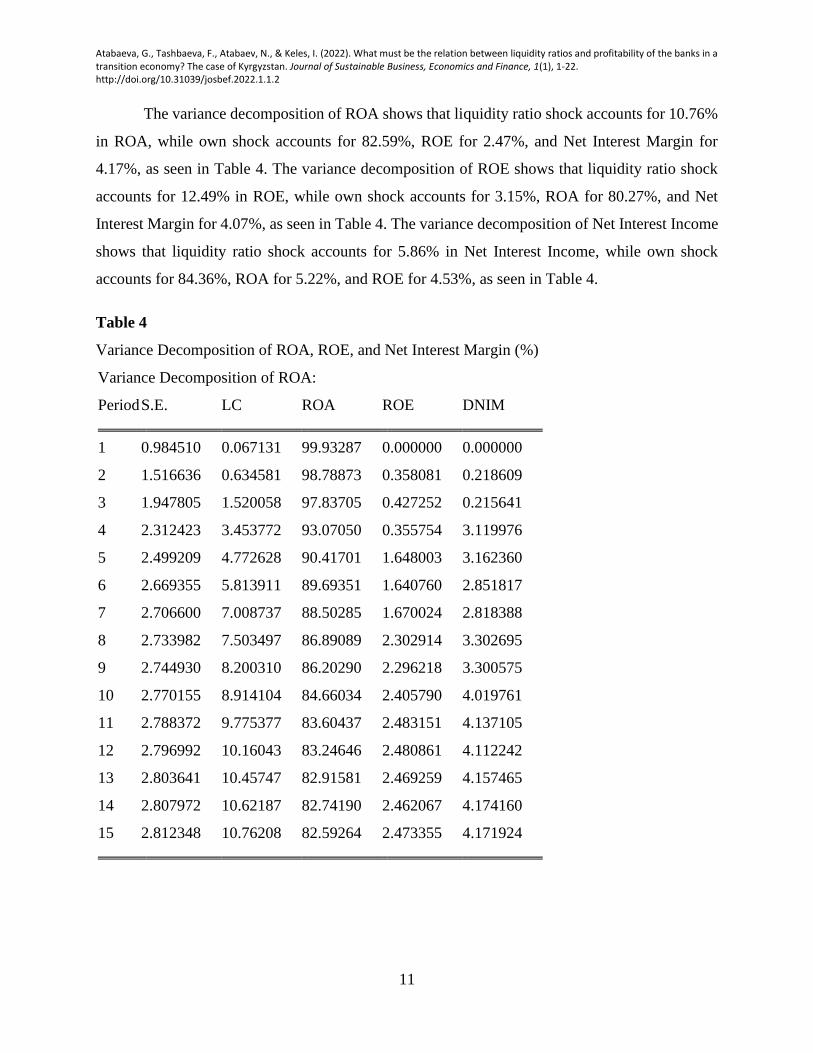

The variance decomposition of ROA shows that liquidity ratio shock accounts for 10.76%

in ROA, while own shock accounts for 82.59%, ROE for 2.47%, and Net Interest Margin for

4.17%, as seen in Table 4. The variance decomposition of ROE shows that liquidity ratio shock

accounts for 12.49% in ROE, while own shock accounts for 3.15%, ROA for 80.27%, and Net

Interest Margin for 4.07%, as seen in Table 4. The variance decomposition of Net Interest Income

shows that liquidity ratio shock accounts for 5.86% in Net Interest Income, while own shock

accounts for 84.36%, ROA for 5.22%, and ROE for 4.53%, as seen in Table 4.

Table 4

Variance Decomposition of ROA, ROE, and Net Interest Margin (%)

Variance Decomposition of ROA:

Period S.E. LC ROA ROE DNIM

1 0.984510 0.067131 99.93287 0.000000 0.000000

2 1.516636 0.634581 98.78873 0.358081 0.218609

3 1.947805 1.520058 97.83705 0.427252 0.215641

4 2.312423 3.453772 93.07050 0.355754 3.119976

5 2.499209 4.772628 90.41701 1.648003 3.162360

6 2.669355 5.813911 89.69351 1.640760 2.851817

7 2.706600 7.008737 88.50285 1.670024 2.818388

8 2.733982 7.503497 86.89089 2.302914 3.302695

9 2.744930 8.200310 86.20290 2.296218 3.300575

10 2.770155 8.914104 84.66034 2.405790 4.019761

11 2.788372 9.775377 83.60437 2.483151 4.137105

12 2.796992 10.16043 83.24646 2.480861 4.112242

13 2.803641 10.45747 82.91581 2.469259 4.157465

14 2.807972 10.62187 82.74190 2.462067 4.174160

15 2.812348 10.76208 82.59264 2.473355 4.171924

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

12

Variance Decomposition of ROE:

Period S.E. LC ROA ROE DNIM

1 5.328915 0.369208 94.22092 5.409867 0.000000

2 7.156804 1.285809 95.60918 3.042462 0.062544

3 9.461017 2.354330 95.31680 1.757557 0.571311

4 11.64761 5.055575 90.23009 1.210260 3.504078

5 12.75013 6.732489 88.39101 1.951935 2.924562

6 13.87186 7.983150 87.58220 1.963790 2.470863

7 14.10312 9.385589 86.21066 1.980005 2.423747

8 14.28283 10.09933 84.24931 2.750917 2.900446

9 14.35931 10.99959 83.35673 2.758045 2.885634

10 14.53330 11.71787 81.38986 3.030788 3.861492

11 14.63679 12.49131 80.27598 3.152785 4.079921

12 14.68806 12.97274 79.79534 3.173532 4.058389

13 14.73583 13.40563 79.31299 3.165886 4.115500

14 14.76714 13.66503 79.06387 3.154682 4.116412

15 14.79728 13.88775 78.82807 3.170565 4.113620

Variance Decomposition of DNIM:

Period S.E. LC ROA ROE DNIM

1 0.443915 6.159289 8.376131 6.583373 78.88121

2 0.577457 5.867585 5.228730 4.535277 84.36841

3 0.592086 6.178213 5.138722 4.658427 84.02464

4 0.594358 6.248373 5.139947 4.628454 83.98323

5 0.601030 6.110714 5.027138 4.680915 84.18123

6 0.602224 6.092092 5.087788 4.891720 83.92840

7 0.614536 6.679141 4.886429 7.719392 80.71504

8 0.624793 6.701384 6.403982 8.740043 78.15459

9 0.628899 6.750838 7.012473 8.848175 77.38851

10 0.631541 6.763020 6.998260 8.829071 77.40965

11 0.638480 6.640623 6.998935 8.950969 77.40947

12 0.644384 6.524919 6.871367 8.951108 77.65261

13 0.644702 6.590419 6.873077 8.942887 77.59362

14 0.645868 6.600795 6.853201 8.967308 77.57870

15 0.646201 6.614120 6.847271 8.969683 77.56893

Cholesky Ordering: LC ROA ROE DNIM

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

13

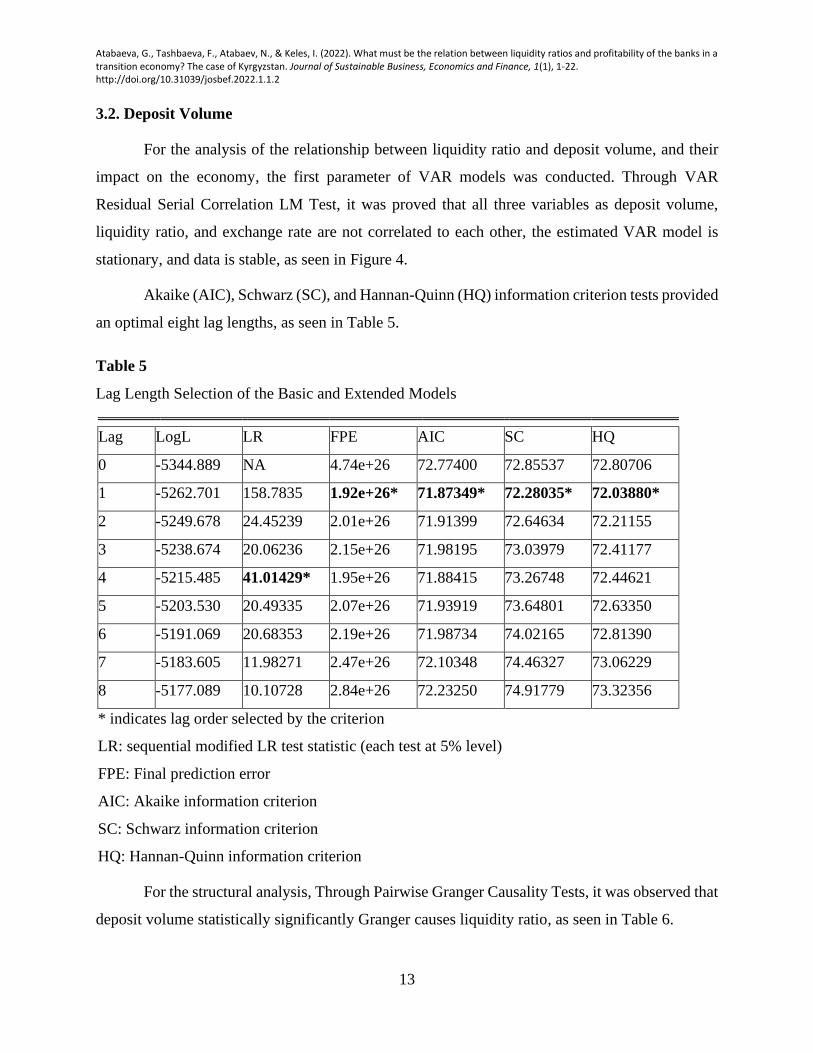

3.2. Deposit Volume

For the analysis of the relationship between liquidity ratio and deposit volume, and their

impact on the economy, the first parameter of VAR models was conducted. Through VAR

Residual Serial Correlation LM Test, it was proved that all three variables as deposit volume,

liquidity ratio, and exchange rate are not correlated to each other, the estimated VAR model is

stationary, and data is stable, as seen in Figure 4.

Akaike (AIC), Schwarz (SC), and Hannan-Quinn (HQ) information criterion tests provided

an optimal eight lag lengths, as seen in Table 5.

Table 5

Lag Length Selection of the Basic and Extended Models

Lag LogL LR FPE AIC SC HQ

0 -5344.889 NA 4.74e+26 72.77400 72.85537 72.80706

1 -5262.701 158.7835 1.92e+26* 71.87349* 72.28035* 72.03880*

2 -5249.678 24.45239 2.01e+26 71.91399 72.64634 72.21155

3 -5238.674 20.06236 2.15e+26 71.98195 73.03979 72.41177

4 -5215.485 41.01429* 1.95e+26 71.88415 73.26748 72.44621

5 -5203.530 20.49335 2.07e+26 71.93919 73.64801 72.63350

6 -5191.069 20.68353 2.19e+26 71.98734 74.02165 72.81390

7 -5183.605 11.98271 2.47e+26 72.10348 74.46327 73.06229

8 -5177.089 10.10728 2.84e+26 72.23250 74.91779 73.32356

* indicates lag order selected by the criterion

LR: sequential modified LR test statistic (each test at 5% level)

FPE: Final prediction error

AIC: Akaike information criterion

SC: Schwarz information criterion

HQ: Hannan-Quinn information criterion

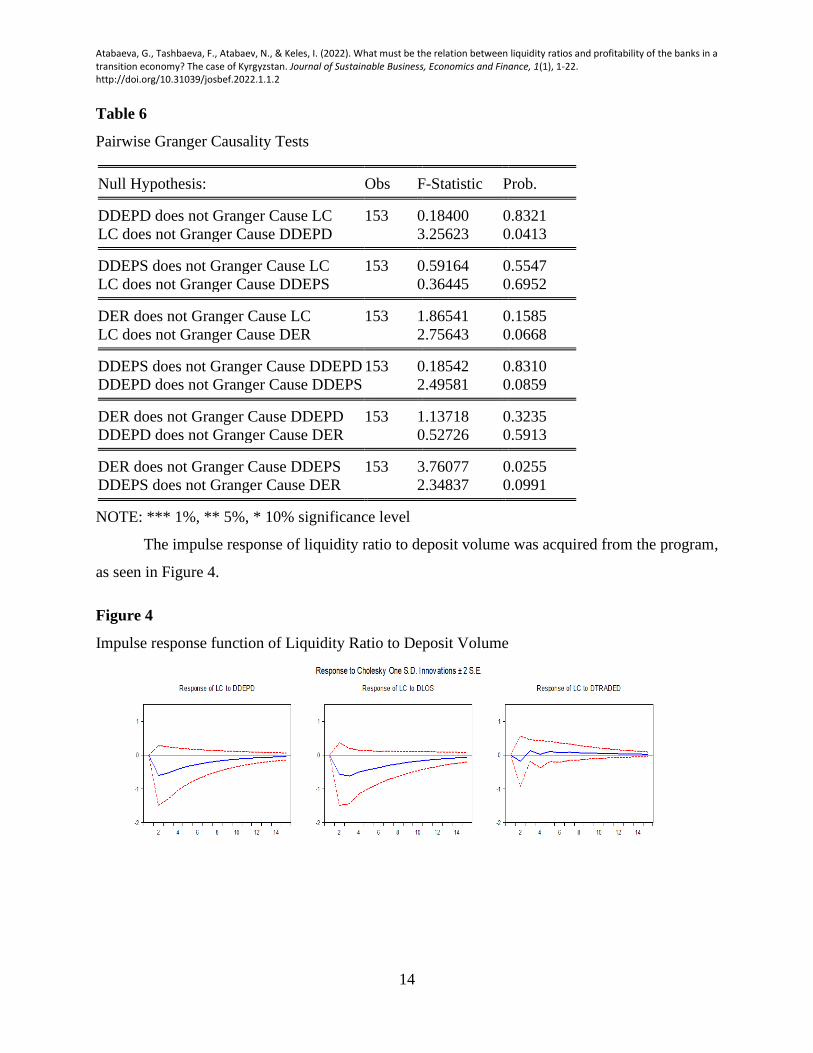

For the structural analysis, Through Pairwise Granger Causality Tests, it was observed that

deposit volume statistically significantly Granger causes liquidity ratio, as seen in Table 6.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

14

Table 6

Pairwise Granger Causality Tests

Null Hypothesis: Obs F-Statistic Prob.

DDEPD does not Granger Cause LC 153 0.18400 0.8321

LC does not Granger Cause DDEPD 3.25623 0.0413

DDEPS does not Granger Cause LC 153 0.59164 0.5547

LC does not Granger Cause DDEPS 0.36445 0.6952

DER does not Granger Cause LC 153 1.86541 0.1585

LC does not Granger Cause DER 2.75643 0.0668

DDEPS does not Granger Cause DDEPD 153 0.18542 0.8310

DDEPD does not Granger Cause DDEPS 2.49581 0.0859

DER does not Granger Cause DDEPD 153 1.13718 0.3235

DDEPD does not Granger Cause DER 0.52726 0.5913

DER does not Granger Cause DDEPS 153 3.76077 0.0255

DDEPS does not Granger Cause DER 2.34837 0.0991

NOTE: *** 1%, ** 5%, * 10% significance level

The impulse response of liquidity ratio to deposit volume was acquired from the program,

as seen in Figure 4.

Figure 4

Impulse response function of Liquidity Ratio to Deposit Volume

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

15

The positive shock on a deposit volume increases the liquidity ratio in the first month and

decreases in the second and third months. Then, there is a negative impact response for the last ten

months. The increase of the liquidity ratio in the first month is due to the banks' cash expansions

through a high deposit volume. The decrease in the second, third, and fourth months occurs due to

increasing liabilities as an accrued interest expense, which raises a current liability and decreases

a liquidity ratio. Moreover, according to the NBKR (2017) statement, if the commercial banks'

liquidity is high, then deposit volume will be increased because the banks will be more secured.

The depositors will put more money. In other words, NBKR believes that the higher liquidity ratio

leads to the public confidence in the banking sector and the higher deposit volume. However, if

the liquidity ratio increases, the Deposit volume decreases, and vice versa, where the deposit

impulse response is negative at last up ten months. This illustrates that the NBKR's statement is a

mistake.

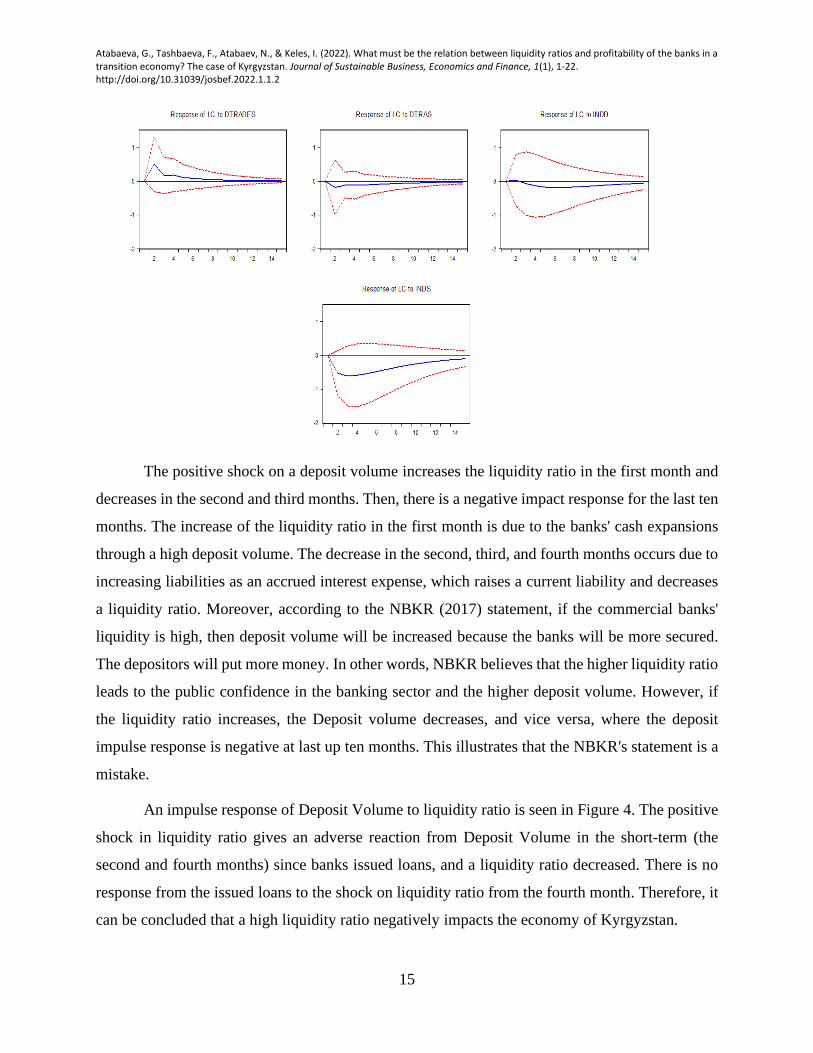

An impulse response of Deposit Volume to liquidity ratio is seen in Figure 4. The positive

shock in liquidity ratio gives an adverse reaction from Deposit Volume in the short-term (the

second and fourth months) since banks issued loans, and a liquidity ratio decreased. There is no

response from the issued loans to the shock on liquidity ratio from the fourth month. Therefore, it

can be concluded that a high liquidity ratio negatively impacts the economy of Kyrgyzstan.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

16

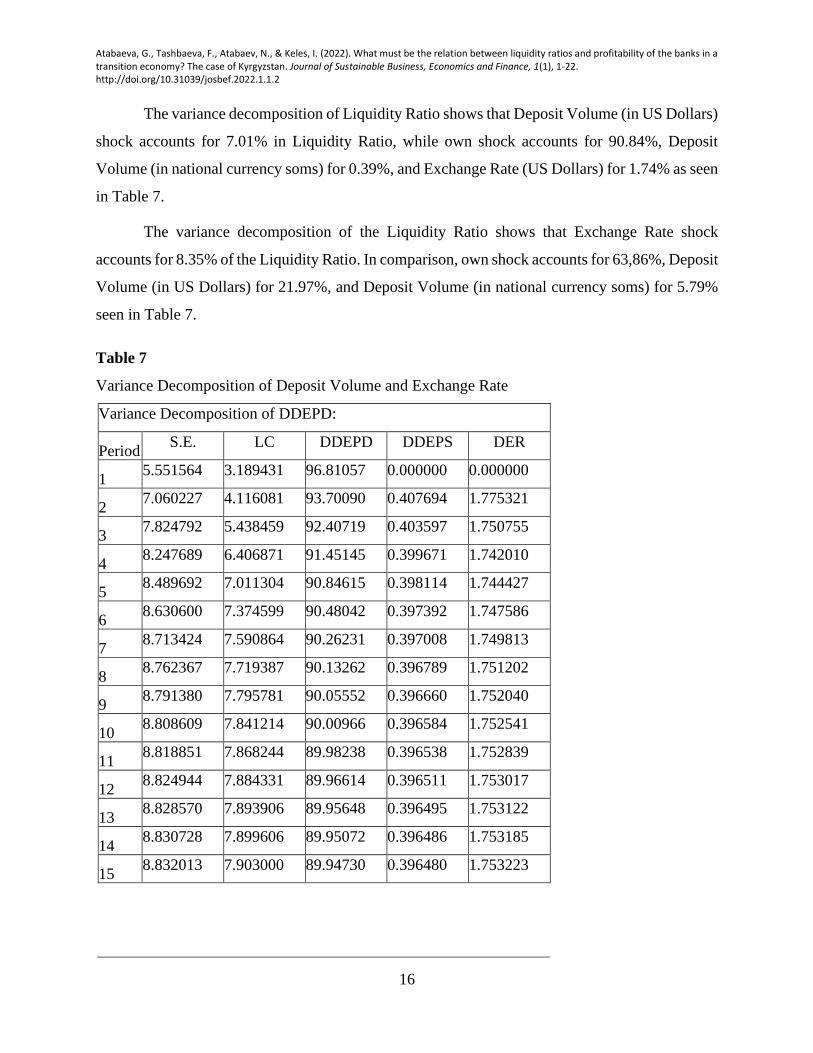

The variance decomposition of Liquidity Ratio shows that Deposit Volume (in US Dollars)

shock accounts for 7.01% in Liquidity Ratio, while own shock accounts for 90.84%, Deposit

Volume (in national currency soms) for 0.39%, and Exchange Rate (US Dollars) for 1.74% as seen

in Table 7.

The variance decomposition of the Liquidity Ratio shows that Exchange Rate shock

accounts for 8.35% of the Liquidity Ratio. In comparison, own shock accounts for 63,86%, Deposit

Volume (in US Dollars) for 21.97%, and Deposit Volume (in national currency soms) for 5.79%

seen in Table 7.

Table 7

Variance Decomposition of Deposit Volume and Exchange Rate

Variance Decomposition of DDEPD:

Period S.E. LC DDEPD DDEPS DER

1 5.551564 3.189431 96.81057 0.000000 0.000000

2 7.060227 4.116081 93.70090 0.407694 1.775321

3 7.824792 5.438459 92.40719 0.403597 1.750755

4 8.247689 6.406871 91.45145 0.399671 1.742010

5 8.489692 7.011304 90.84615 0.398114 1.744427

6 8.630600 7.374599 90.48042 0.397392 1.747586

7 8.713424 7.590864 90.26231 0.397008 1.749813

8 8.762367 7.719387 90.13262 0.396789 1.751202

9 8.791380 7.795781 90.05552 0.396660 1.752040

10 8.808609 7.841214 90.00966 0.396584 1.752541

11 8.818851 7.868244 89.98238 0.396538 1.752839

12 8.824944 7.884331 89.96614 0.396511 1.753017

13 8.828570 7.893906 89.95648 0.396495 1.753122

14 8.830728 7.899606 89.95072 0.396486 1.753185

15 8.832013 7.903000 89.94730 0.396480 1.753223

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

17

Variance Decomposition of DDEPS:

Period S.E. LC DDEPD DDEPS DER

1 1855087. 2.494009 2.115653 95.39034 0.000000

2 1891920. 2.486760 4.305637 93.02784 0.179759

3 1907048. 2.515571 4.303149 92.94729 0.233990

4 1917348. 2.551359 4.307849 92.90690 0.233890

5 1923865. 2.578479 4.307427 92.88002 0.234075

6 1927819. 2.595616 4.306998 92.86296 0.234426

7 1930186. 2.606025 4.306695 92.85260 0.234681

8 1931598. 2.612259 4.306508 92.84639 0.234844

9 1932438. 2.615978 4.306394 92.84269 0.234942

10 1932938. 2.618194 4.306327 92.84048 0.235001

11 1933236. 2.619513 4.306286 92.83916 0.235037

12 1933414. 2.620299 4.306262 92.83838 0.235058

13 1933519. 2.620767 4.306248 92.83792 0.235070

14 1933582. 2.621045 4.306240 92.83764 0.235078

15 1933620. 2.621211 4.306234 92.83747 0.235082

Variance Decomposition of DER:

Period S.E. LC DDEPD DDEPS DER

1 1337949. 5.828269 21.42390 5.695186 67.05265

2 1358648. 5.761054 22.41264 5.971513 65.85480

3 1359517. 6.560612 22.37390 5.914776 65.15071

4 1359812. 7.244109 22.23635 5.869115 64.65043

5 1360009. 7.688999 22.13597 5.840302 64.33473

6 1360134. 7.960081 22.07299 5.822953 64.14398

7 1360210. 8.122263 22.03498 5.812616 64.03014

8 1360256. 8.218840 22.01229 5.806468 63.96241

9 1360283. 8.276298 21.99877 5.802812 63.92212

10 1360299. 8.310484 21.99073 5.800637 63.89815

11 1360309. 8.330828 21.98594 5.799343 63.88388

12 1360315. 8.342937 21.98310 5.798572 63.87539

13 1360318. 8.350145 21.98140 5.798114 63.87034

14 1360320. 8.354437 21.98039 5.797841 63.86733

15 1360321. 8.356992 21.97979 5.797678 63.86554

Cholesky Ordering: LC DDEPD DDEPS DER

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

18

4. Discussion

According to the result, the banking sector's high liquidity ratio hurts the banking sector's

profitability in the long run. Firstly, by analyzing the cause-effect of return on assets, return on

equity, and net interest margin, it was found that these variables have a positive impact on the

negative shock on liquidity ratio in the short-term. This happens since banks hold profitable

government securities that increase their revenue and profitability in the short-term. In the long-

term, the positive shock on the liquidity ratio negatively impacts the net interest margin. Due to

the low investment from banks into the loan portfolio, the net interest margin of the banking sector

decreases in the long-run that reaffirms Brealey et al.'s (2011) and Westerfield's (1921) claims that

high liquidity shortens loan investments opportunities for the banks and decreases the banks'

profitability.

Second, the VAR model showed no evidence that a high liquidity ratio in the banking

sector leads to the increased deposit volume, as stated by NBKR (2017). Even more, the liquidity

ratio has a negative effect in the short run. Therefore, it can be implied that the judgment of NBKR

that the high liquidity ratio leads to the people's confidence and higher deposit volume is not a

reasonable policy for the Kyrgyz Republic's banking sector.

Thirdly, it was found that the liquidity ratio has a positive effect on the treasury bills

volume. This means that banks buy a high amount of government securities, and as a result, it

increases their liquidity ratio. Additionally, VAR model analysis found that there is no evidence

that a high liquidity ratio leads to the people's confidence in the banking sector, and as a result, to

the increased deposit volume as NBKR stated it.

Finally, regarding the impact of liquidity ratio on the Kyrgyz Republic economy, we found

that commercial banks hold a lot of liquidity because they receive income from interest on these

securities by purchasing short-term government securities during the year.

Overall, it can be inferred from the results that a high liquidity ratio hurts the banking

sector's profitability.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

19

5. Conclusion

Analyzing the relationship between bank profitability and liquidity of Kyrgyz Republic

banks for 2001-2019 with the ADF test and VAR model analyses was the main objective of this

research. Specifically, the impact of high liquidity ratio on the banks' revenue, profitability, deposit

volume, credit volume, and exchange rate. The findings of the study proved that liquidity

management has an important impact on the banks profits. The future and health of the banks

associated with liquidity and profitability. The above findings of the study showed that there is a

relationship between Liquidity ratio and net interest margin, return on equity, and return on assets.

The Vector Auto Regression model assessments the independent variable coefficient is valid for

the net interest margin and liquidity, but the coefficient is not valid in other cases.

The Vector Auto Regression model analysis found that the liquidity ratio in the Kyrgyz

Republic's banking sector hurts the net interest margin, return on assets, and return on equity that

measures the banking sector's profitability. Accordingly, bank can face unexpected market

conditions and need to decrease liabilities or increase assets in its balance sheet. Hence, when the

bank's liquid (current) assets are high, the bank's profitability decreases.

Liquidity and profitability are two essential aspects of banking operations and are

monitored by all banking system stakeholders. This study's primary concern was to figure out if

the banks' liquidity affects their profitability as these two issues are much important to the banks'

main stakeholders.

Finally, this study contributes to banking literature by analyzing the profitability and

liquidity aspects of a developing country, on one side, profit maximization expectations (return on

investment) of shareholders and, on the other side, risk awareness of depositors.

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

20

References

Abdullah, M. N., & Jahan, N. (2014). The impact of liquidity on profitability in banking sector

of Bangladesh: a case of Chittagong stock exchange. EPRA International Journal of

Economic and Business Review, 2(10), 17-22.

Banks, E. (2004). Alternative risk transfer: Integrated risk management through insurance,

reinsurance, and the capital markets. John Wiley & Sons.

Becht, M., Bolton, P., & Röell, A. (2011). Why bank governance is different. Oxford Review of

Economic Policy, 27(3), 437-463. https://doi.org/10.1093/oxrep/grr024

Brunnermeier, M. K., & Pedersen, L. H. (2009). Market liquidity and funding liquidity. The

Review of Ffinancial Studies, 22(6), 2201-2238. https://doi.org/10.1093/rfs/hhn098

Djalilov, K., & Piesse, J. (2016). Determinants of bank profitability in transition countries: What

matters most?. Research in International Business and Finance, 38, 69-82.

https://doi.org/10.1016/j.ribaf.2016.03.015

Eichengreen, B., & Gibson, H. D. (2001). Greek banking at the dawn of the new

millennium. Available at SSRN 269391. https://ssrn.com/abstract=269391

Erdogan, M., & Aksoy, E. E. (2016). Banking regulation and determinants of banks profits:

Empirical evidence from Turkey. Eurasian Journal of Business and economics, 9(17),

109-124. https://doi.org/10.17015/ejbe.2016.017.07

Faizulayev, A., & Wada, I. (2019). What drives the banking performance? Case of Eurasian

economic union countries. In N. Ozatac, & K. Gokmenoglu (Eds.), Global issues in

banking and finance (pp. 27-33). Springer, Cham. https://doi.org/10.1007/978-3-030-

30387-7_3

Shijaku, G. (2017). Bank stability and competition: Evidence from Albanian banking market.

Eurasian Journal of Business and Economics, 10(19), 127-154.

https://doi.org/10.17015/ejbe.2017.019.07

Haji-Zada, E. (2017). The macroeconomic determinants of credit risk in the banking sector of

Kyrgyzstan [Unpublished master thesis]. Eastern Mediterranean University, Institute of

Graduate Studies and Research, Deptartment of Banking and Finance, North Cyprus.

http://irep.emu.edu.tr:8080/xmlui/bitstream/hand-

le/11129/3871/hajizadaevelina.pdf?sequence=1

Humphrey, T. M. (1982). The real bills doctrine. Federal Reserve Bank of Richmond Economic

Review, 68(5), 3-13. https://ssrn.com/abstract=2120000

International Monetary Fund. (2003). Kyrgyz Republic: Financial system stability assessment

including reports on the observance of standards and codes on the following topics:

Monetary and financial policy transparency, banking supervision, and payment systems.

IMF Staff Country Reports 2003/052. https://doi.org/10.5089/9781451821390.002

International Monetary Fund. (2016). Kyrgyz Repiblic: Second review under the three-year

arrangement under the extended credit facility, and request for modification of

performance criteria-press release; staff report; and statement by the executive director

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

21

for the Kyrgyz Republic. IMF Staff Country Reports 2016/186.

https://doi.org/10.5089/9781475519198.002

Kichurchak, M. (2019). Bank deposit activity in Ukraine: Directions and factors of development

activation. Journal of Eastern European and Central Asian Research, 6(1), 145-160.

https://doi.org/10.15549/jeecar.v6i1.275

Malik, M. S., Awais, M., & Khursheed, A. (2016). Impact of liquidity on profitability: A

comprehensive case of Pakistan’s private banking sector. International Journal of

Economics and Finance, 8(3), 69-74. http://dx.doi.org/10.5539/ijef.v8n3p69

Met, O., Torobekova, V. & Keles, I. (2008). Financial system developments in transition

economies: The case of Kyrgyz financial system. Manas Üniversitesi Sosyal Bilimler

Dergisi, 10(19), 1-11. https://dergipark.org.tr/en/pub/manassosyal/issue/49945/640034

Mitchell, W. F. (1923). The institutional basis for the shiftability theory of bank

liquidity. University Journal of Business, 1(3), 334-356.

https://www.jstor.org/stable/2354871

Morris, S., & Shin, H. S. (2016). Illiquidity component of credit risk–the 2015 Lawrence R.

Klein lecture. International Economic Review, 57(4), 1135-1148.

https://doi.org/10.1111/iere.12192

National Bank of the Kyrgyz Republic. (2017). Regulation on economic ratios and requirements

binding to be fulfilled by the commercial banks of the Kyrgyz Republic. National Bank of

the Kyrgyz Republic.

https://www.nbkr.kg/contout.jsp?item=103&lang=ENG&material=86830

National Bank of the Kyrgyz Republic. (2020). The financial sector stability report of the Kyrgyz

Republic. National Bank of the Kyrgyz Republic.

https://www.nbkr.kg/DOC/21082020/000000000055183.pdf

Osborne, M., Fuertes, A., & Milne, A. (2012). Capital and profitability in banking: Evidence

from US banks. In 3rd Emerging Scholars in Banking and Finance Conference, Cass

Business School (pp. 1-54).

Pak, O. (2019). The impact of state ownership and business models on bank stability: Empirical

evidence from the Eurasian Economic Union. The Quarterly Review of Economics and

Finance, 71, 161-175. https://doi.org/10.1016/j.qref.2018.07.008

Pak, O. (2020). Bank profitability in the Eurasian Economic Union: Do funding liquidity and

systemic importance matter?. The North American Journal of Economics and

Finance, 54, Article: 101265. https://doi.org/10.1016/j.najef.2020.101265

Prochnow, H. V. (1949). Bank liquidity and the new doctrine of anticipated income. The Journal

of Finance, 4(4), 298-314. https://doi.org/2975424

Brealey, R. A., Myers, S. C. & Allen, F. (2011). Principles of corporate finance. The McGraw-

Hill/Irwin.

Sobolieva-Tereshchenko, O., & Zhukova, Y. (2020). Stress testing the banking systems:

Approach of Ukraine. Journal of Eastern European and Central Asian Research, 7(2),

205-218. https://doi.org/10.15549/jeecar.v7i2.358

Atabaeva, G., Tashbaeva, F., Atabaev, N., & Keles, I. (2022). What must be the relation between liquidity ratios and profitability of the banks in a transition economy? The case of Kyrgyzstan. Journal of Sustainable Business, Economics and Finance, 1(1), 1-22. http://doi.org/10.31039/josbef.2022.1.1.2

22

Tovar-García, E. D., & Kozubekova, R. (2016). The Third Pillar of the Basel Accord: Evidence

of borrower discipline in the Kyrgyz banking system. Journal of Eurasian Studies, 7(2),

195-204. https://doi.org/10.1016/j.euras.2016.02.002

Tran, V. T., Lin, C. T., & Nguyen, H. (2016). Liquidity creation, regulatory capital, and bank

profitability. International Review of Financial Analysis, 48, 98-109.

https://doi.org/10.1016/j.irfa.2016.09.010

Tursoy, T. (2018). Risk management process in the banking industry. MPRA Paper No. 86427.

https://mpra.ub.uni-muenchen.de/86427/ MPRA Paper No. 86427

Waleed, A., Pasha, A. & Akhtar, A. (2016). Exploring the Impact of Liquidity on Profitability:

Evidence from Banking Sector of Pakistan. Journal of Internet Banking and Commerce,

Vol. 21, No. 3, Dec. 2016,

Waleed, A., Pasha, A., & Akhtar, A. (2016). Exploring the impact of liquidity on profitability:

Evidence from banking sector of Pakistan. Journal of Internet Banking and

Commerce, 21(3). http://dx.doi.org/10.2139/ssrn.2899817

Westerfield, R. B. (1921). Banking principles and practice. Vol. 1 & II, The Roland Press

Company.