Embed Size (px)

Citation preview

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 159

Impact of Dividend Policy and Capital Structure on Profitability of Firms:

A Comparative study between Food and Cement Sector of Pakistan Stock

Exchange

Hidayat Ali Khan

Federal Urdu University of Arts, Science and Technology, Islamabad

Qasim Ali

Federal Urdu University of Arts, Science and Technology, Islamabad

Abstract

This study was aimed at identifying the impact of “dividend policy and capital structure” on

“profitability of firms” listed in Pakistan Stock Exchange. The data regarding “dividend

payout ratio, debt to equity ratio and return on equity” was collected from published annual

audited reports obtained from official website of firms for four years, from 2012 to 2015.

“Ordinary Least Square model” for regression analysis was utilized to assess the insights of

these relationships. Return on equity was used as proxy for profitability of firms. Findings

showed mixed results. In “Food and Personal care Product” sector both dividend policy and

capital structure were found positively significant to profitability, but in “cement” sector

dividend policy is found insignificant to profitability, and capital structure is found positively

significant. “Food and Cement” sectors of Pakistan stock exchange have been studied for

identifying the impact of dividend policy and capital structure on profitability of firms. Also

comparison is carried out in these sectors.

Keywords – Dividends, Capital structure, Profitability, Debt to Equity, Payout

1.0 Introduction:

Financial analyses of firms play a vital role in assessing the financial health and

performance of the firms and in achieving their financial objectives. There are different types

of financial analysis like comparative financial statement analysis, cash flow analysis,

valuation analysis, ratio analysis and common-size financial statement analysis. These all

types of analyses have an important role in a business success. Out of these types of analysis,

ratio analysis is a simplest and most common way of analyzing any organization’s accounts

(Babalola & Abiola, 2013). Financial ratios of companies are important indicators to analyze

any company’s financial health. Ratios show mirror view of a company. These ratios are

helpful to managers, shareholders, directors, labor unions, customers, regulators and stake

holders of a company (Babalola & Abiola, 2013). It can be defined as “financial ratio

analysis is a process of determining and interpreting relationships between the items of

financial statements to provide a meaningful understanding of the performance and financial

position of an enterprise” (Babalola & Abiola, 2013). Similarly Kabajeh, Al Nu’aimat and

Dahmash (2012) defines financial ratios as “a relationship between two individual

quantitative financial information connected with each other in some logical manner, and this

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 160

connection, is considered as a meaningful financial indicator which can be used by the

different financial information users”. Some important ratios related to firm performance

includes dividend payout ratio, earning per share, leverage ratio, return on equity, current

ratio, quick ratio, inventory turnover ratio, return on assets, debtor’s turnover ratio, price

earnings ratio, and assets turnover ratio etc. Coming towards definitions, Dividend payout

ratio can be defined as “the percentage of profits paid as dividend” (Amidu & Abor, 2006).

Likewise “the debt-to-equity ratio (D/E) is a financial ratio indicating the relative proportion

of shareholders' equity and debt used to finance a company's assets” (Peterson & Pamela,

1999). In other words, leverage ratio can be defined as portion of debt that a company uses to

finance its assets in respect of its equity. In the same way, return on equity can be defined as,

“ROE is the percentage of profit the company makes for every monetary unit of equity

invested in the company” (Berzkalne & Zelgalve, 2014). A company’s profitability can be

influenced by external as well as internal factors. External factors consists of a country’s

economic and political situation etc. while internal factors consists of a company’s

management, capital structure decisions, working capital management, capital budgeting

decisions and dividend policy etc. Out of these internal and external factors, capital structure

and dividend policy of a company play a vital role in determination of profitability of a

company.

1.1 Research Gap based on Literature:

Although research on payout ratio and leverage ratio to profitability (ROE) has been

carried out, however, there exist gaps in literature for example, a) only a few researchers have

examined the impact of payout ratio and leverage ratio on profitability (ROE)

simultaneously, b) minimal work is seen on payout ratio and leverage ratio in emerging

countries like Pakistan, c) to the best of authors’ knowledge, food & personal care products

and cement sector have not been studied in respect of knowing the impact of dividend payout

ratio and leverage ratio on profitability (ROE) in case of Pakistan. So this is a pioneer study

to analyse these sectors.

1.2 Research Question:

Based on the above argument, the research question arises that what is the impact of

dividend payout ratio and leverage ratio on profitability (ROE) of firms in case of Pakistan?

So, this study is aimed at answering above stated research question by examining the impact

of dividend pay-out ratio and leverage ratio on profitability (ROE) of firms in case of

Pakistan.

1.3 Significance/ Importance of Study:

By addressing above research gaps, this study will contribute to the literature by

analysing impact of financial ratios of different organizations. In essence, managers and other

stakeholders of different organizations will benefit in different ways, like it will help

managers to be able to make optimal use of its resources for the best interest of company. It

will also help managers to make their policies according to the nature and behaviour of its

shareholders and basic structure of organization. If managers are aware of the impact of pay-

out policy then they can increase or decrease the level of pay-out ratio on the basis of its

influence on shareholders, if they find no impact of pay-out policy then they can spare capital

for other investment opportunities. Shareholders can get more insights into the performance

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 161

of any organization for the purpose of making investment decision. They can assess a

company’s profitability, after knowing about its pay-out ratio, so they can take decision join

it or not. Additionally, this study will help managers to take decision for selection of its basic

capital structure by taking in mind the impact of capital structure on profitability of firms. If

they find debt financing beneficial for their company, they can increase debt financing, but if

they find equity financing more beneficial for organization, so they can focus on equity

financing in the firm, which can be driving force to increase profitability of firms.

2.0 Literature Review:

2.1 Profitability (Return on Equity)

In literature there are two major groups of profitability model, Structure-Conduct-

Performance (SCP) and Firm Effect Models (Stierwald, 2009). Bain’s Structure-conduct-

performance model of 1951 suggests that perfectly competitive markets are less profitable

than concentrated markets and firm effect models suggests that profitability is based on

characteristics of firm, like organizational structure and level of its efficiency (Stierwald,

2009). Similarly, Demsetz (1973) gave superior firm hypothesis which states that firms are

different from each other on the basis of efficiency level of cost or production. Moreover

Jovanovic (1982) states that firms which are more efficient than rivals are more profitable

and can grow and survive in market better than its rivals. Cowling and Waterson (1976)

argued that the rate of profitability of firms is a function of its concentration. In a study of

firm’s profitability, Stierwald (2009) argues that the factors like concentration factors and

strategic management factors are important and are dominant factors for profitability of

firms. Even a lot of work (Feeny, 2000; Stierwald 2009; Zaid, Ibrahim, & Zulqernain 2014;

Pratheepan, & Banda, 2016) is carried out to find out the drivers which influence profitability

of companies.

Profitability of any company is measured by using different profitability ratios (along

with other measures) like return on equity, return on asset and net profit margin. These

profitability ratios can be used as an indicator of the company’s profitability. Financial

institutions and companies frequently use these ratios to determine the financial performance

of the company. Kabajeh et al., (2012) suggested that return on asset (ROA) and return on

equity (ROE) are important ratios to make an assessment of the profitability of companies.

Berzkalne and Zelgalve (2014) define return on equity as “ROE tells what percentage of

profit the company makes for every monetary unit of equity invested in the company”. We

can calculate return on equity (ROE) by dividing net profit by average shareholders’ equity.

The other ratio return on asset is obtained by dividing profit after tax with total assets, and

this ratio tells how much profit is generated through use of assets of firm (Kabajeh et al.,

2012).

Return on equity has been investigated by many researchers. Acheampong (2000)

states that country and company factors have a significant impact on changes in return on

equity. He further added that return on equity is an important tool that investors use to

measure performance and profitability of firm and to take investment decision (Acheampong,

2000). Herciu, Ogrean and Belascu (2011) states that profits are irrelevant to investors to the

extent of some other indicators. Warusawitharana (2013) states that future return on equity is

expected to be low as compared to past realized returns. Finally, Berzkalne and Zelgalve

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 162

(2014) argue that return on equity is an important indicator of a firm’s profitability that

cannot be isolated from other indicators. So, its association with other characteristics of

companies should also be studied.

By analyzing literature it can be argued that return on equity is an important indicator

for profitability measure, and variations in ROE are based on different factors, like factors

related to overall economy and internal factors of a company.

2.2 Dividend Pay-out policy:

Dividend Pay-out policy has been an indispensable part of studies in finance due to its

importance in corporate world. Many scholars have taken this important concept into

account, some have proved it to be positively related and others as negatively related to the

value of firms (Al-Hasanet al.,2013). The dividend Pay-out ratio measures the proportion of

after tax profits that are given to shareholders in the form of dividends during the year. After

calculation of the percentage of dividend payments out of net profit, this ratio can also be

used to find out the portion of profit the company decides to keep in order to fund future

operations and profitable investment projects. Linter (1956) was probably the first researcher

who opted to discover insights of dividend policy and conclude that dividend payments are

necessary for long-term and sustainable earnings. Broadly speaking, in literature there are

two major schools of thought regarding dividend pay-out policy, one school of thought

considers dividend policy relevant to value of firm and the other is in favour of irrelevance of

dividend policy towards the value of firm (Al-Hasanet al., 2013).

The school of thought which is in favour of relevance of dividend policy to value of

firm consists of two models, Walter’s model and Gordon model. Walter’s model was

presented in 1963 which states that the firm’s value is always affected by its dividend policy

(Al-Hasan et al., 2013). The other argument given in favour of relevance of dividend policy

was presented by Gordon (1962), which states that the value of share always influenced by

the dividend policy of organizations even in the case of equivalence of cost of capital and

expected return (as cited in Al-Hasan et al., 2013). The second school of thought regarding

dividend policy is related to irrelevance of dividend policy. This school of thought states that

dividend policy of a firm has no impact on firm’s value (Modigliani & Miller, 1958). Since

then numerous studies have paid attention to this phenomena. Murhadi (2008) states that

stock prices are influenced by dividend policy. Similarly, researchers have argued that price

changes are significantly correlated in response to dividend yield (Asghar, Shah, Hamid &

Suleman, 2011). Moreover Uwuigbe, Jafaru and Ajayi, (2012) proved a positive significant

impact of dividend policy on performance of firm. Furthermore, Gill, Biger, and Tiberwala

(2010) argued that the dividend pay-out ratio help the company to maintain its market share.

In contrast, another research that was conducted by Allen and Michaely (2003) noted that

dividend pay-out ratio of firm will not impact company’s profitability. Similarly Brav,

Graham, Harvey and Michaely (2005) carried out a survey on top executives of different

companies to know whether dividend pay-out ratio effects company’s profitability, so the

answer of executives was no, almost all the executive agreed on the same point stating that

the company’s profitability is not related to its dividend policy. Moreover, Amidu and Abor

(2006) found dividend pay-out ratio to be positively associated with the company’s

profitability.

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 163

Based on literature one can argue that dividend pay-out policy is still an ambiguous

phenomena because we observed different views of scholars on this important variable. It is

important to take it to further investigation to know actual insights of its impact on overall

performance or profitability of firm. Based on literature following hypotheses are posed.

H1: Dividend pay-out policy has significant positive impact on profitability of firms in Food

and personal care product sector of Pakistan Stock Exchange.

H2: Dividend pay-out policy has significant positive impact on profitability of firms in

Cement sector of Pakistan Stock Exchange

2.3 Capital Structure (Debt-to-equity ratio)

The debate for irrelevance of capital structure to firm’s value was carried out by

Modigliani and Miller (1958) in theory of capital structure. They gave a proposition in which

it was argued that capital structure is irrelevant to the value of a firm. It was also argued that

the firm’s value is a function of its earning power and riskiness of its assets. This debate is

still under discussion by various scholars, whether capital structure is relevant to firm’s

profitability/performance or not. Numerous studies have focused on this relationship.

Recently, Ippolito, Steri, and Tebaldi (2017) investigated the impact of capital structure on

levered returns and found it relevant to returns of a firm. In the same way Rehman (2013)

conducted a research in listed sugar companies of Pakistan stock exchange to check the

association between debt-to-equity ratio and profitability(ROE and ROA), the results showed

negative relationship between leverage(D/E) and return on equity, but positive relationship

between leverage and return on asset. Similarly Ojo (2012) found that the corporate

performance of pharmaceutical companies in Nigeria is significantly affected by their

financial leverage. Ojo (2012) also suggested that the traditional theories of capital structures

should not be employed in emerging countries same as in developed or advanced countries. A

firm should consider its industry and country factors while implementing these theories.

Likewise, Akhtar, Javed, Maryam and Sadia (2012) conducted a study to examine

relationship between financial leverage and financial performance in fuel and energy sectors

of Pakistan. The results revealed a positive relationship between financial leverage and

financial performance in the two sectors. Likewise Berger and Patti (2006) also found a

negative relationship between debt-to-equity ratio and company’s performance.

Correspondingly, Yoon and Jang (2005) examined the impact of debt-to-equity on

profitability and risk of restaurant firms. They found that debt-to-equity ratio does not

influence the restaurant firm’s profitability. Another study by Deesomsak, Paudyal and

Pescetto (2004) reported a negative association between leverage ratio and net profitability of

companies in Malaysia.

By considering literature it can be argued that since capital structure theory of

Modigliani and Miller, no scholar have reached to a terminating argument for capital

structure’s impact on profitability of firms. So, further inquiry should be carried out to know

insights of relevance or irrelevance of capital structure to firm’s profitability. Based on this

argument following hypotheses are posed.

H3: Capital structure of firms has significant positive impact on profitability of firms in Food

and personal care product sector of Pakistan Stock Exchange.

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 164

H4: Capital structure of firms has significant positive impact on profitability of firms in

Cement Sector of Pakistan Stock Exchange.

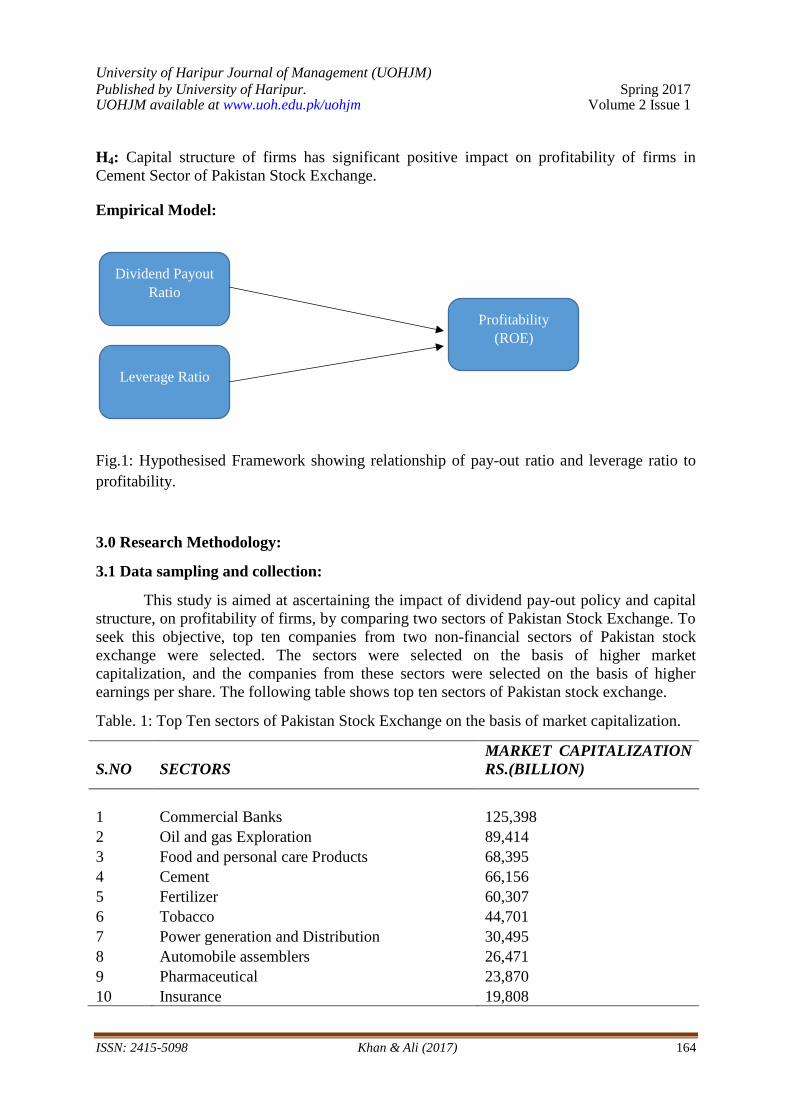

Empirical Model:

Fig.1: Hypothesised Framework showing relationship of pay-out ratio and leverage ratio to

profitability.

3.0 Research Methodology:

3.1 Data sampling and collection:

This study is aimed at ascertaining the impact of dividend pay-out policy and capital

structure, on profitability of firms, by comparing two sectors of Pakistan Stock Exchange. To

seek this objective, top ten companies from two non-financial sectors of Pakistan stock

exchange were selected. The sectors were selected on the basis of higher market

capitalization, and the companies from these sectors were selected on the basis of higher

earnings per share. The following table shows top ten sectors of Pakistan stock exchange.

Table. 1: Top Ten sectors of Pakistan Stock Exchange on the basis of market capitalization.

S.NO SECTORS

MARKET CAPITALIZATION

RS.(BILLION)

1 Commercial Banks 125,398

2 Oil and gas Exploration 89,414

3 Food and personal care Products 68,395

4 Cement 66,156

5 Fertilizer 60,307

6 Tobacco 44,701

7 Power generation and Distribution 30,495

8 Automobile assemblers 26,471

9 Pharmaceutical 23,870

10 Insurance 19,808

Dividend Payout

Ratio

Leverage Ratio

Profitability

(ROE)

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

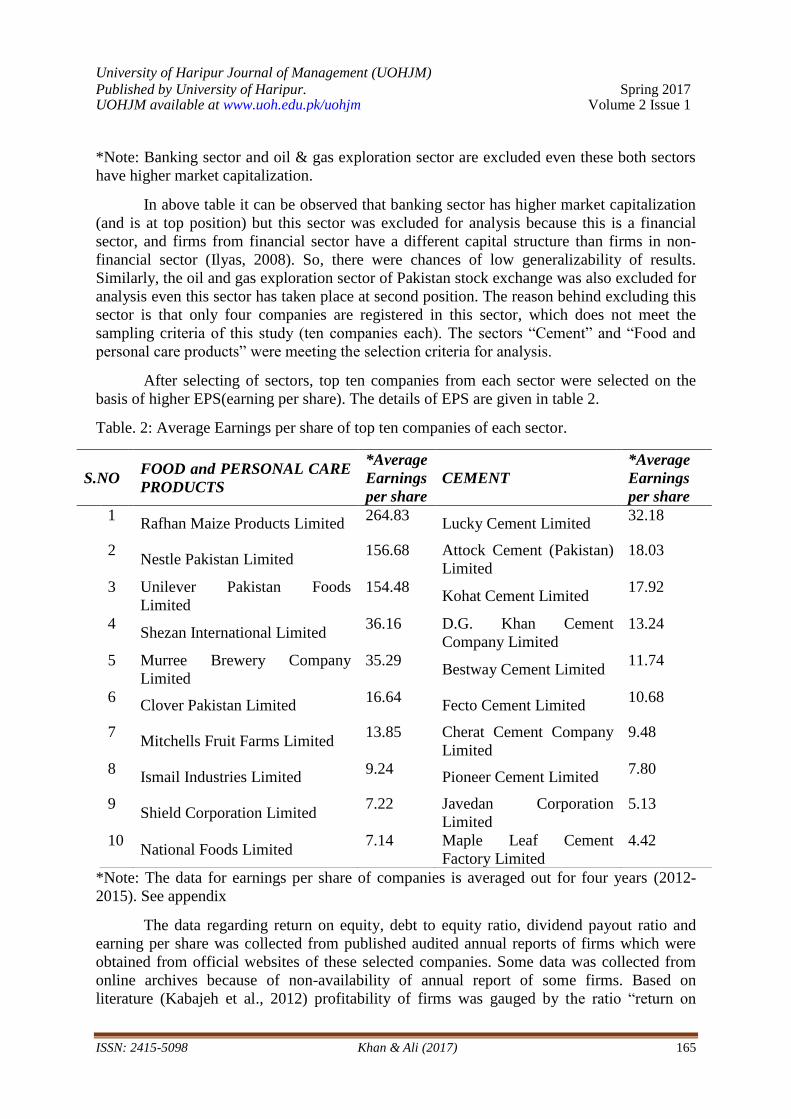

ISSN: 2415-5098 Khan & Ali (2017) 165

*Note: Banking sector and oil & gas exploration sector are excluded even these both sectors

have higher market capitalization.

In above table it can be observed that banking sector has higher market capitalization

(and is at top position) but this sector was excluded for analysis because this is a financial

sector, and firms from financial sector have a different capital structure than firms in non-

financial sector (Ilyas, 2008). So, there were chances of low generalizability of results.

Similarly, the oil and gas exploration sector of Pakistan stock exchange was also excluded for

analysis even this sector has taken place at second position. The reason behind excluding this

sector is that only four companies are registered in this sector, which does not meet the

sampling criteria of this study (ten companies each). The sectors “Cement” and “Food and

personal care products” were meeting the selection criteria for analysis.

After selecting of sectors, top ten companies from each sector were selected on the

basis of higher EPS(earning per share). The details of EPS are given in table 2.

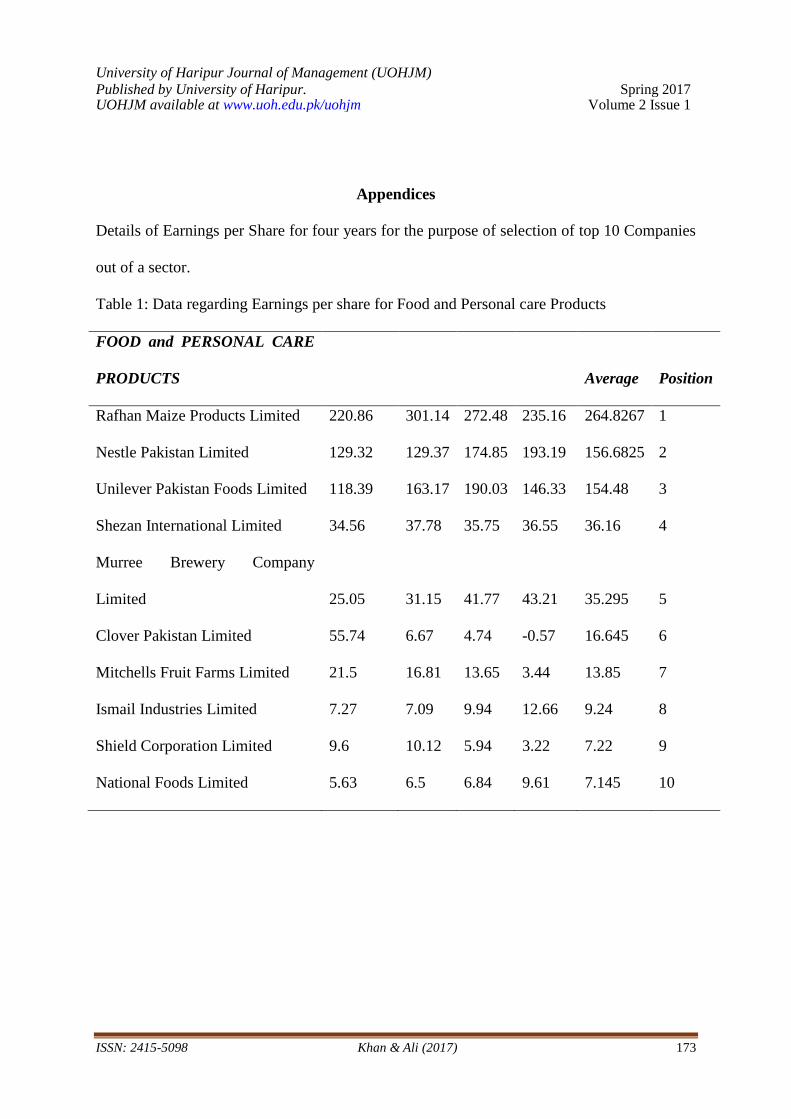

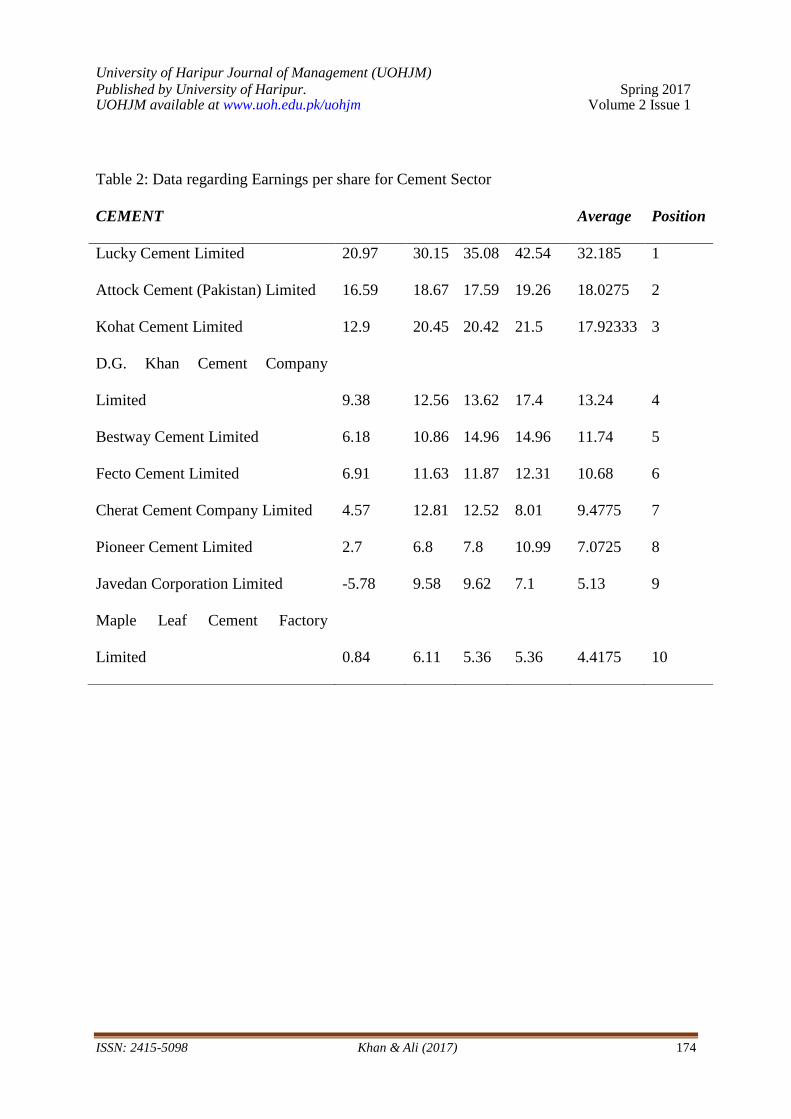

Table. 2: Average Earnings per share of top ten companies of each sector.

*Note: The data for earnings per share of companies is averaged out for four years (2012-

2015). See appendix

The data regarding return on equity, debt to equity ratio, dividend payout ratio and

earning per share was collected from published audited annual reports of firms which were

obtained from official websites of these selected companies. Some data was collected from

online archives because of non-availability of annual report of some firms. Based on

literature (Kabajeh et al., 2012) profitability of firms was gauged by the ratio “return on

S.NO FOOD and PERSONAL CARE

PRODUCTS

*Average

Earnings

per share

CEMENT

*Average

Earnings

per share

1 Rafhan Maize Products Limited

264.83 Lucky Cement Limited

32.18

2 Nestle Pakistan Limited

156.68 Attock Cement (Pakistan)

Limited

18.03

3 Unilever Pakistan Foods

Limited

154.48 Kohat Cement Limited

17.92

4 Shezan International Limited

36.16 D.G. Khan Cement

Company Limited

13.24

5 Murree Brewery Company

Limited

35.29 Bestway Cement Limited

11.74

6 Clover Pakistan Limited

16.64 Fecto Cement Limited

10.68

7 Mitchells Fruit Farms Limited

13.85 Cherat Cement Company

Limited

9.48

8 Ismail Industries Limited

9.24 Pioneer Cement Limited

7.80

9 Shield Corporation Limited

7.22 Javedan Corporation

Limited

5.13

10 National Foods Limited

7.14 Maple Leaf Cement

Factory Limited

4.42

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 166

equity”, the capital structure’s impact was analyzed by company’s ratio “debt to equity ratio”,

while dividend payout was assessed through “dividend payout ratio” of firms. The data for

calculating these ratios was obtained for four years, ranging 2012 to 2015. Statistical Package

for Social Sciences (SPSS 20) was used to analyze the data. The Ordinary Least Square

Regression (OLS) method was used to find out the important insights of these ratios.

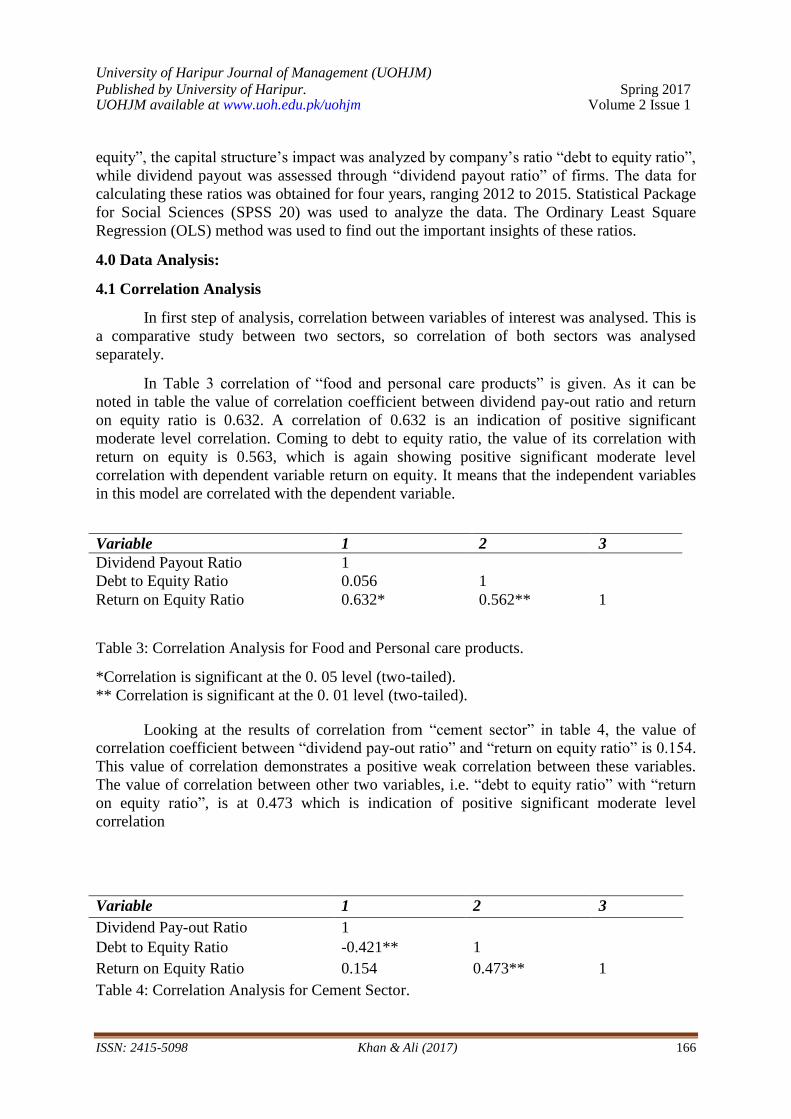

4.0 Data Analysis:

4.1 Correlation Analysis

In first step of analysis, correlation between variables of interest was analysed. This is

a comparative study between two sectors, so correlation of both sectors was analysed

separately.

In Table 3 correlation of “food and personal care products” is given. As it can be

noted in table the value of correlation coefficient between dividend pay-out ratio and return

on equity ratio is 0.632. A correlation of 0.632 is an indication of positive significant

moderate level correlation. Coming to debt to equity ratio, the value of its correlation with

return on equity is 0.563, which is again showing positive significant moderate level

correlation with dependent variable return on equity. It means that the independent variables

in this model are correlated with the dependent variable.

Table 3: Correlation Analysis for Food and Personal care products.

*Correlation is significant at the 0. 05 level (two-tailed).

** Correlation is significant at the 0. 01 level (two-tailed).

Looking at the results of correlation from “cement sector” in table 4, the value of

correlation coefficient between “dividend pay-out ratio” and “return on equity ratio” is 0.154.

This value of correlation demonstrates a positive weak correlation between these variables.

The value of correlation between other two variables, i.e. “debt to equity ratio” with “return

on equity ratio”, is at 0.473 which is indication of positive significant moderate level

correlation

Table 4: Correlation Analysis for Cement Sector.

Variable 1 2 3

Dividend Payout Ratio 1

Debt to Equity Ratio 0.056 1

Return on Equity Ratio 0.632* 0.562** 1

Variable 1 2 3

Dividend Pay-out Ratio 1

Debt to Equity Ratio -0.421** 1

Return on Equity Ratio 0.154 0.473** 1

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 167

*Correlation is significant at the 0. 05 level (two-tailed).

** Correlation is significant at the 0. 01 level (two-tailed).

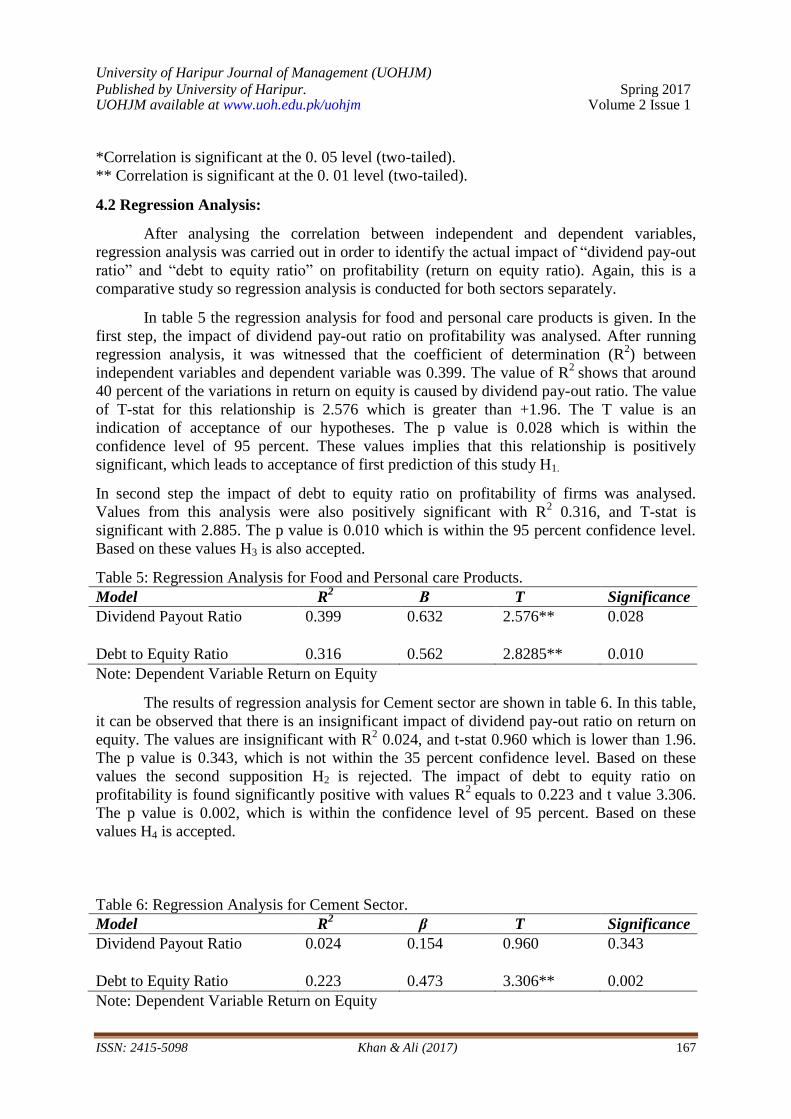

4.2 Regression Analysis:

After analysing the correlation between independent and dependent variables,

regression analysis was carried out in order to identify the actual impact of “dividend pay-out

ratio” and “debt to equity ratio” on profitability (return on equity ratio). Again, this is a

comparative study so regression analysis is conducted for both sectors separately.

In table 5 the regression analysis for food and personal care products is given. In the

first step, the impact of dividend pay-out ratio on profitability was analysed. After running

regression analysis, it was witnessed that the coefficient of determination (R2) between

independent variables and dependent variable was 0.399. The value of R2

shows that around

40 percent of the variations in return on equity is caused by dividend pay-out ratio. The value

of T-stat for this relationship is 2.576 which is greater than +1.96. The T value is an

indication of acceptance of our hypotheses. The p value is 0.028 which is within the

confidence level of 95 percent. These values implies that this relationship is positively

significant, which leads to acceptance of first prediction of this study H1.

In second step the impact of debt to equity ratio on profitability of firms was analysed.

Values from this analysis were also positively significant with R2 0.316, and T-stat is

significant with 2.885. The p value is 0.010 which is within the 95 percent confidence level.

Based on these values H3 is also accepted.

Table 5: Regression Analysis for Food and Personal care Products.

Model R2

Β T Significance

Dividend Payout Ratio 0.399 0.632 2.576** 0.028

Debt to Equity Ratio 0.316 0.562 2.8285** 0.010

Note: Dependent Variable Return on Equity

The results of regression analysis for Cement sector are shown in table 6. In this table,

it can be observed that there is an insignificant impact of dividend pay-out ratio on return on

equity. The values are insignificant with R2 0.024, and t-stat 0.960 which is lower than 1.96.

The p value is 0.343, which is not within the 35 percent confidence level. Based on these

values the second supposition H2 is rejected. The impact of debt to equity ratio on

profitability is found significantly positive with values R2

equals to 0.223 and t value 3.306.

The p value is 0.002, which is within the confidence level of 95 percent. Based on these

values H4 is accepted.

Table 6: Regression Analysis for Cement Sector.

Model R2

β T Significance

Dividend Payout Ratio 0.024 0.154 0.960 0.343

Debt to Equity Ratio 0.223 0.473 3.306** 0.002

Note: Dependent Variable Return on Equity

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 168

4.3 Comparison of Statistics of sectors of interest:

Based on analysis one can observe that the relationship of dividend pay-out ratio in

“Food and Personal care Products” sector has significant positive impact on profitability of

firms as compared to “Cement” sector of Pakistan Stock Exchange in which this relationship

is found insignificant.

Coming to the other hypothesised relationship in which the impact of capital structure

on profitability is analysed. It can be observed that capital structure has a significant positive

impact on profitability of firms in cement sector firms listed on Pakistan Stock Exchange.

From the analyses, we can also observe that the “Food and Personal care Products” sector of

Pakistan stock Exchange has higher R2 value “0.316” as compared to “Cement” sector in

which R2 is “0.223”, also β value is higher in “Food and personal care product” sector, but t

stat is opposite to these values. The t stat for “Food and personal care product” is lower

“2.8285” as compared to “cement” sector “3.306”.

4.4 Discussion and Implications:

The basic objective of this study was to examine the impact of dividend policy and

capital structure on profitability of firms listed in food and cement sector of Pakistan Stock

Exchange. To seek this objective four predictions were made on the basis of related literature.

The details of acceptance or rejection of hypothesis is given in table 7.

Table 7: Hypothesis with Acceptance or Rejection.

S.NO

Hypothesis

Acceptance/

Rejection

H1 Dividend Pay-out policy has significant positive impact on profitability of

firms in Food and personal care product sector of Pakistan Stock Exchange

Accepted

H2 Dividend Pay-out policy has significant positive impact on profitability of

firms in Cement sector of Pakistan Stock Exchange

Rejected

H3 Capital Structure of firms have significant positive impact on profitability of

firms in Food and personal care product sector of Pakistan Stock Exchange

Accepted

H4 Capital Structure of firms have significant positive impact on profitability of

firms in Cement Sector of Pakistan Stock Exchange

Accepted

4.5 Food and personal care product sector:

The first hypothesised relationship H1 is related to food and personal care product

sector of Pakistan Stock Exchange. This hypothesis is accepted, parallel to analysis of Amidu

and Abor (2006). The acceptance of this relationship in this sector implies that profitability of

firms listed in this sector is influenced by its dividend pay-out policy, if firms are paying

more dividends, it will lead to higher profitability, which will ultimately lead to maximization

of firm’s value. Now managers of firms registered in this sector should formulate firm’s

strategies in a manner in which there is high dividend pay-out trend. If firms in this sector

will pay high dividends, it will attract new investors, which will increase demand of shares of

these firms, which will lead to higher share price of shares of these firms; ultimately it will

lead to value maximization of the firms.

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 169

The third hypothesised relationship H3 is also related to food and personal care

product sector of Pakistan Stock Exchange. As suggested by analysis, this supposition is also

accepted comparable to the study of Akhtar et al., (2012). Based on this acceptance it can be

argued that the profitability of firms is influenced positively for those firms which are having

higher debt to equity ratio in their capital structure as compared to firms with lower debt to

equity ratio. Now the prime focus of managers of firms registered in this sector should be to

increase the level of debt financing as compared to its equity financing. This act will help a

manager to increase profitability of firm by utilizing less financing from equity, because

taking loan is beneficial for these firms as compared to bringing equity finance in business.

4.6 Cement Sector:

The hypothesis H2 and H4 were posed for Cement sector of Pakistan Stock Exchange.

Contrary to the supposition, H2 was found insignificant in this sector, similar to the study of

Brav et al., (2005). This insignificance of impact of pay-out policy on profitability of firms

infers that high dividend pay-out will not influence the profitability of firms registered in this

sector. So now it’s up to managers to pay high dividend or pay lower dividends. Managers

can also reinvest dividends of its shareholders, which can benefit shareholders and also firms

in term of availability of finance to respond to new opportunities,

The aim of hypothesis H4 was to identify impact of capital structure of firms

registered in cement sector of Pakistan Stock Exchange. Similar to the findings of Akhtar et

al., (2012), the findings of this prediction were also found positively significant. Considering

these findings, one can conclude that in Cement sector of Pakistan Stock Exchange,

profitability of firms is influenced by its capital structure. It means that the firms in cement

sector having more debt in their capital structure will earn higher profitability. So, here in

cement sector the cost of debt financing is lower as compared to using equity finance.

Furthermore, debt financing is less risky. Managers in cement sector should focus on debt

financing more as compared to equity finance; ultimately it will increase overall profitability

of firms.

5.0 Conclusion:

The main focus of this study was to identify and compare the impact of pay-out policy

and capital structure on profitability of companies in two important sectors “Food and

personal care Products” and “Cement” sectors of Pakistan Stock Exchange. Dividend pay-out

ratio and debt to equity ratio were used as independent variable, while return on equity(proxy

for profitability) was used as dependent variable in this specific study. The data for the years

2012 to 2015 was taken from annual audited reports of the companies. Ordinary Least

Squares model was utilized to extract the impact of pay-out policy and capital structure on

profitability. Mixed results were observed as a result of the analysis of collected data. In

“food and personal care product” sector, significant positive impact of dividend policy and

capital structure was found on profitability of firms. Coming to “Cement” sector, impact of

dividend policy on profitability was found insignificant; however the impact of capital

structure was found positively significant. These results are consistent with previous studies,

conducted to investigate these relationships. On the basis of these findings, it can be

concluded that firms in food and personal care products should focus on higher dividend

payments and should also use debt financing instead of equity financing. Furthermore, in

“Cement” sector, it is not mandatory for firms to pay any regular cash dividend, as findings

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 170

of this study suggests insignificant impact of pay-out policy on profitability of firms.

Additionally, firms should utilize debt financing to increase profitability as compared to

equity financing.

Limitations and Future research:

The major source of data collection was annual audited financial reports, but one

problem which occurred while data collection was that some data is collected from online

archives. The reason is that annual reports of some firms were not available on official

website of firms. Although this data is reliable but data from firm’s source can be considered

more reliable. Data for 2016 of some firms were also not available so that is why recent year

is excluded for this analysis. Additionally this past data is related to the time period on which

Karachi stock exchange was not merged to Pakistan stock exchange and after merger the

growth of Pakistan stock exchange has magnificently increased. Moreover the sample size

consists of only four years, this time period is small for this analysis. In future sample size

should be increased to at least recent six years. Furthermore data should be collected from

only annual audited reports, which are issued by company. Another thing which should be

considered in future is to add more independent variables to this relationship proposed in this

study.

References

Acheampong, S. Y., & Hess, J. W. (2000). Origin of the shallow groundwater system in the

southern Voltaian Sedimentary Basin of Ghana: an isotopic approach. Journal of

Hydrology, 233(1), 37-53.

Akhtar, S., Javed, B., Maryam, A., & Sadia, H. (2012). Relationship between financial

leverage and financial performance: Evidence from fuel & energy sector of

Pakistan. European Journal of Business and Management, 4(11), 7-17.

Al-Hasan, M. A., Asaduzzaman, M., & Karim, R. A. (2013). The effect of dividend policy on

share price: An evaluative study. IOSR Journal of Economics and Finance, 1(4), 6-11.

Allen, F., & Michaely, R. (2003). Payout policy. Handbook of the Economics of Finance, 1,

337-429.

Amidu, M., & Abor, J. (2006). Determinants of dividend payout ratios in Ghana. The Journal

of Risk Finance, 7(2), 136-145.

Asghar, M., Shah, S. Z. A., Hamid, K., & Suleman, M. T. (2011). Impact of dividend policy

on stock price risk: Empirical evidence from equity market of Pakistan. Far East

Journal of Psychology and Business. 4(1),

Babalola, Y. A., & Abiola, F. R. (2013). Financial ratio analysis of firms: A tool for decision

making. International Journal of Management Sciences, 1(4), 132-137.

Berger, A. N., & Di Patti, E. B. (2006). Capital structure and firm performance: A new

approach to testing agency theory and an application to the banking industry. Journal

of Banking & Finance, 30(4), 1065-1102.

Brav, A., Graham, J. R., Harvey, C. R., & Michaely, R. (2005). Payout policy in the 21st

century. Journal of Financial Economics, 77(3), 483-527.

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 171

Cowling, K., & Waterson, M. (1976). Price-cost margins and market Structure. Economica,

43(171), 267-274.

Deesomsak, R., Paudyal, K., & Pescetto, G. (2004). The determinants of capital structure:

evidence from the Asia Pacific region. Journal of Multinational Financial

Management, 14(4), 387-405.

Demsetz, H. (1973). Industry structure, market rivalry, and public policy. The Journal of Law

and Economics, 16(1), 1-9.

Feeny, S. (2000). Determinants of profitability: an empirical investigation using Australian

tax entities. Melbourne Institute working paper No. 1/00 ISSN 1328-4991, ISBN 0

7340 1481 3 March 2000.

Gill, A., Biger, N., & Tibrewala, R. (2010). Determinants of dividend payout ratios: evidence

from United States. The Open Business Journal, 3(1), 8-14.

Gordon, M. J. (1959). Dividends, earnings, and stock prices. The Review of Economics and

Statistics, 41(2), 99-105.

Herciu, M., Ogrean, C., & Belascu, L. (2011). A Du Pont analysis of the 20 most profitable

companies in the world. International Conference on Business and Economics

Research, 13(1), 18-93.

Ilyas, J. (2008). The determinants of capital structure: Analysis of non-financial firms listed

in Karachi stock exchange in Pakistan. Journal of Managerial Sciences, 2(2), 279-

307.

Ippolito, F., Steri, R., & Tebaldi, C. (2017). Levered Returns and Capital Structure

Imbalances.

Jovanovic, B. (1982). Selection and the Evolution of Industry. Econometrica: Journal of the

Econometric Society, 50(3), 649-670.

Kabajeh, M. A. M., Al Nu’aimat, S. M. A., & Dahmash, F. N. (2012). The relationship

between the ROA, ROE and ROI ratios with Jordanian insurance public companies

market share prices. International Journal of Humanities and Social Science, 2(11),

115-120.

Lintner, J. (1956). Distribution of incomes of corporations among dividends, retained

earnings, and taxes. The American Economic Review, 46(2), 97-113.

Modigliani And Miller's Capital Structure Theories - Complete Guide To Corporate Finance.

(2014, June 03). Retrieved January 17, 2017, from

http://www.investopedia.com/walkthrough/corporate-finance/5/capital-structure/modigliani-

miller.aspx

Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the

theory of investment. The American Economic Review, 40, 261-297.

Murhadi, W. R. (2008). Study on dividend policy in Indonesian capital market.

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 172

Ojo, S.A. (2012). The Effects of Financial Leverage on Corporate Performance of Some

Selected Companies in Nigeria. Canadian Social Science, 8 (1), 85- 91.

Pratheepan, T., & Yatiwella, W. B. (2016). The Determinants of Capital Structure: Evidence

from Selected Listed Companies in Sri Lanka. International Journal of Economics

and Finance, 8(2), 94-106.

Shah, F.R.S. (2013). Relationship between financial leverage and financial performance:

Empirical evidence of listed sugar companies of Pakistan. Global Journal of

Management and Business Research, 13(8).

Stierwald, A., (2009). Determinants of firm profitability – the effect of productivity and its

persistence. Retrieved from https://editorialexpress.com/cgibin/conference/

download.cgi?db_name=ESAM09&paper_id=152

Uwuigbe, U., Jafaru, J., & Ajayi, A. (2012). Dividend policy and firm performance: A study

of listed firms in Nigeria. Accounting and Management Information Systems, 11(3),

442-454

Warusawitharana, M. (2013). The expected real return to equity. Journal of Economic

Dynamics and Control, 37(9), 1929-1946.

Yoon, E., & Jang, S. (2005). The effect of financial leverage on profitability and risk of

restaurant firms. The Journal of Hospitality Financial Management, 13(1), 35-47.

Zaid, N. A. M., Ibrahim, W. M. F. W., & Zulqernain, N. S. (2014, February). The

Determinants of profitability: Evidence from Malaysian construction companies.

In Proceedings of 5th Asia-Pacific Business Research Conference (17-18).

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 173

Appendices

Details of Earnings per Share for four years for the purpose of selection of top 10 Companies

out of a sector.

Table 1: Data regarding Earnings per share for Food and Personal care Products

FOOD and PERSONAL CARE

PRODUCTS

Average Position

Rafhan Maize Products Limited 220.86 301.14 272.48 235.16 264.8267 1

Nestle Pakistan Limited 129.32 129.37 174.85 193.19 156.6825 2

Unilever Pakistan Foods Limited 118.39 163.17 190.03 146.33 154.48 3

Shezan International Limited 34.56 37.78 35.75 36.55 36.16 4

Murree Brewery Company

Limited 25.05 31.15 41.77 43.21 35.295 5

Clover Pakistan Limited 55.74 6.67 4.74 -0.57 16.645 6

Mitchells Fruit Farms Limited 21.5 16.81 13.65 3.44 13.85 7

Ismail Industries Limited 7.27 7.09 9.94 12.66 9.24 8

Shield Corporation Limited 9.6 10.12 5.94 3.22 7.22 9

National Foods Limited 5.63 6.5 6.84 9.61 7.145 10

University of Haripur Journal of Management (UOHJM) Published by University of Haripur. Spring 2017 UOHJM available at www.uoh.edu.pk/uohjm Volume 2 Issue 1

ISSN: 2415-5098 Khan & Ali (2017) 174

Table 2: Data regarding Earnings per share for Cement Sector

CEMENT

Average Position

Lucky Cement Limited 20.97 30.15 35.08 42.54 32.185 1

Attock Cement (Pakistan) Limited 16.59 18.67 17.59 19.26 18.0275 2

Kohat Cement Limited 12.9 20.45 20.42 21.5 17.92333 3

D.G. Khan Cement Company

Limited 9.38 12.56 13.62 17.4 13.24 4

Bestway Cement Limited 6.18 10.86 14.96 14.96 11.74 5

Fecto Cement Limited 6.91 11.63 11.87 12.31 10.68 6

Cherat Cement Company Limited 4.57 12.81 12.52 8.01 9.4775 7

Pioneer Cement Limited 2.7 6.8 7.8 10.99 7.0725 8

Javedan Corporation Limited -5.78 9.58 9.62 7.1 5.13 9

Maple Leaf Cement Factory

Limited 0.84 6.11 5.36 5.36 4.4175 10