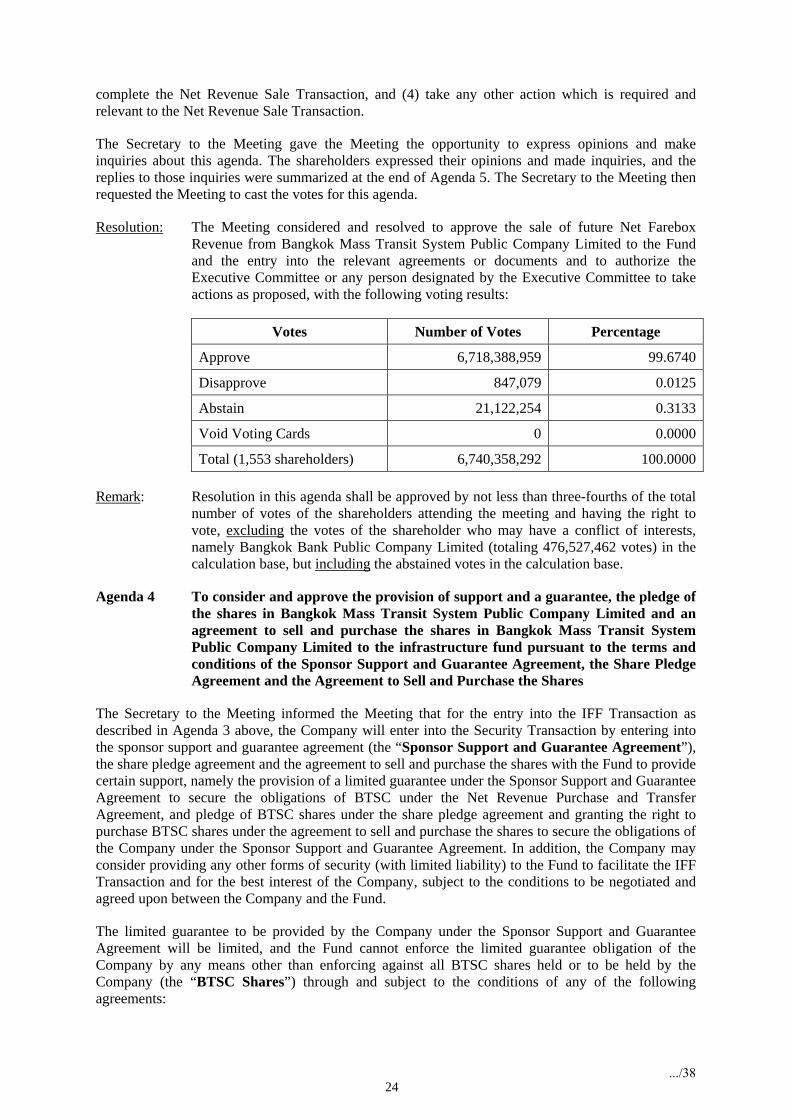

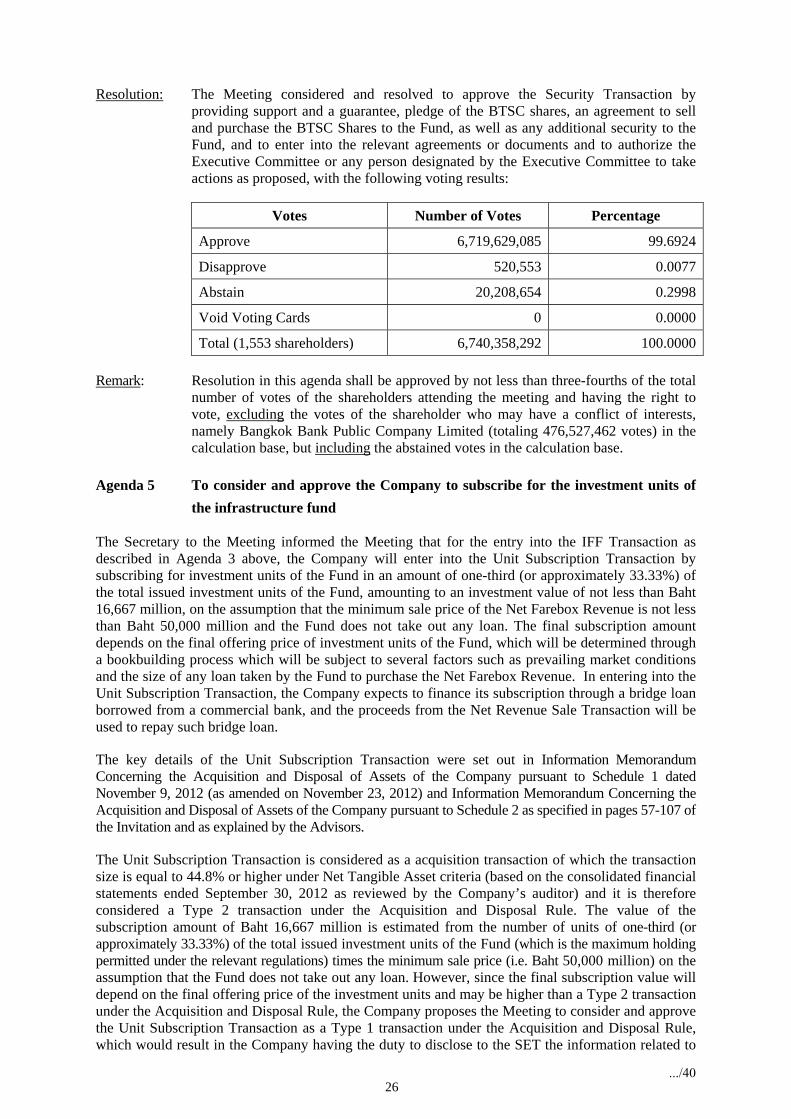

Embed Size (px)

Citation preview

Invitation to the 2013 Annual

General Meeting of Shareholders

BTS GroupHoldings Public Company Limited

The 2013 Annual General Meeting of Shareholders

To be held on Friday July 26, 2013, at 13.30 hrs.

Rama Gardens Hotel Bangkok, Convention Center,

9/9 Vibhavadi Rangsit Road, Laksi, Bangkok

BTS Group Holdings Public Company Limited14 -15 Floor, TST Tower, 21 Soi Choei Phuang, Viphavadi-Rangsit Road, Chomphon, Chatuchak, Bangkok 10900

Tel: +66 2273 8511-5, +66 2273 8611-5 Fax: +66 2273 8610, +66 2273 8616 www.btsgroup.co.th

th th

Table of Contents

Page

Invitation to the 2013 Annual General Meeting of Shareholders 1

Registration Form (Please bring this document to the meeting)

(Enclosure 1) Please see the separate document

Annual Report 2012/13 and Sustainability Report in CD-ROM

(Enclosure 2) As enclosed

Copy of the Minutes of the Extraordinary General Meeting of Shareholders No. 1/2012

dated December 18, 2012

(Enclosure 3) 15

Profiles of the persons nominated as Directors of the Company and Definition of Independent

Director of the Company

(Enclosure 4) 45

Profiles and working experience of auditors

(Enclosure 5) 52

Guideline for the appointment of proxy, the registration, documents to be presented on the

meeting date, the voting procedures and votes counting and the meeting procedures

(Enclosure 6) 55

Proxy Form B.

(Enclosure 7) Please see the separate document

Profiles of Independent Directors for appointment of proxy by the shareholders

(Enclosure 8) 61

The Company’s Articles of Association

(Enclosure 9) 62

Location Map

(Enclosure 10) Inside back cover

…/2

Agenda 2 To consider and adopt the Minutes of the Extraordinary General Meeting of

Shareholders No. 1/2012

The Company had prepared the Minutes of the Extraordinary General Meeting of Shareholders No.

1/2012 dated December 18, 2012 and submitted the copy as appeared in Enclosure 3, to the Stock

Exchange of Thailand within 14 days from the meeting date. The said minutes are also available on

the Company’s website. The shareholders’ meeting is proposed to adopt the Minutes of the

Extraordinary General Meeting of Shareholders No. 1/2012 dated December 18, 2012.

Opinion of the

Board of Directors:

The Board of Directors considers that the Minutes of the Extraordinary General

Meeting of Shareholders No. 1/2012 dated December 18, 2012 were correctly

and completely recorded and deems appropriate to propose to the shareholders’

meeting to adopt the said minutes.

Remark: Resolution in this agenda shall be adopted by the majority votes of the

shareholders attending the meeting and casting their votes, excluding the

abstained votes from the calculation base.

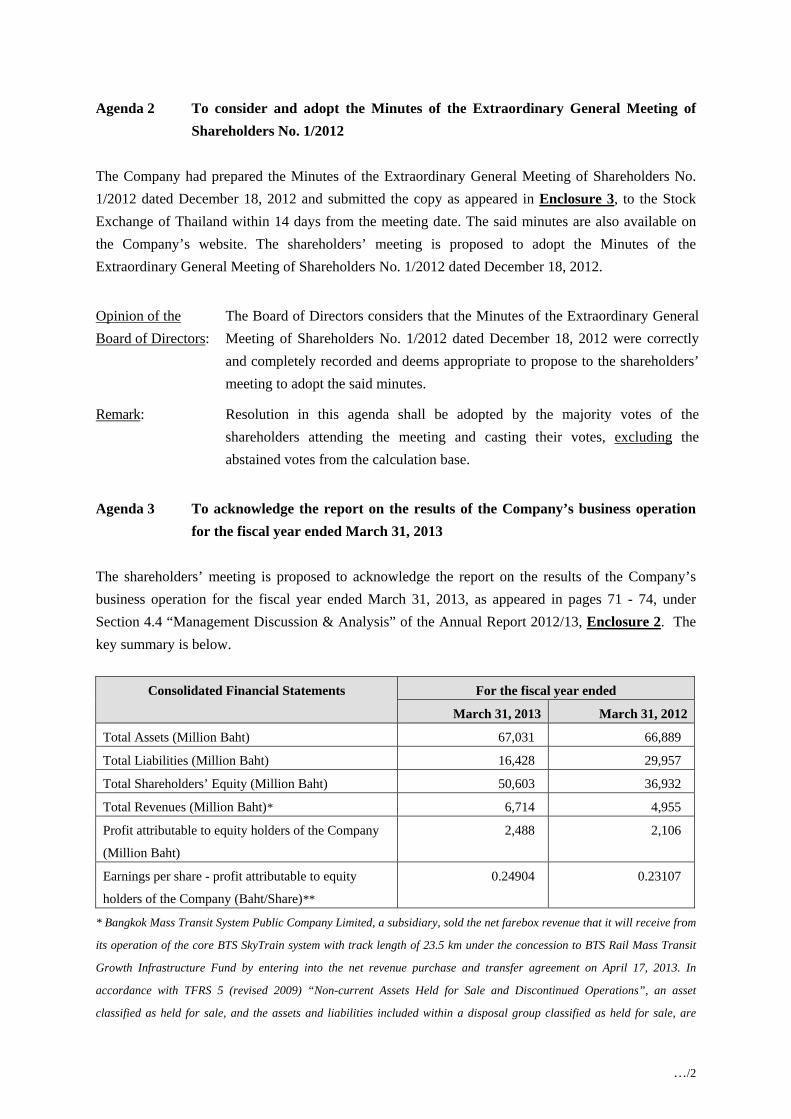

Agenda 3 To acknowledge the report on the results of the Company’s business operation

for the fiscal year ended March 31, 2013

The shareholders’ meeting is proposed to acknowledge the report on the results of the Company’s

business operation for the fiscal year ended March 31, 2013, as appeared in pages 71 - 74, under

Section 4.4 “Management Discussion & Analysis” of the Annual Report 2012/13, Enclosure 2. The

key summary is below.

Consolidated Financial Statements For the fiscal year ended

March 31, 2013 March 31, 2012

Total Assets (Million Baht) 67,031 66,889

Total Liabilities (Million Baht) 16,428 29,957

Total Shareholders’ Equity (Million Baht) 50,603 36,932

Total Revenues (Million Baht)* 6,714 4,955

Profit attributable to equity holders of the Company

(Million Baht)

2,488 2,106

Earnings per share - profit attributable to equity

holders of the Company (Baht/Share)**

0.24904 0.23107

* Bangkok Mass Transit System Public Company Limited, a subsidiary, sold the net farebox revenue that it will receive from

its operation of the core BTS SkyTrain system with track length of 23.5 km under the concession to BTS Rail Mass Transit

Growth Infrastructure Fund by entering into the net revenue purchase and transfer agreement on April 17, 2013. In

accordance with TFRS 5 (revised 2009) “Non-current Assets Held for Sale and Discontinued Operations”, an asset

classified as held for sale, and the assets and liabilities included within a disposal group classified as held for sale, are

…/3

presented separately in the statement of financial position. As a result, as at March 31, 2013, the Company classified the

assets derecognized from its accounts on April 17, 2013 as non-current assets classified as held for sale, and presented them

as a separate item in the statement of financial position. Thus, in the statement of financial position as at March 31, 2013,

the Company presented the information on the total revenues after removing the revenues relating to such non-current assets

classified as held for sale (the farebox revenues – net at Baht 4,896 million). For two fiscal-year comparative purposes, the

total revenues for the fiscal year ended March 31, 2012 was restated by removing the farebox revenues – net at Baht 4,297

million from the total revenues of Baht 9,252 million and, therefore, the information of the total revenues for the fiscal year

ended March 31, 2012 was presented as Baht 4,955 million.

** The Company completed the share consolidation and the change in par value of shares from Baht 0.64 per share to Baht

4 per share on August 7, 2012 resulting in the change in the number of ordinary shares during the year. For comparative

purposes, the Company adjusted the number of ordinary shares as if the share consolidation and change in par value of

shares had occurred at the beginning of the earliest period reported. In addition, for two fiscal-year comparative purposes,

the earnings per share for the fiscal year ended March 31, 2012 was restated as if the share consolidation and change in par

value of shares had occurred since the fiscal year ended March 31, 2012.

Opinion of the

Board of Directors:

The Board of Directors deems appropriate to report the results of the Company’s

business operation for the fiscal year ended March 31, 2013 to the shareholders’

meeting for acknowledgement.

Remark: This agenda is for acknowledgement and no casting of vote.

Agenda 4 To consider and approve the Company and its subsidiaries report and

consolidated financial statements for the fiscal year ended March 31, 2013

The shareholders’ meeting is proposed to consider and approve the Company and its subsidiaries

report and consolidated financial statements for the fiscal year ended March 31, 2013, as appeared in

pages 113 - 204, under Section 6.3 “Independent Auditor’s Report”, Section 6.4 “Audited Financial

Statements” and Section 6.5 “Notes to Consolidated Financial Statements” of the Annual Report

2012/13, Enclosure 2.

Opinion of the

Board of Directors:

The Board of Directors deems appropriate to propose to the shareholders’ meeting

to consider and approve the Company and its subsidiaries report and

consolidated financial statements for the fiscal year ended March 31, 2013,

which have been audited by the Company’s Certified Public Accountant,

reviewed by the Audit Committee and approved by the Board of Directors.

Remark: Resolution in this agenda shall be approved by the majority votes of the

shareholders attending the meeting and casting their votes, excluding the abstained

votes from the calculation base.

…/4

Agenda 5 To consider and approve the allocation of profit for the results of the operation

in the fiscal year ended March 31, 2013 and dividend distribution

Dividend Payment Policy

The Company has a policy of paying dividend at the rate of no less than 50% of the net income after

tax in accordance with the Company’s financial statements (on a standalone basis). The Company

shall pay dividend in the following fiscal year taking into consideration the cashflow from the

operation of the business. The annual dividend payment announcement must be approved at the

Annual General Meeting of Shareholders. As for the interim dividend payment, the Company’s Board

of Directors may deem it appropriate to pay interim dividend if the Company has sufficient profits

and working capital for business operation after the interim dividend payment. The Board of Directors

has the responsibility to inform the shareholders of such payment in the subsequent shareholders’

meeting.

The Board of Directors shall take the following factors into account when considering dividend

payment to the shareholders, namely, the Company’s performance, liquidity, current cashflow and

financial status, regulations and conditions regarding dividend payment as set forth in the loan

agreements, bonds, any contracts imposing the Company’s liabilities, including agreements or

contracts that the Company is obliged to comply with; future business plan and capital investment

requirement; and other factors as the Board of Directors deems appropriate.

Moreover, the Company must comply with the Public Company Limited Act B.E. 2535 (1992)

(as amended), which states that the Company cannot pay dividend if the Company still has retained

loss though the Company has net income in that particular year. Additionally, the Public Company

Limited Act B.E. 2535 (1992) (as amended) states that the Company is required to reserve an amount

equal to 5% of the annual net income after deduction of the retained loss (if any) as legal reserve fund

until such legal reserve fund is equal to not less than 10% of the registered capital. In addition to the

legal reserve fund, the Board of Directors may consider making other types of reserve fund as it

deems appropriate.

Subject to the compliance with the Public Company Limited Act B.E. 2535 (1992) (as amended) and

provided that there is no material adverse change to the business operation or financial conditions of

the Company, in the next 3 fiscal years, namely the fiscal year ended March 31, 2014 - March 31,

2016, the Company has a policy to pay out the dividend to the shareholders from its net income and/or

retained earnings at the amount of:

1. No less than Baht 6,000 million for the fiscal year ended March 31, 2014;

2. No less than Baht 7,000 million for the fiscal year ended March 31, 2015; and

3. No less than Baht 8,000 million for the fiscal year ended March 31, 2016.

…/5

The Company’s ability to pay the dividend in the aggregate amount of no less than Baht 21,000

million in the next 3 fiscal years will be supported by the profits from operation as well as the

extraordinary profits from the infrastructure fund transaction.

Allocation of Profit for Dividend Payment

The operating results for the fiscal year ended March 31, 2013 show that the Company has net income

after corporate income tax (financial statements on a standalone basis) in the amount of Baht 5,469.8

million. The Company already allocated the fund as legal reserve in the amount of Baht 273.5 million

(equivalent to 5% of the annual net income as required by laws). Thus, the Company proposed to pay

dividend for the fiscal year ended March 31, 2013 to the shareholders in the total amount of not

exceeding Baht 4,359.1 million (equivalent to 79.7% of the net income after corporate income tax -

financial statements on a standalone basis), which is in line with the dividend payment policy of the

Company. The Company made the interim dividend payment No. 1 on February 8, 2013 in the

amount of Baht 1,793.8 million and the interim dividend payment No. 2 on May 17, 2013 in the

amount of Baht 2,052.2 million. Therefore, the aggregate interim dividend already paid to the

shareholders is Baht 3,845.9 million.

After the payment of interim dividend to the shareholders, the Company can pay the rest of dividend

for the fiscal year ended March 31, 2013 in the amount not exceeding Baht 513.1 million or

equivalent to the dividend payment at the rate of Baht 0.045 per share (4.5 Satang per share) to the

shareholders whose names appear on the date for determining the names of shareholders who shall be

entitled to receive dividend (Record Date) on June 18, 2013 and the date to gather the names of

shareholders under Section 225 of the Securities and Exchange Act B.E. 2535 (as amended) by

closure of the share register book and suspension of share transfer on June 19, 2013 and set the

payment date of the dividend on August 9, 2013, after having the approval from the shareholders’

meeting. In this regard, the shareholders who are disqualified to receive the dividend under the law

will not be entitled to this dividend payment. In addition, as this dividend is exempted from the

corporate income tax and, therefore, the individual shareholders are not entitled to any dividend tax

credits under Section 47 bis of the Revenue Code.

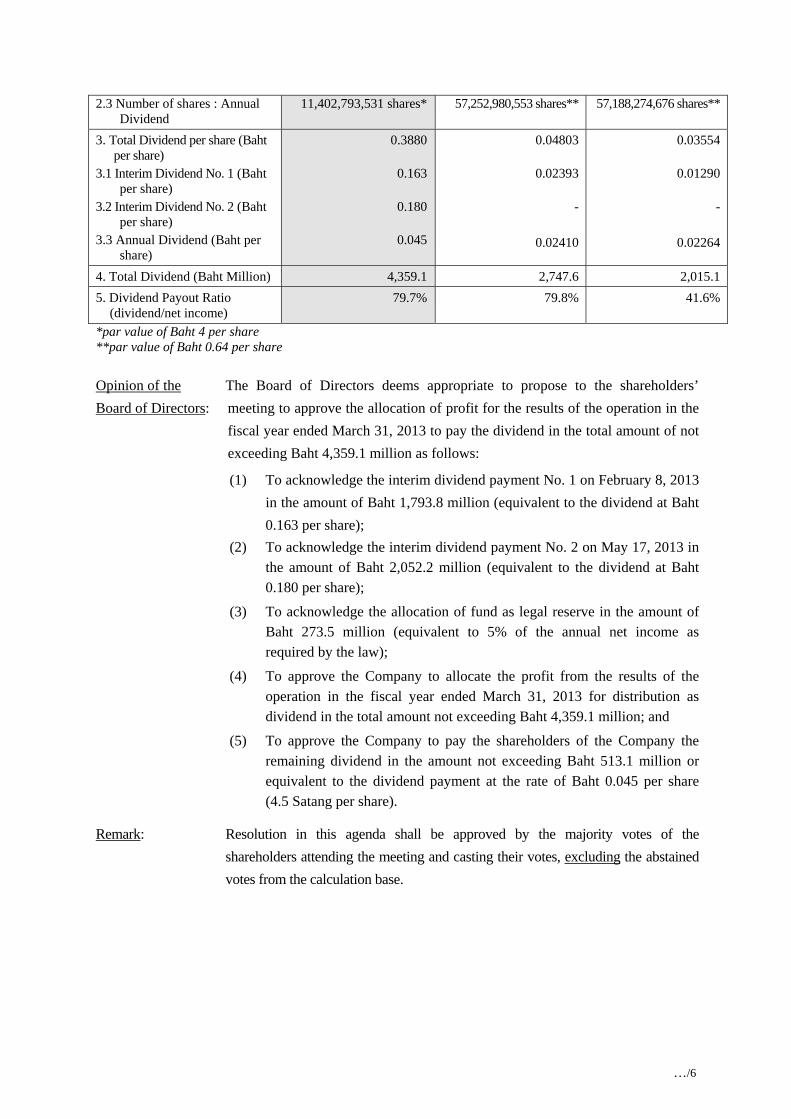

Details of the dividend payment for the fiscal year ended March 31, 2013, 2012 and 2011 in comparison are as follows:

Details For the fiscal year ended

March 31, 2013 March 31, 2012 March 31, 2011

1. Net Income (Baht Million) (financial statements on a standalone basis)

5,469.8 3,443.2 4,840

2. Number of Shares 2.1 Number of shares : Interim

Dividend No.1 2.2 Number of shares : Interim

Dividend No. 2

11,006,834,594 shares*

11,402,793,531 shares*

57,188,274,676 shares**

-

55,889,275,885 shares**

-

…/6

2.3 Number of shares : Annual Dividend

11,402,793,531 shares* 57,252,980,553 shares** 57,188,274,676 shares**

3. Total Dividend per share (Baht per share)

3.1 Interim Dividend No. 1 (Baht per share)

3.2 Interim Dividend No. 2 (Baht per share)

3.3 Annual Dividend (Baht per share)

0.3880

0.163

0.180

0.045

0.04803

0.02393

-

0.02410

0.03554

0.01290

-

0.02264

4. Total Dividend (Baht Million) 4,359.1 2,747.6 2,015.1

5. Dividend Payout Ratio (dividend/net income)

79.7% 79.8% 41.6%

*par value of Baht 4 per share **par value of Baht 0.64 per share

Opinion of the

Board of Directors:

The Board of Directors deems appropriate to propose to the shareholders’

meeting to approve the allocation of profit for the results of the operation in the

fiscal year ended March 31, 2013 to pay the dividend in the total amount of not

exceeding Baht 4,359.1 million as follows:

(1) To acknowledge the interim dividend payment No. 1 on February 8, 2013

in the amount of Baht 1,793.8 million (equivalent to the dividend at Baht

0.163 per share);

(2) To acknowledge the interim dividend payment No. 2 on May 17, 2013 in the amount of Baht 2,052.2 million (equivalent to the dividend at Baht 0.180 per share);

(3) To acknowledge the allocation of fund as legal reserve in the amount of Baht 273.5 million (equivalent to 5% of the annual net income as required by the law);

(4) To approve the Company to allocate the profit from the results of the operation in the fiscal year ended March 31, 2013 for distribution as dividend in the total amount not exceeding Baht 4,359.1 million; and

(5) To approve the Company to pay the shareholders of the Company the remaining dividend in the amount not exceeding Baht 513.1 million or equivalent to the dividend payment at the rate of Baht 0.045 per share (4.5 Satang per share).

Remark: Resolution in this agenda shall be approved by the majority votes of the

shareholders attending the meeting and casting their votes, excluding the abstained

votes from the calculation base.

…/7

Agenda 6 To determine the directors’ remuneration

The shareholders’ meeting is proposed to determine the directors’ remuneration for year 2013 and the

directors’ bonus for the fiscal year ended March 31, 2013. The Board of Directors, in concurrence

with the Nomination and Remuneration Committee, considered and determined the directors’

remuneration by using the same criteria as previous years, namely to consider the remuneration from

the size of business and the responsibilities of the Board of Directors in comparison with other

companies with the same range of market capitalization and listed in the Stock Exchange of Thailand.

The details are as follows:

1. Fixed Remuneration To keep the fix remuneration the same as the previous year (as

approved by the 2012 Annual General Meeting of Shareholders), namely

Monthly Directors’ Remuneration

Chairman of the Board of Directors Baht 60,000 / month

Chairman of the Audit Committee Baht 50,000 / month

Directors Baht 30,000/ person / month

Meeting Allowance for the Members of the Audit Committee

Chairman of the Audit Committee Baht 20,000 / attendance

Members of the Audit Committee Baht 20,000 / person / attendance

2. Directors’ Bonus In order to reflect and to be consistent with the Company’s

operating results for the fiscal year ended March 31, 2013, to determine the directors’

bonus for year 2013 at the rate of 0.5% of the total dividend of the Company payable

to the shareholders for the fiscal year ended March 31, 2013 which is equivalent to

the directors’ bonus of not exceeding Baht 21.8 million. The directors’ bonus shall be

allocated among the Directors at their discretion after the shareholders’ meeting

approves the directors’ bonus. (Remark: In the previous year, the Company paid the

directors’ bonus at the rate of 0.5% of the total dividend payment of the Company payable to

the shareholders for the fiscal year ended March 31, 2012, equivalent to the directors’ bonus

in the amount of Baht 13.7 million.)

Opinion of the

Board of Directors:

The Board of Directors, in concurrence with the thorough consideration of the

Nomination and Remuneration Committee, deems appropriate to propose to the

shareholders’ meeting to determine the directors’ remuneration as per the details

above.

Remark: Resolution in this agenda shall be approved by not less than two-thirds of the total

numbers of votes of the shareholders attending the meeting, including the abstained

votes in the calculation base.

…/8

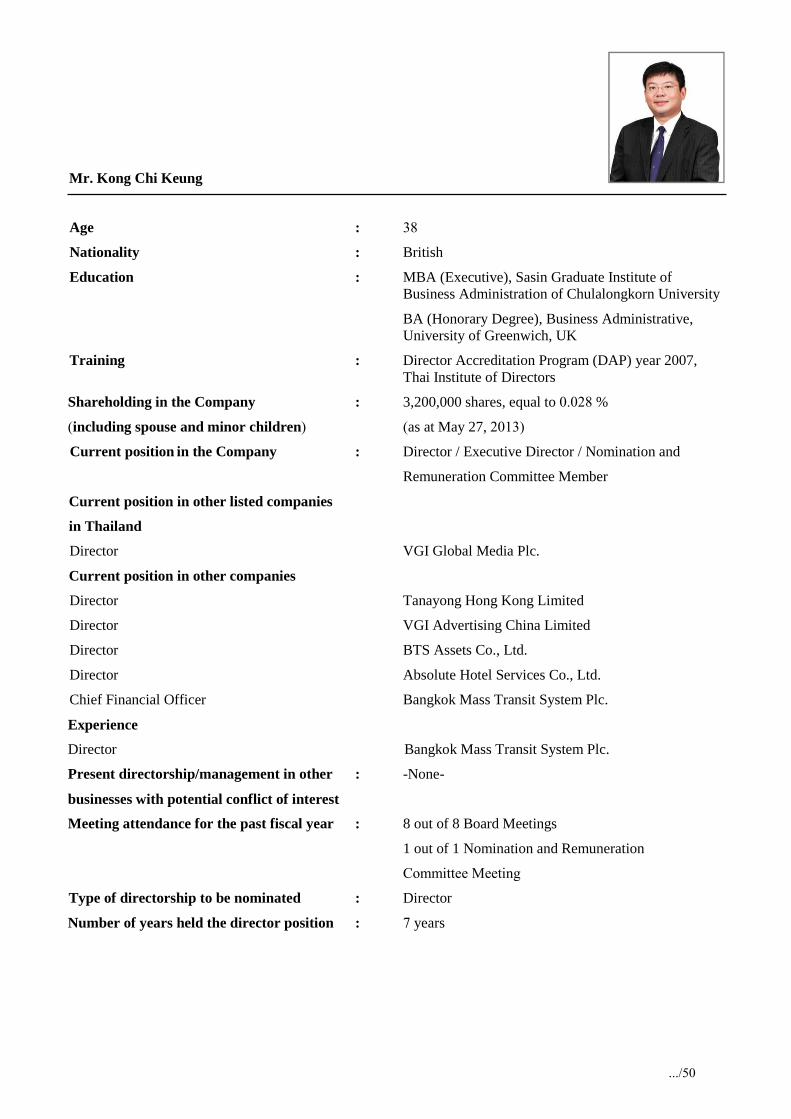

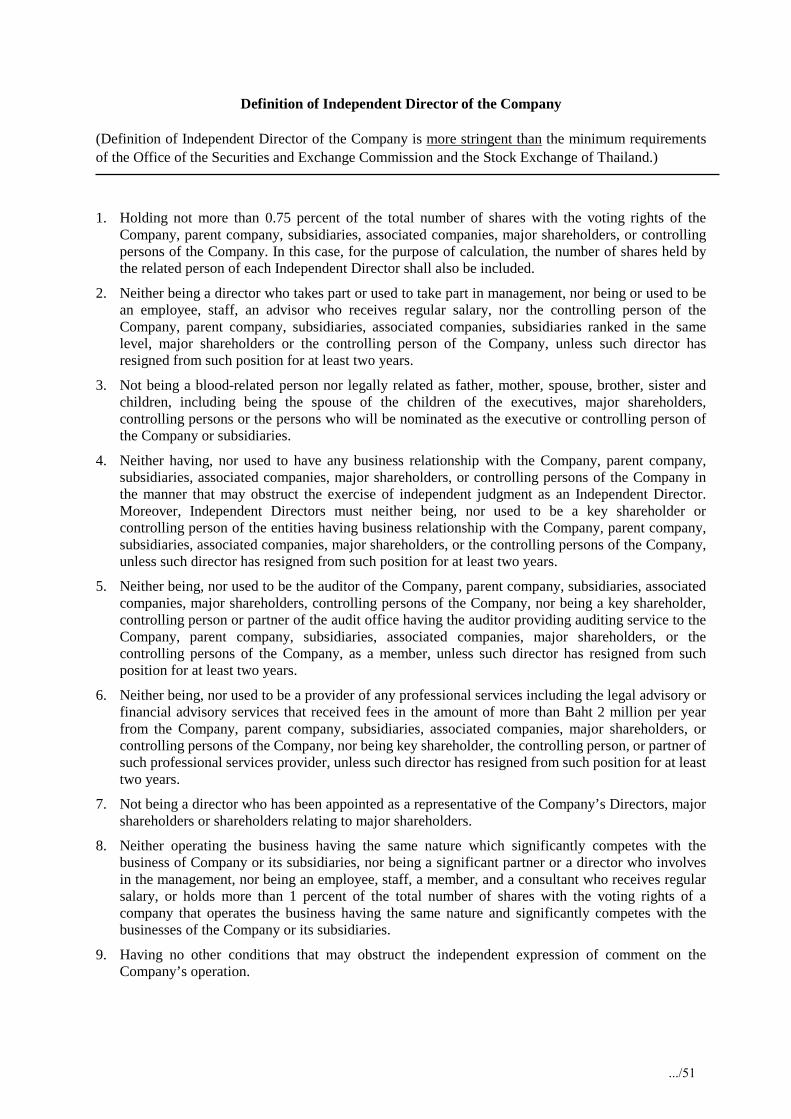

Agenda 7 To consider the election of Directors to replace those who must retire by rotation

According to the Public Company Limited Act B.E. 2535 (1992) (as amended) and Article 14. of the

Company’s Articles of Association, at least one-third of the total number of directors must retire by

rotation at the Annual General Meeting of Shareholders in each year and if the number of directors

cannot be divided into three, the closest number to one-third shall retire and the retired directors are

eligible for re-election. There are 4 directors who will retire by rotation at the 2013 Annual General

Meeting of Shareholders, namely

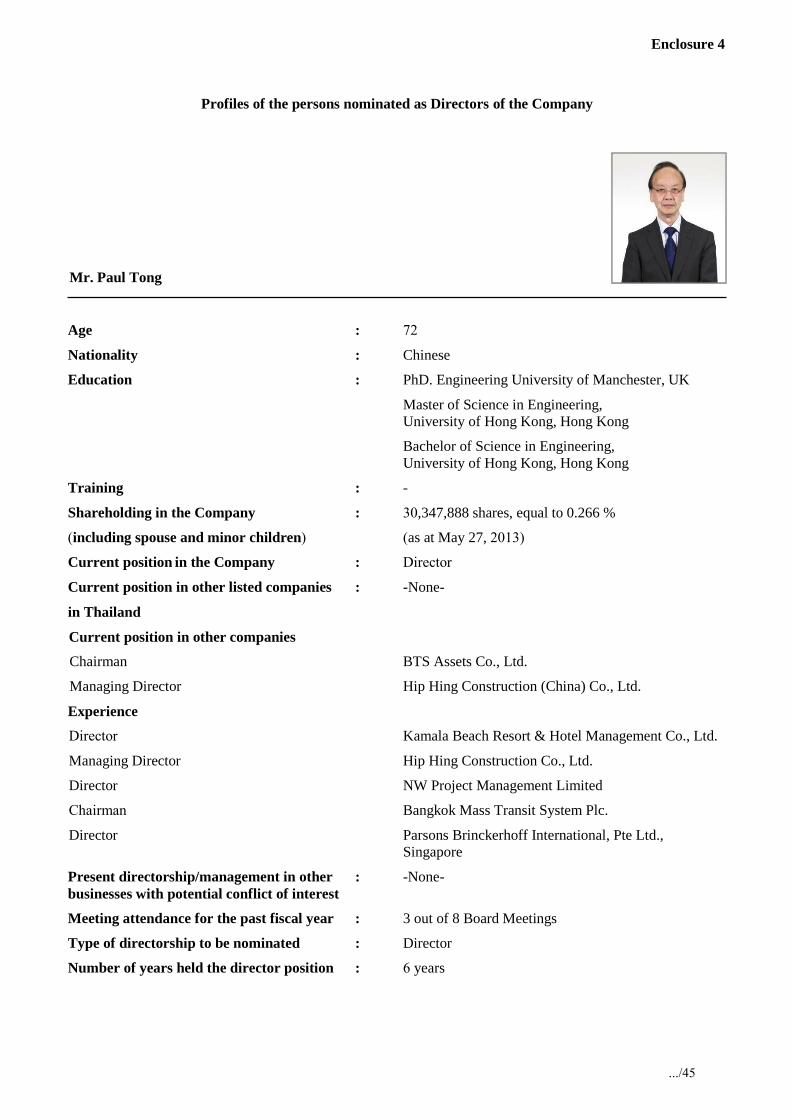

(1) Mr. Paul Tong – Director

(2) Mr. Amorn Chandara-Somboon – Independent Director

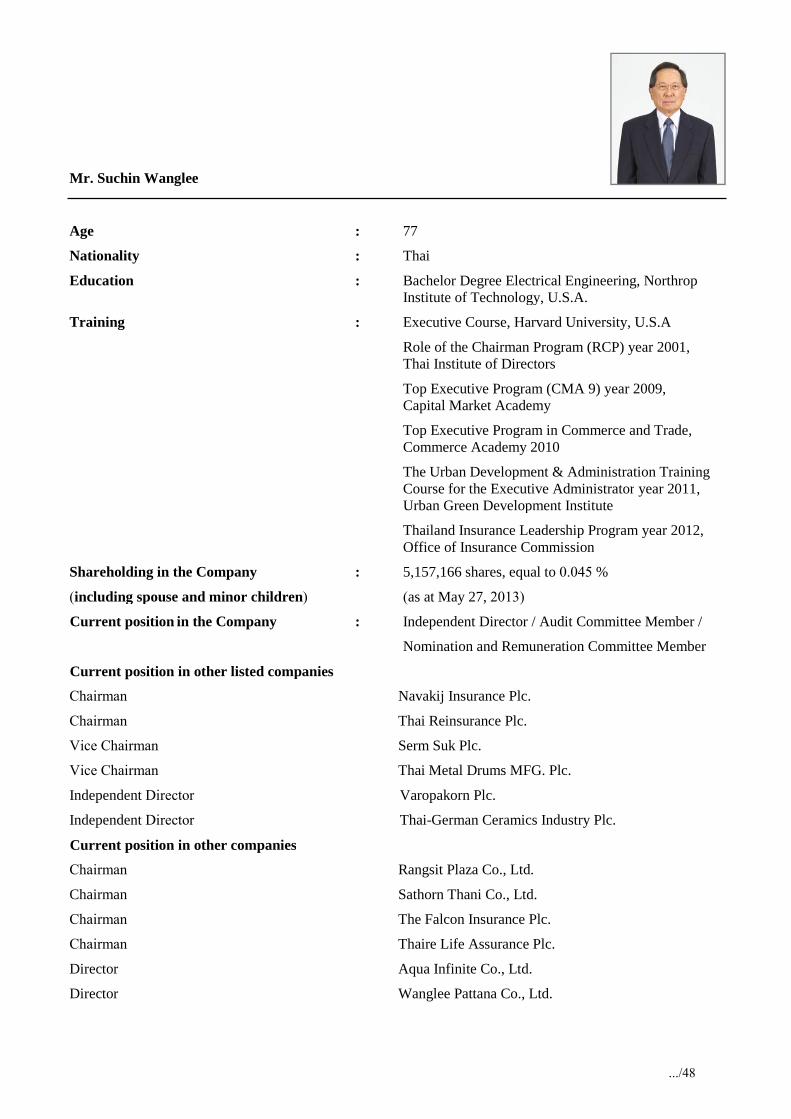

(3) Mr. Suchin Wanglee – Independent Director

(4) Mr. Kong Chi Keung – Director

To promote the good corporate governance practice, the Company invited the minority shareholders

who are collectively holding at least 3% of the Company’s total issued shares and continually holding

those shares for at least 6 months, to nominate candidate(s) to be elected as Director for the 2013

Annual General Meeting of Shareholders during the period from December 28, 2012 to March 31,

2013. Nonetheless, there was no shareholder nominating any candidate to be elected as the Director of

the Company.

The Nomination and Remuneration Committee (by the members of the Nomination and

Remuneration Committee having no conflict of interest) had reviewed the qualifications of these 4

Directors who would retire by rotation at the 2013 Annual General Meeting of Shareholders and of

the opinion that these 4 Directors are knowledgeable, experienced and skillful in benefit to the

Company’s operations and have full qualification and do not have any prohibited characteristics under

the Public Limited Company Act B.E. 2535 (1992) (as amended), the Securities and Exchange Act

B.E. 2535 (1992) (as amended), and other relevant regulations. In addition, the Independent Directors

also possess the qualification in accordance with the Definition of Independent Director of the

Company which is more stringent than the minimum requirement of the Office of the Securities and

Exchange Commission and the Stock Exchange of Thailand. The profiles of these 4 persons and the

Definition of the Independent Director of the Company are as appeared in Enclosure 4. Therefore, it

is proposed that the shareholders’ meeting consider the election of these 4 persons to be the Directors

of the Company for another term.

Opinion of the

Board of Directors:

The Board of Directors (by the Directors having no conflict of interest) deems

appropriate to propose to the shareholders’ meeting to consider and approve the

election of these 4 persons, namely Mr. Paul Tong, Mr. Amorn Chandara-

Somboon, Mr. Suchin Wanglee and Mr. Kong Chi Keung, who will retire by

rotation to be the Directors of the Company for another term.

…/9

Remark: Resolution in this agenda shall be approved by the majority votes of the

shareholders attending the meeting and casting their votes, excluding the abstained

votes from the calculation base.

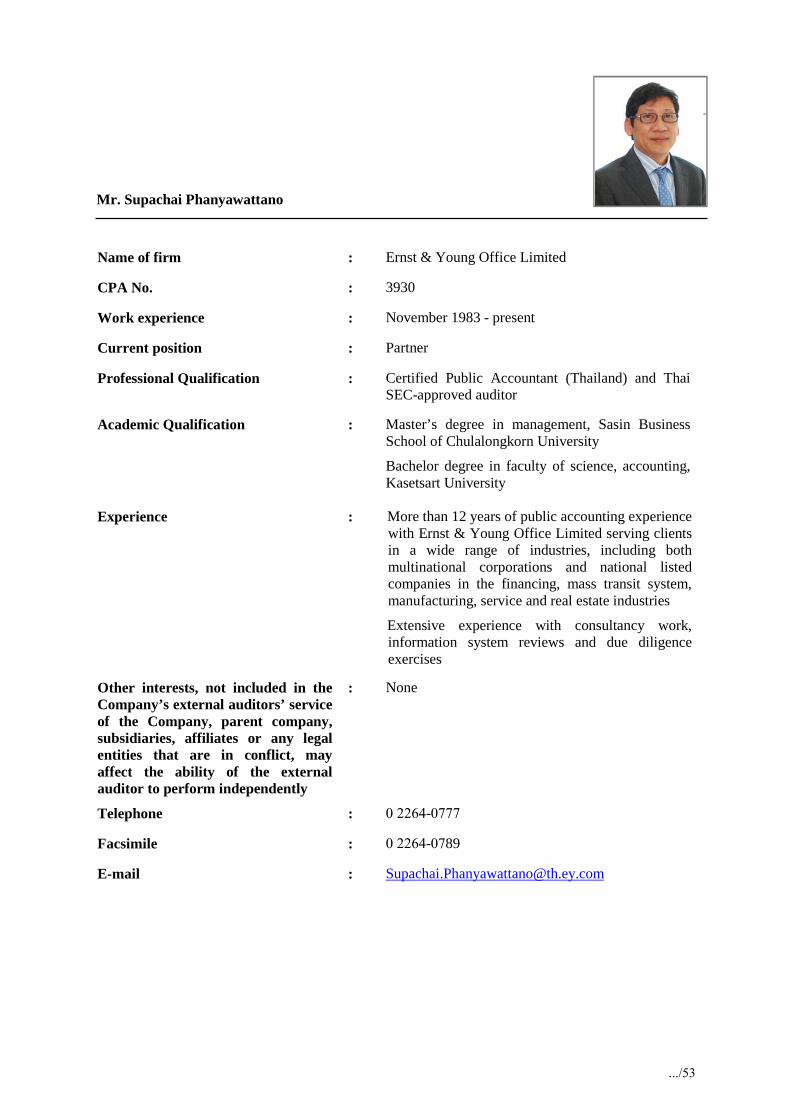

Agenda 8 To consider and approve the appointment of auditors and determination of the

audit fee for the fiscal year ended March 31, 2014

To comply with Section 120 of the Public Company Limited Act B.E. 2535 (1992) (as amended)

which requires the Annual General Meeting of Shareholders to appoint the auditors and determine the

audit fee of the Company every year, the Audit Committee has selected the auditors in accordance

with the criteria of the Public Company Limited Act B.E. 2535 (1992) (as amended) and the relevant

Notification of the Capital Market Supervisory Board. The Audit Committee considered the

performance of the auditors from Ernst & Young Office Limited for the past year and was of the view

that the auditors from Ernst & Young Office Limited were independent, proper and duly performed

duties with their responsibilities. In addition, the proposed audit fee for the fiscal year ended March

31, 2014 is appropriate considering the scope of audit. The Audit Committee therefore proposed to the

Board of Directors to further propose to the shareholders’ meeting for consideration.

The Board of Directors, by the recommendation of the Audit Committee, deems appropriate to

propose to the shareholders’ meeting to consider and approve the appointment of auditors from Ernst

& Young Office Limited as the Company’s auditors for the fiscal year ended March 31, 2014, any of

the following auditors being authorized to review and give opinion on the Company’s financial

statements:

(1) Mr. Narong Puntawong: Certified Public Accountant (Thailand) No. 3315; and/or

(has never signed the Company’s financial statements)

(2) Mr. Supachai Phanyawattano: Certified Public Accountant (Thailand) No. 3930; and/or

(signed the Company’s financial statements during the fiscal year ended March 31, 2004 –

fiscal year ended March 31, 2008)

(3) Miss Siraporn Ouaanunkun: Certified Public Accountant No. 3844

(signed the Company’s financial statements during the fiscal year ended March 31, 2012 –

fiscal year ended March 31, 2013).

None of the auditors whose names are proposed has any relationship with nor interest in the

Company, subsidiaries, management, major shareholders or the related persons of such persons and,

therefore, they are independent to audit and give opinion on the Company’s financial statements. In

addition, neither Mr. Narong Puntawong nor Miss Siraporn Ouaanunkun has audited or reviewed and

gave opinion on the Company’s financial statements for five consecutive fiscal years. For

Mr. Supachai Phanyawattano, though he has audited and reviewed and gave opinion on the

Company’s financial statements for five consecutive fiscal years, he already ceased his role as the

Company’s auditor for more than two fiscal years. Therefore, all of the proposed auditors possess the

…/10

qualification as required by the Notification of Capital Market Supervisory Board No. TorChor

11/2552 re: Rules, Conditions and Procedures for Disclosure of Information Relating to the Financial

Status and Operating Results of the Company issuing the Securities. The profiles and working

experience of these 3 auditors are as appeared in Enclosure 5.

Moreover, the Board of Directors, by the recommendation of the Audit Committee, deems appropriate

to propose to the shareholders’ meeting to consider and approve the audit fee of the Company for the

fiscal year ended March 31, 2014 in the amount of not exceeding Baht 3.3 million, which is Baht 0.3

million or 10% increase from the fee paid in previous fiscal year due to business expansion of the

Company.

The auditors from Ernst & Young Office Limited will be the auditors of 24 subsidiaries for the fiscal

year ended March 31, 2014. However, one subsidiary, VGI Advertising China Co., Ltd., incorporated

in People’s Republic of China, will appoint BDO China Shu Lun Pan CPAs Ltd, the member of BDO

International with worldwide network of public accounting firms, as the auditor of VGI Advertising

China Co., Ltd. by the reason that there are few transactions for VGI Advertising China Co., Ltd. and

BDO China Shu Lun Pan CPAs Ltd offered more favorable audit fee. The preliminary audit fee for 25

subsidiaries for the fiscal year ended March 31, 2014 is in the amount of approximately Baht 9.8

million, which is Baht 0.9 million or 9.6% increase from the fee paid in previous fiscal year. The

increase of the audit fee is mainly resulting from the increase of transaction volumes in certain

subsidiaries.

Opinion of the

Board of Directors:

The Board of Directors, in concurrence with the thorough consideration of the Audit

Committee, deems appropriate to propose to the shareholders’ meeting to consider

and approve the appointment of auditors from Ernst & Young Office Limited,

namely Mr. Narong Puntawong and/or Mr. Supachai Phanyawattano and/or Miss

Siraporn Ouaanunkun as the Company’s auditors for the fiscal year ended March

31, 2014 and determine the audit fee of the Company in the amount of not

exceeding Baht 3.3 million and to acknowledge the auditors and preliminary audit

fee of 25 subsidiaries, as per details above.

Remark: Resolution in this agenda shall be approved by the majority votes of the

shareholders attending the meeting and casting their votes, excluding the abstained

votes from the calculation base.

Agenda 9 To consider and approve the amendment of Article 3. of the Company’s Articles

of Association

In year 2010, the Company had amended Article 3. of the Company’s Articles of Association to

accommodate the exercise of the conversion right of the convertible bonds issued and offered to the

foreign investors in January 2011 in order to allow the foreign investors to be able to exercise their

conversion right of the convertible bonds without being obstructed by the restriction on the ratio of

…/11

the shareholding by the non-Thai persons. However, at present, Baht 10,000 million convertible bonds

have been converted into the ordinary shares of the Company in full amount. It is therefore

appropriate to propose that the Meeting consider and approve the amendment of Article 3. of the

Articles of Association, as detailed below:

The existing Articles of Association:

“3. The shares of the Company may be transferred without any restriction, except for any transfer

of shares resulting in non-Thai person(s) holding more than 30 percent of the total issued shares

in the Company.

The non-Thai persons may acquire ordinary shares of the Company in excess of the restricted

ratio prescribed above by converting the convertible bonds which are wholly issued to non-Thai

investors pursuant to the Extraordinary General Meeting of Shareholders No. 2/2010 held on

November 16, 2010, even though the ratio of the shareholding by the non-Thai persons has

reached 30 percent of the total issued shares of the Company. However, such shareholding shall

not cause the total number of the shareholding ratio of the non-Thai persons to exceed 49

percent of the total issued shares of the Company. The holding of shares by the non-Thai

persons exceeding 30 percent up to 49 percent shall apply to the case of any transfer of shares

by non-Thai persons, who have acquired new shares by means of the exercise of conversion

right of convertible bonds under this paragraph two, by their transferees and subsequent

transferees in every stage of transfers.”

The proposed amendment of the Articles of Association:

“3. The Company’s shares can be freely transferred without any restriction, except for the case that

such transfer may cause the non-Thai persons to hold more than 49 percent of the total issued

shares of the Company. However, if any transfer will increase the ratio of aggregate shares

held by the non-Thai persons over the limit specified above, the Company reserves the right to

refuse to register such transfer of shares.”

Opinion of the

Board of Directors:

The Board of Directors deems appropriate to propose to the shareholders’ meeting

to consider and approve the amendment of Article 3. of the Company’s Articles of

Association as per the details above.

Remark: Resolution in this agenda shall be approved by not less than three-fourths of the

total number of votes of the shareholders attending the meeting and having the

right to vote, including the abstained votes in the calculation base.

…/12

Agenda 10 To consider other business (if any)

The Company has prepared and delivered to the shareholders the Annual Report 2012/13 in CD-

ROM. If any shareholder wishes to obtain the Annual Report 2012/13 in booklet, please contact the

Investor Relations to obtain at the Company’s office during the business hours, telephone nos.

0-2273-8631, 0-2273-8636, 0-2273-8637, or to obtain on the meeting date at Rama Gardens Hotel

Bangkok, Convention Center.

To promote the good corporate governance practice, the Company invited the minority shareholders

to propose agenda in advance. The shareholders, who are collectively holding at least 3% of the

Company’s total issued shares and continually holding such shares for at least 6 months, are entitled

to propose agenda for the 2013 Annual General Meeting of Shareholders during the period from

December 28, 2012 to March 31, 2013. The Company published such criteria on the Company’s

website as well as announced the news through the website of the Stock Exchange of Thailand.

Nonetheless, there was no shareholder proposing any agenda.

In order to allow the 2013 Annual General Meeting of Shareholders to be carried out efficiently, the

shareholders are invited to send the questions for the 2013 Annual General Meeting of Shareholders

by email to [email protected] or by a registered mail to the Company Secretary

Office at TST Tower, 15th Floor, 21 Soi Choei Phuang, Viphavadi-Rangsit Road, Chomphon,

Chatuchak, Bangkok 10900 in advance. For this purpose, please specify the questions and include

your name, address, telephone number, email address (if any) and have the documents delivered to the

Company no later than Wednesday July 24, 2013.

The Company set the date of determining the names of shareholders who shall be entitled to attend the

2013 Annual General Meeting of Shareholders (Record Date) on June 18, 2013 and the date to gather

the names of shareholders under Section 225 of the Securities and Exchange Act B.E. 2535 (as

amended) by closing the share register book and suspension of share transfer on June 19, 2013.

The shareholders are cordially invited to attend the 2013 Annual General Meeting of Shareholders on

Friday July 26, 2013 at 13.30 hrs., at Rama Gardens Hotel Bangkok, Convention Center, 9/9

Vibhavadi Rangsit Road, Laksi, Bangkok 10210. The shareholders are recommended to study the

registration procedure and to prepare all documents that are required to present on the meeting date,

and to study the voting and meeting procedures as detailed in Enclosure 6. The Company will

conduct the meeting in accordance with the meeting procedure as detailed in Enclosure 6 and the

Company’s Articles of Association in Enclosure 9. In order to protect the rights and interests of the

shareholders in the event that any shareholder is unable to attend the meeting and would like to

appoint the Company’s Independent Director as their proxy to attend the meeting and cast votes on

his/her behalf, the shareholders can appoint the Independent Director of the Company as per the

details in Enclosure 8 and deliver Proxy Form B. as appeared in Enclosure 7 together with the

supporting documents to the Company Secretary Office at TST Tower, 15th Floor, 21 Soi Choei

…/13

Phuang, Viphavadi-Rangsit Road, Chomphon, Chatuchak, Bangkok 10900, telephone no. 0-2273-

8611-15 Ext. 1525, 1531. For convenience of reviewing the documents, please kindly have the

documents delivered to the Company no later than Wednesday July 24, 2013.

In order to allow the registration for the attendance of the 2013 Annual General Meeting of

Shareholders to be carried out smoothly and efficiently, the shareholders and proxies can register for

the meeting attendance from 11.30 hrs. onwards at Rama Gardens Hotel Bangkok, Convention

Center. The Company will use the Barcode system to facilitate the registration and votes counting in

this meeting; therefore, the shareholders and proxies are requested to present the Registration Form,

Enclosure 1 and other supporting documents as detailed in Enclosure 6 at the Registration Desk.

Please be informed accordingly.

Sincerely yours,

BTS Group Holdings Public Company Limited

-Mr. Keeree Kanjanapas-

Chairman / Executive Chairman

Enclosure 2

Enclosure 1

Registration Form (Please see the separate document)

Annual Report 2012/13 and Sustainability Report in CD-ROM (as enclosed)

.../14

.../15

2

Limited (“BBLAM”), a subsidiary of Bangkok Bank Public Company Limited, may be the management company of the infrastructure fund. Therefore, Bangkok Bank Public Company Limited, a major shareholder and the controlling person of BBLAM, may have a conflict of interests in voting in Agenda 3 and 4.

The Secretary to the Meeting informed the Meeting that the Company used the Barcode System of the Thailand Securities Depository Co., Ltd. for the registration and vote counting and that Mr. Kom Vachiravarakarn, the representative from Weerawong, Chinnavat and Peangpanor Limited, the legal advisor, acted as a witness to the vote counting. In addition, in order to promote the Company’s good corporate governance, the Secretary to the Meeting also invited minority shareholders to act as a witness to the vote counting. However, no shareholder expressed his/her interest in acting as a witness to the vote counting.

The Secretary to the Meeting introduced the Directors, the Executives and the Advisors who attended the Meeting today as follows:

Directors presented at the Meeting

Mr. Keeree Kanjanapas Chairman of the Board of Directors / Executive Chairman / Chairman of the Corporate Governance Committee

Dr. Anat Arbhabhirama Executive Director / Member of the Corporate Governance Committee

Mr. Surapong Laoha-Unya Executive Director

Mr. Kavin Kanjanapas Executive Director

Mr. Rangsin Kritalug Executive Director / Chief Operating Officer / Member of the Nomination and Remuneration Committee / Member of the Corporate Governance Committee

Mr. Kong Chi Keung Executive Director / Member of the Nomination and Remuneration Committee

Prof. (Special) Lt. Gen. Phisal Thepsithar

Independent Director / Chairman of the Audit Committee / Chairman of the Nomination and Remuneration Committee

Dr. Amorn Chandara-Somboon Independent Director

Mr. Suchin Wanglee Independent Director / Member of the Audit Committee / Member of the Nomination and Remuneration Committee

Prof. (Special) Charoen Wattanasin Independent Director / Member of the Audit Committee / Member of the Nomination and Remuneration Committee / Member of the Corporate Governance Committee

Mr. Cheong Ying Chew, Henry Independent Director

Executives presented at the Meeting

Mr. Surayut Thavikulwat Chief Financial Officer

Mrs. Duangkamol Chaichanakajorn Accounting Director

.../16

3

Mrs. Patchaneeya Pootme Corporate Communications Director

Mr. Daniel Ross Financial Director

Miss Chawadee Rungruang Financial Controller

Miss Chayada Yodyingtammakul Legal Director / Company Secretary

Advisors presented at the Meeting

Financial Advisor Phatra Securities Public Company Limited

Mr. Chainarong Rojanasintu

Legal Advisor Weerawong, Chinnavat and Peangpanor Limited

Miss Peangpanor Boonklum

Independent Financial Advisor Sage Capital Company Limited

Miss Rutchanee Chatbunchachai

Auditor Earnst & Young Limited

Miss Siraporn Ouaanunkun

Mr. Keeree Kanjanapas (Mr. “Keeree”), Chairman of the Board of Directors and Executive Chairman, acted as the Chairman of the Meeting, declared the Extraordinary General Meeting of Shareholders No. 1/2012 open and proceeded with Agenda 1 accordingly.

Agenda 1 Message from the Chairman to the Meeting

Mr. Keeree expressed his appreciation to all shareholders and advisors attending the Meeting. He informed the Meeting that the most important matter of this Meeting is to consider raising funds through the infrastructure fund, which Mr. Keeree would give a summary of the overall picture in brief, and the advisors would further give more details to the Meeting.

The BTS Group is determined to operate the continual and sustainable SkyTrain business. As of December 5, 2012, Bangkok Mass Transit System Public Company Limited or BTSC, our subsidiary, has been operating the SkyTrain business for 13 years and there are another 17 years remaining under the concession. As the Government has a policy to encourage the establishment of an infrastructure fund, the Company believes that this will be a way to raise funds for expanding the Company’s business. The expansion of the SkyTrain business requires a large amount of investment. If the Company has a strong financial position and is supported by its capability and experience in operating SkyTrain system, the Company believes that the Government will witness such and this will assist the Company to accelerate the expansion of its SkyTrain business. Compared to other countries, Bangkok still has very few SkyTrain networks. As the Government has a policy to encourage the establishment of an infrastructure fund, the Company believes that this will be an opportunity to sell the future net farebox revenue for the next 17 years of the core SkyTrain system (the Green Line) with an approximate track length of 23.5 km to the infrastructure fund (the “Fund”). The achievement of this project will strengthen the Company’s financial liquidity and investment capacity. The book value of such farebox revenue is approximately Baht 40,000 million. With regard to the approval from the Meeting, the Company will not sell the net farebox revenue if the selling price is less than Baht 50,000 million. However, the Company has an opportunity to sell the net farebox revenue for more than Baht 50,000 million, depending on several factors, including market conditions and investors’ demand and interest.

.../17

4

After the establishment of the Fund, the Company will be able to invest in this Fund. The Company will invest by subscribing for 33.33% of the total investment units of the Fund by using a part of the proceeds derived from the sale of the net farebox revenue by BTSC. With such investment, the Company will hold 33.33% of the total investment units of the Fund, which is the maximum percentage permitted by law.

BTSC would not sell to the Fund the Long Term Operation and Maintenance Agreement and continues to operate and receive the benefits and revenues from such. The Fund will be listed on the Stock Exchange of Thailand and the Fund’s investment units can be traded in the same manner as shares. If demand is high, the price of investment units may increase. However, if demand is low, the price of investment units may decrease. For this project, the Company only sells the net farebox revenue of BTSC, a subsidiary in which the Company holds 97.46% of the total issued shares, to the Fund, but the Company still operates other businesses.

Some shareholders may wonder what will happen after BTSC sells its net farebox revenue, which is one of the Company’s core revenue stream. The answer to this question as a role of the management is, if this project is complete, not only our cash position will be strengthen, but the operating result is also likely to perform better as a result of, among the other things, tax privileges, details of which will be further provided by the advisors. After the advisors have given their presentation and explanation, if there are any further questions, the Company will be pleased to respond.

Remark: This agenda is for acknowledgement and no casting of vote.

After Agenda 1 was completed, Mr. Keeree assigned the Secretary to the Meeting to conduct the Meeting from Agenda 2 onwards. The Secretary to the Meeting conducted the Meeting in accordance with the agenda as follows:

Agenda 2 To consider and adopt the Minutes of the 2012 Annual General Meeting of Shareholders

The Secretary to the Meeting informed the Meeting that the Company had prepared the Minutes of the 2012 Annual General Meeting of Shareholders dated July 26, 2012 and submitted the copy of the said minutes to the Stock Exchange of Thailand within 14 days from the meeting date and to the Ministry of Commerce as required by laws, as well as made available on the Company’s website. The copy of the minutes of the 2012 Annual General Meeting of Shareholders was delivered to the shareholders along with the Invitation in pages 14-56.

The Secretary to the Meeting gave the Meeting an opportunity to express opinion and make inquiries with regard to this agenda. The shareholders expressed their opinion and made inquiries, and the answers to those inquiries were summarized at the end of this agenda. The Secretary to the Meeting then asked the Meeting to consider and adopt the Minutes of the 2012 Annual General Meeting of Shareholders dated July 26, 2012.

Resolution: The Meeting considered and resolved to adopt the Minutes of the 2012 Annual General Meeting of Shareholders dated July 26, 2012 as proposed, with the following voting results:

Votes Number of Votes Percentage

Approve 7,202,305,274 99.9984

Disapprove 108,334 0.0015

Abstain 10,875,958 -

Void Voting Cards 0 -

Total (1,481 shareholders) 7,213,289,566 -

.../18

5

Remark: Resolution in this agenda shall be adopted by the majority votes of the shareholders attending the meeting and casting their votes, excluding the abstained votes from the calculation base.

Agenda 2 – Comments/ Inquiries/ Replies

Shareholder Mr. Sakchai Sakulsrimontree asked about the effect on BTS of a statement made in the Invitation “Not for publication or distribution, directly or indirectly, in or into the United States”.

Miss Peangpanor Boonklum

The legal advisor clarified that, as certain parts of the information regarding the infrastructure fund stipulated in the Invitation may be considered an offering of securities under the laws of certain countries, such as the U.S. securities law, it was necessary for such a statement be included in the Invitation. However, the Company has the duty to deliver the Invitation to all shareholders; therefore, the English Invitation includes a similar statement that, “This document is not an offering of securities”.

Before proceeding to Agenda 3, the Secretary to the Meeting informed the Meeting that, since the matters in Agenda 3-5 are related to the infrastructure fund transaction (the “IFF Transaction”), and are related to one another. If any of these agenda items are not approved by the Meeting, all of those agenda items shall be deemed disapproved by the Meeting.

In order for the Meeting to understand the details of the IFF Transaction to be considered in Agenda 3 through 5 before casting their votes, all details of Agenda 3 through Agenda 5 will be given to the Meeting, and then the votes on each Agenda will be cast accordingly. The Secretary to the Meeting invited Mr. Chainarong Rojanasintu, the financial advisor from Phatra Securities Public Company Limited (“Mr. Chainarong”) and Miss Peangpanor Boonklum, the legal advisor from Weerawong, Chinnavat and Peangpanor Company Limited (“Miss Peangpanor”) to give details about Agenda 3 through Agenda 5 to the Meeting. In addition, the Secretary to the Meeting also invited Miss Rutchanee Chatbunchachai, the independent financial advisor from Sage Capital Company Limited (“Miss Rutchanee”), to give opinions on the IFF Transaction to the Meeting.

Mr. Chainarong gave an explanation of the IFF Transaction to the Meeting, the key details of which are summarized as follows:

1. Benefits of the IFF Transaction

The IFF Transaction will mutually benefit three parties as follows:

(1) The Thai Government – The Government wishes to develop the country’s transportation system, especially the SkyTrain system in Bangkok and its vicinity, which is one of the first priorities of the Government. The development of the SkyTrain system is one way to drive the country’s economy and to increase people’s quality of life in society. According to the current National Economic and Social Development Plan (2010 - 2029), the Government plans to expand the SkyTrain system to a total of 12 lines, with a total length of 508 km., which will substantially increase from the current length of approximately 80 km.

(2) Bangkok Mass Transit System Public Company Limited (“BTSC”) – BTSC is the leader in providing rapid mass transit services in Thailand, with more than 10 years’ experience in operating the SkyTrain system. BTSC wishes to continuously expand the SkyTrain business in order to improve the quality of life of people in Bangkok. The investment in the SkyTrain system, which is an infrastructure project, requires a substantial amount of funds to expand, and the need for investment is urgent in order to promptly provide the SkyTrain services to the public as soon as possible. Moreover, this will increase BTSC’s revenue, especially when the current concession

.../19

6

agreement expires in the next 17 years, so it will create long-term sustainable value for the Company.

(3) The Capital Market – The Stock Exchange of Thailand (the “SET”) and the Office of the Securities and Exchange Commission (the “SEC”) promote the establishment and investment in the infrastructure fund in order to be a new channel of investment which provides a stable return to investors, and gives investors an opportunity to be an owner of the country’s key infrastructure business, with several beneficial schemes, especially tax privileges. The investment in the infrastructure fund will provide investors with the following tax privileges in accordance with the terms and conditions as required by law:

(a) Individuals: Dividends received are exempt from personal income tax for a period of 10 years from the date of the establishment of the Fund.

(b) Companies listed on the SET: Dividends received are exempt from corporate income tax.

(c) Companies incorporated under Thai law, but not listed on the SET: 50% of the dividends received are exempt from corporate income tax.

The infrastructure fund is one of alternatives for raising funds from the public for the purpose of investment in and development of new infrastructure networks.

2. Principle and Rationale for Conducting the IFF Transaction

The concession agreement for BTSC, which has a 30-year term, has been in operation for 13 years, and expires in the next 17 years. After the concession expires, it will result in a loss of certain parts of the Company’s revenue: (i) the farebox revenue from the core BTS SkyTrain system through the Sukhumvit Line (from On Nut Station to Mo Chit Station) and the Silom Line (from the National Stadium Station to Saphan Taksin Station), which are the two major lines operated under the concession agreement; and (ii) the revenue from advertising space on the core SkyTrain system. BTSC is required to transfer the trains to the Bangkok Metropolitan Administration (“BMA”), the grantor of the concession. As a result, BTSC’s business size will be smaller. However, BTSC will still earn revenue from the operation of other businesses, including revenue from the 30-year Long Term Operation and Maintenance Agreement entered into by BTSC and Krungthep Thanakom Company Limited, and the revenue from advertising space in areas other than the core SkyTrain system. Therefore, the Company is required to raise funds to expand its business, especially the mass transit business.

3. Investment Opportunity to which the Company Gives Priority

The Company will consider the investment opportunity by giving priority to the four main lines of the SkyTrain system, as the Company has an advantage over the competition in operating these mass transit lines.

(1) Green Line: Consisting of two lines: from Mo Chit to Saphan Mai, and from Bearing to Samut Prakarn, with a combined track length of 25 km., consisting of 21 stations. It is expected to commence operation by April 2017, with a total project value of approximately Baht 64,500 million, and the bidding process is expected to start in 2013. This project is a strategic line covering areas with a dense population, and directly connects to BTSC’s current Green Line, from Mo Chit Station and Bearing Station. If the Company becomes the operator of this project, the Company will have a competitive advantage due to low costs from economies of scale, and can facilitate passengers who wish to go to these destinations easily as passengers do not have to leave one train to connect to another train.

.../20

7

(2) Pink Line: From Khae Rai to Minburi, with a track length of 34.5 km., consisting of 30 stations. It is expected to commence operation around October 2017, with a total project value of approximately Baht 42,000 million, and the bidding process is expected to start in 2013. This project will connect to the Green Line at Laksi Turnabout Station.

(3) Light Rail Transit Line (LRT): From Bangna to Suvarnabhumi, with a track length of approximately 18 km., consisting of 15 stations. It is expected to commence operation by 2017, with a total project value of approximately Baht 25,000 million. This project is in the process of awaiting for the Cabinet’s approval. The project will connect to the Green Line at Bangna Station.

The total value of investment for these three projects is approximately Baht 130,000 million.

4. Overall Structure of the Transaction

BTSC, a subsidiary of the Company and the concessionaire of the two core lines of the SkyTrain system, will enter into the IFF Transaction by selling the net farebox revenue from the core BTS SkyTrain system to the Fund: the Sukhumvit Line and the Silom Line with a combined track length of 23.5 km., consisting of 23 stations. The revenue from the 30-year Long Term Operation and Maintenance Agreement remains with BTSC. Other businesses of BTSC, such as the business of VGI Global Media Public Company Limited (“VGI”), media business and shares in VGI held by BTSC, as well as the service business of Bangkok Smartcard System Company Limited or Rabbit Card, and other businesses are still owned by BTSC and having opportunities to continue growing in the future. The Fund will raise money by offering investment units to both domestic and international investors, and will use the entire proceeds to invest in the net farebox revenue, which will be at least Baht 50,000 million. The Company will invest in this Fund by subscribing for 33.33% of the total issued investment units of the Fund, which is the maximum investment percentage permitted by law.

The net farebox revenue to be sold to the Fund by BTSC is all farebox revenue to be generated from the operation of the core SkyTrain system, and compensation and money to be received by BTSC from the BMA arising out of or related to the concession agreement less operating expenses, such as labor, electricity, maintenance, administrative expenses or SG&A (Selling, General & Administrative Expenses), and capital expenditures (for example, investment in rolling stocks to provide services to passengers).

In addition, the Fund will pay a management fee and/or incentive fee as an incentive for BTSC if the actual net farebox revenue is higher than the projection, at the rate set out in the agreement.

5. Management Structure of the Fund

The Company, as a shareholder of BTSC, will support these transactions by supporting the performance of BTSC’s obligations having toward the Fund. The Company will provide a guarantee (with limited liability) to secure the obligations of BTSC, and will pledge all shares in BTSC held by the Company to secure the obligations of BTSC. Where BTSC breaches its obligations, the Fund may enforce such security and become BTSC’s shareholder. However, the support and guarantee will be limited to the shares that the Company holds in BTSC.

Moreover, the fund management company that will manage the Fund will take part in BTSC’s management. The structure of BTSC’s Board of Directors will consist of the following: (1) one-third of the directors will be representatives from the Company, (2) one-third of the directors will be independent directors and (3) one-third of the directors will be representatives from the Fund in order to oversee the performance of BTSC’s obligations having toward the Fund. In addition, a fund supervisor will be appointed to oversee the interests of the unitholders.

.../21

8

6. The Holding of Investment Units by the Company

The Company will obtain a bridge loan from a commercial bank to invest in the Fund by subscribing for one-third of the total investment units of the Fund. After fund raising from the public and the establishment of the Fund, the Fund will use such proceeds to purchase the net farebox revenue. BTSC will distribute the proceeds for, among other things, dividend payments, capital reduction, loans or other debt instruments, and the Company will use such proceeds to repay the bridge loan.

7. Objective for the Use of Proceeds

Assuming that the net farebox revenue will be sold for Baht 60,000 million, the Company will invest the first portion of approximately Baht 20,000 million in the Fund by subscribing for one-third of the total investment units of the Fund; the second portion of approximately Baht 10,600 million will be deposited by BTSC with a financial institution to guarantee the principal and interest of BTSC’s debentures; and the remaining portion of approximately Baht 29,000 million will be allocated by BTSC for investing in the four priority mass transit projects as mentioned above. If there is any remaining cash and the Company has good liquidity, the Board of Directors or the shareholders’ meeting may consider the declaration of a special dividend to shareholders. However, in paying the special dividend, the Company will consider it together with the future business plan and capital investment requirements, as well as any legal restrictions and other factors.

8. Benefits to the Company’s Shareholders

The IFF Transaction will benefit the Company’s shareholders as follows:

(1) Create long-term value of the Company for shareholders;

(2) Create opportunities to invest in new lines of the mass transit system in order to increase the long-term revenue of the Company;

(3) The Company will have sufficient cash and the ability to invest in the mass transit system projects which are opened for participation, including both Green Line extensions and other lines.

(4) The Company will receive a stable return from the investment in the Fund in the form of dividends, which will have the opportunity to increase in line with the number of passengers when the extension lines are in operation in the near future.

Miss Peangpanor, the legal advisor from Weerawong, Chinnavat and Peangpanor Limited, provided an explanation regarding the IFF Transaction and legal issues related to the concession agreement to the Meeting; the key details of which are summarized as follows:

1. Agreements related to the IFF Transaction and their Material Terms (All of these agreements were under negotiation)

(1) The Net Revenue Purchase and Transfer Agreement, to be entered into between BTSC and the Fund, has the following material terms and conditions:

(a) The net farebox revenue to be sold under this agreement is all farebox revenue to be generated from the operation of the core BTS SkyTrain system less all costs and expenses in connection with the operation and maintenance of the core BTS SkyTrain system. In addition, the revenue to be sold includes all cash or revenue arising from any claims, awards, or judgments. Please see the Invitation on pages 3-4 for further details.

.../22

9

(b) The selling price of the net farebox revenue is expected to be approximately Baht 50,000 to 60,000 million, or may be higher. However, it shall not be lower than Baht 50,000 million. The final price of the net farebox revenue will be agreed on between BTSC and the Fund. In this respect, the Fund may procure a loan in a certain amount in order to pay the price, but this will be subject to negotiations between the Fund and its lender.

(c) The key obligations of BTSC are:

1) BTSC shall deliver to the Fund the net farebox revenue on a daily basis.

2) BTSC shall deposit the O&M expenses of the core BTS SkyTrain system according to the daily projection in the account opened by BTSC with the fund supervisor, and the O&M expenses can be withdrawn from the account at the end of each month, and will be reconciled quarterly.

3) Where the net farebox revenue received for any particular period exceeds the selling price allocated for that period, the Revenue Department may consider the Fund to be engaging in a business having the nature of a commercial bank, and will be subject to specific business tax of 3.3%. In that case, BTSC has agreed to reimburse the Fund for the specific business tax. However, at present, the Revenue Department is considering this issue, and if specific business tax is exempt, BTSC will not have that tax burden.

(d) BTSC will grant the Fund the right to purchase and the right of first refusal to purchase certain projects under: 1) any extension of the concession agreement after its expiration in next 17 years; 2) the 30-year Long Term Operation and Maintenance Agreement; and 3) other agreements in relation to the mass transit system in Bangkok and its vicinity. The purchase price will be subject to negotiation between the parties. If they fail to reach an agreement, the parties shall follow the procedures and conditions set out in the agreement. The price for the right to purchase shall, in no case, be less than the investment cost of the asset plus the rate of return set out in the agreement. The exercise of the right to purchase shall be made in accordance with the procedures set out in the agreement, including obtaining approval from the board of directors and the shareholders’ meeting in compliance with the law. With regard to the right of first refusal, if any third party offers to purchase the asset, BTSC shall inform the Fund of such an offer, and the Fund will have the right of first refusal to purchase at the same price offered by that third party. The right is given for a period of 17 years, provided that that period may be extended according to the term of the relevant project. For example, the right to purchase and the right of first refusal to purchase the assets under the 30-year Long Term Operation and Maintenance Agreement will be extended according to the term of that agreement.

(e) BTSC will give the Fund a right to participate in its management. For this purpose, the Fund will be entitled to nominate persons to be appointed as the directors of BTSC for one-third of the board of directors. Passing resolutions in the reserved matters, including the incurrence of expenditure or new indebtedness in the amount or type not permitted, making new investment, appointment or removal of certain senior management members, capital restructuring (such as the capital reduction or amalgamation) or change of auditor, shall require approval from the directors nominated by the Fund.

.../23

10

(f) BTSC will be entitled to receive the management fee and incentive fee at the prescribed rate. If the actual net farebox revenue is exceeding the projected net farebox revenue for such period, BTSC’s incentive fee shall increase accordingly.

(g) There are certain undertakings that BTSC shall comply with or is restricted from carrying out, including engaging in a new business, amending or terminating the concession agreement, incurring any new indebtedness in the amount or type not permitted, and amending the agreements in connection with the operation and maintenance of the core BTS SkyTrain system, unless the approval of the Fund is obtained in advance.

(h) Events of default, such as,

1) Failure to deliver the net farebox revenue, unless such a failure is caused by a technical error, and payment is made within 5 days of its due date;

2) Failure to comply with any obligation under the agreement, and failure to remedy such breach within the specified period;

3) Breach of other financing agreements for the specified amount (cross default);

4) Business reorganization, a composition or compromise with creditors in general, or entering into bankruptcy proceedings; and

5) Unenforceability of the agreements in connection with the IFF Transaction.

(i) Consequences of Events of Default

1) The Fund will become the creditor and be entitled to enforce the pledge of BTSC shares made by the Company, or to exercise the right to purchase BTSC shares from the Company under the Agreement to Purchase and to Sell Shares.

2) If the event of default is due to a breach of the concession agreement, the Fund may exercise its step-in right as the creditors’ representative under the concession agreement.

3) The Fund agrees to cause BTSC to separate the revenue to be generated from the assets which are not bought by the Fund, or to transfer the assets which are not bought (except for the assets which are required for the operation of the core BTS SkyTrain system), such as VGI shares, to the Company or any person designated by the Company.

The Fund will assume both risks and rewards; namely, if the net farebox revenue obtained exceeds the purchase price paid by the Fund, such premium will belong to the Fund. However, if there are expenses and maintenance costs incurred or any related problems arise, the Fund shall also assume such risks.

(2) The Sponsor Support and Guarantee Agreement, to be entered into between the Company and the Fund, has the following material terms and conditions:

(a) The Company shall give a guarantee to secure the obligations of BTSC, but not the payment obligation. As a result, the Fund will receive the actual net

.../24

11

farebox revenue. The Company has no obligation to pay the projected net farebox revenue.

(b) The Company shall maintain its current shareholding percentage in BTSC.

(c) The Company shall support BTSC’s operation in accordance with the Net Revenue Purchase and Transfer Agreement, such as appointing people nominated by the Fund to be one-third of BTSC’s directors, and carrying out the reserved matters.

(d) The Company will pledge its shares in BTSC to secure its obligations under the agreement.

(e) The Fund cannot enforce the Company to perform its obligations by any means other than enforcing against all BTSC shares held by the Company under the Share Pledge Agreement or the Agreement to Purchase and to Sell Shares, and, upon transfer of BTSC shares to the Fund, the Company will be released from its guarantee obligation.

(f) The Company and the Fund may agree that the Company makes the payment to the Fund in place of enforcement upon BTSC shares. However, this agreement will be subject to further negotiation between the Fund and the Company in the future.

(g) In the event that the Concession Agreement expires and the Fund releases the pledge of BTSC shares under the Share Pledge Agreement, but any claim which the Fund is entitled to obtain and for which BTSC is exercising its rights or is about to deliver to the Fund remains, the Company agrees to guarantee the obligations of BTSC to deliver to the Fund the payment obtained or to be obtained by BTSC.

(h) The Company (including its affiliates) will grant the Fund the right to purchase and the right of first refusal to purchase the projects in relation to the mass transit system in Bangkok and its vicinity, in the same manner as BTSC.

(3) The Share Pledge Agreement, to be entered into between the Company and the Fund, has the following material terms and conditions:

(a) The Company shall pledge all of its BTSC shares (currently 97.46%) to the Fund in order to secure its obligations under the Sponsor Support and Guarantee Agreement.

(b) To enforce the share pledge, the parties agree to set a condition for the public auction that the third-party awarded bidder is required to enter into an agreement in the form and substance substantially similar to the Sponsor Support and Guarantee Agreement.

(4) The Agreement to Purchase and to Sell Shares, to be entered into between the Company and the Fund, has the following material terms and conditions:

(a) The Company agrees to sell its BTSC shares to the Fund upon the occurrence of an event of default under the Net Revenue Purchase and Transfer Agreement and the exercise notice being delivered by the Fund.

(b) The exercise of the right to purchase shares is for setting off the purchase price against the Company’s obligations under the Sponsor Support and Guarantee Agreement.

.../25

12

2. Unit Subscription Transaction

The Company will subscribe for one-third of the total investment units of the Fund. Moreover, the Company may have an agreement with the underwriters that it will not sell or dispose of any investment units for a certain period in order to give investors confidence in the Fund. The Company will finance its subscription through a bridge loan from a commercial bank, and when BTSC receives the proceeds from the sale of the net farebox revenue and distributes such proceeds to the Company in the form of an intercompany loan, the Company will use that intercompany loan to repay the bridge loan to the commercial bank.

3. Legal Issues in Entering into the IFF transaction and Concession Agreement

Weerawong, Chinnavat and Peangpanor Limited, as the legal advisor, provided its opinions to

the SEC and BTSC, which can be summarized as follows:

(1) Having reviewed the concession agreement and the agreements in connection with the IFF Transaction, the legal advisor views that this transaction is the sale of net farebox revenue, and does not constitute any amendment to the concession agreement. As a result, it is not required to comply with the law on private sector participation in a government undertaking.

(2) Having reviewed the concession agreement and the agreements in connection with the IFF Transaction, the legal advisor views that the IFF Transaction does not constitute any breach to the concession agreement entered into between BTSC and the BMA. BTSC is entitled to collect the farebox revenue under the concession agreement and therefore, as the owner of the asset, BTSC can manage its asset in whatever manner it wishes, including selling the net farebox revenue to the Fund.

4. Events of Default for Termination of the Concession Agreement by BMA

The concession agreement may be terminated in any of the following three circumstances. The first circumstance is in relation to system testing, which was already conducted and completed. The remaining two circumstances are as follows:

(1) BTSC becoming bankrupt; or

(2) BTSC’s willful breach of the concession agreement in a material and continuing nature.

The BMA is required to give one month’s prior notice of termination if the default cannot be remedied. If the default is capable of being remedied, then not less than six months’ prior notice of termination must be given. In an emergency case, to ensure that the system continues to provide service to the public, the BMA in cooperation with BTSC’s creditors may operate the core BTS SkyTrain system on a temporary basis. If BTSC is unable to cure the default within the specified period, BTSC’s creditors (represented by the Fund as notified to the BMA pursuant to the instructions given to the BMA) will be entitled to procure another party to accept an assignment of the rights and obligations under the concession agreement within 6 months of the date of the BMA’s written notice to the representative of the creditors. If the creditors can procure a party to accept the assignment of the rights and obligations within the specified period, the BMA is required to accept the assignment and not to terminate the concession agreement.

5. Conditions Precedent for the Sale and Transfer of the Net Farebox Revenue

(1) The shareholders’ meeting of BTSC and the shareholders’ meeting of the Company resolve to approve the entry into the transaction. In this regard, the shareholders’ meeting of BTSC convened earlier this morning already approved the transaction.

.../26

13

(2) The approval or consent required under the relevant agreements has been obtained. BTSC set the date of the meeting of debentureholders on December 19, 2012 and will procure a letter of guarantee to the debentureholders by placing the proceeds received from the sale of net farebox revenue with the bank in an amount equal to the principal and interest to be repaid throughout the term of debentures to secure the issue of the letter of guarantee. BTSC will seek approval of the amendment of the terms and conditions of the debentures. If the meeting of the debentureholders approves the amendment, BTSC will give the debentureholders a put option for early redemption, to be exercised by January 2013, regardless of whether or not the IFF Transaction takes place. Upon the letter of guarantee being effective, certain conditions and restrictions will be cancelled or amended so that BTSC has the flexibility to operate the business, such as capital reduction or loans to be granted to its parent company.

(3) The SEC approves the establishment of the Fund.

(4) The offering of investment units is successful.

In addition, on the closing date for the sale and transfer of the net farebox revenue, which will occur after the offering of investment units and the establishment of Fund have been completed, BTSC shall amend its Articles of Association by setting out certain reserved matters to the extent permitted by law, register the appointment of directors representing the Fund to the board of directors of BTSC, register the share pledge, and deliver share certificates to the Fund or a person designated by the Fund.

Miss Rutchanee, the Independent Financial Advisor from Sage Capital Company Limited, expressed the financial advisor’s opinion on the following transactions: the Net Revenue Sale Transaction, the Security Transaction, and the Unit Subscription Transaction. The opinions consist of two parts: 1) an opinion on the fairness of entering into the transactions, meaning whether or not the value of the sale of the net farebox revenue at the minimum price of Baht 50,000 million is fair; and 2) an opinion on the reasonableness for the entry into those transactions. The key details of this opinion can be summarized as follows:

1. Fairness of the Sale Price of the Net Revenue

With regard to the fairness of the price of the net farebox revenue to be sold to the Fund, the Independent Financial Advisor assessed the fair value of this transaction as if all of the assets of the business of the core BTS SkyTrain system had been sold to the Fund, using the following four approaches:

(1) Net Book Value of Assets: Based on BTSC’s reviewed carve-out financial statements as of September 30, 2012, the book value of assets of the core BTS SkyTrain system is Baht 43,162.5 million.

(2) Market Comparables: The assessment using this approach was made by making a comparison to Bangkok Metro Public Company Limited (“BMCL”), which is the only company listed on the SET whose business is similar to that of BTSC. The ratios used by the Independent Financial Advisor in the comparison are: 1) Price to Earnings Ratio (P/E Ratio); and 2) Price to Book Value Ratio (P/BV Ratio).

However, the P/E Ratio could not be used, as BMCL reported a loss in its 4 previous quarters. Although the P/BV Ratio of BMCL could be used, the result is quite high compared to the industry or the P/BV Ratio of companies listed on the SET. As BMCL has continued making loss in its operating results, its book value is quite low, while the market price of BMCL shares is quite stable. As a result, the P/BV Ratio of BMCL is quite high. The Independent Financial Advisor, therefore, was of the opinion that it is not appropriate to use this approach as a benchmark for this valuation.

.../27

14

(3) Enterprise Value of Assets: Under this approach, the market price of the Company’s shares will be used to determine the Company’s business value, and the value of other businesses which form part of the Company will then be assessed. In regard to the media business, as VGI is a company listed on the SET, the market price of VGI shares was used to assess the value of VGI’s business. In regard to the property business, the value appraised by the independent appraiser for all land and buildings owned by the Company and its subsidiaries was assessed. The book value of the service business was applied as there is no market value to be used for this assessment. Consequently, the value of the core BTS SkyTrain system is ranging from Baht 42,262.2 to Baht 45,402.4 million.

(4) Discounted Cash Flow: The Independent Financial Advisor estimated the cash flow from the core BTS SkyTrain system business throughout the remaining concession term (17 years). The estimate of the net farebox revenue was conducted by Systra MVA (Thailand) Limited (“MVA”), while the estimate of the expenses was conducted by PB Asia Limited (“PB”). Both MVA and PB are consulting firms to domestic and international transportation companies with expertise in the transportation business, and are reliable internationally. Under this approach, the net present value of the net farebox revenue of the core BTS SkyTrain system is Baht 51,608.0 million for the base case. In addition, the Independent Financial Advisor conducted a sensitivity analysis by adjusting the ridership estimated by MVA at the rate of 2.5% (upwards and downwards) and by adjusting the SET market return at the rate of approximately 1% (upwards and downwards), which resulted in the net present value of the net farebox revenue of the core BTS SkyTrain system ranging from Baht 47,027.9 to Baht 56,644.9 million.

It is of the Independent Financial Advisor’s view that the Net Book Value of Assets approach is not suitable, as it does not reflect either the fair value of BTSC’s liabilities or assets, nor the operating results and ability to generate profits in the future.

With regard to the Market Comparables approach, it is common and appropriate to use this approach for valuing a business if there is more than one company in a similar industry and of comparable size to be used as a benchmark. However, in the case of BTSC, BMCL is the only company listed on the SET having a business similar to BTSC. The Independent Financial Advisor believes that using only one company might not be appropriate for establishing an industry benchmark to be used for comparison and for determining the value of BTSC’s business. Moreover, BMCL has sustained a loss, and its P/E Ratio could not be determined, while its P/BV Ratio is too high compared to the overall industry and the SET. Therefore, the Independent Financial Advisor believes that the Market Comparables approach is not suitable for determining the value of the core BTS SkyTrain system.

As to the Enterprise Value of Assets approach, the Independent Financial Advisor found that only the market value of the Company and VGI is available, while other businesses which are components of the Company do not have a market price and do not reflect the appropriate value of such businesses. As a result, it is not appropriate to use this approach to determine the fair value.