Embed Size (px)

Citation preview

Maximising the Benefits and Minimising the Risk of Drawdown

Sustainable Income Needs:

Personal MIR

Retirement income planning in 2015 A NEW ERA

Accelerated Income needs?

Tax Free Cash

Additional cash needs?

Retirees

3 Key Choices

Learning Outcomes

Describe the purpose of Drawdown reviews, HMRC and FCA requirements

Calculate relevant and personalised critical yields

Evaluate when conversion to an annuity might be considered

Understand what an appropriate process for Drawdown reviews might look like

Handset Question 1

What does your Drawdown Review process currently look like for clients under 75?

1.Annual review by post, email or telephone.

2.Three yearly review by post, email or telephone.

3.Annual review face to face.

4.Three yearly review face to face.

The purpose of Drawdown Reviews

AdviserRetirees

• HMRC Requirement• GAD Review to ensure fund

doesn’t deplete too quickly• Ongoing review post 2015?

FCA Rules for Drawdown Reviews

COBS 9.3.3

Outcomes =

personal

recommendations

Regulatory updates 55 and 67

Best Practice for Drawdown Reviews – COBS 9.3.3

“When a firm is making a personal recommendation to a retail client about income withdrawals or purchase of short-term annuities, it should consider all the relevant circumstances including:

(1)the client's investment objectives, need for tax-free cash and state of health;

(2) current and future income requirements, existing pension assets and the relative importance of the plan, given the client's financial circumstances;

(3) the client's attitude to risk, ensuring that any discrepancy is clearly explained between his attitude to an income withdrawal or purchase of a short-term annuity and other investments.

COBS 9.3.3

An appropriate process – meeting the needs of COBS 9.3.3

Frequent reviewsCharge an

explicit facilitated fee

Conduct full fact find

Check Drawdown ATR

Capacity for lossState of health –

self and dependants

Change in circumstances

Relevant Critical Yields

Issue relevant annuity quotes

Discuss options with client

Make recommendation

Is anything missing from your Drawdown Review Process?

“A process which doesn’t include both health questions and the practical use of the answers to those questions is likely to result in more clients remaining in drawdown, possibly to their detriment”

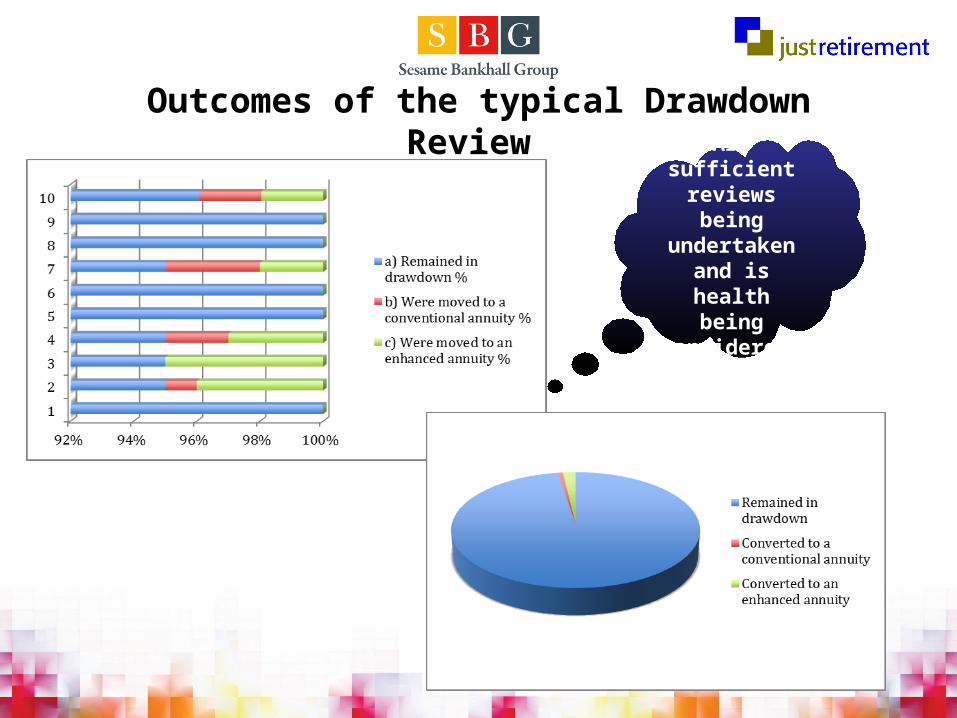

Outcomes of the typical Drawdown Review

Are sufficient reviews being

undertaken and is health

being considered?

Two key questions

What are the outcomes of the typical Drawdown

review?

Based on the requirements of COBS 9.3.3. is anything missing

from your Drawdown review process?

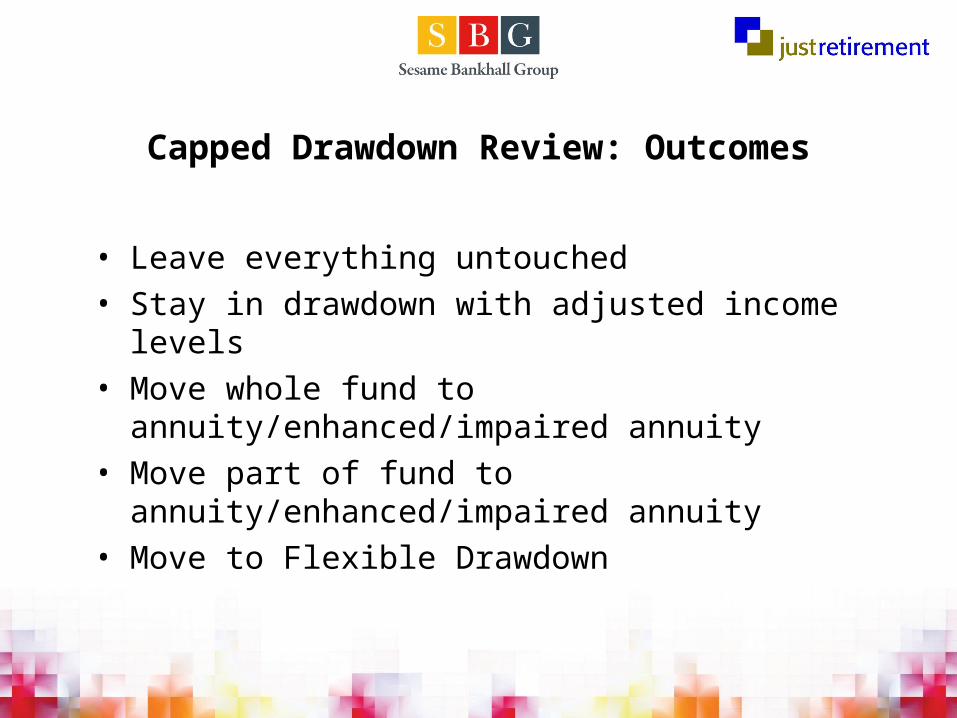

Capped Drawdown Review: Outcomes

• Leave everything untouched• Stay in drawdown with adjusted income levels• Move whole fund to annuity/enhanced/impaired annuity• Move part of fund to annuity/enhanced/impaired annuity• Move to Flexible Drawdown

Outcomes of the typical Drawdown Review

Income requirements

Construct investment

portfolio

Assess risk profile

Critical Yield

Enhanced annuity rate?

Underwrite

Income Shape

Personal Critical Yield

Three Steps to a Personalised Critical Yield

Impact on Critical Yield calculation

Quoted CY from Capped DD quotation

6.51%

Step 3Income 12.67%

Step 2Shape 6.45%

Step 1Underwrite 7.14%

0.00% 5.00% 10.00%

Source: Avelo Exchange & Just Retirement Limited 16.04.14. Based on an individual aged 65, with a £100k fund, monthly in arrears, no escalation, no value protection, 50% spouses pension, 5 year guarantee period, based on RH2 7RT postcode. An annual management charge of 2% has been assumed when calculating critical yields.

15.00%

Personalised Critical Yield

Handset Question 2

Would you like a copy of the Critical Yield Calculator?

1.Yes

2.No

When might a conversion to annuity be considered?

Health

LTC

Death of spouse

Assets depleted

Mortality drag

Now fully retired

Concerns re performance

required

ATR changed

Gtd income now

important

Legislation, GAD, etc

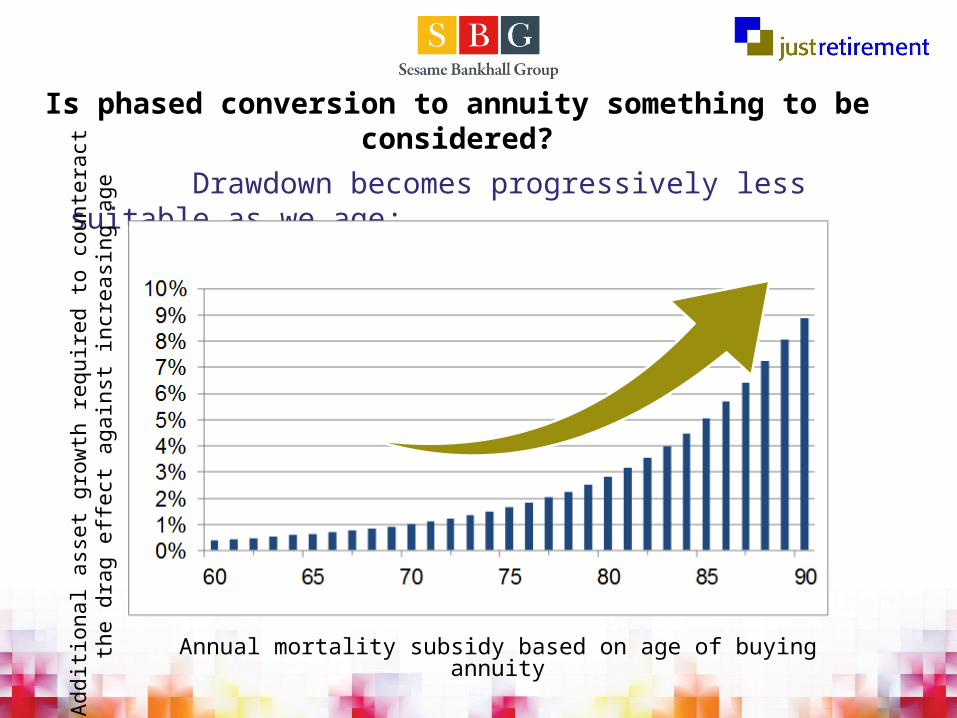

Is phased conversion to annuity something to be considered?

Drawdown becomes progressively less suitable as we age;

Annual mortality subsidy based on age of buying annuity

Add

ition

al a

sset

gro

wth

req

uire

d to

cou

nter

act

the

drag

effe

ct a

gain

st in

crea

sing

age

Exit strategies are important because of mortality drag

When should annuitisation start?

Annual mortality subsidy based on age of buying annuity

0%1%2%3%4%5%6%7%8%9%

10%

60 65 70 75 80 85 90

Financial sense of annuitising

increases

Add

ition

al a

sset

gro

wth

req

uire

d to

cou

nter

act

the

drag

effe

ct a

gain

st in

crea

sing

age

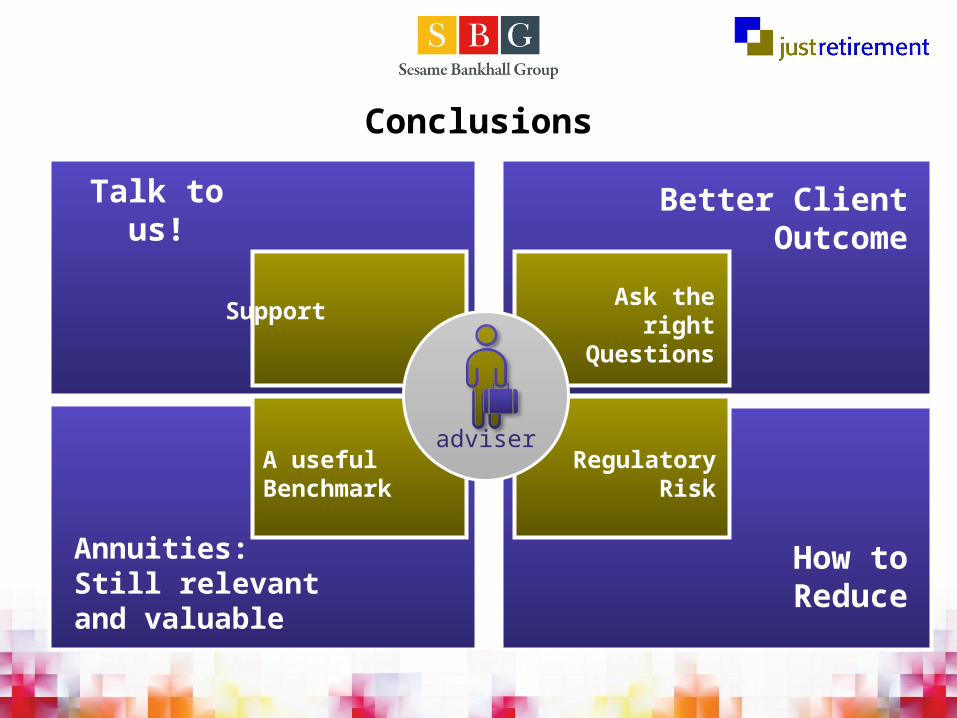

Talk to us!

Annuities: Still relevant and valuable

Better Client Outcome

How to Reduce

Ask the right Questions

A useful Benchmark

Regulatory Risk

Support

adviser

Conclusions

Handset Question 3

Following this presentation, to what extent will you now consider changes to your review process?

1.May consider making significant changes.

2.May consider a few changes.

3.Am unlikely to make any changes.

Thank You

Learning Outcomes

Describe the purpose of Drawdown reviews, HMRC and FCA requirements

Calculate relevant and personalised critical yields

Evaluate when conversion to an annuity might be considered

Understand what an appropriate process for Drawdown reviews might look like

Important Information

It is our intention that the information contained within this presentation is accurate. We have taken all reasonable steps to ensure that it is up-to-date and where relevant, reflects the current views of our experts. However, we do not accept any liability for errors or omissions in the information supplied and if you require clarification on anything, our recommendation is that you contact us at the address below for verification, or call 0845 302 2287.Our registered address:Just Retirement LimitedVale House, Roebuck Close, Bancroft Road, Reigate, Surrey RH2 7RU.

Regulatory information: Just Retirement Limited (Registered in England Number 05017193). Registered Office: Vale House, Roebuck Close, Bancroft Road, Reigate Surrey, RH2 7RU. Just Retirement Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.