Embed Size (px)

Citation preview

Pergamon

Journal of Accounting Education, Vol. 14, No. 1, pp. 57-67, 1996 Copyright © 1996 Elsevier Science Ltd

Printed in Great Britain. All rights reserved 0748-5751/96 $15.00 + 0.00

0748-5751(95)00030-5

USING INFORMATION SYSTEMS AS A BASIS FOR TEACHING ACCOUNTING

Marshall B. Ronmey J. Owen Cherrington

Eric L. Demma BRIGHAM YOUNG UNIVERSITY

Abstract: This paper describes how Brigham Young University reorganized the way it teaches financial, managerial, auditing, tax, law, and information systems (the accounting core). It discusses why information systems (IS) is the first topic taught, why it is a central focus throughout the core, and how teaching the functional areas of accounting is integrated.

The paper discusses the results of a survey of core students. The survey shows that studying systems first helped these students integrate IS and accounting concepts, understand the underlying accounting framework, and understand other areas of accounting. Integrating systems with other subjects helped the students understand the role of systems in accounting and how systems relates to other accounting areas. Survey results show systems concepts can be taught in an intensive manner without reducing the level of coverage or affecting student comprehension. Finally, the results show professors can receive high teacher evaluations in systems courses and students can have both a quality and an enjoyable learning experience.

INTRODUCTION

Recently there have been a number of calls for significant changes in accounting and information systems (IS) education (AAA, 1986; AECC, 1990). A recurring theme of the Bedford report and the AECC position statement is the critical need for IS to be a fundamental part of accounting education. Historically, accounting has been taught in separate functional courses such as auditing, financial, law, managerial, systems, and tax. This "stovepipe" approach (Elliot, 1992) makes it difficult for students to integrate the concepts and to see why IS is such an important part of accounting education. For example, a managerial class may discuss how to use information to make decisions, but never discuss how the information is collected, stored, or made available to the decision maker. Likewise, the systems course may discuss how information is collected, stored, and made available but never discuss the use of the information.

The Bedford report also emphasized that IS should be one of the first topics taught. Unfortunately, this is not the model most schools use as most schools view accounting information systems (AIS) as tangential to accounting. The AIS course is rarely among the more popular accounting classes and AIS courses and instructors receive lower student evaluations

57

58 M.B. Romney et al.

(Raval, 1991). As a result, the AIS course is usually a senior level class students take just before graduation. It has little impact on shaping student perceptions of the accounting profession.

Brigham Young University (BYU) developed a new and highly integrated approach to teaching financial, managerial, auditing, tax, law, and systems (Albrecht, Clark, Smith, Stocks, & Woodfield, 1994). This article describes how the change affected one group of students' ability to learn IS and accounting. An essential part of the change is that IS is the first core topic and remains a central focus throughout the year. By teaching systems as the first foundation topic of the core we hoped it would help students understand the fundamental change in accounting itself--from transaction processing to a systems/business process orienta- tion. IS topics are not taught in isolation of other topics; instead they are integrated with them. Students are taught that accounting is a process that requires them to identify, gather, measure, summarize, analyze, com- municate, and use information. To do so, they must understand the concepts, methods, and processes used to design an effective system. They must also understand current and future roles of computer-based technology.

The remainder of the paper is organized as follows. The next section discusses the systems portion of the BYU accounting core. One section explains how teaching the different functional areas of accounting is integrated, using the sales collection cycle as an example. Another discusses the results of a survey that measured student satisfaction and their perceived learning. The final section discusses the conclusions, implications, and limitations of the survey.

THE SYSTEMS PORTION OF THE BYU ACCOUNTING CORE

The systems portion of the accounting core provides students with a blend of conceptual systems concepts and hands-on systems experience. The first assignment is a Systems Understanding Aid (Kieso, Arens, & Ward, 1991) that helps students understand a manual system. The Aid is followed by ten hands-on computer assignments designed to help them understand operating systems, a spreadsheet, database technology, and a general ledger package. The students use the Aid data to develop financial statements for the general ledger assignment and for the last two Paradox assignments. That is, they use the same data to prepare the same financial statements using a manual system, a general ledger package, and a relational database system.

For the conceptual portion of the systems core, the faculty selected from the many potential systems topics those they felt were most important for accounting students. Two separate texts are used to help teach this conceptual material: A traditional systems text (Cushing & Romney, 1994)

Information Systems in Teaching Accounting 59

Table 1. Information system topics taught in 15.5 3-hour core blocks

Reading Day" Conceptual topic Hands-on assignment

Foundation phase 1 Intro to AIS DOS C&R 1 2 Transaction processing Pacioli (G/L package) C&R 2 3 Information technology Spreadsheet-- intro C&R 4-6 4 Systems development process Spreadsheets--advanced C&R 8 5 Alternative development - - C&R 11

approaches DCAH 1-3 6 Business events Paradox--creat ing tables DCAH 5 7 Developing data models Paradox-- forms C&R 7 8 Evaluating data models Paradox--s imple queries DCAH 6-7 9A Computer fraud - - C&R 14

DCAH 4 9B Computer controls Paradox--complex queries C&R 12

10A Computer controls Paradox-- income statement 10B Computer controls Paradox--balance sheet C&R 13 11A Computer controls 11B Careers in IS

Business cycles 12; Sales/collection information C&R 16 13A systems 13B Acquisition payment information C&R 17

systems 14A Payroll/performance information C&R 19

systems 14B; Conversion/inventory information C&R 18 15A systems 15B; Financial information systems C&R 20 16A

C&R=Accounting Information Systems by Cushing and Romney (1993). DCAH=Event Driven Business Solutions by Denna et al. (1993). =Each day equals a 3 hour teaching block.

and a book written for business professionals on the events-driven approach to systems development (Denna, Cherrington, Andros, & Hollander, 1993). Table 1 shows the major topics discussed during each of the 15.5 3-hour teaching blocks allocated to systems. It also shows the computer and reading assignments.

STUDENT RESPONSE TO THE SYSTEMS PORTION OF THE ACCOUNTING CORE

To measure student perceptions, a questionnaire was administered in class the first day of the second semester. The students surveyed were members of the third group through the core; no comparable surveys were conducted during the first 2 years of the core. The students had completed the foundation phase and the sales/collection cycle. Three separate four-

60 M.B . Romney et al.

page questionnaires were developed. The first two pages were the same and gathered primarily demographic information. The last two pages asked different questions about the core content and teaching approach. The questionnaires were completed during class and all 233 students in attendance that day completed a questionnaire. Students were randomly assigned questionnaires. Approximately one-third of the students com- pleted each version of the questionnaire (81, 75, and 77 students, respectively).

DEMOGRAPHICS

The survey revealed the following about the students:

• 85% owned their own computer • 65% had taken a spreadsheet course • 59% had taken a word processng course • 47% had taken other computer courses • before the core, 5.2% described themselves as advanced computer

users, 33% as intermediate users, 49.4% as beginners, and 12.4% as novices

• after the first semester, 10.7% described themselves as advanced users, 73.8% as intermediate, and 15.5% as beginners.

COVERAGE OF THE MATERIAL

One concern with the way the core is taught is the amount of systems material the students must absorb in such a short amount of time. Except for four 1.5 hour sessions spread throughout the second half of the first semester, all of the systems foundation material is taught in the first 4 weeks of the integrated core. During this time students read over 470 textbook pages, complete six hands-on computer assignments, and turn in one or more written homework assignments per class period.

Questions were asked about the amount of material covered, the depth of coverage, and the speed of coverage. The responses are shown in Table 2. The three questions were phrased in the negative; that is, they could agree or disagree that too much material was covered too quickly or in insufficient depth. Significantly more students (38.3%) felt that the material was covered too quickly than felt it was not covered in sufficient depth (17.3%) or that too much material was covered (14.3%).

These results are surprising, inasmuch as the systems faculty felt the systems workload was quite h~vy. One possible explanation is that the students felt the systems workload was lighter than that of the other functional areas. Students were asked to rate the average workload per day for each functional area. As shown in Figure 1, students felt tax had

Information Systems in Teaching Accounting 61

Table 2. Coverage of material

SD a D N A SA

2.7% 50.7% 29.3% 13.3% 4.0% For the t ime allowed, we did NOT co~,er the material in the systems portion of the core in sufficient depth

For the t ime allowed, we covered too much material in the systems portion of the core

For the t ime allowed, we covered the material in the systems portion of the core too quickly

10.4% 42.9% 32.5% 9.1% 5.2%

3.7% 35.8% 22.2% 30.9% 7.4%

aSD=strongly disagree; D=disagree; N=neutral; A=agree; SA=strongly agree.

Average Workload per Day by Subject Areas

. . n g e = n t Accounting

L u .

,s

Financial Accounting ~////////////////~ Legend

[ ] . . t ing: ! =,oa.i.t. Audit 6 = Lightest

i I i I I I I 0 1 2 3 4 5 6

Figure 1 . Average workload per day by subject areas.

the heaviest workload and managerial accounting had the lightest workload per day. In comparison to the other functional areas, the systems workload was not excessive.

MEASURES OF LEARNING

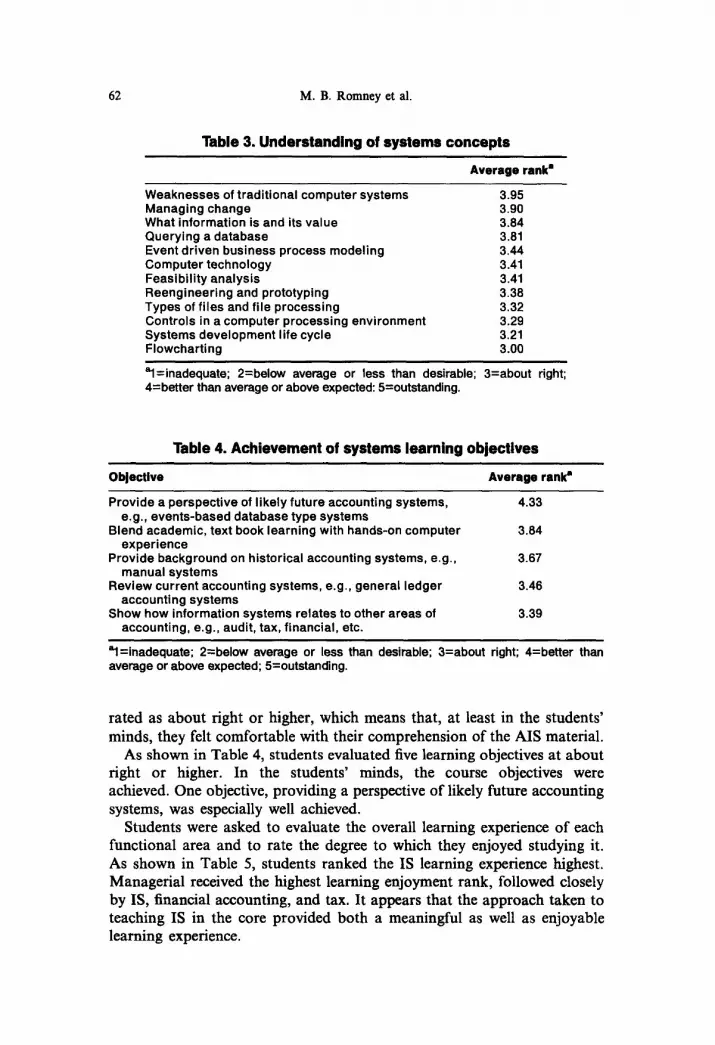

Another concern with compressing the systems material into such a short learning span was how well the students would understand the concepts presented. Students were asked to rate how well they understood twelve major systems topics. As shown in Table 3, all twelve topics were

62 M.B. Romney et al.

Table 3. Understanding of systems concepts

Average rank-

Weaknesses of traditional computer systems Managing change What information is and its value Querying a database Event driven business process modeling Computer technology Feasibility analysis Reengineering and prototyping Types of files and file processing Controls in a computer processing environment Systems development life cycle Flowcharting

3.95 3.90 3.84 3.81 3.44 3.41 3.41 3.38 3.32 3.29 3.21 3.00

al=inadequate; 2=below average or less than desirable; 3=about right; 4=better than average or above expected: 5=outstanding.

Table 4. Achievement of systems learning objectives

Objective Average rank"

Provide a perspective of likely future accounting systems, 4.33 e.g., events-based database type systems

Blend academic, text book learning with hands-on computer 3.84 experience

Provide background on historical accounting systems, e.g., 3.67 manual systems

Review current accounting systems, e.g., general ledger 3.46 accounting systems

Show how information systems relates to other areas of 3.39 accounting, e.g., audit, tax, financial, etc.

=1=inadequate; 2=below average or less than desirable; 3=about right; 4=better than average or above expected; 5=outstanding.

rated as about right or higher, which means that, at least in the students' minds, they felt comfortable with their comprehension of the AIS material.

As shown in Table 4, students evaluated five learning objectives at about right or higher. In the students' minds, the course objectives were achieved. One objective, providing a perspective of likely future accounting systems, was especially well achieved.

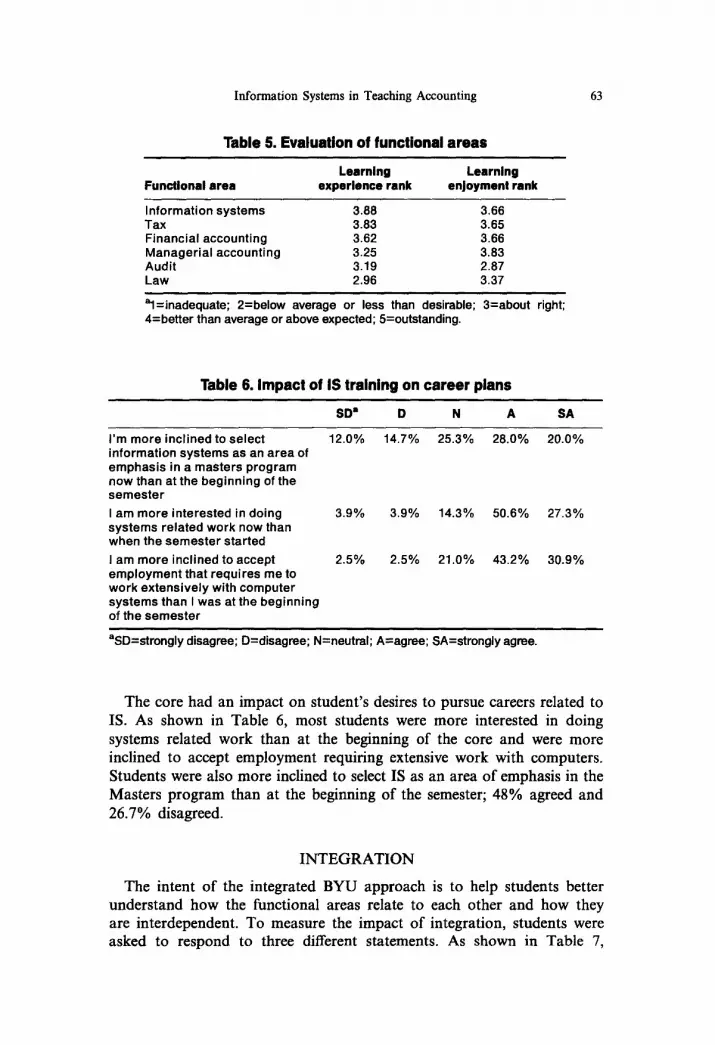

Students were asked to evaluate the overall learning experience of each functional area and to rate the degree to which they enjoyed studying it. As shown in Table 5, students ranked the IS learning experience highest. Managerial received the highest learning enjoyment rank, followed closely by IS, financial accounting, and tax. It appears that the approach taken to teaching IS in the core provided both a meaningful as well as enjoyable learning experience.

Information Systems in Teaching Accounting 63

Table 6. Evaluation of functional areas

Learning Learning Functional area experience rank enjoyment rank

Information systems 3.88 3.66 Tax 3.83 3.65 Financial accounting 3.62 3.66 Managerial accounting 3.25 3.83 Audit 3.19 2.87 Law 2.96 3.37

al=inadequate; 2=below average or less than desirable; 3=about right; 4=better than average or above expected; 5=outstanding.

Table 6. Impact of IS training on career plans

SD = D N A SA

12.0% 14.7% 25.3% 28.0% 20.0% I'm more inclined to select information systems as an area of emphasis in a masters program now than at the beginning of the semester

I am more interested in doing systems related work now than when the semester started

I am more inclined to accept employment that requires me to work extensively with computer systems than I was at the beginning of the semester

3.9% 3.9% 14.3% 50.6% 27.3%

2.5% 2.5% 21.0% 43.2% 30.9%

aSD=strongly disagree; D=disagree; N=neutral; A=agree; SA=strongly agree.

The core had an impact on student's desires to pursue careers related to IS. As shown in Table 6, most students were more interested in doing systems related work than at the beginning of the core and were more inclined to accept employment requiring extensive work with computers. Students were also more inclined to select IS as an area of emphasis in the Masters program than at the beginning of the semester; 48% agreed and 26.7% disagreed.

I N T E G R A T I O N

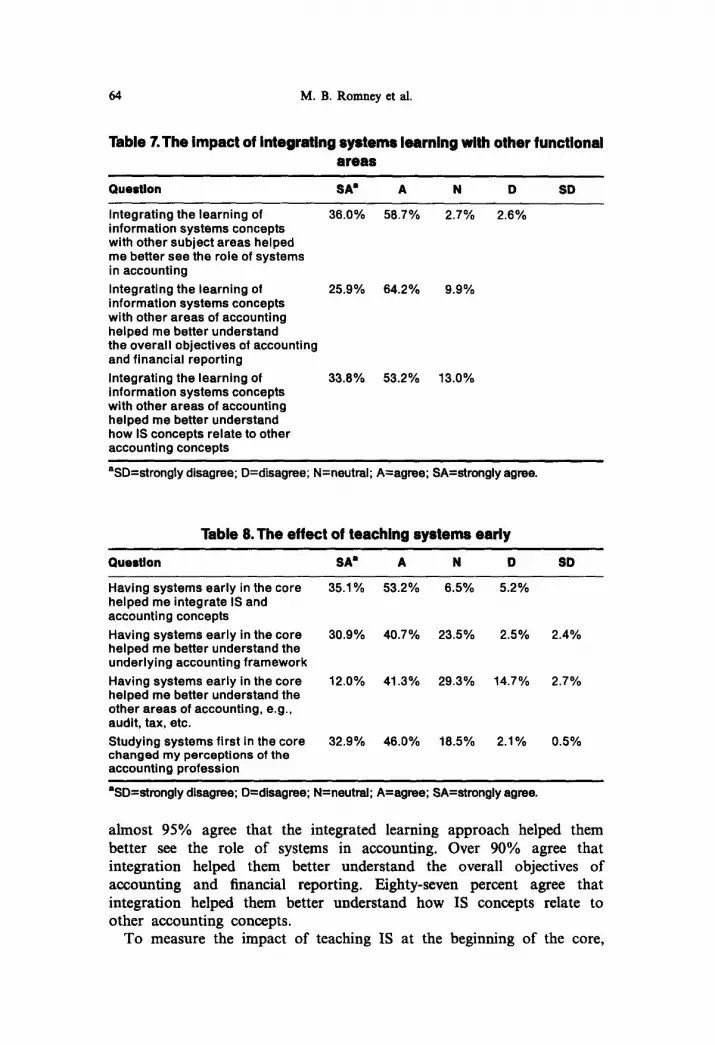

The intent of the integrated BYU approach is to help students better understand how the functional areas relate to each other and how they are interdependent. To measure the impact of integration, students were asked to respond to three different statements. As shown in Table 7,

64 M.B. Romncy ct al.

Table 7. The impact of Integrating systems learning with other functional areas

Question SA a A N D SD

Integrating the learning of 36.0% 58.7% 2.7% 2.6% information systems concepts with other subject areas helped me better see the role of systems in accounting Integrating the learning of 25.9% 64.2% 9.9% information systems concepts with other areas of accounting helped me better understand the overall objectives of accounting and financial reporting Integrating the learning of 33.8% 53.2% 13.0% information systems concepts with other areas of accounting helped me better understand how IS concepts relate to other accounting concepts

aSD=strongly disagree; D=disagree; N=neutral; A=agree; SA=strongly agree.

Table 8. The effect of teaching systems early

Question SA" A N D SD

Having systems early in the core 35.1% 53.2% 6.5% 5.2% helped me integrate IS and accounting concepts Having systems early in the core 30.9% 40.7% 23.5% 2.5% 2.4% helped me better understand the underlying accounting framework Having systems early in the core 12.0% 41.3% 29.3% 14.7% 2.7% helped me better understand the other areas of accounting, e.g., audit, tax, etc. Studying systems first in the core 32.9% 46.0% 18.5% 2.1% 0.5% changed my perceptions of the accounting profession

=SD=strongly disagree; D=disagree; N=neutrel; A:agree; SA=strongly agree.

almost 95% agree that the integrated learning approach helped them better see the role of systems in accounting. Over 90% agree that integration helped them better understand the overall objectives of accounting and financial reporting. Eighty-seven percent agree that integration helped them better understand how IS concepts relate to other accounting concepts.

To measure the impact of teaching IS at the beginning of the core,

Information Systems in Teaching Accounting 65

students were asked to respond to a number of statements. As shown in Table 8, having systems early in the core helped 88,3% of the students integrate IS and accounting concepts; 71.6% to better understand the accounting framework; and 53.3% to better understand the other areas of accounting. In addition, 78.9% felt that studying systems first changed their perceptions of the accounting profession.

STUDENT TEACHER/COURSE EVALUATIONS

The School of Accountancy and Information Systems at BYU requires every faculty member to be evaluated in every course, every semester. The evaluations are used to determine annual salary adjustments and in promotion and tenure decisions. The evaluation form uses a 7-point scale, with 1 being "very poor" and 7 being "exceptional." For the period covered by the survey, the three IS core faculty had an average instructor rating of 6.19, compared to a non-IS faculty rating of 5.65. The average course rating for the IS portion of the core was 5.84 compared to 5.40 for other accounting areas. These results are in marked contrast to the evidence presented by Raval (1991) that AIS courses and instructors receive lower student evaluations.

The higher ratings could be due to the faculty assigned to teach the core. Although faculty assignments could be part of the explanation, we think a major portion of the results can be attributed to the methods used to teach AIS. There are two reasons for this belief. First, these three faculty members received higher ratings teaching IS in the core than they did when teaching AIS as a stand-alone course. Second, one of the three instructors taught one of the other functional areas in the core during the Winter semester to the same students and received lower teacher and course ratings.

LIMITATIONS AND IMPLICATIONS

The intent of this paper is to describe the way BYU teaches information systems to its accounting students. From a pure research standpoint, there are a number of limitations to our survey results. One limitation is a lack of comparative data. We did not administer the questionnaire to our precore students. Because of differences in pedagogy, instructors, objectives, and structure of IS courses we lack comparative data from other universities. Notwithstanding these limitations, this paper does serve an important purpose. Although further reseach is needed to confirm some of our results, it appears that:

• Systems concepts may be taught in an intensive manner without reducing the level of coverage or affecting student comprehension.

66 M.B. Romney et al.

• Systems may be taught in a way that provides students with both a quality and an enjoyable learning experience.

• Systems can be a fun course to teach and professors can receive high teacher evaluations in IS courses.

• Integrating IS concepts with other subject areas may help students better understand (a) the role of systems in accounting, (b) how IS concepts relate to other accounting areas, and (c) the overall objectives of accounting and financial reporting.

• Student's perceptions of accounting may change as they study IS topics. This argues for having systems concepts taught at the beginning of their accounting classes, not at the end. The tack-on approach of teaching systems at the end of the curriculum makes it much more difficult for students to understand the importance of systems concepts.

• Studying systems first may help students (a) integate IS and accounting concepts, (b) understand the underlying accounting framework, and (c) better understand other functional areas of accounting.

The study opens the door to further research topics. For example:

• Is this approach transferable to other universities? • Can the same results be achieved without integrating all six functional

areas? For example, can the same or better results be achieved by integrating IS and managerial accounting or IS and auditing?

• Are there other approaches that can produce similar results? • Why do students feel the way they do? Exactly what is it about the

approach that they like and what do they not like? • Are these results an anomaly? Will longitudinal data over several

years produce the same results?

It is hoped that this article will provide some help and guidance to faculty, department chairs, and deans who are struggling with how to teach accounting information systems.

REFERENCES

Accounting Education Change Commission [AECC]. (1990). Objectives of education for accountants: Position Statement No. 1.

Albrecht, W. S., Clark, D. C., Smith, J. M., Stocks, K. D., & Woodficld, L. W. (1994). An accounting curriculum for the next century. Issues in Accounting Education.

American Accounting Association [AAA]. Committee on the Future Structure, Content, and Scope of Accounting Education [The Bedford Committee l (1986). Future accounting education: Preparing for the expanding profession. Issues in Accounting Education, I, 168- 195.

Arthur Andersen & Co., Arthur Young, Coopers & Lybrand, Deloitte Haskins & Sells, Ernst & Whinney, Peat Marwick Main & Co., Price Waterhouse, & Touche Ross [The Big

Information Systems in Teaching Accounting 67

Eight]. (1989). Perspectives on education: Capabilities for success in the accounting profession. New York: Authors.

Cherrington, J. O., Denna, E. L., & Romney, M. B. (1994). Teaching IS: The new philosophy. Marriott School of Management, Working Paper Collection #99, an Innovative Accounting Information Systems (AIS) Course.

Cushing, B. E., & Romney, M. B. (1993). Accounting information systems, (6th edition). Reading, MA: Addison-Wesley.

Denna, E. L., Cherrington, J. O., Andros, D. P., & Hollander, A. S. (1993). Event-driven business solutions. Homewood, IL: Business One Irwin.

Deppe, L. A., Sonderegger, E. O., Stice, J. D., Clark, D. C., & Streuling, G. F. (1991). Emerging competencies for the practice of accountancy. Journal of Accounting Education, 257-290.

Elliott, R. K. (1992). The third wave breaks on the shores of accounting. Accounting Horizons, 61-85.

Kieso, D. E., Arens, A. A., & Ward, D. D. (1991). Systems understanding aid for finuncial accounting, (3rd edition). Williamston, MI: Dalton.

Mueller, G. G., & Simmons, J. K. (1989). Change in accounting education. Issues in Accounting Education, 247-251.

Raval, V. (1991). Perspectives on students' teaching evaluations of AIS courses. Journal of Information Systems, 62-72.

Romney, M. B. (1984). Teaching accounting information systems using a case study approach. Journal of Accounting Education, 145-154.

Williams, D. Z., & Sundem, G. L. (1990). Grants awarded for implementing improvements in accounting education. Issues in Accounting Education, 313-329.