Embed Size (px)

Citation preview

Determinants of corporate debt

structure in a privately dominated

debt market: a study of the

Spanish capital market

Kalu Ojaha and Justo Manriqueb,*

aSchool of Economic and Business Sciences, University of theWitwatersrand, Johannesburg, Private Bag 3, Wits 2050, South AfricabFACIS Department, School of Business, University of Houston–Downtown,One Main Street–Suite 1007N, Houston, TX 77079, USA

To date, corporate debt structure research has focused largely on nationaldebt markets characterized by both public and private debts supplies.However, given that most national debt markets are characterized by theabsence of public debt supply, the representative debt market of Spain isused to extend the research on corporate debt structure. A double-hurdletest approach reveals that the likelihood of using bank debt is positivelyrelated to firm size and information availability but negatively related tofirm credit worthiness, while the likelihood of using non-bank private debtis positively related to firm size, growth potential, relative firm size anddegree of leverage. Further, it is found that the amount of bank debt firmshold is positively related to firm size, growth potential, informationasymmetry, and age but negatively related to information availability.The amount of non-bank private debt is positively related to firm sizebut negatively to growth potential and age. Moreover, it is found thatthough some roles of private debt providers are similar in the two distinctnational debt markets, some roles of public debt suppliers are supplantedby non-bank private debt suppliers in a debt market bereft of public debtsupply.

I. Introduction

Unlike major developed capital markets such as those

of the USA, Japan, and Britain, and like most emerg-

ing capital markets, Spain’s capital market is domina-

ted by private (bank and non-bank) debt providers.

In fact, these latter markets have thin or no public

debt supply; thin because their public debt supply is

almost exclusively of government issues: treasury and

municipal debts. This kind of debt market no doubt

adds a curious complexion to the evolving state of

capital structure research, which has advanced

beyond looking at the optimum divide between

equity and debt sources of financing to ascertaining

*Corresponding author. E-mail: [email protected]

Applied Financial Economics ISSN 0960–3107 print/ISSN 1466–4305 online # 2005 Taylor & Francis Group Ltd 455

http://www.tandf.co.uk/journalsDOI: 10.1080/0960310042000319228

Applied Financial Economics, 2005, 15, 455–468

why corporations employ a mix of debt sources in

meeting their debt financing.1 There is therefore a

need to examine how debt funding mix is determined

in a debt market characterized by private (bank and

non-bank) debt suppliers, with little or no competi-

tion from public debt suppliers. It is specifically

examined whether the same set of factors that deter-

mine corporate debt structure in the USA, Japan and

other major capital markets that supply both private

and public debts (Houston and James, 1996;

Johnson, 1997; Anderson and Makhija, 1999; Denis

and Mihov, 2003) similarly determines corporate

debt structure in a privately dominated debt market

such as Spain’s.

The Spanish market is particularly suited to this

examination of potential differences in corporate

debt structures in dissimilar capital markets. Spain’s

capital market has salient features that distinguish it

from most major capital markets of the world. As

Saa-Requejo (1996) points out, most Spanish banks

are at the core of large industrial groups in ways that

they serve as both the main creditors and the main

shareholders of firms in those groups. That is, they

have historically played and continue to play a role

akin to those of German and Japanese banks

(Meerschwarm, 1991). Unlike the very developed

securities markets of Japan and the USA, for

instance, Spain’s securities market is relatively under-

developed in that it has (1) small transaction volumes,

(2) high transaction and flotation costs, and (3) few

players (mostly financial services companies) that

wield substantial market powers. Importantly,

Spain’s public debt market is almost exclusively for

government issues. Its bankruptcy and tax laws have

features that further distinguish its financial system:

bankruptcy laws give control of distressed firms to

a pool of major creditors, who are mostly banks.

In this research, the universality of current findings

on firms’ debt structure is examined along the lines

of Johnson (1997), Anderson and Makhija (1999),

and Denis and Mihov’s (2003) analyses by focusing

on Spain. Particularly, it is wondered whether the

factors affecting a firm’s mix of bank and non-bank

private debts differ in an environment where compa-

nies have no access to domestic public debt than in an

environment where companies have access to both

public and private debts. For instance, it is possible

that non-bank private debt serves the role of mitigat-

ing hold-up cost of borrowing from banks in an

environment bereft of public debt supply (Rajan,

1992; Houston and James, 1996). It is equally con-

ceivable that banks’ specialization in information

gathering and monitoring better place them as the

appropriate debt fund providers to risky firms

whereas well-heeled firms may be more capable of

accessing non-bank private debt sources in a debt

market that has no public debt. In other words, in

contrast to Johnson’s (1997) observation about a

debt market encompassing both public and private

debts, small and less heeled firms may not be screened

out of bank financing in a debt market characterized

by the absence of public debt.2 These possible differ-

ences in debt providers’ roles are examined by com-

paring the present study’s result to results of two

empirical studies that explore simultaneously roles

of bank, non-bank private and public debt providers

in corporate debt structure (Johnson, 1997; Denis and

Mihov, 2003). Finally, in light of credit supplies being

limited to mainly private debts in Spain, the extent to

which companies’ preference for credit types align

with the market’s supply of credit types is examined.

Using a double-hurdle empirical test approach, it is

shown that the likelihood of using bank debt is

positively related to firm size and information avail-

ability but negatively related to firm credit worthiness,

while the likelihood of using non-bank private debt is

positively related to firm size, growth potential (qual-

ity projects), relative firm size and degree of leverage.

Further, it is found that the amount of bank debt

firms hold is positively related to firm size, growth

potential, information asymmetry and age, but

negatively related to information availability in terms

1Both theoretical and empirical works have began addressing specific debt structure issues such as (1) why there is a mix ofpublic and private sources of debt for corporations as exemplified by Blackwell and Kidwell (1988), Diamond (1991a),Easterwood and Kadapakkan (1991), Rajan (1992), Hoshi et al. (1993), Chemmanur and Fulghieri (1994), Detragiache(1994), Houston and James (1996), Johnson (1997), Anderson and Makhija (1999), Hooks (2003) and Denis and Mihov(2003); and (2) what a firm’s optimal debt maturity structure should be as in Brick and Ravid (1985), Flannery (1986),Diamond (1991b, 1993), Houston and Venkataraman (1994), Barclay and Smith (1995) and Cai et al. (1999).2 This insight is rather in accord with Diamond (1991a) who notes that less reputed and/or track-record deficient firms are bychoice and prerequisites for gaining access to public debt funds bound to banks, which uniquely and systemically possess thedelegated monitoring know-how. The difference here is that small and less reputed firms build their track record by submittingto bank scrutiny to acquire bonding and reputation as to eventually access the, perhaps, less expensive direct placement debt(non-bank private debt) market. That is, non-bank private debt sources may substitute for public debt sources in this kind ofdebt market.

456 K. Ojah and J. Manrique

of dividend payment. Amount of non-bank private

debt is positively related to firm size and negatively

to potential growth in terms of capital expenditures,

and age. Note that the sets of significant factors in the

mix and amount of debt equations are largely dissim-

ilar, thus suggesting that companies’ preferences for

debt types are not well accommodated by the debt

market’s supply pattern; a situation which in turn

points to a need for market completeness either

through new products creation by debt providers or

through government policy initiative that better

aligns debt supplies with firms’ debt preferences.

On the major question of whether determinants of

debt structure here differ from those in debt markets

characterized by both private and public debt supplies,

it is found that their roles are the same in both kinds

of markets in some respects. Interestingly, however,

the signs of creditworthiness and firm leverage

variables reflect role reversals in corporate debt struc-

ture determination in a market that supplies no public

debt. Unlike in a market that supplies public debt

as well, where creditworthiness is positively related

to bank debt access (e.g., Johnson, 1997; Denis and

Mihov 2003), credit worthiness is negatively related

to preference for bank debt in the market where

firms lack access to public debt supply. Similarly,

high leverage is usually positively related to preference

for bank debt in a market that has public debt supply

as well (e.g., Johnson, 1997) but it is unimportant

in determining a firm’s preference for bank debt in

a market with no public debt supply. Instead and in

contrast to Johnson’s finding, high leverage is

positively related to preference for non-bank debt;

thus suggesting avoidance of further hold-up costs

of bank borrowing. In the same vein, possession of

quality projects which usually enhances access to

public debts, rather enhances preference for non-

bank private debts in this market. In sum, therefore,

the evidence here points to a possible roles substitution

between public debt suppliers and non-bank private

debt suppliers in a national debt market bereft of

public debt.

Furthermore, note that it is found that different

sets of factors determine the amount of bank versus

non-bank private debts that a firm holds. Particularly

where a factor affects both amounts of the two types

of debt, the factor has opposite effects on amounts of

the two debt types. Specifically, size, growth potential

and reputation are found to be the most influential

determinants of the amount of non-bank private

debts a firm holds. Conversely, size, growth potential,

information asymmetry and reputation are the most

influential determinants of the amount of bank debts

a firm holds; with these factors relating to the amount

of bank debt in ways that underline banks’traditional rolesofdelegatedmonitoringandprudence.

Interestingly, the descriptive statistics and trendanalysis of the sample suggest that the majority ofSpanish firms’ debt is short-term in nature (only16% is long-term); which is not surprising given thelack of domestic public debt market. Firms in thissample hold an average 57% of their total capital indebt forms, which is in line with most modern firmsaround the world filling the majority of their externalcapital through debt sources. In the next section, thehypotheses that explain corporations’ mix of debtsources are stated in a way that motivates the empir-ical analysis. Section III describes the sample andprovides descriptive statistics on Spanish firms’ debtstructure. In Section IV, the methodology used toexamine the questions of the study is presented andthe empirical results discussed. Section V concludesthe paper.

II. Background on Determinantsof Firm’s Debt Structure

The debt structure of a firm is a function of the firm’sdemand for and supply of debt funds. Recent workson debt structure have proffered hypotheses of howcorporate debt markets are impacted to yield whatconstitutes an optimal mix of private and publicdebts for individual firms. Though these worksvariously point to several company characteristicsthat can interact with different sources of debt supplyto decide a firm’s optimal mix of private and publicdebts, these factors are classified into three non-mutually exclusive groups that guide the empiricaltests. They are namely (a) cost of information gather-ing and monitoring, (b) mitigation of informationasymmetry, and (c) efficiency of liquidation. In thefollowing paragraphs each of the factors is discussedalong with implied predictions of how they wouldaffect firms’ reliance on bank debt versus non-bankdebt. The slant towards bank debt is motivated bybanks’ dominance of most debt markets.

Cost of information gathering and monitoring

The concentrated ownership of private (bank) debtrelative to the diffused ownership of public debt (orarm’s length private placements) can be readily tracedto differences in information gathering and monitor-ing costs on borrowers of these different types ofdebt. Fama (1985), James (1987), Nakamura (1993),Yosha (1995) and Houston and James (1996) var-iously note that banks have a comparative advantagevis-a-vis other lenders in gathering information

Corporate debt structure in privately dominated debt market 457

on borrowers and subsequently monitoring their

behaviour. Specifically, Fama (1985) argues that firms

who benefit from the more effective monitoring and

information gathering of banks are willing to pay for

the reserve-tax which banks uniquely bear. This wil-

lingness contrasts the resistance of firms that can more

cheaply provide company information to creditors,

such as large firms that are able to reduce informa-

tion disclosure cost via economies of scale as well as

attract substantial investors’ following that closely

monitor their activities.3 Nakamura (1993) stresses

this point by noting that unlike small firms whose

banks can effectively gather information from their

transaction accounts, large firms typically spread

their deposits among several banks. Consequently, a

single bank is not likely to provide comprehensive

information on a large firm. The prediction is that

small-to-medium sized firms rely on bank financing

than large firms who prefer public debt.

James (1987) and Yosha (1995) suggest that bank

financing signals positive information about a firm’s

quality. James shows that refinancing bank debts sig-

nals a firm’s positive future prospects while Yosha

argues that firms that have quality projects would

avoid using public debt as not to reveal information

to rival firms, though that might elicit competitive

responses. In other words, high quality projects

firms see information advantage as outweighing the

costs of both competitive response and high informa-

tion disclosure, and rely on bank debt. Alternatively,

such Yosha-described firms can enjoy the good of

both worlds by privately placing their debts, which

allows them to keep their information confidential

without overtly evoking competition.

Therefore, in attempts to minimize information

provision and monitoring costs, small-to-medium

size firms would rely more on bank debt than large

firms would. Quality project firms would rely on

bank debt. And firms with information advantage

would protect it by relying on bank or non-bank

private debt.

Mitigation of information asymmetry

Jensen and Meckling (1976) in their analysis of firms’

agency problems highlight the importance of moni-

toring as a way of resolving the undue usurpation

of some stakeholders’ benefits by another – caused

mainly by information asymmetry. In the spirit of

Jensen and Meckling, banks provide a much more

effective monitoring of borrowers and thus reduces

information asymmetry than non-bank lenders; an

assertion that is variously supported by Smith and

Warner (1979), Blackwell and Kidwell (1988), and

Diamond (1984, 1991a), among others. Assuming

alignment of managers’ and owners’ interests,

Hoshi et al. (1993) argue that banks monitor man-

agers to discourage unprofitable investment, suggest-

ing that firms with little or no profitable investment

opportunities would benefit more from the kind of

close monitoring banks provide than would firms

with significant profitable investment opportunities.

In instances where a firm has profitable investment

opportunities but is not sizable enough or as well

known as to borrow from non-bank sources (particu-

larly the public) at affordable cost, Diamond (1991a)

suggests that the firm would first build a track record

(reputation) by submitting to bank monitoring.

Consequently, this reduces information asymmetry

between borrowers and lenders. Thus, unlike older

and larger reputed firms, younger and smaller firms

that lack reputation would reduce information

asymmetry by relying more on bank debt than on

public debt.

Among other observations, Rajan (1992) shows

how banks’ monitoring and control of borrowers

are fostered by the threat of non-renewal of crucial

short- to medium-term loans. Under public borrow-

ing, managers face no such threats and can, therefore,

engage in unprofitable projects that serve their inter-

est at the expense of public lenders. It follows there-

fore that firms seeking owners’ wealth maximization

and possessing less profitable projects would prefer

bank debt as to deter the potential moral hazard

problems associated with public debt (Detragiache,

1994). In this vein, Smith and Warner (1979) posit

that risky firms benefit from placing more restrictive

covenants on their debt as to reduce moral hazard

problems such as under-investment which can occur

after a debt is issued. Given that banks provide

similar restrictions vis-a-vis public lenders, risky

firms should prefer bank debt to public debt.4

In order to reduce adverse selection and moral

hazard problems associated with debt financing,

3Alternatively, sizable (medium to large) firms who are ‘capable’ of privately placing debts with non-bank financiers wouldavoid the particularly costly bank debt in a debt market that supplies no public debt.4 See Barclay and Smith (1995, pp. 610–11) for additional exposition on how resolution of the under-investment problem (firstarticulated by Myers, 1977) would induce small and risky firms to rely on bank financing instead of public debt. Recall thatadverse selection and moral hazard are both consequences of information asymmetry. Thus, attempts to forestall them,mitigate information asymmetry.

458 K. Ojah and J. Manrique

a firm would rely more on bank (private) debt

than on public debt if it is predominantly charac-

terized by any or a combination of the following:

(1) unattractive investment opportunities, (2) low

reputation, (3) medium sized and (4) risky.

Efficiency of liquidation

Borrowing long-term from the public requires

a borrower to be both credit-worthy and able to

satisfactorily disseminate material information to

dispersed creditors. An important, and perhaps,

unintended accrual to the borrower for fulfilling

these requirements is the continuation of unattractive

projects that would otherwise be liquidated under a

more closely monitored debt contract that provides

for re-negotiation (i.e., bank debt). Thus, an optimal

debt structure trades off inefficient liquidation

decisions against agency costs of monitoring. Usually

banks conduct the kind of comprehensive investiga-

tions that help avoid such inefficiencies (Berlin and

Loeys, 1988: Berlin and Mester, 1992; Rajan, 1992;

Chemmanur and Fulghieri, 1994; Detragiache, 1994).

Like Rajan (1992) and others, Diamond (1991b,

1993) discusses the likelihood of inefficient liquida-

tion. He suggests that firms possessing favourable

private information on future profitability would

prefer to issue short-term (bank) debt as to foster

efficient liquidation.5 Berlin and Leoys (1988) upon

analysing models of unmonitored debt contract and a

range of monitored debt contracts, conclude that

firms with high liquidation value projects would

welcome the close scrutiny of private lenders

(banks) and its attendant benefits than would firms

with low liquidation value projects. Not only would

low liquidation value firms be subjected to more

frequent liquidation under private debt contract,

they might also incur a higher capital loss in the

process. Berlin and Loeys further predict that

credit-worthy firms face less threat of frequent

liquidation and has the confidence it takes to borrow

from the public, consequently they rely less on bank

debt.

Taking a different tack, Chemmanur and Fulghieri

(1994) posit that otherwise good firms characterized

by a high likelihood of financial distress would

prefer bank financing, which provides re-negotiation

when it is necessary to avoid inefficient liquidation,

despite its high cost. Hence, firms characterized by a

low likelihood of financial distress can and would

borrow from the public (non-bank sources) at a

lower cost. In the same vein, Berlin and Mester

(1992) argue that bank debt cost more – including

harsher covenants – than public debt because it

allows for re-negotiation, especially when covenants

interfere with optimum investment.

In order to foster efficiency of liquidation, firms

possessing the following characteristics would rely

more on banks than on the public and/or non-bank

private source for their debt financing: (1) attractive

investment opportunities, (2) high private informa-

tion advantage, (3) low leverage, (4) high liquidation

value projects and (5) high likelihood for financial

distress.

Summary predictions from the debtstructure literature

In Table 1 the predictions on determinants of corpo-

rate debt structure are restated succinctly. For each of

the predictions, a construct is indicated that is used in

empirical tests. Note that these summarized factors

and their predicted effects are predicated largely on

a debt market characterized by the simultaneity of

viable private and public debt sources. This contrasts

Spain’s debt market which is examined here; its

non-bank debt market is characterized by activities

akin to private placements and public issuance of

government debts. In other words, firms in Spain

lack access to domestic public debt.

Some of Table 1’s constructs require further

comments. Size has traditionally been represented by

total assets or total sales. Here, sales are used because

total asset is highly correlated with many other

independent variables that are standardized by assets,

such as debt ratio, capital investment ratio, and fixed

asset ratio. A firm’s potential growth (quality project)

is usually represented by the ratio of market value of

equity plus book value of liabilities to book value of

assets under the assumption of market efficiency or

by the ratio of capital investments to assets. The

latter is used as it was not possible to obtain market

stock prices because Banco de Espana provides the

data in a form that conceals individual firm’s

identity.6 As Petersen and Rajan (1994) show, the

length of time a firm has been in existence indicates

5He, however, acknowledges that short-term borrowing can expose a firm to excessive liquidation. In fact, he suggests thathighly levered firms may limit the use of bank debt as to avoid excessive liquidation.6Under the same wealth maximization assumption that underlies the market-to-book construct, a firm would increase capitalinvestments only when such an increase is attractive. Consequently, a high capital investment indicates a firm’s pursuit ofquality projects, which in turn enhances potential (future) growth.

Corporate debt structure in privately dominated debt market 459

the kind of reputation it has built over time. If a firmhas survived several years, it follows that its built-upreputation must have sustained it. The medium-sized construct is motivated by Diamond’s (1991a)exposition of how the quest for reputation motivatesfirms’ reliance on bank financing. Just as large(reputed) firms do not rely on bank financing, sodo small firms with no reputation to risk getscreened out by banks. Consequently, medium-sized(reputation-seeking) firms would particularly rely onbank financing. These constructs are used in theempirical tests (see Section IV).

III. Data and Descriptive Statistics

In this section the main data of the study is described,in addition to providing a general description of thepattern of corporate debt structure in Spain.

Data source

The set of data used here to ascertain corporate

debt structure in a national debt market characterized

by private debt dominance and thin public debt

source comes from Central de Balances del Banco

de Espana. It is a confidential databank of annual

financial reports, including balance sheets, income

statements, sources and uses of funds statements,

and employment size for hundreds of Spanish firms.

It is a database assembled essentially for research

purposes. Since it is confidential and contributing

firms receive aggregate information about their

competitors (industry), firms are motivated to report

pertinent data to the Banco de Espana (Central Bank

of Spain), the compiler. Contributing companies’

anonymity is partly ensured by the Bank’s replace-

ment of individual company names with pseudo-

names. In keeping with the thrust of the present

research, those non-financial services firms that are

Table 1. Summary predictions of corporate debt structure determinants as suggested by the literature, with bank financing as the

reference debt financing source

Predicted determinant (factor) Predicted sign Proxy for predicted determinant (factor)

A. Information/monitoring cost reductionSize of firm � Log of total sales (or total sales value)Quality projects þ Ratio of total capital investments to

total assetInformation disadvantage þ Ratio of intangible assets to total assets

B. Avoidance of information asymmetryAttractive investments � Ratio of total capital investments

to total assetsHigh reputation � Firm’s age since inception or incorporationMedium sized þ 0,1 for firms whose employment size is

within Banco de Espana’s classificationof medium-sized firm and above(50–249 employees)

Information availability � 0,1 for firms that pay dividendLow distress potential þ Z-score¼ [Sales/Assetsþ 3.3(EBIT/

Sales)þ 1.4(Retained Earning/Assets)þ 1.2(Working capital/Assets)]

C. Efficient liquidationFinancial leverage � Ratio of sum of short- and long-term

debts to assetsLiquidation value of assets þ Ratio of fixed assets (plant and equipment)

to total assets; or ratio of intangible assetsto total assets (reverse effect)

Credit worthiness � Ratio of operating income to interest expense;or Z-score¼ [Sales/Assetsþ 3.3(EBIT/Sales)þ 1.4(Retained Earning/Assets)þ 1.2(Working capital/Assets)]

Bank ownership þ/� 0,1 for firms that are partly owned byabank/banks

Notes: The predicted signs are based on how the determinants relate to reliance on bank debt per current corporate debtstructure literature.A predicted sign of þ/� connotes an empirical question that has not yet been empirically examined in the literature.

460 K. Ojah and J. Manrique

listed on Bolsa de Madrid and that indicate theirsources of debt for 1998/1999 are culled from thedatabase. Pertinent information on debt sourcesinclude the level of bank debts, long-term debts(long-term is a maturity of >1 year), commercialpaper and other types of privately placed debts, etc.

Pattern of corporate borrowing and related statistics

In Table 2, the trend of corporate debt structure inSpain as at the research period 1998/1999 is pre-sented, along with summary statistics or indicatorsof the debt management status of the samplefirms. It must be noted at this juncture that the non-reporting of pertinent (particularly often footnoteddebt-related) information by sample firms detractsfrom the desired level of detail on debt structurethat was sought. Available information, shown inTable 2, indicates that Spanish firms unsurprisinglysource the majority of their capital funding throughdebt (average debt structure¼ 57%). Interestingly,only an average of 16% of this debt funding is of along-term nature, suggesting that the bulk of theirdebt maturity is short-term. This is logical given theabsence of a viable domestic public debt market,which traditionally provides long-term debts.

In terms of the debt management profile of thesample firms, an average interest expense to totaldebt ratio of 4% and an average interest coverageratio of 8.24 times are recorded. Moreover, an aver-age Altman Z-score of 2.30 is found, which is higherthan the conventional benchmark score of 1.81. Insum, therefore, it can be concluded from this evidencethat Spanish firms’ debt management profile is soundrelatively speaking.7

IV. Empirical Specification and Results

In this section empirical specifications of the studyare described, and the empirical results are reportedand discussed. First, the test methodology used toascertain determinants of corporate debt structure isbriefly described.

Test methodology

A full examination of the debt structure issuesuggests that a two-stage empirical test methodologyis appropriate as it permits use of currently extantdebt structure determinants (per theory and empiricalevidence) in figuring out what drives a firm’s use ofbank and/or non-bank private debt; then conditionalon the decision to hold or not to hold bank andnon-bank private debts, one ascertains which ofthe relevant factors determine the quantity of debteventually held. To this end, binomial probit modelsare used, in the first stage, to ascertain what factorsdetermine the debts mix of Spanish firms. For this,the dependent variable is a dummy taking the valueof one for bank debt (or for non-bank private debt)and zero for no bank debt (or for no non-bankprivate debt), respectively. The independent variablesare as described in Table 1, based on currentcorporate debt structure literature.

For the second stage, the dependent variablesbecome the amount of bank debts and the amount ofnon-bank private debts, respectively. The same set ofindependent variables used in the choice of debt typeequations are retained. The objective is to test whetherthe set of statistically significant factors in the choiceof and amount of debt equations is the same. That is,

7Not reported in the table, 77% of the reporting firms use exclusively non-bank private debts, 10% use exclusively bankdebts, and 13% use both non-bank private and bank debts.

Table 2. Sample corporate debt structure pattern and debt management descriptive statistics

Variable Mean Maximum Minimum Standard deviation

Total debt/total asset 0.57 1.32 0.00 0.25Long-term debt/total debt 0.16 0.82 0 0.19Sales/total debt 3.71 51 0 3.83EBIT/interest expenses 8.24 331 �10.60 24.24Interest expense/total debt 0.04 0.64 0 0.07Z-score (low distress potential) 2.30 10.74 �2.31 1.44Assets (in millions of pesetas) 1096.00 47520 5 3644Sales (in millions of pesetas) 1291.70 57900 0 4204Size of employment 49 710 1 87

Notes: Observations are for 1998/1999 of listed sample firms that have debt outstanding in the database of Central de Balancesdel Banco de Espana. The test variables are as defined in Table 1.

Corporate debt structure in privately dominated debt market 461

are the same factors relevant in the two debt structuredecisions? Theory does not suggest otherwise, thusit is assumed that, a priori, the same factors thatdetermine the preferred mix of debts also determinethe quantity of corresponding debts held. However,due to the number of sample firms not holding eitherbank and/or non-bank private debt, many zeros wereencountered for the dependent variables of theamount of bank and non-bank debts equations.This raised the issue of selectivity bias – i.e., that thezeros and positive values are not randomly assigned.Accordingly, a standard and consistent procedurewas used to correct selectivity bias (Lee, 1978).First, univariate probit estimates were used to com-pute the inverse Mills ratio. Then both a correctionterm for selectivity bias and a new disturbanceterm, with a zero conditional mean, were added tothe debt amount equations. That is, the inverseMills ratio is used as a proxy for selectivity bias.

Univariate probit analysis of determinantsof choice of bank and non-bank debts

Firms decide whether or not to hold bank and/ornon-bank debts, with different sets of variablesexplaining the decision on each debt type. That is,the variables affecting the decision to choose bankdebts and those affecting the decision to choosenon-bank debts are not necessarily the same. Thedesired bank (w�

ba) and non-bank (w�nb) debts are

defined as:

w�ba ¼ �0

bazba þ �ba

w�nb ¼ �0

nbznb þ �nb

ð1Þ

where zba and znb are vectors of explanatory variables;�ba and �nb are parameter vectors; and �ba and �nb

are vectors of disturbance terms. Note that w�ba and

w�nb are latent unobservable variables. However,

two observable dummy variables are identified:wba (dummy variable for bank debt status) and wnb

(dummy variable for non-bank debt status).The dummy variables are specifically defined asfollows: wba¼ 1 if w�

ba>0 and wba¼ 0 otherwise; andwnb¼ 1 if w�

nb>0 and wnb¼ 0 otherwise.As shown in Table 3, the determinants of Spanish

firms’ preferred mix of bank and non-bank privatedebts appear robust with respect to both the sign

and statistical significance of the coefficients.8

Results of a probit model that encompass allindependent variables for the bank and non-bankdebt choice decisions, respectively, are reported. Tobuttress this model’s finding (particularly given thatprobit coefficients do not equal their marginaleffects), the marginal probability elasticity (MPE)technique is used to quantify the magnitude of thepotential effects of a change in any of the explanatory(continuous) variables on the probability of choosingbank and non-bank private debts. The marginalprobability elasticity is computed as

MPE ¼ �ð�0ZÞ�½S=Prðw ¼ 1Þ� ð2Þ

where MPE refers to the marginal probability elasti-city with respect to the Z vector; � is the standardnormal density; S represents the vector of samplemeans of the continuous explanatory variables; andPr(w¼ 1) represents the probability of choosing abank or a non-bank debt. However, since it isnot strictly correct to evaluate the potential effectsof discrete variables by using marginal probabilityelasticity, their potential impacts are assessed bycomputing their marginal effects. Marginal effectsare calculated as the finite changes in these discretevariables as their values change from zero to one,ceteris paribus. The marginal probability elasticitiesand marginal effects of bank and non-bank debtchoices are reported in Table 4.

As reported in Table 3, size, information availabil-ity and credit quality are determinants of Spanishfirms’ preference for bank debt (all at 5% or bettersignificance levels), with size and information avail-ability relating positively to the probability of a firm’sinclusion of bank debt in its debt capital while highcredit quality relates negatively to it. More specifi-cally and per Table 4, note that a 1% increase ina firm’s size increases the probability of the firmelecting to hold bank debts by 0.04%. Conversely,a 1% increase in the level of credit worthinessdecreases the probability of electing to hold bankdebts by 1.1%. Firms that paid dividends (thusmore forthcoming with information) are more likelyto prefer bank debts than firms that did not paydividend. This suggests that size/reputation and pro-vision of information motivate Spanish firms to preferbank debts while firms characterized by high creditworthiness prefer to avoid bank debts. In light of the

8 Bivariate probit analysis was used to test for the hypothesis that the disturbance terms of the choice of bank and non-bankdebt equations were statistically correlated. The empirical results showed that the estimated correlation coefficient of thedisturbance terms was not statistically different from zero, implying that the two equations were statistically independent.Thus bivariate probit regression was not justified and hence not more appropriate than the independent univariate probitregressions, reported in Table 3.

462 K. Ojah and J. Manrique

fact thatasimilarnegativeassociationobtains forfirms’likelihood of selecting non-bank private debt (thoughsignificant at the 20% level), it can be inferred thatsample Spanish firms that have relatively safe finan-cial conditions and, thus can use internal equity,prefer to avoid sourcing debt funds. This seems tosupport the inference, in the analysis of debt structuretrend, that risky borrowers would likely be bound tobanks due to banks’ delegated monitoring.

The reputation implication associated with size isweakly supported by the finding of the age variablebeing positive though insignificant for the bank debtequation. Like the age variable, the quality project(potential growth) variable is positively related to afirm’s likelihood of selecting bank debts (but signifi-cant at the 20% level). A 1% increase in a firm’spotential for growth increases the probability ofselecting bank debts by 0.05%.

For firms’ likely selection of non-bank privatedebt, size, quality project, medium-to-large size andleverage relate positively and significantly to a firm’spreference for a non-bank private debt, with all butthe leverage estimate significant at the 5% or betterlevels. Corresponding results in Table 4 shows that a1% increase in size, quality project and leverageincreases the probability of choosing non-bankdebts by 0.12%, 0.06% and 0.44% respectively.Strikingly, medium-to-large size firms are 25%more likely to prefer non-bank private debts thansmall firms. In other words, in Spain, medium tolarge firms that possess quality projects and lesserdebt capacity tend to prefer non-bank private debtfor filling their debt funding need. Striking in thisresult is the fact that, unlike in debt markets charac-terized by both private and public debt sources,where firms that are protective of information

Table 3. Univariate probit regressions of determinants of companies’ preference for bank and non-bank

private debts (corporate debt structure)

VariableModel of determinantsof bank debt source

Model of determinantsof non-bank debt source

Constant �7.27 �1.870(�0.13) (�3.62)**

Firm size 0.0001 0.0001(2.49)** (2.22)**

Capital investment 0.007 0.0032(quality project) (1.35) (2.22)**

Ratio of intangibles �1.300 0.564(information disadvantage) (�1.02) (1.30)

Paid dividend 1.123 �0.086(information availability) (2.00)** (�0.35)

Age (reputation) 0.003 �0.005(0.30) (�0.82)

Medium to large firm 8.224 0.652(0.15) (3.11)**

Credit worthiness �1.118 �0.121(low distress potential) (�2.67)** (�1.44)

Debt ratio (leverage) �0.735 0.796(�0.68) (1.86)*

Bank ownership �4.246 0.553(�0.01) (0.92)

Year-dummy 0.093 0.058(0.22) (0.32)

�Log-Likelihood 23.19 120.02�Chi-Squared (10)a 72.69 56.42(Significance level) (0.10 E-06) (0.16 E-07)�Per cent of correct predictionsb 97.80 88.90

Notes: The dependent variable is either 1 if the firm uses any bank debt and 0 otherwise or 1 ifthe firm uses non-bank private debt and 0 otherwise. The independent variables are as defined inTable 1.** and * indicate statistical significance at 5% or better and 10% levels, respectively. Asymptotict-values are in parentheses.a The Chi-squared test is valid for the hypothesis that all slopes on the non-constant regressorsare zero.b An observation is judged to be 1 if the predicted probability, P(y¼ 1) is 0.5 or larger, otherwisethe observation is judged to be zero.

Corporate debt structure in privately dominated debt market 463

would seek debt funds from banks, sizable firmspossessing quality projects (high growth potential)that are protective of company information prefernon-bank private debt sources instead in a debtmarket dominated by banks. Perhaps this suggeststhat non-bank private debt sourcing is perceived asa potentially important way of avoiding the hold-upcost of banks’ information monopoly in a debtmarket bereft of public debt supply.

Of particular interest in the non-bank debt probitresults is that of the medium-to-large size variable.Medium to large firms (very few firms in the sampleare large per Bank of Spain’s classification – firms thatemploy �250 people) most strongly determines afirm’s likelihood of selecting non-bank private debtas a source of its debt funding. This finding is in starkcontrast to the literature-based predictions (reportedin Table 1) that medium-size firms largely accessbank-debts as they seek reputation necessary forgaining access to the public debt funds (i.e.,Diamond, 1991a). It seems as though non-bankprivate debt sources substitute certain functions ofpublic debt sources in a debt market that hasno public debt supply. Recall Diamond’s (1991a)life-cycle prediction that a firm’s debt fund sourcewould evolve from bank to public sources as thefirm increases in size.

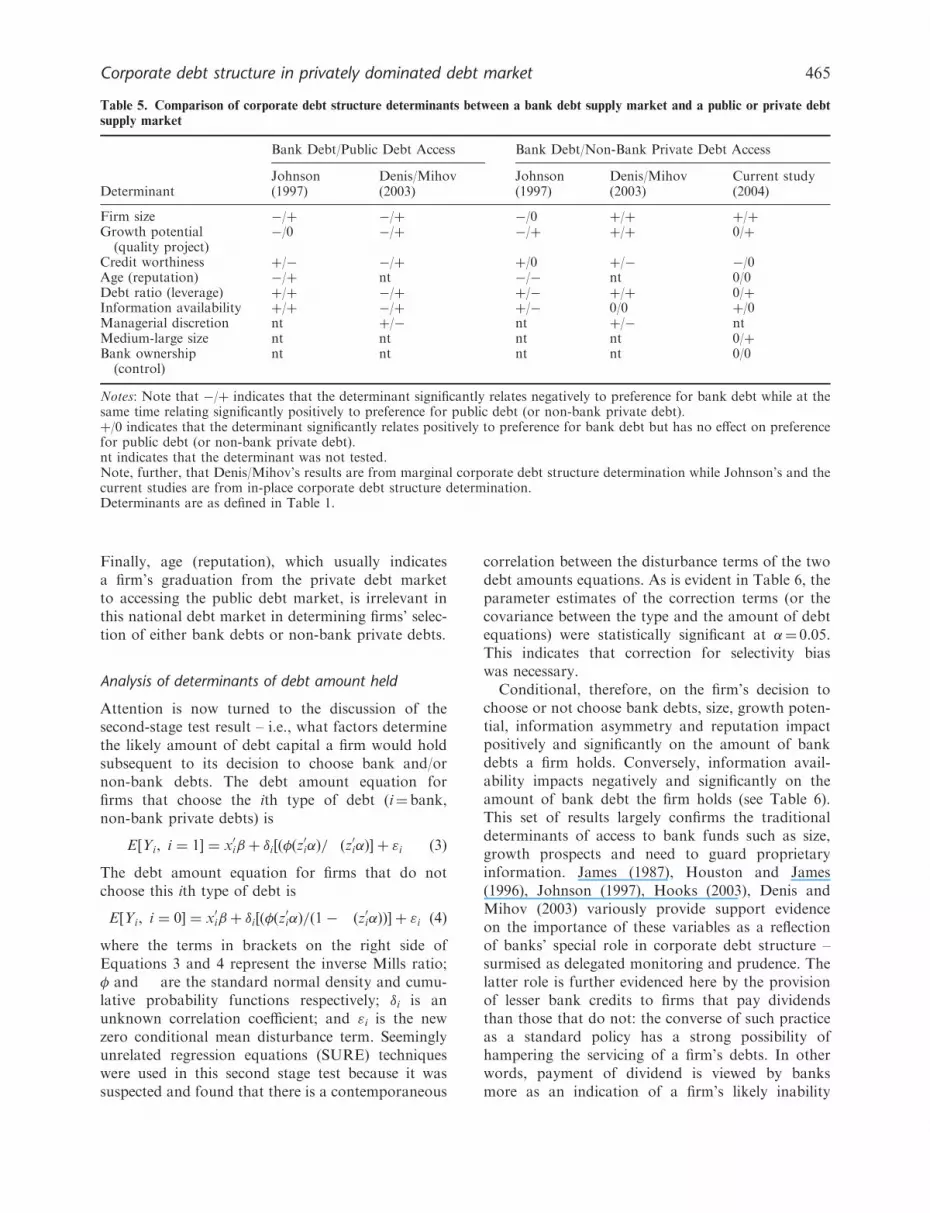

Table 5 is constructed to more clearly highlight theresults of the tests’ relative predictions in light of theliterature (Table 1) as well as contrast the result withthose of the two empirical studies that specificallyexamined determinants of firms’ mix of bank andnon-bank private debts (Johnson, 1997; Denis and

Mihov, 2003). This table is particularly instructivesince the reference studies are based on a debt marketcharacterized by the existence of both public debt andprivate (bank and non-bank) debts suppliers, unlikethe market examined here, which has no public debtand is representative of many national debt marketsof the world; particularly emerging markets. Beforeproceeding with the comparison, attention is drawnto an important nuance in test focus between thetwo reference studies. Denis and Mihov’s focus onmarginal debt structure determination, probablyexplains the slight difference between their resultsand Johnson’s. The comparison here should thereforebe more between the current finding and Johnson’s,who like the current authors studied in-placecorporate debt structure.

Though the roles of the corporate debt structuredeterminants are the same in both kinds of debtmarkets in some respects, it is however interestingto note that credit worthiness and leverage seem toindicate role reversals in corporate debt structuredetermination in a market with no public debt access.Unlike in a market that supplies public debt funds aswell, where credit worthiness is positively related tobank debt access, credit worthiness is negativelyrelated to preference for bank debt in this marketwhere firms lack access to public debt. Similarly,high leverage is positively related to bank debt accessin a market where firms have access to public debtfunds but it is unimportant in determining a firm’spreference for bank debt in a market with no publicdebt funds supply; instead high leverage is positivelyand significantly related to non-bank debt preference.

Table 4. Marginal probability elasticities and marginal effects (for binary variables) of determinants of companies’ preference for

bank or non-bank private debts

VariableModel of determinantsof bank debt source

Model of determinantsof non-bank debt source

Marginal probability elasticityFirm size 0.043 0.115Capital investment (quality project) 0.052 0.055Ratio of intangibles (information disadvantage) �0.194 0.189Age (reputation) 0.022 �0.097Credit worthiness (low distress potential) �1.105 �0.268Debt ratio (leverage) �0.179 0.435

Marginal effectPaid dividend (information availability) 0.0001 �0.033Medium to large firm 0.0002 0.253Bank ownership �0.0002 0.214Year 0.0001 0.022

Notes: Marginal probability elasticity is computed as MPE¼ �(�0Z)�[S/Pr(w¼ 1)], where MPE refers to marginal probabilityelasticity with respect to the Z vector, � is the standard normal density, S is the vector of sample means of the continuousexplanatory variables, and Pr(w¼ 1) represents the probability of choosing bank debt (or non-bank private debt).Marginal effect is calculated as the finite changes in discrete variables as their values change from 0 to 1, ceteris paribus.The variables are as defined in Table 1.

464 K. Ojah and J. Manrique

Finally, age (reputation), which usually indicatesa firm’s graduation from the private debt marketto accessing the public debt market, is irrelevant inthis national debt market in determining firms’ selec-tion of either bank debts or non-bank private debts.

Analysis of determinants of debt amount held

Attention is now turned to the discussion of thesecond-stage test result – i.e., what factors determinethe likely amount of debt capital a firm would holdsubsequent to its decision to choose bank and/ornon-bank debts. The debt amount equation forfirms that choose the ith type of debt (i¼ bank,non-bank private debts) is

E½Yi, i ¼ 1� ¼ x0i�þ �i½ð�ðz0i�Þ=�ðz0i�Þ� þ "i ð3Þ

The debt amount equation for firms that do notchoose this ith type of debt is

E½Yi, i ¼ 0� ¼ x0i�þ �i½ð�ðz0i�Þ=ð1��ðz0i�ÞÞ� þ "i ð4Þ

where the terms in brackets on the right side ofEquations 3 and 4 represent the inverse Mills ratio;� and � are the standard normal density and cumu-lative probability functions respectively; �i is anunknown correlation coefficient; and "i is the newzero conditional mean disturbance term. Seeminglyunrelated regression equations (SURE) techniqueswere used in this second stage test because it wassuspected and found that there is a contemporaneous

correlation between the disturbance terms of the twodebt amounts equations. As is evident in Table 6, theparameter estimates of the correction terms (or thecovariance between the type and the amount of debtequations) were statistically significant at �¼ 0.05.This indicates that correction for selectivity biaswas necessary.

Conditional, therefore, on the firm’s decision tochoose or not choose bank debts, size, growth poten-tial, information asymmetry and reputation impactpositively and significantly on the amount of bankdebts a firm holds. Conversely, information avail-ability impacts negatively and significantly on theamount of bank debt the firm holds (see Table 6).This set of results largely confirms the traditionaldeterminants of access to bank funds such as size,growth prospects and need to guard proprietaryinformation. James (1987), Houston and James(1996), Johnson (1997), Hooks (2003), Denis andMihov (2003) variously provide support evidenceon the importance of these variables as a reflectionof banks’ special role in corporate debt structure –surmised as delegated monitoring and prudence. Thelatter role is further evidenced here by the provisionof lesser bank credits to firms that pay dividendsthan those that do not: the converse of such practiceas a standard policy has a strong possibility ofhampering the servicing of a firm’s debts. In otherwords, payment of dividend is viewed by banksmore as an indication of a firm’s likely inability

Table 5. Comparison of corporate debt structure determinants between a bank debt supply market and a public or private debt

supply market

Bank Debt/Public Debt Access Bank Debt/Non-Bank Private Debt Access

Johnson Denis/Mihov Johnson Denis/Mihov Current studyDeterminant (1997) (2003) (1997) (2003) (2004)

Firm size �/þ �/þ �/0 þ/þ þ/þGrowth potential

(quality project)�/0 �/þ �/þ þ/þ 0/þ

Credit worthiness þ/� �/þ þ/0 þ/� �/0Age (reputation) �/þ nt �/� nt 0/0Debt ratio (leverage) þ/þ �/þ þ/� þ/þ 0/þInformation availability þ/þ �/þ þ/� 0/0 þ/0Managerial discretion nt þ/� nt þ/� ntMedium-large size nt nt nt nt 0/þBank ownership

(control)nt nt nt nt 0/0

Notes: Note that �/þ indicates that the determinant significantly relates negatively to preference for bank debt while at thesame time relating significantly positively to preference for public debt (or non-bank private debt).þ/0 indicates that the determinant significantly relates positively to preference for bank debt but has no effect on preferencefor public debt (or non-bank private debt).nt indicates that the determinant was not tested.Note, further, that Denis/Mihov’s results are from marginal corporate debt structure determination while Johnson’s and thecurrent studies are from in-place corporate debt structure determination.Determinants are as defined in Table 1.

Corporate debt structure in privately dominated debt market 465

to service its debt than an indication of a firm’sproclivity to share material information. Thepositive association of reputation to quantity ofbank debts seems more likely to reflect relationshipbanking than a prerequisite for access to bank credits.Banks’ specialization in information gatheringand post-loan monitoring rationally minimizes theimportance of reputation/credit history as a prerequi-site for granting loans.

Turning now to determinants of amounts of non-bank private debts firms hold, conditional upon thedecision to choose or not choose non-bank privatedebt, the amount of this debt that a firm holds ispositively affected by size but negatively affected bygrowth potential and reputation. Similarly, medium-to-large firms hold lesser amounts of non-bankprivate debts than do small firms. This set of resultsappear to corroborate a recent US study by Denisand Mihov (2003), which documents that non-bankprivate debt providers play an important role ofproviding debt funds to small and risky firms. Theseeming contradiction of having size relate positively

to amounts of non-bank private debts while medium-to-large size relates negatively to same, may beexplained by the denomination of non-bank privatedebts, which is usually small. Therefore, though sizegenerally enhances a firm’s ability to access most debtsources including non-bank private debt sources,non-bank debt providers lack of capacity to puttogether the usually substantial bloc of debt fundsneeded by large firms inadvertently screens themout. This, therefore, leaves small firms as most likelytakers of non-bank private debts.

V. Conclusions

Corporate debt structure in a financial market bereftof public debt supply is examined by analysingthe representative debt market of Spain. The suspi-cion is that the roles of determinants of corporatedebt structure in an environment where firms haveaccess to full complements of public and privatedebts may differ from those in an environment

Table 6. Parameter estimates of the amount of debt held by firms from seemingly unrelated regression

equation (SURE) models

Model of determinants Model of determinants ofVariable of amount of bank debt amount of non-bank debt

Constant 2333 2066(9.56)** (10.46)**

Firm size 0.024 0.081(3.80)** (15.23)**

Capital investment 1.28 �1.69(quality project) (3.22)** (�5.54)**

Ratio of intangibles 240.5 �49.22(information disadvantage) (2.04)** (�0.55)

Paid dividend �113.8 15.17(information availability) (�1.78)* (0.32)

Age (reputation) 3.49 �2.62(2.02)** (�2.00)**

Medium to large firm 81.33 �81.39(1.33) (�1.78)*

Credit worthiness �17.89 �6.19(low distress potential) (�0.91) (�0.41)

Debt ratio (leverage) 16.14 13.39(0.15) (0.16)

Bank ownership �49.19 �128.3(�0.25) (0.87)

Year-dummy �11.20 �5.07(�0.23) (�0.14)

Inverse Mills ratio �3071.0 �2515.4(�12.14)** (�11.8)**

Adjusted R2 0.37 0.62F[11,357] 20.65 56.25

Notes: The dependent variables are amount of bank debt or amount of non-bank private debtwhereas independent variables are as defined in Table 1.** and * indicate statistical significance at 5% or better and 10% levels, respectively.Asymptotic t-values are in parentheses.

466 K. Ojah and J. Manrique

where firms’ access is restricted to only private

(bank and non-bank) debts.

Using a double-hurdle empirical test approach, it is

documented that the likelihood of using bank debt is

positively related to firm size and information avail-

ability but negatively related to firm creditworthiness,

while the likelihood of using non-bank private debt is

positively related to firm size, growth potential (qual-

ity projects), relative firm size and degree of leverage.

Further, it is found that the amount of bank debt

firms hold is positively related to firm size, growth

potential, information asymmetry and age, but nega-

tively related to information availability. The amount

of non-bank private debt is positively related to firm

size and negatively related to growth potential in

terms of capital expenditures, and age. These differ-

ences on determinants of amounts of debt types held

and determinants of preference for mix of debt types

suggest a need for bank and non-bank private debt

providers to up-grade their product lines as to better

meet unfilled needs of corporate customers in the

absence of public debt providers. For instance, large

firms with the requisite wherewithal for accessing

non-bank debt funds show a preference for exactly

that but they actually fill their debt funds need from

banks. Perhaps developing a consortium arrange-

ment can permit non-bank private debt suppliers to

provide large denomination loans that large firms

typically seek.

On the major question of whether debt structure

determinants here differ from those in debt markets

characterized by both private and public debt sup-

plies, it is found that their roles are the same in

both kinds of debt markets in some respects.

Interestingly, however, credit worthiness and leverage

appear to indicate role reversals in corporate debt

structure determination in a market that supplies no

public debt. Unlike in a market that supplies public

debt as well, where credit worthiness is positively

related to bank debt access, credit worthiness is

negatively related to preference for bank debt in the

market where firms lack access to public debt supply.

Similarly, high leverage is usually positively related to

preference for bank debt in a market with public debt

supply but it is unimportant in determining a firm’s

preference for bank debt in a market with no public

debt supply. Instead high leverage is positively related

to preference for non-bank debt, thus suggesting

avoidance of further hold-up costs of bank borrow-

ing. In the same vein, possession of quality projects

which usually enhances access to public debts, rather

enhances preference for non-bank private debts in

this market. In sum, therefore, the evidence here

points to a possible roles substitution between public

debt suppliers and non-bank private debt suppliers

in a national debt market bereft of public debt.

Moreover, it is found that different sets of factors

determine the amount of bank versus non-bank

private debts that a firm holds. Particularly where a

factor affects both amounts of the two types of debt,

the factor has opposite effects on amounts of the two

debt types. This indicates that the two types of debts

are distinct and fill different funding needs for firms.

Importantly, size, growth potential and reputation of

a firm are found to be the most influential determi-

nants of the amount of non-bank private debts

the firm holds. Conversely, size, growth potential,

information asymmetry and reputation are the most

influential determinants of the amount of bank debts

a firm holds; with these factors relating to the amount

of bank debts in ways that underline banks’

traditional rolesofdelegatedmonitoringandprudence.

Interestingly on the trend of debt structure in

Spain, it is found that the majority of firms’ debt is

of a short-term nature (only 16% is long-term); which

is not surprising given the absence of domestic public

debt market. Firms in this sample hold an average

57% of their total capital funds in debt forms,

which is in line with most modern firms around the

world filling the majority of their external capital

funds through debt sources.

Finally, two interesting questions thrown up by

this study are noted. To what extent does the finding

documented here represent corporate debt structure

in similarly privately-dominated national debt mar-

kets, particularly those of emerging capital markets?

Granted the benefit of a more detailed data informa-

tion, could a firm’s access to multiple banks’ credit

supply alter the documented non-bank private debt

suppliers’ role substitution for public debt suppliers’

in a similarly privately-dominated debt market?

References

Anderson, C. W. and Makhija, A. K. (1999) Deregulation,disintermediation, and agency costs of debt: evidencefrom Japan, Journal of Financial Economics, 51,309–39.

Barclay, M. J. and Smith, C. W. (1995) The maturitystructure of corporate debt, Journal of Finance, 50,609–31.

Berlin, M. and Loeys, J. (1988) Bond covenants anddelegated monitoring, Journal of Finance, 43, 397–412.

Berlin, M. and Mester, L. (1992) Debt covenants andrenegotiation, Journal of Financial Intermediation,2, 95–133.

Blackwell, D. W. and Kidwell, D. S. (1988) An investiga-tion of cost differences between public sales and privateplacements of debt, Journal of Financial Economics,22, 253–78.

Corporate debt structure in privately dominated debt market 467

Brick, I. E. and Ravid, S. A. (1985) On the relevanceof debt maturity structure, Journal of Finance, 40,1423–37.

Cai, J., Cheung, J. and Goyal, V. K. (1999) Bank monitor-ing and the maturity structure of Japanese corporatedebt issues, Pacific-Basin Finance Journal, 7, 229–50.

Chemmanur, T. and Fulghieri, P. (1994) Reputation,renegotiation, and the choice between bank loansand publicly traded debt, Review of Financial Studies,7, 475–506.

Denis, D. J. and Mihov, V. T. (2003) The choice amongbank debt, nonbank private debt, and public debt:evidence from new corporate borrowings, Journalof Financial Economics, 70, 2–23.

Detragiache, E. (1994) Public versus private borrowing:a theory with implications for bankruptcy reform,Journal of Financial Intermediation, 3, 327–54.

Diamond, D. W. (1984) Financial intermediation anddelegated monitoring, Review of Economic Studies,51, 393–414.

Diamond, D. W. (1991a) Monitoring and reputation: thechoice between banks loans and directly placed debt,Journal of Political Economy, 99, 689–721.

Diamond, D. W. (1991b) Debt maturity structure andliquidity risk, Quarterly Journal of Economics, 106,709–37.

Diamond, D. W. (1993) Seniority and the maturity ofdebt contracts, Journal of Financial Economics, 33,341–68.

Easterwood, J. and Kadapakkam, P. R. (1991) The roleof private and public debt in capital structures,Financial Management, 20, 49–57.

Fama, E. (1985) What’s different about banks?, Journalof Monetary Economics, 15, 29–39.

Flannery, M. J. (1986) Asymmetric information andrisky debt maturity choice, Journal of Finance, 41,19–37.

Hooks, L. (2003) The impact of firm size on bank debt use,Review of Financial Economics, 12, 173–89.

Hoshi, T., Kashyap, A. and Scharfstein, D. (1993) Thechoice between public and private debt: an analysisof post-deregulation corporate financing in Japan,Working Paper, MIT.

Houston, J. and James, C. (1996) Bank informationmonopolies and the mix of private and public debtclaims, Journal of Finance, 51, 1867–89.

Houston, J. and Venkataraman, S. (1994) Optimal maturitystructure with multiple debts claims, Journal ofFinancial and Quantitative Analysis, 29, 179–97.

James, C. (1987) Some evidence on the uniqueness of bankloans, Journal of Financial Economics, 19, 217–35.

Jensen, M. C. and Meckling, W. H. (1976) Theory of thefirm: managerial behavior, agency cost and ownershipstructure, Journal of Financial Economics, 3, 305–60.

Johnson, S. A. (1997) An empirical analysis of the determi-nants of corporate debt ownership structure, Journal ofFinancial and Quantitative Analysis, 32, 47–69.

Lee, L. F. (1978) Simultaneous equations models withdiscrete and censored dependent variables, in Struc-tural Analysis of Discrete Data with EconometricApplications (Eds) P. Manski and D. McFadden,MIT Press, Cambridge, MA, pp. 197–272.

Meerschwarm, D. M. (1991) Breaking Financial Boundaries:Global Capital, National Deregulation, and FinancialServices Firms, Harvard Business School Press,Harvard.

Myers, S. C. (1977) Determinants of corporate borrowing,Journal of Financial Economics, 5, 147–75.

Nakamura, L. (1993) Commercial bank information:implications for the structure of banking, in StructuralChanges in Banking (Eds) M. Klausner and L. White,Business One/Irwi, Homewood, IL.

Petersen, M. and Rajan, R. (1994) The benefits of lendingrelationships: evidence from small business data,Journal of Finance, 49, 3–37.

Rajan, R. (1992) Insiders and outsiders: the choice betweeninformed and arm’s length debt, Journal of Finance,47, 1367–400.

Saa-Requejo, J. (1996) Financing decisions: lessons from theSpanish experience, Financial Management, 25, 44–56.

Smith, C. W. and Warner, J. B. (1979) On financialcontracting: an analysis of bond covenants, Journalof Financial Economics, 7, 117–61.

Yosha, O. (1995) Information disclosure costs and thechoice of financing source, Journal of FinancialIntermediation, 4, 3–20.

468 K. Ojah and J. Manrique