Embed Size (px)

Citation preview

1

The Value Relevance of Inflation Accounting Disclosure of Quoted Petroleum Firms in Nigeria

By

ABUBAKAR Zaid M.Sc/Admin/4073/2010-2011

BEING THESIS SUBMITTED TO THE POST-GRADUATE SCHOOL, AHAMDU BELLO UNIVERSITY ZARIA IN PARTIAL FULFILLMENT

FOR THE AWARD OF MASTERS DEGREE IN ACCOUNTING AND FINANCE

MARCH 2013

2

Declaration I hereby declare that this thesis titled “The Value Relevance of Inflation

Accounting Disclosure of Quoted Petroleum Firms in Nigeria” is a product of

my modest research effort, carried out under the supervision of Dr. Ahmad

Bello (Major Supervisor) and Mal Isah Shittu. Acknowledgements were duly

observed in respect of all sources from which information were sourced. In

addition, this research work has not been presented anywhere for the award of

any educational certificate.

______________________ _______________

Zaid Abubakar Date

Certification

3

This Thesis titled “The Value Relevance of Inflation Accounting Disclosure of

Quoted Petroleum Firms in Nigeria” by Zaid Abubakar, meets the regulation

governing the award of the degree of Masters in Accounting and Finance of

Ahmadu Bello University, and is approved for its contribution to knowledge

and Literary Presentation

______________________ _______________ ______________

Chairman, Supervisory Committee Signature Date

____________________ _______________ ______________

Member, supervisory committee signature Date

____________________ ________________ ______________

Head of Department Signature Date

____________________ ________________ ______________

Dean school of Postgraduate studies signature Date

4

Acknowledgements

All praises are due to Allah, we praise Him, we thank Him and seek His

forgiveness. We seek refuge in ALLAH from the evils of our souls and that of

our actions. Whomever Allah guides, none can misguide him and whoever

misguides, there is none to guide him. I bear witness that there is no worthy of

worship but Allah, and I bear witness that Muhammad (S.A.W) is His servant

and Messenger.

It is by Allah’s will that; this study comes to its logical conclusion. This

acknowledgement is meant to show my sincere appreciation to a number of

people who have contributed in one way or the other in realizing this dream.

In view of this, my unreserved thanks and appreciation goes to my kind-

hearted supervisor, the amiable Dr, Ahmad Bello,(Major Supervisor) a scholar

per excellence and a professor in the making, for his constructive comments,

contributions and observations that have actually enriched the work. A special

appreciation also goes to Malam Isah Shittu, my minor supervisor, for his

technical inputs, comments and pieces of advice that also make the work what

it is today. In this line, my appreciation also goes to Dr Salisu Abubakar, ( The

M.sc coordinator) for his support and advice. To all of you I say jazakumullahu

khayrah.

5

I sincerely, acknowledge the parental prayers, care and support I receive from

my parents, Fatima Abdulhameed and Malam Abubakar Muhammad Bello, my

granny Alh Abdulhameed, who believe in the continuous pursuit of knowledge.

Also in this angle are my brothers and sisters, Suleiman Abubakar, Najeeb

Abubakar, Fatima Abubakar, Nabeela Abubakar and Ahmad Abubakar, for

their constant prayers. This paragraph shall never be complete without

acknowledging and appreciating the prayers, support, and care of my beloved

wife, Amina Auwal Ahamad, who had to do without me for most of the time

this study is being conducted. I say jazakillah for your understanding and for

some editorial comments you offered.

I also appreciate the kind gesture of some of my lecturers for their

encouragement and support, such as Dr Shehu Usman Hassan, who has been

reviewing this work, right from proposal stage to-date; Dr Ahmad Bello

Dogarawa, Dr Hassan Ibrahim; Mal Idris Ahmad, from Department of

Business Administration, who has proved to be a brother, a lecturer and a guide

at all times. At this point, I would like to acknowledge and appreciate the

fatherly contributions, comments and observations of my Father-in-law Dr

Auwal Yahya Ahmad, he had not only offered his observations but some

editorials on the study. Some other colleagues worth mentioning are: Malam

Jubril Yero and Malam Nasiru Yunusa for their contributions toward the

success of the work.

6

At coursework class level, I acknowledge the support, concern and

observations of Moddibbo Abubakar, a friend and brother indeed, Salami

Suleiman, and Ahmad Abubakar,

7

Abstract

Income is one of the most important economic variables in financial statements that reports the direction of business entities and as well, serve as a decision base for different users of financial information. Unless financial information is adjusted for inflation, income will to certain extent be meaningless. This is because market values and opportunity cost are not reflected. It is in this view; this study examines the individual value relevance of historical cost model, inflation adjusted model, and joint value relevance of inflation accounting disclosure on the quoted petroleum firms in Nigeria. In view of the objectives, three hypotheses were formulated and subjected to OLS estimation initially, and later to the panel models, considering the fixed effects (FE) and random effects (RE); these estimation techniques were later dropped, because of the inability of data for the study to meet the asymptotic assumptions of the Hausman specification test. Thereafter, the study employs the seemingly unrelated estimation technique (SUR), upon which correlation contemporaneous diagnosis was performed to obtain the best linear unbiased estimates of the variables (BLUE). Further, the study uses modified Olhson (1995) price valuation model for analysis. Correlational and Ex facto Research design were employed, and data for the study were sourced from Nigerian stock exchange fact book and available annual reports and accounts of the firms. Price indexes provided by the Central Bank of Nigeria (CBN) website were used to adjust the historical cost financial statements into the inflation adjusted values. The findings of the study revealed that inflation adjusted financial information is slightly more explanatory than the historical cost financial information, and marginal information provided by the inflation adjusted financial information does not mean anything to the financial information users. While on the overall, the inflation adjusted cost model shows a little more relevance if the joint reporting is adopted. The study concludes that, the inflation adjusted financial information is as explanatory as historical financial information, and joint reporting could provide financial information users with broad opportunity to focus on other variables for their decision making rather than earnings and book values. Therefore, it is recommended among others that policymakers, especially the financial reporting council of Nigeria (FRC) should require firms in the petroleum industry to provide inflation adjusted financial information in addition to the historical cost statements; while the financial information users should use the inflation adjusted financial statements as a complementary to historical cost statement rather than alternative.

8

Table of Contents

Page

Title page

Declaration i

Certification ii

Acknowledgement iii

Abstract vi

Table of contents vii

List of Tables x

List of Appendices xi

CHAPTER ONE: INTRODUCTION

1.1 Background to the Study 1 1.2 Statement of the Problem 4 1.3 Objectives of the Study 6 1.4 Research Hypotheses 6 1.5 Scope of the Study 6 1.6 Significance of the Study 7

CHAPTER TWO: LITERATURE REVIEW

2.1 Introduction 9

2.2 Conceptualization 9

2.3 Inflationary Trend in Nigeria: Factors Responsible 18

2.4 Income and Income Measurement 20

2.5 Joint and Marginal Information Content of Financial Reports 28

2.6 Inflation Accounting Technique 29

2.7 Components of Financial Statements Quality 32

9

2.8 Impact of Price Level Changes on Financial Reporting 35

2.9 Effects of Inflation on Decision Making Process 37

2.10 Review of Empirical Studies 39

2.11 Theoretical Framework and Model Development 45

2.12 summary 51

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction 51

3.2 Research Design 51

3.3 Population and Sample of the Study 53

3.4 Sources and Method of Data Collection 53

3.5 Techniques of Data Analysis 53

3.6 Justification of Technique for Data Analysis 55

3.7 summary 55

CHAPTER FOUR: ANALYSIS, RESULTS AND DISCUSSIONS

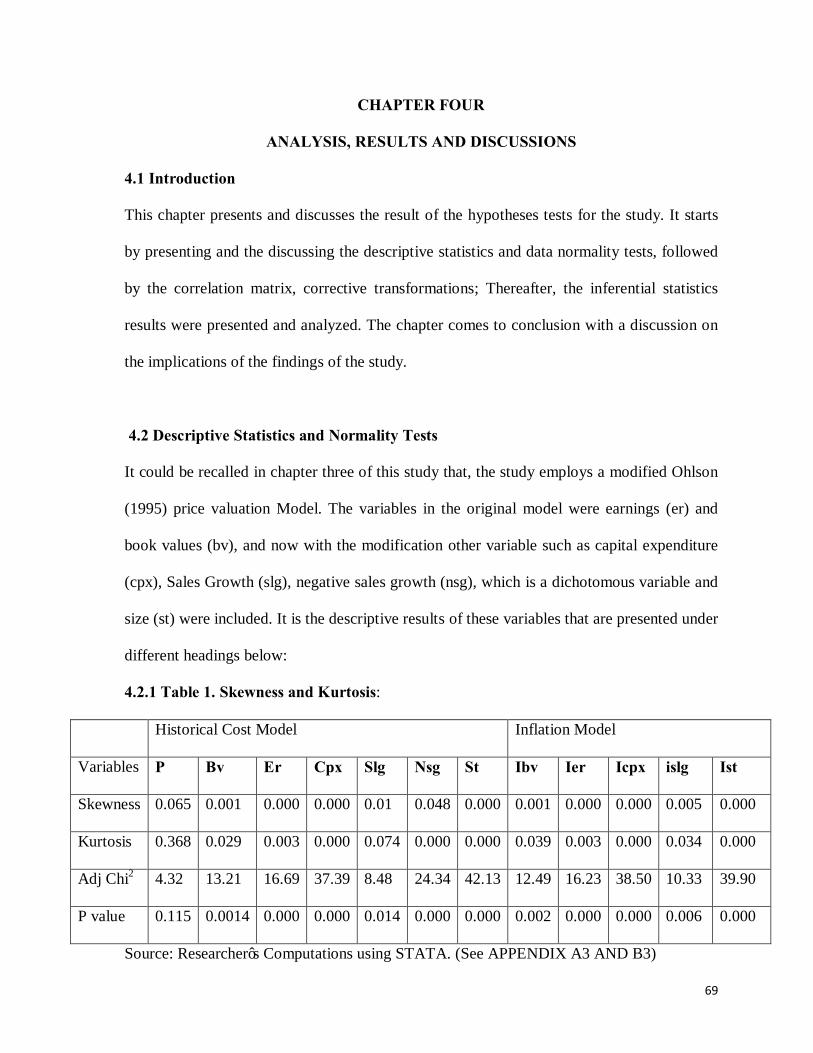

4.1 Introduction 56

4.2 Descriptive Statistics and Normality Test 56

4.3 Corrective Transformation 63

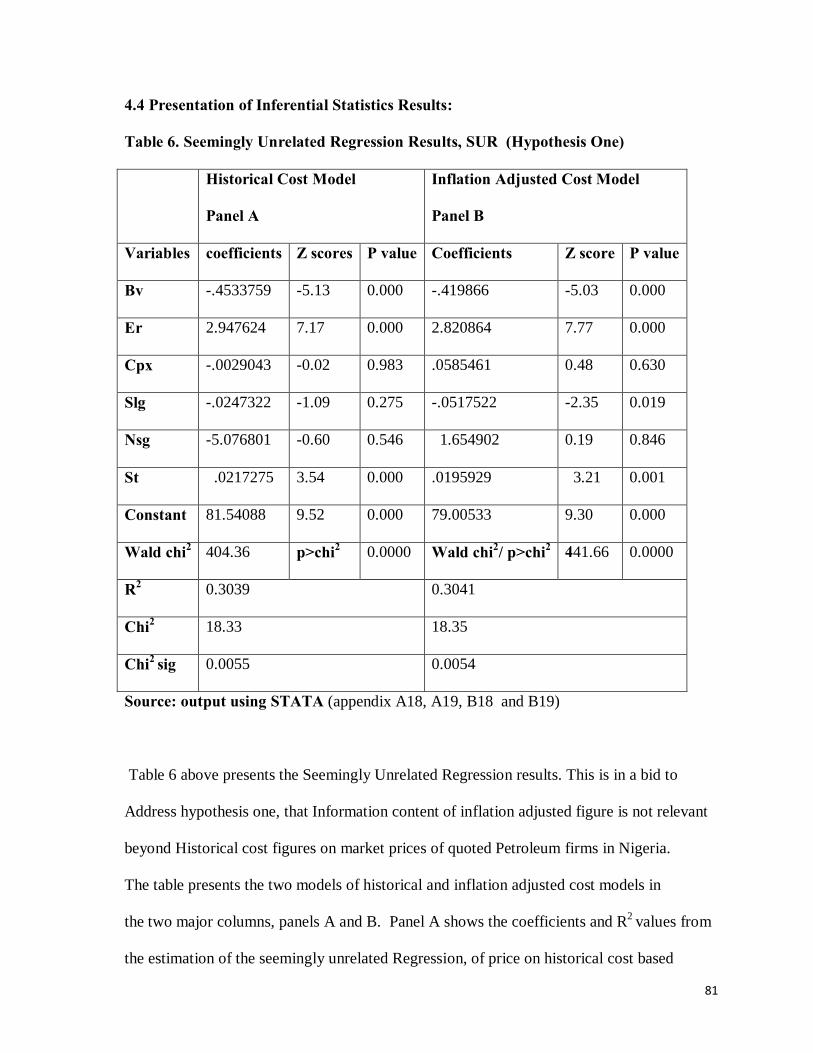

4.4 Presentation of Inferential Statistics Results 67

4.5 Implications of Findings 73

4.6 summary 76

CHAPTER FIVE:SUMMARY, CONCLUSION AND

RECOMMENDATION

10

5.1 Summary 75

5.2 Conclusion 76

5.3 Recommendation 77

5.4 Limitations of the Study 78

5.6 Areas of Further Study 78

Bibliography

Appendices

11

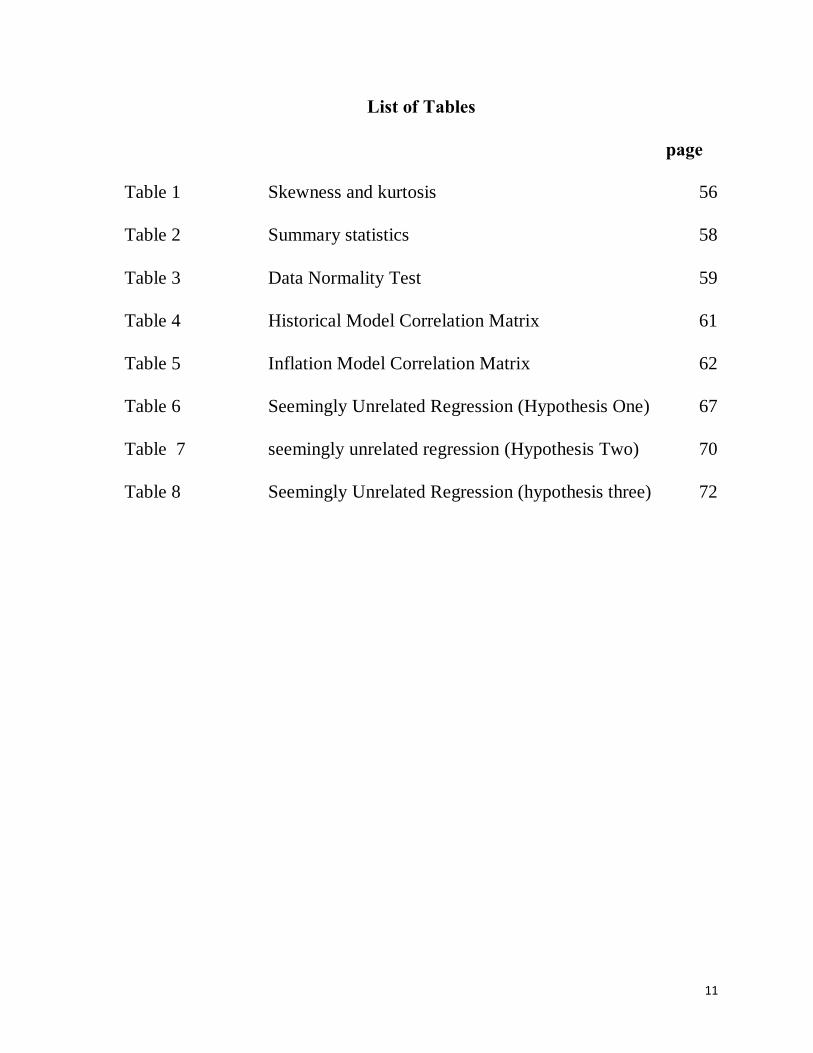

List of Tables

page

Table 1 Skewness and kurtosis 56

Table 2 Summary statistics 58

Table 3 Data Normality Test 59

Table 4 Historical Model Correlation Matrix 61

Table 5 Inflation Model Correlation Matrix 62

Table 6 Seemingly Unrelated Regression (Hypothesis One) 67

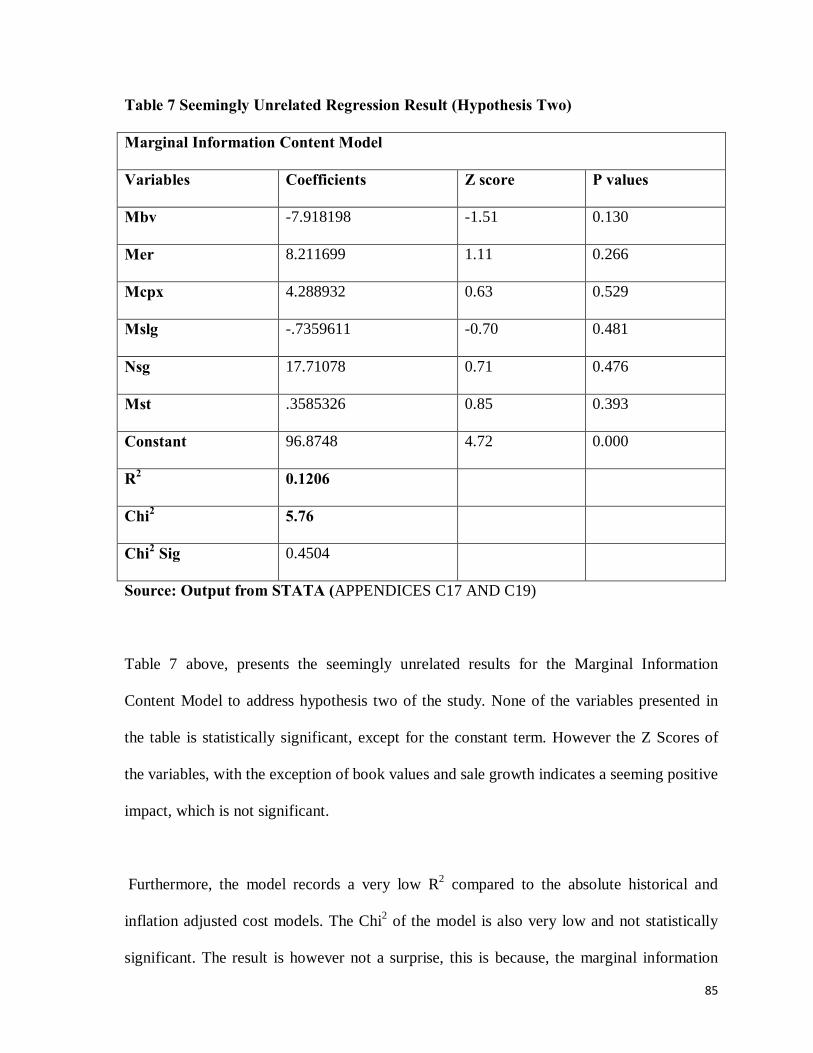

Table 7 seemingly unrelated regression (Hypothesis Two) 70

Table 8 Seemingly Unrelated Regression (hypothesis three) 72

12

List of Appendices

A1-A22 HISTORICAL COST MODEL

B1-B22 INFLATION ADJUSTED MODEL

C1-C18 MARGINAL INFORMATION CONTENT MODEL

D1-D19 JOINT REPORTING MODEL

E1 LIST OF FIRMS

13

CHAPTER ONE

INTRODUCTION

1.1 Background to the Study

The major role of financial accounting is to provide quality financial information on the

activities of entity for economic decisions. Such information should be up-to-date and

should present the true and fair position of the reporting entity. It should be free from bias,

to considerably enhance the users’ reliance and more importantly relevant to current and

future decisions. Thus, the only instrument by which financial information could be related

to users is the financial statements that are often prepared for the purposes of stewardship.

Conventionally, financial statements provide information, using the Historical Cost

Accounting Model (HCA), which has for decades been claimed to be objective, reproducible

and prudent. However, during periods of price changes historical cost based statements

could present financial information in a misleading way. Commenting on the weakness of

HCA, Panton (1920) opines that direct comparison of financial events arising from different

periods might be difficult to achieve. This is because; accountants deal with an unstable

currency. The reliability and objective qualities labeled in favor of HCA could be of little

relevance if it does not measure income, accurately; being an indispensable variable of the

financial statements. (Solomon, 1961)

Therefore, financial statements prepared in inflationary condition could be misleading.

Furthermore, it reduces the Financial Accounting role as input for decision making. Hence

the need for adjustment to the historical cost approach to reflect current economic realities

becomes inevitable. The need for Accounting for changing price levels was not a recently

14

observed issue. It dates back to 1938, an article by Sir Ronald Edwards brought the subject

matter to fore, this was followed by series of write ups from Accounting bodies and

scholars. Effort ranges from issuance of exposure drafts monographs to formulation of

valuation models in light of the phenomenon.

The first inflation standard, issued in the United States by the Financial Accounting

Standard Board was in 1979, Statement of Financial Accounting Standard No. 33 (SFAS 33)

termed financial reporting and changing prices. This was later replaced by statement of

Financial Accounting Standard No. 89 (SFAS 89) in 1984, ‘Financial Reporting and Change

in Prices”.

In the U.K, the story was not different; there was the Accounting for stewardship in a period

of inflation, published in 1968 by the Research foundation of the Institute of Chartered

Accountants of England and Wales (ICAEW), as a result of Exposure Draft No. 8 (ED8).

The ED 8 provided the proposal that companies should be required to publish, in addition to

their conventional financial statements, supplementary statements which would be in effect,

their final financial statements amended to conform to current purchasing power (CPP)

principles.

In 1974, there was also, the Statement of Standard Accounting Practice No. 7 (SSAP 7) in

the UK, which, stipulates that the Retail Price Index (RPI) be used in conversions of

financial statements from Historical Cost. After the release of SSAP 7, the U.K. Government

inaugurated a Committee of Inquiry in 1975, which was popularly known as the Sandilands

Committee. The committee recommended the system of Current Cost Accounting (CCA),

15

approving the Concept of Capital Maintenance as the Maintenance of Operating Capacity

and also led to the emergence of SSAP 16. (Wood and Sangster, 2005).

In Nigeria, no amount of effort could be seen from the regulatory authorities in addressing

the effect of inflation on financial reporting. The Nigerian Accounting Standard Board

(NASB) now Financial Reporting Council of Nigeria (FRC) has not issued any standard in

that regard, or called for compliance with any international existing standard, despite the

persistent inflationary environment, in which entities operate in the country. Some

Developing Countries such as Turkey, did not only issue standards on price changing levels

but also make it compulsory for the entities to comply by supplementing their Historical

Annual Reports and Accounts with the inflation-adjusted ones. This therefore shows the

inactivity and absence of pro activeness on the part of local Accounting Regulatory

Authorities. Hence the need for empirical studies in the area with a view to exposing the

value derivable from additional reporting.

Moreover International Accounting Standard Board (IASB) is a body responsible for

drafting and issuing standards aimed at overcoming country differences. To address the

problem of inflation, the board came up with the international accounting Standards No. 17

in 1981 and No. 29 in 1989 respectively even with this development, a significant

achievement has not been recorded in developing countries, such as Nigeria where neither

an alternative valuation model is developed nor the available one adopted for financial

reporting.

16

The motivation for this study was triggered by the persistent inflationary condition in which

the Nigerian economy operates, which is further aggravated by Government policy

inconsistency over the years. During the democratic regime of Obasanjo (1999 to 2007), lots

of economic tensions came to being as a result of increases in prices of fuel, which brought

about general increases in prices of goods and services across the country, however the fuel

price increase was reversed by the administration of Yar’adua (2007 to 2009), but other

prices never came down. Now with the recent announcement of fuel subsidy removal by

Jonathan’s administration (2012), another fold of inflation has begun to set in. The Nigerian

economy is primarily run on oil, so any slight change on fuel prices will automatically have

an inflationary effect on the entire economy. Hence the need to study the effect of price level

changes on financial reporting.

1.2 Statement of the Problem

As the General Price levels fluctuate overtime, the value of a unit of measurement fluctuates

alongside, (Sweeny, 1936). Therefore, the unit of measurement becomes a unit of different

magnitude. What this signifies is that the value of a Naira today is different from that of

yesterday. As such, Accountants in the guise of conservative historical accounting, report

figures with an implicit assumption that values at the end of a fiscal year are comparable to

values at the beginning; embedded also, with an assumption of price stability. This

assumption has never been true, especially in developing economies, where monetary units

loose values by the day, either at the instances of forces of demand and supply or at a

slightest change or anticipated change in economic policies. Thus, affecting income of

entities; this could in turn impact on market prices in such an environment.

17

In view of the above, Income ,being an important economic variable in financial statements

that measures the direction of business entity as well as decision base by different users, will

to some extent be meaningless in an inflationary environment, because market values and

opportunity cost are not reflected. This therefore leaves the users of financial information

stuck with inadequate data that will disable them to draw an informed decision. They would

be left at the mercy of Historical figures that fail to recognize the time value of money.

Furthermore, in some Developing economies, to which Nigeria belongs, various episodes of

inflations are experienced; ranging from creeping to galloping, running to hyper, yet

accounting regulatory bodies in some of these countries have not been proactive in

formulating standards that will address prices instability in financial reporting. In Nigeria for

instance, the Nigerian Accounting Standard Board (NASB), now Financial Reporting

Council of Nigeria (FRC) has none, out of its 30 issued standards that deals with price

stabilization, this indicates the regulatory laxity and seeming indifference on Accounting

regulation in Nigeria, which is further enhanced by non appreciation of the value derivable

from reporting financial information reflecting current economic reality

Debates about the relevance or otherwise of inflation accounting has been on for decades. It

is in this view that some empirical studies were carried out in the area, with a view to

investigating the value of incremental information content of financial statements as a result

of extra reporting of inflation adjusted figures, some of the studies concluded in slight or

insignificant relevance, this however might not be unconnected with the fact that, bulk of

these studies were conducted in developed economies where inflation is always within

check, while the few carried out in the developing economies suffer from methodological

18

challenges, ranging from inadequacy in model strength and robustness to data paucity, hence

ended up without achieving the set objective. This study addresses the topic by using a more

robust methodological approach and design.

1.3 Objectives of the Study

In view of the problem stated above, the study achieves the following objectives:

a. To examine the value relevance of Inflation adjusted numbers beyond Historical cost

numbers for financial decision purposes on quoted Petroleum firms in Nigeria.

b. To examine the relevance of the Marginal incremental Information of Inflation

adjusted numbers for financial decision purposes on quoted Petroleum firms in

Nigeria.

c. To investigate the value relevance of joint information content of inflation adjusted

and Historical Cost Accounting numbers for financial decision purposes on quoted

Petroleum firms in Nigeria.

1.4 Research Hypotheses

For the purpose of this study, the following hypotheses were tested:

Ho1: Information content of inflation adjusted numbers is not relevant beyond Historical

cost numbers for financial decision purposes of quoted Petroleum firms in Nigeria.

Ho2: Marginal incremental information content of inflation adjusted numbers is not

significant to users of financial information of quoted petroleum firms in Nigeria.

Ho3: Joint Informational Content of Inflation-Adjusted and Historical Cost Accounting

Numbers are not value relevant for financial decision purposes of quoted petroleum

firms in Nigeria.

19

1.5 Scope of the Study

The study covers a period of seven years, from 2005 to 2011. It has been a period that

various economic policies and pronouncements are made in respect to increases in workers’

salaries and fuel prices without a due regard to the purchasing ability of the Naira, as well as

its exchange power against other currencies. During this period, the value of Naira has

assumed the worst shape ever in history, likewise its exchange ability against International

currencies, such as the Dollar. It is also within this period that the world experienced another

fold of Global Economic Crisis, the first of its kind in the New Millennium, forcing

countries currencies to assume various purchasing powers against one another and several

transactions to take different value from what was initially expected.

The study used the down Stream sector of the Nigerian petroleum industry as its domain.

This is because; it is one of the few sectors of the economy that have direct contact with the

International monetary system, as noted in Anyanwu (1992), as such, pressure from global

economy might have effect on it. Further, the study observes it, to be one of the few sectors,

neglected for accounting researches, hence the need to examine its contribution.

The study adopts out of the numerous inflation–Accounting approaches; the current cost

Accounting Technique. This is due its robustness, in its approach to valuation (any of

replacement, net realizable value and discounted cash flow methods) and its flexibility in

both high and low inflationary environments. Its basic principle is in tracking the monetary

price changes; and the units of measurement is the monetary unit itself rather than

purchasing power index.

20

1.6 Significance of the Study

The focal point of Accounting is to periodically measure and report economic wealth and it

changes for informed decisions by financial information users. The financial information

users are numerous and usually require relevant information that will aid them in day-to-day

decisions. This therefore, overemphasis the need for relevance in financial reporting that

addresses current economic reality and has the ability to predict the occurrences in the

future. This study would be of benefit to investors, management, Government, Accounting

Regulatory bodies and the academics.

Investors will have the most current information on companies to enable them assess the

actual performance of their investment, the amount of dividend they expect and more

importantly how market values their investment. This will go a long way in helping

investors in deciding whether to check out their share in pursuance of capital gains, or

maintain their stake in a company.

Management of companies would be enabled to fairly plan for Assets replacement by

providing proportionate asset allowances, based on current economic realities. The

government in its capacity as the custodian of businesses will be able to assess companies

fairly for taxation purposes. While the accounting regulatory bodies could use the findings,

to issue new standards or amend any existing one. This work will add to the existing body of

knowledge, because of its currency and the methodological approach.

21

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This Chapter presents and review relevant empirical studies after review of the variables of

the study. Included in this section are reviews on the inflation Accounting technique and

Model Development for the study.

2.2 Conceptualization

There are various definitions of the term inflation by many scholars. Keynes (1936) views

inflation as an attempt to increase investment in a period of full employment, positing that,

there can be no inflation while there is unemployment. In periods of non-full employment

rising prices indicate rising total real income. Keynes in his definition tried to establish an

inverse relationship between inflation and unemployment. This makes his definition to be

practically wrong in the Nigerian case, where inflation co exist with unemployment.

In view of the above, the concept is further viewed as the time-period of rising prices

because total money spending is increasing faster than the amount of goods being sold,

practically implying that inflation is a general increase in prices that exceeds the increase in

goods and services provided. This has it root cause in the change in total money spending,

relative to the flow of goods offered for sales. (Samuelson, 1948).

Friedman (1963) in his submission defines inflation as a steady and sustained increase in the

general price level. He emphasized the differences between a steady inflation, as one that

proceeds at a more or less constant rate. Intermittent inflation is the one that proceeds by fits

22

and starts. Friedman further opines that, the steady or persistent element of inflation will

tend to be incorporated into expectations and will consequently be comparatively benign,

while the intermittent inflation will be less benign. This definition succeeded only in

separating the less benign form of inflation from the high ones. In reality all forms of

inflation tend to have a negative impact on transactions.

Some scholars, such as (Quah and Vahey, 1985; and Roger, 1998) view the concept from its

core and hyper perspective. In this view, inflation is seen as the component of measured

inflation that has medium-to-long-term impact on real output. Hence, this definition views

inflation as a phenomenon that affects output only.

Furthermore, Salvary (2004) in his submission views inflation as persistent changes in

relative prices which produce a sustained change in the general level of prices in an

economy to the detriment of some members of the economy. His definition tends to be

incomprehensive, because it has not captured all individual customers within an economy.

Sequel to this, inflation is seen as an increase in the supply of money that causes the general

price level to rise, (Saville, 2005).

To accountants, inflation accounting is a method of accounting that includes inflationary

index. One records price changes that affect the purchasing power of current assets and the

value of the company’s long term assets and liabilities, thus, providing a more accurate

picture of a company’s value. It is an alteration of a firm’s financial statement to account for

changes in the purchasing power of money. With inflation accounting, gains and losses from

holding monetary items during periods of changing prices are recognized. Like-wise, long-

23

term assets and liabilities are adjusted for changing price levels. Inflation accounting is used

to supplement regular financial statements. In order to illustrate how changing price levels

can affect a firm, also called general price level accounting, (Woods, 2005).

Finally, Inflation could be seen as the general level rise in prices of goods and services with

a fall in purchasing power of a currency within an economy. It is an upward movement in

the average level of prices, though, It is quite possible that some individual prices may

remain stable even fall, but when prices in general, say a year period are compared with one

another, It will clearly be seen that there has been a significant overall increase in prices.

2.2.1 Causes of Inflation

Inflation causes, are for the purpose of this study explained in relation to demand and supply

forces, as well as impact of exchange rate and the prices of goods and services in the

international economy. The inflation causes could be categorized as follows: Cost push-

inflation, Demand full inflation, Wage spiral inflation. (Saville, 1980; Riley, 2006; and

Bello, 2009)

Cost Push-inflation according to Riley (2006) occurs when businesses respond to rising

production cost, by raising prices in order to maintain their profit margin. There are

numerous reasons why costs might rise, this include: pricing imported raw materials costs,

caused by inflation in countries that are heavily dependent on exports of these commodities

or alternatives, a fall in the value of a particular currency say the Naira in the foreign

exchange markets which increases the prices of imported inputs in the local economy.

24

Secondly, rising labor costs, caused by wage increases which exceed any improvement in

productivity, just as the case in developing economies like Nigeria. The cost is important to

those industries that are Labor-intensive. These firms may decide to pass these higher costs

onto their customers, in the short run, but in the long-run, wage inflation tends to move

closely with price inflation because there are limits to the extent to which any business can

absorb higher wage expense.

Third reason for cost push inflation is the higher indirect taxes imposed by the government.

for example, a rise in the rate of excise duty, increase in government charge for fuel just as

the case in Nigeria, rise in the standard rate of value added tax (VAT) or extension to other

range of product which were hitherto excluded from VAT. (Nwaobi, n.d).

Demand-Pull Inflation occurs when there is full employment of resources and when supply

is inelastic. In this scenario, an increase in Aggregate Demand will lead to an increase in

prices. Aggregate demand might rise for a number of reasons. Some of which occur together

at the same moment of the economic cycle. A depreciation of the exchange rate, which has

the effect of increasing the price of imports and reduces the foreign price of exports. If

consumers buy fewer imports, while foreigners buy more exports, Aggregate Demand will

rise. If the economy is already at full employment, prices are pulled upwards.

Another factor responsible for demand – pull inflation is reduction in direct or indirect

taxation. If direct taxes are reduced consumer have more real disposable income causing

demand to rise. A reduction in indirect taxes will mean that a given amount of income will

now buy a greater real volume of goods and services. Both factors can take aggregate

25

demand and real GDP higher and beyond potential GDP. The monetarist economists believe

that the causes of inflation are monetary in particular when the monetary authorities permit

an excessive growth of the supply of money in circulation beyond what is needed to finance

the volume of transactions produced in the economy. Another factor is for the demand-pull

inflation is the rising consumer confidence and an increase in the rate of growth and house

prices – both of which would lead to an increase in total household demand for goods and

services.

The Wage Price Spiral – “Expectation – Induced Inflation occurs as a result of rising

expectations. When people expect prices to continue rising, they are unlikely to accept a pay

less than an expected inflation rate because they want to protect the real purchasing power of

their incomes. In this scenario, workers will seek to negotiate higher wages and there is then

a danger that this will trigger a wage-price spiral that then requires the introduction of

deflationary policies such as higher interest rates or increase in direct taxation.

Other factors that could trigger inflation could be looked at from productivity point view

(Riley, 2006). Productivity measures output per person employed or output per person hour.

A rise in productivity helps to keep unit cost down. However, if earnings to people in work

are rising faster than productivity, then unit labor costs will increase, thereby a tendency for

price increases occur.

Empirically, a lot of researchers have one thing or the other to say on the cause of inflation.

Friedman (1980) holds the view that inflation is a monetary phenomenon, wherever it exists,

drawing his submission from the quantity theory of money. Following the footsteps of

26

monetarist, Salvary (2004) also concludes that in the absence of monetary dislocation or

collapse of the monetary system, nominal money, the measuring unit used by Accountants is

not defective under general economic conditions, hence positing money to be the prime

cause of inflation. Also commenting on the same subject matter, Bello (2009;25) stated that

“while an increase in the money supply can accommodate or accentuate a rise in the price

level, changes in the general price level is not a monetary phenomenon.”

The foregoing discussion and analysis on the causes of inflation in this study leads us to the

conclusion that factors other than money such as government policies summersaults are

responsible for inflation, especially in developing economies like Nigeria.

2.2.2 Types of Inflation

Going through some of the economic literatures, Inflation could be broadly grouped into

four types according to its magnitude, these are: Creeping, Walking, Running and Hyper

Inflation. Riley (2006) is of the view that creeping Inflation occurs when the rise in price is

very slow. A sustained annual rise in prices of less than 3% per annum falls under this

category. Such an increase in prices is regarded safe and essential for economic growth.

Walking inflation happens when prices rise moderately and annual inflation rate is at single

digit. This occurs when the rate of rise in price is in the intermediate range of 3 to less than

10 percent. Inflation of this rate is a warning signal for the government to control it, before it

turns into running one.

27

Running inflation is when prices rise rapidly at the rate of 10 to 20 percent per annum. At

this point a running inflation is said to have occurred. This type of inflation has tremendous

adverse effects on the poor and middle class. Its control requires strong monetary and fiscal

measures. Hyper inflation occurs when prices rise very fast at double or triple digit rates.

This could get to a situation where the inflation rate can no longer be measurable and

absolutely uncontrollable. Prices could rise many times every single day. Such a situation

brings a total collapse of the monetary system because of the continuous fall in the

purchasing power of money. (Kimberly, n.d)

2.2.3 Measuring Inflation

The simplest way to convert money measurement into a real measure, according to

Alexander (1962) is through an accepted index of the general price level. Because perfect

satisfactory index of the general price level does not exists. Furthermore, it is not only that,

price indices are imperfect because of poor price reporting and inadequate coverage, but

even in theory, it seems impossible to construct a perfect price index no matter how much

information one gathers. This is because all prices do not move together. In view of this, it is

necessary to use an average of different price movements. The average must be weighted

and the appropriate weights change as between the beginning and end of the period over

which price is being measured. However, this approach fails to state the category of goods

on which prices are to be captured.

It is in view of the deficiency in the preceding measurement approach, that Kirkman (1974)

opines that inflation is measured by observing the change in the price level of a large

number of goods and services in an economy. That is the prices of essential commodities

28

within an economy have to be tracked for any inflationary measurement unit to be arrived at.

The problem with this submission is in identifying what constitute essential commodities in

a given economy. This is in addition to the problem of consistent price tracking.

In an attempt to solve the problem of the range of goods to capture in tracking the price

index, Diewert (2005) is of the opinion that one of the simplest choices is to use the inflation

rate for a widely traded commodity, such as gold as the index of general inflation. Another

alternative is to use the rate of increase in the exchange rate of country against a stable

currency. More still, instead of using the price of gold or any single commodity as the

indicator of inflation, the general inflation between the beginning and the end of the

accounting period might be better captured by looking at the price change of a representative

basket of goods. It is in this light that Inflation measurement is viewed as the process

through which changes in the prices of individual goods and services are combined to yield

a measure of general price change (Lebow and Rudd, 2006).

Silver (2007) in his contribution asserts that consumer price Index (CPI) is usually the unit

used in measuring inflation, especially in economies that adopt inflation targeting. To

achieve this measurement, the index to be used should be one that the public is familiar

with. Thus, the consumer price index (CPI) should have requisite high public profile and

prevalence as a target for measurement.

Whichever point of argument we take; there will always be an imperfection in the index to

be used in adjusting the Historical Cost Accounts for inflationary purposes. However, this

does not preclude us from agreeing with Staubus (1975) where he opines that adjusting

29

historical costs for general inflation by an imperfect index will generally be an improvement

over historical cost accounting.

Empirically, some of the recommendations submitted by some scholars, (e.g Lebow and

Rudd, 2006) for the choice of index choice are: cost-of-goods-index, cost-of-living-index,

policy assessment measures, prediction method, consumer price index, gross domestic

product deflator, and misery index. They asserts that, Cost-of-Goods-Index (COGI) tends to

cover a broad enough basket of goods that will provide adequate base of arriving at an

index. COGI comes very close to what most people intuitively mean by an inflation rate.

However, this index is not free from some deficiencies because COGI is for fixed bundle of

goods, it will not be of enough representation when new goods are introduced or when

changes occur in the features of the products covered.

Cost-of-living-index (COLI) is a measure of inflation based on the expenditures needed for

an optimizing consumer to maintain a specified level of utility as price changes. The cost-of-

living index derived its strength from the theory of consumer behavior, which can provide

clear-cut suggestions as to how to deal with such problems as changes in expenditure

patterns or the introduction of new goods. However, cost of-living-index (COLI) provides

little or no guidance about the construction of broader measures of inflation that include

prices for other components of output.

Consumer Price Index (CPI) is a method whereby a bundle of goods and services in a

certain weighted combination is determined. The total price of the bundle is calculated every

month and an annual average is also determined. CPI in the submission of many economists

30

provides more accurate insight into the deeper, underlying inflationary pressures within the

economy. However, CPI has some of its own deficiencies, CPI measures may overstate the

true rate of inflation, because they do not take into account improvements in the quality of

goods and services which may offset, in some cases, some of the rise in their prices, it does

not also provide adequate allowances for changes in the cost of housing and other hard-to-

estimate prices. (Stanford, 2008).

Gross Domestic Product Deflator, is a price index which adjusts the overall value of GDP

according to the average to the average increase in the prices of all output. The GDP deflator

equals the ratio of nominal GDP to real GDP. It is an alternative measure of inflation to the

consumer price index. GDP deflator captures the overall level of inflation in everything that

an economy produces

Misery Index equates economic unhappiness as weighted sum of inflation and

unemployment. (Smith, 1937). Consequently, the choice of a particular index depends on

the needs of the user; in this case we can deduce from the foregoing discussions that CPI

favors the individual consumers and the firms, while Group deflator favors the government.

Furthermore, some researchers (e.g. Silver, 2007; Roberts, 2008) argued that inflation signal

and inflation noise have to be distinctively understood for any meaningful measurement to

be achieved, they defined Inflation signal as a warning in general price increases, with a

great tendency to continue into the future, while inflation noise, is the rise in the prices of

specific goods or services – within an economy; in other words, it is the volatility in prices

of certain goods and services within an economy. Consequently, the study adopts the

consumer price index in adjusting the historical cost accounts to inflation adjusted.

31

2.3 Inflationary Trend in Nigeria: Factors Responsible

Nigerian Inflationary trend is the price of President Babangida’s Structural Adjustment

programme. This is because it assumed a doomsday scenario since its inception in July 1986

(from 5.4% in 1986 inflation rate to 40.9% in 1989), and has also been threatening to

destroy the very fabric of Nigerian society. It has included hyperinflation, depleted external

resources, worsened balance of payment positions and increased personal insecurity as well

as lessening personal satisfaction, (Anyanwu, 1992).

The country has experienced high volatility in inflation rates. From the early 1970s, as a

result of increases in the world price of oil and with oil production expanding, the country

seemed to be on track to prosperity. Because oil revenues allowed for a large investment

programs and rapidly rising government expenditure led to increasing purchasing power for

significant numbers of people (Kuijs, 1998).

However, following the fall in international oil prices and subsequent cut off of Nigeria from

the international capital markets, the government sustained its annual budget by increased

foreign borrowing, which rapidly assisted in building the country’s foreign debt; also at this

period, the government maintained an overvalued exchange rate with distortionary foreign

exchange controls which drove up the parallel market premium against the official market

(Anyanwu, 1992). This however, led to damage to local industry and agriculture, coupled

with highly expansionary monetary policy, powered by monetary financing of deficit

budget, which fuel high inflation in Nigeria.

According to Masha (2000), there have been four major episodes of high inflation, in excess

of 30 percent in Nigeria from the 1970s. The first inflation episode occurred in 1976, the

32

cause of which was the drought experienced in Northern Nigeria which destroyed

agricultural production and pushed up the cost of agricultural food items. Factors

responsible for the second episode of the inflation include: excessive monetization of oil

export revenue, which gave the inflation a monetary character, devaluation of the domestic

currency, causing prices to adjust to the parallel rate of exchange, thereby fuelling inflation

further.

The third inflation episode in Nigeria was characterized by fiscal expansion that

accompanied the 1988 budget, in addition was the debt conversion exercise, through which

debt for equity swaps took place, external debt was repurchased with new local currency.

However, with the drastic monetary contraction coupled with the aforementioned factors,

inflation was brought to a lower level.

The fourth inflationary episode started in 1993 through 1995. The major factor here was the

inability of regulatory authorities to contain the growth of private sector domestic credit and

bank liquidity, which made growth in money supply to move beyond demand.

Finally we view the New Millennium inflation in Nigeria as one, been characterized by poor

governmental policy on fuel prices, announcement of fuel subsidy removal, jumbo salaries

to political office holders, demand for salaries increases by the Labor Unions and worst of

all financial indiscipline by the people in the position of authorities, yet without any

commensurate effort in supply of essential goods and services.

33

2.4 Income and Income Measurement

Income is nothing more than consumption, (Fisher, 1927). From this view, anything besides

consumption is not income. Therefore, income is the net revenue that remained after

deducting the expenses for maintaining fixed assets and the day-to-day expenses as opined

by (Smith, 1937). This view is in line with that of most accountants; however do not provide

any procedure for measurement.

In an attempt to circumvent the measurement problem, Hicks (1950) sees Business income

as the maximum amount which the firm can distribute as dividends and still be as well off at

the end of the period as at the beginning. Thus income is in economies is mostly thought of

in real terms and is the result of balance sheet valuation rather than the residual from income

statement as the case in Accountants view. Thus, being as well off economically is

interpreted as maintaining capital intact in terms of the discounted value of expected future

receipts.

Bedford (1951) views income or profit as an increase of net rights in property. It could be

construed from this definition that an increase of rights in property refers to an increase in

the ability of property to satisfy wants. It is not a mere increase in physical form, or increase

only in money or its equivalent. Therefore, income is the difference between incomings of a

business or proprietor and the outgoings; hence it is the net of gross incomings and the gross

outgoings. (Marshall, 1952)

Generally, according to Chang (1962) Business income is concerned with the residue from

matching revenue realized against costs consumed. In other words, it is the residue or

34

remnants of Revenue realized from business operations after deducting all expenditures

incurred for that sole purpose, meaning that, income is a money concept, measured

periodically for a specific time through the instrument of the income statement. As such, it is

the excess of business revenue over related cost. Hence, the main task of income accounting

is to match revenue realized and cost consumed. This matching process causes an

aggregation of unallocated costs (non monetary assets) together with monetary resources of

an entity after deducting the liabilities, which gave rise to a residue called accounting or

residual equity (kirkman, 1974; Belkaou, 1992).

There have been various views by scholars as demonstrated above,of what income is,

however, some groups such as the Mercantilists, that view business income as the balance

of profit on the merchants book at the end of the year, this view, see business profit as an

annual phenomenon, and do not take into regards procedures needed to arrive at the final

income.

The Physiocrats, in their opinion, income is only the net product of an agricultural

entrepreneur, implying income to be something available for consumption after deducting

land usage allowances, annual expenditure incurred in the course of generating the gross

product; the definition views business income from a narrow perspective, without any

measurement yardstick.

Finally from the economists point of view, income is seen as the money value of the net

accretion to ones economic power between two points of time, while from the accounting

35

perspectives, more procedural approach is emphasized, hence the view that income is the

end result of the process of matching efforts and accomplishments.

Income measurements on the other hand is the process of assigning symbols to selected

objects, so that important class distinction, ordinal status, variations and differences, scales

for establishing comparative magnitude could be disclosed. (Williams and Griffin, 1967),

for any measurement to be significant, there must be a presupposition of purpose or

objective on the part of the measure. Ijiri (1966) views measurement as a special language

which represents real world phenomena by means of numbers that are predetermined within

the number system.

Measurement in accounting is done through the scale of ratio and money or price as

measuring unit. The choice of these two mechanisms is criticized on whether such

assignment can truly represent what is to be measured under different conditions and

circumstances (Bello, 2009), therefore, numbers resulting from applications of measurement

procedures have relevance only as they are identified through the use of formal theoretical,

construct as opined by Campbell (1963).

2.4.1 Income Valuation Approaches

Income is the end product of any measurement yardstick applied, especially in Asset

valuation. Traditionally, income is determined through the historical cost accounting model

which states assets on the basis of its original cost; therefore, the final figure from the

income statement will also be historical in nature. The earnings referred to mostly in

Accounting literature are either income derived from residual income approach or a

36

discounted cash flow approach. Income determined through residual income – measures

according to Fernández (2001), could be through one of the following valuations techniques:

Economic Value Added, economic Profit and Cash Value Added.

Economic Value Added (EVA), which is defined as earnings before interest less firm’s book

value multiplied by the average cost of capital. Economic value added as enunciated by

Stern steward & Co’s, is the measure that correctly takes into account value creation or

destruction in a company, because it measures the true financial performance of a company.

The proponents of this income valuation model argued that income determined through the

method is most directly linked to the creation of shareholder wealth over a time, thus, the

higher the EVA of a company, the higher its stock prices. Furthermore, Mekalainen (1998)

posits that, an essential component of EVA is the weighted Average Cost of Capital

(WACC) determined with the costs of both debt and equity. He further asserted that

theoretically EVA is much better than conventional measures in explaining the market value

of a company. Economic Profit (EP), is a form of income or profit, defined as book profit

less the equity’s book value multiplied by the required return to equity. The income

valuation was propounded by Boston consulting group.

Cash Value Added Model (CVA), is defined as earnings before interest plus amortization

less economic depreciation, less cost of capital employed. The model was also introduced by

the Boston Consulting Group, as an alternative to the EVA. They defined Income as the Net

Operating Profit after Tax (NOPAT), plus book depreciation (DEP) less economic

Depreciation (ED) less cost of capital employed.

37

The aforementioned incomes measurement techniques are categorized as Residual Income

Approach, which could be arrived from both Historical Cost Account and Current Value

Accounts. In continuation of our exploration of Income Determination Technique, Historical

Cost Accounts, as mentioned earlier has its own peculiar advantages. Hence, Posits Daines

(1929), that its greatest advantage is the fact that an original cost method is most easily

subjected to objective verification, thus, the easiest to use in practice. Furthermore, Littleton

(1956) in continuous defense for Historical Cost Accounts reflects the opinion of most

financial accountants, that historical Cost Accounting is best for financial reporting because

of its reproducibility properties, therefore, adjusting the Historical Cost valuations of assets

is best left to management.

However, during periods of price changes, the objectivity and reproducibility properties of

the Historical cost accounts cease to exist, therefore, during this period. The following assets

valuation methods, according to lamberg (n.d), could be considered: Net Realization Value

Method, Replacement Cost Method, Future Discounted Cash Flow Method, Specific Price

Historical Adjustment Method, and Prepaid Expenses Method.

Net Realization Value, is also referred to as exit values. This is the value an asset can fetch

if it is to be sold now at the market. It is the defined as the Asset- realizable value less

consequential cost as a result of Disposal Edwards and Bell (1961) views it in a similar

direction, defining it as the maximum price a currently held asset could be sold for in the

market less the transaction cost of the sale, i.e. the net realizable value for the asset. Net –

realizable value is current value accounting model advocated by many leading –

Accountants and Economist (e.g. Sweeney, 1936; Staubus, 1961 and Chambers, 1965).

38

However, the valuation method is not free from certain deficiencies such as lack of

reproducibility and Additivity problems unlike the historical cost accounts.

Replacement Cost Method is otherwise called Reproduction method or Entry value method.

It is defined by Edward and Bells (1961) as the minimum cost of purchasing a replacement

for a correctly held asset. It is the sum of money which would have to be expended at the

present time to reproduce a physical property identical with that in existence at the present

time and used for the benefit of the public (Hammod and Hayes, 1913).

Though the usage of replacement cost accounting has drastically been reduced as a current

value accounting, some accountants still find it relevant as a basis for computing

depreciation on a current cost basis. The drastic reduction in its usage might not be

unconnected with the same two difficulties that were associated with the use of net

realizable values model of not being generally reproducible and lack of additivity.

Future Discounted Cash flow: In accounting literature, estimating a current asset value as

the discount stream of its future expected returns is known as the economic approach to

asset valuation. This technique as posited by Fisher (1897) is based on the economic concept

of capital maintenance. However, the valuation methods has been criticized for its non-

reliability as the discounted net returns could not be known with any degree of certainty and

even where the returns are known, it is quite difficult or even impossible to allocate

combined revenues generated by aggregate assets to individual assets.

Specific Price Level Adjusted Historical Cost happens to be another current value valuation

concept put forward by Daines (1929) and Sweeney (1934). The method attempts to classify

39

assets into finite numbers of distinct classes at the beginning of an accounting period, called

period zero (0), with an index number attached with same classification, so that during

inflation, the depreciation value of the asset for that year would be zero, while the asset

value will stand at the asset index at the beginning scaled by index at the end. The

distinctive feature of this method is that general index is not used for all Assets; rather, each

class of Asset will take its specific index. However, the difficulty attached in obtaining

individual asset index, is of the deficiencies of the method, even where those indices are

arrived, the certainty is not always guaranteed, hence, subjectivity sets in.

Prepaid Expenses Assets and their allocation is current value accounting model which takes

a rather different approach, from the traditional way to valuing only tangible assets to

intangibles. The method views investments in intangible assets such as research and

development, advertisement and market expenses as well as training expenses. Assets whose

benefits are for more than one accounting period, and are capable of increasing the future

earnings potentials of a company, even though not reflected in the balances sheets of the

companies. The method advocates for allocating the intangible expenditures over estimated

period from which benefits are expected to accrue, thus, arriving at an income that has a fair

share of those expenditures, rather than charging these intangible assets expenditures to the

period when they were incurred. The concept of prepaid expenses is the major attribute of

the valuation model used in this study, with the approach of matching current costs with

future expected revenues. Haffield (1927) correctly noted that this type of Asset is different

from the usual sort of tangible asset, since they cannot readily be converted into cash,

thereby dispossessing opportunity cost value.

40

However, the problems faced in adopting this valuation method is not far from the intangible

assets possessing the nature of fixed cost, which are usually of no consequence for a firms

future strategic behavior. Nevertheless, the method has some utility, hence the conclusion by

Edwards (1954) “Even crude attempts should result in an improvement over present

depreciation practices. During periods of rapidly changing prices crude – measurements of

relevant item are likely to be much more meaningful than accurate measurements of an

irrelevant one”. This valuation model contributed immensely in modifying the model used

for this study.

2.5 Joint and Marginal Information Content of Financial Report

Most of the studies on information content of accounting data, view the announcement

aspects, by examining whether the announcement of some events result in a change in the

characteristics of the stock- return distribution, such as mean or variance. (Leu and Olhson,

1982).

The information content of financial reports could be separated into joint information

content and marginal information content, because different set of accounting income data

are viewed as signals about the attributes of a firm in a particular condition. Therefore, the

dependency of security returns on a given signal is generally defined as the information

content of that signal.

In view of this, Joint Information Content according to Matolcosy (1984) is the sum of the

information contents of simultaneously realized signals, while marginal information

contents of a signal is the information content of that signal beyond the information content

41

of all other simultaneously realized signals. In view of this, it should be noted that, the signal

which the information is sending, is what affects the firms’ values, whether disclosed or not.

Ball and Brown (1968) study signals on earnings announcements in which unexpected

annual earnings changes were correlated with residual stock returns and also tested for the

information content of the earnings. The study concluded that consistent evidence does exist

on the relevance and timeliness of accounting earnings.

However, the difficulties in testing for joint and marginal information content of two or

more signals from accounting data is the potential for compounding effects, in the form of

release of information about the realization of inflation-adjusted accounting – numbers

coinciding with the release of the information on the realization of Historical Cost

accounting income numbers, Matolcosy (1984). However, this study intends to overcome

this problem by coming up with a modified price model that will test for the information

content as against market – return models used by previous studies.

2.6 Inflation Accounting Technique

There are several techniques used in adjusting historical based financial statements to

inflation adjusted statements. The techniques are hereunder discussed as follows:

2.6.1 Current Cost Approach: - This approach is found in a number of different methods.

In general, the approach uses replacement cost as the primary measurement basis, if

however, replacement cost is higher than net realizable value and present value, the higher

of net realizable value and present value is usually used as the measurement basis. (lamberg,

n.d).

42

The replacement cost of a specific asset is normally derived from the current acquisition cost

of a similar asset, new or used, or of an equivalent production capacity or service potential.

While net realizable value usually represents the current selling price of the asset whereas

present value represents a current estimate of future net receipts attributable to the asset,

appropriately discounted.

Furthermore, specific price indices are often used as a means to determine current cost for

items. Particularly if no recent transaction involving these items has occurred, no price lists

are available or the use of price list is not practical. Current costs methods generally require

recognition of the effects on depreciation and cost of sales for changes in prices specific to

the enterprise. The method also require the application of some form of adjustments which

have in common a general recognition of the interaction between changing prices and the

financing of an enterprise.

Current cost methods also require an adjustment reflecting the effects of changing prices on

all net monetary items. Including long-term liabilities, leading to a loss from holding net

monetary assets or to a gain from having net monetary liabilities when prices are rising, and

vice versa. Most often the adjustment in this regard is limited to the monetary assets and

liabilities included in the working capital of the enterprise.

A variant of the current cost method apply a general price – level index to the amount of

shareholders interests. This indicates the extent to which shareholders equity in the

enterprise has been maintained in terms of the general purchasing power when the increase

in the replacement cost of the assets arising during the period is less than the decrease in the

43

purchasing power of the shareholders interest during the same period. Sometimes, this

calculation is merely noted to enable a comparison to be made between net assets in terms of

general purchasing and net assets in terms of current costs. The difference between two net

assets figures is treated as a gain or loss accruing to the shareholders (wood and Sangster,

2005).

However, the valuation methods embedded in current cost technique have proved to be

inadequate to valuation problems, on their individual capacity, hence the proposal by the

Sandilands Committee of Concept “value to the owner” a method which encapsulates the

elements of replacement, net realizable value and present value methods.

Value to the owner is defined as the minimum loess which an entity might incur if it were

deprived of an asset. Values from the three methods are compared to determine the

minimum loss by assuming that the business is deprived of an asset and at the same time

trying to maximize its profits. A way of deferring value to the owner according to Glutier

and Underdown (1986) is by reversing the opportunity cost concept, which is defined as the

least costly sacrifice avoided by owning an Asset. Value to the owner is sometimes referred

to as “Value to the firm”.

However, current cost method or current value Accounting as otherwise called was

criticized for making it difficult to make comparisons over a period of time when the unit of

measurement is unstable, this notwithstanding does not render the method useless , because

relevance of the financial information is of paramounce and superior to comparison.[FASB]

44

2.6.2 General Purchasing Power Approach

This method is known by different names, such as Constant Purchasing Power Accounting

(CPPA), General Price Level Accounting (GPLA), Constant Dollar Accounting, and

General Purchasing Power Accounting (GPPA), which was first highlighted by Sweeny

(1936). The general purchasing power approach involves the restatement of some or all the

items in the financial statements for changes in the general price level proposals. This

subject emphasis that general purchasing power statements change the unit of account but do

not change the underlying measurement bases, under this approach the amount reported in

conventional financial statements are measured in terms of the number of units of money

expanded for the object of measurement.

According to Gynther (1974) the method uses purchasing power unit rather than money, and

the method are not strictly a change from the historical cost based Accounting. It is merely

an attempt to remove the distortions in the financial statements which arises due to changing

price levels. It makes accounting income normally reflects the effects, using an appropriate

index of general price level changes on depreciation, cost of sales and net monetary items is

reported after the general purchasing power of the shareholders equity in the enterprise has

been maintained.

The overall objective of the method is to determine the real changes in well being of the

value of money which do not represent real – changes in the financial position of a business

[Institute of Chartered Accountants of Nigeria, ICAN].

However, the method is not free from its own deficiencies; it is believed to be potentially

misleading for including net gains on monetary items on holding gain in income stated.

45

2.7 Components of Financial Statements Quality

Financial reporting is the most important product of the accounting system, the most

important goal of which is to provide necessary financial data to evaluate the economic

units, function and their ability to make profits (Salehi, 2009b). In the same vein, Telebnia,

Salehi and Kangarluei (2010) stressed that the quality of financial reporting indicates a limit

in which the financial reports of a company, its economic status, and functions which are

measured in a period of time, is presented honestly. Financial reporting is not only the

financial reporting product, but it is also a process which is formed by several components.

The quality of financial reporting ultimately depends on the quality of each part of these

reporting components. In view of this, the Financial Accounting Standard Board (FASB)

outlines the components of quality information: predictive ability, feedback value,

timeliness, verifiability, neutrality and representational faithfulness (Valury and Jenkins,

2006). The International Accounting Standard Board (1989) framework identifies four

principal qualitative characteristics of financial reports, viz: understandability, relevance,

reliability and comparability.

2.7.1 Understandability

Information in financial statements should be readily understandable by users who have

business, economics and accounting knowledge and willingness to study the information

carefully, although financial reports should be understandable, complex matters that are

relevant to economic decision – making should not be excluded merely because they are too

difficult for users to understand.

46

2.7.2 Relevance

Financial information should be relevant to the decision –making needs of users for it to be

useful. According to the IASB framework, information has the quality of relevance when it

influences the economic decisions of users by helping them evaluate past, present or future

events or confirming or correcting their past evaluations. Information may be considered

relevant either because of its nature or because it is material.

Financial information is material if its omission or misstatement could affect the economic

decisions of users. The IASB framework regards materiality as a threshold or cut-off point,

therefore any information that fails the test of materiality need not be disclosed separately in

the financial statements and vice versa.

2.7.3 Reliability

Information is said to be reliable when it is free from material bias and can be depended

upon by users to represent faithfully that which it either purports to represent or could

reasonably be expected to represent,[ICAN]. In view of the inherent difficulties in

identifying certain transactions, or in finding appropriate methods of measurement or

presentation, financial statements cannot be perfectly “accurate” hence faithful

representation might be regarded as describing to the closest that accountants can come

towards total accuracy.

2.7.4 Comparability

Comparability components of financial reporting enables users to compare the financial

statements of an entity through time, that is over a period of time), to identify trends in its

47

financial position and performance. It also enables financial statement users to compare

different entities to determine their relative financial positions, performance and changes in

financial positions, performance and changes in financial position.

Other ingredients of financial statements include; neutrality, prudence, completeness and

timeliness.

However, there is usually a tradeoff between and among these financial statement

ingredients, especially between Relevance and reliability (ICAN). Reliability measures the

degree of verifiability and objectivity of the accounting members, however, lack predictive

ability renders it inappropriate for current and future decision-making, while relevance

shows the extent of accounting numbers, currency, appropriates and fitness to the prevailing

economic reality, hence relevant to decision making. In view of this, relevance as a

component of financial statement quality is one of the key concepts that underscore this

study. In summary, the study rests on relevance of accounting numbers to financial

information users.

2.8 Impact of Price Level Changes on Financial Reports

For more than 65 years, the accounting profession has been reminded that inflation affects

the contents of financial statements. (Schneider, 2000). Earlier, one of leading accounting

researchers, Patton (1920) was not far behind in making a similar observation, he posits:“It

is evident that the whole problem (accounting for effects of changes in price law) is an

unsettled one, with much to be said on both sides. It is a question to be determined on its

own merits with particular reference to the sound needs of business management and not on

the basis of tradition. The accountant in general will do well to concentrate his attention on

48

the development of methods of bringing re-evaluations and their subsequent effects onto the

books in a manner which will not impair the integrity of original cost figures, nor lead to the

misinterpretation of financial reports, rather than take the position that the effects of

revaluation are outlawed for as accounting records are concerned. (Adopted from Wolk et al

1989).

In light of the above quote therefore, it is evident that inflation being the systematic decrease

in purchasing power and it erodes entities capital, is a fundamental fact of economic activity

over item and it creates serious financial reporting and financial management problems

(Gucenme, 2004). Thies and Sturrock (1987) in their study of inflation-adjusted Accounting

Data and the prediction of Bond ratings, established that: During inflationary period, the

traditional Historical Accounting model overstates profitability and misrepresents the

relative financial strengths of firms, hence raises a serious concern to an extent that analysts,

investors and other financial information cannot make informed financial decisions without

understanding the impact of inflation on financial information.

In the same vein, Gucenme (2004) posits that reports that are prepared according to

historical cost principle overstate profitability, weaken equity by causing over taxation and

reduce the accounting reports role in decision making within inflationary environments.

Looking critically at the two accounting valuation methods: Historical and Inflation –

adjusted Accounts, it was an established fact in literatures, that Historical Cost Accounting

model maintains only money capital of entities, by assuming that monetary values at the end

of an accounting period are comparable to monetary values at the beginning of the

accounting period, implicitly assuming stability of price level. The paradox here is that, the

49

capital purported to be maintained loses relevance and is eroded by price level changes in

periods of inflation. While, current value accounting model, maintains the physical capital,

comprising of predictive and operative capacities of entities.

In view of this controversy, the Conceptual framework of the International Accounting

Standard Board (IASB) also recognizes the capital maintenance concept; differentiating it

into financial and physical capital maintenance concepts, without however, emphasizing on

a particular concept. Financial capital maintenance, is defined as a profit earned only if the

amount of net assets at the end of a period exceeds the amount at the beginning of the

period, excluding any inflows from or outflows to owners, such as contribution and

distributions whereas, Physical capital maintenance, defined as income or capital as long as

the entities – productive or operating capacity at the end of a period is mentioned intact.

2.9 Effects of Inflation on Decision Making Process

A major impact on both financial theory and practice of financial decision making has been

the economic instability, especially in Prices (Mills, 1996). Inflation, as general price level

changes affects both internal and external users of financial information in their decision –

making processes. Inflation affects financial management, inventory management, working

capital management and investment decisions.

Financial management defined as the process of financial decision-making, has three

categories, namely: financing decisions, investment decisions and dividend decisions.

During inflationary conditions, the financial decisions should be influenced by the impact of

the declining purchasing power of money on the company. The single and important maxim

50

of financial management that influences every decision is that “time eats money”. This

maxim holds well even in the absence of inflation, because of cost of capital, it gains extra

strength during inflationary conditions. A finance manager should consider the basis of

decision making and pricing decisions while taking such decisions during the inflationary

conditions. (Gupta, 1998).

Basis of Decision – Making: The profit reported by Historical Cost accounting is inflated,

hence should not be the basis for decision making, therefore need to be adjusted. The pricing

policies undergo a dramatic transformation during inflation. Prices must be revised

frequently and sharply to accurately reflect the impact of inflation. Under investment

decisions, capital budgeting is one of the major tools which helps financial managers in

evaluating investment proposals. Inflation according to Kannadhasan (N.d) affects two

aspects of capital budgeting namely: projected cash flows and discounting rate. Inflation will