Embed Size (px)

Citation preview

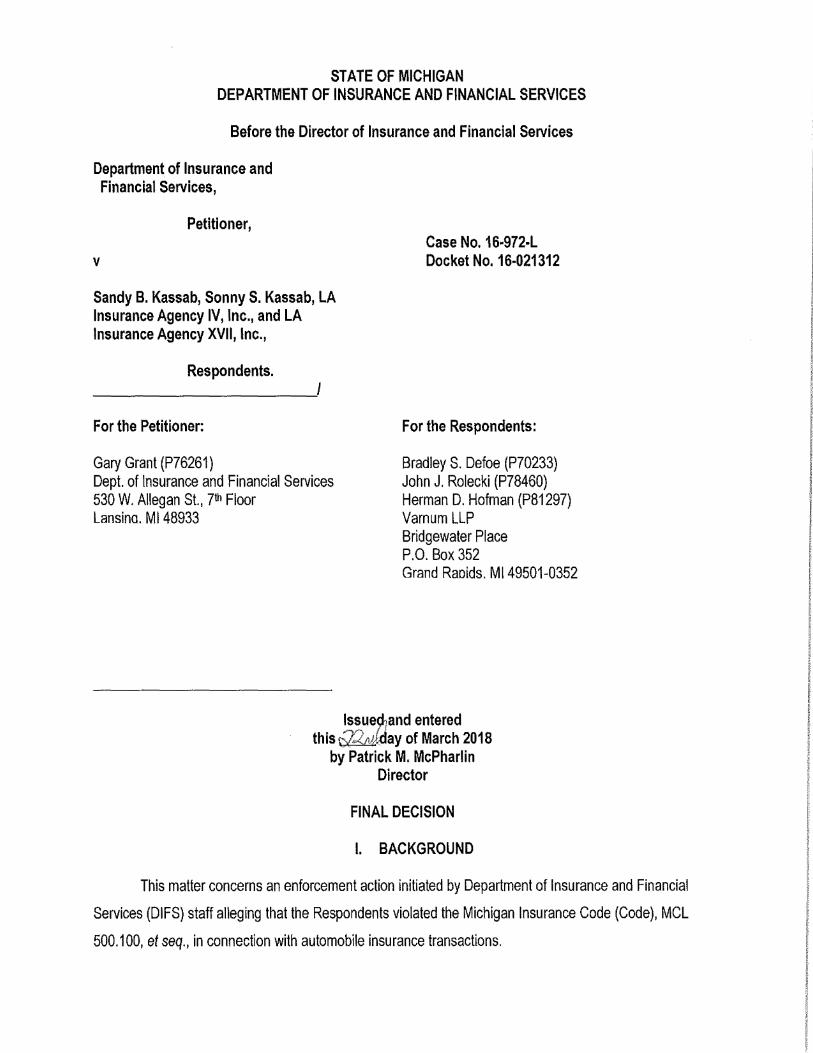

STATE OF MICHIGAN DEPARTMENT OF INSURANCE AND FINANCIAL SERVICES

Before the Director of Insurance and Financial Services

Department of Insurance and Financial Services,

Petitioner,

V

Sandy B. Kassab, Sonny S. Kassab, LA Insurance Agency IV, Inc., and LA Insurance Agency XVII, Inc.,

Respondents. --------~/

For the Petitioner:

Gary Grant (P76261) Dept. of Insurance and Financial Services 530 W. Allegan St., 7th Floor Lansina. Ml 48933

Case No.16-972-L Docket No. 16-021312

For the Respondents:

Bradley S. Defoe (P70233) John J. Rolecki (P78460) Herman D. Hofman (P81297) Varnum LLP Bridgewater Place P.O. Box 352 Grand Raoids. Ml 49501-0352

lssue~and entered this Q""d&fday of March 2018

by Patrick M. McPharlin Director

FINAL DECISION

I. BACKGROUND

This matter concerns an enforcement action initiated by Department of Insurance and Financial

Services (DIFS) staff alleging that the Respondents violated the Michigan Insurance Code (Code), MCL

500.100, et seq., in connection with automobile insurance transactions.

Case No. 16-972-L Docket No. 16-021312 Page 2

Sandy B. Kassab, System ID No. 0143564, is a licensed resident insurance producer with

qualifications in property and casualty and is authorized to transact the business of insurance in Michigan.

Sonny S. Kassab, System ID No. 0234461, is a licensed resident insurance producer with

qualifications in property and casualty and is authorized to transact the business of insurance in Michigan.

L.A. Insurance Agency IV, Inc., System ID No. 0019820 (LA IV), is a Michigan corporation with its

principal place of business located at 10231 Livernois Ave., Detroit, Ml 48204, and is a licensed resident

insurance agency in the state of Michigan with qualifications in property and casualty. Respondent Sandy

Kassab is LA IV's sole shareholder and serves as LA IV's Designated Responsible Licensed Producer

(DRLP).

LA Insurance Agency XVII, LLC, System ID No. 0019815 (LA XVII), is a Michigan limited liability

company with its principal place of business located at 17516 Livernois Ave., Detroit, Ml 48221, and is a

licensed resident insurance producer agency in the state of Michigan with qualifications in property and

casualty. Respondent Sandy Kassab is LA XVll's sole shareholder and serves as its DRLP.

Collectively, the above-named parties are herein referred to as "Respondents." Respondents LA IV

and LA XVII are referred to together as "Agency Respondents."

A hearing was held on August 1 and 2, 2017. The Respondents were represented by counsel at

the hearing. A Proposal for Decision (PFD) was issued on October 27, 2017.

II. EXCEPTIONS

On November 8, 2017, Petitioner and Respondents filed exceptions to the PFD. On November 16,

2017, Respondents filed a Response to Petitioner's Exceptions to the PFD, and Petitioner filed a Response

to Respondents' Exceptions to the PFD.

In its Exceptions to the PFD, Petitioner argued that the PFD should be adopted and a Final

Decision should issue in Petitioner's favor; except that the ALJ's exclusion of five exhibits from evidence

(namely, Exhibits P-2, P-5, P-6, P-8 and P-11) was in error and that the exhibits should be included in the

official records of the proceedings to support sanctions for the Respondents.

Respondents' Exceptions to the PFD argued that the PFD should be rejected in its entirety

because Respondents were prejudiced by "procedural defects": namely, that evidence and testimony was

admitted that should have been excluded pursuant to MCL 24.274 and MCL 24.272(4); that the ALJ's

Case No. 16-972-L Docket No. 16-021312 Page 3

factual findings were unsupported by competent, material, and substantial record evidence; and that the

ALJ committed errors of law in reaching its conclusions of law.

Petitioner's Response to Respondents' Exceptions argued that MCL 24.274 did not require

Petitioner to disclose documents that are confidential under Section 1246 of the Code, MCL 500.1246; that

MCL 24.272(4) did not require the exclusion of hearsay or telephonic evidence; and that there was

sufficient evidence to justify sanctions under the Code.

Respondents' Response to Petitioner's Exceptions argued that the ALJ's decision to exclude

Exhibits P-2, P-5, P-6, P-8, and P-11 was not in error because the exhibits were cumulative and unduly

repetitious under MCL 24.275.

Ill. FINDINGS OF FACT AND CONCLUSIONS OF LAW

The Findings of Fact and Conclusions of Law in the October 27, 2017, Proposal for Final Decision

are adopted and made a part of this Final Decision.

The ALJ excluded Petitioner's proposed Exhibits P-2, P-5, P-6, P-8, and P-11, all of which were

deposition transcripts of customers who also offered in-person testimony. The ALJ excluded these

proposed exhibits on the basis that the witnesses were present to appear in person and/or because an

affidavit of the witnesses had been admitted into evidence, rendering the deposition transcript redundant.

The ALJ did not cite any statute or rule of evidence to support excluding these exhibits. Accordingly, the

Director notes that MCL 24.275 and MRE 403 provide a tribunal with discretion to exclude certain evidence

if it is duplicative or repetitious. MCL 24.275 states that "unduly repetitious evidence may be excluded."

Similarly, MRE 403, which may be "followed as far as practicable," see MCL 24.275, provides for the

exclusion of evidence whose probative value is outweighed by "considerations of undue delay, waste of

time, or needless presentation of cumulative evidence." Although the Director agrees with Petitioner that

MCL 24.272(4) does not require the exclusion of hearsay evidence or telephonic testimony, he nonetheless

finds no basis for overturning the exclusion of Exhibits P-2, P-5, P-6, P-8, and P-11, and does not adopt

Petitioner's exceptions in this regard.

All of Respondents' Exceptions are restatements of arguments made in the Respondents' previous

submissions to the tribunal, including its discovery motions and post-hearing briefs. The Director finds that

these arguments were adequately addressed by the ALJ in the contested case proceeding and the PFD.

Therefore, the Director does not adopt the Respondent's Exceptions. Instead, in response to Respondent's

Case No. 16-972-L Docket No. 16-021312 Page 4

Exceptions, the Director adopts the ALJ's Findings of Fact and Conclusions of Law in the following: Order

Denying Respondent's Motion to Compel Discovery from Petitioner (April 11, 2017; finding that Section

1246(1) protects certain documents and information in Petitioner's possession); Order Denying Motion in

Limine to Bar Testimony of and Any Evidence Regarding [D.W. and S.S.] (July 12, 2017; finding that while

a written statement in lieu of live testimony precludes cross-examination, that goes to the weight of .the

evidence and not its admissibility); Order Granting Petitioner's Motion to Quash Subpoena Duces Tecum

(July 31, 2017; finding that testimony relating to Petitioner's internal procedures was protected under

Section 1246 of the Code); and the PFD (October 27, 2017) (finding, inter alia, that prior statements

provided to Petitioner were confidential under Section 1246 of the Code).

The PFD contains Conclusions of Law supporting findings of knowing and willful violations of the

Code for which enhanced sanctions are appropriate. Accordingly, this Final Decision orders heightened

fines for each knowing and willful violation of the Code.

This Final Decision orders suspension of Respondents' licenses. Suspension, rather than

revocation, is appropriate in this instance because of the relatively minimal economic harm to consumers,

which can be adequately redressed via restitution. In addition, Petitioner did not establish a practice or

pattern of Code violations that would support revocation. However, any finding of additional violations of the

Code shall be grounds for revocation of Respondents' licenses.

IV. ORDER

Therefore, it is ORDERED that:

1. The PFD is adopted and made part of this final decision.

2. Respondents Sandy Kassab and LA IV shall pay restitution to the following consumers within

30 days of the effective date of this Final Decision:

a. $100 to customer M.D.;

b. $100 to customer J.M.; and

c. $100 to customer S.S.

3. Respondents Sonny Kassab and LA XVII shall pay restitution to the following consumers within

30 days of the effective date of this Final Decision:

a. $100 to customer A.S.;

b. $100 to customer R.B.; and

Case No. 16-972-L Docket No. 16-021312 Page 5

c. $100 to customer D.W.

4. Respondent Sandy Kassab shall pay to the State of Michigan civil fines in this matter in the

total amount of $7,000 as follows:

a. $2,500 for Respondent Sandy Kassab's knowing violation of Sections 1239(1)(b), (d),

(e), and (h) of the Code, MCL 500.1239(1)(b), (d), (e), and (h), by failing to fully

disclose the details and costs of the NSD product being sold in the insurance

transaction with customer S. B.;

b. $500 for Respondent Sandy Kassab's violation of Sections 1239(1)(b), (d), (e), and (h)

of the Code, MCL 500.1239(1 )(b), (d), (e), and (h), by failing to fully disclose the details

and costs of the product being sold in the insurance transaction with customer J.M.;

c. $2,500 for Respondent Sandy Kassab's knowing violation of Sections 1239(1)(b), (d),

(e), and (h) of the Code, MCL 500.1239(1)(b), (d), (e), and (h), by failing to fully

disclose the details and costs of the product being sold in the insurance transaction

with customer A.S.1;

d. $500 for Respondent Sandy Kassab's violation of Section 1207(1) of the Code, MCL

500.1207(1), by violating her fiduciary duty to S.B. when she received money from

S.B. intended for the purchase of an insurance policy and applied a portion of that

money to the NSD membership;

e. $500 for Respondent Sandy Kassab's violation of Section 1207(1) of the Code, MCL

500.1207(1), by violating her fiduciary duty to J.M. when she received money from

J.M. intended for the purchase of an insurance policy and applied a portion of that

money to the NSD membership; and

f. $500 for Respondent Sandy Kassab's violation of Section 1207(1) of the Code, MCL

500.1207(1 ), by violating her fiduciary duty to A.S. when she received money from

A.S. intended for the purchase of an insurance policy and applied a portion of that

money to the NSD membership.

5. Respondent Sonny Kassab shall pay to the State of Michigan civil fines in this matter in the

total amount of $3,000 as follows:

1 The PFD refers to customer "A.B." but the context and relevant subheading in the PFD clearly indicate that the intended reference is to customer "A.S." See PFD, p. 28.

Case No. 16-972-L Docket No. 16-021312 Page 6

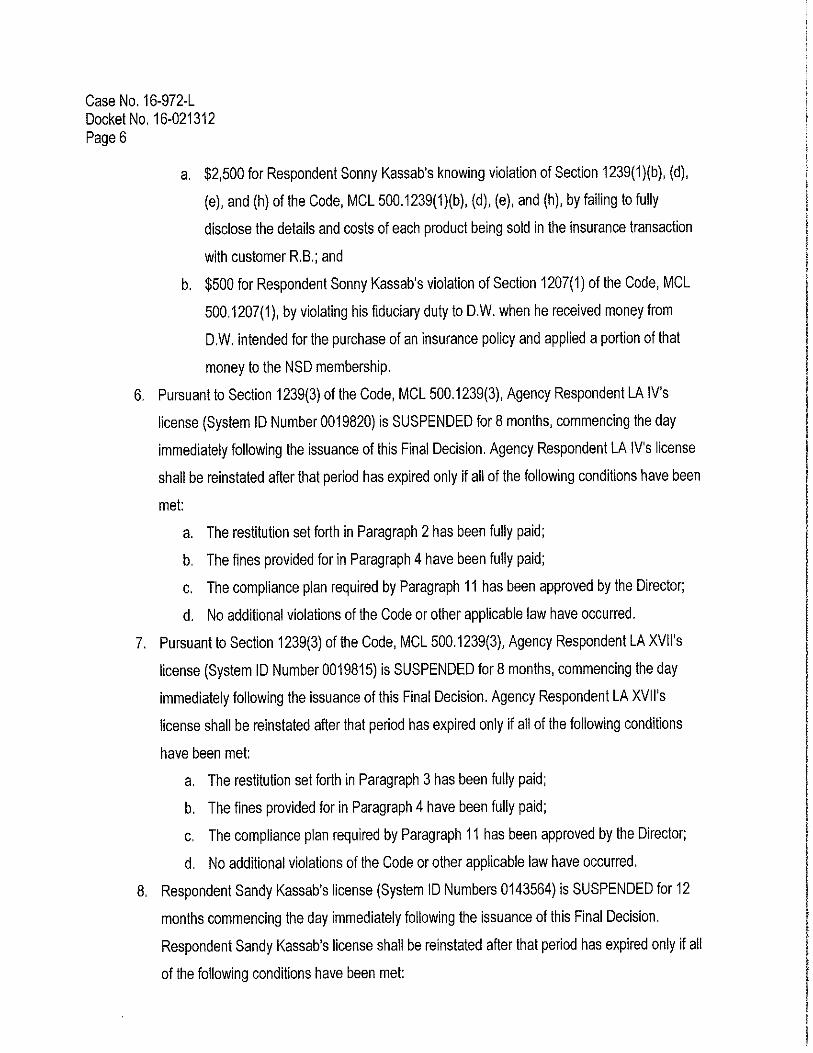

a. $2,500 for Respondent Sonny Kassab's knowing violation of Section 1239(1)(b), (d),

(e), and (h) of the Code, MCL 500.1239(1)(b), (d), (e), and (h), by failing to fully

disclose the details and costs of each product being sold in the insurance transaction

with customer R.B.; and

b. $500 for Respondent Sonny Kassab's violation of Section 1207(1) of the Code, MCL

500.1207(1), by violating his fiduciary duty to D.W. when he received money from

D.W. intended for the purchase of an insurance policy and applied a portion of that

money to the NSD membership.

6. Pursuant to Section 1239(3) of the Code, MCL 500.1239(3), Agency Respondent LA IV's

license (System ID Number 0019820) is SUSPENDED for 8 months, commencing the day

immediately following the issuance of this Final Decision. Agency Respondent LA IV's license

shall be reinstated after that period has expired only if all of the following conditions have been

met:

a. The restitution set forth in Paragraph 2 has been fully paid;

b. The fines provided for in Paragraph 4 have been fully paid;

c. The compliance plan required by Paragraph 11 has been approved by the Director;

d. No additional violations of the Code or other applicable law have occurred.

7. Pursuant to Section 1239(3) of the Code, MCL 500.1239(3), Agency Respondent LA XVll's

license (System ID Number 0019815) is SUSPENDED for 8 months, commencing the day

immediately following the issuance of this Final Decision. Agency Respondent LA XVI l's

license shall be reinstated after that period has expired only if all of the following conditions

have been met:

a. The restitution set forth in Paragraph 3 has been fully paid;

b. The fines provided for in Paragraph 4 have been fully paid;

c. The compliance plan required by Paragraph 11 has been approved by the Director;

d. No additional violations of the Code or other applicable law have occurred.

8. Respondent Sandy Kassab's license (System ID Numbers 0143564) is SUSPENDED for 12

months commencing the day immediately following the issuance of this Final Decision.

Respondent Sandy Kassab's license shall be reinstated after that period has expired only if all

of the following conditions have been met:

Case No. 16-972-L Docket No. 16-021312 Page 7

a. The restitution set forth in Paragraph 2 has been fully paid;

b. The fines provided for in Paragraph 4 have been fully paid;

c. The compliance plan required by Paragraph 11 has been approved by the Director;

d. No additional violations of the Code or other applicable law have occurred.

9. Respondent Sonny Kassab's license (System ID Number 0234461) is SUSPENDED for 8

months commencing the day immediately following the issuance of this Final Decision.

Respondent Sonny Kassab's license shall be reinstated after that period has expired only if all

of the following conditions have been met:

a. The restitution set forth in Paragraph 3 has been fully paid;

b. The fines provided for in Paragraph 5 have been fully paid;

c. No additional violations of the Code or other applicable law have occurred.

10. Respondents shall be on probation for one year after their licenses are reinstated pursuant to

Paragraphs 6 through 9, above. The terms of said probation are as follows:

a. Respondents shall promptly report to DIFS any new investigations, administrative, civil and

criminal proceedings, and consumer complaints (written or oral) brought or made against

them or their agents. They shall provide to DIFS a copy of all pleadings, judgments,

awards, orders, reports, or complaints associated with said matters. All disclosures and

reports must be addressed to: Department of Insurance and Financial Services, Office of

Insurance Licensing and Market Conduct, P.O. Box 30220, Lansing, Ml 48909-7720;

b. Respondents are prohibited from applying for or obtaining any new qualifications;

c. Respondents are prohibited from applying for or obtaining any new insurance company

appointments;

d. Respondents are prohibited from applying for or obtaining any new insurance licenses that

may otherwise be available to them under the Code; and

e. A market conduct examination of the Agency Respondents shall be conducted during the

pendency of the probationary period.

11. With regard to the sale of Nation Safe Driver products or any other product that is not sold as

part of a DIFS-approved insurance policy, the Respondents shall develop a comprehensive

compliance plan regarding sales practices. Such compliance plan shall be submitted to DIFS

for approval within 30 days of the effective date of the Final Decision, and must be approved

Case No. 16-972-L Docket No. 16-021312 Page 8

by DIFS prior to implementation. The compliance plan must include, at a minimum, the

following: detailed sales practices that ensure adequate disclosure of the products being sold,

and a detailed plan to train staff to utilize such sales practices to ensure compliance with the

Code and all other applicable laws and regulations.

12. Any finding of additional violations of the Code shall be grounds for revocation of Respondents'

licenses.

(/~~1$~l2 -··,-Patrick M. McPharlin

Director

STATE OF MICHIGAN MICHIGAN ADMINISTRATIVE HEARING SYSTEM

IN THE MATTER OF:

Department of Insurance and Financial Services,

Petitioner

V

Sandy B. Kassab, Sonny S. Kassab, LA Insurance Agency IV, Inc., and LA Insurance Agency XVII, Inc.,

Respondent

I

Docket No.: 16-021312

Case No.: 16-972-L

Agency: Department of Insurance and Financial Services

Case Type: DIFS-lnsurance

Filing Type: Enforcement

Issued and entered this '2.1 t.ttday of October 2017

by: Thomas A. Halick Administrative Law Judge

PROPOSAL FOR DECISION

PROCEDURAL HISTORY

This proceeding under the Michigan Insurance Code of 1956, being 1956 PA 218, as amended, MCL 500.100 et seq. (hereafter "Insurance Code" or "Code"), commenced with the issuance of a Complaint, Statement of Factual Allegations, and an Order Referring Complaint for Hearing dated July 20, 2016, regarding the resident insurance producer licenses of Sandy B. Kassab, Sonny S. Kassab, LA Insurance Agency IV, Inc., and LA Insurance Agency, Inc. XVII, Respondents.

On August 5, 2016, the Michigan Administrative Hearing System issued a Notice of Hearing pursuant to a Request for Hearing, scheduling a hearing date of October 13, 2016. After several adjournments during which discovery was conducted and numerous motions were filed and decided, the hearing was held on August 1 and 2, 2017.

Petitioner was represented by Gary S. Grant, DIFS Enforcement Attorney.

Respondents were represented by Attorneys Kevin M. Blair and Derrick Mullins, Honigman, Miller, Schwartz and Cohn LLP.

16-021312 Page 2

Procedural Background

This case arises from a consumer complaint1 against Respondents Sandy Kassab and LA Insurance Agency XVII, filed on April 24, 2013, alleging, inter alia, that Sandy Kassab misapplied money that she received that was intended for payment of an auto insurance policy, and rather applied that money to purchase of a motor club membership that the consumer did not ask to purchase. The complaint prompted an investigation by Petitioner that commenced with a visit to Respondent's agency (LA IV) on August 16, 2013, and a subsequent visit to Respondent's other agency (LA XVII), resulting in additional allegations of fact against the other named Respondents with regard to transactions with other customers.

On January 4, 2016, a Notice and Opportunity to Show Compliance was mailed to Respondents. Thereafter, the parties conducted an informal conference without resolution of this dispute.

On July 20, 2016, Petitioners issued a Complaint, including Counts I through V, alleging violations of the Michigan Insurance Code (Code), 1956 PA 218, as amended, MCL 500.100 et seq. Respondents referred this matter to MAHS for an evidentiary hearing to be held in accordance with the Administrative Procedures Act (APA), 1969 PA 306, as amended, MCL 24.201, et seq.

On August 1, 2016, MAHS received a Request for Hearing, and issued a Notice of Hearing on August 5, 2016, scheduling an evidentiary hearing for October 13, 2016.

On September 20, 2016, counsel for Petitioner filed a request to hold a prehearing conference, with the concurrence of opposing counsel.

On September 26, 2016, a prehearing conference was held, resulting in a Scheduling Order establishing dates for preliminary witness lists, discovery cut-off, dispositive motions, and which adjourned the hearings scheduled in this case and several related cases. It was anticipated that after discovery, it could be determined which of the related cases should be consolidated, and that hearings would be held after April 1, 2017.

On October 31, 2016, Petitioner filed its Proposed Witness List, identifying 11 witnesses.

On December 12, 2016, the parties filed a proposed, stipulated order to consolidate three of the related cases, not including this case, and also stipulating to the extension of the discovery deadline from December 31, 2016, to February 28, 2016, which was granted by Order Extending Discovery Deadline, dated December 12, 2016.

1 Insurance Complaint Form, 3/29/2012. Exhibit JT-7.

16-021312 Page3

On January 11, 2017, Respondents requested subpoenas to depose 16 witnesses involved in this case and the related cases, which were issued on January 17, 2017.

On February 14, 2017, Respondents in the related cases requested subpoenas for the deposition of six witnesses, which were signed by the ALJ and issued on February 15, 2017.

On February 27, 2017, a prehearing conference was held by telephone.

On March 13, 2017, the parties submitted a Stipulated Amended Scheduling Order, governing this case and the related cases, which was signed by the ALJ and issued on March 31, 2017. It was agreed, among other matters, that the hearing would be scheduled for no later than July 31, 2017.

On March 31, 2017, Respondent filed a motion to compel discovery.

On April 5, 2017, Petitioner filed a response to the motion to compel.

On April 11, 2017, the ALJ issued an Order Denying Respondent's Motion to Compel Discovery from Petitioner.

On May 15, 2017, Petitioner filed its Final Witness List, identifying nine witnesses by name, and three persons identified as "custodians of records."

On July 12, 2017, this Tribunal issued an Order Denying Respondent's Motion In Limine to Bar Testimony of and any Evidence Regarding [customer D.W.] and [customer S.B].

On July 21, 2017, the parties held a telephonic prehearing conference.

On July 31, 2017, this Tribunal issued an Order Granting Petitioner's Motion to Quash Subpoena Duces Tecum.

The hearing was held on August 1, and 2, 2017.

Petitioner called the following witnesses:

1. R.B., Customer of LA Insurance Agency IV, Inc. 2. S.B., Customer of LA Insurance Agency XVII, Inc. 3. J.M., Customer of LA Insurance Agency IV, Inc. 4. M.D., Customer of LA Insurance Agency IV, Inc. 5. A.S., Customer of LA Insurance Agency XVII, LLC. 6. Justin Blood, DIFS Investigator.

16-021312 Page 4

Respondents called the following witnesses:

1. Sonny Kassab, Respondent. 2. Sandy Kassab, Respondent 3. Cindy Kassab, Insurance Agent at LA Insurance Agency XVII, LLC on August 16,

2017.

The parties offered the following joint exhibits:

JT-1. Verified Return of Service documents for Petitioner's witnesses. JT-2. Audio Recording of Justin Blood investigation of LA Insurance Agency LA XVII. JT-3. Michigan Insurance Division - Licensed Individual Full History. JT-4. Insurance and NSD documents - M.D. JT-5. Insurance and NSD documents - S.B. JT-6. Insurance and NSD documents - J.M. JT-7. Insurance Complaint Form -A.S. JT-8. Insurance and NSD documents and emails - R.B. JT-9. Subpoena and proof of service for the Deposition of D.W., January 17, 2017. JT-10. Insurance and NSD documents and emails - D.W. [Pages 44-51 only]. JT-11. Insurance and NSD documents - G. JT-12. Insurance Bureau Bulletin 81-20; Insurance Bulletin 2015-21; Insurance Bulletin, 2016-20.

Petitioner offered the following exhibits:

P-1. Affidavit of M.D. P-2. Deposition Transcript of M.D. [Excluded]. P-3. Affidavit of S.B. P-4. Affidavit of J.M. P-5. Deposition Transcript of J.M [Excluded]. P-6. Deposition Transcript of A.S. [Excluded]. P-7. Affidavit of R.B. P-8. Deposition Transcript of R.B. [Excluded]. P-9. Affidavit of D.W. P-10. Affidavit of G.B. P-11. Deposition Transcript of G.B. [Excluded].

Objections:

P-1 See discussion regarding P-7, below.

16-021312 Page 5

P-2 The discovery deposition of M.D. was excluded because she was present to testify in person.

P-3 See discussion regarding P-7, below.

P-4 P-3 See discussion regarding P-7, below.

P-5 The discovery deposition of J.M. was excluded because he was present to testify in person.

P-6 The discovery deposition of A.S. was excluded because he was present to testify in person.

P-7 The Affidavit of R.B. was admitted over Respondent's objection based on Petitioner's failure to provide prior statements made by R.B. to DIFS, pursuant to MCL 24.274(2) - "An agency that relies on a witness in a contested case, whether or not an agency employee, who has made prior statements or reports with respect to the subject matter of his testimony, shall make such statements or reports available to opposing parties for use on cross-examination."

Any such statement is confidential by law pursuant to MCL 500.1246. Furthermore, the alleged "prior statements" consist of notes of conversations or answers to questions in emails do not constitute an affirmative "statement" made to DIFS by this witness within the meaning of MCL 24.274(2).

P-8 See discussion regarding P-7.

P-9 See discussion regarding P-7.

P-10 See discussion regarding P-7.

P-11 The discovery deposition of G.B. was excluded as redundant and cumulative and not necessary to establish the relevant facts that are material to reaching a decision. The Affidavit of G.B. was admitted into evidence.

Respondents offered the following exhibits:

R-A. Email. List of customers contacted. R-B. Petitioner's Response to First Set of Discovery Requests. R-C. Insurance Policy - A.S. R-D. Sample Documents related to Insurance and NSD transaction.

16-021312 Page 6

POST HEARING FILINGS

On September 7, 2017, Respondents filed a Post Hearing Brief.

On September 7, 2017, Petitioner filed its written Closing Argument.

On September 14, 2017, Respondents filed a Response to the Department of Insurance and Financial Services' Post-Hearing Brief.

On September 14, 2017, Petitioners filed a Reply to Respondents' Closing Argument.

ISSUES AND APPLICABLE LAW

The issues presented in the Complaint are whether sanction(s) are properly imposed under Section 1244(1)(a)-(d) of the Insurance Code, MCL 500.1244(1)(a)-(d) against Respondents' licenses based on violations of the following sections of the Insurance Code, supra, which provide as follows:

Sec. 249. For the purposes of ascertaining compliance with the provisions of the insurance laws of the state or of ascertaining the business condition and practices of an insurer or proposed insurer, the commissioner, as often as he deems advisable, may initiate proceedings to examine the accounts, records, documents and transactions pertaining to:

(a) Any insurance agent, surplus line agent, general agent, adjuster, public adjuster or counselor.

Sec. 1205. (1) A person applying for a resident insurance producer license shall file with the commissioner the uniform application required by the commissioner and shall declare under penalty of refusal, suspension, or revocation of the license that the statements made in the application are true, correct, and complete to the best of the individual's knowledge and belief. An application for a resident insurer producer license shall not be approved unless the commissioner finds that the individual meets all of the following:

***

(b) The business entity has designated an individual licensed producer responsible for the business entity's compliance with this state's insurance laws, rules, and regulations. [Emphasis added.]

16-021312 Page 7

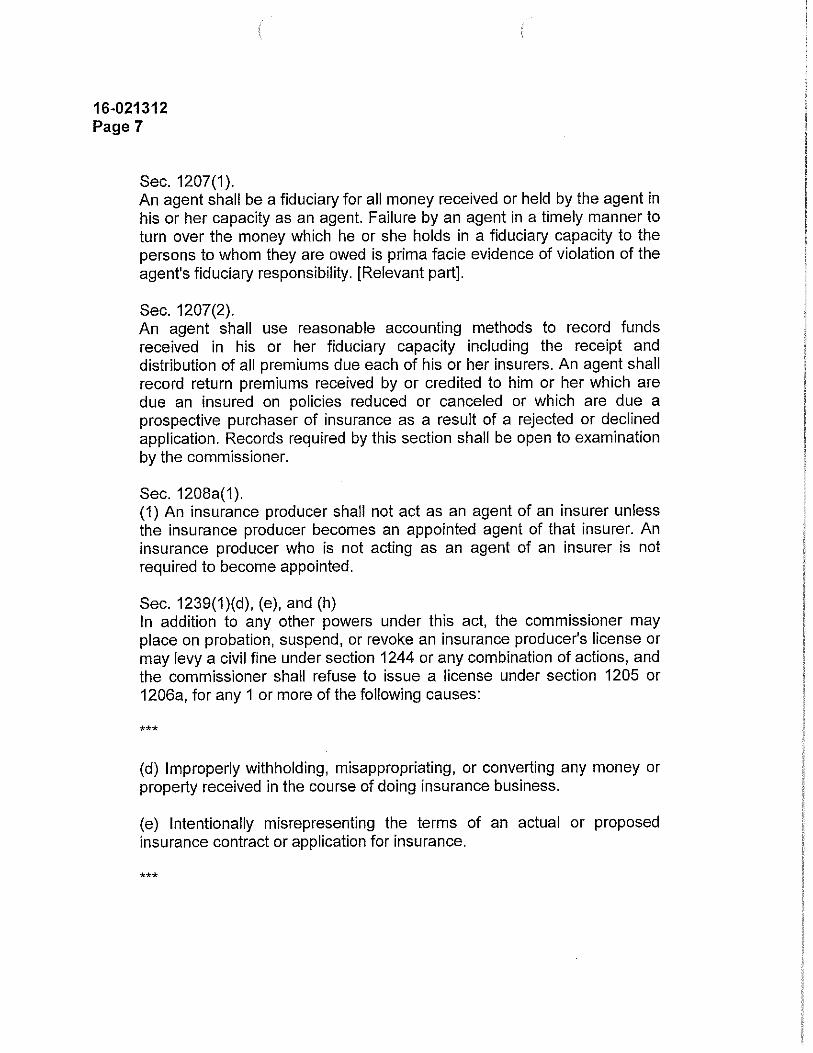

Sec. 1207(1). An agent shall be a fiduciary for all money received or held by the agent in his or her capacity as an agent. Failure by an agent in a timely manner to turn over the money which he or she holds in a fiduciary capacity to the persons to whom they are owed is prima facie evidence of violation of the agent's fiduciary responsibility. [Relevant part].

Sec. 1207(2). An agent shall use reasonable accounting methods to record funds received in his or her fiduciary capacity including the receipt and distribution of all premiums due each of his or her insurers. An agent shall record return premiums received by or credited to him or her which are due an insured on policies reduced or canceled or which are due a prospective purchaser of insurance as a result of a rejected or declined application. Records required by this section shall be open to examination by the commissioner.

Sec. 1208a(1). (1) An insurance producer shall not act as an agent of an insurer unless the insurance producer becomes an appointed agent of that insurer. An insurance producer who is not acting as an agent of an insurer is not required to become appointed.

Sec. 1239(1)(d), (e), and (h) In addition to any other powers under this act, the commissioner may place on probation, suspend, or revoke an insurance producer's license or may levy a civil fine under section 1244 or any combination of actions, and the commissioner shall refuse to issue a license under section 1205 or 1206a, for any 1 or more of the following causes:

***

(d) Improperly withholding, misappropriating, or converting any money or property received in the course of doing insurance business.

(e) Intentionally misrepresenting the terms of an actual or proposed insurance contract or application for insurance.

***

16-021312 Page 8

(h) Using fraudulent, coercive, or dishonest practices or demonstrating incompetence, untrustworthiness, or financial irresponsibility in the conduct of business in this state or elsewhere.

Sec. 1239(3). The license of a business entity may be suspended, revoked, or refused if the commissioner finds, after hearing, that an individual licensee's violation was known or should have been known by 1 or more of the partners, officers, or managers acting on behalf of the partnership or corporation and the violation was neither reported to the commissioner nor corrective action taken.

Sec 150(1) (1) Any person who violates any provision of this act for which a specific penalty is not provided under any other provision of this act or of other laws applicable to the violation shall be afforded an opportunity for a hearing before the commissioner pursuant to the administrative procedures act of 1969, Act No. 306 of the Public Acts of 1969, being sections 24.201 to 24.328 of the Michigan Compiled Laws. If the commissioner finds that a violation has occurred, the commissioner shall reduce the findings and decision to writing and shall issue and cause to be served upon the person charged with the violation a copy of the findings and an order requiring the person to cease and desist from the violation. In addition, the commissioner may order any of the following:

(a) Payment of a civil fine of not more than $500.00 for each violation. However, if the person knew or reasonably should have known that he or she was in violation of this act, the commissioner may order the payment of a civil fine of not more than $2,500.00 for each violation. With respect to filings made under chapters 21, 22, 23, 24, and 26, "violation" means a filing not in compliance with the provisions of those chapters and does not include an action with respect to an individual policy based upon a noncomplying filing. An order of the commissioner under this subdivision shall not require the payment of civil fines exceeding $25,000.00. A fine collected under this subdivision shall be turned over to the state treasurer and credited to the general fund.

(b) The suspension, limitation, or revocation of the person's license or certificate of authority.

16-021312 Page 9

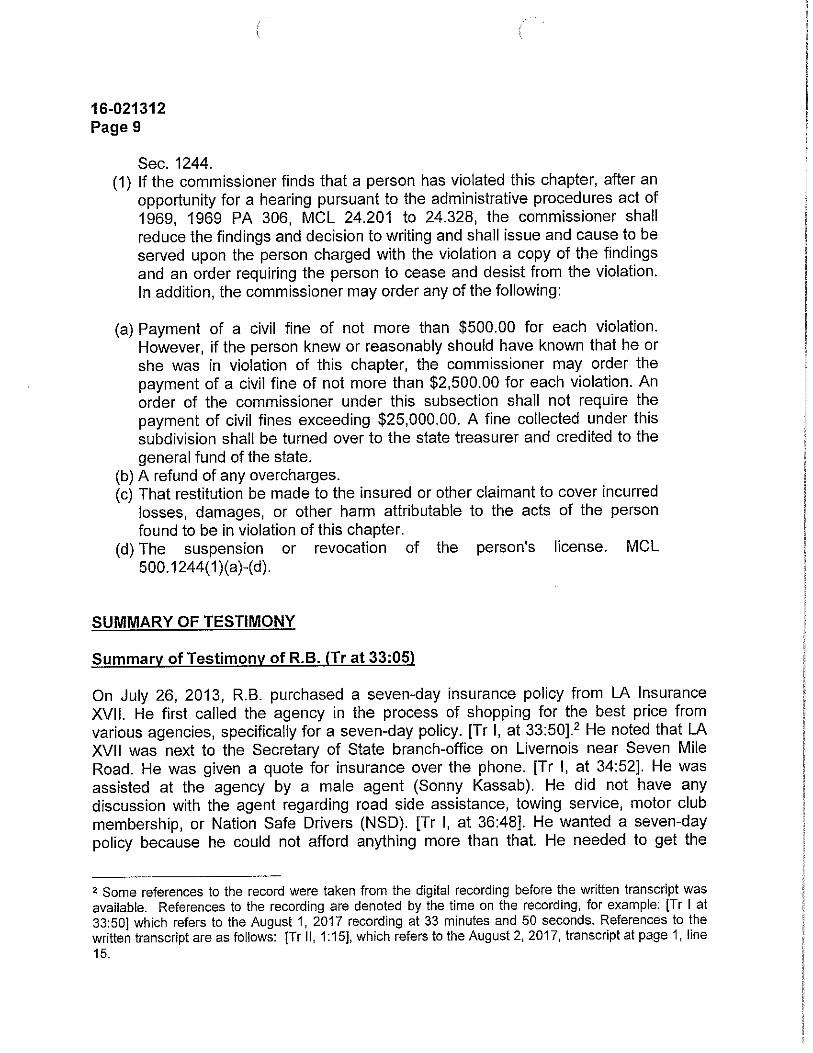

Sec. 1244. (1) If the commissioner finds that a person has violated this chapter, after an

opportunity for a hearing pursuant to the administrative procedures act of 1969, 1969 PA 306, MCL 24.201 to 24.328, the commissioner shall reduce the findings and decision to writing and shall issue and cause to be served upon the person charged with the violation a copy of the findings and an order requiring the person to cease and desist from the violation. In addition, the commissioner may order any of the following:

(a) Payment of a civil fine of not more than $500.00 for each violation. However, if the person knew or reasonably should have known that he or she was in violation of this chapter, the commissioner may order the payment of a civil fine of not more than $2,500.00 for each violation. An order of the commissioner under this subsection shall not require the payment of civil fines exceeding $25,000.00. A fine collected under this subdivision shall be turned over to the state treasurer and credited to the general fund of the state.

(b) A refund of any overcharges. (c) That restitution be made to the insured or other claimant to cover incurred

losses, damages, or other harm attributable to the acts of the person found to be in violation of this chapter.

(d) The suspension or revocation of the person's license. MCL 500.1244(1 )(a)-(d).

SUMMARY OF TESTIMONY

Summary of Testimony of R.B. (Tr at 33:05)

On July 26, 2013, R.B. purchased a seven-day insurance policy from LA Insurance XVI I. He first called the agency in the process of shopping for the best price from various agencies, specifically for a seven-day policy. [Tr I, at 33:50].2 He noted that LA XVII was next to the Secretary of State branch-office on Livernois near Seven Mile Road. He was given a quote for insurance over the phone. [Tr I, at 34:52]. He was assisted at the agency by a male agent (Sonny Kassab). He did not have any discussion with the agent regarding road side assistance, towing service, motor club membership, or Nation Safe Drivers (NSD). [Tr I, at 36:48]. He wanted a seven-day policy because he could not afford anything more than that. He needed to get the

2 Some references to the record were taken from the digital recording before the written transcript was available. References to the recording are denoted by the time on the recording, for example: [Tr I at 33:50] which refers to the August 1, 2017 recording at 33 minutes and 50 seconds. References to the written transcript are as follows: [Tr II, 1:15], which refers to the August 2, 2017, transcript at page 1, line 15.

16-021312 Page 10

seven-day policy to get his vehicle registration. He recalls paying between $200 and $300 for the auto insurance policy. He did not know that any of the price was being applied to any other product (such as road side assistance, towing, motor club membership, or NSD). He believes that he signed documents for the purchase of a seven-day policy only. The agent did not tell him he was signing any document for the purchase of any other product.

R.B. recalls seeing the insurance policy application and documents at his deposition in January of 2017, but does not remember seeing the documents before then. He now knows that the documentation states that the cost of the insurance policy was $104. He first learned that his insurance cost only $104 (and not $200 or $300) when Mr. Blood brought it to his attention prior to the deposition, and also at the time of his deposition. [Tr I, p 35:14].

He admitted that his signature appears on the NSD application. [Tr I, p 35:24]. He says the document was presented to him and he signed it. He did not read the document carefully. He states that the agent did not discuss NSD with him.

R.B. signed an affidavit prepared by DIFS, which was based on questions that he answered by email sent to Mr. Blood. He answered the questions the best he could. He reviewed the affidavit before he signed it and believes it to be true. He stands by the information in his affidavit. He does not recall if Mr. Blood promised that he would receive money back, but that he thought he "was just helping them - helping the case along when" he signed the affidavit. [Tr I, p 40:18].

R.B. does not recall receiving any documents regarding the NSD policy. He only needed the proof of insurance documents that he took to the Secretary of State. When he when to LA XVII, he was on a tight budget and did not want roadside assistance or anything other than a seven-day insurance policy. Nothing occurred at LA XVII that made him change his mind to want to purchase roadside assistance. "I didn't want to purchase any roadside, I was on a tight budget as it was ... I didn't purchase any roadside, I didn't want the roadside assistance because it was going to be more money than what I had ... I wouldn't have gotten it." [Tr I, at 54:10-25; See also, Tr I, p 41].

On cross-examination [Tr I, p 42:22]. R.B. testified that when he was given the full price for the insurance, he believed he paid $200 to $300 for a seven-day policy, he did not know at the time of purchase that the policy only cost $104.

Q. And you understood that $104.00 went to purchase a seven-day policy, right?

A. To my knowledge. From what I'm seeing here, yes, I would say that I - I believe the documentation is showing that it's $104.00 that went towards it. As I stated before, when I was given the full price of what it was. And that's what I - to my knowledge,

16-021312 Page 11

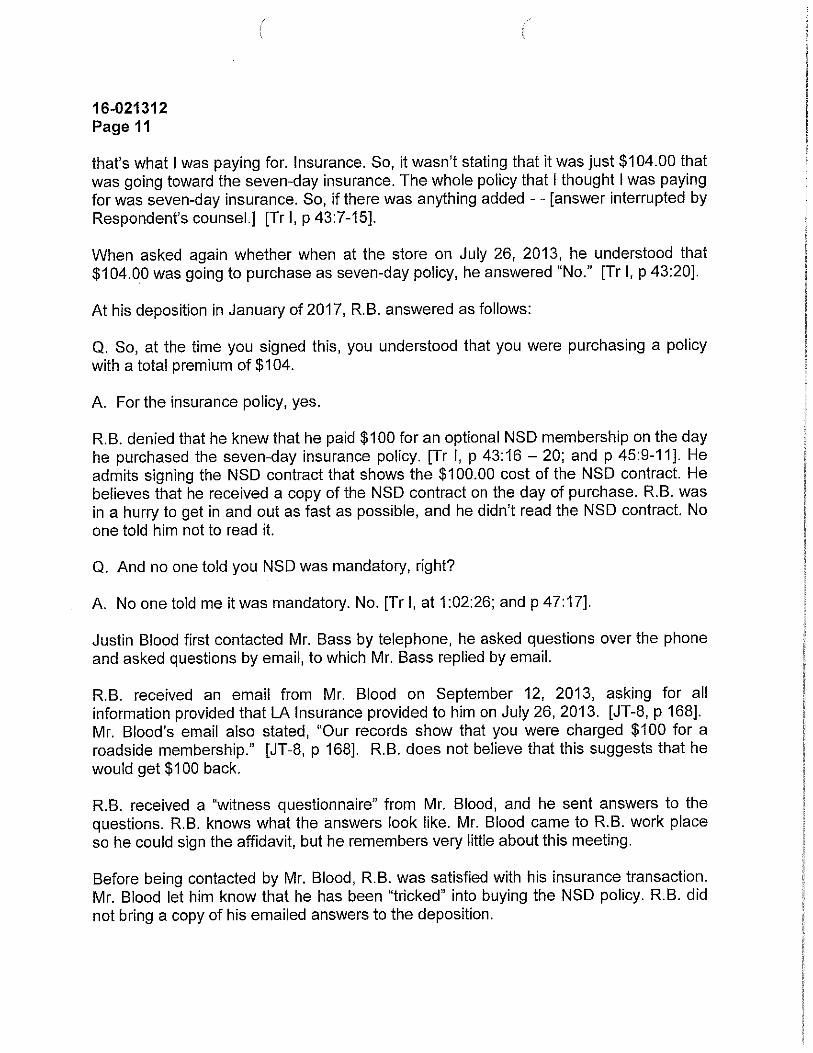

that's what I was paying for. Insurance. So, it wasn't stating that it was just $104.00 that was going toward the seven-day insurance. The whole policy that I thought I was paying for was seven-day insurance. So, if there was anything added - - [answer interrupted by Respondent's counsel.] [Tr I, p 43:7-15].

When asked again whether when at the store on July 26, 2013, he understood that $104.00 was going to purchase as seven-day policy, he answered "No." [Tr I, p 43:20].

At his deposition in January of 2017, R.B. answered as follows:

Q. So, at the time you signed this, you understood that you were purchasing a policy with a total premium of $104.

A. For the insurance policy, yes.

R.B. denied that he knew that he paid $100 for an optional NSD membership on the day he purchased the seven-day insurance policy. [Tr I, p 43:16 - 20; and p 45:9-11]. He admits signing the NSD contract that shows the $100.00 cost of the NSD contract. He believes that he received a copy of the NSD contract on the day of purchase. R.B. was in a hurry to get in and out as fast as possible, and he didn't read the NSD contract. No one told him not to read it.

Q. And no one told you NSD was mandatory, right?

A. No one told me it was mandatory. No. [Tr I, at 1 :02:26; and p 47:17].

Justin Blood first contacted Mr. Bass by telephone, he asked questions over the phone and asked questions by email, to which Mr. Bass replied by email.

R.B. received an email from Mr. Blood on September 12, 2013, asking for all information provided that LA Insurance provided to him on July 26, 2013. [JT-8, p 168]. Mr. Blood's email also stated, "Our records show that you were charged $100 for a roadside membership." [JT-8, p 168]. R.B. does not believe that this suggests that he would get $100 back.

R.B. received a "witness questionnaire" from Mr. Blood, and he sent answers to the questions. R.B. knows what the answers look like. Mr. Blood came to R.B. work place so he could sign the affidavit, but he remembers very little about this meeting.

Before being contacted by Mr. Blood, R.B. was satisfied with his insurance transaction. Mr. Blood let him know that he has been "tricked" into buying the NSD policy. R.B. did not bring a copy of his emailed answers to the deposition.

16-021312 Page 12

He does not recall making any changes to the affidavit that Mr. Blood prepared for this signature.

On re-direct examination, R.B, stated that he was satisfied with the insurance, however, he believed that all the money paid was for the insurance contract, but then Mr. Blood showed him that he paid only $104 for the insurance, and he learned for the first time that he paid $100 for the NSD. The agent at LA Insurance did not say anything about NSD or roadside coverage. When he left LA Insurance Agency in 2013, he believed he had only purchased a seven-day insurance policy.

On re-cross-examination, R.B. answered as follows:

Q. You understood on July 26, 2013 ... that $104 of what you were paying was going to purchase a seven-day policy, right?

A. That's correct. [Tr, at 1 :13:50].

Q. OK. And you know that you also paid $100 for the NSD, correct?

A. I know that now, yes. I didn't know that before.

Q. But on the day you bought the insurance, you knew that only $104 was going to buy the insurance?

A. No, I did not know that the day of the insurance.

R.B. acknowledges that he stated at his deposition that he paid $104 for insurance; however at the hearing, he stated that he did not know he was purchasing roadside coverage. He signed papervilork "just to sign it." He thought he was signing everything to do with insurance. He wouldn't have paid for roadside coverage. He doesn't recall any discussion about roadside service.

[Respondent moved to exclude all of R.B.'s testimony based on his statements that he submitted a written response to DIFS (the witness questionnaire) that were not produced by DIFS during discovery. Respondent argued that MCL 24.274(2) requires the exclusion of the testimony based on the failure to disclose these email communications. This motion was denied. DIFS asserts that the email is not a prior statement under MCL 24.274(2), and even if it is, that it is not required to disclose this information, which is confidential by law under MCL 500.1246.]

DIFS moved for the admission of the Deposition Transcript of R.B. Respondents assert that the deposition was taken for discovery purpose only, and that it is unfair to admit the transcript under these circumstances. The transcript was excluded.

16-021312 Page 13

The Tribunal excluded the deposition transcript as not being the best evidence and redundant, seeing how the witness testified at the hearing, in the presence of the finder of fact and subject to cross-examination.

Summary of the Testimony of S.B.

On July 30, 2013, S.B. went to LA IV to purchase insurance, and decided to purchase a seven-day policy. She told the insurance agent (Sandy Kassab ) that she already had a towing service through AAA, which included services for lockouts or a dead battery. The agent told her the policy would cost "close to $300." [Tr I, p 68].

S.B. testified that she only asked for automobile insurance, and that during the transaction the agent was "all over the place, honestly. She was sending faxes, answering the phone. So she just handed me some paperwork, highlighted the areas that she wanted me to sign." [Tr I, p 68].

On July 30, 2013, S.B. signed an application for a seven-day insurance policy. [See Exh. JT-5, p 27.] The insurance application process required her to sign the documents five times. In addition, S.B.'s signature appears on a document entitled "NSD Motor Club Membership" dated July 30, 2014. [Exh. JT-5, p 118].

S.B. testified that the agent "handed me a stack of papers in which she either highlighted or took her pen and was like, sign here, sign here, sign here. And that's what I did." [Tr I, p 70]. She did not read the documents. She did not realize that she had signed a document for the NSD. She believed that the money she paid to the agent was all for insurance and not for NSD. She did not know she had purchased the NSD until she was contacted by a DIFS investigator. [Tr I, p 71].

Summary of Testimony of J.M.

On July 18, 2013, J.M. went to LA IV, where he spoke with a female insurance agent about purchasing a seven-day automobile insurance policy. He never discussed a motor club membership, towing service, or roadside assistance, with the agent. [Tr I, p 97]. J.M, admits that his signature appears on the NSD form, but that he did not know he purchased the NSD.

In an affidavit signed on September 24, 2013, he stated that he did not remember whether NSD was mentioned during the transaction on July 18, 2013. On crossexamination at the hearing, he testified that he was sure that the agent never mentioned NSD.

16-021312 Page 14

Summary of Testimony of M.D.

On July 18, 2013, M.D. purchased a seven-day automobile insurance policy at LA IV.

Initially she called LA IV by telephone and was given a quote of $225 "out the door." There was no discussion about roadside service.

At the agency, the agent (Sandy Kassab) told her that the insurance policy "comes with roadside assistance." [Tr I, p 135, 136, 137]. M.D. told the agent that she didn't need roadside assistance for only seven days. The agent told M.D. that the roadside assistance was "part of the package." [Tr I, p 139]. She paid $266 to LA IV. [Tr I, p 145]. She believed this amount was solely for the seven-day insurance policy. M.D. stated that had she been given the option whether to purchase the NSD, she would have declined it. [Tr I, p 143]. Although the documents stated that $153 was for insurance, the agent never broke it down for her, but only told her that the total amount of $266 was due for the package. On cross-examination, M.D. testified as follows:

Q. So when you say that you understood that it came with a package, what you understood was that for the price that you'd been quoted, you get the roadside service, correct?

A. Correct.

Q. And during that time, she didn't tell you that you didn't have the option to decline it. You just never asked, right?

A. Correct. She never mentioned it, and I never asked. [Tr I, p 152].

Summary of Testimony of A.S.

In January of 2012, Customer "A.S." went to LA XVII to purchase an insurance policy. Sandy Kassab told her the down payment on a six-month policy would cost $220.00. After purchasing the policy, A.S. learned that the insurance company had received only $120.00. When A.S. inquired with Sandy Kassab, she was told that of the $220.00 paid, $100.00 was applied to purchase NSD, and that the NSD was required in order to keep the insurance. This witness stated emphatically that she did not want NSD, that it was never discussed at any point in the transaction, and that when she discovered the $100.00 payment for NSD, she told Sandy Kassab that she already had roadside assistance through AAA. Sandy Kassab replied that A.S. could cancel the AAA, because she had to keep the NSD, because it was part of the package. [Tr I, p 165-

16-021312 Page 15

170]. This testimony is consistent with the language that A.S. wrote on the complaint form3 that she filed with DIFS in March of 2012. [Joint Exh. JT-7].

Summary of Testimony of Justin Blood

Justin Blood testified that he has been with DIFS for over nine years, currently serving as an insurance investigator. Mr. Blood investigated a consumer complaint filed by customer A.S. regarding LA IV. He first collected a list of customers of LA IV and LA XVII. He also visited each agency on August 16, 2013. He spoke with Sandy Kassab at LA IV regarding a quote for insurance. She provided him with a quote for a six-month and a seven-day policy. She stated that the seven-day policy would cost $290.00 "out the door." This undercover investigation of Sandy Kassab and LA IV was recorded. He has reviewed hundreds of documents related to seven-day insurance policies and transactions. There is one approved, seven-day insurance policy that is approved in Michigan, it is offered by lntegon Insurance Company working together with National General Insurance Company. He has reviewed thousands of such policies and transactions. This policy does not include roadside assistance, towing services, or NSD.

Of the thousands of polices reviewed, the highest premium that Mr. Blood has seen for a seven-day policy is $171.00. [Tr. I, p 198:21].

At the August 16, 2013, encounter with Sandy Kassab, Mr. Blood stated his ZIP code was 48203, which is one of the highest in the State with regard to automobile insurance rates. [Tr. I, p 198:13].

Mr. Blood visited LA XVII on August 16 and 17, 2013. He decided to investigate LA XVII because Sandy Kassab was also the DLRP for that entity.

National Motor Club, Inc. sells the "National Safe Drivers" (NSD) memberships at wholesale to insurance agencies, which sell them to customers at retail. For a membership sold for $100.00, NSD earn $9.00 of revenue and the seller (insurance agency) earns $91.00. [Tr. I, p 219-221].

Summary of Testimony of Sonny S. Kassab

Sonny S. Kassab worked as a licensed insurance agent at LA Insurance XVII. He generally worked there alone, but sometimes his sister, Sandy Kassab would cover for him when he was not there. He testified that he never told a customer that NSD was required or that it was part of an insurance policy; some customers purchased

3 Some of the handwriting on the Complaint form is difficult to decipher, but AS. was able to read most of it while on the witness stand, and confirmed that her statement on the form is consistent with her testimony.

16-021312 Page 16

insurance without NSD; he answered questions for customers about the policy and NSD; he never mislead a customer as to whether NSD was included in an insurance policy; he never signed a customer's name to any document; and, that no customer has ever complained that he mislead them about an insurance policy.

He did not treat customers D.W. or R.B. any differently than any other customer.

Sandy Kassab

The relevant facts pertaining to Sandy Kassab are included in the Findings of Fact section and discussed further in the Conclusions of Law section of this Proposal for Decision.

FINDINGS OF FACT

Based on the entire record in this matter, including the witness testimony and admitted exhibits, the following findings of fact are established by a preponderance of the evidence:

1. At all relevant times, Sandy B. Kassab and Sonny S. Kassab were licensed resident insurance producers with qualifications in property and casualty and were authorized to transact the business of insurance in Michigan.

2. Respondent LA Insurance Agency IV, Inc. ("LA IV") is a Michigan corporation with its principal place of business located at 10231 Livernois Ave., Detroit, Michigan 48204, and is a licensed resident insurance agency in the state of Michigan with qualifications in property and casualty.

3. Respondent Sandy Kassab is an officer of each Agency and their Designated Responsible Licensed Producer (DRLP).

4. LA Insurance Agency XVII, Inc., (LA XVII) is a Michigan corporation that at all relevant times was a licensed resident agency insurance producer with qualifications in property and casualty.

5. On August 16, 2013, DIFS investigators Justin Blood and another DIFS investigator ("Peck") visited LA XVII, at which time Sonny Kassab and Cindy Kassab were present. Mr. Blood conducted an investigation under the assumed name, Nick Davis. After greetings were exchanged between Blood and Cindy Kassab, Blood asked for a quote for a car he intended to buy. Sonny Kassab asked Blood whether he "was looking for no fault or full coverage?" Blood answered, "I just kinda want to price out everything and see what I got . . . ." Cindy Kassab handled a telephone call, then asked Blood for his driver's license

16-021312 Page 17

and for some personal information. She asked Blood whether he currently had insurance, and he stated that he did have insurance through State Farm. Cindy Kassab answered, "If you've had State Farm for the last six months with no lapse in coverage, you're not going to get a cheaper rate. We're a non-standard market ... so, just a heads up." [JT-2 at 4:53]. Cindy Kassab provided a quote for a sixmonth policy with full coverage for the price of $3,275. Blood also asked about a seven-day policy, and Cindy Kassab Explained that "you cannot get a seven-day policy with full coverage." She stated that the seven-day liability policy would cost $265. [JT-2, recording 1, at 8:50]. Blood asked, "What is . . . full coverage?" Cindy Kassab answered, "Comp and collision ... Full coverage is made up of three components, · liability, comprehensive, and then collision coverage." After further explaining the details of the six-month, full coverage policy, she stated, "If you're going to have a six-month policy, then you can just add that car onto your policy" (referring to Blood's existing State Farm policy) it would be cheaper than, probably, $265 for seven days." Blood then asked, "with the State Farm it has roadside assistance and stuff, do you guys have anything like that." Cindy Kassab, "We do." Blood asked, "On the six-month policy?" Cindy Kassab answered, "Mm, hm." Blood then asked, "I think the State Farm comes automatically?" Cindy Kassab answered, "So um, oh, I don't know." Blood asked, "for Progressive, does it cost anything else?" Cindy Kassab answered, "a [?] charge of twelve dollars, but that quote wasn't through Progressive, a six-month policy was through MAIPF, which is the pool, it's the facility . . . your Progressive rate was $5,200." Regarding the road service, Cindy Kassab stated, "And so with the pool, you can get towing and road service, but it doesn't come with it, it's something separate that you have to purchase." She answered Blood's question, stating that roadside and towing does not come with the six-month quote, "I did not even put that in there," she said. Blood then asked, "What about the seven-day policy?" Cindy Kassab answered, "Yep, you can get that too ... you can get road service." Blood inquired further, "ls that automatic, or ... ?" Cindy Kassab stated, "You can do it either way." Blood: "Would it be cheaper if I didn't?" Cindy Kassab, "Um, yeah, like I said, you'll save a little bit, but it depends on whether you are going to do no fault or full coverage. But like I said, if you already have a policy, you're going to be way better off adding [a car] to your policy ... so think about it, I'm going to grab this [phone call], okay, good luck, call your agent . .. it will be way cheaper."

6. With regard to the above discourse between Cindy Kassab and Justin Blood, Cindy Kassab testified that the $265 for the seven-day policy "would include road service." [Tr II, p 257:18]. Cindy Kassab testified that NSD is included in the price quoted to the customer, and stated further that, the reason for doing so was that "I'm giving the quote with the liability and the NSD. At the time of giving the quote they're both included in the pricing." When asked further, "And is that because

16-021312 Page 18

you're trying to sell NSD to the customer," she answered, "Of course." She further clarified that when the customer actually purchased the policy that "we'd break it down to them" and she further denied that she ever told a customer that the NSD was required or that it was part of the insurance policy. [Tr II, p 259].

7. With regard to the investigation involving Cindy Kassab, the price initially quoted for insurance ($265.00) also included the NSD membership, before the customer asked about roadside assistance. She did not say NSD was optional at that point in the conversation. However, to her credit, she later stated that "you could do it either way" (with or without road service) and that "you would save a little bit" without it.

8. Also on August 16, 2013, Blood and Peck visited LA IV, at which time Respondent Sandy B. Kassab was present. Mr. Blood indicated that he was interested in a quote for insurance on a vehicle he intended to purchase. Sandy Kassab asked Blood "Who's name is the car in?" Blood told Sandy Kassab that he was going to buy a 2002 Chevy Impala and that he was "looking for a quote." Blood identified himself as "Nick Davis" and provided an address and other personal information. Blood stated that he was looking for a quote on a six-month policy, and Sandy Kassab stated that the six-month premium would be $2,454, with a down payment of 40% ($982) with the balance due in three monthly payments of $497. Sandy Kassab then offered the following: "The second option they offer is a seven-day policy, which will just allow you to get plates and tabs and get on the road legally, and that's going to be $290." Blood responded, "$290 right out the door?" Sandy Kassab answered, "Out the door, yes. But you do need to bring that title back from that owner, or even a copy of it, and then your license, and then the down payment is cash, credit card, or money order." Blood asked for the name of the insurance company, and Sandy Kassab stated that for the six-month policy it would be through the insurance pool, and would be either State Farm or Citizens. Sandy Kassab then answered a very brief phone call, and answered Blood's question about the insurance pool. Blood then stated that the six-month policy was quite expensive and that he was interested in the seven-day policy because he just wanted to get tabs and plates. Sandy Kassab replied, "You can do that too." Blood asked, "what comes with the seven-day policy?" Sandy Kassab replied, "It's just insurance for the seven days and then you add4 towing and road service also." [Jt-2, recording 2, at 4:38]. Blood then asked for further details, "Oh that comes with it?" Sandy Kassab answered, "Um hm" and Blood replied, "Nice." Again, Sandy Kassab answered "Yes" when Blood asked, "But with the sevenday policy it just comes with it." ("It" meaning roadside assistance.) Sandy

4 It is possible that Cindy Kassab said, "then you have towing and road service also." The ALJ listened to the live recording and also slowed it down to better understand her words, and hears "then you add towing and road service."

16-021312 Page 19

Kassab affirmed that with the six-month policy the roadside could be added for $100.00 but that with the seven-day policy roadside "just comes with it."

9. Of the thousands of policies he has reviewed, the highest premium that Mr. Blood has seen for a seven-day policy is $171.00. [Tr. I, p 198:6].

10. At the August 16, 2013, encounter with Sandy Kassab, Mr. Blood stated his ZIP code was 48203, which is one of the highest in the State with regard to automobile insurance rates. [Tr. I, p 198:13].

11. Mr. Blood visited LA XVII on August 16 and 17, 2013. He decided to investigate LA XVII because Sandy Kassab was also the DLRP for that entity.

12.Customer "A.S." went to LA XVII in January of 2012 to purchase an insurance policy. Sandy Kassab told her the down payment on a six-month policy would cost $220.00. After purchasing the policy, A.S. learned that the insurance company had received only $120.00. When A.S. inquired with Sandy Kassab, she was told that of the $220.00 paid, $100.00 was applied to purchase NSD, and that the NSD was required in order to keep the insurance. This witness stated emphatically that she did not want NSD, that it was never discussed at any point in the transaction, and that when she discovered the $100.00 payment for NSD, she told Sandy Kassab that she already had roadside assistance through AAA. Sandy Kassab replied that A.S. could cancel the AAA, because she had to keep the NSD, because it was part of the package. [Tr, p 165-170]. This testimony is consistent with the language that A.S. wrote on the complaint form5 that she filed with DIFS in March of 2012. [Joint Exh. JT-7].

13.On July 26, 2013, R.B. purchased a seven-day insurance policy from LA Insurance XVII. He first called the agency in the process of shopping for the best price from various agencies. He noted that LA XVII was right next to the Secretary of State branch-office on Livernois near Seven Mile Road. He received a quote over the phone. He was assisted at the agency by a male agent (Sonny Kassab). He did not have any discussion with the agent regarding road side assistance, towing service, motor club membership, or Nation Safe Drivers (NSD). He wanted a seven-day policy because he could not afford anything more than that. He needed to get the seven-day policy to get his vehicle registration. He recalls paying between $200 and $300 for the auto insurance policy. He did not know that any of the price was being applied to any other product (such as road side assistance, towing, motor club membership, or NSD). He believed he

5 Some of the handwriting on the Complaint form is difficult to decipher, but A.S. was able to read most of it while on the witness stand, and confirmed that her statement on the form is consistent with her testimony.

16-021312 Page 20

signed documents for the purchase of a seven-day policy, and the agent did not tell him he was signing any document for the purchase of any other product.

14. Customer D.W. was looking for long-term insurance, in order to renew the tags on his car, but could not afford the price that Sonny Kassab quoted. Instead, he opted for a seven-day policy, and was quoted a price of $370.00, which he paid in cash. The documentary evidence proves that $200.00 of the $370.00 was applied to purchase the NSD membership. He only wanted insurance, and could afford nothing more than a seven-day policy, but ended up paying more for the roadside assistance than for the insurance.

15.On July 30, 2013, S.B. went to LA IV to purchase insurance, and decided to purchase a seven-day policy. She told the insurance agent (Sandy Kassab) that she already had a towing service through AAA, which include services for lockouts or a dead battery. The agent told her the policy would cost "close to $300." [Tr I p 68].

16. S.B. testified that she only asked for automobile insurance, and that during the transaction the agent was "all over the place, honestly. She was sending faxes, answering the phone. So she just handed me some paperwork, highlighted the areas that she wanted me to sign." [Tr I, p 68].

17.On July 30, 2013, S.B. signed an application for a seven-day insurance policy. [Exh. JT-5, p 27]. The insurance application process required her to sign the documents four times. In addition, S.B.'s signature appears on a document entitled "NSD Motor Club Membership" dated July 30, 2014. [Exh. JT-5, p 118].

18.S.B. testified that the agent (Sandy Kassab) "handed me a stack of papers in which she either highlighted or took her pen and was like, sign here, sign here, sign here. And that's what I did." [Tr I, p 70]. She did not read the documents. She did not realize that she had signed a document for the NSD. She believed that the money she paid to the agent was all for insurance and not for NSD. She did not know she had purchased the NSD until she was contacted by a DIFS investigator. [Tr I, p 71].

19.Approximately 50% of revenues for the agencies are from sales of NSD memberships.

20. National Motor Club, Inc. sells the "National Safe Drivers" (NSD) memberships at wholesale to insurance agencies, which sell them to customers at retail. For a membership sold for $100.00, NSD earn $9.00 of revenue and the seller (insurance agency) earns $91.00. [Tr. I, p 219- 221].

16-021312 Page 21

21. Customer M.D. called LA IV and obtained a quote for insurance in the approximate amount of $255.00. She did not ask for any other product. [Tr I, p 133, 136].

22.On July 17, 2013, M.D. went to LA IV, where Sandy Kassab told her that roadside coverage was "part of the package." [Tr I, p 136]. She told the agent that she did not need roadside assistance, and she would have declined to purchase it had she been given the opportunity.

23. The actual cost of the insurance policy that M.D. purchased was $153.00. [Joint Exh. JT- 4].

24.On July 18, 2013, J.M. went to LA IV, where he spoke with a female insurance agent about purchasing a seven-day automobile insurance policy. He never discussed a motor club membership, towing service, or roadside assistance, with the agent. [Tr I, p 97]. J.M, admits that his signature appears on the NSD form, but that he did not know he purchased the NSD.

25.ln an affidavit signed on September 24, 2013, J.M. stated that he did not remember whether NSD was mentioned during the transaction on July 18, 2013. On cross-examination at the hearing, he testified that he was sure that the agent never mentioned NSD. ·

CONCLUSIONS OF LAW

As the complaining party, Petitioner has the burden to prove the truth of the factual and legal allegations set forth in the Complaint by a preponderance of evidence. As the Michigan Supreme Court has stated, "[p]roof by a preponderance of the evidence requires that the fact finder believe that the evidence supporting the existence of the contested fact outweighs the evidence supporting its nonexistence." Blue Cross and Blue Shield of Michigan v Milliken, 422 Mich 1; 367 NW2d 1 (1985).

Pursuant to Section 1239(1) of the Insurance Code, supra, the Commissioner (now Department Director per Executive Order 2013-1) may sanction a license of a resident insurance producer for violations of the Code. MCL 500.1244.

Sec. 1239. (1) In addition to any other powers under this act, the commissioner may

place on probation, suspend, or revoke an insurance producer's license or may levy a civil fine under section 1244 or any combination of actions, and the commissioner shall refuse to issue a license under section 1205 or 1206a, for any 1 or more of the following causes:

16-021312 Page 22

***

(b) Violating any insurance laws or violating any regulation, subpoena, or order of the commissioner or of another state's insurance commissioner.

***

(d) Improperly withholding, misappropriating, or converting any money or property received in the course of doing insurance business.

(e) Intentionally misrepresenting the terms of an actual or proposed insurance contract or application for insurance.

***

(h) Using fraudulent, coercive, or dishonest practices or demonstrating incompetence, untrustworthiness, or financial irresponsibility in the conduct of business in this state or elsewhere.

Sec. 249. For the purposes of ascertaining compliance with the provisions of the insurance laws of the state or of ascertaining the business condition and practices of an insurer or proposed insurer, the commissioner, as often as he deems advisable, may initiate proceedings to examine the accounts, records, documents and transactions pertaining to:

(a) Any insurance agent, surplus line agent, general agent, adjuster, public ;;idjuster or counselor.

Sandy Kassab

The following evidence supports a conclusion that Sandy Kassab violated sections 1239 (b), (d), (e), and (h) of the Insurance Code. MCL 500.1239(b), (d), (e), and (h).

When the state's investigator asked for a quote on an insurance policy, Sandy Kassab offered the following: "The second option they offer is a seven-day policy, which will just allow you to get plates and tabs and get on the road legally, and that's going to be $290."

Blood then asked, "OK, but with the ... seven-day policy, it [towing and road service] just comes with it? And Sandy Kassab answered, "Yeah."

16-021312 Page 23

Respondent attempts to characterize the above exchange as a simple misunderstanding. However, after hearing the entire conversation, it is clear that Sandy Kassab stated that the price for the seven-day policy is $290, with no mention of roadside service at that point. Sandy Kassab testified at the hearing that if an insurance premium was $173.00 she provided a quote of $273.00, which is for the seven-day policy and roadside assistance. [Tr II, p 191 :4]. Therefore, with regard to the statement to Mr. Blood, it is more likely than not that the price of the insurance policy was $190, and that $100 of the total quote was for NSD. Sandy Kassab did not say it was optional. Her statement was misleading, and created the impression that the insurance premium was $290. This is false. This price included the NSD.

We know from other transactions that it was the practice at each agency to quote a price for the policy that included the NSD. [See, e.g., Testimony of Cindy Kassab, Tr II, p 258:13].

The above findings of fact are supported by the ensuing discussion between Mr. Blood and Sandy Kassab. When Mr. Blood (alias, Mr. Davis) asked whether "it just comes with" the insurance he was referring to roadside service, and Sandy Kassab answered "Yeah," meaning yes, roadside assistance does come with the insurance. By quoting the single price for insurance, and then indicating that roadside coverage comes with the insurance for $290, Sandy Kassab intentionally misled the customer. She was content to allow the customer to believe that the roadside assistance came with the insurance policy. She clearly did not explain that he could get "on the road" with a seven-day policy for $190.00, and that he could have optional roadside assistance for an additional $100.00.

It is no defense to claim that she would have explained the deal to him accurately had he proceeded to fill out the paperwork. At that point, the customer would have been under the belief that the agent had offered to sell insurance which included roadside assistance for $290. It is likely that the deal would have closed under that premise, as it did in numerous other transactions involved in this case.

Sandy Kassab was asked how she typically responds if a customer asks for a quote on a seven-day policy and the computer shows that the cost for that policy will be, for example, $173.00.

Q. . .. what would you tell that customer when they say, what's, what's the quote?

A. For $273.00 you would get the seven-day policy, which is liability coverage, and the optional roadside assistance. [Tr II, p 191 :4].

Other than her own testimony, there is no evidence that she ever worded her responses to specify "optional roadside assistance." Even if she did, it is misleading to give a quote

16-021312 Page 24

for insurance and "optional" roadside assistance, when the customer only asked for a quote for an insurance policy.

The fact that the NSD membership agreement states that it is "optional and not required in order to purchase or obtain insurance ... " does not cure the above misleading statements. It is not acceptable to misrepresent the terms of the transaction and present documents for signature that contradict the verbal representations.

It is clear from the recording of the conversation between Sandy Kassab and the investigator that when asked for quote, she stated that cost of the seven-day policy was $290.00. Initially, she did not say that the policy "included" roadside assistance or "came with" roadside assistance. There was no discussion of NSD, towing, or roadside assistance. At this point the customer was led to believe that the cost of the insurance (only) would be $290.00. More likely than not, based on the totality of the evidence, the actual insurance cost was $190.00.

Sandy Kassab stated that "The second option they offer is a seven-day policy, which will just allow you to get plates and tabs and get on the road legally, and that's going to be $290." Blood responded, "$290 right out the door?" Sandy Kassab answered, "Out the door, yes." The conversation was at a natural ending point, and had Mr. Blood walked out, he would have been under the impression that a seven-day policy would cost him $290.00, with no mention of roadside assistance, optional or otherwise.

Of the thousands of policies he has reviewed, the highest premium that Mr. Blood has seen for a seven-day policy is $171.00. [Tr. I, p 198:6]. At the August 16, 2013, encounter with Sandy Kassab, Mr. Blood stated his ZIP code was 48203, which is one of the highest in the State with regard to automobile insurance rates. [Tr. I, p 198:13]. Again, the $290.00 quote included both the insurance premium and $100.00 for the NSD policy that the customer did not ask for.

Later, Blood asked "what comes with the seven-day policy?" Sandy Kassab replied, "It's just insurance for the seven days and then you add6 towing and road service also." [Jt-2, recording 2, at 4:38]. Stating "then you add towing and road service" is different than saying that it is "optional." She did not say it was optional. She stated it as a matter of fact that "you add towing and road service," which would be reasonably understood to mean that the road service is part of the $290.00 quoted price.

Blood then asked for further details, "Oh that comes with it?" Sandy Kassab answered, "Um hm" and Blood replied, "Nice." Again, Sandy Kassab answered "Yes" when Blood asked, "But with the seven-day policy it just comes with it" ("it" meaning roadside

6 It is possible that Cindy Kassab said, "then you have towing and road service also." The ALJ listened to the live recording and also slowed it down to better understand her words, and hears "then you add towing and road service."

16-021312 Page 25

assistance.) Sandy Kassab affirmed that with the six-month policy the roadside could be added for $100.00 but that with the seven-day policy roadside "just comes with it."

Based on the foregoing, it can be concluded that the $290.00 quote also included both insurance and NSD. This is misleading and dishonest.

Customer S.B.

The July 30, 2013, transaction with S.B. also supports the above-cited violations.

On July 30, 2013, S.B. went to LA IV to purchase insurance, and decided to purchase a seven-day policy. She told the insurance agent (Sandy Kassab) that she already had a towing service through AAA, which included services for lockouts or a dead battery. The agent told her the policy would cost "close to $300.00." [Tr I, p 68].

S.B. testified under oath at the hearing that she only asked for automobile insurance and that Sandy Kassab "handed me some paperwork, highlighted the areas that she wanted me to sign." [Tr I, p 68].

The customer, S.B., credibly testified that the agent "handed me a stack of papers in which she either highlighted or took her pen and was like, sign here, sign here, sign here. And that's what I did." [Tr I, p 70]. Ms. Bundy did not realize that she had signed a document for the NSD. She believed that the money she paid to the agent was all for insurance and not for NSD. She did not know she had purchased the NSD until she was contacted by a DIFS investigator. [Tr I, p 71].

The fact that S.B. already had roadside service, towing, lockout, and battery service through AAA lends credibility to Ms. Bundy's claim that she did not want duplicative services through NSD. This is similar to the transaction with A.S. (discussed infra).

Respondents argue that S.B. is not credible because she did not mention in her affidavit that she had roadside assistance through AAA, but that she testified to this fact at the hearing. There is no evidence to prove that Ms. Bundy did not have AAA. Undoubtedly, Respondents could have obtained evidence to prove whether she had AAA roadside assistance or not. There is no reason to believe that S.B. lied about having roadside assistance through AAA. This fact standing alone, without regard to whether she mentioned it when interviewed for the affidavit, makes it highly unlikely that she would knowingly purchase another roadside assistance membership. Respondents have not provided any valid answer to this inconvenient fact. Respondents cite Sandy Kassab's self-interested testimony where she claims that she never misled any customer. The credibility problem lies in Sandy Kassab's testimony. The recorded conversation between Sandy Kassab and Justin Blood is convincing - she led the investigator to believe that the quoted price included roadside assistance. It is entirely reasonable to

16-021312 Page 26

believe that S.B. was also misled to believe that the NSD was required or otherwise included with the insurance policy.

Respondents attempt to impeach S.B.'s credibility by pointing to some alleged inconsistencies in her testimony, regarding her understanding of the NSD policy, specifically whether Sandy Kassab explained it to her, whether it was voluntary, whether it came with the insurance, or was a part of the insurance. Any confusion in this regard is understandable given the misleading tactics employed by Respondents. The fact remains that S.B already had AAA roadside assistance. Under these circumstances, it is highly unlikely that she would have agreed to purchase the NSD membership, unless she was led to believe that it was either part of the insurance policy (not severable) or that it was required to buy the membership in order to get the insurance.

A. There was no option to take this out. I would have gladly taken this extra $100 and put it towards something else. [S.B. testimony, Tr I, p 79-80].

S.B.'s testimony that roadside assistance was "never explained to her" is not inconsistent with her testimony that she was not given the option to buy insurance without the NSD. The testimony that NSD was never explained does not mean or imply that it was discussed at all.

Customer J.M.

J.M.'s testimony is also found to be relevant and credible. On July 18, 2013, J.M. went to LA IV, where he spoke with Sandy Kassab about purchasing a seven-day automobile insurance policy. He never discussed a motor club membership, towing service, or roadside assistance with the agent. [Tr I, p 97]. J.M. admits that his signature appears on the NSD form, but states that he did not know he purchased the NSD. J.M. believed that the entire amount that he paid was for the seven-day policy.

Customer A.S.

In January of 2012, complainant and customer "A.S." went to LA XVII to purchase an insurance policy. Sandy Kassab told her that the down payment on a six-month policy would cost $220.00. After purchasing the policy, A.S. learned that the insurance company had received only $120.00 for the policy. At a later date, A.S. inquired about this discrepancy, and Sandy Kassab told her that of the $220.00 paid, $100.00 was applied to purchase NSD, and that the NSD was required in order to keep the insurance. Customer A.S. stated emphatically that she did not want NSD, that it was never discussed at any point in the transaction, and that when she discovered the $100.00 payment for NSD, she told Sandy Kassab that she already had roadside assistance through AAA. Sandy Kassab replied that A.S. could cancel the AAA, because she had to keep the NSD, because it was part of the package. [Tr, p 165-170].

16-021312 Page 27

This testimony is consistent with the language that A.S. wrote on the complaint form7

that she filed with DIFS in March of 2012. [Joint Exh. JT-7].