Embed Size (px)

Citation preview

The Effects of Mergers and Acquisitions in thePharmaceutical Industry

By

Matthew David Lamb

Union College

March 14, 2014

1

1: Abstract

Corporate management strives to maximize and sustain

revenue and earnings growth, in order to drive shareholder’s

profits. Two key factors in providing long-term growth are

producing new products and possessing strong core operation

activities. The creation of new products primarily derives

from two options, either internal research and development,

or merger acquisition activity. Corporate mergers and

acquisitions (M&A) are a tempting option for senior managers

and board members. The potential to obtain rights to the

next “Blockbuster drug” helps drive demand. Internal

research and development (R&D) has a tendency to be a

sluggish process that does not guarantee to come to fruition

(Wang 2007). Mergers and acquisitions can help companies

obtain current high revenue generating drugs and can help

companies increase efficiency by reducing overhead. Mergers

2

and acquisitions can be used as a tool to help protect a

firm from competition.

The nature of the pharmaceutical industry makes it

extremely susceptible to globalization and industry

competition. In the 20th century, pharmaceutical companies

endured a slight change in development preference. A strong

trend of M&A activity swept across the industry and in 2000

firms spent roughly 1.6 trillion dollars in M&As. Compared

to the 300 billion dollars that firms spent in 1991, 2000’s

M&A activity rate is astronomically high (Hill and Jones

2004). This begs the question why? Have pharmaceutical firms

discovered the secret to rapid corporate growth? Or, are

firms following the industry’s herd mentality in the hopes

of achieving similar returns from particular firm’s M&As?

The long-term demand for M&A’s will be determined by the

success of transactions. In this paper I will be analyzing

the short-term and long-term realized abnormal returns in an

effort to determine if M&A’s increase the firms ability to

generate profit from its assets and increase its operational

efficiency.

3

The analysis will focus on companies in the

pharmaceutical sector, and more specially, the top companies

competing in the Pharmaceutical Preparation Manufacturing

industry (NAICS 325412); according to MergentsOnline. The

data was collected from 1982 to 2013; company’s dates range

due to their availability on MergentOnline. This study will

use a multi prong approach, both looking at four-years

performance pre and post-merger and acquisitions, while

compared to industry weighted averages, among other

benchmarks. This study will be focusing on both horizontal

and cross-sectional M&A activity.

There has been numerous studies on the performance of

M&A activity in the pharmaceutical industry. However, many

economic studies report conflicting results. Wang reports

evidence of both long and short-run abnormal returns for

acquisitions, but not for mergers. There has been no

evidence that mergers produce positive abnormal return,

although one study indicates that mergers do produce some

operational efficiency. The study reports that both return

on assets and cash flows improve post mergers (Wang 2007).

4

Across academic papers today the results are volatile, which

suggests that the effect of M&A activity is still a valid

and debated topic.

Table of Contents

Chapter One: Introduction5

A. Motivation to Participate in Mergers & Acquisitions6

B. Why the Pharmaceutical Manufacturing Industry8

Chapter Two: Literature Review

10

Chapter Three: Data and Methods18

A. Data Description18

5

B. Regression Methods22

Chapter Four: Empirical Results25

A. Event window results for Return on Equity 26

B. Event window results for Gross Profit Margin31

C. Event window results for Return on Investment

37

Chapter Five: Conclusion

42

Chapter One

6

1: Introduction

The overriding goal for a merger is to strengthen a

firm’s share value, generating increases in shareholders’

wealth. However, there is an on going debate between

academic researchers on what effect acquiring companies has

on shareholders’ wealth. There has been a plethora of

studies performed on mergers and acquisitions, indicating

both positive and negative effects on shareholder wealth. A

study by Agrawal reports a statistically significant

decrease in wealth of 10 percent following the merger’s

completion (Agrawal 1992). This study hypothesizes that the

market is slow to adjust to the effect of the merger. Firth

in 1980 reported that mergers and acquisitions do create

value (Firth 1980). Chatterjee’s 1986 study, reports that

acquiring firms indeed creates company value, but not

through the traditional notation of synergies. He indicates

that the value creation stems from unexplored opportunities

within the targeted company, which have either been

previously ignored or were unable to be performed because

the target firm was incapable of such activities (Chatterjee

7

1986). Due to the vast discrepancies in the results on the

firm’s post-performance after a merger and acquisition,

there remains to be unanswered questions. My analysis will

focus on the long-term pre and post-performance effects of

mergers and acquisitions (M&A) in the Pharmaceutical

Preparation Manufacturing industry (NAICS 325412), defined

by MerchantOnline.

The pharmaceutical industry is an attractive setting to

study M&A performance, due to the volume of M&A activity and

the susceptibility for high abnormal returns. This is

because newly invented brand name drugs can generate

substantial revenue. In this analysis we focus on abnormal

returns based on a firm’s return on investment, return on

equity, and gross profit margin.

This section will indicate the quintessential topic

discussed in the paper. The third section will indicate the

motivations behind why these firms will participate in

merger and acquisition activity. The fourth section will

discuss the rationale behind why pharmaceutical industries

are enticing to analyze. The fifth section will discuss the

8

relevant studies previously done in this subject matter. The

sixth section will divulge my data sources. The seventh

section will describe what type of regression methods are

used and how abnormal returns are generated. The eighth

section will consist of the findings from my research and

the analysis of the findings and the final section will

include a conclusion of the results and a discussion of

their limitations.

2: Motivation to Participate in Mergers & Acquisitions

Section two will describe the potential reasons firm part-

take in merger and acquisitions.

In order to have a comprehensive understanding of what

effect M&A’s have on shareholder value and why they have

that effect, it is important to acknowledge what motivates

acquiring firms to participate in M&A activity. “The

overriding goal for merging is maximization of owners’

wealth as reflected in the acquirer’s share price” (Krueger,

2010). However, often mergers are performed for other

9

reasons. According to Principles of Managerial Finance there are two

types of reasons for mergers and acquisitions, strategic and

financial.

In a strategic M&A the operations of the acquiring firm

and target firm are combined to achieve synergies. The

generated synergy or economies of scale result from the

merged firms lowering of overhead by the elimination of

redundant functions and employees. This is most clearly

identifiable when companies merge with other companies in

the industry. M&A’s can also provide rapid growth in size

and diversification of product line. The acquiring firm may

buy a target firm for their new developments, patents, or

the current drugs they produce. This type of merger would

allow them to expand product lines without incurring the

risks associated with designing, manufacturing, and selling

new or additional products. Many companies find M&A a more

cost effective alternative for growth, compared to “organic

growth” through internal research and development funding.

Lastly, strategic M&A activity can increase both managerial

and technological skills. Often companies cannot fulfill

10

their full potential due to insufficiency in particular

aspects of management, or the lack of necessary product

and/or technology (Krueger, 2010).

The motivation for financial M&A activity is that

acquiring companies believe they can restructure the

companies' cash flows, to reveal their untapped potential.

The acquiring company achieves this by cutting costs and

selling off unproductive assets, among other things.

Companies also participate in financial M&As for tax

benefits. This normally takes place when one company has a

tax loss carry-forward. When a merger occurs with a firm

that has a tax loss carry-forward, the company can apply

that tax loss to future earnings to reduce the other

company’s taxable income. The final motivation behind

financial M&A activity is to increase the firm’s ability to

fundraise. In this case a company may acquire a “cash rich”

company (high liquid assets and low liabilities,) to

increase its borrowing power by reducing its financial

leverage. By decreasing financial leverage, the company is

11

able to externally borrow funds at a lower cost (Krueger,

2010).

3: Why the Pharmaceutical Manufacturing Industry

Section three will discuss the rationale on why I chose

the pharmaceutical industry

The Pharmaceutical Industry has been highly influenced

by globalization due to the nature of its products. The

industry is particularly attractive due to the mass quantity

of mergers and acquisition activities. The pharmaceutical

industry has a rich history dating back to the late 19th

Century (Surrey 2005). Early characteristics of this

industry were centered on strong internal research and

developmental, and patent protection. Competition was based

on new product development and not price of certain drugs.

In a study conducted by Hill and Jones they said “The most

recent wave of mergers and acquisitions peaked in 2000 when

US firms spent some $1.6 trillion on 11,000 mergers and

acquisitions up from $300 billion in 1991. (Hill and Jones

12

2004)” It would seem that pharmaceutical firms have adverted

from the early practices to an increasingly preferred system

of mergers and acquisitions. In 1990 the top 10 companies in

this industry represented only 28 percent of the total

market. After an eight-year window, the largest ten

companies increased their market share to 36 percent (Marron

2006). Why has this change occurred? Some point to stricter

regulations on clinical trials by increasing time-to-market

and other development costs. However, the most significant

change may have stemmed from the implementation of a fixed

period on patent protection. For example, sales in Prozac

fell by 22 percent in the first year alone after the patent

expired (Marron 2006).

The drug manufacturing industry is unique in that it

has a high cost of drug development paired with an

incredibly low rate of success. In a study performed on the

top 50 largest pharmaceutical firms by sales, it was

reported that only one sixth of the self-originated drugs

that first entered clinical trials between 1993-2004 and

were observed in June 2009 were approved for retail (DiMasi

13

2010). This trend continued to fall; in a study of

pharmaceutical firms between 2004-2010, only one out of

every ten drugs entered the first phase of clinical trials

received FDA approval (Berkrot 2011). It’s very important to

note that many of the projects these companies fund fail

before they can even enter the first phase of clinical

trials. Pharmaceutical companies inherently understand these

statistics and therefore have an incentive to partake in M&A

activity either to supplement or outsource early stage

research.

In order to indicate the success of the M&A, this study

will be focusing on changes in efficiencies, accounting

ratios and abnormal returns in the firm’s short and long

run. Changes in these categories should “reflect the

synergies claimed in the company’s explanations of their

reasons for merging” (Wang 2007). According to Hassan and

Wang (2007) the pharmaceutical industry has predisposition

to incite M&A activity with firms that have potential

billion-dollar revenue power, referred to as “blockbuster

drugs. ” A prevalent example of this can be seen with the

14

company AstraZeneca. The company, based in London, was

formed in 1999 from Astra AB of Sweden merging with Zeneca

Group PLC of the UK. Two major blockbuster drugs were

developed due to this merger, Prilosec and Nexium. Prilosec,

despite losing its patent protect in 2002 generated 946

million dollars in 2009, while in 2009, still patented,

raked in $4.96 billion as AstraZeneca’s top seller (Berndt

2001). As certain companies exemplified, there is

particularly strong potential for high returns for these

types of M&A activity, leading many firms to correlate M&As

with increases in wealth. However, many studies on this

topic have not been able to conclude this effect. Once a

pharmaceutical company has patent on a new drug, they have

monopoly or oligopoly structure on that particular product-

market. Over this patent-protected period, abnormal returns

stemming from the M&A can be readily observed. In a 2001

study by Berndt, he reports that 80 percent of revenue is

lost after the expiration of the patent period (Berndt

2001). Due to all of the reasons listed, this study will

base its regressions on companies in the pharmaceutical

15

industry.

4: Literature Review

Section four will describe and discuss the finding of

economic studies similar to this study.

The majority of recent publishing on comprehensive

performance valuations for mergers and acquisitions have

been event studies. Event studies measure the statistical

effects of a merger and acquisition on a firm’s value.

Current findings have produced conflicting results depending

on which company the study is focused on: the acquiring or

targets company. Conclusive abnormal return results are

difficult to achieve because studies vary by time periods,

benchmarks, abnormal returns equations, and weighting

methodologies (Wang 2007). An inconsistency among previous

studies' variables makes comparisons difficult as well. Wang

in 2007 analyzed 405 mergers and acquisitions, 78 percent US

based targets and 22 percent foreign-based targets, between

the years of 1981-2004. Wang found no abnormal returns in

16

both short and long run mergers of both US and foreign based

acquiring companies (Wang 2007). Firth in 1980 investigated

434 takeovers (mergers) between the periods of 1969 to 1975.

He uses a market model to measure the effect takeovers have

on shareholder returns. Though the results were

insignificant, identified positive abnormal returns for

acquiring firms after 36 months following the takeover

(Firth 1980). Agrawal in1992 researched post-merger

performance in acquiring firms; he determined that acquiring

firms exhibited significant underperformance after a merger

(Agrawal 1992). Agrawal’s findings were consistent with

other works like Loughran and Vijh (1997), Asquith et al.

(1983) and Andre ́ et al. (2004).

To measure the performance of mergers and acquisitions,

an overwhelming number of studies focus on abnormal returns.

The idea of abnormal returns runs in contrast with the

efficient market hypothesis (EMH), which describes the

market as “perfect”: expected returns are equal to required

returns, prices react swiftly to new information, and stocks

17

are fully and fair priced. If EMH theory were correct,

abnormal returns would not exist ("Efficient Market

Hypothesis"). Abnormal returns are actual returns greater

than average market returns. These are often triggered by an

event. Recent studies have used M&A activity during a time

period as an event to see if there have been changes in

abnormal returns. Wang study uses cumulative abnormal

returns after an event (M&A activity) to see what the long

and short-term effects are (Wang 2007). Wang reports no

abnormal returns for acquiring companies post M&A in both

the short and long run. Sorescu in 2002 identified abnormal

returns on stock price created by M&As in the pharmaceutical

industry. Sorescu uses two methodologies to measure post-

event abnormal returns: the Fama and French three-factor

model and the mean monthly calendar time approach. His data

included 1414 acquisitions for eleven years between 1992 and

2002. Sorescu found that long run abnormal returns were not

statistically significantly, claiming the M&A activity had

no long run effect. Sorescu also analyzed short term effects

for acquiring companies and found a -1 percent return for

18

the three and five day window surrounding the announcement

of the acquisition (Sorescu 2002).

Previous and recent reports on a long-term acquiring

firm’s performance are mixed, but consensus is pointing to

negative post-merger performance. Andre in 2004 did a study

on 267 Canadian mergers and acquisitions between the years

of 1980 to 2000. The study focuses on completed M&A deals

with a minimum value of 10 million US dollars. Andre also

includes companies that performed numerous M&A deals during

this time period, similar to my study. To measure average

long run abnormal returns Andre construction monthly

portfolios in calendar time. He uses this method over an

event time approach because monthly returns are less

subjected to “the bad model problem. (Andre 2004)” Monthly

returns allow cross-correlation examination between the

companies in the sample size. In this model each month’s

returns are calculated from the portfolio of companies that

undertook M&A activity during month k of the calendar month

t. The dependent variable is excess returns, which is derived

19

from given month t’s return on portfolio minus the calculated

risk free rate. Andre found that mergers underperformed

significantly in both the long run and three-year horizon.

The three-year post-acquisition average abnormal returns for

the portfolio of Canadian acquiring firms resulted in a

statistically significant negative return of -0.523% per

month. Over a twelve-month period, that is a negative

abnormal return of -6.28 percent (Andre 2004). Andre was

unable to find significant positive results post M&A

activity.

Loughran and Vijh results indicate similar findings to

Andre (2004). Loughran and Vijh in 1997 collected annual

data and aggregate market value for 947 acquisitions by 639

firms, between the years of 1970-1989. Loughran and Vijh

only includes operating firms found on the NYSE, AMEX, or

Nasdaq, and excludes all ADRs, closed-end funds, and REITs.

To measure long run abnormal returns, the study ran an

annual regression of one-year buy and hold returns. Their

regression was run to find abnormal returns in the company’s

20

stock price. A regression run for the overall sample average

of 947 acquisitions for a five-year buy and hold period

indicated a return of 88.2 percent. The average acquisition

returns were 6.5% lower than that of competing non-

acquisition peers, and were statistically significant.

Loughran and Vijh ran an independent regression for firms

that participated in mergers. The returns indicated mergers

performed even worse. Firms that participated in a merger in

a five-year buy and hold model experienced an

underperformance of 15.9 percent compared to matching firms

(Loughran and Vijh 1997).

The majority of event studies and economic papers focus

on the creation of abnormal returns from the company’s stock

price. Healy study decided to use post-merger cash flow to

find abnormal returns instead of stock price. He says “Our

research is motivated by the inability of stock price

performance studies to determine whether takeovers create

real economic gains (Healy 1992).” One of the major causes

of the inability of stock price studies to successfully

21

determine the effect of M&A is market inefficiencies. A

possible explanation on why a stock price study may produce

positive abnormal returns is the market overvaluing the

equity (Healy 1992). The overvaluation of equities happens

on a day-to-day basis. By using a firm’s post and pre merger

accounting data to find real economic gains in M&A activity,

market inefficiency risk can be mitigated. Healy in 1992

collected data from the 50 largest target firms'

acquisitions between the years of 1979 to 1983. Healy

reports that merger firms have significantly greater return

on operating cash flows, due to greater asset productivity

in comparison to industry average (Healy 1992). Ravenscraft

and Scherer in 1987 also analyzed earnings performance after

takeovers. Their results contradicted Healy’s. They were not

able to identify any post takeover operational improvements

(Healy 1992).

Recent and historical academic literature has also used

operational efficiencies and financial ratios to measure

post M&A performance. Demirbag in 2007 states that value

22

creation and performance of M&A are created by changes in

cost-based and revenue-based synergies. His case study is a

comparative analysis of pharmaceutical companies pre M&A

during the years of 1995 to 1999 and post M&A for the years

of 2000 to 2004. The case study compares six companies,

three large pharmaceutical firms and three similar

pharmaceutical firms that operated through organic growth,

instead of M&A. The variables the study compares are

research productivity, return on investment (ROI), and

profit margin. Demirbag found that research productivity

pre-M&A was significantly higher at 78.7, than post-M&A at

only 12 (Demirbag, 2007). R&D based pharmaceutical firms saw

a similar decline during the same period for research

production, but operated at a higher level between 2000-2004

compared to M&A firms. For ROI post-M&A firms on average

performed better at 20.6 percent than non-M&A firm at 17.3

percent. Results for marginal profit were higher post-M&A

than pre-M&A, but only by a small amount (Demirbag, 2007).

Trivedi in 2013 performed a case study on the effect of

23

M&As on operational performance and shareholder wealth in

the short-run. Trivedi found inconsistencies on the effect

of earnings per share (EPS). The research shows examples of

firms both increasing post-M&A and firms EPS dropping by

half post-M&A. The research concluded that in the short run

post M&A firms endured significant reductions in Return on

Net Worth, Return on Capital Employed, Gross Margin, and Net

Margin. Trivedi notes that in the long run more synergies

may arise to help cope with competition, cut costs, and

increase a company’s market reach (Trivedi 2013).

To complement the first half of Wang's study on

abnormal returns in stock price, Wang also investigated

abnormal returns in operational efficiencies. The study

focused on pre-tax operational cash flows (ORET), Return on

Assets (ROA), and Return on Equity, pre and post-M&A. Wang’s

results indicate that post M&A firms have higher ROA ratios

than pre-M&A. Further, operating cash flows also improved,

but many of the positive returns were insignificant.

However, ROE does not improve post M&A, indicating that

24

larger mergers may not create value (Wang 2007).

Researchers have also analyzed cross-border mergers and

acquisitions. The results are mixed but predominantly

negative. Danzon in 2004 found positive abnormal returns

from both large horizontal and cross-border mergers. This

indicates that shareholders should expect positive value

creation from these types of mergers (Danzon 2004). Black in

2001 also analyzed cross-border M&As. His sample included

361 M&A transactions over the period of 1985 to 1995. Black

focused on abnormal returns to measure M&A performance. In a

three and five year regression of abnormal returns, which

the researchers considered to indicate the long run effects,

Black found negatively significant returns. The study

reports that 53 percent of cross-border M&As resulted in

lower shareholder value one year after M&A (Black 2001). The

negative returns for cross-border firms post M&A in both

three and five-year regressions are consistent with the

domestic findings of both Agrawal and Loughran & Vijh. Conn

in 2001 performed a study comparing domestic and cross-

25

border acquisitions between the years of 1984 to 2000. Conn

concluded that domestic acquisitions did produce negative,

but not cross-border acquisitions. Conn’s regressions showed

significant neutral long-term returns post takeover of

cross-border firms. Their research shows there was no

difference in abnormal returns between domestic and cross-

border M&A’s, in the second and third years (Conn 2001).

With research merger and acquisition performance, there

is a plethora of benchmarks and variables that can alter

findings. In multiple recent academic studies researchers

employ controls for firm size. Andre, Barber and Lyon, and

Kothari and Warner used reference portfolios to control for

firm size (Wang 2007). To construct the size control

portfolio, Andre each month ranked the securities he was

researching by market capitalization. In addition to

controlling for size, recent merger and acquisition studies

on measuring performance also control for book-to-market

ratio. Loughran and Vijh make the connection between book-

to-market ratio and method of payment (Loughran and Vijh

26

1997). Andre’s results show that companies that participated

in M&A activity with target firms with a low book-to-market

ratio outperformed companies that purchased target firms

with high book-to-market ratios, but these results were

insignificant in the long run. Similar to Andre, and

Loughran and Vijh control for market-to-book ratio, Asquith

in 1983 controls for method of payment. Asquith reported

discrepancies on post M&A returns when the form of payment

differs. The study indicated positive returns when M&A

activity was paid in cash, and negative returns for

acquiring companies post M&A that completed the transaction

through stock offering (Asquith 1983).

In order to generate an abnormal return, a benchmark

needs to be incorporated to provide a basis to compare to.

Studies that use stock price to generate abnormal returns

will frequently use tailored industry indexes as a

benchmark. For abnormal returns that focus on accounting

data, indexes will not provide a useful benchmark. Instead

industry averages will be used. Agrawal controlled for

27

changes in company risk or beta on a month-to-month basis.

“When investigating long-run returns over several years,

Dimson and Marsh (1986, especially Fig. 1) present

persuasive evidence that measured performance can be

significantly affected by the firm size effect (Agrawal

1992)” However, Agrawal found that acquiring firms lost 10

percent, five-years post merger. This finding was not

affected by changes in a firm’s beta (Agrawal 1992).

Limited academic research has investigated the various

effects of M&A in the pharmaceutical industry. There is an

abundance of different methods available to measure M&A

performance in the pharmaceutical industry. Because of these

varying methodologies, differentiating time frames, and

changes in the industry regulations, comparison among

different studies proves to be difficult. Danzon (2004)

controls for propensity to merger due to patent expiration,

depleted drug production, and visible firm characteristics.

Danzon (2004) concludes that firms with high propensity to

merge have low internal R&D growth. He further concludes

28

that mergers have a negative effect on internal sales and

R&D growth (Danzon 2004).

My paper will focus on the long and short run effects

of pre & post-M&A for acquiring firms. The methodology this

paper for calculating abnormal returns will use the

traditional market model and abnormal returns equation. We

will be regressing profitability ratios to identify a firm’s

abnormal returns over a period of time. To adjust for cross-

sectional dependency, my study will be weighted according to

size and income generating ability to minimize redundant

detection of long run abnormal returns. To avoid other

potential biases, this analysis will also control for beta,

and firm size. The approaches this paper will participate in

are described in more detail in the proceeding paragraphs.

5: Data and Methods

Section five will present and describe the data I collected and the regression methods used.

Data Description

The data pertaining to the dates of mergers and

29

acquisitions activity is gathered from MergentOnlines and

LexisNexis Company Profiles. MergentOnline gives members

access to all publicly traded company information, which

includes a detailed list of the company’s historic

activities. To reinforce the validity of the collected data,

this analysis fact checked using the LexisNexis resources.

LexisNexis uses the resources of Experian Corpfin, SDC

Mergers and acquisitions, and Mergerstat M&A database, which

display the effective date, the quantitative amount, and

synopsis of the merger or acquisition.

The data includes both United States and foreign

companies merger and acquisition activity on the New York

Stock Exchange. The date of the completion of the merger and

acquisition activity or “effective date” is used to

differentiate the company’s post and pre performance. For

example, if Merck were to acquire Pfizer and the effective

date was June 2005, then 2000 to 2005 would constitute five

years pre merger and 2006 to 2010 would represent five years

post merger. The data collected in this study is considered

30

to be panel data or longitudinal data. Panel data contains

observations where multiple cases (in our case firms) will

be observed multiple times at different time periods. Panel

data is unique because it can provide two types of

information. It can show the difference in performance

between two or more firms, and how the firms performed over

time.

As Healy (1992) states, the use of stock price to

measure the true economic gain of merger and acquisition

activity may not be the best indication of the firm’s

performance. Unlike Loughran and Vijh and Andre who used a

stock price variable to find abnormal returns, this study

uses accounting profitability measures as variables to

generate abnormal returns. Unlike stock price, which is

susceptible to human error and volatile fluctuations,

profitability measures reflect the overall performance of

the company (Healy 1992). If synergies are achieved, then

those synergies should be reflected by an increase in the

company’s profitability. According to investment

31

professionals, the listed measurements are critical in

determining the health and future of the company. The

variables I chose to measure each firm’s profitability were

return on investment, gross profit margin, and return on

equity. The advantage of using profitability ratios is that

inflation does not affect the accounting ratios. This is

because accounting ratios are calculated in the current

fiscal year. The percentage calculated is therefore not

affected by inflation.

The most significant limitation of my data is its

ability to capture the entire effect of M&A activity. In our

estimation we are expecting to be able to identify changes

in the company’s performance within a ten-year window.

However, some firms may take ten years post merger for the

company to be able to benefit from the M&A activity. In

certain situations the beginning M&A activity can produce

negative abnormal returns due to possible redundancies in

operations. In fact, there is not a defined time period when

companies always are able to fully benefit from their

32

acquisition. Our study may not accurately identify all of

the abnormal returns because some of the benefits from the

M&A activity could come to fruition a decade after the

activity took place.

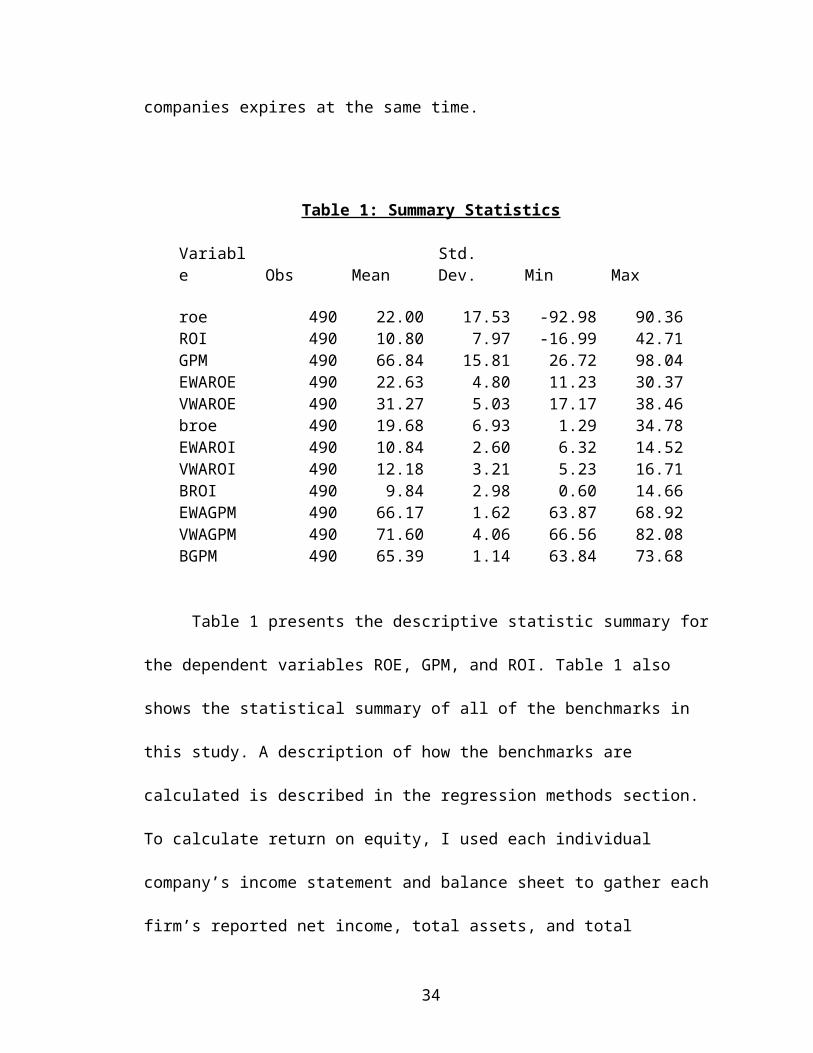

The sample size used in this paper consists of twenty

companies that participated in at least one or more merger

and/or acquisitions, between 1982 and 2013. After omitting

companies with incomplete data on MergentsOnline, or

suspicious merger and acquisition dates, the number of

mergers and acquisitions for gross profit margin (GPM) and

return on equity (ROE) dependent variables is forty-nine.

Return on investment has fifty M&A activity observations,

because there was more historic information on MergentOnline

for this variable. The profitability ratios are calculated

using the firm’s annual fiscal year accounting information.

As stated before, all companies participating in the

following regressions are constituted as operating in the

Pharmaceutical Preparation Manufacturing industry (NAICS

325412). The fiscal year for the majority of the sample

33

companies expires at the same time.

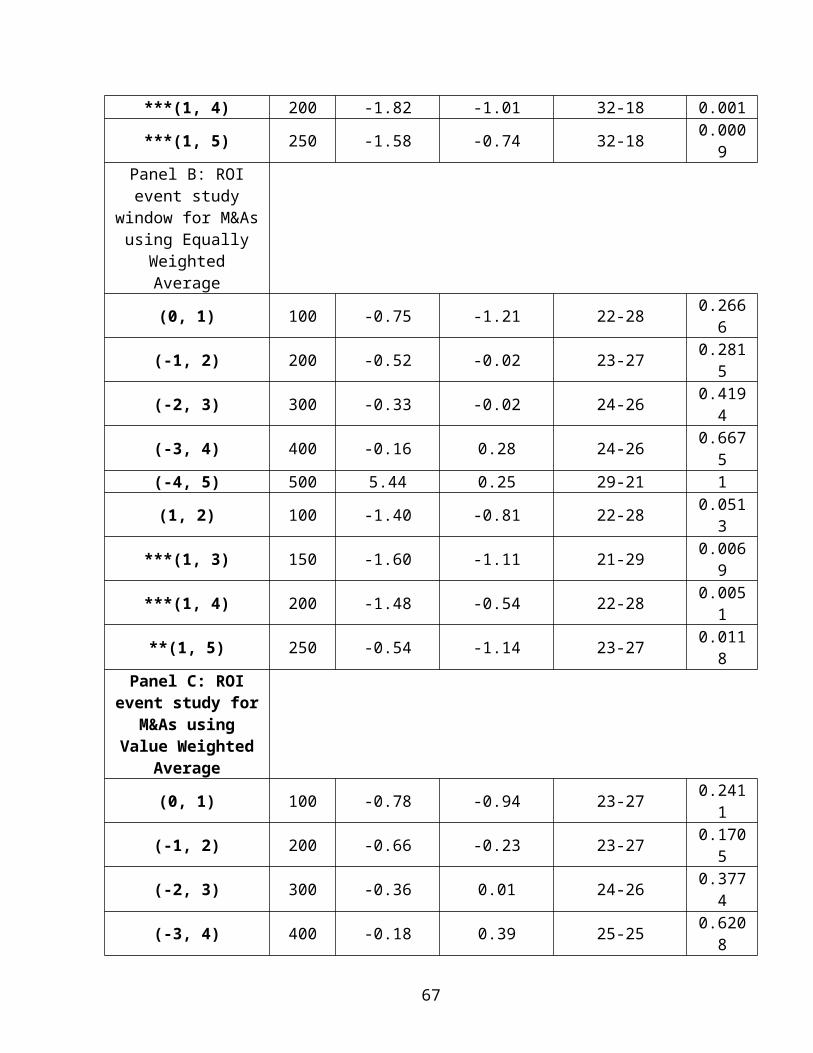

Table 1: Summary Statistics

Variable

Obs Mean

Std. Dev. Min Max

roe 490 22.00 17.53 -92.98 90.36ROI 490 10.80 7.97 -16.99 42.71GPM 490 66.84 15.81 26.72 98.04EWAROE 490 22.63 4.80 11.23 30.37VWAROE 490 31.27 5.03 17.17 38.46broe 490 19.68 6.93 1.29 34.78EWAROI 490 10.84 2.60 6.32 14.52VWAROI 490 12.18 3.21 5.23 16.71BROI 490 9.84 2.98 0.60 14.66EWAGPM 490 66.17 1.62 63.87 68.92VWAGPM 490 71.60 4.06 66.56 82.08BGPM 490 65.39 1.14 63.84 73.68

Table 1 presents the descriptive statistic summary for

the dependent variables ROE, GPM, and ROI. Table 1 also

shows the statistical summary of all of the benchmarks in

this study. A description of how the benchmarks are

calculated is described in the regression methods section.

To calculate return on equity, I used each individual

company’s income statement and balance sheet to gather each

firm’s reported net income, total assets, and total

34

liabilities. This information was collected through the

MergentOnline database. Return on equity is calculated by

net income over average common shareholders’ equity, where

average common shareholders equity is derived from

difference between total assets and total liabilities, then

averaged with the previous years common shareholders equity.

The number of observations for ROE is 500. ROE had a mean of

22%, and a standard deviation of 17.52; this is the largest

out of all of the dependent variables.

The profitability measures return on investment and

gross profit margin were calculated using MergentOnline

resources, these dependent variables included 490

observations. Return on investment can be calculated in

numerous ways but due to some limitations of the data,

return on investment is calculated in the following way:

dividing net income over average total asset, where average

total assets is the average of the current year’s total

assets and the previous year’s total assets. ROI showed the

smallest standard deviation value, suggesting its sample

35

size has the least variation from the mean. Gross profit

margin indicates the firm’s ability to generate profits

through its core operations. This ratio represents the

percentage of each sales dollar remaining after the cost of

goods sold. Gross profit margin is derived by dividing the

difference between revenue and cost of goods sold over

revenue. GPM had a mean of 66.84%, suggesting on average

over the entire time period firms have the ability to retain

66.84 cents per dollar of goods sold. No firm in this sample

size produced a negative GPM.

7: Regression Methods

The following regression is an event study, because it

uses statistical methods to identify the impact of mergers

and acquisitions on firm performance. The data analysis and

statistical software used to perform this event study was

Stata. The event study approach is used to analyze the

reaction of profitability ratios after the completion of a

major merger and/or acquisition. The regression model used

was the random effect model. The random effect model is used

36

because we are assuming that the independent variables are

random and not fixed. The variables in this regression are

random variables because these twenty companies are intended

to help generalize the pharmaceutical market as a whole

(Portland State School, 2006). Similar to Wang, often time

firms would have overlapping mergers, meaning that companies

would perform more than one merger in a five-year span.

Overlapping mergers can cause a cross-sectional dependency

problem (Wang 2007). To control for this, I isolated each

merger as its own individual firm. For example, if Merck

bought Johnson and Johnson in 2000, and Aetna in 2002, the

firm name for the first merger would be Merck and the firm

name for the second merger would be Merck1. In order to run

the regression that corresponded with merger and acquisition

activity, a specific date had to be selected, and estimated

parameters needed to be constructed. To illustrate this,

suppose a company’s effective date for a merger is September

30th 2008. An estimated event window is then constructed for

two defined periods per-merger years (-4, 0) to represent

five year prior to merger, and post-merger years (1, 5) to

37

represent five years performance post merger. In order to

analyze the effect of abnormal return over time, I adjusted

the estimated window range from a ten-year window to smaller

ranges. This allows me to compare the effect of abnormal

returns in both the long and short-run.

To adjust for size bias and to estimate abnormal

returns, I used a market model with three different

benchmarks. The first benchmarked used, BROE, was computed

using the ratios from the firms included in the study plus

twenty companies operating on different exchanges. These

additional companies are classified as working in the

pharmaceutical sector of the market. Additionally, according

to the experts at MergentOnline, all companies added into

the benchmark were characterized as competitors to the

majority companies in the pharmaceutical preparation and

manufacturing industry. The next benchmark I created was an

equally weighted average of each company’s profitability

ratio per year. This benchmark was created by averaging the

ratios of each company equally, implying that each firm’s

38

ratios have the same effect on the average. The last

benchmark used in this analysis was a value weighted

average. The value-weighted benchmark was valued by the

firm’s ability to generate income. For the dependent

variables ROE and ROI net income was used to determine the

company’s impact on the average. The more net income a

company had, the greater impact their ratio has on the

average. For GPM the value of the firm’s ratio on the

benchmark average is determined by the amount of revenue the

company generates. The reason we used value-weighted average

is that larger companies are traditionally viewed as less

volatile and a better indicator of industry performance. The

equally weighted and value weighted benchmark were

calculated using only the companies included directly in the

study. The use of three different benchmarks will help

support the validity of my findings.

The traditional market model to generate estimated

abnormal returns is calculated by:

R i, t = α + Benchmark + ε i, t

39

(1)

Where Ri,t is the return on company i during year t, α is

alpha. The traditional market model only calculates the

firm’s return for a certain time period. The traditional

model helps us generate the predicted return for a certain

time period. To determine if a company benefited or

suffered from M&A activity, we examine each firm’s abnormal

returns over a single time period. To identify a firm’s

abnormal return per year, we used the following equation:

ARi,t = R i, t – predicted return

(2)

The methodology behind finding abnormal returns will be

described in this section. Predicted return is calculated

using the company’s historic performance and industry

benchmarks and previous performance as a tool to estimate

how the company should be performing. The estimated model

implies that a company will continue on its historic trend

within the parameters of the industry as a whole. The actual

40

predicted value was generated using the Stata. When

calculating the difference between the company’s actual

performance and its predicted performance, we are able to

identify if the company has experienced a change in its

trends. If the company continues on its historical trend

then abnormal returns will be zero. If the abnormal return

is a positive number, this indicates that the company,

because of the merger and acquisition activity, was able to

improve on its traditional and expected growth trend. If the

abnormal return is a negative number, then this means that

the M&A activity actually had a negative impact on the

company’s growth trend. The abnormal return will be

statistically important only if the data comes to be

statistically significant, meaning P values are less

than .05. Once the abnormal returns are achieved, averages

are computed for each year across all firms.

8: Empirical Results

In this section we present and discuss our empirical

findings using the model discussed above.

41

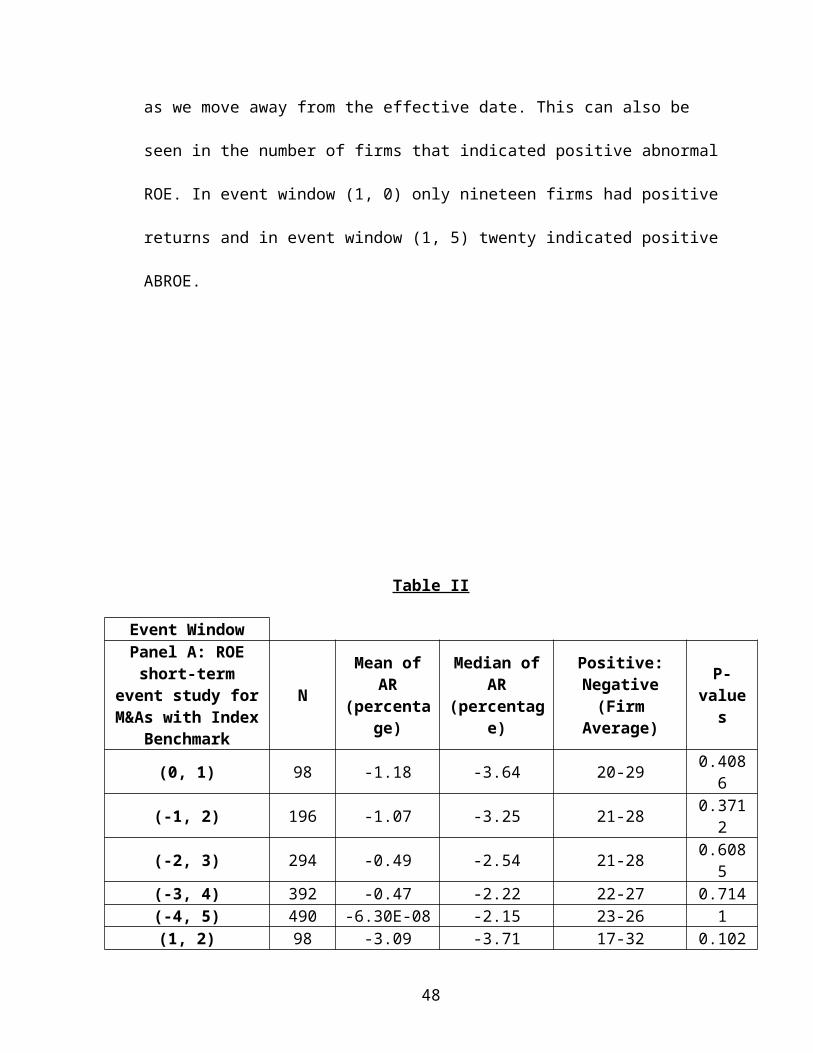

Event window results for Return on Equity

Table II shows the results of the horizon short-term

event study based on return on equity, using the traditional

market model and our abnormal returns equation. Panel A

reports the profitability performance results for M&A

activity based on the company’s return on equity. The

benchmark that Panel A incorporates uses multiple

competitors not located on the New York Stock Exchange; this

provides more broad exposure to the overall performance of

the pharmaceutical industry. Panel B reports the results of

the same information as Panel A; however, Panel B uses the

equally weighted averages as the benchmark. Panel C

integrates the same event windows as both Panels A and B,

while using a different benchmark of value weighted average.

In the preceding tables N represents the number of

observations, and the mean and median are represented as a

percentage. The column Positive: Negative represents the

number of firms that had either a negative or positive mean.

42

The results in Panel A indicate that after a merger or

acquisition occurs, the company’s return on equity ratio is

reduced. The average drop in a company’s ROE two years post

M&A activity is -3.08 percent. Excluding event window (1,

4), which represents the average abnormal ROE four years

post merger, year-over-year the value of ROE increases. The

value of abnormal ROE from two years post merger to five

years post merger increased by thirty percentage points.

Event windows (1, 3), (1, 4), and (1, 5) are all

statistically significant values at alpha .05. This

indicates that our results show with 95% confidents that on

average firms participating in M&A activity three, four, and

five years post merger will produce negative returns.

What is interesting about Panel A’s results is the

trend of how much abnormal ROE has dropped year after year.

Event window (0, 1), which illustrates the abnormal return

on equity for one year post and pre-merger, has a negative

abnormal ROE of -1.18%. Though this number is not

statistically significant, the value is what we would have

predicted. In the first year post and pre merger, the

43

companies produced the worst median and mean abnormal

return. As the study begins to incorporate more years after

and before the “effective date,” the abnormal ROE begins to

increase in value. This can be seen in event windows (-1,

2), (-2, 3), and (-3, 4); the average abnormal ROE increases

by .11 percentage points when expanding the post and pre

merger to a total span of four years. This trend continues

in the six-year (-2, 3) window where the abnormal ROE

increased by .69 percentage points. After the window

incorporates eight years, the average AR increased by .70

percentage points.

Congruent with the increases of mean of abnormal

return, the median abnormal return on equity also increased

as the study incorporates more years after and before the

merger’s effective date. Despite the increase of abnormal

ROE year-over-year, the mean and median abnormal return on

equity four-years pre and post-merger is still negative. It

is also worth noting that as our event windows include more

years, the P values also increase in significance, except

for in event window (-1, 2).

44

Panel B compares the sample size companies’ return on

equity while using the equally weighted benchmark. Similar

to our index benchmark, no positive mean or median abnormal

return on equity was identified in any of the event windows.

Panel B signifies that as we incorporate more years post and

pre merger, the average value of abnormal ROE increases. In

the first year pre and post M&A completion, only twenty-one

companies out of forty-nine produced positive abnormal

returns. However, in event window (-3, 4), which included a

regression of eight years (four pre, and four post), twenty-

five companies were identified as generating a positive

abnormal return on equity. Panel B also displays the fact

that as we expanded our event window period, the P-value

increases. Panel B, in comparison to Panel A, has

significantly lower mean and median abnormal ROE. This may

suggest that the included pharmaceutical companies have

produced higher levels of ROE over the same period than the

companies directly included in this study.

Panel B displays statistically significant results from

event windows (1, 3) and (1, 4) at alpha .05. This

45

indicates that we are 95% confident that on average abnormal

return on equity will be -3.17% three years post merger, and

-3.03% four years post merger. When comparing firms’ average

abnormal return on equity one-year post merger to five years

post merger, the average abnormal return increases by .38

percentage points. This suggests that as firms move away

from the completion date of M&A activity, the average

abnormal return on equity percentage increases. This is

supported by the increase in the number of firms that were

identified with positive mean abnormal ROE. After the first

year post merger, only twenty-one firms produced a positive

mean abnormal ROE. This number increases to twenty-three

firms after a five-year period post M&A activity.

Panel C differs from the other two Panels because it

uses a value weighted index. Despite the different

benchmarks, the trend of the numbers is quite similar to the

other Panels. The results in event window (0, 1) produced

the greatest mean and median negative abnormal return on

equity (ABROE). Again as we include more post and pre M&A

activity years, the mean and median abnormal ROE increases

46

in value. This trend can be supported when looking at the

number of companies that had a negative abnormal ROE one-

year post & pre merger versus four years post & pre merger.

In event window (0, 1) twenty-seven companies were

identified as having a negative abnormal ROE. In event

window (-3, 4) the number of companies experiencing negative

ABROE decreased to twenty-six. The trend of increasing mean

and median ABROE is consistent within A, B, and C Panels.

Panel C also displays the abnormal return on equity

just for years after merger. Only event windows (1, 3), and

(1, 4), representing three and four years post merger, are

statistically significant at alpha .05. For three-year post

M&A activity, firms on average produced -3.13% less abnormal

return on equity. In a four-year period post M&A completion

date, firms had an average 3.35% less abnormal return on

equity. Isolating all of the event windows that strictly

obtain post M&A activity years, the largest percentage

decrease in ABROE was (1, 2), and the smallest decrease in

ABROE was in (1, 5). This is similar to the trend discussed

above where the value of abnormal return on equity increases

47

as we move away from the effective date. This can also be

seen in the number of firms that indicated positive abnormal

ROE. In event window (1, 0) only nineteen firms had positive

returns and in event window (1, 5) twenty indicated positive

ABROE.

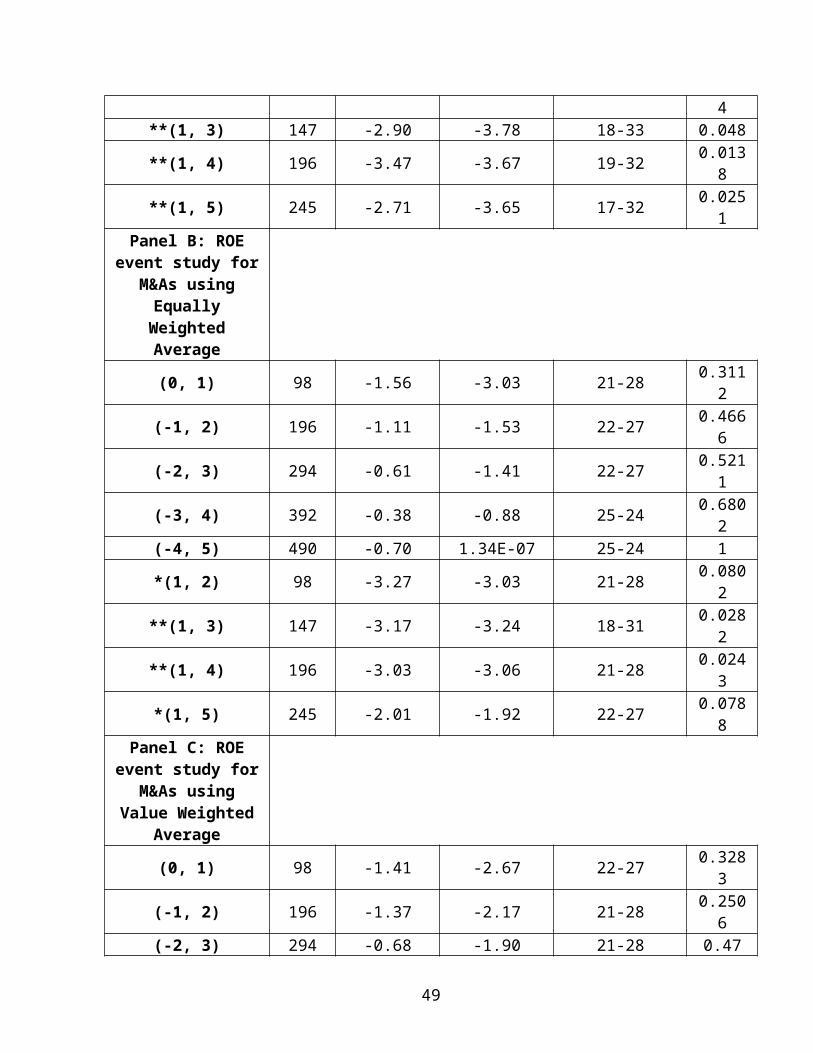

Table II

Event WindowPanel A: ROEshort-term

event study forM&As with Index

Benchmark

N

Mean ofAR

(percentage)

Median ofAR

(percentage)

Positive:Negative(Firm

Average)

P-value

s

(0, 1) 98 -1.18 -3.64 20-29 0.4086

(-1, 2) 196 -1.07 -3.25 21-28 0.3712

(-2, 3) 294 -0.49 -2.54 21-28 0.6085

(-3, 4) 392 -0.47 -2.22 22-27 0.714(-4, 5) 490 -6.30E-08 -2.15 23-26 1(1, 2) 98 -3.09 -3.71 17-32 0.102

48

4**(1, 3) 147 -2.90 -3.78 18-33 0.048

**(1, 4) 196 -3.47 -3.67 19-32 0.0138

**(1, 5) 245 -2.71 -3.65 17-32 0.0251

Panel B: ROEevent study for

M&As usingEquallyWeightedAverage

(0, 1) 98 -1.56 -3.03 21-28 0.3112

(-1, 2) 196 -1.11 -1.53 22-27 0.4666

(-2, 3) 294 -0.61 -1.41 22-27 0.5211

(-3, 4) 392 -0.38 -0.88 25-24 0.6802

(-4, 5) 490 -0.70 1.34E-07 25-24 1

*(1, 2) 98 -3.27 -3.03 21-28 0.0802

**(1, 3) 147 -3.17 -3.24 18-31 0.0282

**(1, 4) 196 -3.03 -3.06 21-28 0.0243

*(1, 5) 245 -2.01 -1.92 22-27 0.0788

Panel C: ROEevent study for

M&As usingValue Weighted

Average

(0, 1) 98 -1.41 -2.67 22-27 0.3283

(-1, 2) 196 -1.37 -2.17 21-28 0.2506

(-2, 3) 294 -0.68 -1.90 21-28 0.47

49

(-3, 4) 392 -0.55 -1.50 23-26 0.5328

(-4, 5) 490 3.31E-08 -0.78 23-26 1

(1, 2) 98 -3.48 -3.60 19-30 0.0652

**(1, 3) 147 -3.13 -3.17 18-31 0.033

**(1, 4) 196 -3.35 -3.00 20-29 0.0168

*(1, 5) 245 -2.20 -2.22 20-29 0.0659

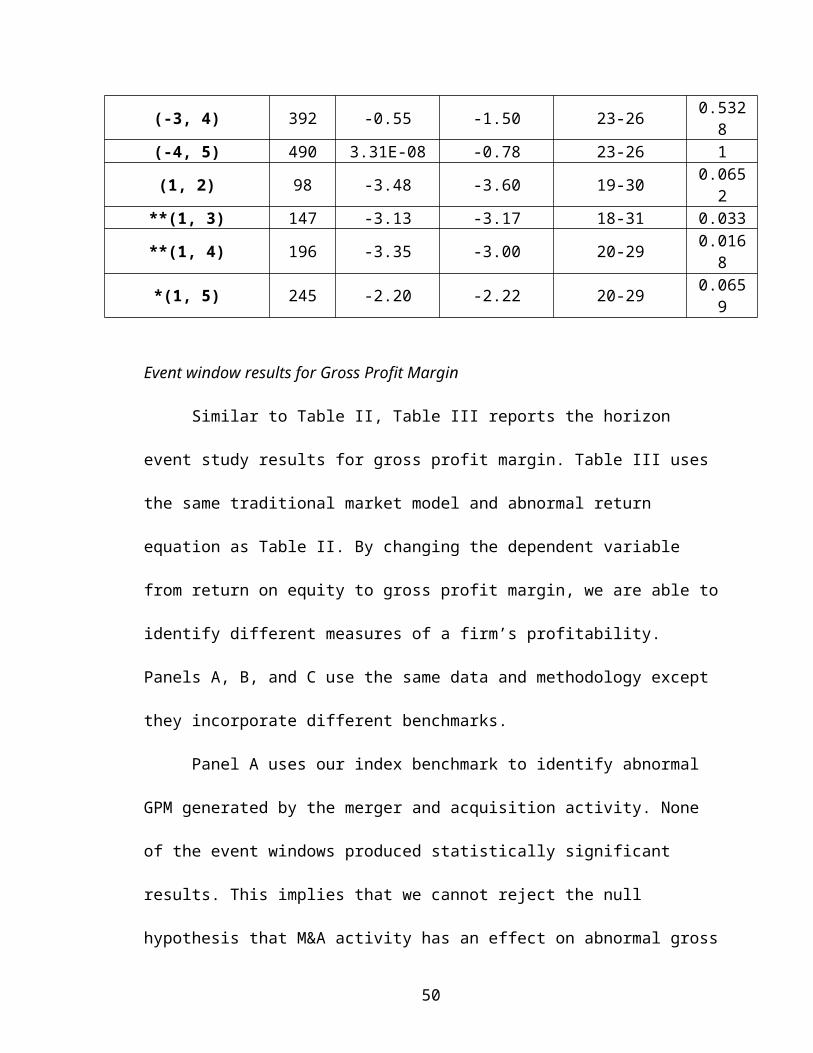

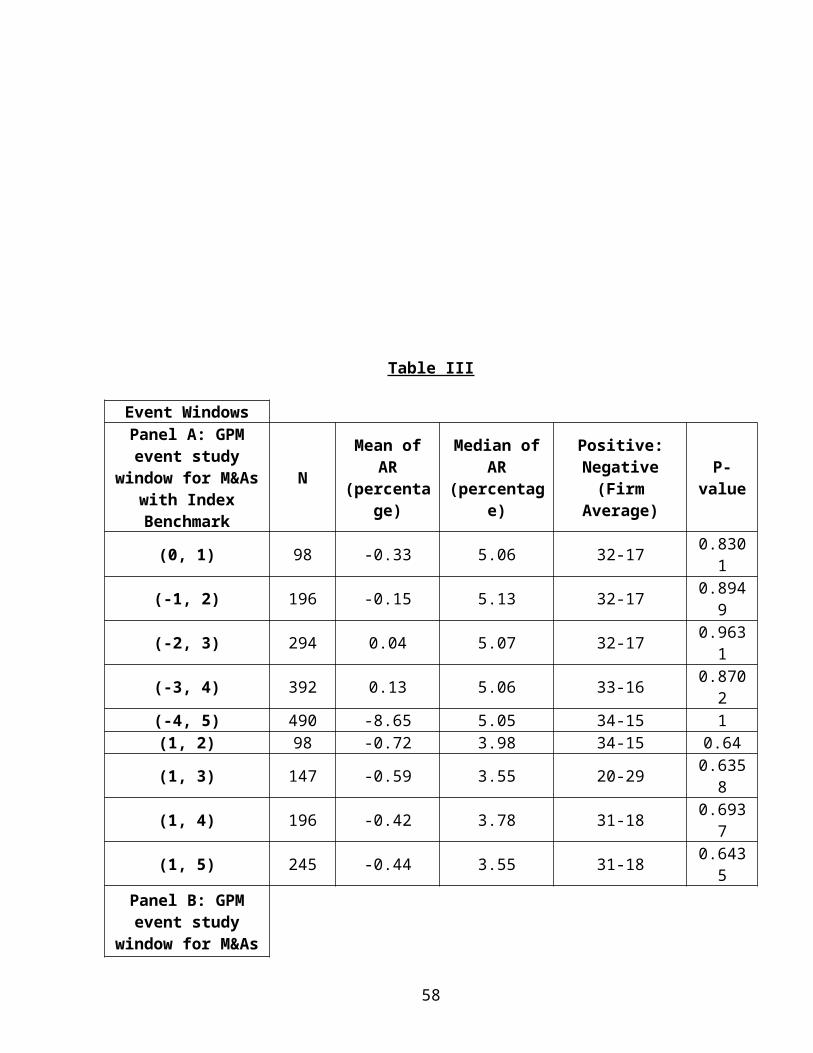

Event window results for Gross Profit Margin

Similar to Table II, Table III reports the horizon

event study results for gross profit margin. Table III uses

the same traditional market model and abnormal return

equation as Table II. By changing the dependent variable

from return on equity to gross profit margin, we are able to

identify different measures of a firm’s profitability.

Panels A, B, and C use the same data and methodology except

they incorporate different benchmarks.

Panel A uses our index benchmark to identify abnormal

GPM generated by the merger and acquisition activity. None

of the event windows produced statistically significant

results. This implies that we cannot reject the null

hypothesis that M&A activity has an effect on abnormal gross

50

profit margin. Event window (0, 1) includes the first year

pre and post merger and acquisition activity. Parallel to

the findings in return on equity, from event windows (1, 0)

to (-3, 4) the mean abnormal GPM value increases. Event

window (-2, 3) had a mean abnormal gross profit margin of

0.04%, while event window (-3,4) had a mean abnormal return

of 0.13% percentage points. Between event windows (1, 0) and

(-3, 4), the mean abnormal return increased by 0.46

percentage points. This helps support the trend that as

mergers and acquisitions over time generates a greater mean

abnormal gross profit margin.

The median abnormal GPM has been predominately

positive. When separating the high values and low values,

the median abnormal gross profit margin overall of the event

windows hovered around 5, when including year’s post and pre

M&A activity. This indicates that more companies saw a

positive abnormal GPM than negative, suggesting that our

mean values may be skewed by disproportionately large

negative abnormal GPM. In event window (0, 1) the number of

firms that had a positive abnormal GPM one-year pre and post

51

effective date is thirty-two. Event window (-3, 4) includes

three more pre and post M&A years. The results report that

over the additional three years post & pre M&A activity, two

additional firms were able to generate a mean positive

abnormal gross profit margin.

When isolating just the performance years post merger,

the mean abnormal gross profit margin is significantly less

than the event windows including pre & post M&A activity

dates. Congruent with the above statement, the mean abnormal

gross profit margin is also significantly less; the average

value hovers around 3.6. Similar to the results for abnormal

ROE, the mean abnormal GPM one-year post merger is the

smallest percentage at -0.72. Event window (1, 5)

representing five years post effective date endured a mean

abnormal GPM increase of .28 percentage points. This is in

line with the trend we identified in return on equity.

However, in contradiction to that trend, the median abnormal

gross profit margin decreases as the study includes more

years post merger. Event window (1, 2) results indicated

highest value median abnormal GPM. The lowest abnormal

52

median gross profit margin was found in event windows (1, 3)

and (1, 5). The decreasing trend of abnormal GPM is also

represented by the number of firms that indicated positive

abnormal GPM. One-year post merger, thirty-four companies

produced positive abnormal GPM; that number decreased by

three firms when including five years post merger.

Panel B uses the same gross profit margin dependent

variable as Panel A, but instead of using the Index

benchmark it uses our equally weighted average benchmark.

Panel B’s mean abnormal gross profit margin reports similar

results to those found in Panel A. Panel B does not include

any statistically significant results. The mean abnormal GPM

in event window (1, 0) is -0.5%. As the event windows

expand, the mean abnormal gross profit margin increases from

a negative to a positive value at (-3, 4). Comparing event

windows (1, 0) through (-4, 5), the number of companies that

were able to obtain positive abnormal gross profit margins

increased from thirty firms to thirty-four firms. This

indicates that the more years companies have post and pre

M&A activity, the more abnormal returns they are able to

53

obtain. Panel B’s median abnormal return is overwhelmingly

positive, similar to Panel A’s. The average median abnormal

GPM over all event windows including pre and post M&A

activity date is 4.82%. This indicates that firms who

participated in M&A activity were able to see more positive

abnormal returns than negative. As I have stated before,

this may indicate that mean abnormal GPM for the event

windows is slanted due to larger negative abnormal returns.

Counter to the trend of mean abnormal GPM, though only

miniscule, the trend of median abnormal GPM between event

windows (0, 1) and (-3, 4) is decreasing. As we incorporate

more years pre and post M&A effective date, the smaller the

median abnormal GPM becomes. This can also be seen in Panel

A.

The trend of increasing mean abnormal GPM can also be

seen when strictly looking at post M&A performance data.

This constitutes only event windows (1, 2), (1, 3), (1, 4),

and (1, 5). In the first year post merger (1, 0), the mean

abnormal GPM was -0.69%. The result was the

greatest underperformance out of all post M&A activity event

54

windows. This makes sense because it takes time for a

company to be able to identify and create synergies. As we

include more post M&A years, the value of the mean abnormal

GPM increases. Though the mean is still negative at -.22%

five years post merger, the mean abnormal GPM increases

by .47 percentage points. This is congruent with the number

of firms that identified positive abnormal GPM. Between

event windows (1, 2) and (1, 5) two additional firms saw

positive mean abnormal return. In contradiction to mean

abnormal GPM, median abnormal GPM decreases as we include

more years post merger.

Panel C uses the value-weighted average benchmark when

regressing the dependent variable gross profit margin. As

the event windows move from the results of the short-term

performance (0, 1) and (-1,2) to a more long-term view (-2,

3) through (-4, 5), the mean abnormal GPM goes from a

negative to positive. Between event windows (0, 1) to (-3,

4) the mean abnormal return increased by .61 percentage

points. This supports the trend we have been able to

identify, that as we expand to include more post and pre M&A

55

activity years, the mean abnormal GPM increases. One factor

supporting this trend’s theory is the number of companies

that produced positive abnormal gross profit margin between

(1, 0) and (-4, 5). In event window (1, 0) thirty companies

saw a positive abnormal GPM while nineteen companies endured

negative abnormal GPM. As we expand the event window to (-4,

5) to include a total of ten years pre and post merger,

three additional companies went from a negative to a

positive abnormal return. Similar to both Panel A & B, Panel

C also reported a declining trend in median abnormal GPM.

The declining median abnormal return deviates less than

Panel B’s; this is because larger companies tend to be less

volatile than smaller ones.

Panel C also displays the results of abnormal GPM

returns solely for post M&A activity; these event windows

are (1, 2,), (1, 3), (1, 4), and (1, 5). All of the event

windows representing post M&A activity indicate negative

mean abnormal GPM. However, an increasing trend over time

can be identified in both mean and median abnormal GPM. For

both mean and median abnormal GPM, the lowest percentage

56

value presented is located in event window (1, 2). As we

include more years by expanding the event window, the

negative mean and median abnormal GPM increases. The trend

is supported by the number of firms that produced positive

abnormal GPM; in (1, 2) twenty-eight firms had positive

abnormal GPM. That number increases to thirty-two firms when

the study moves from one-year post merger to five-years post

merger. Additionally as we expanded the event window to

include more post M&A years, the P-value also increases,

suggesting less and less significant results.

All of the gross profit margin results in Panel A, B,

and C were not statistically significant. This means we are

not confident that we can reject the null hypothesis that

M&A activity does affect abnormal GPM. The trends in Panel

A, B, C are all consistent; the results indicate that in

event windows (0, 1) and (-1, 2), mean gross profit margin

on average will suffer from a negative abnormal return.

However, when expanding the study to four years post and pre

effective date, the abnormal GPM will increase in value.

57

Table III

Event WindowsPanel A: GPMevent study

window for M&Aswith IndexBenchmark

N

Mean ofAR

(percentage)

Median ofAR

(percentage)

Positive:Negative(Firm

Average)

P-value

(0, 1) 98 -0.33 5.06 32-17 0.8301

(-1, 2) 196 -0.15 5.13 32-17 0.8949

(-2, 3) 294 0.04 5.07 32-17 0.9631

(-3, 4) 392 0.13 5.06 33-16 0.8702

(-4, 5) 490 -8.65 5.05 34-15 1(1, 2) 98 -0.72 3.98 34-15 0.64

(1, 3) 147 -0.59 3.55 20-29 0.6358

(1, 4) 196 -0.42 3.78 31-18 0.6937

(1, 5) 245 -0.44 3.55 31-18 0.6435

Panel B: GPMevent study

window for M&As

58

using EquallyWeightedAverage

(0, 1) 98 -0.50 4.54 30-19 0.7477

(-1, 2) 196 -0.27 5.11 32-17 0.8079

(-2, 3) 294 -0.01 4.89 32-17 0.9855

(-3, 4) 392 0.10 4.82 33-16 0.8914

(-4, 5) 490 -3.96E-07 4.73 34-15 1

(1, 2) 98 -0.69 3.42 30-19 0.6579

(1, 3) 147 -0.46 4.07 30-19 0.7106

(1, 4) 196 -0.24 3.83 32-17 0.827

(1, 5) 245 -0.22 3.62 32-17 0.8188

Panel C: GPMevent study for

M&As usingValue Weighted

Average

(0, 1) 98 -0.43 4.67 30-19 0.7795

(-1, 2) 196 -0.20 4.50 31-18 0.8569

(-2, 3) 294 0.02 4.50 32-17 0.9806

(-3, 4) 392 0.12 4.40 32-17 0.8811

(-4, 5) 490 -9.82E-07 4.31 33-16 1

(1, 2) 98 -0.65 3.66 28-21 0.6707

(1, 3) 147 -0.41 3.95 30-19 0.7423

(1, 4) 196 -0.17 3.94 31-18 0.8723

59

(1, 5) 245 -0.11 4.04 32-17 0.9039

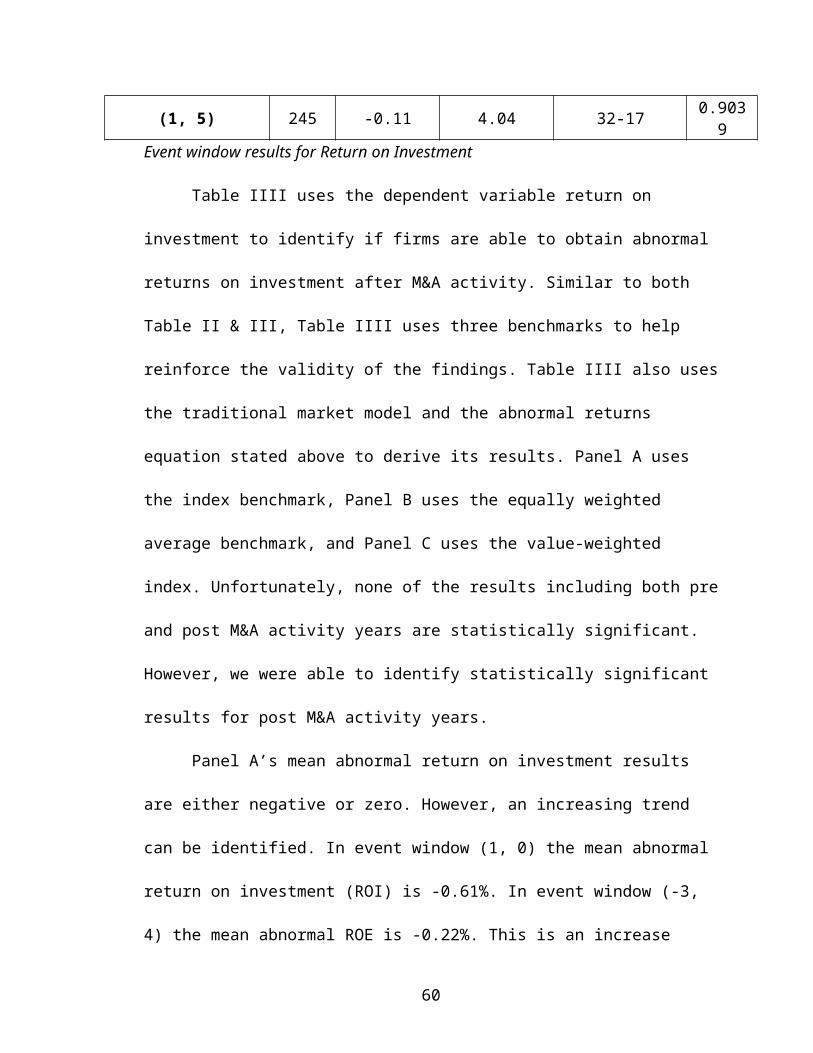

Event window results for Return on Investment

Table IIII uses the dependent variable return on

investment to identify if firms are able to obtain abnormal

returns on investment after M&A activity. Similar to both

Table II & III, Table IIII uses three benchmarks to help

reinforce the validity of the findings. Table IIII also uses

the traditional market model and the abnormal returns

equation stated above to derive its results. Panel A uses

the index benchmark, Panel B uses the equally weighted

average benchmark, and Panel C uses the value-weighted

index. Unfortunately, none of the results including both pre

and post M&A activity years are statistically significant.

However, we were able to identify statistically significant

results for post M&A activity years.

Panel A’s mean abnormal return on investment results

are either negative or zero. However, an increasing trend

can be identified. In event window (1, 0) the mean abnormal

return on investment (ROI) is -0.61%. In event window (-3,

4) the mean abnormal ROE is -0.22%. This is an increase

60

of .39 percentage points. This trend is congruent with the

trends identified in both ROE and GPM. Like the trend of

mean abnormal returns, Panel A shows that as we incorporate

more post and pre M&A activity years, the greater the median

abnormal ROI is. In fact, the median abnormal ROI is

positive 0.23% when the study includes a total of eight

years. However, unlike the results from ROE and GPM, the

number of firms that had a positive abnormal ROI at event

window (0, 1) decreased in comparison to event window (-3,

4). The number of firms with a positive abnormal return went

from twenty-four one-year post & pre mergers to twenty-one

four-years post & pre merger. This trend primarily

contradicts what we found in Table II and III.

Two years after the effective date, firms on average

produced the highest percentage of abnormal ROI on

investment at -1.35%. As the event window expands to include

more years after the effective date, the mean abnormal

return on investment decreases. Though more volatile, the

median abnormal return on investment follows a similar trend

as the mean. Event windows (1, 3), (1, 4), and (1, 5) are

61

all statistically significant at alpha 0.01, indicating that

we are 99% confident that firms on average will produce

negative abnormal return on investment three, four, and five

years post M&A activity.

Panel B uses the equally weighted benchmark to help

generate the predicted abnormal returns. Parallel to the

findings in Panel A, the mean abnormal ROI were either

negative or zero. Additionally, the mean abnormal ROI

increases in value as more years are included in the event

window. The highest percentage abnormal return on investment

occurred in event window (-3, 4) where it produced a value

of -0.16%. Between event windows (1, 0) and (-3, 4) the mean

abnormal return on investment value increased by 0.59

percentage points. Panel B’s first three event windows

produce a negative median abnormal ROI similar to that of

Panel A’s. For return on investment, Panel B presents the

strongest evidence that over time firms are able to generate

the positive abnormal returns, when including both pre and

post M&A activity data. In event window (0, 1) the number of

firms that had a positive abnormal return was only twenty-

62

two, which is less than half of our sample size. However, in

event window (-4, 5), our largest event window, the number

of firms with positive abnormal returns was twenty-nine,

more than half our sample size. This indicates that when

comparing one-year post and post merger versus four-years

pre and post merger, seven additional companies were able to

obtain positive mean abnormal returns.

Panel B also includes event windows that only

incorporate post M&A activity performance data. The three

statistically significant results identified stem from event

window (1, 3), (1, 4), and (1, 5). Event windows (1, 3), and

(1, 4) are statistically significant at alpha 0.01, and

event window (1, 5) is statistically significant at alpha

0.05. These event windows suggest that we can reject the

null hypothesis that M&A activity does not have an effect on

abnormal return on investment ratios. All the significant

event windows produced negative abnormal return on

investment. Between three and five years post M&A activity,

the mean abnormal return on investment increased by 1.06

percentage points. The median abnormal ROI did not follow

63

the same trend as the mean, but between the same time

periods an additional two firms were identified with

positive abnormal ROI.

Panel C uses our value-weighted benchmark to produce

abnormal return results. Consistent with both Panels A and

B, Panel C had all negative mean abnormal ROI. Additionally,

the trend of increasing mean abnormal ROI for event windows

incorporating both pre and post M&A years is also present in

Panel C. From event windows (0, 1) to (-3, 4) the mean

abnormal return on investment increased by 0.60 percentage

points. Unlike the mean abnormal ROI values, the abnormal

ROI median is positive for three event windows: (-2, 3), (-

3, 4), and (-4, 5). Similar to the findings in mean abnormal

ROI, the median abnormal ROI increases as the event windows

expand. This is found in all three of the Panels in Table

IIII. This can also be seen in the number of firms that have

experienced the positive abnormal ROI. In event window (0,1)

only twenty-three companies were identified with positive

abnormal ROI; the number increases to twenty-eight firms in

(-4, 5).

64

Parallel to the finding in Panel B, Panel C’s

significant event windows display increasing abnormal ROI as

the event windows incorporate more years post merger. Both

the mean and median are at their highest value, though still

negative, when we incorporate our greatest sample size of

five years post M&A activity. Event windows (1, 3) and (1,

5) are statistically significant at alpha .05, suggesting

that we are 95% confident that on average firms three and

five years post M&A activity will produce a negative

abnormal return on investment. Event window (1, 4) is

statistically significant at alpha .01, meaning that we can

both reject the null hypothesis and we are 99% confident

that firms on average will produce a negative abnormal

return on investment four years post the effective date.

Unlike the findings in Panels A and B, Panel C median and

mean abnormal ROI for post M&A years follows a correlating

increasing trends.

Overall, Panels A, B, and C all produced similar

results and trends of increased abnormal return on

65

investment for event windows incorporating both pre and post

M&A activity years over time. Additionally when isolating

just the post M&A activity years the mean and number of

firms with positive abnormal ROI for all panels followed

similar trends. This was not the case for the median

abnormal return on investment, as Panel C’s results conflict

with the findings in Panel A and B.

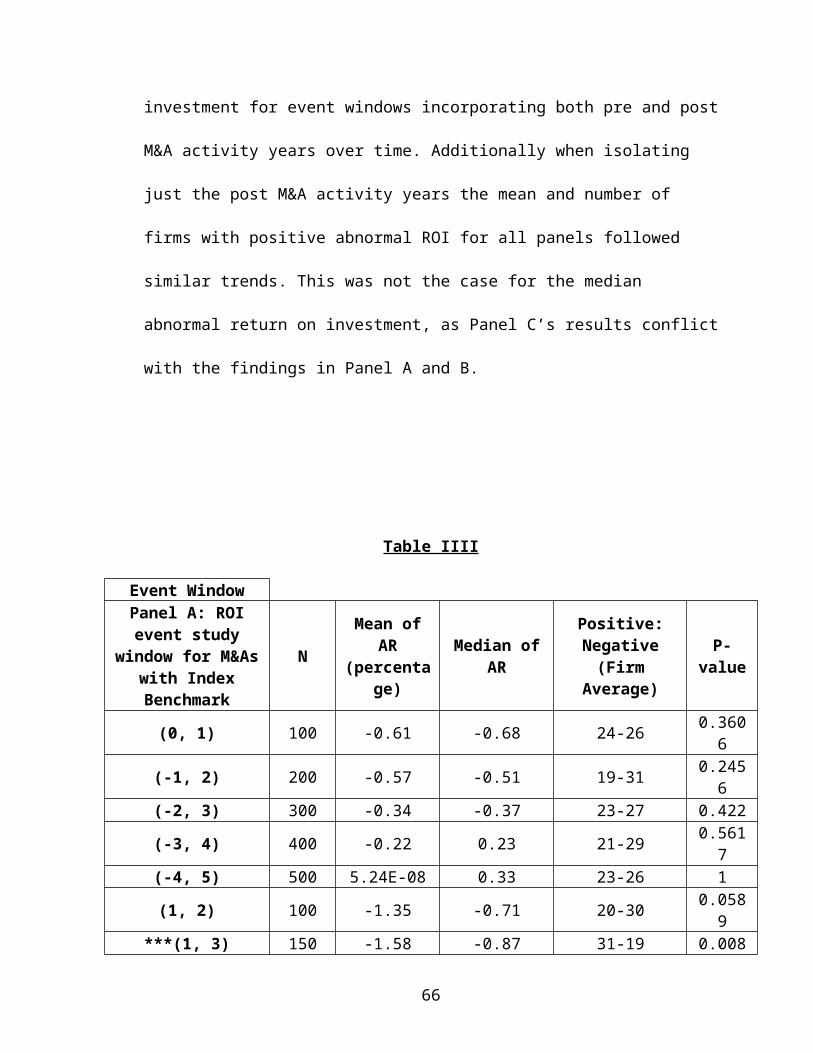

Table IIII

Event WindowPanel A: ROIevent study

window for M&Aswith IndexBenchmark

N

Mean ofAR

(percentage)

Median ofAR

Positive:Negative(Firm

Average)

P-value

(0, 1) 100 -0.61 -0.68 24-26 0.3606

(-1, 2) 200 -0.57 -0.51 19-31 0.2456

(-2, 3) 300 -0.34 -0.37 23-27 0.422

(-3, 4) 400 -0.22 0.23 21-29 0.5617

(-4, 5) 500 5.24E-08 0.33 23-26 1

(1, 2) 100 -1.35 -0.71 20-30 0.0589

***(1, 3) 150 -1.58 -0.87 31-19 0.008

66

***(1, 4) 200 -1.82 -1.01 32-18 0.001

***(1, 5) 250 -1.58 -0.74 32-18 0.0009

Panel B: ROIevent study

window for M&Asusing Equally

WeightedAverage

(0, 1) 100 -0.75 -1.21 22-28 0.2666

(-1, 2) 200 -0.52 -0.02 23-27 0.2815

(-2, 3) 300 -0.33 -0.02 24-26 0.4194

(-3, 4) 400 -0.16 0.28 24-26 0.6675

(-4, 5) 500 5.44 0.25 29-21 1

(1, 2) 100 -1.40 -0.81 22-28 0.0513

***(1, 3) 150 -1.60 -1.11 21-29 0.0069

***(1, 4) 200 -1.48 -0.54 22-28 0.0051

**(1, 5) 250 -0.54 -1.14 23-27 0.0118

Panel C: ROIevent study for

M&As usingValue Weighted

Average

(0, 1) 100 -0.78 -0.94 23-27 0.2411

(-1, 2) 200 -0.66 -0.23 23-27 0.1705

(-2, 3) 300 -0.36 0.01 24-26 0.3774

(-3, 4) 400 -0.18 0.39 25-25 0.6208

67

(-4, 5) 500 -1.74E-08 0.39 28-22 1

(1, 2) 100 -1.29 -0.95 23-27 0.0673

**(1, 3) 150 -1.41 -0.95 21-29 0.0145

***(1, 4) 200 -1.42 -0.88 20-30 0.0065

**(1, 5) 250 -1.01 -0.70 23-27 0.0195

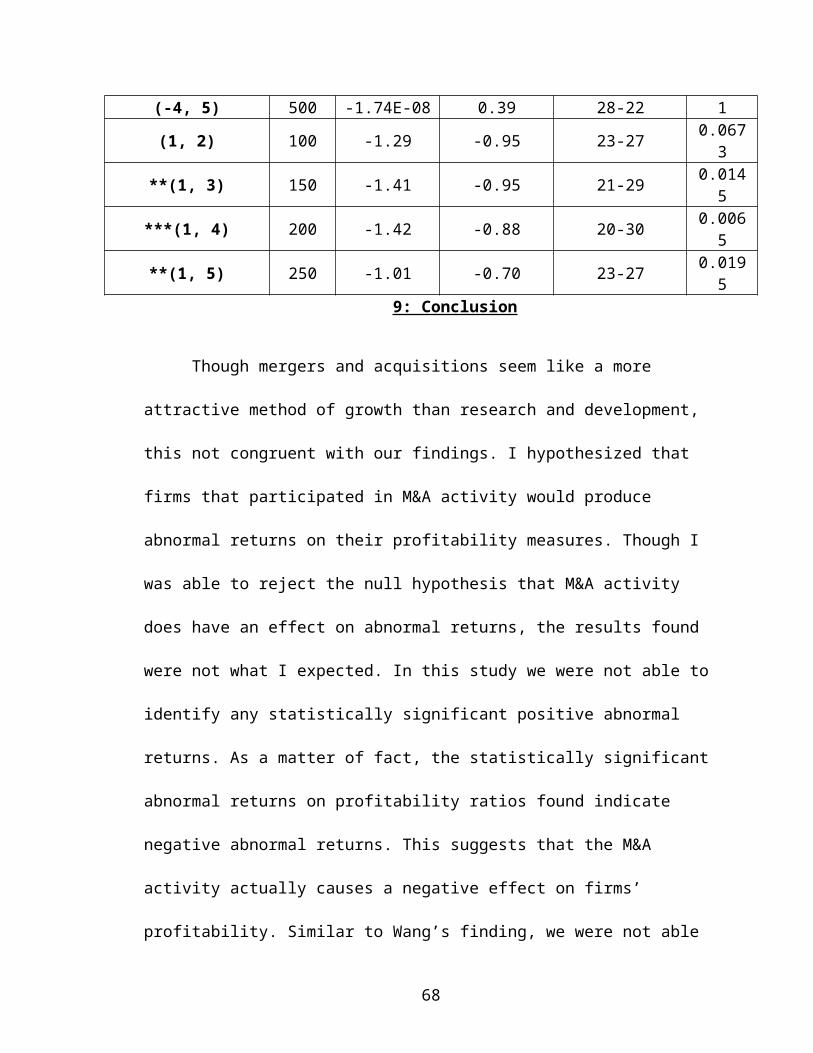

9: Conclusion

Though mergers and acquisitions seem like a more

attractive method of growth than research and development,

this not congruent with our findings. I hypothesized that

firms that participated in M&A activity would produce

abnormal returns on their profitability measures. Though I

was able to reject the null hypothesis that M&A activity

does have an effect on abnormal returns, the results found

were not what I expected. In this study we were not able to

identify any statistically significant positive abnormal

returns. As a matter of fact, the statistically significant

abnormal returns on profitability ratios found indicate

negative abnormal returns. This suggests that the M&A

activity actually causes a negative effect on firms’

profitability. Similar to Wang’s finding, we were not able

68

to identify any improvement in firms’ ROE.

The results from the predominately negative dependent

profitability variables should make readers question the

efficiency of M&A activity. The statistically significant

results for mean and median ROE and ROI post merger indicate

that firms have worse profitability measures than if they

did not partake in the activity. The reason we included the

pre and post M&A event windows is to compare these windows

to the post M&A activity event windows. When comparing the

mean and median abnormal ROI and ROE, the pre and post event

windows significantly outperform. This suggests that on

average firm’s historical profitability trends pre effective

date would predict higher rates than their real

profitability rates post M&A. In our prediction we would

expect that due to synergies and the growth of the

companies, the firms would experience increases in all three

profitability measures. The biggest surprise was that the

dependent variable gross profit margin did not produce an

overwhelmingly positive and significant abnormal return. I

69

would not automatically assume that M&A would cause an

increase in revenues; however, I would expect that GPM would

increase due to a reduction in the cost of goods sold.

The study results beg the question why did M&A activity

cause profitability measure to reduce? Our findings suggest

that target companies are not as easily incorporated as the

acquiring company might have thought. The combining of two

companies is an enormous task, even in horizontal M&A’s each

company is different. Difficulties can arise from

conflicting company cultures, incompatible infrastructures,

and languages. The acquiring company’s management also might

not be effective enough to efficiently incorporate the

assets that they have acquired. Additionally, the post M&A

performance data might be skewed if the acquiring company

and the target company use different account policies, like

FIFO and LIFO.

Despite the strictly negative statistically significant

returns our results indicated M&A activity might not be all-

bad. Discussed in the empirical results section, we were

70

able to identify a trend of increasing abnormal ROI (Panels

B & C) and ROE as we expand the event window. As the study

included more post years the negative abnormal returns

increase in value. This may suggest that M&A do in fact

create positive returns, however it may take the acquiring

company more than five years to achieve.

The question still remains why would pharmaceutical

firms continue to partake in M&A activity when they produce

negative results? Our study’s finding expect that as firms

begin to realize that these activities are actually creating

negative returns, their development preferences will change.

It will be interesting to see if the industries preference

will change, and revert back to heavy dependence on internal

development. Wang suggests that if this preference doesn’t

change, that firm performing M&As knowing that the majority

of them will fail, but the ones that due succeed will makeup

for the ones that don’t (Wang 2007). Additional studies

should be preformed with larger post M&A activity event