Embed Size (px)

Citation preview

Small firm growth in a post-conflict environment:the role of human capital, institutional quality,and managerial capacities

Besnik A. Krasniqi1,2 & Muhamet Mustafa3

# Springer Science+Business Media New York 2016

Abstract Drawing on concepts from earlier theories of firm growth (Gibrat’s Law -GL, Jovanovic’s Learning Theory- JLT, Resource Based View-RBV, and InstitutionalTheory-IT) this paper empirically tests the large sets of variables as predictors of smallfirm growth that accounts for wide range of factors affecting small firm growth inKosova (human capital, institutional quality, and managerial capacities). Using datafrom a sample of 1606 entrepreneurs based on three pooled SME surveys this studycontrols for potential biases in other studies in transition economies (TEs) thatoverlooked internal factors compared to institutional factors. Findings based onProbit and Tobit models show that growth aspirations, managerial capacities andtraining are among the most significant variables associated with growth. Among theinstitutional quality variables, only corruption appears to be significant and negativelyassociated with growth. Other important factors for explaining a small firm growth arefirm size and age, and export involvement. This study contributes to literature on smallfirms growth in TEs and highlights several managerial and policy implications to fostera small firm growth.

Keywords Kosova.Transition .Small firmgrowth.Humancapital . Institutionalquality.

Managerial capacities

Int Entrep Manag JDOI 10.1007/s11365-016-0384-9

* Besnik A. [email protected]; [email protected]

Muhamet [email protected]

1 Staffordshire University, Staffordshire, UK2 University of Prishtina, Prishtina, Kosova3 Riinvest College, Prishtina, Kosova

Introduction

Although research exploring the determinants of small firm growth has attractedinterest of researchers and policymakers in order to promote policies that focus onemployment generation and economic growth (Sleuwaegen and Goedhuys 2002;Wiklund et al. 2009; Hamilton 2012; Obeng et al. 2012), there is still a need to exploreand understand this phenomenon (Wiklund et al. 2009). Despite the growing number ofstudies, (Wiklund et al. 2009; Hashi and Krasniqi 2011; Efendic et al. 2014; Naldi andDavidsson 2014; Lechner and Gudmundsson 2014) the volume of research on smallfirm growth is dominated by studies concentrated on the institutional determinants offirm growth, rather than the internal factors (i.e., the entrepreneurs’ growth aspirations,managerial capacities) and even less on the combination or linkage between the two(Smallbone and Welter 2009). In particular, literature knows very little about thecharacteristics of growing firms, which are main drivers of employment growth(Hölzl 2009). Entrepreneurs’ growth-orientation in empirical research is very importantfrom the policy angle as few small firms intent to grows, and therefore it provideslimited contribution to the economy and therefore questioning the start-up supportpolicies (Santarelli and Vivarelli 2007; Shane 2009; Doern 2011; Román et al. 2013).Studies on transition context usually overemphasis institutional environment at theexpense of the internal factors such as firm, strategy and management factors (Krasniqi2012). In addition to the institutional context which is of paramount importance, itsrelationship to the other aspects of entrepreneurship such as: the knowledge and skillspossessed by the people running a small firm is important too (Veciana and Urbano2008).

In his review of studies in small firm growthWiklund et al. (2009) notes that most ofstudies cover only a limited number of the variables that are important in explainingsmall firm growth. Research in this field is necessary to develop our understanding ofentrepreneurial activities in TEs adapting to a free market economy and, from apractical point of view, it may help entrepreneurs develop their operations by revealingopportunities and constraints in this market (Ojala and Isomäki 2011). Therefore, thispaper contributes to the transition literature by filling an important gap in understandinga small firm growth in the unique post-conflict economy of Kosova. The paperempirically tests variables as predictors of a small firm growth in a particular context,such as Kosova. Kosova is a country often regarded as an extreme and challengingenvironment for entrepreneurship, making it a ‘natural laboratory’ for entrepreneurshipresearchers (Solymossy 2005). In a broader sense, by grounding entrepreneurship innational context, we aim to contribute and value-add to the literature in understanding asmall firm growth in general (see Welter and Lasch 2008). The paper empirically testscomprehensive set of variables affecting small firm growth, such as firms characteris-tics (size, age, location, networking), human capital (training, education, experience),managerial and strategy level factors (exporting, growth aspirations, foreign ownership,separation of ownership and control) and institutional quality (unfair competition,corruption, access to finance, taxes.). The study responds to the current debateconcerning improving and refining the set of explanatory variables that have beenlimited and affect firms growth such as entrepreneurial orientation and strategicmanagement (see Wiklund et al. 2009; Parker et al. 2010; Stam 2010; Hitt et al.2011; Obeng et al. 2012; Sadler-Smith et al. 2003). From a theoretical viewpoint, the

Int Entrep Manag J

findings call for a more balanced approach between internal and external factors andsuggest application of a more integrative model of a small firm growth in TEs –overlooked in previous studies. The empirical analysis uses primary data gatheredthrough SME surveys conducted by Riinvest Institute providing information on a widerange of characteristics of the entrepreneur, the firm and its management and strategy,internal resources and the institutional environment.

The paper proceeds as follows. To begin with, we first introduce the unique featuresin this context of entrepreneurship development in Kosova. Then, theoretical literaturediscusses earlier theories of firm growth and based on these concepts derived fromtheory develops hypothesis to be tested. This follows by an explanation of the data andmethod. The next section presents the results of the determinants of a small firm growthin Kosova, for both whole sample and sample of growing firms; and the final sectionconcludes the paper.

Context: entrepreneurship and SMEs in Kosova

Specific historical and institutional context in Kosova visualizes the opportunities andthreats in development of the private sector dominated by SMEs. The developmentpath begins with so-called Bsmall economy^ during 70’s and 80’s of the last century,with a mixture of the elements of planned and market economy system within Bself-management socialism^ - a specific feature of former Yugoslavia. Private ownership ofland, farms, handicrafts, and small firms was something more pronounce in Kosova ascompared to the other TEs in CEE. The existence of private ownership, althoughlimited has played a vital role in building private sector during the period of reformingafter 1989. Massive job losses of those employed in a state and public (70 % weredismissed by Milosevic regime) heavily influenced the boom in creation of SMEsduring 1990–1993. SMEs mainly in a trade and services were born in self-employmentattempts as a gateway from difficult economic and social conditions, making a rise tonecessity-driven entrepreneurship. This period was followed by a decline in start-upsbecause of the repressive regime and deep recession because of the occupation(Riinvest 1998). During the armed conflict of 1998–1999, 92 % SMEs experiencedlosses and damages in their assets (Riinvest 2000). A period of new developmentstarted at the end of the conflict followed by the UN Administration of the Country(since June 1999) and continued after the country proclaimed its independence(February 2008).

Kosova is amongst less developed European countries with GDP per capita of 2800Euro coming from services (56 %), industry 18 %, agriculture 17 %, and construction10 %. (EU Commission 2014). Deindustrialization marked by the shrink of industryshare of GDP (47 % 1989 to 15 % during early stage of the post conflict period)influenced a heavy imbalance in the macroeconomic configuration. Trade deficitreaching about 40 % of GDP and unemployment rate above 30 % are the key problems.On the other side, macroeconomic and fiscal stability and low inflation persisted with amodest economic growth of 2–4 %. The remittances (about 14 % of GDP) and donorcontribution, especially during the emergent reconstruction phase fuelled the develop-ment of SMEs by causing high aggregate demand. Although the legal framework isalmost completed and in compliance with EU standards, the implementation and weak

Int Entrep Manag J

rule of law remains a severe problem for entrepreneurship development. The unfaircompetition remains the key barrier in doing business, according to perceptions of SMEowners and managers (Riinvest 2013b). Similar trend are reported for corruption,access to finance and taxes. However, entrepreneurs rank the employee knowledgeand managerial abilities as the lowest barriers for their operation and growth. Overall,Kosova private sector and SMEs, although fragmented and with difficulties to benefitfrom efficiency gains remains key for Kosova development as they contribute about70 % to GDP (Riinvest 2013a). The law enforcement and fair competition will remainkey challenges in establishing entrepreneurship friendly business environment inimmediate and midterm future.

Literature review

Despite an emerging body of literature on small firms growth (Davidsson et al. 2002;Wiklund et al. 2009; Yasuda 2005; Coad 2009) theories to explain and predict growthstill remain sparse (Garnsey 1998; Stam 2010), and often contradictory, urging the needfor an expansion of the current set of explanatory variables in the empirical research(Davidsson et al. 2002; Stam 2010). The following discussion takes on to bringtogether the theories of firm growth linking them with modern approaches to smallfirm growth. Earlier theories to explain the growth of small firms include the GL or theLaw of Proportionate Effect (Gibrat 1931), JLT (Jovanovic 1982), RBV (Penrose1959), and IT (North 1990).

Gibrat’ Law and Jovanovic’s Learning GL and JLT have been summarised inliterature as the size-age-growth relationship, which has become a popular theme inrecent small firm growth literature and industrial dynamics. This was motivatedoriginally by the arguments of exploitation of economies of scale discussed by neo-classical theory. The literature based on the so-called GL, maintains that a firm’s growthis independent of its size – a view that became a common wisdom in theoretical andempirical literature (Heshmati 2001). Neoclassical economics' basic assumption is thatthe optimal size is a level of production at which economies of scale are exhausted andthe average long run cost curve reaches its minimum (Carlton and Perloff 2004). In thisview, if firms behave rationally they will achieve the optimal size (minimum efficientscale - MES) and would not have an incentive to grow beyond that point. Theimplication of this theory is that small firms grow faster than larger ones until theyboth reach their optimal size or MES. Another strand of the literature, known as the‘noisy selection’ model developed by Jovanovic (1982), argues that firms learn abouttheir real efficiency over time (thus the relevance of age) and that small firms growfaster than larger firms do. In the post-entry period, firms gradually learn about theirreal cost efficiency and grow during their maturity period due to their ability to learnfrom experience diminishes; this is because of the diminishing returns to experience.Firms enter the market under the MES level and overtime grow to reach this level. Inmarkets with only negligible scale economies, the likelihood of survival is greater fornew entrants, but the opportunity to grow in post-entry period is limited by the gapbetween the MES and size of the firm (Acs and Audretsch 2001). However, the maincritiques to the industrial economics approach relates to the fact that many small firms

Int Entrep Manag J

operate in ‘relatively uncompetitive markets and partly protected local and regionalmarkets’ (O’Farrell and Hitchens 1988, p.1366). Contextualised to the transitioncontext, this critique infers that firms in TEs operate in competitive markets usuallycoupled with weakly installed institutions, thus, the assumption of competitive marketsdoes not hold. In addition, firms do not face the same cost curve and are also marked byother differences in the real world such as their ability to access inter alia managerialresources, skills technology and finance (Deakins and Freel 2003) as recognized by theresources based-view of the firm growth later.

Resource-based view Penrose’s (1959) theory of the firm growth postulates that theavailability of firm resources and knowledge determines the expansion of the firm. InPenrosean view, firms can achieve growth by the accumulation of knowledge in twoways. Firms can accumulate knowledge by learning to use the existing knowledgewithin the firms more efficiently. Alternatively, firms can use new knowledge fromexternal sources, but conditional upon internal absorbing capabilities of firms.Nevertheless, firms will be limited in terms of possibility of these growth opportunitiesbecause of the inherent rigidities of using their existing resource base, and because oftheir need to maintain coherence in their activities (Ghosh and Moran 1998). Sapienzaet al. (2004) points out that the growth of a firm is limited by the speed with which newknowledge and resources is accumulated and by its managers’ ability to quickly learnand respond to ‘accommodate the expanding scope’ of the firm’s operations. In thePenrosean view, it is not the resources itself that yield results within the firm but themanagerial capacity and their increased problem solving and competencies that may bein the form of providing productive opportunities (Garnsey 1998; Nooteboom 2009).The more resources the firm employs, the more likely it is that managers will discovernew combinations of using them in response to the new opportunities providing thebasis for persistent growth. In Penrosean view, firms engaged in the same type ofactivities, using the same technology and employees, are likely to produce differentoutput levels depending on their unique teamwork, knowledge and experiences. Eachfirm is specific in its competencies to create or acquire new knowledge, and is unique inmaking use of this knowledge differently from other firms. Therefore, the prerequisitefor firms to successfully compete in the market is their unique ability (resources) toaccess and combine resources in a distinctive way to gain competitive advantage overtheir competitors. Of course, there are disadvantages of having unique resources or aunique knowledge of operating these resources. For example, in the fast changingexternal market conditions, the firm’s performance and its competitive advantage maybe eroded if it relies heavily on certain specific specialized resources (Coad 2009).

Institutional theory Earlier theories discussed above have neglected the role of marketfailures such as imperfect information and institutional quality. Williamson (2000)posits that neo-classical economics takes institutions for granted by assuming thatlaws and courts are in place to enforce contracts and protect property rights of partiesin a transaction. The New Institutional Economics - NIE literature based on North(1990) has brought the discussion of institutions and their impact on entrepreneurshipand growth to the forefront of academic debate. The debate emerged towards theinvestigation of the role of both formal and informal institutions on entrepreneurialbehaviour (Smallbone and Welter 2009). North (1990, 2005) made a clear distinction

Int Entrep Manag J

between informal and formal institutions influencing a society’s incentive system andso how it shapes an individual’s behaviour. In particular, it is important to distinguishbetween formal institutions such as creation of new laws, procedures and other propertyrights and social institution, which are embodied in the social lives of entrepreneurs andsociety as a whole. Following NIE, a number of studies show that an unfavourableinstitutional framework has an adverse impact on entrepreneurship and small firmgrowth (Smallbone and Welter 2009; Aidis et al. 2008; Aidis and Van Praag 2007;Pissarides et al. 2003; Bartlett and Bukvič 2001; Hashi and Krasniqi 2011).Furthermore, the slow and uneven development of the institutional framework indifferent TEs has been one of the major factors explaining the divergent paths ofdevelopment, particularly the development of SMEs and entrepreneurship, in thesecountries (Frye and Zhuravskaya 2000). Therefore, the IT provides a good guidingframework because of the specific features of the institutional environment that influ-ence entrepreneurship compared with a more mature market economy (Smallbone andWelter 2006).

Hypotheses

Although important for guiding empirical research, earlier theories of firm growthcannot explain small firm growth without the inclusion of a wide range of determinantsof firm growth. The most widely used framework is based on Storey (1994a) whichincorporates firm, entrepreneur and environment. Based on Storey’s (1994a) frame-work and with authors’ extension to account for quality of institutions in TEs wediscuss main determinants classified into four groups of factors: firm, human capital,strategy and growth aspiration, and the institutional environment.

Firm

Based on GL and JLT discussed in the previous section the validity of size-age growththeories has been tested empirically by many studies, using various samples by time,sector, size, and region. These studies generally have contradicted this Law by finding anegative relationship between size, age and growth in both, TEs (Bartlett and Bukvič2001; Krasniqi 2006; Hashi and Krasniqi 2011) and developed economies (Davidssonet al. 2002; Almus 2002; Yasuda 2005). The above literature suggests that refuting GLand JLT is mainly based on ability of small and young firms to exploit economy ofscale because they are far from MES, and hence growth more than larger firms. Thus,we propose following hypotheses:

H1a: Growth is negatively associated with firm sizeH1b: Growth is negatively associated with firm age

Urban location is a factor that influences the growth of firms. Studies of agglomer-ation economies, focusing on the role of positive externalities in developed anddynamic urban areas have highlighted the important role of location for the growthof firms (Black and Henderson 1999; Alcacer and Chung 2007). They claim thatexternalities are particularly associated with knowledge spillover and the role ofurban institutions, which could lead to efficient growth. Maine et al. (2010) argue that

Int Entrep Manag J

firms may have access to some specialized resources that may not be able to developinternally, but it can be found in more urban areas. Recent theories suggest that there areincreasing returns to scale for firms in production that can be realised most effectively ifproduction is concentrated in agglomerations (see, Krugman 1991; Fujita and Thisse2002). Sleuwaegen and Goedhuys (2002) study of firm growth in Nigeria noted thatfirms located in the commercial capital of the country, were more likely to engage innetworking and subcontracting, which provided greater opportunity for growth, thanfirms located in other parts of the country. Urban resources are conducive to developfirms in developing countries. Therefore, we put the following hypothesis:

H2: growth is positively associated with urban location – resources

Many studies have explored the link between the legal form of the firm and its growth.One of the main propositions is that firms operating as limited liability companies haveshown higher rates of growth as firms founded as a limited liability have greater incentivesto peruse riskier projects compared with other counterparts and therefore they are morelikely to have higher growth than other firms (Stiglitz and Weiss 1981). Limited liabilityfirms have more credibility with both customers and banks compared to other legal types(e.g., Storey 1994b). Limited liability firms benefit from an increased reputation, whichplays a key role in accessing external finance. On the other hand, indicates the involve-ment in a higher risk than usual and signals a high-expected return but also a high-expected risk (e.g., Harhoff et al. 1998). To conclude, the legal form seems to have aninfluence on the firm’s growthwith firms operating as limited liability experiencing highergrowth rates. This, we suggest the following hypothesis:

H3: growth is positively associated with limited liability legal form

Firms can also improve their performance through networking – which ease theirgaining from external economies. Knowledge flows are among the key causes inexplaining firm growth in today’s knowledge-based economy. Evidence suggests thatfirms that belong to formal networks are more likely to report innovation and, inaddition, the growth paths of firms in a cluster lay above those of isolated firms, thatdo not belong to any networks (Beaudry and Swann 2009; Maine et al. 2010). Firmscan also benefit from other forms of networking such as membership in businessassociations. These benefits, among others, include the improved information flow,training, facilitating foreign cooperation and others (Brown et al. 2005. Particularly, thisapplies to TEs, as evidence suggest that membership in business associations, alsoseems to have a positive and significant effect on firms (Hashi and Krasniqi 2011).Therefore, our next hypothesis is formulated as follows:

H4: growth is positively associated with networking of entrepreneurs

Human capital

Many researchers in both developed and developing countries recognize the impact ofhuman capital on a firm’s growth by showing that education of employees and

Int Entrep Manag J

managers contributes to better firm performance (Kangasharju and Pekkala 2002;Macpherson and Holt 2007; see van der Sluis et al. 2005). Human capital refers tothe range of skills, knowledge and experience that facilitate growth. However, littleresearch has been conducted to measure the influence of human capital on entrepre-neurial performance and motivation in TEs (Aidis and Van Praag 2007). Haber andReichel (2007) find that human capital of the entrepreneur, especially in the form ofmanagerial skills, is the greatest contributing factor to performance. Other authors pointto the role of training as an alternative mechanism for enhancing employees andmanagers’ skills (Kirby 1990; Cosh et al. 2000). They find a positive relationshipbetween training and employment growth, especially if the training embodies the widerange of management training and human relations practices in the firm (Cosh et al.2000). Training is expected to be directly associated with growth, in particular if thefirm is involved in innovation and competes based on quality rather than simply price(Bryan 2006). Skilled employees are more productive because they have higherproblem-solving abilities, leading to greater efficiency within the firm. To sum up,firms that are strongly motivated to grow and train their workforce to facilitate thegrowth (Hallier and Butts 1999). In TEs, firms often, use training as a way tocompensate for low quality of labour, which indicates low quality of education(Krasniqi 2012). Based on the above discussion, we state following hypotheses:

H5a: Growth is positively associated with higher educationH5b: Growth is positively associated with training, of both, managers andemployees

Entrepreneur’s experience is another dimension of human capital. Several stud-ies reported a positive relationship between entrepreneurial experience and firmgrowth (Capelleras and Rabetino 2008; Lee and Tsang 2001). Beside the fact thatthat entrepreneurs’ experience is crucial for growth, how that experience developsand how it is influenced by the overall context or interactions remains unclear(Macpherson and Holt 2007). For example, in the context of TEs, pre-existingknowledge in the form of experience might not have expected positive effectsbecause as experience develops it interacts with the rapidly changing environment,therefore experience might not be a very useful guide to the entrepreneur’s futureactions. Thus, from the studies above it is shown that the firms of middle age owner/managers experience a higher growth, which leads us to following hypothesis:

H6: growth is positively associated with entrepreneur’s experience

An entrepreneurial team is fundamental to firm growth since the manage-ment of a business requires a range of skills. The synergy effects of theknowledge of founders, especially in teams with those members who havecomplementary skills (Corbett 2007). The synergy effect expands knowledge,increases managerial capabilities and in addition to the knowledge synergy thepartners may act as a signalling for potential creditors and lenders of theseriousness and economic strength of the business leading to higher growth(Schutjens and Wever 2000; Pasanen and Laukkanen 2006). Thus, the follow-ing hypothesis states:

Int Entrep Manag J

H7: Growth is positively associated with the entrepreneurial teams

Managerial capacities, strategy, and growth aspiration

The entrepreneur’s intent to grow has been the subject of a growing debate, as not allsmall firms are growth-oriented or have growth aspirations (Morrison et al. 2003;Doern 2009). Evidence suggests that individuals start and run their businesses forreasons rather than just for profit maximizing, therefore, a broader view of motives andattitudes to grow should be taken into account (Wiklund et al. 2009). Therefore, growthimplies radical changes in the business, which may hinder the owners’ goals such asindependence or ‘life style’ (Wiklund et al. 2009). Different entrepreneurs may followdifferent growth strategies and management practices; some of them, preferring toremain small and others aiming at continuous growth and operating internationally. InTEs context, this is a critical aspect to be considered as a significant share of entrepre-neurs are necessity-driven pursuing an entrepreneurial career as an employment optionto escape from unemployment making a limited contribution to economy (Early andSkaova 2000; Krasniqi 2014). Although firms may adopt various strategies for growth,the entrepreneur’s commitment to grow is the most important factor in explainingfuture growth (Wiklund et al. 2003; Mochrie et al. 2006). This reasoning suggests thefollowing hypothesis:

H8: Growth is positively associated with future growth aspiration of entrepreneurs

Export involvement is considered a growth-oriented strategy of firms. Firms in-volved in exporting may experience higher growth for at least two reasons (i) theirorientation towards new markets and market niches and (ii) their ability to learn fromtheir competitors in the areas of technology and quality. The survey of literature byTybout (2003) suggests that exporting activities have a positive effect on a firmperformance. In the earlier period of transition, there was a lack of managerial skillsand competencies because the older management practices were no longer useful tosupport growth of new enterprises. The so-called ‘learning by exporting’ enhancesinnovation, especially in firms in laggard transition economies (Salomon and Shaver2005). These spillover effects of knowledge transfer (technology, management, andexpertise) are the main reasons for their positive influence of exporting and foreignownership on firm growth. Studies from TEs such as Russia support views that foreignownership has a positive effect on firm performance (Djankov and Murrell 2002;Yudaeva et al. 2003). Foreign ownership contributes to import of advanced technolo-gies, training, and vertical technology transfers through diffusing technology, and moreimportantly, for developing countries capital investment (Taymaz and Özler 2007) andTEs (Hashi and Krasniqi 2011). All these interrelations between firms, both nationallyand internationally, can increase productive opportunities and increase the knowledgebase of the firm as postulated by the RBV. This discussion leads to followinghypotheses:

H9a: growth is positively associated with exporting statusH9b: growth is positively associated with foreign ownership

Int Entrep Manag J

As a firm grows, it faces the managerial capacity challenges such as the needfor more professional managers. Owners of the majority of small firms deal withday-to-day management. As firms start to grow and face the need for professionalmanagers, the owners’ desire to keep control over the firm and their hesitation todelegate decision-making to managers (reluctance to bring professional managers)may inhibit the growth of the firm. Small business owners are sometimes reluctantto grow even though they may face opportunities for expansion (Hart 2000).Serrasqueiro and Nunes (2008) in their study they found that in firms wheremanagement was separated from ownership, the nonowners’ objectives were morelikely to be growth-oriented, suggesting that separating management and ownershiphas a positive impact on firm growth. In developing and transitional contexts,firms have a higher concentration of ownership and control (Porta et al. 1999)despite their needs for a change from small owner-managed to a professionallyoriented firm (Shirokova et al. 2015). For example, entrepreneurs from developingand TEs’ view export markets as a risky business and that they lack knowledgeand expertise (Okpara 2009). Therefore, separating ownership from managementwill unleash growth potential of small firms in TEs. Accordingly, we hypothesizethat:

H10: growth is positively associated with higher levels of professional managers(separation of ownership and management)

Institutional quality

Drawing on IT many studies addressed small firm growth by analysing the funda-mental transformation of institutional settings in unusual and novel context oftransitional environment (Smallbone and Welter 2009; Estrin et al. 2013). Thisliterature suggests that low-level of entrepreneurship and small firms has beenattributed to weakly installed institutional environment, weak legal system, admin-istrative burden, corruption, taxes and restricted access to finance (Smallbone andWelter 2006; Estrin et al. 2013; Aidis et al. 2008). Consequently, institutionsconsisting of formal constraints, such as laws and regulation, and informal con-straints, such as conventions, codes of behaviour, norms and culture, formal andinformal elements strongly influence the goals and beliefs of individuals andorganizations. In this context, institutional factors have been used to explore newventure growth and performance in TEs (Krasniqi et al. 2008; Aidis and Mickiewicz2003; Bartlett and Bukvič 2001). Major findings in the literature point to thecomplicated and excessively regulated environment creates the incentive for entre-preneurs to evade regulations by moving partially or fully into the informal sector(Johnson et al. 2000; Shleifer and Wishny 1994). Furthermore, it also encouragesrent seeking behaviour by public officials and facilitates the development of corrup-tion. Combined, informal activities and corruption contribute to an anticompetitiveenvironment in which the market fails to allocate resources efficiently because somemarket players operate outside the law while those operating within the legal systemface the increased cost of ‘doing business’ legally. Based on this we propose thefollowing hypothesis:

Int Entrep Manag J

H11: Growth is negatively associated with higher perception of barriers of institu-tional quality (corruption, bureaucracy, high taxes, unfair competition, and accessto finance)

Methods and data

Sample and research design

This study is based on a survey responses from 1606 Kosovar entrepreneurs whocompleted questionnaires in a face-to-face interviews during December-January 2002–2003, 2003–2004, 2004–2005 (thereafter 2002, 2003 and 2004). SME surveys wereconducted by Riinvest Institute for Development Research and one of the authors had aleading role in this research project. Samples were selected randomly from the businessregister kept at the Statistical Office of Kosova and the Ministry of Trade and Industry(2005). Experienced and trained final year business students at the University ofPrishtina conducted interviews and the Riinvest research team monitored them care-fully. Respondents were key informants, mainly the owner or the general managers ofcompanies. The response rate was high with an average of 96.4 %. Excluding theseobservations might lead to sample selection bias, but in our case, this is not a concern,as the non-response rate is small (around 3.6 % of total cases) also our sample remainsrepresentative (see, Cameron and Trivedi 2005).

Pooling data The pooled data technique is used to test set of econometric models of firmgrowth. The pooled data contains information from three independent surveys from theperiod 2002, 2003 2004. An Bindependently pooled cross-section^ technique is obtainedby pooling randomly sampled cross-sections at different points in time (Wooldridge2006). The data set used in this study meets the conditions of the surveys being randomand independent of each other, using the same research instrument and identical depen-dent and independent variables in the estimations. From a statistical point of view, theindependently pooled cross sections data has several important features (Wooldridge2006). It rules out the correlation between the error terms across different observations,controls for changes overtime with the inclusion of year dummy variables, provides moreprecise estimates and more powerful diagnostic test statistics, increases the number ofobservations and, hence, has a larger sample size and more robust coefficients. This isimportant to present research which accounts for many variables which otherwise wouldbe econometrically difficult to carry out. To ensure the pure random sampling we havedeleted a few cases in which the same company was sampled more than 1 year (only 23cases). The sample includes SMEs from all regions and in all economic activities.

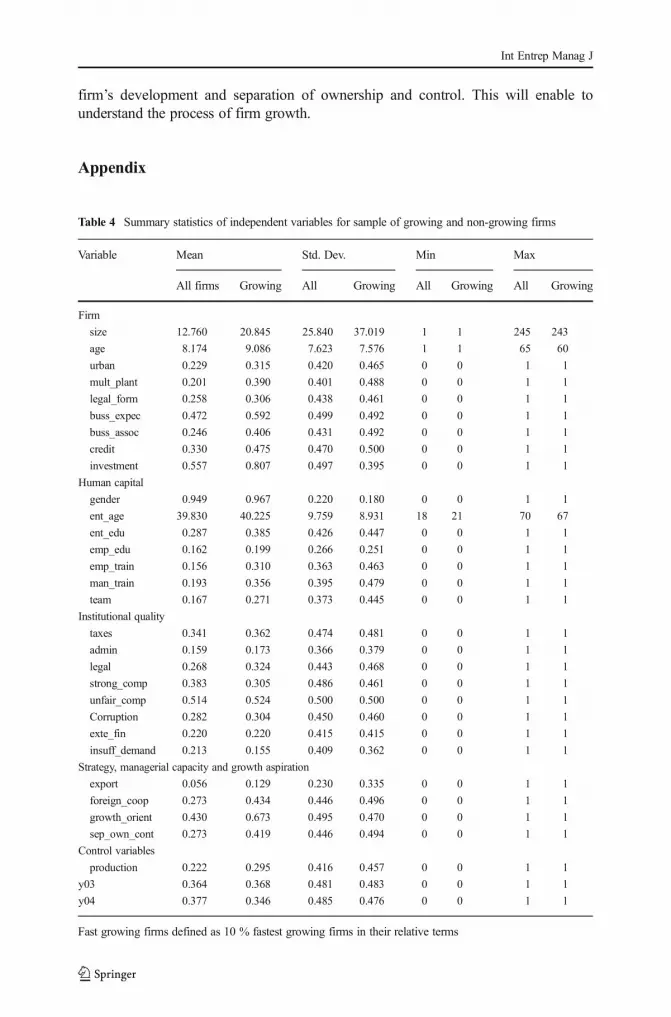

Descriptive statistics Descriptive statistics presented in Table A1 Appendix shows asummary of the statistics, and show that overall the mean size of the companies(measured by number of employees) in the sample are very small, around 13 em-ployees. The surveys indicates the recent origin of the private sector. Around 54 % ofthe firms are 5 years old or younger, and around 70 % of them are no more than10 years old. The overall average age of the companies in the data set is around 8 years.It is important to note that the institutional quality and structure of SMEs has not

Int Entrep Manag J

changed in Kosova, so the problem of corruption and other institutional variables is stillthe most important (BSCK 2012). This evidence suggests that although our study usesrather old data, the results and hence conclusions are coherent with the current situationof SME development in Kosova. Moreover, the results are comparable, and recom-mendations may be applied to the other TEs with similar weak institutional settings.

Growing vs. non-growing firms It is important for the purpose of empiricalestimation of the determinants of SME growth to break down the sample intogrowing and non-growing firms. As discussed, growing SMEs are more impor-tant from the policy perspective as they account for most of the new jobs andincome generation. The survey results show that during the period underconsideration (2002–04) less than a third of the firms experienced employmentgrowth (28.1 %). Comparing the share of growing versus non-growing firmsacross the years in the sample, a slightly decreasing trend of the number ofgrowing firms is noted (2002, 31; 2003, 28.4; 2004, 25.8 %). The decrease ingrowth of small firms maybe due to the decrease in the excessive aggregatedemand for goods and services following the end of the emergency reconstruc-tion phase in the aftermath of the Kosova’s War.

Model and variables

This section discusses econometric models used to estimate small firm growth.For the purposes of empirical estimations and robustness of the results variouseconometric models are employed to test against the same set of parameterssuch as probit, tobit, ordered probit regression models as well as OLS method.Based on the above discussion, the following tobit model estimates the firmgrowth equation (Greene 2003, pp. 905–926; Wooldridge 2002, p. 517–536).The general tobit model can be expressed in terms of latent variable:

y*i ¼ xiβ þ ui ð1Þ

Where yi* is the latent variable, i refers to individual firms, xi is a vector of

explanatory variables, β is the vector of parameter to be estimated, and ui is the errorterm. The assumptions of the tobit model are that the error term is normally distributed,homoscedastic with mean of zero u, u|x ~Normal(0, σ2). The tobit is given by:

yi ¼ y*i ¼ xiβ þ ui if xiβ þ ui > 00 if xiβ þ ui≤ 0

�ð2Þ

As can be seen, yi contains either zero for those firms that did not grow or apositive value for those who did grow. The model combines aspects of thebinomial probit (or logit) for yi = 0 versus yi > 0 and the regression modelE[yi|yi > 1, xi]. This means that we can observe yi through the latent variable ℓonly when it is positive (yi

* > 0) whereas the dependent variable is censored foryi* ≤ 0, therefore in our case is expressed:

Int Entrep Manag J

yi ¼ y*i ¼ xiβ þ ui if growth > 00 if nogrowth≤0

�ð3Þ

In addition, a probit model is developed in order to test the appropriateness of thetobit model. Comparing tobit and probit models allows us to assess: a) the explanatorypower of the independent variables regarding small firm growth, and b) the contribu-tion of these independent variables to growth behaviour, i.e., the probability of a firmgrowing. The following probit model is specified with the same independent variablesas in the above tobit model (Eq. 1);

P y ¼ 1jxð Þ ¼ β0 þ β1x1 þ…þ βkxk ð4Þ

where the outcome y is equal to one if the firm experiences growth in the given yearand zero otherwise; x is a vector of explanatory variables with βi as the correspondingvector of coefficients. Ordered probit model is not discussed as it is used solely forpurposes of comparison with probit and tobit models.

Measures of growth This study uses the employment growth which is most widelyused as an indicator in empirical studies of small firm growth in both, developed firmsand TEs (Bartlett and Bukvič 2001; Reichstein and Dahl 2004; Goddard et al. 2006;Capelleras and Rabetino 2008). In the TE context of Kosova there are more reasons toopt for employment growth. As in other TEs where firms commonly underreport theiractivities, employment growth is more reliable than other measures of firm growth(e.g., sales), because unlike sales, employment figures are less likely to beunderreported, easier to remember by entrepreneurs and also uncontaminated by pricechanges (see Brown et al. 2005; Mochrie et al. 2006; Aidis and Mickiewicz 2006).

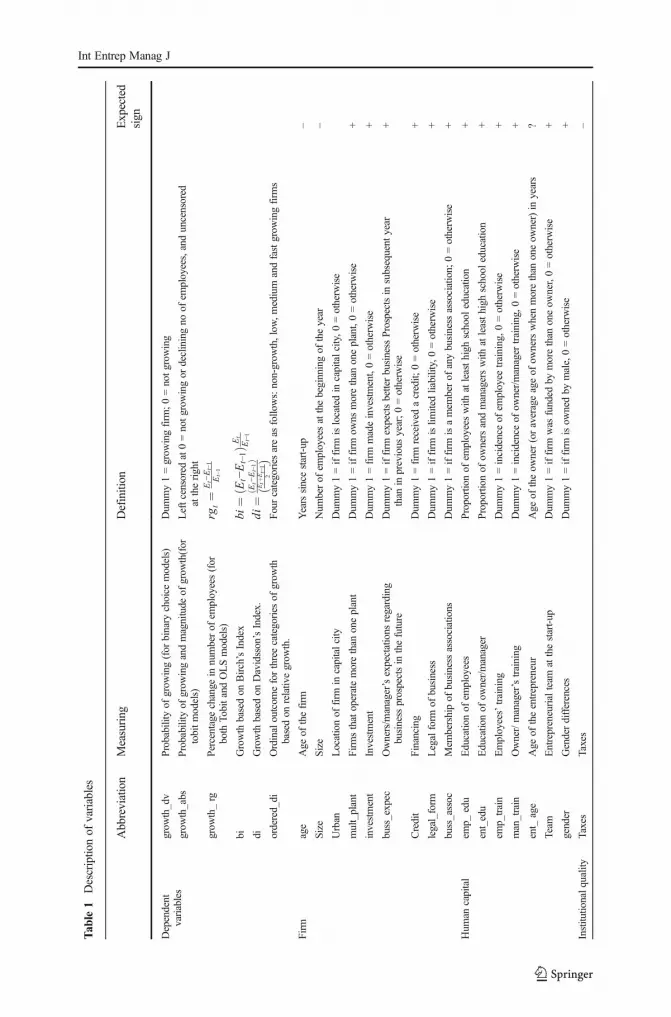

In the empirical studies, growth is measured in absolute or relative terms. This mayhave a significant impact on the empirical results, in particular on the sign of theindependent variable of a firm’s size (Brüderl and Preisendörfer 2000). This is mainlybecause the relative measures of growth favour the small firms compared to largerfirms, while the opposite holds for an absolute measure of growth. This study usesboth, absolute and relative measures of firm growth. Absolute growth (growth_abs) issimply the increase in the number of employees during each year for growing firms andzero for non-growing firms. Relative growth (growth_rg) is measured as a percentagechange in the number of employees (Table 1). Relative growth is zero for non-growingand shrinking firms. In the probit estimation, the dependent variable (growth_dv) is adummy, equal to one for growing firms and zero otherwise. In addition to absolute andrelative measures of growth, we use other measures of firm growth too. Almus (2002)argues that using the relative growth measure will produce biased results towards smallfirms, while using absolute growth measures will lead to biased results towards largefirms. Thus, we construct two other measures of growth, Birch’s (1987) Index (bi) andDavidsson et al. (2002) Index (di). The rationale behind using these measures of growthis to test whether the findings are sensitive to specific measurements of growth (see,Ahmad and Gonnard 2007; Hölzl 2009). Formula for calculating bi and di indicatorsare presented in Table 1. bi multiplies the absolute employment growth with the relativeemployment growth to determine the employment-generation power of firms in

Int Entrep Manag J

different sizes. This measure of firm growth is not biased towards any particular size.The di growth indicator is calculated as final employment minus initial employmentdivided by average of final and initial employment. This measure, too, is not biasedtowards any particular size.

Independent variables Independent variables influencing small firm growth groupedin four categories based on research framework: firm, human capital, institutionalquality, strategy, managerial capacities and growth aspirations. Other factors includecontrol variables in each group. The precise definitions of all independent variables areprovided in Table 1.

Results and discussion

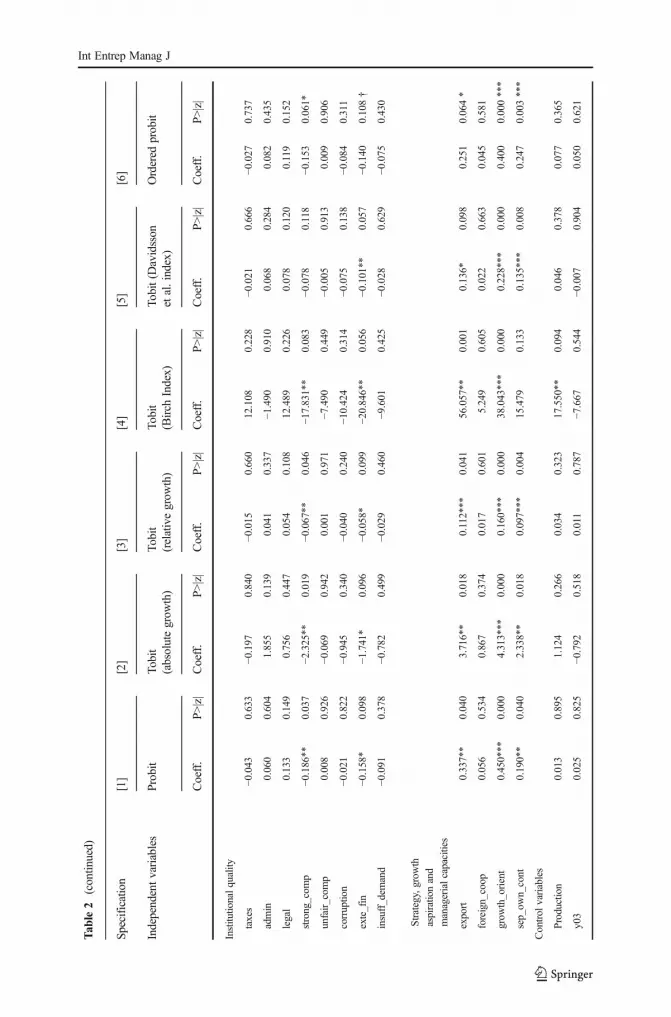

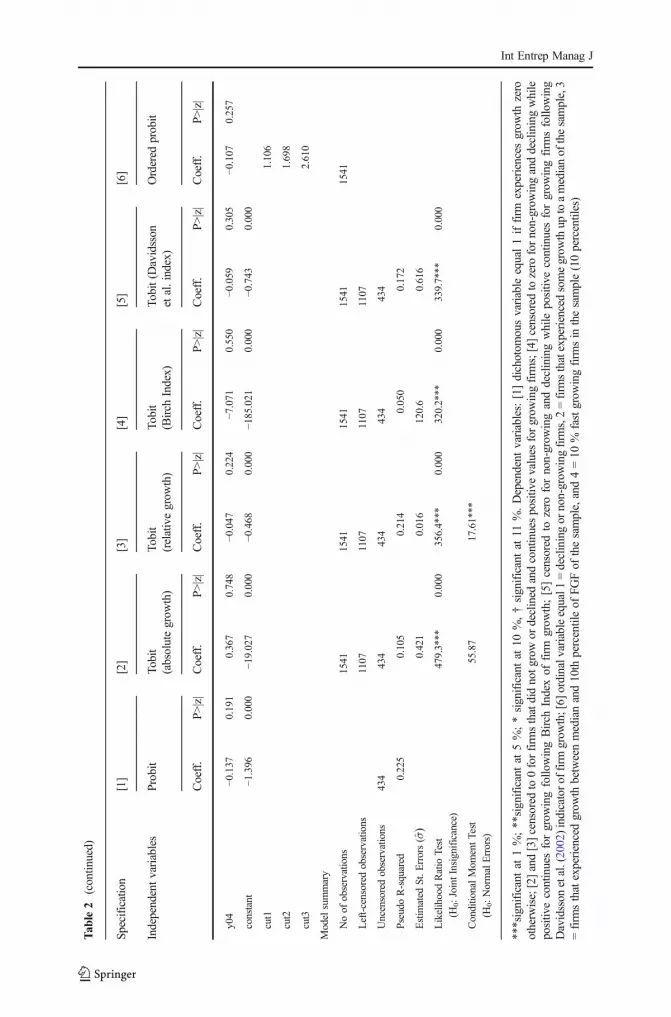

Table 2 presents the estimates of the probit, Tobit, ordered probit models of theassociation between firm growth and the characteristics of the firm, human capital,quality of institutions and strategy, managerial capacities and growth aspirations. Thefollowing discussion focuses only on the direction of the variables and their statisticalsignificance for towards the growth and comparing its consistency between all modelsused. Table 2 shows six specifications of the model. Specification [1] is the probitmodel with the dichotomous dependent variable, taking the value of 1 for growing and0 for non-growing firms. This specification will serve as a comparison check with tobitspecifications. Specifications [2] to [5] are tobit models with the dependent variable leftcensored at zero (for non-growing firms) and continuous uncensored at right takingpositive values (the growth of the number employees using different method ofcalculation). In specification [2] growth is measured in absolute terms and in specifi-cation [3] in relative terms. Specifications [4] and [5] use bi and di measures of growth.For the purposes of ensuring a robust check, we first use an alternative methodology(ordered probit specification [6]) and compare the results with those of the Tobitmodels. The dependent variable is divided into four categories: firms whose growthwas negative or zero; firms whose growth was up to a median of the sample; firmswhose growth was between the median of the sample and ten percentile fastest growingfirms; and 10 % fastest growing firms in the sample. The unconditional marginal effectsare calculated for porbit and tobit models, but we present here only tobit marginaleffects as they are of central interest in this paper and also provide more information ascompared to probit marginal effects (Table A5 in Appendix). They refer to the wholepopulation (i.e., both those that are likely to grow and those that are likely to growmore), and therefore are the effects that are most relevant for policy discussion.

Now we turn to the discussion of econometric results. Table 2 shows that the probitand tobit estimates are very similar (in terms of both sign and the level of significance)except for variables indicating the size of the firm and education of employees. Thevariable age is not statistically significant in explaining the growth of the firm in any ofthe specifications. The size of the firm is significant but does not have the expectednegative sign as postulated by JLT based on the learning theory. However, for a numberof reasons, these two variables, in order to test the validity of GL, should be interpretedwith caution here. First, in previous research, the variable size was calculated as the

Int Entrep Manag J

Tab

le1

Descriptionof

variables

Abbreviation

Measuring

Definition

Expected

sign

Dependent

variables

grow

th_dv

Probabilityof

grow

ing(for

binary

choice

models)

Dum

my1=grow

ingfirm

;0=notgrow

ing

grow

th_abs

Probabilityof

grow

ingandmagnitude

ofgrow

th(for

tobitmodels)

Leftcensored

at0=notgrow

ingor

decliningno

ofem

ployees,anduncensored

attheright

grow

th_rg

Percentagechange

innumberof

employees(for

both

TobitandOLSmodels)

rgt¼

Et−Et−1

Et−1

biGrowth

basedon

Birch’sIndex

bi¼

Et−Et−1

ðÞE

tEt−1

diGrowth

basedon

Davidsson’sIndex.

di¼

Et−Et−1

ðÞ

Etþ

Et−1

2ð

Þordered_di

Ordinaloutcom

eforthreecategories

ofgrow

thbasedon

relativ

egrow

th.

Fourcategories

areas

follows:non-grow

th,low

,medium

andfastgrow

ingfirm

s

Firm

age

Age

ofthefirm

Yearssincestart-up

–

Size

Size

Num

berof

employeesatthebeginningof

theyear

–

Urban

Locationof

firm

incapitalcity

Dum

my1=iffirm

islocatedin

capitalcity,0

=otherw

ise

mult_plant

Firmsthatoperatemorethan

oneplant

Dum

my1=iffirm

owns

morethan

oneplant,0=otherw

ise

+

investment

Investment

Dum

my1=firm

madeinvestment,0=otherw

ise

+

buss_expec

Owners/m

anager’sexpectations

regarding

business

prospectsin

thefuture

Dum

my1=iffirm

expectsbetterbusiness

Prospectsin

subsequent

year

than

inprevious

year;0=otherw

ise

+

Credit

Financing

Dum

my1=firm

received

acredit;

0=otherw

ise

+

legal_form

Legalform

ofbusiness

Dum

my1=iffirm

islim

itedliability,0=otherw

ise

+

buss_assoc

Mem

bershipof

business

associations

Dum

my1=iffirm

isamem

berof

anybusiness

association;

0=otherw

ise

+

Hum

ancapital

emp_

edu

Educationof

employees

Proportionof

employeeswith

atleasthigh

school

education

+

ent_edu

Educationof

owner/manager

Proportionof

ownersandmanagerswith

atleasthigh

school

education

+

emp_train

Employees’training

Dum

my1=incidenceof

employee

training,0

=otherw

ise

+

man_train

Owner/manager’straining

Dum

my1=incidenceof

owner/manager

training,0

=otherw

ise

+

ent_

age

Age

oftheentrepreneur

Age

oftheow

ner(oraverageageof

ownerswhenmorethan

oneow

ner)in

years

?

Team

Entrepreneurialteam

atthestart-up

Dum

my1=iffirm

was

funded

bymorethan

oneow

ner,0=otherw

ise

+

gender

Genderdifferences

Dum

my1=iffirm

isow

nedby

male,0=otherw

ise

+

Institutio

nalq

uality

Taxes

Taxes

–

Int Entrep Manag J

Tab

le1

(contin

ued)

Abbreviation

Measuring

Definition

Expected

sign

Dum

my1=ifentrepreneur

rankslevelof

taxesas

amajor

obstacleto

operation

andgrow

thof

business,0

=otherw

ise

Adm

inEffectof

administrationprocedures

and

bureaucracy

Dum

my1=ifentrepreneur

ranksadministrativeprocedures

asamajor

obstacle

tooperationandgrow

thof

business,0

=otherw

ise

unfair_com

pUnfaircompetition

Dum

my1=ifentrepreneur

ranksunfaircompetitionas

amajor

obstacleto

operation

andgrow

th0=otherw

ise

–

strong_com

pStrongcompetition

Dum

my1=ifentrepreneur

ranksstrong

competitionas

amajor

obstacleto

operation

andgrow

thof

business,0

=otherw

ise

–

exte_fin

Availabilityandconditionsof

externalfinance

Dum

my1=ifentrepreneur

ranksavailabilityandconditionsof

externalfinance

asamajor

obstacleto

operationandgrow

thof

business,0

=otherw

ise

–

Legal

Law

sandlegislation

Dum

my1=ifentrepreneur

ranksthelegalenvironm

entas

amajor

obstacleto

operation

andgrow

thof

business,0

=otherw

ise

–

Corruption

Corruption

Dum

my1=ifentrepreneur

rankscorruptionas

amajor

obstacleto

operationandgrow

thof

business,0

=otherw

ise

–

insuff_dem

and

Insufficient

demand

Dum

my1=ifentrepreneur

ranksinsufficient

demandas

amajor

obstacleto

operation

andgrow

thof

business,0

=otherw

ise

–

Strategy,g

rowth

aspiratio

nand

managerial

capacities

Export

Searching

fornew

marketsandexpansion

Dum

my1=iffirm

exports,0=otherw

ise

+

foreign_coop

Foreign

cooperation

Dum

my1=iffirm

hasperm

anentforeignpartner,0=otherw

ise

+

grow

th_orient

Planforgrow

thof

thefirm

(noof

employees)

Dum

my1=iffirm

plansto

increase

thenumberof

employeesin

thefuture,

0=otherw

ise

+

sep_ow

n_cont

Managerialcapabilitiesanddevelopm

entof

professionalmanagers

Dum

my1=ifow

nershipandmanagem

entareseparated,

0=otherw

ise

+

Control

variables

production

Productionsector

Dum

my1=iffirm

operates

prim

arily

inproductio

nsector,0

=otherw

ise;

+

services

Servicessector

Dum

my1=iffirm

operates

prim

arily

inservices,0

=otherw

ise;

+

y04

Year1

Dum

my1=for2004,0

=otherw

ise

?

y03

Year2

Dum

my1=for2003,0

=otherw

ise

?

y02

Year3

Dum

my1=for2002,0

=otherw

ise

?

Int Entrep Manag J

difference in the number of employees between the start-up year and the current year.Unfortunately, this information is not available in the Riinvest SME survey. Second,many authors use the logarithm of employment growth as the dependent variable whichin our case is impossible as we use tobit or probit models. Finally, the impact of sizeand age depend on whether the relative or absolute definition of growth is used. Themain conclusions emerging from this finding is that the association of variables sizeand age with growth is sensitive to whether the relative or absolute definition of growthis used. This is confirmed by two other tobit models (specifications [2] and [3], Table 2)and ordered probit model (specification [6] Table 2). In specification [2], the variablesize is significant and has a positive sign (when the absolute growth measure is used).In specification [3], when we use the relative growth measure for size, the variablebecomes negative, suggesting that GL does not hold.1 Results of this empirical testsuggest a nonlinear and negative relationship of size with the growth of the firm. On theother hand, age of firm is not statistically significant. In technical terms, the calculatedunconditional marginal effects indicate that there is a one-percent increase in size of thefirm decreases the percentage of growth by 0.014 %. The marginal effects for age arelow and not significant which might be because of the low firm mean age of 8 years(H1a partially supported, H1b not supported). In addition, we find that firms in the urbanlocations (capital city) are more likely to grow than other firms (H2 supported).Unconditional marginal effect show that, keeping other variables constant, transitioningfrom a non-urban firm to an urban firm increases the percentage of growth 0.55 %.However, when we split the sample by sector and size, we find that the smaller firmsand manufacturing firms exploit greater benefits from being located in the capital city(see Table 2).

These findings are in line with research on agglomeration economies, which arguethat the positive externalities enjoyed by firms operating in developed and dynamicurban areas (i.e., a larger number of consumers, better access to resources,networking,knowledge spillovers, human capital, funds, urban institutions etc.) havethe benefit of grow faster (Glaeser et al. 1992; Black and Henderson 1999). Firmslocated in urban areas are more likely to engage in networking and subcontracting,which provide greater opportunity for growth, in comparison to firms located in otherperipheral locations of the country. Firms using bank finance are more likely to growand experience higher growth compared to their counterparts. Firms that made aninvestment during the year experienced higher growth compared to those who did notinvest. The use of bank credit might influence the expansion of a firm’s activities and,in turn, will be associated with employment growth. Age does not seem to have asignificant effect on either the probability of the firm grows or the magnitude of growth– though it always has the expected sign (H1b not supported).

Human capital factors The impact of human capital (entrepreneurs, managers andemployees) on firm growth has been acknowledged by many researchers in bothdeveloped and developing countries supporting the human capital theory that greatereducation benefits the firm’s performance (Kangasharju and Pekkala 2002;Macpherson and Holt 2007; see also van der Sluis et al. 2005 for an overview of

1 We have tried quadratic terms of variable size and age but results but these variables were statisticallyinsignificant.

Int Entrep Manag J

Tab

le2

Determinantsof

smallfirm

grow

th:regression

results

ofprobit,

tobitandorderedprobitmodelsfrom

pooled

data

Specification

[1]

[2]

[3]

[4]

[5]

[6]

Independentvariables

Probit

Tobit

(absolutegrow

th)

Tobit

(relativegrow

th)

Tobit

(Birch

Index)

Tobit(D

avidsson

etal.index)

Ordered

probit

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Firm size

0.003**

0.040

0.069***

0.000

lnsize

−0.056***

0.000

−0.062

0.690

−0.002**

0.017

−0.129

0.000**

lnage

−0.001

0.919

−0.044

0.449

−0.001

0.694

−0.536

0.375

−0.002

0.442

−0.039

0.375

urban

0.174***

0.061

2.512**

0.011

0.055

0.103

19.560**

0.057

0.072

0.155

0.134

0.105†

mult_plant

0.430***

0.000

3.740***

0.000

0.146***

0.000

36.011**

0.001

0.192***

0.000

0.373

0.000***

legal_form

0.011

0.907

1.194

0.220

0.006

0.855

4.191

0.681

0.004

0.936

−0.003

0.970

buss_expec

0.041

0.608

1.372

0.118

0.026

0.388

11.006

0.227

0.034

0.447

0.049

0.506

buss_assoc

0.056

0.571

0.717

0.494

0.023

0.527

−14.540

0.188

0.007

0.904

0.053

0.552

credit

0.180**

0.031

2.488***

0.005

0.068**

0.026

14.374

0.122

0.097**

0.034

0.178

0.018**

Investment

0.592***

0.000

6.045***

0.000

0.253***

0.000

56.845***

0.000

0.378***

0.000

0.612

0.000***

Hum

ancapital

gender

−0.008

0.964

0.395

0.856

−0.007

0.924

8.383

0.713

−0.035

0.741

−0.052

0.767

ent_age

−0.005

0.282

−0.031

0.501

−0.001

0.511

−0.269

0.579

−0.002

0.383

−0.002

0.534

ent_edu

0.098

0.396

1.046

0.395

0.049

0.250

18.702

0.143

0.054

0.388

0.098

0.348

emp_edu

−0.006

0.972

−3.517*

0.060

−0.045

0.470

−35.713*

0.065

−0.018

0.845

−0.067

0.663

emp_train

0.243**

0.039

4.009***

0.001

0.068

0.110

37.809***

0.003

0.077

0.223

0.183

0.079*

man_train

0.249**

0.017

2.741**

0.012

0.105***

0.005

33.643***

0.003

0.165***

0.003

0.245

0.008***

team

0.165

0.113

0.817

0.452

0.056

0.139

12.294

0.276

0.071

0.205

0.124

0.179

Int Entrep Manag J

Tab

le2

(contin

ued)

Specification

[1]

[2]

[3]

[4]

[5]

[6]

Independentvariables

Probit

Tobit

(absolutegrow

th)

Tobit

(relativegrow

th)

Tobit

(Birch

Index)

Tobit(D

avidsson

etal.index)

Ordered

probit

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Institutionalquality

taxes

−0.043

0.633

−0.197

0.840

−0.015

0.660

12.108

0.228

−0.021

0.666

−0.027

0.737

admin

0.060

0.604

1.855

0.139

0.041

0.337

−1.490

0.910

0.068

0.284

0.082

0.435

legal

0.133

0.149

0.756

0.447

0.054

0.108

12.489

0.226

0.078

0.120

0.119

0.152

strong_com

p−0

.186**

0.037

−2.325**

0.019

−0.067**

0.046

−17.831**

0.083

−0.078

0.118

−0.153

0.061*

unfair_com

p0.008

0.926

−0.069

0.942

0.001

0.971

−7.490

0.449

−0.005

0.913

0.009

0.906

corruption

−0.021

0.822

−0.945

0.340

−0.040

0.240

−10.424

0.314

−0.075

0.138

−0.084

0.311

exte_fin

−0.158*

0.098

−1.741*

0.096

−0.058*

0.099

−20.846**

0.056

−0.101**

0.057

−0.140

0.108†

insuff_dem

and

−0.091

0.378

−0.782

0.499

−0.029

0.460

−9.601

0.425

−0.028

0.629

−0.075

0.430

Strategy,grow

th

aspirationand

managerialcapacities

export

0.337**

0.040

3.716**

0.018

0.112***

0.041

56.057**

0.001

0.136*

0.098

0.251

0.064*

foreign_coop

0.056

0.534

0.867

0.374

0.017

0.601

5.249

0.605

0.022

0.663

0.045

0.581

grow

th_orient

0.450***

0.000

4.313***

0.000

0.160***

0.000

38.043***

0.000

0.228***

0.000

0.400

0.000***

sep_ow

n_cont

0.190**

0.040

2.338**

0.018

0.097***

0.004

15.479

0.133

0.135***

0.008

0.247

0.003***

Control

variables

Production

0.013

0.895

1.124

0.266

0.034

0.323

17.550**

0.094

0.046

0.378

0.077

0.365

y03

0.025

0.825

−0.792

0.518

0.011

0.787

−7.667

0.544

−0.007

0.904

0.050

0.621

Int Entrep Manag J

Tab

le2

(contin

ued)

Specification

[1]

[2]

[3]

[4]

[5]

[6]

Independentvariables

Probit

Tobit

(absolutegrow

th)

Tobit

(relativegrow

th)

Tobit

(Birch

Index)

Tobit(D

avidsson

etal.index)

Ordered

probit

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

Coeff.

P>|z|

y04

−0.137

0.191

0.367

0.748

−0.047

0.224

−7.071

0.550

−0.059

0.305

−0.107

0.257

constant

−1.396

0.000

−19.027

0.000

−0.468

0.000

−185.021

0.000

−0.743

0.000

cut1

1.106

cut2

1.698

cut3

2.610

Modelsummary

Noof

observations

1541

1541

1541

1541

1541

Left-censored

observations

1107

1107

1107

1107

Uncensoredobservations

434

434

434

434

434

PseudoR-squared

0.225

0.105

0.214

0.050

0.172

Estim

ated

St.E

rrors( σ̂)

0.421

0.016

120.6

0.616

LikelihoodRatio

Test

(H0:JointInsignificance)

479.3***

0.000

356.4***

0.000

320.2***

0.000

339.7***

0.000

ConditionalMom

entTest

(H0:NormalErrors)

55.87

17.61***

***significant

at1%;**significantat

5%;*significantat

10%,†significantat

11%.Dependent

variables:[1]dichotom

ousvariable

equal1iffirm

experiencesgrow

thzero

otherw

ise;[2]and[3]censored

to0forfirm

sthatdidnotg

rowor

declined

andcontinuespositivevalues

forgrow

ingfirm

s;[4]censored

tozero

fornon-grow

inganddecliningwhile

positivecontinuesforgrow

ingfollo

wingBirch

Indexof

firm

grow

th;[5]censored

tozero

fornon-grow

inganddecliningwhile

positiv

econtinuesforgrow

ingfirm

sfollo

wing

Davidsson

etal.(2002)indicatorof

firm

grow

th;[6]

ordinalvariableequal1

=decliningor

non-grow

ingfirm

s,2=firm

sthatexperiencedsomegrow

thup

toamedianof

thesample,3

=firm

sthatexperiencedgrow

thbetweenmedianand10th

percentileof

FGFof

thesample,and4=10

%fastgrow

ingfirm

sin

thesample(10percentiles)

Int Entrep Manag J

these studies). In contrast to studies that found a positive relationship between educa-tion and growth of the firm (Kangasharju and Pekkala 2002; Macpherson and Holt2007; van der Sluis et al. 2005), our evidence suggests that the education of employeeshas a significant negative relationship with the growth of a firm while the educationalattainment of the entrepreneur has no significant association with growth, calling forcontextual and other interpretation frameworks (H5a not supported). The higher levelsof education of employees (university degree) is a statistically significant and nega-tively associated with growth across all specifications and definitions of growth, exceptin specification [3] when relative growth is used – which gives greater prominence tothe smaller firms in the sample. In this specification, the positive sign indicates thatfirms with a higher proportion of employees with higher education experience smallergrowth rates compared to rest of the firms in the sample (H5a not supported). Theunconditional marginal effects indicate that a one-percent increase in proportion ofemployees with university degree decreases the growth by 0.7 employees (Table A5,Tobit 1, in Appendix,). SMEs that provide on-the-job training for employees andmanagers generate, on average, 0.019 %, or 0.029 more of their growth than doSMEs that do not offer such service to their employees and managers.

Although this finding is not in line with other studies on small firm growth, it is inline with the few studies conducted in both developed and TEs. For example, Bartlettand Bukvič (2001) report similar results in their study of SMEs in Slovenia, Johnson etal. (2000) for UK SMEs operating in the service sector and Xheneti and Bartlett (2012)for Albanian SMEs. This evidence from both developed and TEs justifies the negativeeffect on employment on the ground of the over-qualification of employees generatingdissatisfaction and hence negatively affecting growth. In the context of Kosova, thedissatisfaction effect of employees and particularly highly educated employees mightbe even more pronounced considering the high unemployment rate. Under highunemployment, people generally have a limited choice about where to work. Underthese conditions, people with university degrees might end-up working in jobs they donot like or jobs that do not match their education profile. At the same time, the qualityof the education and therefore the quality of available labour in Kosova is not beneficialto the growth of SMEs in terms of the new knowledge necessary to run businesses in amarket economy. In addition, one should compare the impact of this variable with thesignificance and impact of other proxy variables for human capital in the model –training. Based on this reasoning, findings suggest the positive and statistically signif-icant association of variables suggesting management and employees’ training ongrowth (H5b supported). In line with other studies (McPherson 1996), results suggestthat firms with trained managers grow significantly faster than firms run by untrainedpeople. This may suggest that firms need to incur training costs to compensate for thelow quality of education embodied in the managers and employees’ work. About the‘legal type of business’ we find the results to be the opposite of those of Storey (1994b)and Harhoff et al. (1998) that limited liability companies experience higher growth ratesbecause they are more likely to get involved in riskier projects and therefore enjoygreater returns if they succeed (H3 not supported). The variable team is justabove the accepted statistical significance, suggesting the positive impact of theentrepreneurial team on post start-up performance because of the synergy effectof partners (H7 supported). The variable gender is not a significant indicator forfirm growth either.

Int Entrep Manag J

Institutional factors Among the institutional quality variables, ‘strong competition’and ‘external finance’ are statistically significant and are negatively associated withgrowth of the firm. (H11 partially supported). Keeping other variables constant, SMEsthat consider finance and strong competition to be a barrier, grow on average, 0.014 and0.052 % less, respectively, than SMEs that do not consider finance and strong compe-tition as a high barrier (Table A5 in Appendix).

Corruption is another dimension of the institutions, which is negatively associatedwith growth, but only for sample of growing firms only (see Table 3). The intensity ofcompetition may be perceived as a barrier by entrepreneurs because of the decrease inaggregate demand for goods and services for individual firms, which have to share themarket with an increasingly large number of other firms. As pointed out by Hay andKamshad (1994), when demand is slacking and competition is growing, economictheory does not provide a clear prediction as to whether competition has a negative orpositive impact on the firm. According to them, the negative impact of increasedcompetition may be an outcome of the capacity costs, which are mostly sunk, andlarger firms benefit from decreasing average costs. A lower level of outputs, thecompetition may cause small firms to contract or exit the market because larger firmsmight be operating on the decreasing part of the average cost curve, benefiting fromscale economies.

Strategy, managerial capacities and growth aspirations Firm growth requires both awilling attitude to exploit growth opportunities, and also the availability of suitableopportunities provided by the external environment. Only a small share of small firms isentrepreneurial and oriented toward continuous growth of their market share. Results ofthis is shown in Table A5 in the Appendix shows that exporter are more likely to grow,on average, 0.016%more than non-exporters, suggesting growth aspiring entrepreneursshould seek larger markets by exporting to other countries, in particular in a smalleconomy such as Kosova (H9a supported). This is particularly true for firms with growthambitions that operate in a small economy (Kosova being an example) where growthopportunities are limited. However, surprisingly, foreign cooperation variable does nothave a significant influence on the growth of the firm (H9b not supported).

While growth can be explained by various firm characteristics, the entrepreneur’scommitment to the growth of a firm is a most important factor (Dobbs and Hamilton2007; Mochrie et al. 2006; Heinonen et al. 2004). To operationalize this variable weused proxy as in Efendic et al. (2014), forward-looking growth orientation of the firmmeasured by ‘plans for future increases in the number of employees’. In our model, thisvariable is highly significant and has the expected positive sign, suggesting that growthaspiration is positively associated with growth (H8 supported). The unconditionalmarginal effects in Appendix show that, changing from a not growth-oriented to agrowth oriented firm increases firm growth by 0.026 % (Table A5). The results satisfyScase’s (2003) view that, especially in TEs, one should distinguish between ‘entrepre-neurship’ (growth-oriented entrepreneurs) and ‘proprietorship’ (one-person businesseswithout the aim to grow). The finding may signal that studies that do not control forgrowth aspirations of firms may have biased approach in explaining growth. Not onlyexternal but also internal factors affect small firm growth. Amongst the key internalfactors that are influencing firm growth is the entrepreneur’s willingness to grow andthe firm’s managerial capacity (Hay and Kamshad 1994). If we compare the economic

Int Entrep Manag J

and statistical significance of variables indicating growth aspiration with the coeffi-cients of variables explaining the influence of institutional factors, we find that internalfactors are more important for explaining a firm’s growth, suggesting a need for usingan ‘integrative approach’ in future empirical studies of entrepreneurship in TEs.

Finally, regarding the impact of managerial capacities on firm growth, we find thatfirms that have brought in professional managers (divorcing management from own-ership functions) are more likely to experience growth and show a greater magnitude ofgrowth. The unconditional marginal effects presented in Table A5 in Appendix showthat, change from an owner-managed to a professionally managed firm increasesgrowth by 0.026 %. (H10 supported). These findings are in line with other organiza-tional theory studies, which propose that organizations evolve through their life cyclestages. In their early phase, firms are limited in their managerial capacities and also maynot grow or wish to grow. In later stages as organizations grow more rapidly, firms needto increase the common set of managerial capabilities to overcome growth challengesin performing organizational tasks in complex external interfaces (Boeker and Wiltbank2005). Accordingly, a founder’s involvement in general management activities may bedecreasingly useful or even detrimental to a firm’s success as the firm grows. Findingssuggest that the transfer of decision-making power from owners to managers isimportant for the growth of the firm because it enhances managerial capabilities bybringing professional managers into the firm and creating conditions for growth, thushaving a positive effect on the growth.

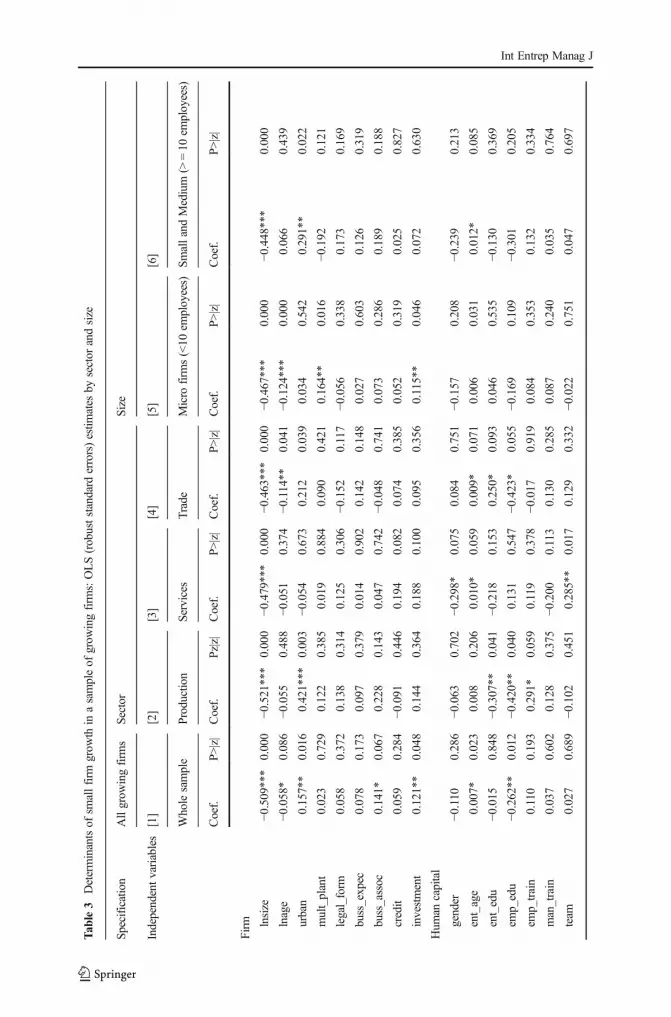

An empirical analysis of small growing firms This section aims to extend currentunderstanding of small business growth in a transitional economy by concentrating onthe subgroup of growing firms in the same dataset. We examine the impact of the samedeterminants of growth in the sample of growing firms and by conducting separateregressions for three main sectors (manufacturing, services and trade) and two sizecategories (micro and small and medium firms). Testing the relationship of the samefactors with growth of a firm within the sample of growing businesses and controlling itfor each size and sector will enable us to overcome some of the empirical drawbacks ofother studies (biased towards larger firms). Our large pooled data set gives the ability toperform this analysis because of a large number of observations.

Table 3 presents the empirical findings based on robust OLS regressions for asample of growing firms. All variables used in this model are the same as thosepresented in Table 1. Several interesting differences that can be noted in terms offindings with whole sample presented in Table 2. Firstly, in specification [1] thevariable age has a negative association with growth. Although it is expected that agewould have a negative association with growth in all sectors, the evidence shows thatthe effect of learning is more important for firms in trade compared to other sectors (H1b

partially supported). As proposed by Jovanovic’s (1982) model, the younger firmsshow higher growth rates as they have less understanding of the true cost related to theirbusiness activities and how these costs change over time. Younger firms are resource-constrained, suffer from the ‘liability of newness’, thus are more likely to make lessefficient use of slack resources than older firms because older firms have had moreopportunity to experiment with the variety of resources and select the ones that best fittheir needs (George 2005). This association is nonlinear, meaning that as firms get olderthere is a diminishing return from learning and experience. Taking into account size

Int Entrep Manag J

Tab

le3

Determinantsof

smallfirm

grow

thin

asampleof

grow

ingfirm

s:OLS(robuststandard

errors)estim

ates

bysector

andsize

Specification

Allgrow

ingfirm

sSector

Size

Independentvariables

[1]

[2]

[3]

[4]

[5]

[6]

Wholesample

Production

Services

Trade

Micro

firm

s(<10

employees)

SmallandMedium

(>=10

employees)

Coef.

P>|z|

Coef.

Pz|z|

Coef.

P>|z|

Coef.

P>|z|

Coef.

P>|z|

Coef.

P>|z|

Firm lnsize

−0.509***

0.000

−0.521***

0.000

−0.479***

0.000

−0.463***

0.000

−0.467***

0.000

−0.448***

0.000

lnage

−0.058*

0.086

−0.055

0.488

−0.051

0.374

−0.114**

0.041

−0.124***

0.000

0.066

0.439

urban

0.157**

0.016

0.421***

0.003

−0.054

0.673

0.212

0.039

0.034

0.542

0.291**

0.022

mult_plant

0.023

0.729

0.122

0.385

0.019

0.884

0.090

0.421

0.164**

0.016

−0.192

0.121

legal_form

0.058

0.372

0.138

0.314

0.125

0.306

−0.152

0.117

−0.056

0.338

0.173

0.169

buss_expec

0.078

0.173

0.097

0.379

0.014

0.902

0.142

0.148

0.027

0.603

0.126

0.319

buss_assoc

0.141*

0.067

0.228

0.143

0.047

0.742

−0.048

0.741

0.073

0.286

0.189

0.188

credit

0.059

0.284

−0.091

0.446

0.194

0.082

0.074

0.385

0.052

0.319

0.025

0.827

investment

0.121**

0.048

0.144

0.364

0.188

0.100

0.095

0.356

0.115**

0.046

0.072

0.630

Hum

ancapital

gender

−0.110

0.286

−0.063

0.702

−0.298*

0.075

0.084

0.751

−0.157

0.208

−0.239

0.213

ent_age

0.007*

0.023

0.008

0.206

0.010*

0.059

0.009*

0.071

0.006

0.031

0.012*

0.085

ent_edu

−0.015

0.848

−0.307**

0.041

−0.218

0.153

0.250*

0.093

0.046

0.535

−0.130

0.369

emp_edu