Embed Size (px)

Citation preview

1

CHAPTER ONE

RESEARCH INTRODUCTION

1.0 Background to the Study

Most businesses all over the world have had it tough to grapple with the management of

working capital. The problem of working capital therefore brings out this question “can

companies that are making profit and has great prospects for the future fail?”

Profitable businesses have collapsed, wind up or liquidated for lack of working capital. Some

businesses have collapsed due to over trading. This occurs if you have sufficient working

capital and try to increase sales and this over stretch the financial resources of the business.

(www.excel.plan.com-2007)

Working capital can be viewed statistically as the balance between current assets and current

liabilities, for example by comparing the balance sheet figures for stock, trade debtors, cash

and trade creditors.

Alternatively, working capital can be viewed dynamically as equilibrium between the income

generating and resource activities of a company (Pacs and Pike, 1984). It is the everyday

term for what accountants call net current assets. The components of organisations working

capital comprise two broad categories. These are current assets and current liabilities.

Trading stocks, trade debtors and cash are the main current assets. Creditors and accrued

expenses form the main current liabilities.

2

Efficient management of an organisation’s working capital is extremely important. Holding

too much working capital is inefficient, holding too little is dangerous to the survival of the

organisation. The importance of management of working capital efficiency is what is typified

by Vedarinayagam Ganesan in the River Academic Journal that “even though firms

traditionally are focused on long term capital budgeting and capital structure, the recent trend

is that many companies across different industries focus on working capital management

efficiency”,(Vedarinyagam, 2002).

Produce Buying Company Limited has been considered for study in this research work with

special interest in how working capital is managed in the organisation. Cocoa buying

companies are registered by the Ghana Cocoa Board. Registered as licensed cocoa buying

companies, their objective is to buy cocoa from farmers from the cocoa growing areas of

Ghana and in turn make the stocks available to Cocoa Marketing Company, a subsidiary of

Ghana Cocoa Board.

Generally, cocoa buying companies operate with huge sums of working capital mostly

financed by Ghana Cocoa Board. According to the Business Financial Times of Monday, 8th

September, 2008, “Ghana Cocoa Board (COCOBOD) has raised $1 billion loan on the local

and international market to finance cocoa purchases for the 2008/2009 crop year”, (Business

and Financial Times, 2008).

In terms of stocks, the Business and Financial Times stated that on the average a total of

670,000 metric tones of cocoa are bought annually since the year 2001. Also, with the high

3

labour intensive of the work and the seasonal nature, all existing companies as of now

operate with both permanent and temporary (commissioned agents) staff.

This thesis aims at a cocoa buying company considering the huge cocoa stocks and very

large cash or bank balances held by that licensed cocoa buying companies and to analyse

effectively how the different components of working capital leads to profit.

Available statistics indicate that Ghana Cocoa Board has over the years licensed over twenty

– seven cocoa buying companies but over the years most of the companies suffer from

liquidity problems due to working capital mismanagement and either collapse or perform

abysmally in subsequent years. It is therefore a common knowledge over few years past that

cocoa buying companies had little stability or job security. Currently, of all the licensed

buying companies just about nine of them operate relatively efficiently and effectively. These

include Produce Buying Company Limited, Federated Commodities Limited, Akuafo

Adamfo, Kuapa Cocoa, Transroyal Ghana Limited, Cocoa Merchants Limited, Adwumapa

Buyers and Armajaro Company Limited.

This research will dwell on the second dynamic approach of working capital definition which

emphasizes more on the cash conversion cycle as whether or not the company experiences

over trading or under trading, liquidity or illiquidity depends upon how it is able to manage

the working capital components especially the cash conversion cycle, efficiently. This

objective above obviously call for efficient management of the stocks, debtors, cash, short

term investments, creditors and accrued expenses of Produce Buying Company Limited.

4

1.1 Research Problem

Between 1993 and 2004 about thirty (30) licensed buying companies had been registered

with the Ghana Cocoa Board to operate alongside the Produce Buying Company.

The market share of the Produce Buying Company has declined over the years from 75% in

1995 to 31% in 2008 as the private Licensed Buying Companies continued to increase their

market share (www.pbcgh.com). Produce Buying Company Limited like many other

businesses is faced with the problem that the value and timing of incoming cash flows are not

sufficient for their operational outflows and the need for efficient and effective working

capital management therefore becomes crucial.

The study thus aimed to assess the working capital strategy employed by Produce Buying

Company Limited in relation to profitability and survival of the company during the period

between 1999 and 2008. The fundamental objective of the study is thus to examine whether

the profitability of Produce Buying Company Limited over the period could be linked to

working capital management problems.

1.2 Objectives of the Study

The objectives of this study have been categorized into two;

i. The main objectives of the research and

ii. Specific objectives

5

Main Objectives

The main aim of this study is to examine the impact of working capital on the profitability of

Produce Buying Company Limited over the period 1999 to 2008. Specifically the study

aimed at:

1. Assessing the trend of working capital components and profitability measures of the

company.

2. Examine the relationship between the working capital components and the cash conversion

cycle.

3. Evaluating the impact of working capital management on profitability of the company.

4. Make recommendations for sustained profitability and growth of the company.

1.3 Significance and need for the Study

In recognition of the important role licensed cocoa buying companies play in the economy of

Ghana, this study is a modest attempt to analyze working capital management of a licensed

buying company. The result of this study therefore is expected to contribute to the existing

literature on working capital management and how companies could apply innovative

policies to achieve positive goals. The study is thus expected to contribute to better

understanding of working capital policies and their impact on profitability especially in an

emerging licensed buying company.

Also, the study is expected to help the government and it agency, the Ghana Cocoa Board to

employ policies that would help the licensed buying companies to improve their working

capital and profitability.

6

The cocoa farmers will also benefit from proper working capital policies of licensed buying

companies in that the companies dealing with the farmers will work hand in hand to produce

best yielding cocoa to produce the best cocoa beans.

1.4 Limitation of the study

Working capital management is an extensive area which cannot be thoroughly researched

within such a limited time. This will be a major limitation to the study because the scope

cannot be defined well. To be able to conduct any meaningful research into the area the

scope of the study must be carefully defined and focused.

Accordingly, this study was limited to the key area of optimum investment in working capital

consistent with the profitability of the company.

Difficulty in obtaining sufficient funds to meet the financial requirements of the study within

the specified time is also identified to be one of the major limiting factors.

Obtaining the needed information to buttress the data took a long time for the researcher.

1.5 Organisation of the Study

Chapter one of the research work focused on the general introduction of the study,

identifying the problems to be analyzed, stating the purpose and specific objectives of the

study and explaining the contributions of the research to business management practice. The

limitations of the study will also be stated.

7

Chapter two looked at the theoretical underpinnings of the study and conducts a review of

prior literature on the topic. This will give a general understanding and some in depth

knowledge of working capital management from different publications such as text books,

articles, magazines, technical papers, journals and other library works. It will also include

prior empirical studies of work done by some other people in the field of working capital

management and the conclusions they arrived at.

Chapter three captured the methods employed in the study including data generation

techniques and analytical tools to be used. It will also look at the profile of Produce Buying

Company (PBC) Limited and its operational processes.

In chapter four, the data representing the management of the components of working capital

in Produce Buying Company (PBC) Limited and the trend of the efficiency ratios over the

years will be analysed. Also to be analysed will be the relationship between the components

of working capital, the cash conversion cycle and profitability of the company

Chapter five will capture the recommendations and conclusions of the study.

This chapter talked about the background information to working capital management. It also

looked at the problem that called for the study and the objectives of the research; “working

capital and profitability: an empirical case from Produce Buying Company Limited”.

8

Research questions were also outlined in this chapter; likewise the significance and need for

the study were also included. Methodology to be used in arriving at the findings has been

included here and the limitation to the study also enumerated with the final sub topic talking

about how the research has been arranged.

From this chapter, the researcher will move to chapter two which dwells mainly on prior

literature on working capital management.

9

CHAPTER TWO

REVIEW OF RELEVANT AND PRIOR LITERATURE

2.0 Introduction

Frustration with the performance of publicly traded corporation abounds in the corporate

world. Even before the Enron debacle in US, Hyundai Corporation in South Korea and

Ghana Airways in Ghana, there was a steadily increasing volume of criticism and complaints

regarding the performance of many companies of which Produce Buying Company Limited

is no exception. This has reached unacceptable level to a growing dissatisfaction among

many stakeholders (Colley Jnr et al, 2003)

Working capital is the comparison of current assets to current liabilities. For most

organizations, current assets exceed current liabilities and working capital therefore

represents the liquid reserves for meeting current obligations. Creditors prefer higher levels

of working capital since they are concerned about receiving payment. However, management

prefers low levels of working capital since working capital earns an extremely low rate of

returns (www.exinfm.com, 2007).

According to Chadwick and Kirkby (1995), working capital represents the difference

between current assets and current liabilities (networking capital).

It is possible to gain a better understanding of how an organization has performed by

examining the numbers contained in its accounts using ratio analyses to;

a. Compare the organizations current performance with that of previous year’s

performance

10

b. Compare the organisations performance with that of other organizations in the

industry.

c.

On their own, however, a company’s accounts do not provide a user with very much

information about how that organisation has performed.

Trends may be analysed using liquidity, profitability, efficiency, leverage and investment

ratios to determine the significant difference that would call for investigation to enable the

users of the account namely stakeholders, employees, trade creditors, government agencies,

public, community, potential investors and financial analysts to obtain much clearer picture

of how an organisation has actually performed. It is in the light of this that the study seeks to

use the accounting analytical tools to critically examine the working capital of Produce

Buying Company in the period of 1999 to 2008 in relation to its profitability, attractiveness,

reliability and efficiency to enable its stakeholders take informed decision.

Many researchers have contributed to our knowledge and understanding of the nature and

importance of working capital management and this chapter seeks to review prior literature

on it.

Luesby Jenny of REL Consultancy Group, a cash flow management advisor in his article

“High cost of idle capital” of March, 2003 issue of the Financial Times argues that working

capital is essential for organizations to meet their continuous operational needs and

represents the cushion or margin of protection an organisation can give to its short term

creditors. Its adequacy therefore influences an organisations ability to meet it trade and short

11

term debt obligations as well as to remain financially viable.

Biereley et al (1999) in an article evaluated financial instability of organisations which often

lead to their liquidation. They observed that organisations failures sometimes occur because

of their inability to restore temporary liquidity problems even though their long term viability

and solvency appear sound. They said organisations need to maintain adequate working

capital to run their business activities if they are to remain in business.

Gamble (2003) in his article “Hoarding Liquidity” comments that organisations face liquidity

problems because their working capital is tied up in inventory, receivables and payables. He

suggested that effective management of all the elements of working capital could release

adequate funds that will reduce organisations over reliance on external sources for working

capital financing.

2.1 The nature of Working Capital

2.1.1 The Concept of Working Capital

Pandy (1991) held the view that working capital is defined as the sum of stocks, accounts

receivable, cash and marketable securities. He focuses attention on two aspects of current

assets management as optimum investments in current assets and financing current assets.

Choyal (1991) describes the concept of working capital and its importance as “a

corporation’s life blood that flows through the veins and arteries of the structure. It engages

every part of the structure, gives courage and morale to the brain (management) and muscles

(personnel), digest to the best degree the raw material used by its constraints and regular flow

12

returns to the heart (cash flow) for another journey and so on. When working capital slows

up, the financial bodies have values only as “junks”. This description was corroborated and

quoted by Philip McCosker (2003).

Net working capital (often referred to simply as working capital) is the difference between a

company’s short term assets and liabilities.

The principal short term assets are cash, current receivable (customer’s unpaid bills) and

inventories of raw materials and finished goods. The principal short term liabilities are

accounts payable – goods that you have not paid, (Brealey and Myers, 2003). Further to the

above, they maintain that working capital summaries the net investment in short assets

associated with a firm, business or a project with most of its important components being

inventory, accounts receivable and accounts payable.

2.1.2 Cash Conversion Cycle

The working capital cycle and its modification, the cash conversion cycle reflects the net

time interval between actual cash expenditures on an organisation’s purchase of productive

resources and the ultimate recovery of cash receipts from product or service sales (Richards

and Laughlin, 1980). Managing cash flow and cash conversion cycle is a critical component

of overall financial management of all firms, especially those which are capital constrained

and more reliant on short term sources of finance (Walker and Petty, 1978; Deakins et al,

2001).

13

According to Padachi (2006) a firm can be very profitable, but if this is not translated into

cash from operating within the same operating cycle, the firm would need to borrow to

support its continued working capital needs. Thus, the twin objectives of profitability and

liquidity must be synchronized and one should not impinge on the other for long.

Investments in current assets are inevitable to ensure delivery of goods or services to the

ultimate customers and a proper management of same should give the desired impact on

either profitability or liquidity.

The cash conversion cycle is defined as the average age of inventory plus the average age of

account receivables less average age of account payables. The cash cycle shows the average

duration of a company’s cash invested in inventory and accounts receivable both of which do

not yield interest. The implication here is that the firm or company stands to gain by keeping

the cycle as short as possible. This is the main set of relationship that is at the heart of

working capital management. The longer the cash conversion cycle, the greater the amount

of investment required in working capital. (Pandy, 2008; Watson and Head, 2007) CCC =

STOCK DAYS + DEBTORS DAYS – CREDITORS DAYS

According to Eugene, Brigham and Michael Ehrhardt “firms typically follow a cycle in

which they purchase inventory, sell goods on credit and then collect accounts receivable.

This cycle is referred to as the cash conversion cycle”. They go further to explain the cash

conversion cycle model “which focuses on the length of time between when the company

makes payments and when it receives cash inflows”.

14

Pandy (op cit) in defining the operating cycle writes: “is the time duration required to convert

sales, after the conversion of resources into inventories, into cash”.

Shin and Soenen (1988) point out that corporation working capital is the result of the time tag

between the expenditure for the purchase goods. As such, it involves many different aspects

of corporate operational management: management of receivables, management of

inventories and management and use of trade credits. They further revealed that Wal-Mart

and Kmart had similar capital structure in 1994, but because Kmart had a cash conversion

cycle of roughly 61 days while Wal-Mart had a cash conversion cycle of 40 days, that Kmart

likely faced an additional $198.3 million per year in financing expenses. Clearly Kmart’s

poor management of its working capital contributed to its going bankrupt.

Gitman (1974) argued that the cash conversion cycle is a key factor in working capital

management. As such it involves many different aspects of corporate operational

management: management of receivables, management of inventories, management and use

of trade credit.

Actually, decisions about how to invest in the customer and inventory accounts and how

much credit to accept from suppliers are reflected in the firm’s cash conversion cycle, which

represents the average number of days between the date when the firm starts paying its

suppliers and the date when it begins to collect payments form its customers. If an

organisation can accelerate the movement of cash through the cycle by effective inventory,

payables and receivables management, the organisation will generate more cash and will

15

need to borrow less to fund working capital, thereby reducing interest costs and increasing

profits.

The cash conversion cycle (also called CCC) is the analytical tool of choice for determining

the investment quality of two critical assets: inventory and accounts receivable. The CCC

tells us the time (number of days) it takes to convert these two important assets into cash. A

fast turnover rate of these assets is what creates real liquidity and is a positive indication of

the quality of and efficient management of inventory and receivables.

The cash conversion cycle captures the amount of time each net input cedi is tied up in the

operational processes of the company from the release of seed fund to the receipt of cheque

for cocoa delivered. It also looks at the amount of time needed to sell inventory, the amount

of time needed to collect receivables and the length of time the company takes to pay its bills

without incurring penalties

2.1.3 Working Capital Policy and Practices

According to Kirkby (1995) it is difficult to lay down any hard and fast rules upon the

amount of working capital required. The working capital requirements will vary from

industry to industry, sector to sector and from company to company.

According to Watson et al (2007), there are three levels of working capital policies. An

Aggressive policy with regards to the level of investment in working capital means that the

company chooses to operate with lower levels of stock, debtors and cash for a given level of

activity or sales. An aggressive policy will increase profitability since less cash will be tied

16

up in current assets but it will also increase risk since the possibility of cash shortages or

running out of stock (stock out) is increased.

A Conservative and more flexible working capital policy for a given level of turnover would

be associated with maintaining a larger cash balance perhaps even investing in short term

securities, offering more generous credit terms to customers and holding higher levels of

stock. Such a policy will give rise to a lower risk of financing problems but at the expense of

reducing profitability.

A Moderate policy would tread a middle path between the aggressive and conservation

approach. The three levels of working capitals was also emphasized by both Van Horne and

Wachowicz (2005) and Brierley et al (1999) by using policy and restricted respectively for

aggressive policy A and relaxed respectively for conservative whilst policy B and moderate

were used respectively for moderate by Watson et al (2007).

Most empirical studies relating to working capital management and profitability support the

fact that aggressive working capital policies enhance profitability. In particular, Jose et al

(1996) provide strong evidence for US companies on the benefits of aggressive working

capital policies. Wang (2000) analyses a sample of Japanese firms from 1985 to 1996 and

finds that the shorter cash conversion cycle is related to better operating performance. the

results can be partially explained by the fact that there are industry benchmarks to which

firms adhere when setting their working capital investment policies(Hawauvini et al, 1986).

Thus firms can increase their profitability by reducing investment on account receivable and

inventories to a reasonable minimum indicated by the benchmarks for their industry.

17

2.2 Working Capital Management

2.2.1Meaning of Working Capital Management

According to Archer et al (1993) working capital management involves managing the level

and mix of current assets and current liabilities. Van Horne (1988) indicates that working

capital management involves the administration of current liabilities. In their study, Van

Horne and Wafchowicz (1992) noted that the administration of current assets and the

financing (especially current liabilities needed to support current assets is the meaning of

working capital management. It involves financial decision making, planning and control

activities related to each of the elements of working capital (McMenamin, 1999).

A study conducted by the treasury department of the New Zealand economy in 1990 on the

treatment of working capital resolved that working capital management takes place on two

levels where ratio analysis can be used to monitor overall trends in working capital and do

identify areas requiring closer management; and where the individual components of

working capital can be effectively managed by using various techniques and strategies

though this depends on the department’s unique mix of working capital components.

(www.wikipedia.com, 2010)

In furtherance to the above, the study noted that “working capital constitutes parts of the

Crown’s investment in the departments”. Associated with this is an opportunity cost to the

Crown that is money invested in one area may cost opportunities for investment in other

areas. If a department is operating with more working capital than is necessary, such an over

investment represents an unnecessary cost to the crown”. (Smith 1980)

18

However, in conclusion, the study noted, working capital management is not an end in itself,

rather is an integral part of the departments overall management. The need of efficient

working capital management, it is noted, must be considered in relation to other aspects of

the department’s financial and non-financial performance (source: www.treasury.gov’t.nz)

Working Capital in this study refers to the amount of capital which is readily available to

meet the recurrent costs of operations of the company. It is the difference between the

resources in cash plus current assets readily convertible into cash and organizational

commitment for which cash would soon be required (current liabilities). Thus it is the net

working capital whereas working capital management refers to policies relating to working

capital and short term financing. In other words, it is referring to all those decisions and

activities Produce Buying Company Limited undertakes to effectively manage the

components of its working capital.

2.2.2 Working Capital Management Components

According to Irani (2008), working capital is the difference between current assets and

current liabilities and it is the amount of liquefiable capital available to a company to build

itself. It does not mean that working capital will always be positive, there are times when it

can be negative and this happens when the current assets are less than the current liabilities.

More importantly a company needs working capital for its day to day activities like those of

paying wages, paying for raw materials and bills. When a company finds itself short of

working capital it uses its current assets to get money. Basically it is needed for the smooth

running of the business. A business in fact requires the right amount of working capital; too

19

much and too little working capital is detrimental to the business. He further points out that

working capital has certain elements and for a business to function smoothly, it needs to be

aware of these elements. The elements according to him are;

CASH: this is probably the most essential element or component of working capital. Without

cash a business cannot run smoothly. However, cash in the business needs to be monitored

carefully along with proper budgeting and forecasting. Cash inflow and cash outflow need to

be monitored properly. (Smith, 1980)

ACCOUNT RECEIVABLE: every business has some debtors; people or other businesses

that owe them money. These in accounts lingo are called account receivables. Simply put,

these are amounts that are yet to be received from debtors. Account receivables have to be

monitored properly and checked. (Smith, 1980)

INVENTORY OR STOCK: inventories are any quantity of items or economic resources

being held in storage for some future use (Federal Reserve Board, 2004). The inventory in a

company usually forms a substantial part of its current assets and hence needs more

monitoring than everything else. Inventory or stock needs to be at a particular level; the rate

of turnover also needs to be monitored closely. All this is an important component of

working capital. (Smith, 1980)

20

ACCOUNTS PAYABLE: like every company having debtors; people who owe it money,

similarly every company has creditors to whom it owes money. Its normal for businesses to

owe money to their suppliers and other businesses, this is because sometimes the amount to

be paid are large and will need some time to be paid off. It is important to track these payable

amounts also called accounts payable for the purpose of working capital and also for

goodwill reasons. (Smith, 1980)

OUTSTANDING EXPENSES AND PAYABLE TAXES: these are certain outstanding

that the company has and that will reflect on the working capital. (Smith, 1980).

Padachi (2006) state that accounts payable is different in the sense that it does not consume

resources; instead it is often used as a short term source of finance. Thus it help firms to

reduce its cash operating cycle, but it has an implicit cost where discount is offered for early

settlement of invoices.

Working capital meets the short term financial requirements of a business enterprise. It is a

trading capital, not retained in the business in particular form for longer than a year. The

money invested in it changes form and substance during the normal cause of business

operations. The objective of working capital management is to maintain the optimist balance

of each of the working capital components.

2.2.3 The Importance of Working Capital Management

Working capital management is important because of its effects on the firm’s profitability

and risk and consequently its value (Smith, 1980). Specifically, working capital investment

involves trade off between profitability and risk. Decisions that tend to increase profitability

21

tend to increase risk and inversely, decisions that focus on risk reduction will tend to reduce

potential profitability. Excessive investment in working capital ties up vital cash resources:

inadequate investment in working capital risks insolvency.

Dow Jones (2003) in his business brief to the Securities and Exchange Commission (SEC) of

New York on the topic “cash sources might dry up by months end”, says that even an

organization that has billions of pounds in fixed assets will quickly find itself in bankruptcy

court if it can not pay its bills as they fall due.

Inadequate working capital therefore leads to financial pressure on an organisation, increased

borrowing and late payments to creditors – all of which result in lower credit rating. A lower

credit rating means banks charge a higher interest rate which can be very expensive to the

organization over time. Adequate working capital therefore places an organization on a

sound financial footing to meet all maturing debts and increases its turnover and profits to

ensure a maximum returns to shareholders, comments Jones.

Narasimhan and Murty (2000) stress on the need for many industries to improve their return

on capital employed by focusing on some critical areas such as cost containment, reducing

investment in working capital and improving working capital efficiency.

The importance of working capital management is not new to the finance literature. Over

twenty – five years ago, Largay and Stickney (1980) reported that the then recent bankruptcy

of W. T. Grant a nationwide chain of departmental stores, should have been anticipated

because the corporation had been running a deficit cash flow form operations for eight of the

last ten years of its corporate life.

22

Theoretical determination of optimal trade credit limits are the subject of many articles over

the years, with scant attention paid to actual accounts receivable management. Across a

limited sample, Weinranb and Visscher (1984) observe a tendency of firms with low levels

of current ratios to also have low levels of current liabilities.

While the performance levels of small businesses have traditionally been attributed to general

managerial factors such as manufacturing, marketing and operations, working, working

capital management may have a consequent impact on small business survival and growth

(Kargar and Blumenthal, 1994).

The management of working capital is important to the financial health of business of all

sizes the amount invested in working capital are often high in proportion to the total assets

employed and so it is vital that these amounts are used in an efficient and effective way.

However, there is evidence that some businesses are not very good at managing their

working capital. Given that many small businesses suffer from under capitalization, the

importance of exerting tight control over working capital investment is difficult to overstate.

As part of a study of the Fortune 500’s financial management practices, Gilbert and Reichert

(1995) find that accounts receivable management models are used in 59% of these firms to

improve working capital projects, while inventory management models were used in 60% of

the companies.

Kieschnick et al (2006) states that corporations appear to pay a great deal of attention on how

well they are doing in managing their working capital and that REL Consultancy group has

23

for years conducted an annual survey of corporate working capital management performance

for CFO Magazine, which then reports. As their 2005 US survey report points out, there is a

high positive correlation between the efficiency of a corporation’s working capital policies

and its return on invested capital.

The ITWorld.com recently posted the results of a study arguing that poor working capital

management practices cost IT companies billions of dollars annually (ITWorld.com, 2002).

Mirroring this, REL, 2005 working capital survey concludes that US corporations had

roughly $450 billion unnecessary tied up in working capital.

Overtrading is selling more than an organization is capable of dealing with (with respect to

its finances and resources). This results in borrowing more money to compensate for the

increased costs (extra wages, materials, etc) of meeting the increased demand and the

problem is aggravated where the organisations sells on credit.

Peter Hanratty (1998), managing director of the U.K. Industrial Fund Limited, said even over

trading is one of the main causes of an organisation’s insolvency at a workshop organised for

a cross-section of the beneficiaries of the fund. Hanratty suggested that to avoid overtrading

and its resultant insolvency; organizations have to budget for enough time between the

receipt of orders and the payment received at the bank.

Another major reasons why organizations face cash flow problems is the failure of business

debtors to settle their invoices on time. If an organisation has debtors who are poor payers, it

24

is bound to face persistent liquidity crises. To overcome this problem, a member of the

American Cash Flow Association suggested that organisations use the services of factoring

companies, who provide support in pre-screening and monitoring customers’ credit

conditions and also provide cash against invoices within forty hours (http://www.finance-

manager.com/factoring-receiveable.htm). It may be the case that an organisation is trading

very profitability, but cash crises can arise through the mismanagement of working capital.

Efficient working capital management is therefore crucial to ensuring the solvency of

organizations says Gamble (2003).

2.2.4 Financing of Working Capital

The most effective way of financing working capital is by optimizing working capital

management practices in an organization, says Payne (2002). While working capital

improvements will not generate cash as quickly as tapping a line of credit, companies can

unlock dramatic amounts of money from their operations in surprisingly short periods of

time, with no obligation to pay back, emphasis Payne.

2.2.5 The Impact of Working Capital Management On Company’s Survival

In his study involving the impact of working capital management and corporate survival,

Bhattacharya (2001) noted that the essential element for the survival of any business is an

inflow of adequate funds. According to him, losses on their own are not strategically as

significant, for there has never been a cash-rich business, which has gone into liquidation

because of losses. That an adequate flow of funds and their proper management is necessary,

not only to save a firm from immediate liquidation but also to finance growth for long term

survival.

25

Some empirical research into the impact of working capital on companies has rather focused

on the components of the subject. This field of study is generally recognized as having

started with liquidity research beginning with the land mark study in 1966 by Beaver. He

tested the ability of thirty (30) standards accounting ratios, four of them cash flow based to

predict the future success of failure of firms.

These ratios were tested on a sample of seventy-nine (79) failed and seventy-nine (79) non-

failed firms and Beaver concluded that ratios, especially those that measure cash flow

coverage of debt, could predict the failure or success of a business as early as five years in

advance. In effect, Beaver’s contention that standard accounting data can predict the financial

performance of firms influenced many studies that followed, having attempted to

demonstrate the predictive values of various techniques for estimating actual business

financial performance.

Deakin (1972) advanced the research of Beaver and Altman by including some fourteen

important variables identifying earlier by Beaver with the multivariate methodology of

Altman. Using a sample of thirty-two failed and thirty-two non-failed firms, Deakin found

that cash flow coverage of total debt was important for predicting failure or bankruptcy.

In a similar study, Blum (1974), also used failed verses non-failed models in his research and

found that cash flow coverage of debt was important to predicting failure for a firm.

Following the preceding landmark studies, many additional research projects were taken in

an attempt to validate the use of financial and liquidity ratios for predicting the success or

26

failure of company. Some of the well known studies include Mensah (1993).

During the 1980’s the research emphasis in the area of predicting business failure shifted to

cash flow analysis following the study of Langay and Stickney (1980), regarding the failure

of W. T. Grant. This study found that liquidity ratio and measures of cash flows from

operations were the best predictors of the future success of a business. However, the

conclusions of the study were questioned by the research findings of Casey and Bartzak

(1984 and 1985). Using a sample of thirty bankrupt firms, with another thirty firms held out

of the study for validating purposes and one hundred and sixty-five non-bankrupt firms with

an equal number held out for validating, the authors found that standard accounting measures

were better for predicting firm bankruptcy than cash flow (liquid assets) measure.

Aziz, Emmanuel and Lawson (1988) combined accrual and cash flow variables in an attempt

to predict firm failure. However, the results of their validating holdout group cast questions

on their conclusions.

Otilson (1980) concluded from his research that, firm size was directly related to its failure or

success, with smaller firms being more likely to become unsuccessful (bankrupt) than large

ones.

2.2.6 The Impact of Working Capital Management on the Profitability and Liquidity of

an Organisation

Working capital management has become one of the most important issues in the

organisations where many financial executives are struggling to identify the basic working

27

capital drivers and that appropriate level of working capital (Lamberson, 1995).

Consequently, companies can minimize risk and improve the overall performance by

understanding the role and drivers of working capital. A firm may adopt an aggressive

working capital management policy with a low level of current assets as percentage of total

assets or it may also use for the financing decisions of the firm in the form of high level of

current liabilities as percentage of total liabilities. Excessive levels of current assets may have

a negative effect on the firm’s profitability whereas a low level of current assets may lead to

lower level of liquidity and stock outs resulting in difficulties in maintaining smooth

operations (Van Horne and Wachowicz, 2004)

The main objective of working capital management is thus to maintain an optimal balance

between each of the working capital components. Business success heavily depends on the

ability of financial executives to effectively manage receivables, inventory and payables

(Filbeck and Krueger, 2005). Thus it is generally appreciated that there is significant

relationship between working capital management and profitability.

Working capital management is a significant area of financial management and the

administration of working capital may have an important impact on the profitability and

liquidity of the firm. Shin and Soenen (1998), examine the relationship between different

accounting profitability measures and net trade cycles, a summary efficiency measure of a

firm’s working capital management. Shin and Soenen’s evidence implies that firms that

manage their working capital more efficiently (that is shorter net trade cycle) experience

higher operating cash flow and are potentially more valuable.

28

However, this last implication does not necessarily follow because firms that have longer net

trade cycles are also investing in short-term assets which may pay off in subsequent periods.

So the valuation issue is whether such investment earns a return above the cost of capital.

Firms can choose between the relative benefits of two basic types of strategies for net

working capital management; they can minimize working capital investment or they can

adopt working capital policies designed to increase sales. Thus, the management of a firm

has to evaluate the trade off between expected profitability and risk before deciding the

optimal level of investment in current assets.

On the one hand, minmising working capital investment (aggressive policies) would

positively affect the profitability of the firm, by reducing the proportion of its total assets in

the form of net current assets. However, Wang (2002) points out that if the inventory levels

are reduced too much, the firm risks loosing increases in sales. Also, a significant reduction

of the trade credit granted may provoke a reduction in sales from customers requiring credit.

Similarly, increasing supplier financing may result in loosing discount for early payments. In

fact, the opportunity cost may exceed twenty percent, depending on the discount period

granted (Wilner, 2000).

On the other hand and contrary to traditional belief, investing heavily in working capital

(conservative policy) may also result in higher profitability. In particular, maintaining high

inventory levels reduces the cost of possible interruptions in the production process and of

loss of business due to the scarcity of products, reduces supply costs and products against

price fluctuations, among other advantages (Blinder and Maccini, 1991). Also, granting trade

credit favours the firm’s sales in various ways. Trade credit can act as an effective price cut,

incentivizes customers to acquire merchandise at times of low demand (Emery, 1987), allows

29

customers to check that the merchandise they receive is as agreed (quantity and quality) and

to ensure that the services contracted are carried out (Smith, 1987), and helps to strengthen

long term relationship with their customer (Ng et al, 1999). However, these benefits have to

offset the reduction in profitability due to the increase of investment in current assets.

As noted earlier, empirical evidence relating working capital management and profitability in

general supports the fact that aggressive working capital policies enhance profitability (Jose

et al, 1996; Shin and Soenen, 1998; for US Companies; Wang, 2002 for Japanese and

Taiwanese firms). This suggests that reducing working capital investment is likely to lead to

higher profits.

2.2.7 The Effects of Working Capital Management on Small – Medium Enterprises

It is said that although working capital is the concern of all firms, it is the small firms which

should address this issue more seriously. Given their vulnerability to a fluctuation in the level

of working capital, they cannot afford to starve of cash. The study undertaken by Peel et al

(2000), revealed that small firms tend to have a relatively high proportion of current assets,

less liquidity, exhibit volatile cash flows and a high reliance on short – term debt. The work

of Howorth and Westhead (2003) suggests that small companies tend to focus on some areas

of working capital management where they can expect to improve marginal returns.

For small and growing business, an efficient working capital management is a vital

component of success and survival; that is both profitability and liquidity (Peel and Wilson,

1996). They further assert that small firms should adopt formal working capital management

30

routines in order to reduce the probability of business closure as well as to enhance business

performance and also emphasized the efficient management of working capital and recently

good credit management practice as being pivotal to the health and performance of the small

firm sector.

Most studies have focused their analysis on larger firms. However, the management of

current assets and liabilities is particularly important in the case of small and medium – sized

companies. Most of these companies’ assets are in the form of current assets. Also, current

liabilities are one of their main source of external finance because they encounter difficulties

in obtaining funding in the long term capital markets (Peterson and Rajan, 1997) and the

financing constraints that they face (Whited, 1992).

2.3 Conclusion

A review of the literature demonstrates that there are diverse views on the nature and

importance of working capital management. But whatever the consensus, it is clear that

working capital which is simply defined as the difference between current assets and current

liabilities is essential for a business to function smoothly and remain viable.

It is noteworthy that efficient working capital management has a significant impact on the

profitability and liquidity of all firms. However, each company has different working capital

requirements. This requirement in turn depends on different factors, including the type of

business size, production policy, process of manufacturing, changes in seasons, working

capital cycle, turnover rate of inventory, policy for credit, business cycles, rate at which

business grows, changes in pricing, dividend policy and capacity of earning.

31

This chapter was devoted to the literatures which are relevant to the topic under study that is

working capital management practices and profitability. The nature of working capital was

discussed which included topics like concept of working capital, the cash conversion cycle

and working capital policies and practices.

Literature on working capital management was also studied under which topics like the

meaning of working capital management, working capital management components, the

importance of working capital management, financing of working capital, the impact of

working capital management on company’s survival, the impact of working capital

management on the profitability and liquidity of an organization and the effect of working

capital management on small and medium scale enterprises.

Also, literature on the causes of insolvency and how to avoid it was also included in the

literature review. The next chapter, which is chapter three, looked at the methods adopted to

gather information on the topic working capital and profitability: an empirical case from

Produce Buying Company Limited.

32

CHAPTER THREE

METHODOLOGY AND PROFILE OF PRODUCE BUYING COMPANY LIMITED

3.0 Introduction

This chapter explained the procedures that were employed to collect the data for the analysis

component of the study. The adoption of both qualitative and quantitative techniques in the

data collection was to ensure cross checking and confirmation or otherwise. Due to resource

constraints the data was for a ten year period. It also captures the profile of Produce Buying

Company Limited.

3.1 Methodology

Perry (1998) describes case study research as consisting of a detailed investigation of one or

more organizations or groups within an organization with a view to providing an analysis of

the context and processes involved in the phenomenon under study. Yin (1993) notes that the

case study approach is not a method but rather a research strategy that is better suited to

‘how’, ‘why’ and ‘what’ questions Within this broad strategy, a number of methods may be

used, such as qualitative or quantitative or both.

The data gathered for this case study have been acquired through a combination of each of

these methods, partly due to the complexity of the subject matter, but more specifically as

part of a triangulation process to improve validity. According to Churchil (1995) research

methodology is a way to systematically solve a research problem.

33

Two conventional approaches to conduct research are: qualitative and quantitative.

Qualitative research is defined as an in-depth inquiry process that seeks to understand a

social or human problem based on building a complex holistic picture, formed by narrative,

reporting detailed views of informants and conducted in a natural setting (Creswell, 2002).

Bell (2001) describes qualitative research as being concerned to understand individuals’

perceptions to the world; they seek insight rather than statistical analysis. Qualitative

research may be used for the examination of attitudes, feelings and motivations of people

(Churchill, 1995). Such research seeks a deeper understanding of individuals and uses a

narrative rather than a numerical approach to explain findings (Beloucif, 2003).

Quantitative research is defined as an-depth inquiry into a social problem, based on testing a

theory composed of variables, measured numerically and analysed with statistical procedures

in order to determine whether the predictive generalisation of the theory holds true (Creswell,

2002).

Creswell, (2002) suggest that combining qualitative and quantitative approaches within the

same piece of research enables the researcher to provide richer detailed analysis. Linking

qualitative and quantitative data ensures the overall effectiveness of the research process as

one can enhance the findings of the other, notes Beloucif (2003).

3.2 Research Strategy

Saunders et al (1997) defined Research Strategy as a general plan of how the researcher will

go about answering the research questions posed. It is concerned with the overall approach to

be used in conducting the research. Robson (1993) identified the three traditional research

34

strategies as: Experimental, Survey and Case Study.

For the purpose of this study, case study research strategy was adopted. The case study has

been accepted as a viable research tool partly because of its convenience and meaningful

techniques which captures time-framed pictures of the research being undertaken (Merriam,

1998). Case studies also appeal to people because they have “face-value credibility”, that was

they can be seen to provide evidence or illustrations with which some readers can readily

identify.

The case study is an ideal methodology when a holistic, in-depth investigation is needed and

it is of particular interest if the researcher wishes to gain a rich understanding of the context

of the research and the process being enacted (Morris and Wood, 1991) including the type

(form) of research question posed, the extent of control of the researcher over actual

behavioural events and the degree of focus on contemporary events.

The research theme of this study relates to ‘how’, ‘why’ and ‘what’ questions. Although any

of the three strategies of experiment, survey and case study stated above would be suitable

for these categories of exploratory questions, only the case study is considered suitable when

the other two criteria need to be satisfied (Perry, 1998).

Given the type of research issues and considering the criteria discussed above, only the case

study method is considered satisfactory for the current research. For instance, Robson (1993)

argued that only the case study approach has the capability to generate answers to the

questions ‘Why’, ‘What’ and ‘How’.

35

Again, the case study approach is the preferred strategy for this research because it enables

the researcher to evaluate how the company’s management of working capital may impact on

the profitability and liquidity of the firm (Shin and Soenen, 1998).

3.3 Data Generation

As in all research, consideration is given to constructive validity, internal validity, external

validity and reliability and as noted by Yin (1993), these can be achieved by using multiple

source of data collection as no single source of data has complete advantage over another;

rather each might be complementary and could be used together and at the same time. In the

current study therefore, secondary and primary data are used.

3.3.1 Secondary Data

Secondary research involves the collection of data from existing sources and the study draws

on secondary data on the following lines:

Analysis of the annual audited accounts (financial statements) for the ten years, 1999

– 2008.

The company’s policy on working capital management practices to evaluate the

management of its working capital and liquidity measures.

Directors’ and auditors reports on the financial statements for the years, paying

attention to issues relating to working capital management.

Analysis of the management reports of the company for the 1999 – 2008.

36

3.3.2 Primary Data

Primary research involves the collection of original data specifically in pursuit of particular

research objectives. To supplement the secondary research activities described above,

primary data were also gathered from the Management of the Company using scheduled in-

depth interviews.

3.4 Rationale of Chosen Strategy

The purpose of the study is to examine and evaluate the working capital and profitability at

Produce Buying Company Limited over a period of ten years (1999-2008). In achieving this

purpose therefore, the methodology needed to be practical and to reflect the day-to-day

practices in the management of the company’s working capital.

3.5 Research Data Analysis

According to Mills and Huberman (1994) there is no standardized approach to the analysis of

research data. The approach adopted depends on the research methodology and data

collection techniques used. To be able to capture the richness and fullness associated with

qualitative and quantitative data, Perry (1998) suggested that the approach should involve

disaggregating the mass of data collected into meaningful and related categories to enhance a

systematic rearrangement and vigorous analysis of the data. The collected data have been

tabulated, analysed and interpreted with the help of different financial ratios and statistical

tools with the aid of SPSS computer software.

37

3.6 Profile of Produce Buying Company Limited

Produce Buying Company Limited (PBC) evolved form the produce department of the

Ghana Cocoa (Marketing) Board. It was incorporated as the Produce Buying Division

Limited on November 13th

, 1981 as a 100% state-owned enterprise and a subsidiary of Ghana

Cocoa Board (COCOBOD). It was granted a certificate to commence business on November

18th

, 1981. By a special resolution of its Board of Directors, the name was changed to

Produce Buying Company Limited on October 27th

, 1983. By a shareholder’s agreement

dated September 15th

, 1999 pursuant to the divestiture objectives of the Ghana Government,

the PBC shareholding was transferred from the Ghana Cocoa Board to the Minister of

Finance on behalf of the Government of Ghana.

VISION

Develop and maintain the Produce Buying Company Limited as the leading cocoa dealer in

Ghana.

MISSION

Purchase high quality cocoa beans from farmers, store and ensure prompt delivery of the

graded and sealed beans to designated Take Over centers in the most efficient and profitable

manner.

COMMITMENT

Produce Buying Company Limited commitment to its stake holders is to ensure:

1. Farmers satisfaction

38

2. Equitable return on shareholders investment

3. Development of a well motivated workforce

The PBC’s business is cocoa, the leading farming crop and a corner stone of the Ghanaian

economy.

The nature of the business which the Company is authorized to carry on is:

To acquire and take over as a going concern the activities and business of the Produce

Buying Division of the Ghana Cocoa (Marketing) Board.

To buy, collect, store, transport or otherwise deal in cocoa, coffee, sheanuts and shea

butter produced in Ghana and to sell same to the Ghana Cocoa (Marketing) Board.

To carry out arrangements, financial or otherwise and to contract with the Ghana

Cocoa (Marketing) Board for the purchase of cocoa, coffee, sheanuts and shea butter.

To appoint agents or enter into arrangements with any company, firm or any person

or group of persons with a view to carrying on the business of the company.

Produce Buying Company Limited basically buys cocoa beans from farmers, stores them in

purpose built sheds at the village/society level and sells to government at a guaranteed price.

The purchased beans are carted to collection depots where they are inspected, graded and

scaled by the Quality Control Division (QCD) of COCOBOD before their final evacuation

and delivery to appointed take-over points of the Cocoa Marketing Company (CMC). The

company is then paid the take-over margin, which is a markup over the producer price paid

to the farmers and linked to the f.o.b. price per ton. The company also earns additional

income from “secondary evacuation” of about 30% of its purchases to takeover centers.

39

3.7.1 Organisational Structure and Employment

The company has its Head Office in Accra (Dzorwulu). It is governed by a 9-member Board

of Directors appointed by the shareholders of the company. An executive management

comprising the Managing Director, a General Manager-Operations, Financial Controller and

six departmental heads, run the daily affairs of the company. Most of this team have worked

in the company for years and also acquired valuable experience working in other divisions

and subsidiaries of the COCOBOD.

PBC has two levels of non-management employees: unionized staff and senior staff. The

unionized staff is covered by a Collective Bargaining Agreement (CBA) between PBC and

the Industrial and Commercial Workers Union (ICU) re-negotiated on 22nd

August, 1999.

The CBA details the relevant terms and conditions of employment. The Senior Staff have up

till date been covered by Ghana Cocoa Board senior staff conditions of service as the

company was a subsidiary of Ghana Cocoa Board. It is expected that subsequent to

privatization, a dedicated PBC Senior Staff Conditions of Service will be put in place.

The Company operates a Provident Fund Scheme into which both employees and the

Company make contributions. Government of Ghana as part of the divestiture is also

allocating 5% of its equity shares in the PBC or 6.2% of the Offer Shares to the Company’s

employees on special terms to provide incentives and motivate them for greater productivity.

- 40 -

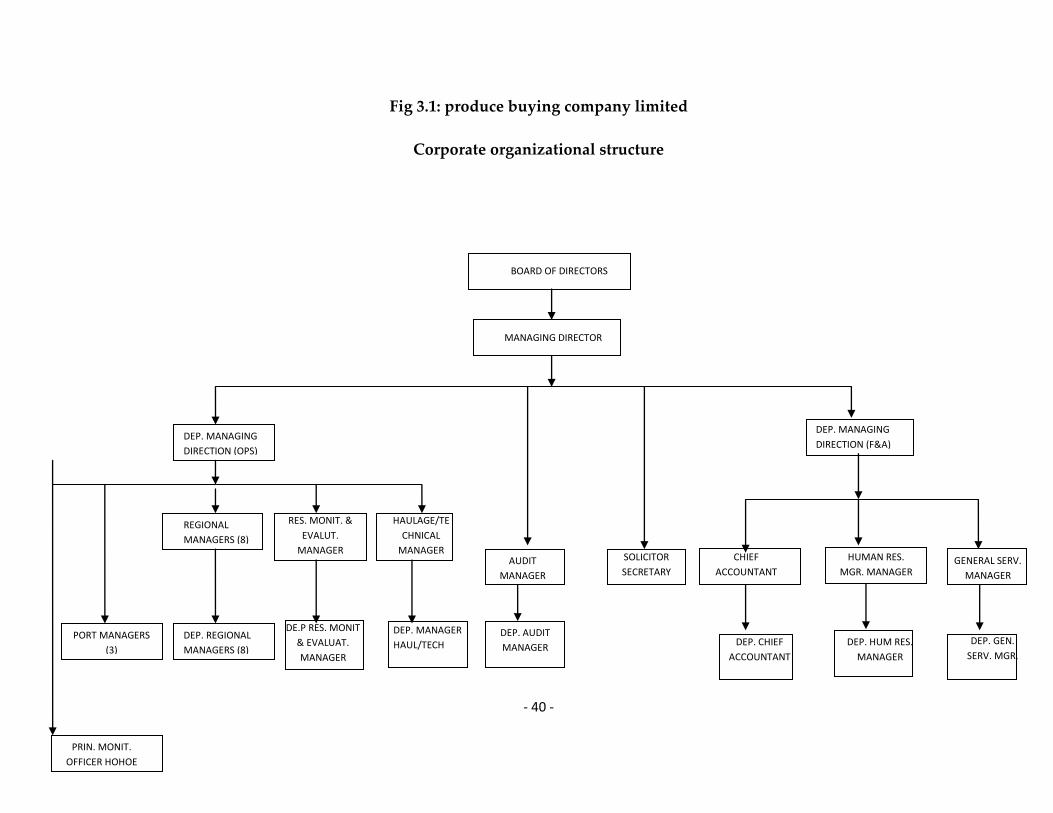

Fig 3.1: produce buying company limited

Corporate organizational structure

BOARD OF DIRECTORS

MANAGING DIRECTOR

DEP. MANAGING

DIRECTION (OPS)

DEP. MANAGING

DIRECTION (F&A)

REGIONAL

MANAGERS (8)

DEP. REGIONAL

MANAGERS (8)

PORT MANAGERS

(3)

RES. MONIT. &

EVALUT.

MANAGER

HAULAGE/TE

CHNICAL

MANAGER AUDIT

MANAGER

DE.P RES. MONIT

& EVALUAT.

MANAGER

DEP. MANAGER

HAUL/TECH DEP. AUDIT

MANAGER

SOLICITOR

SECRETARY

CHIEF

ACCOUNTANT

HUMAN RES.

MGR. MANAGER GENERAL SERV.

MANAGER

PRIN. MONIT.

OFFICER HOHOE

DEP. GEN.

SERV. MGR.

DEP. HUM RES.

MANAGER

DEP. CHIEF

ACCOUNTANT

- 41 -

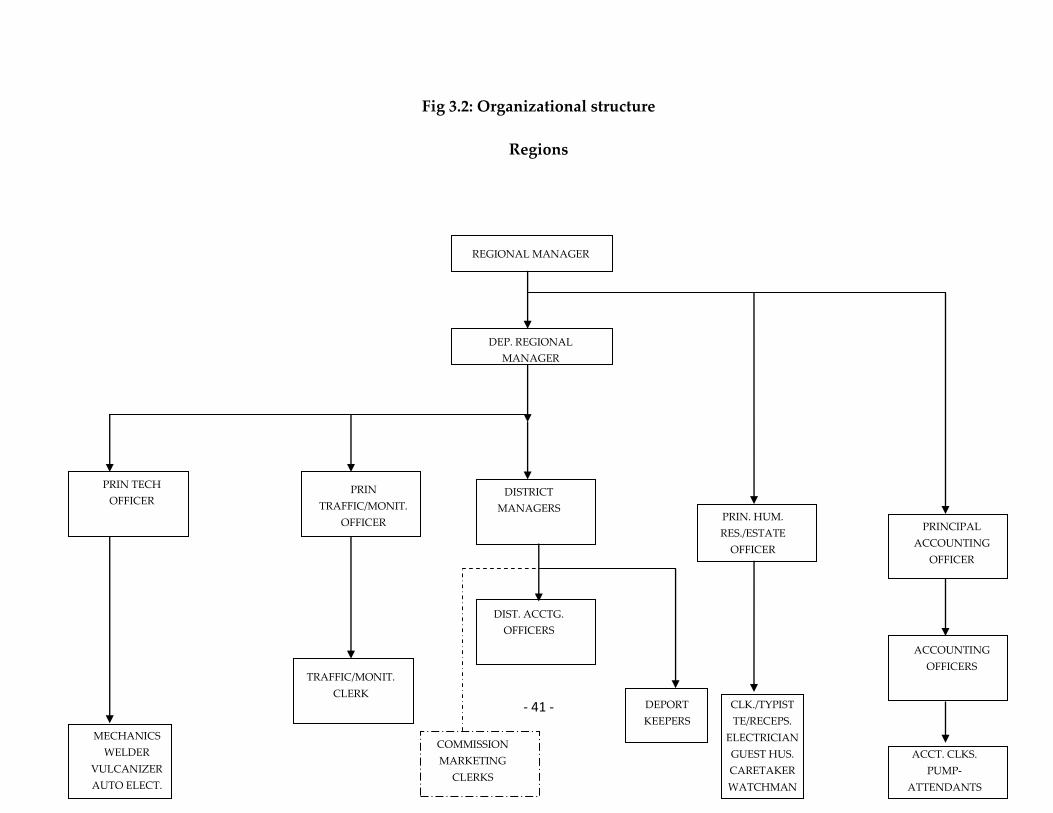

Fig 3.2: Organizational structure

Regions

REGIONAL MANAGER

DEP. REGIONAL

MANAGER

PRIN. HUM.

RES./ESTATE

OFFICER

PRINCIPAL

ACCOUNTING

OFFICER

DISTRICT

MANAGERS

PRIN

TRAFFIC/MONIT.

OFFICER

PRIN TECH

OFFICER

ACCOUNTING

OFFICERS

DIST. ACCTG.

OFFICERS

COMMISSION

MARKETING

CLERKS

ACCT. CLKS.

PUMP-

ATTENDANTS

DEPORT

KEEPERS

CLK./TYPIST

TE/RECEPS.

ELECTRICIAN

GUEST HUS.

CARETAKER

WATCHMAN

TRAFFIC/MONIT.

CLERK

MECHANICS

WELDER

VULCANIZER

AUTO ELECT.

42

3.7.2 Operational Structure

There is a regional structure directly below Head office management which coordinates

the activities of the districts. There are nine regional divisions operating in six political

regions of the country; the Western Region, the largest cocoa producing area has been

divided for administrative purposes into Western North, Western South; which are all

divided into two regions making it four regions in the western region.

The ground operations are handled from the district offices which supervise and

coordinate the activities of the village societies from where the cocoa is actually

purchased.

In addition, the company maintains vehicles and equipment workshops at Tema,

Dzorwulu and Abuakwa near Kumasi to service the operational requirements of the

company’s haulage trucks.

In conclusion, this chapter did talk about the methodology employed by the researcher to

obtain information on the topic; working capital management and profitability at Produce

Buying Company Limited. It also gave the organizational profile of the company PBC

Ltd.

From this chapter comes the next chapter which is on the analysis of the information

gathered with the use of Statistical Package for Social Scientist (SPSS), computer

software.

43

CHAPTER FOUR

DATA ANALYSIS, FINDINGS AND DISCUSSIONS

4.0 Introduction

This chapter assessed the policies employed by Produce Buying Company Limited to

manage its working capital.

The chapter has been divided into three main sections. Section one looks at the financial

operational performance of the company in terms of working capital polices employed

and the resultant trend of the working capital components. The second section is on the

profitability of the company in relation to the efficiency ratios and the final section

examines the survival of the company.

4.1 Management of Working Capital Components

Looking at the nature of Produce Buying Company Limited, its major components of

working capital are inventory, receivables and payables. This section assesses the policies

embarked by the company in managing the components. The management and the trend

of the working capital components are assessed using the efficiency ratios.

4.1.1 Management and Trend of Inventories

The inventories of Produce Buying Company Limited is the management of seed fund

transfer, that is cash and bank less foreign accounts and cocoa advances to societies.

Foreign accounts are excluded because they are not meant for cocoa purchases. This

inventory captures the cycle of the transfer of funds released by COCOBOD through

Head Offices to Societies. The seed fund is likened to raw materials in a manufacturing

enterprise. It takes some days for the funds to go through the transfer process to the

society accounts where it is accessed for cocoa purchases.

44

Funds must be accessed at maximum speed, purchases done quickly and the purchased

beans evacuated to the final destination at a faster rate. The evacuation includes the

preparation of the beans for quality certification by the Quality Control Division and

final evacuation to take over centers for delivery to the Cocoa Marketing Company with

the generation of sales invoice.

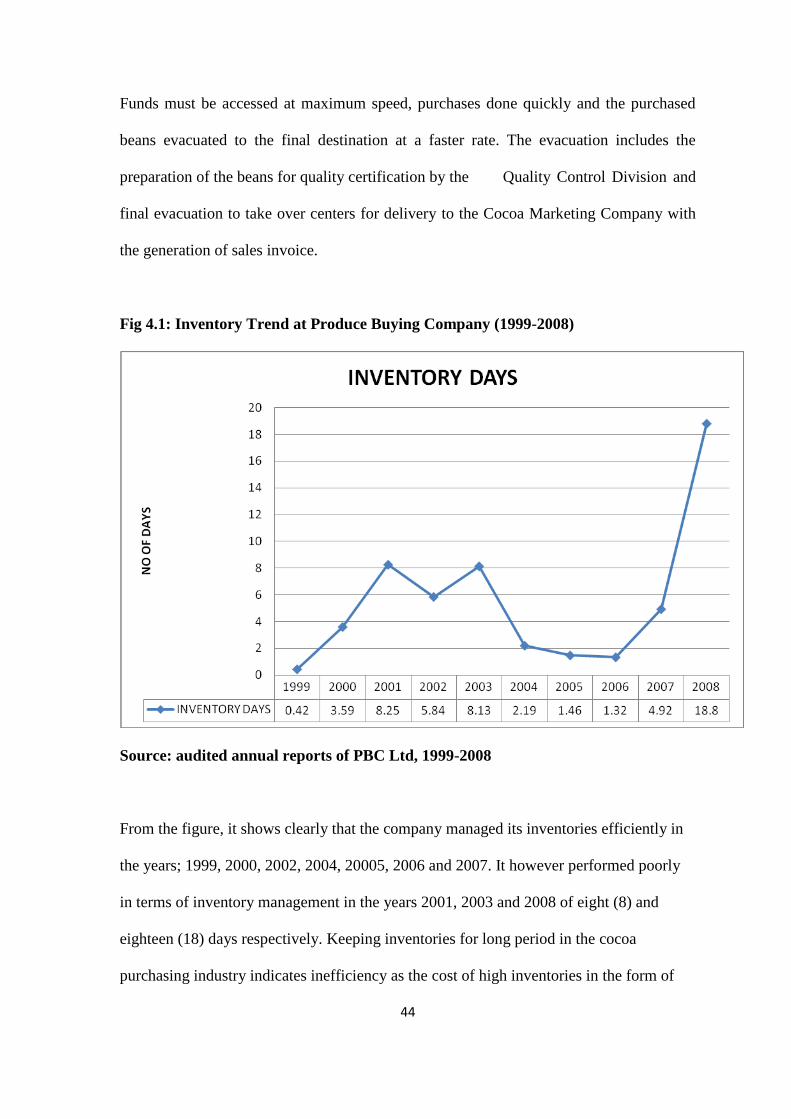

Fig 4.1: Inventory Trend at Produce Buying Company (1999-2008)

Source: audited annual reports of PBC Ltd, 1999-2008

From the figure, it shows clearly that the company managed its inventories efficiently in

the years; 1999, 2000, 2002, 2004, 20005, 2006 and 2007. It however performed poorly

in terms of inventory management in the years 2001, 2003 and 2008 of eight (8) and

eighteen (18) days respectively. Keeping inventories for long period in the cocoa

purchasing industry indicates inefficiency as the cost of high inventories in the form of

45

interest on seed fund and associated cost of carrying stocks reduce profitability. Also,

keeping stocks does not give any advantage to the licensed buying company since the

industry is not characterized by competitive market forces at customer level. The demand

conditions depict monopolistic market since Cocoa Marketing Company is the only buyer

of the commodity.

From 2001, 2003 and 2008 there seems to be lower performance in terms of inventory

management compared to the other years in the ten year period of study. The 2008 season

clearly indicates worst inventory management period by the company during the ten year

period that this study covers. In an interview it was revealed that the there is competition

and the seeds have a fixed value and if kept for long may loose the value and thus reduce

the price. It was revealed that to make evacuation of the cocoa beans as faster as possible

Produce Buying Company Limited has bought a number of its own haulage trucks for the

various centers. All this has accounted for the early evacuation of the beans to the depots.

4.1.2: Trend of Accounts Receivable

Irani (2008) has indicated that every business has some debtors and Produce Buying

Company Limited is no exception. Management of PBC trade debtors is highly monitored

and every effort is made to see to it that deliveries taken over by CMC are promptly paid

for.

46

Fig 4.2: Accounts Receivable days’ trend at Produce Buying Company Limited

(1999-2008)

Source: audited annual reports of PBC Ltd, 1999-2008

Form figure 4.2, the accounts receivables were recollected earlier after the 1999 year of

eight days that is the year 2000, 2001, 2002, 2003. But form the year 2004 to 2008 the

receivable days were increasingly excessively from eleven to nineteen days.

This is partly due to COCOBOD payment policy being the only purchaser of the produce

from PBC and other licensed buying companies. The upward movement in the accounts

receivable days from 2004 to 2008 indicates the company’s inability to collect its

accounts from Cocoa Marketing Company on time. In an interview, it was clear that the

payments to the company by Ghana Cocoa Board is done as the beans arrives at CMC’s

place where a certificate indicating that they have taken over from the licensed buying

companies.

47

4.1.3: Trend of Payables

As every company has debtors, so is every company having creditors who they owe

money. This happens because the amounts they pay are sometimes large and will need

some time to pay off. It is therefore important to track these accounts payable for the

purpose of not only achieving optimum payable period but also maintaining good

relationship with creditors. For account payables, the longer the more encouraging the

performance.

Fig. 4.3: Account Payable days Trend at Produce Buying Company (1999-2008)

Source: audited annual reports of PBC Ltd, 1999-2008

From figure 4.3, the indicators shows that the payables by PBC over the ten year period

was encouraging as the company continuously delayed payment of seed fund to

COCOBOD and thus improved its cash flow for operational activities

48

The company achieved this encouraging performance by maintaining good relationship

with COCOBOD (its major creditors) and other commercial banks by updating them

periodically with its operational activities.

4.2 The Working Capital Components and the Cash Conversion Cycle

This sub-section seeks to evaluate the components of working capital in relation to the

cash conversion cycle, and the policies identified with the cycle.

Fig 4.4: The CCC and the Working Capital Components of Produce Buying

Company (1999-2008)

Source: audited annual reports of PBC Ltd, 1999-2008

49

Figure 4.4 shows the trend of CCC and the working capital component for the years under

review. There was a rise of the CCC from 1999 to 2003 which was not the best for the

company in terms of converting inventories and receivables into cash for the operational

activities. This indicates that the company was not able to deliver its produce to CMC on

time.

However, 2004 to 2006 saw a favourable conversion period but this did not last longer for

the company as there was another rise from 2007 to 2008 which was rapid: almost

nineteen days. 2004 to 2006 yielded a positive cash flow and thus lessened the risk of the

company encountering any liquidity problems as compared to the other eight years of the

study. In the researcher’s interview, it was revealed that the CCC of the company was

really encouraging because it was a policy to convert the stocks to cash within three

weeks as the stocks are obtained.

4.3 Working Capital Management and Profitability

The section examines the relationship between the components of working capital and

profitability of Produce Buying Company Limited from 1999 to 2008.

4.3.1 Profitability

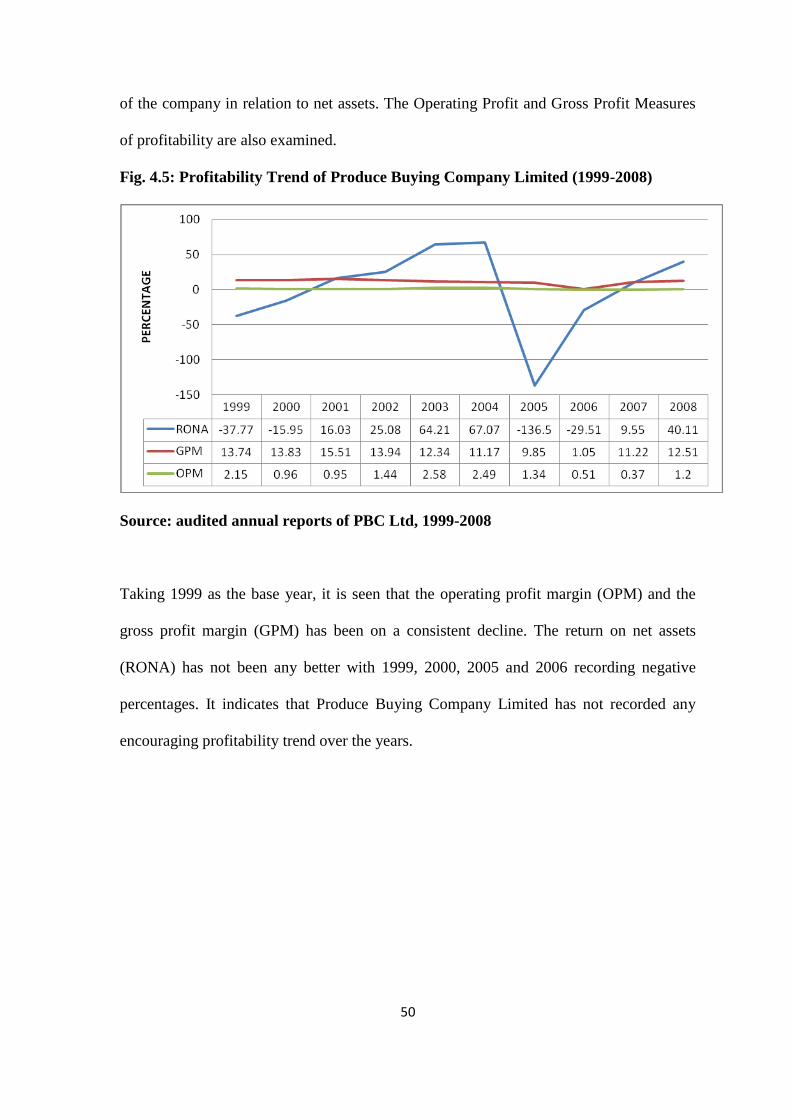

Profitability as used in this study is measured comprehensively by Return on Net Assets

(RONA). This is arrived at by dividing the company’s profit before tax instead of the

widely used profit before interest and tax by its net assets as the finance cost of PBC is

mainly associated with COCOBOD Seed Fund and other short term bank loans, which are

treated by the company as operational cost and therefore captured in arriving at the

operational profit. The RONA is considered more appropriate as it is based on the profit

50

of the company in relation to net assets. The Operating Profit and Gross Profit Measures

of profitability are also examined.

Fig. 4.5: Profitability Trend of Produce Buying Company Limited (1999-2008)

Source: audited annual reports of PBC Ltd, 1999-2008

Taking 1999 as the base year, it is seen that the operating profit margin (OPM) and the

gross profit margin (GPM) has been on a consistent decline. The return on net assets

(RONA) has not been any better with 1999, 2000, 2005 and 2006 recording negative

percentages. It indicates that Produce Buying Company Limited has not recorded any

encouraging profitability trend over the years.

51

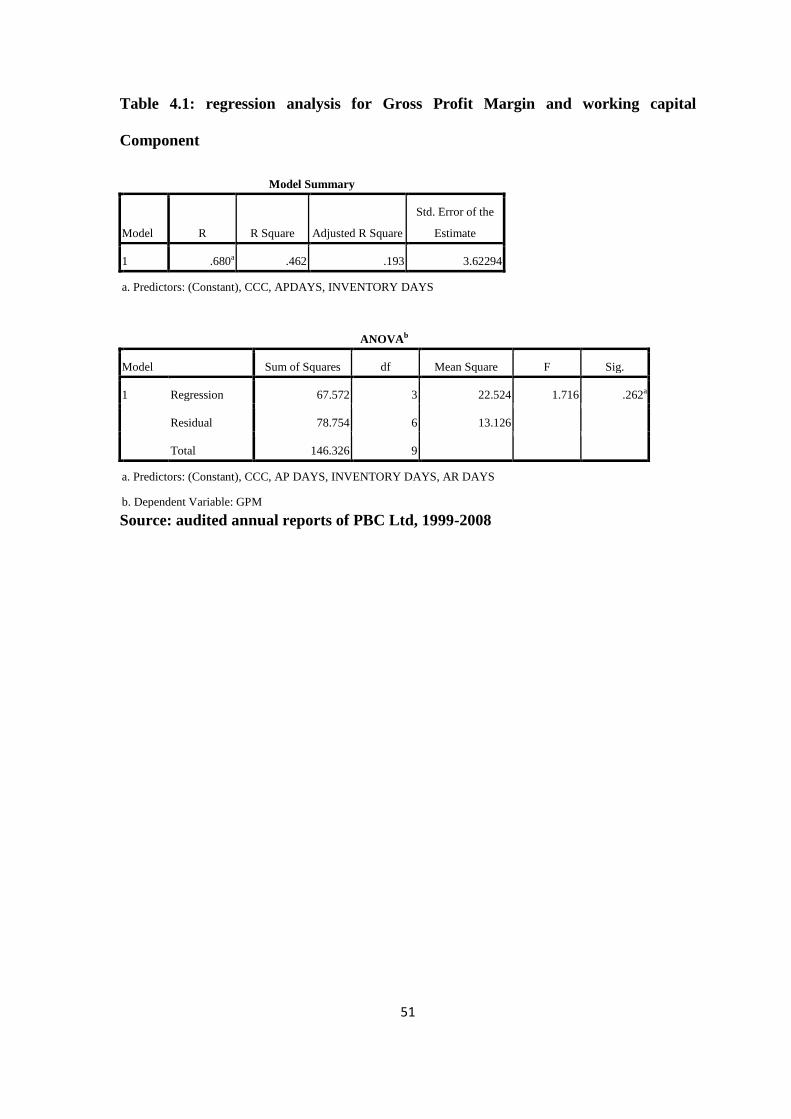

Table 4.1: regression analysis for Gross Profit Margin and working capital

Component

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .680a .462 .193 3.62294

a. Predictors: (Constant), CCC, APDAYS, INVENTORY DAYS

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 67.572 3 22.524 1.716 .262a

Residual 78.754 6 13.126

Total 146.326 9

a. Predictors: (Constant), CCC, AP DAYS, INVENTORY DAYS, AR DAYS

b. Dependent Variable: GPM

Source: audited annual reports of PBC Ltd, 1999-2008

52

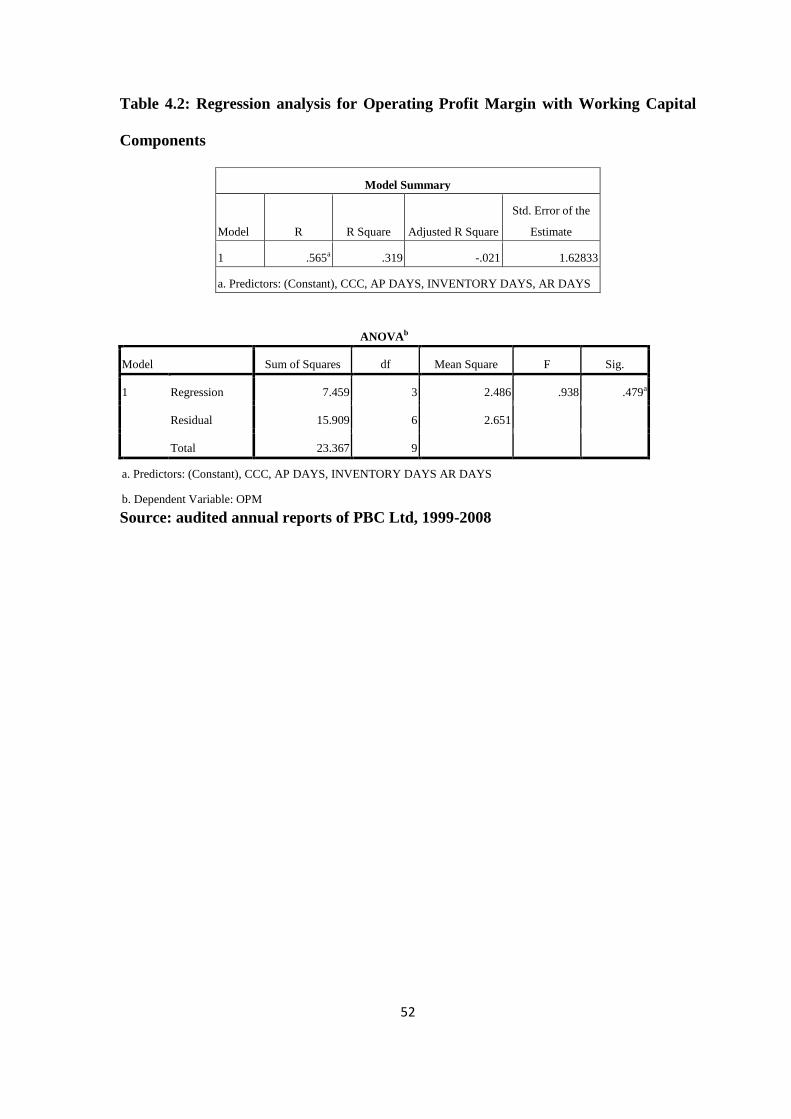

Table 4.2: Regression analysis for Operating Profit Margin with Working Capital

Components

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .565a .319 -.021 1.62833

a. Predictors: (Constant), CCC, AP DAYS, INVENTORY DAYS, AR DAYS

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 7.459 3 2.486 .938 .479a

Residual 15.909 6 2.651

Total 23.367 9

a. Predictors: (Constant), CCC, AP DAYS, INVENTORY DAYS AR DAYS

b. Dependent Variable: OPM

Source: audited annual reports of PBC Ltd, 1999-2008

53

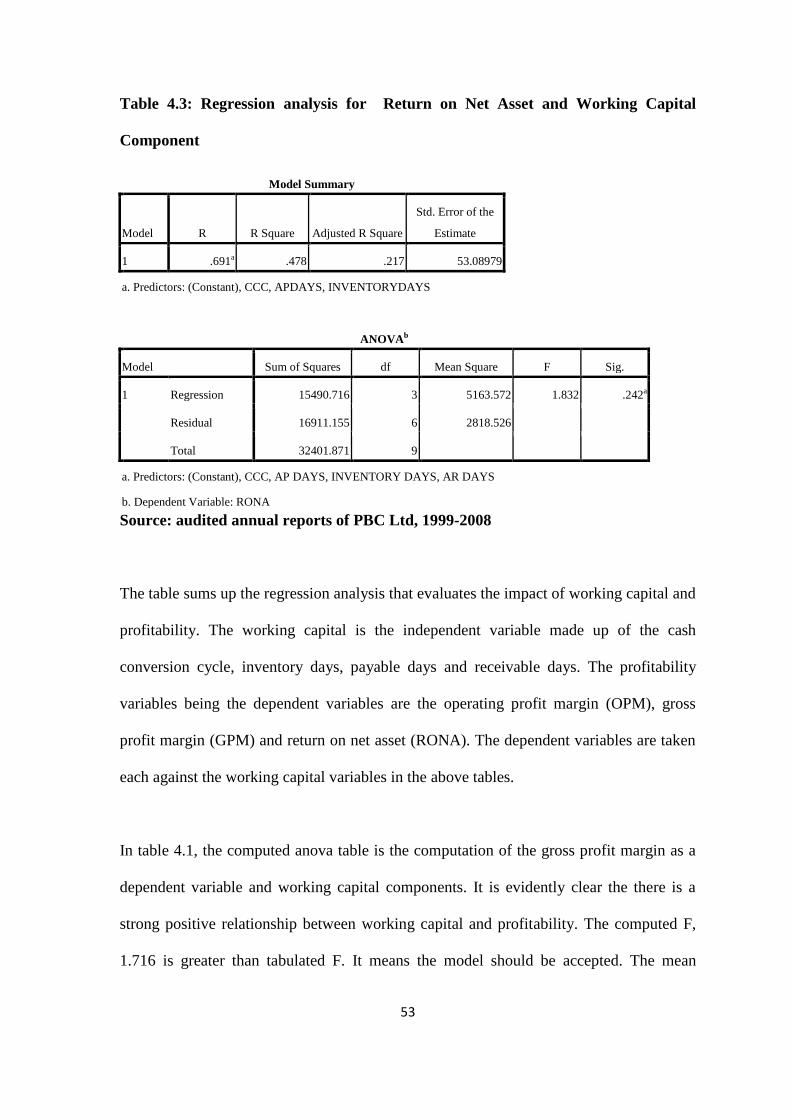

Table 4.3: Regression analysis for Return on Net Asset and Working Capital

Component

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .691a .478 .217 53.08979

a. Predictors: (Constant), CCC, APDAYS, INVENTORYDAYS

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 15490.716 3 5163.572 1.832 .242a

Residual 16911.155 6 2818.526

Total 32401.871 9

a. Predictors: (Constant), CCC, AP DAYS, INVENTORY DAYS, AR DAYS

b. Dependent Variable: RONA

Source: audited annual reports of PBC Ltd, 1999-2008

The table sums up the regression analysis that evaluates the impact of working capital and

profitability. The working capital is the independent variable made up of the cash

conversion cycle, inventory days, payable days and receivable days. The profitability

variables being the dependent variables are the operating profit margin (OPM), gross

profit margin (GPM) and return on net asset (RONA). The dependent variables are taken

each against the working capital variables in the above tables.

In table 4.1, the computed anova table is the computation of the gross profit margin as a

dependent variable and working capital components. It is evidently clear the there is a

strong positive relationship between working capital and profitability. The computed F,

1.716 is greater than tabulated F. It means the model should be accepted. The mean

54

square error which is 13.126 is smaller indicating that the error is minimal, meaning the

model is accepted. The computed F being 1.716 and the mean square error 13.126 is

indicative that the dependent variable and the independent variables above reveal there is

linear relationship between them, that is as working capital improves, profitability of the

company increases and vice versa.

Referring to table 4.2 which is the operation profit margin against the working capital