Embed Size (px)

Citation preview

1

CHAPTER I

RESEARCH BACKGROUND

I. INTRODUCTION

Management of Working capital has become crucial, given

the increasing pressure on operating cycles. Too much or

too low working capital may suffer firms, so an optimum

level of working capital is the key to maximize ensure

firm’s profitability. The management of working capital

refers to management of both current assets and current

liabilities (S.D. Talekar, 2005).

Statistically, about 97.5% of Vietnam's firms are small

and medium-sized enterprise (SME). The greatest weakness

and greatest impact to business operations of these

firms is capital. Vietnam Economy and businesses depend

heavily on bank credit. While the capital structure of

2

the banking system still has many risks, mainly use

short-term funds for medium and long term loans, or

deposits from customers for real estate projects, lead

to the deficiency of medium and long term capital for

the economy. On the other hand due to insufficiency of

capital, cost of capital in Viet Nam is still high

compared to other countries in Southeast Asia. Moreover,

in the period 2008-2011, Vietnam’s government still

prefer curbing inflation to stabilize macroeconomic, the

monetary policy will not be loosened in the short term,

plus the banking system is facing many difficulties so

the credit capital will be tightened more, stock market

and real estate stagnate for a long time will lead to

the fact that businesses would be more difficult to find

capital in the near future. Firms which hold less cash

will lack of capital to maintain operations while cannot

solving the problem of output and, increase the

inventory cost, this can cause bankruptcy for these

firms (Dr. Le Chi Hieu, 2012). According to Deloof, the

3

way that working capital is managed has a

significant impact on profitability of firms. Such

results indicate that firms may have a certain level of

working capital requirements which can maximize their

value.

The impact of Working capital management on firm’s

profitability can be analyzed in several ways, which

consisting of inventory management and accounts

receivables management. As the firm increase the level

of inventory it holds, the risk of running out inventory

is lessened, but the inventory expense are increase

(Krish Rangarajan, Krish Rangarajan; Anil Misra, 2005),

management and control the inventory effectively are the

important duties of the finance manager, inappropriate

decisions or inefficient procedures can add significant

costs, adversely impacting working capital (James

Sagner, 2014). Another component of working capital is

accounts payable. Delaying payments to suppliers allows

a firm to assess the quality of the products bought, and

4

can be an inexpensive and flexible source of financing

for the firm. On the other hand, delaying of such

payables can be expensive if a firm is offered a

discount for the early or instant payment (Deloof M,

2003). By the same token, uncollected accounts

receivables can lead to cash inflow problems for the

firm.

The firm also needs to take into account its cash

conversion cycle, which is the length of time between

the payment of account payables and the collection of

account receivables (Lorenzo Preve, Virginia Sarria-

Allende, 2010). Deloof found that the longer the time

lag, the larger the investment in working capital

(Deloof M, 2003). A long cash conversion cycle might

increase profitability because it leads to higher sales.

However, corporate profitability might decrease with the

cash conversion cycle, if the costs of higher investment

in working capital rise faster than the benefits of

holding more inventories or granting more trade credit

5

to customers. It recommends that managers of firm should

conduct some policy to reduce cash conversion cycle to

gain high firm’s value.

Key work: Working capital, firm’s profitability, SMEs,

Food and Beverage industry, AR, inventory, AP, CCC.

II. GLOBAL CONTEXT

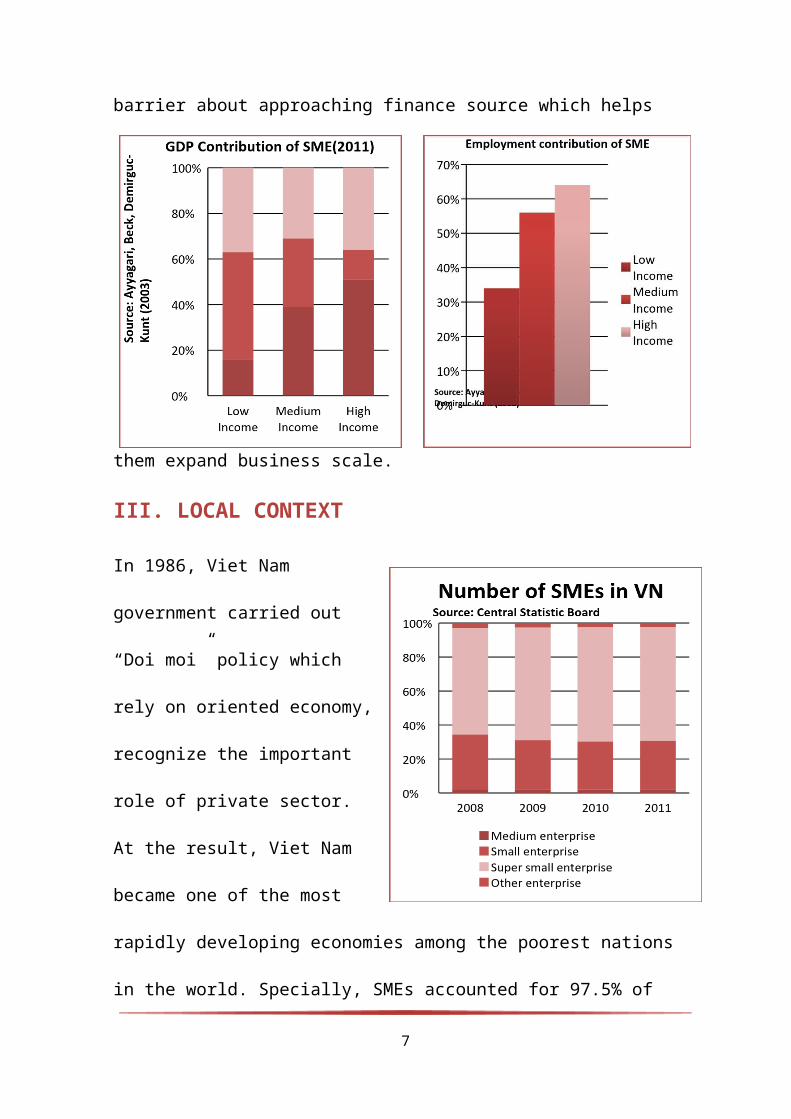

SMEs are a multiform group of businesses which usually

running in the service, trade, agri-business, and

manufacturing sectors. SMEs take approximately for 95%

of total firms around the world (Arancha Gonzalez, 2014)

and it generates 35.3% of GDP on average. For instance,

in the European Union, SMEs occupied 99.8% of registered

firms and it provided 75 million jobs (67.4% of total

employment). In USA, SMEs contributed 29% of export

value. In Asia, especially in Japan, the number of

employees who work in SMEs occupies 81% of total

employees in the whole country. Even though SMEs play an

important role in each economy, they also face with big

6

barrier about approaching finance source which helps

them expand business scale.

III. LOCAL CONTEXT

In 1986, Viet Nam

government carried out

“Doi moi” policy which

rely on oriented economy,

recognize the important

role of private sector.

At the result, Viet Nam

became one of the most

rapidly developing economies among the poorest nations

in the world. Specially, SMEs accounted for 97.5% of

7

total enterprise in Viet Nam (GSO, Number and Event

magazine 5/2013), it become a motivated factor to foster

economy by creating employment and contributing to gross

domestic product. Particularly, in 2011, SMEs area

created 40% GDP. Besides that, SMEs generate 1,000 new

jobs/ year (VINASME, 2014)

Besides above advantages, SMEs Viet Nam also faced with

difficult problems about liquidity and profitability.

According to the report about SMEs for 2011 – 2015, in

2010, SMEs’ income was 80.59 thousand billion VND (which

occupied 22.87% of the whole VN enterprises’ total net

operating income before tax). In 2012, the enterprises’

income sharply went down; it was 22.82 thousand billion

VND that took 7.26% of the whole VN enterprises’ total

net operating income before tax.

Ministry of Planning and Investment also expressed the

worrying about the increasing number of SMEs getting

loss. In 2010, SMEs suffering loss took 25.14% of total

enterprises; at the end of September 2013, this

8

percentage climbed up 65.8%. The percentage of

enterprise getting profit in 2010 and September 2013

were 64.12% and 34.12%, respectively.

Furthermore, in 2009 – 2011, bankruptcy situation took

place in SMEs. According CIEM (2011), 60% SMEs are

forced to cut down their full-time workforce. Total

number of full-time staff of 1,999 samples drop slightly

from 28,174 (2009) to 26,414 (2011), this is equivalent

to 6.2% in 2 years.

According to PhD. Nguyen Manh Quan – Director of

enterprise research and development institute (Inbus),

just 20% of total number of SMEs can live in rival

environment, while 60% of another are trying to survive

and 20% of 2,508 SMEs ,who are studied in 2009, went to

bankrupt in 2011. This percentage is higher than

percentage is observed in period 2007 – 2009.

Another problem exist in SMEs is lack of capital.

According to Cao Sĩ Kiêm (Director of VINASME), low

capital scale also cause disadvantage in access to

9

credit sources. Equity is too small, that leads to D/E

ratio are low. This limits the borrowing capital ability

of SMEs. Furthermore, SMEs often lack the collateral for

the loan amounts. Even in developed countries like USA,

Japan, banks are hesitating to give loans to SMEs

because the credit risk. In particularly, the percentage

of SMEs, whose chartered capital is lower than 7 billion

VND, is 80% and the percentage of SMEs that have demand

to loan from bank accounted for 90%. However, most of

SMEs had difficulties in mobilizing capital because of

lacking of competence to borrow money from banks or

approach international financial institutions.

IV. RATIONALE

According to Brigham and Houston (2003), about 60% of

financial manager’s time is spent for management of

working capital. Working capital management is

undoubtedly an important issue to firms, but in Viet

Nam, less firms use it effectively. For example, SMEs

use the equity as the major source of finance, the

10

equity ratio usually reaches at 90%. Furthermore,

because of difficulties in obtaining long-term loans,

SMEs are willing to use short-term loans to finance

long-term assets and investment; they also bear the high

cost of inventory and interest rate of bank loans (Kack

and Lindgren, 1999) and (Findings of Vuong Quan Hoang,

1998). These require a more detail research about the

application of working capital to SME firm's

profitability, especially in Viet Nam.

For reason above, the group investigates the

relationship between Working capital and firms’

profitability for SMEs in Viet Nam for the 2009-2011.

When selecting the period of time, group wants to study

the accuracy of problem (working capital affects SMEs’

profitability); therefore, group will focus on the

period from 2009 to 2011 in this research. The economic

crisis occurred from 2008, so the data might not reflect

suitably to the topic concepts.

V. RESEARCH QUESTIONS

11

To reach the purpose of this research, it is necessary

to answer: How does working capital affect SMEs'

profitability in 2009 – 2011 in VN?

VI. RESEARCH OBJECTIVES

In order to answer these questions, this study needs to

reach four objectives below:

● Providing the background of working capital, firm’s

profitability and SMEs.

● Offer a descriptive study about the effect of each

component of working capital

● Examining the relationship between working capital

and profitability

● Proposing conclusions and recommendations for

implications. (Evaluating and comparing the results in

Viet Nam context with some previous research)

12

CHAPTER II

LITERATURE REVIEW

I. WORKING CAPITAL

1.1 Definition

“The tradition definition of working capital shows how

much cash (or liquid assets) is available to satisfy the

short-term cash requirements imposed by current

liabilities”- Lorenzo A. Preve, Virginia Sarria-Allende

( 2010). Working capital is specified defined as stocks

of materials, fuels, semi-finished goods, finished

goods; cash and cash equivalent, payment such as rent,

salaries, interests, dividends, purchase of goods and

services; short-term loans, advances towards tax

payments (Arnold, 2008). Working capital is circular

changes of assets from one to other forms. For instance,

beginning with cash, changing to raw materials, shifting

13

to work in progress and finished goods, sales of product

and final ending with sales considered as cash (Weston

and Brigham, 1977). Firms use working capital and cash

inflows to finance materials needs for their operating

activities. When purchased materials have undergone a

manufacturing process and become finished goods, it is

time to get products sold to get money back. Money

earned from sales is used to pay liabilities, give

dividends to shareholders and reinvest. From here the

cycle starts over again (Pass & Hike, 2007).

Working capital is the difference between current assets

and current liabilities, and it may get the negative and

positive results. If the working capital is positive

which means the current assets are greater than

liabilities and this surplus can be used to fulfill

financial commitments and obligation to stockholders

with the aspect for the continuing growth in the future

(Lantz, 2008). On the other hand, the positive working

capital reflects the high level of capital tied up which

14

the capital does not generate any additions value and do

more good in new investment which could bring the

further return (Lantz, 2008). If the working capital is

negative which means firm does not have enough capital

for financing short-term debts and may goes to

bankruptcy.

1.2 Characteristics

According to Gauri Sankar – Senior Manager at Canara

Bank, there are two characteristics should be kept in

mind: short life span and swift transformation. Usually,

current assets have very short life span (within one

year or less than one year); the lifespan of current

assets bases on the time required in activities of

procurement, production process, sales and collection of

bills. The greater the time duration of activities is,

the longer life current assets gets. In addition,

working capital is swift transformation. Because of

short life span, current assets can easily shift to

other forms of asset such as cash, account receivables,

15

inventory for running business. These forms are

interrelated; therefore, a decision of one form may have

influence on other forms. To sum up, when analyzing

working capital, all of these forms must be brought in

account.

1.3 Working capital accounts

According to James S.Sagner, working capital account

consists of Cash accounts and short-term investments

which include in cash on hand or in bank accounts and

any short-term investments expected to be cash converted

within one year. Accounts receivable includes all credit

sales where the customer is expected to pay by a future

date specified on an invoice. Inventory usually is

combination of raw materials, work‐in‐process that

partially manufactured and assembled, and finished

goods. Accounts payables represent the amounts owed to

creditors for purchases. Other working capital accounts

like prepaid expenses and accrued expenses often appear

on balance sheets. Prepaid expenses are assets paid in

16

advance of expenses as incurred. Accrued expenses are

costs that have been incurred as of the date of a

balance sheet but not paid. The infrastructure of

working capital involves those activities that are

essential for managers to proceed. These include

international working capital, information and working

capital, and management of the working capital cycle.

1.4 Working Capital Measurement

In the past, working capital management was

compartmentalized (Sartoris and Hill, 1983). Sartoris

and Hill (1983) argued that there was a need for an

integrated approach, where all the three compartments

are combined. This led to the integration of the

management of inventories, account payables and account

receivables, called Working Capital Management (WCM),

these parts will now be discussed individually.

Companies often allow customers a specified number of

days to pay their invoices. The use of such credits

generates trade receivables, also known as account

17

receivables (Lorenzo Preve, Virginia Sarria-Allende,

2010). Giving these credit terms to customers are an

important way of securing sales (Berry and Jarvis, 2006)

.More specifically, goods or services delivered to

customers on credit will increase the receivables

balance, and payments subsequently received from

customers will decrease this balance (Lorenzo Preve,

Virginia Sarria-Allende , 2010). According to Berry and

Jarvis (2006), a firm sets up a policy for determining

the optimal amount of account receivables have to take

in account the following:

● The trade-off between the securing of sales and

profits and the amount of opportunity cost and

administrative costs of the increasing account

receivables.

● The level of risk the firm is prepared to take when

extending credit to a customer, because this customer

could default when payment is due.

● The investment in debt collection management.

18

A firm’s inventory is the necessary investment that the

firm needs to make to ensure the normal operation of the

business and a certain level of customer service

(Lorenzo Preve, Virginia Sarria-Allende , 2010). The

goal of inventory management is to minimize the costs of

storing and financing goods while maintaining a level of

inventories that satisfies the amounts of sales of a

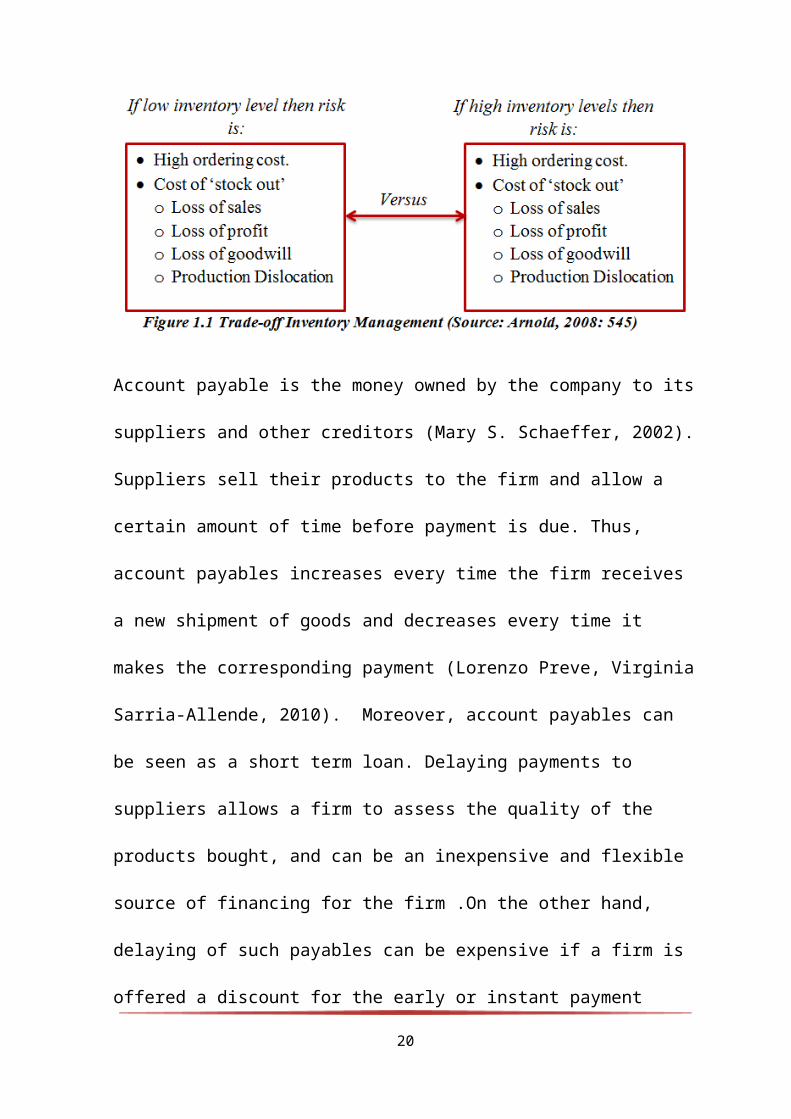

firm (Hampton and Wagner, 1989). Deloof (2003) argues

that with inventory management there is a trade-off

between sales and costs. As the firm increase the level

of inventory it holds, the risk of running out inventory

is lessened, but the inventory expense are increase

(Krish Rangarajan, Krish Rangarajan; Anil Misra, 2005).

In figure 1.1 the different trade-offs a firm faces, are

illustrated.

19

Account payable is the money owned by the company to its

suppliers and other creditors (Mary S. Schaeffer, 2002).

Suppliers sell their products to the firm and allow a

certain amount of time before payment is due. Thus,

account payables increases every time the firm receives

a new shipment of goods and decreases every time it

makes the corresponding payment (Lorenzo Preve, Virginia

Sarria-Allende, 2010). Moreover, account payables can

be seen as a short term loan. Delaying payments to

suppliers allows a firm to assess the quality of the

products bought, and can be an inexpensive and flexible

source of financing for the firm .On the other hand,

delaying of such payables can be expensive if a firm is

offered a discount for the early or instant payment

20

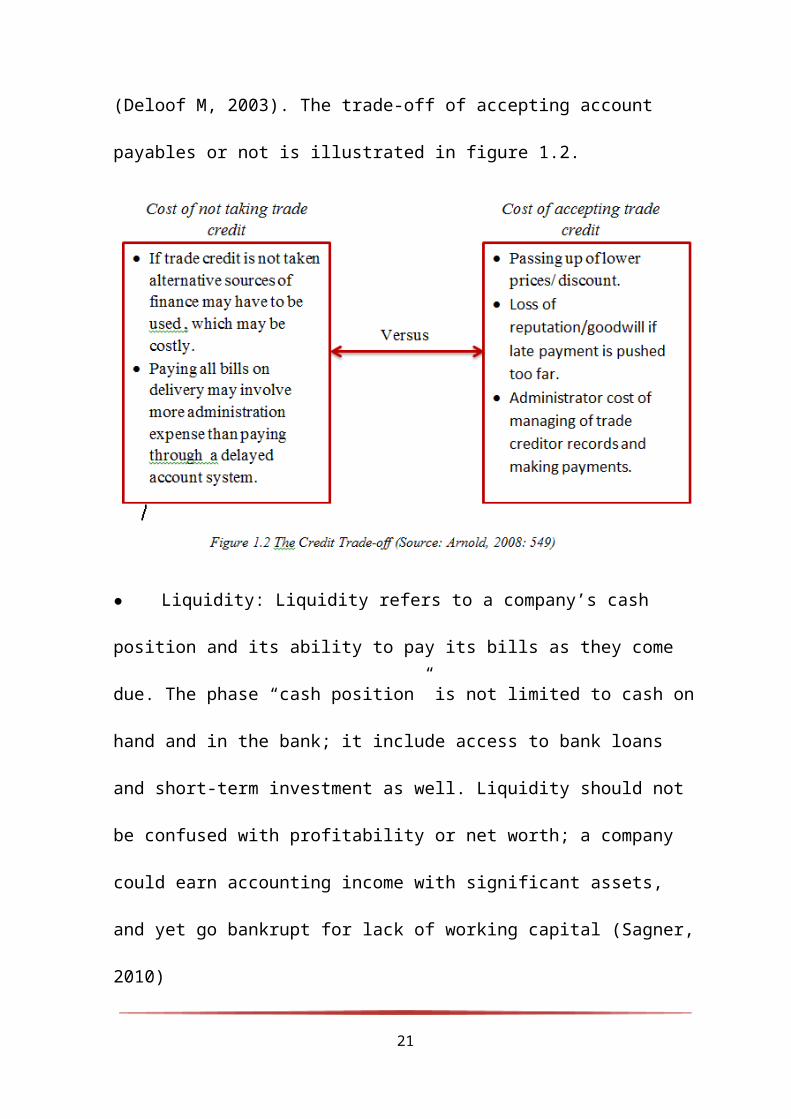

(Deloof M, 2003). The trade-off of accepting account

payables or not is illustrated in figure 1.2.

● Liquidity: Liquidity refers to a company’s cash

position and its ability to pay its bills as they come

due. The phase “cash position” is not limited to cash on

hand and in the bank; it include access to bank loans

and short-term investment as well. Liquidity should not

be confused with profitability or net worth; a company

could earn accounting income with significant assets,

and yet go bankrupt for lack of working capital (Sagner,

2010)

21

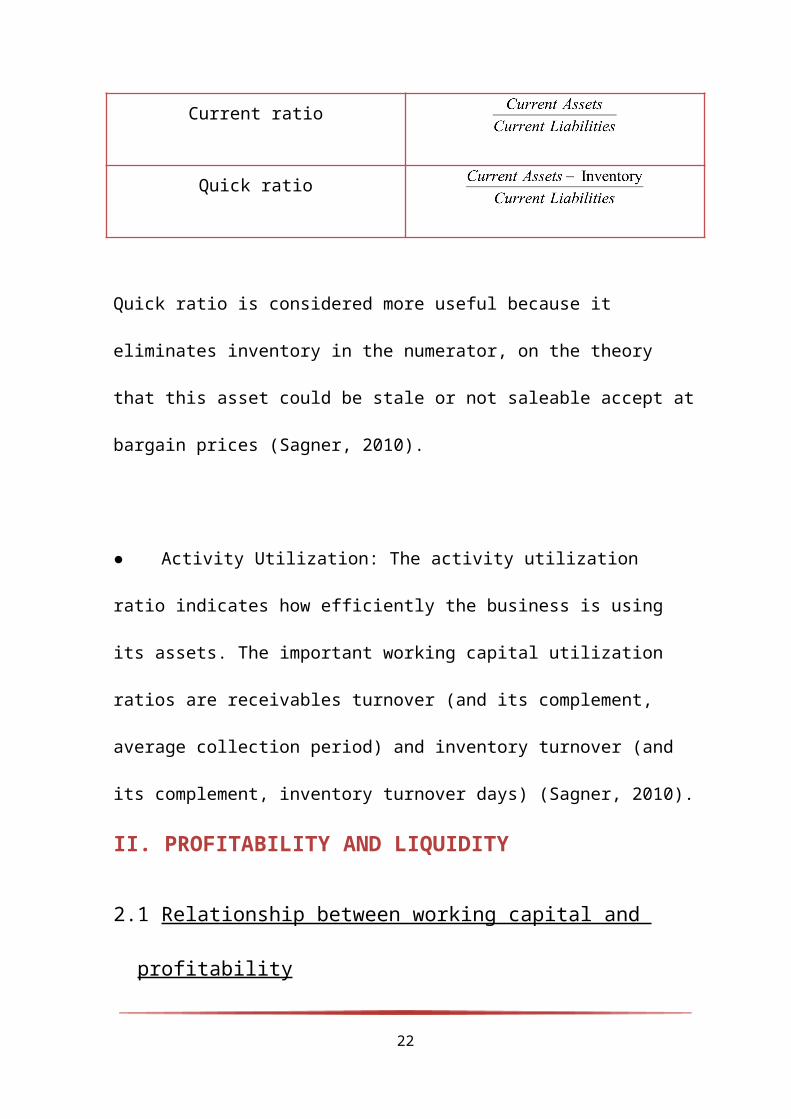

Current ratio

Quick ratio

Quick ratio is considered more useful because it

eliminates inventory in the numerator, on the theory

that this asset could be stale or not saleable accept at

bargain prices (Sagner, 2010).

● Activity Utilization: The activity utilization

ratio indicates how efficiently the business is using

its assets. The important working capital utilization

ratios are receivables turnover (and its complement,

average collection period) and inventory turnover (and

its complement, inventory turnover days) (Sagner, 2010).

II. PROFITABILITY AND LIQUIDITY

2.1 Relationship between working capital and

profitability

22

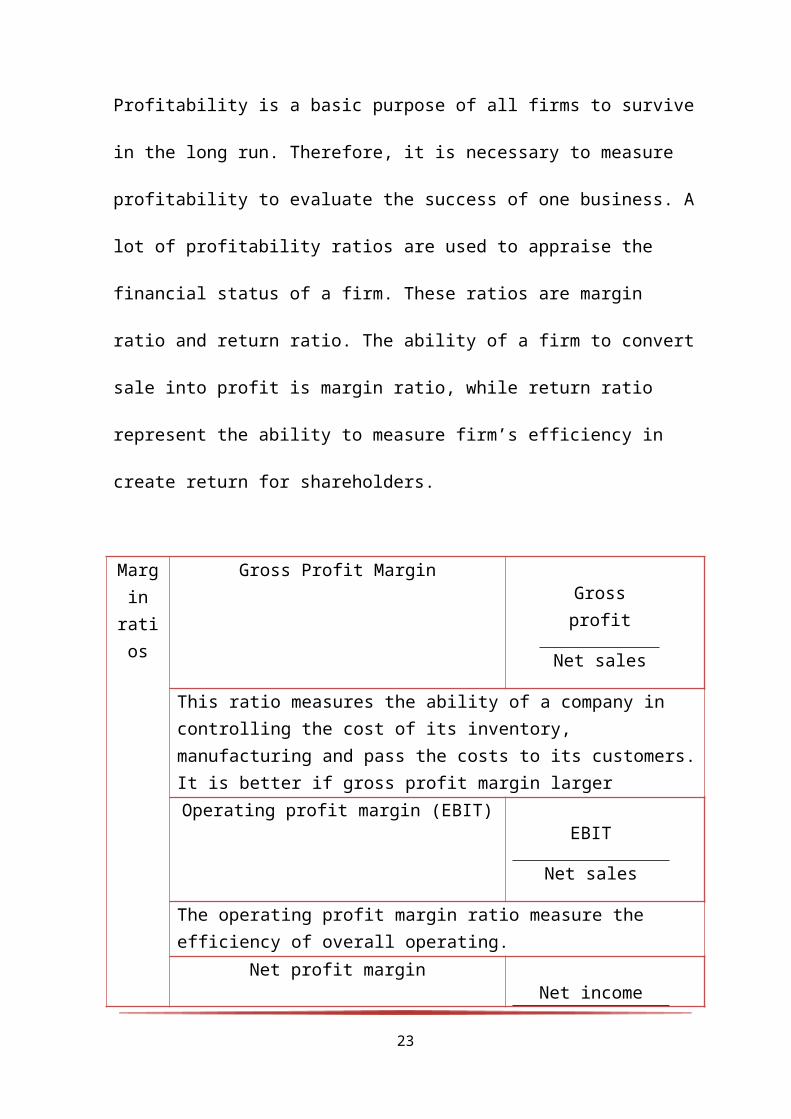

Profitability is a basic purpose of all firms to survive

in the long run. Therefore, it is necessary to measure

profitability to evaluate the success of one business. A

lot of profitability ratios are used to appraise the

financial status of a firm. These ratios are margin

ratio and return ratio. The ability of a firm to convert

sale into profit is margin ratio, while return ratio

represent the ability to measure firm’s efficiency in

create return for shareholders.

Margin

ratios

Gross Profit MarginGrossprofit

Net sales

This ratio measures the ability of a company in controlling the cost of its inventory, manufacturing and pass the costs to its customers.It is better if gross profit margin largerOperating profit margin (EBIT)

EBIT

Net sales

The operating profit margin ratio measure the efficiency of overall operating.

Net profit marginNet income

23

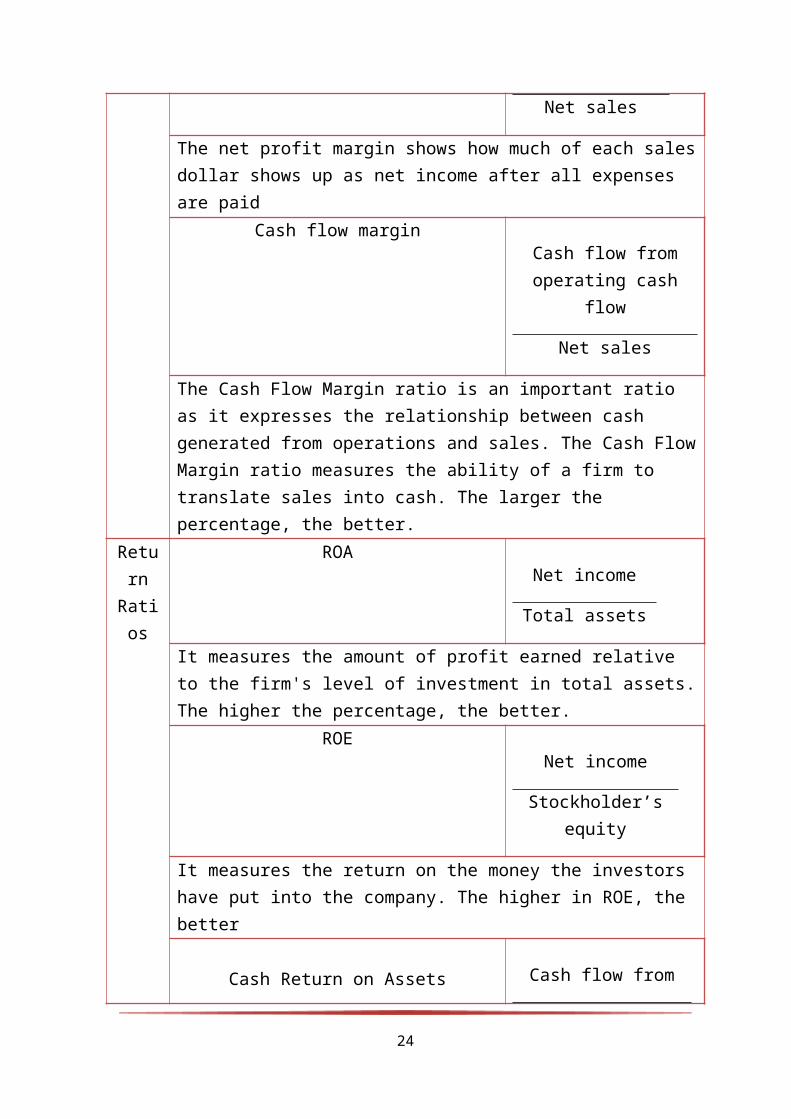

Net sales

The net profit margin shows how much of each salesdollar shows up as net income after all expenses are paid

Cash flow marginCash flow fromoperating cash

flow

Net sales

The Cash Flow Margin ratio is an important ratio as it expresses the relationship between cash generated from operations and sales. The Cash FlowMargin ratio measures the ability of a firm to translate sales into cash. The larger the percentage, the better.

Return

Ratios

ROANet income

Total assets

It measures the amount of profit earned relative to the firm's level of investment in total assets.The higher the percentage, the better.

ROENet income

Stockholder’sequity

It measures the return on the money the investors have put into the company. The higher in ROE, the better

Cash Return on Assets Cash flow from

24

operatingactivities

Total assets

Deloof (2003) conducts a study on Belgian Firms to exam

how the working capital management affects

profitability. At the result, he found that almost firms

invest a large amount of cash invested in working

capital. He recommends that by reducing the number of

day’s account receivable and inventories to reasonable

minimum, manager could improve corporate profitability.

The negative relation between profitability and accounts

payable suggest that companies wait longer to pay their

bills if they are less profitable.

2.2 Relationship between profitability and

liquidity

In a high level of trading activities, some investors

care about the liquidity of assets. The liquidity is the

ability to convert an asset to cash quickly. In

25

accounting, the liquidity reflects the ability of

current assets to match current liability.

According to Chandra (2001, p.72), a high liquidity

reflects the strength of financial. However, according

to some authors as Assaf Neto (2003, p.22), a high

liquidity can be as undesirable as a low because the

current assets are less profitable then the fixed

assets. That is because current assets generate

additional costs for maintenance, thus reducing the

profitability of the company.

According to Eljelly (2004), the virtual role of

managing working capital is maintaining its liquidity in

daily operation to meet its obligation. Therefore, every

firm attempt to optimize the profitability while

preserving the liquidity. Dilemma in liquidity

management is to achieve desired trade-off between

liquidity and profitability (Raheman et all, 2007). That

means the increasing in profits at the cost of liquidity

might lead to financial insolvency. Thus an effective

26

WCM needs to balance two core objectives of the firm.

Because, excessive liquidity don’t make any profits for

the firm and on the other hand, insufficient

liquidity might damage the firm’s goodwill,

deteriorate firm’s credit. That leads to the firm

might face to bankruptcy and insolvency problem.

Liquidity in itself, for the purpose of this research,

is measured in terms of current asset ratios, quick

ratio and operating cash flow.

III. REVIEW OF PREVIOUS STUDIES

3.1 Developed countries

America

Amarjit Gill, Nahum Biger, Neil Mathur (2010) conducted

the research to seek the relationship between working

capital management and profitability. They used the data

of 88 American firms listed on New York Stock Exchange

for a period from 2005 to 2007. The outcomes showed the

positive relationship between the CCC and profitability

estimated GOP. In addition, DSO and GOP have a negative

27

relationship which means firms can create profit by

keeping account receivables at an optimal level.

However, authors could not find the relationship of two

groups of factor firm size – gross operating profit

ratio and DPO – profitability.

Japanese

To study the relationship between working capital

management and firm’s profitability, Nobanee and Al

Hajjar (2009) investigated 2123 Japanese non-financial

firms listed in the Tokyo Stock Exchange for the period

from 1990 to 2004. The results suggest Japanese firms

concentrate on shortening the DPO, DSI and CC to

increase the profit. Authors also recommended

lengthening DPO is not solution because this could

impacts the firms’ credit reputation and profitability

in the long-term.

Thai

28

Kulkanya Napompech (2012) had figured out the

relationship between working capital and profitability

by sampling 255 companies listed on the Stock Exchange

of Thailand from 2007 through 2009. The results revealed

a negative relationship between GOP and DSI, DSO;

Thailand companies can increase the profitability by

shortening the CCC, DSI, and DSO. However, they cannot

increase firm’s profitability by lengthening the DPO.

3.2 Developing countries

Ghana

Examining the effect of working capital management on

firm’s performance for 125 non-listed Ghanaian firms

from 2004 to 2009 was carried out by Albert Amponsah

Addae and Michael Nyarko-Baasi (2013). The study found

that, profitability is negatively related to the length

of cash conversion cycle. This can be understood that

firms will be more profitable if they are able to

shorten the length of Cash conversion cycle. This

examination also indicates the negative relationship

29

between profitability and not only the CCC but also DSI,

DSO, and DPO.

Nigeria

Owolabi, Sunday Ajiao and Alu, Chituru Nkechinyere

(2012) pointed out the significant inverse relationship

between some working capital management factors measured

as DSO, DSI, DPO and profitability of manufacturing

firms. By implication, increases and decreases in any of

these variables affect the firm’s profits in an opposite

direction. Besides, the analysis showed that the size of

firm also influent its profitability such as the firms

increases in size, the ROA also goes up and vice versa.

Vietnam

Investigating relationship between Working capital

management and profitability, Tu and Nguyen (2014)

analyzed a panel data of 208 firms listed on both Ho Chi

Minh City Stock Exchange (HOSE) and Hanoi Stock Exchange

(HNX) in the period from 2006 to 2012. By using

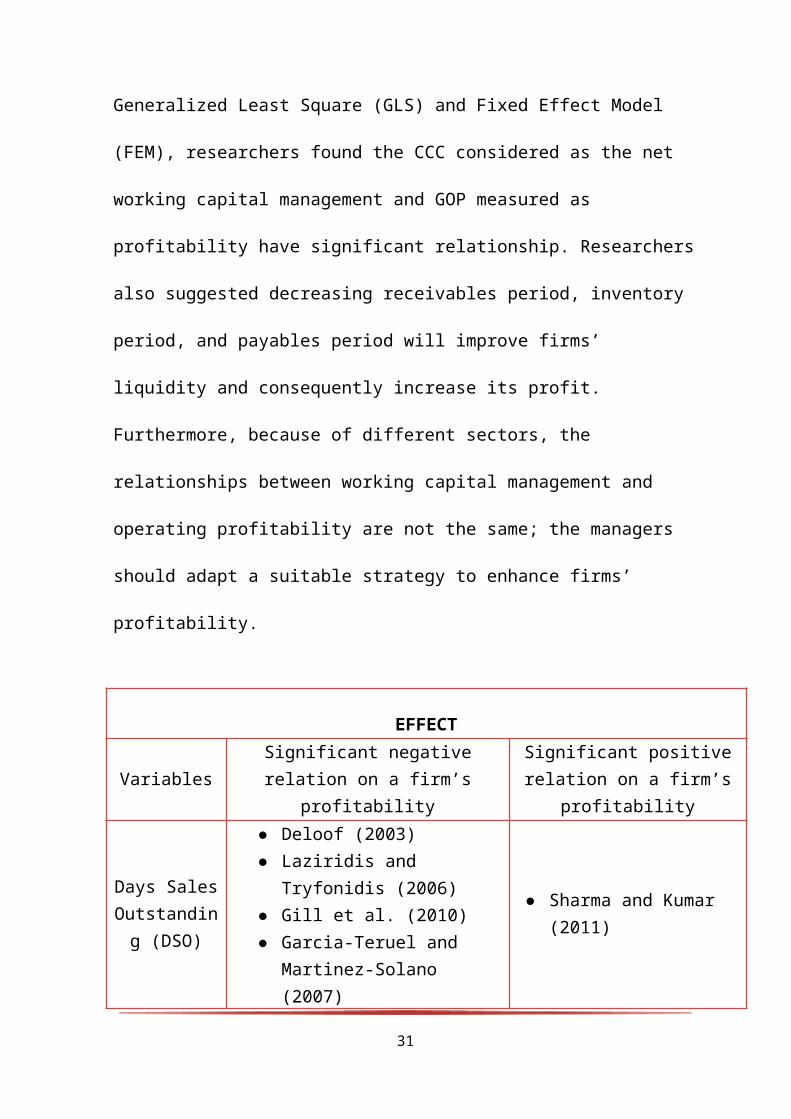

30

Generalized Least Square (GLS) and Fixed Effect Model

(FEM), researchers found the CCC considered as the net

working capital management and GOP measured as

profitability have significant relationship. Researchers

also suggested decreasing receivables period, inventory

period, and payables period will improve firms’

liquidity and consequently increase its profit.

Furthermore, because of different sectors, the

relationships between working capital management and

operating profitability are not the same; the managers

should adapt a suitable strategy to enhance firms’

profitability.

EFFECT

VariablesSignificant negativerelation on a firm’s

profitability

Significant positiverelation on a firm’s

profitability

Days SalesOutstanding (DSO)

● Deloof (2003)● Laziridis and

Tryfonidis (2006)● Gill et al. (2010)● Garcia-Teruel and

Martinez-Solano (2007)

● Sharma and Kumar (2011)

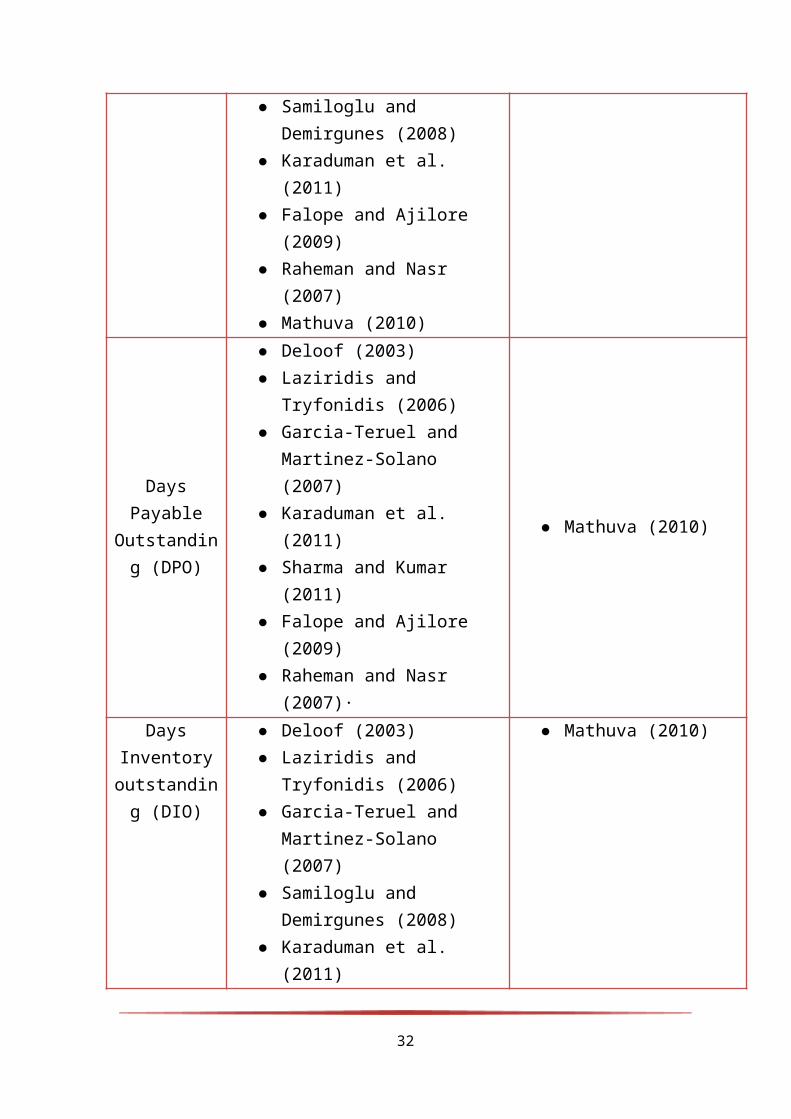

31

● Samiloglu and Demirgunes (2008)

● Karaduman et al. (2011)

● Falope and Ajilore (2009)

● Raheman and Nasr (2007)

● Mathuva (2010)

DaysPayable

Outstanding (DPO)

● Deloof (2003)● Laziridis and

Tryfonidis (2006)● Garcia-Teruel and

Martinez-Solano (2007)

● Karaduman et al. (2011)

● Sharma and Kumar (2011)

● Falope and Ajilore (2009)

● Raheman and Nasr (2007)·

● Mathuva (2010)

DaysInventoryoutstanding (DIO)

● Deloof (2003)● Laziridis and

Tryfonidis (2006)● Garcia-Teruel and

Martinez-Solano (2007)

● Samiloglu and Demirgunes (2008)

● Karaduman et al. (2011)

● Mathuva (2010)

32

● Sharma and Kumar (2011)

● Falope and Ajilore (2009)

● Raheman and Nasr (2007)

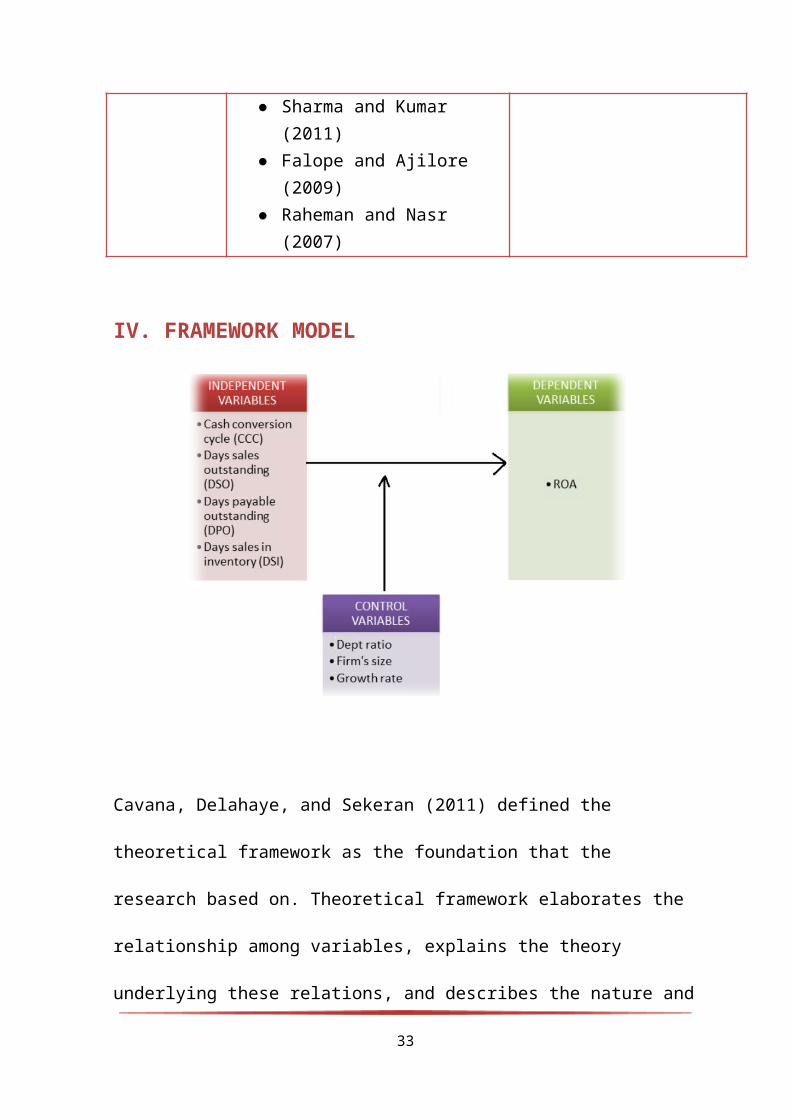

IV. FRAMEWORK MODEL

Cavana, Delahaye, and Sekeran (2011) defined the

theoretical framework as the foundation that the

research based on. Theoretical framework elaborates the

relationship among variables, explains the theory

underlying these relations, and describes the nature and

33

direction of the relationship. After having enough

foundation from literature review, theoretical framework

will provide logical base for developing hypotheses. In

this part, Cash Conversion Cycle (CCC) and its

components will be studied to measure the effect of

working capital on firm’s profitability.

4.1Independent variables

The effect of CCC and its components on firm’s

profitability were tested in numerous articles such as

Sharma and Kumar (2011),Karaduman et al. (2011),

Lazaridis and Tryfonidis (2006), Deloof (2003), Falope

and Ajilore (2009), Garcia-Teruel and Martinez-Solano

(2007), Dong and Su (2010), Matuva (2010) and Raheman

and Nasr (2007).

Eljelly (2004) assesses the relation between

profitability and liquidity through current ratio and

cash gap (cash conversion cycle) of joint stock

companies in Saudi Arabia. She found a negative

relationship between profitability and liquidity, and it

34

was found that CCC had a bigger impact over

profitability then current ratio. Also it was observed

that there was great variation among industries with

respect to the significant measure of liquidity.

Base on above result, in this study, days sales

outstanding (DSO), days inventory outstanding (DIO),

days payable outstanding (DPO) will be used as the

operationalization of the management of trade credit and

inventory. The Cash Conversion Cycle will be used as a

comprehensive measure of Working capital (Deloof, 2003).

H1 There is no relationship between ROA and CCC

H2 There is no relationship between DSO and ROA

H3 There is no relationship between DPO and ROA

H4 There is no relationship between DSI and ROA

4.2 Dependent variables

Firm’s Profitability

35

There are many different measurements of firm

profitability among the researchers who studied the

relation between Working capital and firm’s

profitability. Return on Assets (ROA) is the simplest

measurement, which is measured by dividing net income

with total assets. ROA will be used to evaluate firm’s

profitability in this study, because the largest part of

Working Capital research uses ROA as the dependent

variable .It was used by Sharma and Kumar (2011), Falope

and Ajilore (2009), Wang (2002), Samiloglu and

Demirgunes (2008), Garcia-Teruel and Martinez-Solano

(2007), Nazir and Afza (2009) and Karaduman et al.

(2011). According to Padachi et al. (2006), ROA is a

good measure for firm’s profitability, because it

relates the profitability of a company with its assets.

4.3 Control variables

Debt

36

Leverage refers to the extent to which a firm relies on

debt. The more debt financing a firm uses in its capital

structure, the less profitability firm has .In this

study, debt ratio which is calculated by dividing total

debt with total assets will be used to measure leverage

that is used in the literature on the relationship

between firm profitability and Working Capital. It was

used in the studies of Raheman and Nasr (2007),

Samiloglu and Demirgunes (2008), Sharma and Kumar

(2011), Shin and Soenen (1998) Lazaridis and Tryfonidis

(2006) and Karaduman et al. (2011).

Firm’s Size

This control variable is operationalized by using the

natural logarithm of sales to determine the size of a

firm. It was used in the studies of Padachi et al.

(2010), Dong and Su (2010), Deloof (2003), Raheman and

Nasr (2007) and Karaduman et al. (2011). In this study

the natural logarithm of sales will also be used as a

measurement for size because of its effectiveness in

37

others studies and because this study is about analyzing

the effect of working capital on SME’s firms, so the

firm’s size is an important variable to discriminate the

effect of working capital between SME firms and larger

firms.

Growth

This control variable is calculated as follows: this

year’s sales minus previous year’s sales divided by

previous year’s sales. This control variable, like

firm’s size, is used in this study to better evaluate

the relation between Working capital and profitability

of SME firms, the growth rate of a firm can have

significant impact on its profitability, which have been

tested in many studies like Samiloglu and Demirgunes

(2008), Sharma and Kumar (2011), Shin and Soenen (1998),

Karaduman et al. (2011), Deloof (2003), Falope and

Ajilore (2009) and Zariyawati et al. (2009).

Fixed Financial Assets

38

The last control variable that will be used is the Fixed

Financial Asset ratio and is calculated by dividing

fixed financial assets with total assets. This control

variables is used in the studies of Deloof (2003),

Raheman and Nasr (2007) and Dong and Su (2010). Other

studies didn’t use this variable because of the possible

lack of data regarding fixed financial assets. According

to Lorenzo Preve and Virginia Sarria-Allende (2010) ,it

is crucial to notice that decisions regarding fixed

assets and long-term debt and equity are decisions over

how to set the appropriate level of working capital.

Therefore, this variable will also be used in this study

to better evaluate the working capital management.

Current Ratio

This variable and is calculated by dividing current

assets with current liabilities. It was used in the

studies of Zariyawati et al. (2009), Shin and Soenen

(1998) and Sharma and Kumar (2011). To enhance

39

robustness of this study this control variable will also

be used in the upcoming analyses.

CHAPTER III

METHODOLOGY

I. RESEARCH PHILOSOPHY

“Research philosophy is a term relates to the

development of knowledge and the nature of that

knowledge” (Saunders et al, 2012). Research philosophy

that researchers apply can be considered as assumptions

about the way we observe the world, which support to

build and reinforce specific research strategies and

methods. Base on the research’s topic and objectives,

the group adopts positivism. There are some important

40

components that positivist researchers concentrate on;

firstly, working with observed phenomena to make

credible data. Secondly, according to Remenyi el at

(1998), researchers are not considered as factor

impacting on the subject of research; therefore,

research ought to be carried out in a value – free way.

Moreover, positivist researchers use structured

methodology to collect quantified samples and test data.

1.1 Nature of research

The group adopts descriptive and explanatory study as

our nature of research. First of all, we present a

general view of the topic. Next, we will determine

working capital’s factors influencing on firms’

profitability. To find the relationship between

variables researchers analyze the data’s samples through

statistical test such as correlation, regression

(Saunders et al, 2012).

1.2 Research approaches

41

At very beginning, research must care the design of

research project, and group chooses the deduction. The

generalizability of deduction is describing phenomenon

from the general to specific which means basing on the

theoretical framework researcher will collect data and

do some statistical analyze to test the framework.

1.3 Research method

This study takes quantitative as research method because

researchers will subject the samples’ numerical data for

statistical analysis. Besides that, it is also

appropriate with characteristic with positivism and

deduction approach.

III. DATA ANALYSIS METHODS

3.1 Pearson’s correlation test

A correlation is a measure of the linear relationship

between variables (Field-2007 ). There are several ways

to evaluate sample data to find the association between

variables, if the variables have ordinal (ranked) data;

42

Spearman’s and Kendall’s analysis should be used.

Because the variables in this study contain interval

data and the measures are linear, so Pearson’s

correlation analysis will be the most suitable method to

evaluate the association of working capital and

profitability in this study. Pearson’s correlation

coefficient is a measure of the linear correlation

(dependence) between two variables X and Y, giving a

value ranging from −1 (indicating perfect negative

association) to 0 (no association) to +1 (perfect

positive association) (Kleinbaum, Kupper, Nizam,

Rosenberg-2007). The analysis will include the

correlation test between the dependent variable (GOP)

and others independent and control variables, to find

the nature of these variables ( positive or negative )

and which have the significant impact on firm’s

profitability (LeBlanc-2004).

3.2 Regression analysis

43

In the following part the regression analyses are used

to investigate the impact of working capital on SME

firm’s profitability in 2009-2011 periods. Numerous

regressions are held for this study, but four most

implicating regression models for each regression

equation are selected for the analysis, which are

CCC,DSO,DIO and DPO.

1. Heterokedasticity

In OLS analysis, it is assumed that the variance of

error is the same and not correlated with each other

(Gauss-Markov assumption). If the errors do not have

constant variance, it is call Heteroskedasticity.

Heteroskedasticity happens in panel data when there is a

change in variation in a short period. When using OLS

within presence of Heteroskedasticity, the standard

errors could be wrong, the OLS estimation will not have

the minimum variance among the set of unbiased

estimation. Therefore, the result could be misleading

(Introductory Econometrics for Finance - Chris Brooks,

44

Cambridge University Press, and May 22, 2008 - Business

& Economics) .In order to avoid heteroskedasticity, the

researcher will use Generalized Least Square (GLS) as an

alternative estimation method.

2. Autocorrelation.

Autocorrelation is the assumption that the errors are

uncorrelated with one another. The consequences of that

problem are similar to those of heteroskedasticity, the

standard error could be wrong and affects to the model

(Brooks 2008). In order to detect the autocorrelation ,

Durbin-Watson test is applied. If Durbin-Watson is near

2, there is a little evidence of autocorrelation. In the

case of Durbin-Watson 0 or 4, there is perfect

autocorrelation in the residual (Brooks 2008). In the

case of presence the dependence between two errors, to

deal with it, generalized least square (GLS) can be the

alternative method instead of using OLS. Under GLS, a

weighted sum of the square residuals is minimized

(Brooks 2008)

45

3. Hausman Tests for correlated random effect.

In panel data methodology, researchers have to

determine whether there is fixed effect (FEM) or

random effect (REM) in the models. When use FEM, we

assume the characteristic are unique to the company and

should be correlated with other individual

characteristic. If they do not correlate, FEM is not

suitable to apply and REM will be used instead. (Kohler,

Kreuter-2008). Hausman Test is applied when there is a

selection to choose which method is more appropriate

between FEM and REM. If the p-value is lower than 0.1,

we reject the null hypothesis of no correlation between

them, which means FEM is more suitable. Otherwise, if

null hypothesis is accepted, REM will be chosen instead.

4. Multicollinearity with Variance Inflation

Factor (VIF).

In multiple regression, the dependencies between the

response variable Y and the repressor’s X are expected

to be found. Multicollinearity exists when there are

46

strong dependencies among the regressors variable X.

Multicollinearity can have serious effects on the

estimates of the regression coefficients and on the

general applicability of the estimated model

(Montgomery, RungeIn-2011). In order to measure the

effect of multicollinearity, Variance Inflation Factor

(VIF) is calculated as follow:

VIF(Xh)

=1

1−Rh2 h=1,2,…,k

Where Rh2 is the R2value obtained for the regression

of , as dependent variable, on other X variables on

the original equation aimed at predicting Y. When the

VIF is greater than 5, there are some degree of

multicollinearity exists with respect to the

variables (Aczel and Sounderpandian - 2009). In another

way, when the VIF is lower than 5, there is no

multicollinearity. The results of VIF for each

regression are shown together with the regression

results.

3.3 Descriptive statistics

47

Descriptive statistics is the discipline of

quantitatively describing the main features of a

collection of information (Mann, Prem-1995) or the

quantitative description itself . The descriptive

statistics in this study will provide simple summaries

about the sample and about the observations that have

been made. The most common types of descriptive

statistic are measures of central tendency and measures

of variability (or dispersion) (Kleinbaum, Kupper,

Nizam, Rosenberg-2007).

The central tendency in a sample of data is the “average

value” of the variable being observed. (Kleinbaum,

Kupper, Nizam, Rosenberg-2007) .The three most

frequently encountered indices of central tendency are

the mode, the median, and the mean. The mode is used for

describing nominal data, the median for describing

ordinal data, and the mean for describing interval or

ratio data. As a quantitative measurement study, this

48

study uses an interval scale, so the mean will be the

best choice as a measurement of central tendency.

Measures of variability tell us the extent to which the

values of the measurements in the sample differ from one

another. (Kleinbaum, Kupper, Nizam, Rosenberg-2007) .

The three most often considered are the range, the

quartile deviation, and the standard deviation . The

range is the only appropriate index of variability for

nominal data, and the quartile deviation is the

appropriate index of variability for ordinal data. In

this study, standard deviation is generally the

preferred index because the study uses interval scale of

data.

Besides measures of central tendency and variability,

this study also provides min, max of the data

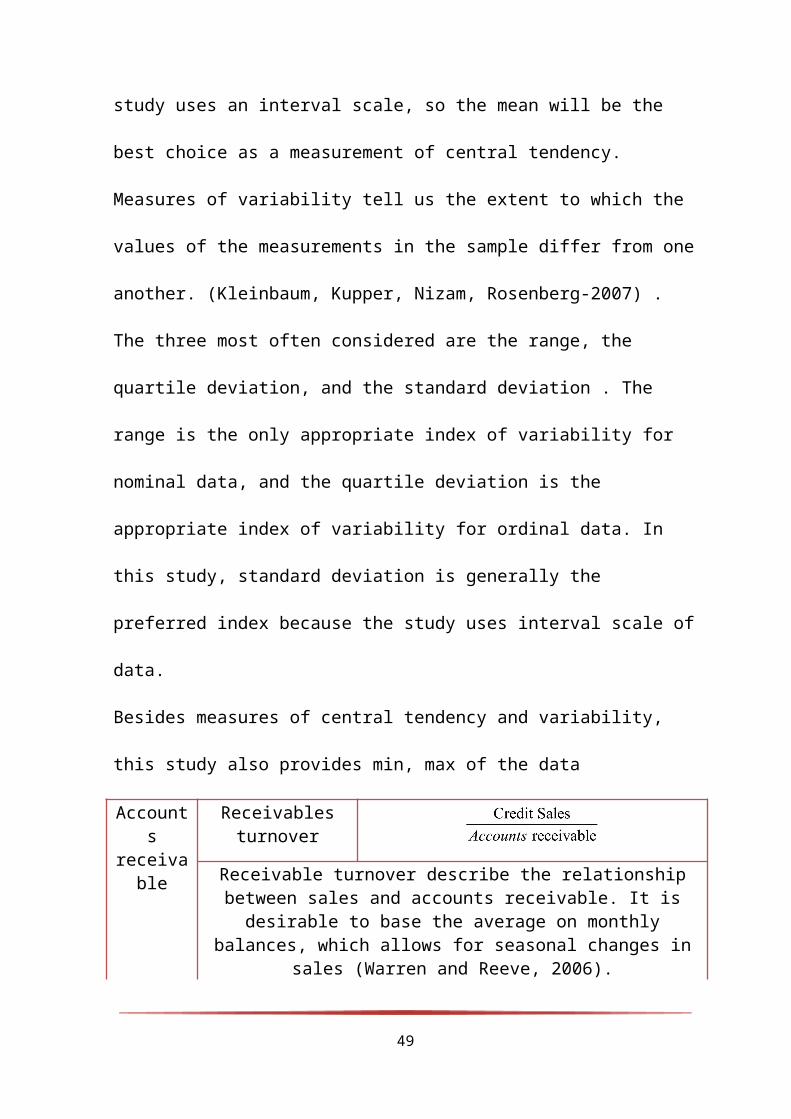

Accounts

receivable

Receivablesturnover

Receivable turnover describe the relationshipbetween sales and accounts receivable. It is

desirable to base the average on monthlybalances, which allows for seasonal changes in

sales (Warren and Reeve, 2006).

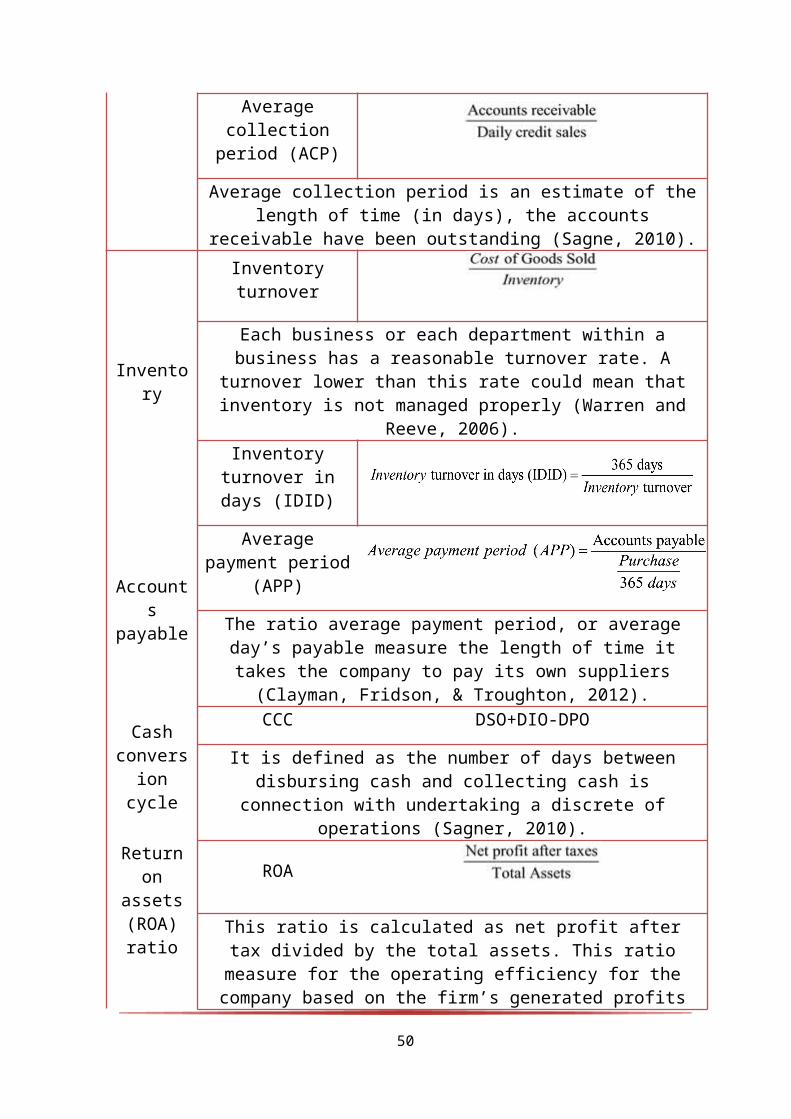

49

Averagecollection

period (ACP)

Average collection period is an estimate of thelength of time (in days), the accounts

receivable have been outstanding (Sagne, 2010).

Inventory

Inventoryturnover

Each business or each department within abusiness has a reasonable turnover rate. A

turnover lower than this rate could mean thatinventory is not managed properly (Warren and

Reeve, 2006).Inventory

turnover indays (IDID)

Accounts

payable

Averagepayment period

(APP)

The ratio average payment period, or averageday’s payable measure the length of time ittakes the company to pay its own suppliers

(Clayman, Fridson, & Troughton, 2012).

Cashconversioncycle

CCC DSO+DIO-DPO

It is defined as the number of days betweendisbursing cash and collecting cash is

connection with undertaking a discrete ofoperations (Sagner, 2010).

Returnon

assets(ROA)ratio

ROA

This ratio is calculated as net profit aftertax divided by the total assets. This ratiomeasure for the operating efficiency for thecompany based on the firm’s generated profits

50

from its total assets (International Journal ofHumanities and Social Science, 2012).

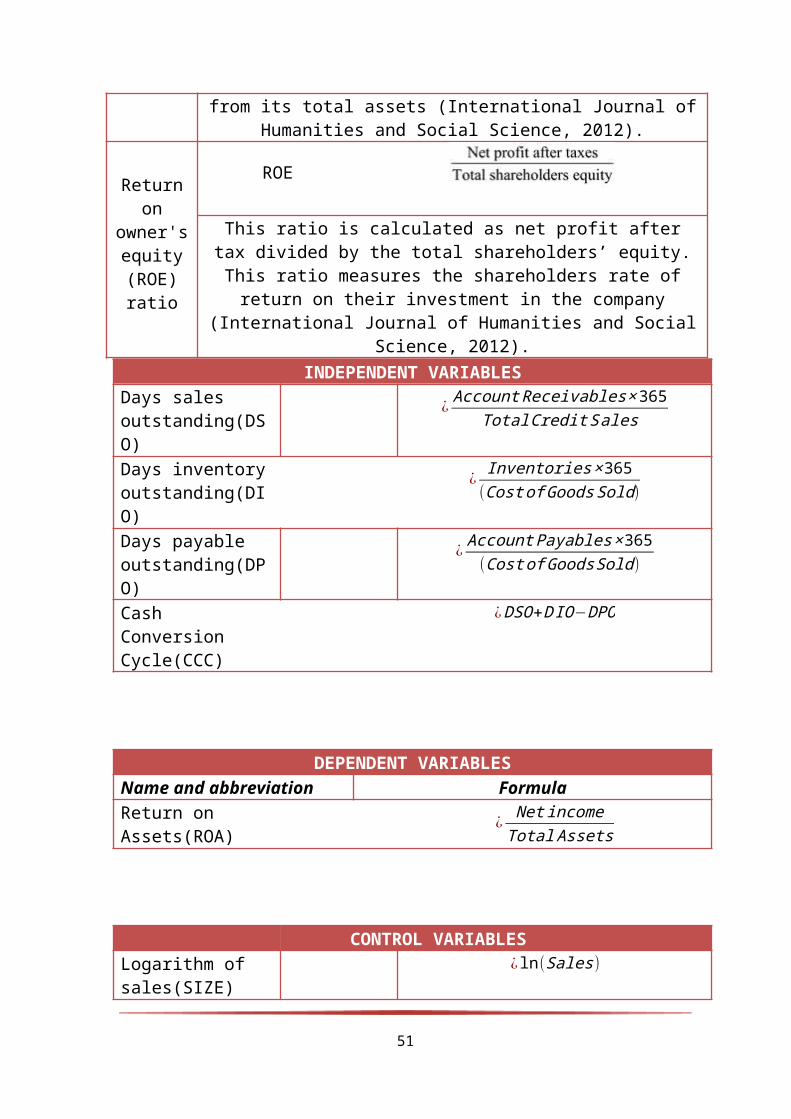

Returnon

owner'sequity(ROE)ratio

ROE

This ratio is calculated as net profit aftertax divided by the total shareholders’ equity.This ratio measures the shareholders rate ofreturn on their investment in the company

(International Journal of Humanities and SocialScience, 2012).

INDEPENDENT VARIABLESDays sales outstanding(DSO)

¿ AccountReceivables×365TotalCreditSales

Days inventoryoutstanding(DIO)

¿Inventories×365

(CostofGoodsSold)

Days payable outstanding(DPO)

¿ AccountPayables×365(CostofGoodsSold)

Cash Conversion Cycle(CCC)

¿DSO+DIO−DPO

DEPENDENT VARIABLESName and abbreviation FormulaReturn on Assets(ROA)

¿NetincomeTotalAssets

CONTROL VARIABLESLogarithm of sales(SIZE)

¿ln(Sales)

51

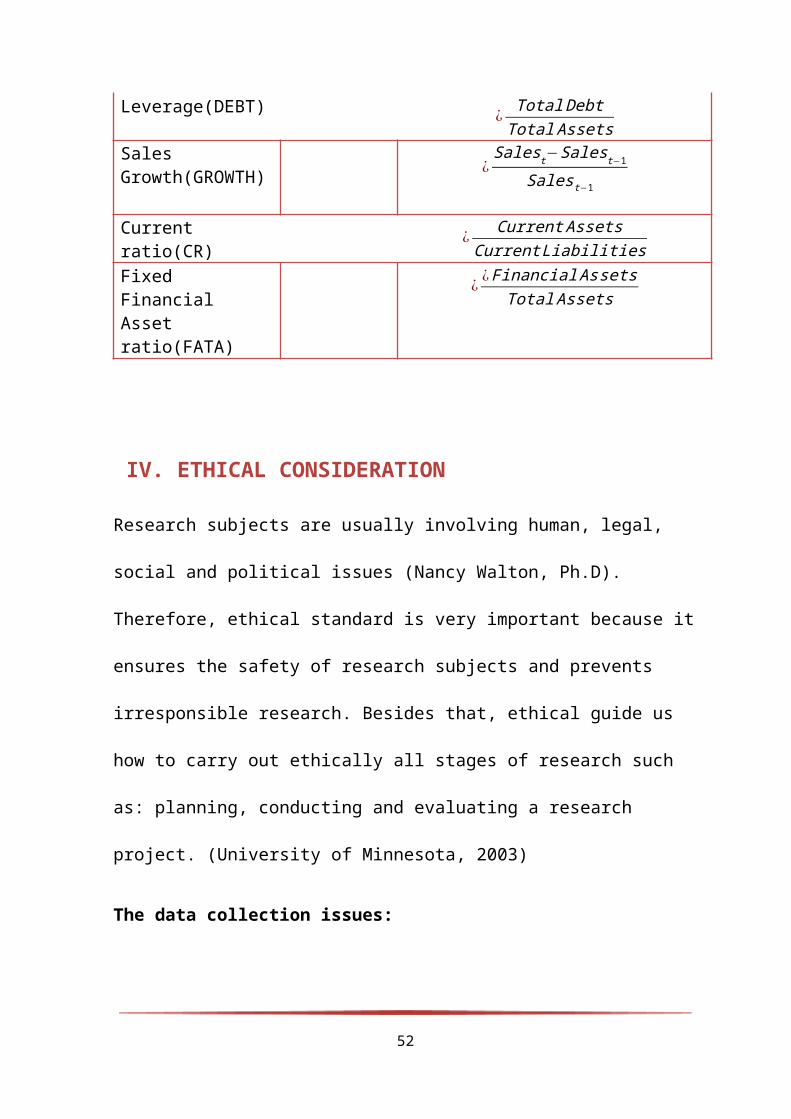

Leverage(DEBT) ¿TotalDebtTotalAssets

Sales Growth(GROWTH) ¿

Salest−Salest−1

Salest−1

Current ratio(CR)

¿CurrentAssets

CurrentLiabilitiesFixed Financial Asset ratio(FATA)

¿¿FinancialAssets

TotalAssets

IV. ETHICAL CONSIDERATION

Research subjects are usually involving human, legal,

social and political issues (Nancy Walton, Ph.D).

Therefore, ethical standard is very important because it

ensures the safety of research subjects and prevents

irresponsible research. Besides that, ethical guide us

how to carry out ethically all stages of research such

as: planning, conducting and evaluating a research

project. (University of Minnesota, 2003)

The data collection issues:

52

The source of financial data is acknowledged and

available in the public domain. The data is taken from

ranking board of the 500 SMEs in Viet Nam through the

period 2009 – 2011 and downloaded on the website

Fast500.vn. We ensure the data is correct with the

statistic of Fast500. In addition, we commit that all

data is used for study purpose, not for any commercial

aims.

The analysis and reporting process issues:

We ensure that the data will be analyzed and reported

honestly and there is no change to get better result.

The information and quote get their sources. The Harvard

style reference is followed as below.

V. LIMITATION OF THE RESEARCH PROJECT

Although 97% of Viet Nam firms are classified as SMEs,

the numbers of companies which have enough conditions to

see as SMEs according World Bank definition are.

Therefore, the result of our study can apply for Vietnam

53

List SMEs. Finally, due to the time and resources

limitation, we cannot update statistics from another

resources; this will effect on our outcome.

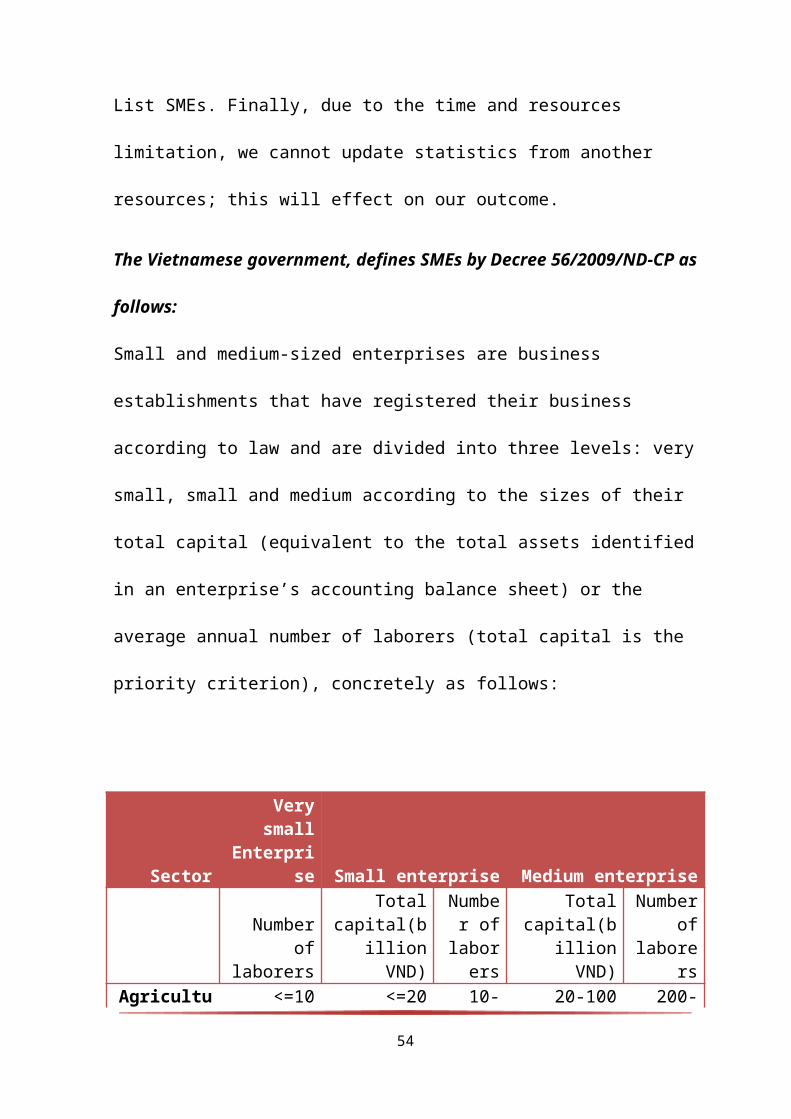

The Vietnamese government, defines SMEs by Decree 56/2009/ND-CP as

follows:

Small and medium-sized enterprises are business

establishments that have registered their business

according to law and are divided into three levels: very

small, small and medium according to the sizes of their

total capital (equivalent to the total assets identified

in an enterprise’s accounting balance sheet) or the

average annual number of laborers (total capital is the

priority criterion), concretely as follows:

Sector

Verysmall

Enterprise Small enterprise Medium enterprise

Numberof

laborers

Totalcapital(b

illionVND)

Number of

laborers

Totalcapital(b

illionVND)

Numberof

laborers

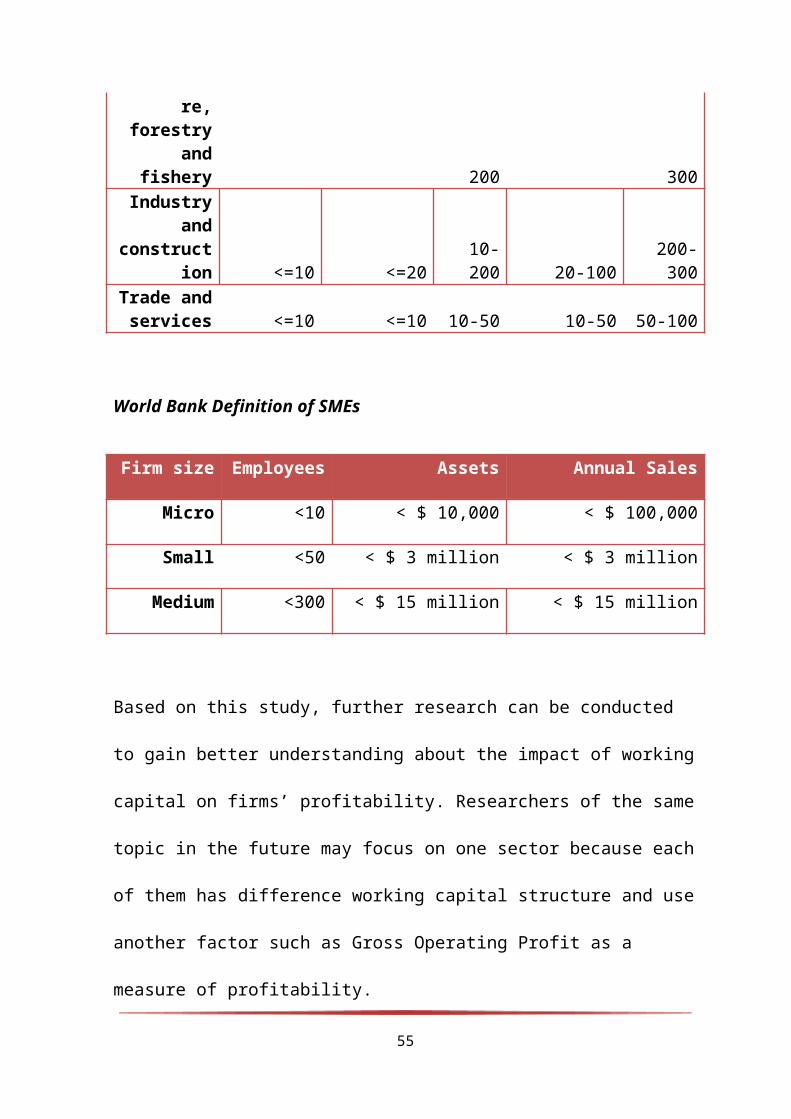

Agricultu <=10 <=20 10- 20-100 200-

54

re,forestry

andfishery 200 300

Industryand

construction <=10 <=20

10-200 20-100

200-300

Trade andservices <=10 <=10 10-50 10-50 50-100

World Bank Definition of SMEs

Firm size Employees Assets Annual Sales

Micro <10 < $ 10,000 < $ 100,000

Small <50 < $ 3 million < $ 3 million

Medium <300 < $ 15 million < $ 15 million

Based on this study, further research can be conducted

to gain better understanding about the impact of working

capital on firms’ profitability. Researchers of the same

topic in the future may focus on one sector because each

of them has difference working capital structure and use

another factor such as Gross Operating Profit as a

measure of profitability.

55

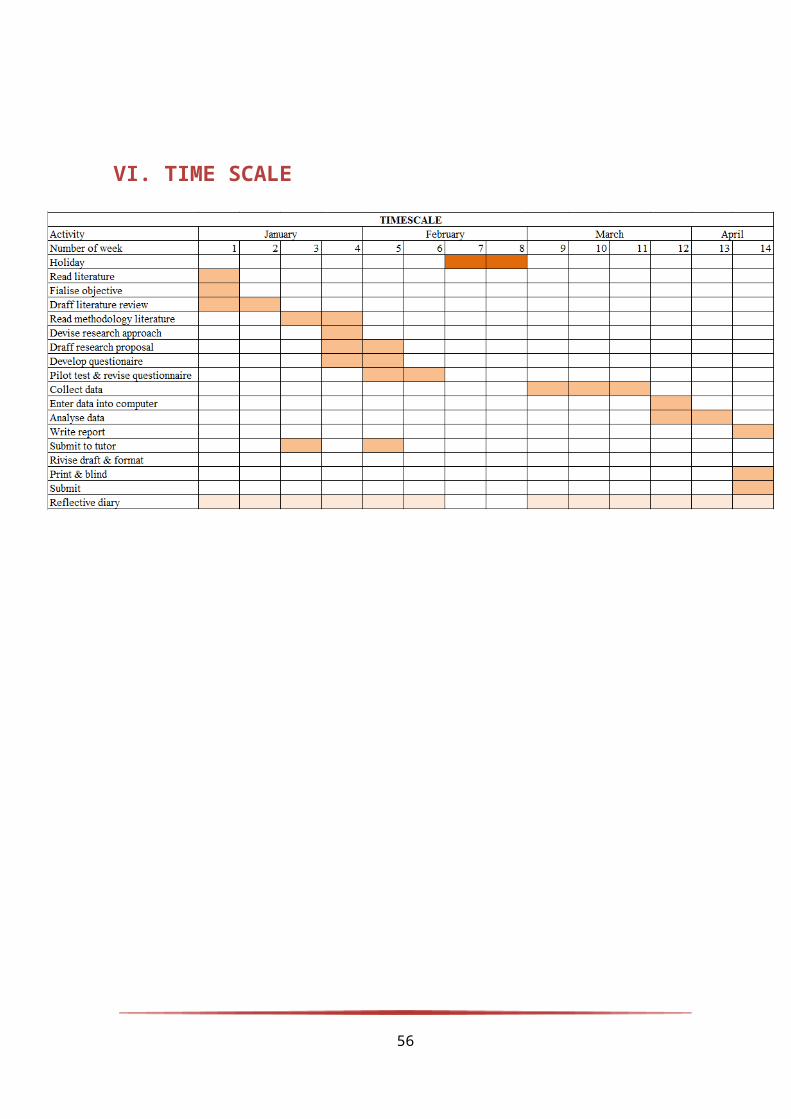

VI. TIME SCALE

56

http://www.researchethics.ca/what-is-research-ethics.htm

http://www.ahc.umn.edu/img/assets/26104/Research_Ethics.pdf

V. REFERENCES

Albert Amponsah Addae and Michael Nyarko-Baasi (2013).

Working Capital Management and Profitability: An empirical Investigation

57

in an Emerging Market. Research Journal of Finance and

Accounting.

Amarjit Gill, Nahum Biger, Neil Mathur (2010). The

Relationship between Working Capital Management and Profitability:

Evidence from the United States. Business and Economics Journal.

Berry, A. and Jarvis ,R. ,Accounting In A Business

Context. 4th edition .(2006)

Brigham, E. F., Houston, J. F., 2003, ‘Fundamentals of

Financial Management’, 10th Edition

Cihan Aktas- Director of Central Bank of the Republic of

Turkey, 2010.”The SMEs in the global world: Issue and Prospects”,

ADFIMI Development Forum 2010

CIEM, 2012. “Characteristics of the Vietnam business environment

evidence from a SME survey in 2011”, Central Institute for

economic management Office.

Cao Sĩ Kiêm (Director of VINASME),2013. “SMEs and support

solutions 2013”, Financial journal number 2-2013.

58

Deloof M, 2003. Does working capital management affect

profitability of Belgian firms? Journal of Business Finance

and Accounting

Dr. Le Chi Hieu, 2012. Economic crisis-Chance to improve

competitiveness of enterprises

Deloof, M. & Jeger, M. (1996). Trade Credit, Product

Quality, and Intragroup Trade: Some European Evidence.

Financial Management, 25(3), pp. 945-968.

Deloof, M. (2003). Does Working Capital Management

Affect Profitability of Belgian Firms?. Journal of

Business Finance & Accounting, 30(3) & (4), pp. 573 –

587.

Dong, H. P. & Su, J. (2010). The Relationship between

Working Capital Management and Profitability: A Vietnam

Case. International Research Journal of Finance and

Economics, 49. pp. 59-67.

Eljelly (2004). The Liquidity-Profitability Tradeoff: An

Empirical Investigation in an Emerging Market.

59

Falope, O. I. & Ajilore, O. T. (2009). Working Capital

Management and Corporate Profitability: Evidence from

Panel Data Analysis of Selected Quoted Companies in

Nigeria. Research Journal of Business Management, 3(3),

pp. 73-84.

Garcia-Teruel, J.P. & Martinez-Solano, P. (2007).

Effects of Working Capital on SME profitability.

International Journal of Managerial Finance, 3(2). pp.

164 –177.

Garcia-Teruel, J.P. & Martinez-Solano, P. (2010).

Determinants of Trade Credit: A Comparative Study of

European SMEs. International Small Business

Journal,28(3). pp. 215-233.

GSO, 2013.“Number and Event magazine 5/2013”, General

Statistics Office

James Sagner ,2014. “Working Capital Management – Application

and Cases” , p. 109.

60

Karaduman, H.A., Akbas, H.E., Caliskan, A.O. & Durer, S.

(2011). The Relationship between Working Capital Management and

Profitability: Evidence from an Emerging Market. International

Research Journal of Finance and Economics, 62(2011), pp.

61-67.

Kack, M and Lindgren, M. (1999), “The financing of private small

and medium size enterprises in Vietnam: A minor study, Department of

Business Studies”, Uppsala University, Sweden

Krish Rangarajan, Krish Rangarajan; Anil Misra , 2005.

“Working Capital Management”, p. 192.

Kulkanya Napompech (2012). Effects of Working Capital Management

on the Profitability of Thai Listed firms. Internal Journal of Trad,

Economics and Finance.

Lorenzo Preve, Virginia Sarria-Allende , 2010.”Working

Capital Management”,p. 67.

Lazaridis, I. & Tryfonidis, D. (2006). Relationship Between

Working Capital Management and Profitability of Listed Companies in the

61

Athens Stock Exchange. Journal of Financial Management and

Analysis, 19(1), pp. 26-35.

Mary S. Schaeffer , Essentials of Accounts Payable

(2002) , p. 2

Mathuva, D. M. (2010). The Influence of Working Capital

Management Components on Corporate Profitability: A Survey on Kenyan

Listed Firms. Research Journal of Business Management,

4(1), pp. 1 – 11.

Ministry Planning and Investment & Agency for enterprise

development, 2011. “SME White Paper 2011”,

http://www.economica.vn/

Nazir, M. S. & Afza, T. (2009). Working Capital Requirements

and the Determining Factors in Pakistan. ICFAI J Journal of

Applied Finance, 15(4), pp. 1109 – 1129.

Owolabi, Sunday Ajiao and Alu, Chituru Nkechinyere

(2012). Effective Working Capital Management and Profitability: A study

of Selected Quoted Manufacturing companies in Nigeria. Economics and

Financa Review.

62

Padachi, K. (2006). Trends in Working Capital Management and its

Impact on Firms’ Performance: An analysis of Mauritian small

manufacturing firms. International Review of Business

Research Papers, 2(2), pp. 45-58.

Padachi, K., Howorth, C., Narasimhan, M.S. & Durbarry,

R. (2010). Working Capital structure and Financing Pattern of

Mauritian SMEs. Oxford Business & Economics Conference

Program.

Raheman, A. & Nasr, M. (2007). Working Capital Management

and Profitability Case in Pakistani firms. ICFAI Journal of Applied

Finance, 54(3), pp. 279-300.

Samiloglu, F. & Demirgunes, K. (2008). The Effects of Working

Capital Management on Firm Profitability: Evidence from Turkey. The

international Journal of Applied Economics and Finance,

2(1), pp. 44 – 50.

Sartoris, W. & Hill, N. (1983). A Generalized Cash Flow

Approach to Short-Term Financial Decisions. Journal of Finance,

38, pp. 349 - 360.

63

Shin, H. & Soenen, L. (1998). Efficiency of Working Capital

Management and Corporate Profitability. Financial Practice and

Education (Now named Journal of Applied Finance) 8. pp.

37 - 45.

Soenen, L. A. (1993). Cash conversion cycle & corporate

profitability. Journal of Cash Management, 13(4), pp. 53-58

Thoa T.K. Tu and Uyen T.U. Nguyen (2014). Relationship

between Working Capital Management and Profitability – Empirical

evidence from Vietnamese listed firms.

S.D. Taleka, 2005. “Management Of Working Capital”, p. 56.

Vuong, Q. H., (1998), SMEs to play a large role in private sector,

Vietnam Investment Review

Wang, Y.J. (2002). Liquidity Management, Operating Performance,

and Corporate value: Evidence from Japan and Taiwan. Journal of

Multinational Financial Management. 12(2), pp. 159-169.

Zariyawati, M., M.N, A., Taufiq, H., & Sazali, A.

(2010). Determinants of Working Capital Management: Evidence from

Malaysia.

64

Introductory Statistics - Mann, Prem S.(1995). Applied

Regression Analysis and Other Multivariable Methods By

David Kleinbaum, Lawrence Kupper, Azhar Nizam, Eli

Rosenberg (2007)

Trochim, William M. K. "Descriptive statistics".

Research Methods Knowledge Base. (2006).

Psychology: A Journey By Dennis Coon, John Mitterer,

(2013), p. 595-596

Discovering Statistics Using SPSS for Windows By Andy P.

Field (2007)

Statistics: Concepts and Applications for Science By

David C. LeBlanc (2004)

Data Analysis Using Stata by Ulrich Kohler, Frauke

Kreuter (2008),p.245

65

Applied Statistics and Probability for Engineers By

Douglas C. Montgomery, George C. RungeIn (2011)

66