Embed Size (px)

Citation preview

25/02/2021

1

Portfolio Management

Risk & Return

• Return

• Income received on an investment (Dividend) plus any

change in market price( Capital gain), usually expressed

as a percent of the beginning market price of the

investment

Dt + (Pt-1 - Pt )

Pt

R =

1

2

25/02/2021

2

• Kamal has purchased shares of A Ltd for Rs. 10 per

share 1 year ago. The stock is currently trading at

Rs.9.50 per share and he just received a Rs1 dividend.

What return was earned over the past year?

Average Rate of Return

3

4

25/02/2021

3

Expected Return

• Expected Rate of Return given a probability distribution of possible returns (ri): E(r)

n

E(R) = S Pi Rii=1

Expected Return

◼ Normal 40% Return 20% = .08

◼ Bad 30% Return 5% = .015

◼ Good 30% Return 35% = .105

=Expected ave return = 20%

5

6

25/02/2021

4

Risk

– Uncertainty - the possibility that the actual

return may differ from the expected return

– Probability - the chance of something

occurring

– Expected Returns - the sum of possible

returns times the probability of each return

Measurement of Risk

• Studies of stock returns indicate they are approximatelynormally distributed. Two statistics describe a normaldistribution, the mean and the standard deviation (which is thesquare root of the variance). The standard deviation shows howspread out is the distribution.

• relevant risk measure is the total risk of expected cash flowsmeasured by standard deviation ()

.

7

8

25/02/2021

5

Standard Deviation

Standard Deviation is a statistical measure of the variability

of a distribution around its mean. It is the square root of

variance

Variance (2) - the expected value of squared deviations

from the mean

Standard deviation is the square root of the variance

=

=n

i 1

i

2

ii

2 P)]E(R-R[)( Variance

i.e• Kamal has invested in A Ltd shares & forecasted

expected returns under different economic conditions are

as follows.

• Depression -20%

• Recession 10%

• Normal 30%

• Boom 50%

• Determine the variance & risk of the security

9

10

25/02/2021

6

Example 2

• Suppose Kamal have predicted the following returns for stocks A and B in three possible states of nature. What are the expected returns?

– State Probability A B

– Boom 0.3 0.15 0.25

– Normal 0.5 0.10 0.20

– Recession 0.2 0.02 0.01

• RA = .3(.15) + .5(.10) + .2(.02) = .099 = 9.99%

• RB = .3(.25) + .5(.20) + .2(.01) = .177 = 17.7%

• Consider the previous example. What are the variance and standard deviation for each stock?

• Stock A

– 2 = .3(.15-.099)2 + .5(.1-.099)2 + .2(.02-.099)2 = .002029

– = .045

• Stock B

– 2 = .3(.25-.177)2 + .5(.2-.177)2 + .2(.01-.177)2 = .007441

– = .0863

11

12

25/02/2021

7

Trade off between risk & return

• When comparing securities, the one with the largest

standard deviation is the riskier

• If returns and standard deviations between two securities

are different, the investor must make a decision between

the tradeoff of the expected return and the standard

deviation of each

Portfolio Theory

• Asset may seem very risky in isolation, but whencombined with other assets, risk of portfolio may besubstantially less—even zero

• When combining different securities, it is important tounderstand how outcomes are related to each other

– Returns of two or more securities are positivelycorrelated indicating they move in same direction

– Returns of two or more securities are negativelycorrelated-move in opposite directions

– Combining a securities would greatly reduce the riskof the portfolio

13

14

25/02/2021

8

• A portfolio is a collection of assets

• An asset’s risk and return is important in how it affects

the risk and return of the portfolio

• The risk-return trade-off for a portfolio is measured by

the portfolio expected return and standard deviation, just

as with individual assets

Portfolios

Covariance & Correlation

• Variance & Standard deviation measures the variability

of individual stock.

• Covariance & Correlation is determine how two variables

are related with each other

• Covariance of Returns measure of the degree to which

two variables “move together” relative to their individual

mean values over time

15

16

25/02/2021

9

Covariance

• Covariance indicates how two variables are related. A positive

covariance means the variables are positively related, while a negative

covariance means the variables are inversely related. The formula for

calculating covariance of sample data is shown below.

• I.e Kamal has invested in A Ltd shares & B ltd shares

forecasted expected returns under different economic

conditions are as follows.

A B

• Depression -20% 5%

• Recession 10% 20%

• Normal 30% -12%

• Boom 50% 9%

Determine the covariance between securities of A & B

17

18

25/02/2021

10

Correlation coefficient

Correlation is another way to determine how two variables are related. In

addition to telling you whether variables are positively or inversely

related, correlation also tells you the degree to which the variables tend

to move together.

The correlation coefficient is obtained by standardizing (dividing) the

covariance by the product of the individual standard deviations

Correlation coefficient varies from -1 to +1

jt

iti

ij

R ofdeviation standard the

R ofdeviation standard the

returns oft coefficienn correlatio ther

:where

Covr

=

=

=

=

j

ji

ij

ij

• This means that returns for the two assets move together in a completely linearmanner. A value of –1 would indicate perfect correlation. This means that thereturns for two assets have the same percentage movement, but in oppositedirections

• If the correlation coefficient is one, the variables have a perfect positivecorrelation. This means that if one variable moves a given amount, the secondmoves proportionally in the same direction. A positive correlation coefficient lessthan one indicates a less than perfect positive correlation, with the strength of thecorrelation growing as the number approaches one.

• If correlation coefficient is zero, no relationship exists between the variables. Ifone variable moves, you can make no predictions about the movement of theother variable; they are uncorrelated.

• If correlation coefficient is –1, the variables are perfectly negatively correlated (orinversely correlated) and move in opposition to each other. If one variableincreases, the other variable decreases proportionally. A negative correlationcoefficient greater than –1 indicates a less than perfect negative correlation, withthe strength of the correlation growing as the number approaches –1.

19

20

25/02/2021

11

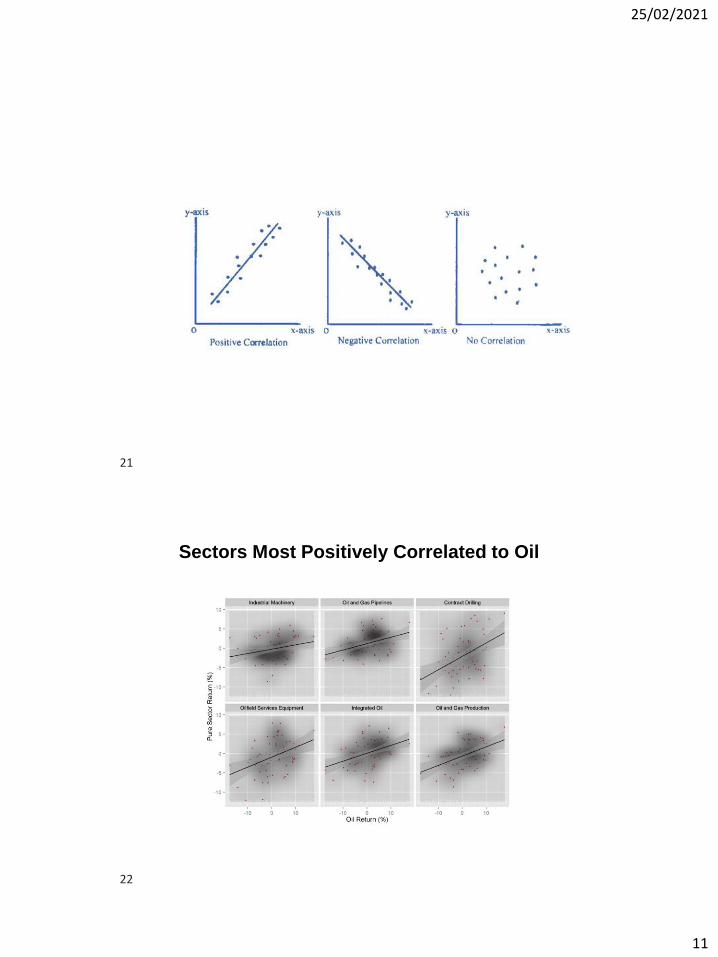

Sectors Most Positively Correlated to Oil

21

22

25/02/2021

12

Sector Oil Correlation p-value

Industrial Machinery 0.29 0.0117

Oil and Gas Pipelines 0.31 0.0075

Contract Drilling 0.37 0.0018

Oilfield Services Equipment 0.38 0.0016

Integrated Oil 0.41 0.0006

Oil and Gas Production 0.43 0.0003

Sectors Most Negatively Correlated to Oil

23

24

25/02/2021

13

Sector Oil Correlation p-value

Real Estate Investment Trusts -0.43 0.0003

Airlines -0.36 0.0021

Aerospace and Defense -0.34 0.0044

Multi Line Insurance -0.33 0.0053

Hotels Resorts Cruiselines -0.32 0.0067

Casinos Gaming -0.28 0.0142

Expected Returns of Portfolio

• The expected return of a portfolio is theweighted average of the expected returns foreach asset in the portfolio

• You can also find the expected return by findingthe portfolio return in each possible state andcomputing the expected value as we did withindividual securities

25

26

25/02/2021

14

• i.e

• Kamal has invested his wealth 60% of security

A & 40% in security B. Expected return from

Security A is 20% & from Security B is 10%

• Determine the portfolio return

Variance & Standard Deviation of portfolio

ji

ijij

ij

2

i

i

port

n

1i

n

1i

ijj

n

1i

i

2

i

2

iport

rCov where

j, and i assetsfor return of rates ebetween th covariance theCov

iasset for return of rates of variancethe

portfolio in the valueof proportion by the determined are weights

whereportfolio, in the assets individual theof weightstheW

portfolio theofdeviation standard the

:where

Covwww

=

=

=

=

=

+= = = =

27

28

25/02/2021

15

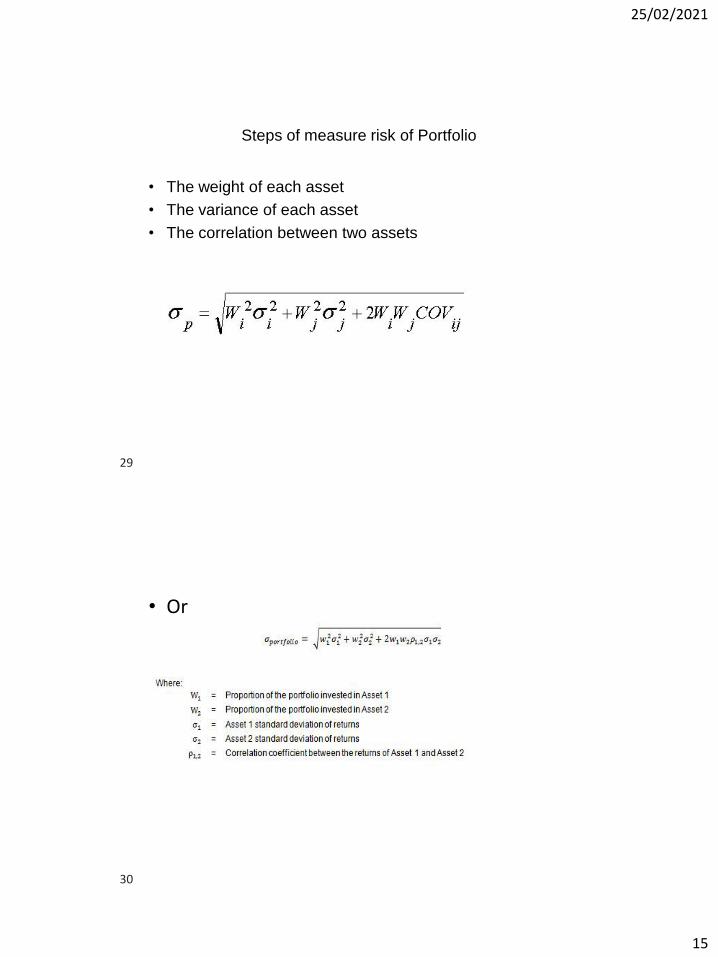

Steps of measure risk of Portfolio

• The weight of each asset

• The variance of each asset

• The correlation between two assets

• Or

29

30

25/02/2021

16

Example 1

Investment 100,000 150,000

Expected Return 10% 15%

Standard Deviation 20% 25%

Correlation coefficient 0.3

• Any asset of a portfolio may be described by two

characteristics:

– The expected rate of return

– The expected standard deviations of returns

• The correlation, measured by covariance, affects the

portfolio standard deviation

• Low correlation reduces portfolio risk while not affecting

the expected return

31

32

25/02/2021

17

• I.e Kamal has invested 60% of wealth in A Ltd shares &

other 40% wealth B ltd shares forecasted expected

returns under different economic conditions are as

follows.

A B

• Depression -20% 5%

• Recession 10% 20%

• Normal 30% -12%

• Boom 50% 9%

Determine the return from the portfolio & standard deviation of the

portfolio

Portfolio Risk-Return Plots for Different

Weights

-

0.05

0.10

0.15

0.20

0.00 0.01 0.02 0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.10 0.11 0.12

Standard Deviation of Return

E(R)

Rij = 0.00

Rij = +1.00

f

gh

ij

k1

2With uncorrelated

assets it is possible

to create a two asset

portfolio with lower

risk than either single

asset

33

34

25/02/2021

18

The Efficient Frontier

• The efficient frontier represents that set of portfolios with

the maximum rate of return for every given level of risk,

or the minimum risk for every level of return

• Frontier will be portfolios of investments rather than

individual securities

– Exceptions being the asset with the highest return and the asset

with the lowest risk

Efficient Frontier for Alternative Portfolios

Efficient Frontier

A

B

C

E(R)

Standard Deviation of Return

35

36

25/02/2021

19

37

Efficient Markets

• Efficient markets are a result of investors trading on the

unexpected portion of announcements

• The easier it is to trade on surprises, the more efficient

markets should be

• Efficient markets involve random price changes because

we cannot predict surprises

38

Systematic Risk

• Risk factors that affect a large number of assets

• Also known as non-diversifiable risk or market

risk

• Includes such things as changes in GDP,

inflation, interest rates, etc.

37

38

25/02/2021

20

39

Unsystematic Risk

• Risk factors that affect a limited number of

assets

• Also known as unique risk and asset-specific

risk

• Includes such things as labor strikes, part

shortages, etc.

40

Diversifiable Risk

• The risk that can be eliminated by combining

assets into a portfolio

• Often considered the same as unsystematic,

unique or asset-specific risk

• If we hold only one asset, or assets in the same

industry, then we are exposing ourselves to risk

that we could diversify away

39

40

25/02/2021

21

41

Total Risk

• Total risk = systematic risk + unsystematic risk

• The standard deviation of returns is a measure of total

risk

• For well diversified portfolios, unsystematic risk is very

small

• Consequently, the total risk for a diversified portfolio is

essentially equivalent to the systematic risk

Measuring Systematic Risk

• How do we measure systematic risk?

• We use the beta coefficient to measure systematic risk

• What does beta tell us?

– A beta of 1 implies the asset has the same systematic risk as the overall market

– A beta < 1 implies the asset has less systematic risk than the overall market

– A beta > 1 implies the asset has more systematic risk than the overall market

41

42

25/02/2021

22

Security Market Line-SML

• The security market line is commonly used by investors

in evaluating a security for inclusion in an

investment portfolio in terms of whether the security

offers a favorable expected return against its level of risk

• SML line drawn on a chart that serves as a graphical

representation of the capital asset pricing model

(CAPM), which shows different levels of systematic, or

market, risk of various marketable securities plotted

against the expected return of the entire market at a

given point in time

43

44