Embed Size (px)

Citation preview

Bargaining, Mergers, and Technology Choice inBilaterally Oligopolistic Industries¤

Roman Indersty

University College LondonChristian Weyz

WZB, CEPR

March 2001

¤The paper was much improved by comments of two anonymous referees and the associate editor.We also thank Helmut Bester, Mathias Dewatripont, Paul Heidhues, Lars-Hendrik Röller and seminarparticipants at the University of Cologne, Humboldt University Berlin, Wissenschaftszentrum Berlin,University College London, Free University Berlin, Nu¢eld College, and ECARES for their comments.An earlier version of this paper was circulated under the title “Market Structure, Bargaining, and Tech-nology Choice” (…rst version June 1999). Financial support from the Deutsche Forschungsgemeinschaft(Ro 2080/1-2) and from the CEPR research network on The Evolution of Market Structure in NetworkIndustries is gratefully acknowledged.

yUniversity College London, Department of Economics, Gower Street, London WC1E 6BT, UK.E-mail: [email protected].

zWissenschaftszentrum Berlin (WZB), Reichpietschufer 50, D-10785 Berlin, Germany. E-mail:[email protected].

1

Abstract

This paper provides a conceptual framework of multilateral bargaining in abilaterally oligopolistic industry to analyze the motivations for horizontal mergers,technology choice, and their welfare implications.

Analyzing the implication of market structure for the distribution of industrypro…ts, we …nd that retailer mergers are more likely (less likely) if suppliers haveincreasing (decreasing) unit costs, while supplier mergers are more likely (lesslikely) if goods are substitutes (complements). In a second step we explore howmarket structure a¤ects suppliers’ technology choice, which re‡ects a trade-o¤between inframarginal and marginal production costs. We …nd that suppliers focusmore on marginal cost reduction if (i) retailers are integrated and (ii) suppliersare non-integrated.

In a …nal step we consider the whole picture where both market structure and(subsequent) technology choice are endogenous. Analyzing the equilibrium marketstructure, we …nd cases where retailers become integrated to induce suppliers tochoose a more e¢cient technology, even though integration weakens their bargain-ing position. In this case the merger bene…ts all parties, i.e., suppliers, retailers,and even consumers. However, we also show that the equilibrium market structuredoes often not maximize welfare.

2

1 Introduction

Supply contracts in markets for intermediate goods are often negotiated. An importantexample are contracts between producers and retailers. Moreover, it is rather excep-tional that either the upstream market (producers) or the downstream market (retail-ers) is fully integrated. Instead, a given producer typically supplies many independentretailers, while a given retailer sells products of many di¤erent suppliers. Despite itsprevalence, bilaterally oligopolistic markets with negotiated supply contracts have beenlargely ignored in the literature.1

This paper develops a model of multilateral bargaining in a bilaterally oligopolisticsetting. In equilibrium each retailer sells all brands, while each producer supplies toall retailers. We subsequently use this model to study two related questions. First,we investigate the incentives for horizontal mergers. Second, we analyze how marketstructure a¤ects technology choice by suppliers.

Precisely, our set-up is as follows. For the main part we assume that demand at bothretailers is independent. This allows us to abstract from monopolization e¤ects on the…nal market when investigating the incentives for horizontal mergers. Our bargainingconcept contains two major ingredients. First, we assume that bargaining is e¢cientas the two sides can write non-linear supply contracts. This seems reasonable for thecase where retailers procure their supply via bilateral negotiations and not via a marketinterface. Second, we assume that bargaining between all parties proceeds simultane-ously, which deprives any party of a …rst-mover advantage. Applying this framework, weproceed in three steps. We …rst analyze equilibrium market structure if this only a¤ectsthe distribution of industry pro…ts. In a second step we introduce (non-contractible)technology choice by suppliers and investigate how this is a¤ected by market structure.Finally, we complete the picture and analyze the case where both market structure andtechnology choices are endogenous.

Focusing on the impact of market structure on the distribution of rents, we deriveexact conditions when suppliers or retailers prefer to become integrated. One implica-tion will be that retailers prefer to merge if the production technologies exhibit strictlyincreasing unit costs. If suppliers have strictly decreasing unit costs, retailers prefer tostay non-integrated. By a¤ecting the distribution of industry pro…ts, market structure

1The standard way to model imperfectly competitive input markets is to consider a two-stage marketgame in which upstream …rms compete as Stackelberg leaders via wholesale prices (see, e.g., Waterson(1980), Salinger (1986), and Kühn and Vives (1999)). In a similar fashion, the literature on verticalagreements typically assumes that suppliers, that are few in numbers, have su¢cient market power toimpose contractual obligations on powerless retailers (see, e.g., recent work by Rasmusen et al. (1991)and Bernheim and Whinston (1998)).

3

also provides incentives for suppliers to choose a particular technology. More speci…-cally, market structure a¤ects the trade-o¤ between inframarginal cost savings and costsavings “on the margin”. By studying the case of linear demand and cost functions, wecan make this trade-o¤ fully explicit. We …nd that the incentives to adopt a technologywith higher marginal costs are reduced if either suppliers become non-integrated or ifretailers become integrated. In contrast to the previous case where market structureonly a¤ected the distribution of industry pro…ts, the size of industry pro…ts and welfaredepends now on the market structure. This may even drive a wedge between retailers’preferred downstream market structure for the cases with and without technology choiceby suppliers. We …nd that retailers may now choose more often to become integratedas this induces suppliers to choose a more e¢cient production technology. Incidentally,implementing the e¢cient technology also bene…ts consumers, implying that in this caseincreased downstream concentration should not be contested by any party. However,we also …nd that a regulator who takes consumer rents into consideration would oftenprefer a di¤erent market structure than that arising endogenously.

Before reviewing some of the related literature, we want to illustrate for the caseof retailer mergers why the issues discussed in this paper are of more than just aca-demic interest. Since the emergence of large retail chains in the 1970s, buying power hasbecome a key feature in the relationship between manufacturers and retailers.2 Whileeconomic analysis has traditionally viewed retailers as lacking in market power on whole-sale markets, recent consolidation in the retailing sector has created market structurescharacterized by bilateral oligopolies, where each retailer accounts for a relatively largeshare of each supplier’s sales and retailers enjoy considerable market power at theiroutlets.3

Buyer power has also become an important issue in competition policy.4 However,2For example, Dell (1996, p. 50) reports that in the United Kingdom and France, the number of

outlets per capita has fallen to one-…fth the level of thirty years ago, and 2 per cent of stores nowaccount for over half of all grocery sales. Similar trends can be observed in other European countries,and to a lesser extent in the U.S. For an overview of recent concentration changes in the retailing sectorsee also Dobson and Waterson (1999) and OECD (1999).

3In fact, market power in the local outlet market, caused by consumers’ preferences for one-stop-shopping and an increasing segmentation of retail formats, has been identi…ed as a critical source ofbuyer power (see OECD (1999)). A good example of such buyer power can be found in the recent UnitedStates Toys “R” Us case, where it was ascertained that it would be very di¢cult for manufacturers toreplace the 30 percent of their sales accounted for by Toys “R” Us (see FTC (1996, 1997) for a review ofthis case). Moreover, in its recent decision in the Tesko/Tuko case, which has been found incompatiblewith the Common Market, the European Commission explicitly referred to the “gatekeeper” role ofthe retail chains which would strengthen the undertaking’s dominant position vis-à-vis suppliers (seeCommission Decision IV/M.784, Nov. 20, 1996).

4The growing concern about buying power in the legal debate is documented in Ehlermann and

4

there is still much controversy about which types of anticompetitive e¤ects may arisefrom horizontal integration in markets where both suppliers and retailers have marketpower and where monopolization e¤ects of mergers on …nal consumer markets are neg-ligible. In particular, this applies to the increasing number of cross-country mergers,take-overs, or alliances between retail chains, which do not a¤ect local downstream mar-ket structure.5 Besides providing a conceptual framework to study bilateral oligopoliesand determining the interaction between bargaining power and market structure, a maincontribution of this paper is to highlight the role of retailer integration for the technologychoice of suppliers. Hence, in our case both the motivation and the welfare implicationof mergers rely on the induced technology choice made by other parties in the valuechain. This also contrasts with more standard merger analysis which has predominantlyanalyzed the cases where …rms merge to either monopolize the …nal good market6 or torealize synergies.7

Negotiated input prices have been previously studied in Horn and Wolinsky (1988a),von Ungern-Sternberg (1996), and Dobson and Waterson (1997). The di¤erences be-tween these papers and our contribution are manyfold. Most importantly, they do notcover the bilaterally oligopolistic case.8 Furthermore, all of these papers consider non-e¢cient bargaining where contracts can only specify a constant unit price. Indeed, the

Laudati (1997), Dobson et al. (1998), Vogel (1998), OECD (1999), Dobson and Waterson (1999). Inthe United States buyer power also enters merger control as an e¢ciency defence via the 1992 HorizontalMerger Guidelines, with the revisions to Section 4 on e¢ciencies in April 8, 1997. The buyer-powerdefence asserts that a merger should not raise competitive concerns when the other market side consitsof large …rms. (For its use in merger cases in the United States see Steptoe (1993).) In the case FTC v.Staples, Inc. the most important e¢ciency claim was that Staples and Depot O¢ce could extract betterprices from its various vendors (see Pitofsky (1998)). The issue of buyer power was also considered inthe EU merger Enso/Stora (Case No IV/M.1225). The merger reduced the number of suppliers ofliquid packaging board to three. As the market was also heavily concentrated on the demand side, theCommission concluded that these circumstances produced a situation of mutual dependence betweenbuyers and sellers, which the merger was unlikely to disturb (see also European Commission (1998)).

5Examples for cross-country activities are the take-over of SHG Makro (Netherland) by Metro AG(Germany) in 1997 or the take-over of BML (Austria) by REWE (Germany) a year earlier. That thisprocess is not con…ned to a pan-European level is documented by Wal-Mart’s acquisition of Wertkauf(Germany).

6For a formal analysis see Salant, Switzer, and Reynolds (1983) for the case of quantity competitionand Deneckere and Davidson (1985) for the case of price competition.

7Since Williamson’s (1968) seminal contribution, the trade-o¤ between monopolization and e¢ciencyhas been studied quite extensively (see, e.g., Perry and Porter (1985) and Farrell and Shapiro (1990)).

8In particular, only Horn and Wolinsky (1988a) consider the case where there may be more than onesupplier. However, they assume that each retailer is locked-in with a particular supplier. The case oflocked-in retailers is also studied in Inderst and Wey (2000a), where the major bene…t of a downstreammerger is to break this lock-in.

5

derived bene…ts from a horizontal (downstream) merger rely on the combination of thiscontractual incompleteness with the assumption that retailers’ demand is interdepen-dent.9 Note …nally that with interdependent demand horizontal mergers have the mainbene…t of monopolizing the …nal product market, which blurs the analysis of a merger’simpact on bargaining power. In addition, none of these papers has addressed the linkbetween input market structure and suppliers’ technology choice.

Our analysis of the interaction between market structure and technology choice isrelated to three di¤erent strands of the literature which analyze incentives for cost re-duction and innovation. (As is explored in more detail below, our results for the choicebetween two technologies can be restated to measure incentives for investing in variousforms of cost reduction.) The …rst strand analyses how …rms’ incentives to reduce theircosts vary with the form of competition (e.g., Bertrand or Cournot), their market share,or the presence of spill-overs (see Bester and Petrakis (1993) and Qiu (1997), Flaherty(1980), and Spence (1984), respectively). The second strand, which is more closely re-lated to our contribution, considers investment incentives under the problem of hold-up.In light of this literature one of our contributions is to combine in one application threeimportant issues. We investigate how incentives to invest in cost reduction are deter-mined by i) the nature of costs, ii) the degree of competition, and iii) the prevailingup- and downstream market structure.10 Finally, our result on how market structurea¤ects technology choice …ts well into the perspective of “innovative markets”, whichrequires to evaluate mergers according to their impact on innovative activities. Thoughthis question has a long history11, it has recently gained much importance in antitrustpolicy. 12 While typically this approach only considers concentration and investment atthe same market “level”, this paper suggests a broader view. Downstream mergers may

9For instance, in Dobson and Waterson (1997) a monopolistic supplier who grants a discount to oneparticular retailer su¤ers from a decrease in his supply to other retailers, who buy at higher unit prices.This negative externality allows the supplier to extract more rents from non-integrated retailers.

10The role of competition has been mostly studied with unit-demand (see Felli and Roberts (2000) fora recent overview). A notable exception is McLaren (2000) who studies the role of vertical integrationon incentives. The role of “bargaining coalitions” in the form of vertical integration is studied in Boltonand Whinston (1993). The basic insights in this case are already obtained in the seminal paper of Hartand Moore (1990).

11See Gilbert and Sunshine (1995) for an overview.12In the U.S. the earliest directive that relevant antitrust markets be de…ned around research and

development activities can be found in the National Cooperative Research Act of 1984. The currentinnovative market approach under Section 7 of the Clayton Act and Section 5 of the Federal TradeCommission Act was …rst applied in 1993, when the DOJ opposed the merger of the Allison TransmissionDivision of General Motors and ZF Friedrichshafen. Since the release of the 1995 Intellectual PropertyGuidelines the FTC has leveled complaints against several additional mergers on the grounds thatinnovation markets would be harmed.

6

a¤ect investment and technology choice at upstream …rms.The paper is organized as follows. Section 2 introduces the economy. In Section

3 we propose and motivate the bargaining concept. Section 4 determines equilibriummarket structure if this has only an impact on the distribution of industry pro…ts. InSection 5 we introduce technology choice by suppliers. Section 6 analyzes the equilibriummarket structure under technology choice. In Section 7 we discuss modi…cations to someassumptions. Section 8 concludes with possible extensions.

2 The Economy

We consider an intermediary goods market in whichN = 2 producers, which are denotedby s 2 S0 = fA;Bg, sell their products to M = 2 retailers, which are denoted byr 2 R0 = fa; bg.13 We assume that each supplier commands over the production ofone di¤erentiated good, where the aggregate cost function is denoted by Ks(¢). Eachretailer owns a single outlet. Demand at di¤erent outlets is independent. Note that thisassumption applies particularly to those cases where retailers are located in di¤erentregions or even countries. This assumption rules out standard monopolization e¤ects ofmergers and allows us to isolate the impact of market structure on bargaining power.We denote the indirect demand function for good s at retailer r by psr(xsr; xs0r), withr 2 R0, where s0 6= s denotes the alternative supplier. A distinguishing feature of supplycontracts in intermediary goods markets, as opposed to …nal goods markets, is thatthey are often negotiated. Consistent with this, supply contracts will be the result ofbargaining. We denote the quantity of good s 2 S0 supplied to retailer r 2 R0 by xsr.

So far we have treated each supplier and each retailer separately. In the following,we distinguish between four market structures, where suppliers or retailers can be inte-grated. We denote a market structure by ! = (n;m), where n stands for the numberof independent suppliers and m stands for the number of independent retailers, withn;m 2 f1; 2g. As demand at the two outlets is independent, mergers will have noimpact on supplied quantities. However, market structure will determine the parties’bargaining power and, thereby, the distribution of rents.

13In Section 6 we argue that most of our results carry over to the case with an arbitrary number ofretailers and producers.

7

3 Bargaining Concept

3.1 Speci…cation of the Bargaining Concept

Negotiations are conducted between all independent suppliers and retailers. We employthe same bargaining concept for all market structures. In Section 3.2 we describe aparticular bargaining procedure, which seems rather natural to us. In particular, it ischaracterized by simultaneous and e¢cient contracting. As discussed in detail below,this procedure gives rise to the Shapley value. For this reason we choose to start out withthe Shapley value as our solution concept to multilateral bargaining, while postponingthe description of the underlying procedure.

We denote total industry pro…ts for given supplies by

W¡fxsrgsr2S0£R0

¢=

X

r2R0[pAr(xAr; xBr)xAr + pBr(xBr; xAr)xBr] ¡

X

s2S0Ks(xsa + xsb):

Denoting the set of all …rms by = fA;B; a; bg, we de…ne W as the maximumindustry pro…ts. Suppose now that supplier s = A leaves the market, which gives usthe subset n fAg. Calculating the maximum industry pro…ts subject to the constraintthat xAa = xAb = 0, we denoted the respective value by WnfAg. We can proceed likethis for any subset ~ µ and derive the resulting maximum pro…ts W~. Of course, itholds that WnfA;Bg = Wnfa;bg = 0. For the calculation of e¢cient supplies under thevarious scenarios, we impose the following assumption, which helps us below to identifyour bargaining procedure with the Shapley value.

Assumption A.1. W (¢) is strictly quasi-concave. It is also continuous on R+ andequal to zero if all supplies are set to zero.14

To calculate the Shapley value, we have to specify a particular market structure toidentify the set of independently negotiating parties, which is denoted by ª. For instance,for ! = (2; 1), we obtain ª = fA;B; (a; b)g, where (a; b) denotes the integrated retailer.According to the Shapley value, the payo¤ of a member à 2 ª is given by15

X

Ã2~ª; ~ª2ª

(¯̄¯~ª

¯̄¯ ¡ 1)!(jªj ¡

¯̄¯~ª

¯̄¯)!

jªj!hW~ª ¡W~ªnfÃg

i(1)

14One important implication of this assumption is that goods are not perfect substitutes.15

¯̄¯~ª

¯̄¯ and jªj denote the numbers of elements in these sets. Observe also that W¢ represents the

characteristic function.

8

and thus re‡ects the incremental contribution of à to various coalitions. While thissolution concept can be justi…ed on axiomatic grounds, we argue next that it is also theoutcome of a rather natural description of simultaneous bargaining in an oligopolisticindustry.

3.2 Bargaining Procedure

Our proposed bargaining procedure contains the following ingredients:

i) Simultaneous bilateral bargaining: We assume simultaneous bilateral negotiationsbetween the representatives of each independent retailer and supplier. For instance,under ! = (1; 2) the integrated supplier employs two sales representatives (agents). Oneof his agents negotiates with retailer a, while the other agent visits retailer b.

ii) E¢cient bargaining and (net) surplus sharing: In all bilateral negotiations therespective agents choose the respective supplies so as to maximize the joint surplus ofthe two parties. When determining supplies, the two parties form rational expectationsabout the outcomes of all other simultaneous negotiations. Moreover, transfers betweenthe two parties are speci…ed so as to split the net surplus equally.

iii) Contingent contracts: In each negotiation the two sides conclude contracts forall possible contingencies, where a contingency describes the set of successful bilateralnegotiations in the industry. For instance, under ! = (1; 2) the agents of the integratedsupplier and retailer a negotiate over two contracts, specifying transfers and supplies forthe cases where simultaneous negotiations with retailer b are successfully concluded ornot. For each of these agreements the requirements of ii), i.e., e¢cient bargaining andsharing of net surplus, apply.

The requirements i)-iii) can be easily formalized. They give rise to an iterativeprocedure, starting from the simplest contingencies where all other negotiations breakdown up to the contingency where all negotiations are successful. We discuss in Section7 how changes in these requirements would a¤ect our results.

We analyze now when this procedure has a unique equilibrium outcome which isidentical to that arising from the Shapley value. Observe that this requires both thatequilibrium supplies are chosen e¢ciently (to maximize industry pro…ts) and that rentsare distributed according to (1). As is easily seen, (A.1) is not su¢cient to ensure thatequilibrium supplies are uniquely determined. For instance, this may be the case if goodsare complements and if a higher supply of good A at r = a makes it also e¢cient tosupply more of good B at this retailer. Decreasing unit costs provide another example.One way to rule out this multiplicity, which is due to the assumption of simultaneity

9

and the resulting problem of co-ordination failure between di¤erent agents, would be toimpose some re…nement, e.g., in the form of coalition-proofness.16 An alternative routeis to invoke additional assumptions on the demand and cost function which ensure thatthis problem does not arise.

The following conditions are su¢cient to establish uniqueness of equilibrium suppliesunder the proposed bargaining procedure. Suppose that only a subset of the four possiblesupplier-retailer “links” sr is active, i.e., that only these supplies can be positive. Ifwe choose the respective supplies xsr to maximize industry pro…ts, we require that allsupplies must be positive. Moreover, if we now consider an additional supplier-retailerlink ~s~r with supplies x~s~r, then maximizing industry pro…ts while keeping the originalsupplies …xed shall imply x~s~r > 0. (Of course, the latter condition is only applicableif we start from a strict subset of all possible supplies.) These requirements are nowre-stated more formally in the following assumption.

Assumption A.2. Exclusion of corner solutions:i) Consider a set of supplier-retailer links L.17 Maximizing W (¢), where xsr = 0 for

all (sr) =2 L, must imply xsr > 0 for all (sr) 2 L. Denote the optimal choices by xsr(L),which is unique by (A.1).

ii) Consider some L and (~s~r) =2 L. Then maximizing W (¢), where xsr = xsr(L) for(sr) 2 L and xsr = 0 for (sr) =2 L [ f(~s~r)g, must imply x~s~r > 0.

Given Assumptions (A.1) and (A.2) it is now easily checked that equilibrium sup-plies are uniquely determined and strictly positive for all bilateral negotiations and allcontingencies. Moreover, all equilibrium supplies are strictly positive.

Given the determination of supplies, we turn next to the question of how pro…tsare distributed. Consider the case with bilateral non-integration. Denote the payo¤of supplier A for the contingency that all negotiations are successful by UA and thatof retailer a by Ua. If bargaining between these two parties breaks down, denote therespective payo¤s under the new contingency by ~UA and ~Ua. Recall now that playerssplit the net surplus in each bilateral negotiation. Clearly, this implies that

UA ¡ Ua = ~UA ¡ ~Ua: (2)

Condition (2) is called “balancedness”, which under our requirements must hold for allbilateral negotiations and all contingencies. As shown by Myerson (1977) and Jacksonand Wolinsky (1996), this condition indeed implies that equilibrium payo¤s are deter-

16This has been used in a slighlty related setting by Bernheim and Whinston (1986).17Formally, L is an element of the power set of S0 £ R0.

10

mined by the Shapley value.18;19 This implication extends clearly to the cases where oneor both sides of the market are integrated.

Admittedly, our speci…cation of the bargaining procedure falls short of the full de-scription of a game. To …ll this gap, consider any bilateral negotiation. We specify thatthe supplier’s agent is chosen to make an o¤er. If the retailer’s agent rejects, then thereis another and last round of bargaining where either side is chosen with equal proba-bility to make a …nal o¤er. Additionally, we assume that with some (arbitrarily) smallprobability " the two sides fail to start negotiations due to some exogenous event. It iseasily checked that an equilibrium of this game supports the equilibrium outcome of ourbargaining procedure.20 ;21

4 Horizontal Integration

4.1 Equilibrium Payo¤s

We now calculate equilibrium payo¤s under the di¤erent market structures. Whilethe calculation of payo¤s is immediate from the Shapley value, we want to use thisopportunity to illustrate the bargaining procedure proposed in Section 3.2. For thispurpose we consider the case ! = (1; 2); where only suppliers are integrated.

18In our speci…c application, where the value (i.e., the maximum of industry pro…ts) is calculated forcertain sub-sets of “links” (or graphs), it is also known as the Myerson value. Originally, these linkswere only considered as “communication” channels, implying that the severance of a particular link didonly a¤ect a player’s position in the graph, but not total surplus. As in Jackson and Wolinsky (1996),a supply-link adds value in our setting.

19Balancedness is also used in Stole and Zwiebel (1996a/b) when showing that their bargainingprocedure obtains the Shapley value.

20The issue of uniqueness is more contrived for two reasons. First, without additional frictions beforethe second round, players are indi¤erent between striking a deal in the …rst round and waiting until eitherside is chosen to make a …nal o¤er. This ambiguity could be easily restored by assuming breakdownafter the …rst round with probability "0 ! 0. Second, simultaneous bargaining with multiple partiesgives rise to the following possibility of rent-extraction. Consider bargaining between A and a. Theircontracts may now specify a substantial (additional) transfer to A if there is agreement in the pair(B; a), while the opposite happens if there is agreement in (A; b). This construction allows the twoparties to extract substantial rents in their simultaneous negotiations with B and b, respectively. InSection 7 we have more to say on this issue.

21The problem with allowing for an open time horizon (as in Binmore et al. (1986)) is the requirementto specify what happens with already signed contracts if there is delay in a particular relation; a problemwhich also arises in two-person multi-issue bargaining situations (see Inderst (2000)).

11

Illustration of the bargaining procedure for the case ! = (1; 2)Denote the respective payo¤ of retailer r by Ur and that of the integrated suppliers

by UAB. Applying the Shapley value yields

UAB =13[W +

12WfA;B;bg +

12WfA;B;ag]; (3)

Ua =13[W ¡WfA;B;bg +

12WfA;B;ag];

Ub =13[W ¡WfA;B;ag +

12WfA;B;bg]:

We show now how we obtain (3) from our bargaining procedure as presented inSection 3.2. The integrated supplier signs with the two retailers r = a; b the followingcontracts. One contract speci…es supplies and transfers for the case when bargainingwith the other retailer is also successful. A second contract is implemented if no con-tract is signed with the other retailer. Moreover, for each contingency supplies arechosen e¢ciently and the net surplus is split equally. Suppose now bargaining betweenthe integrated supplier and retailer b breaks down. It is straightforward that for thiscontingency the contract with retailer b allows the supplier to realize the payo¤ 1

2Wnfbg,i.e., half of the maximum industry pro…ts which are feasible without retailer b. Like-wise the contract with retailer b speci…es that either side realizes 1

2Wnfag if there isno agreement with retailer a. Based on these results we can now determine contractsfor the contingency where all negotiations are successful. Denote for this purpose therespective total transfer from retailer r to the integrated supplier by tr, which is paidfor the supply of xAr; xBr. When bargaining with r = a, the net surplus is equal to

Sa = xAapAa(xAa;xBa) + xBapBa(xBa; xAa)

¡KA(xAa + xAb) ¡KB(xBa + xBb) +KA(xAb) +KB(xBb);

implying that retailer a must realize Ua = 12Sa, while the supplier realizes UAB =

12Wnfag+ 1

2Sa. We can proceed likewise for negotiations with retailer b, where Ub = 12Sb

and UAB = 12Wnfbg+ 1

2Sb. As Ua+Ub+UAB =W, it is straightforward to obtain fromthese requirements the payo¤s stated in (3).

Equilibrium payo¤sTo determine equilibrium market structures in what follows, it is su¢cient to cal-

culate the joint payo¤s of suppliers and retailers. Moreover, as total industry pro…tsare invariant to the choice of market structure, it is su¢cient to state in each case thejoint payo¤s of suppliers. A complete statement of payo¤s for the individual parties iscon…ned to the appendix.

12

Proposition 1. Under the di¤erent market structures we obtain for the aggregatepayo¤s of suppliers:

i) Bilateral integration (! = (1; 1)): 12W

ii) Integrated suppliers (! = (1; 2)): 13

£W + 1

2WfA;B;ag + 12WfA;B;bg

¤

iii) Integrated retailers (! = (2; 1)): 13

£2W ¡ 1

2WfA;a;bg ¡ 12WfB;a;bg

¤

iv) Non-integration (! = (2; 2)): 12W+1

6

£WfA;B;ag +WfA;B;bg ¡WfA;a;bg ¡WfB;a;bg

¤:

Proof. See Appendix.

4.2 Equilibrium Market Structure

To determine the equilibrium market structure, we …rst compare the joint payo¤s ofretailers and suppliers in the di¤erent cases. Simple calculations yield the followingresult.

Proposition 2.i) Regardless of whether retailers are integrated or not, suppliers’ joint payo¤s are

higher under integration if

WfA;a;bg +WfB;a;bg > W; (4)

while their joint payo¤s are lower under integration if the inequality is reversed.ii) Regardless of whether suppliers are integrated or not, retailers’ joint payo¤s are

higher under integration if

WfA;B;ag +WfA;B;bg > W; (5)

while their joint payo¤s are lower under integration if the inequality is reversed.

We say that a market structure is an equilibrium market structure if the joint pro…tsof participants on either side of the market do not increase if they change their respectivemarket structure (while, of course, the structure on the other side remains unchanged).22

Proposition 2 yields the following result.

Corollary 1. We can make the following predictions for the equilibrium marketstructure:

i) Suppliers are integrated if WfA;a;bg+WnfB;a;bg > W and they stay non-integratedif WfA;a;bg +WnfB;a;bg < W.

i) Retailers are integrated if WfA;B;ag +WfA;B;bg > W and they stay non-integratedif WfA;B;ag +WfA;B;bg < W.

22For a precise formulation of these conditions, see e.g., Selten (1973).

13

Before providing some intuition for these results, we brie‡y investigate when con-ditions (4) and (5) should hold. Consider …rst the retailers’ incentives to merge. Wesay that the cost function Ks(¢) exhibits strictly increasing (decreasing) unit costs ifKs(x)=x is strictly increasing (decreasing) on x > 0. It is straightforward that (5) musthold if both cost functions exhibit strictly increasing unit costs, while the converse holdsstrictly if both cost functions exhibit strictly decreasing unit costs.

Consider next suppliers. We say that the two goods are strict substitutes if x00 > x0

and psr(x; x00) > 0 imply psr(x; x0) > psr(x; x00), for any choices s 2 S0 and r 2 R0. Inthis case it is straightforward that (4) holds, implying that suppliers become integrated.If x00 > x0 and psr(x; x0) > 0 imply psr(x; x0) < psr(x; x00), we say that goods are strictcomplements. In this case suppliers prefer to stay non-integrated. We have thus obtainedthe following result.

Corollary 2. If both suppliers have strictly increasing (decreasing) unit costs, re-tailers are integrated (non-integrated) in equilibrium. If products are strict substitutes(complements) at the two outlets, suppliers are integrated (non-integrated) in equilibrium.

Using the bargaining procedure proposed in Section 3.2, we now provide additionalintuition for our results. Consider …rst the incentives of retailers to integrate. As suppliesare not a¤ected by market structure and total rents are therefore left unchanged, inte-gration can only shift rents between retailers and suppliers. If a non-integrated retailer abargains with a supplier, they consider the additional costs incurred by the delivery to a.The same logic applies to negotiations with r = b. In contrast, if retailers are integrated,the two sides negotiate about the total supply of the respective good. Loosely speaking,negotiating separately with two non-integrated retailers allows a supplier to roll-overmore of his additional or “marginal” costs. If unit costs are increasing, the supplier willthus enjoy more of the “infra-marginal” rents. If retailers become integrated in this case,they gain access to a larger share of these rents. The same principle prevails in the caseof supplier integration. For instance, if goods are complements, the positive cross-pricee¤ect implies that the net or additional surplus created by each good is increased. Hence,in case of complements, suppliers prefer to negotiate “at the margin”.

Broadly speaking, integration shifts bargaining away from the margin. If the creatednet surplus is smaller at the margin, which is the case with increasing unit costs orsubstitutes, the respective market side prefers to become integrated. While the explo-ration of this principle in the framework of a (bilaterally) oligopolistic market is to ourknowledge new, the general principle has been already detected by Horn and Wolinsky(1988b) and Jun (1989). Both papers analyze bargaining between one …rm and twoworkers (or groups of workers). Each worker can supply one unit of labor. If their re-spective inputs are complements, workers can extract much of the surplus by bargaining

14

independently.23

Observe that our results qualify the concept of “buyer power”. Indeed, we identifyreasonable circumstances under which retailers would be worse o¤ if they were integrated.This is more likely if the industry exhibits high …xed costs and strong economies of scale.On the other side, if tight capacity implies that unit costs are increasing fast, the bene…tsfor retailers from integration should be rather high.

We consider it worthwhile to brie‡y elaborate more formally on the role of capacityconstraints. Suppose that the economy can be in one of two states, where total demand iseither high or low. In the high-demand state capacity constraints of suppliers are ratherbinding, implying that each retailer becomes more or less dispensable. In fact, even iftotal supply would be sold at only one retailer, this might only slightly depress pricesand revenues. In particular, it may hold that Wnfag +Wnfbg > W, where the upperbar denotes the high-demand state. We know that in this case retailers would preferto become integrated. Consider next the case with low demand and thus more thansu¢cient capacity. If producing involves, however, some …xed costs, this would implyoverall decreasing unit costs and thus Wnfag + Wnfbg < W, where the lower bardenotes the low-demand state Retailers would then be better o¤ to stay non-integrated.If market structure exhibits a su¢cient degree of inertia, which seems to be a realisticassumption, retailers’ choice now depends on their outlook on future demand.

Clearly, Corollary 2 does not exhaust all possible cases. For instance, unit costsmay be decreasing and increasing at di¤erent output levels. Moreover, one of the twosuppliers may enjoy decreasing unit costs while the other supplier has increasing unitcosts. In these case we can still make precise predictions on the equilibrium marketstructure by referring to the conditions (4) and (5) in Proposition 2.

4.3 Extensions of Market Structure Analysis

Our analysis of market structure has been con…ned to the case of a bilateral duopoly.Given our choice of the bargaining procedure and concept, an extension to the generalcase with N suppliers and M retailers is straightforward.24 We con…ne ourselves tobrie‡y discuss some interesting issues which arise if there are more than just two retailers

23The e¤ects have also been exploited by Bolton and Scharfstein (1996), where the individual agree-ments of debtholders have a complementary role. Stole and Zwiebel (1999a/b) consider bargainingbetween one …rm and many workers. Segal (2000) provides a unifying axiomatic approach. For earlierwork see the references in Legros (1987).

24Our restriction to N = 2;M = 2 is motivated by the fact that the previous analysis represents abuilding block to …nally study the interaction of market structure of technology choice, which wouldnot be tractable for more general cases.

15

or suppliers.

(i) Buyer and seller power: Suppose that suppliers’ technologies exhibit decreasingunit costs, while there are more than two retailers. While it is straightforward that inthis case all retailers should merge, this may not be feasible for various reasons. (Forinstance, management or owners may value control.) In this case more integrated largerretailers, e.g., hypermarket chains, get better deals than small retailers, which are forcedto bargain with suppliers over production quantities which lie at the margin of the costfunction. Of course, the same picture applies if goods are substitutes and not all suppliersare integrated. Larger supplier groups can sell goods at higher prices.

(ii) S-shaped cost functions: With many retailers and S-shaped cost functions re-tailer concentration is pro…table “as long as unit costs are increasing”. If concentrationbecomes so large that the supplier-retailer bargaining problem reaches inframarginalproduction levels at which unit costs start to decrease, further concentration becomesunpro…table. S-shaped cost function, therefore, lead to downstream market structureswhere a large retailer may co-exist with small retailers.

5 Horizontal Integration and Technology Choice

In the preceding analysis market structure does not a¤ect equilibrium supplies. In thatsense the industry’s performance is invariant to market structure. Particularly, totalwelfare and consumer surplus are not a¤ected by market structure, implying no role formerger control. In this and the following section we let suppliers choose technologiesand study the interaction with market structure. Among other things, this will implythe possibility of welfare enhancing merger policies.

Precisely, one supplier can choose between two production technologies which di¤erwith respect to inframarginal and marginal cost levels.25 For instance, following anupward shift in total demand, the supplier may face the decision to re-organize hisproduction facilities. This change may lead to lower marginal costs, but may have thedrawback of higher operating costs. Instead of a change in production costs, we couldalso imagine that the supplier can choose between di¤erent distribution strategies. Usinga highly ‡exible computerized logistical system may make it cheaper to ship additionalquantities, but again this may come at higher operating expenses.

Our model isolates the following two e¤ects of market structure on technology choice,where the …rst e¤ect is obtained by separating retailers and the second by separating

25As the two suppliers produce di¤erentiated products, assuming that only one supplier has accessto two technologies is not unrealistic.

16

suppliers.

1. Rent-Sharing E¤ect: By separating retailers, bargaining is shifted towards marginalproduction levels, so that suppliers have to bear a larger share of their inframarginalcosts and a smaller share of their marginal costs compared to the case of retailerintegration. As a result, suppliers have more incentives to trade o¤ lower infra-marginal costs with higher marginal costs if retailers Stay non-integrated.

2. Competition E¤ect: If suppliers become non-integrated, a marginal cost reductionleads to a decreasing output level of the rival supplier. This negative externalityfrom a marginal cost reduction is not internalized if suppliers are not integrated.Hence, disintegrating suppliers increases the incentives to reduce marginal costs atthe expense of higher inframarginal costs.

In what follows, we consider a three stage game. In the …rst stage, suppliers andretailers can become integrated. In the second stage, the supplier commanding overproduction of brand s = A decides which technology to choose, and in the third stagesupply contracts are negotiated. The following section analyzes the second stage of thegame, i.e., optimal technology choice for a given market structure. In Section 7 we willturn to the …rst stage and derive the equilibrium market structure.

5.1 Technology Choice

Throughout this section we restrict consideration to the case where technologies anddemand are both linear. We invoke both speci…cations in turn before proceeding to theanalysis.

TechnologiesWe consider the following problem of technology choice. Goods can be produced

with two technologies indexed by i 2 I = f®; ¯g. Initially, both goods are producedwith the same technology i = ®. However, supplier s = A can switch costlessly tothe technology ¯. We denote the respective cost functions under the two regimes byKi(x) = F i + kix for x > 0, where F i stands for …xed production costs and ki standsfor marginal costs. Fixed production costs are only incurred for positive supply level,while costs are zero if no production takes place. Consequently, …xed costs are not sunkbefore bargaining starts, but are part of the bilateral negotiation between suppliers andretailers. We assume that technology ¯ has lower (constant) marginal but higher …xedcosts; i.e., it holds that 0 · k¯ < k® < 1 and 0 · F® < F ¯. It is convenient to denote¢F = F ¯ ¡ F® > 0 and ¢k = k® ¡ k¯ > 0. Observe that the di¤erence K¯(x) ¡K®(x)

17

is strictly decreasing in x and strictly positive at x = 0. For our analysis, it su¢ces toconcentrate on the case k¯ = 0 and F® = 0, so that ¢F = F ¯ and ¢k = k®.

DemandThe utility of a representative consumer purchasing at outlet r the quantities xsr of

supplier s at prices psr is given by

xAr + xBr ¡ 12

£x2Ar + x

2Br + 2cxArxBr

¤¡ xArpAr ¡ xBrpBr.

As is well-known, this gives rise to a system of linear demand functions, where theinverse demand function for xsr is given by psr = 1¡xsr¡ cxs0r, with s0 6= s. We restrictattention to the case of substitutes where 0 < c < 1. Moreover, to ensure that (A.2)holds, we require that

c < ¹c ´ min½1 ¡ ¢k;

1 ¡ 2p¢F

1 ¡ ¢k

¾: (6)

A derivation of these conditions is contained in the appendix.

We can now proceed to the analysis. It is intuitive that for a given market structure! and …xed values of c and ¢k, technology i = ¯ is only chosen if the increase in …xedproduction costs ¢F is su¢ciently small. Precisely, for any market structure we candetermine a threshold ¢!F such that i = ¯ is strictly preferred if and only if ¢F < ¢!F . Tomake our procedure well-understood, consider the case where both sides are integratedsuch that the aggregate payo¤ of suppliers is half of total industry pro…ts. Comparingthe respective payo¤s under the two technology regimes, we obtain for the threshold¢1;1F the expression

¢1;1F = 2¡,

where ¡ ´ 14

¢k1¡c2 [2(1 ¡ c)(1 ¡ ¢k) + ¢k]. Proceeding as in this case for all market

structures, we obtain the following results.

Lemma 1. In the linear case, technology i = ¯, which has lower marginal and higher…xed costs compared to technology i = ®, is chosen until the …xed cost di¤erence ¢F isnot larger than ¢!F , where26

¢1;1F = 2¡;

¢1;2F =

32¡;

¢2;2F =

32¡ +

18;

¢2;1F = 2¡ +

16;

26For the sake of brevity we do not specify what happens in case of indi¤erence. This is withoutconsequences for the further analysis as we will simply omit these parameters.

18

with ´ c¢k1¡c2 [2(1 ¡ c)(1 ¡ ¢k) ¡ c¢k].

Proof. See Appendix.

Using Lemma 1, we can determine which market structure is more likely to lead toeither technology ® or ¯.27

Proposition 3. In the linear case, thresholds ¢!F for the technology choice satisfythe following ordering:

¢1;2F < ¢2;2

F < ¢1;1F < ¢2;1

F for all c 2 (0; ¹c):

Proof. See Appendix.

Proposition 3 con…rms the stipulated rent-sharing and competition e¤ects. The sup-plier controlling the production at A cares more about marginal cost-savings if eitherretailers become integrated or suppliers stay non-integrated. More formally, by Propo-sition 3 we obtain for m = 1; 2 that ¢m;2F ¡ ¢m;1F < 0, which illustrates the rent-sharinge¤ect, and for n = 1; 2 that ¢2;n

F ¡¢1;nF > 0, which illustrates the competition e¤ect.28 As

a consequence, the market structure ! = (2; 1) yields the strongest incentives to adopttechnology ¯; i.e., for a given reduction in marginal costs, ¢k, this market structureallows the largest …xed cost increase, ¢F . On the other side of the spectrum, the marketstructure ! = (1; 1) implies the lowest incentives to choose technology ¯. Regarding thetwo intermediate cases, the two e¤ects work in opposite directions. It turns out that inour example the rent-sharing e¤ect dominates. However, it is instructive to see how thedi¤erence in the two threshold ¢1;1

F and ¢2;2F changes in the degree of substitutability.

We obtain that ¢1;1F ¡ ¢2;2

F strictly decreases in c, which underlines once again the roleof the competition e¤ect.29

Before proceeding with the analysis, we brie‡y discuss the related case where sup-pliers can invest to reduce costs. Incentives to reduce marginal or infra-marginal costsare now a¤ected di¤erently by the market structure. Focusing again on the linear case,incentives to reduce …xed costs do only depend on the downstream market structure.If retailers are integrated, we know that the supplier can roll-over a larger portion of

27To compare ¢1;1F with ¢2;2

F note that > 0 follows from condition (6).28The impact of coalitional (or ownership) structure on various forms of cost-reducing investment

goes back Hart and Moore (1990). See also more recently Stole and Zwiebel (1996a,b), where a single…rm bargains with its workers. In this setting only the rent-sharing e¤ect is obtained.

29Precisely, we obtain

d[¢1;1F ¡ ¢2;2

F ]dc

= ¡12¢k

1 + c2 ¡ ¢k ¡ c2¢k ¡ 2c + c¢k

(1 ¡ c2)2< 0:

Note that the numerator is strictly positive if ¢k < 1+c2¡2c1+c2¡c , which holds by (6).

19

…xed costs, which reduces his incentives. In contrast, incentives to reduce marginal costsonly depend on the upstream market structure. It is easy to establish that integrationof suppliers decreases the bene…ts from reducing marginal costs.30 If suppliers are notintegrated, supplier A does not internalize the (negative) demand spill-over for goods = B after a reduction in marginal costs.

5.2 E¢ciency Benchmarks

We compare next the respective technology choices with two benchmarks of e¢ciency:industry pro…ts and welfare. First, we consider industry pro…ts. It is immediate thattechnology choice under a bilateral monopoly, ! = (1; 1), maximizes aggregate prof-its. Proposition 3 allows to obtain the parameter regions for which alternative marketstructures lead to a less e¢cient choice.

Corollary 3. In the linear case the following results hold regarding industry pro…ts:(i) If ¢F 2

¡¢1;1F ;¢

2;1F

¢; only ! = (2; 1) implements the less e¢cient technology.

(ii) If ¢F 2¡¢2;2F ;¢

1;1F

¢, only ! = (2; 2) and ! = (1; 2) implement the less e¢cient

technology.(iii) If ¢F 2

¡¢1;2F ;¢

2;2F

¢, only ! = (1; 2) implements the less e¢cient technology.

(iv) For all other cases all market structures implement the e¢cient technology.

We come next to a comparison of social welfare (the sum of industry pro…ts andconsumer surplus). Precisely, we have now in mind the picture of a regulator who canprescribe market structure, but neither directly the choice of technology nor that ofindividual outputs. As the supplied quantities are independent of the market structure,the regulator is thus only concerned with the impact of market structure on technologychoice. By substituting equilibrium quantities, we can determine social welfare underthe two technology regimes. We denote social welfare when technology i 2 I is used bySW i. Comparison of SW® and SW ¯ yields again a unique threshold for the di¤erence

30Di¤erentiating the payo¤ of the non-integrated supplier A w.r.t. his marginal costs kA, we obtain

11 ¡ c2

14[2(1 ¡ kA) ¡ 2c(1 ¡ kB)];

while proceeding analogously for the integrated supplier yields

11 ¡ c2

14[2(1 ¡ kA)

3 ¡ c2

3¡ 4

3c(1 ¡ kB)]:

As (1 ¡ kA)c > 1 ¡ kB holds, the incentives for the non-integrated supplier to reduce his marginalcosts are higher.

20

of …xed costs ¢F , which is now denoted by ¢¤F . We obtain

¢¤F = 3¡.

Hence, the choice i = ¯ maximizes welfare if and only if ¢F · ¢¤F . To determine

whether a given market structure maximizes welfare, it thus remains to compare ¢¤F

with the respective thresholds derived in Proposition 4.

Proposition 4. In the linear case the welfare threshold ¢¤F satis…es

¢¤F > ¢2;1

F .

Proof. See Appendix.

This result is intuitive given that retailers set prices to maximize industry pro…ts.As a consequence, equilibrium supply is always ine¢ciently low. To counteract thismarginalization e¤ect, the regulator has a stronger preference for the technology withsmaller marginal costs and thus a higher equilibrium supply. Proposition 4 implies thefollowing result.

Corollary 4. In the linear case the following results hold regarding total welfare:(i) If ¢F 2

¡¢2;1F ;¢

¤F

¢; all market structures implement the less e¢cient technology.

(ii) If ¢F 2¡¢1;1F ;¢

2;1F

¢; all but ! = (2; 1) implement the less e¢cient technology.

(iii) If ¢F 2¡¢2;2F ;¢

1;1F

¢, all but ! = (2; 1) and ! = (1; 1) implement the less

e¢cient technology.(iv) If ¢F 2

¡¢1;2F ;¢

2;2F

¢, only ! = (1; 2) implements the less e¢cient technology.

(v) For all other cases all market structures implement the e¢cient technology.

As a consequence of Proposition 4 and Corollary 4, a regulator is more likely toprefer the market structure ! = (2; 1), i.e., to integrate retailers, but to keep suppliersdisintegrated.

Given the benchmarks in Corollaries 3-4, the natural question is now which mar-ket structure would arise endogenously. As goods are substitutes and unit costs arenon-increasing, the …rst conjecture would be that suppliers merge while retailers staydisintegrated. This conjecture is, however, wrong for retailers who now take into con-sideration the impact of their organizational form on suppliers’ technology choice.

21

6 Equilibrium Market Structure with TechnologyChoice

We assume that market structure exhibits su¢cient inertia so that it cannot be changed(again) right after the technology has been chosen. Consider …rst the choice of upstreammarket structure. As goods are substitutes, we know that integration allows suppli-ers to extract more of total industry pro…ts. As the decision to implement ® or ¯ ismade optimally by the respective supplier, it is straightforward that regardless of thedownstream market structure suppliers will become integrated. In contrast, as retailerscannot directly control the choice of technology, they must take this into considerationwhen choosing whether to become integrated. If ¢F is below ¢1;2

F , suppliers will alwayschoose technology ¯ regardless of the downstream market structure. Given the resultingstrictly decreasing unit costs at plant A, retailers are better o¤ by staying non-integrated.Similarly, suppliers’ technology choice is also una¤ected by downstream market struc-ture if ¢F exceeds ¢1;1

F . As both goods are now produced with technology ®, which haszero …xed costs, retailers are indi¤erent towards integration.31 Hence, for relatively lowor high values of ¢F the picture has not changed compared to our previous analysis.In contrast, for ¢F 2 (¢1;2

F ;¢1;1F ) we …nd that retailers become integrated, even though

the resulting choice of technology ¯ implies strictly decreasing unit costs.

Proposition 5. In the linear case the equilibrium market structure under technologychoice is ! = (1; 2) for all ¢F < ¢1;2

F and ! = (1; 1) for all ¢F 2 (¢1;2F ;¢

1;1F ). For

¢F > ¢1;1F either ! = (1; 2) or ! = (1; 1) may emerge.

Proof. See Appendix.

Retailers prefer to merge for ¢F 2 (¢1;2F ;¢

1;1F ) as this tilts the suppliers’ choice

of technology towards ¯. Observe that for this interval ¯ maximizes industry pro…ts.While integration reduces retailers’ share of the total surplus as their bargaining positiondeteriorates, this is more than compensated by the resulting increase in total pro…ts,which can be distributed.

In the case where retailers integrate strategically to in‡uence suppliers’ technologychoice, we know from Corollary 4 that this leads also to an increase in total welfare. Theresulting switch to the technology with lower marginal costs boosts output and consumerrents. Hence, in this case all parties, i.e., suppliers, retailers, and consumers, gain from ahigher concentration in the downstream market. In our particular case integration leadsto a monopsonic position for retailers.

31This indi¤erence could be easily resolved by assuming F® > 0. While not a¤ecting the previousresults as long as ¢F > 0, this somewhat complicates all expressions.

22

While our analysis is limited to the linear case, we believe that the point we make ismore general. As we know from Section 4, integration shifts the bargaining problem moretowards inframarginal production quantities. As a consequence, suppliers’ incentives forcost reduction at the margin increase, implying an increase in total output and thusconsumer rents. While the e¤ects of retailer concentration on consumer surplus mayhave to be quali…ed depending on possible monopolization e¤ects at the outlet markets,their positive e¤ects on manufacturers’ investment and technology choices would stillpersist. Finally, our observation that retailer concentration may imply more e¢cientproduction runs counter to a widely held view. As stated, for instance, in Dobsonet al. (1998) and FTC (2001), it is believed that a monopsony reduces productivee¢ciency by erasing suppliers’ rents. However, our analysis suggests that this view hasto be quali…ed in two respects. First, retailer concentration a¤ects di¤erently suppliers’bene…ts from various forms of cost-reduction, i.e., those a¤ecting more infra-marginal ormarginal costs. Second, from consumers’ perspective the latter form of cost-reductionmay matter far more, while suppliers’ incentives to keep down marginal costs may infact increase if retailers are concentrated.

7 Discussion

7.1 Discussion of the Bargaining Procedure

We now comment on the choice of our bargaining procedure as discussed in Section3.2. It is straightforward to show that nothing would change qualitatively if we were toassume a di¤erent sharing rule of (net) surplus, which is not directly a¤ected by marketstructure. If bargaining were to proceed sequentially, the distribution of payo¤s woulddepend crucially on the (arti…cially?) chosen sequence. To see this, suppose that oneside is integrated, implying the presence of exactly three independent parties. Supposealso that players can write rather complicated contracts, which may, for instance, specifya penalty if one of the players subsequently negotiates with the third player. In sucha setting it is typically the case that the two players who start bargaining can extractextremely high rents from the third party. This is, for instance, the case if one supplier(retailer) negotiates sequentially with a series of retailers (suppliers) (see Aghion andBolton (1987), Marx and Sha¤er (1999), and Bernheim and Whinston (1998)). On theother side, if the contractual set is rather constrained and may only permit a …xed cashpayment, the outcome can be markedly di¤erent. To see this, suppose that two supplierswith strictly complementary goods bargain with a single retailer. Once the retailer hasobtained the …rst good, the incremental surplus of obtaining the second good can be

23

extremely high. As this allows the second supplier to extract a high payment, the supplierselling …rst receives far less. This has been formally explored by Cai (2000). While asimultaneous procedure looks more natural in a bilateral oligopoly, it does not avoid theaforementioned issue of (excessive) rent-extraction and its dependence on the contractualset. Allowing for relatively rich contractual sets would give rise to multiple equilibria inwhich the “victims” of rent-extraction change.32 And we also …nd an extreme outcomefor the opposite case where players can only contract on the equilibrium supplies andtransfers (without any strings attached). Indeed, this concept was applied in an earlierversion of this paper (see Inderst and Wey (2000b)). With complements or decreasingunit costs this set-up often yields extreme results where some …rms are left with zeropayo¤s. Intuitively, the possibility to contract on more contingencies under the currentprocedure safeguards …rms against excessive rent-extraction.

Our results on equilibrium market structure and technology choice depend on thefact that bargaining between two …rms proceeds overproportionally on the respective“margin”, i.e., over the net surplus, while the de…nition of this “margin” depends onthe size of the …rms, i.e., on being integrated or not. We conjecture that any bargainingconcept for oligopolistic industries with these features would reproduce our results. Asestablished in Inderst and Wey (2000b), this holds in particular for the case of simulta-neous Nash bargaining over simple (non-contingent) supply contracts.

7.2 Interdependent Demand at the Retail Outlets

We have so far assumed that demand at the two retailers is independent. If this is nolonger the case, the choice of the contractual set discussed above rises another issue.Consider the case of bilateral non-integration. Under our bargaining procedure, con-tracts between supplier s and retailer r can only condition on the set of (dis-)agreementsin the economy. With this speci…cation contracts fail to maximize industry surplus un-der interdependent demand due to opportunistic behavior in the bilateral negotiations(see McAfee and Schwartz (1994)). Precisely, the cross-price e¤ects over the two retail-ers are not taken into consideration. In this case downstream integration would havethe immediate bene…t of monopolizing the …nal market. Instead, if we allow for morecomplex arrangements where bilateral contracts can condition on either the whole setof contracts in the economy, there exists an equilibrium where the …nal market is fullymonopolized. Intuitively, as each supplier serves all retailers in equilibrium, it is fea-

32The related issue of co-ordination failure has been particularly explored in the case of exclusivecontracting, e.g., by Rasmusen et al. (1991) and Innes and Sexton (1994).

24

sible to internalize all externalities (over goods and retailers) by bilateral contracts.33

As noted above, more complex contracts typically give rise to multiple equilibria, someinvolving extreme degrees of rent extraction. We conjecture that under a suitable choiceof equilibrium for varying market structures our results should survive.34

8 Conclusion

This paper makes three related contributions. First, we propose a rather natural form ofnegotiations and contracting in bilateral oligopolistic industries, which happens to giverise to the Shapley value. Second, we explore the motivations for up- and downstreamhorizontal mergers if the only e¤ect of market structure is to determine the distributionof industry pro…ts. Third, we explore the interaction of market structure with technologychoice. As market structure determines how marginal and inframarginal rents are shared,we …nd that i) market structure a¤ects technology choice and that ii) …rms may choose aparticular organizational form in order to in‡uence the technology choice of other …rmsin the value chain. The link between market structure and technology choice providesalso a basis for regulatory interference even though market structure has no direct impacton consumer welfare.

Throughout the paper we have been silent on the possibility of vertical mergers.Extending both the analysis of market structure and that of technology choice to thiscase seems to be a fruitful avenue for further research. For instance, one might askwhether, starting from a non-integrated market structure, either retailers or anothersupplier have more to gain from merging with a particular “target” supplier to strenghtentheir bargaining position. Alternatively, one could ask which market structure maximizessuppliers’ incentives to decrease marginal or inframarginal costs and whether this marketstructure could arise endogenously.

A further extension would be to put exogenous restrictions on the supply patternsin the industry. For instance, we may suppose that certain …rms (retailers) cannotprocure from certain suppliers as they have not previously invested in the necessaryinfrastructure. It may be interesting to analyze how industry surplus is shared under suchrestrictions. Moreover, imposing these restrictions may allow to explore new incentives

33The question of how results depend on the set of feasible contracts is a very active research area.For an overview for the case with “simple” bilateral contracts see Prat and Rustichini (2000), whilemore complex mechanisms are studied in Martimort and Stole (1999) and Epstein and Peters (1999).

34However, with interdependent demand at the two retailers, we would obtain additional incentivesfor downstream integration. Indeed, the logic obtained for suppliers in case of substitutes could now bedirectly applied to downstream merger incentives.

25

for (horizontal) mergers.35

Finally, this paper has con…ned itself to study the impact of market structure ontechnology choice at a single supplier. Exploring further the idea how market structureat one level may a¤ect investment and strategic (non-price) choices at other levels ofthe value chain, the following questions arise naturally. How does downstream marketstructure a¤ect the product choice of suppliers, e.g., their degree of substitutabilityor complementarity? How are incentives for (not full contractible) demand-enhancingactivities, e.g., advertising by retailers or product innovation by suppliers, determinedby the integration of suppliers or retailers respectively?

9 Appendix

Proof of Proposition 1.The proof consists of the application of the Shapley value for the di¤erent market

structures.

i) ! = (1; 1): If both sides are integrated, the two parties share the surplus W

equally.

ii) ! = (1; 2): If only suppliers are integrated, retailer r realizes 13 [W ¡WfA;B;r0g +

12WfA;B;rg], where r0 6= r, while the integrated supplier realizes 1

3 [W + 12WfA;B;r0g +

12WfA;B;rg]:

iii) ! = (2; 1): If only retailers are integrated, supplier s realizes 13 [W ¡Wfs0;a;bg +

12Wfs;a;bg], where s0 6= s, while the integrated retailer realizes 1

3 [W+ 12Wfs0;a;bg+ 1

2Wfs;a;bg]:

iv) ! = (2; 2): If both sides are non-integrated, supplier s realizes

14W +

112

£Wfs;ag +Wfs;bg ¡Wfs0;ag ¡Wfs0;bg

¤

+112

£WfA;B;ag +WfA;B;bg +Wfs;a;bg ¡Wfs0;a;bg

¤;

where s0 6= s, while retailer r realizes

14W +

112

£WfA;rg +WfB;rg ¡WfA;r0g ¡WfB;r0g

¤

+112

£WfA;a;bg +WfB;a;bg +WfA;B;rg ¡ 3WfA;B;r0g

¤;

where r0 6= r.35Similar questions are addressed in the network literature (see Jackson and Wolinsky (1996), Kranton

and Minehart (2000)).

26

Derivation of Condition (6)We show that (A.2) holds for the linear case with substitutes if

1 ¡ ks > c(1 ¡ ks0) + 2pFs (7)

is satis…ed for s0 6= s. Substituting the speci…cations for ks and Fs for the technologyregimes ®; ¯, we obtain the two requirements

c < 1 ¡ ¢k;

c <1 ¡ 2

p¢F

1 ¡ ¢k;

which give rise to (6). To derive (7) from (A.2), note …rst that our linear case exhibitsnon-increasing unit costs at both suppliers. Hence, with substitutes the additional sur-plus of an additional retailer-supplier link eser is smallest if the initial link structure isL = f(s; a); (s; b)g with es 6= s, i.e., if previously only supplies of the other good s werefeasible. To maximize industry pro…ts, xsa and xsb are both equal to (1 ¡ ks)=2 > 0.Given these supplies, the optimal (additional) supply of xeser maximizes

(1 ¡ xes ¡ c1 ¡ k2

2¡ kes)xes ¡ Fes ¡ cxes

1 ¡ k22

. (8)

Maximizing (8) yields a positive value for xeser whenever 1 ¡ c¡ kes + cks > 0, while themaximum additional surplus (8) is positive if 1 ¡ kes > c(1 ¡ ks) + 2

pFes.

Proof of Lemma 1For a given technology i 2 f®; ¯g the payo¤, U!i of the supplier commanding over

production of goodA under a particular market structures, !, is derived form the Shapleyvalue formula, which yields in the general case

U1;1i =

12W i

U1;2i =

13(W i +W inr)

U2;1i =

13(W i ¡W inA +

12W inB)

U2;2i =

112

(3W i + 2W infB;r) ¡ 2W infA;rg + 2W inr +WinB ¡ 3W inA),

where W iC is the industry pro…t for a coalition C, with C = f;nr;nA;nBg, when

27

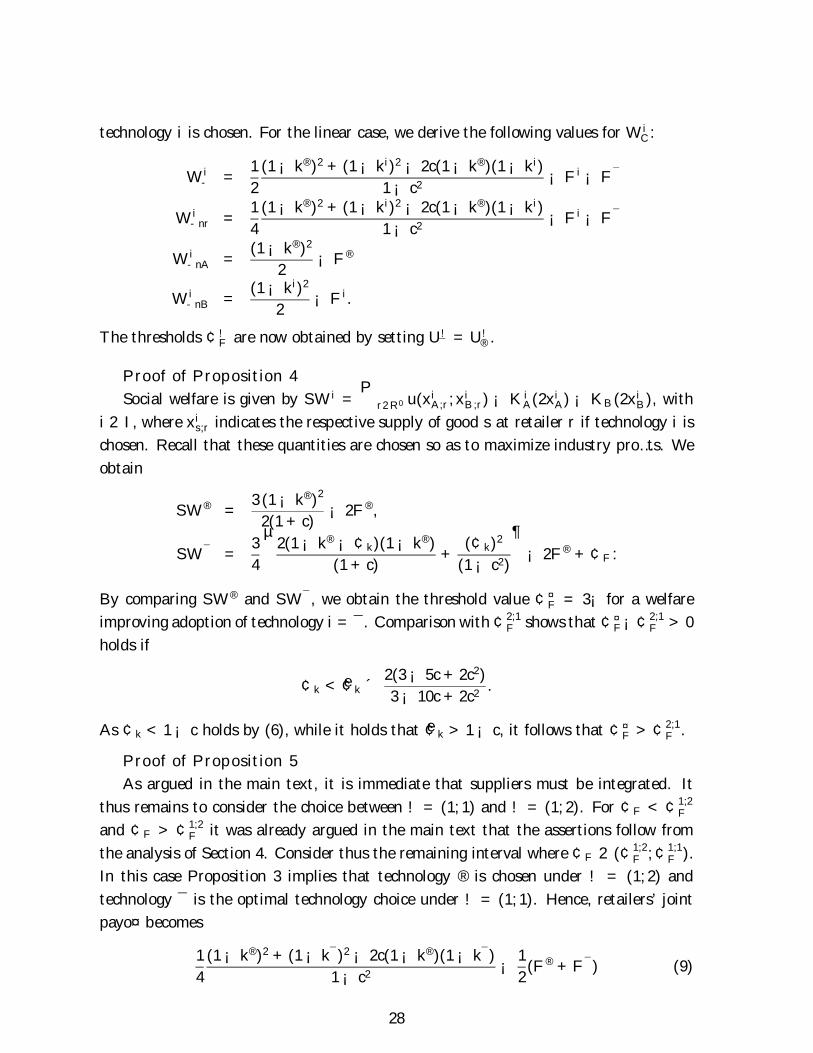

technology i is chosen. For the linear case, we derive the following values for W iC:

W i =12(1 ¡ k®)2 + (1 ¡ ki)2 ¡ 2c(1 ¡ k®)(1 ¡ ki)

1 ¡ c2 ¡ F i ¡ F ¯

W inr =14(1 ¡ k®)2 + (1 ¡ ki)2 ¡ 2c(1 ¡ k®)(1 ¡ ki)

1 ¡ c2 ¡ F i ¡ F ¯

W inA =(1 ¡ k®)2

2¡ F®

W inB =(1 ¡ ki)2

2¡ F i.

The thresholds ¢!F are now obtained by setting U!¯ = U!® .

Proof of Proposition 4Social welfare is given by SW i =

Pr2R0 u(x

iA;r; xiB;r) ¡ KiA(2xiA) ¡ KB(2xiB), with

i 2 I, where xis;r indicates the respective supply of good s at retailer r if technology i ischosen. Recall that these quantities are chosen so as to maximize industry pro…ts. Weobtain

SW® =3 (1 ¡ k®)22(1 + c)

¡ 2F®,

SW ¯ =34

µ2(1 ¡ k® ¡ ¢k)(1 ¡ k®)

(1 + c)+

(¢k)2

(1 ¡ c2)

¶¡ 2F® +¢F :

By comparing SW® and SW ¯, we obtain the threshold value ¢¤F = 3¡ for a welfare

improving adoption of technology i = ¯. Comparison with ¢2;1F shows that ¢¤

F¡¢2;1F > 0

holds if

¢k < e¢k ´ 2(3 ¡ 5c+ 2c2)3 ¡ 10c+ 2c2

.

As ¢k < 1 ¡ c holds by (6), while it holds that e¢k > 1 ¡ c, it follows that ¢¤F > ¢2;1

F .

Proof of Proposition 5As argued in the main text, it is immediate that suppliers must be integrated. It

thus remains to consider the choice between ! = (1; 1) and ! = (1; 2). For ¢F < ¢1;2F

and ¢F > ¢1;2F it was already argued in the main text that the assertions follow from

the analysis of Section 4. Consider thus the remaining interval where ¢F 2 (¢1;2F ;¢

1;1F ).

In this case Proposition 3 implies that technology ® is chosen under ! = (1; 2) andtechnology ¯ is the optimal technology choice under ! = (1; 1). Hence, retailers’ jointpayo¤ becomes

14(1 ¡ k®)2 + (1 ¡ k¯)2 ¡ 2c(1 ¡ k®)(1 ¡ k¯)

1 ¡ c2 ¡ 12(F® + F ¯) (9)

28

for ! = (1; 1) and

13(1 ¡ k®)2 + (1 ¡ k®)2 ¡ 2c(1 ¡ k®)(1 ¡ k®)

1 ¡ c2 (10)

¡ 112

(1 ¡ k®)2 + (1 ¡ k®)2 ¡ 2c(1 ¡ k®)(1 ¡ k®)1 ¡ c2

for ! = (1; 2). The assertion for ¢F 2 (¢1;2F ;¢

1;1F ) holds whenever (9)>(10), which

transforms to the requirement

¢F > e¢F ´ 12¢k

2 ¡ ¢k ¡ 2c + 2c¢k1 ¡ c2 :

Using ¢k < 1 ¡ c from (6), it follows that e¢F is strictly decreasing in ¢k. It thusremains to show that ¢F > e¢F holds at the lower boundary of the considered intervalwhere ¢F = ¢1;2

F = 32(

14

¢k1¡c2 (2(1¡c)(1¡¢k)+¢k)). At this point ¢F > e¢F transforms

to the requirement c < 2¡¢k2(1¡¢k) : As 2¡¢k

2(1¡¢k) > 1, this holds by (6) and ¢k > 0, whichcompletes the proof.

10 References

Aghion,P. and Bolton, P. (1987), Contracts as Barriers to Entry, American EconomicReview 77, 388-401.

Bernheim, B.D. and Whinston, M.D. (1986), Menu Auctions, Resource Allocation, andEconomic In‡uence, Quarterly Journal of Economics 101, 1-31.

Bernheim, B.D. and Whinston, M.D. (1998), Exclusive Dealing, Journal of PoliticalEconomy 106, 64-103.

Bester, H. and Petrakis, E. (1993), The In

Deneckere, R. and Davidson, C. (1985), Incentives to Form Coalitions with BertrandCompetition, Rand Journal of Economics 16, 473-486.

Dobson, P., Waterson, M., and Chu, A. (1998), The Welfare Consequences of theExercise of Buyer Power, O¢ce of Fair Trading Research Paper No. 16, July.

Dobson, P. and Waterson, M. (1997), Countervailing Power and Consumer Prices,Economic Journal 107, 418-430.

Dobson, P. and Waterson, M. (1999), Retailer Power: Recent Developments and PolicyImplications, Economic Policy 28, 133-164.

Ehlermann, C.D. and Laudati, L.L. (1997), Proceedings of the European CompetitionForum, New York, John Wily & Sons.

Epstein, L.G. and Peters, M. (1999), A Revelation Principle for Competing Mecha-nisms, Journal of Economic Theory 88, 119-160.

European Commission (1998), European Community and Competition Policy, 28thReport on Competition Policy, European Communities, Luxembourg.

Farrell, J. and Shapiro, C. (1990), Horizontal Mergers: An Equilibrium Analysis, Amer-ican Economic Review 80, 107-126.

Felli, L. and Roberts, K. (2000), Does Competition Solve the Hold-up Problem?, CA-RESS Working Paper No. 00-04.

Flaherty, T. (1980), Industry Structure and Cost-reducing Investment, Econometrica10, 1187-1209.

FTC (1996), FTC: Toys “R” Us Doesn’t Play Fair - Charges Nation’s Largest Toyretailer Induced Toy makers to Cut O¤ Discounts, Keeping Prices Higher andReducing Choice for Consumers, FTC Press release, May 22, 1996.

FTC (1997), FTC Judge Upholds Charges Against Toys “R” Us: Law Judges Fins thatNation’s Largest Retailer Induced Toy Makers to Cut O¤ Discount WarehouseClubs, FTC Press Release, September 30, 1997.

FTC (2001), Report on the Federal Trade Commission Workshop on Slotting Al-lowances and Other Marketing Practices in the Grocery Industry, Report by FTCSta¤.

30

Gilbert, R. and Sunshine, S.C. (1995), Incorporating Dynamic E¢ciency Concernsin Merger Analysis: The Use of Innovative Markets, Antitrust Law Journal 63,569-601.

Hart, O. and Moore, J. (1990), Property Rights and the Nature of the Firm, Journalof Political Economy 98, 1119-1158.

Horn, H. and Wolinsky, A. (1988a), Bilateral Monopolies and Incentives for Merger,Rand Journal of Economics 19, 408-419.

Horn, H. and Wolinsky, A. (1988b), Worker Substitutability and Patterns of Unionisa-tion, Economic Journal 98, 484-497.

Inderst, R. and Wey, C. (2000a), Cross-Country Mergers and Countervailing Power,Mimeo.

Inderst, R. and Wey, C. (2000b), Market Structure, Bargaining, and Technology Choice,Discussion Paper FS IV 00-12, Wissenschaftszentrum Berlin.

Inderst, R. (2000), Multi-issue Bargaining with Endogenous Agenda, Games and Eco-nomic Behavior 30, 64-82.

Innes, R. and Sexton R. J. (1994), Strategic Buyers and Exclusionary Contracts, Amer-ican Economic Review 84, 566-584.

Jackson, M. O. and Wolinsky, A. (1996), A Strategic Model of Social and EconomicNetworks, Journal of Economic Theory 71, 44-74.

Jun, B.H. (1989), Non-Cooperative Bargaining and Union Formation, Review of Eco-nomic Studies 56, 59-76.

Kranton, R. E. and Minehart, D. F. (2000), A Theory of Buyer-Seller Networks, forth-coming American Economic Review.

Kühn, K.-U. and Vives, X. (1999), Excess Entry, Vertical Integration, and Welfare,Rand Journal of Economics 30, 575-603.

Legros, P. (1987), Diadvantageous Syndicates and Stable Cartels: The Case of theNucleolus, Journal of Economic Theory 42, 30-49.

Martimort, D. and Stole, L. (1999), The Revelation and Taxation Principles in CommonAgency Games, Mimeo.

31

Marx, L. M. and Sha¤er, G. (1999), Predatory Accommodation: Below-Cost Pricingwithout Exclusion in Intermediate Goods Markets, Rand Journal of Economics30, 22-43.

McAfee, R.P. and Schwartz, M. (1994), Opportunism in Multilateral Vertical Contract-ing: Nondiscrimination, American Economic Review 84, 210-230.

McLaren, J. (2000), Globalization and Vertical Structure, American Economic Review90, 1239-54.

Myerson, R.G. (1977), Graphs and Cooperation in Games, Mathematics and OperationsResearch 2, 225-229.

OECD (1999), Buying Power of Multiproduct Retailers, OECD, Paris.

Ordover, J.A., Saloner, G., and Salop S. C. (1990), Equilibrium Vertical Foreclosure,American Economic Review 80, 127-142.

Perry, M.K. and Porter, R.H. (1985), Oligopoly and the Incentives for HorizontalMerger, American Economic Review 75, 219-227.

Pitofsky, R. (1998), E¢ciencies in Defense of Mergers: 18 Month After, FTC, Wash-ington D.C., October 16, 1998.

Prat, A. and Rustichini, A. (2000), Games Played through Agents, mimeo.

Qiu, L.D. (1997), On the Dynamic E¢ciency of Bertrand and Cournot Equilibria,Journal of Economic Theory 75, 213-229.

Rasmusen, E. B., Ramseyer, J. M., and Wiley, J. S. (1991), Naked Exclusion, AmericanEconomic Review 81, 1137-1145.

Salant, S.W., Switzer, S. and Reynolds, R.J. (1983), Losses from Horizontal Merger:The E¤ects of an Exogenous Change in Industry Structure on Cournot-Nash Equi-librium, Quarterly Journal of Economics 98, 187-199.

Salinger, M.A. (1988), Vertical Mergers and Market Foreclosure, Quarterly Journal ofEconomics 103, 345-356.

Segal, I. (2000), Collusion, Exclusion, and Inclusion in Random-Order Bargaining,mimeo.

Selten, R. (1973), A Simple Model of Imperfect Competition Where Four are Few andSix Are Many, International Journal of Game Theory 2, 141-201.

32

Spence, M. (1984), Cost Reduction, Competition and Industry Performance, Econo-metrica 52, 101-121.

Steptoe, M.L. (1993), The Power-Buyer Defense in Merger Cases, Anitrust Law Journal61, 493-504.

Stole, L. and Zwiebel, J. (1996a), Intra-Firm Bargaining Under Non-Binding Contracts,Review of Economic Studies 63, 375-410.

Stole, L. and Zwiebel, J. (1996b), Organizational Design and Technology Choice UnderIntra…rm Bargaining, American Economic Review 86, 195-222.

Vogel, L. (1998), Competition Law and Buying Power: The Case for a New Approachin Europe, European Competition Law Review 1, 4-11.

von Ungern-Sternberg, T. (1996), Countervailing Power Revisited, International Jour-nal of Industrial Organization 14, 507-520.

Waterson, M. (1980), Price-cost Margins and Successive Market Power, Quarterly Jour-nal of Economics 94, 135-150.

Williamson, O.E. (1968), Economies as an Antitrust Defense: The Welfare Tradeo¤s,American Economic Review 58, 18-35.

33