Embed Size (px)

Citation preview

MEXICO OUTLOOK Current situation and challenges

HISTORY AT GLANCE• Spanish colony• 19 Century liberal wars• 20 Century PRI rule • Milagro Mexicano 1950 – 1975

• Lost decades 1980 – 1990• 2000 Democratic transition

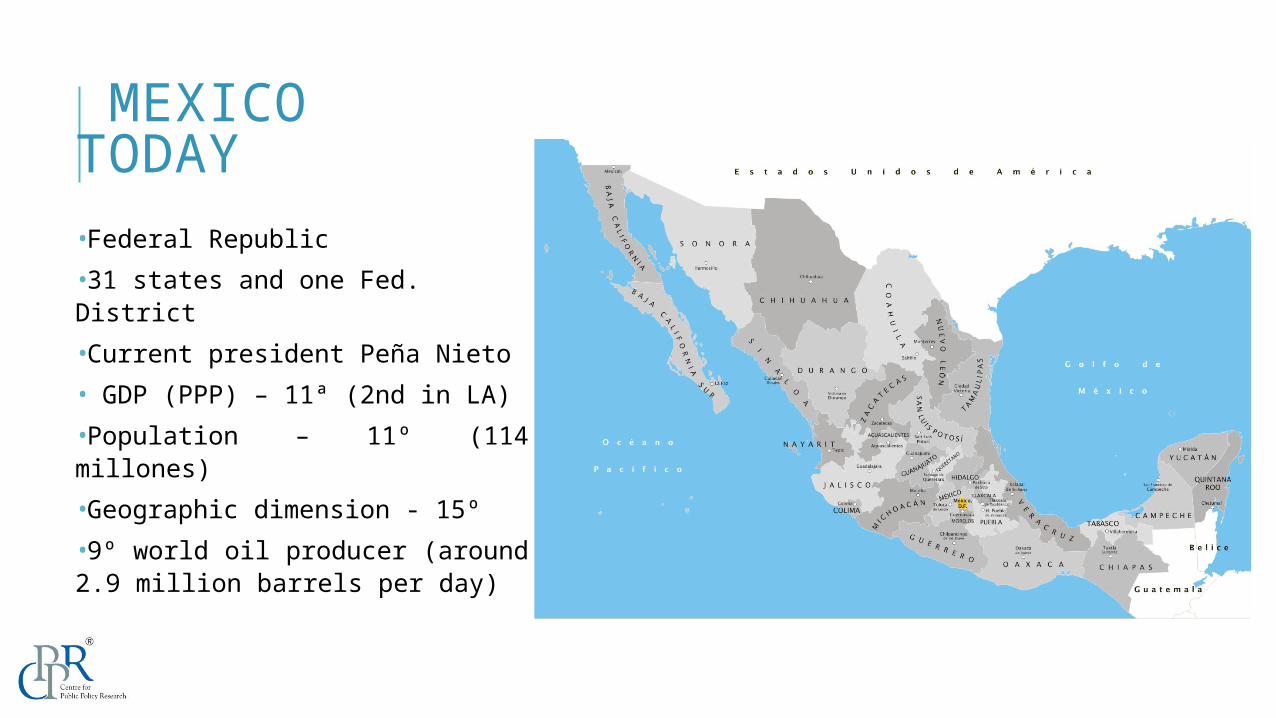

MEXICO TODAY •Federal Republic•31 states and one Fed. District•Current president Peña Nieto• GDP (PPP) – 11ª (2nd in LA)•Population – 11º (114 millones)•Geographic dimension - 15º •9º world oil producer (around 2.9 million barrels per day)

POLITICS The return of the PRI

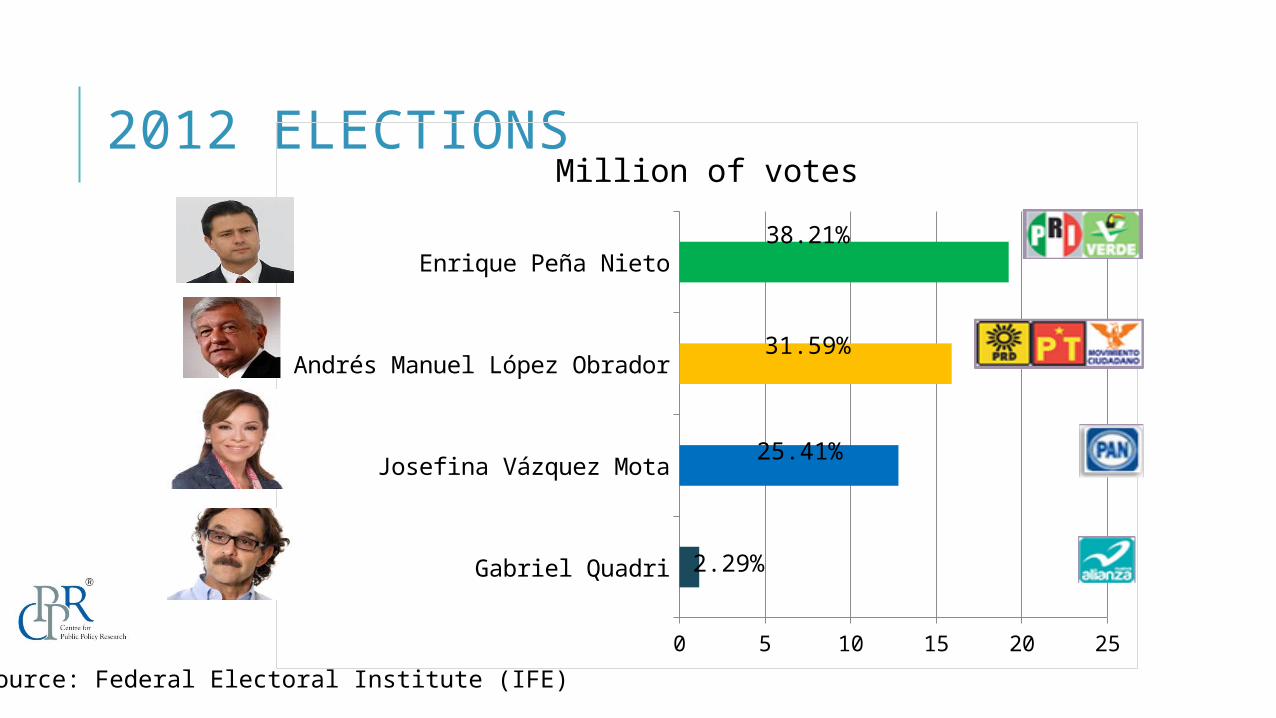

2012 ELECTIONS

Gabriel Quadri

Josefina Vázquez Mota

Andrés Manuel López Obrador

Enrique Peña Nieto

0 5 10 15 20 25

Million of votes38.21%

31.59%

25.41%

2.29%

Source: Federal Electoral Institute (IFE)

2012 ELECTIONS

PRI43%

PAN23%

PRD21%

PVEM6%

MC3%

PT3%

PRI42%

PAN30%

PRD17%

PVEM5%

PT 4%

Congress SenateS/ Grupo. 2%NA 2%

500 seats total 128 seats totalSource: Federal Electoral Institute (IFE)

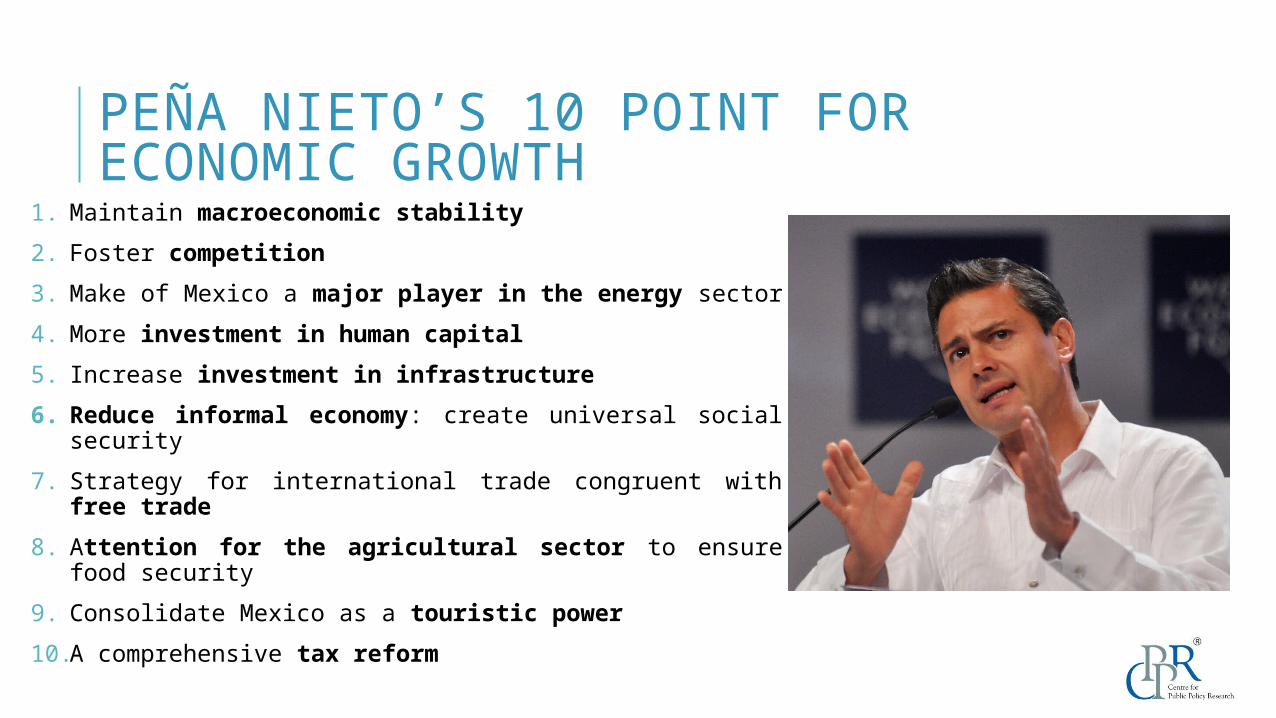

PEÑA NIETO’S 10 POINT FOR ECONOMIC GROWTH

1. Maintain macroeconomic stability2. Foster competition3. Make of Mexico a major player in the energy sector 4. More investment in human capital5. Increase investment in infrastructure6. Reduce informal economy: create universal social

security7. Strategy for international trade congruent with

free trade 8. Attention for the agricultural sector to ensure

food security9. Consolidate Mexico as a touristic power10.A comprehensive tax reform

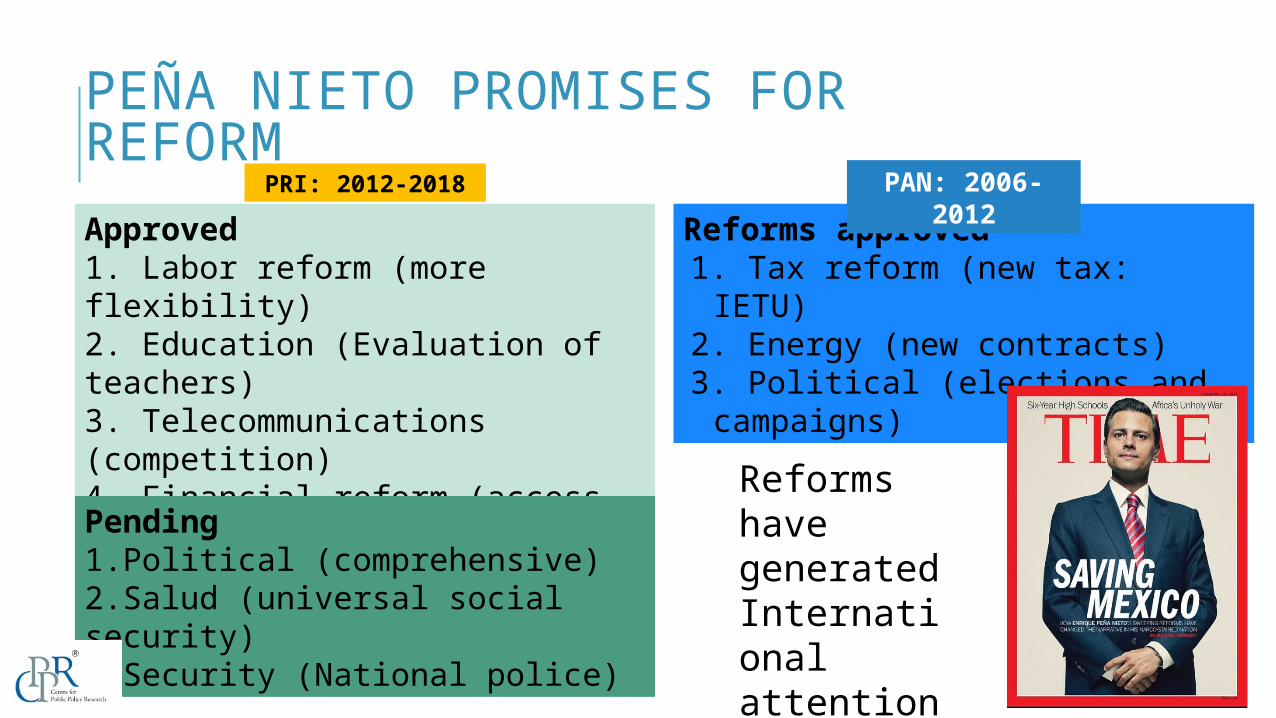

PEÑA NIETO PROMISES FOR REFORMApproved 1. Labor reform (more flexibility)2. Education (Evaluation of teachers)3. Telecommunications (competition)4. Financial reform (access to credit)5. Tax reform (increase in taxes)6. Energy (Open sector)

Reforms approved 1. Tax reform (new tax: IETU)

2. Energy (new contracts)3. Political (elections and campaigns)

PAN: 2006-2012

PRI: 2012-2018

Pending1.Political (comprehensive)2.Salud (universal social security)3.Security (National police)

Reforms have generated International attention

ECONOMY An international comparison

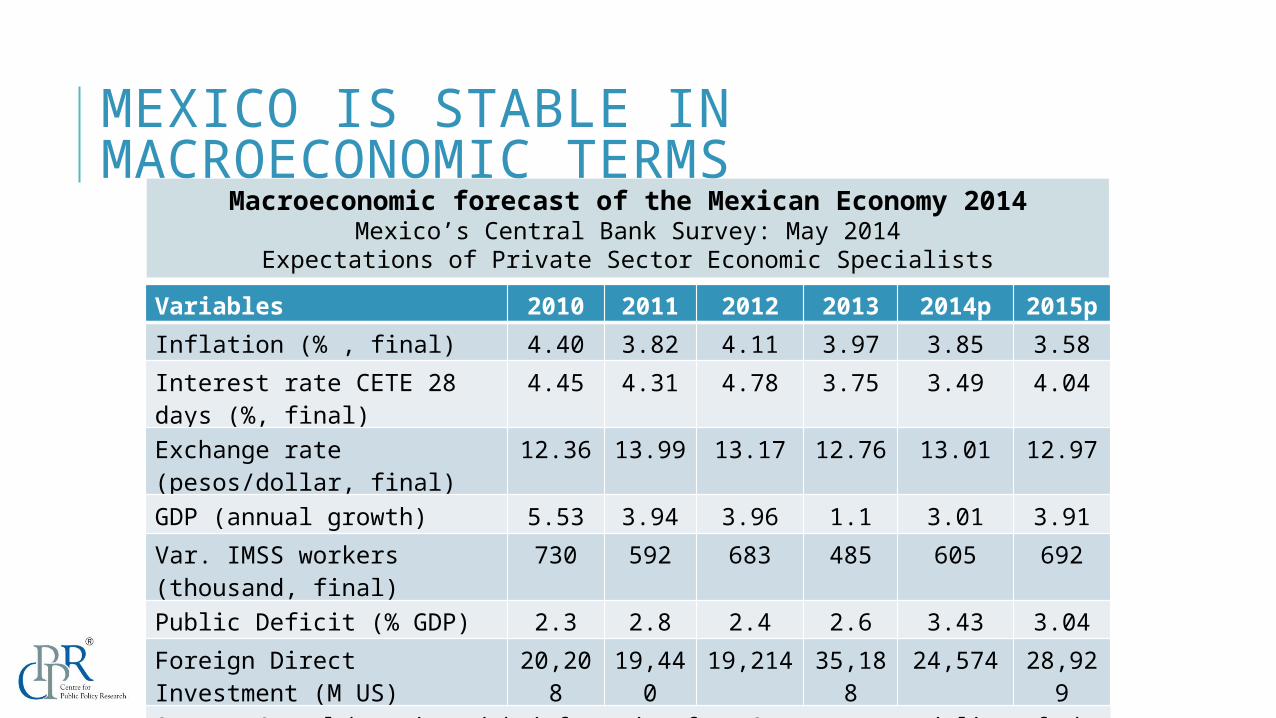

MEXICO IS STABLE IN MACROECONOMIC TERMS

Macroeconomic forecast of the Mexican Economy 2014Mexico’s Central Bank Survey: May 2014

Expectations of Private Sector Economic SpecialistsVariables 2010 2011 2012 2013 2014p 2015pInflation (% , final) 4.40 3.82 4.11 3.97 3.85 3.58Interest rate CETE 28 days (%, final)

4.45 4.31 4.78 3.75 3.49 4.04

Exchange rate (pesos/dollar, final)

12.36 13.99 13.17 12.76 13.01 12.97

GDP (annual growth) 5.53 3.94 3.96 1.1 3.01 3.91Var. IMSS workers (thousand, final)

730 592 683 485 605 692

Public Deficit (% GDP) 2.3 2.8 2.4 2.6 3.43 3.04Foreign Direct Investment (M US)

20,208

19,440

19,214 35,188

24,574 28,929

Source: Own elaboration with information from Survey to specialist of the private sector, May 2014, Mexico’s Central Bank

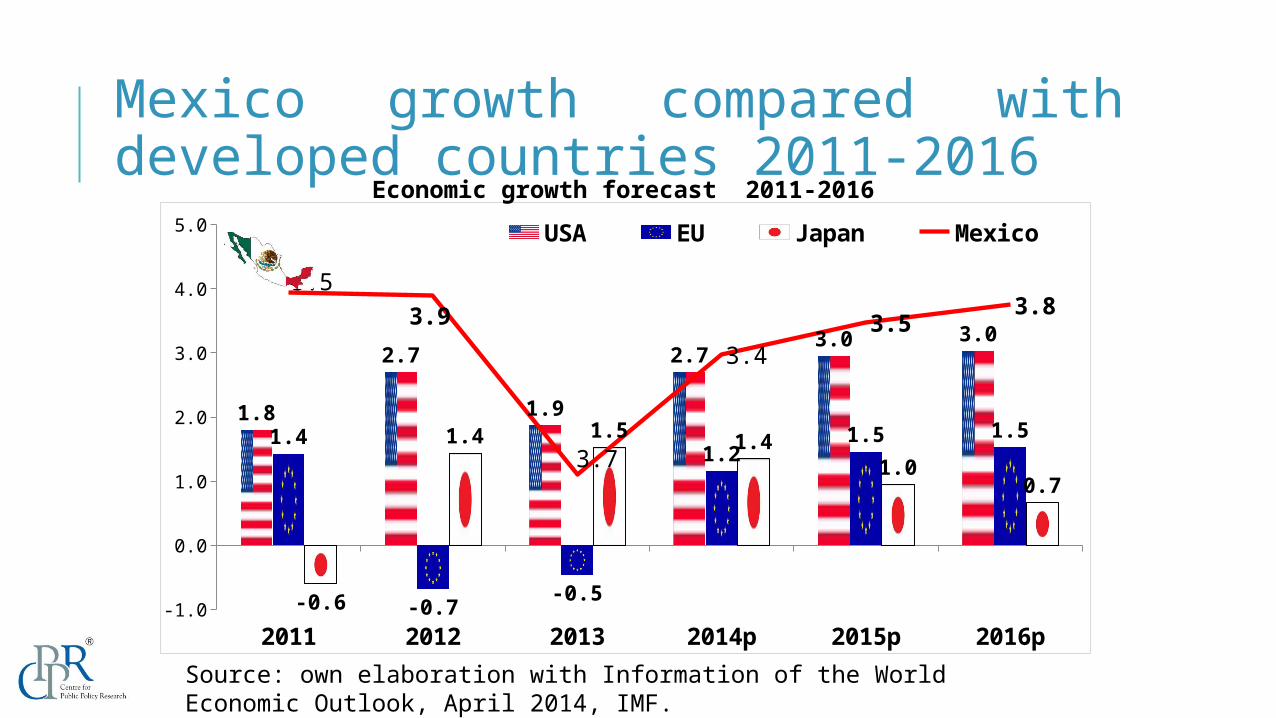

Mexico growth compared with developed countries 2011-2016

2011 2012 2013 2014p 2015p 2016p-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1.8

2.7

1.9

2.7 3.0 3.0

1.4

-0.7 -0.5

1.21.5 1.5

-0.6

1.4 1.5 1.41.0

0.7

5.53.9

3.7

3.43.5 3.8

USA EU Japan Mexico

Source: own elaboration with Information of the World Economic Outlook, April 2014, IMF.

Economic growth forecast 2011-2016

9º in World1º in LA

9º in World1º in LAC

18º in the World

2º in LA

External sector is Mexico’s main economic driver

Exports: 2% of World,

US$349.5 billion

USA

78.6%

Canada

3%

China

1.7%

Colombia

1.6%

USA

49.8%

China

14.8%

Japan

4.7%

South Korea

3.9%

FDIAverage MFN tariff: 4.2% (2013)

Tourism: 12.5 billionRemittances: 24 billionOil: 56.3 billion

Imports:1.9% of World

US$350.8 billion

Trade – 60% of GDP

Stock 2013: US 355 billion

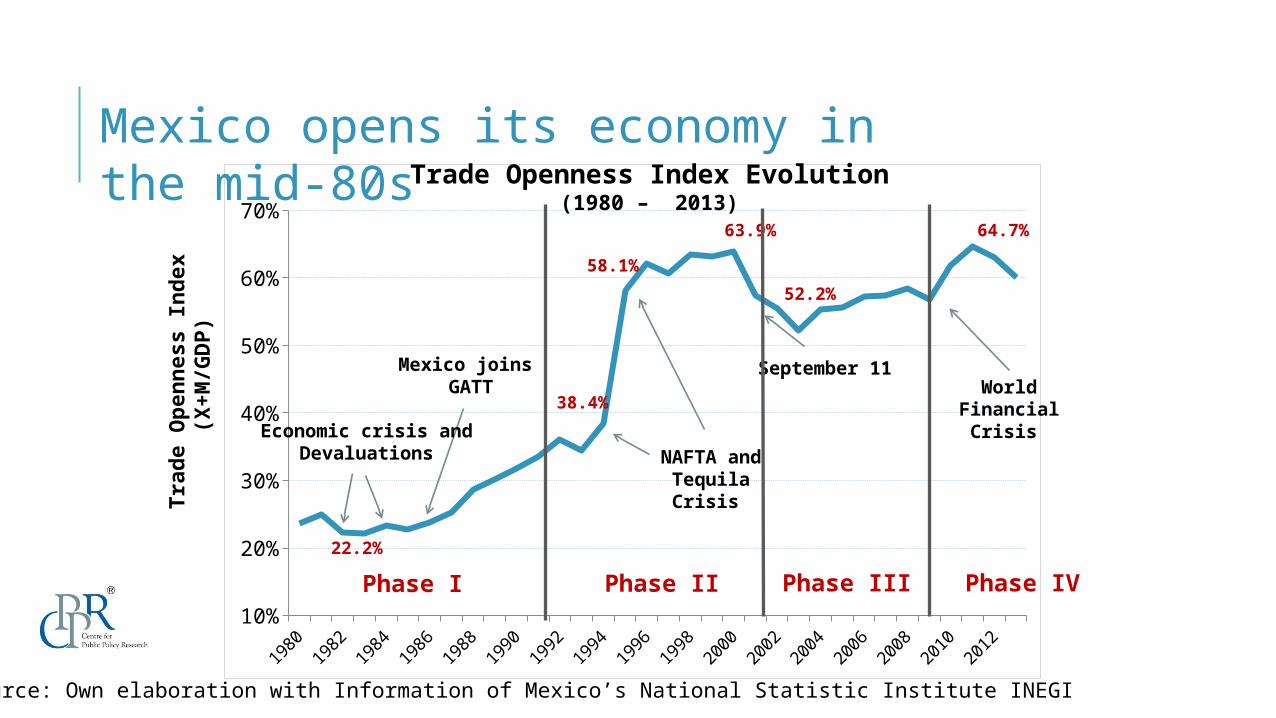

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

10%

20%

30%

40%

50%

60%

70%

Phase II22.2%

NAFTA and Tequila Crisis

September 11

52.2%

World Financial Crisis

Mexico joins GATT

Source: Own elaboration with Information of Mexico’s National Statistic Institute INEGI

Economic crisis andDevaluations

Trad

e Op

enne

ss I

ndex

(X+M/

GDP)

Phase I

64.7%63.9%

58.1%

38.4%

Trade Openness Index Evolution(1980 – 2013)

Phase III Phase IV

Mexico opens its economy in the mid-80s

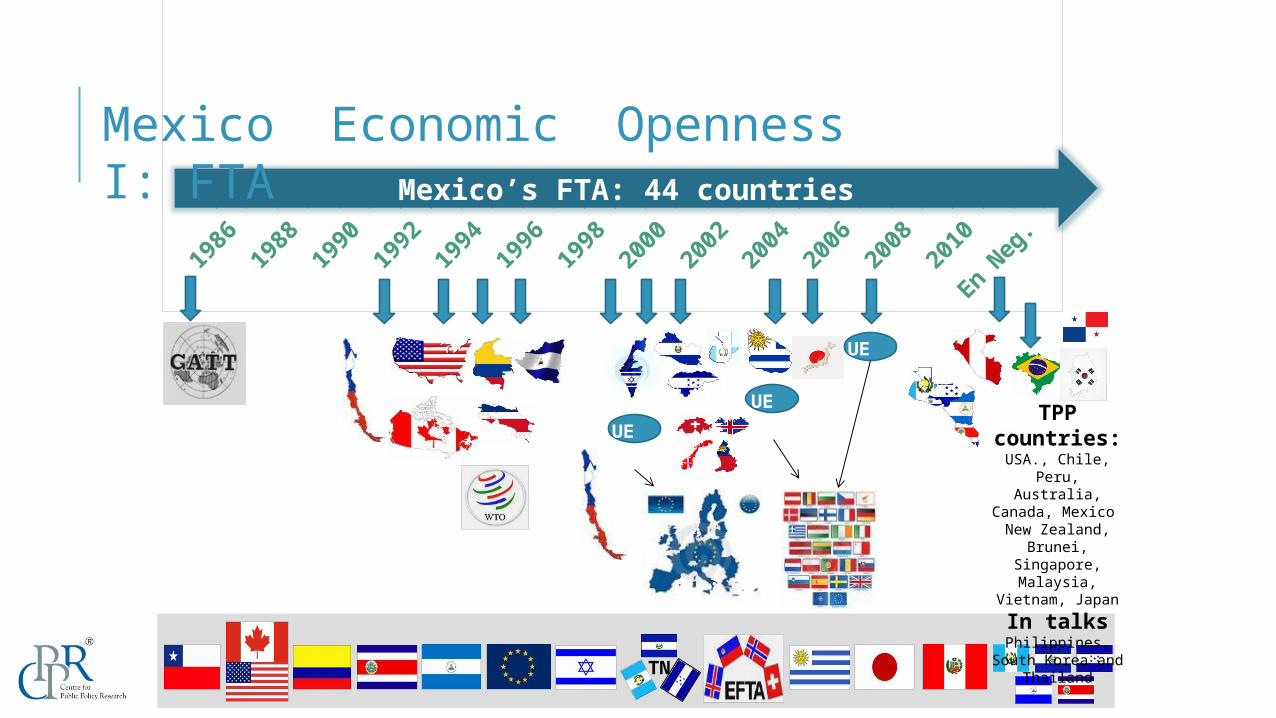

Mexico’s FTA: 44 countries

UE 25UE

15

UE 27

TN

TPP countries:USA., Chile,

Peru, Australia,

Canada, Mexico New Zealand,

Brunei,Singapore, Malaysia,

Vietnam, JapanIn talksPhilippines,

South Korea and Thailand

Mexico Economic Openness I: FTA

ACECuba

FTAHonduras

FTAGuatemala

FTAEl Salvador

FTAColombia

FTANicaragua

FTACosta Rica

AAPPanama

AAPEcuador

FTAPeruACE

BoliviaFTA

Chile

ACEBrazil

AAPParaguay

ACEArgentina

FTAUruguay

5 ACEs 3 AAP

Mexico Economic Openness II: PTA

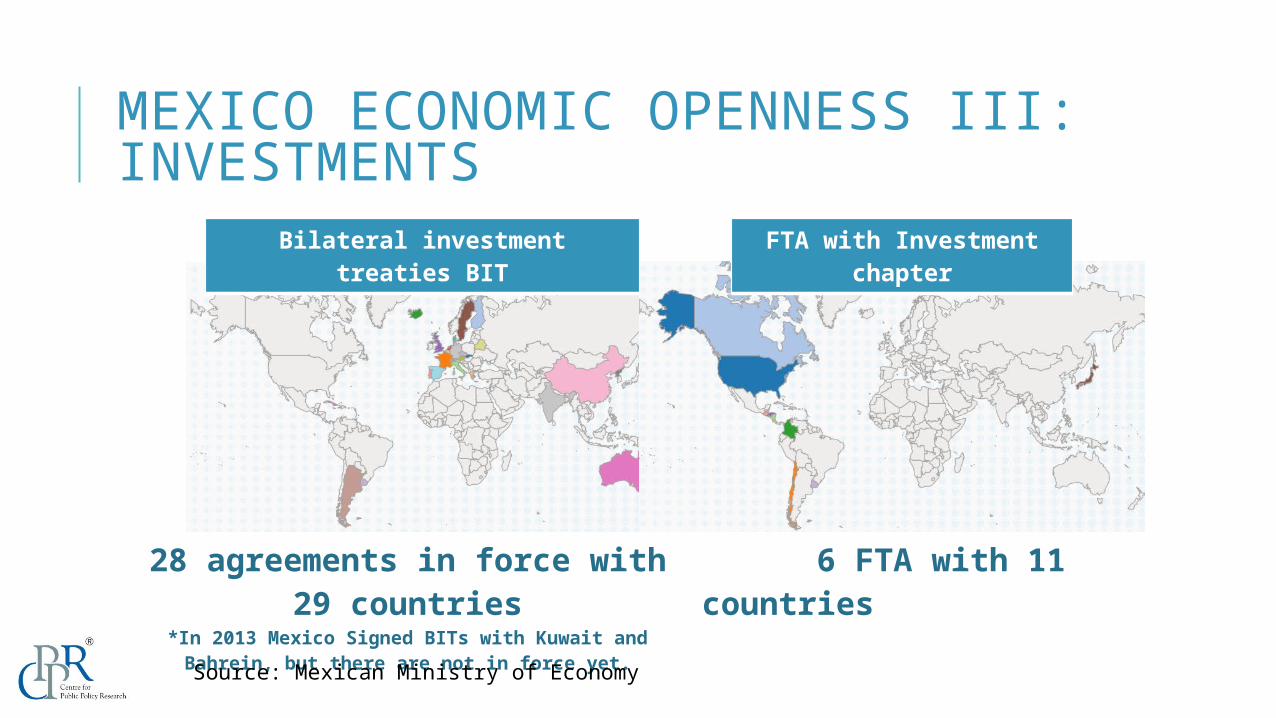

Bilateral investment treaties BIT

FTA with Investment chapter

28 agreements in force with 29 countries

*In 2013 Mexico Signed BITs with Kuwait and Bahrein, but there are not in force yet.

6 FTA with 11 countries

Source: Mexican Ministry of Economy

MEXICO ECONOMIC OPENNESS III: INVESTMENTS

MEXICO’S EXPORTS HAVE ALSO CHANGED

0%

10%

20%30%

40%

50%60%

70%80%

90%

100%Structure of Mexico’s exports

ManufacturesExtractiveAgricultural productsOil

Source: Own elaboration with Information of Mexico’s National Statistic Institute INEGI

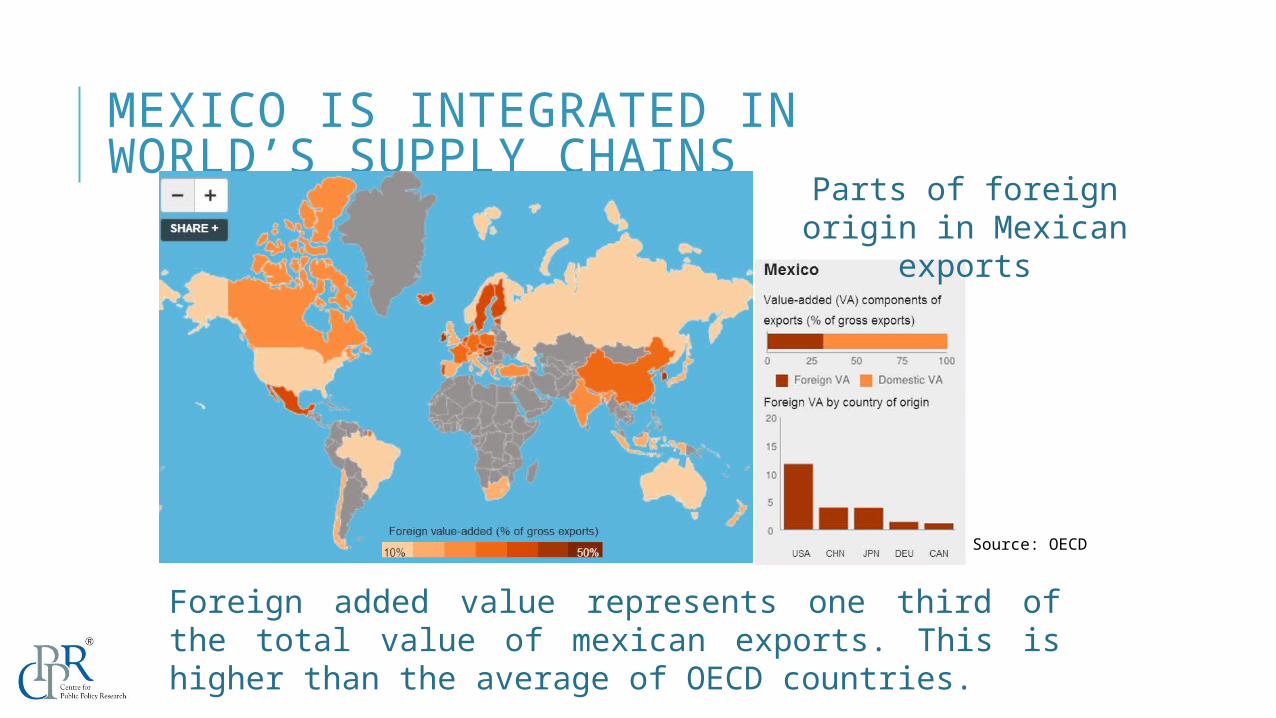

MEXICO IS INTEGRATED IN WORLD’S SUPPLY CHAINS

Source: OECD

Parts of foreign origin in Mexican

exports

Foreign added value represents one third of the total value of mexican exports. This is higher than the average of OECD countries.

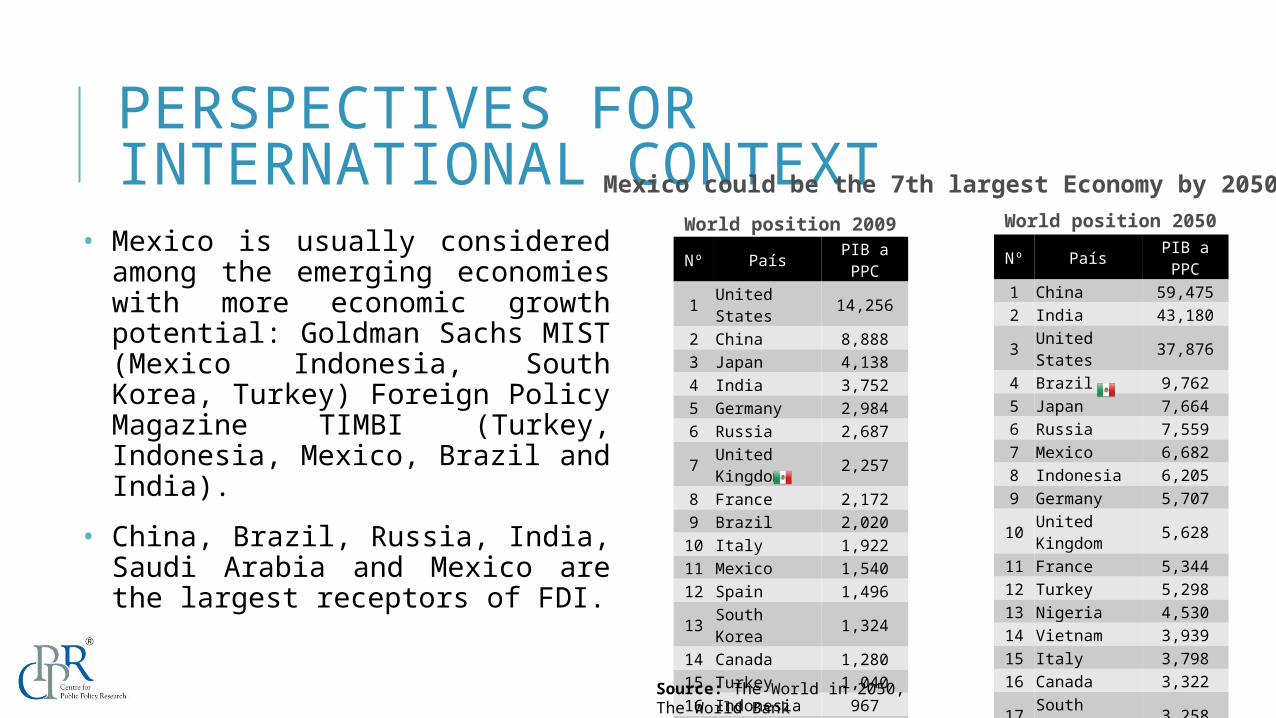

PERSPECTIVES FOR INTERNATIONAL CONTEXT

• Mexico is usually considered among the emerging economies with more economic growth potential: Goldman Sachs MIST (Mexico Indonesia, South Korea, Turkey) Foreign Policy Magazine TIMBI (Turkey, Indonesia, Mexico, Brazil and India).

• China, Brazil, Russia, India, Saudi Arabia and Mexico are the largest receptors of FDI.

Nº País PIB a PPC

1 United States 14,256

2 China 8,888 3 Japan 4,138 4 India 3,752 5 Germany 2,984 6 Russia 2,687

7 United Kingdom 2,257

8 France 2,172 9 Brazil 2,020 10 Italy 1,922 11 Mexico 1,540 12 Spain 1,496

13 South Korea 1,324

14 Canada 1,280 15 Turkey 1,040 16 Indonesia 967 17 Australia 858

18 Saudi Arabia 595

19 Argentina 586

20 South Africa 508

Nº País PIB a PPC

1 China 59,475 2 India 43,180

3 United States 37,876

4 Brazil 9,762 5 Japan 7,664 6 Russia 7,559 7 Mexico 6,682 8 Indonesia 6,205 9 Germany 5,707

10 United Kingdom 5,628

11 France 5,344 12 Turkey 5,298 13 Nigeria 4,530 14 Vietnam 3,939 15 Italy 3,798 16 Canada 3,322

17 South Korea 3,258

18 Spain 3,195

19 Saudi Arabia 3,039

20 Argentina 2,549

Mexico could be the 7th largest Economy by 2050World position 2009 World position 2050

Source: The World in 2050, The World Bank

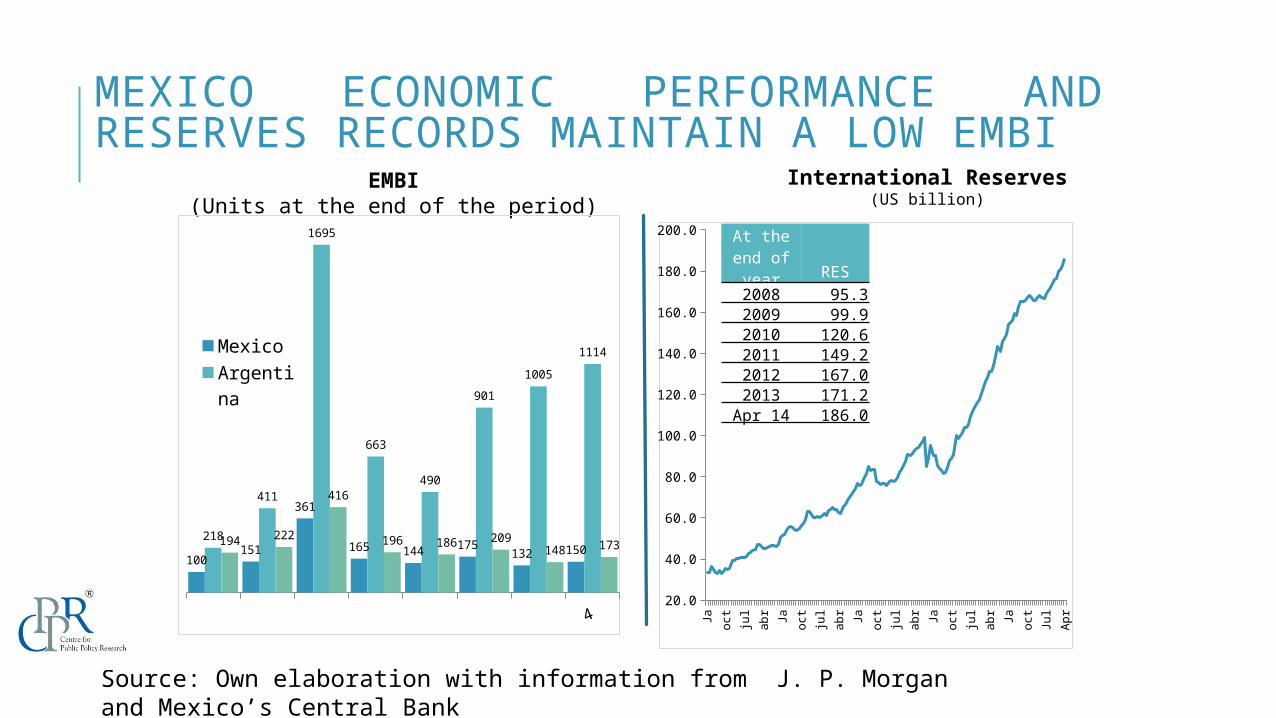

MEXICO ECONOMIC PERFORMANCE AND RESERVES RECORDS MAINTAIN A LOW EMBI

EMBI(Units at the end of the period)

Ja oct

jul

abr Ja oct

jul

abr Ja oct

jul

abr Ja oct

jul

abr Ja oct

Jul

Apr

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

International Reserves(US billion)

4

100151

361

165 144 175 132 150218

411

1695

663

490

9011005

1114

194 222

416

196 186 209148 173

MexicoArgentina

At the end of year RES2008 95.32009 99.92010 120.62011 149.22012 167.02013 171.2

Apr 14 186.0

Source: Own elaboration with information from J. P. Morgan and Mexico’s Central Bank

MEXICO HAS A YOUNG POPULATION AND THE GROWTH OF THE LABOR FORCE IS AMONG THE LARGEST

Source: Mexican National Institute of Statitstics INEGI and Jack A. Goldstone “Rise of TIMBIs” in Foreing Policy, December 2, 2011.

Labor force growth rate (population

between 15 and 59 years) 1959=100

More than 56% of the population is younger than 30 yearsIn the next 30 years the labor force will reach its maximum which represents a demographic bonus

33 40 48 53 57América Latina, 2012

Mexico is relatively well positioned in international competitive indexes: Global Competitiveness Index

MEXICO HAS GOOD INDICATORS OF INTERNATIONAL COMPETITIVENESS AND ECONOMIC FREEDOM

23

Positions in international rankings: competitiveness and economic freedom

Report Mexico Brazil Russia

India China

Doing Business 2013(World Bank) 48 130 112 132 91

Economic Freedom of the 2012 World (Fraser)

91 105 95 111 107

International Competitiveness Index 2011 (IMCO)

32 36 33 42 40

Mexico has a better competitiveness regarding international competitors

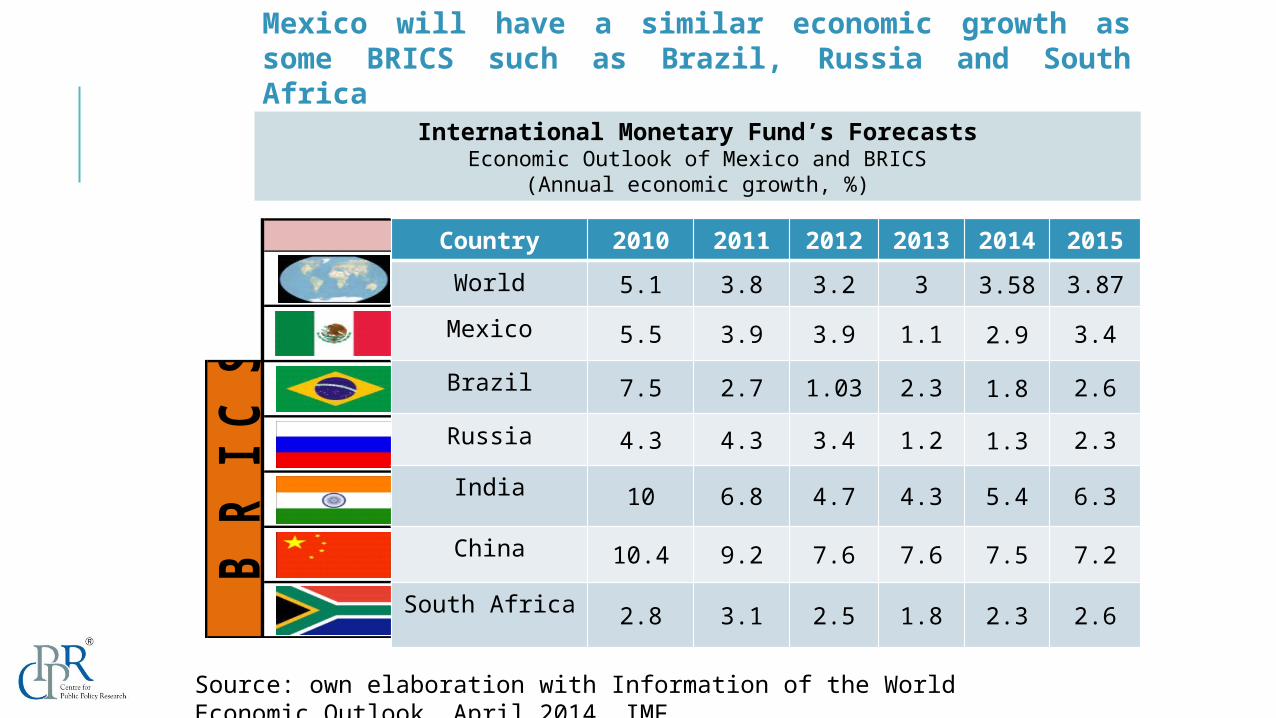

Mexico will have a similar economic growth as some BRICS such as Brazil, Russia and South Africa

2010 2011 2012p 2013pProducción M undial 5.3 3.9 3.5 4.1

M éxico 5.5 4.0 3.6 3.7

Brasil 7.5 2.7 3.0 4.1

Rusia 4.3 4.3 4.0 3.9

India 10.6 7.2 6.9 7.3

China 10.4 9.2 8.2 8.8

Sudáfrica 2.9 3.1 2.7 3.4Fuente: Elaboración propia con datos de Perspectivas de la Econom ía M undial, abril 2012, FM I

PaísB

R I C

SCountry 2010 2011 2012 2013 2014 2015World 5.1 3.8 3.2 3 3.58 3.87Mexico 5.5 3.9 3.9 1.1 2.9 3.4Brazil 7.5 2.7 1.03 2.3 1.8 2.6Russia 4.3 4.3 3.4 1.2 1.3 2.3India 10 6.8 4.7 4.3 5.4 6.3

China 10.4 9.2 7.6 7.6 7.5 7.2

South Africa 2.8 3.1 2.5 1.8 2.3 2.6

International Monetary Fund’s ForecastsEconomic Outlook of Mexico and BRICS

(Annual economic growth, %)

Source: own elaboration with Information of the World Economic Outlook, April 2014, IMF.

Challenges The external sector is not enough

WHAT PRIVATE SECTOR SPECIALISTS THINK

What factors could hinder Mexico’s economic growth 1. Public security problems2. Weakness of the internal market3. Weakness of the world economySource: Own elaboration with information from Survey to specialist of the private sector, May 2014, Mexico’s Central Bank• Other challenges • Poverty• Inequality

• Education• Monopolies

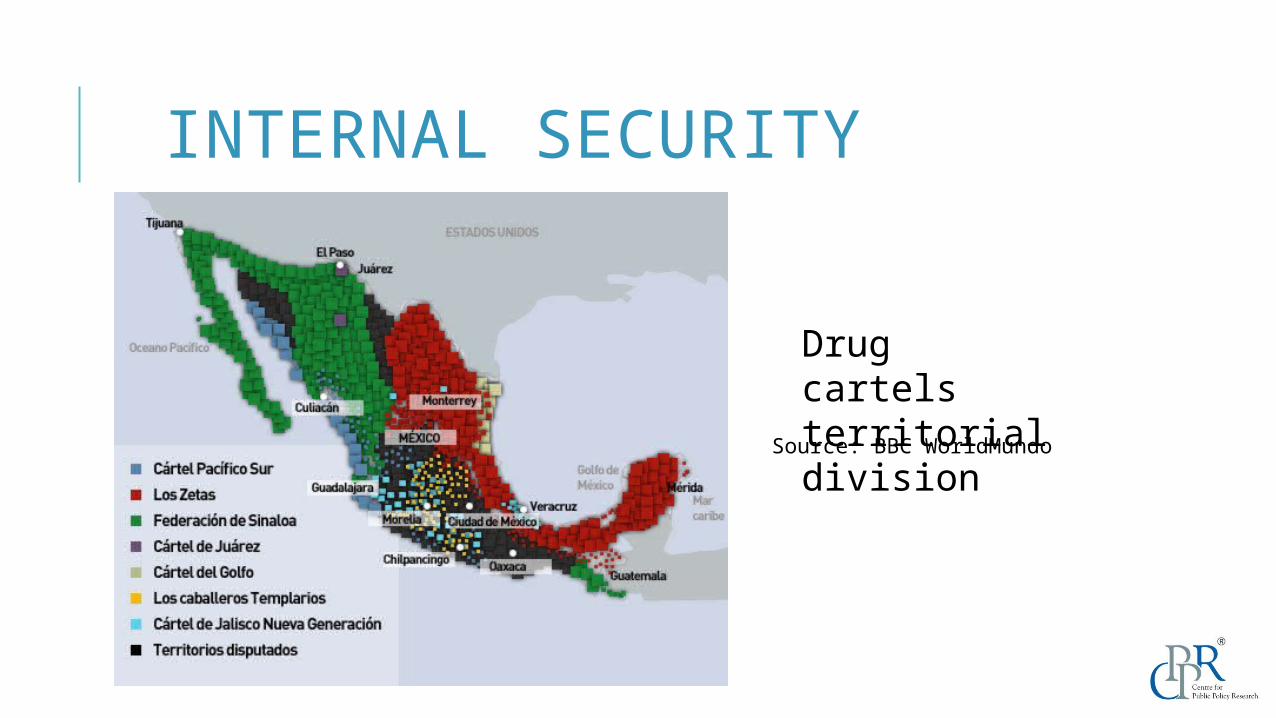

INTERNAL SECURITY

Drug cartels territorial division

Source: BBC WorldMundo

27

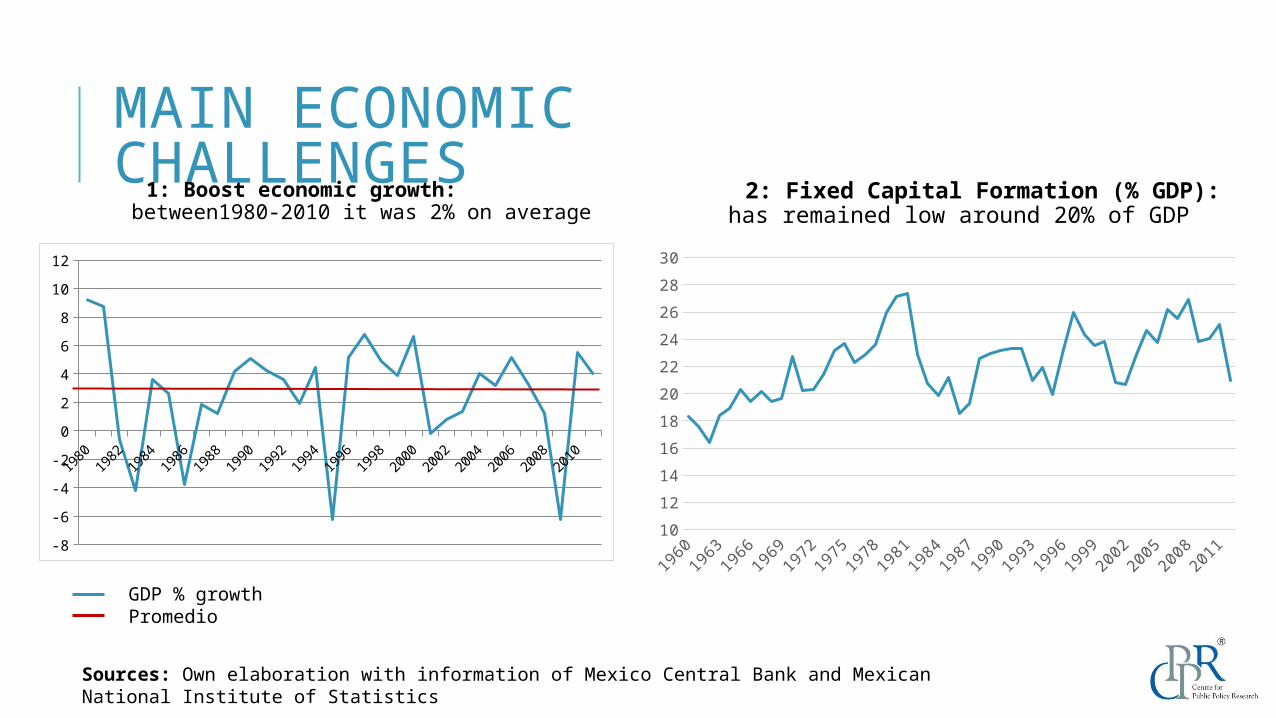

MAIN ECONOMIC CHALLENGES 1: Boost economic growth: between1980-2010 it was 2% on average

1980198

2198

4198

6198

8199

0199

2199

4199

6199

8200

0200

2200

4200

6200

8201

0

-8-6-4-202468

1012

GDP % growthPromedio

Sources: Own elaboration with information of Mexico Central Bank and Mexican National Institute of Statistics

1012141618202224262830

2: Fixed Capital Formation (% GDP): has remained low around 20% of GDP

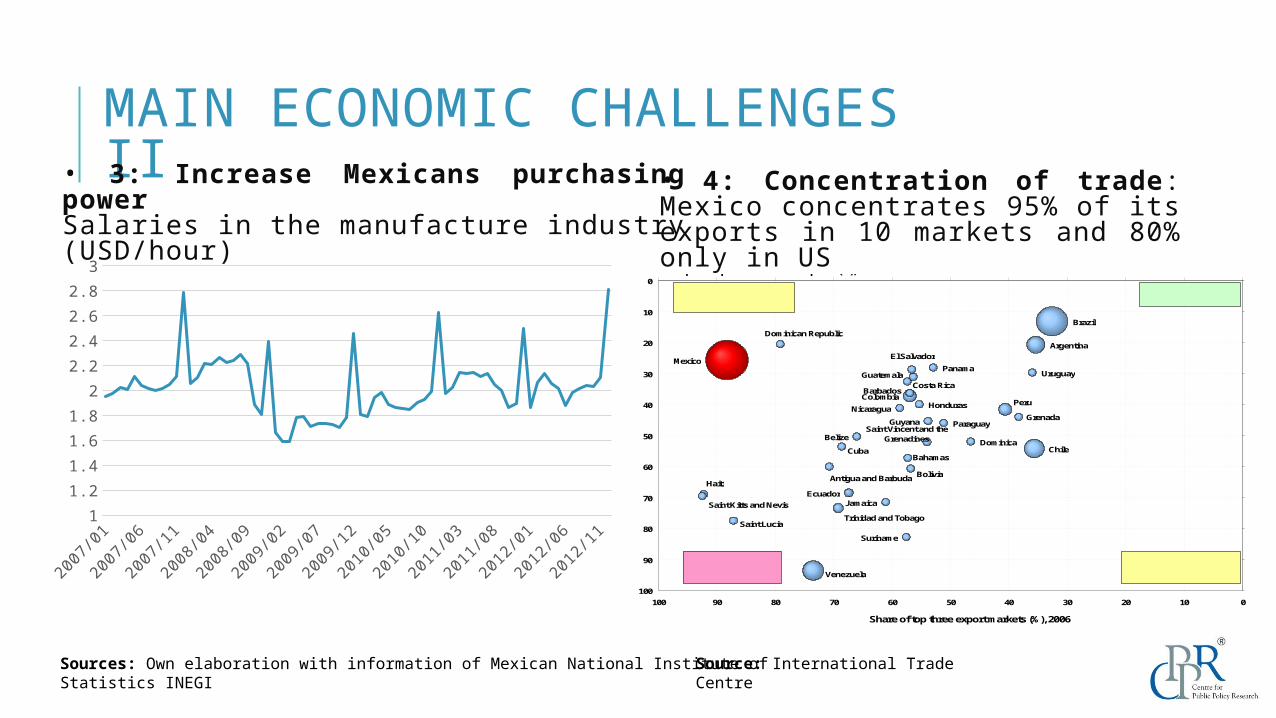

MAIN ECONOMIC CHALLENGES II

29

11.21.41.61.8

22.22.42.62.8

3

Sources: Own elaboration with information of Mexican National Institute of Statistics INEGI

• 4: Concentration of trade: Mexico concentrates 95% of its exports in 10 markets and 80% only in US

Source: International Trade Centre

• 3: Increase Mexicans purchasing powerSalaries in the manufacture industry (USD/hour)

GrenadaSaint Vincent and the

Grenadines

Saint Kitts and Nevis

Dominica

Antigua and Barbuda

Saint Lucia

Belize

Barbados

Guyana

Haiti

Nicaragua

Panama

Suriname

Honduras

El Salvador

Paraguay

Jamaica

BahamasCuba

Guatemala Uruguay

Bolivia

Dominican Republic

Costa Rica

Ecuador

Trinidad and Tobago

PeruColombia

Argentina

Chile

Venezuela

Brazil

Mexico

0

10

20

30

40

50

60

70

80

90

1000102030405060708090100

Share of top three export markets (%), 2006

High product concentrationLow market concentration

Low product andmarket concentration

High product andmarket concentration

Low product concentrationHigh market concentration

Share of top three products in total exports (%), 2006

✓ ✗

IN SUM

30

Strengths Weaknesses• Macroeconomic stability

• Competitiveness

• Trade

• High vulnerability of external sector

• Insufficient economic growth

ChallengeStructural Reforms to activate

internal market