Embed Size (px)

Citation preview

South Korea | March 2022

Korean Hotel Investment Outlook Global interest to fuel recovery

Hotels & Hospitality Group

Korean Hotel Investment Outlook | 3 Korean Hotel Investment Outlook | 2

IntroductionOver the last decade, South Korea has firmly established itself as one of the top global destinations. We anticipate the reopening of borders without quarantine in late March 2022 coupled with the rising interest in Korean popular culture will launch Korean hotel market into a rapid recovery. We expect full recovery to pre-COVID levels by 2024 or 2025.

While COVID-19 has led to a setback in the country’s tourism sector, it has also proved the tourism industry’s resiliency and enabled a “reset” which will poise the sector for a strong recovery. The pent-up demand for visitation is escalating, aided in part by the increasing international penetration of the Korean cultural wave called “Hallyu” which will lead to diversification of source markets.

Further, the favourable supply and demand balance created by the reduction in supply through alternative-use conversion in 2020 and 2021, along with the recovery of international visitation and corporate travel is anticipated to fuel South Korea’s post COVID-19 recovery.

Historical resiliency of the market, pent-up demand, improving vaccination rate against COVID-19 and growing influence of the Korean culture give strong confidence on the recovery and further growth of South Korea’s increasingly dynamic hospitality scene. We anticipate the following five trends will drive the recovery:

Recovery in visitor arrivals will come from more diversified source markets, as demand from Mainland China returns slowly

Provincial markets have benefited from grounded leisure demand, but Seoul will recover more quickly upon return of international visitation

Growing interest from international investors will support an active hotel transaction market

Luxury & Upper-Upscale segment driven by pent-up leisure demand will continue to lead the recovery in the near term

Future supply growth is anticipated to slow down, resulting in a favorable supply and demand environment

1

2

3

4

5Korean Hotel Investment Outlook | 2

Korean Hotel Investment Outlook | 5 Korean Hotel Investment Outlook | 4

South Korea has quickly emerged as one of the most popular destinations not only in Asia but also globally. International visitor arrivals to South Korea reached 17.5 million in 2019, which signifies an increase of approximately three-folds since 2009. The contribution of “Hallyu” cannot be understated: more than 23% of tourists visiting South Korea quoted “K-pop and Hallyu experiences” as their primary purpose of visit in 2019, based on a survey conducted by the Korean Tourism Organization.

Despite the strong momentum in visitation growth,South Korea was no exception to the global downturn caused by the COVID-19 pandemic, which severely impacted hospitality markets worldwide. Although South Korea was one of the first countries to proactively implement contact tracing, testing, and cross-border lockdown, international visitation in 2021 decreased to 967,000, representing 6% of the historical peak in 2019.

Figure 1 South Korea International visitation

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Annu

al g

row

th

Visi

tor a

rriv

als

International Visitor Arrivals Annual Growth

MERS(-7%)

THAAD(-23%)

COVID-19(-86%)

Source: JLL, Korea Tourism Organization

Recovery in visitor arrivals will come from more diversified source markets, as demand from Mainland China returns slowly1

The most striking decrease in visitation was found in arrivals from Mainland China, which has historically been an important source market for South Korea. In 2007, visitors from Mainland China totalled 1.1 million, or 20% of the total visitation. By 2019, the number had grown more than five-folds to 6.0 million, or 34% of the total visitation. With the advent of COVID-19, visitation from Mainland China came to a complete halt. In 2021, annual visitation from Mainland China stood below 200,000, or approximately 3% of visitation in 2019.

We anticipate the visitation from Mainland China will remain well below pre-COVID levels in the near-term. Chinese government is abiding to its “Zero-COVID” policy, and geopolitical tensions are escalating to new heights, casting doubt on the near-term recovery of Chinese visitation. While Chinese travelers should ultimately return to South Korea, visitation from Mainland China is expected to recover slowly, extending to 2024 or even 2025.

Korean Hotel Investment Outlook | 7 Korean Hotel Investment Outlook | 6

Despite the outlook on prolonged recovery of Chinese visitation, South Korea’s tourism industry is anticipated to exhibit strong recovery in the near-to-mid term. The pent-up demand for Korean culture and diaspora of Hallyu is anticipated to draw visitation from more diversified source markets upon return of international travel. Countries in Asia such as Japan, Indonesia, Philippines, Singapore and Malaysia remain the top source markets for Hallyu-related travel, but strong increase in Hallyu following in North America (30% y-o-y in 2020) and Europe (25%) are contributing to the diversity of source markets. We anticipate the diversification of source markets will result in lower occupancy / higher rate environment compared to 2019, as the market relies less on large group travel demand from Mainland China. Further, internationally branded hotels with loyalty programs will be better equipped to capture the more diversified international demand compared to the non-branded Midscale & Economy hotels that rely on Chinese group demand. Nonetheless, full recovery and growth to surpass pre-COVID level performance can be achieved only when the visitation from Mainland China returns.

We anticipate the pent-up demand for business travel to also contribute to the recovery in visitation. Historically, international visitation was primarily driven by leisure demand, while business demand accounted for less than 20% of visitation. Nevertheless, emergence of Hallyu and South Korea’s economic growth to world’s 10th largest economy in terms of nominal gross domestic product will position Korea to benefit from recovery in business travel. South Korea boasts accessible country-wide infrastructure and modern convention spaces totaling more than 386,000 m2, which will allow the tourism sector to benefit from reactivated convention segment during the recovery.

While visitation from Mainland China may be slower to return to pre-COVID levels in the near term, the popularity of Hallyu will drive visitation from more diverse source markets, resulting in lower occupancy but higher ADR environment.

Korean Hotel Investment Outlook | 7

Korean Hotel Investment Outlook | 9 Korean Hotel Investment Outlook | 8

Luxury & Upper-Upscale segment driven by pent-up leisure demand will continue to lead the recovery in the near term 2

Although the economic impact of COVID-19 on the lodging sector is anticipated to linger into 2022 and 2023, trading performance indicators are showing signs of recovery.

The recovery, however, was uneven across segments, as the Luxury & Upper-Upscale segment outpaced the Economy segment in performance recovery.

Figure 2 Monthly RevPAR recovery of the Luxury & Upper-Upscale and the Economy & Midscale segments relative to 2019 levels

86%

66%

0%

20%

40%

60%

80%

100%

120%

140%

Jan-

20

Feb-

20

Mar

-20

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-

21

May

-21

Jun-

21

Jul-2

1

Aug-

21

Sep-

21

Oct

-21

Nov

-21

Dec-

21

Luxury & Upper-Upscale Economy & Midscale

Source: JLL, STR © 2022 CoStar Group

As of December 2021, RevPAR in the Luxury & Upper-Upscale segment recovered to 86% of 2019 level, while the Midscale & Economy segment recovered to 66% of 2019 level. The demand for staycations—or “Hocance”—was a major driver in the recovery of rates and occupancy for the Luxury & Upper-Upscale segments, which is better equipped with amenities (i.e., gyms, pools, spa) and diverse F&B options to capture leisure demand. Economy & Midscale hotels, which relied more on business and group travel, were more severely impacted by COVID-19.

We anticipate the leisure demand to continue spearheading the recovery in the near-term. According to research by STR, leisure travelers exhibit pent-up demand to travel internationally despite the continued impact of COVID-19 in 2022, while propensity for international business trip remains below pre-COVID levels. Although trading performance across all hotel segments remain subdued in the absence of international visitation, high vaccination rate and controlled reopening of borders (i.e., vaccinated travel lanes) show signs of hope for a hastened border reopening.

Trading performance is expected to recover to pre-COVID levels by 2024 or 2025. Leisure demand will continue to lead the recovery in the Luxury & Upper-Upscale segments, followed by the return of MICE and business travelers in the near future.

Korean Hotel Investment Outlook | 9

Korean Hotel Investment Outlook | 11 Korean Hotel Investment Outlook | 10

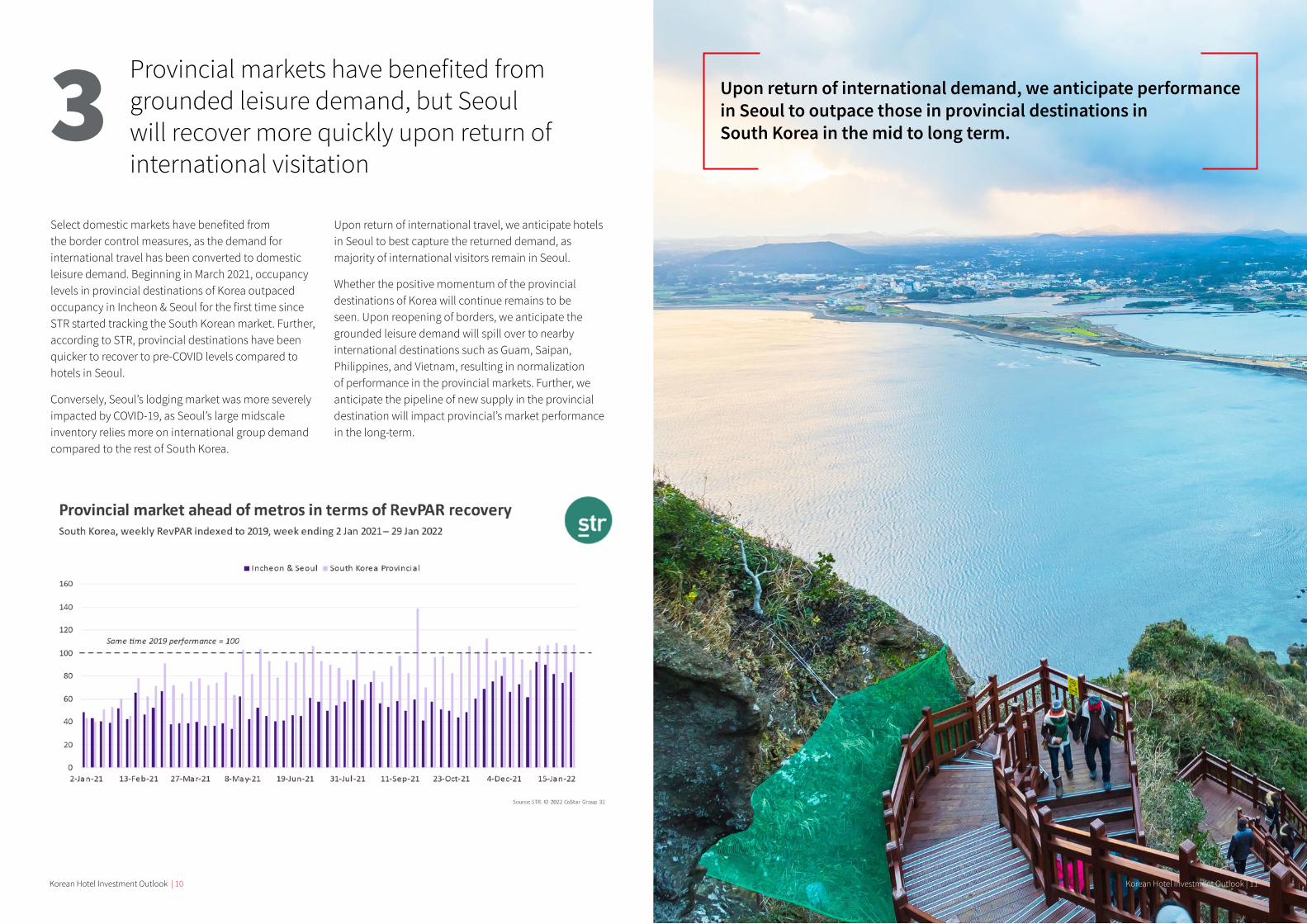

Provincial markets have benefited from grounded leisure demand, but Seoul will recover more quickly upon return of international visitation

3Select domestic markets have benefited from the border control measures, as the demand for international travel has been converted to domestic leisure demand. Beginning in March 2021, occupancy levels in provincial destinations of Korea outpaced occupancy in Incheon & Seoul for the first time since STR started tracking the South Korean market. Further, according to STR, provincial destinations have been quicker to recover to pre-COVID levels compared to hotels in Seoul.

Conversely, Seoul’s lodging market was more severely impacted by COVID-19, as Seoul’s large midscale inventory relies more on international group demand compared to the rest of South Korea.

Upon return of international travel, we anticipate hotels in Seoul to best capture the returned demand, as majority of international visitors remain in Seoul.

Whether the positive momentum of the provincial destinations of Korea will continue remains to be seen. Upon reopening of borders, we anticipate the grounded leisure demand will spill over to nearby international destinations such as Guam, Saipan, Philippines, and Vietnam, resulting in normalization of performance in the provincial markets. Further, we anticipate the pipeline of new supply in the provincial destination will impact provincial’s market performance in the long-term.

Upon return of international demand, we anticipate performance in Seoul to outpace those in provincial destinations in South Korea in the mid to long term.

Korean Hotel Investment Outlook | 11

Korean Hotel Investment Outlook | 13 Korean Hotel Investment Outlook | 12

Future supply growth is anticipated to slow down, resulting in a favorable supply and demand environment4

Between 2012 and 2020, the lodging supply in South Korea nearly doubled, primarily fuelled by public policy which encouraged development of new hotels in preparations for major events such as the 2014 Asian Games and the 2018 Winter Olympics. The policy allowed new hotels to benefit from higher floor-area-ratio and lower parking requirements.

During this growth spurred by policy easing, great majority of new supply was concentrated in the “tourism hotels”—typically unbranded products in the Economy to Upper-Midscale segments. While past supply was concentrated in Economy to Upper-Midscale segments, new entrants will be primarily upper-upscale and luxury products.

Figure 3 South Korea existing supply and pipeline

-

20,000

40,000

60,000

80,000

100,000

120,000

CAGR: +6.5%

Projected CAGR: +2.0%

Existing Supply Added Supply

Source: JLL, STR © 2022 CoStar Group

We anticipate the future supply growth to slow down, thus creating a favorable supply and demand environment in the near term. Due to rising land costs and reduced development incentives, supply growth will be moderate compared to historical periods. Further, the majority of the recently transacted hotels have been converted to alternative uses (i.e., residential or commercial), which reduced the existing supply.

In 2019, approximately 110 hotel rooms were taken off the market through alternative-use conversions; but the number has increased to 755 in 2020, and 2,160 in 2021. Examples of hotels transacting for conversions to alternative-use include Le Meridien (Gangnam), Sheraton Palace (Gangnam), Hankang Hotel Seoul (Gwangjin), and Haeundae Grand Hotel (Busan).

The subdued supply growth and recovering demand are anticipated to create a favourable supply and demand dynamic in the near term.

Korean Hotel Investment Outlook | 13

Korean Hotel Investment Outlook | 15 Korean Hotel Investment Outlook | 14

Growing interest from international investors will support an active hotel transaction market5

South Korea recorded an impressive USD 1.4 billion of total hotel investment volume in 2021, the highest in history followed by 2019. While the great majority of transactions have been smaller hotels and motels priced below USD 30 million, large transactions for alternative-use conversions such as Le Meridien Seoul—the largest hotel sales price in South Korean history and largest across Asia Pacific in 2021—highlighted the year. Other key transactions include Mercure Ambassador Hongdae, Four Points by Sheraton Guro, and D-Cube City Sheraton.

We anticipate the capital market to remain active 2022 with USD 1 billion projected transaction for the full year. Below are a few considerations that investors may consider in the near-term:

South Korean hospitality market attracts both domestic investors seeking redevelopment opportunities and international investors seeking freehold investment opportunities in one of the largest capital cities in Asia.

South Korea offers opportunities to acquire hotels with in-place master leases, albeit more operators have become more reluctant to engage in master leases following COVID-19.

Abundant domestic and international financial institutions enable deal engineering such as sale leasebacks and share sales at relatively affordable fees.

South Korea’s real estate market remain moderately volatile, as real estate values across all asset types, especially in the residential sector, recently reached new historic highs.

Domestic and international investors and lenders remain wary of hotel assets in the near-term.

The pricing expectations of sellers and buyers remain difficult to bridge as sellers continue to hope for impending recovery.

Figure 4: South Korea Hotel Investment Volume (in USD)

-

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

2007 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Cross-border Domestic UnknownSource: JLL

Korea Hotel Investment Outlook | 15

In line with broader interest for commercial real estate, we expect Seoul to continue to attract strong interest from domestic and international investors. We anticipate the hotel capital market in 2022 to remain active, with anticipated transaction volume in excess of USD 1 billion.

Korean Hotel Investment Outlook | 15

+

+

+

JLL is observing increasing levels of interest in the South Korean hospitality market from both domestic and international investors; and we remain optimistic of the projected recovery in the near-term. As a global hotel advisory firm with expertise and track record in the local Korean market, JLL will help investors at any stage of their investment cycle.

We are here to help you achieve your goals. We look forward to hearing from you.

Contact us

Nihat Ercan Head of Investment Sales Asia Pacific [email protected]

Min Joon Kim Vice President South Korea [email protected] +82 10 2588 3521

Xander Nijnens Head of Advisory & Asset Management Asia Pacific [email protected]

Chaehun Chang Managing Director South Korea [email protected]

© 2022 All rights reserved. The information contained in this document has been compiled from sources believed to be reliable. Neither Jones Lang LaSalle nor any of its affiliates accept any liability or responsibility for the accuracy or completeness of the information contained herein. And no reliance should be placed on the information contained in this document.