Embed Size (px)

Citation preview

Taklimat Laporan Tahunan 2017 danLaporan Kestabilan Kewangandan Sistem Pembayaran 2017

Bank Negara Malaysia

28 Mac 2018

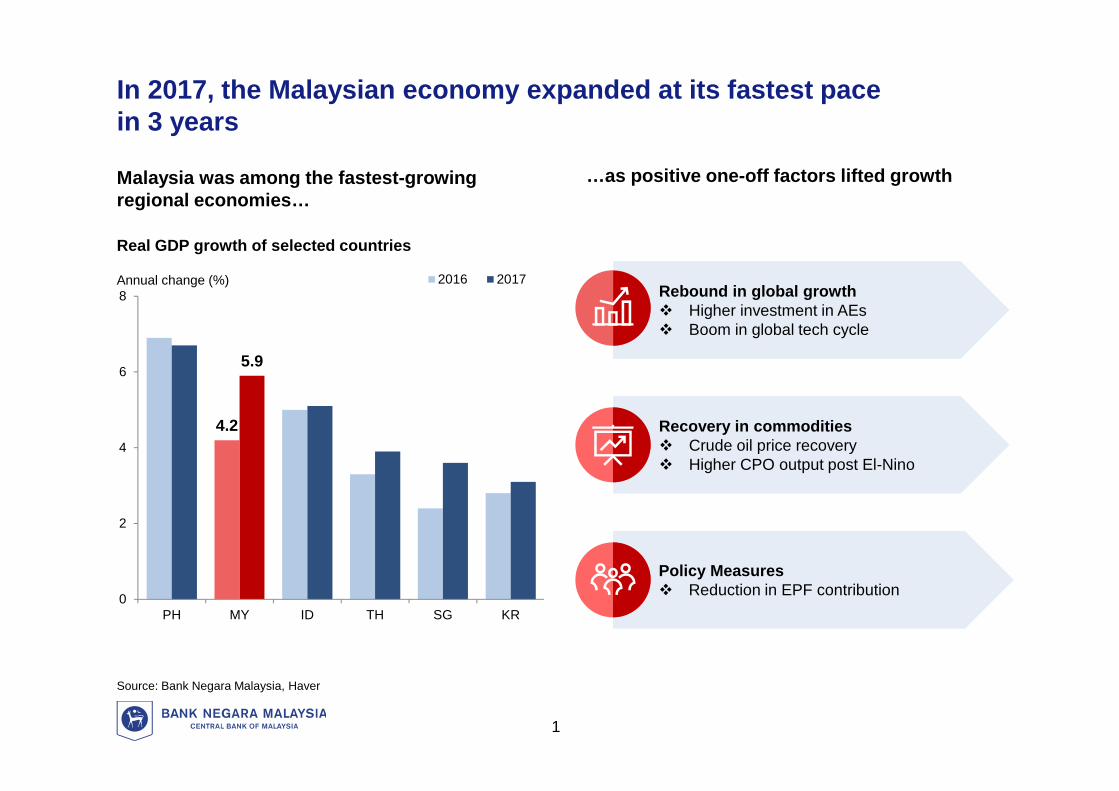

Policy Measures Reduction in EPF contribution

Recovery in commodities Crude oil price recovery Higher CPO output post El-Nino

In 2017, the Malaysian economy expanded at its fastest pacein 3 years

Malaysia was among the fastest-growingregional economies…

…as positive one-off factors lifted growth

Real GDP growth of selected countries

Source: Bank Negara Malaysia, Haver

4.2

5.9

0

2

4

6

8

PH MY ID TH SG KR

2016 2017Annual change (%)Rebound in global growth Higher investment in AEs Boom in global tech cycle

1

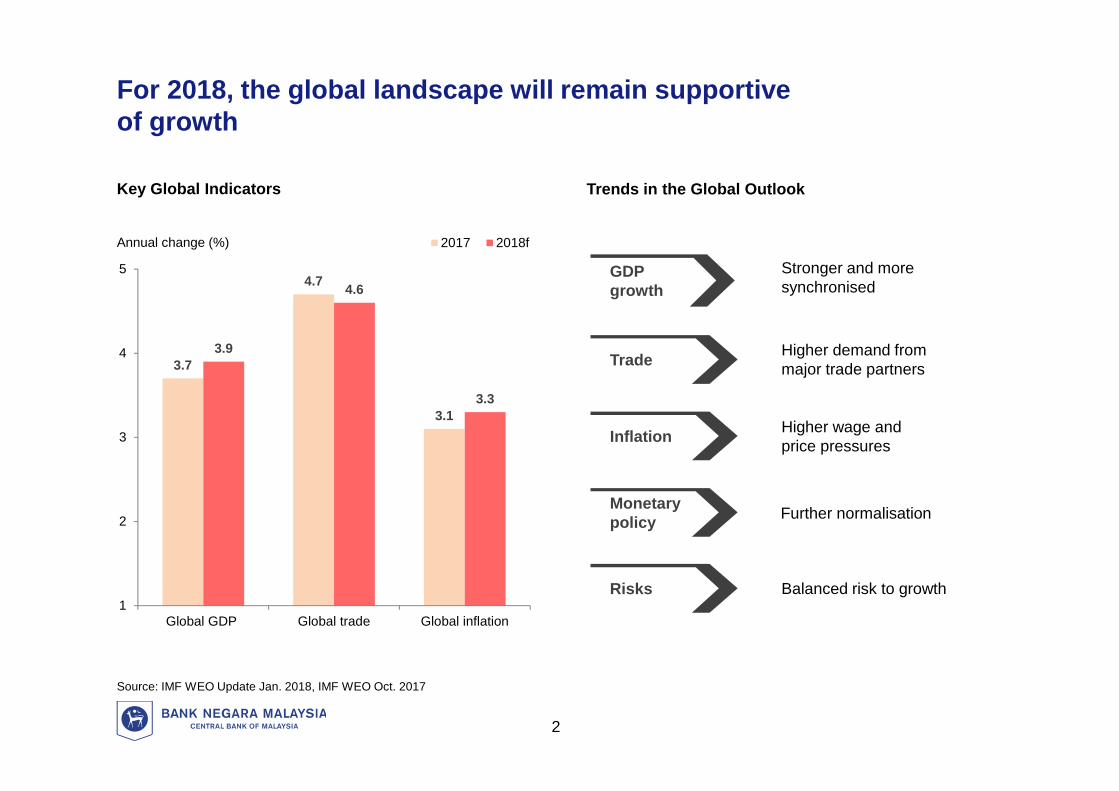

Trends in the Global Outlook

3.7

4.7

3.1

3.9

4.6

3.3

1

2

3

4

5

Global GDP Global trade Global inflation

2017 2018fAnnual change (%)

Source: IMF WEO Update Jan. 2018, IMF WEO Oct. 2017

Stronger and moresynchronised

Higher demand frommajor trade partners

Higher wage andprice pressures

Further normalisation

Balanced risk to growth

GDPgrowth

Trade

Inflation

Monetarypolicy

Risks

Key Global Indicators

For 2018, the global landscape will remain supportiveof growth

2

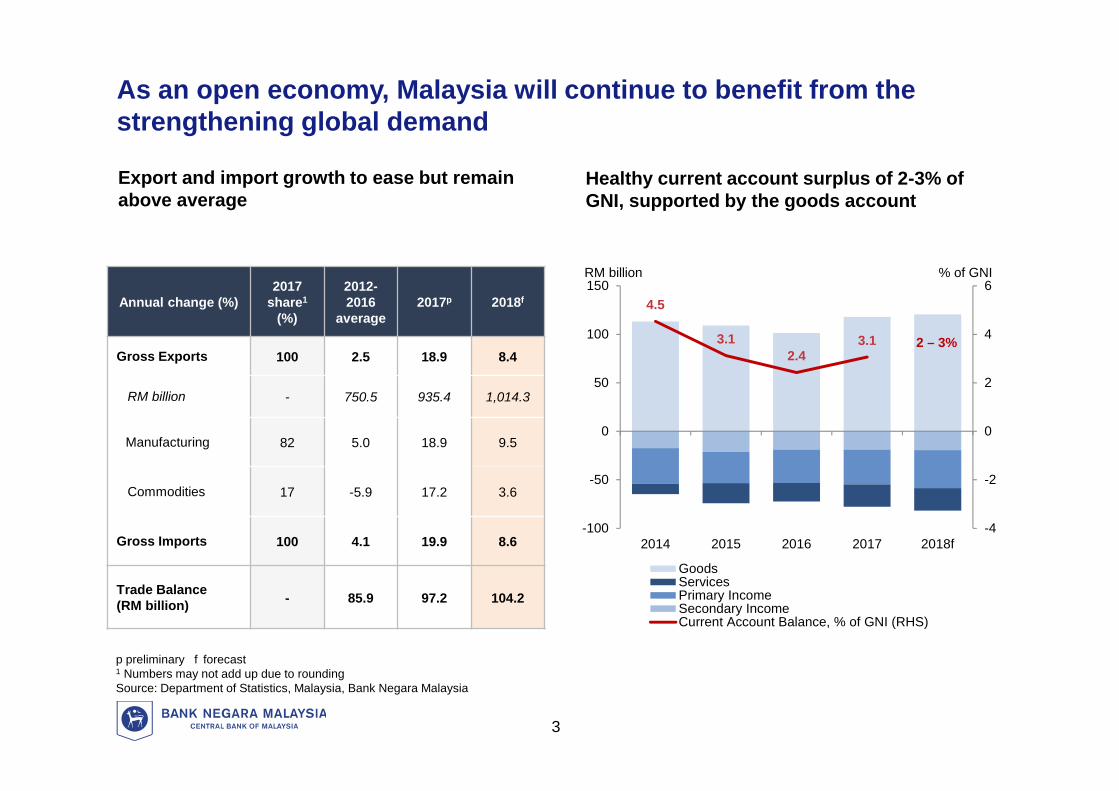

As an open economy, Malaysia will continue to benefit from thestrengthening global demand

Healthy current account surplus of 2-3% ofGNI, supported by the goods account

p preliminary f forecast1 Numbers may not add up due to roundingSource: Department of Statistics, Malaysia, Bank Negara Malaysia

Export and import growth to ease but remainabove average

Annual change (%)2017

share1

(%)

2012-2016

average2017p 2018f

Gross Exports 100 2.5 18.9 8.4

RM billion - 750.5 935.4 1,014.3

Manufacturing 82 5.0 18.9 9.5

Commodities 17 -5.9 17.2 3.6

Gross Imports 100 4.1 19.9 8.6

Trade Balance(RM billion) - 85.9 97.2 104.2

4.5

3.12.4

3.1

-4

-2

0

2

4

6

-100

-50

0

50

100

150

2014 2015 2016 2017 2018f

GoodsServicesPrimary IncomeSecondary IncomeCurrent Account Balance, % of GNI (RHS)

RM billion % of GNI

2 – 3%

3

5.9

2014 2015 2016 2017p 2018f

Annual change (%) 2017 share1

(%) 2017p 2018f

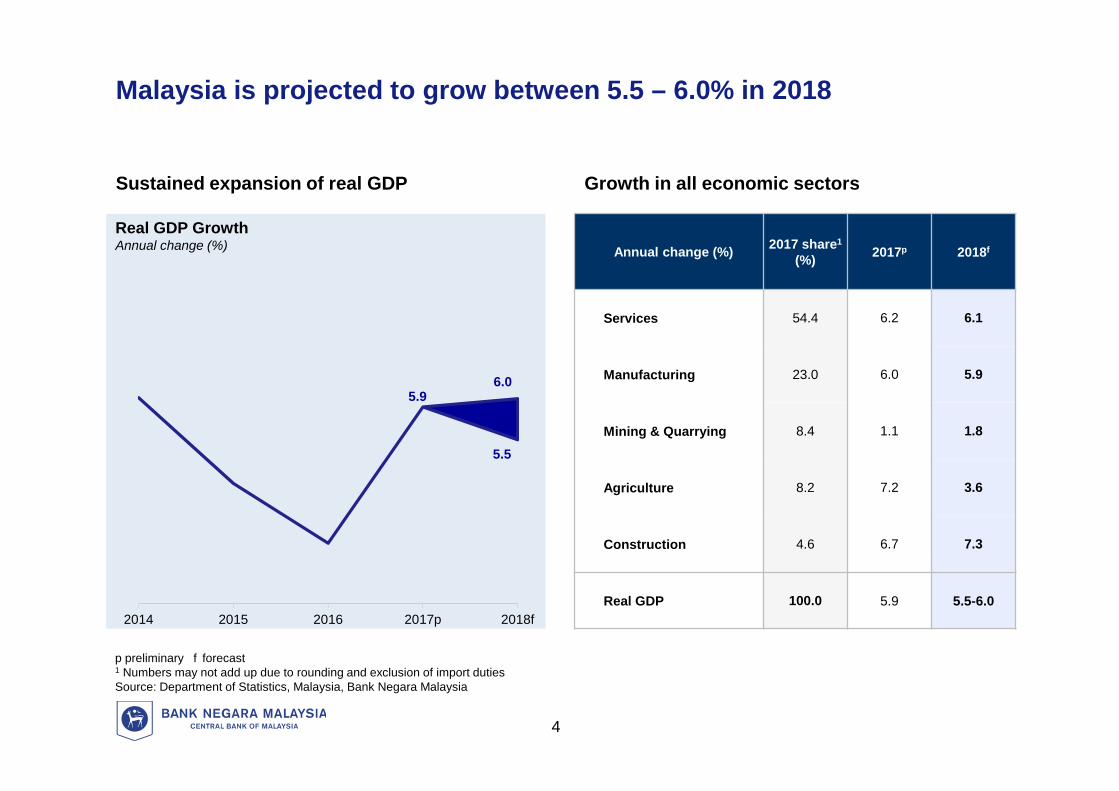

Services 54.4 6.2 6.1

Manufacturing 23.0 6.0 5.9

Mining & Quarrying 8.4 1.1 1.8

Agriculture 8.2 7.2 3.6

Construction 4.6 6.7 7.3

Real GDP 100.0 5.9 5.5-6.0

p preliminary f forecast1 Numbers may not add up due to rounding and exclusion of import dutiesSource: Department of Statistics, Malaysia, Bank Negara Malaysia

10

Updated

Growth in all economic sectors

Malaysia is projected to grow between 5.5 – 6.0% in 2018

Real GDP GrowthAnnual change (%)

6.0

5.5

Sustained expansion of real GDP

4

-1.1

5.5

2014 2016 2018f

9.3 9.1

0.1

-3.2

2014 2016 2018f

7.0 7.2

5.4

0.6

2014 2016 2018f

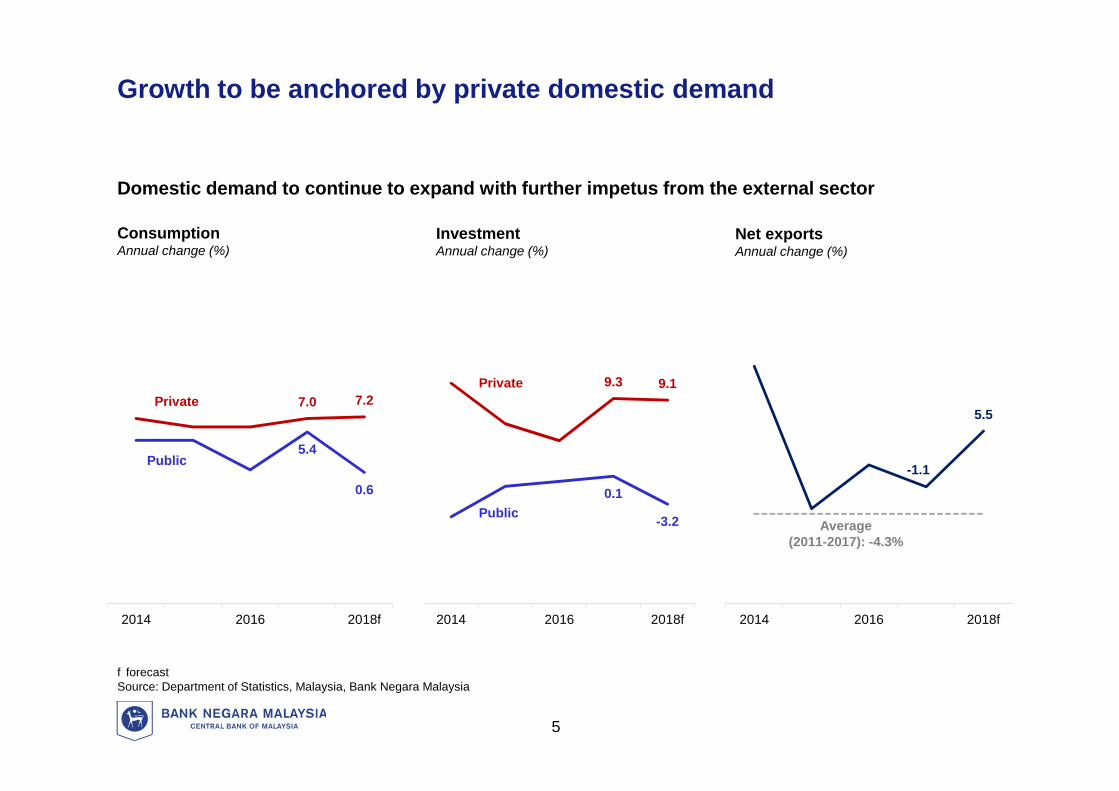

LGrowth to be anchored by private domestic demand

Domestic demand to continue to expand with further impetus from the external sector

ConsumptionAnnual change (%)

InvestmentAnnual change (%)

Net exportsAnnual change (%)

Private

Public

Private

Public

5

Average(2011-2017): -4.3%

f forecastSource: Department of Statistics, Malaysia, Bank Negara Malaysia

0.7

2.1

2015 2016 2017p

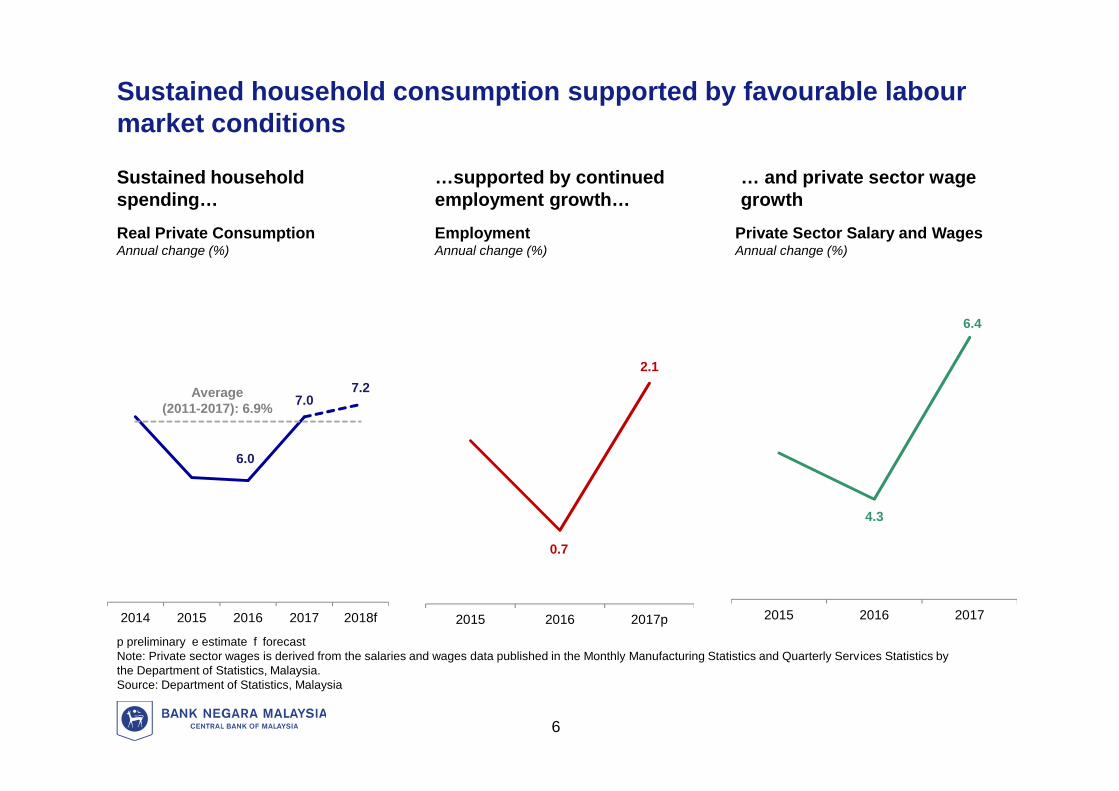

Sustained household consumption supported by favourable labourmarket conditions

Sustained householdspending…

6.0

7.07.2

2014 2015 2016 2017 2018f

… and private sector wagegrowth

…supported by continuedemployment growth…

4.3

6.4

2015 2016 2017

Real Private ConsumptionAnnual change (%)

EmploymentAnnual change (%)

Private Sector Salary and WagesAnnual change (%)

6

Average(2011-2017): 6.9%

p preliminary e estimate f forecastNote: Private sector wages is derived from the salaries and wages data published in the Monthly Manufacturing Statistics and Quarterly Services Statistics bythe Department of Statistics, Malaysia.Source: Department of Statistics, Malaysia

MIER Business Condition IndexPoints

4.3

9.3 9.1

2014 2015 2016 2017p 2018f

13

70

80

90

100

110

120

2Q 16 4Q 16 2Q 17 4Q 17

Optimismthreshold

(100 points)

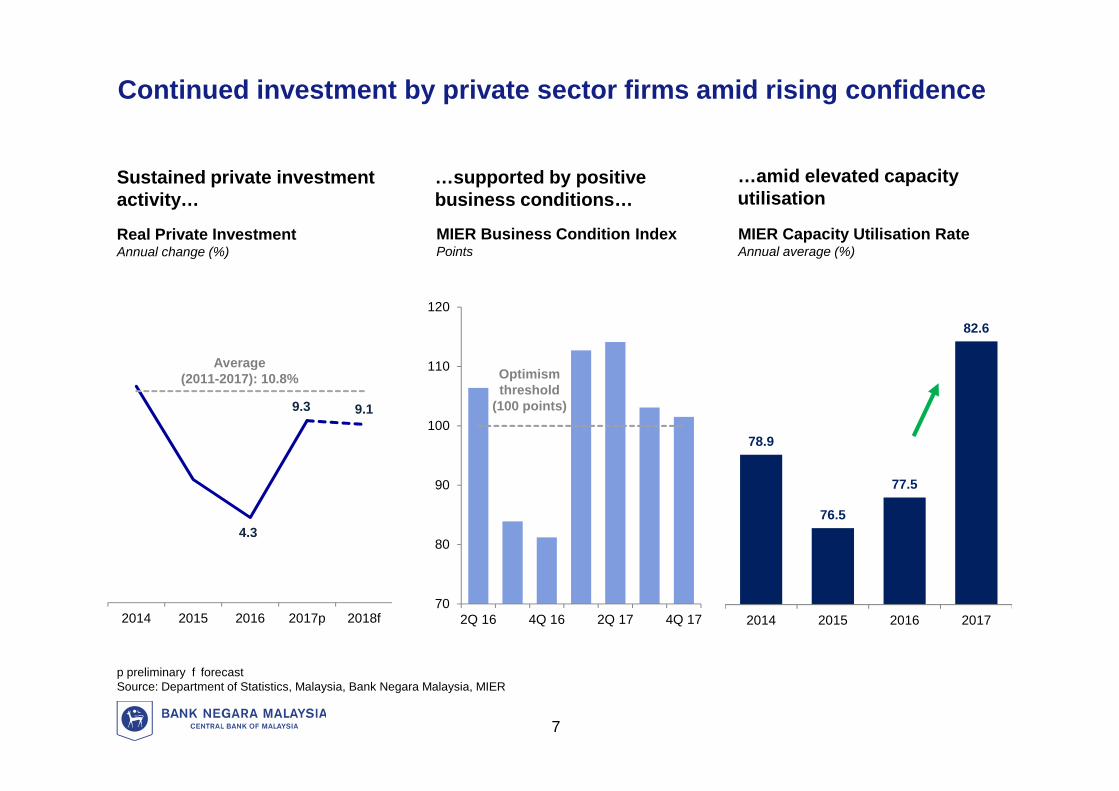

Continued investment by private sector firms amid rising confidence

Sustained private investmentactivity…

…supported by positivebusiness conditions…

…amid elevated capacityutilisation

Real Private InvestmentAnnual change (%)

7

Average(2011-2017): 10.8%

p preliminary f forecastSource: Department of Statistics, Malaysia, Bank Negara Malaysia, MIER

78.9

76.5

77.5

82.6

2014 2015 2016 2017

MIER Capacity Utilisation RateAnnual average (%)

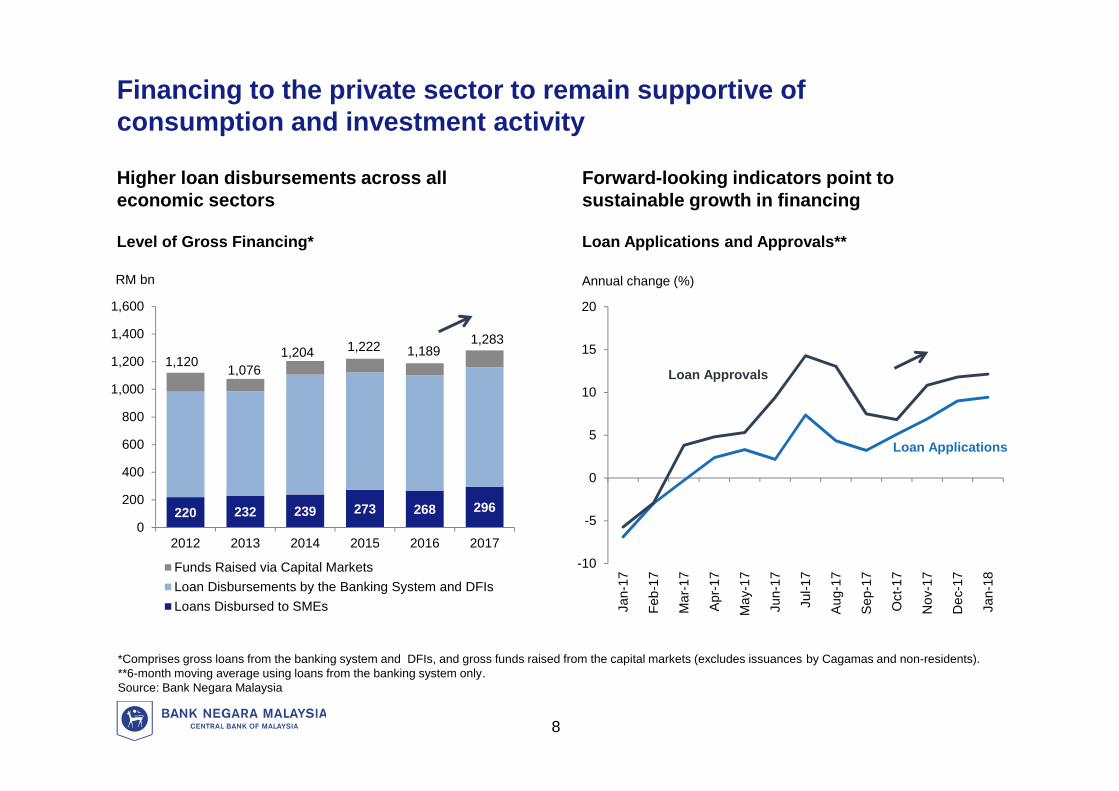

Financing to the private sector to remain supportive ofconsumption and investment activity

Loan Applications and Approvals**

*Comprises gross loans from the banking system and DFIs, and gross funds raised from the capital markets (excludes issuances by Cagamas and non-residents).**6-month moving average using loans from the banking system only.Source: Bank Negara Malaysia

8

220 232 239 273 268 296

1,120 1,0761,204 1,222 1,189

1,283

0

200

400

600

800

1,000

1,200

1,400

1,600

2012 2013 2014 2015 2016 2017

Funds Raised via Capital MarketsLoan Disbursements by the Banking System and DFIsLoans Disbursed to SMEs

RM bn

Level of Gross Financing*

-10

-5

0

5

10

15

20

Jan-

17

Feb-

17

Mar

-17

Apr

-17

May

-17

Jun-

17

Jul-1

7

Aug

-17

Sep

-17

Oct

-17

Nov

-17

Dec

-17

Jan-

18

Annual change (%)

Loan Approvals

Loan Applications

Higher loan disbursements across alleconomic sectors

Forward-looking indicators point tosustainable growth in financing

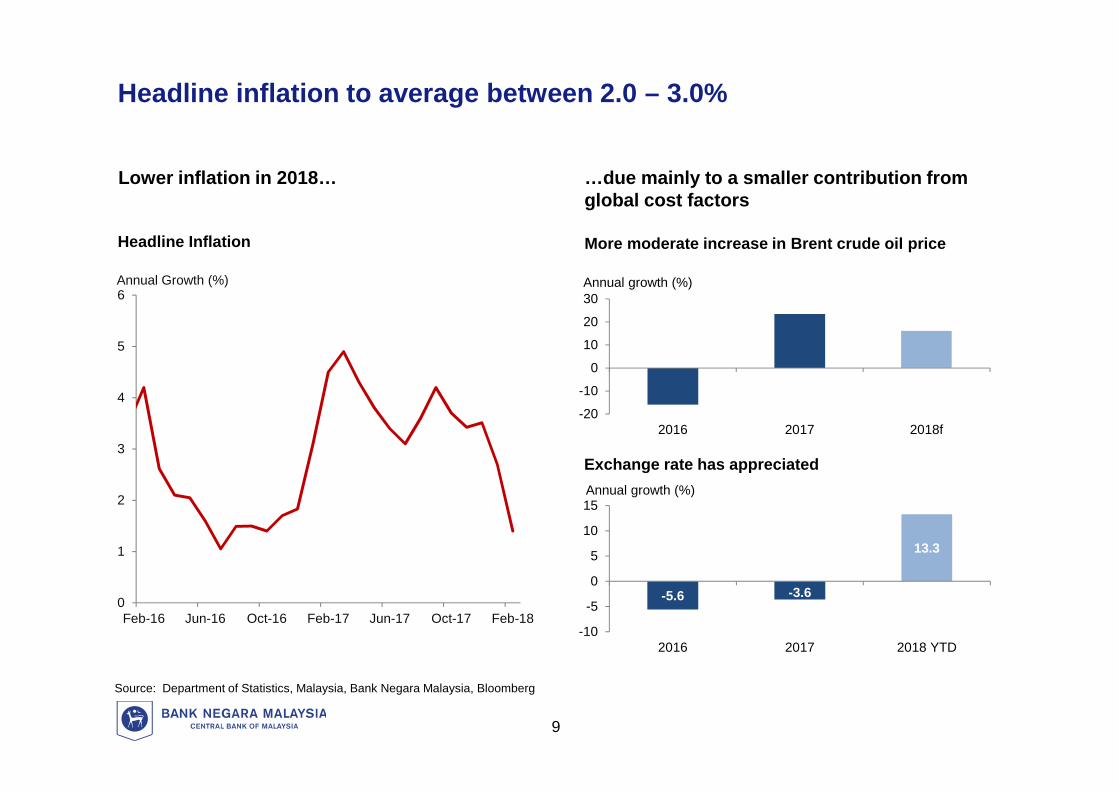

Lower inflation in 2018…

0

1

2

3

4

5

6

Feb-16 Jun-16 Oct-16 Feb-17 Jun-17 Oct-17 Feb-18

Annual Growth (%)

Source: Department of Statistics, Malaysia, Bank Negara Malaysia, Bloomberg

23

Headline inflation to average between 2.0 – 3.0%

-20

-10

0

10

20

30

2016 2017 2018f

Annual growth (%)

-5.6 -3.6

13.3

-10

-5

0

5

10

15

2016 2017 2018 YTD

Annual growth (%)

…due mainly to a smaller contribution fromglobal cost factors

More moderate increase in Brent crude oil price

Exchange rate has appreciated

9

Headline Inflation

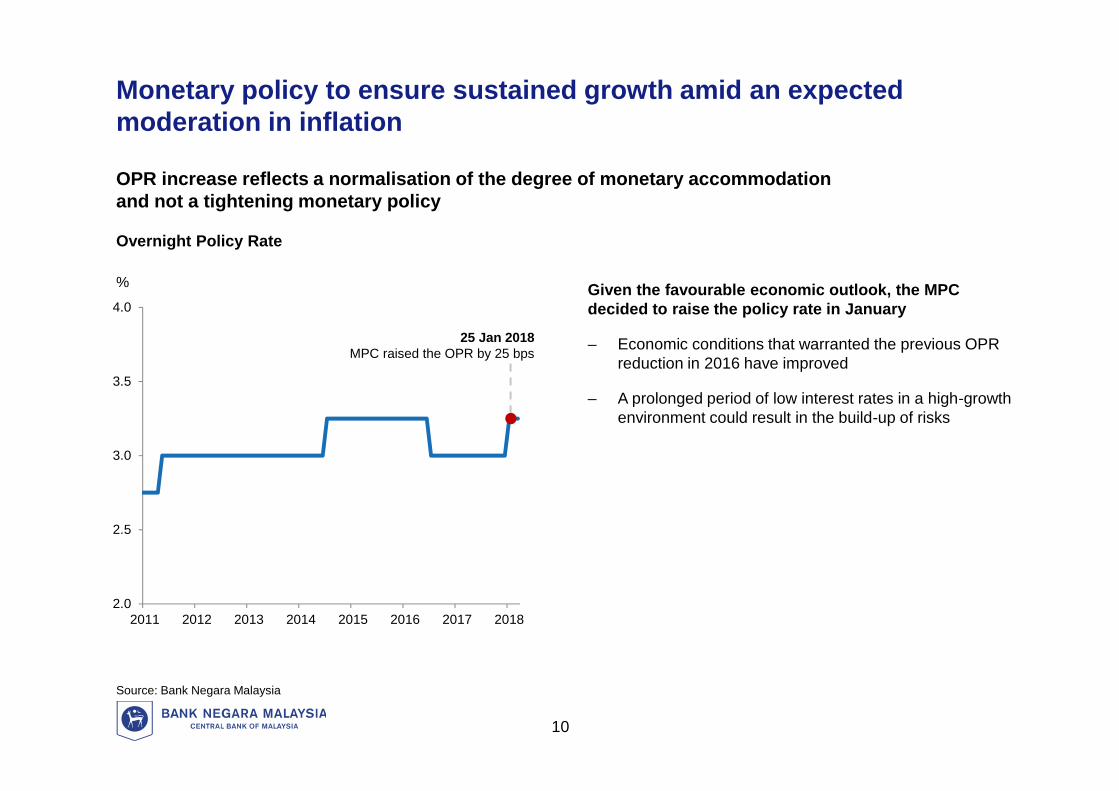

Monetary policy to ensure sustained growth amid an expectedmoderation in inflation

Given the favourable economic outlook, the MPCdecided to raise the policy rate in January

‒ Economic conditions that warranted the previous OPRreduction in 2016 have improved

‒ A prolonged period of low interest rates in a high-growthenvironment could result in the build-up of risks

OPR increase reflects a normalisation of the degree of monetary accommodationand not a tightening monetary policy

Source: Bank Negara Malaysia

%

Overnight Policy Rate

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014 2015 2016 2017 2018

25 Jan 2018MPC raised the OPR by 25 bps

10

3.8

3.9

4.0

4.1

4.2

4.3

4.4

4.5

Jan-17 Apr-17 Jul-17 Oct-17 Jan-1899

101

103

105

107

109

111

113

115

117

MYR/USD

Regional Average(RHS)

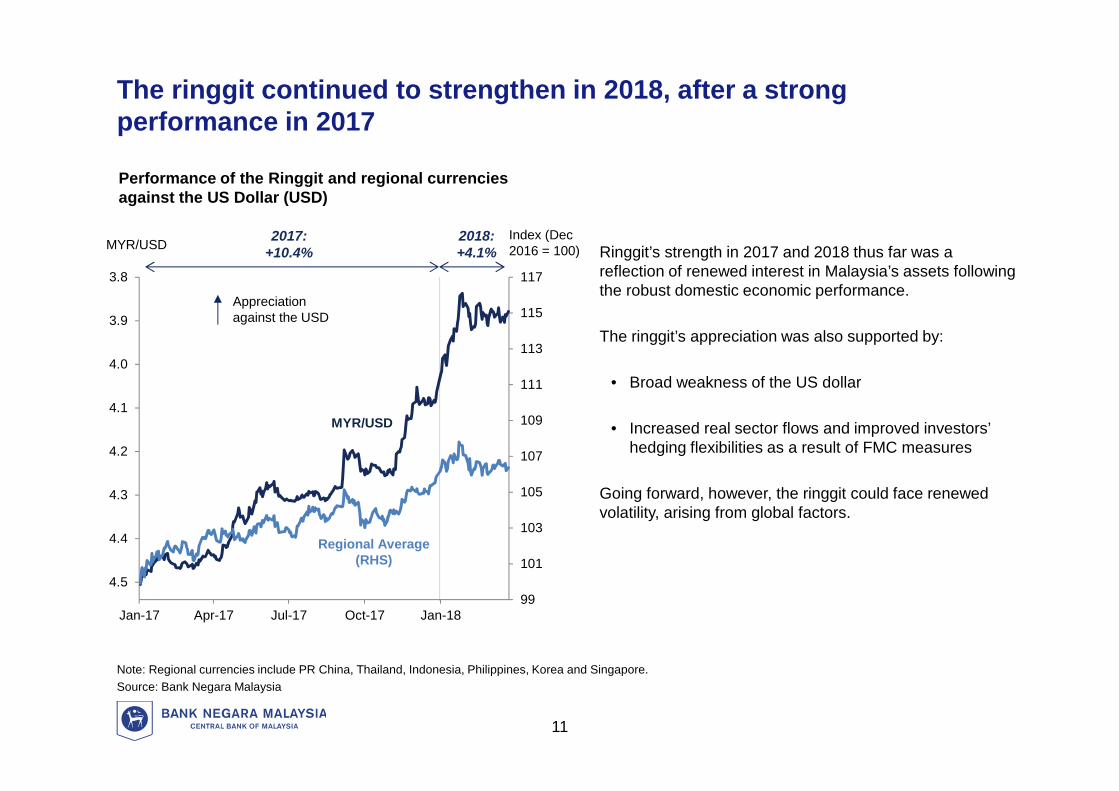

The ringgit continued to strengthen in 2018, after a strongperformance in 2017

Note: Regional currencies include PR China, Thailand, Indonesia, Philippines, Korea and Singapore.Source: Bank Negara Malaysia

MYR/USDIndex (Dec2016 = 100) Ringgit’s strength in 2017 and 2018 thus far was a

reflection of renewed interest in Malaysia’s assets followingthe robust domestic economic performance.

The ringgit’s appreciation was also supported by:

• Broad weakness of the US dollar

• Increased real sector flows and improved investors’hedging flexibilities as a result of FMC measures

Going forward, however, the ringgit could face renewedvolatility, arising from global factors.

Performance of the Ringgit and regional currenciesagainst the US Dollar (USD)

Appreciationagainst the USD

2018:+4.1%

2017:+10.4%

11

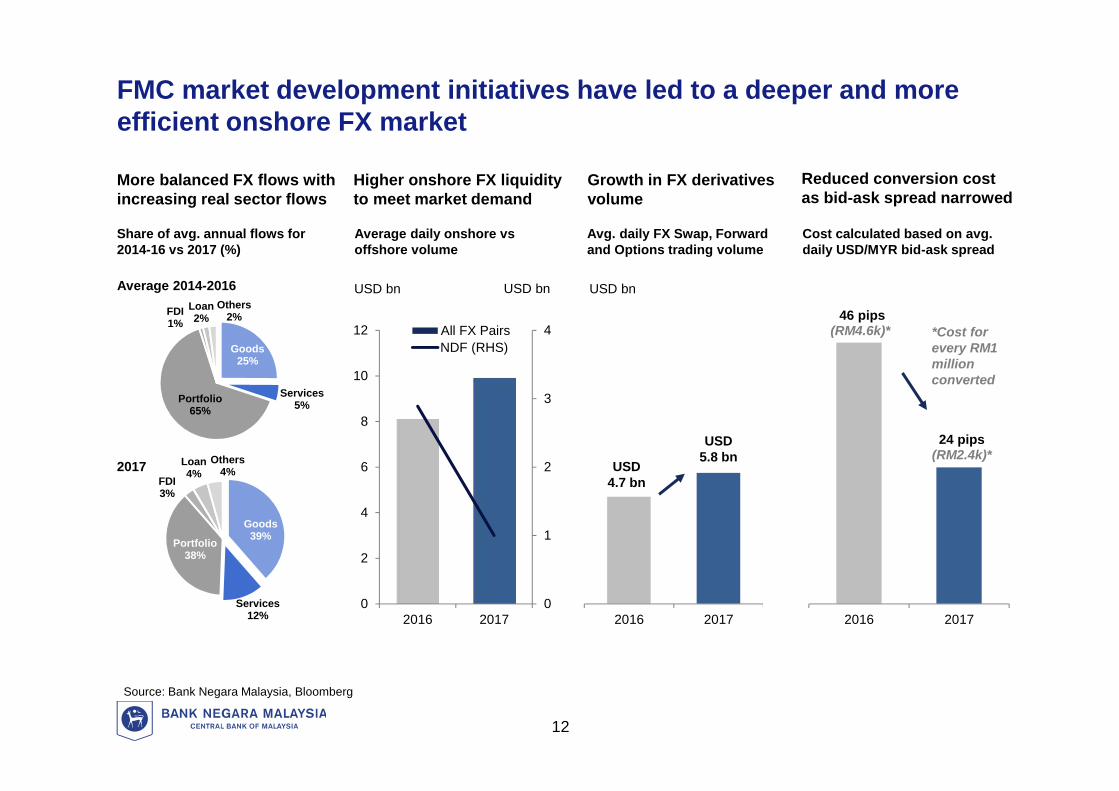

2016 2017

Average daily onshore vsoffshore volume

Avg. daily FX Swap, Forwardand Options trading volume

USD bn USD bn USD bn

More balanced FX flows withincreasing real sector flows

Higher onshore FX liquidityto meet market demand

Growth in FX derivativesvolume

Share of avg. annual flows for2014-16 vs 2017 (%)

Source: Bank Negara Malaysia, Bloomberg

FMC market development initiatives have led to a deeper and moreefficient onshore FX market

Reduced conversion costas bid-ask spread narrowed

Cost calculated based on avg.daily USD/MYR bid-ask spread

2017

Average 2014-2016

0

1

2

3

4

0

2

4

6

8

10

12

2016 2017

All FX PairsNDFGoods

25%

Services5%Portfolio

65%

FDI1%

Loan2%

Others2%

Goods39%

Services12%

Portfolio38%

FDI3%

Loan4%

Others4%

NDF (RHS)

46 pips(RM4.6k)*

24 pips(RM2.4k)*

2016 2017

*Cost forevery RM1millionconverted

12

USD4.7 bn

USD5.8 bn

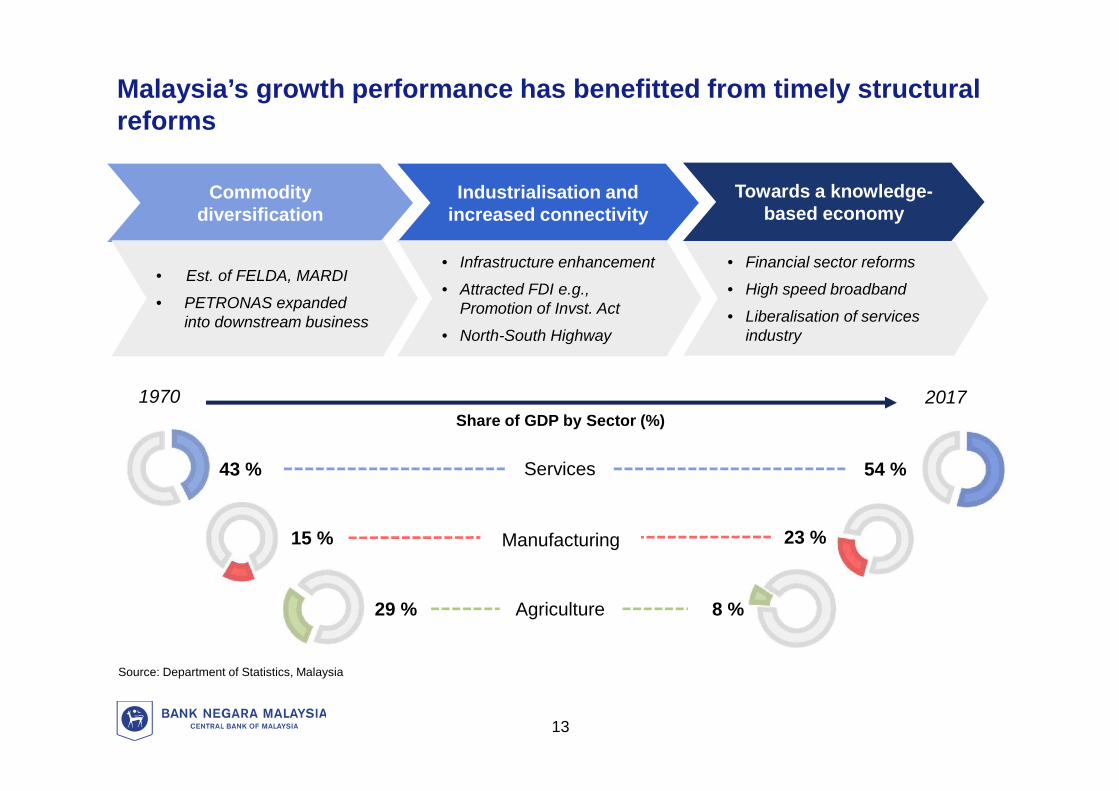

Malaysia’s growth performance has benefitted from timely structuralreforms

Commoditydiversification

Share of GDP by Sector (%)

Services43 % 54 %

Agriculture29 % 8 %

20171970

Manufacturing15 % 23 %

Source: Department of Statistics, Malaysia

• Est. of FELDA, MARDI

• PETRONAS expandedinto downstream business

Industrialisation andincreased connectivity

• Infrastructure enhancement

• Attracted FDI e.g.,Promotion of Invst. Act

• North-South Highway

Towards a knowledge-based economy

• Financial sector reforms

• High speed broadband

• Liberalisation of servicesindustry

13

However, further reforms are necessary to steer the economytowards a sustainable growth path going forward

Vital longer term reforms to enhance economic competitiveness

Labour market reforms Reducing reliance on foreign workers

Creating high quality jobs

Offering more competitive wages

Quality investments Encouraging deeper contributions to the

Malaysian economy

Diversifying into knowledge-intensive products

Embracing new growth areas Accelerating pace of digitalisation

Advancing economic complexity

14

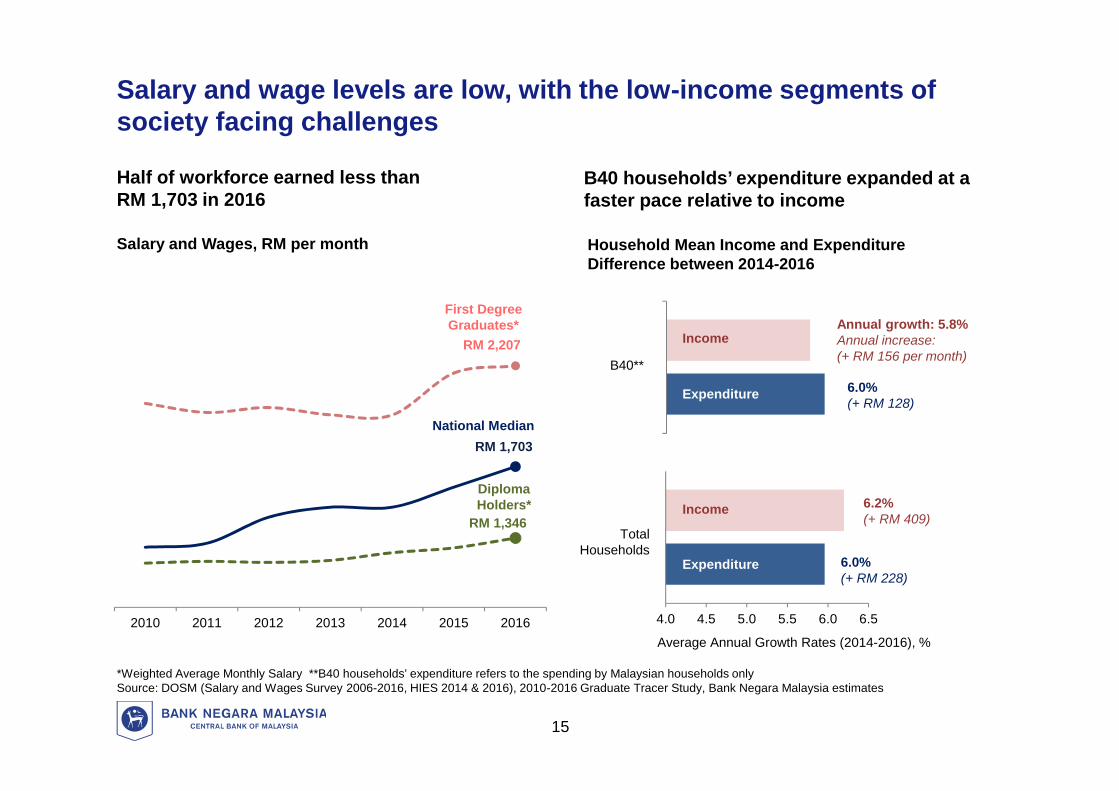

Salary and wage levels are low, with the low-income segments ofsociety facing challenges

Half of workforce earned less thanRM 1,703 in 2016

B40 households’ expenditure expanded at afaster pace relative to income

2010 2011 2012 2013 2014 2015 2016

RM 1,346

RM 1,703

RM 2,207

National Median

First DegreeGraduates*

DiplomaHolders*

15

Household Mean Income and ExpenditureDifference between 2014-2016

Salary and Wages, RM per month

Income

Expenditure

4.0 4.5 5.0 5.5 6.0 6.5

Income

Expenditure

Annual growth: 5.8%Annual increase:(+ RM 156 per month)

Average Annual Growth Rates (2014-2016), %

6.0%(+ RM 128)

6.2%(+ RM 409)

6.0%(+ RM 228)

B40**

TotalHouseholds

*Weighted Average Monthly Salary **B40 households’ expenditure refers to the spending by Malaysian households onlySource: DOSM (Salary and Wages Survey 2006-2016, HIES 2014 & 2016), 2010-2016 Graduate Tracer Study, Bank Negara Malaysia estimates

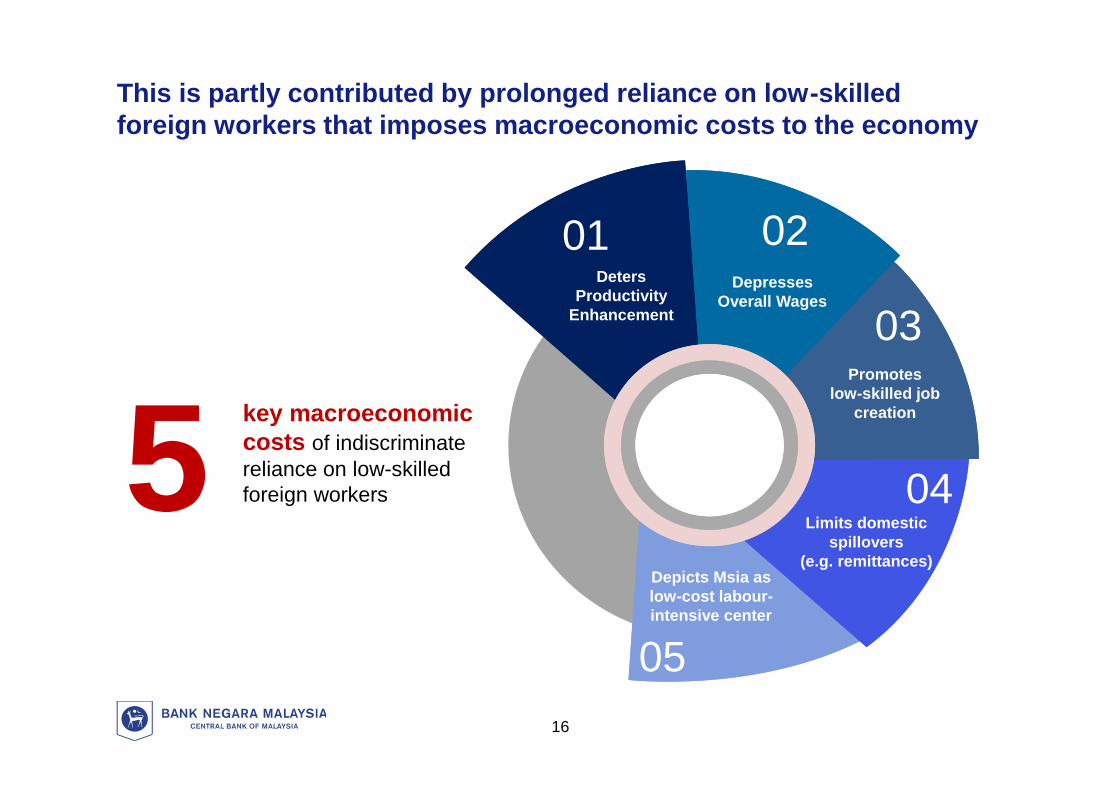

This is partly contributed by prolonged reliance on low-skilledforeign workers that imposes macroeconomic costs to the economy

DepressesOverall Wages

Limits domesticspillovers

(e.g. remittances)

03

04

05

0201Deters

ProductivityEnhancement

key macroeconomiccosts of indiscriminatereliance on low-skilledforeign workers5

16

Depicts Msia aslow-cost labour-intensive center

Promoteslow-skilled job

creation

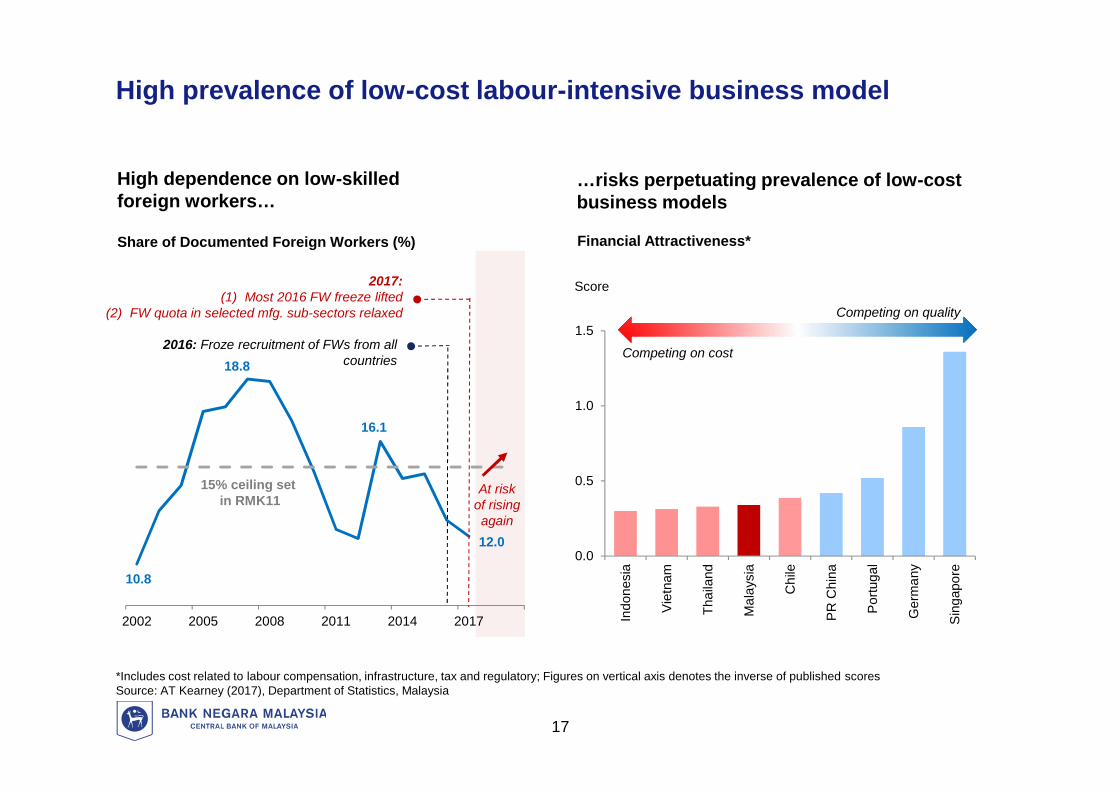

High prevalence of low-cost labour-intensive business model

*Includes cost related to labour compensation, infrastructure, tax and regulatory; Figures on vertical axis denotes the inverse of published scoresSource: AT Kearney (2017), Department of Statistics, Malaysia

Share of Documented Foreign Workers (%)

High dependence on low-skilledforeign workers…

17

10.8

18.8

16.1

12.0

2002 2005 2008 2011 2014 2017

15% ceiling setin RMK11

2016: Froze recruitment of FWs from allcountries

2017:(1) Most 2016 FW freeze lifted

(2) FW quota in selected mfg. sub-sectors relaxed

At riskof risingagain

Indo

nesi

a

Vie

tnam

Thai

land

Mal

aysi

a

Chi

le

PR

Chi

na

Por

tuga

l

Ger

man

y

Sin

gapo

re

0.0

0.5

1.0

1.5

Competing on cost

Competing on quality

Score

Financial Attractiveness*

…risks perpetuating prevalence of low-costbusiness models

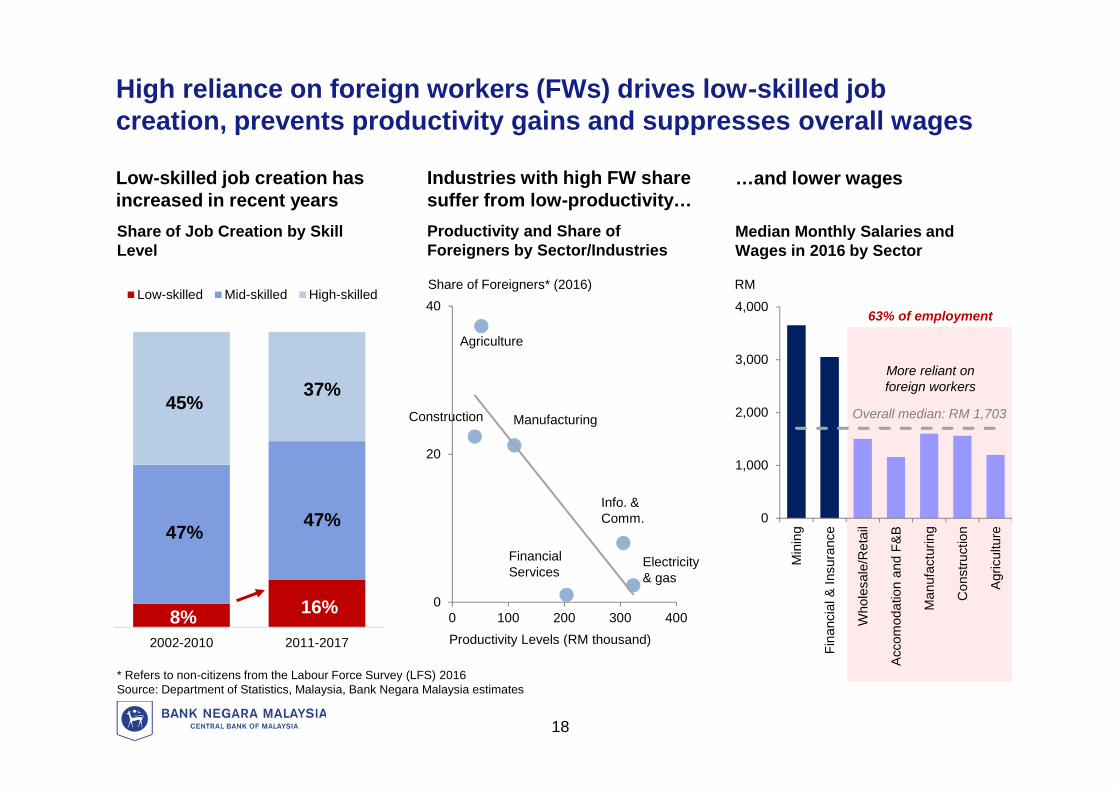

High reliance on foreign workers (FWs) drives low-skilled jobcreation, prevents productivity gains and suppresses overall wages

* Refers to non-citizens from the Labour Force Survey (LFS) 2016Source: Department of Statistics, Malaysia, Bank Negara Malaysia estimates

Productivity and Share ofForeigners by Sector/Industries

Median Monthly Salaries andWages in 2016 by Sector

Low-skilled job creation hasincreased in recent years

Industries with high FW sharesuffer from low-productivity…

…and lower wages

Share of Job Creation by SkillLevel

Min

ing

Fina

ncia

l & In

sura

nce

Who

lesa

le/R

etai

l

Acc

omod

atio

n an

d F&

B

Man

ufac

turin

g

Con

stru

ctio

n

Agr

icul

ture

0

1,000

2,000

3,000

4,00063% of employment

More reliant onforeign workers

Overall median: RM 1,703

0

20

40

0 100 200 300 400

Agriculture

Manufacturing

Info. &Comm.

FinancialServices

Share of Foreigners* (2016)

Productivity Levels (RM thousand)

Electricity& gas

18

Construction

RM

2002-2010 2011-2017

Low-skilled Mid-skilled High-skilled

45%37%

47% 47%

8% 16%

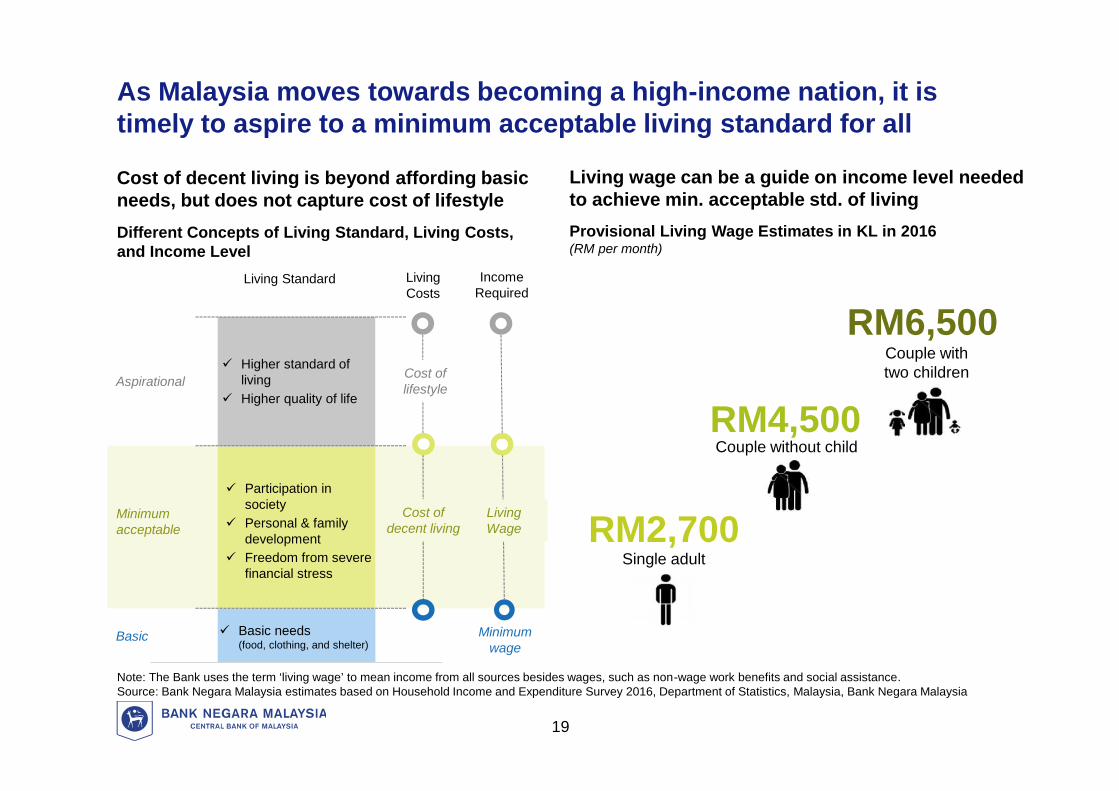

As Malaysia moves towards becoming a high-income nation, it istimely to aspire to a minimum acceptable living standard for all

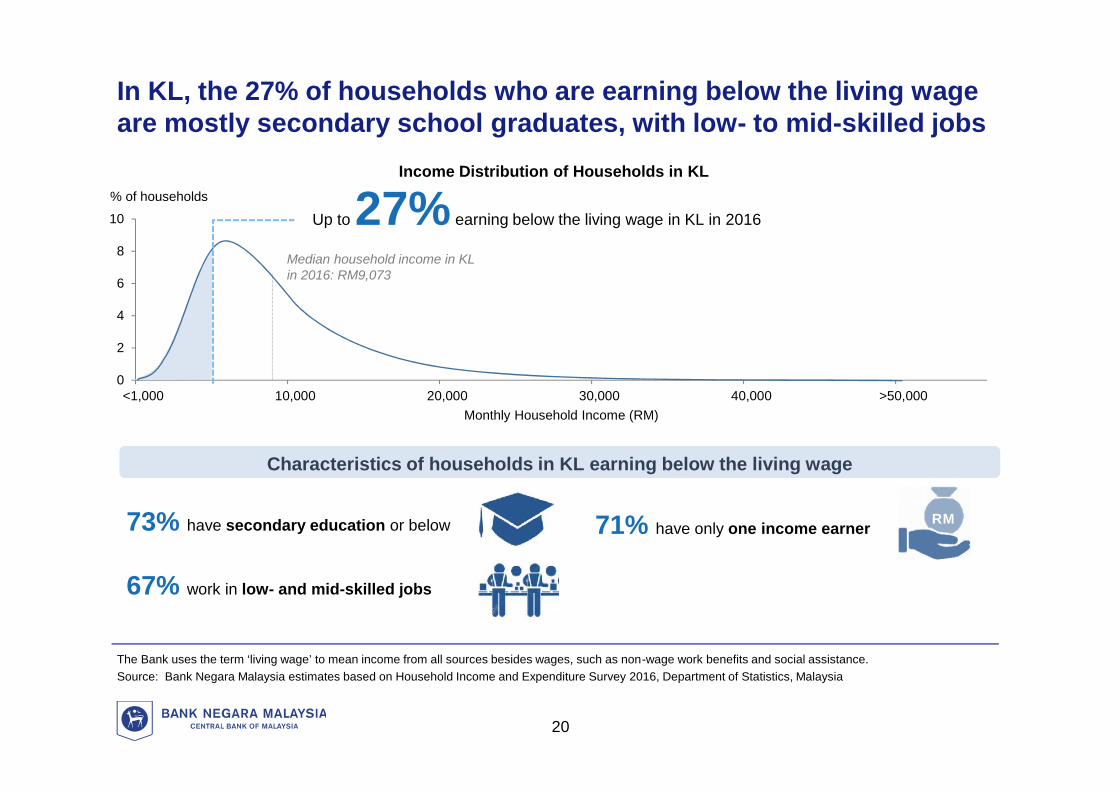

Cost of decent living is beyond affording basicneeds, but does not capture cost of lifestyle

Note: The Bank uses the term ‘living wage’ to mean income from all sources besides wages, such as non-wage work benefits and social assistance.Source: Bank Negara Malaysia estimates based on Household Income and Expenditure Survey 2016, Department of Statistics, Malaysia, Bank Negara Malaysia

Living wage can be a guide on income level neededto achieve min. acceptable std. of living

Different Concepts of Living Standard, Living Costs,and Income Level

Provisional Living Wage Estimates in KL in 2016(RM per month)

Minimumacceptable

Basic

Aspirational Higher standard of

living Higher quality of life

Participation insociety

Personal & familydevelopment

Freedom from severefinancial stress

Basic needs(food, clothing, and shelter)

Living Standard IncomeRequired

LivingWage

Minimumwage

LivingCosts

Cost ofdecent living

Cost oflifestyle

19

Single adultRM2,700

Couple without childRM4,500

Couple withtwo children

RM6,500

0

2

4

6

8

10

<1,000 10,000 20,000 30,000 40,000 >50,000Monthly Household Income (RM)

Median household income in KLin 2016: RM9,073

Up to 27% earning below the living wage in KL in 2016

73% have secondary education or below

67% work in low- and mid-skilled jobs

Income Distribution of Households in KL

71% have only one income earner RM

% of households

In KL, the 27% of households who are earning below the living wageare mostly secondary school graduates, with low- to mid-skilled jobs

The Bank uses the term ‘living wage’ to mean income from all sources besides wages, such as non-wage work benefits and social assistance.Source: Bank Negara Malaysia estimates based on Household Income and Expenditure Survey 2016, Department of Statistics, Malaysia

20

Characteristics of households in KL earning below the living wage

3.5

11.1

4.9 4.6

0

2

4

6

8

10

12

Malaysia India C. Taipei PR China

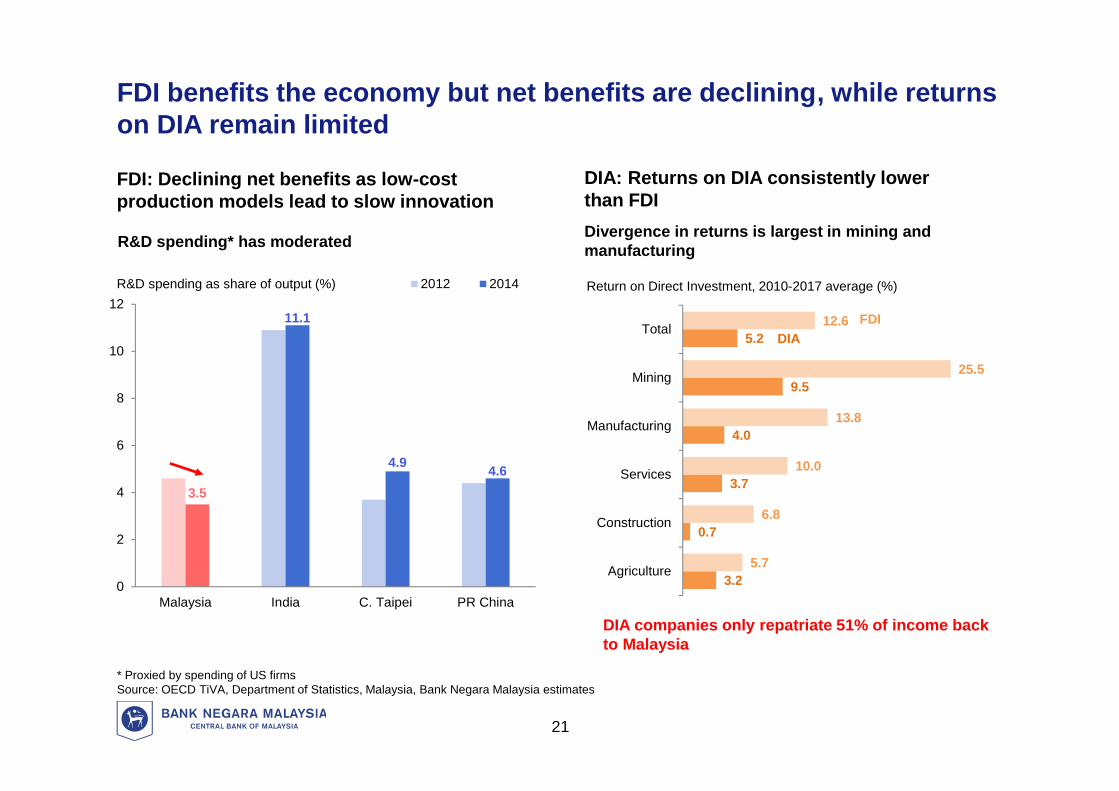

2012 2014R&D spending as share of output (%)

R&D spending* has moderated

FDI benefits the economy but net benefits are declining, while returnson DIA remain limited

FDI: Declining net benefits as low-costproduction models lead to slow innovation

* Proxied by spending of US firmsSource: OECD TiVA, Department of Statistics, Malaysia, Bank Negara Malaysia estimates

DIA: Returns on DIA consistently lowerthan FDI

21

3.2

0.7

3.7

4.0

9.5

5.2

5.7

6.8

10.0

13.8

25.5

12.6

Agriculture

Construction

Services

Manufacturing

Mining

TotalDIA

FDI

Return on Direct Investment, 2010-2017 average (%)

Divergence in returns is largest in mining andmanufacturing

DIA companies only repatriate 51% of income backto Malaysia

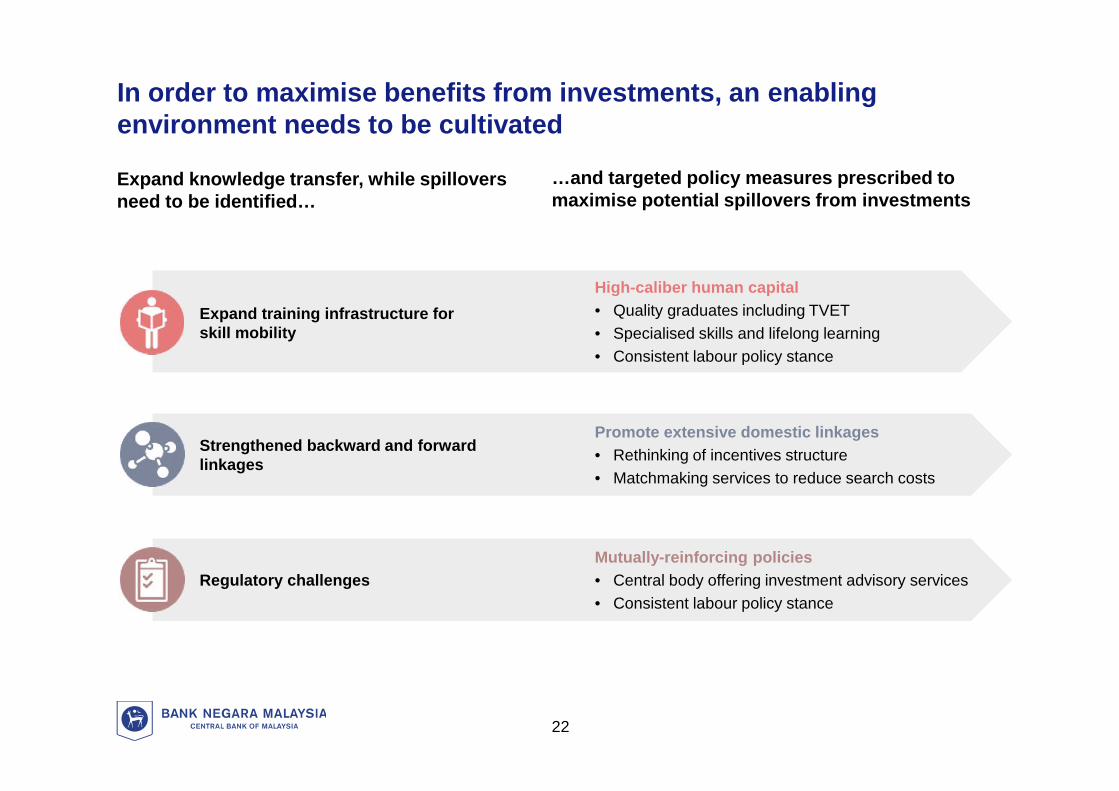

Mutually-reinforcing policies• Central body offering investment advisory services• Consistent labour policy stance

Promote extensive domestic linkages• Rethinking of incentives structure• Matchmaking services to reduce search costs

High-caliber human capital• Quality graduates including TVET• Specialised skills and lifelong learning• Consistent labour policy stance

In order to maximise benefits from investments, an enablingenvironment needs to be cultivated

Expand knowledge transfer, while spilloversneed to be identified…

…and targeted policy measures prescribed tomaximise potential spillovers from investments

Expand training infrastructure forskill mobility

Strengthened backward and forwardlinkages

Regulatory challenges

22

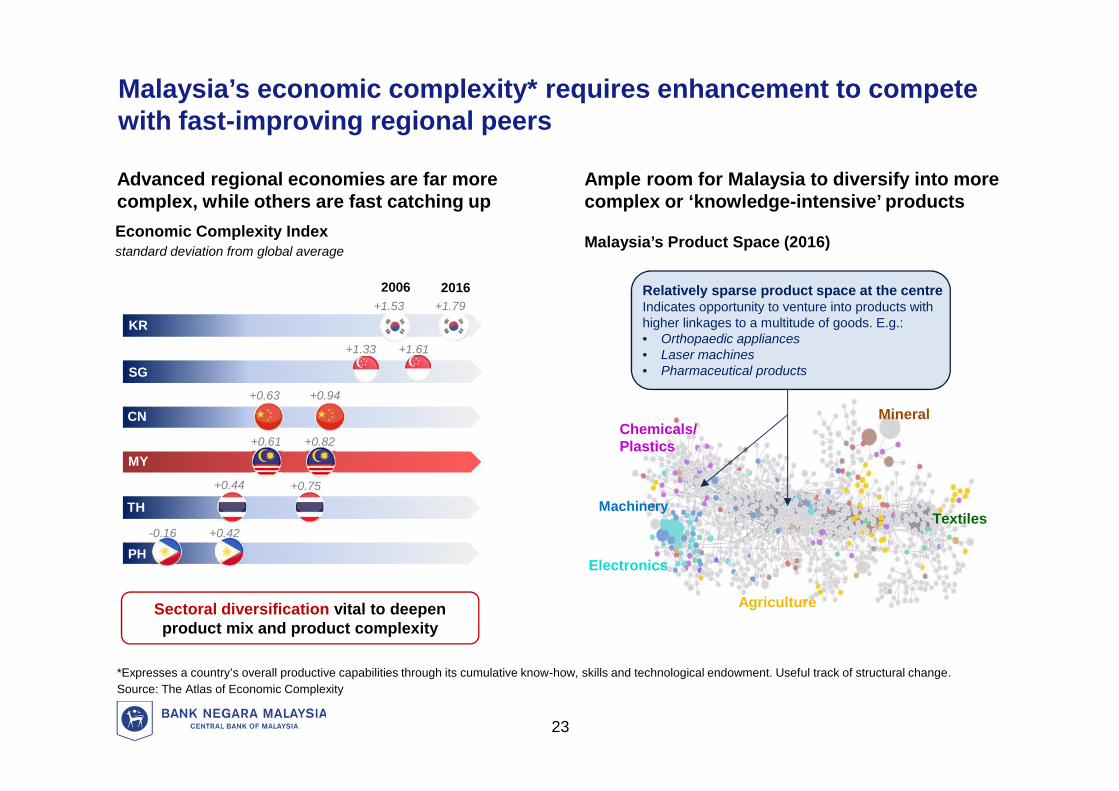

Malaysia’s economic complexity* requires enhancement to competewith fast-improving regional peers

Updated

Economic Complexity Indexstandard deviation from global average

Advanced regional economies are far morecomplex, while others are fast catching up

Sectoral diversification vital to deepenproduct mix and product complexity

Malaysia’s Product Space (2016)

Ample room for Malaysia to diversify into morecomplex or ‘knowledge-intensive’ products

Relatively sparse product space at the centreIndicates opportunity to venture into products withhigher linkages to a multitude of goods. E.g.:• Orthopaedic appliances• Laser machines• Pharmaceutical products

Machinery

Electronics

Chemicals/Plastics

Textiles

Mineral

Agriculture

*Expresses a country’s overall productive capabilities through its cumulative know-how, skills and technological endowment. Useful track of structural change.Source: The Atlas of Economic Complexity

+1.79+1.53

+0.61 +0.82

+0.94+0.63

+0.75+0.44

+0.42-0.16

+1.61+1.33

KR

SG

CN

MY

TH

2006 2016

23

PH

KR

SG

JP

USEE

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0.3 0.5 0.7 0.9 1.1Digital Adoption Index Score

Adopter

Laggard

Malaysia

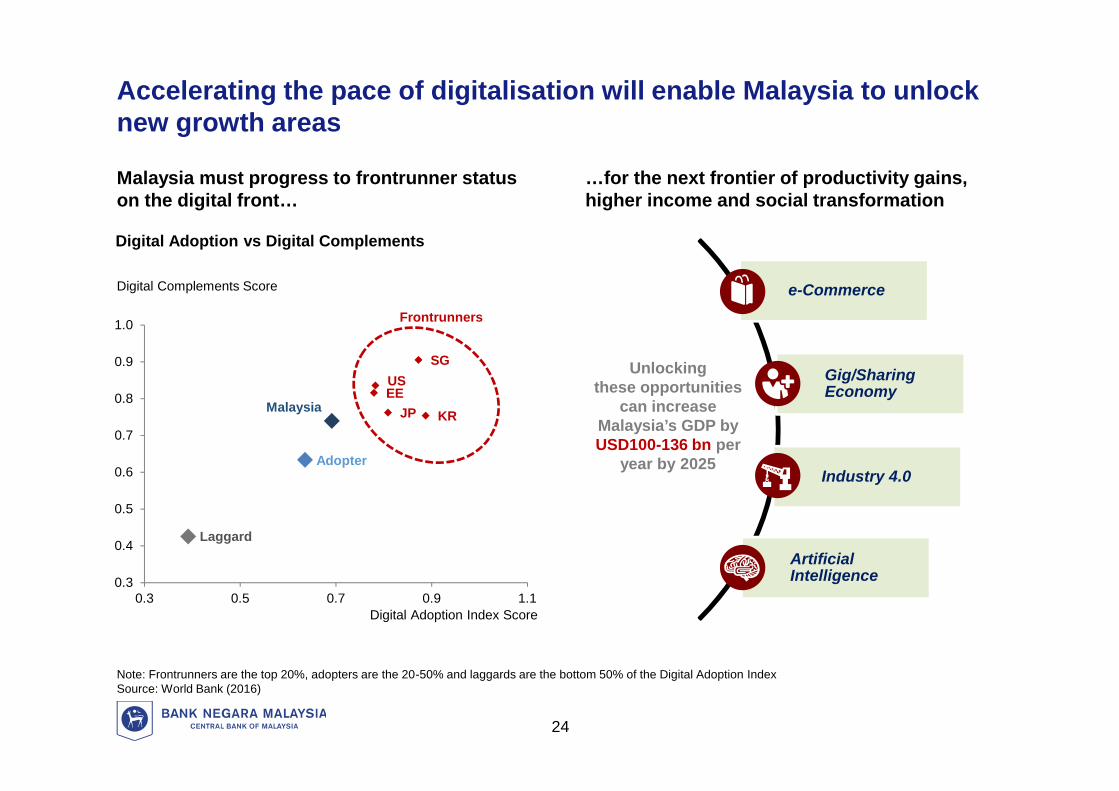

Accelerating the pace of digitalisation will enable Malaysia to unlocknew growth areas

Malaysia must progress to frontrunner statuson the digital front…

…for the next frontier of productivity gains,higher income and social transformation

Digital Complements Score

Frontrunners

e-Commerce

Gig/SharingEconomy

Industry 4.0

ArtificialIntelligence

Unlockingthese opportunities

can increaseMalaysia’s GDP byUSD100-136 bn per

year by 2025

Digital Adoption vs Digital Complements

Note: Frontrunners are the top 20%, adopters are the 20-50% and laggards are the bottom 50% of the Digital Adoption IndexSource: World Bank (2016)

24

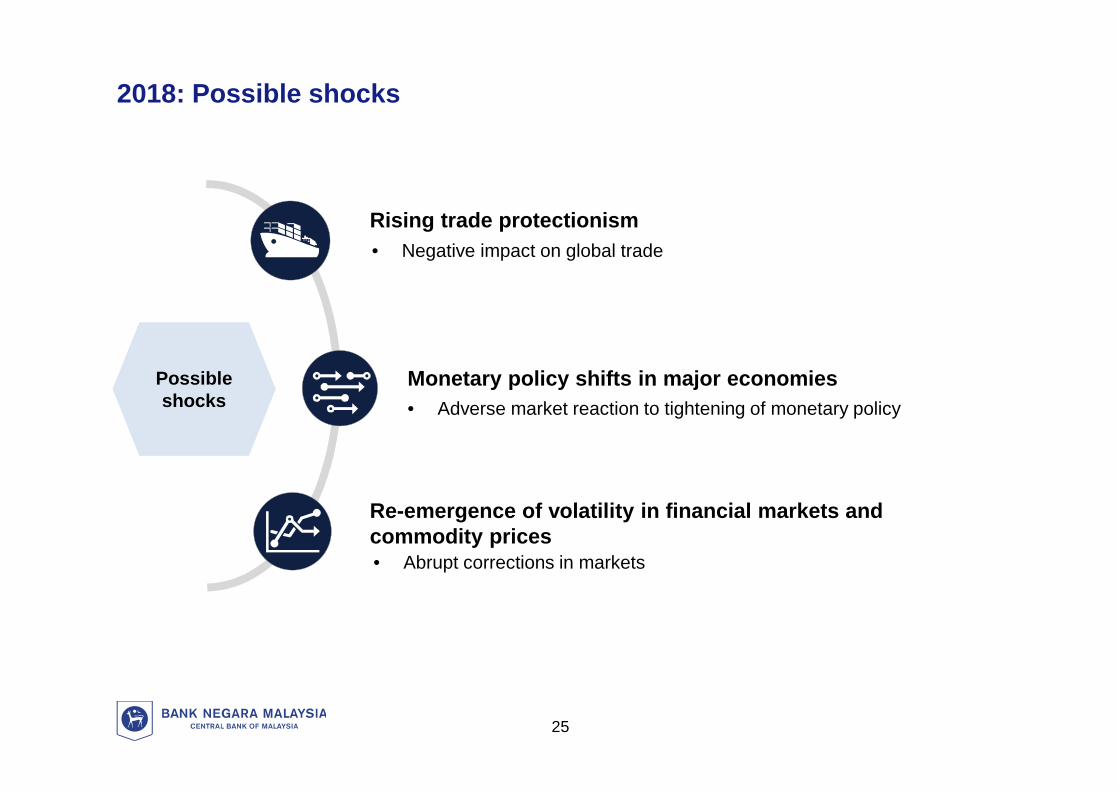

2018: Possible shocks

Rising trade protectionism

Monetary policy shifts in major economies

Re-emergence of volatility in financial markets andcommodity prices

• Adverse market reaction to tightening of monetary policy

• Abrupt corrections in markets

Possibleshocks

25

• Negative impact on global trade

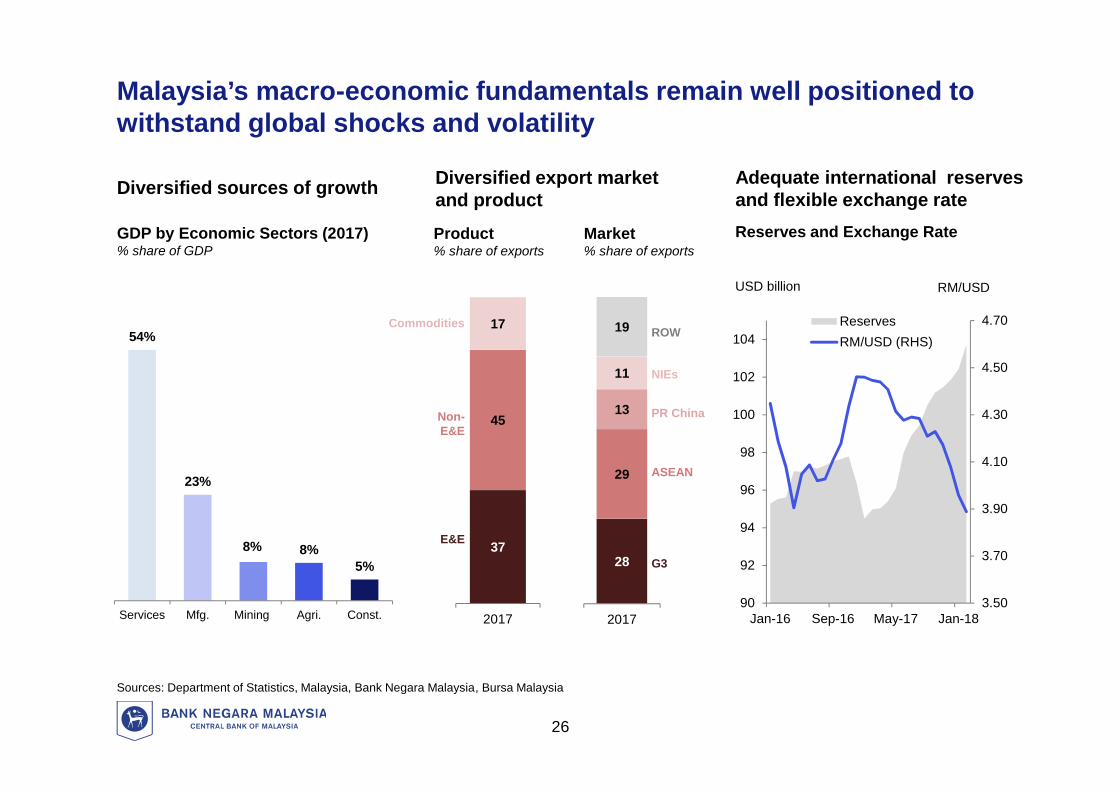

GDP by Economic Sectors (2017)% share of GDP

Reserves and Exchange Rate

Sources: Department of Statistics, Malaysia, Bank Negara Malaysia, Bursa Malaysia

Diversified sources of growth Diversified export marketand product

Market% share of exports

Product% share of exports

Adequate international reservesand flexible exchange rate

26

Malaysia’s macro-economic fundamentals remain well positioned towithstand global shocks and volatility

54%

23%

8% 8%5%

Services Mfg. Mining Agri. Const.

37

45

17

2017

28

29

13

11

19

2017

E&E

Non-E&E

Commodities

G3

ASEAN

PR China

NIEs

ROW

3.50

3.70

3.90

4.10

4.30

4.50

4.70

90

92

94

96

98

100

102

104

Jan-16 Sep-16 May-17 Jan-18

ReservesRM/USD (RHS)

USD billion RM/USD

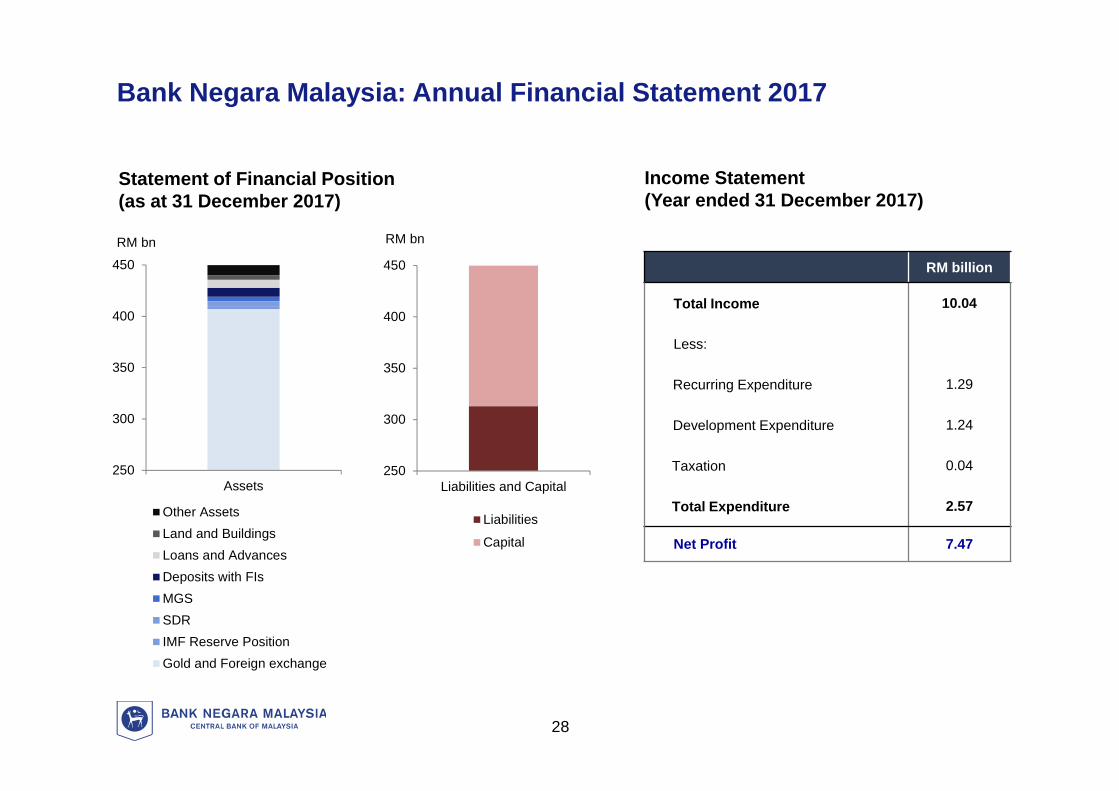

Bank Negara Malaysia: Annual Financial Statement 2017

Financial position remained strong in 2017:

• Total assets of BNM amounted to RM449.85 billion

• Net profit of RM7.47 billion

• 2017 dividend of RM2.5 billion paid to the Government

27

33

Income Statement(Year ended 31 December 2017)

Statement of Financial Position(as at 31 December 2017)

250

300

350

400

450

Assets

Other AssetsLand and BuildingsLoans and AdvancesDeposits with FIsMGSSDRIMF Reserve PositionGold and Foreign exchange

RM bn

250

300

350

400

450

Liabilities and Capital

Liabilities

Capital

RM bn

RM billion

Total Income 10.04

Less:

Recurring Expenditure 1.29

Development Expenditure 1.24

Taxation 0.04

Total Expenditure 2.57

Net Profit 7.47

Bank Negara Malaysia: Annual Financial Statement 2017

28

Laporan Kestabilan Kewangandan Sistem Pembayaran 2017

Bank Negara Malaysia

28 Mac 2018

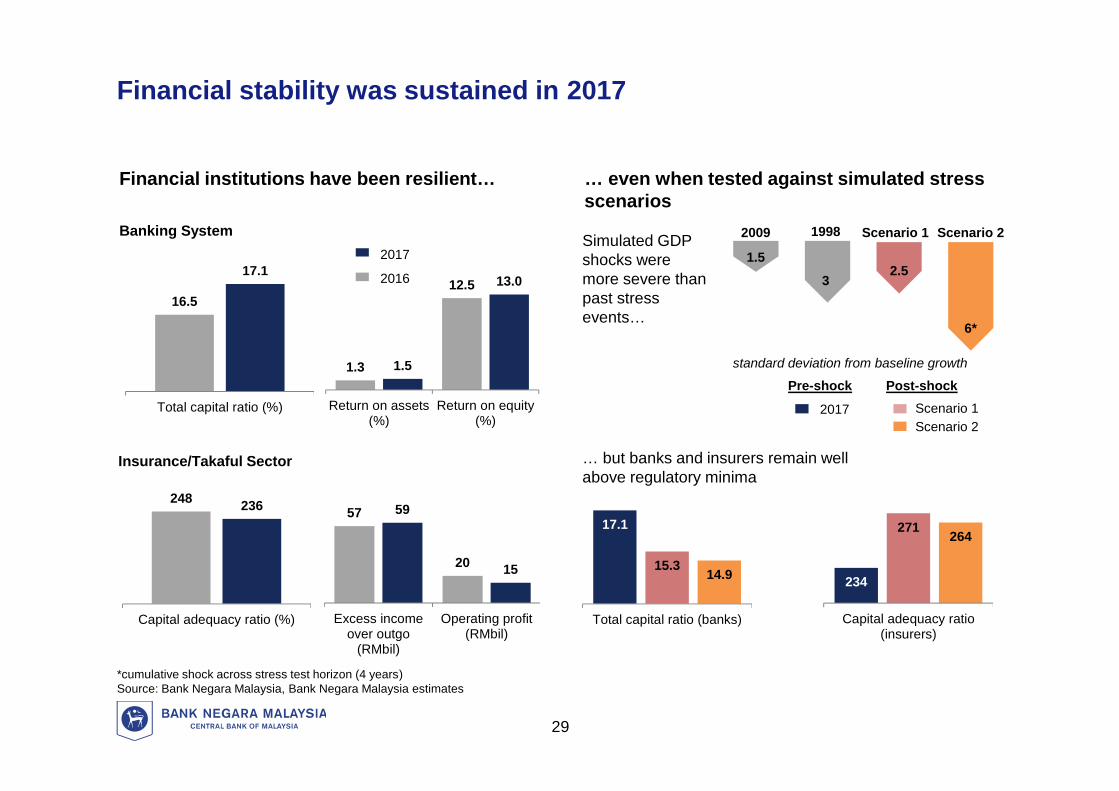

Financial stability was sustained in 2017

*cumulative shock across stress test horizon (4 years)Source: Bank Negara Malaysia, Bank Negara Malaysia estimates

Financial institutions have been resilient… … even when tested against simulated stressscenarios

Simulated GDPshocks weremore severe thanpast stressevents…

Insurance/Takaful Sector

standard deviation from baseline growth

2009

1.5

1998

32.5

Scenario 1

6*

Scenario 2

… but banks and insurers remain wellabove regulatory minima

17.1

15.3 14.9

Total capital ratio (banks)

234

271 264

Capital adequacy ratio(insurers)

16.5

17.1

Total capital ratio (%)

1.3

12.5

1.5

13.0

Return on assets(%)

Return on equity(%)

2017

2016

2017 Scenario 1Scenario 2

Post-shockPre-shock

248 236

Capital adequacy ratio (%)

57

20

59

15

Excess incomeover outgo

(RMbil)

Operating profit(RMbil)

Banking System

29

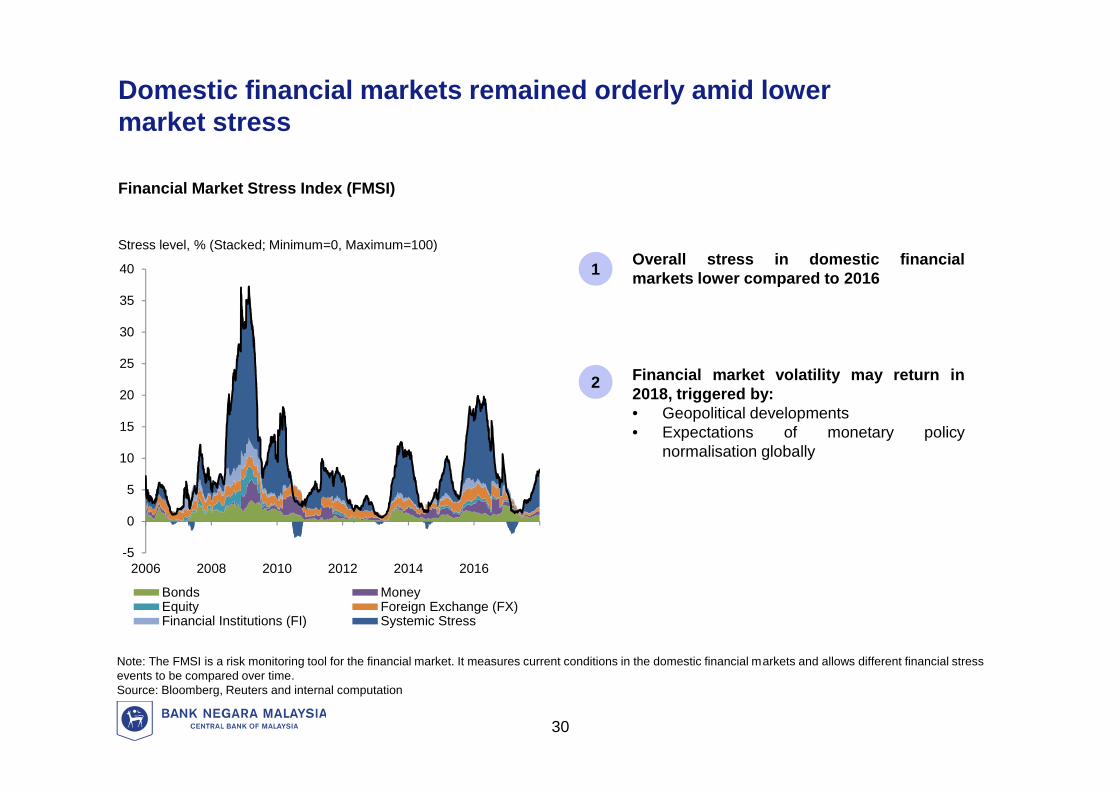

Domestic financial markets remained orderly amid lowermarket stress

Note: The FMSI is a risk monitoring tool for the financial market. It measures current conditions in the domestic financial markets and allows different financial stressevents to be compared over time.Source: Bloomberg, Reuters and internal computation

Stress level, % (Stacked; Minimum=0, Maximum=100)

Financial Market Stress Index (FMSI)

-5

0

5

10

15

20

25

30

35

40

2006 2008 2010 2012 2014 2016

Bonds MoneyEquity Foreign Exchange (FX)Financial Institutions (FI) Systemic Stress

Overall stress in domestic financialmarkets lower compared to 20161

Financial market volatility may return in2018, triggered by:• Geopolitical developments• Expectations of monetary policy

normalisation globally

2

30

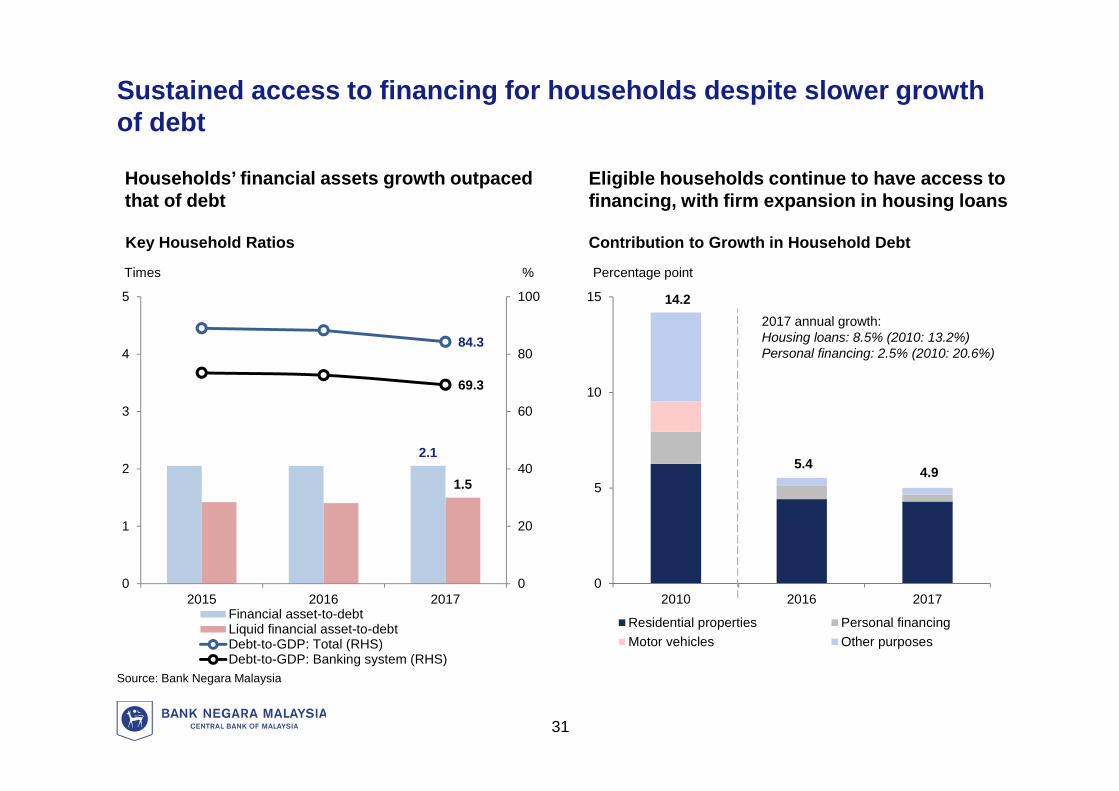

Sustained access to financing for households despite slower growthof debt

Households’ financial assets growth outpacedthat of debt

Key Household Ratios

Source: Bank Negara Malaysia

31

2.1

1.5

84.3

69.3

0

20

40

60

80

100

0

1

2

3

4

5

2015 2016 2017Financial asset-to-debtLiquid financial asset-to-debtDebt-to-GDP: Total (RHS)Debt-to-GDP: Banking system (RHS)

Times %

Eligible households continue to have access tofinancing, with firm expansion in housing loans

Percentage point

Contribution to Growth in Household Debt

14.2

5.4 4.9

0

5

10

15

2010 2016 2017

Residential properties Personal financingMotor vehicles Other purposes

2017 annual growth:Housing loans: 8.5% (2010: 13.2%)Personal financing: 2.5% (2010: 20.6%)

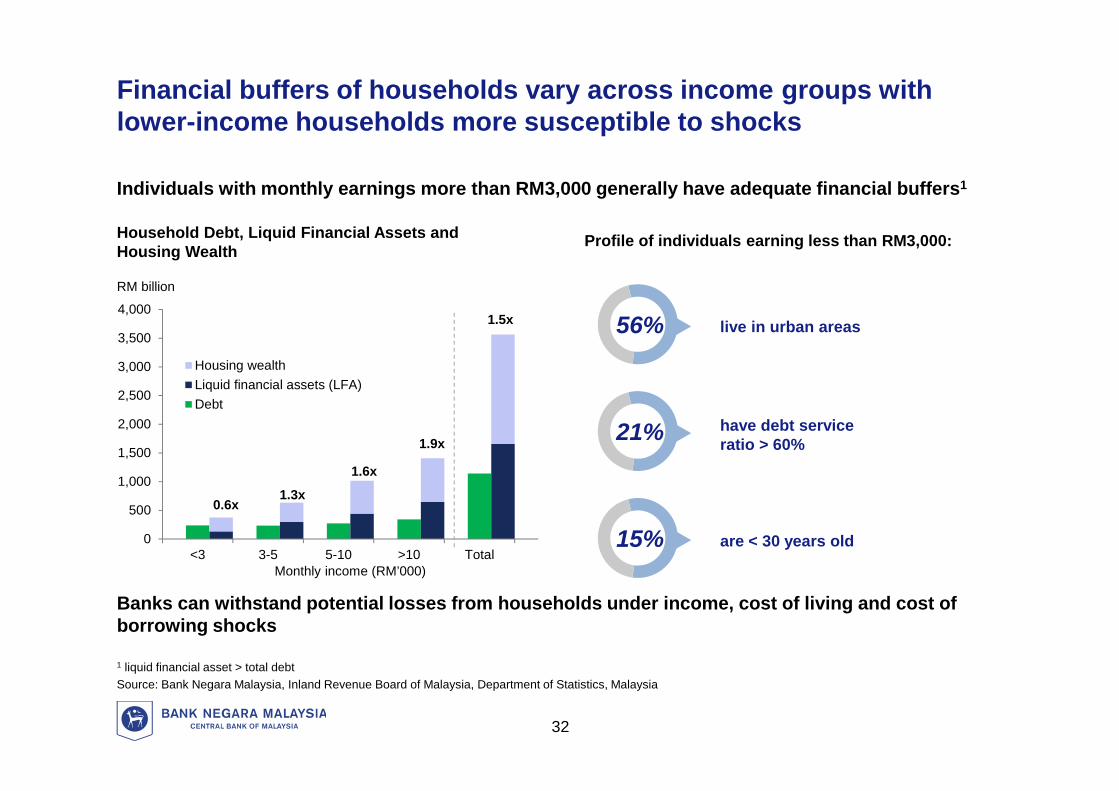

Financial buffers of households vary across income groups withlower-income households more susceptible to shocks

Individuals with monthly earnings more than RM3,000 generally have adequate financial buffers1

1 liquid financial asset > total debtSource: Bank Negara Malaysia, Inland Revenue Board of Malaysia, Department of Statistics, Malaysia

RM billion

Household Debt, Liquid Financial Assets andHousing Wealth

are < 30 years old

56% live in urban areas

have debt serviceratio > 60%

Banks can withstand potential losses from households under income, cost of living and cost ofborrowing shocks

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

<3 3-5 5-10 >10 TotalMonthly income (RM’000)

Housing wealthLiquid financial assets (LFA)Debt

0.6x1.3x

1.6x

1.9x

1.5x

32

Profile of individuals earning less than RM3,000:

21%

15%

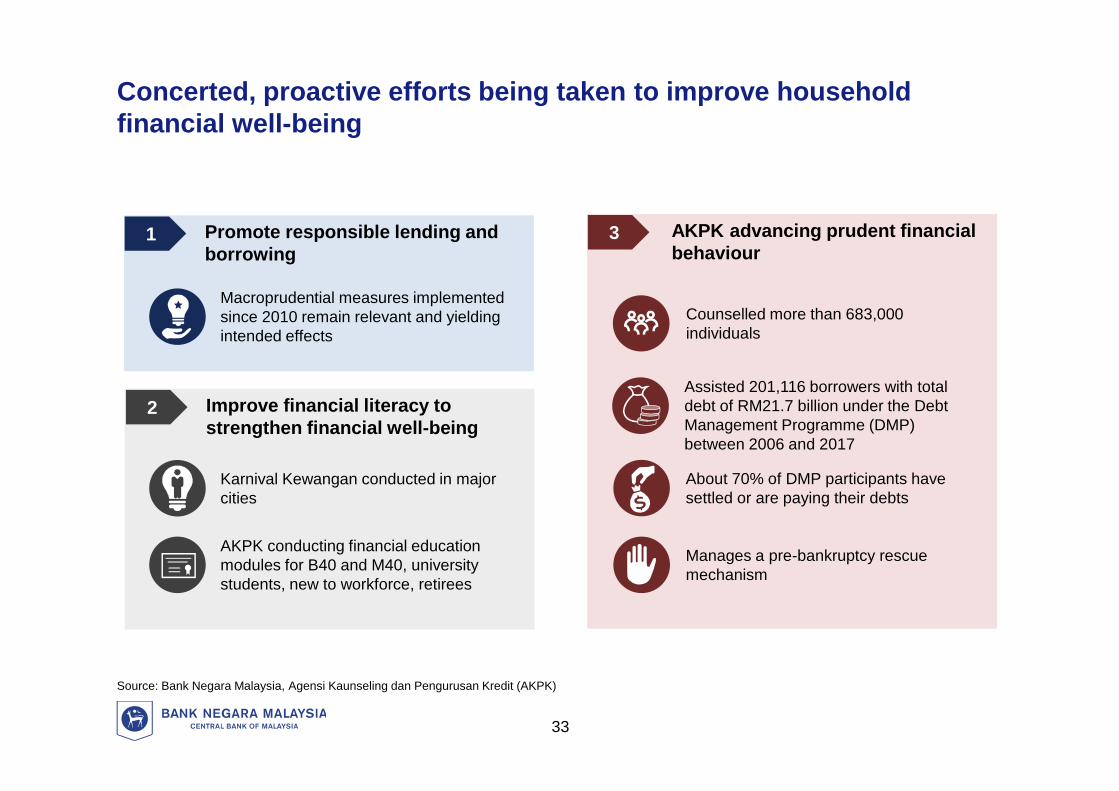

Concerted, proactive efforts being taken to improve householdfinancial well-being

Source: Bank Negara Malaysia, Agensi Kaunseling dan Pengurusan Kredit (AKPK)

1 Promote responsible lending andborrowing

2 Improve financial literacy tostrengthen financial well-being

3 AKPK advancing prudent financialbehaviour

Counselled more than 683,000individuals

Assisted 201,116 borrowers with totaldebt of RM21.7 billion under the DebtManagement Programme (DMP)between 2006 and 2017

About 70% of DMP participants havesettled or are paying their debts

Manages a pre-bankruptcy rescuemechanism

AKPK conducting financial educationmodules for B40 and M40, universitystudents, new to workforce, retirees

Karnival Kewangan conducted in majorcities

Macroprudential measures implementedsince 2010 remain relevant and yieldingintended effects

33

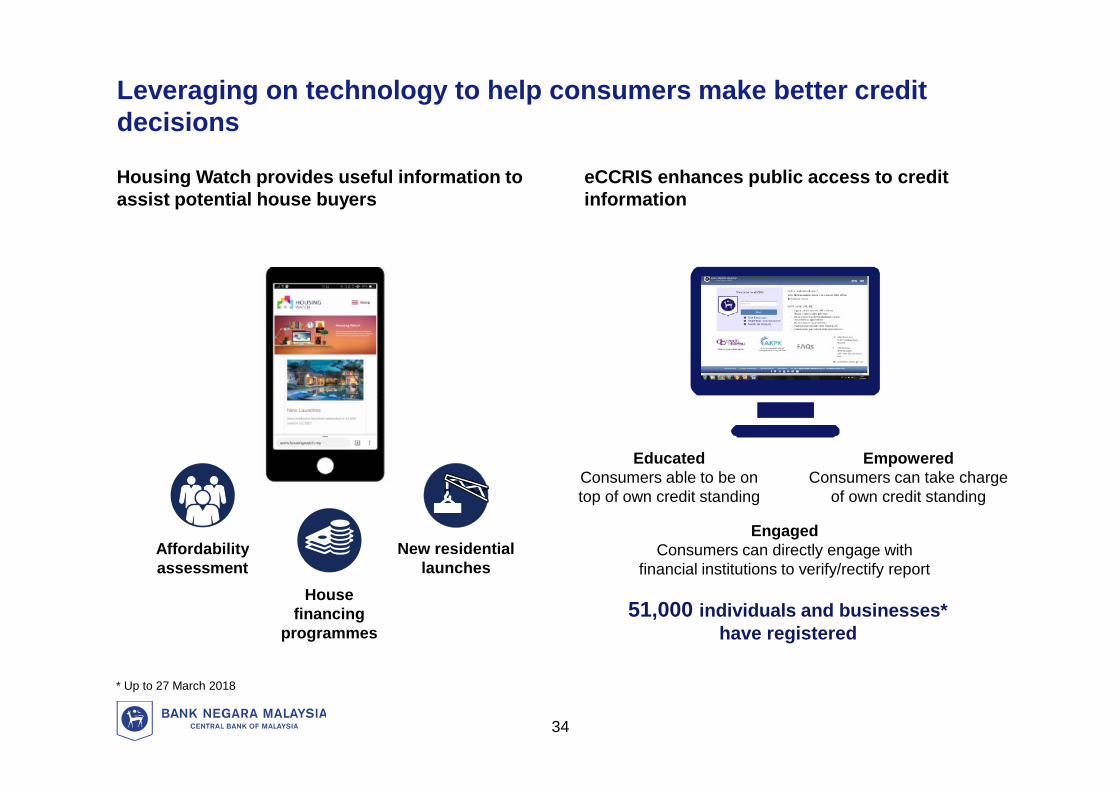

Leveraging on technology to help consumers make better creditdecisions

Housing Watch provides useful information toassist potential house buyers

* Up to 27 March 2018

eCCRIS enhances public access to creditinformation

51,000 individuals and businesses*have registered

Affordabilityassessment

Housefinancing

programmes

New residentiallaunches

34

EducatedConsumers able to be ontop of own credit standing

EmpoweredConsumers can take charge

of own credit standing

EngagedConsumers can directly engage with

financial institutions to verify/rectify report

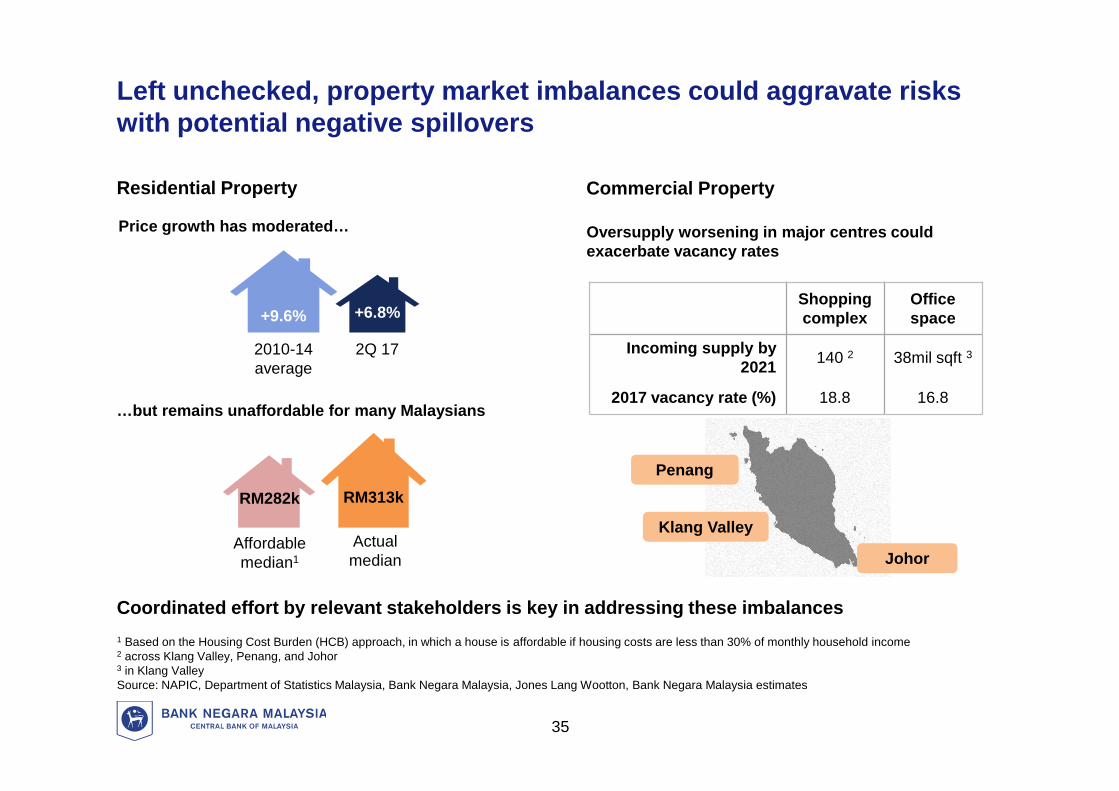

Left unchecked, property market imbalances could aggravate riskswith potential negative spillovers

1 Based on the Housing Cost Burden (HCB) approach, in which a house is affordable if housing costs are less than 30% of monthly household income2 across Klang Valley, Penang, and Johor3 in Klang ValleySource: NAPIC, Department of Statistics Malaysia, Bank Negara Malaysia, Jones Lang Wootton, Bank Negara Malaysia estimates

Coordinated effort by relevant stakeholders is key in addressing these imbalances

Price growth has moderated… Oversupply worsening in major centres couldexacerbate vacancy rates

…but remains unaffordable for many Malaysians

35

Residential Property Commercial Property

Shoppingcomplex

Officespace

Incoming supply by2021 140 2 38mil sqft 3

2017 vacancy rate (%) 18.8 16.8

Johor

Klang Valley

Penang

+6.8%

2Q 17

+9.6%

2010-14average

RM313k

Actualmedian

Affordablemedian1

RM282k

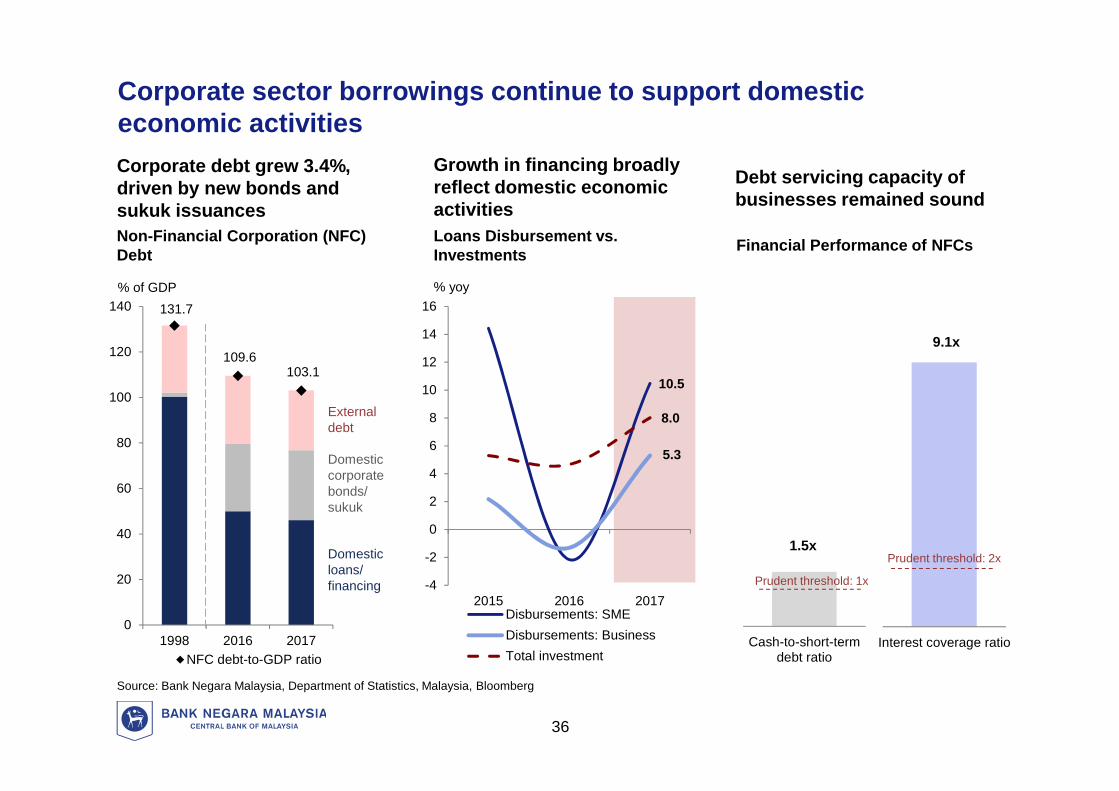

Corporate sector borrowings continue to support domesticeconomic activities

% of GDP

Loans Disbursement vs.Investments

% yoy

Corporate debt grew 3.4%,driven by new bonds andsukuk issuances

Growth in financing broadlyreflect domestic economicactivities

Debt servicing capacity ofbusinesses remained sound

Non-Financial Corporation (NFC)Debt

131.7

109.6103.1

0

20

40

60

80

100

120

140

1998 2016 2017NFC debt-to-GDP ratio

Externaldebt

Domesticcorporatebonds/sukuk

Domesticloans/financing

Financial Performance of NFCs

Interest coverage ratio

Prudent threshold: 2x

Cash-to-short-termdebt ratio

Prudent threshold: 1x

10.5

5.3

8.0

-4

-2

0

2

4

6

8

10

12

14

16

2015 2016 2017Disbursements: SMEDisbursements: BusinessTotal investment

Source: Bank Negara Malaysia, Department of Statistics, Malaysia, Bloomberg

36

9.1x

1.5x

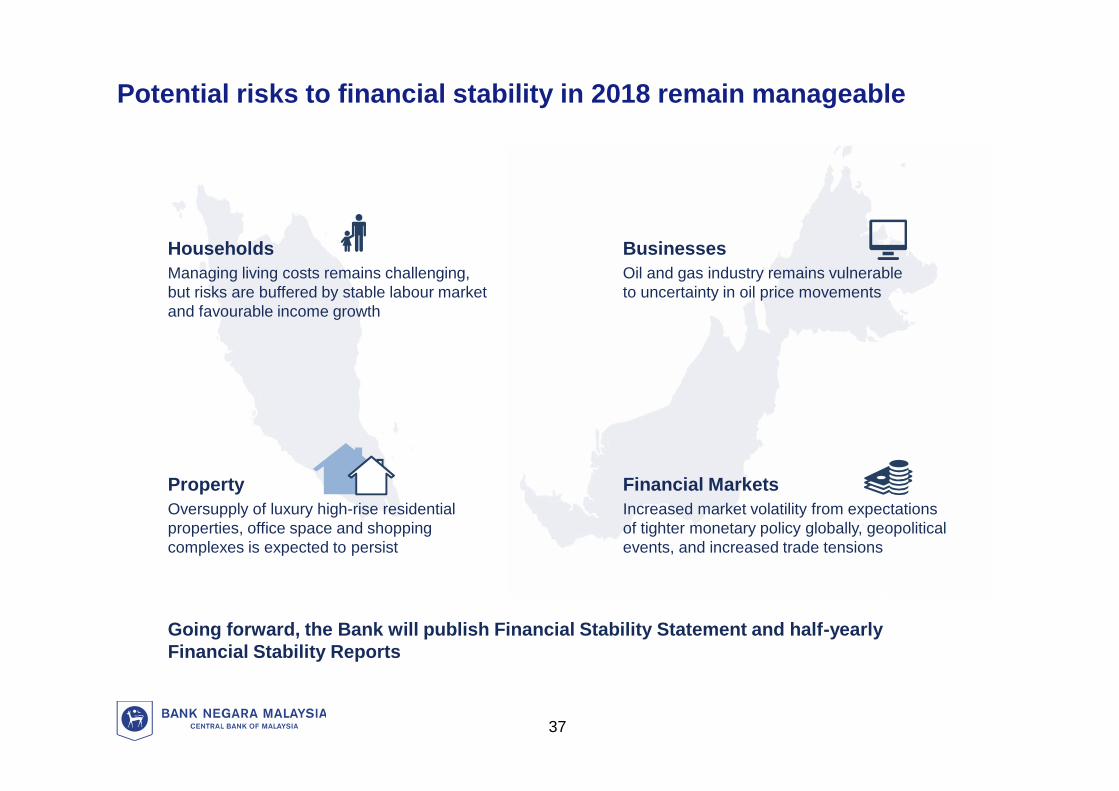

Potential risks to financial stability in 2018 remain manageable

HouseholdsManaging living costs remains challenging,but risks are buffered by stable labour marketand favourable income growth

PropertyOversupply of luxury high-rise residentialproperties, office space and shoppingcomplexes is expected to persist

BusinessesOil and gas industry remains vulnerableto uncertainty in oil price movements

Financial MarketsIncreased market volatility from expectationsof tighter monetary policy globally, geopoliticalevents, and increased trade tensions

37

Going forward, the Bank will publish Financial Stability Statement and half-yearlyFinancial Stability Reports

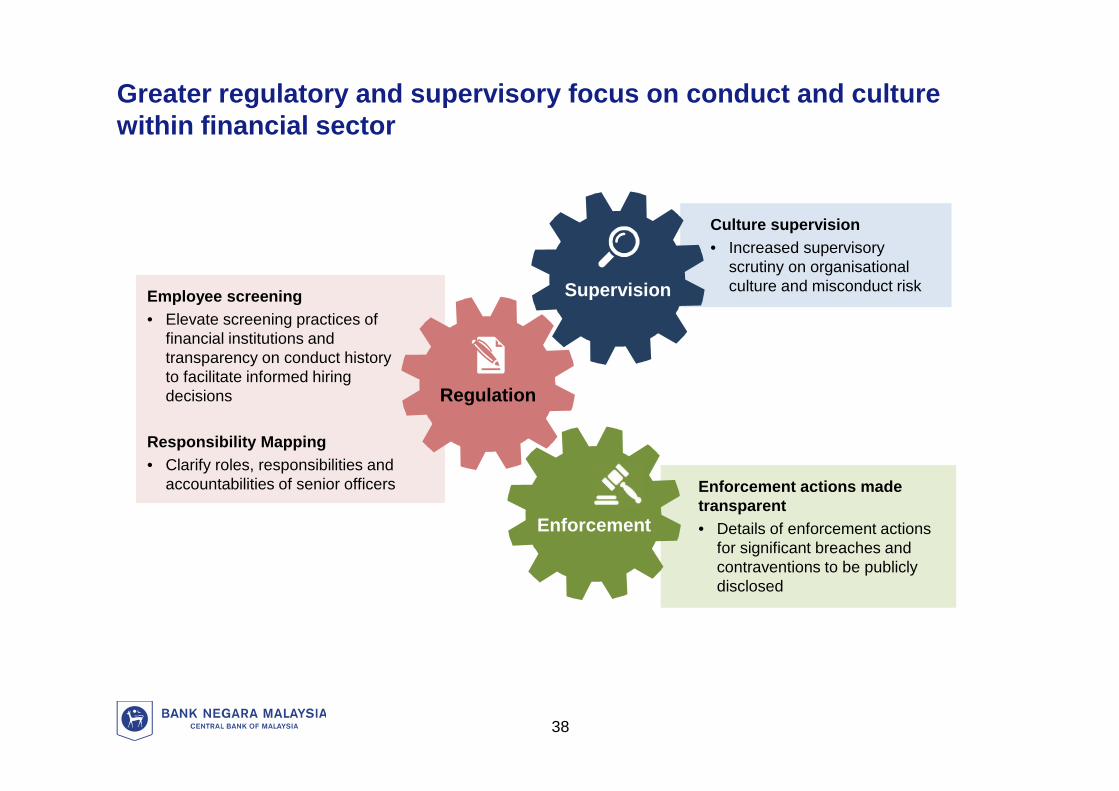

Greater regulatory and supervisory focus on conduct and culturewithin financial sector

Employee screening• Elevate screening practices of

financial institutions andtransparency on conduct historyto facilitate informed hiringdecisions

Responsibility Mapping• Clarify roles, responsibilities and

accountabilities of senior officers

Culture supervision• Increased supervisory

scrutiny on organisationalculture and misconduct risk

Enforcement actions madetransparent• Details of enforcement actions

for significant breaches andcontraventions to be publiclydisclosed

Supervision

Regulation

Enforcement

38

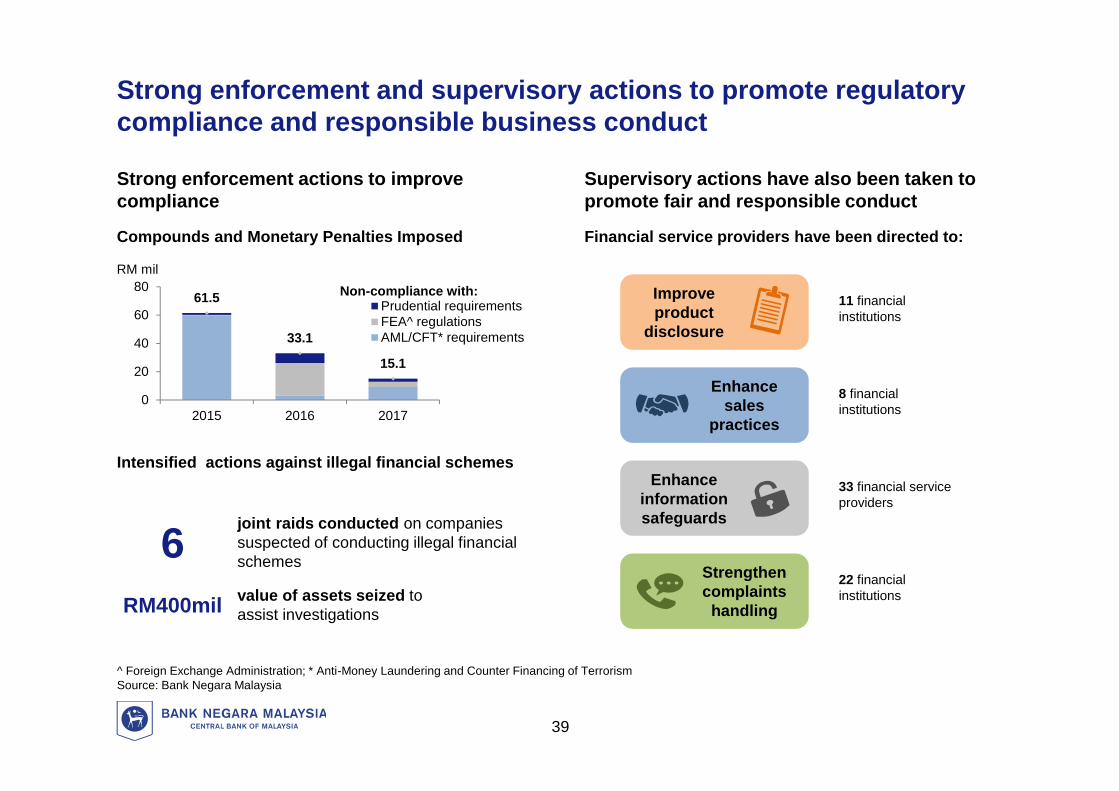

Strong enforcement and supervisory actions to promote regulatorycompliance and responsible business conduct

^ Foreign Exchange Administration; * Anti-Money Laundering and Counter Financing of TerrorismSource: Bank Negara Malaysia

RM mil

Supervisory actions have also been taken topromote fair and responsible conduct

Intensified actions against illegal financial schemes

Compounds and Monetary Penalties Imposed

Strong enforcement actions to improvecompliance

61.5

33.1

15.1

0

20

40

60

80

2015 2016 2017

Prudential requirementsFEA^ regulationsAML/CFT* requirements

Non-compliance with:

joint raids conducted on companiessuspected of conducting illegal financialschemes6

RM400mil value of assets seized toassist investigations

Financial service providers have been directed to:

Improveproduct

disclosure

11 financialinstitutions

Enhancesales

practices

8 financialinstitutions

Enhanceinformationsafeguards

33 financial serviceproviders

Strengthencomplaints

handling

22 financialinstitutions

39

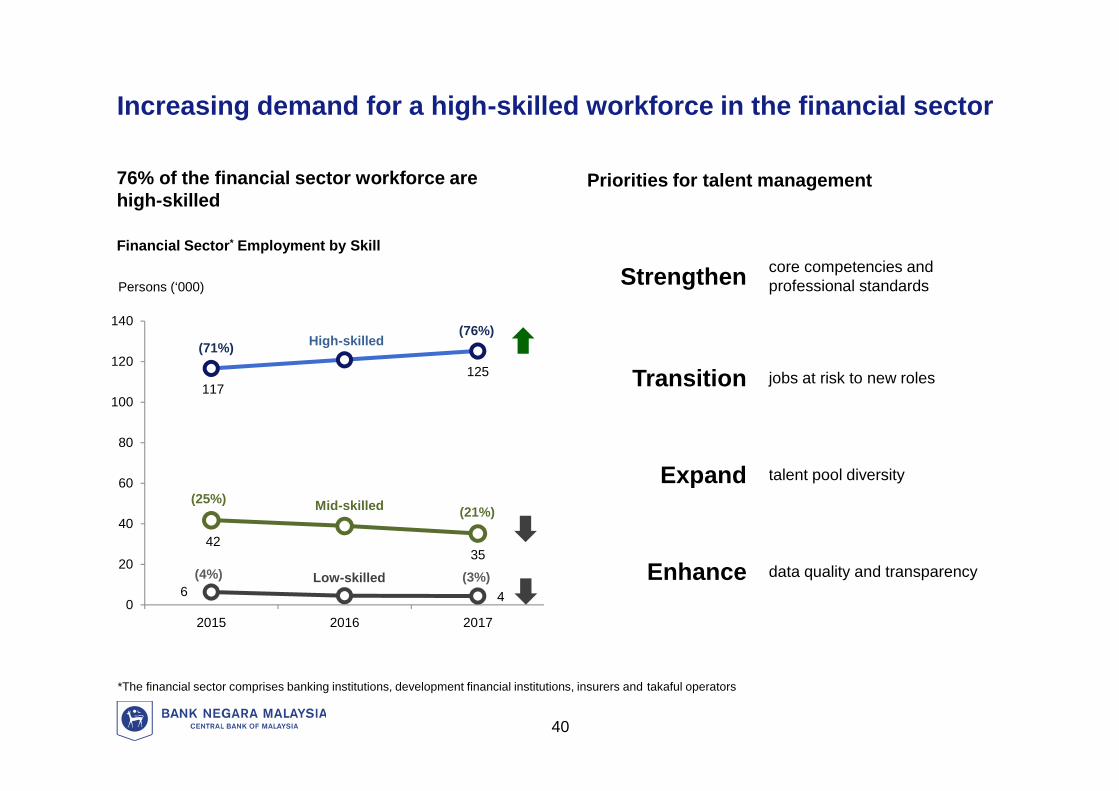

*The financial sector comprises banking institutions, development financial institutions, insurers and takaful operators

Persons (‘000)

Increasing demand for a high-skilled workforce in the financial sector

76% of the financial sector workforce arehigh-skilled

Financial Sector* Employment by Skill

117125

4235

6 40

20

40

60

80

100

120

140

2015 2016 2017

High-skilled

Mid-skilled

Low-skilled

(71%)(76%)

(25%)(21%)

(4%) (3%)

Priorities for talent management

40

Strengthen core competencies andprofessional standards

Transition jobs at risk to new roles

Expand talent pool diversity

Enhance data quality and transparency

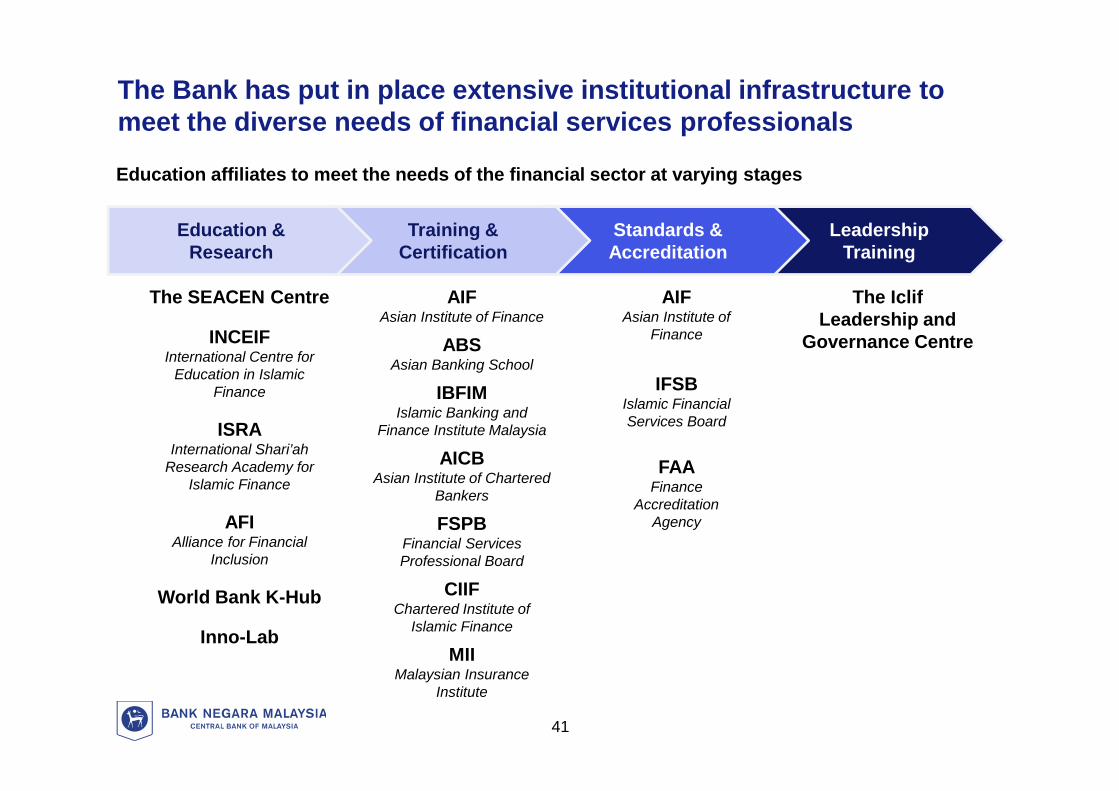

The Bank has put in place extensive institutional infrastructure tomeet the diverse needs of financial services professionals

Education affiliates to meet the needs of the financial sector at varying stages

LeadershipTraining

Standards &Accreditation

Training &Certification

Education &Research

The SEACEN Centre

INCEIFInternational Centre for

Education in IslamicFinance

ISRAInternational Shari’ah

Research Academy forIslamic Finance

AFIAlliance for Financial

Inclusion

World Bank K-Hub

Inno-Lab

AIFAsian Institute of Finance

ABSAsian Banking School

IBFIMIslamic Banking and

Finance Institute Malaysia

AICBAsian Institute of Chartered

Bankers

FSPBFinancial ServicesProfessional Board

CIIFChartered Institute of

Islamic Finance

MIIMalaysian Insurance

Institute

AIFAsian Institute of

Finance

IFSBIslamic FinancialServices Board

FAAFinance

AccreditationAgency

The IclifLeadership and

Governance Centre

41

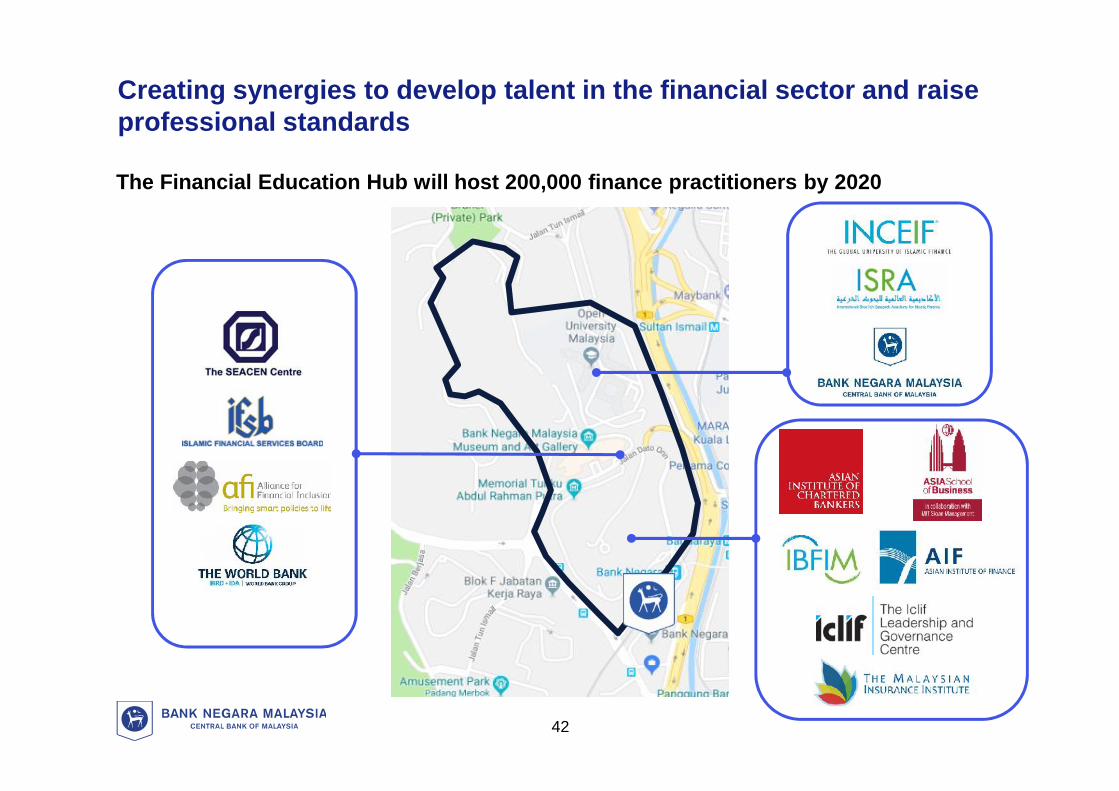

Creating synergies to develop talent in the financial sector and raiseprofessional standards

The Financial Education Hub will host 200,000 finance practitioners by 2020

42

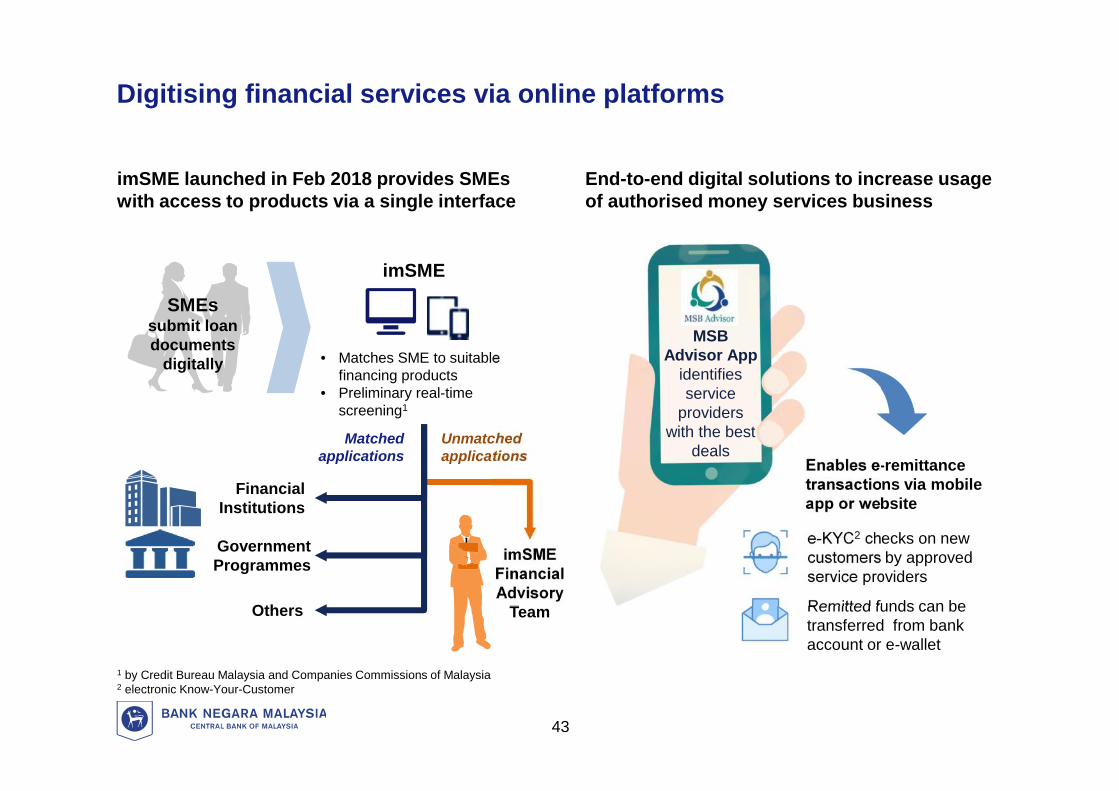

Digitising financial services via online platforms

imSME launched in Feb 2018 provides SMEswith access to products via a single interface

1 by Credit Bureau Malaysia and Companies Commissions of Malaysia2 electronic Know-Your-Customer

End-to-end digital solutions to increase usageof authorised money services business

SMEssubmit loandocuments

digitally

imSME

• Matches SME to suitablefinancing products

• Preliminary real-timescreening1

FinancialInstitutions

Others

Matchedapplications

Unmatchedapplications

imSMEFinancialAdvisory

Team

Enables e-remittancetransactions via mobileapp or website

e-KYC2 checks on newcustomers by approvedservice providers

Remitted funds can betransferred from bankaccount or e-wallet

GovernmentProgrammes

43

MSBAdvisor App

identifiesservice

providerswith the best

deals

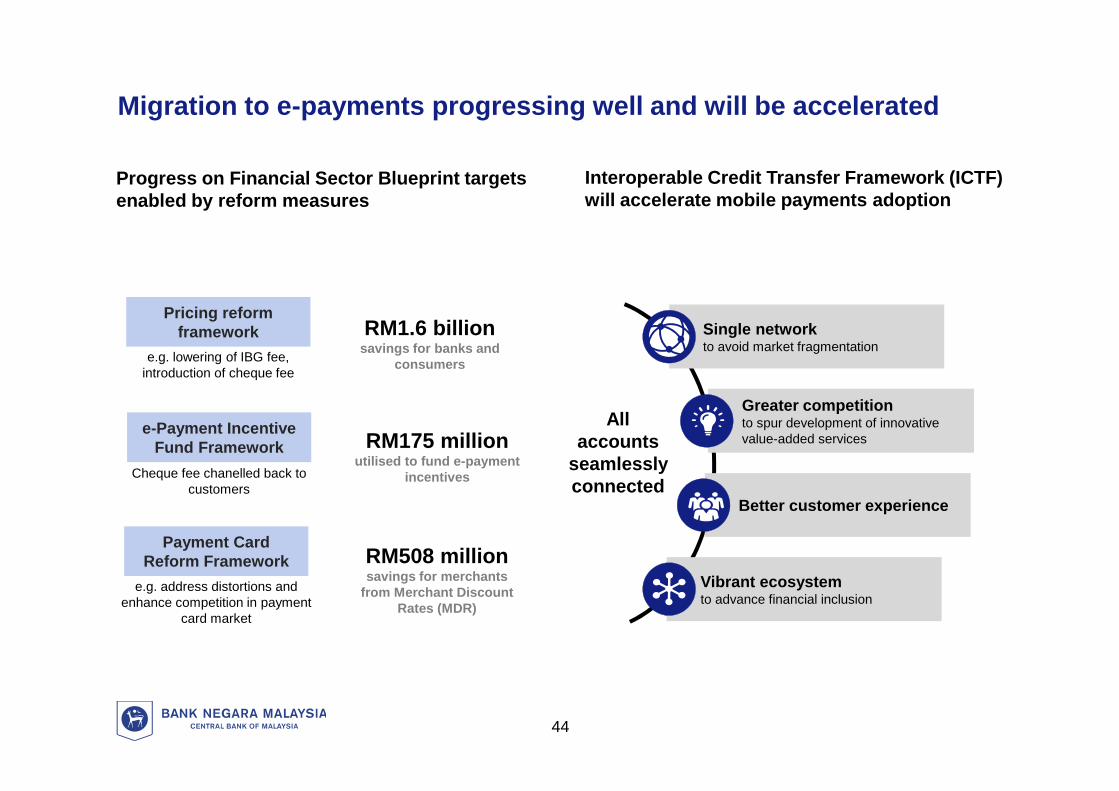

Migration to e-payments progressing well and will be accelerated

Progress on Financial Sector Blueprint targetsenabled by reform measures

Interoperable Credit Transfer Framework (ICTF)will accelerate mobile payments adoption

RM1.6 billionsavings for banks and

consumers

RM175 millionutilised to fund e-payment

incentives

RM508 millionsavings for merchants

from Merchant DiscountRates (MDR)

e-Payment IncentiveFund Framework

Cheque fee chanelled back tocustomers

Allaccounts

seamlesslyconnected

Single networkto avoid market fragmentation

Greater competitionto spur development of innovativevalue-added services

Vibrant ecosystemto advance financial inclusion

44

e.g. address distortions andenhance competition in payment

card market

Payment CardReform Framework

e.g. lowering of IBG fee,introduction of cheque fee

Pricing reformframework

Better customer experience

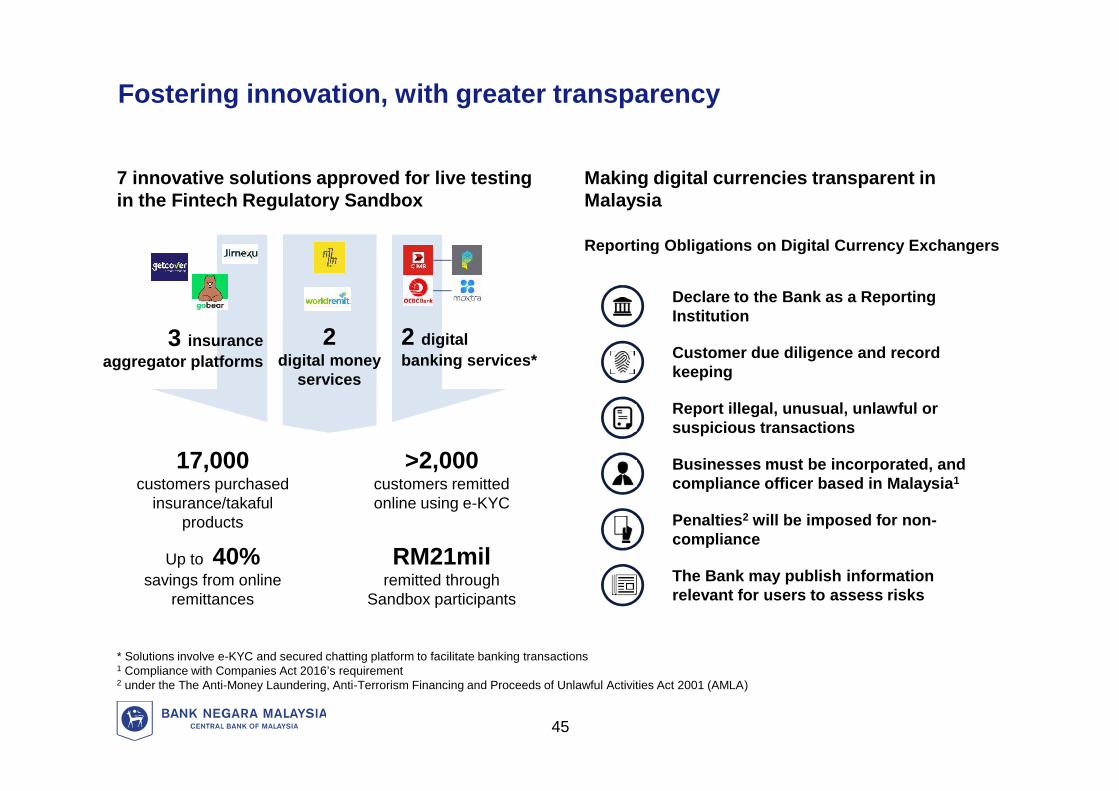

Fostering innovation, with greater transparency

7 innovative solutions approved for live testingin the Fintech Regulatory Sandbox

* Solutions involve e-KYC and secured chatting platform to facilitate banking transactions1 Compliance with Companies Act 2016’s requirement2 under the The Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (AMLA)

Making digital currencies transparent inMalaysia

Reporting Obligations on Digital Currency Exchangers

Declare to the Bank as a ReportingInstitution

Report illegal, unusual, unlawful orsuspicious transactions

Businesses must be incorporated, andcompliance officer based in Malaysia1

Customer due diligence and recordkeeping

The Bank may publish informationrelevant for users to assess risks

Penalties2 will be imposed for non-compliance

3 insuranceaggregator platforms

2digital money

services

2 digitalbanking services*

17,000customers purchased

insurance/takafulproducts

RM21milremitted through

Sandbox participants

>2,000customers remittedonline using e-KYC

Up to 40%savings from online

remittances

45

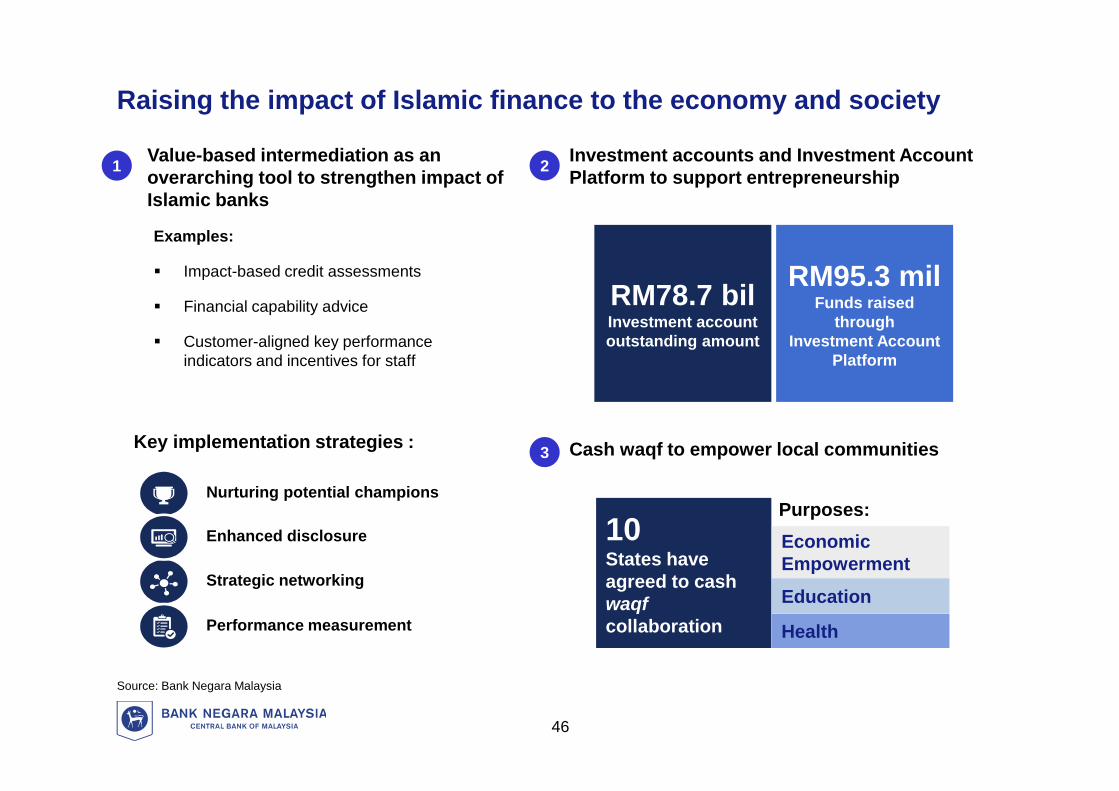

Raising the impact of Islamic finance to the economy and society

Source: Bank Negara Malaysia

Examples:

Impact-based credit assessments

Financial capability advice

Customer-aligned key performanceindicators and incentives for staff

1 Value-based intermediation as anoverarching tool to strengthen impact ofIslamic banks

Key implementation strategies :

Nurturing potential champions

Performance measurement

Enhanced disclosure

Strategic networking

2 Investment accounts and Investment AccountPlatform to support entrepreneurship

3 Cash waqf to empower local communities

RM78.7 bilInvestment accountoutstanding amount

RM95.3 milFunds raised

throughInvestment Account

Platform

10States haveagreed to cashwaqfcollaboration

EconomicEmpowerment

Education

Health

Purposes:

46

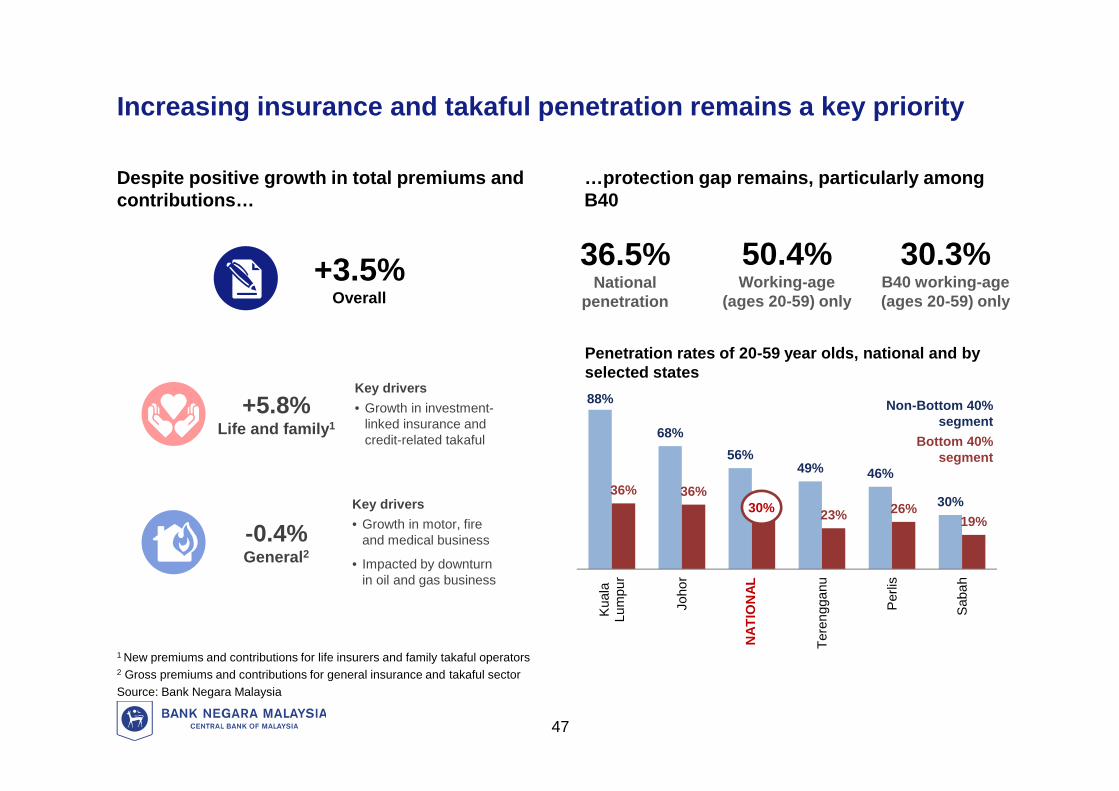

Increasing insurance and takaful penetration remains a key priority

Despite positive growth in total premiums andcontributions…

1 New premiums and contributions for life insurers and family takaful operators2 Gross premiums and contributions for general insurance and takaful sectorSource: Bank Negara Malaysia

…protection gap remains, particularly amongB40

Penetration rates of 20-59 year olds, national and byselected states88%

68%56%

49% 46%

30%36% 36%

30%23% 26%

19%

Kua

laLu

mpu

r

Joho

r

NA

TIO

NAL

Tere

ngga

nu

Per

lis

Sab

ah

Non-Bottom 40%segment

Bottom 40%segment

NAT

ION

AL

30%

Key drivers• Growth in investment-

linked insurance andcredit-related takaful

+5.8%Life and family1

+3.5%Overall

-0.4%General2

Key drivers• Growth in motor, fire

and medical business

• Impacted by downturnin oil and gas business

47

50.4%Working-age

(ages 20-59) only

36.5%National

penetration

30.3%B40 working-age(ages 20-59) only

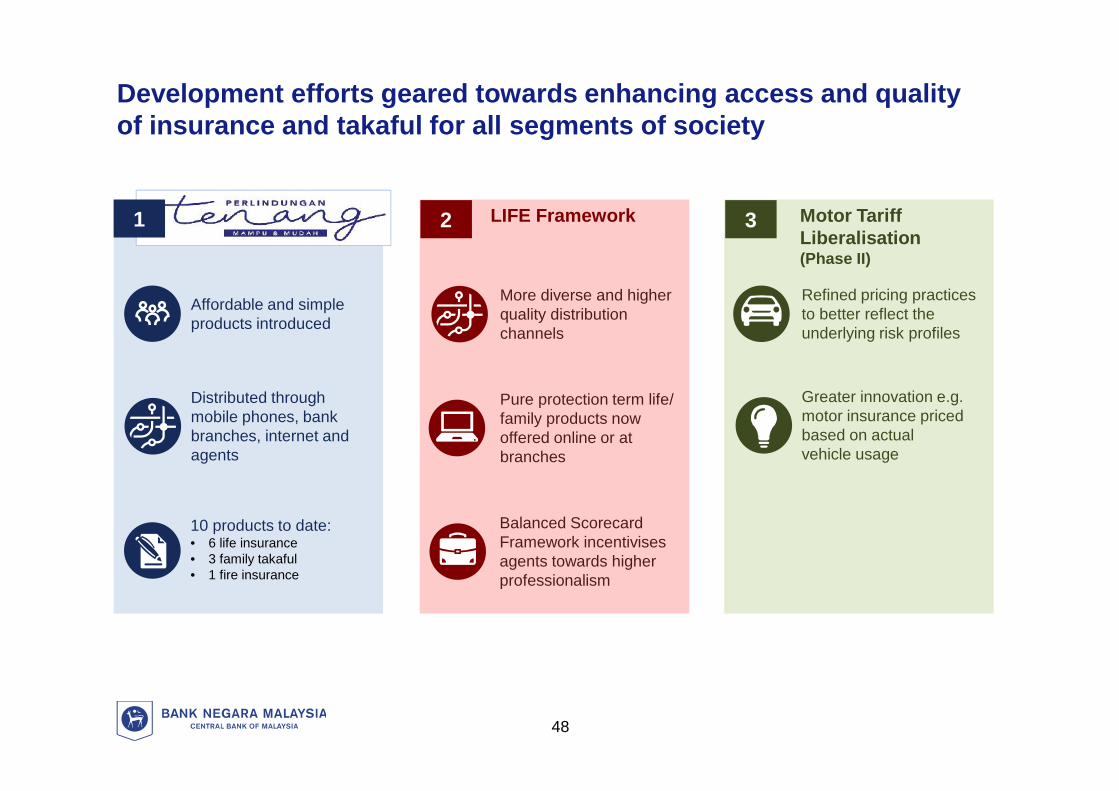

Development efforts geared towards enhancing access and qualityof insurance and takaful for all segments of society

2 3Perlindungan Tenang LIFE Framework Motor TariffLiberalisation(Phase II)

Distributed throughmobile phones, bankbranches, internet andagents

Affordable and simpleproducts introduced

10 products to date:• 6 life insurance• 3 family takaful• 1 fire insurance

More diverse and higherquality distributionchannels

Pure protection term life/family products nowoffered online or atbranches

Balanced ScorecardFramework incentivisesagents towards higherprofessionalism

Greater innovation e.g.motor insurance pricedbased on actualvehicle usage

Refined pricing practicesto better reflect theunderlying risk profiles

48

1

FactWatch.my intended to debunk misinformation

• The Bank has always advocated for greaterdisclosure and transparency to help decision-making, and to build confidence

• A rich information environment, comprising notjust facts, but opinions and experiences, bothpositive and negative, further helps in decision-making and validating the facts

• However, misinformation and “opinionpresented/treated as fact” create confusion andmyths, can mislead and cause harm.

• Debunking misinformation quickly is important tocreate and maintain a healthy informationenvironment

http://factwatch.my

49

FactWatch.my focuses on areas pertaining to the Bank

• FactWatch.my aims to provide factualinformation to correct misinformation andaddress misleading claims

• Does not provide opinions

• Focus is on areas pertaining to the Bank,such as economy, financial sector, financialconsumers

• Complements other fact-checking effortssuch as sebenarnya.my

• Posts will be shared on official social mediaaccounts for more effective dissemination

• Monetary Policy Statement –justifications for OPR decisions

• Rates and statistics on its website &periodicals

• Disclosure of enforcement actionsunder the laws administered by theBank

• Monetary Policy Statement –justifications for OPR decisions

• Rates and statistics on its website &periodicals

• Disclosure of enforcement actionsunder the laws administered by theBank

Some examples over the years include:

50