Embed Size (px)

Citation preview

Equity Market OutlookJune 2021

Source: 1Bloomberg. GARP: Growth at Reasonable PriceDisclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

Second wave of infection, though still underway, has receded as rapidly as it spread. Improved vaccination and more pragmatic approach by governments resulted in shallower impact to economic activity.

We believe that the Indian economy should witness a recovery in 2021, albeit of a slightly lower intensity than before the onset of the second wave and accelerate there after. India is well-positioned to commence on a new economic upcycle over the next few years implying broad-based improvement across a variety of industries.

Consumption will take precedence over savings as real interest rates turn negative; manufacturing sector to continue building on its recovery, while services will be more back ended.

Mild inflation expectations, in the initial growth phase of under-utilized capacity, may offer a conducive environment for corporates to improve profits, leading to an earnings upgrade cycle.

Valuations of leading indices, adjusted for lower cost of capital, in-line with long term average – making risk-reward in the markets more evenly balanced. Mid/small cap valuations at a premium to large cap peers; need a strong earnings cycle to drive incremental gains; stock selection key.

Scare to global growth due to delta variant of the COVID – 19 keeps us vigilant for risks emerging at the margin. Recent collapse in US 10-yr yield curve to below the 1.2%1 handle being an indicator of the same.

We prefer a pro-cyclical outlook as GARP opportunities emerge. We maintain our over-weight positions to financials, consumer discretionary and industrials sectors. We also like technology for its earnings resilience but have moderated our stance, of past 6-9 months, as valuations have re-rated.

An economic recovery along with an earnings upgrade cycle can offer more upside to equities in general, with a better participation from the broader markets, offering a good opportunity to invest for the long term.

2

Equity market outlook

3

Global Macro

13.80%

8.10%7.90%

8.70%

-10%-5%0%5%

10%15%20%25%30%

Jan-

07O

ct-0

7Ju

l-08

Apr-0

9Ja

n-10

Oct

-10

Jul-1

1Ap

r-12

Jan-

13O

ct-1

3Ju

l-14

Apr-1

5Ja

n-16

Oct

-16

Jul-1

7Ap

r-18

Jan-

19O

ct-1

9Ju

l-20

Apr-2

1

% (Y

oY)

US Europe Japan UK

0

5,000

10,000

15,000

20,000

25,000

30,000

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Billio

ns U

SD

Fed BoJ ECB

Since Feb 2020, +$9.2 T in balance sheet assets

Fed: +$3.8T

BoJ: +$1.1T

ECB: +$4.1T

Source: Invesco. Fed: Federal Bank, BoJ: Bank Of Japan, ECB: European Central Bank. GFC: Global Financial Crisis. Data as at 30 June 2021

Large-Scale Asset Purchases Continue to Support RecoveryMajor Central Bank Balance Sheets, Total Assets

Money Supply Growth across Major Developed Economies, % yoyBase Effect Catching Up, Yet Elevated

4

Emergency monetary programs led to broad money growth

Combined monetary stimulus of 3 central banks, to alleviate pandemic pangs, is almost 11% of Global GDP, compared to about 6% during GFC. The coordination amongst the banks was high and implementation was swift. Loose monetary policies still prevail.

Source: Invesco Ltd. For illustrative purposes only.

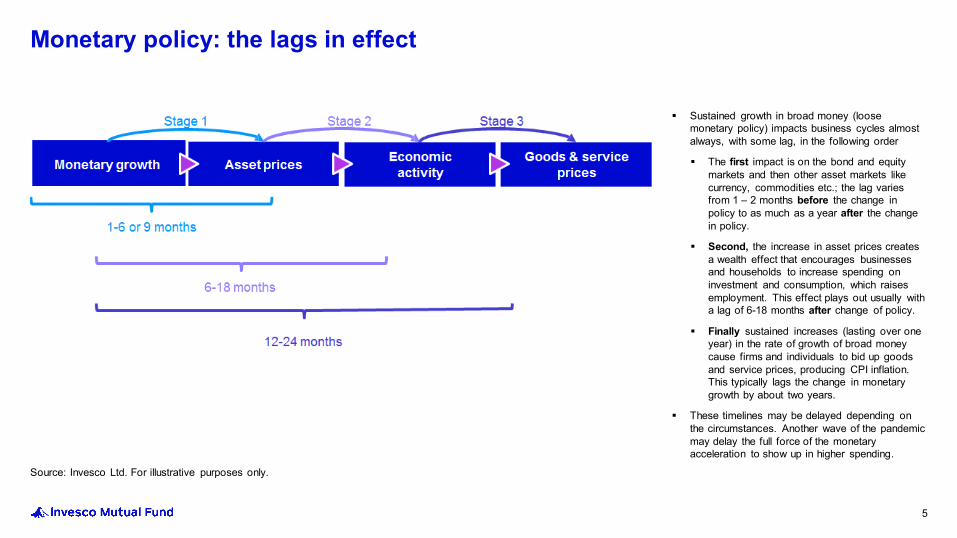

Sustained growth in broad money (loose monetary policy) impacts business cycles almost always, with some lag, in the following order

The first impact is on the bond and equity markets and then other asset markets like currency, commodities etc.; the lag varies from 1 – 2 months before the change in policy to as much as a year after the change in policy.

Second, the increase in asset prices creates a wealth effect that encourages businesses and households to increase spending on investment and consumption, which raises employment. This effect plays out usually with a lag of 6-18 months after change of policy.

Finally sustained increases (lasting over one year) in the rate of growth of broad money cause firms and individuals to bid up goods and service prices, producing CPI inflation. This typically lags the change in monetary growth by about two years.

These timelines may be delayed depending on the circumstances. Another wave of the pandemic may delay the full force of the monetary acceleration to show up in higher spending.

5

Monetary policy: the lags in effect

Source: Invesco Ltd. Data as at 28 June 2021

6

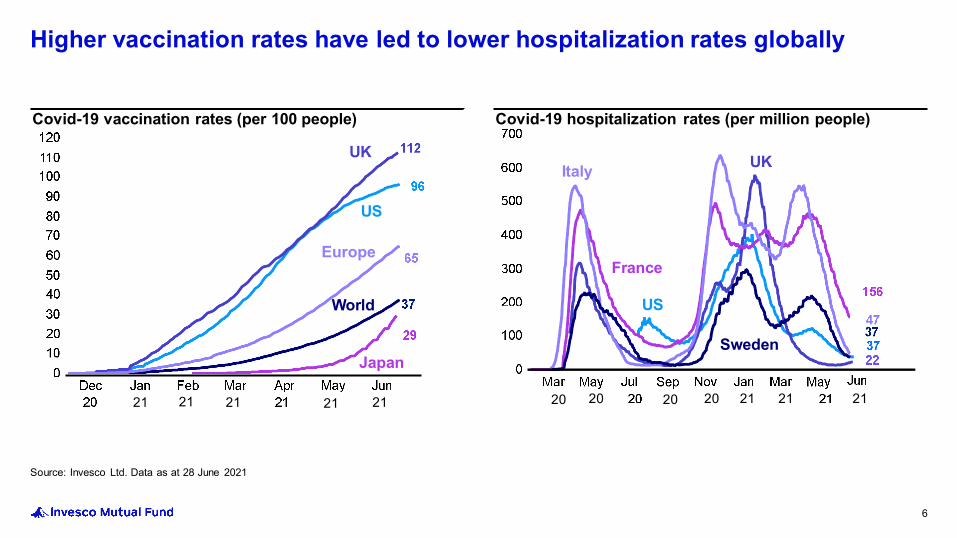

Higher vaccination rates have led to lower hospitalization rates globally

Covid-19 vaccination rates (per 100 people)

UK

US

Europe

World

Japan

Covid-19 hospitalization rates (per million people)

UK

US

Italy

Sweden

France

21 21 21 21 21 21 21 2120202020

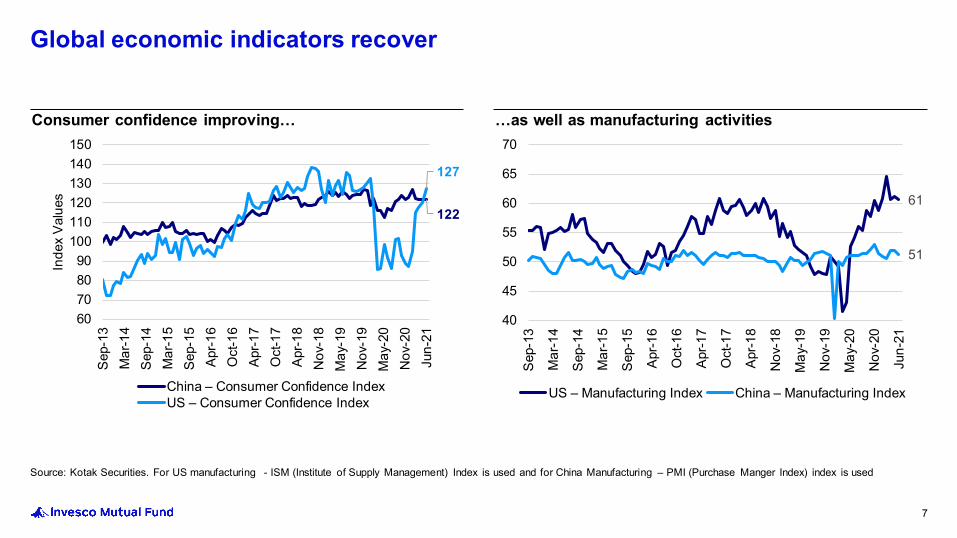

Source: Kotak Securities. For US manufacturing - ISM (Institute of Supply Management) Index is used and for China Manufacturing – PMI (Purchase Manger Index) index is used

122

127

60708090

100110120130140150

Sep-

13M

ar-1

4Se

p-14

Mar

-15

Sep-

15Ap

r-16

Oct

-16

Apr-1

7O

ct-1

7Ap

r-18

Nov

-18

May

-19

Nov

-19

May

-20

Nov

-20

Jun-

21

Inde

x Va

lues

China – Consumer Confidence IndexUS – Consumer Confidence Index

Consumer confidence improving…

61

51

40

45

50

55

60

65

70

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

Apr-1

6

Oct

-16

Apr-1

7

Oct

-17

Apr-1

8

Nov

-18

May

-19

Nov

-19

May

-20

Nov

-20

Jun-

21

US – Manufacturing Index China – Manufacturing Index

…as well as manufacturing activities

7

Global economic indicators recover

8

Indian Macro

Source: Worldometers; Ministry of Health and Family Welfare, GOIDisclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

43 45

- 50

100 150 200 250 300 350 400 450

May

-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec

-20

Jan-

21

Feb-

21

Mar

-21

Apr-2

1

May

-21

Jun-

21

Jul-2

1

New

Cas

es /

Rec

over

ies

(‘000

)

New Cases Recoveries

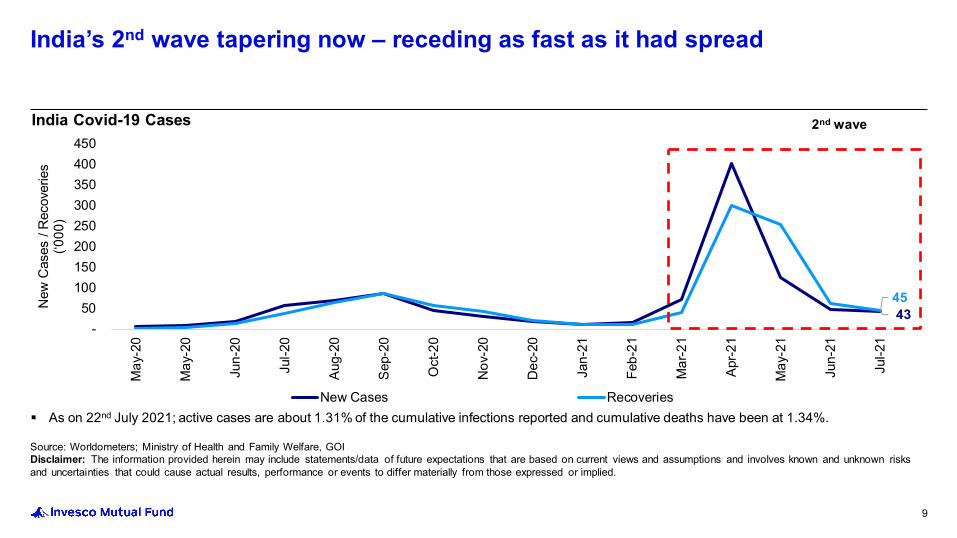

India Covid-19 Cases

9

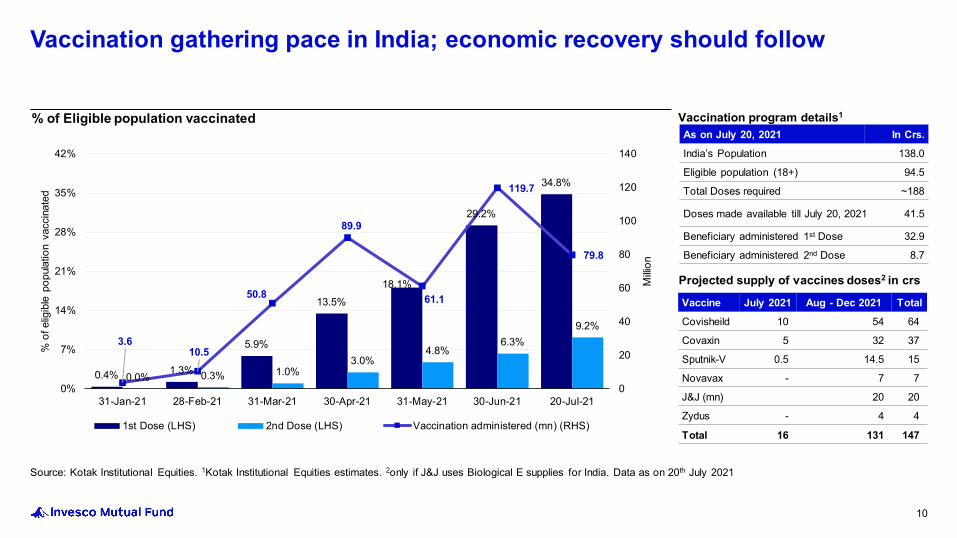

India’s 2nd wave tapering now – receding as fast as it had spread

2nd wave

As on 22nd July 2021; active cases are about 1.31% of the cumulative infections reported and cumulative deaths have been at 1.34%.

0.4% 1.3%

5.9%

13.5%18.1%

29.2%

34.8%

0.0% 0.3% 1.0%3.0%

4.8%6.3%

9.2%3.6

10.5

50.8

89.9

61.1

119.7

79.8

0

20

40

60

80

100

120

140

0%

7%

14%

21%

28%

35%

42%

31-Jan-21 28-Feb-21 31-Mar-21 30-Apr-21 31-May-21 30-Jun-21 20-Jul-21

Milli

on

% o

f elig

ible

pop

ulatio

n va

ccin

ated

1st Dose (LHS) 2nd Dose (LHS) Vaccination administered (mn) (RHS)

Source: Kotak Institutional Equities. 1Kotak Institutional Equities estimates. 2only if J&J uses Biological E supplies for India. Data as on 20th July 2021

% of Eligible population vaccinated

Projected supply of vaccines doses2 in crs

10

Vaccination gathering pace in India; economic recovery should follow

Vaccine July 2021 Aug - Dec 2021 TotalCovisheild 10 54 64

Covaxin 5 32 37

Sputnik-V 0.5 14.5 15

Novavax - 7 7

J&J (mn) 20 20

Zydus - 4 4

Total 16 131 147

As on July 20, 2021 In Crs.India’s Population 138.0

Eligible population (18+) 94.5

Total Doses required ~188

Doses made available till July 20, 2021 41.5

Beneficiary administered 1st Dose 32.9

Beneficiary administered 2nd Dose 8.7

Vaccination program details1

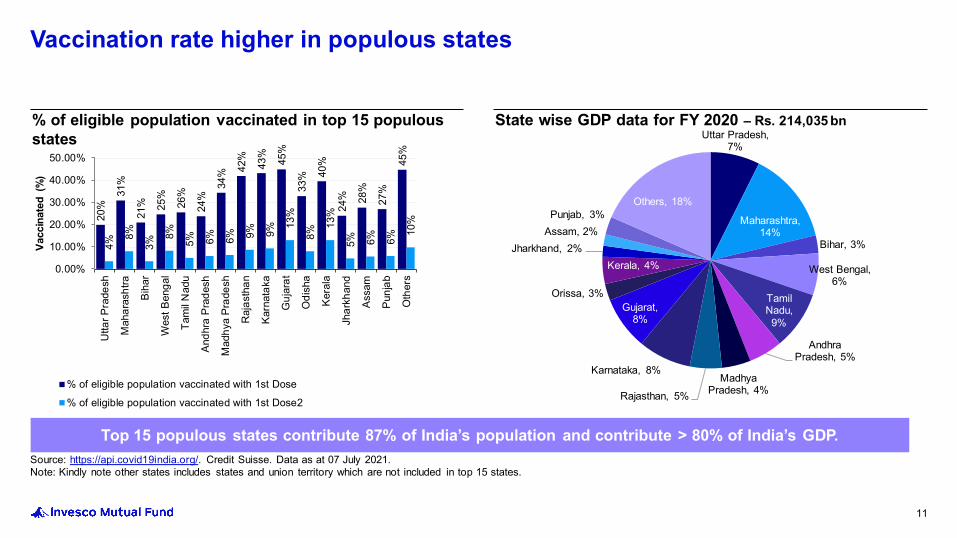

Source: https://api.covid19india.org/. Credit Suisse. Data as at 07 July 2021. Note: Kindly note other states includes states and union territory which are not included in top 15 states.

20%

31%

21% 25

%

26%

24%

34% 42

%

43%

45%

33% 40

%

24% 28

%

27%

45%

4%

8%

3%

8%

5% 6% 6% 9% 9%

13%

8%

13%

5% 6% 6%

10%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

Utta

r Pra

desh

Mah

aras

htra

Biha

r

Wes

t Ben

gal

Tam

il N

adu

Andh

ra P

rade

sh

Mad

hya

Prad

esh

Raj

asth

an

Karn

atak

a

Guj

arat

Odi

sha

Kera

la

Jhar

khan

d

Assa

m

Punj

ab

Oth

ers

Vacc

inat

ed (

%)

% of eligible population vaccinated with 1st Dose

% of eligible population vaccinated with 1st Dose2

% of eligible population vaccinated in top 15 populous states Uttar Pradesh,

7%

Maharashtra, 14%

Bihar, 3%

West Bengal, 6%

Tamil Nadu, 9%

Andhra Pradesh, 5%

Madhya Pradesh, 4%Rajasthan, 5%

Karnataka, 8%

Gujarat, 8%

Orissa, 3%

Kerala, 4%Jharkhand, 2%

Assam, 2%Punjab, 3%

Others, 18%

State wise GDP data for FY 2020 – Rs. 214,035 bn

11

Vaccination rate higher in populous states

Top 15 populous states contribute 87% of India’s population and contribute > 80% of India’s GDP.

Source: Spark Capital

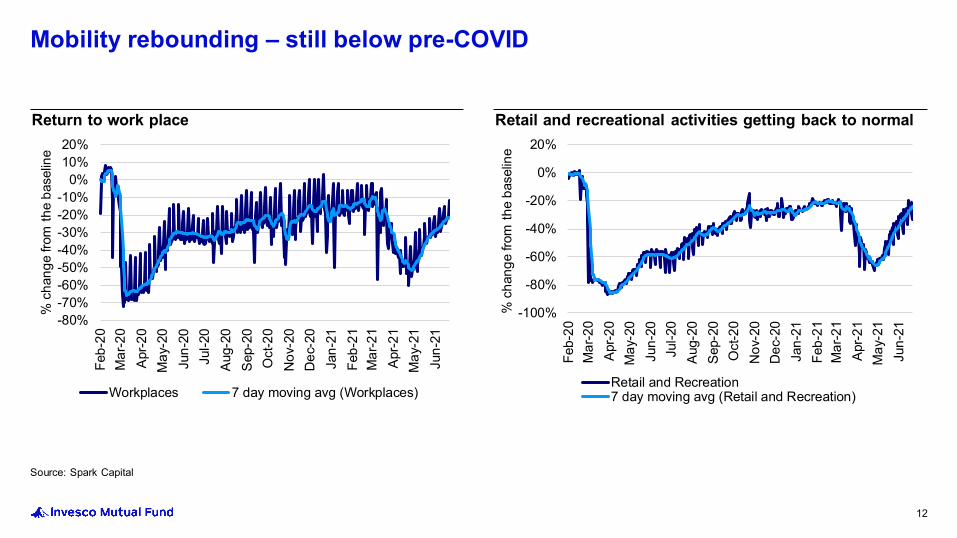

Return to work place Retail and recreational activities getting back to normal

12

Mobility rebounding – still below pre-COVID

-80%-70%-60%-50%-40%-30%-20%-10%

0%10%20%

Feb-

20M

ar-2

0Ap

r-20

May

-20

Jun-

20Ju

l-20

Aug-

20Se

p-20

Oct

-20

Nov

-20

Dec

-20

Jan-

21Fe

b-21

Mar

-21

Apr-2

1M

ay-2

1Ju

n-21

% c

hang

e fro

m th

e ba

selin

e

Workplaces 7 day moving avg (Workplaces)

-100%

-80%

-60%

-40%

-20%

0%

20%

Feb-

20M

ar-2

0Ap

r-20

May

-20

Jun-

20Ju

l-20

Aug-

20Se

p-20

Oct

-20

Nov

-20

Dec

-20

Jan-

21Fe

b-21

Mar

-21

Apr-2

1M

ay-2

1Ju

n-21

% c

hang

e fro

m th

e ba

selin

e

Retail and Recreation7 day moving avg (Retail and Recreation)

Source: Spark capitalNote: The sectors referred above should not be construed as recommendations, advice to buy, sell or in any manner transact in the sector and neither should it be considered as Research Report from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The Scheme may or may not have any present or future positions in these sectors.

302,771

1,442,276

1,432,518

1,191,200

895,130

0

400,000

800,000

1,200,000

1,600,000

Jan-

20Fe

b-20

Mar

-20

Jun-

20Ju

l-20

Aug-

20Se

p-20

Oct

-20

Nov

-20

Dec

-20

Jan-

21Fe

b-21

Mar

-21

Apr-2

1M

ay-2

1Ju

n-21

Uni

ts

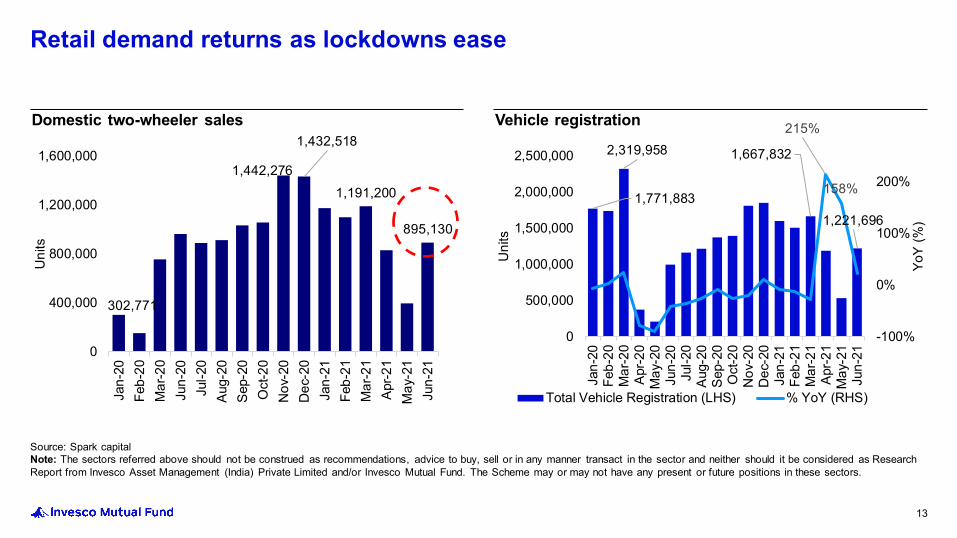

Domestic two-wheeler sales

1,771,883

2,319,958 1,667,832

1,221,696

215%

158%

-100%

0%

100%

200%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Jan-

20Fe

b-20

Mar

-20

Apr-2

0M

ay-2

0Ju

n-20

Jul-2

0Au

g-20

Sep-

20O

ct-2

0N

ov-2

0D

ec-2

0Ja

n-21

Feb-

21M

ar-2

1Ap

r-21

May

-21

Jun-

21

YoY

(%)

Uni

ts

Total Vehicle Registration (LHS) % YoY (RHS)

Vehicle registration

13

Retail demand returns as lockdowns ease

47.3%

-80%

-40%

0%

40%

80%

120%

160%

200%

240%

Apr-1

0D

ec-1

0Au

g-11

Apr-1

2D

ec-1

2Au

g-13

Apr-1

4N

ov-1

4Ju

l-15

Mar

-16

Nov

-16

Jul-1

7M

ar-1

8N

ov-1

8Ju

n-19

Feb-

20O

ct-2

0Ju

n-21

YoY

%

48.1

0

20

40

60

May

-17

Jul-1

7Se

p-17

Nov

-17

Jan-

18M

ar-1

8M

ay-1

8Ju

l-18

Sep-

18N

ov-1

8Ja

n-19

Mar

-19

May

-19

Jul-1

9Se

p-19

Nov

-19

Jan-

20M

ar-2

0M

ay-2

0Ju

l-20

Sep-

20N

ov-2

0Ja

n-21

Mar

-21

May

-21

Valu

e

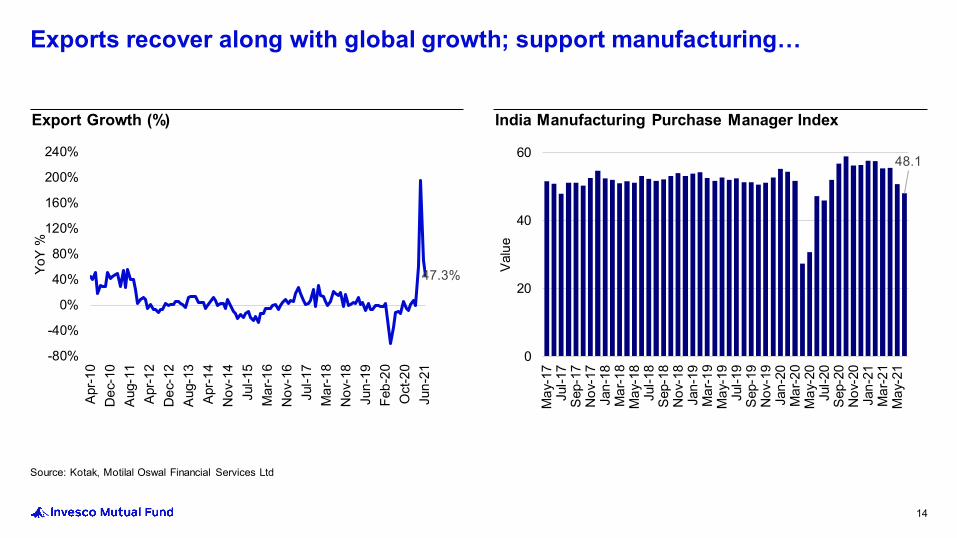

Source: Kotak, Motilal Oswal Financial Services Ltd

Export Growth (%) India Manufacturing Purchase Manager Index

14

Exports recover along with global growth; support manufacturing…

56%

-60%

-30%

0%

30%

60%

90%

120%

Apr-1

0D

ec-1

0Au

g-11

Apr-1

2D

ec-1

2Ju

l-13

Mar

-14

Nov

-14

Jul-1

5M

ar-1

6O

ct-1

6Ju

n-17

Feb-

18O

ct-1

8M

ay-1

9Ja

n-20

Sep-

20M

ay-2

1

YoY

%

3032 30 31 30 30 31 32 33 33 34 24

617

2730

30.534.6

37.8634.73

38.3538 38

43 36 253436

2223 2021 21 222222

23 2324

162

816

19 1922.8

26.3222.99

25.8425 25

2823

1521

23

57.2

71

60

01020304050607080

Apr-1

9

Jun-

19

Aug-

19

Oct

-19

Dec

-19

Feb-

20

Apr-2

0

Jun-

20

Aug-

20

Oct

-20

Dec

-20

Feb-

21

Apr-2

1

Jun-

21

Milli

on

Intra State Inter State Total

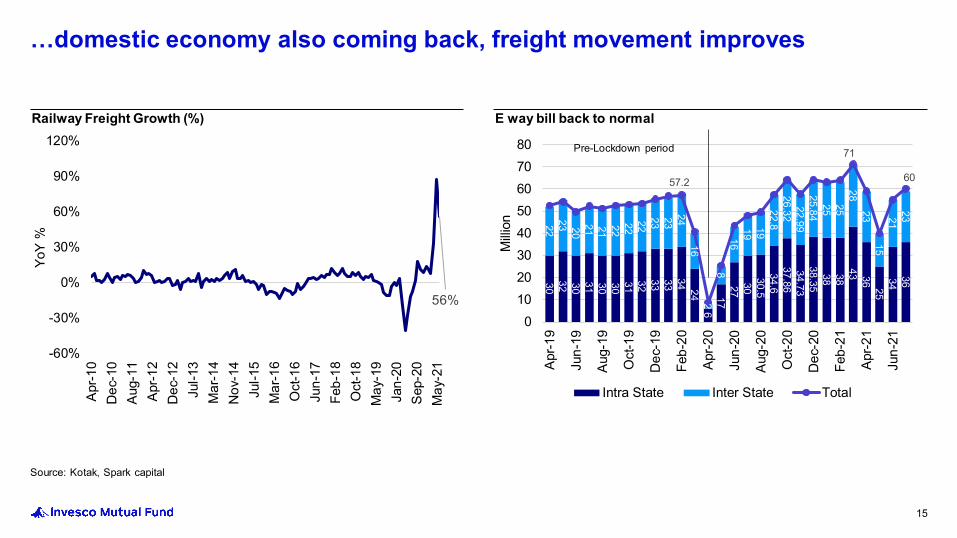

Source: Kotak, Spark capital

Railway Freight Growth (%) E way bill back to normal

15

…domestic economy also coming back, freight movement improves

Pre-Lockdown period

Source: Morgan Stanley, Bloomberg

7.27%

3.00%

5.00%

7.00%

9.00%

11.00%

Aug-

10M

ay-1

1Ja

n-12

Sep-

12M

ay-1

3Ja

n-14

Sep-

14M

ay-1

5Ja

n-16

Sep-

16M

ay-1

7Ja

n-18

Sep-

18M

ay-1

9Ja

n-20

Sep-

20M

ay-2

1

% o

f GD

P

Fiscal Deficit (12 months trailing)

250

350

450

550

650

Sep-

11Fe

b-12

Jul-1

2D

ec-1

2M

ay-1

3O

ct-1

3M

ar-1

4Au

g-14

Dec

-14

May

-15

Oct

-15

Mar

-16

Aug-

16Ja

n-17

Jun-

17O

ct-1

7M

ar-1

8Au

g-18

Jan-

19Ju

n-19

Nov

-19

Apr-2

0Au

g-20

Jan-

21Ju

n-21

USD

Bn

609

Foreign Exchange Reserves (USD bn)

16

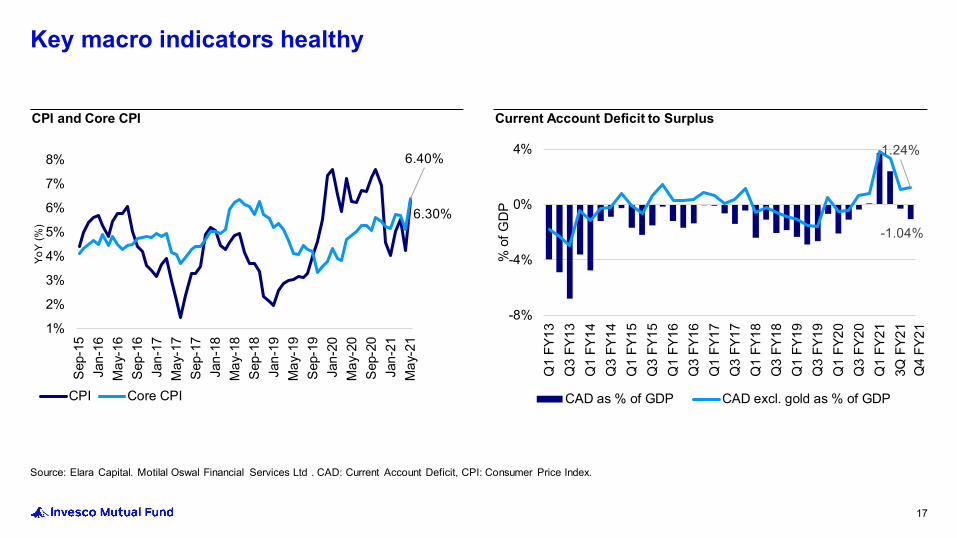

Key macro indicators healthy

Source: Elara Capital. Motilal Oswal Financial Services Ltd . CAD: Current Account Deficit, CPI: Consumer Price Index.

6.40%

1%

2%

3%

4%

5%

6%

7%

8%

Sep-

15Ja

n-16

May

-16

Sep-

16Ja

n-17

May

-17

Sep-

17Ja

n-18

May

-18

Sep-

18Ja

n-19

May

-19

Sep-

19Ja

n-20

May

-20

Sep-

20Ja

n-21

May

-21

YoY

(%)

CPI Core CPI

6.30%

CPI and Core CPI

-1.04%

1.24%

-8%

-4%

0%

4%

Q1

FY13

Q3

FY13

Q1

FY14

Q3

FY14

Q1

FY15

Q3

FY15

Q1

FY16

Q3

FY16

Q1

FY17

Q3

FY17

Q1

FY18

Q3

FY18

Q1

FY19

Q3

FY19

Q1

FY20

Q3

FY20

Q1

FY21

3Q F

Y21

% o

f GD

P

CAD as % of GDP CAD excl. gold as % of GDP

Current Account Deficit to Surplus

17

Key macro indicators healthy

Q4

FY21

14.40%

12.50%

2.41%

1.64% 1.65%

2.49%

1%

2%

2%

3%

3%

7%

10%

13%

16%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

FY22

BE

% o

f GD

P

% o

f GD

P

Revex (LHS) Capex (RHS)

The fiscal stimulus in FY09 was Revex-led while Capex was a

casualty

The fiscal stimulus in FY22 is Capex-led

2.59%

6.57%

9.50%

6.80%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

FY22

BE

Fisc

al d

efic

it (%

of G

DP)

Source: Spark Capital. Revex: Revenue Expenditure. Capex: Capital Expenditure. BE: Budget estimatesDisclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

While fiscal stimulus has increased fiscal deficit, the nature of fiscal stimulus is different this time as…

This time it is CapEx led, unlike 2009 which was RevEx led (aimed at boosting consumption)

18

Fiscal Deficit: driven by necessity – spending better plannedProductive spend than stimulus

• Capital expenditure creates future sources of employment (hence income) compared to revenue expenditure which gets consumed in the present.• Latter has a positive impact to the GDP growth in the near-term; while former creates more sustainable growth levers to long-term GDP growth.

Source: Elara Capital; NFSA: National Food Security Act, 2013; IPDS: Integrated Power Development Scheme; DDUGY: Deen Dayal Upadhyaya Gram Jyoti Yojana; SAUBHAGYA: Pradhan Mantri Sahaj Bijli Har Ghar Yojana. Note: Above table includes those key schemes that had quantifiable monetary impact and which account to ~93% of total amount announced.

Fiscal Deficit: measured spendsEconomic relief package necessary to alleviate 2nd wave pandemic stress

19

Scheme Amount (INR bn) Remarks

Loan Guarantee Scheme for COVID Affected Sectors 1,100 Includes INR 500bn for the health sector and INR 600bn for other sectors. Interest rate capped at 7.95% for health sector and 8.25% for other sectors

Emergency Credit Line Guarantee Scheme (ECLGS) 1,500 ECLGS given as part of Atmanirbhar Bharat Package has been extended by another INR 1.5tn. Overall cap of admissible guarantee has been raised from INR 3.0tn to INR 4.5tn.

Free foodgrains under Pradhan Mantri Garib Kalyan Yojana (PMGKY) 938.69 Scheme relaunched in May 2021 to ensure food security of poor and vulnerable.

5kg of food grains will be provided free of cost to NFSA beneficiaries over May-November 2021.

New Scheme for Public Health 150 The scheme is focused on short-term emergency preparedness with special emphasis on children and paediatric care & beds.

Boost for Project Exports through NEIA 330 Extra corpus to be provided to National Export Insurance Account (NEIA) to underwrite INR 330bn worth of project exports over five years

Boost to Export Insurance Cover 880 Government has announced additional equity infusion in Export Credit Guarantee Corp over five years to bolster exports insurance cover by INR 880bn.

Reforms Based Result Linked Power Distribution Scheme (Budget Announcement) 976.31

INR 3.03tn for a revamped reforms-based, results-linked power distribution scheme. Of this, the Centre’s share would be INR 976.31bn. Ongoing works of IPDS, DDUGJY and SAUBHAGYA will be merged. States have already been allowed additional borrowing for four years of up to 0.5% of gross state domestic product annually (INR 1.05 for FY22) subject to carrying out specified power sector reforms.

Total 6,286.93

Total economic announcements worth INR 6.3 trillion, the actual impact to government’s balance sheet is only INR 1.4 trillion.

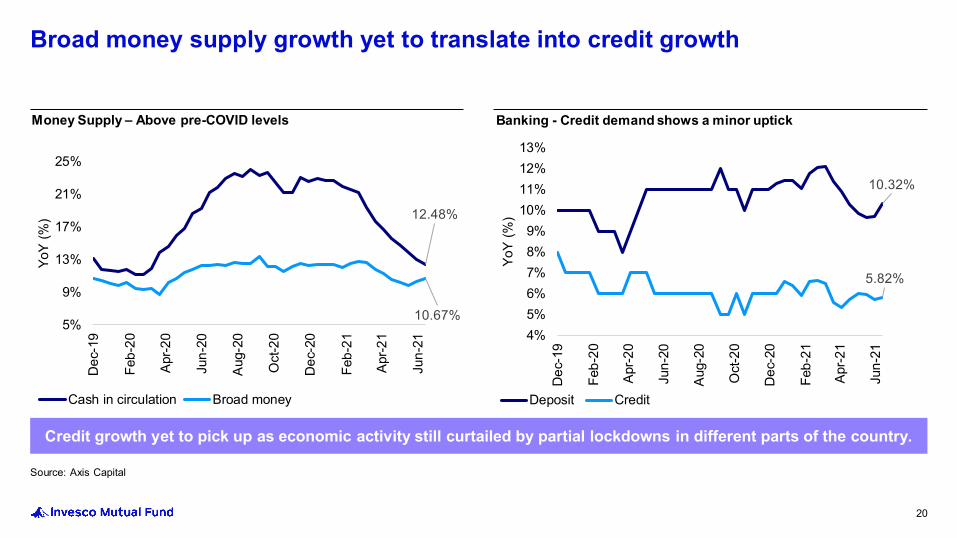

10.32%

5.82%

4%5%6%7%8%9%

10%11%12%13%

Dec

-19

Feb-

20

Apr-2

0

Jun-

20

Aug-

20

Oct

-20

Dec

-20

Feb-

21

Apr-2

1

Jun-

21

YoY

(%)

Deposit Credit

12.48%

10.67%5%

9%

13%

17%

21%

25%

Dec

-19

Feb-

20

Apr-2

0

Jun-

20

Aug-

20

Oct

-20

Dec

-20

Feb-

21

Apr-2

1

Jun-

21

YoY

(%)

Cash in circulation Broad money

Source: Axis Capital

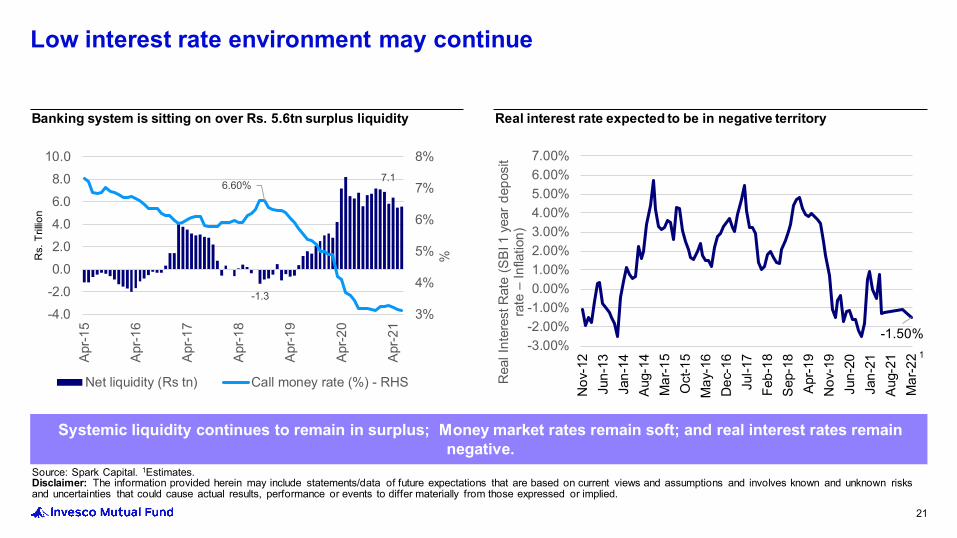

Banking - Credit demand shows a minor uptickMoney Supply – Above pre-COVID levels

20

Broad money supply growth yet to translate into credit growth

Credit growth yet to pick up as economic activity still curtailed by partial lockdowns in different parts of the country.

Source: Spark Capital. 1Estimates.Disclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

-1.3

7.16.60%

3%

4%

5%

6%

7%

8%

-4.0-2.00.02.04.06.08.0

10.0

Apr-1

5

Apr-1

6

Apr-1

7

Apr-1

8

Apr-1

9

Apr-2

0

Apr-2

1

%Rs.

Tril

lion

Net liquidity (Rs tn) Call money rate (%) - RHS

Banking system is sitting on over Rs. 5.6tn surplus liquidity

-1.50%-3.00%-2.00%-1.00%0.00%1.00%2.00%3.00%4.00%5.00%6.00%7.00%

Nov

-12

Jun-

13Ja

n-14

Aug-

14M

ar-1

5O

ct-1

5M

ay-1

6D

ec-1

6Ju

l-17

Feb-

18Se

p-18

Apr-1

9N

ov-1

9Ju

n-20

Jan-

21Au

g-21

Mar

-22

Rea

l Int

eres

t Rat

e (S

BI 1

yea

r dep

osit

rate

–In

flatio

n)

Real interest rate expected to be in negative territory

21

Low interest rate environment may continue

1

Systemic liquidity continues to remain in surplus; Money market rates remain soft; and real interest rates remain negative.

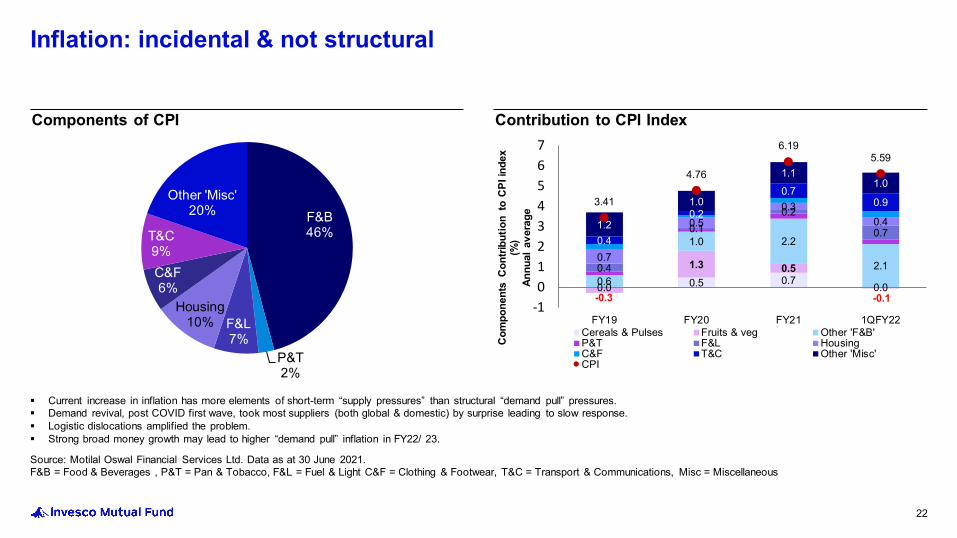

Source: Motilal Oswal Financial Services Ltd. Data as at 30 June 2021. F&B = Food & Beverages , P&T = Pan & Tobacco, F&L = Fuel & Light C&F = Clothing & Footwear, T&C = Transport & Communications, Misc = Miscellaneous

Components of CPI Contribution to CPI Index

22

Inflation: incidental & not structural

F&B46%

P&T2%

F&L7%

Housing10%

C&F6%

T&C9%

Other 'Misc'20%

0.0 0.5 0.7 0.0 -0.3

1.3 0.5

-0.1 0.6

1.0 2.2

2.10.4

0.10.2

0.7

0.7

0.50.3

0.4

0.4

0.2

0.70.9

1.2

1.0

1.11.0

3.41

4.76

6.195.59

-101234567

FY19 FY20 FY21 1QFY22

Com

pone

nts

Con

tribu

tion

to C

PI in

dex

(%)

Annu

al a

vera

ge

Cereals & Pulses Fruits & veg Other 'F&B'P&T F&L HousingC&F T&C Other 'Misc'CPI

Current increase in inflation has more elements of short-term “supply pressures” than structural “demand pull” pressures. Demand revival, post COVID first wave, took most suppliers (both global & domestic) by surprise leading to slow response. Logistic dislocations amplified the problem. Strong broad money growth may lead to higher “demand pull” inflation in FY22/ 23.

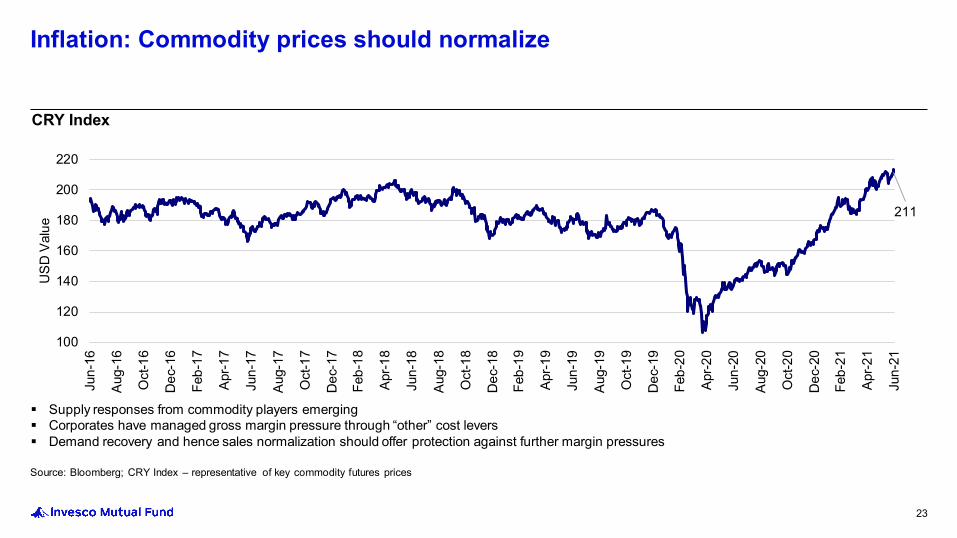

Source: Bloomberg; CRY Index – representative of key commodity futures prices

211

100

120

140

160

180

200

220

Jun-

16

Aug-

16

Oct

-16

Dec

-16

Feb-

17

Apr-1

7

Jun-

17

Aug-

17

Oct

-17

Dec

-17

Feb-

18

Apr-1

8

Jun-

18

Aug-

18

Oct

-18

Dec

-18

Feb-

19

Apr-1

9

Jun-

19

Aug-

19

Oct

-19

Dec

-19

Feb-

20

Apr-2

0

Jun-

20

Aug-

20

Oct

-20

Dec

-20

Feb-

21

Apr-2

1

Jun-

21

USD

Val

ue

CRY Index

23

Inflation: Commodity prices should normalize

Supply responses from commodity players emerging Corporates have managed gross margin pressure through “other” cost levers Demand recovery and hence sales normalization should offer protection against further margin pressures

Past performance may or may not be sustained in future. Source: Spark Capital. Time frame: 20 years since 2001.Disclaimer: The above simulation is for illustrative purpose only and should not be construed as a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Private Limited/Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

4.10%

28.00%

16.00%12.20%

<3% 3<= to <5% 5%<= to <7% >=7%

Nift

y 50

Per

form

ance

(%)

Inflation range (%)

Average performance by Nifty 50

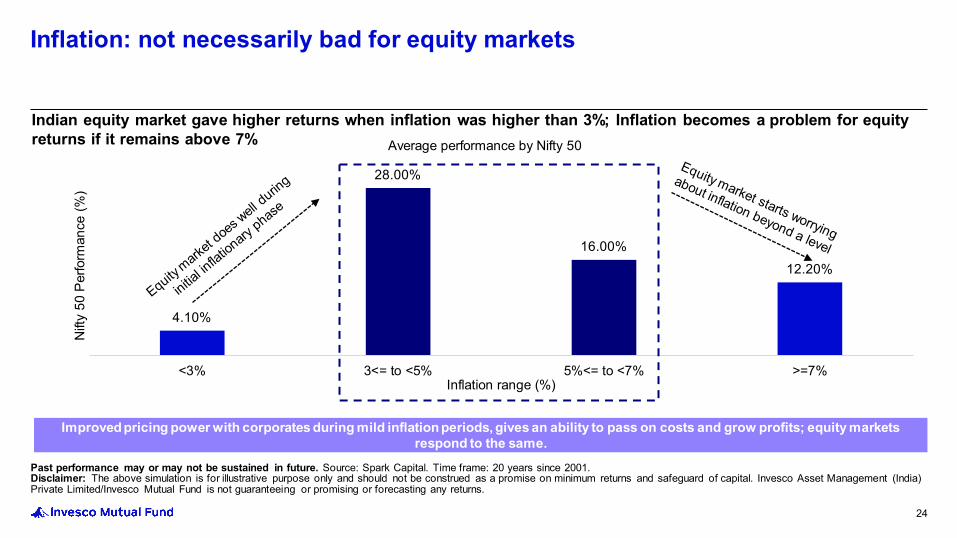

Indian equity market gave higher returns when inflation was higher than 3%; Inflation becomes a problem for equity returns if it remains above 7%

24

Inflation: not necessarily bad for equity markets

Improved pricing power with corporates during mild inflation periods, gives an ability to pass on costs and grow profits; equity markets respond to the same.

25

Outlook

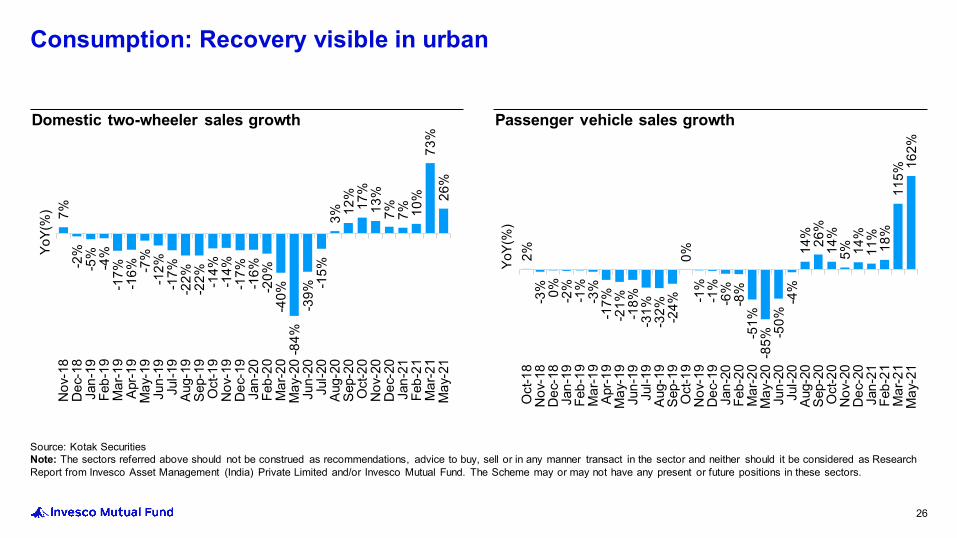

Source: Kotak SecuritiesNote: The sectors referred above should not be construed as recommendations, advice to buy, sell or in any manner transact in the sector and neither should it be considered as Research Report from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The Scheme may or may not have any present or future positions in these sectors.

Domestic two-wheeler sales growth Passenger vehicle sales growth

26

Consumption: Recovery visible in urban7%

-2%

-5%

-4%

-17%

-16% -7

%-1

2%-1

7%-2

2%-2

2% -14%

-14%

-17%

-16%

-20%

-40%

-84%

-39%

-15%

3% 12%

17%

13%

7% 7% 10%

73%

26%

Nov

-18

Dec

-18

Jan-

19Fe

b-19

Mar

-19

Apr-1

9M

ay-1

9Ju

n-19

Jul-1

9Au

g-19

Sep-

19O

ct-1

9N

ov-1

9D

ec-1

9Ja

n-20

Feb-

20M

ar-2

0M

ay-2

0Ju

n-20

Jul-2

0Au

g-20

Sep-

20O

ct-2

0N

ov-2

0D

ec-2

0Ja

n-21

Feb-

21M

ar-2

1M

ay-2

1

YoY(

%)

2%-3

% 0% -2%

-1%

-3%

-17%

-21%

-18%

-31%

-32% -24%

0%-1

%-1

%-6

%-8

%-5

1%-8

5% -50%

-4%

14% 26%

14%

5% 14%

11%

18%

115%

162%

Oct

-18

Nov

-18

Dec

-18

Jan-

19Fe

b-19

Mar

-19

Apr-1

9M

ay-1

9Ju

n-19

Jul-1

9Au

g-19

Sep-

19O

ct-1

9N

ov-1

9D

ec-1

9Ja

n-20

Feb-

20M

ar-2

0M

ay-2

0Ju

n-20

Jul-2

0Au

g-20

Sep-

20O

ct-2

0N

ov-2

0D

ec-2

0Ja

n-21

Feb-

21M

ar-2

1M

ay-2

1

YoY(

%)

Source: Spark CapitalNote: The sectors referred above should not be construed as recommendations, advice to buy, sell or in any manner transact in the sector and neither should it be considered as Research Report from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The Scheme may or may not have any present or future positions in these sectors.

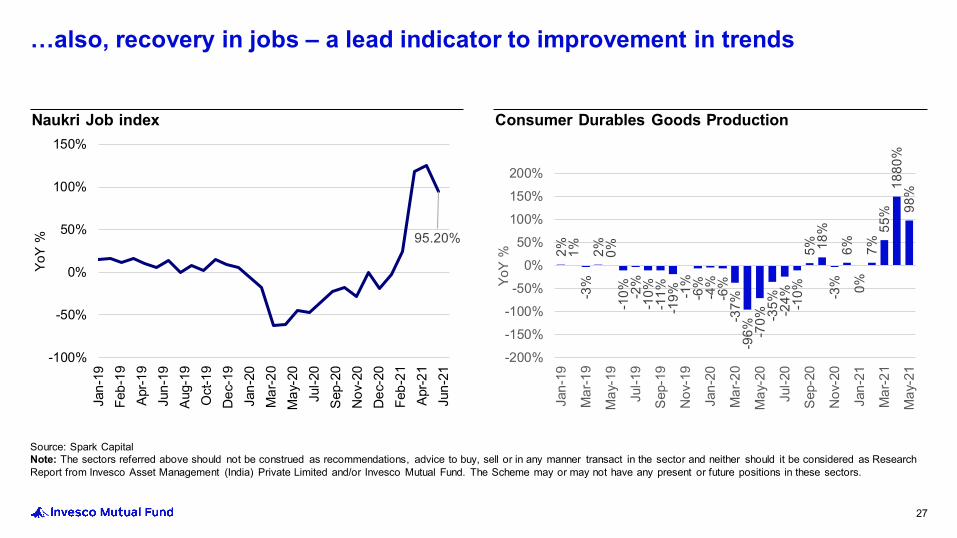

95.20%

-100%

-50%

0%

50%

100%

150%

Jan-

19Fe

b-19

Apr-1

9Ju

n-19

Aug-

19O

ct-1

9D

ec-1

9Ja

n-20

Mar

-20

May

-20

Jul-2

0Se

p-20

Nov

-20

Dec

-20

Feb-

21Ap

r-21

Jun-

21

YoY

%

Naukri Job index

2% 1%-3

%2% 0%

-10% -2

%-1

0%-1

1%-1

9% -1%

-6%

-4%

-6%

-37%

-96% -7

0% -35% -24% -10%

5% 18%

-3%

6%0%

7%55

%18

80%

98%

-200%

-150%

-100%

-50%

0%

50%

100%

150%

200%

Jan-

19

Mar

-19

May

-19

Jul-1

9

Sep-

19

Nov

-19

Jan-

20

Mar

-20

May

-20

Jul-2

0

Sep-

20

Nov

-20

Jan-

21

Mar

-21

May

-21

YoY

%

Consumer Durables Goods Production

27

…also, recovery in jobs – a lead indicator to improvement in trends

2.22

6.56% 0.00

2.00

4.00

0%10%20%30%

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

Rs.

Tril

lion

% Y

oY

Incremental Agri GDP (Rs. tn) - RHS Nominal Agri GDP growth (%, yoy) (LHS)

5.69%

7.00%

0%5%

10%15%

Feb-

15

Jul-1

5

Nov

-15

Apr-1

6

Sep-

16

Feb-

17

Jul-1

7

Dec

-17

May

-18

Oct

-18

Mar

-19

Aug-

19

Jan-

20

Jun-

20

Nov

-20

Mar

-21

%

Rural wage growth: Non agricultural Rural wage growth: Agricultural

-5%

22%

2%

14%

1%10%

11%

-10%0%

10%20%30%

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

E

Farm

inco

me

grow

th

(%,Y

oY)

Source: Spark CapitalDisclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

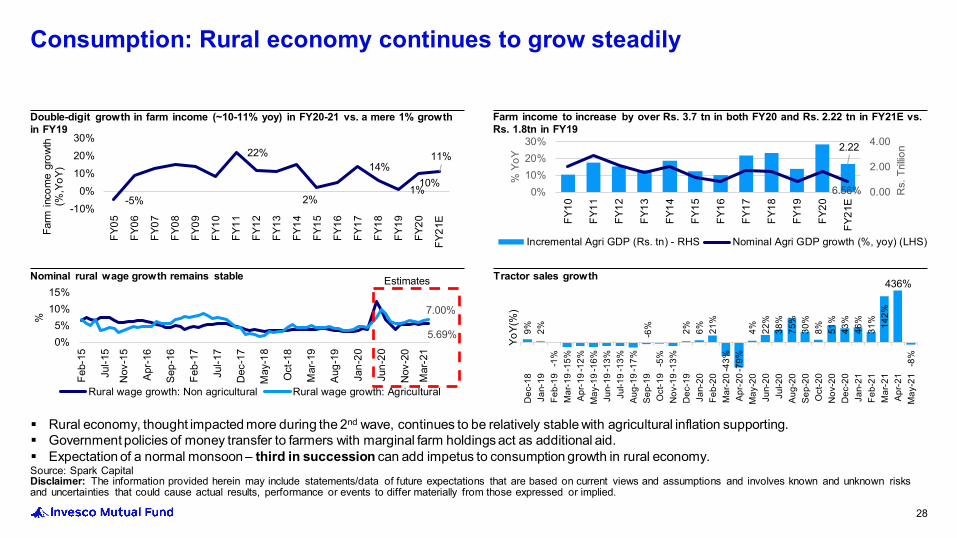

Consumption: Rural economy continues to grow steadily

Double-digit growth in farm income (~10-11% yoy) in FY20-21 vs. a mere 1% growth in FY19

Nominal rural wage growth remains stable Tractor sales growth

28

Rural economy, thought impacted more during the 2nd wave, continues to be relatively stable with agricultural inflation supporting. Government policies of money transfer to farmers with marginal farm holdings act as additional aid. Expectation of a normal monsoon – third in succession can add impetus to consumption growth in rural economy.

Farm income to increase by over Rs. 3.7 tn in both FY20 and Rs. 2.22 tn in FY21E vs. Rs. 1.8tn in FY19

Estimates

9% 2%-1

%-1

5%-1

2%-1

6%-1

3%-1

3%-1

7%-6

%-5

%-1

3%2% 6% 21

%-4

3%-7

9%4% 22

%38

%75

%30

%8% 51

%43

%46

%31

% 142%

-8%

Dec

-18

Jan-

19Fe

b-19

Mar

-19

Apr

-19

May

-19

Jun-

19Ju

l-19

Aug

-19

Sep

-19

Oct

-19

Nov

-19

Dec

-19

Jan-

20Fe

b-20

Mar

-20

Apr

-20

May

-20

Jun-

20Ju

l-20

Aug

-20

Sep

-20

Oct

-20

Nov

-20

Dec

-20

Jan-

21Fe

b-21

Mar

-21

Apr

-21

May

-21

YoY(

%)

436%

Source: Motilal Oswal Financial Services Ltd. DAM Capital Advisors Limited. P: Provisional, BE: Budget Estimates. EPC: Engineering, Procurement and Construction. MHCV: Medium and heavy commercial vehicle.

83 90 89 87 88 88 88 88 86 86 88 87 88 88 84

17 10 11 13 12 12 12 12 14 14 12 13 12 12 16

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

(P)

FY22

BE

%

Revenue spending Capital spending

Capital spending is budgeted to rise as a % of total spending in FY22BE

29

Investments: Government pushBudget’s increased spend in infrastructure sector

Break-up of Capex in key sectors

(INR trn)

FY21BE

FY21RE

FY22BE

YoY growth

(%)Key Beneficiaries

Roads1.6 1.7 1.8 8% Road EPC, Cement, MHCV

Trucks, Construction equipment Railways

1.6 1.6 2.2 34%Rolling stock manufacturers and

its Financiers, Rail EPC companies

Defence1.1 1.3 1.4 0% Local defense equipment

manufacturersWater – Jal Jeevan Mission 0.3 0.2 0.6 253%

EPC contractors, Ductile iron pipes,

PVC pipes Department of Economic affairs – – 0.4 – –

Housing0.8 0.8 0.8 5%

Affordable Real estate developers,

Cement, Steel, EPC companies Other Sectors (Power, Energy and Petroleum)

3.1 2.9 3.1 6% –

24%

18%

17%

12%

8%

7%3%

3%3%2% 1%

1%Energy

Roads

Urban

Railways

Irrigation

Rural Infra

Social infra

Digital Infra

Industrial infra

Agri and food processinginfra

~INR 111 Lakh crores

31%

18%15%

12%

10%

9%1%

1%2%

Power

Roads and Bridges

Urban

Telecommunication

Railways

Irrigation

Ports

Airports

Others

~INR 57 lakh crores

Source: Report of the Task Force Department of Economic Affairs Ministry of Finance Government of India- Volume II.Disclaimer: The data on this slide is just to explain the thrust towards infrastructure sector and should not be construed as recommendations, advice to buy, sell or in any manner transact in these sectors and neither should it be considered as Research Report from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. Schemes of Invesco Mutual Fund may or may not have any present or future positions in these sectors.

FY2013-2019 FY2020-2025

30

Investments: Government pushIncreased spend coupled with facilitating private sector participation

The National Infrastructure Pipeline (NIP) is government’s effort to augment India's infrastructure through an identified investment of INR 111 Lakh crores between FY 2020-25.

Source: Spark Capital. PLI: Product Linked IncentiveNote: The sectors referred above should not be construed as recommendations, advice to buy, sell or in any manner transact in the sector and neither should it be considered as Research Report from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The Scheme may or may not have any present or future positions in these sectors.

Source: Spark Capita 31

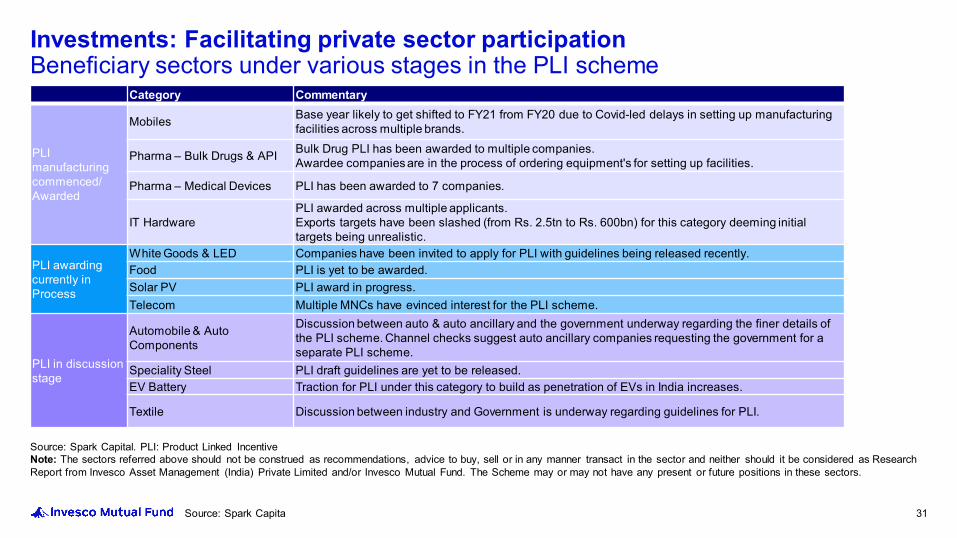

Investments: Facilitating private sector participation Beneficiary sectors under various stages in the PLI scheme

Category Commentary

PLI manufacturingcommenced/Awarded

Mobiles Base year likely to get shifted to FY21 from FY20 due to Covid-led delays in setting up manufacturing facilities across multiple brands.

Pharma – Bulk Drugs & API Bulk Drug PLI has been awarded to multiple companies. Awardee companies are in the process of ordering equipment's for setting up facilities.

Pharma – Medical Devices PLI has been awarded to 7 companies.

IT HardwarePLI awarded across multiple applicants. Exports targets have been slashed (from Rs. 2.5tn to Rs. 600bn) for this category deeming initialtargets being unrealistic.

PLI awardingcurrently inProcess

White Goods & LED Companies have been invited to apply for PLI with guidelines being released recently.Food PLI is yet to be awarded. Solar PV PLI award in progress.Telecom Multiple MNCs have evinced interest for the PLI scheme.

PLI in discussion stage

Automobile & AutoComponents

Discussion between auto & auto ancillary and the government underway regarding the finer details of the PLI scheme. Channel checks suggest auto ancillary companies requesting the government for a separate PLI scheme.

Speciality Steel PLI draft guidelines are yet to be released. EV Battery Traction for PLI under this category to build as penetration of EVs in India increases.

Textile Discussion between industry and Government is underway regarding guidelines for PLI.

Source: Press Information Bureau – Government of India

Some of the key bills which might be tabled in Lok Sabha during the monsoon session to aid future growth/ developments:

1) The Insolvency and Bankruptcy Code (Amendment) Bill, 2021.

2) The Electricity (Amendment) Bill, 2021.

3) The Pension Fund Regulatory and Development Authority (Amendment) Bill, 2021.

4) The Deposit Insurance and Credit Guarantee Corporation (Amendment) Bill, 2021

5) The Limited Liability Partnership (Amendment) Bill, 2021.

6) The Coal Bearing Areas (Acquisition and Development) Amendment Bill, 2021.

7) The Trafficking of Person (Prevention, Protection and Rehabilitation) Bill.

32

Reforms: Continuing with the momentum

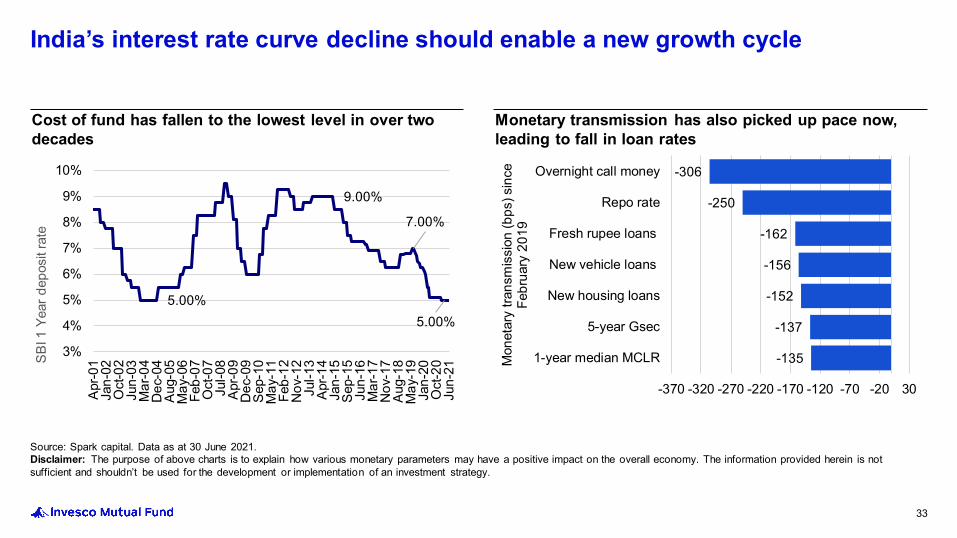

Source: Spark capital. Data as at 30 June 2021.Disclaimer: The purpose of above charts is to explain how various monetary parameters may have a positive impact on the overall economy. The information provided herein is not sufficient and shouldn’t be used for the development or implementation of an investment strategy.

Cost of fund has fallen to the lowest level in over two decades

Monetary transmission has also picked up pace now, leading to fall in loan rates

33

India’s interest rate curve decline should enable a new growth cycle

5.00%

9.00%

7.00%

5.00%

3%

4%

5%

6%

7%

8%

9%

10%

Apr-0

1Ja

n-02

Oct

-02

Jun-

03M

ar-0

4D

ec-0

4Au

g-05

May

-06

Feb-

07O

ct-0

7Ju

l-08

Apr-0

9D

ec-0

9Se

p-10

May

-11

Feb-

12N

ov-1

2Ju

l-13

Apr-1

4Ja

n-15

Sep-

15Ju

n-16

Mar

-17

Nov

-17

Aug-

18M

ay-1

9Ja

n-20

Oct

-20

Jun-

21

SBI 1

Yea

r dep

osit

rate

-135

-137

-152

-156

-162

-250

-306

-370 -320 -270 -220 -170 -120 -70 -20 30

1-year median MCLR

5-year Gsec

New housing loans

New vehicle loans

Fresh rupee loans

Repo rate

Overnight call money

Mon

etar

y tra

nsm

issi

on (b

ps) s

ince

Fe

brua

ry 2

019

6.00%

-2.10%

-10%-5%0%5%

10%15%20%25%30%35%40%

Jul-0

3Ju

l-04

Jul-0

5Ju

l-06

Jun-

07Ju

n-08

Jun-

09Ju

n-10

Jun-

11Ju

n-12

Jun-

13Ju

n-14

Jun-

15M

ay-1

6M

ay-1

7M

ay-1

8M

ay-1

9M

ay-2

0M

ay-2

1

Gro

wth

(%)

Credit Growth (%) Nominal GDP Growth

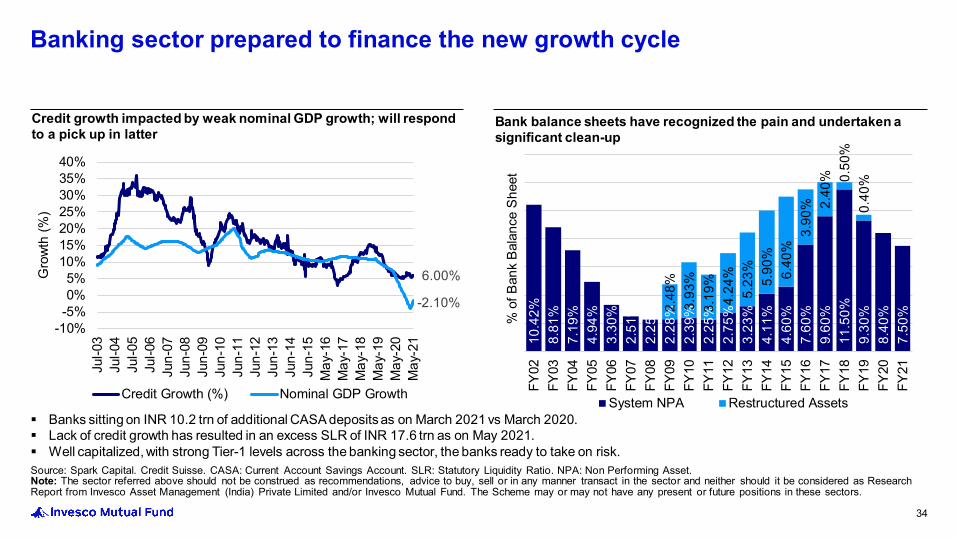

Source: Spark Capital. Credit Suisse. CASA: Current Account Savings Account. SLR: Statutory Liquidity Ratio. NPA: Non Performing Asset.Note: The sector referred above should not be construed as recommendations, advice to buy, sell or in any manner transact in the sector and neither should it be considered as Research Report from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The Scheme may or may not have any present or future positions in these sectors.

Credit growth impacted by weak nominal GDP growth; will respond to a pick up in latter

Bank balance sheets have recognized the pain and undertaken a significant clean-up

34

Banking sector prepared to finance the new growth cycle

10.4

2%8.

81%

7.19

%4.

94%

3.30

%2.

51%

2.25

%2.

28%

2.39

%2.

25%

2.75

%3.

23%

4.11

%4.

60%

7.60

%9.

60%

11.5

0%9.

30%

8.40

%7.

50%2.

48%

3.93

%3.

19%

4.24

%5.

23%

5.90

%6.

40%

3.90

% 2.40

% 0.50

%0.

40%

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

% o

f Ban

k Ba

lanc

e Sh

eet

System NPA Restructured Assets Banks sitting on INR 10.2 trn of additional CASA deposits as on March 2021 vs March 2020. Lack of credit growth has resulted in an excess SLR of INR 17.6 trn as on May 2021. Well capitalized, with strong Tier-1 levels across the banking sector, the banks ready to take on risk.

35

Earnings & Valuations

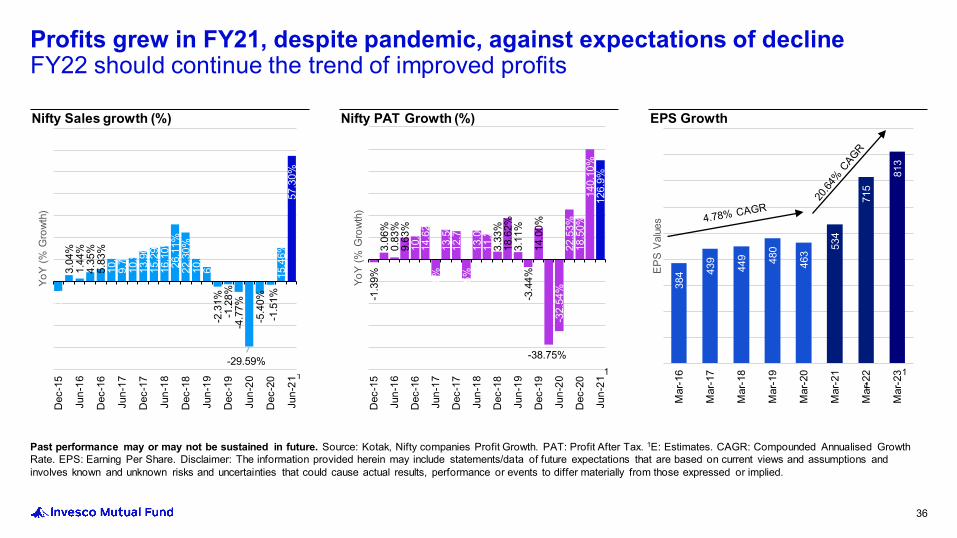

Past performance may or may not be sustained in future. Source: Kotak, Nifty companies Profit Growth. PAT: Profit After Tax. 1E: Estimates. CAGR: Compounded Annualised Growth Rate. EPS: Earning Per Share. Disclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

-4.1

7%3.

04%

1.44

%4.

35%

5.83

%10

.31%

9.72

%10

.90%

13.9

0%15

.29%

16.1

0%26

.11%

22.3

0%10

.43%

6.72

%-2

.31%

-1.2

8%-4

.77%

-29.59%

-5.4

0%-1

.51%

15.4

6%57

.30%

Dec

-15

Jun-

16

Dec

-16

Jun-

17

Dec

-17

Jun-

18

Dec

-18

Jun-

19

Dec

-19

Jun-

20

Dec

-20

Jun-

21

YoY

(% G

rowt

h)

1

Nifty Sales growth (%)

-1.3

9%3.

06%

0.83

%9.

63%

10.4

3%14

.62%

-7.5

5%13

.50%

12.7

0%-8

.85%

13.0

0%11

.23%

3.33

%18

.62%

3.11

%-3

.44%

14.0

0%

-38.75%

-32.

54%

22.5

3%18

.50%

140.

10%

126.

9%

Dec

-15

Jun-

16

Dec

-16

Jun-

17

Dec

-17

Jun-

18

Dec

-18

Jun-

19

Dec

-19

Jun-

20

Dec

-20

Jun-

21

YoY

(% G

rowt

h)1

Nifty PAT Growth (%)

384 43

9

449 48

0

463 53

4

715

813

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21

Mar

-22

Mar

-23

EPS

Value

s

11

EPS Growth

36

Profits grew in FY21, despite pandemic, against expectations of declineFY22 should continue the trend of improved profits

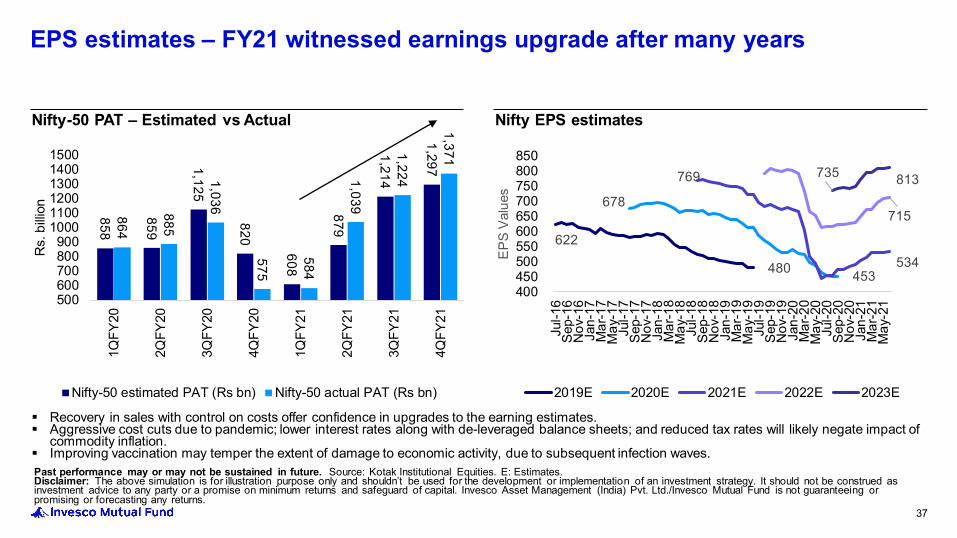

Past performance may or may not be sustained in future. Source: Kotak Institutional Equities. E: Estimates.Disclaimer: The above simulation is for illustration purpose only and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party or a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Pvt. Ltd./Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

Nifty-50 PAT – Estimated vs Actual Nifty EPS estimates

37

EPS estimates – FY21 witnessed earnings upgrade after many years

858

859

1,125

820

608

879

1,214

1,297

864

885

1,036

575

584

1,039

1,224

1,371

500600700800900

100011001200130014001500

1QFY

20

2QFY

20

3QFY

20

4QFY

20

1QFY

21

2QFY

21

3QFY

21

4QFY

21

Rs.

billi

on

Nifty-50 estimated PAT (Rs bn) Nifty-50 actual PAT (Rs bn)

622

480

678

453

769

534

715

735 813

400 450 500 550 600 650 700 750 800 850

Jul-1

6Se

p-16

Nov

-16

Jan-

17M

ar-1

7M

ay-1

7Ju

l-17

Sep-

17N

ov-1

7Ja

n-18

Mar

-18

May

-18

Jul-1

8Se

p-18

Nov

-18

Jan-

19M

ar-1

9M

ay-1

9Ju

l-19

Sep-

19N

ov-1

9Ja

n-20

Mar

-20

May

-20

Jul-2

0Se

p-20

Nov

-20

Jan-

21M

ar-2

1M

ay-2

1

EPS

Valu

es

2019E 2020E 2021E 2022E 2023E

Recovery in sales with control on costs offer confidence in upgrades to the earning estimates. Aggressive cost cuts due to pandemic; lower interest rates along with de-leveraged balance sheets; and reduced tax rates will likely negate impact of

commodity inflation. Improving vaccination may temper the extent of damage to economic activity, due to subsequent infection waves.

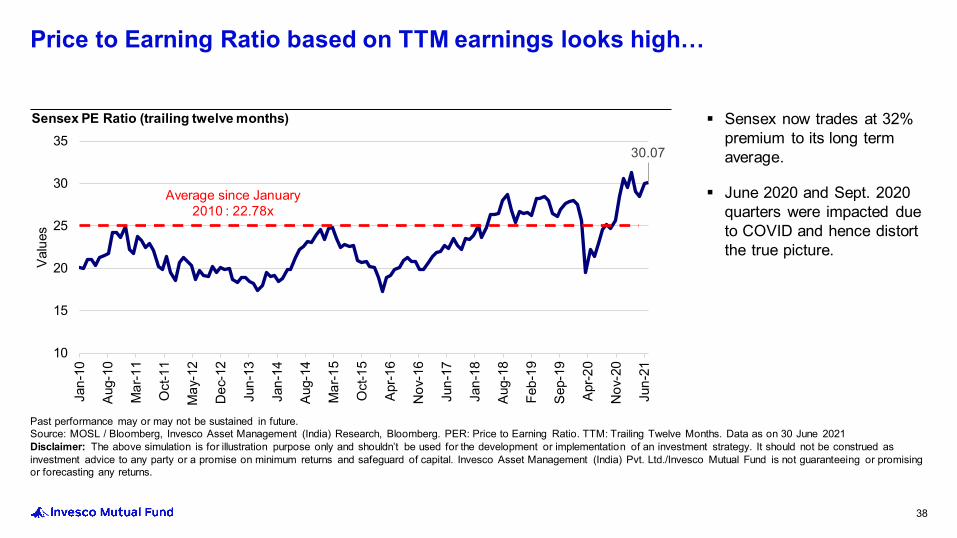

Past performance may or may not be sustained in future.Source: MOSL / Bloomberg, Invesco Asset Management (India) Research, Bloomberg. PER: Price to Earning Ratio. TTM: Trailing Twelve Months. Data as on 30 June 2021Disclaimer: The above simulation is for illustration purpose only and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party or a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Pvt. Ltd./Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

30.07

10

15

20

25

30

35

Jan-

10

Aug-

10

Mar

-11

Oct

-11

May

-12

Dec

-12

Jun-

13

Jan-

14

Aug-

14

Mar

-15

Oct

-15

Apr-1

6

Nov

-16

Jun-

17

Jan-

18

Aug-

18

Feb-

19

Sep-

19

Apr-2

0

Nov

-20

Jun-

21

Valu

es

Average since January 2010 : 22.78x

Sensex PE Ratio (trailing twelve months) Sensex now trades at 32% premium to its long term average.

June 2020 and Sept. 2020 quarters were impacted due to COVID and hence distort the true picture.

38

Price to Earning Ratio based on TTM earnings looks high…

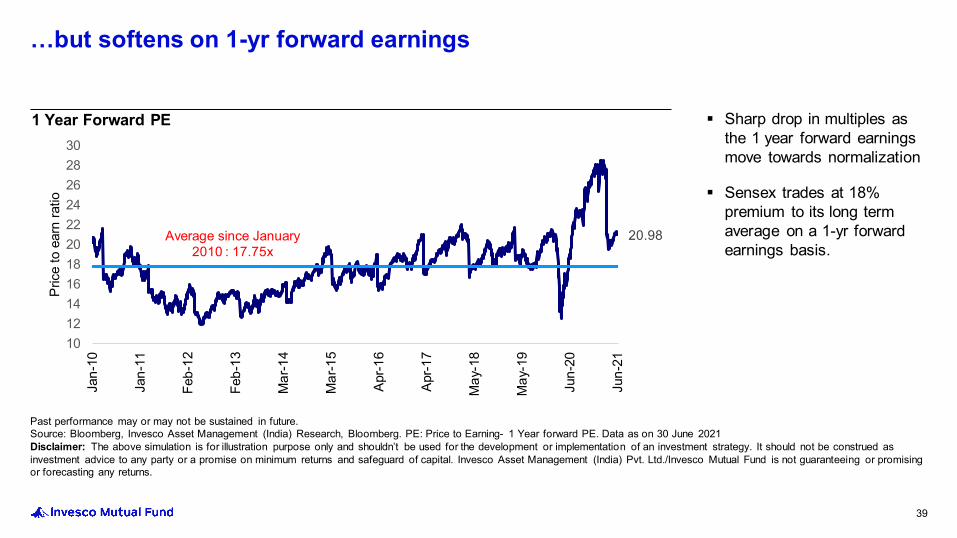

Past performance may or may not be sustained in future.Source: Bloomberg, Invesco Asset Management (India) Research, Bloomberg. PE: Price to Earning- 1 Year forward PE. Data as on 30 June 2021Disclaimer: The above simulation is for illustration purpose only and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party or a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Pvt. Ltd./Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

20.98

1012141618202224262830

Jan-

10

Jan-

11

Feb-

12

Feb-

13

Mar

-14

Mar

-15

Apr-1

6

Apr-1

7

May

-18

May

-19

Jun-

20

Jun-

21

Pric

e to

ear

n ra

tio

Average since January 2010 : 17.75x

1 Year Forward PE

39

…but softens on 1-yr forward earnings

Sharp drop in multiples as the 1 year forward earnings move towards normalization

Sensex trades at 18% premium to its long term average on a 1-yr forward earnings basis.

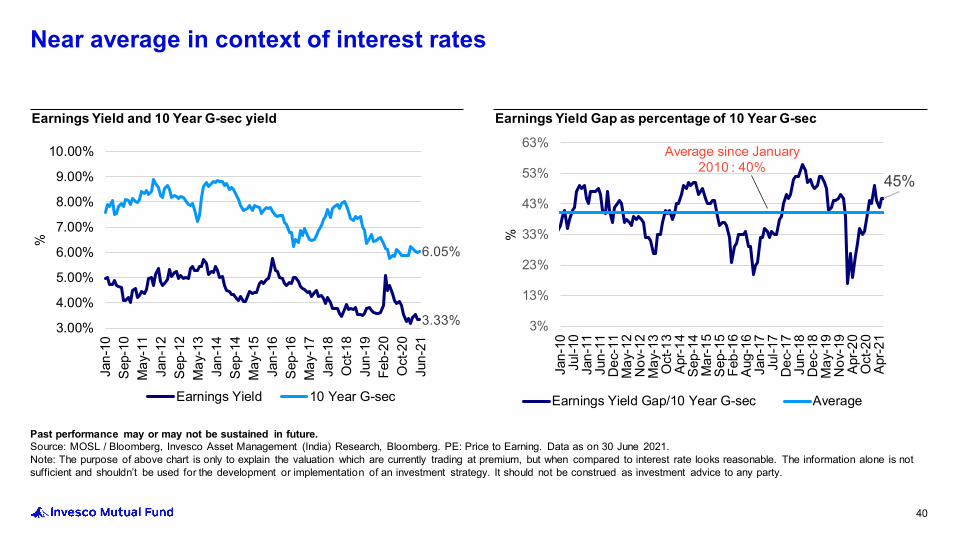

Past performance may or may not be sustained in future.Source: MOSL / Bloomberg, Invesco Asset Management (India) Research, Bloomberg. PE: Price to Earning. Data as on 30 June 2021.Note: The purpose of above chart is only to explain the valuation which are currently trading at premium, but when compared to interest rate looks reasonable. The information alone is not sufficient and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party.

3.33%

6.05%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Jan-

10Se

p-10

May

-11

Jan-

12Se

p-12

May

-13

Jan-

14Se

p-14

May

-15

Jan-

16Se

p-16

May

-17

Jan-

18O

ct-1

8Ju

n-19

Feb-

20O

ct-2

0Ju

n-21

%

Earnings Yield 10 Year G-sec

Earnings Yield and 10 Year G-sec yield

45%

3%

13%

23%

33%

43%

53%

63%

Jan-

10Ju

l-10

Jan-

11Ju

n-11

Dec

-11

May

-12

Nov

-12

May

-13

Oct

-13

Apr-1

4Se

p-14

Mar

-15

Sep-

15Fe

b-16

Aug-

16Ja

n-17

Jul-1

7D

ec-1

7Ju

n-18

Dec

-18

May

-19

Nov

-19

Apr-2

0O

ct-2

0Ap

r-21

%

Earnings Yield Gap/10 Year G-sec Average

Earnings Yield Gap as percentage of 10 Year G-sec

40

Near average in context of interest rates

Average since January 2010 : 40%

3.3

1.7

2.2

2.7

3.2

3.7

4.2

Dec

-15

Aug-

16

Mar

-17

Oct

-17

May

-18

Jan-

19

Aug-

19

Mar

-20

Oct

-20

Jun-

21

PB

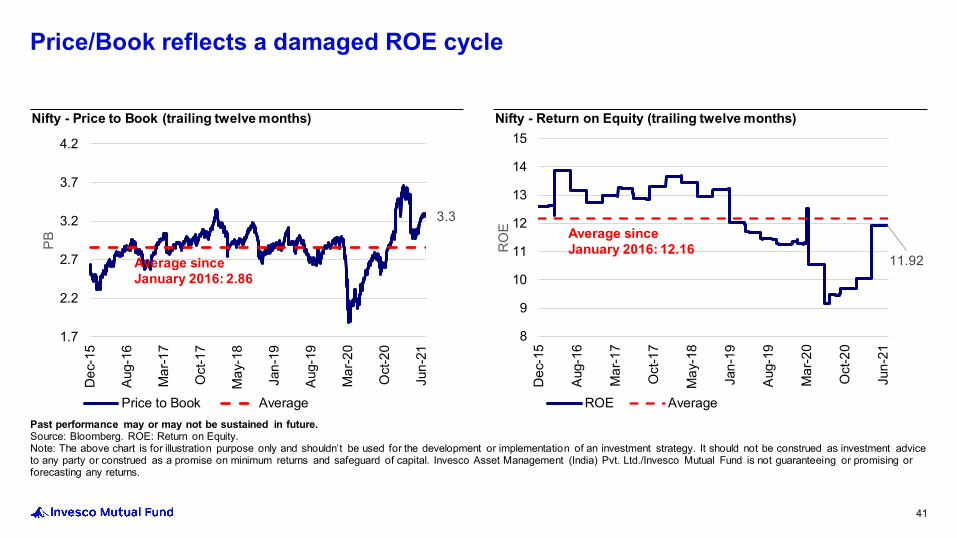

Price to Book Average

Average since January 2016: 2.86

11.92

8

9

10

11

12

13

14

15

Dec

-15

Aug-

16

Mar

-17

Oct

-17

May

-18

Jan-

19

Aug-

19

Mar

-20

Oct

-20

Jun-

21

RO

E

ROE Average

Average since January 2016: 12.16

Past performance may or may not be sustained in future.Source: Bloomberg. ROE: Return on Equity.Note: The above chart is for illustration purpose only and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party or construed as a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Pvt. Ltd./Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

Nifty - Price to Book (trailing twelve months) Nifty - Return on Equity (trailing twelve months)

41

Price/Book reflects a damaged ROE cycle

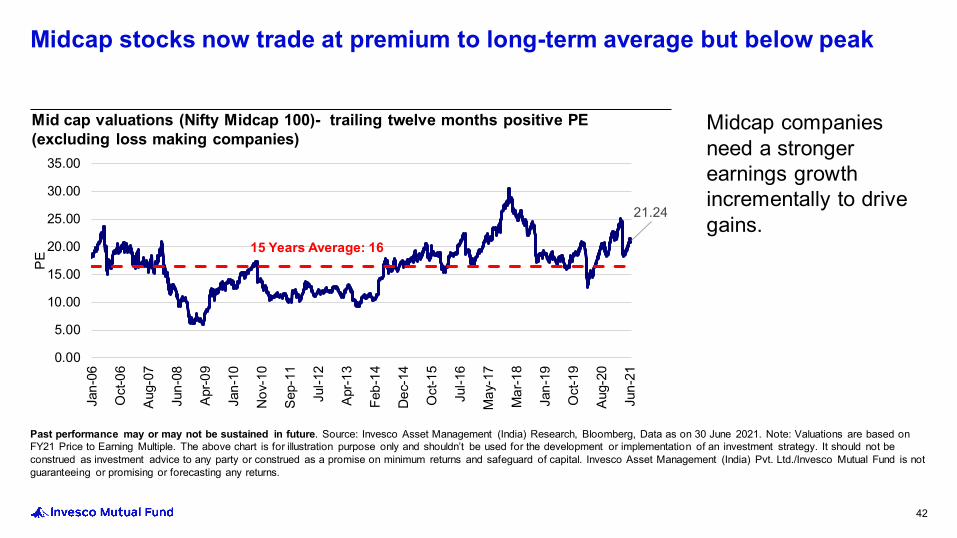

Past performance may or may not be sustained in future. Source: Invesco Asset Management (India) Research, Bloomberg, Data as on 30 June 2021. Note: Valuations are based on FY21 Price to Earning Multiple. The above chart is for illustration purpose only and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party or construed as a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Pvt. Ltd./Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

21.24

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

Jan-

06

Oct

-06

Aug-

07

Jun-

08

Apr-0

9

Jan-

10

Nov

-10

Sep-

11

Jul-1

2

Apr-1

3

Feb-

14

Dec

-14

Oct

-15

Jul-1

6

May

-17

Mar

-18

Jan-

19

Oct

-19

Aug-

20

Jun-

21

PE

15 Years Average: 16

Mid cap valuations (Nifty Midcap 100)- trailing twelve months positive PE (excluding loss making companies)

Midcap companies need a stronger earnings growth incrementally to drive gains.

42

Midcap stocks now trade at premium to long-term average but below peak

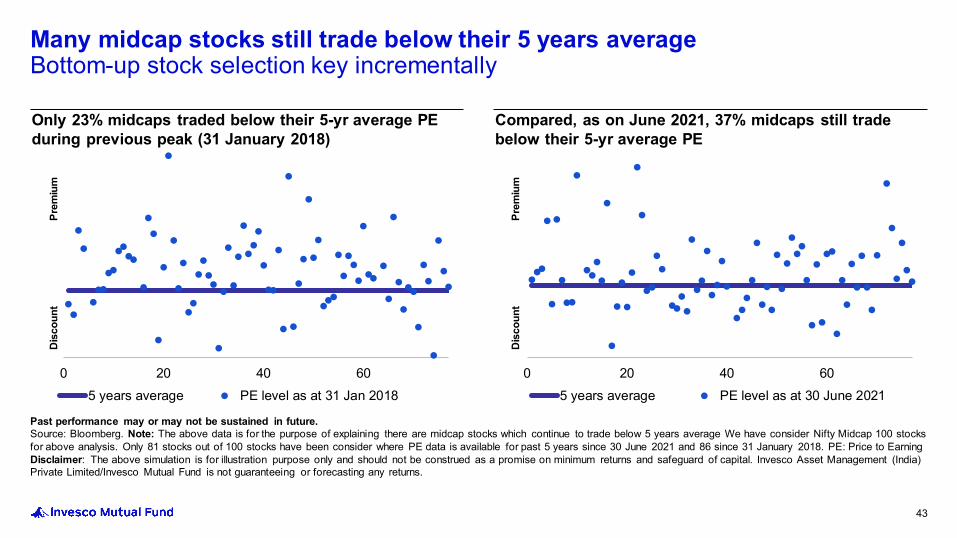

0 20 40 605 years average PE level as at 30 June 2021

0 20 40 605 years average PE level as at 31 Jan 2018

Past performance may or may not be sustained in future.Source: Bloomberg. Note: The above data is for the purpose of explaining there are midcap stocks which continue to trade below 5 years average We have consider Nifty Midcap 100 stocks for above analysis. Only 81 stocks out of 100 stocks have been consider where PE data is available for past 5 years since 30 June 2021 and 86 since 31 January 2018. PE: Price to EarningDisclaimer: The above simulation is for illustration purpose only and should not be construed as a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Private Limited/Invesco Mutual Fund is not guaranteeing or forecasting any returns.

Only 23% midcaps traded below their 5-yr average PE during previous peak (31 January 2018)

Compared, as on June 2021, 37% midcaps still trade below their 5-yr average PE

43

Many midcap stocks still trade below their 5 years averageBottom-up stock selection key incrementally

Prem

ium

Dis

coun

t

Prem

ium

Dis

coun

t

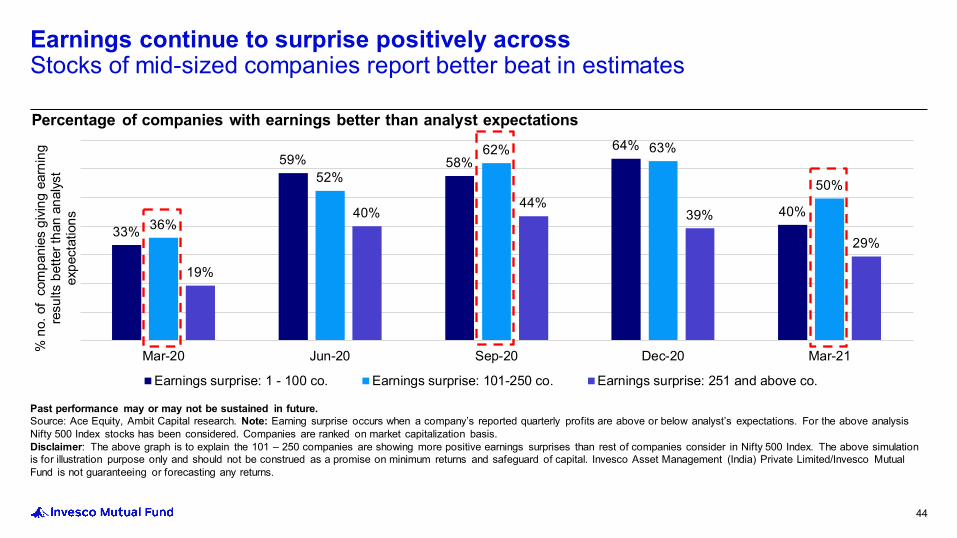

Past performance may or may not be sustained in future.Source: Ace Equity, Ambit Capital research. Note: Earning surprise occurs when a company’s reported quarterly profits are above or below analyst’s expectations. For the above analysis Nifty 500 Index stocks has been considered. Companies are ranked on market capitalization basis.Disclaimer: The above graph is to explain the 101 – 250 companies are showing more positive earnings surprises than rest of companies consider in Nifty 500 Index. The above simulation is for illustration purpose only and should not be construed as a promise on minimum returns and safeguard of capital. Invesco Asset Management (India) Private Limited/Invesco Mutual Fund is not guaranteeing or forecasting any returns.

33%

59% 58%64%

40%36%

52%

62% 63%

50%

19%

40%44%

39%

29%

Mar-20 Jun-20 Sep-20 Dec-20 Mar-21% n

o. o

f co

mpa

nies

givi

ng e

arni

ng

resu

lts b

ette

r tha

n an

alys

t ex

pect

atio

ns

Earnings surprise: 1 - 100 co. Earnings surprise: 101-250 co. Earnings surprise: 251 and above co.

Percentage of companies with earnings better than analyst expectations

44

Earnings continue to surprise positively across Stocks of mid-sized companies report better beat in estimates

Source: 1Bloomberg. GARP: Growth at Reasonable PriceDisclaimer: The information provided herein may include statements/data of future expectations that are based on current views and assumptions and involves known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied.

Second wave of infection, though still underway, has receded as rapidly as it spread. Improved vaccination and more pragmatic approach by governments resulted in shallower impact to economic activity.

We believe that the Indian economy should witness a recovery in 2021, albeit of a slightly lower intensity than before the onset of the second wave and accelerate there after. India is well-positioned to commence on a new economic upcycle over the next few years implying broad-based improvement across a variety of industries.

Consumption will take precedence over savings as real interest rates turn negative; manufacturing sector to continue building on its recovery, while services will be more back ended.

Mild inflation expectations, in the initial growth phase of under-utilized capacity, may offer a conducive environment for corporates to improve profits, leading to an earnings upgrade cycle.

Valuations of leading indices, adjusted for lower cost of capital, in-line with long term average – making risk-reward in the markets more evenly balanced. Mid/small cap valuations at a premium to large cap peers; need a strong earnings cycle to drive incremental gains; stock selection key.

Scare to global growth due to delta variant of the COVID – 19 keeps us vigilant for risks emerging at the margin. Recent collapse in US 10-yr yield curve to below the 1.2%1 handle being an indicator of the same.

We prefer a pro-cyclical outlook as GARP opportunities emerge. We maintain our over-weight positions to financials, consumer discretionary and industrials sectors. We also like technology for its earnings resilience but have moderated our stance, of past 6-9 months, as valuations have re-rated.

An economic recovery along with an earnings upgrade cycle can offer more upside to equities in general, with a better participation from the broader markets, offering a good opportunity to invest for the long term.

45

Equity market outlook

Disclaimer: This presentation is for information purposes only and is not an offer to sell or a solicitation to buy any mutual fund units/securities. The information alone is not sufficient and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party. All opinions, figures, charts/graphs and data included in this presentation are as on date and are subject to change without notice. The sectors referred in this presentation are for illustrative purposes only and should not be construed as recommendations from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. Schemes of Invesco Mutual Fund may or may not have any present or future positions in these sectors. The content of this document is intended solely for the use of the addressee. If you are not the addressee or the person responsible for delivering it to the addressee, any disclosure, copying, distribution or any action taken or omitted to be taken in reliance on it is prohibited and may be unlawful. The data used in this presentation is obtained by Invesco Asset Management (India) Private Limited from the sources which it considers reliable. While utmost care has been exercised while preparing this document, Invesco Asset Management (India) Private Limited does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Neither Invesco Asset Management (India) Private Limited nor any person connected with it accepts any liability arising from the use of this information. The recipient(s) before acting on any information herein should make his/their own investigation and seek appropriate professional advice.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

46

Disclaimer

Get in touch

Corporate Office:Invesco Asset Management (India) Private Limited2101 A, 21st Floor, A- Wing, Marathon Futurex, N.M. Joshi Marg, Lower Parel, Mumbai – 400 013+91 22 67310000 F +91 22 23019422

To invest:Call 1800-209-0007 ∆ sms ‘Invest’ to 56677Invest Online www.invescomutualfund.com