Embed Size (px)

Citation preview

1

A Study of Beijing‘s Competitive Advantage

as an Emergent Media Capital

Angela Lin Huang

Bachelor of Law / Master of Law

A dissertation presented in fulfilment of the requirements for the

degree of Doctor of Philosophy

Creative Industries Faculty,

Queensland University of Technology

2012

i

Keywords

Media capital

Media industries

Media market

Media cluster

Media policy

China

Beijing

Institution

ii

Abstract

The development of creative industries has been connected to urban

development since the end of the 20th

century. However, the causality of why

creative industries always cluster and develop in certain cities hasn‘t been

adequately demonstrated, especially as to how various resources grow, interact

and nurture the creative capacity of the locality. Therefore it is vital to observe

how the local institutional environment nurtures creative industries and how

creative industries consequently change the environment in order to better

address the connection between creative industries and localities.

In Beijing, the relocation of CCTV, BTV and Phoenix to Chaoyang District

raises the possibility of a new era for Chinese media, one in which the

stodginess of propaganda content will give way to exciting new forms and

genres. The mixing of media companies in an open commercial environment

(away from the political power district of Xicheng) holds the promise of more

freedom of expression and, ultimately, to a ‗media capital‘ (Curtin, 2003). These

are the dreams of many media practitioners in Beijing. But just how realistic are

their expectations?

This study adopts the concept of ‗media capital‘ to demonstrate how participants,

including state-media organisations, private media companies and international

media conglomerates, are seeking out space and networks to survive in Beijing.

Drawing on policy analysis, interviews and case studies, this study illustrates

how different agents meet, confront and adapt in Beijing. This study identifies

factors responsible for the media industries clustering in China, and argues that

Beijing is very likely to be the next Chinese media capital, after enough

accumulation and development, although as a lower tier version compared to

other media capitals in the world. This study contributes to Curtin‘s ‗media

capital‘ concept, develops his interpretation on the relationship of media

iii

industries and the government, and suggests that the influence over the

government of media companies and professionals should be acknowledged.

Therefore, empirically, this study assists media practitioners in understanding

how the Chinese government perceives media industries and, consequently, how

media industries are operated in China. The study also reveals that despite the

government‘s aspirations, China‘s media industries are still greatly constrained

by institutional obstacles. Hence Beijing really needs to speed up its pace on the

path of media reform, abandon the old mindset and create more room for

creativity. Policy-makers in China should keep in mind that the only choice left

to them is to further the reform.

iv

Table of Contents

KEYWORDS ................................................................................................................................. I

ABSTRACT .................................................................................................................................. II

TABLE OF CONTENTS ........................................................................................................... IV

LIST OF FIGURES ................................................................................................................... VII

LIST OF TABLES ................................................................................................................... VIII

ABBREVIATIONS....................................................................................................................... X

AUTHORSHIP ........................................................................................................................... XI

ACKNOWLEDGEMENTS ...................................................................................................... XII

CHAPTER 1 INTRODUCTION ................................................................................................. 1

1.1 MEDIA CAPITAL ...................................................................................................................... 2

1.2 RESEARCH QUESTIONS ........................................................................................................... 8

1.3 RESEARCH SIGNIFICANCE ....................................................................................................... 9

1.4 RESEARCH APPROACH AND METHODS .................................................................................. 11

1.4.1 Document analysis ....................................................................................................... 14

1.4.2 Semi-structured interviews ........................................................................................... 16

1.4.3 Case study .................................................................................................................... 17

1.5 CHAPTER BREAKDOWN ........................................................................................................ 19

CHAPTER 2 LITERATURE REVIEW: GLOBALISATION AND REGIONALISATION 21

2.1 GLOBAL MEDIA PRODUCTION: DISPERSAL AND CONCENTRATION ......................................... 22

2.2 MEDIA CAPITAL .................................................................................................................... 24

2.2.1 The cultural turn in economic geography .................................................................... 25

2.2.2 Three operating principles ........................................................................................... 28

2.2.3 The creative field .......................................................................................................... 35

2.3 CRITICISMS OF MEDIA CAPITAL ............................................................................................ 41

2.4 CONCLUDING REMARKS: WHERE IS CHINA‘S MEDIA CAPITAL? ............................................. 43

CHAPTER 3 BACKGROUND: HISTORICAL CONTEXT OF BEIJING AS A MEDIA

CENTRE ...................................................................................................................................... 45

3.1 MEDIA SECTOR REFORM IN CHINA ....................................................................................... 47

3.1.1 Nation building (1978-1991) ....................................................................................... 48

3.1.2 Cultural security (1992-2002) ..................................................................................... 56

3.1.3 Soft power (2002-present) ............................................................................................ 66

3.1.4 The implication of media reform .................................................................................. 67

3.2 MEDIA REGULATORY ENVIRONMENT IN CHINA..................................................................... 73

3.3 THE GEOGRAPHY OF MEDIA INDUSTRIES............................................................................... 77

3.3.1 Beijing .......................................................................................................................... 77

3.3.2 Shanghai ...................................................................................................................... 80

3.3.3 Guangdong Province ................................................................................................... 81

v

3.3.4 Hunan Province ........................................................................................................... 81

3.3.5 Zhejiang Province and Jiangsu Province..................................................................... 82

3.4 CONCLUDING REMARKS: THE PROSPECTS OF INNOVATION .................................................... 83

CHAPTER 4 REFRAMING MEDIA INDUSTRIES’ EXPANSION IN CHINA .................. 85

4.1 MEDIA COMPANIES ............................................................................................................... 85

4.1.1 State-owned media groups ........................................................................................... 85

4.1.2 Private media companies ............................................................................................. 88

4.1.3 Foreign media groups in China ................................................................................... 90

4.1.4 Implications ................................................................................................................. 91

4.2 NEW CHARACTERISTICS ........................................................................................................ 92

4.2.1 Competition. ................................................................................................................. 92

4.2.2 Changing attitudes ....................................................................................................... 93

4.2.3 Development of ICTs. ................................................................................................... 94

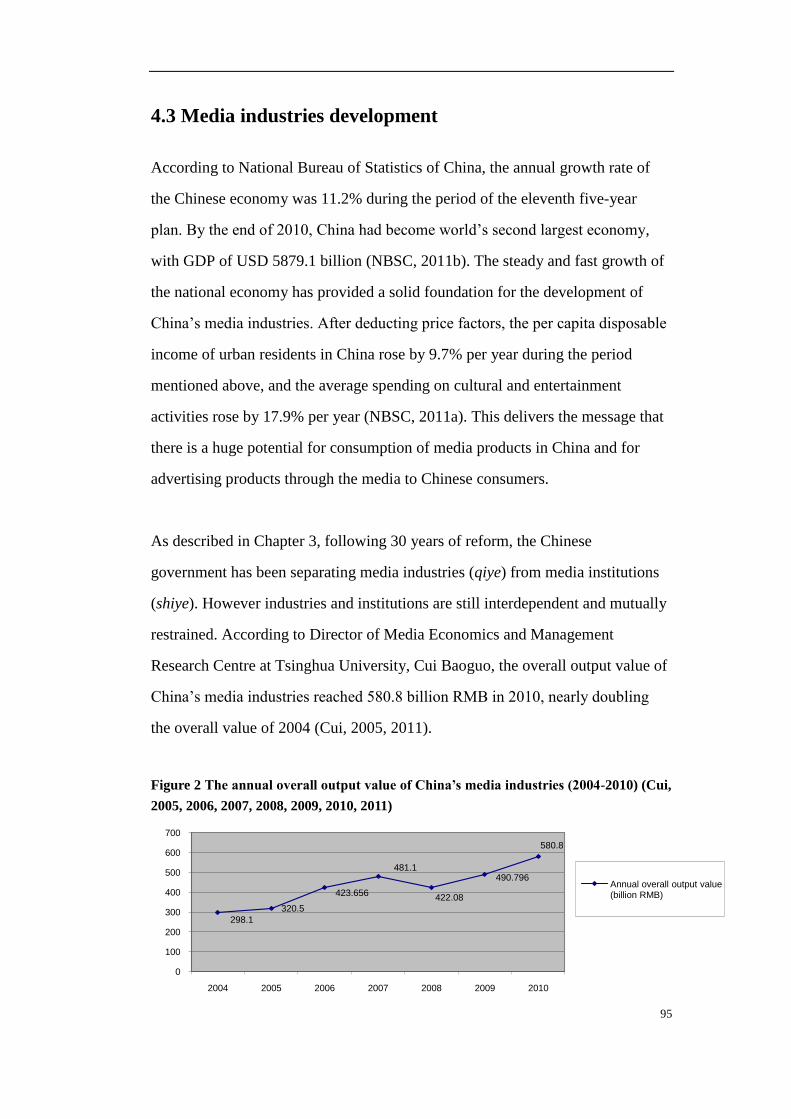

4.3 MEDIA INDUSTRIES DEVELOPMENT ...................................................................................... 95

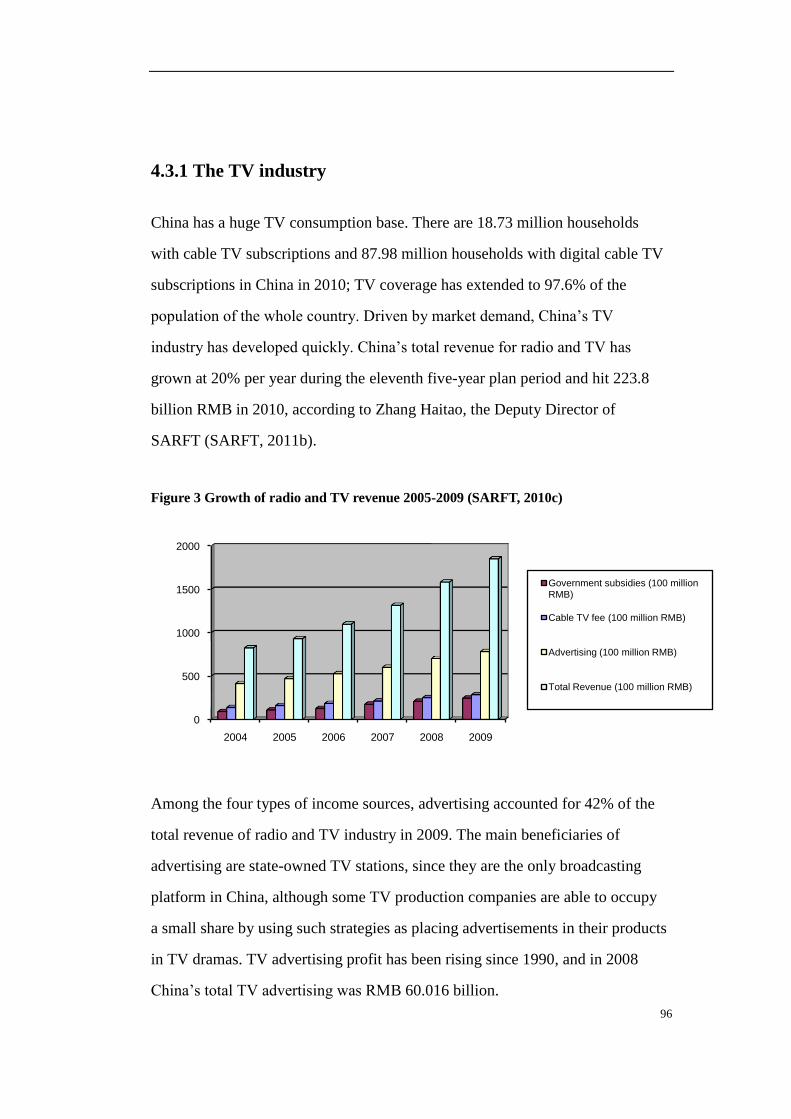

4.3.1 The TV industry ............................................................................................................ 96

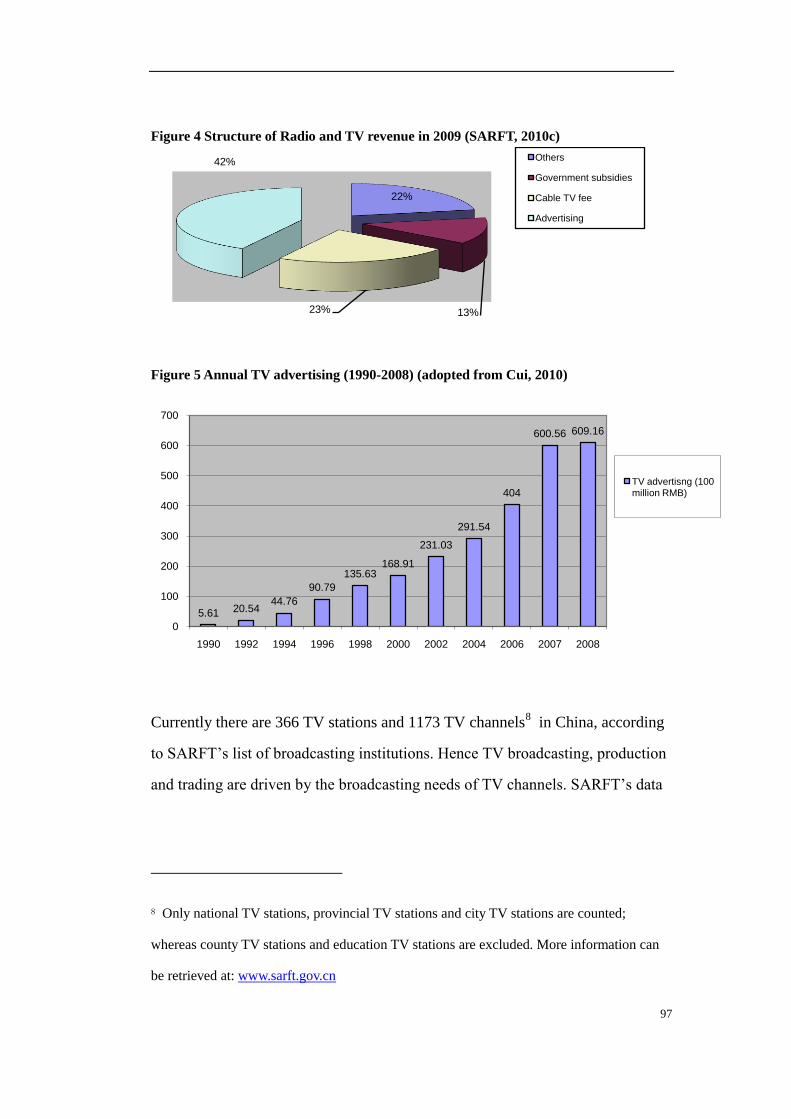

4.3.2 The film industry ........................................................................................................ 101

4.5 SOFT POWER AND INTERNATIONALISATION......................................................................... 106

4.5.1 Media export .............................................................................................................. 106

4.5.2 International capital .................................................................................................. 112

4.5.3 Co-production ............................................................................................................ 115

CHAPTER 5 BEIJING: THREE PRINCIPLES OF MEDIA CAPITAL ............................ 117

5.1 CURTIN 1: FORCES OF BEIJING‘S ACCUMULATION .............................................................. 118

5.1.1 TV industry: forces of accumulation .......................................................................... 118

5.1.2 Film industry: forces of accumulation ....................................................................... 120

5.1.3 Different routes, same destination.............................................................................. 127

5.2 CURTIN 2: TRAJECTORIES OF BEIJING‘S CREATIVE MIGRATION ........................................... 128

5.2.1 Education institutions ................................................................................................ 130

5.2.2 Career opportunities .................................................................................................. 132

5.2.3 Initiated by the capital status ..................................................................................... 133

5.2.4 The mutual learning effect in media migration .......................................................... 135

5.3 CURTIN 3: BEIJING‘S SOCIO-CULTURAL VARIATION ............................................................ 139

5.3.1 Schizophrenic Beijing ................................................................................................ 139

5.3.2 Struggling international conglomerates .................................................................... 143

5.3.3 Confident domestic players ........................................................................................ 145

5.3.4 Regulatory backflips .................................................................................................. 150

5.4 CONCLUDING REMARKS ..................................................................................................... 154

CHAPTER 6: THE CBD INTERNATIONAL MEDIA INDUSTRY CLUSTER IN BEIJING

..................................................................................................................................................... 157

6.1 THE CBD INTERNATIONAL MEDIA INDUSTRY CLUSTER ..................................................... 157

6.1.1 The Central Business District in Beijing .................................................................... 158

6.1.2 The formation of CBD International Media Cluster .................................................. 161

6.1.3 The CBD International Media Cluster and the capital city ....................................... 167

vi

6.2 TENSIONS ........................................................................................................................... 170

6.2.1 Small and medium companies .................................................................................... 171

6.2.2 The content of media products ................................................................................... 176

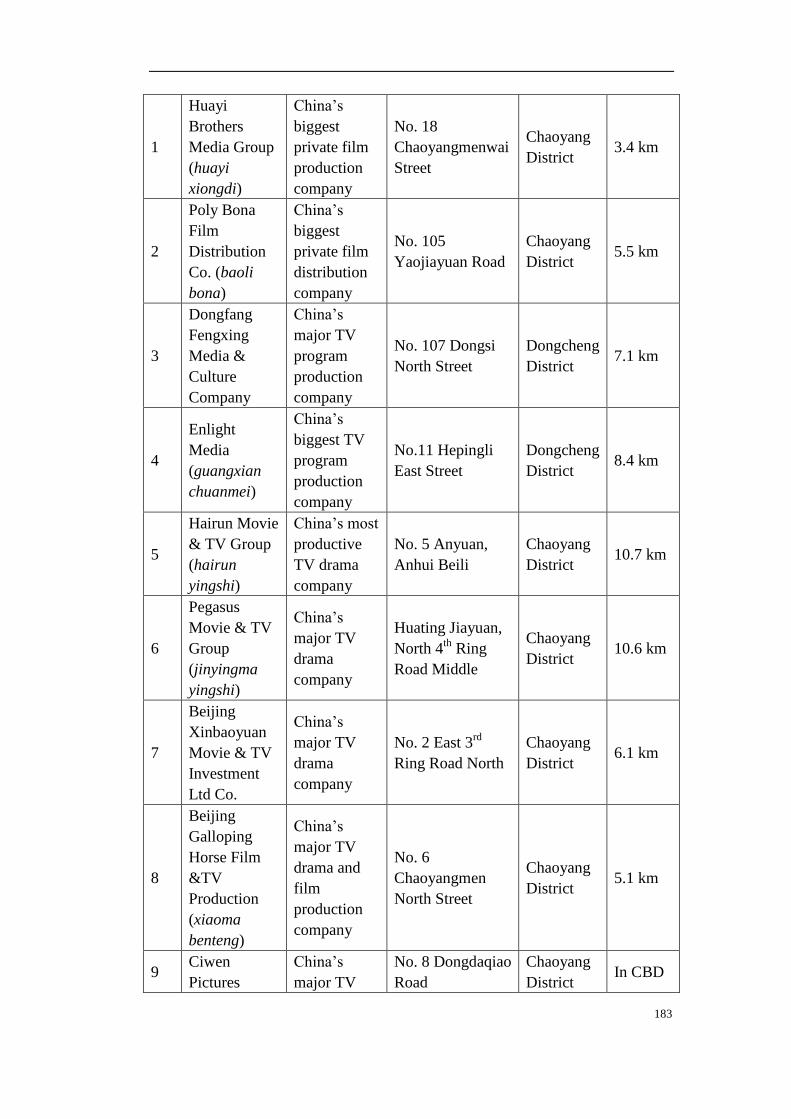

6.2.3 CCTV’s influence ....................................................................................................... 182

6.3 DISCUSSION ....................................................................................................................... 186

CHAPTER 7 BEIJING’S COMPARATIVE ADVANTAGES AS AN EMERGENT MEDIA

CAPITAL ................................................................................................................................... 190

7.1 PREDICTABILITY, CONTROL AND CONVERGENCE ................................................................ 191

7.2 ISSUES ARISING .................................................................................................................. 197

7.3 BEIJING AS A MEDIA CAPITAL IN THE GREAT CHINESE MEDIA MARKET ............................... 202

7.3.1 Adaptive informal institutions .................................................................................... 206

7.3.2 Continuous adaption and convergence of the media regulatory system .................... 210

7.3.3 The generational transition of power in Chinese film directors ................................ 214

7.3.4 Audiences and other issues in the Mainland TV market ............................................ 217

7.4 BEIJING‘S ADVANTAGES AND CHALLENGES ........................................................................ 219

CHAPTER 8 CONCLUSION .................................................................................................. 223

8.1 POSITIONING BEIJING IN CHINESE MEDIA INDUSTRIES........................................................ 223

8.2 REVISITING CURTIN‘S MEDIA CAPITAL ............................................................................... 231

8.3 SIGNIFICANCE OF THIS STUDY ............................................................................................ 233

8.3.1 Implication for theory ................................................................................................ 234

8.3.2 Implication for policy ................................................................................................. 235

8.3.3 Implication for practice ............................................................................................. 236

8.4 LIMITATIONS OF THIS STUDY .............................................................................................. 236

8.5 DIRECTIONS FOR FURTHER STUDY ...................................................................................... 237

APPENDIX I: LIST OF INTERVIEWEES ............................................................................ 238

APPENDIX II SAMPLE QUESTIONS FOR SEMI-STRUCTURED INTERVIEW ........ 241

BIBLIOGRAPHY ..................................................................................................................... 245

vii

List of Figures

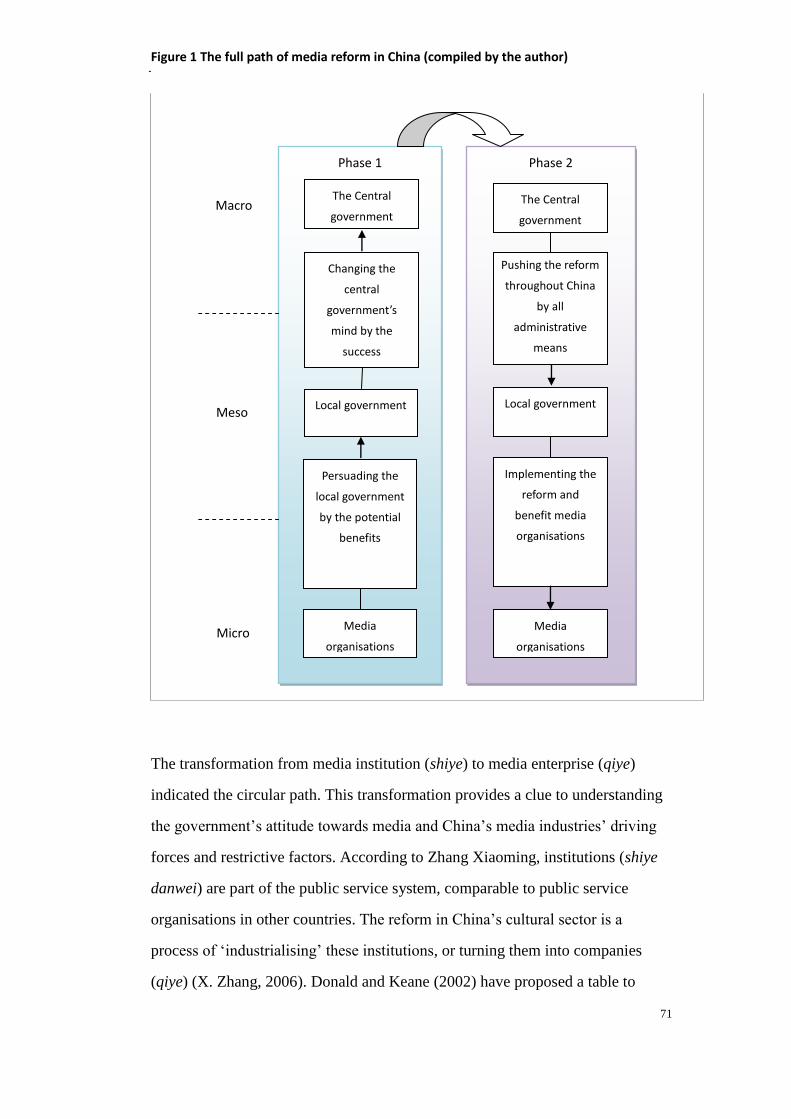

Figure 1 The full path of media reform in China (compiled by the author) ........ 71

Figure 2 The annual overall output value of China‘s media industries

(2004-2010) (Cui, 2005, 2006, 2007, 2008, 2009, 2010, 2011) .......................... 95

Figure 3 Growth of radio and TV revenue 2005-2009 (SARFT, 2010c)............. 96

Figure 4 Structure of Radio and TV revenue in 2009 (SARFT, 2010c) .............. 97

Figure 5 Annual TV advertising (1990-2008) (adopted from Cui, 2010)............ 97

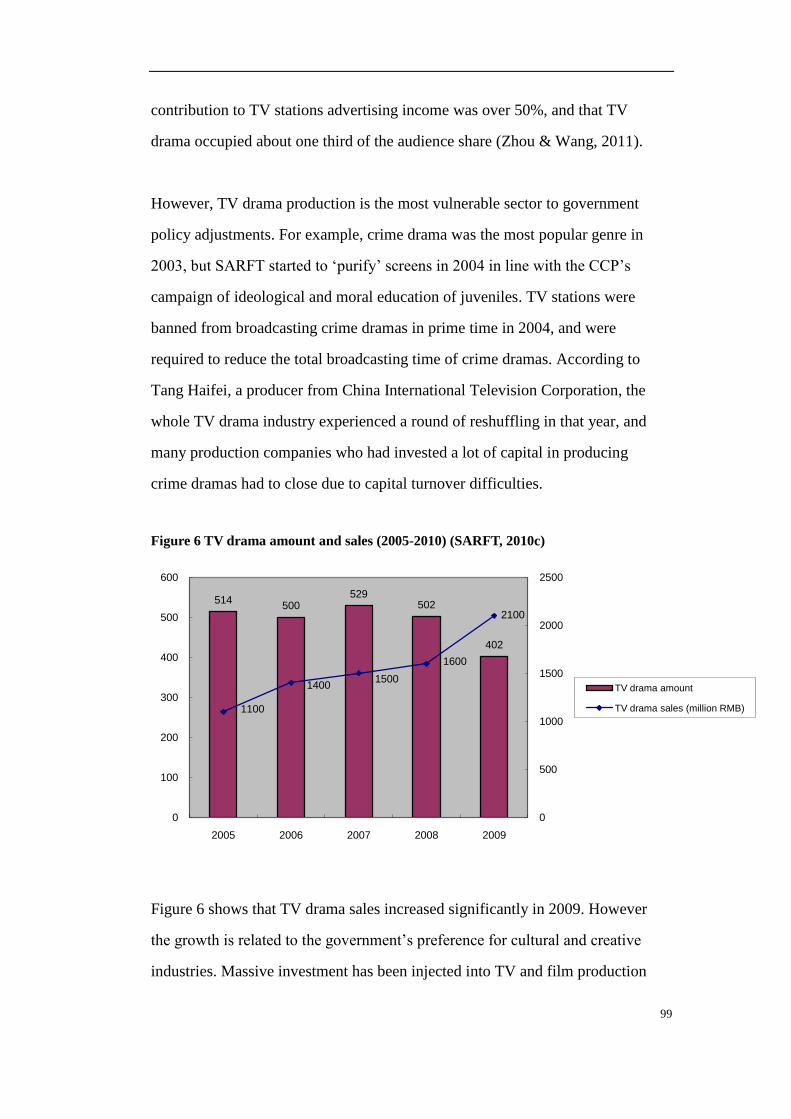

Figure 6 TV drama amount and sales (2005-2010) (SARFT, 2010c).................. 99

Figure 7 Broadcasting and viewing proportion of TV drama (2006-2009) (Cui,

2010) .................................................................................................................. 100

Figure 8 Income of China‘s film industry (2004-2010) (Cui, 2011) ................. 101

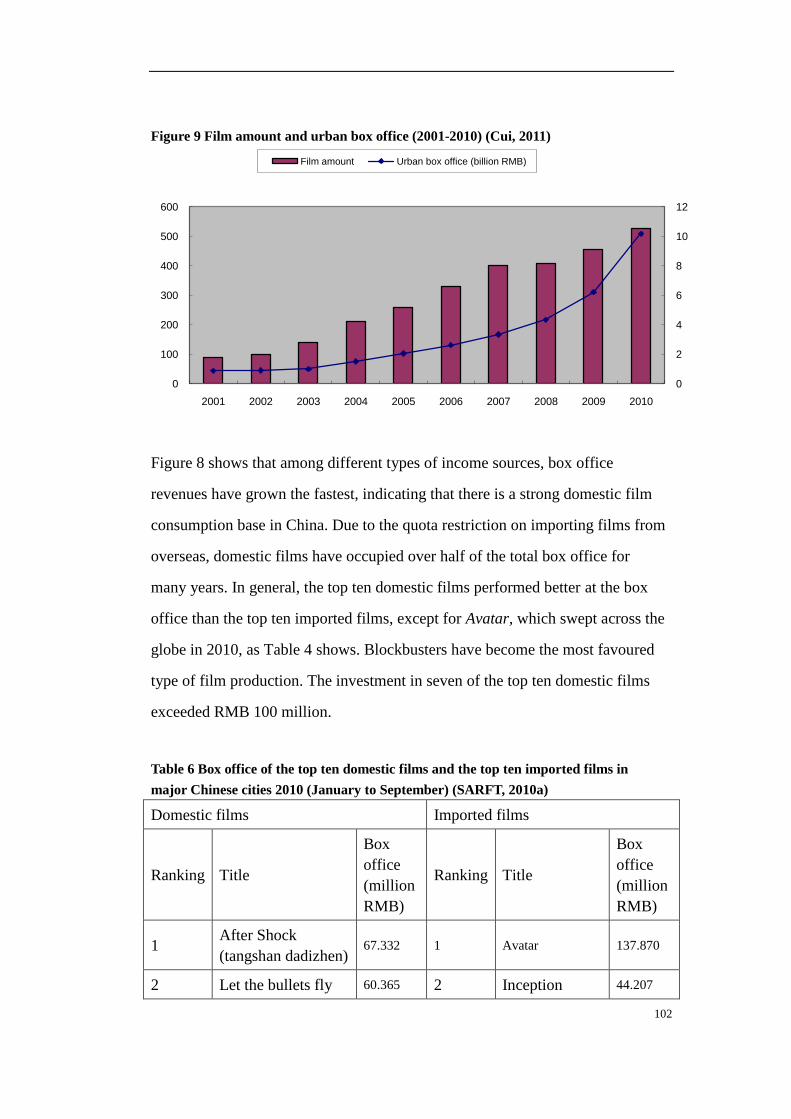

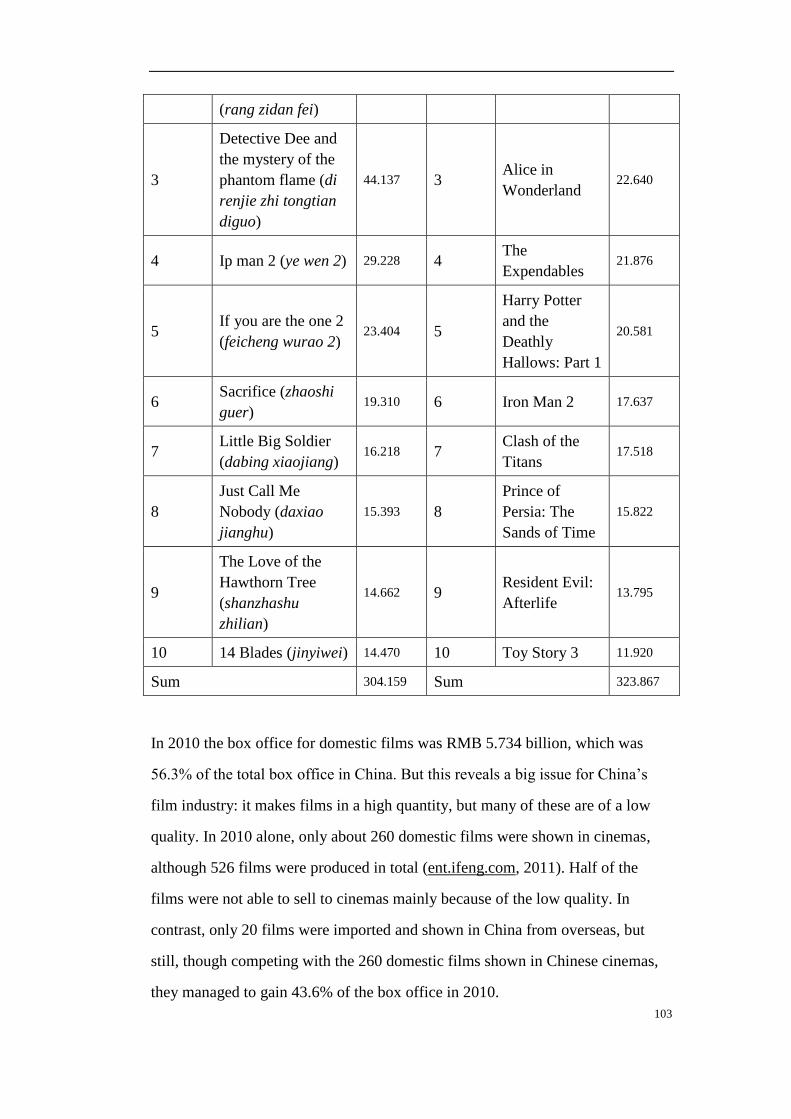

Figure 9 Film amount and urban box office (2001-2010) (Cui, 2011) .............. 102

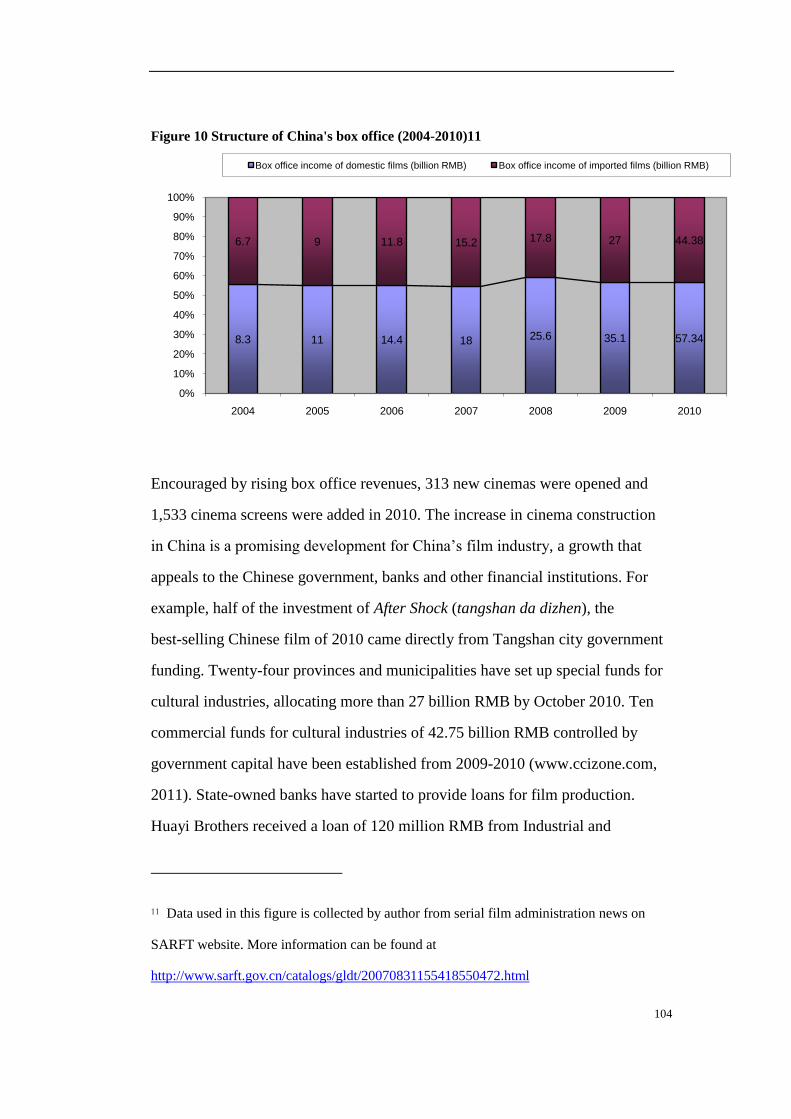

Figure 10 Structure of China's box office (2004-2010) ..................................... 104

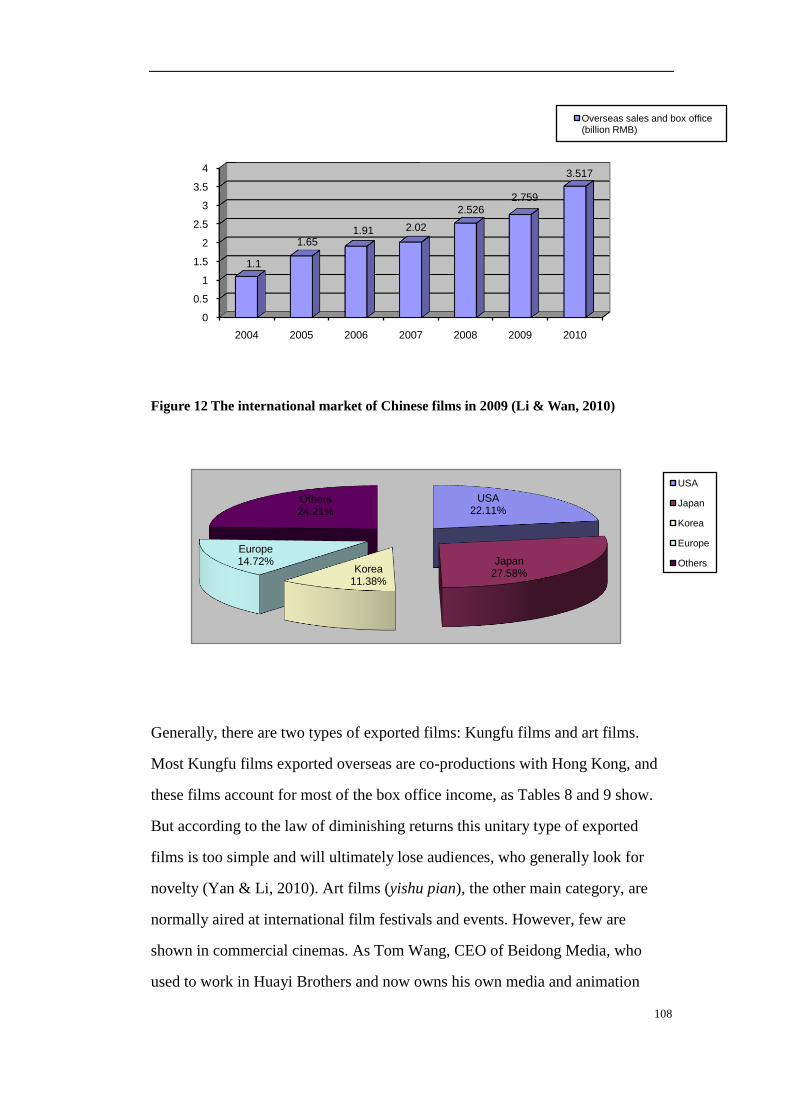

Figure 11 International income of China's film industry (2004-2010) (Cui, 2011)107

Figure 12 The international market of Chinese films in 2009 (H. Li & Wan,

2010) .................................................................................................................. 108

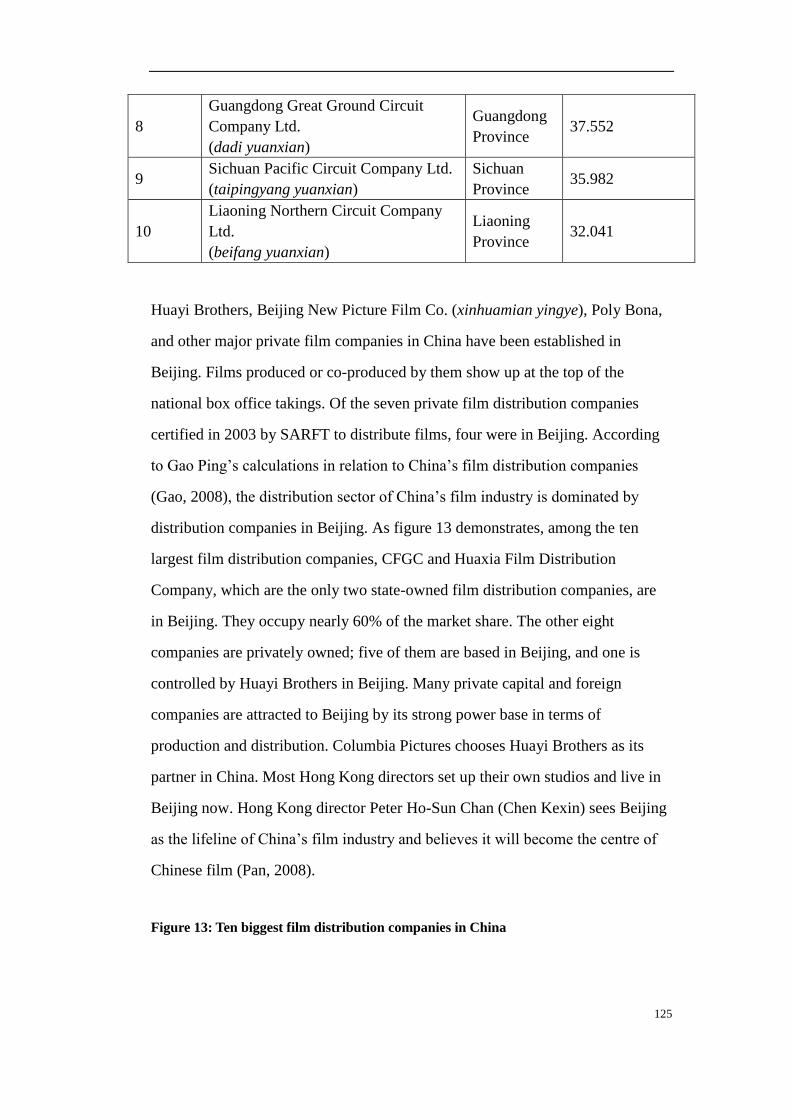

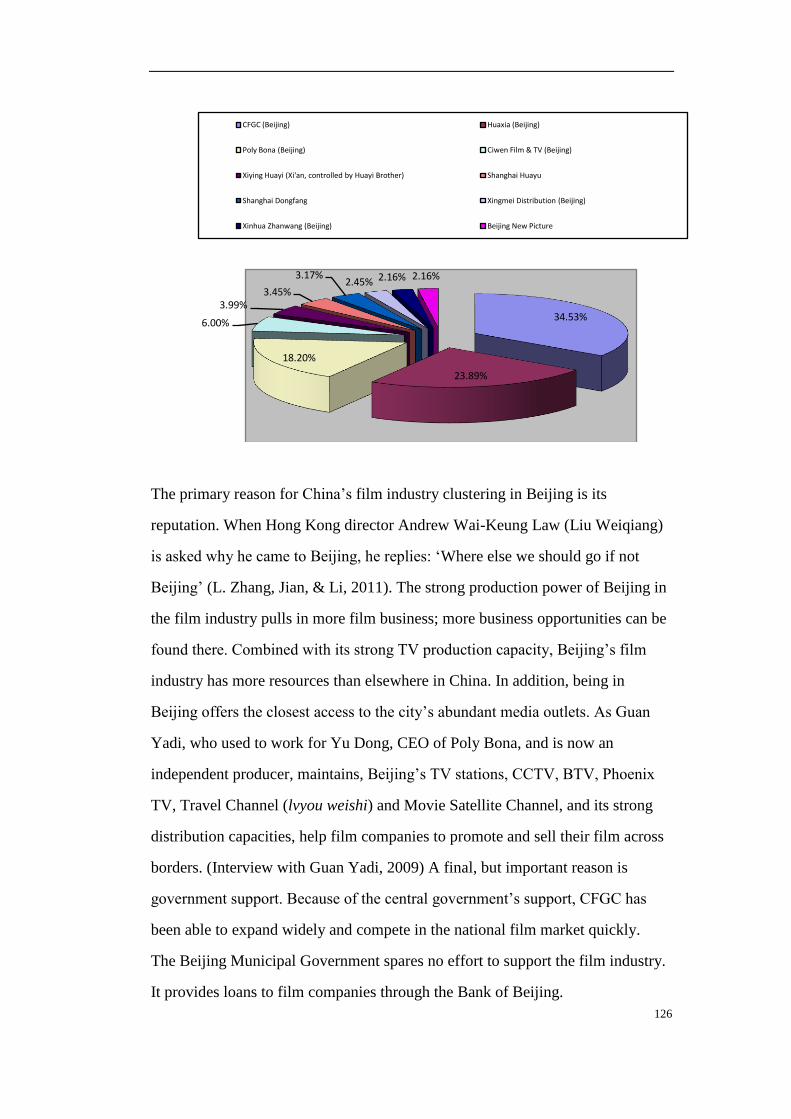

Figure 13: Ten biggest film distribution companies in China ........................... 125

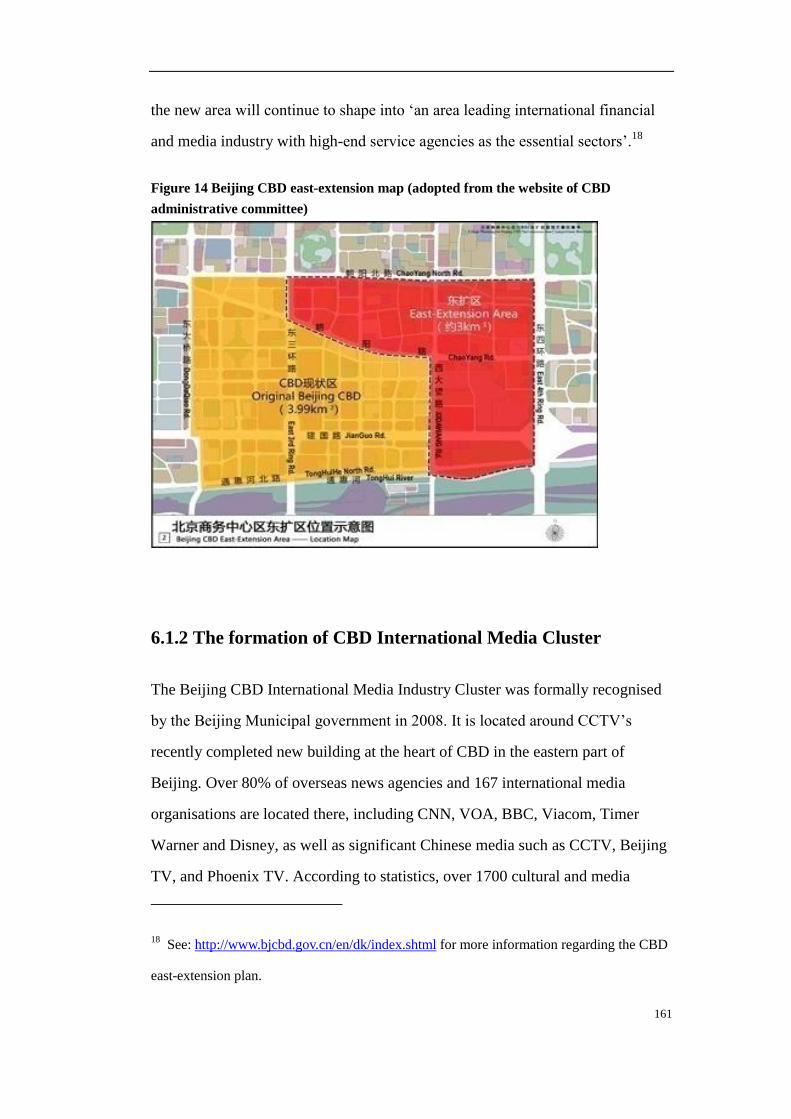

Figure 14 Beijing CBD east-extension map (adopted from the website of CBD

administrative committee) .................................................................................. 161

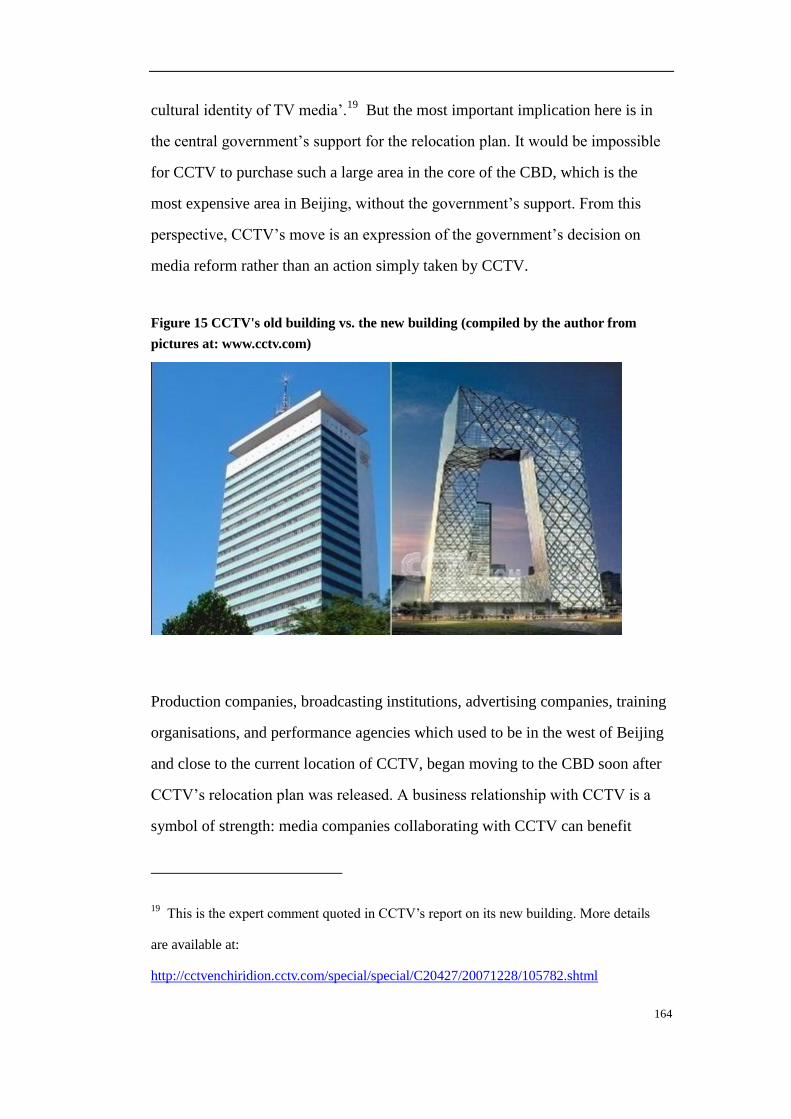

Figure 15 CCTV's old building vs. the new building (compiled by the author

from pictures at: www.cctv.com) ....................................................................... 164

viii

List of Tables

Table 1 The gross income of TV sector in Beijing, Shanghai and Guangdong,

2006-2008 (Source: The Yearbook of Chinese Radio and Television 2007, 2008,

2009) ...................................................................................................................... 5

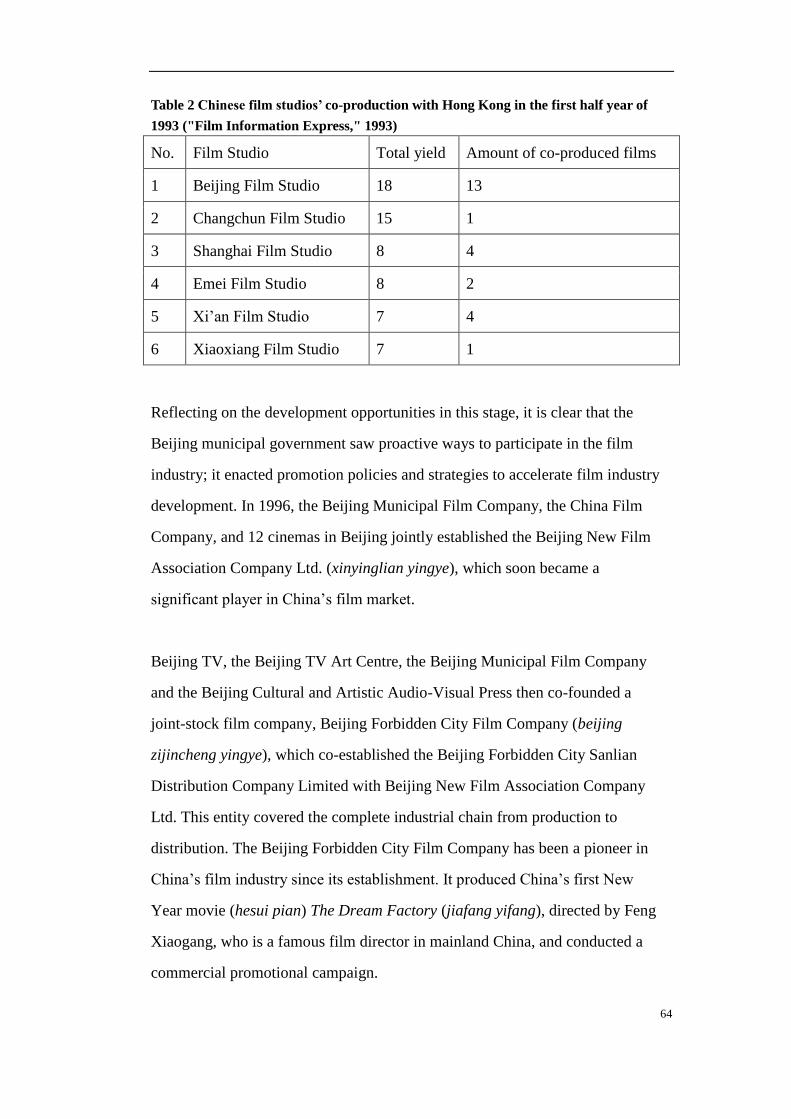

Table 2 Chinese film studios‘ co-production with Hong Kong in the first half

year of 1993 ("Film Information Express," 1993) ............................................... 64

Table 3 Comparison of shiye and qiye (adopted from Donald & Keane, 2002) . 72

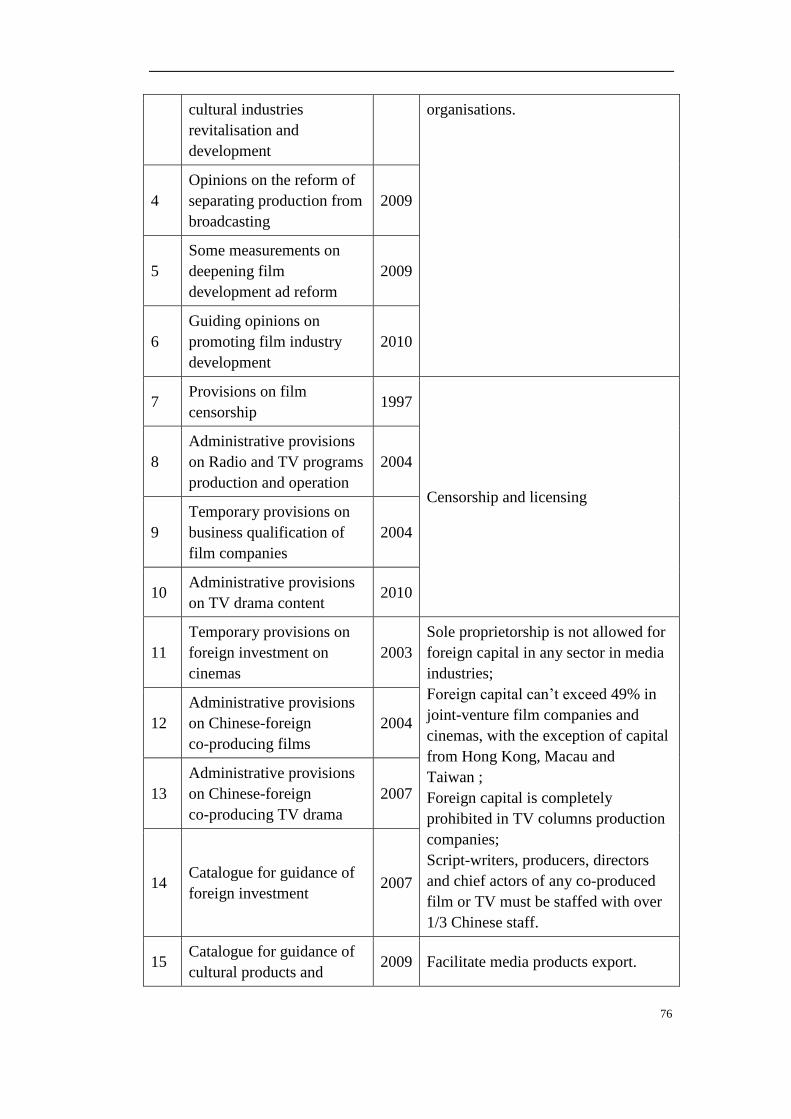

Table 4 Major national media policies in China .................................................. 75

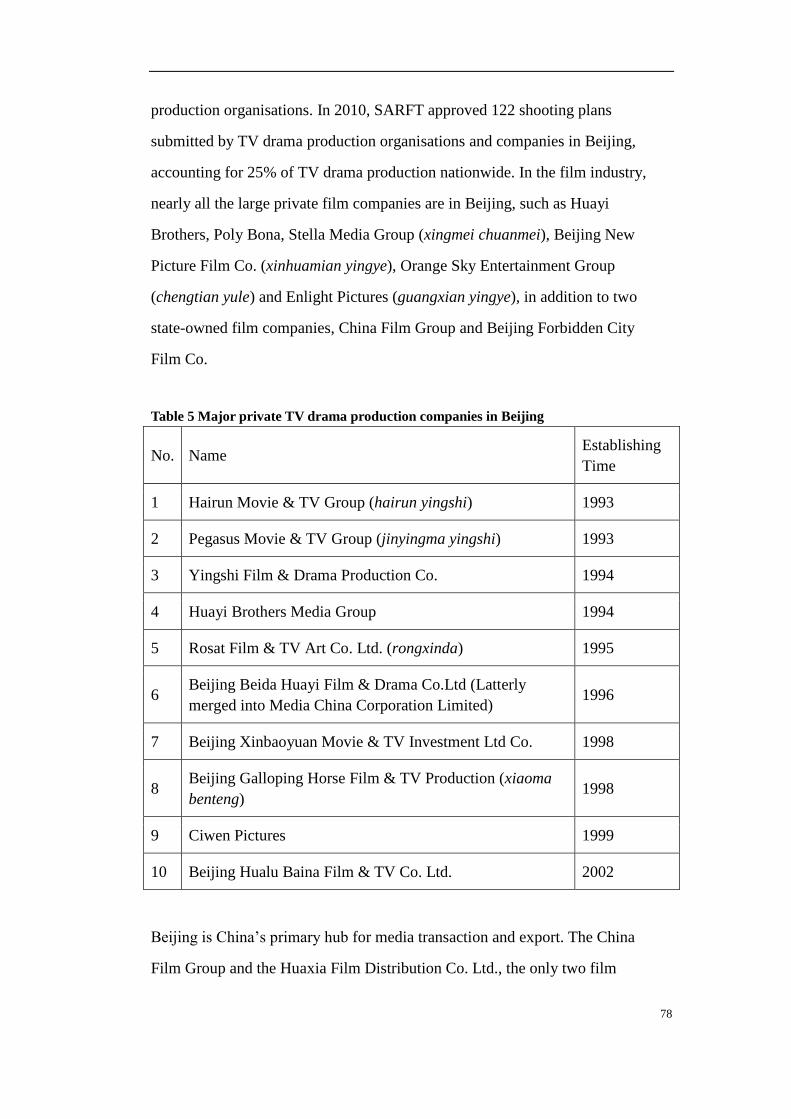

Table 5 Major private TV drama production companies in Beijing .................... 78

Table 6 Box office of the top ten domestic films and the top ten imported films

in major Chinese cities 2010 (January to September) (SARFT, 2010a) ............ 102

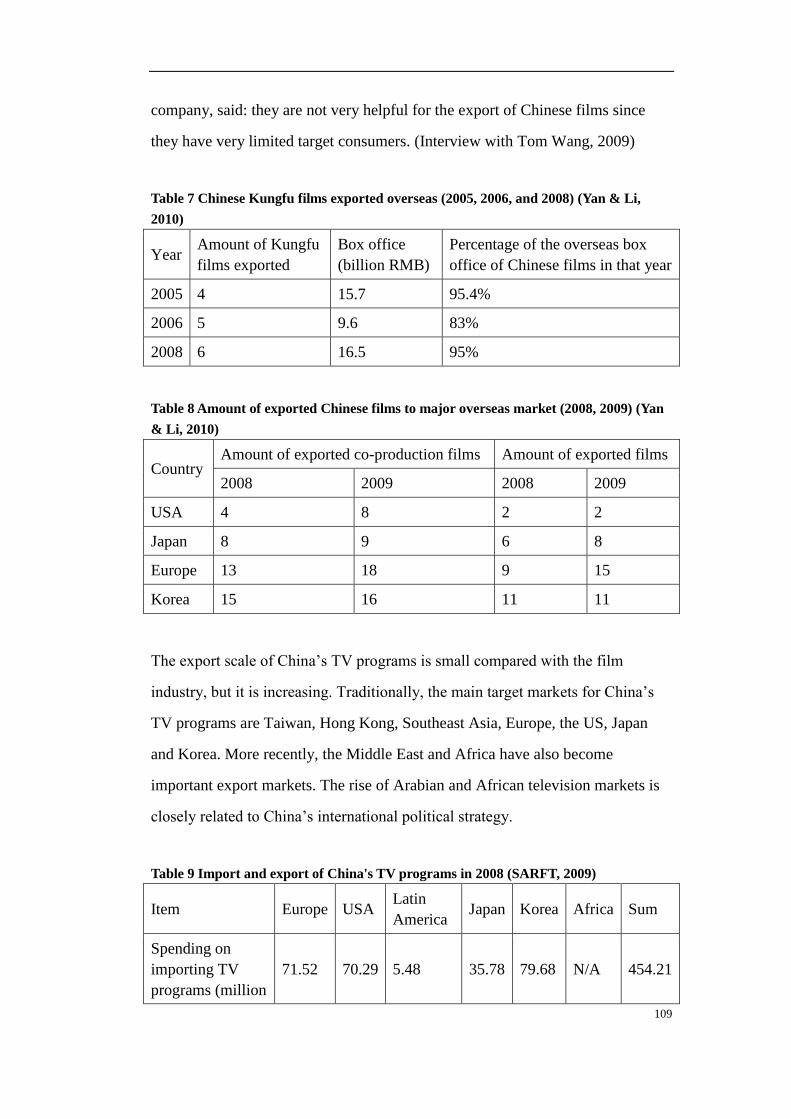

Table 7 Chinese Kungfu films exported overseas (2005, 2006, and 2008) (Yan

& Li, 2010) ......................................................................................................... 109

Table 8 Amount of exported Chinese films to major overseas market (2008,

2009) (Yan & Li, 2010) ..................................................................................... 109

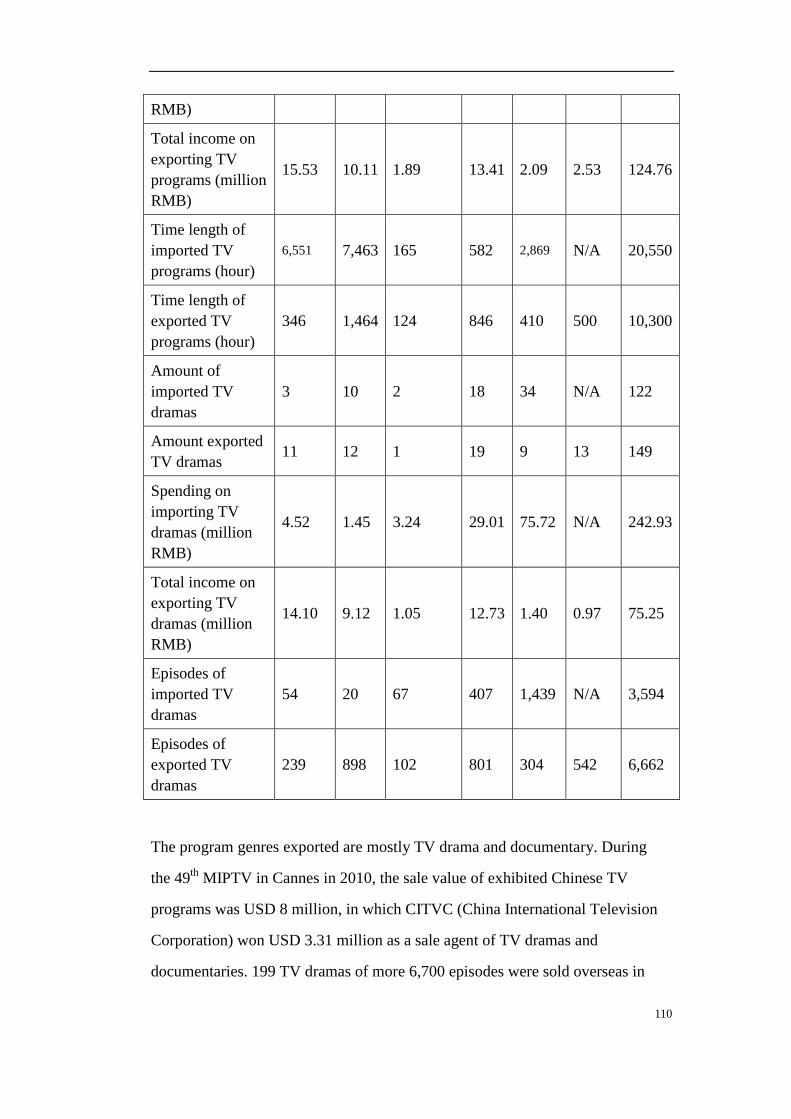

Table 9 Import and export of China's TV programs in 2008 (SARFT, 2009) ... 109

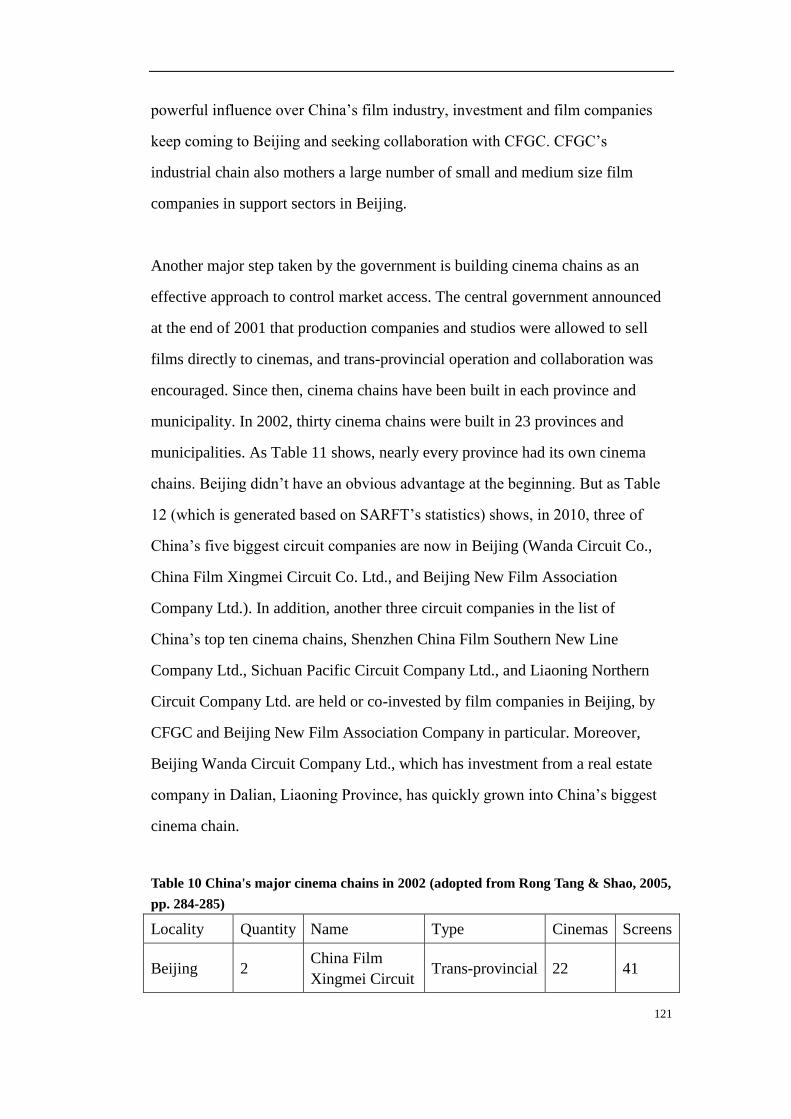

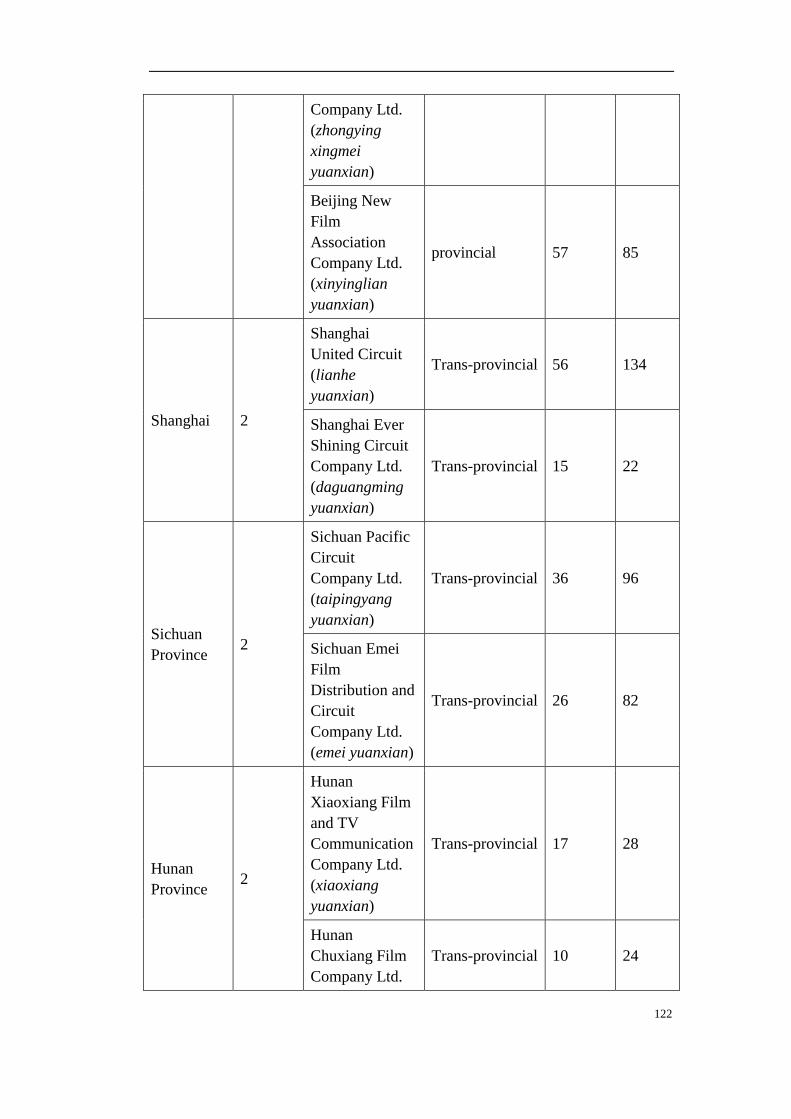

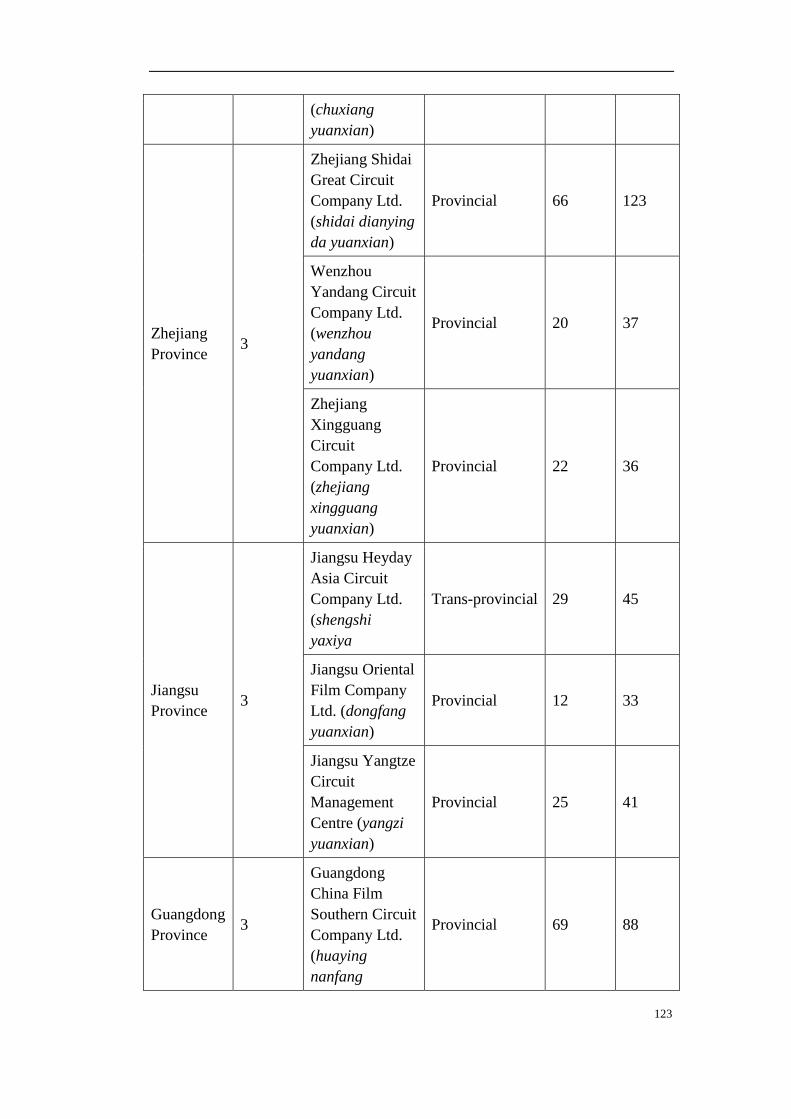

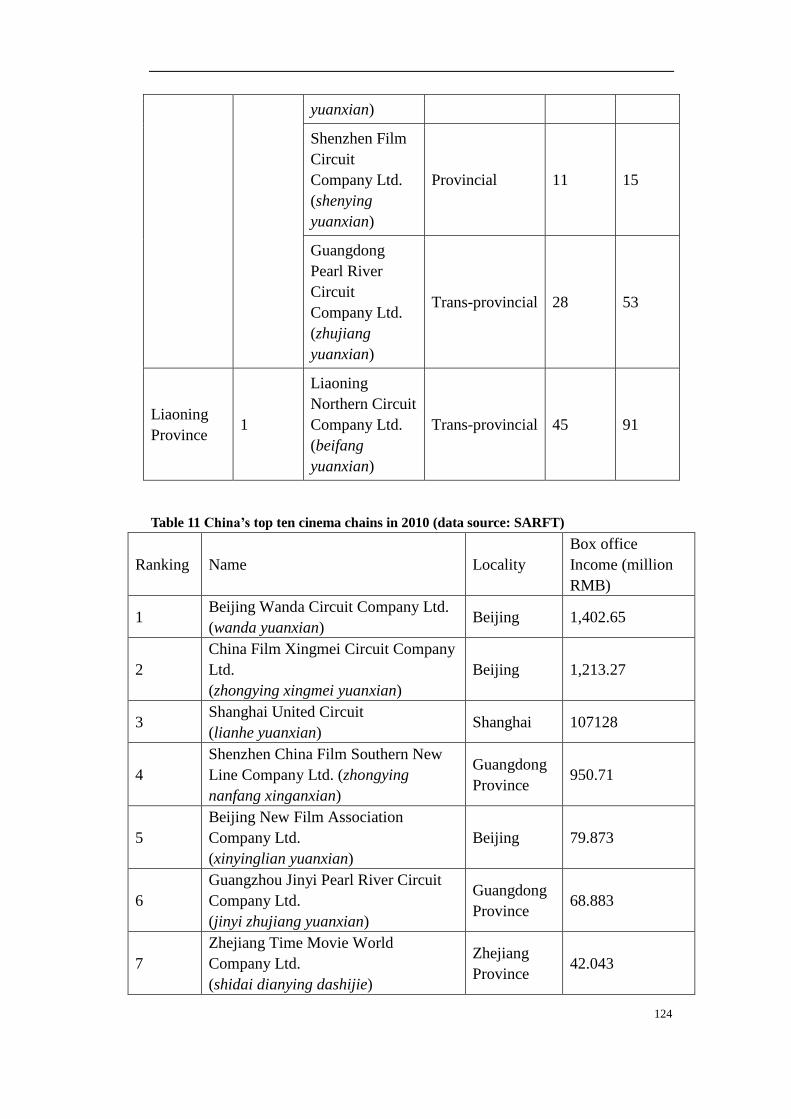

Table 10 China's major cinema chains in 2002 (adopted from Rong Tang &

Shao, 2005, pp. 284-285) ................................................................................... 121

Table 11 China‘s top ten cinema chains in 2010 (data source: SARFT) ........... 124

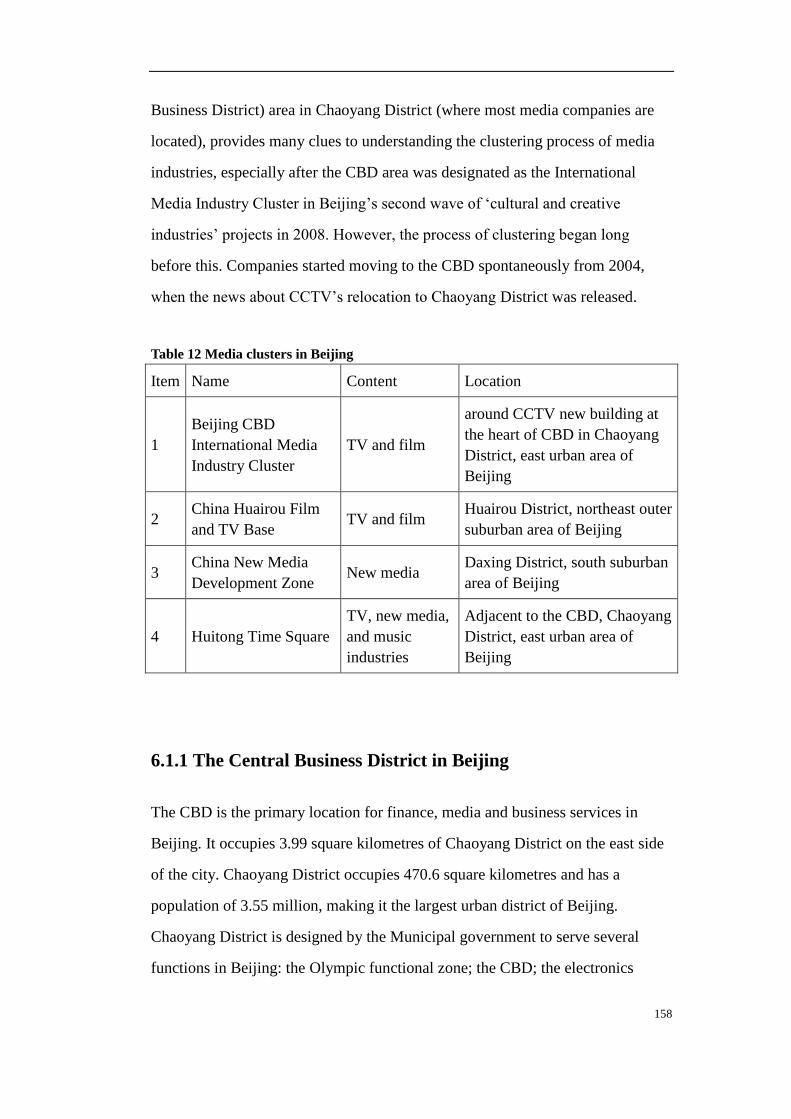

Table 12 Media clusters in Beijing .................................................................... 158

Table 13 Location of major private media companies in Beijing (distance

calculated based on Google Map) ...................................................................... 182

ix

x

Abbreviations

BFA Beijing Film Academy

BGCTV Beijing Gehua Cable TV Networks

BTV Beijing TV

CAD the Central Academy of Drama

CCCCP The Central Committee of Chinese Communist Party

CCFC China Co-production Film Corporation

CCP Chinese Communist Party

CCTV China Central Television

CETV China Education Television

CFGC China Film Group Corporation

CTPC China‘s TV Production Centre

CUC Communication University of China

HSTV Hunan Satellite TV

MoC Ministry of Culture China Central Television

NBSC National Bureau of Statistics of China

NDRC National Development and Reform Committee of China

SARFT State Administration of Radio, Film and Television

SMG Shanghai Media Group

WTO World Trade Organization

xi

Authorship

The work contained in this thesis has not been previously submitted to meet

requirements for an award at this or any other higher education institution. To

the best of my knowledge and belief, the thesis contains no material previously

published or written by another person except where due reference is made.

Signature:

Date: 31 May 2012

QUT Verified Signature

xii

Acknowledgements

It would be impossible for me to complete this thesis without the enormous help

and support that I have received from many individuals in these four years. First

of all, I would like to express my biggest gratitude and thanks to my wonderful

supervisors, Distinguished Professor Stuart Cunningham, Professor Michael

Keane and Professor Terry Flew. Stuart‘s critical queries have compelled me

through my PhD adventure in a very challenging way and finally I could see

more. Whenever I encountered problems, big or small, Michael told me: ‗Don‘t

worry, I will help you.‘ And he always did what he said. Terry has kindly

included me in the work of ARC funded project Creative Suburbia, by which I

was fortunate to get valuable opportunities of conferences and publications. You

guys make an unparalleled team!

Many thanks must go to my interviewees and friends in Beijing. A thousand

thanks go to Yang Li, who not only has contributed her time and insightful

opinions to my field work in Beijing but also generously introduced many of her

friends to me; and to Yao Min, who introduced me two of her important

business partner and my interviews with them have helped me develop a clearer

research direction. Without your continuous support, I would not have come so

far. Special thanks go to Shen Jiao and her husband, Xiao Zhaojun. They always

kindly let me to stay with them in their small cosy apartment and fed me with

their beautiful cooking every time when I was back in Beijing.

I was so lucky to have many friends in Brisbane who have accompanied me

during my PhD journey. They are Linda Watterson, Bonnie Rui Liu, Wen Wen,

Yaxing Zhang, Henry Siling Li, Weihong Zhang, Mimi Yihsin Tsai, Ivy Lau,

Vicki Chihsuan Chiu, Wei Song, Ying Zhou, Judy Tan, Falk Hartig, Mark Ryan,

Thomas Petzold, Tripta Chandola, Barbara Gligorijevic, Emma Felton, Ct Suria,

xiii

Yong Guo, Juncheng Dai and many others whose name are not mentioned here.

I may have been alone from time to time, but I was never lonely because of you.

I would like to thank lovely staff from CIF and CCI – Kate Simmonds, Colleen

Cook, Sue Carson, Cheryl Stock, Sharon Kolar, Jenny Mayes and Aislinn

McConnell, who have been very patient and supportive from the first beginning

till the very end. Your smile has meant so much to me. I must thank the China

Scholarship Council and the education officer from the Consulate General of the

PRC in Brisbane that sponsored and assisted selflessly my study and living in

Australia.

Finally I want to express my deepest love and gratitude to my Mum, Hao

Yuping, my Dad, Huang Jianjun, and my husband, Liu Liyong. I always knew

that I was surrounded by your love and support though we were parted by the

ocean.

1

Chapter 1 Introduction

When I set out on my PhD journey I decided to look at the phenomenon of

clustering. Over the past two decades clusters have become central to economic

development in China; the past several years have seen a wave of cultural and

creative clusters, such as art zones, reconverted factories, film, TV and

animation parks. All cities seem to have similar cluster plans. My interest was

Beijing.

However, much confusion exists about clusters. What constitutes a cluster? How

do they work? At the same time as the cluster fever broke there was a similar

focus on the bigger picture: the nation and the city. How could China be a media

power like the US? How could it stop the wave of imports from Korea? People

spoke about creative cities, world cities, knowledge cities, cities of design and

cities of culture. What kind of city was Beijing? It was the capital of course; it

was trying to be many things at once.

In the course of my early research I came across the concept of ‗media capital‘

(Curtin 2003). This seemed to be a new way of viewing Beijing‘s development,

by bringing the cluster idea together with the city. The media capital concept,

which I will outline below, is based on a high degree of media concentration and

successful media products, especially exports. In effect, media capital is another

form of clustering. Michael Curtin, the US scholar who coined this idea,

believes that Beijing could not be a media capital because it was a media control

centre. I wanted to test this claim.

2

1.1 Media capital

Curtin, together with many other scholars (for instance see Tunstall 2007),

believes that nowadays the global media system is no longer a one-way flow of

(mainly) US programming to other places of the world. Rather, according to

Curtin, the increasing volume and velocity of multi-directional media flows is

emanating from media capitals on the periphery of the world media system, such

as Cairo, Bombay, Hong Kong and, more recently, Miami. Curtin maintains that

media capitals are places where new mass culture forms containing local

specificity are generated and exported while media resources and talent come

together, interact and exchange.

Instead of depicting global media as an extension of Hollywood, the global

media system is de-territorialised and clustered in specific regions where there

are particular attractive resources for international investment. The capacity of

these emergent media capitals is improving as they become hubs for a range of

media flows, which bring resources and new knowledge. Hence media capital is

a dynamic concept, as capital status can be won and lost at different

development stages. Media capital is a relational concept. Geographically, a

media capital must be envisioned in ‗a terrain over which it holds sway and a

constellation of related nodes of cultural endeavour‘ (Curtin, 2007, p. 285). A

media capital must be a geographic centre within a field of interconnected

locales (Curtin, 2010a). A media capital must be able to constantly absorb

resources beyond boundaries, produce distinctive prototypes to its competitors,

and extend circulation as far as possible (Curtin, 2007, p. 287). Managerial and

productive operations of media enterprises are concentrated in a certain location

despite the technological, political, and trade liberalisation that spreads their

markets and products transnationally. Gradually, with the concentration of

resources, reputation, and talent, the city becomes a flux of complex forces and

3

flows from near and far. At the same time, media enterprises are driven by

market forces searching persistently for socio-cultural variations that bring new

market opportunities and stimulate distinctive production. Consequently, they

can produce new exportable cultural forms and circulate products at multiple

geographical locales through flexible and far-reaching distribution operations

that interface effectively with local nodes of exhibition and marketing.

As a result, capital in Curtin‘s context has two meanings: a centre of activity

(geographical) and a concentration of resources, reputation and talent

(economic). Michael Curtin illustrates the temporal dynamism and spatial

complexity of the global media from three aspects:

(a) Logic of accumulation. In this principle, Curtin explains the centripetal

tendencies of production and centrifugal tendencies of distribution through an

economic geography perspective: driven by the pursuit of profit and assisted by

the development of ICTs and other technologies, modern enterprises are able to

operate across borders of states and regions to reduce production costs, extend

the market and increase speed of distribution.

(b) Trajectories of migration. Creativity is a core resource for media industries

and comes from pools of labour that continually acquire new prototypes

motivated by aesthetic innovation and market considerations. With

accumulation of resources, media talent is attracted to the new production

centres because of the growth in work opportunities. The creative migration

stimulated by job opportunities enhances the attractiveness of the region to other

media workers, which in turn drives the growth and expansion of media

industries in the region.

4

(c) Forces of socio-cultural variation. Media products adapted to local

traditions, resources and preferences are more easily accepted by audiences in

particular geo-linguistic regions due to cultural proximity (Straubhaar 1991).

Moreover, national and local institutions, such as ideology, policies and

institutions intervene and complicate the production, distribution and migration.

The question of why Beijing wants to be a media capital and how it might

become a media capital need to be contextualised in recent history. The thesis

argues that Chinese media is at an important crossroads, trying to commercialise

and trying to become stronger in media production exports. In the past decade

there has been a concerted attempt to utilise clustering and regional media

groups as a development strategy. This has obvious limits, which I will discuss

in Chapter 6. However, one of the key driving forces behind media development

in China is the Chinese ‗going out‘ strategy, which has been taken up in media

under the slogan ‗soft power‘ (ruan shili). For Beijing to be a media capital it

therefore has to be a producer of soft power. In this thesis I describe China‘s

media as progressing through three identifiable periods (1) nation-building (2)

cultural security and (3) soft power. It is the last of these that links directly to

media capital.

Beijing is the media centre of China. The Chinese media industry has made

rapid development in recent years, but it is by no means a balanced development.

Beijing, Shanghai and Guangdong Province are the three most prominent ‗media

hotspots‘, or what Chinese scholars term ‗media highlands‘ (chuanmei gaodi)

(Tan & Wang, 2009). The evidence I provide in this thesis shows that Beijing

prevails amongst these competing hotspots. Yu Guoming has evaluated media

development in Chinese cities taking into account five aspects: production,

profit, consumption, advertising and environment. Beijing tops his list (Yu,

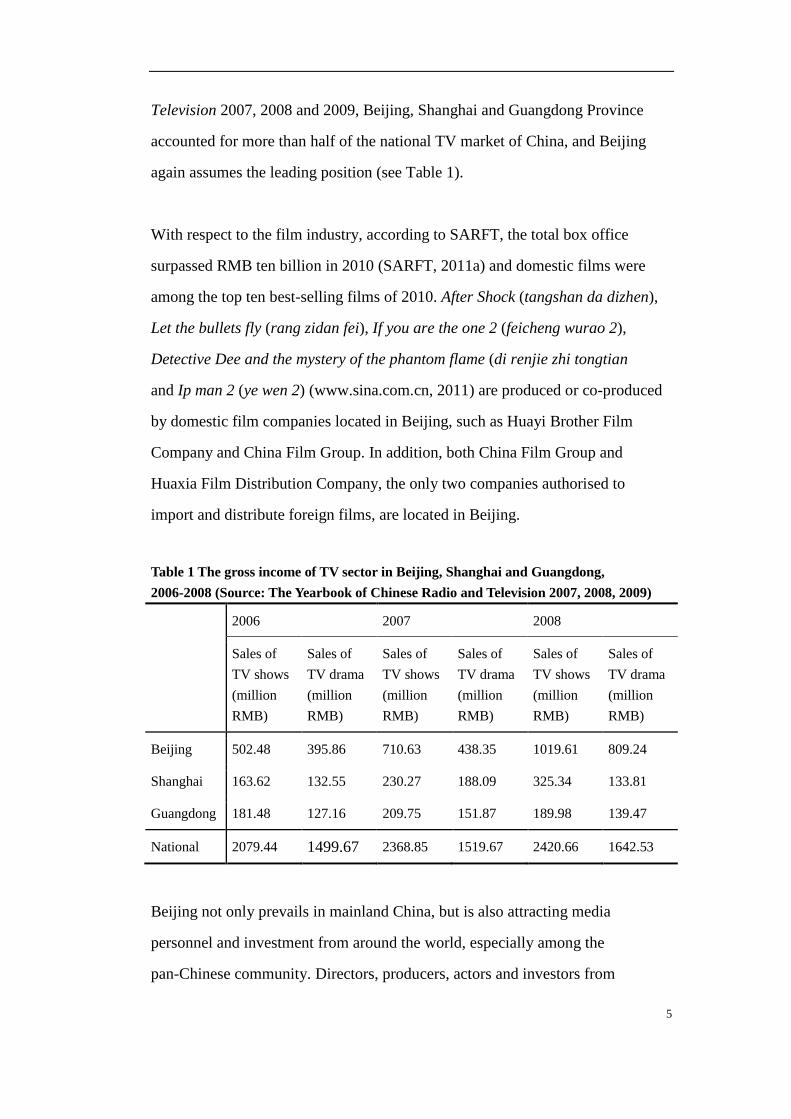

2010). In the TV sector, according to The Yearbook of Chinese Radio and

5

Television 2007, 2008 and 2009, Beijing, Shanghai and Guangdong Province

accounted for more than half of the national TV market of China, and Beijing

again assumes the leading position (see Table 1).

With respect to the film industry, according to SARFT, the total box office

surpassed RMB ten billion in 2010 (SARFT, 2011a) and domestic films were

among the top ten best-selling films of 2010. After Shock (tangshan da dizhen),

Let the bullets fly (rang zidan fei), If you are the one 2 (feicheng wurao 2),

Detective Dee and the mystery of the phantom flame (di renjie zhi tongtian

and Ip man 2 (ye wen 2) (www.sina.com.cn, 2011) are produced or co-produced

by domestic film companies located in Beijing, such as Huayi Brother Film

Company and China Film Group. In addition, both China Film Group and

Huaxia Film Distribution Company, the only two companies authorised to

import and distribute foreign films, are located in Beijing.

Table 1 The gross income of TV sector in Beijing, Shanghai and Guangdong,

2006-2008 (Source: The Yearbook of Chinese Radio and Television 2007, 2008, 2009)

2006 2007 2008

Sales of

TV shows

(million

RMB)

Sales of

TV drama

(million

RMB)

Sales of

TV shows

(million

RMB)

Sales of

TV drama

(million

RMB)

Sales of

TV shows

(million

RMB)

Sales of

TV drama

(million

RMB)

Beijing 502.48 395.86 710.63 438.35 1019.61 809.24

Shanghai 163.62 132.55 230.27 188.09 325.34 133.81

Guangdong 181.48 127.16 209.75 151.87 189.98 139.47

National 2079.44 1499.67 2368.85 1519.67 2420.66 1642.53

Beijing not only prevails in mainland China, but is also attracting media

personnel and investment from around the world, especially among the

pan-Chinese community. Directors, producers, actors and investors from

6

Shanghai, Guangzhou, Hong Kong, Taiwan and Singapore have moved to find

work and make deals in Beijing (see G. Chen, 2004). Desmond Hui (2003) has

observed that Hong Kong is experiencing an inevitable ‗brain drain‘. More

multinational corporations moved their Asian-Pacific headquarters to Beijing

and Shanghai after China‘s accession to the WTO. The small local market has

severely hindered further development of Hong Kong‘s TV and film industry. It

is becoming imperative for Hong Kong producers to seek collaborations in

mainland China. The Hong Kong film producer Wu Siyuan believes Beijing is

China‘s film centre and therefore releasing a film in Beijing is more effective

(cited in Y. Zhang, 2009).

In addition to attracting media resources, Beijing has all the stakeholders in

China‘s media industries and therefore provides a representative case study for

close analysis of how media industries operate in China:

Beijing is the national decision centre of the media industries. Being the

capital of China, it is the locus of government departments related to the

media industry, including the State Administration of Radio, Film and

Television (SARFT), Ministry of culture (MoC), Ministry of Industry and

Information Technology (MIIT) and the General Administration of Press

and Publication (GAPP).

Beijing has the greatest concentrations of domestic media organisations in

China. Beijing serves as the major node of Chinese media industries‘

networks and nearly all the national media enterprises are in Beijing, as it is

the cultural and political centre of China. The two most important

state-owned national media companies, CCTV (which is the biggest TV

group in China and covers one third of the national TV market) and China

Film Group Corporation (CFGC, which accounts for over 50% of the

7

Chinese film market) are both located in Beijing. Furthermore, most

competitive private media companies, such as Enlight Media (guangxian

chuanmei), H.Y. Brother (huayi xiongdi), Poly bona (baoli bona), Orange

Sky (chengtian jiahe) and Galloping Horse Film & TV Production (xiaoma

benteng) are in Beijing.

Beijing has a high proportion of creative talent. It is acclaimed as the

cultural centre of China. Large numbers of cultural workers have migrated

to Beijing. Most renowned Chinese directors, producers, actors and

screenwriters are attracted by the symbiosis of a unique local landscape,

ancient civilisation and modern pop culture. Many settle down in Beijing.

Recently, many entertainers from Hong Kong, Taiwan and even Singapore

have taken up residence in Beijing. In early 2009, the Hong Kong film

director Chen Kexin (Peter Chan) opened his film studio in Beijing. Ma

Chucheng (Jingle Ma), Liu Zhenwei (Jeffery Lau), Chen Jiashang (Gordon

Chan), Wu Yusen (John Woo) and Er Dongsheng (Derek Yee) all followed,

and signed up with media companies in Beijing.

Beijing is the headquarters for most international media companies. In 1995,

Viacom set up its representative office in Beijing and launched its

collaboration with CCTV on entertainment programs and children‘s shows.

In 1999, News Corporation set up a representative office in Beijing. Japan‘s

Fuji TV started to cooperate with CCTV; broadcasting news produced by

CCTV on its news website is a part of their collaboration. At the present

moment, international media companies are only allowed to co-produce TV

and film. So they often establish covert and ‗under the radar‘ joint ventures

with Chinese media organisations and state-owned TV stations, most of

which are located in Beijing.

8

1.2 Research questions

According to Curtin, a media capital exports media product. Though Beijing is

the media centre of China, the question still remains: is Beijing a media capital?

In most cases, so far, Beijing has not even been considered. In order to address

literature gaps related to media capital, I take Beijing, the political capital of

China, as a case study. Therefore the primary research question is:

What are the possibilities of Beijing becoming a media capital?

In order to address the primary research question, five subsidiary research

questions are proposed:

(1) How do media industries operate in Beijing?

(2) Is Curtin‘s media capital framework able to be directly applied to China? In

which way should the media capital notion be revised when it is applied to

China?

(3) What factors differentiate Beijing from other known media capitals?

(4) Is there a push for Beijing to be an international media capital? If yes, where

does it come from? If not, what is holding it back?

(5) What are the strengths and weaknesses of Beijing as a media capital?

9

1.3 Research significance

The research has significance for several reasons. The upsurge of interest in

cultural and creative industries in the past decade has heightened place

competition among Chinese cities (Keane, 2007a, 2011; Liu, Huang, & Zhang,

2008; Zhang, 2008). Shanghai is striving to be a business centre; Beijing, as the

political capital, aspires to be a global city through the enhancement of its media

assets. Media industry, the most vibrant of creative industries, is worthy of close

observation. According to Anke Redl and Rowan Simons, ‗the development of

the media, the most political and commercial of modern industries, provides a

unique insight into the reality of socialism with Chinese characteristics and the

challenges facing China as it emerges as a major world economy and cultural

force‘ (Redl & Simons, 2002, p. 18). Prior studies have demonstrated that local

business networks are both the key driver of industrial agglomeration (Curtin,

2005; Keane, 2006; Porter, 1998; Scott, 2006b) and one of the defining

characteristics of Chinese social, political and communicative organisation

(Shoesmith & Wang, 2002). But existing Western studies of China‘s media do

not deeply investigate the local network of Chinese media industries, nor do

they tend to link cultural studies with geographic deployment. Instead, the focus

appears to be on ‗propaganda‘ or ‗ideology‘, deployed as concepts to critique

Chinese media as technologies of power (Donald & Keane, 2002). As a result,

there is a lack of analysis of the development trajectories arising from the

changing political-economic, institutional and social dynamics of Chinese media

industries.

In relation to Chinese media industry studies, several principles should be borne

in mind: the foremost principle of media regulation in East Asia remains

national sovereignty (Goldsmith, 2003); Chinese media industry is still in the

process of transition in terms of control (Keane, 2006, p. 837); and, most

10

importantly, the context of the media industries in China is one where the

government not only supervises the media but also intervenes in shaping

competition and collaboration between media companies of various scales and

ownership forms for its own national development priorities. By contrast,

Curtin‘s argument is generally based on the observation of the Western free

market model (e.g. Hong Kong and Hollywood). As Michael Keane argues, the

theoretical issue of how media and communication studies ought to connect with

non-Western contexts is urgently needed, because the current Western

theoretical frameworks are incapable of engaging with the field outside the

Western enclaves where it is predominantly practised (Keane, 2006, p. 837).

Therefore, the media capital concept, although it starts from analysing the

historical evolution process of local networks and provides a rational way to

elaborate the ceaselessly changing media industry, needs certain modifications

when it is applied to Beijing, since it has never been adopted in order to study

any part of mainland China.

Based on the above, ‗the tensions, contradictions, compliance, and partial

resolution between the state and the market [in China] harbour great possibilities

for theory building and testing‘ (Ma, 2000, p. 32) whereas a discourse on the

local and the interior of Chinese media industry is still apparently missing both

in Western and Eastern hemispheres. Given the complexity of local networks of

Chinese media industry, an inside-out and bottom-up approach to the Chinese

media industry through the approach of media capital is crucial and vital.

This project will, therefore, be based on the city of Beijing, and will focus on the

geographic redeployment of media industry in Beijing caused by the relocation

of CCTV. It will investigate the changes to the Chinese media industry, such as

infrastructure, business environment, governmental policies and development

features generated by this redeployment. It will investigate the ways in which

11

the network of Chinese media industry relationships are operating in order to

identify major factors influencing the clustering process of China‘s media

industry, thus informing understandings of geographic locations and Chinese

media industry development.

Such an empirical approach enables us to examine the possibilities of Beijing

becoming an international media capital, while also adjusting Michael Curtin‘s

media capitals model into a framework that can be utilised to understand

Chinese media industry from the perspective of cultural and economic

geography. It is anticipated that the research program in this thesis will have

both practical and theoretical applications, and will make an important

contribution to both the Chinese media industry and the research literature.

1.4 Research approach and methods

This research investigates commercial TV and film industries, and excludes

sectors such as news and documentary. This parallels Curtin‘s analysis, which

mainly focuses on the commercial entertainment sector. In the Chinese context,

it is also highly relevant that such sectors as news and documentaries remain

very much as media institutions (shiye). They are heavily regulated, which

leaves little room for competition. This research also excludes new media

services (such as SNS and IPTV), as research on new media requires different

research methods, models, perspectives and approaches (Williams, Rice, &

Rogers, 1988).

Resolving Beijing‘s media capital status presented me with a complicated set of

problems. It would be simple to adopt the approach that Beijing could not be a

media capital because of the state‘s socialist ideology and the legacy of

12

excessive government control and censorship, in line with Curtin‘s media capital

model and his observations on Beijing (Curtin, 2010a, 2011). However, political

power that is heavily concentrated in Beijing enables the clustering of media

industries and provides access for companies to negotiate with the government

and even to change the government‘s approach, which will be discussed in

Chapter 7. Hence it is necessary to identify difficulties in applying Curtin‘s

media capital notion directly in Beijing.

In order to investigate how Beijing might qualify as a media capital I needed to

get inside the system, to talk with a range of players or stakeholders. I made use

of qualitative methods, primarily semi-structured interviews. While my research

interest was specific, at the same time there was a need for flexibility and a

degree of open-endedness in the interviews in order to further explore points

made by interviewees, where their unique characteristics or circumstances make

it necessary or useful (Weerakkody, 2009, p. 167). I used document analysis and

case study to complement my interviews in the first and third phases of this

research. A qualitative way of thinking was adopted, as this project studies

‗meaning‘ (Hesse-Biber & Leavy, 2006, p. 8), namely: how to understand

China‘s media industries clustering and export through Curtin‘s media capital

perspective, and to identify what variables and vectors, and to what extent, we

needed to revise the media capital idea when applying it to China.

The focus of this research is to come up with a more holistic image of China‘s

media industries, one which produces descriptive, interpretive and

culturally-situated knowledge by interplaying Curtin‘s media capital idea with

data collected during my field work in Beijing. According to Stake (2010),

qualitative research relies on human perceptions and understanding. Therefore,

the outcomes of qualitative research are representations and presentations of

salient findings from the analytical synthesis of data, such as new insights and

13

understandings of social complexity, the evaluation of a policy‘s influence, and

a critique of existing social orders (Saldana, Leavy, & Beretvas, 2011, p. 4). In

terms of media and communication studies, Hollifield and Coffey (2006)

observed that qualitative research has been widely used in media and

communication studies, especially by scholars at the crossroads of media

economics and policies, as qualitative research takes nuances and contexts into

account when analysing data, discussing results and forming arguments.

On the other hand, this research is related to geography, as it discusses the

relationships between media industries and the environment in Beijing to

explore how the trajectory of media industries is altered by Beijing‘s physical

and social cultural landscape and how the city‘s landscape develops and changes

along with the development of media industries. Nowadays, qualitative research

is commonly used in geography to address various issues of culture, society,

economy and places (Hay, 2010). Qualitative research is able to help

geographers understand and explain the social and cultural differences through

the perspective of participants in the place. This is more difficult in quantitative

research.

This research uses a range of methods, including document analysis, interviews

and case study analysis, in order to gather useful and usable data to answer the

research questions proposed in this chapter.

According to Al James (2006), research questions should be derived from ‗a

simultaneous revisionist cycling‘ between academic debates, government

documents and evident socio-economic issues; and case study, interview and

social-based qualitative analysis should be adopted to seek the answer to

research questions. Hence this study is designed as follows:

14

I conducted document analysis on relative statistics, policies and other types of

government discourses to discover the status quo of media industry clustering in

Beijing and to identify the rationale of Chinese media industries‘ accumulation

strategies by combining the result with government policies. Informed by the

results of the interviews, I undertook a case study of the change of geographic

deployment of the media industry in Beijing caused by the relocation of CCTV

in order to propose and test answers to research questions.

1.4.1 Document analysis

The first phase of this project is to discover the current situation and

characteristics of development regarding media industry agglomeration in

Beijing. But due to the insufficiency and the inconsistency of authoritative

statistical data in China, statistics are only utilised to provide a broad depiction.

Relevant data can be retrieved from Beijing Statistical Information Net1, Beijing

Cultural and Creative Net2, eBeijing

3, the website of the State Administration of

Radio Film and Television, the website of General Administration of Customs

of China, the website of Beijing Customs and the website of State

Administration of Foreign Exchange. I looked at the Yearbook of Chinese Radio

and Television to examine major events and statistical data regarding radio and

1 Beijing Statistical Information Net is the only dedicated website of Beijing Statistics

Bureau to disclose statistic data. For more information, please see: www.bjstats.gov.cn

2 Beijing Cultural and Creative Net is the only dedicated website of Beijing Cultural and

Creative Promotion Center to release information concerning creative industries in Beijing.

For more information please see: www.bjci.gov.cn

3 eBeijing is the Official Website of the Beijing Municipal Government, please look at:

www.beijing.gov.cn

15

TV sectors, and several series of Blue Books, including the Report on

Development of China’s Radio, Film and Television, the official statistics report

published annually by SARFT, the Report on Development of China’s Media

Industry, the Report on Development of China’s Cultural Industry. By exploring

these data sources, I was able to analyse the development trend of China‘s media

industries and identify the scale and function of Beijing‘s media industries.

Moreover, I conducted a document analysis on relevant government policies to

reveal the major themes that the Chinese government is pursuing. Most

government policies are listed on the websites of the Ministry of Culture, the

State Administration of Radio Film and Television, China‘s General

Administration of Press and Publication, and China‘s General Administration of

Customs.

However, it is necessary to make a connection between the language used in

policies and that of the ‗real world‘, between policy-makers who produce

documents and the audience for whom the documents were intended, if we are

to understand their essential elements. Such policy documents, when read

without contextual background, do not reflect the real situation (Prior, 2011).

Faced with difficult access to government officials, in this phase I used other

document sources, such as political speeches and official commentaries, as

complementary components in the system of government actions and discourses.

This type of governmental discourse that I drew on included: Chinese senior

leaders‘ speeches on Chinese core leadership, which normally can be found at

the www.xinhua.com; articles in party newspapers, including The People’s

Daily (renmin ribao), Enlightenment Daily (guangming ribao) and The

Economic Daily (jingji ribao).

16

1.4.2 Semi-structured interviews

The second research method that I employed as a means of collecting data and

evidence was semi-structured interviews. Weerakkody (2009, p. 166) points out

that in media research, interviews allow researchers to collect information from

interviewees when the phenomenon under study cannot be directly observed or

measured. Moreover, in studies of geography, interviews are often used when

investigating complex behaviours and motivations and in understanding how

meanings differ among different groups of people (Dunn, 2010).

Interviews involved ‗active asking and listening‘ (Hesse-Biber & Leavy, 2006, p.

119) on the ‗theme of mutual interest‘ (Marshall & Rossman, 2011, p. 142), as

these are useful for finding out about people‘s experiences, the way they do

things, their motivations, their attitudes, their knowledge, the way in which they

interpret things or the meaning they attach to things (McGivern, 2003).

It is still widely believed that because of government control, the Chinese media

industry is hamstrung and, accordingly, Beijing will not develop into a media

capital. My hypothesis is that a unique economic-political system is actually

forming in China. In making this claim, I am drawing on remarks that the

Chinese media environment is not like a ‗birdcage‘ (Ma, 2000, p. 28); that is,

the government is not indifferent to the vibrancy of the bird, namely media

industries. Chinese media companies have never stopped searching for a means

to achieve longer sustainability and they have coped with what Ma (2000) called

‗structural coexistence‘ and overt conflicts with government in their own ways.

They have found ways of negotiating with government. Beijing is the best place

to see these deliberative processes in action.

17

In order to comprehensively understand the tension between the government and

the media industry itself, my interviewees included four categories:

managers/directors in Chinese media organisations; media workers; foreign

media personnel; and media scholars. Informed by my document analysis, I

interviewed people from these groupings in order to further identify causal

relationships and patterns of interaction, as well as to access the myriad cultural

assumptions, competing possibilities, trade-offs, historical contingencies and

multiple motives that underpin corporate decisions and non-decisions that are

rendered invisible in survey data (James, 2006, p. 297). For the information of

interviewees, please refer to the list of interviewees in Appendix 1.

1.4.3 Case study

A case study typically examines a group of people, an organisation, an event, a

process, an issue or even a campaign (Gerring, 2007; Weerakkody, 2009).

Multiple realities or diverse perspectives of information are linked up into a

coherent framework. More importantly, a typical case is an exercise in

theory-building and is the most information-rich and fruitful way for junior

scholars to invest their limited resources (James, 2006, p. 294).

For this reason, in the third phase of this project, I conducted a case study on the

most significant media cluster in Beijing, the Beijing CBD International Media

Industry Cluster, around the CCTV new building at the heart of CBD in

Chaoyang District. This is a significant development as China attempts to

up-scale its innovative productivity through new forms of creative organisation

and management (Keane, 2007a). I looked not only at the cluster itself but also

at the migration trend of media industries from the west of Beijing to the CBD

in the east of the city. The purpose of conducting a case study was to show

18

cause-and-effect relationships between government ambitions, local networks

and industrial development.

The Beijing CBD International Media Industry Cluster started forming in 2004

and was officially recognised by the Beijing municipal government in 2008. It is

located around the CCTV new building (which recently finished construction) at

the heart of the CBD in the eastern part of Beijing. Over 80% of overseas news

agencies and 167 international media organisations are located in this cluster,

including CNN, VOA, BBC, Viacom, Timer Warner, Disney as well as

significant Chinese media such as CCTV, Beijing TV and Phoenix TV.

According to statistics, over 1700 cultural and media organisations were situated

in the CBD by September 2010. A Chaoyang District government‘s report

claimed that on average one media company per day has moved into the CBD

since 2006 (The Propaganda Department of Chaoyang District Government,

"Ten years of CBD," 2010). The Beijing CBD International Media Industry

Cluster is the epitome of the clustering process of the media industry in China,

and it includes most of China‘s media companies.

CCTV conceived a plan of moving to the core area of CBD in 2004, and the

construction of the new building began shortly after. This decision arguably

represents a strategic change, from party organ towards an international media

enterprise. Moreover, production companies, broadcasting institutions,

advertising companies, training organisations, and performance agencies, which

used to be in the west of Beijing and close to the current location of CCTV,

began moving to CBD soon after this news was released. The reason for the

change of media landscape is that a business relation with CCTV is a symbol of

strength; a shorter geographical distance to CCTV enhances opportunities for

entering into a contract with CCTV. Media companies collaborating with CCTV

can benefit from economic profit and from reputational effects. Later on, Beijing

19

TV (the local TV station of Beijing) and Phoenix TV (the most popular overseas

TV station based in Hong Kong) moved to the CBD. A huge conglomeration of

media business and media workers has formed since.

In this case study, I collected first-hand data by site visit and combined it with

data collected during the document analysis and interviews in the first and

second phases. I analysed relationships between major institutional factors, such

as media companies, TV stations, administrative sector of clusters, local

governments and independent creative forces to probe into the causality and

implication of the clustering process.

1.5 Chapter breakdown

The remainder of this thesis is organised as follows:

Chapter 2 explores theories related to media capital and clusters to interpret

three principles (logic of accumulation, trajectories of creative migration and

forces of social-cultural variation) and to investigate how they act on each other

in order to describe the research context. Then the literature gaps are identified

and corresponding research questions are proposed.

Chapter 3 begins with a historical review on media reform in China so as to

generalise characteristics of Chinese media industries and to understand the role

of various stakeholders in China‘s media sector. Following this, the chapter

investigates the implications the characteristics of Chinese media industries with

regard to the understanding of media capital.

20

Chapter 4 shows the larger picture of competition in the TV and film industries

in China, the relationships between different types of organisations, the

regulatory environment and the export of China‘s media industries informed by

Chapters 2 and 3.

Chapter 5 focuses on how the three principles of media capital play out in

Beijing in the soft power era. This chapter investigates media production and

export in Beijing and how the intersection of people and social-cultural variables

influences development. In conclusion, I discuss the consequence of the three

principles for media industries in Beijing.

Chapter 6 is a case study on the media cluster around CCTV‘s new building in

the CBD of Beijing in order to investigate the change of the geographical

deployment of media companies and workers. The relocation of CCTV allows

us to take a close look at the relationship between the government, industry and

location; it demonstrates tensions emanating from the process of agglomeration.

Chapter 7 discusses how different factors interact in Beijing and the kind of

ecology that such interaction takes on with regard to media industries; it

analyses issues arising from previous chapters and identifies possibilities and

difficulties for Beijing to become a media capital.

Chapter 8, the concluding chapter, summarises findings in order to answer the

research question of this thesis.

21

Chapter 2 Literature review: Globalisation and

regionalisation

It is often argued that globalisation is engulfing every corner of this earth. For

the boosters of globalisation, it seems that the world is becoming flat, as fast

developing communication technologies and global transportation have

diminished the need for the collocation of management, labour and consumption

(Freeman, 2000); consequently, the impact of geographic location on site

selection has been reduced (Friedman, 2006). However, Dickens maintains that

within the geo-economic map of globalisation we can not only find dispersal but

also economic concentration tendencies that give rise to the agglomeration of

economic activities in localised geographical clusters (Dicken, 2007, p. 21).

This is a core factor in the cultural and creative industries: it is argued that

‗while the distribution and marketing of cultural products spans globally, the

development and production – but not always the reproduction – of them is

highly clustered in a few major cities, such as London, Los Angeles, Paris,

Tokyo, Moscow, Mumbai and so on‘ (Lorenzen & Frederiksen, 2008, p. 155).

In this chapter, I explore the relationship between globalisation, regional identity

and media capital. The first section looks at the bidirectional development trend

of global media production. Though Hollywood still holds its advantageous

position as the global media production centre, the importance of places other

than Hollywood is growing rapidly. Media products are produced in Hong Kong,

Tokyo, Cairo and Mumbai and are spread trans-regionally. These

newly-emerging media centres outside the US demonstrate how satellite

technologies and ICTs enable media companies to transmit technology,

knowledge and products over boundaries. Furthermore, the emergence of new

22

media centres shows that location of production can be a unique component for

competitive media products.

In this context, it is important to note increasing regionalisation in the global

media market while acknowledging that Hollywood still dominates media

industries globally. Following this opening discussion I examine the media

capital notion and its three operating principles: logic of accumulation,

trajectories of creative migration and forces of social-cultural variation. As the

key concept, media capital provides a perspective and an approach, which

combines a range of theories including political economy, urban studies,

economic geography and policy studies, for understanding the development

orbit and driving dynamics of media clusters. This leads into a discussion of

how to win and keep the status of media capital, a question that will be

discussed throughout the following chapters. I introduce theories to illustrate

that the key is to combine agglomerated production systems with the geographic

milieu so as to facilitate accumulation, to accommodate innovation and to

reinforce the cultural identity of the location. Finally in this chapter I offer some

critical perspectives on applying ‗media capital‘ directly in China.

2.1 Global media production: dispersal and concentration

In media industries, globalisation has frequently been used as a synonym for

Westernisation or Americanisation (Giddens, 2002): this reflects the fact that the

best known global movies and TV industry products are produced out of

Hollywood (Miller, Govil, McMurria, & Maxwell, 2001). But the wide

application of satellite technologies and ICTs has enabled flows of capital,

technology, knowledge and people, and has generated a strong multi-directional

tendency. In addition, it has been observed that contemporary media products

23

frequently contain interchangeable elements (Keane & Moran, 2004), although

it is also argued that media conglomerates still keep a firm hand on the

generation and ownership of intellectual property (Miller, et al., 2001).

Therefore, media companies are capable of flexibly choosing suitable

production locations for different purposes. Most scenes from Lord of the Rings

were shot in New Zealand; the CGI of The Matrix was mainly generated in

Australia. Moreover, media companies such as TimeWarner, Disney, News

Corporation and Sony, have stretched out their antennae globally by various

means, including offshore production, joint ventures, production deals and

diagonal mergers. Global media production networks are formed as a result.

Nonetheless, globalisation should not be understood simply as

de-territorialisation (Storper, 1997). The emergence of a range of different

media centres, especially those outside the US, shows a reverse trend to the

simple global dispersal of production. This indicates agglomerations of

knowledge, practitioners, and technology in certain areas. It has been argued that

the global impact of American media is declining and the preference for local

cultural content is still strong despite cultural convergence and globalisation

(Tunstall, 2008). The dispersion of production stems mainly from the general

belief that it is possible to standardise production processes due to the

globalisation of trade, the spread of ideas and access to technologies.

At the same time, a shift from mass production and consumption to ‗flexible

specialization‘ and smaller niche markets (Amin, 1994; Harvey, 1989; Lash &

Urry, 1987, 1994; Lipietz, 1992; O'Connor, 2007; Scott, 1988) validates that

location of production can be a unique component for competitive media

products (Scott, 2006a, p. 10), since culture is interwoven with the lived

experience of consumers (S. Hall, 1986, p. 39), as well as the symbolic content

of media products being highly valued (Harvey, 1989; Lash & Urry, 1994). It is

24

difficult for a program which meets the tastes and concerns of one audience to

have the same merit in a different context (Bielby & Harrington, 2002); as a

result, there is at least the potential for a more polycentric global media

production system and this tendency is even more obvious in the TV sector than

in film. Thus, as Joseph Straubhaar (Straubhaar, 1991, 2010) contends, we see

the increasing interdependence of the global media market, one that bears a

strong regional flavour.

Outsourcing production in the wake of globalisation has in fact generated a

transfer of knowledge or control (Flew, 2007; Storper, 1997), which further

enables the formation of ‗complex‘ international flows of programs and a

‗multilayered‘ global media system (Cunningham & Jacka, 1996a; Sparks,

2007). Other than Hollywood in the USA, cities that used to be deemed as the

periphery are becoming major centres of cultural production for both local and

global markets (Goldsmith, Ward, & O'Regan, 2010; Lorenzen, Scott, & Vang,

2008). TV Globo in Brazil and Televisa in Mexico are not only major national

TV producers but are also major soap opera exporters in the Latin American TV

market. Japan, Korea and Hong Kong have established themselves as major

media producers for pan-Asian markets (Curtin, 2003; Flew, 2007). In terms of

the number of films, India remains the world‘s leading film producer, but

Nigeria is closing the gap after overtaking the United States for second place

(UIS, 2009). Consequently, a polycentric and polycultural global system is

forming (Anheier & Isar, 2008).

2.2 Media capital

In 2003, Michael Curtin provided a perspective through which we can

understand the spatial dynamics of media industry agglomeration, by proposing

25

the concept of ‗media capital‘ (Curtin, 2003). According to Curtin, media

capitals are ‗centres of media activity that have specific logics of their own; sites

of mediation; locations where complex forces and flows interact; meeting places

where local specificity arises out of migration, interaction and exchange; places

where things come together and, consequently, where the generation and

circulation of new mass culture forms become possible‘ (Curtin, 2003, pp.

203-205). Media capital is also a dynamic concept, since although it

acknowledges dominance it is also observed that capital status can be won and

lost, and the term itself has two subtle meanings: capital as a centre of activity

(geographical) and capital as a concentration of resources, reputation and talent

(economic).

As media capital is a key concept informing this study, I investigate its

relationship to a range of other forces, including political economy, urban

studies, cultural economic geography and policy studies, in order to lay out a

theoretical framework for understanding the development orbit and driving

dynamics of media clusters.

2.2.1 The cultural turn in economic geography

Curtin states that media capital is a relational concept. A city‘s status as a media

capital is embodied in its geographical, historical, cultural or industrial relations

with other cities. The point here is to establish that media capital provides an

interpretation of the global media production system through a perspective that

Flew (2009) terms ‗cultural economic geography‘. This approach explains the

distinctive relations between space, knowledge and place. We need to critically

review this approach in order to better examine Curtin‘s media capital idea.

26

Economic geography recognises that the central element of economic life is the

place-specific and clustered nature of many economic activities (Dicken, 2007;

Soja, 2010). Cities and city regions are involved in networks that transcend

national boundaries. Therefore place is a kind of node, or point, where relations

and connections meet across space; the interaction of relations and connections

reshapes the economic landscape of the place (Massey, 1995). However, with

the rise of a global cultural economy, cultural goods are no longer largely the

possession of the upper middle class. In the cultural, or creative, economy,

culture becomes a serial of products that can be sold and purchased in the

market. Place acquires a unique identity and becomes a site for generating

distinct bodies of knowledge. Hence, in media industries, the global media

production system is developing into a ‗polycentric‘ system that embodies a

tendency of increasing diversity in global media industry as the development of

niche markets (Scott, 2005, pp. 167-168) and their distinctive place-based look,

feel and meaning are embedded into their outputs (Lorenzen, et al., 2008, p.

590). All of these propositions signify the ‗cultural turn‘ in economic geography,

which proposes that ‗economic categories are themselves discursively as well as

materially constructed, practised and performed at different spatial scales‘ (c.f.

Flew, 2009; James, Martin, & Sunley, 2007).

Being a complex nexus of diverse disciplinary perspectives rather than a

coherent school, cultural economic geography emphasises the mutual

constitution and fundamental inseparability of the economic sphere and the

cultural sphere (James, 2006). James (2006) holds that, on the one hand, cultural

economic geography is a direct response to the shift towards a post-industrial,

knowledge-based, global capitalist economy in which social relations are of

apparent importance to economic success/failure; and, on the other hand, it

challenges structurally determinist accounts of economic change that have

previously dominated the field, and argues that the economy determines culture

27

in a predefined hierarchy of epistemic significance. In other words, we need to

locate and contextualize the economic within cultural, social and political

relations (Massey, 1995).

Gertler (2003a) outlines three themes relevant to culture‘s implications for

economic geography. Firstly, the increasing significance of niche markets push

firms to shift away from standardised production to customised production: this

requires more flexible production processes and labour divisions, both inside

and between companies; the specialised offerings of external inputs and

suppliers lowers risks and encourages productivity. Secondly, production

processes as well as the process of innovating becomes more and more

socialised, hence the shared social attributes embedded in regional cultures

facilitate knowledge exchange, inter-firm learning and trust bonds. Thirdly,

economic prosperity is increasingly path-dependent as it is conditioned by

historical patterns that are embodied in material objects, the experiences of

individuals and social structures, and increasing returns to scale that result in the

self-reinforcing of economic change, so it is necessary to understand the

historical social, economic and cultural paths taken by production regions.

Thus, the economic geography approach informs the following discussion on

media capital in the following aspects: (1) in which way the tendencies of media

production towards ‗flexible specialization‘ has influenced the formation of

media capital; (2) how the local social attributes, or the ‗untraded

interdependencies‘ (Storper, 1997), facilitate the further growth of media capital;

(3) how habitus and convention alter the development of media capital.

28

2.2.2 Three operating principles

According to Curtin there are three principles of media capital: (1) logic of

accumulation; (2) trajectories of creative migration; and (3) forces of

social-cultural variation.

Logic of accumulation

Stimulated by the pursuit of profit and assisted by the development of ICTs and

other technologies, modern enterprises are able to operate across borders of

states and regions to reduce costs on production and increase the speed of

distribution. The logic of accumulation explains the centripetal tendencies of

production and centrifugal tendencies of distribution through the economic

geography perspective. Geographer David Harvey points out that companies

make the most of productive capacity and realise the greatest possible return by

concentrating productive resources on the one hand and through the extension of

markets on account of the demand for enhancing efficiencies on the other

(Harvey, 2005). Transportation and communications technologies, referred to as

‗time-space shrinking technologies‘ by Peter Dicken (2007), overcome natural

and political borders and transmit tangibles and intangibles internationally,

including materials, products, ideas, images, knowledge and even people.

However this generates uneven development and, accordingly, the New

International Division of Labour (NIDL). MNCs (Multinational Corporations),

the major players in the global economy, subcontract to developing countries for

low-wage labour and tax incentives while leaving the more technical and skilled

aspects of production in the home country (see Flew, 2008; Fröbel, Heinrichs, &

Kreye, 1980).

29

Toby Miller and colleagues (Miller, et al., 2001) have applied this insight into

the media industries in order to illustrate Hollywood‘s domination over the