Embed Size (px)

Citation preview

Taklimat Laporan Tahunan 2015 dan Laporan Kestabilan Kewangan dan Sistem Pembayaran 2015

Gabenor Bank Negara Malaysia 23 Mac 2016

Embargo

Not for publication or broadcast before 1800 hours on Wednesday, 23 March 2016

In 2015, the Malaysian economy is still on a stable growth path despite a challenging environment

Domestic Demand: 2014

Source: IMF, Department of Statistics, Malaysia and Bank Negara Malaysia

6.0 5.0

-2

0

2

4

6

8

2007 2009 2011 2013 2015p

Malaysian economy grew by 5.0% in 2015

Annual change (%)

Within the region, Malaysia was among the faster-growing economies

0.7

2.0

2.6

2.8

4.8

5.0

5.8

6.9

7.3

0 2 4 6 8

Chinese Taipei

Singapore

Korea

Thailand

Indonesia

Malaysia

Philippines

PR China

India

Annual change (%)

Real GDP Growth Real GDP Growth

Global growth: 3.3%

p preliminary

2

3.6 3.6 3.1

1.9 1.8 1.1

0.8 0.6 0.6

0.2

-0.5 -0.1 -1.0

1.1

-0.3 -0.8

-0.6

0.6

-4

-2

0

2

4

6

8

2013 2014 2015p

Change in Stocks Net Exports Public Investment Public Consumption Private Investment Private Consumption GDP Growth

• Private consumption:

- Weighed down by weaker sentiments and households adjusting to rising cost of living

- But supported by continued income growth and stable labour market conditions

• Private investment:

- Driven by the manufacturing and services sectors

• Net exports:

- Weighed down growth as domestic demand-driven imports grew stronger than exports

Private domestic demand continued to anchor growth

3

Contribution to growth (ppt.)

Real GDP Growth

Source: Department of Statistics, Malaysia p preliminary

3

-4

-2

0

2

4

6

8

10

12

14

2008 2010 2012 2014 2016f

Advanced economies Asia Other EMEs Global GDP

GDP Growth By Region

L

• Modest growth momentum in the advanced economies, reflecting:

- Moderate growth in the US

- Slow improvement in the euro area

• In Asia, growth to be underpinned by private domestic demand given:

- Favourable labour market conditions

- Stimulus measures in a number of economies

- Supportive monetary conditions

Global growth to improve at a modest pace in 2016

Annual change (%)

Source: IMF and Bank Negara Malaysia estimates

4

L

5

Moderate expansion in global trade

• Structural and cyclical factors contribute to the decline in trade intensity

− Structural factors:

• Waning impact of previous drivers of trade growth

• Slower expansion of global value chains

• Weaker investment by corporates

− Cyclical factors:

• Modest economic recovery in a number of major advanced economies

• Greater economic and financial uncertainty

0

1

2

3

4

1992 1996 2000 2004 2008 2012 2016f

1990 – 2000

average : 2.1 times 2002 -

2007 average: 1.6 times

2011 - 2016

average: 1.0 times

Lower global trade intensity post-GFC

*The ratio increased significantly in 2009, due to weak world growth

2001: Dot-com bubble

2008 / 2009: GFC

World Trade-to-GDP Ratio* Ratio (No. of times)

Source: IMF and Bank Negara Malaysia estimates

5

Global inflationary pressures to remain subdued amid lower commodity prices

6

Low commodity prices to contain inflationary pressures across economies

Global commodity prices are expected to remain low in 2016 amid excess supply

0

1

2

3

4

5

6

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

G3***

Asia**

* Price index simple average of three spot prices - Brent, West Texas Intermediate, and the Dubai Fateh ** Asia refers to Chinese Taipei, Hong Kong SAR, Indonesia, Korea, Malaysia, the Philippines, PR China, Singapore and Thailand *** G3 refers to the US, euro area and Japan

0

50

100

150

200

250

2000 2004 2008 2012 2016f

Index (2005=100)

Selected Commodity Prices Headline Inflation Rates Annual change (%)

Metal

Crude Oil*

Food

Source: Haver, IMF and Bank Negara Malaysia estimates

6

Divergent but still very accommodative monetary policies in the major economies

0

10

20

30

40

50

60

70

80

Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

…whereas ECB and BOJ continue with monetary accommodation through asset purchases and

negative interest rates Central Bank Balance Sheet Size

% of GDP

ECB

Fed

BOJ

Source: National authorities, Haver and Bank Negara Malaysia estimates

7

0

1

2

3

4

5

Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

Policy Rates of Selected Major Central Banks

The US Federal Reserve has begun a slow-paced interest rate normalisation…

ECB

Fed

BOJ

Rate (%)

The Malaysian economy to expand at between 4.0 – 4.5% in 2016

• Domestic demand will continue to be the

principal driver of growth, sustained primarily

by the private sector

• External sector to provide support to growth

in 2016

• All economic sectors, except for agriculture,

are expected to expand, with the services and

manufacturing sectors remaining as the key

drivers of overall growth.

L

-2

0

2

4

6

8

2008 2009 2010 2011 2012 2013 2014 2015p 2016f

6.0

Annual change (%)

Real GDP Growth

5.0 4.5

4.0

Source: Department of Statistics, Malaysia and Bank Negara Malaysia p preliminary, f forecast

8

Domestic demand will continue to drive growth with support from external demand

Real GDP Annual change (%)

% share of GDP (2015)

2015p 2016f

Domestic demand (excluding stocks) 91.6 5.1 4.3

Private expenditure 69.2 6.1 5.2 Private consumption 52.4 6.0 5.1 Private investment 16.9 6.4 5.5

Public expenditure 22.4 2.1 1.6 Public consumption 13.5 4.3 2.0 Public investment 8.9 -1.0 1.1

Gross Fixed Capital Formation 25.8 3.7 4.0 Net exports of Goods & Services 8.6 -3.7 1.1

Exports of Goods & Services 73.0 0.7 3.2 Imports of Goods & Services 64.4 1.3 3.4

Real GDP 100.0 5.0 4.0 - 4.5

6.0

5.0

4.0 – 4.5

-2

-1

0

1

2

3

4

5

6

7

8

2014 2015p 2016f

Change in Stocks Net Exports Public Investment Public Consumption Private Investment Private Consumption GDP growth

Real GDP Growth Contribution to growth (ppt.)

Source: Department of Statistics, Malaysia and Bank Negara Malaysia p preliminary, f forecast

9

Private consumption to grow by 5.1% in 2016

6.0

5.1

4

5

6

7

8

9

2011 2012 2013 2014 2015p 2016f

Consumer spending to be affected by an environment of higher prices and greater uncertainty…

…but remain supported by continued income and employment growth

Unemployment and Salary Growth

2.9 3.2 3.3-3.5

5.5 5.6 5.5-6.0

0

1

2

3

4

5

6

7

2011 2012 2013 2014 2015p 2016f

Salary increment (Annual change, %)

Unemployment rate (Share of labour force, %)

Annual change (%)

Real Private Consumption Growth

Annual change (%)

Long-term average (1990-2014): 6.7%

Source: Department of Statistics, Malaysia, Bank Negara Malaysia and Malaysian Employers Federation (MEF) p preliminary, f forecast

10

52 72 75

148 153

108

20 14

4

0

50

100

150

200

250

300

2013 2014 2015

Manufacturing Services Primary

11.0

6.4 5.5

0

5

10

15

20

25

2011 2012 2013 2014 2015p 2016f

Long-term average (1990-2014): 8.5%

RM billion Approved Investment

by MIDA

However, growth remains supported by on-going and new investments, particularly in the manufacturing sector

Real Private Investment Growth

Private investment to trend below long-term average in 2016

219 240

187

Private investment to expand by 5.5%

Annual change (%)

Source: Department of Statistics, Malaysia Investment Development Authority (MIDA) and Bank Negara Malaysia p preliminary, f forecast

11

p preliminary, f forecast Note: G3 refers to the US, EU and Japan, NIEs refers to Hong Kong, Korea and Chinese Taipei

Malaysia’s exports supported by a diversified trade structure

Trade Annual change (%)

% share (2015) 2015p 2016f

Gross exports 100.0 1.9 2.4

Manufactured 80.2 6.5 5.6

E&E 35.6 8.5 5.5

Non-E&E 44.6 5.0 5.7

Commodities 19.2 -13.4 -11.1

Gross imports 100.0 0.4 4.9

Capital goods 14.0 0.0 8.9

Intermediate goods 58.2 -2.3 4.7

Consumption goods 9.1 24.1 3.0

Trade balance (RM billion) - 94.6 79.5

Continued expansion in manufactured exports amid a smaller decline in commodity exports

Malaysia’s exports supported by diversified structure across products and markets

19.2

35.6

44.6

0

20

40

60

80

100

2015

% share of total exports

Non-E&E

E&E

Commodities

Exports by Product

18.9

11.0

13.0

28.1

29.0

0

20

40

60

80

100

2015

% share of total exports

G3

China

ROW

ASEAN

NIEs

Exports by Market

Source: Department of Statistics, Malaysia

12

Current account to remain in surplus

p preliminary, f forecast

Narrower current account surplus reflects global developments and domestic structural transformation

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015p 2016f

Gross Capital Formation

Savings-Investment Gap

RM billion

Gross National Savings

Continued expansion of investment activity, particularly to boost productivity and capacity

16.6 17.6

11.2

3.0 1-2

-12 -8 -4 0 4 8 12 16 20 24

-100

-50

0

50

100

150

200

2006 2008 2010 2012 2014 2016f Goods Services Primary income Secondary income % of GNI (RHS)

RM billion % of GNI Current Account Balance Savings-Investment Gap

Source: Department of Statistics, Malaysia

13

While ringgit has strengthened in recent months, volatility is likely to persist going forward

Ringgit has outperformed most regional currencies since end Sept 2015

-11.3

3.3

-29.4

10.6

-30

-20

-10

0

10

20

30

1 Sep 2014- 29 Sep 2015 30 Sep 2015- 22 Mar 2016

Regional Currencies (Average) MYR

NEER: -21.3% REER: -19.6%

NEER: 7.6% REER: 8.1%

Ringgit vis-à-vis USD

Note: Regional currencies include IDR, KRW, SGD, THB, TWD, INR, PHP, CNY

Ringgit volatility since September 2014 has exceeded levels in previous episodes of sharp adjustments

*Average historical volatility of the stated period. Historical volatility defined as a 22-day (trading days in 1 month) rolling standard deviation of daily currency change (%)

Historical Volatility* of Ringgit against USD

Pre-

GFC

GFC

Euro

pean

SD

C

Tape

r Tan

trum

Sinc

e Se

pt ‘1

4

0

1

2

3

4

5

6

7

8

9

10

Past MYR volatility

Annual change (%)

change (%)

Source: Bloomberg and Bank Negara Malaysia

14

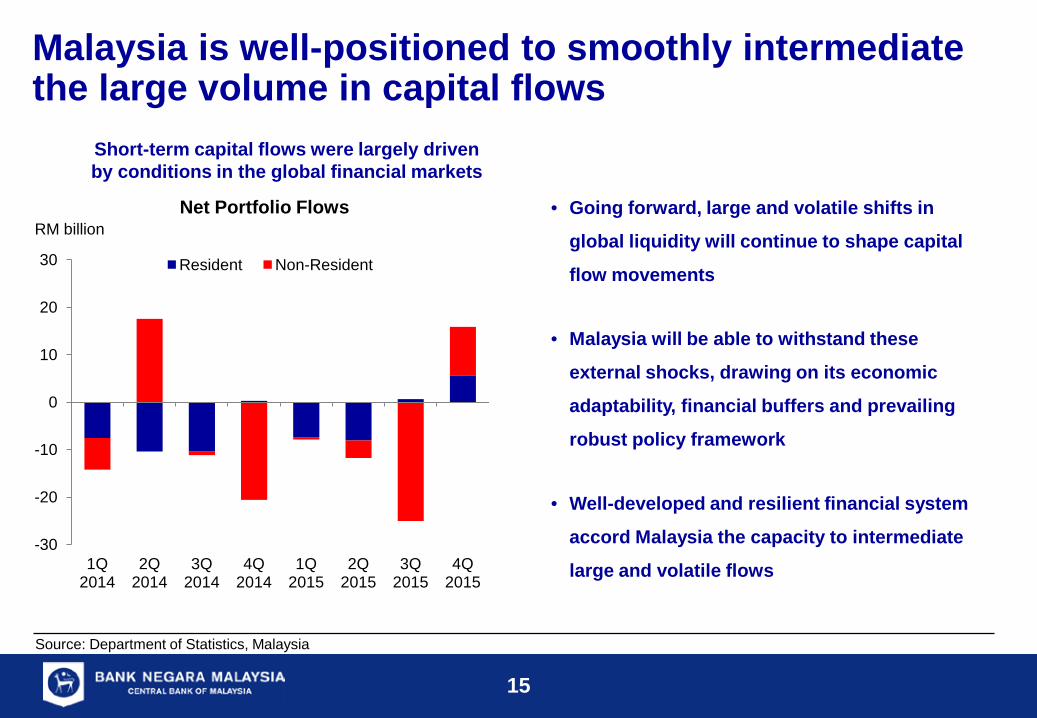

Malaysia is well-positioned to smoothly intermediate the large volume in capital flows

Short-term capital flows were largely driven by conditions in the global financial markets

• Going forward, large and volatile shifts in

global liquidity will continue to shape capital

flow movements

• Malaysia will be able to withstand these

external shocks, drawing on its economic

adaptability, financial buffers and prevailing

robust policy framework

• Well-developed and resilient financial system

accord Malaysia the capacity to intermediate

large and volatile flows -30

-20

-10

0

10

20

30

1Q 2014

2Q 2014

3Q 2014

4Q 2014

1Q 2015

2Q 2015

3Q 2015

4Q 2015

Resident Non-Resident

RM billion Net Portfolio Flows

Source: Department of Statistics, Malaysia

15

1%

1%

2%

10%

13%

29%

44%

0 20 40 60 80 100

Nominees/ Custodians

Others

Insurance Companies

Banks

Pension Funds

Central Bank/ Government

Asset Management

Distribution of Non-resident Holdings in Government Bonds as at end-January’16

Non-resident holdings of Malaysian government bonds are stable, underpinned by long-term investors

29% 30%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

Jan-14 Jun-14 Nov-14 Apr-15 Sep-15

Govt Bond (LHS) % NR of Govt (RHS)

Non-resident holdings of Malaysian government bonds are stable at 30%

Majority of non-residents are long-term investors

15

16

RM billion

Non-Resident Holdings of Malaysian Government Bonds

% NR holding

RM billion

Source: Bank Negara Malaysia Note: *Others include individuals, non-financial corporations and unidentified sectors

Jan-16

USD 118.7 billion USD384.1 billion

International reserves are adequate to provide a buffer against external shocks and facilitate international transactions

8.4

1.2

0

2

4

6

8

10

12

14

0

20

40

60

80

100

120

140

160

180

200

1991 1994 1997 2000 2003 2006 2009 2012 2015

Net International Reserves Retained import cover (RHS) Reserves/ST ext debt (RHS)*

15 Mar. 2016 USD96.1 bil

1997: USD21.7 bil

Reserves position remains at about four-times the level during Asian Financial Crisis

Redefinition of external debt

Net International Reserves

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

0

10

20

30

40

50

60

70

80

90

100

2005 2015

Malaysia’s External Assets1

International reserves Bank & non-bank corporates external assets

2005

59%

25%

41%

75%

% share

Increased holdings of foreign assets by banks and corporations

1 International investment position

2015

USD billion Times

17

External debt remains manageable

696.6 747.5 833.7

0

200

400

600

800

1000

-20

0

20

40

60

80

100

120

140

160

2013 2014 2015 Revaluation changes Changes in external debt, excl. valuation changes Total external debt (RHS)

(68.4% of GDP)

(67.5%) (72.1%)

Contribution to changes in

external debt

• Healthy external debt profile:

- Contained risks of foreign exchange fluctuations as 36% of external debt is denominated in ringgit

- Limited rollover risks as 57.8% of external debt is skewed towards medium- to long-term tenures

- Debt service ratio remained low at 22.6%

Higher external debt in 2015 due mainly to foreign exchange valuation effects

18

RM billion RM billion

Total External Debt

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

Foreign currency debt remains low while short-term external debt is mostly covered by assets

60.0*

41.8

0

20

40

60

1998 2015

% of GDP

262.0

324.8

0

100

200

300

400

2015

RM billion

Short-Term External Position of Banks and Non-bank Corporations

Foreign currency external debt remained stable at 41.8% of GDP

Short-term external debt is mostly covered by the short-term external assets

*Based on previous definition of external debt, which excludes trade credits

19

Short-term external

debt

Short-term external assets

Foreign Currency External Debt

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

• Higher inflation reflects upward adjustment of

administered prices and the weaker ringgit

exchange rate

• Inflationary pressures will be mitigated by:

− Low global energy and commodity prices

− Subdued global inflation

− More moderate domestic demand

• However, rising cost of living continues to

affect low- and middle-income households

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013 2014 2015 2016f

3.5

2.1 2.5

Long-term average (1991-2015) = 3%

While headline inflation to range between 2.5 – 3.5% in 2016, cost of living expected to remain elevated Annual change (%)

Inflation Forecast

Source: Department of Statistics, Malaysia and Bank Negara Malaysia f forecast

20

Monetary policy will focus on sustainable economic growth and price stability

• Monetary policy in 2016 will focus on ensuring

monetary conditions remain supportive of the

sustainable growth of the domestic economy

and price stability

• The Bank will continue to ensure that liquidity

is sufficient, to support the orderly functioning

of the money and foreign exchange markets

3.25

1

2

3

4

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Overnight Policy Rate (OPR) Rate (%)

Source: Bank Negara Malaysia

21

151 184 220 232 239 273 0

300

600

900

1200

1500

2010 2011 2012 2013 2014 2015

Loans Disbursed to SMEs Loan Disbursements by the Banking System and DFIs Funds Raised via Capital Markets

1,084

842 926

1,124

Continued access to financing for private sector

Gross Financing through Banking System and the Capital Markets*

• Going forward, financing activity is expected to remain supportive of economic activity

− Level of loans disbursed to remain healthy, and broad-based across all economic sectors

− Funds raised from the capital market to be sustained given continued investment activity

1,208 1,225

RM billion

*Comprises gross loans from the banking system and DFIs, and gross funds raised from the capital markets Source: Bank Negara Malaysia

22

Borrowing costs for the private sector remain stable

• Private sector will continue to benefit from stable financing costs

− Lending rates in the banking system remains stable. In particular, lending rates to businesses and SMEs remain below their long-run average

− Despite financial market volatility, cost of financing from the capital markets remains attractive for fund-raising

2

3

4

5

6

7

Overall private sector

Overall businesses

SMEs Large Corporate (5y

AAA PDS)

Long-run average* Jan-16

Interest Rates to the Private Sector

Note: * Average (Jan 2002 – Dec 2015)

Rate (%)

Source: Bank Negara Malaysia

23

55.5 97.4

11.8 16.1

0

10

20

0

50

100

150

1998 2015 Size of Bond Market Capital Ratio* (RHS)

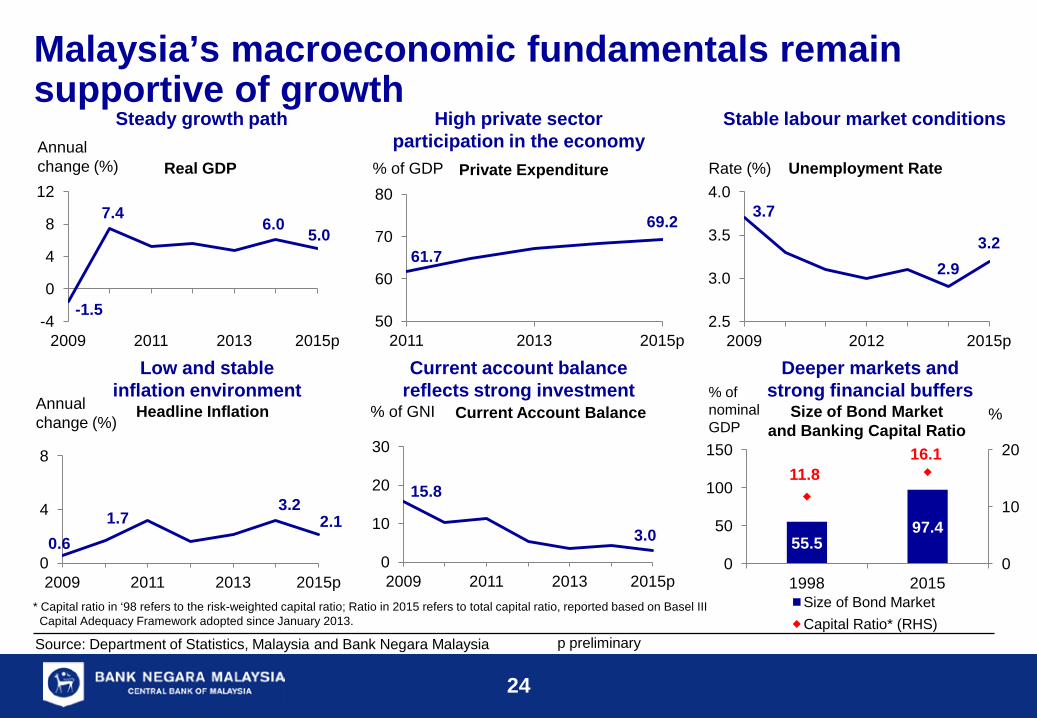

Malaysia’s macroeconomic fundamentals remain supportive of growth

61.7

69.2

50

60

70

80

2011 2013 2015p

% of GDP

3.7

2.9 3.2

2.5

3.0

3.5

4.0

2009 2012 2015p

Rate (%)

0.6 1.7

3.2 2.1

0

4

8

2009 2011 2013 2015p

Annual change (%)

Steady growth path High private sector participation in the economy

Low and stable inflation environment

Stable labour market conditions

Deeper markets and strong financial buffers

-1.5

7.4 6.0 5.0

-4

0

4

8

12

2009 2011 2013 2015p

Current account balance reflects strong investment

15.8

3.0 0

10

20

30

2009 2011 2013 2015p

Annual change (%)

% of GNI Current Account Balance Headline Inflation

Real GDP Private Expenditure Unemployment Rate

% of nominal GDP

Size of Bond Market and Banking Capital Ratio

%

* Capital ratio in ‘98 refers to the risk-weighted capital ratio; Ratio in 2015 refers to total capital ratio, reported based on Basel III Capital Adequacy Framework adopted since January 2013.

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

24

p preliminary

The economy remains resilient with the ability to manage potential downside risks to growth

In this challenging environment, the Malaysian economy is projected to expand by 4.0 – 4.5% in 2016, driven by domestic demand Lower and more stable inflation of 2.5 – 3.5%

Downside risks to growth emanating from global and domestic developments - Moderate recovery in the major economies - Further weakness in global commodity prices - Households’ ongoing adjustments to higher cost of living

Malaysia’s strong fundamentals and benefits from earlier reforms and structural adjustments - Diversified sources of growth - Favourable external position - Well-capitalised banking system and well-developed capital markets

1

3

4

2

25

Financial position remained stable in 2015:

• Total assets of BNM amounted to RM440.6 billion with International Reserves of RM409.1 billion (USD 95.3 billion)

• Net profit of RM7.79 billion

• Dividend of RM3.0 billion to the Government

Bank Negara Malaysia: Annual Financial Statements 2015

26

RM bil

Total Income 11.79

Less:

Recurring Expenditure 1.21

Development Expenditure 2.74

Taxation 0.05

Total Expenditure 4.00

Net Profit 7.79

Income Statement (Year ended 31 December 2015)

0

100

200

300

400

500

Assets Gold and Foreign Exchange IMF Reserve Position SDR MGS Deposits with FIs Loans and Advances Land and Buildings Other Assets

Statement of Financial Position (as at 31 December 2015)

RM billion

0

100

200

300

400

500

Liabilities and Capital

Total Capital Total Liabilities

RM billion

Updated

Bank Negara Malaysia: Annual Financial Statements 2015

27

Laporan Kestabilan Kewangan dan Sistem Pembayaran 2015

28

• Financial institutions continue to

maintain strong capitalisation with ample

liquidity buffers and sustained

profitability

• Malaysian banks adopt global reforms

from a strong starting point

• Stable asset quality, reinforced by sound

provisioning practices

Financial stability in 2016 to remain sound Banking sector (%) 2014 Jan ‘16

Capitalisation Common equity tier 1 ratio Total capital ratio Excess capital buffer (RM bil)

13.3 15.9 107.2

12.8 16.4 120.5

Profitability Return on assets Return on equity

1.5 15.2

1.3 12.2

Asset quality Net impaired loans ratio Loans in arrears (1-<3 mths)

1.2 2.5

1.2 2.2

Liquidity position Liquidity coverage ratio*

-

124.7

Insurance/Takaful sector (%) 2014 2015 Capitalisation

Capital adequacy ratio – Insurance Capital adequacy ratio – Takaful Capital buffer (RM bil)

251.9 190.2 32.3

251.9 190.3 46.0

Profitability Profit (RM bil)

16.9

14.7

* Basel III Liquidity Coverage Ratio requirement implemented from 1 June 2015, superseding the previous Liquidity Framework and Liquidity Framework-i requirements

29

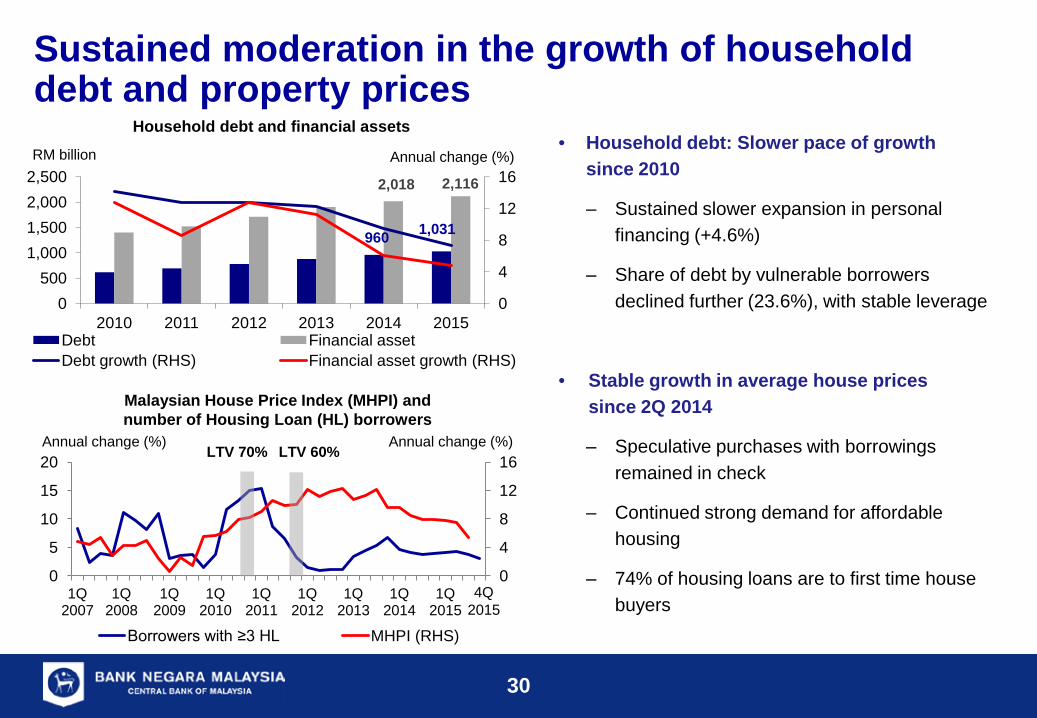

1,031 960

2,116 2,018

0

4

8

12

16

0 500

1,000 1,500 2,000 2,500

2010 2011 2012 2013 2014 2015 Debt Financial asset Debt growth (RHS) Financial asset growth (RHS)

Household debt and financial assets • Household debt: Slower pace of growth

since 2010

‒ Sustained slower expansion in personal financing (+4.6%)

‒ Share of debt by vulnerable borrowers declined further (23.6%), with stable leverage

• Stable growth in average house prices since 2Q 2014

‒ Speculative purchases with borrowings remained in check

‒ Continued strong demand for affordable housing

‒ 74% of housing loans are to first time house buyers

Sustained moderation in the growth of household debt and property prices RM billion Annual change (%)

0

4

8

12

16

0

5

10

15

20

1Q 2007

1Q 2008

1Q 2009

1Q 2010

1Q 2011

1Q 2012

1Q 2013

1Q 2014

1Q 2015

Borrowers with ≥3 HL MHPI (RHS)

LTV 70%

Malaysian House Price Index (MHPI) and number of Housing Loan (HL) borrowers

Annual change (%) Annual change (%) LTV 60%

30

4Q 2015

• Expansion in domestic borrowings (+9.5%) remained close to long term trend

- Driven by capital expenditure for private sector investments and public infrastructure projects

• Higher external borrowings (24.8% of GDP) largely driven by exchange rate valuation effects

- 54% of external debt associated with trade credits, non-resident holdings of RM-denominated securities and intra-group borrowings, with low currency and funding risks

• Overall debt servicing capacity of businesses remained sound

- Relatively low share of debt-at-risk

- Aggregate debt service capacity of large borrowers supported by stable and healthy cash buffers

Expansion in corporate borrowings reflected increased domestic investment activities

0

20

40

60

80

100

2014 2015 2014 2015 2014 2015

Average for regional comparators

Malaysia % of debt

Return on assets >3%

Interest coverage ratio>1.5 times

Debt-to-equity ratio <1 time

131.7%

94.6% 98.5% 96.8% 104.8%

45.5 42.5 40.0

46.8*

25

35

45

55

0

50

100

150

1998 2012 2013 2014 2015 Domestic Loans to GDP Domestic PDS to GDP External debt to GDP Debt-to-Equity ratio (RHS)

% of GDP %

Corporate Leverage and Debt Composition

Distribution of Corporate Debt by Financial Indicators * First nine month

31

32

• Banking system surplus liquidity remained high at RM178.3 billion as at January 2016

• Measures taken by the Bank to ease funding pressures amid heightened deposit competition

‒ Liquidity facilities

‒ Reduction in SRR

• Expansion of liquidity metrics to capture effects of financial deepening on banks funding structure

‒ Publication of loan-to-funds and loan-to-funds and equity ratios from January 2016

Liquidity and funding conditions remained supportive of financing activities

60

80

100

120

140

0

100

200

300

400

500

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16

% RM bil

Banks' surplus liquidity placed with BNM (including SRR) Stock of HQLA Liquidity Coverage Ratio (RHS)

Banking System Surplus Liquidity and LCR

70

75

80

85

90

M J S D M J S D M J S D

% Banking System Funding Ratios

Loan-to-deposit ratio Loan-to-funds ratio 2013 2014 2015

• Domestic banking groups maintained net external asset position reflect operations of overseas branches and subsidiaries

• Net external liability position of locally-incorporated foreign banks reflects parent funding, as operations in Malaysia remain profitable

• Banks continue to maintain prudent risk controls to manage credit risks and currency and maturity mismatches

‒ Capitalisation, profitability and asset quality of overseas operations remain healthy

Risk of contagion from banks’ external exposures were well-contained

0

8

16

24

32

2014 2015 2014 2015 2014 2015

Capital ratio Return on equity Gross impaired loans ratio (RHS)

%

0

2

4

6 % Range of Key FSI of Selected Overseas Operations

-120

-80

-40

0

40

80

-450

-300

-150

0

150

300

2011 2012 2013 2014 2015

RM billion RM billion Banks’ external assets and liabilities

Interbank Deposits & nostro Loans Debt securities Capital funds Securities under custody Others Banking system net exposures Net exposures of LIFBs (RHS) Net exposures of DBGs (RHS)

Assets

Liabilities

33

• Capitalisation of banks and insurers remained above minimum regulatory requirement under simulated stress scenarios:

‒ Synchronised sharp economic slowdown and banking sector distress in several major trade partners;

‒ Heightened geopolitical tensions;

‒ Protracted commodity market rebalancing and extreme global financial market volatility; and

‒ Domestic economy in recession deeper than 2008 with sharp correction across major asset classes.

4

9

14

19

24

2015 2016 2017 2018 2019 2015 2016 2017 2018 2019

%

1st quartile Median 3rd quartile Average

Banks’ post-shock common equity tier 1 capital ratio

Adverse scenario 2 Adverse scenario 1

System-wide post-shock capitalisation from the Bank’s multiyear solvency stress test

Banks Total capital ratio: 10.4% and 9.9% Common equity Tier-1 ratio: 7.6% and 6.9%

Insurers Capital adequacy ratio between 176% and 245%

Banks and insurers well-placed to withstand severe macroeconomic and financial shocks

34

• Malaysia’s admission into the Renminbi Qualified Foreign Institutional Investor (RQFII) programme by PR China in November 2015

- Enables development of more renminbi-denominated financial products

- Guidance Note issued jointly by the Bank and Securities Commission Malaysia to facilitate applications by qualified Malaysian institutions

Measures to further promote the utilisation of renminbi as a settlement currency

Continued expansion in financing for SMEs

1 2

Effective financial intermediation and the further deepening of financial markets have continued to support economic activity

• Financing to SMEs expanded by 14.4% to RM273.3 billion

• Additional RM1 billion funding for the Shariah Compliant SME Financing Scheme

0 50

100 150 200 250 300

2011 2012 2013 2014 2015

RM billion Loans disbursed to SMEs

35

ASEAN financial integration gained further traction

Conclusion of ASEAN Banking Integration Framework

Liberalisation of foreign exchange administration measures

Broad framework on ASEAN Financial Integration post-2015

Operationalisation of first local currency trade settlement framework in

ASEAN currencies

• Greater market access and operational flexibilities for Qualified ASEAN Banks based on mutually agreed commitments between home and host countries in the region

1 3

2 4

• To facilitate cross-border offerings of collective investment scheme (CIS) products within ASEAN under the ASEAN Capital Market Forum

• 10-year plan based on the three pillars of financial integration, financial stability and financial inclusion

• Further integration opportunities to be pursued in areas of financial sector, capital market and cross border payments

• Collaboration with the Bank of Thailand to promote the use of the ringgit and Thai baht for settlement activities

36

Strengthening independence and role of the

appointed actuary

Implementation of capital

management for takaful operators Implementation of

Life Insurance and Family Takaful

Framework

Phased liberalisation of motor and fire insurance

tariffs Standards on

management of participating life

insurance business

Improving consumer outcomes and promoting long-term sustainability in the insurance/takaful sector

37

New

R Further liberalisation of Motor and Fire Tariffs will benefit consumers while ensuring long-term sustainability

* New products/coverage not defined under the Motor/Fire Tariff, or any variation to, or extension of, existing products/coverage.

Roadmap for further liberalisation

Assessment of readiness of consumers and industry for further liberalisation

Removal of tariff rates for Motor

Comprehensive and Motor Third Party Fire

and Theft policies

Gradual adjustments for Motor Third Party

tariff rates

Gradual adjustments to Fire Tariff rates

Insurers may introduce new non-tariff products and optional add-on covers*

Existing tariff-based products will continue to be available

Motor Class Fire Class

1 July 2017 onwards

2019 onwards

Outcomes achieved Initiatives under New Motor Cover Framework

Gradual adjustments to the Motor Tariff (2012-

2015)

Inter-agency committee to drive efficiency

improvements

24-hour nationwide accident call centre

Loss ratio for bodily injury and death claims

improved from 301% to 210%

42% reduction in declined risks

(previously under MMIP)

Claim settlement time reduced by 17%

More than 1,000 calls to Accident Assist

Call Centre per month

Number of complaints reduced by 33%

1 July 2016 onwards

38

55% women

Gender

Age group

46% from age of 15-24 years old

Income

86% no income & low income

33% in East Malaysia

Region

8% of adult population still unbanked

Convenient accessibility

Malaysia’s Financial Inclusion Indicators

• Mukim with at least 2,000 population with at least one access point

• Population living in mukim with at least one access point

• Deposit accounts

• Micro enterprise with financing accounts

2011 2015

Take-up rate (adult population)

Responsible usage

• Customers with active deposit accounts

• Customers with performing financing accounts

Satisfaction level

• Malaysians who are satisfied with overall financial services

46%

98% 82%

91% 92%

73% 51%

92% 87%

98% 97%

73% 61%

96%

3

2

1

4

• Need to improve take-up rate among lower income groups for financial services

• Microsavings, microinsurance/ microtakaful and microfinancing products to be pursued to expand reach

Further progress in financial inclusion

39

Development Financial

Institutions Act (Amendment)

2015

Business Activities

Regulatory Oversight

Shariah Governance

Business Conduct & Consumer Protection

Enforcement Framework

Corporate Governance

Further strengthen the ability of DFIs to support Malaysia’s socio-economic development and promote inclusive growth

Ensure sound financial management and improve the operational efficiency and resilience of DFIs to ensure long-term sustainability

Key outcomes

1

2

3

4

5

6

Enhanced provisions

New provisions

Amendments to DFIA will support more effective role and performance of DFIs

40

Operationalisation of Financial Ombudsman Scheme

My Ringgit My Tabung My BNM BNM MyLINK

• To commence operations in 2Q 2016 with expanded scope and, enhanced governance and operational arrangements

• Progressive integration of financial education into formal school curriculum

• Targeted financial education programmes by AKPK to more than 370,000 adults in 2015

• Launched nationwide Financial Capability and Inclusion Demand Side survey to measure financial capability levels of consumers

• Introduced mobile applications to elevate consumer awareness and skills in money management matters

Supported by sustained financial education agenda

Expansion of AKPK’s Debt Management Programme to non-

bank borrowers

3

2

1

• Services expanded to borrowers of non-banks including credit cooperatives and Malaysia Building Society Berhad

Expansion of redress and debt resolution arrangements for financial consumers

41

Continued development of an efficient Islamic financial system built on strong Shariah foundations

• Expansion of investment accounts

- New investment accounts offered by 8 Islamic banks as part of measures to comply with IFSA

- RM47.1 billion placed in investment accounts as at end December 2015 representing 10% of total funding of Islamic banks

- Investment Account Platform serves as an online market place for entrepreneurs and investors to participate in investment accounts

• Further progress on development of a comprehensive Shariah contract-based regulatory framework

- 13 key Shariah standards and 5 operational guidelines issued to date

42

R

Payment indicators 2011 2015 2020 target

E-payment per capita 49 82 200

Cheques cleared (million) 205 148 100

Card terminals (per 1,000 inhabitants)

7 9 25

Debit card transactions per capita

1 3 30

Five focus areas to accelerate the migration to e-payments

Cheques, IBG and IBFT Transaction Volume

Price signal Industry incentive structure

Awareness and confidence

Quality and value proposition

Access points

• Encouraging progress in the migration away from cheques with accelerated decline rate

• Payment Card Reform Framework to promote wider acceptance and usage of debit cards

Cheques

IBG

0

2

4

6

8

10

12

14

16

18

20

J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N

Million

2015 2014 2013 2012 2011

IBFT

50 sen cheque fee and ePIF framework

IBFT fee capped at 50 sen

IBG fee capped at 10 sen

Increasing momentum in the migration to e-payments

43

Strong leadership

Technically competent

Qualified and certified

Ethical and professional

Creation of comprehensive infrastructure to nurture a deep professional talent pool

Recent Key Outcomes

1

2

3

4

• Training institutes and standard-setters continually enhanced and evolving to deliver highest, globally-benchmarked standards in learning

• Over 50,000 technically-competent banking, insurance and Islamic finance employees produced in past 5 years

• Over 20,000 strong leaders including senior management, Board of Director and Shariah experts nurtured in past 5 years

• Chartered Banker qualifications track benchmarked against the highest standards of industry excellence and professionalism

• Over 1,300 students enrolled/registered

• Industry code of ethics (CoE) published in January 2016 will set a high bar for professionalism and ethics

Lead Institutions

44

Professionalising talent to meet the evolving need of the financial sector

Financial sector is in a stronger position to cope with the more challenging environment

Resilient financial institutions and ample liquidity to support financial intermediation activities - Financial institutions well-placed to withstand severe macroeconomic and financial shocks Deep and diversified financial system will continue to support orderly market conditions Priorities of the Bank going forward include: - Maintaining close vigilance over domestic developments and management of risks by

financial institutions including overseas operations - Continuing with the implementation of global prudential standards and insurance reforms - Strengthening inter-agency and cross-border arrangements for management of financial

stability

1

2

45

3

Financial sector is in a stronger position to cope with the more challenging environment

Resilient financial institutions and ample liquidity to support financial intermediation activities - Financial institutions well-placed to withstand severe macroeconomic and financial shocks Deep and diversified financial system will continue to support orderly market conditions Priorities of the Bank going forward include: - Maintaining close vigilance over domestic developments and management of risks by

financial institutions including overseas operations - Continuing with the implementation of global prudential standards and insurance reforms - Strengthening inter-agency and cross-border arrangements for management of financial

stability

1

2

46

3