Embed Size (px)

Citation preview

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 1 of 29

MASTER OF BUSINESS ADMINISTRATION

INTERNATIONAL PROGRAM

SEMESTER 2 – 2013

ANALYSIS THE FINNANCIAL STATEMENT OF INVESTMENT COMMERCE

FISHERIES CORPORATION - ICF

Lecturer: Dr. Phan Dinh Nguyen

Student Name: Nguyen Manh Ha

ID No: 15030

MBAOUM0313 - Class K08A

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 2 of 29

Preface:

My heart is filled with very gratitude to my dear teacher who inspire and instruct me

how to do research and conduct a case study for how analysing the financial statement of the

ICF Corporation that listed in Hochiminh City’s Stock Exchange. These studies have

revealed the application for analysis any type of businesses, organizations on the financial

market. The fact that the financial statement is very important and the manager of any

business requires a flow of information to make informed, intelligent decisions affecting the

success or failure of its operations. Investors need statements to analyze investment potential

Banks require financial statements to decide whether or not to loan money, and/ or many

companies need statements to ascertain the risk involved in doing business with their

customers and suppliers

I highly appreciate the efforts of Dr. Phan Dinh Nguyen who guided and gave me a

chance to do this assignment.

I also would like to express my thanks to all my friends & ICF Corporation helped

me with very useful information so that I could accomplish this assignment.

I hope that my analysis would serve as a ready reckoned document for students,

research scholars using as a reference source.

With very best regards.

Nguyen Manh Ha

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 3 of 29

Table of contents

I. Introduction

II. General introduction of Incomfish

III. Analysis of financial statements

IV. Conclusion and policy implications

References

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 4 of 29

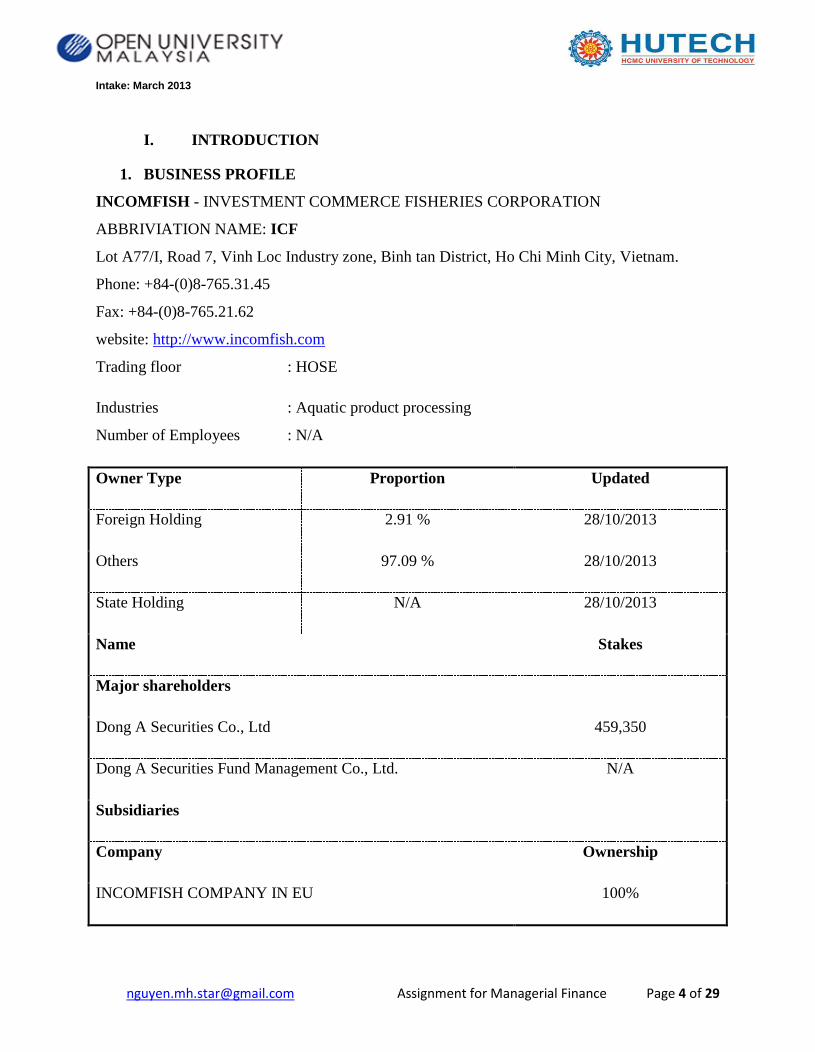

I. INTRODUCTION

1. BUSINESS PROFILE

INCOMFISH - INVESTMENT COMMERCE FISHERIES CORPORATION

ABBRIVIATION NAME: ICF

Lot A77/I, Road 7, Vinh Loc Industry zone, Binh tan District, Ho Chi Minh City, Vietnam.

Phone: +84-(0)8-765.31.45

Fax: +84-(0)8-765.21.62

website: http://www.incomfish.com

Trading floor : HOSE

Industries : Aquatic product processing

Number of Employees : N/A

Owner Type Proportion Updated

Foreign Holding 2.91 % 28/10/2013

Others 97.09 % 28/10/2013

State Holding N/A 28/10/2013

Name Stakes

Major shareholders

Dong A Securities Co., Ltd 459,350

Dong A Securities Fund Management Co., Ltd. N/A

Subsidiaries

Company Ownership

INCOMFISH COMPANY IN EU 100%

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 5 of 29

INCOMFISH COMPANY IN NORTHERN AMERICA 100%

II. GENERAL INTRODUCTION OF INCOMFISH

1. Corporate History

1st Sep1999: Established with the initial chartered capital of VND10 billion

2001: Constructing Seafood Product Processing Manufactory in Vinh Loc industrial park

– Ho Chi Minh City

June 2006: Completing to build Seafood Product Processing Manufactory with the

capacity of 6,500 tons/ year

Increasing its chartered capital to VND118 billion

29/11/2006: Listed on Hose

03/2011: The chartered capital is VND128.07 billion

2. Scopes of Business

Cultivating sea animals

Processing and preserving seafood products and others

Supplying services relating to sea animals as collecting, transporting fresh sea animals,

providing foods, creating fish or shrimp breeds

Processing and preserving meat, products from meat, vegetables and products from

vegetables.

Others under business license

3. Development Strategies

Good quality is the main principle to develop company. Thus, it always increases the role

of quality management to meet higher consumers’ demand on quality.

Keeping diversifying products and market, the company plans to build infrastructures of

industrial parks, congealment manufactory according the economic and social

incorporation programs between Ho Chi Minh City and Dong Thap province from 2007

to 2010.

4. Company Ability

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 6 of 29

Investment Commerce Fisheries Joint Stock Company was established in 1999 and started

operating in 2003. The company mainly produces seafood products (3 main types: fish, shrimp

and processing foodstuff). Company’s products are mainly exported (above 95%) to the US,

Japan and EU. The main manufactory of company located in an area of 21,000 m2 has a capacity

of 1500 tons per year. Moreover, the company has a system of cold storages with capacity of

2,500 ton and applies technology of conveyor belt and sewage disposal system. Especially,

company’s products are permitted to export to Japan without inspections.

5. Company Position

Incomfish applies quality management system as HACCP, BRC (Brittish Retail

Consortium), ISO 9001:2000, IFS (International Food Standard), ACC (Aquaculture

Certificate Council), MSC (Marine Stewardships Council) to guarantee high standard of

quality and food safety. Besides, in 2008, the company was granted SA 8000 (Social

Accountability) by TUV NORD

Their products directly entered EU market, Japan, US and some high demanding markets.

6. Major Projects

Project of congealment manufactory in Dong Thap province: this company invested VND

66,240,000,000 in the manufactory with capacity of 150 tons/ year. It will be put into

operation in July 2009.

Making contributions to establish Incomfish Company in the US and EU with the

investment capital of VND29.16 billion. Investing USD2 million on equipments and

machines of Incomfish Company. It will officially operate in 5/2009.

Project of office building in No.32, Mac Dinh Chi, 1st District, Ho Chi Minh City. The

company contributed VND39.6 billion in this project with Saga Trading &Service Co.

Ltd

Project of building infrastructures of Industrial group in Dong Thap province. Incomfish

mobilized VND250 billion. It will begin executing in 2009.

Project of real estate in Linh Xuan ward, Thu Duc District, HCM city. The company

contributed VND48 billion in this project with Vega Trading &Service Co. Ltd

7. Company Prospects

The manufactory is equipped with modern machines and advanced technology.

The company’s products are evaluated as good quality and safety

Diversifying material resources in domestic and overseas sources to reduce risks about

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 7 of 29

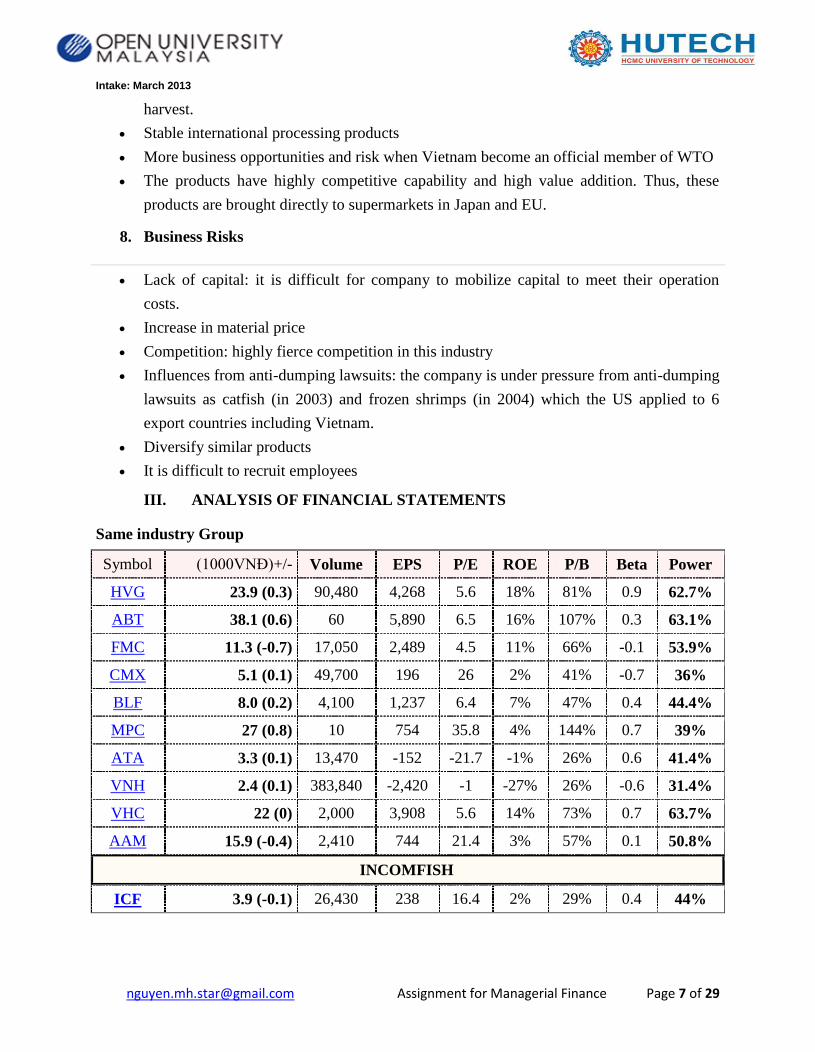

harvest.

Stable international processing products

More business opportunities and risk when Vietnam become an official member of WTO

The products have highly competitive capability and high value addition. Thus, these

products are brought directly to supermarkets in Japan and EU.

8. Business Risks

Lack of capital: it is difficult for company to mobilize capital to meet their operation

costs.

Increase in material price

Competition: highly fierce competition in this industry

Influences from anti-dumping lawsuits: the company is under pressure from anti-dumping

lawsuits as catfish (in 2003) and frozen shrimps (in 2004) which the US applied to 6

export countries including Vietnam.

Diversify similar products

It is difficult to recruit employees

III. ANALYSIS OF FINANCIAL STATEMENTS

Same industry Group

Symbol (1000VNĐ)+/- Volume EPS P/E ROE P/B Beta Power

HVG 23.9 (0.3) 90,480 4,268 5.6 18% 81% 0.9 62.7%

ABT 38.1 (0.6) 60 5,890 6.5 16% 107% 0.3 63.1%

FMC 11.3 (-0.7) 17,050 2,489 4.5 11% 66% -0.1 53.9%

CMX 5.1 (0.1) 49,700 196 26 2% 41% -0.7 36%

BLF 8.0 (0.2) 4,100 1,237 6.4 7% 47% 0.4 44.4%

MPC 27 (0.8) 10 754 35.8 4% 144% 0.7 39%

ATA 3.3 (0.1) 13,470 -152 -21.7 -1% 26% 0.6 41.4%

VNH 2.4 (0.1) 383,840 -2,420 -1 -27% 26% -0.6 31.4%

VHC 22 (0) 2,000 3,908 5.6 14% 73% 0.7 63.7%

AAM 15.9 (-0.4) 2,410 744 21.4 3% 57% 0.1 50.8%

INCOMFISH

ICF 3.9 (-0.1) 26,430 238 16.4 2% 29% 0.4 44%

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 8 of 29

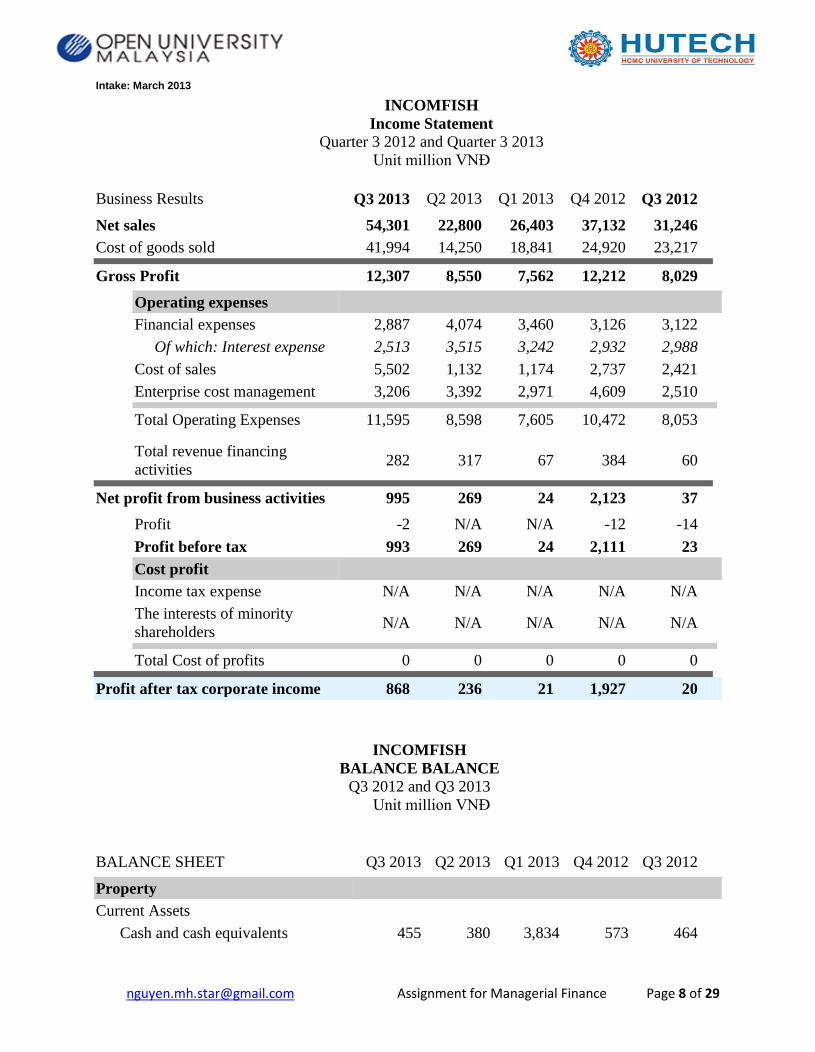

INCOMFISH

Income Statement

Quarter 3 2012 and Quarter 3 2013

Unit million VNĐ

Business Results Q3 2013 Q2 2013 Q1 2013 Q4 2012 Q3 2012

Net sales 54,301 22,800 26,403 37,132 31,246

Cost of goods sold 41,994 14,250 18,841 24,920 23,217

Gross Profit 12,307 8,550 7,562 12,212 8,029

Operating expenses

Financial expenses 2,887 4,074 3,460 3,126 3,122

Of which: Interest expense 2,513 3,515 3,242 2,932 2,988

Cost of sales 5,502 1,132 1,174 2,737 2,421

Enterprise cost management 3,206 3,392 2,971 4,609 2,510

Total Operating Expenses 11,595 8,598 7,605 10,472 8,053

Total revenue financing

activities 282 317 67 384 60

Net profit from business activities 995 269 24 2,123 37

Profit -2 N/A N/A -12 -14

Profit before tax 993 269 24 2,111 23

Cost profit

Income tax expense N/A N/A N/A N/A N/A

The interests of minority

shareholders N/A N/A N/A N/A N/A

Total Cost of profits 0 0 0 0 0

Profit after tax corporate income 868 236 21 1,927 20

INCOMFISH

BALANCE BALANCE

Q3 2012 and Q3 2013

Unit million VNĐ

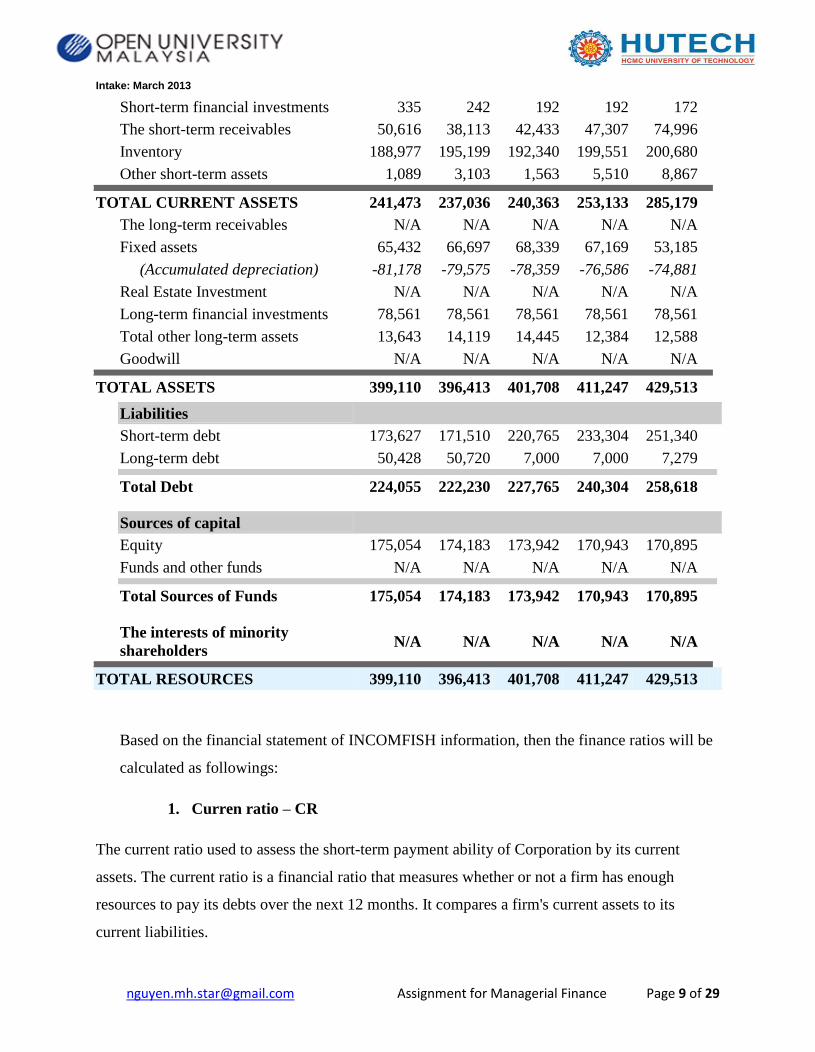

BALANCE SHEET Q3 2013 Q2 2013 Q1 2013 Q4 2012 Q3 2012

Property

Current Assets

Cash and cash equivalents 455 380 3,834 573 464

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 9 of 29

Short-term financial investments 335 242 192 192 172

The short-term receivables 50,616 38,113 42,433 47,307 74,996

Inventory 188,977 195,199 192,340 199,551 200,680

Other short-term assets 1,089 3,103 1,563 5,510 8,867

TOTAL CURRENT ASSETS 241,473 237,036 240,363 253,133 285,179

The long-term receivables N/A N/A N/A N/A N/A

Fixed assets 65,432 66,697 68,339 67,169 53,185

(Accumulated depreciation) -81,178 -79,575 -78,359 -76,586 -74,881

Real Estate Investment N/A N/A N/A N/A N/A

Long-term financial investments 78,561 78,561 78,561 78,561 78,561

Total other long-term assets 13,643 14,119 14,445 12,384 12,588

Goodwill N/A N/A N/A N/A N/A

TOTAL ASSETS 399,110 396,413 401,708 411,247 429,513

Liabilities

Short-term debt 173,627 171,510 220,765 233,304 251,340

Long-term debt 50,428 50,720 7,000 7,000 7,279

Total Debt 224,055 222,230 227,765 240,304 258,618

Sources of capital

Equity 175,054 174,183 173,942 170,943 170,895

Funds and other funds N/A N/A N/A N/A N/A

Total Sources of Funds 175,054 174,183 173,942 170,943 170,895

The interests of minority

shareholders N/A N/A N/A N/A N/A

TOTAL RESOURCES 399,110 396,413 401,708 411,247 429,513

Based on the financial statement of INCOMFISH information, then the finance ratios will be

calculated as followings:

1. Curren ratio – CR

The current ratio used to assess the short-term payment ability of Corporation by its current

assets. The current ratio is a financial ratio that measures whether or not a firm has enough

resources to pay its debts over the next 12 months. It compares a firm's current assets to its

current liabilities.

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 10 of 29

Current ratio = Total Current Asset / Total Current Liabilities or short term debt

Incomfish’s current ratio = 241,473 / 173,627 = 1.39, and the avarage of industry is 1.97.

This index means that every penny of liability, the company can pay by 1.39 penny of current

asset. Because the current ratio greater than one (1) so this shows that the company can afford

to pay short term debt. However, when compare this ratio to avarage of industry 1.97, the

current ration of company is lower, so maintain at this ratio is not good for company.

The current ratio have relationship with net working capital, net working capital equal zero if

current ratio equal 1, net working capital is negative if current ration smaller than 1, and the

net working capital is positive if current ratio greater than 1.

Table: Find out the ratio of same industry: (Unit Million VND)

Stock

Code

Seafood Industry group / name Current

Asset

Current

Liabilities

Current

ratio

HVG Hung Vuong Corporation 6,484,147 5,064,179 1.28

ABT Bentre Aquaproduct Import And Export

Joint Stock Company

419,640 97,825 4.29

FMC Sao Ta Foods Joint Stock Company 630,800 564,433 1.12

CMX Ca Mau Frozen Seafood Processing Import

Export Corporation

368,295 544,553 0.68

BLF Bac Lieu Fisheries Joint Stock Company 291,345 314,099 0.93

MPC Minh Phu Seafood Joint Stock Company 4,833,504 4,966,728 0.97

ATA NTACO Joint Stock Company 598,760 576,820 1.04

VNH Viet Nhat Seafood Corporation 2,527,297 1,869,023 1.35

VHC Vinh Hoan Corporation 2,527,297 1,869,023 1.35

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 11 of 29

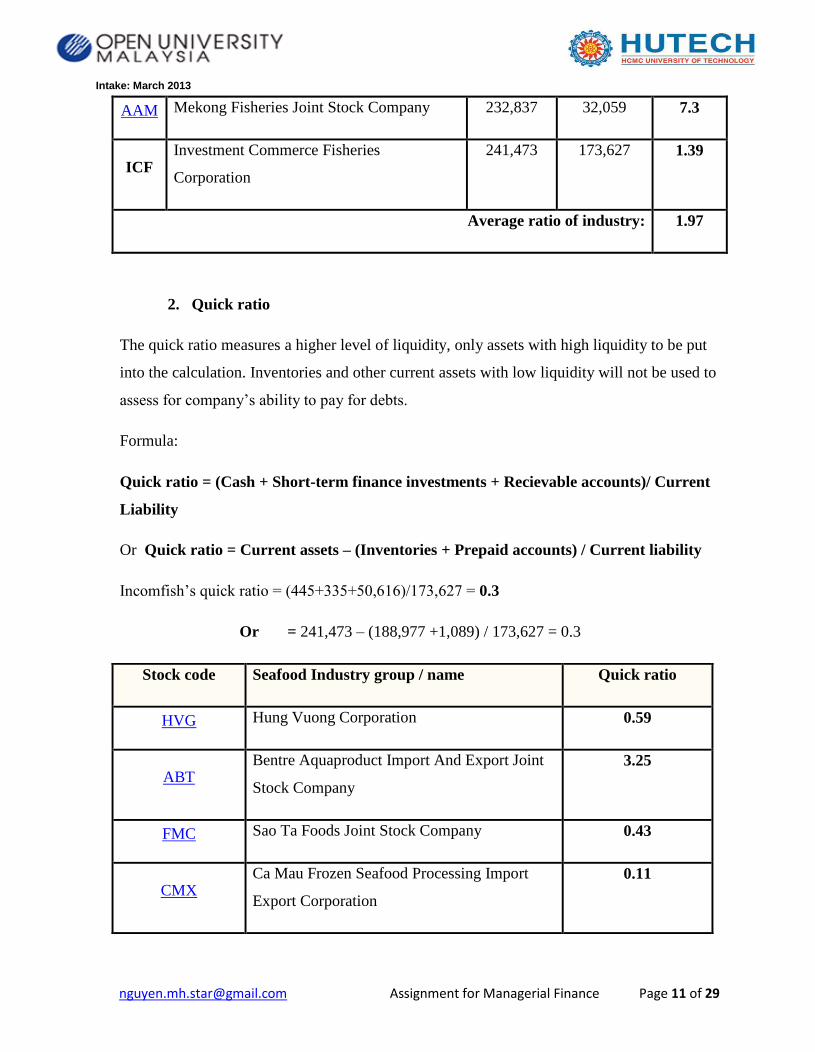

AAM Mekong Fisheries Joint Stock Company 232,837 32,059 7.3

ICF Investment Commerce Fisheries

Corporation

241,473 173,627 1.39

Average ratio of industry: 1.97

2. Quick ratio

The quick ratio measures a higher level of liquidity, only assets with high liquidity to be put

into the calculation. Inventories and other current assets with low liquidity will not be used to

assess for company’s ability to pay for debts.

Formula:

Quick ratio = (Cash + Short-term finance investments + Recievable accounts)/ Current

Liability

Or Quick ratio = Current assets – (Inventories + Prepaid accounts) / Current liability

Incomfish’s quick ratio = (445+335+50,616)/173,627 = 0.3

Or = 241,473 – (188,977 +1,089) / 173,627 = 0.3

Stock code Seafood Industry group / name Quick ratio

HVG Hung Vuong Corporation 0.59

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

3.25

FMC Sao Ta Foods Joint Stock Company 0.43

CMX Ca Mau Frozen Seafood Processing Import

Export Corporation

0.11

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 12 of 29

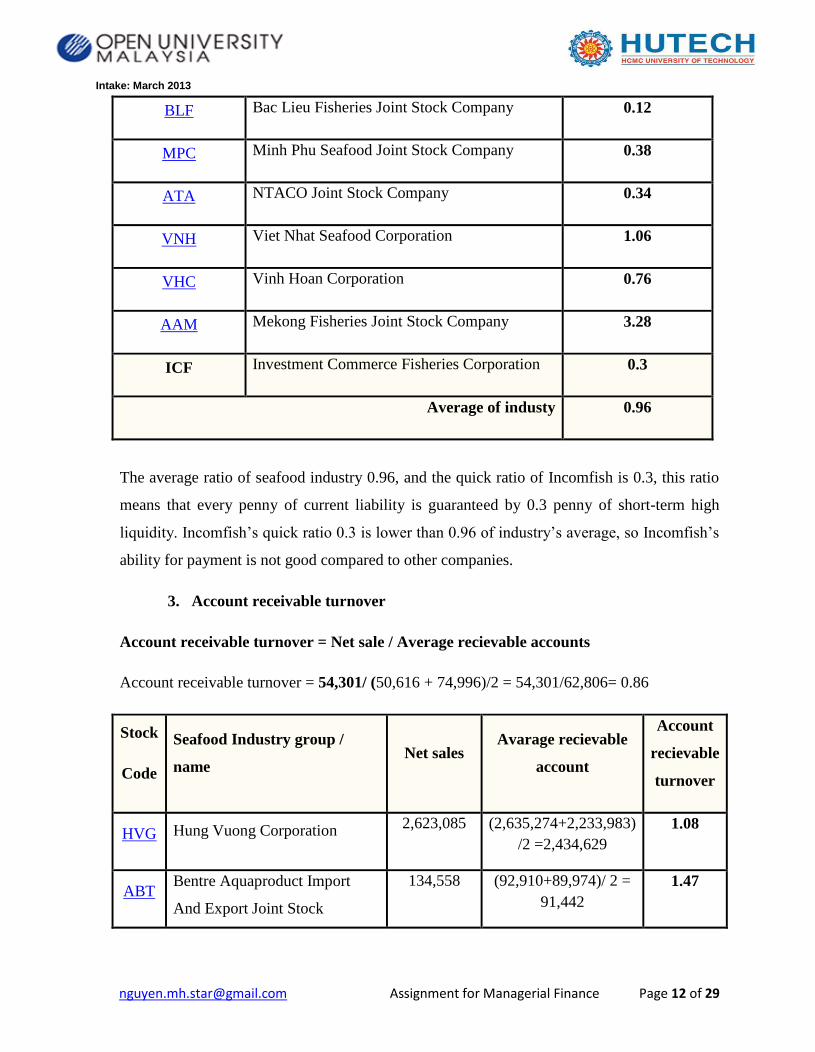

BLF Bac Lieu Fisheries Joint Stock Company 0.12

MPC Minh Phu Seafood Joint Stock Company 0.38

ATA NTACO Joint Stock Company 0.34

VNH Viet Nhat Seafood Corporation 1.06

VHC Vinh Hoan Corporation 0.76

AAM Mekong Fisheries Joint Stock Company 3.28

ICF Investment Commerce Fisheries Corporation 0.3

Average of industy 0.96

The average ratio of seafood industry 0.96, and the quick ratio of Incomfish is 0.3, this ratio

means that every penny of current liability is guaranteed by 0.3 penny of short-term high

liquidity. Incomfish’s quick ratio 0.3 is lower than 0.96 of industry’s average, so Incomfish’s

ability for payment is not good compared to other companies.

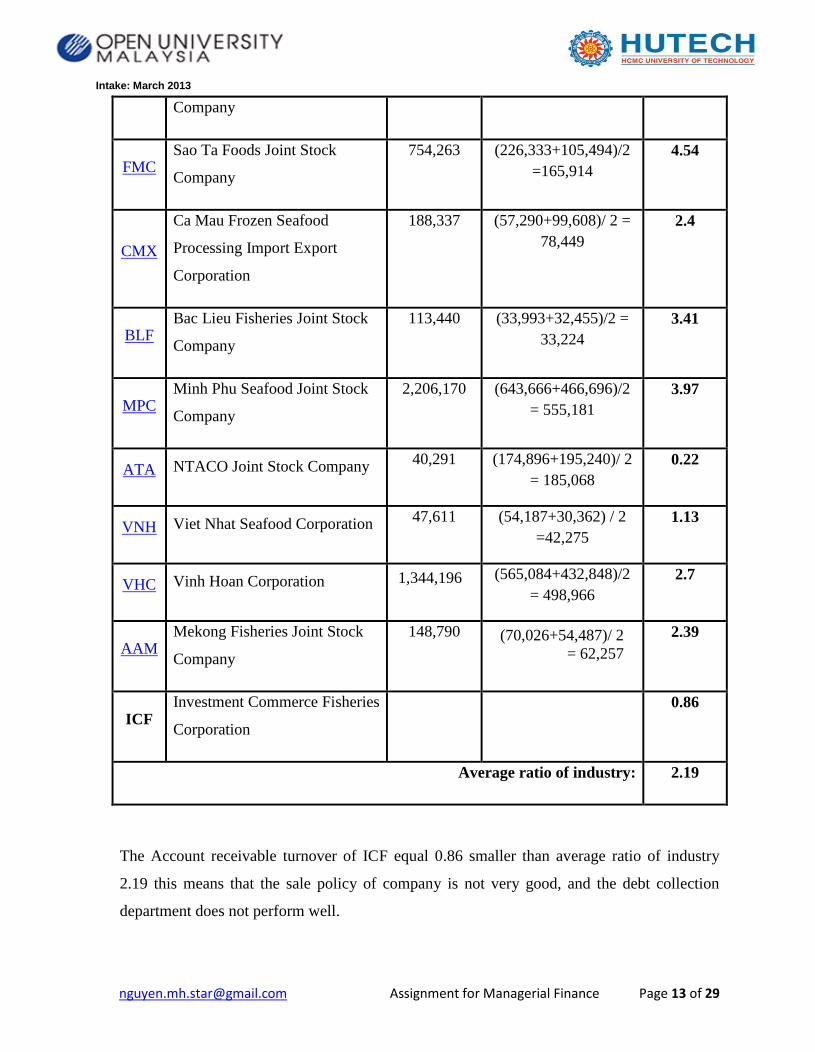

3. Account receivable turnover

Account receivable turnover = Net sale / Average recievable accounts

Account receivable turnover = 54,301/ (50,616 + 74,996)/2 = 54,301/62,806= 0.86

Stock

Code

Seafood Industry group /

name Net sales

Avarage recievable

account

Account

recievable

turnover

HVG Hung Vuong Corporation 2,623,085 (2,635,274+2,233,983)

/2 =2,434,629

1.08

ABT Bentre Aquaproduct Import

And Export Joint Stock

134,558 (92,910+89,974)/ 2 =

91,442

1.47

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 13 of 29

Company

FMC Sao Ta Foods Joint Stock

Company

754,263 (226,333+105,494)/2

=165,914

4.54

CMX

Ca Mau Frozen Seafood

Processing Import Export

Corporation

188,337 (57,290+99,608)/ 2 =

78,449

2.4

BLF Bac Lieu Fisheries Joint Stock

Company

113,440 (33,993+32,455)/2 =

33,224

3.41

MPC Minh Phu Seafood Joint Stock

Company

2,206,170 (643,666+466,696)/2

= 555,181

3.97

ATA NTACO Joint Stock Company 40,291 (174,896+195,240)/ 2

= 185,068

0.22

VNH Viet Nhat Seafood Corporation 47,611 (54,187+30,362) / 2

=42,275

1.13

VHC Vinh Hoan Corporation 1,344,196

(565,084+432,848)/2

= 498,966

2.7

AAM Mekong Fisheries Joint Stock

Company

148,790 (70,026+54,487)/ 2

= 62,257

2.39

ICF Investment Commerce Fisheries

Corporation

0.86

Average ratio of industry: 2.19

The Account receivable turnover of ICF equal 0.86 smaller than average ratio of industry

2.19 this means that the sale policy of company is not very good, and the debt collection

department does not perform well.

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 14 of 29

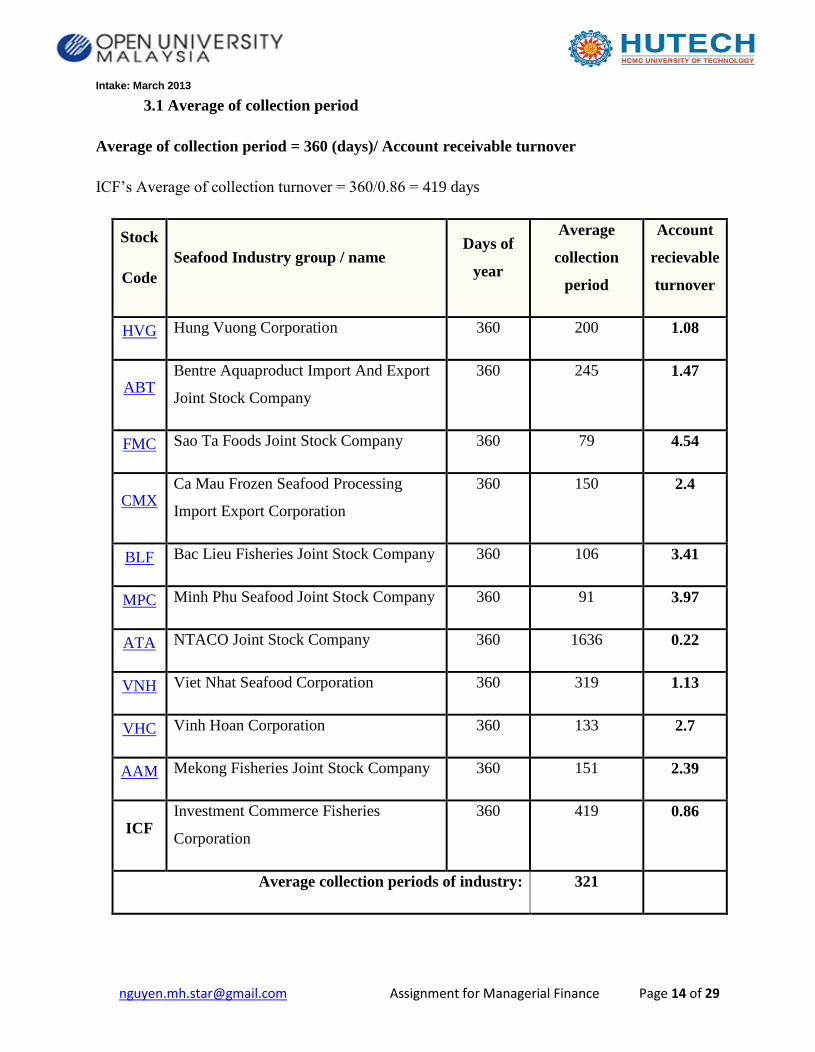

3.1 Average of collection period

Average of collection period = 360 (days)/ Account receivable turnover

ICF’s Average of collection turnover = 360/0.86 = 419 days

Stock

Code

Seafood Industry group / name Days of

year

Average

collection

period

Account

recievable

turnover

HVG Hung Vuong Corporation 360 200 1.08

ABT Bentre Aquaproduct Import And Export

Joint Stock Company

360 245 1.47

FMC Sao Ta Foods Joint Stock Company 360 79 4.54

CMX Ca Mau Frozen Seafood Processing

Import Export Corporation

360 150 2.4

BLF Bac Lieu Fisheries Joint Stock Company 360 106 3.41

MPC Minh Phu Seafood Joint Stock Company 360 91 3.97

ATA NTACO Joint Stock Company 360 1636 0.22

VNH Viet Nhat Seafood Corporation 360 319 1.13

VHC Vinh Hoan Corporation 360 133 2.7

AAM Mekong Fisheries Joint Stock Company 360 151 2.39

ICF Investment Commerce Fisheries

Corporation

360 419 0.86

Average collection periods of industry: 321

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 15 of 29

The Average collection of ICF is 419 days bigger than the average collection period of industry

321days. This analysis show that the company’s collection period too large, and aslo show that

revenue of company is not good, or too small compare to the account receivable, if company

there is no sale policy to increase revenue then it will short of money to investment or

reinvestment.

4. Inventory turnover

Inventory turnover = COGS / average of inventory

ICF’s Inventory turnover = 41,994 / (188,977+200,680)/2 = 41,994/ 194,829= 0.21

Average inventory turnover of industry = 0.83

ICF’s inventory turnover is smaller than average of industry, it means that the speed of ICF’s sale

too slow, consumable goods is small compare to the average of industry, and the inventory

higher than its sale this prove than the sales policy is not effectively.

4.1. Average inventory sales period

Average inventory sales period = 360 (days)/ Inventory turnover

ICF’s Average inventory sales period = 360/ 0.21 = 1714

Industry’s inventory sales poriods = 1285

The industry’s inventory sales period is greater than ICF’s sales period mean that the inventory

of ICF keep in store too long, this cause the company’s cash flow stuck.

5. Total asset turnover

Total asset turnover = Net sale / Total of average asset

ICF’s Total asset turnover = 54,301 / (399,110+429,513)/2 = 0.131

Industry’s Total asset turnover =1.04

The ratio of ICF’s totala asset turnover is too small comparing to the average of industry, means

every 1 penny of asset return 0.131 penny of sales. The return is small and the usage of asset is

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 16 of 29

not efficiency.

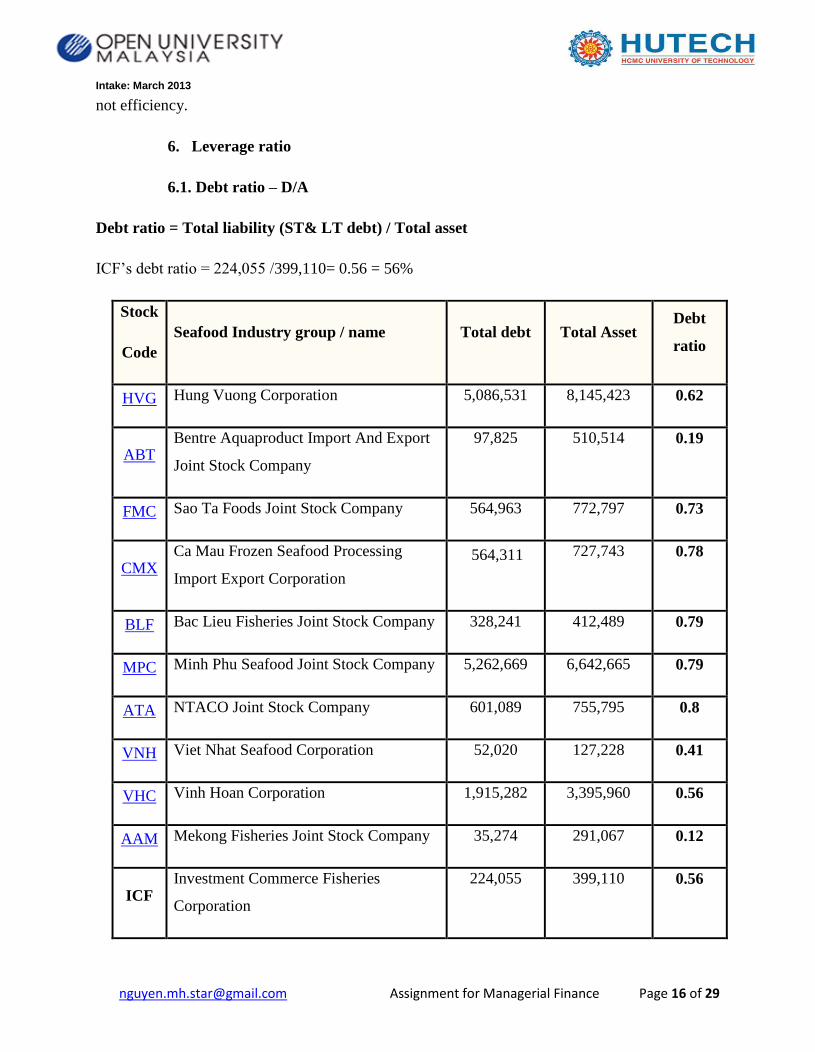

6. Leverage ratio

6.1. Debt ratio – D/A

Debt ratio = Total liability (ST& LT debt) / Total asset

ICF’s debt ratio = 224,055 /399,110= 0.56 = 56%

Stock

Code

Seafood Industry group / name Total debt Total Asset Debt

ratio

HVG Hung Vuong Corporation 5,086,531 8,145,423 0.62

ABT Bentre Aquaproduct Import And Export

Joint Stock Company

97,825 510,514 0.19

FMC Sao Ta Foods Joint Stock Company 564,963 772,797 0.73

CMX Ca Mau Frozen Seafood Processing

Import Export Corporation

564,311

727,743 0.78

BLF Bac Lieu Fisheries Joint Stock Company 328,241 412,489 0.79

MPC Minh Phu Seafood Joint Stock Company 5,262,669 6,642,665 0.79

ATA NTACO Joint Stock Company 601,089 755,795 0.8

VNH Viet Nhat Seafood Corporation 52,020 127,228 0.41

VHC Vinh Hoan Corporation 1,915,282 3,395,960 0.56

AAM Mekong Fisheries Joint Stock Company 35,274 291,067 0.12

ICF Investment Commerce Fisheries

Corporation

224,055 399,110 0.56

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 17 of 29

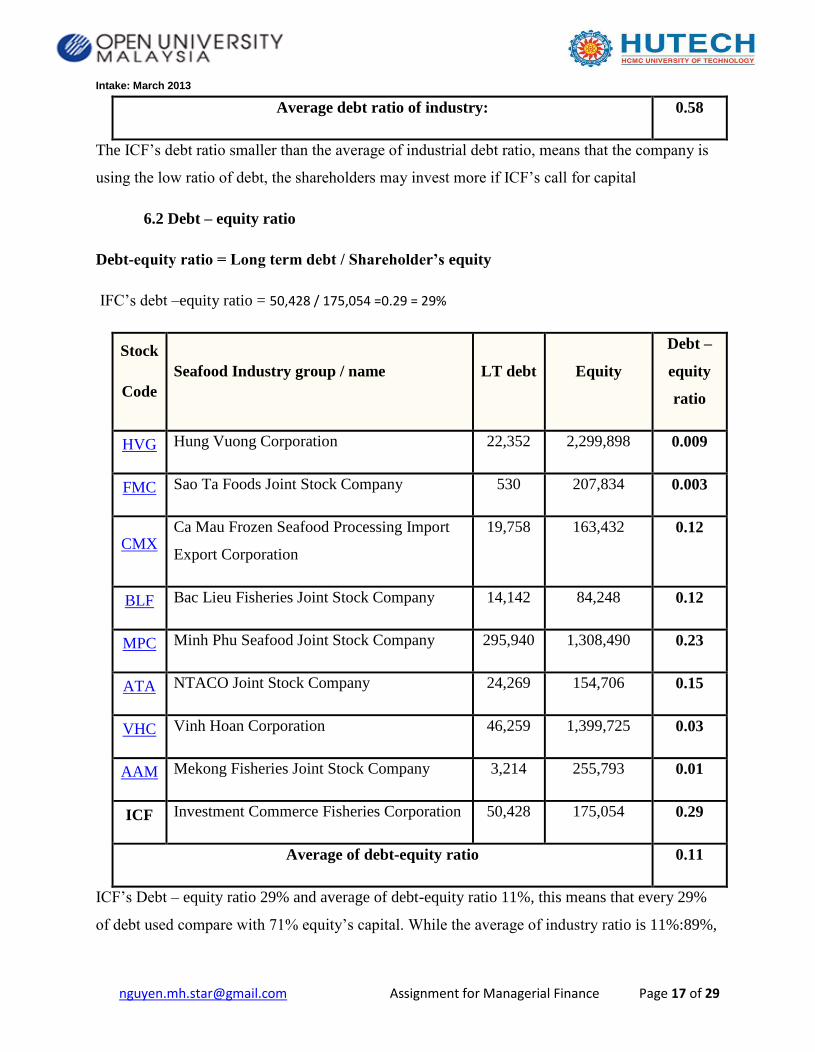

Average debt ratio of industry: 0.58

The ICF’s debt ratio smaller than the average of industrial debt ratio, means that the company is

using the low ratio of debt, the shareholders may invest more if ICF’s call for capital

6.2 Debt – equity ratio

Debt-equity ratio = Long term debt / Shareholder’s equity

IFC’s debt –equity ratio = 50,428 / 175,054 =0.29 = 29%

Stock

Code

Seafood Industry group / name LT debt Equity

Debt –

equity

ratio

HVG Hung Vuong Corporation 22,352 2,299,898 0.009

FMC Sao Ta Foods Joint Stock Company 530 207,834 0.003

CMX Ca Mau Frozen Seafood Processing Import

Export Corporation

19,758 163,432 0.12

BLF Bac Lieu Fisheries Joint Stock Company 14,142 84,248 0.12

MPC Minh Phu Seafood Joint Stock Company 295,940 1,308,490 0.23

ATA NTACO Joint Stock Company 24,269 154,706 0.15

VHC Vinh Hoan Corporation 46,259 1,399,725 0.03

AAM Mekong Fisheries Joint Stock Company 3,214 255,793 0.01

ICF Investment Commerce Fisheries Corporation 50,428 175,054 0.29

Average of debt-equity ratio 0.11

ICF’s Debt – equity ratio 29% and average of debt-equity ratio 11%, this means that every 29%

of debt used compare with 71% equity’s capital. While the average of industry ratio is 11%:89%,

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 18 of 29

ICF’s debt ratio higher than the industry, ICF denpendent on dept higher than the company in the

same industry.

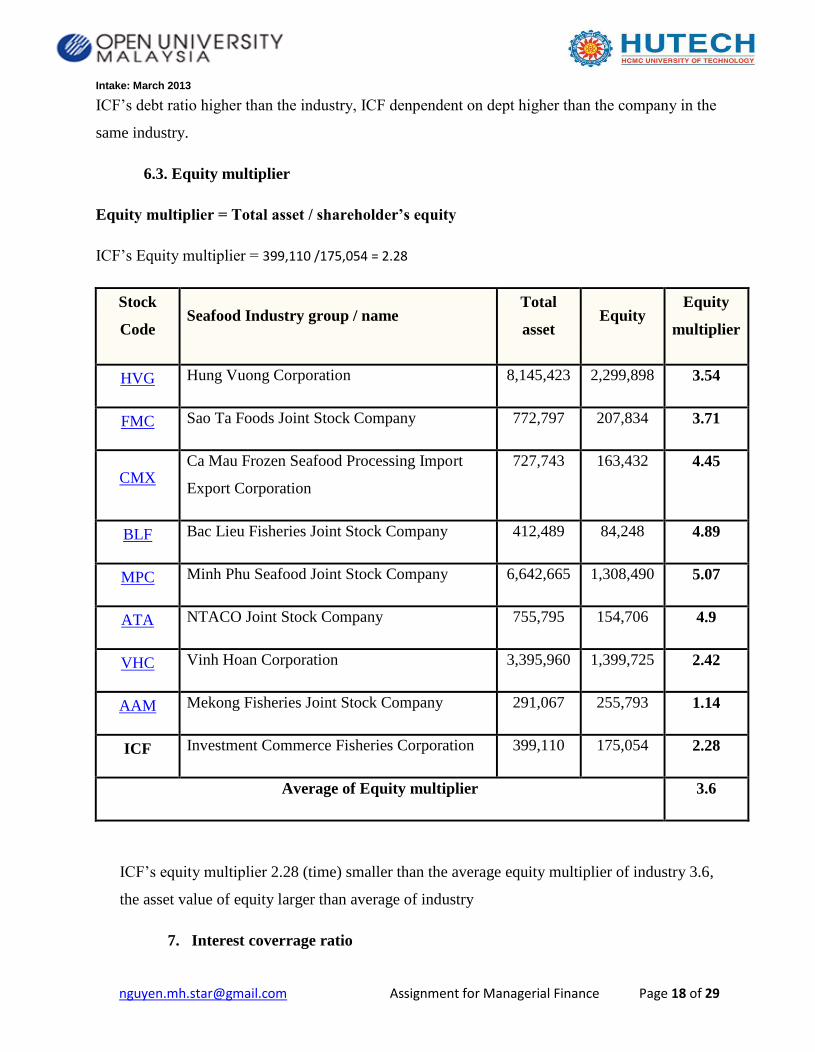

6.3. Equity multiplier

Equity multiplier = Total asset / shareholder’s equity

ICF’s Equity multiplier = 399,110 /175,054 = 2.28

Stock

Code Seafood Industry group / name

Total

asset Equity

Equity

multiplier

HVG Hung Vuong Corporation 8,145,423 2,299,898 3.54

FMC Sao Ta Foods Joint Stock Company 772,797 207,834 3.71

CMX Ca Mau Frozen Seafood Processing Import

Export Corporation

727,743 163,432 4.45

BLF Bac Lieu Fisheries Joint Stock Company 412,489 84,248 4.89

MPC Minh Phu Seafood Joint Stock Company 6,642,665 1,308,490 5.07

ATA NTACO Joint Stock Company 755,795 154,706 4.9

VHC Vinh Hoan Corporation 3,395,960 1,399,725 2.42

AAM Mekong Fisheries Joint Stock Company 291,067 255,793 1.14

ICF Investment Commerce Fisheries Corporation 399,110 175,054 2.28

Average of Equity multiplier 3.6

ICF’s equity multiplier 2.28 (time) smaller than the average equity multiplier of industry 3.6,

the asset value of equity larger than average of industry

7. Interest coverrage ratio

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 19 of 29

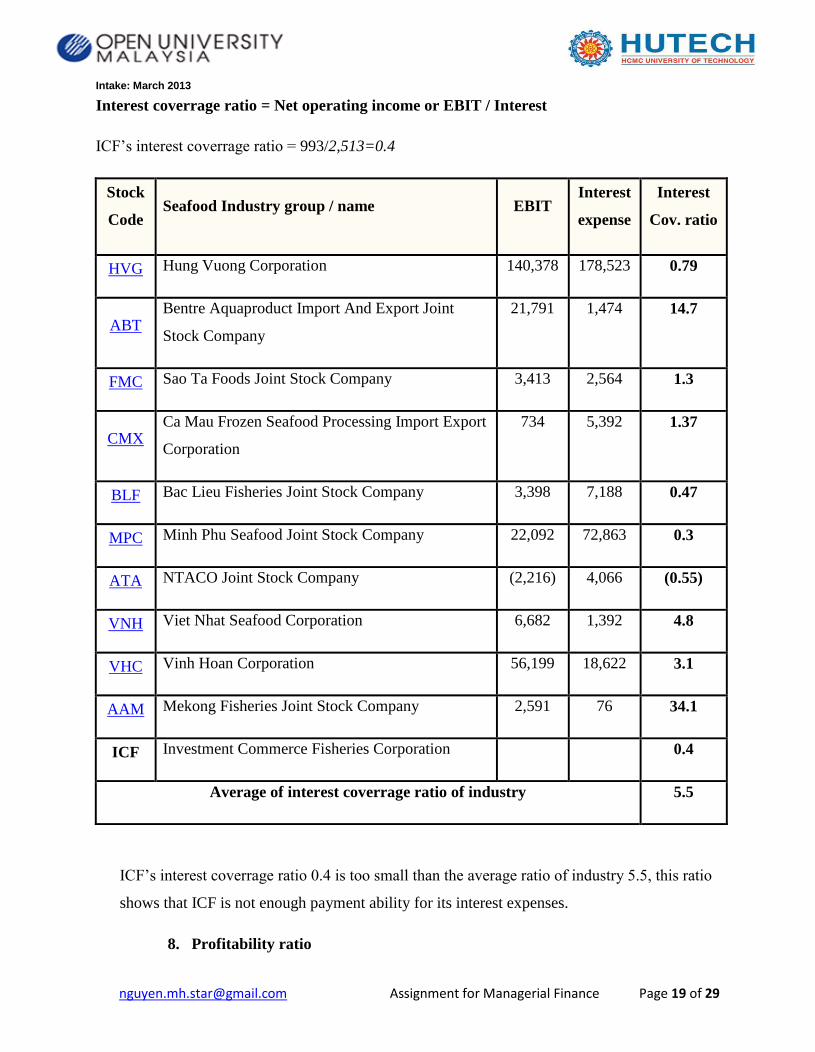

Interest coverrage ratio = Net operating income or EBIT / Interest

ICF’s interest coverrage ratio = 993/2,513=0.4

Stock

Code Seafood Industry group / name EBIT

Interest

expense

Interest

Cov. ratio

HVG Hung Vuong Corporation 140,378 178,523 0.79

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

21,791 1,474 14.7

FMC Sao Ta Foods Joint Stock Company 3,413 2,564 1.3

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

734 5,392 1.37

BLF Bac Lieu Fisheries Joint Stock Company 3,398 7,188 0.47

MPC Minh Phu Seafood Joint Stock Company 22,092 72,863 0.3

ATA NTACO Joint Stock Company (2,216) 4,066 (0.55)

VNH Viet Nhat Seafood Corporation 6,682 1,392 4.8

VHC Vinh Hoan Corporation 56,199 18,622 3.1

AAM Mekong Fisheries Joint Stock Company 2,591 76 34.1

ICF Investment Commerce Fisheries Corporation 0.4

Average of interest coverrage ratio of industry 5.5

ICF’s interest coverrage ratio 0.4 is too small than the average ratio of industry 5.5, this ratio

shows that ICF is not enough payment ability for its interest expenses.

8. Profitability ratio

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 20 of 29

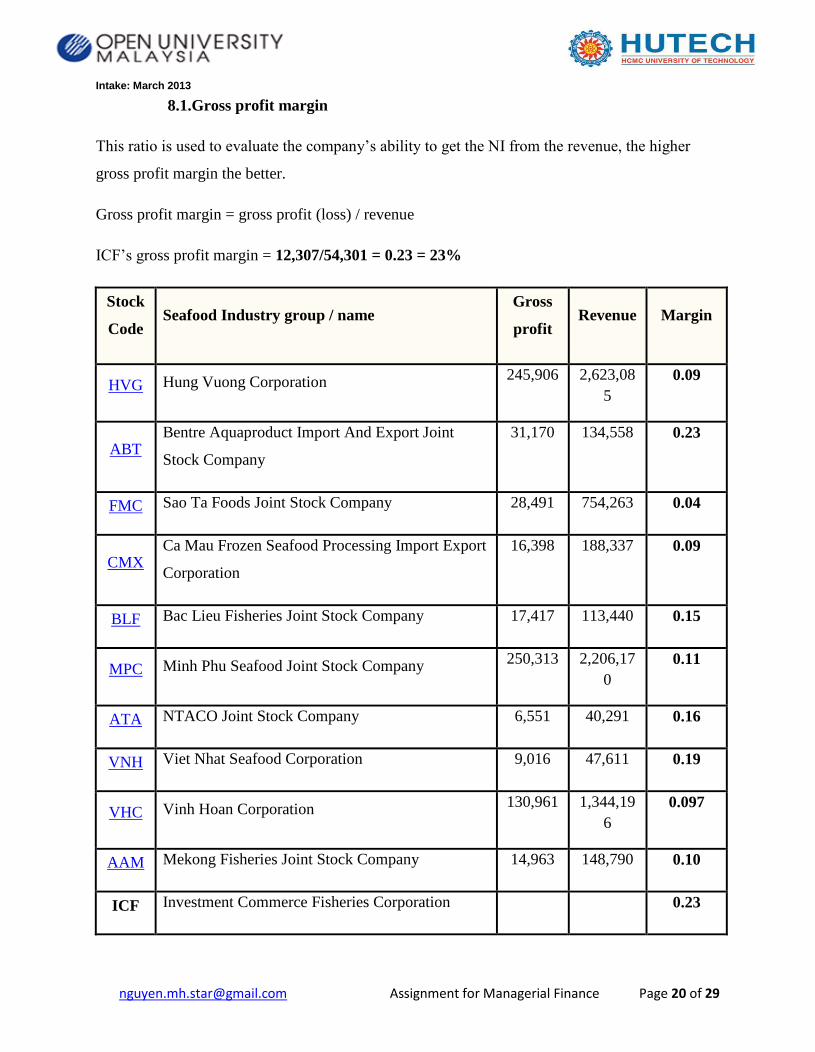

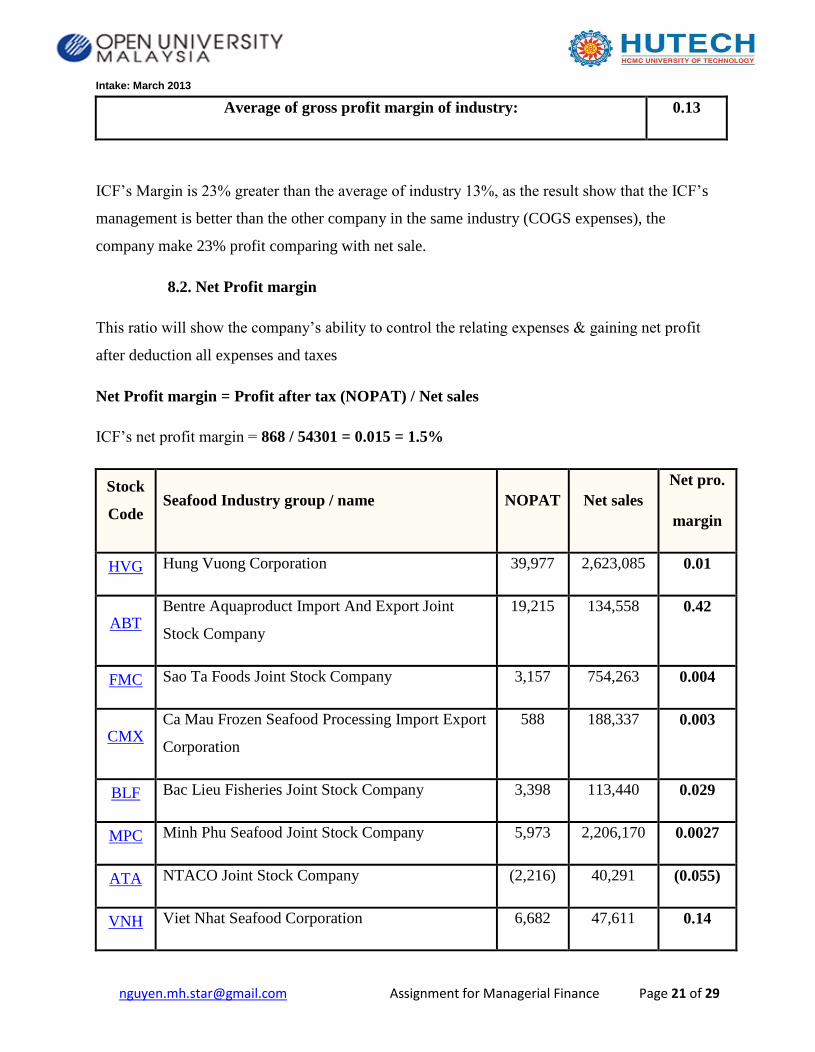

8.1.Gross profit margin

This ratio is used to evaluate the company’s ability to get the NI from the revenue, the higher

gross profit margin the better.

Gross profit margin = gross profit (loss) / revenue

ICF’s gross profit margin = 12,307/54,301 = 0.23 = 23%

Stock

Code Seafood Industry group / name

Gross

profit Revenue Margin

HVG Hung Vuong Corporation 245,906 2,623,08

5

0.09

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

31,170 134,558 0.23

FMC Sao Ta Foods Joint Stock Company 28,491 754,263 0.04

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

16,398 188,337 0.09

BLF Bac Lieu Fisheries Joint Stock Company 17,417 113,440 0.15

MPC Minh Phu Seafood Joint Stock Company 250,313 2,206,17

0

0.11

ATA NTACO Joint Stock Company 6,551 40,291 0.16

VNH Viet Nhat Seafood Corporation 9,016 47,611 0.19

VHC Vinh Hoan Corporation 130,961 1,344,19

6

0.097

AAM Mekong Fisheries Joint Stock Company 14,963 148,790 0.10

ICF Investment Commerce Fisheries Corporation 0.23

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 21 of 29

Average of gross profit margin of industry: 0.13

ICF’s Margin is 23% greater than the average of industry 13%, as the result show that the ICF’s

management is better than the other company in the same industry (COGS expenses), the

company make 23% profit comparing with net sale.

8.2. Net Profit margin

This ratio will show the company’s ability to control the relating expenses & gaining net profit

after deduction all expenses and taxes

Net Profit margin = Profit after tax (NOPAT) / Net sales

ICF’s net profit margin = 868 / 54301 = 0.015 = 1.5%

Stock

Code Seafood Industry group / name NOPAT Net sales

Net pro.

margin

HVG Hung Vuong Corporation 39,977 2,623,085 0.01

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

19,215 134,558 0.42

FMC Sao Ta Foods Joint Stock Company 3,157 754,263 0.004

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

588 188,337 0.003

BLF Bac Lieu Fisheries Joint Stock Company 3,398 113,440 0.029

MPC Minh Phu Seafood Joint Stock Company 5,973 2,206,170 0.0027

ATA NTACO Joint Stock Company (2,216) 40,291 (0.055)

VNH Viet Nhat Seafood Corporation 6,682 47,611 0.14

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 22 of 29

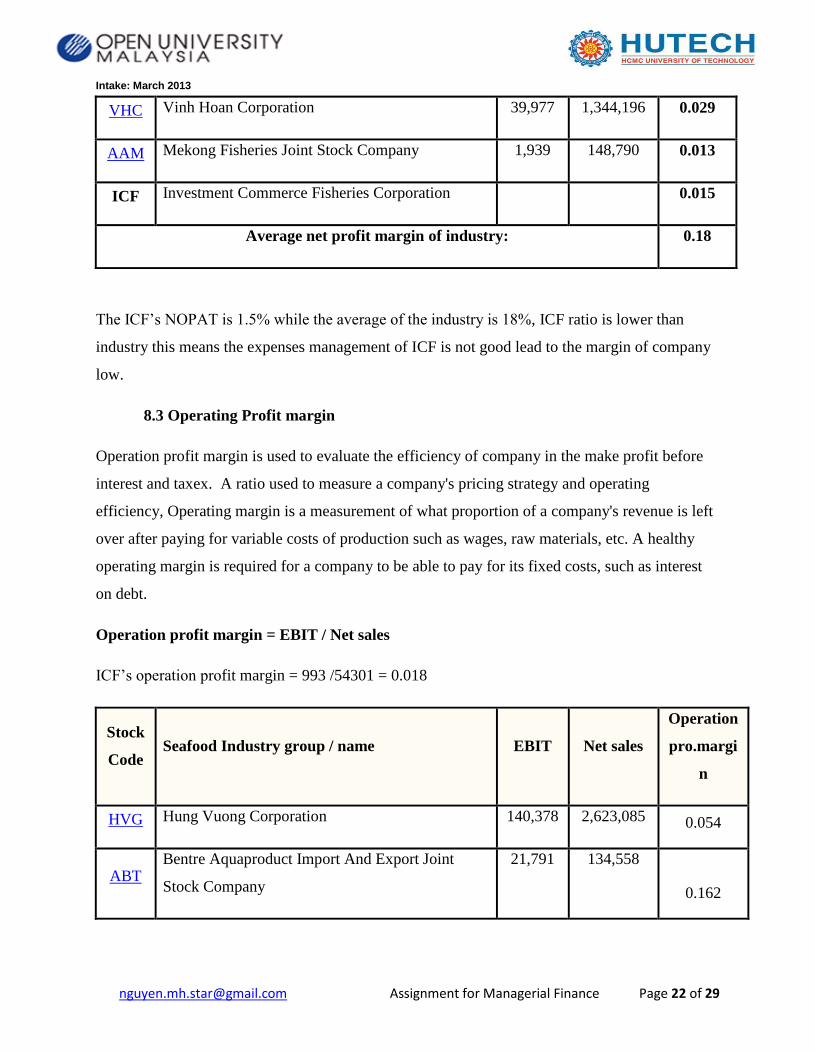

VHC Vinh Hoan Corporation 39,977 1,344,196 0.029

AAM Mekong Fisheries Joint Stock Company 1,939 148,790 0.013

ICF Investment Commerce Fisheries Corporation 0.015

Average net profit margin of industry: 0.18

The ICF’s NOPAT is 1.5% while the average of the industry is 18%, ICF ratio is lower than

industry this means the expenses management of ICF is not good lead to the margin of company

low.

8.3 Operating Profit margin

Operation profit margin is used to evaluate the efficiency of company in the make profit before

interest and taxex. A ratio used to measure a company's pricing strategy and operating

efficiency, Operating margin is a measurement of what proportion of a company's revenue is left

over after paying for variable costs of production such as wages, raw materials, etc. A healthy

operating margin is required for a company to be able to pay for its fixed costs, such as interest

on debt.

Operation profit margin = EBIT / Net sales

ICF’s operation profit margin = 993 /54301 = 0.018

Stock

Code Seafood Industry group / name EBIT Net sales

Operation

pro.margi

n

HVG Hung Vuong Corporation 140,378 2,623,085 0.054

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

21,791 134,558

0.162

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 23 of 29

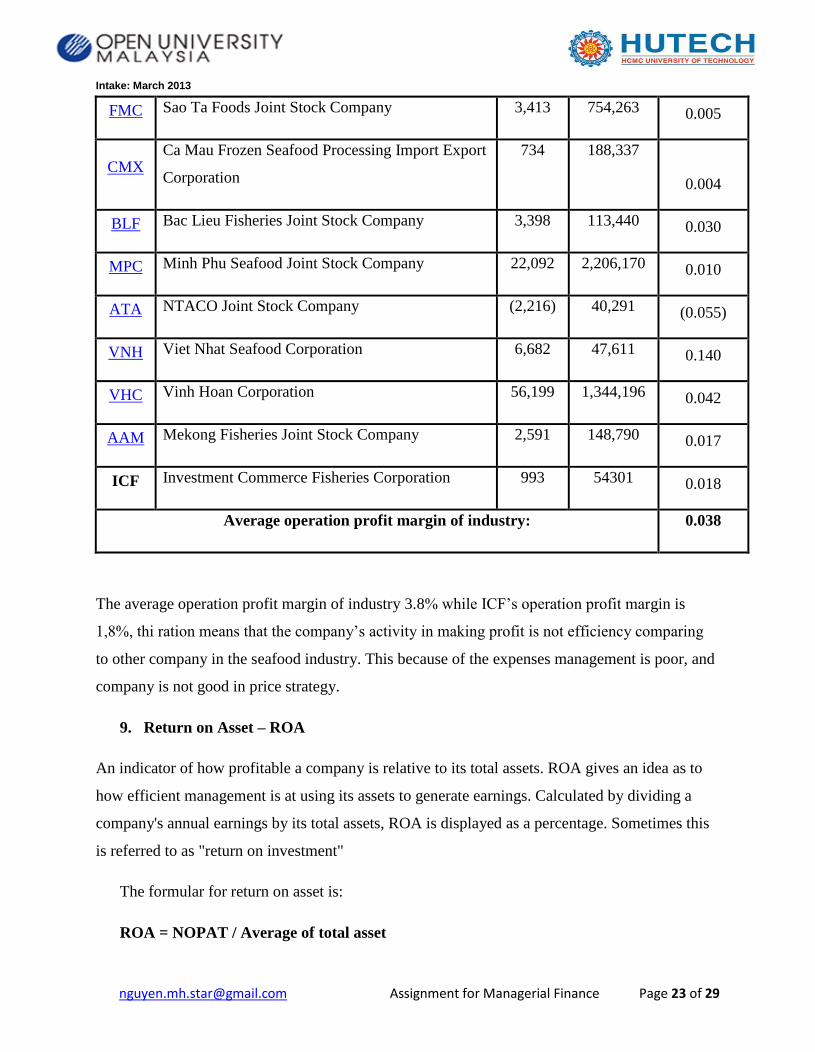

FMC Sao Ta Foods Joint Stock Company 3,413 754,263 0.005

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

734 188,337

0.004

BLF Bac Lieu Fisheries Joint Stock Company 3,398 113,440 0.030

MPC Minh Phu Seafood Joint Stock Company 22,092 2,206,170 0.010

ATA NTACO Joint Stock Company (2,216) 40,291 (0.055)

VNH Viet Nhat Seafood Corporation 6,682 47,611 0.140

VHC Vinh Hoan Corporation 56,199 1,344,196 0.042

AAM Mekong Fisheries Joint Stock Company 2,591 148,790 0.017

ICF Investment Commerce Fisheries Corporation 993 54301 0.018

Average operation profit margin of industry: 0.038

The average operation profit margin of industry 3.8% while ICF’s operation profit margin is

1,8%, thi ration means that the company’s activity in making profit is not efficiency comparing

to other company in the seafood industry. This because of the expenses management is poor, and

company is not good in price strategy.

9. Return on Asset – ROA

An indicator of how profitable a company is relative to its total assets. ROA gives an idea as to

how efficient management is at using its assets to generate earnings. Calculated by dividing a

company's annual earnings by its total assets, ROA is displayed as a percentage. Sometimes this

is referred to as "return on investment"

The formular for return on asset is:

ROA = NOPAT / Average of total asset

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 24 of 29

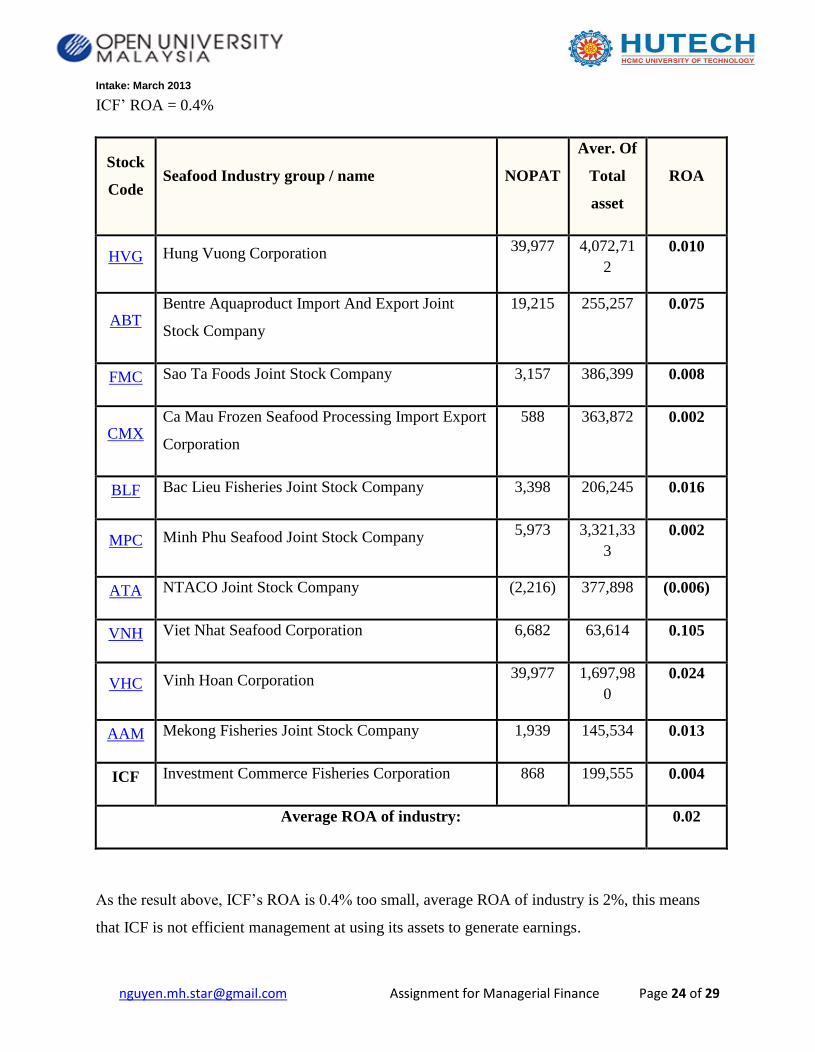

ICF’ ROA = 0.4%

Stock

Code Seafood Industry group / name NOPAT

Aver. Of

Total

asset

ROA

HVG Hung Vuong Corporation 39,977 4,072,71

2

0.010

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

19,215 255,257 0.075

FMC Sao Ta Foods Joint Stock Company 3,157 386,399 0.008

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

588 363,872 0.002

BLF Bac Lieu Fisheries Joint Stock Company 3,398 206,245 0.016

MPC Minh Phu Seafood Joint Stock Company 5,973 3,321,33

3

0.002

ATA NTACO Joint Stock Company (2,216) 377,898 (0.006)

VNH Viet Nhat Seafood Corporation 6,682 63,614 0.105

VHC Vinh Hoan Corporation 39,977 1,697,98

0

0.024

AAM Mekong Fisheries Joint Stock Company 1,939 145,534 0.013

ICF Investment Commerce Fisheries Corporation 868 199,555 0.004

Average ROA of industry: 0.02

As the result above, ICF’s ROA is 0.4% too small, average ROA of industry is 2%, this means

that ICF is not efficient management at using its assets to generate earnings.

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 25 of 29

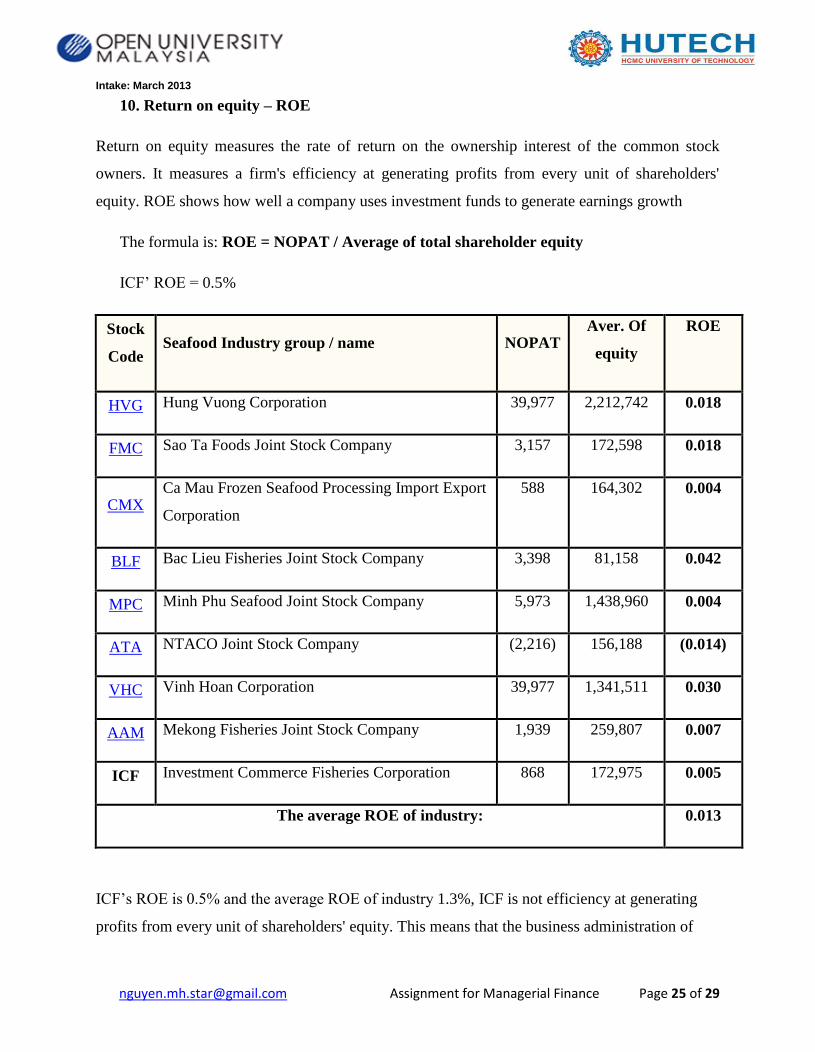

10. Return on equity – ROE

Return on equity measures the rate of return on the ownership interest of the common stock

owners. It measures a firm's efficiency at generating profits from every unit of shareholders'

equity. ROE shows how well a company uses investment funds to generate earnings growth

The formula is: ROE = NOPAT / Average of total shareholder equity

ICF’ ROE = 0.5%

Stock

Code Seafood Industry group / name NOPAT

Aver. Of

equity

ROE

HVG Hung Vuong Corporation 39,977 2,212,742 0.018

FMC Sao Ta Foods Joint Stock Company 3,157 172,598 0.018

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

588 164,302 0.004

BLF Bac Lieu Fisheries Joint Stock Company 3,398 81,158 0.042

MPC Minh Phu Seafood Joint Stock Company 5,973 1,438,960 0.004

ATA NTACO Joint Stock Company (2,216) 156,188 (0.014)

VHC Vinh Hoan Corporation 39,977 1,341,511 0.030

AAM Mekong Fisheries Joint Stock Company 1,939 259,807 0.007

ICF Investment Commerce Fisheries Corporation 868 172,975 0.005

The average ROE of industry: 0.013

ICF’s ROE is 0.5% and the average ROE of industry 1.3%, ICF is not efficiency at generating

profits from every unit of shareholders' equity. This means that the business administration of

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 26 of 29

IFC is not better than the other company in seafood industry.

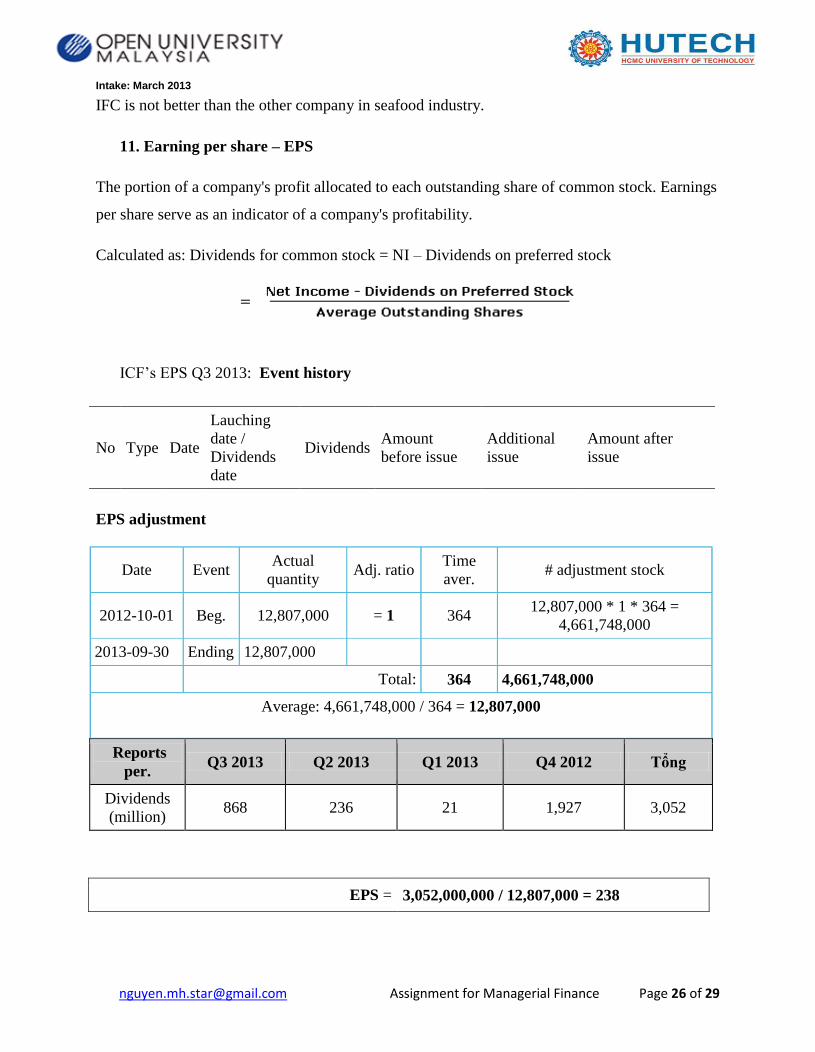

11. Earning per share – EPS

The portion of a company's profit allocated to each outstanding share of common stock. Earnings

per share serve as an indicator of a company's profitability.

Calculated as: Dividends for common stock = NI – Dividends on preferred stock

ICF’s EPS Q3 2013: Event history

No Type Date

Lauching

date /

Dividends

date

Dividends Amount

before issue

Additional

issue

Amount after

issue

EPS adjustment

Date Event Actual

quantity Adj. ratio

Time

aver. # adjustment stock

2012-10-01 Beg. 12,807,000 = 1 364 12,807,000 * 1 * 364 =

4,661,748,000

2013-09-30 Ending 12,807,000

Total: 364 4,661,748,000

Average: 4,661,748,000 / 364 = 12,807,000

Reports

per. Q3 2013 Q2 2013 Q1 2013 Q4 2012 Tổng

Dividends

(million) 868 236 21 1,927 3,052

EPS = 3,052,000,000 / 12,807,000 = 238

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 27 of 29

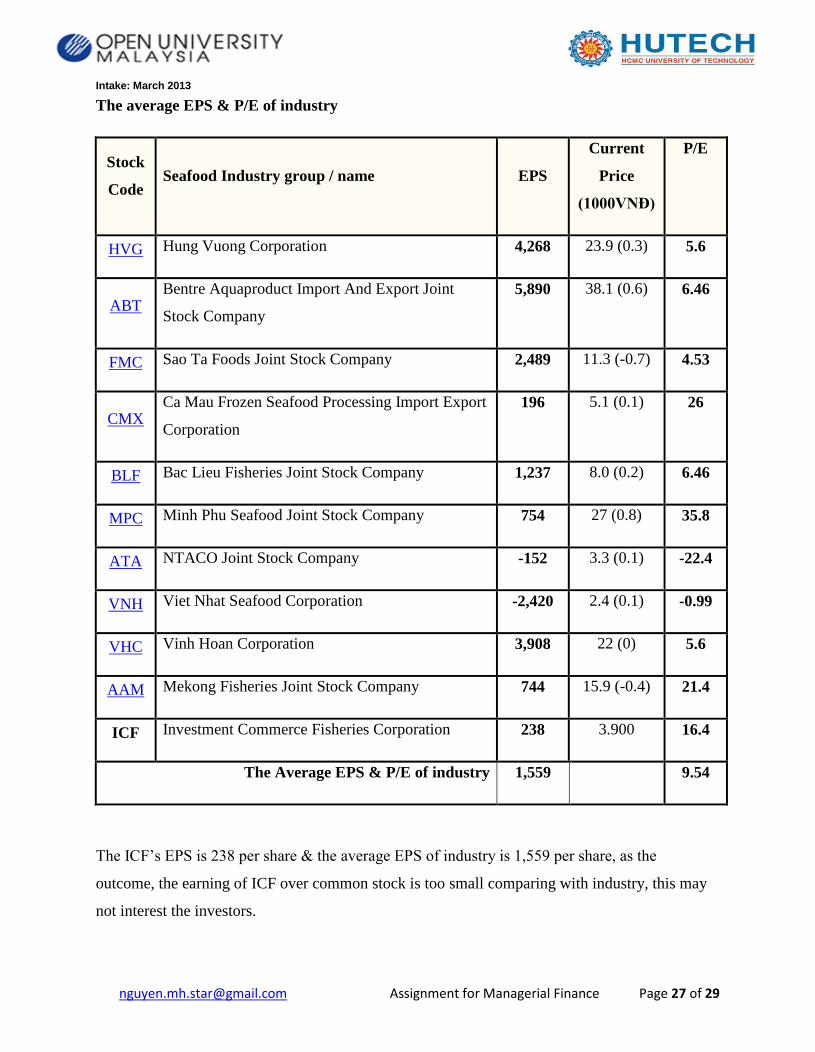

The average EPS & P/E of industry

Stock

Code Seafood Industry group / name EPS

Current

Price

(1000VNĐ)

P/E

HVG Hung Vuong Corporation 4,268 23.9 (0.3) 5.6

ABT Bentre Aquaproduct Import And Export Joint

Stock Company

5,890 38.1 (0.6) 6.46

FMC Sao Ta Foods Joint Stock Company 2,489 11.3 (-0.7) 4.53

CMX Ca Mau Frozen Seafood Processing Import Export

Corporation

196 5.1 (0.1) 26

BLF Bac Lieu Fisheries Joint Stock Company 1,237 8.0 (0.2) 6.46

MPC Minh Phu Seafood Joint Stock Company 754 27 (0.8) 35.8

ATA NTACO Joint Stock Company -152 3.3 (0.1) -22.4

VNH Viet Nhat Seafood Corporation -2,420 2.4 (0.1) -0.99

VHC Vinh Hoan Corporation 3,908 22 (0) 5.6

AAM Mekong Fisheries Joint Stock Company 744 15.9 (-0.4) 21.4

ICF Investment Commerce Fisheries Corporation 238 3.900 16.4

The Average EPS & P/E of industry 1,559 9.54

The ICF’s EPS is 238 per share & the average EPS of industry is 1,559 per share, as the

outcome, the earning of ICF over common stock is too small comparing with industry, this may

not interest the investors.

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 28 of 29

12. Price earning ratio – P/E

The price-to-earnings ratio, or P–E ratio, or P/E ratio, is an equity valuation multiple. It is

defined as market price per share divided by annual earnings per share.

P/E =Current price / EPS

ICF’s P/E = 3900/238 = 16.4

The average P/E of industry is 9.54

As the outcome above, the investor may accept to pay 16.4 times for every share of ICF higher

than other company in the same industry (9.54 times).

IV. CONCLUSION AND POLICY IMPLICATIONS

Based on the analysis of ICF, I have my conclution about the company business situation; ICF

have not built the stable exporting market yet, ICF is heavily influenced by the anti-dumping

lawsuit seafood export to the U.S market. ICF also have been not maintaining the stability export

to other major market such as Japan & EU market.

ICF is not completely proactive about the raw materials, purchased power dependent on directly

purchases and/or imported. All the above elements & factors lead to the revenue and profits over

the years are low, and the other reason is due to the processing plants not operating at full

capacity leading to costly inefficiencis & increasing costs.

This analysis is generated & performed based on the financial statement of Incomfish company

and other truth sources, however I do not guarantee that all information & database is completely

sufficient and/or arcurately 100 percent, so this analysis purpose for case study & reference

source for whom intending to invest into this security.

Intake: March 2013

[email protected] Assignment for Managerial Finance Page 29 of 29

References sources:

Lecture of Dr. Phan Dinh Nguyen Faculty of Accounting, Banking and Finance, HUTECH

University

Financial Management Theory and Practice, authors Eugene F. Brigham University of Florida,

Michael C. Ehrharrdt University of Tennessee.

http://www.cophieu68.vn/profilesymbol.php?id=icf

http://s.cafef.vn/hose/ICF-cong-ty-co-phan-dau-tu-thuong-mai-thuy-san.chn

http://www.vcbs.com.vn/en/Research/Company.aspx?subTab=2&stock_symbol=ICF

http://www.dnb.com/customer-service/understanding-financial-statements.html