Embed Size (px)

Citation preview

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc.

Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in

any form or manner without the prior written permission of Experian. Experian Public.

Unlocking the power of commercial bureau and regional economic data in forecasting loan performance

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 2

Cris deRitis Moody’s Analytics

Dan Meder Experian

Introducing:

@ExperianVision | #vision2015

Follow us on Twitter:

3 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Small business as growth engine

Capital adequacy requirements and small business lending

Correlating macro economic factors and small business performance

Best practices in loss forecasting and stress testing

Summary

Agenda

Data

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 4

Firms with less than

100 employees make up

98% of all businesses

in the U.S.

5 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Growth Firms with less than

100 employees

showed substantial

employment growth

in H1 2014

Insights

6 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Over 50% of Small

and Medium Enterprise

(SME) lending

is conducted by

banks with assets

over $1 billion

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 7

Capital adequacy

requirements and

small business

lending

8 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

WHAT IS REQUIRED? The aim of the annual reviews is to ensure that

large financial institutions have robust,

forward-looking capital planning processes

that account for their unique risks, and to help

ensure that they have sufficient capital to

continue operations throughout times of

economic and financial stress.

– Federal Reserve Board

9 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Economic

Instability in the

economic environment

calls for controlled

growth that balances

portfolio growth with risk

Technology

Potential for shifts in

regulatory, industry,

market and business

dynamics are

demanding more agile

and flexible technology

to minimize business

disruptions and support

real-time decisioning

Regulatory

Increased regulatory

requirements demand

sound development,

implementation and use

of credit models, a

stronger focus on risk

governance and

rigorous management of

liquidity and capital

Social

The Consumer

Protection Bureau

(CFPB) is mandating

more education,

transparency and

inclusive lending

practices to ensure

equal access to credit

and to protect

consumers from unfair

lending practices

Moving beyond the burden of compliance to uncover opportunity

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 10

Correlating macro

economic factors

and small business

performance

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Analytics

11

Best practice combines

business performance

and macroeconomic

factors in determining

capital adequacy

12 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

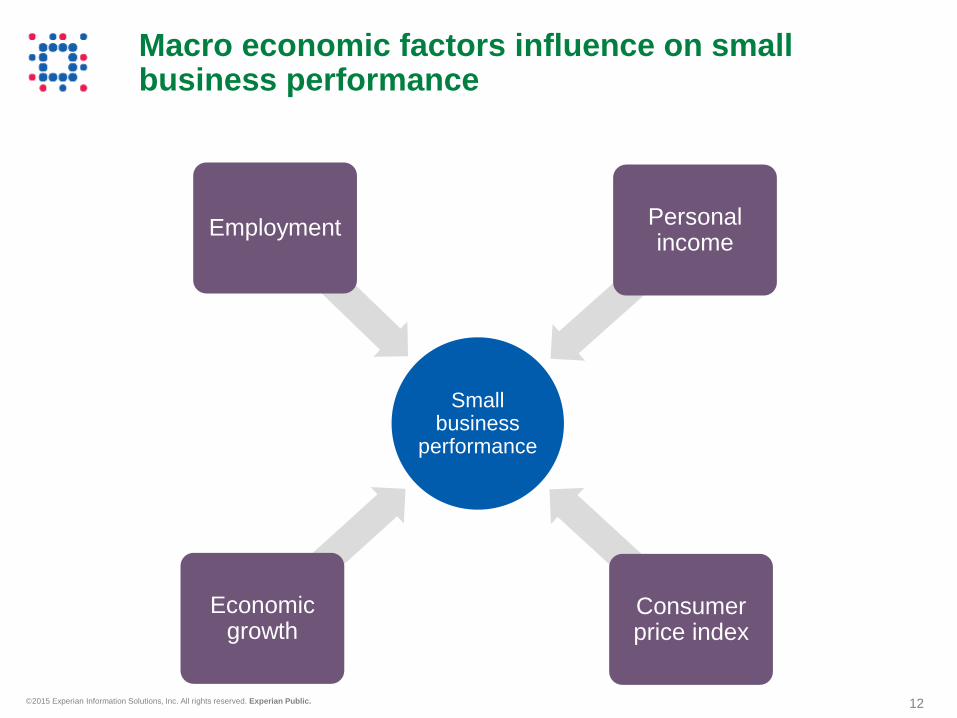

Macro economic factors influence on small business performance

Small business

performance

Economic growth

Employment Personal income

Consumer price index

13 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Payment and risk performance

► Region

► Industry

Economic

► Employment

► Personal income

► Retail sales

► Gross domestic product

► Personal consumption expenditures

► Industrial production

The combined power of economic and performance data

14 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Macro economic factors can affect different types of businesses in different ways

► Example: unemployment impact on retail performance

Correlating macro economic factors with the unique characteristics of your portfolio can increase predictiveness

► Geographic

► Business size

► Industry

Identifying higher risk segments of the portfolio will likely result in better identification of true reserves

Obtaining a well-rounded view of your portfolio

15 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

How payment performance can vary by region…

Percent of balances past due (firms with fewer than 100 workers)

Sources: Experian, Moody’s Analytics

0.80 to 5.43

11.57 to 29.50

5.44 to 11.56

16 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

…and by industry

Best performing industries by delinquency percent

Source: Business Information Map

1%

2%

3%

4%

5%

6%

7%

Q1 2013 Q2 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

Public Services Utilities

Health Services Education Services

Hospitality

0%

5%

10%

15%

20%

Q1 2013 Q2 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

Business Services Real EstateTransportation FinanceConstruction

Worst performing industries by delinquency percent

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 17

Best practices in

loss forecasting

and stress testing

18 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

SEEING THE FUTURE

Prediction is very difficult,

especially if it's about

the future.

– Niels Bohr

19 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Credit loss models for regulatory stress testing requirements:

► Sound, transparent, well-understood and owned by their users

Models need to be sensitive to economic conditions

Documentation is critical

► Conceptual underpinnings/assumptions and forecast results

Objectivity

► Let the models speak

Consider the alternatives

► Data

► Techniques

► Opinions

Best practices in loss forecasting and stress testing

20 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

MOONSTRUCK

MOMENT There are three kinds of pipe. There's what you

have, which is garbage - and you can see where

that's gotten you. There's bronze, which is pretty

good, unless something goes wrong. And

something always goes wrong. Then, there's

copper, which is the only pipe I use. It costs

money. It costs money because it saves money.

— Cosmo Castorini

21 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

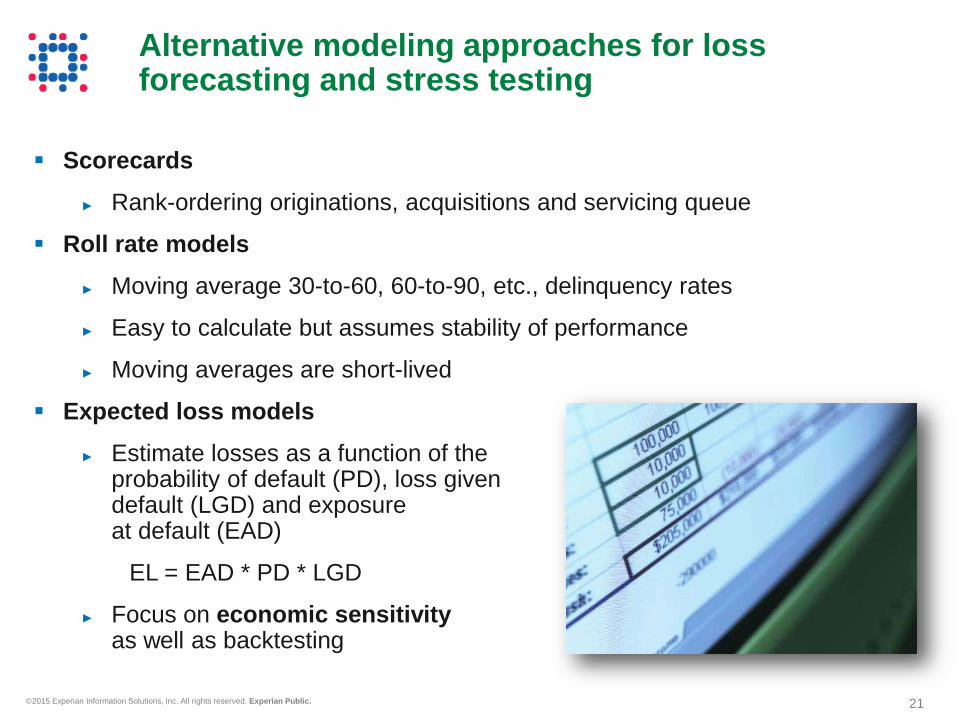

Scorecards

► Rank-ordering originations, acquisitions and servicing queue

Roll rate models

► Moving average 30-to-60, 60-to-90, etc., delinquency rates

► Easy to calculate but assumes stability of performance

► Moving averages are short-lived

Expected loss models

► Estimate losses as a function of the probability of default (PD), loss given default (LGD) and exposure at default (EAD)

EL = EAD * PD * LGD

► Focus on economic sensitivity as well as backtesting

Alternative modeling approaches for loss forecasting and stress testing

22 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

The complex life of a loan

O months delinquent

1 month delinquent

2 months delinquent

3 months delinquent

4 months delinquent

Charge-off (Gross $)

Recovery (=1-LGD)

Net Loss $

Originations/ Sales

Prepayment

Receivable Income

• Interest Income

• Fees

• Collection Expenses

23 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Micro approach: Loan/account level models

► Incorporate borrower and loan level detail (Big Data)

► Longer processing and simulation times

► May be less sensitive to broader economic trends and feedback effects

● Attenuation bias

Macro approach: Cohort level models

► Collapse borrower and loan level information to cohorts

► Shorter processing and simulation times

► Better suited to aggregate economic data

Multiple approaches are ideal

Expected loss model strengths and weaknesses

24 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Microeconomic model used to forecast account or loan level performance

Competing risk framework is common

Estimate discrete-time hazard

X has account-specific and time-varying economic factors

Aggregate economic information is correlated with individuals but may introduce noise

► Metro-level unemployment rate is an imprecise approximation of individual-level unemployment probability

Expected loss models Micro approach

25 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Macroeconomic model used to forecast macro-level performance like portfolio loss

► Capture broader trends, interdependencies and cycles

Portfolio losses especially stress losses are macro-dependent

Credit performance by regional geography may offer better match with regional economic data

► Higher correlation = lower noise

► Greater precision = Less excess capital

Expected loss models Macro approach

26 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Fed favors an aggregated approach for small business loans

Fed favors an aggregated approach for small business loans due to limited data

The other retail lending product portfolios include the small business loan portfolio, the other consumer loan portfolio, the student loan portfolio, the corporate credit card portfolio, and international retail portfolios. Due to data limitations and the relative small size of these portfolios, loan level models of default are not feasible.

Comprehensive Capital Analysis and Review 2012: Methodology for Stress Scenario Projections March 12, 2012

27 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Cohort loss models

Segment portfolio by product, geography, risk segment and vintage

Compute default rates each reporting month by cohort

Estimate PD = f(credit quality, age/maturation, the economy)

Leverage panel data and regional heterogeneity

Economic data is consistent with outcome providing appropriate sensitivity for stress testing:

► Default rate in Philadelphia directly related to unemployment rate in Philadelphia

Expected loss models Macro approach

Age V2011Q1 V2011Q2 V2011Q3 V2011Q4 V2012Q1

1 0.0% 0.0% 0.0% 0.2% 0.0%

2 0.5% 0.1% 1.0% 0.5% 0.3%

3 1.0% 0.1% 1.5% 1.0% 1.0%

4 1.5% 0.4% 1.7% 2.0% 2.4%

28 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Fed provides national scenarios

2015Q1 Severely Adverse Scenario for Unemployment Rate

29 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Local economics matter… Idiosyncratic scenarios stress geographic and industry concentrations

2015Q1 Severely Adverse Scenario

30 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Champion/challenger models give a broader view

► Over-reliance on single model technologies during US recession

► Leverage strengths of multiple approaches

► Fully transparent, back-tested and documented econometric loss forecasting models customized to specific portfolios

Benchmarking

► Experian industry data exist across multiple segments

► Industry data can fill in portfolio data deficiencies for modeling

► For small portfolios, no choice BUT an industry model

Supporting forecasts with external data

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 31

Some final

thoughts…

32 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

If you don’t have a loss forecast policy for your small business portfolio… get one

If you do, strongly consider what we’ve discussed today

But either way, we’re here to help. Come talk to us!

Some final thoughts…

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public. 33

For additional information,

please contact:

@ExperianVision | #vision2015

Follow us on Twitter:

34 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Share your thoughts about Vision 2015!

Please take the time now to give us your feedback about this session. You can complete the survey in the mobile app or request a paper survey.

Select the breakout

session you attended

Select the Survey

button and complete 1 2

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.