Embed Size (px)

Citation preview

International capital �ows and global imbalances

Sewon Hur

University of Pittsburgh

March 3, 2015

International Finance (Sewon Hur) Lecture 4 March 3, 2015 1 / 38

International capital �ows and global imbalances

Lucas (1990) - Why Doesn't Capital Flow from Rich to Poor

Countries?

Gourinchas and Jeanne (2011) - Capital Flows to Developing

Countries: The Allocation Puzzle

Mendoza, Quadrini, Rios-Rull (2009) - Financial Integration,

Financial Development and Global Imbalances

International Finance (Sewon Hur) Lecture 4 March 3, 2015 2 / 38

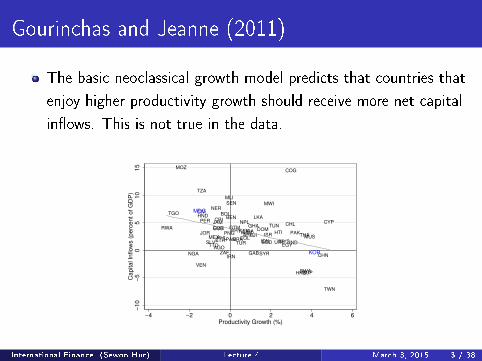

Gourinchas and Jeanne (2011)

The basic neoclassical growth model predicts that countries that

enjoy higher productivity growth should receive more net capital

in�ows. This is not true in the data.

AGO

ARG

BEN

BGD

BOL

BRA

BWA

CHL

CHN

CIV

CMR

COG

COL

CRICYP

DOMECU

EGYETH

FJI

GAB

GHAGTM

HKG

HND

HTI

IDN IND

IRN

ISR

JAM

JOR KEN

LKA

MARMEX

MLI

MOZ

MUS

MWI

MYS

NER

NGA

NPL

PAK

PAN

PER

PHLPNG

PRYRWA

SEN

SGP

SLV

SYR

TGO

THA

TTO

TUN

TUR

TWN

TZA

UGA

URY

VEN

ZAF KOR

MDG

−10

−5

05

10

15

Cap

ita

l In

flo

ws (

perc

en

t of

GD

P)

−4 −2 0 2 4 6Productivity Growth (%)

Figure 1: Average productivity growth and average capital inflows between 1980 and 2000.

wedge that distorts investment decisions, and one wedge that distorts saving decisions. It isthen possible, for each country in our sample, to estimate the saving and investment wedgesthat are required to explain the observed levels of savings and investment (and thereforeof net capital flows). We find that the investment wedge cannot, by itself, explain theallocation puzzle, and that solving the allocation puzzle requires a saving wedge that isstrongly negatively correlated with productivity growth. That is, the allocation puzzle is asaving puzzle.

We then look at a decomposition of international capital flows into public and privateflows, similar to Aguiar and Amador (2011). We confirm that paper’s finding that the alloca-tion puzzle is mostly a feature of public flows, and in addition find that the accumulation ofinternational reserves plays a role in generating the puzzle. However, we do not find robustevidence that private flows conform to the predictions of theory.

What can explain this puzzling allocation of capital flows across developing countries?Our wedge analysis shows that the explanation must involve the relationship between savingsand growth, and our flow decomposition suggests that reserve accumulation plays an impor-tant role. This suggests to us that the solution to the allocation puzzle should be lookedfor at the nexus between growth, saving, and reserve accumulation. Why do countries thatgrow more also accumulate more reserves, and why is this reserve accumulation not offsetby capital inflows to the private sector? We discuss possible explanations at the end of thepaper—some of which were developed since the first version of this paper was circulated. Noattempt is made to discriminate empirically between these explanations —the objective ofthe last section of the paper being to propose a road map for future research rather than toestablish new results.

This paper lies at the confluence of different lines of literature. First, it is related to the

2

International Finance (Sewon Hur) Lecture 4 March 3, 2015 3 / 38

Model

Small open economy that can borrow and lend at world interest

rate R∗

Time is discrete and there is no uncertainty

Technology: Yt = Kαt (AtLt)

1−α

Labor supply is exogenous, equal to the population Lt = Nt

Resource constraint:

Ct + It + R∗D = Yt + Dt+1

It = Kt+1 − (1− δ)Kt

Country's external debt Dt

International Finance (Sewon Hur) Lecture 4 March 3, 2015 4 / 38

Model

Capital in�ows Dt+1 − Dt is equal to domestic investment It

minus savings St = Yt − (R∗ − 1)Dt − Ct

Rt = α(kt/At)α−1 + 1− δ where kt = Kt/Nt

Since Rt = R∗ in equilibrium,

kt = k∗ ≡(

α

R∗ + δ − 1

)1/(1−α)

where k = k/A (capital stock per e�cient unit of labor)

International Finance (Sewon Hur) Lecture 4 March 3, 2015 5 / 38

Model

Exogenous, deterministic productivity path, {At}t=0,..∞,

At ≤ A∗t = A∗0 (g ∗)t

where g ∗ − 1 is the growth rate of the world technology frontier

Gap between domestic productivity and the productivity with no

�catch-up�

πt ≡At

A0 (g ∗)t− 1

Growth rate always converges to g ∗ , and π ≡ limt→∞ πt is

well-de�ned.

International Finance (Sewon Hur) Lecture 4 March 3, 2015 6 / 38

Model

Representative household solves

max∞∑

s=0

βsu(ct+s)

s.t. Ct + Kt+1 ≤ R∗Kt + (Dt+1 − R∗Dt) + wtNt

where u(c) = log(c), wt = (1− α)kαt A1−αt

Euler equation

1

ct= βR∗

1

ct+1

Assume R∗ =g ∗

β, which holds if ROW is composed of developed

economies that have the same preferences and are in steady

state BGP.International Finance (Sewon Hur) Lecture 4 March 3, 2015 7 / 38

Capital Flows and Productivity Catch-Up

1 If k0 = k∗ (optimal initial capital) and d0 = 0 (no initial debt),

then the country receives positive net capital in�ows i� π > 0.

Capital �ows into the developing countries whose TFP catches

up relative to the world frontier, and �ows out of the countries

whose TFP falls behind.

2 If identical except for long-run productivity catch-up, then

country A receives more capital in�ows i� it catches up more

than country B, i.e. πA > πB .

Other things equal, countries that grow faster should receive

more capital �ows.

The opposite is true in the data, hence the puzzle.

International Finance (Sewon Hur) Lecture 4 March 3, 2015 8 / 38

Capital Flows and Productivity Catch-Up

Data: 65 non-OECD countries + Korea, Mexico, Turkey (1980-2000)

KOR

TWN

BGD

HKG

PNG

CHN

IDNPHL

SGP

LKA

PAK

FJI INDTUR

MYS

THANPL

BOL

PAN

VEN

HTI

COLPRYCRIMEXSLVTTO

PER

ARG

URYBRAGTM DOM

JAM

HNDECU

CHL

ISRBEN

NGA

MOZ

TGO

TZAJOR

CIV

MAR MUSIRN

MLI

COG

SYRZAF

NER MWIGHA

RWA

AGOSEN

KEN

MDG UGA

BWA

TUN CYP

ETHGAB EGY

CMR

-2.0

0-1

.00

0.00

1.00

2.00

Capi

tal I

nflow

s (re

lativ

e to

initia

l out

put)

-0.75 -0.50 -0.25 0.00 0.25 0.50 0.75 1.00Productivity Catch-Up

Predicted: investment saving

Figure 2: Productivity catch-up (π) and change in external debt (∆D/Y0) together withpredicted investment

(∆DI/Y0

)and predicted saving

(∆DS/Y0

)terms.

significant at the 1 percent level.21

In addition to confirming, with different measures, the basic correlation already shownin Figure 1, Figure 2 compares the data to the prediction of the basic neoclassical growthframework. We observe that capital flows are not only negatively correlated with the modelpredictions but also tend to be smaller in absolute value. This is especially true if we look atthe saving component, which implies that a one percentage point increase in the productivitycatch-up variable π should raise capital inflows by 5.25 percent of initial output.22 For acountry such as Korea, with a productivity catch up π equal to 0.61, the model predictsinvestment and saving components of net capital inflows each in excess of 130 percent ofinitial output. Conversely, for Madagascar, with a relative productivity decline π equal to-0.47, the model predicts investment and saving components of net capital outflows each inexcess of 100 percent of initial output!

As noted at the end of section 2, the saving component is very responsive to growth in themodel because of the assumption that consumers are infinitely-lived and can perfectly smoothconsumption. Introducing financial frictions or assuming different preference structures couldreduce significantly the importance of the saving component.23 By contrast, observed flows

21The slope of the regression line in figure 2 is -0.68 with a s.e. of 0.18 (p-value smaller than 0.01).22The slope of the investment term ∆Di/Y0 is (ng∗)20 = 2.14 while the slope of the saving term ∆Ds/Y0

is (1 + (1− α)k∗(α−1)/R∗∑19t=0 (ng∗)t (1− t/20) (ng∗)20 = 5.25.

23In the limit case where households cannot access financial markets, the saving component would equalzero.

13

International Finance (Sewon Hur) Lecture 4 March 3, 2015 9 / 38

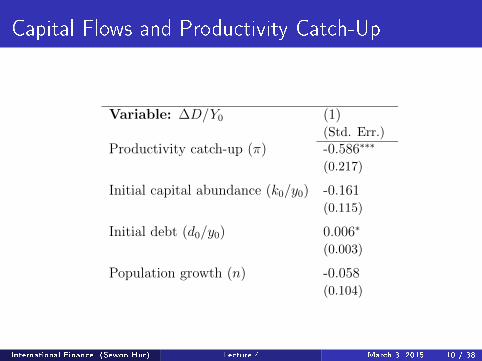

Capital Flows and Productivity Catch-Up

Variable: ∆D/Y0 (1) (2) (3)(Std. Err.) (Std. Err.) (Std. Err.)

Productivity catch-up (π) -0.586∗∗∗ -0.456∗∗ -0.697∗∗∗

(0.217) (0.209) (0.227)

Initial capital abundance (k0/y0) -0.161 -0.126 -0.081(0.115) (0.109) (0.107)

Initial debt (d0/y0) 0.006∗ 0.004 0.001(0.003) (0.003) (0.003)

Population growth (n) -0.058 -0.098 -0.073(0.104) (0.099) (0.096)

Openness (Chinn-Ito) -0.141∗∗ -0.115∗

(0.063) (0.062)

Openness x π -0.455∗

(0.197)

Intercept 0.516 0.576 0.536(0.315) (0.299) (0.289)

Number of observations 68 67 67Adjusted-R2 0.174 0.157 0.214

Table 2: Estimation results : Regression of observed capital inflows ∆D/Y0 on initial condi-tions (capital abundance, external debt), population growth, productivity catch-up (π) andthe Chinn and Ito (2008) index of capital account openness.

International Finance (Sewon Hur) Lecture 4 March 3, 2015 10 / 38

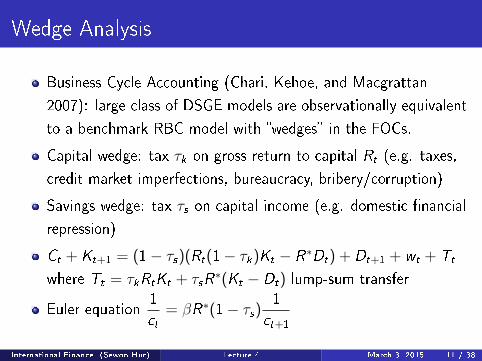

Wedge Analysis

Business Cycle Accounting (Chari, Kehoe, and Macgrattan

2007): large class of DSGE models are observationally equivalent

to a benchmark RBC model with �wedges� in the FOCs.

Capital wedge: tax τk on gross return to capital Rt (e.g. taxes,

credit market imperfections, bureaucracy, bribery/corruption)

Savings wedge: tax τs on capital income (e.g. domestic �nancial

repression)

Ct + Kt+1 = (1− τs)(Rt(1− τk)Kt − R∗Dt) + Dt+1 + wt + Tt

where Tt = τkRtKt + τsR∗(Kt − Dt) lump-sum transfer

Euler equation1

ct= βR∗(1− τs)

1

ct+1

International Finance (Sewon Hur) Lecture 4 March 3, 2015 11 / 38

Capital Wedge

Capital and savings wedges can be calculated to match

investment and savings rates

Capital wedge lower in high productivity growth economies

(better institutions and lower distortions)

AGO

ARG

BEN

BGDBOL

BRA

BWA

CHLCHN

CIV CMR

COG

COL

CRI

CYP

DOM

ECU

EGY

ETH

FJI

GAB

GHAGTM

HKG

HND

HTI

IDN

IND

IRNISRJAM

JOR

KEN

KOR

LKA

MAR

MDG

MEX

MLI

MOZ

MUSMWI

MYS

NERNGA

NPL

PAK

PANPER

PHL

PNG

PRY

RWA

SEN

SGP

SLV

SYR

TGO

THA

TTOTUN

TURTWN

TZA

UGA

URY

VEN

ZAF

01

02

03

04

05

0

Capital W

edge (

%)

−.75 −.5 −.25 0 .25 .5 .75 1

Productivity Catch−Up

Figure 3: Productivity catch-up (π) and capital wedge (τ k).

AGO ARG

BEN

BGD

BOL

BRA

BWA

CHL

CHN

CIV

CMR

COG

COL

CRI

CYP

DOM

ECU

EGY

ETH

FJIGABGHA

GTM

HKG

HND

HTIIDN

IND

IRN

ISR

JAM

JOR

KEN

LKA

MAR

MEX

MLI

MOZ

MUS

MWI

MYS

NER

NGA

NPL

PAK

PAN

PER

PHLPNGPRY

RWA

SEN

SGP

SLV

SYR

TGO

THA

TTO

TUN

TUR

TWN

TZA

UGA

URY

VEN

ZAF

KOR

MDG

−2

0−

10

01

02

0

Pre

dic

ted C

hange in E

xte

rnal D

ebt (r

ela

tive to initia

l outp

ut)

−.75 −.5 −.25 0 .25 .5 .75 1

Productivity Catch−Up

Figure 4: Productivity catch-up (π) and capital inflows(

∆DY0

)predicted by the model with

capital wedges.

18

International Finance (Sewon Hur) Lecture 4 March 3, 2015 12 / 38

Capital Wedge

This worsens the allocation puzzle

Plot of productivity catch-up and capital in�ows predicted by the

model with capital wedges

AGO

ARG

BEN

BGDBOL

BRA

BWA

CHLCHN

CIV CMR

COG

COL

CRI

CYP

DOM

ECU

EGY

ETH

FJI

GAB

GHAGTM

HKG

HND

HTI

IDN

IND

IRNISRJAM

JOR

KEN

KOR

LKA

MAR

MDG

MEX

MLI

MOZ

MUSMWI

MYS

NERNGA

NPL

PAK

PANPER

PHL

PNG

PRY

RWA

SEN

SGP

SLV

SYR

TGO

THA

TTOTUN

TURTWN

TZA

UGA

URY

VEN

ZAF

01

02

03

04

05

0

Capital W

edge (

%)

−.75 −.5 −.25 0 .25 .5 .75 1

Productivity Catch−Up

Figure 3: Productivity catch-up (π) and capital wedge (τ k).

AGO ARG

BEN

BGD

BOL

BRA

BWA

CHL

CHN

CIV

CMR

COG

COL

CRI

CYP

DOM

ECU

EGY

ETH

FJIGABGHA

GTM

HKG

HND

HTIIDN

IND

IRN

ISR

JAM

JOR

KEN

LKA

MAR

MEX

MLI

MOZ

MUS

MWI

MYS

NER

NGA

NPL

PAK

PAN

PER

PHLPNGPRY

RWA

SEN

SGP

SLV

SYR

TGO

THA

TTO

TUN

TUR

TWN

TZA

UGA

URY

VEN

ZAF

KOR

MDG

−2

0−

10

01

02

0

Pre

dic

ted C

hange in E

xte

rnal D

ebt (r

ela

tive to initia

l outp

ut)

−.75 −.5 −.25 0 .25 .5 .75 1

Productivity Catch−Up

Figure 4: Productivity catch-up (π) and capital inflows(

∆DY0

)predicted by the model with

capital wedges.

18

International Finance (Sewon Hur) Lecture 4 March 3, 2015 13 / 38

Private Returns Equalization

Naive private returns Rn ≡ αY /K − δWedge-adjusted returns (1− τk)(1 + Rn)− 1

AGO

ARG

BEN

BGDBOL

BRA

BWA

CHLCHN

CIV

CMRCOG COL

CRICYP

DOM

ECU

EGY

ETH

FJIGAB

GHAGTM

HKGHND

HTI

IDN

IND

IRNISRJAM

JOR

KEN

KOR

LKAMAR

MDG

MEX

MLI

MOZ

MUS

MWI

MYS

NER

NGANPL

PAK

PANPERPHL

PNGPRY

RWA

SEN

SGP

SLVSYR

TGO

THA

TTOTUNTUR TWN

TZA

UGA

URYVEN

ZAF

020

40

60

80

100

120

Naiv

e M

PK

(perc

ent)

0 10000 20000 30000

Real GDP per capita (2000)

AGO ARGBENBGDBOL BRABWACHLCHNCIV

CMR

COG

COLCRI CYPDOMECUEGY

ETH FJI GABGHAGTM HKGHND

HTI

IDNIND

IRNISRJAM

JORKEN KORLKAMAR

MDGMEX

MLIMOZ MUS

MWI

MYS

NER

NGA

NPLPAK PANPERPHLPNGPRYRWA

SEN SGPSLVSYR

TGOTHA

TTOTUNTUR TWN

TZA

UGA

URYVENZAF0

20

40

60

80

100

120

Wedge−

Adju

ste

d M

PK

(perc

ent)

0 10000 20000 30000

Real GDP per capita (2000)

Figure 5: Naıve and Wedge-adjusted Marginal Product of Capital in year 2000.

As a final comment, it is interesting to note that the capital wedge plays a similar roleas adjusting for non-reproducible capital and relative price effects discussed in Caselli andFeyrer (2007). Those authors argue that, while naıve estimates of the marginal productof capital vary enormously across countries, the returns to capital are essentially the sameonce the estimates are adjusted for cross-country differences in the share of non-reproduciblecapital in total capital and in the price of reproducible capital in terms of output, whichare both higher in less advanced countries. Our approach leads to the same cross-countrycompression in the estimates of the returns on capital, but this is achieved by the capitalwedge τ k.

To illustrate this point, Figure 5 compares the naive estimate of private returns (leftpanel), defined as RN = αY/K − δ, and the wedge-adjusted return (right panel), RW =(1− τ k) (1 +RN) − 1, against 2000 income per capita. The left panel indicates enormousvariation in the naıve estimate, between 3.6 percent (Singapore) and 110 percent (Haiti),with a mean of 22.3 percent. By contrast, the wedge-adjusted return varies between -2.5percent (Nigeria) and 43 percent (Haiti, a clear outlier), with a mean of 6.3 percent. Theamount of compression is remarkable, given that the capital wedge is not calibrated to ensureprivate returns equalization. Our results thus parallel those of Caselli and Feyrer (2007):private returns to capital appear remarkably similar across countries.34

To summarize, introducing investment wedges to match observed investment rates intothe model does not help to solve the allocation puzzle, but is consistent with the equalizationof private returns to capital across countries. We now turn to the saving wedges.

34In Gourinchas and Jeanne (2007) we also look at the correlation between productivity growth and capitalinflows when productivity is measured based on the model with non-reproducible capital of Caselli and Feyrer(2007). We find the same negative correlation.

19

International Finance (Sewon Hur) Lecture 4 March 3, 2015 14 / 38

Savings Wedge

Savings wedge lower in high productivity growth economies

(subsidize vs tax)

AGO

ARG

BEN

BGD

BOL

BRA

BWA

CHL

CHN

CIV

CMR

COG

COL

CRI

CYP

DOM

ECU

EGY

ETH

FJIGABGHA

GTM

HKG

HND

HTIIDN

IND

IRN

ISR

JAMJOR

KEN

LKA

MAR

MEX

MLI

MOZ

MUS

MWI

MYS

NERNGA

NPL

PAK

PAN

PER

PHLPNG

PRY

RWA

SEN

SGP

SLV

SYR

TGO

THA

TTO

TUN

TUR

TWN

TZA

UGA

URY

VEN

ZAF

KOR

MDG

−5

05

Savin

g W

edge (

perc

ent)

−.75 −.5 −.25 0 .25 .5 .75 1

Productivity Catch−Up

Figure 6: Productivity catch-up (π) and saving wedges (τ s).

productivity catch-up and distortions in the accumulation of domestic capital summarizedby the capital wedge τ k. Not surprisingly, the convergence component is positive for Asiaand Latin America (capital scarce regions) and negative for Africa (capital abundant), whilethe investment component is positive for Asia (productivity catch-up) and negative for LatinAmerica and Africa (productivity decline). The sum of these two terms is negatively corre-lated with observed capital inflows.

This illustrates the extent to which the allocation puzzle is a saving puzzle: adjustinginvestment rates to account for physical capital accumulation is not enough to account forpatterns of capital flows across countries. The saving wedge is essential to account forthe observed pattern of net capital flows across developing countries. Our wedge analysisindicates that Asia subsidizes saving (τ s = −1.14 percent) whereas Latin America and Africatax savings similarly (τ s = 1.8 percent). Similarly, the saving tax decreases with levels ofdevelopment.

5 Public vs. private flows

Having established that the allocation puzzle is a saving puzzle, we now offer a different cutof the data. This section documents differences between the behavior of public capital flows(defined as flows that go to or emanates from the public sector) and that of private flows(defined as the residual). We look first at official aid flows, and then at broader measures ofpublic flows.38 One could argue that the basic neoclassical framework may not be appropriate

38Our results on aid flows were reported in previous versions of this paper. The analysis was extended topublic flows as defined by Aguiar and Amador (2011) following a suggestion of the editor and referees.

21

International Finance (Sewon Hur) Lecture 4 March 3, 2015 15 / 38

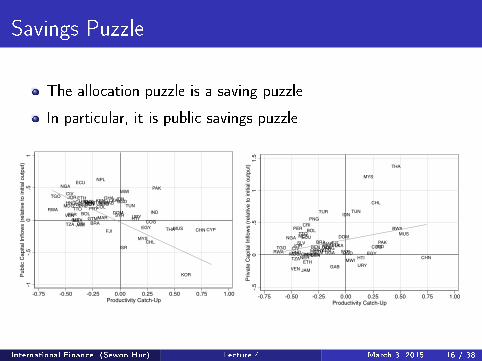

Savings Puzzle

The allocation puzzle is a saving puzzle

In particular, it is public savings puzzle

PHLIND

PAK

KOR

MYS

CHNTHA

IDN

NPL

FJI

PNG BGDTUR LKA

ECU

BOLGTM

COL

HTI

PAN

SLVURYVEN

BRACRI

HND

PERPRY

DOMTTO

CHL

JAM

ARG

MEX

MWI

TUNCMR

SYR

KEN

MUS

NER GAB

TZA

SENRWA

JOR

COG

ISR

BENTGO

CYPEGY

CIVNGA

ETHMDG

UGA

MAR

MLIGHA

-1-.5

0.5

1Pu

blic

Capi

tal I

nflow

s (re

lativ

e to

initia

l out

put)

-0.75 -0.50 -0.25 0.00 0.25 0.50 0.75 1.00Productivity Catch-Up

(a) Net Public Capital Inflows

PNG

FJI PAK

THA

IND

MYS

LKABGD

NPL

PHL

IDN

CHN

TUR

URYVEN

HND

BRACOL

DOM

JAM

ECU

HTI

PER BOL

GTMPAN

MEX

ARGPRY

CHL

SLV

TTO

CRI

BEN MAR

EGYSYR

MWI

COGTGO CIVRWA CMRNERETH

TUN

GHA

SENMDG

NGA

BWA

JORMLI UGA

TZAKEN

GAB

MUS

-.50

.51

1.5

Priva

te C

apita

l Infl

ows

(rela

tive

to in

itial o

utpu

t)

-0.75 -0.50 -0.25 0.00 0.25 0.50 0.75 1.00Productivity Catch-Up

(b) Net Private Capital Inflows

Note: top panel reports ∆Dpub/Y0 against π. Bottom panel reports ∆Dpriv/Y0 against π.

Figure 8: Productivity catch-up (π) and change in public and private external debt.

26

PHLIND

PAK

KOR

MYS

CHNTHA

IDN

NPL

FJI

PNG BGDTUR LKA

ECU

BOLGTM

COL

HTI

PAN

SLVURYVEN

BRACRI

HND

PERPRY

DOMTTO

CHL

JAM

ARG

MEX

MWI

TUNCMR

SYR

KEN

MUS

NER GAB

TZA

SENRWA

JOR

COG

ISR

BENTGO

CYPEGY

CIVNGA

ETHMDG

UGA

MAR

MLIGHA

-1-.5

0.5

1Pu

blic

Capi

tal I

nflow

s (re

lativ

e to

initia

l out

put)

-0.75 -0.50 -0.25 0.00 0.25 0.50 0.75 1.00Productivity Catch-Up

(a) Net Public Capital Inflows

PNG

FJI PAK

THA

IND

MYS

LKABGD

NPL

PHL

IDN

CHN

TUR

URYVEN

HND

BRACOL

DOM

JAM

ECU

HTI

PER BOL

GTMPAN

MEX

ARGPRY

CHL

SLV

TTO

CRI

BEN MAR

EGYSYR

MWI

COGTGO CIVRWA CMRNERETH

TUN

GHA

SENMDG

NGA

BWA

JORMLI UGA

TZAKEN

GAB

MUS

-.50

.51

1.5

Priva

te C

apita

l Infl

ows

(rela

tive

to in

itial o

utpu

t)

-0.75 -0.50 -0.25 0.00 0.25 0.50 0.75 1.00Productivity Catch-Up

(b) Net Private Capital Inflows

Note: top panel reports ∆Dpub/Y0 against π. Bottom panel reports ∆Dpriv/Y0 against π.

Figure 8: Productivity catch-up (π) and change in public and private external debt.

26

International Finance (Sewon Hur) Lecture 4 March 3, 2015 16 / 38

Savings Puzzle

Why are emerging economies accumulating so much foreign

reserves (savings)?

Recent papers on reserves accumulation

reserves to smooth consumption against exogenous crises: Alfaro

and Kanczuk (2009), Bianchi et al. (2012), Caballero and

Panageas (2007), Jeanne and Ranciere (2011)

NFA prevents crises: Durdu et al (2009), Mendoza (2010)

reserves prevent crises: Hur and Kondo (2013), Kim (2008)

International Finance (Sewon Hur) Lecture 4 March 3, 2015 17 / 38

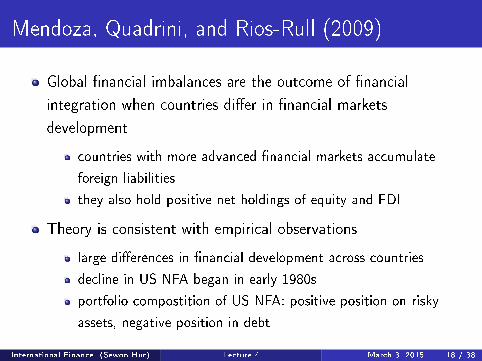

Mendoza, Quadrini, and Rios-Rull (2009)

Global �nancial imbalances are the outcome of �nancial

integration when countries di�er in �nancial markets

development

countries with more advanced �nancial markets accumulate

foreign liabilities

they also hold positive net holdings of equity and FDI

Theory is consistent with empirical observations

large di�erences in �nancial development across countries

decline in US NFA began in early 1980s

portfolio compostition of US NFA: positive position on risky

assets, negative position in debt

International Finance (Sewon Hur) Lecture 4 March 3, 2015 18 / 38

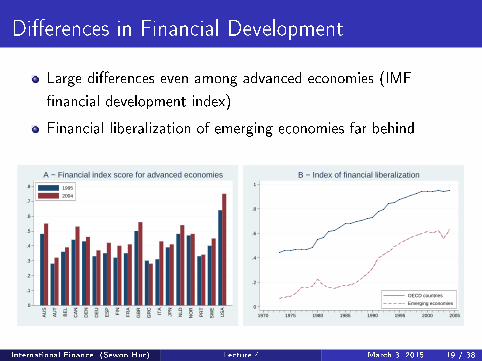

Di�erences in Financial Development

Large di�erences even among advanced economies (IMF

�nancial development index)

Financial liberalization of emerging economies far behind

0

.1

.2

.3

.4

.5

.6

.7

.8

AU

S

AU

T

BE

L

CA

N

DE

N

DE

U

ES

P

FIN

FR

A

GB

R

GR

C

ITA

JPN

NLD

NO

R

PR

T

SW

E

US

A

A − Financial index score for advanced economies

1995

2004

0

.2

.4

.6

.8

1

1970 1975 1980 1985 1990 1995 2000 2005

OECD countries

Emerging economies

B − Index of financial liberalization

Figure 1: Indices of financial markets heterogeneity. The index in panel Ais from IMF (2006). The index in panel B is from Abiad, Detragiache andTressel (2007). See appendix A for the definition of variables.

3

0

.1

.2

.3

.4

.5

.6

.7

.8

AU

S

AU

T

BE

L

CA

N

DE

N

DE

U

ES

P

FIN

FR

A

GB

R

GR

C

ITA

JPN

NLD

NO

R

PR

T

SW

E

US

A

A − Financial index score for advanced economies

1995

2004

0

.2

.4

.6

.8

1

1970 1975 1980 1985 1990 1995 2000 2005

OECD countries

Emerging economies

B − Index of financial liberalization

Figure 1: Indices of financial markets heterogeneity. The index in panel Ais from IMF (2006). The index in panel B is from Abiad, Detragiache andTressel (2007). See appendix A for the definition of variables.

3

International Finance (Sewon Hur) Lecture 4 March 3, 2015 19 / 38

Composition of NFA

US increased risky assets and reduced riskless assets (net)

Emerging economies reduced risky assets and increased riskless

assets (net)

−10

−8

−6

−4

−2

0

2

4

Per

cent

of w

orld

GD

P

1970 1975 1980 1985 1990 1995 2000 2005

United States

OECD countries except US

Emerging economies

A − NFA in debt and international reserves

−10

−8

−6

−4

−2

0

2

4

Per

cent

of w

orld

GD

P

1970 1975 1980 1985 1990 1995 2000 2005

United States

OECD countries except US

Emerging economies

B − NFA in portfolio equity and FDI

Figure 3: Net foreign asset positions in debt instruments and risky assets.The graphs are constructed using data from Lane and Milesi-Ferretti (2006).See appendix A.

5

−10

−8

−6

−4

−2

0

2

4

Per

cent

of w

orld

GD

P

1970 1975 1980 1985 1990 1995 2000 2005

United States

OECD countries except US

Emerging economies

A − NFA in debt and international reserves

−10

−8

−6

−4

−2

0

2

4

Per

cent

of w

orld

GD

P

1970 1975 1980 1985 1990 1995 2000 2005

United States

OECD countries except US

Emerging economies

B − NFA in portfolio equity and FDI

Figure 3: Net foreign asset positions in debt instruments and risky assets.The graphs are constructed using data from Lane and Milesi-Ferretti (2006).See appendix A.

5

International Finance (Sewon Hur) Lecture 4 March 3, 2015 20 / 38

Model

Multi-country DSGE model with incomplete markets

Idiosyncratic shocks to endowment and investment

Two frictions: limited enforcement and limited liability

International Finance (Sewon Hur) Lecture 4 March 3, 2015 21 / 38

Simple Model

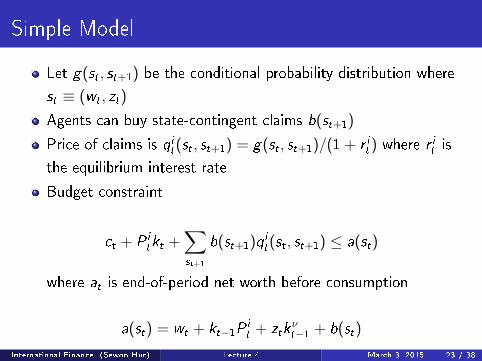

Two countries, i = 1, 2, each populated by continuum of agents

Each country endowed with unit supply of non-reproducible,

international immobile asset, traded at price P it

This asset can be used to produce yt+1 = zt+1kνt where zt+1 is

an idiosyncratic investment shock. Agents can invest

domestically or abroad, but not diversify (relaxed later)

Agents receive an idiosyncratic stochastic endowment wt , which

follows a Markov process

Maximize∑∞

t=0 βtU(ct)

No aggregate uncertainty

International Finance (Sewon Hur) Lecture 4 March 3, 2015 22 / 38

Simple Model

Let g(st , st+1) be the conditional probability distribution where

st ≡ (wt , zt)

Agents can buy state-contingent claims b(st+1)

Price of claims is qit(st , st+1) = g(st , st+1)/(1 + r it ) where r it is

the equilibrium interest rate

Budget constraint

ct + P itkt +

∑

st+1

b(st+1)qit(st , st+1) ≤ a(st)

where at is end-of-period net worth before consumption

a(st) = wt + kt−1Pit + ztk

νt−1 + b(st)

International Finance (Sewon Hur) Lecture 4 March 3, 2015 23 / 38

Financial Frictions

If markets were complete, agents would perfectly insure against

endowment and investment risks

Agents can divert 1− φi of income; φi represents degree of

enforcement

Two frictions: limited enforcement and limited liability

a(sj)− a(s1) ≥ (1− φi) [wj − w1 + (zj − z1)kνt ]

a(sj) ≥ 0

where s1 denotes the worst possible realization

φi = 1 implies constant consumption and φi = 0 implies no

insurance

International Finance (Sewon Hur) Lecture 4 March 3, 2015 24 / 38

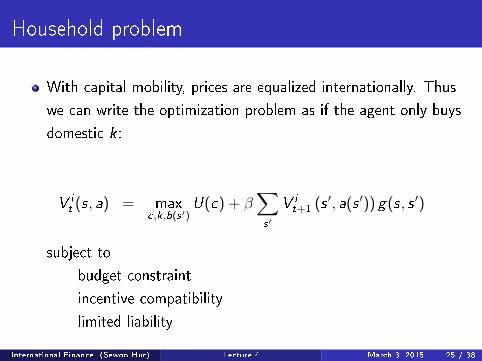

Household problem

With capital mobility, prices are equalized internationally. Thus

we can write the optimization problem as if the agent only buys

domestic k :

V it (s, a) = max

c,k,b(s′)U(c) + β

∑

s′

V it+1 (s ′, a(s ′)) g(s, s ′)

subject to

budget constraint

incentive compatibility

limited liability

International Finance (Sewon Hur) Lecture 4 March 3, 2015 25 / 38

Autarky Equilibrium

Given �nancial development φi and initial distributions M it(s, k , b) for

i = 1, 2, an autarky equilibrium is policy functions, value functions,

prices, and distributions such that

1 policy functions and value functions solve household problem

2 asset markets clear :´s,k,b

k itM

it(s, k , b) = 1,´

s,k,b,s′bit(s, a, s

′)M it(s, k , b)g(s, s ′) = 0 for i = 1, 2

3 distributions are consistent with initial distributions, individual

policies, and stochastic processes for idiosyncratic shocks

International Finance (Sewon Hur) Lecture 4 March 3, 2015 26 / 38

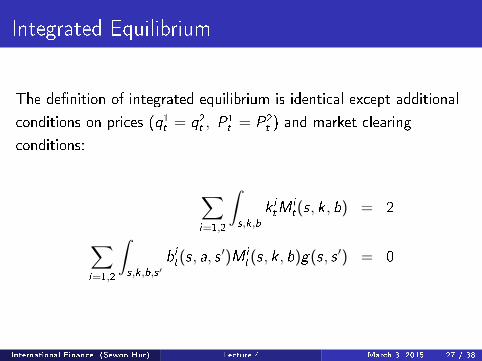

Integrated Equilibrium

The de�nition of integrated equilibrium is identical except additional

conditions on prices (q1t = q2

t , P1t = P2

t ) and market clearing

conditions:

∑

i=1,2

ˆs,k,b

k itM

it(s, k , b) = 2

∑

i=1,2

ˆs,k,b,s′

bit(s, a, s′)M i

t(s, k , b)g(s, s ′) = 0

International Finance (Sewon Hur) Lecture 4 March 3, 2015 27 / 38

Net foreign asset position

NFA of country i is given by

NFAit =

ˆs,k,b

bit(s, a, s′)M i

t(s, k , b)g(s, s ′)+

ˆs,k,b

[k it − 1

]PtM

it(s, k , b)

International Finance (Sewon Hur) Lecture 4 March 3, 2015 28 / 38

Characterization

First consider the case with endowment shocks only.

Financial autarky regime and φ = φ (such that IC not binding).

Then r = 1/β − 1 since agents can perfectly insure against

idiosyncratic risk, and there are no precautionary savings. Also

Rt+1 = 1 + rt

Financial autarky regime and φ = 0 (no state-contingent

claims). Then r < 1/β − 1 since agents cannot perfectly insure

against idiosyncratic risk, and there are precautionary savings

(since U ′ is convex). Also Rt+1 = 1 + rt

All agents invest k = 1 since marginal return on productive asset

is equal to the interest rate

International Finance (Sewon Hur) Lecture 4 March 3, 2015 29 / 38

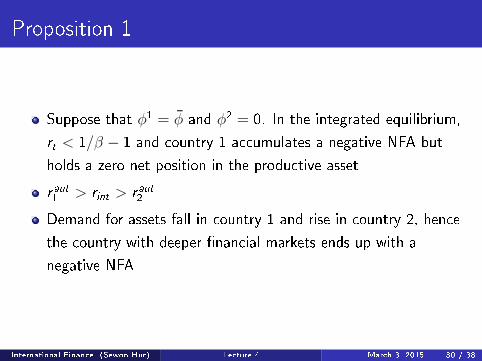

Proposition 1

Suppose that φ1 = φ and φ2 = 0. In the integrated equilibrium,

rt < 1/β − 1 and country 1 accumulates a negative NFA but

holds a zero net position in the productive asset

r aut1 > rint > r aut2

Demand for assets fall in country 1 and rise in country 2, hence

the country with deeper �nancial markets ends up with a

negative NFA

International Finance (Sewon Hur) Lecture 4 March 3, 2015 30 / 38

Characterization

Now consider the case with investment shocks only.

Financial autarky regime and φ = φ (such that IC not binding).

Then r = 1/β − 1 since agents can perfectly insure against

idiosyncratic risk. Now ERt+1 = 1 + rt , but still all agents invest

k = 1

Financial autarky regime and φ = 0 (no state-contingent

claims). Then r < 1/β − 1 since agents cannot perfectly insure

against idiosyncratic risk (precautionary savings). But now there

is a marginal risk premium for the risky asset

ERt+1 − (1 + rt) = −Cov(Rt+1,U′(c(z ′))

EU ′(c(z ′))> 0

International Finance (Sewon Hur) Lecture 4 March 3, 2015 31 / 38

Proposition 2

Suppose that φ1 = φ and φ2 = 0. In the integrated equilibrium,

rt < 1/β − 1. Country 1 has a negative NFA but a positive

position on the productive asset. Moreover, the average return of

country 1's foreign assets is larger than the cost of its liabilities.

The same proposition holds for the case with both endowment

and investment shocks.

International Finance (Sewon Hur) Lecture 4 March 3, 2015 32 / 38

General Model

Extend the simple model

N countries

diversi�able managerial capital yt+1 =∑N

i=1 zi ,t+1A1−νit kνit with∑N

i=1 Ait = 1

second source of �nancial heterogeneity (a(sj) ≥ ai limited

liability) in addition to φ

di�erences in economic size of countries

International Finance (Sewon Hur) Lecture 4 March 3, 2015 33 / 38

US vs ROW

µ1 = 0.3 to match US share of world GDP, 30 percent

φ1 = 0.3, φ2 = 0 (contingent claims partly available in US)

International Finance (Sewon Hur) Lecture 4 March 3, 2015 34 / 38

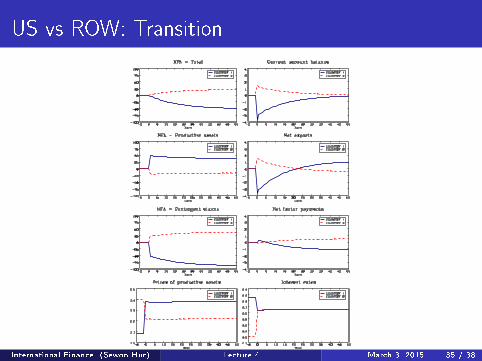

US vs ROW: Transition

Figure 6: Transition dynamics after capital markets liberalization.

28

International Finance (Sewon Hur) Lecture 4 March 3, 2015 35 / 38

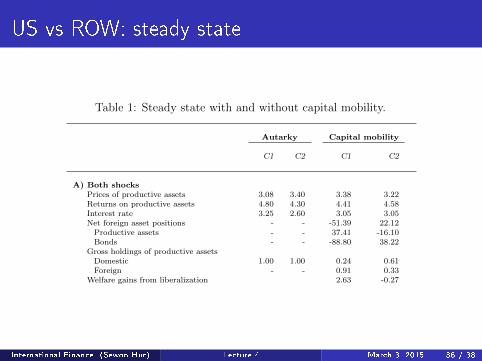

US vs ROW: steady state

Table 1: Steady state with and without capital mobility.

Autarky Capital mobility

C1 C2 C1 C2

A) Both shocksPrices of productive assets 3.08 3.40 3.38 3.22Returns on productive assets 4.80 4.30 4.41 4.58Interest rate 3.25 2.60 3.05 3.05Net foreign asset positions - - -51.39 22.12Productive assets - - 37.41 -16.10Bonds - - -88.80 38.22

Gross holdings of productive assetsDomestic 1.00 1.00 0.24 0.61Foreign - - 0.91 0.33

Welfare gains from liberalization 2.63 -0.27

B) Endowment shocks onlyPrices of productive assets 2.95 3.22 3.14 3.14Returns on productive assets 5.08 4.66 4.78 4.78Interest rate 3.81 3.49 3.58 3.58Net foreign asset positions - - -38.69 16.58Productive assets - - 0.00 0.00Bonds - - -38.69 16.58

Gross holdings of productive assetsDomestic 1.00 1.00 1.00 1.00Foreign - - 0.00 0.00

Welfare gains from liberalization 1.66 -0.77

C) Investment shocks onlyPrices of productive assets 1.41 1.37 1.45 1.38Returns on productive assets 10.63 10.90 10.41 10.83Interest rate 7.35 6.58 7.33 7.33Net foreign asset positions - - -5.38 2.31Productive assets - - 14.08 -6.04Bonds - - -19.46 8.35

Gross holdings of productive assetsDomestic 1.00 1.00 0.23 0.61Foreign - - 0.91 0.33

Welfare gains from liberalization 0.60 0.20

Notes: Foreign asset positions are in percentage of domestic income (endowment plusdomestic investment income). Gross positions of productive assets are units of k per-capita. Welfare gains are in percentage of consumption.

26

International Finance (Sewon Hur) Lecture 4 March 3, 2015 36 / 38

US vs ROW: welfare

Two sources of welfare gains/losses

diversi�cation of investment risk

cost of borrowing/lending

In country 1, all agents gain from liberalization, and the gains

are especially high for low wealth agents

In country 2, agents also gain from diversi�cation of risk, but

the increase in interest rates relative to autarky hurt the poor.

Overall, they su�er a welfare loss.

International Finance (Sewon Hur) Lecture 4 March 3, 2015 37 / 38

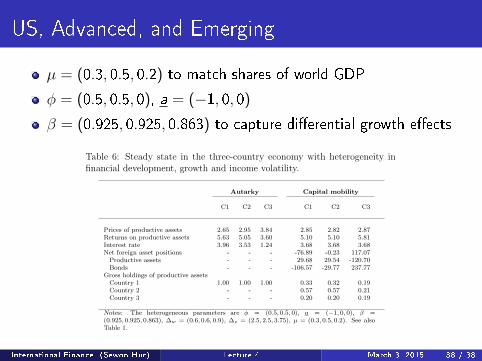

US, Advanced, and Emerging

µ = (0.3, 0.5, 0.2) to match shares of world GDP

φ = (0.5, 0.5, 0), a = (−1, 0, 0)

β = (0.925, 0.925, 0.863) to capture di�erential growth e�ects

with greater uncertainty at the individual level.14 Therefore, if we want tocapture the differences between industrialized and emerging economies thatare relevant for savings, we should allow for three sources of heterogeneity:financial markets development, economic growth and income volatility.

We add heterogeneity in growth and income volatility to the three-countrymodel examined above. An easy way to capture differences in growth ratesis to assume that countries have different discount rates. If β is the discountfactor for industrialized countries and the growth rate differential betweenemerging and industrialized countries is 1 + g, then the discount factor ofemerging countries is β = β/(1 + g)σ. Assuming an annual growth differ-ential of 3.5 percent, and given the baseline parametrization β = 0.925 andσ = 2, the discount factor for C3 is β = 0.925/1.0352 = 0.863. Under theseassumptions, if C1 and C2 grow at about 2 percent per year, emerging coun-tries (C3) grow at 5.5 percent per year. To account for the higher uncertaintyfaced by agents in emerging economies, we assume that the standard devia-tions of endowment and investment shocks in C3 are 50 percent higher thanin C1 and C2.

Table 6: Steady state in the three-country economy with heterogeneity infinancial development, growth and income volatility.

Autarky Capital mobility

C1 C2 C3 C1 C2 C3

Prices of productive assets 2.65 2.95 3.84 2.85 2.82 2.87Returns on productive assets 5.63 5.05 3.60 5.10 5.10 5.81Interest rate 3.96 3.53 1.24 3.68 3.68 3.68Net foreign asset positions - - - -76.89 -0.23 117.07Productive assets - - - 29.68 29.54 -120.70Bonds - - - -106.57 -29.77 237.77

Gross holdings of productive assetsCountry 1 1.00 1.00 1.00 0.33 0.32 0.19Country 2 - - - 0.57 0.57 0.21Country 3 - - - 0.20 0.20 0.19

Notes: The heterogeneous parameters are φ = (0.5, 0.5, 0), a = (−1, 0, 0), β =(0.925, 0.925, 0.863), ∆w = (0.6, 0.6, 0.9), ∆z = (2.5, 2.5, 3.75), µ = (0.3, 0.5, 0.2). See alsoTable 1.

14An indicator of this is that inequality tends to increase during phases of rapid growth.See Khan & Riskin (2001) and Naughton (2007). Also, several emerging economies haveexperienced Sudden Stops after entering the global financial markets.

39

International Finance (Sewon Hur) Lecture 4 March 3, 2015 38 / 38

![fJi)uEZíg j s5 - OAK Centralcentral.oak.go.kr/repository/journal/13228/BBROBV_2014_v...^ t½{ v \ fJi)uEZíg j s5 \ fJu)fI Iv Eh]{ v \ fJi)uEz¡Z±uîue Zíg j s5u1gµf E\ tñ a`Ñu9ZéZu-sÝ[Yj](https://img.dokumen.tips/doc/110x75/5b1bc6487f8b9a1e258f280a/fjiuezig-j-s5-oak-t-v-fjiuezig-j-s5-fjufi-iv-eh-v-fjiuezzuiue.jpg)