Embed Size (px)

Citation preview

INTRODUCTION TO OPERATING COST

The information concerning the businessenterprise is very helpful to the management to control it in an efficiently way.

As the other branches like financial accountancy and management accountancy, the cost accountancy also serves the important information to the management regarding the operating efficiency of the business. It becomes very easy for management to lay down management policies, to guide management decisions or evaluate operating management performance with the information provided by cost accounting.

The term operation in business terminology refers to an activity of the business. It is very important to study the operations of the business in detail becausedepends on the operations, which it performs. The management should always concentrate on the efficiency of the operation and also the costs associated to the operations. It is very important to control the costs associated tothe operations for the enterprises like manufacturing companies, companies engaged in the process of extraction of materials from earth like, coal mines etc.

Generally, the above mentioned business enterprises depend on the operation that it has to be performed in to produce in to produce the final output. The costs associated with such operations are generallyhigher. These costs are called as“operating costs”.

The costs, which are incurred to perform the operation of the enterprise, arecalled as operating costs.

1

These costs are to be accounted forin order to arrive at the total costs ofoperation or process, which helps indetermining the price of the final product.

“Cost accounting is the classifying, recording and appropriate allocation of expenditure for the determination of the costs of products or services, and to the presentation of suitably; arranged data forthe purposes of control and guidance of management.”

It includes the ascertainment of the costs of every process, operation, services or contrast as may be appropriate. It deals with the cost of production, selling and distribution. It thus, the provision of suchanalysis and classification of expenditure as will enable the total cost of any particular unit of production to be ascertained with reasonable degree of accuracy and at the same time to disclose exactly how such total cost is constituted (i.e. the value of material used, the amountof labour and other expenses incurred) so asto control and reduce the cost.

THE FEATURES OF COST ACCOUNTING:

1. It is a process of accounting for costs.

2. It records income and expenditure relating to goods and services.

2

3. It provides statistical data on thebasis of which future estimates are prepared

4. and quotations are submitted.

5. It is concerned with cost ascertainment, cost control and cost reduction.

6. Finally it involves the preparation of right information to the right person at the right time so that it may be helpful to management for planning, evaluation ofperformance, control and decision-making.

:

ADVANTAGES OF COST ACCOUNTANCY

1. It enables a concern to measure the efficiency and than to maintain and improve it. This can be done with the help of comparison of data made available of the previous periods and

current period.

2. It provides information upon which estimates and tenders are based.

3

3. It guides for future production polices. It explains the cost incurredand there by provides data on the basis of which production can be appropriately planned.

4. The extract cause of decrease or increase in profit/loss can be detected. A concern may suffer not because of the cost of production is high or prices are low but also because the output is much below the capacity of the concern.

5. Efficiency of public enterprises. Costing has a more important role to playin public enterprises than in private enterprises. The primary objective of thepublic enterprises is not to raise profits but it is to serve the society byproviding quality good at cheaper rates.

The efficiency of a public sector can be judged by comparing its cost of production of its counterparts.

STATEMENT OF THE PROBLEM:

The main focus is on the operating costs of acoal mine in the

Singareni collieries company limited.

OBJECTIVES OF THE STUDY:The study of “operating costs of a

coal mine” proposes the following:

To identify the operations of the coalmines.

4

To identify the different technologies used to extract the coalfrom earth.To find the associated with the process under various technologies.

SCOPE OF STUDY:

The area of the study was restricted to the Singareni collieries company limited and its operations.

METHODOLOGY OF THE STUDY:

Data collection methodsThe study is based on both secondary

and examines the total costs vs. operating costs. The results are drawn mainly from theprimary and secondary data collected.

Secondary data has been collected from the various sources such as

Publications of the company. Business magazines. Journal, text books. Websites. Annual reports.

In order to gain information on currentprocess and operations the area chosen for

study is the BHOOPALPALLY IN WARANGALDISTRICT.

5

TOOLS & TECHNIQUES OF DATA COLLECTION:

1. This phase of the project deals with the various techniques adopted in gathering information.

2. The information and data was collected during my visit to the coal mine and GM office of Bhupalpally area.

3. The study required observation method,which has both of direct and indirect in NATURE.

4. A questionnaire was adopted was designed to collect the relevant information. Questionnaire consists ofboth open ended and close-ended questions.

5. The direct approach was adopted to gather as much information as possible, by interacting with persons working in organization such as operational engineers of the mine, additional GeneralManager (finance), deputy General Manager(finance), accounts officers and other executives and so on.

6. The direct approach was also adoptedto gather was also adopted to gather the relevant

7. Information for the study.

Limitations of the study:1. Coverage area was only limited to one coal mine in the company.

2. The financial data of the mines is limited to one year.3. The study is based on secondary data.4. There may be approximation.

6

C OMP AN Y PR OF IL E

INTRODUCTION OF COAL MINING IN INDIA:

Man had blessed with abundance of

natural resources, including mineral

wealth. That playvital role

in the development of a

country and promote the economic growth

when explored and made best use of them.

Coal, which is one if the

important minerals, is known to man

since ages and this natural wealth has

put to diverse use in the modern world.

Coal regarded as the fuel for growth,

the coal is animportant input for

power generation and many other

industries like iron and steel,

railway, shipping and construction

industries etc, a vital infrastructure

for economic development.

Despite the development of alternative

fuel sources like electricity, petrol

7

and solar energy, coal continues to be

major fuel material in many industries.

Thus coal industry plays an important

role in the industrial development of any

country, like India.

The world coal consumption is projected

to go up from 4.7 billion tines in 1999

to 6.4 billion tones by 2020, primarily

in china and India, which are expected

tom account for 75% of the increased

consumption.

In India coal mining was started

in 1774 and is still

significantly under the Government

control and ownership with coal India

Limited (CIL), along with Government

with its following subsidiaries are

become number onecoal producer in

India.

1. Eastern coal fields India limited (ECFIL) – Sanctrica, west

Bengal.

2.Bharath cooking coal limited (BCCL) – Dhanbad, Bihar

3. Central coal fields limited (CCL) – Ranchi, Bihar.

4. Northern coal fields limited (NCFL)Singrauli, Madhya

Pradesh

8

5. Western coal fields limited (WCFI) – Nagpur, Maharashtra.

6. Mahanadi coal fields limited (MCL) – Sambalpur, Orissa

7. Central mining planning &Designinstitute Limited

(CMPDIL) - Ranchi, Bihar

8. Singareni Collieries Company

Limited (SCCL) – Kothagudem,

Andhra Pradesh.

SINGARENI COLLIERIES COMPANY LIMITED:

ORIGIN:

A remarkable little adventure gave

birth to this giant corporate entity that

us today the Singareni Collieries Company

Limited.

Way back on a dark night in 1870 a

group of Pilgrims whoon their way

to havea Darshan of Lord Rama

at Bhadrachalam Temple (near Singareni

Village) has lit a fire to prepare their

meal. One of the supporting stones

on their

9

makeshift stove caught fire. The

incident was immediately reported to the

local Government.

This led to an extensive survey by

Dr. William King, an eminent Geologist,

which confirmed the

revolutionary discovery of mammoth

deposits of coal in the Godavari Valley.

The rest, as they say, is HISTORY :

The year 1886 witnessed the

formation of the Hyderabad Deccan

Company Private Limited and It acquires

the mining rights for exploiting

the coal reserves. The first

commercial operation commenced

at Yellandu (Khammam District) in

Andhra Pradesh in 1889. In 1921 the

company was re-christened the “Singareni

Collieries Company Limited” and its script

listed on the London Stock Exchange.

The mining rights for exploiting the

coal reserves were acquiredby the

Hyderabad DeccanCompany,which

was incorporated at London Exchange.

Hence the first extracting of coal was

started at Yellandu in 1886 by Hyderabad

Deccan Company.

10

The companybecome Government Companyafter

Nizam purchased its shares from LondonStock Exchange in1945.With this SCCL became the

first-ever government

management Coal Company in India. Later in

the year 1949, SCCL came under the

control of Government of India and

Andhra Pradesh as a joint venture with

equity ratio of 49% and

51%respectively.

The Bhupalpally Area was started the

ensuing the coal since the year 1997. Till

it has working as five underground mines

and one opencast sector – I project. The

life of the coal mines nearly 75 years.

So, the village of the Bhupalpally had

changed as Mandal and it has developing

Area.

The SCCL is engaged in coal mining in

four districts of Andhra Pradesh namely,

Khammam, Karimnagar, Adilabad and Warangal.

In overall India it spreads to 6%

geographical area producing 10% of total

coal.

The Operation Areas of SCCL areas follows:

KHAMMAM DISTRICT Kothagudem, Yellanduand

Manuguru.

11

ADILABAD DISTRICT Bellampalli,Mandamarriand

Srirampur

KARIMNAGAR DISTRICT Ramagundem I,

II, III WARANGAL DISTRICT

Bhupalpally.

The Coal reserves stretch over

350 squares Kms. of Pranahitha Godavari

valley of above Districts of Andhra

Pradesh with provide geological reserves of

9384, million tones of coal.

SCCL now operates Thirty Six (36)

under Ground Mines and fourteen (14)

open cast Mines in these four (4)

Districts.

MILE STONES OF TECHNOLOGY INTRODUCTION :

1948 Introduction of machine mining (Shuttle car)

1951 Electric Coal Drills.

1953 Electric cap Lamps.

12

1954 Flame proof Mining Machinery.

1975 Open Cast mining.

1979 Side Dump Loaders (SDL s)

1981 Load hauls Dumpers.

1983 Mechanized Long wall.

1986 Introduction of computers and walking

Dragline

in

Opencast Mines.

1989 French Blasting Gallery Technology.

1994 In pit crushing & conveying Technology.

Vision , Mission and Principles GuidingSustainable

Developmen

t:

Vision :

13

a. Vision shall bring into view

untapped potentials and unutilized

opportunities that await exploitation

as well as problems and challenges

that may impede progress. The vision

must identify catalytic forces that can

be harnessed.

b. It must express aspirations,

determination and commitment for self

realization.

c. Though planning and prediction over

long time horizon is difficult, desired

end results must be dreamt and strategies

to accomplish them shall be drawn. Vision

needs a subtle blend of humility and

courage to dare.

d. Vision is realizable only when it

neither has lofty optimism nor extreme

pessimism.

The Vision ofSingareni is,

“Singareni Collieries to produce coalqualitatively and cost

14

effectivelyina socially and

environmentally

sustainable manner, valued by

customers, employees, and the community”.

To achieve this vision,

a.It aims to achieve a best safety performance.

b. Adopt best environmental

practices strive to bring back the

nature to the best possible original

extent.

c. Attain a sustainable competitive

advantage in the marketplace.

d. Align production to meet market demand.

e. And, continuously improve

operational performance.

SCCL – MISSION :

To retain role of a premier coal

producing company and excel in a

competitive business environments.

15

To strive for self – reliance by

optimum utilization of existing

resources and earn adequate returns

on capital employed.

To exploit the available mining

blocks with maximum conservation

and utmost safety by

adopting suitable technologies and

practices and constantly upgrading

them against international bench marks.

To supply reliable and qualitative coal

in adequate quantities and strive to

satisfy customers needs by constantly

sharing their experience and customizing

our product.

To emerge as a modal employer and

maintain harmonious industrial relations

with the legal and social frame work of

the state.

To emerge as a responsible company

through good corporate governance, by

laying emphasis on protection of

16

environment & ecology and with due regard

for corporate social obligations.

Gloom to Glory :

The SCCL was receiving budgetary

support from both Government of India and

government of Andhra Pradesh till some time

age, but they later abandoned. Also the

pricing of coal was decided by government of

India keeping its impact on other major

sectors like, power, Railways, cement etc.

The prices were not revised regularly; also

hike in input cost due to periodical

revisions of national coal wage agreements

(NCWA), stores and interest were also not

fully compensated by Government. The

frequent strikes by the workers, law and

order problems, low productivity, apart from

un remunerative coal price vis-à-vis cost of

production during the period 1989-90 to

1991-92 affected the financial health of the

company and refer referred to BIFR in 1992,

but due to liberal financial package extended

by the Govt. of in India

17

consultation with Govt. of AP, and sustained

efforts made by the management of SCCL

and Trade Unions, a modest financial

turnaround was achieved. The

company earned profit of

Rs.17.76Crore and 26.64Crore in 1993-94

and 1994-95 respectively. My

March 1994, SCCL came out of the

BIFR purview. Following remedial

measures/reforms were taken by the company

for Success:

i. Unifying Trade Unions through Path Breaking

Elections.

ii. High Pitch

Communication Drive

harnessing media, launching

literacy programs.

iii. Focused multi-faceted

worker’s welfare program. Iv.

Establishing outsourcing of

non-core and ancillary

activities.

18

v Innovative programs Launched (Dial-your-GM, Field

Visits, Interactions and Follow-ups).

vi. Fuel Supply Agreements – Technology infusion for

Quality Testing, Workforce visits to client sites.

vii. Focus on Safety, Environment Protection and Labour

Welfare.

The process of turning around a Sick

Company, which commenced in 1997-98,

reached its logical conclusion when SCCL

totally wiped out its accumulated losses

and entered the financial year 2003-04

with a net profit of RS.80.45core after

issuing a dividend of

RS.86.70Crore. DETAILS OF LOCATION

OF VARIOUS UNITS:

SCCL operates 51 mines including 14 open

cast mines in 10 operating areas in the

state of Andhra Pradesh.

Area UG Mines, OC mines, Total & District.

a) Area / Region – wise production :

19

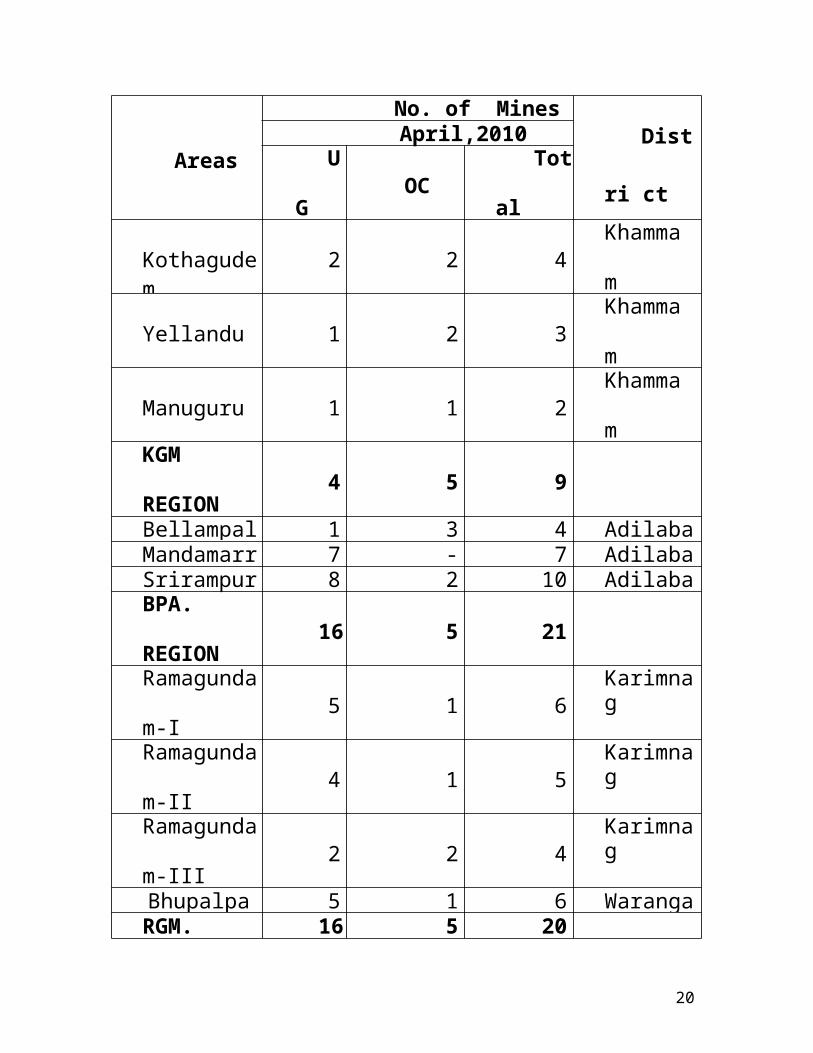

Areas

No. of MinesDist

ri ct

April,2010U

GOC

Tot

al

Kothagudem

2 2 4Khamma

m

Yellandu 1 2 3Khamma

m

Manuguru 1 1 2Khamma

mKGM

REGION4 5 9

Bellampalli

1 3 4 AdilabadMandamarr

i7 - 7 Adilaba

dSrirampur 8 2 10 AdilabadBPA.

REGION16 5 21

Ramagunda

m-I5 1 6

Karimnag

Ramagunda

m-II4 1 5

Karimnag

Ramagunda

m-III2 2 4

Karimnag

Bhupalpally

5 1 6 WarangalRGM. 16 5 20

20

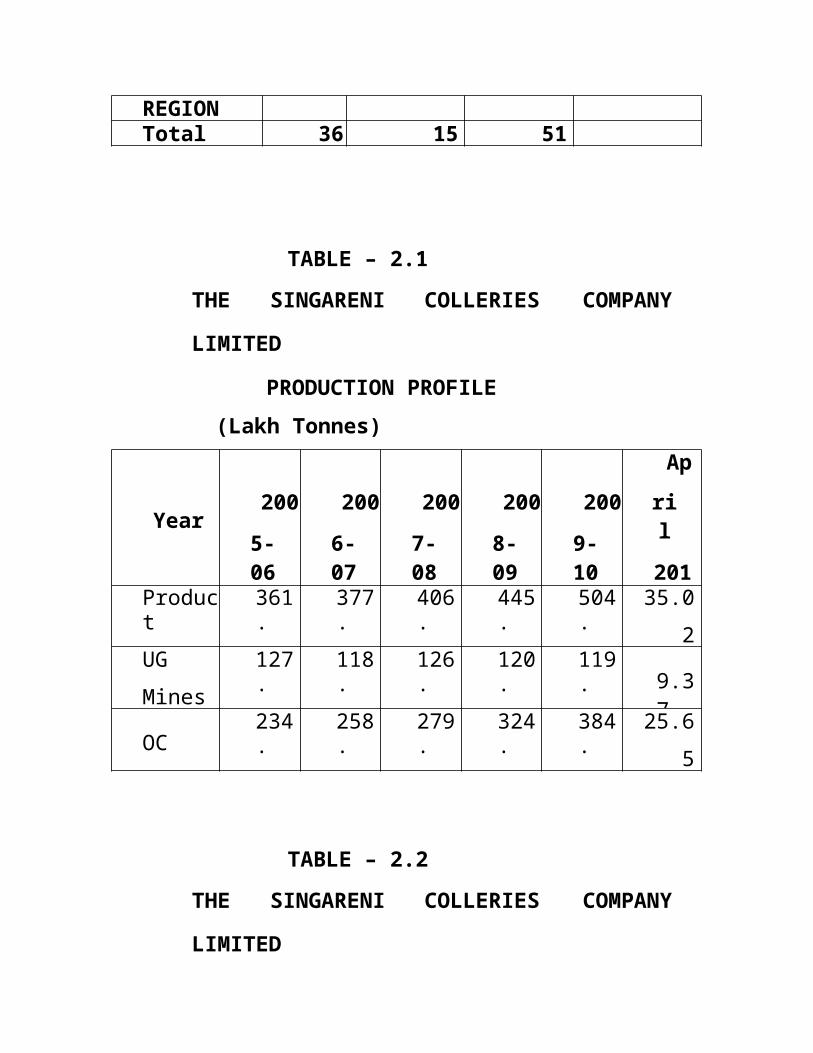

REGIONTotal SCCL

36 15 51

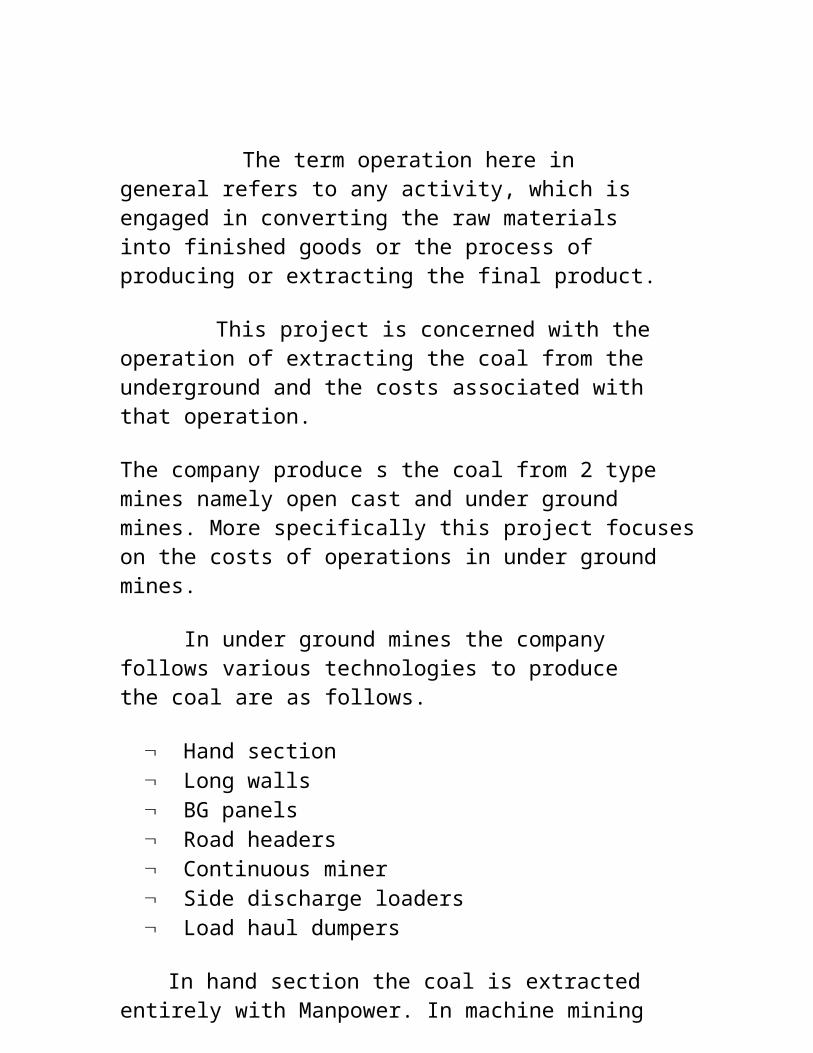

TABLE – 2.1THE SINGARENI COLLERIES COMPANY

LIMITED

PRODUCTION PROFILE(Lakh Tonnes)

Year2005-06

2006-07

2007-08

2008-09

2009-10

April201

Product

361.

377.

406.

445.

504.

35.02

UGMines

127.

118.

126.

120.

119. 9.3

7OC

234.

258.

279.

324.

384.

25.65

TABLE – 2.2THE SINGARENI COLLERIES COMPANY

LIMITED

21

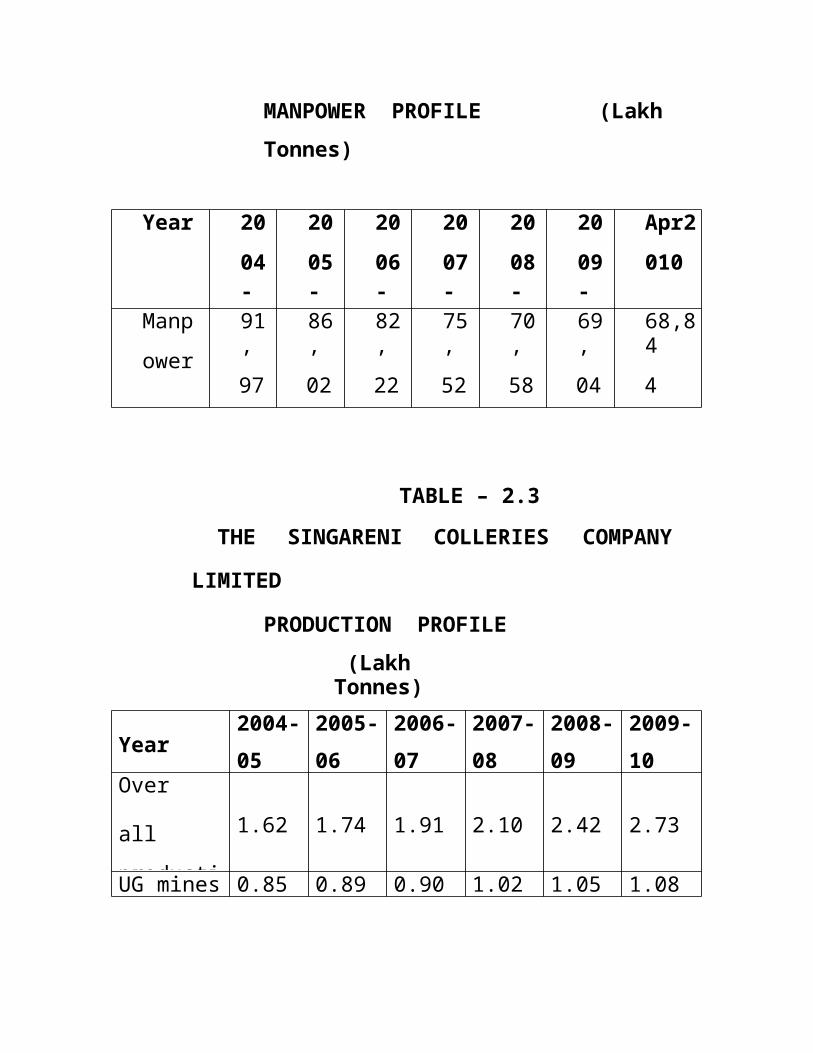

MANPOWER PROFILE (LakhTonnes)

Year 2004-

2005-

2006-

2007-

2008-

2009-

Apr2010

Manpower

91,97

86,02

82,22

75,52

70,58

69,04

68,844

TABLE – 2.3THE SINGARENI COLLERIES COMPANY

LIMITED

PRODUCTION PROFILE(Lakh

Tonnes)

Year2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

Over

allproducti

1.62 1.74 1.91 2.10 2.42 2.73

UG mines 0.85 0.89 0.90 1.02 1.05 1.08

22

The term operation here in general refers to any activity, which is engaged in converting the raw materials into finished goods or the process of producing or extracting the final product.

This project is concerned with the operation of extracting the coal from the underground and the costs associated with that operation.

The company produce s the coal from 2 type mines namely open cast and under ground mines. More specifically this project focuseson the costs of operations in under ground mines.

In under ground mines the company follows various technologies to produce the coal are as follows.

Hand section Long walls BG panels Road headers Continuous miner Side discharge loaders Load haul dumpers

In hand section the coal is extracted entirely with Manpower. In machine mining

the coal is produced with the help of machines. In machine mining the production process depends largely on machines but it requires some skilled manpower also. The study focuses on the machines called side discharge loaders.

23

For the purpose of the detailed study of the production process of coal in singareni collieries the coal mine Bhupalpally area was observed.

In the mine, the coal is produced with the help of machines called SDL s (Side Discharge Loaders) besides the hand section.

Extraction of coal in hand section entirely depends on the

man power. The process of extraction of coalfrom an underground mine which is using the technology of hand section is as follows.

Blasting the faces with the help of explosives. The face is the place where the coal is located; the coal will be separated from the earth using these explosives.

The process of blasting makes it easy toremove the coal from the earth. This processis known as coal cutting. The men ho do thisprocess are known as coal cutters. After cutting into pieces the coal will be filled into tub trains. The men who perform this process are known as coal fillers. The tub trains bring the coal from under ground to the surface using track.

From the surface the coal is transportedto the coal screening plant (CSP) for cleaning and other process the coal can be transported to the customers of Singareni.

Another technology of extracting of coal is using SDL s, the main objective of introducing SDL s is to improve safety, avoidthe human drudgery of carrying baskets at work space and also better

24

conservation of coal. In the mains where thetechnology of SDL s is using the coal can beextracted as follows.

Blasting of coal with the help of explosives to separate it from the earth.The machines instead of men can fill the coal.These machines are called as Side Discharge Loaders (SDL s) after the blasting of the coal SDL s move towards the face, takes thecoal into its bucket and comes back (in thesame direction without turning back) anddischarge the coal onto a belt. The belttakes the coal and dumps into the tubs ofthe trains and these tubs will bring thecoal to the surface.

The capacity of the bucket of the machine is one tonne. The time taken by themachines to move from the coverage belt to the face where the coal is blasted, to liftcoal into the bucket and to discharge the coal onto the coverage belt is called lead time. The lead time takes the major part incomputing the cost of the production. Shorter the lead time larger the productionand vice e versa.

The process will generally include

the following costs.

1. Wages (Filling and Time rated )2. Wages of other executives.3. Explosives.4. Other stores.5. Power.6. Coal transportation.7. Stand stowing8. Mine over heads.9. Work shop over heads.10. CSP over heads

25

11. Depreciation of mines.12. Depreciation of common assets.13. Interest.14. Area over heads.

The system being followed band the steps involved in preparation of cost sheet under the present costing system involved in preparation of cost sheet under the present costing system are explained as follows.

i. A perform cost sheet followedin presentation of costsheets

for hand section andother technologies isfurnished. Theexpenditure is presented

through the cost sheet undervarious elements of cost.

ii. Cost ascertainment is donethrough cost centers allotted tothe various activities in underground and surface operations atthe mine and overhead costs

for the expenditure onserviceand administrative

department.

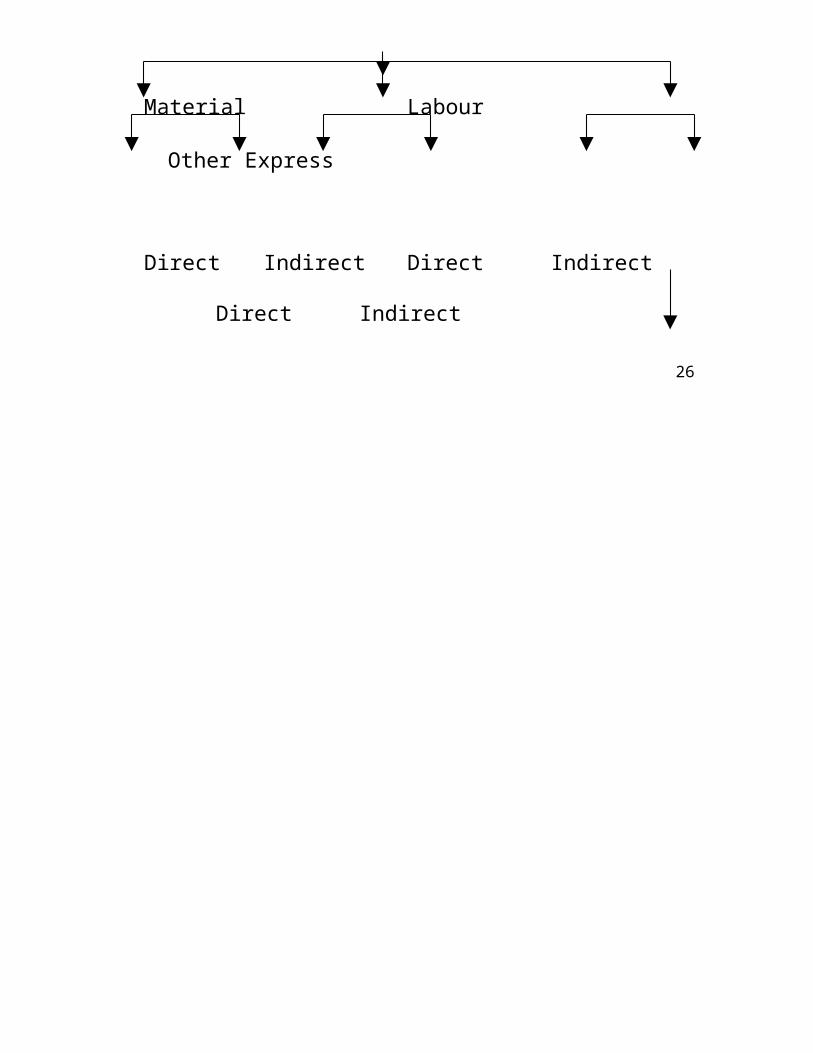

Elements of costs: Elements of Costs

Material Labour

Other Express

Direct Indirect Direct Indirect

Direct Indirect

26

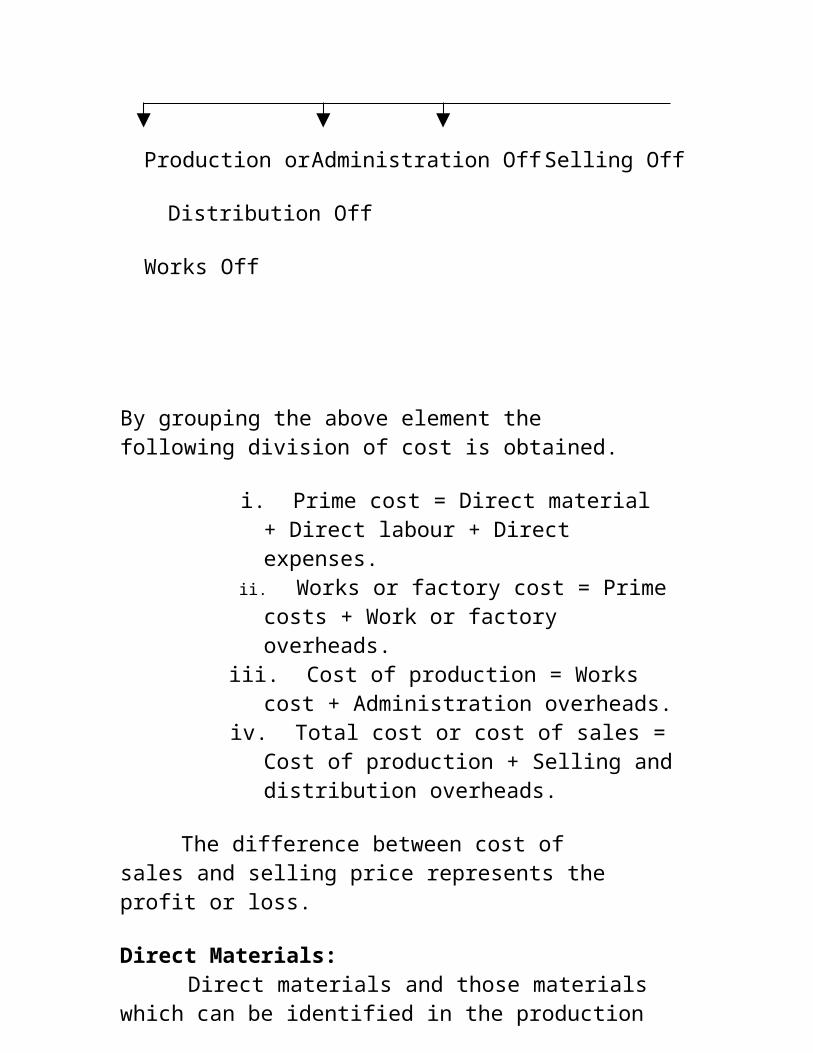

Production orAdministration OffSelling Off

Distribution Off

Works Off

By grouping the above element the following division of cost is obtained.

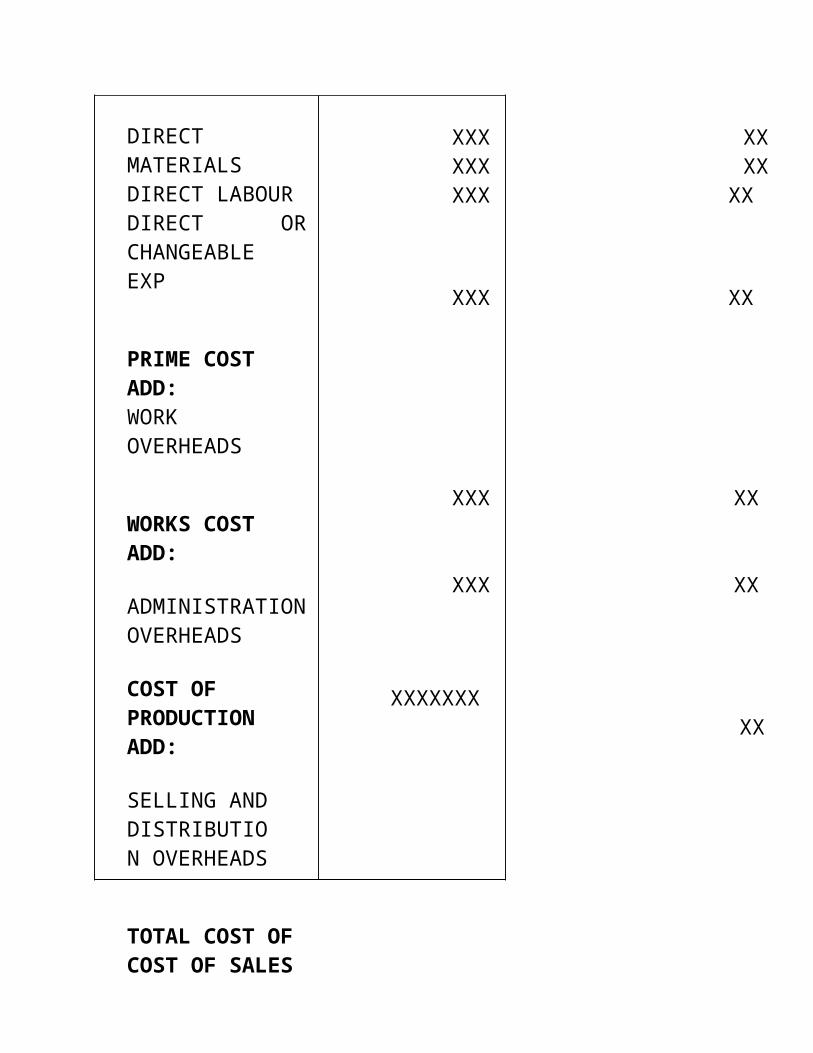

i. Prime cost = Direct material+ Direct labour + Direct expenses.

ii. Works or factory cost = Primecosts + Work or factory overheads.

iii. Cost of production = Works cost + Administration overheads.

iv. Total cost or cost of sales = Cost of production + Selling anddistribution overheads.

The difference between cost of sales and selling price represents the profit or loss.

Direct Materials:Direct materials and those materials

which can be identified in the production

and can be conveniently measured and directly charges to the product. Thus, thesematerials directly enter the production and form a part of the finished product. Forexample timber in furniture making clothe in dress making and bricks in building a house.

27

The following are normally classified asdirect materials

i. All raw materials like jute in the manufacturing of gunny bags, pig iron in foundry and fruits incanning industry.

ii. Material specifically purchased for a specific job, process or order like glue for a book building, starch powder for dressing yarn etc...

iii. Parts or components purchasedor produced like batteries for transistor radios and tries for cycles.

iv. Primary packing materials likecartoons, wrappings, cardboard, boxes, etc... Used to protect finished product from climate conditions or far easy handling inside the factory.

Indirect materials are those materialswhich cannot be classified as direct materials. For examples, consumables like cotton waste, lubricants, brooms, rags, cleaning materials, materials for repairs and maintenance of fixed assets, high speeddiesel used in power generators etc.

Direct Labour:

Direct labour is all labour expendedin altering, construction, composition, confirmation or condition of the product.In simple words it is that labour which can be conveniently identified or attributed wholly to a particular job, product of extended in converting raw materials into finished goods.

Indirect wages are the wages paid to supervisors, inspectors etc...Through not direct labour.

Direct Expenses:

28

All expenses, which can be identified toa particular cost center and hence directly charged to the center, are known as direct expenses. In other words all expenses (other than direct materials and direct labour) incurred specifically for a particular, job, department etc., are called direct expenses. These are directly charged to the product, job, department etc.

Examples of such expenses are royalty, excise duty, hire charges of a specific plant and equipment.

Overheads:

Overheads may be defined as the aggregate of the costs of indirect materials, indirect labour such other expenses including services as cannot conveniently be charged direct to specific cost units. Thus, overheads are all expensesother that direct expenses.

Overheads are sub-divided as

a. Manufacturing expenses. b. Administration overheads. c. Selling overheads.d. Distribution overheads.

e. Research and development overheads.

Expenses included from costs:The total of a product should

include only those items of expenses which are a charge against profit. Items of expenses which are relating to capital assets which are relating to capital assets,capital losses, payments by way of distribution of profits matters of pure finance should not from a part of the costs.

29

MINING:Mining is an economic activity. It

does not belong to a service sector where expenditure is permitted without matching financial returns. Coal mining activity, therefore, is undertaken not only to meet thecoal demand but also to enhance financial resources of the coal producer for further advancement and growth. Even when coal pricesare controlled or regulated by the Govt., a coal producing organization is either given an average price forcoal that is expected to yield a reasonablereturn on overall investments by the producer or is given a subsidy as comprehensive for activities required to bedone but are not economical. The coal miningindustry in India is largely in publicsector and guidelines of the Govt., presently (1998), are that, while approving any coal mining new, reorganization or expansion project, the project should indicate a return (to be precise- internal rate of return- IRR) on investment of minimum 17% at 85% levelof projected output. It is, therefore, clear that even the public sector coal mining activity is expected to be an economic activity. The private sector, obviously, willlike to have similar or more return

on investment. Any mining activity, therefore, has to be viable. Not only just viable but also that which will give minimumacceptable return on investment, of course, following law of the land. Thus all economicactivities, including mining are permitted activities that incur least cost and are viable.

IMPORTANT OF TRENDS:

1. It has been started that, opencast costs are rising at a rate slower than costsfor under ground. Consequently, many properties, economical today for underground mining, will become opencast able in near future as has happened in the past. A portionof kargali underground mine was converted to opencast in1950’s.similarly, a portion of kurasia underground was converted

30

to opencast in 1960’s. Today, many erstwhileunderground mining properties. In full or part, are being worked and are being converted to be worked by opencast. This trend music must be given due consideration while deciding whether a property shouldbe worked by opencast or by underground mining to be cheaper by10-15% or so compared to opencast mining, the property should not be worked by underground. After all, an underground minemay have a life of 15 to 20 years and more with in which time opencast mining become more viable in many cases, by the timedepth is worked by opencast, deeper depth mayalso become viable for opencast.

2. Similarly, transport costs byrope haulage are rising sharply thantransport costs by belt conveyor. This isdue to the fact that, a rope haulagesystem is manpower oriented and wagecost is increasing substantially each year.Therefore, if there is only a sightdifference between estimated mining costs forrope haulage and belt system should bepreferred if the installation is to last fora few years. Further, belt conveyors can dealwith increased outputin future more affectivity.

3. Shaft versus incline is another case which can be cited. Supremacy of shaft

to meet ventilation requirements is undisputed. As far as coal raising is concerned, an incline equipped with the beltconveyor for coal raising with a rail track for supply issuperior to a shaft for similar duties expect perhaps for depths more than 250m at present. In olden days, say three decades ago, initial depths exceeding 70m were planned with shafts only as mine openings. Today, coal raising from such depths is planned through inclines with belt conveyor.Recent mines have been planned with inclinesfor coal raising from depth exceeding 200m.

4. Marginally better estimated viability for imported technology, not sufficiently field proven, should not be considered for adoption. Only when substantial advantages of such a technology calls for a trail only in geo-mining conditions suitable

31

for such a technology have not yielddesired results on sustained basis and suchequipments have ultimately become a Burdonon the industry.

Trends and experience, therefore, have tobe given due importance before taking final decisions on current estimates. Trends and experiences are facts well established whileestimates are projections only, through wellintended, which may or may not come true further, estimates are always coloured by subjective thinking of the estimator which can be made more objective by considering past and current trends and experience in similar circumstances. It only means that, realistic and sustainable improvements should improvements should be planned and executed.

SCOPE:

The scope of operation costing is very wide and includes the following.

Where there is only one process or operation (unit costing)

When they concern rendering some services rather than manufacturing the goods called service costing (operating cost)

When in one process there are different operations which are to beperformed to convert the raw

material into finished product (operating costing)

When the raw material in order tobe converts or into finishedproducts has to per certain stagesor process called process costing.

1. ONE OPERATING (UNIT)COSTING:

32

This is a method of costing by units of production and it adopted where production is uniform and a continuous affair, units of output are identical and the cost units are physical and natural. Thecost per unit is determined by dividing the total cost during a given period by the number of units produced during that period.This method of costing is generally adopted where an undertaking is engaged in producingonly one type of product or two or more products of the same kind but of varying grades of quality. The industries where thismethod of costing is used are collieries,sugar, mills, cement works, brick works, paper mills etc. In all these cases, workis a natural unit of cost.

2. OPERATING (SERVICE) COST:

Service costing is that form of operation costing which applies where standardized services are provided either byan undertaking or by a service cost center with in an undertaking. The method may be used where service is not completely standardized, but where it is continent to regard it is such, and to calculate average cost per period in relation to the standardized unit of measurement. Thus it isthe cost of producing and maintaining a

service. It is a method of costing applied to undertaking which provides service ratherthan production of commodities. The icesto be costed could either be:

1. Transport service:Tramways, Railways, Bus, Transport.

2. Supply service:Gas supply, Electricity supply, Watersupply.

3. Welfare service:Hospitals, canteen, Libraries.

33

4. Municipal service:Street lighting, Road maintenance etc.

INPUT AND OUTPUT COSTS:

Input costs are constantly changing, actually constantly rising. Further, due to recent change in favour of global market economy, the price of coal has to be competitive with imported coal of better quality. The market forces will, thus, restrict selling price of coal requiring mining to be more and more effective. A visible mine of today, therefore, may not beviable tomorrow due to rising input costs and limitations on raising coal price. The situation will require fresh look on the exiting system of mining to evolve a system that will keep the production costs contained. Planning, therefore, is a continuous process. Even profit earning mines should be given a fresh look every nowand than for improving economics and reducing costs. Or else, they will also become uneconomic in near future.

In any activity, only a few key items constitute major share of costs. In opencasts. In opencast, the activities of

drilling, blasting and transport are the keyactivities where attention should first be diverted. In medium mechanized underground mines, the important activities may be supports, coal availability for SDL/LHD and coal clearance. Costs of these key items have to be keenly and constantly watched andimproved upon.

For any worthwhile assessment, it is veryessential that item wise and activity wise cost data are correctly recorded, stored andanalyzed. Further, they should be made available to the concerned executives at regular intervals and well in time before they become too old to be effective. If theydata are not correctly recorded and

34

timely furnished, improvements for cannot be properly planned and executed.

From the above, we can conclude that,while calculating economics and preparing estimates, we have to consider:

1. Nature of deposit2. Quantum of projected production and degree of mechanization. Effect of reduced or increased production than projected.

3. Requirement and availability of recourses and their phasing:

i. Financial (including loan)ii. Equipment (including hire),

particularly from indigenous sources.

iii. Manpower (including contact).4. Proximately of coal consumer and willingness to pay higher price, if required.

5. Capabilities of management.6. Law of land.7. Intrastate required and infrastructure available.8. Past trends and future projects.9. Social atmosphere and expectations of the people likely to be disturbed.

10. Possibilities of early return on capital and rate of return on capital to

be invested.11. Period for which a facility is to becreated and the time it takes to be created.

It will, thus, be seen that, economics of a mine is not a mere theoretical exercise. It is sum total of possibilities and restrictions.

35

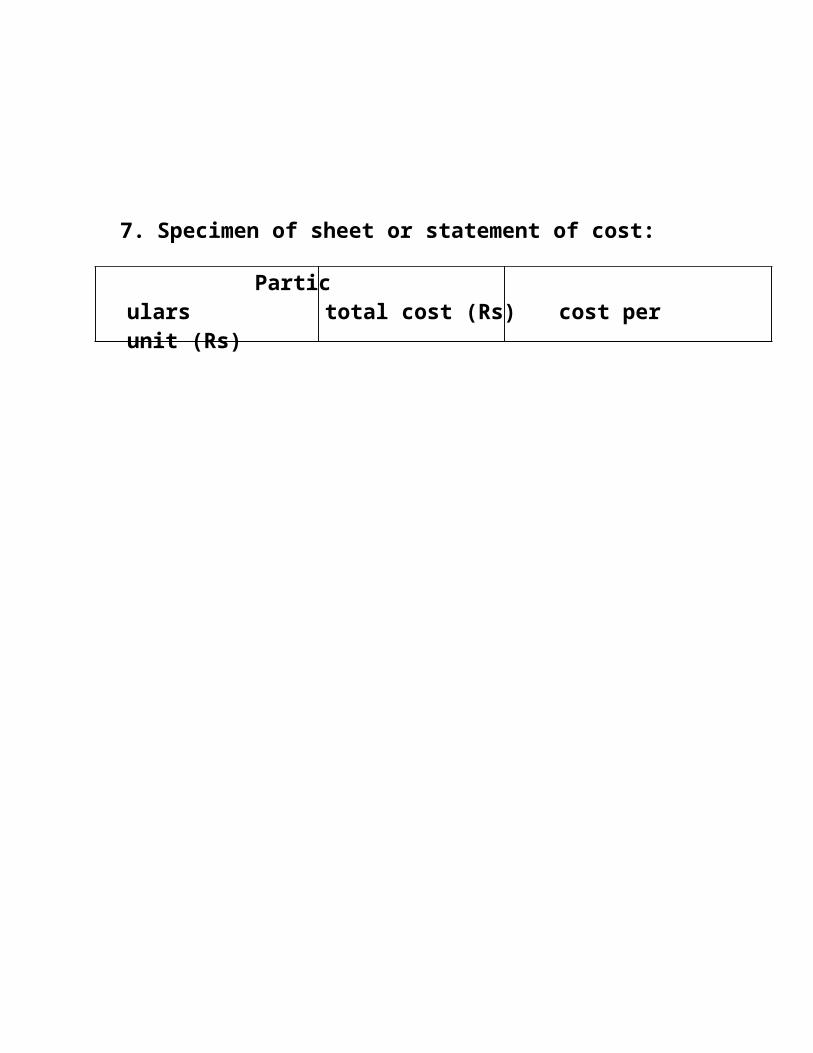

7. Specimen of sheet or statement of cost:

Particulars total cost (Rs) cost per unit (Rs)

36

DIRECT MATERIALS DIRECT LABOUR DIRECT ORCHANGEABLEEXP

PRIME COSTADD:WORK OVERHEADS

WORKS COST ADD:

ADMINISTRATIONOVERHEADS

COST OF PRODUCTION ADD:

SELLING ANDDISTRIBUTION OVERHEADS

TOTAL COST OFCOST OF SALES

XXX XXXXX XXXXX XX

XXX XX

XXX XX

XXX XX

XXXXXXXXX

37

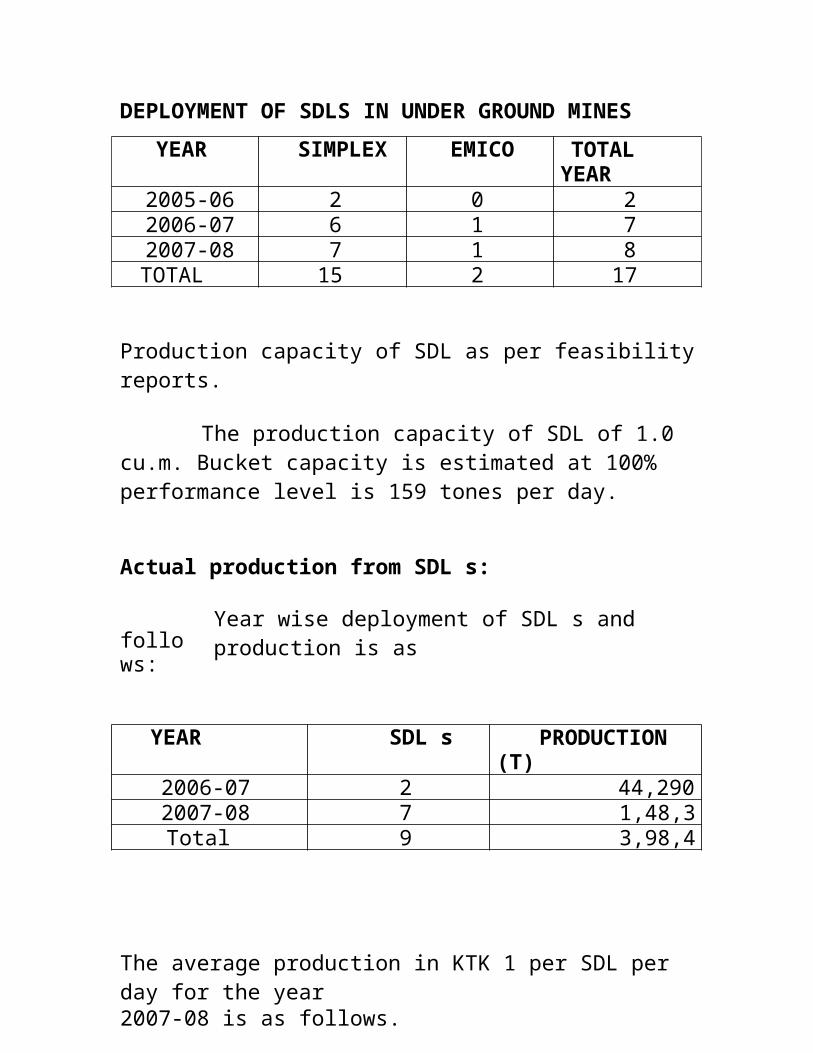

DEPLOYMENT OF SDLS IN UNDER GROUND MINESYEAR SIMPLEX EMICO TOTAL

YEAR2005-06 2 0 22006-07 6 1 72007-08 7 1 8TOTAL 15 2 17

Production capacity of SDL as per feasibility reports.

The production capacity of SDL of 1.0cu.m. Bucket capacity is estimated at 100% performance level is 159 tones per day.

Actual production from SDL s:

follows:

Year wise deployment of SDL s and production is as

YEAR SDL s PRODUCTION (T)

2006-07 2 44,2902007-08 7 1,48,3

88Total 9 3,98,455

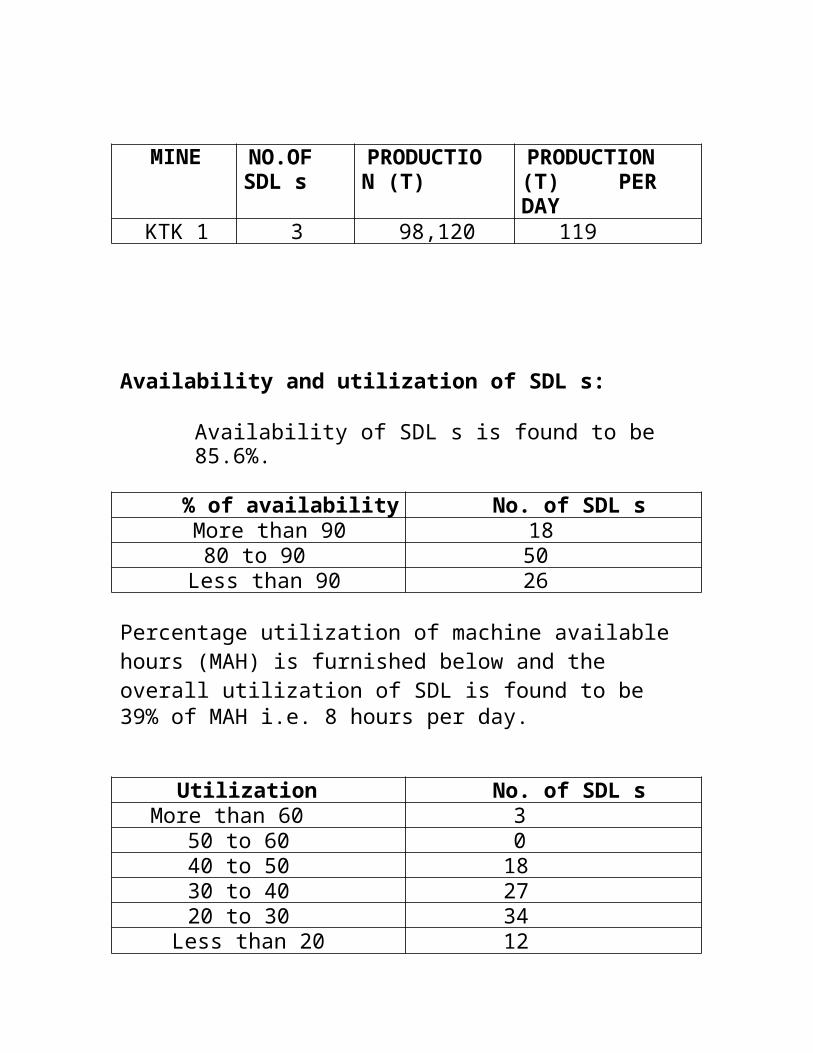

The average production in KTK 1 per SDL per day for the year2007-08 is as follows.

38

MINE NO.OFSDL s

PRODUCTIO N (T)

PRODUCTION (T) PER DAY

KTK 1 3 98,120 119

Availability and utilization of SDL s:

Availability of SDL s is found to be 85.6%.

% of availability No. of SDL sMore than 90 1880 to 90 50

Less than 90 26

Percentage utilization of machine availablehours (MAH) is furnished below and the overall utilization of SDL is found to be39% of MAH i.e. 8 hours per day.

Utilization (%MAH)

No. of SDL sMore than 60 3

50 to 60 040 to 50 1830 to 40 2720 to 30 34

Less than 20 12

39

No of SDL s

2 3 4Man shifts 129 159 186Men in roll 156 185 217

Detailed analysis of the idle hours:

SDL s is idle for 52% of available time. The reasons for idleness are analyzed and furnished below:

1 Idle due to shift 15%2.Idle due to roof supporting

19%3 Idle due to machine 3%4.Idle due to out by problem

15%

Total 52%

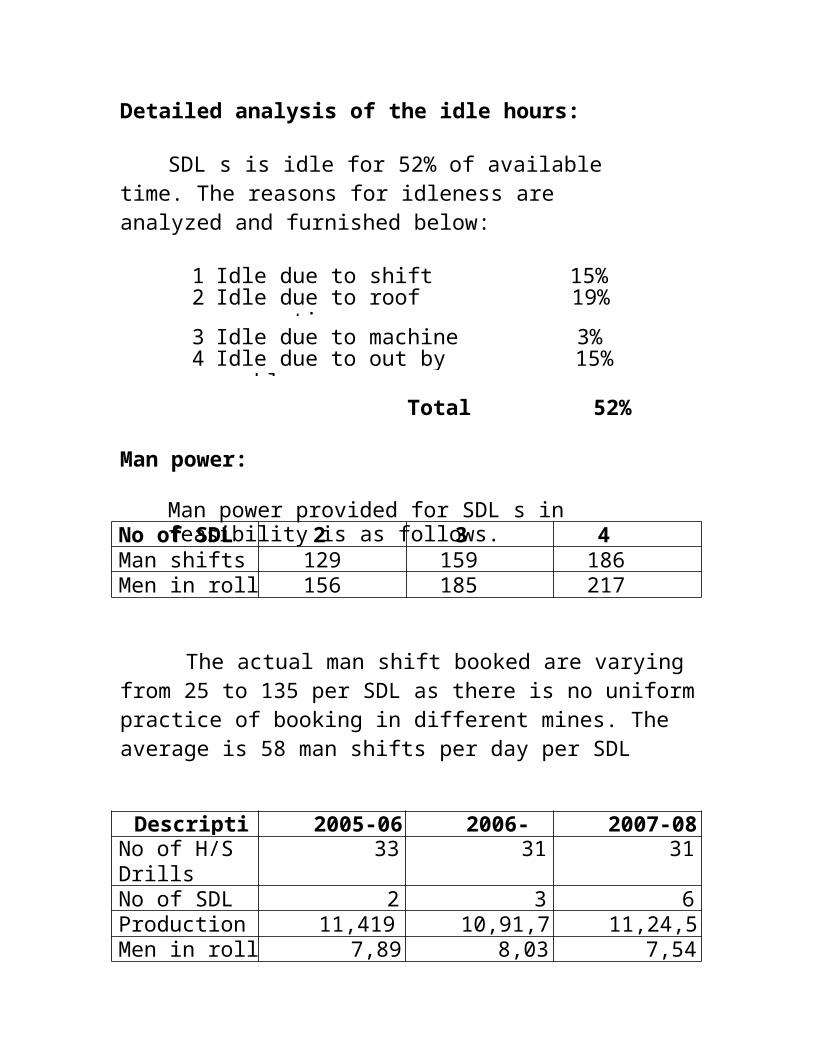

Man power:

Man power provided for SDL s in feasibility is as follows.

The actual man shift booked are varying from 25 to 135 per SDL as there is no uniformpractice of booking in different mines. The average is 58 man shifts per day per SDL

Description

2005-06 2006-07

2007-08No of H/SDrills

33 31 31

No of SDL s

2 3 6Production (t)

11,41903

10,91,767

11,24,566Men in roll 7,89

78,033

7,542

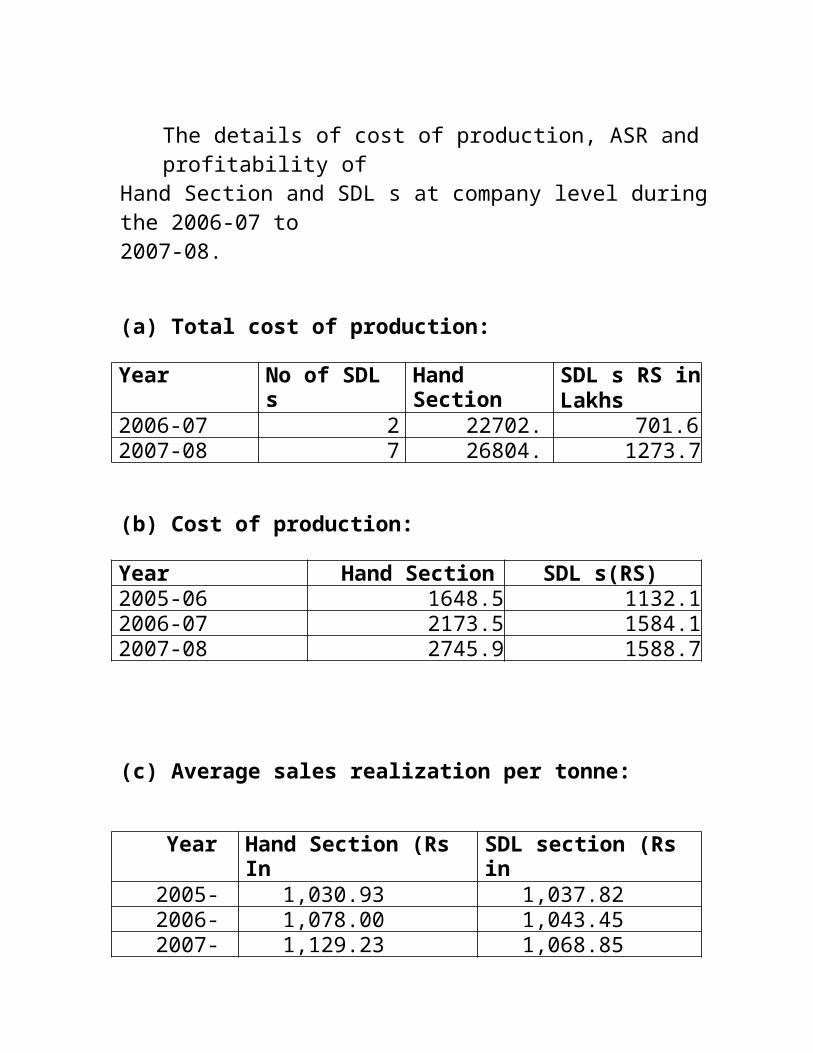

Cost of production from SDL s and Hand Section at company level:

40

The details of cost of production, ASR andprofitability of

Hand Section and SDL s at company level duringthe 2006-07 to2007-08.

(a) Total cost of production:

Year No of SDL s

Hand SectionRs. In

SDL s RS inLakhs

2006-07 2 22702.60

701.612007-08 7 26804.

691273.70

(b) Cost of production:

Year Hand Section SDL s(RS)2005-06 1648.5

91132.132006-07 2173.5

91584.122007-08 2745.9

91588.77

(c) Average sales realization per tonne:

Year Hand Section (Rs InLakhs)

SDL section (Rs inLakhs)2005-

061,030.93 1,037.82

2006-07

1,078.00 1,043.452007-08

1,129.23 1,068.85

41

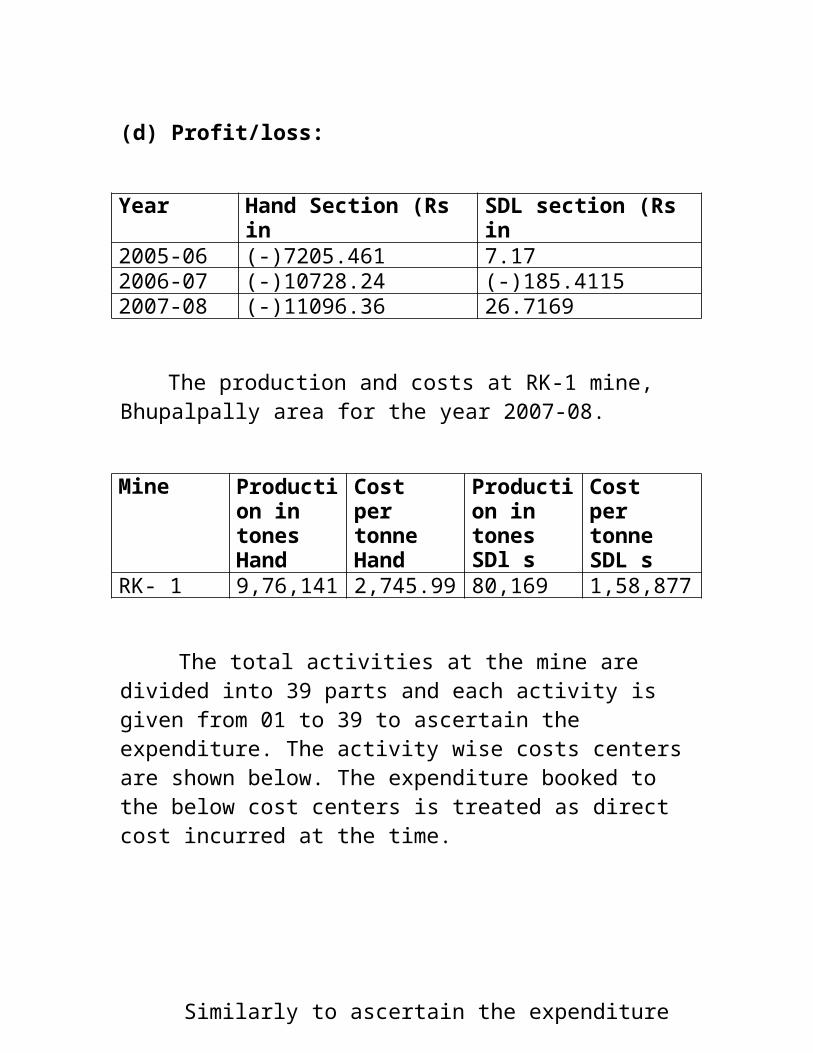

(d) Profit/loss:

Year Hand Section (Rs inLakhs)

SDL section (Rs inLakhs)2005-06 (-)7205.461 7.17

2006-07 (-)10728.24 (-)185.41152007-08 (-)11096.36 26.7169

The production and costs at RK-1 mine, Bhupalpally area for the year 2007-08.

Mine Production in tones Hand

Cost per tonne Hand

Production in tonesSDl s

Cost per tonne SDL s

RK- 1 9,76,141 2,745.99 80,169 1,58,877

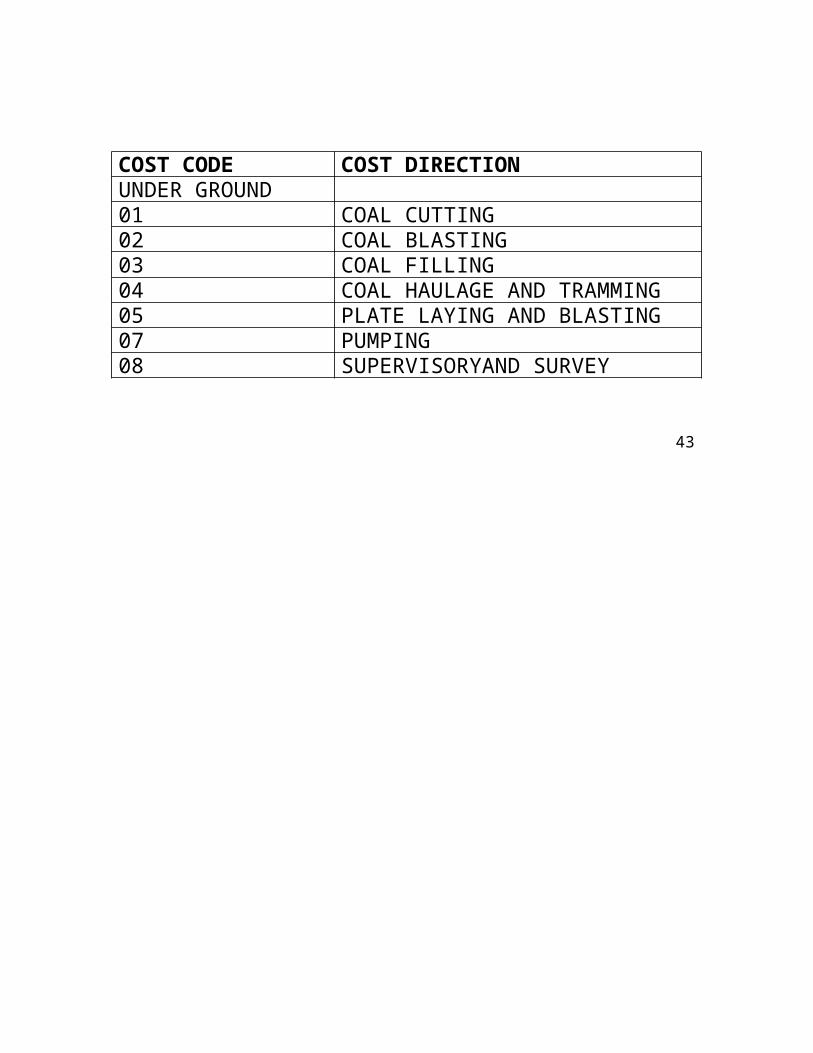

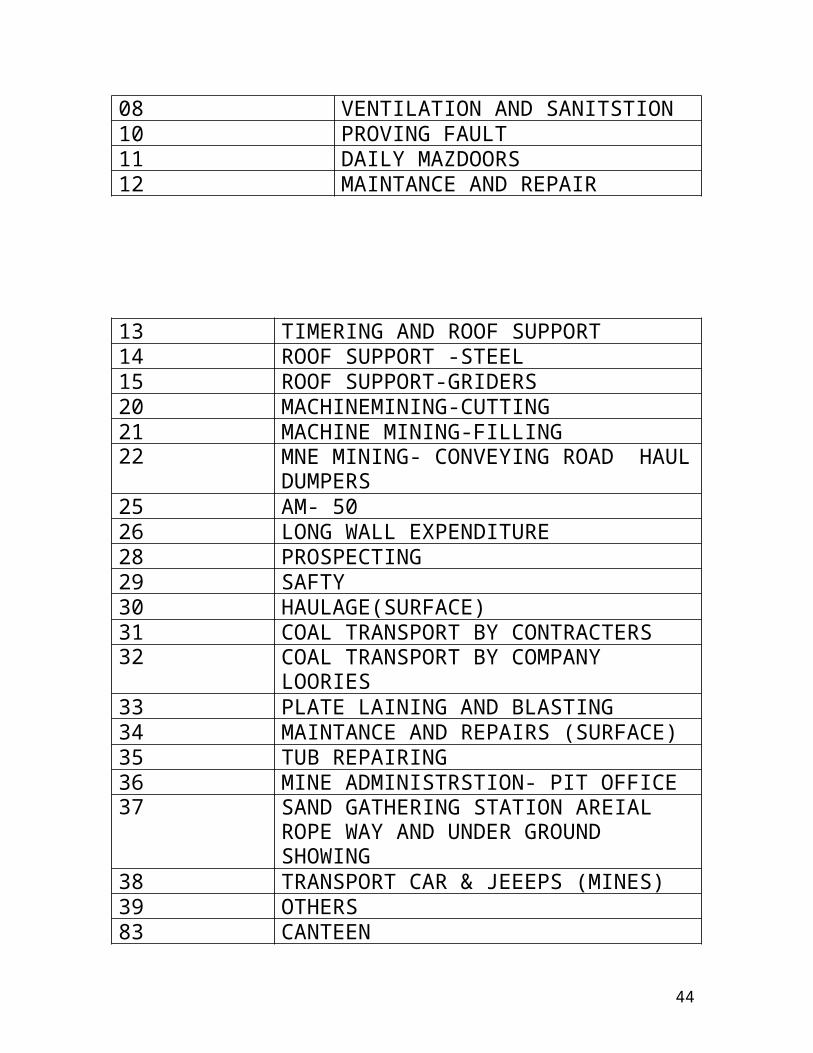

The total activities at the mine are divided into 39 parts and each activity is given from 01 to 39 to ascertain the expenditure. The activity wise costs centers are shown below. The expenditure booked to the below cost centers is treated as direct cost incurred at the time.

Similarly to ascertain the expenditure

on various surface cost codes from 40 to 102are allocated which are used to book the

42

expenditure on the activities on the service and administrative department etc.the expenditure incurred at workshop. CSP and G.M. office etc are the examples of the indirect cost booked through below cost centers.

The indirect cost is grouped into 2 parts for the presentation

in the mine cost sheet. They are overheads and area overheads. The mine overhead, while represents the incidental, costs to the direct wages like LTC/ LLTC, leave enhancement, women compensation free issue ofgas etc. paid to the employees have been taken as direct expenditure and the actuarialprovision of been taken asdirect expenditure and the actual provisionof Gratuity allocated to the mine is treatedas mine overheads and apportioned on thebasis of production as per the procedure.

Thus, the total cost of production is ascertained by way of allocation of direct expenditure and apportionment of overhead costs books through various cost centers. The expenditure thus ascertained is divided with the production to arrive at the cost ofproduction per tonne. The profit/ loss is the difference the average sales realizationplus surface transport charges and total cost of production.

COST CODE COST DIRECTIONUNDER GROUND01 COAL CUTTING02 COAL BLASTING03 COAL FILLING04 COAL HAULAGE AND TRAMMING05 PLATE LAYING AND BLASTING07 PUMPING08 SUPERVISORYAND SURVEY

43

08 VENTILATION AND SANITSTION10 PROVING FAULT11 DAILY MAZDOORS12 MAINTANCE AND REPAIR

13 TIMERING AND ROOF SUPPORT14 ROOF SUPPORT -STEEL15 ROOF SUPPORT-GRIDERS20 MACHINEMINING-CUTTING21 MACHINE MINING-FILLING22 MNE MINING- CONVEYING ROAD HAUL

DUMPERS25 AM- 5026 LONG WALL EXPENDITURE28 PROSPECTING29 SAFTY30 HAULAGE(SURFACE)31 COAL TRANSPORT BY CONTRACTERS32 COAL TRANSPORT BY COMPANY

LOORIES33 PLATE LAINING AND BLASTING34 MAINTANCE AND REPAIRS (SURFACE)35 TUB REPAIRING36 MINE ADMINISTRSTION- PIT OFFICE37 SAND GATHERING STATION AREIAL

ROPE WAY AND UNDER GROUND SHOWING

38 TRANSPORT CAR & JEEEPS (MINES)39 OTHERS83 CANTEEN

44

COSTSSTATEMENT SHOWING THE OPERATION

OF BHOOPALPALLY AREA FOR 2008-09

45

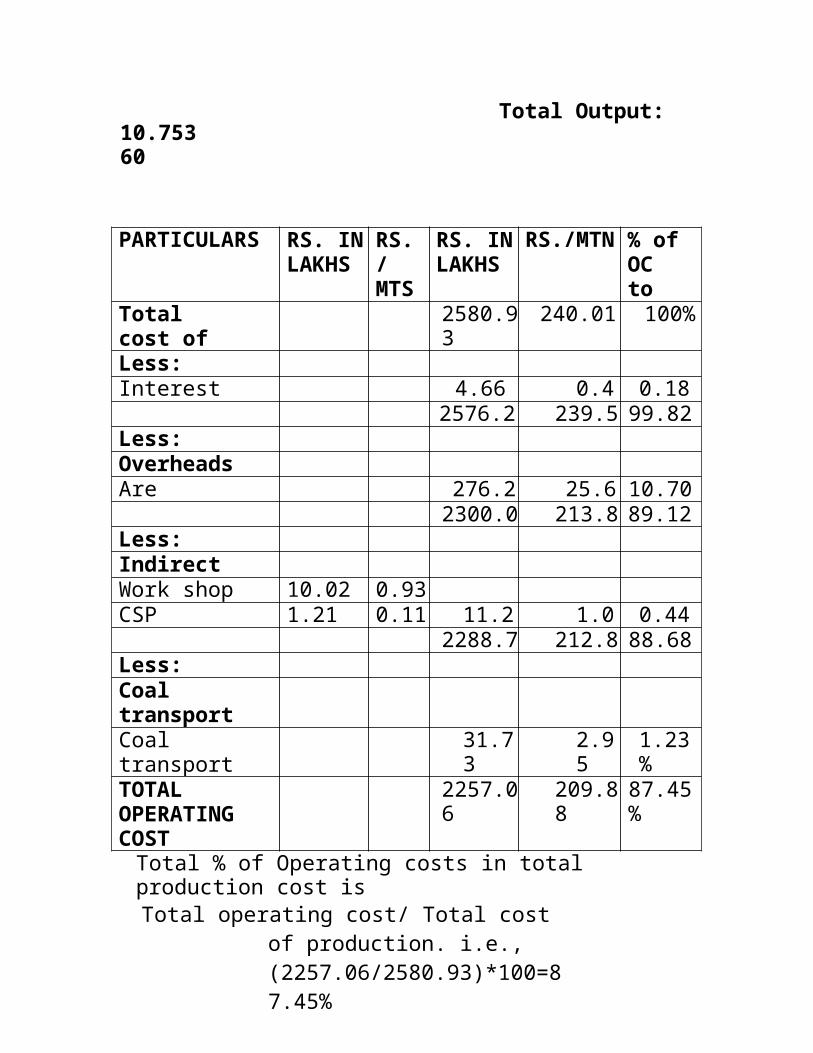

10.75360

Total Output:

PARTICULARS RS. INLAKHS

RS./ MTS

RS. INLAKHS

RS./MTN % ofOC to

Total cost of

2580.93

240.01 100%

Less:Interest 4.66 0.4

30.18%2576.2

7239.57

99.82%Less:

OverheadsAre overheads

276.25

25.68

10.70%2300.0

2213.88

89.12%Less:

Indirect cost forWork shop 10.02 0.93CSP 1.21 0.11 11.2

31.04

0.44%2288.7

9212.83

88.68%Less:

Coal transport Coal transport

31.73

2.95

1.23%

TOTAL OPERATING COST

2257.06

209.88

87.45%

Total % of Operating costs in total production cost isTotal operating cost/ Total cost

of production. i.e., (2257.06/2580.93)*100=87.45%

46

COSTSSTATEMENT SHOWING THE OPERATION

OF BHOOPALPALLY AREA FOR 2007-08

47

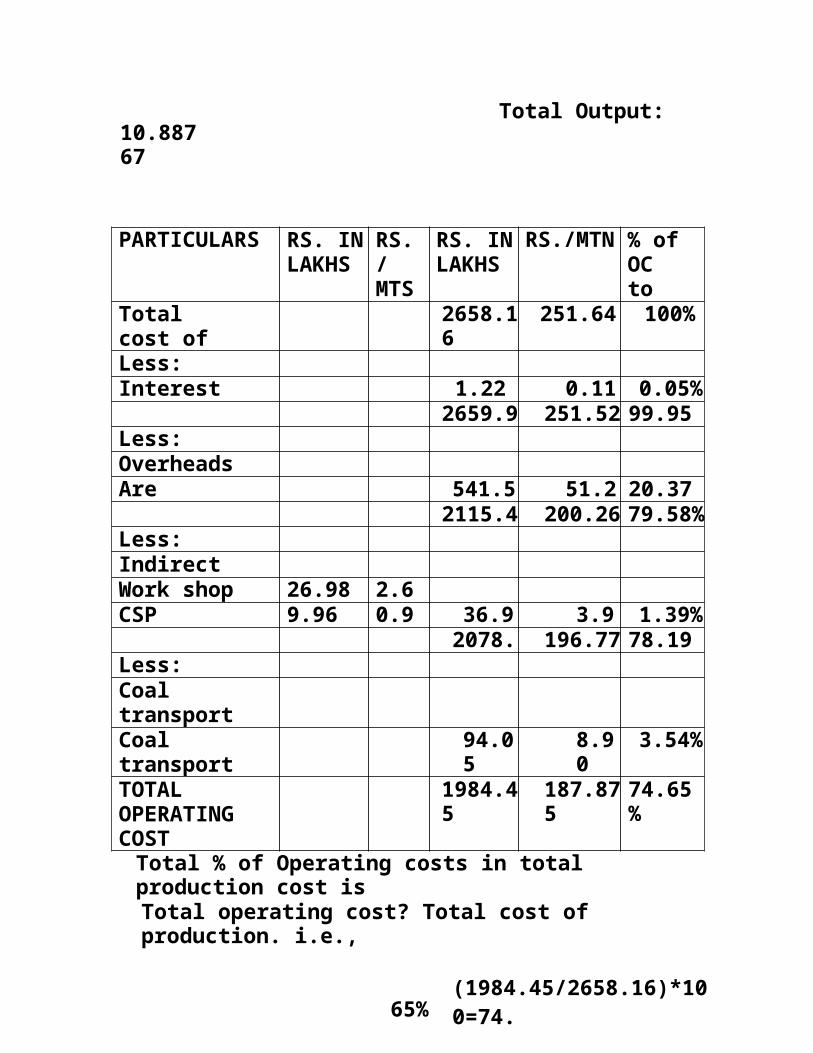

10.88767

Total Output:

PARTICULARS RS. INLAKHS

RS./ MTS

RS. INLAKHS

RS./MTN % ofOC to

Total cost of

2658.16

251.64 100%

Less:Interest 1.22 0.11

50.05%

2659.94

251.525

99.95%Less:

OverheadsAre overheads

541.50

51.26

20.37%2115.4

4200.265

79.58%Less:Indirect cost forWork shop 26.98 2.6CSP 9.96 0.9 36.9

43.94

1.39%2078.5

196.775

78.19%Less:

Coal transport Coal transport

94.05

8.90

3.54%

TOTAL OPERATING COST

1984.45

187.875

74.65%

Total % of Operating costs in total production cost isTotal operating cost? Total cost of production. i.e.,

65%(1984.45/2658.16)*100=74.

48

COSTSSTATEMENT SHOWING THE OPERATION

OF BHOOPALPALLY AREA FOR 2006-07

49

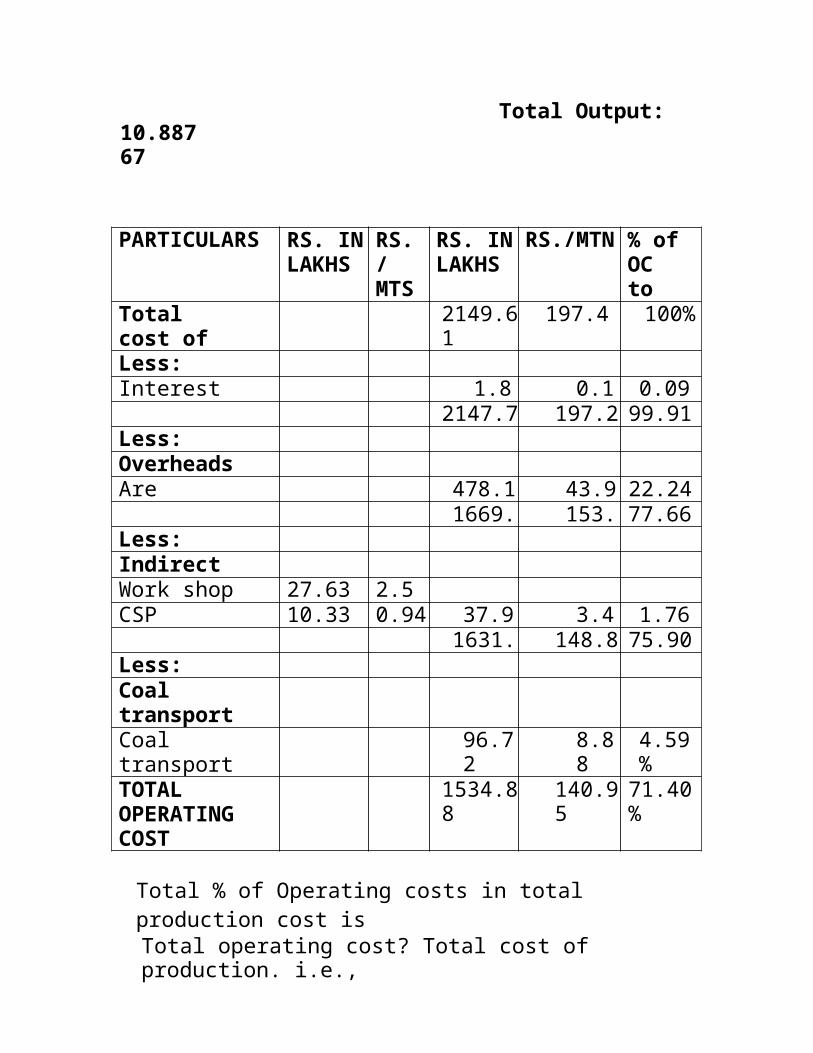

10.88767

Total Output:

PARTICULARS RS. INLAKHS

RS./ MTS

RS. INLAKHS

RS./MTN % ofOC to

Total cost of

2149.61

197.4 100%

Less:Interest 1.8

60.17

0.09%2147.7

5197.23

99.91%Less:

OverheadsAre overheads

478.19

43.92

22.24%1669.

5153.3

77.66%Less:

Indirect cost forWork shop 27.63 2.5CSP 10.33 0.94 37.9

63.48

1.76%1631.

6148.83

75.90%Less:

Coal transport Coal transport

96.72

8.88

4.59%

TOTAL OPERATING COST

1534.88

140.95

71.40%

Total % of Operating costs in total production cost isTotal operating cost? Total cost of production. i.e.,

50

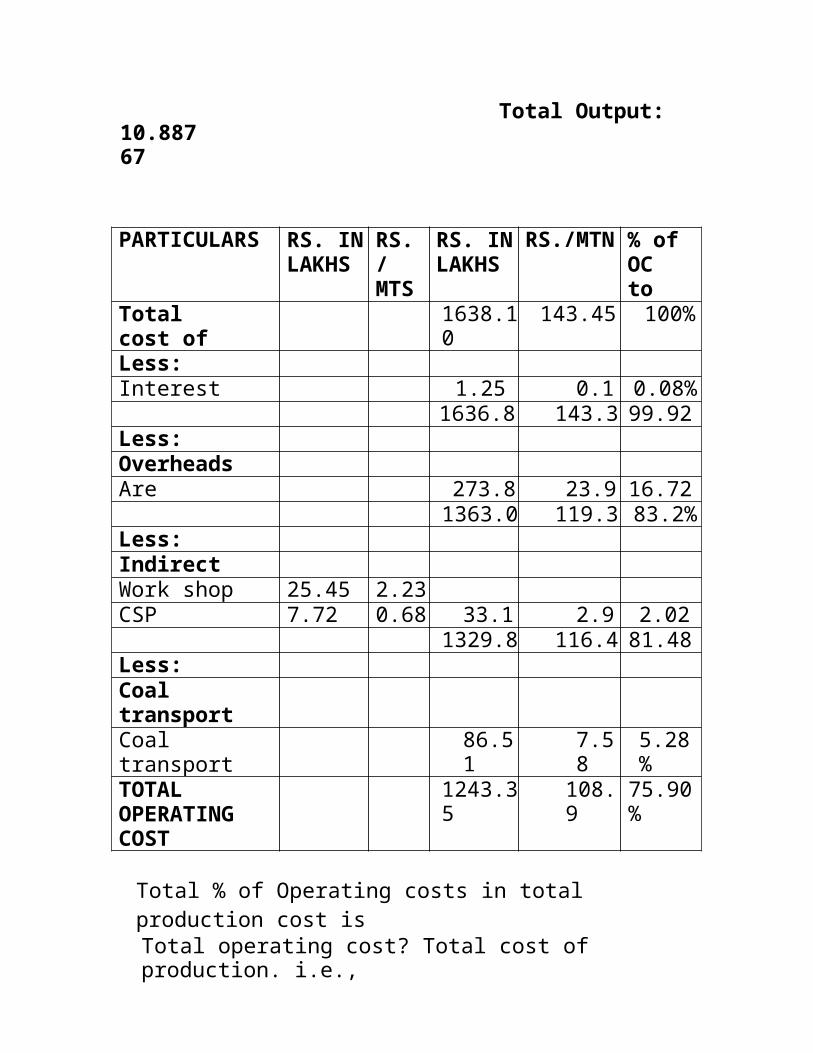

40%(1534.88/2149.61)*100=71.

COSTSSTATEMENT SHOWING THE OPERATION

OF BHOOPALPALLY AREA FOR 2005-06

51

10.88767

Total Output:

PARTICULARS RS. INLAKHS

RS./ MTS

RS. INLAKHS

RS./MTN % ofOC to

Total cost of

1638.10

143.45 100%

Less:Interest 1.25 0.1

00.08%

1636.85

143.35

99.92%Less:

OverheadsAre overheads

273.82

23.97

16.72%1363.0

3119.38

83.2%Less:Indirect cost forWork shop 25.45 2.23CSP 7.72 0.68 33.1

72.90

2.02%1329.8

6116.48

81.48%Less:

Coal transport Coal transport

86.51

7.58

5.28%

TOTAL OPERATING COST

1243.35

108.9

75.90%

Total % of Operating costs in total production cost isTotal operating cost? Total cost of production. i.e.,

52

90%(1243.35/1638.10)*100=75.

COSTSSTATEMENT SHOWING THE OPERATION

OF BHOOPALPALLY AREA FOR 2004-05

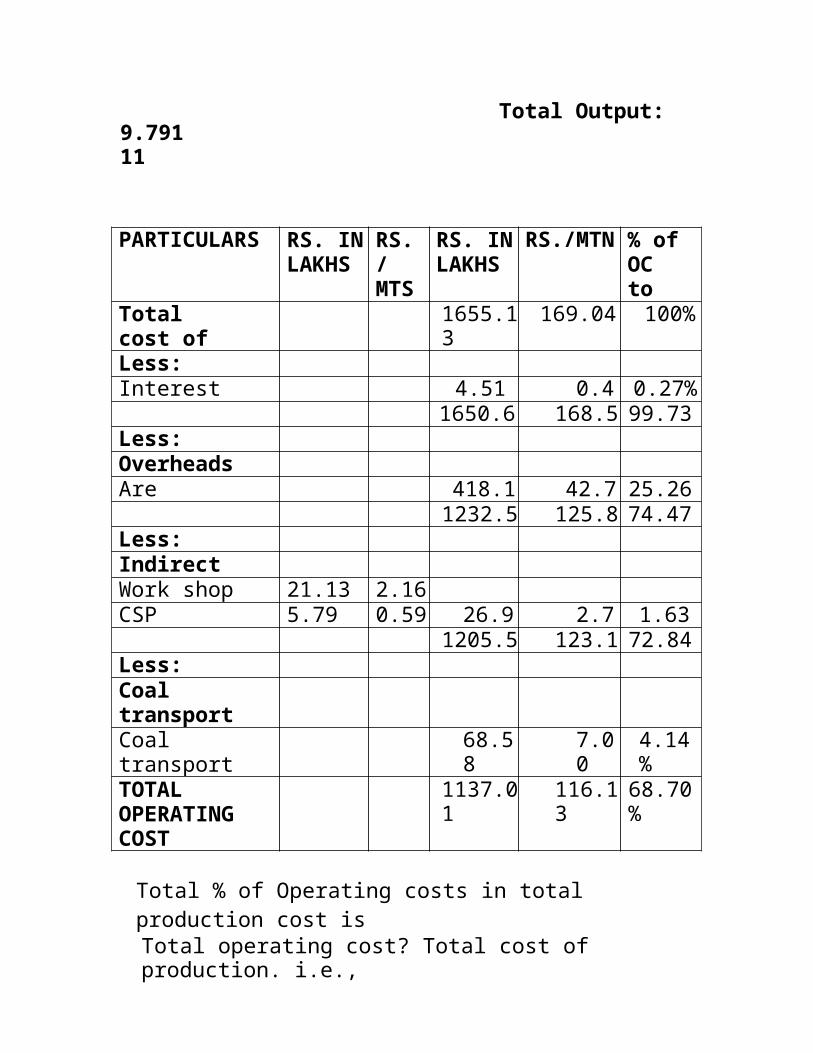

53

9.79111

Total Output:

PARTICULARS RS. INLAKHS

RS./ MTS

RS. INLAKHS

RS./MTN % ofOC to

Total cost of

1655.13

169.04 100%

Less:Interest 4.51 0.4

60.27%

1650.62

168.58

99.73%Less:

OverheadsAre overheads

418.11

42.70

25.26%1232.5

1125.88

74.47%Less:

Indirect cost forWork shop 21.13 2.16CSP 5.79 0.59 26.9

22.75

1.63%1205.5

9123.13

72.84%Less:

Coal transport Coal transport

68.58

7.00

4.14%

TOTAL OPERATING COST

1137.01

116.13

68.70%

Total % of Operating costs in total production cost isTotal operating cost? Total cost of production. i.e.,

54

70%(1137.01/1655.13)*100=68.

C ONCLU SION S

One of the objectives of introducing SDL s is to save manpower and thereby reducing the cost of production. A study of technology wise cost sheet shows that SDL s technology. In the present 2007-08 the SIMPLEX provides 6, EMICO-1 in 2006-07SIMPLEX-2 and EMICO– nill. The productioncapacity of SDL s of 1.0.cu.m. and theactual production from SDL s for year 2007-08 is 205777 which was increased compared to 2006-07. The average production per dayfor the year 2007-08 is 119 tonnes.

The availability and utilization of SDLs is found to be

85.6% and Man Power is 39% where the IdleHours are 52% the average Man Shifts per day

of SDL is 58.cost of production from SDL sand Hand Section at company level for theyear 2007-08 is no. SDL s is 7 and HandSection production is 26804.69 lakhs and1273.70 lakhs. The profit/loss of HandSection is (-) 11096.36 andSDL is26.7169.

55

The total operating cost is 2257.06 with the total output of

10.75360 by which the operating cost to totalcost % is 87.45 in the year 2008-09. The total operating cost is 1984.45 with the total output of 10.56310 by which operating cost to total cost % is 74.65 in the 2007-08.In 2006-07 the total output production is10.388767 and the total cost % is 71.40%. In 2005-06 the total output production is 11.41903 and the total cost % is 75.90%. Inthe year of 2004-05 the % is 68.70% with the total output production of 9079111.

SU GGE ST ION S

by…The operating cost in the underground mines can be reduced

Controlling the ratio of absenteeismof employees. Decreasing the company losses by the effective utilization ofresources.

56

Reduce the cost of area. Reduce the area overheads. Increase the production which canbe done by the increase themechanization in the totalproduction process.

Reduce the indirect cost of workshopand CSP. Reduce the cost of transport contract.

57

h

58