Embed Size (px)

Citation preview

ASIA PACIFIC REGIONCIVIL HELICOPTERS

Year End 2015

Beijing

PenglaiSeoul

Shanghai

Hong Kong

Manila

Chengdu

Shenzhen

Bangkok

ASIAN SKY GROUP (ASG), headquartered in Hong Kong with offices throughout Asia, has assembled the most experienced aviation team in the Asia-Pacific region to provide a wide range of independent services for both fixed and rotary-wing aircraft. ASG also provides access to a significant customer base around the world with the help of its exclusive partners.

ASG is backed by SEACOR Holdings Inc., a publically listed US company (NYSE: “CKH”) with over US$1 billion in revenue and US$3 billion in assets, and also by Avion Pacific Limited, a mainland China-based general aviation service provider with over 20 years of experience and 6 offices and bases throughout China.

ASG provides its clients with four main business aviation services:1. Sales & Acquisitions including Transactional Advisory2. Market Research and Consulting including Special Projects3. Operation Oversight including Completion Management, Audits, Invoice Review and Aircraft Appraisals, and4. Luxury Charter Services.

The acclaimed Asian Sky Fleet Reports are produced by ASG’s Market Research and Consulting group. ASG has a growing portfolio of business aviation reports designed to provide valued information so that the reader can make better informed business decisions. Included in the portfolio are Asian Sky Asia-Pacific Fleet Reports for both Civil Helicopters and Business Jets, the Africa Business Jet Fleet Report and the all new industry leading Asian Sky Quarterly magazine.

Asian Sky Group would like to acknowledge the gracious contributions made by numerous organisations, including aircraft operators, OEMs, aviation authorities and JETNET LLC in providing data for this report.

Should you wish to reproduce or distribute any portion of this report, in part or in full, you may do so by mentioning the source as: “Asian Sky Group, a Hong Kong based business aviation consulting group”.

Thank you for your interest in this report. We hope you will find the information useful. If you would like to receive further information about our other aviation reports and services, please contact us at [email protected] or visit us at www.asianskygroup.com.

ABOUT ASIAN SKY GROUP

CONTRIBUTION

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 1

INTRODUCTION

Asian Sky Group (ASG) is pleased to present the 3rd edition of its Civil Helicopter Fleet Report. Originally just covering the Greater China region, this edition covers the Asia Pacific region for the second time and now also includes the important Asia Pacific markets of India, Australia and New Zealand. ASG’s Fleet Reports provide the most comprehensive coverage and breakdown of the civil helicopter fleet in the Asia Pacific region and have established themselves as an indispensable source of valued information. For copies of ASG’s various industry reports, please visit at www.asianskygroup.com.

TABLE OF CONTENTSEXECUTIVE SUMMARY AND KEY FINDINGS…………………………………………………….4 OFFSHORE ACTIVITY………...………………...............................……………………...........…8

FLEET BREAKDOWN NORTHEAST ASIA

GREATER CHINA……………………………………………..........................................12JAPAN……..............………………………………………………....................................27SOUTH KOREA .........………………………………………….....................................36

CENTRAL ASIAINDIA.................…………………………………………..............................................46

SOUTHEAST ASIATHAILAND..........…………………………………………..............................................55PHILIPPINES.................……………………….....…….............................................65MALAYSIA........................……........................…….............................................73INDONESIA..………………….............................……..........................................85MYANMAR..………………….............................……...........................................93LAOS..…….…………….............................…….....................................................94CAMBODIA……………….............................……...........................................94VIETNAM……………….............................……...........................................95BRUNEI……………….............................……...........................................96SINGAPORE……………….............................……...........................................96

OCEANIAPAPUA NEW GUINEA...……....................................…….........................98 AUSTRALIA....................……………..........……..................................................105NEW ZEALAND................……........................……...........................................114

PRE-OWNED AIRCRAFT GLOBAL AVAILABILITY…………....…………...…...….............123

AIRCRAFT MODELS POSITIONING……………...………………………………………………124

SUPPORT INFRASTRUCTURE……..........…….......……….......…………………………......130

Note (1): Fleet distribution is based on helicopters in service and their active base of operation.Note (2): 2014 data for Australia, India, New Zealand and other Oceania Islands has been determined by deducting from 2015 fleet totals new

and pre-owned deliveries including any aircraft that are known to have left a country but remained in the Asia Pacific region.Note (3): Other Islands include Maldives, Micronesia, Northern Mariana Islands, Palau and Solomon Islands.

782 762

Indonesia +8%

Australia +3%

Macau

Myanmar

Laos

Bangladesh

India

Nepal +4%

Cambodia -11%

Guam +4%

Hong Kong

Vietnam

Thailand +1%

Taiwan -5%

South Korea +2%

Japan -3%China +20%

Mongolia

Sri Lanka

Singapore

Brunei

Papua New Guinea +9%

130

6

1327

130

6

1327

1 1

6

576

6

694

9 8

10 10

20

26304

20

27304

28 29

41 39

111 112

105185 114199

6 6

212 216

2,028 2,094

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 20152

2014 5,758

2015 6,015+4.5%

FrenchPolynesia

Fiji +25%

New Zealand +7%

New Caledonia

Vanuatu

Philippines +8%

Malaysia -2%

186

169

200

165

7 7

20

47

788

8

20

47

841

10

ASIA PACIFIC REGION – CIVIL HELICOPTERS

Other Islands37 7

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 3

EXECUTIVE SUMMARY

KEY FINDINGS

At the end of 2015, the Asia Pacific civil helicopter fleet numbered 6,015 helicopters in active service, an increase of 4.5% over year end 2014.

As with 2014, the growth leader in percentage and number of units was China, with 20% growth and 118 helicopters added by year end 2015. This, however, represented a slowdown compared with 2014, when growth was 31% and 135 helicopters were added. Overall, of the 34 markets analyzed in this report, only a third experienced growth in 2015, with the other two-thirds either contracting or remaining stagnant.

The Asia Pacific region is currently dominated by 4 countries and 3 manufacturers: with 73% of the helicopter fleet based in Australia, New Zealand, Japan and China, and 78% of those units being either a Robinson, Airbus Helicopters or Bell Helicopter.

In terms of Replacement Cost, the “big four” OEMs (Airbus Helicopters, Bell Helicopter, Sikorsky and AgustaWestland) make up nearly 90% of the market, with Airbus Helicopters leading at 46% and the other three combining for 42%.

Australia represents the largest market overall and is the largest market for Robinson and Bell Helicopter. In terms of unit numbers, New Zealand is next, and is the largest market for MD Helicopters. These are followed by Japan, which is the largest market for AgustaWestland and Airbus Helicopters, and finally China, the fastest growing market overall and the largest for Sikorsky.

In terms of units, approximately 45% of the Asia Pacific fleet operates in a multi-mission role, followed by corporate or private missions at 28%, and offshore operations at 6%; though in terms of Replacement Cost, offshore operations make up approximately 20% of the market.

Offshore Activity: The downturn in oil prices significantly impacted the Asia Pacific region in 2015. In previous years, offshore oil and gas service providers were one of the main growth drivers for the region, however in 2015 there was limited to zero growth, and overall utilisation of the existing offshore fleet came down significantly, with nearly a third of the existing fleet likely idle or preparing for another mission role at year end.

Greater China: Growth slowed in 2015 due a number of factors including the overall economic environment, expected currency depreciation, the downturn in oil and gas activity, negative sentiment resulting from certain government actions, and airspace taking longer to open up than previously anticipated. China will continue to see growth in the number of helicopters delivered during 2016 however, but at a much more moderate pace compared to prior years.

Japan: The Japanese fleet contracted 3% in 2015, with only Sikorsky and AgustaWestland showing increases. This occurred due to greater numbers of older piston, single engine and medium size helicopters either being retired or replaced by fewer but newer helicopter models like the S-76D and AW139. The net decrease was 20 helicopters, though the overall market size grew in terms of Replacement Cost.

South Korea: Despite its advanced aviation industry, there has been only moderate growth in the Korean fleet over the past few years, with 2015 being no exception at just 2%. The largest portion of the fleet is used in a multi-mission role, with 50% used in firefighting operations and being primarily Kamov and Mil helicopters.

India: India saw limited growth in 2015 compared to expectations, but new regulations from the DGAC aimed specifically at the helicopter market could spur growth in 2016. The Indian helicopter market is also sensitive to the oil and gas business, which will continue to impact fleet growth and utilisation. Thailand: The net increase of only 1 helicopter in 2015 was predominantly the result of importation restrictions on helicopters older than 5 years, while the oil and gas market and political factors also contributed to slower growth.

Philippines: Growth in 2015 was a healthy 8% with 14 net helicopters added, which mostly consisted of single and piston categories operated by individuals or corporations. Elections in May 2016 will play a significant factor in the country’s helicopter market, as will overall economic conditions.

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 20154

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 5

Asia Pacific Fleet Breakdown by Size & Replacement Cost

RobinsonAirbus Helicopters

Bell HelicopterAgustaWestland

MDSikorsky

SchweizerAmateur-Built Aircraft

EnstromKamov

MilGuimbal

HALAvicopter

HarbinBoeing Rotocraft

BrantlyKaman

KAIOthers2

1,882

Total Fleet

Total Fleet 6,015 $20,647M

Replacement Cost (USD)

572

67 38

4124

248 369

23 223

34

1,599 9,424

67 348

21

206 2,762

15 26

19

1,195 3,578

62 501

31

182 66

10

303 2,412

29 12

29

90 19

7110

Note (1): Replacement Cost is used to determine the overall dollar value of the civil helicopter fleet. The cost values are based on 2015 OEM list prices for new aircraft models, and 2015 Conklin & de Decker pre-owned prices for equivalent models with the same mission configuration. In some cases, an estimate was used, particularly with regard to aircraft models no longer in production.

Note (2): Others include Aérospatiale Gazelle, Fairchild Hiller, Hiller Aircraft and VTOL.

Malaysia: The fleet contracted slightly in 2015, which was expected given that nearly a third of the total fleet is configured for offshore oil and gas support. Malaysian offshore operators faced significant challenges during the later part 2015, and will likely attempt to move into other missions or other countries in 2016.

Indonesia: Growth in 2015 was almost 8% with 14 net helicopters added to the fleet. However, new regulations restricting in-service helicopters to under 30 years of age and restricting new imported helicopters to under 5 years of age, combined with the downturn in offshore oil and gas, may cause growth in the fleet to stagnate in 2016.

Australia: The fleet grew at just a modest 3% in 2015, but is not expected to grow further in 2016 due to the negative impact of a significantly weakened Australian dollar, the rapid decrease in mineral exports and the downturn in oil and gas prices. The country has a staggering 1,017 operators, including many individuals and corporations, with an average of 2 helicopters per operator (one of which on average is a Robinson), and many of them are very sensitive to changes in the economic conditions and currency movements.

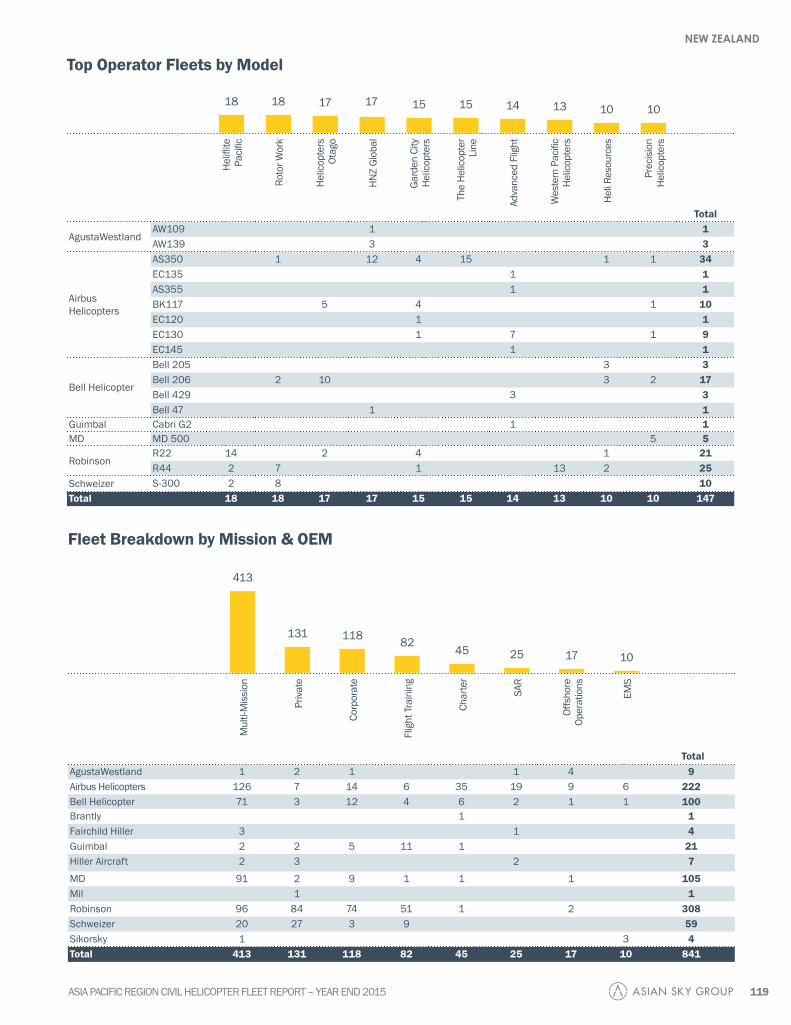

New Zealand: Growth was a healthy 7% in 2015, with a net 53 helicopters added to the market. Pre-owned helicopters made up 81% of the additions which is characteristic of the New Zealand market. New Zealand has the largest fleet of MD helicopters in Asia Pacific, most of which are utilised for multi-mission operations.

Papua New Guinea: The fleet grew 9% in 2015. A typical PNG helicopter can be characterised as pre-owned, aging, and a single-engine turbine from either Bell Helicopter or Airbus Helicopters, and engaged in multi-mission applications. However this profile may begin to change in 2016, with several new helicopters already set to deliver.

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 20156

Fleet Breakdown by OEM & Country6,015 in Total

100+44+38+35+16+11+10+10+8+6+6+2+2+1Au

stra

lia

Chin

a

Phili

ppin

es

Papu

aN

ew G

uine

a

Taiw

an

New

Zeal

and

Indi

a

Indo

nesi

a

Thai

land

Hon

g Ko

ng &

M

acau

Japa

n

Sout

h Ko

rea

Mal

aysi

a

Vanu

atu

AgustaWestland 48 9 87 35 38 15 14 7 33 8 6 1 2 303 5%

Airbus Helicopters 298 222 340 151 120 55 84 72 83 34 34 3 13 9 15 18 2 8 5 7 2 8 6 5 2 1 2 1,599 27%

Amateur-Built Aircraft

90 90 1%

Avicopter 15 15 -

Bell Helicopter 447 100 130 91 88 44 43 74 19 70 52 19 1 3 8 2 1 2 1 1,195 20%

Boeing Rotocraft 4 3 7 -

Enstrom 18 2 20 2 3 2 18 1 1 67 1%

Guimbal 4 21 2 2 29 -

HAL 21 2 23 -

Harbin 10 10 -

Hiller Aircraft 7 7 1 15 -

Kamov 1 12 51 3 67 1%

MD 27 105 15 4 4 8 9 4 40 5 27 248 4%

Mil 1 11 5 9 3 4 5 10 5 4 1 4 62 1%

Robinson 1,061 308 149 233 17 4 45 2 15 5 4 2 11 1 10 9 2 2 1 1 1,882 31%

Schweizer 56 59 4 56 4 2 1 182 3%

Sikorsky 35 4 31 52 5 24 1 16 11 1 13 2 7 4 206 3%

Others2 3 5 3 2 2 15 -

Total 2,094 841 762 694 304 216 200 199 165 114 112 47 39 31 29 27 27 20 20 13 10 10 8 7 6 6 6 1 7 6,015

% of Total 34% 14% 13% 12% 5% 4% 3% 3% 3% 2% 2% 1% 1% 1% - - - - - - - - - - - - - - -

2,094

841

114

762

112

694

47

304

39

216

31

200 199 165

Note (1): Please refer to Page 129 for Multi-Mission descriptions. Note (2): Others include Aérospatiale Gazelle, KAI, Kaman and VTOL.

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 7

Fleet Breakdown by MissionVi

etna

m

New

Cale

doni

a

Cam

bodi

a

Fren

ch

Poly

nesi

a

Brun

ei

Nep

al

Mya

nmar

Laos

Othe

r Is

land

s

Sing

apor

e

Bang

lade

sh Fiji

Sri L

anka

Mon

golia

Gua

m

AgustaWestland 48 9 87 35 38 15 14 7 33 8 6 1 2 303 5%

Airbus Helicopters 298 222 340 151 120 55 84 72 83 34 34 3 13 9 15 18 2 8 5 7 2 8 6 5 2 1 2 1,599 27%

Amateur-Built Aircraft

90 90 1%

Avicopter 15 15 -

Bell Helicopter 447 100 130 91 88 44 43 74 19 70 52 19 1 3 8 2 1 2 1 1,195 20%

Boeing Rotocraft 4 3 7 -

Enstrom 18 2 20 2 3 2 18 1 1 67 1%

Guimbal 4 21 2 2 29 -

HAL 21 2 23 -

Harbin 10 10 -

Hiller Aircraft 7 7 1 15 -

Kamov 1 12 51 3 67 1%

MD 27 105 15 4 4 8 9 4 40 5 27 248 4%

Mil 1 11 5 9 3 4 5 10 5 4 1 4 62 1%

Robinson 1,061 308 149 233 17 4 45 2 15 5 4 2 11 1 10 9 2 2 1 1 1,882 31%

Schweizer 56 59 4 56 4 2 1 182 3%

Sikorsky 35 4 31 52 5 24 1 16 11 1 13 2 7 4 206 3%

Others2 3 5 3 2 2 15 -

Total 2,094 841 762 694 304 216 200 199 165 114 112 47 39 31 29 27 27 20 20 13 10 10 8 7 6 6 6 1 7 6,015

% of Total 34% 14% 13% 12% 5% 4% 3% 3% 3% 2% 2% 1% 1% 1% - - - - - - - - - - - - - - -

Total% of Total

45+16+12+6+6+5+4+3+3+GMulti-Mission1 2,684 (45%)

Corporate 941 (16%)

EMS 190 (3%)

Charter 210 (3%)

SAR 262 (4%)

Law Enforcement 294 (5%)

Offshore Operations 356 (6%)

Flight Training 374 (6%)

Private 704 (12%)

29 20 10 6 1 727 20 10 627 13 8 7 61+1+1+1+1+1+1+1+1+1+1+1+1+1+1

OFFSHORE ACTIVITYAt year-end 2015, helicopters used for offshore oil and gas support in the Asia Pacific region numbered 356 out of a total of 6,015 (unchanged from 2014), and making up 6% of total fleet by numbers but 20% in terms of Replacement Cost. When excluding the Oceania fleet of nearly 3,000, the number of offshore-configured helicopters represent more than 10% of the total Asia Pacific fleet. In Southeast Asia alone, the offshore-configured fleet represents over 15% of the fleet by numbers and 40% by Replacement Cost.

This report provides a statistical snapshot of the current offshore support helicopter fleet, however, and does not necessarily capture the true difficulties currently faced by operators, OEMs, leasing companies, investors, service providers and the oil and gas producers themselves.

As with other regions around the world, the global downturn in the oil and gas industry is also impacting the Asia Pacific region significantly. Between 2012 and 2014 one of the main growth drivers for the Asia Pacific fleet was helicopter deliveries to offshore oil and gas service providers and operators. However towards the end of 2015, OGP helicopter utilisation decreased significantly, a trend that will impact growth severely in the short term.

Capital spending on exploration and production in Asia Pacific is expected to be down 20% in 2016, following an already reduced spending rate in 2015. This reduction reflects lower capital expenditures from several projects reaching completion in 2015, while anticipated new projects are deferred across the region and primarily in Indonesia, Malaysia, Myanmar, India, China and Australia.

Major oil and gas producers in Asia Pacific have been gradually downsizing their operations, cancelling new exploration and drilling plans, in some extreme cases suspending or shutting down existing projects all together, and reducing their workforces considerably.

Oil and gas drilling rig utilisation worldwide is down to 70% compared to a 95% several years ago, with the Asia Pacific offshore rig market reflecting similar trends. This triggers serious concerns across the helicopter industry with stakeholders now trying to predict how deep this decline will be and how it will impact their clients, contracts and future demand for services.

Offshore helicopter operators have been severely impacted by this downturn as many of the helicopters ordered over the last year or two – sometimes speculatively – were expected to support the industry’s continued growth and development. Utilisation levels throughout the Asia Pacific region in 2015 varied significantly; while in some protected countries, offshore activity was lightly affected, in other large oil and gas producing countries there was a severe decline, with even the more protected and resilient markets now expected to show increasing signs of stress in 2016.

It is important to note that the number of aircraft in the fleet listed in this report does not reflect actual offshore activity, as the true number of helicopters servicing contracts today is considerably lower in many of the countries covered in this report. In certain cases over a third of the offshore fleet is hangared and not flying, or have been redirected toward other missions.

The number of heavy and medium helicopters on the ground has increased significantly this year as operators have been forced to adjust to the new market conditions and realities. Just a few years ago, operators were not only looking to replace their ageing helicopters, but also were seeking to transit longer distances, requiring more resilient helicopters with greater endurance and payload from the offshore industry. This was before oil prices plummeted to where they were at year-end 2015.

Operator difficulties have been compounded by the global nature of the down turn and the oversupply of helicopters in most markets, limiting their opportunities to sell aircraft or find work for these helicopters in other markets. Helicopter values have consequently come under tremendous pressure.

In the Asia Pacific market, the changing nature of helicopter age regulations is also impacting demand. In countries with strict age related importation restrictions such as China, Thailand, Myanmar and recently Indonesia, older aircraft that are already in-country may become more valuable locally and may find continued employment. While in countries where oil companies have imposed strict age limits on the helicopters they are willing to contract, such as India, certain pre-owned helicopters become less appealing locally once they become too old for offshore oil and gas operations.

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 20158

Much like some of the large energy companies capable of keeping production levels even if oil prices continue to go further down, helicopter operators who are either large enough or involved in other activities might have the strength to wait-out or overcome the downturn. But smaller operators who have been relying solely on oil and gas contracts are facing more difficult times and are not positioned as well as others to prosper in a low oil price environment.

As a response to these difficulties, some Asia Pacific offshore operators are gravitating towards other missions such as EMS, SAR, firefighting and even corporate transport, while others have no choice but to wait for oil and gas prices to rebound. There are some niche applications across non-traditional markets that may be undertaken by helicopters configured for offshore transport, but at a certain cost and risk, and operators are as a result forced to take a more cautious approach.

Despite the slump in spending and operations, several projects in the region are still set to see investments and many existing projects will at least continue production for the foreseeable future. This will enable the operators relying on those contracts to remain active throughout the downturn.

These are challenging times no doubt, and there are likely to be more difficult times ahead in 2016. While it is too early to predict any kind of meaningful recovery, we expect this downturn to eventually give way to recovery, and ultimately the oversupply in the market should work its way through the system and toward a more balanced state. From a historical perspective, and while downside risks remain, Asian Sky Group expects the demand for energy and natural resources will continue to grow on a global basis over time. Increasing global demand requires increasing global production, and when an eventual recovery does take place, we expect the Asia Pacific region to continue its vital role in that production.

Philippines

JapanChina

Indonesia Papua New Guinea

Brunei

Thailand

Australia

Malaysia

Myanmar 16 159

5

5

70

21 21

47

9

5

5

68

India

South Korea

Vietnam

New Zealand

26 31

12

50

3

47

6

1

6

80 81

17 17

2014 356

2015 356

48

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 9

OFFSHORE ACTIVITY

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201510

Asia Pacific Offshore Fleets – Breakdown by Operator (2 or more helicopters) 294 in Total

37

28

26

22

18

18

16

15

13

13

10

10

10

9

9

8

7

7

6

6

6

5

5

5

5

5

3

3

3

3

2

2

2

2

2

Citic Offshore Helicopter

Bristow Helicopters Australia

Weststar Aviation

China Southern Helicopters

Lloyd Helicopters

Pawan Hans Helicopters

MHS Aviation

Vietnam Helicopter

Global Vectra Helicorp

Travira Air

HNZ Global

Pelita Air Service

Thai Aviation Services

CHC Helicopters (Australia)

China Eastern GA

Heligo Charters

Awan Inspirasi

Bond Helicopters Australia

Esso Australia Resources

Hevilift

SFS Aviation

Brunei Shell Petroleum

Heli-Union

INAEC Aviation

Pacific Helicopters

United Offshore Aviation

Heli Korea

Helicopter Resources

McDermott Aviation

United Helicharters

FI Helicopters

Gulf Helicopters

Heli Niugini

Jayrow Helicopters

Reliance Industries

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201510

OFFSHORE ACTIVITY

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 11

As seen in previous years, the Greater China civil helicopter fleet continued to grow strongly in 2015, leading the Asia Pacific region. Greater China grew at 17.9% in 2015, increasing from 648 helicopters in total to 764. All of this growth occurred in the China market itself as Taiwan contracted and Hong Kong remained flat.

Growth in 2015 was slower however dropping from 2014’s 26.8%. Growth is being impacted by a number of major factors – some unique to China, and some the same world over. China’s economic growth is at its lowest in 25 years with its big state-owned helicopter operators being significantly impacted by the oil and gas crisis around the world. Buying sentiment is also being negatively impacted by government policy and the regulatory environment and airspace are taking longer to relax, discouraging new entrants.

Despite the drawbacks, the advantage the China market has is its ability to absorb these specific shocks due to the very diverse nature of the missions the fleet is performing. For instance, offshore operations only represent 9% of the fleet, corporate and private just 3%, whereas multi-mission represents 58%. Flight Training, SAR and Law Enforcement are all growing year to year. Consequently, Asian Sky Group expects growth to continue in 2016, though similar to 2015, the growth is expected to be moderated and in the area of 10%, with the prospect of even dipping into the single-digit category.

Almost 70% of the Greater China fleet is represented by 3 manufacturers: Robinson 32%, Airbus Helicopters 23% and Bell Helicopter 14%, which overall is in line with the Asia Pacific region as a whole. The Robinson fleet in Greater China grew the most in 2015 (29%), followed by Sikorsky (26%), and then Airbus Helicopters (17%). By size category, the single-engine category grew the highest at 25%, followed by pistons at 19%. Given all of these indicators, it is not too surprising then to find the fleet of helicopters engaged in multi-mission applications grew the highest at 24%. Most other missions grew at only around 10%. Looking at turbine helicopters only, the most popular types in Greater China are the AS350, followed by the Bell 206/407 and then the Sikorsky S-76 family.

Examining the net fleet additions in 2015, the Greater China market added 116 new helicopters and 21 pre-owned helicopters, but the market also saw 26 helicopters leave this region. It is significant to note the slow emergence of a pre-owned market, representing just 15% of the additions in 2015. By model type, the biggest net gainers were the R44, AS350 and the Bell 407, with decreases, also coming from Bell 206s, R22s and Schweizer 300s for instance.

The two biggest operators are China National Police (CNP) and CITIC Offshore Helicopters (COHC) – both with a fleet of 57 helicopters, representing 23% of the total turbine fleet. Whereas CNP has a very diverse fleet from across the spectrum of helicopter manufacturers, COHC is predominately an Airbus Helicopters operator focused on medium to heavy helicopters – AS332s, EC155s, EC225s, Kamov KA-32s and the Sikorsky S-92s.

China

576

694

441

40 3041 3139 31

Taiwan Hong Kong & Macau

Note: 2014 fleet growth figures in Greater China are based on Asian Sky Group’s adjusted numbers for 2013

2015

2014

2013

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201512

GREATER CHINA

NORTHEAST ASIA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 13

764 in Total

Shanghai51

Jiangsu24

Shandong32

Tianjin17

Beijing99

Heilongjiang36

Jilin3

Liaoning9

Shaanxi13

Shanxi2

Inner Mongolia5

Gansu2

Qinghai2

Xinjiang8

Sichuan51

Chongqing22

Hunan12

Hubei31

Jiangxi2

Fujian7

Guangdong132

Hainan16

Zhejiang16

Guizhou5

Guangxi9

Yunnan19

Hebei21

Henan42

Anhui6

Hong Kong30Macau

1

Taiwan39

Fleet Growth

Note: 2014 fleet growth figures in Greater China are based on Asian Sky Group’s adjusted and updated 2013 numbers.

2009 2010 2011 2012 2013 2014 2015 2016 EST

900

800

700

600

500

400

300

200

100

0

260

+16.2%+18.2%

+17.4%

+22.0%

+26.8%

+17.9%

+10.0%

302357

419

511

648

764

840

Civil Helicopters in Greater China

GREATER CHINA

14

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 15

Net Fleet Growth by Mission

Net Fleet Growth by Size Category

Net Fleet Growth by OEM

Agus

taW

estla

nd

Airb

us H

elic

opte

rs

Avic

opte

r

Bell

Helic

opte

r

Boei

ng R

otoc

raft

Bran

tly

Enst

rom

Guim

bal

Harb

in

Kam

ov MD Mil

Robi

nson

Schw

eize

r

Siko

rsky

Mul

ti-M

issi

on

Flig

ht Tr

aini

ng

Offs

hore

Ope

ratio

ns

Law

Enf

orce

men

t

SAR

Char

ter

Corp

orat

e

Priva

te

EMS

Pist

on

Sing

le

Ligh

t Tw

in

Med

ium

Heav

y

2015 (764)

2014 (648)

2013 (511)

2015 (764)

2014 (648)

2013 (511)

2015 (764)

2014 (648)

2013 (511)

36

148

4132

2 2 2 22 23 7 14203 315 1010 10 2 127 6 161111

122

246

191

50 565839

5443

9711

89

131

173

110105

254

173

252

301

126

175

219

34 42 40

131131150

47 48 54

360

446

5118 23 29

7 12 14 10 8 11 5 6 7

73 7073 68 50 5748 45 46 5379

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201516

Breakdown by Size Category764 in Total

Breakdown by Mission764 in Total

Breakdown by OEM Fleet Size

58+10+10+7+7+4+2+1+1+GPiston 301 (39%)

Light Twin 40 (5%)Heavy 54 (7%)

Robisnon246 (32%)

Airbus Helicopters(41%)

Airbus Helicopters173 (23%)

Sikorsky (24%)

AgustaWestland(9%)

Bell Helicopter(9%)Bell Helicopter

110 (14%)

Schweizer 56 (7%)

Sikorsky 54 (7%)

AugustaWestland41 (5%)

Enstrom 20 (3%)

Mil (4%)

Avicopter 15 (2%) Others 7 (1%)

Harbin (3%)

Robinson (3%)

Kamov 12 (2%)

Mil 11 (2%) Harbin 10 (1%)

Kamov (2%)

Schweizer (1%)MD 9 (1%) Avicopter (1%)

Others (2%)

MD (1%)

Multi-Mission 446 (58%)

EMS 7 (1%)

FlightTraining79 (10%)

OffshoreOperations68 (9%)

LawEnforcement57 (8%)

SAR 53 (7%)

Charter 29 (4%) Corporate 14 (2%)

Private 11 (1%)

Medium 150 (20%)

Single 219 (29%)

Note: The market share of Enstrom’s replacement cost is less than 1%.

Replacement Cost (USD)

764 $3,102M

Multi-Mission58%

Turbine 61%

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 17

Breakdown by Mission764 in Total

OEM Market Share – Hong Kong and Macau

OEM Market Share – Taiwan

OEM Market share – Mainland China

36+29+19+16+G50+32+8+5+5+G

MD 5 (16%)

Bell Helicopter 91 (13%)

Schweizer 56 (8%)

Sikorsky 52 (7%)

AgustaWestland 35 (5%)

Enstrom 20 (3%)

Others 8 (1%)

Avicopter 15 (2%)

Kamov 12 (2%)

Mil 11 (2%) Harbin 10 (1%)

Robinson 11 (36%)

Robinson 233 (34%)

Airbus Helicopters 151 (22%)

AugustaWestland 6 (19%)

Airbus Helicopters 9 (29%)

Robinson 2 (5%)

Sikorsky 2 (5%)

Boeing Rotocraft 3 (8%)

Airbus Helicopters 13 (33%)

Bell Helicopter 19 (49%)

694

31

39

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201518

19+14+6+2+0+60+23+21+20+15+15+6+5+4+3+1+0+13+1+1+0+40+39+16+11+3+1+0+3+0+15+0+7+3+0+12+0+4+2+2+1+0+8+3+0+9+0+1+0+17+14+7+6+5+2+1AW139AW109AW119

SW-4

AS350EC155EC135EC120AS365EC225

AS332L1EC130

AS332L2BK117

AS332L

Bell 206Bell 407Bell 205Bell 429Bell 212Bell 427

Z-9Z-11

KA-32

MD 900MD 520MD 500MD 600

S-76C++S-92

S-76DS-76C+

S-76AS-76B

S-76A++

Mi-8Mi-26

S-333

R66

BV234

EN480

AC311AC312AC301

1914

62

6023

2120

1515

65

43

1

113

4039

1611

31

3

15

73

12

422

1

83

9

1

1714

96

52

1

1

Breakdown by Helicopter Model – Turbine Only463 in Total

AgustaWestland 41 (9%)

Airbus Helicopters 173 (37%)

Avicopter 15 (3%)

Bell Helicopter 110 (24%)

Boeing Rotocraft 3 (1%)

Enstrom 15 (3%)

Harbin 10 (2%)

Kamov 12 (3%)

MD 9 (2%)

Mil 11 (2%)

Robinson 9 (2%)

Schweizer 1

Sikorsky 54 (12%)

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 19

4+4+4+4+4+4+4+3+3+3+3+3+3+3+3+3+3+3+3+3+3+3+357+57+31+22+22+21+21+20+17+14+14+14+13+12+11+10+10+10+9+9+8+8+7+7+7+7+7+6+6+5+5+5+5+5+5+5+5+5+5+5Breakdown by Operator

Top 62 – Out of 178 Operators (3 or more helicopters)

Hainan Aviation Academy

Heliservices

Ju Xiang GA

NUAA Academy

Qiqihar KunFeng GA

Ruoer GA

Shandong Qixiang

Baiyangdian General Aviation

Chongqing Shenlong GAC

Elm GA

Emerald Pacific Airlines

Guangxi UUG

Hebei Xiang Hua GA

Henan Da Di

Huayu GA

Hubei Tuncang GA

Hunan Hengyang GA

Hunan Xiangwei GA

Sichuan Luozhengtong GA

Sichuan Xihua GA

Tianjin Tianhang

Xinjiang Kaiyuan GA

Yunnan Hexie

57

14

9

6

22

13

5

21

10

4

3

3

4

3

3

7

5

57

14

22

12

7

5

20

10

4

3

3

4

3

3

4

3

3

7

5

5

5

31

14

8

5

21

11

7

5

17

10

4

3

3

4

3

3

3

7

5

5

19+14+6+2+0+60+23+21+20+15+15+6+5+4+3+1+0+13+1+1+0+40+39+16+11+3+1+0+3+0+15+0+7+3+0+12+0+4+2+2+1+0+8+3+0+9+0+1+0+17+14+7+6+5+2+1China National Police

Citic offshore Helicopter

Taiwan NASC

China Flying Dragon

China Southern Helicopters

Beijing Reignwood GA

State Grid

Ministry of Transport

Sichuan Xilin Fengteng

China Eastern GA

Guangzhou Suilian Helicopter

Hubei Tongcheng GA

Beijing Capital Helicopter

Hainan Sanya Yalong GA

Tianjin Top GA

Civil Aviation Academy

Shanghai Kingwing

Tuofeng GA

Chongqing GA

Henan Yongxiang GA

Henan Guan Chen GA

Shanghai Heli

Anyang Aero

Beijing Tian Xin Ai GA

Government Flying Service

Guangdong Bai Yun GA

Shanghai Skyway

Beidahuang GA

Tangshan Lianwang

GaoXiang Shandong GA

Hong Kong Aviation Club

Hubei Yinyan GA

Qingdao Helicopter

Shandong GA

Sky Shuttle Helicopters

Wuhan Helicopter

Yunnan FengXiang

Zhejiang Huayi GA

Zhongshan Eagle GA

9

8

6

3

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201520

Top Operator Fleets by Model – Greater China

Citic

Offs

hore

He

licop

ter

Stat

e Gr

id

Beijin

g Re

ignw

ood

GA

Min

istry

of

Tran

spor

t

Guan

gzho

uSu

lian

Helic

opte

r

Chin

a Na

tiona

lPo

lice

Chin

a Fl

ying

Drag

on

Chin

a So

uthe

rnHe

licop

ters

Sich

uan

Xilin

Feng

teng

Hube

iTo

ngch

eng

GA

Chin

a Ea

ster

n GA

Total

AgustaWestlandAW109 7 2 9AW119 2 2AW139 7 1 8

AirbusHelicopters

AS350 3 7 7 1 7 25EC155 3 15 18EC225 1 9 1 4 15EC135 6 1 1 8AS332L 1 1AS332L1 6 6AS332L2 1 1AS365 4 10 1 15EC120 2 1 1 1 5

AvicopterAC301 1 1AC311 4 4AC312 1 1

BellHelicopter

Bell 205 16 16Bell 206 3 1 6 3 13Bell 212 1 2 3Bell 407 9 4 1 14Bell 429 3 2 5

Boeing Rotocraft BV234 3 3Enstrom EN480 3 3

HarbinZ-11 2 1 3Z-9 3 2 2 7

Kamov KA-32 2 8 10Mil Mi-26 2 2

RobinsonR22 3 2 4 9R44 6 5 5 4 3 23R66 1 2 3

Schweizer S-300 1 8 7 3 2 4 25

Sikorsky

S-76A 4 1 5S-76A++ 1 1S-76B 2 2S-76C+ 2 4 6S-76C++ 7 4 6 17S-76D 8 8S-92 3 9 1 13

Total 57 57 31 22 22 21 21 20 17 14 14 14 310

57+57+31+22+22+21+21+18+17+14+14+1457 57

22 22 21 21 20 17 14 14 14

Taiw

an N

ASC

31

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 21

Fleet Breakdown by Mission & OEM – Greater China

Mul

ti-M

issi

on

Offs

hore

Oper

atio

ns

SAR

Coro

pora

te

EMS

Flig

ht Tr

aini

ng

Law

Enf

orce

men

t

Char

ter

Priva

te

100+27+25+23+21+16+13+12+11AgustaWestland 11 2 16 11 1 41Airbus Helicopters 95 1 31 12 23 4 2 5 173Avicopter 9 6 15Bell Helicopter 75 4 4 12 10 2 3 110Boeing Rotocraft 1 2 3Brantly 2 2Enstrom 13 4 3 20Guimbal 2 2

Harbin 6 1 3 10Kamov 10 2 12MD 7 1 1 9Mil 11 11Robinson 170 47 10 3 8 8 246Schweizer 34 20 1 1 56Sikorsky 2 34 16 2 54Total 446 79 68 57 53 29 14 11 7 764

446

79 68 57 53 29 14 11 7

Total Fleet Age Distribution764 in Total

Year of Manufacture

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

120

100

80

60

40

20

0

Total

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201522

Si Rui, General ManagerDepartment of Strategic Planning

Eastern General Aviation (EGAC), a subsidiary of China Eastern Airlines was developed from China General Aviation, which in turn was developed from the No. 1 Civil Aviation Flying Corps, established in 1952. The company’s mission is to develop China’s general aviation business.

Since 1998, EGAC’s scale and footprint has changed after a series of reforms and adjustments in the market. Currently, the company is focused on offshore oil and gas exploration, and an anticipated expansion of its aircraft management business. Although the company offers some land-based services, EGAC focuses mainly on offshore operations, located mostly in the Bohai Sea area, with bases in Tianjin and Shandong. With more than thirty years of experience, the company is confident that it fully meets its customer’s requirements, especially with its offshore oil & gas services and risk management capabilities.

“Although the Bohai Sea area has relatively low oil and gas production compared to the South China Sea, our operational and safety management control capabilities are on par with international operation standards,” said Si Rui, EGAC’s General Manager, Department of Strategic Planning. “Our services include aerial mapping, security patrol and protection of oil and gas pipelines for energy companies; emergency rescue, aerial forest fire protection, aviation touring, and aircraft management.”

For offshore oil and gas services, EGAC’s major competitors are Zhuhai Helicopter Company and COHC (CITIC Offshore Helicopter Co., Ltd.). While safety is fundamental, advanced safety concepts and a culture of safety management are equally important. Since the late 1990’s, EGAC has been cooperating

with international oil and gas suppliers, and integrating their systems knowledge and concepts into its own safety culture.

“Zhuhai Helicopter and COHC compete with each other, and each has subsequently carved out its own market share in the South China Sea. If EGAC were to enter the fray, it would mean greater stress and risks. From the viewpoint of the customers, the goal is to achieve a competitive balance in offshore oil and gas supplies. Alternately, customers do not want to see a monopoly in this market so, while keeping a healthy level of sufficient competition, the three companies pursue excellence in our respective competitive advantages. The present competitive environment enables us to avoid price wars. Compared with Zhuhai Helicopter and COHC, we do not have an advantage in scale, but we can continue to pursue excellence in our own market segments,” says Si.

When asked about their heritage and operational culture, Si remarked that in 1999 EGAC recruited experienced foreign captains, who trained their pilots as they conducted operations. It was during this period that they were introduced to an advanced concept of flight safety and standards.

“Since 2000, in order to standardize operations, we ensured that each pilot receives overseas simulator training twice a year. Now that there is a simulator training center in Zhuhai, most of our pilots are trained domestically. Because some aircraft types are still not available in China, a small number of our pilots are still trained overseas,” said Si, who continued, “Since 2010, we adopted the EVXP system, an enhanced health and usage monitoring system, to improve our safety management. EVXP indicates whether the operations made by the pilots during a flight comply with standard procedures. Additionally, we have

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 23

adopted the HUMS system for our helicopters, another primary measure for us to monitor flight quality. In 2012, we received Safety Management System (SMS) certification, a first for any general aviation company in China.”

The journey to developing China’s General Aviation industry is no easy route. Si noted that EGAC has faced stressful times. “The key challenges we are facing include reduced petroleum revenue and the contradiction in available human resources, such as pilot and maintenance personnel. In terms of numbers, we have a relatively large number of maintenance personnel, but the portion of high-tech trained staff is still relatively low. Another issue is the need to renew the fleet with new aircraft. All of these issues have some impact on us,” noted Si.

In addressing these challenges, expansion is not seen as a competitive advantage to pursue. “We will wait for an upturn in the market, while continuing to pursue excellence in all we do. Further, during this down period, we will increase our investment in training to resolve the issues in our human resource structure. Finally, we aim to become an integrated service provider with advanced technology, so we are enhancing our management and flight training business, and initiating market-oriented reforms for our maintenance personnel,” said Si.

EGAC has developed their thirteenth five year plan. In the next five years, it has to replace older aircraft in their fleet with new ones, and enlarged the fleet from 13 to 16 aircraft. Additionally, the company aims to further expand their leasing business. “We estimate that, five years from now, the total quantity of our fleet, including aircraft we acquire, lease, and manage, will reach a total of twenty-four or -five. On a side note, I expect the petroleum business to continue to linger at a low point in 2016. So we’ll have to watch out for that,” Si noted.With China on the forefront of a booming general

aviation market, EGAC and other players are keeping a keen eye on easing regulations and investment opportunities. With enough patience and dedication from the players, China’s general aviation is set to rival that of other developed countries soon - perhaps just over the horizon.

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201524

Pre-owned Additions

Deductions

New Deliveries

38+29+14+9+5+5+G

31+23+19+19+4+4+G

45+19+11+8+6+4+2+3+2+GMD 3 (14%)

Robinson 6 (29%)

Avicopter 1 (5%)

Schweizer 1 (5%)

Airbus Helicopters 8 (38%)

Robinson 5 (19%)

Enstrom 1 (4%)

MD 1 (4%)

Schweizer 5 (19%) Bell Helicopter 8 (31%)

Airbus Helicopters 6 (23%)

Robinson 54 (45%)

Airbus Helicopters 23 (19%)

Bell Helicopter 13 (11%)

Sikorsky 11 (9%)

Enstrom 7 (6%)

AgustaWestland 5 (4%)

Kamov 3 (2%) Schweizer 2 (2%)

Kamov 2 (9%)

Avicopter 3 (2%)

+121

+21

-26

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 25

Additions & Deductions Per Model116 in total

Deductions (-26)

New Deliveries (+121)

Pre-owned (+21)

3

33

3

3

3

4

316

2

2

111

11

1

12

7

1111

1

1

3

2

18

-3-2

-5

35

-1

-1

-3

-5

-1

-1

-2-2

AW139AW119

AS350EC225EC120AS365EC135EC155EC130AS355BO105SA315

AC311

EN480

Bell 407Bell 429Bell 206

KA-32

S-300

R44R22R66

MD 520MD 500MD 900

S-76DS-92

+4+5

+5+5

5+2

-2+1

1+6

Agus

ta

Wes

tland

Airb

us

Hel

icop

ters

Avic

opte

rBe

ll H

elic

opte

rEn

stro

mM

DRo

bins

onSc

hwei

zer

Siko

rsky

+5+2

5

Kam

ov

8

GREATER CHINA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201526

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 27

JAPAN

Japan has the 3rd largest helicopter fleet in the Asia Pacific region – 762 in total. The country’s geographic characteristics make it a natural place for helicopter operations. The archipelago comprises four main islands and over 2,000 underlying islands across the country’s territory and the Japan Sea.

Japan also has the largest fleet of AgustaWestland and Airbus Helicopters in the Asia Pacific region: Japan’s fleet represents 29% of the total Asia Pacific AgustaWestland fleet and 21% of the total Asia Pacific Airbus Helicopters fleet. When including Bell Helicopter and Robinson, among these 4 manufacturers, 93% of the Japanese fleet of helicopters is represented.

The only manufacturers to succeed in growing their Japanese fleets in 2015 were Sikorsky (+29%) and AgustaWestland (+6%) with the total Japanese fleet actually contracting 3% in 2015. This phenomenon occur as a number of older piston helicopters (primarily R22/44s), single-engine (Bell 206s & AS350s primarily) and medium size helicopters (Bell 212s & AS365s primarily) were all retired and replaced by fewer, new helicopters like the S-76D and AW139. Eight S-76Ds entered service in 2015 with the Japanese Coast Guard (JCG) for SAR, as well as four AW139s, two of which are with the Japan National Police Agency (JNPA). In total there were 29 new deliveries in 2015 and 2 pre-owned helicopters delivered, but 51 helicopters left the Japanese fleet through 2015, yielding a net growth of a negative 20 helicopters.

The Japanese fleet is dominated by medium and light twin size helicopters – 58% of the fleet – with the fleet involved primarily in multi-mission, EMS, law enforcement, and SAR applications, these missions comprising 76% of the fleet. Japan’s climate and geography make the country prone to large scale natural disasters and extreme weather conditions, in addition to having many active volcanoes, frequent earthquakes, and typhoons. Such characteristics lend themselves to multi-mission and para-public operations, which in turn require the use of heavy and medium-sized helicopters. Medium-sized helicopters are also favoured by the considerably large corporate segment.

There are 237 operators in the country, many of which are corporations and private users operating their helicopters independently. However, Japan’s 5 largest helicopter operators represent almost 37% of the total fleet, performing a wide variety of missions including EMS, SAR, disaster relief, charter services, industrial utility, aerial photography, electronic news gathering, and other activities. The biggest operator is Aero Asahi whose largest shareholder is Toyota Motor Corporation. Aero Asahi has a very diverse fleet including 14 different helicopter types, with the largest types being AS350s and AS355s. The 2nd largest operator is Nakanihon Air Service, part of All Nippon Airways Co., Ltd. It too has a very diverse fleet with 12 types, though the largest types are EC135s and AS350s. The remaining 3

762 in Total

operators in the Top 5 are the Prefectural Police Departments, JCG and JNPA operating AW139s & Bell 412s, AW139s & S-76Ds and AW109s respectively.

SAR and disaster relief operations are performed primarily by prefectural authorities throughout the archipelago, using advanced medium to heavy sized helicopters. Medium-sized helicopters represent 37% of the total Japanese fleet. The heavy and medium helicopter segments’ popularity in Japan is attributed to the operational needs of these para-public missions. Light single and twin-engine helicopters also hold a large market share representing 41% of the fleet. There are 147 piston-engine helicopters in Japan representing 19% by number, but only 1% by replacement cost.

Airbus Helicopters holds 45% of the market followed by Robinson with 20%, and Bell Helicopter with 17%. AgustaWestland make up 11% of the market followed by Sikorsky with 4%.

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201528

JAPAN

67+0 78+0 65+0 100+0 18+00+62 0+65 0+66 0+100 0+18

100+0 47+0 45+0 39+0 28+0 26+0 20+0 0+0 1+00+98 0+44 0+43 0+37 0+30 0+24 0+19 0+1 0+1

34+0 100+0 53+0 2+0 3+0 1+0 14+0 56+0 5+0 17+00+36 0+100 0+48 0+2 0+3 0+1 0+14 0+53 0+4 0+19Net Fleet Growth by Mission

Net Fleet Growth by Size Category

Net Fleet Growth by OEM

Agus

taW

estla

nd

Airb

us H

elic

opte

rs

Bell

Helic

opte

r

Enst

rom

Kam

an

Kam

ov MD

Robi

nson

Schw

eize

r

Siko

rsky

Mul

ti-M

issi

on

Corp

orat

e

EMS

Law

Enf

orce

men

t

SAR

Priva

te

Flig

ht Tr

aini

ng

Char

ter

Offs

hore

Ope

ratio

ns

Pist

on

Sing

le

Ligh

t Tw

in

Med

ium

Heav

y

130

87

32

159

52415

132

149

4

31151

340

149

82

342

310

115 109

309

107 105 10050

1

3067

9345

11

2972

159 155

281

23

164147 157

281

22

155

2015 (762)

2014 (782)

2015 (762)

2014 (782)

2015 (762)

2014 (782)

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 29

JAPAN

Breakdown by Size Category762 in Total

Breakdown by Mission762 in Total

Breakdown by OEM Fleet Size

45+20+17+11+4+2+1+G

41+14+14+13+8+6+4+GHeavy 22 (3%)

Sikorsky 31 (4%)

Piston 147 (19%)

Bell Helicopter 130 (17%)

Law Enforcement93 (12%)

SAR 72 (9%)

Private 45 (6%)

Flight Training 29 (4%)

Single 155 (20%)

Robinson 149 (20%)

Corporate 107 (14%)

EMS105 (14%)

Light Twin 157 (21%)

Airbus Helicopters340 (45%)

Multi-Mission 311 (41%)

Medium 281 (37%)

MD 15 (2%)

56+18+14+9+1+1+1+GAirbus Helicopters(56%)

BellHelicopter(14%)

Sikorsky (9%)

MD (1%) Robinson (1%)

Others (1%)

Replacement Cost (USD)

AgustaWestland (18%)

AgustaWestland 87 (11%)Others 10 (1%)

Note: Multi-Mission includes one charter and one offshore operations.

762 $4,198M

Multi-Mission41%Turbine

81%

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201530

JAPAN 44+41+1+184+69+51+43+26+24+8+6+6+6+4+4+4+3+1Breakdown by Helicopter Model – Turbine Only615 in Total

AW139 44

AS350

AS355 26

EC130 6

BO105 4

AW109 41

EC135 6984

EC145 24

SA315 6

EC120 3

AW119 1

AS365 51

EC225 8

AS332L 4

AS332L2 1

Bell 412 57

Bell 430 12

Bell 407 4

Bell 212 2

Bell 205 11EN480

R66 6

MD 900

S-76D 11

K-Max 3KA-32 1

S-76C++ 4

MD 500

S-76C+ 6

S-76C 3

MD 600 6 113

1

S-76B 4

S-76A+ 2S-92

S-333

1

1

AW101 1

BK117 43

AS332L1 7

EC155 4

Bell 206 36

Bell 204 7Bell 427 6

Bell 429 4

Bell 214 1

AgustaWestland87 (14%)

Airbus Helicopters 340 (55%)

Bell Helicopter130 (21%)

Enstrom 1

MD 15 (2%)

Robinson 6 (1%)

Kaman 3Kamov 1

Sikorsky 31 (5%)

Schweizer 1

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 31

JAPAN76+61+53+49+42+27+24+18+17+16+12+12+10+10+9+7+7+6+6+5+4+4+4+4+3+3+3+3+3+3+3+3+3+3+3+3 3+3+3+3Breakdown by OperatorTop 40 – Out of 237 Operators (2 or more helicopters)

Aero Asahi

Nakanihon Air

Prefectural Police Departments

Japan Coast Guard

National Police Agency

Toho Air Service

Akagi Helicopter

Nishi Nihon Air Services

Hirata Gakuen

All Nippon Helicopter

Alpha Aviation

Shin-Nihon Helicopter

Tohoku Air Service

Tokyo Fire Department

Ogawa Air

Kagoshima Air

Shikoku Air

Central Helicopter

Rosen Air

Hokkaido Air

Asahi Shimbun

Honda Airways

S.G.C. Saga Aviation

Sato Jitsugyo

Auto Panther

Chunichi Shimbun

Dai Ichi Air

DHC

Fukuoka Fire Department

Gov’t of Japan - Min of Transport

Hideyuki- Private

Japan Digital Laboratory

Mainichi Newspapers

Ministry of Land & Infrastructure

Nihon Flight Safety

Noevir Aviation

Shizuoka Air

Teikyo Daigaku

Tsukuba Aviation

Yomiuri Shimbun

76

61

53

49

42

27

24

18

17

16

12

10

12

10

9

7

6

7

6

5

4

4

4

4

3

3

3

3

3

3

3

3

3

3

3

3

3

3

3

3

6

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201532

JAPAN

76+61+53+49+42+27+24+18+17+16Top Operator Fleets by Model

Aero

Asa

hi

Pref

ectu

ral P

olic

eDe

partm

ents

Natio

nal P

olic

eAg

ency

Akag

i Hel

icop

ter

Hira

ta G

akue

n

Naka

niho

n Ai

r

Japa

n Co

ast

Guar

d

Toho

Air

Serv

ice

Nish

i Nih

on A

irSe

rvic

es

All N

ippo

nHe

licop

ter

Total

AgustaWestlandAW101 1 1AW109 3 20 23AW139 1 10 17 4 3 35

Airbus Helicopters

AS332L 2 1 1 4AS332L1 2 3 5AS332L2 1 1AS350 17 16 8 5 5 1 52AS355 10 5 5 20AS365 2 1 7 5 1 7 23BK117 1 8 5 1 2 17EC135 20 4 5 3 13 6 51EC145 8 1 4 13EC155 2 1 1 4EC225 5 5SA315 6 6

Bell Helicopter

Bell 204 2 2 2 6Bell 206 9 3 4 3 2 7 28Bell 212 2 2Bell 412 3 1 12 5 4 2 27Bell 427 3 3Bell 429 1 1 2Bell 430 6 6 12

Kaman K-Max 3 3Kamov KA-32 1 1MD MD 500 3 3

MD 900 9 9Robinson R22 3 3

Sikorsky

S-76B 2 2S-76C 2 1 3S-76C+ 4 1 1 6S-76C++ 1 1 2S-76D 11 11

Total 76 61 53 49 42 27 24 18 17 16 383

7661

53 49 4227 24 18 17 16

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 33

JAPAN

100+40+40+35+24+15+5+1+1

Total Fleet Age Distribution762 in Total

Year of Manufacture

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

45

40

35

30

25

20

15

10

5

0

Mul

ti-M

issi

on

EMS

SAR

Flig

ht Tr

aini

ng

Char

ter

Offs

hore

Op

erat

ions

Corp

orat

e

Law

Enf

orce

men

t

Priva

te

AgustaWestland 9 11 5 40 22 87Airbus Helicopters 184 26 67 31 27 4 1 340Bell Helicopter 71 5 24 20 9 1 130Enstrom 1 1 2Kaman 3 3Kamov 1 1MD 6 3 6 15

Robinson 25 56 1 38 29 149Schweizer 1 1 2 4Sikorsky 8 5 2 2 14 31Total 309 107 105 93 72 45 29 1 1 762

309

107 105 9372

4529 1 1

Fleet Breakdown by Mission & OEM

Total

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201534

JAPAN

Pre-owned Additions

Deductions

New Deliveries

50+50+G41+29+24+2+2+2+G

45+28+17+7+3+GAgustaWestland 1 (50%)Robinson 1 (50%)

Robinson 13 (26%)

AgustaWestland 1 (2%)Sikorsky 1 (2%)

Schweizer 1 (2%)

Airbus Helicopters 15 (29%) Bell Helicopter 20 (39%)

Airbus Helicopters 13 (45%)AgustaWestland 5 (17%)

Robinson 2 (7%)

Sikorsky 8 (28%)

Bell Helicopter 1 (3%)

+29

+2

-51

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 35

JAPAN

Additions & Deductions Per Model-20 in total

Deductions (-51)

New Deliveries (+29)

Pre-owned (+2)

AW139

AW109 -1

-1

-1

-2

-3

-7

-10

-6

-7

-3

-4

-4

Agus

ta

Wes

tland

Airb

us

Hel

icop

ters

Bell

Hel

icop

ter

Robi

nson

Schw

eize

rSi

kors

ky

EC135

EC155

BK117

EC225

AS365

AS350

SA315

AS332L1

Bell 412

Bell 206

Bell 212

R66

R22

R44

S-300

S-76D

S-76B

+5-2

-1+7

-19

-10

-1

-1

8

1

1

1

1

2

3

1

4

1

1 1

4

2

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201536

SOUTH KOREA

The South Korean Helicopter fleet numbered 216 helicopters at year-end 2015 with para-public operations such as SAR, firefighting, marine patrol, and police work being the dominant mission category in the country.

Despite its developed economy and advanced aviation industry, the Korean helicopter fleet has not grown much in recent years. In 2015 the Korean fleet remained unchanged with no significant growth drivers and a net 4 helicopter additions.

In the para-public segment, 50% of the multi-mission fleet is used by the government for firefighting operations during the Korean summer and dry seasons. These helicopters are operated by Korean provincial authorities and ministries, and in many cases are leased from local operators granted with government contracts.

The Ministry of Forestry operates a large fleet of 47 helicopters, of which 30 are Russian-built Kamov helicopters, many having been in service for over 15 years. In 2015, the Ministry placed an order for several new Surion helicopters from Korean Aerospace Industries (KAI). The Surion was initially developed by KAI together with Airbus Helicopters to provide an indigenous option for replacing some of South Korea’s military helicopters as well as meeting other national rotary requirements.

Airbus Helicopters make-up 25% of the market alongside Russian Helicopters, Mil, and Kamov, which combined represent nearly 30% of the fleet. Out of all the Asia Pacific countries, Russian-designed helicopters in South Korea have the strongest presence in terms of the number of helicopters in operation.

Multi-mission operations are the largest mission segment in the country (66%) followed by helicopters used by large corporations for the transportation needs of their senior management. This corporate segment represents 13% if the total fleet.

216 in Total

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201536

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 37

6+0 55+0 14+0 100+0 13+00+6 0+56 0+16 0+100 0+13

12+0 54+0 44+0 3+0 0+0 2+0 52+0 8+0 9+0 5+0 23+00+15 0+55 0+44 0+3 0+1 0+2 0+51 0+8 0+9 0+4 0+24Net Fleet Growth by Mission

Net Fleet Growth by Size Category

Net Fleet Growth by OEM

Agus

taW

estla

nd

Airb

us H

elic

opte

rs

Bell

Helic

opte

r

Enst

rom

Hille

r Airc

raft

KAI

Kam

ov MD Mil

Robi

nson

Siko

rsky

Mul

ti-M

issi

on

Corp

orat

e

SAR

Law

Enf

orce

men

t

Flig

ht Tr

aini

ng

Offs

hore

Ope

ratio

ns

EMS

Pist

on

Sing

le

Ligh

t Tw

in

Med

ium

Heav

y

12

5444

3 2

52

8 9 5

2315

5544

3 1 2

51

8 9 4

24

4 32

15

2822

4 33

15

2821

614 13

55

616 13

56

138142

124 125

2015 (216)

2014 (212)

2015 (216)

2014 (212)

2015 (216)

2014 (212)

SOUTH KOREA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201538

63+13+10+8+3+2+1+G

25+24+20+11+7+4+4+2+1+1+1+G

Breakdown by Size Category216 in Total

Breakdown by OEM Fleet Size

Breakdown by Mission216 in Total

Piston 6 (3%)

Flight Training 4 (2%)

Offshore Operations 3 (1%)

Heavy 13 (6%)

EMS 3 (1%)

Light Twin 16 (7%)

Law Enforcement 15 (7%)SAR 21 (10%)

Single 56 (26%)

Corporate 28 (13%)

Mil 9 (4%)

Robinson 4 (2%)

MD 8 (4%)

Bell Helicopter 44 (20%)

Sikorsky 24 (11%)

AugustaWestland 15 (7%)

KAI 2 (1%)

Enstrom 3 (1%)

Airbus Helicopters55 (25%)

Kamov 51 (24%)

Medium 125 (58%) Multi-Mission 142 (66%)

27+26+21+9+9+4+3+1+GAirbus Helicopters

(27%)

Sikorsky (26%)Kamov (21%)

BellHelicopter(9%)

AugustaWestland(9%)

Mil (4%) KAI (3%)

MD (1%)

Replacement Cost (USD)

Hiller Aircraft 1 (1%)

Note: The market share of Enstrom, Hiller Aircraft and Robinson’s replacement cost are less than 1%.

216 $1,292M

Turbine 97%

Multi-Mission66%

SOUTH KOREA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 39

11+2+1+116+11+10+6+6+3+1+1+125+8+6+2+2+122517+16+37+5+3+3+2+2+1+1Breakdown by Helicopter Model – Turbine Only210 in Total

AW139 11

AS350 16

Bell 206 25

S-76C+ 7

EC135 6

Bell 430 2

S-76D 2

S-58 1

AW109 2

AS365 11

Bell 214 8

S-61 5

EC155 3

Bell 230 1

S-76C++ 2

AW119 1

BK117 10

Bell 412 6

S-76B 3

EC145 1

SW-4 1

B0105 6

Bell 407 2

S-64 3

S-92 1

AS355 1

EN480 2

2

EC225 1

Surion

KA-32 51

MD 500 7MD 520 1

Mi-2 6Mi-8 3

AgustaWestland15 (7%)

Airbus Helicopters 55 (26%)

Bell Helicopter 44 (21%)

Enstrom2 (1%)

KAI2 (1%)

Kamov51 (24%)

MD8 (4%)

Mil9 (4%)

Sikorsky24 (11%)

SOUTH KOREA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201540

47+17+16+15+11+9+8+7+6+6+5+5+5+5+4+3+3+2+2+2+2+2+2+2+2+2+2+1+1+1+1+1+1+1+1+1+1+1Breakdown by Operator51 Operators

47

17

9

6

5

2

2

16

8

5

4

2

2

12

1

15

7

5

3

2

2

12

1

11

6

5

3

2

2

1

1

1

1

1

1

11

1

1

11

1

1

11

1

1

1

1

Gov’t Forestry Department

National Police

Heli Korea

Gov’t Coast Guard

Hongik Air

Sejin Aviation

Tongil Air

Yecheon Astro Space Center

Korean Air Lines

Samsung Techwin

Air Palace

Central SAR 119

UB Air

UI Helijet

Hanseo University

Gyeonggi Fire Department

Seoul Fire Department

Busan Fire Department

Changwoon Aviation

Daegu Metro Fire Department

Deajin Air

Gov’t of South Korea

Incheon Fire Department

Jeollanam-do State Gov’t

LG

POSCO

Woori Aviation

Ace Air

Blue Airline

Chungbuk Fire Department

Chungcheongnam-do

Donghae & Machinery Airlines

EMS Air

Farm & Copter

Gangwon Province

Gangwon-do Fire Department

Hana Air

Hanwha Chemical

Hyundai Motor

Korea Air Express

Korean Broadcasting System

Kyungbuk Fire Department

Munhwa Broadcasting Corporation

National Park Authority

Pearl Korea

Samsung Hospital

SK Telecom

SN Air

Sung Joon Airlines

TransHeli

Uslan Fire Department

1+1+1+1+1+1+1+1+1+1+1+1+1SOUTH KOREA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 41

47+17+16+15+11+9+8+7+6+6+5+5+5+5+4+3+3+2+2+2+2+2+2+2+2+2+2+1+1+1+1+1+1+1+1+1+1+147+17+16+15+11+9+8+7+6+6

Top Operator Fleets by Model

Gov’

t For

estry

Depa

rtmen

t

Heli

Kore

a

Hon

gik

Air

Sejin

Avia

tion

Yech

eon

Asto

Spac

e Ce

nter

Natio

nal P

olic

e

Gov’

t Coa

stGu

ard

Tong

il Ai

r

Sam

sung

Te

chw

in

Kore

anAi

r Lin

es

Total

AgustaWestland

AW109 2 2AW119 1 1AW139 2 4 6

AirbusHelicopters

AS350 4 6 1 11EC155 2 2EC135 1 5 6AS365 4 4BK117 1 1 1 1 4BO105 6 6

BellHelicopter

Bell 206 8 6 2 1 2 19Bell 214 4 2 1 7Bell 407 1 1Bell 412 1 3 4

KAI Surion 2 2Kamov KA-32 30 3 8 41

MDMD 500 2 1 3MD 520 1 1

MilMi-2 5 5Mi-8 3 3

RobinsonR22 1 1R44 1 1

Sikorsky

S-61 4 4S-64 3 3S-76C+ 3 1 4S-92 1 1

Total 47 17 16 15 11 9 8 7 6 6 142

47

17 16 15 11 9 8 7 6 61+1+1+1+1+1+1+1+1+1+1+1+1SOUTH KOREA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201542

100+40+30+21+5+4+4Fleet Breakdown by Mission & OEM

TotalAgustaWestland 6 4 2 3 15Airbus Helicopters 35 10 9 1 55Bell Helicopter 32 2 1 7 1 1 44Enstrom 1 2 3Hiller Aircraft 1 1KAI 2 2Kamov 43 8 51MD 8 8Mil 5 3 1 9Robinson 3 1 4Sikorsky 9 11 1 3 24Total 142 28 21 15 4 3 3 216

Mul

ti-M

issi

on

Copo

rate

SAR

Law

Enfo

rcem

ent

Offs

hore

Oper

atio

ns

Flig

ht Tr

aini

ng

EMS

142

33415

2128

Total Fleet Age Distribution216 in Total

0

12

4

2

14

6

16

8

18

20

10

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0 2+0 1+0 1 0 0 1 3 0+0 0+0 0 0 0 0 0 0+1 0+1 0 1 1 0SOUTH KOREA

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 43

0 2+0 1+0 1 0 0 1 3 0+0 0+0 0 0 0 0 0 0+1 0+1 0 1 1 0Additions & Deductions Per Model4 in total

3AW139

KA-32

UH-12+1

R22

S-76B

BO105

AS365+1

Bell 206

Bell 214

2

-1

-1

-1

-1

1

1

1

-1-1

+1

Deductions (-4)

New Deliveries (+3)

Pre-owned (+5)

Agus

ta

Wes

tland

Hill

erAi

rcra

ftKa

mov

Robi

nson

Siko

rsky

Airb

us

Hel

icop

ters

Bell

H

elic

opte

r

+3

SOUTH KOREA

In the business aviation sector, helicopter operators have been hit especially hard by the current struggles of the global oil and gas industry. Many operators have chosen therefore to reduce risks by leasing helicopters, instead of tying up capital resources and taking on even greater risks by purchasing one. In choosing a leasing company, it is imperative that one find a well-capitalized company with solid assets, headed by entrepreneurial managers who know the helicopter business and for whom leasing helicopters is the core business. No company fits the bill better than Waypoint Leasing, the world’s largest independent helicopter leasing company.

Waypoint was founded in 2013 by a team of helicopter industry veterans, most of whom had firsthand experience as helicopter operators. Waypoint’s three major long term investors are MSD Capital, L.P., Quantum Strategic Partners, and Cartesian Capital Group LLC. Collectively these three fund investors lead the way, giving the Ireland-based Waypoint financial depth and reliability to face any challenges that may show up on the world economy’s radar. The company now has $1.4 billion in helicopter assets, representing a fleet of over 120 helicopters which are leased to operators in more than

Vice PresidentSales and Relationship Management, Asia

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 201544

20 countries around the world. Its clients value the integrity, experience, and commitment of Waypoint’s leadership team and financial sponsors. Over the years the company has expanded from its roots in Ireland to open offices in Australia, Brazil, Singapore, South Africa, and the UK, making it more easily accessible to its clients around the world.

Philip Stransky, Waypoint’s Vice President of Sales and Relationship Management, Asia, leads the company’s work in the Asia region. Philip came to the helicopter leasing business when he took a year off to attend business school after nearly a decade with SEACOR, principally in the marine business. While studying at MIT, he was regularly in touch with Ed Washecka, CEO of Waypoint, and his team, who were busy raising capital and getting Waypoint Leasing off the ground. Philip says, “Ed offered me the unique opportunity to return to Singapore, where I had spent three and a half years with SEACOR, to help catapult Waypoint’s efforts in the region with the goal of becoming the largest independent helicopter leasing company. By late 2014, when I came back to Singapore, Waypoint had already successfully negotiated and signed a number of leases in Asia. Our goal was then to provide current and potential customers with a local contact and the ability to act immediately and follow up swiftly. Being on the ground has been tremendously successful, giving us the ability to work on opportunities with regional clients and to ensure that we provide exciting solutions in a time sensitive manner.”

As a multi-national (France, USA, and UK) Philip grew up fascinated by aviation, clocking up a good number of air miles. He was given his first taste of the helicopter business in 2009 which only further increased his longing to be in the industry. “The opportunity of joining Waypoint was the ideal way of matching my personal passion for aviation with a background in business development,” says Philip.

Philip and his senior management team bring clients decades of experience, giving them a unique insight into the customers’ needs for high quality aircraft, innovative financing options, and long-standing relationships with service providers. Philip approaches the company’s role from the perspective of the operator and the end user. Waypoint’s leasing solutions address not only the present needs of the client, but also anticipate the cyclical realities of the helicopter industry, positioning Waypoint to be able to address the needs and challenges that lie just beyond the horizon as well.

Waypoint’s expertise is firmly fixed on the helicopter market. The company’s fleet of technologically advanced helicopters include aircraft manufactured by Finmeccanica (formerly AugustaWestland), Bell Helicopter, Airbus Helicopters, and Sikorsky. Its fleet ranges from heavy to medium to light-twin models,

ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2015 45