Embed Size (px)

Citation preview

Aligninganorganisation’ssustainability

needsanditsstakeholders’requests:

TheMaterialityBalancedScorecard

by

MireiaGuix

SubmittedfortheDegreeofDoctorofPhilosophy

SchoolofHospitalityandTourismManagement

FacultyofArtsandSocialSciences

Supervisors:XavierFont,JasonStienmetzandMariaJesúsBonilla-Priego

©MireiaGuix2019

II

DeclarationoforiginalityThis thesisand thework towhich it refersare theresultsofmyownefforts.Any ideas,data,

imagesortextresultingfromtheworkofothers(whetherpublishedorunpublished)arefully

identifiedassuchwithintheworkandattributedtotheiroriginatorinthetext,bibliographyorin

footnotes.Thisthesishasnotbeensubmittedinwholeorinpartforanyotheracademicdegree

orprofessionalqualification.IagreethattheUniversityhastherighttosubmitmyworktothe

plagiarismdetectionserviceTurnitinUKfororiginalitychecks.Whetherornotdraftshavebeen

so-assessed, the University reserves the right to require an electronic version of the final

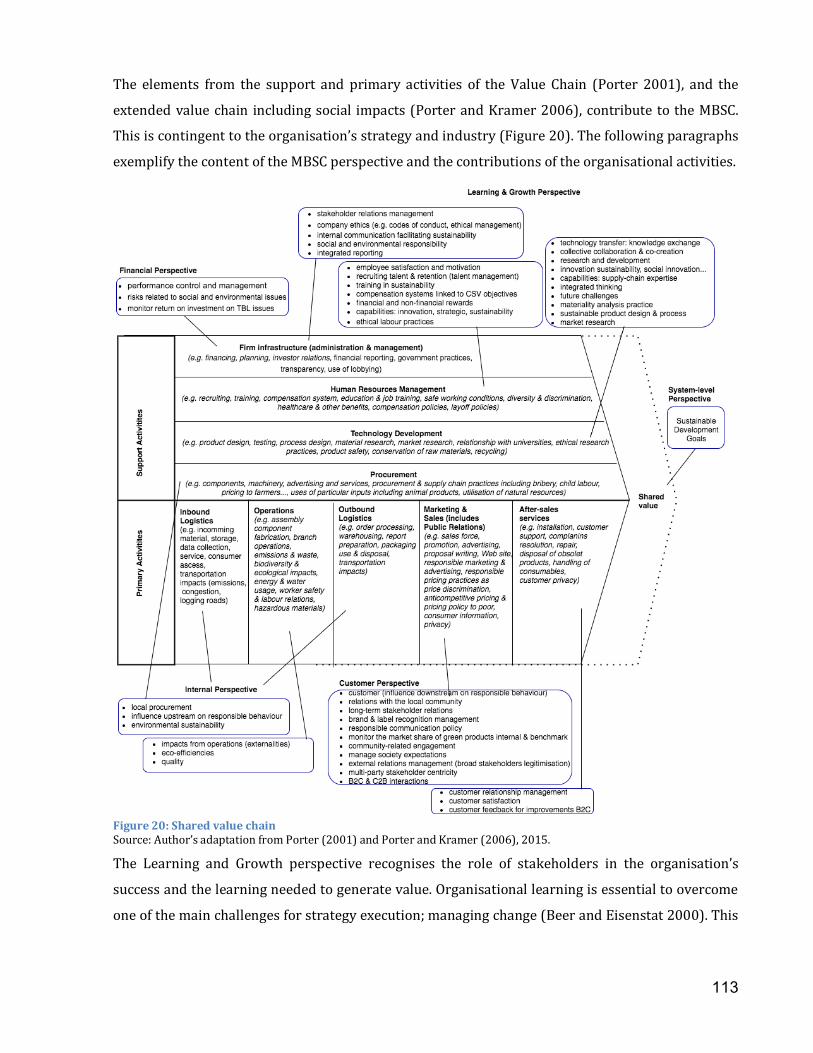

document(assubmitted)forassessmentasabove.

Signature:

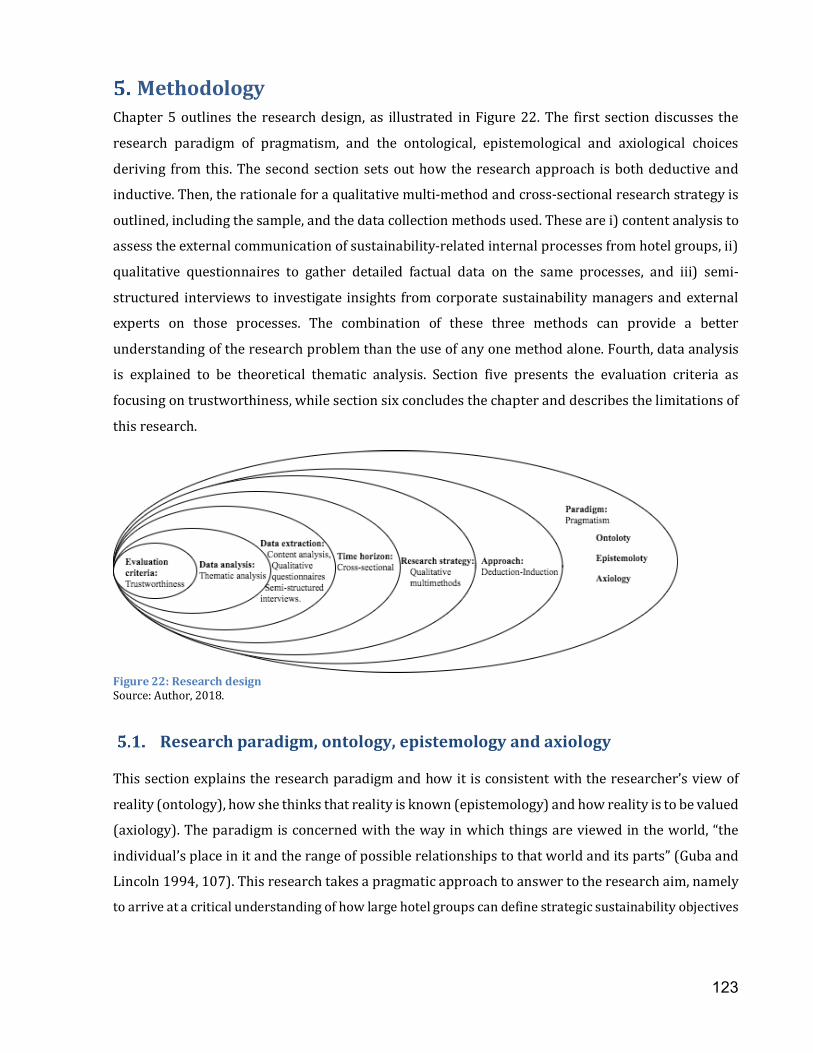

MireiaGuixNavarrete

Date:7thMarch2019

Theauthorconfirmsthattheworksubmittedisherown,exceptwhereworkwhichhasformed

partofjointlyauthoredpublicationshasbeenincluded.Thecontributionofthecandidateandthe

otherauthorstothisworkhasbeenexplicitlyindicated.Appropriatecredithasbeengiveninthe

thesiswherereferencehasbeenmadetotheworkofothers.

Publicationstatusandcollaboratorcontribution

Materialcontainedinchapter2ofthisthesisappearsinajointlyauthoredpublishedpaperand

twojointlyauthoredpublishedbookchapters:

• Literaturereviewrelatedtothesharedvalueframework:

o Font,X.,Guix,M.andBonilla-Priego,M.J.(2016)Corporatesocialresponsibilityin

cruising:Usingmaterialityanalysistocreatesharedvalue.TourismManagement,

53,175-186.Doi:10.1016/j.tourman.2015.10.007

• Literaturereviewrelatedtocorporatesocialresponsibility:

o Font,X.,Bonilla,MJ.andGuix.M.Chapter5Corporatesocialresponsibilitiesinthe

cruisesector,86-105.InDowling,R.andWeeden,C.(2016)HandbookofCruise

ShipTourism,2ndEd.Wallingford,UK:CABI.ISBN:9781780646084.

o Font,X.&Guix,M.Chapter37CorporateSocialResponsibilityintourism,567-580.

In Cooper C. Gartner, B., Scott, N. & Volo, S. (2018) SageHandbook of Tourism

Management.London,UK:Sage.ISBN:9781526461131.

III

Materialcontainedinchapter3ofthisthesisrelatedtotheAA1000SESPrinciplesappearsina

jointlyauthoredpublishedpaper:

• Guix,M,Bonilla-Priego,MJ.andFont,X.(2018)Theprocessofsustainabilityreportingin

international hotel groups: an analysis of stakeholder inclusiveness, materiality and

responsiveness, Journal of Sustainable Tourism, 12(7), 1063-1084. Doi:

10.1080/09669582.2017.1410164

Materialcontainedinchapter6and7ofthisthesisappears intwo jointlyauthoredpublished

papersandanindustryreport:

• Publicationofanabridgedversionofthecontentanalysisresults:Guix,M.,Bonilla-Priego,

MJ. and Font, X. (2018) The process of sustainability reporting in international hotel

groups:ananalysisofstakeholderinclusiveness,materialityandresponsiveness,Journal

ofSustainableTourism,12(7),1063-1084.Doi:10.1080/09669582.2017.1410164

• Publication of the interview results on materiality assessment: Guix, M., Font, X. and

Bonilla-Priego,M.J.(2018)Materiality:therationalebehindsustainabilitychoicesinhotel

groups, International Journal of Contemporary Hospitality Management (on-line) Doi:

10.1108/IJCHM-05-2018-0366

• PublicationofajointInfographicwithUNEPshowcasingpreliminaryresultsofthecontent

analysis.

IV

AbstractThisexploratorystudyaims todevelopacriticalunderstandingofhowlargehotelgroupscan

definestrategicsustainabilityobjectives inordertocreatesharedvalue. It isthe firststudy to

conductacomparativeanalysisofthepubliclyavailablesustainabilityreportsfromthe50largest

hotelgroupsintheworld,andtocombinethesewithinterviewresponsesfromasampleoftheir

CorporateSocialResponsibility(CSR)managersandindustrysustainabilityexperts.Therichness

of this data enables the investigation of complex and interdependent factors that influence

strategicsustainabilityplanning,measurement,managementandreporting.

Thisstudyfirstproposesastrategicmanagementframework,theMaterialityBalancedScorecard

(MBSC),todesign,communicateandrealiseCSRstrategiesthatcreatesharedvalue.TheMBSC

combines the Balanced Scorecard, and its sustainability adaptations, with the principles of

inclusiveness,materialityandresponsivenessoftheAA1000StakeholderEngagementStandard.

The MBSC constitutes a theoretical contribution in the emerging literature addressing the

relationshipbetweensustainabilityperformancemanagementandreporting.

This study then attempts to characterise and identify the internal determinants of the CSR

managementandreportingof largehotelgroups, inorder thence toappraise the feasibilityof

implementingtheMBSCwithinthehotelindustry.Thisstudyaddressesthegapintheliterature

abouthotel groups integratingCSRagendas into their organisational strategies, practices and

processes.Itextendsearlierknowledgebyincluding(1)cognitivedeterminants(inrespecttothe

stakeholderculture,thestakeholdermanagementcapability,thestakeholderinfluencecapacity,

as well as the capacity building in respect to stakeholder engagement and materiality), (2)

organisationaldeterminants (CSR rolesand responsibilities, internalaccountabilityand cross-

departmentalcoordination)and(3)technicaldeterminants(integrationofCSRwithintheoverall

business management, and the accuracy and comprehensiveness of the performance

management systems). The research establishes the implications of the determinants for the

mismanagementofsustainabilityandprogresstowardsadoptingthesharedvalueapproach.

The study also critically assesses the adoption by large hotel groups of the inclusiveness,

materialityand responsivenessprinciples that are central to theMBSC. It constitutes the first

study to assess those three principles in tandem, and together with their effect on the

organisations’accountability.Itisalsothefirstempiricalstudyonthedisclosureofandbarriers

to materiality. The study identifies the symbolic adoption of reporting guidelines and

characterises the process of managerial capture of the reporting process. The comparison

between sustainability disclosure, environmental performance and sustainability integration

revealsthatthesustainabilityreportsdonotreflectthemanagementofsustainability,addingto

thebodyofknowledgethatsuggestssustainabilityreportingdoesnotdeliveraccountabilityto

V

stakeholders. Based on these findings, a refined conceptualisation of the principles of

inclusiveness, materiality and responsiveness embedded in the MBSC is proposed to help

organisations to develop shared value strategies, thereby making a practical contribution to

addressthelimitedguidanceavailableontheimplementationofsharedvalue.

Overall,theMBSCisratheridealisticwhencomparedtotherealityofthehotelindustry,because

therequirementtoadoptsharedvaluestrategiesseemsmostlyinfeasible.Nonetheless,theMBSC

maybeapplicableinproactiveorganisationsaslongastheyarewillingi)tocommittoshared

value and ii) to engage with the principles of inclusiveness, materiality and responsiveness

openly,asameanstooperationalisethiscommitment.

VI

AcknowledgementsIwouldliketoexpressmygratitudetoallthosewhograntmethepossibilitytocompletethis

Ph.D.Forthoseunlisted,Ithankyouallforyoureffortandhelpalongtheway.

First and foremost, Iwould like to recognisemy supervisor,Dr. XavierFont,whohasbeena

tremendousmentorforme,notonlyforhisinvaluableinsightintodoingthisresearchbutalsofor

theencouragementandinspirationthatkeptmyresearchpassionalive.IwouldliketothankDr.

MariaJesúsBonillaforherconstantguidance,constructivecriticism,patienceandsupportduring

theresearchprocess.ThankyoutoDr.StephenHenderson.ThankyoutoDr.JasonStienmetz,for

hisinvaluableinsightsonmanagementconcepts.

Iwouldliketoacknowledgethecrucialroleoftheparticipantsinthisresearch.Withoutyou,this

Ph.D. would not have been possible. My sincere appreciation, therefore, goes to those who

participated.

Aspecialthankyoutomyfamily.WordscannotexpresshowgratefulIamtomymotherMªAngels

NavarreteandmyfatherJoanMªGuixforgivingmethestrengthandsupportinthedifficulttimes.

My deepest gratitude goes to Dr. Guillem Roig for his endless support and invaluable advice

throughtheemotionaljourneythathasbeenthisPh.D.

VII

TableofContentsDeclarationoforiginality.............................................................................................................II

Abstract............................................................................................................................................IV

Acknowledgements.......................................................................................................................VI

TableofContents.........................................................................................................................VII

TableofFigures.............................................................................................................................XI

ListofTables................................................................................................................................XIII

IndexofAcronyms.....................................................................................................................XVI

Introduction...........................................................................................................................17

Contextandrationale................................................................................................17

Researchaim,objectivesandscope......................................................................22

Structureofthethesis...............................................................................................24

FromCorporateSocialResponsibilitytoCreatingSharedValue............................28

Sustainablebehaviourbyorganisations.............................................................28

Towardsbeingmorestrategic............................................................................................28

Improvingperformancethroughresponsiblemanagement...............................30

Connectingsocialandeconomicprogress..........................................................38

Pursuingthefuturecompetitivefrontiers....................................................................38

Contestingsharedvalue.........................................................................................................40

Puttingsharedvaluetowork..................................................................................44

Threepathwaystocompetitiveadvantage..................................................................44

Re-evolutionoftheorganisation.......................................................................................46

Influencingtransformationsbeyondtheorganisation..........................................50

Conclusions..................................................................................................................52

Instrumentstoachievesharedvalue..............................................................................54

BSC:aperformancemanagementtool.................................................................55

Advantages....................................................................................................................................56

Challenges......................................................................................................................................63

BSCmodifications:Overcomingthechallenges.................................................66

Toincludesustainabilityissues.........................................................................................72

DeterminingthedesignoftheMBSCfrompreviousscholars’work..............73

Toincreasestakeholders’accountability......................................................................80

AdvantagesandshortcomingsofBSCmodification................................................83

VIII

Sustainabilityreportingtoincreasestakeholderaccountability.................87

Inclusiveness:stakeholderidentificationandengagement................................88

Materialityassessment:amultiplepurposetool......................................................91

Responsiveness:addressingstakeholder’sexpectations.....................................98

Assurance:increasingcredibilityofreports................................................................99

Conclusions................................................................................................................100

MaterialityBalanceScorecard.......................................................................................105

Step1.IntegratingsustainabilityintotheBalancedScorecard..................106

Step2:Recognisingstakeholdervalue(InclusivenessandResponsiveness)109

Step3:Determiningenvironmentalandsocialexposureofstrategicbusiness

units(Materialityassessment)..........................................................................................110

Step4:TheMaterialityBalancedScorecard.....................................................112

DiscussionoftheadvantagesanddisadvantagesoftheMBSC....................118

Conclusions................................................................................................................121

Methodology........................................................................................................................123

Researchparadigm,ontology,epistemologyandaxiology..........................123

Researchstrategy:qualitativemulti-methods.................................................126

Stage1A&B:Contentanalysis........................................................................................129

Stage2:Qualitativequestionnaires...............................................................................133

Stage3:Semi-structuredinterviews............................................................................136

Dataanalysis:thematicanalysis..........................................................................145

Ethicalconsiderationsandevaluationcriteria:Trustworthiness..............151

Credibility...................................................................................................................................151

Transferability..........................................................................................................................154

Dependability............................................................................................................................154

Confirmability...........................................................................................................................155

Methodologicallimitations....................................................................................155

Samplelimitations..................................................................................................................155

Limitationsofcontentanalysis........................................................................................155

Limitationsofqualitativequestionnaires..................................................................156

Limitationsofsemi-structuredinterviews................................................................156

Conclusions................................................................................................................156

Acomparativeanalysisofthedisclosureofsustainabilityreportingprocessesand

sustainabilityintegrationofhotelgroups..........................................................................158

Organisations’profiles...........................................................................................159

IX

Step0.Strategicplanningandinformationsharing.......................................163

Step1.IntegratingsustainabilityintotheBSC.................................................167

Step2.Recognisingstakeholdervalue...............................................................176

Step3.Determiningtheenvironmentalandsocialexposureofstrategic

businessunits.........................................................................................................................188

Acomparativeanalysisbetweensustainabilitydisclosure,environmental

performanceandsustainabilityintegration..................................................................206

TheAccountabilityMatrix..................................................................................................206

Therelationshipbetweensustainabilitydisclosureandenvironmental

performance....................................................................................................................................................209

TheSustainabilityIntegrationMatrix..........................................................................212

Conclusions................................................................................................................219

ThevalueoftheMBSCtowardstransitioningfromreactiveCSRtosharedvalue225

Arehotelgroups’actionsresponsiveCSRorsharedvalue?.........................225

Internalfactorsshapingthehotels’CSRpracticesandthelikelihoodof

implementingtheMBSCintheindustry..........................................................................231

Cognitivebarriersbasedonorganisationalcultureandvalues.....................233

Organisationalbarriersbasedonstructure..............................................................237

Technicalbarriersbasedonsystemsandprocesses...........................................239

Thehotels’approachtoInclusiveness,MaterialityandResponsiveness:

Consequencesforsharedvalue.........................................................................................242

Conclusions:TheMBSCasavehicleforsharedvalue....................................248

Conclusions..........................................................................................................................258

8.1. Conclusionswithregardstotheaimandobjectives......................................258

8.2. Theoreticalcontribution........................................................................................265

8.3. Practicalimplications.............................................................................................269

8.4. Limitationsanddirectionsforfutureresearch...............................................271

References............................................................................................................................273

Appendices...........................................................................................................................318

Appendix1:Listofthe50largesthospitalitygroupsintheworld(Hotels

Magazine,2015).....................................................................................................................318

Appendix2:Contentanalysisthemesandresearchquestions...................320

Appendix3:Coverletterforhotelgroupswithsustainabilityinformation

publiclyavailable...................................................................................................................323

X

Appendix4:Coverletterforhotelgroupswithoutsustainabilityinformation

publiclyavailable...................................................................................................................324

Appendix5:Participantinformationsheet(CSRmanagers).......................325

Appendix6:Questionnairequestions................................................................328

Appendix7:InfographicAnalysingthequalityandcredibilityofCorporate

SocialReportingintheHospitalitySector,2016..........................................................332

Appendix8:CSRmanager’sinterviewguide....................................................339

Appendix9:Participantinformationsheetandconsentform(Experts).340

Appendix10:Expert’sinterviewguide..............................................................342

Appendix11:Interviewthemes,categories,subcategoriesandillustrative

quotes344

Appendix12:Transcriptionsymbols.................................................................382

XI

TableofFiguresFigure1:BSCperspectives.................................................................................................................................................57

Figure2:Thecause-and-effectrelationships’strategyintheBSC................................................................59

Figure3:Strategymapappliedintoanorganisation...........................................................................................61

Figure4:ExampleofanappliedSBSC.ThestrategymapofShell.................................................................73

Figure5:VariationsofgenericSBSCarchitectures...............................................................................................74

Figure6:FrequenciesofgenericSBSCarchitectures...........................................................................................75

Figure7:ExampleofNon-hierarchicalSBSCs..........................................................................................................78

Figure8:ResponsibleScorecardarchitecture.........................................................................................................79

Figure9:ExampleofahierarchicalextendedSBSC..............................................................................................80

Figure10:ExampleofNon-hierarchicalStakeholderScorecard...................................................................81

Figure11:ExampleofHierarchicalStakeholderScorecard.............................................................................82

Figure12:TheBSCfornon-profitorganisations....................................................................................................85

Figure13:HotelindustrymaterialitymatrixfromInternationalTourismPartnership...................94

Figure14:ComparisonbetweenGRImaterialitymatrixandadaptedversions....................................96

Figure15:StepsbuildingtheMaterialityBalanceScorecard........................................................................105

Figure16:Step1–IntegratingsustainabilityintotheBSC.............................................................................106

Figure17:Step2–StakeholdervalueintheBSC.................................................................................................109

Figure18:Step3–MaterialityassessmentintheBSC......................................................................................110

Figure19:TheMBSC...........................................................................................................................................................112

Figure20:Sharedvaluechain........................................................................................................................................113

Figure21:ThegenericMBSCStrategyMap............................................................................................................117

Figure22:Researchdesign..............................................................................................................................................123

Figure23:Visualdiagramofthemulti-methodsapproach............................................................................128

Figure24:SustainabilityintegrationthemesinhotelgroupsbyMBSCsteps......................................159

Figure25:Organisationalsustainabilityintegration.........................................................................................159

Figure26:Step0Strategicplanningandinformationsharing.....................................................................164

XII

Figure27:Step1IntegratingsustainabilityintotheBSC................................................................................167

Figure28:Step2Recognisingstakeholdervalue................................................................................................176

Figure29:Matrixofthedisclosureofnarroworbroadstakeholderidentificationandsymbolicor

substantivestakeholderengagement..............................................................................................................179

Figure30:Step3Determiningenvironmentalandsocialexposureofstrategicbusinessunits.188

Figure 31: Accountability Matrix based on the disclosure on Inclusiveness, Materiality and

Responsiveness...........................................................................................................................................................208

Figure32:Comparisonofdisclosureinthesustainabilityreportingprocessandenvironmental

indicators.......................................................................................................................................................................210

Figure33:Sustainabilityintegrationmatrix...........................................................................................................217

Figure34:EffectofsustainabilitybarriersontheMBSC.................................................................................232

XIII

ListofTablesTable1:Structureofthethesis........................................................................................................................................24

Table2:ValuetypesfromCSR.........................................................................................................................................39

Table3:CSVchallenges........................................................................................................................................................40

Table4:Multi-stageprocesstodevelopCSV............................................................................................................46

Table5:Genericorganisationandsocialresultsbylevelsofsharedvalue..............................................48

Table6:DevelopmentoftheBSCconceptbyKaplanandNorton.................................................................56

Table7:CategoriesofchallengesassociatedwiththeBSC...............................................................................63

Table8:ReviewofpreviousSustainabilityBalanceScorecards....................................................................68

Table9:CategoriesofspecificshortcomingsassociatedwithanSBSC......................................................83

Table10:Engagementlevelsandmethodsofengagement..............................................................................90

Table11:Comparisonofthedefinitionsofmateriality......................................................................................92

Table12:Similaritiesbetweenthetools...................................................................................................................101

Table13:Synergiesbetweenthetools......................................................................................................................102

Table14:IssuesinrespecttoCustomer,InternalprocessandLearningandGrowthperspectives

oftheMBSC...................................................................................................................................................................107

Table15:Examplesofnegativeandpositiveexternalitiesinthehotelindustry................................108

Table16:Hospitalitygroupswithpublishedsustainabilityreportsfromthetop50organisations

accordingtothenumberofroomsin2014..................................................................................................130

Table17:Literatureinformingtheresearchquestionsforcontentanalysis........................................131

Table18:Criteriaandcodingscheme........................................................................................................................132

Table19:CriteriafortheEnvironmentalSDGs.....................................................................................................133

Table20:Literatureinformingthequalitativequestionnaires....................................................................135

Table21:SamplecompositionofCSRmanagers’interviewsandcodes.................................................137

Table22:Organisations’interviewquestionsandrationale.........................................................................139

Table23:Samplecompositionofexperts’interviewsandcodes................................................................142

Table24:Experts’interviewquestionsandrationale.......................................................................................143

Table25:Thematicanalysisphasesfortheinterviewanalysis....................................................................147

XIV

Table 26: Synthesis of the dimensions of sustainability integration broken down by the

organisationalvariablesofthe7-SFramework.........................................................................................148

Table 27: Themes identified, classified into the 7-S Framework variables, sustainability

integrationlevels,andMBSCsteps...................................................................................................................150

Table28:Researcher’sstrategiestoaddresstrustworthiness.....................................................................151

Table29:Peerscrutiny......................................................................................................................................................153

Table30:Organisationsize(Numberofroomsby31stDecember2014)andownershipofhotel

groupsby31stDecember2015(%)................................................................................................................160

Table31:Responsibilitiesforsustainabilitymanagementfrominterviewees....................................161

Table32:Departmentsinvolvedinreporting........................................................................................................163

Table33:Disseminationformatsofsustainabilityinformation...................................................................166

Table34:Environmentalindicatorsmeasuredfromquestionnairesand%disclosurefromcontent

analysis............................................................................................................................................................................168

Table35:Intensitymetricsused...................................................................................................................................170

Table36:Rewardssystems.............................................................................................................................................174

Table37:Differencebetweenenvironmentalindicatorsmeasuredanddisclosed...........................175

Table38:Comparisonbetween%identificationofenvironmentalmaterialissuesanddisclosure

ofperformance............................................................................................................................................................175

Table39:Quantitativecodingscoresforstakeholderidentificationandengagement....................177

Table40:Stakeholdersengagedinsustainabilityfromthequestionnaires..........................................178

Table41:Stakeholderengagementlevelsfromthequestionnaires..........................................................180

Table42:Levelofengagementandmethodsofengagementbystakeholdergroup........................181

Table43:Stakeholderengagementmechanismsbystakeholdergroupandorganisationfromthe

questionnaires.............................................................................................................................................................182

Table44:Responsivenessfromcontentanalysis.................................................................................................186

Table45:Hotelgroupswithpublishedsustainabilityreportsfromthetop50largestbynumber

ofroomsin2014........................................................................................................................................................190

Table46:Quantitativecodingscoresformaterialityassessment...............................................................193

Table47:Materialityassessmentstepsdisclosed...............................................................................................194

XV

Table48:DisclosedSErelatedactionsforMA.......................................................................................................194

Table49:Assuranceofsustainabilityreports.......................................................................................................198

Table50:Sustainabilityreportassurancecharacteristics..............................................................................199

Table51:Keydriverstoproduceasustainabilityreport................................................................................201

Table52:TransparencypercriterionandorganisationtobuildtheAccountabilityMatrix........207

Table 53: Comparison of disclosure on sustainability reporting process and environmental

indicatorsbyquantityandquality....................................................................................................................209

Table54:CriteriaandscoresfortheSustainabilityIntegrationMatrix...................................................213

Table55:Interviewees’scoresfortheSustainabilityIntegrationMatrix...............................................216

Table56:Criteriaforidentifyingmaterialissues.................................................................................................253

XVI

IndexofAcronyms• AA1000SES:AccountAbilityAA1000StakeholderEngagementStandard

• BSC:BalanceScorecard

• CDP:CarbonDisclosureProject

• CSR:CorporateSocialResponsibility

• CSV:CreatingSharedValue

• GISR:GlobalInitiativeforSustainabilityRatings

• GRI:GlobalReportingInitiative

• IIRC:InternationalIntegralReportingCouncil

• IR:IntegratedReporting

• MA:MaterialityAnalysis

• MBSC:MaterialityBalancedScorecard

• NGOs:Non-GovernmentalOrganisations

• PM:PerformanceManagement

• RRM:ReputationandRiskManagement

• SASB:SustainabilityAccountingStandardsBoard

• SAMEs:SmallandMediumsizeEnterprises

• SBSC:SustainabilityBalancedScorecard

• SDGs:SustainableDevelopmentGoals

• SE:StakeholderEngagement

• SI:StakeholderIdentification

• SR:SustainabilityReporting

• TBL:TripleBottomLine

17

IntroductionThe introduction chapter outlines the research problem, context and rationale for a Materiality

BalancedScorecard,aframeworkforintegratedsustainabilitymanagementwithinthehotelindustry.

Thenthefocusturnstotheaimandobjectivesenvisagedforansweringtheresearchquestion:How

cananorganisationdefine strategic sustainabilityobjectives to create sharedvalue and translate

themintoaction,measureoutputsandreport?Finally,thechapterexaminesthestructureandscope

oftheresearch.Thechapterconcludeswiththethesisoverview,whichincludesabriefsynopsisofits

eightchaptersandtherelatedpublishedoutputs.

Contextandrationale

As the adverse impacts of tourism on the environment and society attract increasing attention,

organisationsareexpectedtotakemoreresponsibilityforthesustainableuseofresourcesandtheir

impactonsocieties.Hospitalityorganisations faceincreasinginternationalcompetitionwithever-

growing customer expectations (Han, Kim, and Kim 2011), declining resources (Laszlo and

Zhexembayeva2011),slowergrowthratesandoversuppliedandmaturemarkets(Soetal.2013).

Within this context, the researcher takes the view from van Marrewijk (2003) that corporate

sustainabilityistheultimategoalofanorganisationinitscontributiontosustainabledevelopment;

meetingtheneedsofthepresentwithoutcompromisingtheabilityoffuturegenerationstomeettheir

own needs (World Commission on Environment and Development 1987). A growing number of

organisationshaveengagedinsustainabilityactivities,socialresponsibilityandethicalbehaviours

throughCorporateSocialResponsibility(henceforthCSR)programmes(deGrosbois2012,Yunus,

Moingeon, and Lehmann-Ortega 2010, Elkington and Hartigan 2008). CSR encompasses the

economic,legal,ethicalanddiscretionaryexpectationsthatsocietyhasoforganisationsatanygiven

pointintime,anddefinestheresponsibilitiesofbusinessestowardssocietyandtheenvironmentwe

livein(CarrollandShabana2010,Carroll1999).Thethesisdistinguishescorporatesustainability,as

theultimategoalofanorganisationinitscontributiontosustainabledevelopment,fromCorporate

SocialResponsibility,astheactivitiesundertakentoachievecorporatesustainability.Thegreaterthe

attentionthatisattractedbytheorganisation’simpactsontheenvironmentandsociety,themore

responsiblearehotels’practices inmanagingthose impacts. Indeed, thisholdstrue forbothlarge

(Fontetal.2012)andmediumsizedandsmallhotels(GarayandFont2012).

18

Theprevioustrendsshapethenewphaseofcompetitiveadvantage,whereCSR,embeddedintothe

corestrategiesofhospitalityorganisations,canplayaconstructiverole.Competitiveadvantageisthe

valuecreatedbyanorganisationforitscustomersthatexceedstheorganisation’scostincreatingit

(Porter1985).Competitiveadvantageoccurswhentheorganisationdevelopsattribute(s)suchas

skills,resourcesormarketposition,allowingittooutperformitscompetition,bycostleadershipor

differentiation.Besidescompetitiveadvantage,strategicCSRdrivesperformance(GarayandFont

2013,Kirk1995),improvedrelationshipwithexternalstakeholders(MurilloandLozano2006)and

viabilityandmarketlegitimacy(Suchman1995).UntilCSRstrategieslinktosocietalexpectations,

however,organisationswillbeviewedasacauseofsocialandenvironmentalproblems(Porterand

Kramer2011).TheprincipleofCreatingSharedValue(henceforthCSV) ispreciselyrooted in the

mutualdependencybetweenorganisationsandsociety for long-termsuccess (PorterandKramer

2011).ScholarsforecastthatcompetitiveadvantagewilldrivestrategicCSR(VázquezandRodríguez

2013),withtheorganisationcontributingtothesocietywhereitoperates(Bonilla-Priego,Font,and

Pacheco-Olivares2014),andeveninconstrainedeconomictimes,organisationshaveincreasedtheir

strategic commitments to responsibility (Bansal, Jiang, and Jung 2015). Corporate and academic

worlds increasingly use CSV (Beschorner and Hajduk 2017, Corazza, Scagnelli, and Mio 2017,

Dembek, Singh, and Bhakoo 2016). Nevertheless, the exploration of shared value in hospitality

literatureremainslimited(e.g.HsiaoandChuang2016).

Aclearimplicationoftheaboveisthatanorganisation’scommitmenttosustainabilitydemandsa

strategicapproachtoensurethatitisanintegratedpartofthestrategyandprocesses(Engert,Rauter,

andBaumgartner2016).ConductingstrategicandeffectiveCSRplanningthatresultsinaclearand

demonstrable impact on the organisation’s and community is a process that still challenges

organisations(Wangetal.2016),however,andthehotelindustryisnotanexception(GarayandFont

2012). Organisations require an explicit linkage between strategic, operational and financial

objectives as well as the ability to monitor the results continuously with quantifiable outcomes

(Cokins2010).Theincreasedattentionpaidtothestrategicenvironmentalandsocialperformance

ofanorganisationintensifiesthedemandforcorporatesustainabilityperformancemeasurementand

management systems (Hansen and Schaltegger 2017, Searcy 2012). Performance management

systemshelptostrikeabalancebetweenconflictsandtotranslatestrategiesandplansintoresults.

CSV,however,entailschangingperformancemanagementsystemstoreflectnewemphasesonwhat

isrelevanttomorestakeholders.CSRresearchcapturesaconceptualshiftfromfinancialoutcomes

andappliesittothemanagementofnon-financial,socialandorganisationaloutcomes(Wangetal.

19

2016). Strategies have changed to manage intangible assets, such as customer relationships,

employee skills, innovative products and responsive operating processes, in order to create

competitive advantage (KaplanandNorton2001b). In sodoing, the valueof anorganisationhas

shifted from tangible to intangible and knowledge-based assets yet performance measurements

systemsstillreflectout-datedmodels(KaplanandNorton2001b).Inevitably,thisconditionlimitsthe

potentialtoalignCSRactivitieswiththeorganisation’sstrategyandwiththedemandsofmultiple

stakeholders–apreconditiontocreatingsharedvalue.

Theincreasedimportanceofmanagingsustainabilityforthesurvivalandsuccessoforganisations

(Cresti2009)hasshiftedresearchtohowsustainabilityissuescouldbeintegratedintoorganisational

systems and processes (Maas, Crutzen, and Schaltegger 2014, Epstein 2008). Sustainability,

incorporated intoperformancemanagement systems, enables aholistic focusonperformanceby

implementing strategic goals and adapting the organisation to operational circumstances (Otley

2001).Thistranslatesintobettermanagementandcontrolofsustainabilityperformance(Georgeet

al. 2016) and value for society (Husted and de Jesus Salazar2006, Hart andMilstein2003).The

BalancedScorecard(BSC)hasemergedasapreferredtoolforevaluatinghowmanagersperformin

CSRandformotivatingtheminthepursuitofthesegoals(Bento,Mertins,andWhite2017).Indeed,

thesustainabilityadaptationsoftheBSCareoneofthemostpromisingstrategictoolstosupportthe

implementation of a sustainability strategy (Journeault 2016) and are seen as an important

sustainability-oriented management accounting innovation of the last two decades (Hansen and

Schaltegger2017).

Stakeholders are defined as those groups or individuals who can affect, or are affected by, the

achievementof theorganisation’spurpose (DonaldsonandPreston1995). Stakeholderspressure

organisations tomeasure,manageandreportsustainabilityperformance(SchalteggerandBurritt

2010) in a manner that links with established strategic, operational and financial objectives

(Calabrese,Costa,andRosati2015,Searcy2012).Whilecorporatesustainabilityrequiresintegrative

measurementandmanagementofsustainabilityissuesratherthanseparateapplicationsofdifferent

toolsintheorganisation(Maas,Schaltegger,andCrutzen2016),however,suchintegrationremainsa

fragileconcept(Battagliaetal.2016).

Existingresearchdealsinanisolatedwaywithspecificmethodsofcapturingsustainability.Authors

have examined the role of sustainability management tools (e.g., Bonacchi and Rinaldi 2007,

Schaltegger andWagner 2006, Johnson and Schaltegger 2016) and accounting and reporting to

20

supportsustainabilityprocesses(BurrittandSchaltegger2010,Bebbington,Unerman,andO'Dwyer

2014,BakerandSchaltegger2015).Therehavebeenfewattemptstodevelopmorecomprehensive

and integratedapproaches (seeDent1990,Chenhall2003,MalmiandBrown2008),whichrarely

integrateaccounting,managementcontrolandreporting(Maas,Schaltegger,andCrutzen2016).For

instance, previous research has studied the link between sustainability balanced scorecards and

performancemanagementcontrol(Schaltegger2011), theroleofmanagementcontrolsystems in

integratingsustainabilityintoorganisationalstrategy(Baker,Brown,andMalmi2012,Crutzenand

Herzig2013)orthedevelopment,structureanduseofsustainabilitycontrolsystems(DitilloandLisi

2014).Researchaddressingtherelationshipbetweensustainabilityperformancemanagementand

reportingisstilllimitedandremainsinanexplorativestage(seedeVilliers,Rouse,andKerr2016for

a first case study). At present, few researchers have addressed the link between sustainability

reporting, organisational change and internal performance improvement (e.g. Adams, Larrinaga-

González,andMcNicholas2007,AdamsandWhelan2009).

Sustainability reporting “is a process that assists organisations in setting goals, measuring

performanceandmanagingchangetowardsasustainableglobaleconomy”(GRI2013b,85).It isa

formofdiscourseaimedoutsidetheorganisationtoachievesustainedcompetitiveadvantage.The

efforts to standardise sustainability reports take two avenues. First, creating sector standards to

determine what is sustainable, through sustainability ecolabels. Such market solutions to

sustainabilityproblemsought tobe reconsidered (Rex andBaumann2007) since thesehavenot

succeededindifferentiatingtheservicesinawaythatdevelopsmarkettraction(Font2013,Gössling

andBuckley2016). Second, by implementingmethodologies for organisations todeterminewhat

their stakeholders consider a priority, such as the Global Reporting Initiative’s requirement to

conductaMaterialityAssessment(henceforthMA).MAisatoolforprioritisingissueswithinstrategic

planning,allowinganintegratedapproachtodefiningasustainabilitystrategyandreportingonit

(GRI2013a).Theconceptofmaterialityisusedtoexplaintowhichextentasustainabilityreportis

informed by the process of engaging which prioritised stakeholders, and how. Materiality is

effectively the process of engaging with stakeholders jointly to determine shared priorities, so

organisationscanrealigntheirpracticesandreportwhatisimportanttotheaudienceoftheirreports.

ReportingorganisationssuchasSustainabilityAccountingBoard(2016a),GlobalReportingInitiative

(2013a)or the IntegratedReportingFramework(IIRC2013) advocate for increasedstakeholder-

focusedcommunication.Yet,therehavebeenfewstudiesintomaterialityforsustainabilityreporting

21

(e.g.,FasanandMio2017)andfewerstillconsideritsroleinconnectionwithsustainabilitystrategy

(Edgley2014).

Thehotel industry faces the challengeof increasing transparency about thedisclosureof current

practices(Fontetal.2012).Also,whilematerialityhasbecomearelevant issue forsustainability

disclosure,materialityisnottreatedcomprehensivelywithinthehotelindustry,whichundermines

thecredibilityofitssustainabilityreportingprocess(Jones,Hillier,andComfort2016).

This thesis studies materiality coupled with the Inclusiveness, Responsiveness and Assurance

principles of the stakeholder engagement standard AA1000SES (AccountAbility 2015). The

AA1000SES principles parallel the reporting process. First, managers identify and engage

stakeholders (inclusiveness). Second, managers use stakeholder insights to determine the

importance of sustainability issues (materiality). Third, the organisation discloses enough

informationtoallowstakeholderstojudgetheorganisation’ssustainabilityperformancebasedon

the issues that they considered important in the first place (responsiveness). And fourth, the

organisation provides confidence regarding the content and process of sustainability reporting

(assurance). The accountability approach may assist organisations in responding to stakeholder

expectationsacrossthecriticalprocesseswithintheorganisation.

This thesis contributes to the literature by investigating how sustainability performance can be

integratedintothebusinessstrategy,managementandreporting(e.g.Figgeetal.2002a,Schaltegger

andWagner2006,Chen,Hsu,andTzeng2011,Zollo,Cennamo,andNeumann2013,deVilliers,Rouse,

andKerr2016).Specifically,thisthesisaddressesthefactthatnoacademicresearchhasexamined

how theprinciples fromAA1000SES couldbe incorporated in existingperformancemanagement

systems,suchastheBalancedScorecard,todefine,implementandreportonasustainabilitystrategy.

The thesis also contributes to the CSR process-based literature that intends to understand the

‘process’ of CSR decision-making and implementation, particularly for the hotel industry. The

process-based researchhas resurged since2000, reflecting the increasing interest in an in-depth

understandingofCSRdecision-makingandimplementation(Wangetal.2016).Thethesistakesa

qualitative approach, to complement the existingquantitative researchonboth the Sustainability

BalancedScorecard literature(HansenandSchaltegger2016)and the ethicalstudies in thehotel

industry(Köseoğluetal.2016).Aqualitativestudyprovidesopportunitiesfortheorybuildingandan

in-depthunderstandingofthecontext(Wangetal.2016).Thisqualitativeresearchassessesthemost

commonchallengesincorporatedecision-making,implementationandreportingofCSRthatconcern

22

thehotelindustry,andthatinturnhampermoreproactivesustainabilitystrategiessuchascreating

sharedvalue.

Researchaim,objectivesandscope

Theaimof thisPhD is to arrive at a critical understandingof how largehotel groups candefine

strategic sustainability objectives to create sharedvalue. It does sobydeveloping theMateriality

BalancedScorecard(henceforthMBSC)inthecontextofthehotelindustry.TheMBSCisanintegrated

framework that links sustainability reporting processes with sustainability performance and

management,usingtheconceptsofsharedvalue(PorterandKramer2011),theBalancedScorecard

(Kaplan and Norton 1993), the Sustainability Balanced Scorecard (Figge et al. 2002a), and the

stakeholder engagement standard AA100SES (AccountAbility 2015). This thesis expands on the

researcher’spreviousworkinmaterialityassessment,togetherwithhersupervisors(Font,Guix,and

Bonilla-Priego2016).Theresearchobjectivesare:

Objective1.Toproposeastrategicmanagementframework,theMaterialityBalancedScorecard,to

design,communicateandrealiseCSRstrategiesthatcreatesharedvalue.

Objective2.TocharacterisetheCSRmanagementandreportingoflargehotelgroupsandidentifythe

internaldeterminants.

Objective3.ToofferacriticalappraisalofthevalueoftheMaterialityBalancedScorecardwithinthe

hotelindustry.

This PhD advances the theoretical and empirical knowledge of how an organisation can define

sustainablestrategicobjectivestocreatesharedvalueandtranslatethisintoactionsusingtheMBSC

framework. CSV entails a progressive reorientation of how an organisation understands its

relationshipwithsociety.Theliteraturereviewdemonstratescomplementaritiesbetweencreating

shared value, the balanced scorecard and themateriality principle from the AA1000SES.Making

socialresponsibilityinternaltoanorganisationrepresentsachangeintheorganisationalcultureand

themindsetof themanagers.Nevertheless, thedifferentCSV implementationguidelinesprovided

(e.g.PorterandKramer2011,BockstetteandStamp2011,Pfitzer,Bockstette,andStamp2013,Tate

andBals2018,Matinheikki,Rajala,andPeltokorpi2017)donotexplainhowtoinvolvestakeholders

oridentifykeysustainabilityissues,orhowtoprioritiseandmeasurethem.Theintegrationofshared

valuewithintheMBSCstandardisestheprocessofidentifyingthesocialissues,prioritisingthemand

measuringstakeholdervalue,linkedwiththefinancialvaluethroughcause-and-effectrelationships,

23

whilemonitoringtheCSVstrategyinacontinualprocess.Themeasurementofsharedvaluemustbe

embeddedintoexistingmanagement(PorterandKramer2011,Porteretal.2012).Accordingly,the

MBSCisbasedonboththeBalancedScorecard(henceforthBSC),widelyusedwithinorganisationsto

increasetheirstrategiceffectiveness(Neely2008a),andtheMaterialityassessment(henceforthMA),

which ismainlyused forsustainabilityreporting(GRI2013a).Anorganisation integratingshared

value within the BSC can track its progress on the link between sustainability and organisation

results,whichcansubsequentlycreatenewvalueandimproveperformance.

Effectivedefinitionofthesustainabilitystrategy,aswellaseffectivemanagement,measurementand

reporting, require a good interplay between different tools and actors within and outside the

organisationforthecollection,analysisandcommunicationofrelevantdata.Thisthesisisgrounded

on ‘Instrumental Stakeholder Theory’, which identifies “the connections, or lack of connections,

between stakeholder management and the achievement of traditional corporate objectives (e.g.

profitability, growth)” (Donaldson and Preston 1995, 71). The MBSC is underpinned by the

instrumental stakeholder theory entailing listening to relevant stakeholders and considering the

issuesthatarematerialtothemandintegratingthoseconcernsintheorganisationaloperations.The

recognition of a broader set of sustainability issues and stakeholders leads to improved

organisationalperformance(e.g.Johnson1998,Sundin,Granlund,andBrown2010).TheMBSCisa

framework to understand better how organisations address the stakeholder claims in respect to

sustainability through their operations, and as a result, improve performance from a wider

perspective. Full integration into the core organisation’s activities and impacts results in amore

cohesive and efficient approach to sustainabilitymanagement. Indeed, theMBSC builds into the

performance an improvement-oriented perspective as a framework for change management for

which;i)stakeholderexpectationssteerperformanceimprovements, ii) internaldevelopmentand

reportingusessustainabilityperformancedataandiii)transparencymustbeadvancedtolegitimise

the organisation’s actions through the wider stakeholder engagement. This research argues that

MBSC,anintegratedtooloftheBSCandtheAA1000SESprinciples,shouldbeasuitableinstrument

todrivechangewithinanorganisation towardsadvancedsustainabilitystrategies,culminating in

creatingsharedvalue.

Thecontributionofferedbythisthesishasbothacademicandpracticalimplications.Ontheacademic

side,totheauthor’sknowledge,thecurrentliteraturedoesnotprovidemethodsforthesimultaneous

andsystematicintegrationofthesustainabilityreportingeffortsintotheorganisationperformance

managementsystem.Onthepracticalside,theresearcherdevelopsaframeworkforintegratingthe

24

concernsofkeystakeholdersintoaperformancemanagementsystem,whichpermitsorganisations

tomonitorandaccountfortheefficiencyandeffectivenessofaddressingstakeholderconcernsand

assessesitspotentialusewithinthehotelindustry.

Structureofthethesis

Thethesisconsistsofeightchapters(Table1).

Table1:Structureofthethesis

Chapter Content PhDobjectives Publicationoutput

1:Introduction • Contextandrationale.• Aimandobjectives.• Thesisstructure.

2: Literaturereview

• Corporate SocialResponsibility.

• Theoretical andcontextualperspectives.

• CreatingSharedValue.

Objective 1,and2

Publicationrelatedtothesharedvalueframework(from a Master’s thesis): Font, X., Guix, M. andBonilla-Priego, M. J. (2016) Corporate socialresponsibility in cruising: Using materialityanalysis to create shared value. TourismManagement, 53, 175-186. Doi:10.1016/j.tourman.2015.10.007Publication related to corporate socialresponsibility (from amaster’s thesis): Font, X.,Bonilla, MJ. and Guix. M. Chapter 5 Corporatesocialresponsibilitiesinthecruisesector,86-105.InDowling,R.andWeeden,C.(2016)HandbookofCruiseShipTourism,2ndEd,86-105.Wallingford:CABI.ISBN:9781780646084Publication related to corporate socialresponsibility: Font, X. & Guix, M. Chapter 37Corporate Social Responsibility in tourism, 567-580. InCooperC.Gartner,B., Scott,N.&Volo, S.(2018) Sage Handbook of Tourism Management.London,UK:Sage.ISBN:9781526461131.

3: Literaturereview

• BalancedScorecard.• Sustainability

BalancedScorecard.• Sustainability

reporting:AA1000SES

Objective1 Publication of the AA1000SES principles in theliterature review in thearticle:Guix,M,Bonilla-Priego, MJ. and Font, X. (2018) The process ofsustainability reporting in international hotelgroups:ananalysisofstakeholder inclusiveness,materiality and responsiveness, analysis ofstakeholder inclusiveness, materiality andresponsiveness, Journal of Sustainable Tourism,12(7), 1063-1084. Doi:10.1080/09669582.2017.1410164

4: Theoreticalcontribution

• Theoreticalframework: TheMateriality BalancedScorecard.

Objective1

5:Methodology • Methodology. Objective 1,2and3

25

6: Findings &Discussions

• Sustainabilityreporting within thehotelindustry.

• Perceptions ofhospitality managerson the sustainabilitymanagement andreporting.

• Interpretation ofdegree ofsustainabilityintegration.

Objective 2and3

Publication of a joint Infographic with UNEPshowcasing preliminary results of the contentanalysis.Publicationofanabridgedversionofthecontentanalysis results: Guix, M, Bonilla-Priego, MJ. andFont, X. (2018) The process of sustainabilityreportingininternationalhotelgroups:ananalysisof stakeholder inclusiveness, materiality andresponsiveness, Journal of Sustainable Tourism,12(7), 1063-1084. Doi:10.1080/09669582.2017.1410164

7: Findings &Discussion

• Experts’ insights onbarriers forsustainabilityintegration.

• Interpretation of thebarriers in lightof theapplication of theMBSC in the hotelindustry.

Objective 2and3

Publicationoftheinterviewresultsonmaterialityassessment:Guix,M., Font, X. and Bonilla-Priego,M.J. (2018)Materiality: the rationale behind sustainabilitychoices in hotel groups, International Journal ofContemporary Hospitality Management (on-line)Doi:10.1108/IJCHM-05-2018-0366

8: Conclusions,contribution toknowledge

• Conclusion.• Contribution to

knowledge.

Aim andobjectives 1,2,and3

Source:Author,2017

Chapter1comprisestheintroductiontothecontext,rationale,scopeandaimsofthethesis.

Chapter2reviewsliteratureintheevolutionofthesustainablebehaviourofanorganisationfromthe

traditionalCSRtowardsbeingmorestrategicbycreatingsharedvalue.Thefirstsectionintroduces

CSRandfour theories,allofwhichrelatetohowanorganisationmanages theperceptionof itself

within society to achieve competitive advantage: the resource based view, reputation and risk

management,legitimacyandstakeholdertheory.Thesecondsectionprogressivelynarrowsthetopic

ofconnectingsocialandeconomicprogressandpresentstheconceptoftheCreatingSharedValue

framework,togetherwithitsapplicationandchallenges.

Chapter3introducestheinstrumentstoachievesharedvalue,whichincludetheBalancedScorecard

asawell-establishedperformancemanagementsystemand itssustainabilityadaptations,andthe

AA1000SESprinciplestorespondtostakeholderexpectationsacrossthecriticalprocesseswithinthe

organisation.DuetotherelationshipbetweenCSV,sustainabilityandbroadstakeholderconcerns,

thesectionalsoreviewsextendedBSCstructuresthataddresssustainabilityissuesandstakeholder

accountabilitymoreinclusively.ThelastpartdiscussesthecomplementaritybetweentheBSCand

MAasthecentralelementintheAA1000SESforrealisingsustainabilitystrategiesthatcreateshared

value,whichunderpintheMaterialityBalanceScorecard.

26

Chapter4developstheMaterialityBalanceScorecardasasuitableinstrumenttodefine,communicate

and operationalise strategic sustainability objectives that create value through the organisation’s

operations.ThechapterdetailsthestepstobuildtheMBSC.Step1outlinestheSustainabilityBSC

characteristics to address sustainability issuesmore inclusively. Step 2 acknowledgeswhere the

organisationcreatesvalue for itsmultiplestakeholders.Later,Step3incorporates theMateriality

Assessmentasatooltoincreasestakeholderaccountability.Chapter4isthetheoreticalcontribution

ofthePhD(Objective2)developingaconceptualframeworkinalignmentwiththegrowingbodyof

research on Sustainability BSCs (Hansen and Schaltegger 2016). The Sustainability BSC is a

developing field where further conceptual and empirical research is needed to improve

understandingofitsbenefitsanddrawbacksinorganisations(HansenandSchaltegger2016,2017,

Journeault2016).

Chapter5exploresthephilosophical,methodological,analyticalandinterpretativeapproachestothe

dataandfindings.Thechapterbeginswithanoverviewofthepragmatismparadigminformingthe

research and the ontological, epistemological and axiological choices. Afterwards, the chapter

outlinestherationaleforaqualitativemulti-methodandcross-sectionalresearchstrategy,including

the sample and thedata collectionmethodsused. It justifies thequalitativemethodsadopted, by

complementingtheexistingcasestudies(27.7%),multi-casestudy(13%)andquantitativeresearch

(13%) on Sustainability BSCs (Hansen and Schaltegger 2016). Then, the chapter presents a

justification and detailed description of the research methods: content analysis, qualitative

questionnaires and semi-structured interviews. The chapter describes the data analysis to be

theoretical thematic analysis. Finally, the section outlines the evaluation criteria as focusing on

trustworthiness,anddescribesthelimitationsofthisresearch.

Chapter6presentsthecharacteristicsandfactorsinfluencingandhinderingsustainabilityintegration

intomanagementandreportingbyhotelgroupsaccordingto thedatacollected(contentanalysis,

qualitative questionnaires and semi-structured interviews). It does so by addressing the seven

elementsfromthe7-SFramework(strategy,structure,systems,style,skills,staffandsharedvalues)

(Waterman,Peters,andPhillips1980).Thisenablesastructuredanalysisoforganisationalvariables

drivingvariousmanagementprocesses,fromstrategyformulation(GalliersandSutherland1991),

employeeempowerment(Lin2002)tosustainabilityreporting(Thijssens,Bollen,andHassink2016).

BecausethisPh.D.paysparticularattentiontosustainabilityintegrationwithinPMS,thisresearch

incorporatesthethreedimensionsofintegrationintothe7-SFramework(cognitive,organisational

andtechnical)(Gondetal.2012,Georgeetal.2016).Cognitiveintegrationentailshowpeoplethink

27

withintheorganisation,thesharedcognitions,andthechangesinfocusandbeliefs.Organisational

integrationinvolveshowprocessesareorganisedconcerningtheorganisations’formalstructureand

rolestofacilitatecommonpractices.Technicalintegrationinvolveshoworganisationsusetoolsand

methodologies for sustainability. Finally the chapter makes a comparative analysis between the

sustainabilitydisclosure, environmental performance and sustainability integrationof largehotel

groups, and presents two tools to assess their sustainability integration (the Sustainability

IntegrationMatrix)andtheiraccountabilitytostakeholders(theAccountabilityMatrix).Finally,the

chapterconcludesbyrevisitingthemainfindings.

Chapter 7 returns to objective 3 ‘To critically appraise the value of the MBSC within the hotel

industry.’First,itdiscussessomeexamplesofhotels’CSRpracticesinlightofthethreepathwaysfor

creatingsharedvalue:reconceivingproductsandservices,reimaginingthevaluechain,andenabling

cluster development. Afterwards, the section turns to the internal cognitive, organisational and

technicaldeterminantstoCSRmanagementandthereportingoflargehotelgroups,andthencethe

likelihoodofimplementingtheMBSCintheindustry.Then,thechapterdiscussesthehotelgroups’

approachestoengagingstakeholders,identifyingmaterialissuesandrespondingtothose,asaresult

of the determinants of CSR management and reporting, and discusses the implications for the

mismanagementof sustainability and the symbolic adoptionof reporting guidelines.The chapter

concludes by refining the MBSC from Chapter 4, including new guidance on the Accountability

principlestofitthesharedvaluepurpose.

Chapter 8 reflects on the attainment of the aim and objectives of the Ph.D. It also considers its

significance foracademicknowledgeandmanagementpractice, specifically for thehotel industry,

andendsbysurveyingwiththestudy’slimitationsanddirectionsforfutureresearch.

28

From Corporate Social Responsibility to Creating SharedValue

Thischapterexplainsthetheoreticalbasesrelatingtosustainablebehaviourbyorganisationsandthe

evolution towards more strategic and value-creating strategies. The first section introduces

CorporateSocialResponsibility(henceforthCSR)andthesecondsectionrevisitsthetheoriesmost

usedtoresearchCSR:theResourceBasedView,ReputationandRiskManagement,andLegitimacy

and Stakeholder theories. Later, the chapter examines how organisations develop a sustainable

competitiveadvantagethroughtheCreatingSharedValueframework(henceforthCSV).Theprocess

of narrowing down the topic helps define the problem and identify the need for theMateriality

BalanceScorecard(henceforthMBSC)tooperationalisesharedvalue-creatingstrategies.

Sustainablebehaviourbyorganisations

ThesectionintroducesCSR,itscomplexdefinitionanditsterminology.ItplacesCSRasastrategictool

for an organisation’s long-term performance, and provides insights into the different theories

justifyingthebusinesscaseforCSR.Thesectionstressestheimportanceofembeddingstakeholder

concernsandsustainabilitywithintheDNAoftheorganisation,notingthatthesearefundamental

ideasshapingtheMBSCframework.

Towardsbeingmorestrategic

The concept andunderstandingofCSR isdynamic, shifting in linewith environmental andsocial

changes,externaldemandsandthemoralmaturityoftheorganisation.Differentschoolsofthought

havedevelopeddifferentCSRdiscourses,allofwhichincludetakingintoaccountthevoluntarinessof

the activity, the stakeholders’ relations and the triple bottom line impacts of an organisation’s

operations (Dahlsrud2008).TheTripleBottomLine approach (henceforthTBL) assessesCSRby

focusingontheeconomic,socialandenvironmentaldimensionsofsustainability(McElhaney2008).

CSR helps to create economic and brand value by focusing an organisation on sustainable

development.ThisthesistakesthedefinitionofCarroll,whichhasnowbeenusedforsome35years;

“the social responsibility of business encompasses the economic, legal, ethical, and discretionary

expectationsthatsocietyhasoforganisationsatagivenpointintime”(Carroll1979,500).CSRis

thereforeaboutmanagingtheorganisation’soperationsinawaythatbothmaximisesthebenefitsto

societyandminimisestheriskandcosttosociety.

The multiple definitions and terms that are used to refer to the sustainable behaviour of an

29

organisationincreaseconfusionforstakeholders,andmakeitdifficulttoembraceCSR.Theseterms,

oftenused interchangeably, include:citizenship,sustainability,corporateresponsibility,corporate

accountabilityandsocialresponsibility(Carroll1999,deGrosbois2012,Coles,Fenclova,andDinan

2013).CSRisasocialconstructwithinaspecificcontext,andthemultiplevariantsoftheconceptcan

make it difficult to engagewith (Van Beurden and Gössling2008, Orlitzky, Siegel, andWaldman

2011). As a consequence, organisations take into account the multiplicity of approaches when

definingstrategies(Dahlsrud2008).OrganisationspursuedifferentCSRobjectives,whichdirectly

influencehowtheymanagetheirresponsibilitiesandstrategies(Hawkins2006,Freeman,Harrison,

andWicks2007,McElroy, Jorna, andvanEngelen2008).Thevoluntarynature and scopeofCSR

meansthatthechoiceofwhetherandhowtodevelopitislefttotheorganisation.

OrganisationscanthereforechooseamongmultipleCSRactivities,whichcanbebroadlycategorised

asResponsiveorStrategic,dependingontheissuesaddressed.ResponsiveCSRaddressesi)generic

socialissues,whicharethosethatarenotaffectedsignificantlybytheorganisation’sactivitiesanddo

notmateriallyaffectthelong-termcompetitiveness,andii)valuechainimpacts,whichresultfrom

the organisation’s operations (Porter and Kramer 2006, 2011). Responsive CSR has been the

traditionalmodel,whereorganisationsfocusonphilanthropyandoutsourcingtheirresponsibilityto

thesupplychain,buthasreceivedmuchcriticism(Laufer2003).StrategicCSR,meanwhile,addresses

i) the value chain issues and ii) the competitive context issues, which are those factors in the

organisation’sexternalenvironmentaffectingtheunderlyingdriversofcompetitivenesswherethe

organisationoperates(PorterandKramer2006,2011).StrategicCSR isamoreholisticapproach

whereby an organisation purposefully matches internal resources (e.g. employee skills,

organisational culture) with external community-specific needs (e.g. related to food access,

education)increasingthebenefitstotheorganisationanditspositiveimpactonthecommunity.This

thesisfocusesonhowtoadvanceCSRtowardsbeingmorestrategicthroughtheMBSC.

Despite therelativeconsensusonCSR, thebusinesscase forsustainabilityremainscontestedand

researchersarecontinuingtoinvestigatehowstrategicCSRleadstocompetitiveadvantage(Porter

andKramer2011)andimprovesrelationshipswithexternalstakeholders(MurilloandLozano2006,

Bhattacharya,Korschun,andSen2009).ThenextsectiondiscussestherelationshipbetweenCSRand

organisationalperformance.

30

Improvingperformancethroughresponsiblemanagement

AkeyareaofresearchhasbeentoidentifytheconditionsunderwhichCSRhasapositiveimpacton

anorganisation’sfinancialperformance,arguablyasawayofprovidingabusinesscaseargumentfor

organisations to engage more intensively in CSR. Scholars have found negative relationships

(Aupperle,Carroll,andHatfield1985,WrightandFerris1997),neutralrelationships(Teoh,Welch,

and Wazzan 1999, Lindgreen and Swaen 2005, Ioannou and Serafeim 2015) and positive

relationships(e.g.WaddockandGraves1997,StanwickandStanwick1998,MargolisandWalsh2003,

Orlitzky,Schmidt,andRynes2003,Vogel2005,GalbreathandGalvin2008,VanBeurdenandGössling

2008). These studies address the association between CSR and performancewhile other studies

researchhow to achieve aperformance increase (RowleyandBerman2000,MargolisandWalsh

2003,LuoandBhattacharya2006,BrancoandRodrigues2006,GalbreathandShum2012,Saeidiet

al.2015).ArticlesresearchinghotelperformanceinthecontextofCSRhavegrownfrom2.3%to3.7%

outofasampleofarticlespublishedinleadinghospitalityandtourismmanagementjournalsfrom

1992to2005,andthisfigureisexpectedtocontinueincreasing(Sainaghi,Phillips,andCorti2013).

While some scholars have found that CSR positively affects performance through savings from

efficiencies,avoidingfuturefinesandbrandpositioning,othershavefoundanegativeimpactdueto

increasedcosts(Nicolau2008,LeeandPark2009,Kang,Lee,andHuh2010,Pereira-Molineretal.

2012,Pereira-Molineretal.2015).Researchersareattemptingtoexplaintherelationshipbetween

CSR and performance using complementary theories as ameans to build the CSR business case

(CarrollandShabana2010).

Multiple theories overlap, providing different butuseful insights on the sustainable behaviour of

organisations.Thissectionaddressesfourtheories,allofwhichlinkhowanorganisationmanages

howitisperceivedwithinsocietyandhowCSRcanbringaboutcompetitiveadvantage.Thechapter

presentstheoriesorganisedaccordingtotheuseofmoreinternaltomoreexternalelementswhen

determining theCSRstrategy.First, theResourceBasedViewtheorypresentsCSRasadiscourse

intendedtomanagestrategicresourcese.g.reputation.Second,theReputationandRiskmanagement

theory sees CSR as a discourse that minimises risks through managing reputation. Third, the

Legitimacy theory postulates that CSR is a discourse serving to gain, maintain or repair the

organisation’srighttooperatebymanagingtheperceptionsofwidersociety.Fourth,theStakeholder

theoryunderstandsCSRasadiscourseimprovingtherelationshipbetweentheorganisationandthe

keystakeholdersbymanagingtheirperceptions.

31

ResourceBasedView

TheResourceBasedViewtheorypostulatesthatanorganisationactsresponsiblytomaximiseand

sustainitscompetitiveadvantageinwayscompetitorscannoteasilyimitate(Wernerfelt1984,Russo

andFouts1997).Theorganisationreachesasustainablecompetitiveadvantagethroughtheunique

mix of rare, valuable, inimitable, non-tradable, non-substitutable, and organisation-specific

resources,capabilitiesandcompetencies(Porter1985,Barney1991,Barney,Wright,andKetchen

2001).CSRfavoursvaluablecapabilitiessuchasstakeholderintegration,innovationororganisational

learning (Garay and Font 2012) and, therefore, CSR practices enable an organisation to acquire

resourcesanddevelopskills thatcannoteasilybe imitatedbycompetitors(Barney1991,Barney,

Wright,andKetchen2001,BrancoandRodrigues2006).Thisformofvaluecreationadvancesthe

understandingofCSRasmorestrategic(Orlitzky,Siegel,andWaldman2011),andthecharacteristics

ofthesecapabilitiesdefinethestrategicleveloftheCSRinitiatives.

Ahotelcandeveloparesource-basedadvantageand increase itsperformancebycreatingservice

brandvalue thatiscultivatedby topmanagementtransformationalleadershipthroughbuildinga

servicecultureandemployeeinvestment(ChangandMa2015).Forinstance,byutilisingemployees

tocreatepositiverelationshipswithguests,Ritz-Carltonenhancestheservicestandardsthatcreate

aconsistentandsuperiorserviceimage(KandampullyandHu2007,Drohan,Lynch,andFoley2009).

Similarly,MarriottHotels attains superior customer loyalty by utilising its culture that facilitates

employeestoofferconsistentlevelsofguestrecognitionandservice(ByeongandHaemoon2004).

Nevertheless,whileResourceBasedViewcanfacilitatesustainedcompetitiveadvantage,determining

thestrategyonlybasedonwhattheorganisationpossessesratherthanthesharedresourcesacquired

throughalliances,orwhattheexternalenvironmentdemands,maybeincomplete.

TheassumptionoftheResourceBasedViewapproachthatorganisationsmustown,oratleastfully

control,theresourcesconferringcompetitiveadvantageturnsouttobeincorrect(Lavie2006).For

example, the resources of partners also influence the competitive advantage of an organisation

(Saxton 1997, Stuart 2000), and issues of reputationmay arise from the relationshipwith those

partners(GrayandWood1991,WestleyandVredenburg1991).TheResourceBasedViewtheory

postulates that reputation is a resource that can yield significant competitive advantage (Barney

1991, Deephouse 2000, Roberts and Dowling 2002), which leads to a discussion of the relation

betweenCSRandReputationandRiskManagement,asinthenextsection.

32

Reputationandriskmanagement(henceforthRRM)

RRM theory has two perspectives: management and sociological, which focus respectively on

reputationasaresourceorasanoutcomeofthereportingprocess.Reputationasastrategicresource

producestangiblebenefits,whichincludepremiumpricesforproducts,lowercostsforcapitaland

labour, improved loyalty from employees and better decision making (Beatty and Ritter 1986,

MilgromandRoberts1986,FombrunandShanley1990,Fombrun1996,LittleandLittle2000).As

such,reputationisanintangibleassetwiththepotentialforvaluecreation(LittleandLittle2000,

RobertsandDowling2002).Alternatively,reputationistheaggregateoftheassessmentsofmultiple

actorsontheorganisation’sperformancerelativetotheirexpectationsandnorms(FombrunandVan

Riel1997).Assuch,itisperceivedasbeinganoutcomeoftheprocessofmanagingtheorganisation’s

pastactionsandresultsaimedatdeliveringvaluetomultiplestakeholders(ScottandWalsham2005).

This approach suggests that reputation is one of the main drivers of sustainability reporting

(FriedmanandMiles2001,ScottandWalsham2005,Bebbington,Larrinaga,andMoneva2008).The

difficulty in studying the notion of reputation systematically (Unerman 2008) has hampered the

understandingofthespecificreportingstrategiesadoptedtomanagereputation.

Under both perspectives, reputation is “a generalised expectation about an organisation’s future

behaviourorperformancebasedoncollectiveperceptions(eitherdirector,moreoften,vicarious)of

past behaviour or performance” (Deephouse and Suchman 2008, 60). RRM links CSR and

performanceinachainofrelationships(Anderson,Fornell,andRust1997)onthebasisthatsocially

responsiblepracticesimproveproductqualityandthencecustomersatisfaction(Carroll1979,2004).

CSR can increase customer identification with the organisation, which in turn builds trust and

increases customer satisfaction (Martínez and del Bosque 2013). Higher levels of customer

satisfactionlead to increased financialperformanceviacustomer loyalty (RustandZahorik1993,

Cronin,Brady, andHult 2000,Gallarza,Gil-Saura, andHolbrook2011, Lombart andLouis2012).

Reputationmediates the loyalty and performance increase (Clarkson 1995, Galbreath and Shum

2012). Hence, there often is a positive relationship between reputation and an organisation’s

performancewithboth financialandnon-financialbenefits (FombrunandShanley1990,Albinger

andFreeman2000,Black,Carnes,andRichardson2000,Helm2007,Ghoogassian2015).

RRMisbasedontheavoidanceoffactorsthatnegativelyinfluencecorporatebrands,avoidingpublic

relationsscandals (Bebbington,Larrinaga,andMoneva2008).This theory includes 'cause-related

marketing',whichisastrategywherethebenefitsoftheproductarelinkedtoappealsforcharitable

33

insuchawayastocomplementtheproduct'sadvantages(FaracheandPerks2010).Forexample,

hotelgroupsincreasinglydevelopCSRstrategiesinvolvingstakeholdersthroughvariousdistribution

channels (Heikkurinen2010).Bydisclosingtheethicalprinciplesandactions tostakeholders,the

hotellegitimisesitsactions,andcreatesadirectionofpurposefortheemployee(PayneandRaiborn