Embed Size (px)

Citation preview

Oando Plc

Market Memorandum

The Oando Corporate Journey - At The Regulators Gate

December 2017

1599-8842 Vol.1 No.161

Contents

Executive Summary

OandoPlc – Origin, Roots and Structurea. Shareholding structure of Oando Plc as at 2017b. The Oando Energy Resources (OER) Acquisitionsi. The Exile Resources Acquisition in Torontoii. The ConocoPhillips Acquisitioniii. How Was This Funded?c. Corporate Governance in Oando Plc

Oando Plc's History with Regulators

The Company - Oando Plca. Who are The Real Shareholders,b. Oando's Relationship With Its Subsidiaries and Its Holdings in These

Subsidiariesc. Who are The Owners of OODP?d. Financial Position of Oandoe. Dividend History of Oando and Relationship with Shareholders

The Petition Itselfa. What is the Petition(s) About, Issues and Parties Involved?i. The Ansbury Investment Inc's Petitionii. The Alhaji Dahiru Barau Mangal's Petitioniii. The Oando response to SEC on Ansbury's Petition

The SEC Decision to Suspend Oandoa. The Timeline of the Petition & SEC's Correspondence with Oandob. SEC's Findings/Decision on Oando Plc c. Processes for Technical Suspension – Meaning, Steps, Process & Implications

Implications of the SEC Decisiona. Analysing the SEC Decisionb. Conclusions

Appendixes & Acknowledgments

Related News& References

Contacts Us

1

16171818181920

22

232325

25252528

2929293334

43464646

474751

52

55

59

In suspending trading on the shares of Oando Plc on October 18, 2017 as part of a series of actions taken by the Securities & Exchange Commission (SEC), the Nigerian regulatory landscape sent out a bold statement that it can act when motivated to do so.

When the move came, it came against a background of recent actions taken by the SEC which reflected a long-awaited clamour for enforcement actions in our market place (with a few false-steps), an increased regulatory enforcement from NCC, NSE, CBN and lately the Financial Reporting C o u n c i l ( F R C ) o n c o r p o r a t e governance practices, and a public perception of Oando Plc as being corporate governance challenged.

The market, while not unaware of the stories in the public space and dealers' trading desks about Oando's executive management's investment dispute with two separate entities which the SEC was looking into, found the actions taken unclear as to intent, precedence and end-game; even as they were expectant of an action to put the matter to rest.

While SEC argued that the action was necessitated by its desire to protect investors' interests, the apparent lack of a scope and determinable time for a resolution raised considerable concerns; none the least the execution of the roll-out plan.

At this stage, the market welcomed a move away from self-denial about concerns over Oando Plc and looked to

Page 1www.proshareng.com

Executive Summary

“…Manipulate the truth long enough and eventually you're selling

something that doesn't exist.”

the SEC for clarity through its actions; one that does not deliver uncertainty, create collateral damages and open up unintended consequences.

Regulatory authorities in this age, as we have seen with the Debt Management Office (DMO) under Dr Abraham Nwankwo and sustained under a new leadership understand that their ultimate responsibility is to build businesses to be viable entities, stronger and not destroy value. Sanctions arising from regulatory action therefore must be in accordance with extant rules and regulations, severe relative to infractions, precise and satisfy the deterrence principle. In delivering on this mandate therefore, best practice regulators understand the need for prompt and clear intervent ions that u l t imate ly enhances the market trust and helps organisations build institutional learning on how to better conduct their businesses and arrangements.

There is thus a growing conviction amongst market analysts that in the i n t e r e s t o f f u l l d i s c l o s u r e , t r a n s p a r e n c y , e q u i t y a n d accountability (the underlying value base for the SEC and other regulators) that regulatory intervention/action must engender trust, integrity and confidence in the market rules and regulations.

Those who support the action of SEC predicate this on a number of long held perceptions including the separation of principals from the institution, the role of risk management to mitigate

excesses arising from ambitious growth pursuits and founder-led management decisions as well as processes within the company. The recent opinion from the independent auditors as contained in its financial statements simply adds another layer of credence to the uncertainty around its gearing/leveraged status and governance concerns.

Even the critics of SEC acknowledge that a clear understanding of the macro and micro challenges faced by the Company's and its management of those challenges that may have led to the above perceptions would be in the best interest of the market; even as they admit that the SEC has acted in ways recently that could benefit from a n u n d e r s t a n d i n g o f h o w “negotiated regulation” works.

The question around the Oando regulatory intervention thus becomes one of answering “what were the issues known to and available before SEC that impacts market rules and regulations and what were the commensurate actions taken?”

This information has remained largely unanswered or was unavailable to the public in a formal manner devoid of sentiments and selective memory.

The Proshare multi-disciplinary project team formed to provide such an “issues update” thus understood that the most important task here was that outcomes and observations reached must be in the best interest of the market to allow it gain critical insight into processes, best practice, offer clarity and an understanding of the possible end game.

The following stood out for us and represent our take-away from the exercise.

1. There is a lot of misconception about the Oando Plc business model and structure, which is in part a function of its evolution, management style and business practices in the sector it plays in as well as the f i n a n c i n g o p p o r t u n i t i e s available for such an inorganic business growth;

2. There are crucial learning points / case study opportunity for corporate organisations on:

a. listing in stock exchanges outside Nigeria – qualification, due diligence, reporting and governance standards;

b. inter-jurisdictional regulatory requirements, collaboration and overlaps;

c. clarity in the rules guiding rights issues and transfer of shares;

d. investor friendly laws and vehicles that aid private equity, trade finance and FDI's for companies with international linkages; and

e. overcoming associated political risk with doing business in Nigeria.

3. There seems to be a failing in adequate risk management implementation in Oando as c o u l d b e d e d u c e d f r o m outcomes in its exposures and consequential outcomes. Evidently and arising from its compliance requirements with TXE, a robust risk management architecture exists in Oando. The question is whether it was always applied in key decisions particularly when certain

Page 2

Page 1www.proshareng.com

unforeseen risks emerged in the course of transactions (e.g. CoP and the Consent Issues – as it can be reasonably argued of they should we have continued with the transaction or exited and perhaps lost the deposit when there were u n f o r e s e e n d e l a y s w i t h obtaining the Honourable M i n i s t e r s ' c o n s e n t f o r example).

4. There is a reputational risk, s o m e a f u n c t i o n o f misconception and others mainly self-inflicted, which underscores the need for Oando to pay attention to d e t a i l s r e l a t e d t o governance ethos if it is serious about addressing the pervading perception of a company that is corporate governance challenged. A few examples will suffice:

a. The public understanding of the appointment process of the executive director of finance. From the evidence reviewed, there was nothing untoward with the appointment of the GCFO to the Board of Oando Plc. The GCFO was employed as an 'employee' but was not automatically appointed as a member of the Board. His remuneration was therefore fixed by negotiation between h i m s e l f a n d t h e G C E O . S u b s e q u e n t l y , h e w a s appointed as a director to the Board of Oando PLC to fill a casual vacancy until the next AGM. There was no evidence o f a c h a n g e t o h i s remuneration. At the next AGM following his appointment to the Board; he formally resigned and came up for re-election,

and was duly elected to the Board by the shareholders. Again, there was no change to his remuneration.This is where it gets curious and opens the doors for questions at to the role of the Board Audit C o m m i t t e e a n d t h e responsibility for fixing and adopting the remuneration of executive directors. The last Board review on executive remunerations took place in 2011 with a next date expected to take place in 2014. This did not take place and whatever the reasons, remains a procedural issue for the SEC to raise and p r o m p t a c t i o n o n ; a n d rightfully so.

b. The non-inclusion of Oando in the NSE Premium Board was a matter that elicited interest from the market, on account of the importance of the project and the timing relevance to listed entities seeking global recognition. Fact is, Oando scored the required mark to qualify for consideration in thepilot CGRS assessment as the model provided for. It however poured water on the next step which was 'an application for the NSE Premium Board listing' when it became clear that it would not/did not meet certain requirements,more obvious of which was the late filings of returns to the market (x-compliance requirements) which Oando explained away as due to its treatment of losses posted for two years in a row and delayed resolution of issues given the multiple reporting levels it had to pass through as a multi-exchange entity (considered part of its

Page 3

Page 1www.proshareng.com

learning curve).

5. There exist a clear and unambiguous basis for the SEC to 'look into” the affairs and governance practices at Oando Plc within the rules and regulations of the market in fulfilment of its investor p r o t e c t i o n m a n d a t e a s evidenced here;

a. the treatment/recognition of unearned revenue and its p o s s i b l e u t i l i s a t i o n f o r d iv idend pay-out ( t ime, motive, representation and pattern analysis drivers) ahead of a planned capital raising

b. t h e e x t e r n a l a u d i t o r s comments about its going concern status after two profit warnings;

c. the appointment process of an executive director ratified at the AGM but with issues around the audit committee r e s p o n s i b i l i t y f o r remunerations.

General Electric (U.S) offers such an example of how regulatory work occurs and should be conducted on the above instances (with or without petitions).

On September 16, 2002; General Electric agreed to cooperate with a Securities and E x c h a n g e C o m m i s s i o n i n v e s t i g a t i o n i n t o a c o m p e n s a t i o n agreement with its former chief executive, John F. Welch Jr., after Mr. Welch came under widespread public criticism over the perks he has been receiving from the company.

This was after U.S. SEC sent a request for voluntary cooperation in what it termed "an informal investigation" in connection with the employment and post-retirement agreement with John Welch jr. who in the end agreed that beyond the undisputed portion of his retirement package, he would "at no cost to the company" act as a consultant and teach management courses; thus restoring confidence in the r e g u l a t o r y i n t e r v e n t i o n process. Immediately after this announcement was made, trading in G.E. shares gained 45 cents to $27.50 on the New York Stock Exchange (NYSE).

On September 23, 2004, the U.S. SEC instituted settled enforcement proceedings against General Electric Company. The Commission charged that GE failed to fully describe the substantial benefits it had agreed to provide its former chairman and CEO John F. "Jack" Welch, Jr., under an "employment and post-retirement consulting agreement." SEC found that in proxy statements and annual r e p o r t s f i l e d w i t h t h e Commission from 1997-2002, GE failed to fully and accurately descr ibe the re t i rement benefits Welch was entitled to receive from the company. The Commission further found that in the first year following W e l c h ' s r e t i r e m e n t i n September 2001 , Welch received approximately $2.5 million in benefits under the agreement, which included access to GE aircraft for unlimited personal use and for

Page 4

Page 1www.proshareng.com

business travel; exclusive use of a furnished New York City apartment that, according to GE, in 2003, had a rental value of approximately $50,000 a month and a resale value in e x c e s s o f $ 1 1 m i l l i o n ; unrestricted access to a chauffeured limousine driven by professionals trained in security measures; a leased Mercedes Benz; office space in both New York City and in Connecticut; the services of professional estate and tax advisors; the services of a p e r s o n a l a s s i s t a n t ; communications systems and networks at Welch's homes, including television, fax, phone and computer systems, with technical support; bodyguard security for various speaking engagements, including a book t o u r t o p r o m o t e h i s autobiography Jack: Straight from the Gut; and installation of a security system in one of Welch's homes and continued maintenance of security s y s t e m s G E p r e v i o u s l y installed in three of Welch's other homes.The Commission c o n c l u d e d t h a t G E ' s inadequate disclosures violated Sections 13(a) and 14(a) of the Securities Exchange Act of 1934 and Rules 13a-1, 14a-3 and 14a-9 t h e r e u n d e r . W i t h o u t admitting or denying the Commission's findings, GE settled the proceedings by consenting to the entry of an Order that it cease and desist from violating the proxy solicitation and periodic reporting provisions of the f e d e r a l s e c u r i t i e s laws."Shareholders have a clear interest in knowing how public companies

compensate their top executives," said Paul R. Berger, Associate Director of t h e S E C ' s D i v i s i o n o f Enforcement. "Compliance with SEC disclosure rules ensures that shareholders are provided a full and accurate understanding of senior executives' compensation arrangements."

On August 4, 2009, the U.S. SEC alleged that GE used improper accounting methods to increase i ts reported earnings or revenues and avoid reporting negative financial results. GE, without admitting o r d e n y i n g t h e S E C ' s allegations agreed to pay a $50 million penalty to settle the S E C ' s c h a r g e s . T h e S E C uncovered the accounting violations in a risk-based investigation of GE's accounting practices. In a risk-based investigation, the SEC identifies a potential risk in an industry or at a particular i s s u e r a n d d e v e l o p s a n investigative plan to test whether the problem actually exists. In this case, the SEC identified the potential misuse of hedge accounting as a possible risk area. The SEC's i n v e s t i g a t i o n u l t i m a t e l y uncovered four separate accounting violations, and GE corrected the last of the violations in 2008. According to Robert Khuzami, Director of t h e S E C ' s D i v i s i o n o f Enforcement"GE bent the accounting rules beyond the breaking point. Overly aggressive accounting can distort a company's true financial condition and mislead investors."In

Page 5

Page 1www.proshareng.com

one instance, the improper accounting allowed GE to avoid m i s s i n g a n a l y s t s ' f i n a l consensus EPS expectations. In reaching its decision, the SEC took into account the remedial acts taken by GE and its audit c o m m i t t e e d u r i n g t h e i n v e s t i g a t i o n , i n c l u d i n g improvements to its internal audit and controllership operations.

On 27 July, 2010, the U.S. SEC charged General Electric C o m p a n y a n d t w o G E subsidiaries — along with two other subsidiaries of public companies that have since been acquired by GE; with violations o f t h e F o r e i g n C o r r u p t Practices Act (FCPA) for its involvement in a $3.6 million kickback scheme with Iraqi government agencies to win contracts to supply medical e q u i p m e n t a n d w a t e r p u r i f i c a t i o n equipment.Without admitting o r d e n y i n g t h e S E C ' s allegations, GE agreed to pay $23.4 million to settle the SEC's charges against the company as well as the two subsidiaries for which GE a s s u m e d l i a b i l i t y u p o n acquiring. The fines were far higher than the benefits w h i c h s u p p o r t a n d promotes what deterrence is truly meant to deliver in regulatory interventions. "Bribes and kickbacks are bad business, period," said Robert Khuzami, Director of the SEC's Division of Enforcement. GE c o o p e r a t e d w i t h t h e investigation.

6. For the above, it becomes apparent that there is a

premium that accrues from co-operat ing with the SEC investigators and taking remedial actions after the fact and during investigations. In this case, it is evident that Oando fully cooperated with the investigators and ought to have enjoyed the benefit of mitigation and process.

7. The decision by the DG, SEC not to refer the petitions to the Administrative Procedures Committee (APC) as prescribed under the Investment and Securities Act 2007 but rather to a Special Task Team and a special purpose Technical Committee made up of both SEC personnel and non-SEC personnel, reporting to the SEC's Corporate Governance Standing Committee, sets a precedence, the consequence of which may open the regulatory process to a legal challenge.

There are a few issues which this immediately throws up, viz:

a. The SEC itself as currently constituted has not been operating with a properly and competently constituted board to oversee its affairs since the DG, SEC was appointed. This is not the norm and does not reflect corporate governance best practice.

b. Neither the Special Task Team's report, the Technical Committee's report nor any other Committee report has been made available to the public, the House Committee on Capital Markets (to whom the SEC offered to give a report in two weeks from their

Page 6

Page 1www.proshareng.com

September 27, 2017 meeting) and to parties as best known to us at the time of concluding this memorandum.

c. The Technical Committee's report was not referred to in the SEC letter and notice on October 17, 2017 where the SEC based its reasons for imposing a technical suspension on the shares of Oando and ordering a forensic audit on certain "weighty" findings it made in the course of a "comprehensive review of the petitions".

d. The import of the above (without prejudice to the competence and capability of the professionals appointed to these Committees and/or working in the SEC) impacts on its best efforts at providing the b e n e f i t o f f a i r n e s s , transparency and best practice.

e. The fact that Ansbury, one of the petitioners is in arbitration with its co-venturer outside the jurisdiction of Nigeria in respect of shares held indirectly in Oando ought to have been obvious to the SEC and the matter, being sub judice (under judicial consideration and therefore prohibited from public discussion elsewhere), s h o u l d n o t h a v e b e e n deliberated upon by the SEC in the exercise of its regulatory powers and in contravention of its own rules. It was expected that at most, the SEC would have chosen to discipline itself t o a c t o n t h e m a t e r i a l information that bothered on its investor protection mandate as part of its supervision role; thus eliminating the accusation

of bias noted in point 8 below.

f. The second petitioner, Alhaji Mangal, only sought for clarification on certain matters contained in the Company's published 2016 Financial Statements which have since been responded to by Oando; and it is for the SEC to d e t e r m i n e i f t h i s w a s satisfactory or not.

g. What will happen in the market place where the details of the Technical Committee report and recommendations are made public and found to contradict the actions of SEC (in some ways or in the main). To eliminate this, the authors of the market laws, rules and regulations recognised the need for an all parties meeting and internal investigation function. It is yet uncertain thatthis was done and if so, not available for an informed commentary.

8. The October 17, 2017 SEC letter to the Chairman of Oando, responding to the August 24 and 28 letters detai l ing concerns about possible bias on the part of the DG, SEC in his handling of the petitions and subsequent investigations (including allegations of a d e n i a l o f f a i r representation and access to outcomes/technical committee reports) came on the same day that SEC issued letters to the managing director of Oando and notices to the market informing all of the suspension of the shares of t h e c o m p a n y a n d t h e 'appointment' of a forensic team to audit the affairs of

Page 7

Page 1www.proshareng.com

Oando. This does little to assuage concerns about intent, m o t i v e a n d r e g u l a t o r y processes.

9. T h e r e a r e o b v i o u s inconsistencies in the SEC position as evident in the following instances:

a. In their October 17, 2017 letter to Oando Plc, the SEC variously used concerns, allegations, and findings interchangeably. Their inability to agree on what was the basis of the action lends grounds for doubt where clarity was required.

b. This lack of clarity was further expanded when it became unclear whether to treat this intervention as a derivative of an allegation or a finding. The request therefore for a forensic audit without a clear scope and t ime frame immediately became untenable.

c. More closely associated to that concern was the question of how the SEC arrived at a figure of N160million without a defined scope of work, a timeframe and a reporting g u i d e l i n e ? H o w d o e s a corporate board pay for such a sum without these details? In anyway, where is the payment of an audit by a regulated entity provided for in the market rulebook or made clear in its extant laws?

d. I n t h e s p i r i t o f g o o d governance, did the SEC validate that none of the entities appointed to conduct the forensic audit is a related party or has a principal/agent relationship with Oando Plc,

currently or in the past?

e. Given that the SEC did not acknowledge the cooperation of Oando Plc and indeed did not acknowledge the volumes of exchanges made available to its Technical Committeemonths e a r l i e r o r / a n d i f t h e information provided were satisfactory or not; - how did it arrive at a decision without reference to such.

f. The SEC,whilst predicating its decision to act on “the weighty findings it made i n t h e c o u r s e o f a comprehensive review of the petitions” also made it clear in its October 17, 2017 letter that the petitioners had a situation that made its acting on same sub judice. What informed the actions of SEC? The evidence available and reviewed would indicate that other matters outside the petition would not have been considered by the Technical C o m m i t t e e t h a t m a d e recommendations and issued a report that guided the DG's actions.

g. The SEC listed out a number of violations which had clear and commensurate sanctions for each as charged based on its findings. These findings were summarized in the SEC Circular to the General Public o f 18 October , 2017 as “weighty” enough to require the suspension of the shares and a forensic audit of Oando. This goes to the fundamental flaw in the letter that seeks to expressly talk about violations not as “possible infractions or violations ahead of an

Page 8

Page 1www.proshareng.com

investigation” but in clear terms which should at this stage give room to a report / decision highlighting penalties for such violations. Point (a) above becomes more relevant therefore because it remains unclear if this is the request to investigate or an outcome of an investigation that gives room to a request to the NSE to suspend trading in the shares of Oando Plc. The understanding of and resolution of this uncertainty is important not just for the precedence setting nature but its impact on rule making and market actions. Who were those who knew about this decision before it was taken and what was the last one week market activity on Oando like? Who were the most active traders and beneficiaries? This should interest the regulators and indeed the entire market.

h. In the SEC's May 18, 2017 letter to Oando, wherein it forwarded the petitions from Messrs Ansbury Investments Inc. and AlhajiDahairu Mangal; and requested a response not later than five days thereafter; it did nothing to apprise itself of the issues at stake, the legal status of same and its role or lack of thereof. This was further continued in its July 10, 2017 letter to Oando subsequent to their May 24, 2017 response. Soat what stage did Messrs Ansbury Inc. referred to as a petitioner on May 18, 2017 become a whistle-blower on October 17, 2017 if that status was not already determined ab-initio?

10. The key market question that should interest the market is

the determination of “who is a n d w h e n d o e s o n e b e c o m e a w h i s t l e -blower?” We had done some extensive research on this principle when reviewing the Laurence D'rogo status in the ETI case with the SEC on January 21, 2014. Then, we took on board legal advice on the interpretation of S. 306 of ISA 2007 as applicable and undertook some review of its applicability to the whistle-blower definition in Nigeria. In this case, we struggled with how a petitioner became a whistle-blower in a case where he/she is a beneficiary of the outcome and has not been engaged as a witness under extant laws or information acquisition program under common and criminal laws. It will be beneficial to the market to understand how this process works to aid other shareholders who may have similar issues with companies they have holdings in.

11. The claim of 'suspected' insider dealing against the company is curious given that the critical test here relates to determining that there existed 'buying or selling' of Oando shares by someonenot the company (as it does not trade in its own shares) who had access to material price sensitive and non-public information. The burden of proof is on the SEC to d e t e r m i n e t h r o u g h a painstaking process that requires it to keep watch or have records on unusual share movements before a big announcement, and make preliminary inquiries before instituting an investigation.

Page 9

Page 1www.proshareng.com

The requirement to dig deeper m a y o f t e n i n v o l v e t h e u s e / a p p o i n t m e n t o f a n accountant and a lawyer (if it does not have this skill-set in its enforcement unit) who act independent ly and have c o n s i d e r a b l e p o w e r s t o e x a m i n e a n d d e m a n d documents. They produce a report upon which it would act and it can do this without throwing up wild allegations that it “observed that certain persons classified as insiders”. The definition of an insider is w i d e a n d a s v a r i e d a s established in the Martha Stewart case where she was charged by the U.S. SEC with obstruction of justice and securities fraud – including insider trading – for her part in the 2001 ImClone case even though she was not a director in the company.

Thus, a slightly different approach was expected from the SEC on this matter deriving from the statements it made thus:

a. SEC affirmed that between January – October 2015, it had evidence of trades that took place before the release of the company's 2014 financial statements where Oando r e p o r t e d a l o s s o f N183.8billion.

b. S E C w a s s u s p e n d i n g i n v e s t i g a t i o n a g a i n s t A l h a j i D a h i r u M a n g a l , a shareholder of Oando on the grounds of it being “sub judice” given that Oando had filed a suit in courts alleging insider

dealings against Alh. Mangal.

12. It was apparent that until the petitions were received, Oando had obtained all necessary regulatory approvals from the SEC on all the matters raised in the case file reviewed. It therefore raises concerns about the process for regulatory review after the fact. It is well w i t h i n t h e r i g h t s a n d responsibilities of SEC to take up any issue based on new facts and evidence and if this were the case as we envision, the SEC had the obligation to act and guide its actions as such – a regulatory review that may include possible forensic audit at its own cost which (based on the professional advice from its supervision/enforcement unit) will be recoverable from the fines and penalties that will be given.

13. The issues around related party transactions is yet unclear and underscores the lack of clarity on the path of S E C . R e l a t e d p a r t y transactions are not illegal commercial transactions but the management of it reflects on the highest levels of governance and reporting and as shown in point 5 above can become a matter of routine interest for the SEC. It is in this same breadth that the issue of a corporate jet and its utilisation (separating between corporate usage and personal use and linking same with the attendant tax treatment of same in the books) will suffice and fall under.

Page 10

Page 1www.proshareng.com

Now, it is imperative to debunk the conspiracy of silence often attached to regulators when it comes to big businesses and the absence of regulatory action.

This is important because it fits into the traditional narrative on why entities deploy technical arguments to get away from “seemingly obvious infractions in the absence of hard evidence”.

In the first place, the SEC made this intervention a response to a petition, which after the formal intervention agreed was sub judice. Thus the evidence that offered such technical construction was offered by the SEC and not Oando, whom we have established above deserved to have been “looked into/investigated” by the SEC long before now, without prompting.

More important is that the theory of reflexivity becomes manifest here.

The principle of reflexivity was perhaps first enunciated by the sociologist William Thomas (1923, 1928) and known as the Thomas theorem: that 'the situations that men define as true, become true for them.'

Sociologist Robert K. Merton (1948, 1949) built on the Thomas principle to define the notion of a self-fulfilling prophecy: that once a prediction or prophecy is made, actors may accommodate their behaviours and actions so that a statement that would have been false becomes true or, conversely, a statement that would have been true becomes false - as a consequence of the prediction or prophecy being made. The prophecy

has a constitutive impact on the outcome or result, changing the outcome from what would otherwise have happened.

An example of this is the interaction between beliefs and observations in a marketplace - if traders believe that prices will fall, they will sell - thus driving down prices, whereas if they believe prices will rise, they will buy - thereby driving prices up. Thus, the trigger for results lies in the belief that guides action/conduct.

If the SEC learnt anything from the post-financial crisis, it most certainly failed to deploy same in its handling of this case. While it is perfectly normal to assume that there may exist a c e r t a i n l e v e l o f i n c e s t u o u s relationships that would have been cultivated by a player in the dominant sector of the economy – Oil export, marketing and servicing; and this can and will be deployed when faced with regulatory chal lenges; i t was incumbent on the SEC to “line up all its ducks in a row”.

The stage was thus set for what we find today, three (3) weeks after that intervention with al legations, counter-allegations, exposes, scandals and sensational stories put out in the public space. We wish our financial market professionals and regulators had read the book by George Soros on the subject matter - we would not be where we are today!

It really is time that egos get checked at the door, and we start adopting a general understanding of what is real, and what are lies or concoctions to achieve an end. This, according to the theory of reflexivity holds true for the SEC, Oando and the entire market.

Reflexivity as a tool

Page 11

Page 1www.proshareng.com

In managing the SEC v Oando matter before the market, it quickly became apparent to us while reviewing the body of information available that some thought ought to have been given to the unintended consequences of any action from the SEC and parties involved. Indeed, it is almost assuming a personal scorecard mind-set, revealing an absence of the much needed professional introspection on issues such as:

1. Messrs Ansbury Investments Inc at no time stated it was a shareholder in Oando Plc in their May 02, 2017 petition to SEC. They stated that they were majority shareholders in Ocean and Oil Development (BVI) which holds 99 percent of OOOP Nigeria (holders of 56% equity stake in Oando Plc), an information hitherto unknown to the SEC. Was the SEC required to be in the know of such a transaction in the affairs of a majority shareholder of an entity under its jurisdiction? What evidence and details of the transaction documents between the owners of OOOP Nigeria and Ansbury has the SEC availed itself of or demanded when the petitions were received?

2. That Messrs AnsburyInc, not being direct shareholders of O a n d o P l c s h o u l d h a v e petitioned through the legal shareholder on record, OODP Nigeria. In the absence of their ability to do that the SEC should have treated Ansbury's petition as mere information, which the SEC should have t h e n c o n s i d e r e d i n d e t e r m i n i n g w h e t h e r

reasonable cause had been established to necessitate the need to engage the Company further in a SEC initiated enquiry on the matters alleged. Any further action by SEC would have had to consider issues such as jurisdiction, applicable Nigerian Law, SEC's powers of investigation and m i n o r i t y s h a r e h o l d e r protection as well as acting in the best interests of the company and the capital markets. But yet again, did the SEC seek to establish this claim a n d t o c o n f i r m i f t h e transaction under reference was conducted under Nigerian laws and done in the best interest (and to the knowledge) of shareholders. This is important because if Ansbury's claims are correct (and it has not been disputed from the evidence seen) a significant portion of the ownership of Oando Plc (above the 5 percent threshold) changed hands w i t h o u t a n y a c t i v e involvement, knowledge of and approval of the SEC. This is of serious concern.

3. The thinking above equally applies to Alhaji Mangal, whom by law ought to inform the company whenever his direct and indirect shareholding passes the regulated threshold. Why is the SEC not interested in the transactions that delivered this situation and the parties involved? If the interest of regulatory intervention is consistent, it will be proper to recognise that this issue goes to the heart of market practice and should be “looked into”.

Identifying the Unintended Consequences

Page 12

Page 1www.proshareng.com

4. T h e M e s s r s A n s b u r y Investment Inc shareholding in Ocean and Oil Development ( B V I ) a n d O O D P B V I ' s investment in OODP Nigeria offers a unique opportunity for t h e S E C t o e x p a n d i t s regulatory coverage and review of business practices that can aid our business environment here in Nigeria but more importantly, is that the SEC should have expanded its investigation to cover tax compliance, foreign exchange control requirements and reporting standards if nothing but to gain knowledge of what r e g u l a t o r s n e e d t o p a y a t t e n t i o n t o a n d h o w businesses has moved far ahead of regulation. Such learnings may require new r u l e s , r e g u l a t i o n s a n d amendments of existing laws to be able to put local regulation in tandem with international business practice.

5. SEC does not have the mandate to make business profitable or to question why a Company is not being profitable. There will always be an element of risk in investing in capital markets and the SEC cannot take away the responsibility of individual i n v e s t o r s , p a r t i c u l a r l y sophisticated high net-worth investors to make informed

investment decisions. SEC's role is not to act as “nanny” to investors but to create an enabling, transparent and accountable market with easy access to information to enable investors make the informed investment decisions. To do o t h e r w i s e w o u l d b e t o overreach its authority and mandate as conferred under the ISA and the SEC Rules. Unless there are matters of c a p i t a l m a r k e t f r a u d , i n f r a c t i o n s o r m a r k e t manipulation; the SEC should restrict itself to its clear mandate or seek legislative change where its current p o w e r s a p p e a r t o b e inadequate in the larger interest of the market as best practice requires.

6. The implications of the “noise” thus far created on possible Nigerian entities that may seek to list in other markets and how the management of this intervention will impact on them. At this time, it does not suggest that we are deploying an helicopter view on such issues at a time we are working assiduously to promote our “ease of doing business” and e x p a n s i o n o f N i g e r i a n businesses to international markets that would open up the growth potential the economy seeks.

The End Game

This was the least challenging aspect of the engagement. We had combed through the corporate governance rules applicable and realised that taken separately, there is “none there” in the allegations contained in the SEC

intervention but a series of infractions for which appropriate sanctions are applicable.

Taken together however, it would seem that the SEC can make a case of a

Page 13

Page 1www.proshareng.com

sustained series of corporate governance failures and exposure of the investors' funds to risk and inevitable going-concern issue.

The SEC can argue that failure to act would represent a failure of its mandate and despite the obvious clumsiness in the presentation and articulation of a case against the board of Oando, it is capable of advancing successfully this argument/point; assuming the basis of his/its action to preserve status quo in suspending trading on the shares of Oando can hold water.

The immediate market learning from this and critical question to ask is that “Is the going concern issue of a Company in itself part of the SEC Mandate?”

How significant are the corporate governance failures mentioned in the “findings” of SEC relating to failure to conduct a Board Evaluation and clarity on whether the Board approves the remuneration of all executive directors have a significant bearing on the overall assessment of the company serious enough to warrant the actions taken by SEC, particularly since the Company had always self-disclosed its own non-compliance with the SEC Code to the SEC; who acknowledged, did and said nothing for years until now.

The SEC letter of October 17, 2017 basically excludes the validity of the initial premise of its actions and rather than argue on the merit of the points available for a needed intervention; it presented a shopping l is t of infractions which had been responded to by Oando. The decision as to whether this was satisfactory and offers a resolution of substantive market issues however remains the prerogative of the SEC.

The determination and exclusion of routine and statutory issues contained in SEC statement of claims/findings and perhaps its yet-to-be publicly sighted Technical Committee report would allow the market to properly understand what and why Oando shares were suspended and the company placed under expanded scrutiny and investigations.

Suffice to say however, had the Financial Reporting Council (FRC) corporate governance code not been suspended, it would have been an applicable rule that would see those in charge of the governance structure of Oando Plc from inception impacted by. This is not available as part of the regulatory options open to the SEC.

Thus, i t is possible to agree conclusively that the end-game would seem to be the removal of Adewale Tinubu and Mofe Boyo; pioneer executives and founders of Oando Plc and the replacement of its leadership.

The money on the street is that these gentlemen represent the heart and soul of the company and the management of their exit can be better achieved through a negotiated regulatory intervention i.e. to enforce investor protection and corporate governance mandates in such a way that corporate value, viability, sustainability and future prospects is protected and enhanced.

For the existing, intended and prospective shareholders of Oando Plc and those in litigation; the share price suspension can only protect current value up to a limit. In fact, it offers little protection if share price suspension is lifted under a cloud of darkness.

It is worth reminding the market that

Page 14

Page 1www.proshareng.com

in spite of the easily identified flaws, drawbacks and challenges; Oando Plc has achieved an impressive list of landmarks from the dreams of three young men in a country not usually associated with “beyond local market” entrepreneurship endeavours.

Yet, in the final analysis, we see a scenario that allows the SEC to learn lessons necessary to support a transcendent market and accelerate the introduction of new policies which management of this intervention offers it in addressing the current concerns of shareholders, petitioners, founders and the current board of Oando Plc.

We envisage that Oando will recognise that as an industry pioneer, there exist learning opportunities for the organisation to benefit from a new leadership and present it with the opportunity of being termed a visionary in years to come.

For the petitioners, it should quickly dawn on them that their goal is to increase shareholder value and that this can be done under a process that is less antagonistic and filled with suspicion but one that elevates the core objective of the company.

Under this scenario, the need to wait for the conclusion of a possible investigation of Oando may end up being a drawn out dream, but the review of key issues via a formal audit would be beneficial for all parties to clarify pre-existing beliefs and thoughts in the minds of business partners, shareholders, investing public, analysts and creditors of the company.

How this plays out is a decision we will revisit in the future.

For now, we leave you to make your own judgement and conclusions from the submissions in this important memo to the market. Thank you.

Olufemi [email protected]

Yours to serve,

Page 15

Page 1www.proshareng.com

Oando Plc – Origin, Roots and Structure

“…Start by doing what's necessary; then do what's possible; and suddenly you are doing the impossible.”– Francis of Assisi

Oando Plc within the past four (4) decadeshas emerged from the defunct Esso Africa (a subsidiary of Exxon Mobil) to becoming Nigeria's leading locally owned integrated oil company.

The journey started in 1976 when the Federal Government of Nigeria acquired a controlling stakein Esso Africa, transforming the brand into what was then known as Unipetrol Ltd which later became a key player in the oil and gas downstream sector.

The Nigerian Government then took another major step in the industry, by selling 60% equity to the public, through an Initial Public Offer. Eventually, Unipetrolincorporated on 25thJuly, 1969, with the objective of being producers, manufacturers, refiners, suppliers etc, of oil, gas, lubricants, insecticides and other petroleum productswas listed on the floor of the Nigerian Stock Exchange on 27th February, 1992 and acquired a 40% stake in Gaslink Nigeria Limited, a gas utility company.”

Adewale Tinubu, Omamofe Boyo, OnajiteOkoloko and Benedict Peters were founding members of the Ocean and Oil Group, a group of young entrepreneurs that

acquired a controlling 30% interest in U n i p e t r o l P l c . F u r t h e r t o this,Unipetrol increased its stake in Gaslink Nigeria to 51%, with a 250km gas pipeline infrastructure. This spurred an increase in Ocean and Oil's stake in Unipetrolto 42%, through an irredeemable convertible loan stock issue.

C o n s i d e r i n g t h e i m m e n s e opportunities in the Nigerian oil and gas (downstream) sector, Ocean and Oil led a Unipetrol bid for a 60% stake inAgip Nigeria Plc, a competitor in the Industry owned by AgipPetroli BV, an Italian-based oil company.

“By a court order dated 22nd January 2003, a merger between Agip Nigeria Plc RC no. 2714 and Unipetrol Nigeria Plc RC no. 6474 was approved and a resolution dated 9th December 2002 was filed at Corporate Affairs Commission (CAC) to that effect”.

The successful merger between Unipetrol and Agip, led to a rebranding and name changeto the notable brand name Oando Plc on 22nd July 2003, thereby positioning it as the largest downstream petroleum marketing company in Nigeria.

Preamble

Page 16

Page 1www.proshareng.com

Figure 1: Oando Trademark Ownership

Source: Trade Journal

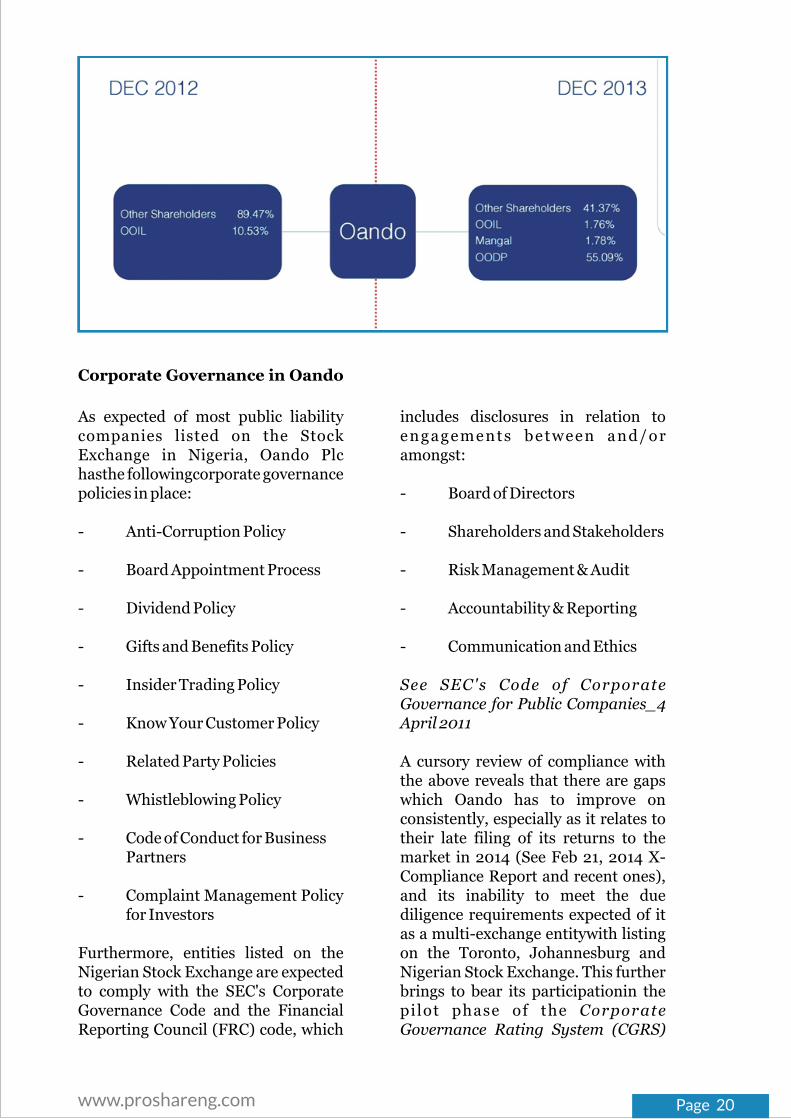

As filed with the Corporate Affairs Commission (CAC), Oando Plc's Current Share Capital amounts to N7,500,000,000 ordinary shares.

Its Shareholding structure is as shown below:

- A n s b u r y ( 4 0 % ) a n d

Whitmore(60%) jointly own OODP BVI

- OODP BVI is 99% owned by OODP Nigeria Oando PLC is o w n e d b y O O D P N i g e r i a ( 5 7 . 3 7 % ) , OOIL(1.28%), Mangal (4%) and Others (37.75%)

Oando PLC's Current Board of Directors are:

1. HRM Oba M.A Gbadebo CFR -Chairman

2. Jubril Adewale Tinubu -Group Chief Executive

3. Omamofe Boyo -Deputy Group Chief Executive

4. MobolajiOsunsanya -Group Executive Director

5. Olufemi Adeyemo -Group Executive Director

6. OghoghoAkpata -Independent Non-Executive Director

7. Chief Sena Anthony -Independent Non-Executive Director

Shareholding Structure of Oando Plc As At 2017

Page 17

Page 1www.proshareng.com

In 2012, Oando PLC completed the reverse takeover of Exile Resources through the use of short term debt. Subsequently, it changed its name to Oando Energy Resources and listed on the Toronto Stock Exchange with a target oil production of 100,000 barrel of oil per day by 2018.

The rationale behind the listing on the Toronto Stock Exchange (TSX) was to explore a veritable platform for capital raising, as the International exchange

and Toronto Stock Exchange had the most hydrocarbon listing across all exchanges in the globe. It was also an avenue to raise equity to pay back the debt the company had acquired to expand its business.

However, in 2016 OER delisted from the TSX since it was unable to meet the target it set towards raising equity, while the post listing cost implication and requirements became enormous compared to the value realised.

8. Dr.Tanimu Yakubu -Independent Non-Executive Director

9. Ademola AkinreleSAN -Independent Non-Executive Director

10. Ikeme Osakwe -Independent Non-Executive Director

11. Ayotola Jagun -Company Sec.& Chief Compliance Officerz

The Oando Energy Resources(OER) Acquisitions

O a n d o P l c h a v i n g i d e n t i f i e d opportunities in other climes and specifically Nigeria's oil & gas exploration sector, sought to acquire

Exile Resources and ConocoPhillips, in order to create value and achieveinorganic growth.

The Exile Resources Acquisition in Toronto

had a responsibility of ensuring that it got an approval from the Department of Petroleum Resources (DPR), the Ministry of Petroleum and the Securities and Exchange Commission (SEC) as stipulated under Section 118 subsection 1 of the ISA 2007, “Notwithstanding anything to the contrary contained in any other enactment, every merger, acquisition or business combination between or among companies shall be subject to the prior review and approval of the Commission”.

In the same year, ConocoPhillips in the process of restructuring its business globally moved to sell its assets in the upstream oil and gas sector in Nigeria. This was in line with the local content policy of the previous administration which had as its focus the encouragement of indigenous participation in the oil and gas sector. Oando Plc saw this as an opportunity to expand its business frontiers into the upstream segment.Oando despite informing the investment community of this move

The ConocoPhillips(COP) Acquisition

Page 18

Page 1www.proshareng.com

Table 1: Funding the COP Acquisition

Date Funding Source AmountBefore the Minister’s Consent

December 21, 2012

Loan from Oando PLC

$345million

December 21, 2012

Secured bridge loans from local Nigerian Banks

$90million

December 6,2013

Increased Deposit

$15million

Total

$450millionFebruary 28, 2014

In order to extend the outside date for the completion of the deal from January 31, 2014 to February 28, 2014

Oando Plc made additional deposit

$50million

Total

$500millionApril 17, 2014

Additional deposit paid since the Hon. Minister of Petroleum Resources approval was not received before/on April 11, 2014

$25million

May 30, 2014 Increased deposit with ConocoPhillips

$25million

Total paid before the Minister’s Consent $550millionAfter the Minister’s Consent for a total cash consideration of $1.65billionJuly 30, 2014 Cash Consideration paid upon

completion of the deal after customary adjustment

$917million

July 30, 2014 Deferred Consideration $33billionTotal paid after the Minister’s Consent $1.5billion

Source: Oando Plc Historical Timeline

The ConocoPhillips acquisition by Oando Energy Resources (OER) was financed with an approximate 50/50 debt to equity ratio. Upon signing of the Sale and Purchase Agreements in December 2012, Oando paid a cash deposit of $435m to ConocoPhillips which was financed by a $345m loan from Oando Plc and $90m funding through secured bridge loans from local Nigerian banks guaranteed by Oando.

On December 6, 2013, OER and ConocoPhillips agreed to an increase in the deposit by $15m making a total of $450m as at the period stated. In February 2014, OER entered into an a m e n d m e n t a g r e e m e n t w i t h ConocoPhillips to extend the outside date for completion of the acquisition from January 31, 2014 to February 28, 2014.OER was expected to pay an additional deposit of $50m pursuant to the agreement which will now take t h e t o t a l d e p o s i t f o r t h e ConocoPhillips acquisition to $500m.

Another agreement was reached to increase the deposit from $500m to $525m on April 17, 2014 provided the consent of the Honourable Minister of Petroleum Resources was not received on or before April 11, 2014. OER further increased total deposit on the acquisition to $550m on May 30, 2014.

On June 18, 2014, OER announced the r e c e i p t o f t h e c o n s e n t o f theHonourable Minister of Petroleum Resources of Nigeria for the acquisition of the Nigerian Upstream O i l a n d G a s B u s i n e s s o f ConocoPhillips for a total cash consideration of US$1.65bn and the acquisition was completed on July 30, 2014 with a total cash consideration of $1.5bn after customary adjustments plus a deferred consideration of US$33 million. Half of the deferred consideration of US$33m is due six months after closing with the balance due 12 months after closing.

So How Was This Funded?

Page 19

Page 1www.proshareng.com

As expected of most public liability companies listed on the Stock Exchange in Nigeria, Oando Plc hasthe followingcorporate governance policies in place:

- Anti-Corruption Policy

- Board Appointment Process

- Dividend Policy

- Gifts and Benefits Policy

- Insider Trading Policy

- Know Your Customer Policy

- Related Party Policies

- Whistleblowing Policy

- Code of Conduct for Business Partners

- Complaint Management Policy for Investors

Furthermore, entities listed on the Nigerian Stock Exchange are expected to comply with the SEC's Corporate Governance Code and the Financial Reporting Council (FRC) code, which

includes disclosures in relation to engagements between and/or amongst:

- Board of Directors

- Shareholders and Stakeholders

- Risk Management & Audit

- Accountability & Reporting

- Communication and Ethics

See SEC's Code of Corporate Governance for Public Companies_4 April 2011

A cursory review of compliance with the above reveals that there are gaps which Oando has to improve on consistently, especially as it relates to their late filing of its returns to the market in 2014 (See Feb 21, 2014 X-Compliance Report and recent ones), and its inability to meet the due diligence requirements expected of it as a multi-exchange entitywith listing on the Toronto, Johannesburg and Nigerian Stock Exchange. This further brings to bear its participationin the pilot phase of the Corporate Governance Rating System (CGRS)

Corporate Governance in Oando

Page 20

Page 1www.proshareng.com

with a score of 70% asthe pass mark.

It should be noted that “the CGRS score is a composite of various a s s e s s m e n t s i n c l u d i n g : ( i ) Compliance Assessment which takes account of the entity's compliance with codes, regulations and best practice; (ii) Fiduciary Awareness based on the certification of the entity's directors to ensure they are versed in their legal and regulatory duties, roles and responsibilities and (iii) Corporate Integrity based on the

assessment of the views and opinions of a range of the entity's stakeholders and other experts, on how their compliance works in practice”.

In addition, the CGRS assessment process is entirely based on areas covered in the SEC Nigeria Code of Corporate Governance and thus not in itself investigative but subject to information provided by staff members and vendors of the entity as well as key stakeholders that participate in the assessment survey.

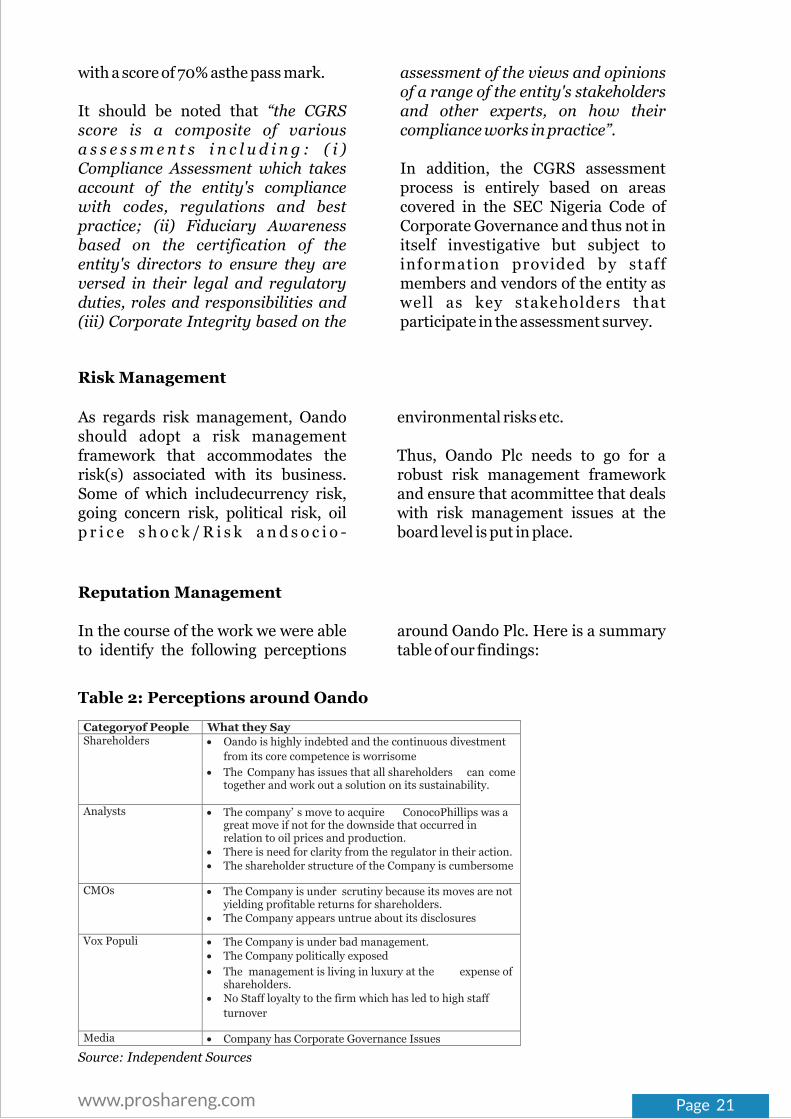

Table 2: Perceptions around Oando

Categoryof People What they Say Shareholders

?

Oando is highly indebted

and the continuous divestment

from its core competence

is worrisome

?

The Company has issues that all shareholders can come together and work out a solution on its sustainability.

Analysts

?

The company’ s move to acquire ConocoPhillips was a great move if not for the downside that occurred inrelation to oil prices and

production.?

There is need for clarity from the regulator in their action.?

The shareholder structure of the Company is cumbersome

CMOs

?

The Company is under

scrutiny because its moves are not yielding profitable returns for shareholders.

?

The Company appears untrue about its disclosures

Vox Populi

?

The Company is under bad management.?The Company politically exposed

?The management is living in luxury at the expense of shareholders.

?No Staff loyalty to the firm which has led to high staff

turnover

Media ?Company has Corporate Governance Issues

Source: Independent Sources

As regards risk management, Oando should adopt a risk management framework that accommodates the risk(s) associated with its business. Some of which includecurrency risk, going concern risk, political risk, oil p r i c e s h o c k / R i s k a n d s o c i o -

environmental risks etc.

Thus, Oando Plc needs to go for a robust risk management framework and ensure that acommittee that deals with risk management issues at the board level is put in place.

Risk Management

In the course of the work we were able to identify the following perceptions

around Oando Plc. Here is a summary table of our findings:

Reputation Management

Page 21

Page 1www.proshareng.com

Recently, Oando Plc has been the most reported quoted company listed on NSE within the media space due to its investigation by SEC. The recent struck out of its court case by the Federal High Court, Lagos and subsequent reference of the plaintiff to the Investment and Securities Tribunal (IST) is another dent on its image which leaves the company at the mercy of the market regulator.

Venturing into the Upstream marked a

new chapter for Oando Plc which was opened through its subsidiary, Oando Energy Resources (OER). This was majorly through the acquisition of ConocoPhillips, a key player in the segment at the time. Oando Plc is one of the few quoted companies in Nigeria that has listings outside the s h o r e s o f t h e c o u n t r y ( t h e Johannesburg Stock Exchange) and a stint of OER on the Toronto Stock Exchange.

Oando Plc's History with Regulators

“…The only way to kill a company is by doing it little by little. If you shoot it in the heart, it survives bleeding for a long time. A company must be poisoned or malnourished, all of its parts must be pushed into a process of irreversible decay. So long as any one of its parts remain alive, the company can be regenerated from this single part.” - Pedro Nueno

For listed companies, infractions can occur at various levels such as the A d m i n i s t r a t i v e P r o c e e d i n g s Committee (APC) of SEC, the Investment Securities Tribunal (IST), the Nigerian Stock Exchange, the Regulator of the Entity's Industry and the Nigerian Judiciary.

Since its listing as Unipetrol, and subsequent rebranding as Oando PLC, the known infractions traced to Oando Plc are the late filings of its Q3 2013 Interim Account and Audited Financial Statement of 2014.Our o b s e r v a t i o n s h o w s t h a t t h e s e infractions are a fall out of its move into the upstream segment of the oil & gas sector in 2013. After which it has faced regulatory headwinds, which hinges on its operations, several allegations and petitions on its shareholding structure, insider trading, related party issues and adherence to corporate governance

provisions as stipulated by the Investments Securities Act (ISA) 2007 of the Federal Republic of Nigeria.

The Securi t ies and Exchange Commission of Nigeria on October 18, 2017 listed the following issues against Oando PLC

a. Fixing of the remuneration of the Executive Directors of Oando PLC board by the GCEO, violating Part B, Section 14.3 of the SEC Code of Corporate Governance.

b. The last board evaluation of Oando PLC was done by KPMG in 2012. A violation of Part B, Section 15.1 of the SEC Code of Corporate Governance

c. Oando's disposal of Oando E x p l o r a t i o n P r o d u c t i o n Limited(OEPL), to Greenpark

Page 22

Page 1www.proshareng.com

Limited without approval from SEC, breaching ISA 2007 provisions

d. Misstatements in the 2013 and 2014 Audited financial statements of Oando PLC a r i s i n g f r o m t h e O E P L transaction, breaching ISA 2007

e. M i s l e a d i n g i n f o r m a t i o n contained in Oando PLC's 2014 R i g h t s I s s u e C i r c u l a r , breaching ISA 2007 Sections 85(1), 86(1) and 87(1)

f. Breach of SEC Rules and Regulations 44(1) in the payment of dividends

g. Going concern of Oando PLC as contained in the 2016 FY report pages 63-68 by the Independent auditors Ernest and Young

h. Suspected Insider dealings under the provisions of Section

315 of the ISA 2007

i. Allegations of Related Party Transactions in accordance with SEC Code of Corporate Governance, NSE Listing Rules and the IFRS provisions

j. That Oando PLC declared dividends in 2013 and 2014 from unrealized profits. And

k. SEC discovered discrepancies in the shareholding structure of Oando PLC, particularly AlhajiDahiru Mangal.

Oando PLC has responded to the issues raised and also secured an injunction from the Federal High Court (FHC), restraining SEC and NSE from technically suspending trading on its shares and SEC carrying out a forensic audit on the company. Eventually, the FHC struck out the case claiming it does not have the jurisdiction to hear the case and referred Oando Plc to the Investment and Securities Tribunal (IST).

The Company - Oando Plc

“…The only way to kill a company is by doing it little by little. If you shoot it in the heart, it survives bleeding for a long time. A company must be poisoned or malnourished, all of its parts must be pushed into a process of irreversible decay. So long as any one of its parts remain alive, the company can be regenerated from this single part.” - Pedro Nueno

Oando Plc, going by its shareholding structure, is owned by:

1. Ocean and Oil Development Partners Ltd (OODP Nigeria)

2. OOIL

3. AlhajiDahiru Mangal; and

4. Other shareholders.

Who Are The Real Shareholders?

Page 23

Page 1www.proshareng.com

Ocean and Oil Development Partners Ltd (OODP Nigeria) owns 57.37% of Oando Plc. Effectively, OODP Nigeria is the majority shareholderin OANDO while OOIL Owns 1.28% AlhajiDahiru Mangal owns 4% of OANDO shares as other shareholders own the remaining 37.75%.

It is pertinent to state that OODP Nigeria which is the majority

Figure 2: Oando Plc's Shareholding Structure as at October 2017

Source: Oando Plc

Figure 3: Growthin Oando Plc's Shareholding Structure between 2013 and 2016

Source: Oando Plc Shareholding Structure

Page 24

Page 1www.proshareng.com

Oando Plc has four (4) major subsidiaries and they are as follows:

1. Oando Energy Resources (OER)

2. Axxela Group (Former Oando Gas and Power)

3. OVH Energy (Former Oando Downstream); and

4. Oando Trading

- Oando Energy Resources (OER) –OER is 100% owned by Oando Plc. Its asset base covers exploration, development and p r o d u c t i o n a s s e t s f o r

both oil and gas situated onshore and offshore in Nigeria.

- Axxela Group– Oando Plc owns 25% stake in Axxela Group which was formerly known as Oando Gas and Power.

- OVH Energy – OVH Energy is owned 40% by Oando and it was formerly known as Oando Downstream.

- Oando Trading – Oando Trading is 100% owned by Oando Plc and is a supply and trading company.

Oando's Relationship with its Subsidiaries and its Holdings in These Subsidiaries

Ansbury Investments Inc and Whitmore Assets Management Ltd jointly own OODP BVI while OODP BVI owns 99% stake in OODP Nigeria.

Ansbury Investments Inc is a company incorporated in Panama and owned by Mr. Gabriel Volpi and family.

Whitmore Asset Mgt Ltd, on the other

hand, is a company incorporated in the British Virgin Islands and owned by Adewale Tinubu and Omamofe Boyo.

Thus, Gabriel Volpi and family own 40% stakes in OODP BVI, Adewale Tinubu owns 40% stakes and Omamofe Boyo owns the remaining 20%.

Who are The Owners of OODP?

Analysing the financial position of Oando for the past 6years, we observed that Oando has been quiet profitable prior to the significant loss of N183billion recorded in 2014, the highest ever recorded by the company.

The loss can be attributed to the debt incurred as a result of the acquisition of ConocoPhillips which the company saw as an opportunity to improve its margins considering the low profit

margins it had continually recorded in the downstream sector. In 2015, the company recorded further loss of N 4 9 b i l l i o n a n d r e t u r n e d t o profitability in 2016 following the “restructuring of its loans, raising of over N120billion in assets disposal and exiting the service business as well as the liabilities that came with them” as stated by the company in its last Annual General Meeting (AGM).

Financial Position of Oando

Page 25

Page 1www.proshareng.com

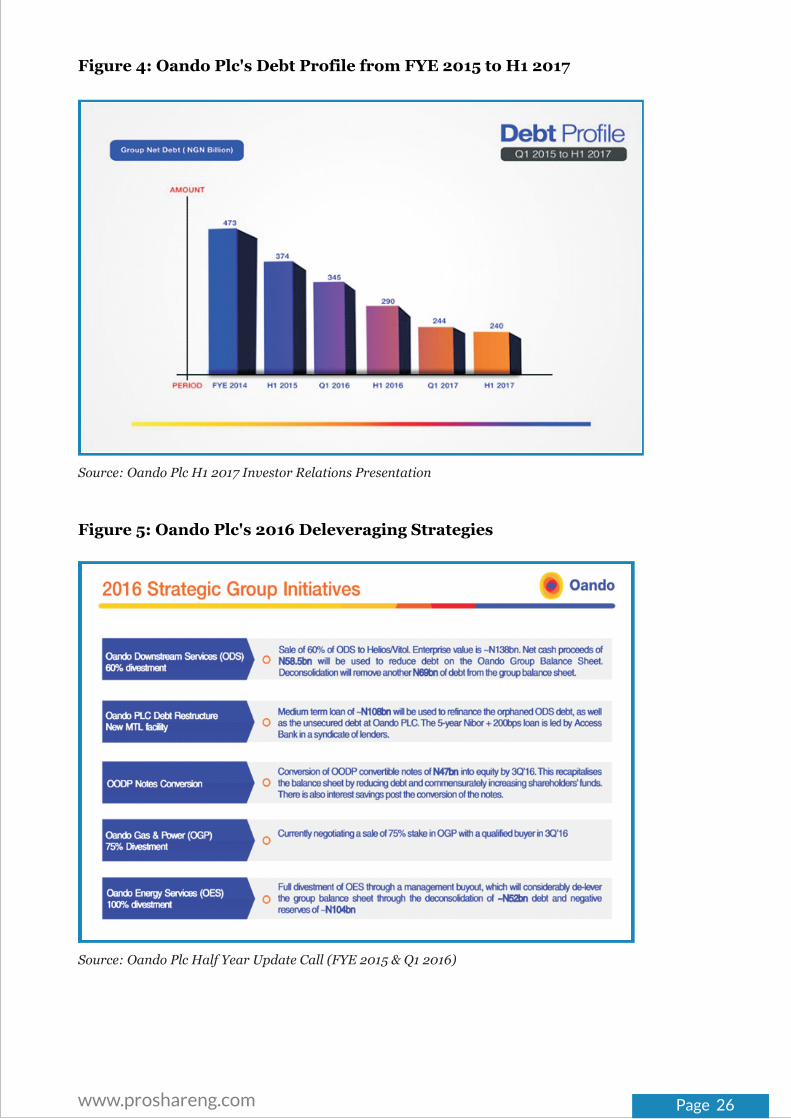

Figure 4: Oando Plc's Debt Profile from FYE 2015 to H1 2017

Source: Oando Plc H1 2017 Investor Relations Presentation

Figure 5: Oando Plc's 2016 Deleveraging Strategies

Source: Oando Plc Half Year Update Call (FYE 2015 & Q1 2016)

Page 26

Page 1www.proshareng.com

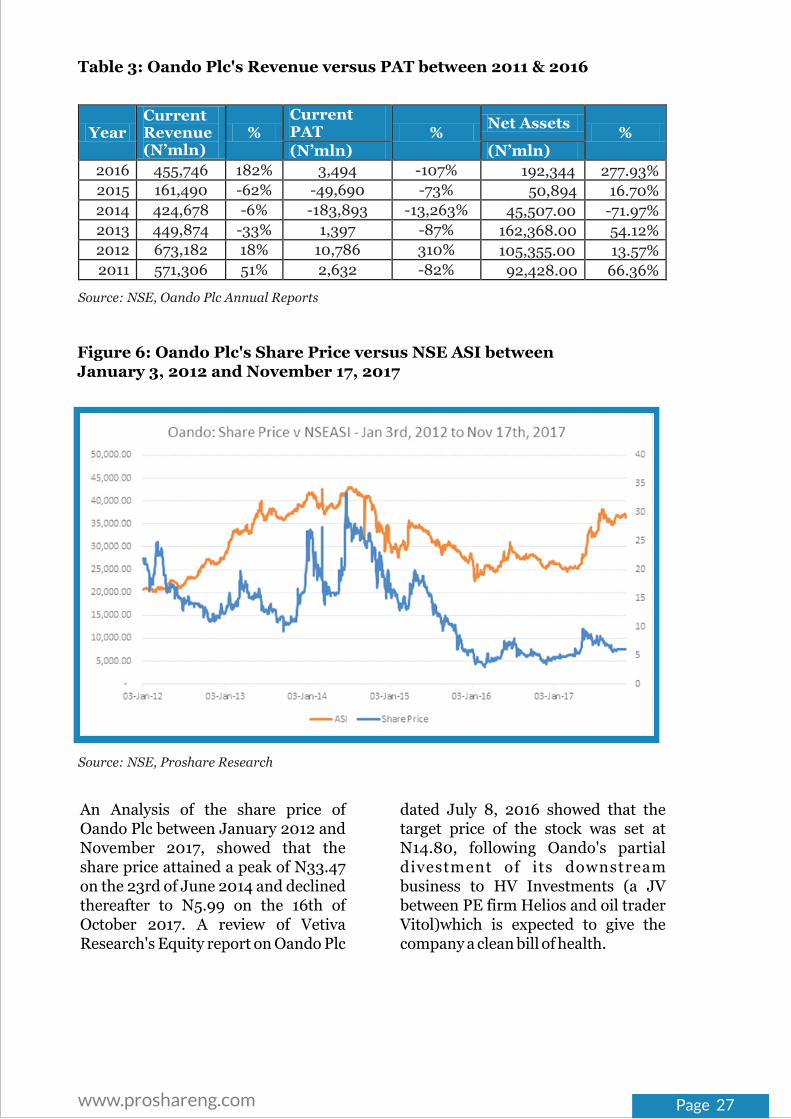

Table 3: Oando Plc's Revenue versus PAT between 2011 & 2016

Year Current Revenue (N’mln)

% Current PAT %

Net Assets %

(N’mln) (N’mln) 2016 455,746 182% 3,494 -107% 192,344 277.93%

2015 161,490 -62% -49,690 -73% 50,894 16.70%

2014 424,678 -6% -183,893 -13,263% 45,507.00 -71.97%

2013 449,874 -33% 1,397 -87% 162,368.00 54.12%

2012 673,182 18% 10,786 310% 105,355.00 13.57%

2011 571,306 51% 2,632 -82% 92,428.00 66.36%

Source: NSE, Oando Plc Annual Reports

Figure 6: Oando Plc's Share Price versus NSE ASI between January 3, 2012 and November 17, 2017

Source: NSE, Proshare Research

An Analysis of the share price of Oando Plc between January 2012 and November 2017, showed that the share price attained a peak of N33.47 on the 23rd of June 2014 and declined thereafter to N5.99 on the 16th of October 2017. A review of Vetiva Research's Equity report on Oando Plc

dated July 8, 2016 showed that the target price of the stock was set at N14.80, following Oando's partial divestment of its downstream business to HV Investments (a JV between PE firm Helios and oil trader Vitol)which is expected to give the company a clean bill of health.

Page 27

Page 1www.proshareng.com

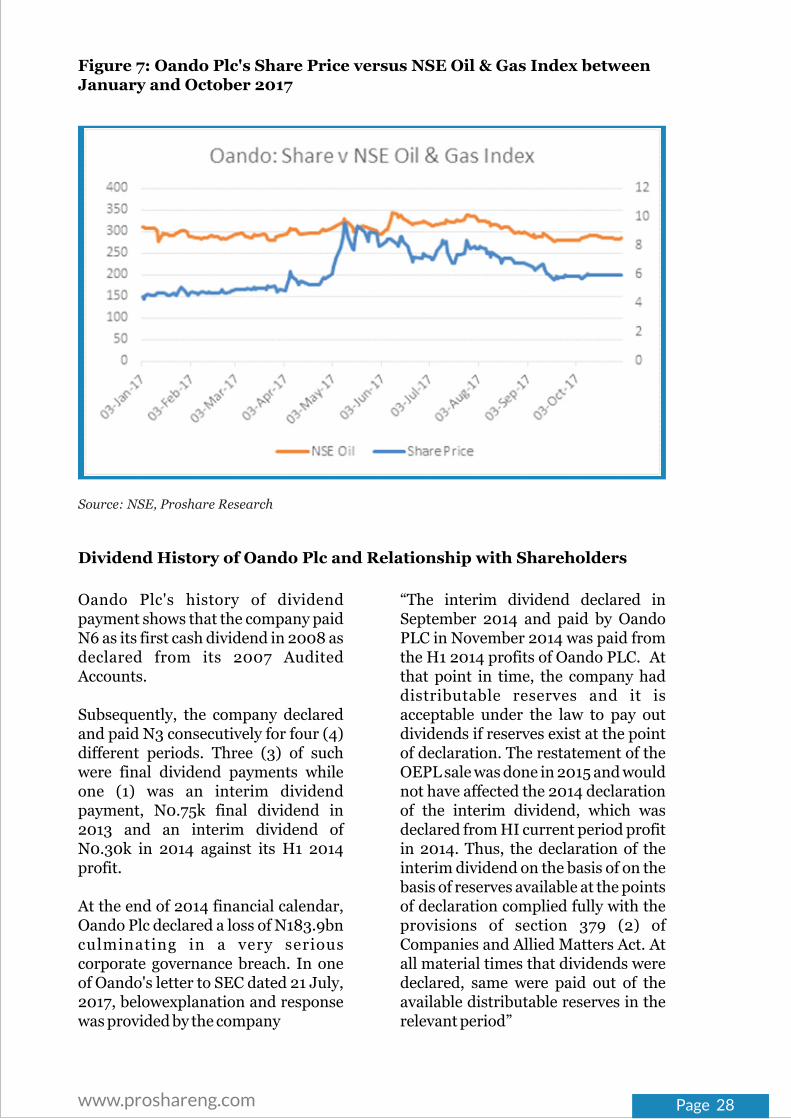

Figure 7: Oando Plc's Share Price versus NSE Oil & Gas Index between January and October 2017

Source: NSE, Proshare Research

Oando Plc's history of dividend payment shows that the company paid N6 as its first cash dividend in 2008 as declared from its 2007 Audited Accounts.

Subsequently, the company declared and paid N3 consecutively for four (4) different periods. Three (3) of such were final dividend payments while one (1) was an interim dividend payment, N0.75k final dividend in 2013 and an interim dividend of N0.30k in 2014 against its H1 2014 profit.

At the end of 2014 financial calendar, Oando Plc declared a loss of N183.9bn culminating in a very serious corporate governance breach. In one of Oando's letter to SEC dated 21 July, 2017, belowexplanation and response was provided by the company

“The interim dividend declared in September 2014 and paid by Oando PLC in November 2014 was paid from the H1 2014 profits of Oando PLC. At that point in time, the company had distributable reserves and it is acceptable under the law to pay out dividends if reserves exist at the point of declaration. The restatement of the OEPL sale was done in 2015 and would not have affected the 2014 declaration of the interim dividend, which was declared from HI current period profit in 2014. Thus, the declaration of the interim dividend on the basis of on the basis of reserves available at the points of declaration complied fully with the provisions of section 379 (2) of Companies and Allied Matters Act. At all material times that dividends were declared, same were paid out of the available distributable reserves in the relevant period”

Dividend History of Oando Plc and Relationship with Shareholders

Page 28

Page 1www.proshareng.com

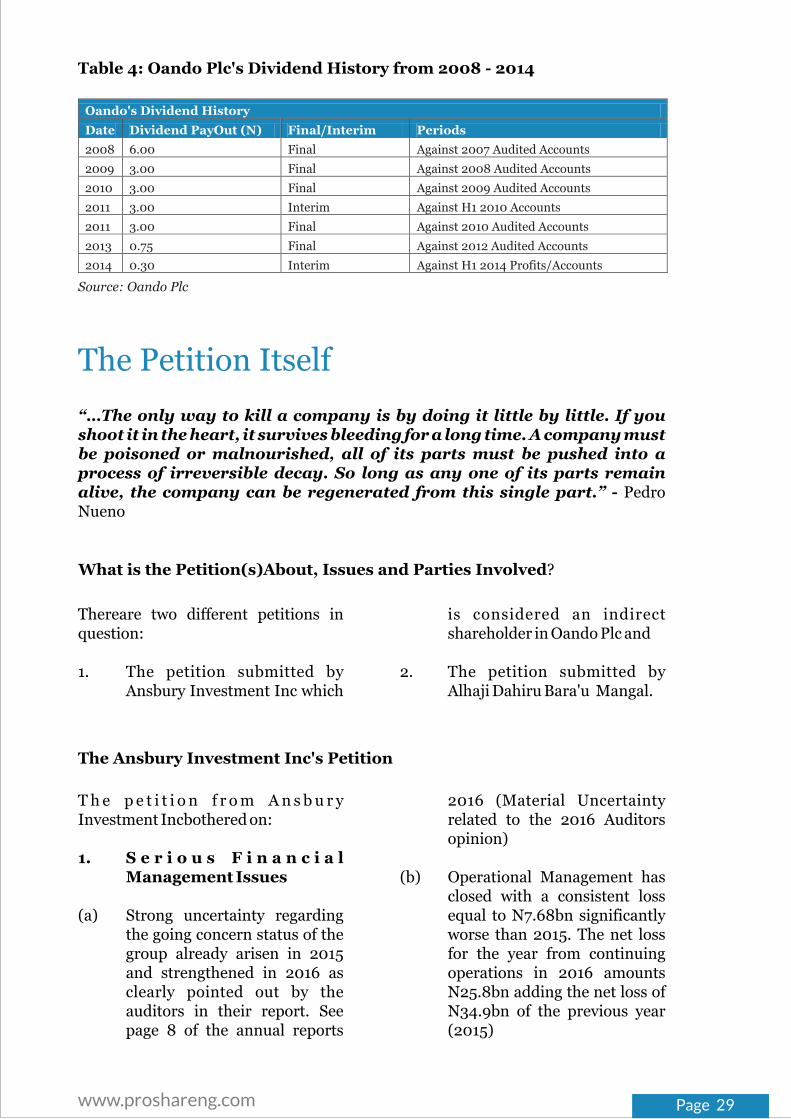

Table 4: Oando Plc's Dividend History from 2008 - 2014

Oando's Dividend History

Date Dividend PayOut (N) Final/Interim Periods

2008 6.00 Final Against 2007 Audited Accounts 2009 3.00 Final Against 2008 Audited Accounts 2010 3.00 Final Against 2009 Audited Accounts 2011

3.00

Interim

Against H1 2010 Accounts

2011

3.00

Final

Against 2010 Audited Accounts

2013

0.75

Final

Against 2012 Audited Accounts

2014 0.30 Interim Against H1 2014 Profits/Accounts

Source: Oando Plc

The Petition Itself

“…The only way to kill a company is by doing it little by little. If you shoot it in the heart, it survives bleeding for a long time. A company must be poisoned or malnourished, all of its parts must be pushed into a process of irreversible decay. So long as any one of its parts remain alive, the company can be regenerated from this single part.” - Pedro Nueno

Thereare two different petitions in question:

1. The petition submitted by Ansbury Investment Inc which

is considered an indirect shareholder in Oando Plc and

2. The petition submitted by Alhaji Dahiru Bara'u Mangal.

What is the Petition(s)About, Issues and Parties Involved?

T h e p e t i t i o n f r o m A n s b u r y Investment Incbothered on:

1. S e r i o u s F i n a n c i a l Management Issues

(a) Strong uncertainty regarding the going concern status of the group already arisen in 2015 and strengthened in 2016 as clearly pointed out by the auditors in their report. See page 8 of the annual reports

2016 (Material Uncertainty related to the 2016 Auditors opinion)

(b) Operational Management has closed with a consistent loss equal to N7.68bn significantly worse than 2015. The net loss for the year from continuing operations in 2016 amounts N25.8bn adding the net loss of N34.9bn of the previous year (2015)

The Ansbury Investment Inc's Petition

Page 29

Page 1www.proshareng.com

(c) The profit for the year 2016 (equal to N3.94bn) only derives from the positive cash flow generated from the sale of consistent part of the group assets which:

(i) Was not enough to fully repay the outstanding debt and

(ii) Has significantly decreased the possibility to generate future positive cash flow to repay our current liabilities.

(d) The current liabilities as at December 31st, 2016 far exceeds the current assets by N263.7bn confirming serious financial imbalance from the previous financial year.

(e) The already severe debt

s i t u a t i o n o f t h e g r o u p h i g h l i g h t e d b y t h e management under notes will deteriorates even further if certain potential liabilities became due such as:

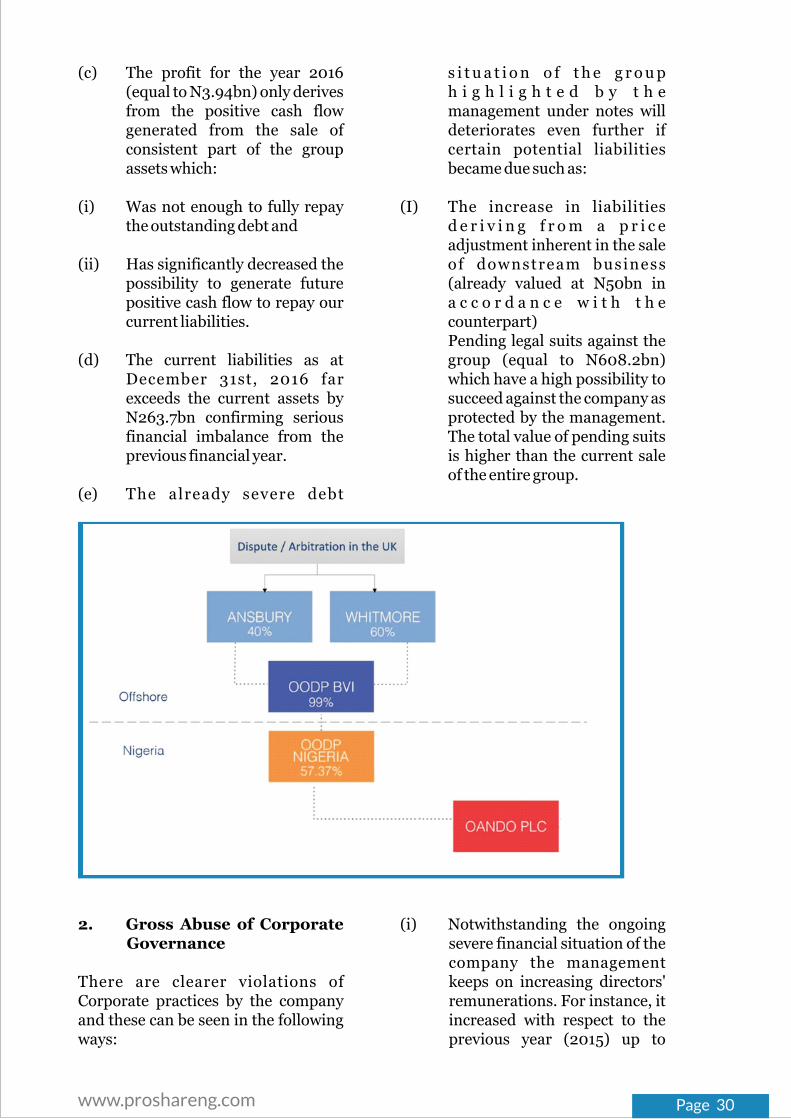

(I) The increase in liabilities d e r i v i n g f r o m a p r i c e adjustment inherent in the sale of downstream business (already valued at N50bn in a c c o r d a n c e w i t h t h e counterpart)Pending legal suits against the group (equal to N608.2bn) which have a high possibility to succeed against the company as protected by the management. The total value of pending suits is higher than the current sale of the entire group.

2. Gross Abuse of Corporate Governance

There are clearer violations of Corporate practices by the company and these can be seen in the following ways:

(i) Notwithstanding the ongoing severe financial situation of the company the management keeps on increasing directors' remunerations. For instance, it increased with respect to the previous year (2015) up to

Page 30

Page 1www.proshareng.com

N1.9bn (See page 43 of the Annual Reports 2016)

(ii) In the previous financial statement, the management had proceeded to liquidate part of the assets of the company and many are going to be liquidated and, in particular, under the notes to the account, management intends to sell its participation in OER (the last asset attributable to the company) in the name of r e s t r u c t u r i n g o r r e -establishing the group going concern. This action and the progressive impoverishment of the group seems directed towards a liquidation of the l a t t e r m o r e t h a n t h e r e s t r u c t u r i n g a n d reorganisation taking into consideration the fact that both the strategy adopted by the management till now and the projected divestiture are not sufficient to service the existing debt.

Ansbury Investment Inc in its petition went on to state the actions it has taken before a formal petition was submitted to SEC Nigeria.

3. Action Taken on Our Side

(i) In order to protect our interest and current litigation between the shareholders we have started taking all necessary measures in relation to our investment in Ocean and Oil Development BVI Limited

(ii) On 6/3/2017 a formal notice was sent from our company to Ocean and Oil (BVI) to order the payment of the expired credit amounting to $470m out of which $270m is made up of

amount indirectly owed us and related matured interest (sums h a v e b e e n u t i l i z e d f o r investment in Oando Plc)

(iii) To this day this credit is yet to be paid and are subject of litigation between us and our partners in Ocean and Oil Development BVI Limited

(iv) This ongoing situation between the parties of Ocean and Oil Nigeria Ltd and is also of great concern which itself as a c o n s e q u e n c e c a n n o t appropriately intervene in the management of Oando Plc despite being the majority shareholder.

4. Mandate of the SEC

Based on the foregoing, we hereby request that the SEC should urgently intervene and adopt all measures deemed appropriate in order to protect the interest of investors which is one of the principal mandate of the SEC most especially the interest of shareholders of Oando Plc in view of the severe financial situation an imminent disruption of the affairs of the company which the current management of the company does not seem to be able to cope with.

T h e S E C h a s a n i m p o r t a n t responsibility to intervene on the issues because the investment and Securities Act (ISA) empowers the SEC as the apex regulator of the Nigerian Capital Market to regulate and ensure the protection of investors including shareholders, maintain fair, efficient and transparent market. Thus section 13 of the ISA empowers the commission to regulate and register the securities of public companies which entails regulating all the activities of those companies to

Page 31

Page 1www.proshareng.com

ensure that the interest of the shareholders are well protected and the section mandate the SEC to act in the public interest having regards to the protection of the investors.

The ISA also empowers the SEC to protect the integrity of the securities market against all forms of abuses including insider abuses or dealings and in our opinion, the action of Oando Plc management constitutes an insider abuse or abuse of management power that could cause serious jeopardy to the corporate existence of the company as a going concern. And in order to ensure the SEC discharges such responsibilities, the ISA mandates the SEC to request their activities are conducted in a transparent manner and in this case, Oando Plc falls under such category.

In our review of the SEC code of corporate governance and specifically rule 28 provides that all capital market operators and other regulated entities shall comply with the SEC rules and regulations for capital market operators and code of governance for public companies and the schedule of the code provides that all participants shall;

(i) Make all efforts to protect the interest of investors

(ii) Always ensure among others that grievances of investors are redressed without delay; and

(iii) Maintain high standard of integrity in all dealings with c l i e n t s a n d o t h e r intermediaries in the conduct of its business.

5. Our Prayers

(i) That the securi t ies and Exchange Commission should

as a matter of urgency look into these issues and cause to convene in the shortest possible t ime an Extra-Ordinary General Meeting (EGM) of Oando Plc in order to c h a n g e t h e c u r r e n t management and board of the company and a l low the shareholders of the company freely express themselves and put in new management, while the current management be made to face the consequences of their action, and this can only be achieved a regulatory i n t e r v e n t i o n w h i c h t h e commission has the mandate as provided both in ISA and the code and in the past, the SEC has taken similar action in a public company.

(ii) Allow Ansbury in its capacity as a n i n d i r e c t m a j o r i t y shareholder of the Oando Plc to intervene in the management of the company through its team and consultants or alternatively to carry out an investigation into the activities of Oando Plc without the hindrance in order to look into the control and most sensitive operations carried out by the current management.

And on its part, Ansbury will continue w i t h a l l i t s s t r e n g t h e n a n d determination to protect in the most appropriate means of its interest and the interest of other shareholders and 3rd party investors made up of Nigerian Banks and Nigerian pensioners whose funds are invested in Oando Plc by Pension Fund Administrators.

We therefore, invite the Securities and Exchange Commission, the apex regulator of the Nigerian Capital

Page 32

Page 1www.proshareng.com

M a r k e t c h a r g e d w i t h t h e responsibi l i t ies of regulating, developing and protecting investors as provided under the Investment and Securities Act (ISA) to please

intervene based on the gravity of the issues in Oando Plc for the interest of all shareholders and the Nigerian Capital Market.

As a shareholder holding 17.9% of the share capital of Oando Plc. I submit to your good self this humble prayer in light of the severe observations arisen from the examination of the 2016 financial statements.

(i) Risk regarding the going concern of the company brought up by the external auditors (Page 7)

(ii) As underlined also by the auditors (page 15), the current liabilities (equal to around N400bn) greatly exceed (by around (2.3x) the current a s s e t s ( t h a t o n l y r e a c h (N140bn). What action can the company take to manage the liquidity problem driving from the fact that Oando still has to define the agreement with some banks for the debt rescheduling that, following the default, was reclassified from mid-long term of short term, as indicated in pages 61 and 76.

(iii) More clarity on the actions that the management wants to undertake to ensure the company's going concern (page 76). In particular: