Embed Size (px)

Citation preview

Corporate logistics strategies have an im-

pact on the volume of freight transporta-

tion and in turn on the environment as well

as land resources. But new corporate be-

havior can increase as well as reduce

freight transportation. This paper tries to

shed some light on this “terra incognita,”

that is the interface between corporate lo-

gistics and freight transportation. Although

it is obvious that corporate behavior today

is heterogeneous, our empirical case study

produces some clusters of key factors

which determine corporate logistics. Over-

all it is evident that environmental issues do

not play any significant role with the re-

sponding firms – due to lack of awareness

and of data. Public-private partnerships

seem to hold some promise of benefit to

corporate performance, the environment

and regional development.

1 Introduction

1.1 The Purpose of the PaperCorporate strategies and the decisionwhere to locate their strategic activitiesis of growing concern not only to thecorporate world but also to the policy-maker, especially when regional devel-opment and the environment are con-cerned.

In the wake of the discussion of inter-nationalization of the economy, it is evi-dent that corporate behavior shapes so-cial development. New corporate strate-gies such as outsourcing of individualproduction processes, have an impacton the volume of freight transportation.Due to concentration of core competen-cies, new logistics trends, and the grow-ing importance of services and liberal-ization of markets, corporate strategiesundergo rapid changes. Their spatialimpact is of interest, especially whentaking into account that new corporatebehavior can increase as well as reducefreight transportation. As a conse-quence, this increase is linked to vehi-

cle-kilometers, emissions and finally tothe conditions of the environment.

This paper tries to shed some light onthe very intricate relationships betweencorporate strategies, corporate logisticsbehavior and the resulting freight trans-port.

Three basic questions are at the be-ginning of this research:• What impacts do structural changesin the economy (e.g. outsourcing, chan-ges in telecommunication) have on thevolume of freight transportation?• In what types of companies does thedivision of labor lead to increased traf-fic and where can freight transportationbe reduced by means of improved com-munications systems?• What potential for reducing freighttransportation is available due to co-operative, public-private efforts, e.g. inthe sense of so-called “client servicetransportation,” improved logistics,etc.?

First, a survey on the pertinent litera-ture reveals only very scattered informa-tion on these issues. Either it is case-study material for specific economicbranches or activities, or studies dealwith certain spatial contexts.

The empirical background for this pa-per stems from a postal survey of com-panies located in the region of Zug,Switzerland. This is part of the researchproject “Corporate Strategies andFreight Transportation” (Thierstein,Schnell and Schwegler, 1999) fundedwithin the framework of the Swiss Na-tional Research Foundation Programme41: “Transport and Environment.”

1.2 Paper OverviewThe paper is organized as follows: Sec-tion 2 will give an overview on corpo-rate strategies, especially on trends incorporate strategies and logistics aswell as on some assumptions about theirimpact on freight transport and environ-ment. Section 3 sets the stage for theempirical study. Our basic working hy-potheses are developed and some se-lected findings for the corporate worldand for cooperative public-private solu-tions are presented. Section 4 presentsour conclusions and suggestions for fiveareas of action.

2 Changes in Corporate Strategiesand Their Spatial Impacts

2.1 Trends in Corporate Strategies and LogisticsThe literature on trends in corporatestrategies and logistics is innumerableand complex. The driving forces andmain causes for these changes or trendsare said to be numerous. There are veryintricate interlinkages between the development of freight transport, eco-nomic structural change, techno-organi-zational innovation and impact on theenvironment. On the one hand there isthe argument of increased trade flows inthe world economy, fuelled by globaltrade agreements like WTO, liberaliza-tion of markets or utilization of new,faster and cost-cutting technologies.There is a growing importance of serv-ices in the economy, one obvious reasonbeing that firms concentrate on their corecompetencies, outsourcing individualproduction processes, just-in-time pro-duction and so on. But despite all this,there is evidence of the importance of re-gional or territorial specificities. Not alleconomic activities are deterritorializedbut instead depend partly on territorialeconomic organization (Storper 1997).

But taking all the arguments together,one can structure the stage by differenti-ating the changes in framework condi-tions as well as changes which stemfrom either the supply side or from thedemand side of the firm.

Looking at the economic frameworkone can detect the following changes,which have major impacts on regionaldevelopment and transport infrastruc-ture (Cooper et al. 1994; Nijkamp1993; Drewe and Janssen 1995):• A shift from seller-markets to buyer-markets: customer orientation is increas-ing and thus diversity of products is in-creasing.• Globalization is the trend towards in-ternationally organized enterprises.

The technological framework showssome profound changes:• Information and communication tech-nologies gain more and more in impor-tance with every size and activity ofcompany. This brings about the accele-ration of processes.

DISP 148 69 2002

A l a i n T h i e r s t e i n , K l a u s - D i e t e r S c h n e l l

Corporate Strategies, Freight Transport and Regional Development

REFEREED

• Integration of transport into produc-tion chains and informational networksof companies.

The ecological framework is also si-multaneously changing:• Carbon dioxide emissions and othergreenhouse gases threaten the globalclimate but may damage regional or lo-cal production systems even worse andin a shorter period of time.• Traffic congestion is increasing ra-pidly in many agglomerated areas,which in turn increases the cost of trans-portation time as well as the accuracy ofdelivery.• Energy prices in real terms havebeen decreasing since the seventies thusfuelling the long distance exchange ofgoods, products and people.

The social framework also is chang-ing, often in an unrecognizable fashion:• Regional systems of production or local networks are being broken upthrough international sourcing strate-gies, also destroying informal informa-tion exchange between producers andcustomers. Innovation is often “only”technology driven and not based on thebottom-up exchange with needs of regional social capital or local diversityof resources.

The political framework changes ondifferent spatial levels:• On the global scale, trade as libera-lized by the World Trade Organization(WTO) speeds up at least large-scale re-gional trade.• The transportation infrastructure inmany countries, especially the totalamount of investment over time, still favors developing road transportationover innovative rail transport systems.

Nevertheless, the question remains,which corporate strategies influence thevolume of freight transportation? Logis-tics have significantly gained impor-tance for the competitiveness of firms intrade and industry. In a very narrowsense, market performance depends onthree significant factors for a firm’s com-petitiveness: product quality, productprice and product supply (ECMT 1997).All three factors are directly affected bylogistics. Taken altogether, one can de-tect three main logistics trends, which

help increase a company’s productivity(ECMT 1997, 11):• further reduction in the level of in-house production;• globalization of all economic proces-ses;• a growing importance of services formarketing industrially finished goods.

Transport needs are changing accord-ingly and are affecting the structuresused to provide transport services. Thechange in the patterns of division of la-bor and the increasing international ex-change of goods and services show atendency of producing higher volumesof freight transport. The reason lies withthe tendency towards zero-stocks pro-duction and distribution which meansthat processes must be linked togetheron a just-in-time basis which ensures theregular and punctual transfer of goodsfrom one producer stage to the next orout of production to the customer. All inall developments lead to an increasinglyindividualized demand for transportservices: “No two shippers have exactlythe same need for transport services,even though they may operate in thesame sector, produce and distribute sim-ilar products and perhaps even supplythe same markets and customers.”(ECMT 1997, 16)

2.2 Assumptions About Impact onFreight Transport and EnvironmentCompanies need supplies for their prod-ucts and services and the distribution ofthese products and services to cus-tomers of every kind. Thus changes insupply chain design and operation haveimportant consequences for transport,most notably through increasing theaverage length of haul for goods (Coo-per et al. 1996). This statement seems tobe one of the core problems with empi-rical representative studies: today, thedegrees of freedom for corporations todevelop strategic-logistics options areso numerous, that it is almost impossibleto develop a stringent model which linkscorporate behavior with its respectivevolume of freight transport.

In some instances the resulting spatialpattern of corporate organization leadsto a clear increase of goods transported

and oftentimes also to an increase in en-vironmental impacts (for example CO2-emissions). But on the other hand, intel-ligent redeployment of transport vehi-cles, included technological advance-ments, can bring along a decrease inthese same indicators. Thus, the bal-ance of net effects is very hard to estab-lish and there seem to exist very fewconvincing approaches to do so. Or, toput it this way: “While rationalizing logistics systems often leads to fewer,more focused manufacturing facilitiesand fewer, more market-spanning distri-bution facilities, it may also result in asecond level of complexity [emphasis bythe author]. Many more transportationmoves result, a greater percentage ofwhich are cross-border hauls. Manag-ing the flow and storage of materialsand information across this supply-chainnetwork requires better information sys-tems and more precise coordination.”(Kobler 1997, 11)

In order to systematize the impacts ofcorporate strategies on freight trans-portation, it is helpful to structure thestrategies along the following lines –which in an ideal case can be coordi-nated properly:• supply• production• distribution

If one wants to identify the impact ofthese different strategic aspects onfreight transportation, knowledge aboutwhere in a firm’s hierarchy and func-tional structure which decisions in logis-tics and transportation are being takenis necessary.

2.2.1 SupplyCertain strategies obviously lead to in-creased vehicle movement like “globalsourcing” which leads to a enlargedspatial supply network or like just-in-time(JIT) delivery which cuts down deliveryfrequency and volume of freight per de-livery (Frigo-Mosca et al., 1996). But“just-in-time” also can have the oppositeimpact: postponing delivery allows forbetter calculating the exact volume ofmaterial or number of parts thus reduc-ing inefficient vehicle movements. Thelocation of the suppliers seems to be thedetermining factor for the net effect; re-

DISP 148 70 2002

cent studies support the argument thatJIT favors regional suppliers and thushelps to reduce the volume of freighttransportation (Jäcker 1997). On theother hand, strategies like “single sourc-ing” or “modular sourcing,” which in-tend to reduce the number of suppliers,normally result in fewer spatial interac-tions. In general, the following seems tohold: the transportation impact of modu-lar sourcing is lower the closer the sup-plier is located to the manufacturer.(Jäcker, 1997)

2.2.2 ProductionVarious studies in all the three aspects oflogistics strategies and across differenteconomic branches show more or lessthat the reduction of the level of in-houseproduction in general leads to an in-crease in freight transportation (Dreheret al. 1995; Haubold 1995; Jäcker1997; Holzapfel and Vahrenkamp1993). But it is important to state thatthe individual case can easily show theopposite effects. For example, one as-pect of changing supply-chain manage-ment is reducing the level of in-houseproduction, which may multiply the num-ber of suppliers. They in turn deliver therequired parts more frequently but insmaller batches thus increasing the vol-ume of freight transportation. On theother hand the manifest trend towardthe concentration and bundling of singlesuppliers in the form of component orsystems suppliers tends to reduce freighttransportation for production inputs.Outsourcing of logistics services to spe-cialized firms is another trend today.This results in less transportation be-cause these specialists are more capa-ble of bundling transportation more effi-ciently.

2.2.3 DistributionMore and more, specialized transportfirms collect all the orders in one areaand deliver them directly to the customerthus reducing the vehicle movement. Thesame effect seems to develop with theupcoming “Euro-logistics concept,”which replaces national logistic con-cepts for spatially, more integrated onesthus cutting down on overall transporta-tion although this strategy may region-

ally lead to an increase of vehicle move-ment.

2.2.4 ConclusionFor the purpose of the project describedin this paper, we produced the follow-ing synopsis. It illustrates the manifoldrecent corporate strategies and theirpresumed impact on the volume offreight transportation (VFT). The twocolumns on the extreme right differenti-ate between vehicle-kilometers (VK) andtransport performance in kilometers(TK).

Fig. 1 shows that we face contradict-ing trends: on the one hand, new cor-porate strategies may increase transportvolume; on the other, these changesmay also prove to have potential for re-ducing the input of resources in thewhole supply chain.

2.3 Regional and Spatial ImpactsRegional science has since long dealtwith the link between infrastructure, es-pecially transport infrastructure and re-gional development. The European sin-gle market spurred research in this ques-tion. One early finding was, that “lowgrowth leads to stable international-na-tional-regional development, whereasvery fast growth tends to destabilize an integrated international-national-re-gional economic system” (Nijkamp1990, 5). As we enter a new millen-nium, we are witnessing very dynamicinternational economic development,from which one can assume in turnleads to the speeding-up of corporatereorganization in the direction thetrends describe in section 2. But despitethe logic of this argument, the link be-tween corporate logistics behavior and

DISP 148 71 2002

Strategic Elements Reflections on Transport Possible Impact

VFT VK TK

Inadequate consideration of real transport costs � �

Hope for planning of goods transport that is �closer to actual needs

Building of increasingly finely-meshed production � � �and value creation chains

Growing need for exchange of information and �goods

Chance to bundle transportation � � �

Lower levels of in-house-production for producers � � �

The percentage of cargo for bulk goods � �decreases; there are more joint loadings andindividual parcels

Distribution by way of express services with � �hub-and-spoke concepts increases vehicle mileage

Change of modal-split in favor of road transport �

More frequent transport movement but with less � �use of cargo room to capacity

Counterbalancing tendencies of delivery security � �and road traffic capacity

Change of modal-split due in part to the existing �rail infrastructure

Suppliers in close proximity � �

Chance for traffic bundling � � �

Logistics (supply and distribution)

Production

Lean Management

Flat hierarchies

Optimization of production depth

Product differentiation

Customer orientation

Product innovation

Procurement logisticsstrategies• Just-in-Time-procure-

ment with variousclearances

New procurement strategies

• Global vs. RegionalSourcing

• Modular Sourcing

• Single Sourcing

Concentration on core competencies

Building of strategic alliances

VFT = Volume of freight transportationVK = Vehicle-kilometersTK = Transport performance in kilometers

Fig. 1: Aspects of strategic change and theirpossible impact on freight transportation

regional or spatial development is veryrarely evaluated. This might be attrib-uted to the very complexity between ini-tial software – that is the strategies –and the final outcome of these strate-gies. The latter – the impact of hardwareon regional development – is treatedquite often in scientific research (see forexample: Vickerman 1991). Variousstudies of different methodologicalbackground agree in stating that newcorporate behavior can increase as wellas reduce freight transportation. Theoverall impact of these changes is veryunclear and little empirical evidence isavailable besides various casual obser-vations and insights originating mainlyin the automotive sector (Womack et al.1991). However, there seems to be evi-dence – at least on a very general level– that spatial concentration of mobility,and accessibility and amenities will of-fer the best changes for sustainability ona spatial level as seen in the DutchRandstad (Nijkamp et al. 1996).

The next subsection of the paper willpresent our four main hypotheses.

2.4 HypothesesAs a result of a survey of theoretical lit-erature and empirical analyses we havebeen able to generate four main work-ing hypotheses, each of which were dif-ferentiated into 3–4 detailed subhy-potheses during the process of their evo-lution. The following four main hypothe-ses were further discussed with selectedexperts in the field of freight transporta-tion and logistics management. Belowwe only present the key aspects.• Corporate division of labor and theintegration of the value-added chaintend to change in a way that affect thenet volume of freight transport.• Taking a closer look, there are cer-tain recent or new corporate (logistic)strategies that tend to increase the amount of vehicle movement and thusthe volume of freight transport, whileother (logistic) strategies seem to reduceor compensate these former trends.• Potential impacts on volume of freighttransport very seldom are a decisive cri-teria for corporate strategic decisions.These decisions focus on the lowering of

costs of transportation and of handlingand storing of goods.• Cooperative approaches either be-tween firms – like multi-firm chains of logistics – or between firms and publicadministration develop and are sup-posed to have a growing influence oncorporate logistics decisions.

These four hypotheses eventuallyserved as a basis for elaborating aquestionnaire (see section 3).

3 The Empirical StudyHowever, knowledge of the effects offreight transport is, as opposed to pas-senger transport, fairly limited. One re-striction we face is the lack of appropri-ate data. Another reason that limitsknowledge about effects on freighttransportation is the absence of an inte-grative analysis of corporate strategiesand trends in freight transportation. Atbest, there are very few scattered exam-ples of innovative and proactive public-private cooperation in this field.

3.1 The Design of the StudyWe expected to find the necessary in-sights on the• macro level: the economic structure,spatial interlinkages, regional input-out-put relations, modal split of transporta-tion;• meso level: regional production sys-tems, regional economic specialization,regional volume of freight transporta-tion;• micro level: corporate (logistics) stra-tegies and organizational features.

Our analytical framework tries to inte-grate the strategic options of firms andtheir corporate behavior in relation tofreight transportation. But to be frank,data which covers exactly this field ofresearch, does not yet exist and is nei-ther available on a private nor on apublic basis. The reasons are pretty ob-vious. Private companies are not inter-ested in such data, because transporta-tion costs in general are but a very mi-nor cost factor in their overall calculus.On the other hand, public authorities focus their attention on private motor vehicle traffic and its various impacts.

Our initial interviews with experts ofshipping companies, that is firms whichdistribute or ship their goods them-selves, and suppliers of innovative logis-tic concepts quickly proved that valu-able data will be gained only by ana-lyzing the enterprises themselves. Thus,the crucial point is to approach “reality”from two sides and find an appropriatelink between strategic corporate behav-ior and volume of freight transportation,which transforms into usable data. Toface this challenge, we opted for amixed methodology:• secondary analysis of federal statis-tics on number of firms, employees,freight transport;• a company survey with questionnaireand additional interviews with logisticsexperts;• case studies with companies havingundergone internal reorganization pro-cesses and where these strategic chan-ges can clearly be identified with a startand a finish date;• a feedback workshop with privateand public firms and public authoritiesprovided a discussion forum for our find-ings regarding their reasonability andto develop approaches for cooperativeefforts to reduce impacts of freight trans-portation on the region and the environ-ment.

To reduce complexity and in order tohandle the empirical approaches wechose to study the interlinkages and im-pacts for the Swiss region of Zug, lo-cated in central Switzerland. This regionwas selected based on the followingfactors:• its central location within the Swissrail and road infrastructure; • the limited spatial scale of an agglo-meration having eight communes andaround one hundred thousand inhabi-tants; • a highly developed and structurallydiversified economy which is based onproduction as well as services such aswholesale or financial services; • finally, because we cooperated witha private foundation which supportedthe survey financially and logistically forthis region.

This paper concentrates on the resultsof the company survey. We next discuss

DISP 148 72 2002

the database of that survey, which wascreated in March and April of 1998.

3.2 The Data Base for the Postal SurveyThe agglomeration of Zug consists ofeight communes and around 6,400firms. The survey excludes firms withless than ten employees and excludesbranches with presumably no direct re-gional freight transportation, like publicadministration and certain services.Questionnaires were sent out to 536firms in early March of 1998; 118 re-sponses were received from which 77were ready for analysis; thus the re-sponse rate was about 14%, which isreasonable compared to the question-naire’s level of complexity.

Concerning the structure of busi-nesses, we can speak of a representa-tive sampling. The division of compa-nies by branches represents approxi-mately that of the Canton of Zug (2ndand 3rd sectors): production businesses32%, construction businesses 22%,trade/maintenance/hospitality busines-ses 34%, and wholesale/transport busi-nesses 12%.

The distribution of firm size can beseen in Fig. 2. We observe the usualfact that the response frequency of smallfirms is far below the share of establish-ments in the sample. Firms with 20 to 49employees comprise the largest share ofall firms responding; companies withmore than 500 employees are largelyover-represented. One reason for non-response of small firms is the unfamiliar-ity with topics like logistics and strategicmanagement whereas these issues aredaily business with large companies.

The status of the plant: More than50% of all firms are single plant firms,whereas 22% are the head plant of anenterprise to which belong also branchplants or subsidiary companies. The restis about evenly distributed as a branch

plant or a subsidiary of an out-of-cantonSwiss company and as a branch plantor a subsidiary of a foreign company.

Export activities are a vital element forSwiss competitiveness. The respondingfirms export slightly more intensivelythan regional average. 12% of the re-sponding firms make more than twothirds of their turnover from exports com-pared to 9% of all firms in Zug. In con-trast, 77% of all firms in Zug do not ex-port compared to 61% of the respond-ing firms.

The development of turnover reflectsthe rather depressed economic situationat the time of the survey (April 1998).Still, two fifths of the firms said they hadincreased turnover compared to the pre-vious year, 34% had stable turnoverwhereas a fourth stated their figures haddecreased. The employment figuressomehow reflect the difficult economicsituation for Swiss companies. One thirdof all firms reported decreasing employ-ment compared to the previous year,while only a fourth had increased.

The Swiss economy traditionally hashad a dual structure. A third of all firmsgenerate their turnover within the Euro-pean Union, their most important mar-ket. However, for over 80% of all com-panies, Switzerland is the most impor-tant market. Rather typical for small andmedium-sized enterprises is the fact that

60% of the firms produce their turnoverwith one single group of products orservices.

3.3 Selected ResultsThis section presents selected resultsfrom the company survey and concen-trates on markets and corporate strate-gies, on corporate transport and on thelink between logistics and environment.

3.3.1 Markets and Corporate StrategiesCorporate behavior or strategies arestrongly shaped by the dynamics andcharacteristics of their respective mar-kets. So we asked the firms: “Which fea-tures characterize the principal marketsof your company?” Answers could begiven with the following key factors tobe rated according to “very high,”“rather high,” “rather low,” and “verylow.” The answers were transferred intonumbers ranging from 4 for “very high”to 1 for “very low.” The ranking of themeans for the key factors is presented asfollows:

This list makes clear that for most com-panies a certain combination of price,quality and time to market are the cru-cial ingredients for competition; logisticsand environment seem to be just a func-tion of these core requirements.

Now with the above ranking in mindwe present a list of factors determiningcorporate logistics. We asked: “Whichare the five most important factors thatshape the way your company organizesfreight transportation?” And the an-swers were as follows in Fig. 4.

This ranking makes quite clear that thefirst six to seven factors seem of moreimportance than the rest. Neverthelessone has to bear in mind that firms ingeneral not only define their logisticsstrategies according to one or two sin-gle requirements. Instead they follow acertain bundle of factors which deter-mine what they are going to do with re-gard to freight transportation and loca-tional decisions. A survey of empiricalliterature prior to our own firm surveysuggested that there must be some kindof typology of corporate behavior in thisregard. On the other hand the rapidproliferation of logistics or strategic op-tions for firms indicated the opposite:

DISP 148 73 2002

0%

10%

20%

30%

40%

50%

60%

10-19 20-49 50-99 100-199 200-499 500-999 1000+

Number of Employees

Sample n = 536

Response nr = 77

Fig. 2: Distribution of firm size

Key factors Mean rating

Intensity of cost / price competition 3.6Intensity of quality competition 3.1Intensity of ‘time’ competition(time to market, order-cycle, delivery) 3.0Frequency of innovations 3.0Importance of information andcommunication technologies 2.6Ecological requirements 2.4

Fig. 3: Characterization of the firms’ respec-tive markets

there were almost no two single compa-nies displaying the same logistics fea-tures.

So best thing is to analyze the abovedata to see if there are certain clustersof key factors which determine logisticbehavior. According to the original re-search plan, the impact of the market sit-uation on a firms’ strategic transporta-tion planning was to be determined withthe help of an ordered probit model.Therefore, clusters of firms should beproduced and then be taken as a start-ing-point for weighted ordered probit re-gressions. Because of various problemswe changed this procedure. A regres-sion with a too small database wouldproduce statistical distortion. This distor-tion would be increased when severalstatistical methods would be executedone after the other. For that reason, westarted with the cluster analysis, but thencontinued with a discriminant analysis.

The hierarchical cluster analysisshows the following characteristics.

First, there are two distinct clusters ofkey factors representing clearly differenteconomic activities (see Fig. 5). The first

cluster is characterized by the factors“reliability/accuracy of delivery,” “flexi-bility/short order-cycle time” and “care-ful handling of goods.” This threesomeof key factors seems to be typical forwholesale activities. But also buildingtraders tend to be linked with this clus-ter. The second cluster encompasses thefactors “transportation cost (percentageof total),” “weight of goods” and “vol-ume of goods” which is typical forheavy and bulky material, e.g. in the in-dustrial sector. The cluster analysis alsoshows that the key factor “price per kilo-gram of goods” is loosely related to thefirst of these clusters. This somehow is asurprise because the firm survey also de-picts that for most companies, the “in-tensity of cost and price competition” intheir main markets is very high – notonly those who rate “price per kilo-gram” as a crucial factor for transporta-tion.

A second finding is, that corporate lo-gistics strategies tend to be very hetero-geneous (see also chapter 2). Neverthe-less, our firm survey produced threeclusters of strategic options, although

they do not reveal much differentiation.The following Fig. 6 gives an overviewof the three clusters and their configura-tion. Strategic options were listed in or-der of their frequency of being men-tioned in the survey, top down and fromleft to right.• First, a basic set of strategies seemsto exist which form a “must” for everyfirm which wants to stay competitive to-day and maybe also in the future. Thiscluster contains the majority of the re-sponding firms (46).

On top of these strategical “basics,”the responding firms seem to subscribeto two more clusters of options.• The second cluster is characterizedby rather “soft” strategies that focus onintra-firm processes and can be labeledas “focus.” This second cluster contains11 firms.• The third cluster, with 26 firms, is call-ed “basics plus” and encompasses a wi-der range of strategic features.

A discriminant analysis was con-ducted to examine significant featuresfor the statistical clustering of firms’strategic behavior. First, we found nottoo much differentiation in the divisionof branches between the three clusters.Small differences could be establishedwithin the cluster “focus,” which couldbe explained by the small number offirms in this cluster. In the “basics” groupwe find more retailers, the two otherclusters contain a few more manufactur-ing firms. As a result of further analysiswe found that neither the number of a

DISP 148 74 2002

Factors for transportation strategy frequency

1 reliability/accuracy of delivery IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 612 flexibility/short order-cycle time IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 543 transportation cost (percentage of total) IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 444 careful handling of goods IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 375 weight of goods IIIIIIIIIIIIIIIIIIIIIIIIIIIIIII 316 volume of goods IIIIIIIIIIIIIIIIIIIIIIII 247 length of transportation itinerary IIIIIIIIIIIIIIIII 178 willingness of customers to wait for goods IIIIIIIIIII 119 ‘time-sensitivity’ of goods IIIIIIII 810 price per kilogram of goods IIIIIII 711 branch of firm IIIIII 612 energy cost (percentage of total) IIIII 513 position within value added chain IIIII 514 availability of infrastructure IIIII 5

Fig. 4: Factors for transportation strategy (fre-quencies)

weight of goods

reliability/accuracy of delivery

flexibility/short order-cycle time

careful handling of goods

transportation cost

volume of goods

Fig. 5: Clusters of factors for transportationstrategy

Fig. 6: Three clusters in strategic behavior

Ÿ Deepen cooperation withcustomers

Ÿ Intensify cooperation withsuppliers

Ÿ Simplify procedures

Ÿ Transparency on goals andperformance within firm

Ÿ Increase ability for productinnovation

Ÿ Simplify product structureŸ Skip activities with low

value addedŸ Reduce level of inhouse

productionŸ Assess environmental

impacts systematicallyŸ Decentralize decision and

commandFocu

s

Basics +

Basi

cs

firm’s employees, nor its position in thevalue added chain was a significantfeature for the classification of the firmsto the clusters. What seems to have acertain impact on this classification isthe self-characterization of a firm’s mar-ket situation. On this matter most of theresponding firms judged the cost andprice competition to be very intensive.

3.3.2 Input-Side of Corporate Freight TransportationThe volume of freight transportation in1997 represented in the survey is about700,000 tons, two thirds of which wereminerals and building material. The sec-ond large statistical class (15%) are theso-called “other products,” which con-tain machines, electrical products, auto-mobiles and other high-value finishedproducts. Only 14% of responding firmsreport a decrease in input-side goodscompared to the previous year. 43% offirms report increasing or constant input-tonnage.

Regional impacts are supposed to belinked strongly with the amount of kilo-meters driven. Thus, we asked for pre-cise data on transportation with com-pany-owned vehicles (kilometers, tonsper kilometer, kind of vehicle). But, forreasons of lack of data or lack of timetoo few responses were submitted tomake valid statements on this aspect.

The more suppliers of parts or compo-nents a single manufacturer has themore vehicle movement will occur – thisis one of our standard assumptions. Oursurvey shows that an average firm haseleven suppliers with significant volumeof freight. The bulk of these suppliersare producing single parts or goods,while comparably few are supplyingcomponents or modules and even fewerare so-called “systems suppliers.”

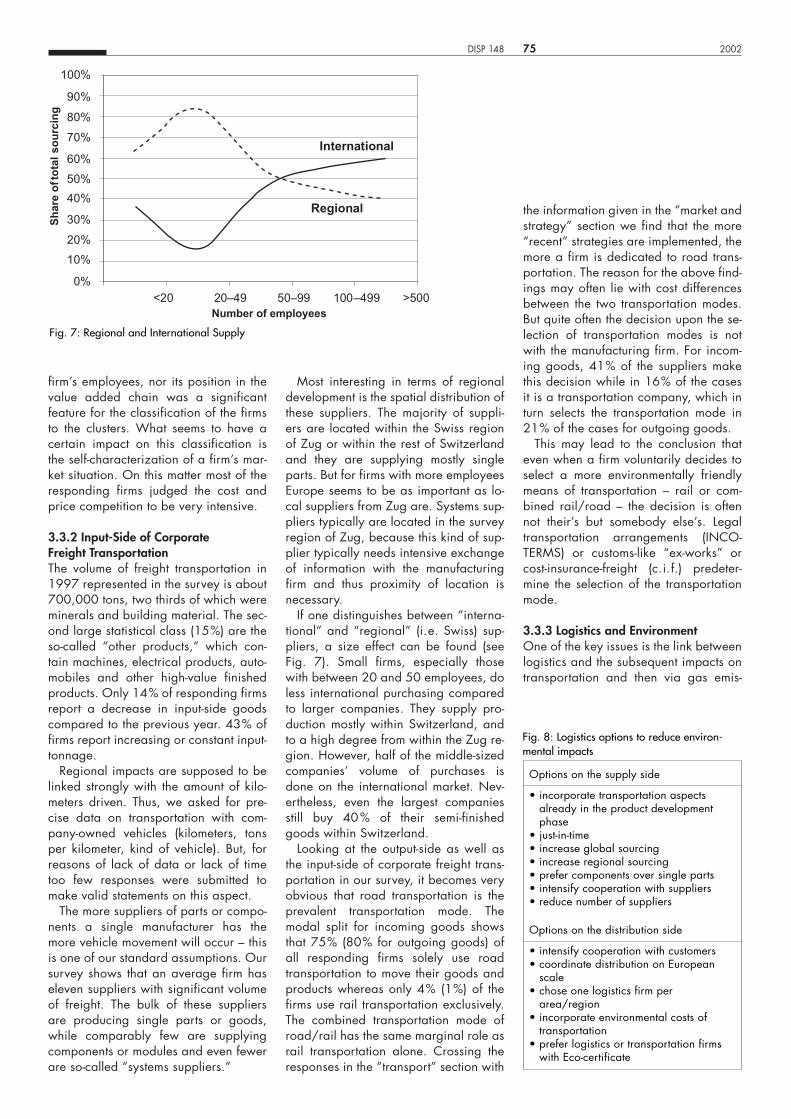

Most interesting in terms of regionaldevelopment is the spatial distribution ofthese suppliers. The majority of suppli-ers are located within the Swiss regionof Zug or within the rest of Switzerlandand they are supplying mostly singleparts. But for firms with more employeesEurope seems to be as important as lo-cal suppliers from Zug are. Systems sup-pliers typically are located in the surveyregion of Zug, because this kind of sup-plier typically needs intensive exchangeof information with the manufacturingfirm and thus proximity of location isnecessary.

If one distinguishes between “interna-tional” and “regional” (i.e. Swiss) sup-pliers, a size effect can be found (seeFig. 7). Small firms, especially thosewith between 20 and 50 employees, doless international purchasing comparedto larger companies. They supply pro-duction mostly within Switzerland, andto a high degree from within the Zug re-gion. However, half of the middle-sizedcompanies’ volume of purchases isdone on the international market. Nev-ertheless, even the largest companiesstill buy 40% of their semi-finishedgoods within Switzerland.

Looking at the output-side as well asthe input-side of corporate freight trans-portation in our survey, it becomes veryobvious that road transportation is theprevalent transportation mode. Themodal split for incoming goods showsthat 75% (80% for outgoing goods) ofall responding firms solely use roadtransportation to move their goods andproducts whereas only 4% (1%) of thefirms use rail transportation exclusively.The combined transportation mode ofroad/rail has the same marginal role asrail transportation alone. Crossing theresponses in the “transport” section with

the information given in the “market andstrategy” section we find that the more“recent” strategies are implemented, themore a firm is dedicated to road trans-portation. The reason for the above find-ings may often lie with cost differencesbetween the two transportation modes.But quite often the decision upon the se-lection of transportation modes is notwith the manufacturing firm. For incom-ing goods, 41% of the suppliers makethis decision while in 16% of the casesit is a transportation company, which inturn selects the transportation mode in21% of the cases for outgoing goods.

This may lead to the conclusion thateven when a firm voluntarily decides toselect a more environmentally friendlymeans of transportation – rail or com-bined rail/road – the decision is oftennot their’s but somebody else’s. Legaltransportation arrangements (INCO-TERMS) or customs-like “ex-works” orcost-insurance-freight (c.i.f.) predeter-mine the selection of the transportationmode.

3.3.3 Logistics and EnvironmentOne of the key issues is the link betweenlogistics and the subsequent impacts ontransportation and then via gas emis-

DISP 148 75 2002

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

<20 20–49 50–99 100–499 >500

Number of employees

Sh

are

of to

tal

so

urc

ing

ternatio

Regional

In nal

Fig. 7: Regional and International Supply

Options on the supply side

• incorporate transportation aspectsalready in the product developmentphase

• just-in-time• increase global sourcing• increase regional sourcing• prefer components over single parts• intensify cooperation with suppliers• reduce number of suppliers

Options on the distribution side

• intensify cooperation with customers• coordinate distribution on European

scale• chose one logistics firm per

area/region• incorporate environmental costs of

transportation• prefer logistics or transportation firms

with Eco-certificate

Fig. 8: Logistics options to reduce environ-mental impacts

sions and noise on the environment. Inour survey we offered the companiesthe following introductory statement:“There are two main approaches forfreight transportation which is environ-mentally sound and at the same timeeconomical: lesser hauls and intelligentdesign of freight transportation.” Thefirms were then asked to choose from alist those logistic concepts which in theirperception could contribute in a certaindegree to the above-described objec-tive, that is to reduce environmental im-pacts. The logistics options were differ-entiated in a supply side and a distribu-tion side:

According to more than 80% of thefirms, intensified cooperation with sup-pliers and a higher rate of regionalsourcing seem to contribute verystrongly to both lesser hauls and intelli-gent design of freight transportation.For almost two thirds of the firms, amore intelligent method of transporta-tion will be strongly supported by just-in-time supply and intensified cooperationwith customers. The previous statementis also a crucial factor for lesser freighthauls. The firms ascribe a strong contri-bution at least to both main approachesto very early incorporation of trans-portation aspects in production plan-ning.

4 Conclusions and Suggestions for Action4.1 ConclusionsThe results of the study clearly show thata multitude of both external and internalfactors influence companies’ behavior.As external influences of firm’s behaviorwe can cite the conditional factor oftransport cost. The study lets us draw theconclusion that transport costs or ratherenergy prices are too low to play a rolein firms’ calculations. The use of envi-ronmental or natural resources does notproduce sufficient price signals, and istherefore ignored or neglected by man-agement.

For the majority of businesses, theconscious planning of goods’ transportis not a pressing topic. But the survey re-sponses reveal that each firm acts in aspecific manner to changes in their envi-

ronment. This impression was stronglycertified within the discussions with ex-perts.

A clear typology – as new businessstrategies demonstrate – is not recogniz-able. Consequently it is not possible todetermine a “typology of goods trans-port burden” that could then be used ina general form for state planning or im-plemented in business planning. How-ever, it is possible to observe a group-ing of businesses that forms around thelevel of logistics integration: on the onehand there are businesses that have acontinuous logistics organization andsee the value chain creation as an en-tirety. On the other hand, there are busi-nesses that promise nothing of this andremain true to the conventional conceptsof manufacturing and product manage-ment. These companies can raise, forexample, few figures on the spatial im-pact of their logistics. For that reasonthey are much less capable of actingstrategically. The analysis shows thatthis qualitative jump in the developmentphase of logistics is highly dependenton the market pressure facing each com-pany. In the region of Zug, this seems tohave no relation to structural character-istics such as the size of the business orsector of operation.

The paper so far gives the correct im-pression that the link or interface be-tween corporate strategies and freighttransportation is blurred and some kindof “terra incognita.” Our own survey offirms aimed – among other things – atproducing quantitative data about thisinterface. This hope proved to bewrong. One of the main reasons is thelack of appropriate information andknowledge within the firms about this is-sue, which in turn is due to a still ratherisolated view of questions of logistics.Therefore, appropriate controlling toolsare lacking.

4.2 Suggestions for ActionCorporate logistics decisions have animpact on the environment. The problemis: who cares? Public administration isinclined to fend off harm done to thepublic but private or public companiesare to produce profit. Our survey offirms shows that in many cases the link

between logistics behavior and volumeof freight transportation is not within themental or pecuniary perception of afirm’s management.

Based on the project results, sugges-tions for future action apply to variousplayers. These suggestions are groupedin five areas of action: Corporate level,Politics, Law, Infrastructure and “Soft-ware.”

4.2.1 Corporate Level All to often, logistics is still a purely op-erational approach. Only if a firm is be-ginning to perceive its performance invalue added chains does it realize thatintegrated logistics concepts are able tooptimize performance all along thisvalue added chain. The more single lo-gistic measures are integrated, the morea firm begins to develop control instru-ments which in turn enable the companyto better perceive its impact on the vol-ume of freight transportation and subse-quently on environment and spatial de-velopment. Raising awareness aboutthis issue requires two things: first mov-ing logistics up the hierarchical ladderof a firm into top management and sec-ond an appropriate control instrument tobetter quantify the interface betweenstrategic logistics decision and volumeof freight transportation. Within thisframework for action, the main ap-proach for better corporate logisticsplanning is to foster regional coopera-tion. Appropriate means are, for in-stance, to participate in cooperationmarkets, to aspire the common use ofcorporate infrastructure, to use flexible-platform pools, or to develop efficientcommunication means.

4.2.2 PoliticsWhat is primarily addressed here is theformation of conditions, such as the setting of price signals countrywide.Thereby external traffic costs such as en-ergy taxes or energy incentives will beincreasingly considered in firms’ costcalculations.

It is urgent that the interface of railand road be made more utilizable. Forthis, public and private entities mustwork together. Only in this manner canthere be an efficient fusion of rail trans-

DISP 148 76 2002

port’s potential for development with thechallenges of businesses. The coopera-tion between state entities and privateenterprise has taken on particular mean-ing largely due to the introduction of theSwiss Alpeninitiative. The survey of busi-nesses in and around Zug confirmedthat transport costs do not belong to thedeciding criteria in business decisions –not even in the area of logistics. The rec-ognized measures of supply-side eco-nomics and free enterprise such as LSVA(flexible tax on road freight transporta-tion) do not provide enough force. Be-yond that, there is a need for coopera-tive development – for example in jointshipping – which not only creates at-tractive business conditions but alsobreaks down emotional barriers be-tween rail transport, its competitors andcustomers.

4.2.3 LawThe need for a broad-based site conceptfor combined traffic is undisputed. Sucha concept must be supported on variouslevels. On the national level, for exam-ple, a new start was made at the begin-ning of 1999 with the legislative pro-posal for rail reform. It is also possibleto envision a federal plan on Rail Trans-portation and Combined Transport In-frastructure.

On the regional level, the basis of thecanton’s strategic traffic planning mustbe improved. As companies do not fittheir activities to political borders, thecanton has to create its bases for plan-ning on a transborder level. This leadsto the question of whether a Swiss na-tional development strategy for the cur-rent environment is needed, to create aframework for this spatially variable co-operation of Swiss cantons.

Based on the results of this project, werecommend that communities pursuemore vigilantly the efficient use of spacein transport and traffic infrastructure intheir plans. This becomes even more im-portant as many key players in the Zugregion consider traffic to be the “Motorof City Development.” The opportunitiesrange from the elimination of certain sitecharacteristics for newly-locating firmsto planning shutdowns for business rea-sons or the application of cooperative

tools in the planning process. Therebythe state asks businesses to cooperateand provides these private entities withuseful information. In this manner, com-panies begin to learn the needs and mo-tives of public offices. It is important thata regional level for cooperation isfound. In the near future, the canton andcommunities of Zug must get closer tothe customer than ever before and there-fore closer to the needs of the economyand the general population.

4.2.4 InfrastructureAs the demand for intermodality oftransport rises, a need for an appro-priate physical infrastructure also arises.Business decisions on transport contain-ers, transport methods and transport de-pend on the network for joint trans-portation being available. For example,at the Rotkreuz railway station the Zugregion has a strategically favorable sitewhose infrastructure still needs develop-ment.

Until now infrastructure policy was al-ways one-sidedly based on supply: thatis to say that when there was a trafficjam, it was counteracted by an expan-sion of traffic infrastructure. Recently,availability and networking of functionssuch as working, living or shopping arebeing demanded locally. For that rea-son, efforts are to be judged on the ba-sis of their contribution to sustainablespatial development and their spatialand environmental effects.

4.2.5 “Software”This term – in contrast to hardware –refers to the “soft infrastructure.” Whatis needed first of all is information. Asan example, few firms know that it ispossible to get subsidies for investmentin a works siding – provided by theCanton of Zug as a clean air measure.A first step toward overcoming this com-munications deficit is the newly createdOffice for Long-term Promotion in thecanton’s Office for Economic Develop-ment. Moreover, “software” also coversvoting processes in logistics as well asthe availability of knowledge and skillsin the region. In this area, deciding fac-tors stem from spatial planning and sitepolicy.

The administration’s proximity to thecustomer should not be restricted to busi-ness. On the one hand, nontrans-parency in traffic processes and impactlinks make it more difficult to lead a dis-cussion oriented toward future abilities.On the other hand, the population in-creasingly views the ever-smaller livingspace as a problem. This situation callsfor public discussion (about values andquality of life). The public administrationhas the obligation to take the needs ofall constituents seriously and to providethem with a forum for exchange.

Notes

This research was funded by the Swiss Na-tional Science Foundation (SNF) within theframework of National Research Programme41 “Transport and Environment – InteractionsSwitzerland/Europe.” Additional supportcame from the “Stiftung Lebens- undWirtschaftsraum Zug,” which prepared theground for our regional case study.

References

COOPER, J., BROWNE, M. and PETERS, M.,1994. European Logistics. Markets, Man-agement and Strategy. Second Edition, Ox-ford: Blackwell.

COOPER, J., BLACK, I. and PETERS, M.,1996. Linking the environmental impact offreight transport to the restructuring of supplychains. Cranfield University.

DREHER, C. et al., 1995. Neue Produktions-konzepte in der deutschen Industrie. Be-standesaufnahme, Analyse und wirtschafts-politische Implikationen. Heidelberg: Physica(Wirtschaft, Technik, Politik – Schriftenreihedes ISI-FHG 18).

DREHER , C. and KÖNIG, R., 1996. Szena-rien technisch-organisatorischer Innovationenund ihrer Auswirkungen auf den Güter-verkehr. Strukturierung wesentlicher Ein-flussfaktoren und Projektion alternativerSzenarien. Karlsruhe: Fraunhofer Institut fürSystemtechnik und Innovationsforschung ISI.

European Conference of Ministers of Trans-port ECMT (Eds.), 1997. New trends in lo-gistics in Europe. Paris: OECD, 1997 (Reportof the 104th Round Table on transport eco-nomics).

DISP 148 77 2002

FRIGO-MOSCA, F., BRÜTSCH, D., HAFEN,U. and TETTAMANTI, S., 1996. Logistic Part-nership: Supply Chain Management in derSchweizer Industrie. Zürich: vdf.

HARMSEN, D.M. 1998. Auswirkungen tech-nisch-organisatorischer Innovationen auf denGüterverkehr – Ergebnisse einer empirischenUntersuchung bei der verladenden Industrie.Vortrag an der Traffic98, Internationale Kon-ferenz in Berlin, 5.–6.2.1998.

HAUBOLD, V., 1995. Umstrukturierungs-prozesse in der zwischenbetrieblichen Ar-beitsteilung der Industrie: Eine theoretischeund empirische Analyse unter besondererBerücksichtigung logistischer Aspekte. Göt-tingen: Vandenhoek und Rupprecht.

JÄCKER, A., 1997. Verkehrliche Wirkungenneuer Produktionskonzepte. Eine theoretischeund empirische Analyse am Beispiel derdeutschen Elektroindustrie. Göttingen: Van-denhoek und Rupprecht.

KOBLER, R.A., 1997. Strategic EuropeanDistribution Logistics Design. Bamberg, Diss.1997 (Dissertation Nr. 2059 der UniversitätSt. Gallen).

NIJKAMP , P., 1990. Spatial Developmentsin the United States of Europe: Glorious Vic-tories or Great Defeats. Free University ofAmsterdam: Department of Economics.

NIJKAMP, P., BAGGEN, J. and VAN DERKNAAP, B., 1996. Spatial Sustainability andthe Tyranny of Transport: A causal path sce-nario analysis. Papers in regional science,75: 501–524.

THIERSTEIN, A., SCHNELL, K.D. andSCHWEGLER, U., 1999. Unternehmens-strategien und Güterverkehr. Wirkungen undZusammenhänge – gezeigt am Beispiel derRegion Zug. Nationales Forschungspro-gramm 41 Verkehr und Umwelt. Bericht B3.Bern: EDMZ.

VICKERMAN, R.W., (Ed.), 1991. Infrastruc-ture and Regional Development. London:Pion (European Research in Regional Sci-ence, Nr. 1).

WOMACK, James P., JONES, Daniel T. andROOS, Daniel (1991): Die zweite Revolutionin der Automobilindustrie: Konsequenzen ausder weltweiten Studie aus dem Massachu-setts Institute of Technology. Frankfurt/M.:Campus.

Prof. Dr. Alain ThiersteinInstitut für Orts-, Regional-und LandesplanungETH HönggerbergCH-8093 Zü[email protected]

Klaus-Dieter SchnellIDT-HSGVarnbüelstrasse 19CH-9000 St. [email protected]

DISP 148 78 2002