Embed Size (px)

Citation preview

Zoona: A Case Study on Third Party Innovation in Digital Finance

Jungwon Byun

AcknowledgementsThis case study would not have been possible without the generous support of Joanna Ledgerwood, Ignacio Mas, and Financial Sector Deepening Zambia. I’d also like to thank Keith Davies and the rest of the team at Zoona for their gracious help in compiling data and conducting interviews. Their openness and commitment made it a joy to write this paper.

Jungwon Byun is a Growth Strategy and Marketing Associate at Upstart, a financial technology startup that provides a marketplace lending platform driven by an alternative credit scoring approach. Previously, she was a management consultant at Oliver Wyman, where she modeled capital markets revenues and devised digital operating models for large international banks. She also has experience working in digital financial services in Zambia, with Financial Sector Deepening Zambia, and leading Elmseed, microfinance organization in New Haven, Connecticut. She enjoys writing,

cooking, and lengthy discussions about long-form articles.

August 2015

1

Zoona

A. IntroductionA discussion about mobile payments and advancing financial inclusion never fails to mention M-Pesa. Often touted as the holy grail for how mobile technology and finance can stimulate economic activity, M-Pesa is virtually synonymous with mobile money in the developing world. But it has been eight years since M-Pesa launched and became the big success story.1 Is it still the only one in digitising financial services? M-Pesa’s success makes capitalizing on mobile money look simple. But in fact, the sober reality is that most mobile money providers have been stuck in a sub-scale trap. The sub-scale trap is a chicken-and-egg problem, as visible in Zambia as in many other developing countries. Mobile money relies heavily on network effects to generate value to end-users and encourage usage. If there aren’t enough use cases for mobile money, or if it does not provide a compelling enough value proposition as an alternative to cash, people have no incentive to use it. For there to be enough use cases and value, there have to be enough merchants who accept/disburse it and enough agents willing to exchange mobile credit for cash. Unfortunately, agents and merchants also need incentives to adopt mobile money transacting capabilities. Thus, mobile operators must figure out how to get enough agents to attract customers while simultaneously getting enough customers to attract agents. Given these market barriers, the types of providers who have the most advantages naturally seem to be the larger mobile network operators (MNOs), like M-Pesa’s Safaricom. The likes of Airtel, MTN, and Safaricom already have massive national networks of agents selling airtime that are easily converted into mobile money agents. They also have relationships with retail businesses and extensive capital resources for flashy marketing campaigns. In rural Zambia, towns outside of the capital city Lusaka are painted in Airtel reds, MTN yellows, and Zamtel greens.2 Not too far behind the mobile operators are the banks. Banks also have a reasonably strong distribution network, though easily dwarfed by those of the MNOs. Additionally, they have the advantages of financial expertise and infrastructure, as well as deep knowledge of financial regulation. In most countries, banks are recognized as trusted, legitimate institutions. In the shadow of these two major competitors, third party providers who want to compete in mobile money appear to be at a significant disadvantage. They have neither the reach nor resources of the MNOs, nor the expertise or legitimacy of the banks. But that has not stopped Zoona, a third party mobile money provider in Zambia, from challenging the status quo and delivering quality money transfer services to Zambians. Zoona hopes to eventually roll out this to the rest of Africa.

This paper explores Zoona’s story in detail, with the hopes that other third party providers operating in digital finance and mobile money will be encouraged by Zoona’s success in Zambia and glean key insights from its experiences. Specifically, the Zoona story demonstrates that:

1. Small players can be competitive in an industry dominated by MNOs; 2. There are alternative business models for delivering digital finance/mobile money that have

not been fully explored; and,3. The journey to identifying the value proposition of digital finance is hardly straight forward.

1 Mas, Ignacio and Morawczynski, Olga, Designing Mobile Money Services: Lessons from M-PESA (April 1, 2009). Innovations, Vol. 4, No. 2, 2009. Airtel, MTN, and Zamtel are the three mobile operators in Zambia whose logos are red, yellow, and green, respectively. Airtel and MTN are multi-national mobile network operators.2 Zamtel is quasi-public and has yet to launch mobile money.

2

A Case Study on Third Party Innovation in Digital FinanceZoona

B. The Zambian climate and Zoona’s success to date Zambia is a young nation whose people humbly understate the uniqueness of their history. Despite having over 70 languages and 50 ethnic tribes, the country has avoided the devastating ethnic conflicts that plagued bordering Zimbabwe and the Democratic Republic of Congo.3 Zambians say, with facetious self-deprecation and a touch of pride, its people come from the tribes who fled conflict from nearby countries and thus have no interest in creating it. The Zambian rural-urban divide is vast, especially in terms of financial services. According to the most recent FinScope (2015), 70.3 percent of urban adults have access to financial services within 30 minutes, but only 50.1 percent of rural adults can claim the same. Overall, 61.8 percent of the population was unbanked and financial exclusion from both formal and informal services was 40.7 percent with women more likely to be excluded compared to males at 42.6 percent and 38.8 percent respectively.4 Zoona is one of many companies trying to extend the reach of financial services to those currently excluded by the financial market. While it has launched numerous products and services (discussed in greater detail below), its core product today is money transfers. People looking to transfer money approach a Zoona agent (found in bright green Zoona booths and kiosks) who processes the transfer on their mobile phone.5 Ninety-four percent of Zoona’s revenues (exceeding USD8 million in 2014) come from the transaction fees charged on its person-to-person (P2P) over-the-counter (OTC) money transfer service.6 A smaller portion of revenue is driven by cashing out remittances sent through a local remittance service, namely Mukuru, and through bill payments.7 The mobile money industry is a tricky one to subdivide, and Zoona’s position within it trickier still to pinpoint. The following graphic categorizes the various providers in Zambia by the financial services offered to the user and the technology through which it is provided.8

3 “Zambia.” The World Factbook. June 24, 2015. 4 FinScope Zambia 2015.5 Zoona is also available through agent managers such as Cactus Financial Services and PostDotNet. These companies are exclusively a distribution channel: neither has its own money transfer service, but serves as cash-in/cash-out agents for many other services, such as MTN Money, Zoona, Zanaco Xpress, etc.6 OTC refers to a transaction in which the end user interacts with an agent to conduct the transaction. Zoona’s transactions are predominantly person to person (P2P) so the sender gives one Zoona agent cash, the agent converts this into digital money in Zoona’s system, and the recipient collects cash from any other Zoona agent. 7 Zoona has a partnership with Zambian Breweries to process payments for approximately 400 distributors. It also offers services such as airtime top-up for consumers. It is still offering vouchers in Zimbabwe and Mozambique with WFP but that is no longer a core product for the company. Mukuru is another international remittance provider for which Zoona offers cashing in/out services.8 From left to right, the companies are divided by the complexity of the financial services they offer to the end-user of the product. A simple P2P money transfer is the most basic service offered, whereas a full banking service includes access to information about a retail bank account and the ancillary services it provides (such as statement history). From top to bottom, the companies are organized by the complexity of the technology that the service is delivered through, again from the perspective of the end-user. For an agent-based transaction, the customer interfaces with a salesperson, or representative of the company (be they an agent in a booth or a teller at a bank branch). For point-of-sale (POS) transactions, a customer interfaces with a terminal or similar device to conduct a transaction. Cell phone and internet banking require greater degrees of technological familiarity andaccess

3

Zoona

Figure 1: Digital finance competitive landscape

Figure 1 illustrates the point that there are many distinct kinds of providers, many of which would actually not be considered direct competitors of Zoona. There are four broad categories of providers within digital finance/mobile money: mobile banking, hardware providers, mobile wallets, and money transfer. Barclays, FBZ, Stanbic, and the other banks have mobile apps and SMS-based banking that aim to provide an additional layer of service and convenience for their existing clients. By definition, these products only target banked individuals, thereby excluding most of the rural or poor population. Typically, these services allow a user to check account statements and history, transfer money, and pay bills. Zanaco is the only exception. The largest commercial bank in Zambia, Zanaco is the only one whose mobile product aims to deliver banking services to under served clients, as opposed to being an additional customer service. Kazang and Broadpay are mostly hardware providers. Kazang sells point-of-sale (POS) devices to small mom-and-pop retailers who can use it to sell airtime or allow customers to pay basic utility bills. Kazang services are typically provided as an extension of an existing business, rather than a standalone revenue source. Broadpay is a new company that has begun establishing ATM-like terminals in urban commercial centers such as shopping malls. The functionality and penetration is quite limited – people can purchase airtime or pay bills. Besides mobile banking and bill payments, there are mobile wallets. MTN and Airtel have mobile wallets that cell phone users can access through USSD. On these wallets, users can purchase airtime, pay basic utility bills, pay at certain retailers, and transfer money to other wallet holders in the same network.

The incentive for MNOs to develop a mobile wallet is to facilitate the process by which users purchase airtime – the product that has the highest profit margin for mobile operators. In essence, the mobile wallet is primarily a retention strategy. Lastly, there are money transfer service providers. Western Union, MoneyGram, ZamPost (the national post office that offers a money transfer service called SwiftCash), and Zoona process person to person (P2P) money transfer transactions throughout the country.

4

A Case Study on Third Party Innovation in Digital FinanceZoona

These companies only conduct money transfers and do not require the user to engage with any technology–only agents sitting at booths. Western Union and MoneyGram generally target international remittances and have a limited presence in rural parts of the country. Thus, while there are a variety of providers in the industry Zoona’s actual competitors can be narrowed to the three presented in Figure 2.9 ZamPost, MTN, and Airtel are the only ones with a focus on domestic P2P transfers and a sizable agent network. Figure 2 Zoona’s direct competitors

Zoona’s agents operate in 84 out of Zambia’s 89 districts, making the service more geographically available than all other banks and money transfer services. Only the MNOs Airtel and MTN have coverage in so many districts, and only Airtel Money has more agents: roughly 1,000 agents are active over a 30 day period compared to Zoona’s 730.10 Zanaco has 172 cash-in/cash-out locations.11 Zampost has 139 locations. Other providers offering money transfer services, PostDotNet and Cactus Financial Services, have 23 and 34 locations, respectively.12

Zoona’s sizable agent network is necessary to support their 700,000 active users. In a given month, approximately 300,000 people conduct at least one transaction.13 This customer base grew organically at an average of more than 65,000 new users each month in 2014. As of November 2014, over 500,000 transactions were being performed every month, at a valueexceeding USD25 million, making Zoona one of the leading money transfer providers in the country. Zoona has managed to grow in such a competitive environment by doing what no one else does: focusing on the agent experience. 9 Agent and active user estimates are as of November 2014. A more quantitative comparison among the four providers cannot be conducted because data on transaction value/count per month and active usage is unavailable or unreliable. These estimates are derived from a combination of internal data and publicly available data. The purpose of this graphic is largely illustrative and should not be taken as definitive. While reasonable estimates for the number of active users and number of agents were available for Airtel, Zoona, and MTN and for the number of agents of SwiftCash, the numbers of active users and agents of SwiftCash and ShopRite (a more recent competitor) are not available.10 Airtel has 6,834 registered mobile money agents. Of these, approximately 2,581 are active over a 90-day period. Precise data for agents active over a 30-day period is not available but based on daily transaction numbers, 1,000 is a reasonable estimate.11 Cash in/out locations include proprietary agents, contracted agents, and bank branches.12 PostDotNet and Cactus Financial Services each provide a variety of money transfer options, including Zoona. At one PostDotNet location a customer can conduct a transfer using MTN Mobile Money, Zanaco Xpress, Zoona, or Western Union.13 The 300,000 includes both senders and receivers.

5

Zoona

C. Zoona’s innovationsMany successful digital finance providers can leverage an existing network of agents and distributors to serve as cash-in/cash-out points. ZamPost already had its post offices, MTN and Airtel already had local distributors selling airtime. Zoona, however, has had to build its agent network one by one. Recognizing that agents are the primary interface with the customer and the key to ensuring quality service, Zoona makes it a focus to understand and empathize with the agent experience at every step, effectively becoming a vertically integrated agent network manager. Zoona internally refers to agents as its primary “customers,” reflecting the attitude that agents are more than just a means to an end. It uses a framework of “touchlines” which maps every single point in the Zoona agent’s journey, from the moment she first hears about the company to the point at which she expands to multiple locations.

Starting agents are eligible for resources such as booths, cell phones, and marketing materials, which are supported by Kiva loans.14 Agents repay Zoona for the value of the materials over time.

Agents then receive a personal account on Zoona’s online portal, home to a suite of services. A simplified version of the portal is accessible via phone (even on feature phones), which agents use to process transactions. The web-based portal contains an extended menu of features, including full transaction histories, statements and account reconciliation. Account reconciliation is a critical part of business management in the money transfer business. Zoona’s agents typically link their own bank accounts to the Zoona system. They can then convert cash and electronic credit between the amount registered in their Zoona accounts and their personal bank accounts to manage float. Zoona has agreements with seven banks allowing agents to deposit cash. Converting electronic credit to cash is done through a process referred to as “Send-to-Bank,” accessible through the website. These internet transfers are processed at set times throughout the day. Because Zoona is integrated fully with Barclay’s reconciliation system, transfers between an agent’s account and Zoona’s accounts are processed in near-real time.

Rural agents, who sometimes travel up to 60km to get to a bank, tend to rebalance once a week. Urban agents rebalance more frequently. Overall, the average outlet rebalances about three or four times a day, more often than agents of many other providers.15 Recognizing the importance of liquidity in managing a money transfer business, Zoona offers an agent financing product so that agents have enough float to trade on and don’t bounce customers.16

The average Zoona agent makes USD1,450 in monthly commissions. The median commission monthly is USD525. Per booth or outlet, the average commission is USD553 and the median closer to USD356.17 By comparison, the median monthly commission on all transactions is USD213 per outlet in Bangladesh, USD117 in Kenya, USD136 in Uganda, USD126 in Tanzania.18 The minimum wage for a sales assistant (a job comparable to being a Zoona agent) in Zambia is ZMW1,300 or USD107 a month.19 Compared to these options, being a Zoona agent is very enticing.

14 Kiva is a P2P lending portal that allows individuals to donate directly to financial institutions that, in turn, disburse microloans to borrowers. 15 Mike McCaffrey et al., Agent Network Accelerator Survey. (Helix Institute of Digital Finance, 2014).16 https://zoona.zendesk.com/hc/en-us/articles/202726469-Zoona-Cash.17 Certain agents run multiple booths.18 Mike McCaffrey et al., Agent Network Accelerator Survey. (Helix Institute of Digital Finance, 2014).19 “Minimum Wages in Zambia with Effect from 01-07-2012,” Mywage.org, last modified November 11, 2014, http://www.mywage.org/zambia/main/ salary/minimum-wage. Exchange rate 1 USD = 12, 389 ZMK, provided by XE currency converter on October 2, 2015.

Agent Touchlines

6

A Case Study on Third Party Innovation in Digital FinanceZoona

This vertical integration sets Zoona apart as an agent manager and reflects a viewpoint different from that of most mobile operators, who see agents as little more than a delivery channel. “Mobile operators use distribution channels to grow sales. Then, as soon as they have sales, they cut the margins and squeeze as much as possible out of the agents,” says Brett Magrath, Zoona’s co-founder and COO.

Zoona is now developing ways to deliver these services to agents and manage their performance more efficiently, with data driving forward the innovation. “Our philosophy is to focus on the high-performing agents, not on the lagging tail,” says Keith Davies, the company’s Head of Finance, Data Analytics & Risk. “So long as the total number of inactive agents doesn’t surpass a certain threshold, it’s more important for us to focus on growing the high-performing guys.”

Zoona manages this through its analytics team, based in Cape Town. The dashboard team produces the reports that monitor and analyze the state of business. This team keeps an eye on agents’ float to manage in real time the amount of cash that agents can access. The predictive analytics team is developing algorithms to identify what an agent’s performance is compared to what it should be.

Zoona has a system in place that allows them to use data to remotely track and manage agent

performance. This allows Zoona to deploy its resources more effectively, instead of expending them to visit every single agent.

It is also using data to develop internal “scorecards” for agents. These scorecards will effectively function as credit scores to determine eligibility for the loans that Zoona extends to cover startup costs. Having a rigorous, data-driven method of determining credit eligibility will help Zoona on board new agents faster and more efficiently. Being open minded about its identity has helped Zoona pivot and refine its strategy. Rather than take a cookie-cutter approach to building out the agent network, Zoona chose to start with delivering a high-quality agent experience. While the money transfer is Zoona’s core product, this has not always been the case. In fact, the money transfer product was largely discounted up until 2014. Zoona has taken a circuitous journey riddled with pivots and battle scars, resembling the coming of age journey of most technology start-ups. Its story begins with Mobile Transactions Zambia, Ltd. (MTZL), in 2008.

D. Zoona’s historyIn July 2008, Brad and Brett Magrath founded MTZL with funding from USAID and Dunavant to develop a product for digitizing payments and communication to rural cotton farmers.20 Brett recalls the mobile money industry at the time consisting of “people with AK47s on vehicles driving cash into the bush.” Presented with the chance to receive their payments electronically, a mere six of Dunavant’s farmers opted to do so. Over the next five seasons, the product expanded to a few thousand farmers but never reached the critical mass that would make the cost savings

20 Dunavant one of the largest cotton buyers in Zambia.

7

Zoona

Around 2009, MTZL started developing the software to process money transfers, ultimately being approved by the Bank of Zambia (BOZ) to be a payment systems provider. The growth strategy in the beginning was nothing if not creative. To recruit agents in rural areas, members of the sales team were sent out with three days per diem and a one-way bus ticket. The recruiter had three days to find a person in the town to cash out a money transfer so that he could buy a bus ticket back to Lusaka. The person willing to cash out for the recruiter became the agent in that town.

Unfortunately, the needle did not move past three to five transactions per day. The team quickly realized that agent location was essential to business success. As part of their first marketing strategy, Brad Magrath and Mike Quinn (CEO) decided to distribute flyers inside the main post office in Lusaka, directly competing with Zampost’s own money transfer service. When an angry post master general came after them, Brad was placed under citizen’s arrest and escorted to the post master general’s office by a security guard and an AK-47. To this day, no one knows what transpired in that office, but Brad walked out with a “gentleman’s agreement” under which Brad and Mike could distribute flyers elsewhere, just not inside the post office. The first outlet was then established in the parking lot of the post office. Almost overnight, the number of transactions jumped to 30 per day. That outlet next to the post office on Cairo Road is still one of Zoona’s biggest outlets. While money transfers grew steadily, the founding team (now Brad, Brett, Mike, and Keith Davies, who joined as CFO in 2010), still did not believe that money transfers alone could keep the company alive. “We thought the MNOs would come into the market and dominate us,” says Brett. “So the whole time we thought, ‘It will just keep us alive until our next great idea because this is too simple’” To avoid getting crushed by a massive telecommunications provider implementing a local version of M-Pesa, MTZL presented an idea to a USAID-funded project named PROFIT.21 In 2010, PROFIT contracted MTZL to improve the distribution of fertilizer and inputs to rural farmers. It wanted to develop electronic vouchers to ensure that the input subsidies went to the right farmers and to ensure farmers used their subsidy payments to purchase inputs from local retailers, not importers.

The product was successful and eventually adopted by the World Food Programme (WFP) who distributed the vouchers to its beneficiaries. These vouchers were redeemable at local retailers for a product basket of staple items such as oil, sugar, or maize. Usage grew rapidly and it wasn’t long until 50,000 vouchers were being distributed every month. Excited by the success of the voucher project with WFP, MTZL developed an initial investment pitch to ACCION’s Frontiers Investment Group. The entire investment case was based on scaling with WFP. Three weeks later, MTZL was about to sign an extension contract when WFP suddenly announced that it was terminating all food subsidy activities in Zambia. Left now with a payments product, voucher product, and back-end reconciliation systems, the MTZL team went out to find more clients and partnerships. “We were always trying to build our next revenue stream. We spent a huge amount of time building these ordering systems, building these bill payment systems, building loads of anything having to do with payment,” says Brett. “We would walk in to meetings and say ‘What do you want?’” This was exactly what happened when MTZL (now rebranded as Zoona) pitched the ordering system to Zambian Breweries in 2011. “We took it to Zambian Breweries but they didn’t have an ordering problem, they had a payment problem.So we started building a supplier payments offering.” Zambian Breweries used Zoona technology to collect payments from its micro beverage distributors, paying Zoona a percentage of the fees on the payments it received. While Zoona still serves roughly 400 of Zambian Breweries’ distributors today, this product did not reach the scale that the team expected.

21 PROFIT has since ended and a new organization, Musika, is continuing much of the work PROFIT was doing in Zambia.

8

A Case Study on Third Party Innovation in Digital FinanceZoona

Finally, in 2012, the day of reckoning came: Airtel and MTN both launched mobile money with fanfare and glitzy marketing campaigns. Surprisingly, Zoona saw no loss in business with the added competition. There was no decrease in numbers and money transfers kept growing.

Still, Zoona was not convinced it could take on the goliaths. In 2013, it entered into an exclusive partnership agreement with Airtel. Through the partnership, all Zoona customers would be migrated on to the Airtel wallets. In exchange, Zoona would receive a fixed percentage of revenue and expand with Airtel. Zoona actually offered higher commissions to agents and lower fees to end-users on Airtel transactions to incentivize the Airtel product. Nevertheless Zoona’s transfers were not significantly affected. Instead, agents and users alike began complaining about technical malfunctions with the product, eventually leading to the dissolution of the partnership.

A year later, in 2014, the mobile operators were still struggling to keep their agents and users active and Zoona made the strategic decision to focus their entire strategy on growing money transfers. “It took us quite a long time to get to actually put our necks out and say we are a money transfer business at our core,” says Mike. “We needed to be sure that we have a value proposition that can compete with those of other providers and we learned that we have.” E. Looking aheadWhile it may be premature to say that Zoona has established a new, successful model for delivering financial services, things look good. The focus since 2014 has been on scaling. This time, Zoona is innovating around a core proven offer instead of focusing on a variety of services. Growth in 2014, demonstrated below, was steady and strong.

However, competition is fierce, with entrants joining the fray on a regular basis. Zoona is still fleshing out what it means to focus entirely on money transfers. For example, Zoona has begun rolling out its newest agent model, which creates a tiered management system of agents by adding a middle class of agents called “aggregators”. The aggregator model is similar to the master agent model in many other countries, such as Kenya and India. High-performing Zoona agents will be trained as aggregators, responsible for recruiting new agents. These aggregators will train and support new agents, splitting the new agents’ commissions. Essentially, Zoona is slowly outsourcing its recruitment, onboarding and training functions to existing agents, hoping to minimize the investment necessary to expand the agent network.

The implications of this new model should not be underestimated: recruiting, onboarding and managing agents is one of the most difficult aspects of delivering financial services. Just because one agent has succeeded on their own does not necessarily mean that they can teach others as well. As of now, there is no plan for graduating these aggregated agents; the aggregated agent splits his commission with the aggregator indefinitely. However, once new agents are established, they will no longer need the training and support services of the aggregator agent and will have no incentive to continue splitting commission.

9

Zoona

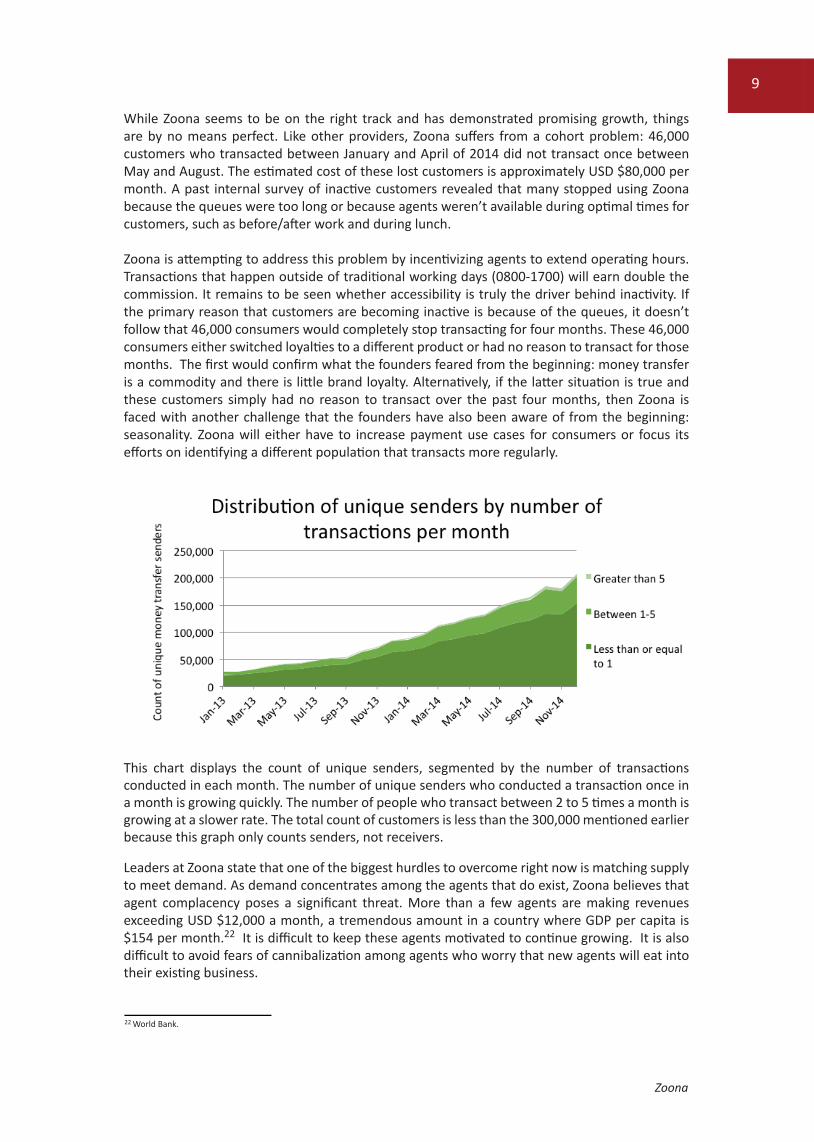

While Zoona seems to be on the right track and has demonstrated promising growth, things are by no means perfect. Like other providers, Zoona suffers from a cohort problem: 46,000 customers who transacted between January and April of 2014 did not transact once between May and August. The estimated cost of these lost customers is approximately USD $80,000 per month. A past internal survey of inactive customers revealed that many stopped using Zoona because the queues were too long or because agents weren’t available during optimal times for customers, such as before/after work and during lunch.

Zoona is attempting to address this problem by incentivizing agents to extend operating hours. Transactions that happen outside of traditional working days (0800-1700) will earn double the commission. It remains to be seen whether accessibility is truly the driver behind inactivity. If the primary reason that customers are becoming inactive is because of the queues, it doesn’t follow that 46,000 consumers would completely stop transacting for four months. These 46,000 consumers either switched loyalties to a different product or had no reason to transact for those months. The first would confirm what the founders feared from the beginning: money transfer is a commodity and there is little brand loyalty. Alternatively, if the latter situation is true and these customers simply had no reason to transact over the past four months, then Zoona is faced with another challenge that the founders have also been aware of from the beginning: seasonality. Zoona will either have to increase payment use cases for consumers or focus its efforts on identifying a different population that transacts more regularly.

This chart displays the count of unique senders, segmented by the number of transactions conducted in each month. The number of unique senders who conducted a transaction once in a month is growing quickly. The number of people who transact between 2 to 5 times a month is growing at a slower rate. The total count of customers is less than the 300,000 mentioned earlier because this graph only counts senders, not receivers.

Leaders at Zoona state that one of the biggest hurdles to overcome right now is matching supply to meet demand. As demand concentrates among the agents that do exist, Zoona believes that agent complacency poses a significant threat. More than a few agents are making revenues exceeding USD $12,000 a month, a tremendous amount in a country where GDP per capita is $154 per month.22 It is difficult to keep these agents motivated to continue growing. It is also difficult to avoid fears of cannibalization among agents who worry that new agents will eat into their existing business.

22 World Bank.

10

A Case Study on Third Party Innovation in Digital FinanceZoona

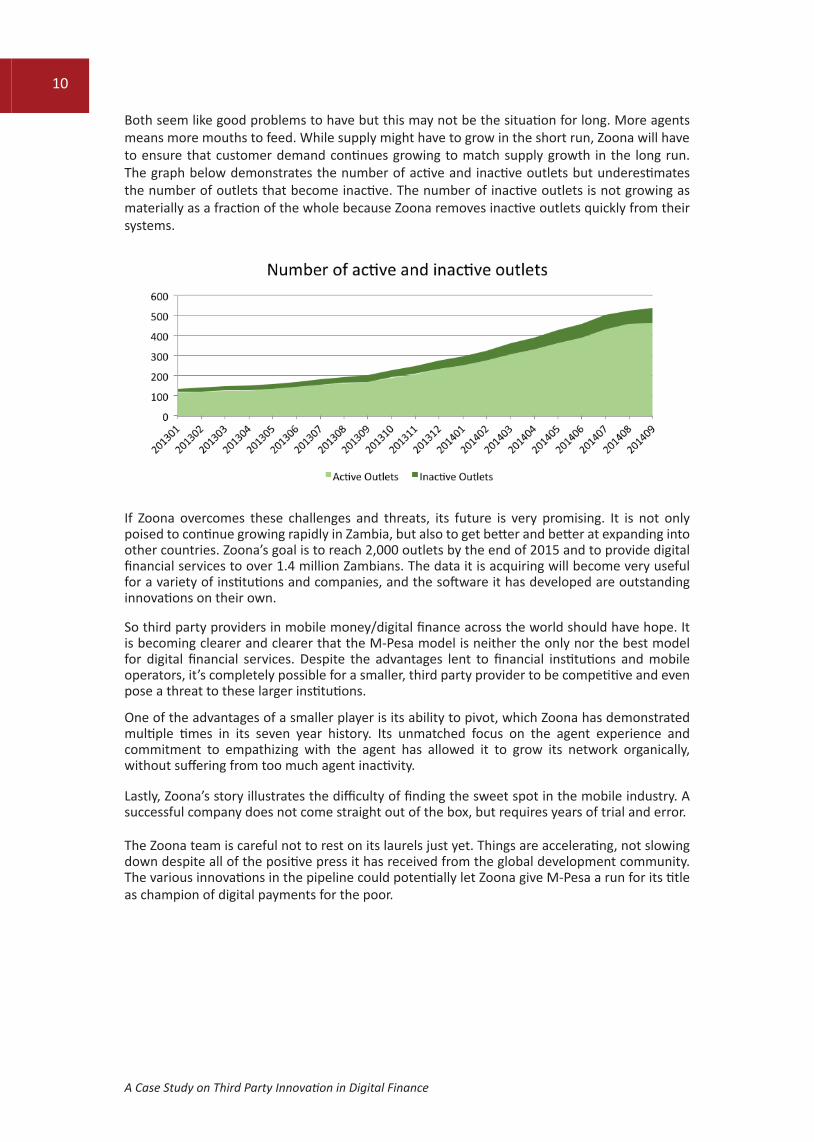

Both seem like good problems to have but this may not be the situation for long. More agents means more mouths to feed. While supply might have to grow in the short run, Zoona will have to ensure that customer demand continues growing to match supply growth in the long run. The graph below demonstrates the number of active and inactive outlets but underestimates the number of outlets that become inactive. The number of inactive outlets is not growing as materially as a fraction of the whole because Zoona removes inactive outlets quickly from their systems.

If Zoona overcomes these challenges and threats, its future is very promising. It is not only poised to continue growing rapidly in Zambia, but also to get better and better at expanding into other countries. Zoona’s goal is to reach 2,000 outlets by the end of 2015 and to provide digital financial services to over 1.4 million Zambians. The data it is acquiring will become very useful for a variety of institutions and companies, and the software it has developed are outstanding innovations on their own.

So third party providers in mobile money/digital finance across the world should have hope. It is becoming clearer and clearer that the M-Pesa model is neither the only nor the best model for digital financial services. Despite the advantages lent to financial institutions and mobile operators, it’s completely possible for a smaller, third party provider to be competitive and even pose a threat to these larger institutions.

One of the advantages of a smaller player is its ability to pivot, which Zoona has demonstrated multiple times in its seven year history. Its unmatched focus on the agent experience and commitment to empathizing with the agent has allowed it to grow its network organically, without suffering from too much agent inactivity.

Lastly, Zoona’s story illustrates the difficulty of finding the sweet spot in the mobile industry. A successful company does not come straight out of the box, but requires years of trial and error.

The Zoona team is careful not to rest on its laurels just yet. Things are accelerating, not slowing down despite all of the positive press it has received from the global development community. The various innovations in the pipeline could potentially let Zoona give M-Pesa a run for its title as champion of digital payments for the poor.

About FSDZFinancial Sector Deepening Zambia was established in 2013 by the UK’s Department for International Development (DFID) with the mandate to increase financial inclusion in Zambia. FSDZ aims to support public and private sector efforts to develop an efficient and vibrant financial sector offering a wide range of financial services through diverse channels to individuals, households and micro, small and medium enterprises. FSDZ provides temporary and catalytic support to key stakeholders with the ultimate goal to support the development of a financial market system that works better for lower income communities.

The Zambian financial services market operates in an information-poor environment. In particular, there is very limited understanding of demand—how low-income households manage their financial lives and the type of financial services they need—and the service and policy implications that flow from this. Addressing these fundamental information constraints is at the heart of the market development challenge and therefore of FSDZ’s mission. FSDZ’s work is shaped by a common, central role: knowledge generation. To this end, FSDZ seeks to provide independent, high quality, insightful analyses on financial services (and especially financial inclusion). Specifically, it seeks to better understand demand and supply through quantitative research.

This report was commissioned by FSD Zambia. The findings, interpretations and conclusions are those of the author and do not necessarily represent those of FSD Zambia and partner organizations.

Financial Sector Deepening ZambiaIncito II 377A Kabulonga Road, Lusaka, Zambia

T: +260 211 848 065/6 | E: [email protected] | W: www.fsdzambia.org@fsdzambia Financial Sector Deepening Zambia Financial Sector Deepening Zambia