Accounting Regulation in Nigeria: Institutionalisation,

Accounting Quality Effects and Capital Market Effects.

Zayyad Abdul-Baki

(ACA, CPFA)

Thesis submitted in fulfilment of the requirement for the

degree of Doctor of Philosophy.

Heriot-Watt University

Department of Accountancy, Economics and Finance

December 2018.

The copyright in this thesis is owned by the author. Any quotation from the thesis or use

of any of the information contained in it must acknowledge this thesis as the source of the

quotation or information.

ii

Abstract

This study examines three different aspects of accounting regulation in Nigeria. The first

empirical chapter (chapter 2) examines the process of the institutionalisation of IFRS in

Nigeria and its outcome. Using data from documents, interviews and survey, the chapter

finds that IFRS is substantively adopted by Nigerian listed firms, as they use it for internal

reporting. Furthermore, the institutionalisation process involves three levels of social

order (i.e., Social, political and economic level; organisational field; and organisational

level) at which different agents reinforce one another to ensure that institutionalisation of

IFRS in Nigeria is substantive.

The second empirical chapter examines whether accounting regulation in the form

of IFRS adoption and/or enforcement of accounting standards lead(s) to higher

accounting quality. The effects of these two regulatory mechanisms were assessed on

three dimensions of accounting quality using fixed-effect regressions for earnings

management, binary logistic regression for timely loss recognition, and a system dynamic

panel model for earnings persistence on a sample of non-financial companies listed on

the Nigerian Stock Exchange. The chapter finds that IFRS adoption significantly

increases earnings management and reduces earnings persistence, while institutional

reform, through the setting up of the Financial Reporting Council of Nigeria (FRCN) to

enforce and monitor compliance with accounting standards, reduces earnings

management.

The third empirical chapter examines the effect of accounting regulation in the

form of IFRS adoption and enforcement on market liquidity in Nigeria. The chapter

adopts a longitudinal research design and analyses hand-collected panel data sets from

semi-structured archives. Three proxies of market liquidity (i.e., bid-ask spread, zero

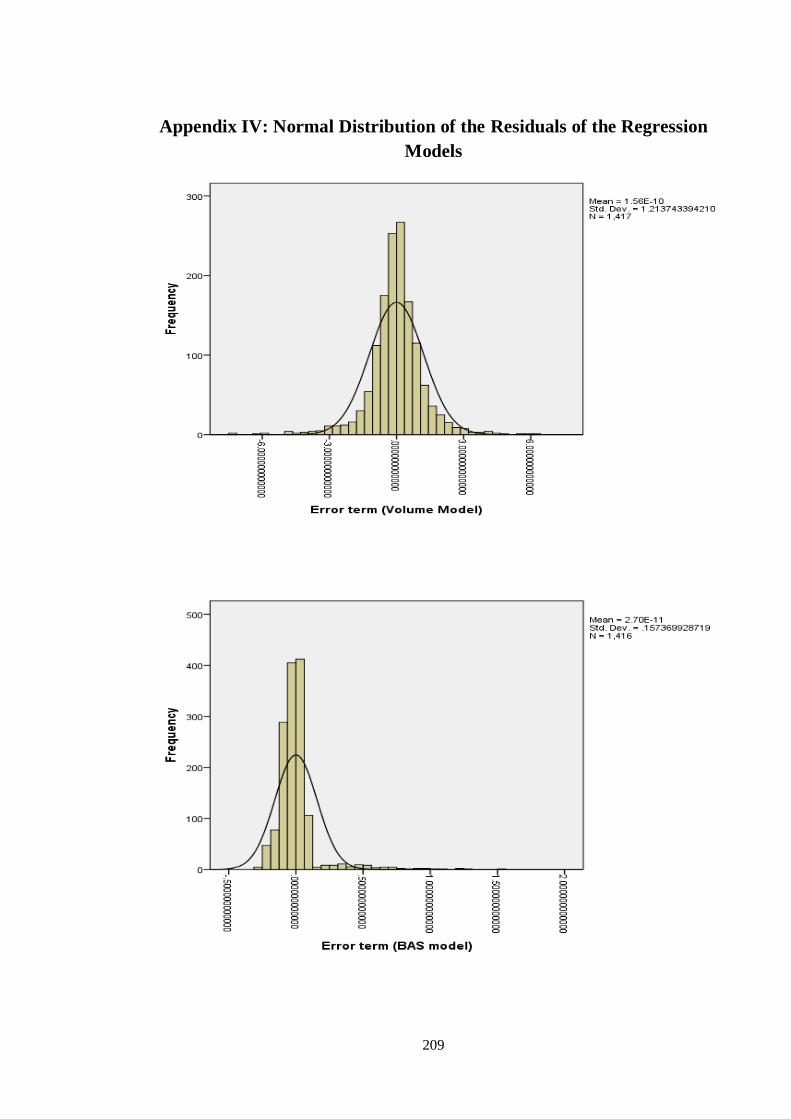

returns, and volume) were adopted for the study. Firm-quarter observations of 1,416,

1,417 and 1,418 were analysed using a random-effect model for bid-ask-spread and a

fixed-effect regression for both zero returns and volume, respectively. The chapter finds

that both IFRS adoption and enforcement significantly improve the Nigerian stock market

liquidity.

iii

Dedication

This thesis is dedicated to my wife, Sofiyyah Muhyideen Ajoke, and daughters, Ikram,

Nabeelah, and Manaar.

iv

Acknowledgements

All praise is due to Allah (Subhanahu Wa ta’aala), the All-Perfect and the All-Knowing,

for bringing me to the successful completion of this arduous journey.

I am deeply grateful to the School of Social Sciences for the PhD scholarship,

which has enabled me to study at Heriot-Watt University. My immense gratitude goes to

my supervisor, Prof. Ros Haniffa, for her constructive comments, understanding,

attention, and constant readiness to give much needed pieces of advice throughout my

PhD journey.

My profound gratitude goes to my parents, Dr A.G.I. Abdul-Baki and Mrs

Ibironke Adamo Afolabi, for their prayers and support. I wish to express my indebtedness

to my beloved wife, Mrs Sofiyat Muhyideen, for her prayers, unrelenting dedication, and

looking after the kids in the best way possible in my absence.

I would like to extend a very heartfelt thank you to Mr Tajudeen Ayinla for his

assistance towards getting respondents for the interview data for this study. I am grateful

to all the questionnaire respondents and the interviewees who have provided the data used

in this study. I thank Dr and Mrs Abdulraheem for their support towards the data

collection for this study.

v

Table of Contents

Abstract -------------------------------------------------------------------------------------------- ii

Dedication ---------------------------------------------------------------------------------------- iii

Acknowledgements ----------------------------------------------------------------------------- iv

List of Tables ---------------------------------------------------------------------------------- viii

List of Figures ----------------------------------------------------------------------------------- ix

Figure 4.4 Factors Affecting Stock Market Liquidity------ -------------------------------- ix

Chapter 1 ------------------------------------------------------------------------------------------ 1

Introduction --------------------------------------------------------------------------------------- 1

1.1 Motivation for the Study ----------------------------------------------------------------------------- 1

1.1.1 The Institutionalisation of IFRS --------------------------------------------------------------- 1

1.1.2 IFRS, Enforcement and Accounting Quality ------------------------------------------------ 4

1.1.3 IFRS, Enforcement and Capital Market Outcomes ----------------------------------------- 6

1.2 Epistemological and Ontological Considerations ------------------------------------------------ 7

1.3 Contributions of the Study -------------------------------------------------------------------------- 10

1.4 Structure of the Thesis ------------------------------------------------------------------------------- 11

Chapter 2 ---------------------------------------------------------------------------------------- 13

The Institutionalisation of IFRS in Nigeria -------------------------------------------------- 13

2.1 Introduction ------------------------------------------------------------------------------------------- 13

2.1 Statement of the Problem --------------------------------------------------------------------------- 14

2.3 Objective of the Study ------------------------------------------------------------------------------- 15

2.4 Significance of the Study --------------------------------------------------------------------------- 15

2.5 Contextual Framework ------------------------------------------------------------------------------ 15

2.5.1 Accounting development in Nigeria --------------------------------------------------------- 15

2.5.2 The Nigerian Accounting Standards Board ------------------------------------------------- 19

2.6 Conceptual Framework ------------------------------------------------------------------------------ 22

2.6.1 Differences in Accounting Practices across Jurisdictions -------------------------------- 22

2.6.2 Evolution of IFRS ------------------------------------------------------------------------------ 25

2.6.3 IFRS adoption by Developing Countries ---------------------------------------------------- 30

2.6.4 Institutionalisation of IFRS at the Organisational Level ---------------------------------- 35

2.7 Neo-institutional Theory ---------------------------------------------------------------------------- 37

2.7.1 Studies on IFRS based on institutional theory---------------------------------------------- 40

2.8 Research Methods and Data Analysis ------------------------------------------------------------- 43

2.8.1 Research Design -------------------------------------------------------------------------------- 43

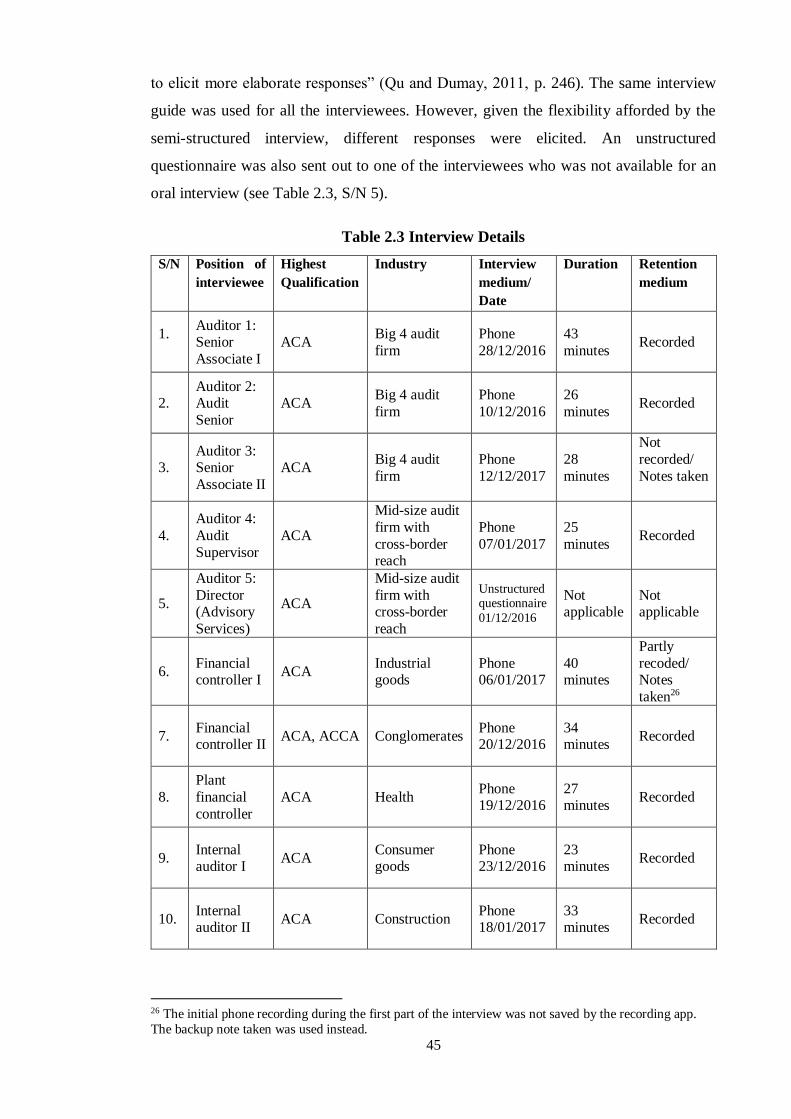

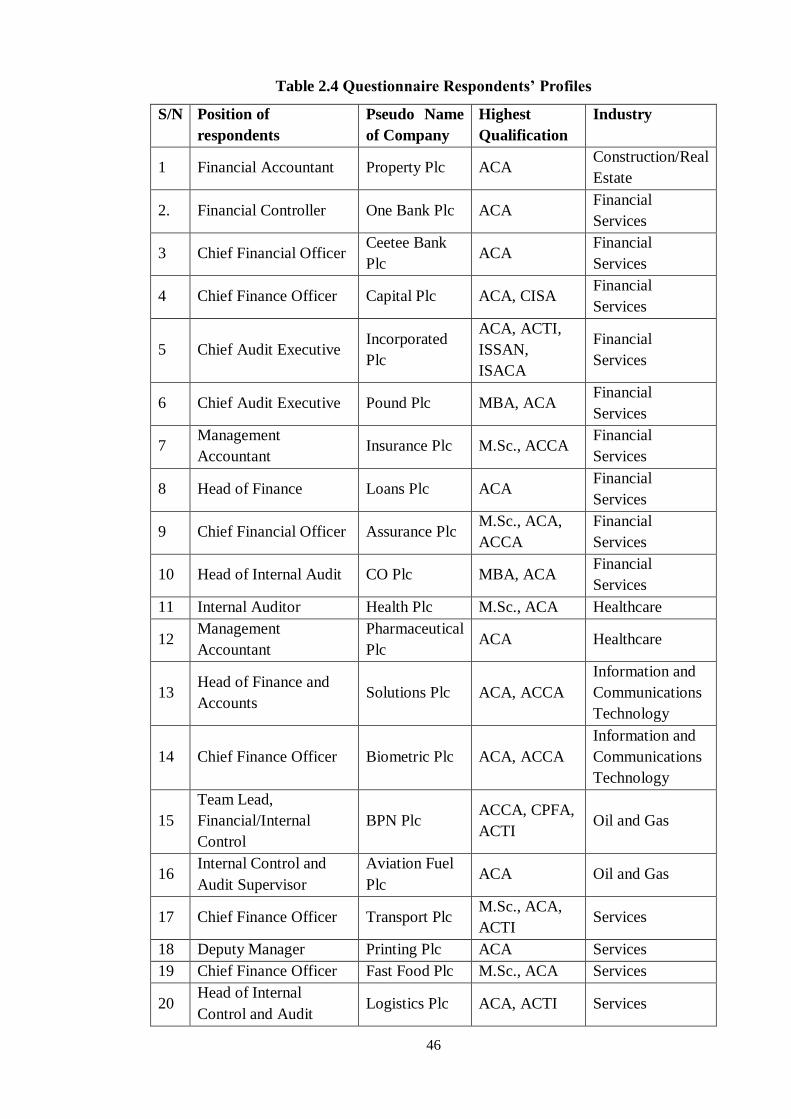

2.8.2 Data gathering ----------------------------------------------------------------------------------- 44

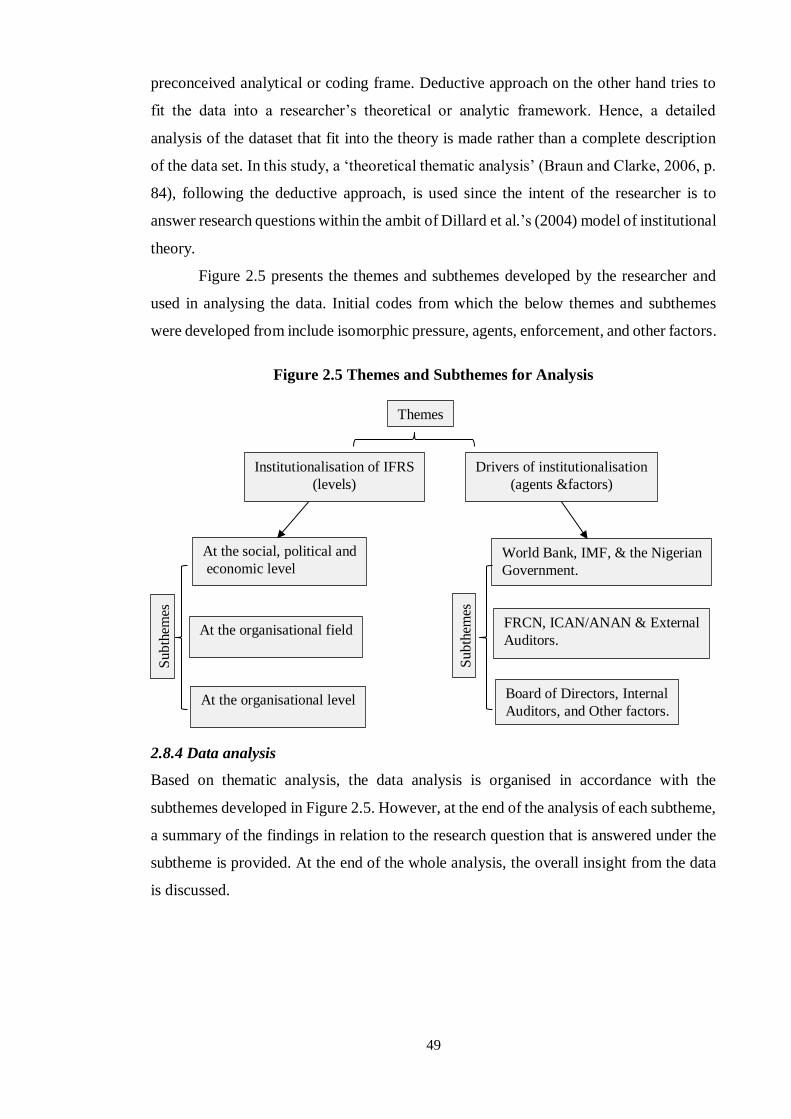

2.8.3 Thematic analysis ------------------------------------------------------------------------------- 47

vi

2.8.4 Data analysis ------------------------------------------------------------------------------------- 49

2.9 Discussion of Findings and Conclusion ---------------------------------------------------------- 65

Chapter 3 ---------------------------------------------------------------------------------------- 67

The Effects of Financial Reporting Regulation on Accounting Quality: The Case of

Nigeria ------------------------------------------------------------------------------------------- 67

3.1 Background to the Study ---------------------------------------------------------------------------- 67

3.2 Statement of the Problem --------------------------------------------------------------------------- 69

3.3 Research Objectives and Research Questions --------------------------------------------------- 70

3.4 Significance of the Study --------------------------------------------------------------------------- 70

3.5 Literature Review ------------------------------------------------------------------------------------ 71

3.5.1 Contextual Framework ------------------------------------------------------------------------- 71

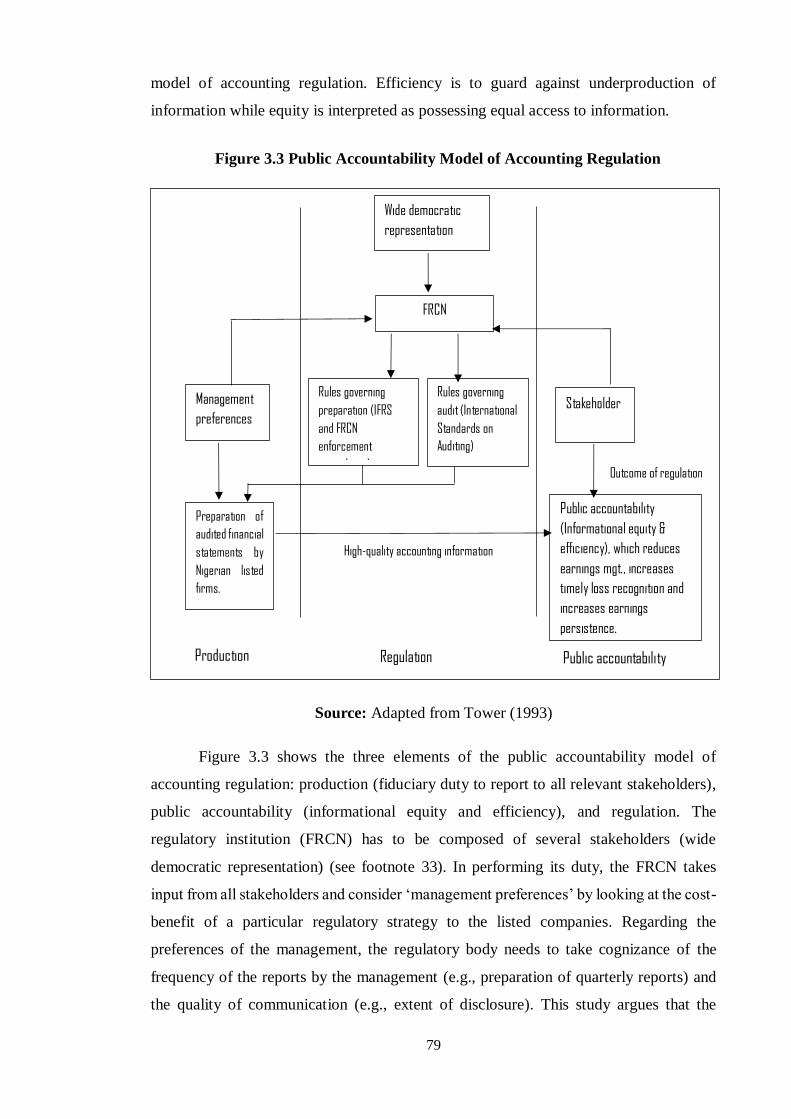

3.5.2 Theoretical framework: public accountability model of accounting regulation ------- 78

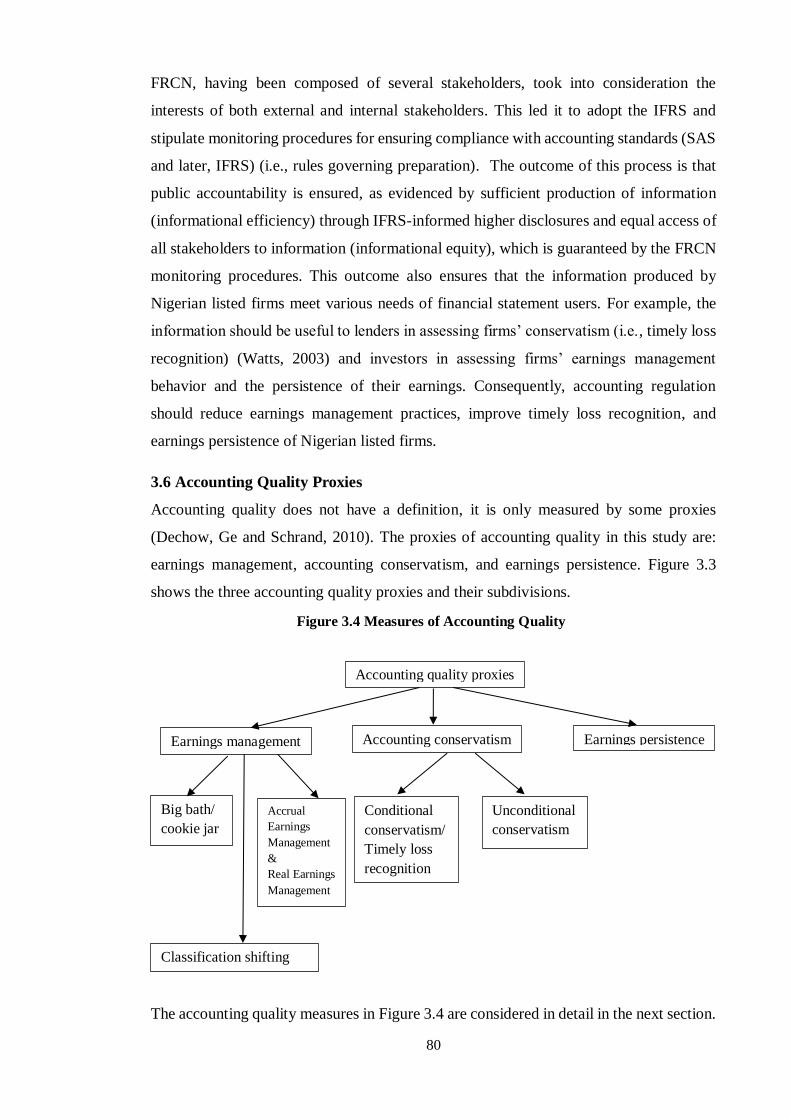

3.6 Accounting Quality Proxies ------------------------------------------------------------------------ 80

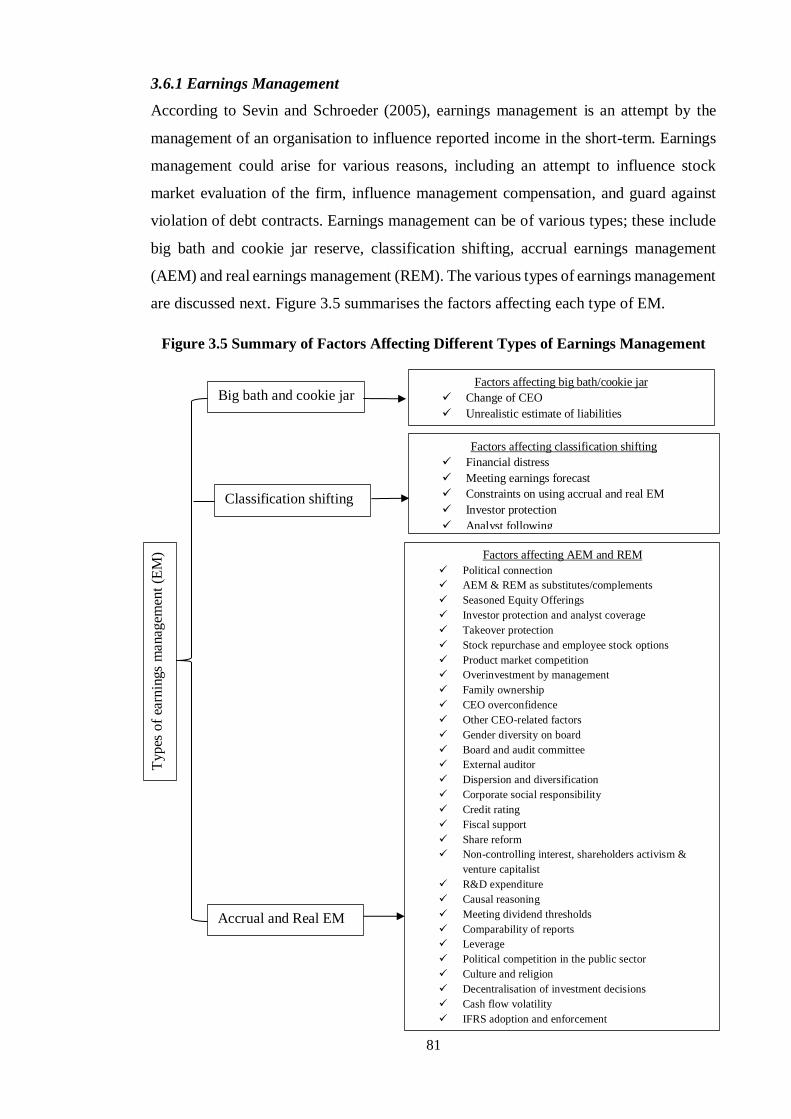

3.6.1 Earnings Management ------------------------------------------------------------------------- 81

3.6.2 Accounting Conservatism ------------------------------------------------------------------- 101

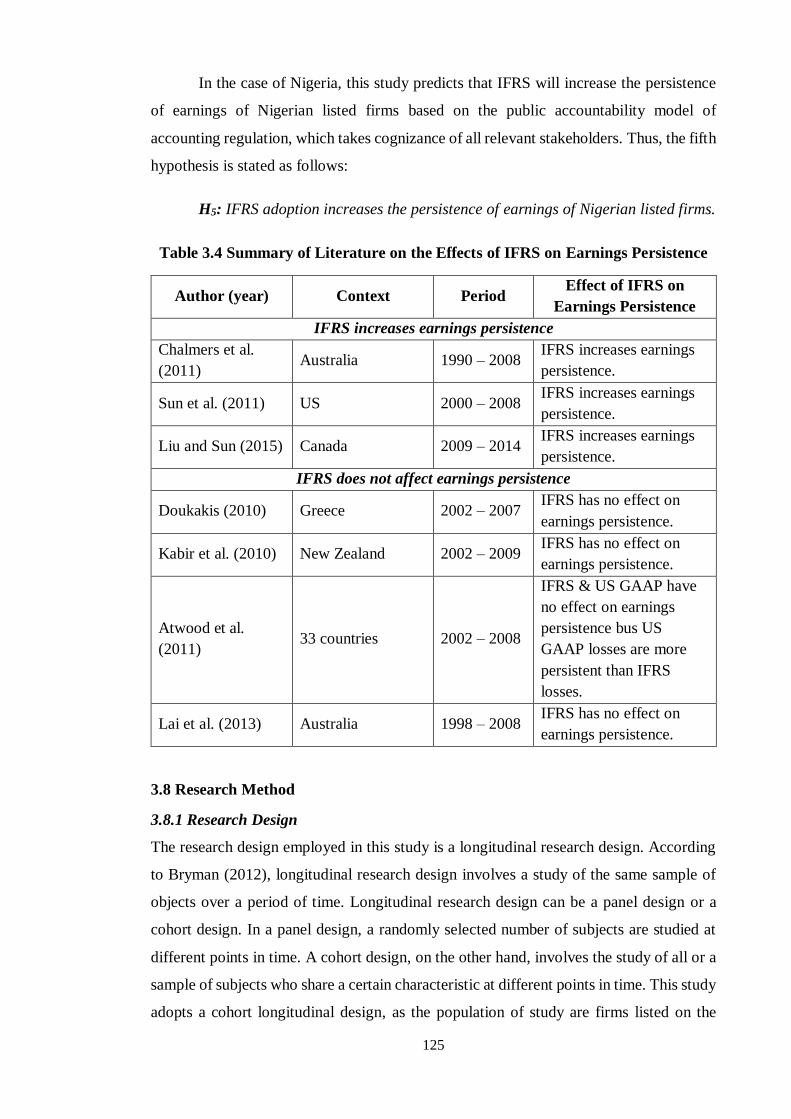

3.6.3 Earnings Persistence -------------------------------------------------------------------------- 110

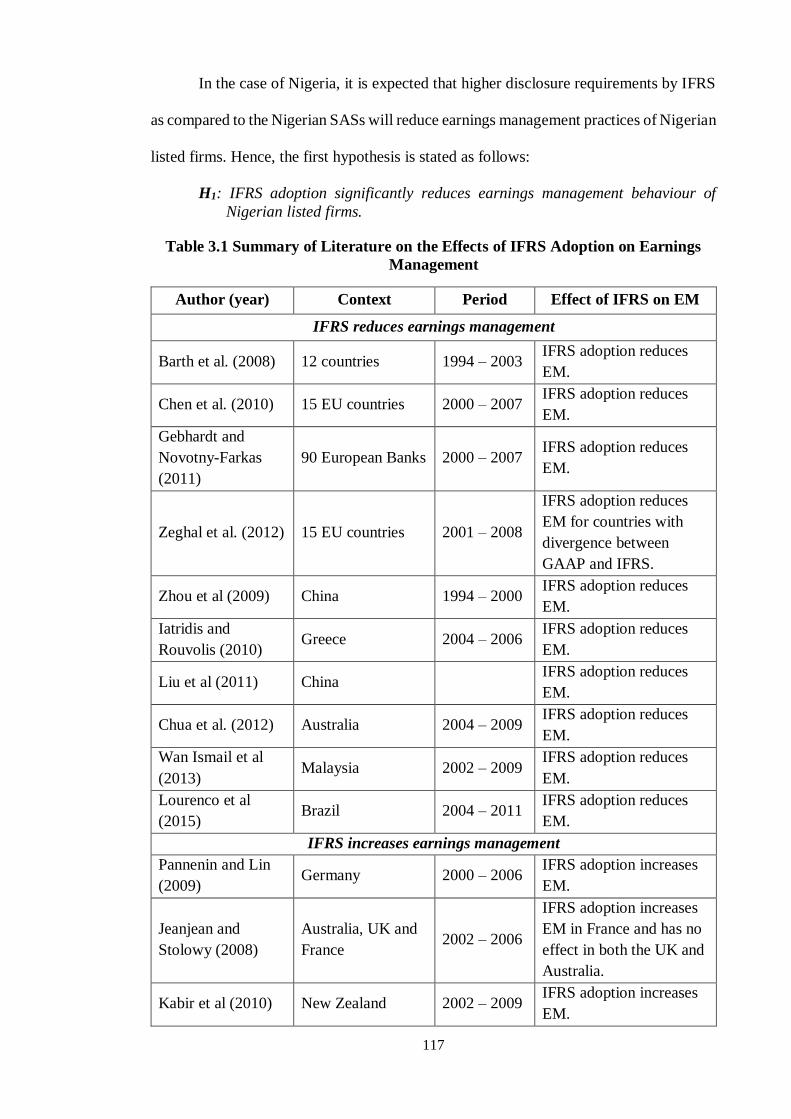

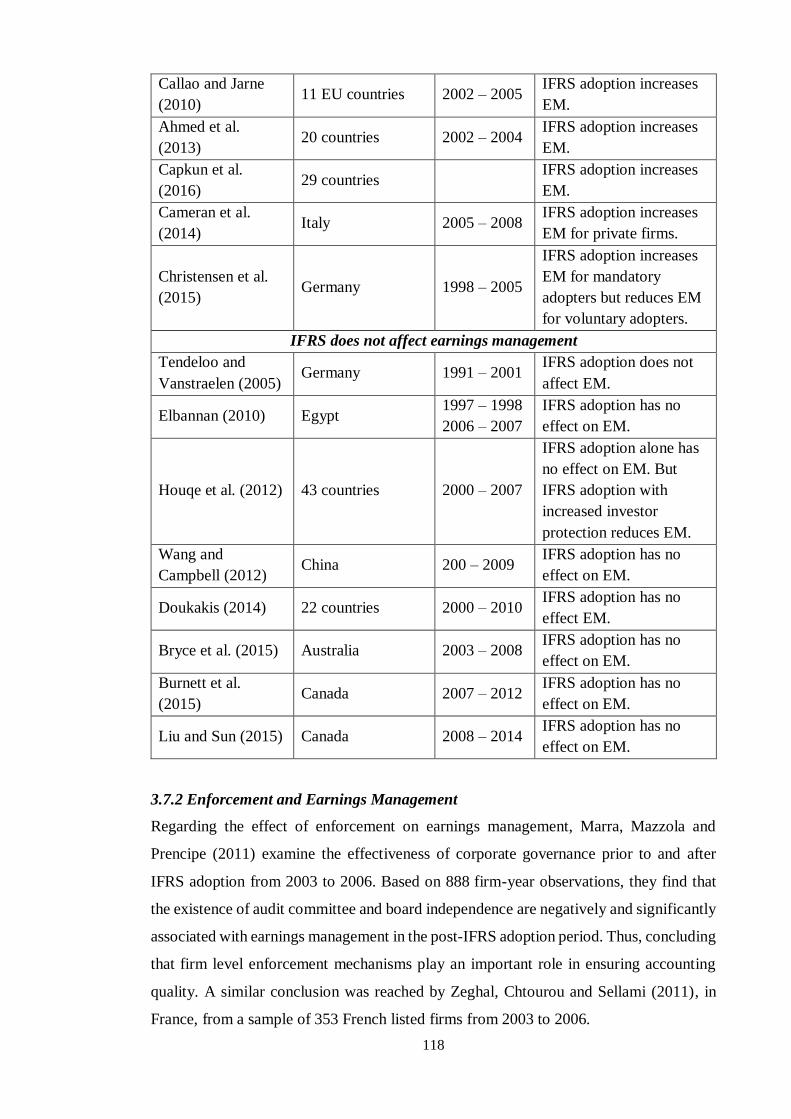

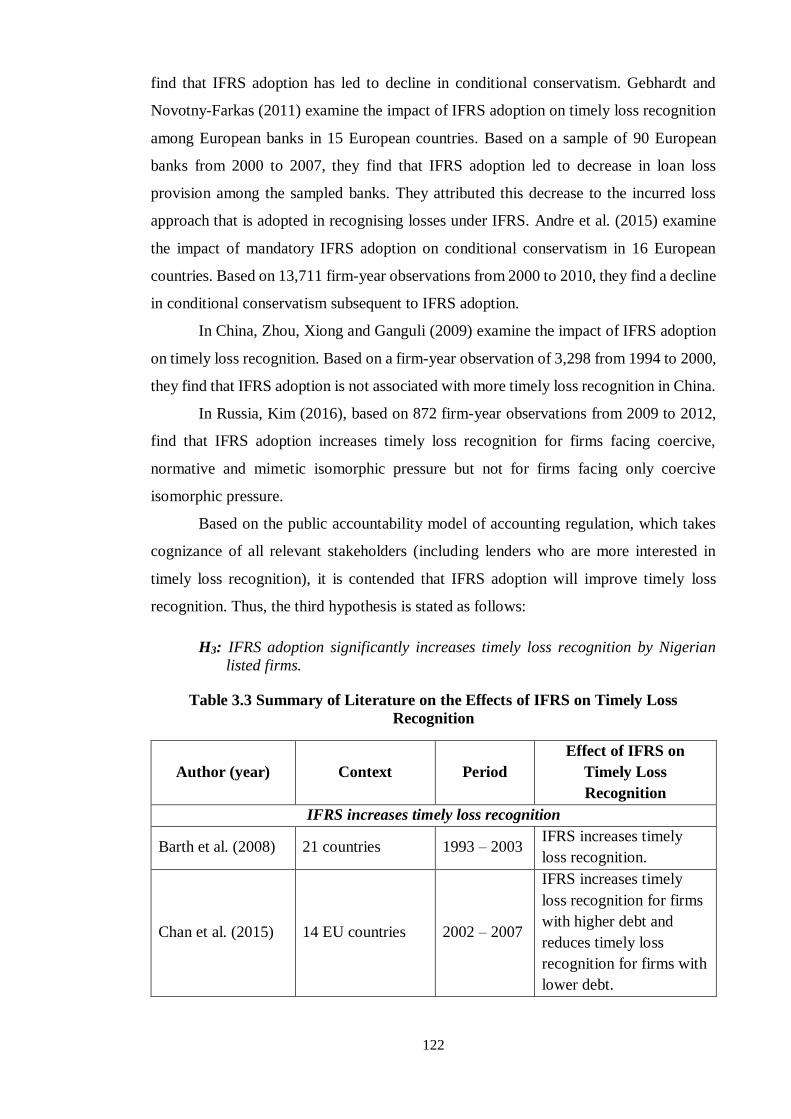

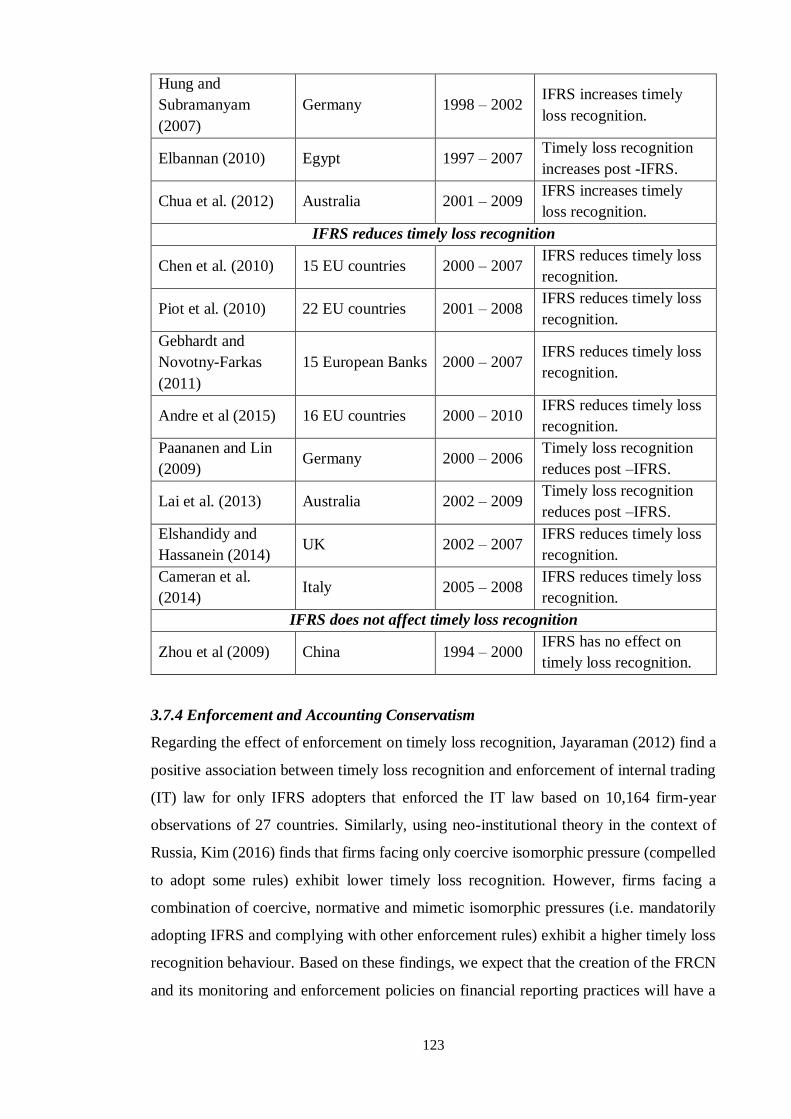

3.7 Review of Empirical Evidence and the Development of Hypotheses ---------------------- 114

3.7.1 IFRS Adoption and Earnings Management ----------------------------------------------- 114

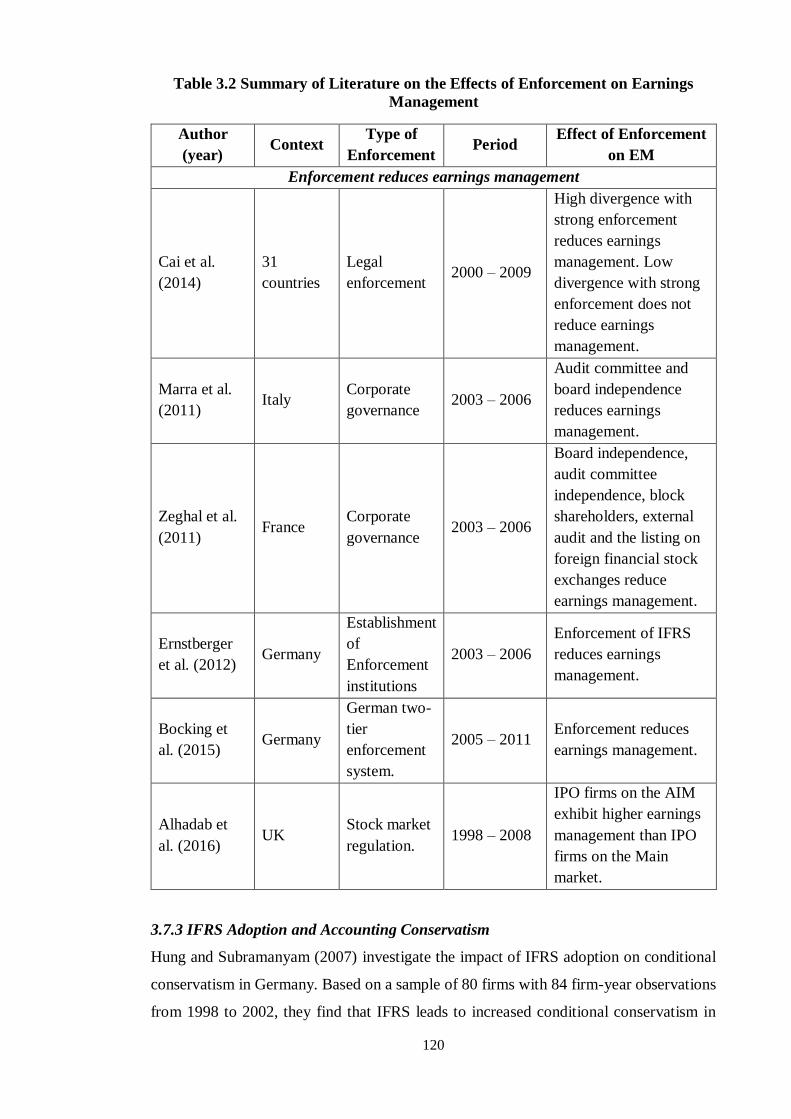

3.7.2 Enforcement and Earnings Management -------------------------------------------------- 118

3.7.3 IFRS Adoption and Accounting Conservatism------------------------------------------- 120

3.7.4 Enforcement and Accounting Conservatism---------------------------------------------- 123

3.7.5 IFRS Adoption and Earnings Persistence ------------------------------------------------- 124

3.8 Research Method ----------------------------------------------------------------------------------- 125

3.8.1 Research Design ------------------------------------------------------------------------------ 125

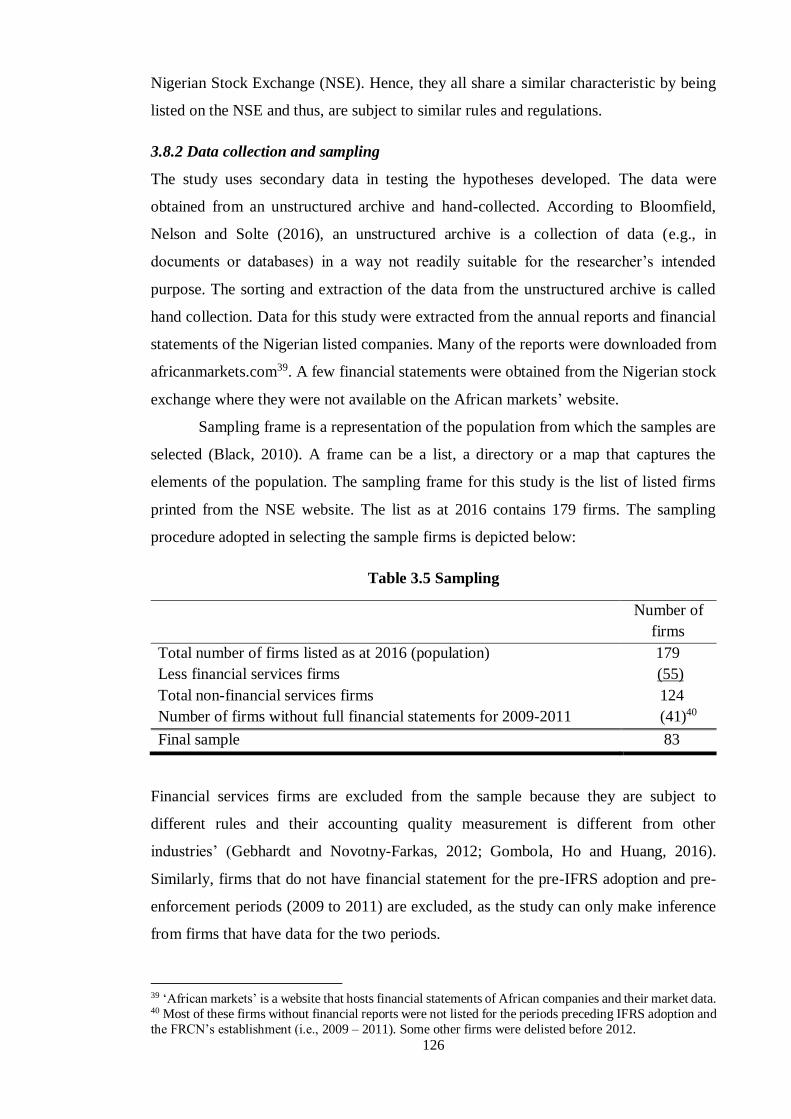

3.8.2 Data collection and sampling --------------------------------------------------------------- 126

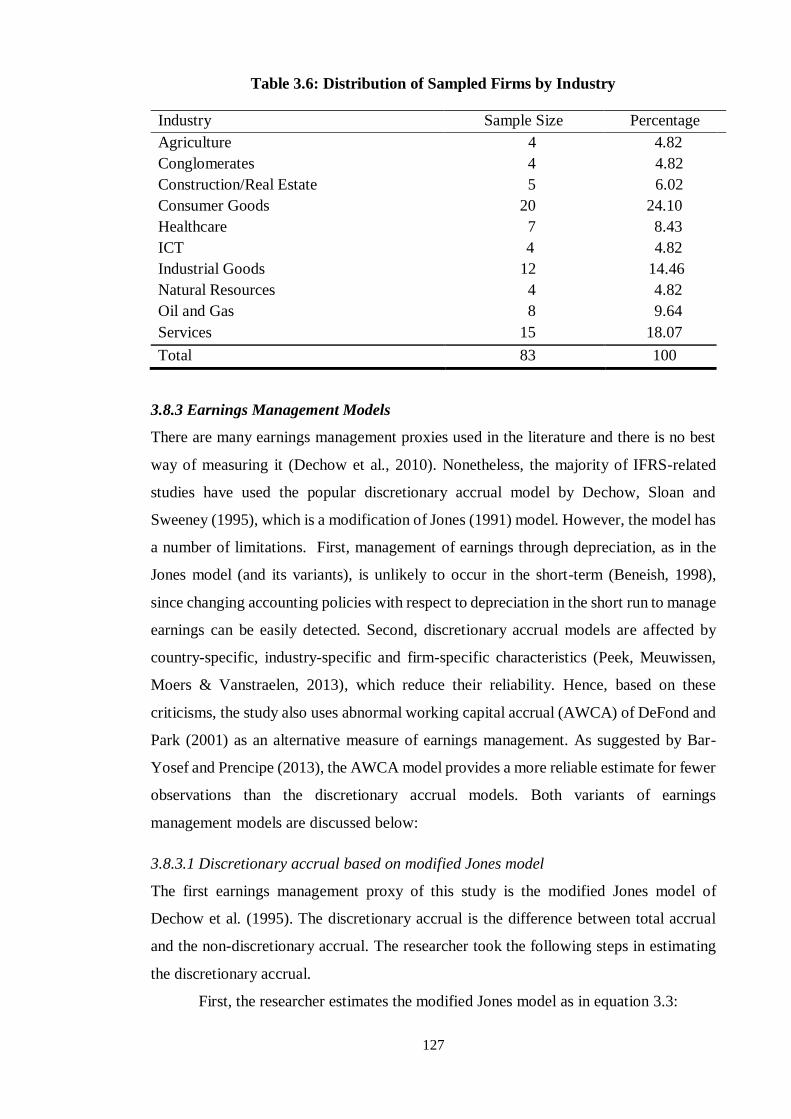

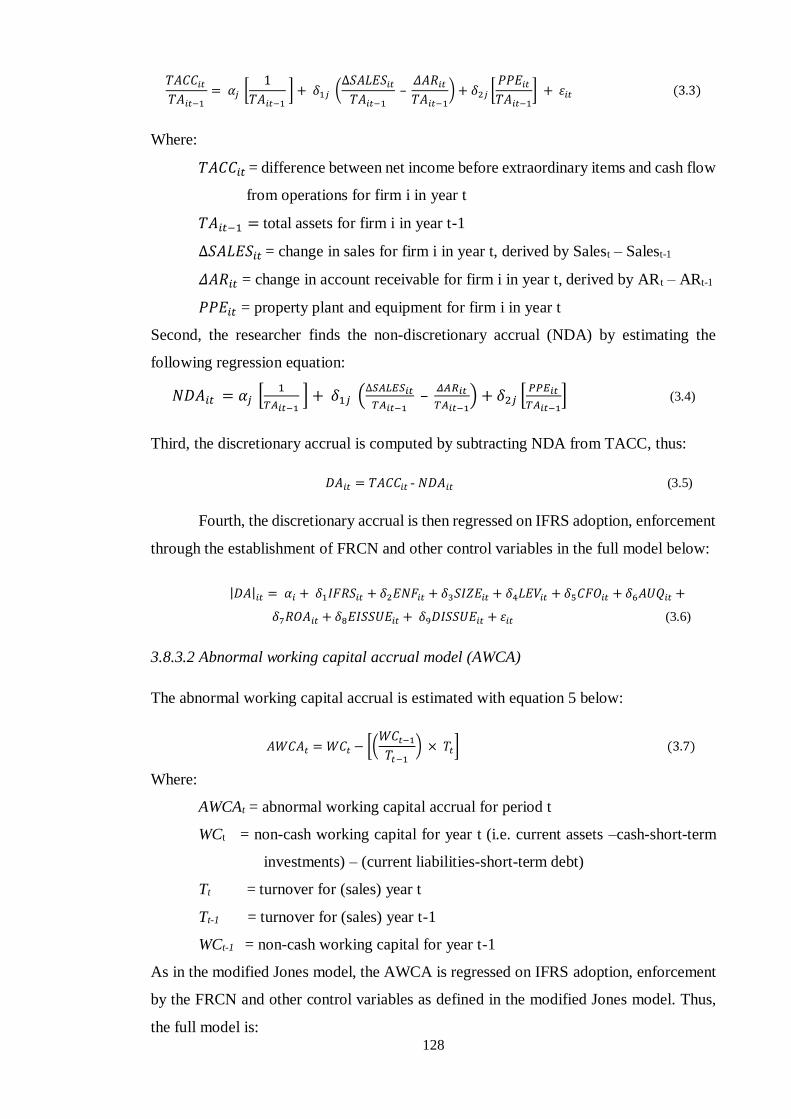

3.8.3 Earnings Management Models-------------------------------------------------------------- 127

3.8.4 Timely Loss Recognition (Conditional Conservatism) ------------------------------------ 129

3.8.5 Earnings Persistence ----------------------------------------------------------------------------- 129

3.8.6 Independent and Control Variables ----------------------------------------------------------- 129

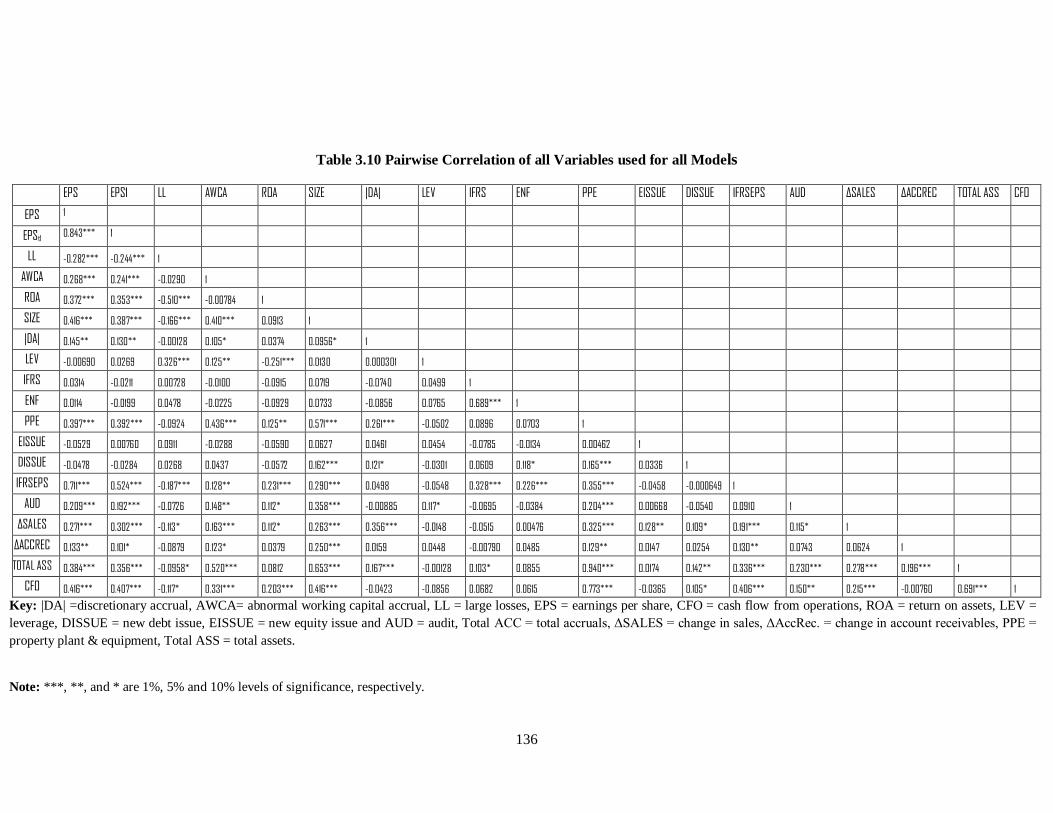

3.9 Data Analysis --------------------------------------------------------------------------------------- 131

3.9.1 Descriptive statistics -------------------------------------------------------------------------- 131

3.9.3 Multivariate Analysis------------------------------------------------------------------------- 133

3.10 Conclusion ----------------------------------------------------------------------------------------- 142

Chapter 4 --------------------------------------------------------------------------------------- 144

The Effect of Accounting Regulation on Stock Market Liquidity in Nigeria ---------- 144

4.1 Background to the Study -------------------------------------------------------------------------- 144

4.2 Statement of the Problem ------------------------------------------------------------------------- 145

vii

4.3 Research Objective --------------------------------------------------------------------------------- 146

4.4 Significance of the Study ------------------------------------------------------------------------- 146

4.5 Scope of the Study --------------------------------------------------------------------------------- 146

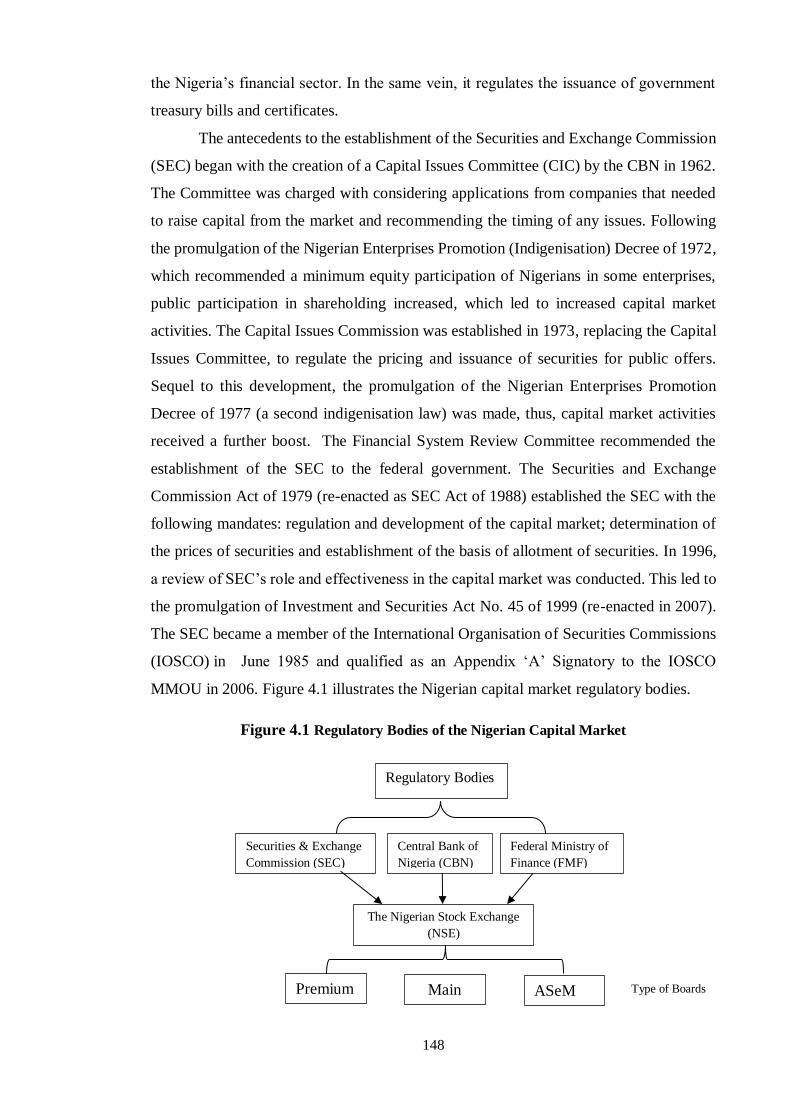

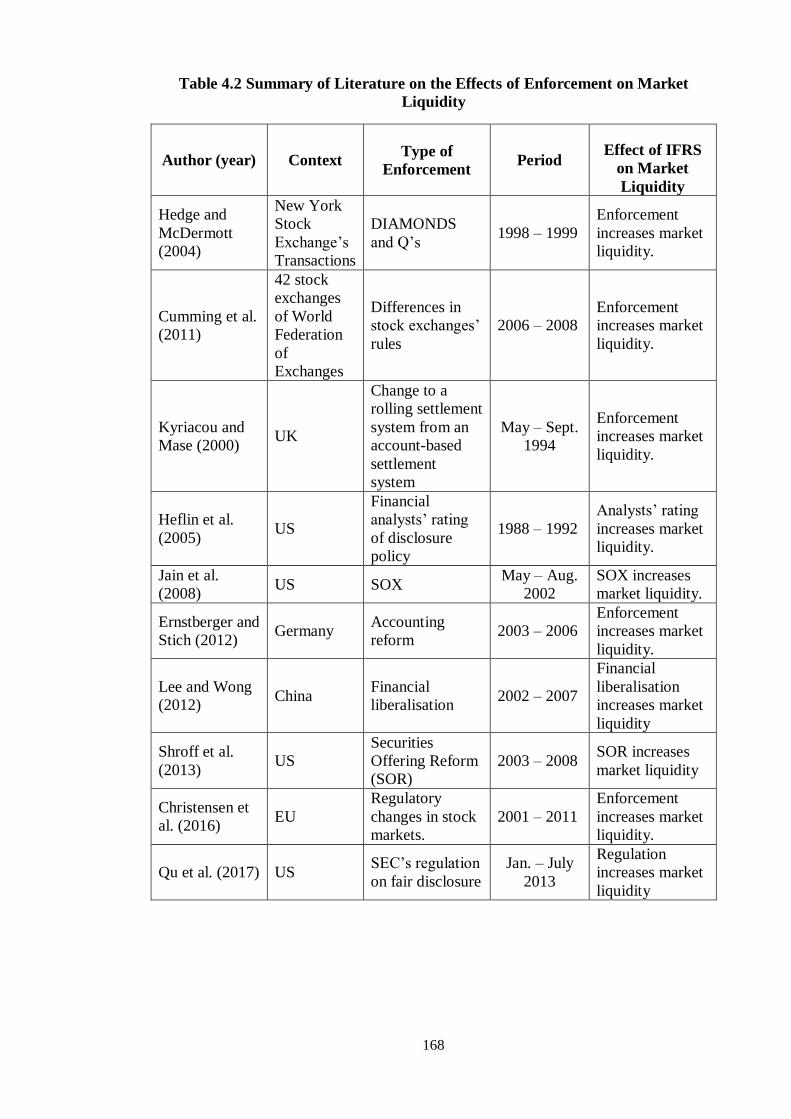

4.6 Literature Review ---------------------------------------------------------------------------------- 147

4.6.1 Regulatory Bodies for the Nigerian Capital Market ------------------------------------- 147

4.6.2 The Nigerian Stock Market before IFRS adoption and FRCN Establishment ------ 149

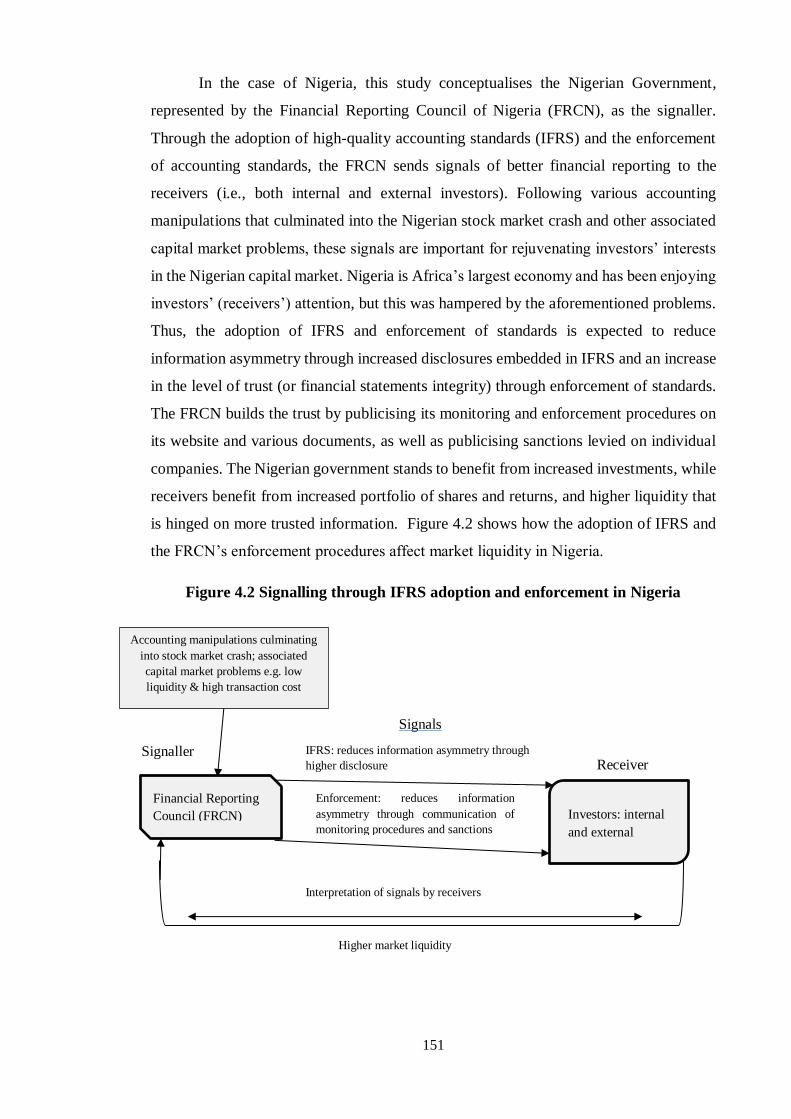

4.6.3 Signalling Theory ----------------------------------------------------------------------------- 150

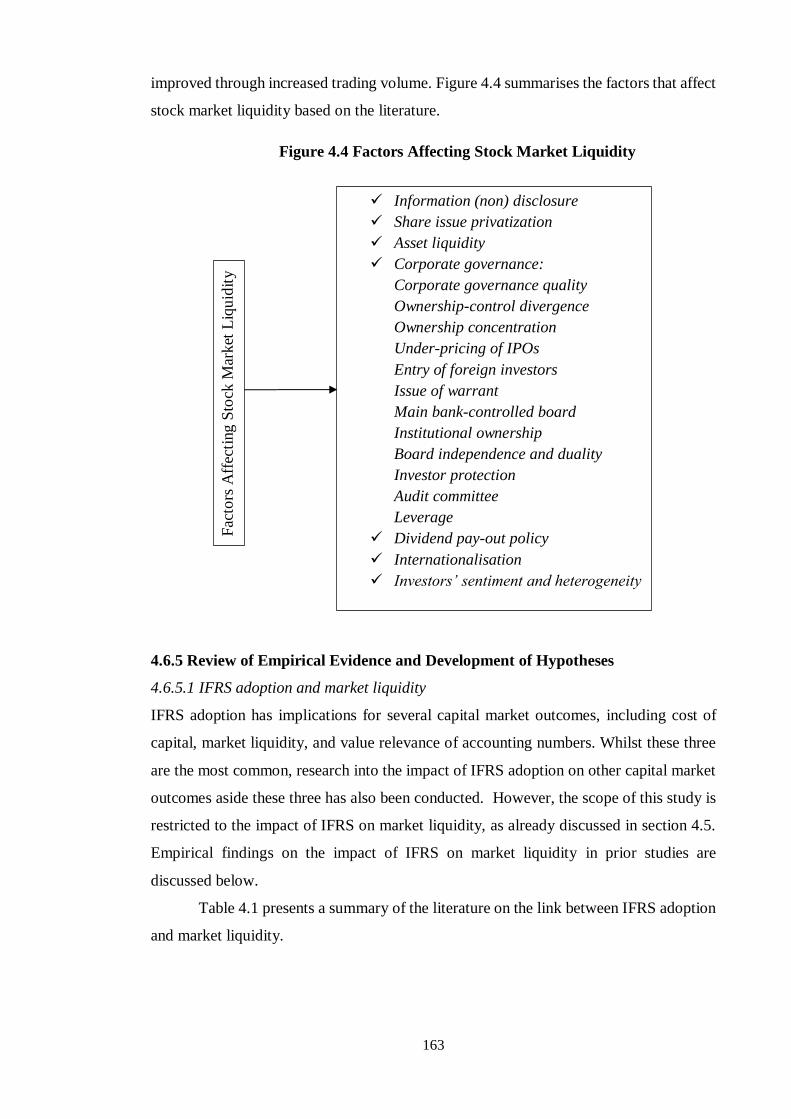

4.6.4 Market Liquidity ------------------------------------------------------------------------------ 155

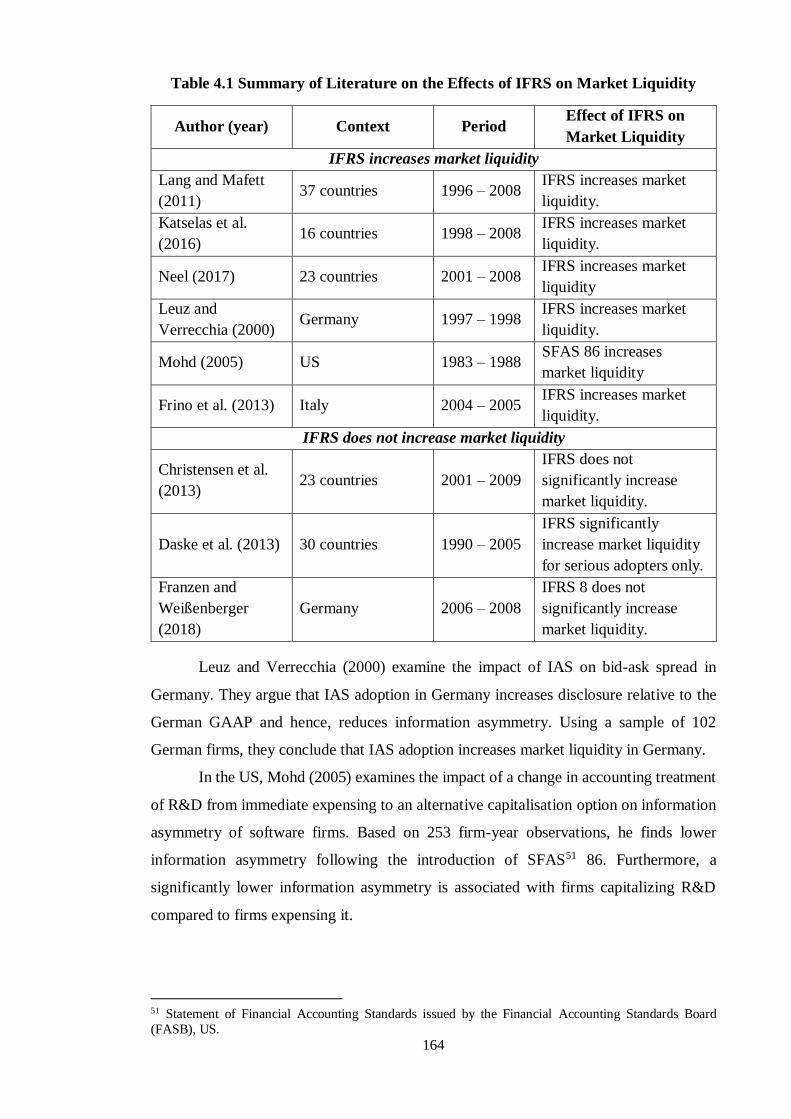

4.6.5 Review of Empirical Evidence and Development of Hypotheses --------------------- 163

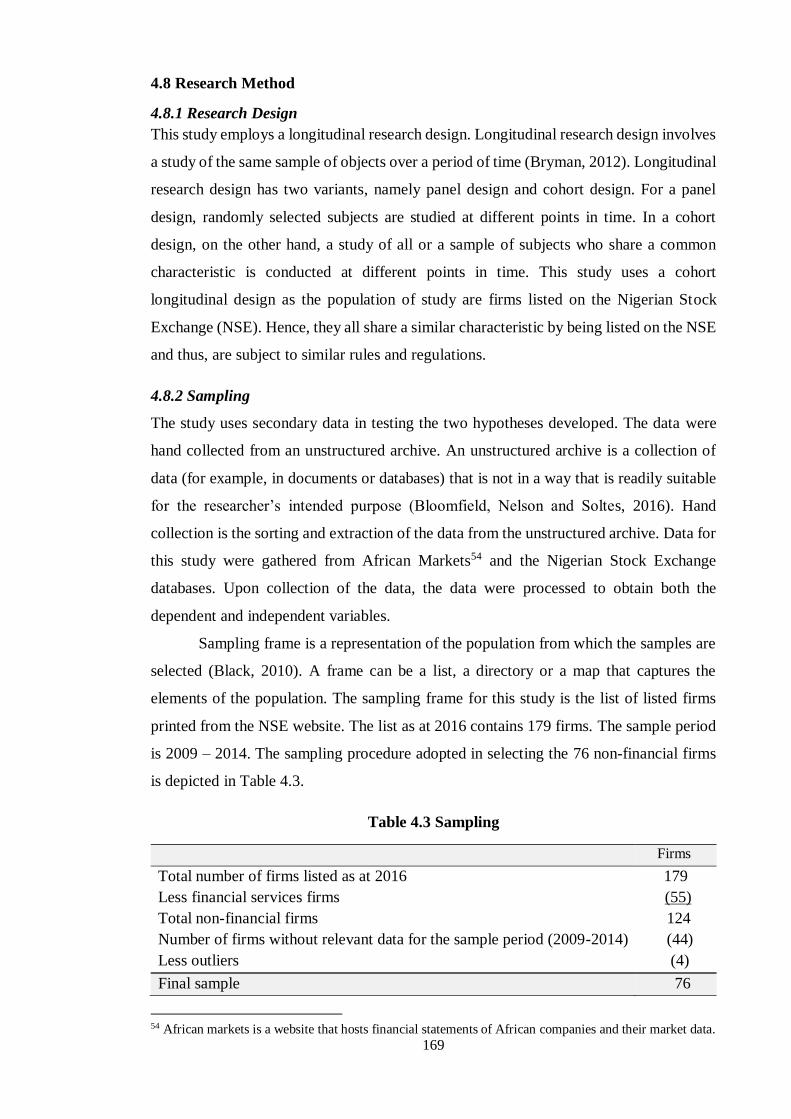

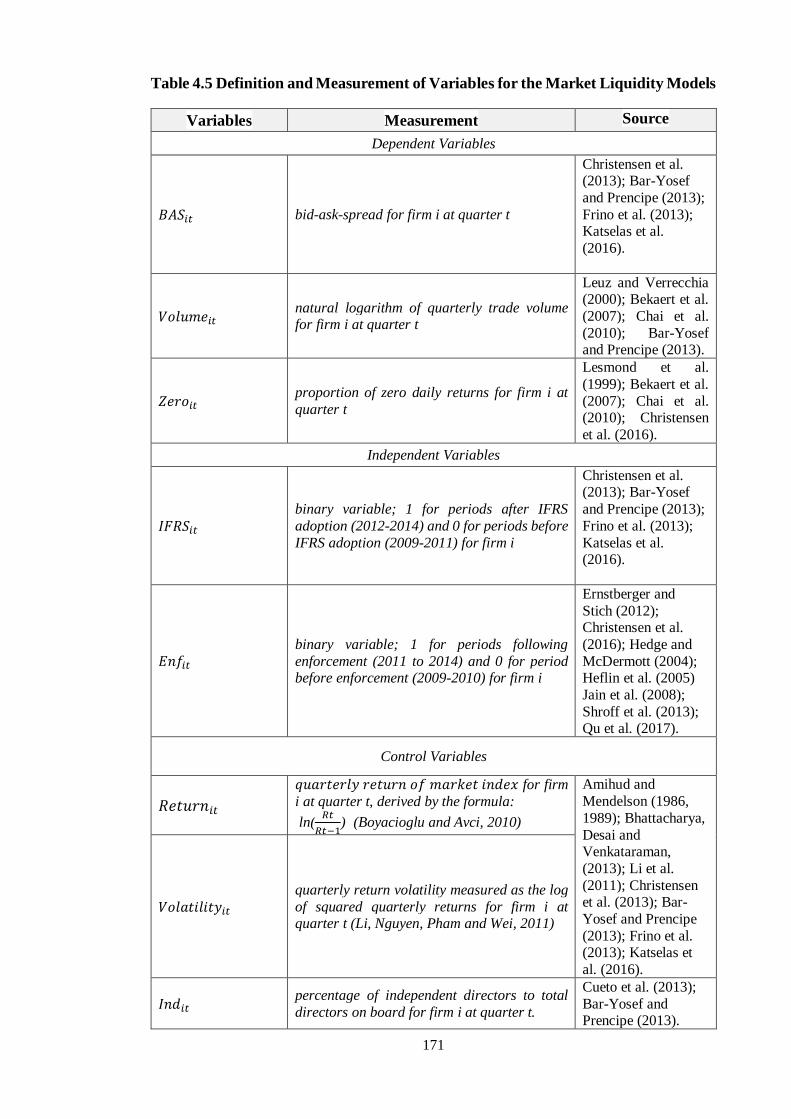

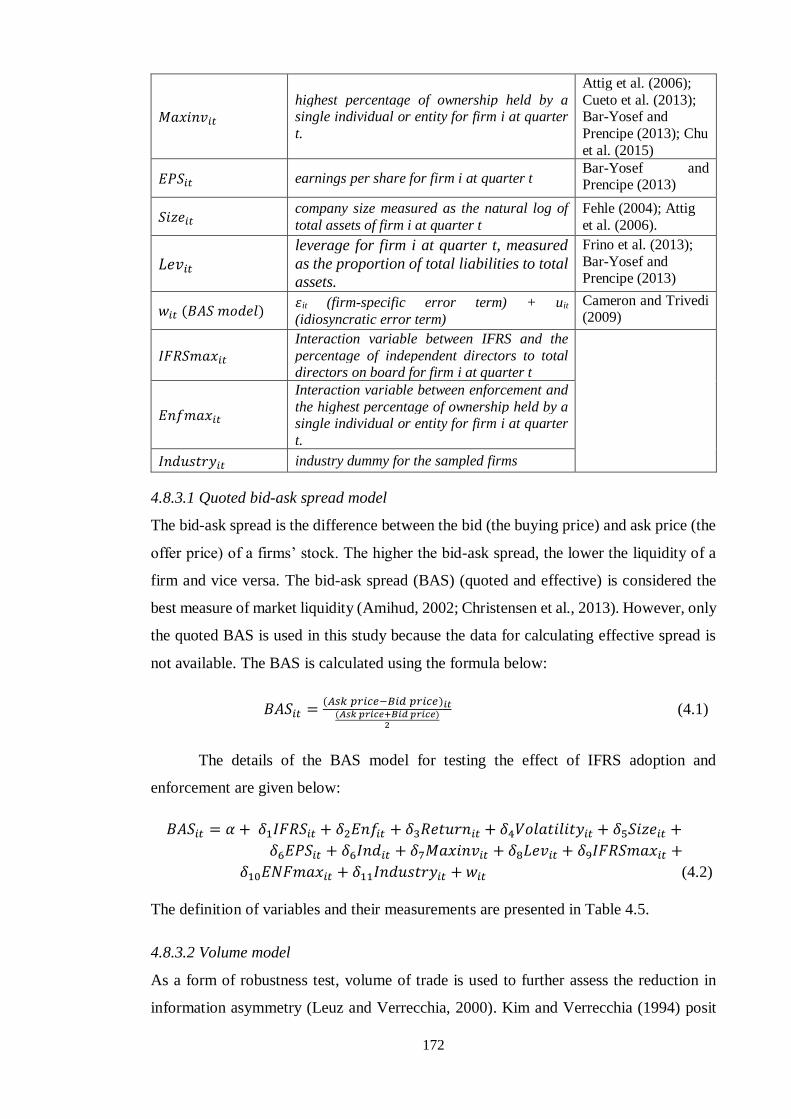

4.8 Research Method ----------------------------------------------------------------------------------- 169

4.8.1 Research Design ------------------------------------------------------------------------------ 169

4.8.2 Sampling --------------------------------------------------------------------------------------- 169

4.8.3 Market Liquidity Models (Dependent Variable) ----------------------------------------- 170

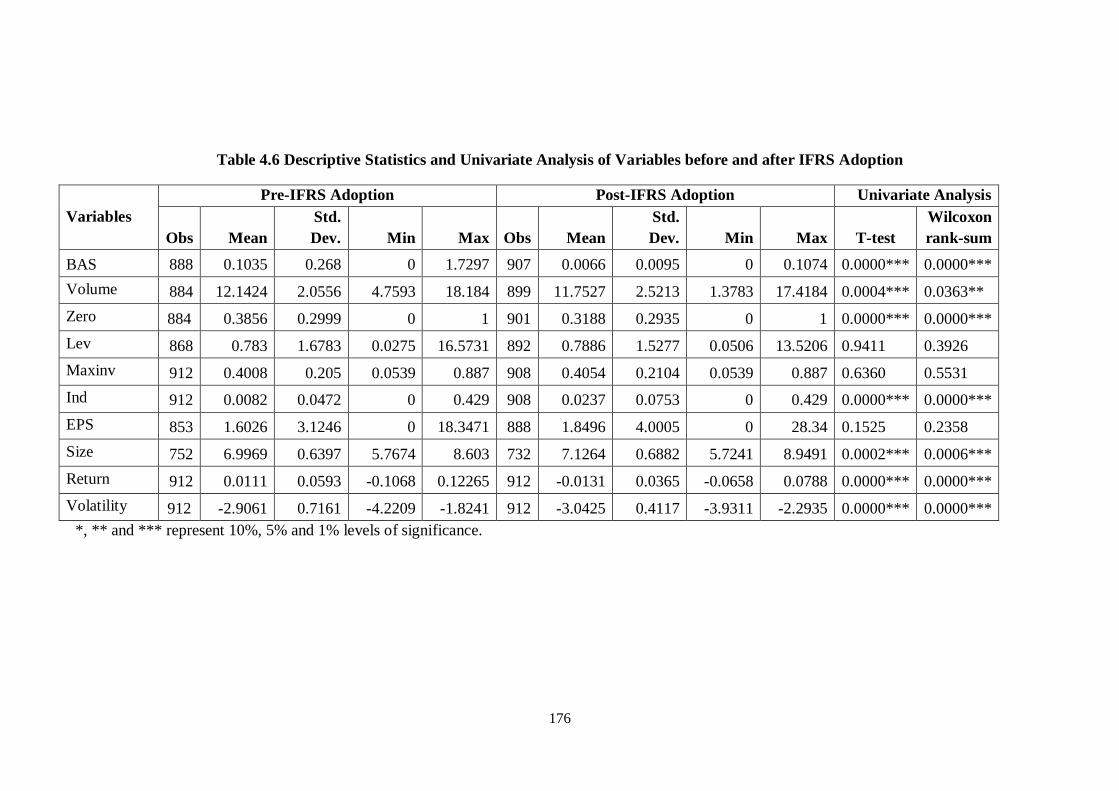

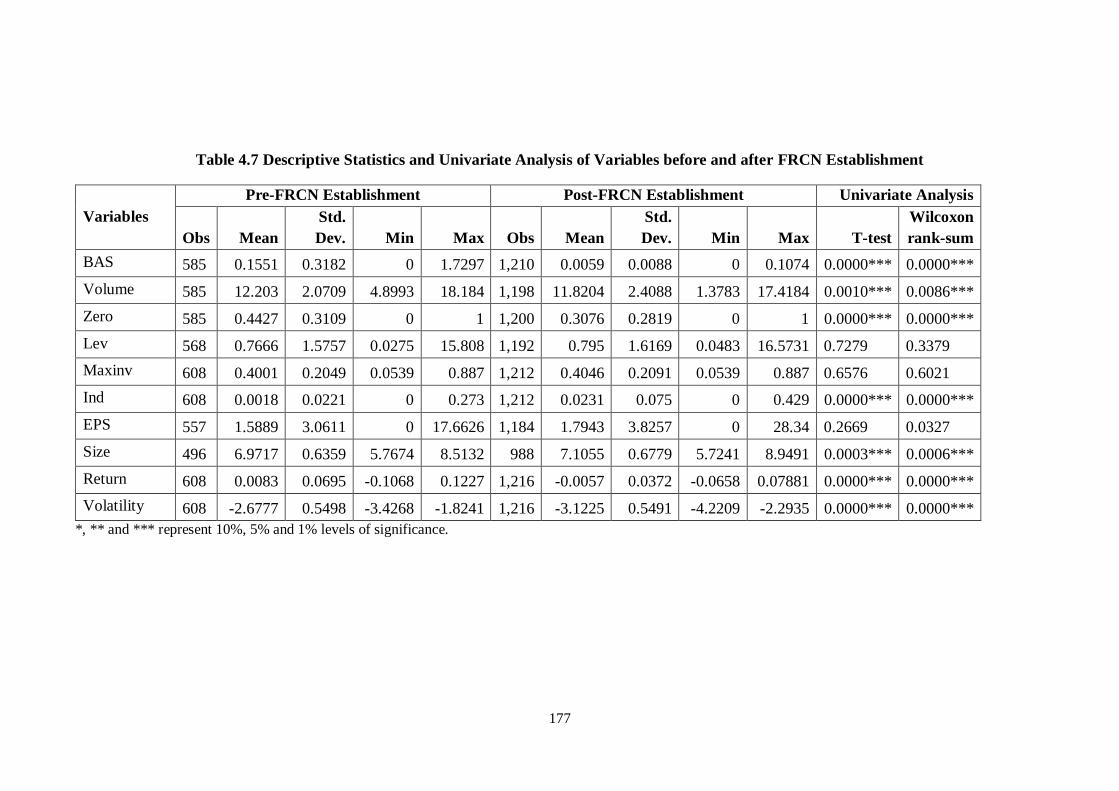

4.9 Data Analysis --------------------------------------------------------------------------------------- 174

4.9.1 Descriptive Statistics ------------------------------------------------------------------------- 174

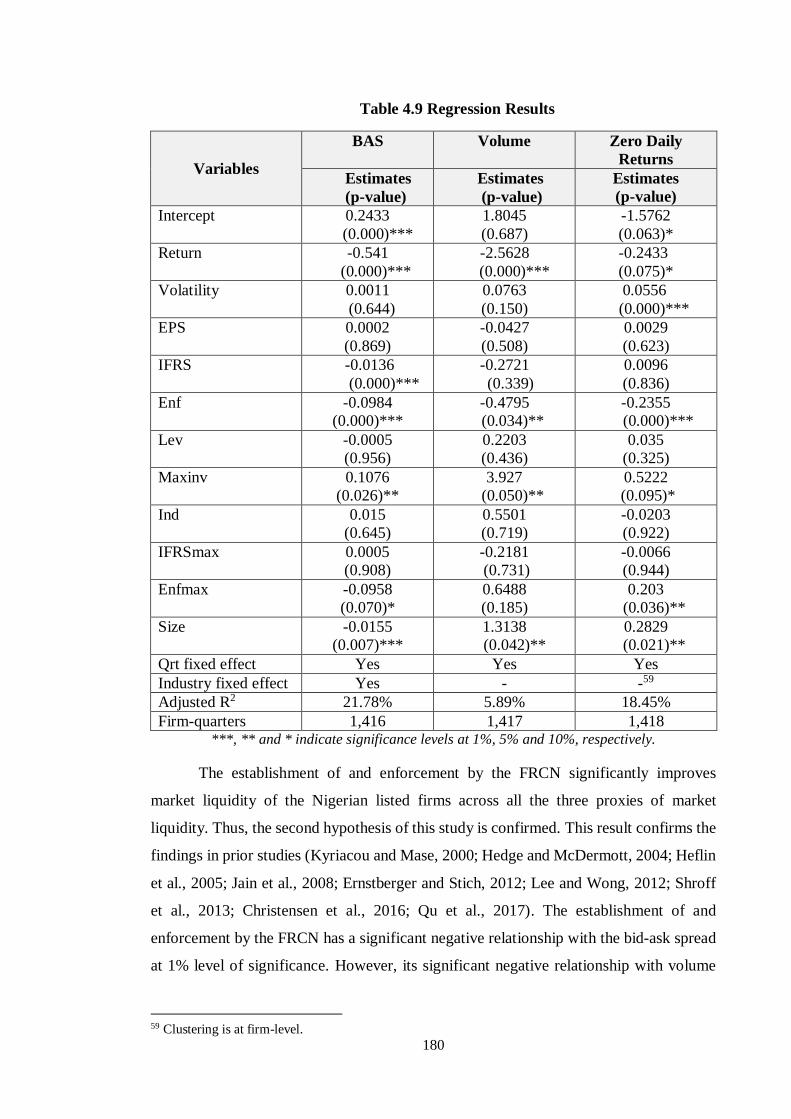

4.9.2 Regression Analysis -------------------------------------------------------------------------- 178

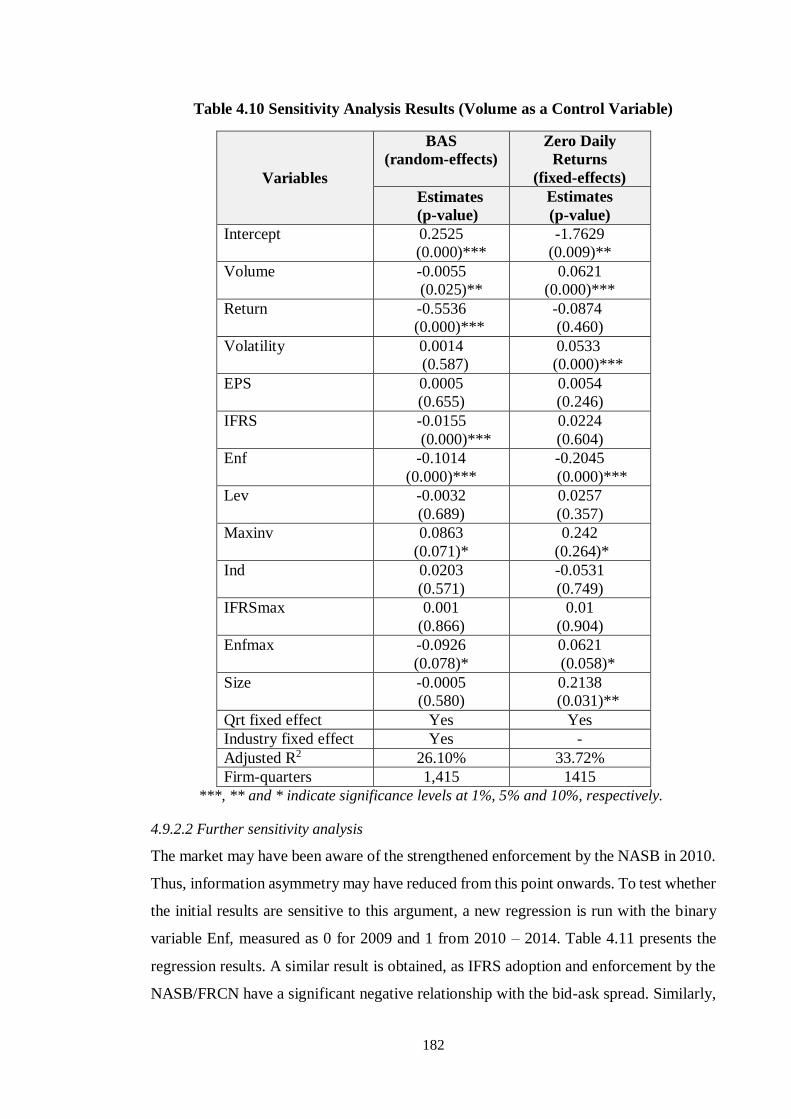

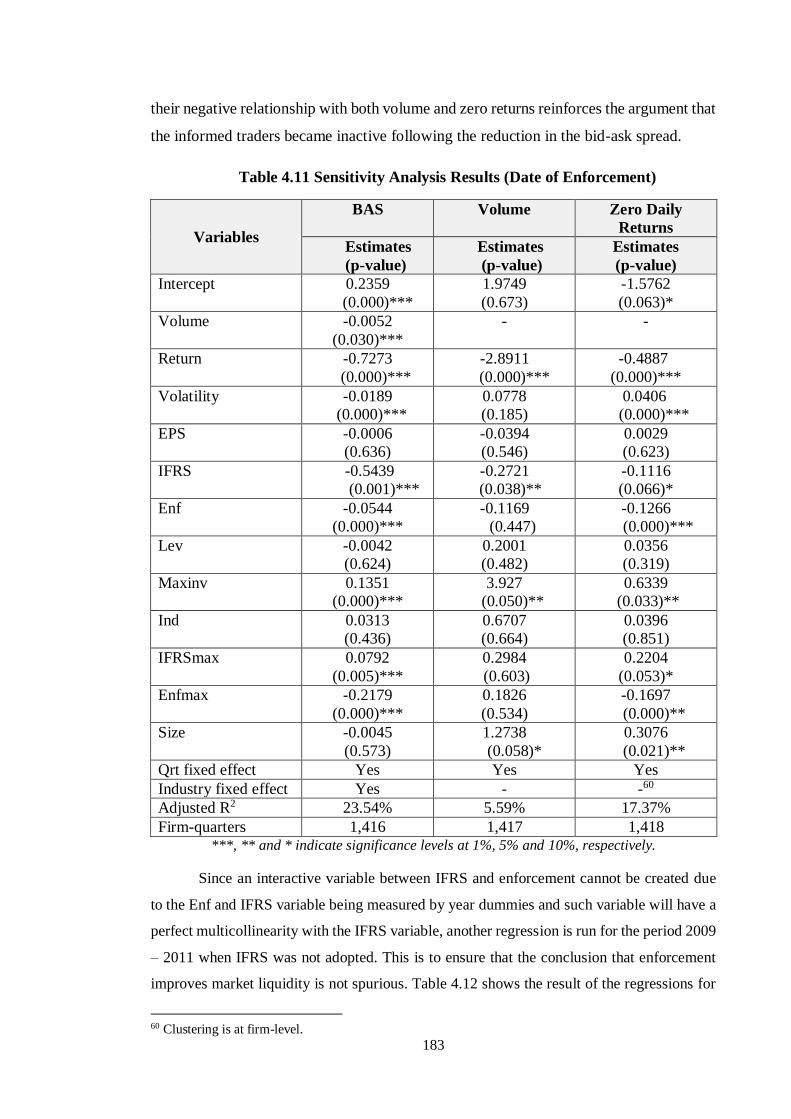

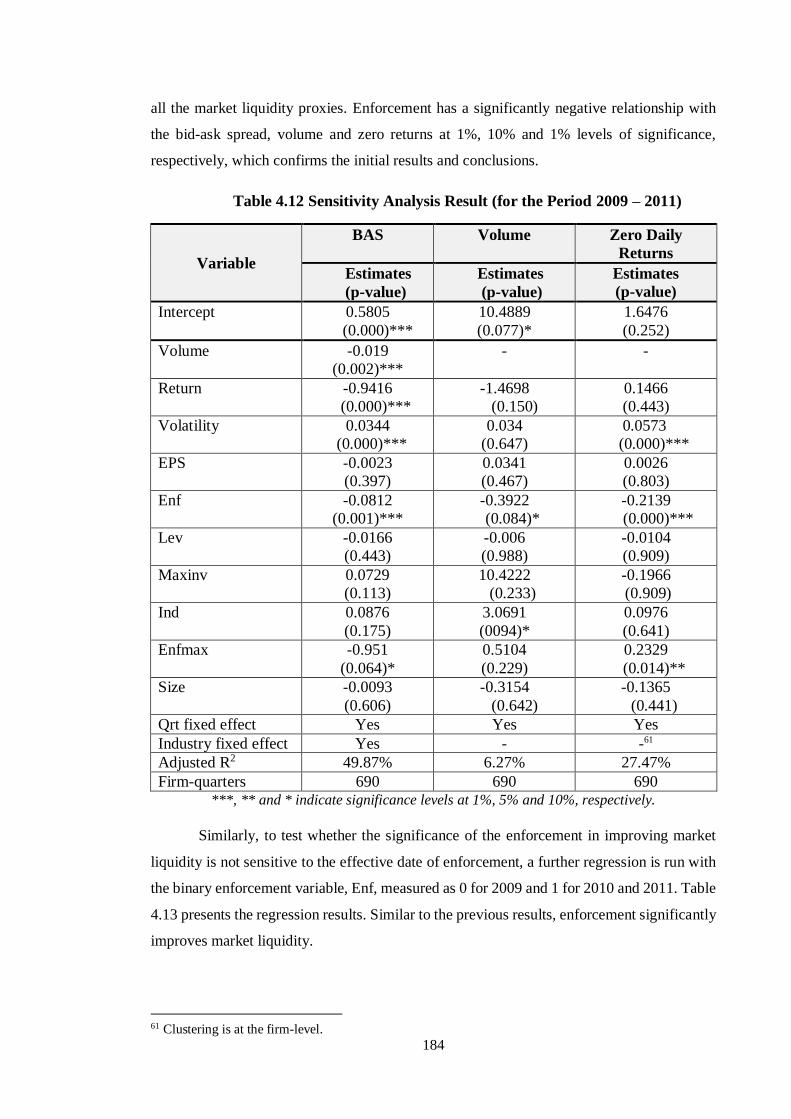

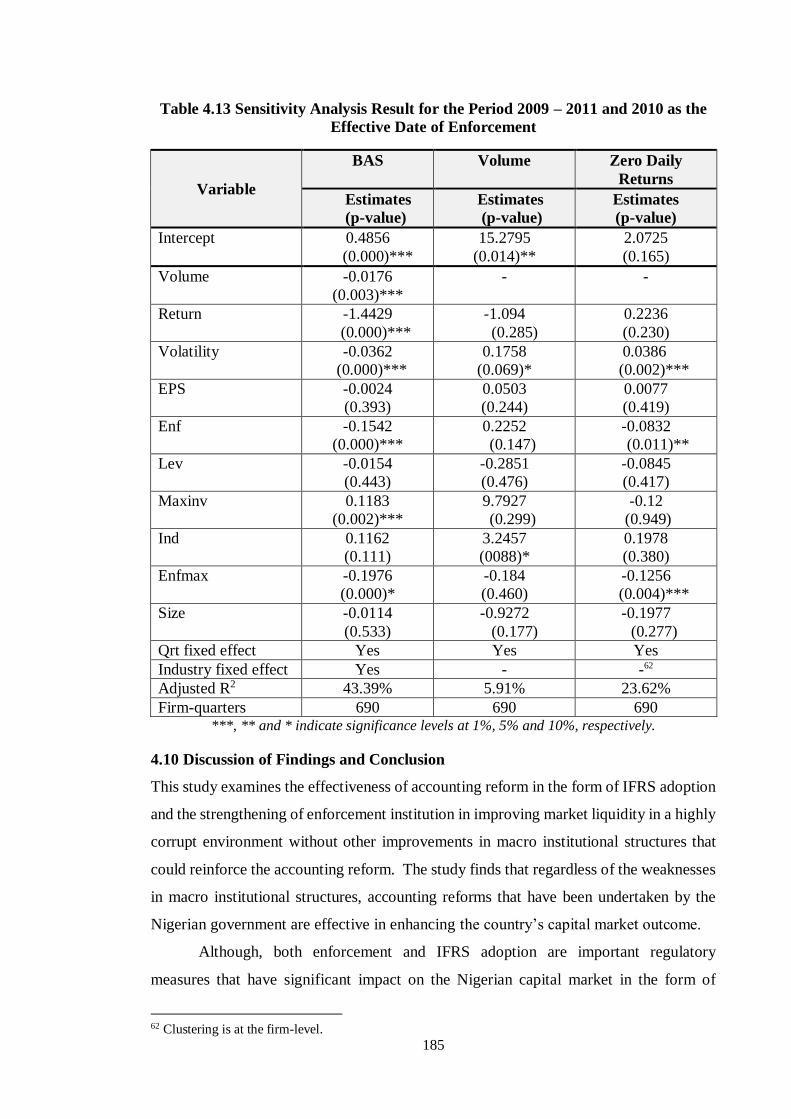

4.10 Discussion of Findings and Conclusion ------------------------------------------------------- 185

Chapter 5 --------------------------------------------------------------------------------------- 187

Summary and Conclusion -------------------------------------------------------------------- 187

5.1 Summary and Reflection -------------------------------------------------------------------------- 187

5.2 Implications of the Study ------------------------------------------------------------------------- 190

5.3 Limitations of the Studies and Avenues for Further Research ------------------------------ 190

Appendix I: Interview Protocol -------------------------------------------------------------- 192

Appendix II: Questionnaire ------------------------------------------------------------------ 194

Appendix III: Analysis of Responses to Questionnaire ----------------------------------- 199

Appendix IV: Normal Distribution of the Residuals of the Regression Models ------- 209

References -------------------------------------------------------------------------------------- 212

viii

List of Tables

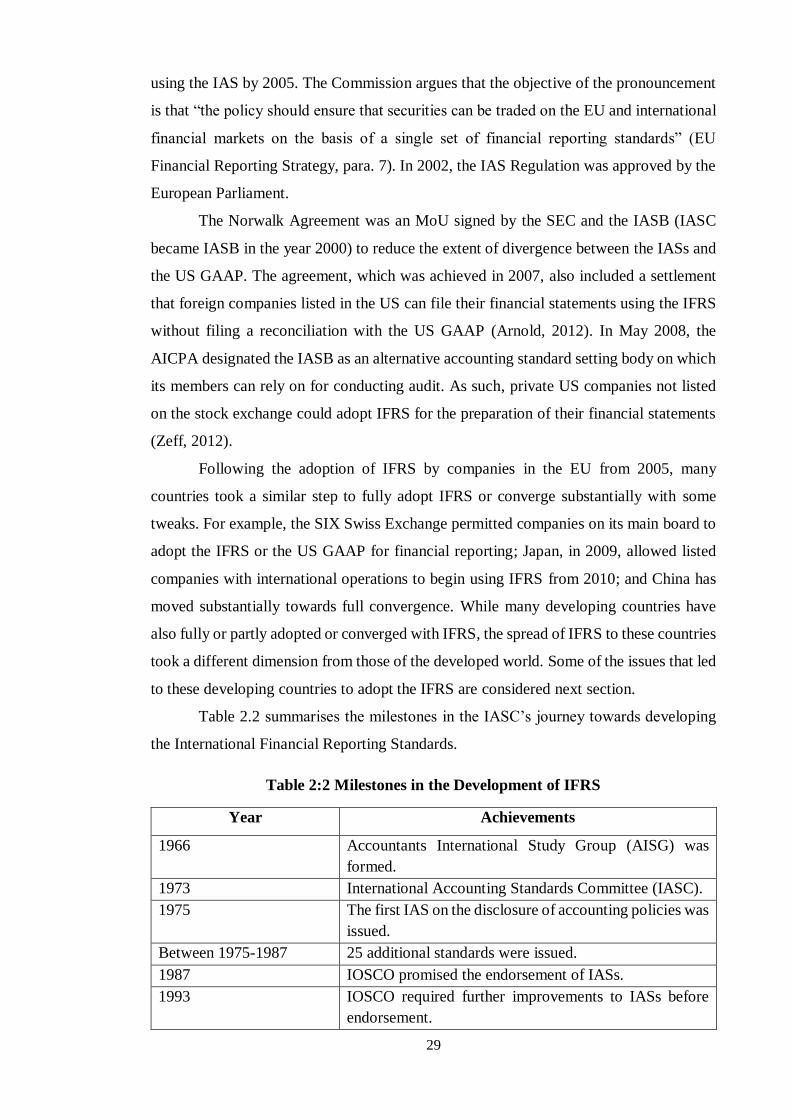

Table 2.1 Nigerian Statement of Accounting Standards before Full IFRS Adoption 17

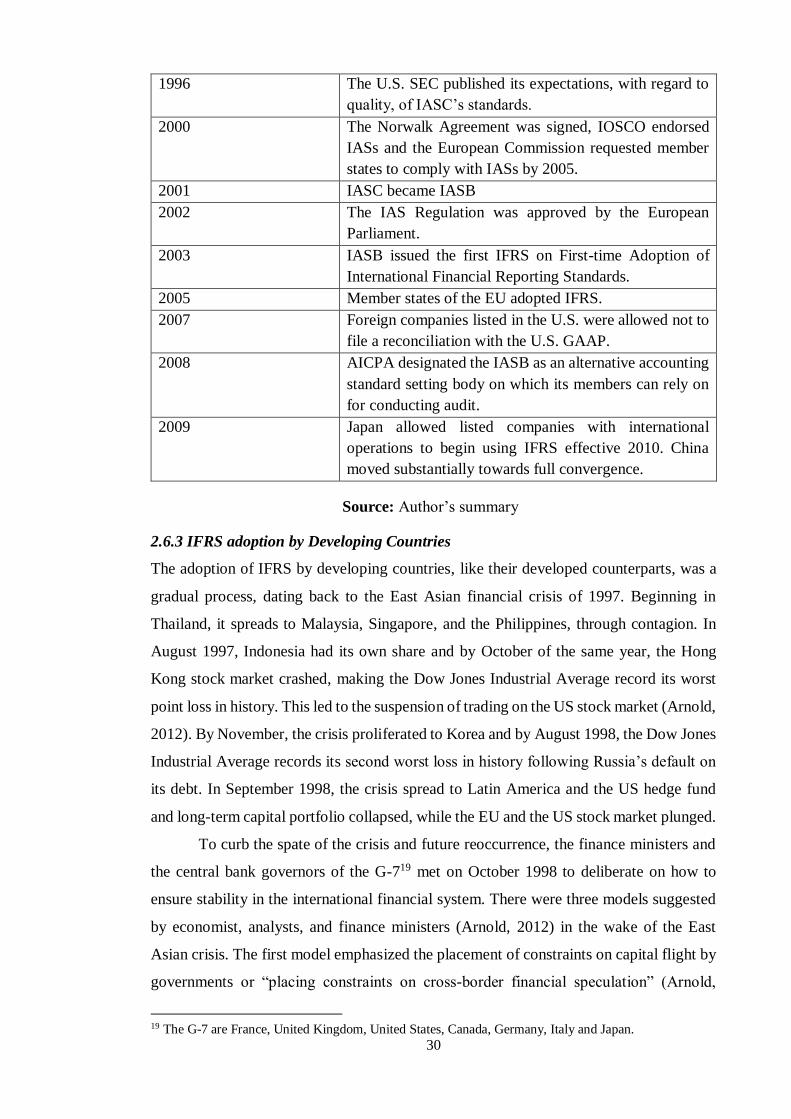

Table 2:2 Milestones in the Development of IFRS 24

Table 2.3 Interview Details 41

Table 2.4 Questionnaire Respondents’ Profiles 42

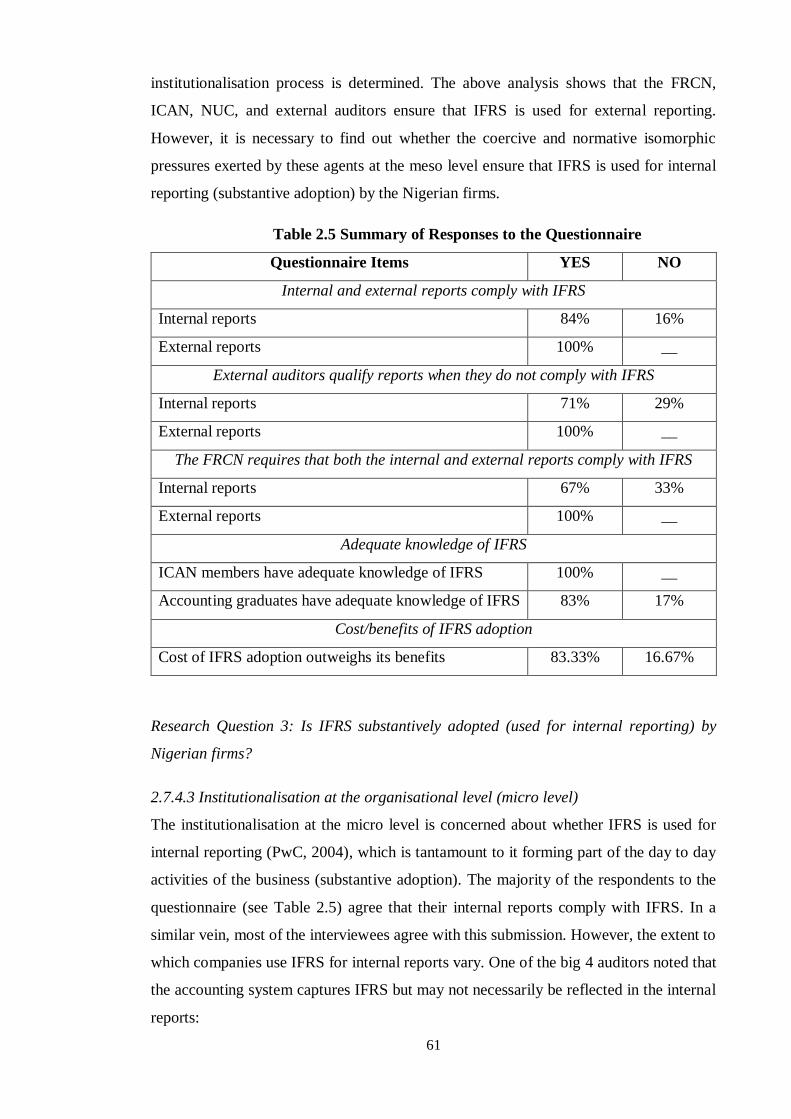

Table 2.5 Summary of Responses to the Questionnaire 61

Table 3.1 Summary of Literature on the Effects of IFRS Adoption on Earnings Mgt. 112

Table 3.2 Summary of Literature on the Effects of Enforcement Adoption on Earn. Mgt. 115

Table 3.3 Summary of Literature on the Effects of IFRS on Timely Loss Recognition 117

Table 3.4 Summary of Literature on the Effects of IFRS on Earnings Persistence 120

Table 3.5 Sampling 121

Table 3.6 Distribution of Firms by Industry 122

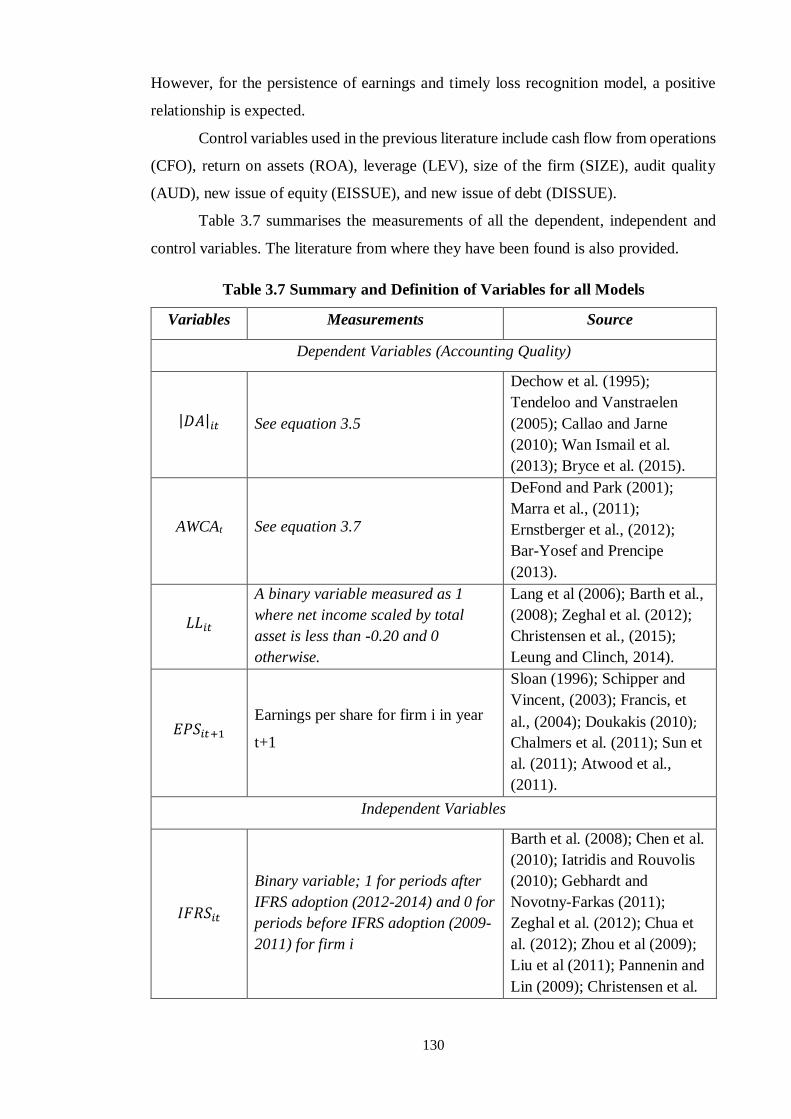

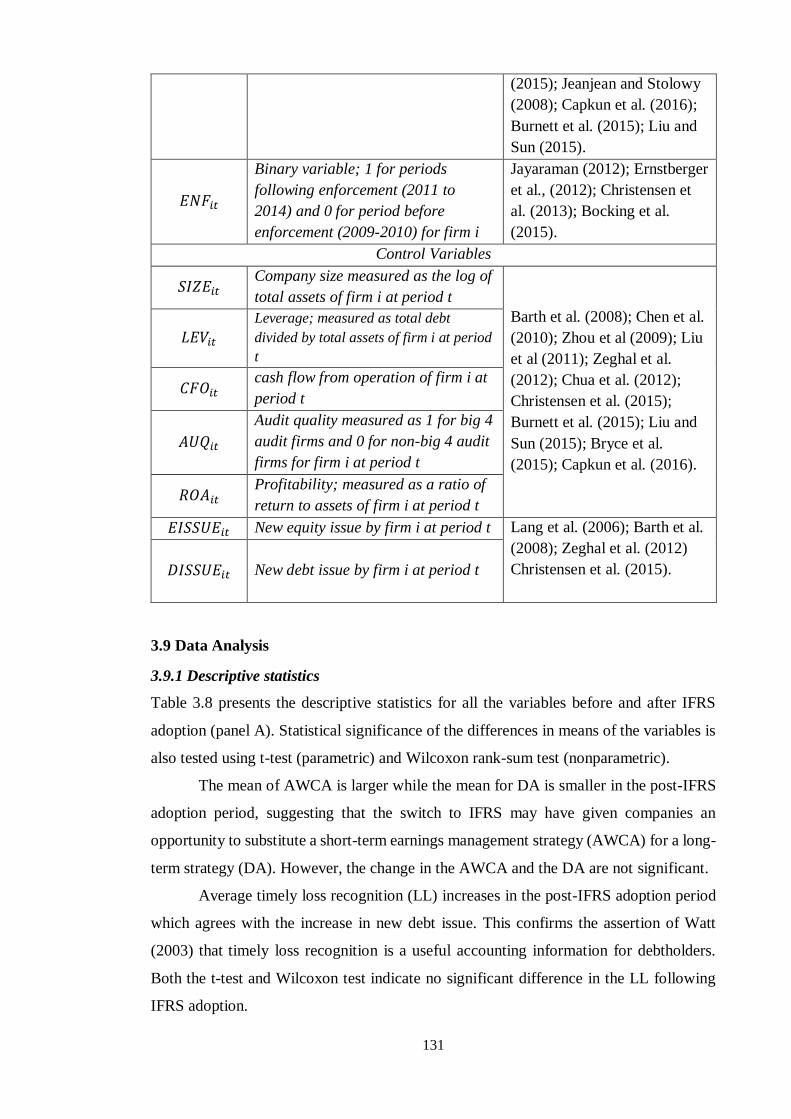

Table 3.7 Summary and Definition of Variables for all Models 125

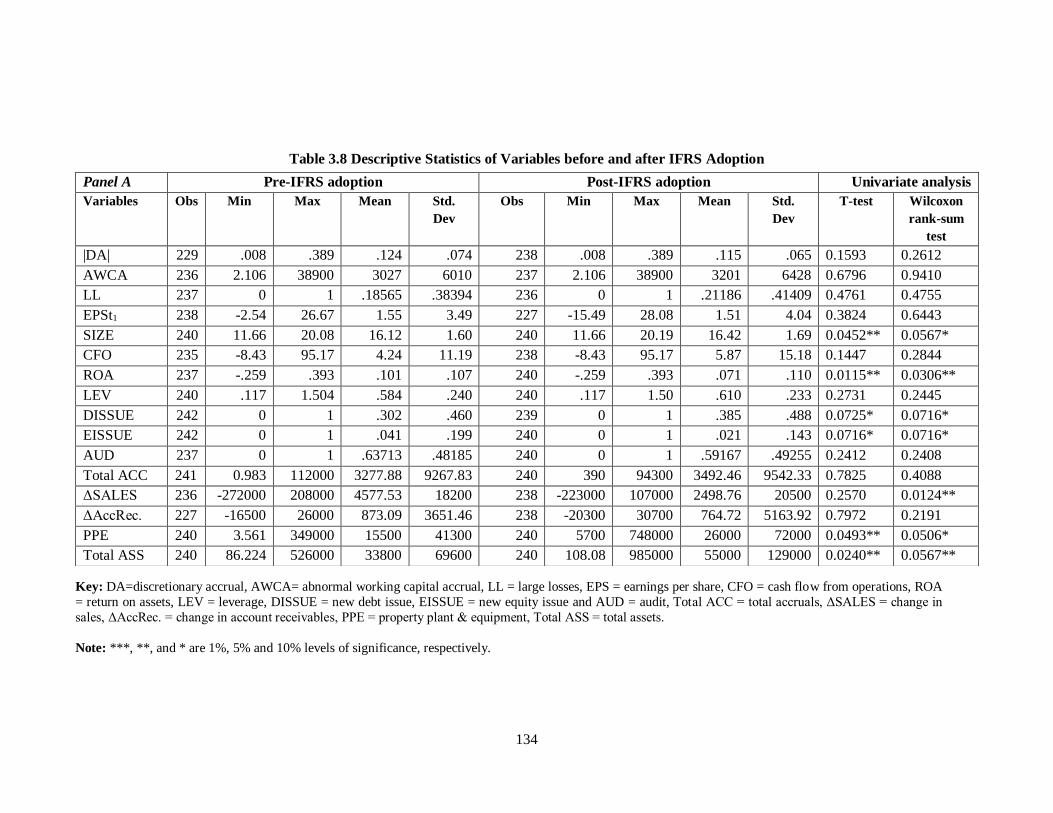

Table 3.8 Descriptive Statistics of Variables before and after IFRS Adoption 129

Table 3.9 Descriptive Statistics of Variables before and after FRCN Establishment 130

Table 3.10 Pairwise Correlation of all Variables used for all Models 131

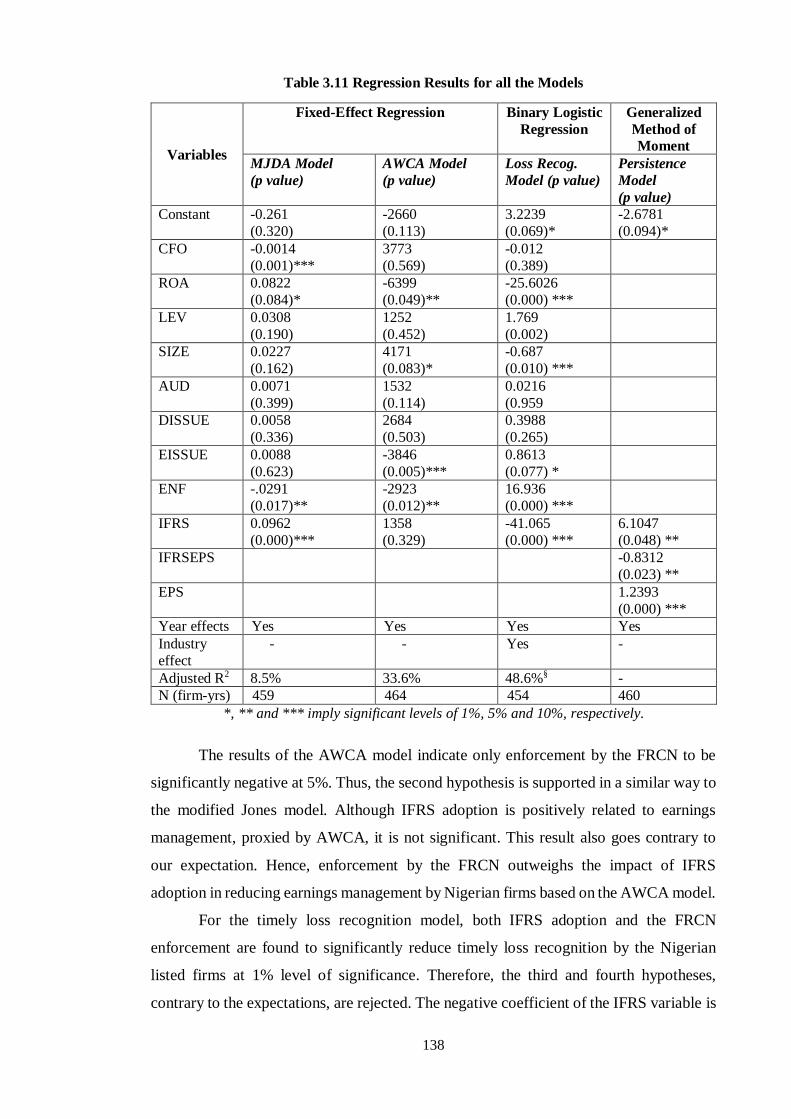

Table 3.11 Regression results for all the models 133

Table 3.12 Sensitivity Analysis Results (Effective Date of Enforcement) 135

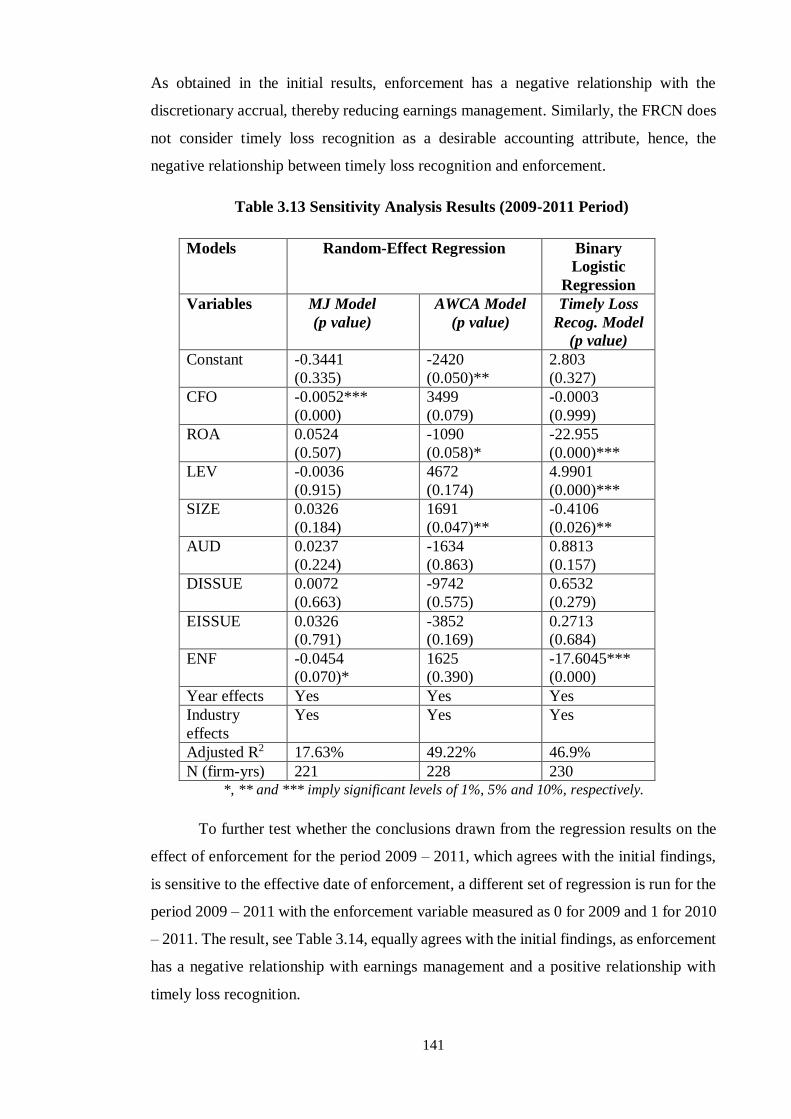

Table 3.13 Sensitivity Analysis Results (2009-2011 Period) 136

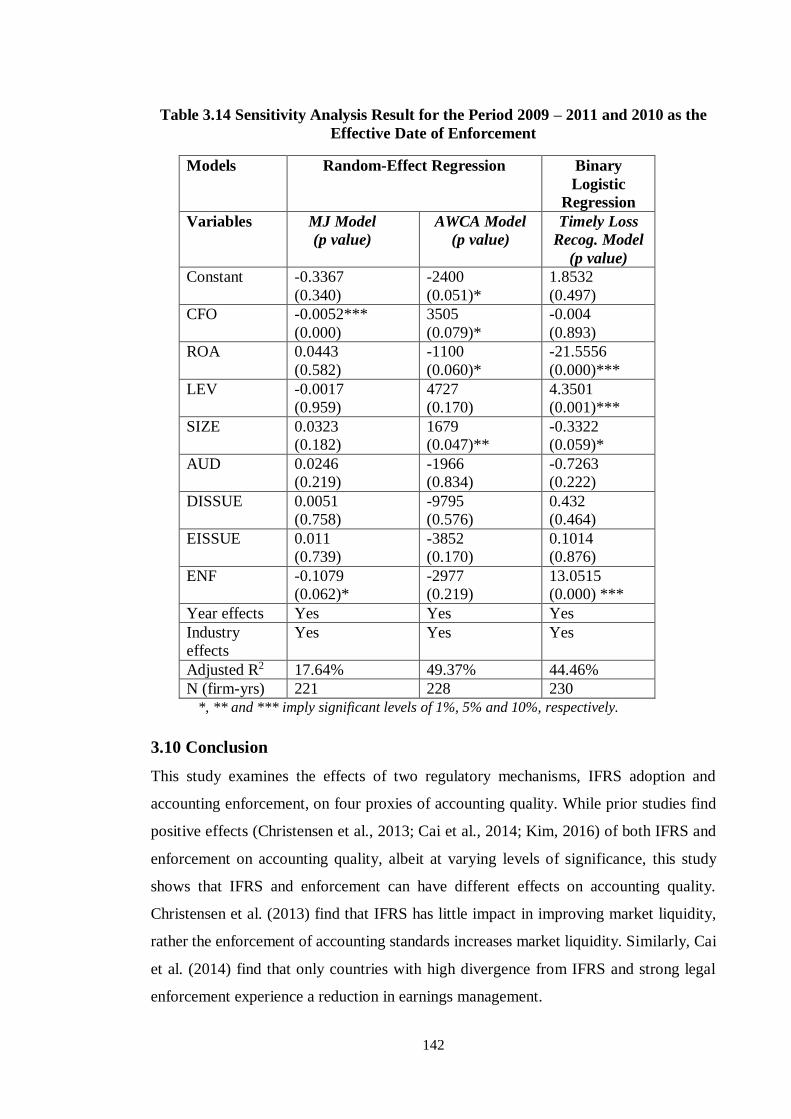

Table 3.14 Sensitivity Analysis Result for the Period 2009 – 2011 and 2010 as the Effective

Date of Enforcement 137

Table 4.1 Summary of Literature on the Effects of IFRS on Market Liquidity 159

Table 4.2 Summary of Literature on the Effects of Enforcement on Liquidity 163

Table 4.3 Sampling 164

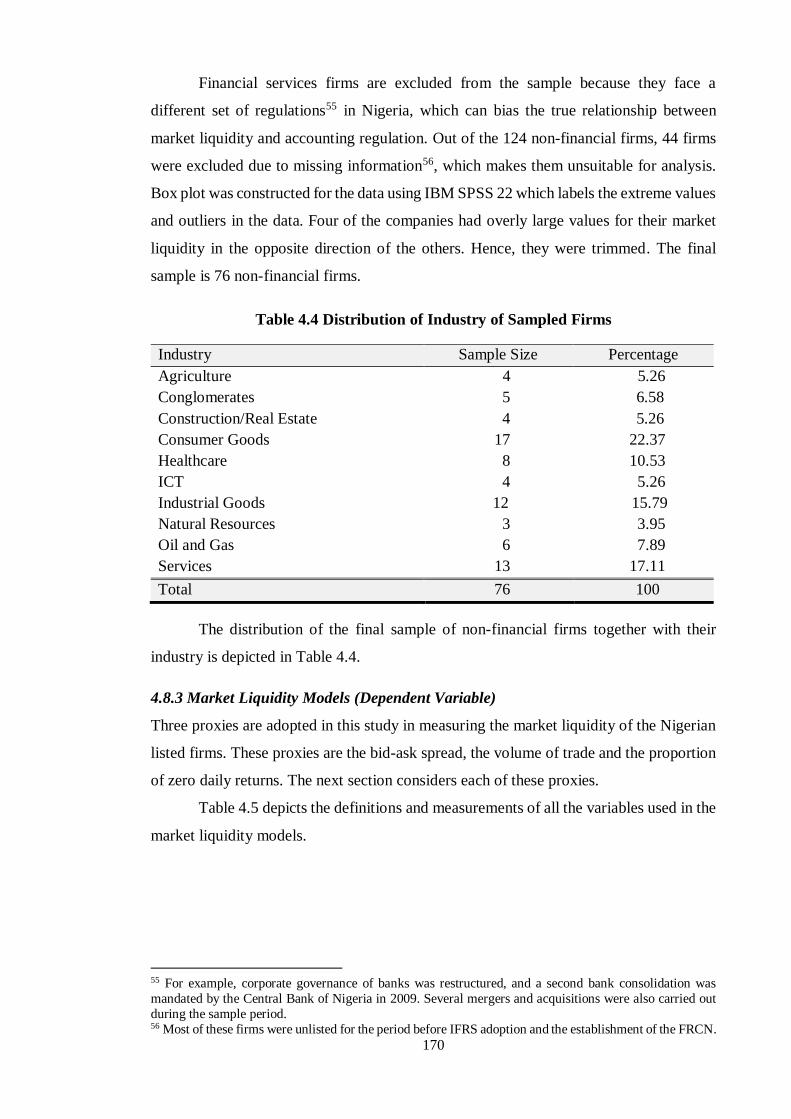

Table 4.4 Distribution of Industry of Sampled Firms 165

Table 4.5 Definition and Measurement of Variables for the Liquidity Models 166

Table 4.6 Descriptive Statistics and Univariate Analysis of Variables (IFRS) 171

Table 4.7 Descriptive Statistics and Univariate Analysis of Variables (FRCN) 172

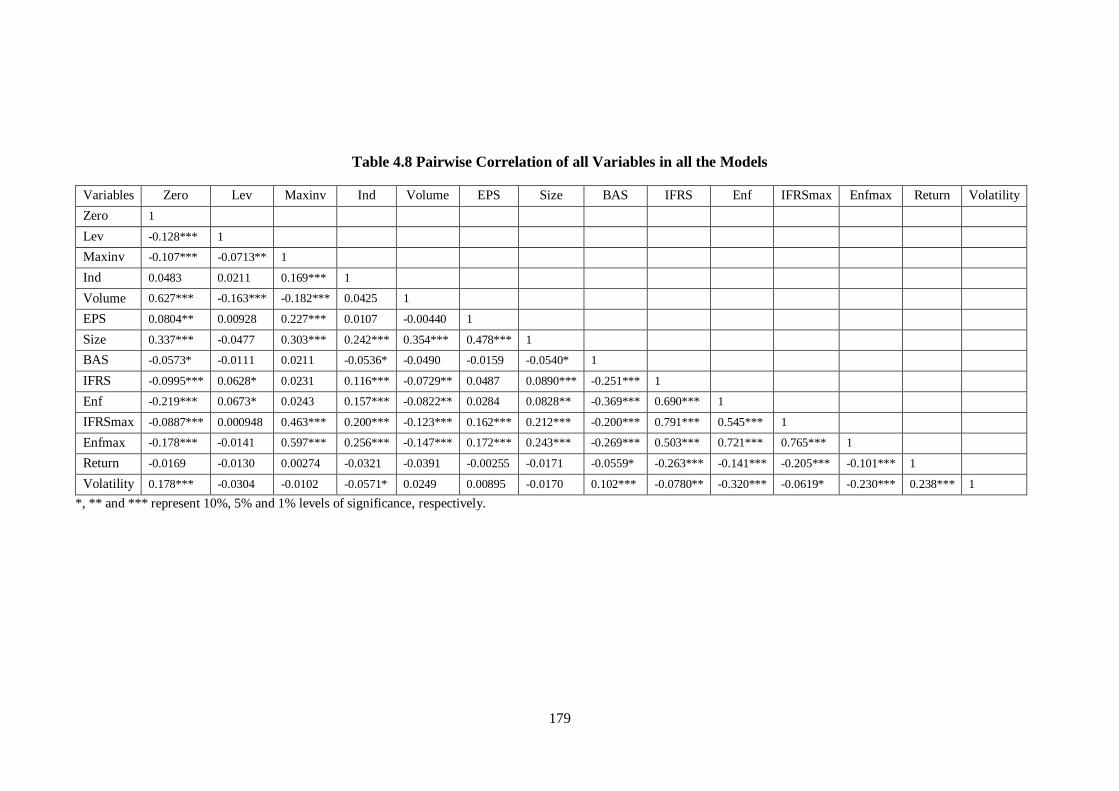

Table 4.8 Pairwise Correlation of all Variables in all the Models 174

Table 4.9 Regression Results 175

Table 4.10 Sensitivity Analysis Results (Volume as a Control Variable) 177

Table 4.11 Sensitivity Analysis Results (Date of Enforcement) 178

Table 4.12 Sensitivity Analysis Result (for the Period 2009 – 2011) 179

Table 4.13 Sensitivity Analysis Result for the Period 2009 – 2011 and 2010 as the Effective

Date of Enforcement 180

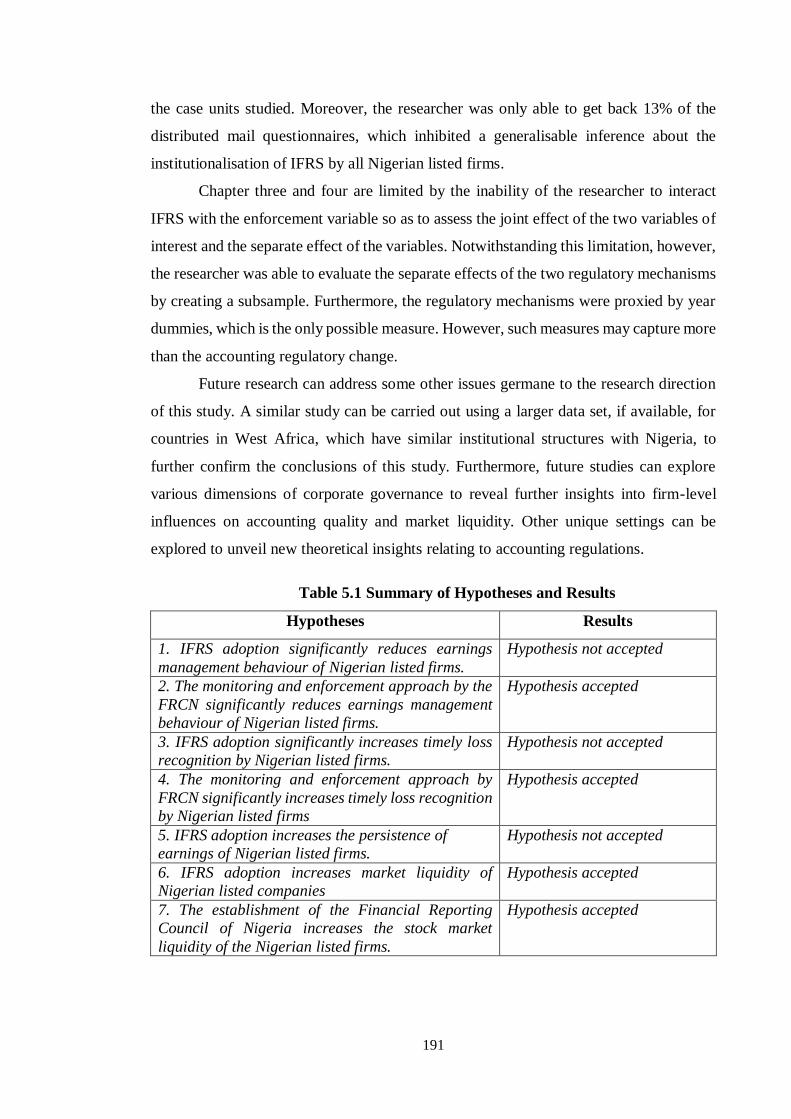

Table 5.1 Summary of Hypotheses and Results 191

ix

List of Figures

Figure 1.1 Overview of Thesis 11

Figure 2.1 Reasons for Differences in Accounting Practices across Jurisdictions 19

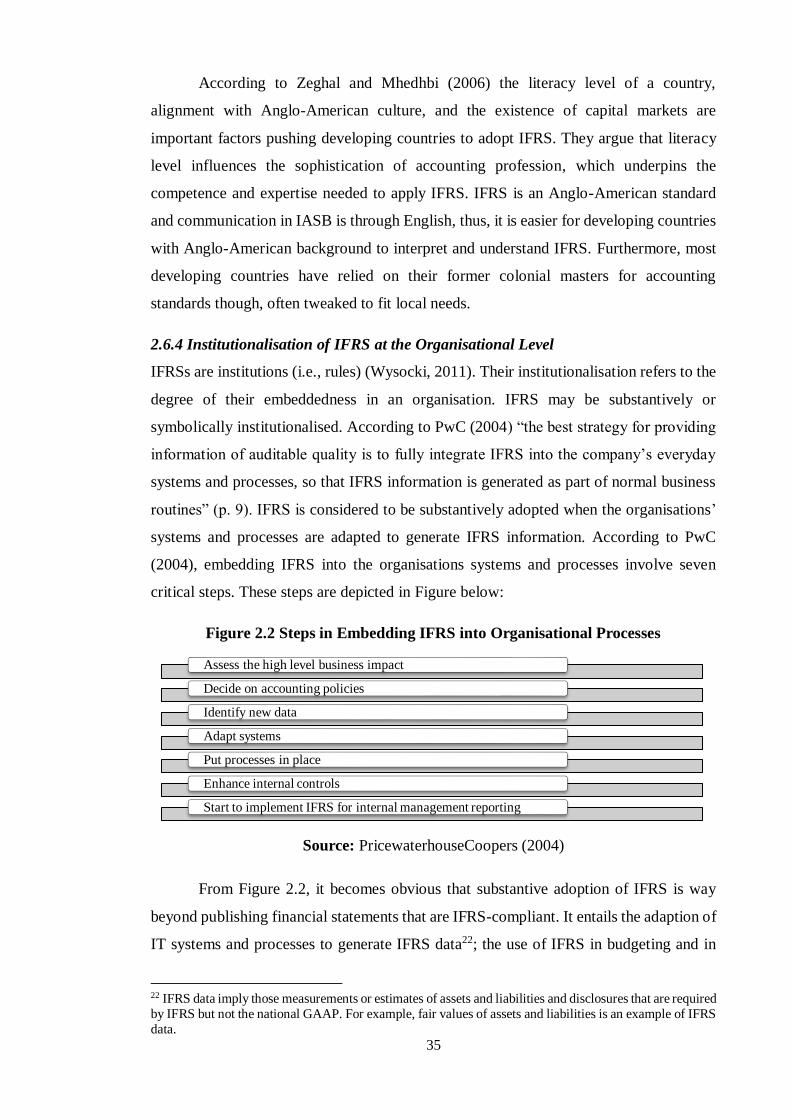

Figure 2.2 Steps in Embedding IFRS into Organisational Processes 31

Figure 2.3 Three levels of institutionalisation 35

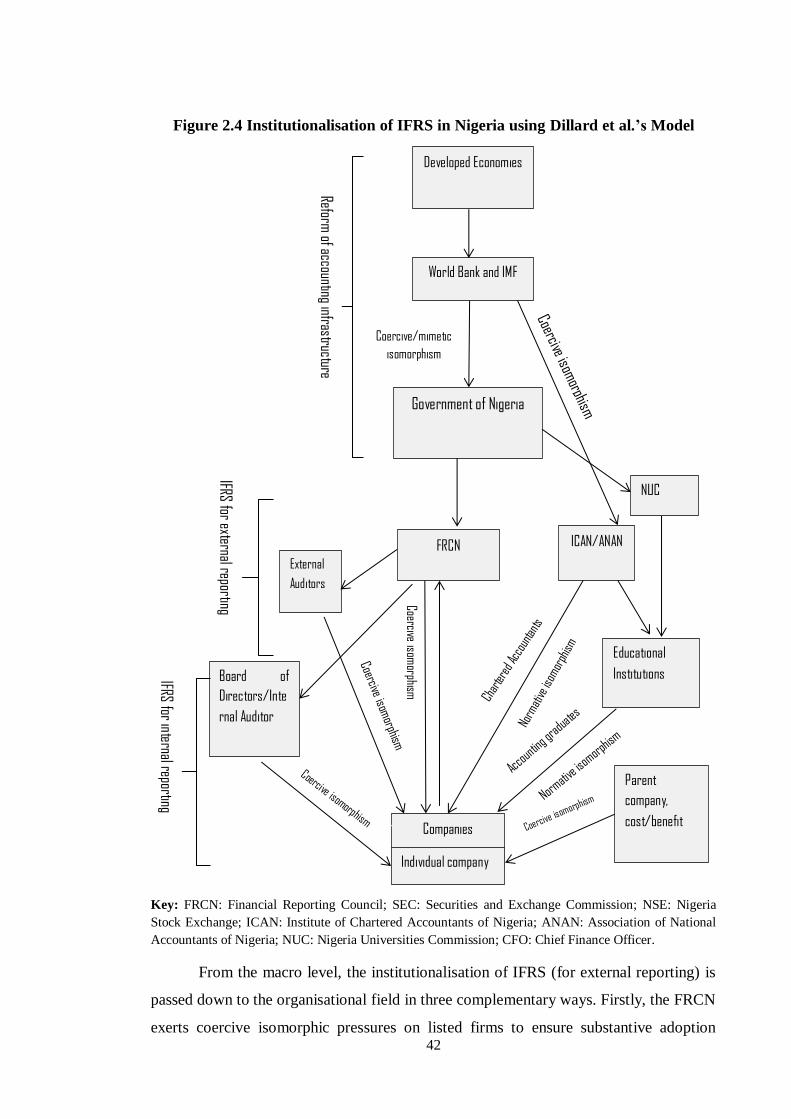

Figure 2.4 Institutionalisation of IFRS in Nigeria using Dillard et al.’s Model 38

Figure 2.5 Themes and Subthemes for Analysis 45

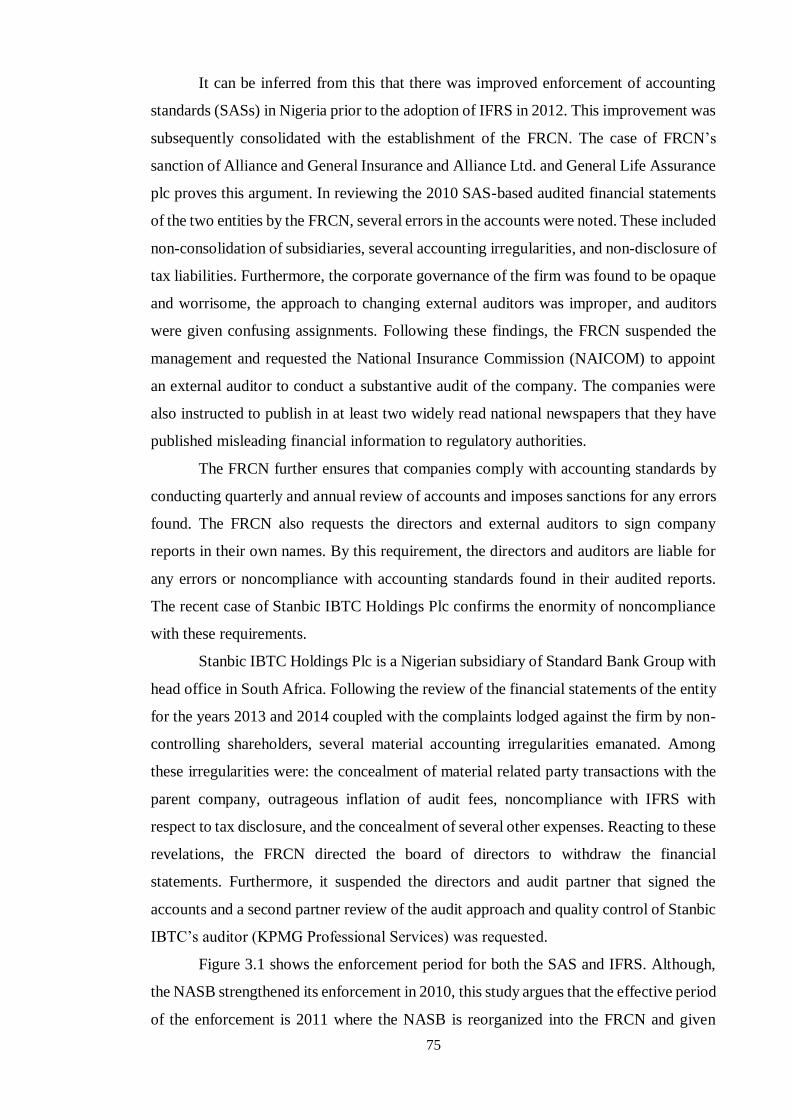

Figure 3.1 Effective Date of Enforcement 71

Figure 3.2 The Demand for Accounting Reform in Nigeria 72

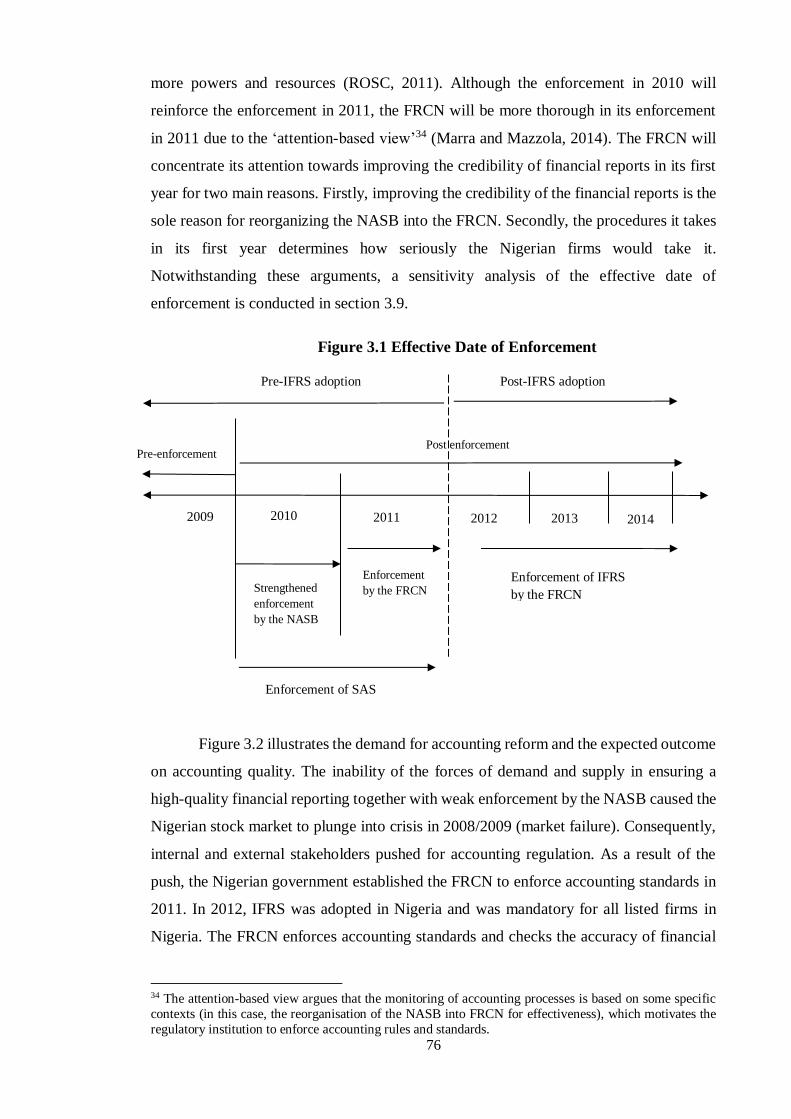

Figure 3.3 Public Accountability Model of Accounting Regulation 74

Figure 3.4 Measures of Accounting Quality 75

Figure 3.5 Summary of Factors Affecting Different Types of Earnings Management 76

Figure 3.6 Summary of Factors Affecting Accounting Conservatism 98

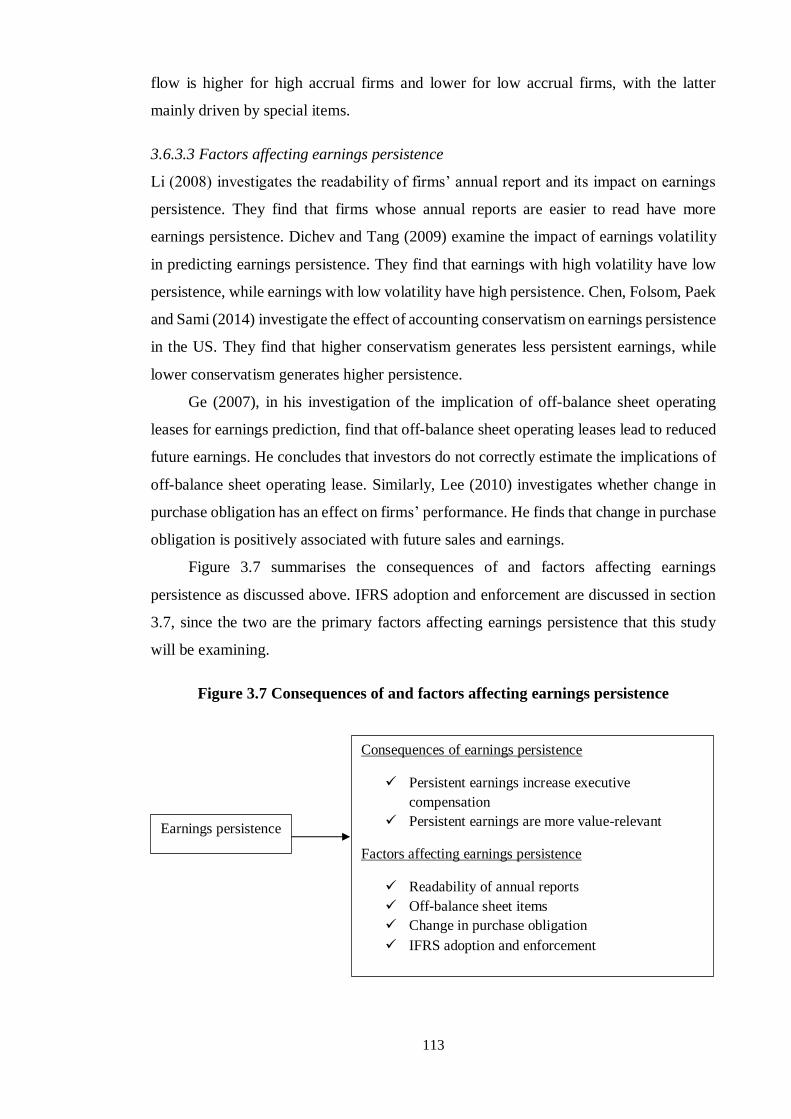

Figure 3.7 Consequences of and factors affecting earnings persistence 108

Figure 4.1 Regulatory Bodies of the Nigerian Capital Market 143

Figure 4.2 Signalling through IFRS adoption and enforcement in Nigeria 146

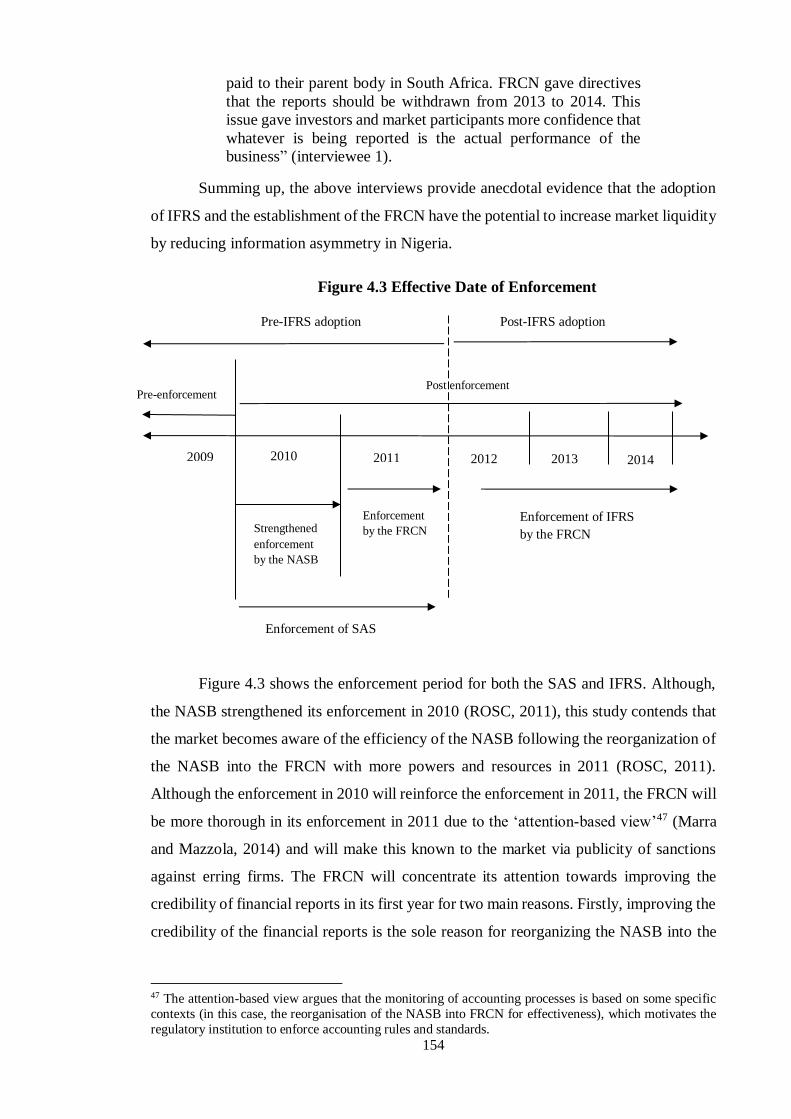

Figure 4.3 Effective Date of Enforcement 149

Figure 4.4 Factors Affecting Stock Market Liquidity 158

1

Chapter 1

Introduction

1.1 Motivation for the Study

The motivation for this study stems from the 2008 Nigerian capital market crisis that

wiped away investors’ funds to the tune of $13.33 billion and led to the pull out of both

foreign and local investors from the Nigerian capital market. In the aftermath of the crisis,

the Securities and Exchange (SEC) report (2009) noted that the unease in the valuation

of assets, arising from non-transparent reporting by the Nigerian listed firms, precipitated

the exist of investors. The World Bank/IMF through their Report on the Observance of

Standards and Codes (ROSC) (2011) recommended the adoption of IFRS and the

establishment of the Financial Reporting Council of Nigeria (FRCN) to improve the

integrity of the financial statements of listed companies in Nigeria. To facilitate the

smooth adoption of IFRS and obviate the potential knowledge gap, the report further

recommends the reform of professional accounting education in the country. It is the

implications of these bundle of accounting reforms that this study seeks to assess.

The adoption of IFRS across numerous parts of the world is considered the

greatest accounting change ever (Leuz and Wysocki, 2016). More than one hundred

countries, developing and developed countries, have adopted IFRS (Bova and Pereira,

2012). In recent times, several studies to examine various dimensions of issues related to

this unprecedented accounting change. These issues revolve around three main themes

which are IFRS adoption and accounting quality, IFRS adoption and capital market

outcome, and the institutionalisation of IFRS in developing countries given their weak

accounting infrastructure. This study is divided into three parts; the first part (Chapter 2)

examines the institutionalisation of IFRS in Nigeria, the second part (Chapter 3) examines

the impact of IFRS adoption and the enforcement of accounting standards on accounting

quality in Nigeria, while the third part (Chapter 4) examine the implications of IFRS

adoption and the enforcement of accounting standards on market liquidity in Nigeria.

1.1.1 The Institutionalisation of IFRS

IFRS was advanced by the developed countries through the International Accounting

Standards Board (IASB). These countries have necessary infrastructures such as

developed capital markets, strong accounting profession and strong enforcement

institutions, which aid proper adoption of and compliance with IFRS by companies in

these countries. These infrastructures are lacking in many developing countries (Chand

2005; Chand and White, 2007; Bova and Pereira, 2012). Hence, the extent of their

2

compliance with IFRS is often very low. Arising from these weak accounting

infrastructures, extant studies (e.g., Irvine, 2008; Albu and Albu, 2011) have discussed

the failure of firms in the developing countries to comply with IFRS, albeit it has been

adopted by the countries in which they operate. However, some developing countries, for

example Nigeria, have implemented reforms such as the establishment of the Financial

Reporting Council of Nigeria and the strengthening of its accounting profession to

enhance the adoption of IFRS. The effectiveness of such reforms is yet to be explored in

extant literature (Nyamori, Abdul-Rahaman and Samkin, 2017). Thus, the objective of

the second chapter of this study is to examine the process and outcome of the

institutionalisation of IFRS in Nigeria.

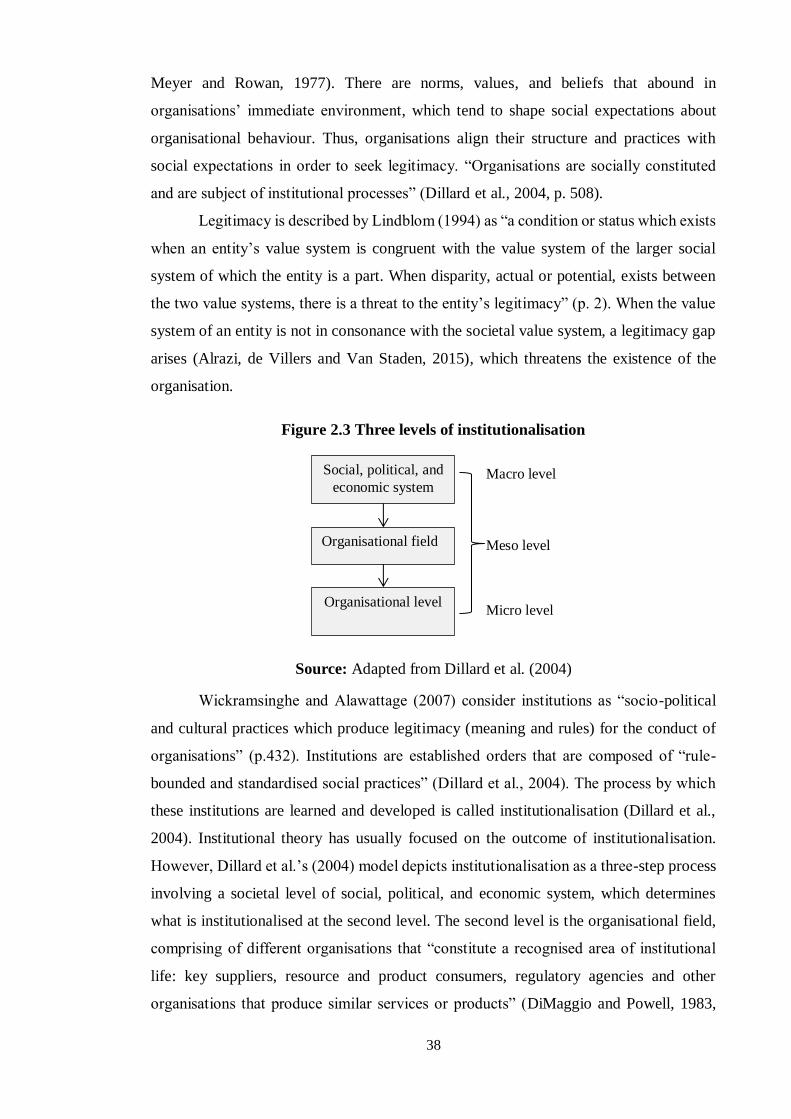

Institutionalisation is the process by which a rule or practice (i.e., an institution)

expected in different social settings is developed and learned (Dillard, Goodman and

Rigsby, 2004). The ‘rule’ here is IFRS (Wysocki, 2011). Institutionalisation takes place

at three levels of social order, namely social, political, and economic level; organisational

field; and organisational level (Dillard et al., 2004). According to DiMaggio (1988), the

outcome of the institutionalisation process is determined by “the relative power of the

actors who support, oppose, or otherwise strive to influence it” (p. 13) at the three levels

of social order.

The outcome of the institutionalisation process is either a symbolic or a

substantive adoption of IFRS. IFRS is symbolically adopted when it is not fully embedded

in organisational processes (e.g., used for internal reporting), while it is substantively

adopted when it is fully embedded in organisational processes (PwC, 2004). Many studies

on the institutionalisation of IFRS in the developing countries (e.g., Chand 2005; Chand

and White, 2007; Chand and Patel, 2008; Irvine, 2008; Albu and Albu, 2012; Albu, Albu

and Alexander, 2014; Nurunnabi, 2015) find IFRS to be symbolically adopted in the

developing countries. In many cases, this symbolic adoption is ascribed to the motive for

adopting IFRS by these countries, which is a symbolic portrayal of an improved reporting

environment. However, many of these countries lack necessary infrastructures (e.g., weak

accounting profession and weak or non-existent enforcement institutions) to support IFRS

implementation.

Given the improved accounting infrastructures in Nigeria, through the

establishment of the FRCN and the reform of the professional accountancy education1,

the objective of this part of the study is to examine the influence of these developments

1 Institute of Chartered Accountants of Nigeria. (ICAN).

3

on the institutionalisation of IFRS in Nigeria and the outcome of the institutionalisation

process. Using Dillard et al.’s (2004) model of neo-institutional theory, this objective is

fulfilled by examining the institutionalising agents and the type of isomorphic pressure

exerted by the agents at the different levels of social order – the social, political, and

economic level (macro); the organisational field (meso); and the organisational level

(micro).

1.1.1.1 Research questions

The following research questions are answered under this theme:

i) Who are the agents and what type of isomorphic pressure do they exert at the

macro level to institutionalise IFRS?

ii) Who are the agents and what type of isomorphic pressure do they exert at the

meso level to institutionalise IFRS?

iii) Who are the agents and what type of isomorphic pressure do they exert at the

micro level to institutionalise IFRS?

1.1.1.2 Research method

To answer the research questions above, a qualitative research approach was adopted.

Data were gathered from multiple sources to adequately capture the three levels of

analysis (i.e., three levels of social order). Due to the historical nature of the

institutionalisation process at the social, political, and economic level, data for this level

were mainly gathered from documents (see Bowen, 2009). Data for the organisational

field were gathered through interviews, while data for the organisational level were

gathered through both interviews and semi-structured questionnaire to cater for the

multitude of stakeholders at this level. Thematic analysis was used in analysing the data

gathered. Thematic analysis is used for the study because the study is theory-driven (i.e.,

neo-institutional theory) (Braune and Clarke, 2005) and the theory formed the framework

within which the data gathered were analysed.

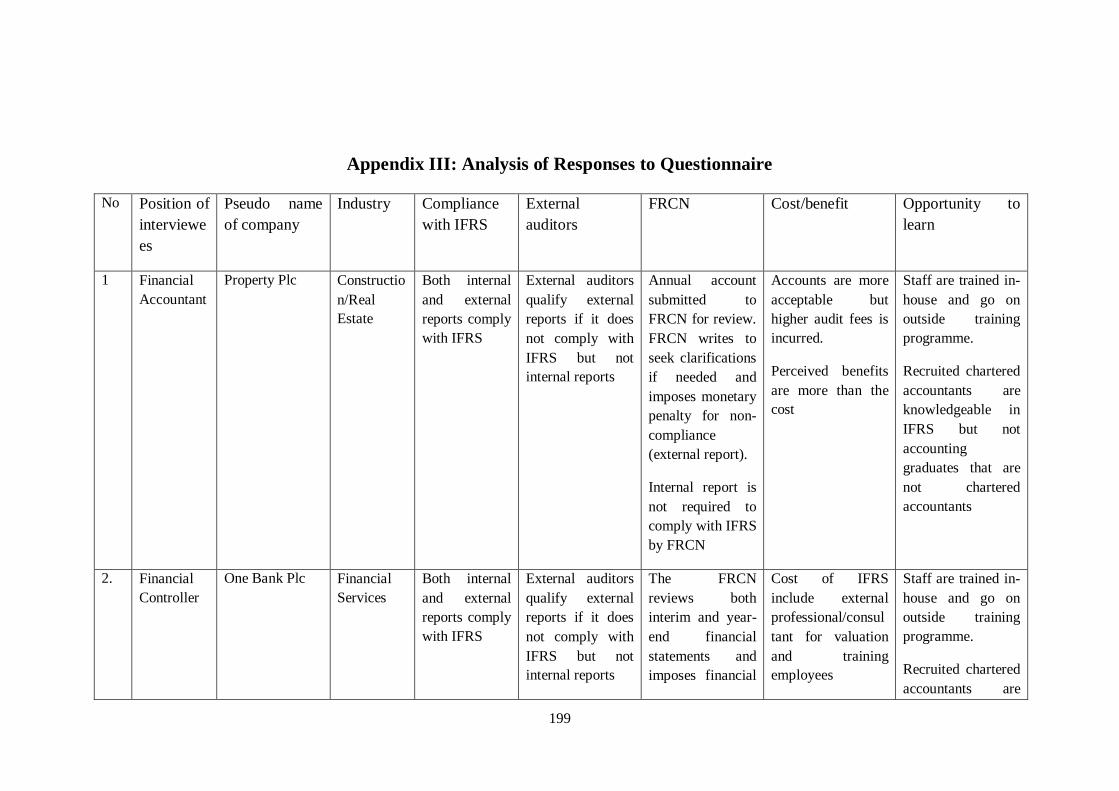

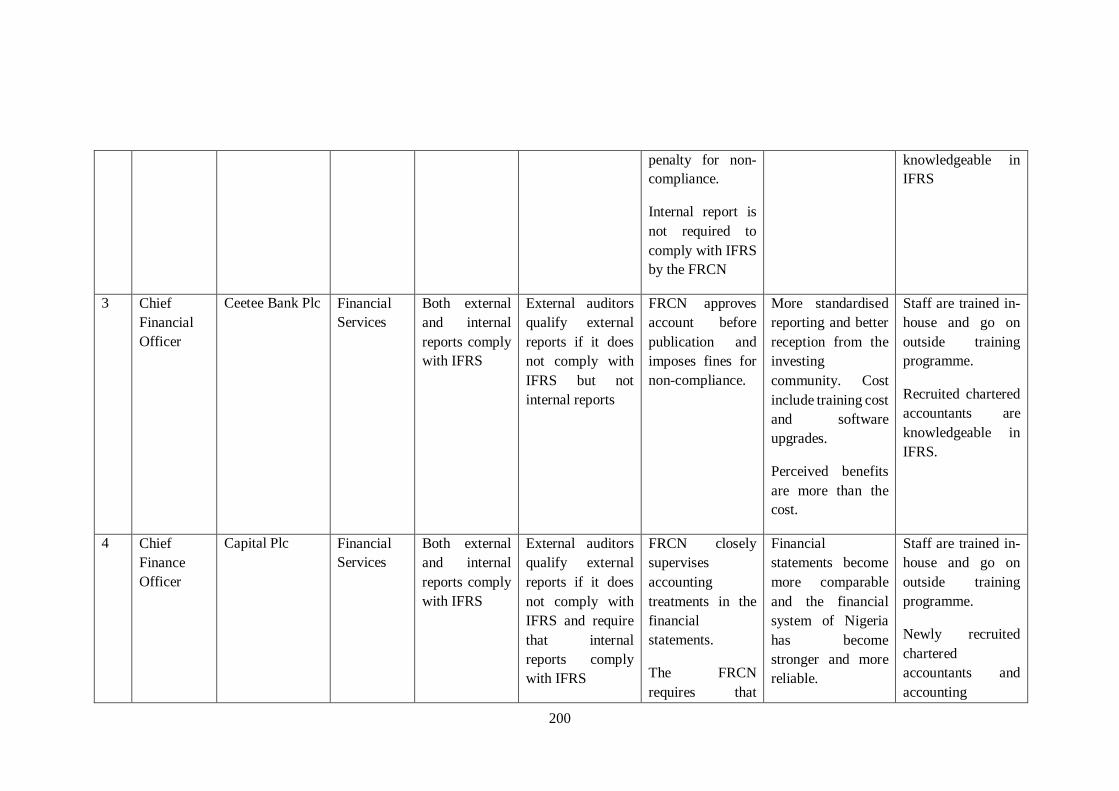

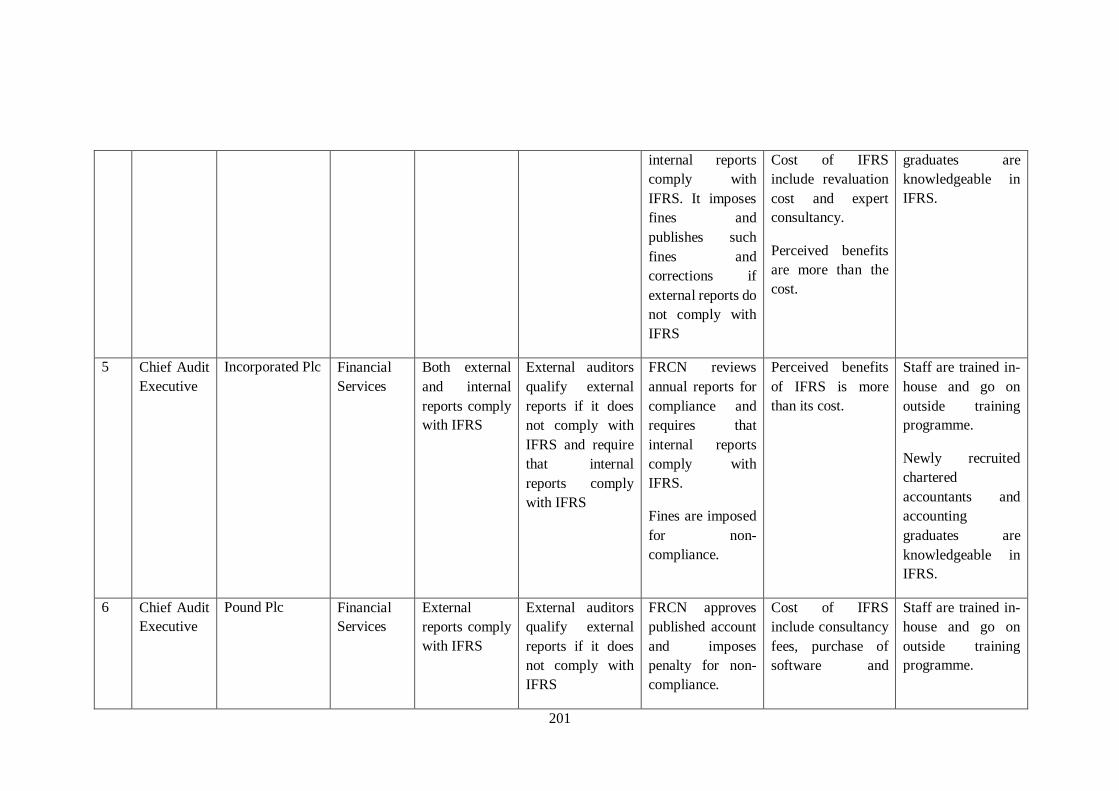

1.1.1.3 Summary of findings

IFRS is substantively adopted by the Nigerian listed firms. This outcome is facilitated by

the creation of the FRCN, the reform of professional accountancy education and other

institutionalising agents at the three levels of social order. At the macro level, the World

Bank exerts coercive pressure on the Nigerian government by making IFRS adoption a

requirement for access to future grants and investments in the country. Coupled with the

desire by the Nigerian government to improve the outlook of the country’s accounting

4

environment, following the capital market crisis in the country in 2008, the FRCN was

established in 2011. The FRCN and the ICAN are the institutionalising agents at the

meso level. The FRCN exerts coercive isomorphic pressures on external auditors and

directly conducts annual review of companies’ reports to ensure that audited reports

comply with IFRS. The ICAN exerts normative isomorphic pressure on companies

through the training of chartered accountants and accounting graduates in line with IFRS.

At the micro level, the board of directors and internal auditors are the agents responsible

for institutionalising IFRS by ensuring that IFRS is used for internal reporting. Other

agents at this level are the cost-benefit of non-compliance with IFRS for internal reporting

and the pressure exerted by a parent company on a Nigerian subsidiary to ensure that their

internal reports comply with IFRS alongside other members of the group.

1.1.2 IFRS, Enforcement and Accounting Quality

IFRS, according to the IASB, is a high-quality accounting standard that will improve

accounting quality once adopted by countries. This assertion has been tested by many

studies in different jurisdictions across the globe (e.g., Barth, Landsman and Lang, 2008;

Ahmed, Neel and Wang, 2013; Cai, Rahman and Courtenay, 2014; Zeghal, Chtourou and

Fourati, 2012; Capkun, Collins and Jeanjean, 2016), which has generated a large pool of

mixed results (Brüggemann, Hitz and Sellhorn, 2013). However, recent arguments by

Christensen, Lee, Walker and Zeng (2015) show that the enforcement of accounting

standards rather than the adoption of IFRS is a better explanation for a higher accounting

quality for mandatory IFRS adopters. Similarly, Capkun et al. (2016) observe that

amendments made to IFRS in 2005 increased the flexibility of IFRS, thereby making the

‘high-quality’ accounting standard to reduce accounting quality rather than improve it.

While cross-country analyses have been criticised for generalising findings

beyond homogeneous settings, Leuz and Wysocki (2016) and De George, Lee and

Shivakumar (2016) recently called for more single-country studies to unveil new insights.

Nigeria is one unique setting to examine the true impact (negative or positive) of IFRS.

This is because the enforcement of accounting standard, through the establishment of the

FRCN, was made a year before IFRS adoption, which provides the opportunity to separate

the effect of IFRS on accounting quality from the effect of enforcement on accounting

quality.

To this end, the objective of the third chapter of this thesis is to disentangle the

impact of enforcement and IFRS adoption on accounting quality in Nigeria. To address

5

this objective, three dimensions of accounting quality are examined. These dimensions

are earnings management, timely loss recognition and earnings persistence.

1.1.2.1 Research questions

The following research questions are answered to address the research objective above:

a) What is the effect of IFRS adoption on earnings management following market

failure in Nigeria?

b) What is the effect of the establishment of the FRCN to enforce accounting

standards on earnings management following market failure in Nigeria?

c) What is the effect of IFRS adoption on timely loss recognition following market

failure in Nigeria?

d) What is the effect of the establishment of the FRCN to enforce accounting

standards on timely loss recognition following market failure in Nigeria?

e) What is the effect of IFRS adoption on earnings persistence following market

failure in Nigeria?

1.1.2.2 Research method

The hypotheses developed in this part of the study were tested using various multivariate

regression techniques. Hand-collected panel data were sourced from annual reports of the

listed Nigerian firms. For the earnings management models, fixed-effect regression was

used to test the hypotheses. A binary logistic regression model developed by Lang, Raedy

and Wilson (2005) was used to test the hypotheses related to timely loss recognition,

while a generalised method of moment model was used in testing the hypothesis related

to earnings persistence.

1.1.2.3 Summary of findings

The study finds that IFRS increases earnings management and reduces timely loss

recognition and earnings persistence of the Nigerian listed firms. This result implies that

IFRS reduces accounting quality of the Nigerian listed firms. On the contrary,

enforcement reduces earnings management and increases timely loss recognition of the

Nigerian listed firms. Overall, the study finds that although IFRS and enforcement were

part of the same accounting regulation bundle, aimed at improving accounting quality in

Nigeria, the two regulatory mechanisms have different effects on accounting quality. The

finding is robust to alternative accounting quality proxies and several control variables.

The study employed public accountability model of accounting regulation (Tower, 1993)

to illuminate the effect of the two regulatory mechanisms on accounting quality.

6

1.1.3 IFRS, Enforcement and Capital Market Outcomes

The IASB has attached numerous capital market benefits to IFRS adoption. These

benefits include increased Foreign Direct Investment (FDI) flow, lower cost of capital,

higher market liquidity, and higher value relevance of accounting numbers among others.

While many studies (Daske, Hail, Leuz and Verdi, 2008; 2013; Florou and Pope, 2012;

Christensen et al., 2013; Florou and Kosi, 2015) have found a positive relationship

between IFRS adoption and the aforementioned capital market benefits, they have linked

these results to the underlying characteristics of the study areas. These characteristics

include the extent of divergence of a country’s local GAAP2 from IFRS (Florou and Pope,

2012, Florou and Kosi, 2015), the quality of investor protection and rule of law (Daske et

al., 2008), and the quality of enforcement mechanisms (Florou and Pope, 2012;

Christensen et al., 2013). Furthermore, Hail and Leuz (2006) show that cost of capital

varies from one country to the other based on the degree of enforcement, security

regulation, and the extent of disclosure. Similarly, Nnadi and Soobaroyen (2015) find that

improvement in the rule of law and a reduction in the level of corruption are the important

explanatory factors for an increase in FDI in African countries.

Given the above findings, it can be concluded that the impact of IFRS on capital

market outcomes needs further exploration in order to ascertain whether the adoption of

IFRS alone without these supporting infrastructures (enforcement, the rule of law and the

degree of divergence of GAAP from IFRS) is sufficient to have positive capital market

outcomes More importantly, understanding the effect of IFRS on capital market requires

a setting with fewer of these cofounding variables (supporting infrastructure) or where

their effects can be separated.

Nigeria is a unique setting for exploring this issue because it has fewer of the

cofounding variables. Nigeria has a weak rule of law, investor protection is low, and there

is a low divergence of the Nigerian GAAP from IFRS. These characteristics make it

possible to largely isolate the effect of IFRS on capital market outcomes from other

possible explanations. Furthermore, the effect of enforcement on capital market outcome

can be separated from the effect of IFRS, since the FRCN was established in 2011 while

IFRS was adopted in 2012.

The fourth chapter of this study, therefore, explores the impact of IFRS adoption

and enforcement on market liquidity in Nigeria. Market liquidity is the choice of capital

market outcome examined in this study because data is not available for examining the

2 Generally Accepted Accounting Principles

7

cost of capital and the value-relevance argument does not have a justifiable theoretical

underpinning (Christensen et al., 2013).

1.1.3.1 Research questions

The following research questions are answered to fulfil the objective of this chapter:

i) Does IFRS adoption increase the market liquidity of Nigerian listed

companies?

ii) Does the establishment of the FRCN to enforce accounting standards increase

the stock market liquidity of Nigerian listed firms?

1.1.3.2 Research methods

Panel data for chapter four of this thesis was hand collected from ‘African markets’3 and

the Nigerian Stock Exchange archives. Fixed-effect and random-effect regression models

were run to test the hypotheses of this chapter. Three proxies were adopted as the

measurements for market liquidity. These proxies are the bid-ask spread, trade volume

and the proportion of zero daily returns (Chai, Faff and Gharghori, 2010).

1.1.3.3 Summary of findings

Both IFRS adoption and enforcement (establishment of the FRCN) were found to

significantly increase market liquidity of Nigerian listed firms. The findings are robust to

several control variables, including corporate governance variables. Furthermore, the

unique setting of Nigeria makes it possible to use the signalling theory to illuminate the

study. This is so because the two regulatory mechanisms were adopted following the 2008

market crisis in Nigeria, which was caused by accounting irregularities and opaque

information environment. Thus, the regulatory mechanisms were attempts to signal to

both foreign and local investors that the information environment had improved, and

accounting irregularities have been curtailed.

1.2 Epistemological and Ontological Considerations

Epistemology is all about what is considered acceptable knowledge in a particular

discipline (Bryman, 2012). In social sciences, the argument is often between whether the

social world can be studied with reference to the principles, techniques, and procedures

used in the natural science or by adopting a different standpoint.

Positivism is an epistemological position that assumes the principles and

procedures in the natural science can be used in studying the social world (Snape and

3 A website, hosting market data of African stock markets.

8

Spencer, 2003). Positivism assumes that only phenomena that can be confirmed by the

senses can be genuinely considered knowledge. In positivism, hypotheses are generated

from a theory, which are tested to prove or disprove the theory (i.e., deductive approach).

Alternatively, theories can be generated by gathering and analysing data from the field

(i.e., inductive approach). Furthermore, scientific inquiries must be objective, that is, free

from the researcher’s influence.

Interpretivism is the opposite of positivism. It assumes that the social science is

different from the natural science as its subjects - people and institutions - are different

from the natural science’s subjects. Interpretivism disregards the existence of a single

truth that could be uncovered by scientific procedures. In contrast, it aims to “grasp the

subjective meaning of social action” (Bryman, 2012, p. 30) by interpreting the social

actions from the actors’ view point. Interpretivism involves three levels of interpretation.

Firstly, the actors interpret the situation. Secondly, their interpretations are interpreted by

the researcher while collecting the data. Thirdly, the researcher interprets his findings

within a theoretical frame, a conceptual frame, and the literature within a discipline.

Realism is the third epistemological philosophy that balances between positivism

and interpretivism. According to the realist, like the positivist, there exist a reality that is

independent of the researcher, which he or she tries to unveil. Realism can be naïve

realism (i.e., empirical realism) or critical realism (Easton, 2010; Bryman, 2012). The

naïve realist espouse that such reality can be readily accessed and that our description of

reality is reality itself. Critical realists assume that our construction of reality only

facilitates our understanding of the reality but not reality itself. The crux of critical realism

is causal explanation (Easton, 2010). Unlike positivism that assumes that the occurrence

of events in a regular pattern implies causality, and interpretivism that does not attempt

to discern into causality but merely interprets it (Easton, 2012), critical realists move

further to explain the causal mechanism(s) of events by paying special attention to the

context (Bryman, 2012).

Ontology refers to how social entities and social actors and their relationships are

perceived. Ontological traditions can either be objectivism or constructionism.

Objectivism assumes that social entities are independent of social actors. They are

external realities or facts that can neither be constructed nor influenced by social actors.

For example, an organisation has a set of rules and codes that individuals working in it

must abide by. Objectivism assumes that such rules and codes exert influence on the

workers who do not have influence in the construction of the rules and their application.

On the other hand, constructionism asserts that social entities and their meanings are not

9

just constructed by social actors but are also constantly being revised by them. Hence, in

organisations, rules are not independent of social actors but are constructed, interpreted,

and often revised by them to suit various social contexts. Objectivism is a feature of

epistemological tradition of positivism while constructionism is a feature of

interpretivism (Bryman, 2012).

In this study, both objectivism and interpretivism are adopted. Specifically,

chapter two uses interpretivism while chapters three and four use positivism. The reasons

for adopting these two philosophies is that chapter two examines the processes by which

IFRS has become institutionalised in Nigerian listed firms. This is done by collecting data

from interviewees based on their interpretations, which is further interpreted by the

researcher within the theoretical framing of neo-institutional theory. Chapters three and

four investigate the impact of accounting regulation (IFRS adoption and enforcement) on

accounting quality and market liquidity respectively in Nigeria. Hypotheses were

developed to test the public accountability model of accounting regulation and signalling

theory in chapters three and four, respectively. Thus, the two chapters follow the

epistemological position of positivism.

The study adopts multiple theoretical framings since a single theory cannot

capture all the objectives of the study. Chapter 2 examine the how IFRS institutionalised,

the influence of the reform of other accounting infrastructure in the institutionalisation

process and the outcome of the process. The Dillard et al.’s (2004) model of

institutionalisation theory is used to illuminate the institutionalisation process. According

to the theory, organisations face different isomorphic pressure to comply with societal

expectations at different levels. The overarching norm (institution) is created at the social,

political and economic level which is then transferred to the organisational field by

actors/agent. From the organisational field, the norm is further transferred to the

organisational level at which the outcome of the institutionalisation process is determined.

The successful institutionalisation of the norm at each level is dependent on the relative

power/influence of the actors at each level.

In Chapter 3, the public accountability model of accounting regulation is used to

theorise the expected impact of IFRS adoption and the enforcement of accounting

standards on accounting quality. The theoretical faming provides a more nuanced link

between accounting reform and accounting quality as perceived by multiple stakeholders.

The theory suggests that the essence of accounting reform is to bring about public

accountability to all stakeholders that have legitimate interests in an organisation. Based

on this theory, it is expected that IFRS adoption and the enforcement of accounting

10

standards should improve various dimensions of accounting quality that are relevant to

different stakeholders. For example, lower earnings management is relevant for

regulators, the government, investors and creditors. Similarly, timely loss recognition is

relevant to creditors.

In Chapter 4, signalling theory is used to argue that after the Nigerian capital

market crisis, the adoption of IFRS and the establishment of the FRCN, as recommended

by the World Bank, are used as signals by the Nigerian government to the investors of a

better reporting regime and more transparent information environment in Nigeria. It is

expected that the signals will stimulate a positive response, through higher market

liquidity, from both internal and external investors who had initially renounced trading in

the Nigerian capital market.

1.3 Contributions of the Study

This study makes several contributions to theory and practice. Contrary to the findings

that the outcome of the institutionalisation of IFRS in most developing countries is

symbolic, chapter two shows that the establishment of an effective enforcement

institution with well-developed strategies will ensure substantive adoption of IFRS. The

chapter also contributes to theory by showing that the institutionalisation of IFRS follows

three levels of social order as posited by Dillard et al. (2004). This is the first study as far

as the researcher knows that uses the Dillard et al.’s (2004) model of institutional theory

to showcase the institutionalisation of IFRS at three levels of social order. Through this

theory, the researcher finds that there are important strategies employed by the agent(s)

at each level of social order to ensure IFRS is substantively adopted at the organisational

level. Subsequent studies can adopt this rich theoretical framing in IFRS-related studies.

Chapter three contributes to the literature in several ways. Firstly, contrary to the

findings of Kim (2016) that enforcement without IFRS does not improve accounting

quality, the researcher finds that enforcement and IFRS have different effects on

accounting quality in Nigeria. Specifically, IFRS reduces accounting quality while

enforcement increases it. Secondly, contrary to the findings of Nnadi and Soobaroyen

(2015), the researcher finds that socio-political factors (e.g., rule of law and investor

protection) do not have to change to have an improvement in accounting quality. The

establishment of an independent enforcement institution (e.g., the FRCN in Nigeria) is

sufficient to have improvements in accounting quality. Thirdly, contrary to the findings

of Cai et al. (2014) that IFRS adoption has an insignificant effect on earnings management

in countries whose national standards have low divergence from IFRS, the researcher

11

finds that despite the low divergence of the Nigerian GAAP from IFRS, the latter is found

to significantly reduce accounting quality. Fourthly, the chapter explores a theoretical link

– public accountability model of accounting regulation – between accounting regulation

and accounting quality. This theory predicts that accounting regulation is needed to

ensure public accountability to all relevant stakeholders. The theory gives a more nuanced

explanation of why accounting regulation is needed by showing that accounting

regulation is needed for informational equity and efficiency. This theory can be explored

by future research in accounting regulation.

The last empirical chapter also finds that sociopolitical variables like the rule of

law and investor protection, as argued by Daske et al. (2008) and Nnadi and Soobaroyen

(2015), may not necessarily improve to have an increase in market liquidity. For a

developing country with weak accounting standard and enforcement institution, adopting

IFRS and establishing a capable enforcement institution are important steps to realizing

improvements in the capital market. Furthermore, contrary to the argument of Christensen

et al. (2013) that enforcement is the major explanatory variable for increased market

liquidity in many countries that adopted IFRS, the situation in Nigeria, with opaque

information environment, is different. IFRS adoption has a significant effect in reducing

information asymmetry alongside the enforcement by the FRCN. The study uses

signaling theory to illuminate the impact of IFRS adoption and enforcement on market

liquidity by exploring the unique nature of the Nigerian setting. IFRS adoption and

enforcement were signals to the capital market that the Nigerian accounting information

environment has improved after the 2008 market crisis. This theory creates a more

nuanced theoretical link among IFRS adoption, enforcement, and market liquidity. This

theory can be employed in similar contexts to Nigeria, especially after a market crisis, to

unveil new insights.

1.4 Structure of the Thesis

This thesis is divided into five chapters, of which three are empirical chapters. The first

chapter is an introduction to the whole study, charting out its aims and approaches.

Chapters 2, 3 and 4 are empirical chapters that explore the issues discussed under the

background to the study. Each of these chapters is structured into sections exploring the

introduction and problem statement of the chapter, literature review (conceptual and

empirical review), research methods and data analysis, and conclusion. Chapter 5

concludes the whole thesis, makes recommendations, and provides future research areas

that may be explored.

12

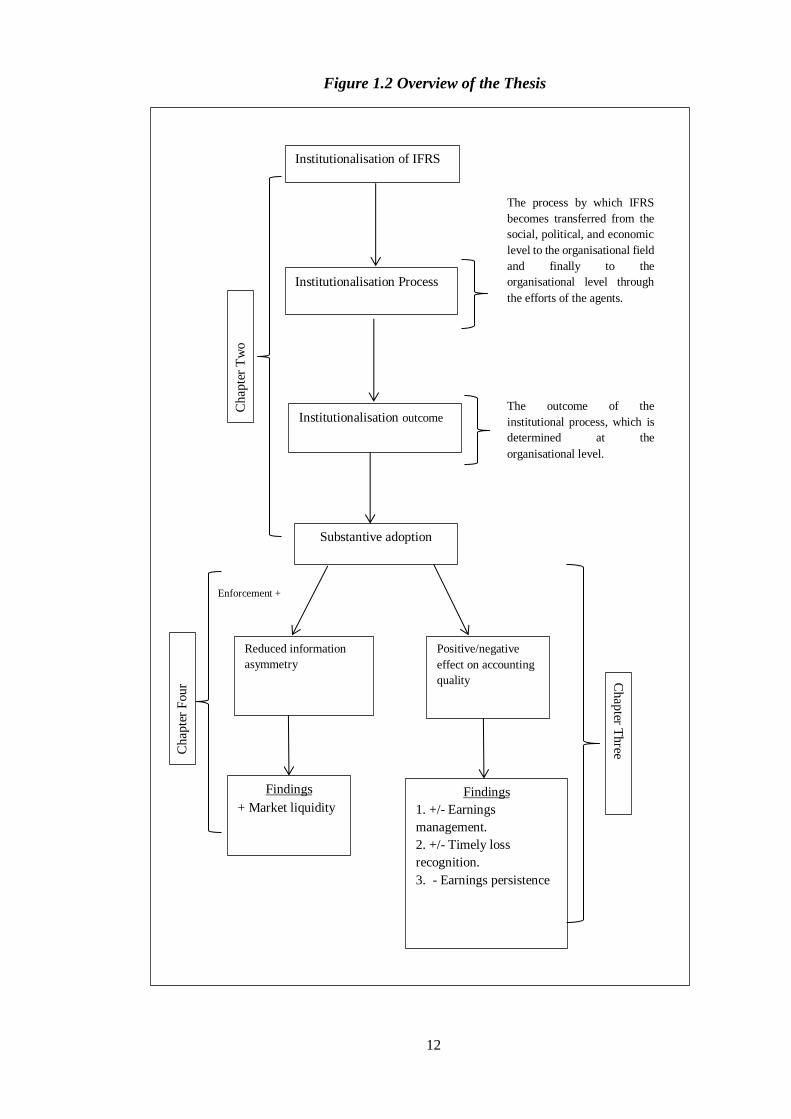

Figure 1.2 Overview of the Thesis

+ Enforcement

Institutionalisation of IFRS

Institutionalisation Process

Substantive adoption

Institutionalisation outcome

Reduced information

asymmetry

Findings

1. +/- Earnings

management.

2. +/- Timely loss

recognition.

3. - Earnings persistence

Findings

+ Market liquidity

Positive/negative

effect on accounting

quality

The process by which IFRS

becomes transferred from the

social, political, and economic

level to the organisational field

and finally to the

organisational level through

the efforts of the agents.

The outcome of the

institutional process, which is

determined at the

organisational level.

Enforcement +

Chap

ter

Tw

o

Ch

apte

r F

ou

r Ch

apter T

hree

13

Chapter 2

The Institutionalisation of IFRS in Nigeria

2.1 Introduction

Financial reporting practices vary markedly across jurisdictions. Among the factors

leading to this variation are economic systems, legal systems, taxation systems, and the

mode of financing (Haller and Walton, 2003; Roberts, Weetman and Gordon, 2008;

Nobes and Parker, 2016). The development of multinational corporations, the spread of

trade liberalisation, and most importantly, the Asian financial crisis of 1997 have led to

the call for the use of high-quality accounting standards across developed and developing

countries (Zeff, 2012).

A strong financial reporting system is dependent on interconnected socio-political

and economic infrastructures such as the adequacy of the rule of law, enforcement quality,

quality of accounting standards, and capital market quality. With the spread of IFRS

across jurisdictions with different accounting infrastructures (i.e., weak and strong),

several studies (Chand, 2005; Zeff, 2012; Perera, 2012; Albu, Albu and Alexander, 2014;

Hopper, Lassou and Soobaroyen, 2017) have questioned whether IFRS is really adopted

to bring about the acclaimed benefits often ascribed to it by the IASB. Specifically, IFRS

adoption by developing economies is perceived by several studies to be symbolic, as a

mere legitimation strategy lacking proper commitment, because they lack necessary

infrastructures (e.g., enforcement institution and developed capital market) to realise the

potentials of IFRS (Mir and Rahaman, 2005; Chand, 2005; Carneiro, Rodrigues and

Craig, 2017). Their adoption of IFRS is often a response to external pressure from the

World Bank and IMF (Irvine, 2008; Albu and Albu, 2012; Hassan, Rankin and Lu, 2014).

However, in some developing countries including Nigeria, there have been

substantial efforts made to build some supporting infrastructures (e.g., the establishment

of the Financial Reporting Council of Nigeria and the reform of professional accounting

education) to ensure that the adoption of IFRS is substantive. While not all supporting

infrastructures have been overhauled4, it would be interesting to investigate whether the

reforms made are significant in ensuring substantive adoption of IFRS by Nigerian

companies. The result of this inquiry is particularly important for policy making, not only

in Nigeria but also in other developing countries, as a possible model to be adopted as a

part of a longer-term plan of reforming other supporting infrastructures.

4 For example, the rule of law is still weak and corruption is still very high.

14

2.1 Statement of the Problem

The establishment of an enforcement institution and the reform of professional

accounting bodies in many developing countries involve substantial costs and efforts. For

example, the World Bank gave a grant of $200,000 to the Bangladeshi Government in

1999 to enhance the institutional capacity of the Institute of Chartered Accountants of

Bangladesh (Mir and Rahaman, 2005). Similarly, in Nigeria, the World Bank gave a grant

of $485,0005 to reform the institutional capacity of the Institute of Chartered Accountants

of Nigeria. Listed Nigerian firms and registered professionals that are connected with the

preparation of financial statements also pay annual subscriptions to the FRCN.

Furthermore, the staff of the FRCN are public officers that are paid salary and pension by

the Nigerian government. These costs are enormous and can be channelled to alternative

productive uses if the purpose for all these reforms are not achieved. Thus, are these

reforms meeting the purpose for which they have been made (i.e., substantive adoption

of IFRS)? This is an important question that needs to be answered.

The reliability of financial statement, as being a true reflection of the summary of

the day to day business transactions of a firm, is dependent on the reliability of the

underlying data and structure (e.g., internal control). ‘IFRS-based’ financial statements

can only be deemed to be IFRS-based if IFRS data forms part of the daily routine of the

business. This means that IFRS data such as fair value, impairment test of assets, and

value-in-use are captured by the accounting system, and structures (e.g., effective internal

control system) are in place to ensure IFRSs are complied with (Wilford, 2016).

Ultimately, internal reports to the management must reflect IFRS information (PwC,

2004). If these structures are not in place in a firm, any IFRS-based financial statement

from such firm will not be reliable. A workaround approach, where IFRS information is

captured at one point in time (usually at year end), is usually adopted by such firms in

preparing IFRS-based statements. Whereas such approach shows that IFRS is not

integrated into the accounting system of the company. The consequence of this is that any

decision made based on such financial statement may be misleading.

This study aims to address the issues related to the institutionalisation of IFRS

across the three levels of social order in Nigeria and examine the outcome of the process.

The objectives of the study and related research questions are stated below.

5 Nigeria: P121511 - Capacity Strengthening of ICAN to Support National and Regional Accountancy

Development, IDF Grant No. TF097436. Available at

http://projects.worldbank.org/procurement/noticeoverview?id=OP00017093&lang=en&print=Y

15

2.3 Objective of the Study

The objective of this study is to examine the process of institutionalising IFRS in Nigeria

across the three levels of social order, and the role played by the establishment of the

FRCN and the professional accounting education reform. Secondly, the study will also

examine whether these reforms lead to substantive adoption of IFRS by Nigerian listed

firms (i.e., whether it is used for internal reporting). These research objectives are

achieved by answering the following research questions:

i) Who are the agents and what type of isomorphic pressure do they exert at the

macro level to institutionalise IFRS?

ii) Who are the agents and what type of isomorphic pressure do they exert at the

meso level to institutionalise IFRS?

iii) Is IFRS substantively adopted (used for internal reporting) by Nigerian firms?

iv) Who are the agents and what type of isomorphic pressure do they exert at the

micro level to institutionalise IFRS?

2.4 Significance of the Study

This is the first study, as far as the researcher is aware, that investigates whether IFRS is

substantively adopted (when used for internal reporting) and if so, the processes leading

to its substantive adoption in a developing country context (i.e., Nigeria).

Although some recent studies on the institutionalisation of IFRS in developing

countries have been conducted, much of these studies (e.g., Mir and Rahaman, 2005;

Irvine, 2008; Albu and Albu, 2012; Albu et al., 2014; Mantzari, Sigalas and Hines, 2017)

have concentrated on the outcome of institutionalisation rather than the process. The

process of institutionalisation is a corollary to its outcome, so it is important to examine

the procedures that lead to the outcome in order to make informed policies. Secondly,

most studies have focused on the symbolic adoption of IFRS in developing countries,

while this study focuses on how the reform of accounting infrastructures may lead to

substantive adoption of IFRS in Nigeria.

2.5 Contextual Framework

2.5.1 Accounting development in Nigeria

The institutionalisation of IFRS in Nigeria becomes more comprehensible if the historical

background of accounting practice in Nigeria is explored. Modern accounting in Nigeria

was a British import through the colonisation of the country. The halt, after more than

300 years, in slave trade and the subsequent growth in agricultural produce led to the

ceding of Lagos in 1861 by the then Oba (king) Dosunmu (Wallace, 1992). This transition

16

informed the need for the modern practice of accounting to cope with the new form of

trade. In 1905, Charles Ernest Dale, the first qualified accountant (Incorporated

Accountant6) arrived in Nigeria as the financial commissioner and treasurer to the

colonial government. While the British government laid down no infrastructure for the

development and sustainability of modern accounting practices in Nigeria, the agitation

for self-rule towards 1957 affected the accounting profession as well. The Companies

Ordinance of 1922 provided that registered companies prepare balance sheets, which

must be audited by auditors approved by a supervising Minister. Approved auditor status

was based on the possession of a practicing certificate issued by the professional

accountancy bodies in the UK or serving in the government audit department for not less

than 15 years and having passed the intermediate level of the examinations of the UK

accountancy bodies. Obviously, many Nigerians did not have these opportunities and

were relegated to performing routine jobs as clerks or some other office duties (Wallace,

1992).

The first qualified accountant in Nigeria was Mr Benjamin Bankole Akinpelu

Osundiya (Wallace 1992). He qualified with the London Corporation of Accountants and

the Association of Certified Accountants in 1928 and 1929 respectively. However, till his

death in 1957, he was neither employed as an accountant nor recognised as an approved

auditor. As at independence in 1960, there were 41 indigenous qualified accountants in

Nigeria. The composition of their professional bodies is as follows:

Cost and Work Accountants 3

Municipal Treasurers and Accountants 1

Certified Accountants 22

Chartered Accountants 15

There was a surge in the growth of expatriate firms with the “coming of

development plans and political independence in the 1950s and 1960s” (Wallace, 1992,

p. 30), as Nigerians were not recruited as accountants and the qualified accountants

amongst them were also limited in number. The expatriate firms initially worked over a

short cycle with a partner coming to Nigeria for short-term audits. But as businesses grew,

there was a need to have local offices in Nigeria. The first of such transnational audit

firms to come to Nigeria was Lewis and Mounsey & Co (LMC) in 1905 (Wallace, 1992).

LMC was short-lived as the firm mainly served the tin mining companies. Thus, following

6 The Society of Accountants was founded in England in 1885, became Society of Incorporated Accountants

and Auditors in 1908 through 1954 and Society of Incorporated Accountants from 1954 to 1957. It

eventually merged with ICAEW in 1957.

17

the decline in tin mining alongside the appointment of supervising agents and internal

auditors (including chartered accountants) by businesses, there was less need for LMC’s

expertise. The West African Services offered accounting services (such as bookkeeping

and internal audit services) to businesses whose owners were not in Nigeria. West African

Services was acquired by Cassleton Elliot in 1929 following the latter’s appointment as

the auditor of Amalgamated Tin Mines of Nigeria in 1928. In 1949, Pannell, Crewson

and Hardy (now Pannell Kerr Forster- PKF) and Midgley, Snelling and Barnes opened

offices in Nigeria, while Cooper Brothers & Co came in 1953. It is worth mentioning that

none of these accountancy firms appointed a Nigerian as a partner in their firms up to

1966. With these “extra territorial” (Wallace, 1992) firms obviously in charge of

accountancy and audit practices in Nigeria, it will not be inconceivable to say that many

qualified Nigerian accountants experienced difficulty in getting audit jobs.

In 1957, Nigerians and expatriates that were members of the ACCA (Associate

Certified and Corporate Accountants) formed a local branch of the professional

accountancy body and they gained recognition of the UK body in 1960. But the

sustainability of the new body suffered from the same little recognition the mother body

suffered in the UK. Thus, as suggestions were raised to bring all qualified Nigerians under

one local umbrella body, the ACCA members gladly embraced the idea. In 1959, the

Association of Accountants of Nigeria was formed to include both qualified Nigerians

and expatriates across all professional accountancy bodies in existence in the UK. The

association followed the Institute of Chartered Accountants of England and Wales

(ICAEW) structure in all ramifications including examinations, codes of conduct for

members, and the use of the designation ‘Chartered Accountant’ (Wallace, 1990).

However, this move was non-consensual because expatriates and Nigerians that were

qualified chartered accountants with ICAEW were unhappy because of the possible

“dilution of the notion of chartered accountancy which might arise from admission of

accountants who were not trained as chartered accountants and the prospect of being

disadvantaged in the Nigerian market for auditing services which permitted easy access

to non-Nigerian (especially British) chartered accountants” (Wallace, 1992, p. 36).

Following this opposition, they sought to establish a rival body - the Institute of Chartered

Accountants of Nigeria (ICAN) - comprising of qualified Nigerians with the ICAEW.

Subsequently, ICAN absorbed the members of the Association of Accountants of Nigeria.

18

In 1965, the Nigerian Parliament passed the ICAN Act with relative ease for three

major reasons. Firstly, the founders7 of ICAN were known for their integrity and

independence. Secondly, a desire to develop local capacity in sustaining independence,

and thirdly, the notion that Nigerian accountants were capable of establishing a viable

accountancy profession.

The ICAN Act of 1965 gave a number of privileges to the Institute, which led to

some internal struggles between ICAN and some other accounting bodies that perceived

such privileges as a basis for ICAN’s monopoly of the accounting profession in Nigeria.

“Up until the enactment of the ICAN Act, no organisation had the duty of regulating the

accounting and auditing profession. Under the Companies Ordinance of 1922 anybody

could act as an auditor to a company” (Uche, 2002, p. 480) except employees of the

companies. However, the ICAN Act made only ICAN members appointable as auditors

of companies in Nigeria as well as the control of education, training and certification of

chartered accountants (Wallace, 1992). As a result of the monopoly of audit assignments

that ICAN members now enjoy, many other Nigerians decided to join ICAN to enjoy the

privilege together. However, some Nigerians of other accounting bodies that have no

recognition by the international accounting bodies were not qualified for the membership

of ICAN. These unrecognised bodies included the Association of International

Accountants (AIA); The Society of Company and Commercial Accountants and; the

British Association of Accountants and Auditors. The Nigeria Society of International

Accountants (SIA), which comprised of the members of the Association of International

Accountants of Nigeria, became a major threat to ICAN monopoly since their members

were not admissible by ICAN. In 1972, the SIA wrote a petition to the Nigerian

government demanding that the ICAN Act be modified to accept members of the SIA.

ICAN swiftly responded to the petition arguing that such move would make “accountancy

qualification obtainable in Nigeria [to] be considered inferior to that of any other country”

(Anibaba, 1990, p. 150). Again, the plan to join ICAN by the SIA was thwarted by

ICAN’s rejoinder. After several failed attempts of persuasive efforts to join ICAN or

make the Nigerian government amend the ICAN Act, the SIA “spearheaded the formation

of a wider accounting body named the Association of National Accountants of Nigeria

(ANAN)” in 1979 (Uche, 2002, p. 484).

ANAN members began a major push for the recognition of their association under

the guise that the number of chartered accountants produced by ICAN was extremely

7 These are Akintola Williams, F. C. O. Coker, Z. O. Ososanya and E. A. Osindero

19

below what the country needed for its increasing growth. Although this argument was

true, ICAN devised several strategies to forestall the recognition of ANAN by the

Nigerian government. The signing of the ANAN Decree8 (1993) by the then Head of

State, General Ibrahim Badamosi Babangida, brought an end to ICAN’s monopoly. The

duties assigned to ANAN are similar to the statutory duties of ICAN. Section 1 of the

ANAN Act highlights the duties of the body as follows: (a) advancing the science of

accountancy (in this Act referred to as ‘the Profession’); (b) determining the standards of

knowledge and skill, to be attained by persons seeking to become registered members of

the profession and reviewing those standards, from time to time as circumstance may

require; (c) promoting the highest standard of competence, practice and conduct among

the members of the profession; (d) securing, in accordance with the provisions of this Act,

the establishment and maintenance of register of members of the profession and the

publication, from time to time, of lists of these persons; (e) doing such things as may

advance and promote the advancement of the profession of accountancy in both the public

and private sector of the economy; and (f) performing through the Council established

under section 3 of this Act, the functions conferred on it by this Act”.

Despite the statutory duties of ANAN being similar to the statutory duties of

ICAN, the hegemony over the Nigerian accounting profession is still maintained by

ICAN. ICAN has enjoyed international recognition as the major accounting professional

body in Nigeria9. Furthermore, only ICAN members can audit listed companies on the

Nigerian Stock Exchange (NSE).

2.5.2 The Nigerian Accounting Standards Board

The NASB was established by ICAN in 1982 and became a Federal Government

parastatal in 199210. The NASB was charged with setting and monitoring compliance

with accounting standards in Nigeria. The board of the NASB comprised:

i. A chairman who shall be a professional accountant with considerable

professional experience in accounting practice.

ii. Two representatives each of the following: Institute of Chartered

Accountants of Nigeria; Association of National Accountants of Nigeria;

8 Now ANAN Act (1993) 9 The International Federation of Accountants (IFAC) had recognised ICAN since 1977 as one of the

founding members (https://www.ifac.org/about-ifac/membership/members/institute-chartered-

accountants-nigeria), while ANAN was only admitted in 2014 (https://www.ifac.org/about-

ifac/membership/members/association-national-accountants-nigeria) 10 Under the then Federal Ministry of Trade and tourism (now Federal Ministry of Industry, Trade &

Investment).

20

iii. A representative each of the following: Federal Ministry Commerce;

Federal Ministry of Finance; Central Bank of Nigeria; Corporate Affairs

Commission; Federal Inland Revenue Service; Nigerian Deposit

Insurance Corporation; Securities and Exchange Commission; Accountant

General of the Federation; Auditor General for the Federation; Chartered

Institute of Taxation of Nigeria; Nigerian Accounting Association;

Nigerian Association of Chambers of Commerce, Industries, Mines and

Agriculture; and

iv. The Executive Secretary of the Board

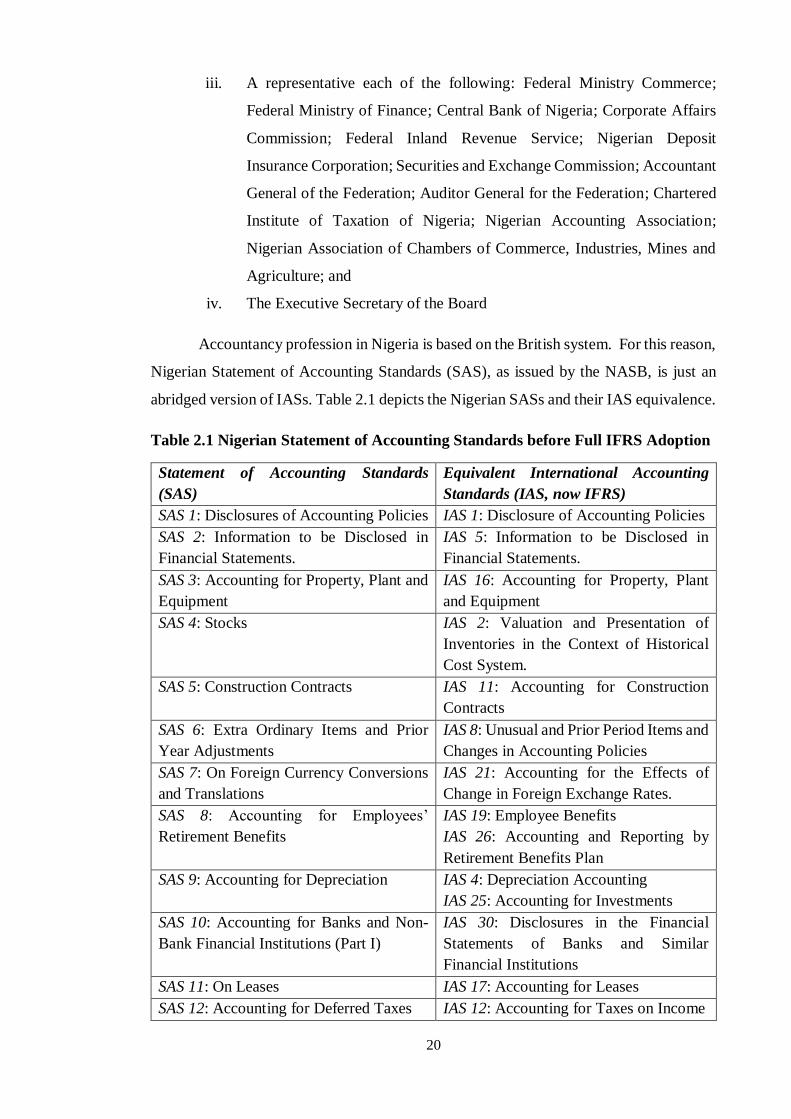

Accountancy profession in Nigeria is based on the British system. For this reason,

Nigerian Statement of Accounting Standards (SAS), as issued by the NASB, is just an

abridged version of IASs. Table 2.1 depicts the Nigerian SASs and their IAS equivalence.

Table 2.1 Nigerian Statement of Accounting Standards before Full IFRS Adoption

Statement of Accounting Standards

(SAS)

Equivalent International Accounting

Standards (IAS, now IFRS)

SAS 1: Disclosures of Accounting Policies IAS 1: Disclosure of Accounting Policies

SAS 2: Information to be Disclosed in

Financial Statements.

IAS 5: Information to be Disclosed in

Financial Statements.

SAS 3: Accounting for Property, Plant and

Equipment

IAS 16: Accounting for Property, Plant

and Equipment

SAS 4: Stocks IAS 2: Valuation and Presentation of

Inventories in the Context of Historical

Cost System.

SAS 5: Construction Contracts IAS 11: Accounting for Construction

Contracts

SAS 6: Extra Ordinary Items and Prior

Year Adjustments

IAS 8: Unusual and Prior Period Items and

Changes in Accounting Policies

SAS 7: On Foreign Currency Conversions

and Translations

IAS 21: Accounting for the Effects of

Change in Foreign Exchange Rates.

SAS 8: Accounting for Employees’

Retirement Benefits

IAS 19: Employee Benefits

IAS 26: Accounting and Reporting by

Retirement Benefits Plan

SAS 9: Accounting for Depreciation IAS 4: Depreciation Accounting

IAS 25: Accounting for Investments

SAS 10: Accounting for Banks and Non-

Bank Financial Institutions (Part I)

IAS 30: Disclosures in the Financial

Statements of Banks and Similar

Financial Institutions

SAS 11: On Leases IAS 17: Accounting for Leases

SAS 12: Accounting for Deferred Taxes IAS 12: Accounting for Taxes on Income

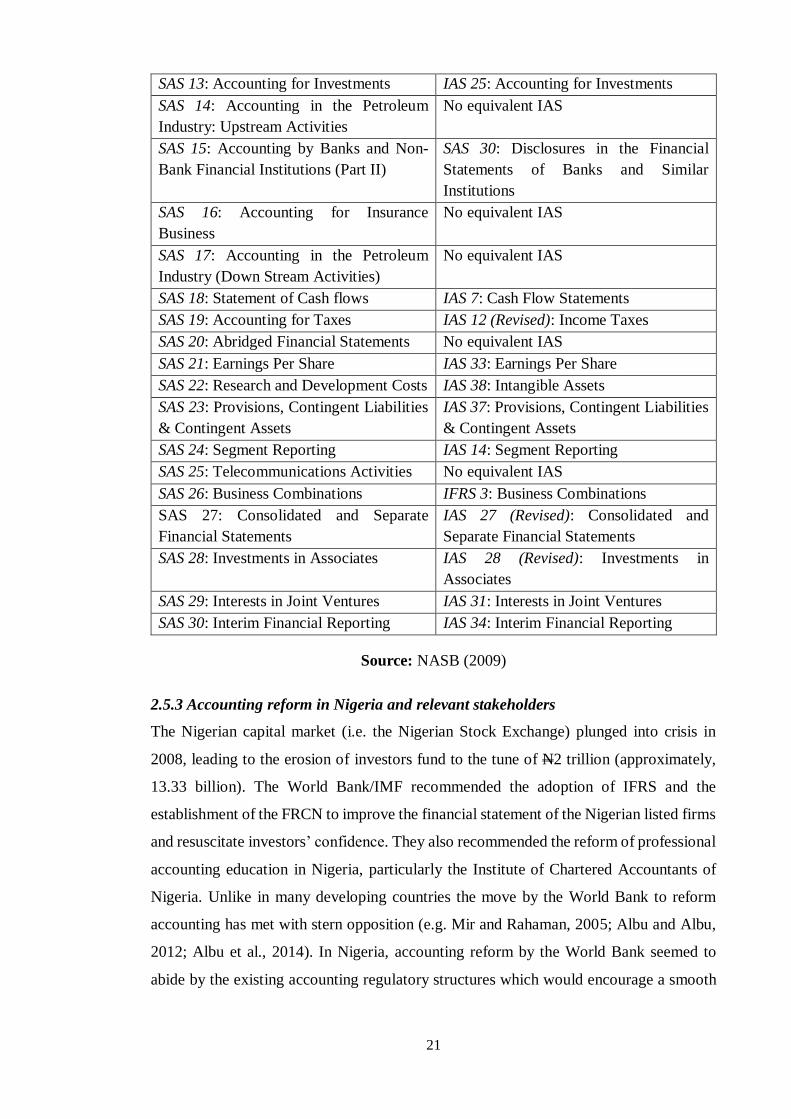

21

SAS 13: Accounting for Investments IAS 25: Accounting for Investments

SAS 14: Accounting in the Petroleum

Industry: Upstream Activities

No equivalent IAS

SAS 15: Accounting by Banks and Non-

Bank Financial Institutions (Part II)

SAS 30: Disclosures in the Financial

Statements of Banks and Similar

Institutions

SAS 16: Accounting for Insurance

Business

No equivalent IAS

SAS 17: Accounting in the Petroleum

Industry (Down Stream Activities)

No equivalent IAS

SAS 18: Statement of Cash flows IAS 7: Cash Flow Statements

SAS 19: Accounting for Taxes IAS 12 (Revised): Income Taxes

SAS 20: Abridged Financial Statements No equivalent IAS

SAS 21: Earnings Per Share IAS 33: Earnings Per Share

SAS 22: Research and Development Costs IAS 38: Intangible Assets

SAS 23: Provisions, Contingent Liabilities

& Contingent Assets

IAS 37: Provisions, Contingent Liabilities

& Contingent Assets

SAS 24: Segment Reporting IAS 14: Segment Reporting

SAS 25: Telecommunications Activities No equivalent IAS

SAS 26: Business Combinations IFRS 3: Business Combinations

SAS 27: Consolidated and Separate

Financial Statements

IAS 27 (Revised): Consolidated and

Separate Financial Statements

SAS 28: Investments in Associates IAS 28 (Revised): Investments in

Associates

SAS 29: Interests in Joint Ventures IAS 31: Interests in Joint Ventures

SAS 30: Interim Financial Reporting IAS 34: Interim Financial Reporting

Source: NASB (2009)

2.5.3 Accounting reform in Nigeria and relevant stakeholders

The Nigerian capital market (i.e. the Nigerian Stock Exchange) plunged into crisis in

2008, leading to the erosion of investors fund to the tune of N2 trillion (approximately,

13.33 billion). The World Bank/IMF recommended the adoption of IFRS and the

establishment of the FRCN to improve the financial statement of the Nigerian listed firms

and resuscitate investors’ confidence. They also recommended the reform of professional

accounting education in Nigeria, particularly the Institute of Chartered Accountants of

Nigeria. Unlike in many developing countries the move by the World Bank to reform

accounting has met with stern opposition (e.g. Mir and Rahaman, 2005; Albu and Albu,

2012; Albu et al., 2014). In Nigeria, accounting reform by the World Bank seemed to

abide by the existing accounting regulatory structures which would encourage a smooth

22

accounting reform. All the key stakeholders have maintained their usual role in the

reform.

The Nigerian government has been in control of the NASB, which has been a

parastatal of the government since has been 1992. Similarly, the FRCN was established

as a parastatal of the Ministry of Industry, Trade and Investment. Accounting reform is

not the first reform encouraged by the World Bank in Nigeria. In the past, the Nigerian

government has been receptive to economic reforms advocated by the World Bank, such

as the Structural Adjustment Programme (SAP) in 1986 and the due process in public

procurement introduced in 2001. Hence accounting reform was not resisted by the

Nigerian government.

The World Bank also recognised the hegemony of the Institute of Chartered

Accountants of Nigeria, whose members have the sole authority to certify listed

companies’ accounts. Hence, the reform of accounting education was tailored towards

the ICAN’s training of chartered accountants. Furthermore, the structure of the defunct

NASB was retained in the newly established FRCN. There was no meddling with the

composition of its board which was a fusion of all relevant stakeholders. Also, the

Statement of Accounting Standards (SAS) that was issued by the NASB borrowed

significantly from the IASs. The expected knowledge gap upon the adoption of IFRS

would not be wide.

Collectively, it is expected that the preservation of the existing accounting

regulatory structures will encourage a less repulse to the World Bank’s advocated

accounting reform in Nigeria.

2.6 Conceptual Framework

2.6.1 Differences in Accounting Practices across Jurisdictions

Accounting is an ‘economic language’ (Haller and Walton, 2003, p.1) that evolves from

the needs of the immediate environment in which it is spoken. Thus, accounting is often

adapted to meet specific local purposes of the people and institutions ‘speaking’ it.

Essentially, the language of accounting in a country will not usually be understood in

another country11 as the two are rooted in different cultures. More so, recipients of

accounting information in the two countries are different.

11 That is, as in natural language, a German will not understand ‘come’ as implying ‘come’ if he has never

learnt English.

23

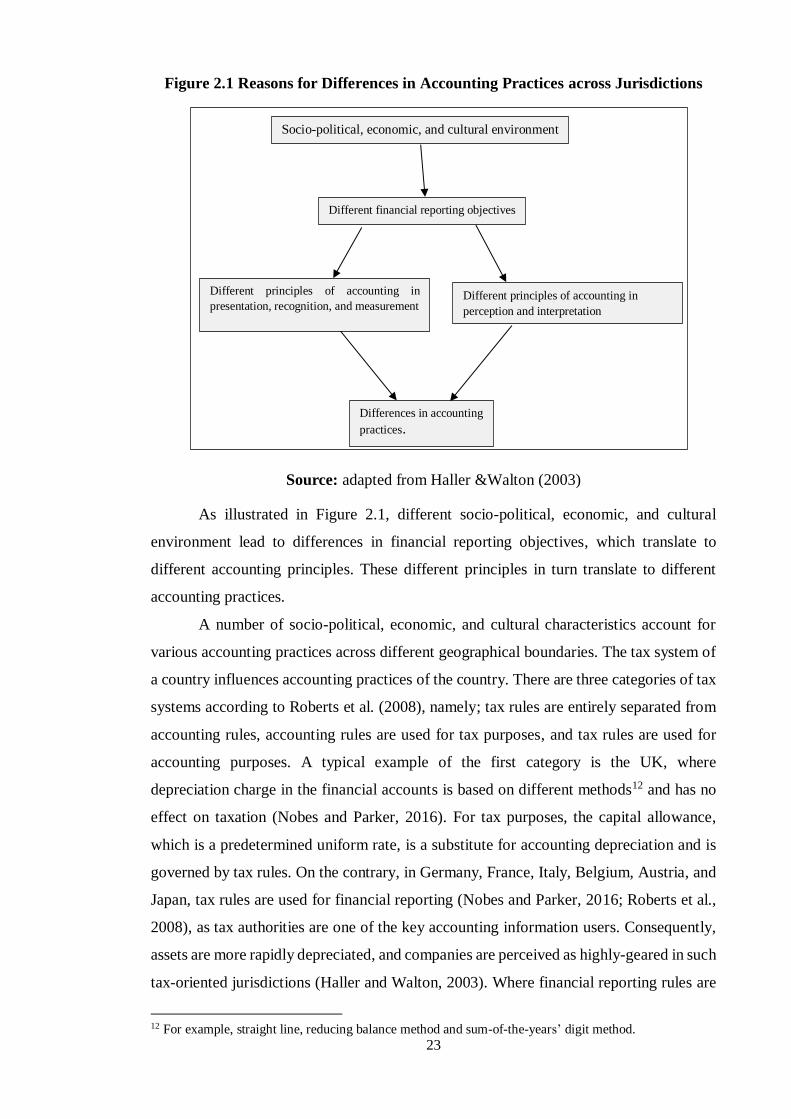

Figure 2.1 Reasons for Differences in Accounting Practices across Jurisdictions

Source: adapted from Haller &Walton (2003)

As illustrated in Figure 2.1, different socio-political, economic, and cultural

environment lead to differences in financial reporting objectives, which translate to

different accounting principles. These different principles in turn translate to different

accounting practices.

A number of socio-political, economic, and cultural characteristics account for

various accounting practices across different geographical boundaries. The tax system of

a country influences accounting practices of the country. There are three categories of tax

systems according to Roberts et al. (2008), namely; tax rules are entirely separated from