Embed Size (px)

Citation preview

Looking back, the times of UPAGovernment experienced a darkphase where the fiscal deficit,the revenue deficit and thecurrent account deficit wasconsiderably high, and hencethe country was suffering fromtremendous amount of inflation.

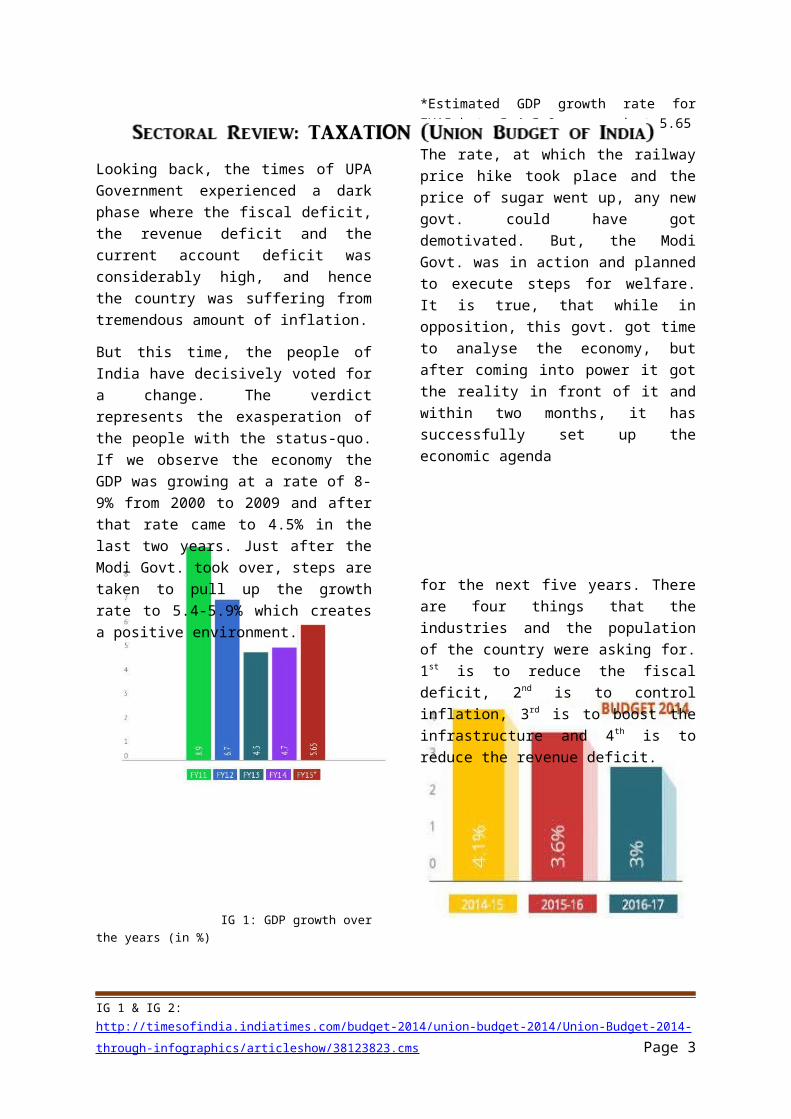

But this time, the people ofIndia have decisively voted fora change. The verdictrepresents the exasperation ofthe people with the status-quo.If we observe the economy theGDP was growing at a rate of 8-9% from 2000 to 2009 and afterthat rate came to 4.5% in thelast two years. Just after theModi Govt. took over, steps aretaken to pull up the growthrate to 5.4-5.9% which createsa positive environment.

IG 1: GDP growth overthe years (in %)

*Estimated GDP growth rate forFY15 bet. 5.4-5.9 averaged at 5.65

The rate, at which the railwayprice hike took place and theprice of sugar went up, any newgovt. could have gotdemotivated. But, the ModiGovt. was in action and plannedto execute steps for welfare.It is true, that while inopposition, this govt. got timeto analyse the economy, butafter coming into power it gotthe reality in front of it andwithin two months, it hassuccessfully set up theeconomic agenda

for the next five years. Thereare four things that theindustries and the populationof the country were asking for.1st is to reduce the fiscaldeficit, 2nd is to controlinflation, 3rd is to boost theinfrastructure and 4th is toreduce the revenue deficit.

IG 1 & IG 2: http://timesofindia.indiatimes.com/budget-2014/union-budget-2014/Union-Budget-2014-through-infographics/articleshow/38123823.cms Page 3

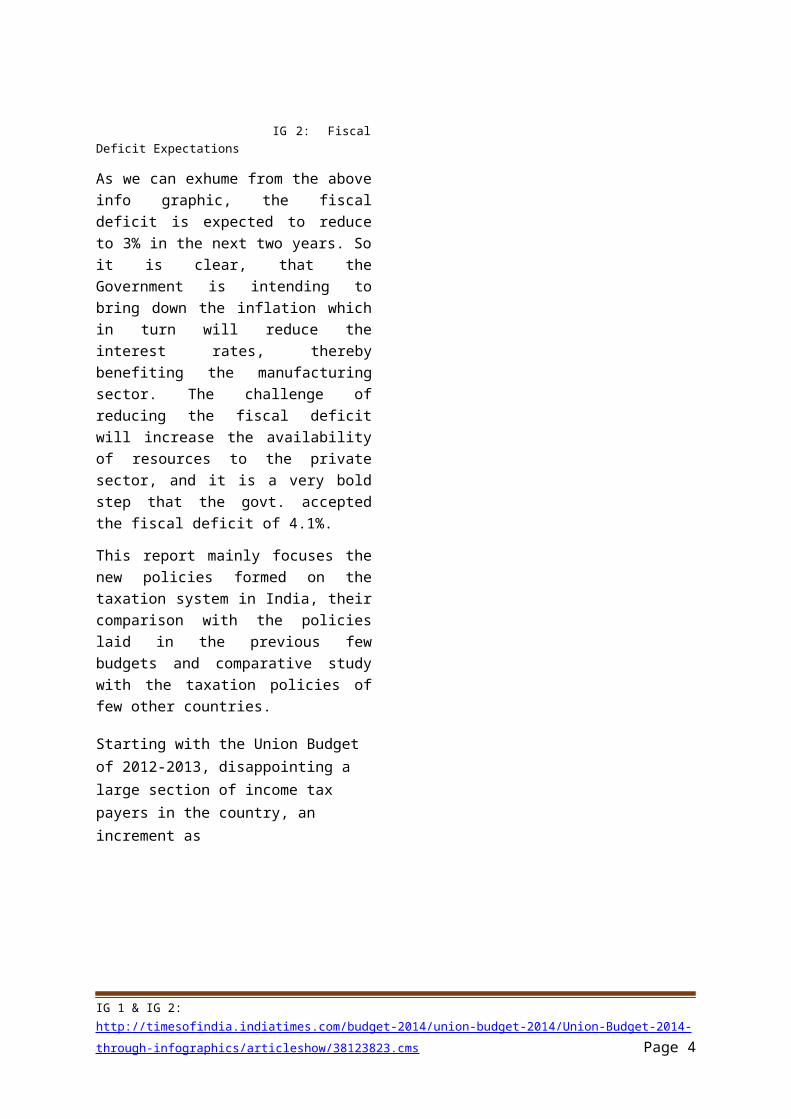

IG 2: FiscalDeficit Expectations

As we can exhume from the aboveinfo graphic, the fiscaldeficit is expected to reduceto 3% in the next two years. Soit is clear, that theGovernment is intending tobring down the inflation whichin turn will reduce theinterest rates, therebybenefiting the manufacturingsector. The challenge ofreducing the fiscal deficitwill increase the availabilityof resources to the privatesector, and it is a very boldstep that the govt. acceptedthe fiscal deficit of 4.1%.

This report mainly focuses thenew policies formed on thetaxation system in India, theircomparison with the policieslaid in the previous fewbudgets and comparative studywith the taxation policies offew other countries.

Starting with the Union Budget of 2012-2013, disappointing a large section of income tax payers in the country, an increment as

IG 1 & IG 2: http://timesofindia.indiatimes.com/budget-2014/union-budget-2014/Union-Budget-2014-through-infographics/articleshow/38123823.cms Page 4

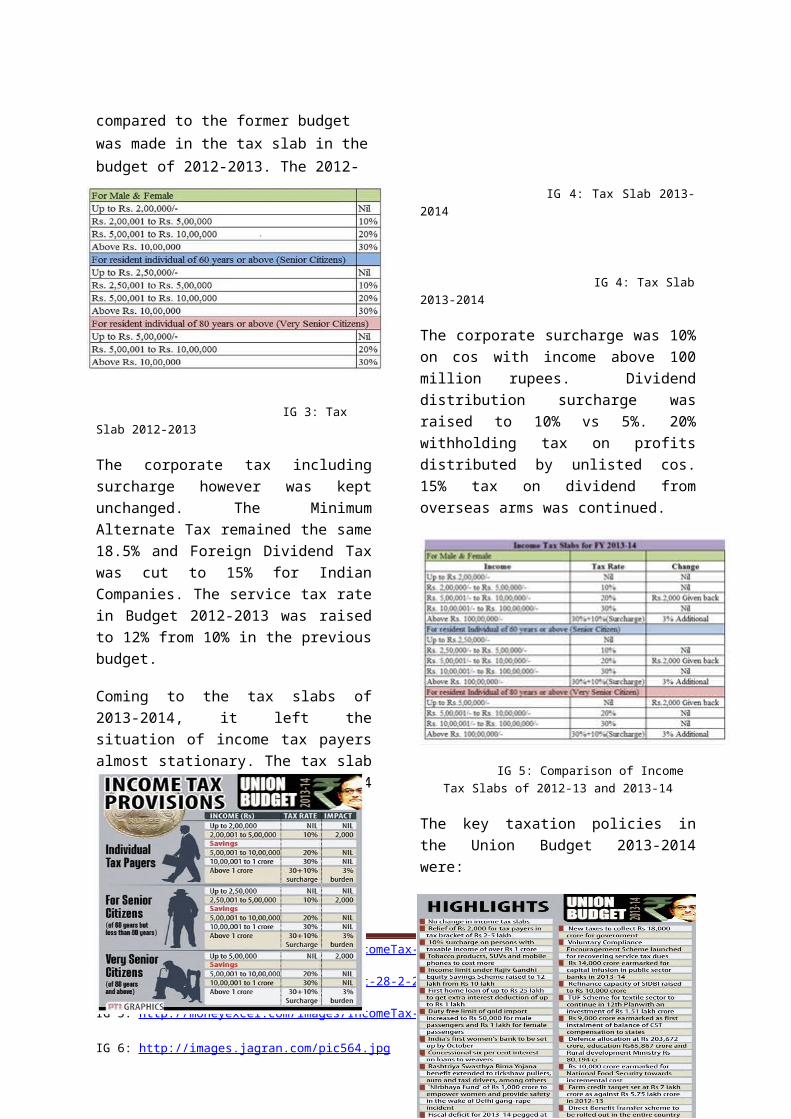

compared to the former budget was made in the tax slab in thebudget of 2012-2013. The 2012-2013 tax slab was as follows:

IG 3: Tax Slab 2012-2013

The corporate tax includingsurcharge however was keptunchanged. The MinimumAlternate Tax remained the same18.5% and Foreign Dividend Taxwas cut to 15% for IndianCompanies. The service tax ratein Budget 2012-2013 was raisedto 12% from 10% in the previousbudget.

Coming to the tax slabs of2013-2014, it left thesituation of income tax payersalmost stationary. The tax slabin the Union Budget 2013-2014was:

IG 4: Tax Slab 2013-2014

IG 4: Tax Slab2013-2014

The corporate surcharge was 10%on cos with income above 100million rupees. Dividenddistribution surcharge wasraised to 10% vs 5%. 20%withholding tax on profitsdistributed by unlisted cos.15% tax on dividend fromoverseas arms was continued.

IG 5: Comparison of IncomeTax Slabs of 2012-13 and 2013-14

The key taxation policies inthe Union Budget 2013-2014were:

IG 3: http://moneyexcel.com/images/IncomeTax-Slab_2012.jpg

IG 4: http://images.jagran.com/9budget-28-2-2013.jpg

IG 5: http://moneyexcel.com/images/IncomeTax-Slab_2013.jpg

IG 6: http://images.jagran.com/pic564.jpg Page 3

IG 6: Key Features of the UnionBudget 2013-2014

The current budget (UnionBudget 2014-2015)gains maximum impression byincreasing the

IG 3: http://moneyexcel.com/images/IncomeTax-Slab_2012.jpg

IG 4: http://images.jagran.com/9budget-28-2-2013.jpg

IG 5: http://moneyexcel.com/images/IncomeTax-Slab_2013.jpg

IG 6: http://images.jagran.com/pic564.jpg Page 3

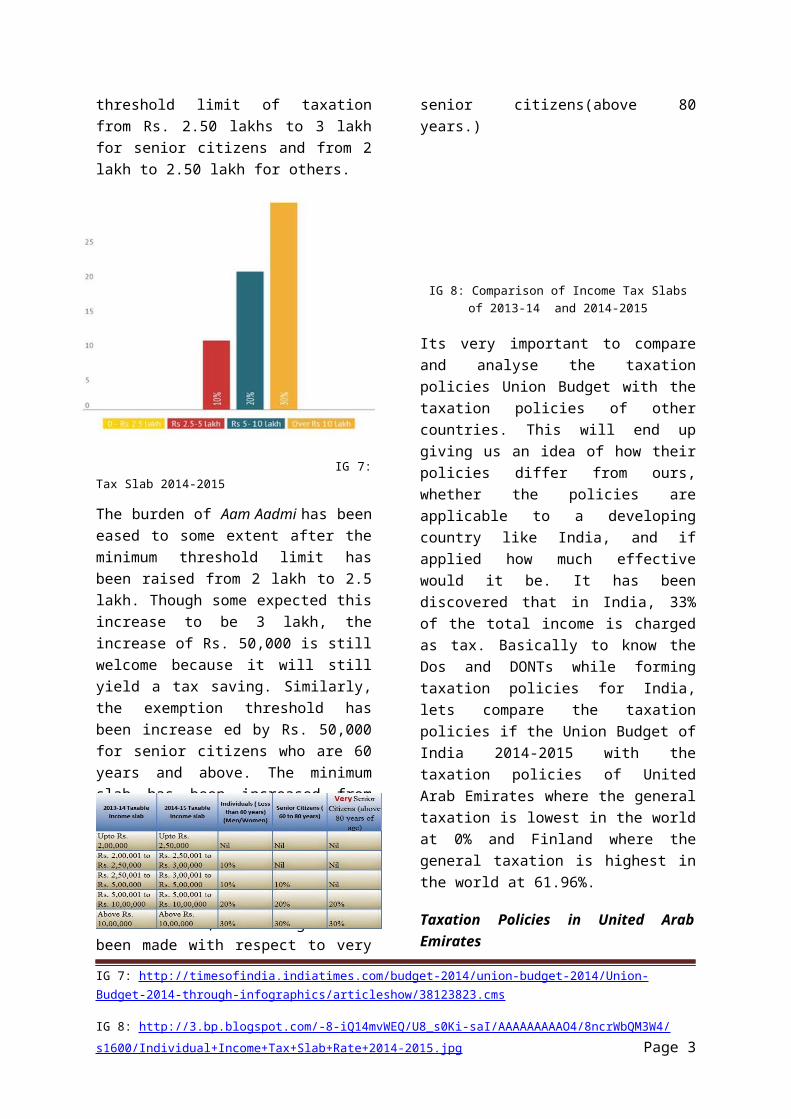

threshold limit of taxationfrom Rs. 2.50 lakhs to 3 lakhfor senior citizens and from 2lakh to 2.50 lakh for others.

IG 7:Tax Slab 2014-2015

The burden of Aam Aadmi has beeneased to some extent after theminimum threshold limit hasbeen raised from 2 lakh to 2.5lakh. Though some expected thisincrease to be 3 lakh, theincrease of Rs. 50,000 is stillwelcome because it will stillyield a tax saving. Similarly,the exemption threshold hasbeen increase ed by Rs. 50,000for senior citizens who are 60years and above. The minimumslab has been increased fromRs. 2.50 lakh to Rs. 3 lakhwhich will provide greaterrelief to the senior citizenswho are mainly dependant onpension, income from depositsetc. However, no changes havebeen made with respect to very

senior citizens(above 80years.)

IG 8: Comparison of Income Tax Slabsof 2013-14 and 2014-2015

Its very important to compareand analyse the taxationpolicies Union Budget with thetaxation policies of othercountries. This will end upgiving us an idea of how theirpolicies differ from ours,whether the policies areapplicable to a developingcountry like India, and ifapplied how much effectivewould it be. It has beendiscovered that in India, 33%of the total income is chargedas tax. Basically to know theDos and DONTs while formingtaxation policies for India,lets compare the taxationpolicies if the Union Budget ofIndia 2014-2015 with thetaxation policies of UnitedArab Emirates where the generaltaxation is lowest in the worldat 0% and Finland where thegeneral taxation is highest inthe world at 61.96%.

Taxation Policies in United ArabEmirates

IG 7: http://timesofindia.indiatimes.com/budget-2014/union-budget-2014/Union-Budget-2014-through-infographics/articleshow/38123823.cms

IG 8: http://3.bp.blogspot.com/-8-iQ14mvWEQ/U8_s0Ki-saI/AAAAAAAAAO4/8ncrWbQM3W4/s1600/Individual+Income+Tax+Slab+Rate+2014-2015.jpg Page 3

The United Arab Emirates is afederation of seven emirateswith autonomous emirate andlocal government. There is noenforced federal income tax legislationfor general business over there.There is an income tax decreein each Emirate, but inpractice, the enforcement ofthese decrees is restrictedto foreign banks and to oilcompanies.

In the emirates of Abu Dhabi,Dubai and Sharjah, foreignbanks are taxed at 20% of theirtaxable income. The tax isrestricted to the taxableincome which is earned ordeemed to be earned in thatparticular Emirate. OilCompanies (which include anychargeable person that deals inoil or right to oil both off-shore and on-shore) pay a flatrate of 55 percent on theirtaxable income in Dubai and 50percent in the other Emirates.In addition, they pay royaltieson production.

IG 7: http://timesofindia.indiatimes.com/budget-2014/union-budget-2014/Union-Budget-2014-through-infographics/articleshow/38123823.cms

IG 8: http://3.bp.blogspot.com/-8-iQ14mvWEQ/U8_s0Ki-saI/AAAAAAAAAO4/8ncrWbQM3W4/s1600/Individual+Income+Tax+Slab+Rate+2014-2015.jpg Page 3

In most Emirates Municipal taxes on annual rental paid at 5 percent are levied for residential premises and 1 % for commercial premises.Other local taxes include a 5 percent tax on hotel services and entertainment.Taxation Policies in Finland

Taxation in Finland is carriedout by the State of Finland,mainly through Finnish TaxAdministration, an agency ofMinistry of Finance. FinnishCustoms and Finnish TransportAgency Trafi also collecttaxes. Taxes collected aredistributed to theGovernment,municipalities,church, and social securityinstitution Kela.

The types of taxation inFinland are:

Earned Income Taxes: Earned gross income is taxed by a progressive state tax. and proportional communal taxes paid to municipalities and parishes The permanent residents of Finland have also to pay health insurance contributions, medical care fee and dailyallowance contribution. There is an earned income tax credit for local

taxes, making them slightly progressive despite their fixed rate. The tax-like mandatory insurance fees are withheld from the wages. They are fully credited from the income taxes. Theemployee's pension and unemployment insurance fees have rates varying according to the person's age but they are usually at 4.7% and 0.6%, respectively.

Indirect Income Taxes: There are also indirect tax-like mandatory social security contributions andinsurance fees paid by employer in addition to the gross income. The social security contribution is 2.12% of the gross income. The pension and unemployment insurance fees depend on the age of the employee and the size of the employer, they are usually18.3% and 3.2% of gross income, respectively.

Corporate Tax: The corporate income tax rate is 20.0%. The corporate tax was fully credited in dividendtax before 2004, but because the neutrality requirements by EU, the tax credits allowed for dividends are now more

[1] http://www.independent.ie/business/world/finland-to-lower-corporate-tax-rate-by-45pc-29146886.html

[2] https://www.vero.fi/en-US/Precise_information/Value_added_tax/Changes_in_VAT_on_1_January_2013%2825751%29 Page 9

complex. The corporate taxwas lowered from 24.5% to 20.0% in January 2014[1].

Dividend and Capital Gain Taxes: The income from dividends, rents, andcapital gains are taxed with investment income tax. The investment income is taxed at fixed rate of 30%or 32% for income that exceeds 50 000 euro. Whether listed or unlistedlimited company, at least 30% of dividends received are categorized as tax free income. Rest of the dividends received is categorized as capital income from listed limitedcompanies and as capital income and/or earned income from unlisted limited companies.

Property Tax: Municipal property taxes are low, since municipalities mostly meet their funding needs via direct income taxes and state subsidies.Tax rates are higher for leisure properties like summer cottages. Property taxes are levied annually on present market value. General rates are 0.60–1.35%, 0.32-0.75% on regular housing and 0.50-1.00% on leisure properties. First-time home buyers home are exempt.

VAT & Excise Taxes: VAT islevied at a standard rate of 24% (January 2013), andtwo reduced rates of 14% on food, restaurant services, catering services and animal feed, and 10% on books, pharmaceutical products, services creating opportunities for physicalexercise, passenger transportation and accommodation[2].

[1] http://www.independent.ie/business/world/finland-to-lower-corporate-tax-rate-by-45pc-29146886.html

[2] https://www.vero.fi/en-US/Precise_information/Value_added_tax/Changes_in_VAT_on_1_January_2013%2825751%29 Page 10

Excise taxes are in place for alcohol, tobacco, sweets, lotteries, insurances, transport fuels and automobiles(2011). Pharmacies pay only theexcise tax from their yearly income; no VAT is levied on medications. There is a tax credit for pharmacies that keepsubsidiary pharmacies (sivuapteekki). The aim of this policy is to support keeping pharmacies in sparsely populated regions[3].

Pension Fees: The mandatory pension fees arepaid directly to the pension insurance company selected by the employer or entrepreneur. The voluntary pension insurance fees or transfers to a personal pension account are credited in earned income taxation up to 5000 € per year.

Church Tax: Taxes are collected from members of the two official churches, Evangelical Lutheran Church of Finland and Finnish Orthodox Church, and two country-wide Lutheran parishes; the German parish in Finland and Olaus Petri parish Olaus Petri parish for citizens of Sweden living in Finland. The tax rates

vary from 1 to 2% of earned income. Persons that are not members of these churches are exempted from paying. A small percentage (2.55% asof 2011[4]) of corporate taxes is also distributed to parishes. Corporates pay church tax regardless of corporations' religiousstatus.

Taxation of Non residents

Anyone who has arrived inFinland and stayed longer than6 months will become, from TaxAdministrator's view, aresident. The residents'worldwide income is subject toFinnish tax, so that nodistinction exists between thesource country. Non-residentsare subjected only to taxationof Finnish-sourced income[5].

ID No. & Tax No.: Personsworking in Finland for ashort period can get theirFinnish personal ID at thetax office. The FinnishTax Administration isentitled to enterinformation into thePopulation Register Systemand distribute identitycodes jointly with LocalRegister Offices if thematter concerns foreigners

[3] http://www.fimea.fi/apteekit/apteekkimaksu

[4] http://www.vm.fi/vm/fi/10_verotus/03_elinkeinoverotus/01_yhteisovero/index.jsp

[5] http://www.vero.fi/en-US/Individuals/Arriving_in_Finland Page 11

[6] http://www.vero.fi/en-US/Precise_information/International_tax_situations/Finnish_personal_identity_codes_for_shor%2821271%29

who arrive for temporaryperiods, i.e. less thanone year to work inFinland. ID requiresfollowing informationentered to the system:Full name, Date of birth,Sex, Place of birth,Address, Citizenship,Native language andOccupation[6]

Withholding tax for foreign wage earners with special expertise: Under the Act on Withholding Tax for Foreign Wage Earners with Special Expertise (1995), a withholding tax of 35% is levied instead of State income tax on earned income and communal tax. The withholding tax is applied to foreign employees under the following conditions:

the individual becomes resident in Finland at the beginning of the period of employment towhich the Act applies

the pecuniary salary for this employment is at least 5,800 euros a month during the total period of employment towhich the Act applies

his tasks require special expertise

he is not a Finnish national and he has notbeen resident in Finland in the five years preceding the year in which this employment began.

[3] http://www.fimea.fi/apteekit/apteekkimaksu

[4] http://www.vm.fi/vm/fi/10_verotus/03_elinkeinoverotus/01_yhteisovero/index.jsp

[5] http://www.vero.fi/en-US/Individuals/Arriving_in_Finland Page 12

[6] http://www.vero.fi/en-US/Precise_information/International_tax_situations/Finnish_personal_identity_codes_for_shor%2821271%29

A taxpayer is deemed to be a foreign expert for a maximum of48 months from the beginning ofthe employment.The structural change in the Union Budget of India 2014-2015is the willingness to listen. It has clearly been identified that what are the challenges that the economic growth or in that context, business is facing.

It can be said that an open mind and a broad agenda is given. There are many positiveand knotty approaches are thereto which we have to give time and observe whether they work well or not.

Page 13