Embed Size (px)

Citation preview

1INTERNATIONAL TAX & FINANCE CONFERENCE 2011

Shri H. Padamchand Khincha, B.Com, LLB, FCA, 5th Rank in B.Com, Bangalore University 25th Rank in CA Final (November 1982). Presently partner in M/s. H. C. Khincha & Co.

Other Activities:

TEACHING:

(a) Visiting Faculty at IIM, Bangalore; (b) Was a Faculty at the intensive coaching classes of ICAI teaching Income Tax for CA final students; (c) Visiting faculty at the Direct Taxes Training Institute of the Income Tax Department.

PROFESSIONAL:

(a) Was writing a monthly column on ‘Tax Patrika’ – a magazine in Hindi devoted to Direct & Indirect Taxes; (b) Presented papers at various Seminars, Conferences all over the country; (c) Was a panel member for answering queries at the ‘NRI Taxation – on line’ of the Economic Times; (d) Was on the advisory board for answering queries of Lex Site.Com a legal portal; (e) Convenor of the Study Group formed to prepare the approach paper on the “Transfer Pricing Guidance Note”.

AUTHORSHIP:

(a) Co-author of “Tax Holiday U/s.10A and 10B – An analysys; (b) Author of Comparitive Analysis of Indian Tax Treaties published by BCAS; (c) Author of three booklets: (i) Capital Gains of Non-Residents; (ii) Tax Deduction at Source; (iii) Concept of Indexation under Capital Gains; (d) Articles published in Current Tax Reporter, BCAJ, Taxwatch, Journal of CA Institute etc;

SPORTS ACHIEVEMENTS:

(a) Was a keen cricket player. Was selected to represent All India Colts Vs the visiting West Indies team at Pune in 1978; (b) Won prizes in middle distance running in St Joseph’s College Athletic Meet.

OTHERS:

Adjudged the ‘Best Outgoing Student’ of St Joseph’s College of Commerce in 1979.

Shri K.K. Chythanya, B.com, FCA, LLB, Eighth Rank in Karnataka State, • First Rank in Mysore University B.com • Forty seventh Rank (All India) in CA Intermediate • Fifteenth Rank (All India) topping Karnataka State in CA Final

Professional :

Articleship in Price Waterhouse Coopers, Bangalore, Industrial Training in Hindustan Lever Limited, Bangalore. Practice as Chartered Accountant for fourteen years specialising in taxation matters, Now as an Advocate in Bangalore

Others :

1. Guest/Visiting Faculty at • IIM, Bangalore • MDP of ICAI, New Delhi • MDP of ICAI, Bangalore • Direct Taxes Training Centre of Income Tax Department

2. Presented papers in Income Tax and VAT at various Metros and other cities

3. Member of Study Group of ICAI for framing Guidance Note on Transfer Pricing.

4. Co-authored a book on Tax Holiday under Sections 10A & 10B published by Wolters Kluwer, a reputed German published and authored a book on Special Economic Zone

5. Contributed articles for the ‘Chartered Accountant’, BCAJ, Taxman, CTR, and other journals.

Case Studies on International Taxation

International Tax & Finance Conference, 2011 1

Case Studies on International Taxation — Panel Discussion

CA H. Padamchand Khincha and Adv. K. K. Chaitanya

CASE STUDY 1

Fact sheet

Name of the assessee Buildcon India Pvt Ltd. (BPL), India

Name of foreign enterprise Moricon AG (MG), Germany

PE MG, Canada

Other information 1. BPL is in construction industry

2. BPL engages MG to render certain management services

3. Canadian PE of MG provides the said services to BPL

4. Canadian PE invoices BPL and receives the consideration

Issues a) Treaty applicability : Which DTA is applicable to the facts of the case : Indo-Canada

or Indo-Germany?

b) Income characterization

i) as per domestic law,

ii) as per Indo-Canada DTA and

iii) as per Indo-Germany DTA?

c) PE creation and attribution

i) Does the stay of MG’s employees in India create a service PE?

ii) Would it make a difference if BPL and MG are closely associated?

iii) Would it make a difference if HO raises the bill and receives the payment?

iv) Transfer pricing vs. Article 7(2) vs. Rule 10.

v) Relevance of Rule 10 in the light of (a) insertion of rules 10A to 10E and (b) Article 7(2)

d) TDS applicability with reference to payment in question

e) Employees tax liability and ‘Employer’ determination

Case Studies on International Taxation

2 International Tax & Finance Conference, 2011

f) Will it make any difference if MG seeks the assistance of Candy Inc, Canada an independent and unrelated company;

a) By outsourcing fully

b) By outsourcing partly

c) By simply seeking manpower assistance

— “Through Secondment”

— Otherwise than through secondment

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

International Tax & Finance Conference, 2011 3

CASE STUDY 2

Fact sheet

Name of the assessee Storetech India Pvt Ltd. (SPL), India

Name of foreign enterprise Storetech Inc (SL), Singapore

Relationship SPL is a 100% subsidiary of SL

Other information 1. SL and SPL are storage solution providers

2. SL as part of HR development, organizes seminars/workshops/training in various areas

3. Training could be

• Both general as well as specific

• Long term as well as short-term

• With or without course material

• In-house or outsourced to third party trainer

4. One of the third party trainers is Chang of Singapore and other is Chandru of India

5. SPL’s employees attend some of these programmes both in India as well in Singapore

6. SL cross charges SPL for the costs incurred

Issues a) Treaty applicability

1. When SPL pays SL - Is Indo-Singapore DTA applicable?

2. When SL pays Chang – Is Indo-Singapore DTA applicable?

3. When SL pays Chandru – Is Indo-Singapore DTA applicable?

b) Income characterisation

1. Is reimbursement income?

2. Is training income FTS?

3. Does training make available technology when training is

• Both general as well as specific

• Long term as well as short-term

• With or without course material

• In-house or outsourced to third party trainer

c) Will the tax position change depending on

(a) whether such training is imparted in India or in Singapore?

Case Studies on International Taxation

4 International Tax & Finance Conference, 2011

(b) when such outsourcing is done to an individual, Chang or Chandru?

(c) when SL asks SPL to pay Chang or Chandru directly to the extent of 50% [representing SPL’s share]?

d) Obligation of SL in India

1) Return under sec. 139(1)

2) Tax audit report under sec. 44AB

3) TP documentation under sec. 92D and certificate under sec. 92E

e) Applicability of sections 271F, 271G, 271B and 271BA

f) Transfer pricing

1) SPL and SL both suffer income enhancement due to differential TP treatment in India

a) By two different TPOs

b) Applying Cup for SPL’s expenditure and applying TNMM for SL’s income

2) Applicability of Explanation 7 to section 271(1)(c)

g) PE creation

1. If training is FTS and

• Taxed under Article 12

• Not taxed under Article 12 because of Article 12(5)

2. If training is not FTS

• When only training –

Duration in days

Total India Singapore

28 28 0

28 0 28

35 28 7

• When training as also other services are provided –

Duration in days

Training Other services

Total India Singapore Total India Singapore

28 28 0 14 0 14

28 0 28 14 14 0

35 28 7 14 2 12

Case Studies on International Taxation

International Tax & Finance Conference, 2011 5

• Chandru is in India for 365 days but SL engages him for training in India for 24 days

h) TDS applicability

1) In the following circumstances

• When SPL pays SL

• When SL pays Chang

• When SL pays Chandru

• When SPL pays Chang/Chandru directly

2) Applicability of section 206AA and section 94A [assuming that the country under discussion is Notified Jurisdictional Area [NJA]]

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

6 International Tax & Finance Conference, 2011

CASE STUDY 3

Fact sheet

Name of the assessee Globe India Pvt Ltd. (GPL), IndiaName of associated enterprise Globe Inc (GL), USARelationship GPL is a 100% subsidiary of GLAssessment year 2008-09Other tax information 1. GPL is claiming sec. 10A deduction 2. Entire turnover is export turnover 3. Operating costs ` 100 crores 4. GPL’s ALP : 10% 5. TPO’s ALP : 20% 6. Assessment order is appealed against ALP

determination and method of computation of section 10A deduction

7. GL initiates MAP with USA authorities

MAP proceedings are concluded as follows: 1. ALP to be worked at 15% on operating costs2. Operating costs were not disturbed3. GL to send the remittance to India of incremental value of turnover4. GPL to withdraw the appeal in so far as the appeal related to ALP computation5. GL to get credit in USA for taxes paid by GPL AO gives a notice to GPL seeking its consent. GPL gives its consent but asserting its

right to claim deduction under section 10A in respect of income added as a result of ALP adjustment as per MAP. AO finalizes the assessment ignoring the claim under section 10A.

Issues 1. Is the final order of AO appealable?2. Can GPL give a conditional consent for implementing MAP order?3. Need and eligibility of GPL as regards the deduction under sec. 10A in respect of

incremental income?4. Would it make a difference, if the operating costs are increased to ` 130 crores by TPO

but fixed at ` 110 crores by MAP —a) Where ALP is retained at 10%

b) Where ALP is fixed at 15%

5. Would it make a difference if the claim of tax holiday is under section 10AA?

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

International Tax & Finance Conference, 2011 7

CASE STUDY 4

Fact sheet

Name of the assessee Mfaber India Pvt Ltd. (MPL), India

Foreign PE Factory in Australia (MA)

Other information 1. MPL is engaged in manufacture of high end pre-fab sheet

2. MA has a factory where the semi finished goods of MPL are imported and sold in local market after finishing

3. MPL invoices MA for sale of semi finished goods

4. MPL debits MA for certain HO expenses and interest

5. MPL also debits MA for 50% of certain payment made by it to one X-Corp in New Zealand for some services provided to MPL and MA

Issues

a) Total Income and its computation1. MPL proposes not to include the profits of MA in its tax return. Is it justified in

its stand?

2. How are profits of MA computed? Should the computation factor the expenses incurred by MPL whether cross charged to MA or not?

3. Would it make a difference if X-Corp was engaged by MA solely for its use and MPL is paying the same [with or without cross charge]?

b) TDS1. Should MA deduct tax in respect of payment of interest to MPL?

2. Should MPL deduct tax in respect of payment made to X-corp?

c) Transfer pricing1. Will transfer pricing provisions apply in respect of transactions between MPL and

MA?

2. Will it make a difference MPL is in Australia and MA is in India?

Case Studies on International Taxation

8 International Tax & Finance Conference, 2011

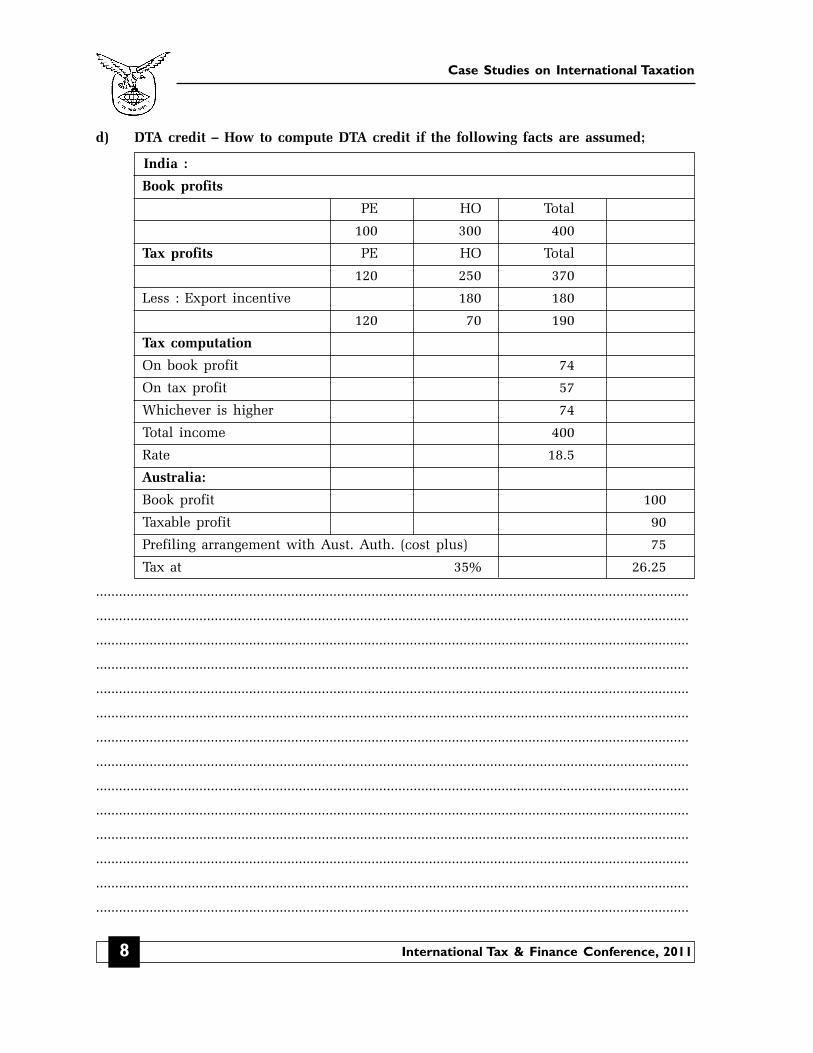

d) DTA credit – How to compute DTA credit if the following facts are assumed;

India :

Book profits

PE HO Total

100 300 400

Tax profits PE HO Total

120 250 370

Less : Export incentive 180 180

120 70 190

Tax computation

On book profit 74

On tax profit 57

Whichever is higher 74

Total income 400

Rate 18.5

Australia:

Book profit 100

Taxable profit 90

Prefiling arrangement with Aust. Auth. (cost plus) 75

Tax at 35% 26.25

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

International Tax & Finance Conference, 2011 9

CASE STUDY 5

Fact sheet

Name of the USA company Orange Inc, USA [Orange] engaged in Bio Tech Industry

Name of the Singapore Crimson Pte, Singapore, [Crimson] specialized in trainingCompany in Bio Technology

Nature of the activity Specialised Training in Bio Technology

Place of training Emerging Pvt Ltd., [Emerging] an Indian company has an extensive Bio tech facility including a training centre in Bangalore where outside trainers are permitted to provide training on professional basis

Other information 1. Orange has engaged Crimson for training its APAC employees (no employees based in India)

2. Part of the training is to be carried out at Emerging’s training centre

3. Three trainers from Crimson visit the training centre in India and train about 20 employees of Orange:

• Classroom training for 10 days

• Training also consists of assignment using trainer’s equipment (for raising molecules) for 30 days

• Consideration payable by Orange to Crimson is as follows:

— For training USD 75,000

— For equipment use USD 30,000

— For comprehensive information in the training module USD 5,000

— For certificates USD 1,000

Issues a) Income characterization

1. In the light of section 9(1)(vi) – Explanation 2(iva) and the applicable DTA

2. In the light of section 9(1)(vii) – Explanation 2 and the applicable DTA

3. Should all types of payments be viewed in isolation or as an aggregate?

4. If viewed in isolation, what is the nature of payment for

• Information in training manual

• Certificates

Case Studies on International Taxation

10 International Tax & Finance Conference, 2011

b) Total income – Place of accrual under IT Act and DTA

1. Which treaty is applicable – Indo-USA or Indo Singapore or Singapore-USA?

2. In the light of Section 5 vs. section 9 (Actual accrual vs. deemed accrual)

3. In the light of Article 12(7)(b) – Its applicability, significance and role

4. In the light of Section 9(1)(vi)(c) and section 9(1)(vii)(c).

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

International Tax & Finance Conference, 2011 11

CASE STUDY 6

Facts sheet

Name of the assessee 6Sigma-India Pvt Ltd., India (SPL)

Foreign holding company 6Sigma-Pte, USA (SUK)

Nature of the activity Manufacture and sale of high end tiles and bricks

Other information 1. SPL is a unit entitled to benefit of deduction under section 10AA

2. SPL pays royalty of USD 1 Mn to SUK after deducting tax for technology relating to tiles

3. SPL determines the ALP of the royalty at USD 0.75 Mn resulting in a suo motu addition of USD 0.25 Mn

4. TPO revises the royalty to USD 0.50 Mn resulting in a further addition of USD 0.25 Mn

5. SPL further pays a lump sum of USD 5 Mn to SUK for acquiring technology to manufacture bricks on an exclusive basis for the territory of India with a clause for payment of additional royalty of 1 USD per brick for production in excess 2.5 Mn bricks

Issues a) Royalty for tiles technology

1. Can SPL claim deduction under section 10AA in respect of suo motu addition?

2. Can SPL claim deduction under section 10AA in respect of TPO’s addition?

3. Can SUK claim refund of tax paid on USD 0.5 Mn in India relying on Article 10(2) notwithstanding section 92C(4)?

b) Royalty for bricks technology

1. What is the nature of income of lump sum royalty and additional royalty?

2. Would the tax treatment be different if lump sum royalty is paid by way of allotment of shares?

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

12 International Tax & Finance Conference, 2011

Other Case Studies

CASE STUDY 7

Fact sheet

Name and status of the assessee Nita is presently a resident in India and a citizen of India

Receipts during the year 1. Pension from Citibank NA

2. Alimony from Rakesh

3. Payment from Rakesh for Nita’s daughter’s education in USA

4. Capital gains on sale of shares (ESOP shares) allotted to her by Citibank NA

5. Capital gains on sale of shares (ESOP shares) given to her by Rakesh at the time of divorce as part of settlement

Other information 1. Nita worked for Citibank NA for 30 years. During her employment, she was posted in different countries and she was in USA at the time of retirement

2. Nita was married to Rakesh in India and the marriage lasted for 20 years before a divorce in an Indian court

3. Rakesh continues to live in USA whereas Nita has moved to India

Issues1. Is pension taxable? If so, in which country?

2. Is alimony taxable? If so, in which country?

3. Is payment to daughter’s education taxable? If so, in which country?

4. Is capital gain on sale of ESOP shares taxable? If so, quantum thereof and in which country?

5. Will the tax position change if Nita is a citizen of USA and a POI in India?

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

International Tax & Finance Conference, 2011 13

CASE STUDY 8

Fact sheet

Name of the assessee Air America Inc, USA (AA)

Nature of business 1. Running Airlines

2. Cargo handling

3. Ticketing

India operations AA runs a sales office in India and

a) sells its tickets as well as of Woodpecker Airlines for international travel (both inbound and outbound)

b) books cargo for itself as well as for other courier companies for international transportation

Issues 1. Does AA have a PE in India?

2. What is the scope of taxation of AA in respect of its India operations?

3. If AA hires Sujay Mallya an Indian resident as a pilot of one of its aircraft, what is the scope of taxation of Sujay Mallya in India?

4. Will Direct Taxes Code make any difference to the above?

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

14 International Tax & Finance Conference, 2011

CASE STUDY 9

Fact sheet

Name of the first foreign Eden Pte, Singaporecompany

Name of the second foreign Bush Inc, USAcompany

Other information 1. Eden runs the business of chip design with its branches in Singapore, Hong Kong and India

2. Eden holds shares in a software company in India

3. Eden amalgamates with Bush

Issues 1. What is the scope of taxation in the hands of Eden?

2. What is the scope of taxation in the hands of Bush?

3. Is tax withholding applicable?

4. Will the position change if, instead of amalgamation, Eden demerges its Indian and HK units to Bush?

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Case Studies on International Taxation

International Tax & Finance Conference, 2011 15

CASE STUDY 10

Facts sheet

Name and status of the assessee Ranga is a budding cricketer and a student of commerce

Other information 1. Leads Club of UK identifies Ranga’s talent and offers him a package

2. Package consists of

a) Ranga to move to UK for two years

b) Ranga will continue his studies in UK and Leads will pay for his stay and education

c) Leads pays a monthly stipend of 500 pounds to him

d) Ranga is obliged to play for Leads in the county matches for two years

e) There were 80 matches played during Ranga’s stay. Out of the same, Ranga was not in the playing 11 for 16 matches. He did not play in 8 matches due to injury. 4 matches were not played due to rain

f) Ranga earned prize moneys of 2500 pounds on account of his team’s wins, man of the match awards and overall performance

g) Ranga earned ad money of 1,000 pounds and coaching fee of 1000 pounds

h) Ranga leaves India on 1-9-2009 and returns on 15-8-2011

i) When Ranga returns to India, he was allowed to retain the car which was given for his use during his UK stay.

Issues 1. What is the residential status of Ranga for each of the years?

2. What is the scope of taxation of following incomes;

a) Stipend

b) Cost of stay and education paid by Leads

c) Ad revenue

d) Coaching fee

Case Studies on International Taxation

16 International Tax & Finance Conference, 2011

e) Prize money

f) Use and transfer of car

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

...........................................................................................................................................................

Reference Material

International Tax & Finance Conference, 2011 17

Reference Material

CASE STUDY 1: Germany & Canada

Article 12 — Royalties and fees for technical services – Germany1. Royalties and fees for technical services arising in a Contracting State and paid to a resident of

the other Contracting State may be taxed in that other State.

2. However, such royalties and fees for technical services may also be taxed in the Contracting State in which they arise and according to the laws of that State, but if the recipient is the beneficial owner of the royalties, or fees for technical services, the tax so charged shall not exceed 10 per cent of the gross amount of the royalties or the fees for technical services.

3. The term “royalties” as used in this Article means payments of any kind received as a consideration for the use of, or the right to use, any copyright of literary, artistic or scientific work, including cinematograph films or films or tapes used for radio or television broadcasting, any patent, trade mark, design or model, plan, secret formula or process, or for the use of, or the right to use, industrial, commercial or scientific equipment, or for information concerning industrial, commercial or scientific experience.

4. The term “fees for technical services” as used in this Article means payments of any amount in consideration for the services of managerial, technical or consultancy nature, including the provision of services by technical or other personnel, but does not include payments for services mentioned in Article 15 of this Agreement.

5. The provisions of paragraphs 1 and 2 shall not apply if the beneficial owner of the royalties or fees for technical services, being a resident of a Contracting State, carries on business in the other Contracting State in which the royalties or fees for technical services arise, through a permanent establishment situated therein, or performs in that other State independent personal services from a fixed base situated therein, and the right, property or contract in respect of which the royalties or fees for technical services are paid is effectively connected with such permanent establishment or fixed base. In such case, the provisions of Article 7 or Article 14, as the case may be, shall apply.

6. Royalties and fees for technical services shall be deemed to arise in a Contracting State when the payer is that State itself, a land or a political sub-division, a local authority or a resident of that State. Where, however, the person paying the royalties or fees for technical services, whether he is a resident of a Contracting State or not, has in a Contracting State a permanent establishment or a fixed base in connection with which the liability to pay the royalties or fees for technical services was incurred, and such royalties or fees for technical services are borne by such permanent establishment or fixed base, then such royalties or fees for technical services shall be deemed to arise in the State in which the permanent establishment or fixed base is situated.

7. Where, by reason of special relationship between the payer and the beneficial owner or between both of them and some other person, the amount of royalties or fees for technical services paid exceeds the amount which would have been paid in the absence of such relationship, the provisions of this Article shall apply only to the last-mentioned amount. In such case, the excess

Reference Material

18 International Tax & Finance Conference, 2011

part of the payments shall remain taxable according to the laws of each Contracting State, due regard being had to the other provisions of this Agreement.

Article 12 — Royalties and fees for included services – Canada1. Royalties and fees for included services arising in a Contracting State and paid to a resident of

the other Contracting State may be taxed in that other State.

2. However, such royalties and fees for included services may also be taxed in the Contracting State in which they arise and according to the laws of that State; but if the beneficial owner of the royalties or fees for included services is a resident of the other Contracting State, the tax so charged shall not exceed :

(a) in the case of royalties referred to in sub-paragraph (a) of paragraph 3 and fees for included services as defined in this Article (other than services described in sub-paragraph (b) of this paragraph) :

(i) during the first five taxable years for which this Agreement has effect,

(A) 15 per cent of the gross amount of the royalties or fees for included services as defined in this Article, where the payer of the royalties or fees is the Government of that Contracting State, a political sub-division or a public sector company; and

(B) 20 per cent of the gross amount of the royalties or fees for included services in all other cases; and

(ii) during the subsequent years, 15 per cent of the gross amount of the royalties or fees for included services; and

(b) in the case of royalties referred to in sub-paragraph (b) of paragraph 3 and fees for included services as defined in this Article that are ancillary and subsidiary to the enjoyment of the property for which payment is received under paragraph 3(b) of this Article, 10 per cent of the gross amount of the royalties or fees for included services.

3. The term ‘royalties’ as used in this Article means :

(a) payment of any kind received as a consideration for the use of, or the right to use, any copyright of a literary, artistic, or scientific work including cinematograph films or work on film tape or other means of reproduction for use in connection with radio or television broadcasting, any patent, trademark, design or model, plan, secret formula or process, or for information concerning industrial, commercial or scientific experience, including gains derived from the alienation of any such right or property which are contingent on the productivity, use, or disposition thereof; and

(b) payments of any kind received as consideration for the use of, or the right to use, any industrial, commercial, or scientific equipment, other than payments derived by an enterprise described in paragraph 1 of Article 8 from activities described in paragraph 3(c) or 4 of Article 8.

4. For the purposes of this Article, ‘fees for included services’ means payments of any kind to any person in consideration for the rendering of any technical or consultancy services (including through the provision of services of technical or other personnel) if such services :

(a) are ancillary and subsidiary to the application or enjoyment of the right, property or information for which a payment described in paragraph 3 is received; or

(b) make available technical knowledge, experience, skill, know-how, or processes or consist of the development and transfer of a technical plan or technical design.

Reference Material

International Tax & Finance Conference, 2011 19

5. Notwithstanding paragraph 4, ‘fees for included services’ does not include amount paid:

(a) for services that are ancillary and subsidiary, as well as inextricably and essentially linked, to the sale of property other than a sale described in paragraph 5(a);

(b) for services that are ancillary and subsidiary to the rental of ships, aircraft, containers or other equipment used in connection with the operation of ships or aircraft in international traffic;

(c) for teaching in or by educational institutions;

(d) for services for the personal use of the individual or individuals making the payment; or

(e) to an employee of the person making the payments or to any individual or firm of individuals (other than a company) for professional services as defined in Article 14.

6. The provisions of paragraphs 1 and 2 shall not apply if the beneficial owner of the royalties or fees for included services, being a resident of a Contracting State, carries on business in the other Contracting State in which the royalties or the fees for included services arise, through a permanent establishment situated therein, or performs in that other State independent personal services from a fixed base situated therein, and the right, property or contract in respect of which the royalties or fees for included services are paid is effectively connected with such permanent establishment or fixed base. In such a case the provisions of Article 7 or Article 14, as the case may be, shall apply.

7. Royalties and fees for included services shall be deemed to arise in a Contracting State when the payer is that State itself, a political sub-division, a local authority or a resident of that State. Where, however, the person paying the royalties or the fees for included services, whether he is a resident of a Contracting State or not, has in a Contracting State a permanent establishment or a fixed base in connection with which the obligation to pay the royalties or the fees for included services was incurred, and such royalties or fees for included services are borne by that permanent establishment or fixed base, then such royalties or fees for included services shall be deemed to arise in the Contracting State in which the permanent establishment or fixed base is situated.

8. Where by reason of a special relationship between the payer and the beneficial owner or between both of them and some other person, the amount of the royalties or fees for included services, having regard to the use, right, information or services for which they are paid, exceeds the amount which would have been agreed upon by the payer and the beneficial owner in the absence of such relationship, the provisions of this Article shall apply only to the last mentioned amount. In that case, the excess part of the payments shall remain taxable according to the law of each Contracting State, due regard being had to the other provisions of this Agreement.

Article 5 — Permanent Establishment – Germany1. For the purposes of this Agreement, the term “permanent establishment” means a fixed place of

business through which the business of an enterprise is wholly or partly carried on.

2. The term “permanent establishment” includes especially,—

(a) a place of management;

(b) a branch;

(c) an office;

(d) a factory;

(e) a workshop;

Reference Material

20 International Tax & Finance Conference, 2011

(f) a mine, an oil or gas well, a quarry or any other place of extraction of natural resources, including an installation or structure used for the exploration or exploitation;

(g) a warehouse or sales outlet;

(h) a farm, plantation or other place where agricultural, forestry, plantation or related activities are carried on; and

(i) a building site or construction, installation or assembly project or supervisory activities in connection therewith, where such site, project or activities continue for a period exceeding six months.

3. An enterprise shall be deemed to have a permanent establishment in a Contracting State and to carry on business through that permanent establishment if it provides services or facilities in connection with, or supplies plant and machinery on hire used for or to be used in the prospecting for or extraction or exploitation of mineral oils in that State.

4. Notwithstanding the preceding provisions of this Article, the term “permanent establishment” shall be deemed not to include,—

(a) the use of facilities solely for the purpose of storage, display or delivery of goods or merchandise belonging to the enterprise;

(b) the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of storage, display or delivery;

(c) the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of processing by another enterprise;

(d) the maintenance of a fixed place of business solely for the purpose of purchasing goods or merchandise or of collecting information, for the enterprise;

(e) the maintenance of a fixed place of business solely for the purpose of carrying on, for the enterprise, any other activity of a preparatory or auxiliary character;

(f) the maintenance of a fixed place of business solely for any combination of activities mentioned in sub-paragraphs (a) to (e), provided that the overall activity of the fixed place of business resulting from this combination is of a preparatory or auxiliary character.

5. Notwithstanding the provisions of paragraphs 1 and 2, where a person - other than an agent of an independent status to whom paragraph 6 applies - is acting in a Contracting State on behalf of an enterprise of the other Contracting State that enterprise shall be deemed to have a permanent establishment in the first-mentioned State, if this person,—

(a) has and habitually exercises in that State an authority to conclude contracts on behalf of the enterprise, unless his activities are limited to the purchase of goods or merchandise for the enterprise ;

(b) has no such authority, but habitually maintains in the first-mentioned State a stock of goods or merchandise from which he regularly delivers goods or merchandise on behalf of the enterprise ; or

(c) habitually secures orders in the first-mentioned State, wholly or almost wholly for the enterprise itself or for the enterprise and other enterprises controlling, controlled by, or subject to the same common control, as that enterprise.

6. An enterprise shall not be deemed to have a permanent establishment in a Contracting State merely because it carries on business in that State through a broker, general commission agent or any other agent of an independent status, provided that such persons are acting in the ordinary course of their business and in their commercial and financial relations to the

Reference Material

International Tax & Finance Conference, 2011 21

enterprise no conditions are agreed or imposed which differ from those usually agreed between independent persons.

7. The fact that a company which is a resident of a Contracting State controls or is controlled by a company which is a resident of the other Contracting State or which carries on business in that other State (whether through a permanent establishment or otherwise), shall not of itself constitute either company a permanent establishment of the other.

Article 5 — Permanent Establishment – Canada1. For the purposes of this Agreement, the term ‘permanent establishment’ means a fixed place of

business through which the business of an enterprise is wholly or partly carried on.

2. The term ‘permanent establishment’ shall include especially :

(a) a place of management;

(b) a branch;

(c) an office;

(d) a factory;

(e) a workshop;

(f) a mine, an oil or gas well, a quarry or any other place of extraction of natural resources;

(g) a warehouse, in relation to a person providing storage facilities for others;

(h) a farm, plantation or other place where agriculture, forestry, plantation or related activities are carried on;

(i) a store or premises used as a sales outlet;

(j) an installation or structure used for the exploration or exploitation of natural resources, but only if so used for a period of more than 120 days in any twelve-month period;

(k) a building site or construction, installation or assembly project or supervisory activities in connection therewith, where such site, project or activities (together with other such sites, projects or activities, if any) continue for a period of more than 120 days in any twelve-month period;

(l) the furnishing of services other than included services as defined in Article 12, within a Contracting State by an enterprise through employees or other personnel, and only if :

(i) activities of that nature continue within that State for a period or periods aggregating to more than 90 days within any twelve-month period; or

(ii) the services are performed within that State for a related enterprise (within the meaning of paragraph 1 of Article 9).

3. Notwithstanding the preceding provisions of this Article, the term ‘permanent establishment’ shall be deemed not to include any one or more of the following :

(a) the use of facilities solely for the purpose of storage, display, or occasional delivery of goods or merchandise belonging to the enterprise;

(b) the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of storage, display, or occasional delivery;

(c) the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of processing by another enterprise;

Reference Material

22 International Tax & Finance Conference, 2011

(d) the maintenance of a fixed place of business solely for the purpose of purchasing goods or merchandise or of collecting information, for the enterprise;

(e) the maintenance of a fixed place of business solely for the purpose of advertising, for the supply of information, for scientific research or for other activities which have a preparatory or auxiliary character, for the enterprise.

4. Notwithstanding the provisions of paragraphs 1 and 2, where a person - other than an agent of an independent status to whom paragraph 5 applies - is acting in a Contracting State on behalf of an enterprise of the other Contracting State, that enterprise shall be deemed to have a permanent establishment in the first-mentioned State if :

(a) he has and habitually exercises in the first-mentioned State an authority to conclude contracts on behalf of the enterprise, unless his activities are limited to those mentioned in paragraph 3 which, if exercised through a fixed place of business, would not make that fixed place of business a permanent establishment under the provisions of that paragraph;

(b) he has no such authority but habitually maintains in the first-mentioned State a stock of goods or merchandise from which he regularly delivers goods or merchandise on behalf of the enterprise, and some additional activities conducted in that State on behalf of the enterprise have contributed to the sale of the goods or merchandise; or

(c) he habitually secures orders in the first-mentioned State, wholly or almost wholly for the enterprise.

5. An enterprise of a Contracting State shall not be deemed to have a permanent establishment in the other Contracting State merely because it carries on business in that other State through a broker, general commission agent, or any other agent of an independent status, provided that such persons are acting in the ordinary course of their business. However, when the activities of such an agent are devoted wholly or almost wholly on behalf of that enterprise and the transactions between the agent and the enterprise are not made under arm’s length conditions, he shall not be considered an agent of independent status within the meaning of this paragraph.

6. The fact that a company which is a resident of a Contracting State controls or is controlled by a company which is a resident of the other Contracting State, or which carries on business in that other State (whether through a permanent establishment or otherwise), shall not of itself constitute either company a permanent establishment of the other.

Rule 10 of the Income-tax Rules, 1962

10. Determination of income in the case of non-residents In any case in which the Assessing Officer is of opinion that the actual amount of the income

accruing or arising to any non-resident person whether directly or indirectly, through or from any business connection in India or through or from any property in India or through or from any asset or source of income in India or through or from any money lent at interest and brought into India in cash or in kind cannot be definitely ascertained, the amount of such income for the purposes of assessment to income-tax may be calculated :—

(i) at such percentage of the turnover so accruing or arising as the Assessing Officer may consider to be reasonable, or

(ii) on any amount which bears the same proportion to the total profits and gains of the business of such person (such profits and gains being computed in accordance with the provisions of the Act), as the receipts so accruing or arising bear to the total receipts of the business, or

(iii) in such other manner as the Assessing Officer may deem suitable.

Reference Material

International Tax & Finance Conference, 2011 23

Article 7 — Business profits – Germany1. The profits of an enterprise of a Contracting State shall be taxable only in that State unless the

enterprise carries on business in the other Contracting State through a permanent establishment situated therein. If the enterprise carries on business as aforesaid, the profits of the enterprise may be taxed in the other State but only so much of them as is attributable to that permanent establishment.

2. Subject to the provisions of paragraph 3, where an enterprise of a Contracting State carries on business in the other Contracting State through a permanent establishment situated therein, there shall in each Contracting State be attributed to that permanent establishment the profits which it might be expected to make, if it were a distinct and separate enterprise engaged in the same or similar activities under the same or similar conditions and dealing wholly independently with the enterprise of which it is a permanent establishment.

3. In the determination of the profits of a permanent establishment, there shall be allowed as deductions, expenses which are incurred for the purposes of the business of the permanent establishment including executive and general administrative expenses so incurred, whether in the State in which the permanent establishment is situated or elsewhere, and according to the domestic law of the Contracting State in which the permanent establishment is situated.

4. Insofar as in a Contracting State and in exceptional cases the determination of the profits to be attributed to a permanent establishment in accordance with paragraph 2 is impossible or gives rise to unreasonable difficulties, nothing in paragraph 2 shall preclude the determination of the profits to be attributed to a permanent establishment by means of either apportioning the total profits of the enterprise to that permanent establishment or estimating on any other reasonable basis; the method of apportionment or estimation adopted shall, however, be such that the result shall be in accordance with the principles contained in this Article.

5. No profits shall be attributed to a permanent establishment by reason of the mere purchase by that permanent establishment of goods or merchandise for the enterprise.

6. For the purposes of the preceding paragraphs, the profits to be attributed to the permanent establishment shall be determined by the same method year by year unless there is good and sufficient reason to the contrary.

7. Where profits include items of income which are dealt with separately in other Articles of this Agreement, then the provisions of those Articles shall not be affected by the provisions of this Article.

Article 7 — Business profits – Canada1. The profits of an enterprise of a Contracting State shall be taxable only in that State unless the

enterprise carries on business in the other Contracting State through a permanent establishment situated therein. If the enterprise carries on or has carried on business as aforesaid, the profits of the enterprise may be taxed in the other State but only so much of them as is attributable to :

(a) that permanent establishment, and

(b) sales of goods and merchandise of the same or similar kind as those sold, or from other business activities of the same or similar kind as those effected, through that permanent establishment.

2. Subject to the provisions of paragraph 3, where an enterprise of a Contracting State carries on business in the other Contracting State through a permanent establishment situated therein, there shall in each Contracting State be attributed to that permanent establishment the profits which it might be expected to make if it were a distinct and separate enterprise engaged

Reference Material

24 International Tax & Finance Conference, 2011

in the same or similar activities under the same or similar conditions and dealing wholly independently with the enterprise of which it is a permanent establishment. In any case, where the correct amount of profits attributable to a permanent establishment is incapable of determination or the ascertainment thereof presents exceptional difficulties, the profits attributable to the permanent establishment may be estimated on a reasonable basis provided that the result shall be in accordance with the principles laid down in this Article.

3. In the determination of the profits of a permanent establishment, there shall be allowed those deductible expenses which are incurred for the purposes of the business of the permanent establishment, including executive and general administrative expenses, whether incurred in the State in which the permanent establishment is situated or elsewhere as are in accordance with the provisions of and subject to the limitations of the taxation laws of that State. However, no such deduction shall be allowed in respect of amounts, if any, paid (otherwise than as a reimbursement of actual expenses) by the permanent establishment to the head office of the enterprise or any of its other offices, by way of royalties, fees or other similar payments in return for the use of patents, know-how or other rights, or by way of commission or other charges, for specific services performed or for management, or, except in the case of a banking enterprise, by way of interest on moneys lent to the permanent establishment. Likewise, no account shall be taken in the determination of the profits of a permanent establishment, for amounts charged (otherwise than towards reimbursement of actual expenses), by the permanent establishment to the head office of the enterprise or any of its other offices, by way of royalties, fees or other similar payments in return for the use of patents, know-how or other rights, or by way of commission or other charges for specific services performed or for management, or, except in the case of a banking enterprise, by way of interest on moneys lent to the head office of the enterprise or any of its other offices.

4. Subject to the provisions of paragraph 3, insofar as it has been customary in a Contracting State to determine the profits to be attributed to a permanent establishment on the basis of an apportionment of the total profits of the enterprise to its various parts, nothing in paragraph 2 shall preclude that Contracting State from determining the profits to be taxed by such an apportionment as may be customary; the method of apportionment adopted shall, however, be such that the result shall be in accordance with the principles contained in this Article.

5. No profits shall be attributed to a permanent establishment by reason of the mere purchase by that permanent establishment of goods or merchandise for the enterprise.

6. For the purposes of the preceding paragraphs, the profits to be attributed to the permanent establishment, shall be determined by the same method year by year unless there is good and sufficient reason to the contrary.

7. Where profits include items of income which are dealt with separately in other Articles of this Agreement, then the provisions of those Articles shall not be affected by the provisions of this Article.

CASE STUDY 2: Singapore

Article 12 — Royalties and fees for technical services – Singapore1. Royalties and fees for technical services arising in a Contracting State and paid to a resident of

the other Contracting State may be taxed in that other State.

2. However, such royalties and fees for technical services may also be taxed in the Contracting State in which they arise and according to the laws of that Contracting State, but if the recipient is the beneficial owner of the royalties or fees for technical services, the tax so charged shall not exceed 10 per cent.

Reference Material

International Tax & Finance Conference, 2011 25

3. The term “royalties” as used in this Article means payments of any kind received as a consideration for the use of, or the right to use :

(a) any copyright of a literary, artistic or scientific work, including cinematograph film or films or tapes used for radio or television broadcasting, any patent, trade mark, design or model, plan, secret formula or process, or for information concerning industrial, commercial or scientific experience, including gains derived from the alienation of any such right, property or information ;

(b) any industrial, commercial or scientific equipment, other than payments derived by an enterprise from activities described in paragraph 4(b) or 4(c) of Article 8.

4. The term “fees for technical services” as used in this Article means payments of any kind to any person in consideration for services of a managerial, technical or consultancy nature (including the provision of such services through technical or other personnel) if such services :

(a) are ancillary and subsidiary to the application or enjoyment of the right, property or information for which a payment described in paragraph 3 is received ; or

(b) make available technical knowledge, experience, skill, know-how or processes, which enables the person acquiring the services to apply the technology contained therein ; or

(c) consist of the development and transfer of a technical plan or technical design, but excludes any service that does not enable the person acquiring the service to apply the technology contained therein.

For the purposes of (b) and (c) above, the person acquiring the service shall be deemed to include an agent, nominee, or transferee of such person.

5. Notwithstanding paragraph 4, “fees for technical services” does not include payments:

(a) for services that are ancillary and subsidiary, as well as inextricably and essentially linked, to the sale of property other than a sale described in paragraph 3(a);

(b) for services that are ancillary and subsidiary to the rental of ships, aircraft, containers or other equipment used in connection with the operation of ships or aircraft in international traffic;

(c) for teaching in or by educational institutions ;

(d) for services for the personal use of the individual or individuals making the payment;

(e) to an employee of the person making the payments or to any individual or firm of individuals (other than a company) for professional services as defined in Article 14;

(f) for services rendered in connection with an installation or structure used for the exploration or exploitation of natural resources referred to in paragraph 2(j) of Article 5;

(g) for services referred to in paragraphs 4 and 5 of Article 5.