Embed Size (px)

Citation preview

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

1

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

The Financial Companies Association – ALB Romania

1. Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession policies

2. Romanian Leasing Market – June, 2011

Adriana AhciarliuSecretary General

www.alb-leasing.ro

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

2

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession policies

Perception versus tradition: What is leasing? Asset financing or delivery of

goods? How should it work? Under special leasing

legislation? Under Central Bank Supervision? Free under provisions of Civil Code or Commercial law?

Are there criteria that make the difference?: Corporate governance? Accounting standards? Is there need for border between financial &

operational leases? Does fiscal treatment matter? What matters more: the lessor or the lessee?

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

3

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession policies

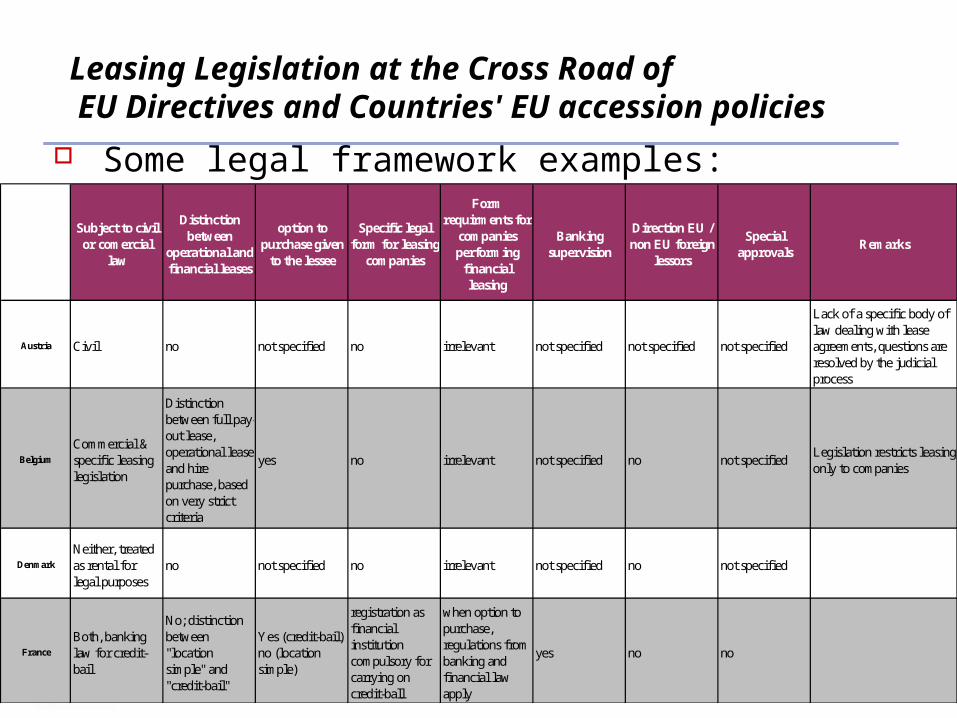

Some legal framework examples:

Subject to civil or comercial

law

Distinction between

operational and financial leases

option to purchase given

to the lessee

Specific legal form for leasing

companies

Form requirments for

companies performing

financial leasing

Banking supervision

Direction EU / non EU foreign

lessors

Special approvals

Remarks

Austria Civil no not specified no irrelevant not specified not specified not specified

Lack of a specific body of law dealing with lease agreements, questions are resolved by the judicial process

Belgium

Commercial & specific leasing legislation

Distinction between full pay-out lease, operational lease and hire purchase, based on very strict criteria

yes no irrelevant not specified no not specifiedLegislation restricts leasing only to companies

Denmark

Neither, treated as rental for legal purposes

no not specified no irrelevant not specified no not specified

France

Both, banking law for credit-bail

No; distinction between "location simple" and "credit-bail"

Yes (credit-bail) no (location simple)

registration as financial institution compulsory for carrying on credit-ball

when option to purchase, regulations from banking and financial law apply

yes no no

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

4

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession policies

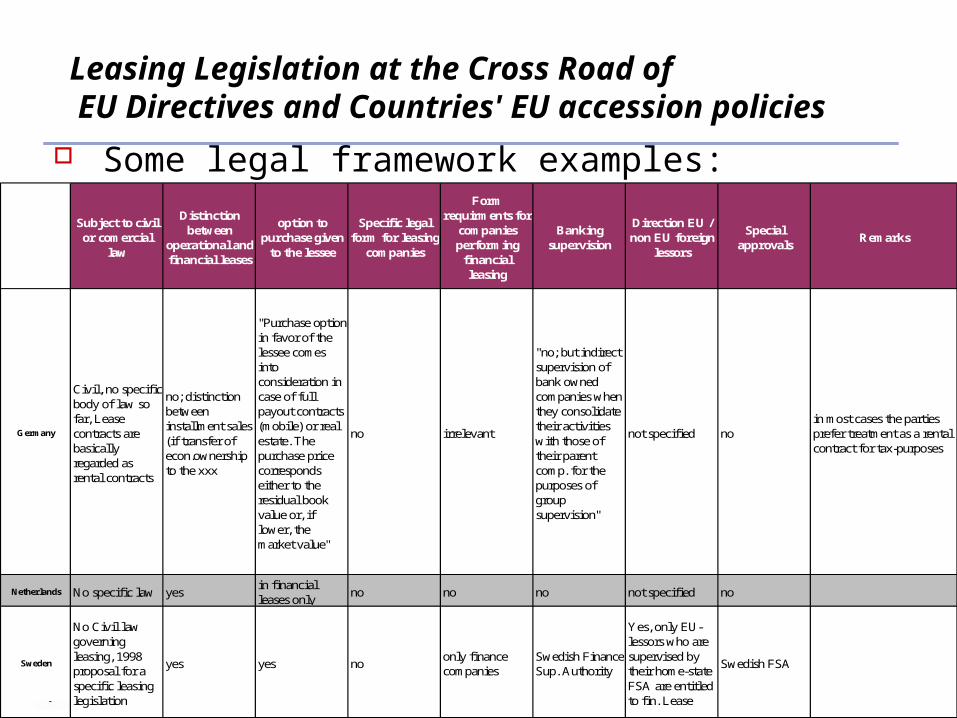

Some legal framework examples:

Subject to civil or comercial

law

Distinction between

operational and financial leases

option to purchase given

to the lessee

Specific legal form for leasing

companies

Form requirments for

companies performing

financial leasing

Banking supervision

Direction EU / non EU foreign

lessors

Special approvals

Remarks

Germany

Civil, no specific body of law so far, Lease contracts are basically regarded as rental contracts

no; distinction between installment sales (if transfer of econ.ownership to the xxx

"Purchase option in favor of the lessee comes into consideration in case of full payout contracts (mobile) or real estate. The purchase price corresponds either to the residual book value or, if lower, the market value"

no irrelevant

"no; but indirect supervision of bank owned companies when they consolidate their activities with those of their parent comp. for the purposes of group supervision"

not specified noin most cases the parties prefer treatment as a rental contract for tax-purposes

Netherlands No specific law yesin financial leases only

no no no not specified no

Sweden

No Civil law governing leasing, 1998 proposal for a specific leasing legislation

yes yes noonly finance companies

Swedish Finance Sup. Authority

Yes, only EU-lessors who are supervised by their home-state FSA are entitled to fin. Lease

Swedish FSA

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

5

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession policies

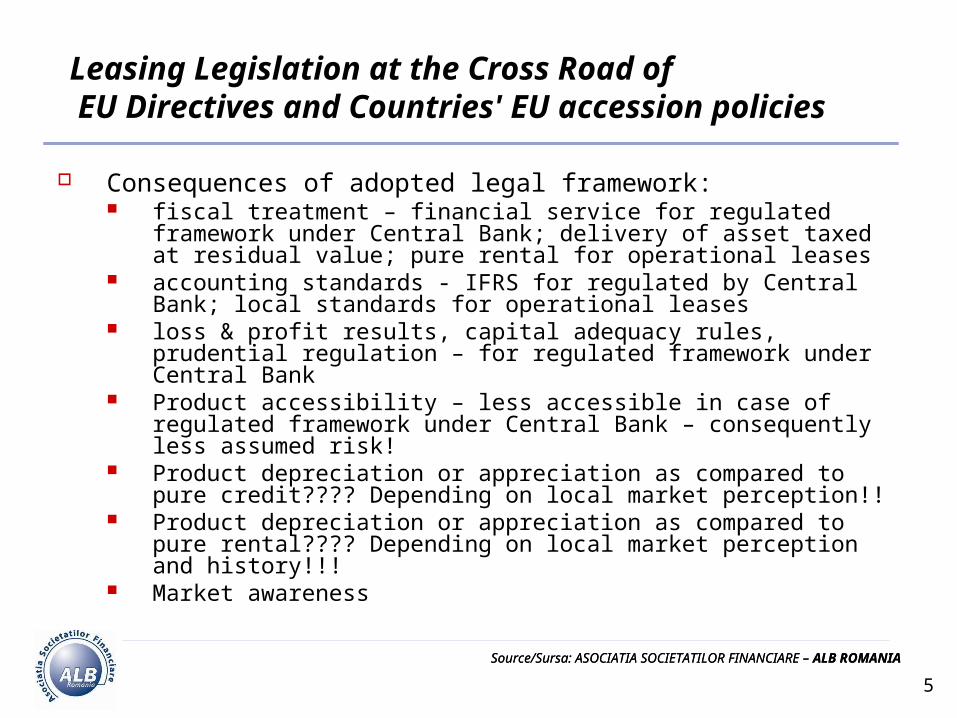

Consequences of adopted legal framework: fiscal treatment – financial service for regulated framework under

Central Bank; delivery of asset taxed at residual value; pure rental for operational leases

accounting standards - IFRS for regulated by Central Bank; local standards for operational leases

loss & profit results, capital adequacy rules, prudential regulation – for regulated framework under Central Bank

Product accessibility – less accessible in case of regulated framework under Central Bank – consequently less assumed risk!

Product depreciation or appreciation as compared to pure credit???? Depending on local market perception!!

Product depreciation or appreciation as compared to pure rental???? Depending on local market perception and history!!!

Market awareness

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

6

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession – Case of Romania

Leasing legal framework before country’s accession to EU: Leasing law defining the terminology Tax incentive: custom duties to be applied

at a maximum RV of 20% at the termination of contract

No rule of authorization No supervision of central bank Romanian accounting standards for LTD

companies

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

7

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession - – Case of Romania

Leasing legal framework after legal harmonizing with EU legislation : Leasing law updated to some EU practice – no

compulsory EU Directive!! Fiscal separation between financial and operational

leasing – there is the VAT Directive offering the framework of VAT treatment according to country’s decision to treat leasing as financial service or delivery of goods

Supervision of financial leasing by Central Bank – operational leasing stays as rental activity under provisions of Commercial Law

Banking Romanian accounting standards for financial leasing (very similar to IFRS), Romanian accounting standards for operational leasing contracts.

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

8

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession – Case of Romania

Leasing legal framework after country’s accession to EU: Romania has followed the example of Italy

& UK with double standard supervision ( small versus big leasing company) VAT treatment for financial leasing =

financial service = VAT EU Directive for credit activity

E.U. Customs Code

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

9

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession – Case of Romania

What happens after harmonization?– is EU a support for lobbying better & healthier business environment? Infringement procedure is an efficient

support towards correct harmonization and implementation of EU legislation at the level of EU member states;

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

10

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession

Is EU a support for lobbying better & healthier business environment? Explanation of procedure for non-compliance with European

Union law Principles Each Member State is responsible for the implementation (transposition

by the deadline, conformity and proper application) of European Union law in its internal legal system. The European Commission ensures that European Union law is properly applied. Consequently, where a Member State fails to comply with European Union law, the Commission has powers of its own (action for non-compliance) which it may use in an attempt to terminate the infringement and, if necessary, it may refer the case to the Court of Justice. The Commission takes whatever action it deems appropriate whether in response to a complaint or after detecting indications of infringements itself.

Non-compliance means failure by a Member State to fulfill its obligations under European Union law. It may consist either of action or omission. The term State is taken to mean the Member State which infringes European Union law, irrespective of the authority - central, regional or local - to which the non-compliance is attributable.

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

11

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession

Is EU a support for lobbying better & healthier business environment? Admissibility of complaints

To be admissible, a complaint has to relate to an infringement of European Union law by a Member State. It cannot therefore concern a private dispute. It is very important for the complaint papers to be complete and accurate, particularly as regards the facts complained of in relation to the Member State in question, any steps which you have already taken at any level and, as far as possible, the provisions of European Union law which you consider to have been infringed and any involvement of a European Union funding scheme.

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

12

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession

Is EU a support for lobbying better & healthier business environment?

Stages of infringement proceedings Research phase Opening of infringement proceedings: formal

contacts between the Commission and the Member State concerned:

If the Commission considers that there may be an infringement of European Union law which warrants the opening of infringement proceedings, it will address a "letter of formal notice" to the Member State concerned, requesting it to submit its observations by a specified date. The Member State has to adopt a position on the points of fact and of law on which the Commission bases its decision to open the infringement proceedings.

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

13

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Leasing Legislation at the Cross Road of EU Directives and Countries' EU accession

Is EU a support for lobbying better & healthier business environment? In the light of the reply or absence of a reply from the

Member State concerned, the Commission may decide to address a "reasoned opinion" to the Member State, clearly and definitively setting out the reasons why it considers there to have been an infringement of European Union law and calling on the Member State to comply with European Union law within a specified period (normally two months).

In the light of the reply, the Commission may also decide not to pursue the infringement proceedings any further, for example where the Member State provides credible assurances as to its intention to amend its legislation or administrative practice. Most cases can be resolved in this way.

The procedure ensures confidentiality of source.

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

14

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

The Financial Companies Association – ALB Romania

Financial Leasing Market in RomaniaH1 2011

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

15

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Evolution of Non Performing Loans from Total Granted Credits Evolutia creditelor neperformante din total credite acordate

29.0%

25.5%

31.6%

12.5%

23.2%21.6%

29.8%

28.5%27.5%27.4%

27.8%

15.1%

17.9%

13.6%13.8%

13.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb

-08

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb

-09

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb

-10

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb

-11

Apr

-11

Jun-

11

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

16

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Growth rates / Rate de crestereEuropean Financial Leasing Market / Piata de leasing financiar in EuropaH1 2010 vs. H1 2011

Source: Leasurope

AT25.0%

BE19.4%

BG45.0%

CH9.6%

CZ16.1%

DE14.4%

EE70.8%

ES-23.9%

FI10.4%

FR10.1%

GR-51.7%

HU11.3%

IT-2.6%

LV128.5%

NL9.1%

NO14.4%

PL27.5%

PT-34.4%

RO22%

RS32.4%

RU101.3%

SE-1.9%

SI-3.6%

SK32.6%

UK5.3%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

17

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Financial Leasing Market Evolution (Biannual Growth Rates) in Romania Evolutia pietei de leasing financiar (cresteri semestriale) in RomaniaH1 2005- H1 2011

776,653

1,484,822

543,719 663,314

109,320117,307

296,450184,220

1,131,779

507,149338,992 397,756

152,197

95,40756,593 81,338

H1 2006 H1 2007 H1 2008 H1 2009 H1 2010 H1 2011

(000

eur

o)

TOTAL Equipment/Echipamente Vehicles/Vehicule Real Estate/Imobiliar

177,54%

69%

-15%

22%

17%

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

18

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Financial Leasing Market - Weight per Good Segment / Piata de Leasing Financiar in Romania - Ponderea segementelor in total finantariH1 2005 - H1 2011

28%

12%

22%22%20%17%

15%

20%

65%

71%71%76%

81%

62% 60%

18%2% 4%

7% 7%

20%

0%10

%20

%30

%40

%50

%60

%70

%80

%90

%

H1 2005 H1 2006 H1 2007 H1 2008 H1 2009 H1 2010 H1 2011

Equipment/Echipamente Vehicles/Vehicule Real Estate/Imobiliar

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

19

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Financial Leasing Market Structure by Type of Lessor/Piata de leasing financiar din Romania dupa categoria societatilor de leasingH1 2009 ÷ H1 2011

60%

28%

12%

64%

22%

14%

65%

20%

15%

0%

10%

20%

30%

40%

50%

60%

70%

H1 2009 H1 2010 H1 2011

BANK S̀ SUBSIDIARES/ Subsidiare banci CAPTIVE/ Captive INDEPENDENT/ Independente

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

20

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Financial Leasing Market Structure by Origin/Piata de leasing financiar din Romania dupa originea bunului H1 2009 ÷ H1 2011

71%

14% 22%

78%

10% 12%

92%

8%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

H1 2009 H1 2010 H1 2011

Domestic RO Domestic EU Import

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

21

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Leasing Market Structure by Acquisition Type/Piata de leasing din Romania dupa tipul achizitieiH1 2009 ÷ H1 2011

86%

14%

79%

21%

82%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

(000

Eur

o)

H1 2009 H1 2010 H1 2011

BRAND NEW / Noi USED / Second Hand

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

22

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Financial Leasing Market Structure by Customer Type/Piata de leasing financiar din Romania dupa categoria utilizatoruluiH1 2009 ÷ H1 2011

89%

9%

2%

91%

7%

2%

95%

4%

1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

H1 2009 H1 2010 H1 2011

CORPORATE/ Companii RETAIL / Retail PUBLIC / Public

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

23

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

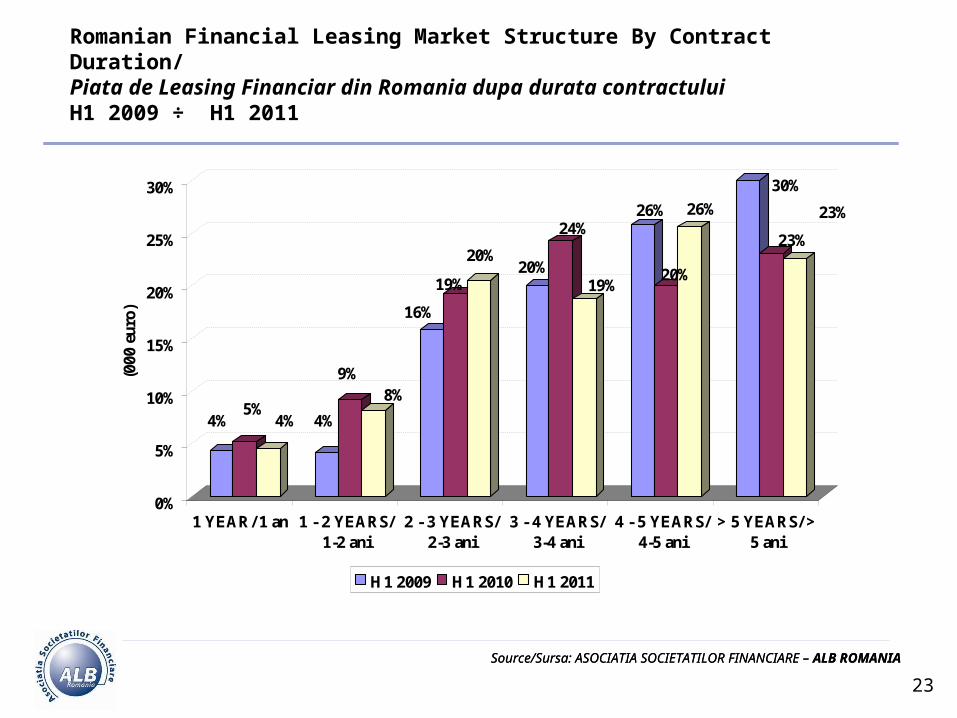

Romanian Financial Leasing Market Structure By Contract Duration/Piata de Leasing Financiar din Romania dupa durata contractuluiH1 2009 ÷ H1 2011

4%5%

4% 4%

9%8%

16%

19%

20%20%

24%

19%

26%

20%

26%

30%

23%

23%

0%

5%

10%

15%

20%

25%

30%

(000

eur

o)

1 YEAR/ 1 an 1 - 2 YEARS/1-2 ani

2 - 3 YEARS/2-3 ani

3 - 4 YEARS/3-4 ani

4 - 5 YEARS/4-5 ani

> 5 YEARS/ >5 ani

H1 2009 H1 2010 H1 2011

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

24

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Leasing Market Equipment Financing/Piata de leasing din Romania finantarea echipamentelorH1 2010 Vs. H1 2011

Construction14%

Office 1%

Others34%

Plastics & Rubber1%

Car Service1%

IT8%Medical care

8%

Petroleum & Derivatives2%

Printing & Packaging1%

Electrical devices1%

Agriculture13%

Chemical Industry3%

Wood processing2%

Food & Beverage4%

Metal processing5%

Construction17%

Metal processing4%

Food & Beverage7%

Car Service4%

Agriculture22%

O thers19%

Electrical devices14%

Medical6%

O ffice + IT4%

Wood processing3% H1 2010

H1 2011

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

25

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

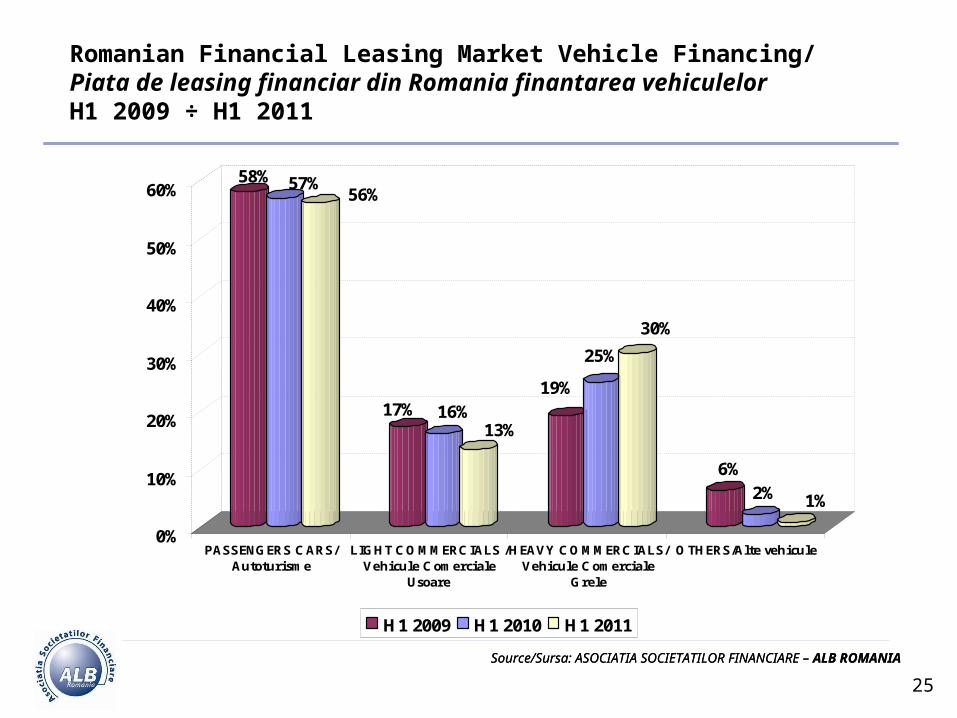

Romanian Financial Leasing Market Vehicle Financing/Piata de leasing financiar din Romania finantarea vehiculelorH1 2009 ÷ H1 2011

58% 57%56%

17% 16%13%

19%

25%

30%

6%

2% 1%

0%

10%

20%

30%

40%

50%

60%

PASSENGERS CARS/Autoturisme

LIGHT CO MMERCIALS /Vehicule Comerciale

Usoare

HEAVY CO MMERCIALS/Vehicule Comerciale

Grele

O THERS/Alte vehicule

H1 2009 H1 2010 H1 2011

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

26

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Romanian Financial Leasing Market Real - Estate Financing/Piata de leasing din Romania - finantarea sectorului imobiliarH1 2009 ÷ H1 2011

65%

18%

40%

22%

39%

18%

1% 0% 1% 0%

31%

5% 5% 5% 5%7% 7%

31%

0%

10%

20%

30%

40%

50%

60%

70%

INDUSTRIAL /Industriale

OFFICE HOTEL / Hoteluri RETAIL OUTLETS RESIDENTIAL/Rezidential

LAND/ Teren

H1 2009 H1 2010 H1 2011

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

27

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

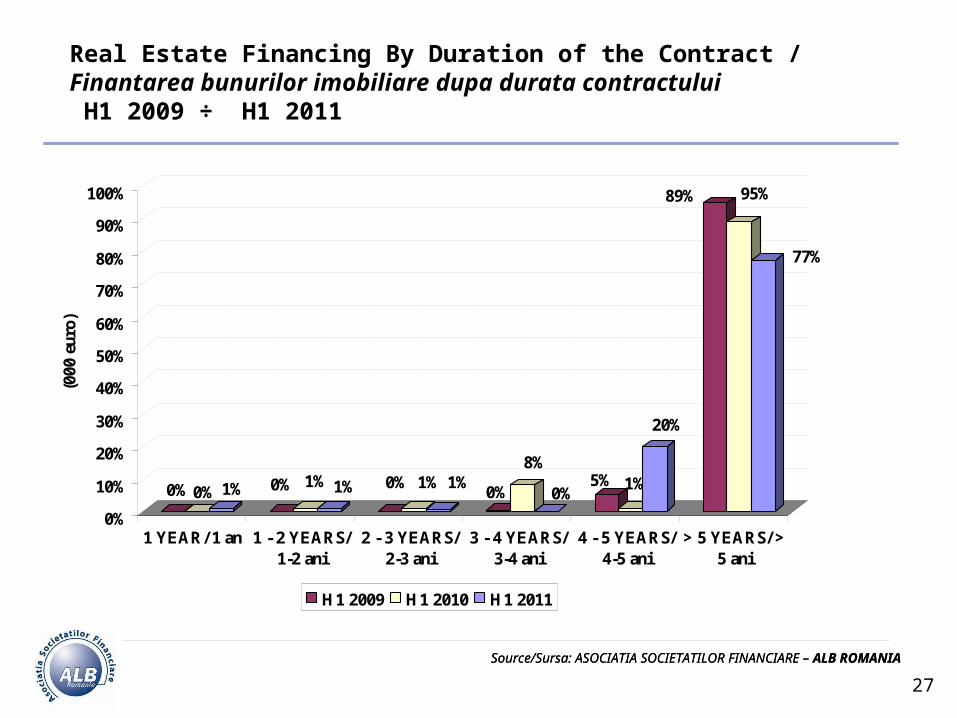

Real Estate Financing By Duration of the Contract /Finantarea bunurilor imobiliare dupa durata contractului H1 2009 ÷ H1 2011

0%0% 1% 0% 1% 1% 0% 1% 1%0%

8%

0%5% 1%

20%

95%89%

77%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

(000

eur

o)

1 YEAR/ 1 an 1 - 2 YEARS/1-2 ani

2 - 3 YEARS/2-3 ani

3 - 4 YEARS/3-4 ani

4 - 5 YEARS/4-5 ani

> 5 YEARS/ >5 ani

H1 2009 H1 2010 H1 2011

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

28

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

Real-estate Financing by Customer Type/Finantarea bunurilor imobiliare dupa categoria utilizatoruluiH1 2009 ÷ H1 2011

100%

0% 0%

100%

0%0%

100%

0%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

H1 2009 H1 2010 H1 2011

CORPORATE/ Companii RETAIL / Retail PUBLIC / Public

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

29

Source/Sursa: ASOCIATIA SOCIETATILOR FINANCIARE – ALB ROMANIA

The Financial Companies Association – ALB Romania

www.alb-leasing.ro

Thank you!