Embed Size (px)

Citation preview

BRAZIL

Danone in Brazil: 42 years history...

4. WATER starts in 2008… 3. BABY (re)starts in 2007…

2. MEDICAL starts in 1996…1. DAIRY starts in 1970…

Economics: solid ground

1. GDP moderate growth… 2. … inflation under control

3. Robust Intl reserves… 4. … liberating Selic

x5

Demographics: robust domestic market

2005 175MM

7%

38%

27%

A/B (> USD

2,400 month)

C(USD 550 -

2,400 month)

D(USD 275 -550 month)

E: (USD 275/ month I D (275 – 550)/ C ( 550 – 2,400) / A/B (> 2,400)

Income Allocation: 20% pop. = 64% income / 40% pop. = 2% income

E(USD 275 month )

28%

2009 188MM

11%

51%

23%

A/B

C

D

E 15% E

2014 200MM

16%

57%

20%

A/B

C

D

8%

+7MM

People

+18MM

People

+11MM

People

+30MM

People

Brazil takes off

GDP

Toward the 5th rank!

Brazil

France

Germany

Internal MarketHuge emerging middle class

2003 2014AB C DE

Mariano LOZANOGM Dairy

Danone Brazil: from successful turnaround to

sustainable growth

Fresh Dairy Products: middle class pushing PCC, Danone earning market share

Fresh Dairy Product PCC (kg)

4.75.7

6.7

2004 2008 2012 2016

2,9

29.838.0

26.9

19.02004 2005 2006 2007 2008 2009 2010 2011 YTD

2012

192,9

Fresh Dairy Product market share

2004 2005 2006 2007 2008 2009 2010 2011 E1 2012

Actimel + Densia

Danoninho

Activia

Granadda

CAGR (2012 vs 2004) = 14.7%

Danone Brazil: mid-teens growth

KEY SUCCESS FACTORS (Growth)

1. PEOPLE DEVELOPMENTSenior (local) Management Team Intra Entrepreneurship Spirit

2. PORTFOLIO MANAGEMENTADDA (Activia / Danoninho) GranADDA (Danone Mother Brand)

3. SALES FORCE MACHINEExecution @POS (PUMA) BU Northeast

4. STRONG OPERATIONS MACHINEIndustrial & Supply Chain capabilities Common IT&IS platform (SAP)

1. People development (Intra Entrepreneurship)

2. Portfolio management

GranADDA ADDA

2. Portfolio management (VOL)

~200 000 tons ~200 000 tons

2. Portfolio management (Activia)

1. COMMUNICATION…

4. TAILORED STUDY!

2. SALES X 10…

3. Exploring PACK Format…

2. Portfolio management (Danoninho)

1. Tailored STUDY…

4. Most visited WEBSITE!

2. SALES X 2…

2008 2009 2010 2011 2012

85% 84%86% 83%

3º1º

Top

two

boxe

s

2º 4º76%

5º

3. Building a DESIRED Character…

2. Portfolio management (Danone)

3. Sales force machine (Puma)

3. Sales force machine (Nordeste BU)

1. FOCUSED Team…

4. EARNED LEADERSHIP!

2. SALES X 3.5…

3. DEDICATED Factory…

2007 2008 2009 2010 20122011

BU NE - Diretoria

Gerente do Negócio

MKT Trade MktCanalIndireto

SupplyOperações

Vendas InspetoriaFinançasCanalKA

IndustrialCanalDireto

30.6

32.930.8

5.7

2007 2008 2009 2010 2011 YTD12

-14.3

DANONE Comp.1 Comp. 2 Comp.3

+2.1

Tons

4. Strong operation machine (supply)

1.86m

1.86m

2 796 km

4. Strong operation machine (IT&IS)

DANONE BRAZIL moving forward...

We count with...

... PASSIONATED (entrepreneurial) PEOPLE

... GREAT EQUITY behind our BRANDS

... STRONG SALES FORCE MACHINE

... ROBUST OPERATIONS POWERHOUSE

We are bullish in…

… developing YOGHURT CONSUMPTION (1YD)... Growing FASTER than COMPETITORS (SOM)… Creating ACCRETIVE VALUE

Waters

Mauricio CAMARA

THE BIG SIZE OF THE MARKET

Brazilian Water Market Per capita Consumption Bottled Water

THE VERY LOW PCP

€1.0bn

(Liters of Still Water – Zenith)

3x lower

In 2008 the decision to start up a water business in Brazil was based on ....

THE LACK OF INVESTMENT

Advertising InvestmentAVG M€ / YR Brazil

Clearly an underdeveloped market with no active competition

CSD = Carbonated Soft Drinks

Also based on...

AND LACK OF BRAND EQUITY

Source: Perceptor - Brand Equity researh

0

1

2

3

4

5

6

7

8

9

10

Brand Equity Evaluation Note 1 to 10 - Perceptor

1% No brand differentiation

Brand 1

Brand 2Brand 3

Brand 4

Brand 5

DEVELOP THE MARKET USING ATOUT

MODEL

Strong Media support & POS animation

3 strategic pillars to tackle the opportunity

ROLLOUT BONAFONT

MEXICAN MODEL

Elimination Positioning

REGIONAL FOCUSSÃO PAULO STATE

GDP (B€) 470POP (M INHAB) 40

Of total water market

CAGR = 55% (2010 – 2012)

The results 4 years later

Edna GIACOMINIGeneral Manager Danone Baby Nutrition Brazil

Baby Nutrition

Beginning of history in Brazil

NumicoIMF brands: Aptamil & Bebelac

Master brand: Support

A regional company playing only in SP metro

Danone bought

Numicoglobally

Danone became the master brand

Geographical expansion to SPI and RJ

+ MG and South

2007: the beginning of Danone Baby Nutrition history

+ West CenterNortheast

€ 168mln

The IMF market (2007)

PCC: 4.7kg

Penetration: 14%

Powder milk for healthy babies (0 to 12 months)

Unhealthy babies with special needs (0 to 12 months):Soy; Anti Reflux; Allergy & Preterm

Market sharesIMF Market Split

The Baby Food category in 2007

Regulatory environment: consumer communication forb idden

Competitor

Lack of innovation

2007 diagnosis

Under-developed market for “Specials”

Low investment in category development

Creating Category Recognition (Credibility )

Leading Category Innovation

Improving Presence Geographic Expansion

2007 action plan

2007 action plan

Creating Category Recognition (Credibility )

Leading Category Innovation

Improving Presence Geographic Expansion

1. Aptamil (Danone) 78%

2. Brand1 (competitor) 70%

Spontaneous Awareness

97%

95%

Total Awareness

99%

99%

HCP Recommendation (babies till 12 months)

Brand1: 83%

Aptamil: 87%Aptamil: 87%

Creating Category Recognition (Credibility )

Competitor

Competitor

2007 action plan

Creating Category Recognition (Credibility)

Leading Category Innovation

Improving Presence Geographic Expansion

Pregomin

Till 2007

MS: 7.8%

2012 MS:

38.9%

2008

2010

2011

AR (Anti-Reflux) best in class formula

PretermSoy 1 & 2

Aptamil PeptiExclusiveMild Allergy Treatment

Lactose Free

HA

Leading Category Innovation

Pregomin PeptiSevere Allergy

Treatment

2007 action plan

Creating Category Recognition (Credibility)

Leading Category Innovation

Improving Presence Geographic Expansion

WD: 83%2012

2007 2011

From 5 (2007) to 130 (2012) sales employeesSynergy with Medical: Tenders & Distributors

Synergy with Dairy : KA distribution

WD: 35%2007

We are moving to a national company

Improving Presence Geographic Expansion

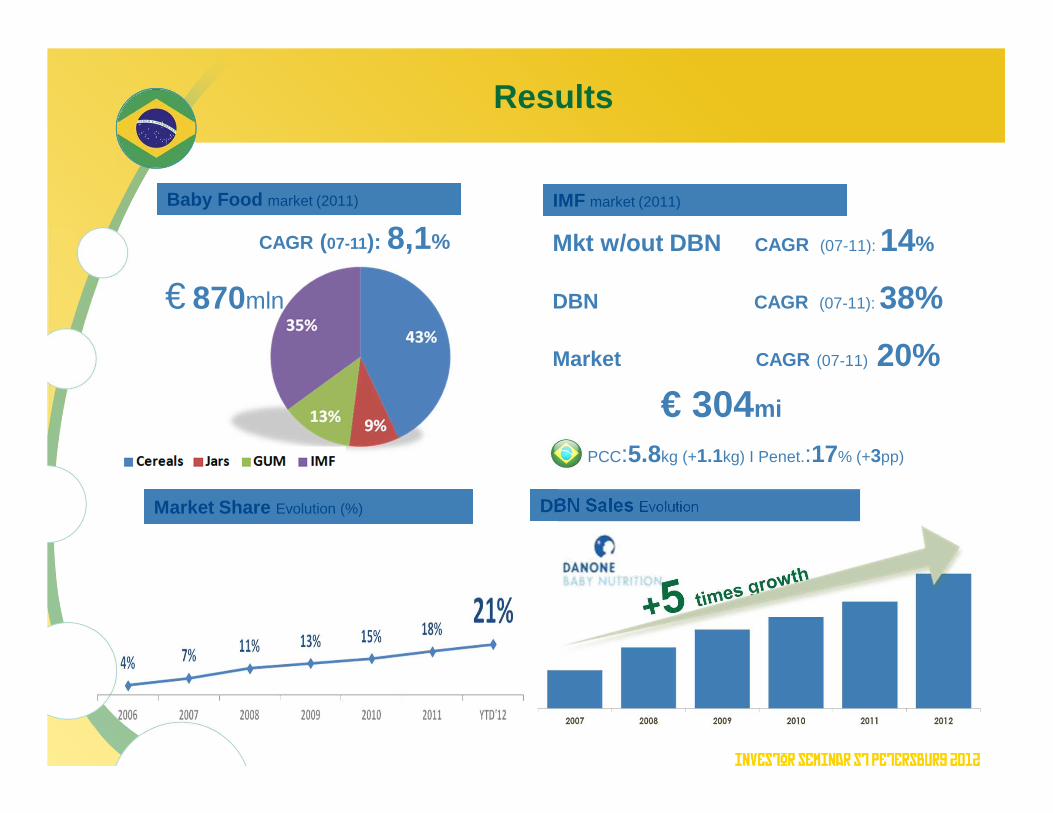

Results

Mkt w/out DBN CAGR (07-11): 14%

DBN CAGR (07-11): 38%

Market CAGR (07-11) 20%

CAGR (07-11): 8,1%

PCC:5.8kg (+1.1kg) I Penet.:17% (+3pp)

€ 870mln

Baby Food market (2011) IMF market (2011)

DBN Sales EvolutionMarket Share Evolution (%)

€ 304mi

Voluntary work (Medical reps)

Objectives:

• Tell histories for hospitalized infant patients

• Create a happy moments in a delicate situation, contributing to health treatment

• Since Sep/12: open to All Danoners

PROJECT BENEFITS

• Provides a unique experience to all involved

• Engages Danoners with the company values

• Establishes partnership with key stakeholders

Being socially responsible

Marcelo BORGES

Medical Nutrition : playing the future

Agenda

Large target populationand increasing purchasing power

(1) Sources: Observador Brasil 2010 – Ipsos/Cetelem; Brazilian Institute of Geography and Statistics; Grupemef and internal data(2) Note: use of WRI available countries (27) to calculate NBC segments through extrapolations in different zones and overall ITC

(3) Sources: World Resource Institute; EIU; UN human development report; BCG analysis * Target Brasil/IMS

2010 2050

Social-economic profile evolution*

Middle class growth (+ 28%)

Purchasing Power is increasing,especially in emerging middle class

Demography is changing very fast.Country is getting older,

but still with a high number of children

Country% of GDP*

Public Private Total

France 8.7% 2.3% 11.0%

UK 6.9% 1.5% 8.4%

Italy 6.7% 2.0% 8.7%

Significant Expenditure in Healthand Growing Pharmaceutical Industry

• Pharma Market is expect to grow more than 50% by 2013 (1)

• OTC represents more than 30%of Pharma market

• Non-reimbursed market Source: * Total Private and Public Health Expenditure OECD 2007

**Sistema de Informações de Beneficiários - ANS/MS - 06/2009 e Cadastro de Operadoras/ANS/MS - 06/2009

Health Insurance

€ 22.8

Others€ 9.6

Medicines € 12.6

Private€ 45.0

Public€ 41.3

Source: MS (estimated 2008)

28% ofall Privateexpenses

22% ofPopulation

withaccess**

3.9%of GDP

3.6%of GDP

Brazilian Pharmaceutical Marketto become the 4 th in the ranking

Total of Expenditure with Health86.3 Billion and 7.5% of GDP

Nutricia is a leading player in Hospital.Community shows a huge potential

COMMUNITYHOSPITAL

Potential€ 200 m

Nutricia14%

Potential€ 287 m

Nutricia39%

Hospital€ 152 m

Out-Patient Mkt€ 25 m

Nutricia

56%

PAED/Allergy€ 54 m

Nutricia

26% CommunityAdult/Pediatric

€ 53 m

Brazilian company

SUPPORTfounded (medical

nutrition and generic-type company)

Brazilian company

SUPPORTfounded (medical

nutrition and generic-type company)

NutriciaLeader

in the Hospital Market:

34%

NutriciaLeader

in the Hospital Market:

34%

Danone Medical Nutrition History in Brazil

NUTRICIAInternational

acquiredSupport

NUTRICIAInternational

acquiredSupport

Introduction

GI-Allergy and

Metabolic

Introduction

GI-Allergy and

Metabolic

DANONEacquired

Numico

DANONEacquired

Numico

6th subsidiary in Sales

4th in absolute Sales growth

6th subsidiary in Sales

4th in absolute Sales growth

4th subsidiary in Sales

3rd in absolute Sales growth

4th subsidiary in Sales

3rd in absolute Sales growth

Nutricia Brazil plays important role in the Medical Division

Strong Growth and Profitability

Sales EBIT EBIT margin

Nutricia holds the leadership of the Total Market

Nutricia holds the leadership of the market• Market: Hospital + OTX Pharmacy + Allergy (Public + Pharmacy)• Excludes Souvenaid and FortiFit markets

33,38% 34,90% 35,24%

2010 2011 2012

Nutricia market share

Vision

Stronger Organization and very competitive player in the market

Leader in the Hospitaland Out-Patient segments

Recognized as Innovative Companyin the Elderly Care thanks to the success of Souvenaid and FortiFit

New route to market with Directto Consumer approach

Sustainable business model with Hospital, OTX (Adult) and Paediatric pillars

BusinessFocus

GroupStrength

&

4 separate independent CBUs

specialization to maximize focusand respect business specificities

Business Focus

to maximize presence, opportunities, productivity …

STRENGTH

Joint actionsRoute to market

Media Congresses

Stakeholder ManagementTender Management

Shared ServicesBack officeSystemsOffices

SynergiesBonafont birth through FDP

Baby re-start-up through Medical

Great Place to WorkGreater People Development opportunities through “migrations”

Group Strength

THANK YOU!OBRIGADO!