PROJECT REPORT

on

A STUDY ON WORKING CAPITAL MANAGEMENT

BY

SAGAR P L

1NZ18MBA72

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BENGALURU

In partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

SANTOSH KUMAR S

PROFESSOR

2018 - 2020

CERTIFICATE

This is to certify that SAGAR P L bearing USN 1NZ18MBA72, is a bonafide student of Master of Business Administration course of the Institute BATCH 18, autonomous program, affiliated to Visvesvaraya Technological University, Belgaum. Project report on A STUDY ON WORKING CAPITAL MANAGEMENT is prepared by him under the guidance of SANTOSH KUMAR S, in partial fulfillment of requirements for the award of the degree of Master of Business Administration of Visvesvaraya Technological University, Belgaum Karnataka. Signature of Internal Guide Signature of HOD Principal

Name of the Examiners with affiliation Signature with date 1. External Examiner 2. Internal Examiner

4

DECLARATION

I, SAGAR P L, hereby declare that the project report on “A STUDY ON WORKING CAPITAL

MANAGEMENT” with reference to “EXIDE INDUSTRIES LIMITED” prepared by me under

the guidance of SANTOSH KUMAR S, faculty of M.B.A Department, New Horizon College

of Engineering.

I also declare that this project report is towards the partial fulfilment of the university

regulations for the award of the degree of Master of Business Administration by Visvesvaraya

Technological University, Belgaum.

I have undergone an industry project for a period of Twelve weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the award

of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

5

ACKNOWLEDGEMENT

The successful completion of the project would not have been possible without

the guidance and support of many people. I express my sincere gratitude to S H

KHAN, MANAGER-PLANT HR, EXIDE INDUSTRIES LIMITED,

BENGALURU, for allowing to do my project at EXIDE INDUSTRIES

LIMITED.

I thank the staff of EXIDE INDUSTRIES LIMITED, Bengaluru for their support

and guidance and helping me in completion of the report.

I am thankful to my internal guide SANTOSH KUMAR S, for his constant

support and inspiration throughout the project and invaluable suggestions,

guidance and also for providing valuable information.

Finally, I express my gratitude towards my parents and family for their

continuous support during the study.

SAGAR P L

1NZ18MBA72

6

TABLE OF CONTENTS

SL. NUMBER CONTENTS PAGE NUMBERS

1 Theoretical Background Of The Study 07

2 Industry Profile &Company Profile 17

3 Research and Methodology 45

4 Analysis And Interpretation Of Financial

Statements And Reports 48

5 Learning Experience- Findings, Suggestions And

Conclusion 86

6 Bibliography 89

7

CHAPTER 1

THEORETICAL BACKGROUND OF THE STUDY

WORKING CAPITAL MANAGEMENT

Working capital management is the process of identifying the financial strengths and weakness of the firm. It is done by establishing relationships between the items of financial statements viz., balance sheet and profit and loss account. Working capital management can be undertaken by management of the firm, viz., owners, creditors, investors and others.

Objectives of the working capital management

Analysis of financial statements may be made for a particular purpose in view:

1. To find out the financial stability and soundness of the business enterprise.

2. To assess and evaluate the earning capacity of the business

3. To estimate and evaluate the fixed assets, stock etc., of the concern.

4. To estimate and determine the possibilities of future growth of business.

5. To assess and evaluate the firm’s capacity and ability to repay short and long term loans.

Parties interested in working capital management:

The users of working capital management can be divided into two broad groups.

Internal users:

1. Financial executives

2. Top management

External users:

1. Investors

2. Creditor.

3. Workers

4. Customers

8

5. Government

6. Public

7. Researchers

Significance of working capital management

Working capital management serves the following purpose:

To know the operational efficiency of the business: The working capital management enables the management to find out the overall efficiency of the firm. This will enable the management to locate the weak Spots of the business and take necessary remedial action.

Help filling measuring the solvency of the firm: The working capital management helps the decision makers in taking appropriate decisions for strengthening the short-term as well as long-term solvency of the firm.

Comparison of past and present results: Financial statements of the previous years can be compared and the trend regarding various expenses, purchases, sales, gross profit and net profit can be ascertained.

Helps in measuring the profitability: Financial statements show the gross profit, & net profit.

Inter‐firm comparison: The working capital management makes it easy to make interfere comparison. This comparison can also be made for various time periods.

Bankruptcy and Failure: Financial statement analysis is significant tool in predicting the bankruptcy and the failure of the business enterprise. Financial statement analysis accomplishes this through the evaluation of the solvency position.

Helps in forecasting: The working capital management will help in assessing future development by making forecasts and preparing budgets.

9

METHODS OF ANALYSIS:

A financial analyst can adopt the following tools for analysis of the financial statements. These are also termed as methods of working capital management.

A. Comparative statement analysis

B. Common-size statement analysis

C. Trend analysis

D. Funds flow analysis

E. Ratio analysis

NATURE OF RATIO ANALYSIS

Ratio Analysis is a powerful tool of working capital management. A ratio is defined as "the indicated quotient of mathematical expression" and as "the relationship between two or more things". A ratio is used as benchmark for evaluating the financial position and performance of the firm. The relationship between two accounting figures, expressed mathematically, is known as a financial ratio.

Ratio helps to summarizes large quantities of financial data and to make qualitative judgment about the firm's financial performance. The persons interested in the analysis of financial statements can be grouped under three head owners (or) investors who are desired primarily a basis for estimating earning capacity. Creditors who are concerned primarily with Liquidity and ability to pay interest and redeem loan within a specified period. Management is interested in evolving analytical tools that will measure costs, efficiency, liquidity and profitability with a view to make intelligent decisions.

STANDARDS OF COMPARISON

The ratio analysis involves comparison for a useful interpretation of the financial statements. A single ratio in itself does not indicate favourable or unfavourable condition. It should be compared with some standard. Standards of comparison are:

1. Past Ratios

2. Competitor’s Ratios

3. Industry Ratios.

4. Projected Ratios

Past Ratio: Ratios calculated from the past financial statements of the same firm.

10

Competitor's Ratio: Ratios of some selected firms, especially the most progressive and successful competitor at the same point in time.

Industry Ratios: Ratios of the industry to which the firm belongs.

Projected Ratios: Ratios developed using the projected financial statements of the same firm.

TIME SERIES ANALYSIS

The easiest way to evaluate the performance of a firm is to compare its present ratios with past ratios. When financial ratios over a period of time are compared, it is known as the time series analysis or trend analysis.

It gives an indication of the direction of change and reflects whether the firm's financial performance has improved, deteriorated or remind constant over time.

CROSS SECTIONAL ANALYSIS

Another way to comparison is to compare ratios of one firm with some selected firms in the industry at the same point in time. This kind of comparison is known as the cross-sectional analysis. It is more useful to compare the firm's ratios with ratios of a few carefully selected competitors, who have similar operations.

INDUSTRY ANALYSIS

To determine the financial conditions and performance of a firm. Its ratio may be compared with average ratios of the industry of which the firm is a member. This type of analysis is known as industry analysis and also it helps to ascertain the financial standing and capability of the firm & other firms in the industry. Industry ratios are important standards in view of the fact that each industry has its characteristics which influence the financial and operating relationships.

TYPES OF RATIOS

Management is interested in evaluating every aspect of firm's performance. In view of the requirement of the various users of ratios, we may classify them into following four important categories:

1. Liquidity Ratio

2. Leverage Ratio

3. Activity Ratio

4. Profitability Ratio

11

Liquidity Ratio

It is essential for a firm to be able to meet its obligations as they become due. Liquidity Ratios help in establishing a relationship between cast and other current assets to current obligations to provide a quick measure of liquidity. A firm should ensure that it does not suffer from lack of liquidity and also that it does not have excess liquidity. A very high degree of liquidity is also bad, idle assets earn nothing.

The firm's funds will be unnecessarily tied up in current assets. Therefore it is necessary to strike a proper balance between high liquidity. Liquidity ratios can be divided into three types:

• Current Ratio

• Quick Ratio

• Cash Ratio

Current Ratio

Current ratio is an acceptable measure of firm’s short-term solvency Current assets includes cash within a year, such as marketable securities, debtors and inventors. Prepaid expenses are also included in current assets as they represent the payments that will not made by the firm in future. All obligations maturing within a year are included in current liabilities. These include creditors, bills payable, accrued expenses, short-term bank loan, income-tax liability in the current year. The current ratio is a measure of the firm's short term solvency. It indicated the availability of current assets in rupees for every one rupee of current liability.

Quick Ratio

Quick Ratio establishes a relationship between quick or liquid assets and current liabilities. An asset is liquid if it can be converted into cash immediately or reasonably soon without a loss of value. Cash is the most liquid asset, other assets that are considered to be relatively liquid asset and included in quick assets are debtors and bills receivables and marketable securities (temporary quoted investments).

Quick ratio is a more penetrating test of liquidity than the current ratio, yet it should be used cautiously. A company with a high value of quick ratio can suffer from the shortage of funds if it has slow- paying, doubtful and long duration outstanding debtors. A low quick ratio may really be prospering and paying its current obligation in time.

Cash Ratio

Cash is the most liquid asset; a financial analyst may examine Cash Ratio and its equivalent current liabilities. Cash and Bank balances and short-term marketable securities are the most liquid assets of a firm, financial analyst stays look at cash ratio. Indeed, one can argue that it is overly stringent. Lack of immediate cash may not matter if the firm stretch its payments or borrow money at short notice.

12

LEVERAGE RATIOS

Financial leverage refers to the use of debt finance while debt capital is a cheaper source of finance: it is also a riskier source of finance. It helps in assessing the risk arising from the use of debt capital. Two types of ratios are commonly used to analyze financial leverage.

1. Structural Ratios

2. Coverage ratios

Structural Ratios are based on the proportions of debt and equity in the financial structure of firm. Coverage Ratios shows the relationship between Debt Servicing, Commitments and the sources for meeting these burdens. The short-term creditors like bankers and suppliers of raw material are more concerned with the firm's current debt-paying ability. These ratios indicated mix of funds provided by owners and lenders. There should be an appropriate mix of Debt and owner's equity in financing the firm's assets. The process of magnifying the shareholder's return through the use of Debt is called "financial leverage" or "financial gearing" or "trading on equity". Leverage Ratios are calculated to measure the financial risk and the firm's ability of using Debt to share holder's advantage. Leverage Ratios can be divided into five types.

• Debt equity ratio.

• Debt ratio.

• Interest coverage ratio Proprietary ratio.

• Capital gearing ratio

Debt equity ratio

It indicates the relationship describing the lenders contribution for each rupee of the owner's contribution is called debt-equity ratio. Debt equity ratio is directly computed by dividing total debt by net worth. Lower the debt-equity ratio, higher the degree of protection. A debt-equity ratio of 2:1 is considered ideal.

The debt consists of all short term as well as long-term and equity consists of net worth plus preference capital plus Deferred Tax Liability.

Debt ratio

Several debt ratios may used to analyze the long-term solvency of a firm. The firm may be interested in knowing the proportion of the interest-bearing debt in the capital structure. It may, therefore, compute debt ratio by dividing total total-debt by capital employed on net assets. Total debt will include short and long-term borrowings from financial institutions, debentures/bonds, deferred payment arrangements for buying equipments, bank borrowings, public deposits and any other interest-bearing loan. Capital employed will include total debt net worth.

13

Interest Coverage Ratio

The interest coverage ratio or the time interest earned is used to test the firms’ debt servicing capacity. The interest coverage ratio is computed by dividing earnings before interest and taxes by interest charges. The interest coverage ratio shows the number of times the interest charges are covered by funds that are ordinarily available for their payment. We can calculate the interest average ratio as earnings before depreciation, interest and taxes divided by interest.

Proprietary ratio

The total shareholder's fund is compared with the total tangible assets of the company. This ratio indicates the general financial strength of concern. It is a test of the soundness of financial structure of the concern. The ratio is of great significance to creditors since it enables them to find out the proportion of share holders funds in the total investment of business.

Capital gearing ratio:

This ratio makes an analysis of capital structure of firm. The ratio shows relationship between equity share capital and the fixed cost bearing i.e., preference share capital and debentures.

ACTIVITY RATIOS

Turnover ratios also referred to as activity ratios or asset management ratios, measure how efficiently the assets are employed by a firm. These ratios are based on the relationship between the level of activity, represented by sales or cost of goods sold and levels of various assets. The improvement turnover ratios are inventory turnover, average collection period, receivable turn over, fixed assets turnover and total assets turnover. Activity ratios are employed to evaluate the efficiency with which the firm manages and utilize its assets. These ratios are also called turnover ratios because they indicate the speed with which assets

are being converted or turned over into sales. Activity ratios thus involve a relationship between sales and assets.

A proper balance between sales and assets generally reflects that asset utilization.

• Activity ratios are divided into four types:

• Total capital turnover ratio

• Working capital turnover ratio

• Fixed assets turnover ratio

• Stock turnover ratio

14

Total capital turnover ratio:

This ratio expresses relationship between the amounts invested in this assets and the resulting in terms of sales. This is calculated by dividing the net sales by total sales. The higher ratio means better utilization and vice-versa.

Some analysts like to compute the total assets turnover in addition to or instead of net assets turnover. This ratio shows the firm's ability in generating sales from all financial resources committed to total assets.

Working capital turnover ratio:

This ratio measures the relationship between working capital and sales.

The ratio shows the number of times the working capital results in sales. Working capital as usual is the excess of current assets over current liabilities. The following formula is used to measure the ratio:

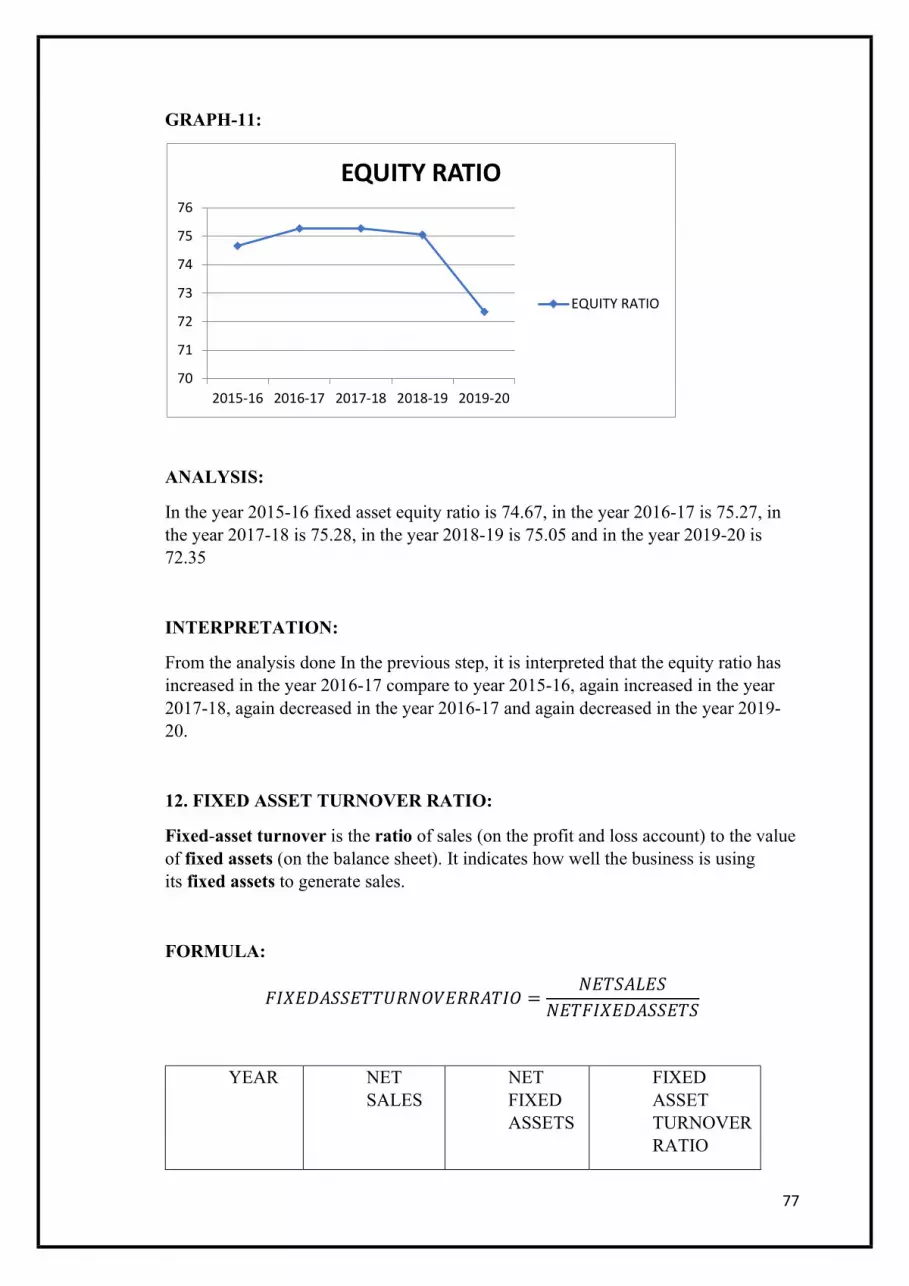

Fixed asset turnover ratio:

The firm may which to know its efficiency of utilizing fixed assets and current assets separately. The use of depreciated value of fixed assets in computing the fixed assets turnover may render comparison of firm's performance over period or with other firms.

The ratio is supposed to measure the efficiency with which fixed assets employed a high ratio indicates a high degree of efficiency in asset utilization and a low ratio reflects inefficient use of assets. However, in interpreting this ratio, one caution should be borne in mind, when the fixed assets of firm are old and substantially depreciated the fixed assets turnover ratio tends to be high because the denominator of ratio is very low.

Stock turnover ratio

Stock turnover ratio indicates the efficiency of firm in producing and selling its product. It is calculated by dividing the cost of goods sold by the average stock. It measures how fast the inventory is moving through the firm and generating sales. The stock turnover ratio reflects the efficiency of inventory management. The higher the ratio, the more efficient the management of inventories and vice versa .However, this may not always be true. A high inventory turnover may be caused by a low level of inventory which may result if frequent stock outs and loss of sales and customer goodwill.

PROFITABILITY RATIOS

A company should earn profits to survive and grow over a long period of time. Profits are essential but it would be wrong to assume that every action initiated by management of a company should be aimed at maximizing profits. Profit is the difference between revenues and expenses over a period .Profit is the ultimate 'output' of a company and it will have no future if it fails to make sufficient profits. The financial manager should continuously evaluate the efficiency of company in terms of profits. The profitability ratios are calculated to measure the operating efficiency of company. Creditors want to get interest and repayment

15

of principal regularly. Owners want to get a required rate of return on their investment. Generally, two major types of profitability ratios are calculated:

•Profitability in relation to sales

•Profitability in relation to investment

Profitability Ratio can be divided into six types:

• Gross profit ratio

• Operating profit ratio

• Net profit ratio

• Return on investment

• Earns per share

• Operating expenses ratio

Gross profit ratio

First profitability ratio in relation to sales is the gross profit margin the gross profit margin reflects. The efficiency with which management produces each unit of product. This ratio indicates the average spread between the cost of goods sold and the sales revenue. A high gross profit margin is a sign of good management. A gross margin ratio may increase due to any of following factors: higher sales prices cost of goods sold remaining constant, lower cost of goods sold, sales prices remaining constant. A low gross profit margin may reflect higher cost of goods sold due to firm's inability to purchase raw materials at favourable terms, inefficient utilization of plant and machinery resulting in higher cost of production or due to fall in prices in market. This ratio shows the margin left after meeting manufacturing costs. It measures the efficiency of production as well as pricing. To analyse the factors underlying the variation in gross profit margin, the proportion of various elements of cost (Labour, materials and manufacturing overheads) to sale may studied in detail.

Operating profit ratio

This ratio expresses the relationship between operating profit and sales. It is worked out by dividing operating profit by net sales. With the help of this ratio, one can judge the managerial efficiency which may not be reflected in the net profit ratio.

Net profit ratio

Net profit is obtained when operating expenses, interest and taxes are subtracted from the gross profit. Net profit margin ratio established a relationship between n

16

et profit and sales and indicates management’s efficiency in manufacturing, administering and selling products. This ratio also indicates the firm's capacity to withstand adverse economic conditions. A firm with a high net margin ratio would be in an advantageous position to survive in the face of falling

Selling prices, rising costs of production or declining demand for product

This ratio shows the earning left for share holders as a percentage of net sales. It measures overall efficiency of production, administration, selling, financing. Pricing and tax management. Jointly considered, the gross and net profit margin ratios provide a valuable understanding of the cost and profit structure of the firm and enable the analyst to identify the sources of business efficiency / inefficiency.

Return on investment:

This is one of the most important profitability ratios. It indicates the relation of net profit with capital employed in business. Net profit for calculating return of investment will mean the net profit before interest, tax, and dividend. Capital employed means long term funds.

Earnings per share

This ratio is computed by earning available to equity share holders by the total amount of equity share outstanding. It reveals the amount of period earnings after taxes which occur to each equity share. This ratio is an important index because it indicates whether the wealth of each share holder on a per share basis as changed over the period.

Operating expenses ratio

It explains the changes in the profit margin ratio. A higher operating expenses ratio is unfavourable since it will leave a small amount of operating income to meet interest, dividends. Operating expenses ratio is a yardstick of operating efficiency, but it should be used cautiously. It is affected by a number of factors such as external uncontrollable factors, internal factors. This ratio is computed by dividing operating expenses by sales. Operating expenses equal cost of goods sold plus selling expenses and general administrative expenses by sales.

17

CHAPTER 2

INDUSTRY PROFILE AND COMPANY PROFILE

MANUGACTURING INDUSTRY OVERVIEW

Manufacturing industry refers to those industries which involve in the manufacturing and processing of items and indulge in either creation of new commodities or in value addition. The manufacturing industry accounts for a significant share of the industrial sector in developed countries. The final products can either serves as a finished good for sale to customers or as intermediate goods used in the production process.

EVOLUTION OF MANUFACTURING INDUSTRY

Manufacturing industries came into being with the occurrence of technological and socio-economic transformations in the Western countries in the 18th-19th century. This was widely known as industrial revolution. It began in Britain and replaced the labour intensive textile production with mechanization and use of fuels.

Working of manufacturing industry:

Manufacturing industries are the chief wealth producing sectors of an economy. These industries use various technologies and methods widely known as manufacturing process management. Manufacturing industries are broadly categorized into engineering industries, construction industries, electronics industries, chemical industries, energy industries, textile industries, food and beverage industries, metalworking industries, plastic industries, transport and telecommunication industries.

Manufacturing industries are important for an economy as they employ a huge share of the labour force and produce materials required by sectors of strategic importance such as national infrastructure and defence. However, not all manufacturing industries are beneficial to the nation as some of them generate negative externalities with huge social costs. The cost of letting such industries flourish may even exceed the benefits generated by them.

ANALYSIS OF MANUFACTURING INDUSTRY

It suggests that the manufacturing industry has served as the pivotal factor in the economic development of a country. The same applies for the United States Of America, whose economy has been growing rapidly owing to the successful manufacturing industry. Manufacturing industry analysis also indicates that the manufacturing industry provides employment to many thereby contributing to the gross domestic product and per capita income of the country. Approximately 75% of the engineers as well as the scientists get employed in the manufacturing industry as recorded by a manufacturing industry analysis.

18

The Census bureau categorizes a particular manufactured product depending on the primary goods produced by the manufacturing industry.

Statistical data showing the impact of the manufacturing industry on economy:

In the year 1992, the expenditure incurred on the research and development by the manufacturing establishments was USD$91.2 billion in the United States of America. Out of this Non Governmental manufacturing establishments registered 79.4% of USD$91.2 billion

18% of GDP or gross domestic product in the year 1993 was due to revenues generated by the manufacturing industry, established according to reports of manufacturing industry analysis.

46.4 was the result obtained in order to find out the number of workers employed in every establishment. This figure was registered in the year 1992.

15% of shipments in the manufacturing segment were due to the material industry.

Capital stock has registered a steady rise for all the sectors of the manufacturing industry since 1982.

Employment opportunity in the manufacturing industry has declined comparatively. Manufacturing industry analysis also suggests that in some countries like China, technological knowhow has to be developed. Despite the fact that China is ranked fourth in the manufacturing productivity, due to technological lacunae, it is not being able to compete in the world market. Also needed are professionals well versed in the technological knowhow.

BATTERY MANUFACTURING INDUSTRY PROFILE

The Indian storage batteries market is approximately estimated at US$ 500 million with the automotive batteries segment 60 to 70 percent of the overall market value. In terms of volumes, the overall consumption of the automotive batteries could be around 6.3 million units with the 40 QE segment comprising around 1.2 to 1.3 million units per annum, Various batteries (clockwise from bottom left): two 9-volt, two AA, one D, a handheld ham radio battery, a cordless phone battery, a camcorder battery, one C, and three AAA.

There are two types of batteries, primary (disposable) and secondary (rechargeable), both of which convert chemical energy to electrical energy. Primary batteries can only be used once because they use up their chemicals in an irreversible reaction. Secondary batteries can be recharged because the chemical reactions they use are reversible; they are recharged by running a charging current through the battery, but in the opposite direction of the discharge current. Secondary, also called rechargeable batteries can be charged and discharged many times before wearing out. After weaning out some of the batteries can be recycled.

19

ABOUT BATTERY

A battery is perhaps the only gift of science where electric is stored by means of elector chemical potentials guided by electro comical reaction. Chemical reaction initiated by electricity. Which take place with the means of electron exchange between the reactions, as and when required the stored energy can be counted back to electro chemical reaction. In certain cases the electrical chemical reactions guiding the energy transformation is not reversible. Such batteries are called ordinary cells. Where the electro chemical reaction guiding energy transformation is reversible hence they can be reused through only after outing a required amount of electric energy once it gets exhausted. These batteries are called secondary batteries.

BATTERY HISTORY

A battery, which is actually an electric cell, is a device that produces electricity from a chemical reaction. Strictly speaking, a battery consists of two or more cells connected in series or parallel, but the term is generally used for a single cell. A cell consists of a negative electrode; an electrolyte, which conducts ions; a separator, also an ion conductor; and a positive electrode.

TIMELINE OF BATTERY HISTORY

1748 - Benjamin Franklin first coined the term "battery" to describe an array of charged glass plates.

1780 to 1786 - Luigi Galvani demonstrated what we now understand to be the electrical basis of nerve impulses and provided the cornerstone of research for later inventors like Volta.

1800 - Alessandro Volta invented the voltaic pile and discovered the first practical method of generating electricity. Constructed of alternating discs of zinc and copper with pieces of cardboard soiled in between the metals, the voltaic pile produced electrical current. The metallic conducting; - arc was used to carry the electricity over a greater distance. Alessandro Volta's voltaic pile was the first "wet cell battery" that produced a reliable, steady current of electricity.

1836 - Englishman, John F. Daniel invented the Daniel Cell that used two electrolytes: copper sulfate and zinc sulfate. The Daniel Cell was somewhat safer and less corrosive then the Volta cell.

1839 - William Robert Grove developed the first fuel cell, which produced electrical by combining hydrogen and oxygen.

20

1839 to 1842 - Inventors created improvements to batteries that used liquid electrodes to produce electricity. Bunsen (1842) and Grove (1839) invented the most successful.

1859 - French inventor, Gaston Planet developed the first practical storage lead-acid battery that could be recharged (secondary battery). This type of battery is

1899 - Wald mar Jenner invented the first nickel-cadmium rechargeable battery.

1901 - Thomas Alva Edison invented the alkaline storage battery. Thomas Edison's alkaline cell had iron as the anode material (-) and nickelic oxide as the cathode material (+).

1949 - Lew Urry developed the small alkaline battery in 1949. The inventor was working for the Eveready Battery Co. at their research laboratory in Parma, Ohio. Alkaline batteries last five to eight times as long as zinc-carbon cells, their predecessors.

1964 - Duracell was incorporated.

COMPANY PROFILE

INTRODUCTION

Incorporated in January 1947.

EXIDE is Asia’s largest exporter of batteries.

A veteran with 52 years of experience.

It has seven manufacturing units in India and five units apart from India.

It has corporate alumni of chloride group PLC, UK.

It provides 4.2 million SLI automotive batteries and 3 million industrial batteries with 300Ah capacity.

The types of batteries manufactured by EXIDE are:

Automotive Batteries

Industrial Batteries

Submarine batteries

The two main manufacturing units of EXIDE which are present in all its manufacturing plants are:

Automotive

VRLA (industrial)

It has products which has capacity ranging from 2.5Ah to 10,000Ah and more.

21

EXIDE also acquired the industrial/ manufacturing units of standard batteries ltd located at Taloja & kanchurmarg (Maharashtra), Guindy (Tamil Nadu), and plant at Ahmednagar (Maharashtra) from Cosepa Fiscal industries ltd as a going concern.

The manufacturing plants of EXIDE in India are:

Shamnagar (West Bengal)

Chinchwad (Pune)

Haldia (West Bengal)

Hosur (Tamil Nadu)

Talia (Maharashtra)

Ahmednagar (Maharashtra)

Bawal (Haryana)

The company’s Submarine batteries is mainly manufactured in the Pune manufacturing plant

It is the first company to design battery powered electrical boat and maintenance free batteries, traction batteries for wheel chairs and flat plate batteries for automated guided vehicles.

EXIDE today is a Rs 3606 cores power storage company.

22

HISTORY:

1916- Chloride Electric Storage Co. (CESCO) UK sets up trading operations in India as an import house.

1946- First factory set up in Shamnagar, West Bengal.

1947- Incorporated as Associated Battery Makers (Eastern) Limited on 31 January 1947 under the Companies Act.

1947- Incorporated Chloride International Limited (previously Exide Products Limited)

2000- Acquisition of 100% stake in Chloride Batteries S E Asia Pvt Ltd., Singapore and 49% stake in Associated Battery Manufacturers (Ceylon) Limited, Sri Lanka.

2003- Commissioned plant at Bawal, Haryana

2003- New joint venture in UK, ESPEX, with 51% holding.

2004- Associated Battery Manufacturers (Ceylon) Limited, Sri Lanka became a subsidiary consequent to acquiring further 12.50% Equity holding.

2005- Investment in 50% shareholding of ING VYSYA Life Insurance Company Limited

2007- Caldyne Automatics Ltd becomes 100% subsidiary consequent to acquiring the balance 49% shareholding.

2007- Investment with 26% shareholding in CEIL Motive Power Pty Ltd. A Joint Venture in Australia.

2007- Acquired 100% stake in Tandon Metals Ltd.

2008- Acquired 51% stake in Lead Age Alloys India Ltd.

2009- Divestment of shareholding in CEIL Motive Power Pty Ltd.

2012- Acquisition of Inverter manufacturing facility at Roorkee, Uttarakhand

2012- Technical Collaboration with East Penn Manufacturing Co., USA

2012- Acquisition of second Inverter manufacturing facility at Haridwar, Uttarakhand.

2012- Acquisition of balance 49% shares in ESPEX Batteries Limited, UK.

2013- Acquisition of remaining 26% shares of ING VYSYA Life Insurance Company adding a total of 100% stake.

2014- ING VYSYA renamed as “EXIDE LIFE INSURANCE COMPANY LTD.

23

PRESENT STATUS

Largest manufacturers and exporter of batteries in Asia.

Developed vast range of batteries through research and developments and has number of patents to its name

Manufacturing specific batteries for specific applications that tough the daily lives of millions of people and costumers of India

Thus justifies the slogan “India moves on EXIDE”

WHY EXIDE INDIA?

1) CLAIM LEADERSHIP

EXIDE is a dominant player in the industrial battery segment. The company exports batteries which have captured niches in south East Asian and European markets.

2) GLOBAL QUALITY

Developed and produced accordingly to international standards and ISO9001, 14001 and ISO/ TS- 16949.

Longer warranty time.

Lower total cost of ownership.

24

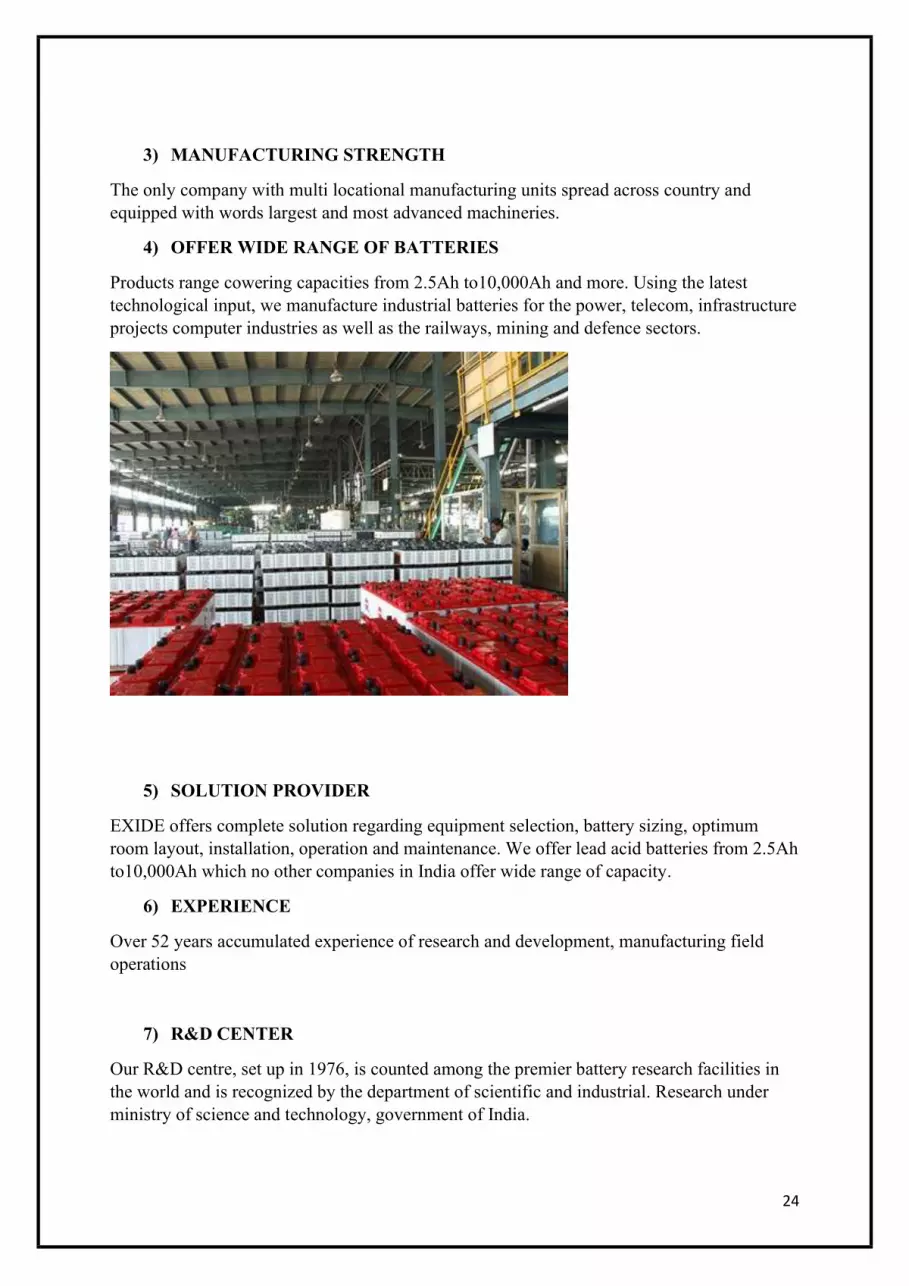

3) MANUFACTURING STRENGTH

The only company with multi locational manufacturing units spread across country and equipped with words largest and most advanced machineries.

4) OFFER WIDE RANGE OF BATTERIES

Products range cowering capacities from 2.5Ah to10,000Ah and more. Using the latest technological input, we manufacture industrial batteries for the power, telecom, infrastructure projects computer industries as well as the railways, mining and defence sectors.

5) SOLUTION PROVIDER

EXIDE offers complete solution regarding equipment selection, battery sizing, optimum room layout, installation, operation and maintenance. We offer lead acid batteries from 2.5Ah to10,000Ah which no other companies in India offer wide range of capacity.

6) EXPERIENCE

Over 52 years accumulated experience of research and development, manufacturing field operations

7) R&D CENTER

Our R&D centre, set up in 1976, is counted among the premier battery research facilities in the world and is recognized by the department of scientific and industrial. Research under ministry of science and technology, government of India.

25

8) SAFETY CONSCIOUS

Underwriters laboratories Inc. USA certifications for the products and available on request.

MANUFACTURING PLANTS OF EXIDE

MANUFACTURING PLANTS

STATE ESTABLISHED YEAR

Shamnagar

Chinchwad

Haldia

Hosur

West Bengal

Pune

West Bengal

Tamil Nadu

1946

1969

1981

1997

26

Taloja

Ahmednagar

Bawal

Maharashtra

Maharashtra

Haryana

1998

1998

2003

EXECUTIVE COMMITTEE

Mr. G. Chatterjee

Mr. A. K. Mukherjee

Mr. Nadeem Kazim

Mr. Subir Chakraborty

Mr. Arun Mittal

Mr. Jitendra Kumar

Mr. Achim Luelsdorf

Mr. Arnab Saha

BOARD OF DIRECTORS

Mr. R. G. Kapadia, Chairman & Independent Director

Mr. R. B. Raheja ,Vice-Chairman & Non-Executive Director

Mr. P. K. Kataky, Managing Director & Chief Executive Officer (till April 30, 2016)

Mr. G. Chatterjee, Managing Director & Chief Executive Officer (w.e.f May 01, 2016)

Mr. A. K. Mukherjee, Director- Finance & Chief Financial Officer

Mr. Nadeem Kazim, Director-HR & Personnel

Mr. Subir Chakraborty, Director-Automotive

Mr. Arun Mittal, Director-Industrial (i.e. May 01, 2016)

Mr. Vijay Aggarwal, Independent Director

Ms. Mona N. Desai, Independent Director

Mr. Sudhir Chand, Independent Director

Mr. Bharat D. Shah, Independent Director

Mr. Nawshir H. Mirza, Independent Director

27

FACTORY PROFILE

Fourth factory

Established in 20th may, 1996

It manufactures two type of batteries

Automotive batteries

Industrial batteries (VRLA)

Manufacturing and operation started on June 1997

Floor space: 50,000 sq.

Industrial plant

VRLA plant inauguration- April 1997

VRLA commercial production- June 1997

ISO 9001 certification- October 1998

UL certification- December 2000

Automotive plant

Auto project commenced- October 1997

Auto plant inauguration- July 1998

Auto new plant project started- February 2000

New plant inauguration- December 2000

28

NATURE OF BUSINESS CARRIED

Exide HOSUR plant is the fourth factory for Exide industry with a turnover of 6900 crores in the year 2015-16. It is found in 1997.It has total land area of 74.5 of which 42% is green zone. HOSUR Exide plant is the more productive unit. It has been the two productive plants like Auto and VRLA type batteries.

Auto plant batteries are used for car, truck, and tractor.

VRLA plant batteries are used for railways, ship.

Automotive Batteries

In the domestic market, the Company sells its products under EXIDE, SF, SONIC and Standard Furukawa Brands. ‘EXIDE’ and ‘SF” are its flagship brands. In the international market the products are sold mainly under DYNEX, INDEX & SONIC brands. The Company supplies batteries to almost all the car and two-wheeler manufacturers in the country.

The Company has a market share of 72% in case of Automotive OEM and 70% in case of Organized Retail. The Company also manufactures submarine batteries

Industrial Batteries

The Company designs and manufacture its industrial batteries in a wide range from 2.5 Ah to 20,600 Ah in conventional flooded and Valve Regulated Lead Acid (VRLA) design. In domestic market, the Company sell its products mainly under EXIDE, INDEX, SF, CEIL & POWER SAFE brands and in the international markets mainly under CEIL, CHLORIDE and INDEX brands. Lead acid and Nickel-Cadmium batteries.

Submarine Batteries

The Company also manufactures high-end submarine batteries (Type 1, 2 & 3). The Company manufactures two to three submarine batteries a year to meet the country’s defence requirements. The Company is one of the five companies in the World which has the capability to make submarine batteries for both Russian and German types. With the government’s permission, in recent years, the Company has exported to Algeria

EXIDE HOSUR- DREAM

To become a formidable global enterprise through manufacturing excellence.

FOCUS OF EXIDE- HOSUR

Quality

29

Productivity

Cost

Delivery

Safety and cleaner environment

Highly motivated team

Fast response (before and after sales)

Long lasting term costumer relationship

VISION

Providing credible value addition to customers, employees and shareholders while simultaneously being recognized by society as a responsible corporate citizen. In addition, achieving operational excellence while addressing and taking steps towards environmental protection.

MISSION

Strive to carefully balance the interest of all stakeholders; to fulfil aspirations of the employees and to passionately pursue excellence without deviating from our core values.

CORE VALUES

Customer Orientation

Personal Integrity and Commitment

Teamwork and Mutual Support

Employee Development and Involvement

Striving for Excellence

Management by Processes and Facts

Responsible Corporate Citizenship

OBJECTIVES AND GOALS OF THE COMPANY

To modernize , upgrade and improve facilities or higher production and productivity

To achieve better Quality in Products.

To Strengthen the Marketing Organization to effectively Compete in National and international markets.

30

AWARDS/ CERTIFICATES AND RECOGNITION

Exide wins CFO of the year award in automotive and auto-ancillary category from CNBC-TV18

Frost & Sullivan Sustainability 4.0 Awards - 2016

WORK FLOW MODEL

31

PRODUCTION DEPARTMENT PRINCIPLE

“TO ACHIEVE ZERO DEFECTS”

In production area they are using many process to produce a battery, some process are grid casting, small parts casting, assembling the parts, acid filling, heat sealing, pole bearing, air leakage testing & charging and testing.

BRIEF OUTLINE OF THE PROCESS OF MANUFACTURE OF VALUE REGULATED LEAD ACID BATTERIES AND the basic raw material for manufacturing a lead acid battery &AUTOMOTIVE BATTERIES.

32

Automotive battery (a captive rechargeable source of energy) is lead. The essential steps for manufacture are as follows.

QUALITY POLICY OF THE COMPANY

The aim of the company is to always provide satisfaction to customers.

The company will develop design, produce and market products and services that cater continuously to the needs and expectation of customer and succeed in gaining/retaining a competitive edge.

A quality system meeting international standards will be implemented and maintained.

T P M POLICY

The members of Exide Industrial Limited in our pursuit of excellence and customer satisfaction are committed to achieve optimum utilization of all available resources by implementation of total productive maintenance

AIM OF ORGANIZATION

1. Improve the overall equipment efficiency by eliminating all losses.

Strive for zero break downs, zero defects and zero accidents.

2. Train, involve and empower people.

3. Create a safe and clean working environment.

33

ENVIRONMENT POLICY

We, the member of Exide Industries Limited., in the pursuit of core value of responsible corporate citizenship are committed to the issues addressed in the policy at all our locations during the marketing, design, manufacture sales and after sales support of lead – acid batteries.

It is the policy of the company to:

1. Minimize the adverse impact of our activities, products and service by implementing an environmental management system.

2. Prevent pollution through waste minimization at source, recovery / treatment of emission and releases conservation of energy, recycling & optimum use of resources.

3. Continuously improve our environmental performance through setting and reviewing and associate objectives and targets and periodic evaluation.

PRODUCTS AND SERVICE PROFILE

1. Automotive batteries For cars, Jeeps and commercial vehicles,

Passenger cars, two wheelers to tractors,

2. Heavy duty batteries For trucks and tractors

3. Light weight batteries For wireless transmission batteries

4. Transaction batteries For material handling equipment

5. Train lighting cells For railway coaches

6. Stationary batteries For telecommunications, telephone, Emergency lighting

34

Lead acid storage for automobile, motorcycle, genets, trawlers, VLRA, industrial stand by, motive power, submarines (2.5 Ah to 12600 Ah)

SPECIAL FEATURES

Maintenance free

Easy handling easy installation

Ready to use

Long service life

Excellent charge retention and recovery ability

High reliability

PRODUCT PROFILE

Types of batteries produced in VRLA plant

SL.NO Type Voltage Ampere hour

Customer Car type

1 4AH/6V 6V 4Ah BPL Lantern

2 4AH/6VR 6V 4Ah BPL Lantern

3 5AH/12V 12V 4.5Ah APC UPS

4 4.5H/12V 12V 7Ah APC UPS

5 7AH 12V 7Ah APC UPS

6 9AHR 12V 9Ah APC UPS

7 9AHR 12V 10Ah APC UPS

8 10AH 12V 10Ah APC UPS

9 10AHR 12V 10Ah APC UPS

7. Submarine batteries

For defence Requirements Company Manufacturers, two or three submarine batteries a year, for new generation Submarine to the Indian navy

35

10 12AH 12V 12Ah APC UPS

11 12AHR 12V 12Ah APC UPS

Type of Batteries products in Auto plant

SL.NO Type voltage Ampere hour Customer

1 38B20L(MF) 12.40V 35 MARKET

2 38B20R(MF) 12.40V 35 MARKET

3 55B24L(MF) 12.40V 45 HYUNDAI

4 55B24R(MF) 12.40V 45 MARUTHI

5 95D31L(MF) 12.40V 80 HM LANCER

6 95D31R(MF) 12.40V 80 HM LANCER

7 MF50Z 12.40V 60 MARKET

8 MF70Z 12.40V 75 ASHOKA LYLAND

9 MF75T 12.40V 75 MARKET

10 MF88T 12.40V 88 MARKET

36

11 MF99T 12.40V 99 MARKET

12 MFS40SV 12.40V 32 MARKET

13 55B24(MF) 12.40V 45 HYUNDAI

14 95D31L(MF) 12.40V 80 HM LANCER

15 MF40SV 12.40V 35 HYUNDAI

16 MF70Z 12.40V 75 ASHOKA LYLAND

17 MF70L 12.40V 65 TOYOTA

18 38B20L(MF) 12.40V 86 HYUNDAI

19 55B20L(MF 12.40V 45 HYUNDAI

AREA OF OPERATION

Exide industrial limited manufacturing and distributing the batteries in globally, It has National and regional customers where the activities takes place according to the order given by customers that to the legal right. The distribution net work is as follows

COMPETITORS INFORMATION

The company faces competition on two fronts. It faces competition from new player in the organized sector who is focusing on advertising and publicity for promoting their brands. The company also faces competition from low cost products from the unorganized sector. There are many firms or agencies dealing with batteries. They produces, markets the product. EXIDE industries ltd facing a huge competition from companies like:

For automotive batteries

PANASONIC

AMARON

WIPRO

MICROTEX

AMCO-YUASA

PRESTOLITE

OKAYA

VARTA

37

For industrial batteries

AMRAJA

HBL

STAR

NED ENERGY SYSTEM

KIRL OSKAR

PANASONIC

BB-CHINA

ROCKET-KOREA

MAJOR CUSTOMERS

AUTOMOTIVE BATTERIES

HYUNDAI

HMT LTD.

MARUTI

TATA

TOYOTA

BAJAJ AUTO

FIAT

HERO

HONDA

PIAGGO

ESCORTS

MAHINDRA

ASHOK LEYLAND

GENERAL MOTORS

SWARAJ MAZADA

MITSUBISHI MOTORS

JOHN DERE

38

EICHER

MNC’S

INDUSTRIAL BATTERIES

MOTOROLA

ERICSSON

EMERSON

SIEMENS

DUBAS

BHEL

BSNL

VSNL

BEL

NTPC

GAIL

ABB

GODREJ

KPCL

INDIAL RAILWAYS

LUCENT TECHNOLOGY

TVS ELECTRONICS

BRANDS OF EXIDE

CHLORIDE

INDEX

DYNEX

Standard Furukawa(sf sonic)

JUPITER

CONREX

CHAMPION

LITTLE CHAMP

39

BOSS

INFRASTRECTURAL FACILITIES

The Exide has eight manufacturing plants producing world class products. Exide factories are located strategically around the country to provide logistic support for its production of over five million batteries per annum.

A technology tie up with Shin Kobe the makers of world class Hitachi VRLA batteries has given Exide the technological edge in maintenance free catteries. Other strategic technology agreement with Furukawa, Japan and Oldham, U, K. has given Exide competitive edge in proving the most reliable solutions for packaged power.

Environmental policy

Safety measures facilities

Medical facilities

Effluents training

Transportation facilities

Canteen facilities

FUTURE GROWTH AND PROSPECTUS

To further expand the business to other regions of Karnataka, Tamil Nadu and Andhra Pradesh.

To set up a sophisticated research and development so that the company may have its own new styles and designs of products that suits the modern fast moving life style.

Objectives and Goals of Company

To modernize , upgrade and improve facilities or higher production and productivity

To achieve better Quality in Products.

To Strengthen the Marketing Organization to effectively Compete in National and international markets.

To get ISO certifications

To maintain and developed highly motivated human Resources to achieve Professional competence and ensure career development of its work force.

To maintain Market Shares in Industry.

ORGANIZATIONAL STRUCTURE

40

SYSTEM

Procedure and process such as information system manufacturing process of budgeting and control process.

Systematic doing day to day work.

All the information catching on SAP.

Production and planning improvement.

EXECUTIVE CHAIRMAN

M D & CEO

DIRECTOR (INDUSTRIAL)

CHIEF OPERATING MANAGER

PRODUCTION

AUTOMOTIVE

PRODUCTION

INDUSTRIAL

PERSONNEL

ACCOUNTS

MATERIAL

CUSTOMER SUPPORT

SERVICE

HEAD

PRODUCTION

AUTOMOTIVE

HEAD

PRODUCTION

INDUSTRIAL

HEAD

ACCOUNTS

HEAD

MATERIAL

HEAD CUSTOMER

SUPPORT SERVICE

HEAD

PERSONNEL

ASSISTANT

MANAGER

MANAGER

ASSISTANT

MANAGER

ASSISTANT

MANAGER

ASSITTMANAGE

R

ASSISTANT

MANAGER

ASSISTANT

MANAGER

MANAGER

41

Accounting procedure:

Maintenance of record as per the accounting standards is maintained.

Ensuring correct & proper material accounting in & out of the factory.

Pay roll accounting.

Creditors bill passing &all payments.

Stock transfer &direct sales invoicing.

Product costing.

Budgeting & budgetary controls.

Fixed assets accounting.

STYLE

Democratic style of industry.

Management style is vertical style.

Democratic style

Here leadership style is democratic because all the heads of departments will have meeting daily so all takes decision. So it is called as democratic style and suggestion committee takes suggestions

Management style

TOP

LEVEL

MIDDLE LEVEL

MANAGEMENT

LOWER LEVEL

MANAGEMENT

42

STAFF

The people in the enterprise and their socialization into the organization.

Roles & Responsibilities of Employees

It is the responsibility of every employee’s to perform work in safe manner.

Suggestion for improvement.

Suggestion for poke – yoke techniques.

Short & separate hazardous wastes.

SHARED VALUE

Fundamental axioms that organization believes in and people respect and work towards. Core values also set the tone of the organization culture the core value of our organization are given bellows:

Customer orientation.

Personal integrity and commitment.

Team work and mutual support.

People development and involvement.

Striving for excellence.

Management by processes and facts.

SKILLS

Technical skill requirement: ITI, Diploma, Mechanical engineers

Nontechnical skill requirement: MBA at top management, BBM & B.com at operational level

CSR ACTIVITIES OF EXIDE

eradicating hunger, poverty and malnutrition, (promoting health care including preventive health care) and sanitation including contribution to the Swach Bharat Kosh set-up by the Central Government for the promotion of sanitation and making available safe drinking water

Castes, the Scheduled Tribes, other backward classes, minorities and women

Contribution or funds provided to technology incubators located within academic institutions which are approved by the Central Government

Rural development projects

43

Any other projects or activities as may be approved by the Central Government pursuant to section 135 of the Companies Act, 2013, from time to time

SWOT ANALYSIS

S-Strengths:

EXIDE is a super brand

It has wide distribution network

Appropriate infrastructure for condition of training

Partnership with various technical & management institution for providing a continuous supply of fresh graduate

Streamlined system of recruitment

Providing the necessary welfare facilities for the employees in the comfort zone & increasing the retention level of the employees

IR/LR relation very conductive for the smooth functioning of the unit

W-Weakness:

Difficult to change to an alternative line production with the existing machinery

High employee turnover

Lack of clarity and transparency in upward/down ward communication.

Evaluation of effectiveness of training programmers being imparted.

No clear job description for various levels resulting in dual reporting relationships.

Performance appraisal system: its approach, effectiveness acceptability.

Effectiveness of organization health study.

44

O-Opportunities:

Opportunity to expand globally

To have in-house online dilution plant for sulphuric acid. This will not only reduce the cost of acid procurement but also will help us to consume the recovered acidic water from plate washing thereby achieving reduction in effluent generation.

To convert the accumulated calcium sulphate solid sludge to useful products in construction industry with the help of IISc Bangalore.

Further reduction in tank formation by increasing the jar formation of VRLA batteries.

To start using rain water in process after necessary treatment. At present we are this only for the green belt development. Storage caexidity of rain water reservoir is 30000KL.

To extend green belt in additional to hectares.

T-Threats:

Fast changing consumer’s tastes & preferences

Liberalization policy of the government of India

Fast changing market conditions

High costs price in view of overheads

Importing components at the low cost from china

Increasing competition (Nationality & Globally)

Unfavourable duty structure

Slow growth rate in profits expected.

45

CHAPTER 3

RESEARCH AND METHODOLOGY

NEED OF THE STUDY

The study enables us to have access to various facts of the organization. It helps in understanding the needs for the importance and advantage of materials in the organization, the study also helps to exposure our minds to the integrated materials management the various procedures, methods and technique adopted by the organization.

The study provides knowledge about how the theoretical aspects are put in the organization.

OBJECTIVES OF STUDY

To analyze the profitability position of the company.

To assess the return on investment.

To analyze the asset turnover ratio.

To determine the solvency position of company.

LIMITATIONS

• The study was limited to only FIVE years Financial Data.

46

•The study is purely based on secondary data which were taken primarily from Published annual reports of EXIDE INDUSTRIES LTD.

•The ratio is calculated from past financial statements and these are not indicators of future.

•The study is based on only on the past records.

• Non availability of required data to analysis the performance.

•The short span of the time provided also one of limitations.

Research Methodology:

Research is designed as a systematic, gathering recording and analysis of data about problem relating to any particular field.

It determines strength reliability and accuracy of the project.

Research Design:

Research design pertains to the great research approach or strategy adopted for a particular project. A research project has to be conducted making sure that the data is collected adequately and economically.

The study used Descriptive research design for the purpose of getting an insight over the issue. It is to provide an accurate picture of some aspects of market environment. Descriptive research is used when the objective is to provide systematic description that is as factual and accurate as possible.

Method of data collection:

Secondary data - Through the internet and published data.

In view of the objects of the study listed above an exploratory research design has been adopted. Exploratory research is one which is largely interprets and already available information and it lays particular emphasis on analysis and interpretation of the existing and available information.

•To know the financial status of the company.

47

•To know the credit worthiness of the company.

•To offer suggestions based on research finding.

48

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

Schedule of changes in working capital:

As the study is confined to working capital management more attention is given towards preparation of schedule of changes in working capital. Schedule of changes in working capital is a statement prepared with the help of current account balances appearing in Balance sheet of two dates increase or decrease in the values of current accounts is noted and its effect on working capital is ascertained.

STATEMENT OF CHANGES IN WORKING CAPITAL OF 2015-16&2016-17

PARTICULARS 2015-16

2016-17 STATEMENT OF CHANGES IN WORKING CAPITAL

INCREASE DECREASE

A. CURRENT ASSETS

Current investment

inventories

trade receivables

cash and cash equivalents

short term loans and advances

other current assets

649.07

1160.71

426.05

62.79

131.33

0.21

324.68

1407.39

591.81

220.51

63.17

782.61

324.39

346.68

165.76

157.72

68.16

782.4

TOTAL CURRENT ASSETS (A)

2430.16 3390.17 1352.56 392.55

49

B. CURRENT LIABILITIES

Short term borrowings

Trade payables

Other current liabilities

Short term provisions

24.52

689.82

244.75

115.82

48.61

995.39

593.04

183.24

24.09

305.57

348.29

67.42

TOTAL CURRENT LIABILITIES (B)

1074.91 1820.28 745.37

NET WORKING CAPITAL (A-B)

1355.25 1569.89 607.19 392.55

NET INCREASE IN WORKING CAPITAL

214.64 214.64

TOTAL 1569.89 1569.89 607.19 607.19

STATEMENT OF CHANGES IN WORKING CAPITAL OF 2017-18&2018-19

PARTICULARS 2016-17

2017-18 STATEMENT OF CHANGES IN WORKING CAPITAL

INCREASE DECREASE

A. CURRENT ASSETS

Current investment

inventories

trade receivables

cash and cash equivalents

short term loans and advances

other current assets

324.68

1407.39

591.81

220.51

63.17

782.61

609.52

1302.86

658.42

286.82

76.13

595.69

284.84

104.53

66.61

66.31

12.96

186.92

50

TOTAL CURRENT ASSETS (A)

3390.17 3529.44 430.72 291.45

B. CURRENT LIABILITIES

Short term borrowings

Trade payables

Other current liabilities

Short term provisions

48.61

995.39

593.04

183.24

10.51

1120.86

352.91

199.12

38.1

125.47

240.13

15.88

TOTAL CURRENT LIABILITIES (B)

1820.28 1683.4 141.35 278.28

NET WORKING CAPITAL (A-B)

1569.89 1846.04 289.37 13.22

NET INCREASE IN WORKING CAPITAL

276.15 276.15

TOTAL 1846.04 1846.04 289.37 289.37

51

STATEMENT OF CHANGES IN WORKING CAPITAL OF 2017-18& 2018-19

PARTICULARS 2017-18

2018-19

STATEMENT OF CHANGES IN WORKING CAPITAL

INCREASE DECREASE

A. CURRENT ASSETS

Current investment

inventories

trade receivables

cash and cash equivalents

short term loans and advances

other current assets

609.52

1302.86

658.42

286.82

76.13

595.69

478.90

1646.36

690.15

207.47

100.68

596.83

130.62

343.5

31.73

79.35

24.55

1.14

TOTAL CURRENT ASSETS (A)

3429.44 3720.39 400.92 209.97

B. CURRENT LIABILITIES

Short term borrowings

Trade payables

Other current liabilities

Short term provisions

10.51

1120.86

352.91

199.12

51.36

1045.63

365.07

257.03

40.85

75.23

12.16

57.91

TOTAL CURRENT LIABILITIES (B)

1683.4 1719.09 110.92 75.23

NET WORKING CAPITAL (A-B)

1846.04 2001.3 290 134.74

155.26 155.26

TOTAL 2001.3 2001.3 290 290

52

STATEMENT OF CHANGES IN WORKING CAPITAL OF 2018-19&2019-20

PARTICULARS 2018-19

2019-20

STATEMENT OF CHANGES IN WORKING CAPITAL

INCREASE DECREASE

A. CURRENT ASSETS

Current investment

inventories

trade receivables

cash and cash equivalents

short term loans and advances

other current assets

478.90

1646.36

690.15

207.47

100.68

596.83

1254.69

1245.88

722.16

293.99

132.57

527.97

775.79

400.48

32.01

86.52

31.89

68.86

TOTAL CURRENT ASSETS (A)

3720.39 4177.26 926.21 469.34

B. CURRENT LIABILITIES

Short term borrowings

Trade payables

Other current liabilities

Short term provisions

51.36

1045.63

365.07

257.03

108.80

1132.14

501.94

285.47

57.44

86.51

136.87

28.44

TOTAL CURRENT LIABILITIES (B)

1719.09 2028.35 309.26

NET WORKING CAPITAL (A-B)

2001.3 2148.91 616.95 469.34

NET INCREASE IN WORKIN CAPITAL

147.61 147.61

TOTAL 2148.91 616.95 616.95

53

CONSOLADATED BALANCE SHEET OF EXIDE COMPANY

Apr 19-Mar 20

Apr 18-

Mar 19

Apr 17-

Mar 18

Apr16-

Mar 17

Apr 15-

Mar 16

EQUITIES AND LIABILITIES

SHAREHOLDER'S FUNDS

Equity Share Capital

85.00 85.00 85.00 85.00 85.00

Total Share Capital

85.00 85.00 85.00 85.00 85.00

Revaluation Reserves

50.40 36.61 38.68 40.37 42.22

Reserves and Surplus

4,194.99 3,719.43 3,335.98 2,954.32 2,560.13

Total Reserves and Surplus

4,245.39 3,756.04 3,374.66 2,994.69 2,602.35

Total Shareholders Funds

4,330.39 3,841.04 3,459.66 3,079.69 2,687.35

Minority Interest

14.61 12.78 11.68 11.16 12.50

Policy Holders Funds

8,634.83 8,040.89 7,149.73 6,257.44 0.00

NON-CURRENT LIABILITIES

Long Term Borrowings

1.90 2.62 4.30 2.38 2.58

54

Deferred Tax Liabilities [Net]

130.51 131.47 111.78 103.66 87.02

Other Long Term Liabilities

143.87 104.62 46.41 7.36 4.39

Long Term Provisions

41.50 34.84 26.92 26.74 57.08

Total Non-Current Liabilities

317.78 273.55 189.41 140.14 151.07

CURRENT LIABILITIES

Short Term Borrowings

108.80 51.36 10.51 48.61 24.52

Trade Payables

1,132.14 1,045.63 1,120.86 995.39 689.82

Other Current Liabilities

501.94 365.07 352.91 593.04 244.75

Short Term Provisions

285.47 257.03 199.12 183.24 115.82

Total Current Liabilities

2,028.35 1,719.09 1,683.40 1,820.28 1,074.91

Total Capital And Liabilities

15,325.96 13,887.35 12,493.88 11,308.71 3,925.83

ASSETS

NON-CURRENT ASSETS

Tangible Assets

1,382.61 1,175.96 1,079.75 1,075.76 1,045.55

Intangible Assets

27.07 23.37 24.47 19.62 11.98

55

Capital Work-In-Progress

192.46 114.57 62.72 60.77 27.39

Fixed Assets 1,602.14 1,313.90 1,166.94 1,156.15 1,084.92

Non-Current Investments

6,992.36 5,869.18 4,794.30 3,696.64 344.38

Deferred Tax Assets [Net]

0.00 0.00 0.00 0.00 0.15

Long Term Loans And Advances

128.76 199.05 131.68 105.59 18.41

Other Non-Current Assets

1,843.54 2,202.93 2,289.62 2,378.26 1.10

Total Non-Current Assets

11,148.70 10,166.96 8,964.44 7,918.54 1,495.67

CURRENT ASSETS

Current Investments

1,254.69 478.90 609.52 324.68 649.07

Inventories 1,245.88 1,646.36 1,302.86 1,407.39 1,160.71

Trade Receivables

722.16 690.15 658.42 591.81 426.05

Cash And Cash Equivalents

293.99 207.47 286.82 220.51 62.79

Short Term Loans And Advances

132.57 100.68 76.13 63.17 131.33

Other Current Assets

527.97 596.83 595.69 782.61 0.21

Total Current Assets

4,177.26 3,720.39 3,529.44 3,390.17 2,430.16

56

Total Assets 15,325.96 13,887.35 12,493.88 11,308.71 3,925.83

OTHER ADDITIONAL INFORMATION

CONTINGENT LIABILITIES, COMMITMENTS

Contingent Liabilities

732.44 407.70 470.73 443.35 280.95

BONUS DETAILS

Bonus Equity Share Capital

54.15 54.15 54.15 54.15 54.15

NON-CURRENT INVESTMENTS

Non-Current Investments Quoted Market Value

7,037.20 6,063.85 4,604.58 3,742.88 17.99

Non-Current Investments Unquoted Book Value

176.72 85.81 8.21 8.72 318.16

CURRENT INVESTMENTS

Current Investments Quoted Market Value

322.19 332.59 229.91 140.43 100.00

Current Investments Unquoted Book Value

932.84 148.56 379.33 184.26 549.07

57

CONSOLADATED PROFIT AND LOSS A/C OF EXIDE COMPANY

Apr 19-

Mar 20

Apr 18-

Mar 19

Apr 17-

Mar 18

Apr16-

Mar 17

Apr 15

Mar 16

Revenue From Operations [Gross]

9,986.42 9,946.12 8,859.71 7,154.71 5,882.31

Less: Excise/Service Tax/Other Levies

920.83 786.11 793.38 793.58 563.64

Revenue From Operations [Net]

9,065.59 9,160.01 8,066.33 6,361.13 5,318.67

Other Operating Revenues 413.85 374.94 242.52 4.76 0.00

Total Operating Revenues 9,479.44 9,534.95 8,308.85 6,365.89 5,318.67

Other Income 135.09 95.15 70.80 56.05 41.46

Total Revenue 9,614.53 9,630.10 8,379.65 6,421.94 5,360.13

EXPENSES

Cost Of Materials Consumed

4,121.90 4,827.48 3,917.17 4,208.69 3,467.88

Purchase Of Stock-In Trade 66.83 113.14 100.37 74.03 49.85

58

Changes In Inventories Of FG,WIP And Stock-In Trade

240.11 -289.02 -11.69 -200.30 -56.89

Employee Benefit Expenses 851.10 760.93 682.12 403.17 330.38

Finance Costs 1.65 3.21 7.61 9.06 14.91

Depreciation And Amortization Expenses

179.96 155.32 140.40 122.00 108.37

Other Expenses 3,144.39 3,185.51 2,756.96 1,028.16 783.00

Total Expenses 8,605.94 8,756.57 7,592.94 5,644.81 4,697.50

Profit/Loss Before Exceptional, Extraordinary Items And Tax

1,008.59 873.53 786.71 777.13 662.63

Profit/Loss Before Tax 1,008.59 873.53 786.71 777.13 662.63

Tax Expenses-Continued Operations

Current Tax 293.27 235.83 232.94 220.61 182.04

Less: MAT Credit Entitlement

0.00 0.53 0.00 0.00 0.00

Deferred Tax -1.10 21.90 7.61 16.52 15.90

Total Tax Expenses 292.17 257.20 240.55 237.13 197.94

Profit/Loss After Tax And Before Extraordinary Items

716.42 616.33 546.16 540.00 464.69

Profit/Loss From Continuing Operations

716.42 616.33 546.16 540.00 464.69

Profit/Loss For The Period

716.42 616.33 546.16 540.00 464.69

Minority Interest -2.72 -1.78 -1.50 -1.87 -3.05

Share Of Profit/Loss Of Associates

0.00 0.00 0.00 11.22 -15.58

Consolidated Profit/Loss After MI And Associates

713.70 614.55 544.66 549.35 446.06

59

OTHER ADDITIONAL INFORMATION

EARNINGS PER SHARE

Basic EPS (Rs.) 8.00 7.00 6.00 6.00 5.00

Diluted EPS (Rs.) 8.00 7.00 6.00 6.00 5.00

DIVIDEND AND DIVIDEND PERCENTAGE

Equity Share Dividend 204.00 187.00 153.00 136.00 127.50

Tax On Dividend 41.01 33.74 25.77 22.45 20.67

Liquidity Ratio

It measures the ability of the firm to meet its short-term obligations that is capacity of the firm to pay its current liabilities as and when they fall due. Thus these ratios reflect the short-term financial solvency of a firm. A firm should ensure that it does not suffer from lack of liquidity. The failure to meet obligations on due time may result in bad credit image, loss of creditors confidence, and even in legal proceedings against the firm on the other hand very high degree of liquidity is also not desirable since it would imply that funds are idle and earn nothing. So therefore it is necessary to strike a proper balance between liquidity and lack of liquidity.

1. CURRENT RATIO:

The current ratio is a liquidity ratio that measures a company's ability to pay short-term and long-term obligations. To gauge this ability, the current ratio considers the current total assets of a company (both liquid and illiquid) relative to that company's current total liabilities.

FORMULA:

𝐶𝑈𝑅𝑅𝐸𝑁𝑇𝑅𝐴𝑇𝐼𝑂 =𝐶𝑈𝑅𝑅𝐸𝑁𝑇𝐴𝑆S𝐸𝑇𝑆

𝐶𝑈𝑅𝑅𝐸𝑁𝑇𝐿𝐼𝐴𝐵𝐼𝐿𝐼𝑇𝐼𝐸𝑆

60

TABLE-1

YEAR CURRENT ASSETS(RS)

CURRENT LIABILITIES(RS)

CURRENT RATIO

2015-16

2430.16 1074.91 2.26

2016-17

3390.17 1820.28 1.86

2017-18

3529.44 1683.40 2.10

2018-19

3720.39 1719.09 2.16

2019-20

4177.26 2028.35 2.06

GRAPH-1:

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2015-162016-17 2017-18 2018-19 2019-20

CURRENT RATIO

CURRENT RATIO

61

ANALYSIS:

The current ratio in the year 2018-19 is 2.26, in the year 2016-17 is 1.86, in the year 2017-18 is 2.10, in the year 2015-16 is 2.16 and in the year 2016-17 is 2.06.

INTERPRETATION:

From the analysis done in the previous step, it is interpreted that the current ratio has decreased in2016-17 compared to 2012-13, again increased in the year 2017-18 , again increased in 2018-19 and again decreased in the year 2016-17.

2. QUICK / LIQUID RATIO:

The quick ratio is a measure of how well a company can meet its short-term financial liabilities, also known as the acid-test ratio. It is used to supplement the information given by the current ratio.

FORMULA:

𝑄𝑈𝐼𝐶𝐾𝑅𝐴𝑇𝐼𝑂 =𝑄𝑈𝐼𝐶𝐾 (𝑂𝑅) 𝐿𝐼𝑄𝑈𝐼𝐷𝐴𝑆𝑆𝐸𝑇𝑆

𝐶𝑈𝑅𝑅𝐸𝑁𝑇𝐿𝐼𝐴𝐵𝐼𝐿𝐼𝑇𝐼𝐸𝑆

TABLE-2:

YEAR LIQUID ASSETS

CURRENT LIABILITIES

QUICK ASSETS

2015-16 488.84 1074.91 0.45

2016-17 812.32 1820.28 0.44

2017-18 945.24 1683.40 0.56

2018-19 897.62 1719.09 0.52

2019-20 1016.15 2028.35 0.50

62

GRAPH 2

ANALYSIS:

The quick ratio in the year2012-13 is 0.45, in the year2019-20 is 0.44, in the year 2018-19 is 0.56, in the year 2019-20 is 0.52 and in the year 2018-19 is 0.50.

INTERPRETATION:

From the analysis done In the previous step, it is interpreted that the quick ratio has decreased in the year 2019-20 compare to year 2012-13, again increased in the year 2018-19, again decreased in the year 2019-20 and again decreased in the year 2018-19.

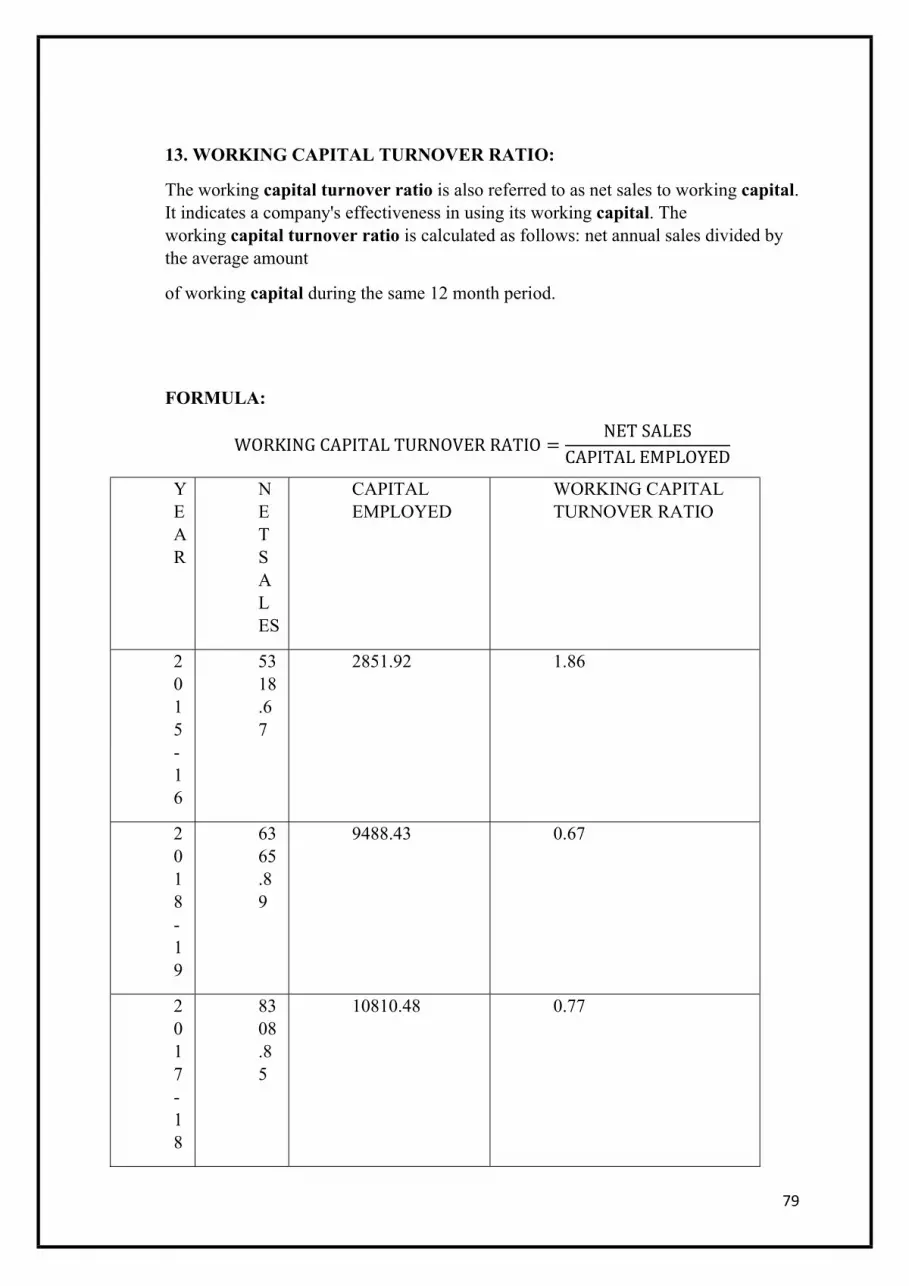

3. WORKING CAPITAL TURNOVER RATIO:

The working capital turnover ratio is also referred to as net sales to working capital. It indicates a company's effectiveness in using its working capital. The working capital turnover ratio is calculated as follows: net annual sales divided by the average amount of working capital during the same 12 month period.

0

0.1

0.2

0.3

0.4

0.5

0.6

2015-16 2016-17 2017-18 2018-19 2019-20

QUICK ASSETS

quick assets

63

FORMULA:

𝑊𝑂𝑅𝐾𝐼𝑁𝐺𝐶𝐴𝑃𝐼𝑇𝐴𝐿𝑇𝑈𝑅𝑁𝑂𝑉𝐸𝑅𝑅𝐴𝑇𝐼𝑂 =𝑁𝐸𝑇𝑆𝐴𝐿𝐸𝑆

𝑁𝐸𝑇𝑊𝑂𝑅𝐾𝐼𝑁𝐺𝐶𝐴𝑃𝐼𝑇𝐴𝐿

TABLE-3:

YEAR NET SALES

NET WORKING CAPITAL

WORKING CAPITAL TURNOVER RATIO

2015-16 5318.67 1355.21 3.92

2016-17 6365.89 1569.89 4.05

2017-18 8308.85 1846.04 4.50

2018-19 9534.95 2001.30 4.76

2019-20 9479.44 2148.91 4.41

GRAPH-3:

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2015-16 2016-17 2017-18 2018-19 2019-20

WORKING CAPITAL TURN OVER RATIO

WORKING CAPITALTURN OVER RATIO

64

ANALYSIS:

In the year 2012-13 working capital turnover ratio is 3.92, in the year 2019-20 is 4.05, in the year 2018-19 is 4.50, in the year 2019-20 is 4.76 and in the year 2018-19 is 4.41.

INTERPRETATION:

From the analysis done In the previous step, it is interpreted that the working capital turnover ratio has increased in the year 2019-20 compare to year 2012-13, again increased in the year 2018-19, again increased in the year 2019-20 and again decreased in the year 2018-19.

4. CURRENT ASSET TURNOVER RATIO:

The asset turnover ratio is an efficiency ratio that measures a company's ability to generate sales from its assets by comparing net sales with average total assets. In other words, this ratio shows how efficiently a company can use its assets to generate sales.

FORMULA:

𝐶𝑈𝑅𝑅𝐸𝑁𝑇𝐴𝑆𝑆𝐸𝑇𝑇𝑈𝑅𝑁𝑂𝑉𝐸𝑅𝑅𝐴𝑇𝐼𝑂 =𝑁𝐸𝑇𝑆𝐴𝐿𝐸𝑆

𝐶𝑈𝑅𝑅𝐸𝑁𝑇𝐴𝑆𝑆𝐸𝑇𝑆

65

TABLE-4

YEAR NET SALES

CURRENT ASSETS

CURRENT ASSETS TURNOVER RATIO

2015-16 5318.67 2430.16 2.19

2016-17 6365.89 3390.17 1.88

2017-18 8308.85 3529.44 2.35

2018-19 9534.95 3720.39 2.56

2019-20 9479.44 4177.26 2.27

GRAPH-4:

0

0.5

1

1.5

2

2.5

3

2015-16 2016-17 2017-18 2018-19 2019-20

CURRENT ASSET TURNOVER RATIO

CURRENT ASSETTURNOVER RATIO

66

ANALYSIS:

In the year 2012-13 current asset turnover ratio is 2.19, in the year 2017-18 is 1.88, in the year 2018-19 is 2.35, in the year 2017-18 is 2.56 and in the year 2018-19 is 2.27.

INTERPRETATION:

From the analysis done in the previous step, it is interpreted that the current asset turnover ratio has decreased in the year 2017-18 compare to year 2012-13, again increased in the year 2018-19, again increased in the year 2017-18 and again decreased in the year 2018-19.

5. STOCK TURNOVER RATIO/ INVENTORY TURNOVER RATIO:

The inventory turnover ratio is an efficiency ratio that shows how effectively inventory is managed by comparing cost of goods sold with average inventory for a period. This measures how many times average inventory is "turned" or sold during a period.

FORMULA:

𝑆𝑇𝑂𝐶𝐾𝑇𝑈𝑅𝑁𝑂𝑉𝐸𝑅𝑅𝐴𝑇𝐼𝑂 =𝐶𝑂𝑆𝑇𝑂𝐹𝐺𝑂𝑂𝐷𝑆𝑆𝑂𝐿𝐷 (𝑁𝐸𝑇 𝑆𝐴𝐿𝐸𝑆)

𝐴𝑉𝐸𝑅𝐴𝐺𝐸𝑆𝑇𝑂𝐶𝐾(𝐼𝑁𝑉𝐸𝑁𝑇𝑂𝑅𝑌)

TABLE-5

YEAR NET SALES AVERAGE STOCK

STOCK TURN OVER RATIO

2015-16

5318.67 1160.71 4.58

67

2016-17

6365.89 1407.39 4.52

2017-18

8308.85 1302.86 6.38

2018-19

9534.95 1646.36 5.79

2019-20

9479.44 1245.88 7.61

GRAPH-5

ANALYSIS:

In the year 2012-13 stock turnover ratio is 4.58, in the year 2015-16 is 4.52, in the year 2019-20 is 6.38, in the year 2015-16 is 5.79 and in the year 2018-19 is 7.61.

0

1

2

3

4

5

6

7

8

2015-16 2016-17 2017-18 2018-19 2019-20

STOCK TURN OVER RATIO

STOCK TURN OVERRATIO

68

INTERPRETATION:

From the analysis done in the previous step, it is interpreted that the stock turnover ratio has decreased in the year 2015-16 compare to year 2012-13, again increased in the year 2019-20, again decreased in the year 2015-16 and again increased in the year 2018-19.

6. NET PROFIT RATIO:

The net profit percentage is the ratio of after-tax profits to net sales. It reveals the remaining profit after all costs of production, administration, and financing have been deducted from sales, and income taxes recognized.

FORMULA:

𝑁𝐸𝑇𝑃𝑅𝑂𝐹𝐼𝑇𝑅𝐴𝑇𝐼𝑂 = 𝑁𝐸𝑇𝑃𝑅𝑂𝐹𝐼𝑇𝐴𝐹𝑇𝐸𝑅𝑇𝐴𝑋

𝑁𝐸𝑇𝑆𝐴𝐿𝐸𝑆

TABLE-6

YEAR NET PROFIT AFTER TAX

NET SALES

NET PROFIT RATIO