Embed Size (px)

Citation preview

EDO UNIVERSITY IYAMHO

Department of Accounting ACC 311 Intermediate Accounting

Instructor: Dr. Alexander Olawumi Dabor: email: [email protected]

Lectures: Wednesday, 1pm – 2.00 pm, LC3, Thursday, 2.00pm-3.00pm phone: (+234)

8161610466

Office hours: Monday, 2.30 to 3.30 PM, Office: Floor1 Rm 10

General overview of lecture: The course content basically focuses on intermediate Accounting. It is aimed at making students

to understand the accounting practice. It aimed at preparing students for interpreting financial

reporting.

Prerequisite: The students are expected to have a strong background in Financial Accounting

Learning outcomes: At the completion of this course, students are expected to: 1. know the how to prepare final account .

2. understand miscellaneous issues in accounting

3. 4. be able to interpret financial report

Assignments: Students are expected to do three take home assignments during this course in

addition to a Mid-Term Test and a Final Exam. Quizzes will also be administered at interval during

the course, this will serve as an acid test to ascertain if students understood what was imparted to

them,

Grading: In this course assign forms 10% of the final marks while assignment and mid-test form

10% and 10% respectively. The final exam forms 70% of the final mark. Students are expected to

sit for a comprehensive examination at the end of the semester.

Textbook: The recommended textbook for this class are as stated:

Title: International Financial Reporting Standard”. In International Finance and Accounting

Handbook

Authors: Paul, P., and Deloitte, T. T

Publisher: Wiley & Sons

Year: 2009

Title: Accounting, An International Perspective

Author(s): Gernon, H. and Meek, G. K. (2001),

Publisher: McGraw-Hill Higher Education.

Year: 2006

Lesson note: - ACC 311 – Intermediate Accounting

The following documents outline the course for the course ACC311- International Accounting.

1. CHANGE IN CONSTITUTION OF PARTNERSHIP

Three principles issues to be dealt with in a change of constitution of partnership include:

1. Goodwill

2. Revaluation

3. Apportionment

A change in partnership constitution is any circumstance that alters the profit sharing ratio as

between partners. These circumstance include:

1. Retirement of a partner

2. Admission of a partner

3. Death of partner

4. Change in profit sharing ratio

5. A combination of any of the above

Admission of new partner

A partner is said to be admitted into a partnership where he/she joins an existing partnership. In

such circumstances he or she is expected to contribute his capital and may be required to pay for

the goodwill which the partnership has earned over the period of its existence the partner is deemed

to have retired and the partnership business continues to exist.

Retirement of partner

This is the withdrawal of interest by a partner from a partnership . In other words, a partner may

willingly withdraw his membership as partner in business owing to reason(s) best known to him.

In such circumstance

Revaluation

When there is a sudden appreciation or depreciation in the value of assets due to economic changes,

the new stand the chance or risk of gaining or losing greatly hence it is imperative for partners to

revalue asset and on admission of a new partner in any other way the business might have changed.

Revaluation Account

The revaluation account is a miniature profit or loss account which is used to determine the capital

profit or capital losses on the revaluation of assets when a partner is to admitted, a partner dies or

retired. The balance of the profit or loss on the revaluation are credited or debited to the partners’

current account as the case may be.

There are two methods of revaluation of assets: Total and difference methods.

Method I

Step 1

Open a revaluation account

i. Dr Revaluation account

Cr Partnership account

With book value of the assets revalued

ii. Dr Particular Asset account

Cr Revaluation account

With the reversed (new) value of assets

Iii Dr Particular liability account

Cr Revaluation account

With book value of only liabilities revalued

iv. Reduction or depreciation in value of assets eg debtors, stock, investment are treated by creating

appropriate provision for them. In other words the book value remain intact and are not passed

through the revaluation account then:

Dr Revaluation

Cr Provision

Step II : Close the revaluation account and share the profit or loss in accordance to profit or loss

sharing ratio of old partners. Then post to the current account as the case may be.

Method II: Difference Method

i. Dr :Revaluation Account

Cr: Liabilities Account

For amount of increases in liabilities

ii. Dr Revaluation account

Cr Assets

For amount increase in value of asset ( note in the case of investment, debtors and stock, the old

book value will be undisturbed and credit will be to a provision a/c)

Iii. Dr Liabilities account

Cr Revaluation account

Amount of decrease in liabilities

iv. Dr Assets

Cr Revaluation account

For amount of increase in asset valuation

The balance of revaluation a/c which could be either be profit or loss will be shared accordingly.

Definition of Goodwill.

SSAP 22 defines by as the difference between the value of a business as a whole and the aggregate

of fair values of its separable net assets. Fair value is amount for which an asset or liability could

be exchange in an arm’s length transaction. Separable net assets are essentially those assets which

can be sold or disposed of separately from the rest of the business.

Goodwill can be purchased or internally generated. It is purchased if is acquired and it is not

purchased if it develop internally. Valuation of goodwill present a problem. Some factors that

create goodwill include:

1. Superior management team.

2. Weakness in management of competitor

3. Effective advertising

4. Goodwill labour relations

5. Secret of patented manufacturing process.

6. Strategic location

7. Product quality and reliability

8. Establishment market with wide and varied outlets.

9. Discovery of talents of resource.

VALUTION OF GOODWILL

Goodwill can be valued in any of the following ways:

1. A number of years purchase of average profit

2. A number of years purchase average gross income of the business

3. A number of years purchase of the average super profits of the business

4. Excess value of business over value of tangible net assets.

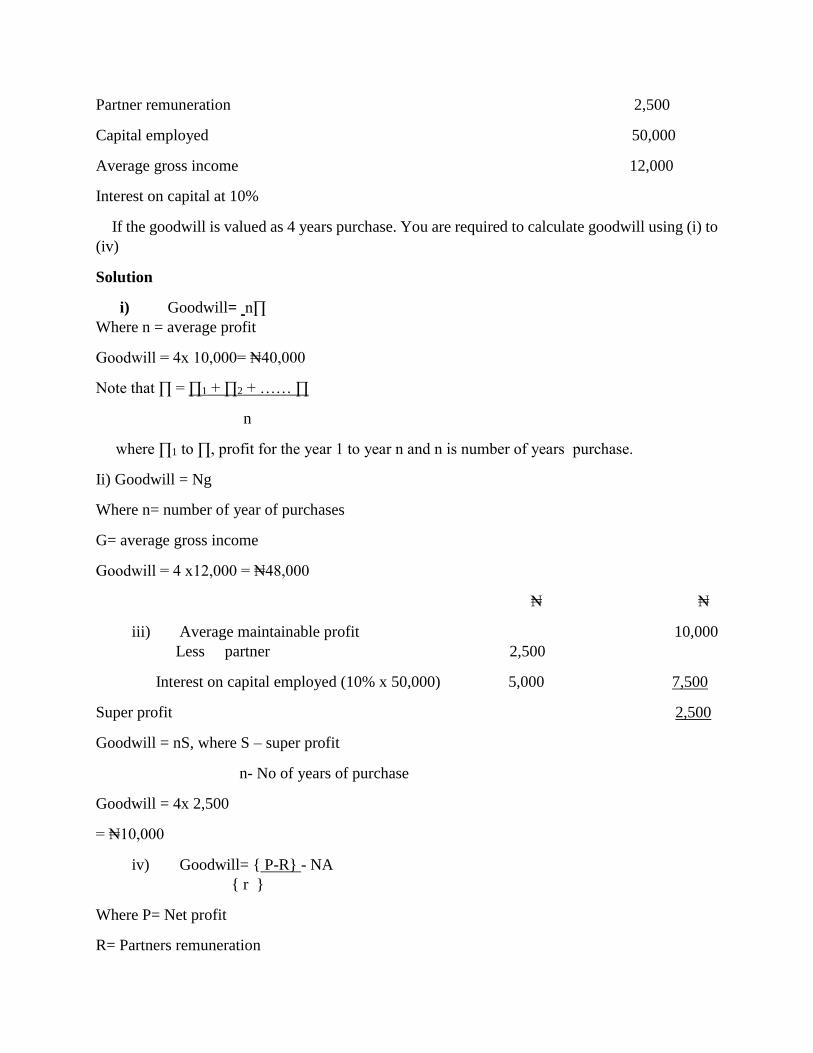

Illustration 1 Valuation of Goodwill

The information below was extracted from ABS Ltd

₦

Average maintainable profit 10,000

Partner remuneration 2,500

Capital employed 50,000

Average gross income 12,000

Interest on capital at 10%

If the goodwill is valued as 4 years purchase. You are required to calculate goodwill using (i) to

(iv)

Solution

i) Goodwill= n∏

Where n = average profit

Goodwill = 4x 10,000= ₦40,000

Note that ∏ = ∏1 + ∏2 + …… ∏

n

where ∏1 to ∏, profit for the year 1 to year n and n is number of years purchase.

Ii) Goodwill = Ng

Where n= number of year of purchases

G= average gross income

Goodwill = 4 x12,000 = ₦48,000

₦ ₦

iii) Average maintainable profit 10,000

Less partner 2,500

Interest on capital employed (10% x 50,000) 5,000 7,500

Super profit 2,500

Goodwill = nS, where S – super profit

n- No of years of purchase

Goodwill = 4x 2,500

= ₦10,000

iv) Goodwill= { P-R} - NA

{ r }

Where P= Net profit

R= Partners remuneration

r = Capitalization rate

NA= Net tangible assets

Goodwill = {10,000- 2500} - 50,000

{ 0.1}

75,000- 50,000= ₦25,000.

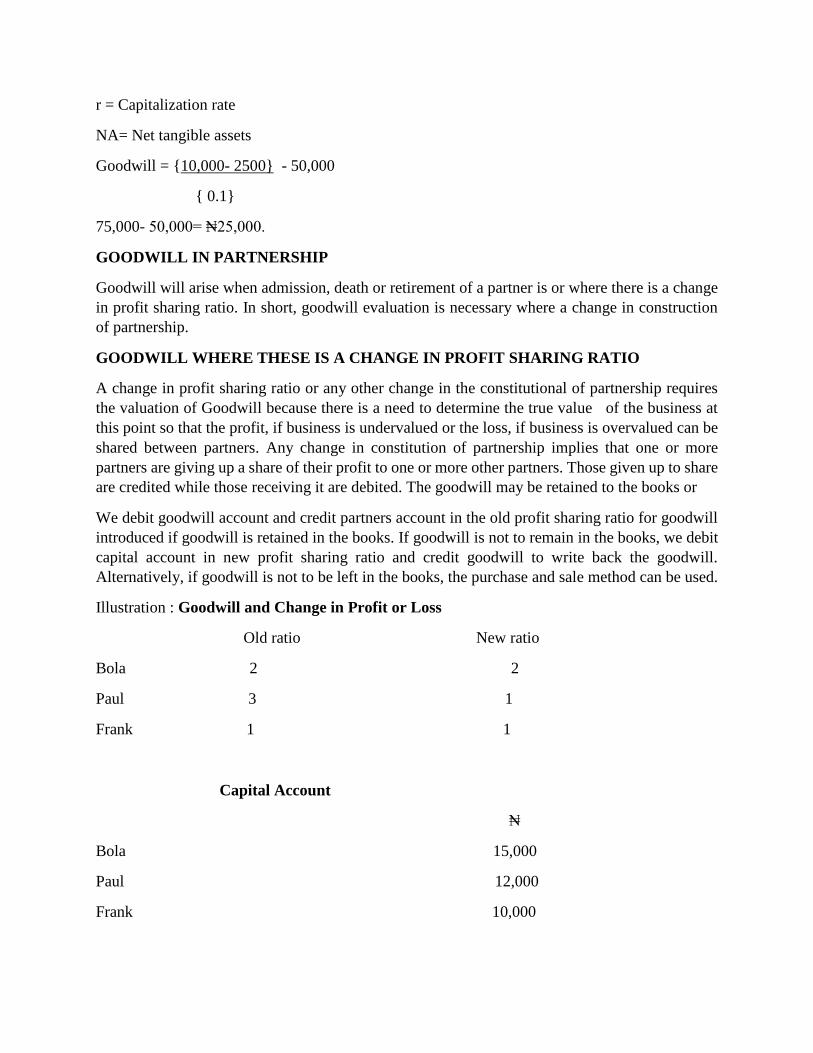

GOODWILL IN PARTNERSHIP

Goodwill will arise when admission, death or retirement of a partner is or where there is a change

in profit sharing ratio. In short, goodwill evaluation is necessary where a change in construction

of partnership.

GOODWILL WHERE THESE IS A CHANGE IN PROFIT SHARING RATIO

A change in profit sharing ratio or any other change in the constitutional of partnership requires

the valuation of Goodwill because there is a need to determine the true value of the business at

this point so that the profit, if business is undervalued or the loss, if business is overvalued can be

shared between partners. Any change in constitution of partnership implies that one or more

partners are giving up a share of their profit to one or more other partners. Those given up to share

are credited while those receiving it are debited. The goodwill may be retained to the books or

We debit goodwill account and credit partners account in the old profit sharing ratio for goodwill

introduced if goodwill is retained in the books. If goodwill is not to remain in the books, we debit

capital account in new profit sharing ratio and credit goodwill to write back the goodwill.

Alternatively, if goodwill is not to be left in the books, the purchase and sale method can be used.

Illustration : Goodwill and Change in Profit or Loss

Old ratio New ratio

Bola 2 2

Paul 3 1

Frank 1 1

Capital Account

₦

Bola 15,000

Paul 12,000

Frank 10,000

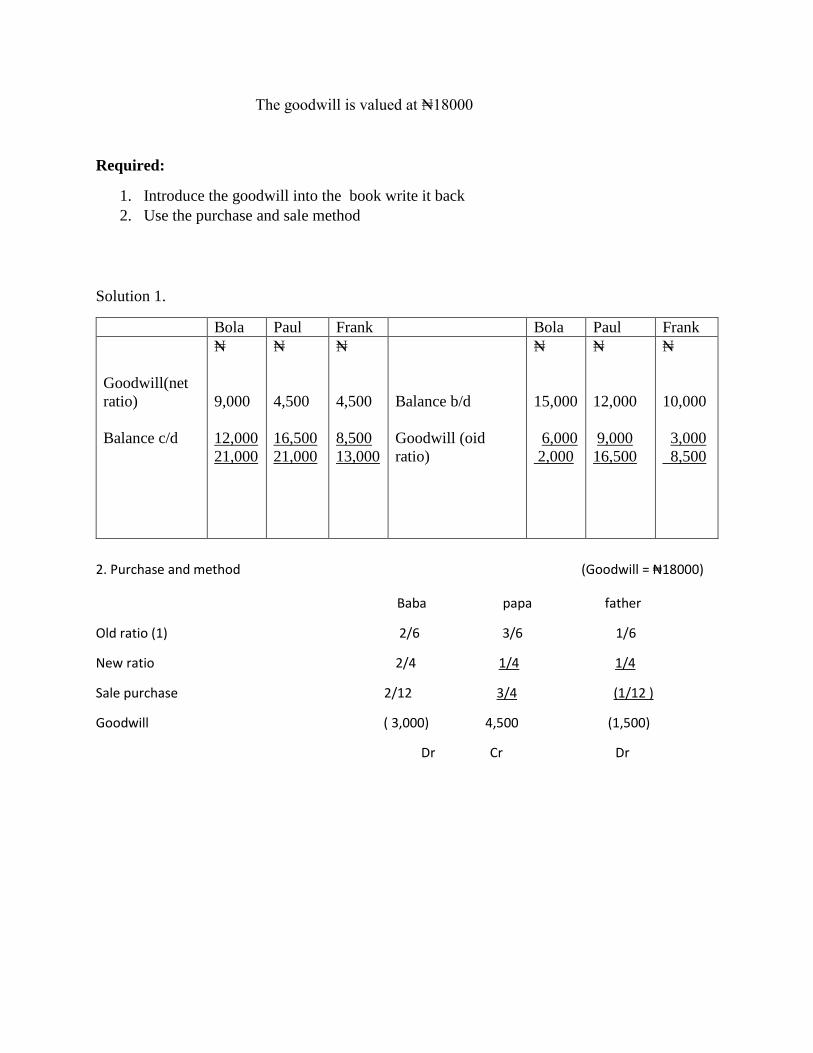

The goodwill is valued at ₦18000

Required:

1. Introduce the goodwill into the book write it back

2. Use the purchase and sale method

Solution 1.

2. Purchase and method (Goodwill = ₦18000)

Baba papa father

Old ratio (1) 2/6 3/6 1/6

New ratio 2/4 1/4 1/4

Sale purchase 2/12 3/4 (1/12 )

Goodwill ( 3,000) 4,500 (1,500)

Dr Cr Dr

Bola Paul Frank Bola Paul Frank

Goodwill(net

ratio)

Balance c/d

₦

9,000

12,000

21,000

₦

4,500

16,500

21,000

₦

4,500

8,500

13,000

Balance b/d

Goodwill (oid

ratio)

₦

15,000

6,000

2,000

₦

12,000

9,000

16,500

₦

10,000

3,000

8,500

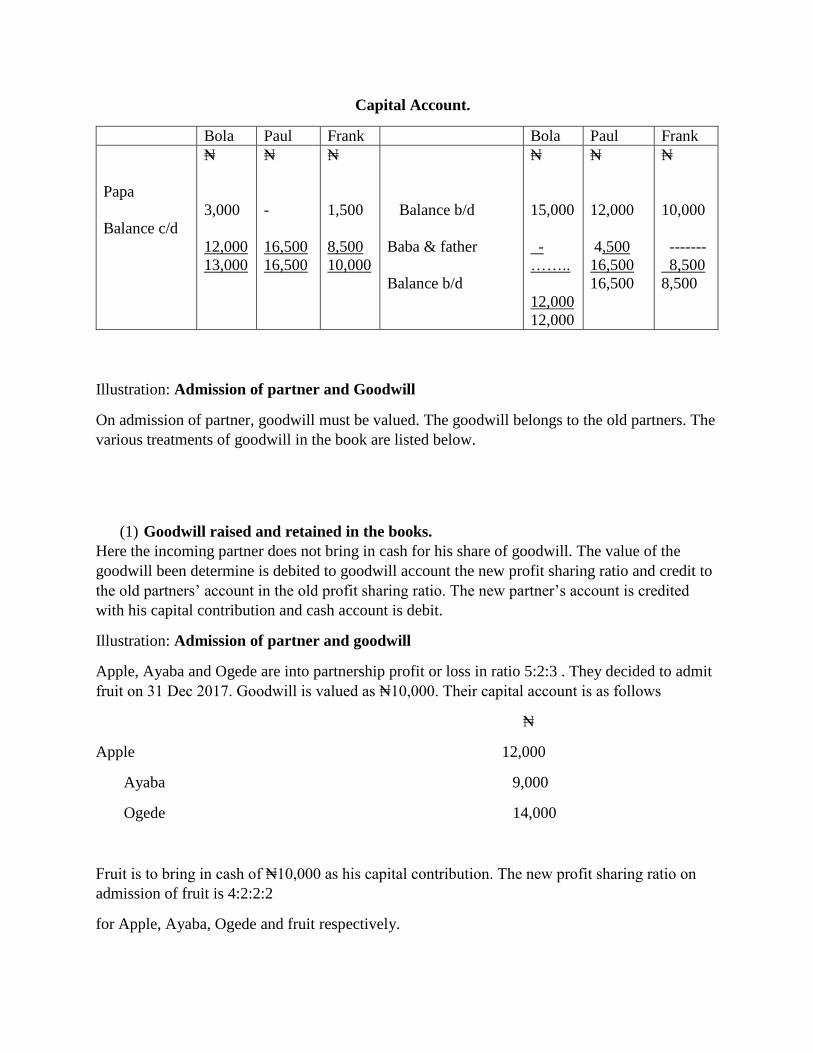

Capital Account.

Illustration: Admission of partner and Goodwill

On admission of partner, goodwill must be valued. The goodwill belongs to the old partners. The

various treatments of goodwill in the book are listed below.

(1) Goodwill raised and retained in the books.

Here the incoming partner does not bring in cash for his share of goodwill. The value of the

goodwill been determine is debited to goodwill account the new profit sharing ratio and credit to

the old partners’ account in the old profit sharing ratio. The new partner’s account is credited

with his capital contribution and cash account is debit.

Illustration: Admission of partner and goodwill

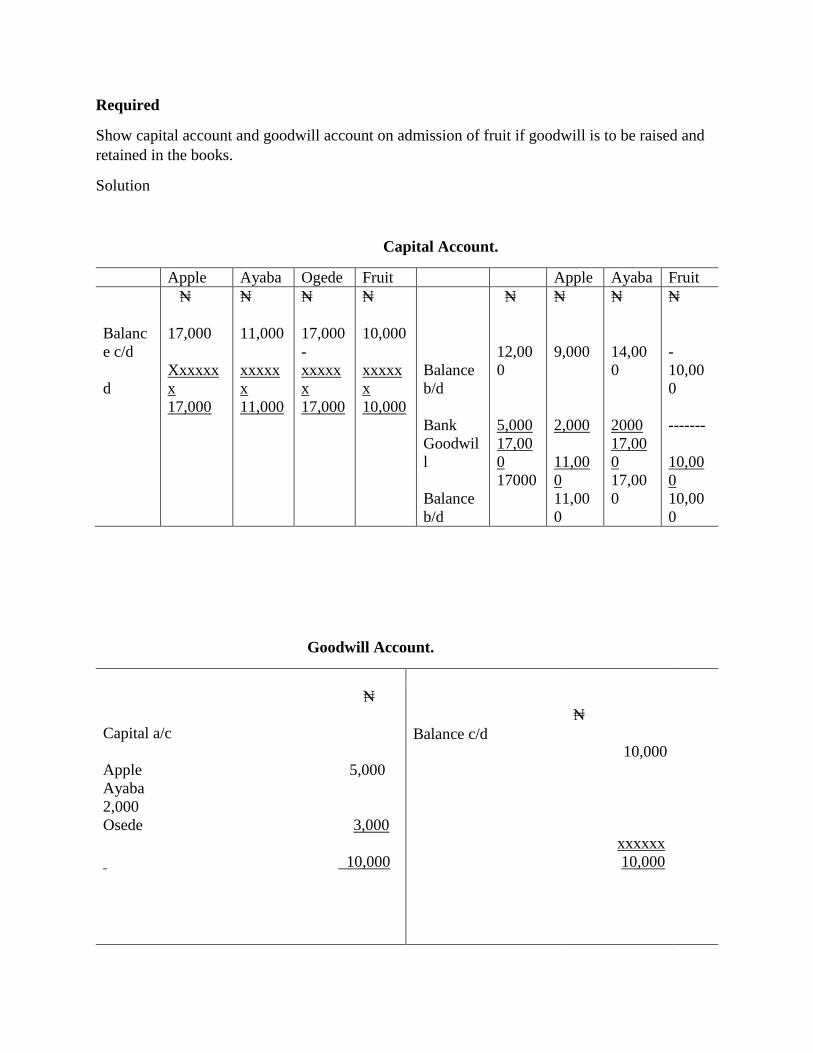

Apple, Ayaba and Ogede are into partnership profit or loss in ratio 5:2:3 . They decided to admit

fruit on 31 Dec 2017. Goodwill is valued as ₦10,000. Their capital account is as follows

₦

Apple 12,000

Ayaba 9,000

Ogede 14,000

Fruit is to bring in cash of ₦10,000 as his capital contribution. The new profit sharing ratio on

admission of fruit is 4:2:2:2

for Apple, Ayaba, Ogede and fruit respectively.

Bola Paul Frank Bola Paul Frank

Papa

Balance c/d

₦

3,000

12,000

13,000

₦

-

16,500

16,500

₦

1,500

8,500

10,000

Balance b/d

Baba & father

Balance b/d

₦

15,000

-

……..

12,000

12,000

₦

12,000

4,500

16,500

16,500

₦

10,000

-------

8,500

8,500

Required

Show capital account and goodwill account on admission of fruit if goodwill is to be raised and

retained in the books.

Solution

Capital Account.

Goodwill Account.

Apple Ayaba Ogede Fruit Apple Ayaba Fruit

Balanc

e c/d

d

₦

17,000

Xxxxxx

x

17,000

₦

11,000

xxxxx

x

11,000

₦

17,000

-

xxxxx

x

17,000

₦

10,000

xxxxx

x

10,000

Balance

b/d

Bank

Goodwil

l

Balance

b/d

₦

12,00

0

5,000

17,00

0

17000

₦

9,000

2,000

11,00

0

11,00

0

₦

14,00

0

2000

17,00

0

17,00

0

₦

-

10,00

0

-------

10,00

0

10,00

0

₦

Capital a/c

Apple 5,000

Ayaba

2,000

Osede 3,000

10,000

₦

10,000

xxxxxx

10,000

Balance c/d

II. Goodwill raised and written back

In this case the goodwill will not be retained in the books. The entries in the situation i) is first

passed then in addition to that to that

Dr Capital a/c of partners in new profit sharing ratio

Cr Goodwill a/c with value of goodwill

Goodwill raised and written back

Assuming the same in illustration above but goodwill is not retained in the book.

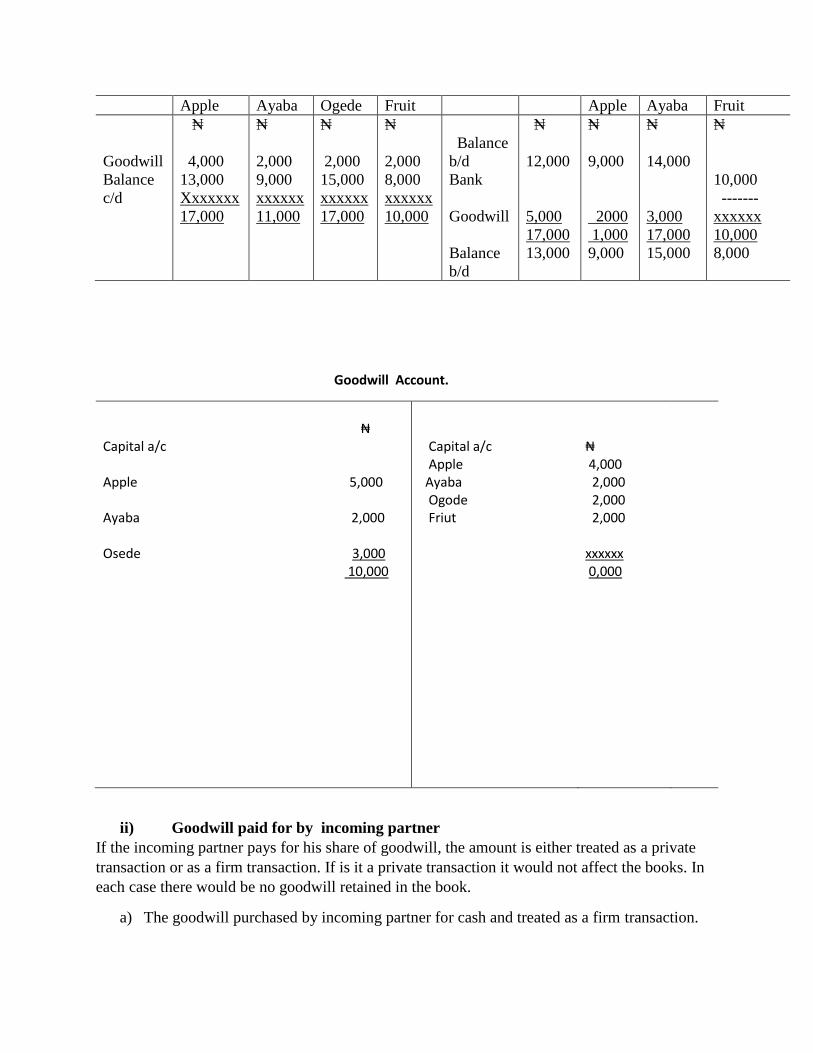

Capital Account.

Goodwill Account.

ii) Goodwill paid for by incoming partner

If the incoming partner pays for his share of goodwill, the amount is either treated as a private

transaction or as a firm transaction. If is it a private transaction it would not affect the books. In

each case there would be no goodwill retained in the book.

a) The goodwill purchased by incoming partner for cash and treated as a firm transaction.

Apple Ayaba Ogede Fruit Apple Ayaba Fruit

Goodwill

Balance

c/d

₦

4,000

13,000

Xxxxxxx

17,000

₦

2,000

9,000

xxxxxx

11,000

₦

2,000

15,000

xxxxxx

17,000

₦

2,000

8,000

xxxxxx

10,000

Balance

b/d

Bank

Goodwill

Balance

b/d

₦

12,000

5,000

17,000

13,000

₦

9,000

2000

1,000

9,000

₦

14,000

3,000

17,000

15,000

₦

10,000

-------

xxxxxx

10,000

8,000

₦ Capital a/c Apple 5,000 Ayaba 2,000 Osede 3,000 10,000

Capital a/c Apple Ayaba Ogode Friut

₦ 4,000 2,000 2,000 2,000 xxxxxx 0,000

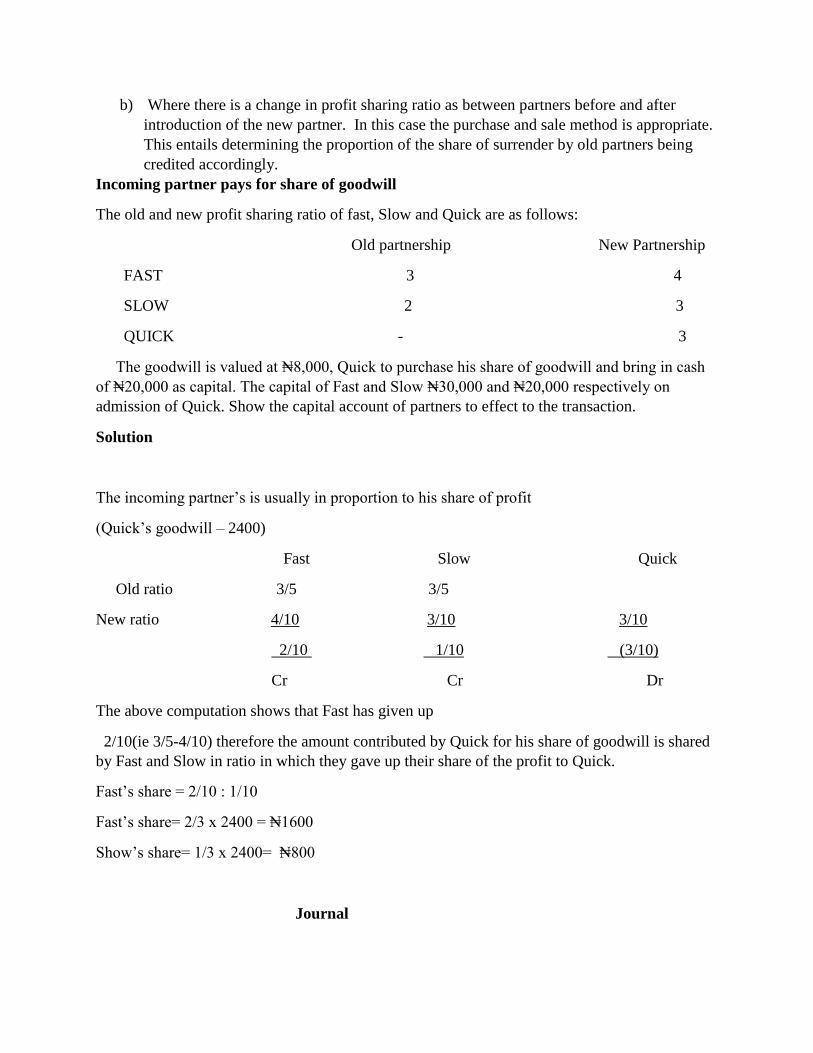

b) Where there is a change in profit sharing ratio as between partners before and after

introduction of the new partner. In this case the purchase and sale method is appropriate.

This entails determining the proportion of the share of surrender by old partners being

credited accordingly.

Incoming partner pays for share of goodwill

The old and new profit sharing ratio of fast, Slow and Quick are as follows:

Old partnership New Partnership

FAST 3 4

SLOW 2 3

QUICK - 3

The goodwill is valued at ₦8,000, Quick to purchase his share of goodwill and bring in cash

of ₦20,000 as capital. The capital of Fast and Slow ₦30,000 and ₦20,000 respectively on

admission of Quick. Show the capital account of partners to effect to the transaction.

Solution

The incoming partner’s is usually in proportion to his share of profit

(Quick’s goodwill – 2400)

Fast Slow Quick

Old ratio 3/5 3/5

New ratio 4/10 3/10 3/10

2/10 1/10 (3/10)

Cr Cr Dr

The above computation shows that Fast has given up

2/10(ie 3/5-4/10) therefore the amount contributed by Quick for his share of goodwill is shared

by Fast and Slow in ratio in which they gave up their share of the profit to Quick.

Fast’s share = 2/10 : 1/10

Fast’s share= 2/3 x 2400 = ₦1600

Show’s share= 1/3 x 2400= ₦800

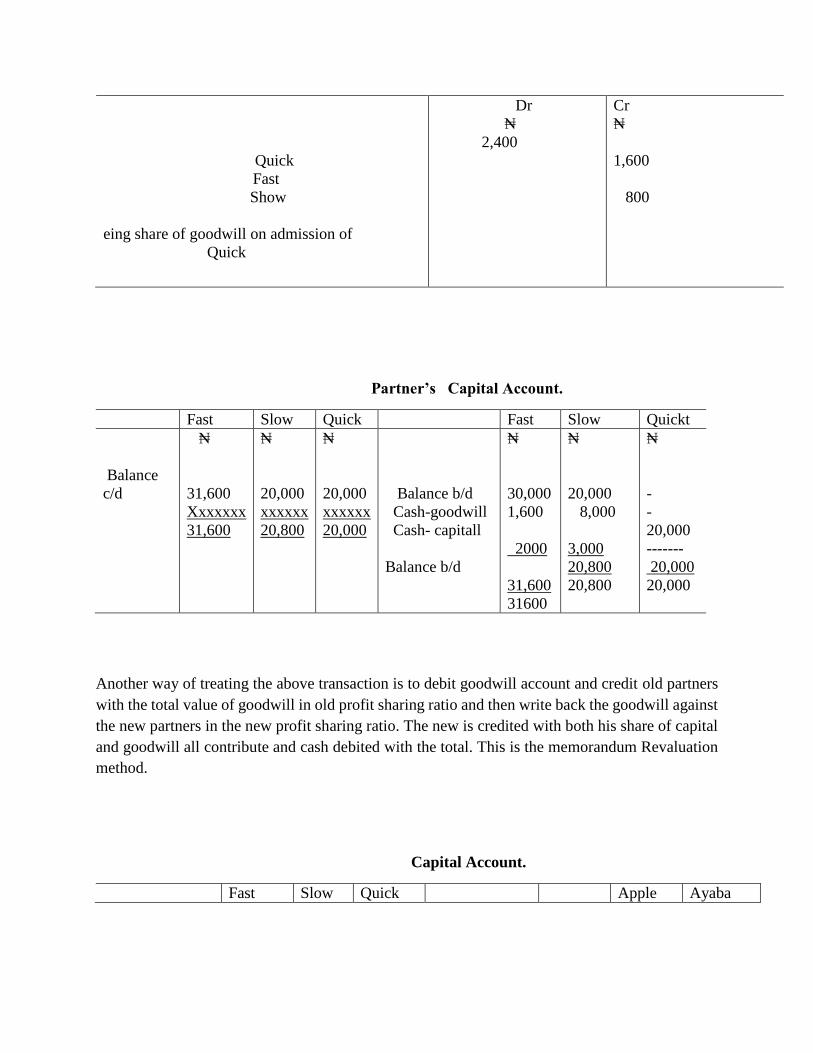

Journal

Quick

Fast

Show

eing share of goodwill on admission of

Quick

Dr

₦

2,400

Cr

₦

1,600

800

Partner’s Capital Account.

Another way of treating the above transaction is to debit goodwill account and credit old partners

with the total value of goodwill in old profit sharing ratio and then write back the goodwill against

the new partners in the new profit sharing ratio. The new is credited with both his share of capital

and goodwill all contribute and cash debited with the total. This is the memorandum Revaluation

method.

Capital Account.

Fast Slow Quick Fast Slow Quickt

Balance

c/d

₦

31,600

Xxxxxxx

31,600

₦

20,000

xxxxxx

20,800

₦

20,000

xxxxxx

20,000

Balance b/d

Cash-goodwill

Cash- capitall

Balance b/d

₦

30,000

1,600

2000

31,600

31600

₦

20,000

8,000

3,000

20,800

20,800

₦

-

-

20,000

-------

20,000

20,000

Fast Slow Quick Apple Ayaba

Goodwill Account.

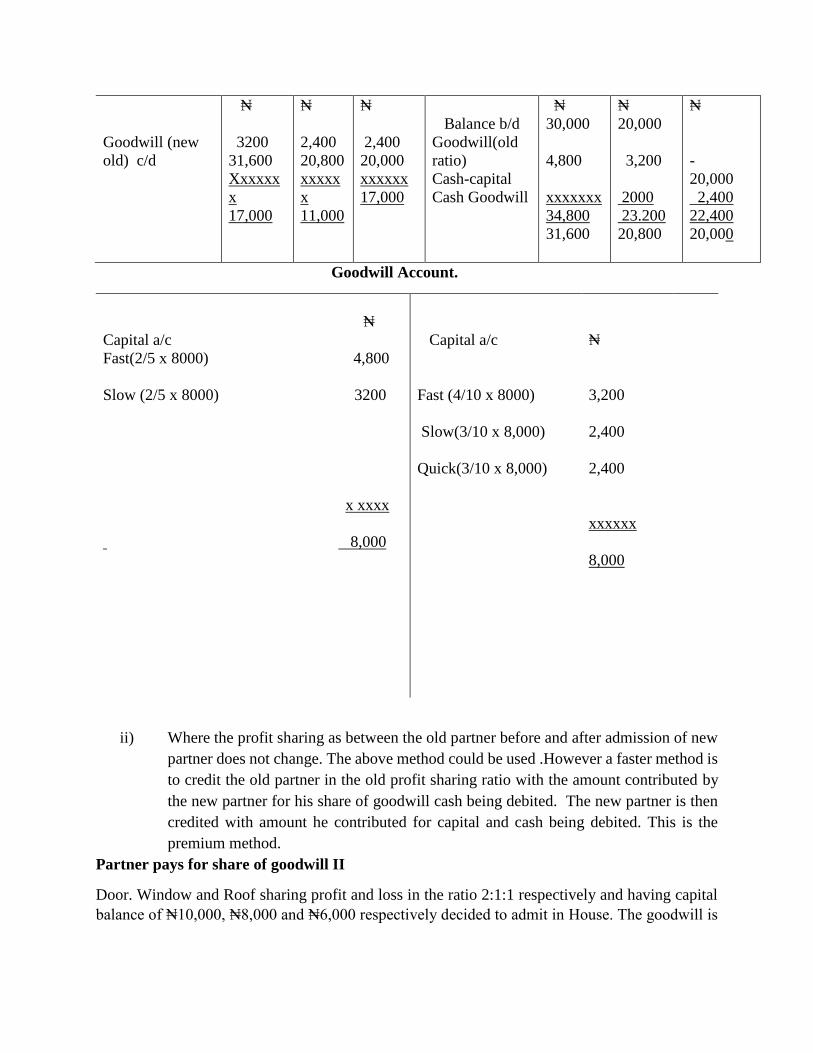

ii) Where the profit sharing as between the old partner before and after admission of new

partner does not change. The above method could be used .However a faster method is

to credit the old partner in the old profit sharing ratio with the amount contributed by

the new partner for his share of goodwill cash being debited. The new partner is then

credited with amount he contributed for capital and cash being debited. This is the

premium method.

Partner pays for share of goodwill II

Door. Window and Roof sharing profit and loss in the ratio 2:1:1 respectively and having capital

balance of ₦10,000, ₦8,000 and ₦6,000 respectively decided to admit in House. The goodwill is

Goodwill (new

old) c/d

₦

3200

31,600

Xxxxxx

x

17,000

₦

2,400

20,800

xxxxx

x

11,000

₦

2,400

20,000

xxxxxx

17,000

Balance b/d

Goodwill(old

ratio)

Cash-capital

Cash Goodwill

₦

30,000

4,800

xxxxxxx

34,800

31,600

₦

20,000

3,200

2000

23.200

20,800

₦

-

20,000

2,400

22,400

20,000

₦

Capital a/c

Fast(2/5 x 8000) 4,800

Slow (2/5 x 8000) 3200

x xxxx

8,000

Capital a/c

Fast (4/10 x 8000)

Slow(3/10 x 8,000)

Quick(3/10 x 8,000)

₦

3,200

2,400

2,400

xxxxxx

8,000

valued as ₦6,000 and House is to purchase his share of the goodwill. House is to bring in ₦10,000

cash for capital. The new profit ratio is 2:1:1:1, for Door, Window, Roof and House respectively.

Required :

Show the capital account as it would appear using method i and ii

2.OIL and GAS ACCOUNTING

Definition of the term Petroleum

The term petroleum is said to have been derived from two Latin words Petra , meaning rock and

Oleum meaning oil. Eventually, the term petroleum came to refer to both crude oil and natural

gas. More broadly defined as , Petroleum refers to mixture of hydrocarbons that are molecular in

nature, in various shape and sizes of hydrogen and carbon atoms found in small connected pore

spaces of some underground rock formation . While crude oil refers hydrocarbon mixture produced

from underground reservoirs that are liquid at normal atmospheric pressure and temperature.

Hydrocarbons are compounds containing only the elements hydrogen and carbon, which may exist

as solids, liquid or gases.

Origin of Petroleum

Over the years two theories- the inorganic theory and the organic theory have been advanced to

explain the formation of oil and gas. Although no one theory have achieved universal acceptance,

most scientist and professionals believe in organic origin of petroleum. The inorganic theory

recognizes that hydrogen and carbon are present in natural form below the surface of the earth.

Different related theories explain the combination of the two elements into hydrocarbon. These

theories include: the alkali theory, carbide theory, volcanic emanation theory, hydrogenation

theory and temperature intrusion theory. Except for the intrusion theory, most of the inorganic

theory have largely discounted.

3. INTERNATIONAL FINANCIAL REPORTINING STANDARD

International standardization Introduction

As individual countries have pursued a policy of standardisation, so too a number of bodies have

become concerned with international standardisation. Both the United Nations (UN) and the

Organisation for Economic Co-operation and Development (OECD) have been concerned with the

regulation of accounting and, as might be expected, these bodies have been primarily concerned

with the regulation of disclosure by multinationals.

The International Accounting Standards Committee

Although the possibility of international standards had been debated during the first half of the

twentieth century, the most successful programme began with the formation of the IASC in 1973.

The founder members were drawn from professional accountancy bodies in the following

countries: Australia, Canada, France, Germany, Japan, Mexico, the Netherlands, the UK, the

Republic of Ireland and the USA. By the time it was replaced by the IASB in 2001, the membership

of the IASC consisted of 153 professional accountancy bodies from 112 countries.

The objectives of the IASC include to:

(a) formulate and publish in the public interest accounting standards to be observed in the

presentation of financial statements and to promote their worldwide acceptance and observance,

and

(b) to work generally for the improvement and harmonisation of regulations, accounting standards

and procedures relating to the presentation of financial statements.

Barriers to harmonization

Barriers to harmonization includes:

(a) differences in background and traditions of countries;

(b) differences in the needs of various economic environments;

(c) the challenge to the sovereignty of states in making and enforcing standards.

The International Accounting Standards Board

The completion of the core international accounting standards provided a suitable opportunity

to address the rather anachronistic structure of the IASC and, in 2001, a new foundation was

formed to take over the international setting activities from IASC. This is new is the International

Accounting Standard Board (IASB). IASB, which assumed responsibility for setting International

Accounting Standards from 1 April 2001. The IASB consists of 14 members, 12 full-time and 2

part-time, and its first Chairman is Sir David Tweedie, the distinguished first Chairman of the UK

Accounting Standard Board for its first ten years of operation.

Objectives of IASB provides:

1. To develop, in the public interest, a single set of high quality, understandable and enforceable

global accounting standards that require high quality, transparent and comparable information in

financial statements and other financial reporting to help participants in the world’s capital markets

make economic decisions.

2. To promote the use and rigorous application of those standards.

3. To bring about convergence of national accounting standards and International Accounting

Standards to high quality solutions.

International Accounting Standards at 1 January 2003

IAS 1 Presentation of Financial Statements 1997*

IAS 2 Inventories 1993*

IAS 7 Cash Flow Statements 1992

IAS 8 Net Profit or Loss for Period, Fundamental Errors and Changes in

Accounting Policies 1993*

IAS 10 Contingencies and Events Occurring After the Balance Sheet Date 1999*

IAS 11 Construction Contracts 1993

IAS 12 Income Taxes 2000

IAS 14 Segment Reporting 1997

IAS 15 Information Reflecting the Effects of Changing Prices 1994

IAS 16 Property, Plant and Equipment 1998*

IAS 17 Leases 1997*

IAS 18 Revenue 1993

IAS 19 Employee Benefits 2000

IAS 20 Accounting for Government Grants and Disclosure of

Government Assistance 1994

IAS 21 The Effects of Changes in Foreign Exchange Rates 1993*

IAS 22 Business Combinations 1998*

IAS 23 Borrowing Costs 1993

IAS 24 Related Party Disclosures 1994*

IAS 26 Accounting and Reporting by Retirement Benefit Plans 1994

IAS 27 Consolidated Financial Statements and Accounting for Investments

in Subsidiaries 2000*

IAS 28 Accounting for Investments in Associates 2000*

IAS 29 Financial Reporting in Hyperinflationary Economies 1994

IAS 30 Disclosures in the Financial Statements of Banks and Similar

Financial Institutions 1994

IAS 31 Financial Reporting of Interests in Joint Ventures 2000

IAS 32 Financial Instruments: Disclosure and Presentation 1998*

IAS 33 Earnings per Share 1997*

IAS 34 Interim Financial Reporting 1998

IAS 35 Discontinuing Operations 1998

IAS 36 Impairment of Assets 1998

IAS 37 Provisions, Contingent Liabilities and Contingent Assets 1998

IAS 38 Intangible Assets 1998

IAS 39 Financial Instruments: Recognition and Measurement 2000*

IAS 40 Investment property 2000*

IAS 41 Agriculture 2001