Embed Size (px)

Citation preview

B R A Z I L | 2 0 1 8

SECTORAL REPORTFOOTWEAR INDUSTRY

Presented by:

Sponsored by:

B R A Z I L | 2 0 1 8

SECTORAL REPORTFOOTWEAR INDUSTRY

01. LOGO + DECODIFICADOR

ADVISORYClarissa Black

Marcos Tadeu Lélis

TECHNICAL COORDINATIONPriscila Linck

TECHNICAL TEAMAlessandra Roehrig

PROOFREADINGAlice RodriguesDiego Rosinha

Maristela Kirst de Lima Girola

GRAPHIC DESIGNGabriel Dias

Sectoral report: Brazilian footwear industry 2018Brazilian Footwear Industries Association. Novo Hamburgo: Abicalçados, 2018.

ISBN: 978-85-93812-04-0

PRESIDENTRosnei Alfredo da Silva

BOARD MEMBERSAdão Oscar Wolff, Caetano Bianco Neto, Caio Borges Ferreira, Danilo Cristófoli, Ernani Reuter, Haroldo Ferreira, José Carlos Brigagão do Couto, Júnior César Silva, Lioveral Bacher, Marco Antônio Coutinho,

Marco Lourenço Müller, Nilson Erineu Spohr, Paulo Roberto Konrath, Paulo Roberto Schefer, Paulo Vicente Bender, Renato Klein, Ricardo Wirth, Sérgio Gracia e Werner Arthur Muller Júnior

EXECUTIVE PRESIDENT

Heitor Klein

CONTACT USRua Júlio de Castilhos, 561 - Novo Hamburgo/RS –Zip code: 93510-130

Phone number: +55 51 [email protected]

www.abicalcados.com.br

B R A Z I L | 2 0 1 8

SECTORAL REPORTFOOTWEAR INDUSTRY

01. LOGO + DECODIFICADOR

SUMÁRIO

5

6

7

7

8

9

11

13

16

17

18

18

23

23

25

31

34

36

36

37

37

38

39

40

41

44

48

49

52

53

54

54

55

55

1. EDITORIAL

2. WORLD2.1 Global Economic Panorama

2.2 Global Footwear Panorama

2.2.1 Main Producing Countries

2.2.2 Main Consuming Countries

2.2.3 Main Exporting Countries

2.2.4 Main Importing Countries

3. BRAZIL3.1 Footwear Production

3.1.1 Installed Capacity Utilization Rate (ICUR)

3.1.2 Production Segmentation

3.2 Footwear Consumption

3.3 Foreign Trade

3.3.1 Exports

3.3.2 Imports

3.4 Employment and Establishments

3.5 Economic Indicators

3.5.1 Exchange Rate

3.5.2 Trade Behavior

3.5.3 Manufacturing Industry

3.5.4 Domestic Inflation

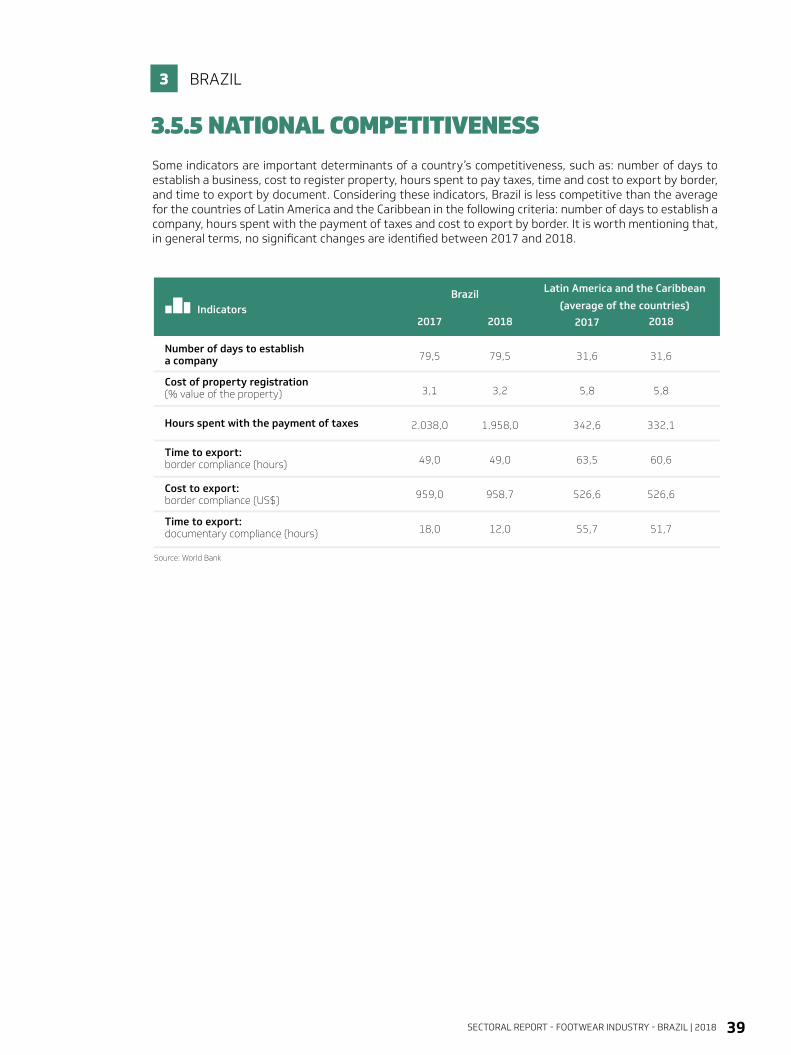

3.5.5 National Competitiveness

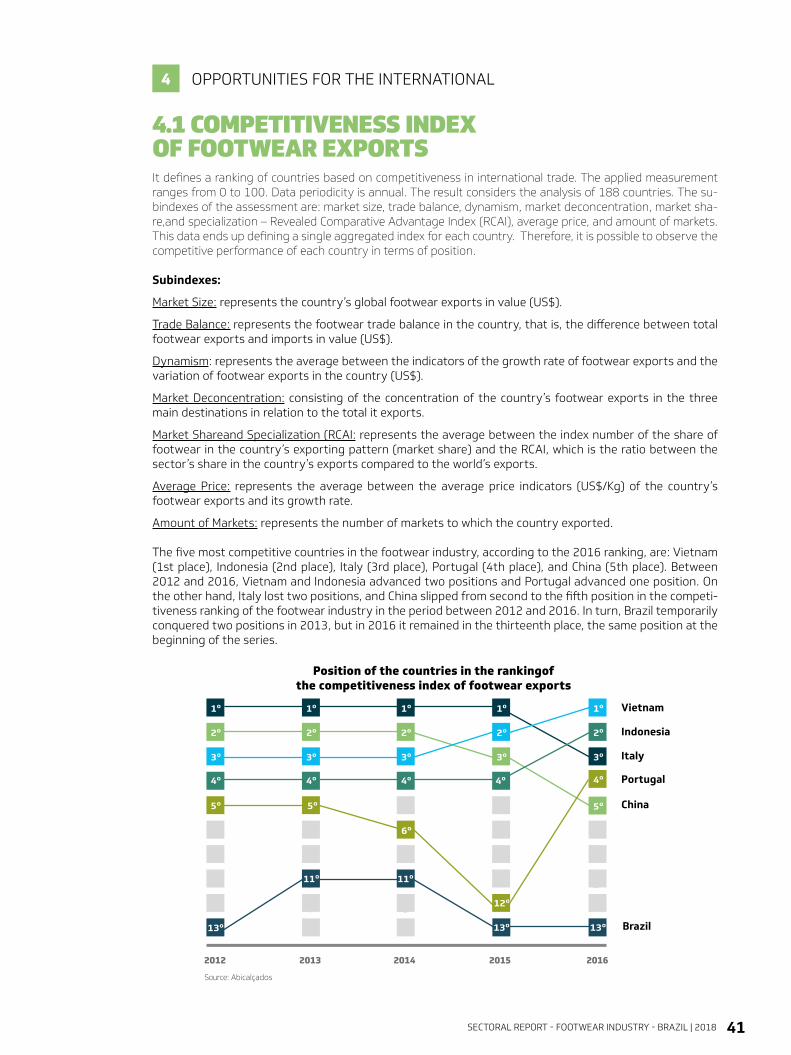

4. OPPORTUNITIES FOR THE INTERNATIONAL MARKET 4.1 Competitiveness Index of Footwear Exports

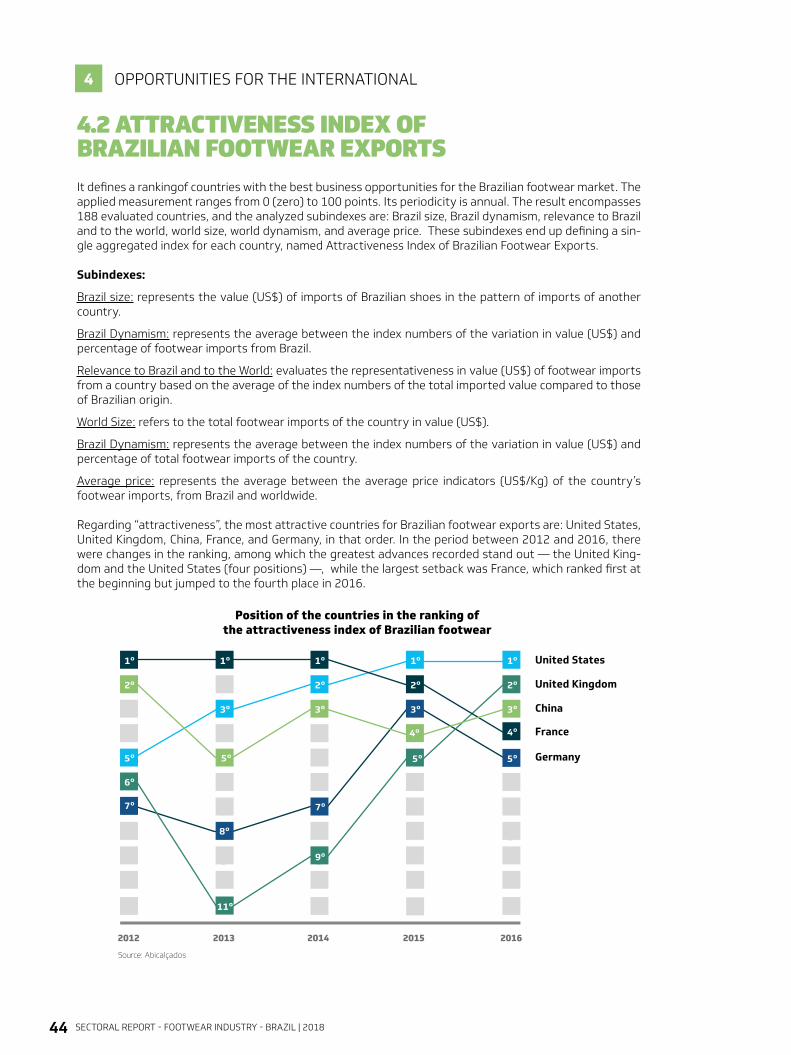

4.2 Attractiveness Index of Brazilian Footwear Exports

5. EXPERT ANALYSIS5.1 The growth dynamics of footwear production in 2017

6. METHODOLOGY6.1 Production Data

6.2 Statistical Projections

6.3 Sources

6.4 Classification of the Harmonized Commodity Description and Coding System

6.5 Definition of the Footwear Clusters

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 5

EDITORIAL

For the third year in a row, Abicalçados publishes the Sectoral Report of the Footwear Industry independently, through its Intelligence Unit. The compilation features figures relating to the footwear industry gathered in surveys by offi-cial sources such as Instituto Brasileiro de Geografia e Estatística (IBGE) [Bra-zilian Institute of Geography and Statistics], Ministério do Trabalho e Emprego (MTE] [Ministry of Labor and Employment], and Banco Central do Brasil [Brazi-lian Central Bank], among others. These figures were combined with a thorough production survey conducted with members of the organization – who account for over 70% of the domestic production. The quality of the research makes the material assertive and also provides a basis for projections for the current year, made by economists who specialize in analyzing data relating to the footwear industry.

The data was gathered not only to inform and to assist companies in the deci-sion-making process and to set commercial strategies, but also to alert them about the current moment of the footwear industry. A loss of competitiveness has been noticed in recent years, both in the domestic and foreign markets. However, global footwear production has increased by 10% since 2014, rea-ching 22 billion pairs, while ours has plunged by 7.3% during the same period,

reaching 909 million pairs in 2017. One position was also lost in the ranking of manufacturers, falling to the fourth place, behind China, India, and Vietnam, and followed closely by Indonesia. In the ranking of industry exporters, we are already in the 11th place, behind countries with no tradition in footwear manufacture, such as the Netherlands, for example, which acts as a re-exporter.

The reasons are well known and consist mainly of the high cost of production in Brazil, since the tax burden is among the highest in the world, logistics is expensive and inefficient, there are excessive regulations, bure-aucracy, indirect labor costs, and exchange rate dis-crepancy, among many other problems that hinder the development of the industry. For 2018, stability is expected, with a modest yet gradual recovery of the domestic demand. But what can be done to improve the situation of competitiveness loss? The answer is a concerted effort to adapt companies to the new reality of the market, increasingly demanding in terms of products and processes. Competition based on price alone should be discarded. We already know the Asians are unbeatable when it comes to this. Naturally, Abicalçados, as the representative of the Brazilian footwear industry, will continue to fight for better competitiveness conditions, taking our appeals to governments and to the legislature. But we know that in order to grow again, we cannot depend on the good will of the Public Power. Our mission is to create an environment of improvement of productive processes, with the lowest possible cost, an industry that develops distinguished fashion products with embedded technology, seeking to stimulate new business models, adjus-ted to the new customer.

Abicalçados, presenting the third issue of this publication, seeks, as mentioned before, to inform and to alert, with the intention of engaging more companies in this fight for a segment as economically and socially impor-tant as the footwear industry, due to its strategic position in the domestic economy, a result of the potential of the complete, integrated production chain, of the installed capacity, and of its exporting character and high employability.

“FOR 2018, STABILITY IS

EXPECTED,

WITH A MODEST YET GRADUAL

RECOVERY OF THE DOMESTIC

DEMAND.”

FIGURES TO INFORM AND TO ALERT

HEITOR KLEINABICALÇADOS EXECUTIVE PRESIDENT

1

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 20186

WORLD2

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 7

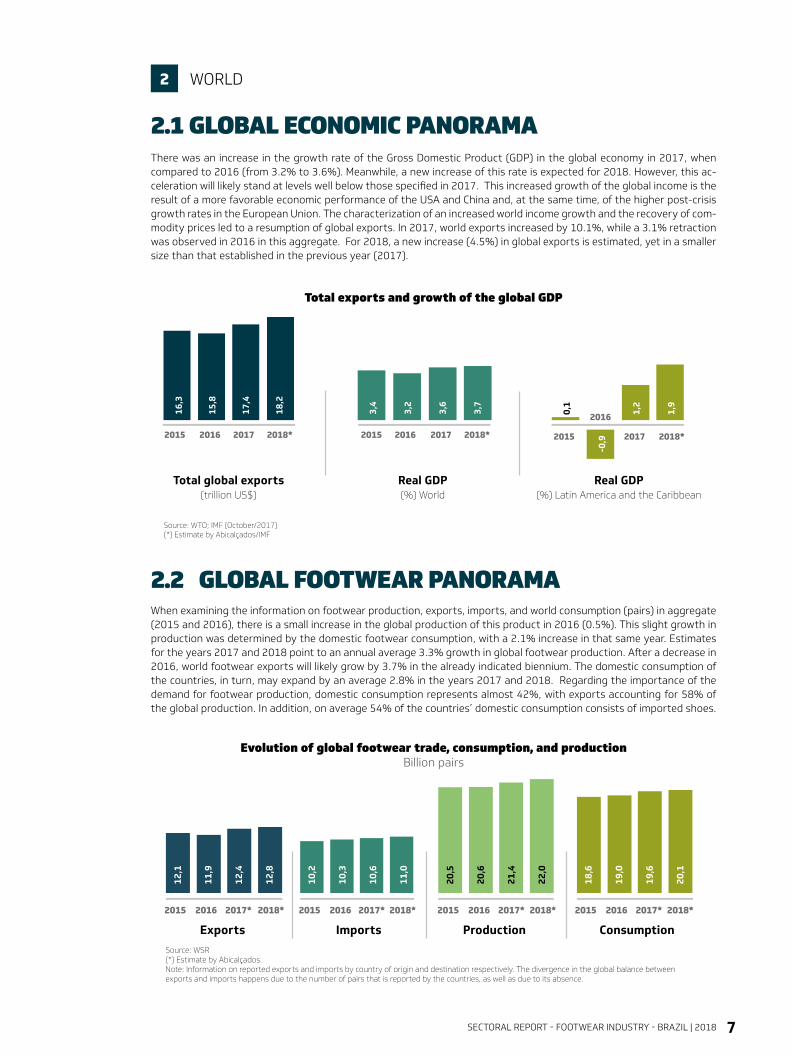

There was an increase in the growth rate of the Gross Domestic Product (GDP) in the global economy in 2017, when compared to 2016 (from 3.2% to 3.6%). Meanwhile, a new increase of this rate is expected for 2018. However, this ac-celeration will likely stand at levels well below those specified in 2017. This increased growth of the global income is the result of a more favorable economic performance of the USA and China and, at the same time, of the higher post-crisis growth rates in the European Union. The characterization of an increased world income growth and the recovery of com-modity prices led to a resumption of global exports. In 2017, world exports increased by 10.1%, while a 3.1% retraction was observed in 2016 in this aggregate. For 2018, a new increase (4.5%) in global exports is estimated, yet in a smaller size than that established in the previous year (2017).

Total exports and growth of the global GDP

Evolution of global footwear trade, consumption, and production Billion pairs

When examining the information on footwear production, exports, imports, and world consumption (pairs) in aggregate (2015 and 2016), there is a small increase in the global production of this product in 2016 (0.5%). This slight growth in production was determined by the domestic footwear consumption, with a 2.1% increase in that same year. Estimates for the years 2017 and 2018 point to an annual average 3.3% growth in global footwear production. After a decrease in 2016, world footwear exports will likely grow by 3.7% in the already indicated biennium. The domestic consumption of the countries, in turn, may expand by an average 2.8% in the years 2017 and 2018. Regarding the importance of the demand for footwear production, domestic consumption represents almost 42%, with exports accounting for 58% of the global production. In addition, on average 54% of the countries’ domestic consumption consists of imported shoes.

2.1 GLOBAL ECONOMIC PANORAMA

2.2 GLOBAL FOOTWEAR PANORAMA

WORLD2

Total global exports(trillion US$)

16,3

15,8

17,4

18,2

3,4

3,2

3,6

3,7

Real GDP(%) World

0,1

1,2

1,9

Real GDP(%) Latin America and the Caribbean

2015 2016 2017 2018* 2015 2016 2017 2018* 2015

2016

2017 2018*

Source: WTO; IMF (October/2017) (*) Estimate by Abicalçados/IMF

-0,9

Exports

12,1

11,9

12,4

12,8

10,2

10,3

10,6

11,0

20,5

20,6

21,4

22,0

18,6

19,0

19,6

20,1

Imports Production ConsumptionSource: WSR(*) Estimate by Abicalçados. Note: Information on reported exports and imports by country of origin and destination respectively. The divergence in the global balance between exports and imports happens due to the number of pairs that is reported by the countries, as well as due to its absence.

2015 2016 2017* 2018* 2015 2016 2017* 2018* 2015 2016 2017* 2018* 2015 2016 2017* 2018*

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 20188

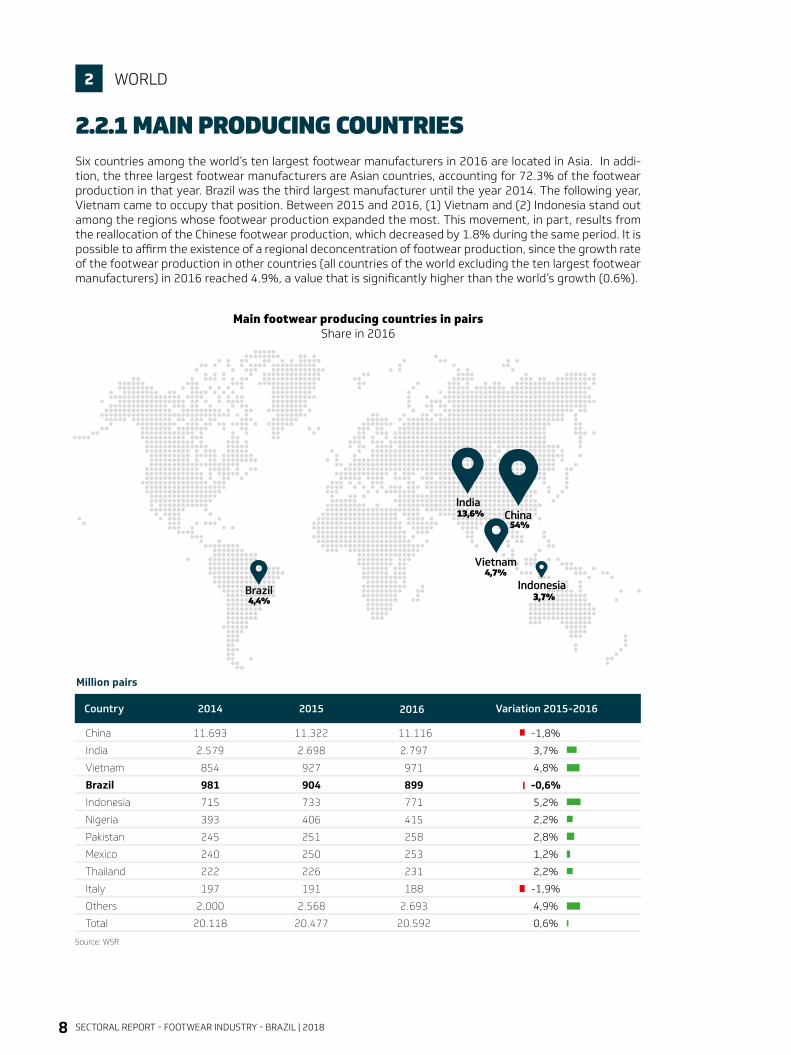

2.2.1 MAIN PRODUCING COUNTRIES

WORLD2

Six countries among the world’s ten largest footwear manufacturers in 2016 are located in Asia. In addi-tion, the three largest footwear manufacturers are Asian countries, accounting for 72.3% of the footwear production in that year. Brazil was the third largest manufacturer until the year 2014. The following year, Vietnam came to occupy that position. Between 2015 and 2016, (1) Vietnam and (2) Indonesia stand out among the regions whose footwear production expanded the most. This movement, in part, results from the reallocation of the Chinese footwear production, which decreased by 1.8% during the same period. It is possible to affirm the existence of a regional deconcentration of footwear production, since the growth rate of the footwear production in other countries (all countries of the world excluding the ten largest footwear manufacturers) in 2016 reached 4.9%, a value that is significantly higher than the world’s growth (0.6%).

Main footwear producing countries in pairsShare in 2016

Country

China

India

Vietnam

Brazil

Indonesia

Nigeria

Pakistan

Mexico

Thailand

Italy

Others

Total

2014

11.693

2.579

854

981

715

393

245

240

222

197

2.000

20.118

2015

11.322

2.698

927

904

733

406

251

250

226

191

2.568

20.477

Million pairs

Source: WSR

11.116

2.797

971

899

771

415

258

253

231

188

2.693

20.592

2016

Brazil

India

Vietnam

China54%

13,6%

4,4%

4,7%Indonesia

3,7%

Variation 2015-2016

-1,8%

3,7%

4,8%

-0,6%

5,2%

2,2%

2,8%

1,2%

2,2%

-1,9%

4,9%

0,6%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 9

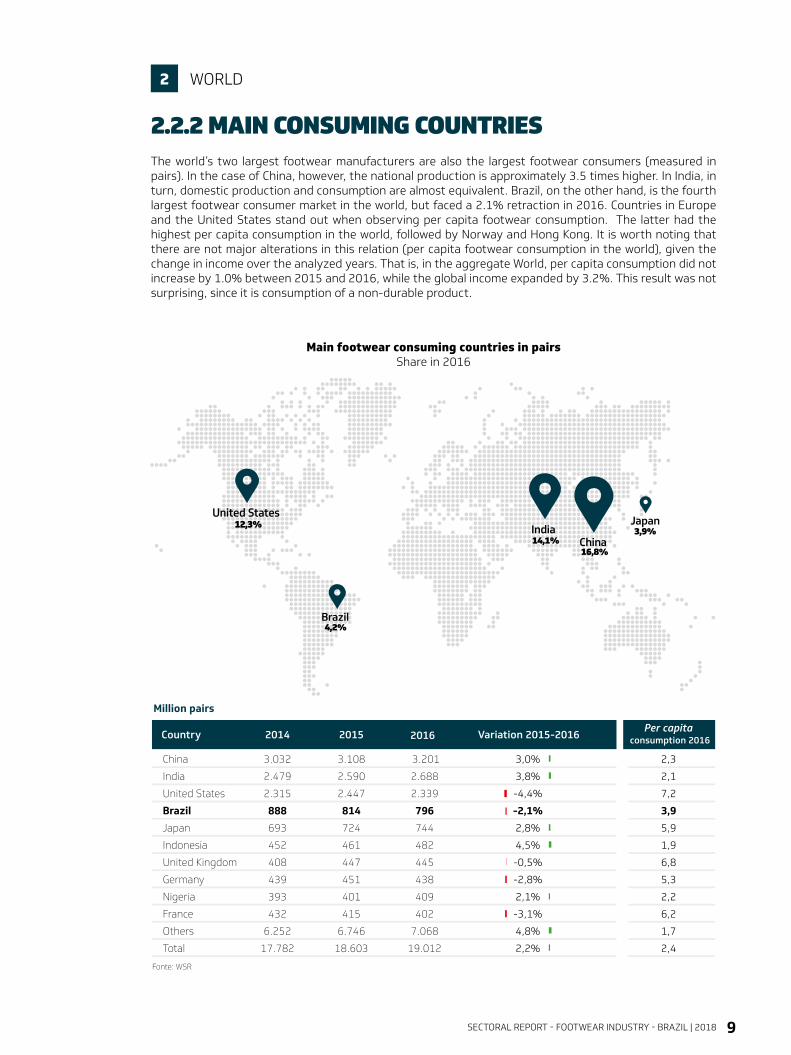

The world’s two largest footwear manufacturers are also the largest footwear consumers (measured in pairs). In the case of China, however, the national production is approximately 3.5 times higher. In India, in turn, domestic production and consumption are almost equivalent. Brazil, on the other hand, is the fourth largest footwear consumer market in the world, but faced a 2.1% retraction in 2016. Countries in Europe and the United States stand out when observing per capita footwear consumption. The latter had the highest per capita consumption in the world, followed by Norway and Hong Kong. It is worth noting that there are not major alterations in this relation (per capita footwear consumption in the world), given the change in income over the analyzed years. That is, in the aggregate World, per capita consumption did not increase by 1.0% between 2015 and 2016, while the global income expanded by 3.2%. This result was not surprising, since it is consumption of a non-durable product.

Main footwear consuming countries in pairsShare in 2016

2.2.2 MAIN CONSUMING COUNTRIES

WORLD2

Country 2014 Variation 2015-2016

China

India

United States

Brazil

Japan

Indonesia

United Kingdom

Germany

Nigeria

France

Others

Total

3.032

2.479

2.315

888

693

452

408

439

393

432

6.252

17.782

2015

3.108

2.590

2.447

814

724

461

447

451

401

415

6.746

18.603

3.201

2.688

2.339

796

744

482

445

438

409

402

7.068

19.012

3,0%

3,8%

-4,4%

-2,1%

2,8%

4,5%

-0,5%

-2,8%

2,1%

-3,1%

4,8%

2,2%

Million pairs

Fonte: WSR

2016

Brazil

IndiaJapan

China16,8%

14,1%

4,2%

3,9%

2,3

2,1

7,2

3,9

5,9

1,9

6,8

5,3

2,2

6,2

1,7

2,4

Per capita consumption 2016

United States12,3%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201810

WORLD2

Main per capita footwear consuming countries Pairs in 2016

Country 2014 Variation 2015-2016

United States

Norway

Hong Kong

United Kingdom

Netherlands

Ireland

Austria

France

Switzerland

Japan

Brazil (31º)

World

7,3

6,7

6,8

6,3

6,8

6,1

6,9

6,7

5,7

5,5

4,4

2,5

2015

7,6

7,0

7,0

6,9

7,2

6,9

6,2

6,4

5,9

5,7

4,0

2,6

7,2

7,1

7,1

6,8

6,6

6,6

6,2

6,2

5,9

5,9

3,9

2,6

-5,3%

1,4%

1,4%

-1,4%

-8,3%

-4,3%

0,0%

-3,1%

0,0%

3,5%

-2,5%

0,0%

Per capita pairs (pairs/inhabitant)

Source: Abicalçados

2016

Brazil

Hong Kong

United Kingdom

Norway

United States7,2

7,1

7,1

6,8

3,9

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 11

Country 2014

8.780

569

354

228

228

155

215

165

158

163

130

1.179

12.322

China

Vietnam

Indonesia

Germany

Belgium

United Kingdom

Italy

India

Spain

Netherlands

Brazil (11°)

Others

Total

2015

8.341

617

366

237

239

191

208

177

158

142

124

1.252

12.053

Million pairs

8.049

654

387

252

236

213

206

181

160

146

126

1.276

11.886

2016

Brazil

Germany

Vietnam

China67,7%

2,1%

1,1%

5,5%

Indonesia3,3%

Variation 2015-2016

-3,5%

6,0%

5,5%

6,5%

-1,0%

11,3%

-0,8%

2,2%

1,1%

3,0%

1,2%

1,9%

-1,4%

Source: WSR

Main footwear exporting countries in pairsShare in 2016

2.2.3 MAIN EXPORTING COUNTRIESNot unlike the ranking of the world’s largest footwear producing countries, in 2016 China remained the world’s largest exporter of this product, both in value (US$) and in pairs. However, there is a retraction in this country’s ex-ports in both units of measures in the year indicated above. Despite this retraction, China is in a privileged position in terms of share in global footwear exports (67.7% in pairs and 41.8% in value). When comparing the position in the ranking in terms of value and pairs, it is possible to arrive at conclusions on the positioning of the countries in average price of exported shoes. This highlights Italy’s position as the 7th largest exporter in the world in pairs and the world’s 2nd largest exporter in terms of value. It is therefore confirmed that the shoes exported by Italy remain among those with the highest prices in the international market. Indonesia, in turn, is in the 3rd position in terms of pairs and in the 5th position in relation to the value of its footwear exports, indicating its average price is below the price set globally.

WORLD2

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201812

Main footwear exporting countries in US$Share in 2016

WORLD2

País 2014

53.836

10.318

11.154

5.565

5.400

3.972

3.095

3.554

3.507

4.014

1.067

26.059

131.542

China

Vietnam

Italy

Belgium

Germany

Indonesia

France

Netherlands

Spain

Hong Kong

Brazil (17°)

Others

Total

2015

51.096

12.013

9.597

5.403

4.868

4.386

3.083

2.992

3.253

3.578

960

23.880

125.106

Million US$

44.886

12.996

9.831

5.948

5.586

4.526

3.308

3.208

2.916

2.765

998

23.448

120.418

2016

Brazil

Vietnam

Italy

China37,3%

10,8%

0,8%

8,2%

Belgium4,9%

Variation 2015-2016

-12,2%

8,2%

2,4%

10,1%

14,8%

3,2%

7,3%

7,2%

-10,3%

-22,7%

3,9%

-1,8%

-3,7%

Source: UNComtrade

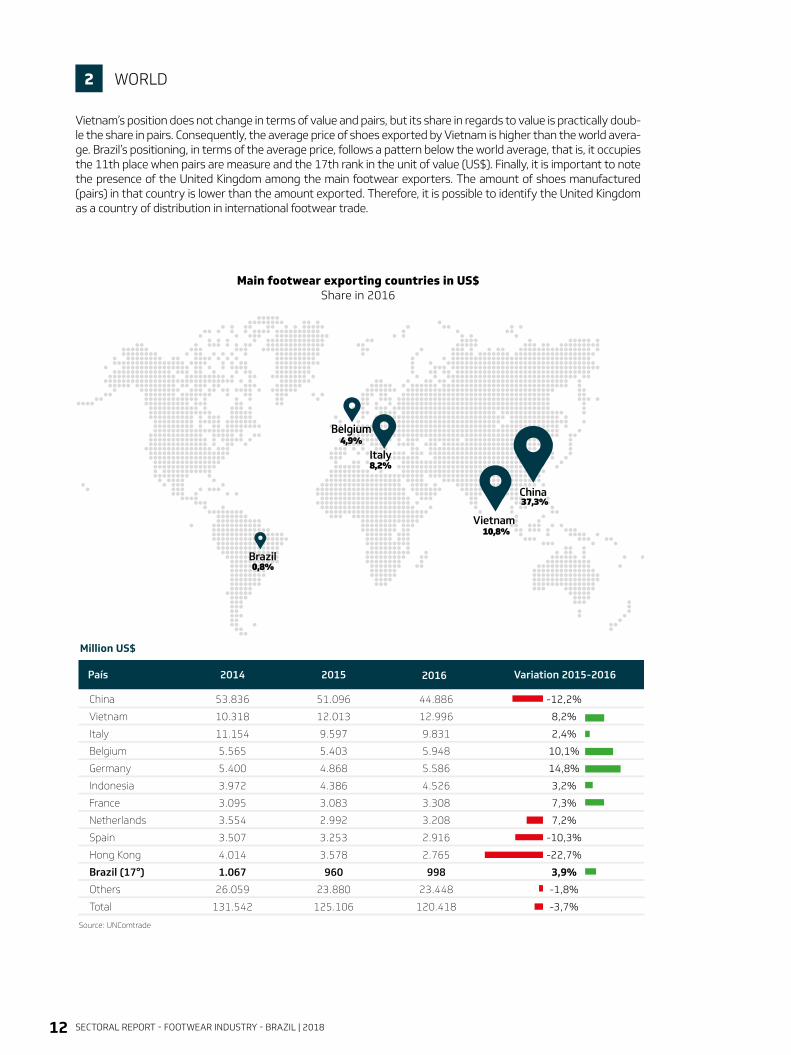

Vietnam’s position does not change in terms of value and pairs, but its share in regards to value is practically doub-le the share in pairs. Consequently, the average price of shoes exported by Vietnam is higher than the world avera-ge. Brazil’s positioning, in terms of the average price, follows a pattern below the world average, that is, it occupies the 11th place when pairs are measure and the 17th rank in the unit of value (US$). Finally, it is important to note the presence of the United Kingdom among the main footwear exporters. The amount of shoes manufactured (pairs) in that country is lower than the amount exported. Therefore, it is possible to identify the United Kingdom as a country of distribution in international footwear trade.

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 13

Country 2014

2.333

610

641

559

509

330

316

283

277

164

37

3.928

9.986

United States

Japan

Germany

United Kingdom

France

Italy

Spain

Belgium

Netherlands

South Africa

Brazil (55°)

Others

Total

2015

2.466

642

654

633

500

328

283

302

264

168

33

3.906

10.179

Million pairs

2.338

665

654

652

486

336

294

290

259

170

23

4.140

10.306

2016

Brazil

Germany

Japan

United Kingdom 6,3%

6,3%

0,2%

6,4%United States22,7%

Variation 2015-2016

-5,2%

3,5%

-0,1%

3,0%

-2,6%

2,4%

3,9%

-3,8%

-2,1%

0,9%

-31,6%

6,0%

1,2%

Source: WSR

Main footwear importing countries in pairsShare in 2016

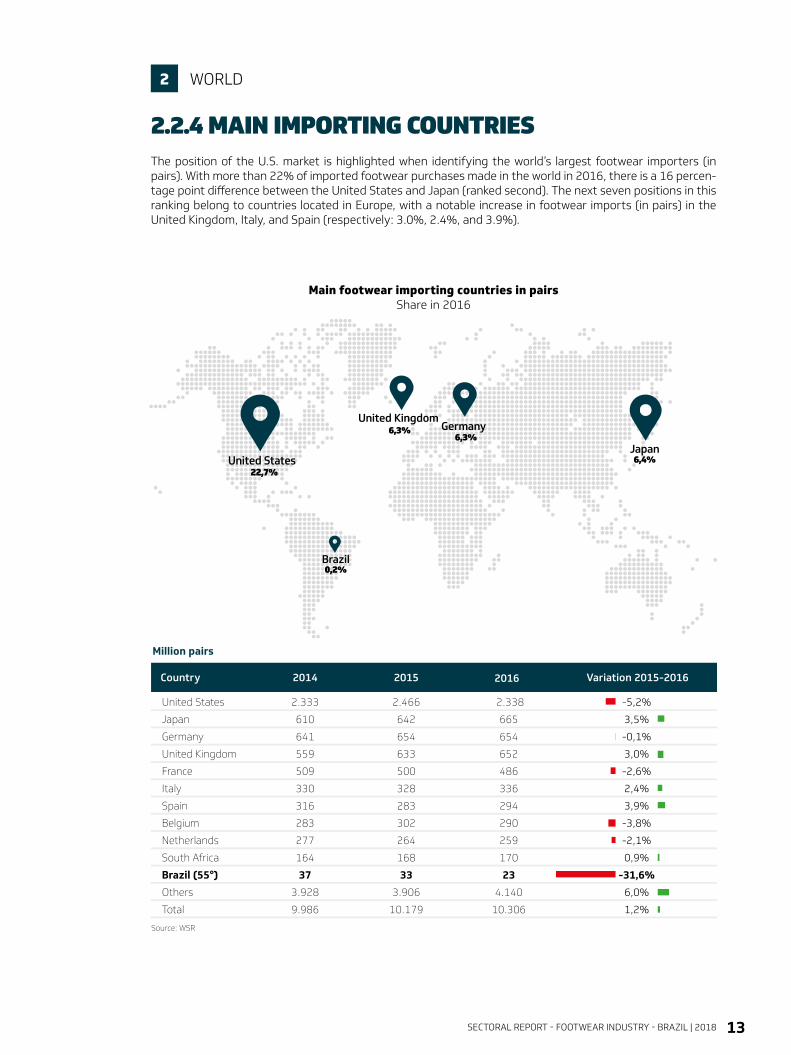

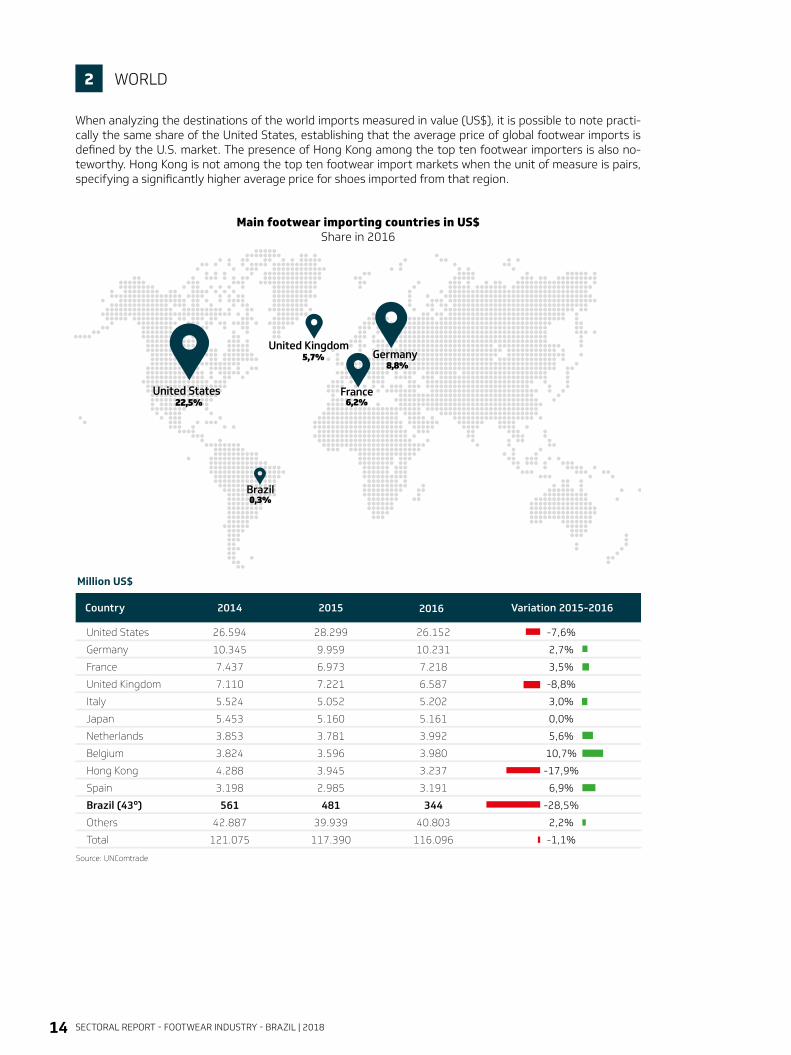

The position of the U.S. market is highlighted when identifying the world’s largest footwear importers (in pairs). With more than 22% of imported footwear purchases made in the world in 2016, there is a 16 percen-tage point difference between the United States and Japan (ranked second). The next seven positions in this ranking belong to countries located in Europe, with a notable increase in footwear imports (in pairs) in the United Kingdom, Italy, and Spain (respectively: 3.0%, 2.4%, and 3.9%).

2.2.4 MAIN IMPORTING COUNTRIES

WORLD2

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201814

Main footwear importing countries in US$Share in 2016

WORLD2

Country 2014

26.594

10.345

7.437

7.110

5.524

5.453

3.853

3.824

4.288

3.198

561

42.887

121.075

United States

Germany

France

United Kingdom

Italy

Japan

Netherlands

Belgium

Hong Kong

Spain

Brazil (43º)

Others

Total

2015

28.299

9.959

6.973

7.221

5.052

5.160

3.781

3.596

3.945

2.985

481

39.939

117.390

Million US$

26.152

10.231

7.218

6.587

5.202

5.161

3.992

3.980

3.237

3.191

344

40.803

116.096

2016

Brazil

Germany

France

United Kingdom5,7%

8,8%

0,3%

6,2%United States

22,5%

Variation 2015-2016

-7,6%

2,7%

3,5%

-8,8%

3,0%

0,0%

5,6%

10,7%

-17,9%

6,9%

-28,5%

2,2%

-1,1%

Source: UNComtrade

When analyzing the destinations of the world imports measured in value (US$), it is possible to note practi-cally the same share of the United States, establishing that the average price of global footwear imports is defined by the U.S. market. The presence of Hong Kong among the top ten footwear importers is also no-teworthy. Hong Kong is not among the top ten footwear import markets when the unit of measure is pairs, specifying a significantly higher average price for shoes imported from that region.

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 15

AF_Anúncio Orisol iCOS_21x28cm + sangra 5mm

quinta-feira, 29 de março de 2018 13:59:27

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201816

BRASIL3 BRAZIL3

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 17

Million pairs Million R$

2015 2016 2017 2018* 2018*

3,5%

6,6%

0,4%

4,5%

904,

4

899,

0

908,

9

940,

7

912,

5

2015 2016 2017

23.0

76

22.6

21

20.4

29

20.6

95

21.6

47

Source: IBGE/Abicalçados(*) Estimate by Abicalçados

Pairs R$

-0,6

-7,8

1,1%

4,5%

6,6%

1,3%

0,0%

4,6%

0,4%

3,5%

2015 2016 2017 2018* 2015 2016 2017 2018*

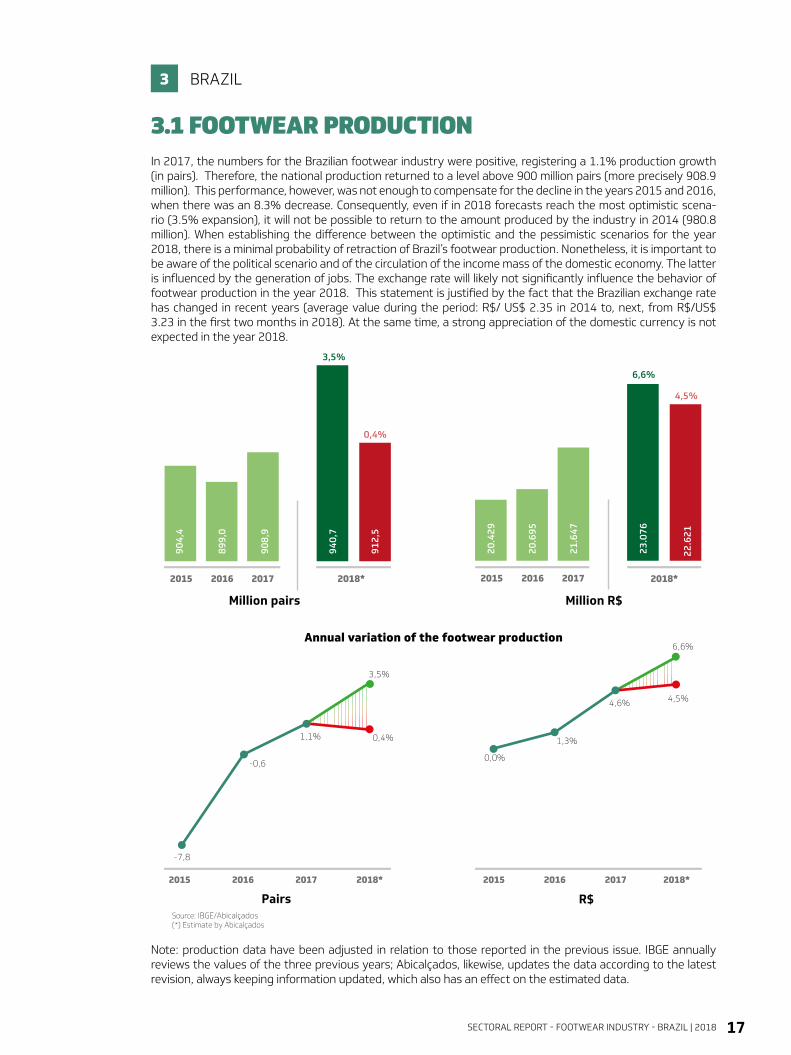

In 2017, the numbers for the Brazilian footwear industry were positive, registering a 1.1% production growth (in pairs). Therefore, the national production returned to a level above 900 million pairs (more precisely 908.9 million). This performance, however, was not enough to compensate for the decline in the years 2015 and 2016, when there was an 8.3% decrease. Consequently, even if in 2018 forecasts reach the most optimistic scena-rio (3.5% expansion), it will not be possible to return to the amount produced by the industry in 2014 (980.8 million). When establishing the difference between the optimistic and the pessimistic scenarios for the year 2018, there is a minimal probability of retraction of Brazil’s footwear production. Nonetheless, it is important to be aware of the political scenario and of the circulation of the income mass of the domestic economy. The latter is influenced by the generation of jobs. The exchange rate will likely not significantly influence the behavior of footwear production in the year 2018. This statement is justified by the fact that the Brazilian exchange rate has changed in recent years (average value during the period: R$/ US$ 2.35 in 2014 to, next, from R$/US$ 3.23 in the first two months in 2018). At the same time, a strong appreciation of the domestic currency is not expected in the year 2018.

Note: production data have been adjusted in relation to those reported in the previous issue. IBGE annually reviews the values of the three previous years; Abicalçados, likewise, updates the data according to the latest revision, always keeping information updated, which also has an effect on the estimated data.

3.1 FOOTWEAR PRODUCTION

BRAZIL3

Annual variation of the footwear production

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201818

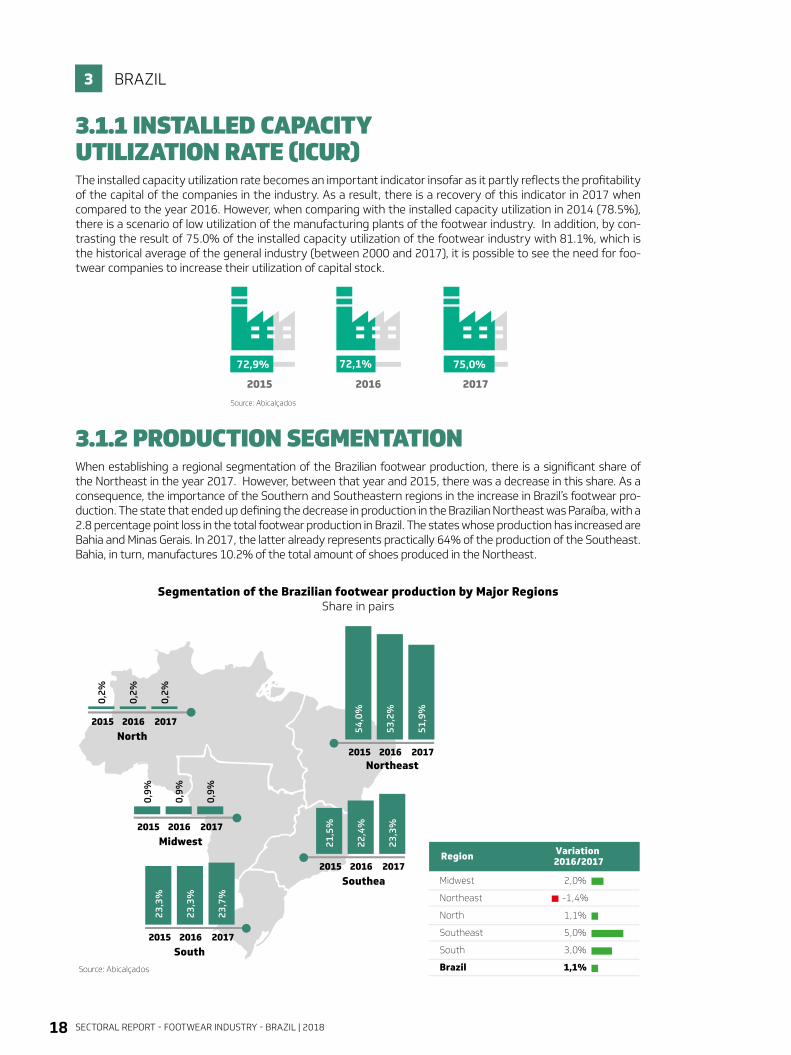

When establishing a regional segmentation of the Brazilian footwear production, there is a significant share of the Northeast in the year 2017. However, between that year and 2015, there was a decrease in this share. As a consequence, the importance of the Southern and Southeastern regions in the increase in Brazil’s footwear pro-duction. The state that ended up defining the decrease in production in the Brazilian Northeast was Paraíba, with a 2.8 percentage point loss in the total footwear production in Brazil. The states whose production has increased are Bahia and Minas Gerais. In 2017, the latter already represents practically 64% of the production of the Southeast. Bahia, in turn, manufactures 10.2% of the total amount of shoes produced in the Northeast.

Segmentation of the Brazilian footwear production by Major RegionsShare in pairs

3.1.2 PRODUCTION SEGMENTATION

BRAZIL3

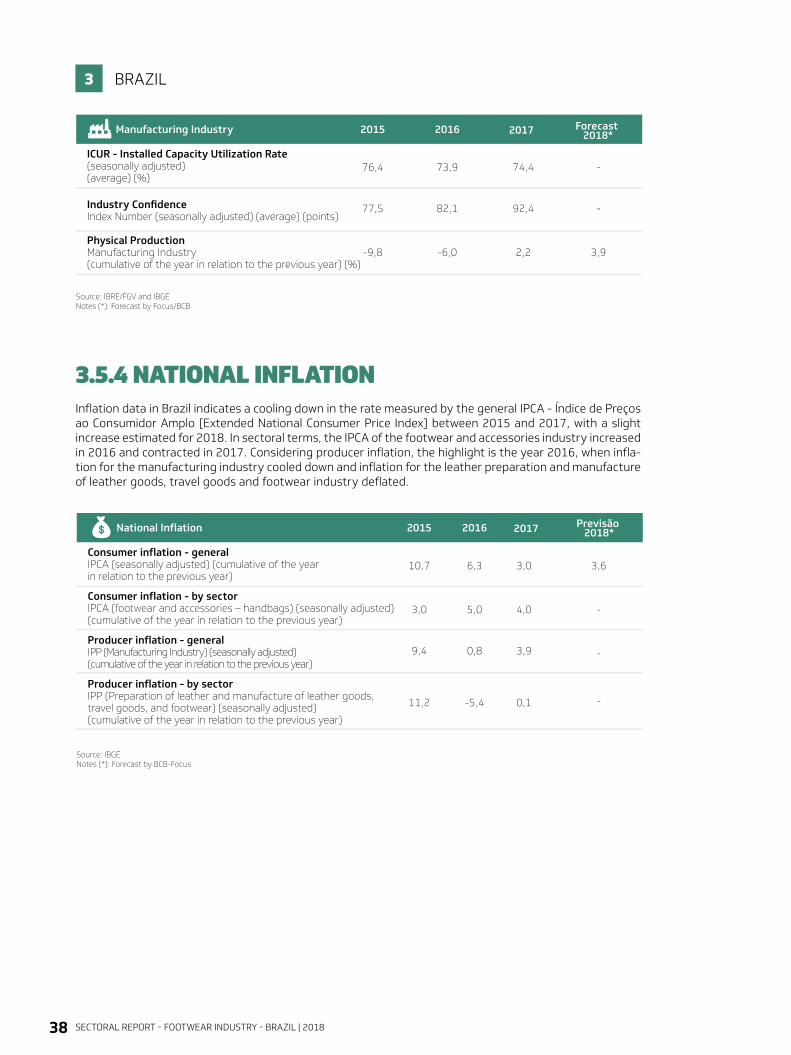

The installed capacity utilization rate becomes an important indicator insofar as it partly reflects the profitability of the capital of the companies in the industry. As a result, there is a recovery of this indicator in 2017 when compared to the year 2016. However, when comparing with the installed capacity utilization in 2014 (78.5%), there is a scenario of low utilization of the manufacturing plants of the footwear industry. In addition, by con-trasting the result of 75.0% of the installed capacity utilization of the footwear industry with 81.1%, which is the historical average of the general industry (between 2000 and 2017), it is possible to see the need for foo-twear companies to increase their utilization of capital stock.

3.1.1 INSTALLED CAPACITY UTILIZATION RATE (ICUR)

Source: Abicalçados

2015 2016 2017

72,9% 72,1% 75,0%

Source: Abicalçados

Midwest

Northeast

North

Southeast

South

Brazil

2,0%

-1,4%

1,1%

5,0%

3,0%

1,1%

Region Variation 2016/2017

54,0

%

2016

53,2

%

2017

51,9

%

Source: Abicalçados

2015State

Share

Ceará

Rio Grande do Sul

Paraíba

Minas Gerais

São Paulo

Bahia

Santa Catarina

Paraná

Sergipe

Mato Grosso do Sul

Others

Brazil

28,0%

20,4%

20,5%

12,9%

7,9%

4,7%

1,9%

1,1%

1,0%

0,9%

0,7%

100%

26,8%

20,3%

20,6%

14,2%

7,6%

5,1%

1,8%

1,1%

0,9%

0,9%

0,6%

100%

28,1%

20,6%

17,7%

14,9%

7,9%

5,3%

1,9%

1,2%

0,9%

0,9%

0,6%

100%

2016 2017

255,7

186,9

Others

Brazil

5,1908,9

CE

160,7

PB

8,6

SE

8,0

MS135,1

MG48,4

BA

71,7

SP

11,0

PR

17,7

SC

RS

2015Northeast

23,3

%

2016

23,3

%

2017

23,7

%

2015South

21,5

%

2016

22,4

%

2017

23,3

%

2015Southea

0,9%

2016

0,9%

2017

0,9%

2015Midwest

0,2%

2016

0,2%

2017

0,2%

2015North

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 19

Segmentation of the Brazilian footwear production by state in 2017Million pairs

BRAZIL3

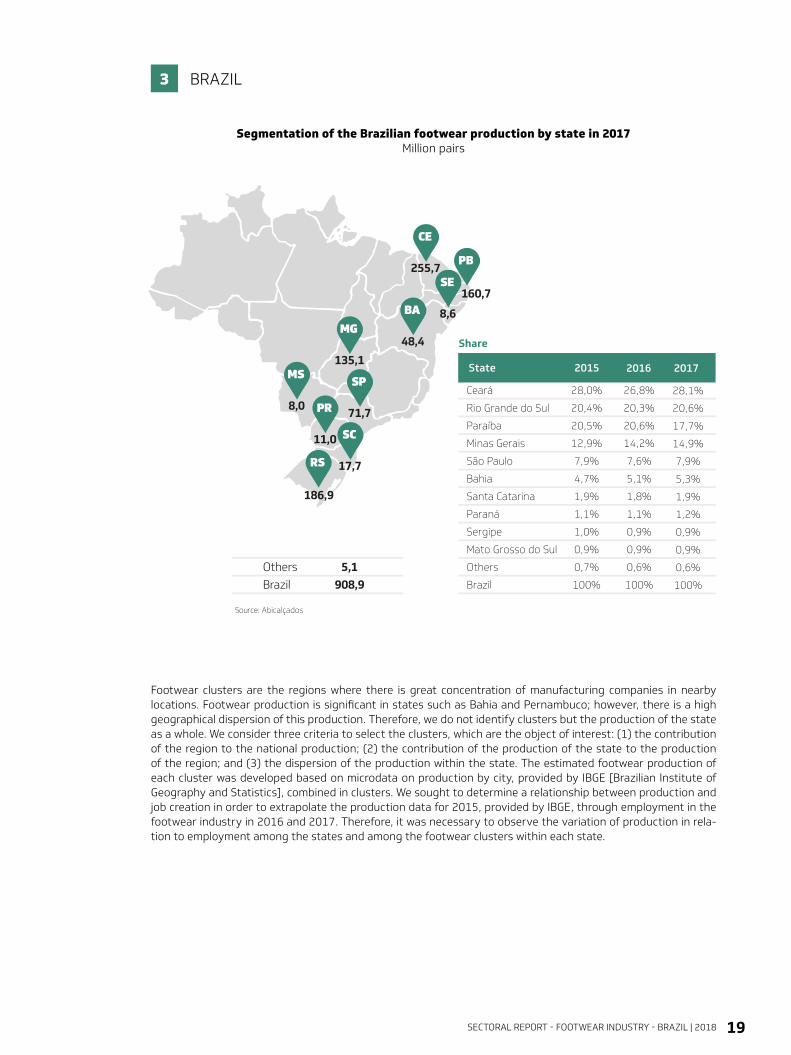

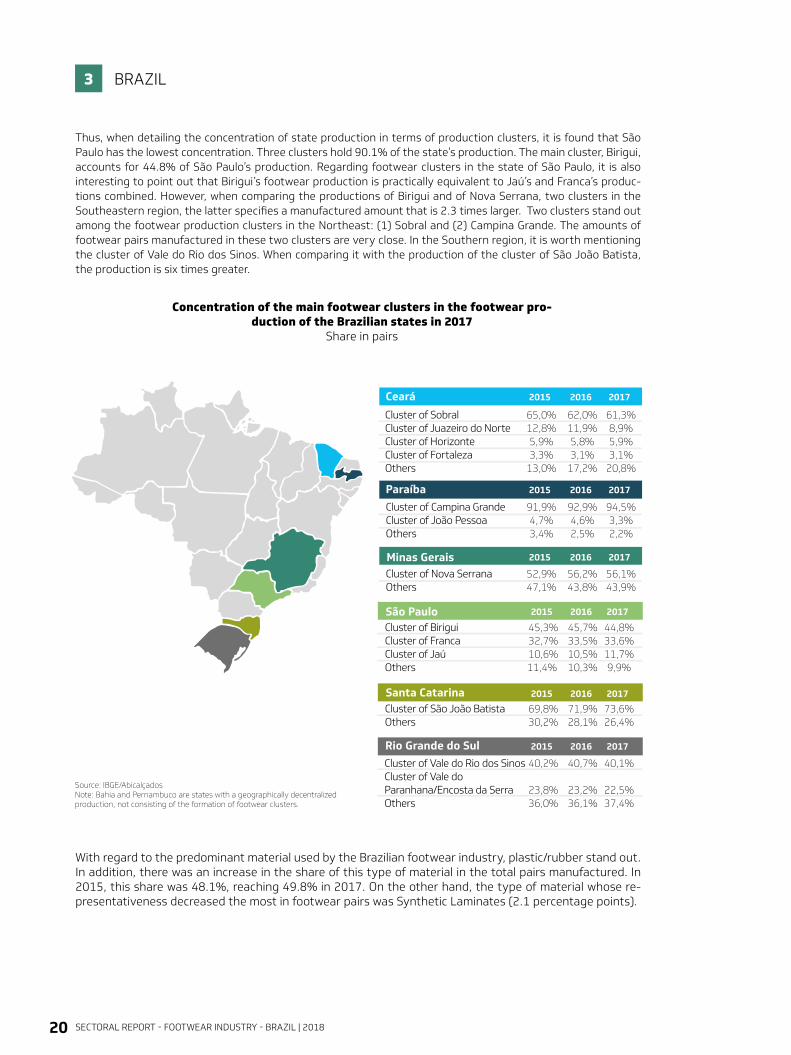

Footwear clusters are the regions where there is great concentration of manufacturing companies in nearby locations. Footwear production is significant in states such as Bahia and Pernambuco; however, there is a high geographical dispersion of this production. Therefore, we do not identify clusters but the production of the state as a whole. We consider three criteria to select the clusters, which are the object of interest: (1) the contribution of the region to the national production; (2) the contribution of the production of the state to the production of the region; and (3) the dispersion of the production within the state. The estimated footwear production of each cluster was developed based on microdata on production by city, provided by IBGE [Brazilian Institute of Geography and Statistics], combined in clusters. We sought to determine a relationship between production and job creation in order to extrapolate the production data for 2015, provided by IBGE, through employment in the footwear industry in 2016 and 2017. Therefore, it was necessary to observe the variation of production in rela-tion to employment among the states and among the footwear clusters within each state.

Source: Abicalçados

Midwest

Northeast

North

Southeast

South

Brazil

2,0%

-1,4%

1,1%

5,0%

3,0%

1,1%

Region Variation 2016/2017

54,0

%

2016

53,2

%

2017

51,9

%

Source: Abicalçados

2015State

Share

Ceará

Rio Grande do Sul

Paraíba

Minas Gerais

São Paulo

Bahia

Santa Catarina

Paraná

Sergipe

Mato Grosso do Sul

Others

Brazil

28,0%

20,4%

20,5%

12,9%

7,9%

4,7%

1,9%

1,1%

1,0%

0,9%

0,7%

100%

26,8%

20,3%

20,6%

14,2%

7,6%

5,1%

1,8%

1,1%

0,9%

0,9%

0,6%

100%

28,1%

20,6%

17,7%

14,9%

7,9%

5,3%

1,9%

1,2%

0,9%

0,9%

0,6%

100%

2016 2017

255,7

186,9

Others

Brazil

5,1908,9

CE

160,7

PB

8,6

SE

8,0

MS135,1

MG48,4

BA

71,7

SP

11,0

PR

17,7

SC

RS

2015Northeast

23,3

%

2016

23,3

%

2017

23,7

%

2015South

21,5

%

2016

22,4

%

2017

23,3

%

2015Southea

0,9%

2016

0,9%

2017

0,9%

2015Midwest

0,2%

2016

0,2%

2017

0,2%

2015North

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201820

Fonte: IBGE/Abicalçados(*) Estados com a produção descentralizada geograficamente, onde não há elos regionais na indústria, proximidade.

Source: IBGE/AbicalçadosNote: Bahia and Pernambuco are states with a geographically decentralized production, not consisting of the formation of footwear clusters.

Cluster of Campina GrandeCluster of João PessoaOthers

91,9%4,7%3,4%

Paraíba 2015

Cluster of SobralCluster of Juazeiro do NorteCluster of HorizonteCluster of FortalezaOthers

65,0%12,8%5,9%3,3%

13,0%

Ceará 2015

2015

2015

2015

Cluster of Nova SerranaOthers

52,9%47,1%

Minas Gerais

Cluster of BiriguiCluster of FrancaCluster of JaúOthers

45,3%32,7%10,6%11,4%

São Paulo

Cluster of São João BatistaOthers

69,8%30,2%

Santa Catarina

2015

Cluster of Vale do Rio dos SinosCluster of Vale do Paranhana/Encosta da SerraOthers

40,2%

23,8%36,0%

92,9%4,6%2,5%

2016

62,0%11,9%5,8%3,1%

17,2%

2016

2016

2016

2016

56,2%43,8%

45,7%33,5%10,5%10,3%

71,9%28,1%

2016

40,7%

23,2%36,1%

94,5%3,3%2,2%

2017

61,3%8,9%5,9%3,1%

20,8%

2017

2017

2017

2017

56,1%43,9%

44,8%33,6%11,7%9,9%

73,6%26,4%

2017

40,1%

22,5%37,4%

Rio Grande do Sul

Concentration of the main footwear clusters in the footwear pro-duction of the Brazilian states in 2017

Share in pairs

BRAZIL3

Thus, when detailing the concentration of state production in terms of production clusters, it is found that São Paulo has the lowest concentration. Three clusters hold 90.1% of the state’s production. The main cluster, Birigui, accounts for 44.8% of São Paulo’s production. Regarding footwear clusters in the state of São Paulo, it is also interesting to point out that Birigui’s footwear production is practically equivalent to Jaú’s and Franca’s produc-tions combined. However, when comparing the productions of Birigui and of Nova Serrana, two clusters in the Southeastern region, the latter specifies a manufactured amount that is 2.3 times larger. Two clusters stand out among the footwear production clusters in the Northeast: (1) Sobral and (2) Campina Grande. The amounts of footwear pairs manufactured in these two clusters are very close. In the Southern region, it is worth mentioning the cluster of Vale do Rio dos Sinos. When comparing it with the production of the cluster of São João Batista, the production is six times greater.

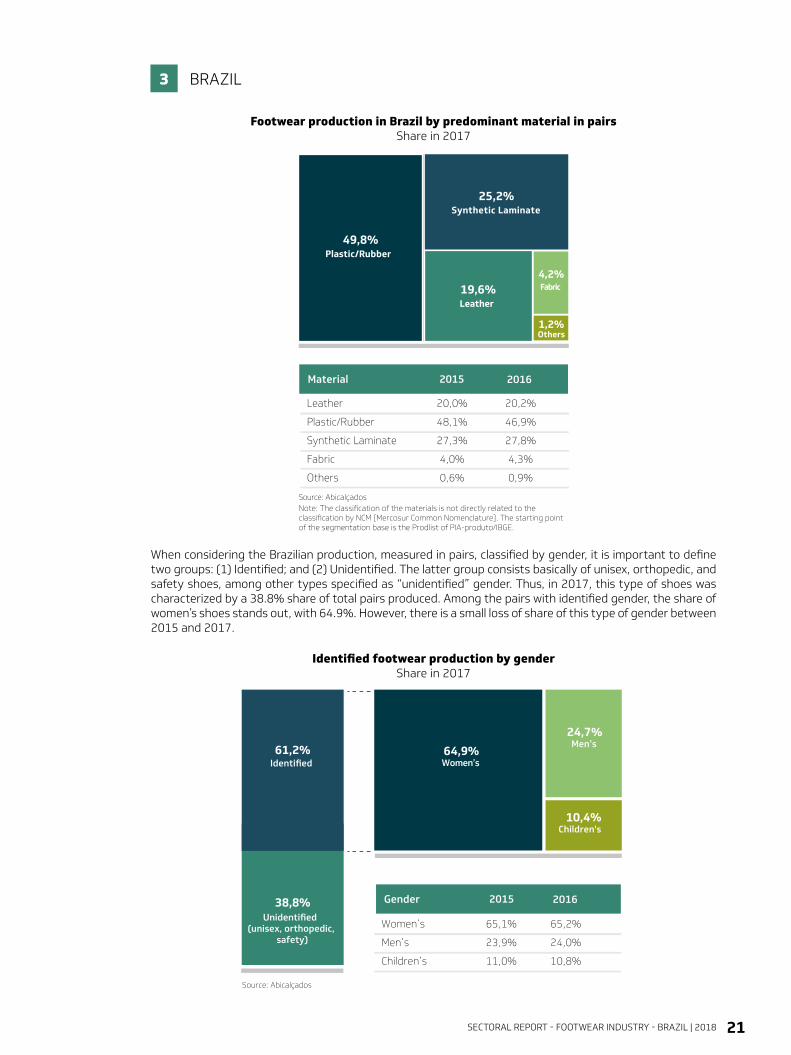

With regard to the predominant material used by the Brazilian footwear industry, plastic/rubber stand out. In addition, there was an increase in the share of this type of material in the total pairs manufactured. In 2015, this share was 48.1%, reaching 49.8% in 2017. On the other hand, the type of material whose re-presentativeness decreased the most in footwear pairs was Synthetic Laminates (2.1 percentage points).

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 21

Identified footwear production by genderShare in 2017

Footwear production in Brazil by predominant material in pairsShare in 2017

BRAZIL3

When considering the Brazilian production, measured in pairs, classified by gender, it is important to define two groups: (1) Identified; and (2) Unidentified. The latter group consists basically of unisex, orthopedic, and safety shoes, among other types specified as “unidentified” gender. Thus, in 2017, this type of shoes was characterized by a 38.8% share of total pairs produced. Among the pairs with identified gender, the share of women’s shoes stands out, with 64.9%. However, there is a small loss of share of this type of gender between 2015 and 2017.

(Participação em 2017)

Produção de calçados no Brasil por material predominante em pares(Participação em 2017)

Fonte: Abicalçados*Nota: Bahia e Pernambuco são estados com a produção descentralizada geograficamente, não consistindo na formação de polos calçadistas.

Source: AbicalçadosNote: The classification of the materials is not directly related to the classification by NCM [Mercosur Common Nomenclature]. The starting point of the segmentation base is the Prodlist of PIA-produto/IBGE.

Outros 32,6%

Participação

Polo do Vale do Rio dos SinosPolo do Vale do Paranhana/Encosta da SerraOutros

41,3%

26,6%32,1%

Rio Grande do Sul

19,6%Leather

25,2%Synthetic Laminate

49,8%Plastic/Rubber

1,2%Others

4,2%Fabric

Source: Abicalçados

Women’s

Men’s

Children’s

2015

65,1%

23,9%

11,0%

2016

65,2%

24,0%

10,8%

10,4%Children's

24,7%Men’s

64,9%Women’s

61,2%

38,8%Unidentified

(unisex, orthopedic, safety)

Identified

Escala de Cores

Leather

Plastic/Rubber

Synthetic Laminate

Fabric

Others

20,0%

48,1%

27,3%

4,0%

0,6%

20,2%

46,9%

27,8%

4,3%

0,9%

Material 2015 2016

Gender 2015 2016

(Participação em 2017)

Produção de calçados no Brasil por material predominante em pares(Participação em 2017)

Fonte: Abicalçados*Nota: Bahia e Pernambuco são estados com a produção descentralizada geograficamente, não consistindo na formação de polos calçadistas.

Source: AbicalçadosNote: The classification of the materials is not directly related to the classification by NCM [Mercosur Common Nomenclature]. The starting point of the segmentation base is the Prodlist of PIA-produto/IBGE.

Outros 32,6%

Participação

Polo do Vale do Rio dos SinosPolo do Vale do Paranhana/Encosta da SerraOutros

41,3%

26,6%32,1%

Rio Grande do Sul

19,6%Leather

25,2%Synthetic Laminate

49,8%Plastic/Rubber

1,2%Others

4,2%Fabric

Source: Abicalçados

Women’s

Men’s

Children’s

2015

65,1%

23,9%

11,0%

2016

65,2%

24,0%

10,8%

10,4%Children's

24,7%Men’s

64,9%Women’s

61,2%

38,8%Unidentified

(unisex, orthopedic, safety)

Identified

Escala de Cores

Leather

Plastic/Rubber

Synthetic Laminate

Fabric

Others

20,0%

48,1%

27,3%

4,0%

0,6%

20,2%

46,9%

27,8%

4,3%

0,9%

Material 2015 2016

Gender 2015 2016

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201822

Segmentation of the Brazilian footwear production by type of use in pairsShare in 2017

SEASONALITY OF FOOTWEAR PRODUCTION, EXPORTS, AND RETAIL SALES IN BRAZIL

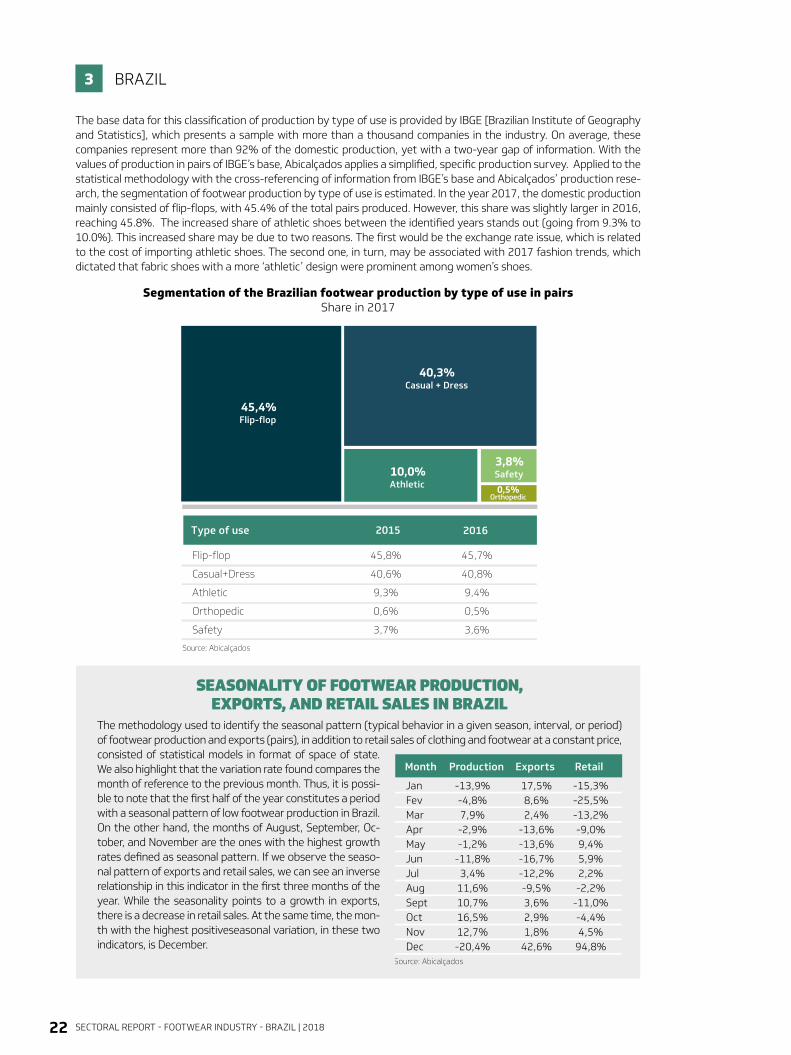

The base data for this classification of production by type of use is provided by IBGE [Brazilian Institute of Geography and Statistics], which presents a sample with more than a thousand companies in the industry. On average, these companies represent more than 92% of the domestic production, yet with a two-year gap of information. With the values of production in pairs of IBGE’s base, Abicalçados applies a simplified, specific production survey. Applied to the statistical methodology with the cross-referencing of information from IBGE’s base and Abicalçados’ production rese-arch, the segmentation of footwear production by type of use is estimated. In the year 2017, the domestic production mainly consisted of flip-flops, with 45.4% of the total pairs produced. However, this share was slightly larger in 2016, reaching 45.8%. The increased share of athletic shoes between the identified years stands out (going from 9.3% to 10.0%). This increased share may be due to two reasons. The first would be the exchange rate issue, which is related to the cost of importing athletic shoes. The second one, in turn, may be associated with 2017 fashion trends, which dictated that fabric shoes with a more ‘athletic’ design were prominent among women’s shoes.

The methodology used to identify the seasonal pattern (typical behavior in a given season, interval, or period) of footwear production and exports (pairs), in addition to retail sales of clothing and footwear at a constant price, consisted of statistical models in format of space of state. We also highlight that the variation rate found compares the month of reference to the previous month. Thus, it is possi-ble to note that the first half of the year constitutes a period with a seasonal pattern of low footwear production in Brazil. On the other hand, the months of August, September, Oc-tober, and November are the ones with the highest growth rates defined as seasonal pattern. If we observe the seaso-nal pattern of exports and retail sales, we can see an inverse relationship in this indicator in the first three months of the year. While the seasonality points to a growth in exports, there is a decrease in retail sales. At the same time, the mon-th with the highest positiveseasonal variation, in these two indicators, is December.

BRAZIL3

Source: Abicalçados

45,4%Flip-flop

40,3%Casual + Dress

10,0%Athletic

3,8%Safety

0,5%Orthopedic

Flip-flop

Casual+Dress

Athletic

Orthopedic

Safety

2015

45,8%

40,6%

9,3%

0,6%

3,7%

2016

45,7%

40,8%

9,4%

0,5%

3,6%

Type of use 2015 2016

Material

Jan

Fev

Mar

Abr

Mai

Jun

Jul

Ago

Set

Out

Nov

Dez

Produção

-13,9%

-4,8%

7,9%

-2,9%

-1,2%

-11,8%

3,4%

11,6%

10,7%

16,5%

12,7%

-20,4%

Exportação

17,5%

8,6%

2,4%

-13,6%

-13,6%

-16,7%

-12,2%

-9,5%

3,6%

2,9%

1,8%

42,6%

Varejo

-15,3%

-25,5%

-13,2%

-9,0%

9,4%

5,9%

2,2%

-2,2%

-11,0%

-4,4%

4,5%

94,8%

Fonte: Abicalçados

Month

JanFevMarAprMayJunJulAugSeptOctNovDec

Production

-13,9%-4,8%7,9%-2,9%-1,2%

-11,8%3,4%

11,6%10,7%16,5%12,7%-20,4%

Exports

17,5%8,6%2,4%

-13,6%-13,6%-16,7%-12,2%-9,5%3,6%2,9%1,8%

42,6%

Retail

-15,3%-25,5%-13,2%-9,0%9,4%5,9%2,2%-2,2%

-11,0%-4,4%4,5%

94,8%Source: Abicalçados

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 23

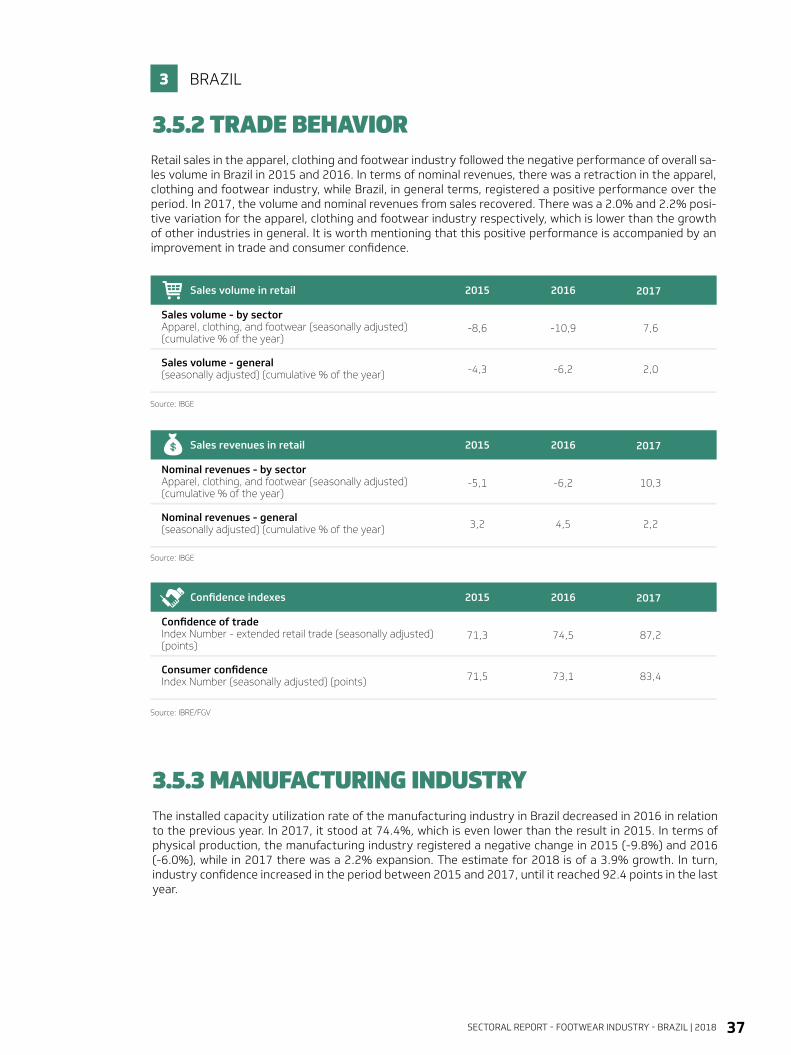

In 2017, the apparent consumption of footwear in Brazil recovered, after the retraction in 2016. Conse-quently, a 1.2% expansion was observed, compared to a 2.1% decline in the previous year. The difference between these two rates also points to a negative value. As a result, the total pairs defined as apparent consumption in the year 2017 is lower than the one specified in the year 2015. It is important to remem-ber that the growth rate of the apparent consumption in 2017 is very close to the growth of the footwear production in Brazil (1.1% expansion). Thus, given the representativeness of this consumption in the total produced by the footwear industry in Brazil, it can be established that the domestic production was in-fluenced by domestic demand vis-a-vis in relation to the foreign demand.

There is an almost linear tendency for increase of the surplus of the Brazilian footwear trade balance (in US$) between 2015 and 2017. Therefore, on average, it specifies a US$ 135.5 million increase for each year in its surplus. However, in 2017, this value was US$ 96.2 million, lower than the average value of the last two years. The lower result was corroborated by the rising of the domestic market compared to the year 2016. The changes in the exchange rate between 2016 and 2017, in turn, defined a small nominal devaluation of the national currency, which did not compensate for the recovery of domestic demand, diminishing the growth rate of the trade balance in the footwear industry.

Apparent consumption of footwearMillion pairs

3.2 FOOTWEAR CONSUMPTION

3.3 FOREIGN TRADE

Footwear trade balance in BrazilMillion US$

BRAZIL3

Consumo aparente de calçados(Milhões de pares)

813,6

796,2

805,5

2015

2016

2017

Escala de Cores

Source: Abicalçados

Balança comercial de calçados no Brasil (Milhões US$)

96

0,4

48

1,0

99

8,0

34

3,7

1.0

90

,5

34

0,0

2015 2016 2017

Exports

Imports

Balance

Source: MDIC

479,4

654,3750,5

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201824

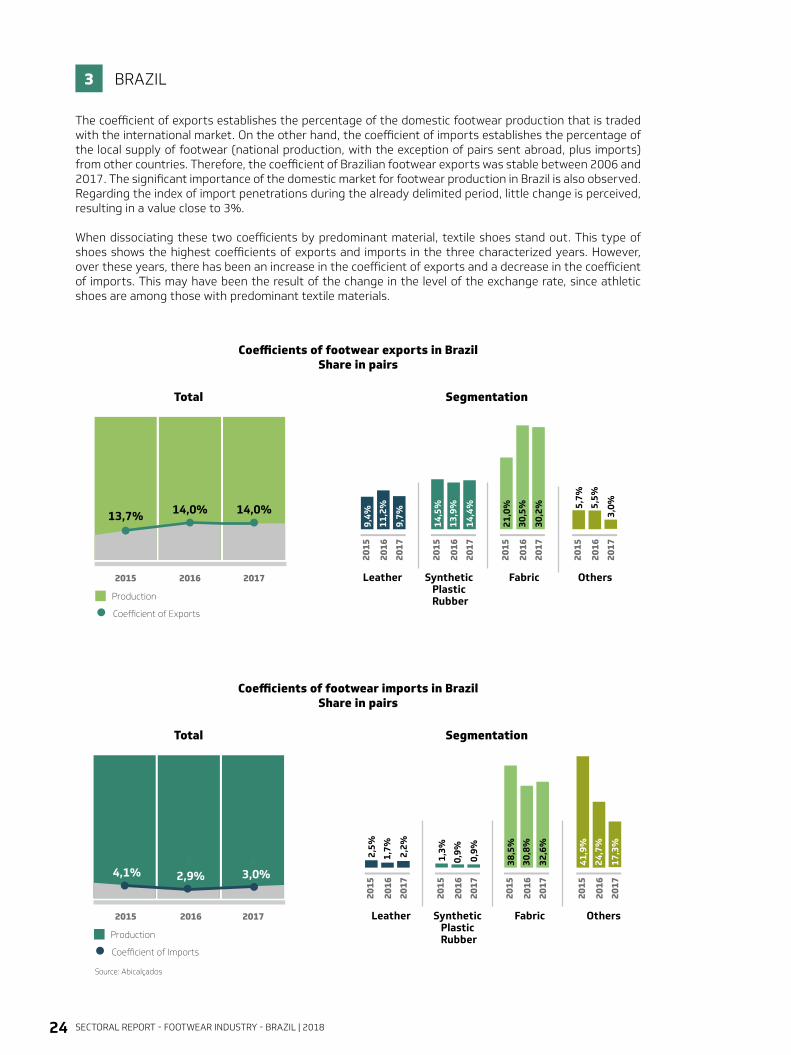

The coefficient of exports establishes the percentage of the domestic footwear production that is traded with the international market. On the other hand, the coefficient of imports establishes the percentage of the local supply of footwear (national production, with the exception of pairs sent abroad, plus imports) from other countries. Therefore, the coefficient of Brazilian footwear exports was stable between 2006 and 2017. The significant importance of the domestic market for footwear production in Brazil is also observed. Regarding the index of import penetrations during the already delimited period, little change is perceived, resulting in a value close to 3%.

When dissociating these two coefficients by predominant material, textile shoes stand out. This type of shoes shows the highest coefficients of exports and imports in the three characterized years. However, over these years, there has been an increase in the coefficient of exports and a decrease in the coefficient of imports. This may have been the result of the change in the level of the exchange rate, since athletic shoes are among those with predominant textile materials.

Coefficients of footwear exports in BrazilShare in pairs

Coefficients of footwear imports in BrazilShare in pairs

Total

Total

Segmentation

Segmentation

BRAZIL3

Coeficiente de Exportações

2015 2016 2017

Source: Abicalçados

Fonte: Abicalçados

14,0%

Production

Coefficient of Exports

Coeficiente de Importações

Coeficiente de Exportações Coeficiente de Importações

2015 2016 2017

4,1% 2,9% 3,0%

Production

Coefficient of Imports

13,7% 14,0%

Leather Fabric OthersSynthetic Plastic Rubber

Leather Fabric OthersSynthetic Plastic Rubber

11,2

%

9,4%

9,7%

2015

2016

2017

13,9

%

14,5

%

14,4

%

2015

2016

2017

30,5

%

21,0

%

30,2

%

2015

2016

2017

5,5%

5,7%

3,0%

2015

2016

2017

1,7%2,5%

2,2%

2015

2016

2017

0,9%

1,3%

0,9%

2015

2016

2017

30,8

%

38,5

%

32,6

%

2015

2016

2017

24,7

%

41,9

%

17,3

%

2015

2016

2017

Coeficiente de Exportações

2015 2016 2017

Source: Abicalçados

Fonte: Abicalçados

14,0%

Production

Coefficient of Exports

Coeficiente de Importações

Coeficiente de Exportações Coeficiente de Importações

2015 2016 2017

4,1% 2,9% 3,0%

Production

Coefficient of Imports

13,7% 14,0%

Leather Fabric OthersSynthetic Plastic Rubber

Leather Fabric OthersSynthetic Plastic Rubber

11,2

%

9,4%

9,7%

2015

2016

2017

13,9

%

14,5

%

14,4

%

2015

2016

2017

30,5

%

21,0

%

30,2

%

2015

2016

2017

5,5%

5,7%

3,0%

2015

2016

2017

1,7%2,5%

2,2%

2015

2016

2017

0,9%

1,3%

0,9%

2015

2016

2017

30,8

%

38,5

%

32,6

%

2015

2016

2017

24,7

%

41,9

%

17,3

%

2015

2016

2017

Coeficiente de Exportações

2015 2016 2017

Source: Abicalçados

Fonte: Abicalçados

14,0%

Production

Coefficient of Exports

Coeficiente de Importações

Coeficiente de Exportações Coeficiente de Importações

2015 2016 2017

4,1% 2,9% 3,0%

Production

Coefficient of Imports

13,7% 14,0%

Leather Fabric OthersSynthetic Plastic Rubber

Leather Fabric OthersSynthetic Plastic Rubber

11,2

%

9,4%

9,7%

2015

2016

2017

13,9

%

14,5

%

14,4

%

2015

2016

2017

30,5

%

21,0

%

30,2

%

2015

2016

2017

5,5%

5,7%

3,0%

2015

2016

2017

1,7%2,5%

2,2%

2015

2016

2017

0,9%

1,3%

0,9%

2015

2016

2017

30,8

%

38,5

%

32,6

%

2015

2016

2017

24,7

%

41,9

%

17,3

%

2015

2016

2017

Coeficiente de Exportações

2015 2016 2017

Source: Abicalçados

Fonte: Abicalçados

14,0%

Production

Coefficient of Exports

Coeficiente de Importações

Coeficiente de Exportações Coeficiente de Importações

2015 2016 2017

4,1% 2,9% 3,0%

Production

Coefficient of Imports

13,7% 14,0%

Leather Fabric OthersSynthetic Plastic Rubber

Leather Fabric OthersSynthetic Plastic Rubber

11,2

%

9,4%

9,7%

2015

2016

2017

13,9

%

14,5

%

14,4

%

2015

2016

2017

30,5

%

21,0

%

30,2

%

2015

2016

2017

5,5%

5,7%

3,0%

2015

2016

2017

1,7%2,5%

2,2%

2015

2016

2017

0,9%

1,3%

0,9%

2015

2016

2017

30,8

%

38,5

%

32,6

%

2015

2016

2017

24,7

%

41,9

%

17,3

%

2015

2016

2017

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 25

BRAZIL3

In the year 2017, Brazilian footwear exports returned to a level of more than US$ 1 billion, more preci-sely, US$ 1.09 billion. This result is due to a 9.3% growth, a very significant result considering the three previous years. When analyzing footwear exports measured in pairs, there is an 1.2% expansion, a result 7.8 times smaller than the increase in terms of value (US$). In addition, the growth rate observed in 2017 is the same as in 2016, since the decline in the year 2015 was 4.2%. Consequently, two conclusions are important: (1) in 2017, the variation in footwear exports was mainly characterized by a rise in the ave-rage price; (2) in that same year, the number of exported pairs was lower than the number of exported pairs in 2015. For the year 2018, the growth of exports measured in pairs is estimated ranging from 0.5% and 1.3%. That is, a decrease in footwear exports in terms of quantity is not expected. However, when highlighting the forecasts in value (US$), the expected range stands at -1.2% to 2.2%. Thus, the variable that will establish the change in the value of footwear exports is the dynamics of prices of this product.

Brazilian footwear exports

3.3.1 EXPORTS

Exportações brasileiras de calçados

960,

4

1.09

0,5

998,

0

2015 2016 2017

Million US$

-1,2%2,2%

2018*

1.07

7,4

(pes

sim

isti

c)

1.11

4,5

(opt

imis

tic)

125,

6

124,

1

127,

1

2015 2016 2017

Million pairs

0,5%1,3%

2018*

127,

8(p

essi

mis

tic)

(opt

imis

tic)

128,

8

Escala de Cores

Source: MDIC(*) Estimate by Abicalçados

Pairs US$

1,2%

-4,2%

1,2%2,2%

-1,2%

3,9%

-10,0%

9,3%

0,5%

1,3%

2015 2016 2017 2018* 2015 2016 2017 2018*

Annual variation of footwear exports

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201826

Main destinations of footwear exports in US$Share in 2017

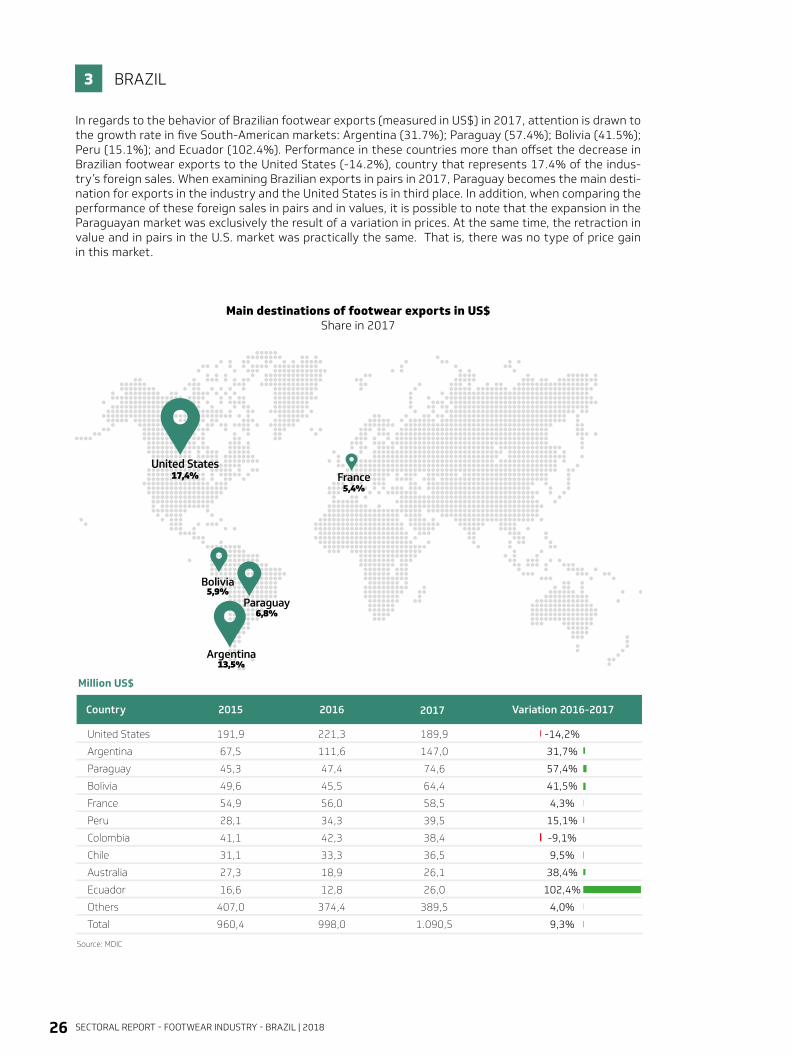

In regards to the behavior of Brazilian footwear exports (measured in US$) in 2017, attention is drawn to the growth rate in five South-American markets: Argentina (31.7%); Paraguay (57.4%); Bolivia (41.5%); Peru (15.1%); and Ecuador (102.4%). Performance in these countries more than offset the decrease in Brazilian footwear exports to the United States (-14.2%), country that represents 17.4% of the indus-try’s foreign sales. When examining Brazilian exports in pairs in 2017, Paraguay becomes the main desti-nation for exports in the industry and the United States is in third place. In addition, when comparing the performance of these foreign sales in pairs and in values, it is possible to note that the expansion in the Paraguayan market was exclusively the result of a variation in prices. At the same time, the retraction in value and in pairs in the U.S. market was practically the same. That is, there was no type of price gain in this market.

BRAZIL3

Country 2015 2016

Million US$

2017

France

Bolivia5,9%

5,4%

Argentina13,5%

Paraguay6,8%

United States17,4%

Variation 2016-2017

Source: MDIC

United States

Argentina

Paraguay

Bolivia

France

Peru

Colombia

Chile

Australia

Ecuador

Others

Total

191,9

67,5

45,3

49,6

54,9

28,1

41,1

31,1

27,3

16,6

407,0

960,4

221,3

111,6

47,4

45,5

56,0

34,3

42,3

33,3

18,9

12,8

374,4

998,0

189,9

147,0

74,6

64,4

58,5

39,5

38,4

36,5

26,1

26,0

389,5

1.090,5

-14,2%

31,7%

57,4%

41,5%

4,3%

15,1%

-9,1%

9,5%

38,4%

102,4%

4,0%

9,3%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 27

Main destinations of footwear exports in pairsShare in 2017

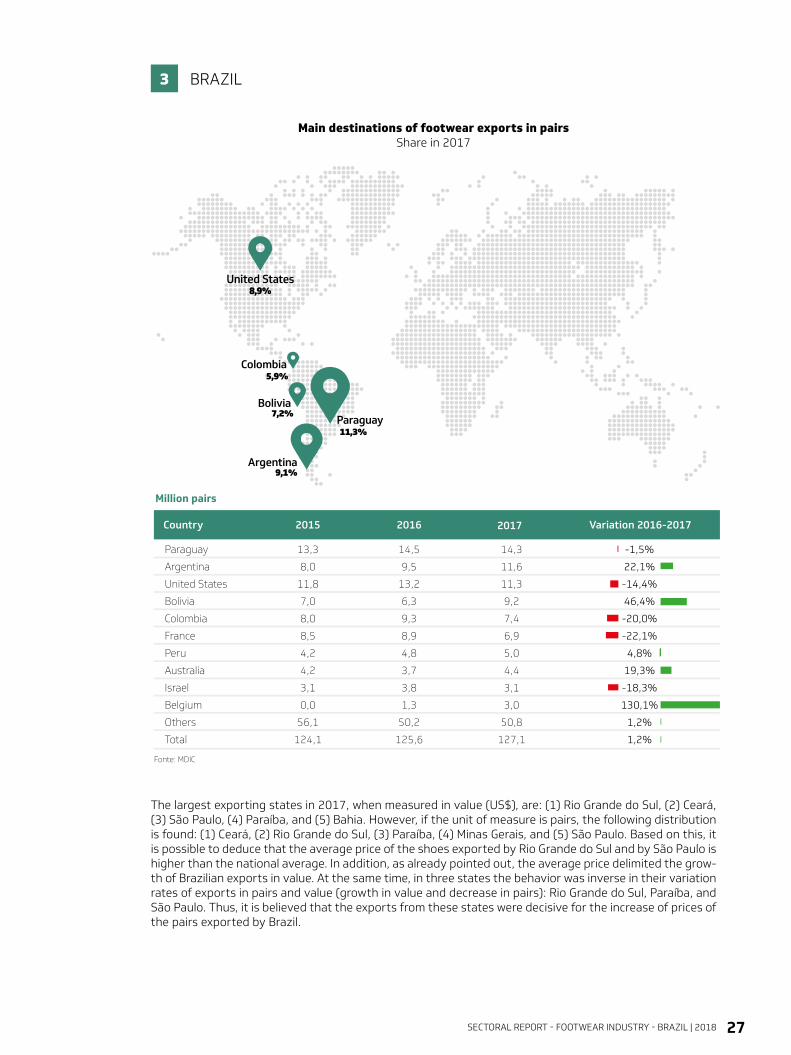

The largest exporting states in 2017, when measured in value (US$), are: (1) Rio Grande do Sul, (2) Ceará, (3) São Paulo, (4) Paraíba, and (5) Bahia. However, if the unit of measure is pairs, the following distribution is found: (1) Ceará, (2) Rio Grande do Sul, (3) Paraíba, (4) Minas Gerais, and (5) São Paulo. Based on this, it is possible to deduce that the average price of the shoes exported by Rio Grande do Sul and by São Paulo is higher than the national average. In addition, as already pointed out, the average price delimited the grow-th of Brazilian exports in value. At the same time, in three states the behavior was inverse in their variation rates of exports in pairs and value (growth in value and decrease in pairs): Rio Grande do Sul, Paraíba, and São Paulo. Thus, it is believed that the exports from these states were decisive for the increase of prices of the pairs exported by Brazil.

BRAZIL3

Country 2015 2016

Million pairs

2017

Bolivia7,2%

Colombia5,9%

Argentina9,1%

Paraguay11,3%

United States8,9%

Variation 2016-2017

Fonte: MDIC

Paraguay

Argentina

United States

Bolivia

Colombia

France

Peru

Australia

Israel

Belgium

Others

Total

13,3

8,0

11,8

7,0

8,0

8,5

4,2

4,2

3,1

0,0

56,1

124,1

14,5

9,5

13,2

6,3

9,3

8,9

4,8

3,7

3,8

1,3

50,2

125,6

14,3

11,6

11,3

9,2

7,4

6,9

5,0

4,4

3,1

3,0

50,8

127,1

-1,5%

22,1%

-14,4%

46,4%

-20,0%

-22,1%

4,8%

19,3%

-18,3%

130,1%

1,2%

1,2%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201828

Footwear exports by state in US$ Share in 2017

Footwear exports by state in pairs Share in 2017

BRAZIL3

Source: MDIC

2015State

77,8 115,673,5 57,3%

960,4 1.090,5998,0 9,3%

2016 2017 Variation 2016-2017

2015State

Others

Brazil

2016 2017 Variation 2016-2017

Participação das exportações de calçados por Unidade da Federação (Milhões de US$)

CE26,5%

PB6,8%

BA4,2%

SP10,4%

RS41,4%

Fonte: MDIC

CE39,3%

PB17,2%

MG6,2%SP

5,8%

RS22,1%

Million US$

Million Pairs

Paraíba 21,926,5 23,5 -7,1%

Rio Grande do Sul 28,120,5 28,7 -1,9%

Brazil 127,1124,1 125,6 1,2%

Minas Gerais 7,97,5 5,7 39,5%

Others 11,88,9 11,0 8,1%

São Paulo 7,410,0 9,0 -18,0%

88,4 74,666,4 12,5%Paraíba

263,0 289,1 269,7 7,2%Ceará

122,6 113,7107,7 5,5%São Paulo

370,0 451,8435,9 3,6%Rio Grande do Sul

38,6 45,644,7 1,9%Bahia

Ceará 50,050,7 47,7 4,8%

Others

Brazil

9,3%100%

Others

Brazil

10,6%100%

Source: MDIC

2015State

77,8 115,673,5 57,3%

960,4 1.090,5998,0 9,3%

2016 2017 Variation 2016-2017

2015State

Others

Brazil

2016 2017 Variation 2016-2017

Participação das exportações de calçados por Unidade da Federação (Milhões de US$)

CE26,5%

PB6,8%

BA4,2%

SP10,4%

RS41,4%

Fonte: MDIC

CE39,3%

PB17,2%

MG6,2%SP

5,8%

RS22,1%

Million US$

Million Pairs

Paraíba 21,926,5 23,5 -7,1%

Rio Grande do Sul 28,120,5 28,7 -1,9%

Brazil 127,1124,1 125,6 1,2%

Minas Gerais 7,97,5 5,7 39,5%

Others 11,88,9 11,0 8,1%

São Paulo 7,410,0 9,0 -18,0%

88,4 74,666,4 12,5%Paraíba

263,0 289,1 269,7 7,2%Ceará

122,6 113,7107,7 5,5%São Paulo

370,0 451,8435,9 3,6%Rio Grande do Sul

38,6 45,644,7 1,9%Bahia

Ceará 50,050,7 47,7 4,8%

Others

Brazil

9,3%100%

Others

Brazil

10,6%100%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 29

Footwear exports by segment

BRAZIL3

Footwear exports by predominant materialMillion US$

Material 2015

3,3

435,5

226,0

209,5

442,0

74,5

5,1

960,4

Injected

Synthetic

Flip-flops

Others

Leather

Fabric

Other Materials

Total

2016

1,5

411,6

175,9

235,7

471,6

107,6

5,6

998,0

2017

1,6

503,3

198,2

305,2

445,2

134,2

5,8

1.090,5

Share 2017

0,1%

46,2%

18,2%

28,0%

40,8%

12,3%

0,5%

100%

Variation 2016-2017

4,6%

22,3%

12,6%

29,5%

-5,6%

25,1%

2,9%

9,3%

Source: MDIC

Footwear exports by predominant materialMillion pairs

Material 2015

0,4

98,8

76,4

22,3

17,1

7,5

0,3

124,1

Injected

Synthetic

Flip-flops

Others

Leather

Fabric

Other Materials

Total

2016

0,3

92,7

66,5

26,2

20,4

11,8

0,4

125,6

2017

0,3

97,6

66,8

30,8

17,4

11,5

0,3

127,1

Share 2017

0,2%

76,8%

52,5%

24,3%

13,7%

9,1%

0,3%

100,0%

Variation 2016-2017

-1,3%

5,3%

0,4%

17,7%

-14,7%

-2,1%

-25,0%

1,2%

Source: MDIC

ATHLETIC 2015

12,0

979,2

Value (million US$)

Pairs (thousand units)

2016

27,1

2.065,2

2017

43,5

2.753,1

Share 2017

4,0%

2,2%

Variation 2016-2017

60,4%

33,3%

FLIP-FLOPS 2015

226,0

76.437,3

Value (million US$)

Pairs (thousand units)

2016

175,9

66.517,8

2017

198,2

66.798,0

Share 2017

18,2%

52,5%

Variation 2016-2017

12,6%

0,4%

OTHER SHOES 2015

722,4

46.665,2

Value (million US$)

Pairs (thousand units)

2016

794,9

56,989,1

2017

848,8

57.587,2

Share 2017

77,8%

45,3%

Variation 2016-2017

6,8%

1,0%

Source: MDIC

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201830

Year

20012002200320042005200620072008200920102011201220132014201520162017

50%

40%

30%

20%

10%

0%

-10%

-20%

-30%

-40%

-50%

Value

4,5%-10,3%7,0%

16,9%4,3%-1,5%2,6%-1,6%

-27,7%9,3%

-12,8%-15,7%0,2%-2,6%

-10,0%3,9%9,3%

Quantum

3,4%-3,5%5,7%7,6%

-11,8%-10,3%-13,2%-21,4%-24,0%-1,5%

-24,5%-13,7%2,5%-0,7%-1,4%15,3%-1,4%

Price

1,1%-7,1%1,2%8,6%

18,2%9,8%

18,2%25,2%-4,8%11,0%15,5%-2,3%-2,2%-1,9%-8,7%-9,9%10,8%

Source: AbicalçadosNote: The price and quantum indexes consist of a geometric mean, so that their sum does not constitute the total variation in the value of footwear exports.

Source: BCB, Abicalçados

Effect price (%)

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Exchange rate fluctuation (%) Polynomial (Exchange rate fluctuation (%))Polynomial (Effect price (%))

Year

20012002200320042005200620072008200920102011201220132014201520162017

50%

40%

30%

20%

10%

0%

-10%

-20%

-30%

-40%

-50%

Value

4,5%-10,3%7,0%

16,9%4,3%-1,5%2,6%-1,6%

-27,7%9,3%

-12,8%-15,7%0,2%-2,6%

-10,0%3,9%9,3%

Quantum

3,4%-3,5%5,7%7,6%

-11,8%-10,3%-13,2%-21,4%-24,0%-1,5%

-24,5%-13,7%2,5%-0,7%-1,4%15,3%-1,4%

Price

1,1%-7,1%1,2%8,6%

18,2%9,8%

18,2%25,2%-4,8%11,0%15,5%-2,3%-2,2%-1,9%-8,7%-9,9%10,8%

Source: AbicalçadosNote: The price and quantum indexes consist of a geometric mean, so that their sum does not constitute the total variation in the value of footwear exports.

Source: BCB, Abicalçados

Effect price (%)

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Exchange rate fluctuation (%) Polynomial (Exchange rate fluctuation (%))Polynomial (Effect price (%))

BRAZIL3

QUANTUM INDEX OF BRAZILIAN FOOTWEAR EXPORTS

The Fisher index was the methodology used to establish the quantum indexes and the prices of footwear exports in Brazil. Thus, it is possible to identify that in the delimited years the positive variations in the value of footwear exports were defined by the behavior of prices. That is, it is possible to note a decrease of Brazilian exports mea-sured in quantum, while the price variable is determinant for the expansion of foreign sales.

In addition, the performance of the prices of Brazilian footwear exports followed a pattern inversely related to the exchange rate (R$/US$) in recent years (2002-2017). In other words, when the exchange rate rises, that is, when the Brazilian currency is devalued, the price of foreign sales of shoes decreases and vice versa. It is worth noting that the behavior of these prices, in part, compensated for the decrease in exported volume, which predomina-ted in most of the observed years.

Variation (%) of the prices of Brazilian footwear exports and variation (%) of the nominal exchange rate (R$/US$)

Decomposition of the growth of Brazilian footwear exports

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 31

Origin of Brazilian footwear imports in US$Share in 2017

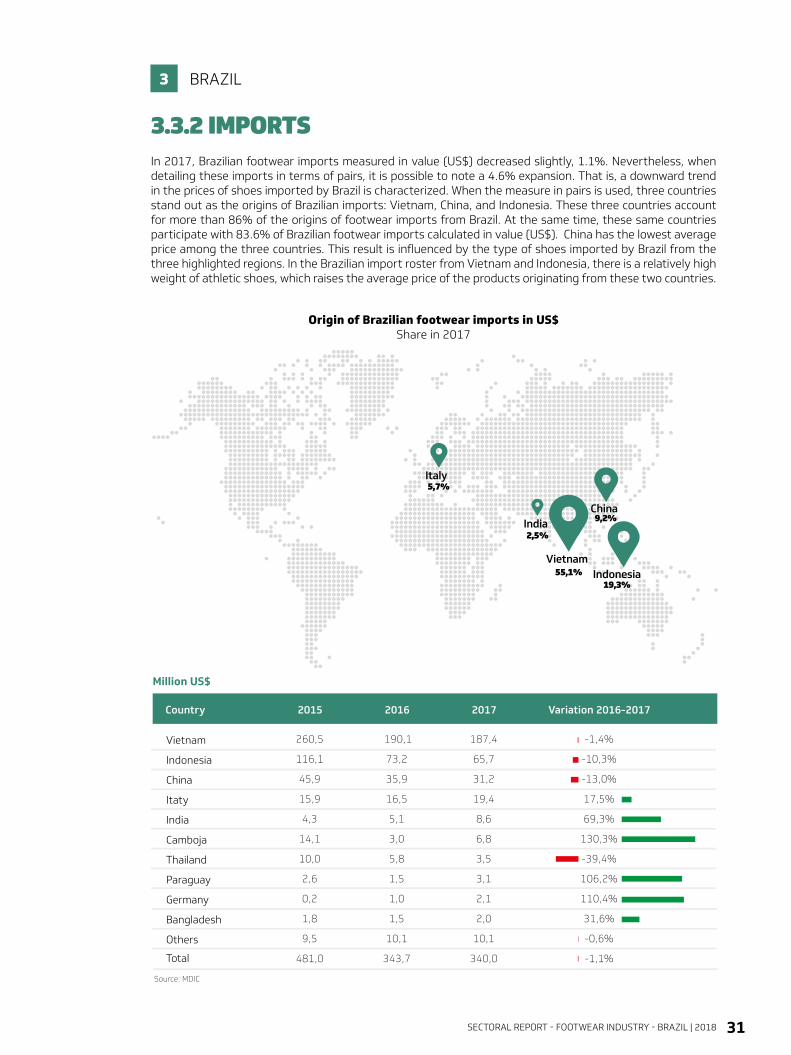

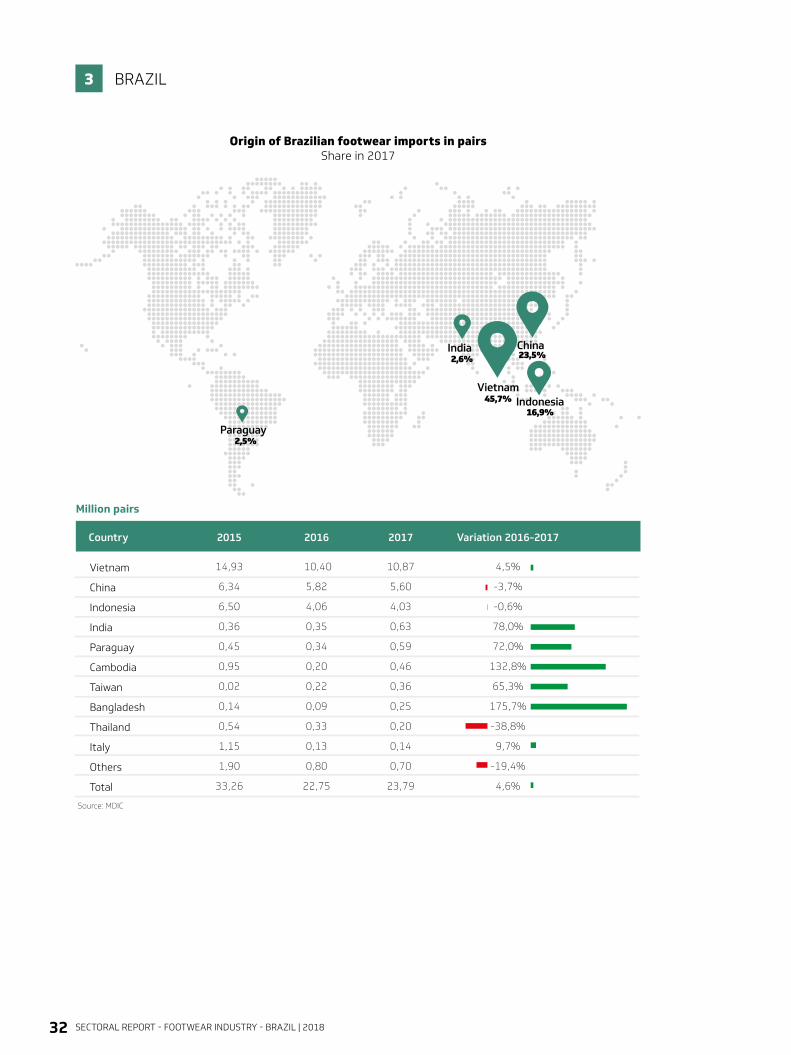

In 2017, Brazilian footwear imports measured in value (US$) decreased slightly, 1.1%. Nevertheless, when detailing these imports in terms of pairs, it is possible to note a 4.6% expansion. That is, a downward trend in the prices of shoes imported by Brazil is characterized. When the measure in pairs is used, three countries stand out as the origins of Brazilian imports: Vietnam, China, and Indonesia. These three countries account for more than 86% of the origins of footwear imports from Brazil. At the same time, these same countries participate with 83.6% of Brazilian footwear imports calculated in value (US$). China has the lowest average price among the three countries. This result is influenced by the type of shoes imported by Brazil from the three highlighted regions. In the Brazilian import roster from Vietnam and Indonesia, there is a relatively high weight of athletic shoes, which raises the average price of the products originating from these two countries.

3.3.2 IMPORTS

BRAZIL3

Vietnam

Indonesia

China

Itaty

India

Camboja

Thailand

Paraguay

Germany

Bangladesh

Others

Total

Source: MDIC

Country

260,5

116,1

45,9

15,9

4,3

14,1

10,0

2,6

0,2

1,8

9,5

481,0

2015

190,1

73,2

35,9

16,5

5,1

3,0

5,8

1,5

1,0

1,5

10,1

343,7

2016

187,4

65,7

31,2

19,4

8,6

6,8

3,5

3,1

2,1

2,0

10,1

340,0

2017

-1,4%

-10,3%

-13,0%

17,5%

69,3%

130,3%

-39,4%

106,2%

110,4%

31,6%

-0,6%

-1,1%

Variation 2016-2017

Million US$

IndonesiaVietnam

China

55,1%

India2,5%

9,2%

Italy5,7%

19,3%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201832

Origin of Brazilian footwear imports in pairsShare in 2017

BRAZIL3

Country 2015

14,93

6,34

6,50

0,36

0,45

0,95

0,02

0,14

0,54

1,15

1,90

33,26

Vietnam

China

Indonesia

India

Paraguay

Cambodia

Taiwan

Bangladesh

Thailand

Italy

Others

Total

2016

10,40

5,82

4,06

0,35

0,34

0,20

0,22

0,09

0,33

0,13

0,80

22,75

2017

10,87

5,60

4,03

0,63

0,59

0,46

0,36

0,25

0,20

0,14

0,70

23,79

Variation 2016-2017

4,5%

-3,7%

-0,6%

78,0%

72,0%

132,8%

65,3%

175,7%

-38,8%

9,7%

-19,4%

4,6%

Source: MDIC

Million pairs

India

IndonesiaVietnam

China

45,7%

23,5%2,6%

Paraguay2,5%

16,9%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 33

Footwear imports by predominant materialMillion US$

Footwear imports by predominant materialMillion pairs

Footwear imports by segment

BRAZIL3

Material 2015

0,24

7,52

0,67

6,85

4,19

17,67

3,64

33,26

Injected

Synthetic

Flip-flops

Others

Leather

Fabric

Other Materials

Total

2016

0,17

5,37

0,85

4,52

2,84

11,93

2,44

22,75

2017

0,29

4,85

0,67

4,18

3,56

12,90

2,19

23,79

Share 2017

1,2%

20,4%

2,8%

17,6%

15,0%

54,2%

9,2%

100,0%

Variation 2016-2017

69,3%

-9,7%

-21,4%

-7,5%

25,5%

8,1%

-10,0%

4,6%

Source: MDIC

Material 2015

1,0

99,4

3,2

96,2

82,4

292,4

5,9

481,0

Injected

Synthetic

Flip-flops

Others

Leather

Fabric

Other Materials

Total

2016

1,0

65,0

2,3

62,7

60,0

214,4

3,3

343,7

2017

1,2

56,6

1,6

55,0

67,9

210,8

3,4

340,0

Share 2017

0,4%

16,7%

0,5%

16,2%

20,0%

62,0%

1,0%

100,0%

Variation 2016-2017

19,3%

-12,9%

-29,8%

-12,3%

13,2%

-1,7%

5,0%

-1,1%

Source: MDIC

2015

206,4

9.173,0

2016

120,3

4.658,7

2017

101,9

4.659,3

30,0%

19,6%

-15,2%

0,0%

2015

3,2

670,5

2016

2,3

849,0

2017

1,6

667,5

0,5%

2,8%

-29,8%

-21,4%

2015

271,5

23.420,5

2016

221,1

17.240,3

2017

236,4

18.465,7

69,5%

77,6%

6,9%

7,1%

Source: MDIC

ATHLETIC

Value (million US$)

Pairs (thousand units)

Share 2017

FLIP-FLOPS

Value (million US$)

Pairs (thousand units)

Share 2017

OTHER SHOES

Value (million US$)

Pairs (thousand units)

Share 2017

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201834

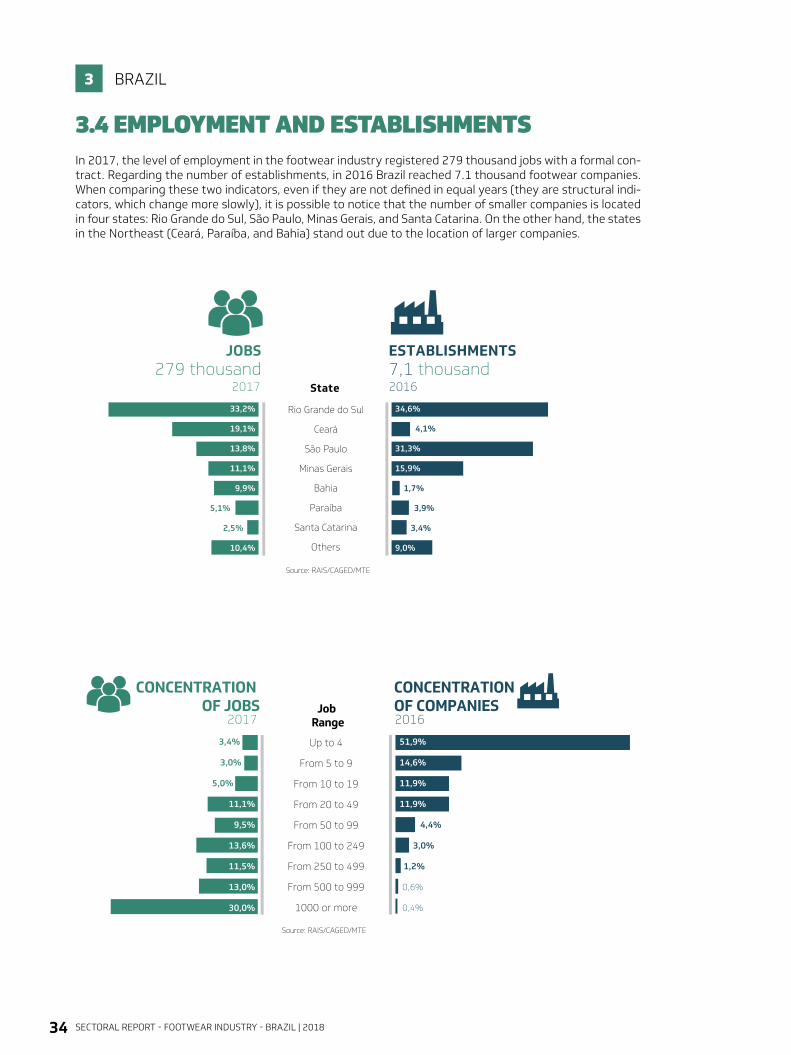

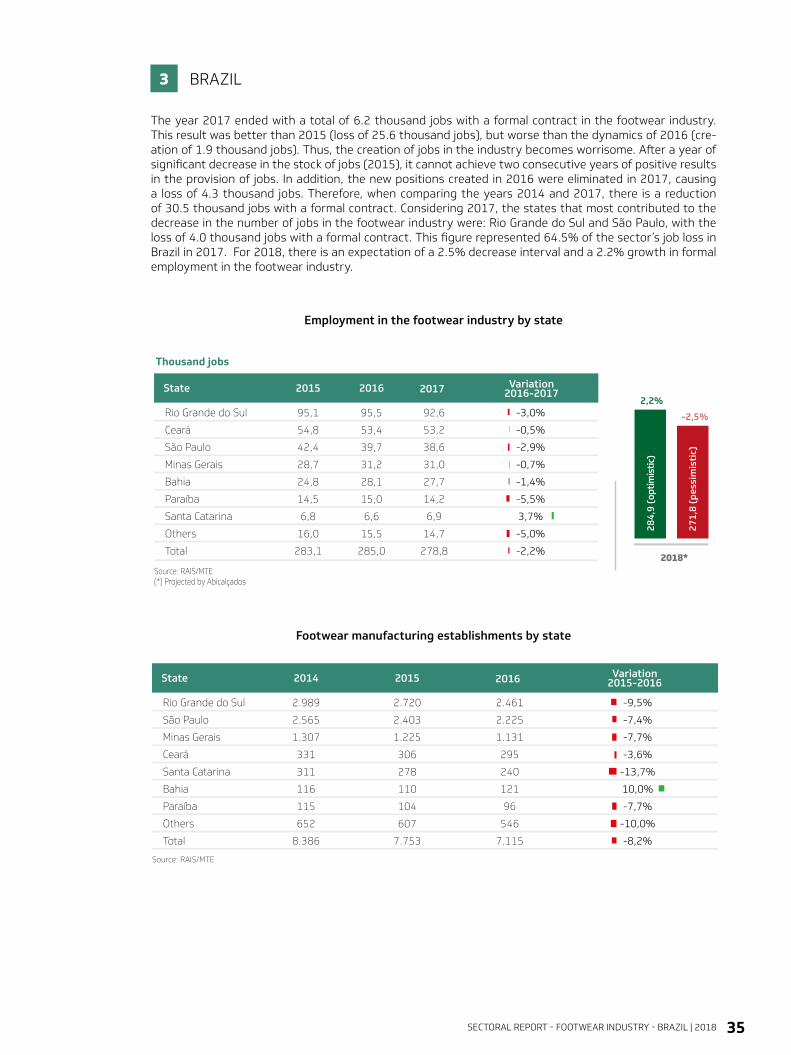

In 2017, the level of employment in the footwear industry registered 279 thousand jobs with a formal con-tract. Regarding the number of establishments, in 2016 Brazil reached 7.1 thousand footwear companies. When comparing these two indicators, even if they are not defined in equal years (they are structural indi-cators, which change more slowly), it is possible to notice that the number of smaller companies is located in four states: Rio Grande do Sul, São Paulo, Minas Gerais, and Santa Catarina. On the other hand, the states in the Northeast (Ceará, Paraíba, and Bahia) stand out due to the location of larger companies.

3.4 EMPLOYMENT AND ESTABLISHMENTS

BRAZIL3

JOBS ESTABLISHMENTS

State

Rio Grande do Sul

Ceará

São Paulo

Minas Gerais

Bahia

Paraíba

279 thousand2017

7,1 thousand2016

33,2%

19,1%

13,8%

11,1%

9,9%

34,6%

4,1%

31,3%

15,9%

1,7%

5,1%

2,5%

3,9%

3,4%

Escala de Cores

Santa Catarina

Others10,4% 9,0%

Source: RAIS/CAGED/MTE

Source: RAIS/CAGED/MTE

CONCENTRATION OF JOBS

CONCENTRATION OF COMPANIES Job

Range

Up to 4

From 5 to 9

From 10 to 19

From 20 to 49

From 50 to 99

From 100 to 249

From 250 to 499

From 500 to 999

1000 or more

2017 2016

51,9%

14,6%

11,9%

11,9%

4,4%

3,0%

1,2%

0,6%

0,4%

3,4%

3,0%

5,0%

11,1%

9,5%

13,6%

11,5%

13,0%

30,0%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 35

Employment in the footwear industry by state

Footwear manufacturing establishments by state

BRAZIL3

The year 2017 ended with a total of 6.2 thousand jobs with a formal contract in the footwear industry. This result was better than 2015 (loss of 25.6 thousand jobs), but worse than the dynamics of 2016 (cre-ation of 1.9 thousand jobs). Thus, the creation of jobs in the industry becomes worrisome. After a year of significant decrease in the stock of jobs (2015), it cannot achieve two consecutive years of positive results in the provision of jobs. In addition, the new positions created in 2016 were eliminated in 2017, causing a loss of 4.3 thousand jobs. Therefore, when comparing the years 2014 and 2017, there is a reduction of 30.5 thousand jobs with a formal contract. Considering 2017, the states that most contributed to the decrease in the number of jobs in the footwear industry were: Rio Grande do Sul and São Paulo, with the loss of 4.0 thousand jobs with a formal contract. This figure represented 64.5% of the sector’s job loss in Brazil in 2017. For 2018, there is an expectation of a 2.5% decrease interval and a 2.2% growth in formal employment in the footwear industry.

State 2014 2015

Footwear manufacturing establishments by state

2016

Source: RAIS/MTE

Rio Grande do Sul

São Paulo

Minas Gerais

Ceará

Santa Catarina

Bahia

Paraíba

Others

Total

2.989

2.565

1.307

331

311

116

115

652

8.386

2.720

2.403

1.225

306

278

110

104

607

7.753

2.461

2.225

1.131

295

240

121

96

546

7.115

-9,5%

-7,4%

-7,7%

-3,6%

-13,7%

10,0%

-7,7%

-10,0%

-8,2%

Variation2015-2016

State 2015

Thousand jobs

Source: RAIS/MTE(*) Projected by Abicalçados

Rio Grande do Sul

Ceará

São Paulo

Minas Gerais

Bahia

Paraíba

Santa Catarina

Others

Total

95,1

54,8

42,4

28,7

24,8

14,5

6,8

16,0

283,1

2016

95,5

53,4

39,7

31,2

28,1

15,0

6,6

15,5

285,0

2017

92,6

53,2

38,6

31,0

27,7

14,2

6,9

14,7

278,8

Variation2016-2017

-3,0%

-0,5%

-2,9%

-0,7%

-1,4%

-5,5%

3,7%

-5,0%

-2,2%2018*

2,2%

-2,5%

284,

9 (o

ptim

istic

)

271,

8 (p

essi

mis

tic)

Aguardando dados

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 201836

3.5 ECONOMIC INDICATORS

3.5.1 EXCHANGE RATE

Exchange Rate R$/US$

BRAZIL3

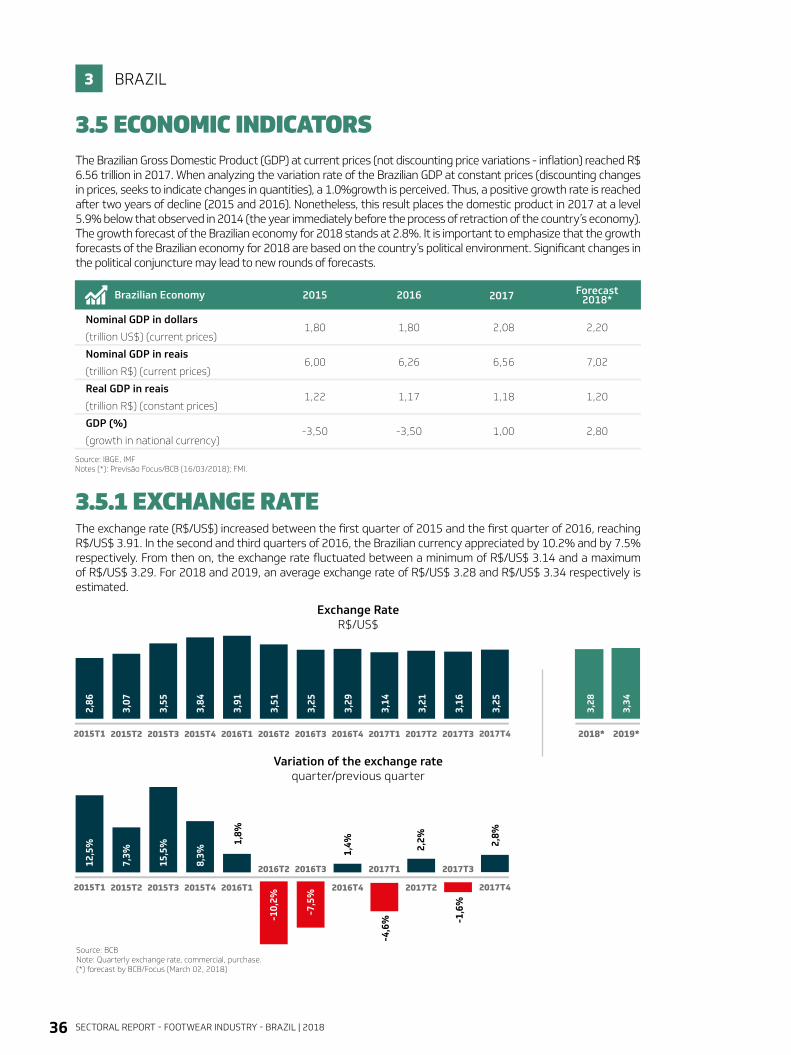

The Brazilian Gross Domestic Product (GDP) at current prices (not discounting price variations - inflation) reached R$ 6.56 trillion in 2017. When analyzing the variation rate of the Brazilian GDP at constant prices (discounting changes in prices, seeks to indicate changes in quantities), a 1.0%growth is perceived. Thus, a positive growth rate is reached after two years of decline (2015 and 2016). Nonetheless, this result places the domestic product in 2017 at a level 5.9% below that observed in 2014 (the year immediately before the process of retraction of the country’s economy). The growth forecast of the Brazilian economy for 2018 stands at 2.8%. It is important to emphasize that the growth forecasts of the Brazilian economy for 2018 are based on the country’s political environment. Significant changes in the political conjuncture may lead to new rounds of forecasts.

The exchange rate (R$/US$) increased between the first quarter of 2015 and the first quarter of 2016, reaching R$/US$ 3.91. In the second and third quarters of 2016, the Brazilian currency appreciated by 10.2% and by 7.5% respectively. From then on, the exchange rate fluctuated between a minimum of R$/US$ 3.14 and a maximum of R$/US$ 3.29. For 2018 and 2019, an average exchange rate of R$/US$ 3.28 and R$/US$ 3.34 respectively is estimated.

Brazilian Economy

Source: IBGE, IMFNotes (*): Previsão Focus/BCB (16/03/2018); FMI.

Nominal GDP in dollars

(trillion US$) (current prices)

Nominal GDP in reais

(trillion R$) (current prices)

Real GDP in reais

(trillion R$) (constant prices)

GDP (%)

(growth in national currency)

2015

1,80

6,00

1,22

-3,50

2016

1,80

6,26

1,17

-3,50

2017

2,08

6,56

1,18

1,00

Forecast2018*

2,20

7,02

1,20

2,80

Variation of the exchange rate quarter/previous quarter

Taxa de câmbio(R$/US$)

3,28

3,34

2015T1 2015T2 2015T3 2015T4 2018* 2019*

Source: BCBNote: Quarterly exchange rate, commercial, purchase. (*) forecast by BCB/Focus (March 02, 2018)

2016T1 2016T2 2016T3 2016T4 2017T1 2017T2 2017T3 2017T4

2,86

3,07

3,55

3,84

3,91

3,51

3,25

3,29

3,14

3,21

3,16

3,25

2015T1 2015T2 2015T3 2015T4 2016T1

2016T2 2016T3

2016T4

2017T1

2017T2

2017T3

2017T4

12,5

%

7,3%

15,5

%

8,3%

-10,

2%

-7,5

%

-4,6

%

-1,6

%

-10,

2%

-7,5

%

-1,6

%

1,4% 2,

2%1,8%

-4,6

%

2,8%

Taxa de câmbio(R$/US$)

3,28

3,34

2015T1 2015T2 2015T3 2015T4 2018* 2019*

Source: BCBNote: Quarterly exchange rate, commercial, purchase. (*) forecast by BCB/Focus (March 02, 2018)

2016T1 2016T2 2016T3 2016T4 2017T1 2017T2 2017T3 2017T4

2,86

3,07

3,55

3,84

3,91

3,51

3,25

3,29

3,14

3,21

3,16

3,25

2015T1 2015T2 2015T3 2015T4 2016T1

2016T2 2016T3

2016T4

2017T1

2017T2

2017T3

2017T4

12,5

%

7,3%

15,5

%

8,3%

-10,

2%

-7,5

%

-4,6

%

-1,6

%

-10,

2%

-7,5

%

-1,6

%

1,4% 2,

2%1,8%

-4,6

%

2,8%

SECTORAL REPORT - FOOTWEAR INDUSTRY - BRAZIL | 2018 37