Embed Size (px)

Citation preview

SAJINEE SRICHAWLA

IS E-COMMERCE SHOPPER JOURNEY TRULY DIGITAL?

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

Is e-commerce shopper journey

truly digital?

MARKET DEVELOPMENTS of online vs offline retail

WHAT DRIVES CONSUMER in shopping online vs offline

What we will be discussing today

WORKSHOP Future Trends of Online Shopping Behavior

MARKET DEVELOPMENTS OF ONLINE VS OFFLINE RETAIL

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

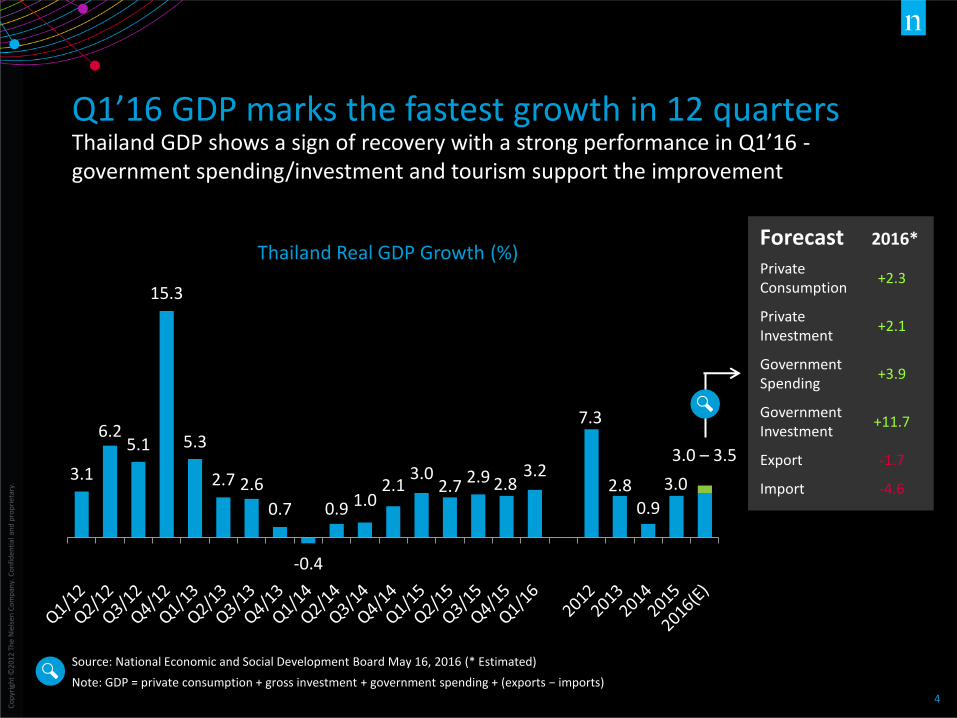

3.1

6.2 5.1

15.3

5.3

2.7 2.6

0.7

-0.4

0.9 1.0 2.1

3.0 2.7

2.9 2.8 3.2

7.3

2.8 0.9

3.0

Thailand Real GDP Growth (%)

Q1’16 GDP marks the fastest growth in 12 quarters Thailand GDP shows a sign of recovery with a strong performance in Q1’16 - government spending/investment and tourism support the improvement

Source: National Economic and Social Development Board May 16, 2016 (* Estimated)

Note: GDP = private consumption + gross investment + government spending + (exports − imports)

Private Consumption

+2.3

Private Investment

+2.1

Government Spending

+3.9

Government Investment

+11.7

Export -1.7

Import -4.6

3.0 – 3.5

Forecast 2016*

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

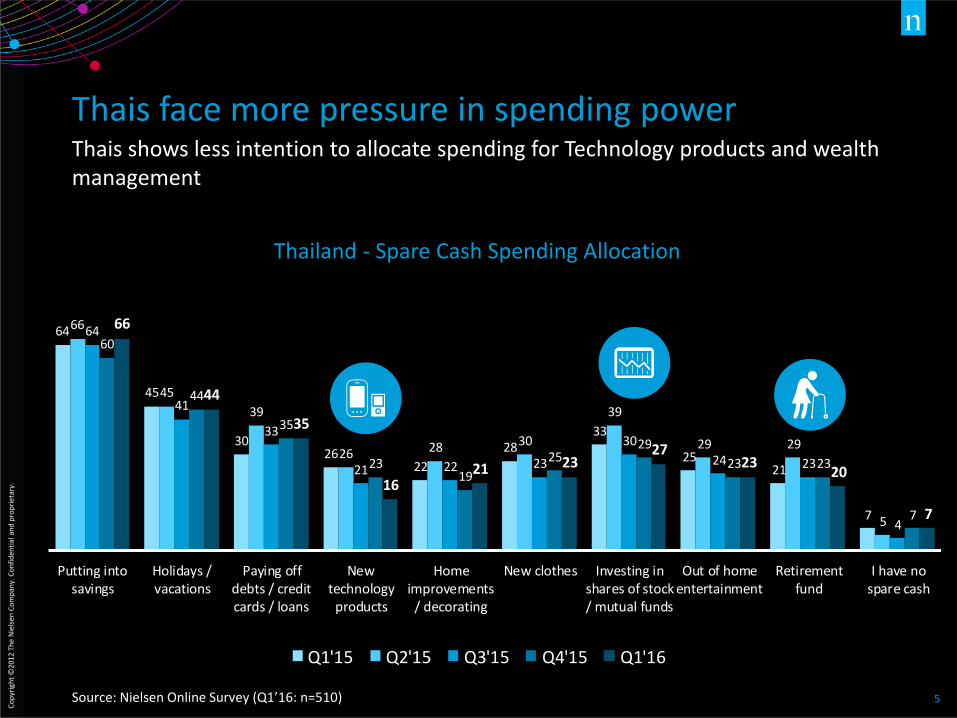

Thais face more pressure in spending power Thais shows less intention to allocate spending for Technology products and wealth management

Source: Nielsen Online Survey (Q1’16: n=510)

64

45

3026

22

2833

2521

7

66

45

39

26 28 30

39

29 29

5

64

41

33

21 22 23

30

24 23

4

60

44

35

2319

2529

23 23

7

66

44

35

1621 23

2723

20

7

Putting intosavings

Holidays /vacations

Paying offdebts / creditcards / loans

Newtechnology

products

Homeimprovements

/ decorating

New clothes Investing inshares of stock/ mutual funds

Out of homeentertainment

Retirementfund

I have nospare cash

Q1'15 Q2'15 Q3'15 Q4'15 Q1'16

Thailand - Spare Cash Spending Allocation

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

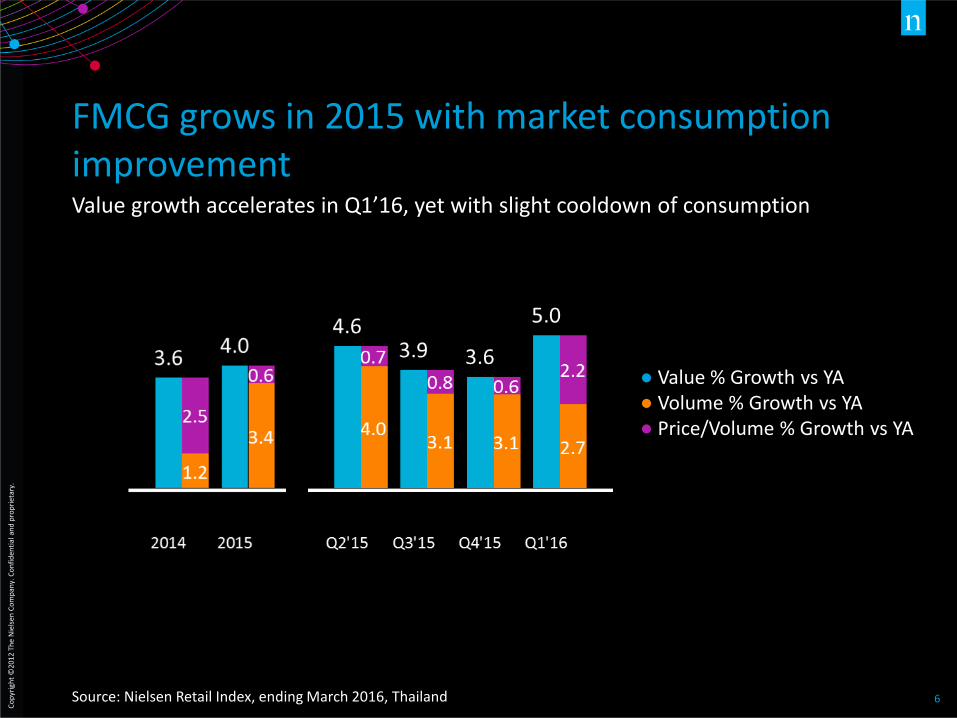

FMCG grows in 2015 with market consumption improvement Value growth accelerates in Q1’16, yet with slight cooldown of consumption

Source: Nielsen Retail Index, ending March 2016, Thailand

● Value % Growth vs YA ● Volume % Growth vs YA ● Price/Volume % Growth vs YA

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

RETAIL OUTLETS IN THAILAND

456,412

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

Traditional Trade remains large in contribution, but Convenience Stores lead in term of growth Competition between offline stores remain; what’s the implication for online stores?

Source: Nielsen Retail Index, March 2016, Thailand

25%

26%

50%

SUPER/HYPERMARKET

TRADITIONAL TRADE

CONVENIENCE STORE

+2.1%

+3.1%

+7.9%

Thailand Offline Retail Trade Channel Contribution as of 2015

TOTAL THAILAND +4%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

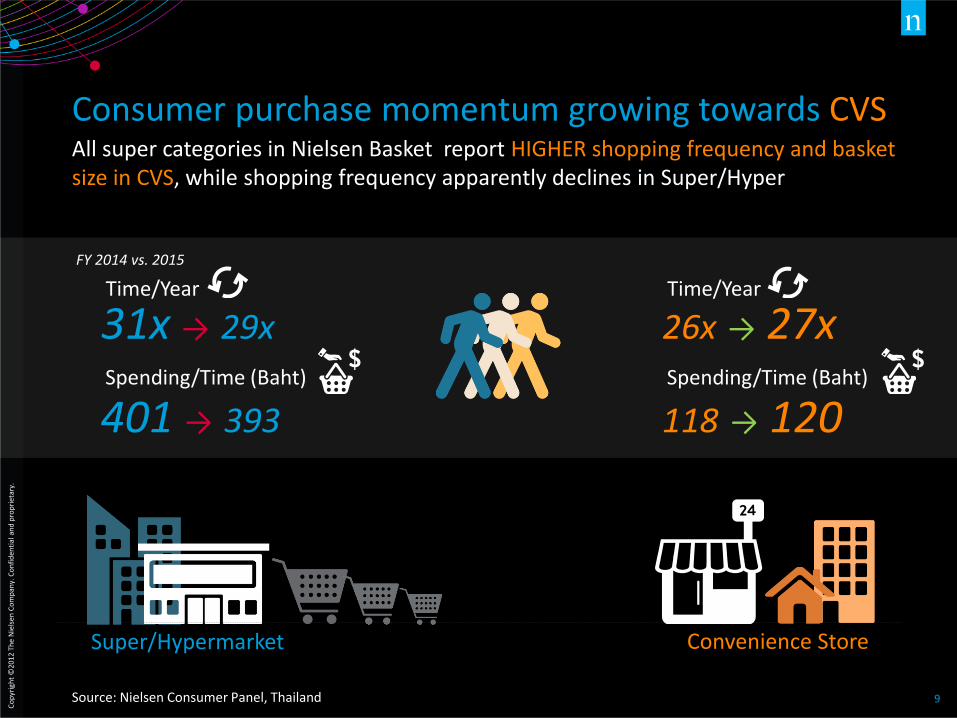

Super/Hypermarket Convenience Store

31x → 29x Time/Year

401 → 393

Spending/Time (Baht)

26x → 27x Time/Year

118 → 120 Spending/Time (Baht)

FY 2014 vs. 2015

Consumer purchase momentum growing towards CVS All super categories in Nielsen Basket report HIGHER shopping frequency and basket size in CVS, while shopping frequency apparently declines in Super/Hyper

Source: Nielsen Consumer Panel, Thailand

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

ONLINE STORE OWNERS According to Department of Business Development (DBD), Thailand

1,005,000

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

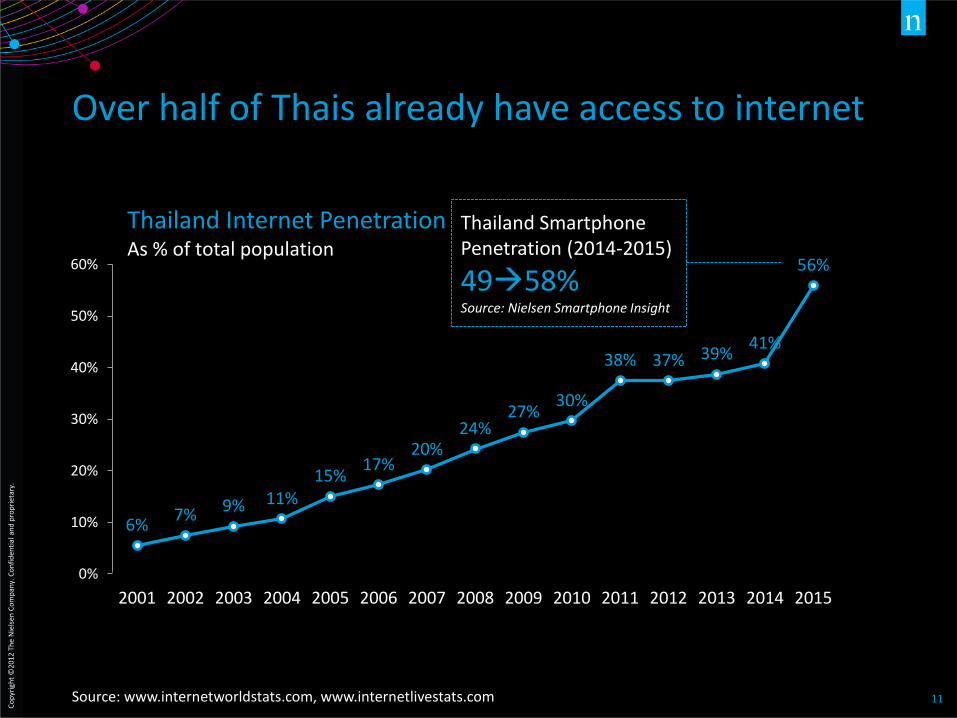

11 Source: www.internetworldstats.com, www.internetlivestats.com

6% 7% 9% 11%

15% 17%

20% 24%

27% 30%

38% 37% 39% 41%

56%

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Thailand Internet Penetration As % of total population

Thailand Smartphone Penetration (2014-2015)

4958% Source: Nielsen Smartphone Insight

Over half of Thais already have access to internet

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12 *Thailand Urban

of ‘online’ Thais shop online according to e-Commerce Landscape Report (Q4’15)*

22%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

58% 41% 38% 32% 32% 30%

Fashion Grocery Electronics Travel HealthProducts

Cosmetics

WHAT PRODUCTS THAIS SHOP ONLINE? Fashion still lead followed by Grocery

Source: Nielsen e-Commerce Landscape Report Q4’15, Thailand

KEY PRODUCT TYPES SHOP ONLINE (Thai Online Shoppers – Q4’15)

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

WHAT DRIVE CONSUMER IN SHOPPING ONLINE VS OFFLINE

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

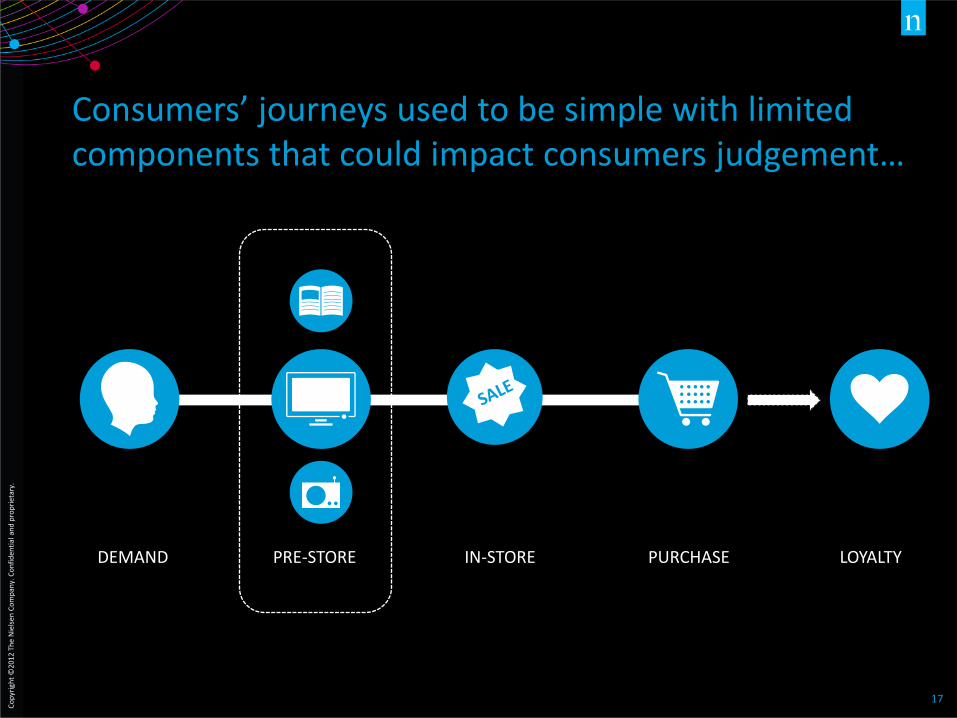

PRE-STORE IN-STORE PURCHASE DEMAND LOYALTY

Consumers’ journeys used to be simple with limited components that could impact consumers judgement…

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

Digital TV

Connected Experience

PRE-STORE IN-STORE PURCHASE DEMAND LOYALTY

They are not that simple anymore…

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

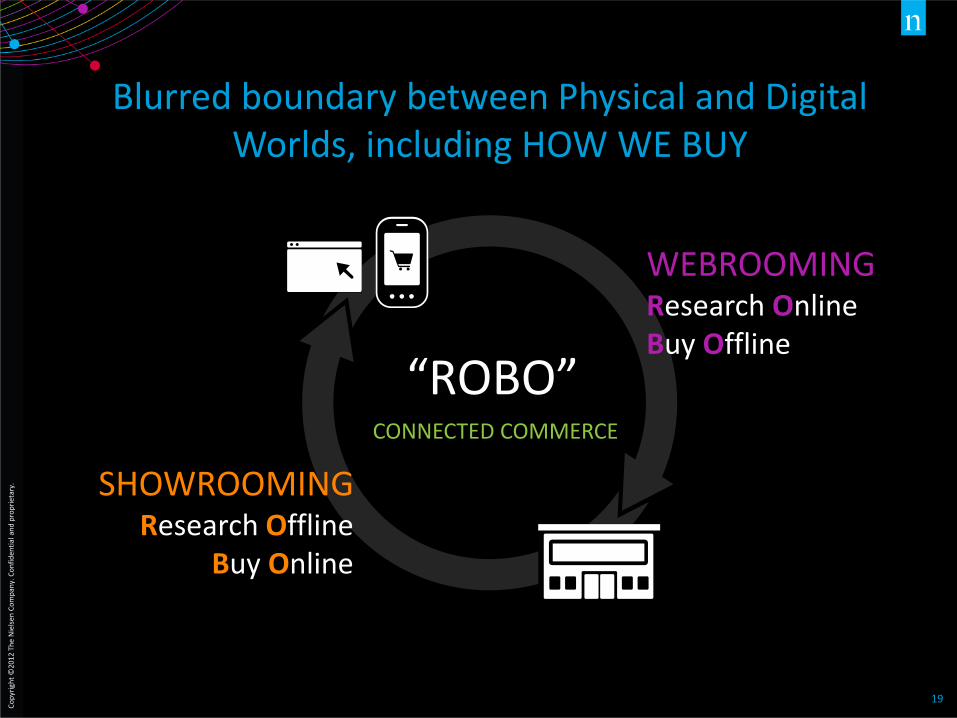

Blurred boundary between Physical and Digital Worlds, including HOW WE BUY

“ROBO”

WEBROOMING Research Online Buy Offline

SHOWROOMING Research Offline

Buy Online

CONNECTED COMMERCE

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

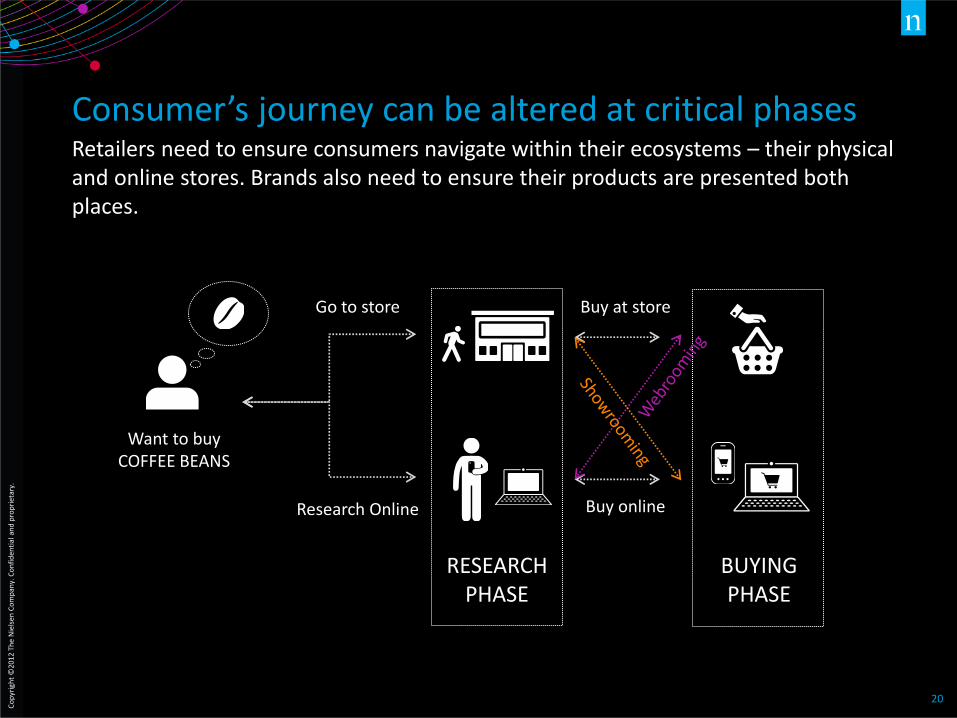

Consumer’s journey can be altered at critical phases Retailers need to ensure consumers navigate within their ecosystems – their physical and online stores. Brands also need to ensure their products are presented both places.

Research Online

Want to buy COFFEE BEANS

Go to store Buy at store

Buy online

RESEARCH PHASE

BUYING PHASE

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

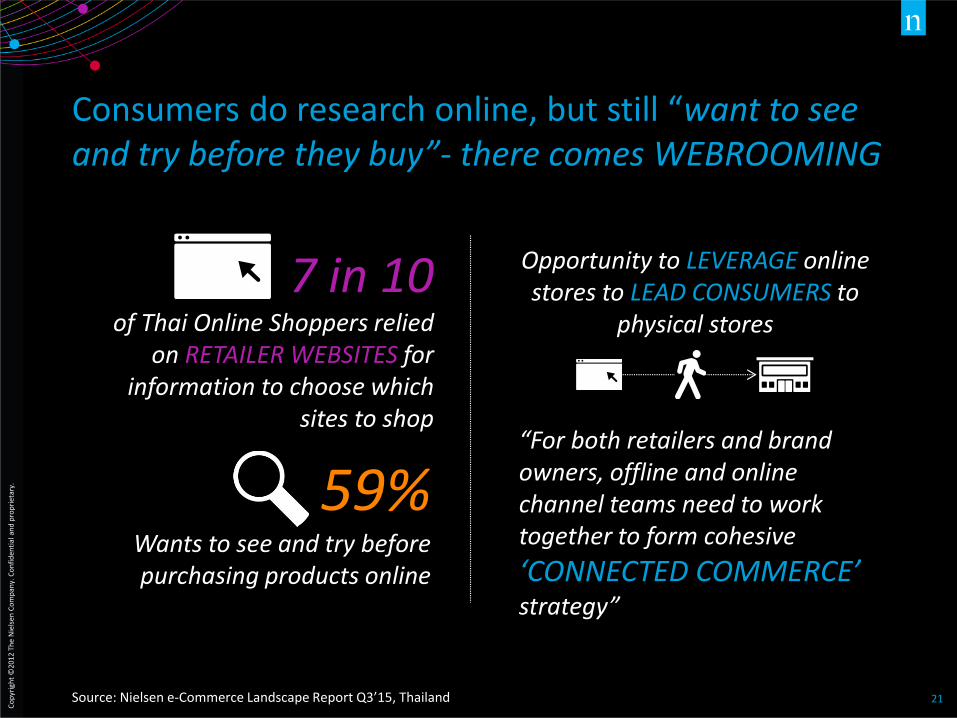

Consumers do research online, but still “want to see and try before they buy”- there comes WEBROOMING

Source: Nielsen e-Commerce Landscape Report Q3’15, Thailand

59% Wants to see and try before purchasing products online

7 in 10 of Thai Online Shoppers relied

on RETAILER WEBSITES for information to choose which

sites to shop “For both retailers and brand

owners, offline and online channel teams need to work together to form cohesive

‘CONNECTED COMMERCE’ strategy”

Opportunity to LEVERAGE online stores to LEAD CONSUMERS to

physical stores

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

26

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

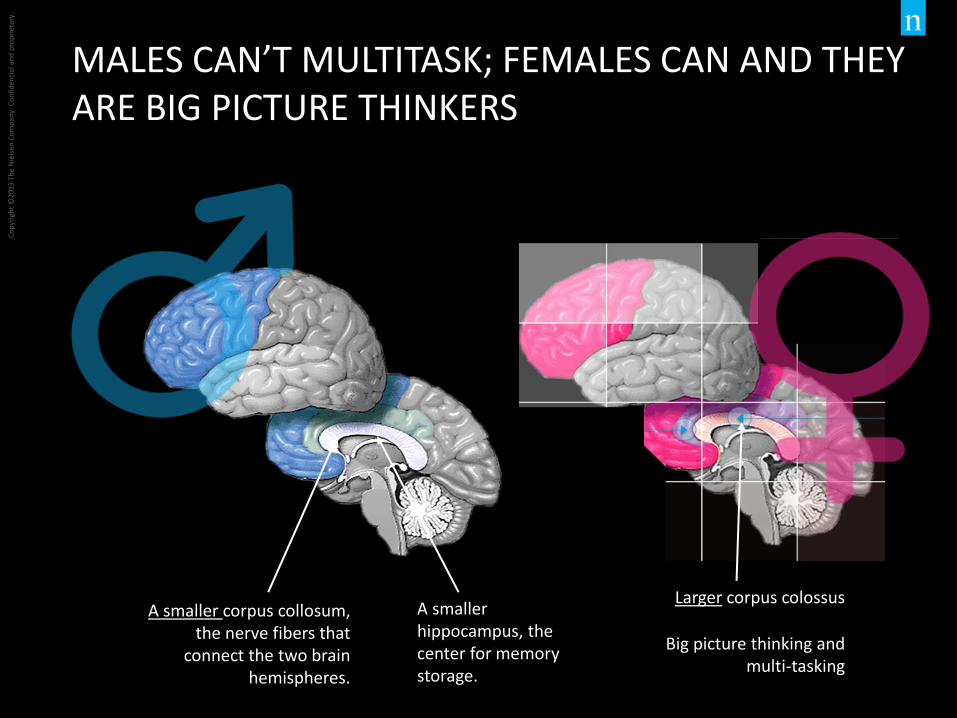

MALES CAN’T MULTITASK; FEMALES CAN AND THEY ARE BIG PICTURE THINKERS

A smaller corpus collosum, the nerve fibers that

connect the two brain hemispheres.

A smaller hippocampus, the center for memory storage.

Larger corpus colossus

Big picture thinking and multi-tasking

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

27

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

FEMALE VS MALE

SOCIAL

EMPATHETIC

VERBAL

MULTI-TASK & BIG PICTURE THINKER GUIDED BY EMOTIONAL MEMORY

INDEPENDENT

IMPULSIVE

COMPETITIVE

CONCRETE/FACTUAL

SEXUAL

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

28

WHAT ARE THEY WATCHING?

Drama/Soap Opera Movie

News/Current Affairs/Panel

Discussion Shows

News/Current Affairs/Panel

Discussion Shows

Sports Sitcoms

Music show Music Show

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

29

IN SUMMARY

ECOMMERCE WILL ACCELERATE THE RETAIL INDUSTRY

THAI’S ARE HUNGRY FOR CONVENIENCE

BE PRESENT IN OFFLINE AND ONLINE

KNOW YOUR SHOPPERS AND TAILOR YOUR STRATEGIES TO DRIVE TRIGGERS AND OVERCOME BARRIERS

WORKSHOP SESSION FUTURE TRENDS OF ONLINE

SHOPPING BEHAVIOR

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

31

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

32

The Macro Trends

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

33