Embed Size (px)

Citation preview

2

Where we left off Diversification

It is a growth strategy, associated with the granulating strat. Ansoff Matrix, and closeness measures Diversification Discounts 2 Dimensions for Categorizing

Concentric, Horizontal, Vertical, Conglomerate

Defensive, Offensive

Organizational Structure Definition Dimensions: Specialization, Standardization, Formalization,

Centralization, Configuration, Flexibility Organigrams Forms of organizational Structure

U-Form, M-Form (cooperative, competitive), H-Form, X-Form, Matrix organization

Matrix organization: Advantages, disadvantages

3

Overview

Merger, Acquisition, Buyout

Types of Mergers Getting a picture of

global M&A Reasons for M&A

NPV, 7 Motivation theories Examples: Entering

markets, Restructuring, Strategic Moves, Complementaries

Steps of a M&A Success/Failure reasons

4

Success rates of M&As

Studies show that about two thirds of all M&As fail on average (anywhere from 50 percent to 80, depending on the measure) .

e.g. Allen, 1999; Hudson & Barnfield, 2001; OECD, 2001; Schuler & Jackson, 2001; Slowinski, 2002.

5

What the expert says...

“There is a ‘gin rummy school of management’... you pick up a few businesses here, discard a few there.

The sad fact is that most acquisitions display an egregious imbalance - they are a bonanza for the shareholders of the acquiree; they increase the income and the status of the acquirer’s management; and they are a honey pot for the investment bankers and the other professionals on both sides.

But alas, they usually reduce the wealth of the acquirer’s shareholders, often to a substantial amount.”

-Warren Buffet, Chairman Berkshire Hathaway

6

Definition Mergers & Acquisition

An ‘acquisition’ normally involves the purchase of another firm’s assets and liabilities, with the acquired firm continuing to exist as a legally owned subsidiary of the acquirer. ‘Takeover’ is often used for hostile acquisitions.

A ‘merger’ of equals on the other hand is a combination of two firms where a new corporate entity is created by exchanging the shares of both companies for shares in the new company.

Most M&As, however, are simple acquisitions since only around three percent of all deals can be classified as real mergers between equals (Buckley & Ghauri, 2002).

7

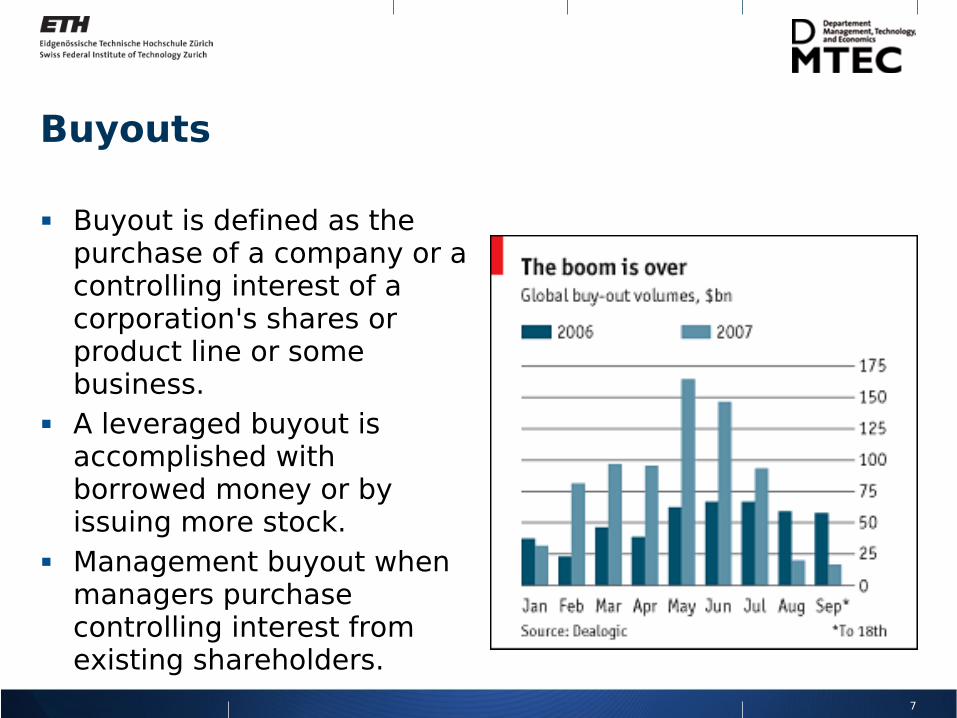

Buyouts

Buyout is defined as the purchase of a company or a controlling interest of a corporation's shares or product line or some business.

A leveraged buyout is accomplished with borrowed money or by issuing more stock.

Management buyout when managers purchase controlling interest from existing shareholders.

8

Buyouts

9

Types of Mergers

Horizontal mergers: two companies in the same industry

Vertical mergers: along the value chain of a good/service

Product-extension: access to complementary products

Market-extension: access to complementary markets

Conglomerate mergers: different industries

src: Federal Trade Commission (FTC)

10

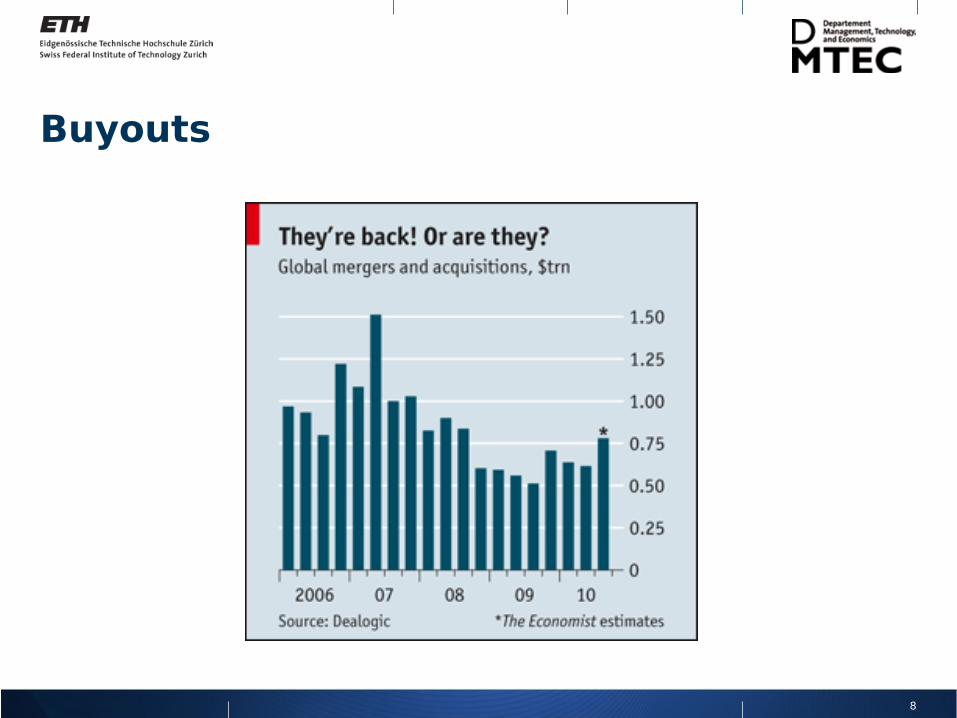

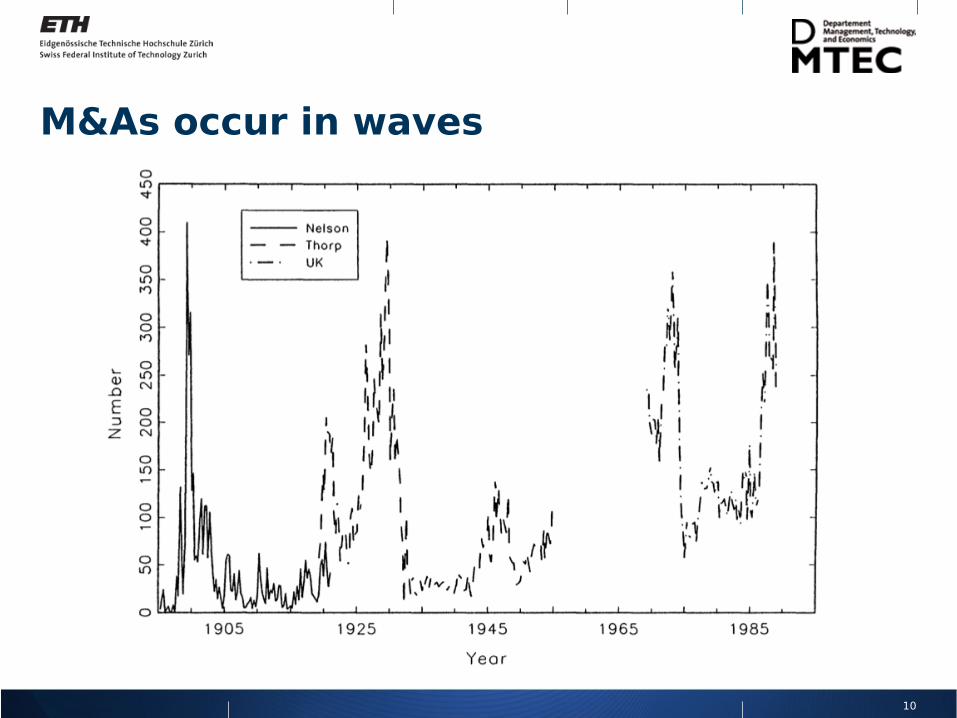

M&As occur in waves

11

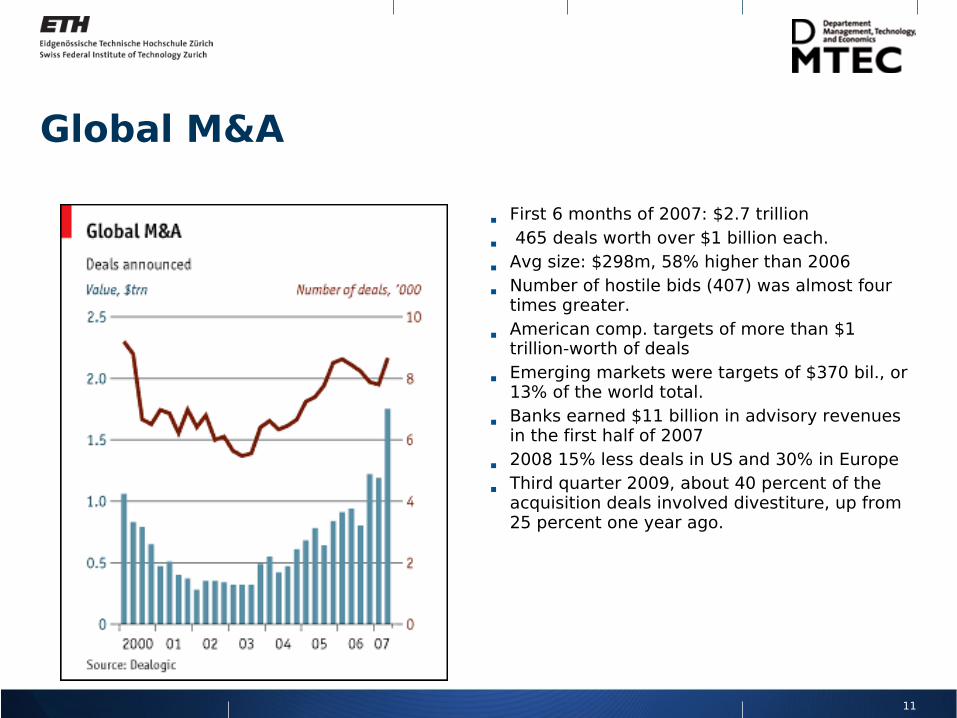

Global M&A

First 6 months of 2007: $2.7 trillion

465 deals worth over $1 billion each.

Avg size: $298m, 58% higher than 2006

Number of hostile bids (407) was almost four times greater.

American comp. targets of more than $1 trillion-worth of deals

Emerging markets were targets of $370 bil., or 13% of the world total.

Banks earned $11 billion in advisory revenues in the first half of 2007

2008 15% less deals in US and 30% in Europe

Third quarter 2009, about 40 percent of the acquisition deals involved divestiture, up from 25 percent one year ago.

12

13

Reasons for M&A

Do they differ from Growth & Diversification reasons? How?

NPV (A + B) > NPV (A) + NPV (B)

NPV := Net Present Value

14

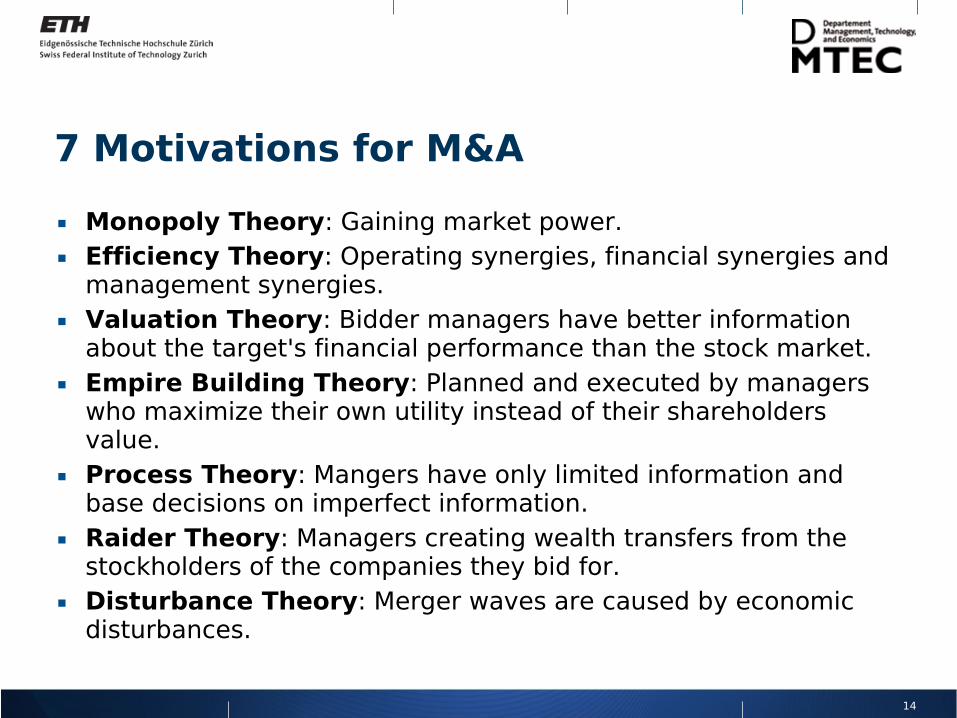

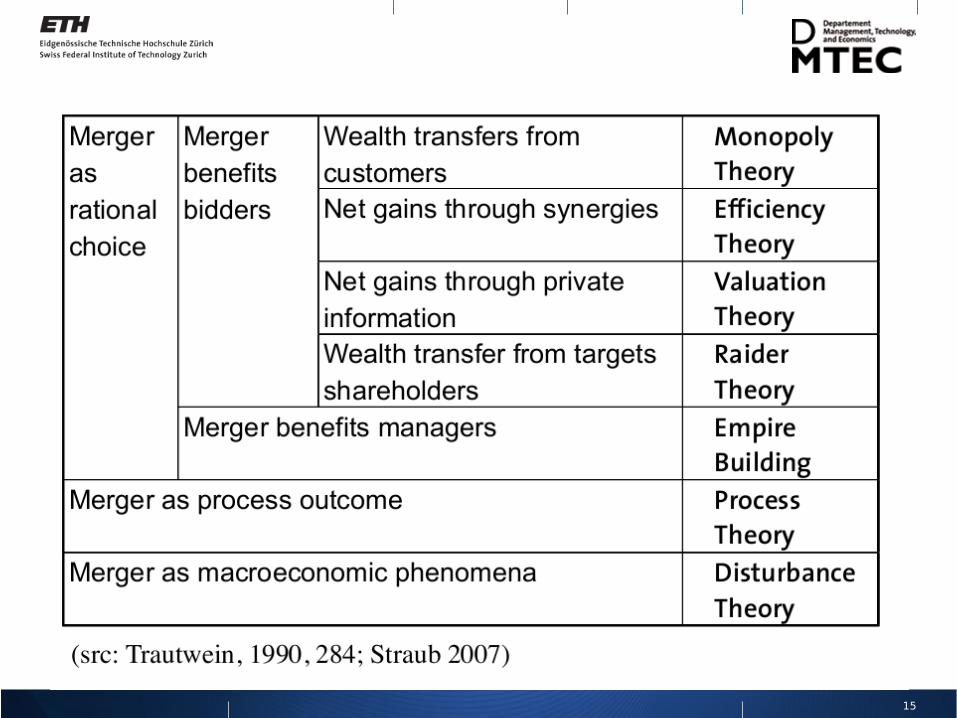

7 Motivations for M&A

Monopoly Theory: Gaining market power.

Efficiency Theory: Operating synergies, financial synergies and management synergies.

Valuation Theory: Bidder managers have better information about the target's financial performance than the stock market.

Empire Building Theory: Planned and executed by managers who maximize their own utility instead of their shareholders value.

Process Theory: Mangers have only limited information and base decisions on imperfect information.

Raider Theory: Managers creating wealth transfers from the stockholders of the companies they bid for.

Disturbance Theory: Merger waves are caused by economic disturbances.

15

16

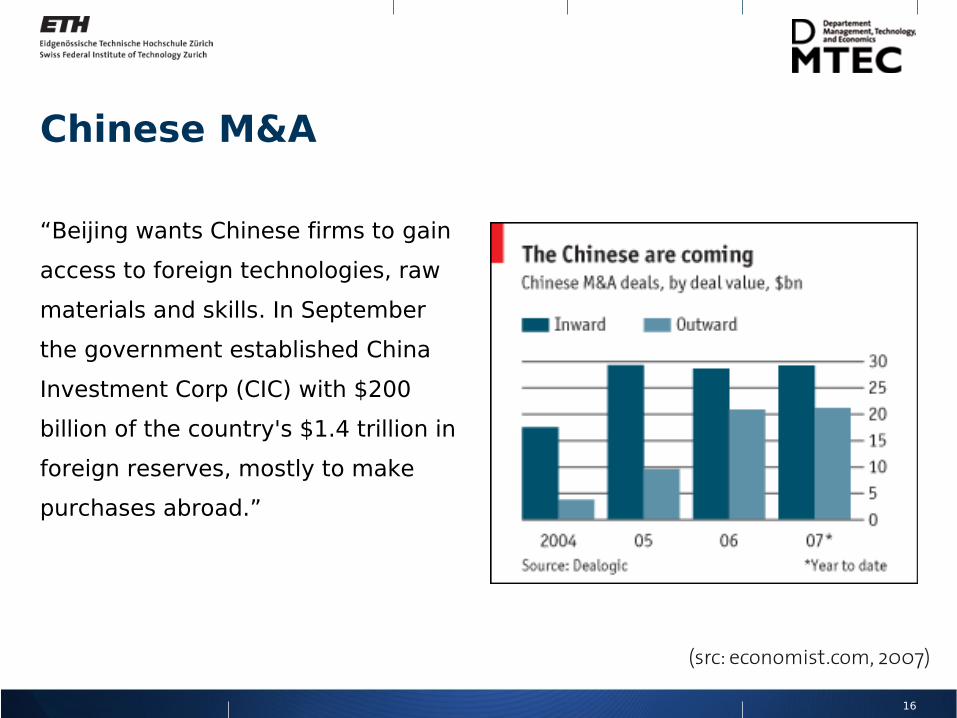

Chinese M&A

“Beijing wants Chinese firms to gain

access to foreign technologies, raw

materials and skills. In September

the government established China

Investment Corp (CIC) with $200

billion of the country's $1.4 trillion in

foreign reserves, mostly to make

purchases abroad.”

(src: economist.com, 2007)

17

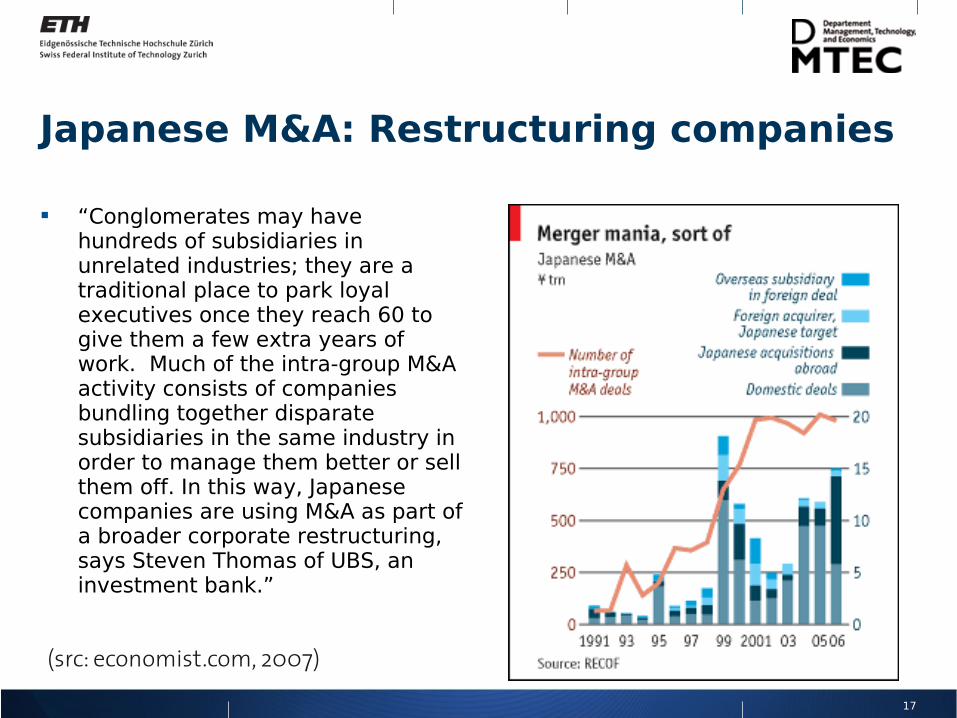

Japanese M&A: Restructuring companies

“Conglomerates may have hundreds of subsidiaries in unrelated industries; they are a traditional place to park loyal executives once they reach 60 to give them a few extra years of work. Much of the intra-group M&A activity consists of companies bundling together disparate subsidiaries in the same industry in order to manage them better or sell them off. In this way, Japanese companies are using M&A as part of a broader corporate restructuring, says Steven Thomas of UBS, an investment bank.”

(src: economist.com, 2007)

18

M&A as a strategic move: Oracle and SAP

Oracle first tried to move beyond databases and other “infrastructure” software (which together produce two-thirds of its revenues) and break into enterprise applications with its own programes. When this failed, it decided to lead consolidation of the software industry and “surround” SAP with acquisitions, in the words of Larry Ellison, its chief executive. Since 2003 Oracle has bought more than 30 firms for about $25 billion in total. BEA does not sell applications, but it will help Oracle win new customers.(The Economist, Oct 18th, 2007)

19

M&A for complementary products:Ebay’s purchase of Skype in 2005 “Skype will provide eBay

with communication platform as a complementary product.”

$2.6 billion with up to 1.5bn more if Skype met certain targets

Skype had 7mio USD turnover in 2004

20

The story goes on...

“This week eBay said that it would take a $1.4 billion charge in relation to the purchase. The bigger part, a so-called impairment write-down, represents eBay's loss on its ill-fated investment.” (The Economist, Oct 4th, 2007)

Wanted to sell 65% of shares for 1,9bn USD to an Investment firm in September 2009. But got sued by Skype founders: Ebay had forgotten to buy the IP rights for all technology used in Skype...

21

Steps of an M&A

1. Formulate Focus or Diversify Strengths to build on and use to create synergies Opportunities Matching Resources and Opportunities

2. prospect (locate, investigate) Search process Looking behind the figures Evaluation: shared resources, transfer of skills, econ. of scale/scope

3. Negotiate & acquire

4. Integrate: people, culture, structures, systems & procedures

(src: adapted, Galpin & Herndon, Thompson & Martin, 2005)

22

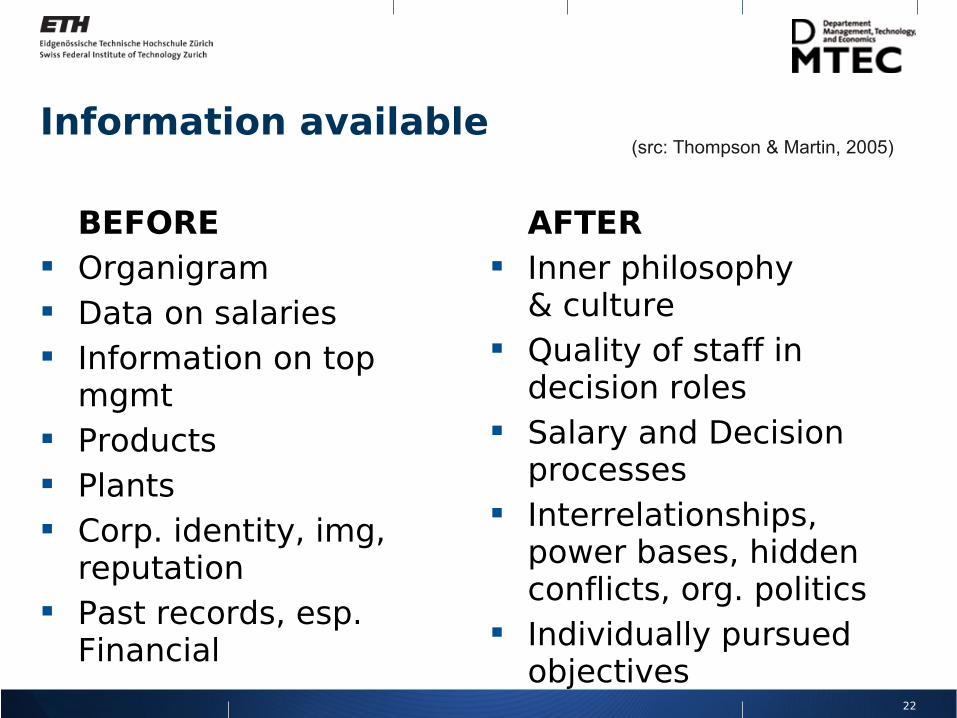

Information available

BEFORE Organigram Data on salaries Information on top

mgmt Products Plants Corp. identity, img,

reputation Past records, esp.

Financial

(src: Thompson & Martin, 2005)

AFTER Inner philosophy

& culture Quality of staff in

decision roles Salary and Decision

processes Interrelationships,

power bases, hidden conflicts, org. politics

Individually pursued objectives

23

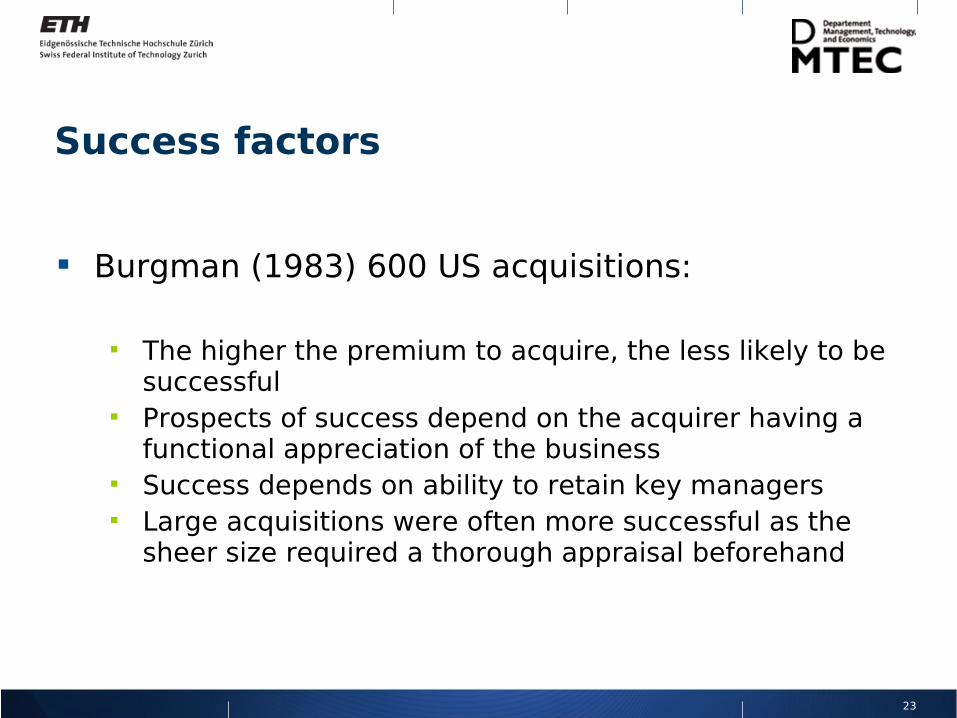

Success factors

Burgman (1983) 600 US acquisitions:

The higher the premium to acquire, the less likely to be successful

Prospects of success depend on the acquirer having a functional appreciation of the business

Success depends on ability to retain key managers Large acquisitions were often more successful as the

sheer size required a thorough appraisal beforehand

24

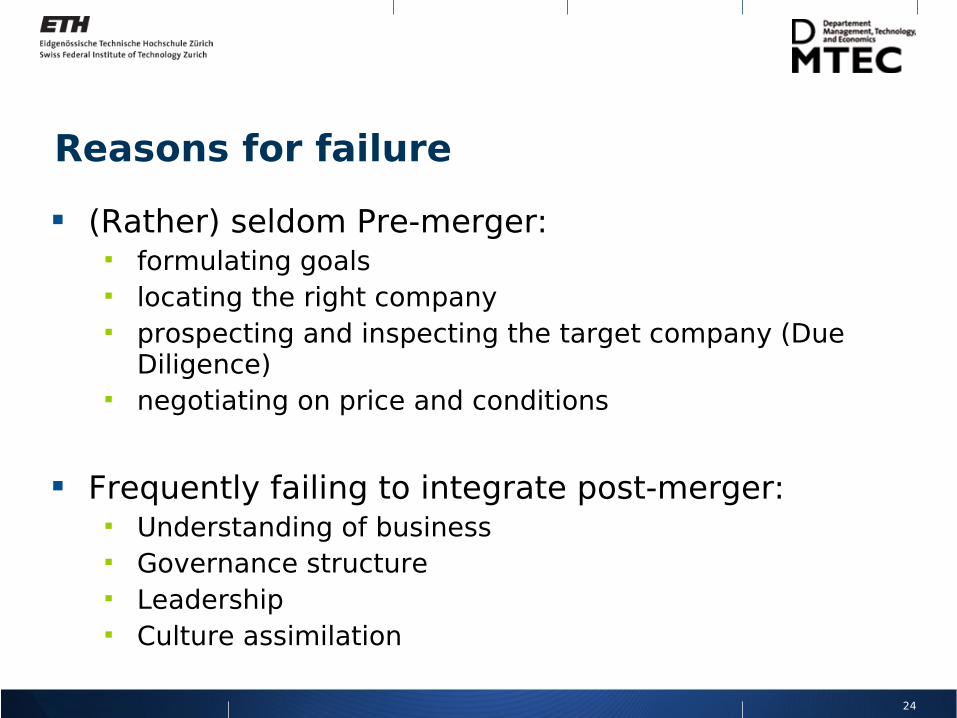

Reasons for failure

(Rather) seldom Pre-merger: formulating goals locating the right company prospecting and inspecting the target company (Due

Diligence) negotiating on price and conditions

Frequently failing to integrate post-merger: Understanding of business Governance structure Leadership Culture assimilation

25

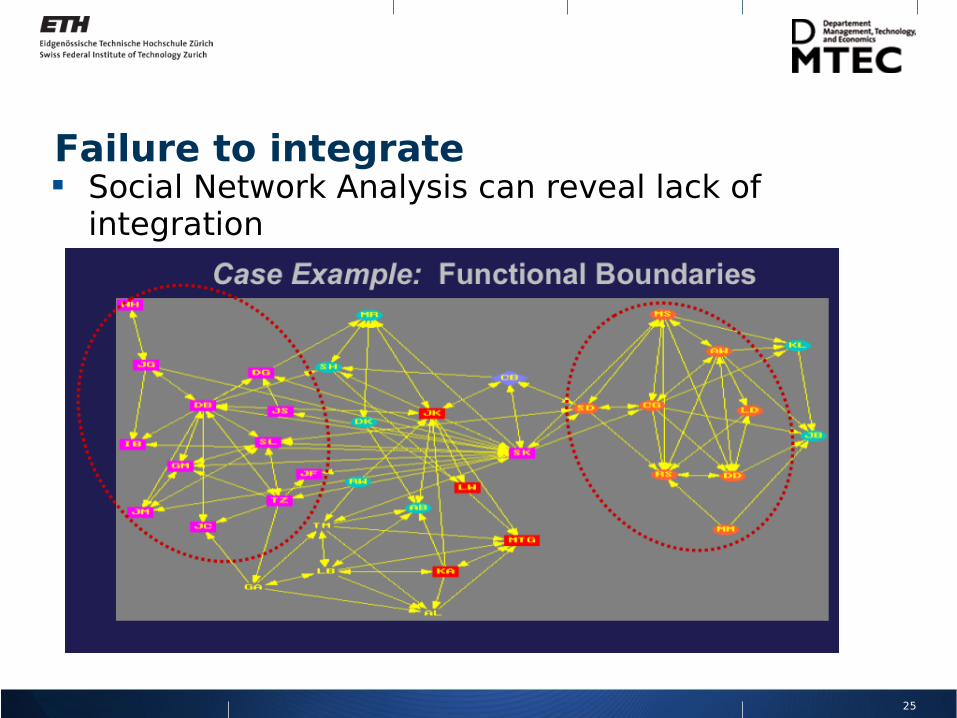

Failure to integrate Social Network Analysis can reveal lack of

integration

26

Wrap up

Definitions Merger, Acquisition, Buyout

Types of Mergers Horizontal, Vertical, Product-extension, Market-extension,

Conglomerate mergers

Getting a picture of global M&A Reasons for M&A

NPV, 7 Motivation theories Examples: Entering markets, Restructuring, Strategic

Moves, Complementaries

Steps of a M&A Success/Failure reasons

Seldom premerger, often failure to integrate

27

References

Burgman, R. J. A strategic explanation of corporate acquisition success Purdue University, 1983 (quoted in quoted in: Mc Lean R.J. April 1985 How to make acqisitions work, Chief Executive)

Thompson, J. & Martin, F. Strategic Management: Awareness and Change Thomson Learning, 2005

Harford, J. What drives merger waves? Journal of Financial Economics, 2005, 77, 529-560

Additional reading: Lubatkin, M. 1983. `Mergers and the Performance

of the Acquiring Firm.' Academy of Management Journal, 8(2), 218-225.