Embed Size (px)

Citation preview

The economics of indirect regulation: A costs analysis vis-à-vis traditional regulation

Roberto D. Taufick12

ABSTRACT: Regulation has been traditionally studied from the perspective that the state will operate as a central regulatory authority. Our experience says, however, that some states can and have, sometimes, behaved as quasi-irresistible market leaders instead of coercive regulatory authorities. This paper claims that the use of market dominance can work as a powerful and less costly tool to drive market behavior than traditional regulation. We also claim that the success of this strategy will depend, however, on the level of competition faced by the public undertaking on the market, the constraints of the market over its management and on the degree of control that the state exerts over the firm. Keywords: indirect regulation, double regulation, regulatory costs, minority shareholding, price leadership, state capitalism, capitalism of ties

1 2015 Gregory Terrill Cox Summer Research Fellow, John Olin Program in L&E, Stanford Law. Master in Law, Science and Technology, Stanford Law School. PGD in EU Competition Law, King's College London. Expert in Competition Law, Fundaçao Getulio Vargas. Bachelor of Laws from the Universidade de Sao Paulo, with extended Education in Competition Law from Universidade de Brasília. 2 The paper was written during my term as 2015 Gregory Terrill Cox Summer Research Fellow in the John Olin Program in L&E at Stanford Law School. I thank professor A. Mitchell Polinsky for his teaching and for recommending me for the fellowship. I also thank Ms. Elan Dagenais for her office hours in the Autumn of 2014.

Roberto D. Taufick

2

TABLE OF CONTENTS

I Background ..................................................................................................................................... 3 II T-‐regulation, I-‐regulation, and double regulation ........................................................ 7 III why the state should regulate v why the state regulates ...................................... 10 IV The costs of regulation ......................................................................................................... 11 IV.1 Why compare costs? ..................................................................................................... 11 IV.2 The costs ............................................................................................................................ 12

V The economics of I-‐regulation ............................................................................................ 22 V.1 Introducing the Concept and Some Benefits ....................................................... 22 V.II Shortcomings .................................................................................................................... 28

VI I-‐regulation vis-‐à-‐vis T-‐regulation .................................................................................. 39 VII Double regulation ................................................................................................................. 44 VIII Final remarks ........................................................................................................................ 50

The economics of indirect regulation

3

I BACKGROUND

Regulation has been studied long before the inception of economics as an

autonomous science in the XIX century -- particularly in political sciences and

philosophy. But economists have been particularly concerned about regulatory costs

at least from the second half of the twentieth century on, when they have called

attention to the relevance of regulatory impact analysis. Over the last century,

regulation has been seen as a task undertaken by the state or that it delegates to third

parties, even to market players, in order to correct market failures. In all these

instances, there was an entity that was clearly assigned by the state the task to

supervise and dictate the rules of specific niches: The regulator.

Yet, no one has taken serious efforts to report and study the use of market

tools by public undertakings3 as a means to indirectly regulate industries. In this case,

the public undertaking is a market player with no regulatory power to set rules or

apply penalties -- in other words, without statutory coercive power. Actually, what we

have been calling indirect regulation4 (aka, I-regulation) incorporates the use of

market power by the public undertaking to induce market behavior (including lower

prices) by the competitors in situations (a) where there is no regulatory obligation to

do so or (b) where regulation fails to do so5.

In general terms, I-regulation works by means of inducement, usually by price

leadership6. This means that I-regulation is a carrot whereas traditional regulation

(aka, T-regulation) is the stick. This characterization of I-regulation as an incentive is

more accurate for the markets where the competitors have room to respond to the

market leader's strategy by innovating and differentiating their products -- thereby

3 Because they are more common outside the US, we opted to use here the terminology used in Article 106 of the TFEU -- Treaty on the Functioning of the European Union -- to refer to what the American literature refers to as state-owned enterprises (Lazzarini & Musacchio, 2014) or public enterprise (Viscusi, 2005). 4 Taufick (2013) and Taufick (2014). 5 As we shall see, case (b) is a case of double regulation. 6 Price controls by the government can range from an attempt to price competitively -- simulating perfect competition and marketing at marginal costs -- to predatory pricing. We assume predatory pricing as an inherently anticompetitive behavior for a market leader, but understand that by setting prices equal to marginal costs the market leader engages in a valid market behavior -- even if it is not a profit-maximizing strategy followed by a public undertaking.

Roberto D. Taufick

4

avoiding becoming close substitutes to the public undertaking's products or services.

There are, of course, other cases where price leadership leaves virtually no room for

alternative strategies and there is lower managerial difference from traditional price

regulation. But even in these cases I-regulation does not incorporate regulatory costs

incurred by both the government agency and the market players7. It is also correct to

say that it will allow much more flexibility in terms of scrutiny -- no one will audit the

decisions of the private undertakings -- and of scope -- market leadership can only

dictate very specific behaviors, usually finalistic ones, like price and quality.

Insofar as I-regulation depends directly on the market behavior of the public

undertaking, it is correct to claim that the public undertaking is not just a yardstick8

that helps a public agency regulate private undertakings against which it competes on

the market. On top of that, unlike T-regulation, I-regulation does not involve legal

coercion -- although it involves market constraints.

There is no a priori reason why I-regulation could not be implemented in any

non-monopolistic regulated market and, as we will see, I-regulation is expected to

work best -- and be less costly -- in markets where there is substantial room for

product differentiation and, hence, where the public undertaking is subject to more

competitive pressure9. We also expect that, as the state shifts majority control to

(control through) minority shareholding and lists the company, the public undertaking

will be less subject to bias and more exposed to market constraints. As consequence,

we believe that I-regulation can be a more efficient tool than T-regulation if both

conditions are present.

We do not know of any case where I-regulation is consistently used as the

only tool for market intervention. The most notorious case resembling I-regulation

that we mention in this work is actually a situation of double regulation10 -- as we will

7 To say the least, in I-regulation the market players are not subject to massive regulatory paperwork. 8 "During the US New Deal of the 1930s, advocates of intervention stressed creating US government owned electric-power generating facilities as 'yardsticks' against which private performance could be compared." (Gordon (1994). P. 73) 9 Although it is true that highly contestable markets will turn I-regulation unfeasible, because it becomes virtually impossible to exert market dominance, we would, on the other hand, expect that highly contestable markets will not be regulated or, at least, not be subject to broad and costly regulatory oversight. 10 Because the oil sector in Brazil is subject to double regulation, I-regulation is ancillary to a parallel T-regulation and the public undertaking is used to reach public policies that could not

The economics of indirect regulation

5

develop further -- in the oil industry11 in Brazil. From what will be said, PetroBRas,

subject to double regulation, majority control by the state and low competition (even

when it comes to a disruptive but remote and slow substitution of oil by green energy)

is not an example of the efficient I-regulation that could replace T-regulation, which

confirms that, to the best of our knowledge, the I-regulation model we propose has

not been tested yet. Still, PetroBRas will be mentioned very often in this work to

make clear where double regulation fails to achieve the efficiency that we see in I-

regulation and to show where double regulation can help identify where I-regulation

might also fail.

In Brazil, the state has constitutional monopoly over virtually all the

production chain (research, mining, refining, importation, exportation, maritime and

duct transportation) and has strategically franchised the right to exploit the oil fields

and the downstream markets to private undertakings under very strict conditions --

including, very often, the establishment of joint ventures with the public undertaking,

PetroBRas12. The state has used the market power of the mammoth oil company to

keep prices down13 along the whole production chain and to influence price behavior

at the retailer gas stations -- including by announcing on TV and in advance changes

in the price of gas14.

be achieved by means of the regulatory agency -- that, as mentioned in Lazzarini and Musacchio (2014. P. 188), has a reputation of been biased and corrupt. 11 As summarized in Taverne (2008. P. 25),

"In many countries the State concerned owns one or more commercial oil enterprises. This is the case not only in countries with a centrally organized or developing economy but also, at least in the past, in countries with a free market economy. In the latter case, governments expected their state-owned enterprise to compete with the private sector with the ultimate aim to safeguard the supply of oil to the domestic market." 12 The Brazilian government is the major shareholder and controller. 13 Lazzarini and Musacchio (2015. P. 167) claimed that national oil companies "are the most important or only actor in the politically sensitive commercialization of gasoline and gas, sectors that affect household income and business profitability directly and thus make governments more tempted to control their prices." 14 In Brazil, those who distribute gas are not allowed to sell it to the end consumer (Article 26 of Resolution ANP 41 of 2013. The prohibition already existed under Article 12 of Resolution ANP 116 of 2000). However, distributors are allowed to license the use of their brands to the owners of gas stations on exclusive basis and hence influence consumer behavior. As evidence of that, in 2007 the Brazilian Competition Commission (Cade) agreed with the Brazilian oil and gas regulator (ANP) that clause 3.2 of the agreements between the PetroBRas acting as a distributor and owners of gas stations had the effect to illegally fix resale prices. (AC 08012.003409/2004-92, involving mergers in the gas retail market (2007)). It is quite possible that deeper antitrust scrutiny of the gas market would show that persisting

Roberto D. Taufick

6

In the given example, the public undertaking may also underprice its products

and, conflicting with antitrust laws, engage in resale price maintenance in order to

protect national consumers from international price shocks. But I-regulation may also

help implement market strategies not associated with price maintenance, like the

adoption of desirable safety standards (the downstream plastic division of the public

undertaking may adopt a green label for environmentally-friendly products) or the

adoption of specific policies by retailers or distributors (as a monopolist in the

extraction of oil the public undertaking may refuse to deal with distributors which do

not follow its specifications -- like it would be in the case of selective distribution).

One should have in mind that the use of market mechanism by public

undertakings in cases of double regulation and I-regulation alike does not mean that

they will always compete on the merits. Public undertakings are, by definition, subject

to more favorable treatment15 by chauvinistic politicians and conflicts of interest by

government officials, as I have already stressed elsewhere16. This will show to be

quite a relevant issue when it comes to sustaining market power in price leadership

strategies, in which case the public undertaking must count with lenient approaches

from antitrust agencies in the competitive markets (like the distribution market in the

Brazilian oil sector).

As exemplificative as it might be, in the Brazilian oil case market leadership is

sustained, among others, by holding insider information17 and because PetroBRas

price homogeneity and low rivalry at the retail level is but the outcome of price coordination by the government. 15 "The government will be more protective in every sense of the word. Greater insulation from competition will be given the firm. The nationalized firm will be sheltered from the takeover threats and bankruptcy that constrain private firms. The ability to attract, discipline, and fire workers may be restricted.

Price levels and structures will be established to subsidize influential consumer blocs. The government may lend money below-market rates, be lax about ensuring repayment, and be lenient about regulating government owned ventures as stringently as private ones."(Gordon (1994), P. 73)

However, as we will discuss in this work, Lazzarini and Musacchio (2014. PP. 198 and 201) claimed that some of these incentives stop existing when the state is a minority shareholder, especially in developed capital markets. 16 Taufick (2013 e 2014). 17 Because PetroBRas was a monopolist in the oil sector in Brazil until the second half of the 1990s, it held all the strategic field information concerning oil extraction in the country. Although the creation of the regulatory agency -- ANP -- in 1997 that followed the 1995 constitutional authorization to open the oil sector to private competition implied the transfer

The economics of indirect regulation

7

becomes an obvious strategic partner for companies who seek important projects that

depend on political support18. And, insofar as the weakening of PetroBras' dominant

position could affect its ability to dictate the rules of the market, biased antitrust

decisions have prioritized fostering fringe competition (leaving PetroBRas as hors

concours) -- leading to decisions that create a competitive niche below PetroBRas,

instead of seeking a countervailing power to the public undertaking.19

But public undertakings' strategies can also collide with existing regulation --

like the one we mentioned in footnote 14, where an anticompetitive practice was

scrutinized and challenged by both the regulatory and the antitrust agencies. In cases

alike, the entities responsible for the market oversight will traditionally face fierce

political pressure to forbear regulation -- and then issue a decision that looks like a

legitimate one -- or, afflicted by the perception that penalties would impair the market

value of a public company and also lead to disinvestment, issue only a cease and

desist order forbearing fines for the regulatory violation.

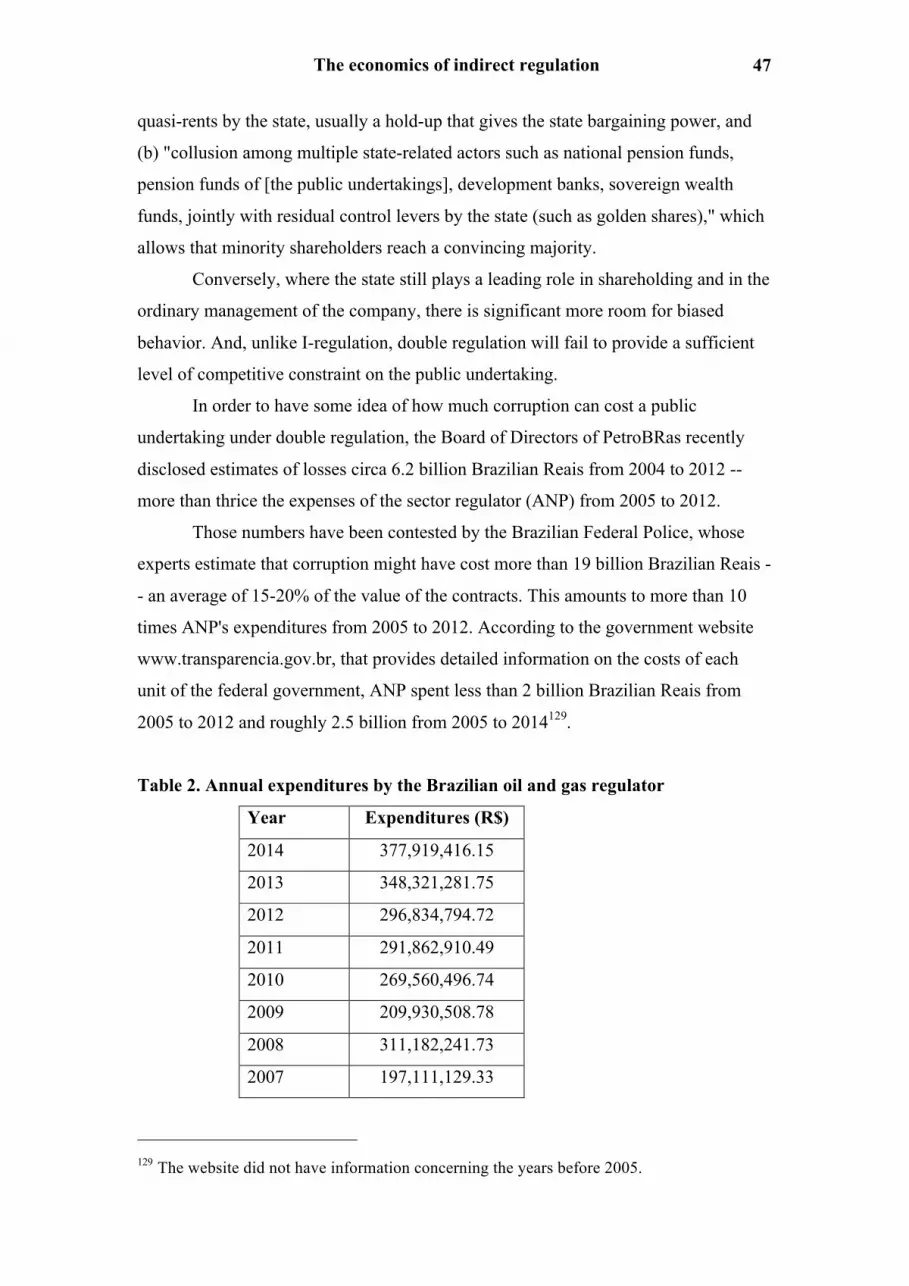

II T-REGULATION, I-REGULATION, AND DOUBLE REGULATION

Regulation is traditionally studied by experts in the economic analysis of the

law as a matter of costs as compared to the free market solution. Although most

would admit that the costs might be worth incurring if they are outweighed by the

benefits20, the vast majority of the economic studies we are acquainted with are

skeptical about the existence of effective analyses of regulatory impact -- either

because the costs are underrated or because the benefits are overrated by the state21.

of the knowledge to the regulatory agency, it is widely accepted that PetroBRas retained copies of the data and witheld information from the agency itself. 18 For instance, the Gemini joint venture between PetroBRas and White Martins involved the transportation of gas from Bolivia and created incentives for price squeeze. 19 The merger Shell/Cosan (AC 08012.001656/2010-01) is an example of a case where the Brazilian Competition Commission has struggled to subject a merger to conditions that enhance fringe competition at the expenses of the creation of a countervailing power against PetroBRas. 20 As Viscusi et alli mention (2005. P. 43), "if the regulations generate benefits that exceed the costs, then it is desirable to promote such regulation rather than discourage it." 21 "Obviously the existence of transaction costs implies that less reform is appropriate than if no transaction cost arose. Such conclusions are useful because prior reform proposals seemed to ignore transaction costs and particularly the severe difficulties of determining where to act. Thus, as this books stresses, the efficacy of governments is overrated." (Gordon (1994). P. 63)

Roberto D. Taufick

8

Two major hearings from the US Congress and the House of Representatives in

197922 and 2002, respectively, have listed but burdens brought by regulations --

although they sporadically mentioned that regulation could eventually lead to net

social benefits.

What this article proposes is another view of regulation. Our task here is,

assuming that regulation was chosen as the most appropriate way to approach a

certain market, help understand a less intrusive way to influence or even dictate

market behavior. Because we will discuss only the relative cost-efficiencies between

forms of regulation, our study aims neither to revisit the economics of regulation nor

to explain why should markets be regulated.

Having that in mind, our research departs from the assumption that there is no

a priori reason why the state cannot determine market behavior as a market player

instead of acting as an oversight regulatory entity23, and we study the regulatory costs

imposed by T-regulation and how they are aggravated or alleviated by I-regulation.

The whole criticism over T-regulation comes from its exacerbated costs.

Sectorial policies require massive human and financial resources spent on the design,

implementation and detection activities -- reason why a certain level of under-

deterrence is welcome in order to avoid that sky-high costs extrapolate the benefits24.

Still, regulation is not cheap. According to Weidenbaum ,25 in 1977 the costs to

operate and costs induced in the private sector summed up $79.1 billion. The author

also estimated that the numbers would achieve $96.7 billion in 1978 and 102.7 billion

in 1979. The Small Business Administration's Office of Advocacy calculated the costs

of regulation to the US economy at impressive $843 billion per year in 200126.

Unlike regulatory discussions over excessive costs of enforcement, I-

regulation involves the use of incentives and market strategies from the public

undertaking instead that might also lead to suboptimal allocation of resources. So the

decision between opting for T-regulation or I-regulation is not based on the

comparative costs to enforce the law (because under I-regulation there is none), but

22 Congress of the United States (1978) and US House of Representatives (2002). 23 Elhauge (1992). P. 1202. 24 Becker (1968). 25 Weidenbaum & DeFina (1978). 26 US House of Representatives (2002).

The economics of indirect regulation

9

rather on the assessment of regulatory enforcement costs under T-regulation vis-à-vis

the market efficiency losses that can be assigned to behavior that is not profit-

maximizing under I-regulation.

As mentioned, this work also distinguishes the application of I-regulation as

an independent tool from the use of I-regulation as ancillary to T-regulation --

something we have already called double regulation. The former happens when there

is the use of a public undertaking alone to induce a certain market behavior in a free

market environment that, instead of increasing profits, is expected to increase the

general welfare of society27. Double regulation, on the other hand, happens when

there are both a separate central regulatory body within the state that is responsible for

the regulation of that specific market and an ancillary public undertaking that uses its

market power to constrain the market options of the competing private undertakings

in a regulated environment towards a socially desirable behavior -- either where there

is no outstanding regulatory obligation compelling said private undertakings to pursue

such a socially desirable behavior or where, even though there is an obligation to

pursue said societal welfare, the regulator fails to enforce it against the regulated

companies. As we already know, the PetroBras case in Brazil is, in fact, a case of

double regulation.

It is not the purpose of this work to give definitive answers on a subject whose

variables change from industry to industry and from place to place. The study sheds

some light, however, on typical or expected results, but only when such conclusions

are backed by empirical evidence or overwhelming literature. As Baldwin et alli 28

advocated, strong convictions based on assumptions where there are not reliable data

available are but expressions of taste and political preferences.

27 This view is also shared by Lazzarini and Musacchio (2014. PP. 60-62). 28 "This prompts comparisons between the outcomes produced by the given regulatory system and the hypothetical outcomes that would have been produced by doing nothing or by implementing some other regime of control. In both cases, it will be difficult to obtain reliable data with which to effect comparisons. Such exercises will be based on underlying assumptions and weightings and, as a result, what constitutes a failure and how much it matters when compared with other 'failures' will turn on tastes and political preferences. The matter of trade-offs constitutes a further evaluation difficulty, since real-life comparisons will often involve looking at regulatory interventions that produce a certain trade-off between numbers of risks against possible other interventions that produce other sets of risk trade-offs." (2012. P. 69.)

Roberto D. Taufick

10

III WHY THE STATE SHOULD REGULATE v WHY THE STATE

REGULATES

There are important reasons why the state should regulate and they are

traditionally associated with what economists call market failures. In general terms,

regulation is needed where competition alone -- read the market alone -- would not

bring prices down to marginal cost or would not substitute for a liability rule that

disciplines the quality of the products. Regulation only makes sense where its benefits

are greater than costs -- although economists have never found it easy to trust

government assessments or to find reliable data that they could use on their own

researches.

As Sappington and Stiglitz29 pointed out, regulation usually tries to solve three

groups of market failure: Imperfect competition, imperfect information and

externalities.

Others prefer to explain why the state chooses to regulate instead of why it

should regulate. One clear example lies in Baldwin et alli30, who listed natural

monopolies, windfall profits, externalities, information inadequacies, continuity and

availability of service, anticompetitive behavior, public goods, unequal bargaining

power, scarcity and rationing, rationalization and coordination, planning, among

others as reasons why the state chooses to regulate. As the authors make it clear, 31 the

state will not necessarily regulate only where there are market failures:

Thus society may, as a matter of policy, decide to act in the face of drivers' desires and demand that seat belts be worn in motor vehicles. In the strongest form of such paternalism, the decision is taken to regulate even where it is accepted that the citizens involved would not support regulation and that they are possessed of full information on the relevant issue.

However, as mentioned, earlier, the scope of this paper does not include a

discussion on why the state should or should not regulate. We leapfrog the analysis of

the justifications to regulate and depart from the assumption that the state officials

have already decided that regulation is a better option than the market solution. What

we ask in this paper is if I-regulation can be a better option than T-regulation under

29 Sappington & Stiglitz (1987). P. 4. 30 Baldwin, R., Cave, M., & Lodge, M. (2012). Understanding regulation: theory, strategy, and practice. 2nd ed. Oxford: Oxford University Press. PP. 15-24. 31 Baldwin (2012), P. 23.

The economics of indirect regulation

11

this scenario. And we might incidentally ask what was the reason why the state chose

to regulate insofar as it shows relevant to clarify which option -- I-regulation, T-

regulation or double regulation -- was the most effective one.

In order to address this question, we must first find out what is commonly

described as costs of T-regulation and then compare these costs with losses of

efficiency caused by substituting I-regulation for the market. For simplicity, we will

now on call costs also the losses of efficiency caused by I-regulation.

Naturally, I-regulation only makes sense when CT-r ≥ CI-r

Where:

CI-r = costs of I-regulation

CT-r = costs of T-regulation

IV THE COSTS OF REGULATION

IV.1 WHY COMPARE COSTS?

Our first task in this section is to identify the burdens that T-regulation lays on

the economy. Although a thorough benchmark analysis should include variables like

effectiveness and efficiency and hence compare the net costs or benefits that arise as a

consequence of T-regulation with those created by I-regulation and double regulation,

due to a lack of reliable information on the benefits caused by regulation the

economists have opted to gauge proxies or, more constantly, to prove how costly

regulation is and how unlikely it would be to find benefits that outweigh costs.

The harder (or more costly) it gets to pursue reliable information regarding the

quantification of the benefits involved in regulatory policies, the more relevant

becomes the cost analysis. First, because, as costs rise, the benefits that regulation

brings must rise accordingly. Second, because, as costs' information becomes the sole

reliable data available, the administration of the costs -- and not the maximization of

the benefits -- becomes the core if not the sole tangible purpose of the regulatory

studies. And, as a consequence, the regulatory authorities -- whose regulations mirrors

academic studies -- become victims of their own lack of transparency and prioritize

Roberto D. Taufick

12

models that minimize costs, even if they would eventually show to be less cost-

efficient32.

For all we have said, the measure of regulatory costs is relevant in our study

when we compare T-regulation with the alternative I-regulation and double regulation

and assume that they lead to the same level of efficacy and efficiency. Or, in jargon, if

we assume that, taking out costs, everything stays equal (coeteris paribus).

IV.2 THE COSTS

Although they are not few, most of the costs are quite predictable and widely

known. The first we address is the so-called regulatory capture and can be enunciated

by Stigler's words that "regulation is acquired by the industry and is designed and

operated primarily for its benefit."33 Stigler claimed that groups want from the

government "direct subsidy of money," "control over entry by new rivals," "price-

fixing." The interest group economic theory has as great merit an open criticism over

the use of regulation for rent seeking -- to say different, money that is spent on

lobbying activity to foreclose entry instead of investing in innovation.

In 2010, the parties to the OECD roundtable for the International Transport

Forum have expressed concerns with capture, political influence and also ossification

-- the inability to respond to necessary changes due to inflexible regulatory practices.

Unlike market decisions, regulations depend on a series of formalities that take time --

which might include amending previous rules or even laws -- and are often taken

blindly, or in trial-and-error "strategies." Because regulators know in advance that

complex rules will have to be adjusted from time to time until they become

sufficiently adequate, seldom do public officials care in making efforts to issue ex

ante and ex post34 regulatory impact analysis.

32 In other words, because we do not know how large are the benefits, we might be opting for lower costs where the option with higher costs would also lead to higher net benefits. 33 Stigler (1971). P. 2. 34 Ex ante and ex post assessments belong to different phases of the strategic planning process: While the former is part of the planning, the latter is the main component of the evaluation.

The economics of indirect regulation

13

Corruption comes high in the literature of regulatory costs. Although not

circumscribed to regulated markets, corruption is easier to be purged from listed

companies and more difficult to affect those who do not suffer from entrenchment.

Listed companies have high incentives to behave properly insofar as the market --

both investors and consumers -- responds negatively on the stock market to signs of

corruption that tarnish the image of the company. And as Viscusi et alli (2005)35 told

us, bad management also presents a good opportunity for investors, who can buy

devaluated shares, replace the managers and resell the shares at a higher price.

The same is not true of unlisted companies, whose bad managers cannot be

efficiently punished by the stock market. Unlisted companies can, however, be

punished by the impact of corruption on sales -- a quite unlikely market behavior,

though. The impact here is unlikely because, even though corruption affects the

credibility of the manager as someone looking after the interests of the investors --

reason why the shareholders of listed companies will respond promptly on the stock

market -, rarely36 will corruption alone affect, coeteris paribus, the credibility of the

product itself.

In its turn, entrenched companies, even the ones that are listed, have lower

incentives to respond in a timely fashion. This happens because the entrenched

managers take into consideration the benefits that they receive while they are on the

board. If the manager is also a shareholder, she will have a greater incentive to step

down if the company is listed. But, even so, there might be gains in staying further --

usually resulting from the association of the goodwill of the company with the

personal prestige of the corruptor, who aggregates value to the brand. In the case

where the managers is not a shareholder, the decision is clearer: She maximizes her

profits by holding to the position as far as she can, with no concern whatsoever with

the value of the company's shares37. But because entrenched boards of non-

35 P. 508. 36 We say rarely because the company's goodwill might be linked to a specific niche of consumers directly affected by the corrupt activity (including religious groups and children's toys) or its brand might have been built over moralistic campaigns. 37 Even though it is clear that, if the company crumbles, the officer loses her position, she can still leave the company any moment between the time when the market starts to penalize her management until the moment before the company goes bankrupt. If the corruption scandal happens at time n and bankruptcy happens at time b, she will be better off anytime she leaves the company between both tempos (in other words, at n + 1, n + 2, n + 3...., n < b).

Roberto D. Taufick

14

shareholders is a phenomenon associated with listed companies38 -- including the so-

called classified or staggered boards -, there will usually be mechanisms that trigger

protection for the shareholders, including the stock purchases mentioned in Viscusi et

alli (2005)39.

Corruption in the public sector is even more critical. There, public officials are

elected or belong to a career and have to face long processes before been discharged.

On top of that, public goods are subject to the dilemma of the commons: No one is

really paying attention to the day-to-day managerial acts of the regulatory entities. But

what makes it worse than private corruption is the snowball effect on the market:

Corruption in the public sector will usually involve the core business and correlated

markets and lay heavy burdens on the consumers than cannot be solved by the market

alone. To our subject of study, it must stay clear that, coeteris paribus, corruption that

affects only the distribution of welfare within a private company (interna corporis),

even if we talk about a regulated undertaking, does not affect public goods -- only

private property. It is only when corruption affects the welfare of the taxpayers and of

the consumers who were supposed to be protected by the regulation that it becomes

relevant for us. And in these cases that matter to us corruption is the outcome of both

regulated entities and public officials colluding to harm competition or to lay lax

rules.

It is also possible that bribery does not lead to an evasion of the regulatory

rules by the private undertakings -- it might actually be the only means for the public

service to work in certain countries. This is the case of a port operator that illegally

asks for money in order to grant access to the harbor. Although the operator would

not succeed if no one paid a penny, the best strategic reply taking into consideration

the expected behavior of the competitors would be bribing40. In these cases,

corruption works as a tax that burdens the private sector and, depending on its

magnitude, diverts money that could have been invested in public goods. It also

prevents entry from potential competitors who decide not to bribe -- and, by lowering

competition and innovation, the regulator is damaging the quality of the service and

38 The presence of independent members in the board has been adopted to improve corporate governance and has become a condition have the shares listed in more advanced stock markets. 39 "[T]he threat of being fired can arise quite effectively via the capital market." (P. 508) 40 A Nash equilibrium.

The economics of indirect regulation

15

raising prices. Because it is a burden to the efficiency of the market, this kind of

corruption interests us.

Asymmetry of information will usually create another problem for regulators:

It impairs the state's ability to make correct assessments of the reality and to respond

efficiently. Asymmetries of information do not allow the regulator to know marginal

costs and to have a good estimate of the competitive price levels. Moreover, they also

lead to models that fail in their attempts to replicate market incentives and increase

transparency, like price cap, cost-of-service and rate of return regulation. Professor

Stiglitz41 stressed that "the structure of the regulator's policy is highly dependent on

what she knows, what she can monitor, and how quickly she can learn. (...) Thus the

magnitude of the informational problem is related to how fast the environment

changes and how fast the regulator learns."

In this same path, Breyer (1982) describes how regulation may lead to

incorrect choices as to what and to whom will play on the market. In other words, the

state might pick up the wrong winners and losers, as compared to what the market

alone would choose. He describes how, depending on the standards set for a public

bid -- (i) technical qualification, (ii) financial qualification, (iii) proposed program

service and (iv) legal qualification --, mavericks may be prevented from entry and

monopolies may be raised. The same applies to standard setting, where the regulators

might set standards that are costly and later abandoned because they are inefficient,

ineffective or impractical -- but have been established by the pressure of consumer

groups that do not understand of technical requirements. As the author explains,

"[o]btaining accurate, relevant information constitutes the central problem for the

agency engaged in standard setting. It has difficulty finding knowledgeable,

trustworthy sources."

But bad regulation commonly arises out of lack of expertise, instead of

imperfect information. Probably most countries are understaffed and/or have public

policies defined and implemented by non-experts. The regulator can also set standards

that are demanded by particular groups -- the same kind of criticism present in

Stigler's paper (1971). Baldwin et alli (2012. P. 73) invoked the futility42, jeopardy43

41 Bailey (1987). P. 22. 42 "[R]egardless of regulatory effort, no change to the existing problem will occur."

Roberto D. Taufick

16

and perversity44 arguments to recall relevant literature claiming that regulation is

usually a worthless expenditure of resources and only aggravates the original

problems.

Regulation implies costs of detection and enforcement by the regulator. And,

obviously, there are also the costs to operate a regulatory agency. According to

professor Weidenbaum (1978), the costs to operate a regulatory agency reached $3.1

billion in 1976. He also showed preliminary figures of $4.8 billion to 1979.

Yet, also critical to regulation are the expenses that regulation imposes on the

regulated companies. Breyer (1982) makes reference to the costs to comply with the

law, in particular when compliance involves expensive studies, like phase 2 double-

blind tests for agencies that regulate drugs. In this case, the costs are not only

monetary, but also flow from uncertainty caused by the non-uniform application of

the law to the different cases45. This is also true of uncertainty caused by conflicts

between the understandings of regulatory and antitrust authorities, which increase the

transaction costs between the regulated entities and the regulatory agencies.

In this regard, Baldwin et alli (2012, P. 77) claimed that "[i]t is particularly

difficult to measure efficiency when the mandate fails to set down consistent or

coherent objectives, or where a regulator's functions intermesh with those of other

agencies and departments." This framework is also called layering theory, "side-

effects of multiple regulatory regimes with different understandings and objectives

operating side-by-side and overlapping." Although guidelines designed by the

authorities are usually helpful to the regulated entities, they are far from sufficient.

Conflicts can still arise as a result of overlapping authority of agencies and also out of

conflicts between sovereign states (US) and countries (EU).46

43 "[D]espite the worthwhile character of a particular regulatory instrument, its deployment would risk wider achievements and/or lead to a chain of undesirable side-effects." 44 "[R]egulatory interventions achieve the exact opposite of their intended outcomes." 45 Having worked from 2011-2014 in the technical committee that decided upon the appeals of the pharmaceutical companies in Brazil, I can certify that the rules for drug approval are very often insufficient to lead to a consistent body of decisions and that the degree of strictness varied from case handler to case handler. 46 The state action doctrine in the US and the loyalty clause in the EU are few examples of tools that address, but do not eliminate conflicts of jurisdiction. For more, see ICN 2004.

The economics of indirect regulation

17

Regulation involves many multiple sources of cost. Gordon (1994)47 argued

that "even determining whether reform is justified involves costs; so, limits must be

set on efforts to evaluate claims that action is needed." And added that ", since

reforms often require substantial transaction costs, the evils must be large enough to

repay the expenditures. Only great inefficiencies justify government intervention."

And in order to assess whether there are such great inefficiencies that require

regulation, public officials "must have the same sort of intuition as a successful

business pioneer." And, as the common sense dictates, the public service lacks market

incentives to be efficient and succeed: The state regulator competes against no one.

Critically high regulatory costs might send away desirable investors and

attract highly-risk-preferred companies interested in monopolizing explosive markets,

where the risks and payoffs are large, or politically insured players moved by moral

hazard. Stiglitz48 also reminded us of moral hazard in the post-bidding behavior of the

winner. As he pointed out, insofar as the regulator lacks the capacity to observe the

actions of the winner (lower detection), it is not able to enforce regulation against it49.

He also sees adverse selection in the cases where the bidder holds information (like

relevant technology) from the regulator. Stiglitz50 also criticizes how regulators

"capture the rents [from established firms] through an auction."51

Professor Weidenbaum (1978) claimed 4 decades ago that the costs to comply

with regulation were already rampant, and that "[t]he aggregate cost of complying

47 PP. 62-63. 48 Bailey (1987). 49 Gary Becker defended (1968) that, for risk averse and risk neutral individuals, deterrence is optimal where fines are equivalent to the wealth of the individual -- because detection costs would be minimal. He argued, however, that a certain level of under-deterrence would be recommended to minimize costs. Applying the Becker solution, Stiglitz' concern (Bailey (1987)) could be addressed by raising the fines to the wealth of the regulated entity. But, as Polinsky (2011. P. 83) makes clear, the Becker solution "is not descriptive of actual enforcement policies." 50 P. 18. 51 Viscusi et alli (2005) brought to our attention that even when a public undertaking is privatized the state extracts rents by charging the expected present value of the future profit stream -- usually meaning that "the sale price (...) should exceed the value of the enterprise had it not been privatized." Citing Spanish Endesa as example, Viscusi et alli showed how the government might increase the dominance of the public undertaking previous to the privatization in order to charge more for the market power, the so-called monopoly premium. (PP. 520-521) The same view is shared by Pargendler (2012) in her recent study about corporate governance of public undertakings in Brazil.

Roberto D. Taufick

18

with Federal regulation came to $62.9 billion in 1976 (...)." And because regulatory

costs were so high and passed on to the consumers, the prices of the products to end-

user were also significantly affected. In other words, high regulatory costs also have

inflationary impact. The Small Business Administration's Office of Advocacy

calculated the costs of regulation to the US economy at $843 billion per year in

200152.

Viscusi et alli (2005)53 called attention to the high monetary costs: According

to the authors, in 1995 alone, the equivalent to 9.2% of the US GDP ($668 billion out

of $7.3 trillion) was spent in regulation. Such costs included both transfers -- like

minimum wage, accounting for $147 billion, where "[t]he gains to workers offset the

losses to firms", so "[f]rom an economic standpoint this is not an efficiency loss (...)"-

- and paperwork requirements: Process regulation, accounting for $218 billion, which

is "[o]ne of the most striking aspects of the regulatory cost mix".54

Weidenbaum (1978) explained that businesses paid $25-30 billion a year in

paperwork. The hearings before the Congress of the United States (1978) also

clarified that in 1976 Dow Chemical USA spent over $20 million in paperwork and

that expenses in paperwork is money diverted from investment:

In one sense, the cost to society was the value of the travel that did not occur. Parallel examples from other areas of regulation include television stations not broadcasting, beneficial drugs not on the market, and freight not carried in empty trucking backhauls.

As less money is used in investment because of regulation, the level of

innovation is also lowered. And as a matter of consequence, claimed Weidenbaum

(1978), because costly regulation lowers investment and curbs innovation, it also

leads to lower employment55 and, as mentioned earlier, to inflation -- in the latter

case, because lower productivity leads to lower output and, according to supply and

52 US House of Representatives (2002). 53 PP. 40 and following. 54 Viscusi et alli (2005. P. 41). 55 Lazzarini and Musacchio (2014. PP. 33-36) also showed numbers confirming that even when the participation of public undertakings in the economy peaked in the 1970s, their share in employment was quite low when the state prioritized the nationalization of "capital-intensive industries such as electricity, telecommunications, oil, and steel."

The economics of indirect regulation

19

demand laws, higher scarcity leads to higher prices56. Because all these costs lead to

lower levels of consumption than there would be absent market regulation, we can say

that they lead to deadweight losses.

Other costs are not so obvious. The competitive costs are one of those.

Weidenbaum (1978) reported before the Congress of the United States in 1978 that "

Federal rules and regulations would cost consumers $102.7 billion and homeowners

$4 billion in fiscal year 1979" and that "5 million small businesses spend $15-$20

billion, or an average of over 3,000 each on federal paperwork." 24 years later, in a

hearing before the US House of Representatives (2002), Professor John D. Graham

stated that

That leads to the key finding of the Crain/Hopkins Report commissioned by the Small Business Administration. Firms with less than 20 employees face 60 percent larger regulatory burdens per employee than firms with greater than 500 employees. So I think it is important to realize that regulation for— particularly for larger companies, in certain circumstances they see that as a competitive advantage relative to small companies.

The words of former Congressman David MCintosh were even more

compelling:

In fact, when I worked with Vice President Quayle, a well-intended lobbyist from one of the Nation’ s large businesses came in and said, we like what you are doing in cutting back on unnecessary regulation, but do not forget there are some regulations that are good. And I said, which ones do you have in mind? He said, well, there are some that we like because our competitors cannot quite comply with them yet. A moment of candor, and it gave me a great insight into what perhaps some of the motivation was behind different programs.

Whereas it might be feasible for larger and consolidated businesses to pass the

burden on to the consumers or even to afford it, start-ups and small businesses in

general might not be able to afford such level of sunk costs in paperwork and are

unlikely to be able to pass it on to the consumers. Starting businesses are expected to

price aggressively to earn clientele and market share, while smaller businesses'

customers are expected to show higher price elasticity or, in other words, to be less

loyal to the brand.

56 It is hard to determine, however, the net impact of unemployment on inflation vis-à-vis other variables like lower productivity. While we expect that unemployment lead to lower inflationary pressure (due to a drop in the demand), lower levels of productivity can actually lead to stagflation (encompassing both unemployment and inflation). Brazil has been subject to stagflation both in the aftermath of democratization and at the present moment.

Roberto D. Taufick

20

It becomes easier now to understand the numbers disclosed by Mr. Mike

Pence, who was the Chairman on Regulatory Reform and Oversight of the Committee

on Small Business of the US House of Representatives in 2002. He showed57 that

half of the US workforce was employed by small businesses and that 2/3 to 3/4 of net

new jobs are created by them. The obvious implication of this data is that, if small

businesses are the ones that are most affected by regulation, then regulation has an

even clearer implication on unemployment.

Interesting enough, professor Stigler (1971) claimed that regulation could, in

fact, subvert market choices and empower groups that have political, instead of

economic strength. According to him, the problem with regulation lies in that it

artificially constrains the power of the largest players when the small firms have

political influence (an issue we mentioned en passant before).

In an unregulated industry each firm's influence upon price and output is proportional to its share of industry output (at least in a simple arithmetic sense of direct capacity to change output). The political decisions take account also of the political strength of the various firms, so small firms have a larger influence than they would possess in an unregulated industry.

Political strength is usually expressed by groups of interest and, specifically in

the US, by means of powerful lobbies.

Costly regulations also affect the international competitiveness of national

companies, who cannot compete abroad on a level playing field. And also influence

jurisdictional arbitrage, leading to a lower attractiveness of the country to foreign

investors (because of the regulatory risk or cost).

Red tape might create unbalance and artificial competitive advantages

between competitors that use different technologies as well. It is true that sunset

clauses, forbearance and regulatory holidays are asymmetric regulatory tools that

exempt new technologies from burdensome regulatory costs, including paperwork. It

is, however, not less true that interest groups might put pressure to be classified into

categories that are exempt from heavy regulation. This is the case, for instance, of lax

network neutrality rules that permit that Internet Service Providers (ISPs) discriminate

between classes of applications -- allowing that different rules apply to each class,

even knowing that interest groups just want to be able to place their own applications

57 US House of Representatives (2002).

The economics of indirect regulation

21

in different classes than their competitors'58 and then charge the competitors for fast

lanes.

Another complication brought by regulation is bias. There are three particular

types of bias that interest us: (a) conflicts of interest, that is, the beneficial treatment

that public undertakings receive from public officials; (b) pressures for government

policies to benefit narrow interests59 -- a subject we have already addressed -- and (c)

changes in political priorities, easily identified when a different group takes charge of

the government -- which professor Stiglitz60 calls policy swings.

At this point, we can summarize the costs laid by T-regulation as follows:

private capture, rent seeking, political influence, ossification, corruption, conflicts of

interest, detection, enforcement, compliance, conflicting regulations (layering), policy

swings, transaction costs, adverse selection, moral hazard (from the regulated private

undertakings), inflation, low investment, less innovation, unemployment, lower

productivity, higher entry barriers, weaker international competitiveness of the

national industry, jurisdictional arbitrage and regulatory asymmetry. However, most

of the aforementioned costs share common features that help us aggregate them into

classes. For simplicity, we have aggregated the costs into 7 classes: bias, intrinsic

flaws, asymmetric information, regulator's expenditures, private expenditures,

competition and macroeconomic impact. Although the division is open to criticism

and is not intended to provide a universal and definitive methodology for the

aggregation of the regulatory costs, we understand that it provides an important tool

for an easier comparison with the alternative regulatory models we will discuss from

the next section on.

• bias (ß): private capture, political influence, policy swings, corruption and

conflicts of interest.

58 The subject is quite complicated to be explained in a footnote. But one example might make it clear. Even though few would disagree that Comcast's Xfinity and Netflix compete for the market of online streaming movies, Xfinity and Netflix could eventually end up in different classes of applications. Comcast could claim that, unlike other online platforms like Netflix, Xfinity has not been provided as open Internet content and therefore both services should be treated differently. Following this rationale Comcast could, working as an ISP, discriminate against Netflix, Youtube and others and demand that they pay for fast lanes. This kind of discrimination is made easier because the definition of which application fits each class is left to the ISPs, subject to ex post confirmation by the regulatory authority. 59 Gordon (1994). PP 62-63. 60 Bailey (1987).

Roberto D. Taufick

22

• intrinsic flaws (ƒ): ossification and layering.

• asymmetric information (α): adverse selection and moral hazard.

• regulator's expenditures (εr): detection and enforcement costs.

• private expenditures with regulation (εp): compliance and transaction costs.

• (lower) competition (κ): lack of investment, lack of innovation, lack of

efficiency, lower competitiveness of the national industry, jurisdictional

arbitrage, entry barriers and regulatory asymmetry.

• macroeconomic impact (µ): inflation and unemployment.

We can now also mathematically define T-regulation, in terms of costs, as:

CT-r = f (ß, ƒ, α, εr, εp, κ, µ)

In the next sections we will introduce the costs involved in I-regulation and

see how they are minimized or magnified as compared to T-regulation.

V THE ECONOMICS OF I-REGULATION

V.1 INTRODUCING THE CONCEPT AND SOME BENEFITS

I-regulation is a mechanism whereby a market player holding market power

disciplines the market using market tools. Unlike T-regulation, I-regulation does not

depend on the policymaking, rulemaking and enforcement of the rules by a central

regulatory authority. It does not need to rely on top-down or bottom-up costs models

either, as market participation eliminates important asymmetry of information faced

by traditional regulation. Because I-regulation does not fit the traditional regulatory

structure, it does not incur intrinsic regulatory costs, like ossification and layering. It

also frees the government from massive regulatory expenditures in detection

mechanisms, including personnel61.

Although working as market players, public undertakings do not share all the

characteristics of the competing private undertakings. A good example can be

extracted from the application of the dividends as state revenue. The profits earned by

the state as a controller shareholder are ideally invested in the country's economy, in

61 We have refrained from mentioning the costs to comply, because, as it should become clear, the use of market mechanisms by public undertakings to exert pressure towards a desirable behavior is, to some extent, a kind of enforcement that also leads to losses of efficiency. For clarity, we use the term enforcement for T-regulation and quasi-enforcement for I-regulation.

The economics of indirect regulation

23

particular in sectors that are key to state programs. Such profits -- that account for

100% of the dividends in wholly owned undertakings -- can also help subsidize lower

prices or stabilize price oscillation of merit goods, or be reinvested in the company,

leveraging its position against competitors62.

One could argue that the claimed power to leverage the public undertaking

against the competition fails to take into consideration the inefficiencies that arise

when the state drives the management of a market company -- an error that can be

compared to the failure to take into account regulatory costs when comparing

unregulated competitive markets and regulated ones. Figure 1 below (Wolak, 2010)

replicates the latter argument that the regulated industries could provide the same

services as free competition, but for a lower price -- insofar as cost-oriented

regulation aims at charging always (since t0) the marginal cost -, increasing consumer

welfare.

Figure 1. Cost-of-service regulation v perfect competition

In the latter case, as professor Wolak explains (2010), what seems plausible in

theory is unlikely to be achieved in reality, because the high costs of regulation lead

to deadweight losses and higher marginal costs that are not incorporated in Figure 1. 62 Lazzarini and Musacchio (2014. P. 167) confirmed this view by claiming that one of the high rents that can be extracted from oil companies are the main reason that lead governments to use national oil companies to pursue social goals. The authors actually claim (PP. 218-219) that this is a characteristic shared with natural resource sectors (the natural resource curse), like mining, where Brazilian Vale is an example of extraction of high rents by the government -- although, this time, using minority shareholding. Conversely, the authors (P. 6) stressed that shocks in the economy can actually lead to astronomic losses to the public undertakings that will be translated into national budget deficits by paternalistic governments.

Roberto D. Taufick

24

The same is not true of I-regulation, though. As mentioned before, the most

distinctive characteristic of I-regulation is that public and private undertakings

compete against one another in a deregulated market, but the rules of the market are

dictated by the dominant public undertaking. In other words, it is, at least in theory,

feasible to achieve the outcome represented in Figure 1 by means of price leadership

exerted by a dominant and efficient public undertaking whose marginal costs are at

least similar to the marginal costs of the most efficient private undertaking.

The problem with the practical implementation of this strategy lies in the

common sense that the state still lacks the same incentives to behave as efficiently as

private managers in a deregulated market -- this fact alone implying that the

inefficient public undertakings cannot sustain a position of market leadership under

free competition by competing on the merits alone. Rephrasing it: If public

undertakings lack the necessary market incentives to be more efficient than private

undertakings, they cannot hold, in the long run, any given market power that is not

artificially sustained and, as a consequence, without said artificial tools not only the

outcome outlined in Figure 1, but also I-regulation itself becomes unfeasible. This is

to say that, following the common sense, in the cases of I-regulation the public

undertaking must necessarily be in charge of strategic input (including privileged

information) or facilities that help shield its market power. Public undertakings can

also indulge in paternalistic behaviors of government officials.

However, as we will point out along this paper, empirical studies have often

raised doubt about the validity of the argument that public undertakings are always

less efficient than the private counterparts. On top of that, minority shareholding,

exposure of listed companies to market constraints and market competition have

shown to be important forces driving public undertakings towards a more efficient

behavior -- which corroborate about perception that, under certain conditions (listed

company, minority shareholding by the state, existence of rivalry on the market and

the implementation of I-regulation alone63), I-regulation can create not only a less

intrusive environment to drive market behavior, but also replicate market incentives

to behave efficiently.

I-regulation relies on market power to dictate the rules of the market. Price

leadership is the tool that dominant public undertakings use to set prices that will be

63 As apposed to an ancillary I-regulation under double regulation.

The economics of indirect regulation

25

followed by competitors. Dominance is also required to put pressure on the

competitors to follow a certain standard -- the competitors know that, if they do not,

they lose the clientele to the market's Leviathan. Nevertheless, because the dominant

public undertaking in a scenario of I-regulation cannot curb the surge of maverick

competitors by an act of regulatory fiat, dominance can only be sustained if it shows

the ability to retain consumers. The need to sustain its dominant position, therefore,

should then work for the creation of a more competitive environment in I-regulation.

This goes in line with what Lazzarini and Musacchio (2014) claimed in their work64:

(...) hundreds of papers have compared the performance of SOEs [public undertakings] and private companies, almost invariably finding that the former underperform the latter, except under some circumstances such as when SOEs face competition (Bartel and Harrison 2005) or when SOEs have been able to act as private companies, with professional management and boards of directors that monitor them closely (Kole and Mulherin 1997).

Studying 17 subsidiaries of German or Japanese firms in which the US

government held stakes of 35-100% (median stake of 75%) for average 7 years

starting in World War II -- 7 of them with shares traded publicly -, Kole and Mulherin

(1997) actually concluded that the existence of competitive markets, external

valuation, internal valuation and incentive devices to monitor managers create a level

playing field for the performance of both public and private undertakings. Even

though these companies were not subject to public policies that privileged social goals

in lieu of the pursuit of profits -- probably influenced by the fact that they were under

interim government custodianship -, it is possible to infer from their study that, being

consistent with our theory for I-regulation, market constrains or forces that replicate

market constrains are likely to improve the performance of both public and private

undertakings.

In its turn, using panel data from Indonesia from 1982 through 1995 and

focusing on ownership and environment incentives to market performance, Bartel and

Harrison (2005) assessed the role of easy access to subsidized loans65 from state

banks and low competition, including imports barriers, to poor public sector behavior.

The authors built a model where public undertakings would be subject to higher

transfers from the government in order to hire extra labor: Whereas more jobs create

64 P. 144. 65 "However, anecdotal evidence suggests that government loans have a large subsidy component, and that many of these loans are never repaid at all." (P. 21)

Roberto D. Taufick

26

more political capital to politicians, excessive labor also leads to lower productivity.

As they claimed66, "[i]t should be clear (...) that public or private ownership is not the

issue here: what determines excess employment (inefficiency) is the magnitude of

transfers, bribes, and other factors." However, they67 tested that, while for private

undertakings there is no significant correlation between government loans and labor

shares, for public undertakings the correlations are significant. In other words, there is

no independent impact of public ownership on the magnitude of excess employment

and "the effect of public ownership on excess labor operates via government loans."68

Bartel and Harrison also argued that because public undertakings are typically

located in sectors shielded from import competition ", failing to control for

differences in import competition could lead to the incorrect conclusion that public

sector enterprises are more inefficient, if lack of import competition is correlated with

poor performance."69 And their study showed evidence that "import penetration has a

positive and significant effect for public sector firms (...), indicating that public sector

firms that were shielded from import competition had inferior performance."70

The incentive to conserve a dominant position is a necessary, although not a

sufficient condition to avoid moral hazard and bring rivalry to the market. The

incentives to be efficient depend heavily on the ability that the competitors have to

differentiate their products instead of following the behavior dictated by the market

leader. The broader the alternatives to the leadership of the public undertaking, the

more the public undertaking will have to be efficient to captivate the consumer.

Although the degree of differentiation counts against the feasibility of I-

regulation, if a differentiation is such that it places the service or product of the

competitor in another relevant market -- meaning that they do not compete anymore -,

then the competitive pressure over the public undertaking is lower, since the relevant

consumer to the public undertaking -- usually the one with lower income -- will not

divert to a premium product or service. But the position of the public undertaking is

never comfortable enough to foreclose the chances that disruptive innovations shift

66 P. 14. 67 P. 26. 68 P. 27. 69 P. 17. 70 P. 31.

The economics of indirect regulation

27

consumers from one market or product to the other. Even undertakings holding

consolidated market positions in the oil industry cannot indefinitely rely that green

technology will not progressively replace conventional fuels. And because in a

scenario of I-regulation there is not a central government authority that the public

undertakings could recur to in order to deter innovation, the competitive pressure is

even greater71.

The public undertaking might also opt to place its product both in the regular

and in the premium markets. In this case, premium products are not usually subject to

I-regulation: Actually, we may expect that high end products be priced according to

the laws of supply-demand.

Besides allowing a greater degree of flexibility, I-regulation also distinguishes

from T-regulation for solving the imperfect information market failure that the latter

failed to address72. Inasmuch as a public undertaking under I-regulation is a dominant

market player, it will be able to have a better assessment of the costs incurred by the

market players. With better information, the decisions of the state (as controller) are

more accurate and quasi-enforcement73 (through market mechanisms), absent moral

hazard from he private undertakings, becomes possible.

Last: Although sharing some similarities -- both are forms of government

interventions in the economy and share the feature of public undertakings competing

against private undertakings -, I-regulation distinguishes from the cases where the

state delegates the function of central regulatory authority to one of the competitors.

Central regulatory authorities are common features of both T-regulation and, as we

will see, double regulation -, but are also familiar, in some European countries, to

models where the regulatory power is officially granted to private74 or to public75

undertakings.

71 Public undertakings could still appeal to the paternalism of the Congress to impose barriers to innovation in the market. One quite recent example lies in the laws approved in Brazil and in European countries against Über. However, besides the slower track, Congress is subject to political accountability, is sensitive to mass mobilization and owes allegiance to certain groups of voters that can counter the presurre coming from the public undertaking/government. 72 Although, as we will see, it creates incentives for moral hazard behavior from the managers of the public undertaking. 73 See footnote 61. 74 See Case C-179/90 Merci Convenzionali Porto di Genoa v Siderurgica Gabrielli SpA [1991] ECR I -5889.

Roberto D. Taufick

28

Insofar economic agents are assumedly rational, the cases where the roles of

market players and regulatory authorities overlap have no other outcome than

foreclosure to competition. Conversely, the features of I-regulation make it a less

intrusive instrument to alter market behavior.

V.II SHORTCOMINGS

If, on the one hand, I-regulation is less intrusive, on the other hand, the

traditional remedies used by regulation are not extended to it: As market participants,

public undertakings cannot award fines or demand behavior from competitors or any

other market player -- the only constraints that a public undertaking can impose on a

competing undertaking are those provided by the market. That is the difference

between enforcement and what we have called quasi-enforcement for the purposes of

this article76.

Because market power is an essential feature of it, I-regulation is, by

definition, stigmatized with a market failure (imperfect competition). I-regulation

demands that the state directly participate in the market as an undertaking and that it

hold such a market power that would allow it be a price maker instead of a price

taker. Not only hold market power, but hold it continuously, in order to allow the

public undertaking to uninterruptedly determine market behavior -- an outcome that,

according to the common sense, is unlikely to happen just by competing on the

merits.

If we follow the common sense that public undertakings cannot be as efficient

as private undertakings -- with which we generally agree under double regulation, but

not under I-regulation -, it would also be correct to say that the use of artificial means

to help sustain market power leads the public undertaking not to feel fully constrained

by market forces and to accommodate, lowering efficiency levels. And by artificially

not allowing the market to be taken over by a more efficient competitor -- be it by

forbidding market acquisitions by private market players, by not privatizing the assets

of the public undertaking, by recurring to administrative biases that curb the

75 See Commission Decision 94/119/EC of 21 December 1993 concerning a refusal to grant access to the facilities of the port of Rødby, OJ [1994] L 55/52. 76 Ibidem.

The economics of indirect regulation

29

emergence of mavericks or by getting privileged access to relevant commercial

information -, the whole market becomes constrained by the lower efficiency levels of

the market leader.

Under this rationale, I-regulation can drive the market away from disruptive

and forward-looking strategies in order to prioritize more conservative policies. This

is the case of spending too much in the oil market -- where the public undertaking is a

market leader -- instead of leading the shift to clean energy -- where private

undertakings will probably take head of the market. The absence of significant shifts -

- that is a common characteristic of both flagrant market dominance and the public

service -- has been reported by the literature77 as a commonplace for market leaders

defending their dominance against disruptive entrants. But it also leads to a widening

gap between the perception of the population towards forward-looking ideas (like

clean energy) and the stagnant world of the dominant undertaking.

As we have mentioned earlier, however, such a level of power stability aimed

by the state when it fosters the presence of a dominant public undertaking to

determine market behavior in a strategic market cannot be expected in a deregulated

industry subject to free competition. Because innovation can anytime disrupt the

market structure, even public undertakings with a high degree of dominance -- in the

oil sector, for instance -- are subject to greenfield technologies -- like clean energy --

that bring competition where the public undertakings have no constraint power. So,

even though it is still true that a successful environment of I-regulation depends on

the public undertaking continuously holding market power, the most desirable

environment to flourish I-regulation is that where rivalry is high and its dominance is

weaker -- because it is there that the public undertaking will behave more

aggressively in order to sustain the ability to at least influence market behavior.

Reality shows us that in the oil market in Brazil, subject to double regulation,

escaping competition on the merits has preserved dominance from the public

undertaking. Conversely, we believe that, where competition is high and state

interference is minimal, a public undertaking can sustain I-regulation without

recurring to artificial means.

77 Christensen (2000) and Wu (2010).

Roberto D. Taufick

30

The market behavior of public undertakings is also subject to strategies that

are not market driven -- the literature78 usually mentions the pursuit of social welfare -

- and which may have controversial effects on the market. Probably the most relevant

distinction between private and public undertakings comes from how each reacts to

market incentives -- and no market incentive is more appealing than the profit-

maximizing rationale. If, for the private undertaking, the search for profits creates the

incentives for the necessary efficient behavior, for a public undertaking profits are a

priority only when they collide with neither macroeconomic policies nor public

policies designed for the sector. On top of that, the state can always subsidize the

reorganization and recoupment of a bankrupt public undertaking (the too big to fail

argument), creating incentives for moral hazard behavior among its managers.

Viscusi et alli (2005)79 claimed that public undertakings, as compared to

private ones, price lower, practice less price discrimination, earn lower profits and are

less efficient: They "use more capital and labor in order to reap nonpecuniary

benefits, such as fewer consumer complaints and an absence of labor strife." They

claimed that the prioritization of political support from voters leads to overinvestment

in characteristics that are more visible to the average voter (like lower prices and

reliability) and underinvestment in innovation. Because public undertakings prioritize

political support instead of profits, their managers are not subject to the constraints

towards a more efficient management that the capital market exerts over the private

undertakings and are constantly appointed by patronage80. But here, again, market