Embed Size (px)

Citation preview

Introduction The constitution empowers the Federal Government to collect taxes

on income other than agricultural income, taxes on capital value,

customs, excise duties and sales taxes. The Central Board of

Revenue (CBR) and its subordinate departments administer the tax

system. Each of the three principal taxes has a different history

and different set of issues. For a large number of income tax

payers the core of the business process is pre-audit and

assessment by a tax official. This process gives considerable

discretion to tax officials, with potential for abuse. Moreover,

this process is also not tenable as the number of taxpayers

increase. The report is focused on a total overhaul of the

process and organization of income tax. Sales tax is recent and

its process and organization is adjusted to the needs of an

expanding tax base. These are based on self-assessment and

selective audit. Similarly, in customs the accent is on

accelerating and broadening the changes begun in recent years.

Before long, central excise will be subsumed in sales tax.

During the nineties, despite many changes in the tax regime and

introduction of withholding and presumptive taxes, Federal

Government tax to GDP ratio has varied narrowly around eleven

percent. The tax base has grown but still remains narrow and

skewed. The number of income tax filers is around one million. At

less than one per cent of the population, it is a lower

proportion than in many developing countries.

Pakistan’s fiscal crisis is deep and cannot be easily resolved.

Taxes are insufficient for debt service and defense. If the tax

1

to GDP ratio does not increase significantly, Pakistan cannot be

governed effectively, essential public services cannot be

delivered and high inflation is inevitable.

Pakistan’s Taxation System

Federal taxes in Pakistan like most of the taxation systems in

the world are classified into two broad categories, viz., direct

and indirect taxes. A broad description regarding the nature of

administration of these taxes is explained below:

Basic concepts of taxation

The Federal levy, tax, on income (Income Tax) is governed by the

Income Tax Ordinance, 2001 and Income Tax Rules, 2002. It is an

annual charge on the taxable income, income subject to separate charge

and income subject to final tax of a person for a tax year.

Levy of tax on taxable income is divided into two parts:

Fixed Tax on separate block of income; and

Income Tax on taxable income excluding separate block of income

subject of fixed tax.

In this brochure from now onwards taxable income refers to is

taxable income excluding separate block of income subject of fixed tax.

“Taxable Income” means total income reduced by: Donations qualifying for

straight deductions; and

2

Following deductible allowances:

- Zakat paid under the Zakat and Ushr Ordinance, 1980; (Zakat

paid on a debt, the profit of which is chargeable to tax under

the head “Income from Other Sources” is not deductible from total

income. Such Zakat is an admissible deduction against profit on

debt);

- Workers Welfare Fund paid under the Workers Welfare Fund

Ordinance, 1971 (applies to certain specified industrial

establishments); and

- Worker‟s Participation Fund paid under the Companies Profit

(Worker‟s Participation) Act, 1968 (applies to companies only).

“Total Income” is the aggregate of income chargeable to tax under

each of head of income:

“Head of Income” – Under the Income Tax Ordinance, 2001, all

income are broadly divided into following five head of income:

Salary;

Income from property;

Income from business;

Capital gains; and

Income from other sources [like dividend, royalty, profit on

debt, rent from sub-lease of land or building, income from lease

3

of any building together with plant or machinery, prize on bonds,

winnings from a raffle, lottery or crossword puzzle, or a loan,

advance, deposit or gift (subject to certain conditions)].

Different set of rules apply for determination of income

chargeable to tax under each head of income. These are briefly

explained latter in this brochure.

Generally, income under a head of income is the total of the

amounts derived as reduced by the admissible deductions against

such income, if any. Expenditures attributable to exempt income,

income subject to separate charge, income subject to final tax and separate block

of income are deductible against income chargeable to tax as total

income/taxable income.

Chargeable income under each head of income is further dependent

on the residential status of a taxpayer. In case of resident, it is

both Pakistan source income and foreign source income, while in case of

non-resident it is restricted to Pakistan source income only.

“Resident”

An association of persons is resident for a tax year if the control and

management of its affairs is situated wholly or partly in

Pakistan at any time in the year;

A company is resident for a tax year if –

4

- it is incorporated or formed by or under any law in force in

Pakistan;

- the control and management of its affairs is situated wholly in

Pakistan at any time in the year; or

- it is a Provincial Government or a local Government in

Pakistan.

An individual is resident for a tax year if he/she –

- is present in Pakistan for a period of, or periods amounting in

aggregate to, 183 days or more in the tax year; or

- is an employee or official of the Federal Government or a

Provincial Government posted abroad in the tax year.

In order to compute the number of days an individual is present in Pakistan in a tax

year, the following rules apply: -

A part of a day that an individual is present in Pakistan (including the day of arrival in,

and the day of departure from, Pakistan) counts as a whole day of such presence;

However, a day or part of a day where an individual is in Pakistan solely by reason of

being in transit between two different places outside Pakistan does not count as a day

present in Pakistan.

The following days in which an individual is wholly or partly present in Pakistan count as

a whole day of such presence:-

- a public holiday;

- a day of leave, including sick leave;

- a day that the individual’s activity in Pakistan is interrupted because of a strike, lock-

out or delay in receipt of supplies; or

5

- a holiday spent by the individual in Pakistan before, during or after any activity in

Pakistan.

“Non-Resident” – An association of persons, a company and an

individual are non-resident for a tax year if they are not a

resident for that year.

“Pakistan source income” is defined in section 101 of the Income

Tax Ordinance, 2001, which caters for incomes under different

heads and situations. Some of the common Pakistan source incomes

are as under: -

Salary received from any employment exercised in Pakistan

wherever paid;

Salary paid by, or on behalf of, the Federal Government, a

Provincial Government, or a

local Government in Pakistan, wherever the employment is

exercised;

Dividend paid by resident company;

Profit on debt paid by a resident person;

Property or rental income from the lease of immovable property in

Pakistan;

Pension or annuity paid by a resident or permanent establishment

of a non-resident;

“Foreign source income” is any income, which is not a Pakistan

source income.

“Person” means:

6

An individual;

A company or association of persons incorporated, formed, organized or

established in Pakistan or elsewhere;

The Federal Government, a foreign government, a political

subdivision of a foreign government, or public international

organization

“Company” means –

A company as defined in the Companies Ordinance, 1984 (XLVII of

1984);

A body corporate formed by or under any law in force in Pakistan;

A modaraba;

A body incorporated by or under the law of a country outside

Pakistan relating to incorporation of companies;

A trust, a co-operative society or a finance society or any other

society established or constituted by or under any law for the

time being in force;

A foreign association, whether incorporated or not, which the

Board has, by general or special order, declared to be a company

for the purposes of this Ordinance;

A Provincial Government;

A Local Government in Pakistan;

“Association of persons” includes a firm (the relation between

persons who have agreed to share the profits of a business carried

on by all or any of them acting for all), a Hindu undivided

7

family, any artificial juridical person and any body of persons

formed under a foreign law, but does not include a company.

“Tax Year” is a period of twelve months ending on 30th day of

June i.e. the financial year and is denoted by the calendar year

in which the said date falls. For example, tax year for the

period of twelve months from July 01, 2010 to June 30, 2011 shall

be denoted by calendar year 2011 and the period of twelve months

from July 01, 2011 to June 30, 2012 shall be denoted by calendar

year 2012.

Tax year includes special tax year, which means any period of

twelve months (subject to certain conditions and restrictions)

and is denoted by the calendar year relevant to the normal tax

year in which closing date of the special tax year falls. For

example, tax year for the period of twelve months from January

01, 2010 to December 31, 2010 shall be denoted by calendar year

2011 and the period of twelve months from October 01, 2010 to

September 30, 2011 shall be denoted by calendar year 2012.

Income subject to a separate charge, which do not form part of

total income or taxable income and are subject to tax on the

basis of gross income, e.g.:-

Dividend;

Royalty of non-resident;

Fee for technical services of non-resident;

Shipping income of non-resident; and

Air transport income of non-resident.

8

For further details, please refer to our brochure “Income subject to

separate charge, final tax and fixed tax regimes of Income Tax”.

Income subject to Final Tax, which are subject to collection or

deduction of tax at source and such tax collected or deducted at

source is treated as final tax liability in respect of such

income e.g.:

Income arising from salary in respect of:

- Retirement or termination benefits of an employee;

- Arrears of salary of an employee; and

- Flying and submarine allowance of certain employees.

Property income;

- Rental income from house or commercial property

Business income:

- Of certain retailers;

- From services rendered outside Pakistan;

- From construction contracts executed out-side Pakistan;

- Of certain manufacturers of cooking oil or vegetable ghee or

both; and

- Of resident from shipping business.

Capital gains from:

9

- Sale of securities; and

- Sale of shares or assets by a private limited company to

Private Equity and Venture Capital Fund.

For further details, please refer to our brochure “Income subject to

separate charge, final tax and fixed tax regimes of Income Tax”.

“Tax” is the amount computed by applying the applicable rate of

tax, on taxable income, income subject to a separate charge, income

subject to final tax and separate block of income subject to

fixed tax.

Tax payable on taxable income is called Income Tax.

“Income tax” payable on taxable income is:

Gross income tax (Calculated on taxable income by applying

applicable rate of income tax);

Reductions in tax liability (refer to our brochure Tax Reductions,

Rebates and Credits); minus

Foreign tax credit (refer to our brochure Tax Reductions, Rebates and

Credits); minus

Tax credits on donations, investments etc. (refer to our brochure

Tax Reductions, Rebates and Credits); minus

Tax credit on exempt share from association of persons (refer to

our brochure Tax Reductions, Rebates and Credits).

To arrive at the net income tax payable or refundable, income tax

payable determined as above is reduced by:

Advance tax already paid; and

10

Adjustable tax collected or deducted at source.

“Adjustable tax collected or deducted at source” is the amount of

tax collected or deducted at source, other than the tax collected

or deducted at source which is treated as final tax. For further

details refer to our brochures “Collection and Deduction of Tax

at Source” and “Income subject to separate charge, final tax and

fixed tax regimes of Income Tax”

Agricultural Income is chargeable to tax (Agricultural Income Tax)

separately by the respective Provincial Governments and hence is

specifically declared exempt from levy of tax under the Income

Tax Ordinance, 2001. Accordingly such income does not form part

of total income / taxable income.

“Agricultural income” is defined broadly to include direct and

indirect income from land situated in Pakistan used for

agriculture purposes. Rental income for the use of cultivated

land and rent of a building on or in the vicinity of cultivated

land occupied by the cultivator or by the receiver of rental

income from cultivated land are some of the examples of indirect

agriculture income.

Tax Calculation in Pakistan

Income Tax is a Federal levy on income governed by the Income Tax

Ordinance, 2001 consisting of thirteen chapters, 240 sections and

seven schedules along with Income Tax Rules, 2002Income Tax is an

annual tax on total income of a person for a tax year computed in

11

accordance with the provisions of Income Tax Ordinance, 2001.

Every tax year is distinct and independent of any other tax year.

The term “person” is divided in following main categories for the

determination of residential status:

a) An individual

b) A company

c) Small Company

d) An association of persons/Firm

Computation Of Income Tax For Individuals In Pakistan

Under the Income Tax Ordinance 2001, every person whose income is

assessable for any Tax year , will furnish a return of its total

income. The income tax returns may be furnished either by

registered post or by hand to the Income Tax authorities. The

acknowledgement receipt must be taken from the Income Tax

authorities, at the time of filing of Income Tax returns.

Calculation Of Gross Income Tax

Gross income tax for total income can be calculated by applying

the table of rates given for a particular tax year on taxable

income.

12

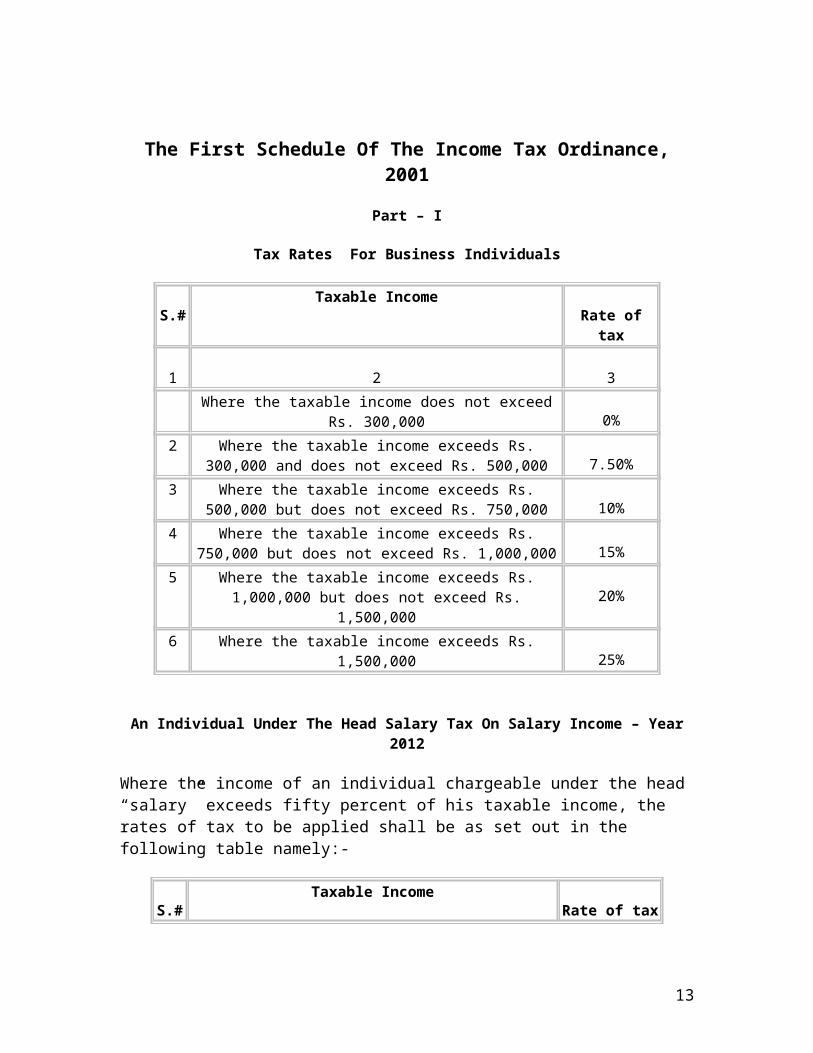

The First Schedule Of The Income Tax Ordinance,2001

Part – I

Tax Rates For Business Individuals

S.#Taxable Income

Rate oftax

1 2 3Where the taxable income does not exceed

Rs. 300,000 0%2 Where the taxable income exceeds Rs.

300,000 and does not exceed Rs. 500,000 7.50%3 Where the taxable income exceeds Rs.

500,000 but does not exceed Rs. 750,000 10%4 Where the taxable income exceeds Rs.

750,000 but does not exceed Rs. 1,000,000 15%5 Where the taxable income exceeds Rs.

1,000,000 but does not exceed Rs.1,500,000

20%

6 Where the taxable income exceeds Rs.1,500,000 25%

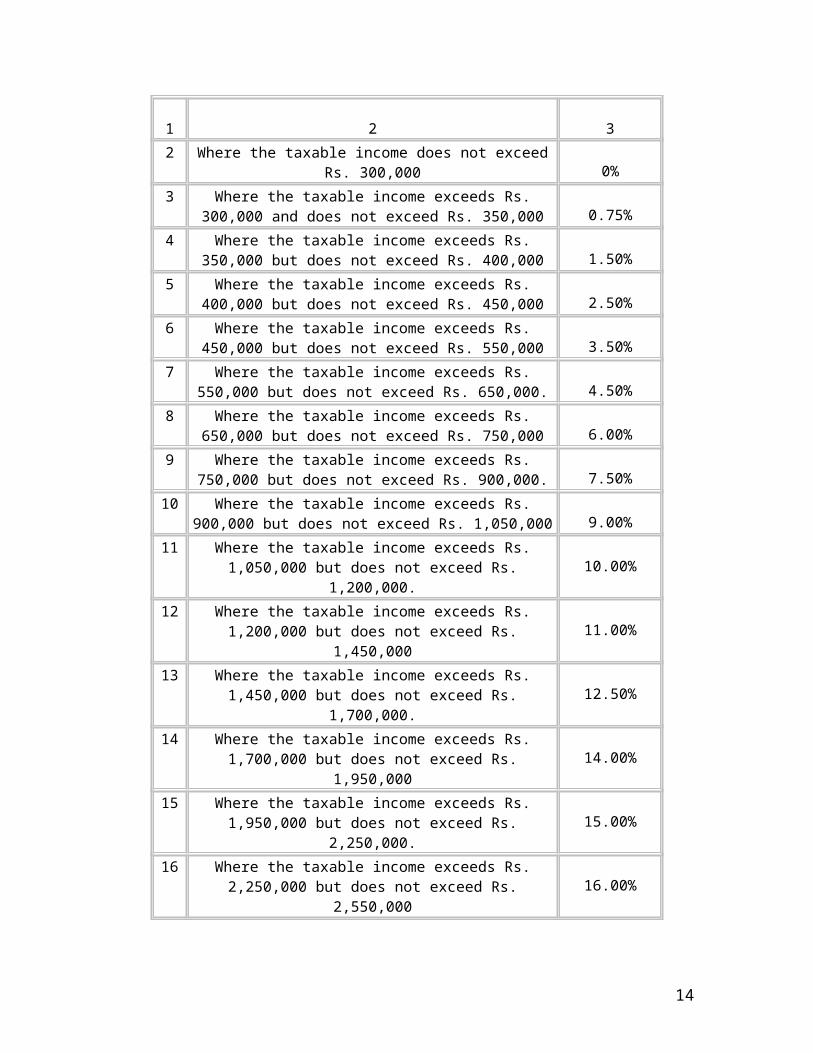

An Individual Under The Head Salary Tax On Salary Income – Year2012

Where the income of an individual chargeable under the head “salary” exceeds fifty percent of his taxable income, the rates of tax to be applied shall be as set out in the following table namely:-

S.#Taxable Income

Rate of tax

13

1 2 32 Where the taxable income does not exceed

Rs. 300,000 0%3 Where the taxable income exceeds Rs.

300,000 and does not exceed Rs. 350,000 0.75%4 Where the taxable income exceeds Rs.

350,000 but does not exceed Rs. 400,000 1.50%5 Where the taxable income exceeds Rs.

400,000 but does not exceed Rs. 450,000 2.50%6 Where the taxable income exceeds Rs.

450,000 but does not exceed Rs. 550,000 3.50%7 Where the taxable income exceeds Rs.

550,000 but does not exceed Rs. 650,000. 4.50%8 Where the taxable income exceeds Rs.

650,000 but does not exceed Rs. 750,000 6.00%9 Where the taxable income exceeds Rs.

750,000 but does not exceed Rs. 900,000. 7.50%10 Where the taxable income exceeds Rs.

900,000 but does not exceed Rs. 1,050,000 9.00%11 Where the taxable income exceeds Rs.

1,050,000 but does not exceed Rs.1,200,000.

10.00%

12 Where the taxable income exceeds Rs.1,200,000 but does not exceed Rs.

1,450,00011.00%

13 Where the taxable income exceeds Rs.1,450,000 but does not exceed Rs.

1,700,000.12.50%

14 Where the taxable income exceeds Rs.1,700,000 but does not exceed Rs.

1,950,00014.00%

15 Where the taxable income exceeds Rs.1,950,000 but does not exceed Rs.

2,250,000.15.00%

16 Where the taxable income exceeds Rs.2,250,000 but does not exceed Rs.

2,550,00016.00%

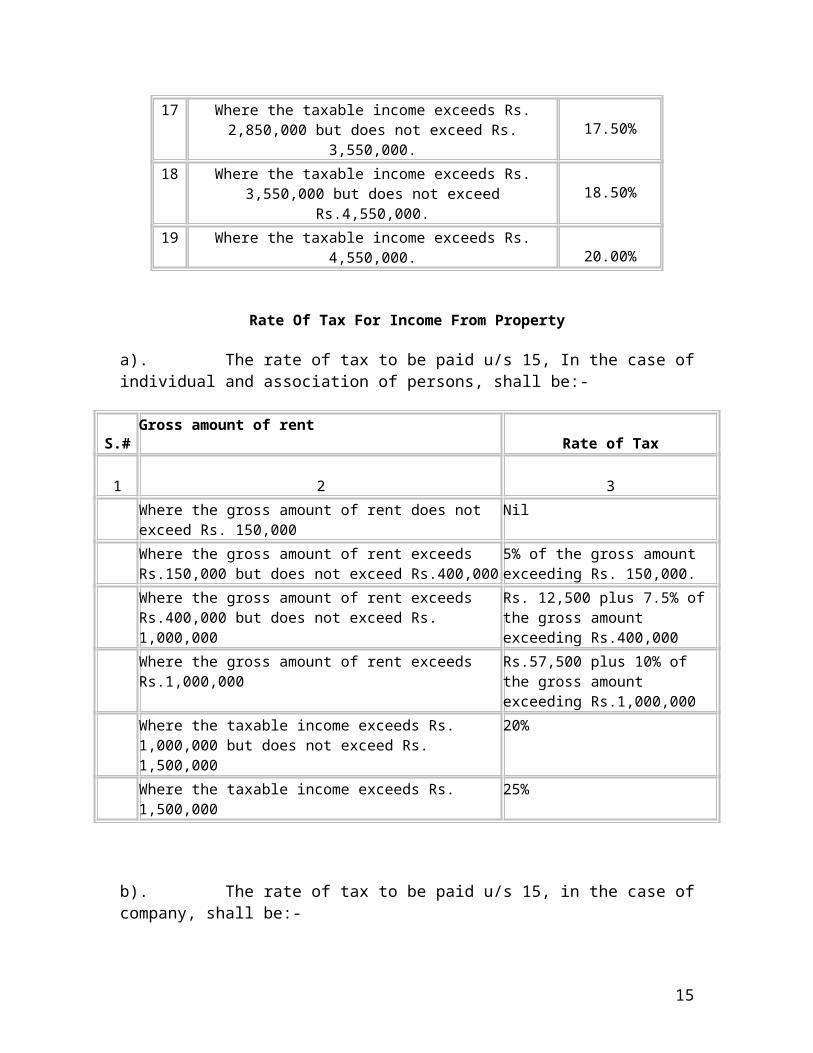

14

17 Where the taxable income exceeds Rs.2,850,000 but does not exceed Rs.

3,550,000.17.50%

18 Where the taxable income exceeds Rs.3,550,000 but does not exceed

Rs.4,550,000.18.50%

19 Where the taxable income exceeds Rs.4,550,000. 20.00%

Rate Of Tax For Income From Property

a). The rate of tax to be paid u/s 15, In the case ofindividual and association of persons, shall be:-

S.#Gross amount of rent

Rate of Tax

1 2 3 Where the gross amount of rent does not

exceed Rs. 150,000Nil

Where the gross amount of rent exceeds Rs.150,000 but does not exceed Rs.400,000

5% of the gross amount exceeding Rs. 150,000.

Where the gross amount of rent exceeds Rs.400,000 but does not exceed Rs. 1,000,000

Rs. 12,500 plus 7.5% of the gross amount exceeding Rs.400,000

Where the gross amount of rent exceeds Rs.1,000,000

Rs.57,500 plus 10% of the gross amount exceeding Rs.1,000,000

Where the taxable income exceeds Rs. 1,000,000 but does not exceed Rs. 1,500,000

20%

Where the taxable income exceeds Rs. 1,500,000

25%

b). The rate of tax to be paid u/s 15, in the case ofcompany, shall be:-

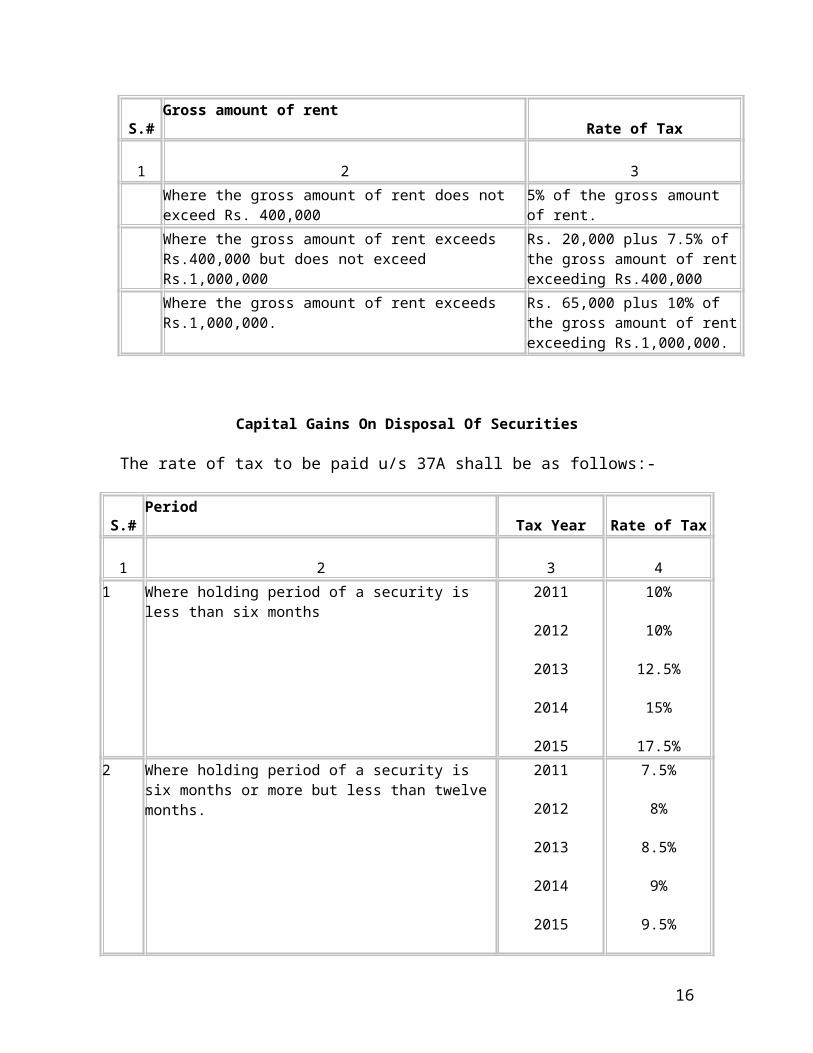

15

S.#Gross amount of rent

Rate of Tax

1 2 3 Where the gross amount of rent does not

exceed Rs. 400,0005% of the gross amount of rent.

Where the gross amount of rent exceeds Rs.400,000 but does not exceed Rs.1,000,000

Rs. 20,000 plus 7.5% of the gross amount of rentexceeding Rs.400,000

Where the gross amount of rent exceeds Rs.1,000,000.

Rs. 65,000 plus 10% of the gross amount of rentexceeding Rs.1,000,000.

Capital Gains On Disposal Of Securities

The rate of tax to be paid u/s 37A shall be as follows:-

S.#Period

Tax Year Rate of Tax

1 2 3 41 Where holding period of a security is

less than six months2011

2012

2013

2014

2015

10%

10%

12.5%

15%

17.5%2 Where holding period of a security is

six months or more but less than twelve months.

2011

2012

2013

2014

2015

7.5%

8%

8.5%

9%

9.5%

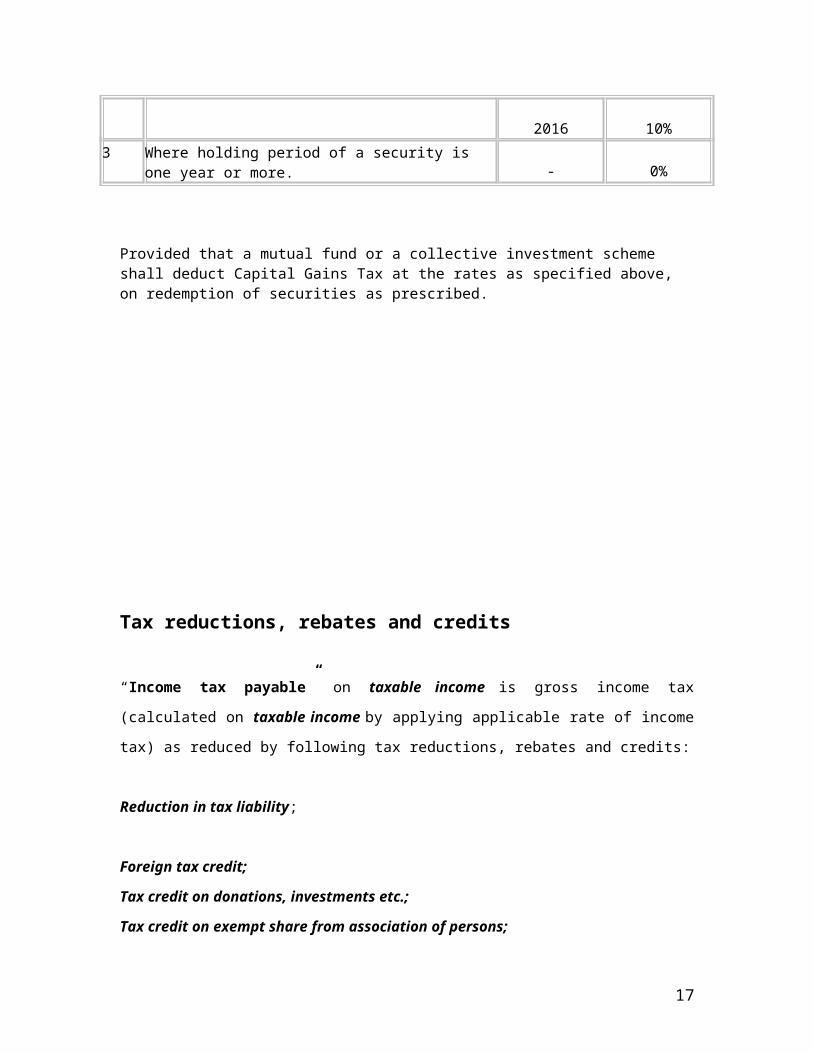

16

2016 10%3 Where holding period of a security is

one year or more. - 0%

Provided that a mutual fund or a collective investment scheme shall deduct Capital Gains Tax at the rates as specified above, on redemption of securities as prescribed.

Tax reductions, rebates and credits

“Income tax payable” on taxable income is gross income tax

(calculated on taxable income by applying applicable rate of income

tax) as reduced by following tax reductions, rebates and credits:

Reduction in tax liability;

Foreign tax credit;

Tax credit on donations, investments etc.;

Tax credit on exempt share from association of persons;

17

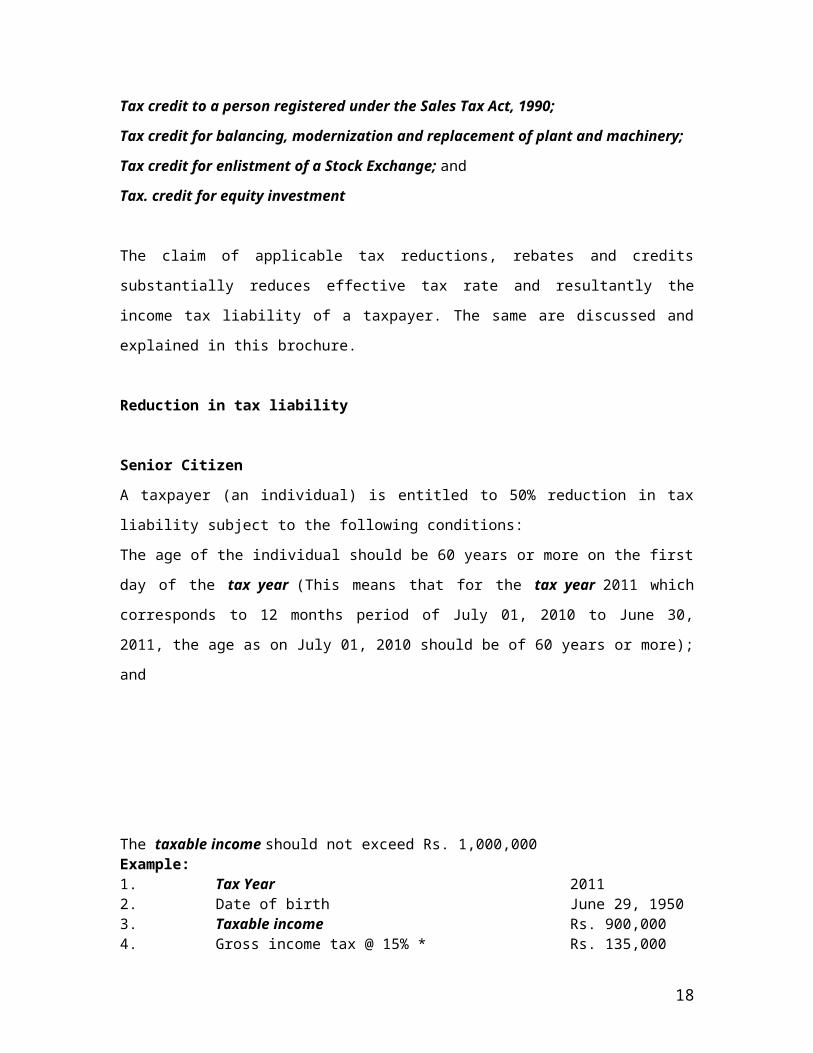

Tax credit to a person registered under the Sales Tax Act, 1990;

Tax credit for balancing, modernization and replacement of plant and machinery;

Tax credit for enlistment of a Stock Exchange; and

Tax. credit for equity investment

The claim of applicable tax reductions, rebates and credits

substantially reduces effective tax rate and resultantly the

income tax liability of a taxpayer. The same are discussed and

explained in this brochure.

Reduction in tax liability

Senior Citizen

A taxpayer (an individual) is entitled to 50% reduction in tax

liability subject to the following conditions:

The age of the individual should be 60 years or more on the first

day of the tax year (This means that for the tax year 2011 which

corresponds to 12 months period of July 01, 2010 to June 30,

2011, the age as on July 01, 2010 should be of 60 years or more);

and

The taxable income should not exceed Rs. 1,000,000 Example:1. Tax Year 2011 2. Date of birth June 29, 19503. Taxable income Rs. 900,000 4. Gross income tax @ 15% * Rs. 135,000

18

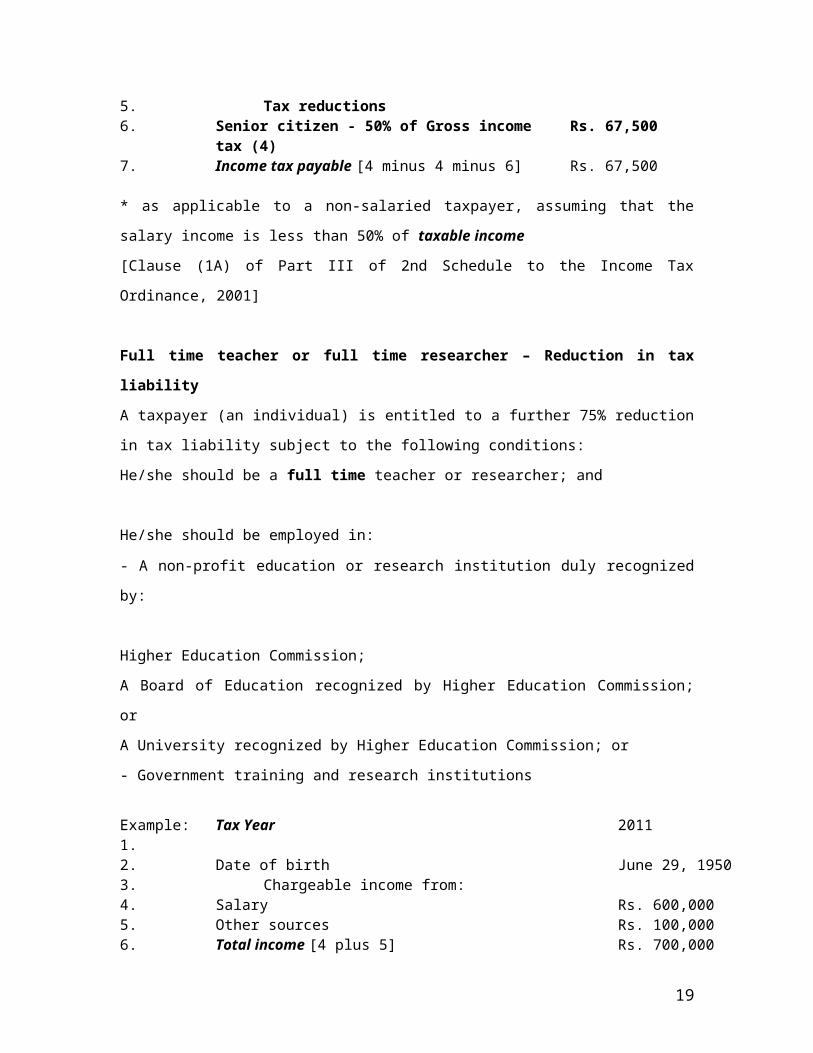

5. Tax reductions 6. Senior citizen - 50% of Gross income

tax (4) Rs. 67,500

7. Income tax payable [4 minus 4 minus 6] Rs. 67,500

* as applicable to a non-salaried taxpayer, assuming that the

salary income is less than 50% of taxable income

[Clause (1A) of Part III of 2nd Schedule to the Income Tax

Ordinance, 2001]

Full time teacher or full time researcher – Reduction in tax

liability

A taxpayer (an individual) is entitled to a further 75% reduction

in tax liability subject to the following conditions:

He/she should be a full time teacher or researcher; and

He/she should be employed in:

- A non-profit education or research institution duly recognized

by:

Higher Education Commission;

A Board of Education recognized by Higher Education Commission;

or

A University recognized by Higher Education Commission; or

- Government training and research institutions

Example: 1.

Tax Year 2011

2. Date of birth June 29, 1950 3. Chargeable income from: 4. Salary Rs. 600,000 5. Other sources Rs. 100,000 6. Total income [4 plus 5] Rs. 700,000

19

7. Deductible allowances 8. Zakat Rs. 10,000 9. Taxable income [6 – 8] Rs. 690,000 10. Gross income tax @ 6% * Rs. 41,400 11. Tax reductions 12. Senior citizen 50% of gross income tax (10) Rs. 20,700 13. Teacher/Researcher (as per calculations

below) Rs. 10,125

14. Income tax payable [10 minus 12 minus 13] Rs. 10,575

as applicable to a salaried taxpayer, since salary income is more than 50% of taxable income

Calculation of 75% tax reduction for a full timeteacher or a full time researcher. 15.

Income from salary Rs. 600,000

16. Gross income tax on salary @ 4.5% Rs. 27,000

17. Senior citizen reduction 50% of gross income tax (16)

Rs. 13,500

18. Income tax payable on salary [16 minus 17]

Rs. 13,500

19. Teacher or Researcher Reduction 75% of income tax payable on salary (18)

Rs. 10,125

[Clause (2) of Part III of 2nd Schedule to the Income TaxOrdinance, 2001]

Yield or profit on Behbood and Pensioners Certificates/Accounts –

Reduction in tax liability

Profit on debt (yield or profit) on Behbood and Pensioners‟

certificates or accounts under the National Savings Scheme are

not subject to deduction of tax at source and are chargeable to

tax as total/taxable income. This is contrary to all other profit on

debts which are subject to deduction of tax at source at the rate

of 10% and the tax so deducted is the final tax, except for a

company.

20

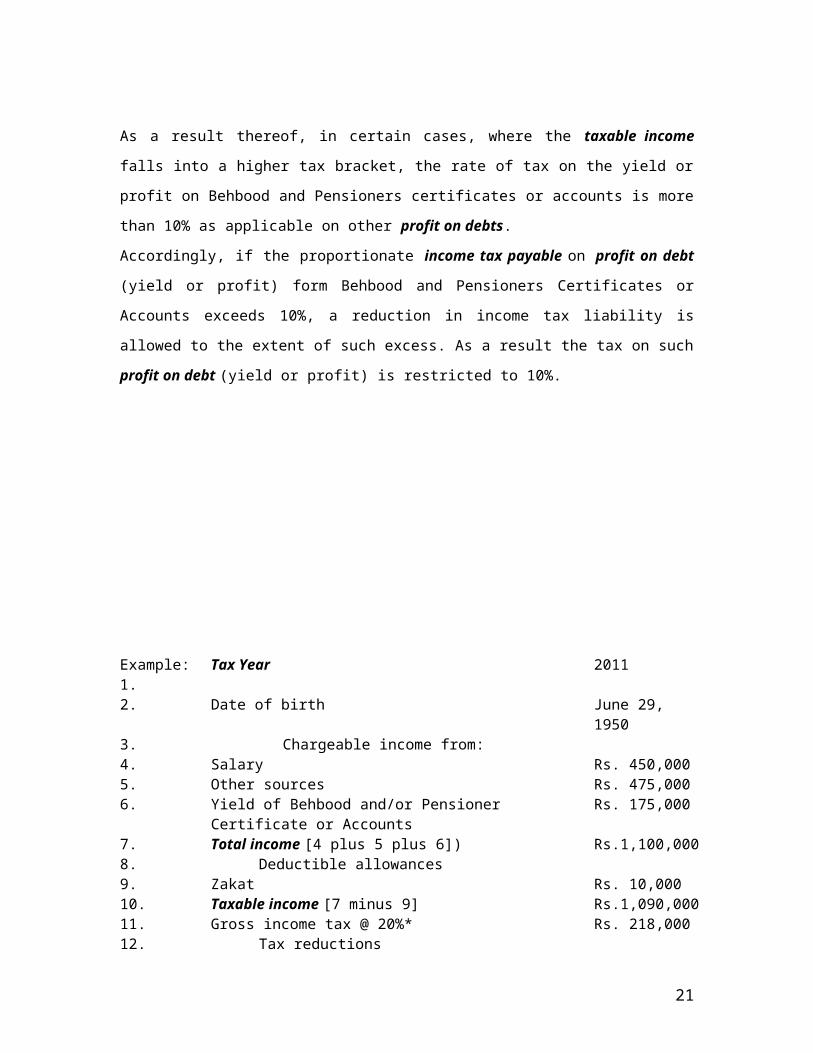

As a result thereof, in certain cases, where the taxable income

falls into a higher tax bracket, the rate of tax on the yield or

profit on Behbood and Pensioners certificates or accounts is more

than 10% as applicable on other profit on debts.

Accordingly, if the proportionate income tax payable on profit on debt

(yield or profit) form Behbood and Pensioners Certificates or

Accounts exceeds 10%, a reduction in income tax liability is

allowed to the extent of such excess. As a result the tax on such

profit on debt (yield or profit) is restricted to 10%.

Example:1.

Tax Year 2011

2. Date of birth June 29, 1950

3. Chargeable income from: 4. Salary Rs. 450,000 5. Other sources Rs. 475,000 6. Yield of Behbood and/or Pensioner

Certificate or Accounts Rs. 175,000

7. Total income [4 plus 5 plus 6]) Rs.1,100,0008. Deductible allowances 9. Zakat Rs. 10,000 10. Taxable income [7 minus 9] Rs.1,090,00011. Gross income tax @ 20%* Rs. 218,000 12. Tax reductions

21

13. Senior citizen **Nil 14. Teacher/researcher ***Nil 15. On Yield or Profit of Behbood and/or

Pensioner Certificates or Accounts (as percalculations below)

Rs. 17,500

16. Income tax payable [11 minus 13 minus 14 minus 15]

Rs. 200,500

* As applicable to a non-salaried taxpayer, since salary income is less than 50% of taxable income ** Since, taxable income exceeds Rs. 1,000,000 *** Assuming the taxpayer is not a teacher or researcher

Calculation of Reduction in tax liability on Yield orprofit on Behbood andPensioners Certificates / Accounts 17.

Income tax payable (11) as reduced by senior citizen reduction (13) and teacher orresearcher reduction (14)

Rs. 218,000

18. Proportionate income tax payable on yield or profit ofBehbood and/or Pensioners Certificates or Accounts [17 divided by 10 multiply by 6]

Rs. 35,000

19. Maximum income tax payable atthe rate of 10% on yield or profit of Behbood and/or Pensioners Certificates or Accounts [6 multiply by 10%]

Rs. 17,500

20. Reduction in tax liability onyield or profit on Behbood and/or Pensioners Certificates / Accounts [18 minus 19]

Rs. 17,500

[Clause (5) of Part III of 2nd Schedule to the Income TaxOrdinance, 2001]

Foreign tax credit

22

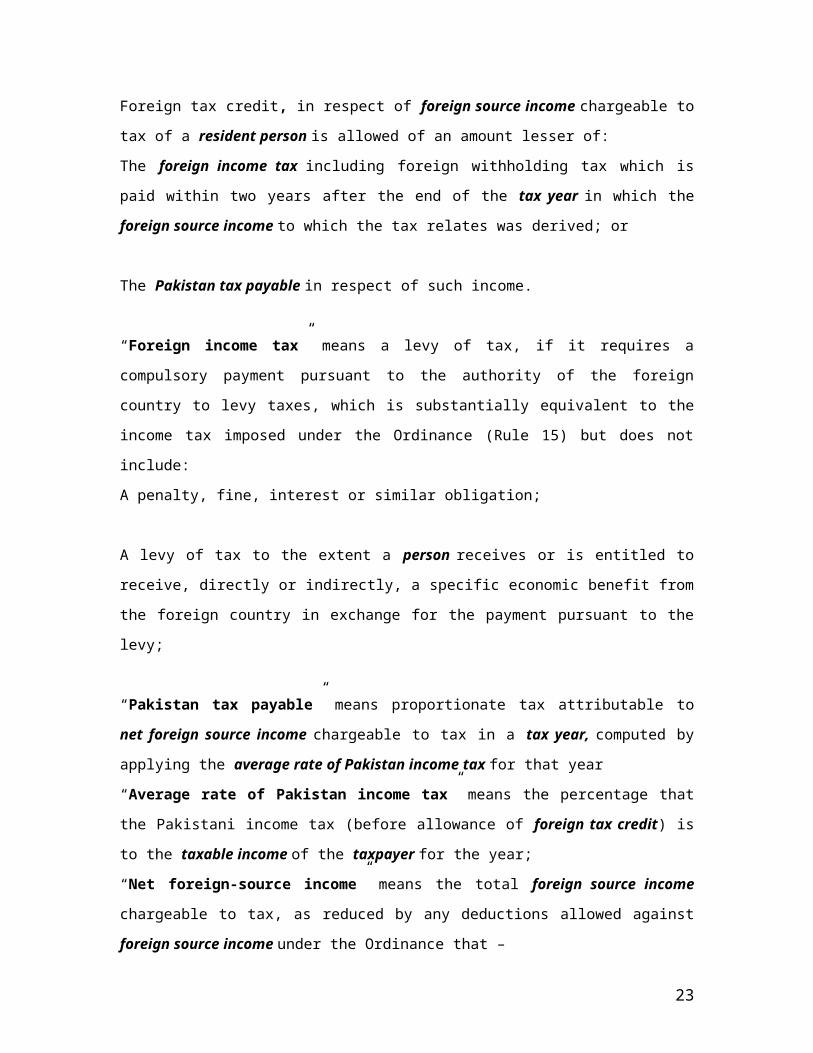

Foreign tax credit, in respect of foreign source income chargeable to

tax of a resident person is allowed of an amount lesser of:

The foreign income tax including foreign withholding tax which is

paid within two years after the end of the tax year in which the

foreign source income to which the tax relates was derived; or

The Pakistan tax payable in respect of such income.

“Foreign income tax” means a levy of tax, if it requires a

compulsory payment pursuant to the authority of the foreign

country to levy taxes, which is substantially equivalent to the

income tax imposed under the Ordinance (Rule 15) but does not

include:

A penalty, fine, interest or similar obligation;

A levy of tax to the extent a person receives or is entitled to

receive, directly or indirectly, a specific economic benefit from

the foreign country in exchange for the payment pursuant to the

levy;

“Pakistan tax payable” means proportionate tax attributable to

net foreign source income chargeable to tax in a tax year, computed by

applying the average rate of Pakistan income tax for that year

“Average rate of Pakistan income tax” means the percentage that

the Pakistani income tax (before allowance of foreign tax credit) is

to the taxable income of the taxpayer for the year;

“Net foreign-source income” means the total foreign source income

chargeable to tax, as reduced by any deductions allowed against

foreign source income under the Ordinance that –

23

Relate exclusively to the derivation of the foreign source income;

and

Are reasonably related to the derivation of foreign source income in

accordance with „apportionment of deductions‟ and the applicable

Rules.

Where, a taxpayer has foreign source income under more than one head

of income or sub-classification of income from business, the foreign

source income, deductible expenditures, net foreign source income, foreign

income tax paid, etc. are determined separately for each head of

income and sub-classifications of income from business (non-

speculation business income and speculation business income) as well.

To claim a foreign tax credit, an application, in the form

prescribed by Rule 16 accompanied by following documents, is

required to be submitted along with the return of income:

Where the foreign tax has been deducted at source:

A declaration by the payer of the income that tax has been

deducted; and

A certified copy of the receipt that the payer has received from

the foreign tax authority for the deducted tax or such secondary

evidence of the deduction acceptable to the Commissioner; and

In any other case the original or a certified copy of the receipt

that the taxpayer has received from the foreign tax authority for

the tax paid.

24

Foreign tax credit or part of a tax credit allowed for a tax year

that can not be adjusted against the income tax payable for that

year is neither refunded nor carried forward to a subsequent tax

year or carried back to a preceding tax year.

Example – See Annexure – I

[Section 103 of the Income Tax Ordinance, 2001]

Tax credit for Charitable donation, Investment in shares and life insurance,

Contribution or premium paid to an Approved Pension Fund and Profit on

debt etc.

A taxpayer is entitled for a tax credit (rebate in income tax

payable) on eligible amounts of Charitable Donation, Investment in Shares,

Investment in Life Insurance (with effect from tax year 2012),

Contribution to an Approved Pension Fund and Profit on Debt Etc. (subject to

certain conditions and restrictions discussed and explained under

the respective headings of eligible amounts).

“Tax Credit” (rebate in income tax payable) is calculated at the

average rate of income tax payable on eligible amounts.

“Average Rate of Income Tax Payable” for the purposes of

calculation of this tax credit is the ratio of tax assessed

(gross income tax as reduced by reductions in tax liability, if any) to

the taxable income. Thus the amount of this tax credit (rebate in

income tax payable) is calculated as under:

Gross income tax Minus Reduction in tax liability Multiply by Total eligible amounts Divided by Taxable income Example

1. Taxable income Rs. 500,000 2. Gross income tax. Rs. 50,000

25

3. Reductions in tax liability (assumed) Rs. 6,000 4. Balance income tax [2 minus 3] Rs. 44,000 5. Total eligible amounts for tax credit Rs. 60,000 6. Tax credit [4 multiply by 5 divided by 1] Rs. 5,280

“Eligible Amount” of charitable donation for the purposes of tax

credit is lower of:

Amount of charitable donations; or

30% of taxable income of an individual or association of persons and 20%

of the taxable income of a company.

Example I Example II 1. Amount of charitable donations Rs. 40,000 Rs. 20,000 2. 30% of taxable income Rs. 30,000 Rs. 30,000 3. Eligible amounts (lower of 1 or 2) Rs. 30,000 Rs. 20,000

The limit of 20% and 30% of the taxable income stated above does

not apply to donations made to Agha Khan Hospital and Medical

College, Karachi “Charitable Donations” for the purpose of tax

credit means amount paid through crossed cheque drawn on a bank

or fair market value of any property given in kind as donation

to:

Any board of education or any university in Pakistan established

by, or under, a Federal or a Provincial law;

Any educational institution, hospital or relief fund established

or run in Pakistan by Federal Government or a Provincial

Government or a local Government; or

A non-profit organization.

26

Non-profit organization is an organization formed or registered under any law

and approved by the Commissioner [under sub-section (26) of section 2], which is

established for religious, educational, charitable, welfare or development purposes, or

for the promotion of an amateur sport.

[Section 61 of the Income Tax Ordinance, 2001]

“Eligible Amount” of Investment in Shares and Life Insurance for the

purposes of tax credit is lower of:

Amount of investment in shares and Life Insurance; or

10% of the taxable income for the tax year 2011 and 15% of the taxable

income with effect from tax year 2012; or

Rs. 300,000 for tax year 2011 and Rs. 500,000 with effect from tax

year 2012.

Example I Example II1. Amount invested in shares and life Insurance Rs. 305,000

Rs. 5,000 2. 10% of taxable income as applicable for 2011 Rs. 15,000

Rs 15,000 3. Maximum eligible amount as applicable for 2011 Rs. 300,000

Rs. 300,000 4. Eligible amount (lower of 1, 2 or 3) Rs. 15,000

Rs. 5,000

“Investment in Shares” for the purpose of tax credit means cost

of acquiring:

New shares offered to public by a public company listed on a

stock exchange in Pakistan, as an original allottee; or

Shares acquired from the Privatization Commission of Pakistan.

27

“Investment in Life Insurance” for the purpose of tax credit

means life insurance premium paid on a policy to a Life Insurance

Company registered by the Securities and Exchange Commission of

Pakistan under the Insurance Ordinance, 2000.

Tax credit for investment in shares is available only to:

An individual (for the tax year 2011);

A resident individual with effect from tax year 2012; and

An association of persons.

Tax credit for investment in Life Insurance is available only to a

resident individual deriving income chargeable to tax under the

head „salary‟ or „income from business‟, and with effect from tax

year 2012.

[Section 62 of the Income Tax Ordinance, 2001]

“Eligible Amount” of contribution or premium paid to an Approved

Pension Fund for the purposes of tax credit is lower of:

Amount of contribution or premium paid by an eligible person to an

Approved Pension Fund; or

20% of the taxable income; or

Rs. 500,000 for tax year 2011 and without any maximum limit with

effect from tax year 2012.

Example I Example II1. Amount of contribution or premium Rs. 205,000

Rs. 5,000 2. 20% of taxable income Rs. 15,500

Rs 15,000

28

3. Maximum eligible amount as applicable for 2011 Rs. 500,000 Rs. 500,000

4. Eligible amount (lower of 1, 2 or 3) Rs. 15,500 Rs. 5,000

“Approved Pension Fund” means approved under the Voluntary

Pension System Rules, 2005.

Eligible Person for tax credit means an individual who is:

A Pakistani National;

Holding a valid National Tax Number (NTN); or Computerized

National Identity Card (CNIC) or National Identity Card for

Overseas Pakistanis (NICOP) issued by the National Database and

Registration Authority; and

Derives income chargeable under the head “salary” or “income from

business”.

Contribution or premium does not include transfer of existing balance

from approved employment pension or annuity scheme or approved

occupational saving scheme to individual pension accounts

maintained with one or more pension fund managers.

[Section 63 of the Income Tax Ordinance, 2001]

“Eligible Amount” of Profit on Debt etc. for the purposes of tax

credit is lower of:

Amount of profit on debt etc.; 50% of the taxable income; or Rs. 750,000

Example I Example II

29

1. Amount of profit etc. Rs. 20,000 Rs. 30,000

2. 50% of taxable income Rs. 25,000 Rs 25,000

3. Maximum eligible amount Rs. 750,000 Rs. 750,000

4. Eligible amount (lower of 1, 2 or 3) Rs. 20,000Rs. 25,000

“Profit on debt etc.” for the purpose of tax credit means profit

or share in rent and share in appreciation of value of house paid

on a loan or advance for the construction of a new house or the

acquisition of house obtained from the following:

Scheduled bank;

Non-banking finance institution regulated by Securities and

Exchange Commission of Pakistan;

Statutory body;

Public company listed on a registered stock exchange in Pakistan;

or

The Federal Government, Provincial Government or a Local

Government.

[Section 64 of the Income Tax Ordinance, 2001]

Surrender of Tax Credit

Where a tax credit for investment in shares has been allowed in

an earlier tax year and the shares are disposed of within 36*

30

months from the date of acquisition, the amount of tax credit

allowed earlier has to be surrendered in the year of disposal.

* This is with effect from tax year 2012. Earlier the time limit

was 12 months.

[Sub-section (3) Section 62 of the Income Tax Ordinance, 2001]

Tax credit for exempt share from association of persons In case of an

individual

Share of profit from an association of persons derived by an

individual is exempt from tax and does not form part of

total/taxable income.

However, where the individual has any income chargeable to tax as

total/taxable income, other than the share of profit from an

association of person, then such share of profit is included in the

total/taxable income for rate purposes, i.e.:

First, the income tax payable is calculated on taxable income inclusive

of exempt share of profits from the association of persons; and

Thereafter, proportionate income tax payable is calculated on the

income chargeable to tax, other than the share of profit from an

association of person.

Technically this is not a tax credit (rebate in income tax

payable) but for the sake of simplicity this is termed as a tax

credit. Accordingly –:

Exempt share of profits from the association of persons is not treated

as exempt income and included in the taxable income; and

31

A tax credit is allowed on such exempt share of profits from the

association of persons calculated like other tax credits by applying

the average rate of income tax.

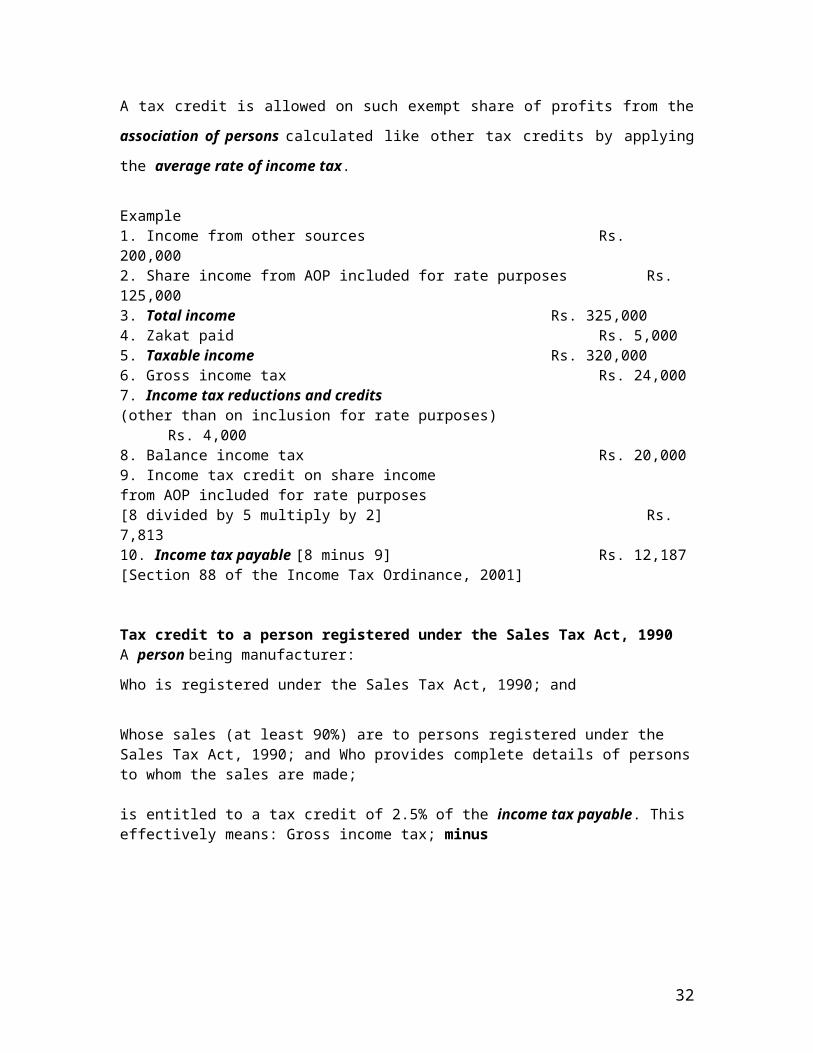

Example 1. Income from other sources Rs. 200,000 2. Share income from AOP included for rate purposes Rs. 125,000 3. Total income Rs. 325,000 4. Zakat paid Rs. 5,000 5. Taxable income Rs. 320,000 6. Gross income tax Rs. 24,0007. Income tax reductions and credits (other than on inclusion for rate purposes)

Rs. 4,000 8. Balance income tax Rs. 20,0009. Income tax credit on share income from AOP included for rate purposes [8 divided by 5 multiply by 2] Rs. 7,813 10. Income tax payable [8 minus 9] Rs. 12,187[Section 88 of the Income Tax Ordinance, 2001]

Tax credit to a person registered under the Sales Tax Act, 1990 A person being manufacturer:

Who is registered under the Sales Tax Act, 1990; and

Whose sales (at least 90%) are to persons registered under the Sales Tax Act, 1990; and Who provides complete details of personsto whom the sales are made;

is entitled to a tax credit of 2.5% of the income tax payable. This effectively means: Gross income tax; minus

32

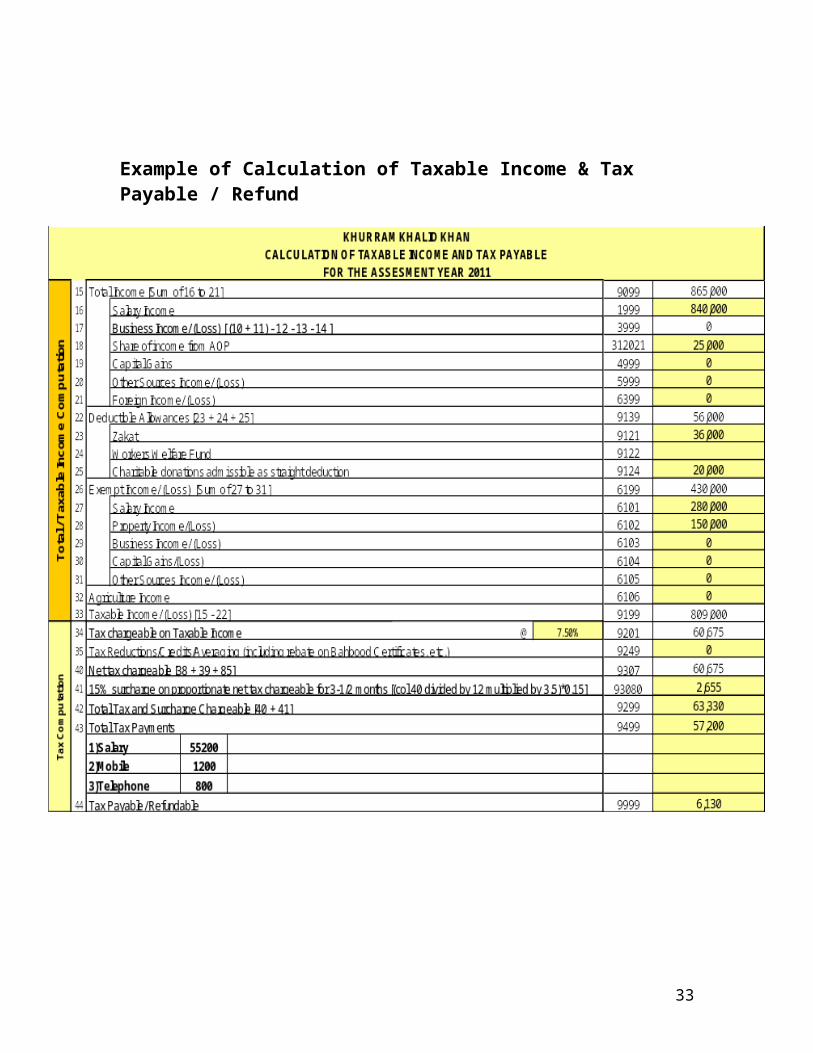

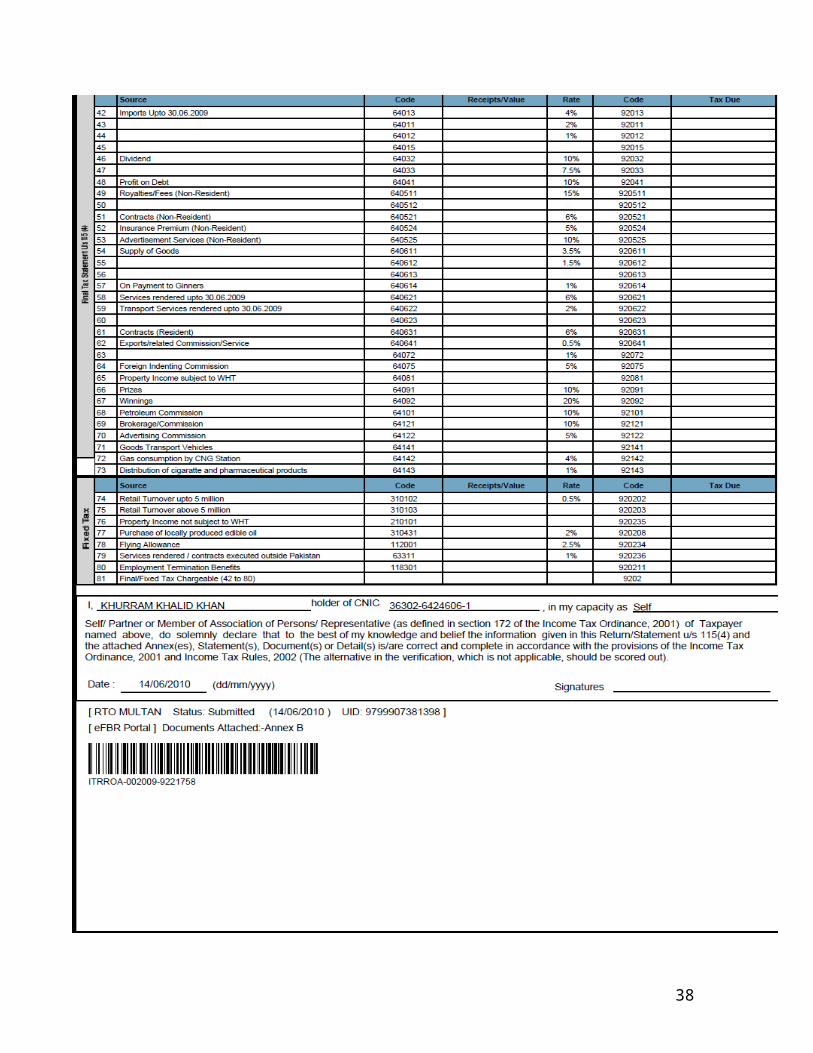

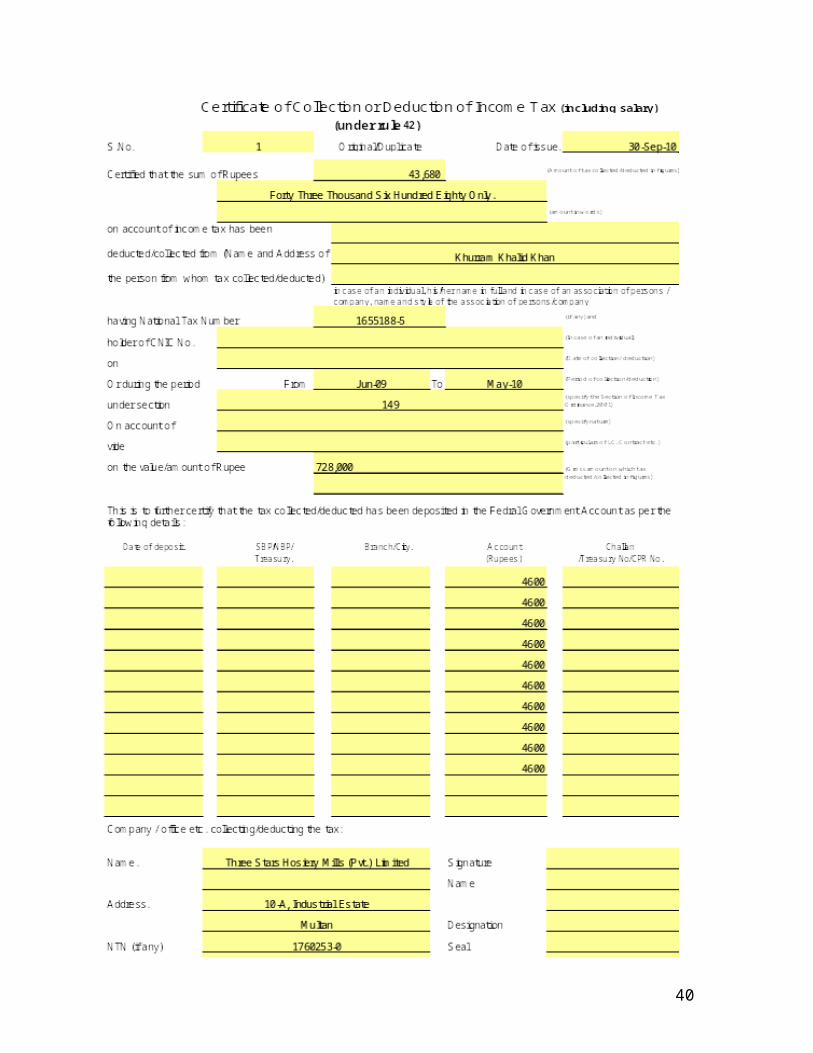

Example of Calculation of Taxable Income & Tax Payable / Refund

33

Calculation of Taxable on Employees and Directors Salaries and Income in ABC (Pvt.) Limited

ABC (Pvt.) Limited (TSH) is liable to deduct tax on thesalaries and wages being paid to its employees and directorsof the company. It has also a system to account for any sortof tax credit and adjustment of taxable income afterobtaining relevant proof from the employees and thedirectors.

There’s a separate department, within the domain of accountsdepartment who calculate tax on salary. The responsibilityof this department is to maintain and keep proper record ofeach taxable employee and director for tax purposes. Thefollowing information is available in the tax file of everyemployee and director.

Copy of computerized national identity card (CNIC) Copy of national tax number (NTN)

A computation of tax showing his salary and otherincome, if any.

Monthly deduction of tax.

Copy of tax payment challan

Proof of tax deductions on mobile, electric, telephonebills.

Proof of any other income.

Final tax calculation sheet

Copy of Income tax deduction certificate, issued by thecompany.

34

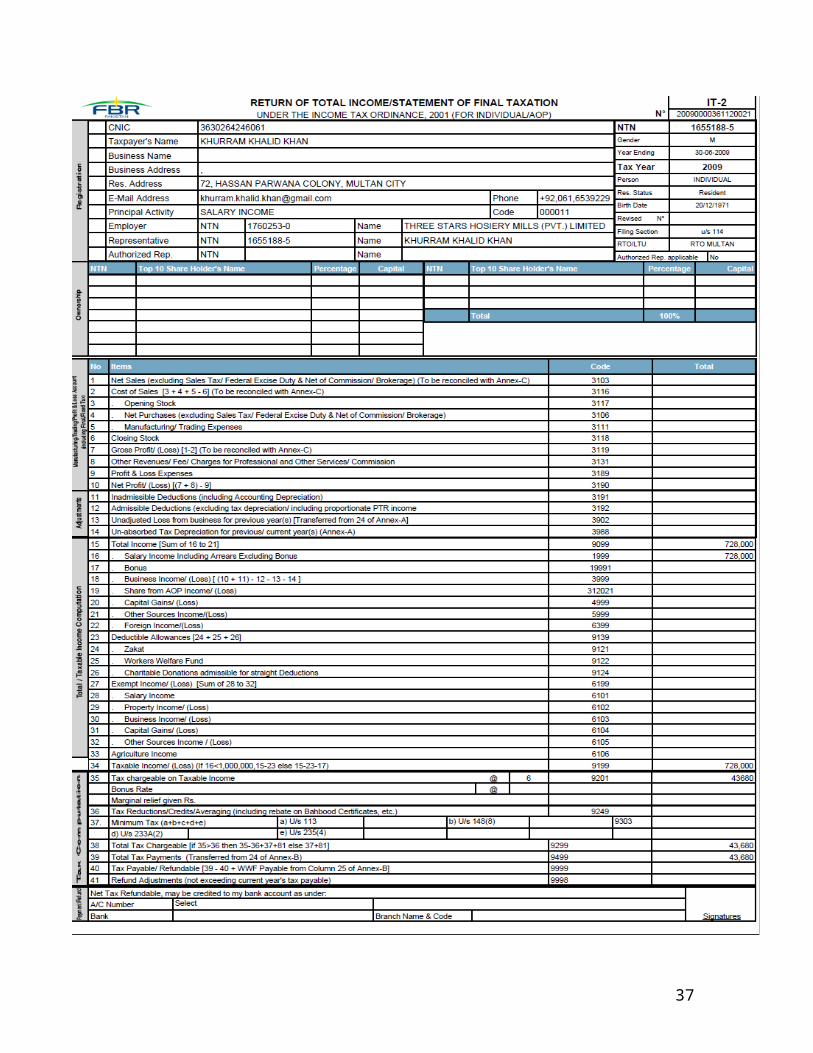

Copy of income tax return and wealth statement, ifrequired, for every assessment year.

Following are the extract of some of the documents beingmaintained by the tax department of the company.

35

36

37

38

39

40