Embed Size (px)

Citation preview

Freight Market Intelligence A Better Way to Control Transportation Costs

March 29, 2012

CHAINalytics

2

Today’s Speakers

Rob Hair Sr. Director, Global Transportation

Processes & Systems

Rodney Noble Sr. Director, Carrier Operations &

Procurement

Gary Girotti Vice President, Transportation

Practice CHAINalytics

Fabrizio Brasca Vice President, Global Logistics

Michael Levans Group Editorial Director, Supply

Chain Group

Moderator

3

Agenda

Introduction to Chainalytics’ Freight Market Intelligence

Consortium

Overview of PepsiCo’s Transportation Procurement Model

How Freight Market Intelligence Enhances PepsiCo’s

Procurement Process

Discussion

4

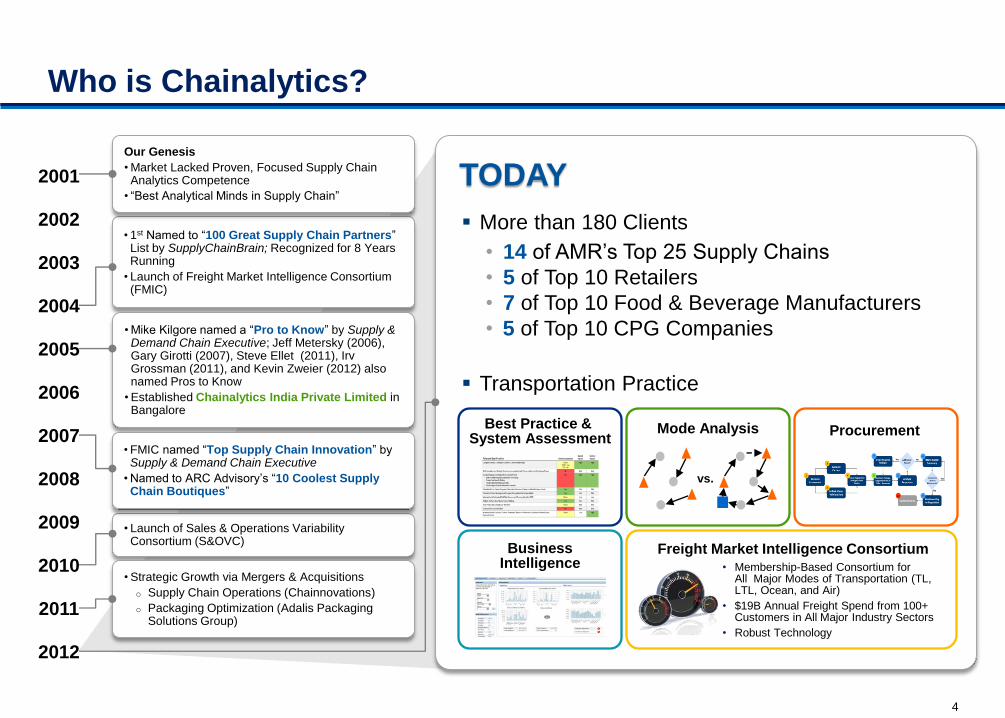

Who is Chainalytics?

More than 180 Clients

• 14 of AMR’s Top 25 Supply Chains

• 5 of Top 10 Retailers

• 7 of Top 10 Food & Beverage Manufacturers

• 5 of Top 10 CPG Companies

Transportation Practice

TODAY

• 1st Named to “100 Great Supply Chain Partners” List by SupplyChainBrain; Recognized for 8 Years Running

• Launch of Freight Market Intelligence Consortium (FMIC)

Our Genesis

• Market Lacked Proven, Focused Supply Chain Analytics Competence

• “Best Analytical Minds in Supply Chain”

• Launch of Sales & Operations Variability Consortium (S&OVC)

• Mike Kilgore named a “Pro to Know” by Supply & Demand Chain Executive; Jeff Metersky (2006), Gary Girotti (2007), Steve Ellet (2011), Irv Grossman (2011), and Kevin Zweier (2012) also named Pros to Know

• Established Chainalytics India Private Limited in Bangalore

• Strategic Growth via Mergers & Acquisitions

o Supply Chain Operations (Chainnovations)

o Packaging Optimization (Adalis Packaging Solutions Group)

• FMIC named “Top Supply Chain Innovation” by Supply & Demand Chain Executive

• Named to ARC Advisory’s “10 Coolest Supply Chain Boutiques”

2001

2002

2003

2004

2005

2006

2007

2009

2010

2011

2008

2012

Procurement Mode Analysis

vs.

Best Practice & System Assessment

Business Intelligence • Membership-Based Consortium for

All Major Modes of Transportation (TL, LTL, Ocean, and Air)

• $19B Annual Freight Spend from 100+ Customers in All Major Industry Sectors

• Robust Technology

Freight Market Intelligence Consortium

5

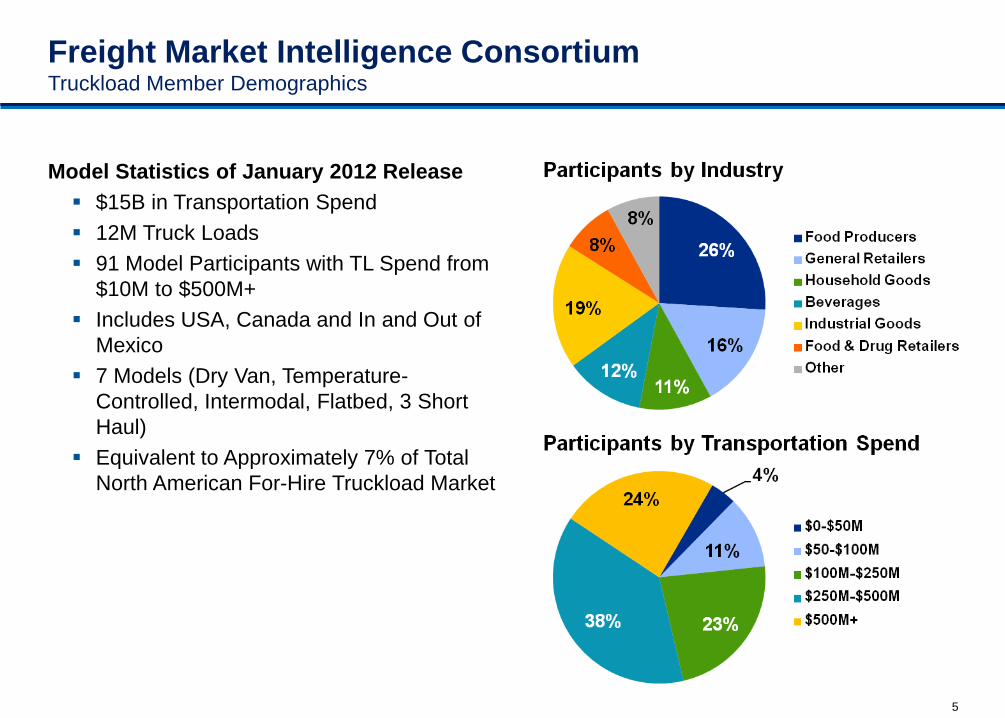

Freight Market Intelligence Consortium Truckload Member Demographics

Model Statistics of January 2012 Release

$15B in Transportation Spend

12M Truck Loads

91 Model Participants with TL Spend from

$10M to $500M+

Includes USA, Canada and In and Out of

Mexico

7 Models (Dry Van, Temperature-

Controlled, Intermodal, Flatbed, 3 Short

Haul)

Equivalent to Approximately 7% of Total

North American For-Hire Truckload Market

6

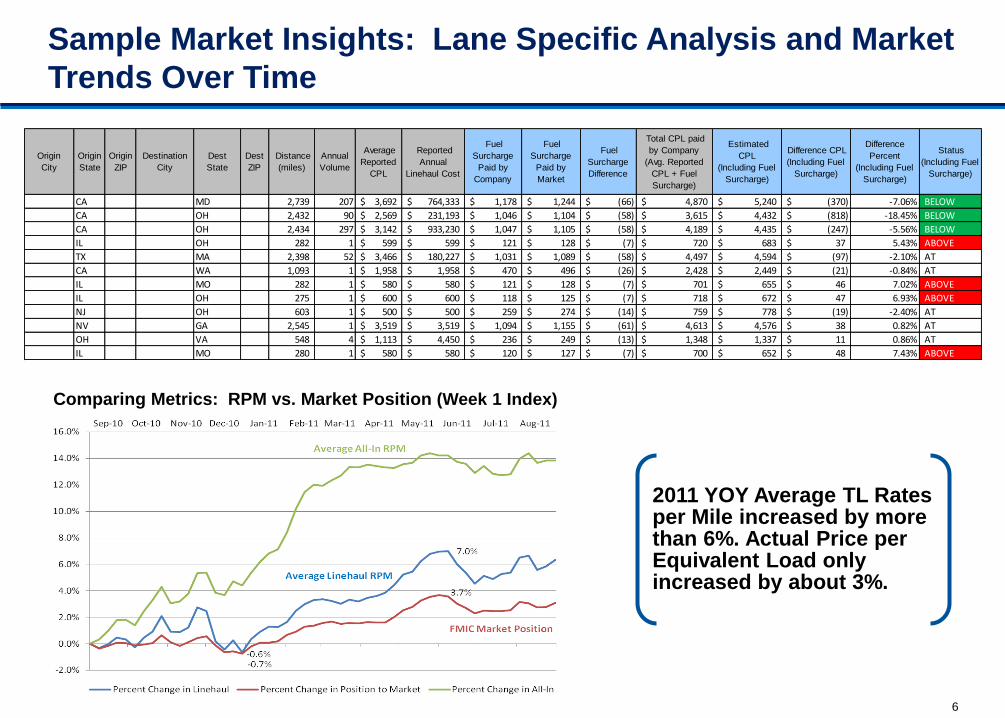

Sample Market Insights: Lane Specific Analysis and Market

Trends Over Time

2011 YOY Average TL Rates per Mile increased by more than 6%. Actual Price per Equivalent Load only increased by about 3%.

Comparing Metrics: RPM vs. Market Position (Week 1 Index)

Origin

City

Origin

State

Origin

ZIP

Destination

City

Dest

State

Dest

ZIP

Distance

(miles)

Annual

Volume

Average

Reported

CPL

Reported

Annual

Linehaul Cost

Fuel

Surcharge

Paid by

Company

Fuel

Surcharge

Paid by

Market

Fuel

Surcharge

Difference

Total CPL paid

by Company

(Avg. Reported

CPL + Fuel

Surcharge)

Estimated

CPL

(Including Fuel

Surcharge)

Difference CPL

(Including Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including Fuel

Surcharge)

CA MD 2,739 207 3,692$ 764,333$ 1,178$ 1,244$ (66)$ 4,870$ 5,240$ (370)$ -7.06% BELOW

CA OH 2,432 90 2,569$ 231,193$ 1,046$ 1,104$ (58)$ 3,615$ 4,432$ (818)$ -18.45% BELOW

CA OH 2,434 297 3,142$ 933,230$ 1,047$ 1,105$ (58)$ 4,189$ 4,435$ (247)$ -5.56% BELOW

IL OH 282 1 599$ 599$ 121$ 128$ (7)$ 720$ 683$ 37$ 5.43% ABOVE

TX MA 2,398 52 3,466$ 180,227$ 1,031$ 1,089$ (58)$ 4,497$ 4,594$ (97)$ -2.10% AT

CA WA 1,093 1 1,958$ 1,958$ 470$ 496$ (26)$ 2,428$ 2,449$ (21)$ -0.84% AT

IL MO 282 1 580$ 580$ 121$ 128$ (7)$ 701$ 655$ 46$ 7.02% ABOVE

IL OH 275 1 600$ 600$ 118$ 125$ (7)$ 718$ 672$ 47$ 6.93% ABOVE

NJ OH 603 1 500$ 500$ 259$ 274$ (14)$ 759$ 778$ (19)$ -2.40% AT

NV GA 2,545 1 3,519$ 3,519$ 1,094$ 1,155$ (61)$ 4,613$ 4,576$ 38$ 0.82% AT

OH VA 548 4 1,113$ 4,450$ 236$ 249$ (13)$ 1,348$ 1,337$ 11$ 0.86% AT

IL MO 280 1 580$ 580$ 120$ 127$ (7)$ 700$ 652$ 48$ 7.43% ABOVE

7

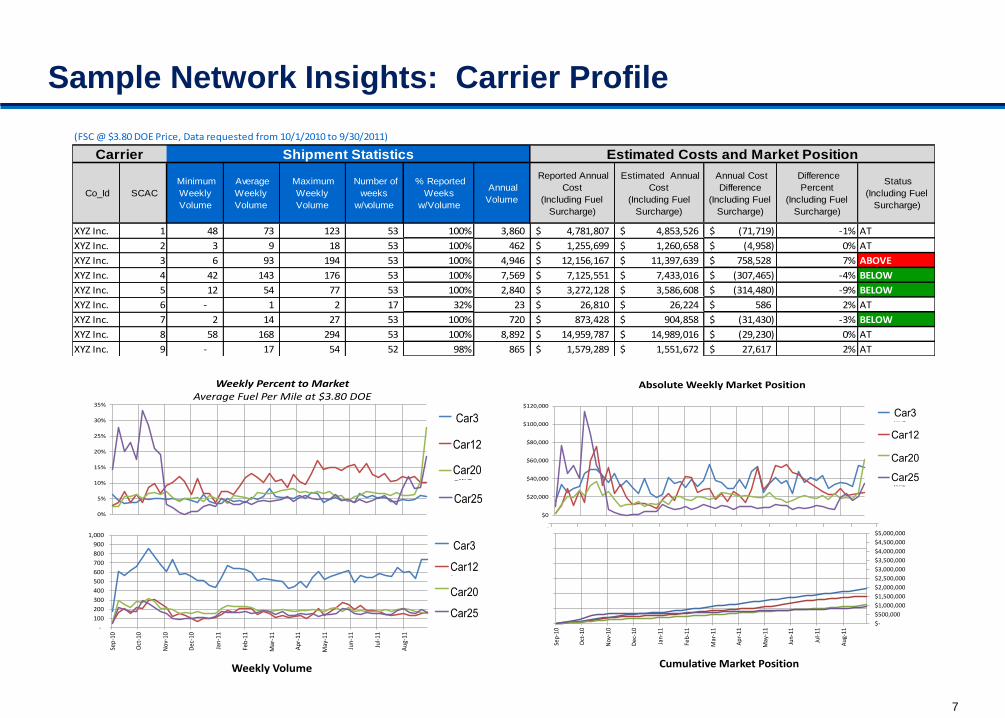

Sample Network Insights: Carrier Profile XYZ Inc.

(FSC @ $3.80 DOE Price, Data requested from 10/1/2010 to 9/30/2011)

Co_Id SCAC

Minimum

Weekly

Volume

Average

Weekly

Volume

Maximum

Weekly

Volume

Number of

weeks

w/volume

% Reported

Weeks

w/Volume

Annual

Volume

Reported Annual

Cost

(Including Fuel

Surcharge)

Estimated Annual

Cost

(Including Fuel

Surcharge)

Annual Cost

Difference

(Including Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including Fuel

Surcharge)

XYZ Inc. 1 48 73 123 53 100% 3,860 4,781,807$ 4,853,526$ (71,719)$ -1% AT

XYZ Inc. 2 3 9 18 53 100% 462 1,255,699$ 1,260,658$ (4,958)$ 0% AT

XYZ Inc. 3 6 93 194 53 100% 4,946 12,156,167$ 11,397,639$ 758,528$ 7% ABOVE

XYZ Inc. 4 42 143 176 53 100% 7,569 7,125,551$ 7,433,016$ (307,465)$ -4% BELOW

XYZ Inc. 5 12 54 77 53 100% 2,840 3,272,128$ 3,586,608$ (314,480)$ -9% BELOW

XYZ Inc. 6 - 1 2 17 32% 23 26,810$ 26,224$ 586$ 2% AT

XYZ Inc. 7 2 14 27 53 100% 720 873,428$ 904,858$ (31,430)$ -3% BELOW

XYZ Inc. 8 58 168 294 53 100% 8,892 14,959,787$ 14,989,016$ (29,230)$ 0% AT

XYZ Inc. 9 - 17 54 52 98% 865 1,579,289$ 1,551,672$ 27,617$ 2% AT

XYZ Inc. 10 1 12 20 53 100% 635 599,163$ 689,347$ (90,185)$ -13% BELOW

XYZ Inc. 11 28 68 97 53 100% 3,585 4,910,758$ 5,062,026$ (151,268)$ -3% BELOW

XYZ Inc. 12 - 14 54 46 87% 627 1,311,745$ 1,043,715$ 268,030$ 26% ABOVE

XYZ Inc. 13 1 14 26 53 100% 730 513,450$ 546,610$ (33,160)$ -6% BELOW

XYZ Inc. 14 143 492 665 53 100% 26,059 30,249,440$ 31,149,423$ (899,983)$ -3% BELOW

XYZ Inc. 15 41 126 186 53 100% 6,661 12,957,732$ 13,458,719$ (500,988)$ -4% BELOW

XYZ Inc. 16 4 23 47 53 100% 1,216 1,998,122$ 2,163,900$ (165,778)$ -8% BELOW

XYZ Inc. 17 10 37 66 53 100% 1,968 2,381,559$ 2,380,354$ 1,205$ 0% AT

XYZ Inc. 18 9 66 146 53 100% 3,475 4,763,127$ 4,999,324$ (236,197)$ -5% BELOW

XYZ Inc. 19 11 37 53 53 100% 1,960 3,085,733$ 2,715,967$ 369,765$ 14% ABOVE

Carrier Shipment Statistics Estimated Costs and Market Position

2011- Annual Truckload Model 2

Carrier Report

0%

5%

10%

15%

20%

25%

30%

35%

Weekly Percent to MarketAverage Fuel Per Mile at $3.80 DOE

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WAL

Car3

Car12

Car20

Car25

-

100

200

300

400

500

600

700

800

900

1,000

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Weekly Volume

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Absolute Weekly Market Position

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

0

0.2

0.4

0.6

0.8

1

1.2

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Cumulative Market Position

XYZ Inc.

(FSC @ $3.80 DOE Price, Data requested from 10/1/2010 to 9/30/2011)

Co_Id SCAC

Minimum

Weekly

Volume

Average

Weekly

Volume

Maximum

Weekly

Volume

Number of

weeks

w/volume

% Reported

Weeks

w/Volume

Annual

Volume

Reported Annual

Cost

(Including Fuel

Surcharge)

Estimated Annual

Cost

(Including Fuel

Surcharge)

Annual Cost

Difference

(Including Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including Fuel

Surcharge)

XYZ Inc. 1 48 73 123 53 100% 3,860 4,781,807$ 4,853,526$ (71,719)$ -1% AT

XYZ Inc. 2 3 9 18 53 100% 462 1,255,699$ 1,260,658$ (4,958)$ 0% AT

XYZ Inc. 3 6 93 194 53 100% 4,946 12,156,167$ 11,397,639$ 758,528$ 7% ABOVE

XYZ Inc. 4 42 143 176 53 100% 7,569 7,125,551$ 7,433,016$ (307,465)$ -4% BELOW

XYZ Inc. 5 12 54 77 53 100% 2,840 3,272,128$ 3,586,608$ (314,480)$ -9% BELOW

XYZ Inc. 6 - 1 2 17 32% 23 26,810$ 26,224$ 586$ 2% AT

XYZ Inc. 7 2 14 27 53 100% 720 873,428$ 904,858$ (31,430)$ -3% BELOW

XYZ Inc. 8 58 168 294 53 100% 8,892 14,959,787$ 14,989,016$ (29,230)$ 0% AT

XYZ Inc. 9 - 17 54 52 98% 865 1,579,289$ 1,551,672$ 27,617$ 2% AT

XYZ Inc. 10 1 12 20 53 100% 635 599,163$ 689,347$ (90,185)$ -13% BELOW

XYZ Inc. 11 28 68 97 53 100% 3,585 4,910,758$ 5,062,026$ (151,268)$ -3% BELOW

XYZ Inc. 12 - 14 54 46 87% 627 1,311,745$ 1,043,715$ 268,030$ 26% ABOVE

XYZ Inc. 13 1 14 26 53 100% 730 513,450$ 546,610$ (33,160)$ -6% BELOW

XYZ Inc. 14 143 492 665 53 100% 26,059 30,249,440$ 31,149,423$ (899,983)$ -3% BELOW

XYZ Inc. 15 41 126 186 53 100% 6,661 12,957,732$ 13,458,719$ (500,988)$ -4% BELOW

XYZ Inc. 16 4 23 47 53 100% 1,216 1,998,122$ 2,163,900$ (165,778)$ -8% BELOW

XYZ Inc. 17 10 37 66 53 100% 1,968 2,381,559$ 2,380,354$ 1,205$ 0% AT

XYZ Inc. 18 9 66 146 53 100% 3,475 4,763,127$ 4,999,324$ (236,197)$ -5% BELOW

XYZ Inc. 19 11 37 53 53 100% 1,960 3,085,733$ 2,715,967$ 369,765$ 14% ABOVE

Carrier Shipment Statistics Estimated Costs and Market Position

2011- Annual Truckload Model 2

Carrier Report

0%

5%

10%

15%

20%

25%

30%

35%

Weekly Percent to MarketAverage Fuel Per Mile at $3.80 DOE

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WAL

Car3

Car12

Car20

Car25

-

100

200

300

400

500

600

700

800

900

1,000

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Weekly Volume

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Absolute Weekly Market Position

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

0

0.2

0.4

0.6

0.8

1

1.2

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Cumulative Market Position

XYZ Inc.

(FSC @ $3.80 DOE Price, Data requested from 10/1/2010 to 9/30/2011)

Co_Id SCAC

Minimum

Weekly

Volume

Average

Weekly

Volume

Maximum

Weekly

Volume

Number of

weeks

w/volume

% Reported

Weeks

w/Volume

Annual

Volume

Reported Annual

Cost

(Including Fuel

Surcharge)

Estimated Annual

Cost

(Including Fuel

Surcharge)

Annual Cost

Difference

(Including Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including Fuel

Surcharge)

XYZ Inc. 1 48 73 123 53 100% 3,860 4,781,807$ 4,853,526$ (71,719)$ -1% AT

XYZ Inc. 2 3 9 18 53 100% 462 1,255,699$ 1,260,658$ (4,958)$ 0% AT

XYZ Inc. 3 6 93 194 53 100% 4,946 12,156,167$ 11,397,639$ 758,528$ 7% ABOVE

XYZ Inc. 4 42 143 176 53 100% 7,569 7,125,551$ 7,433,016$ (307,465)$ -4% BELOW

XYZ Inc. 5 12 54 77 53 100% 2,840 3,272,128$ 3,586,608$ (314,480)$ -9% BELOW

XYZ Inc. 6 - 1 2 17 32% 23 26,810$ 26,224$ 586$ 2% AT

XYZ Inc. 7 2 14 27 53 100% 720 873,428$ 904,858$ (31,430)$ -3% BELOW

XYZ Inc. 8 58 168 294 53 100% 8,892 14,959,787$ 14,989,016$ (29,230)$ 0% AT

XYZ Inc. 9 - 17 54 52 98% 865 1,579,289$ 1,551,672$ 27,617$ 2% AT

XYZ Inc. 10 1 12 20 53 100% 635 599,163$ 689,347$ (90,185)$ -13% BELOW

XYZ Inc. 11 28 68 97 53 100% 3,585 4,910,758$ 5,062,026$ (151,268)$ -3% BELOW

XYZ Inc. 12 - 14 54 46 87% 627 1,311,745$ 1,043,715$ 268,030$ 26% ABOVE

XYZ Inc. 13 1 14 26 53 100% 730 513,450$ 546,610$ (33,160)$ -6% BELOW

XYZ Inc. 14 143 492 665 53 100% 26,059 30,249,440$ 31,149,423$ (899,983)$ -3% BELOW

XYZ Inc. 15 41 126 186 53 100% 6,661 12,957,732$ 13,458,719$ (500,988)$ -4% BELOW

XYZ Inc. 16 4 23 47 53 100% 1,216 1,998,122$ 2,163,900$ (165,778)$ -8% BELOW

XYZ Inc. 17 10 37 66 53 100% 1,968 2,381,559$ 2,380,354$ 1,205$ 0% AT

XYZ Inc. 18 9 66 146 53 100% 3,475 4,763,127$ 4,999,324$ (236,197)$ -5% BELOW

XYZ Inc. 19 11 37 53 53 100% 1,960 3,085,733$ 2,715,967$ 369,765$ 14% ABOVE

Carrier Shipment Statistics Estimated Costs and Market Position

2011- Annual Truckload Model 2

Carrier Report

0%

5%

10%

15%

20%

25%

30%

35%

Weekly Percent to MarketAverage Fuel Per Mile at $3.80 DOE

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WAL

Car3

Car12

Car20

Car25

-

100

200

300

400

500

600

700

800

900

1,000

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Weekly Volume

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Absolute Weekly Market Position

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

0

0.2

0.4

0.6

0.8

1

1.2

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Cumulative Market Position

XYZ Inc.

(FSC @ $3.80 DOE Price, Data requested from 10/1/2010 to 9/30/2011)

Co_Id SCAC

Minimum

Weekly

Volume

Average

Weekly

Volume

Maximum

Weekly

Volume

Number of

weeks

w/volume

% Reported

Weeks

w/Volume

Annual

Volume

Reported Annual

Cost

(Including Fuel

Surcharge)

Estimated Annual

Cost

(Including Fuel

Surcharge)

Annual Cost

Difference

(Including Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including Fuel

Surcharge)

XYZ Inc. 1 48 73 123 53 100% 3,860 4,781,807$ 4,853,526$ (71,719)$ -1% AT

XYZ Inc. 2 3 9 18 53 100% 462 1,255,699$ 1,260,658$ (4,958)$ 0% AT

XYZ Inc. 3 6 93 194 53 100% 4,946 12,156,167$ 11,397,639$ 758,528$ 7% ABOVE

XYZ Inc. 4 42 143 176 53 100% 7,569 7,125,551$ 7,433,016$ (307,465)$ -4% BELOW

XYZ Inc. 5 12 54 77 53 100% 2,840 3,272,128$ 3,586,608$ (314,480)$ -9% BELOW

XYZ Inc. 6 - 1 2 17 32% 23 26,810$ 26,224$ 586$ 2% AT

XYZ Inc. 7 2 14 27 53 100% 720 873,428$ 904,858$ (31,430)$ -3% BELOW

XYZ Inc. 8 58 168 294 53 100% 8,892 14,959,787$ 14,989,016$ (29,230)$ 0% AT

XYZ Inc. 9 - 17 54 52 98% 865 1,579,289$ 1,551,672$ 27,617$ 2% AT

XYZ Inc. 10 1 12 20 53 100% 635 599,163$ 689,347$ (90,185)$ -13% BELOW

XYZ Inc. 11 28 68 97 53 100% 3,585 4,910,758$ 5,062,026$ (151,268)$ -3% BELOW

XYZ Inc. 12 - 14 54 46 87% 627 1,311,745$ 1,043,715$ 268,030$ 26% ABOVE

XYZ Inc. 13 1 14 26 53 100% 730 513,450$ 546,610$ (33,160)$ -6% BELOW

XYZ Inc. 14 143 492 665 53 100% 26,059 30,249,440$ 31,149,423$ (899,983)$ -3% BELOW

XYZ Inc. 15 41 126 186 53 100% 6,661 12,957,732$ 13,458,719$ (500,988)$ -4% BELOW

XYZ Inc. 16 4 23 47 53 100% 1,216 1,998,122$ 2,163,900$ (165,778)$ -8% BELOW

XYZ Inc. 17 10 37 66 53 100% 1,968 2,381,559$ 2,380,354$ 1,205$ 0% AT

XYZ Inc. 18 9 66 146 53 100% 3,475 4,763,127$ 4,999,324$ (236,197)$ -5% BELOW

XYZ Inc. 19 11 37 53 53 100% 1,960 3,085,733$ 2,715,967$ 369,765$ 14% ABOVE

Carrier Shipment Statistics Estimated Costs and Market Position

2011- Annual Truckload Model 2

Carrier Report

0%

5%

10%

15%

20%

25%

30%

35%

Weekly Percent to MarketAverage Fuel Per Mile at $3.80 DOE

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WAL

Car3

Car12

Car20

Car25

-

100

200

300

400

500

600

700

800

900

1,000

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Weekly Volume

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Absolute Weekly Market Position

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

0

0.2

0.4

0.6

0.8

1

1.2

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Cumulative Market Position

XYZ Inc.

(FSC @ $3.80 DOE Price, Data requested from 10/1/2010 to 9/30/2011)

Co_Id SCAC

Minimum

Weekly

Volume

Average

Weekly

Volume

Maximum

Weekly

Volume

Number of

weeks

w/volume

% Reported

Weeks

w/Volume

Annual

Volume

Reported Annual

Cost

(Including Fuel

Surcharge)

Estimated Annual

Cost

(Including Fuel

Surcharge)

Annual Cost

Difference

(Including Fuel

Surcharge)

Difference

Percent

(Including Fuel

Surcharge)

Status

(Including Fuel

Surcharge)

XYZ Inc. 1 48 73 123 53 100% 3,860 4,781,807$ 4,853,526$ (71,719)$ -1% AT

XYZ Inc. 2 3 9 18 53 100% 462 1,255,699$ 1,260,658$ (4,958)$ 0% AT

XYZ Inc. 3 6 93 194 53 100% 4,946 12,156,167$ 11,397,639$ 758,528$ 7% ABOVE

XYZ Inc. 4 42 143 176 53 100% 7,569 7,125,551$ 7,433,016$ (307,465)$ -4% BELOW

XYZ Inc. 5 12 54 77 53 100% 2,840 3,272,128$ 3,586,608$ (314,480)$ -9% BELOW

XYZ Inc. 6 - 1 2 17 32% 23 26,810$ 26,224$ 586$ 2% AT

XYZ Inc. 7 2 14 27 53 100% 720 873,428$ 904,858$ (31,430)$ -3% BELOW

XYZ Inc. 8 58 168 294 53 100% 8,892 14,959,787$ 14,989,016$ (29,230)$ 0% AT

XYZ Inc. 9 - 17 54 52 98% 865 1,579,289$ 1,551,672$ 27,617$ 2% AT

XYZ Inc. 10 1 12 20 53 100% 635 599,163$ 689,347$ (90,185)$ -13% BELOW

XYZ Inc. 11 28 68 97 53 100% 3,585 4,910,758$ 5,062,026$ (151,268)$ -3% BELOW

XYZ Inc. 12 - 14 54 46 87% 627 1,311,745$ 1,043,715$ 268,030$ 26% ABOVE

XYZ Inc. 13 1 14 26 53 100% 730 513,450$ 546,610$ (33,160)$ -6% BELOW

XYZ Inc. 14 143 492 665 53 100% 26,059 30,249,440$ 31,149,423$ (899,983)$ -3% BELOW

XYZ Inc. 15 41 126 186 53 100% 6,661 12,957,732$ 13,458,719$ (500,988)$ -4% BELOW

XYZ Inc. 16 4 23 47 53 100% 1,216 1,998,122$ 2,163,900$ (165,778)$ -8% BELOW

XYZ Inc. 17 10 37 66 53 100% 1,968 2,381,559$ 2,380,354$ 1,205$ 0% AT

XYZ Inc. 18 9 66 146 53 100% 3,475 4,763,127$ 4,999,324$ (236,197)$ -5% BELOW

XYZ Inc. 19 11 37 53 53 100% 1,960 3,085,733$ 2,715,967$ 369,765$ 14% ABOVE

Carrier Shipment Statistics Estimated Costs and Market Position

2011- Annual Truckload Model 2

Carrier Report

0%

5%

10%

15%

20%

25%

30%

35%

Weekly Percent to MarketAverage Fuel Per Mile at $3.80 DOE

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WAL

Car3

Car12

Car20

Car25

-

100

200

300

400

500

600

700

800

900

1,000

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Weekly Volume

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Absolute Weekly Market Position

TNTI_WAL

RTS_WAL

GRDN_WAL

EPES_WALCar25

Car3

Car12

Car20

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

0

0.2

0.4

0.6

0.8

1

1.2

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun

-11

Jul-

11

Au

g-11

Cumulative Market Position

8

Overview of PepsiCo’s Transportation Procurement Model

9

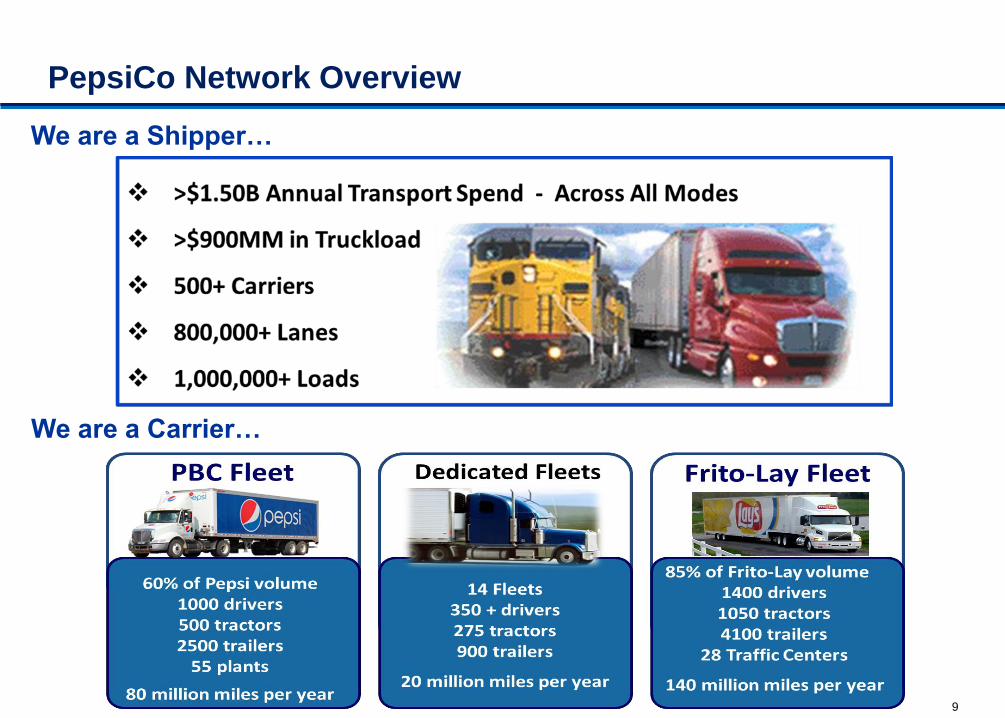

PepsiCo Network Overview

We are a Shipper…

We are a Carrier…

10

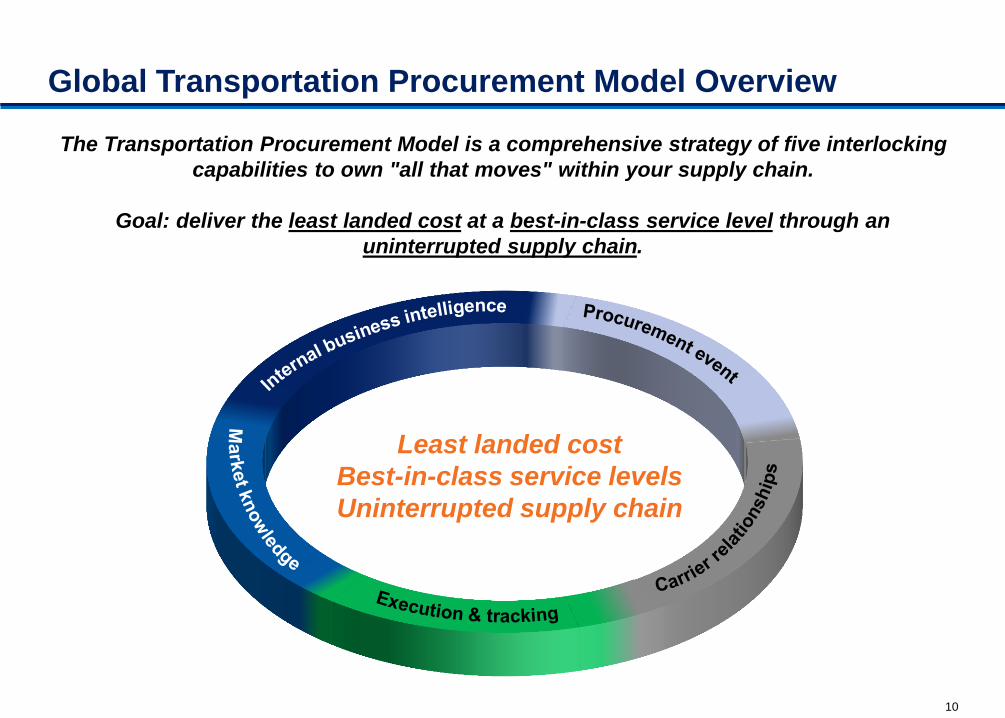

Global Transportation Procurement Model Overview

Least landed cost

Best-in-class service levels

Uninterrupted supply chain

The Transportation Procurement Model is a comprehensive strategy of five interlocking

capabilities to own "all that moves" within your supply chain.

Goal: deliver the least landed cost at a best-in-class service level through an

uninterrupted supply chain.

11

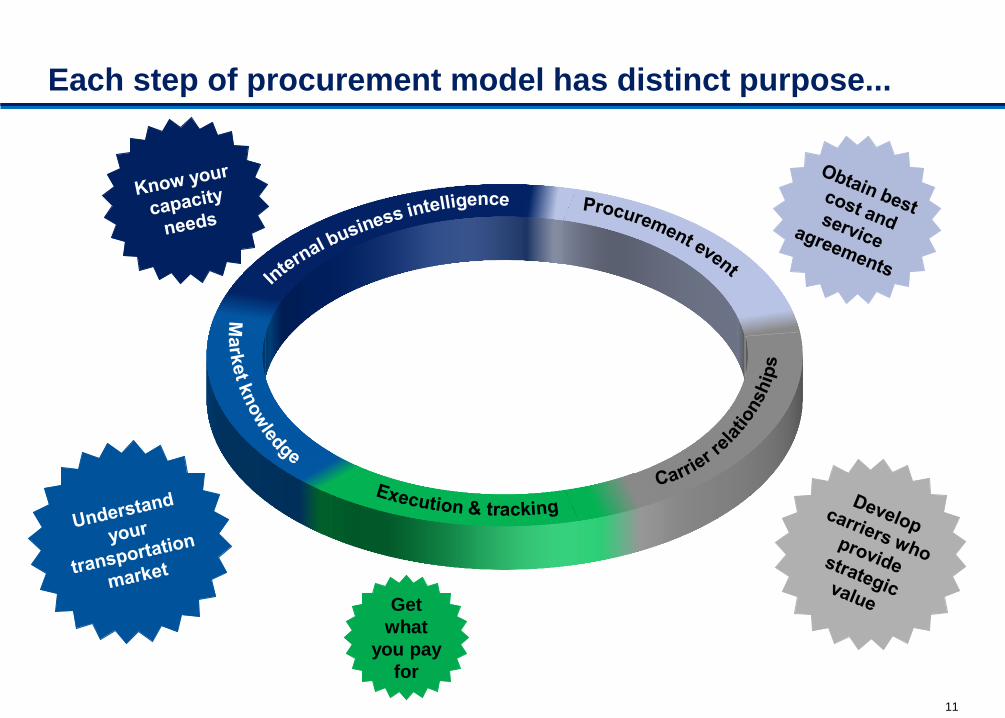

Each step of procurement model has distinct purpose...

Get

what

you pay

for

12

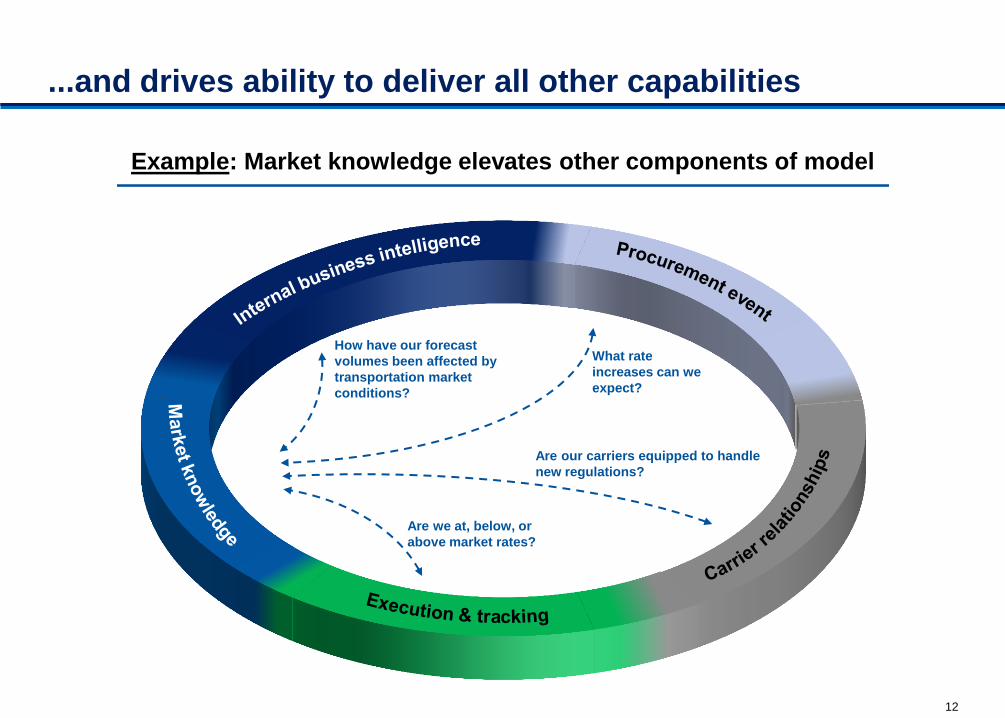

...and drives ability to deliver all other capabilities

How have our forecast

volumes been affected by

transportation market

conditions?

What rate

increases can we

expect?

Are our carriers equipped to handle

new regulations?

Are we at, below, or

above market rates?

Example: Market knowledge elevates other components of model

13

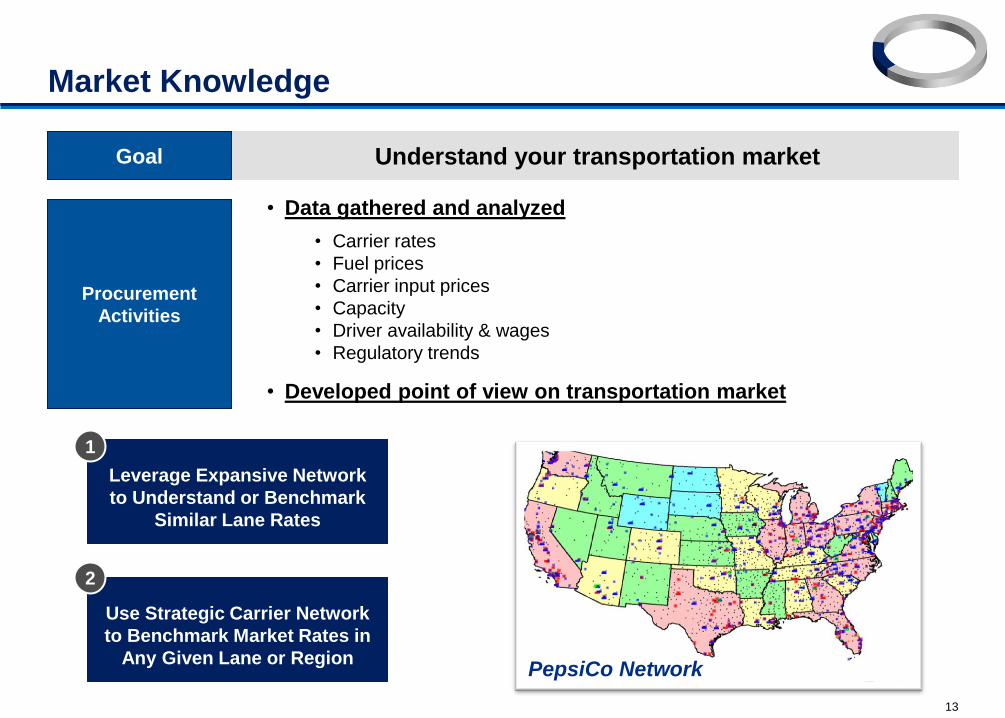

Market Knowledge

Understand your transportation market Goal

Procurement

Activities

• Data gathered and analyzed

• Carrier rates

• Fuel prices

• Carrier input prices

• Capacity

• Driver availability & wages

• Regulatory trends

• Developed point of view on transportation market

Leverage Expansive Network

to Understand or Benchmark

Similar Lane Rates

Use Strategic Carrier Network

to Benchmark Market Rates in

Any Given Lane or Region

1

2

PepsiCo Network

14

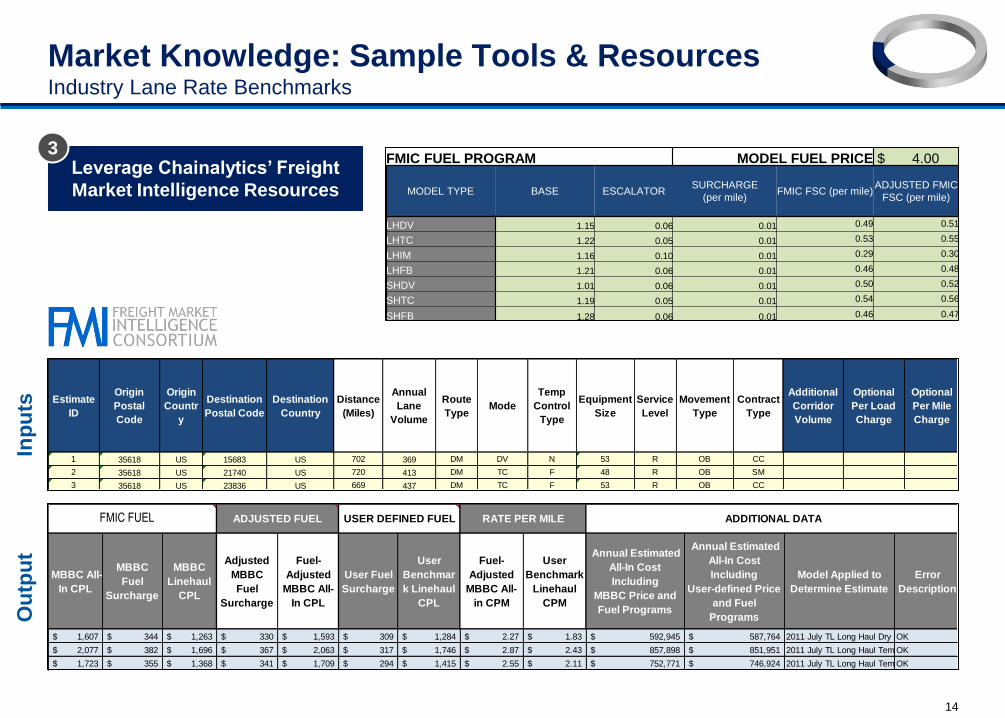

Market Knowledge: Sample Tools & Resources Industry Lane Rate Benchmarks

Leverage Chainalytics’ Freight

Market Intelligence Resources

3

FMIC BATCH UPLOAD TEMPLATE

FOR TRUCKLOAD SHIPPERS

FMIC FUEL PROGRAM MODEL FUEL PRICE $ 4.00

MODEL TYPE BASE ESCALATORSURCHARGE

(per mile)FMIC FSC (per mile)

ADJUSTED FMIC

FSC (per mile)

LHDV 1.15 0.06 0.01 0.49 0.51

LHTC 1.22 0.05 0.01 0.53 0.55

LHIM 1.16 0.10 0.01 0.29 0.30

LHFB 1.21 0.06 0.01 0.46 0.48

SHDV 1.01 0.06 0.01 0.50 0.52

SHTC 1.19 0.05 0.01 0.54 0.56

SHFB 1.28 0.06 0.01 0.46 0.47

USER DEFINED FUEL PROGRAM CURRENT FUEL PRICE $ 4.10

MODEL TYPE

DISTANCE or

PERCENTAGE

BASED?

BASE ESCALATOR SURCHARGE FSC RATE

LHDV 0.00

LHTC 0.00

LHIM 0.00

LHFB 0.00

SHDV 0.00

SHTC 0.00

SHFB 0.00

Estimate

ID

Origin

Postal

Code

Origin

Countr

y

Destination

Postal Code

Destination

Country

Distance

(Miles)

Annual

Lane

Volume

Route

TypeMode

Temp

Control

Type

Equipment

Size

Service

Level

Movement

Type

Contract

Type

Additional

Corridor

Volume

Optional

Per Load

Charge

Optional

Per Mile

Charge

1 35618 US 15683 US 702 369 DM DV N 53 R OB CC

2 35618 US 21740 US 720 413 DM TC F 48 R OB SM

3 35618 US 23836 US 669 437 DM TC F 53 R OB CC

4 35618 US 30439 US 400 508 DM DV N 53 R IB CC

5 35618 US 36750 US 152 348 DM DV N 53 X OB CC

6 35618 US 42101 US 195 352 MS DV N 53 R OB CC

7 35618 US 46320 US 547 504 DM DV N 53 R OB CC

Inp

uts

MBBC All-

In CPL

MBBC

Fuel

Surcharge

MBBC

Linehaul

CPL

Adjusted

MBBC

Fuel

Surcharge

Fuel-

Adjusted

MBBC All-

In CPL

User Fuel

Surcharge

User

Benchmar

k Linehaul

CPL

Fuel-

Adjusted

MBBC All-

in CPM

User

Benchmark

Linehaul

CPM

Annual Estimated

All-In Cost

Including

MBBC Price and

Fuel Programs

Annual Estimated

All-In Cost

Including

User-defined Price

and Fuel

Programs

Model Applied to

Determine Estimate

Error

Description

1,607$ 344$ 1,263$ 330$ 1,593$ 309$ 1,284$ 2.27$ 1.83$ 592,945$ 587,764$ 2011 July TL Long Haul Dry VanOK

2,077$ 382$ 1,696$ 367$ 2,063$ 317$ 1,746$ 2.87$ 2.43$ 857,898$ 851,951$ 2011 July TL Long Haul Temperature ControlledOK

1,723$ 355$ 1,368$ 341$ 1,709$ 294$ 1,415$ 2.55$ 2.11$ 752,771$ 746,924$ 2011 July TL Long Haul Temperature ControlledOK

890$ 196$ 694$ 188$ 882$ 176$ 706$ 2.21$ 1.77$ 452,230$ 448,166$ 2011 July TL Long Haul Dry VanOK

534$ 76$ 458$ 73$ 531$ -$ 531$ 3.49$ 3.49$ 185,819$ 184,761$ 2011 July TL Short Haul Dry VanOK

585$ 98$ 487$ 94$ 581$ -$ 581$ 2.98$ 2.98$ 205,763$ 204,390$ 2011 July TL Short Haul Dry VanOK

997$ 268$ 729$ 257$ 986$ 241$ 745$ 1.80$ 1.36$ 502,363$ 496,850$ 2011 July TL Long Haul Dry VanOK

MBBC FUEL ADJUSTED FUEL USER DEFINED FUEL RATE PER MILE ADDITIONAL DATAFMIC FUEL

Ou

tpu

t

15

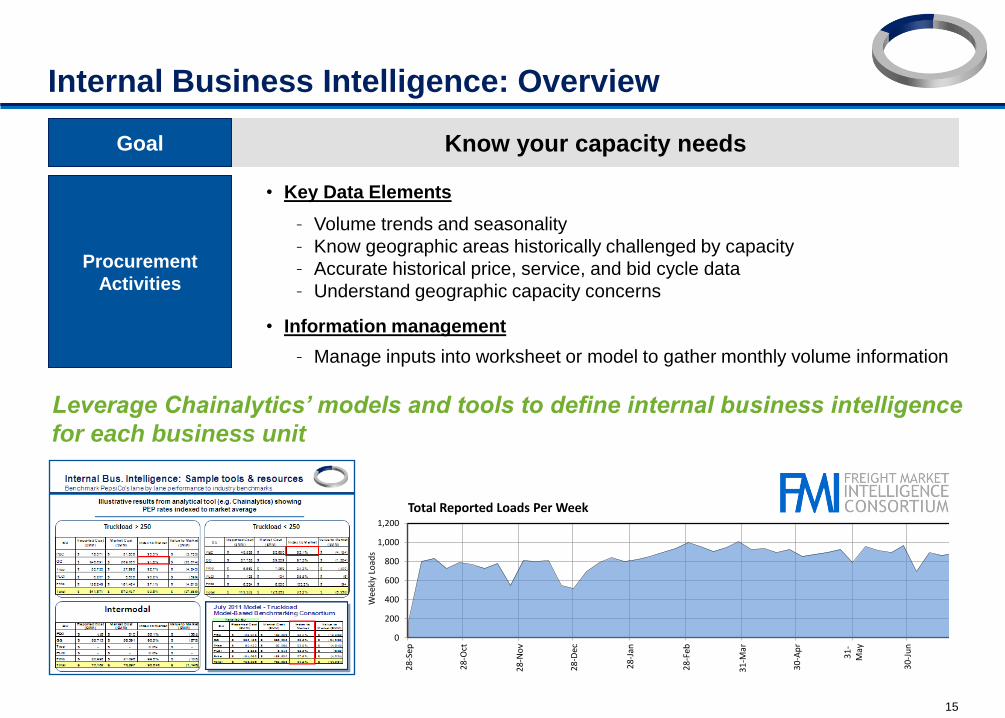

Internal Business Intelligence: Overview

Procurement

Activities

• Key Data Elements

– Volume trends and seasonality

– Know geographic areas historically challenged by capacity

– Accurate historical price, service, and bid cycle data

– Understand geographic capacity concerns

• Information management

– Manage inputs into worksheet or model to gather monthly volume information

Leverage Chainalytics’ models and tools to define internal business intelligence

for each business unit

Goal Know your capacity needs

0

200

400

600

800

1,000

1,200

28

-Sep

28

-Oct

28

-No

v

28

-Dec

28

-Jan

28

-Feb

31

-Mar

30

-Ap

r

31

-M

ay

30

-Ju

n

31

-Ju

l

31

-Au

g

Wee

kly

Load

s

Total Reported Loads Per Week

0

200

400

600

800

1,000

1,200

28

-Sep

28

-Oct

28

-No

v

28

-Dec

28

-Jan

28

-Feb

31

-Mar

30

-Ap

r

31

-M

ay

30

-Ju

n

31

-Ju

l

31

-Au

g

Wee

kly

Load

s

Total Reported Loads Per Week

16

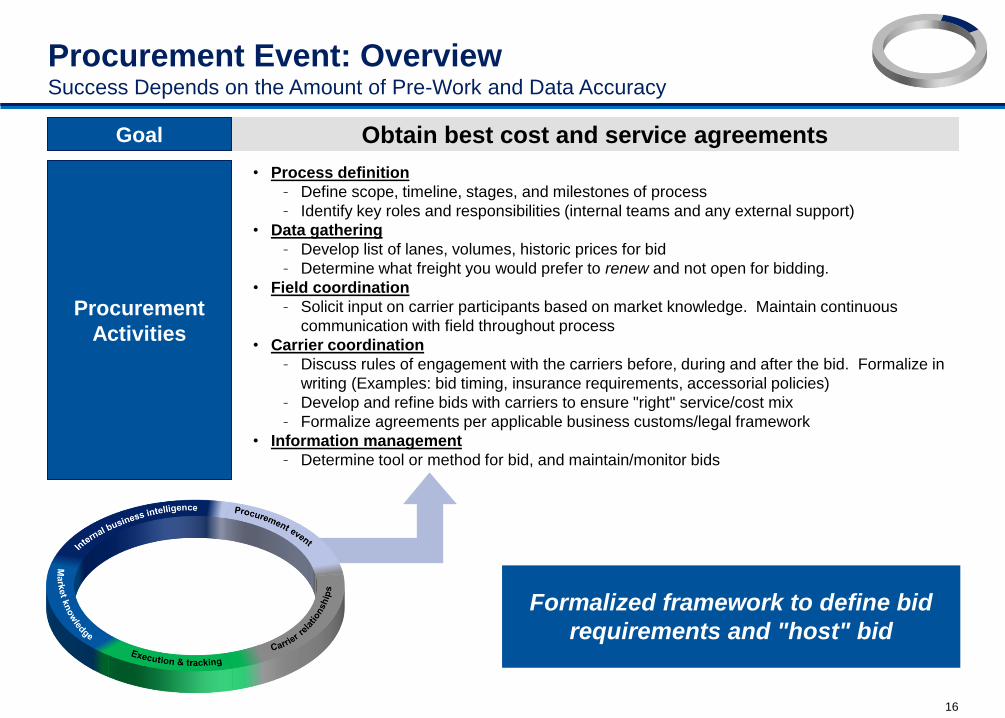

Obtain best cost and service agreements

Procurement Event: Overview Success Depends on the Amount of Pre-Work and Data Accuracy

Procurement

Activities

• Process definition

– Define scope, timeline, stages, and milestones of process

– Identify key roles and responsibilities (internal teams and any external support)

• Data gathering

– Develop list of lanes, volumes, historic prices for bid

– Determine what freight you would prefer to renew and not open for bidding.

• Field coordination

– Solicit input on carrier participants based on market knowledge. Maintain continuous

communication with field throughout process

• Carrier coordination

– Discuss rules of engagement with the carriers before, during and after the bid. Formalize in

writing (Examples: bid timing, insurance requirements, accessorial policies)

– Develop and refine bids with carriers to ensure "right" service/cost mix

– Formalize agreements per applicable business customs/legal framework

• Information management

– Determine tool or method for bid, and maintain/monitor bids

Goal

Formalized framework to define bid

requirements and "host" bid

17

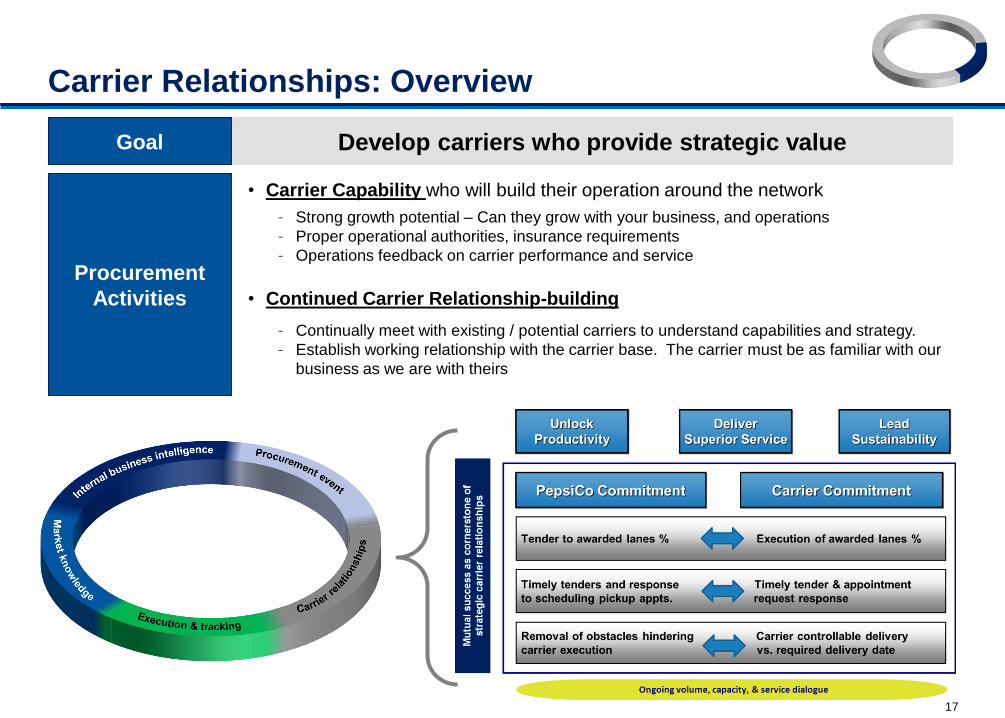

Carrier Relationships: Overview

Develop carriers who provide strategic value

Procurement

Activities

• Carrier Capability who will build their operation around the network

– Strong growth potential – Can they grow with your business, and operations

– Proper operational authorities, insurance requirements

– Operations feedback on carrier performance and service

• Continued Carrier Relationship-building

– Continually meet with existing / potential carriers to understand capabilities and strategy.

– Establish working relationship with the carrier base. The carrier must be as familiar with our

business as we are with theirs

Goal

18

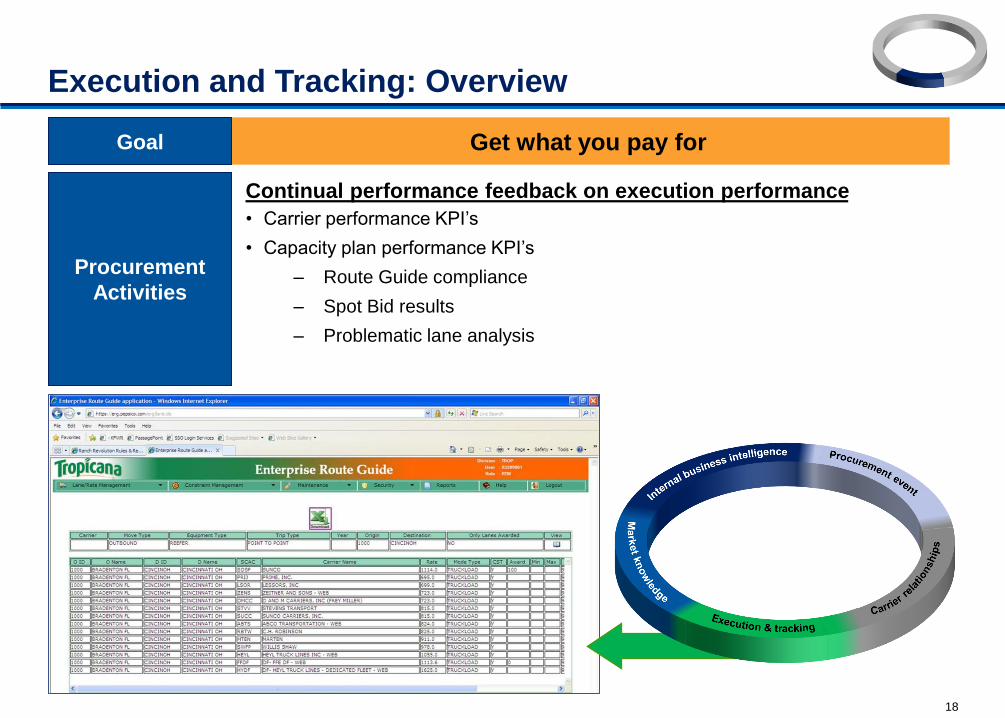

Execution and Tracking: Overview

Get what you pay for Goal

Procurement

Activities

Continual performance feedback on execution performance

• Carrier performance KPI’s

• Capacity plan performance KPI’s

– Route Guide compliance

– Spot Bid results

– Problematic lane analysis

19

Discussion

20

Discussion

Rob Hair Sr. Director, Global Transportation

Processes & Systems

Rodney Noble Sr. Director, Carrier Operations &

Procurement

Gary Girotti Vice President, Transportation

Practice CHAINalytics

Fabrizio Brasca Vice President, Global Logistics

Michael Levans Group Editorial Director, Supply

Chain Group

Moderator