Embed Size (px)

Citation preview

October 4, 2018

Orient Paper & Industries Ltd.

Growth catalysts in place; rerating potential…

CMP INR 43 Target INR 57 Initiating Coverage –BUY

SKP Securities Ltd www.skpsecurities.com Page 1 of 26

Key Share Data

Face Value (INR) 1.0

Equity Capital (INR Mn) 212.2

Market Cap (INR Mn) 9,124.4

52 Week High/Low (INR) 62/25

6 months Avg. Daily Volume (NSE) 763,091

BSE Code 502420

NSE Code ORIENTPPR

Reuters Code ORPP.NS

Bloomberg Code OPI:IN

Shareholding Pattern (as on June 2018)

39%

21%

40%Promoter

FII/MF

Puiblic & Other

Source: Company

Particulars FY17 FY18 FY19E FY20E

Net Sales 5,114.9 6,613.6 6,838.6 7,613.0

Growth (%) 29.3% 3.4% 11.3%

EBITDA 315.4 1,118.8 1,354.0 1,583.5

PAT 108.8 492.9 941.3 1,011.4

Growth (%) 353.2% 91.0% 7.4%

EPS (INR) 0.5 2.3 4.4 4.8

BVPS (INR) 59.1 62.1 65.6 69.4

Key Financials (INR Million)

Particulars FY17 FY18 FY19E FY20E

P/E (x) 129.1 13.3 9.7 9.0

P/BVPS (x) 1.2 0.5 0.7 0.6

Mcap/Sales (x) 2.7 1.0 1.3 1.2

EV/EBITDA (x) 50.1 6.1 6.8 6.0

ROCE (%) 0.5% 6.0% 7.3% 8.3%

ROE (%) 0.9% 3.7% 6.8% 6.9%

EBITDA Mar (%) 6.2% 16.9% 19.8% 20.8%

PAT Mar (%) 2.1% 7.5% 13.8% 13.3%

Debt - Equity (x) 0.1 0.1 0.0 0.1

Key Financials Ratios

Source: Company, SKP Research

1 Yr price performance OPIL; vis-à-vis BSE Mid Cap

-50%

0%

50%

100%

28

-Sep

-17

26

-Oct-

17

23

-Nov-1

7

21

-Dec-1

7

18

-Ja

n-1

8

15

-Fe

b-1

8

15

-Ma

r-1

8

12

-Apr-

18

10

-Ma

y-…

7-J

un

-18

5-J

ul-

18

2-A

ug-1

8

30

-Aug

-18

27

-Sep

-18

OPIL BSE MID Cap

Company Background

Orient Paper and Industries Limited (Orient Paper), promoted by CK Birla Group, is India’s largest manufacturer and exporter of tissue paper with ~17% domestic market share. Its integrated manufacturing facility is located at Amlai in Madhya Pradesh (MP) having a total installed paper capacity of 100,000 MTPA viz. 50,000 MTPA each of Tissue and Writing & Printing (W&P) Paper. It also has 72,500 MTPA of pulp capacity and a 55 MW captive power plant. It also has 36,000 MTPA capacity of Caustic Soda, contributing ~18% to revenue. Vide a process of sequential demergers, its erstwhile cement and consumer durables businesses are now parts of two separate listed entities. Investment Rationale

India’s largest tissue paper producer; buoyant demand puts Orient in a sweet spot India is expected to emerge as the fastest-growing paper market, growing at a rate of

~7% per annum. The Indian tissue paper market is relatively small (1% of total global demand) but has been recording double-digit growth on the back of increasing hygiene awareness and rising disposable income. In addition there is a good demand for quality tissue paper in global markets where Indian tissue paper industry has demonstrated its ability to provide desired quality at competitive prices.

Orient Paper enjoys a first mover advantage in the tissue paper segment having ventured in it in 1997 by setting up 10,000 MTPA capacity, when the total tissue paper industry size was only 5,000 MTPA. This was expanded to 25,000 MTPA in FY10 and currently is 50,000 MTPA, making it the largest tissue paper player in the country.

The Company has an edge over its peers in tissue paper segment as existing tissue paper players are not able to ramp up capacity and key domestic paper producers are yet to enter this segment. Therefore, absence of competition in the domestic market and sprawling export opportunity (Middle East and newer markets such as South Africa, Australia, Zimbabwe, Tanzania, and Ghana) puts Orient Paper in a sweet spot.

Pulp capex will lead to raw material security and an additional tissue capacity To eliminate its dependency on the more expensive market pulp (<10% of total pulp

requirement at >50% higher cost than own manufacturing), Orient Paper has planned to increase its pulp capacity from 72,500 MTPA to 100,000 MTPA at a cost of Rs 450 mn. It is also setting up a new recovery boiler at a cost of ~Rs 1.65 bn and upgrading its pulp capacity to become ECF (elemental chlorine free) complaint at a cost of ~Rs 150 mn. The proposed capex will be commissioned by Q3FY20 and will be funded majorly through internal accruals and marginal borrowings. Post expansion the enhanced pulp capacity will support paper production of 120,000-125,000 MTPA as against current paper capacity of 100,000 MTPA.

To augment its enhanced pulp capacity of 100,000 MTPA, surplus power (>15 MW) and huge land bank at M.P, Orient Paper may take up brownfield tissue paper expansion of ~20,000 MTPA as its existing tissue capacity is expected to reach optimum utilization in few years. This expansion can be done at minimal incremental cost and will take approx 1.5 years to get commissioned.

Strong entry barriers restricting entry of new players in the industry Strong entry barriers like huge capital outlay, high gestation period of ~24-30 months

including requisite environmental clearances, availability of land & water, cost of upgrading technology regularly, growing wood plantations, establishing a distribution network and high energy cost, augurs well for Orient Paper.

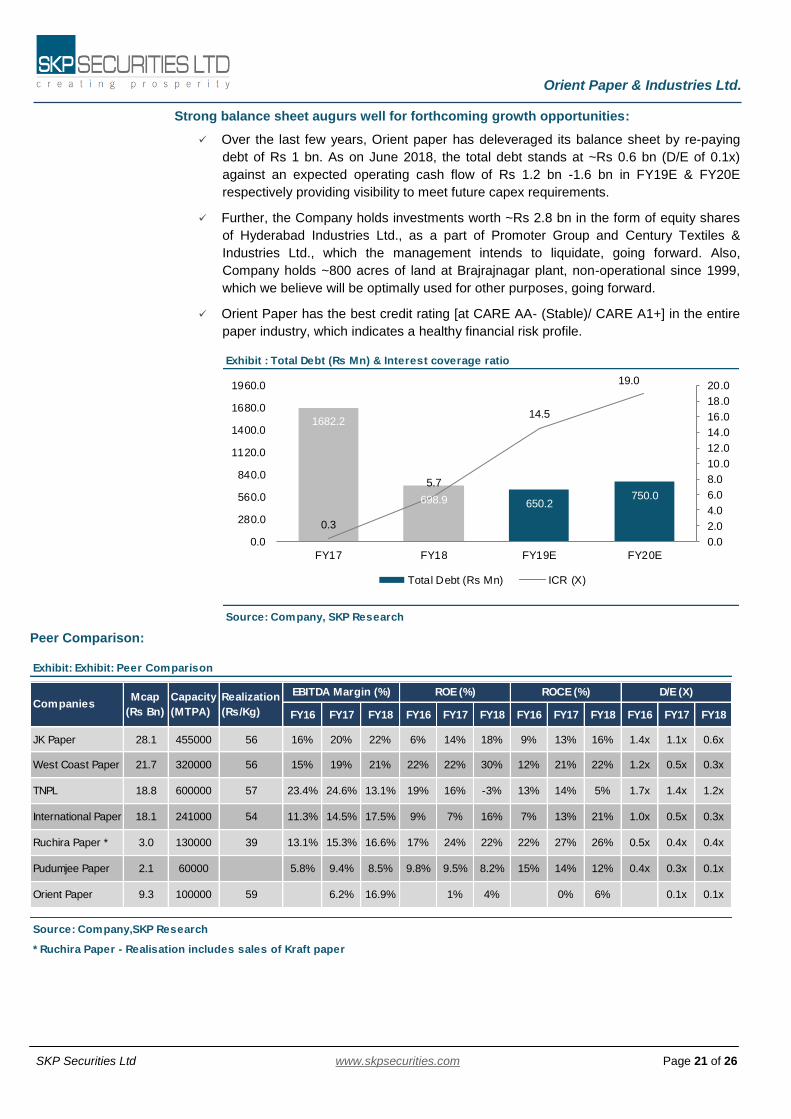

Balance sheet strength bodes well Over last few years, Orient Paper has deleveraged its balance sheet by repaying debt

of Rs 1 bn. As on June 2018, total debt stands at ~Rs 0.6 bn (D/E of 0.1x) against an expected operating cash flow of Rs 1.2-1.6 bn in FY19E & FY20E respectively, providing visibility to meet future capex requirements comfortably.

Further, Orient paper holds investments worth ~Rs 2.8 bn in equity shares of Hyderabad Industries Ltd., as a part of the Promoter Group and Century Textiles & Industries Ltd., in which the management intends to liquidate stake going forward. It also holds ~800 acres of land at its erstwhile plant at Brajrajnagar, closed since 1999, which, we believe, will be used for other purposes going forward.

Valuation Orient Paper has moved up the value chain into tissue paper, which has higher growth

potential and better realizations, leading to a self-sustained model (increasing profitability) backed by favourable demand-supply equilibrium and muted domestic wood prices. Additionally, with internal cost controls and effective management, this business is showing signs of: (1) improvement in utilization (asset turnover), (2) healthy margins, and (3) strong free cash flow generation, providing visibility to comfortably meet future capex requirements and better return ratios.

We have valued the stock on SOTP basis valuing Orient’s core paper business at 7x EV/EBITDA of FY20E and investments (except Brajrajnagar land) at Rs 8/-share. We recommend a BUY on the stock with a target price of Rs 57/- in 15 months, although the long term story looks even better. Any monetization of Brajrajnagar land will trigger an upside potential of Orient Paper profitability and stock price.

Anik Das

Tel No: +91-33-40077020;

Mobile: +91-8017914822

E-mail: [email protected]

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 2 of 26

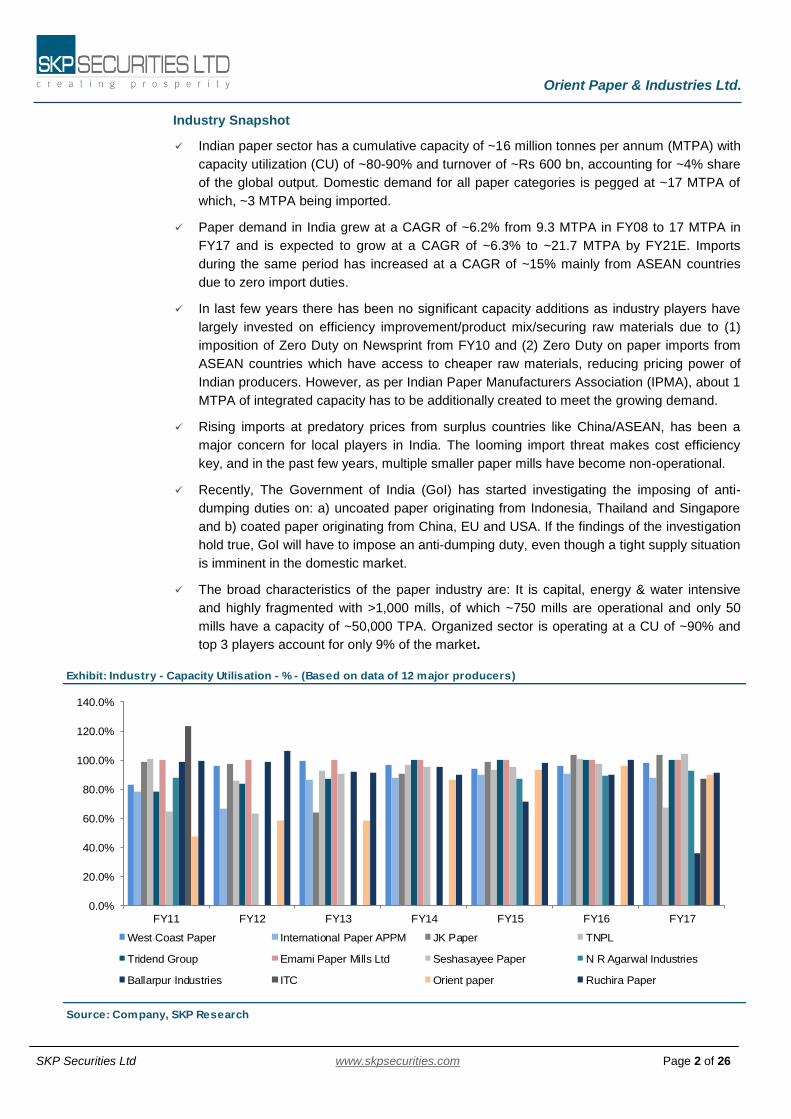

Exhibit: Industry - Capacity Utilisation - % - (Based on data of 12 major producers)

Source: Company, SKP Research

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

FY11 FY12 FY13 FY14 FY15 FY16 FY17

West Coast Paper International Paper APPM JK Paper TNPL

Tridend Group Emami Paper Mills Ltd Seshasayee Paper N R Agarwal Industries

Ballarpur Industries ITC Orient paper Ruchira Paper

Industry Snapshot

Indian paper sector has a cumulative capacity of ~16 million tonnes per annum (MTPA) with

capacity utilization (CU) of ~80-90% and turnover of ~Rs 600 bn, accounting for ~4% share

of the global output. Domestic demand for all paper categories is pegged at ~17 MTPA of

which, ~3 MTPA being imported.

Paper demand in India grew at a CAGR of ~6.2% from 9.3 MTPA in FY08 to 17 MTPA in

FY17 and is expected to grow at a CAGR of ~6.3% to ~21.7 MTPA by FY21E. Imports

during the same period has increased at a CAGR of ~15% mainly from ASEAN countries

due to zero import duties.

In last few years there has been no significant capacity additions as industry players have

largely invested on efficiency improvement/product mix/securing raw materials due to (1)

imposition of Zero Duty on Newsprint from FY10 and (2) Zero Duty on paper imports from

ASEAN countries which have access to cheaper raw materials, reducing pricing power of

Indian producers. However, as per Indian Paper Manufacturers Association (IPMA), about 1

MTPA of integrated capacity has to be additionally created to meet the growing demand.

Rising imports at predatory prices from surplus countries like China/ASEAN, has been a

major concern for local players in India. The looming import threat makes cost efficiency

key, and in the past few years, multiple smaller paper mills have become non-operational.

Recently, The Government of India (GoI) has started investigating the imposing of anti-

dumping duties on: a) uncoated paper originating from Indonesia, Thailand and Singapore

and b) coated paper originating from China, EU and USA. If the findings of the investigation

hold true, GoI will have to impose an anti-dumping duty, even though a tight supply situation

is imminent in the domestic market.

The broad characteristics of the paper industry are: It is capital, energy & water intensive

and highly fragmented with >1,000 mills, of which ~750 mills are operational and only 50

mills have a capacity of ~50,000 TPA. Organized sector is operating at a CU of ~90% and

top 3 players account for only 9% of the market.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 3 of 26

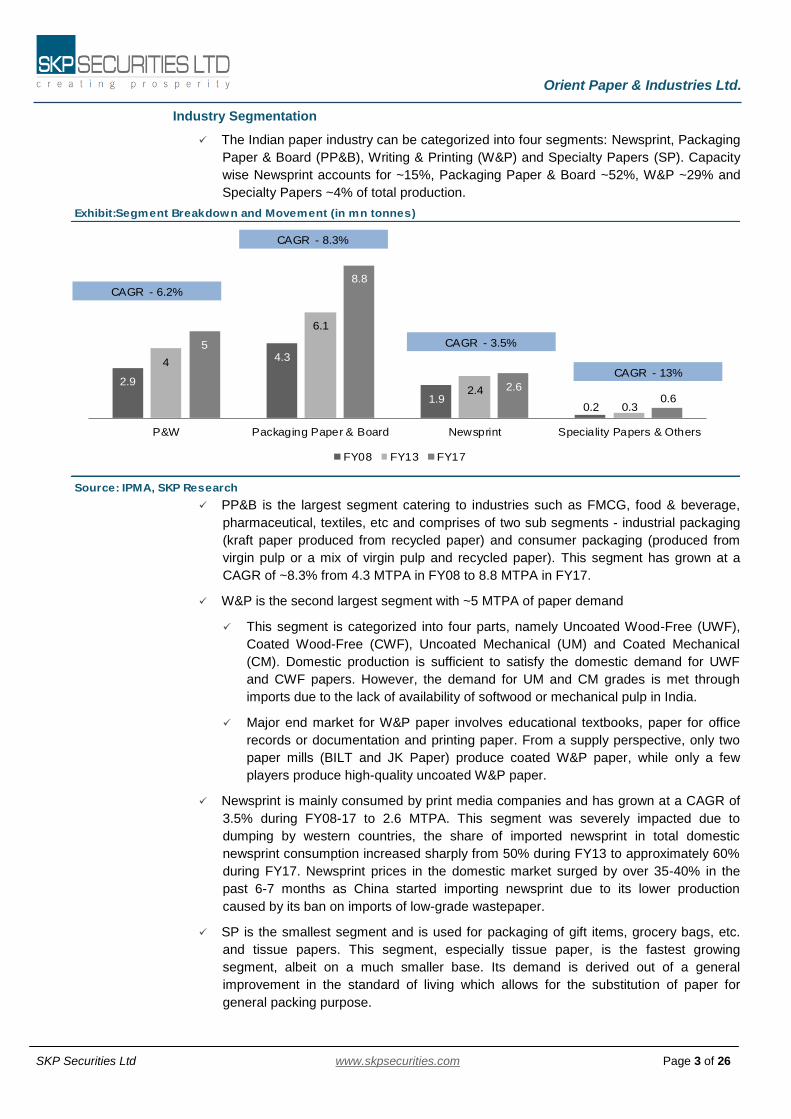

Exhibit:Segment Breakdown and Movement (in mn tonnes)

Source: IPMA, SKP Research

2.9

4.3

1.90.2

4

6.1

2.4

0.3

5

8.8

2.60.6

P&W Packaging Paper & Board Newsprint Speciality Papers & Others

FY08 FY13 FY17

CAGR - 6.2%

CAGR - 8.3%

CAGR - 3.5%

CAGR - 13%

Industry Segmentation

The Indian paper industry can be categorized into four segments: Newsprint, Packaging

Paper & Board (PP&B), Writing & Printing (W&P) and Specialty Papers (SP). Capacity

wise Newsprint accounts for ~15%, Packaging Paper & Board ~52%, W&P ~29% and

Specialty Papers ~4% of total production.

PP&B is the largest segment catering to industries such as FMCG, food & beverage,

pharmaceutical, textiles, etc and comprises of two sub segments - industrial packaging

(kraft paper produced from recycled paper) and consumer packaging (produced from

virgin pulp or a mix of virgin pulp and recycled paper). This segment has grown at a

CAGR of ~8.3% from 4.3 MTPA in FY08 to 8.8 MTPA in FY17.

W&P is the second largest segment with ~5 MTPA of paper demand

This segment is categorized into four parts, namely Uncoated Wood-Free (UWF),

Coated Wood-Free (CWF), Uncoated Mechanical (UM) and Coated Mechanical

(CM). Domestic production is sufficient to satisfy the domestic demand for UWF

and CWF papers. However, the demand for UM and CM grades is met through

imports due to the lack of availability of softwood or mechanical pulp in India.

Major end market for W&P paper involves educational textbooks, paper for office

records or documentation and printing paper. From a supply perspective, only two

paper mills (BILT and JK Paper) produce coated W&P paper, while only a few

players produce high-quality uncoated W&P paper.

Newsprint is mainly consumed by print media companies and has grown at a CAGR of

3.5% during FY08-17 to 2.6 MTPA. This segment was severely impacted due to

dumping by western countries, the share of imported newsprint in total domestic

newsprint consumption increased sharply from 50% during FY13 to approximately 60%

during FY17. Newsprint prices in the domestic market surged by over 35-40% in the

past 6-7 months as China started importing newsprint due to its lower production

caused by its ban on imports of low-grade wastepaper.

SP is the smallest segment and is used for packaging of gift items, grocery bags, etc.

and tissue papers. This segment, especially tissue paper, is the fastest growing

segment, albeit on a much smaller base. Its demand is derived out of a general

improvement in the standard of living which allows for the substitution of paper for

general packing purpose.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 4 of 26

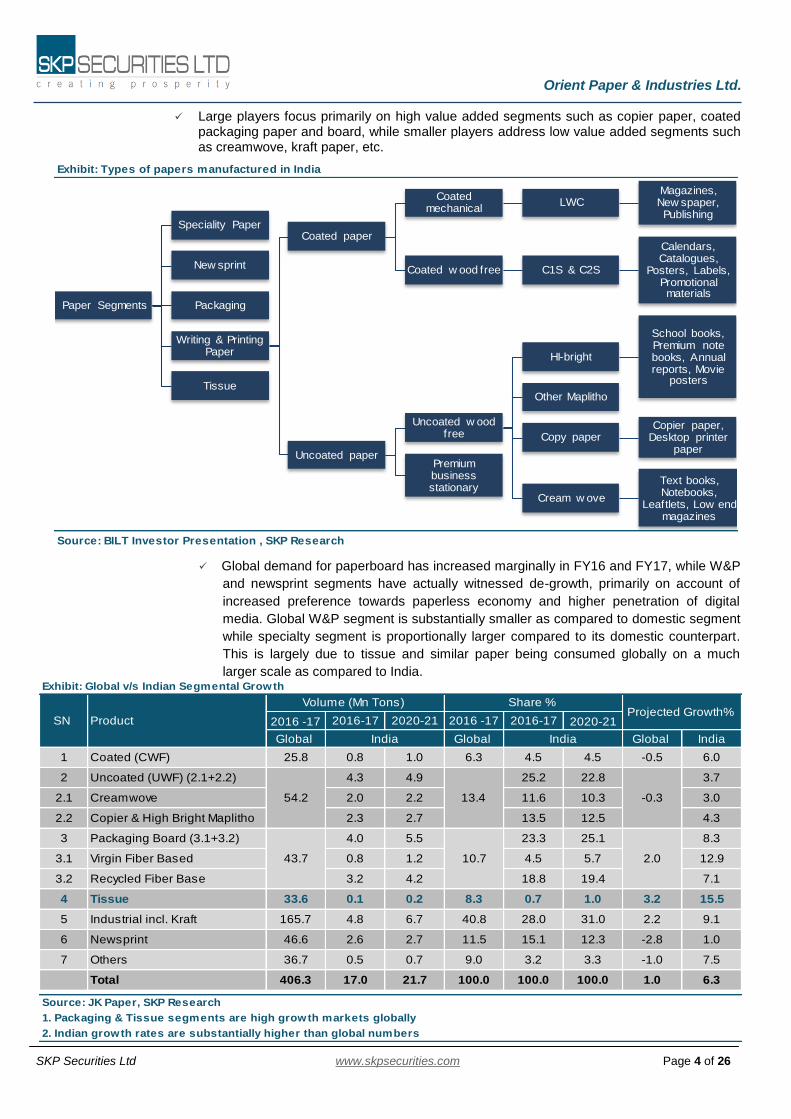

Exhibit: Types of papers manufactured in India

Source: BILT Investor Presentation , SKP Research

Paper Segments

Speciality Paper

New sprint

Packaging

Writing & Printing Paper

Coated paper

Coated mechanical

LWCMagazines, New spaper, Publishing

Coated w ood free C1S & C2S

Calendars, Catalogues,

Posters, Labels, Promotional materials

Uncoated paper

Uncoated w ood free

HI-bright

School books, Premium note books, Annual reports, Movie

posters

Other Maplitho

Copy paperCopier paper,

Desktop printer paper

Cream w ove

Text books, Notebooks,

Leaftlets, Low end magazines

Premium business stationary

Tissue

Large players focus primarily on high value added segments such as copier paper, coated packaging paper and board, while smaller players address low value added segments such as creamwove, kraft paper, etc.

Global demand for paperboard has increased marginally in FY16 and FY17, while W&P

and newsprint segments have actually witnessed de-growth, primarily on account of

increased preference towards paperless economy and higher penetration of digital

media. Global W&P segment is substantially smaller as compared to domestic segment

while specialty segment is proportionally larger compared to its domestic counterpart.

This is largely due to tissue and similar paper being consumed globally on a much

larger scale as compared to India.

Exhibit: Global v/s Indian Segmental Growth

2016 -17 2016-17 2020-21 2016 -17 2016-17 2020-21

Global Global Global India

1 Coated (CWF) 25.8 0.8 1.0 6.3 4.5 4.5 -0.5 6.0

2 Uncoated (UWF) (2.1+2.2) 4.3 4.9 25.2 22.8 3.7

2.1 Creamwove 2.0 2.2 11.6 10.3 3.0

2.2 Copier & High Bright Maplitho 2.3 2.7 13.5 12.5 4.3

3 Packaging Board (3.1+3.2) 4.0 5.5 23.3 25.1 8.3

3.1 Virgin Fiber Based 0.8 1.2 4.5 5.7 12.9

3.2 Recycled Fiber Base 3.2 4.2 18.8 19.4 7.1

4 Tissue 33.6 0.1 0.2 8.3 0.7 1.0 3.2 15.5

5 Industrial incl. Kraft 165.7 4.8 6.7 40.8 28.0 31.0 2.2 9.1

6 Newsprint 46.6 2.6 2.7 11.5 15.1 12.3 -2.8 1.0

7 Others 36.7 0.5 0.7 9.0 3.2 3.3 -1.0 7.5

Total 406.3 17.0 21.7 100.0 100.0 100.0 1.0 6.3

1. Packaging & Tissue segments are high growth markets globally

2. Indian growth rates are substantially higher than global numbers

Projected Growth%

Source: JK Paper, SKP Research

54.2 13.4 -0.3

43.7 10.7 2.0

SN Product

Volume (Mn Tons) Share %

India India

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 5 of 26

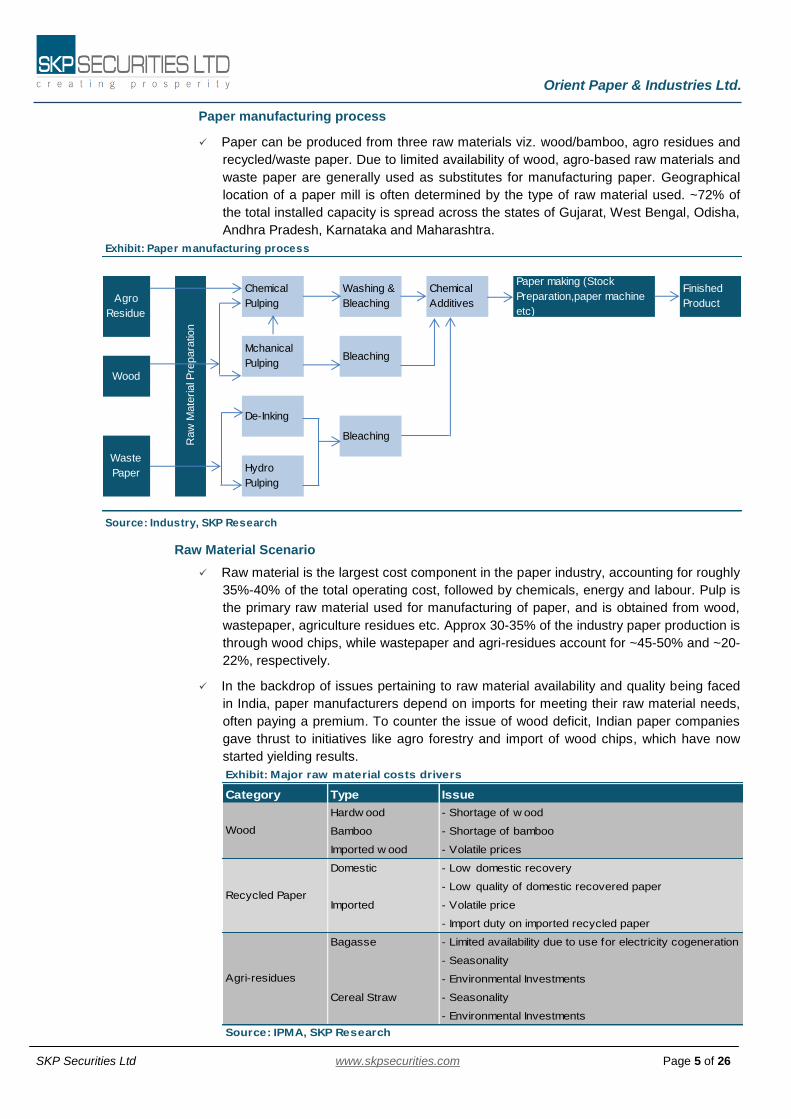

Exhibit: Paper manufacturing process

Source: Industry, SKP Research

De-Inking

Hydro

Pulping

Bleaching

Raw

Mate

rial P

repara

tion

Agro

Residue

Wood

Waste

Paper

Chemical

Pulping

Washing &

Bleaching

Chemical

Additives

Paper making (Stock

Preparation,paper machine

etc)

Finished

Product

Mchanical

PulpingBleaching

Paper manufacturing process

Paper can be produced from three raw materials viz. wood/bamboo, agro residues and

recycled/waste paper. Due to limited availability of wood, agro-based raw materials and

waste paper are generally used as substitutes for manufacturing paper. Geographical

location of a paper mill is often determined by the type of raw material used. ~72% of

the total installed capacity is spread across the states of Gujarat, West Bengal, Odisha,

Andhra Pradesh, Karnataka and Maharashtra.

Raw Material Scenario

Raw material is the largest cost component in the paper industry, accounting for roughly

35%-40% of the total operating cost, followed by chemicals, energy and labour. Pulp is

the primary raw material used for manufacturing of paper, and is obtained from wood,

wastepaper, agriculture residues etc. Approx 30-35% of the industry paper production is

through wood chips, while wastepaper and agri-residues account for ~45-50% and ~20-

22%, respectively.

In the backdrop of issues pertaining to raw material availability and quality being faced

in India, paper manufacturers depend on imports for meeting their raw material needs,

often paying a premium. To counter the issue of wood deficit, Indian paper companies

gave thrust to initiatives like agro forestry and import of wood chips, which have now

started yielding results.

Exhibit: Major raw material costs drivers

Category Type Issue

Hardw ood - Shortage of w ood

Bamboo - Shortage of bamboo

Imported w ood - Volatile prices

Domestic - Low domestic recovery

- Low quality of domestic recovered paper

Imported - Volatile price

- Import duty on imported recycled paper

Bagasse - Limited availability due to use for electricity cogeneration

- Seasonality

- Environmental Investments

Cereal Straw - Seasonality

- Environmental Investments

Source: IPMA, SKP Research

Wood

Recycled Paper

Agri-residues

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 6 of 26

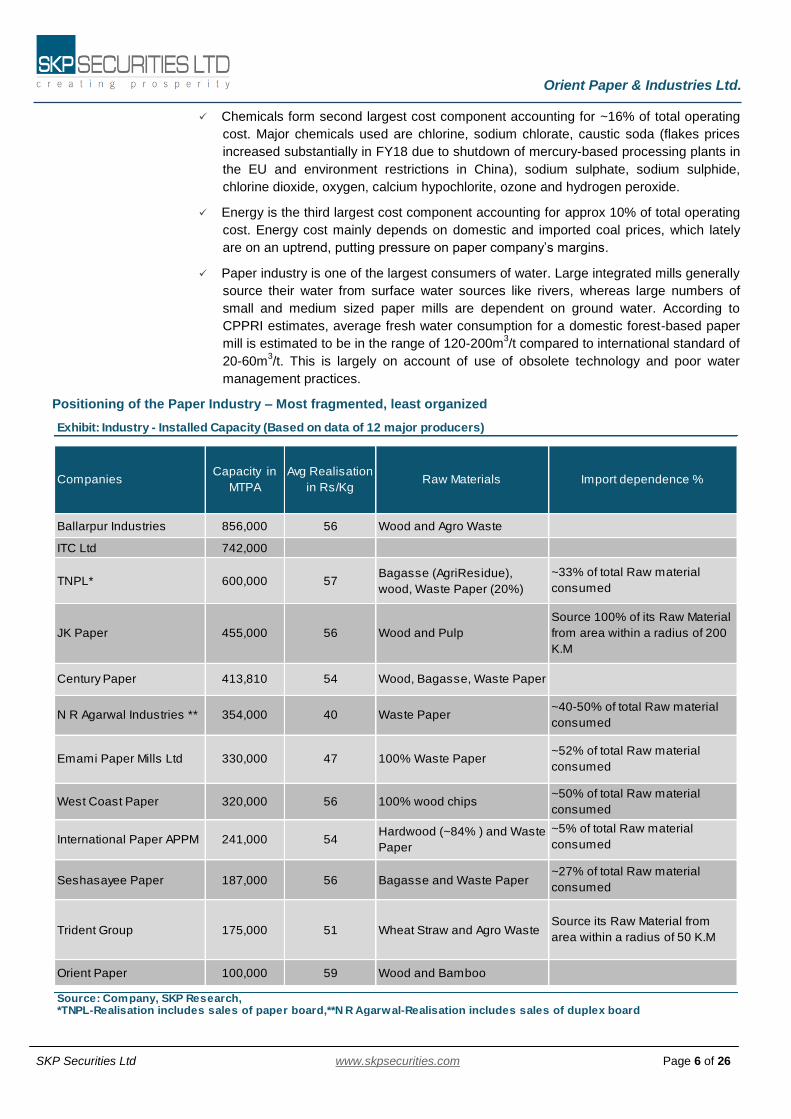

Exhibit: Industry - Installed Capacity (Based on data of 12 major producers)

Ballarpur Industries 856,000 56 Wood and Agro Waste

ITC Ltd 742,000

TNPL* 600,000 57Bagasse (AgriResidue),

wood, Waste Paper (20%)

Seshasayee Paper 187,000 56 Bagasse and Waste Paper

Trident Group 175,000 51 Wheat Straw and Agro Waste

Orient Paper 100,000 59 Wood and Bamboo

*TNPL-Realisation includes sales of paper board,**N R Agarwal-Realisation includes sales of duplex board

N R Agarwal Industries ** 354,000 40 Waste Paper ~40-50% of total Raw material

consumed

~5% of total Raw material

consumed

~27% of total Raw material

consumed

Source its Raw Material from

area within a radius of 50 K.M

Source: Company, SKP Research,

~50% of total Raw material

consumed

International Paper APPM 241,000

56 100% wood chips

54Hardwood (~84% ) and Waste

Paper

West Coast Paper 320,000

47 100% Waste Paper~52% of total Raw material

consumed Emami Paper Mills Ltd 330,000

54 Wood, Bagasse, Waste Paper Century Paper 413,810

~33% of total Raw material

consumed

JK Paper 455,000 56 Wood and Pulp

Source 100% of its Raw Material

from area within a radius of 200

K.M

Companies Capacity in

MTPA

Avg Realisation

in Rs/Kg Raw Materials Import dependence %

Chemicals form second largest cost component accounting for ~16% of total operating

cost. Major chemicals used are chlorine, sodium chlorate, caustic soda (flakes prices

increased substantially in FY18 due to shutdown of mercury-based processing plants in

the EU and environment restrictions in China), sodium sulphate, sodium sulphide,

chlorine dioxide, oxygen, calcium hypochlorite, ozone and hydrogen peroxide.

Energy is the third largest cost component accounting for approx 10% of total operating

cost. Energy cost mainly depends on domestic and imported coal prices, which lately

are on an uptrend, putting pressure on paper company’s margins.

Paper industry is one of the largest consumers of water. Large integrated mills generally

source their water from surface water sources like rivers, whereas large numbers of

small and medium sized paper mills are dependent on ground water. According to

CPPRI estimates, average fresh water consumption for a domestic forest-based paper

mill is estimated to be in the range of 120-200m3/t compared to international standard of

20-60m3/t. This is largely on account of use of obsolete technology and poor water

management practices.

Positioning of the Paper Industry – Most fragmented, least organized

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 7 of 26

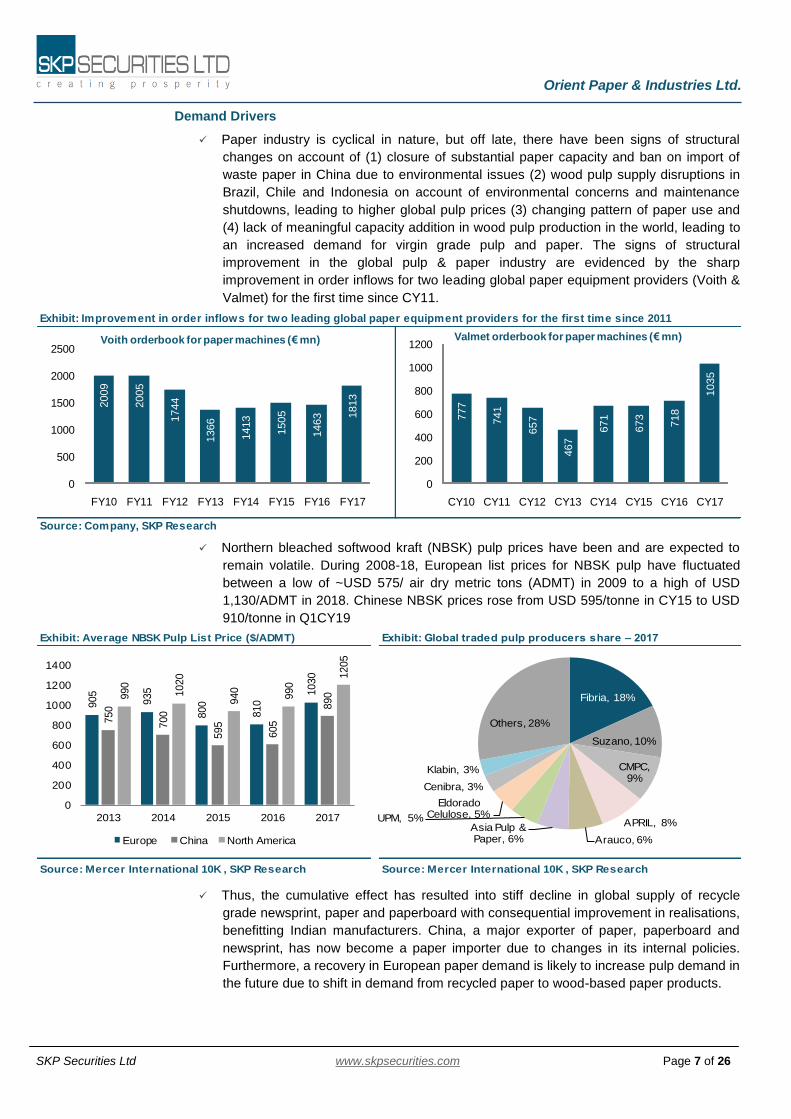

Exhibit: Average NBSK Pulp List Price ($/ADMT) Exhibit: Global traded pulp producers share – 2017

Source: Mercer International 10K , SKP Research Source: Mercer International 10K , SKP Research

Fibria, 18%

Suzano, 10%

CMPC, 9%

APRIL, 8%

Arauco, 6%

Asia Pulp & Paper, 6%

UPM, 5%

Eldorado Celulose, 5%

Cenibra, 3%

Klabin, 3%

Others, 28%

905

935

800

810

1030

750

700

595

605

890990

1020

940

990

1205

0

200

400

600

800

1000

1200

1400

2013 2014 2015 2016 2017

Europe China North America

Demand Drivers

Paper industry is cyclical in nature, but off late, there have been signs of structural

changes on account of (1) closure of substantial paper capacity and ban on import of

waste paper in China due to environmental issues (2) wood pulp supply disruptions in

Brazil, Chile and Indonesia on account of environmental concerns and maintenance

shutdowns, leading to higher global pulp prices (3) changing pattern of paper use and

(4) lack of meaningful capacity addition in wood pulp production in the world, leading to

an increased demand for virgin grade pulp and paper. The signs of structural

improvement in the global pulp & paper industry are evidenced by the sharp

improvement in order inflows for two leading global paper equipment providers (Voith &

Valmet) for the first time since CY11.

Northern bleached softwood kraft (NBSK) pulp prices have been and are expected to

remain volatile. During 2008-18, European list prices for NBSK pulp have fluctuated

between a low of ~USD 575/ air dry metric tons (ADMT) in 2009 to a high of USD

1,130/ADMT in 2018. Chinese NBSK prices rose from USD 595/tonne in CY15 to USD

910/tonne in Q1CY19

Thus, the cumulative effect has resulted into stiff decline in global supply of recycle

grade newsprint, paper and paperboard with consequential improvement in realisations,

benefitting Indian manufacturers. China, a major exporter of paper, paperboard and

newsprint, has now become a paper importer due to changes in its internal policies.

Furthermore, a recovery in European paper demand is likely to increase pulp demand in

the future due to shift in demand from recycled paper to wood-based paper products.

Exhibit: Improvement in order inflows for two leading global paper equipment providers for the first time since 2011

Source: Company, SKP Research

2009

2005

1744

1366

1413

1505

1463 1

813

0

500

1000

1500

2000

2500

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Voith orderbook for paper machines (€ mn)

777

741

657

467

671

673

718

1035

0

200

400

600

800

1000

1200

CY10 CY11 CY12 CY13 CY14 CY15 CY16 CY17

Valmet orderbook for paper machines (€ mn)

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 8 of 26

Exhibit: Per capita indicators (Rs '000 at current prices) Exhibit: Age distribution of Indian population

Source: : Central Statistics Office (CSO), IBEF, SKP Research

73.5 82.4 91.9

100.2

108.6

119.3

71.6 80.5 89.8 98.1

106.6

117.4

40.3

45.9

52.3

57.4

61.6 6

80

20

40

60

80

100

120

140

FY12 FY13 FY14 FY15 FY16 FY17

Per Capita GNDI Indian GDP Per Capita Per Capita PFCE

46.9 37.9 37.1 30.1 26.7

55.456.9 63.4

66.2 66.2

7.37.7 5.8 6.1 5.8

0

20

40

60

80

100

120

Japan US China World India

0-14 years 15-64 years >64 years

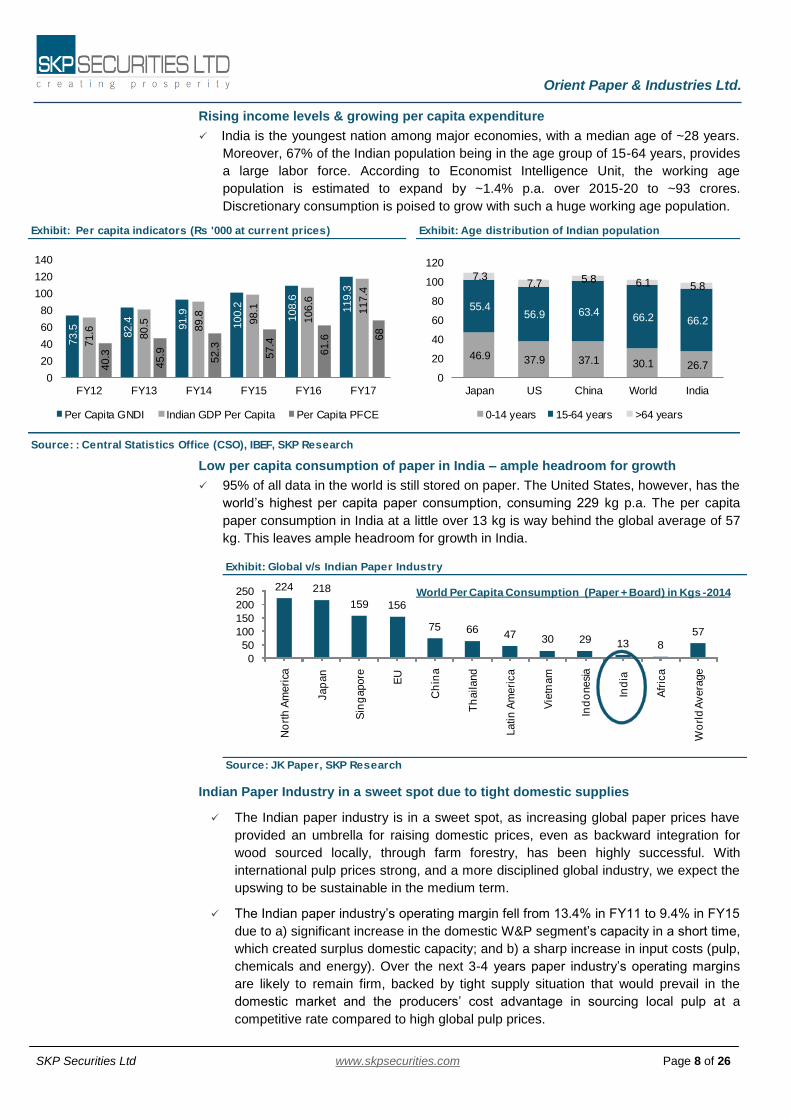

Rising income levels & growing per capita expenditure

India is the youngest nation among major economies, with a median age of ~28 years.

Moreover, 67% of the Indian population being in the age group of 15-64 years, provides

a large labor force. According to Economist Intelligence Unit, the working age

population is estimated to expand by ~1.4% p.a. over 2015-20 to ~93 crores.

Discretionary consumption is poised to grow with such a huge working age population.

Low per capita consumption of paper in India – ample headroom for growth

95% of all data in the world is still stored on paper. The United States, however, has the

world’s highest per capita paper consumption, consuming 229 kg p.a. The per capita

paper consumption in India at a little over 13 kg is way behind the global average of 57

kg. This leaves ample headroom for growth in India.

Indian Paper Industry in a sweet spot due to tight domestic supplies

The Indian paper industry is in a sweet spot, as increasing global paper prices have

provided an umbrella for raising domestic prices, even as backward integration for

wood sourced locally, through farm forestry, has been highly successful. With

international pulp prices strong, and a more disciplined global industry, we expect the

upswing to be sustainable in the medium term.

The Indian paper industry’s operating margin fell from 13.4% in FY11 to 9.4% in FY15

due to a) significant increase in the domestic W&P segment’s capacity in a short time,

which created surplus domestic capacity; and b) a sharp increase in input costs (pulp,

chemicals and energy). Over the next 3-4 years paper industry’s operating margins

are likely to remain firm, backed by tight supply situation that would prevail in the

domestic market and the producers’ cost advantage in sourcing local pulp at a

competitive rate compared to high global pulp prices.

Source: JK Paper, SKP Research

Exhibit: Global v/s Indian Paper Industry

224 218

159 156

75 6647 30 29 13 8

57

0

50

100

150

200

250

No

rth

Am

eri

ca

Jap

an

Sin

gapore

EU

Ch

ina

Th

ailand

Latin

Am

eri

ca

Vie

tnam

Ind

onesi

a

Ind

ia

Afr

ica

Wo

rld A

vera

ge

World Per Capita Consumption (Paper + Board) in Kgs -2014

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 9 of 26

Exhibit: Industry - Financial Synopsis

Source: Company, SKP Research

20.9%

10.2%

14.8%16.0%

4.3%

10.9%

14.6%

8.1%13.4%

10.1% 10.3% 9.8%

9.4%

11.1%

14.7%15.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Industry's margin & revenue growth (%)

Margin(%) Revenue Growth (%)

2.3

1.9

1.0

1.3

1.0

1.31.4

1.7

1.0 1.0 1.1 1.2 1.2

1.41.4

0.8

0.0

0.5

1.0

1.5

2.0

2.5

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

D/E (X) & ICR (X)

D/E (X) ICR (X)

Unlike in the previous cycle where players added capacity in uncoated paper

segment, future capex creation would be in a different vertical of the paper industry

(specialty paper, packaging board) by strong players and the weak balance sheet of

key paper producers (such as BILT) would restrict them from aggressively

participating in the current cycle.

After receiving environmental and other clearance, it usually takes 18-24 months for a

brownfield expansion and 24-30 months for a greenfield expansion. As per industry

estimates, as against an estimated annual increase in demand of ~1 MTPA for virgin-

pulp-based uncoated paper, only two players have received environmental clearance

for brownfield expansion for an aggregate capacity of ~150 KTPA. Therefore, we

believe the industry is likely to face a tight supply situation over next 3-4 years, giving

enhanced pricing power to existing paper manufacturers.

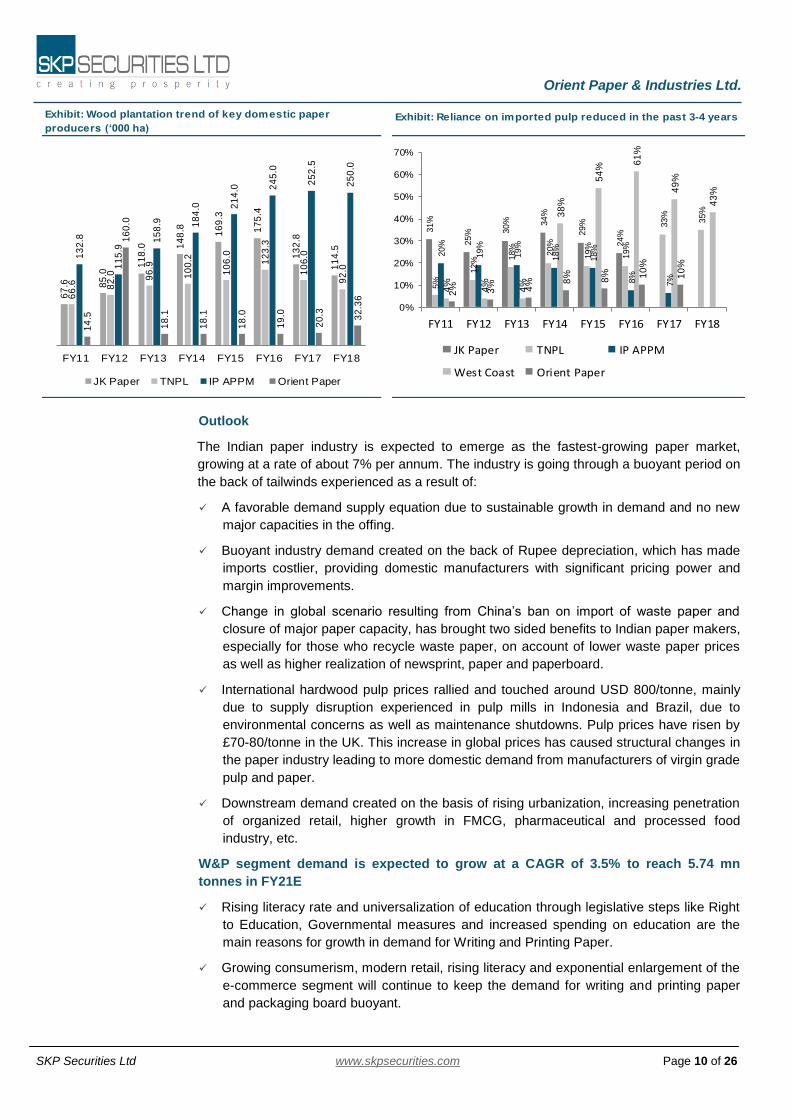

Domestic wood prices to remain weak on increased plantation of wood & bamboo

reclassification

Over the past decade, key focus area for wood-based domestic paper manufacturers

has been on improving farm forestry near the plant area (within a radius of 200 KM) for

better wood availability at reasonable prices. This also helps in reducing freight cost and

less reliance on costlier imported wood/pulp.

This commitment was reinforced through various initiatives such as training of farmers

to enhance plantation yields and assisting farmers seeking loans for plantation

reinvestment. The farm forestry initiative has also helped enhancing sustainable

livelihoods across rural districts, provided farmers a stable customer and the prospect of

equitable realizations (income out of eucalyptus, subabul and casuarina wood

cultivation is estimated to be far better than other cash crops).

The GoI is now seriously considering utilization of waste lands for plantations to

generate revenue, thereby generating job opportunities in rural segment and reducing

reliance on imported wood/pulp. Further, the recent draft National Forest Policy 2018

and the Government’s reclassification of bamboo from forest produce to non-forest

produce (for bamboo grown outside reserved forest areas) in November 2017 are

positive steps to increase wood/bamboo supply in the domestic market.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 10 of 26

Exhibit: Wood plantation trend of key domestic paper

producers (‘000 ha)Exhibit: Reliance on imported pulp reduced in the past 3-4 years

67

.6 85

.0

11

8.0 1

48

.8 16

9.3

17

5.4

13

2.8

11

4.5

66

.6 82

.0 96

.9

10

0.2

10

6.0

12

3.3

10

6.0

92

.0

13

2.8

11

5.9

15

8.9 18

4.0 2

14

.0 24

5.0

25

2.5

25

0.0

14

.5

16

0.0

18

.1

18

.1

18

.0

19

.0

20

.3 32

.36

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

JK Paper TNPL IP APPM Orient Paper

31%

25% 3

0% 34

%

29

%

24%

5%

12% 1

8%

20

%

19%

19%

33%

35%

20%

19

%

19

%

18%

18

%

8%

7%

4%

4%

4%

38

%

54

%

61

%

49

%

43

%

2% 3% 4% 8

% 8% 10

%

10

%

0%

10%

20%

30%

40%

50%

60%

70%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

JK Paper TNPL IP APPM

West Coast Orient Paper

Outlook

The Indian paper industry is expected to emerge as the fastest-growing paper market,

growing at a rate of about 7% per annum. The industry is going through a buoyant period on

the back of tailwinds experienced as a result of:

A favorable demand supply equation due to sustainable growth in demand and no new

major capacities in the offing.

Buoyant industry demand created on the back of Rupee depreciation, which has made

imports costlier, providing domestic manufacturers with significant pricing power and

margin improvements.

Change in global scenario resulting from China’s ban on import of waste paper and

closure of major paper capacity, has brought two sided benefits to Indian paper makers,

especially for those who recycle waste paper, on account of lower waste paper prices

as well as higher realization of newsprint, paper and paperboard.

International hardwood pulp prices rallied and touched around USD 800/tonne, mainly

due to supply disruption experienced in pulp mills in Indonesia and Brazil, due to

environmental concerns as well as maintenance shutdowns. Pulp prices have risen by

£70-80/tonne in the UK. This increase in global prices has caused structural changes in

the paper industry leading to more domestic demand from manufacturers of virgin grade

pulp and paper.

Downstream demand created on the basis of rising urbanization, increasing penetration

of organized retail, higher growth in FMCG, pharmaceutical and processed food

industry, etc.

W&P segment demand is expected to grow at a CAGR of 3.5% to reach 5.74 mn

tonnes in FY21E

Rising literacy rate and universalization of education through legislative steps like Right

to Education, Governmental measures and increased spending on education are the

main reasons for growth in demand for Writing and Printing Paper.

Growing consumerism, modern retail, rising literacy and exponential enlargement of the

e-commerce segment will continue to keep the demand for writing and printing paper

and packaging board buoyant.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 11 of 26

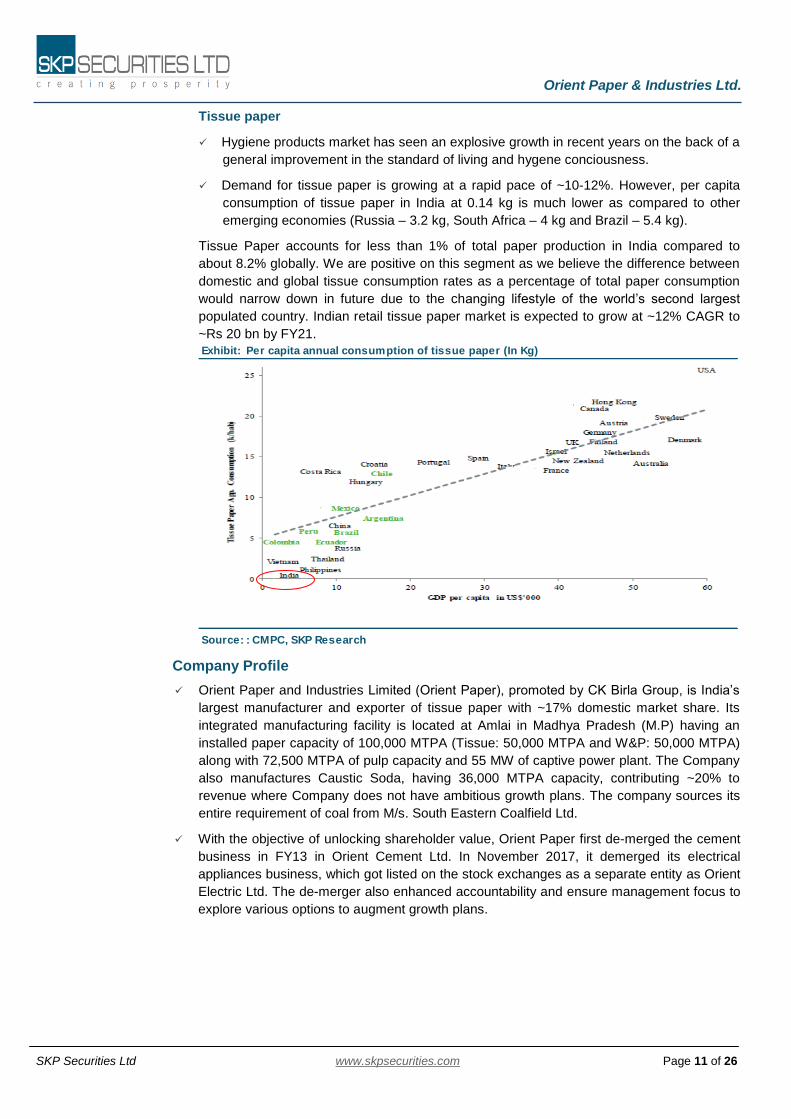

Exhibit: Per capita annual consumption of tissue paper (In Kg)

Source: : CMPC, SKP Research

Tissue paper

Hygiene products market has seen an explosive growth in recent years on the back of a

general improvement in the standard of living and hygene conciousness.

Demand for tissue paper is growing at a rapid pace of ~10-12%. However, per capita

consumption of tissue paper in India at 0.14 kg is much lower as compared to other

emerging economies (Russia – 3.2 kg, South Africa – 4 kg and Brazil – 5.4 kg).

Tissue Paper accounts for less than 1% of total paper production in India compared to

about 8.2% globally. We are positive on this segment as we believe the difference between

domestic and global tissue consumption rates as a percentage of total paper consumption

would narrow down in future due to the changing lifestyle of the world’s second largest

populated country. Indian retail tissue paper market is expected to grow at ~12% CAGR to

~Rs 20 bn by FY21.

Company Profile

Orient Paper and Industries Limited (Orient Paper), promoted by CK Birla Group, is India’s

largest manufacturer and exporter of tissue paper with ~17% domestic market share. Its

integrated manufacturing facility is located at Amlai in Madhya Pradesh (M.P) having an

installed paper capacity of 100,000 MTPA (Tissue: 50,000 MTPA and W&P: 50,000 MTPA)

along with 72,500 MTPA of pulp capacity and 55 MW of captive power plant. The Company

also manufactures Caustic Soda, having 36,000 MTPA capacity, contributing ~20% to

revenue where Company does not have ambitious growth plans. The company sources its

entire requirement of coal from M/s. South Eastern Coalfield Ltd.

With the objective of unlocking shareholder value, Orient Paper first de-merged the cement

business in FY13 in Orient Cement Ltd. In November 2017, it demerged its electrical

appliances business, which got listed on the stock exchanges as a separate entity as Orient

Electric Ltd. The de-merger also enhanced accountability and ensure management focus to

explore various options to augment growth plans.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 12 of 26

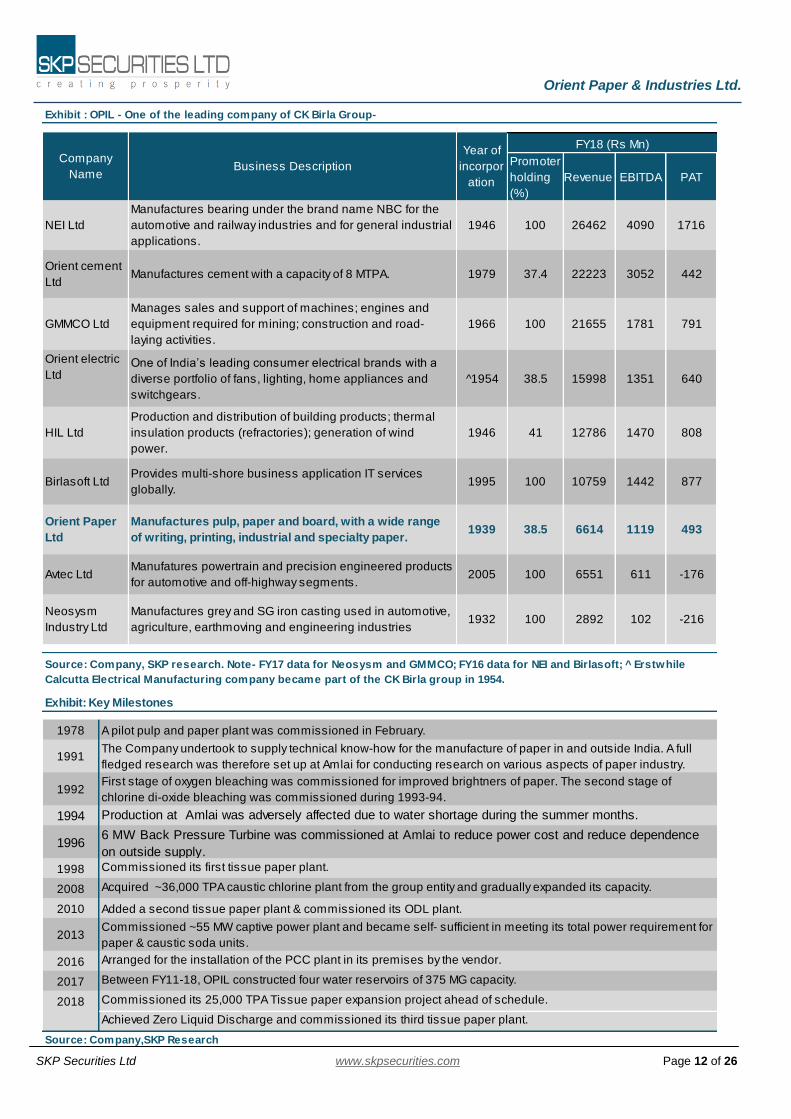

Exhibit : OPIL - One of the leading company of CK Birla Group-

Promoter

holding

(%)

Revenue EBITDA PAT

FY18 (Rs Mn)Company

Name Business Description

Year of

incorpor

ation

Source: Company, SKP research. Note- FY17 data for Neosysm and GMMCO; FY16 data for NEI and Birlasoft; ^ Erstwhile

Calcutta Electrical Manufacturing company became part of the CK Birla group in 1954.

-216

611

102

493

-176

1716

442

791

640

808

877

6614

6551

2892

4090

3052

1781

1351

1470

1442

1119

26462

22223

21655

15998

12786

10759

100

37.4

100

38.5

41

100

38.51939

2005

1932

100

100

Manufactures bearing under the brand name NBC for the

automotive and railway industries and for general industrial

applications.

NEI Ltd

Orient cement

LtdManufactures cement with a capacity of 8 MTPA.

Birlasoft LtdProvides multi-shore business application IT services

globally.

GMMCO Ltd

Manages sales and support of machines; engines and

equipment required for mining; construction and road-

laying activities.

1946

1979

1966

^1954

1946

1995

Avtec LtdManufatures powertrain and precision engineered products

for automotive and off-highway segments.

Neosysm

Industry Ltd

Manufactures grey and SG iron casting used in automotive,

agriculture, earthmoving and engineering industries

Orient electric

LtdOne of India’s leading consumer electrical brands with a

diverse portfolio of fans, lighting, home appliances and

switchgears.

HIL Ltd

Production and distribution of building products; thermal

insulation products (refractories); generation of wind

power.

Orient Paper

Ltd

Manufactures pulp, paper and board, with a wide range

of writing, printing, industrial and specialty paper.

Exhibit: Key Milestones

1978 A pilot pulp and paper plant was commissioned in February.

1991The Company undertook to supply technical know-how for the manufacture of paper in and outside India. A full

fledged research was therefore set up at Amlai for conducting research on various aspects of paper industry.

1992First stage of oxygen bleaching was commissioned for improved brightners of paper. The second stage of

chlorine di-oxide bleaching was commissioned during 1993-94.

1994 Production at Amlai was adversely affected due to water shortage during the summer months.

19966 MW Back Pressure Turbine was commissioned at Amlai to reduce power cost and reduce dependence

on outside supply.

1998 Commissioned its first tissue paper plant.

2008 Acquired ~36,000 TPA caustic chlorine plant from the group entity and gradually expanded its capacity.

2010 Added a second tissue paper plant & commissioned its ODL plant.

2013Commissioned ~55 MW captive power plant and became self- sufficient in meeting its total power requirement for

paper & caustic soda units.

2016 Arranged for the installation of the PCC plant in its premises by the vendor.

2017 Between FY11-18, OPIL constructed four water reservoirs of 375 MG capacity.

2018 Commissioned its 25,000 TPA Tissue paper expansion project ahead of schedule.

Achieved Zero Liquid Discharge and commissioned its third tissue paper plant.

Source: Company,SKP Research

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 13 of 26

Parameter Paper & Board Caustic soda Others

Key competitors

Demand drivers

Source: Company, SKP Research

Key risks

3%

3%

Exhibit : Orient Paper and Industries Limited - Business Mix

Geographic presence

Sales growth (FY14-FY18 – 4-yr CAGR)

Sales forecast (FY18-FY20 – 2-yr CAGR)

18%

14%

Revenue contribution (FY17) 79%

(12%) (7% growth in volume and 4% growth in realization CAGR)

(7%) (4% growth in volume and 5% growth in realization CAGR)

Capital Allocation

Credit Rating

Domestic: 83%, Exports: 17% (UAE and Rest of the world)

A prominent player in the writing & printing (W&P) paper segment with a capacity of

50,000 TPA. It also has a diversified presence in all the high-value tissue segments

(Tissue Capacity – 50,000 TPA) with manufacturing facilities located in AMLAI, Madhya

Pradesh.

Orient has been prudent in capital allocation. To eliminate its dependency on the

more expensive market pulp), Orient Paper has planned to increase its pulp capacity

from 72,500 MTPA to 100,000 MTPA at a cost of Rs 450 mn. It is also setting up a new

recovery boiler at a cost of ~Rs 1.65 bn and upgrading its pulp capacity to become

ECF (elemental chlorine free) complaint at a cost of ~Rs 150 mn. Post expansion the

enhanced pulp capacity will support paper production of 120,000-125,000 MTPA as

against current paper capacity of 100,000 MTPA.

Revenue contribution (FY20E)

Market position

JK Papers Ltd, BILT, TNPL, Century, ITC, WCPM and Emami Paper

The increasing rates of literacy rate, consumerism, economic activity,changing

lifestyles and e-commerce transactions are key revenue drivers in this industry.

CARE Ratings assigned CARE AA-; Stable / CARE A1+ (Double A minus; Outlook:

Stable/ A One plus) rating in view of long and satisfactory track record of the company.

Volatility in raw material (Bamboo/wood,pulp,chemical) prices of paper division

Threat from imports, though limited in tissue paper segment

83%

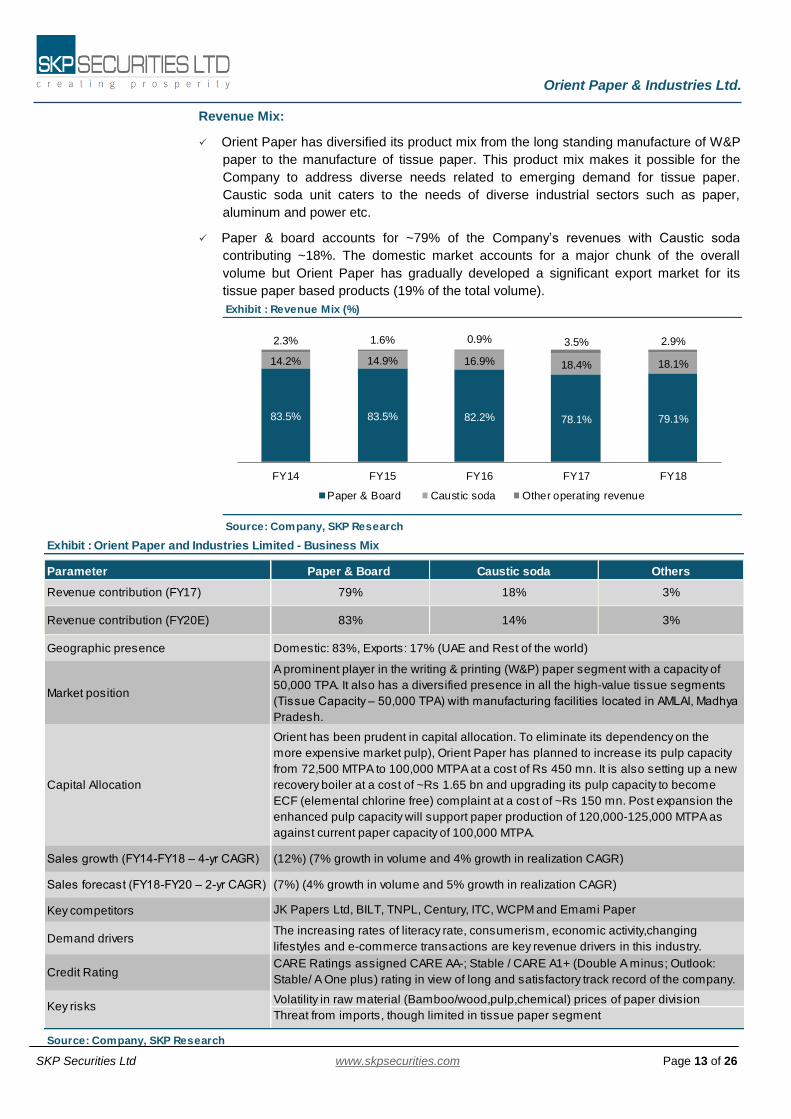

Exhibit : Revenue Mix (%)

Source: Company, SKP Research

83.5% 83.5% 82.2% 78.1% 79.1%

14.2% 14.9% 16.9% 18.4% 18.1%

2.3% 1.6% 0.9% 3.5% 2.9%

FY14 FY15 FY16 FY17 FY18

Paper & Board Caustic soda Other operating revenue

Revenue Mix:

Orient Paper has diversified its product mix from the long standing manufacture of W&P

paper to the manufacture of tissue paper. This product mix makes it possible for the

Company to address diverse needs related to emerging demand for tissue paper.

Caustic soda unit caters to the needs of diverse industrial sectors such as paper,

aluminum and power etc.

Paper & board accounts for ~79% of the Company’s revenues with Caustic soda

contributing ~18%. The domestic market accounts for a major chunk of the overall

volume but Orient Paper has gradually developed a significant export market for its

tissue paper based products (19% of the total volume).

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 14 of 26

Exhibit: OPIL - Largest tissue paper manufacturer in India

Source: : SKP Research

50000

36000 36000

25200 22000

0

10000

20000

30000

40000

50000

60000

Orient Century Textile ITC Arjun pulp and

paper

Pudumjee Paper

Capacity (TPA)

Investment Rationale

Largest player in Tissue paper with integrated production facilities, robust demand in

tissue paper puts Orient Paper in a sweet spot

The tissue paper industry is emerging as a new sub-segment within the Specialty Paper

market. Globally, tissue paper segment, accounts for 8% of global paper demand and in

terms of growth, tissue and packaging paper are the fastest growing segments in the world

due to improving lifestyles, increasing hygiene awareness and rising disposable income.

India’s share of tissue paper in terms of total global paper demand is quite low (1%).

However, growth potential for tissue paper is strong given that per capita tissue paper

consumption is amongst the lowest in the world. With rising disposable income and

increasing hygiene awareness, difference between domestic and global tissue consumption

rates as a percentage of total paper consumption would narrow down in future. Therfore,

domestic demand for tissue paper is expected to remain buoyant over the long-term.

Even if per capita consumption increases by 1 kg, it will lead to an increase of paper

production by 1 MTPA. As per IPMA, tissue paper demand in India is expected to grow at a

rate of ~10-12% p.a. FY18 demand stands at 50,000 TPA. Competitiveness of Indian tissue

players has improved due to sharp increase in global pulp prices, weaker Rupee ably

supported by moderate domestic wood prices.

Orient Paper is the largest player in tissue paper segment in India (50,000 TPA), followed

by Century Textile & Industries Ltd (36,000 TPA), ITC (36,000 TPA), Arjun Pulp & Paper

(25,200 TPA) and Pudumjee Paper Products Ltd (22,000 TPA). Orient Paper was a pioneer

in setting up a tissue paper capacity of 10,000 TPA at a time when the total Indian market

for tissue paper was not 5,000 TPA.

The leadership in this segment was strengthened in FY17-18 following the addition of a new

capacity of 25,000 TPA with a capex of Rs 800 mn. Orient commissioned its tissue

expansion project ahead of schedule on 1st May 2017, making it the largest producer of

tissue paper in India. Tissue paper accounts for ~37% of its production, ~50% of which is

exported. In contrast, existing players are not able to ramp up the capacity to optimal

level and key domestic paper producers are yet to enter this segment. This puts

Orient Paper in a sweet spot due to its established presence in both the domestic

and international markets.

In tissue paper segment, Orient Paper enjoys higher realisations (tissue paper has ~Rs

10/kg higher realization than W&P paper) and better margins. Its state-of-the art machines

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 15 of 26

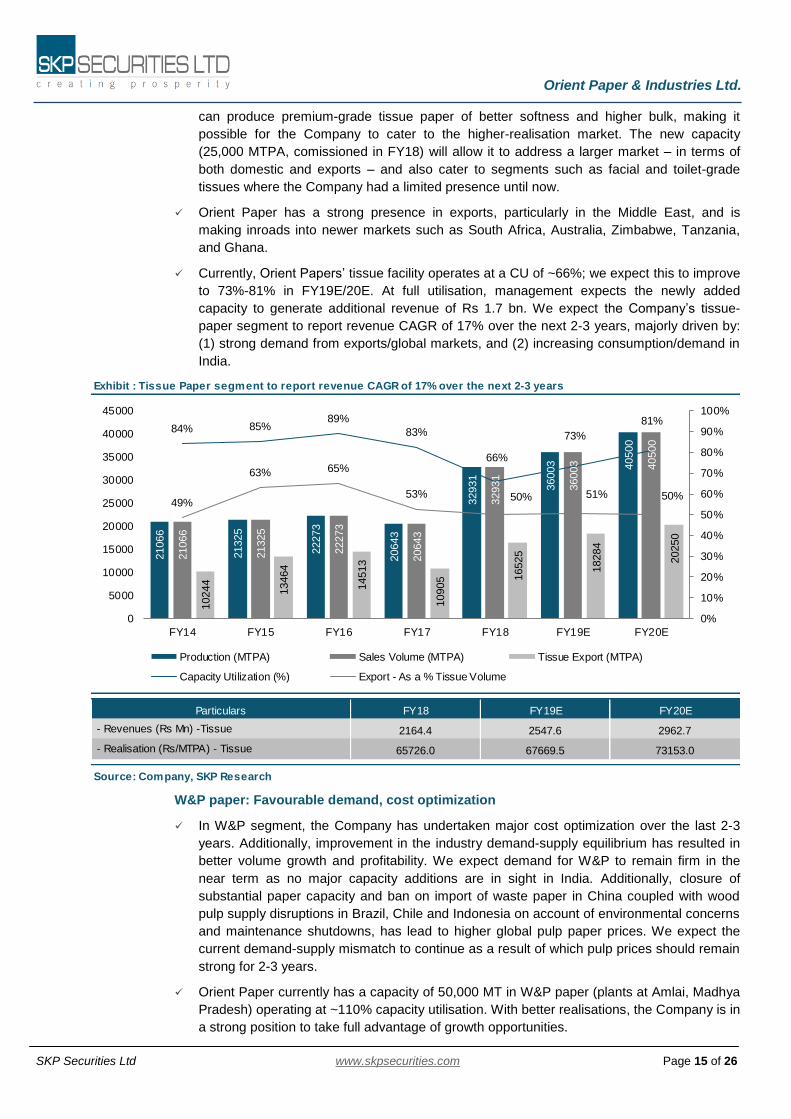

Exhibit : Tissue Paper segment to report revenue CAGR of 17% over the next 2-3 years

Source: Company, SKP Research

- Revenues (Rs Mn) -Tissue

- Realisation (Rs/MTPA) - Tissue

FY20EFY19EFY18Particulars

2164.4

65726.0

2547.6

67669.5

2962.7

73153.0

21066

21325

22273

20643

32931

36003 40500

21066

21325

22273

20643

32931

36003 40500

10244

13464

14513

10905 1

6525

18284

20250

84% 85%89%

83%

66%

73%

81%

49%

63% 65%

53% 50% 51% 50%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Production (MTPA) Sales Volume (MTPA) Tissue Export (MTPA)

Capacity Utilization (%) Export - As a % Tissue Volume

can produce premium-grade tissue paper of better softness and higher bulk, making it

possible for the Company to cater to the higher-realisation market. The new capacity

(25,000 MTPA, comissioned in FY18) will allow it to address a larger market – in terms of

both domestic and exports – and also cater to segments such as facial and toilet-grade

tissues where the Company had a limited presence until now.

Orient Paper has a strong presence in exports, particularly in the Middle East, and is

making inroads into newer markets such as South Africa, Australia, Zimbabwe, Tanzania,

and Ghana.

Currently, Orient Papers’ tissue facility operates at a CU of ~66%; we expect this to improve

to 73%-81% in FY19E/20E. At full utilisation, management expects the newly added

capacity to generate additional revenue of Rs 1.7 bn. We expect the Company’s tissue-

paper segment to report revenue CAGR of 17% over the next 2-3 years, majorly driven by:

(1) strong demand from exports/global markets, and (2) increasing consumption/demand in

India.

W&P paper: Favourable demand, cost optimization

In W&P segment, the Company has undertaken major cost optimization over the last 2-3

years. Additionally, improvement in the industry demand-supply equilibrium has resulted in

better volume growth and profitability. We expect demand for W&P to remain firm in the

near term as no major capacity additions are in sight in India. Additionally, closure of

substantial paper capacity and ban on import of waste paper in China coupled with wood

pulp supply disruptions in Brazil, Chile and Indonesia on account of environmental concerns

and maintenance shutdowns, has lead to higher global pulp paper prices. We expect the

current demand-supply mismatch to continue as a result of which pulp prices should remain

strong for 2-3 years.

Orient Paper currently has a capacity of 50,000 MT in W&P paper (plants at Amlai, Madhya

Pradesh) operating at ~110% capacity utilisation. With better realisations, the Company is in

a strong position to take full advantage of growth opportunities.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 16 of 26

Exhibit : Writing/printing (WP) paper

Source: Company, SKP Research

3341.3

60751.0

- Revenues (Rs Mn) -Writing/printing (WP)

- Realisation (Rs/MTPA) - Writing/printing (WP)

FY20EFY19EFY18Particulars

3063.6

55632.8

3004.4

58414.5

47367

53487

54657

52074

55068

51432

55000

47367

53487

54657

52074

55068

51432

55000

86%

97% 99% 95%

110%

94%100%

0%

20%

40%

60%

80%

100%

120%

42000

44000

46000

48000

50000

52000

54000

56000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Production (MTPA) Sales Volume (MTPA) Capacity Utilization (%)

The company had a three-week maintenance shutdown in June 2018, longer than the

seven-day shutdown in FY17. Therefore, we expect revenue CAGR of about 4.4% for this

segment over the next 2-3 years.

Projected pulp capacity increase will lead to raw material security & an additional tissue

capacity

Orient Paper has recently announced its plan to increase pulp capacity from 72,500 TPA to

100,000 TPA to eliminate its dependency on expensive market pulp (<10% of total pulp

requirement and cost is >50% higher than own manufacturing) at a cost of Rs 450 mn. The

Company is also setting up a new recovery boiler at a cost of ~Rs 1.65 bn and upgrading its

pulp capacity to become ECF (elemental chlorine free) complaint at a cost of ~Rs 150 mn.

The proposed capex will be commissioned by Q3FY20 and will be funded majorly through

internal accruals and marginal borrowings. Post expansion the enhanced pulp capacity will

support paper production of 120,000-125,000 MTPA as against current paper capacity of

100,000 MTPA.

Furthermore, Orient Paper may go for a brownfield tissue paper expansion of ~20,000

MTPA (existing tissue capacity is expected reach optimum utilization in few years) to

augment its enhanced pulp capacity of 100,000 MTPA, surplus power (>15 MW) and huge

land bank at M.P. If it happens, expansion will be done at a minimal cost and will take

approx 1.5 years to get commissioned.

Margins to improve with better product mix and cost rationalization

In the paper sector, marketing focuses on selling the largest volume at the highest

realizations. This, in turn, warrants the creation of a superior product mix that enhances

margins and return on employed capital. Therefore, Orient Paper has diversified from the

longstanding manufacture of W&P paper to the manufacture of tissue paper.

Orient Paper has upgraded the quality of its tissue paper to address all segments i.e. facial,

toilet, toweling and napkin grades for domestic and export markets. In the writing & printing

segment, Orient Paper has developed suitable publishing grade papers in addition to its

stronghold in the notebook segment.

With its strong product profile, Orient Paper is focusing on higher-margin divisions (tissue

paper – which has ~Rs 10/kg higher realization). In FY18, tissues’ revenue contribution was

32%; with an increased capacity, we expect the share to increase to 39% by FY20.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 17 of 26

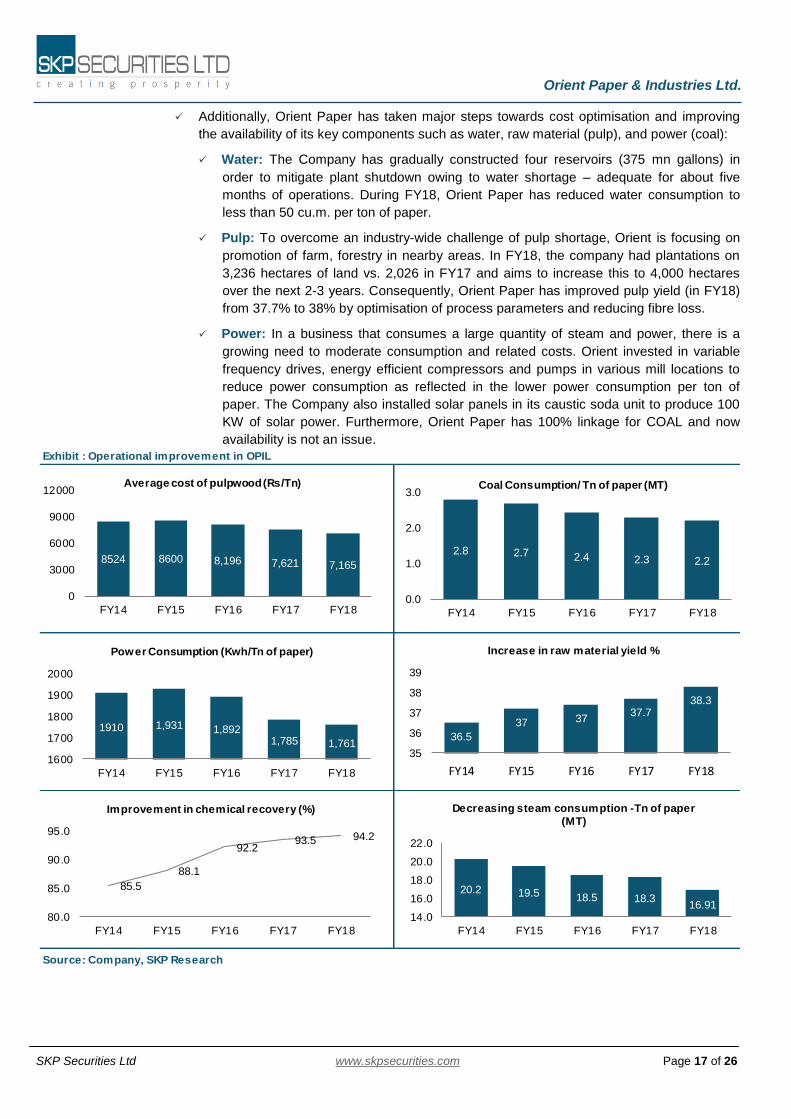

Additionally, Orient Paper has taken major steps towards cost optimisation and improving

the availability of its key components such as water, raw material (pulp), and power (coal):

Water: The Company has gradually constructed four reservoirs (375 mn gallons) in

order to mitigate plant shutdown owing to water shortage – adequate for about five

months of operations. During FY18, Orient Paper has reduced water consumption to

less than 50 cu.m. per ton of paper.

Pulp: To overcome an industry-wide challenge of pulp shortage, Orient is focusing on

promotion of farm, forestry in nearby areas. In FY18, the company had plantations on

3,236 hectares of land vs. 2,026 in FY17 and aims to increase this to 4,000 hectares

over the next 2-3 years. Consequently, Orient Paper has improved pulp yield (in FY18)

from 37.7% to 38% by optimisation of process parameters and reducing fibre loss.

Power: In a business that consumes a large quantity of steam and power, there is a

growing need to moderate consumption and related costs. Orient invested in variable

frequency drives, energy efficient compressors and pumps in various mill locations to

reduce power consumption as reflected in the lower power consumption per ton of

paper. The Company also installed solar panels in its caustic soda unit to produce 100

KW of solar power. Furthermore, Orient Paper has 100% linkage for COAL and now

availability is not an issue.

Exhibit : Operational improvement in OPIL

Source: Company, SKP Research

8524 8600 8,196 7,621 7,165

0

3000

6000

9000

12000

FY14 FY15 FY16 FY17 FY18

Average cost of pulpwood (Rs/Tn)

2.8 2.7 2.4 2.3 2.2

0.0

1.0

2.0

3.0

FY14 FY15 FY16 FY17 FY18

Coal Consumption/ Tn of paper (MT)

1910 1,931 1,8921,785 1,761

1600

1700

1800

1900

2000

FY14 FY15 FY16 FY17 FY18

Power Consumption (Kwh/Tn of paper)

36.5

37 3737.7

38.3

35

36

37

38

39

FY14 FY15 FY16 FY17 FY18

Increase in raw material yield %

85.5

88.1

92.293.5 94.2

80.0

85.0

90.0

95.0

FY14 FY15 FY16 FY17 FY18

Improvement in chemical recovery (%)

20.2 19.5 18.5 18.316.91

14.0

16.0

18.0

20.0

22.0

FY14 FY15 FY16 FY17 FY18

Decreasing steam consumption -Tn of paper

(MT)

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 18 of 26

Strong entry barriers restricting the entry of new players into the industry:

A technology intensive industry: Indian paper industry is gradually moving towards

advanced technologies, where size of the company and capital outlay comes into play.

Those who can adapt to new technologies will survive, while others will feel the heat, as the

cost of non-wood based raw material for making paper is gradually coming at par with

wood-based raw materials. Small paper making units could find it increasingly difficult to

survive the cut-throat competition in the sector.

Highly capital intensive industry: Setting up new capacities in paper requires substantial

capital outlay. Given the importance of captive power generation and mandatory ECF

compliance, it is estimated that setting a new venture would entail an investment of Rs.

80,000-100,000/mt, with a minimum viable plant size of 50,000 mt, implying a capex of over

Rs 5 bn. Also investment needed for upgrading technology, growing wood plantations and

establishing a distribution network; all make manufacturing paper a capital intensive task.

Adding to the woes, the industry is cyclical. Thus, small players might not be able to keep

up with heavy investments that are required to make them competitive.

High gestation period & tough environmental clearances: The pulp and paper industry

is among the world’s largest producers of water pollutants and waste products. This makes

the industry heavily regulated, and requires heavy investment from companies to be

environmentally compliant. Therefore, besides the huge capital outlays, requisite

environmental clearances and availability of land & water also pose significant challenges to

new projects, thereby restricting entry of new players

Indian paper industry is actively promoting agro-forestry, which has a five year cycle, to

meet its raw material needs. Here also a long gestation period acts as a hindrance.

It takes about 24-30 months for a greenfield project to commission in India, which

includes 12-15 months of erection of infrastructure and another 12-15 months for

getting requisite environmental clearances from the regulatory authorities.

High energy intensive industry with high energy cost: The Indian paper industry is

energy intensive which is scarce in India. Manufacturing one tonne of paper requires, 1,500

kWh of power and 850-1,000 kgs of coal.

Further, the cost of own power generation is increasing due to consistent increase in

coal prices. Thus, high energy consumption and high energy costs also act as a good

entry barrier.

Advent of GST: GST has been introduced at 12-18% for most paper categories. This

implies that the margin cushion available to small companies may be pressured; this along

with the high cost of environment compliance should drive the industry towards

consolidation.

Economies of scale: The average capacity of an Indian paper mill is about 21,373 TPA,

which is less than 1/5th of the average capacity of European mills, and about 1/9th the size

of the average US mill. The water, power and chemical requirements for paper production

reduce as the mills grow larger.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 19 of 26

Exhibit : Realisation & Revenue

Source: Company, SKP Research

54.859.4

63.166.0

0.0

15.0

30.0

45.0

60.0

75.0

FY17 FY18 FY19E FY20E

Net Realisations (Rs/Kg)

5114.9

6613.6 6838.67613.0

0.7%

29.3%

3.4%

11.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

0.0

1500.0

3000.0

4500.0

6000.0

7500.0

9000.0

FY17 FY18 FY19E FY20E

OPIL’s revenue to grow at 7.3% CAGR during FY18-20E

Revenue (Rs Mn) Growth (%)

Financial Highlights:

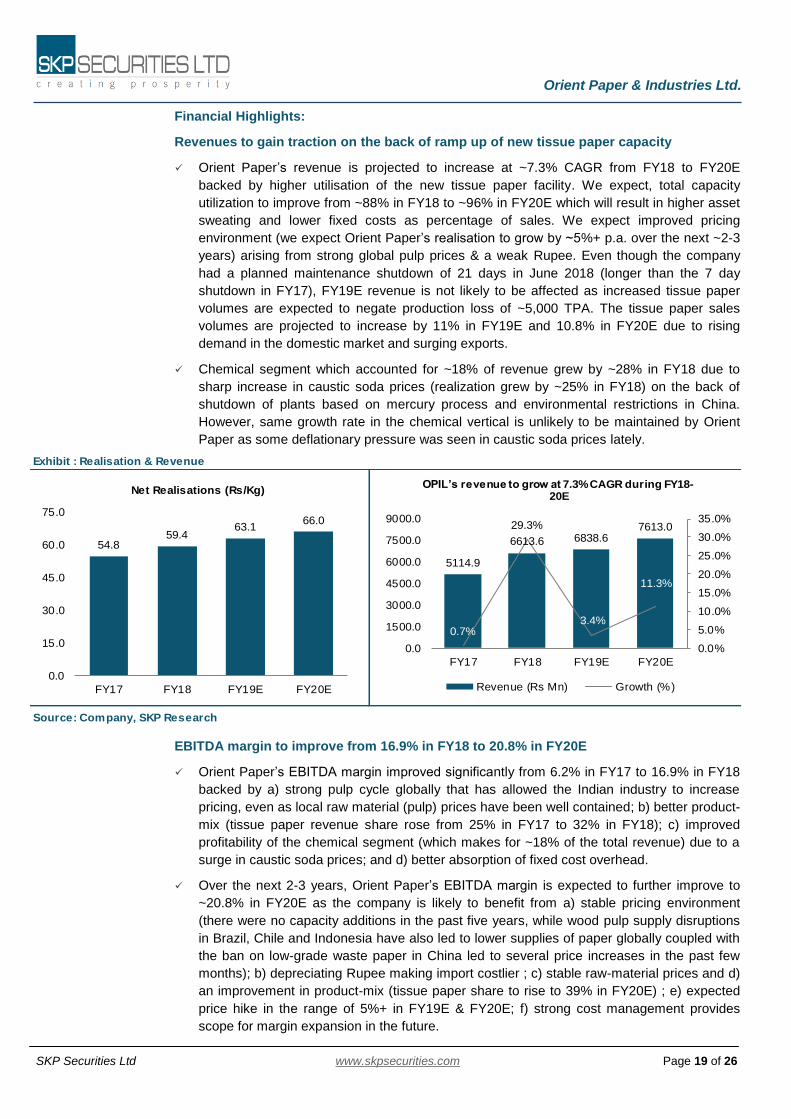

Revenues to gain traction on the back of ramp up of new tissue paper capacity

Orient Paper’s revenue is projected to increase at ~7.3% CAGR from FY18 to FY20E

backed by higher utilisation of the new tissue paper facility. We expect, total capacity

utilization to improve from ~88% in FY18 to ~96% in FY20E which will result in higher asset

sweating and lower fixed costs as percentage of sales. We expect improved pricing

environment (we expect Orient Paper’s realisation to grow by ~5%+ p.a. over the next ~2-3

years) arising from strong global pulp prices & a weak Rupee. Even though the company

had a planned maintenance shutdown of 21 days in June 2018 (longer than the 7 day

shutdown in FY17), FY19E revenue is not likely to be affected as increased tissue paper

volumes are expected to negate production loss of ~5,000 TPA. The tissue paper sales

volumes are projected to increase by 11% in FY19E and 10.8% in FY20E due to rising

demand in the domestic market and surging exports.

Chemical segment which accounted for ~18% of revenue grew by ~28% in FY18 due to

sharp increase in caustic soda prices (realization grew by ~25% in FY18) on the back of

shutdown of plants based on mercury process and environmental restrictions in China.

However, same growth rate in the chemical vertical is unlikely to be maintained by Orient

Paper as some deflationary pressure was seen in caustic soda prices lately.

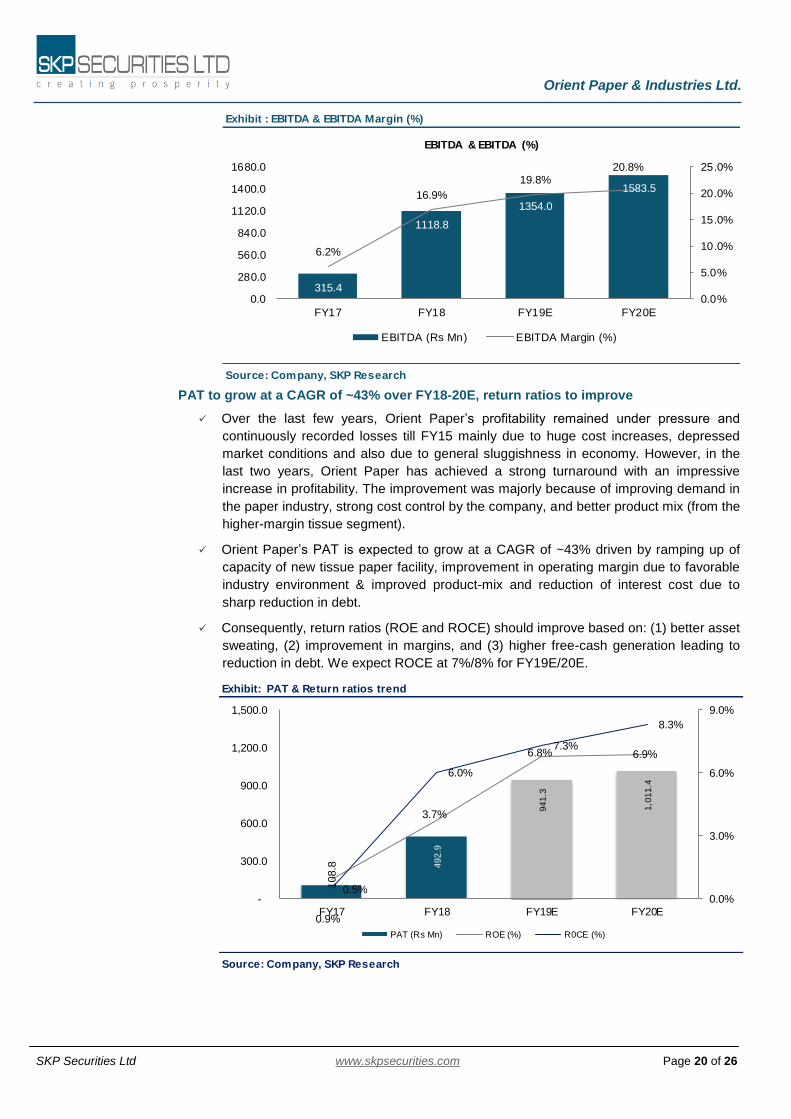

EBITDA margin to improve from 16.9% in FY18 to 20.8% in FY20E

Orient Paper’s EBITDA margin improved significantly from 6.2% in FY17 to 16.9% in FY18

backed by a) strong pulp cycle globally that has allowed the Indian industry to increase

pricing, even as local raw material (pulp) prices have been well contained; b) better product-

mix (tissue paper revenue share rose from 25% in FY17 to 32% in FY18); c) improved

profitability of the chemical segment (which makes for ~18% of the total revenue) due to a

surge in caustic soda prices; and d) better absorption of fixed cost overhead.

Over the next 2-3 years, Orient Paper’s EBITDA margin is expected to further improve to

~20.8% in FY20E as the company is likely to benefit from a) stable pricing environment

(there were no capacity additions in the past five years, while wood pulp supply disruptions

in Brazil, Chile and Indonesia have also led to lower supplies of paper globally coupled with

the ban on low-grade waste paper in China led to several price increases in the past few

months); b) depreciating Rupee making import costlier ; c) stable raw-material prices and d)

an improvement in product-mix (tissue paper share to rise to 39% in FY20E) ; e) expected

price hike in the range of 5%+ in FY19E & FY20E; f) strong cost management provides

scope for margin expansion in the future.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 20 of 26

Exhibit: PAT & Return ratios trend

Source: Company, SKP Research

108.8

492

.9

94

1.3

1,0

11

.4

0.9%

3.7%

6.8% 6.9%

0.5%

6.0%

7.3%

8.3%

0.0%

3.0%

6.0%

9.0%

-

300.0

600.0

900.0

1,200.0

1,500.0

FY17 FY18 FY19E FY20E

PAT (Rs Mn) ROE (%) R0CE (%)

Exhibit : EBITDA & EBITDA Margin (%)

Source: Company, SKP Research

315.4

1118.8

1354.0

1583.5

6.2%

16.9%

19.8%20.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0.0

280.0

560.0

840.0

1120.0

1400.0

1680.0

FY17 FY18 FY19E FY20E

EBITDA & EBITDA (%)

EBITDA (Rs Mn) EBITDA Margin (%)

PAT to grow at a CAGR of ~43% over FY18-20E, return ratios to improve

Over the last few years, Orient Paper’s profitability remained under pressure and

continuously recorded losses till FY15 mainly due to huge cost increases, depressed

market conditions and also due to general sluggishness in economy. However, in the

last two years, Orient Paper has achieved a strong turnaround with an impressive

increase in profitability. The improvement was majorly because of improving demand in

the paper industry, strong cost control by the company, and better product mix (from the

higher-margin tissue segment).

Orient Paper’s PAT is expected to grow at a CAGR of ~43% driven by ramping up of

capacity of new tissue paper facility, improvement in operating margin due to favorable

industry environment & improved product-mix and reduction of interest cost due to

sharp reduction in debt.

Consequently, return ratios (ROE and ROCE) should improve based on: (1) better asset

sweating, (2) improvement in margins, and (3) higher free-cash generation leading to

reduction in debt. We expect ROCE at 7%/8% for FY19E/20E.

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 21 of 26

Exhibit : Total Debt (Rs Mn) & Interest coverage ratio

Source: Company, SKP Research

1682.2

698.9 650.2750.0

0.3

5.7

14.5

19.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

0.0

280.0

560.0

840.0

1120.0

1400.0

1680.0

1960.0

FY17 FY18 FY19E FY20E

Total Debt (Rs Mn) ICR (X)

Exhibit: Exhibit: Peer Comparison

FY16 FY17 FY18 FY16 FY17 FY18 FY16 FY17 FY18 FY16 FY17 FY18

JK Paper 28.1 455000 56 16% 20% 22% 6% 14% 18% 9% 13% 16% 1.4x 1.1x 0.6x

West Coast Paper 21.7 320000 56 15% 19% 21% 22% 22% 30% 12% 21% 22% 1.2x 0.5x 0.3x

TNPL 18.8 600000 57 23.4% 24.6% 13.1% 19% 16% -3% 13% 14% 5% 1.7x 1.4x 1.2x

International Paper 18.1 241000 54 11.3% 14.5% 17.5% 9% 7% 16% 7% 13% 21% 1.0x 0.5x 0.3x

Ruchira Paper * 3.0 130000 39 13.1% 15.3% 16.6% 17% 24% 22% 22% 27% 26% 0.5x 0.4x 0.4x

Pudumjee Paper 2.1 60000 5.8% 9.4% 8.5% 9.8% 9.5% 8.2% 15% 14% 12% 0.4x 0.3x 0.1x

Orient Paper 9.3 100000 59 6.2% 16.9% 1% 4% 0% 6% 0.1x 0.1x

Source: Company,SKP Research

* Ruchira Paper - Realisation includes sales of Kraft paper

ROE (%) ROCE (%) D/E (X)Companies

Mcap

(Rs Bn)

Realization

(Rs/Kg)

EBITDA Margin (%)Capacity

(MTPA)

Strong balance sheet augurs well for forthcoming growth opportunities:

Over the last few years, Orient paper has deleveraged its balance sheet by re-paying

debt of Rs 1 bn. As on June 2018, the total debt stands at ~Rs 0.6 bn (D/E of 0.1x)

against an expected operating cash flow of Rs 1.2 bn -1.6 bn in FY19E & FY20E

respectively providing visibility to meet future capex requirements.

Further, the Company holds investments worth ~Rs 2.8 bn in the form of equity shares

of Hyderabad Industries Ltd., as a part of Promoter Group and Century Textiles &

Industries Ltd., which the management intends to liquidate, going forward. Also,

Company holds ~800 acres of land at Brajrajnagar plant, non-operational since 1999,

which we believe will be optimally used for other purposes, going forward.

Orient Paper has the best credit rating [at CARE AA- (Stable)/ CARE A1+] in the entire

paper industry, which indicates a healthy financial risk profile.

Peer Comparison:

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 22 of 26

Valuations

Orient Paper has moved up the value chain which has higher growth potential and better

realizations, leading to a self-sustained model (increasing profitability) backed by

favourable demand-supply equilibrium and muted domestic wood prices. Additionally, with

internal cost controls and effective management, this business is showing signs of: (1)

improvement in utilization (asset turnover), (2) healthy margins, and (3) strong free cash

flow generation, providing visibility to meet future capex requirements and better return

ratios.

We have valued the stock on SOTP basis valuing Orient’s core paper business at 7x

EV/EBITDA of FY20E and investments (except Brajrajnagar land) at Rs 8/-share. We

recommend a BUY on the stock with a target price of Rs 57/- in 15 months, although the

long term story looks even better. Any monetization of Brajrajnagar land will trigger an

upside potential on Orient Paper profitability and stock price.

Risks & Concerns

Competition from unorganised players: As mentioned earlier, Indian paper industry is highly fragmented with ~825 small to large mills. Any increase in the competitive intensity from unorganized segment may be detrimental for the Company.

Import from ASEAN countries and China: Increase in cheap inflow under the Free Trade Agreement (FTA), may cause pricing pressure on some segments of the paper industry. Paper demand in India grew at a CAGR of ~6.2% from 9.3 MTPA in FY08 to 17 MTPA in FY17. Imports during the same period has increased at a CAGR of ~15% mainly from ASEAN countries due to zero import duties, affecting fresh capacity creation.

In order to provide a level playing field to the domestic industry and encourage farming of wood in India, there is a need to review the current import duty structure and re-examine existing FTAs and the new ones under formulation.

Unfavourable forex fluctuations: Sharp Rupee appreciation: may reduce the competitive advantage of domestically sourced wood vs imported pulp.

Shortage or rise in prices of raw materials: Traditionally, woodchips supply has been much lower than the actual demand. Also, diversion or increase in demand for wood from competing industries like MDF & construction may cause shortage or rise in price.

Exhibit: SOTP based target price

EV/EBIDTA FY20E

EBIDTA (Rs mn) 1584

Est EV/EBIDTA (x) 7

EV (Rs mn) 11085

Net Debt (Rs mn) 605

Add

30% Discount - Century Textiles & Industries Limited 719

40% Discount - Hyderabad Industries Limited 920

Shareholders' Value (Rs mn) 12119

O/s Shares (mn Shares in FY20E) 212

Fair Value (Rs per share) 57

CMP (Rs) 43

Return (%) 33%

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 23 of 26

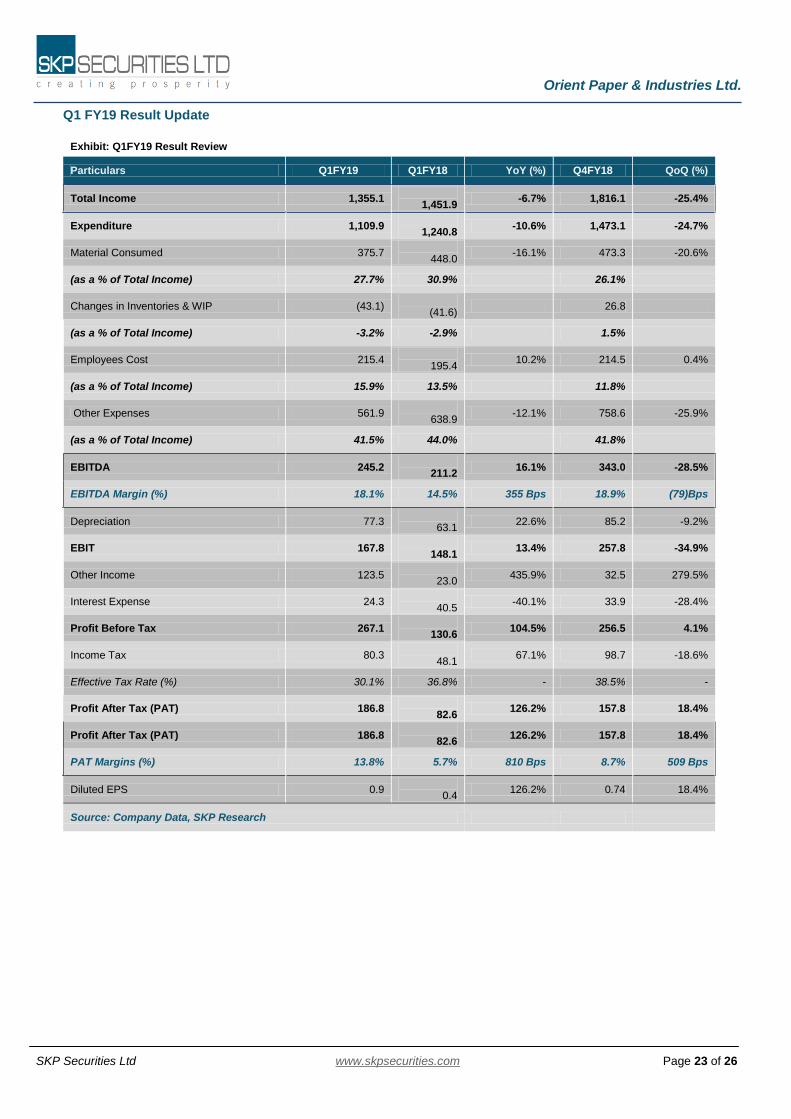

Q1 FY19 Result Update

Exhibit: Q1FY19 Result Review

Particulars Q1FY19 Q1FY18 YoY (%) Q4FY18 QoQ (%)

Total Income 1,355.1

1,451.9 -6.7% 1,816.1 -25.4%

Expenditure 1,109.9

1,240.8 -10.6% 1,473.1 -24.7%

Material Consumed 375.7

448.0 -16.1% 473.3 -20.6%

(as a % of Total Income) 27.7% 30.9% 26.1%

Changes in Inventories & WIP (43.1)

(41.6) 26.8

(as a % of Total Income) -3.2% -2.9% 1.5%

Employees Cost 215.4

195.4 10.2% 214.5 0.4%

(as a % of Total Income) 15.9% 13.5% 11.8%

Other Expenses 561.9

638.9 -12.1% 758.6 -25.9%

(as a % of Total Income) 41.5% 44.0% 41.8%

EBITDA 245.2

211.2 16.1% 343.0 -28.5%

EBITDA Margin (%) 18.1% 14.5% 355 Bps 18.9% (79)Bps

Depreciation 77.3

63.1 22.6% 85.2 -9.2%

EBIT 167.8

148.1 13.4% 257.8 -34.9%

Other Income 123.5

23.0 435.9% 32.5 279.5%

Interest Expense 24.3

40.5 -40.1% 33.9 -28.4%

Profit Before Tax 267.1

130.6 104.5% 256.5 4.1%

Income Tax 80.3

48.1 67.1% 98.7 -18.6%

Effective Tax Rate (%) 30.1% 36.8% - 38.5% -

Profit After Tax (PAT) 186.8

82.6 126.2% 157.8 18.4%

Profit After Tax (PAT) 186.8

82.6 126.2% 157.8 18.4%

PAT Margins (%) 13.8% 5.7% 810 Bps 8.7% 509 Bps

Diluted EPS 0.9

0.4 126.2% 0.74 18.4%

Source: Company Data, SKP Research

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 24 of 26

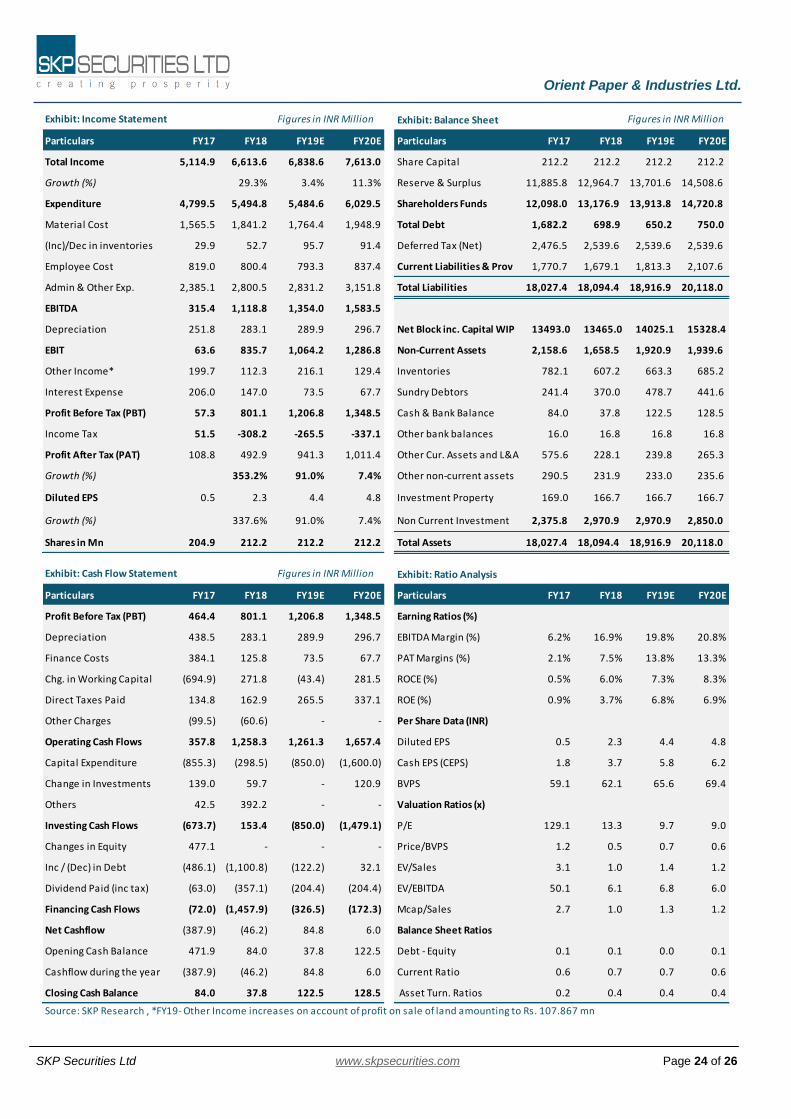

Exhibit: Balance Sheet

Particulars FY17 FY18 FY19E FY20E Particulars FY17 FY18 FY19E FY20E

Total Income 5,114.9 6,613.6 6,838.6 7,613.0 Share Capital 212.2 212.2 212.2 212.2

Growth (%) 29.3% 3.4% 11.3% Reserve & Surplus 11,885.8 12,964.7 13,701.6 14,508.6

Expenditure 4,799.5 5,494.8 5,484.6 6,029.5 Shareholders Funds 12,098.0 13,176.9 13,913.8 14,720.8

Material Cost 1,565.5 1,841.2 1,764.4 1,948.9 Total Debt 1,682.2 698.9 650.2 750.0

(Inc)/Dec in inventories 29.9 52.7 95.7 91.4 Deferred Tax (Net) 2,476.5 2,539.6 2,539.6 2,539.6

Employee Cost 819.0 800.4 793.3 837.4 Current Liabilities & Prov 1,770.7 1,679.1 1,813.3 2,107.6

Admin & Other Exp. 2,385.1 2,800.5 2,831.2 3,151.8 Total Liabilities 18,027.4 18,094.4 18,916.9 20,118.0

EBITDA 315.4 1,118.8 1,354.0 1,583.5

Depreciation 251.8 283.1 289.9 296.7 Net Block inc. Capital WIP 13493.0 13465.0 14025.1 15328.4

EBIT 63.6 835.7 1,064.2 1,286.8 Non-Current Assets 2,158.6 1,658.5 1,920.9 1,939.6

Other Income* 199.7 112.3 216.1 129.4 Inventories 782.1 607.2 663.3 685.2

Interest Expense 206.0 147.0 73.5 67.7 Sundry Debtors 241.4 370.0 478.7 441.6

Profit Before Tax (PBT) 57.3 801.1 1,206.8 1,348.5 Cash & Bank Balance 84.0 37.8 122.5 128.5

Income Tax 51.5 -308.2 -265.5 -337.1 Other bank balances 16.0 16.8 16.8 16.8

Profit After Tax (PAT) 108.8 492.9 941.3 1,011.4 Other Cur. Assets and L&A 575.6 228.1 239.8 265.3

Growth (%) 353.2% 91.0% 7.4% Other non-current assets 290.5 231.9 233.0 235.6

Diluted EPS 0.5 2.3 4.4 4.8 Investment Property 169.0 166.7 166.7 166.7

Growth (%) 337.6% 91.0% 7.4% Non Current Investment 2,375.8 2,970.9 2,970.9 2,850.0

Shares in Mn 204.9 212.2 212.2 212.2 Total Assets 18,027.4 18,094.4 18,916.9 20,118.0

Exhibit: Ratio Analysis

Particulars FY17 FY18 FY19E FY20E Particulars FY17 FY18 FY19E FY20E

Profit Before Tax (PBT) 464.4 801.1 1,206.8 1,348.5 Earning Ratios (%)

Depreciation 438.5 283.1 289.9 296.7 EBITDA Margin (%) 6.2% 16.9% 19.8% 20.8%

Finance Costs 384.1 125.8 73.5 67.7 PAT Margins (%) 2.1% 7.5% 13.8% 13.3%

Chg. in Working Capital (694.9) 271.8 (43.4) 281.5 ROCE (%) 0.5% 6.0% 7.3% 8.3%

Direct Taxes Paid 134.8 162.9 265.5 337.1 ROE (%) 0.9% 3.7% 6.8% 6.9%

Other Charges (99.5) (60.6) - - Per Share Data (INR)

Operating Cash Flows 357.8 1,258.3 1,261.3 1,657.4 Diluted EPS 0.5 2.3 4.4 4.8

Capital Expenditure (855.3) (298.5) (850.0) (1,600.0) Cash EPS (CEPS) 1.8 3.7 5.8 6.2

Change in Investments 139.0 59.7 - 120.9 BVPS 59.1 62.1 65.6 69.4

Others 42.5 392.2 - - Valuation Ratios (x)

Investing Cash Flows (673.7) 153.4 (850.0) (1,479.1) P/E 129.1 13.3 9.7 9.0

Changes in Equity 477.1 - - - Price/BVPS 1.2 0.5 0.7 0.6

Inc / (Dec) in Debt (486.1) (1,100.8) (122.2) 32.1 EV/Sales 3.1 1.0 1.4 1.2

Dividend Paid (inc tax) (63.0) (357.1) (204.4) (204.4) EV/EBITDA 50.1 6.1 6.8 6.0

Financing Cash Flows (72.0) (1,457.9) (326.5) (172.3) Mcap/Sales 2.7 1.0 1.3 1.2

Net Cashflow (387.9) (46.2) 84.8 6.0 Balance Sheet Ratios

Opening Cash Balance 471.9 84.0 37.8 122.5 Debt - Equity 0.1 0.1 0.0 0.1

Cashflow during the year (387.9) (46.2) 84.8 6.0 Current Ratio 0.6 0.7 0.7 0.6

Closing Cash Balance 84.0 37.8 122.5 128.5 Asset Turn. Ratios 0.2 0.4 0.4 0.4

Source: SKP Research , *FY19- Other Income increases on account of profit on sale of land amounting to Rs. 107.867 mn

Figures in INR MillionExhibit: Income Statement

Figures in INR MillionExhibit: Cash Flow Statement

Figures in INR Million

Orient Paper & Industries Ltd.

SKP Securities Ltd www.skpsecurities.com Page 25 of 26

Notes: The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg and Thomson First Call. DISCLAIMER: This document has been prepared by SKP Securities Ltd, hereinafter referred to as SKP to provide information about the

company (ies)/sector(s), if any, covered in the report and may be distributed by it and/or its affiliates. SKP Securities Ltd., offers

broking and depository participant services and is regulated by Securities and Exchange Board of India (SEBI). It also distributes

investment products/services like mutual funds, alternative investment funds, bonds, IPOs, etc., renders corporate advisory

services and invests its own funds in securities and investment products. We declare that no material disciplinary action has

been taken against SKP by any regulatory authority impacting Equity Research Analysis. As a value addition to its clients, it

offers its research services and reports in various formats to its clients and prospects. As such, SKP is making these disclosures

under SEBI (Research Analysts) Regulations, 2014.

Terms & Conditions and Other Disclosures: This research report (“Report”) is for the personal information of the selected recipient(s), does not construe to be any

investment, legal or taxation advice, is not for public distribution and should not be copied, reproduced or redistributed to any

other person or in any form without SKP’s prior permission. The information provided in the Report is from publicly available

data, which we believe, are reliable. While reasonable endeavours have been made to present reliable data in the Report so far

as it relates to current and historical information, but SKP does not guarantee the accuracy or completeness of the data in the