Embed Size (px)

Citation preview

MANAGEMENTACCOUNTING

PUBLISHED BY THE NATIONAL ASSOCIATION OF ACCOUNTANTS/ FEBRUARY 1973

THE BUSINESSMAN'S ROLE

PRICE -LEVEL CHANGES AND COMPANY WEALTH

INTERNATIONAL TAX MANAGEMENTCMA: FIRST EXAMINATION

'C : . . �

''� /--�•� ili�

NAA'sManagement Advisory Service

Isn't For Sale .. .(But a Lot Of People Are Buying It!)

For the disadvantaged, needy person wanting to establish hisown small business properly, confidential accounting andfinancial management advice is available from a number ofNAA Chapters . .. without charge.

This advisory service is provided by volunteer managementaccountants, corporate treasurers, controllers, financialexecutives and CPAs with membership in NAA.

The purpose of the advisory program is to make the smallbusinessman aware of his financial management needs and toget him started in the right direction.

NAA does not do the detail work. Carrying out of advice mustbe accomplished by competent employees or qualifiedprofessionals. NAA advisors withdraw once the business issuccessfully under way. The problem is, there are still a lot ofareas, where help is needed, not now being served by an NAAChapter Socio- Economic Committee.

If you'd like to start one —or otherwise help out — contact:

• Your local Chapter President

• ROBERT F. CLAIRMONTSocio-Economic Program

National Association of Accountants919 Third AvenueNew York, N.Y. 10022(212) 759 -3444 or 371 -9124

Participation is not limited to NAA members. Anyone whowould like to join the NAA Socio- Economic Program is alsoinvited to contact us.

PRESIDENT'S PERSPECTIVE

ImprovingFinancial ReportingA great deal of concern has been expressed in recent yearsabout financial reporting and disclosure. Auditors have comeunder fire for attest ing to statements later viewed as misleading.Corporate accountants and company management have alsoreceived their share of criticism for information deemedmisleading and for omission of material facts. Financial publicrelations consultants are now the latest group to fall under SECscrut iny. In the landmark Pig 'N Whist le injunction and consentdecree the concept of liability was extended to financial publicrelations counselors, placing on them the obligation ofinvestigat ing facts received from management , as well asinvestigation of management's creditability.

A positive effort to improve financial reporting to the presshas been launched in recent months by the Public Relat ionsSociety of America. Its local chapters have held seminars ondisclosure requirements and account ing principles, which weredeveloped in cooperation with one of the Big Eight account ingfirms.

Although the seminars principally involved CPAs and financialpublic relations consultants, it was apparent in many cases therewas a lack of communication between P -R consultants andin -house accounting staff. Corporate accountants were notheld legally responsible in this particular instance but in light ofthe recent public crit icism it would seem that at the veryminimum they have a professional responsibility to improvetheir working relationship with all the other parties involved infinancial reporting.

The inter - disciplinary approach to financial reporting, asillustrated by the discussion seminars between P -R consultantsand CPAs, is a significant new development and one which canonly lead to bet ter communications. Management accountantscan inaugurate similar efforts to improve disclosure and thusbolster the public's faith in the basic integrity of the privateenterprise system.

ROBERT BEYERPresident, 1972 -73

MANAGEMENT ACCOUNTING /FEBRUARY 1973

2

MANAGEMENTACCOUNTING

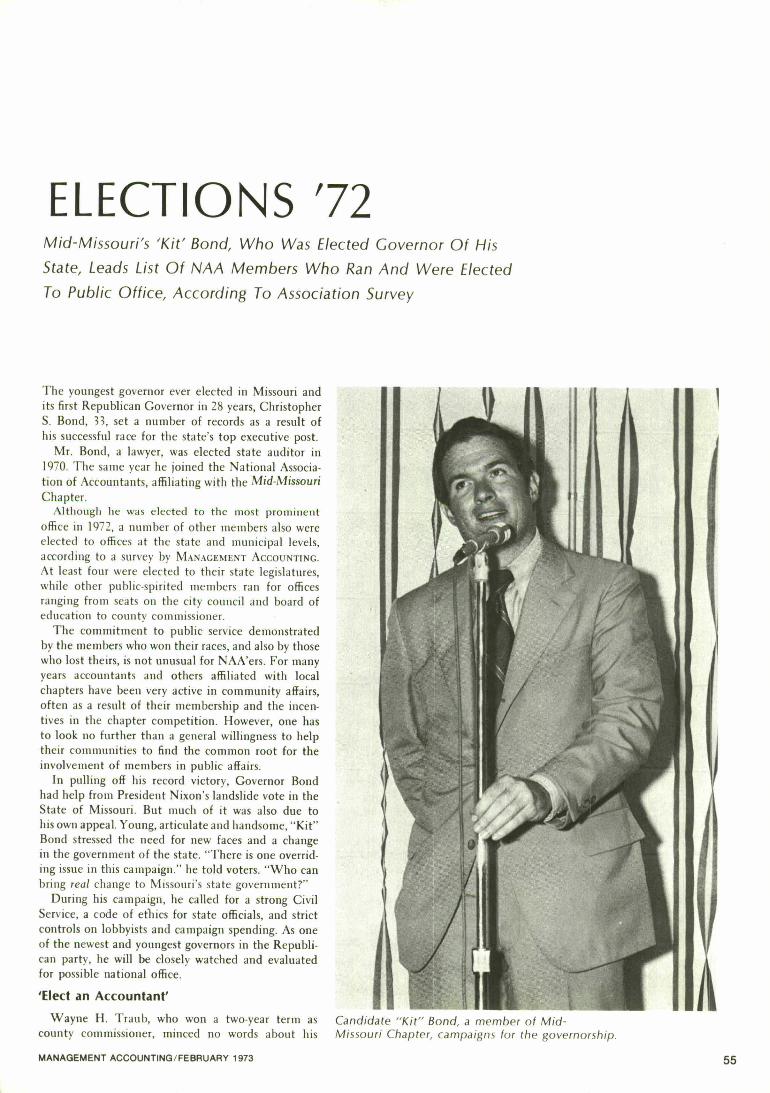

15 THE BUSINESSMAN'S ROLEBy Robinson F. BarkerA review of the problems facing business today and the role the businessman mustplay in contributing to public policy.

Cover: 17 PRICE -LEVEL CHANGES AND COMPANY WEALTHCMA test scene inManhattan was By Russell J. Petersen

duplicated at 21 other Changes in price levels may affect the purchasing power of a company and thereforesites across the its comparative wealth. In this article, the author describes a procedure for the

country. See p. 61. measurement of gains or losses resulting from price -level changes.

21 CONTROL AND MANAGEMENT OF INDIRECT EXPENSESBy Harold E. SharpIndirect expenses are of prime concern to buyers for governmental agencies andprivate companies. In this article, the author reviews various aspects of the subjectand illustrates the approaches used to best allocate these costs in order to remaincompetitive.

26 ACCOUNTING CHANGES: WHY CPAs MUST CONFORMBy George D. Cameron, III; Ralph W. Gudmundsen, Jr.; and Jack R. BallDespite the natural urge to resist change in financial statements, management shouldconsider why the change is necessary and why the CPA insists on it. The authors feelthat the CPA must make these changes and they give three reasons why.

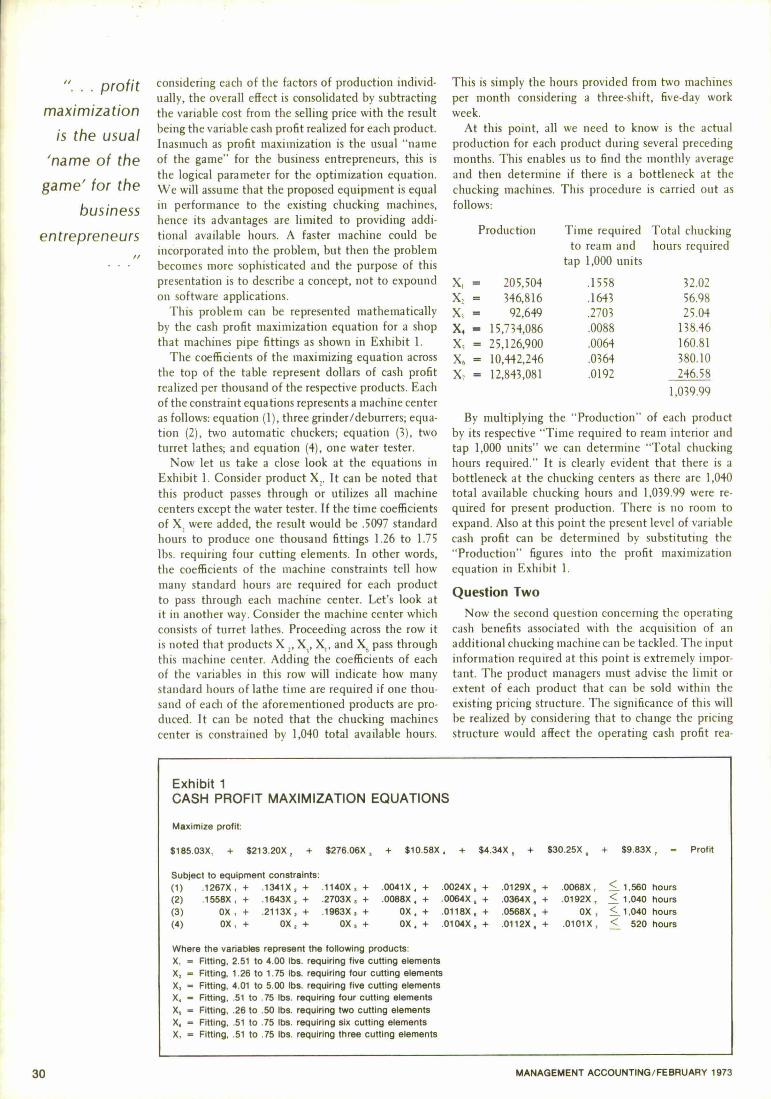

29 A SYSTEMS APPROACH TO CASH FLOW DETERMINATIONBy Walter J. Thrun, Sr.The author presents three questions that budget administrators should ask to obtaininformation for an investment decision. He shows how to answer them with asystems concept.

An award-winning article: Certificate of Recognition

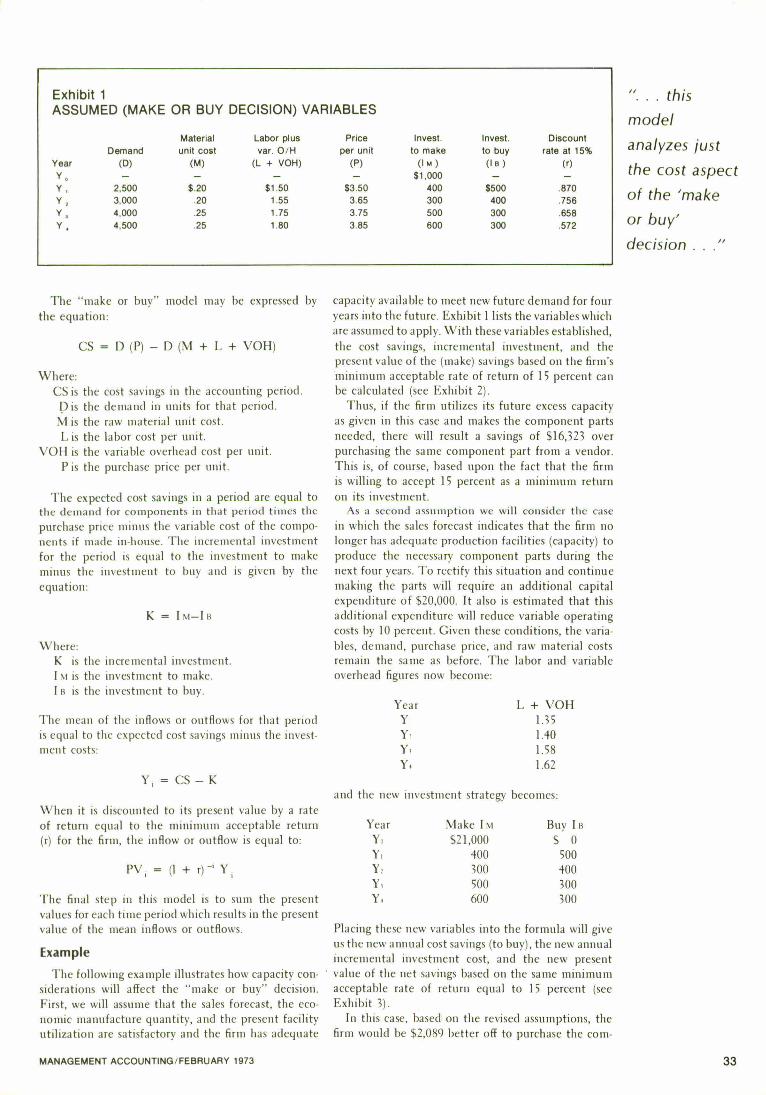

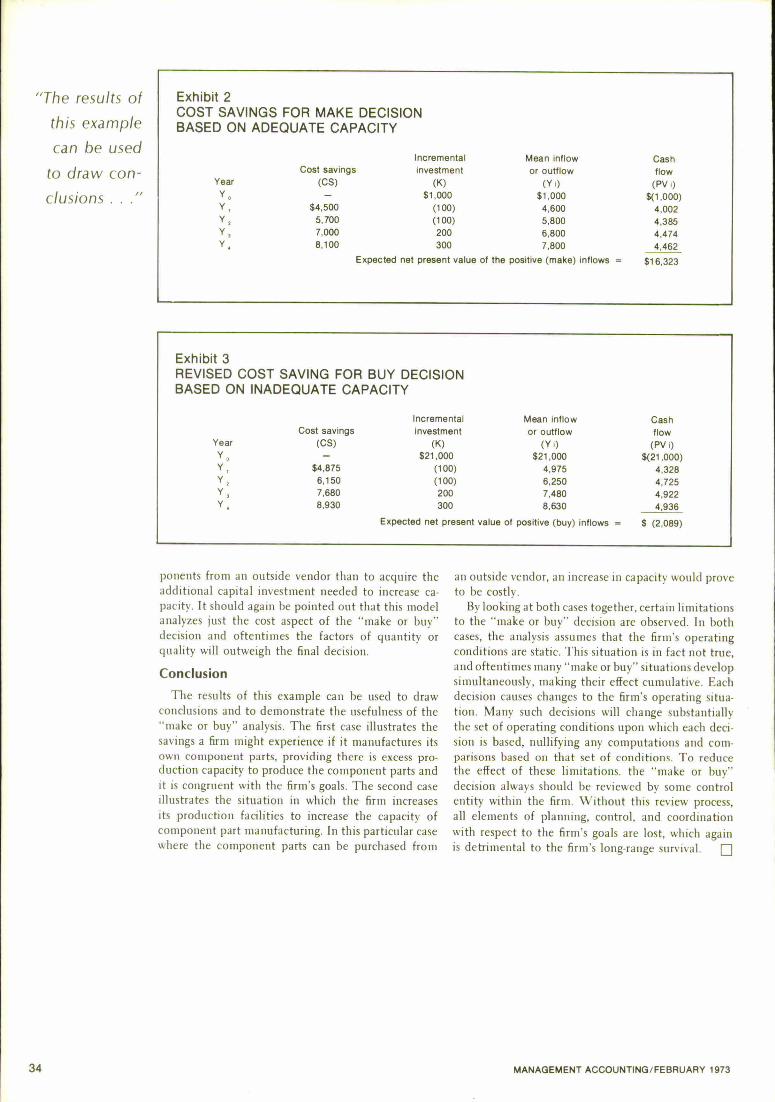

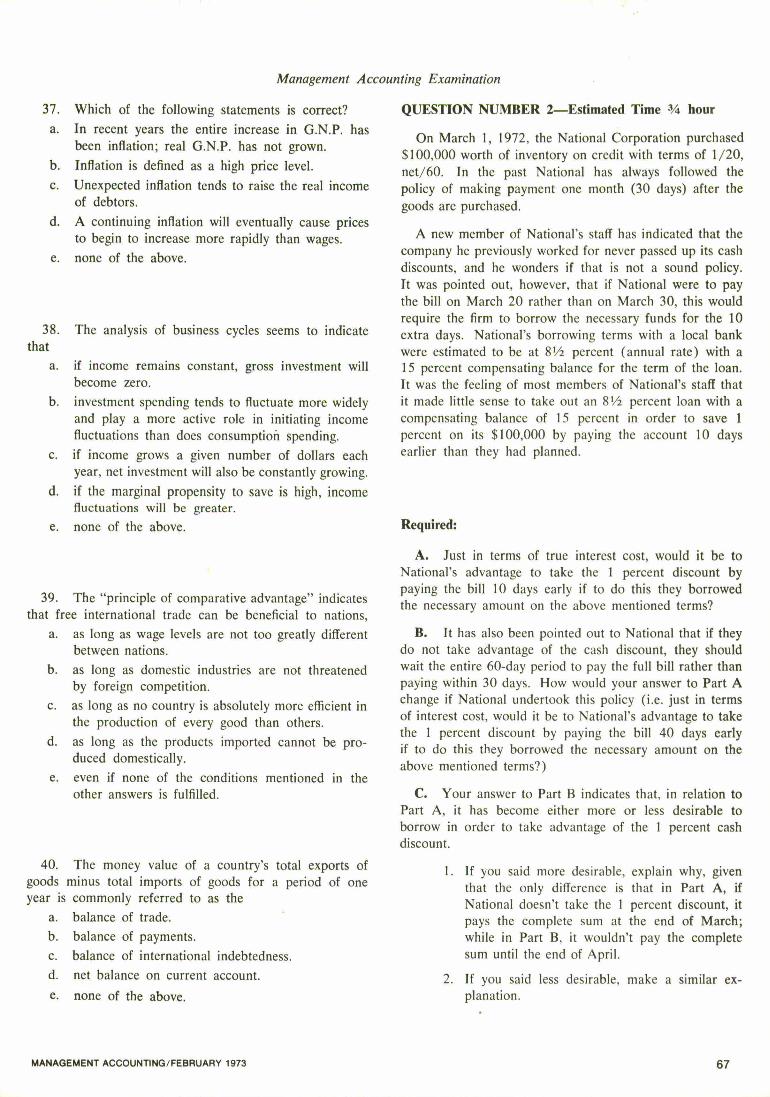

32 THE 'MAKE OR BUY' DECISIONBy Jim MadisonThe cost analysis of "make or buy" decisions can best be made using a mathematicalmodel. In this article, the author discusses suc h a model and offers an example wherethe firm's capacity to produce is the determining consideration.

35 A CASE FOR CURRENT -COST REPORTINGBy Arthur E. CarlsonThe author asserts that data for reporting purposes must take cognizance of the factthat future orientation is a prime requisite of accounting information for decisionmaking purposes. He reviews three sets of current standards to substantiate hisassertion.

38 CONTRACT TERMINATION AND UNABSORBED OVERHEADBy Paul M. TruegerAlthough it is generally agreed that the overall public interest is best served by givingthe Government the right to halt activities and related costs which are determined tobe unproductive, this author believes that the Government should move to help the

el

contractor to extricate himself from the cancelled project and to compensate himequitably for the financial consequences.

MANAGEMENT ACCOUNTING /FEBRUARY 1973

FEBRUARY 1973

41 ASPR: SOME SUGGESTED CHANGESBy Douglas G. CordermanAccording to the author, defense contract accounting procedures do not alwaysconform to generally accepted accounting principles. To remedy the situation, he

proposes a number of changes.

45 BUSINESS COMBINATIONS: POOLING OR PURCHASE?By David J. RetzWhen two corporations decide to combine, the accounting methods used to effectthat combination will be subject to conflicting interpretations. In this article, theauthor presents a strong case for the "purchase method" over the "pooling of

interests" method.

47 INTERNATIONAL TAX MANAGEMENTBy Ernst K. BrinerInternational corporations face special tax problems in terms of United States taxesand the taxes of other countries. An insight into some of these problems is offered

in this article.

53 NAA TESTIFIES ON FORECASTSText of MAP statement on forecasts at SEC hearings.

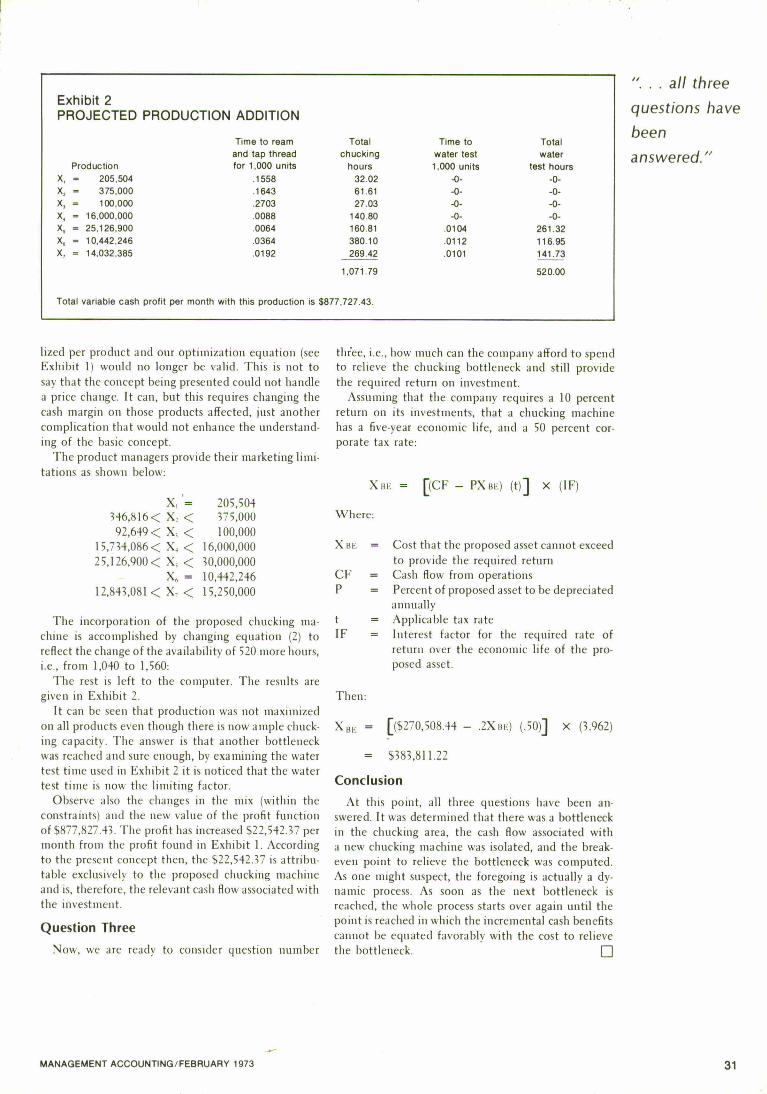

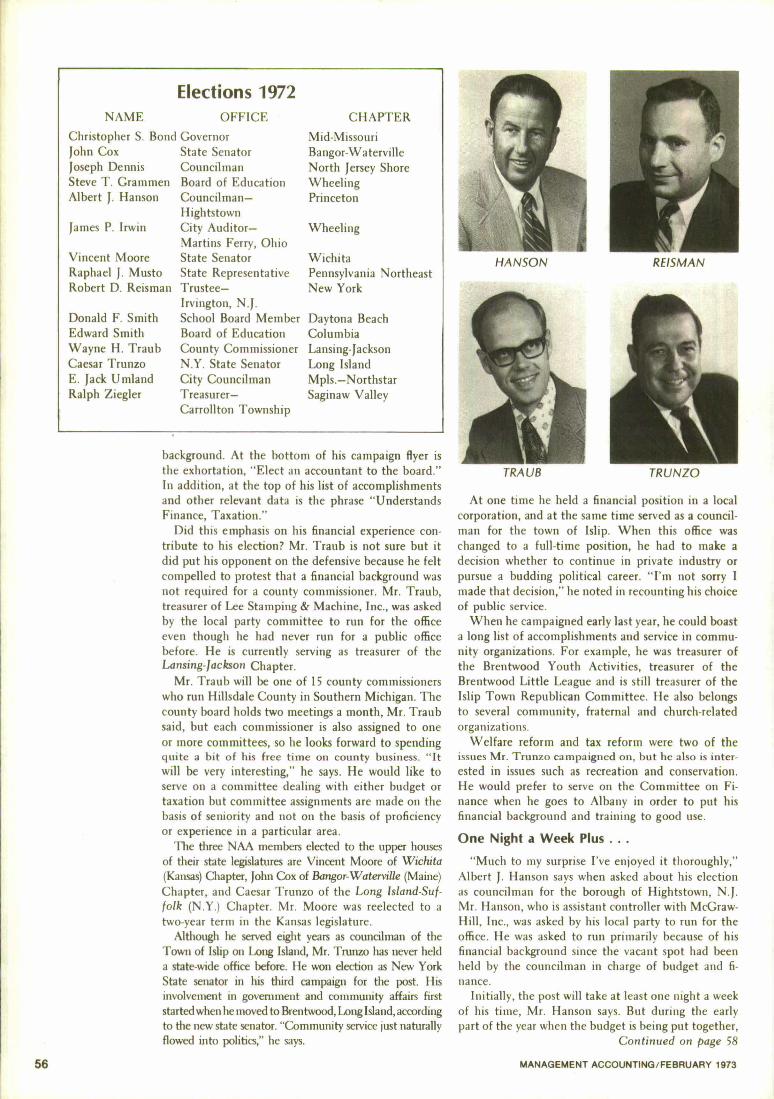

55 ELECTIONS '72Mid - Missouri's "Kit" Bond, who was elected governor of his state, leads list of NAAmembers who ran and were elected to public office last November.

57 THE GAMES ACCOUNTANTS PLAYWith magnifying glass and trenchant wit, Prof. Briloff dissects the anatomy of recentfinancial reports; finds "Hot Pants" accounting and "Inflated Bosoms."

61 CMA EXAMINATIONS HELD FOR FIRST TIMEInitial Certificate testing program attracts many; questions and unofficial answers toPart 1 are offered for future guidance.

DEPARTMENTS1 PRESIDENT'S PERSPECTIVE6 LETTERS to the editor

14 DATA SHEET items of interest for the businessman

52 BOOKS for the management accountant59 CHAPTER /MEMBER NEWS all about chapters and members60 TIME OFF the l ighter side of the ledger

Views expressed herein are authors' and do not represent Association policy unless sostated. Reprints of articles appearing in any issue of MANAGEMENT ACCOUNTING are availa-ble from NAA's Reprint Department.

MANAGEMENT ACCOUNTING /FEBRUARY 1973 3

COMMENT

Is There A Forecast In Your Future?

Corporate financial management may soon be faced wi th an addi-tional annual reporting problem— forecasting. It appears that the Se-curities & Exchange Commission may permit, if not require, compa-nies to include in their annual financial reports, predictions of nextyear's profit status.

Some companies seem to believe the SEC will require such fore-casts, and because of this belief one company included in an unusual1972 "preliminary" annual report (dated Dec. 28) estimates for 1973.The company's (Fuqua Industries, Inc.) Chairman, J. B. Fuqua, saidof the forecast, "While we are not fully convinced of the merits ofmaking public projections of future earnings, if this is the kind ofmusic we will have to march to, we are willing to lead the band."

At the SEC hearings in November and December, some testimonywas favorable to forecasting in annual reports, but most financialgroups were opposed to mandatory forecasts while in favor of volun-tary forecasts. Because of such great opposition, some observersbelieve required forecasting will not come about.

NAA is involved in the forecasting. issue through the Committeeon Management Accounting Practices. The MAP Committee sug-gested the SEC permit forecasting if companies so desire but shouldnot require forecasts because of the problems which could resultfrom presentation of such predictions. (See page 53 for text of thestatement.) The Financial Executives Institute took a similar position.

Since forecasting soon may become a reality, NAA members shouldstay abreast of developments as reported in newspaper and magazineartic les . MANAGEMENT ACCOUNTING has pr inted art ic les On forecasting

and undoubtedly will print more. NAA invites you to participatedirectly in the forecasting issue through letters to MAP and MANAGE-MENT AC CO U NT IN G Or t h r o u g h s u b m i s s i o n o f articles discussingthe ramifications and feasibility of forecasting.

C o m i n g U p i n MANAGEMENT ACCOUNTING

Everyone compla ins about r i sing heal th care cos ts ; in "Hospi t al Cos tControls , " Isaac Smal ls does something about i t . . . Seeking sophis-ticated pricing guides? Al J. Betley provides them with "Contribut ionPricing" . . . Sett ing work standards for profess ionals requires re-sourcefulness, ski l lfully di splayed in "Controll ing Professional Man-

power Costs" by J. Kent Oehm . . . In "The Investment Credit,"Will iam A. Cole and Stephen H. Wales, Sr., discuss appl ications ofthe five Investment Credit Acts passed since 1962.

MANAGEMENTACCOUNTING

VOL. LIV NO. 8 FEBRUARY 1973

Published monthly, for members only, by theNATIONAL ASSOCIATION

OF ACCOUNTANTS919 Third Avenue, New York, N.Y. 10022

rnonpo

dR =EXECUTIVE DIRECTORWilliam M. Young, Jr.

DIRECTOR OF PUBLICATIONSJames D. Collier

MANAGING EDITORErwin S. Koval

SENIOR TECHNICAL EDITORAlbert Cohen

FEATURE EDITORRobert F. Randall

ASSOCIATE EDITORSDonald StabileKathy Williams

EDITORIAL ASSISTANTSDebbie VoutsasLucile Lawrence

CIRCULATION MANAGERRaymond Goldstein

B o

Secondclasspostage paid at New York, N.Y.,and at additional mailing offices. To ensureuninterrupted mail service, please notify usimmediately of any change of address. Sendpresent address label and new address, in-cluding Zip number, to Member RelationsDept., NAA, 919 Third Ave., New York, N.Y.10022. Allow six weeks for change. Price $1.25per copy. Single subscriptions available onlyto NAA members, libraries, and college -levelaccounting students. Subscription rates, peryear: NAA members, $10.00 (included in an-nual dues); libraries, $9.00, college students,$5.00.

ADVERTISING REPRESENTATIVES

Mead Irwin Associates, 520 Fifth Avenue, NewYork, N. Y. 10036, (212) 986 -9781.E. W. Carlson, Union Trust Building, Pitts-burgh, Pa. 15219, (412) 471 -1410.

James K. Millhouse, 919 N. Michigan Avenue,Chicago, ill. 60611, (312) 641 -6625.

WESTERN STATESRoy McDonald Associates, Inc.

Dallas, Tex. —(214) 637 -2444Denver, Colo. —(303) 825 -3325Houston, Tex. —(713) 529 -6711

Los Angeles, Calif. —(213) 483 -1304Portland, Ore. —(503) 292 -8521

San Francisco, Calif. —(415) 397 -5377Copyright © 1973 by the

Nat ional Association of Accountants

MANAGEMENT ACCOUNTING/ FEBRUARY 1973

NewNCR18=22Designed for the business office, with features for business problems.

Now, NCR brings you a new, low- pricedone - memory calculator especially designed for officefigure work. The new NCR 18 -22 has all the featuresto do the kind of jobs you encounter every day inbusiness.

Two MOS /LSI chips make it tick. It has 12 -digitdisplay for your big problems. True memory withdirect access from plus, minus, equals /plus andequals /minus. Overflow protection. Automaticconstants. Selection of automatic round -off or noround -off. Floating /in, fixed /out decimal system. 0 -9decimal selection. Convenient signals for minusfactor, overflow, and amount in memory.

The keyboard is not cramped. Extra long "zero"bar extends to the left of amount keys for natural handpositioning. Arithmetic function keys and memorykeys are spaced so anyone can operate the 18 -22

\1

with ease. Yet its compact size -8.8" x 11.2" —takes no more space than a business letter, and itslight weight —only 3 lbs. —makes it easy to movefrom desk to desk, or even take it home if you like.

When you see the NCR 18 -22, we're sure you'llagree it's the ideal display calculator for your businessneeds at a price you can afford. Only $279.For more information call your nearest NCR BranchOffice or NCR Office Products Dealer. Or write OfficeProducts Division, Dayton, Ohio 45409.

Office Products Division

MANAGEMENT ACCOUNTING/ FEBRUARY 1973

Letters TO THE EDITOR

Will Accountants Recognize Social Changesand Adapt . . . 3

I read with interest the article, "Pilots of Social Progress," byMr. Robert Beyer in the July 1972 issue of MANAGEMENTACCOUNTING. It is true that accountants in public and corporateaccounting practices have historically had a role in corporate socialresponsibility and that the role has expanded considerably duringthe last twenty years. There is little doubt that future socialchanges will have even greater influences on the profession ofaccountancy. The real question appears to be whether accountantswill be able to recognize social changes and adapt to them.

Social changes have resulted from expanding technology, declineof the family unit, greater educational opportunities, failure ofthe market mechanism, and political philosophies. Whether thesefactors represent root causes of social change or are results ofintensified human interaction is difficult to determine. However,the effects of these factors can be seen in attitude changes towardmanagement and accounting, as well as in the quantity and sophis-tication of accounting data required to satisfy social demands.

Causes of social change are primarily external to the businessorganization. In many instances, a positive business response tosocial demands has resulted, principally due to government coer-cion. Some social groups have expressed antagonism towards busi-ness management and accountants because certain social needsand changing attitudes have not been recognized. Many corpora-tions would not have invested in pollution controls, engaged inminority employment, or used good accounting and reportingpractices if it were not for government intervention.

Accountants and professional accounting organizations need torevise their perspectives of the accountant's service role and rela-tionship to social progress. Social progress is people- oriented, andsince accountants generally have had little training in the behav-ioral sciences, any reference to the accountant as a pilot of socialprogress may be misleading. Social progress will occur becauseelements in society change. The role played by accountants insocial progress will depend on their ability to recognize and respondto social changes and causal factors.

Elliot SlocumDepartment of Accounting

Georgia S ta te UniversityAtlanta, Ga.

A Giant Step Forward

As I was reading the article by William J. Sullivan of Youngs-town State University in the August 1972 Issue Of MANAGEMENTACCOUNTING, I discovered that through his system of budget re-porting to department heads on a monthly basis, he has takena giant step forward in solving the age -old problem of com-munications between financial personnel and others in an organi-zation.

As most of us know, a budget, in order to be effective, mustbe communicated so that adequate planning can be done. Ade-quate communication means an understanding of the budget byall concerned and frequent reporting on the budgetary progress.Once the budgetary or financial division of an organization under-stands all other facets of the organization, and once all nonfinan-cial people in an organization understand budgetary responsibility,

one of the problems that has plagued financial officers for yearswill have been solved.

It seems that Youngstown State University through its budgetofficer, William J. Sullivan, has reminded us again that there ismore to finance than facts and figures, and that communicationis essential to productive, workable relations between persons inany organization.

Jeffery W. BarryPresident —Walsh College

of Accounting and Business AdministrationTroy, Mich.

Listening Is a Two -Way Operation

"The Auditor Should Be Welcomed Into the Data ProcessingFamily ..." This concept, mentioned in Harry L. Brown's article"Auditing Computer Systems" (September 1972), represents achallenge to both the auditor and data processing personnel.

Mr. Brown pointed out that the auditor has more to offer thanjust "checks and balances." The auditor for years has been a"systems analyst." The auditor has the ears of top management,a corporate overview, access to all company information and knowsthe value of good controls. With this background the auditor hasmany things to offer in designing a system. One wonders why,with all of this going for him, the auditors have not been moreinvolved in the design of major systems. He suggests that dataprocessing personnel listen to the auditor. I suggest that the listen-ing is a two -way operation. However, being a "member of thefamily," he does link his experience factor as an auditor and hiscontrol concepts to data processing operations. This closer tie tendsto expedite the solution of problems of control in the design stages.

Ken PenderThe Detroit Edison Co.

Detroit, Mich.

Re: Information Services

I feel that I would be remiss in my duty if I did not reporton the excellent service that I received from your Mr. DonaldMackenzie, the Manager of your Technical Information Service.

Mr. Mackenzie gave himself entirely to a problem which Isubmitted to him for his assistance. 1 am sure that if prospectivemembers knew of his devotion to duty, and that of the nationalstaff, they would not hesitate to join our Association.

I am more than pleased to call at tention to the high class of"service" that Mr. Mackenzie gives on behalf of the Association,and he deserves every consideration.

Joseph de AmbrosisMember -at -Large

Winnipeg, ManitobaCanada

A Very Useful and Timely Article

Mr. Pagano's article in the September 1972 issue of MANAGEMENT

MANAGEMENT ACCOUNTING/ FEBRUARY 1973

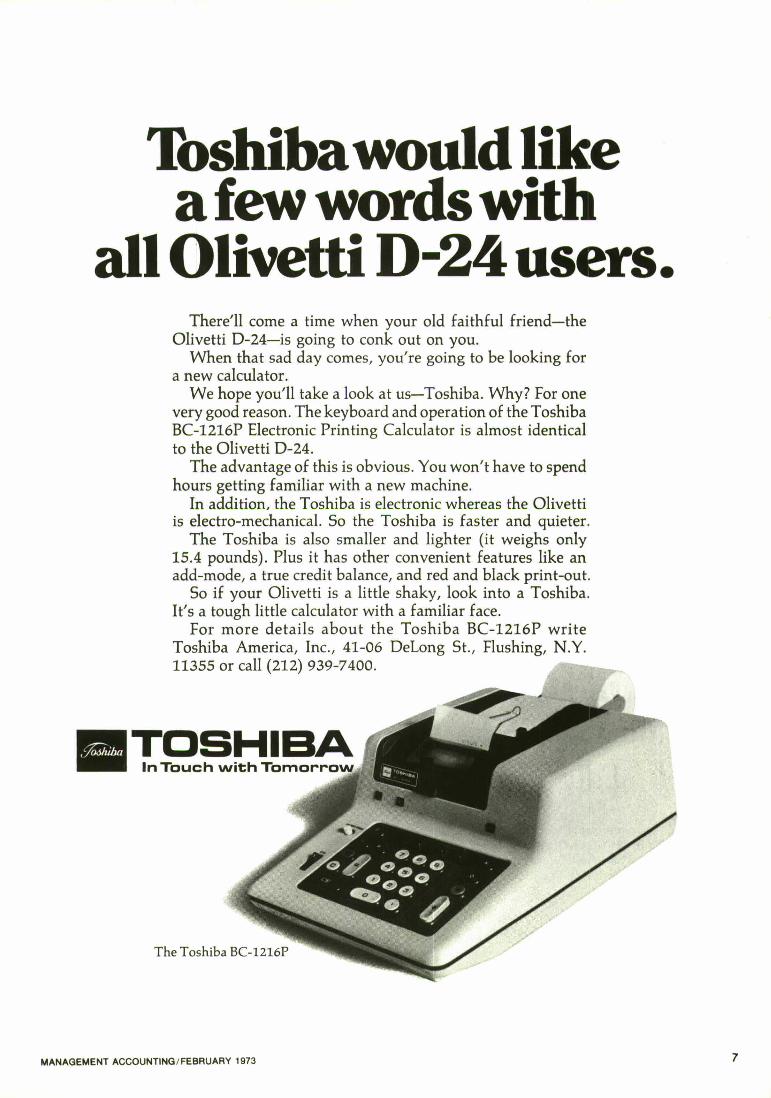

Toshi*,ba would Ii0kea few words wi6th

all 0111ietti* Dm24 users.There'll come a time when your old faithful friend —the

Olivetti D-24—is going to conk out on you.When that sad day comes, you're going to be looking for

a new calculator.We hope you'll take a look at us— Toshiba. Why? For one

very good reason. The keyboard and operation of the ToshibaBC -1216P Electronic Printing Calculator is almost identicalto the Olivetti D-24.

The advantage of this is obvious. You won't have to spendhours getting familiar with a new machine.

In addition, the Toshiba is electronic whereas the Olivettiis electro- mechanical. So the Toshiba is faster and quieter.

The Toshiba is also smaller and lighter (it weighs only15.4 pounds). Plus it has other convenient features like anadd -mode, a true credit balance, and red and black print -out.

So if your Olivetti is a little shaky, look into a Toshiba.It's a tough little calculator with a familiar face.

For more details about the Toshiba BC -1216P writeToshiba America, Inc., 41 -06 DeLong St., Flushing, N.Y.11355 or call(212) 939 -7400.

W T O SI n T o u ch

R I B Aw i t h T o m o r r o w

The Toshiba BC-1216P

MANAGEMENT ACCOUNTING/ FEBRUARY 1973

ACCOUNTING titled "The Line Manager 's Role In Bakery Opera.tions" is a very complete discussion of line functions in a bakeryoperation. He correctly identifies the primary objectives of theline manager as "efficient production output" and "high qualityof merchandise."

His statement that the line manager must work closely withthe Scheduling Department indicates one very important and veryessential consideration. The line manager should not be burdenedWith the responsibility for production scheduling in addition todirect production responsibilities. For greatest efficiency, a sched-uling function or department distinct from the line functionshould be maintained. The overall line responsibility for produc-tion setup, production runs, packaging, production reporting, andmaterial and supply usage reporting is essentially a completeoperation.

James D. PascoeAccounting Manager

Fred Sanders Co.Detroit, Mich.

Software Costs — Expense or Capital Expenditure

Software associated with a data processing facility, regardlessof whether purchased or developed with in -house capabilities, posesa serious accounting question. From both an accounting theoryand a management information standpoint, what is the properaccounting treatment for the costs of such software? This questioncomes to light because the IRS has changed the rules governing

the method of accounting for software costs for tax purposes.The IRS originally took the position that software, when pur-

chased together with hardware, should be depreciated over a five -year period. Left unclear was the problem of what a purchaserof software should do when his systems engineering and program-ming services were purchased separately from his hardware. TheIRS has since changed its position. Its latest ruling provides thatcompanies obtaining software either bundled with new equipment,purchased separately from an equipment supplier or softwarehouse, or developed in- house, have the option of either expensingit during the year of purchase or capitalizing the costs with sub-sequent amortization over a five -year period. The IRS also askedthat companies be consistent in their accounting for software, andif a company wishes to change from one method to another fora new purchase, permission must be obtained from the IRSCommissioner. It appears that by changing i ts ruling, the IRShas taken a "middle of the road" position and left the accountingfor software costs to the discretion of the companies using dataprocessing equipment.

One cannot argue with the fact that a tax advantage wouldaccrue to a company that expensed i ts software costs. From anaccounting theory standpoint, it seems that an asset has beenacquired and should be capitalized and depreciated. It is a knownfact that the hardware cannot operate without software, i.e., theprograms to perform the various data processing operations,whether for accounting analyses or other types of managementinformation needs, depend on software for implementation. If thehardware must be capitalized and depreciated, why shouldn't thesame rules apply to the software?

Continued on page 28

Vir niaris

f0rlOVerSwho will love Richmond

too during Garden Week in Virginia. . .

Educational, Historical &BeautifulFor information write to: APR I L 26-28,1973

MR. CHARLES D. SANDS7104 Wheeler Road

Richmond, Virginia 23229 HOTEL

RICHMOND, VIRGINIA

MID - ATLANTIC REGIONAL CONFERENCE■ Richmond Chapter of

■

NATIONAL ASSOCIATION OF ACCOUNTANTS

MANAGEMENT ACCOUNTING/ FEBRUARY 1973

Stake it to aailas

.. md11 do the rest!The Texas Council has helped prepare an exciting program for the1973 Annual International Conference for you and your family— one as big as Texas itself.Your trip to Dallas will span the excitement of a real Texas Rodeo,where big prize money is at stake, to a sample of the life style of

the sophisticated super -rich.

If you have never attended an informal Texas Chuck WagonDinner, then this is your chance. (Of course you'll have a chance todress -up at the Annual Dinner.)

Children of all ages rave about the Six Flags of Texas, which isacres and acres of fun and Texas history.

Plan now to attend one of the best National Association ofAccountants' Annual International Conferences ever. If you havenever attended before — don't miss this one!

Speakers and topics for the Technical Program and details about thecomplete schedule at the Big "D" in '73 will be in the mail shortly.

■ NATIONAL ASSOCIATION OF ACCOUNTANTS

■� � NqlCONFER�N� �

0).

GE's nZw Mark IIIextends time- sharingacross 17 time zones.

In t er n a t i on a l n e t wor k s er v i c e sa r e be i n g i n t r od u c e d i n J a p a n .

Balancing the comput ing needsof user s on 3 cont inent sr eaching across 17 t ime zonesa llows process ing economieswhich can help GE cut yourtime - sharing costs by a third.

An information processing network ofnearly 100 integrated computers linking over275 locations on 3 continents provides youwith the most economical time - sharingavailable today. And whether you're locatedin Tokyo, New York, Paris, or all three, youcan have instant information processingfrom common data files available througha local phone call.

Whatever your needs — responsive, interactivetime - sharing, a world -wide order processingor financial reporting network, or economicalremote processing —GE's new Mark IIIis the answer.

For all the details, phone 800 - 638 -0971 orwrite us at 7735 Old Georgetown Road,Bethesda, Maryland 20014.We're ready to help.

�WORLD LEADER

GENERAL � ELECTRIC IN INFORMATIONSERVICES

If you can't attend ourC "Effective Cash

Management" in New York,March

1 2 m 1 6 , 1 1 1 1 1 1 1 1 1 1

New York /March 12- 16 /Statler- Hilton /13 Courses

Developing and Using Standard Costs (Mon. /Tue.)

Flexible Budgeting & Performance Reporting (Wed. /Thu. /Fri.)

Effective Cash Management (Mon. /Tue.)

Economic Evaluation of Capital Expenditures (Thu. /Fri.)

Accounting Information for Pricing — Policies and Decisions (Mon. /Tue.)

Management Accounting for Banks (Thu. /Fri.)

Management Accounting for Executives & Managers (Mon. /Tue.)

Management Accounting for Hospitals (Mon. /Tue.)

Data Processing— Concepts & Techniques for Managers (Mon. /Tue. /Wed.)

Computers and Internal Control (Thu. /Fri.)

Management Science for Budgeting and Profit Planning (Mon. /Tue.)

Linear Programming: Accounting Applications (Thu. /Fri.)

Marketing Fundamentals for the Management Accountant (Thu. /Fri.)

12 MANAGEMENT ACCOUNTING/ FEBRUARY 1973

u1s rhow about' n St. LoMarch 26 -30?

St. Louis /March 26 -30 /Chase -Park Plaza /6 Courses

Developing and Using Standard Costs (Mon. /Tue.)

Flexible Budgeting & Performance Reporting (wed. /Thu. /Fri.)

Direct Costing & Contribution Accounting (Thu. /Fri.)

Effective Cash Management (Mon. /Tue.)

Economic Evaluation of Capital Expenditures (Thu. /Fri.)

Data Processing— Concepts & Techniques for Managers (Mon. /Tue. /Wed.)

RegiSter nowfor New York or St. Louis

Spring'73C E P

Continuing Education Program

Write or call: CEP RegistrarNational Association of Accountants919 Third Avenue, New York, N.Y. 10022(212) 759 -3444

MANAGEMENT ACCOUNTING/ FEBRUARY 1973 13

Data Sheet FEBRUARY 1973

Disclosure of Accounting Policies and Tax Discrepancies Proposed by SEC

New disclosure proposals by the Securities & Exchange Commission would affect reportingof accounting policies use0and reporting of Federal taxes in earnings reports. Under the SECproposal, companies would be required to submit in reports to the agency "a summary ofsignificant accounting policies to be included in the financial statements either separately oras the first note." "Under certain circumstances and where significant" a company would haveto include an estimate of the dollar impact on net income of use of the principle followedas compared to an alternative acceptable principle. Such disclosure would be required whena company uses more than one accounting principle in reporting similar types of transactions,when it changes its accounting policy within the past two years, or when the principle usedis not the prevailing principle used by companies in the same industry. An accounting changeregarded as "significant" by the agency is one that affects net income by at least 5% or affectsthe improvement or worsening of earnings by more than 25 %, as compared to the prior period.The agency also wants to see improved disclosure of the reason why total income tax expensereported by the company differs from the amount which would result from multiplying thestatutory United States Federal corporate income tax rate by the income before tax.

Take Joint Responsibility for Disclosure, SEC Chief Accountant Urges Auditors

Speaking before the N.Y. State Society of CPAs, SEC Chief Accountant John C. Burton urgedthe auditors to take joint responsibility with corporate management for what is disclosed infinancial statements. If the financial statement which the auditor is attesting to is not preparedas he would prepare it, then he should so note that fact in his report and not tuck it awayin a footnote, Mr. Burton advised. He told the Society members that the costs would be muchhigher if they let the potential liability from shareholder lawsuits prevent them from innovatingand improving their functions.

AICPA Expands Washington, D.C. Staff

In recognition of the increasing impact of the Federal Government on the accounting profession,the American Institute of CPAs has expanded its staff in the U.S. capital. In announcing thenew direction in Washington, Gilbert Simonetti, Jr., vice president — government relations, ac-knowledged the influence of government in the past, on a number of matters of great significanceto the accounting profession. The Institute will concentrate on developing a more effectiverelationship with Congress and the Executive Branch by working "toward becoming a positivesource of advice on public policy relating to accounting, auditing, financial controls, taxationand . . . related m at ters. . . . "

Big Demand for Accounting and Financial Executives Seen in 1973

There will be a 20% increase in corporate demand for accounting and financial executives thisyear, according to a nationwide survey of 475 major corporations conducted by Boyden As-sociates, Inc., an executive search firm. This was the largest increase by job category projectedby the survey. The biggest demand for accounting and financial executives with minimum salariesof $25,000 will be in the East and Southeast. The firm noted that the demand for multinationalexecutives is also rising. "The executive with international experience and expertise in marketing,sales, finance and general management is being sought in almost every corner of the globe,"says Frederick M. Linton, president of Boyden Associates.

CASB Secretary Says MAP's Statement on Contract Costs the Only One Available

One quote you may have missed. Speaking before the Federal Government Accountants Assn.,Arthur Schoenhaut, executive secretary of the Cost Accounting Standards Board, said, "The NAAhas a subcommittee of its Management Accounting Practices Committee that interfaces withthe staff of the Board. The MAP Committee has made some constructive suggestions in thepast and, in fact, developed a statement of contract cost concepts which was published inthe March 1972 issue of MANAGEMENT ACCOUNTING. Although one can find fault with the state-ment of contract cost concepts, it is the only such statement available, and it emanates froman authoritative group."

14 MANAGEMENT ACCOUNTING /FEBRUARY 1973

THE BUSINESSMAN'S ROLEOf All Our Institutions, Business Is The Only One That Society

Will Let Disappear

By Robinson F. Barker

In our free enterprise system, business traditionallyhas been held responsible for the supply of goods andjobs, for costs, prices, wages, hours of work, and forstandards of living. Today, business also is being askedto take on the responsibili ty for the quality of lifein our society. The expectation is that business —inaddition to its traditional accountability for economicperformapce and results — should assume responsibilityfor the health of society. Not only is business beingasked to solve those social problems that have defeatedothers, but i t is expected to anticipate them and toprevent their emergence in the first place.

This challenge does not, of course, come as a com-plete surprise. For some time, there have been businessleaders who have heeded Thomas Paine's warning:"Those who expect to reap the blessings of freedommust, like men, undergo the fatigue of supporting it. "'These are the men who share the concern voiced bystudents and others that not all in our nation haveparticipated in the most prosperous economic era inthe history of man. More important, these same busi-nessmen have begun to take steps to try to mitigatethe problem.' Similarly, the business community rec-ognizes and is working on other associated social prob-lems. The nation's top scientists and engineers —amongthem representatives of industry— working under theauspices of the National Academy of Engineering andthe National Academy of Sciences, have begun totackle the problem of assessing technology. Their goalquite simply is to create a mechanism —now lackingin the economy— whereby the broad social effects ofexploiting and restricting a technological developmentcould be considered and effectively expressed.

Good Business Or Good Citizenship?

More and more the distinction traditionally drawnbetween corporate citizenship and corporate businessis becoming less and less delineated. Are companytraining programs for school dropouts good businessor good citizenship? Does a large corporation's massivestudy of the effects of automation on society mostsignificantly serve the company planners or the com-munity at large? Is the sponsorship of an art showsound advertising or does it fal l under the headingof culture? If you're a pragmatist, as most businessmenare trained to be, the answers are irrelevant. It isactivity itself which is important.

Obviously, a great deal more activity is required.

In many areas we have merely begun to scratch thesurface and in others —if we subject ourselves to objec-tive self - analysis —we have not accomplished even that.We still have to substitute deeds for words if we wishto plead innocent to the charge of preaching andpromising while running in place. There is however,concrete evidence that the first steps —the most impor-tant in any journey —have been taken and others willfollow.

However, it is not that simple. Business does notoperate in a vacuum. While it does have a distinctimpact on society, distinct capabilities and charac-teristics, and distinct opportunities, business is notalone. Other institutions such as the university, thehospital, the government, the military, and labor playa role, and as such must be held fully as accountableas business for the quality of life in our society. Justas we now recognize that government does not offera panacea for society's problems, we also must recog-nize that business of and by itself will produce nomiracles.

The Problem of Environment

Consider the problem of environment. Business doesnot have the capability to solve the problem by itself.Even the most stringent self - policing will result innothing better than a diffused, disorganized overallapproach. This is an area that is responsible only toenlightened government regulation which accuratelyreflects the demands of the total populace.

Too often, I'm afraid, we tend to ignore the com-plexity of the problem in a search for easy solutions.Take the case of electric utilities. How many of ourpower demands are we willing to sacrifice in the nameof preserving the environment? Before answering,however, pause to consider that the makeup of manyof our power plants today was determined by govern-ment regulations responding to a public plea for powerat the cheapest cost.

Again, business' efforts in an area such as housingwill be governed by the attempt to update buildingcodes at the local level and the efforts of unions inthe building trades to cooperate. Nor can business beexpected to unleash the technology and capability that

'Thomas Paine, The American Crisis IV, September 12, 1777.' Members of the National Alliance of Businessmen, an organization re resentingsome 47,500 American industrial companies, during the past four and one -halfyears found jobs for approximately 1,000,000 disadvantaged persons. Of thisgroup —made up of those formerly considered chronically unemployed becauseof their environment and lack of education —some 500,000 were still on the jobafter six months. Pittsburgh Office of the National Alliance of Businessmen.

R. F. BARKER

is Chairman of theBoard, PPG Industries,Inc., Pittsburgh, Pa.He is a graduate ofHarvard College andthe AdvancedManagement Programin the HarvardGraduate School ofBusinessAdministration. Mr.Barker serves asdirector to severalprivate and publicinstitutions.

This article is adaptedfrom a speech to thePittsburgh Chapter inOctober 1970, andwas submittedthrough that chapter.

MANAGEMENT ACCOUNTING /FEBRUARY 1973 15

"What many

. . . fail to

recognize isthat business

is ... an organof innovation."

exist to solve the problem under a property tax struc-ture that harnesses the profit motive in reverse bymaking it more profitable to let buildings decay thanto improve or replace them.

Similarly, can business attempts to help solve theproblems of the hardcore unemployed and minoritygroups be effective unless accompanied by a similareffort on the part of unions in their membership andlicensing practices?

None of the foregoing comments are to imply inany way that it is not clearly in the self - interest ofbusiness and businessmen to accept this responsibilityfor the quality of life in our society and to build itinto the vision of business executives. Three immedi-ate reasons come to mind to support such a move.First, the consequences for neglecting this area areso very great. Second, there is the obvious and moreimportant fact that a healthy business and a sicksociety are not compatible. Healthy businesses requirea healthy, or at least a functioning, society. The healthof a community is a prerequisite for successful andgrowing business. Finally, the quality of life in oursociety should be a tremendous business opportunity.It is, after all, the job of business to convert the needsof society into profitable business opportunities —toconvert social change into constructive innovation.And it is a poor businessman who thinks that innova-tion refers to technology alone. The major industriesof the nineteenth century resulted, to a very largeextent, from the conversion of the new social environ-ment —the industrial city —into a business opportunityand into a business market.

Business . . . An Economic Institution

Yet, one must wonder if the demand that businesstake responsibility for the quali ty of life has beencarefully thought through by its advocates. Business,for example, cannot accomplish these tasks by behav-ing like anything but what it is, an economic institu-tion that acts in terms of economic rationality, aninstitution that must be motivated by profit incentivesin order to function efficiently. Profitability mustremain the yardstick of business whether its activitiesare concerned with the quality or quantity needs ofsociety.

This is a pressing point, and one, I suspect, thatis not fully recognized. For example, businessmen oftoday cannot help but be struck by the lack of under-standing regarding the profit motive. It may well bethat the greatest failure of businessmen is their inabil-ity, or lack of effort, to educate others about theoperation and meaning of the profit system. You asaccountants, better than anyone, should understandthe system. Yet how many of you go home eachevening and complain about the rat -race? Is it anywonder that most wives can't go beyond naming thecompany their husbands work for in answer to a re-quest to describe what their husbands do for a living?Or is it surprising that so many of the youth in ourcolleges —sons and daughters of businessmen —swearthat business and industry is the last place they wantto end up. It is readily apparent, and becomes moreso each day, that while as a nation we reap the benefitsof our economic system, we have little understandingof it.

An Organ of Innovation

At a time when increasing numbers of individualsand groups are demanding that business accept moreresponsibility— because of its demonstrated ability tomanage and get things done —there is underway alsoan attack at the very foundations of business —profitand competit ion. What many unfortunately fail torecognize is that business is predominantly an organof innovation. Of all social institutions, it is the onlyone created for the express purpose of making andmanaging change.

Specifically, business has an advantage where gov-ernment, for example, is weak. Business can abandonan activity. Indeed, it is forced to do so if it operatesin a competitive market. There is a point beyondwhich even the most stubborn businessman cannotargue with the market test , no matter how rich hemay be. (Even Henry Ford had to abandon the ModelT when it no longer could be sold.)

Of all our institutions, business is the only one thatsociety will let disappear. Attempts to close a uni-versity or a hospital, no matter how superfluous andunproductive they might be, create a storm of protest.

Precisely because business can make a profit, it alsomust run the risk of loss. This risk, in turn, goes backto a second strength of business: It alone among allinstitutions must pass the test of performance. Nomatter how inadequate the test of profitability, it isa test nonetheless for all to see.

Support for an obsolete hospital in a communityis usually based on the argument that it will one daybe needed again. Advocates for even the poorest uni-versity contend that it is better than none. The com-munity is easily moved by a sense of "moral duty"to save either institution. The consumer, however, isunsentimental. He is unmoved when he is told thathe has a duty to buy the product of a company becauseit has been around a long time. The consumer alwaysasks: "And what will the product do for me to-morrow?" If the answer is "nothing" he will see itsmanufacturer disappear without the slightest regret.And so will the investor.

This is the strength of business as an institution.And it is the best reason for keeping it under privateownership. The argument that the capitalist shouldnot be allowed to make profits is a popular one. Butthe real role of the capitalist is to be expendable. Hisrole is to take risks and, sometimes, to take losses asa result. This is a role that the private investor, ratherthan the public one, is much better equipped to dis-charge. Business is the one institution that, from thebeginning, has adapted to change, the one institutionthat has proved its right to survival again and again.This is what business is designed for, precisely becauseit is designed to make and to manage change.

The Proper Role of Government

For many years people have expected miracles ofgovernment because it was widely believed that gov-ernment would produce a great many things for noth-ing. It could eliminate wicked private interests andthe dirty profi t motive. It could solve many of ourproblems by dividing the wealth as opposed to the

Continued on page 25

16 MANAGEMENT ACCOUNTING /FEBRUARY 1973

PRICE -LEVEL CHANGESAND COMPANY WEALTHThe Funds Approach To The Measurement Of Net Monetary Gain Or Loss

By Russell J. Petersen

During a period in which there is a change in thegeneral price level, a company may experience a changein its wealth in the form of reduced or increasedpurchasing power. In certain circumstances this impactcan be material, particularly for companies that holdlarge net monetary positions during periods of signifi-cant changes in the general price level. The purposeof this article is to describe a procedure for the mea-surement of general price -level gains and losses, whichis an amplification of material contained in ARS No.6 and APB Statement No. 3.'

Approach

The general procedure to be described may beviewed as a problem in estimating price- stabilized netmonetary fund flows during a specific time period.Accountants have become experts at measuring andreporting other fund flows when the fund is definedas cash, net working capital, or net quick assets. Aswe will illustrate, they also may develop a funds state-ment to report the flow of net monetary magnitudes(during a specific time period) using the same conceptsand procedures which are appropriate for the develop-ment of the more classical funds statements. Themeasurement of net monetary gains and losses in-volves, in essence, the measuring of price- stabilizednet flows to determine a computed net magnitudeat the end of the t ime period. Comparison of thiscomputed magnitude with the actual net monetaryposition will yield the period gain or loss.

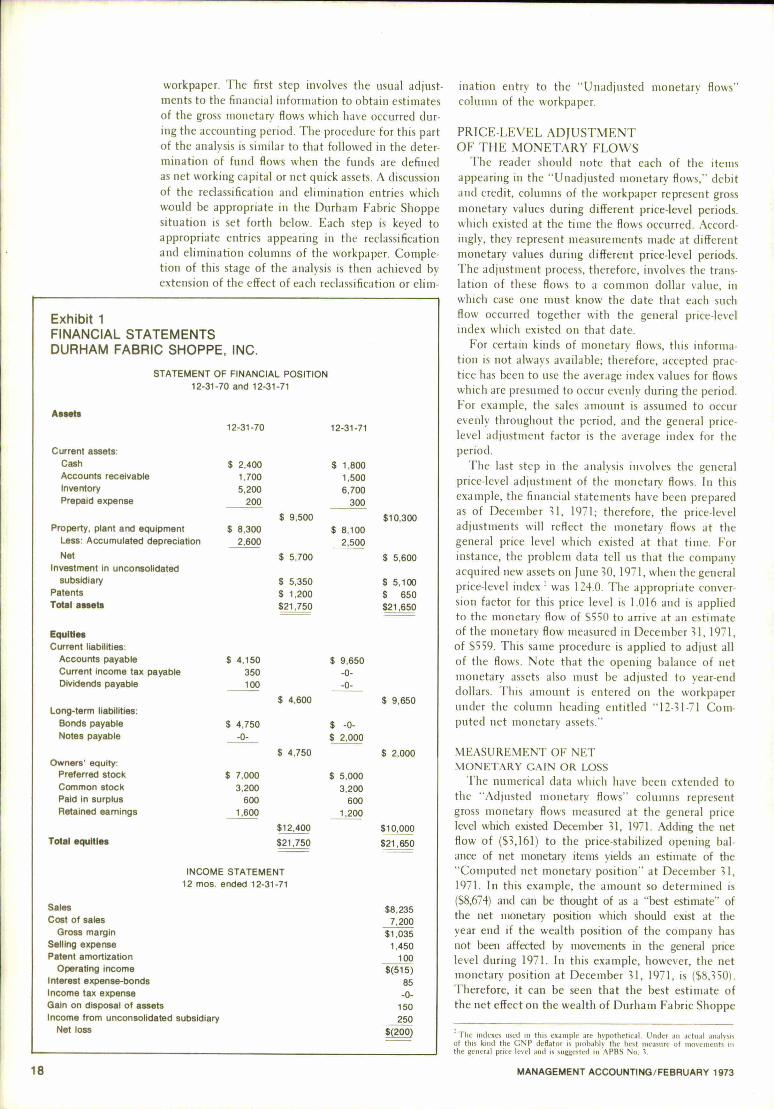

ExampleThe financial statements of the Durham Fabric

Shoppe, Exhibit 1, are used to illustrate the principalideas in this procedure. In addition to the financialstatements, the following information is required inorder to complete the analysis.

1. Depreciation expense for 1971 was $500 and isincluded in cost of sales.

2. Assets disposed of during the year were depre-ciated to a net 20 percent salvage value. Theywere sold on March 31, 1971, and all new assetswere acquired on June 30, 1971.

MANAGEMENT ACCOUNTING/ FEBRUARY 1973

3. Bonds were redeemed on March 31, 1971, at theirbook value at that time. They were six percent,$5,000 face value bonds.

4. Preferred stock valued at $2,000 was redeemedon June 30, 1971, in exchange for notes payable.

5. Cash dividends of $100 were declared on June30 and December 31,1971.

6. The company maintains its investment in itsunconsolidated subsidiary account on an equitybasis. The subsidiary declares and pays cash divi-dends on September 30 of every year.

7. Prepaid expenses are entirely salesmen's supplies.8. The company sold patents which cost $450 for

book value on September 30,1971.9. Interest is paid on December 31 of each year.

10. Sales, purchases, and selling expense have beenrealized or incurred evenly throughout the year.

In addition to the above information, the generalprice -level index data is assumed to be as follows:

Date GNP Conversiondeflator factor*

12 -31-70 120.0 1.0503 -31-71 122.0 1.0336 -30-71 124.0 1.0169-30-71 125.0 1.00812 -31-71 126.0 1.000Average(1971) 123.0 1.024

*ConversionEnd of period index

factorIndex of time of monetary flow

Average CF (1971) — 126.0— 1.024

123.0

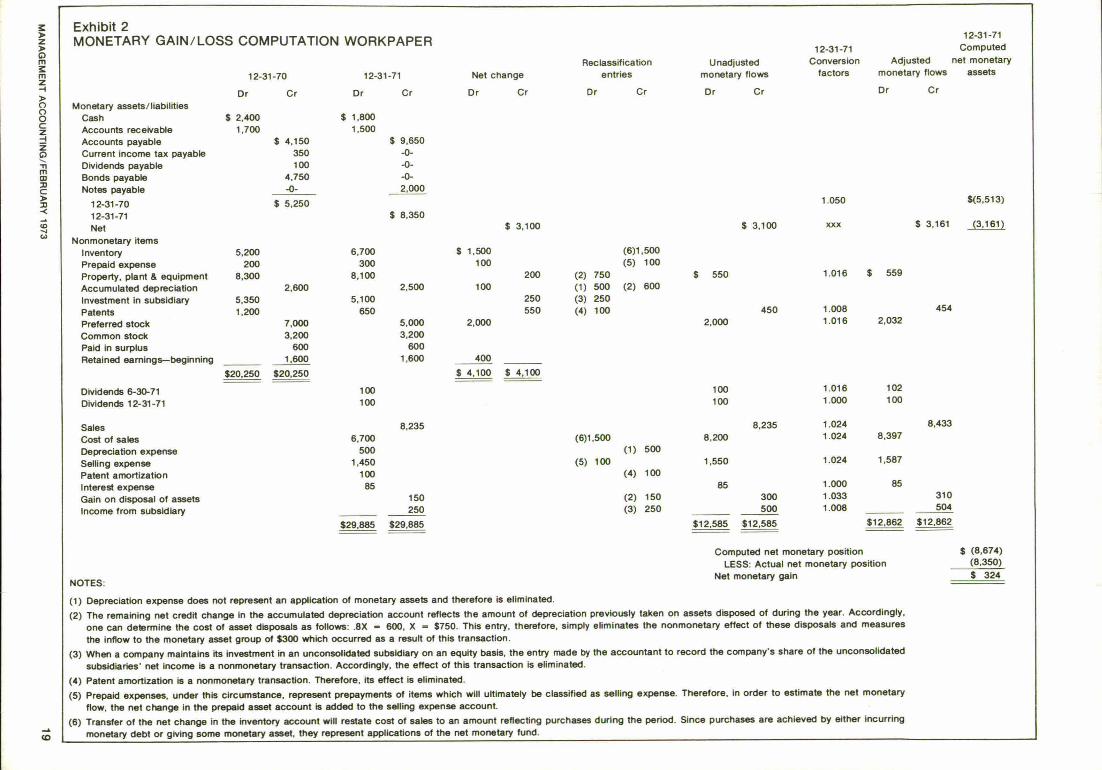

MEASUREMENT O F N ET MO NETARY FLOWSThe Monetary Gain /Loss Computation Work -

paper, Exhibit 2,reflects the complete computationalprocedure from which we will derive the ComparativeFunds Statement illustrated in Exhibit 3. Essentially,there are two principal steps required to complete the

Reporting the Financial Effects of Price -Level Changes, ARS No. 6, AIOPA,New York 1963.— Financial Statements Restated forCentral Price -Level Changes.APB Statement No. 3, AICPA, New York. 1969.

R. J. PETERSEN

is an AssistantProfessor at theGraduate School ofBusiness, DukeUniversity. He is alsoa CPA and holds a B.S.degree from OregonState University, anM.S. degree from theUniversity of Oregon,and a Ph.D. degreefrom the University ofWashington.

17

workpaper. The first step involves the usual adjust-ments to the financial information to obtain estimatesof the gross monetary flows which have occurred dur-ing the accounting period. The procedure for this partof the analysis is similar to that followed in the deter-mination of fund flows when the funds are definedas net working capital or net quick assets. A discussionof the reclassification and elimination entries whichwould be appropriate in the Durham Fabric Shoppesituation is set forth below. Each step is keyed toappropriate entries appearing in the reclassificationand elimination columns of the workpaper. Comple-tion of this stage of the analysis is then achieved byextension of the effect of each reclassification or elim-

Exhibit 1FINANCIAL STATEMENTSDURHAM FABRIC SHOPPE, INC.

STATEMENT OF FINANCIAL POSITION12 -31 -70 and 12 -31 -71

Assets

12 -31 -70 12 -31 -71

Current assets:Cash $ 2,400 $ 1,800Accounts receivable 1,700 1,500Inventory 5,200 6,700Prepaid expense 200 300

$ 9.500 $10,300Property, plant and equipment $ 8,300 $ 8,100

Less: Accumulated depreciation 2,600 2,500Net $ 5,700 $ 5,600

Investment in unconsolidatedsubsidiary $ 5,350 $ 5,100

Patents $ 1,200 $ 650Total assets $21,750 $21,650

EquitiesCurrent liabilities:

Accounts payable $ 4,150 $ 9 1850Current income tax payable 350 -0-Dividends payable 10_0 -0-

$ 4,600 $ 9,650Long -term liabilities:

Bonds payable $ 4,750 $ -0-Notes payable -0- $ 2,000

$ 4,750 $ 2,000Owners' equity:

Preferred stock $ 7,000 $ 5,000Common stock 3.200 3,200Paid in surplus 600 600Retained eamings 1,600 1,200

$12,400 $10,000Total equities $21,750 $21,650

INCOME STATEMENT12 mos. ended 12 -31-71

Sales $8,235Cost of sales 7,200

Gross margin $1,035Selling expense 1,450Patent amortization 100

Operating income $(515)Interest expense -bonds 65Income tax expense -0-Gain on disposal of assets 150Income from unconsolidated subsidiary 250

Net loss $(200)

ination entry to the "Unadjusted monetary flows"column of the workpaper.

PRICE -LEVEL ADJUSTMENTOF THE MONETARY FLOWS

The reader should note that each of the itemsappearing in the "Unadjusted monetary flows," debitand credit, columns of the workpaper represent grossmonetary values during different price -level periods.which existed at the time the flows occurred. Accord-ingly, they represent measurements made at differentmonetary values during different price -level periods.The adjustment process, therefore, involves the trans-lat ion of these flows to a common dollar value, inwhich case one must know the date that each suchflow occurred together with the general price -levelindex which existed on that date.

For certain kinds of monetary flows, this informa-tion is not always available; therefore, accepted prac-tice has been to use the average index values for flowswhich are presumed to occur evenly during the period.For example, the sales amount is assumed to occurevenly throughout the period, and the general price -level adjustment factor is the average index for theperiod.

The last step in the analysis involves the generalprice -level adjustment of the monetary flows. In thisexample, the financial statements have been preparedas of December 31, 1971; therefore, the price -leveladjustments will reflect the monetary flows at thegeneral price level which existed at that t ime. Forinstance, the problem data tell us that the companyacquired new assets on June 30, 1971, when the generalprice -level index' was 124.0. The appropriate conver-sion factor for this price level is 1.016 and is appliedto the monetary flow of $550 to arrive at an estimateof the monetary flow measured in December 31, 1971,of $559. This same procedure is applied to adjust allof the flows. Note that the opening balance of netmonetary assets also must be adjusted to year -enddollars. This amount is entered on the workpaperunder the column heading entitled "12 -31 -71 Com-puted net monetary assets."

MEASUREMENT OF NET

MONETARY GAIN OR LOSSThe numerical data which have been extended to

the "Adjusted monetary flows" columns representgross monetary flows measured at the general pricelevel which existed December 31, 1971. Adding the netflow of ($3,161) to the price- stabilized opening bal-ance of net monetary items yields an estimate of the"Computed net monetary position" at December 31,1971. In this example, the amount so determined is($8,674) and can be thought of as a "best estimate" ofthe net monetary position which should exist at theyear end if the wealth posit ion of the company hasnot been affected by movements in the general pricelevel during 1971. In this example, however, the netmonetary position at December 31, 1971, is ($8,350).Therefore, i t can be seen that the best est imate ofthe net effect on the wealth of Durham Fabric Shoppe

The indexes used in this example are hypothetical. Under an actual analysisof this kind the GNP deflator is probably the hest measure of movements inthe general price level and is suggested in APBS No, 1.

18 MANAGEMENT ACCOUNTING /FEBRUARY 1973

DZDOm

r

mZ

Dn

n

OC2

ZO

mm

c

D

co

vw

tD

Exhibit 2MONETARY GAIN /LOSS COMPUTATION WORKPAPER

12 -31 -70 12 -31 -71

Dr Cr Dr Cr

Monetary ass ets/ l i ab i l i t i es

Cash $ 2,400 $ 1,800

Ac c ounts rec e i vab le 1,700 1,500

Ac c ounts payab le $ 4,150 $ 9,650

Curren t i nc om e tax payab le 350 -0-

Di vi dends payab le 100 -0-

Bonds payab le 4,750 -0-

Notes payab le -0 - 2,000

12 -31 -70 $ 5,250

12 -31 -71 $ 8,350

Net c ha nge

D r Cr

Net $ 3,100

Nonm oneta ry i tem s

Inven to ry 5.200 6,700 $ 1,500

Prepa id expens e 200 300 100

Propert y, p l an t 8 equ ipm ent 8,300 8,100 200

Ac c um ula ted deprec i a t i on 2,600 2,500 100

Investm ent i n s ubs id ia ry 5,350 5,100 250

Patents 1,200 650 550

Pre fe rred s toc k 7,000 5,000 2,000

Com m on s toc k 3,200 3,200

Pa id i n s u rpl us 600 600

Reta i ned earn i ngs - beg inn ing 1,600 1,600 400

$20,250 $20,250 $ 4,100 $ 4,100

Dividends 6 -30-71 100

Dividends 12 -31 -71 100

Sales

Cost of s a les

Deprec i a t i on expens e

Se l l i ng expens ePaten t am ort i za t i on

In te res t expens e

Gain on di s pos a l of as s e ts

Inc om e f rom s ubs id i a ry

8,235

6,700

500

1,450

100

85150

250

$29,885 $29,885

Reclas si f i ca ti on

en t r i es

Dr Cr

(6 )1 ,500

(5) 100

(2) 750(1) 500 (2 ) 600

(3) 250

(4) 100

(6)1,500(1) 500

(5) 100(4) 100

(2 ) 150

(3) 250

Unad jus ted

m oneta ry f l ow s

Dr Cr

$ 3,100

$ 550

450

2,000

100

100

8,235

8,200

1.550

85

12 -31 -71

12 -31 -71 Co m p ut ed

Conve rs i on Ad jus ted ne t m one ta ry

fac to rs m onet a ry f l ow s ass ets

Dr Cr

1.050 $(5 ,513)

xxx $ 3,161 (3 ,161)

1.016 $ 559

1.008 454

1.016 2,032

1.016 102

1.000 100

1.024 8,433

1.024 8,397

1.024 1,587

1.000 85300 1.033 310

500 1.008 504

$12,585 $12,585 $12,862 $12,862

Com put ed ne t m o net a ry po s i t i on $ (8 ,674)

LESS: Ac t ua l ne t m onet a ry pos i t i on (8 ,350)

NOTES: Net m onet a ry ga in $ 324

(1) Deprec i a t i on expens e does no t repr es en t an app l i c a t i on o f m oneta ry a s s e ts and there fo re i s e l im ina ted .

(2 ) The re m a in i n g ne t c red i t c han ge i n the ac c um ul a ted d eprec i a t i on ac c o unt re f l ec ts the am o unt o f dep rec i a t i on p revi ou s l y tak en o n a s s e ts d i s p os ed o f du r i ng th e ye ar . Ac c ord i ng l y,

one c a n de te rm ine the c os t o f as s e t d i s p os a l s as fo l l ow s .8X = 600, X = $750. Th i s en t ry, there fo r e , s im p l y e l im in a tes the nonm on eta ry e f fec t o f thes e d i s pos a l s and m eas ures

the i n f l o w to the m oneta ry as s e t g r oup o f $ 300 w h i c h oc c urre d as a re s u l t o f th i s t ran s ac t i on .

(3 ) W hen a c om pany m ain ta i ns i t s i nvestm ent i n an unc ons o l i dated subs id ia ry on an equ i ty bas i s, the en t ry m ade by th e ac c oun t an t t o re c ord the c om pa ny' s s har e o f the u nc on s o l i d a ted

subs id i a r i es ' ne t i nc ome i s a nonm oneta ry t rans ac t i on . Ac c ord i ng l y, the e f fec t o f th i s t rans ac t i on i s e l im ina ted .

(4 ) Pa ten t am ort iza t i on i s a nonm oneta ry t rans ac t i on . There fo re , i t s e f fec t i s e l im ina ted .

(5 ) P repa id expens es , under th i s c i rc u m s tanc e , repres en t p repaym ents o f i tem s w h i c h w i l l u l t im ate l y be c l as s i f i ed as s e l l i ng expens e . Ther e fo re , i n o rd er to es t im at e t he ne t m one ta ry

f l ow , the ne t c han ge i n the p repa id as s e t ac c oun t i s a dded to t he s e l l i n g expens e ac c oun t .

(6 ) Trans fe r o f t he ne t c hang e i n th e i nve n to ry ac c oun t w i l l res ta t e c os t o f s a l es to an am o unt re f l ec t i ng purc has es dur i ng the p er i od . S inc e pu rc ha s es a re ac h i eved by e i th er i nc ur r i ng

Il m oneta ry deb t o r g i vi ng s om e m oneta ry as s e t , they repres en t app l i c a t i ons o f the ne t m o neta ry fund .

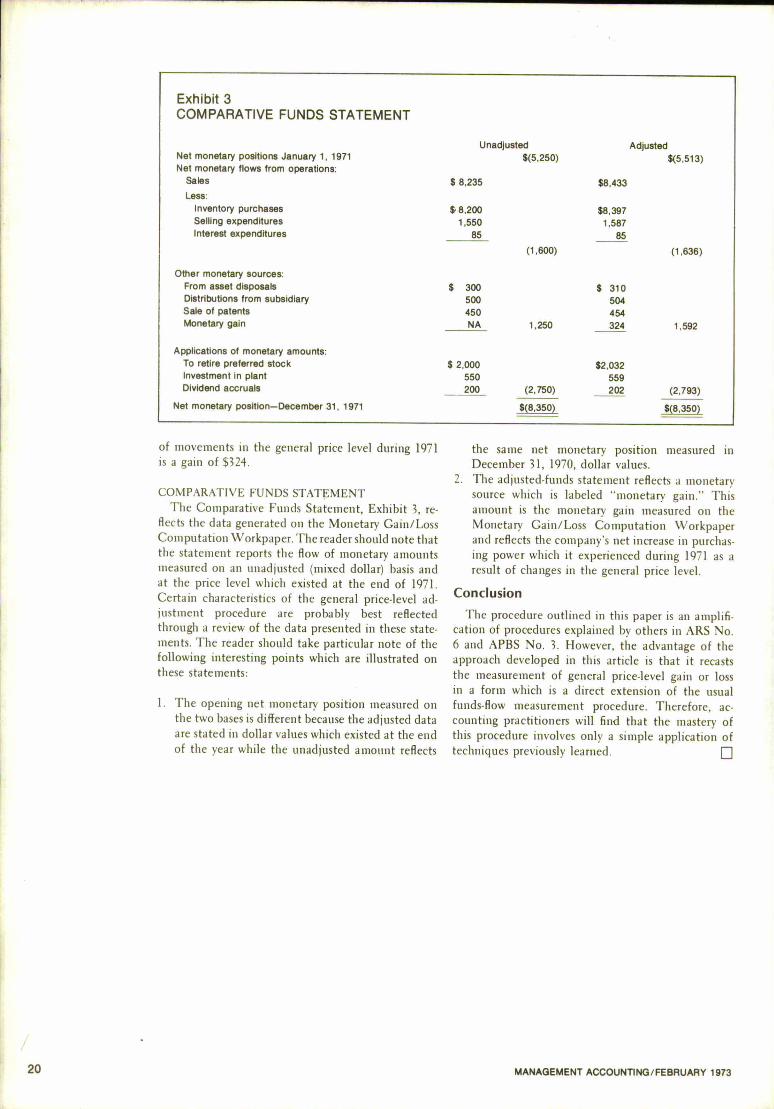

Exhibit 3COMPARATIVE FUNDS STATEMENT

Unadjusted AdjustedNet monetary positions January 1, 1971 $(5,250) $(5,513)Net monetary flows from operations:

Sales $ 8,235 $8,433

Less:Inventory purchases $, 8,200 $8,397Selling expenditures 1,550 1,587Interest expenditures 85 85

(1,600) (1,636)

Other monetary sources:From asset disposals $ 300 $ 310Distributions from subsidiary 500 504Sale of patents 450 454Monetary gain NA 1,250 324 1,592

Applications of monetary amounts:To retire preferred stock $ 2,000 $2,032Investment in plant 550 559Dividend accruals 200 (2,750) 202 (2,793)

Net monetary position— December 31, 1971 $(8,350) $1.350L

of movements in the general price level during 1971is a gain of $324.

COMPARATIVE FUND S STATEMENT

The Comparative Funds Statement, Exhibit 3, re-flects the data generated on the Monetary Gain /LossComputation Workpaper. The reader should note thatthe statement reports the flow of monetary amountsmeasured on an unadjusted (mixed dollar) basis andat the price level which existed at the end of 1971.Certain characteristics of the general price -level ad-justment procedure are probably best reflectedthrough a review of the data presented in these state-ments. The reader should take particular note of thefollowing interesting points which are illustrated onthese statements:

1. The opening net monetary position measured onthe two bases is different because the adjusted dataare stated in dollar values which existed at the endof the year while the unadjusted amount reflects

the same net monetary position measured inDecember 31, 1970, dollar values.

2. The adjusted -funds statement reflects a monetarysource which is labeled "monetary gain." Thisamount is the monetary gain measured on theMonetary Gain /Loss Computation Workpaperand reflects the company's net increase in purchas-ing power which it experienced during 1971 as aresult of changes in the general price level.

Conclusion

The procedure outlined in this paper is an amplifi-cation of procedures explained by others in ARS No.6 and APBS No. 3. However, the advantage of theapproach developed in this article is that it recaststhe measurement of general price -level gain or lossin a form which is a direct extension of the usualfunds -flow measurement procedure. Therefore, ac-counting practitioners will find that the mastery ofthis procedure involves only a simple application oftechniques previously learned. ❑

20 MANAGEMENT ACCOUNTING /FEBRUARY 1973

CONTROL ANDMANAGEMENTOF INDIRECT EXPENSESThe Control And Management Of Indirect Expenses Is One Of

The Most Important Contributions The Management Accountant

Makes Toward The Profit Objective Of His Company

By Harold E. Sharp

It is common today for buyers representing both gov-emmental agencies and private companies to obtaindetailed cost estimates from the seller for the purposeof establishing a price for his various products andservices. Because the subject of overhead is generallytoo complex to be readily understood by most buyers,they base their purchase decisions on the size of theoverhead rate. It is, therefore, important for the sellerto find answers to the following questions: "Is a lowrate better than a high rate ?" "Does a more efficientcompany have low overhead rates?' "Do lower over-head rates mean lower total costs ?" The answers arenot easily determined. In order to please the customer,and to remain competitive, many companies havedeviated from the academic approach of classifyingdirect and indirect costs. The trend has been to reclas-sify many indirect costs as direct, under the assumptionthat whenever a cost can be charged direct it is morereasonable to do so. Some companies also attemptto reduce their overhead expense rate through ac-counting reclassifications. An example of this is dem-onstrated below:

Companies A and B have the same facilities, basicexpenses, and produce the same products. CompanyA is 10 percent more efficient than Company B inthe areas of direct and indirect labor. However, Com-pany B has reclassified 20 percent of its indirect laboras direct. A comparison of costs and rates before andafter the accounting change is illustrated by Exhibit1. The example shows that before the accountingchange, Company B was the high cost producer, buthad a lower overhead rate. After the accountingchange, Company B's total costs did not change, butthe overhead rate dropped considerably.

Indirect Expense Rates

The development of indirect expense rates as a partof the company's estimating and accounting proce-dures permits it to: (1) estimate its rates so that it

can bid on new work and plan internal operations;(2) record and allocate expenses to the various workorders as actual costs are incurred; and (3) at the endof each fiscal year (shorter periods may be used), closeits books and make final adjustments to accuratelyreflect the period's costs. These three processes resultin the following types of rates:

BIDDING RATESBidding rates are used for estimating the price for

work to be performed in the future. They are estimatesusually based on historical costs modified by estimates(statistical and /or direct) to reflect anticipated futureconditions.

BILLING RATESBilling rates are interim overhead rates used to

allocate overhead expenses to the various work ordersor other cost objectives during the company's fiscalyear. Actual overhead rates may fluctuate widelythroughout the year because of seasonal fluctuationsof expenses and workload changes. Overriding theseconditions is the fact that at the close of the fiscalyear overhead charges to all work performed duringthe year will be adjusted to reflect the final overheadrate. The billing rate thus represents the company'sbest estimate of what the final rate will be for thefiscal year.

The cycles which billing rates normally follow are:(1) At the beginning of the company's fiscal year thebidding and billing rates will probably be the same;and (2) Periodically, based on experience and othercurrent data (as it becomes known), the rates fordistributing indirect costs will be revised to be asrealistic as possible. Each time the billing rate is re-vised, all overhead costs allocated to the specific costobjectives during the current fiscal year are adjustedto equal the revised rate.

FINAL OVERHEAD RATES

Final overhead rates are the rates established at the

H. E. SHARP

is CorporateAdministrativeContracting Officer atthe Lockheed AircraftCorp., Burbank, Calif.He holds a B.A.degree in Accountingfrom California StateCollege at LosAngeles, and has beenan Instructor at theU.C.L.A. GovernmentContracts Program.

This article wassubmitted through theSouthwest LosAngeles Chapter.

MANAGEMENT ACCOUNTING/ FEBRUARY 1973 21

". . . somecompanies

establish a

number of

indirect

expensePOWs."

close of the company's fiscal year after all expensesare in and accruals, as appropriate, are made. Theseare the final rates which will be used to allocate indi-rect expenses to all work orders or other cost objectiveswhich incur costs of the type included in the baseused to allocate indirect costs. The following exampleillustrates the effect of adjustment from interim ratesused for allocating costs during the fiscal year to reflectthe allocation of the final rates for the fiscal year.In this case, direct labor cost is used to allocate manu-facturing overhead.

Rate AmountDirect labor (base) $5,000,000Applied overhead 118% 5,900,000Actual overhead 121% 6,050,000Adjustment (increase) to

work orders 3% 150,000

The $5,900,000 of applied overhead is the amountapplied to work orders by use of interim billing ratesof 118 percent. The overhead expense actually experi-enced during the company's fiscal year was $6,050,000,or 121 percent. The three percent difference, $150,000,represents the addit ional cost to be applied to thespecific cost objectives.

Indirect Expense Pools

For purposes of controlling and estimating, over-head expenses are generally classified as fixed, semi -variable, and variable expenses in relation to somebase. Some of the more typical categories to be foundin a manufacturing plant follow:

FIXEDRentTaxesInsurance (property)UtilitiesCommunication

SEMI - VARIABLE

PensionsEmployee insurance

Exhibit 1COMPARISON OF OVERHEAD RATEBEFORE AND AFTER ACCOUNTING CHANGE

Company A Company B

Before AfterDirect labor $900 $1,000 $1,200

OverheadIndirect labor $ 900 $1,000 $ 800Other expenses 1,000 1,000 1,000

Total overhead $1,900 $2,000 $1,800

Total cost $2,800 $3,000 $3,000

Overhead rate 211% 200% 150%

Vacation & sick leavePayroll taxAccountingMaintenance

VARIABLE

Indirect laborTrainingSuppliesRecruitment expense

Fixed expenses usually do not vary much unlessmanagement decides, for example, to increase or de-crease facilities and other capital equipment. Semi -variable expenses usually relate to payroll orientedexpenses that have fixed limits, and do not vary pro-portionately to the payroll. Variable expenses usuallyvary directly with the base to which they are applied,such as payroll cost, or labor hours. In many cases,management decisions can vary the amounts to beexpended without a direct relationship to the base.Indirect expense is thus allocated to the various costobjectives by the application of a rate which is devel-oped by relating total indirect expenses for the yearto a base. To account for these costs, some companiesestablish a number of indirect expense pools.

The number of expense pools established by theaccounting system determines the number of differentrates the company must manage and use in estimatingthe prices of its products. From a management aspect,the smaller the size of each pool the better visibilitymanagement has in controlling indirect expenses.Some companies use a large number of small pools,usually at the departmental or burden center level,and therefore have many different overhead rates. Thefollowing list is an example of an organization withmany pools:

ENGINEERIN G EXPENSE PO OLS

Advanced technologies 110%Systems engineering 115%Design engineering 117%Material engineering 116%Analytical support 120%Laboratories 150%Test operations 175%Engineering shops 165%Logistics 105%Training 112%

TEST SITES EXPENSE POOLS

Eastern test range 100%Western test range 115%Happy island 90%Go -Go mountain 95%Boondock haven 105%

MAN UFACTURING EXPEN SE POO LSDevelopment machine shop 210%Development sheet metal 195%Development assembly 180%Processing & plating 250%Heat treating 220%Production machine shop 160%Production sheet metal 155%

22 MANAGEMENT ACCOUNTING /FEBRUARY 1973

Production subassembly 140%Production final assembly 130%Tool design 120%Tool fabrication 170%Planning 115%

G & A EXPENSE POOLSContract & administration 10%Research & development 2%

The disadvantage of having many small overheadpools and rates is that fluctuations in the allocationbase (i.e., direct labor dollars) causes the rates to varysignificantly. This in turn makes forecasting realisticrates a difficult task. When business is slack for acertain department, its rates are high, and it is moredifficult to estimate prices for new business. Also, theaccounting for historical costs, and cost distributions,are more complex and t ime consuming. In order toavoid these difficulties, many companies prefer to usea small number of large pools, such as the following:

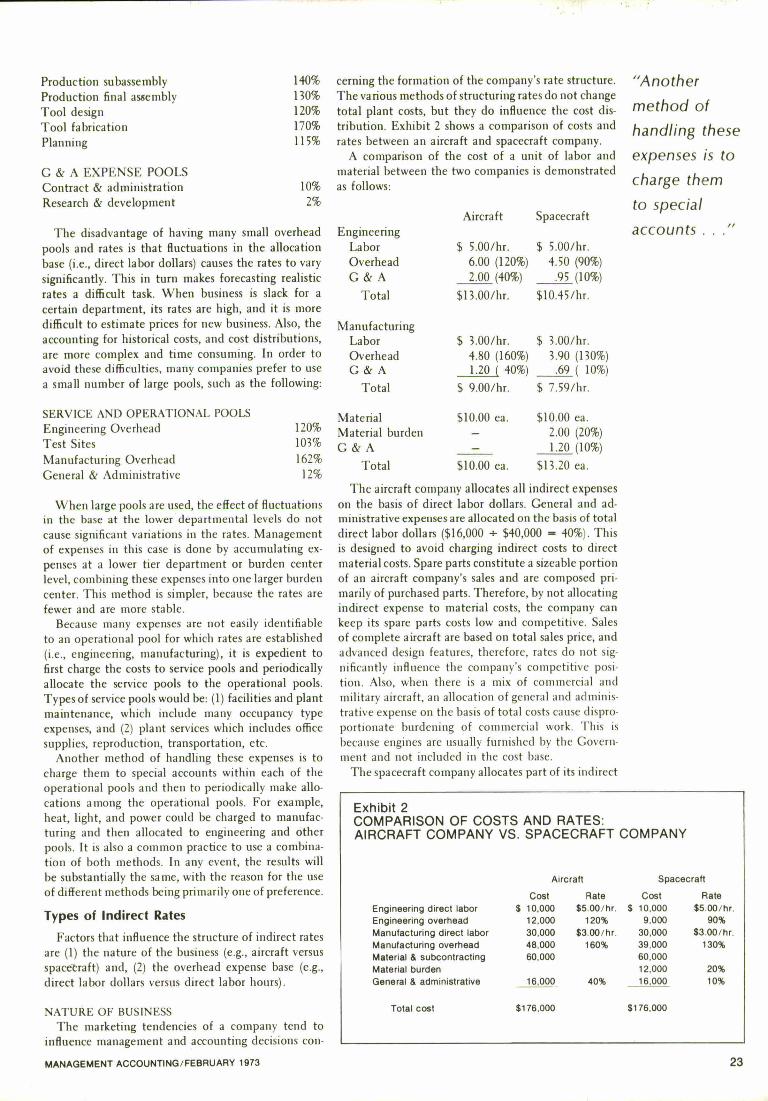

cerning the formation of the company's rate structure. "AnotherThe various methods of structuring rates do not change

method oftotal plant costs, but they do influence the cost dis-tribution. Exhibit 2 shows a comparison of costs and handling theserates between an aircraft and spacecraft company.

A comparison of the cost of a unit of labor and expenses is tomaterial between the two companies is demonstrated

charge thema s follows:

to specialAircraft Spacecraft

Engineering accounts ..."Labor $ 5.00 /hr. $ 5.00 /hr.Overhead 6.00 (120 %) 4.50 (90 %)G & A 2.00 (40 %) .95 (10 %)

Total $13.00 /hr. $10.45 /hr.

ManufacturingLabor $ 3.00 /hr. $ 3.00 /hr.Overhead 4.80 (160 %) 3.90 (130 %)G & A 1.20 ( 40 %) .69 ( 10 %)

Total $ 9.00 /hr. $ 7.59/hr.

SERVICE AND OPERATIONAL POOLS Material $10.00 ea. $10.00 ea.Engineering Overhead 120% Material burden

—

2.00 (20 %)Test Sites 103% G & A

—

1.20 (10 %)Manufacturing Overhead 162% Total $10.00 ea. $13.20 ea.General & Administrative 12%

When large pools are used, the effect of fluctuationsin the base at the lower departmental levels do notcause significant variations in the rates. Managementof expenses in this case is done by accumulating ex-penses at a lower tier department or burden centerlevel, combining these expenses into one larger burdencenter. This method is simpler, because the rates arefewer and are more stable.

Because many expenses are not easily identifiableto an operational pool for which rates are established(i.e., engineering, manufacturing), it is expedient tofirst charge the costs to service pools and periodicallyallocate the service pools to the operational pools.Types of service pools would be: (1) facilities and plantmaintenance, which include many occupancy typeexpenses, and (2) plant services which includes officesupplies, reproduction, transportation, etc.

Another method of handling these expenses is tocharge them to special accounts within each of theoperational pools and then to periodically make allo-cations among the operational pools. For example,heat, light, and power could be charged to manufac-turing and then allocated to engineering and otherpools. It is also a common practice to use a combina-tion of both methods. In any event, the results willbe substantially the same, with the reason for the useof different methods being primarily one of preference.

Types of Indirect Rates

Factors that influence the structure of indirect ratesare (1) the nature of the business (e.g., aircraft versusspacecraft) and, (2) the overhead expense base (e.g.,direct labor dollars versus direct labor hours).

NATURE OF BUSINESSThe marketing tendencies of a company tend to

influence management and accounting decisions con-

The aircraft company allocates all indirect expenseson the basis of direct labor dollars. General and ad-ministrative expenses are allocated on the basis of totaldirect labor dollars ($16,000 + $40,000 — 40 %). Thisis designed to avoid charging indirect costs to directmaterial costs. Spare parts constitute a sizeable portionof an aircraft company's sales and are composed pri-marily of purchased parts. Therefore, by not allocatingindirect expense to material costs, the company cankeep its spare parts costs low and competitive. Salesof complete aircraft are based on total sales price, andadvanced design features, therefore, rates do not sig-nificantly influence the company's competitive posi-tion. Also, when there is a mix of commercial andmilitary aircraft, an allocation of general and adminis-trative expense on the basis of total costs cause dispro-portionate burdening of commercial work. This isbecause engines are usually furnished by the Govern-ment and not included in the cost base.

The spacecraft company allocates part of its indirect

Exhibit 2COMPARISON OF COSTS AND RATES:AIRCRAFT COMPANY VS. SPACECRAFT COMPANY

Aircra ft Spacecraft

Cost Rate Cost RateEngineeri ng di rect labor $ 10,000 $5.00 /hr. $ 10,000 $5.00 /hr.Eng ineer i ng overhead 12,000 120% 9,000 90%Manufac tur i ng d i rec t labor 30,000 $3.00 /hr. 30,000 $3.00 /hr.Manufac tu r i ng overhead 48,000 160% 39,000 130%Material & subc on t ract i ng 60,000 60,000Mater i al bu rden 12,000 2 0 %

General & adm ini strati ve 16.000 40% 16,000 10%

Total cost $176,000 $176,000

MANAGEMENT ACCOUNTING/FEBRUARY 1973 23

"Indirect labor,

payrollexpenses, andfringe benefits

usually relateto direct labor

dollars."

expense to material and subcontract direct costs. Gen-eral and administrative expenses are allocated on thebasis of total costs (direct labor, overhead, mate-rial /subcontracting and material burden) which pro-duces a lower rate ($16,000 + $160,000 — 10%). Theprinciple sales of the company are in the form of itsengineering capabilities; therefore, the cost of an engi-neering hour must be competitive. Although the com-pany does get involved in hardware production, sparessales are low, and the company is usually 'locked in"on its products because of its engineering capabilities.

OVERHEAD EXPENSE BASEOverhead expenses are commonly distributed as a

percentage of direct labor dollars; however, some firmsuse a percentage rate based on direct labor hours. Thisis shown by the following examples:

Expense Base RateEngineering Direct labor

overhead dollars 120%Engineering Direct labor

overhead hours $6.00 /hrMaterial handling Direct material

expense & sub - contractdollars 12%

G &A Total costs 10%G &A Direct labor

dollars 50%G &A Direct labor

hours $1.10 /hr

The percentage methods have the following advan-tages and disadvantages:

Advantages1. Fluctuations in expense dollars do not "appear"

to affect the rate significantly, for example:

Before Afterchange change

Overhead expense $1,200,000 $1,240,000Direct labor dollars 1,000,000 1,000,000Direct labor hours 200,000 200,000Rate — percent 120% 124%Rate — dollars per hour $6.00 /hr. $6.20 /hr

A four percent increase appears less significant thana 20 cent per hour increase.Since direct labor dollar escalation trends are sig-nificantly higher than for overhead trends, theeffect of adverse fluctuations in either the directlabor or overhead expense will tend to be offsetby the difference in escalation trends.Percentages are easier to compare between depart-ments or companies than are the rates per hour.

Disadvantages1. If most of the overhead expense items are not

directly related to direct labor dollars, but ratherto direct labor hours, headcount, floorspace, orsome other identifiable relationship, then the useof percentages for management purposes is mis-leading.

2. Since direct labor rates normally escalate at a

higher rate than other costs, judging fluctuationsof other expenses in relation to direct labor dollarswill result in distortions.

Forecasting Indirect Expense Rates

Forecasted rates are used for bidding and cost man-agement purposes. However, there are two significantproblems in forecasting: (1) determining the futuresales in terms of units to be used for establishing thebase for each indirect expense pool (i.e., direct labordollars, cost of sales, etc.), and (2) the cost of futureexpenses (i.e., labor, material, taxes, etc.). Commonly,seat -of- the -pants forecasting is done by starting withthe current rates and adjusting them for knownchanges, such as tax increases, union agreements, etc.,and ignoring the sales base and the other effects offuture costs. Today, most major concerns attempt tobe more exacting in their estimates.

Forecasting the base of each indirect expense poolrequires a determination of future sales, based on firm,as well as anticipated business. The value of futuresales can be developed on a bottom -up or top -downbasis. Bottom -up estimates are used when hardwarequantities for current products are estimated (i.e.,number of airplanes, missiles, etc.). Then manhoursand materials can be estimated using statistical meanssuch as learning curves and other historical costs andproviding for anticipated escalation trends. Bottom -upestimating, although more exacting, is time consumingand the least preferred methods by most people. Top -down estimates usually consider cost escalation in agross manner. The base for each overhead pool (i.e.,engineering direct labor, etc.). is usually determinedon a statistical basis.