Embed Size (px)

Citation preview

INTERNATIONAL BANKING AND FINANCE

BANKING REGULATION – CAPITAL ADEQUACY

INTRODUCTION Substantial decline in banks earnings and increased numbers of bank failure between 1980s highlighted the interest in capital management.

Capital is a fundamental building block of the banking business that is essential to survival and growth

Bankers – to use less capital to magnify asset earnings and earn higher equity rates return

Regulators – banks should increase their capital to ensure safety and soundness in the event earnings become negative

SUMMARY This chapter covers:o Definition of bank capital o Important of bank capitalo Role of bank capital in managing bank operation and financial risks

o Issues of capital adequacy from the view points of regulators and bank shareholders

o International (IBS) risk base capital requirements applicable to today’s bank.

Bank Capital – Definition Capital = equity + long term debts.Bank capital o includes reserves that are set aside to meet anticipated bank operating losses

o subject to regulatory requirements that attempt to endure adequate capital to absorb losses on investment to protect depositors and deposit insurer.

Bank Capital – Definition(i) Accounting Approach Capital = difference between the accounting book value of assets and liabilities.

(ii) Economist ApproachCapital / Owners’ Equity / Net Worth = difference between the market value of assets and liabilities

(iii) Regulators ApproachCapital and Required Leverage ratio (i.e. the Core Capital / Asset ratio) are based partly on book value accounting concept.

Bank Capital – DefinitionRegulators: two types of capital i.e. core capital (Tier-I) and supplementary capital (Tier II)

Core Capital: constituent of core capital funds should possess following features:Fully paid-up and permanently available;Freely available and not earmarked to particular assets of banking activities;

Ability to absorb losses occurring in the curse of an on-going business; and

Represents no fixed charged on the earnings of an institution.

Bank Capital – DefinitionCore Capital – represent resources that can be used to meet current losses while enabling the financial institution to continue operation as a going concern.

Types of Core CapitalPaid-up ordinary sharesNon-repayable share premium accountGeneral reservesRetained earningsNon-cumulative irredeemable preference sharesMinority interests in subsidiaries consistent with

foregoing components.

Bank Capital – DefinitionSupplementary Capital – Capital comprises elements which are available to meet losses, but which have certain drawbacks compared with the Core Capital

Types of Supplementary CapitalGeneral provisions for doubtful debts. Asset revaluation reserves.Cumulative irredeemable preference sharesPerpetual subordinated debtLimited-life redeemable preference sharesTerm subordinated debt.

Bank Capital – DefinitionSupplementary Capital

Goodwill, which cannot be used to support losses on an on-going basis, is deducted from this core capital.

Investment in subsidiaries and other financial institutions’ capital are also deducted in assessing capital adequacy.

Net Future income tax benefits should be excluded from the computing of core capital and total capital.

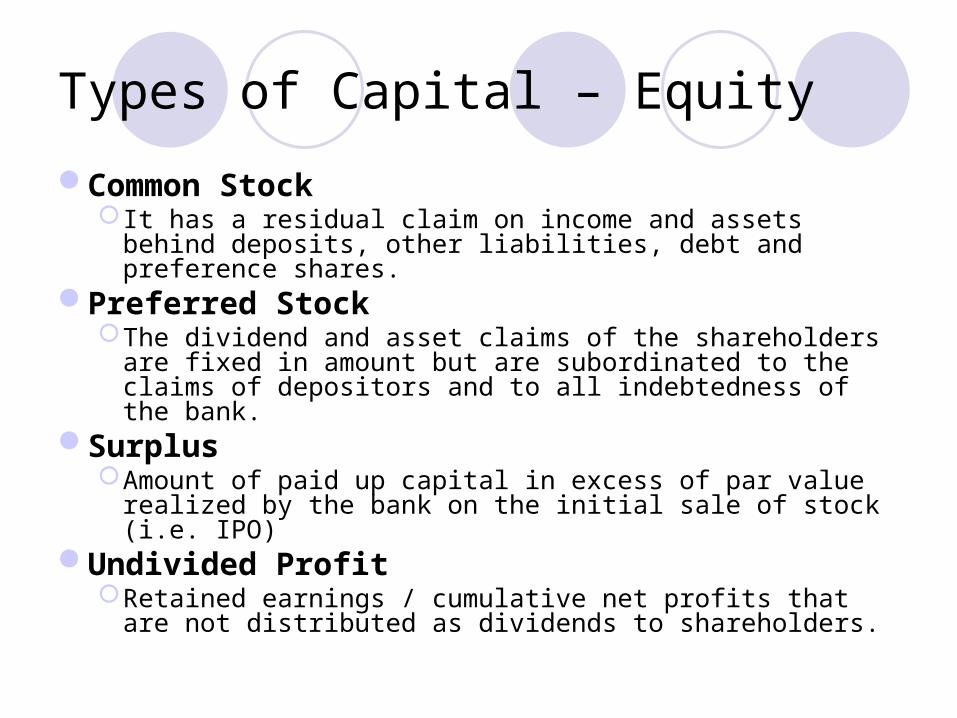

Types of Capital – Equity Common Stock

It has a residual claim on income and assets behind deposits, other liabilities, debt and preference shares.

Preferred StockThe dividend and asset claims of the shareholders are fixed in amount but are subordinated to the claims of depositors and to all indebtedness of the bank.

SurplusAmount of paid up capital in excess of par value realized by the bank on the initial sale of stock (i.e. IPO)

Undivided ProfitRetained earnings / cumulative net profits that are not distributed as dividends to shareholders.

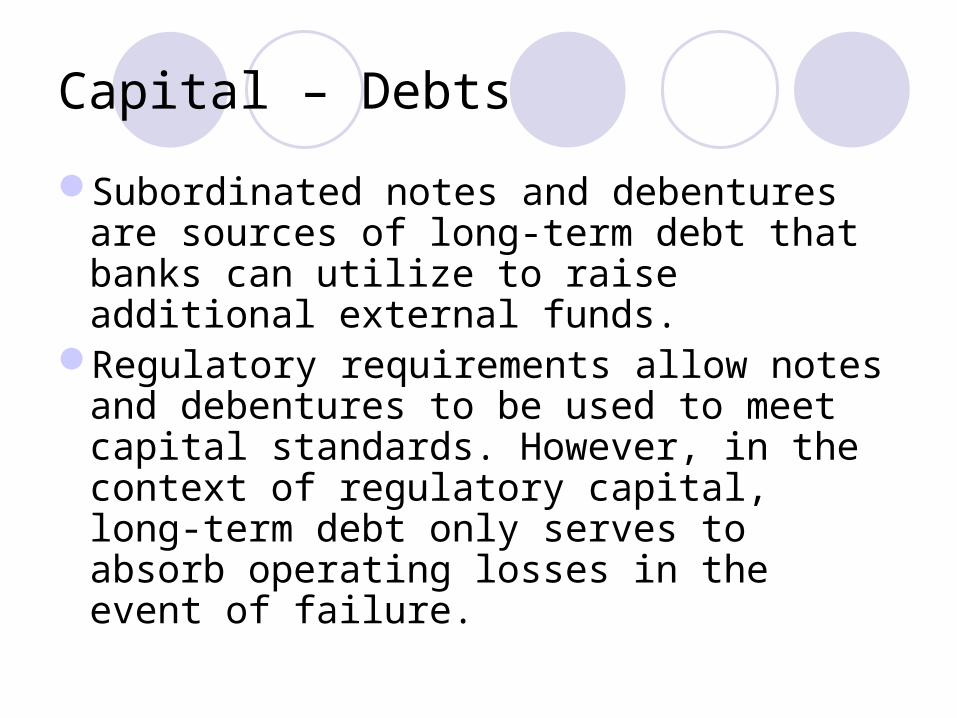

Capital – Debts Subordinated notes and debentures are sources of long-term debt that banks can utilize to raise additional external funds.

Regulatory requirements allow notes and debentures to be used to meet capital standards. However, in the context of regulatory capital, long-term debt only serves to absorb operating losses in the event of failure.

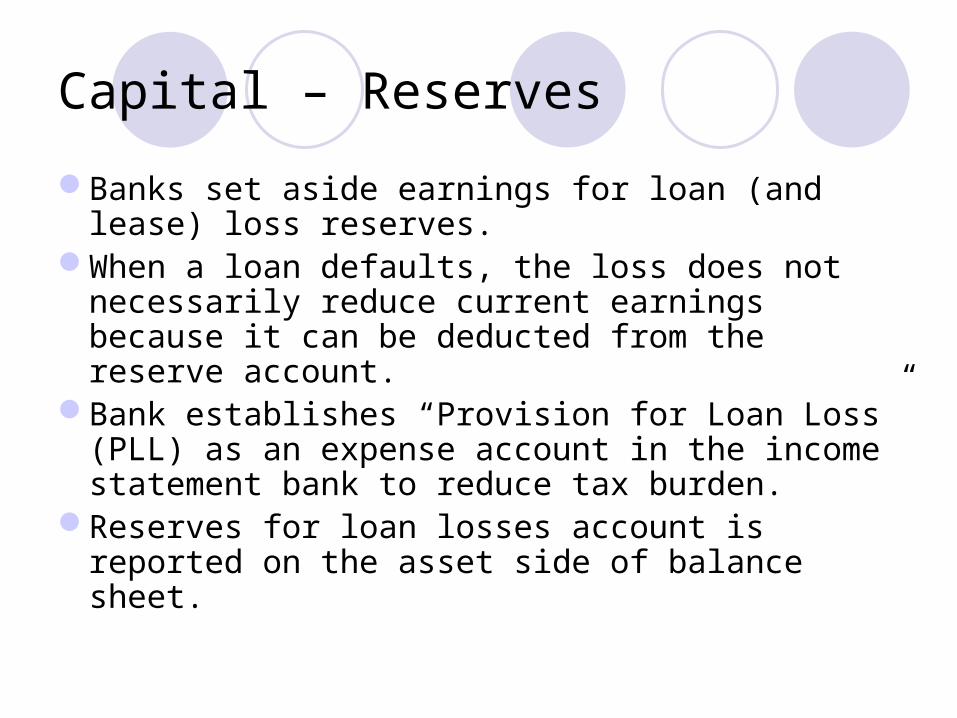

Capital – Reserves Banks set aside earnings for loan (and lease) loss reserves.

When a loan defaults, the loss does not necessarily reduce current earnings because it can be deducted from the reserve account.

Bank establishes “Provision for Loan Loss” (PLL) as an expense account in the income statement bank to reduce tax burden.

Reserves for loan losses account is reported on the asset side of balance sheet.

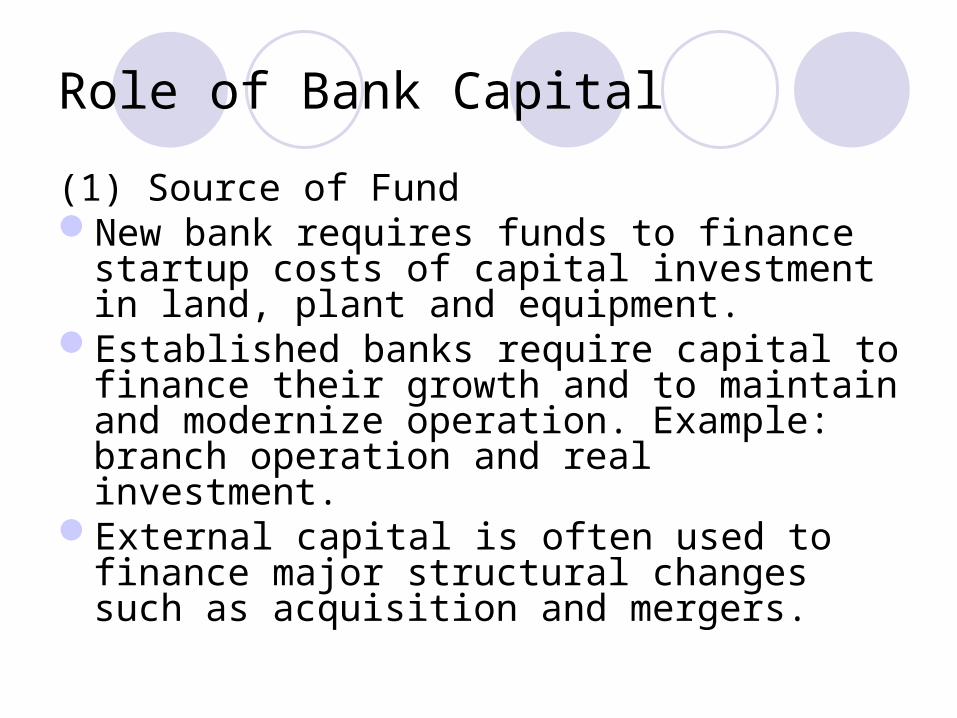

Role of Bank Capital (1) Source of Fund New bank requires funds to finance startup costs of capital investment in land, plant and equipment.

Established banks require capital to finance their growth and to maintain and modernize operation. Example: branch operation and real investment.

External capital is often used to finance major structural changes such as acquisition and mergers.

Role of Capital (2) To Serve as Cushion to Absorb Unexpected Operation Losses

Bank’s capital is the primary means of protection against the risk of insolvency and failure.

Insufficient large capital could lead to inability to cushion unexpected losses and hence force the bank to declare insolvent.

Long term debt instruments are capital source of funds that cannot be used to absorb losses except in a liquidation of a failed bank.

Therefore long term debt only weakly satisfies the role of capital as a cushion to absorb losses.

Role of Bank Capital Example:o The dept of economic downturn in 1997 in many Asian countries caused many banks loss substantially. These losses surpassed the loan loss provisio0ns of many banks, causing them to use capital to absorb unanticipated losses. Banks with insufficient capital to absorb losses are declared insolvent by their regulatory agency. The consequences: many banks are forced to merge or being acquired by other banks or financial institutions.

Role of Bank CapitalThe third function of bank capital bears on the question of Adequate Capital.

Bank generally has less than 10% of assets funded by capital. Therefore relatively small percentage of asset losses can significantly affect bank capital and threaten bank solvency.

Role of Bank CapitalBank regulator establishes minimum requirements (Adequate Capital) (i) To promote safety and soundness in the banking system.

(ii) To protect uninsured depositors, bondholders and creditors in the event of insolvency and liquidation.

(iii) To protect the shareholder of banks against increase in insurance premium. Insurance premiums are paid out of the net profit of the bank. Adequate capital will reduce the risk of insolvency. This protects the banking industry from paying larger insurance premiums.

Role of Bank Capital(iv) Market confidence is another factor in evaluating adequate capital. If market perceives a shortage of bank capital, bank stock prices will be affected.

(v) To protect Taxpayers and Bank Insurance Funds. (For the U.S.) When banks insolvent, the regulator would intervene to protect depositors and insured claimants. Adequate capital offers protection to taxpayers who bear cost of bailing-out insolvent bank and insurance funds. (For the U.S.)

Market Value of Capital In market value terms, bank assets and liabilities are valued at current prices on a mark-to-market basis.

On market value basis, the bank is economically solvent and imposes no failure costs on depositors or regulators if it were liquidated today.

Market Value of CapitalMarket Value of Capital and Credit Risk Inability of borrowers to keep up their promised loan repayment Decline in the current and expected future cash flows would lower the market value of the loan portfolio held by the bank.

Market Value of Capital and Interest Rate Risk

Increase in interest rates reduce the market value of bank’s long term fixed income securities and loans while floating rate instruments, if instantaneously re-priced, find their market values largely unaffected.

Market Value of CapitalMarket Value and Credit and Interest Rate Risk

o Credit risk and interest rate risk shocks that result in losses in the market value of assets are borne directly by the equity holders in the sense that such losses are charges against the value of their ownership claims in the bank.

o Market valuation of the balance sheet produces an economically accurate picture of the net worth, and thus, the solvency position of a bank.

Book Value of CapitalBook value capital and capital rules based on book values are most commonly used by banks regulators.

Under this valuation method of capital, both assets and liabilities are valued at their historical book values.

Book value of capital, (assets less liabilities) comprises the following four componentsPar value of sharesSurplus value of sharesRetained earnings and,Loan loss reserve.

Book Value of CapitalBook Value of Capital and Credit Risko Book value accounting systems do recognize credit risk problems, but only partially and usually with a long and discretionary time lag.

o There is a tendency for the bank to defer write-downs.

o When the loan customers having difficulty regarding repayment schedules, the revaluation of cash flows leads to an immediate downward adjustment of the loan portfolio’s market value. By contrast, under historic book value accounting methods, banks have greater discretion in regulating or timing problem loan loss recognition on their balance sheets and thus in the impact of such losses on capital

Book Value of Capital Book Value of Capital and Interest Rate Risk

o The effects of interest rate change are not recognized in book value accounting method.

o The failure of book value accounting method to recognize the impact of interest rate risk is even more extreme.

o In the book value accounting method, all assets and liabilities reflect their original cost of purchase. The rise in interest rates has no effect on the value of assets, liabilities, or book value of equity. That is the balance sheet remains unchanged.

Book Value of CapitalDiscrepancy between Market and Book value of equity

Degree of difference between book value and true economic market value depends on the following factors:

o Interest Rate Volatility: The higher the interest volatility, the greater the discrepancy.

o Examination and Enforcement: The more frequent the on-site and off-site examinations and the stiffer the examiner / regulator standards regarding charging off problem loans, the smaller the discrepancy

Capital Adequacy in Commercial BankActual Capital Ruleso Commercial Banks faced two different capital requirements: a capital-assets (leverage) ratio and a risk-based capital ratio.

o Risk-based capital ratio is in turn subdivided into a Tier I capital risk-based ratio and a total capital. (Tier I + Tier II capital) risk-based ratio.

Capital Adequacy in Commercial BankThis ratio measures the ratio of a bank’s book value of primary or core capital to the book value of its assets.

The lower this ratio is, the more highly leveraged the bank is.

Primary or core capital is a bank’s common equity plus qualifying cumulative perpetual preferred stock plus minority interests in equity accounts or consolidated subsidiaries.

L = core capital / assets

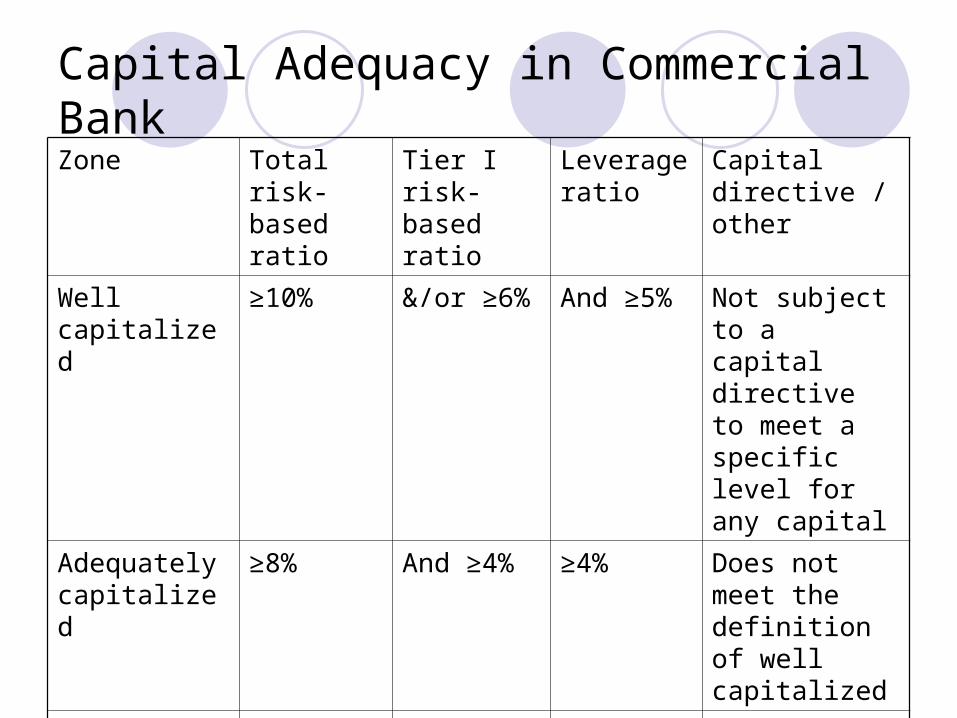

Capital Adequacy in Commercial BankZone Total

risk-based ratio

Tier I risk-based ratio

Leverage ratio

Capital directive /other

Well capitalized

≥10% &/or ≥6% And ≥5% Not subject to a capital directive to meet a specific level for any capital

Adequately capitalized

≥8% And ≥4% ≥4% Does not meet the definition of well capitalized

Significantly

<8% Or <4% Or <4%

Under-capitalized

<6% Or <3% Or <3%

Critically under capitalized

≤2% ≤2% ≤2%

Capital Adequacy in Commercial BankProblems of leverage ratio

Market value: There is no assurance that depositors and regulators (include taxpayers) is adequately protected against losses. This is because even if a bank is closed when the leverage ratio falls below 2%, a 2% book capital-asset ratio could be consistent with a massive negative market value net worth.

Asset Risk – the leverage ratio fails to take into account the different credit, interest rate and other risks of the assets.

Off-balance-sheet activities: no capital is required to meet the potential insolvency risks involving contingent assets and liabilities.

CAR – Risk Base Capital Ratio This section will examine

(i) how capital is used as a cushion against credit using the BIS approach (Basel I)

(ii) capital as a cushion against credit risk using Basel II

(iii) the required add-on to capital under Basel II that cushion a bank against market and operational risk.

CAR – Risk Base Capital RatioThe Basel AgreementBasel Agreement: The requirement to impose risk-based capital ratios on banks in major industrialized countries.

1993 Basel Agreement (Basel I) explicitly incorporated the different credit risks of assets (both on- and off-balance sheet) into Capital Adequacy measures.

Basel I was revised in 1998: Market risk was incorporated into risk-based capital.

CAR- Risk Base Capital Ratio (Basel II)(a) Pillar I: Credit, Market and Operational Risks

MeasurementCredit Risk:

Standardized approach: Similar to Basel except it is more risk sensitive.

Internal Rating Based (IRB): Banks are allowed to use their internal estimates of borrower creditworthiness to assess credit risk in their portfolios.

Operational risk: Three approaches: Basic indicator, Standardized and Advanced Measurement Approaches.

Market Risk: Same as Basel I proposal.

Risk Base Capital Ratio (Basel II) (b) Pillar II: Regulatory Review Process on

Minimum Capital RequirementsBIS recommended review procedures for Regulator to ensure that Bank has sound internal processes to assess capital adequacy

Bank has set targets for capital that are commensurate with the bank’s specific risk profile and control environment.

Risk Base Capital Ratio (Basel II)(c) Pillar III: Detailed Guidance on DisclosureBasel II proposal provides detailed guidance on the disclosure of capital structure, risk exposures, and capital adequacy.

These disclosure requirements allow market participants to assess critical information describing the risk profile and capital adequacy of banks.

Risk Base Capital Ratio (Basel II)The calculation of risk-based capital adequacy measures Distinguish among the different credit risks of assts on the balance sheet and,

Identify the credit risk inherent in instruments off the balance sheet by using a risk-adjusted assets denominator in these capital adequacy ratios.

In these measurements, bank’s capital is the standard by which each of credit risk, operational risk and market risk is measured.

Risk Base Capital Ratio (Basel II)Enforced alongside traditional leverage ratio

Minimum requirement of 8% total capital (Tier I core plus Tier II supplementary capital) to risk-adjusted assets ratio and,

Tier (core) capital ratio = Core Capital (Tier I) / Risk-adjusted ≥ 4%.

It is crudely mark to market on- and off-balance sheet positions.

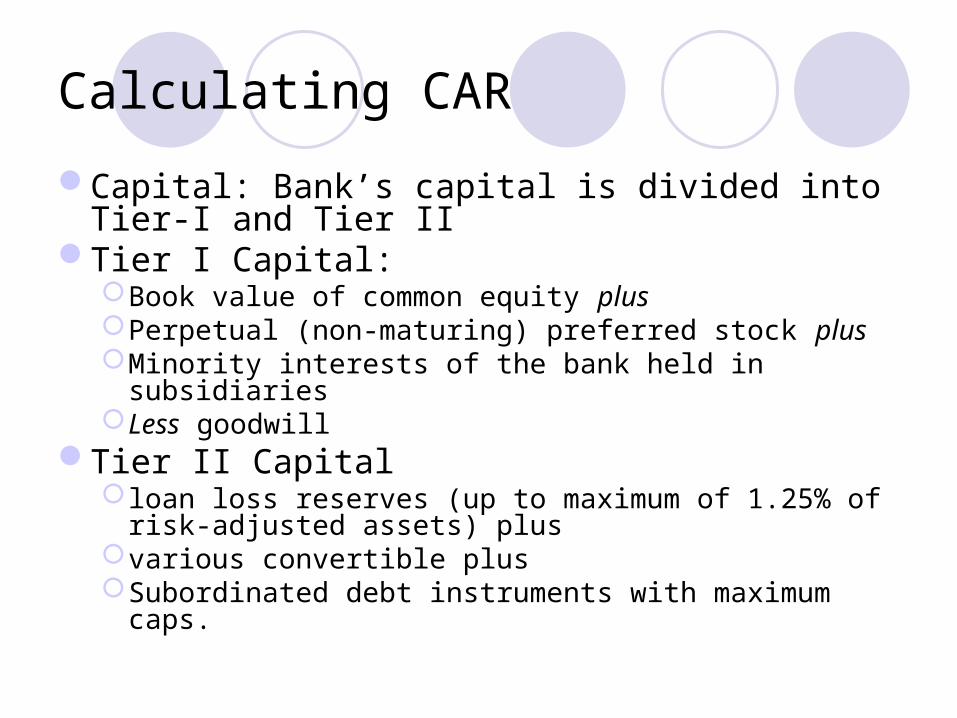

Calculating CAR Capital: Bank’s capital is divided into Tier-I and Tier II

Tier I Capital: Book value of common equity plusPerpetual (non-maturing) preferred stock plusMinority interests of the bank held in subsidiaries

Less goodwillTier II Capital

loan loss reserves (up to maximum of 1.25% of risk-adjusted assets) plus

various convertible plus Subordinated debt instruments with maximum caps.

Calculating CARCredit Risk-Adjusted AssetsTwo components o Credit risk-adjusted on-balance-

sheet assetso Credit risk-adjusted off-balance-

sheet assets.

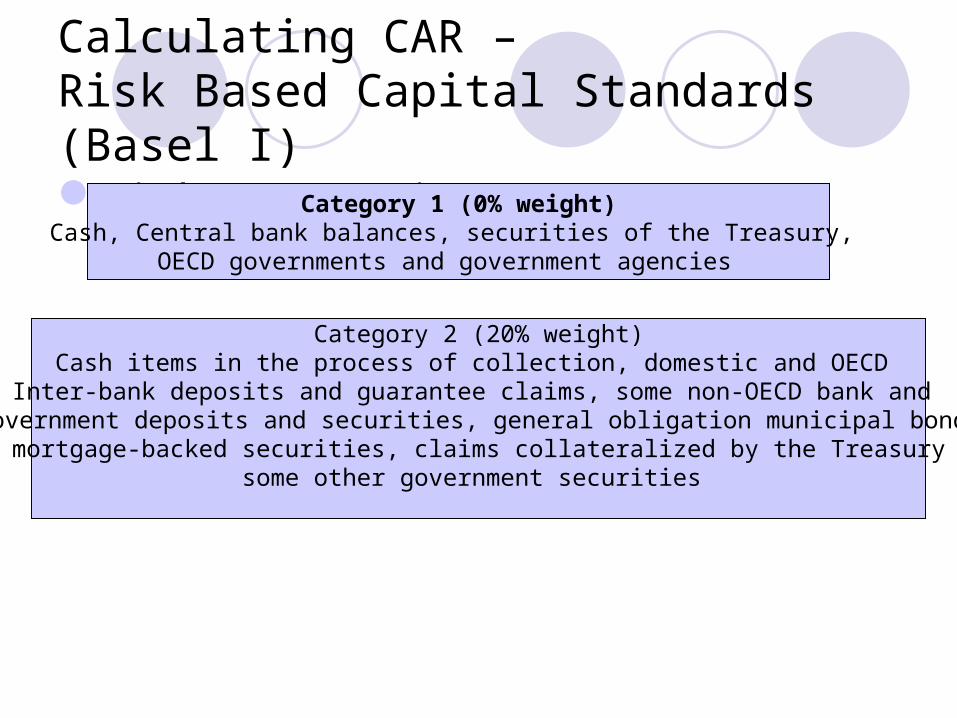

Calculating CAR – Risk Based Capital Standards (Basel I) Risk Categories Category 1 (0% weight)Cash, Central bank balances, securities of the Treasury,

OECD governments and government agencies

Category 2 (20% weight)Cash items in the process of collection, domestic and OECD

Inter-bank deposits and guarantee claims, some non-OECD bank and government deposits and securities, general obligation municipal bonds

Some mortgage-backed securities, claims collateralized by the Treasury and some other government securities

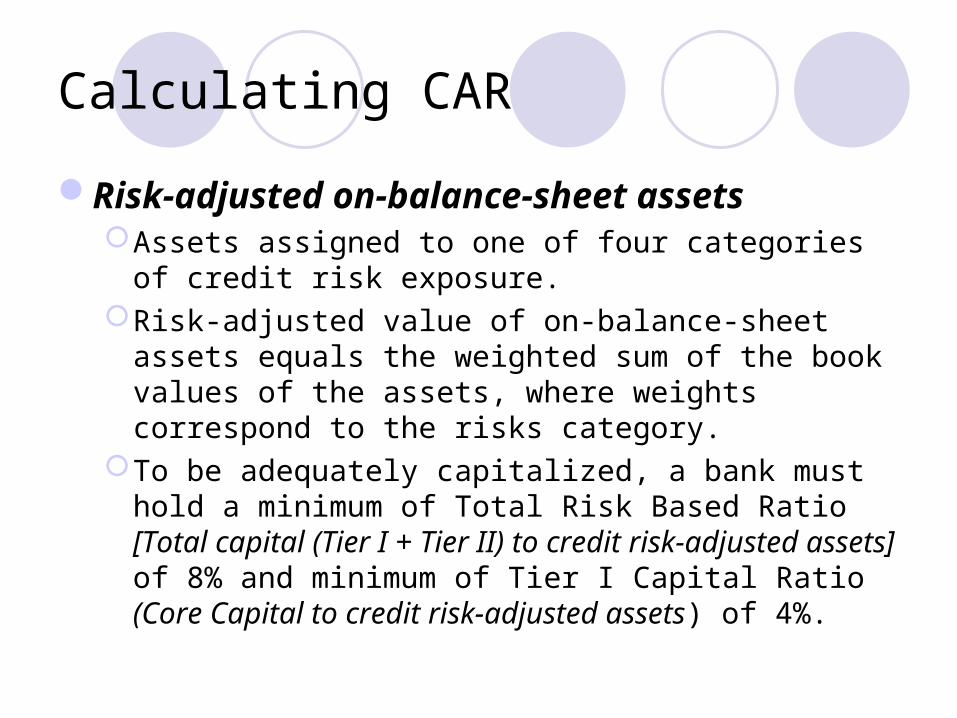

Calculating CARRisk-adjusted on-balance-sheet assets

Assets assigned to one of four categories of credit risk exposure.

Risk-adjusted value of on-balance-sheet assets equals the weighted sum of the book values of the assets, where weights correspond to the risks category.

To be adequately capitalized, a bank must hold a minimum of Total Risk Based Ratio [Total capital (Tier I + Tier II) to credit risk-adjusted assets] of 8% and minimum of Tier I Capital Ratio (Core Capital to credit risk-adjusted assets) of 4%.

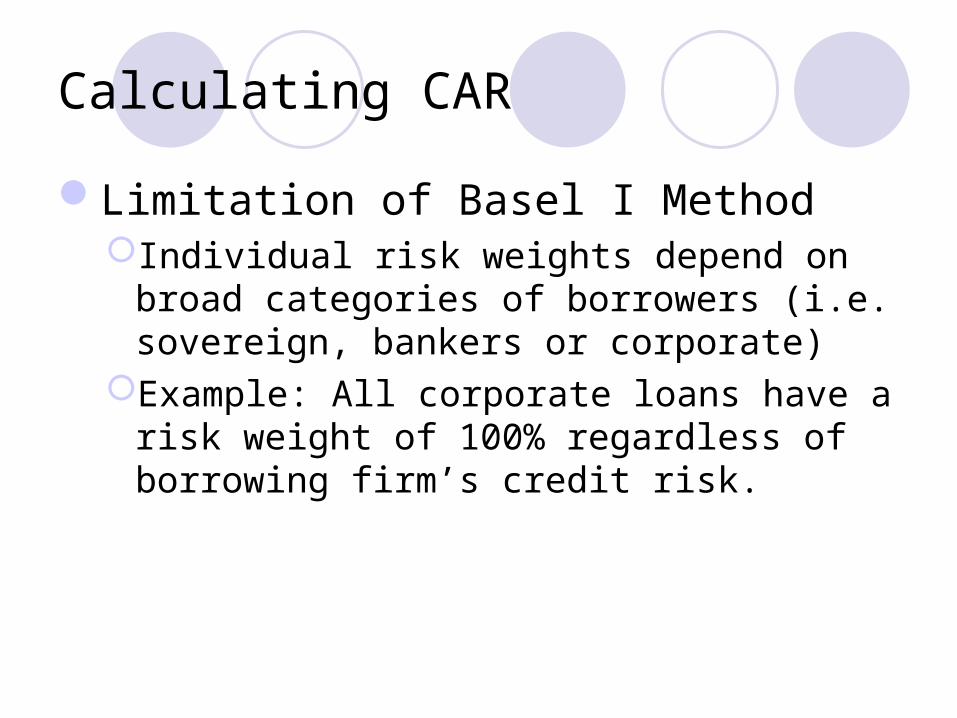

Calculating CARLimitation of Basel I Method

Individual risk weights depend on broad categories of borrowers (i.e. sovereign, bankers or corporate)

Example: All corporate loans have a risk weight of 100% regardless of borrowing firm’s credit risk.

Calculating CAR (On-Balance Sheet)Credit Risk-Adjusted On-Balance-Sheet Assets

Under Basel IIIt introduces a wider differentiation of credit risk weights.

Risk weights are refined by reference to a rating provided by external credit rating agency (S&P).

Therefore Basel II should produce Capital Ratio more in line with actual economic risk that depository institutions / banks are facing.

Calculating CAR (Off-Balance-Sheet) Credit Risk Adjusted (CRA) Off-Balance-

Sheet ActivitiesThe calculation CRA values of OBS involves

Two StepsStep I– Derive the Credit Equivalent Amounts: Find the risk-adjusted asset value for these OBS items and multiply the amount outstanding of these items with the conversion factors.

Step II – Multiply these Credit Equivalent amounts by their appropriate risk weights.

Calculating CAR (Off-Balance-Sheet)Off-balance-sheet continent guaranty

contractsConversion factors used to convert into credit equivalent amounts – amounts equivalent to an on-balance-sheet item. Conversion factors used depend on the guaranty type.

Calculating CAR (Off-Balance-Sheet)For example: Direct credit substitute SLC issues by banks – 100% conversion factor rating.

Performance-related SLC and unused loan commitments of more than 1 year – 50% conversion factor.

Other loan commitments, those with one year or less to maturity – 0% credit conversion factor. (Basel II: this conversion factor will increase to 20%)

Calculating CAR (Off-Balance-Sheet)Risk weights assigned to OBS contingent guaranty contracts are the same as if the bank had entered into the transactions as a principal.

For Example:o The credit rating used to assign a credit risk weight for in-balance-sheet assets are also used to assign credit risk weights on these OBS activities.

Calculating CAR (Off-Balance-Sheet)The CRA Asset Value of OBS Market

Contracts or Derivative Instrumentso Banks engage in buying and selling OBS futures, options, forward, caps and other derivative securities are exposes to counter party credit risk.

o Counterparty Credit Risk: The risk that the other side of a contract will default on payment obligations.

Calculating CAR (Off-Balance-Sheet)The calculation of Risk-adjusted asset values of OBS market contracts involves two steps:

o Step I: Calculate a conversion factor to create credit equivalent amounts.

o Step II: Multiply the credit equivalent amounts by the appropriate risk weights.

The Credit Equivalent (CE) amount is divided into a potential exposure element and a Current exposure element

That is CE = potential exposure ($) + current exposure ($)

Calculating CAR (Off-Balance-Sheet)Potential Exposure: The risk of counterparty to a derivative securities contract defaulting in the future. (Refer to Table 20-15, page 534 for potential exposure conversion factor)

Calculating CAR (Off-Balance-Sheet)Current Exposure: The cost of replacing a derivative securities contract at today’s prices. The calculation is by replacing the rate or price initially in the contract with the current rate or price for a similar contract and recalculates all the current and future cash flows that would have bee generated under current rate or price terms.

o Risk-adjusted asset value of OBS market contracts = Total credit equivalent amount X risk weight.

o Limitation: This method ignores the netting of exposure.

Calculating CAR (Off-Balance-Sheet)Risk-Adjusted Asset Value of OBS Derivatives with

Nettingo With netting, the bank requires to estimate the net current exposure and net potential exposure of bilateral netting contracts.

o Total credit equivalent amount = Net Current exposure + Net potential exposure

o Net Current Exposure = sum of all positive and negative replacement costs. If the sum is positive, then net current exposure equals the sum. If negative, net current exposure equals zero.

Calculating CAR (Off-Balance-Sheet)The net potential exposure is defined by the following formula:

o A net = (0.4 X A gross ) + (0.6 X NGR X A gross )

o A net = the net potential exposure o A gross = the sum of the potential exposures of each contract

o NGR = the ratio of net current exposure to gross current exposure

o 0.6 = the amount of potential exposure that is reduced as a result of netting.

Calculating CARInterest Rate Risk, Market Risk, and Risk-Based

CapitalFrom a regulatory perspective, a credit risk-based capital ratio adequate only as long as a bank is not exposed to undue interest rate or market risk.

This is because the risk-based capital ratio takes into account only the adequacy of a bank’s capital to meet both its on- and off-balance-sheet credit risks.

This method does not explicitly accounted for the insolvency risk resulted from interest rate risk (duration mismatches) and market (trading) risk.

Calculating CAR – Operational Risk & Risk-Based Capital Operational Risk and Risk-Based

CapitalBasel II on amendments to capital adequacy rules: BIS proposed an additional add-on to capital for operational risk.

Basel committee proposed 3 methods to Capital to protect against operational risk: Basic Indicator Approach, the Standardized Approach, and the Advanced Measurement Approach.

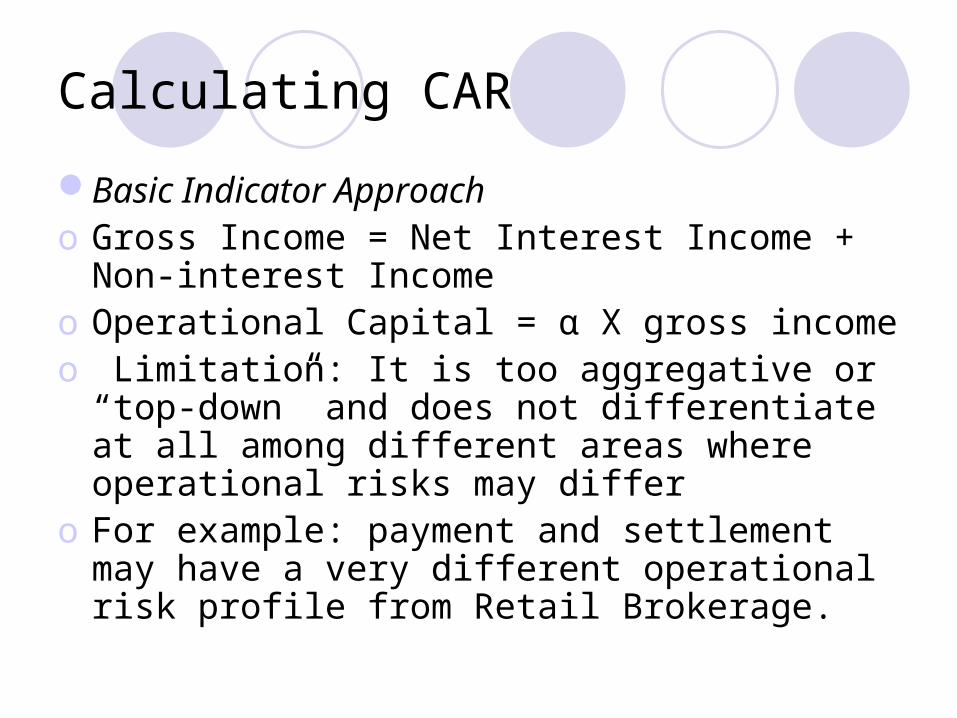

Calculating CARBasic Indicator Approacho Gross Income = Net Interest Income + Non-interest Income

o Operational Capital = α X gross incomeo Limitation: It is too aggregative or “top-down” and does not differentiate at all among different areas where operational risks may differ

o For example: payment and settlement may have a very different operational risk profile from Retail Brokerage.

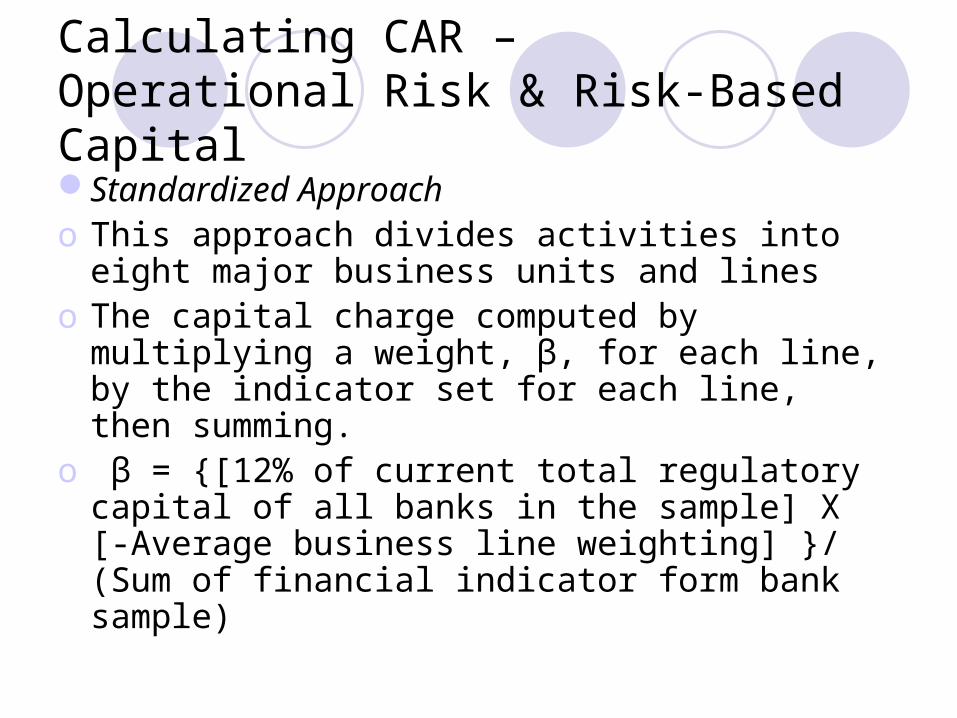

Calculating CAR – Operational Risk & Risk-Based CapitalStandardized Approacho This approach divides activities into eight major business units and lines

o The capital charge computed by multiplying a weight, β, for each line, by the indicator set for each line, then summing.

o β = {[12% of current total regulatory capital of all banks in the sample] X [-Average business line weighting] }/ (Sum of financial indicator form bank sample)

Calculating CAR – Operational Risk & Risk-Based CapitalAdvanced Measurement Approach:This model allows individual banks to rely on internal data for regulatory capital purposes.

Calculating CAR – Operational Risk & Risk-Based Capital3 broadly categories are currently under development:

(a) Internal Measurement Approach (IMA): based on a framework that separates a bank’s operational risk exposures into lines of business and operational risk event types.

Calculating CAR – Operational Risk & Risk-Based Capital(b) Loss Distribution Approach (LDA): Similar to IMA except that this method assesses unexpected losses at the 99.9 percentile directly rather than via an assumption about the relationship between expected loss and unexpected loss.

Calculating CAR – Operational Risk & Risk-Based Capital(c) Scorecard Approach (SA):Under this method, banks determine an initial level of operational risk capital at the firm or business line level, and then modify these amounts over time on the basis of scorecards that attempt to capture the underlying risk profile and risk control environment of the various lines of business.

Risk-Based Capital Ratio – Criticisms The risk-based capital requirement seeks to improve on the simple leverage ratio byIncorporating credit, market, and operational risks into the determination of capital adequacy

More systematically accounting ofr credit risk differences among assets

Incorporating off-balance-sheet exposures, and

Applying a similar capital requirement across the entire major DI in the world.

Risk-Based Capital Ratio – CriticismsLimitation: The requirements have a number of conceptual and applicability weaknesses in achieving these objectives:

Risk Weights – The four (five) weight categories may not reflect true credit risk. For example: relative weight does not imply the exact additional risk of one type of loan on the other type of loan

Risk-Based Capital Ratio – CriticismsRisk Weights based on external credit rating agencies – Measuring of credit risk depend on external credit rating. It is unclear whether the risk weights accurately measure the relative (or absolute) risk exposures of individual borrowers. Moreover S&P and Moody’s rating are ofthen accused of lagging rather than leading the business. As a result, “required” capital may peak during a recession when banks are least able to meet the requirements.

Risk-Based Capital Ratio – CriticismsPortfolio Aspects: BIS plans largely ignore credit risk portfolio diversification opportunities.

Bank Specialness: Private sector’s commercial loans have moderate and highest risk weighting. This may reduce incentives for banks to make loans to these businesses.

Risk-Based Capital Ratio – CriticismsOther Risks: BIS plan does not account for other risks, such as interest rate risk, foreign exchange risk, and liquidity risk.

Competition: Tax and accounting standard differences across banking systems and in safety net coverage, the risk-base capital requirement has not created competition among banks.