Embed Size (px)

Citation preview

0

LSC

MBAFinance-Semester2

Financial Markets and Investment Analysis

Assigment & Report of the given questions

Module Leader: Palan Ambikai

Written by: Yhlas Sovbetov

Student ID: L0072KEKE0212

December-2012

1

Q1. Why distinctions between Debt & Equity are disappearing?

According to the theory and traditional view of debt - equity relations, there are

significant distinctions between Debt financing and Equity such as:

Debt is a loan that is borrowed from investors via non-relational contract between firm

and investors, that promises an annual fixed payment (interest) to pay back the loan

amount within agreed period.

Whereas, the Equity is relational contract between equity holders and firm, that makes

the equity holders part of the firm ownership and gives a claim on current and future

earnings of the firm as dividend. But dividends are not fixed, and sometimes it can be

reduced or suspended as well. In addition to this, the stock market returns are higher than

bond markets, but otherwise if in any trouble cases of the firm, the debt holders will be

paid first, and equity holders will be in the end of the queue. Therefore, due to higher

risk, these securities are generally expensive than debt bonds. However, this security

gives to its holder, the voting rights and decision making on how to employ the assets.

The firms can increase their capital by 2 ways: issuing bonds or issuing shares. The

relation between them determines the leverage of the firm. Till recent years, firms were

considering the leverage balance while they planned to increase the capital. But in recent years,

asset financing with debt has exceeded the equity one. The reasons of this, can be pointed as new

innovations in the financial markets and new understanding of the capital structure theory. The

main understanding was high geared companies have high risk of capital structure, so that

shareholders will require risk premium for the extra risks. But the modern understanding of the

capital structure by Modigliani and Miller which makes the leverage risk irrelevant was the

first challenge against the distinctions between debt and equity. The theory says that financing

with debt or equity won't affect the cost of capital. (Kopcke & Rosengren, 1989)

Secondly, the taxation regulations led the bond markets to be more attractive. Paying

high corporate tax always was main consideration for the firms. In the debt financing, firms pay

interest to the investors that is tax deductible. Whereas, in equity financing, the firms cannot

seize the taxation advantage, and also shareholder will pay income tax on the dividend they got.

Thirdly, with new innovations of the financial instruments in the bond market, such as

convertible bonds that are convertible to the ordinary share at a specific price; dated bonds that

can be bought back by the firm at specific date and price; undated bonds that are not redeemable,

secured bonds that are backed by mortgages such as CMO, CARD, CAR, CLEO, and FRENDs;

unsecured bonds, debt with equity warrants, and etc, the significant distinctions between

borrowed capital and equity are blurred. These developments in the bond market provided more

flexibility to the firms as well as to investors. For instance; If the firm issues the callable bonds

(redeemable) at % 10 interest rate, and in future when the interest rates fall down to % 6, the firm

2

will collect all bonds back, and will re-issue them at % 6. Due to these flexibilities the bond

markets have become more preferable than stock markets. (Kopcke & Rosengren, 1989)

Moreover, the potential risk and return of these new financial instruments, were

mitigated by new hedging instruments such as Butterfly spread, Cancelable Forward

Exchange Contracts, Synthetic instruments, Carrots and Stick bonds, Convertible Premium Puts,

Dual-Currency bonds, COP (Covered Options), ECU (European Currency Unit) bonds, ICON

(Indexed Options), PERL (Principal Exchange Rate Linked), FRN (Floating Rate Notes), Swap

Agreements, Certificated Securities and etc.

Lastly, beside the bond market, the developments in the stock markets such as auctions

(MMP, CAMPS, CMPS, DARTS, STARS, PIK), options and resets, in its turn, contributed to

the distinctions between stocks and bonds be melted.

In conclusion, with the new progresses and diversifications in the financial instruments,

the debt bonds start to include more equity characteristics. On other hand, the tax deductibility

and flexibility advantages of the financial products make the bond markets more attractive with

the consideration of the modern theory of capital structure of leverage irrelevancy.

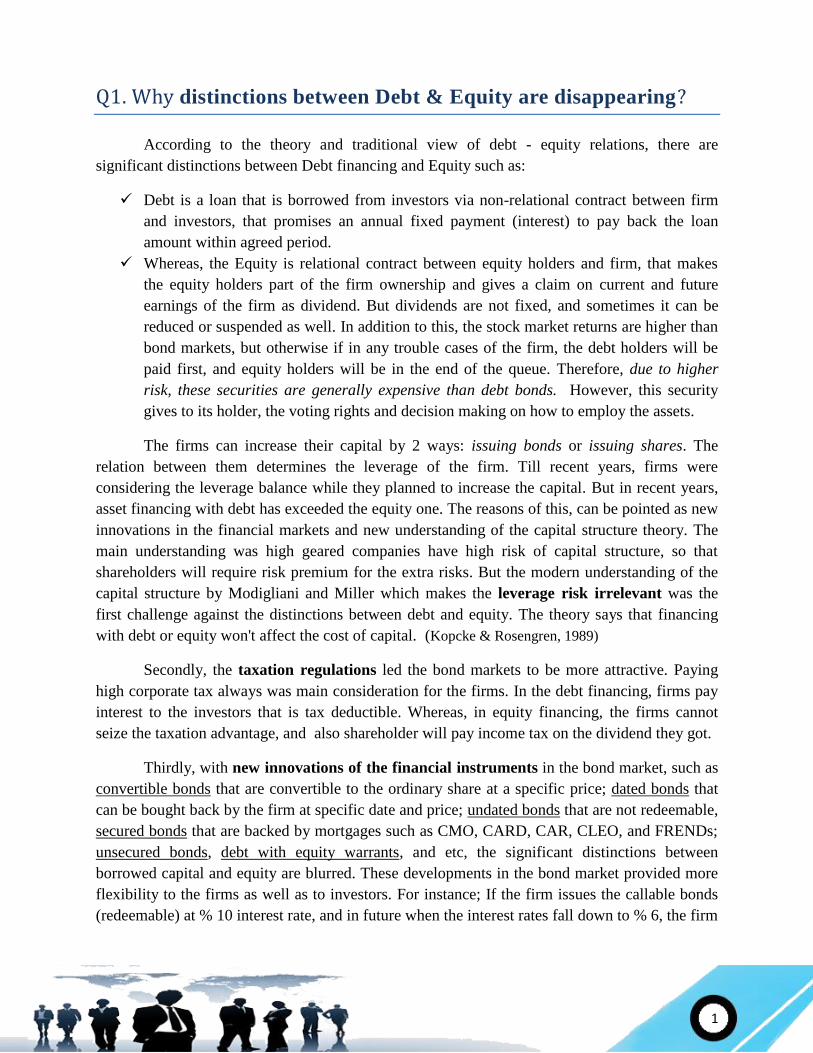

Here in graphic 1 and in table 1 & 2, the financial structures of 2 different PLC

companies are shown below for overview the effect of the developments that mentioned above.

Example 1: Financial Structure of the BP Plc (2011) and Vodafone Group Plc (2012)

Source: (BP Plc LSE, 2012) & (Vodafone Group Plc LSE, 2012)

Table 1: Past 4 years balance sheet figure of Vodafone Group Plc

VODAFONE PLC (million £) 2009 2010 2011 2012

Total Assets 152,699 156,985 151,220 139,576

Short Term Debt 27,947 28,616 27,075 24,025

Long Term Debt 39,975 37,559 36,584 37,349

Total Equity 84,777 90,810 87,561 78,202

Source: (Vodafone Group Plc LSE, 2012)

3

Table 2: Past 4 years balance sheet figure of BP Plc

Source: (BP Plc LSE, 2012)

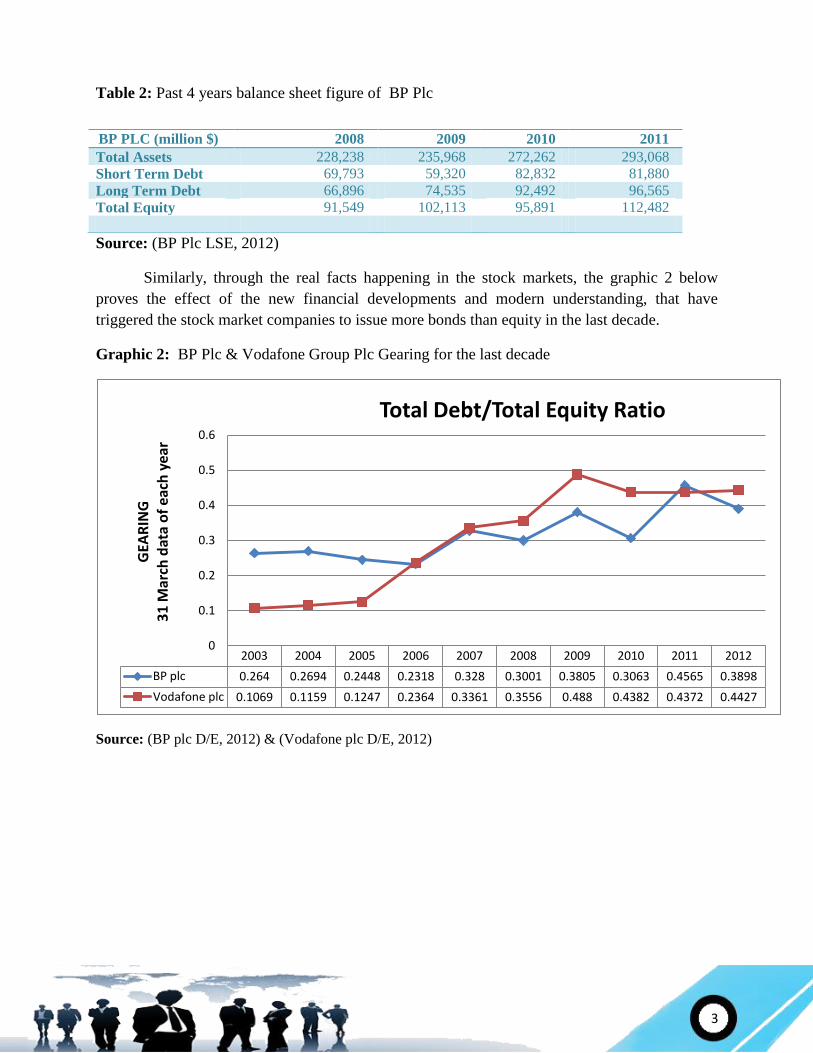

Similarly, through the real facts happening in the stock markets, the graphic 2 below

proves the effect of the new financial developments and modern understanding, that have

triggered the stock market companies to issue more bonds than equity in the last decade.

Graphic 2: BP Plc & Vodafone Group Plc Gearing for the last decade

Source: (BP plc D/E, 2012) & (Vodafone plc D/E, 2012)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

BP plc 0.264 0.2694 0.2448 0.2318 0.328 0.3001 0.3805 0.3063 0.4565 0.3898

Vodafone plc 0.1069 0.1159 0.1247 0.2364 0.3361 0.3556 0.488 0.4382 0.4372 0.4427

0

0.1

0.2

0.3

0.4

0.5

0.6

GEA

RIN

G

31

Mar

ch d

ata

of

each

yea

r

Total Debt/Total Equity Ratio

BP PLC (million $) 2008 2009 2010 2011

Total Assets 228,238 235,968 272,262 293,068

Short Term Debt 69,793 59,320 82,832 81,880

Long Term Debt 66,896 74,535 92,492 96,565

Total Equity 91,549 102,113 95,891 112,482

4

London School of Commerce

MBA Finance

Financial Markets Investment Analysis

Assignment Question No.3

REPORT: Overview of foreign exchange markets for a small local company

TO: Company "Z"

FROM: Ihlas Sovbetov Nobatovich

DATE: December 11, 2012

Abstract

This is a report for the company "Z" about foreign exchange markets due to their first

international contract. In the case, company can face with four types of risks such as translation,

transaction, economic, and political risks. But as it was asked in particular the exchange rate risk

that company can face within the contract period, only the transaction risk management

techniques will be considered in this report. More briefly, as it is the company's first international

contract, the internal hedging tools will be ignored, and only the external one, especially forward

and money market hedging tools will be analyzed.

1. Introduction

Transaction risk occurs when sellers agree to get the payment of their products or

services, within specific period of future time in different currency units. Here the involved risk

is currency movements against the seller company. Some reasons of these movements can be

pointed as a change in demand & supply of the currency, a change in balance trade of the

country, as well as the differentiation of interest and inflation rates. To eliminate or mitigate

the risk of these currency fluctuations, the hedging tools are used. Basically, here, the main focus

will be on forward and money markets hedging tools, others (Swap, Options) won't be discussed.

2. Money Market Hedging Techniques

The main idea behind this tool is to lock the current spot rate of payables or receivables

by matching the assets or liabilities in trading currency, then convert and invest it to the home

currency. Accordingly to this, if the company sells to overseas, then company will have

receivable that is an asset. To lock the spot rate of the receivables, the company should create a

liability to match. On contrast, if the company buys from overseas on credit, then the company

will have payable that is a liability. To hedge it, the company should create an asset to match.

5

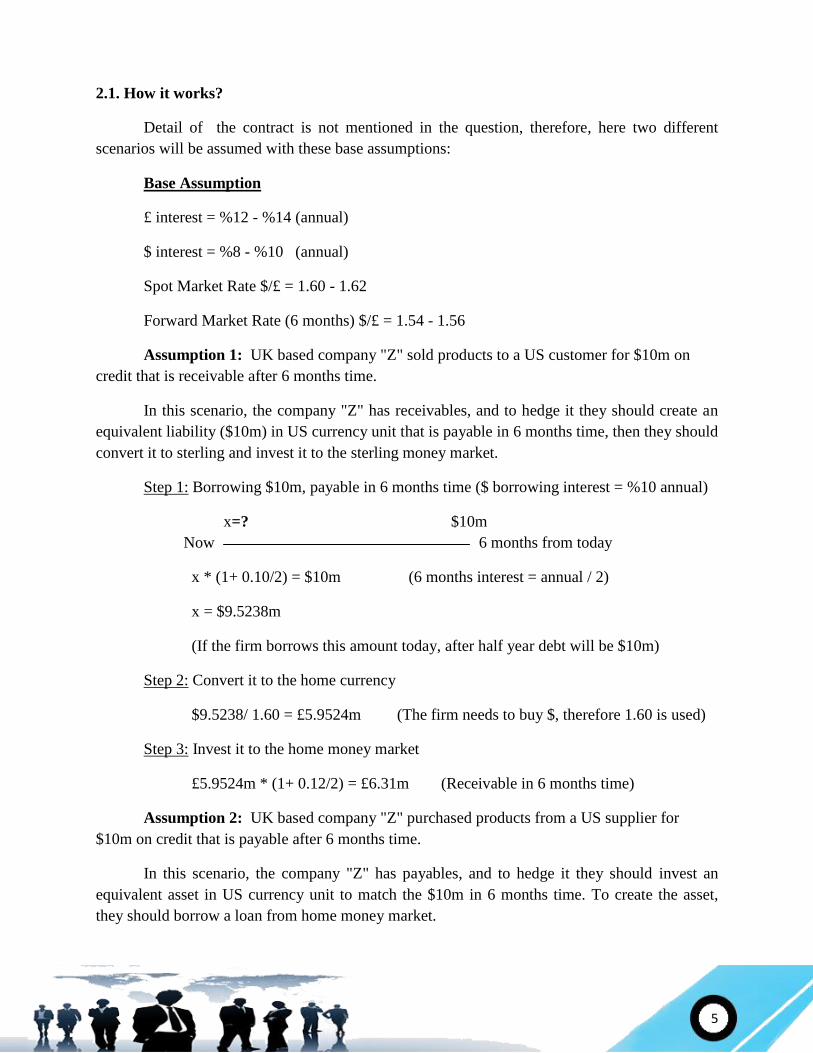

2.1. How it works?

Detail of the contract is not mentioned in the question, therefore, here two different

scenarios will be assumed with these base assumptions:

Base Assumption

£ interest = %12 - %14 (annual)

$ interest = %8 - %10 (annual)

Spot Market Rate $/£ = 1.60 - 1.62

Forward Market Rate (6 months) $/£ = 1.54 - 1.56

Assumption 1: UK based company "Z" sold products to a US customer for $10m on

credit that is receivable after 6 months time.

In this scenario, the company "Z" has receivables, and to hedge it they should create an

equivalent liability ($10m) in US currency unit that is payable in 6 months time, then they should

convert it to sterling and invest it to the sterling money market.

Step 1: Borrowing $10m, payable in 6 months time ($ borrowing interest = %10 annual)

x=? $10m

Now 6 months from today

x * (1+ 0.10/2) = $10m (6 months interest = annual / 2)

x = $9.5238m

(If the firm borrows this amount today, after half year debt will be $10m)

Step 2: Convert it to the home currency

$9.5238/ 1.60 = £5.9524m (The firm needs to buy $, therefore 1.60 is used)

Step 3: Invest it to the home money market

£5.9524m * (1+ 0.12/2) = £6.31m (Receivable in 6 months time)

Assumption 2: UK based company "Z" purchased products from a US supplier for

$10m on credit that is payable after 6 months time.

In this scenario, the company "Z" has payables, and to hedge it they should invest an

equivalent asset in US currency unit to match the $10m in 6 months time. To create the asset,

they should borrow a loan from home money market.

6

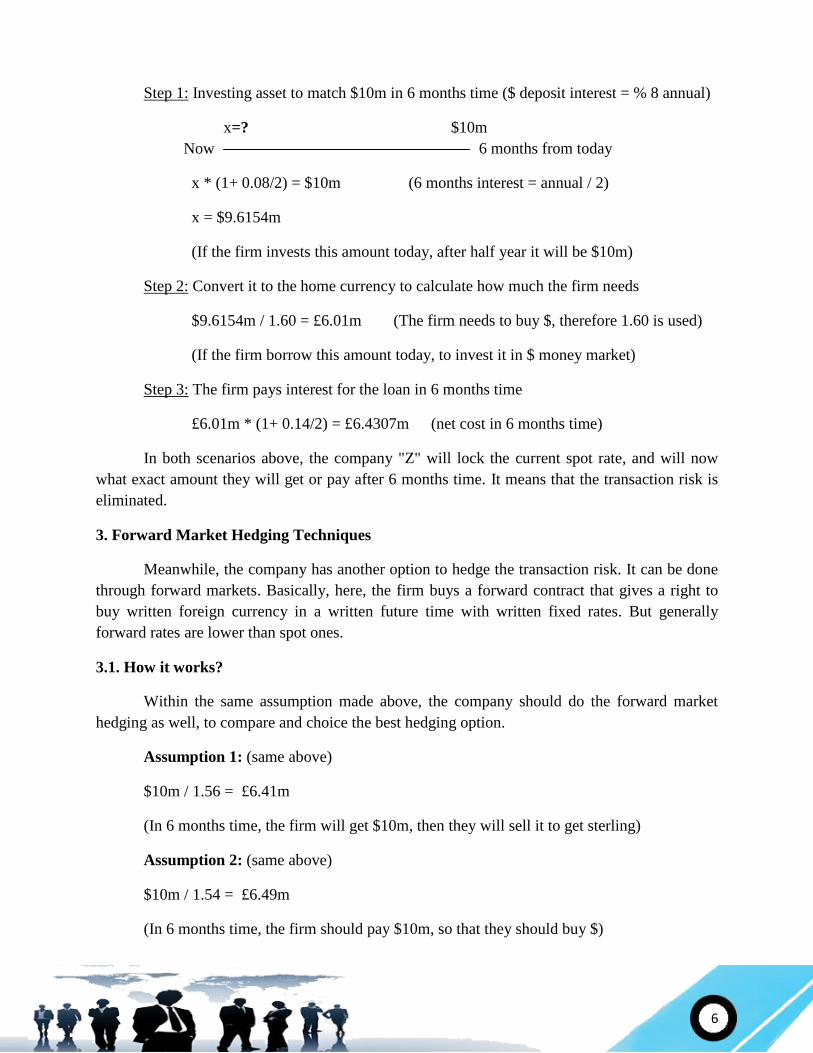

Step 1: Investing asset to match $10m in 6 months time ($ deposit interest = % 8 annual)

x=? $10m

Now 6 months from today

x * (1+ 0.08/2) = $10m (6 months interest = annual / 2)

x = $9.6154m

(If the firm invests this amount today, after half year it will be $10m)

Step 2: Convert it to the home currency to calculate how much the firm needs

$9.6154m / 1.60 = £6.01m (The firm needs to buy $, therefore 1.60 is used)

(If the firm borrow this amount today, to invest it in $ money market)

Step 3: The firm pays interest for the loan in 6 months time

£6.01m * (1+ 0.14/2) = £6.4307m (net cost in 6 months time)

In both scenarios above, the company "Z" will lock the current spot rate, and will now

what exact amount they will get or pay after 6 months time. It means that the transaction risk is

eliminated.

3. Forward Market Hedging Techniques

Meanwhile, the company has another option to hedge the transaction risk. It can be done

through forward markets. Basically, here, the firm buys a forward contract that gives a right to

buy written foreign currency in a written future time with written fixed rates. But generally

forward rates are lower than spot ones.

3.1. How it works?

Within the same assumption made above, the company should do the forward market

hedging as well, to compare and choice the best hedging option.

Assumption 1: (same above)

$10m / 1.56 = £6.41m

(In 6 months time, the firm will get $10m, then they will sell it to get sterling)

Assumption 2: (same above)

$10m / 1.54 = £6.49m

(In 6 months time, the firm should pay $10m, so that they should buy $)

7

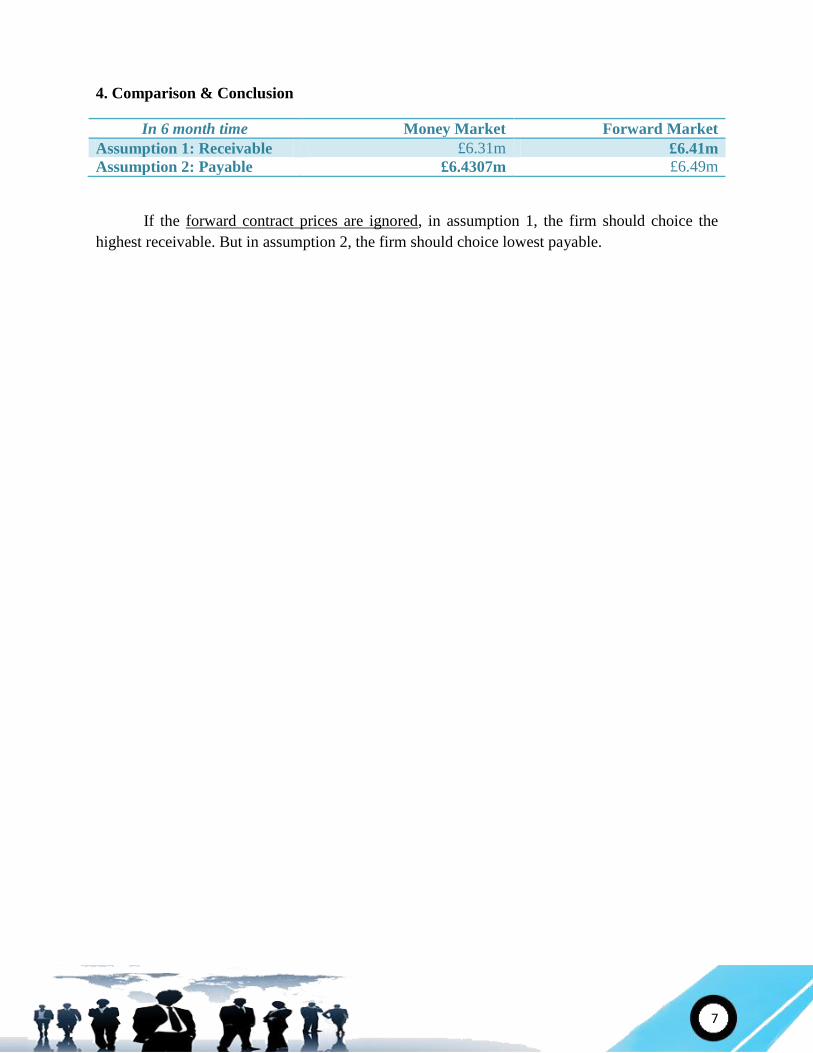

4. Comparison & Conclusion

In 6 month time Money Market Forward Market

Assumption 1: Receivable £6.31m £6.41m

Assumption 2: Payable £6.4307m £6.49m

If the forward contract prices are ignored, in assumption 1, the firm should choice the

highest receivable. But in assumption 2, the firm should choice lowest payable.

8

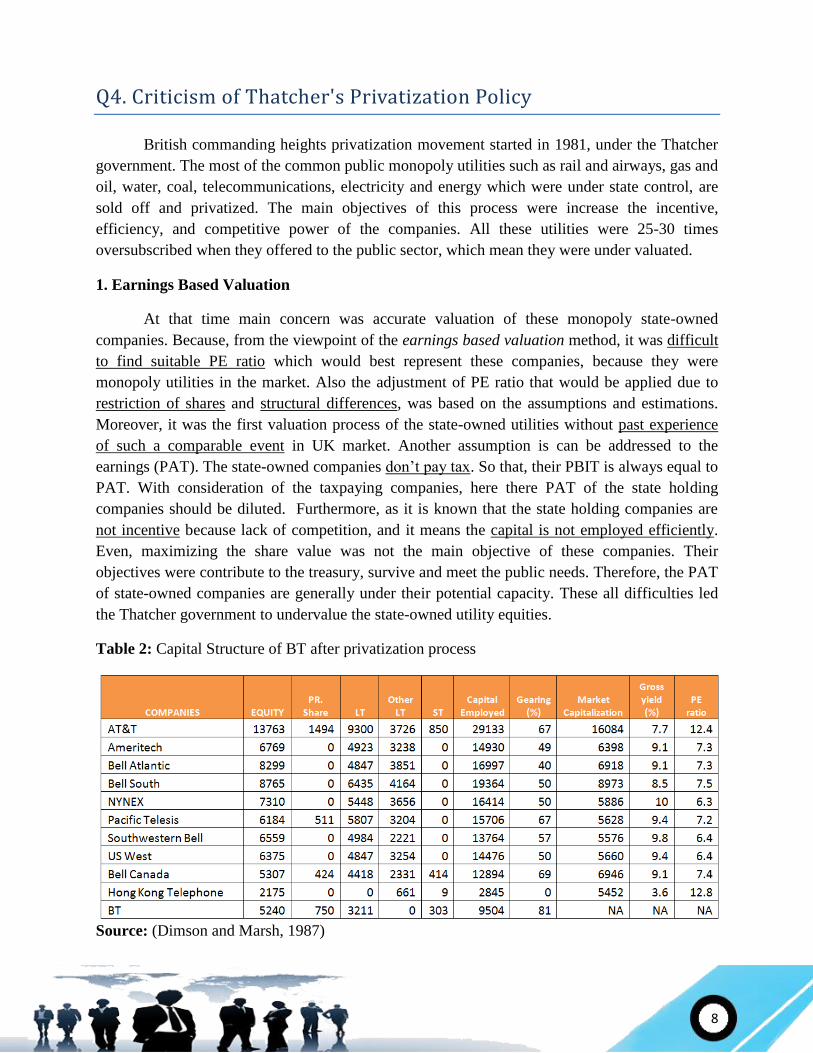

Q4. Criticism of Thatcher's Privatization Policy

British commanding heights privatization movement started in 1981, under the Thatcher

government. The most of the common public monopoly utilities such as rail and airways, gas and

oil, water, coal, telecommunications, electricity and energy which were under state control, are

sold off and privatized. The main objectives of this process were increase the incentive,

efficiency, and competitive power of the companies. All these utilities were 25-30 times

oversubscribed when they offered to the public sector, which mean they were under valuated.

1. Earnings Based Valuation

At that time main concern was accurate valuation of these monopoly state-owned

companies. Because, from the viewpoint of the earnings based valuation method, it was difficult

to find suitable PE ratio which would best represent these companies, because they were

monopoly utilities in the market. Also the adjustment of PE ratio that would be applied due to

restriction of shares and structural differences, was based on the assumptions and estimations.

Moreover, it was the first valuation process of the state-owned utilities without past experience

of such a comparable event in UK market. Another assumption is can be addressed to the

earnings (PAT). The state-owned companies don’t pay tax. So that, their PBIT is always equal to

PAT. With consideration of the taxpaying companies, here there PAT of the state holding

companies should be diluted. Furthermore, as it is known that the state holding companies are

not incentive because lack of competition, and it means the capital is not employed efficiently.

Even, maximizing the share value was not the main objective of these companies. Their

objectives were contribute to the treasury, survive and meet the public needs. Therefore, the PAT

of state-owned companies are generally under their potential capacity. These all difficulties led

the Thatcher government to undervalue the state-owned utility equities.

Table 2: Capital Structure of BT after privatization process

Source: (Dimson and Marsh, 1987)

9

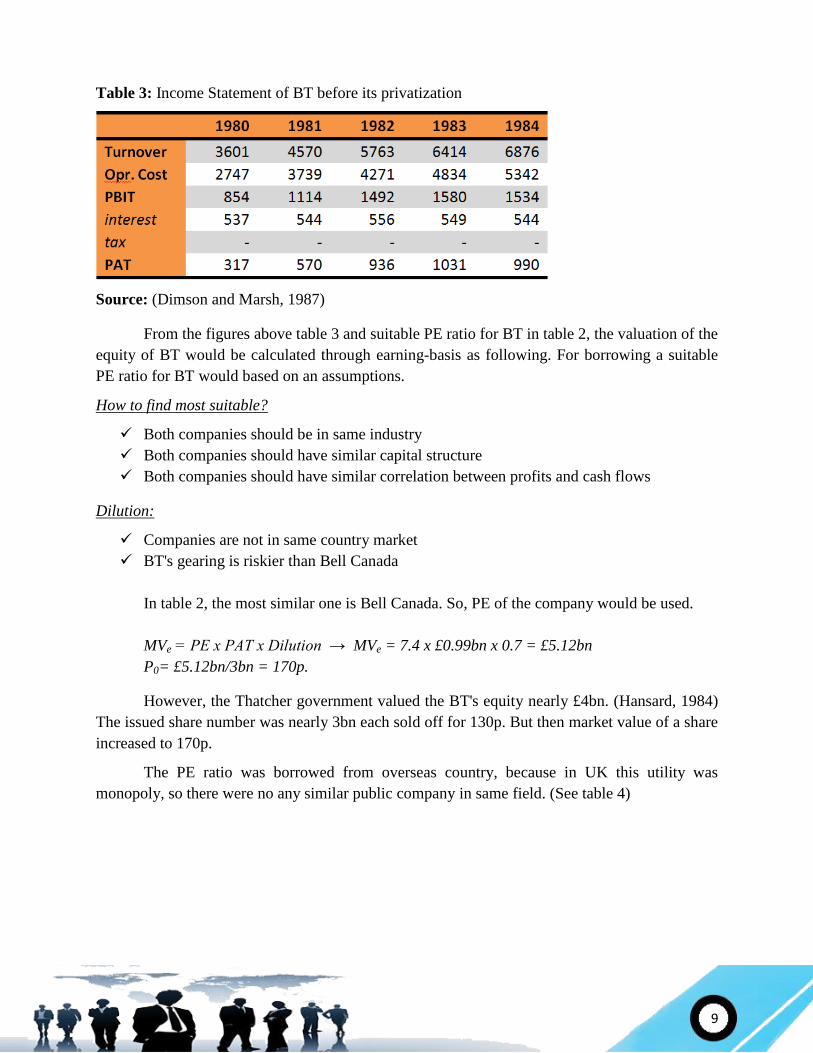

Table 3: Income Statement of BT before its privatization

Source: (Dimson and Marsh, 1987)

From the figures above table 3 and suitable PE ratio for BT in table 2, the valuation of the

equity of BT would be calculated through earning-basis as following. For borrowing a suitable

PE ratio for BT would based on an assumptions.

How to find most suitable?

Both companies should be in same industry

Both companies should have similar capital structure

Both companies should have similar correlation between profits and cash flows

Dilution:

Companies are not in same country market

BT's gearing is riskier than Bell Canada

In table 2, the most similar one is Bell Canada. So, PE of the company would be used.

MVe = PE x PAT x Dilution → MVe = 7.4 x £0.99bn x 0.7 = £5.12bn

P0= £5.12bn/3bn = 170p.

However, the Thatcher government valued the BT's equity nearly £4bn. (Hansard, 1984)

The issued share number was nearly 3bn each sold off for 130p. But then market value of a share

increased to 170p.

The PE ratio was borrowed from overseas country, because in UK this utility was

monopoly, so there were no any similar public company in same field. (See table 4)

10

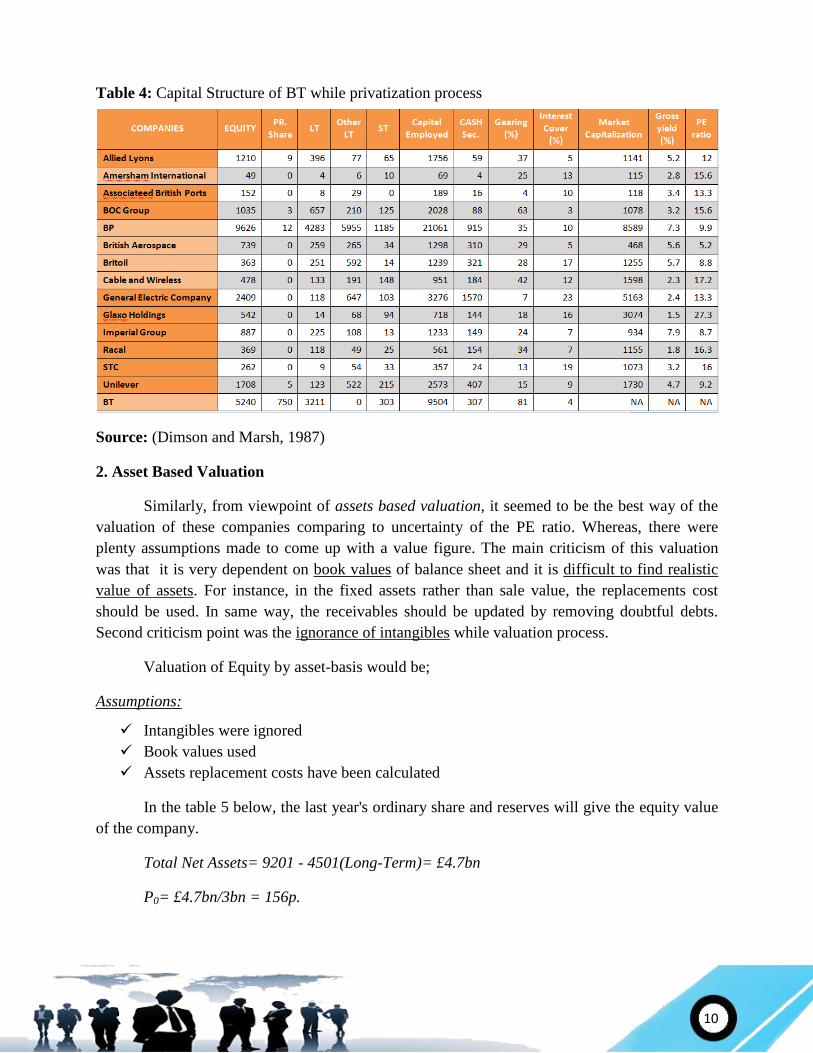

Table 4: Capital Structure of BT while privatization process

Source: (Dimson and Marsh, 1987)

2. Asset Based Valuation

Similarly, from viewpoint of assets based valuation, it seemed to be the best way of the

valuation of these companies comparing to uncertainty of the PE ratio. Whereas, there were

plenty assumptions made to come up with a value figure. The main criticism of this valuation

was that it is very dependent on book values of balance sheet and it is difficult to find realistic

value of assets. For instance, in the fixed assets rather than sale value, the replacements cost

should be used. In same way, the receivables should be updated by removing doubtful debts.

Second criticism point was the ignorance of intangibles while valuation process.

Valuation of Equity by asset-basis would be;

Assumptions:

Intangibles were ignored

Book values used

Assets replacement costs have been calculated

In the table 5 below, the last year's ordinary share and reserves will give the equity value

of the company.

Total Net Assets= 9201 - 4501(Long-Term)= £4.7bn

P0= £4.7bn/3bn = 156p.

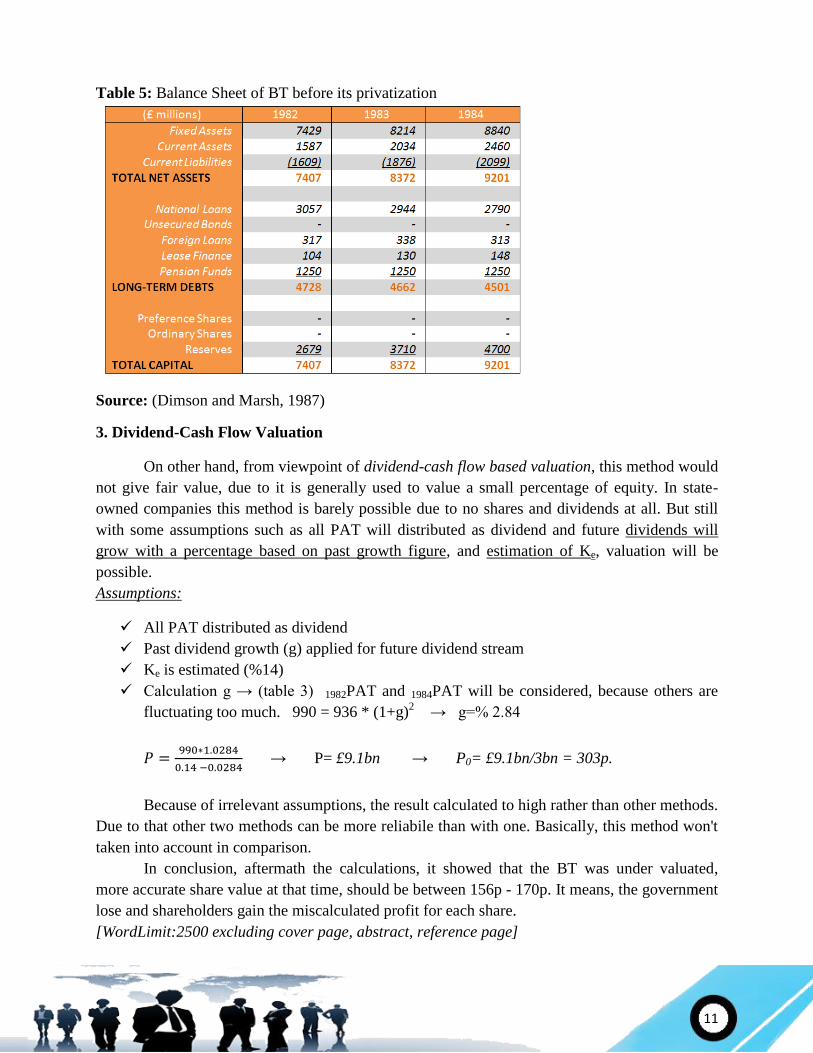

11

Table 5: Balance Sheet of BT before its privatization

Source: (Dimson and Marsh, 1987)

3. Dividend-Cash Flow Valuation

On other hand, from viewpoint of dividend-cash flow based valuation, this method would

not give fair value, due to it is generally used to value a small percentage of equity. In state-

owned companies this method is barely possible due to no shares and dividends at all. But still

with some assumptions such as all PAT will distributed as dividend and future dividends will

grow with a percentage based on past growth figure, and estimation of Ke, valuation will be

possible.

Assumptions:

All PAT distributed as dividend

Past dividend growth (g) applied for future dividend stream

Ke is estimated (%14)

Calculation g → (table 3) 1982PAT and 1984PAT will be considered, because others are

fluctuating too much. 990 = 936 * (1+g)2 → g=% 2.84

→ P= £9.1bn → P0= £9.1bn/3bn = 303p.

Because of irrelevant assumptions, the result calculated to high rather than other methods.

Due to that other two methods can be more reliabile than with one. Basically, this method won't

taken into account in comparison.

In conclusion, aftermath the calculations, it showed that the BT was under valuated,

more accurate share value at that time, should be between 156p - 170p. It means, the government

lose and shareholders gain the miscalculated profit for each share.

[WordLimit:2500 excluding cover page, abstract, reference page]

12

REFERENCE

Kopcke, R. and Rosengren, E.; (1989), Are the Distinctions between Debt and Equity

Disappearing?, Federal Reserve Bank of Boston, Vol.x, No.x, Conference Series No.33, New

Hampshire

Mulyono, P.; Suhardianto, M. and Sihotang, R.; (2009), Hedging Transaction and Economic

Exposure, Journal of Applied Finance and Accounting, vol. 1 no.2, p.231

Dimson, E. and Marsh, P.; (1987), British Telecom, London Business School, pp.202-221

Hansard (1984), British Telecom (Privatisation), HC Deb, vol.59, p.354

BP plc (2012), ADVFN, [online], Available:

<http://uk.advfn.com/p.php?pid=financials&symbol=L%5EBP.> (10 December, 2012)

Vodafone Group plc (2012), ADVFN, [online], Available:

<http://uk.advfn.com/p.php?pid=financials&symbol=L%5EVOD> (09 December, 2012)

BP plc D/E (2012), YCHARTS, [online], Available:

<http://ycharts.com/companies/BP/debt_equity_ratio> (09 December, 2012)

Vodafone plc D/E (2012), YCHARTS, [online], Available:

<http://ycharts.com/companies/VOD/debt_equity_ratio> (09 December, 2012)